UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number: | | 811-04304 |

| | | |

| Exact name of registrant as specified in charter: | | Delaware Group® Government Fund |

| | | |

| Address of principal executive offices: | | 2005 Market Street |

| | Philadelphia, PA 19103 |

| | | |

| Name and address of agent for service: | | David F. Connor, Esq. |

| | 2005 Market Street |

| | Philadelphia, PA 19103 |

| | | |

| Registrant’s telephone number, including area code: | | (800) 523-1918 |

| | | |

| Date of fiscal year end: | | July 31 |

| | | |

| Date of reporting period: | | July 31, 2013 |

Item 1. Reports to Stockholders

Annual report Delaware Core Plus Bond Fund Fixed income mutual fund |

| Carefully consider the Fund’s investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Fund’s prospectus and, if available, its summary prospectus, which may be obtained by visiting delawareinvestments.com or calling 800 523-1918. Investors should read the prospectus and, if available, the summary prospectus carefully before investing. |

You can obtain shareholder reports and prospectuses online instead of in the mail.

Visit delawareinvestments.com/edelivery. |

Experience Delaware Investments

Delaware Investments is committed to the pursuit of consistently superior asset management and unparalleled client service. We believe in our investment processes, which seek to deliver consistent results, and in convenient services that help add value for our clients.

If you are interested in learning more about creating an investment plan, contact your financial advisor.

You can learn more about Delaware Investments or obtain a prospectus for Delaware Core Plus Bond Fund at delawareinvestments.com.

Manage your investments online

- 24-hour access to your account information

- Obtain share prices

- Check your account balance and recent transactions

- Request statements or literature

- Make purchases and redemptions

Delaware Management Holdings, Inc. and its subsidiaries (collectively known by the marketing name of Delaware Investments) are wholly owned subsidiaries of Macquarie Group Limited, a global provider of banking, financial, advisory, investment and funds management services.

Investments in Delaware Core Plus Bond Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies (Macquarie Group), and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Fund, the repayment of capital from the Fund, or any particular rate of return.

Table of contents

| Portfolio management review | 1 |

| Performance summary | 4 |

| Disclosure of Fund expenses | 8 |

| Security type/sector allocation | 10 |

| Statement of net assets | 12 |

| Statement of assets and liabilities | 45 |

| Statement of operations | 46 |

| Statements of changes in net assets | 48 |

| Financial highlights | 50 |

| Notes to financial statements | 60 |

| Report of independent registered | |

| public accounting firm | 78 |

| Other Fund information | 79 |

| Board of trustees/directors and | |

| officers addendum | 80 |

| About the organization | 88 |

Unless otherwise noted, views expressed herein are current as of July 31, 2013, and subject to change.

Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Fund’s distributor, Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

© 2013 Delaware Management Holdings, Inc.

All third-party marks cited are the property of their respective owners.

| Portfolio management review |

| Delaware Core Plus Bond Fund | | August 6, 2013 |

| Performance preview (for the year ended July 31, 2013) |

| Delaware Core Plus Bond Fund (Class A shares) | 1-year return | | -1.51% |

| Barclays U.S. Aggregate Index (benchmark) | 1-year return | | -1.91% |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Core Plus Bond Fund, please see the table on page 4.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. |

Throughout most of the Fund’s fiscal year ended July 31, 2013, central bank policy was the dominant factor impacting fixed income markets worldwide. Shortly after the period began, European Central Bank (ECB) President Mario Draghi, reacting to severe stress in peripheral European bond markets, promised to do “whatever it takes” to keep the euro currency alive. Shortly thereafter, U.S. Federal Reserve Chairman Ben Bernanke launched a third round of bond buying, known as quantitative easing or QE3. Bernanke’s pledge was particularly notable in that, for the first time, the Fed publicly linked its policies to explicit levels of employment and inflation. The Bank of England and the Bank of Japan subsequently enacted their own quantitative easing measures that mirrored those of the Fed, especially in regard to forward guidance.

Initially, the resulting tidal wave of central bank liquidity — combined with a further deceleration of global economic growth — pushed bond yields sharply lower. With the Fed buying $85 billion in Treasury and mortgage securities each month — and with investors confident that the liquidity spigot would remain wide open indefinitely — credit spreads tightened and nominal yields declined

A flood of central bank liquidity drove fixed income markets worldwide:

- Nominal and real yields declined to historic lows until April

- Anticipation of the looming end to QE3 caused a sharp backup in rates in May and June

- Credit spreads tightened, then widened, amid uncertainty regarding Fed policy

1

Portfolio management review

Delaware Core Plus Bond Fund

to levels last visited in the 1950s. Meanwhile, the Fed also maintained its pledge to keep benchmark interest rates at virtually zero until unemployment falls to 6.5%.

As the year progressed, investors also relearned a difficult lesson: what central banks give, they also can take away. Though monetary policy in the euro zone, United Kingdom, and Japan remained highly expansionary, Chairman Bernanke hinted in mid-May that U.S. policy makers could begin scaling back, or “tapering,” the central bank’s monthly bond purchases by the end of 2013, if not before. Given that the U.S. economy remained mired in slow-growth mode and that the Fed itself forecasted a further deceleration in growth, a large number of shocked investors reacted by exiting the Treasury market. Most Treasury bond yields rose by at least 1% — a particularly dramatic move off of what had been historically low levels — causing double-digit declines among longer-dated securities. Furthermore, in a notable departure from normal cyclical patterns, corporate debt (with the exception of bank loans) did not absorb much of the backup in Treasury rates, causing credit spreads to widen as well. As such, prices of investment grade and high yield corporate bonds also fell sharply during a roughly six-week period amid fears of an imminent withdrawal of Fed liquidity. Those concerns were partially assuaged in July as various Fed officials seemed to clarify their messages about tapering.

Overall, the strongest-performing sectors of the fixed income market during the Fund’s fiscal year were those that offered relatively generous income potential (high yield), indirect exposure to the equity market (convertibles), and minimal duration risk (bank loans). Despite the tepid pace of U.S. and global economic growth, corporate fundamentals generally remained solid, emboldening investors to push corporate yields lower, and credit spreads tighter. The 7.2% average yield on sub-investment-grade bonds, for example, plunged to a low of about 5% in the spring and finished the fiscal period at 6.5%. Notably, the default rate in the high yield sector remained below the historical norm, in part because companies have been able to refinance outstanding debt on favorable terms. The relatively weak and uncertain nature of the economic recovery has also made corporate executives hesitant to begin capital projects or take on additional leverage.

Conversely, interest-rate-sensitive areas such as 10- and 30-year Treasurys and mortgage-backed securities mostly lagged throughout the Fund’s fiscal year. Losses were especially severe at the longer-term end of the Treasury yield curve, with the bulk of the rise in long rates (roughly 1.10%) coming during the turbulent May–June period. On a total return basis, investment grade corporates finished the fiscal year roughly flat throughout the fiscal period, while mortgage-backed bonds fell 1.7% and Treasury inflation-protected securities declined 5.5%.

2

Fund performance

For its fiscal year ended July 31, 2013, Delaware Core Plus Bond Fund (Class A shares) returned -1.51% at net asset value and -5.91% at maximum offer price (both returns reflect all distributions reinvested). In comparison, the Fund’s benchmark, the Barclays U.S. Aggregate Index, returned -1.91% during the same period. For complete annualized performance of Delaware Core Plus Bond Fund, please see table on page 4.

For most of the Fund’s fiscal year, we positioned the Fund to have more interest-rate sensitivity than that of its benchmark. Beginning in May, however, we took a defensive measure to move to a below-average level of duration, or interest rate risk, as it became apparent to us that the Fed indeed seemed serious about reducing the magnitude of its monthly bond purchases.

Our moves to add exposure to high yield bonds, bank loans, and convertibles (the three strongest-performing areas) during the fiscal year also contributed to the Fund’s relative performance, as did the Fund’s allocation toward the domestic banking and finance sectors. From an individual corporate bond perspective, the Fund’s holdings in issues from Taminco Global Chemical, Nara Cable Funding, and JBS USA LLC contributed to Fund performance during the year while issues from the Republic of South Africa, New South Wales Treasury Corp, and Treasury Corp Victoria detracted.

Meanwhile, early in the year hedges against the euro and euro-zone bonds held within the Fund detracted marginally from relative performance. After ECB President Draghi issued his “whatever it takes” proclamation, however, we unwound those positions as investors took a more positive reading on the situation in the euro zone.

Raising the Fund’s exposure to emerging market debt and emerging market currencies also undermined relative performance, especially as those sectors sold off in May and June.

During the Fund’s fiscal year, we invested in single-name (sovereign) credit default swaps, credit default swap baskets, forward foreign currency contracts, interest rate swaps, futures, and options. The credit default swaps and credit default swap baskets were used primarily for potential protection against economic contagion risk stemming from Europe. The forward foreign currency contracts were used to hedge the currency risk of securities denominated in foreign currencies (or to more generally manage foreign currency exposures within the Fund). The interest rate swaps, futures, and options were used primarily to seek to hedge interest rate risks and to seek to capitalize on volatility levels. Though the aggregate derivative positions generally detracted from absolute and relative performance by approximately 0.75%, we were comfortable holding them as risk management tools in an uneven macroeconomic environment.

3

| Performance summary | |

| Delaware Core Plus Bond Fund | July 31, 2013 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| Fund and benchmark performance1,2 | Average annual total returns through July 31, 2013 |

| 1 year | | 5 years | | 10 years | |

| Class A (Est. Aug. 16, 1985) | | | | | | |

| Excluding sales charge | -1.51% | | +7.07% | | +5.19% | |

| Including sales charge | -5.91% | | +6.10% | | +4.71% | |

| Class B (Est. May 2, 1994) | | | | | | |

| Excluding sales charge | -1.97% | | +6.34% | | +4.57% | |

| Including sales charge | -5.78% | | +6.10% | | +4.57% | |

| Class C (Est. Nov. 29, 1995) | | | | | | |

| Excluding sales charge | -2.24% | | +6.30% | | +4.44% | |

| Including sales charge | -3.19% | | +6.30% | | +4.44% | |

| Class R (Est. June 2, 2003) | | | | | | |

| Excluding sales charge | -1.74% | | +6.88% | | +4.96% | |

| Including sales charge | -1.74% | | +6.88% | | +4.96% | |

| Institutional Class (Est. June 1, 1992) | | | | | | |

| Excluding sales charge | -1.26% | | +7.37% | | +5.48% | |

| Including sales charge | -1.26% | | +7.37% | | +5.48% | |

| Barclays U.S. Aggregate Index | -1.91% | | +5.24% | | +4.89% | |

1 Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. Expenses for each class are listed on the “Fund expense ratios” table on page 6. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.30% of average daily net assets. This fee has been contractually limited to 0.25% of average daily net assets from Nov. 28, 2012, through Nov. 28, 2013. Furthermore, the Board has adopted a formula for calculating 12b-1 plan fees for the Fund’s Class A shares that went into effect on June 1, 1992. The Fund’s Class A shares are currently subject to a blended 12b-1 fee equal to the sum of: (i) 0.10% of average daily net assets representing shares acquired prior to June 1, 1992, and (ii) 0.30% of average daily net assets representing shares acquired on or

4

after June 1, 1992. All Class A shares currently bear 12b-1 fees at the same rate, the blended rate, based on the formula described above. This method of calculating Class A 12b-1 fees may be discontinued at the sole discretion of the Board. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. This fee has been contractually limited to 0.25% of average daily net assets from March 1, 2013, through Feb. 28, 2014. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Ten-year performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Class R shares are available only for certain retirement plan products. They are sold without a sales charge and have an annual distribution and service fee of 0.60% of average daily net assets, which has been limited contractually to 0.50% from Nov. 28, 2012, through Nov. 28, 2013.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

High yielding, noninvestment grade bonds (junk bonds) involve higher risk than investment grade bonds. The high yield secondary market is particularly susceptible to liquidity problems when institutional investors, such as mutual funds and certain other financial institutions, temporarily stop buying bonds for regulatory, financial, or other reasons. In addition, a less liquid secondary market makes it more difficult for the Fund to obtain precise valuations of the high yield securities in its portfolio.

The Fund may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the

5

Performance summary

Delaware Core Plus Bond Fund

opposite direction from what the portfolio manager anticipated. A derivative transaction depends upon the counterparties’ ability to fulfill their contractual obligations.

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations.

Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

If and when the Fund invests in forward foreign currency contracts or uses other investments to hedge against currency risks, the Fund will be subject to special risks, including counterparty risk.

The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

Per Standard & Poor’s credit rating agency, bonds rated AA and A are more susceptible to the adverse effects of changes in circumstances and economic conditions than those in the higher-rated AAA category, but the obligor’s capacity to meet its financial commitment on the obligation is still strong. Bonds rated BBB exhibit adequate protection parameters, although adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitments. Bonds rated BB, B, and CCC are regarded as having significant speculative characteristics, with BB indicating the least degree of speculation of the three.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total annual fund operating expenses (excluding certain fees and expenses) from exceeding 0.65% of the Fund’s average daily net assets from Nov. 28, 2012, through Nov. 28, 2013. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| Fund expense ratios | | Class A | | Class B | | Class C | | Class R | | Institutional Class |

| Total annual operating expenses | | 1.18% | | 1.88% | | 1.88% | | 1.48% | | 0.88% |

| (without fee waivers) | | | | | | | | | | |

| Net expenses | | 0.90% | | 1.65% | | 1.65% | | 1.15% | | 0.65% |

| (including fee waivers, if any) | | | | | | | | | | |

| Type of waiver | | Contractual | | Contractual | | Contractual | | Contractual | | Contractual |

6

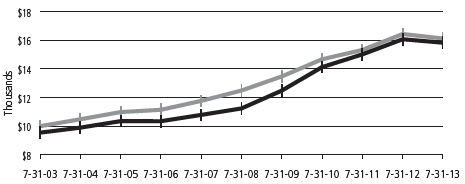

Performance of a $10,000 investment1

Average annual total returns from July 31, 2003, through July 31, 2013

| For period beginning July 31, 2003, through July 31, 2013 | | Starting value | | Ending value | |

| | Barclays U.S. Aggregate Index | | | $ | 10,000 | | | $16,121 | |

| | Delaware Core Plus Bond Fund — Class A shares | | | $ | 9,550 | | | $15,844 | |

1 The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A shares of the Fund on July 31, 2003, and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 6. Please note additional details on pages 4 through 7.

The chart also assumes $10,000 invested in the Barclays U.S. Aggregate Index as of July 31, 2003. The Barclays U.S. Aggregate Index is a broad composite that tracks the investment grade domestic bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Performance of other Fund classes will vary due to different charges and expenses.

| | Nasdaq symbols | | CUSIPs | |

| Class A | | DEGGX | | 246094205 | |

| Class B | | DEGBX | | 246094601 | |

| Class C | | DUGCX | | 246094700 | |

| Class R | | DUGRX | | 246094809 | |

| Institutional Class | | DUGIX | | 246094502 | |

7

Disclosure of Fund expenses

For the six-month period from February 1, 2013 to July 31, 2013 (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period from Feb. 1, 2013 to July 31, 2013.

Actual expenses

The first section of the table shown, “Actual Fund return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second section of the table shown, “Hypothetical 5% return,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The Fund’s expenses shown in the table reflect fee waivers in effect. The expenses shown in the table assume reinvestment of all dividends and distributions.

8

Delaware Core Plus Bond Fund

Expense analysis of an investment of $1,000

| | Beginning | | Ending | | | | | Expenses |

| | Account Value | | Account Value | | Annualized | | Paid During Period |

| | 2/1/13 | | 7/31/13 | | Expense Ratio | | 2/1/13 to 7/31/13* |

| Actual Fund return† | | | | | | | | | | | | | | | |

| Class A | | $ | 1,000.00 | | | $ | 977.70 | | | 0.90 | % | | $ | 4.41 | |

| Class B | | | 1,000.00 | | | | 976.70 | | | 1.13 | % | | | 5.54 | |

| Class C | | | 1,000.00 | | | | 974.10 | | | 1.65 | % | | | 8.08 | |

| Class R | | | 1,000.00 | | | | 977.70 | | | 1.15 | % | | | 5.64 | |

| Institutional Class | | | 1,000.00 | | | | 978.90 | | | 0.65 | % | | | 3.19 | |

| Hypothetical 5% return (5% return before expenses) | | | | | | | | |

| Class A | | $ | 1,000.00 | | | $ | 1,020.33 | | | 0.90 | % | | $ | 4.51 | |

| Class B | | | 1,000.00 | | | | 1,019.19 | | | 1.13 | % | | | 5.66 | |

| Class C | | | 1,000.00 | | | | 1,016.61 | | | 1.65 | % | | | 8.25 | |

| Class R | | | 1,000.00 | | | | 1,019.09 | | | 1.15 | % | | | 5.76 | |

| Institutional Class | | | 1,000.00 | | | | 1,021.57 | | | 0.65 | % | | | 3.26 | |

*“Expenses Paid During Period” are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

†Because actual returns reflect only the most recent six-month period, the returns shown may differ significantly from fiscal year returns.

9

| Security type/sector allocation | |

| Delaware Core Plus Bond Fund | As of July 31, 2013 (Unaudited) |

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications, which may result in the sector designations for one fund being different than another fund’s sector designations.

| Security type/sector | Percentage of net assets |

| Agency Collateralized Mortgage Obligations | 2.91 | % |

| Agency Mortgage-Backed Securities | 24.44 | % |

| Commercial Mortgage-Backed Securities | 4.95 | % |

| Convertible Bonds | 0.86 | % |

| Corporate Bonds | 48.13 | % |

| Banking | 7.23 | % |

| Basic Industry | 4.13 | % |

| Brokerage | 0.50 | % |

| Capital Goods | 1.51 | % |

| Communications | 5.80 | % |

| Consumer Cyclical | 2.29 | % |

| Consumer Non-Cyclical | 3.58 | % |

| Electric | 5.52 | % |

| Energy | 4.55 | % |

| Finance Companies | 1.72 | % |

| Insurance | 2.91 | % |

| Natural Gas | 3.28 | % |

| Real Estate | 1.83 | % |

| Technology | 2.62 | % |

| Transportation | 0.66 | % |

| Municipal Bonds | 0.17 | % |

| Non-Agency Asset-Backed Securities | 2.31 | % |

| Non-Agency Collateralized Mortgage Obligations | 0.36 | % |

| Regional Bonds | 0.95 | % |

| Senior Secured Loans | 7.84 | % |

| Sovereign Bonds | 1.35 | % |

| Supranational Bank | 0.06 | % |

| U.S. Treasury Obligations | 3.44 | % |

| Convertible Preferred Stock | 0.16 | % |

| Preferred Stock | 0.93 | % |

10

| Security type/sector | Percentage of net assets |

| Short-Term Investments | 19.13 | % |

| Securities Lending Collateral | 0.02 | % |

| Total Value of Securities | 118.01 | % |

| Obligation to Return Securities Lending Collateral | (0.02 | %) |

| Other Liabilities Net of Receivables and Other Assets | (17.99 | %) |

| Total Net Assets | 100.00 | % |

11

| Statement of net assets | |

| Delaware Core Plus Bond Fund | July 31, 2013 |

| | | | Principal amount° | | Value (U.S. $) |

| Agency Collateralized Mortgage Obligations – 2.91% | | | | | | | |

| Fannie Mae Grantor Trust | | | | | | | |

| Series 2002-T1 A2 7.00% 11/25/31 | | USD | | 54,363 | | $ | 63,668 |

| Fannie Mae Interest Strip | | | | | | | |

| Series 35-2 12.00% 7/1/18 | | | | 21,349 | | | 24,021 |

| Fannie Mae REMICs | | | | | | | |

| Series 1988-15 A 9.00% 6/25/18 | | | | 415 | | | 435 |

| Series 1996-46 ZA 7.50% 11/25/26 | | | | 65,540 | | | 75,313 |

| Series 2002-83 GH 5.00% 12/25/17 | | | | 233,496 | | | 247,822 |

| Series 2011-80 CB 4.00% 8/25/26 | | | | 1,953,713 | | | 2,050,759 |

| û•Series 2012-122 SD 5.91% 11/25/42 | | | | 227,627 | | | 58,360 |

| û•Series 2012-124 SD 5.96% 11/25/42 | | | | 320,457 | | | 74,915 |

| ûSeries 2013-26 ID 3.00% 4/25/33 | | | | 309,217 | | | 51,287 |

| ûSeries 2013-38 AI 3.00% 4/25/33 | | | | 311,633 | | | 51,450 |

| ûSeries 2013-44 DI 3.00% 5/25/33 | | | | 918,291 | | | 152,907 |

| • | Fannie Mae Whole Loan | | | | | | | |

| Series 2002-W1 2A 6.756% 2/25/42 | | | | 72,269 | | | 85,889 |

| Freddie Mac REMICs | | | | | | | |

| Series 2557 WE 5.00% 1/15/18 | | | | 197,327 | | | 209,586 |

| Series 3131 MC 5.50% 4/15/33 | | | | 24,816 | | | 24,934 |

| Series 3173 PE 6.00% 4/15/35 | | | | 109,904 | | | 112,970 |

| Series 3656 PM 5.00% 4/15/40 | | | | 235,000 | | | 257,399 |

| û•Series 4148 SA 5.909% 12/15/42 | | | | 376,644 | | | 90,338 |

| ûSeries 4185 LI 3.00% 3/15/33 | | | | 229,630 | | | 38,295 |

| ûSeries 4191 CI 3.00% 4/15/33 | | | | 98,900 | | | 16,539 |

| t | Freddie Mac Structured Pass Through Securities | | | | | | | |

| Series T-42 A5 7.50% 2/25/42 | | | | 28,171 | | | 33,113 |

| GNMA | | | | | | | |

| Series 2010-42 PC 5.00% 7/20/39 | | | | 545,000 | | | 617,858 |

| Series 2010-113 KE 4.50% 9/20/40 | | | | 245,000 | | | 267,287 |

| NCUA Guaranteed Notes | | | | | | | |

| Series 2010-C1 A2 2.90% 10/29/20 | | | | 80,000 | | | 83,078 |

| Total Agency Collateralized Mortgage | | | | | | | |

| Obligations (cost $4,631,117) | | | | | | | 4,688,223 |

| |

| Agency Mortgage-Backed Securities – 24.44% | | | | | | | |

| Fannie Mae | | | | | | | |

| 2.27% 1/1/23 | | | | 213,102 | | | 198,711 |

| 4.50% 5/1/41 | | | | 102,021 | | | 106,917 |

| 10.50% 6/1/30 | | | | 10,672 | | | 10,969 |

12

| | | | | Principal amount° | | Value (U.S. $) |

| Agency Mortgage-Backed Securities (continued) | | | | | | | |

| • | Fannie Mae ARM | | | | | | | |

| | 2.81% 11/1/35 | | USD | | 42,992 | | $ | 45,658 |

| | 4.296% 7/1/36 | | | | 74,954 | | | 81,235 |

| | 5.157% 8/1/35 | | | | 22,488 | | | 24,078 |

| Fannie Mae S.F. 15 yr | | | | | | | |

| | 2.50% 2/1/28 | | | | 367,766 | | | 367,981 |

| | 2.50% 5/1/28 | | | | 49,173 | | | 49,195 |

| | 3.00% 11/1/27 | | | | 106,952 | | | 110,153 |

| | 3.50% 7/1/26 | | | | 120,184 | | | 126,285 |

| | 3.50% 10/1/26 | | | | 109,066 | | | 114,396 |

| | 4.00% 11/1/25 | | | | 239,706 | | | 257,166 |

| | 5.00% 5/1/21 | | | | 73,280 | | | 78,120 |

| | 8.00% 10/1/16 | | | | 27,803 | | | 29,244 |

| Fannie Mae S.F. 15 yr TBA | | | | | | | |

| | 2.50% 9/1/28 | | | | 8,521,000 | | | 8,495,701 |

| | 3.00% 9/1/28 | | | | 5,073,000 | | | 5,204,383 |

| | 3.50% 9/1/28 | | | | 566,000 | | | 591,802 |

| Fannie Mae S.F. 20 yr | | | | | | | |

| | 5.00% 11/1/23 | | | | 9,542 | | | 10,357 |

| | 5.50% 8/1/28 | | | | 187,889 | | | 204,992 |

| | 5.50% 12/1/29 | | | | 16,411 | | | 17,942 |

| Fannie Mae S.F. 30 yr | | | | | | | |

| | 3.50% 7/1/42 | | | | 13,857 | | | 13,984 |

| | 3.50% 6/1/43 | | | | 36,842 | | | 37,192 |

| | 4.00% 11/1/40 | | | | 46,269 | | | 48,097 |

| | 4.00% 1/1/41 | | | | 223,898 | | | 232,743 |

| | 4.00% 2/1/41 | | | | 289,928 | | | 302,385 |

| | 4.00% 9/1/41 | | | | 31,842 | | | 33,096 |

| | 4.00% 10/1/41 | | | | 153,856 | | | 159,934 |

| | 4.00% 12/1/41 | | | | 787,542 | | | 818,654 |

| | 4.00% 3/1/42 | | | | 455,730 | | | 473,893 |

| | 4.00% 1/1/43 | | | | 633,444 | | | 658,401 |

| | 4.00% 4/1/43 | | | | 105,993 | | | 110,181 |

| | 4.50% 7/1/36 | | | | 36,879 | | | 39,068 |

| | 4.50% 4/1/40 | | | | 44,727 | | | 47,445 |

| | 4.50% 8/1/40 | | | | 207,285 | | | 219,611 |

| | 4.50% 11/1/40 | | | | 113,899 | | | 120,820 |

| | 4.50% 2/1/41 | | | | 53,726 | | | 57,010 |

| | 4.50% 3/1/41 | | | | 236,015 | | | 250,444 |

| | 4.50% 5/1/41 | | | | 38,036 | | | 40,418 |

13

Statement of net assets

Delaware Core Plus Bond Fund

| | | | | Principal amount° | | Value (U.S. $) |

| Agency Mortgage-Backed Securities (continued) | | | | | | | |

| Fannie Mae S.F. 30 yr (continued) | | | | | | | |

| | 4.50% 8/1/41 | | USD | | 260,279 | | $ | 276,191 |

| | 4.50% 10/1/41 | | | | 135,017 | | | 143,272 |

| | 4.50% 11/1/41 | | | | 117,072 | | | 124,229 |

| | 8.00% 2/1/30 | | | | 19,908 | | | 20,537 |

| | 10.00% 7/1/20 | | | | 5,015 | | | 5,806 |

| | 10.00% 5/1/22 | | | | 4,832 | | | 5,430 |

| | 10.00% 2/1/25 | | | | 82,211 | | | 92,801 |

| Fannie Mae S.F. 30 yr TBA | | | | | | | |

| | 3.00% 9/1/43 | | | | 11,558,000 | | | 11,169,725 |

| | 3.50% 9/1/43 | | | | 2,746,000 | | | 2,760,588 |

| | 4.50% 9/1/43 | | | | 2,173,000 | | | 2,296,929 |

| • | Freddie Mac ARM | | | | | | | |

| | 2.502% 7/1/36 | | | | 32,783 | | | 34,942 |

| | 5.393% 10/1/36 | | | | 61,639 | | | 65,312 |

| Freddie Mac S.F. 15 yr 5.00% 6/1/18 | | | | 31,397 | | | 33,207 |

| Freddie Mac S.F. 30 yr | | | | | | | |

| | 3.00% 11/1/42 | | | | 113,320 | | | 109,649 |

| | 4.00% 10/1/40 | | | | 125,964 | | | 130,708 |

| | 4.00% 11/1/40 | | | | 79,762 | | | 82,766 |

| | 4.50% 10/1/39 | | | | 158,162 | | | 166,711 |

| | 4.50% 11/1/39 | | | | 265,086 | | | 279,417 |

| | 4.50% 1/1/41 | | | | 207,556 | | | 214,287 |

| | 4.50% 3/1/42 | | | | 484,711 | | | 511,226 |

| | 6.00% 8/1/38 | | | | 272,181 | | | 299,663 |

| | 6.00% 10/1/38 | | | | 399,043 | | | 435,067 |

| | 8.00% 5/1/31 | | | | 84,143 | | | 97,640 |

| | 10.00% 1/1/19 | | | | 7,727 | | | 8,773 |

| | 11.50% 6/1/15 | | | | 743 | | | 755 |

| | 11.50% 8/1/15 | | | | 454 | | | 456 |

| | 11.50% 2/1/16 | | | | 5,489 | | | 5,611 |

| | 11.50% 3/1/16 | | | | 1,143 | | | 1,168 |

| GNMA I GPM 12.25% 3/15/14 | | | | 1,397 | | | 1,405 |

| GNMA I S.F. 15 yr 6.50% 7/15/14 | | | | 12,466 | | | 12,815 |

| GNMA I S.F. 30 yr | | | | | | | |

| | 7.50% 1/15/32 | | | | 10,192 | | | 12,396 |

| | 8.00% 5/15/30 | | | | 12,830 | | | 13,209 |

| | 9.50% 10/15/19 | | | | 2,730 | | | 2,744 |

| | 9.50% 8/15/21 | | | | 9,572 | | | 10,580 |

| | 9.50% 3/15/23 | | | | 12,582 | | | 13,722 |

14

| | | | | Principal amount° | | Value (U.S. $) |

| Agency Mortgage-Backed Securities (continued) | | | �� | | | | |

| GNMA I S.F. 30 yr (continued) | | | | | | | |

| | 10.00% 9/15/18 | | USD | | 6,719 | | $ | 6,756 |

| | 11.00% 8/15/15 | | | | 2,044 | | | 2,066 |

| | 12.00% 4/15/14 | | | | 2,001 | | | 2,010 |

| | 12.00% 5/15/14 | | | | 608 | | | 618 |

| | 12.00% 6/15/14 | | | | 267 | | | 269 |

| | 12.00% 3/15/15 | | | | 827 | | | 831 |

| | 12.00% 5/15/15 | | | | 3,564 | | | 3,583 |

| | 12.00% 6/15/15 | | | | 8,234 | | | 8,378 |

| | 12.50% 12/15/13 | | | | 267 | | | 268 |

| | 12.50% 1/15/16 | | | | 11,080 | | | 11,293 |

| GNMA II S.F. 30 yr | | | | | | | |

| | 7.50% 9/20/30 | | | | 15,251 | | | 18,542 |

| | 8.00% 6/20/30 | | | | 8,631 | | | 10,412 |

| | 10.00% 11/20/15 | | | | 198 | | | 202 |

| | 10.00% 5/20/19 | | | | 980 | | | 1,003 |

| | 10.00% 6/20/20 | | | | 3,247 | | | 3,739 |

| | 10.00% 8/20/20 | | | | 1,715 | | | 1,996 |

| | 10.00% 1/20/21 | | | | 2,525 | | | 2,962 |

| | 10.00% 2/20/21 | | | | 8,151 | | | 9,393 |

| | 10.00% 5/20/21 | | | | 3,329 | | | 3,896 |

| | 10.00% 6/20/21 | | | | 893 | | | 1,043 |

| | 10.50% 3/20/16 | | | | 415 | | | 438 |

| | 10.50% 1/20/18 | | | | 321 | | | 327 |

| | 10.50% 12/20/18 | | | | 325 | | | 372 |

| | 10.50% 2/20/19 | | | | 122 | | | 123 |

| | 10.50% 6/20/19 | | | | 362 | | | 417 |

| | 10.50% 9/20/19 | | | | 338 | | | 393 |

| | 10.50% 1/20/20 | | | | 994 | | | 1,012 |

| | 10.50% 5/20/20 | | | | 5,468 | | | 5,621 |

| | 10.50% 8/20/20 | | | | 472 | | | 475 |

| | 10.50% 10/20/20 | | | | 4,468 | | | 5,225 |

| | 10.50% 2/20/21 | | | | 18,158 | | | 18,261 |

| | 11.00% 5/20/15 | | | | 216 | | | 217 |

| | 11.00% 7/20/19 | | | | 445 | | | 448 |

| | 12.00% 3/20/14 | | | | 39 | | | 39 |

| | 12.00% 4/20/14 | | | | 225 | | | 228 |

| | 12.00% 5/20/15 | | | | 68 | | | 69 |

| | 12.50% 10/20/13 | | | | 124 | | | 124 |

| | 12.50% 12/20/13 | | | | 272 | | | 274 |

15

Statement of net assets

Delaware Core Plus Bond Fund

| | | | Principal amount° | | Value (U.S. $) |

| Agency Mortgage-Backed Securities (continued) | | | | | | | |

| GNMA II S.F. 30 yr (continued) | | | | | | | |

| 12.50% 5/20/14 | | USD | | 135 | | $ | 136 |

| 12.50% 7/20/15 | | | | 294 | | | 296 |

| Total Agency Mortgage-Backed Securities | | | | | | | |

| (cost $39,132,853) | | | | | | | 39,352,153 |

| |

| Commercial Mortgage-Backed Securities – 4.95% | | | | | | | |

| Bank of America Merrill Lynch Commercial | | | | | | | |

| Mortgage Securities | | | | | | | |

| •Series 2006-2 A4 5.73% 5/10/45 | | | | 115,000 | | | 126,468 |

| Series 2006-4 A4 5.634% 7/10/46 | | | | 200,000 | | | 219,609 |

| • | Bear Stearns Commercial Mortgage Securities | | | | | | | |

| Series 2005-T20 A4A 5.143% 10/12/42 | | | | 60,000 | | | 64,561 |

| Series 2006-PW12 A4 5.715% 9/11/38 | | | | 55,000 | | | 60,618 |

| Citigroup Commercial Mortgage Trust | | | | | | | |

| Series 2012-GC8 A4 3.024% 9/10/45 | | | | 180,000 | | | 171,431 |

| • | Commercial Mortgage Pass Through Certificates | | | | | | | |

| Series 2005-C6 A5A 5.116% 6/10/44 | | | | 95,000 | | | 101,460 |

| Series 2013-CR8 A5 3.612% 6/10/46 | | | | 235,000 | | | 231,375 |

| • | Commercial Mortgage Trust | | | | | | | |

| Series 2005-GG5 A5 5.224% 4/10/37 | | | | 340,000 | | | 363,618 |

| • | Credit Suisse Mortgage Capital Certificates | | | | | | | |

| Series 2006-C1 AAB 5.392% 2/15/39 | | | | 51,710 | | | 52,936 |

| # | DBUBS Mortgage Trust | | | | | | | |

| Series 2011-LC1A A3 144A 5.002% 11/10/46 | | | | 850,000 | | | 942,938 |

| #• | FREMF Mortgage Trust | | | | | | | |

| Series 2012-K21 B 144A 3.939% 7/25/45 | | | | 105,000 | | | 96,790 |

| Goldman Sachs Mortgage Securities II | | | | | | | |

| •Series 2004-GG2 A6 5.396% 8/10/38 | | | | 420,000 | | | 430,836 |

| Series 2005-GG4 A4A 4.751% 7/10/39 | | | | 450,000 | | | 471,957 |

| •Series 2006-GG6 A4 5.553% 4/10/38 | | | | 435,000 | | | 473,277 |

| #Series 2010-C1 A2 144A 4.592% 8/10/43 | | | | 245,000 | | | 265,485 |

| #•Series 2010-C1 C 144A 5.635% 8/10/43 | | | | 150,000 | | | 160,452 |

| #Series 2012-ALOHA B 144A 4.049% 4/10/34 | | | | 100,000 | | | 99,692 |

| JPMorgan Chase Commercial | | | | | | | |

| Mortgage Securities | | | | | | | |

| •Series 2005-LDP5 A4 5.20% 12/15/44 | | | | 280,000 | | | 302,288 |

| Series 2011-C5 A3 4.171% 8/15/46 | | | | 165,000 | | | 173,546 |

16

| | | | Principal amount° | | Value (U.S. $) |

| Commercial Mortgage-Backed Securities (continued) | | | | | | | |

| Lehman Brothers-UBS Commercial | | | | | | | |

| Mortgage Trust | | | | | | | |

| Series 2004-C1 A4 4.568% 1/15/31 | | USD | | 103,124 | | $ | 104,640 |

| •Series 2005-C3 B 4.895% 7/15/40 | | | | 60,000 | | | 62,097 |

| Merrill Lynch Mortgage Trust | | | | | | | |

| Series 2005-CIP1 A2 4.96% 7/12/38 | | | | 53,245 | | | 53,721 |

| •Series 2005-CKI1 A6 5.282% 11/12/37 | | | | 286,832 | | | 307,218 |

| Morgan Stanley Capital I | | | | | | | |

| Series 2005-HQ6 A4A 4.989% 8/13/42 | | | | 592,000 | | | 628,067 |

| •Series 2005-HQ7 5.206% 11/14/42 | | | | 480,000 | | | 476,562 |

| •Series 2007-T27 A4 5.647% 6/11/42 | | | | 375,000 | | | 423,900 |

| # | OBP Depositor Trust | | | | | | | |

| Series 2010-OBP A 144A 4.646% 7/15/45 | | | | 115,000 | | | 124,882 |

| # | Timberstar Trust | | | | | | | |

| Series 2006-1A A 144A 5.668% 10/15/36 | | | | 185,000 | | | 207,170 |

| # | VNO Mortgage Trust | | | | | | | |

| Series 2012-6AVE 144A 2.996% 11/15/30 | | | | 350,000 | | | 329,181 |

| WF-RBS Commercial Mortgage Trust | | | | | | | |

| Series 2012-C9 A3 2.87% 11/15/45 | | | | 130,000 | | | 121,936 |

| Series 2013-C11 A5 3.071% 3/15/45 | | | | 115,000 | | | 109,234 |

| Series 2013-C14 A5 3.337% 6/15/46 | | | | 210,000 | | | 202,582 |

| Total Commercial Mortgage-Backed Securities | | | | | | | |

| (cost $7,703,292) | | | | | | | 7,960,527 |

| |

| Convertible Bonds – 0.86% | | | | | | | |

| Advanced Micro Devices 6.00% | | | | | | | |

| exercise price $28.08, | | | | | | | |

| expiration date 4/30/15 | | | | 22,000 | | | 22,784 |

| # | Alaska Communications Systems Group 144A | | | | | | | |

| 6.25% exercise price $10.28, | | | | | | | |

| expiration date 4/27/18 | | | | 24,000 | | | 19,425 |

| Alere 3.00% exercise price $43.98, | | | | | | | |

| expiration date 5/15/16 | | | | 27,000 | | | 28,536 |

| Ares Capital 5.75% exercise price $19.13, | | | | | | | |

| expiration date 2/1/16 | | | | 27,000 | | | 29,531 |

| *Φ | ArvinMeritor 4.00% exercise price $26.73, | | | | | | | |

| expiration date 2/12/27 | | | | 52,000 | | | 48,489 |

| BGC Partners 4.50% exercise price $9.84, | | | | | | | |

| expiration date 7/13/16 | | | | 25,000 | | | 25,641 |

17

Statement of net assets

Delaware Core Plus Bond Fund

| | | | Principal amount° | | Value (U.S. $) |

| Convertible Bonds (continued) | | | | | | | |

| # | Blucora 144A 4.25% exercise price $21.66, | | | |

| expiration date 3/29/19 | | USD | | 17,000 | | $ | 19,752 |

| * | Chesapeake Energy 2.50% exercise price $50.90, | | | |

| expiration date 5/15/37 | | | | 11,000 | | | 10,581 |

| # | Ciena 144A 3.75% exercise price $20.17, | | | |

| expiration date 10/15/18 | | | | 26,000 | | | 35,214 |

| # | Clearwire Communications 144A 8.25% | | | |

| exercise price $7.08, | | | | | | | |

| expiration date 11/30/40 | | | | 22,000 | | | 24,475 |

| Dendreon 2.875% exercise price $51.24, | | | |

| expiration date 1/13/16 | | | | 33,000 | | | 24,131 |

| Equinix 4.75% exercise price $84.32, | | | |

| expiration date 6/13/16 | | | | 5,000 | | | 11,050 |

| Φ | General Cable 4.50% exercise price $36.55, | | | |

| expiration date 11/15/29 | | | | 43,000 | | | 48,401 |

| Gilead Sciences 1.625% exercise price $22.71, | | | |

| expiration date 5/1/16 | | | | 12,000 | | | 32,475 |

| Helix Energy Solutions Group 3.25% | | | |

| exercise price $25.02, | | | | | | | |

| expiration date 3/12/32 | | | | 29,000 | | | 38,679 |

| *Φ | Hologic 2.00% exercise price $31.17, | | | |

| expiration date 2/27/42 | | | | 34,000 | | | 36,338 |

| Iconix Brand Group 2.50% exercise price $30.75, | | | |

| expiration date 5/31/16 | | | | 14,000 | | | 17,054 |

| # | Illumina 144A 0.25% exercise price $83.55, | | | |

| expiration date 3/11/16 | | | | 16,000 | | | 18,110 |

| Intel 3.25% exercise price $21.94, | | | |

| expiration date 8/1/39 | | | | 19,000 | | | 23,619 |

| Jefferies Group 3.875% exercise price $45.72, | | | |

| expiration date 10/31/29 | | | | 32,000 | | | 33,980 |

| Leap Wireless International 4.50% | | | |

| exercise price $93.21, | | | | | | | |

| expiration date 7/10/14 | | | | 46,000 | | | 47,063 |

| # | Lexington Realty Trust 144A 6.00% | | | |

| exercise price $6.84, | | | | | | | |

| expiration date 1/11/30 | | | | 12,000 | | | 22,298 |

| # | Liberty Interactive 144A 0.75% | | | |

| exercise price $1,000.00, | | | | | | | |

| expiration date 3/30/43 | | | | 23,000 | | | 25,933 |

18

| | | | Principal amount° | | Value (U.S. $) |

| Convertible Bonds (continued) | | | | | | | |

| Linear Technology 3.00% exercise price $41.46, | | | |

| expiration date 4/30/27 | | USD | | 225,000 | | $ | 244,405 |

| MGM Resorts International 4.25% | | | | | | | |

| exercise price $18.58, | | | | | | | |

| expiration date 4/10/15 | | | | 32,000 | | | 37,380 |

| Mylan 3.75% exercise price $13.32, | | | | | | | |

| expiration date 9/15/15 | | | | 9,000 | | | 23,012 |

| Nuance Communications 2.75% | | | | | | | |

| exercise price $32.30, | | | | | | | |

| expiration date 11/1/31 | | | | 37,000 | | | 37,879 |

| NuVasive 2.75% exercise price $42.13, | | | |

| expiration date 6/30/17 | | | | 54,000 | | | 52,919 |

| # | Opko Health 144A 3.00% exercise price $7.07, | | | |

| expiration date 1/28/33 | | | | 8,000 | | | 8,600 |

| # | Owens-Brockway Glass Container 144A 3.00% | | | |

| exercise price $47.47, | | | | | | | |

| expiration date 5/28/15 | | | | 37,000 | | | 38,434 |

| * | Peabody Energy 4.75% exercise price $57.95, | | | |

| expiration date 12/15/41 | | | | 19,000 | | | 14,381 |

| PHH 4.00% exercise price $25.80, | | | | | | | |

| expiration date 8/27/14 | | | | 27,000 | | | 29,548 |

| Rovi 2.625% exercise price $47.36, | | | | | | | |

| expiration date 2/10/40 | | | | 14,000 | | | 14,403 |

| # | Ryman Hospitality Properties 144A 3.75% | | | |

| exercise price $21.96, | | | | | | | |

| expiration date 9/29/14 | | | | 15,000 | | | 25,688 |

| SanDisk 1.50% exercise price $52.37, | | | | | | | |

| expiration date 8/11/17 | | | | 35,000 | | | 44,516 |

| SBA Communications 4.00% | | | | | | | |

| exercise price $30.38, | | | | | | | |

| expiration date 9/29/14 | | | | 8,000 | | | 19,685 |

| Steel Dynamics 5.125% exercise price $17.21, | | | |

| expiration date 6/15/14 | | | | 9,000 | | | 9,771 |

| TIBCO Software 2.25% exercise price $50.57, | | | |

| expiration date 4/30/32 | | | | 57,000 | | | 57,783 |

| Titan Machinery 3.75% exercise price $43.17, | | | |

| expiration date 4/30/19 | | | | 26,000 | | | 24,278 |

| • | Vector Group 2.50% exercise price $18.50, | | | |

| expiration date 1/14/19 | | | | 8,000 | | | 9,573 |

19

Statement of net assets

Delaware Core Plus Bond Fund

| | | | | Principal amount° | | Value (U.S. $) |

| Convertible Bonds (continued) | | | | | | | |

| VeriSign 3.25% exercise price $34.37, | | | | | | | |

| | expiration date 8/15/37 | | USD | | 22,000 | | $ | 32,560 |

| # | WellPoint 144A 2.75% exercise price $75.38, | | | | | | | |

| | expiration date 10/15/42 | | | | 16,000 | | | 20,930 |

| Total Convertible Bonds (cost $1,306,596) | | | | | | | 1,389,304 |

| |

| Corporate Bonds – 48.13% | | | | | | | |

| Banking – 7.23% | | | | | | | |

| # | Banco BTG Pactual 144A 4.00% 1/16/20 | | | | 245,000 | | | 210,700 |

| # | Banco do Brasil 144A 3.75% 7/25/18 | | EUR | | 170,000 | | | 224,430 |

| # | Banco Santander Mexico 144A 4.125% 11/9/22 | | USD | | 300,000 | | | 279,375 |

| Bancolombia 5.95% 6/3/21 | | | | 180,000 | | | 188,550 |

| # | Bank Nederlandse Gemeenten 144A | | | | | | | |

| | 1.375% 3/19/18 | | | | 350,000 | | | 344,559 |

| Bank of America | | | | | | | |

| | 3.875% 3/22/17 | | | | 195,000 | | | 206,500 |

| | 4.10% 7/24/23 | | | | 150,000 | | | 150,385 |

| • | 5.20% 12/29/49 | | | | 235,000 | | | 212,675 |

| • | Bank of New York Mellon 4.50% 12/31/49 | | | | 155,000 | | | 144,731 |

| * | Barclays Bank 7.625% 11/21/22 | | | | 400,000 | | | 399,000 |

| BB&T 5.25% 11/1/19 | | | | 627,000 | | | 704,183 |

| # | BBVA Banco Continental 144A 3.25% 4/8/18 | | | | 205,000 | | | 200,388 |

| BBVA U.S. Senior 4.664% 10/9/15 | | | | 200,000 | | | 206,556 |

| • | Branch Banking & Trust 0.592% 9/13/16 | | | | 280,000 | | | 276,125 |

| City National 5.25% 9/15/20 | | | | 160,000 | | | 172,848 |

| • | Deutsche Bank 4.296% 5/24/28 | | | | 200,000 | | | 181,975 |

| • | Fifth Third Bancorp 5.10% 12/31/49 | | | | 200,000 | | | 189,500 |

| • | Fifth Third Capital Trust IV 6.50% 4/15/37 | | | | 510,000 | | | 511,913 |

| Goldman Sachs Group 2.90% 7/19/18 | | | | 420,000 | | | 421,227 |

| #• | HBOS Capital Funding 144A 6.071% 6/29/49 | | | | 790,000 | | | 762,349 |

| JPMorgan Chase | | | | | | | |

| | 2.92% 9/19/17 | | CAD | | 170,000 | | | 165,116 |

| • | 5.15% 12/29/49 | | USD | | 150,000 | | | 139,875 |

| | 6.00% 12/29/49 | | | | 30,000 | | | 29,588 |

| KeyBank 5.45% 3/3/16 | | | | 500,000 | | | 551,616 |

| Morgan Stanley 4.10% 5/22/23 | | | | 535,000 | | | 503,240 |

| Oesterreichische Kontrollbank | | | | | | | |

| | 1.125% 5/29/18 | | | | 175,000 | | | 171,071 |

20

| | | | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | | |

| Banking (continued) | | | | | | | |

| PNC Bank | | | | | | | |

| | 3.80% 7/25/23 | | USD | | 250,000 | | $ | 247,372 |

| | 6.875% 4/1/18 | | | | 250,000 | | | 300,749 |

| • | PNC Financial Services Group | | | | | | | |

| | 4.494% 5/29/49 | | | | 260,000 | | | 260,325 |

| | 4.85% 5/29/49 | | | | 170,000 | | | 155,125 |

| PNC Funding 5.125% 2/8/20 | | | | 210,000 | | | 235,043 |

| Regions Financial 2.00% 5/15/18 | | | | 215,000 | | | 207,208 |

| Royal Bank of Scotland Group 6.10% 6/10/23 | | | | 45,000 | | | 43,233 |

| # | Russian Agricultural Bank 144A 5.10% 7/25/18 | | | | 200,000 | | | 201,100 |

| # | Sberbank 144A 4.95% 2/7/17 | | | | 200,000 | | | 210,240 |

| # | Standard Chartered 144A 3.95% 1/11/23 | | | | 290,000 | | | 272,764 |

| State Street 3.10% 5/15/23 | | | | 245,000 | | | 229,787 |

| SVB Financial Group 5.375% 9/15/20 | | | | 150,000 | | | 164,171 |

| U.S. Bank North America 4.95% 10/30/14 | | | | 250,000 | | | 263,135 |

| *• | USB Capital IX 3.50% 10/29/49 | | | | 705,000 | | | 627,449 |

| #• | USB Realty 144A 1.415% 12/22/49 | | | | 100,000 | | | 87,000 |

| Wachovia | | | | | | | |

| *• | 0.638% 10/15/16 | | | | 95,000 | | | 93,800 |

| | 5.25% 8/1/14 | | | | 105,000 | | | 109,546 |

| Zions Bancorp | | | | | | | |

| | 4.50% 3/27/17 | | | | 275,000 | | | 284,211 |

| | 7.75% 9/23/14 | | | | 95,000 | | | 101,697 |

| | | | | | | | 11,642,430 |

| Basic Industry – 4.13% | | | | | | | |

| ArcelorMittal 10.35% 6/1/19 | | | | 330,000 | | | 400,125 |

| # | Barrick Gold 144A | | | | | | | |

| | 2.50% 5/1/18 | | | | 70,000 | | | 65,029 |

| | 4.10% 5/1/23 | | | | 190,000 | | | 161,909 |

| CF Industries | | | | | | | |

| | 6.875% 5/1/18 | | | | 210,000 | | | 248,064 |

| | 7.125% 5/1/20 | | | | 275,000 | | | 327,840 |

| Dow Chemical 8.55% 5/15/19 | | | | 479,000 | | | 617,079 |

| # | Freeport-McMoRan Copper & Gold 144A | | | | | | | |

| | 3.875% 3/15/23 | | | | 155,000 | | | 140,506 |

| Georgia-Pacific 8.00% 1/15/24 | | | | 520,000 | | | 675,475 |

| # | Gerdau Trade 144A 4.75% 4/15/23 | | | | 200,000 | | | 183,000 |

| # | Glencore Funding 144A 2.50% 1/15/19 | | | | 285,000 | | | 261,814 |

21

Statement of net assets

Delaware Core Plus Bond Fund

| | | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | | |

| Basic Industry (continued) | | | | | | | |

| International Paper | | | | | | | |

| 6.00% 11/15/41 | | USD | | 230,000 | | $ | 252,900 |

| 9.375% 5/15/19 | | | | 55,000 | | | 72,828 |

| LYB International Finance 4.00% 7/15/23 | | | | 680,000 | | | 676,221 |

| Nucor 4.00% 8/1/23 | | | | 95,000 | | | 93,704 |

| *# | Phosagro 144A 4.204% 2/13/18 | | | | 200,000 | | | 194,500 |

| Plains Exploration & Production | | | | | | | |

| 6.50% 11/15/20 | | | | 130,000 | | | 140,069 |

| Rio Tinto Finance USA 2.25% 12/14/18 | | | | 135,000 | | | 131,945 |

| Rock Tenn | | | | | | | |

| 3.50% 3/1/20 | | | | 60,000 | | | 59,207 |

| 4.00% 3/1/23 | | | | 55,000 | | | 53,052 |

| Rockwood Specialties Group 4.625% 10/15/20 | | | | 260,000 | | | 265,200 |

| Southern Copper | | | | | | | |

| 3.50% 11/8/22 | | | | 40,000 | | | 36,366 |

| 5.25% 11/8/42 | | | | 160,000 | | | 128,032 |

| # | Taminco Global Chemical 144A 9.75% 3/31/20 | | | | 940,000 | | | 1,064,551 |

| * | Teck Resources 3.75% 2/1/23 | | | | 140,000 | | | 126,922 |

| Vale Overseas 5.625% 9/15/19 | | | | 70,000 | | | 76,297 |

| # | Vedanta Resources 144A 6.00% 1/31/19 | | | | 200,000 | | | 196,000 |

| | | | | | | | 6,648,635 |

| Brokerage – 0.50% | | | | | | | |

| Jefferies Group | | | | | | | |

| 5.125% 1/20/23 | | | | 285,000 | | | 288,976 |

| 6.45% 6/8/27 | | | | 60,000 | | | 62,283 |

| 6.50% 1/20/43 | | | | 50,000 | | | 50,130 |

| Lazard Group 6.85% 6/15/17 | | | | 366,000 | | | 409,674 |

| | | | | | | | 811,063 |

| Capital Goods – 1.51% | | | | | | | |

| # | Ardagh Packaging Finance 144A | | | | | | | |

| 7.00% 11/15/20 | | | | 925,000 | | | 913,437 |

| Ball 5.75% 5/15/21 | | | | 495,000 | | | 527,175 |

| # | Cemex Espana Luxembourg 144A | | | | | | | |

| 9.25% 5/12/20 | | | | 250,000 | | | 274,375 |

| # | Ingersoll-Rand Global Holding 144A | | | | | | | |

| 4.25% 6/15/23 | | | | 380,000 | | | 379,735 |

22

| | | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | | |

| Capital Goods (continued) | | | | | | | |

| # | URS 144A | | | | | | | |

| 4.35% 4/1/17 | | USD | | 25,000 | | $ | 25,585 |

| 5.50% 4/1/22 | | | | 125,000 | | | 128,171 |

| # | Votorantim Cimentos 144A 7.25% 4/5/41 | | | | 200,000 | | | 190,000 |

| | | | | | | | 2,438,478 |

| Communications – 5.80% | | | | | | | |

| American Tower 5.90% 11/1/21 | | | | 250,000 | | | 275,330 |

| # | American Tower Trust I 144A | | | | | | | |

| 1.551% 3/15/18 | | | | 85,000 | | | 83,003 |

| 3.07% 3/15/23 | | | | 210,000 | | | 200,636 |

| Bell Canada 3.35% 3/22/23 | | CAD | | 50,000 | | | 45,836 |

| CC Holdings GS V 3.849% 4/15/23 | | USD | | 445,000 | | | 420,131 |

| CenturyLink 5.80% 3/15/22 | | | | 265,000 | | | 265,663 |

| # | Clearwire Communications 144A | | | | | | | |

| 12.00% 12/1/15 | | | | 220,000 | | | 233,750 |

| # | Columbus International 144A 11.50% 11/20/14 | | | | 100,000 | | | 108,500 |

| # | Cox Communications 144A 3.25% 12/15/22 | | | | 420,000 | | | 384,517 |

| # | Crown Castle Towers 144A 4.883% 8/15/20 | | | | 800,000 | | | 852,427 |

| # | Digicel Group 144A 10.50% 4/15/18 | | | | 200,000 | | | 218,000 |

| # | Intelsat Jackson Holdings 144A 5.50% 8/1/23 | | | | 345,000 | | | 332,925 |

| # | Millicom International Cellular 144A | | | | | | | |

| 4.75% 5/22/20 | | | | 200,000 | | | 194,500 |

| # | Myriad International Holding 144A | | | | | | | |

| 6.375% 7/28/17 | | | | 200,000 | | | 217,240 |

| # | Nara Cable Funding 144A 8.875% 12/1/18 | | | | 500,000 | | | 527,500 |

| # | Qtel International Finance 144A 3.25% 2/21/23 | | | | 200,000 | | | 184,500 |

| Qwest 6.75% 12/1/21 | | | | 185,000 | | | 207,362 |

| # | SBA Tower Trust 144A 2.24% 4/16/18 | | | | 160,000 | | | 158,030 |

| # | SES 144A 3.60% 4/4/23 | | | | 365,000 | | | 347,157 |

| Sinclair Television Group 6.125% 10/1/22 | | | | 430,000 | | | 436,450 |

| # | Softbank 144A 4.50% 4/15/20 | | | | 240,000 | | | 232,260 |

| Sprint Nextel | | | | | | | |

| 6.00% 12/1/16 | | | | 110,000 | | | 117,150 |

| 8.375% 8/15/17 | | | | 130,000 | | | 147,550 |

| # | TBG Global 144A 4.625% 4/3/18 | | | | 200,000 | | | 197,500 |

| # | Telefonica Chile 144A 3.875% 10/12/22 | | | | 200,000 | | | 184,393 |

| Telefonica Emisiones 3.192% 4/27/18 | | | | 600,000 | | | 593,378 |

| # | Telemar Norte Leste 144A 5.50% 10/23/20 | | | | 265,000 | | | 250,425 |

23

Statement of net assets

Delaware Core Plus Bond Fund

| | | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | | |

| Communications (continued) | | | | | | | |

| Time Warner Cable 8.25% 4/1/19 | | USD | | 385,000 | | $ | 448,697 |

| # | UPCB Finance III 144A 6.625% 7/1/20 | | | | 250,000 | | | 268,750 |

| Virgin Media Secured Finance 6.50% 1/15/18 | | | | 500,000 | | | 523,750 |

| # | Vivendi 144A | | | | | | | |

| 3.45% 1/12/18 | | | | 455,000 | | | 459,867 |

| 6.625% 4/4/18 | | | | 2,000 | | | 2,288 |

| Vodafone Group 2.95% 2/19/23 | | | | 230,000 | | | 213,283 |

| | | | | | | | 9,332,748 |

| Consumer Cyclical – 2.29% | | | | | | | |

| ADT 4.125% 6/15/23 | | | | 150,000 | | | 129,200 |

| Amazon.com 2.50% 11/29/22 | | | | 370,000 | | | 340,282 |

| # | Daimler Finance North America 144A | | | | | | | |

| 2.25% 7/31/19 | | | | 250,000 | | | 244,957 |

| Ford Motor Credit | | | | | | | |

| 5.875% 8/2/21 | | | | 400,000 | | | 444,274 |

| 12.00% 5/15/15 | | | | 200,000 | | | 236,832 |

| Historic TW 6.875% 6/15/18 | | | | 540,000 | | | 654,478 |

| Host Hotels & Resorts | | | | | | | |

| 3.75% 10/15/23 | | | | 45,000 | | | 41,848 |

| 4.75% 3/1/23 | | | | 175,000 | | | 176,732 |

| 5.25% 3/15/22 | | | | 180,000 | | | 187,813 |

| 5.875% 6/15/19 | | | | 75,000 | | | 80,784 |

| # | Hyundai Capital America 144A 2.125% 10/2/17 | | | | 130,000 | | | 126,995 |

| # | QVC 144A 4.375% 3/15/23 | | | | 435,000 | | | 415,767 |

| # | SACI Falabella 144A 3.75% 4/30/23 | | | | 200,000 | | | 183,655 |

| Western Union | | | | | | | |

| 2.875% 12/10/17 | | | | 130,000 | | | 130,998 |

| 3.65% 8/22/18 | | | | 95,000 | | | 98,475 |

| Wyndham Worldwide | | | | | | | |

| 4.25% 3/1/22 | | | | 100,000 | | | 98,807 |

| 5.625% 3/1/21 | | | | 90,000 | | | 96,922 |

| | | | | | | | 3,688,819 |

| Consumer Non-Cyclical – 3.58% | | | | | | | |

| # | BFF International 144A 7.25% 1/28/20 | | | | 100,000 | | | 111,000 |

| Boston Scientific 6.00% 1/15/20 | | | | 145,000 | | | 165,584 |

| # | BRF - Brasil Foods 144A 5.875% 6/6/22 | | | | 255,000 | | | 259,463 |

24

| | | | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | | |

| Consumer Non-Cyclical (continued) | | | | | | | |

| CareFusion | | | | | | | |

| # | 144A 3.30% 3/1/23 | | USD | | 185,000 | | $ | 174,523 |

| | 6.375% 8/1/19 | | | | 475,000 | | | 547,756 |

| Celgene 3.95% 10/15/20 | | | | 120,000 | | | 123,571 |

| Constellation Brands | | | | | | | |

| | 3.75% 5/1/21 | | | | 110,000 | | | 103,125 |

| | 4.25% 5/1/23 | | | | 75,000 | | | 70,875 |

| # | Cosan Luxembourg 144A 5.00% 3/14/23 | | | | 200,000 | | | 188,000 |

| Covidien International Finance 2.95% 6/15/23 | | | | 165,000 | | | 157,501 |

| Del Monte 7.625% 2/15/19 | | | | 55,000 | | | 57,750 |

| Energizer Holding 4.70% 5/24/22 | | | | 360,000 | | | 364,163 |

| Fomento Economico Mexicano 4.375% 5/10/43 | | | | 150,000 | | | 129,383 |

| # | Korea Expressway 144A 1.875% 10/22/17 | | | | 200,000 | | | 194,813 |

| Kroger 3.85% 8/1/23 | | | | 150,000 | | | 149,280 |

| Laboratory Corporation of America Holdings | | | | | | | |

| | 2.20% 8/23/17 | | | | 190,000 | | | 188,931 |

| # | Mylan 144A | | | | | | | |

| | 3.125% 1/15/23 | | | | 105,000 | | | 95,901 |

| | 6.00% 11/15/18 | | | | 245,000 | | | 265,063 |

| Newell Rubbermaid 2.05% 12/1/17 | | | | 120,000 | | | 118,497 |

| # | Pernod-Ricard 144A 5.75% 4/7/21 | | | | 660,000 | | | 744,997 |

| Quest Diagnostics 4.70% 4/1/21 | | | | 235,000 | | | 248,631 |

| # | SABMiller Holdings 144A 3.75% 1/15/22 | | | | 400,000 | | | 408,182 |

| # | Want Want China Finance 144A 1.875% 5/14/18 | | | | 200,000 | | | 190,374 |

| Yale University 2.90% 10/15/14 | | | | 125,000 | | | 128,592 |

| Zimmer Holdings 4.625% 11/30/19 | | | | 240,000 | | | 264,231 |

| # | Zoetis 144A 3.25% 2/1/23 | | | | 330,000 | | | 313,922 |

| | | | | | | | 5,764,108 |

| Electric – 5.52% | | | | | | | |

| AES 7.375% 7/1/21 | | | | 535,000 | | | 607,225 |

| Ameren Illinois 9.75% 11/15/18 | | | | 769,000 | | | 1,037,736 |

| # | American Transmission Systems 144A | | | | | | | |

| | 5.25% 1/15/22 | | | | 225,000 | | | 239,697 |

| # | APT Pipelines 144A 3.875% 10/11/22 | | | | 95,000 | | | 88,207 |

| CenterPoint Energy 5.95% 2/1/17 | | | | 165,000 | | | 187,957 |

| CMS Energy 6.25% 2/1/20 | | | | 190,000 | | | 221,073 |

| ComEd Financing III 6.35% 3/15/33 | | | | 190,000 | | | 189,063 |

| #• | Electricite de France 144A 5.25% 12/29/49 | | | | 325,000 | | | 311,351 |

25

Statement of net assets

Delaware Core Plus Bond Fund

| | | | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | | |

| Electric (continued) | | | | | | | |

| # | Eskom Holdings 144A 6.75% 8/6/23 | | USD | | 200,000 | | $ | 198,380 |

| Exelon Generation 4.25% 6/15/22 | | | | 400,000 | | | 402,678 |

| Great Plains Energy | | | | | | | |

| 4.85% 6/1/21 | | | | 90,000 | | | 97,044 |

| 5.292% 6/15/22 | | | | 305,000 | | | 334,183 |

| • | Integrys Energy Group 6.11% 12/1/66 | | | | 295,000 | | | 309,982 |

| LG&E & KU Energy | | | | | | | |

| 3.75% 11/15/20 | | | | 115,000 | | | 117,733 |

| 4.375% 10/1/21 | | | | 380,000 | | | 393,341 |

| # | Narragansett Electric 144A 4.17% 12/10/42 | | | | 135,000 | | | 122,470 |

| • | National Rural Utilities Cooperative Finance | | | | | | | |

| 4.75% 4/30/43 | | | | 230,000 | | | 222,525 |

| NextEra Energy Capital Holdings | | | | | | | |

| | 3.625% 6/15/23 | | | | 100,000 | | | 97,057 |

| • | 6.35% 10/1/66 | | | | 440,000 | | | 457,926 |

| NV Energy 6.25% 11/15/20 | | | | 240,000 | | | 283,378 |

| Pennsylvania Electric 5.20% 4/1/20 | | | | 175,000 | | | 191,234 |

| • | PPL Capital Funding 6.70% 3/30/67 | | | | 150,000 | | | 156,126 |

| Public Service Company of Oklahoma | | | | | | | |

| 5.15% 12/1/19 | | | | 550,000 | | | 627,601 |

| Puget Energy 6.00% 9/1/21 | | | | 65,000 | | | 71,915 |

| • | Puget Sound Energy 6.974% 6/1/67 | | | | 525,000 | | | 549,342 |

| SCANA 4.125% 2/1/22 | | | | 815,000 | | | 801,625 |

| • | Wisconsin Energy 6.25% 5/15/67 | | | | 535,000 | | | 563,560 |

| | | | | | | | 8,880,409 |

| Energy – 4.55% | | | | | | | |

| Apache 2.625% 1/15/23 | | | | 85,000 | | | 78,942 |

| Continental Resources 4.50% 4/15/23 | | | | 170,000 | | | 165,750 |

| # | Gazprom 144A 4.95% 5/23/16 | | | | 200,000 | | | 210,500 |

| # | Gazprom Neft 144A 4.375% 9/19/22 | | | | 200,000 | | | 186,040 |

| Halliburton 3.50% 8/1/23 | | | | 265,000 | | | 264,817 |

| # | KazMunayGas National 144A 9.125% 7/2/18 | | | | 210,000 | | | 256,463 |

| # | Korea Gas 144A 2.875% 7/29/18 | | | | 200,000 | | | 200,165 |

| Lukoil International Finance 6.125% 11/9/20 | | | | 335,000 | | | 361,030 |

| Newfield Exploration 5.625% 7/1/24 | | | | 175,000 | | | 175,875 |

| Noble Holding International | | | | | | | |

| 3.95% 3/15/22 | | | | 245,000 | | | 240,633 |

| 5.25% 3/15/42 | | | | 35,000 | | | 32,883 |

26

| | | | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | | |

| Energy (continued) | | | | | | | |

| ONGC Videsh 2.50% 5/7/18 | | USD | | 200,000 | | $ | 189,932 |

| # | Pacific Rubiales Energy 144A 7.25% 12/12/21 | | | | 100,000 | | | 108,000 |

| # | Pertamina Persero 144A 4.875% 5/3/22 | | | | 350,000 | | | 333,375 |

| Petrobras Global Finance 3.00% 1/15/19 | | | | 220,000 | | | 204,836 |

| Petrobras International Finance 5.375% 1/27/21 | | | | 300,000 | | | 300,251 |

| Petrohawk Energy 7.25% 8/15/18 | | | | 340,000 | | | 373,150 |

| Petroleos de Venezuela 9.00% 11/17/21 | | | | 381,000 | | | 318,135 |

| Petroleos Mexicanos | | | | | | | |

| # | 144A 2.286% 7/18/18 | | | | 10,000 | | | 10,275 |

| # | 144A 3.50% 1/30/23 | | | | 225,000 | | | 206,438 |

| | 5.50% 6/27/44 | | | | 110,000 | | | 101,035 |

| Pride International 6.875% 8/15/20 | | | | 475,000 | | | 569,253 |

| Range Resources 8.00% 5/15/19 | | | | 175,000 | | | 189,875 |

| # | Samson Investment 144A 10.00% 2/15/20 | | | | 775,000 | | | 825,374 |

| * | SandRidge Energy 8.75% 1/15/20 | | | | 235,000 | | | 247,925 |

| Statoil 3.95% 5/15/43 | | | | 110,000 | | | 100,293 |

| Talisman Energy 5.50% 5/15/42 | | | | 470,000 | | | 474,731 |

| Weatherford International 9.625% 3/1/19 | | | | 150,000 | | | 192,662 |

| # | Woodside Finance 144A | | | | | | | |

| 8.125% 3/1/14 | | | | 280,000 | | | 290,893 |

| 8.75% 3/1/19 | | | | 85,000 | | | 109,068 |

| | | | | | | | 7,318,599 |

| Finance Companies – 1.72% | | | | | | | |

| # | CDP Financial 144A | | | | | | | |

| 4.40% 11/25/19 | | | | 280,000 | | | 308,850 |

| 5.60% 11/25/39 | | | | 250,000 | | | 287,488 |

| General Electric Capital | | | | | | | |

| | 2.10% 12/11/19 | | | | 65,000 | | | 63,683 |

| | 4.375% 9/16/20 | | | | 230,000 | | | 244,981 |

| | 6.00% 8/7/19 | | | | 470,000 | | | 548,472 |

| • | 6.25% 12/15/49 | | | | 300,000 | | | 313,294 |

| • | 7.125% 12/15/49 | | | | 100,000 | | | 112,688 |

| General Electric Capital Canada Funding | | | | | | | |

| 2.42% 5/31/18 | | CAD | | 9,000 | | | 8,650 |

| #• | ILFC E-Capital Trust II 144A 6.25% 12/21/65 | | USD | | 210,000 | | | 194,775 |

| International Lease Finance | | | | | | | |

| 5.875% 4/1/19 | | | | 85,000 | | | 89,250 |

| 6.25% 5/15/19 | | | | 88,000 | | | 93,280 |

| 8.75% 3/15/17 | | | | 100,000 | | | 115,250 |

27

Statement of net assets

Delaware Core Plus Bond Fund

| | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | |

| Finance Companies (continued) | | | | | | |

| PHH 9.25% 3/1/16 | USD | | 145,000 | | $ | 164,575 |

| # | Temasek Financial I 144A 2.375% 1/23/23 | | | 250,000 | | | 226,365 |

| | | | | | | 2,771,601 |

| Insurance – 2.91% | | | | | | |

| American International Group 8.25% 8/15/18 | | | 245,000 | | | 307,198 |

| • | Chubb 6.375% 3/29/67 | | | 680,000 | | | 739,499 |

| # | Highmark 144A | | | | | | |

| 4.75% 5/15/21 | | | 200,000 | | | 189,766 |

| 6.125% 5/15/41 | | | 30,000 | | | 26,936 |

| *• | ING Groep 5.775% 12/29/49 | | | 85,000 | | | 85,000 |

| # | ING US 144A | | | | | | |

| 2.90% 2/15/18 | | | 85,000 | | | 84,870 |

| 5.50% 7/15/22 | | | 160,000 | | | 173,038 |

| •5.65% 5/15/53 | | | 220,000 | | | 207,350 |

| # | Liberty Mutual Group 144A | | | | | | |

| 4.25% 6/15/23 | | | 170,000 | | | 167,059 |

| 4.95% 5/1/22 | | | 215,000 | | | 223,199 |

| 6.50% 5/1/42 | | | 190,000 | | | 212,511 |

| MetLife 6.817% 8/15/18 | | | 165,000 | | | 201,632 |

| # | Metropolitan Life Global Funding I 144A | | | | | | |

| 3.00% 1/10/23 | | | 300,000 | | | 286,445 |

| 3.875% 4/11/22 | | | 475,000 | | | 485,776 |

| Prudential Financial | | | | | | |

| 3.875% 1/14/15 | | | 65,000 | | | 67,827 |

| *4.50% 11/15/20 | | | 50,000 | | | 54,059 |

| •5.625% 6/15/43 | | | 95,000 | | | 92,388 |

| •5.875% 9/15/42 | | | 245,000 | | | 248,063 |

| 6.00% 12/1/17 | | | 120,000 | | | 138,505 |

| • | XL Group 6.50% 12/29/49 | | | 160,000 | | | 158,000 |

| #• | ZFS Finance USA Trust II 144A 6.45% 12/15/65 | | | 500,000 | | | 536,249 |

| | | | | | | 4,685,370 |

| Natural Gas – 3.28% | | | | | | |

| AmeriGas Finance 7.00% 5/20/22 | | | 650,000 | | | 695,500 |

| El Paso Pipeline Partners Operating | | | | | | |

| 6.50% 4/1/20 | | | 295,000 | | | 344,919 |

| • | Enbridge Energy Partners 8.05% 10/1/37 | | | 265,000 | | | 300,957 |

| Energy Transfer Partners 9.70% 3/15/19 | | | 127,000 | | | 165,236 |

28

| | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | |

| Natural Gas (continued) | | | | | | |

| Enterprise Products Operating | | | | | | |

| •7.034% 1/15/68 | USD | | 450,000 | | $ | 505,612 |

| 9.75% 1/31/14 | | | 130,000 | | | 135,657 |

| # | GDF Suez 144A 2.875% 10/10/22 | | | 210,000 | | | 196,212 |

| Kinder Morgan Energy Partners | | | | | | |

| | 4.15% 2/1/24 | | | 65,000 | | | 65,010 |

| 9.00% 2/1/19 | | | 415,000 | | | 534,167 |

| NiSource Finance | | | | | | |

| 3.85% 2/15/23 | | | 100,000 | | | 98,289 |

| 4.80% 2/15/44 | | | 210,000 | | | 195,402 |

| 5.80% 2/1/42 | | | 150,000 | | | 159,968 |

| Plains All American Pipeline 8.75% 5/1/19 | | | 195,000 | | | 254,099 |

| # | Regency Energy Partners 144A 4.50% 11/1/23 | | | 370,000 | | | 348,725 |

| Spectra Energy Capital 3.30% 3/15/23 | | | 55,000 | | | 49,820 |

| Sunoco Logistics Partners Operations | | | | | | |

| 3.45% 1/15/23 | | | 185,000 | | | 174,019 |

| TransCanada Pipelines | | | | | | |

| 3.80% 10/1/20 | | | 100,000 | | | 104,994 |

| •6.35% 5/15/67 | | | 310,000 | | | 325,684 |

| Williams Partners 7.25% 2/1/17 | | | 535,000 | | | 622,978 |

| | | | | | | 5,277,248 |

| Real Estate – 1.83% | | | | | | |

| Alexandria Real Estate Equities 4.60% 4/1/22 | | | 510,000 | | | 523,652 |

| BRE Properties 3.375% 1/15/23 | | | 210,000 | | | 197,100 |

| # | Corporate Office Properties 144A | | | | | | |

| 3.60% 5/15/23 | | | 150,000 | | | 139,201 |

| DDR | | | | | | |

| 4.625% 7/15/22 | | | 80,000 | | | 82,349 |

| 4.75% 4/15/18 | | | 80,000 | | | 86,939 |

| 7.875% 9/1/20 | | | 90,000 | | | 111,180 |

| 9.625% 3/15/16 | | | 150,000 | | | 179,501 |

| Digital Realty Trust | | | | | | |

| 5.25% 3/15/21 | | | 450,000 | | | 472,463 |

| 5.875% 2/1/20 | | | 95,000 | | | 103,628 |

| Duke Realty 3.625% 4/15/23 | | | 150,000 | | | 140,350 |

| National Retail Properties | | | | | | |

| 3.30% 4/15/23 | | | 100,000 | | | 92,751 |

| 3.80% 10/15/22 | | | 90,000 | | | 87,151 |

29

Statement of net assets

Delaware Core Plus Bond Fund

| | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | |

| Real Estate (continued) | | | | | | |

| Realty Income 4.65% 8/1/23 | USD | | 185,000 | | $ | 189,836 |

| Regency Centers | | | | | | |

| | 4.80% 4/15/21 | | | 55,000 | | | 58,379 |

| 5.875% 6/15/17 | | | 95,000 | | | 106,111 |

| # | WEA Finance 144A 4.625% 5/10/21 | | | 210,000 | | | 222,437 |

| Weingarten Realty Investors 3.50% 4/15/23 | | | 165,000 | | | 154,387 |

| | | | | | | 2,947,415 |

| Technology – 2.62% | | | | | | |

| Agilent Technologies 3.875% 7/15/23 | | | 100,000 | | | 97,546 |

| Apple 2.40% 5/3/23 | | | 380,000 | | | 349,342 |

| Baidu 3.25% 8/6/18 | | | 245,000 | | | 246,136 |

| EMC 2.65% 6/1/20 | | | 50,000 | | | 49,665 |

| Fidelity National Information Services | | | | | | |

| 3.50% 4/15/23 | | | 205,000 | | | 189,358 |

| GXS Worldwide 9.75% 6/15/15 | | | 240,000 | | | 247,050 |

| Microsoft 2.125% 11/15/22 | | | 195,000 | | | 179,049 |

| National Semiconductor 6.60% 6/15/17 | | | 255,000 | | | 300,281 |

| NetApp | | | | | | |

| 2.00% 12/15/17 | | | 125,000 | | | 122,755 |

| 3.25% 12/15/22 | | | 145,000 | | | 134,016 |

| Oracle 2.375% 1/15/19 | | | 325,000 | | | 327,631 |

| # | Samsung Electronics America 144A | | | | | | |

| 1.75% 4/10/17 | | | 200,000 | | | 198,189 |

| Symantec 4.20% 9/15/20 | | | 125,000 | | | 128,728 |

| # | Tencent Holdings 144A 3.375% 3/5/18 | | | 200,000 | | | 202,478 |

| Total System Services | | | | | | |

| 2.375% 6/1/18 | | | 40,000 | | | 38,944 |

| 3.75% 6/1/23 | | | 180,000 | | | 167,489 |

| # | VeriSign 144A 4.625% 5/1/23 | | | 705,000 | | | 680,325 |

| Xerox 6.35% 5/15/18 | | | 490,000 | | | 565,688 |

| | | | | | | 4,224,670 |

| Transportation – 0.66% | | | | | | |

| # | Brambles USA 144A | | | | | | |

| 3.95% 4/1/15 | | | 80,000 | | | 83,441 |

| 5.35% 4/1/20 | | | 205,000 | | | 223,416 |

| # | DP World Sukuk 144A 6.25% 7/2/17 | | | 100,000 | | | 109,750 |

30

| | | Principal amount° | | Value (U.S. $) |

| Corporate Bonds (continued) | | | | | | |

| Transportation (continued) | | | | | | |

| # | ERAC USA Finance 144A 5.25% 10/1/20 | USD | | 370,000 | | $ | 411,936 |

| | United Parcel Service 5.125% 4/1/19 | | | 200,000 | | | 230,298 |

| | | | | | | 1,058,841 |

| Total Corporate Bonds (cost $76,589,749) | | | | | | 77,490,434 |

| |

| Municipal Bonds – 0.17% | | | | | | |

| Golden State Tobacco Securitization, | | | | | | |

| California Settlement Revenue Refunding | | | | | | |

| Asset-Backed Senior Series A-1 | | | | | | |

| 5.125% 6/1/47 | | | 100,000 | | | 71,409 |

| 5.75% 6/1/47 | | | 75,000 | | | 58,568 |

| Grand Parkway Transportation Tax System Toll | | | | | | |

| Revenue Series B 5.00% 4/1/53 | | | 10,000 | | | 9,714 |

| State of Georgia Series D 5.00% 2/1/23 | | | 115,000 | | | 137,599 |

| Total Municipal Bonds (cost $293,796) | | | | | | 277,290 |

| |

| Non-Agency Asset-Backed Securities – 2.31% | | | | | | |

| AEP Texas Central Transition Funding | | | | | | |

| Series 2012-1 A2 1.976% 6/1/21 | | | 395,000 | | | 390,379 |

| • | Ally Master Owner Trust | | | | | | |

| Series 2011-1 A1 1.061% 1/15/16 | | | 140,000 | | | 140,339 |

| Series 2013-2 A 0.641% 4/15/18 | | | 200,000 | | | 199,022 |

| # | Avis Budget Rental Car Funding AESOP | | | | | | |

| Series 2011-2A A 144A 2.37% 11/20/14 | | | 135,000 | | | 137,101 |

| Bank of America Auto Trust | | | | | | |

| Series 2012-1 A3 0.78% 6/15/16 | | | 450,000 | | | 450,411 |

| # | California Republic Auto Receivables Trust | | | | | | |

| Series 2013-1 A2 144A 1.41% 9/17/18 | | | 100,000 | | | 99,665 |

| Capital One Multi-Asset Execution Trust | | | | | | |

| Series 2007-A7 A7 5.75% 7/15/20 | | | 100,000 | | | 116,299 |

| •Series 2013-A2 A2 0.371% 2/15/19 | | | 440,000 | | | 438,320 |

| CenterPoint Energy Transition Bond | | | | | | |

| Series 2012-1 A2 2.161% 10/15/21 | | | 120,000 | | | 119,465 |

| # | Enterprise Fleet Financing | | | | | | |

| Series 2012-1 A2 144A 1.14% 11/20/17 | | | 158,942 | | | 159,399 |

31

Statement of net assets

Delaware Core Plus Bond Fund

| | | Principal amount° | | Value (U.S. $) |

| Non-Agency Asset-Backed Securities (continued) | | | | | | |

| General Electric Capital Credit Card Master | | | | | | |

| Note Trust | | | | | | |

| Series 2012-2 A 2.22% 1/15/22 | USD | | 100,000 | | $ | 99,788 |

| | Series 2012-6 A 1.36% 8/17/20 | | | 170,000 | | | 167,546 |

| John Deere Owner Trust | | | | | | |

| Series 2011-A A4 1.96% 4/16/18 | | | 145,000 | | | 146,527 |

| Mercedes-Benz Auto Lease Trust | | | | | | |

| Series 2013-A A4 0.72% 12/17/18 | | | 180,000 | | | 179,245 |

| # | Navistar Financial Owner Trust | | | | | | |