UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-03651

Touchstone Strategic Trust

(Exact name of registrant as specified in charter)

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Address of principal executive offices) (Zip code)

Jill T. McGruder

303 Broadway, Suite 1100

Cincinnati, Ohio 45202-4203

(Name and address of agent for service)

Registrant's telephone number, including area code: 800-638-8194

Date of fiscal year end: March 31

Date of reporting period: March 31, 2015

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

March 31, 2015

Annual Report

Touchstone Strategic Trust

Touchstone Flexible Income Fund

Touchstone Focused Fund

Touchstone Growth Opportunities Fund

Touchstone International Value Fund

Touchstone Large Cap Growth Fund

Touchstone Mid Cap Growth Fund

Touchstone Sands Capital Emerging Markets Growth Fund

Touchstone Small Cap Growth Fund

Table of Contents

This report identifies the Funds' investments on March 31, 2015. These holdings are subject to change. Not all investments in each Fund performed the same, nor is there any guarantee that these investments will perform as well in the future. Market forecasts provided in this report may not occur.

Letter from the President

Dear Shareholder:

We are pleased to provide you with the Touchstone Strategic Trust Annual Report. Inside you will find key financial information, as well as manager commentaries for the Funds, for the 12 months ended March 31, 2015.

During the period, the U.S. economy began to accelerate amid a strengthening labor market and improving consumer confidence. The economy was sufficiently strong for the U.S. Federal Reserve Board (Fed) to end its Quantitative Easing (QE) program and turn its attention to the timing of its first interest rate increase in nearly 10 years. Combined with weak economic growth abroad, the prospect of higher U.S. interest rates resulted in a strong rally for the U.S. dollar during late 2014 and early 2015. Energy markets fell sharply during the year. Weak global demand and a surge in new supply from North American producers led to a roughly 50 percent decline in the price of oil.

On the strength of the U.S. economy, equity markets continued to move higher during the 12-month period. The U.S. market environment generally favored larger capitalization stocks and companies with stronger growth characteristics. Economic weakness abroad and a rapidly appreciating U.S. dollar led to flat returns for developed international and emerging market equities.

Despite the end of QE and the potential for further tightening of monetary policy by the Fed, interest rates declined during the period, driving bonds to a year of solid gains. Credit spreads widened slightly, causing high yield bonds to lag the investment grade sector.

After an eventful year in the financial markets, a review of your current asset allocation and long-term investment goals is particularly timely. A financial professional can help to assess whether your portfolio’s positioning provides a risk-return profile that is consistent with your financial situation and goals.

We greatly appreciate your continued support. Thank you for including Touchstone as part of your investment plan.

Sincerely,

Jill T. McGruder

President

Touchstone Strategic Trust

Management's Discussion of Fund Performance (Unaudited)

Touchstone Flexible Income Fund

Sub-Advised by ClearArc Capital, Inc.

Investment Philosophy

The Touchstone Flexible Income Fund invests in a variety of income-producing asset classes, including debt securities, common stock and preferred stock. The Fund’s investment approach employs a top-down macro perspective along with a bottom-up security selection analysis emphasizing quality, relative value and high current income consistent with reasonable risk. Correlation analysis, the statistical measure of how two securities move in relation to each other, is conducted between asset classes in an effort to build a portfolio with low correlation to both stocks and bonds. Fundamental research, quantitative modeling and capital structure analysis are used to help maximize risk-adjusted returns.

Fund Performance

Touchstone Flexible Income Fund (Class A Shares) underperformed its benchmark, the Barclays U.S. Aggregate Bond Index, for the 12-month period ended March 31, 2015. The Fund’s total return was 5.22 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 5.72 percent.

Market Environment

The primary story for the period was the strong downward movement in interest rates. In the U.S., the rate yield curve flattened as longer-term rates declined more than intermediate and shorter-term rates. Declining interest rates were mainly due to lower-than-expected inflation across the globe and falling energy prices, while the U.S. Federal Reserve Board (Fed) concluded its taper of quantitative easing (QE) in the face of a slowly improving employment market and modest gross domestic product (GDP) growth. Yet the European Central Bank (ECB), Bank of Japan and many emerging market central banks continued to enact expansionary monetary policies such as QE and/or cutting short-term interest rates. This divergence of monetary policies between the U.S. and most developed and emerging markets led to a strengthening U.S. dollar. This lower global interest rate environment provided a performance tailwind for both preferred and real estate investment trust (REIT) equities. Stocks in the U.S. posted strong returns, however European and Japanese equity markets generally posted weak returns.

Portfolio Review

The Fund’s effective duration was about one year shorter than the benchmark. This shorter duration position overall detracted from performance as the Fund sacrificed some upside performance in both preferred and REIT equities over the period. Within the Fund’s preferred equity allocation, we have favored the hybrid (fixed to floating structure) portion of the preferred market. These securities have less interest rate sensitivity but with rates falling, they underperformed fixed-rate preferred equities. We believe that rate volatility is likely to pick up as the Fed’s decision to raise rates is an ongoing debate, and therefore believe hybrid preferred equities offer the most appropriate positioning. As mentioned previously, equity REITs had a strong year and the Fund’s underweight to this sector combined with security selection detracted from performance. Overall, REITs benefited from the rate movement. The Fund’s allocation was heavier in mortgage REITs which offered more yield, but did not perform as well as non-mortgage REITs when longer-term rates declined.

Within the Fund’s bond allocation, we saw the potential for weakness in credit early in the period, and therefore reduced the Fund’s corporate bond exposure and increased its U.S. Treasury exposure. This move contributed to the Fund’s performance. However, credit does appear to be on the rebound due to demand exceeding supply, so we are selectively adding to higher quality bonds where appropriate. Outside of credit sectors, security selection across structured bonds was mixed. Asset-Backed Securities (ABS) contributed to performance while the Fund’s Commercial Mortgage-Backed Securities (CMBS) allocation detracted.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Within the Fund’s common stock exposure, security selection detracted from the Fund’s performance. This was primarily driven by poor performance from positions in Eastman Chemical Co., BP PLC, and LyondellBasell Industries NV. In the final quarter of the period, some U.S. equity exposure was shifted to Japanese and European equities because of what we believed to be more attractive valuations and easier monetary policies in those markets.

The Fund was appropriately positioned for U.S. dollar strength and hedged many of the Fund’s foreign currency holdings. The Fund was also positioned appropriately for weakening emerging market currencies such as short positions in the Brazilian real, South African rand, Columbian peso, and the Indonesian rupiah. Additionally, the Fund had some relative value currency trades that saw small success.

Outlook

We believe equity markets in Japan, Europe and China are likely to outperform the U.S. going forward. We also believe rates have settled into a new range. Absent stronger fundamentals than expected, we anticipate rates will likely hover between 1.6 percent to 2.2 percent on the 10-year U.S. Treasury, held back by QE in Europe and Japan. We believe the U.S. dollar may strengthen further but at a slower rate of appreciation. Higher volatility may represent opportunity and the Fund is positioned for a more normal environment there. Since current inflation measures are well below their target, GDP growth is still moderate, and inflation expectations remain weak, we believe raising rates too soon may be a policy error. Finally, we believe there is a chance for an emerging market crisis at some point during the year.

We would be concerned if the Fed tightened policy too early, as the U.S. dollar’s strength has already acted as de facto tightening. The effects of an emerging markets crisis are difficult to predict. That is why the flexibility afforded in the Fund is so important. Although we don’t expect a Fed move in the short term, we remain ready to adjust to such a scenario. Real GDP growth over three percent for several quarters, accompanied by strong wage growth and a rise in inflation expectations, would threaten our expectations.

We believe the environment remains favorable for the Fund. It is hard to overstate the benefit of a yield advantage within an unlevered and high quality context in a low (to zero) interest rate environment. While the Fund may struggle to keep up in return, we believe our measured approach is proper in a more volatile environment.

Dividend-paying investments may not experience the same price appreciation as non-dividend paying instruments, dividend-issuing companies may choose not to pay a dividend, or the dividend may be less than what is anticipated.

Diversification neither assures a profit nor guarantees against loss in a declining market.

Management's Discussion of Fund Performance (Unaudited) (Continued)

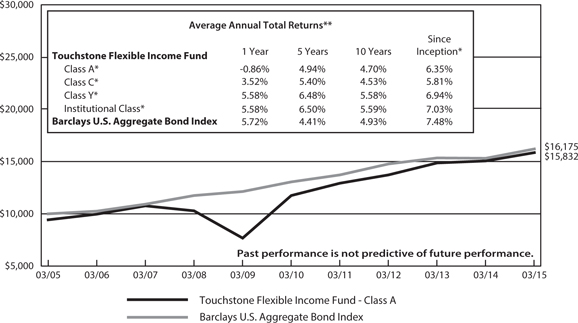

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Flexible Income Fund - Class A* and the Barclays U.S. Aggregate Bond Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was April 1, 2004, October 29, 2001, September 1, 1998 and September 10, 2012, respectively. Class A shares, Class C shares and Class Y shares performance information was calculated using the historical performance of the Fifth Third/Maxus Income Fund Investor shares, with an inception date of March 10, 1985, for periods prior to April 1, 2004, October 29, 2001 and September 1, 1998, respectively. Institutional Class shares performance information was calculated using the historical performance of Class Y shares for the periods prior to September 10, 2012. The returns have been restated to reflect sales charges and fees applicable to Class A, Class C, Class Y and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum applicable sales charges, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00% that will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed if redeemed within a one-year period from date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

Barclays U.S. Aggregate Bond Index is an unmanaged index comprised of U.S. investment grade, fixed rate bond market securities, including government, government agency, corporate and mortgage-backed securities between one and ten years.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Focused Fund

Sub-Advised by Fort Washington Investment Advisors, Inc.

Investment Philosophy

The Fund seeks to invest in companies of all capitalizations that are trading below what is believed to be the estimate of their intrinsic value and have a sustainable competitive advantage or a high barrier to entry in place. The barrier(s) to entry can be created through a cost advantage, economies of scale, high customer loyalty or a government barrier (e.g., license or subsidy). Management believes that the strongest barrier to entry is the combination of economies of scale and high customer loyalty.

Fund Performance

The Touchstone Focused Fund (Class A Shares) underperformed its benchmark, the Russell 3000® Index, for the 12-month period ended March 31, 2015. The Fund’s total return was 6.99 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 12.37 percent.

Market Environment

Equity markets continued to climb and set record highs as investors assessed a wide range of issues. Job growth was healthy and commodity prices generally declined over the last year. The Energy sector was the only sector in the benchmark that experienced an absolute decline in value as investors responded to a 50 percent drop in the price of crude oil as well as the lowest level of natural gas prices seen since April 2012. Performance of the Materials, Industrials, Telecommunication Services, Utilities and Financials sectors also lagged. The Health Care sector outperformed all sectors. Information Technology, Consumer Staples and Consumer Discretionary sector stocks also outperformed.

Portfolio Review

Most of the underperformance of the Touchstone Focused Fund can be attributed to stock selection, with sector allocation accounting for the remainder. From a sector allocation perspective, an underweight to the Health Care sector detracted the most from performance. Other sectors that underperformed the benchmark included Industrials, Consumer Staples and Financials. Sectors that outperformed the benchmark included Consumer Discretionary, Energy, Materials, Telecommunication Services and Information Technology. International companies also underperformed the benchmark.

Royal Caribbean Cruises Ltd. (Consumer Discretionary sector) was the top performing stock during the past 12 months. Throughout the year, it benefited from an improving core business and falling fuel prices. Berry Plastics Group Inc. (Materials sector) was also a top performer as the company gave strong cash flow guidance for 2015 aided by falling oil prices which should result in lower resin costs in the future. World Fuel Services Corp. (Energy sector) also performed strongly as the company benefited from the recent volatility in bunker fuel prices which led to increased volumes from its highly captive customer base.

Stocks that detracted from performance included Tesco (Consumer Staples sector) which felt the negative impact from increased competition from discount food retailers and negative sentiment surrounding an accounting issue announced in the fourth quarter of 2014. Bank of America Corp. (Financials sector) lagged due to concerns over its ability to return capital to shareholders after conditionally passing regulatory stress tests. Joy Global Inc. (Industrials sector) reported a weak fourth quarter and warned investors of continued weakness due to the impact from falling commodity prices, particularly iron ore and copper.

Management's Discussion of Fund Performance (Unaudited) (Continued)

From a market cap perspective, the Fund’s allocation to smaller-cap businesses was reduced. The Fund maintained an overweight to mid-cap companies. While the Fund has increased its exposure to larger-cap businesses it remained underweight to the benchmark. This allocation decision had no impact on performance during the year.

In general, as the market has moved higher over the past 12 months, our assessment of the quality of the overall Fund’s portfolio remained high. The weighted average return on capital for the companies held in the Fund (excluding the Financials sector stocks) is currently estimated to be above the weighted average cost of capital. Moreover, the Fund is invested in companies that we believe have high barriers to entry indicating that these businesses should continue to earn attractive returns on capital in the future.

Outlook

The market marked the sixth anniversary of the current bull market, which began on March 10, 2009. It is worth noting that determining when to call the market top for equities based on nothing more than the age of a bull market is fraught with problems, given their varying lengths throughout history. We believe the approach that should be taken is to examine the quality of the bull market. Today, breadth (a measure of the number of stocks participating in a market movement) in mid-cap and large-cap businesses is still good with only deterioration in the small-cap area. In other words, market breadth is providing little indication of a market top. Beyond breadth, we believe market valuation is reasonable. Additionally, lending standards are favorable so we are comfortable with the credit cycle. We believe that inflation is under control which is also indicative of a positive backdrop to the equity market.

The Fund is structured to benefit from a decline in the U.S. dollar; for Chinese, U.S. and European consumers to grow their rate of consumption; and for oil and interest rates to increase from current levels. We will continue to select companies for the Fund that we believe can generate excess returns on capital and have high barriers to entry, and yet are priced as if they are mature businesses with little expectation for future growth.

Management's Discussion of Fund Performance (Unaudited) (Continued)

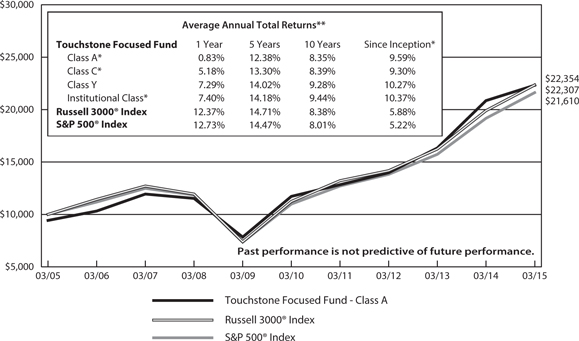

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Focused

Fund - Class A*, the Russell 3000® Index and the S&P 500® Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was September 30, 2003, April 12, 2012, February 12, 1999 and December 20, 2006, respectively. Class A shares, Class C shares and Institutional Class shares performance information was calculated using the historical performance of Class Y shares for the periods prior to September 30, 2003, April 12, 2012 and December 20, 2006, respectively. The returns have been restated to reflect sales charges and fees applicable to Class A, Class C and Institutional Class shares. The returns of the indexes listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum applicable sales charges, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00% that will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed if redeemed within a one-year period from date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell 3000® Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

S&P 500® Index is a group of 500 widely held stocks and is commonly regarded to be representative of the large capitalization stock universe.

Management's Discussion of Fund Performance (Unaudited)

Touchstone Growth Opportunities Fund

Sub-Advised by Westfield Capital Management LP

Investment Philosophy

The Touchstone Growth Opportunities Fund seeks long-term capital appreciation by primarily investing in stocks of U.S. companies with large, medium and small market capitalizations. The Fund’s portfolio managers place focus on companies they believe to have demonstrated records of achievement with excellent prospects for earnings growth over a 1-3 year period and incorporate a proprietary, research driven, bottom-up approach that seeks to identify quality growth companies with strong management teams, sustainable business models and solid financials.

Fund Performance

The Touchstone Growth Opportunities Fund (Class A Shares) underperformed its benchmark, the Russell 3000® Growth Index, for the 12-month period ended March 31, 2015. The Fund’s total return was 14.99 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 15.76 percent.

Market Environment

Most domestic stock indices delivered double-digit gains in the past 12 months, extending the current bull market that began six years ago. The advance, however, was not uniform across sectors and companies, as investors wrestled with the implications of a number of macroeconomic factors. For example, the dramatic collapse of crude oil prices pushed Energy sector stocks across all market capitalizations into deeply negative territory, while the rapid ascent of the U.S. dollar put pressure on the earnings outlooks of many multinational firms. The timing of the U.S. Federal Reserve Board’s (Fed) monetary policy tightening continued to be a significant source of uncertainty for investors. While the U.S. economy was on a stronger footing than economies of other countries around the world, fears of global economic contagion lingered. The Health Care sector delivered the top returns across the market capitalization spectrum, by far outpacing more economically-sensitive sectors such as Energy, Materials, and Industrials. Health Care sector performance was powered in part by a robust mergers and acquisitions (M&A) environment within the biotechnology and pharmaceutical industries. Growth-oriented stocks generally outperformed their value counterparts. The performance dichotomy highlighted investors’ sharpened focus on those segments that were able to deliver earnings growth in an uncertain economic backdrop.

Portfolio Review

Four economic sectors contributed positively to relative returns, but it was the Fund’s investments in Health Care, Energy and Financials that generated the majority of incremental gains, offsetting weakness within the Materials, Consumer Staples and Industrials sectors.

The Health Care sector was the Fund’s top relative and absolute performer. The outperformance was broad based, with particular strength exhibited by the Fund’s pharmaceutical and biotechnology stocks. The pharmaceuticals industry, which remains the Fund’s largest active weight, continued to be fueled by M&A activity. Most transactions to this point have been highly accretive, with commercial scale and cost synergies representing the primary drivers. Actavis PLC, a pharmaceutical firm focused on manufacturing generic and over-the-counter products, was one of the performance highlights. Its acquisitions of Forest Laboratories in early 2014 and Warner Chilcott in 2013 expanded the earnings growth of the company, which is domiciled in tax-advantaged Ireland. In November, it announced it would acquire Allergan Inc., a global multi-specialty health care company. We liked the deal from a strategic fit perspective and for its meaningful tax and cost savings. Allergan’s book of products, which is diversified across neurology, ophthalmology and medical aesthetics, represents a high-visibility cash flow

Management's Discussion of Fund Performance (Unaudited) (Continued)

generation machine that would underwrite Actavis’ further M&A activity. Endo International PLC., an Irish-domiciled, specialty pharmaceutical company, reached an all-time high in mid-March. The company’s seasoned management team has repositioned its portfolio of healthcare brands, selling less profitable assets and pursuing accretive acquisitions. During an industry-wide conference in early January, the company emphasized the strength of its generics pipeline, an area where Endo has a lot of pricing power, and highlighted its continued focus on growth through strategic acquisitions. We trimmed the stock several times to manage the position size, and following Endo’s surprisingly high bid for Salix Pharmaceuticals on March 13, we sold the Fund’s remaining position. Cubist Pharmaceuticals, Inc. surged in December following the buyout news of this acute care biopharmaceutical company by Merck. The largest holding within the sector, Celgene Corporation, also contributed meaningfully to excess returns. We believe that the company has the ability to drive double-digit growth on the top and bottom line given its robust, low-risk product pipeline. Celgene’s key product Revlimid is the standard of care for the treatment of multiple myeloma patients in the U.S. and the drug’s sales continue to accelerate, driven by market share gains and increased treatment duration. The company’s newer franchises include Abraxane for breast, lung and pancreatic cancers and Otezla for inflammation disorders.

The Energy sector contributed positively to relative Fund performance, however the sector’s performance, in general, reflected the downward trajectory of crude oil – the commodity price began to decline in the summer of 2014, and did not find support until late February/early March 2015 at around $50 per barrel. A combination of the Fund’s strategic underweight to oil/gas exploration and production companies and a stock within the refining industry, Tesoro Corporation, drove the bulk of the outperformance within the sector. Refining had been a poor industry for 30 years in the U.S., but we saw a fundamental shift driven by shale oil production and management commitment to change. The Fund originally invested in refiners three years ago when they traded at a mere three times EBITDA (Earnings Before Interest, Depreciation and Amortization) because Wall Street analysts did not understand the paradigm shift that would take place. We believe refiners are still mispriced by Wall Street, with valuation multiples based on their refining merits alone, while these companies often have significant mid-stream assets, which in some cases represent up to 40 percent of their value. While we continue to like Tesoro’s fundamental characteristics and long-term appreciation potential, we have trimmed the Fund’s position, as we think that slowing domestic oil supply will be a headwind for the company near term. The Fund’s exposure to the sector decreased over the past 12 months, and we are becoming incrementally more positive on those companies within the Energy sector that benefit from rising commodity prices. The oil rig count is already down over 40 percent year-to-date, and we project U.S. production will slow significantly during the second half of 2015. It is our opinion that a more balanced oil market will require higher oil prices to meet global demand. Some oil producers already trade at valuations reflecting $80 per barrel of oil despite their stretched balance sheets. However, we believe that oil service companies possessing next-generation technologies and oil exploration firms that have the highest quality geological assets will offer the potential for solid returns going forward.

The Financials sector also contributed to excess returns. The sector, heavily influenced by global interest rates trends, delivered uneven performance, underperforming the broad market during the period. Generally speaking, stocks with fixed-income-like characteristics, such as property REITs (real estate investment trusts), advanced, while interest rate-sensitive banks underperformed. Although the Fund is generally underweight REITs, we continue to believe that commercial mortgage companies behave differently than their equity REIT brethren. Given less leverage and floating rate loans with commercial mortgage, we believe REITs should exhibit less interest rate risk. CBRE Group, Inc., a provider of commercial real estate services, was the sector’s top contributor to relative returns. The Fund owns the company based on our outlook for the non-residential construction market and the health of commercial real estate in general. CBRE continued to take market share from the middle market operators who are not able to compete with the reach and service capabilities of the bigger players in this highly fragmented industry. In late March, the company announced that it would acquire Johnson Controls’ Global Workplace Solutions business segment. We view the move as representative of the secular

Management's Discussion of Fund Performance (Unaudited) (Continued)

shift within the industry, with clients gravitating to larger industry participants who are better able to provide a full suite of services than smaller players. Given its dominant position in most markets, CBRE is the likely candidate for continued market share gains, in our opinion. The Fund has an overweight position in the sector following the purchase of Discover Financial Services, a direct banking and payment services company. We like Discover’s loan and revenue growth and believe its payment network is a unique asset that has the potential to be acquired in the future.

The Materials sector was the Fund’s largest detractor. The sector underperformed the broad market during the period, as investors’ already negative outlook on the earnings prospects of large capitalization Materials sector companies was exacerbated by uncertainty around crude oil prices, unfavorable currency trends and weak emerging markets. The Fund’s exposure to the sector was reduced during the period partially due to the sale of specialty chemicals developer FMC Corp. The trade was motivated by a change in the company’s strategy. Our initial sum-of-the-parts analysis of FMC’s intrinsic value was based on the company’s proposed split into two publicly traded entities, and when FMC abandoned its divesture plans and announced a decision to acquire a global crop chemical company instead, we sold the Fund’s investment in the stock. Also restraining performance results was Axiall Corporation, a producer of vinyl-based products, which traded lower over the summer months. The company posted disappointing quarterly earnings, citing weather and operational mishaps at one of its vinyl-chloride plants among the reasons for the weakness. Our analysis of the industry trends confirmed that growth in the U.S. housing sector was not strong enough to drive PVC price increases and expand the company’s profit margins, and the stock was sold. We continue to be selective in the Fund’s holdings within the sector, favoring innovation-driven companies that exhibit secular growth from new material use or market share gains. For instance, the Fund remains invested in Monsanto Company. It has the largest innovation pipeline in the industry and has demonstrated robust share gains in corn and soybeans, coming at the expense of DuPont’s Pioneer and Syngenta. We believe its earnings will continue to accelerate through a combination of secular growth in new technologies, new market opportunities and share buybacks.

The Consumer Staples sector also detracted from Fund performance, restrained primarily by stock-specific weakness within the packaged foods and meats sub-industry. Underperforming during the time period, and sold last summer, was confectionary maker Hershey Company. Although we like the company’s innovation pipeline and international business opportunities, we were concerned about the sluggish earnings growth prospects near term. B&G Foods, Inc., a manufacturer and distributor of packaged foods, was also sold from the Fund. The company, which had been growing through tuck-in acquisitions, underperformed due to some execution issues with its recent transactions, particularly snack maker Pirate’s Booty. We remain constructive on the sector, seeking investments that present a growth opportunity in excess of the average Consumer Staples company growth rate. Mead Johnson Nutrition Company, a manufacturer of infant and children’s nutrition products, was added to the Fund. The nutritional market has secular tailwinds, including job growth and rising incomes, and we think the company will benefit from its exposure to rapidly-growing emerging markets.

The Industrials sector also detracted from relative performance. A complex and multifaceted sector, Industrials delivered uneven results, lagging behind the broader index’s advance. Companies in globally-oriented industries declined, while companies in acyclical industries, such as employment services and diversified support services, rose. The top performers were airlines and transportation companies, the beneficiaries of lower crude oil prices. While the Fund’s airline investment – United Continental Holdings, Inc. – provided a sizable boost to relative returns, its positive contribution was offset by declines across several sub-industries. Hexcel Corporation, a manufacturer of lightweight aerospace composites, had a negative impact on absolute and relative returns, and the stock was sold. While we are optimistic about the company’s growth prospects associated with the Airbus A350 and the Boeing 787, we were concerned about the lack of near-term catalysts and management’s reluctance to provide sufficient detail on its capital deployment strategy. IHS Inc., a consulting services firm, declined after the company lowered organic subscription revenue guidance for the fourth quarter. According to management,

Management's Discussion of Fund Performance (Unaudited) (Continued)

certain discontinued products that came as part of prior acquisitions, have been moved to the organic base in the books, necessitating the guidance reduction. This Fund investment was sold as well. Also underperforming, but maintained in the Fund, was Caterpillar Inc., a manufacturer of heavy equipment and industrial engines and turbines. The company’s energy-related business put a damper on the earnings, held back by the sharp decline in exploration and production capital expenditures. Despite this weakness, we continued to view Caterpillar’s global franchise as one of the best in the construction machinery segment. Given the company’s top-of-the-line products, its dividend yield and low capital expenditures, we believe Caterpillar should demonstrate significant price appreciation when industry demand for the company’s products picks up.

Outlook

The U.S. economy appeared to have hit a soft patch in the first quarter of the year, restrained by unusually harsh winter conditions across major parts of the Midwest and Northeast as well as a prolonged stoppage at West Coast ports. We think that the weakness is transient and that economic growth will resume, fueled by low inflation, a benign interest rate environment, and improving consumer spending. The first quarter earnings reporting season that begins in the second week of April 2015, will help to identify those segments of the economy that are struggling and those that are expanding. In addition to continued strength here in the U.S., our analysis also indicates the start of an economic recovery in Europe. We believe massive monetary stimulus launched by the European Central Bank in early 2015 should promote growth in the eurozone and help all economies dependent on global trade.

Volatility of risky assets did pick up in the past few months, but we remain enthusiastic about the prospects of domestic growth equities. Although their valuations have expanded during the current bull market, equities remain attractive, specifically those companies with solid fundamentals, organic growth and reasonable valuations.

Dividend-paying investments may not experience the same price appreciation as non-dividend paying instruments, dividend-issuing companies may choose not to pay a dividend, or the dividend may be less than what is anticipated.

Management's Discussion of Fund Performance (Unaudited) (Continued)

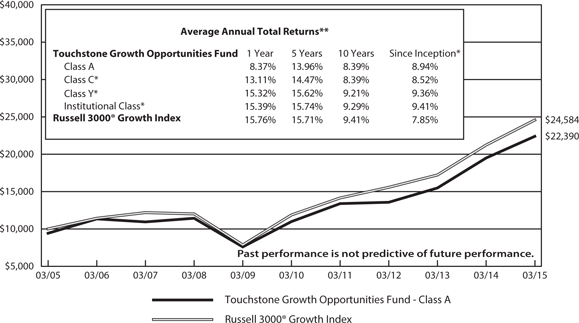

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Growth Opportunities Fund - Class A* and the Russell 3000® Growth Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was September 29, 1995, August 2, 1999, February 2, 2009 and February 2, 2009, respectively. Class C shares, Class Y shares and Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to August 2, 1999, February 2, 2009 and February 2, 2009, respectively. The returns have been restated to reflect sales charges and fees applicable to Class C, Class Y and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum applicable sales charges, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00% that will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed if redeemed within a one-year period from date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

Russell 3000® Growth Index measures the performance of those Russell 3000® companies with higher price-to-book ratios and higher forecasted growth values.

Management's Discussion of Fund Performance (Unaudited)

Touchstone International Value Fund

Sub-Advised by Barrow, Hanley, Mewhinney & Strauss, LLC

Investment Philosophy

The Touchstone International Value Fund seeks long-term capital growth by primarily investing in equity securities of non-U.S. companies believed to be undervalued and searches for companies that have price-to-earnings and price-to-book ratios below the market, free cash flow ratios at or below the market and dividend yields above the market.

Fund Performance

The Touchstone International Value Fund (Class A Shares) underperformed its benchmark, the MSCI EAFE Index, for the 12-month period ended March 31, 2015. The Fund’s total return was -4.95 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was -0.92 percent.

Market Environment

During the 12-month period, many of the world’s economies, currencies, central banks and interest rates were on very diverse paths, with this divergence magnified by a surging U.S. dollar and a collapse in oil prices. Investors were highly focused on the U.S. economy, with particular attention paid to those indicators that might presage a change in the monetary policy stance of the U.S. Federal Reserve Board (Fed). After the Fed’s massive, multi-year quantitative easing program that reflated U.S. financial markets and helped the economy recover, the Fed is now looking to return to more “normal” monetary conditions. The U.S. economy grew at a stronger rate than the rest of the developed world during the last 12 months, increasing the likelihood that the Fed would increase short-term interest rates to normalize its monetary policy. However, concerns over rising interest rates and the impact of a stronger dollar caused the U.S. market to stall and underperform Europe and Japan during the final quarter of the period.

Although European and Japanese economies struggled through most of the 12-month period, monetary easing efforts from each of their central banks began to gain traction early in 2015. The European Central Bank (ECB) announced its long-awaited quantitative easing plan, which was received positively by the market, and many countries in the region posted strong performance in local-currency terms toward the end of the period. Japan’s economy was supported by its easy monetary policy and government’s move to purchase equities, which also created positive momentum for that country’s economy.

Portfolio Review

For the period, the Fund’s stock selection within the Utilities, Materials and Industrials sectors benefited performance, along with the Fund’s underweight position to the Energy and Materials sectors. Conversely, stock selection within the Financials, Consumer Staples and Consumer Discretionary sectors were the primary detractors from performance. Among the individual stocks that contributed to Fund performance during the period were Mabuchi Motor Co. Ltd., AMADA Holdings Co. Ltd. (both from the Industrials sector), Teva Pharmaceutical Industries Ltd. (Health Care sector) and Imperial Tobacco Group PLC (Consumer Staples sector). Mabuchi Motor Co. is a Japan-based manufacturer of small motors that are used in automobiles and electric components. Mabuchi performed strongly as a recovery in global auto production benefitted the company. This tailwind was particularly pronounced due to a shift in product mix toward the higher-margin automotive motors. Automobile motors made up the majority of the company’s business, which contributed to an acceleration in the company’s growth and margin expansion. Mabuchi also announced a dividend increase and a share buyback, which further benefited the stock. AMADA Holdings Co., a plate- and press-products manufacturing company based in Japan, produced strong performance, as the company’s profits for its fiscal year 2014 exceeded expectations. AMADA also increased its earnings guidance for fiscal year 2015 above market estimates, increased its dividend payout target and

Management's Discussion of Fund Performance (Unaudited) (Continued)

repurchased some of the company’s outstanding shares. Additionally, we believe the company should benefit from strong levels of domestic demand going forward, as a result of the country’s ongoing reconstruction activity and Japan’s winning bid to host the 2020 winter Olympics. Teva Pharmaceutical Industries, an Israel-based generic pharmaceutical company, climbed higher as a result of a new delivery method for its Copaxone drug. Previously taken daily, Copaxone can now be effectively administered thrice-weekly, a change that extended the drug’s patent life. Furthermore, the company’s new management team executed well on its strategy to convert Copaxone patients over to the improved version of the drug, and implemented a large cost-reduction plan. Imperial Tobacco Group, a U.K.-based tobacco products company, outperformed during the annual period. Earlier in the year, the stock was supported by the company’s defensive characteristics, including its high-cash dividend yield. Management was forthright in stating its intention to increase the dividend in both 2014 and 2015, pledging to devote balance sheet assets to finance the increase. In the summer of 2014, Imperial Tobacco unexpectedly announced that it would be involved in a long-rumored deal between rival tobacco companies Reynolds American Inc. and Lorillard, Inc. (neither company is a Fund holding). Specifically, Imperial Tobacco will purchase five brands—KOOL, Salem, Winston, Maverick and blu eCigs—from Reynolds American and Lorillard, and will also acquire Lorillard’s manufacturing facilities and U.S. sales force. Following U.S. regulatory approval, Imperial Tobacco’s market share in the U.S. is expected to experience a strong increase.

Among the stocks that detracted from Fund performance were Delta Lloyd NV, Erste Group Bank AG (both from the Financials sector), Casino Guichard-Perrachon SA (Consumer Staples sector) and Joy Global Inc. (Industrials sector). Delta Lloyd is a Netherlands-based financial services provider offering insurance products, fund management and banking products and services. The company is sensitive to interest rate movements, and the stock underperformed as the 10-year interest rates in both the U.S. and Europe declined. Furthermore, there was concern about Delta Lloyd’s capital adequacy relative to its peers, resulting in speculation that the company may have to initiate an equity issuance. Although interest rate movements mask most fundamental changes, we still like Delta Lloyd going forward. The company continues to see improvement in its underlying business as earnings from one of its largest segments, the Dutch pension buyout market, is growing at a double-digit pace. We believe the company has an attractive valuation and will benefit strongly from an increase in interest rates. Erste Group Bank AG, an Austria-based banking company, underperformed in the period as a result of negative regulatory decisions in the first half of the year. These actions included a forced acceleration of loan loss reserves and a restatement of the currency impact on foreign loans. These write-downs ultimately depressed earnings. Looking ahead, we expect the regulatory environment to soften for Erste Group as the bank transitions to the ECB regulatory regime. Given the company’s strong capital position and attractive valuation, we remain positive on the prospects for Erste Group. During the first half of the fiscal period, the stock of Casino Guichard-Perrachon performed strongly. A France-based operator of retail stores and outlets, Casino executed a radical price repositioning in France, which drove improved trends at its French hypermarkets and supermarkets. The company also experienced resilient growth in emerging market regions, particularly its Brazilian subsidiary, and the monetization of its e-commerce assets via a pending IPO of e-commerce company Cnova NV. During the second half of the fiscal year, however, concerns mounted that a price war would break out among the grocery retailers in France, where pricing is more aggressive because of a soft consumer economy. Additionally, Casino’s stock was negatively impacted by the Cnova IPO valuation, which fell short of expectations and the depreciation of the Brazilian real and the Colombian peso, which hurt Casino’s overseas earnings. Over the long term, we believe Casino’s international portfolio is positioned well in structurally attractive emerging markets, including Brazil, Colombia and Thailand. In France, Casino has leading positions in retailers (from convenience stores to hypermarkets) and its market share is stabilizing. Joy Global is a U.S.-based manufacturer and distributor of mining equipment for the extraction of minerals and ores. Joy Global underperformed during the period as the company cut its full-year earnings outlook due to declining prices for commodities such as copper. Additionally, demand for coal fell due to lower prices for natural gas, which is often used as a substitute for coal in power generation. The depressed commodity prices reduced the need for capital expenditures and

Management's Discussion of Fund Performance (Unaudited) (Continued)

maintenance expenses among Joy Global’s mining customers. However, we believe the company has a strong competitive position, attractive valuation and a meaningful earnings upside driven in part by Joy Global’s move into hardrock and consumables.

Outlook

We believe the outlook for global equities remains positive overall, but is dependent in many cases on geographic location and valuations. Several positive developments in Europe have bolstered our confidence in this region and we maintain our positive view on European stocks and remain overweight this region. Going forward, we believe the recent announcement by the ECB to commence its own quantitative easing program, a weaker euro and lower oil prices should stimulate growth within the region and provide a better operating environment for European companies. Risks within the region remain, though, such as the still unresolved Greek debt situation. We are cautious on our outlook for Japan, as we believe its stimulus program does not address broader corporate management issues relating to profitability and shareholder value. However, there are signs that a subtle shift in management psychology is occurring and, as such, we have added to the Fund’s underweight position and are searching for more opportunities. While many areas within Emerging Markets are trading on compelling valuations, we believe risks remain elevated. A slowing Chinese economy, weakened currencies relative to the U.S. dollar and lower commodity prices have all put pressure on a recovery. We believe these risks will abate and the holdings in Emerging Markets should benefit the Fund going forward.

Our investment discipline is driven by fundamental research, which includes analyzing and building our own appraisals of fair value one company at a time. The Fund strives to comprise a relatively concentrated basket of companies that we believe offer a better return profile relative to the market.

Dividend-paying investments may not experience the same price appreciation as non-dividend paying instruments, dividend-issuing companies may choose not to pay a dividend, or the dividend may be less than what is anticipated.

Management's Discussion of Fund Performance (Unaudited) (Continued)

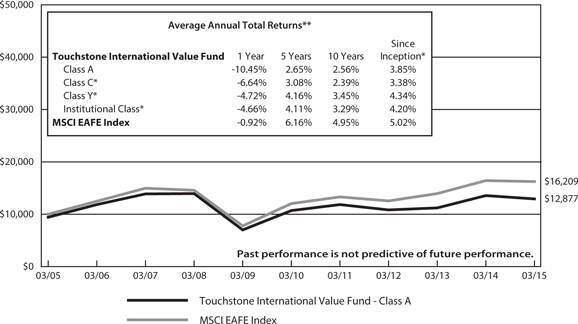

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone International Value Fund - Class A* and the MSCI EAFE Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class C shares, Class Y shares and Institutional Class shares was August 18, 1994, April 25, 1996, October 9, 1998 and September 10, 2012, respectively. Class C shares, Class Y shares and Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to April 25,1996, October 9, 1998 and September 10, 2012, respectively. The returns have been restated to reflect sales charges and fees applicable to Class C, Class Y, and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum applicable sales charges, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class C shares are subject to a contingent deferred sales charge (“CDSC”) of 1.00% that will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed if redeemed within a one-year period from date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance excluding the U.S. and Canada.

Management's Discussion of Fund Performance (Unaudited)

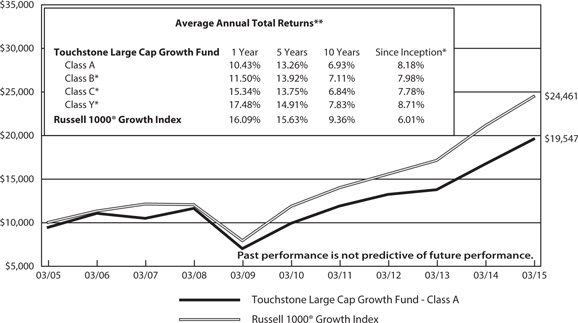

Touchstone Large Cap Growth Fund

Sub-Advised by Navellier & Associates, Inc.

Investment Philosophy

The Touchstone Large Cap Growth Fund seeks long-term growth of capital. The Fund primarily invests in common stocks of large-cap U.S. companies believed to possess strong appreciation potential.

Fund Performance

The Touchstone Large Cap Growth Fund (Class A Shares) outperformed its benchmark, the Russell 1000® Growth Index, for the 12-month period ended March 31, 2015. The Fund’s total return was 17.17 percent (calculated excluding the maximum sales charge), while the total return of the benchmark was 16.09 percent.

Market Environment

During the period, the U.S. economy began to accelerate amid a strengthening labor market and improving consumer confidence. The economy was sufficiently strong for the U.S. Federal Reserve Board (Fed) to end its quantitative easing (QE) program and turn its attention to the timing of a first interest rate increase in nearly 10 years. Combined with weak economic growth abroad, the prospect of higher U.S. interest rates resulted in a strong rally for the U.S. dollar during late 2014 and early 2015. Energy markets fell sharply during the year. Weak global demand and a surge in new supply from North American producers led to a roughly 50 percent decline in the price of oil.

On the strength of the U.S. economy, equity markets continued to move higher during the 12-month period. The U.S. market environment generally favored larger-capitalization stocks and companies with stronger growth characteristics. Strong returns among large-cap growth stocks was broad-based, with six of the 10 economic sectors posting double-digit returns. However, economic weakness abroad and a rapidly appreciating U.S. dollar led to flat returns for developed international and emerging market equities.

Despite the end of QE and the potential for further tightening of monetary policy by the Fed, interest rates declined during the period, driving bonds to a year of solid gains. Credit spreads widened slightly, causing high yield bonds to lag the investment grade sector.

Portfolio Review

Although the exposure to Health Care stocks was trimmed over the past 12 months, the Fund continued to have a significant overweight position in the Health Care sector which contributed to performance. Also, the Fund’s overweight position in the Information Technology sector contributed to performance. Conversely, the Energy and Materials sectors were the biggest detractors to performance due to the drop in oil and other commodity prices.

The top stock contributors to the Fund’s returns over the 12-month period were Amerisource Bergen Corp. (Health Care sector), Southwest Airlines Co. (Industrials sector), Skyworks Solutions Inc. (Information Technology sector), Actavis PLC (Health Care sector) and Avago Technologies Ltd. (Information Technology sector).

The largest detractors to performance came from: Amkor Technology Inc. (Information Technology sector), Salix Pharmaceuticals Ltd. (Health Care sector), U.S. Silica Holdings Inc. (Energy sector), Century Aluminum Co. (Materials sector) and Helmerich & Payne Inc. (Energy sector).

Outlook

Overall, we remain in an environment with low interest rates, a cautious Fed, and positive gross domestic product (GDP) growth. A strong U.S. dollar and low crude oil prices are causing the trade deficit to shrink dramatically.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the

Touchstone Large Cap Growth Fund - Class A* and the Russell 1000® Growth Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class B shares, Class C shares and Class Y shares based on the differences in loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class B shares, Class C shares and Class Y shares was December 19, 1997, October 4, 2003, October 4, 2003 and November 10, 2004, respectively. Class B shares, Class C shares and Class Y shares performance information was calculated using the historical performance of Class A shares for periods prior to October 4, 2003, October 4, 2003 and November 10, 2004, respectively. The returns have been restated to reflect sales charges and fees applicable to Class B, Class C and Class Y shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum applicable sales charges, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class B shares are subject to a contingent deferred sales charge (“CDSC”) of 5.00% in the event of a shareholder redemption within a one-year period of purchase. The CDSC will be incrementally reduced over time. After the 6th year, there is no CDSC. Class C shares are subject to a CDSC of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed if redeemed within a one-year period from date of purchase. Class Y shares shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Notes to Chart

Russell 1000® Growth Index measures the performance of those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values.

Management's Discussion of Fund Performance (Unaudited)

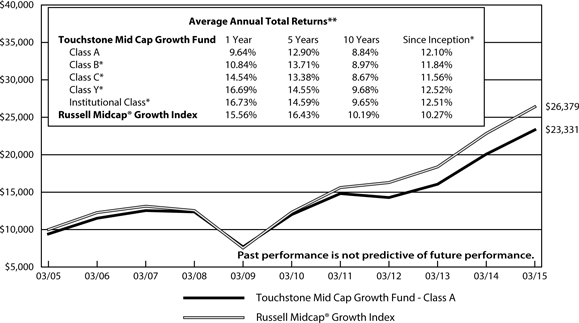

Touchstone Mid Cap Growth Fund

Sub-Advised by Westfield Capital Management LP

Investment Philosophy

The Touchstone Mid Cap Growth Fund seeks long-term growth by primarily investing in stocks of mid-cap U.S. companies. The Fund’s portfolio managers place focus on companies that they believe to have demonstrated records of achievement with excellent prospects for earnings growth over a 1-3 year period and incorporate a proprietary, research driven, bottom-up approach that seeks to identify quality growth companies with strong management teams, sustainable business models and solid financials.

Fund Performance

The Touchstone Mid Cap Growth Fund (Class A Shares) outperformed its benchmark, the Russell Midcap® Growth Index, for the 12-month period ended March 31, 2015. The Fund’s total return was 16.34 percent (calculated excluding the maximum sales charge), while the total return on the benchmark was 15.56 percent.

Market Environment

Most domestic stock indices delivered double-digit gains in the past 12 months, extending the current bull market that began six years ago. The advance, however, was not uniform across sectors and companies, as investors wrestled with the implications of a number of macroeconomic factors. For example, the dramatic collapse of crude oil prices pushed Energy sector stocks across all market capitalizations into deeply negative territory, while the rapid ascent of the U.S. dollar put pressure on the earnings outlooks of many multinational firms. The timing of the U.S. Federal Reserve Board’s (Fed) monetary policy tightening continued to be a significant source of uncertainty for investors. While the U.S. economy was on a stronger footing than economies of other countries around the world, fears of global economic contagion lingered. The Health Care sector delivered the top returns across the market capitalization spectrum, by far outpacing more economically-sensitive sectors such as Energy, Materials and Industrials. Health Care sector performance was powered in part by a robust mergers and acquisition (M&A) environment within the biotechnology and pharmaceutical industries. Growth-oriented stocks generally outperformed their value counterparts. The performance dichotomy highlights investors’ sharpened focus on those segments that are able to deliver earnings growth in an uncertain economic backdrop.

Portfolio Review

Six economic sectors contributed positively to relative returns, but it was the Fund’s investments in the Information Technology and Energy sectors that generated the majority of incremental gains, offsetting weakness within the Materials and Consumer Discretionary sectors.

The Information Technology sector contributed to relative returns, driven by stock selection within the semi-conductors industry. Skyworks Solutions, Inc., which designs, manufactures and markets semiconductor products to multimedia platforms and smart phones, was the Fund’s top performer within the sector. The company supplies the robust smart phone market and has been gaining market share on leading customer platforms, such as the Apple iPhone and Samsung Galaxy. In addition, the company’s radio frequency semi-conductor business is complemented by strong growth in non-mobile Internet-of-Things applications. NXP Semiconductors NV is a broad-based, global Information Technology (IT) company specializing in high performance, mixed signal semi-conductors; it contributed meaningfully to relative returns. NXP Semiconductors has been able to consistently deliver solid quarterly earnings, powered by product-cycle-specific growth drivers for automotive, identification and wireless applications. The company delivered double-digit organic revenue and earnings growth as a result of a robust product cycle and management’s focus on cost control and profit margins. In March 2015, NXP Semiconductors announced its plan to merge with Freescale Semiconductor, and the stock surged on the news, exceeding our

Management's Discussion of Fund Performance (Unaudited) (Continued)

internal price target. As a result, we exited the Fund’s investment in the company. Although the Fund has been underweight the Information Technology sector relative to the benchmark, we continue to be active in the sector. We are focusing on areas of secular growth, such as Internet, cloud and security software, as well as segments with solid and predictable growth, such as data processing.

The Energy sector also contributed positively to relative performance. Energy was the only segment of the broad market to post negative absolute returns in the past 12 months, and it underperformed the benchmark by over 35 percent. The performance was a reflection of the downward trajectory of crude oil. Oil prices began to decline in the summer of 2014 and did not stabilize until late in the first quarter, falling over 50 percent from its summer price of more than $100 a barrel. The Fund’s strategic underweight to oil & gas exploration and production companies and investments within the refining industry — Valero Energy Corporation and Tesoro Corporation — drove the bulk of the outperformance within the sector. While the refining industry remains the Fund’s largest active exposure, positions in both Valero and Tesoro were trimmed over the course of the past several months. While we continued to like their fundamental characteristics and long-term appreciation potential, slowing domestic oil supply will be a headwind for these stocks in the near term. Lately we have become incrementally more positive on those companies within the Energy sector that benefit from rising commodity prices. The oil rig count has already declined over 40 percent year-to-date, and we project U.S. production to slow significantly during the second half of 2015. It is our opinion that a more balanced oil market will require higher oil prices to meet global demand, and the stock prices of some oil producers already reflect expectations for higher oil prices. We think oil service companies that possess next-generation technologies and oil exploration firms that have the highest quality geological assets will offer solid returns going forward. We recently added Pioneer Natural Resources Company to the Fund’s portfolio. Pioneer is an independent oil & gas exploration company with significant holdings in the Permian Basin, one of the most productive and fastest growing energy regions in the U.S.

The Consumer Discretionary sector detracted from relative results. Urban Outfitters, Inc., an operator of brand-name clothing stores, declined after lowering its sales projections for the fourth quarter of 2014. Although we still like the company for its long-term positioning, we felt that the inventory buildup would take several months to resolve, and therefore, we sold the Fund’s investment. Deckers Outdoor Corp., which manages popular footwear brands such as UGGS and Teva, traded sharply lower in the beginning of 2015 after the company disappointed investors by missing consensus estimates for quarterly revenue and earnings. Management noted that the revenue shortfall was due to the weak sales of Decker’s UGG brand. We ultimately felt that the company’s upbeat guidance for sales in the UGG wholesale and direct-to-consumer business might prove too optimistic given the recent lackluster results and exited the Fund’s investment in the company.

The Materials sector detracted from excess returns. Earnings prospects for most Materials sector companies are closely tied to global economic health. Over the past 12 months, we received clearer signals that economies outside North America were, in fact, deteriorating. The Fund’s exposure to the sector was reduced partially due to the sale of specialty chemicals developer FMC Corp. The trade was motivated by a change in the company’s strategy. Our initial analysis of FMC’s intrinsic value was based on the company’s proposed split into two publicly traded entities. When FMC abandoned its divesture plans and announced a decision to instead acquire a global crop chemical company, we sold the Fund’s investment in the stock. Celanese Corp., a producer of industrial chemicals, also delivered lackluster returns, declining after missing expectations for quarterly sales. The shortfall in reported revenues was driven by those business segments where declines in raw material costs are passed through in the form of lower prices. Though earnings actually came in ahead of Wall Street estimates for the quarter, our analysis of the company indicated continued weakness in its near-term earnings power. Given the limited visibility of Celanese’s business, we exited the Fund’s position in the stock.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Outlook

The U.S. economy appeared to have hit a soft patch in the first quarter of the year, restrained by unusually harsh winter conditions across major parts of the Midwest and Northeast as well as a prolonged stoppage at West Coast ports. We think that the weakness is transient and that economic growth will resume, fueled by low inflation, a benign interest rate environment and improving consumer spending. The first quarter earnings reporting season that begins in the second week of April, will help to identify those segments of the economy that are struggling and those that are expanding. In addition to continued strength here in the U.S., our analysis also indicated the start of an economic recovery in Europe. We believe massive monetary stimulus launched by the European Central Bank in early 2015 should promote growth in the eurozone and help all economies dependent on global trade.

Volatility of risky assets did pick up in the past few months, but we remain enthusiastic about the prospects of domestic growth equities. Although their valuations have expanded during the current bull market, equities remain attractive, specifically those companies with solid fundamentals, organic growth and reasonable valuations.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Comparison of the Change in Value of a $10,000 Investment in the Touchstone Mid Cap

Growth Fund - Class A* and the Russell Midcap® Growth Index

| * | The chart above represents performance of Class A shares only, which will vary from the performance of Class B shares, Class C shares, Class Y shares and Institutional Class shares based on the differences in loads and fees paid by shareholders in the different classes. The inception date of Class A shares, Class B shares, Class C shares, Class Y shares and Institutional Class shares was October 3, 1994, May 1, 2001, October 3, 1994, February 2, 2009 and April 1, 2011. Class B shares, Class Y shares and Institutional Class shares performance information was calculated using the historical performance of Class A shares for periods prior to May 1, 2001, February 2, 2009 and April 1, 2011, respectively. The returns have been restated to reflect sales charges and fees applicable to Class B, Class Y, and Institutional Class shares. The returns of the index listed above are based on the inception date of the Fund. |

| ** | The average annual total returns shown above are adjusted for maximum applicable sales charges, if applicable. The maximum offering price per share of Class A shares is equal to the net asset value (“NAV”) per share plus a sales load equal to 6.10% of the NAV (or 5.75% of the offering price). Class B shares are subject to a contingent deferred sales charge (“CDSC”) of 5.00% in the event of a shareholder redemption within a one-year period of purchase. The CDSC will be incrementally reduced over time. After the 6th year, there is no CDSC. Class C shares are subject to a CDSC of 1.00%. The CDSC will be assessed on an amount equal to the lesser of (1) the NAV at the time of purchase of the shares being redeemed or (2) the NAV of such shares being redeemed if redeemed within a one-year period from date of purchase. Class Y shares and Institutional Class shares are not subject to sales charges. |

The performance of the above Fund does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Note to Chart

Russell Midcap® Growth Index measures the performance of those Russell Midcap® companies with higher price-to-book ratios and higher forecasted growth values.

Management's Discussion of Fund Performance (Unaudited)

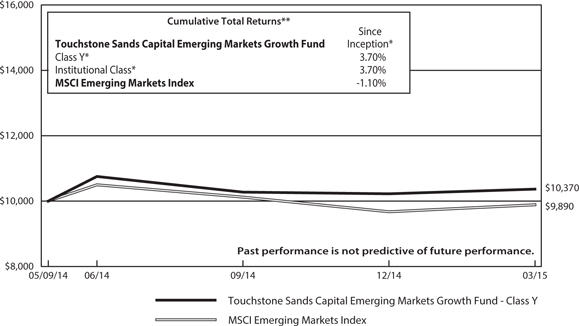

Touchstone Sands Capital Emerging Markets Growth Fund

Sub-Advised by Sands Capital Management, LLC

Investment Philosophy

The Touchstone Sands Capital Emerging Markets Growth Fund seeks long-term capital appreciation. The Fund primarily invests in companies located in emerging market countries and opportunistically, in frontier market countries. Sands Capital generally seeks leading growth businesses with sustainable above average earnings growth and with capital appreciation potential. In addition, Sands Capital looks for companies that have a significant competitive advantage, a leadership position or proprietary niche, a clear mission in an understandable business, financial strength and are valued rationally in relation to comparable companies, the market and the business prospects for that particular company.

Fund Performance

The Touchstone Sands Capital Emerging Markets Growth Fund (Class Y Shares) outperformed its benchmark, the MSCI Emerging Markets Index, since the Fund’s inception on May 9, 2014, through March 31, 2015. The Fund’s total return was 3.70 percent, while the total return of the benchmark was -1.10 percent.

Market Environment

While we continually monitored and assessed the impact of macroeconomic factors on the Fund’s holdings, as bottom-up, fundamental investors, it did not drive our stock selection process. We sought emerging markets growth businesses that were driven by local structural demand factors that we believed should have less sensitivity to short-term macroeconomic changes. Nevertheless, the Fund’s mandate to invest in emerging markets means that we did pay close attention to these secondary drivers.

The escalating conflict between Russia and Ukraine was in focus throughout much of the first half of the year, which affected the stock price performance of related equity markets. Despite the uncertainty created by this geopolitical conflict, we believe the Fund’s two Russian holdings (Magnit OSJC and Mail.ru Group Ltd., which together represent just over three percent of the Fund’s portfolio as of March 31, 2015) have the ability to grow despite the challenges of doing business in Russia, due to their wide competitive moats, established leadership positions and tailwinds from strong secular trends.

Russia, as well as other oil-exporting nations such as Brazil and Saudi Arabia, have also been affected by lower commodity prices throughout much of the past year. The depressed oil price environment has different implications for certain emerging market economies. Countries that are net commodity importers (i.e. China, India and Indonesia) continue to benefit from low oil and gas prices, while the economies of net exporters face challenges. Although the majority of the Fund’s holdings operate in countries that benefit from low oil prices, the Fund has some holdings in net exporter economies. We remain confident in the performance of these businesses as we believe their growth relies on sound secular drivers that are less impacted by macroeconomic volatility.

Positive news came out of India during the year as Narendra Modi led the pro-business Bharatiya Janata Party’s (BJP) return to power with a clear majority. Our view of India’s economic situation started to turn positive nearly two years ago, as our research began to indicate the government was committed to pushing reforms necessary to address the dysfunctions and bottlenecks that hamper growth. As we found new opportunities within the country, including Larsen & Toubro Ltd. and Adani Ports & Special Economic Zone Ltd. (and sold Nestlé India Ltd., which was no longer a strong fit with our investment criteria), we increased the Fund’s portfolio exposure to the country. We continued to see progress being made on reforms and our conviction in India’s growth prospects and our Indian businesses has grown stronger. We continue to be highly optimistic about India’s growth prospects and believe the country is in the process of implementing real reforms that

Management's Discussion of Fund Performance (Unaudited) (Continued)

should create an environment where consumers want to consume and investors want to invest. The Fund has exposures to Indian businesses in the Consumer, Financials, Health Care and Industrials sectors.

The strength of the U.S. dollar, relative to many other global currencies, is one theme currently dominating the broader emerging markets macroeconomic landscape. Historically, a strong dollar environment has caused emerging markets to experience capital outflows, rising debt service costs (particularly for countries with dollar-denominated debt), trade and fiscal imbalances and currency weakness. We believe emerging markets in general are likely to face near-term challenges due to the U.S. dollar’s recent rise, however, we caution against painting all emerging market equities with the same broad brush. We believe business fundamentals and long-term growth prospects will be the primary drivers of wealth creation over time, and have positioned the Fund’s portfolio to benefit from growth drivers we believe are more immune to foreign currency fluctuations and, in so doing, generate sustainable, above-average growth.

Porfolio Review