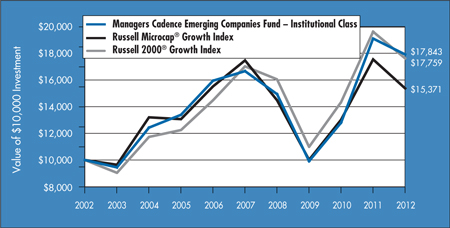

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-03752

The Managers Funds

(Exact name of registrant as specified in charter)

800 Connecticut Avenue, Norwalk, Connecticut 06854

(Address of principal executive offices) (Zip code)

Managers Investment Group LLC

800 Connecticut Avenue, Norwalk, Connecticut 06854

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203) 299-3500

Date of fiscal year end: May 31

Date of reporting period: July 1, 2011 – May 31, 2012

(Annual Shareholder Report)

| Item 1. | Reports to Shareholders |

ANNUAL REPORT

Managers Funds

May 31, 2012

Managers Cadence Capital Appreciation Fund

Managers Cadence Focused Growth Fund

Managers Cadence Mid-Cap Fund

Managers Cadence Emerging Companies Fund

Managers Funds

Annual Report — May 31, 2012

| | | | |

TABLE OF CONTENTS | | Page | |

| |

LETTER TO SHAREHOLDERS | | | 1 | |

| |

ABOUT YOUR FUND’S EXPENSES | | | 3 | |

| |

INVESTMENT MANAGER’S COMMENTS, FUND SNAPSHOTS, AND SCHEDULES OF PORTFOLIO INVESTMENTS | | | | |

| |

Managers Cadence Capital Appreciation Fund | | | 5 | |

| |

Managers Cadence Focused Growth Fund | | | 11 | |

| |

Managers Cadence Mid-Cap Fund | | | 16 | |

| |

Managers Cadence Emerging Companies Fund | | | 22 | |

| |

NOTES TO SCHEDULES OF PORTFOLIO INVESTMENTS | | | 28 | |

| |

FINANCIAL STATEMENTS | | | | |

| |

Statements of Assets and Liabilities | | | 29 | |

Balance sheets, net asset value (NAV) per share computations and cumulative undistributed amounts | | | | |

| |

Statements of Operations | | | 31 | |

Detail of sources of income, expenses, and realized and unrealized gains (losses) during the fiscal year | | | | |

| |

Statements of Changes in Net Assets | | | 32 | |

Detail of changes in assets for the past three fiscal periods | | | | |

| |

FINANCIAL HIGHLIGHTS | | | 35 | |

Historical net asset values per share, distributions, total returns, income and expense ratios, turnover ratios and net assets | | | | |

| |

NOTES TO FINANCIAL STATEMENTS | | | 43 | |

Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | | | | |

| |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | | | 53 | |

| |

TRUSTEES AND OFFICERS | | | 54 | |

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the Managers Family of Funds. Such offering is made only by Prospectus, which includes details as to offering price and other material information.

Letter to Shareholders

Dear Shareholder:

Our foremost goal at Managers Investment Group is to structure and manage mutual funds that will help our shareholders and clients successfully reach their investment goals and objectives.

Each of our funds is geared to provide you with exposure to a specific asset class or style of investing. The Managers Cadence Capital Appreciation Fund and the Managers Cadence Focused Growth Fund invest in large-cap growth companies, while the Managers Cadence Mid-Cap Fund emphasizes mid-cap growth stocks and the Managers Cadence Emerging Companies Fund focuses on small-cap and micro-cap growth names.

The U.S. equity market generated slightly negative returns as the Russell 3000® Index, a popular barometer for the broad U.S. equity market, returned (-1.87%) through May 31, 2012 over the trailing 12 months. During the last 12 months, large-cap stocks outperformed small-cap stocks and growth beat value. Investors favored safety more often than risk as the financials sector struggled and falling commodity prices hurt the energy sector. Poor performance within the financials sector was a contributing factor to growth stocks’ relative outperformance. As a result of market preferences, the best performing segment of the U.S. equity market was large-cap growth. The Russell 1000® Growth Index returned (+1.49%) and handily outperformed the Russell 1000® Value Index, which returned (-3.88%). Over the same time period the Russell 1000® Index returned (-1.23%), compared to (-8.88%) for the Russell 2000® Index. Micro-cap stocks performed even worse as the Russell Microcap® Index returned (-9.20%) during a volatile 12-month period ended May 31, 2012.

The above-mentioned returns do not tell the full story of the 12 months ended May 31, 2012, which were dominated by macro, global developments such as the Arab Spring and the European debt crisis. During the third quarter of 2011, markets turned negative after a decent start to 2011. This was most attributable to increased concerns about a double-dip recession in the U.S. and a hard landing in developing countries. The U.S. debt ceiling debate, and a subsequent S&P downgrade of U.S. long-term debt, added to investor uncertainty. Between June 1, 2011 and September 30, 2011, the Russell 3000® Index returned roughly (-17%). This quickly changed in early-October, as domestic economic data improved. This caused investor concerns of a double-dip recession to evaporate and a strong rally ensued. Additionally, signs of progress in resolving the European debt crisis comforted investors and led to a return to the “risk-on” trade. The rally continued into the first quarter of 2012. In fact, the first quarter of 2012 was the strongest first quarter since 1998. Between October 1, 2011 and March 31, 2012, the Russell 3000® Index rallied nearly (+27%). Unfortunately, those developments have not led to much change in Europe as we continue to await a long-term solution. The European debt crisis reappeared on center stage during the second quarter and investors quickly adopted the “risk off” trade. Through May 31, 2012 the Russell 3000® Index was down nearly (+7%) during the second quarter. The end result of this choppy period was a modestly negative 12-month return for the Russell 3000® Index. Markets were volatile and investors remain uneasy. Most of the macro factors that caused markets to turn negative in mid-2011 remain.

Against this backdrop, the Managers Cadence Funds generated negative returns and, with the exception of Managers Cadence Emerging Companies Fund, lagged their respective benchmarks.

| | | | | | | | | | | | | | | | | | | | |

Periods Ended 05/31/2012 | | Six Months | | | One Year | | | Three Years | | | Five Years | | | Ten Years | |

Managers Cadence Capital Appreciation Fund | | | | | | | | | | | | | | | | | | | | |

Institutional Class | | | 1.17 | % | | | (5.10 | )% | | | 12.11 | % | | | (2.57 | )% | | | 2.80 | % |

Russell 1000® Growth Index | | | 6.82 | % | | | 1.49 | % | | | 16.89 | % | | | 2.01 | % | | | 4.72 | % |

Managers Cadence Focused Growth Fund | | | | | | | | | | | | | | | | | | | | |

Institutional Class | | | 1.82 | % | | | (5.13 | )% | | | 11.20 | % | | | (3.29 | )% | | | 4.15 | % |

Russell 1000® Growth Index | | | 6.82 | % | | | 1.49 | % | | | 16.89 | % | | | 2.01 | % | | | 4.72 | % |

Managers Cadence Mid-Cap Fund | | | | | | | | | | | | | | | | | | | | |

Institutional Class | | | 1.06 | % | | | (7.96 | )% | | | 16.01 | % | | | (0.78 | )% | | | 5.07 | % |

Russell Midcap® Growth Index | | | 4.50 | % | | | (6.31 | )% | | | 18.45 | % | | | 1.17 | % | | | 7.00 | % |

1

Letter to Shareholders (continued)

| | | | | | | | | | | | | | | | | | | | |

Periods Ended 05/31/2012 | | Six Months | | | One Year | | | Three Years | | | Five Years | | | Ten Years | |

Managers Cadence Emerging Companies Fund | | | | | | | | | | | | | | | | | | | | |

Institutional Class | | | 3.96 | % | | | (6.60 | )% | | | 21.63 | % | | | 1.38 | % | | | 5.96 | % |

Russell Microcap® Growth Index | | | 5.47 | % | | | (12.37 | )% | | | 15.37 | % | | | (2.52 | )% | | | 4.39 | % |

Russell 2000® Growth Index | | | 3.24 | % | | | (9.46 | )% | | | 17.37 | % | | | 0.85 | % | | | 5.91 | % |

For the fiscal year ended May 31, 2012, the Managers Cadence Capital Appreciation Fund returned (-5.10%), compared to (+1.49%) for the Russell 1000® Growth Index. The primary causes of underperformance were poor performance in the information technology and energy sectors, a slight tilt towards higher-beta stocks, and headwind from an unfavorable investment environment that often ignored fundamentals and was very macro driven. Decent results within the consumer staples sector were the most noteworthy positive during the fiscal year.

For the fiscal year ended May 31, 2012, the Managers Cadence Focused Growth Fund returned (-5.13%), compared to (+1.49%) for the Russell 1000® Growth Index. The primary causes of underperformance were poor performance in the information technology, industrials and energy sectors, and headwind from an unfavorable investment environment that often ignored fundamentals and was very macro driven. Strong performance in the consumer staples and consumer discretionary sectors partly offset the above detractors.

For the fiscal year ended May 31, 2012, the Managers Cadence Mid-Cap Fund returned (-7.96%), compared to Russell Midcap® Growth Index’s return of (-6.31%). Negative absolute results are consistent with the market’s preference for large-cap stocks during “risk off” time periods. The modest underperformance is due to a combination of factors. Poor performance within the industrials sector and unfavorable positioning in a challenging investment environment were the most notable detractors. Conversely, decent performance within the consumer staples sector helped relative performance and offset some of the detractors.

For the fiscal year ended May 31, 2012, the Managers Cadence Emerging Companies Fund returned (-6.60%) during the trailing 12 months and significantly outperformed the Russell Microcap® Growth Index, which returned (-12.37%). Disappointing absolute returns were driven by market preferences for large-cap stocks. Nevertheless, the Fund held up better than its Index due to strong performance within the consumer discretionary and materials sectors. Conversely, beta positioning relative to the Index and a challenging investment environment detracted from relative results.

The Cadence portfolio management team has provided a more detailed discussion of the performance of the Funds during the last year and its perspective on the investment environment in the management discussion and analysis section of this report.

The following report covers the one-year period ended May 31, 2012. Should you have any questions about this report, or if you’d like to receive a prospectus and additional information, including fees and expenses for these or any of the other Funds in our family, please feel free to contact us at 1-800-835-3879, or visit our Web site at www.managersinvest.com. As always, please read the prospectus carefully before you invest or send money.

You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

We thank you for your continued confidence and investment in The Managers Funds.

|

| Respectfully, |

|

/s/ Keitha Kinne |

| Keitha Kinne |

| Managing Partner |

| Managers Investment Group LLC |

2

About Your Fund’s Expenses

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The first line of the following table provides information about the actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| | | | | | | | | | | | | | | | |

Six Months Ended May 31, 2012 | | Expense

Ratio for

the Period | | | Beginning

Account Value

12/01/2011 | | | Ending

Account Value

05/31/2012 | | | Expenses

Paid During

the Period* | |

Managers Cadence Capital Appreciation Fund | | | | | | | | | | | | | | | | |

Class A | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.12 | % | | $ | 1,000 | | | $ | 936 | | | $ | 5.42 | |

Hypothetical (5% return before expenses) | | | 1.12 | % | | $ | 1,000 | | | $ | 1,019 | | | $ | 5.65 | |

Class B | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.87 | % | | $ | 1,000 | | | $ | 933 | | | $ | 9.03 | |

Hypothetical (5% return before expenses) | | | 1.87 | % | | $ | 1,000 | | | $ | 1,016 | | | $ | 9.42 | |

Class C | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.88 | % | | $ | 1,000 | | | $ | 933 | | | $ | 9.08 | |

Hypothetical (5% return before expenses) | | | 1.88 | % | | $ | 1,000 | | | $ | 1,016 | | | $ | 9.47 | |

Class D | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.12 | % | | $ | 1,000 | | | $ | 937 | | | $ | 5.42 | |

Hypothetical (5% return before expenses) | | | 1.12 | % | | $ | 1,000 | | | $ | 1,019 | | | $ | 5.65 | |

Institutional Class | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 0.72 | % | | $ | 1,000 | | | $ | 938 | | | $ | 3.49 | |

Hypothetical (5% return before expenses) | | | 0.72 | % | | $ | 1,000 | | | $ | 1,021 | | | $ | 3.64 | |

Administrative Class | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 0.97 | % | | $ | 1,000 | | | $ | 937 | | | $ | 4.70 | |

Hypothetical (5% return before expenses) | | | 0.97 | % | | $ | 1,000 | | | $ | 1,020 | | | $ | 4.90 | |

Class P | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 0.79 | % | | $ | 1,000 | | | $ | 938 | | | $ | 3.83 | |

Hypothetical (5% return before expenses) | | | 0.79 | % | | $ | 1,000 | | | $ | 1,021 | | | $ | 3.99 | |

Class R | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.37 | % | | $ | 1,000 | | | $ | 935 | | | $ | 6.63 | |

Hypothetical (5% return before expenses) | | | 1.37 | % | | $ | 1,000 | | | $ | 1,018 | | | $ | 6.91 | |

3

About Your Fund’s Expenses (continued)

| | | | | | | | | | | | | | | | |

Six Months Ended May 31, 2012 | | Expense

Ratio for

the Period | | | Beginning

Account Value

12/01/2011 | | | Ending

Account Value

05/31/2012 | | | Expenses

Paid During

the Period* | |

Managers Cadence Focused Growth Fund | | | | | | | | | | | | | | | | |

Class A | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.07 | % | | $ | 1,000 | | | $ | 930 | | | $ | 5.16 | |

Hypothetical (5% return before expenses) | | | 1.07 | % | | $ | 1,000 | | | $ | 1,020 | | | $ | 5.40 | |

Class C | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.85 | % | | $ | 1,000 | | | $ | 927 | | | $ | 8.91 | |

Hypothetical (5% return before expenses) | | | 1.85 | % | | $ | 1,000 | | | $ | 1,016 | | | $ | 9.32 | |

Class D | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.13 | % | | $ | 1,000 | | | $ | 931 | | | $ | 5.45 | |

Hypothetical (5% return before expenses) | | | 1.13 | % | | $ | 1,000 | | | $ | 1,019 | | | $ | 5.70 | |

Institutional Class | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 0.76 | % | | $ | 1,000 | | | $ | 932 | | | $ | 3.67 | |

Hypothetical (5% return before expenses) | | | 0.76 | % | | $ | 1,000 | | | $ | 1,021 | | | $ | 3.84 | |

Administrative Class | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 0.79 | % | | $ | 1,000 | | | $ | 932 | | | $ | 3.81 | |

Hypothetical (5% return before expenses) | | | 0.79 | % | | $ | 1,000 | | | $ | 1,021 | | | $ | 3.99 | |

Class P | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 0.82 | % | | $ | 1,000 | | | $ | 932 | | | $ | 3.96 | |

Hypothetical (5% return before expenses) | | | 0.82 | % | | $ | 1,000 | | | $ | 1,021 | | | $ | 4.14 | |

Managers Cadence Mid-Cap Fund | | | | | | | | | | | | | | | | |

Class A | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.12 | % | | $ | 1,000 | | | $ | 909 | | | $ | 5.34 | |

Hypothetical (5% return before expenses) | | | 1.12 | % | | $ | 1,000 | | | $ | 1,019 | | | $ | 5.65 | |

Class B | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.87 | % | | $ | 1,000 | | | $ | 906 | | | $ | 8.91 | |

Hypothetical (5% return before expenses) | | | 1.87 | % | | $ | 1,000 | | | $ | 1,016 | | | $ | 9.42 | |

Class C | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.87 | % | | $ | 1,000 | | | $ | 906 | | | $ | 8.91 | |

Hypothetical (5% return before expenses) | | | 1.87 | % | | $ | 1,000 | | | $ | 1,016 | | | $ | 9.42 | |

Class D | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.12 | % | | $ | 1,000 | | | $ | 909 | | | $ | 5.35 | |

Hypothetical (5% return before expenses) | | | 1.12 | % | | $ | 1,000 | | | $ | 1,019 | | | $ | 5.65 | |

Institutional Class | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 0.72 | % | | $ | 1,000 | | | $ | 911 | | | $ | 3.44 | |

Hypothetical (5% return before expenses) | | | 0.72 | % | | $ | 1,000 | | | $ | 1,021 | | | $ | 3.64 | |

Administrative Class | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 0.97 | % | | $ | 1,000 | | | $ | 910 | | | $ | 4.63 | |

Hypothetical (5% return before expenses) | | | 0.97 | % | | $ | 1,000 | | | $ | 1,020 | | | $ | 4.90 | |

Class P | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 0.84 | % | | $ | 1,000 | | | $ | 910 | | | $ | 4.01 | |

Hypothetical (5% return before expenses) | | | 0.84 | % | | $ | 1,000 | | | $ | 1,021 | | | $ | 4.24 | |

Class R | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.37 | % | | $ | 1,000 | | | $ | 908 | | | $ | 6.53 | |

Hypothetical (5% return before expenses) | | | 1.37 | % | | $ | 1,000 | | | $ | 1,018 | | | $ | 6.91 | |

Managers Cadence Emerging Companies Fund | | | | | | | | | | | | | | | | |

Institutional Class | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.42 | % | | $ | 1,000 | | | $ | 899 | | | $ | 6.74 | |

Hypothetical (5% return before expenses) | | | 1.42 | % | | $ | 1,000 | | | $ | 1,018 | | | $ | 7.16 | |

Administrative Class | | | | | | | | | | | | | | | | |

Based on Actual Fund Return | | | 1.64 | % | | $ | 1,000 | | | $ | 897 | | | $ | 7.78 | |

Hypothetical (5% return before expenses) | | | 1.64 | % | | $ | 1,000 | | | $ | 1,017 | | | $ | 8.27 | |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (183), then divided by 366. |

4

Managers Cadence Capital Appreciation Fund

Investment Manager’s Comments

For the fiscal year ended May 31, 2012, the Managers Cadence Capital Appreciation Fund (the “Fund”) returned (-5.10%), lagging its benchmark, the Russell 1000® Growth Index, which returned (+1.49%).

Market Review

While we had some good news and periods of strong performance, the fiscal year ending May 31, 2012 started on a shaky note. After months of carefully planned financial stimulus and cautiously optimistic reports of a strengthening economy, even the Federal Reserve had to admit in Spring 2011 that the economic data was worse than expected. Not coincidentally, U.S. equity market benchmarks turned negative during the middle of 2011 before a sharp decline in late-Summer. The market volatility reflected growing concern over the Federal Reserve’s withdrawal of its Quantitative Easing policy (QE2), which was recently extended in June 2012, and questions over the U.S. economy’s ability to self-sustain without the cash infusion. Continued social unrest in the Middle East, decelerating growth in China, continued concerns over Eurozone sovereign debt and a potential collapse of the Euro added to the fears. Even though the U.S. did not double-dip into a recession, the modest (+2%) growth rate continued to feel recessionary to many Americans.

Macroeconomic drivers returned to the forefront of the investment landscape in the fall of 2011, and the backdrop turned gloomy. The U.S. continued to face high unemployment, volatile commodity prices, a persistently weak housing sector and widening credit spreads, indicating market stress. Fiscal and political turmoil in Washington led to a U.S. debt downgrade, and expectations for growth in America were muted at best. Abroad, Eurozone countries continued to struggle through their financial crisis, while growth in China slowed and Greece hovered on the precipice of default.

Understandably, investors were nervous. In the fall of 2011, we saw many investors questioning their investment strategies, and even large institutions pulling out of stocks at potentially the worst time. Yet at the same time, counter-intuitively, we saw companies thriving across all sectors. We were able to make sound, well-priced investments in companies with strong revenues and earnings, high levels of productivity, and record cash on their balance sheets. While market downturns are often painful, they can provide compelling buying opportunities for long-term investors.

During October the market rebounded sharply. Some broad indexes were up over (+20%). Strong performance was driven by increased confidence about the U.S. recovery and that the Eurozone crisis would be resolved. The last two months of 2011 were relatively flat, but volatile, after the sharp October rebound. The first quarter of 2012 saw an acceleration of the upward trend. Most U.S. equity indexes were up another 15-20% before markets turned downward in April as Eurozone issues returned to the forefront. Additionally, U.S. economic data was less favorable and caused investors to, again, question the sustainability of the economic recovery. Investors were also concerned about slowing growth in China and if emerging market growth would be enough to overshadow major fiscal issues in developed nations. Markets fell 5-10% during the first two months of 2012.

Performance Review

The Fund generated a negative absolute return and lagged its benchmark during the trailing 12-month period. The Fund was hurt by an unfavorable investment environment that created headwind for the process, poor performance within the information technology and energy sectors, and a tilt towards higher-beta stocks. During the trailing 12-month period, macro factors frequently dominated and fundamentals were often ignored. This often creates headwind for our fundamentally-based, growth-at-a-reasonable-price investment strategy. Correlations across stocks were often elevated and volatility indicators fluctuated with macro concerns. This creates a less favorable environment for fundamentally-based investment managers. We believe volatility creates good long-term investment opportunities, but the macro-environment was a headwind.

From an attribution perspective, stock selection within the information technology sector was the key detractor. The largest individual detractor, on a relative basis, was Apple, Inc. (“Apple”). Apple returned (+66.1%) during the fiscal year. We like Apple as an investment and held it in the Fund throughout the fiscal year. However, our investment process limits us from matching the position size within the Index. As a result, our underweight was a significant contributor to relative returns. BMC Software, Inc. (-42.7%) and Autodesk, Inc. (-37.0%) were additional information technology stocks that hurt performance.

Our investment process and quantitative screens have produced a tilt towards higher-beta stocks relative to the Index. This is primarily a bottom-up decision because these stocks have a more attractive combination of growth potential and valuations. Many “defensive” stocks appear overvalued relative to their history. This tilt hurt performance because during the trailing 12-month period, the highest-beta quintile of the Russell 1000® Growth Index returned (-20.6%), compared to (+10.4%) for the lowest-beta quintile. The Fund had a slight overweight to higher-beta stocks and a slight underweight to lower-beta stocks. We continue to believe our patience will be rewarded as these stocks remain attractive.

The abovementioned detractors were partly offset by decent performance within the consumer staples sector. Whole Foods Market, Inc. (+45.9%), The Hershey Company (+10.8%) and Estee Lauder Co., Class A (+10.5%) all helped relative performance. Very good results in this sector were not enough to overcome headwind from market preferences, portfolio positioning and the information technology sector.

Outlook

We believe the remainder of 2012 is likely to feature a slow-growth world and a slowly recovering market. We believe the Cadence portfolios should do well in this environment. The data show that while cheapness tends to move stocks off their troughs, quality and dependability buoy companies in tough markets. This is because when growth is perceived as scarce, investors tend to be skeptical and will therefore pay up for quality, growing companies. Our disciplined strategies thrived in a similar environment in 2004, as we transitioned away from the sharp initial upturn in 2003.

5

Managers Cadence Capital Appreciation Fund

Investment Manager’s Comments (continued)

Overall, we have taken a balanced approach to investing in growth companies, including both secular and cyclical growers in the Fund. We have also remained true to our valuation discipline, buying growing companies at prices that make sense. Short-term our insistence on good value has been a headwind, but long-term it has served our investors well. We believe the Fund is comprised of high-quality companies purchased at reasonable prices. While larger companies have been more affected by global macroeconomic events in general, Cadence portfolios tend to exhibit greater percentages of rising estimates and positive surprises than the Russell 1000® Growth Index. Similarly, the Fund has often produced a smaller percentage of negative surprises than the index.

In this environment, we feel patience is the key. With the market so distracted by macroeconomic events — and market swings a reaction to broad-based news rather than specific company fundamentals — bottom-up investors who pick each stock based on its individual merit must weather the storm. We continue to believe fundamentals matter and our disciplined investment process will be rewarded.

This commentary reflects the viewpoints of Cadence Capital Management, LLC as of May 31, 2012 and is not intended as a forecast or guarantee of future results.

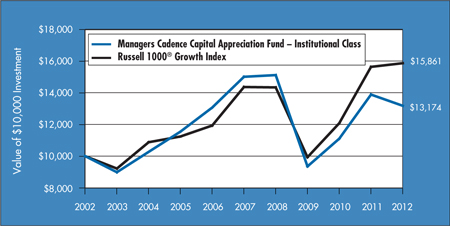

CUMULATIVE TOTAL RETURN PERFORMANCE

Managers Cadence Capital Appreciation Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in Managers Cadence Capital Appreciation Fund’s Institutional Class on May 31, 2002, compared to a $10,000 investment made in the Russell 1000® Growth Index for the same time period. Performance for periods longer than one year is annualized. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Past performance is not indicative of future results. Total returns would have been lower had certain expenses not been reduced.

6

Managers Cadence Capital Appreciation Fund

Investment Manager’s Comments (continued)

CUMULATIVE TOTAL RETURN PERFORMANCE (continued)

The table below shows the average annual total returns for the Managers Cadence Capital Appreciation Fund since inception through May 31, 2012, and the Russell 1000® Growth Index for the same periods.

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | Average Annual Total Returns1 | |

| | | | | One Year | | | Five Years | | | Ten Years | | | Since

Inception | | | Inception

Date | |

Managers Cadence Capital Appreciation Fund 2,3,4,5,6,* | | | | | | | | | | | | | | | | | | | | |

Class A | | No Load | | | (5.50 | )% | | | (2.96 | )% | | | 2.38 | % | | | 4.62 | % | | | 01/20/1997 | |

Class A | | With Load | | | (10.93 | )% | | | (4.11 | )% | | | 1.78 | % | | | 4.22 | % | | | 01/20/1997 | |

Class B | | No Load | | | (6.24 | )% | | | (3.69 | )% | | | 1.61 | % | | | 3.84 | % | | | 01/20/1997 | |

Class B | | With Load | | | (10.93 | )% | | | (4.04 | )% | | | 1.61 | % | | | 3.84 | % | | | 01/20/1997 | |

Class C | | No Load | | | (6.22 | )% | | | (3.67 | )% | | | 1.63 | % | | | 3.85 | % | | | 01/20/1997 | |

Class C | | With Load | | | (7.16 | )% | | | (3.67 | )% | | | 1.63 | % | | | 3.85 | % | | | 01/20/1997 | |

Class D | | | | | (5.52 | )% | | | (2.96 | )% | | | 2.39 | % | | | 2.48 | % | | | 04/08/1998 | |

Institutional Class | | | | | (5.10 | )% | | | (2.57 | )% | | | 2.80 | % | | | 8.62 | % | | | 03/08/1991 | |

Administrative Class | | | | | (5.38 | )% | | | (2.81 | )% | | | 2.56 | % | | | 6.17 | % | | | 07/31/1996 | |

Class P | | | | | (5.18 | )% | | | — | | | | — | | | | (0.99 | )% | | | 07/07/2008 | |

Class R | | | | | (5.75 | )% | | | (3.20 | )% | | | — | | | | 4.62 | % | | | 12/31/2002 | |

Russell 1000® Growth Index 7 | | | 1.49 | % | | | 2.01 | % | | | 4.72 | % | | | — | 8 | | | 03/08/1991 | † |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end, please call (800) 835-3879 or visit our Web site at www.managersinvest.com.

Performance differences among the share classes are due to differences in sales charge structures and class expenses. Returns shown reflect maximum sales charge of 5.75% on Class A shares. Maximum sales charge on Class B shares is 5.00% up to six years from the date of purchase. Class C shares held for less than one year are subject to a 1.00% contingent deferred sales charge (CDSC).

|

Investors should carefully consider the Fund’s investment objectives, risks, charges, and expenses before investing. For this and other information, please call 800.835.3879 or visit |

| | |

www.managersinvest.com for a free prospectus. Read it carefully before investing or sending money. Funds are distributed by Managers Distributors, Inc., a member of FINRA. † Date reflects inception date of the Fund, not the index. * The Fund changed its fiscal year end from June 30 to May 31 in 2011. 1 Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the Prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of May 31, 2012. All returns are in U.S. dollars ($). 2 From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. 3 A greater percentage of the Fund’s holdings may be focused in a smaller number of securities which may place the Fund at greater risk than a more diversified fund. 4 The Fund invests in growth stocks, which may be more sensitive to market movements because their prices tend to reflect future investor expectations rather than just current profits. Growth stocks may underperform value stocks during given periods. |

5 | | The Fund invests in large-capitalization companies that may underperform other stock funds (such as funds that focus on small-and medium-capitalization companies) when stocks of large-capitalization companies are out of favor. |

6 The Fund is subject to special risk considerations similar to those associated with the direct ownership of real estate. Real estate valuations may be subject to factors such as changing general and local economic, financial, competitive, and environmental conditions. 7 The Russell 1000® Growth Index is a market capitalization weighted index that measures the performance of those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values. Unlike the Fund, the Russell 1000® Growth Index is unmanaged, is not available for investment and does not incur expenses. 8 Since the Russell 1000® Growth Index’s Inception date of June 1, 1995, the average annual total return for the index was 6.68%. The Russell 1000® Growth Index is a registered trademark of Russell Investments. Russell® is a trademark of Russell Investments. Not FDIC insured, nor bank guaranteed. May lose value. |

7

Managers Cadence Capital Appreciation Fund

Fund Snapshots

May 31, 2012

Portfolio Breakdown (unaudited)

| | | | | | | | |

Industry | | Managers Cadence Capital

Appreciation Fund** | | | Russell 1000®

Growth Index | |

Information Technology | | | 30.0 | % | | | 29.6 | % |

Consumer Discretionary | | | 19.9 | % | | | 14.8 | % |

Industrials | | | 12.7 | % | | | 12.2 | % |

Health Care | | | 11.0 | % | | | 10.7 | % |

Energy | | | 8.3 | % | | | 9.5 | % |

Consumer Staples | | | 7.3 | % | | | 12.7 | % |

Financials | | | 6.2 | % | | | 4.3 | % |

Materials | | | 3.8 | % | | | 5.2 | % |

Telecommunication Services | | | 0.0 | % | | | 0.9 | % |

Utilities | | | 0.0 | % | | | 0.1 | % |

Other Assets and Liabilities | | | 0.8 | % | | | 0.0 | % |

| ** | As a percentage of net assets |

Top Ten Holdings (unaudited)

| | | | |

Security Name | | % of

Net Assets | |

Google, Inc., Class A* | | | 2.5 | % |

QUALCOMM, Inc.* | | | 2.5 | |

JPMorgan Chase & Co. | | | 1.8 | |

Procter & Gamble Co., The | | | 1.6 | |

Paychex, Inc. | | | 1.5 | |

Norfolk Southern Corp. | | | 1.5 | |

Stryker Corp. | | | 1.4 | |

Clorox Co., The | | | 1.4 | |

Cooper Cos., Inc., The | | | 1.4 | |

Occidental Petroleum Corp. | | | 1.4 | |

| | | | |

Top Ten as a Group | | | 17.0 | % |

| | | | |

| * | Top Ten Holding at November 30, 2011 |

|

| Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report. |

8

Managers Cadence Capital Appreciation Fund

Schedule of Portfolio Investments

May 31, 2012

| | | | | | | | |

| | | Shares | | | Value | |

| | | | | | | | |

Common Stocks - 99.2% | | | | | | | | |

Consumer Discretionary - 19.9% | | | | | |

Bed Bath & Beyond, Inc.* | | | 99,920 | | | $ | 7,219,220 | |

CBS Corp., Class B | | | 250,340 | | | | 7,990,853 | |

Chipotle Mexican Grill, Inc.* | | | 16,790 | | | | 6,935,445 | |

Coach, Inc. | | | 116,880 | | | | 7,883,556 | |

Ford Motor Co. | | | 743,720 | | | | 7,853,683 | |

Genuine Parts Co. | | | 105,650 | | | | 6,655,950 | |

Harley-Davidson, Inc. | | | 165,790 | | | | 7,987,762 | |

Limited Brands, Inc. | | | 147,620 | | | | 6,548,423 | |

Lululemon Athletica, Inc.* | | | 69,940 | | | | 5,080,442 | |

McDonald’s Corp. | | | 72,650 | | | | 6,490,551 | |

NIKE, Inc., Class B | | | 76,140 | | | | 8,236,825 | |

Nordstrom, Inc. | | | 155,200 | | | | 7,351,824 | |

Omnicom Group, Inc. | | | 175,270 | | | | 8,356,874 | |

priceline.com, Inc.* | | | 9,730 | | | | 6,086,018 | |

PVH Corp. | | | 67,750 | | | | 5,487,750 | |

Ralph Lauren Corp. | | | 53,490 | | | | 7,959,312 | |

Starbucks Corp. | | | 125,260 | | | | 6,875,521 | |

TJX Cos., Inc. | | | 161,910 | | | | 6,874,699 | |

Total Consumer Discretionary | | | | | | | 127,874,708 | |

Consumer Staples - 7.3% | | | | | |

Clorox Co., The | | | 135,440 | | | | 9,318,272 | |

Costco Wholesale Corp. | | | 96,270 | | | | 8,316,765 | |

Kroger Co., The | | | 343,530 | | | | 7,561,095 | |

Philip Morris International, Inc. | | | 95,620 | | | | 8,080,846 | |

Procter & Gamble Co., The | | | 165,380 | | | | 10,301,520 | |

Whole Foods Market, Inc. | | | 42,270 | | | | 3,745,545 | |

Total Consumer Staples | | | | | | | 47,324,043 | |

Energy - 8.3% | | | | | | | | |

Anadarko Petroleum Corp. | | | 145,460 | | | | 8,873,060 | |

Chevron Corp. | | | 79,260 | | | | 7,792,051 | |

Halliburton Co. | | | 275,090 | | | | 8,269,205 | |

Murphy Oil Corp. | | | 155,130 | | | | 7,232,161 | |

National Oilwell Varco, Inc. | | | 134,610 | | | | 8,985,218 | |

Occidental Petroleum Corp. | | | 115,030 | | | | 9,118,428 | |

Range Resources Corp. | | | 49,880 | | | | 2,865,107 | |

Total Energy | | | | | | | 53,135,230 | |

Financials - 6.2% | | | | | | | | |

Discover Financial Services | | | 211,460 | | | | 7,001,441 | |

JPMorgan Chase & Co. | | | 356,340 | | | | 11,812,671 | |

Northern Trust Corp. | | | 150,080 | | | | 6,480,454 | |

T. Rowe Price Group, Inc. | | | 109,260 | | | | 6,292,283 | |

| | | | | | | | |

| | | Shares | | | Value | |

| | | | | | | | |

Wells Fargo & Co. | | | 255,620 | | | $ | 8,192,621 | |

Total Financials | | | | | | | 39,779,470 | |

Health Care - 11.0% | | | | | | | | |

Abbott Laboratories | | | 134,310 | | | | 8,299,015 | |

Agilent Technologies, Inc. | | | 193,010 | | | | 7,847,787 | |

Biogen Idec, Inc.* | | | 56,010 | | | | 7,323,308 | |

Cardinal Health, Inc. | | | 188,230 | | | | 7,788,957 | |

Cooper Cos., Inc., The | | | 107,680 | | | | 9,172,182 | |

Covidien PLC | | | 157,160 | | | | 8,137,745 | |

Intuitive Surgical, Inc.* | | | 9,880 | | | | 5,168,228 | |

Johnson & Johnson | | | 128,670 | | | | 8,032,868 | |

Stryker Corp. | | | 182,220 | | | | 9,375,219 | |

Total Health Care | | | | | | | 71,145,309 | |

Industrials - 12.7% | | | | | | | | |

Chicago Bridge & Iron Co., N.V. | | | 170,360 | | | | 6,122,738 | |

Cummins, Inc. | | | 59,100 | | | | 5,729,745 | |

Expeditors International of Washington, Inc. | | | 221,170 | | | | 8,459,753 | |

Honeywell International, Inc. | | | 137,020 | | | | 7,626,533 | |

Joy Global, Inc. | | | 117,152 | | | | 6,544,111 | |

Norfolk Southern Corp. | | | 143,190 | | | | 9,381,809 | |

Owens Corning* | | | 199,520 | | | | 6,157,187 | |

PACCAR, Inc. | | | 211,840 | | | | 7,958,829 | |

Parker Hannifin Corp. | | | 79,230 | | | | 6,476,260 | |

Stericycle, Inc.* | | | 96,830 | | | | 8,449,386 | |

United Technologies Corp. | | | 119,750 | | | | 8,874,673 | |

Total Industrials | | | | | | | 81,781,024 | |

Information Technology - 30.0% | | | | | |

Accenture PLC, Class A | | | 118,980 | | | | 6,793,758 | |

Adobe Systems, Inc.* | | | 256,960 | | | | 7,978,608 | |

Amphenol Corp., Class A | | | 144,920 | | | | 7,708,295 | |

Apple, Inc.* | | | 14,330 | | | | 8,278,871 | |

Applied Materials, Inc. | | | 683,080 | | | | 7,056,216 | |

Autodesk, Inc.* | | | 204,120 | | | | 6,535,922 | |

Broadcom Corp.,

Class A* | | | 229,260 | | | | 7,416,561 | |

Cisco Systems, Inc. | | | 144,080 | | | | 2,352,826 | |

Citrix Systems, Inc.* | | | 85,800 | | | | 6,270,264 | |

Cognizant Technology Solutions Corp.,

Class A* | | | 119,680 | | | | 6,971,360 | |

EMC Corp.* | | | 381,030 | | | | 9,087,566 | |

F5 Networks, Inc.* | | | 71,600 | | | | 7,409,168 | |

Fortinet, Inc.* | | | 244,230 | | | | 5,189,888 | |

Google, Inc., Class A* | | | 27,360 | | | | 15,892,330 | |

Lam Research Corp.* | | | 128,410 | | | | 4,789,693 | |

Marvell Technology Group, Ltd. | | | 479,700 | | | | 6,010,641 | |

The accompanying notes are an integral part of these financial statements.

9

Managers Cadence Capital Appreciation Fund

Schedule of Portfolio Investments (continued)

| | | | | | | | |

| | | Shares | | | Value | |

| | | | | | | | |

Information Technology - 30.0% (continued) | | | | | | | | |

Microsoft Corp. | | | 285,130 | | | $ | 8,322,945 | |

Paychex, Inc. | | | 314,260 | | | | 9,418,372 | |

QUALCOMM, Inc. | | | 276,640 | | | | 15,854,238 | |

Red Hat, Inc.* | | | 106,880 | | | | 5,491,494 | |

Teradata Corp.* | | | 75,210 | | | | 4,999,961 | |

TIBCO Software, Inc.* | | | 271,680 | | | | 7,267,440 | |

Trimble Navigation, Ltd.* | | | 164,170 | | | | 7,743,078 | |

VeriFone Systems, Inc.* | | | 193,630 | | | | 6,991,979 | |

Visa, Inc., Class A | | | 43,560 | | | | 5,018,112 | |

VMware, Inc., Class A* | | | 67,530 | | | | 6,280,965 | |

Total Information Technology | | | | | | | 193,130,551 | |

Materials - 3.8% | | | | | | | | |

CF Industries Holdings, Inc. | | | 46,430 | | | | 7,937,673 | |

| | | | | | | | |

| | | Shares | | | Value | |

| | | | | | | | |

Cliffs Natural Resources, Inc. | | | 130,540 | | | $ | 6,237,201 | |

Freeport-McMoRan Copper & Gold, Inc., Class B | | | 206,832 | | | | 6,626,897 | |

Sherwin-Williams Co., The | | | 26,410 | | | | 3,423,792 | |

Total Materials | | | | | | | 24,225,563 | |

Total Common Stocks

(cost $638,471,882) | | | | | | | 638,395,898 | |

Other Investment Companies - 0.7%1 | | | | | | | | |

Dreyfus Cash Management Fund, Institutional Class Shares, 0.09%

(cost $4,516,454) | | | 4,516,454 | | | | 4,516,454 | |

Total Investments - 99.9%

(cost $642,988,336) | | | | | | | 642,912,352 | |

Other Assets, less Liabilities - 0.1% | | | | 541,781 | |

Net Assets - 100.0% | | | | | | $ | 643,454,133 | |

The accompanying notes are an integral part of these financial statements.

10

Managers Cadence Focused Growth Fund

Investment Manager’s Comments

For the fiscal year ended May 31, 2012, the Managers Cadence Focused Growth Fund (the “Fund”) returned (-5.13%), lagging its benchmark, the Russell 1000® Growth Index, which returned (+1.49%).

Market Review

While we had some good news and periods of strong performance, the fiscal year ending May 31, 2012 started on a shaky note. After months of carefully planned financial stimulus and cautiously optimistic reports of a strengthening economy, even the Federal Reserve had to admit in Spring 2011 that the economic data was worse than expected. Not coincidentally, U.S. equity market benchmarks turned negative during the middle of 2011 before a sharp decline in late-Summer. The market volatility reflected growing concern over the Federal Reserve’s withdrawal of its Quantitative Easing policy (QE2), which was recently extended in June 2012, and questions over the U.S. economy’s ability to self-sustain without the cash infusion. Continued social unrest in the Middle East, decelerating growth in China, continued concerns over Eurozone sovereign debt and a potential collapse of the euro added to the fears. Even though the U.S. did not double-dip into a recession, the modest (+2%) growth rate continued to feel recessionary to many Americans.

Macroeconomic drivers returned to the forefront of the investment landscape in the fall of 2011, and the backdrop turned gloomy. The U.S. continued to face high unemployment, volatile commodity prices, a persistently weak housing sector and widening credit spreads, indicating market stress. Fiscal and political turmoil in Washington led to a U.S. debt downgrade, and expectations for growth in America were muted at best. Abroad, Eurozone countries continued to struggle through their financial crisis, while growth in China slowed and Greece hovered on the precipice of default.

Understandably, investors were nervous. In the fall of 2011, we saw many investors questioning their investment strategies, and even large institutions pulling out of stocks at potentially the worst time. Yet at the same time, counter-intuitively, we saw companies thriving across all sectors. We were able to make sound, well-priced investments in companies with strong revenues and earnings, high levels of productivity, and record cash on their balance sheets. While market downturns are often painful, they can provide compelling buying opportunities for long-term investors.

During October the market rebounded sharply. Some broad indexes were up over (+20%). Strong performance was driven by increased confidence about the U.S. recovery and that the Eurozone crisis would be resolved. The last two months of 2011 were relatively flat, but volatile, after the sharp October rebound. The first quarter of 2012 saw an acceleration of the upward trend. Most U.S. equity indexes were up another 15-20% before markets turned downward in April as Eurozone issues returned to the forefront. Additionally, U.S. economic data was less favorable and caused investors to, again, question the sustainability of the economic recovery. Investors were also concerned about slowing growth in China and if emerging market growth would be enough to overshadow major fiscal issues in developed nations. Markets fell 5-10% during the first two months of 2012.

Performance Review

The Fund generated a negative absolute return and meaningfully lagged its benchmark during the trailing 12-month period. A combination of factors contributed to the underperformance. In particular, the Fund was hurt by an unfavorable investment environment that created headwind and poor performance within the information technology, industrials and energy sectors. Beta positioning relative to the Index also hurt performance. During the trailing 12-month period, macro factors frequently dominated and fundamentals were often ignored. This often creates headwind for our fundamentally-based, growth-at-a-reasonable-price investment strategy. Correlations across stocks were often elevated and volatility indicators fluctuated with macro concerns. This creates a less favorable environment for fundamentally-based investment managers. We believe volatility creates good long-term investment opportunities, but the macro-environment was a headwind.

From an attribution perspective, stock selection within the information technology sector was the key detractor. The largest individual detractor, on a relative basis, was Apple, Inc. (“Apple”). Apple returned (+66.1%) during the fiscal year. We like Apple as an investment and held it in the Fund throughout the fiscal year. However, our investment process limits us from matching the position size within the Index. As a result, our underweight was a significant contributor to relative returns. Juniper Networks, Inc. (-42.3%) and Applied Materials, Inc. (-30.2%) were other information technology holdings that weighed on relative results. Additionally, performance within industrials and energy hurt performance. Notable detractors include Joy Global, Inc. (-37.0%), SPX Corp. (-32.9%), Halliburton Co.

(-42.5%) and Baker Hughes, Inc. (-32.5%).

Our investment process and quantitative screens have produced a slight tilt towards higher-beta stocks relative to the Index. This is primarily a bottom-up decision because these stocks have a more attractive combination of growth potential and valuations. Many “defensive” stocks appear overvalued relative to their history. This tilt hurt performance because during the trailing 12-month period.

The abovementioned detractors were partly offset by decent performance within the consumer staples and consumer discretionary sectors. TJX Cos., Inc. (+62.1%), Starbucks Corp. (+51.3%) and McDonald’s Corp. (+24.3%) were strong consumer discretionary performers that helped relative and absolute returns. Within consumer staples, Whole Foods Market, Inc. (+45.9%) and The Hershey Company (+10.8%) led the way. Very good results in these sectors were not enough to overcome significant headwind from market preferences and portfolio positioning.

Outlook

We believe the remainder of 2012 is likely to feature a slow-growth world and a slowly recovering market. We believe the Cadence portfolios should do well in this environment. The data shows that while cheapness tends to move stocks off their troughs, quality and dependability buoy companies in tough markets. This is because when growth is perceived as scarce, investors tend to be skeptical and will therefore pay up for quality, growing companies. Our

11

Managers Cadence Focused Growth Fund

Investment Manager’s Comments (continued)

disciplined strategies thrived in a similar environment in 2004, as we transitioned away from the sharp initial upturn in 2003.

Overall, we have taken a balanced approach to investing in growth companies, including both secular and cyclical growers in the Fund. We have also remained true to our valuation discipline, buying growing companies at prices that make sense. Short-term our insistence on good value has been a headwind, but long-term it has served our investors well. We believe the Fund is comprised of high-quality companies purchased at reasonable prices. While larger companies have been more affected by global macroeconomic events in general, Cadence portfolios tend to exhibit greater percentages of rising estimates and positive surprises than the Russell 1000® Growth Index. Similarly the Fund has often produced a smaller percentage of negative surprises than the Index.

In this environment, we feel patience is the key. With the market so distracted by macroeconomic events — and market swings a reaction to broad-based news rather than specific company fundamentals — bottom-up investors who pick each stock based on its individual merit must weather the storm. We continue to believe fundamentals matter and our disciplined investment process will be rewarded.

This commentary reflects the viewpoints of Cadence Capital Management, LLC as of May 31, 2012 and is not intended as a forecast or guarantee of future results.

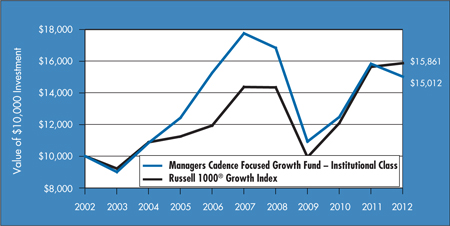

CUMULATIVE TOTAL RETURN PERFORMANCE

Managers Cadence Focused Growth Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in Managers Cadence Focused Growth Fund’s Institutional Class on May 31, 2002, compared to a $10,000 investment made in the Russell 1000® Growth Index for the same time period. Performance for periods longer than one year is annualized. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Past performance is not indicative of future results. Total returns would have been lower had certain expenses not been reduced.

12

Managers Cadence Capital Appreciation Fund

Investment Manager’s Comments (continued)

CUMULATIVE TOTAL RETURN PERFORMANCE (continued)

The table below shows the average annual total returns for the Managers Cadence Focused Growth Fund since inception through May 31, 2012, and the Russell 1000® Index for the same time periods.

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | Average Annual Total Returns1 | |

| | | | | One Year | | | Five Years | | | Ten Years | | | Since

Inception | | | Inception

Date | |

Managers Cadence Focused Growth Fund 2,3,4,5,6,* | | | | | | | | | | | | | | | | | | | | |

Class A | | No Load | | | (5.47 | )% | | | (3.63 | )% | | | — | | | | (0.40 | )% | | | 07/05/2006 | |

Class A | | With Load | | | (10.93 | )% | | | (4.76 | )% | | | — | | | | (1.40 | )% | | | 07/05/2006 | |

Class C | | No Load | | | (6.07 | )% | | | (4.34 | )% | | | — | | | | (1.14 | )% | | | 07/05/2006 | |

Class C | | With Load | | | (6.94 | )% | | | (4.34 | )% | | | — | | | | (1.14 | )% | | | 07/05/2006 | |

Class D | | | | | (5.47 | )% | | | (3.64 | )% | | | — | | | | (0.09 | )% | | | 07/05/2006 | |

Institutional Class | | | | | (5.13 | )% | | | (3.29 | )% | | | 4.15 | % | | | 0.40 | % | | | 08/31/1999 | |

Administrative Class | | | | | (5.14 | )% | | | (3.38 | )% | | | — | | | | 0.15 | % | | | 09/15/2006 | |

Class P | | | | | (5.20 | )% | | | — | | | | — | | | | (1.02 | )% | | | 07/07/2008 | |

Russell 1000® Growth Index7 | | | 1.49 | % | | | 2.01 | % | | | 4.72 | % | | | 0.36 | % | | | 08/31/1999 | † |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end, please call (800) 835-3879 or visit our Web site at www.managersinvest.com.

Performance differences among the share classes are due to differences in sales charge structures and class expenses. Returns shown reflect maximum sales charge of 5.75% on Class A shares, as well as the applicable contingent deferred sales charge (CDSC) on Class C shares. Class C shares held for less than one year are subject to a 1% CDSC.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For this and other information, please call 800.835.3879 or visit www.managersinvest.com for a free prospectus. Read it carefully before investing or sending money. Funds are distributed by Managers Distributors, Inc., a member of FINRA.

|

† Date reflects inception date of the Fund, not the index. * The Fund changed its fiscal year end from June 30 to May 31 in 2011. 1 Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the Prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of May 31, 2012. All returns are in U.S. dollars ($). 2 From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. 3 A greater percentage of the Fund’s holdings may be focused in a smaller number of securities which may place the Fund at greater risk than a more diversified fund. 4 The Fund invests in growth stocks, which may be more sensitive to market movements because their prices tend to reflect future investor expectations rather than just current profits. Growth stocks may underperform value stocks during given periods. 5 The Fund invests in large-capitalization companies that may underperform other stock funds (such as funds that focus on small- and medium-capitalization companies) when stocks of large-capitalization companies are out of favor. 6 The Fund is subject to special risk considerations similar to those associated with the direct ownership of real estate. Real estate valuations may be subject to factors such as changing general and local economic, financial, competitive, and environmental conditions. 7 The Russell 1000® Growth Index is a market capitalization weighted index that measures the performance of those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values. Unlike the Fund, the Russell 1000® Growth Index is unmanaged, is not available for investment and does not incur expenses. The Russell 1000® Growth Index is a registered trademark of Russell Investments. Russell® is a trademark of Russell Investments. Not FDIC insured, nor bank guaranteed. May lose value. |

13

Managers Cadence Focused Growth Fund

Fund Snapshots

May 31, 2012

Portfolio Breakdown (unaudited)

| | | | | | | | |

Industry | | Managers Cadence Focused

Growth Fund** | | | Russell 1000®

Growth Index | |

Information Technology | | | 31.4 | % | | | 29.6 | % |

Consumer Discretionary | | | 15.3 | % | | | 14.8 | % |

Industrials | | | 12.8 | % | | | 12.2 | % |

Health Care | | | 11.6 | % | | | 10.7 | % |

Financials | | | 9.0 | % | | | 4.3 | % |

Energy | | | 8.6 | % | | | 9.5 | % |

Consumer Staples | | | 6.9 | % | | | 12.7 | % |

Materials | | | 3.7 | % | | | 5.2 | % |

Telecommunication Services | | | 0.0 | % | | | 0.9 | % |

Utilities | | | 0.0 | % | | | 0.1 | % |

Other Assets and Liabilities | | | 0.7 | % | | | 0.0 | % |

| ** | As a percentage of net assets |

Top Ten Holdings (unaudited)

| | | | |

Security Name | | % of

Net Assets | |

Google, Inc., Class A* | | | 3.2 | % |

QUALCOMM, Inc.* | | | 2.9 | |

Philip Morris International, Inc.* | | | 2.9 | |

JPMorgan Chase & Co. | | | 2.8 | |

Omnicom Group, Inc. | | | 2.6 | |

Mastercard, Inc., Class A | | | 2.6 | |

Adobe Systems, Inc. | | | 2.6 | |

Paychex, Inc. | | | 2.6 | |

Coach, Inc.* | | | 2.5 | |

Stryker Corp. | | | 2.5 | |

| | | | |

Top Ten as a Group | | | 27.2 | % |

| | | | |

| * | Top Ten Holding at November 30, 2011 |

|

| Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report. |

14

Managers Cadence Focused Growth Fund

Schedule of Portfolio Investments

May 31, 2012

| | | | | | | | |

| | | Shares | | | Value | |

| | | | | | | | |

Common Stocks - 99.3% | | | | | | | | |

Consumer Discretionary - 15.3% | | | | | |

Coach, Inc. | | | 3,170 | | | $ | 213,817 | |

Nordstrom, Inc. | | | 3,310 | | | | 156,795 | |

Omnicom Group, Inc. | | | 4,690 | | | | 223,619 | |

priceline.com, Inc.* | | | 260 | | | | 162,627 | |

Ralph Lauren Corp. | | | 1,010 | | | | 150,288 | |

Starbucks Corp. | | | 3,320 | | | | 182,235 | |

TJX Cos., Inc. | | | 4,860 | | | | 206,356 | |

Total Consumer Discretionary | | | | | | | 1,295,737 | |

Consumer Staples - 6.9% | | | | | | | | |

Clorox Co., The | | | 2,870 | | | | 197,456 | |

Philip Morris International, Inc. | | | 2,850 | | | | 240,854 | |

Whole Foods Market, Inc. | | | 1,620 | | | | 143,548 | |

Total Consumer Staples | | | | | | | 581,858 | |

Energy - 8.6% | | | | | | | | |

Anadarko Petroleum Corp. | | | 2,640 | | | | 161,040 | |

Halliburton Co. | | | 5,520 | | | | 165,931 | |

National Oilwell Varco, Inc. | | | 2,930 | | | | 195,577 | |

Occidental Petroleum Corp. | | | 2,530 | | | | 200,553 | |

Total Energy | | | | | | | 723,101 | |

Financials - 9.0% | | | | | | | | |

Discover Financial Services | | | 5,530 | | | | 183,098 | |

JPMorgan Chase & Co. | | | 7,080 | | | | 234,702 | |

T. Rowe Price Group, Inc. | | | 2,880 | | | | 165,859 | |

Wells Fargo & Co. | | | 5,470 | | | | 175,314 | |

Total Financials | | | | | | | 758,973 | |

Health Care - 11.6% | | | | | | | | |

Cardinal Health, Inc. | | | 4,750 | | | | 196,555 | |

Cooper Cos., Inc., The | | | 2,360 | | | | 201,025 | |

Covidien PLC | | | 3,620 | | | | 187,444 | |

Johnson & Johnson | | | 2,860 | | | | 178,550 | |

Stryker Corp. | | | 4,150 | | | | 213,518 | |

Total Health Care | | | | | | | 977,092 | |

Industrials - 12.8% | | | | | | | | |

Expeditors International of Washington, Inc. | | | 5,080 | | | | 194,310 | |

| | | | | | | | |

| | | Shares | | | Value | |

| | | | | | | | |

Honeywell International, Inc. | | | 3,700 | | | $ | 205,942 | |

Joy Global, Inc. | | | 3,070 | | | | 171,490 | |

Norfolk Southern Corp. | | | 3,040 | | | | 199,181 | |

PACCAR, Inc. | | | 4,750 | | | | 178,458 | |

Parker Hannifin Corp. | | | 1,560 | | | | 127,514 | |

Total Industrials | | | | | | | 1,076,895 | |

Information Technology - 31.4% | | | | | |

Accenture PLC, Class A | | | 3,040 | | | | 173,584 | |

Adobe Systems, Inc.* | | | 6,990 | | | | 217,039 | |

Apple, Inc.* | | | 310 | | | | 179,096 | |

Applied Materials, Inc. | | | 18,640 | | | | 192,551 | |

Autodesk, Inc.* | | | 5,550 | | | | 177,711 | |

Cisco Systems, Inc. | | | 3,510 | | | | 57,318 | |

Citrix Systems, Inc.* | | | 2,270 | | | | 165,892 | |

Google, Inc., Class A* | | | 460 | | | | 267,196 | |

Mastercard, Inc., Class A | | | 540 | | | | 219,515 | |

Paychex, Inc. | | | 7,200 | | | | 215,784 | |

QUALCOMM, Inc. | | | 4,310 | | | | 247,006 | |

Red Hat, Inc.* | | | 3,180 | | | | 163,388 | |

Teradata Corp.* | | | 2,390 | | | | 158,887 | |

VMware, Inc., Class A* | | | 2,270 | | | | 211,133 | |

Total Information Technology | | | | | | | 2,646,100 | |

Materials - 3.7% | | | | | | | | |

Freeport-McMoRan Copper & Gold, Inc., Class B | | | 5,580 | | | | 178,783 | |

Sherwin-Williams Co., The | | | 1,030 | | | | 133,529 | |

Total Materials | | | | | | | 312,312 | |

Total Common Stocks

(cost $8,273,101) | | | | | | | 8,372,068 | |

Other Investment Companies - 0.4%1 | | | | | | | | |

Dreyfus Cash Management Fund, Institutional Class Shares, 0.09%

(cost $38,884) | | | 38,884 | | | | 38,884 | |

Total Investments - 99.7%

(cost $8,311,985) | | | | | | | 8,410,952 | |

Other Assets, less Liabilities - 0.3% | | | | 22,200 | |

Net Assets - 100.0% | | | | | | $ | 8,433,152 | |

The accompanying notes are an integral part of these financial statements.

15

Managers Cadence Mid-Cap Fund

Investment Manager’s Comments

For the fiscal year ended May 31, 2012, the Managers Cadence Mid-Cap Fund (the “Fund”) returned (-7.96%) lagging its benchmark, the Russell MidCap® Growth Index, which returned (-6.31%).

Market Review

While we had some good news and periods of strong performance, the fiscal year ending May 31, 2012 started on a shaky note. After months of carefully planned financial stimulus and cautiously optimistic reports of a strengthening economy, even the Federal Reserve had to admit in Spring 2011 that the economic data was worse than expected. Not coincidentally, U.S. equity market benchmarks turned negative during the middle of 2011 before a sharp decline in late-Summer. The market volatility reflected growing concern over the Federal Reserve’s withdrawal of its Quantitative Easing policy (QE2), which was recently extended in June 2012, and questions over the U.S. economy’s ability to self-sustain without the cash infusion. Continued social unrest in the Middle East, decelerating growth in China, continued concerns over Eurozone sovereign debt and a potential collapse of the euro added to the fears. Even though the U.S. did not double-dip into a recession, the modest (+2%) growth rate continued to feel recessionary to many Americans.

Macroeconomic drivers returned to the forefront of the investment landscape in the fall of 2011, and the backdrop turned gloomy. The U.S. continued to face high unemployment, volatile commodity prices, a persistently weak housing sector and widening credit spreads, indicating market stress. Fiscal and political turmoil in Washington led to a U.S. debt downgrade, and expectations for growth in America were muted at best. Abroad, Eurozone countries continued to struggle through their financial crisis, while growth in China slowed and Greece hovered on the precipice of default.

Understandably, investors were nervous. In the fall of 2011, we saw many investors questioning their investment strategies, and even large institutions pulling out of stocks at potentially the worst time. Yet at the same time, counter-intuitively, we saw companies thriving across all sectors. We were able to make sound, well-priced investments in companies with strong revenues and earnings, high levels of productivity, and record cash on their balance sheets. While market downturns are often painful, they can provide compelling buying opportunities for long-term investors.

During October the market rebounded sharply. Some broad indexes were up over (+20%). Strong performance was driven by increased confidence about the U.S. recovery and that the Eurozone crisis would be resolved. The last two months of 2011 were relatively flat, but volatile, after the sharp October rebound. The first quarter of 2012 saw an acceleration of the upward trend. Most U.S. equity indexes were up another 15-20% before markets turned downward in April as Eurozone issues returned to the forefront. Additionally, U.S. economic data was less favorable and caused investors to, again, question the sustainability of the economic recovery. Investors were also concerned about slowing growth in China and if emerging market growth would be enough to overshadow major fiscal issues in developed nations. Markets fell 5-10% during the first two months of 2012.

Performance Review

The Fund generated a negative absolute return and lagged its benchmark during the trailing 12-month period. Several factors contributed to the underperformance. In particular, the Fund was hurt by an unfavorable investment environment, poor performance within the industrials sector and unfavorable portfolio positioning. During the trailing 12-month period, macro factors frequently dominated and fundamentals were often ignored. This often creates headwind for our fundamentally-based, growth-at-a-reasonable-price investment strategy. Correlations across stocks were often elevated and volatility indicators fluctuated with macro concerns. This creates a less favorable environment for fundamentally-based investment managers. We believe volatility creates good long-term investment opportunities, but the macro-environment was a headwind.

From an attribution perspective, stock selection within the industrials sector was the key detractor. The largest individual detractors were Gardner Denver, Inc. (-38.2%), SPX Corp. (-32.9%) and Joy Global, Inc. (-34.3%). In aggregate our industrials holdings returned (-10.8%), compared to (-3.7%) during the prior 12-months. Our information technology stocks also hurt relative returns. Bankrate, Inc. (-27.3%), Skyworks Solutions, Inc. (-18.6%) and Atmel Corp. (-35.0%) struggled the most. We subsequently liquidated Skyworks Solutions, Inc. and Atmel Corp., but continue to hold Bankrate, Inc. as of May 31, 2012.

Our investment process and quantitative screens have produced a tilt towards higher-beta stocks relative to the Index. This is primarily a bottom-up decision because these stocks have a more attractive combination of growth potential and valuations. Many “defensive” stocks appear overvalued relative to their history. Nevertheless, the highest-beta quintile of the Russell MidCap® Growth Index returned (-19.6%), compared to (+6.1%) for the lowest-beta quintile. The Fund had a slight overweight to higher-beta stocks and a slight underweight to lower-beta stocks. This tilt hurt relative results during the fiscal year. We continue to believe our patience will be rewarded as these stocks remain attractive. The Fund was also hurt by overweights to the energy and information technology sectors, which were the two worst performing sectors within the Index. Information technology stocks appear very attractively valued, especially relative to other investment alternatives and their valuation history.

The abovementioned detractors were partly offset by decent performance within the consumer staples sector. Monster Beverage Corp. (+102.7%) and Whole Foods Market, Inc. (+45.9%) were up significantly and notable positive contributors to relative results. Underweights to the financials and consumer discretionary sectors also made modesly positive contributions to relative returns.

Outlook

We believe the remainder of 2012 is likely to feature a slow-growth world and a slowly recovering market. We believe the Cadence portfolios should do well in this environment. The data shows that while cheapness tends to move stocks off their troughs, quality and dependability buoy companies in tough markets. This is because

16

Managers Cadence Mid-Cap Fund

Investment Manager’s Comments (continued)

when growth is perceived as scarce, investors tend to be skeptical and will therefore pay up for quality, growing companies. Our disciplined strategies thrived in a similar environment in 2004, as we transitioned away from the sharp initial upturn in 2003.

Overall, we have taken a balanced approach to investing in growth companies, including both secular and cyclical growers in the Fund. We have also remained true to our valuation discipline, buying growing companies at prices that make sense. Short-term our insistence on good value has been a headwind, but long-term it has served our investors well. We believe the Fund is comprised of high-quality companies purchased at reasonable prices.

In this environment, we feel patience is the key. With the market so distracted by macroeconomic events — and market swings a reaction to broad-based news rather than specific company fundamentals — bottom-up investors who pick each stock based on its individual merit must weather the storm. We continue to believe fundamentals matter and our disciplined investment process will be rewarded.

This commentary reflects the viewpoints of Cadence Capital Management, LLC as of May 31, 2012 and is not intended as a forecast or guarantee of future results.

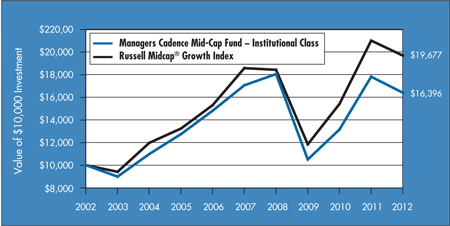

CUMULATIVE TOTAL RETURN PERFORMANCE

Managers Cadence Mid-Cap Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in Managers Cadence Mid-Cap Fund’s Institutional Class on May 31, 2002, compared to a $10,000 investment made in the Russell Midcap® Growth Index for the same time period. Performance for periods longer than one year is annualized. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Past performance is not indicative of future results. Total returns would have been lower had certain expenses not been reduced.

17

Managers Cadence Capital Appreciation Fund

Investment Manager’s Comments (continued)

CUMULATIVE TOTAL RETURN PERFORMANCE (continued)

The table below shows the average annual total returns for the Managers Cadence Mid-Cap Fund since inception through May 31, 2012, and the Russell Midcap® Growth Index for the same time periods.

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | Average Annual Total Returns1 | |

| | | | | One Year | | | Five Years | | | Ten Years | | | Since

Inception | | | Inception

Date | |

Managers Cadence Mid-Cap Fund 2,3,4,5,* | | | | | | | | | | | | | | | | | | | | |

Class A | | No Load | | | (8.33 | )% | | | (1.18 | )% | | | 4.65 | % | | | 6.25 | % | | | 01/13/1997 | |

Class A | | With Load | | | (13.59 | )% | | | (2.34 | )% | | | 4.03 | % | | | 5.84 | % | | | 01/13/1997 | |

Class B | | No Load | | | (9.02 | )% | | | (1.92 | )% | | | 3.86 | % | | | 5.46 | % | | | 01/13/1997 | |

Class B | | With Load | | | (13.57 | )% | | | (2.27 | )% | | | 3.86 | % | | | 5.46 | % | | | 01/13/1997 | |

Class C | | No Load | | | (8.97 | )% | | | (1.91 | )% | | | 3.87 | % | | | 5.46 | % | | | 01/13/1997 | |

Class C | | With Load | | | (9.88 | )% | | | (1.91 | )% | | | 3.87 | % | | | 5.46 | % | | | 01/13/1997 | |

Class D | | | | | (8.31 | )% | | | (1.18 | )% | | | 4.66 | % | | | 4.33 | % | | | 04/08/1998 | |

Institutional Class | | | | | (7.96 | )% | | | (0.78 | )% | | | 5.07 | % | | | 9.44 | % | | | 08/26/1991 | |

Administrative Class | | | | | (8.19 | )% | | | (1.02 | )% | | | 4.82 | % | | | 9.07 | % | | | 11/30/1994 | |

Class P | | | | | (8.06 | )% | | | — | | | | — | | | | 0.12 | % | | | 07/07/2008 | |

Class R | | | | | (8.57 | )% | | | (1.42 | )% | | | — | | | | 7.09 | % | | | 12/31/2002 | |

Russell Midcap® Growth Index6 | | | (6.31 | )% | | | 1.17 | % | | | 7.00 | % | | | — | 7 | | | 08/26/1991 | † |

The performance data shown represents past performance, which is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end please call (800) 835-3879 or visit our Web site at www.managersinvest.com.

Performance differences among the share classes are due to differences in sales charge structures and class expenses. Returns shown reflect maximum sales charge of 5.75% on Class A shares. Maximum sales charge on Class B Shares is 5.00% up to six years from the date of purchase. Class C shares held for less than one year are subject to a 1.00% contingent deferred sales charge (CDSC).

| | |

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For this and other information, please call 800.835.3879 or visit www.managersinvest.com for a free prospectus. Read it carefully before investing or sending money. Funds are distributed by Managers Distributors, Inc., a member of FINRA. † Date reflects inception date of the Fund, not the index. * The Fund changed its fiscal year end from June 30 to May 31 in 2011. 1 Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the Prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of May 31, 2012. All returns are in U.S. dollars ($). 2 From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. 3 The Fund invests in growth stocks, which may be more sensitive to market movements because their prices tend to reflect future investor expectations rather than just current profits. Growth stocks may underperform value stocks during given periods. |

| 4 | | The Fund is subject to risks associated with investments in mid-capitalization companies such as erratic earnings patterns, competitive conditions, limited earnings history, and a reliance on one or a limited number of products. |