UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

INVESTMENT COMPANIES

Investment Company Act file number: 811-04547

Exact name of registrant as specified in charter:

Voyageur Mutual Funds III

Voyageur Mutual Funds III

Address of principal executive offices:

2005 Market Street

Philadelphia, PA 19103

2005 Market Street

Philadelphia, PA 19103

Name and address of agent for service:

David F. Connor, Esq.

2005 Market Street

Philadelphia, PA 19103

David F. Connor, Esq.

2005 Market Street

Philadelphia, PA 19103

Registrant’s telephone number, including area code: (800) 523-1918

Date of fiscal year end: April 30

Date of reporting period: April 30, 2010

Item 1. Reports to Stockholders

Annual report Delaware Select Growth Fund April 30, 2010 Growth equity mutual fund |

This annual report is for the information of Delaware Select Growth Fund shareholders, but it may be used with prospective investors when preceded or accompanied by a current prospectus for Delaware Select Growth Fund. The figures in the annual report for Delaware Select Growth Fund represent past results, which are not a guarantee of future results. The return and principal value of an investment in the Fund will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. You should consider the investment objectives, risks, charges, and expenses of the Fund carefully before investing. The Delaware Select Growth Fund prospectus contains this and other important information about the Fund. Prospectuses for all open-end funds in the Delaware Investments® Family of Funds are available from your financial advisor, online at www.delawareinvestments.com, or by phone at 800 523-1918. Please read the prospectus carefully before you invest or send money. |

| You can obtain shareholder reports and prospectuses online instead of in the mail. Visit www.delawareinvestments.com/edelivery. |

Experience Delaware Investments

Delaware Investments is committed to the pursuit of consistently superior asset management and unparalleled client service. We believe in our investment processes, which seek to deliver consistent results, and in convenient services that help add value for our clients.

If you are interested in learning more about creating an investment plan, contact your financial advisor.

You can learn more about Delaware Investments or obtain a prospectus for Delaware Select Growth Fund at www.delawareinvestments.com.

Manage your investments online

- 24-hour access to your account information

- Obtain share prices

- Check your account balance and recent transactions

- Request statements or literature

- Make purchases and redemptions

On January 4, 2010, Delaware Management Holdings, Inc., and its subsidiaries (collectively known by the marketing name of Delaware Investments) were sold by a subsidiary of Lincoln National Corporation to Macquarie Group Limited, a global provider of banking, financial, advisory, investment and funds management services. Please see your Fund’s prospectus and any supplements thereto for more complete information.

Investments in Delaware Select Growth Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies (Macquarie Group), and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Fund, the repayment of capital from the Fund, or any particular rate of return.

| Table of contents | |

| Portfolio management review | 1 |

| Performance summary | 4 |

| Disclosure of Fund expenses | 7 |

| Sector allocation and top 10 holdings | 9 |

| Statement of net assets | 10 |

| Statement of operations | 14 |

| Statements of changes in net assets | 16 |

| Financial highlights | 18 |

| Notes to financial statements | 28 |

| Report of independent registered public accounting firm | 39 |

| Other Fund information | 40 |

| Board of trustees/directors and officers addendum | 50 |

| About the organization | 60 |

Unless otherwise noted, views expressed herein are current as of April 30, 2010, and are subject to change.

Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Fund’s distributor Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

© 2010 Delaware Management Holdings, Inc.

All third-party trademarks cited are the property of their respective owners.

| Portfolio management review | |

| Delaware Select Growth Fund | May 11, 2010 |

| Performance preview (for the period ended April 30, 2010) | ||||

| Delaware Select Growth Fund (Class A shares) | 1-year return | +48.20% | ||

| Russell 3000® Growth Index (benchmark) | 1-year return | +38.69% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Select Growth Fund please see the table on page 4.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

For complete, annualized performance for Delaware Select Growth Fund please see the table on page 4.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

What a difference a year makes. At the end of the Fund’s previous fiscal year (April 30, 2009), many investors did not know what to make of the equity market rally that began in the prior month. After all, the economy was still mired in recession and a stimulus package had recently been enacted; consumer activity was lackluster at best and unemployment figures continued to rise. Cautious optimism among investors, however, was supported in time by early signs of an economic recovery and helped stocks in the second calendar quarter of 2009, which became the best quarter for the S&P 500 Index since 1998. (Source: Bloomberg.) Please see page 6 for a description of the S&P 500 Index.

Previously down-and-out sectors like financials led the charge in the stock market. The technology sector also enjoyed a bit of a rebound as signs of a recovery prompted analysts to predict significant investment in information technology. Confidence seemed to return to corporate boardrooms, as initial public offerings and merger and acquisition proposals began to make some headlines. A “new and improved” General Motors emerged from bankruptcy protection in time to participate in the federal government’s cash-for-clunkers program, which took effect in August 2009 and increased auto sales nationally.

Given the severity of the recent recession, however, plenty of concerns remained throughout the Fund’s fiscal year. While employment data trends improved, unemployment remained high as many companies were hesitant to add new employees; the U.S. housing rebound in the second half of the year remained muted at best, despite government incentives; and a European debt crisis, in which the European Union and International Monetary Fund bailed out Greece, rattled stock markets in April 2010 and threatened the nascent global economic recovery. (Source: Bloomberg.)

Within the Fund

For its fiscal year ended April 30, 2010, Delaware Select Growth Fund (Class A shares) returned +48.20% at net asset value and +39.68% at maximum offer price (both figures reflect all distributions reinvested). The Fund outperformed its benchmark, the Russell 3000 Growth Index, which advanced +38.69% for the same period. For the complete annualized performance of Delaware Select Growth Fund, please see the table on page 4.

1

Portfolio management review

Delaware Select Growth Fund

Delaware Select Growth Fund

It was another year in which macroeconomic and geopolitical factors greatly affected the markets. Despite the occasionally volatile macroeconomic environment, our stock selection process remained bottom-up. Rather than turn defensive or try to position the Fund to benefit from a turn in the economy, we held true to our philosophy and continued to seek what we viewed as high-quality companies with good competitive positions that we believed could outperform the benchmark index regardless of the market cycle.

Apple was the Fund’s largest holding, and its stock price more than doubled during the 12-month period. While the iPhone exceeded all expectations in terms of sales and profitability, its popularity also drove successes for some of the company’s traditional product lines, such as Mac desktops and laptops. Additionally, the recently launched iPad sold more than one million units in its initial month and helped push Apple’s stock price to an all-time high.

Netflix was another significant holding. The company continued growing its subscriber base and dominating its market for mail-order DVDs and online movie and television packages. Its management team also had the foresight to recognize the evolution of the digital content market and has forged distribution partnerships with manufacturers of televisions, DVD players, and game consoles, and with other relevant industry leaders like Microsoft.

During the fiscal year, Heartland Payment Systems advanced more than 120%. Heartland has continued to deliver solid operating performance after overcoming a high-profile security breach last year that interrupted its growth trajectory. The company agreed to a settlement with Visa regarding that breach, which seemed to further ease investors’ minds on that particular issue. We wrote about these circumstances in this space last year, expressing our confidence in the company’s ability to resolve the issues.

Detractors from performance included biotech company Gilead Sciences, which in December 2009 received news of a failed clinical trial involving a potential cardiovascular treatment. While some investors worried about Gilead’s existing drug pipeline and prospects for future growth, we chose to hang on to the stock and remain confident in the company’s leading competitive position within the field of HIV care and prevention.

Weight Watchers International appeared to continue to frustrate many investors. The diet plan specialist rose to a 52-week high in February 2010 as it enhanced its profitable food licensing and online operations. However, a poor earnings report did not sit well with investors. While we have generally been pleased with the company’s ability to shift its revenue mix toward licensing and online product offerings — both of which carry high margins and recurring revenues — we have been concerned with the lack of improvement in its core meeting attendance business. We believe the lack of growth in this core business is mostly attributable to the economic environment, and continue to hold what we believe to be a cash-generative and attractively valued company.

Finally, athenahealth posted disappointing performance toward the end of the fiscal period. In late February 2010, the company delayed its earnings release and ultimately restated earnings from a prior period. While the

2

restatement was relatively small, the incident created enough investor uncertainty to cause a selloff in the stock. We remain confident, however, that the company’s medical billing solution can help it continue to increase market share.

Among financial stocks, we have long advocated investing in transaction-oriented companies as opposed to institutions that operate businesses dependent on interest rate “spreads” (such as most banks, for instance). Two exchanges, IntercontinentalExchange and CME Group, have been core holdings in the Fund. We believe investors tended to associate the companies with other financials during the market downturn, despite having very different business models. During the Fund’s fiscal year, both companies benefited from increased trading volume as the markets began to rebound. Some investors became concerned as the government looked to tighten regulations on derivatives markets, though others view both companies as integral players in the future evolution and transparency of these markets. For the 12-month period, both stocks were solid performers.

Cautious optimism

Many investors are now wondering if the equity market has come too far, too fast. In our view, the magnitude and duration of the equity market rally of the last year may be based more on expectations for continued improvement than on current fundamentals. At some point, corporate earnings must reflect meaningful revenue growth and not just prior cost cutting. Additionally, much of the economic recovery has been the result of government intervention. We believe that, as these stimulus measures wind down, the markets must prove they can thrive without ongoing fiscal assistance. Our sense is that equity investors may become impatient or disappointed with inconsistent economic data if there isn’t a return to meaningful revenue growth across the economy.

Regardless of the economic outlook, we remain consistent in our long-term investment philosophy: We want to own strong secular-growth companies with solid business models and competitive positions that we believe can grow market share and deliver shareholder value in a variety of market environments.

3

| Performance summary | |

| Delaware Select Growth Fund | April 30, 2010 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our Web site at www.delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

You should consider the investment objectives, risks, charges, and expenses of the investment company carefully before investing. The Delaware Select Growth Fund prospectus contains this and other important information about the investment company. Please request a prospectus through your financial advisor or by calling 800 523-1918 or visiting our Web site at www.delawareinvestments.com. Read the prospectus carefully before you invest or send money.

| Fund performance | Average annual total returns through April 30, 2010 | ||||||

| 1 year | 5 years | 10 years | Lifetime | ||||

| Class A (Est. March 16, 1994) | |||||||

| Excluding sales charge | +48.20% | +6.43% | -2.60% | +9.27% | |||

| Including sales charge | +39.68% | +5.17% | -3.17% | +8.87% | |||

| Class B (Est. April 16, 1996) | |||||||

| Excluding sales charge | +47.12% | +5.63% | -3.19% | +8.38% | |||

| Including sales charge | +43.12% | +5.26% | -3.19% | +8.38% | |||

| Class C (Est. May 20, 1994) | |||||||

| Excluding sales charge | +47.15% | +5.63% | -3.33% | +8.45% | |||

| Including sales charge | +46.15% | +5.63% | -3.33% | +8.45% | |||

| Class R (Est. June 2, 2003) | |||||||

| Excluding sales charge | +47.87% | +6.15% | n/a | +5.84% | |||

| Including sales charge | +47.87% | +6.15% | n/a | +5.84% | |||

| Institutional Class (Est. Aug. 28, 1997) | |||||||

| Excluding sales charge | +48.59% | +6.70% | -2.36% | +9.49% | |||

| Including sales charge | +48.59% | +6.70% | -2.36% | +9.49% | |||

Returns reflect the reinvestment of all distributions and any applicable sales charges as noted in the following paragraphs.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Expense limitations were in effect for certain classes during the periods shown in the “Fund performance” chart and in the “Performance of a $10,000 investment” chart. The current expenses for each class are listed on the “Fund expense ratios” chart. (Note that all charts and graphs referred to in the “Performance summary” section of this report are found on pages 4 through 6.) Performance would have been lower had the expense limitations not been in effect.

4

The Fund offers Class A, B, C, R, and Institutional Class shares.

Class A shares are sold with a maximum front-end sales charge of up to 5.75%, and have an annual distribution and service fee of up to 0.25% of average daily net assets.

Class B shares may only be purchased through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B purchase and sales charges. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held.

Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets.

Ten-year and lifetime performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of up to 1.00% of average daily net assets.

Class R shares were first made available June 2, 2003, and are available only for certain retirement plan products. They are sold without a sales charge and have an annual distribution and service fee of up to 0.60% of average daily net assets, which has been limited contractually to 0.50% from Sept. 1, 2009, through Aug. 31, 2010.

Institutional Class shares were first made available Aug. 28, 1997, and are available without sales or asset-based distribution charges only to certain eligible institutional accounts.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Instances of high double-digit returns are unusual, cannot be sustained, and were primarily achieved during favorable market conditions.

The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” chart. Delaware Investments has agreed to (1) voluntarily waive all or a portion of its investment advisory fees and/or reimburse certain expenses (excluding certain expenses) to prevent total annual fund operating expenses from exceeding 1.25% of the Fund’s average daily net assets from Sept. 1, 2009, until the voluntary cap is discontinued; and (2) contractually limit the Class R shares distribution and service fees from Sept. 1, 2009, through Aug. 31, 2010, to 0.50%. Please see the most recent prospectus or supplements thereto for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | Class A | Class B | Class C | Class R | Institutional Class | |||||

| Total annual operating expenses | 1.85% | 2.60% | 2.60% | 2.20% | 1.60% | |||||

| (without fee waivers) | ||||||||||

| Net expenses | 1.50% | 2.25% | 2.25% | 1.75% | 1.25% | |||||

| (including fee waivers, if any) | ||||||||||

| Type of waiver | Voluntary | Voluntary | Voluntary | Voluntary | Voluntary | |||||

| and contractual | ||||||||||

5

Performance summary

Delaware Select Growth Fund

Delaware Select Growth Fund

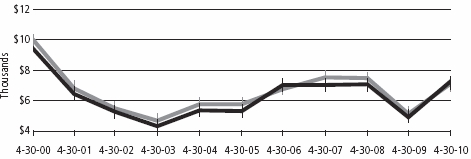

Performance of a $10,000 Investment

Average annual total returns from April 30, 2000, through April 30, 2010

| For period beginning April 30, 2000, through April 30, 2010 | Starting value | Ending value | ||

| Delaware Select Growth Fund — Class A Shares | $9,425 | $7,243 | ||

| Russell 3000 Growth Index | $10,000 | $7,098 | ||

The chart assumes $10,000 invested in the Fund on April 30, 2000, and includes the effect of a 5.75% front-end sales charge and the reinvestment of all distributions. Please note additional details on these fees in the “Performance summary” section of this report, which includes pages 4 through 6.

The chart also assumes $10,000 invested in the Russell 3000 Growth Index as of April 30, 2000.

The Russell 3000 Growth Index measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 3000 companies with higher price-to-book ratios and higher forecasted growth values.

The S&P 500 Index, mentioned on page 1, measures the performance of 500 mostly large-cap stocks weighted by market value, and is often used to represent performance of the U.S. stock market.

An index is unmanaged and does not reflect the costs of operating a mutual fund, such as the costs of buying, selling, and holding securities. You cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

The “Fund performance” chart and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares.

| Stock symbols and CUSIP numbers | |||||||

| Nasdaq symbols | CUSIPs | ||||||

| Class A | DVEAX | 928931104 | |||||

| Class B | DVEBX | 928931849 | |||||

| Class C | DVECX | 928931203 | |||||

| Class R | DFSRX | 928931740 | |||||

| Institutional Class | VAGGX | 928931757 | |||||

6

Disclosure of Fund expenses

For the period November 1, 2009 to April 30, 2010

For the period November 1, 2009 to April 30, 2010

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from November 1, 2009 to April 30, 2010.

Actual expenses

The first section of the table shown, “Actual Fund return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second section of the table shown, “Hypothetical 5% return,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The Fund’s expenses shown in the table reflect fee waivers in effect.

7

Disclosure of Fund expenses

Delaware Select Growth Fund

Expense analysis of an investment of $1,000

Expense analysis of an investment of $1,000

| Beginning | Ending | Expenses | ||||||||||||

| Account Value | Account Value | Annualized | Paid During Period | |||||||||||

| 11/1/09 | 4/30/10 | Expense Ratio | 11/1/09 to 4/30/10* | |||||||||||

| Actual Fund return | ||||||||||||||

| Class A | $1,000.00 | $1,202.70 | 1.50% | $ | 8.19 | |||||||||

| Class B | 1,000.00 | 1,197.90 | 2.25% | 12.26 | ||||||||||

| Class C | 1,000.00 | 1,198.10 | 2.25% | 12.26 | ||||||||||

| Class R | 1,000.00 | 1,201.00 | 1.75% | 9.55 | ||||||||||

| Institutional Class | 1,000.00 | 1,204.20 | 1.25% | 6.83 | ||||||||||

| Hypothetical 5% return (5% return before expenses) | ||||||||||||||

| Class A | $1,000.00 | $1,017.36 | 1.50% | $ | 7.50 | |||||||||

| Class B | 1,000.00 | 1,013.64 | 2.25% | 11.23 | ||||||||||

| Class C | 1,000.00 | 1,013.64 | 2.25% | 11.23 | ||||||||||

| Class R | 1,000.00 | 1,016.12 | 1.75% | 8.75 | ||||||||||

| Institutional Class | 1,000.00 | 1,018.60 | 1.25% | 6.26 | ||||||||||

*“Expenses Paid During Period” are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

8

| Sector allocation and top 10 holdings | |

| Delaware Select Growth Fund | As of April 30, 2010 |

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications, which may result in the sector designations for one fund being different than another fund’s sector designations.

| Sector | Percentage of net assets | |

| Common Stock² | 96.80 | % |

| Consumer Discretionary | 17.54 | % |

| Consumer Staples | 5.11 | % |

| Energy | 4.92 | % |

| Financial Services | 15.63 | % |

| Health Care | 19.03 | % |

| Materials & Processing | 4.68 | % |

| Producer Durables | 0.65 | % |

| Technology | 27.91 | % |

| Utilities | 1.33 | % |

| Discount Note | 3.92 | % |

| Securities Lending Collateral | 19.10 | % |

| Total Value of Securities | 119.82 | % |

| Obligation to Return Securities Lending Collateral | (19.50 | %) |

| Liabilities Net of Receivables and Other Assets | (0.32 | %) |

| Total Net Assets | 100.00 | % |

²Narrow industries are utilized for compliance purposes for diversification whereas broad sectors are used for financial reporting.

Holdings are for informational purposes only and are subject to change at any time. They are not a recommendation to buy, sell, or hold any security.

| Top 10 holdings | Percentage of net assets | |

| Apple | 7.88 | % |

| Peet’s Coffee & Tea | 4.20 | % |

| Allergan | 3.49 | % |

| Gilead Sciences | 3.39 | % |

| IntercontinentalExchange | 3.36 | % |

| NetFlix | 3.23 | % |

| VeriSign | 3.07 | % |

| Perrigo | 3.05 | % |

| CME Group | 2.92 | % |

| EOG Resources | 2.81 | % |

9

| Statement of net assets | |

| Delaware Select Growth Fund | April 30, 2010 |

| Number of shares | Value | ||||

| Common Stock – 96.80%² | |||||

| Consumer Discretionary – 17.54% | |||||

| † | DineEquity | 41,200 | $ | 1,694,556 | |

| † | eBay | 22,200 | 528,582 | ||

| ± | Intertek Group | 64,534 | 1,466,367 | ||

| † | Interval Leisure Group | 237,500 | 3,512,625 | ||

| Lowe’s | 239,900 | 6,506,088 | |||

| Natura Cosmeticos | 246,800 | 5,240,639 | |||

| *† | NetFlix | 81,500 | 8,049,755 | ||

| NIKE Class B | 23,000 | 1,745,930 | |||

| *† | priceline.com | 26,625 | 6,977,081 | ||

| * | Ritchie Bros Auctioneers | 90,000 | 2,106,000 | ||

| * | Staples | 55,200 | 1,298,856 | ||

| * | Strayer Education | 5,100 | 1,239,912 | ||

| * | Weight Watchers International | 124,800 | 3,315,936 | ||

| 43,682,327 | |||||

| Consumer Staples – 5.11% | |||||

| *† | Peet’s Coffee & Tea | 264,000 | 10,459,680 | ||

| *† | Whole Foods Market | 58,300 | 2,274,866 | ||

| 12,734,546 | |||||

| Energy – 4.92% | |||||

| * | Core Laboratories | 35,000 | 5,246,150 | ||

| * | EOG Resources | 62,375 | 6,993,485 | ||

| 12,239,635 | |||||

| Financial Services – 15.63% | |||||

| † | Affiliated Managers Group | 31,000 | 2,609,580 | ||

| Bank of New York Mellon | 103,781 | 3,230,703 | |||

| *† | CB Richard Ellis Group Class A | 175,200 | 3,034,464 | ||

| CME Group | 22,150 | 7,274,282 | |||

| * | Heartland Payment Systems | 158,300 | 2,909,554 | ||

| † | IntercontinentalExchange | 71,825 | 8,376,949 | ||

| * | MasterCard Class A | 17,950 | 4,452,318 | ||

| † | optionsXpress Holdings | 147,100 | 2,611,025 | ||

| Schwab (Charles) | 16,700 | 322,143 | |||

| * | Visa Class A | 45,300 | 4,087,419 | ||

| 38,908,437 | |||||

| Health Care – 19.03% | |||||

| *† | ABIOMED | 129,100 | 1,244,524 | ||

| Allergan | 136,500 | 8,693,684 | |||

| *† | athenahealth | 159,700 | 4,634,494 | ||

10

| Number of shares | Value | |||||

| Common Stock (continued) | ||||||

| Health Care (continued) | ||||||

| † | Gilead Sciences | 212,650 | $ | 8,435,826 | ||

| † | Medco Health Solutions | 110,250 | 6,495,930 | |||

| Novo Nordisk ADR | 74,900 | 6,149,290 | ||||

| * | Perrigo | 124,558 | 7,601,775 | |||

| Techne | 21,100 | 1,397,875 | ||||

| UnitedHealth Group | 90,100 | 2,730,931 | ||||

| 47,384,329 | ||||||

| Materials & Processing – 4.68% | ||||||

| * | BHP Billiton ADR | 17,650 | 1,284,744 | |||

| Monsanto | 29,700 | 1,872,882 | ||||

| * | Newmont Mining | 40,700 | 2,282,456 | |||

| * | Praxair | 12,000 | 1,005,240 | |||

| Syngenta ADR | 102,850 | 5,194,953 | ||||

| 11,640,275 | ||||||

| Producer Durables – 0.65% | ||||||

| * | Expeditors International Washington | 36,400 | 1,482,936 | |||

| ±† | Hansen Transmissions International | 88,206 | 135,207 | |||

| 1,618,143 | ||||||

| Technology – 27.91% | ||||||

| † | Adobe Systems | 115,200 | 3,869,568 | |||

| † | Apple | 75,125 | 19,616,640 | |||

| *† | Crown Castle International | 181,100 | 6,854,635 | |||

| † | Google Class A | 8,265 | 4,342,762 | |||

| † | Intuit | 131,800 | 4,765,888 | |||

| QUALCOMM | 144,500 | 5,597,930 | ||||

| † | Research in Motion | 27,000 | 1,922,130 | |||

| *† | SBA Communications Class A | 98,800 | 3,494,556 | |||

| *† | Sybase | 32,980 | 1,430,672 | |||

| † | Symantec | 120,600 | 2,022,462 | |||

| † | Teradata | 108,900 | 3,165,723 | |||

| *† | VeriFone Holdings | 249,732 | 4,752,400 | |||

| * | VeriSign | 280,550 | 7,650,599 | |||

| 69,485,965 | ||||||

| Utilities – 1.33% | ||||||

| *† | j2 Global Communications | 137,800 | 3,318,224 | |||

| 3,318,224 | ||||||

| Total Common Stock (cost $190,045,754) | 241,011,881 | |||||

11

Statement of net assets

Delaware Select Growth Fund

Delaware Select Growth Fund

| Principal amount | Value | |||||

| ≠Discount Note – 3.92% | ||||||

| Federal Home Loan Bank 0.06% 5/3/10 | $ | 9,755,058 | $ | 9,755,025 | ||

| Total Discount Note (cost $9,755,025) | 9,755,025 | |||||

| Total Value of Securities Before Securities | ||||||

| Lending Collateral – 100.72% (cost $199,800,779) | 250,766,906 | |||||

| Number of shares | ||||||

| Securities Lending Collateral** – 19.10% | ||||||

| Investment Companies | ||||||

| Mellon GSL DBT II Collateral Fund | 43,060,659 | 43,060,659 | ||||

| BNY Mellon SL DBT II Liquidating Fund | 4,511,427 | 4,461,801 | ||||

| @†Mellon GSL Reinvestment Trust II | 988,494 | 42,011 | ||||

| Total Securities Lending Collateral (cost $48,560,580) | 47,564,471 | |||||

| Total Value of Securities – 119.82% | ||||||

| (cost $248,361,359) | 298,331,377 | © | ||||

| Obligation to Return Securities | ||||||

| Lending Collateral** – (19.50%) | (48,560,580 | ) | ||||

| Liabilities Net of Receivables | ||||||

| and Other Assets – (0.32%) | (783,039 | ) | ||||

| Net Assets Applicable to 9,063,906 | ||||||

| Shares Outstanding – 100.00% | $ | 248,987,758 | ||||

| Net Asset Value – Delaware Select Growth Fund | ||||||

| Class A ($150,016,139 / 5,367,410 Shares) | $27.95 | |||||

| Net Asset Value – Delaware Select Growth Fund | ||||||

| Class B ($15,011,424 / 606,240 Shares) | $24.76 | |||||

| Net Asset Value – Delaware Select Growth Fund | ||||||

| Class C ($29,502,208 / 1,204,407 Shares) | $24.50 | |||||

| Net Asset Value – Delaware Select Growth Fund | ||||||

| Class R ($806,850 / 29,413 Shares) | $27.43 | |||||

| Net Asset Value – Delaware Select Growth Fund | ||||||

| Institutional Class ($53,651,137 / 1,856,436 Shares) | $28.90 | |||||

12

| Components of Net Assets at April 30, 2010: | |||

| Shares of beneficial interest (unlimited authorization – no par) | $ | 434,803,880 | |

| Accumulated net investment loss | (92,972 | ) | |

| Accumulated net realized loss on investments | (235,692,708 | ) | |

| Net unrealized appreciation of investments | |||

| and foreign currencies | 49,969,558 | ||

| Total net assets | $ | 248,987,758 |

| ² | Narrow industries are utilized for compliance purposes for diversification whereas broad sectors are used for financial reporting. |

| † | Non income producing security. |

| © | Includes $48,081,040 of securities loaned. |

| * | Fully or partially on loan. |

| ** | See Note 9 in “Notes to financial statements.” |

| ≠ | The rate shown is the effective yield at the time of purchase. |

| ± | Security is being valued based on international fair value pricing. At April 30, 2010, the aggregate amount of international fair value priced securities was $1,601,574, which represented 0.64% of the Fund’s net assets. See Note 1 in “Notes to financial statements.” |

| @ | Illiquid security. At April 30, 2010, the aggregate amount of illiquid securities was $42,011, which represented 0.02% of the Fund’s net assets. See Note 10 in “Notes to financial statements.” |

ADR — American Depositary Receipts

| Net Asset Value and Offering Price Per Share – | ||

| Delaware Select Growth Fund | ||

| Net asset value Class A (A) | $ | 27.95 |

| Sales charges (5.75% of offering price) (B) | 1.71 | |

| Offering price | $ | 29.66 |

| (A) | Net asset value per share, as illustrated, is the amount which would be paid upon redemption or repurchase of shares. |

| (B) | See the current prospectus for purchase of $50,000 or more. |

See accompanying notes

13

| Statement of operations | |

| Delaware Select Growth Fund | Year Ended April 30, 2010 |

| Investment Income: | ||||||||

| Dividends | $ | 1,457,560 | ||||||

| Securities lending income | 166,045 | |||||||

| Interest | 6,600 | |||||||

| Foreign tax withheld | (51,833 | ) | $ | 1,578,372 | ||||

| Expenses: | ||||||||

| Management fees | 1,940,968 | |||||||

| Dividend disbursing and transfer agent fees and expenses | 1,455,239 | |||||||

| Distribution expenses – Class A | 329,600 | |||||||

| Distribution expenses – Class B | 172,859 | |||||||

| Distribution expenses – Class C | 267,797 | |||||||

| Distribution expenses – Class R | 4,648 | |||||||

| Reports and statements to shareholders | 120,433 | |||||||

| Accounting and administration expenses | 103,275 | |||||||

| Registration fees | 68,730 | |||||||

| Legal fees | 58,800 | |||||||

| Audit and tax | 25,522 | |||||||

| Trustees’ fees | 15,626 | |||||||

| Custodian fees | 14,053 | |||||||

| Insurance fees | 5,317 | |||||||

| Pricing fees | 4,579 | |||||||

| Dues and services | 4,253 | |||||||

| Consulting fees | 2,877 | |||||||

| Trustees’ expenses | 1,086 | 4,595,662 | ||||||

| Less fees waived | (586,536 | ) | ||||||

| Less waived distribution expenses – Class R | (774 | ) | ||||||

| Total operating expenses | 4,008,352 | |||||||

| Net Investment Loss | (2,429,980 | ) |

14

| Net Realized and Unrealized Gain (Loss) on Investments | |||

| and Foreign Currencies: | |||

| Net realized gain (loss) on: | |||

| Investments | $ | 38,970,785 | |

| Foreign currencies | (187,327 | ) | |

| Net realized gain | 38,783,458 | ||

| Net change in unrealized appreciation/depreciation of | |||

| investments and foreign currencies | 63,092,292 | ||

| Net Realized and Unrealized Gain on Investments | |||

| and Foreign Currencies | 101,875,750 | ||

| Net Increase in Net Assets Resulting from Operations | $ | 99,445,770 |

See accompanying notes

15

Statements of changes in net assets

Delaware Select Growth Fund

Delaware Select Growth Fund

| Year Ended | ||||||||

| 4/30/10 | 4/30/09 | |||||||

| Increase (Decrease) in Net Assets from Operations: | ||||||||

| Net investment loss | $ | (2,429,980 | ) | $ | (835,340 | ) | ||

| Net realized gain (loss) on investments and | ||||||||

| foreign currencies | 38,783,458 | (68,399,378 | ) | |||||

| Net change in unrealized appreciation/depreciation | ||||||||

| of investments and foreign currencies | 63,092,292 | (22,025,813 | ) | |||||

| Net increase (decrease) in net assets resulting | ||||||||

| from operations | 99,445,770 | (91,260,531 | ) | |||||

| Capital Share Transactions: | ||||||||

| Proceeds from shares sold: | ||||||||

| Class A | 18,629,185 | 33,119,294 | ||||||

| Class B | 206,648 | 344,304 | ||||||

| Class C | 1,799,685 | 1,986,293 | ||||||

| Class R | 252,368 | 96,447 | ||||||

| Institutional Class | 90,342,397 | 39,439,327 | ||||||

| 111,230,283 | 74,985,665 | |||||||

| Cost of shares repurchased: | ||||||||

| Class A | (26,291,216 | ) | (31,669,576 | ) | ||||

| Class B | (11,280,764 | ) | (31,483,335 | ) | ||||

| Class C | (5,500,832 | ) | (10,282,576 | ) | ||||

| Class R | (405,510 | ) | (283,229 | ) | ||||

| Institutional Class | (113,200,890 | ) | (12,042,543 | ) | ||||

| (156,679,212 | ) | (85,761,259 | ) | |||||

| Decrease in net assets derived from capital | ||||||||

| share transactions | (45,448,929 | ) | (10,775,594 | ) | ||||

| Net Increase (Decrease) in Net Assets | 53,996,841 | (102,036,125 | ) | |||||

| Net Assets: | ||||||||

| Beginning of year | 194,990,917 | 297,027,042 | ||||||

| End of year (including accumulated net investment | ||||||||

| loss of $92,972 and $38,325 respectively) | $ | 248,987,758 | $ | 194,990,917 | ||||

See accompanying notes

16

Financial highlights

Delaware Select Growth Fund Class A

Delaware Select Growth Fund Class A

Selected data for each share of the Fund outstanding throughout each period were as follows:

| Net asset value, beginning of period |

| Income (loss) from investment operations: |

| Net investment loss1 |

| Net realized and unrealized gain (loss) on investments and foreign currencies |

| Total from investment operations |

| Net asset value, end of period |

| Total return2 |

| Ratios and supplemental data: |

| Net assets, end of period (000 omitted) |

| Ratio of expenses to average net assets |

| Ratio of expenses to average net assets |

| prior to fees waived and expense paid indirectly |

| Ratio of net investment loss to average net assets |

| Ratio of net investment loss to average net assets |

| prior to fees waived and expense paid indirectly |

| Portfolio turnover |

1 The average shares outstanding method has been applied for per share information.

2 Total investment return is based on the change in net asset value of a share during the period and assumes reinvestment of dividends and distributions at net asset value and does not reflect the impact of a sales charge. Total investment return during all periods shown reflects a waiver by the manager. Performance would have been lower had the waiver not been in effect.

See accompanying notes

18

| Year Ended | ||||||||||||||||

| 4/30/10 | 4/30/09 | 4/30/08 | 4/30/07 | 4/30/06 | ||||||||||||

| $18.860 | $27.300 | $27.110 | $27.180 | $20.470 | ||||||||||||

| (0.209 | ) | (0.041 | ) | (0.119 | ) | (0.193 | ) | (0.086 | ) | |||||||

| 9.299 | (8.399 | ) | 0.309 | 0.123 | 6.796 | |||||||||||

| 9.090 | (8.440 | ) | 0.190 | (0.070 | ) | 6.710 | ||||||||||

| $27.950 | $18.860 | $27.300 | $27.110 | $27.180 | ||||||||||||

| 48.20% | (30.92% | ) | 0.70% | (0.26% | ) | 32.78% | ||||||||||

| $150,016 | $106,919 | $157,366 | $160,170 | $187,319 | ||||||||||||

| 1.50% | 1.49% | 1.48% | 1.50% | 1.55% | ||||||||||||

| 1.73% | 1.85% | 1.62% | 1.64% | 1.70% | ||||||||||||

| (0.89% | ) | (0.20% | ) | (0.42% | ) | (0.77% | ) | (0.35% | ) | |||||||

| (1.12% | ) | (0.56% | ) | (0.56% | ) | (0.91% | ) | (0.50% | ) | |||||||

| 49% | 66% | 61% | 51% | 124% | ||||||||||||

19

Financial highlights

Delaware Select Growth Fund Class B

Delaware Select Growth Fund Class B

Selected data for each share of the Fund outstanding throughout each period were as follows:

| Net asset value, beginning of period |

| Income (loss) from investment operations: |

| Net investment loss1 |

| Net realized and unrealized gain (loss) on investments and foreign currencies |

| Total from investment operations |

| Net asset value, end of period |

| Total return2 |

| Ratios and supplemental data: |

| Net assets, end of period (000 omitted) |

| Ratio of expenses to average net assets |

| Ratio of expenses to average net assets |

| prior to fees waived and expense paid indirectly |

| Ratio of net investment loss to average net assets |

| Ratio of net investment loss to average net assets |

| prior to fees waived and expense paid indirectly |

| Portfolio turnover |

1 The average shares outstanding method has been applied for per share information.

2 Total investment return is based on the change in net asset value of a share during the period and assumes reinvestment of dividends and distributions at net asset value and does not reflect the impact of a sales charge. Total investment return during all periods shown reflects a waiver by the manager. Performance would have been lower had the waiver not been in effect.

See accompanying notes

20

| Year Ended | ||||||||||||||||

| 4/30/10 | 4/30/09 | 4/30/08 | 4/30/07 | 4/30/06 | ||||||||||||

| $16.830 | $24.550 | $24.560 | $24.810 | $18.820 | ||||||||||||

| (0.355 | ) | (0.182 | ) | (0.304 | ) | (0.365 | ) | (0.252 | ) | |||||||

| 8.285 | (7.538 | ) | 0.294 | 0.115 | 6.242 | |||||||||||

| 7.930 | (7.720 | ) | (0.010 | ) | (0.250 | ) | 5.990 | |||||||||

| $24.760 | $16.830 | $24.550 | $24.560 | $24.810 | ||||||||||||

| 47.12% | (31.45% | ) | (0.04% | ) | (1.01% | ) | 31.83% | |||||||||

| $15,012 | $19,222 | $67,344 | $126,866 | $199,863 | ||||||||||||

| 2.25% | 2.24% | 2.23% | 2.25% | 2.30% | ||||||||||||

| 2.48% | 2.60% | 2.37% | 2.39% | 2.45% | ||||||||||||

| (1.64% | ) | (0.95% | ) | (1.17% | ) | (1.52% | ) | (1.10% | ) | |||||||

| (1.87% | ) | (1.31% | ) | (1.31% | ) | (1.66% | ) | (1.25% | ) | |||||||

| 49% | 66% | 61% | 51% | 124% | ||||||||||||

21

Financial highlights

Delaware Select Growth Fund Class C

Delaware Select Growth Fund Class C

Selected data for each share of the Fund outstanding throughout each period were as follows:

| Net asset value, beginning of period |

| Income (loss) from investment operations: |

| Net investment loss1 |

| Net realized and unrealized gain (loss) on investments and foreign currencies |

| Total from investment operations |

| Net asset value, end of period |

| Total return2 |

| Ratios and supplemental data: |

| Net assets, end of period (000 omitted) |

| Ratio of expenses to average net assets |

| Ratio of expenses to average net assets |

| prior to fees waived and expense paid indirectly |

| Ratio of net investment loss to average net assets |

| Ratio of net investment loss to average net assets |

| prior to fees waived and expense paid indirectly |

| Portfolio turnover |

1 The average shares outstanding method has been applied for per share information.

2 Total investment return is based on the change in net asset value of a share during the period and assumes reinvestment of dividends and distributions at net asset value and does not reflect the impact of a sales charge. Total investment return during all periods shown reflects a waiver by the manager. Performance would have been lower had the waiver not been in effect.

See accompanying notes

22

| Year Ended | ||||||||||||||||

| 4/30/10 | 4/30/09 | 4/30/08 | 4/30/07 | 4/30/06 | ||||||||||||

| $16.650 | $24.290 | $24.300 | $24.540 | $18.620 | ||||||||||||

| (0.357 | ) | (0.173 | ) | (0.302 | ) | (0.362 | ) | (0.251 | ) | |||||||

| 8.207 | (7.467 | ) | 0.292 | 0.122 | 6.171 | |||||||||||

| 7.850 | (7.640 | ) | (0.010 | ) | (0.240 | ) | 5.920 | |||||||||

| $24.500 | $16.650 | $24.290 | $24.300 | $24.540 | ||||||||||||

| 47.15% | (31.45% | ) | (0.04% | ) | (0.98% | ) | 31.79% | |||||||||

| $29,502 | $23,030 | $44,972 | $59,271 | $84,458 | ||||||||||||

| 2.25% | 2.24% | 2.23% | 2.25% | 2.30% | ||||||||||||

| 2.48% | 2.60% | 2.37% | 2.39% | 2.45% | ||||||||||||

| (1.64% | ) | (0.95% | ) | (1.17% | ) | (1.52% | ) | (1.10% | ) | |||||||

| (1.87% | ) | (1.31% | ) | (1.31% | ) | (1.66% | ) | (1.25% | ) | |||||||

| 49% | 66% | 61% | 51% | 124% | ||||||||||||

23

Financial highlights

Delaware Select Growth Fund Class R

Delaware Select Growth Fund Class R

Selected data for each share of the Fund outstanding throughout each period were as follows:

| Net asset value, beginning of period |

| Income (loss) from investment operations: |

| Net investment loss1 |

| Net realized and unrealized gain (loss) on investments and foreign currencies |

| Total from investment operations |

| Net asset value, end of period |

| Total return2 |

| Ratios and supplemental data: |

| Net assets, end of period (000 omitted) |

| Ratio of expenses to average net assets |

| Ratio of expenses to average net assets |

| prior to fees waived and expense paid indirectly |

| Ratio of net investment loss to average net assets |

| Ratio of net investment loss to average net assets |

| prior to fees waived and expense paid indirectly |

| Portfolio turnover |

1 The average shares outstanding method has been applied for per share information. |

2 Total investment return is based on the change in net asset value of a share during the period and assumes reinvestment of dividends and distributions at net asset value. Total investment return during all periods shown reflects waivers by the manager and/or distributor. Performance would have been lower had the waivers not been in effect. |

See accompanying notes

24

| Year Ended | ||||||||||||||||

| 4/30/10 | 4/30/09 | 4/30/08 | 4/30/07 | 4/30/06 | ||||||||||||

| $18.550 | $26.930 | $26.810 | $26.940 | $20.340 | ||||||||||||

| (0.265 | ) | (0.092 | ) | (0.188 | ) | (0.257 | ) | (0.154 | ) | |||||||

| 9.145 | (8.288 | ) | 0.308 | 0.127 | 6.754 | |||||||||||

| 8.880 | (8.380 | ) | 0.120 | (0.130 | ) | 6.600 | ||||||||||

| $27.430 | $18.550 | $26.930 | $26.810 | $26.940 | ||||||||||||

| 47.87% | (31.12% | ) | 0.45% | (0.48% | ) | 32.45% | ||||||||||

| $807 | $671 | $1,266 | $1,432 | $1,485 | ||||||||||||

| 1.75% | 1.74% | 1.73% | 1.75% | 1.82% | ||||||||||||

| 2.08% | 2.20% | 1.97% | 1.99% | 2.05% | ||||||||||||

| (1.14% | ) | (0.45% | ) | (0.67% | ) | (1.02% | ) | (0.62% | ) | |||||||

| (1.47% | ) | (0.91% | ) | (0.91% | ) | (1.26% | ) | (0.85% | ) | |||||||

| 49% | 66% | 61% | 51% | 124% | ||||||||||||

25

Financial highlights

Delaware Select Growth Fund Institutional Class

Delaware Select Growth Fund Institutional Class

Selected data for each share of the Fund outstanding throughout each period were as follows:

| Net asset value, beginning of period |

| Income (loss) from investment operations: |

| Net investment income (loss)1 |

| Net realized and unrealized gain (loss) on investments and foreign currencies |

| Total from investment operations |

| Net asset value, end of period |

| Total return2 |

| Ratios and supplemental data: |

| Net assets, end of period (000 omitted) |

| Ratio of expenses to average net assets |

| Ratio of expenses to average net assets |

| prior to fees waived and expense paid indirectly |

| Ratio of net investment income (loss) to average net assets |

| Ratio of net investment loss to average net assets |

| prior to fees waived and expense paid indirectly |

| Portfolio turnover |

1 The average shares outstanding method has been applied for per share information. |

2 Total investment return is based on the change in net asset value of a share during the period and assumes reinvestment of dividends and distributions at net asset value. Total investment return during all periods shown reflects a waiver by the manager. Performance would have been lower had the waiver not been in effect. |

See accompanying notes

26

| Year Ended | ||||||||||||||||

| 4/30/10 | 4/30/09 | 4/30/08 | 4/30/07 | 4/30/06 | ||||||||||||

| $19.450 | $28.090 | $27.820 | $27.820 | $20.900 | ||||||||||||

| (0.150 | ) | 0.010 | (0.048 | ) | (0.128 | ) | (0.024 | ) | ||||||||

| 9.600 | (8.650 | ) | 0.318 | 0.128 | 6.944 | |||||||||||

| 9.450 | (8.640 | ) | 0.270 | 0.000 | 6.920 | |||||||||||

| $28.900 | $19.450 | $28.090 | $27.820 | $27.820 | ||||||||||||

| 48.59% | (30.76% | ) | 0.97% | 0.00% | 33.11% | |||||||||||

| $53,651 | $45,149 | $26,079 | $35,399 | $46,152 | ||||||||||||

| 1.25% | 1.24% | 1.23% | 1.25% | 1.30% | ||||||||||||

| 1.48% | 1.60% | 1.37% | 1.39% | 1.45% | ||||||||||||

| (0.64% | ) | 0.05% | (0.17% | ) | (0.52% | ) | (0.10% | ) | ||||||||

| (0.87% | ) | (0.31% | ) | (0.31% | ) | (0.66% | ) | (0.25% | ) | |||||||

| 49% | 66% | 61% | 51% | 124% | ||||||||||||

27

| Notes to financial statements | |

| Delaware Select Growth Fund | April 30, 2010 |

Voyageur Mutual Funds III (Trust) is organized as a Delaware statutory trust and offers two series: Delaware Large Cap Core Fund and Delaware Select Growth Fund. These financial statements and the related notes pertain to Delaware Select Growth Fund (Fund). The Trust is an open-end investment company. The Fund is considered diversified under the Investment Company Act of 1940, as amended, and offers Class A, Class B, Class C, Class R and Institutional Class shares. Class A shares are sold with a maximum front-end sales charge of up to 5.75%. Class A share purchases of $1,000,000 or more will incur a contingent deferred sales charge (CDSC) of 1% if redeemed during the first year and 0.50% during the second year, provided that Delaware Distributors, L.P. (DDLP) paid a financial advisor a commission on the purchase of those shares. Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges. Prior to June 1, 2007, Class B shares were sold with a CDSC that declined from 4% to zero depending upon the period of time the shares were held. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Class C shares are sold with a CDSC of 1%, if redeemed during the first twelve months. Class R and Institutional Class shares are not subject to a sales charge and are offered for sale exclusively to certain eligible investors.

The investment objective of the Fund is to seek long-term capital appreciation, which the Fund attempts to achieve by investing primarily in equity securities of companies the manager believes have the potential for sustainable free cash flow growth.

1. Significant Accounting Policies

The following accounting policies are in accordance with U.S. generally accepted accounting principles (U.S. GAAP) and are consistently followed by the Fund.

Security Valuation — Equity securities, except those traded on the Nasdaq Stock Market, Inc. (Nasdaq), are valued at the last quoted sales price as of the time of the regular close of the New York Stock Exchange (NYSE) on the valuation date. Securities traded on the Nasdaq are valued in accordance with the Nasdaq Official Closing Price, which may not be the last sales price. If on a particular day an equity security does not trade, then the mean between the bid and ask prices will be used. Securities listed on a foreign exchange are valued at the last quoted sales price on the valuation date. Investment companies are valued at net asset value per share. Short-term debt securities are valued at market value. Foreign currency exchange contracts are valued at the mean between the bid and ask prices. Interpolated values are derived when the settlement date of the contract is an interim date for which quotations are not available. Generally, other securities and assets for which market quotations are not readily available are valued at fair value as determined in good faith under the direction of the Fund’s Board of Trustees (Board). In determining whether market quotations are readily available or fair valuation will be used, various factors will be taken into consideration, such as market closures or suspension of trading in a security. The Fund may use fair value pricing more frequently for securities traded primarily in non-U.S. markets because, among other things, most foreign markets close well before the Fund values its securities

28

at 4:00 p.m. Eastern time. The earlier close of these foreign markets gives rise to the possibility that significant events, including broad market moves, government actions or pronouncements, aftermarket trading, or news events may have occurred in the interim. To account for this, the Fund may frequently value foreign securities using fair value prices based on third-party vendor modeling tools (international fair value pricing).

Federal Income Taxes — No provision for federal income taxes has been made as the Fund intends to continue to qualify for federal income tax purposes as a regulated investment company under Subchapter M of the Internal Revenue Code of 1986, as amended, and make the requisite distributions to shareholders. The Fund evaluates tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether the tax positions are “more-likely-than-not” of being sustained by the applicable tax authority. Tax positions not deemed to meet the more-likely-than-not threshold are recorded as a tax benefit or expense in the current year. Management has analyzed the Fund’s tax positions taken on federal income tax returns for all open tax years (April 30, 2007 – April 30, 2010), and has concluded that no provision for federal income tax is required in the Fund’s financial statements.

Class Accounting — Investment income, common expenses and realized and unrealized gain (loss) on investments are allocated to the various classes of the Fund on the basis of daily net assets of each class. Distribution expenses relating to a specific class are charged directly to that class.

Repurchase Agreements — The Fund may invest in a pooled cash account along with other members of the Delaware Investments® Family of Funds pursuant to an exemptive order issued by the Securities and Exchange Commission. The aggregate daily balance of the pooled cash account is invested in repurchase agreements secured by obligations of the U.S. government. The respective collateral is held by the Fund’s custodian bank until the maturity of the respective repurchase agreements. Each repurchase agreement is at least 102% collateralized. However, in the event of default or bankruptcy by the counterparty to the agreement, realization of the collateral may be subject to legal proceedings. At April 30, 2010, the Fund held no investments in repurchase agreements.

Foreign Currency Transactions — Transactions denominated in foreign currencies are recorded at the prevailing exchange rates on the valuation date. The value of all assets and liabilities denominated in foreign currencies is translated into U.S. dollars at the exchange rate of such currencies against the U.S. dollar daily. Transaction gains or losses resulting from changes in exchange rates during the reporting period or upon settlement of the foreign currency transaction are reported in operations for the current period. The Fund does not isolate that portion of realized gains and losses on investments which are due to changes in foreign exchange rates from that which are due to changes in market prices. The Fund reports certain foreign currency related transactions as components of realized gains (losses) for financial reporting purposes, whereas such components are treated as ordinary income (loss) for federal income tax purposes.

29

Notes to financial statements

Delaware Select Growth Fund

Delaware Select Growth Fund

1. Significant Accounting Policies (continued)

Use of Estimates — The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Other — Expenses directly attributable to the Fund are charged directly to the Fund. Other expenses common to various funds within the Delaware Investments® Family of Funds are generally allocated amongst such funds on the basis of average net assets. Management fees and some other expenses are paid monthly. Security transactions are recorded on the date the securities are purchased or sold (trade date) for financials reporting purposes. Costs used in calculating realized gains and losses on the sale of investment securities are those of the specific securities sold. Dividend income is recorded on the ex-dividend date and interest income is recorded on the accrual basis. Taxable non-cash dividends are recorded as dividend income. Foreign dividends are also recorded on the ex-dividend date or as soon after the ex-dividend date that the Fund is aware of such dividends, net of all non-rebatable tax withholdings. Withholding taxes on foreign dividends have been recorded in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. The Fund declares and pays dividends from net investment income and distributions from net realized gain on investments, if any, annually.

Subject to seeking best execution, the Fund may direct certain security trades to brokers who have agreed to rebate a portion of the related brokerage commission to the Fund in cash. Such commission rebates are included in realized gain on investments in the accompanying financial statements and totaled $37,247 for the year ended April 30, 2010. In general, best execution refers to many factors, including the price paid or received for a security, the commission charged, the promptness and reliability of execution, the confidentiality and placement accorded the order, and other factors affecting the overall benefit obtained by the Fund on the transaction.

The Fund receives earnings credits from its custodian when positive cash balances are maintained, which are used to offset custody fees. There were no earnings credits for the year ended April 30, 2010.

On July 1, 2009, the Financial Accounting Standards Board (FASB) issued the FASB Accounting Standards Codification (Codification). The Codification became the single source of authoritative nongovernmental U.S. GAAP, superseding existing literature of the FASB, American Institute of Certified Public Accountants, Emerging Issues Task Force and other sources. The Codification is effective for interim and annual periods ending after September 15, 2009. The Fund adopted the Codification for the year ended April 30, 2010. There was no impact to financial statements as the Codification requirements are disclosure-only in nature.

30

2. Investment Management, Administration Agreements and Other Transactions with Affiliates

In accordance with the terms of its investment management agreement, the Fund pays Delaware Management Company (DMC), a series of Delaware Management Business Trust and the investment manager, an annual fee which is calculated daily at the rate of 0.75% on the first $500 million of average daily net assets of the Fund, 0.70% on the next $500 million, 0.65% on the next $1.5 billion, and 0.60% on average daily net assets in excess of $2.5 billion.

Effective September 1, 2009, DMC has voluntarily agreed to waive that portion, if any, of its management fee and reimburse the Fund to the extent necessary to ensure that total annual operating expenses (excluding any 12b-1 plan expenses, taxes, interest, inverse floater program expenses, short sale and dividend interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations) do not exceed 1.25% of average daily net assets of the Fund until such time as the waiver is discontinued. This expense waiver and reimbursement applies only to expenses paid directly by the Fund, and may be discontinued at any time because it is voluntary. Prior to September 1, 2009, DMC had contractually agreed to waive its management fee to the extent necessary to ensure that total annual operating expenses (excluding any 12b-1 plan expenses, taxes, interest, inverse floater program expenses, short sale and dividend interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations) did not exceed 1.25% of the Fund’s average daily net assets.

Delaware Service Company, Inc. (DSC), an affiliate of DMC, provides fund accounting and financial administration oversight services to the Fund. For these services, the Fund pays DSC fees based on the aggregate daily net assets of the Delaware Investments® Family of Funds at the following annual rate: 0.0050% of the first $30 billion; 0.0045% of the next $10 billion; 0.0040% of the next $10 billion; and 0.0025% of aggregate average daily net assets in excess of $50 billion. The fees payable to DSC under the service agreement described above are allocated among all Funds in the Delaware Investments Family of Funds on a relative net asset value basis. For the year ended April 30, 2010, the Fund was charged $12,940 for these services.

DSC also provides dividend disbursing and transfer agency services. The Fund pays DSC a monthly fee based on the number of shareholder accounts for dividend disbursing and transfer agent services.

Pursuant to a distribution agreement and distribution plan, the Fund pays DDLP, the distributor and an affiliate of DMC, an annual distribution and service fee not to exceed 0.25% of the average daily net assets of the Class A shares, 1.00% of the average daily net assets of the Class B and C shares and 0.60% of the average daily net assets of the Class R shares. Institutional Class shares pay no distribution and service expenses. DDLP has contracted to limit the Class R shares 12b-1 fees through August 31, 2010 to no more than 0.50% of average daily net assets.

31

Notes to financial statements

Delaware Select Growth Fund

Delaware Select Growth Fund

2. Investment Management, Administration Agreements and Other Transactions with Affiliates (continued)

At April 30, 2010, the Fund had liabilities payable to affiliates as follows:

| Investment management fee payable to DMC | $ | 74,813 |

| Dividend disbursing, transfer agent and fund accounting | ||

| oversight fees and other expenses payable to DSC | 47,116 | |

| Distribution fees payable to DDLP | 68,173 | |

| Other expenses payable to DMC and affiliates* | 41,515 |

*DMC, as part of its administrative services, pays operating expenses on behalf of the Fund and is reimbursed on a periodic basis. Such expenses include items such as printing of shareholder reports, fees for audit, legal and tax services, registration fees and trustees’ fees.

As provided in the investment management agreement, the Fund bears the cost of certain legal and tax services, including internal legal and tax services provided to the Fund by DMC and/or its affiliates’ employees. For the year ended April 30, 2010, the Fund was charged $ 17,461 for internal legal and tax services provided by DMC and/or its affiliates’ employees.

For the year ended April 30, 2010, DDLP earned $18,822 for commissions on sales of the Fund’s Class A shares. For the year ended April 30, 2010, DDLP received gross CDSC commissions of $-, $13,041 and $2,078 on redemption of the Fund’s Class A, Class B and Class C shares, respectively, and these commissions were entirely used to offset up-front commissions previously paid by DDLP to broker/dealers on sales of those shares.

Trustees’ fees include expenses accrued by the Fund for each Trustee’s retainer and meeting fees. Certain officers of DMC, DSC and DDLP are officers and/or Trustees of the Trust. These officers and Trustees are paid no compensation by the Fund.

3. Investments

For the year ended April 30, 2010, the Fund made purchases of $119,890,671 and sales of $170,282,327 of investment securities other than short-term investments.

At April 30, 2010, the cost of investments for federal income tax purposes was $250,275,452. At April 30, 2010, net unrealized appreciation was $48,055,925, of which $55,077,914 related to unrealized appreciation of investments and $7,021,989 related to unrealized depreciation of investments.

U.S. GAAP defines fair value as the price that the Fund would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants at the measurement date under current market conditions. A three level hierarchy for fair value measurements has been established based upon the transparency of inputs to the valuation of an asset or liability. Inputs may be observable or unobservable and refer broadly to the assumptions that market

32

participants would use in pricing the asset or liability. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions that market participants would use in pricing the asset or liability developed based on the best information available under the circumstances. The Fund’s investment in its entirety is assigned a level based upon the observability of the inputs which are significant to the overall valuation. The three level hierarchy of inputs is summarized below.

Level 1 – inputs are quoted prices in active markets

Level 2 – inputs are observable, directly or indirectly

Level 3 – inputs are unobservable and reflect assumptions on the part of the reporting entity

The following table summarizes the valuation of the Fund’s investments by fair value hierarchy levels as of April 30, 2010:

| Level 1 | Level 2 | Level 3 | Total | ||||||||

| Common Stock | $ | 239,410,307 | $ | 1,601,574 | $ | — | $ | 241,011,881 | |||

| Short-Term | — | 9,755,025 | — | 9,755,025 | |||||||

| Securities Lending Collateral | 43,060,659 | 4,461,801 | 42,011 | 47,564,471 | |||||||

| Total | $ | 282,470,966 | $ | 15,818,400 | $ | 42,011 | $ | 298,331,377 | |||

The following is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value:

| Securities | ||

| Lending | ||

| Collateral | ||

| Balance as of 4/30/09 | $ | 99 |

| Net change in unrealized appreciation/depreciation | 41,912 | |

| Balance as of 4/30/10 | $ | 42,011 |

| Net change in unrealized appreciation/depreciation from | ||

| investments still held as of 4/30/10 | $ | 41,912 |

In January 2010, the FASB issued an Accounting Standards Update, Improving Disclosures about Fair Value Measurements, which introduces new disclosure requirements and clarifies certain existing disclosure requirements around fair value measurements currently presented above. The new disclosures and clarifications of existing disclosures are generally effective for the Fund’s year ending April 30, 2011 and interim periods therein. Management is evaluating the impact of this update on its current disclosures.

33

Notes to financial statements

Delaware Select Growth Fund

Delaware Select Growth Fund

4. Dividend and Distribution Information

Income and long-term capital gain distributions are determined in accordance with federal income tax regulations, which may differ from U.S. GAAP. Additionally, distributions from net gains on foreign currency transactions and net short-term gains on sales of investment securities are treated as ordinary income for federal income tax purposes. There were no dividends and distributions paid for the years ended April 30, 2010 and 2009.

5. Components of Net Assets on a Tax Basis

As of April 30, 2010, the components of net assets on a tax basis were as follows:

| Shares of beneficial interest | $ | 434,803,880 | |

| Post-October currency losses | (92,972 | ) | |

| Capital loss carryforwards | (233,778,615 | ) | |

| Unrealized appreciation of investments | |||

| and foreign currencies | 48,055,465 | ||

| Net assets | $ | 248,987,758 |

The differences between book basis and tax basis components of net assets are primarily attributable to tax deferral of losses on wash sales.

Post-October currency losses represent losses realized on foreign currency transactions from November 1, 2009 through April 30, 2010 that, in accordance with federal income tax regulations, the Fund has elected to defer and treat as having arisen in the following year.

For financial reporting purposes, capital accounts are adjusted to reflect the tax character of permanent book/tax differences. Reclassifications are primarily due to tax treatment of net operating losses, gain (loss) on foreign currency transactions and capital loss carryforward expiration. Results of operations and net assets were not affected by these reclassifications. For the year ended April 30, 2010, the Fund recorded the following reclassifications:

| Accumulated net investment loss | $ | 2,375,333 | |

| Accumulated net realized gain | 357,983,603 | ||

| Paid-in capital | (360,358,936 | ) |

For federal income tax purposes, at April 30, 2010, capital loss carryforwards of $233,778,615 may be carried forward and applied against future capital gains. $357,796,276 expired in 2010. Capital loss carryforwards remaining at April 30, 2010 will expire as follows: $185,917,705 expires in 2011, $18,530,411 expires in 2012, $21,490,547 expires in 2017 and $7,839,952 expires in 2018.

34

6. Capital Shares

Transactions in capital stock shares were as follows:

| Year Ended | |||||

| 4/30/10 | 4/30/09 | ||||

| Shares sold: | |||||

| Class A | 799,379 | 1,557,580 | |||

| Class B | 9,629 | 17,122 | |||

| Class C | 86,267 | 111,377 | |||

| Class R | 10,157 | 4,546 | |||

| Institutional Class | 3,745,535 | 1,968,498 | |||

| 4,650,967 | 3,659,123 | ||||

| Shares repurchased: | |||||

| Class A | (1,102,488 | ) | (1,651,316 | ) | |

| Class B | (545,493 | ) | (1,618,162 | ) | |

| Class C | (265,058 | ) | (579,812 | ) | |

| Class R | (16,910 | ) | (15,373 | ) | |

| Institutional Class | (4,210,692 | ) | (575,418 | ) | |

| (6,140,641 | ) | (4,440,081 | ) | ||

| Net decrease | (1,489,674 | ) | (780,958 | ) | |

For the years ended April 30, 2010 and 2009, 363,005 Class B shares were converted to 322,972 Class A shares valued at $7,518,237 and 1,015,729 Class B shares were converted to 910,682 Class A shares valued at $20,207,902, respectively. The respective amounts are included in Class B redemptions and Class A subscriptions in the table above and the statements of changes in net assets.

7. Line of Credit

The Fund, along with certain other funds in the Delaware Investments® Family of Funds (Participants), participates in a $35,000,000 revolving line of credit with The Bank of New York Mellon (BNY Mellon) to be used for temporary or emergency purposes as an additional source of liquidity to fund redemptions of investor shares. Under the agreement, the Participants are charged an annual commitment fee, which is allocated across the Participants on the basis of each Participant’s allocation of the entire facility. The Participants may borrow up to a maximum of one third of their net assets under the agreement. The agreement expires on November 16, 2010. The Fund had no amounts outstanding as of April 30, 2010 or at any time during the year then ended.

8. Derivatives

U.S. GAAP requires enhanced disclosures that enable investors to understand: 1) how and why an entity uses derivatives, 2) how they are accounted for, and 3) how they affect an entity’s results of operations and financial position.

35

Notes to financial statements

Delaware Select Growth Fund

Delaware Select Growth Fund

8. Derivatives (continued)

Foreign Currency Exchange Contracts — The Fund may enter into foreign currency exchange contracts as a way of managing foreign exchange rate risk. The Fund may enter into these contracts to fix the U.S. dollar value of a security that it has agreed to buy or sell for the period between the date the trade was entered into and the date the security is delivered and paid for. The Fund may also use these contracts to hedge the U.S. dollar value of securities it already owns that are denominated in foreign currencies. The change in value is recorded as an unrealized gain or loss. When the contract is closed, a realized gain or loss is recorded equal to the difference between the value of the contract at the time it was opened and the value at the time it was closed.

The use of foreign currency exchange contracts does not eliminate fluctuations in the underlying prices of the securities, but does establish a rate of exchange that can be achieved in the future. Although foreign currency exchange contracts limit the risk of loss due to a decline in the value of the hedged currency, they also limit any potential gain that might result should the value of the currency increase. In addition, the Fund could be exposed to risks if the counterparties to the contracts are unable to meet the terms of their contracts. The Fund’s maximum risk of loss from counterparty credit risk is the value of its currency exchanged with the counterparty. The risk is generally mitigated by having a netting arrangement between the Fund and the counterparty and by the posting of collateral by the counterparty to the Fund to cover the Fund’s exposure to the counterparty. No foreign currency exchange contracts were outstanding at April 30, 2010.

9. Securities Lending