Item 1. Reports to Stockholders

Annual report

Fixed income mutual fund

Delaware Core Plus Bond Fund

July 31, 2016

Carefully consider the Fund’s investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Fund’s prospectus and its summary prospectus, which may be obtained by visiting delawareinvestments.com/literature or calling 800 523-1918. Investors should read the prospectus and the summary prospectus carefully before investing.

You can obtain shareholder reports and prospectuses online instead of in the mail.

Visit delawareinvestments.com/edelivery.

Experience Delaware Investments

Delaware Investments is committed to the pursuit of consistently superior asset management and unparalleled client service. We believe in our investment processes, which seek to deliver consistent results, and in convenient services that help add value for our clients.

If you are interested in learning more about creating an investment plan, contact your financial advisor.

You can learn more about Delaware Investments or obtain a prospectus for Delaware Core Plus Bond Fund at delawareinvestments.com/literature.

Manage your investments online

| • | | 24-hour access to your account information |

| • | | Check your account balance and recent transactions |

| • | | Request statements or literature |

| • | | Make purchases and redemptions |

Delaware Management Holdings, Inc. and its subsidiaries (collectively known by the marketing name of Delaware Investments) are wholly owned subsidiaries of Macquarie Group Limited, a global provider of banking, financial, advisory, investment, and funds management services.

Neither Delaware Investments nor its affiliates referred to in this document are authorized deposit-taking institutions for the purpose of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of Macquarie Bank Limited (MBL), a subsidiary of Macquarie Group Limited and an affiliate of Delaware Investments. MBL does not guarantee or otherwise provide assurance in respect of the obligations of these entities, unless noted otherwise. The Fund is governed by U.S. laws and regulations.

Table of contents

Unless otherwise noted, views expressed herein are current as of July 31, 2016, and subject to change for events occurring after such date.

The Fund is not FDIC insured and is not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Fund’s distributor, Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

© 2016 Delaware Management Holdings, Inc.

All third-party marks cited are the property of their respective owners.

| | | | |

| Portfolio management review | | | | |

| Delaware Core Plus Bond Fund | | | August 9, 2016 | |

| | | | | | | | |

| Performance preview (for the year ended July 31, 2016) | | | | | | |

| |

Delaware Core Plus Bond Fund (Institutional Class shares) | | | 1-year return | | | | +4.40% | |

| |

Delaware Core Plus Bond Fund (Class A shares) | | | 1-year return | | | | +4.15% | |

| |

Bloomberg Barclays U.S. Aggregate Index* (benchmark) | | | 1-year return | | | | +5.94% | |

| |

Past performance does not guarantee future results.

For complete, annualized performance for Delaware Core Plus Bond Fund, please see the table on page 4.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible accounts.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. Please see page 7 for a description of the index.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

*Formerly known as the Barclays U.S. Aggregate Index.

Commodity prices continued to decline during the first half of the Fund’s fiscal year ended July 31, 2016, but began to recover early in 2016, boosting investor confidence and increasing interest in down-in-quality assets (source: Bloomberg). China’s decision to devalue its currency in August 2015, along with signs of its economic deceleration, led Chinese officials to take additional stimulus measures in February 2016. However, questions remained regarding China’s short-term growth trajectory, partly fed by uncertainty over the government’s willingness to take further actions to support its economy.

The U.S. Federal Reserve raised the federal funds rate by 0.25 percentage points in December 2015, the first increase since 2006. However, other central banks, including the European Central Bank (ECB) and the Bank of Japan, flooded markets with liquidity. We believe this divergence in central bank policy caused asset prices to separate from fundamentals, complicating the Fed’s efforts to implement its policy of gradual monetary tightening. The full implementation of Fed policy was also hampered by currency markets, where the dollar rallied whenever anticipation of a Fed rate hike increased, seemingly forcing the U.S. central bank to back off. (A stronger dollar tends to restrain the earnings of American multinationals, and thereby acts as a modest brake on domestic economic growth.)

The following factors affected the fixed income market during the Fund’s fiscal year:

| | ● | | Commodity prices recovered after falling sharply |

| | ● | | Divergent global monetary policy triggered a disconnect between asset prices and fundamentals |

| | ● | | Uncertainty related to China, U.S. monetary policy, and global populism argued for maintaining liquidity. |

1

Portfolio management review

Delaware Core Plus Bond Fund

Late in the Fund’s fiscal year, the ECB introduced its corporate sector purchase program (CSPP), which provided a major non-price-sensitive buyer in the markets. While helping to reduce risk premiums and overall yields, the CSPP also had the effect of encouraging greater risk taking and, as a result, further contributed to a divergence between fundamentals and asset prices.

Within the Fund

For the fiscal year ended July 31, 2016, Delaware Core Plus Bond Fund underperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Index. The Fund’s Institutional Class shares returned +4.40%. The Fund’s Class A shares returned +4.15% at net asset value and -0.57% at maximum offer price. These figures reflect all distributions reinvested. During the same period, the benchmark returned +5.94%. For complete, annualized performance of Delaware Core Plus Bond Fund, please see the table on page 4.

The Fund’s underperformance was largely due to asset allocation. The Fund was generally overweight mortgage-backed securities (MBS) and underweight U.S. Treasurys, which performed well relative to MBS and asset-backed securities (ABS). The Fund’s exposure to out-of-benchmark and below-investment-grade assets also detracted from performance. While the Fund’s bank loan holdings gained in absolute terms, they significantly lagged the overall benchmark. An underweight allocation to the more volatile industrials sector also detracted from performance, particularly in the second half of the Fund’s fiscal year, when energy and metals-and-mining securities rallied strongly.

Weak security selection, notably in the commodity space, was costly to performance as well. The Fund was hurt by its exposure to energy and commodities securities in the first half of the fiscal year, including down-in-quality holdings such as Chesapeake Energy, which we sold in its entirety

before the rebound in commodity prices. Another detractor was Energy Transfer Equity, which owns an equity interest in a limited partnership in the natural gas midstream business. As of the end of the Fund’s fiscal year, the Fund did not hold that security.

BJ’s Wholesale, an operator of membership warehouse clubs in the Eastern United States, generated a negative return and was sold during the fiscal year as we continued to favor higher quality issuers.

Additionally, the junior guaranteed debentures of the wireless telecommunications provider, Sprint, generated a negative return. The Fund sold this debt during the year and purchased the senior guaranteed debt within the company’s capital structure.

While the Fund’s overweight to MBS detracted from performance, results were stronger in the commercial mortgage-backed securities (CMBS) sector, where the Fund’s overweight position performed in line with the benchmark’s CMBS component, which outpaced the overall benchmark. The Fund’s allocation to ABS was a slight detractor, trailing the overall benchmark and its ABS component.

Overall, the fiscal year was a challenging environment for the Fund, which adheres to a bottom-up (bond by bond), fundamentals-focused approach. In the more momentum-driven market that characterized the fiscal period, fundamentals generally deteriorated despite positive market performance.

On the positive side, the Fund’s security selection in U.S. Treasurys was helpful. The Fund used Treasurys to source longer-dated and somewhat higher yielding assets and therefore attempted to counteract exposure to the intermediate part of the yield curve in corporate credit. The benefit was limited, however, because an underweight to the sector detracted from the Fund’s returns.

2

Strong security selection within investment grade credit also aided performance. The Fund’s securities within financials benefited from a supportive regulatory environment that forced a number of banks to increase capital and focus on balance sheet improvement. Some stronger-performing holdings in this group included Wells Fargo, U.S. Bancorp, and JPMorgan Chase.

Throughout the Fund’s fiscal year (and particularly in the first half), we adjusted the portfolio to achieve a higher-quality bias, while attempting to reduce overall risk. For example, the Fund was overweight utilities, which generally have less idiosyncratic risk than healthcare companies, in part due to their reduced exposure to foreign exchange volatility and shareholder-friendly activity. This allocation to a less volatile sector reflected our conservative view and our desire to try to limit those risks.

Although security selection among utilities was a slight detractor for the Fund, it was more than offset by the Fund’s significant sector overweight, as utilities significantly outperformed other high grade credit. Leading performers included MidAmerican Energy and First Mortgage bonds, Duke Energy senior unsecured bonds, and some longer-dated Alabama Power unsecured bonds.

We believe that central bank policy could continue to drive market volatility, while lower yields will likely continue to present challenges for investors. The global wave of populism, that was reflected in

the British vote to leave the European Union (Brexit) and in the U.S. presidential campaign, also continues to be a source of uncertainty. Until those issues are resolved, we think it unlikely that confidence will be strong enough for companies to aggressively invest in their businesses.

From a risk management standpoint, we continue to focus on liquidity given our expectation that volatility will likely persist. We see opportunities, particularly in credits that, in our view, have strong enough balance sheets to weather uncertain times, and we will continue to maintain exposure to sectors such as banking and utilities. Finally, we will maintain a higher-quality bias when seeking incremental yield through high yield bonds and bank loans.

A note about derivatives

The Fund benefited modestly from the use of futures, which added some duration to the Fund. During the fiscal year, the Fund utilized fixed income options to hedge interest rate volatility. Interest rate swaps were utilized as a source of duration and to capture the decline in swap spreads. We also had a small position in credit default swaps in an attempt to protect against emerging market volatility, and we used S&P e-mini futures as a slight hedge. Overall, however, the use of derivatives did not have a material effect on performance (that is, it amounted to less than 0.50 percentage points).

3

| | |

| Performance summary | | |

| Delaware Core Plus Bond Fund | | July 31, 2016 |

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data current for the most recent month end by calling 800 523-1918 or visiting our website at delawareinvestments.com/performance. Current performance may be lower or higher than the performance data quoted.

| | | | | | | | | | | | |

| Fund and benchmark performance1,2 | | Average annual total returns through July 31, 2016 | |

| | | 1 year | | | 5 years | | | 10 years | |

Class A (Est. Aug. 16, 1985) | | | | | | | | | | | | |

Excluding sales charge | | | +4.15% | | | | +3.33% | | | | +5.50% | |

Including sales charge | | | -0.57% | | | | +2.38% | | | | +5.01% | |

Class C (Est. Nov. 29, 1995) | | | | | | | | | | | | |

Excluding sales charge | | | +3.37% | | | | +2.56% | | | | +4.73% | |

Including sales charge | | | +2.37% | | | | +2.56% | | | | +4.73% | |

Class R (Est. June 2, 2003) | | | | | | | | | | | | |

Excluding sales charge | | | +3.88% | | | | +3.07% | | | | +5.27% | |

Including sales charge | | | +3.88% | | | | +3.07% | | | | +5.27% | |

Institutional Class (Est. June 1, 1992) | | | | | | | | | | | | |

Excluding sales charge | | | +4.40% | | | | +3.59% | | | | +5.78% | |

Including sales charge | | | +4.40% | | | | +3.59% | | | | +5.78% | |

Bloomberg Barclays U.S. Aggregate Index | | | +5.94% | | | | +3.57% | | | | +5.06% | |

1Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund and benchmark performance” table. Expenses for each class are listed on the “Fund expense ratios” table on page 6. Performance would have been lower had expense limitations not been in effect.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible accounts.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.25% of average daily net assets. The Board has adopted a formula for calculating 12b-1 plan fees for the Fund’s Class A shares. The Fund’s Class A shares are currently subject to a blended 12b-1 fee equal to the sum of: (i) 0.10% of average daily net assets representing shares acquired prior to June 1, 1992, and (ii) 0.25% of average daily net assets representing shares acquired on or after June 1, 1992. All Class A shares currently bear 12b-1 fees at the same rate, the blended rate, currently 0.25% of average daily net assets, based on the formula described above. This method of calculating Class A 12b-1 fees may be discontinued at the sole discretion of the Board. Performance for Class A shares, excluding sales

4

charges, assumes that no front-end sales charge applied.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. Performance for Class C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Class R shares are available only for certain retirement plan products. They are sold without a sales charge and have an annual distribution and service fee of 0.50% of average daily net assets.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

High yielding, noninvestment grade bonds (junk bonds) involve higher risk than investment grade bonds. The high yield secondary market is particularly susceptible to liquidity problems when institutional investors, such as mutual funds and certain other financial institutions, temporarily stop buying bonds for regulatory, financial, or other reasons. In addition, a less liquid secondary market makes it more difficult for the Fund to obtain precise valuations of the high yield securities in its portfolio.

The Fund may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the opposite direction from what the portfolio manager anticipated. A derivative transaction depends

upon the counterparties’ ability to fulfill their contractual obligations.

Investments in mortgage-backed securities (MBS) may involve risks. MBS represent an ownership interest in a pool of mortgage loans. The individual mortgage loans are packaged or “pooled” together for sale to investors. These mortgage loans may have either fixed or adjustable interest rates.

Because the Fund may invest in bank loans and other direct indebtedness, it is subject to the risk that the Fund will not receive payment of principal, interest, and other amounts due in connection with these investments, which primarily depend on the financial condition of the borrower and the lending institution.

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations.

Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

If and when the Fund invests in forward foreign currency contracts or uses other investments to hedge against currency risks, the Fund will be subject to special risks, including counterparty risk.

The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

Per Standard & Poor’s credit rating agency, bonds rated AA and A are more susceptible to the adverse effects of changes in circumstances and economic conditions than those in the higher-rated AAA category, but the obligor’s capacity to meet its financial commitment on the obligation is still strong. Bonds rated BBB exhibit adequate protection parameters, although adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of

5

Performance summary

Delaware Core Plus Bond Fund

the obligor to meet its financial commitments. Bonds rated BB, B, and CCC are regarded as having significant speculative characteristics, with BB indicating the least degree of speculation of the three.

2The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total annual fund operating expenses (excluding any 12b-1 fees, acquired fund fees and expenses, taxes, interest, short sale and dividend interest expenses, brokerage fees, certain insurance costs, and nonroutine expenses or costs, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations (collectively, nonroutine expenses)) from exceeding 0.65% of the Fund’s average daily net assets during the period from Aug. 1, 2015 through July 31, 2016.* Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

| | | | | | | | |

| Fund expense ratios | | Class A | | Class C | | Class R | | Institutional Class |

Total annual operating expenses (without fee waivers) | | 1.20% | | 1.95% | | 1.45% | | 0.95% |

Net expenses (including fee waivers, if any) | | 0.90% | | 1.65% | | 1.15% | | 0.65% |

Type of waiver | | Contractual | | Contractual | | Contractual | | Contractual |

*The aggregate contractual waiver period covering this report is from Nov. 28, 2014, through Nov. 28, 2016.

6

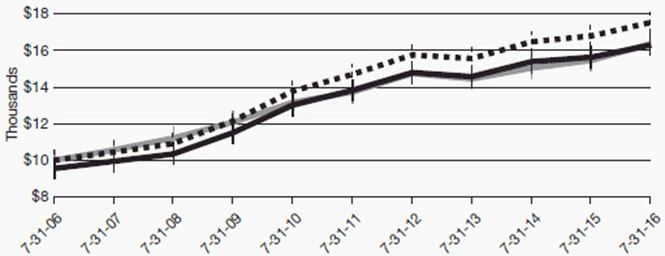

Performance of a $10,000 investment1

Average annual total returns from July 31, 2006, through July 31, 2016

| | | | | | | | | | |

| For period beginning July 31, 2006, through July 31, 2016 | | Starting value | | | | | Ending value |

| | Delaware Core Plus Bond Fund — Institutional Class shares | | | $10,000 | | | | | $17,544 |

| | Bloomberg Barclays U.S. Aggregate Index | | | $10,000 | | | | | $16,379 |

| | Delaware Core Plus Bond Fund — Class A shares | | | $9,550 | | | | | $16,310 |

1The “Performance of a $10,000 investment” graph assumes $10,000 invested in Institutional Class and Class A shares of the Fund on July 31, 2006, and includes the effect of a 4.50% front-end sales charge (for Class A shares) and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Expenses are listed in the “Fund expense ratios” table on page 6. Please note additional details on pages 4 through 7.

The graph also assumes $10,000 invested in the Bloomberg Barclays U.S. Aggregate Index as of

July 31, 2006. The Bloomberg Barclays U.S. Aggregate Index (formerly known as the Barclays U.S. Aggregate Index) measures the performance of publicly issued investment grade (Baa3/BBB- or better) corporate, U.S. government, mortgage-and asset-backed securities with at least one year to maturity and at least $250 million par amount outstanding.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| | | | | | | | |

| | | Nasdaq symbols | | CUSIPs | | | | |

Class A | | DEGGX | | 246094205 | | | | |

Class C | | DUGCX | | 246094700 | | | | |

Class R | | DUGRX | | 246094809 | | | | |

Institutional Class | | DUGIX | | 246094502 | | | | |

7

Disclosure of Fund expenses

For the six-month period from February 1, 2016 to July 31, 2016 (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire six-month period from Feb. 1, 2016 to July 31, 2016.

Actual expenses

The first section of the table shown, “Actual Fund return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical example for comparison purposes

The second section of the table shown, “Hypothetical 5% return,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The Fund’s expenses shown in the table reflect fee waivers in effect. The expenses shown in the table assume reinvestment of all dividends and distributions.

8

Delaware Core Plus Bond Fund

Expense analysis of an investment of $1,000

| | | | | | | | | | | | | | | | |

| | | Beginning Account Value 2/1/16 | | | Ending Account Value 7/31/16 | | | Annualized Expense Ratio | | | Expenses Paid During Period 2/1/16 to 7/31/16* | |

Actual Fund return† | | | | | | | | | | | | | | | | |

Class A | | | $1,000.00 | | | | $1,040.70 | | | | 0.90% | | | | $4.57 | |

Class C | | | 1,000.00 | | | | 1,036.80 | | | | 1.65% | | | | 8.36 | |

Class R | | | 1,000.00 | | | | 1,039.30 | | | | 1.15% | | | | 5.83 | |

Institutional Class | | | 1,000.00 | | | | 1,041.90 | | | | 0.65% | | | | 3.30 | |

Hypothetical 5% return (5% return before expenses) | | | | | | | | | |

Class A | | | $1,000.00 | | | | $1,020.39 | | | | 0.90% | | | | $4.52 | |

Class C | | | 1,000.00 | | | | 1,016.66 | | | | 1.65% | | | | 8.27 | |

Class R | | | 1,000.00 | | | | 1,019.14 | | | | 1.15% | | | | 5.77 | |

Institutional Class | | | 1,000.00 | | | | 1,021.63 | | | | 0.65% | | | | 3.27 | |

| * | “Expenses Paid During Period” are equal to the Fund’s annualized expense ratio, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period). |

| † | Because actual returns reflect only the most recent six-month period, the returns shown may differ significantly from fiscal year returns. |

9

| | |

| Security type / sector allocation | | |

| Delaware Core Plus Bond Fund | | As of July 31, 2016 (Unaudited) |

Sector designations may be different than the sector designations presented in other Fund materials. The sector designations may represent the investment manager’s internal sector classifications.

| | | | | |

| Security type / sector | | Percentage of net assets |

Agency Collateralized Mortgage Obligations | | | | 4.42 | % |

Agency Commercial Mortgage-Backed Securities | | | | 1.67 | % |

Agency Mortgage-Backed Securities | | | | 28.77 | % |

Collateralized Debt Obligations | | | | 1.62 | % |

Convertible Bonds | | | | 0.19 | % |

Corporate Bonds | | | | 38.12 | % |

Banking | | | | 7.31 | % |

Basic Industry | | | | 1.90 | % |

Brokerage | | | | 0.23 | % |

Capital Goods | | | | 1.16 | % |

Communications | | | | 4.60 | % |

Consumer Cyclical | | | | 2.86 | % |

Consumer Non-Cyclical | | | | 5.41 | % |

Electric | | | | 6.20 | % |

Energy | | | | 1.91 | % |

Finance Companies | | | | 0.86 | % |

Insurance | | | | 1.42 | % |

Natural Gas | | | | 0.07 | % |

REITs | | | | 1.28 | % |

Technology | | | | 1.65 | % |

Transportation | | | | 1.26 | % |

Municipal Bonds | | | | 1.10 | % |

Non-Agency Asset-Backed Securities | | | | 6.65 | % |

Non-Agency Collateralized Mortgage Obligations | | | | 1.38 | % |

Non-Agency Commercial Mortgage-Backed Securities | | | | 4.34 | % |

Regional Bonds | | | | 0.43 | % |

Senior Secured Loans | | | | 2.99 | % |

Sovereign Bonds | | | | 0.45 | % |

U.S. Treasury Obligations | | | | 2.00 | % |

Convertible Preferred Stock | | | | 0.02 | % |

Preferred Stock | | | | 0.95 | % |

Short-Term Investments | | | | 14.69 | % |

Total Value of Securities | | | | 109.79 | % |

Liabilities Net of Receivables and Other Assets | | | | (9.79 | %) |

Total Net Assets | | | | 100.00 | % |

10

| | |

| Schedule of investments | | |

| Delaware Core Plus Bond Fund | | July 31, 2016 |

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Agency Collateralized Mortgage Obligations – 4.42% | | | | | | | | |

| |

Fannie Mae Grantor Trust | | | | | | | | |

Series 2002-T1 A2 7.00% 11/25/31 | | | 38,249 | | | $ | 46,641 | |

Fannie Mae Interest Strip | | | | | | | | |

Series 35 2 12.00% 7/25/18 | | | 4,548 | | | | 4,902 | |

Fannie Mae REMIC Trust | | | | | | | | |

Series 2002-W1 2A 6.221% 2/25/42 • | | | 47,628 | | | | 56,570 | |

Fannie Mae REMICs | | | | | | | | |

Series 1988-15 A 9.00% 6/25/18 | | | 81 | | | | 85 | |

Series 1996-46 ZA 7.50% 11/25/26 | | | 35,661 | | | | 40,366 | |

Series 2002-83 GH 5.00% 12/25/17 | | | 33,292 | | | | 33,948 | |

Series 2005-70 PA 5.50% 8/25/35 | | | 9,505 | | | | 10,818 | |

Series 2008-15 SB 6.112% 8/25/36 •S | | | 25,185 | | | | 5,292 | |

Series 2010-129 SM 5.512% 11/25/40 •S | | | 162,702 | | | | 27,906 | |

Series 2011-80 CB 4.00% 8/25/26 | | | 1,953,713 | | | | 2,182,584 | |

Series 2012-122 SD 5.612% 11/25/42 •S | | | 304,429 | | | | 68,796 | |

Series 2013-26 ID 3.00% 4/25/33 S | | | 225,260 | | | | 28,641 | |

Series 2013-38 AI 3.00% 4/25/33 S | | | 217,415 | | | | 24,692 | |

Series 2013-43 IX 4.00% 5/25/43 S | | | 635,096 | | | | 132,109 | |

Series 2013-44 DI 3.00% 5/25/33 S | | | 673,740 | | | | 89,683 | |

Series 2013-55 AI 3.00% 6/25/33 S | | | 267,543 | | | | 31,729 | |

Series 2014-68 BS 5.662% 11/25/44 •S | | | 226,845 | | | | 48,627 | |

Series 2014-90 SA 5.662% 1/25/45 •S | | | 641,387 | | | | 139,382 | |

Series 2015-27 SA 5.962% 5/25/45 •S | | | 85,420 | | | | 19,340 | |

Series 2015-44 Z 3.00% 9/25/43 | | | 197,301 | | | | 197,791 | |

Series 2016-55 SK 5.517% 8/25/46 •S | | | 165,000 | | | | 43,313 | |

Freddie Mac REMICs | | | | | | | | |

Series 2557 WE 5.00% 1/15/18 | | | 29,286 | | | | 29,901 | |

Series 3656 PM 5.00% 4/15/40 | | | 143,128 | | | | 159,337 | |

Series 4109 AI 3.00% 7/15/31 S | | | 440,449 | | | | 38,160 | |

Series 4120 IK 3.00% 10/15/32 S | | | 343,217 | | | | 38,725 | |

Series 4146 IA 3.50% 12/15/32 S | | | 180,767 | | | | 26,457 | |

Series 4159 KS 5.669% 1/15/43 •S | | | 158,857 | | | | 38,508 | |

Series 4181 DI 2.50% 3/15/33 S | | | 109,648 | | | | 11,291 | |

Series 4184 GS 5.639% 3/15/43 •S | | | 180,703 | | | | 43,139 | |

Series 4185 LI 3.00% 3/15/33 S | | | 166,419 | | | | 19,320 | |

Series 4191 CI 3.00% 4/15/33 S | | | 73,388 | | | | 9,162 | |

Series 4435 DY 3.00% 2/15/35 | | | 162,000 | | | | 170,312 | |

Series 4592 WT 5.50% 6/15/46 | | | 390,207 | | | | 438,441 | |

Series 4594 SG 5.519% 6/15/46 •S | | | 445,399 | | | | 116,694 | |

Freddie Mac Strips | | | | | | | | |

Series 267 S5 5.519% 8/15/42 •S | | | 237,298 | | | | 54,140 | |

Series 299 S1 5.519% 1/15/43 •S | | | 176,841 | | | | 38,907 | |

Series 326 S2 5.469% 3/15/44 •S | | | 118,461 | | | | 27,061 | |

11

Schedule of investments

Delaware Core Plus Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Agency Collateralized Mortgage Obligations (continued) | | | | | | | | |

| |

Freddie Mac Structured Agency Credit Risk Debt Notes | | | | | | | | |

Series 2015-HQA2 M2 3.288% 5/25/28 • | | | 250,000 | | | $ | 257,243 | |

Freddie Mac Structured Pass Through Securities | | | | | | | | |

Series T-42 A5 7.50% 2/25/42 ¿ | | | 19,826 | | | | 23,912 | |

GNMA | | | | | | | | |

Series 2010-42 PC 5.00% 7/20/39 | | | 545,000 | | | | 622,015 | |

Series 2010-113 KE 4.50% 9/20/40 | | | 245,000 | | | | 277,430 | |

Series 2013-113 AZ 3.00% 8/20/43 | | | 202,986 | | | | 203,841 | |

Series 2015-133 AL 3.00% 5/20/45 | | | 214,000 | | | | 221,411 | |

| | | | | | | | |

Total Agency Collateralized Mortgage Obligations (cost $6,068,391) | | | | | | | 6,098,622 | |

| | | | | | | | |

| | | | | | | | |

| |

Agency Commercial Mortgage-Backed Securities – 1.67% | | | | | | | | |

| |

Freddie Mac Multifamily Structured Pass Through Certificates | | | | | | | | |

Series K041 A2 3.171% 10/25/24 ¿ | | | 240,000 | | | | 262,928 | |

Series K055 A2 2.673% 3/25/26 ¿ | | | 245,000 | | | | 258,159 | |

Series K056 A2 2.525% 5/25/26 ¿ | | | 85,000 | | | | 87,546 | |

Series K716 A2 3.13% 6/25/21 ¿ | | | 100,000 | | | | 107,341 | |

Series K722 A1 2.183% 5/25/22 ¿ | | | 89,880 | | | | 92,379 | |

FREMF Mortgage Trust | | | | | | | | |

Series 2011-K10 B 144A 4.631% 11/25/49 #• | | | 110,000 | | | | 120,216 | |

Series 2011-K14 B 144A 5.167% 2/25/47 #• | | | 50,000 | | | | 56,312 | |

Series 2011-K15 B 144A 4.948% 8/25/44 #• | | | 75,000 | | | | 83,380 | |

Series 2012-K18 B 144A 4.255% 1/25/45 #• | | | 55,000 | | | | 60,131 | |

Series 2012-K22 B 144A 3.686% 8/25/45 #• | | | 85,000 | | | | 89,744 | |

Series 2012-K23 C 144A 3.656% 10/25/45 #• | | | 30,000 | | | | 30,036 | |

Series 2012-K708 B 144A 3.751% 2/25/45 #• | | | 110,000 | | | | 113,845 | |

Series 2012-K708 C 144A 3.751% 2/25/45 #• | | | 25,000 | | | | 25,048 | |

Series 2013-K30 C 144A 3.557% 6/25/45 #• | | | 25,000 | | | | 24,097 | |

Series 2013-K33 B 144A 3.503% 8/25/46 #• | | | 65,000 | | | | 67,249 | |

Series 2013-K35 C 144A 3.942% 8/25/23 #• | | | 20,000 | | | | 19,810 | |

Series 2013-K712 B 144A 3.369% 5/25/45 #• | | | 125,000 | | | | 128,395 | |

Series 2013-K712 C 144A 3.369% 5/25/45 #• | | | 300,000 | | | | 305,804 | |

Series 2013-K713 B 144A 3.165% 4/25/46 #• | | | 75,000 | | | | 76,594 | |

Series 2013-K713 C 144A 3.165% 4/25/46 #• | | | 140,000 | | | | 139,961 | |

Series 2014-K716 C 144A 3.953% 8/25/47 #• | | | 150,000 | | | | 149,527 | |

| | | | | | | | |

Total Agency Commercial Mortgage-Backed Securities (cost $2,264,684) | | | | 2,298,502 | |

| | | | | | | | |

| | | | | | | | |

| |

Agency Mortgage-Backed Securities – 28.77% | | | | | | | | |

| |

Fannie Mae | | | | | | | | |

10.50% 6/1/30 | | | 10,009 | | | | 10,205 | |

Fannie Mae ARM | | | | | | | | |

2.413% 5/1/43 • | | | 60,911 | | | | 62,903 | |

12

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Agency Mortgage-Backed Securities (continued) | | | | | | | | |

| |

Fannie Mae ARM | | | | | | | | |

2.553% 6/1/43 • | | | 21,778 | | | $ | 22,494 | |

2.612% 8/1/35 • | | | 17,826 | | | | 18,802 | |

2.731% 7/1/36 • | | | 54,798 | | | | 58,350 | |

2.913% 7/1/45 • | | | 36,012 | | | | 37,481 | |

2.966% 4/1/46 • | | | 20,314 | | | | 21,204 | |

3.21% 4/1/44 • | | | 38,621 | | | | 40,475 | |

3.231% 3/1/44 • | | | 77,509 | | | | 81,686 | |

3.276% 9/1/43 • | | | 52,379 | | | | 54,882 | |

Fannie Mae S.F. 15 yr | | | | | | | | |

2.50% 5/1/31 | | | 170,955 | | | | 177,482 | |

3.00% 11/1/26 | | | 263,700 | | | | 278,314 | |

3.00% 9/1/30 | | | 102,535 | | | | 108,064 | |

3.00% 12/1/30 | | | 283,398 | | | | 298,902 | |

3.00% 2/1/31 | | | 252,472 | | | | 266,107 | |

3.00% 3/1/31 | | | 589,665 | | | | 620,899 | |

3.50% 4/1/26 | | | 232,882 | | | | 248,009 | |

3.50% 7/1/26 | | | 60,940 | | | | 64,722 | |

3.50% 11/1/26 | | | 27,491 | | | | 29,198 | |

3.50% 8/1/29 | | | 120,689 | | | | 127,823 | |

3.50% 4/1/30 | | | 56,992 | | | | 61,042 | |

4.00% 11/1/25 | | | 121,826 | | | | 130,055 | |

4.00% 12/1/26 | | | 38,896 | | | | 41,704 | |

4.00% 1/1/27 | | | 281,603 | | | | 300,204 | |

Fannie Mae S.F. 20 yr | | | | | | | | |

3.00% 8/1/33 | | | 35,234 | | | | 37,106 | |

3.00% 1/1/36 | | | 269,112 | | | | 283,129 | |

3.00% 5/1/36 | | | 178,916 | | | | 188,236 | |

Fannie Mae S.F. 30 yr | | | | | | | | |

3.50% 2/1/45 | | | 313,148 | | | | 333,064 | |

3.50% 2/1/46 | | | 948,369 | | | | 1,001,526 | |

3.50% 3/1/46 | | | 84,045 | | | | 88,780 | |

3.50% 5/1/46 | | | 151,909 | | | | 160,471 | |

4.00% 11/1/42 | | | 334,302 | | | | 364,092 | |

4.00% 4/1/46 | | | 576,478 | | | | 624,685 | |

4.50% 7/1/36 | | | 27,655 | | | | 30,251 | |

4.50% 6/1/38 | | | 72,786 | | | | 79,801 | |

4.50% 4/1/39 | | | 81,620 | | | | 88,909 | |

4.50% 6/1/39 | | | 660,952 | | | | 720,864 | |

4.50% 9/1/39 | | | 21,246 | | | | 23,216 | |

4.50% 11/1/39 | | | 65,350 | | | | 72,675 | |

4.50% 1/1/40 | | | 886,102 | | | | 976,709 | |

4.50% 4/1/40 | | | 32,489 | | | | 35,562 | |

13

Schedule of investments

Delaware Core Plus Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Agency Mortgage-Backed Securities (continued) | | | | | | | | |

| |

Fannie Mae S.F. 30 yr | | | | | | | | |

4.50% 6/1/40 | | | 68,826 | | | $ | 76,307 | |

4.50% 8/1/40 | | | 21,708 | | | | 23,881 | |

4.50% 9/1/40 | | | 104,238 | | | | 114,128 | |

4.50% 11/1/40 | | | 59,123 | | | | 64,743 | |

4.50% 2/1/41 | | | 246,247 | | | | 269,639 | |

4.50% 3/1/41 | | | 77,676 | | | | 85,058 | |

4.50% 4/1/41 | | | 94,431 | | | | 103,166 | |

4.50% 7/1/41 | | | 208,871 | | | | 231,129 | |

4.50% 8/1/41 | | | 39,608 | | | | 44,124 | |

4.50% 10/1/41 | | | 78,348 | | | | 85,640 | |

4.50% 12/1/41 | | | 168,785 | | | | 184,262 | |

4.50% 1/1/42 | | | 590,898 | | | | 646,373 | |

4.50% 4/1/42 | | | 23,183 | | | | 25,376 | |

4.50% 8/1/42 | | | 1,173,486 | | | | 1,289,165 | |

4.50% 9/1/42 | | | 685,150 | | | | 748,726 | |

4.50% 1/1/43 | | | 109,386 | | | | 119,655 | |

4.50% 9/1/43 | | | 90,539 | | | | 99,071 | |

4.50% 10/1/43 | | | 478,983 | | | | 527,548 | |

4.50% 11/1/43 | | | 124,276 | | | | 135,553 | |

4.50% 4/1/44 | | | 219,923 | | | | 239,740 | |

4.50% 5/1/44 | | | 58,412 | | | | 63,657 | |

4.50% 6/1/44 | | | 435,594 | | | | 476,343 | |

4.50% 10/1/44 | | | 417,324 | | | | 456,676 | |

4.50% 12/1/44 | | | 72,981 | | | | 79,759 | |

4.50% 1/1/45 | | | 590,939 | | | | 644,549 | |

4.50% 2/1/45 | | | 323,099 | | | | 353,095 | |

4.50% 4/1/45 | | | 420,169 | | | | 460,071 | |

4.50% 3/1/46 | | | 26,391 | | | | 29,099 | |

5.00% 2/1/35 | | | 7,978 | | | | 8,872 | |

5.00% 10/1/35 | | | 41,319 | | | | 45,811 | |

5.00% 11/1/35 | | | 19,910 | | | | 22,070 | |

5.00% 4/1/37 | | | 11,610 | | | | 12,843 | |

5.00% 8/1/37 | | | 3,018 | | | | 3,349 | |

5.00% 12/1/39 | | | 32,949 | | | | 36,761 | |

5.00% 1/1/40 | | | 7,265 | | | | 8,144 | |

5.00% 11/1/44 | | | 404,540 | | | | 448,863 | |

5.50% 12/1/32 | | | 2,221 | | | | 2,514 | |

5.50% 2/1/33 | | | 29,288 | | | | 33,058 | |

5.50% 6/1/33 | | | 17,710 | | | | 20,028 | |

5.50% 4/1/34 | | | 12,455 | | | | 14,098 | |

5.50% 5/1/34 | | | 122,472 | | | | 138,723 | |

5.50% 7/1/34 | | | 3,963 | | | | 4,492 | |

14

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Agency Mortgage-Backed Securities (continued) | | | | | | | | |

| |

Fannie Mae S.F. 30 yr | | | | | | | | |

5.50% 9/1/34 | | | 48,080 | | | $ | 54,506 | |

5.50% 11/1/34 | | | 12,002 | | | | 13,600 | |

5.50% 12/1/34 | | | 268,345 | | | | 304,109 | |

5.50% 3/1/35 | | | 24,367 | | | | 27,559 | |

5.50% 4/1/35 | | | 70,297 | | | | 79,176 | |

5.50% 5/1/35 | | | 67,084 | | | | 75,971 | |

5.50% 6/1/35 | | | 7,982 | | | | 8,945 | |

5.50% 12/1/35 | | | 11,649 | | | | 13,165 | |

5.50% 1/1/36 | | | 54,494 | | | | 61,790 | |

5.50% 4/1/36 | | | 279,394 | | | | 315,240 | |

5.50% 5/1/36 | | | 5,742 | | | | 6,493 | |

5.50% 7/1/36 | | | 3,407 | | | | 3,863 | |

5.50% 9/1/36 | | | 66,656 | | | | 75,454 | |

5.50% 11/1/36 | | | 9,894 | | | | 11,135 | |

5.50% 1/1/37 | | | 41,444 | | | | 46,604 | |

5.50% 2/1/37 | | | 28,739 | | | | 32,323 | |

5.50% 4/1/37 | | | 83,085 | | | | 93,472 | |

5.50% 8/1/37 | | | 58,816 | | | | 66,581 | |

5.50% 9/1/37 | | | 56,306 | | | | 63,271 | |

5.50% 1/1/38 | | | 613,393 | | | | 694,181 | |

5.50% 2/1/38 | | | 98,966 | | | | 111,928 | |

5.50% 6/1/38 | | | 99,094 | | | | 111,402 | |

5.50% 7/1/38 | | | 19,885 | | | | 22,370 | |

5.50% 9/1/38 | | | 87,910 | | | | 99,506 | |

5.50% 12/1/38 | | | 381,594 | | | | 431,876 | |

5.50% 1/1/39 | | | 64,464 | | | | 73,087 | |

5.50% 2/1/39 | | | 149,154 | | | | 168,659 | |

5.50% 6/1/39 | | | 57,319 | | | | 64,721 | |

5.50% 12/1/39 | | | 113,302 | | | | 128,493 | |

5.50% 3/1/40 | | | 326,168 | | | | 369,684 | |

5.50% 7/1/40 | | | 84,515 | | | | 95,661 | |

5.50% 3/1/41 | | | 250,721 | | | | 283,852 | |

5.50% 6/1/41 | | | 145,131 | | | | 164,283 | |

5.50% 9/1/41 | | | 618,954 | | | | 698,121 | |

6.00% 6/1/36 | | | 4,013 | | | | 4,594 | |

6.00% 9/1/36 | | | 21,873 | | | | 25,477 | |

6.00% 12/1/36 | | | 3,987 | | | | 4,577 | |

6.00% 2/1/37 | | | 13,629 | | | | 15,589 | |

6.00% 6/1/37 | | | 2,277 | | | | 2,625 | |

6.00% 7/1/37 | | | 155,737 | | | | 180,386 | |

6.00% 8/1/37 | | | 43,056 | | | | 49,467 | |

6.00% 9/1/37 | | | 4,443 | | | | 5,079 | |

15

Schedule of investments

Delaware Core Plus Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Agency Mortgage-Backed Securities (continued) | | | | | | | | |

| |

Fannie Mae S.F. 30 yr | | | | | | | | |

6.00% 11/1/37 | | | 682 | | | $ | 778 | |

6.00% 5/1/38 | | | 27,241 | | | | 31,128 | |

6.00% 9/1/38 | | | 167,082 | | | | 191,459 | |

6.00% 10/1/38 | | | 6,251 | | | | 7,153 | |

6.00% 9/1/39 | | | 119,773 | | | | 136,911 | |

6.00% 10/1/39 | | | 192,159 | | | | 222,876 | |

6.00% 3/1/40 | | | 18,088 | | | | 20,681 | |

6.00% 4/1/40 | | | 31,082 | | | | 35,554 | |

6.00% 9/1/40 | | | 16,537 | | | | 18,915 | |

6.00% 11/1/40 | | | 6,434 | | | | 7,458 | |

6.00% 5/1/41 | | | 402,486 | | | | 460,600 | |

6.00% 7/1/41 | | | 344,289 | | | | 394,875 | |

8.00% 2/1/30 | | | 16,607 | | | | 16,891 | |

10.00% 7/1/20 | | | 1,937 | | | | 2,086 | |

10.00% 5/1/22 | | | 1,127 | | | | 1,210 | |

10.00% 2/1/25 | | | 22,005 | | | | 23,808 | |

Fannie Mae S.F. 30 yr TBA | | | | | | | | |

3.00% 8/1/46 | | | 5,105,000 | | | | 5,312,391 | |

3.00% 10/1/46 | | | 5,147,000 | | | | 5,335,187 | |

4.50% 8/1/46 | | | 529,000 | | | | 576,852 | |

Freddie Mac ARM | | | | | | | | |

2.434% 10/1/36 • | | | 39,097 | | | | 41,415 | |

2.831% 9/1/45 • | | | 272,821 | | | | 283,089 | |

2.944% 10/1/45 • | | | 72,566 | | | | 75,883 | |

2.949% 11/1/44 • | | | 24,877 | | | | 25,764 | |

3.107% 3/1/46 • | | | 103,486 | | | | 108,527 | |

Freddie Mac S.F. 20 yr | | | | | | | | |

3.00% 6/1/34 | | | 20,126 | | | | 21,149 | |

3.00% 6/1/36 | | | 32,744 | | | | 34,425 | |

Freddie Mac S.F. 30 yr | | | | | | | | |

3.50% 2/1/45 | | | 69,467 | | | | 73,341 | |

3.50% 8/1/45 | | | 370,534 | | | | 394,496 | |

3.50% 11/1/45 | | | 59,275 | | | | 62,580 | |

3.50% 6/1/46 | | | 300,567 | | | | 317,329 | |

4.50% 10/1/35 | | | 3,806 | | | | 4,161 | |

4.50% 4/1/39 | | | 11,757 | | | | 12,924 | |

4.50% 5/1/40 | | | 439,475 | | | | 489,867 | |

4.50% 8/1/40 | | | 93,671 | | | | 102,511 | |

4.50% 3/1/41 | | | 76,198 | | | | 83,384 | |

4.50% 4/1/41 | | | 52,901 | | | | 57,792 | |

4.50% 3/1/42 | | | 266,744 | | | | 293,070 | |

4.50% 7/1/42 | | | 116,983 | | | | 128,795 | |

16

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Agency Mortgage-Backed Securities (continued) | | | | | | | | |

| |

Freddie Mac S.F. 30 yr | | | | | | | | |

4.50% 8/1/44 | | | 168,094 | | | $ | 185,011 | |

4.50% 7/1/45 | | | 361,000 | | | | 395,149 | |

5.00% 6/1/36 | | | 234,244 | | | | 259,991 | |

5.50% 3/1/34 | | | 4,837 | | | | 5,459 | |

5.50% 12/1/34 | | | 4,560 | | | | 5,159 | |

5.50% 12/1/35 | | | 531,895 | | | | 600,481 | |

5.50% 6/1/36 | | | 2,803 | | | | 3,158 | |

5.50% 11/1/36 | | | 6,097 | | | | 6,824 | |

5.50% 9/1/37 | | | 6,205 | | | | 6,972 | |

5.50% 7/1/38 | | | 22,318 | | | | 25,125 | |

5.50% 6/1/39 | | | 23,211 | | | | 26,072 | |

5.50% 3/1/40 | | | 15,224 | | | | 17,088 | |

5.50% 8/1/40 | | | 54,919 | | | | 61,629 | |

5.50% 1/1/41 | | | 17,601 | | | | 19,796 | |

5.50% 6/1/41 | | | 209,597 | | | | 236,239 | |

6.00% 2/1/36 | | | 9,934 | | | | 11,440 | |

6.00% 1/1/38 | | | 6,033 | | | | 6,907 | |

6.00% 6/1/38 | | | 16,137 | | | | 18,473 | |

6.00% 8/1/38 | | | 101,741 | | | | 118,420 | |

6.00% 5/1/40 | | | 38,272 | | | | 44,137 | |

6.00% 7/1/40 | | | 84,982 | | | | 97,682 | |

10.00% 1/1/19 | | | 1,985 | | | | 2,110 | |

GNMA II S.F. 30 yr | | | | | | | | |

5.50% 5/20/37 | | | 35,440 | | | | 39,548 | |

5.50% 4/20/40 | | | 36,130 | | | | 39,649 | |

6.00% 2/20/39 | | | 54,477 | | | | 62,024 | |

6.00% 4/20/46 | | | 53,417 | | | | 61,414 | |

| | | | | | | | |

Total Agency Mortgage-Backed Securities (cost $39,406,094) | | | | | | | 39,668,389 | |

| | | | | | | | |

| | | | | | | | |

| |

Collateralized Debt Obligations – 1.62% | | | | | | | | |

| |

Avery Point III CLO | | | | | | | | |

Series 2013-3A A 144A 2.079% 1/18/25 #• | | | 250,000 | | | | 247,957 | |

Benefit Street Partners CLO IV | | | | | | | | |

Series 2014-IVA A1A 144A 2.186% 7/20/26 #• | | | 500,000 | | | | 498,418 | |

BlueMountain CLO | | | | | | | | |

Series 2015-2A A1 144A 2.109% 7/18/27 #• | | | 250,000 | | | | 248,267 | |

Cent CLO | | | | | | | | |

Series 2014-21A A1B 144A 2.124% 7/27/26 #• | | | 250,000 | | | | 246,411 | |

Magnetite IX | | | | | | | | |

Series 2014-9A A1 144A 2.135% 7/25/26 #• | | | 495,000 | | | | 495,109 | |

Neuberger Berman CLO XIX | | | | | | | | |

Series 2015-19A A1 144A 2.10% 7/15/27 #• | | | 250,000 | | | | 249,102 | |

17

Schedule of investments

Delaware Core Plus Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Collateralized Debt Obligations (continued) | | | | | | | | |

| |

Shackleton CLO | | | | | | | | |

Series 2014-5A A 144A 2.132% 5/7/26 #• | | | 250,000 | | | $ | 248,371 | |

| | | | | | | | |

Total Collateralized Debt Obligations (cost $2,242,603) | | | | | | | 2,233,635 | |

| | | | | | | | |

| | | | | | | | |

| |

Convertible Bonds – 0.19% | | | | | | | | |

| |

Alaska Communications Systems Group 6.25% exercise price $10.28, maturity date 5/1/18 @ | | | 24,000 | | | | 23,370 | |

Blucora 4.25% exercise price $21.66, maturity date 4/1/19 | | | 5,000 | | | | 4,675 | |

Ciena 144A 3.75% exercise price $20.17, maturity date 10/15/18 # | | | 14,000 | | | | 16,695 | |

General Cable 4.50% exercise price $32.36, maturity date 11/15/29 @f | | | 28,000 | | | | 18,900 | |

Helix Energy Solutions Group 3.25% exercise price $25.02, maturity date 3/15/32 | | | 9,000 | | | | 8,348 | |

Hologic 2.00% exercise price $31.18, maturity date 3/1/42 f | | | 19,000 | | | | 25,864 | |

Intel 3.25% exercise price $21.18, maturity date 8/1/39 | | | 19,000 | | | | 32,490 | |

Jefferies Group 3.875% exercise price $44.19, maturity date 11/1/29 | | | 32,000 | | | | 32,720 | |

Meritor 4.00% exercise price $26.73, maturity date 2/15/27 f | | | 39,000 | | | | 37,952 | |

Nuance Communications 2.75% exercise price $32.30, maturity date 11/1/31 | | | 27,000 | | | | 27,236 | |

Titan Machinery 3.75% exercise price $43.17, maturity date 5/1/19 @ | | | 26,000 | | | | 22,441 | |

Vector Group 2.50% exercise price $15.98, maturity date 1/15/19 • | | | 8,000 | | | | 11,495 | |

| | | | | | | | |

Total Convertible Bonds (cost $249,734) | | | | | | | 262,186 | |

| | | | | | | | |

| | | | | | | | |

| |

Corporate Bonds – 38.12% | | | | | | | | |

| |

Banking – 7.31% | | | | | | | | |

Bank Nederlandse Gemeenten 144A 1.625% 4/19/21 # | | | 182,000 | | | | 184,644 | |

Bank of America 4.45% 3/3/26 | | | 745,000 | | | | 801,667 | |

Bank of New York Mellon | | | | | | | | |

2.15% 2/24/20 | | | 30,000 | | | | 30,676 | |

2.50% 4/15/21 | | | 270,000 | | | | 279,913 | |

2.80% 5/4/26 | | | 65,000 | | | | 67,760 | |

4.625% 12/29/49 • | | | 120,000 | | | | 120,000 | |

BB&T 2.05% 5/10/21 | | | 640,000 | | | | 651,091 | |

Citizens Bank 2.55% 5/13/21 | | | 250,000 | | | | 255,432 | |

Citizens Financial Group 4.30% 12/3/25 | | | 115,000 | | | | 122,301 | |

Compass Bank 3.875% 4/10/25 | | | 250,000 | | | | 241,705 | |

Cooperatieve Rabobank 2.50% 1/19/21 | | | 250,000 | | | | 258,120 | |

Credit Suisse Group 144A 6.25% 12/29/49 #• | | | 200,000 | | | | 194,029 | |

18

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Banking (continued) | | | | | | | | |

Credit Suisse Group Funding Guernsey 144A | | | | | | | | |

4.55% 4/17/26 # | | | 615,000 | | | $ | 650,368 | |

Fifth Third Bancorp 2.875% 7/27/20 | | | 50,000 | | | | 52,079 | |

Fifth Third Bank | | | | | | | | |

2.25% 6/14/21 | | | 200,000 | | | | 204,136 | |

3.85% 3/15/26 | | | 200,000 | | | | 213,752 | |

JPMorgan Chase | | | | | | | | |

2.95% 10/1/26 | | | 135,000 | | | | 136,485 | |

4.25% 10/1/27 | | | 635,000 | | | | 685,866 | |

KeyBank 3.40% 5/20/26 | | | 545,000 | | | | 561,443 | |

KFW 1.50% 6/15/21 | | | 130,000 | | | | 131,678 | |

Morgan Stanley | | | | | | | | |

2.50% 4/21/21 | | | 45,000 | | | | 45,571 | |

3.125% 7/27/26 | | | 475,000 | | | | 479,404 | |

3.95% 4/23/27 | | | 155,000 | | | | 160,463 | |

PNC Bank | | | | | | | | |

1.85% 7/20/18 | | | 250,000 | | | | 252,966 | |

2.30% 6/1/20 | | | 335,000 | | | | 344,715 | |

2.45% 11/5/20 | | | 250,000 | | | | 258,465 | |

State Street | | | | | | | | |

2.55% 8/18/20 | | | 120,000 | | | | 124,895 | |

3.55% 8/18/25 | | | 150,000 | | | | 165,071 | |

SunTrust Bank 3.30% 5/15/26 | | | 200,000 | | | | 207,820 | |

Swedbank 144A 2.65% 3/10/21 # | | | 200,000 | | | | 208,213 | |

Toronto-Dominion Bank | | | | | | | | |

2.125% 4/7/21 | | | 115,000 | | | | 117,101 | |

2.50% 12/14/20 | | | 150,000 | | | | 155,248 | |

U.S. Bancorp | | | | | | | | |

3.10% 4/27/26 | | | 50,000 | | | | 52,219 | |

3.60% 9/11/24 | | | 125,000 | | | | 136,047 | |

UBS Group Funding Jersey 144A 4.125% 4/15/26 # | | | 350,000 | | | | 370,800 | |

USB Capital IX 3.50% 10/29/49 @• | | | 705,000 | | | | 607,181 | |

Wells Fargo | | | | | | | | |

4.30% 7/22/27 | | | 45,000 | | | | 49,337 | |

4.40% 6/14/46 | | | 375,000 | | | | 398,587 | |

Zions Bancorporation 4.50% 6/13/23 | | | 105,000 | | | | 109,903 | |

| | | | | | | | |

| | | | | | | 10,087,151 | |

| | | | | | | | |

Basic Industry – 1.90% | | | | | | | | |

Bahia Sul Holdings 144A 5.75% 7/14/26 # | | | 300,000 | | | | 295,875 | |

CF Industries 6.875% 5/1/18 | | | 210,000 | | | | 227,644 | |

Dow Chemical 8.55% 5/15/19 | | | 479,000 | | �� | | 570,765 | |

19

Schedule of investments

Delaware Core Plus Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Basic Industry (continued) | | | | | | | | |

Eastman Chemical | | | | | | | | |

3.80% 3/15/25 | | | 25,000 | | | $ | 26,561 | |

4.65% 10/15/44 | | | 315,000 | | | | 332,005 | |

Georgia-Pacific | | | | | | | | |

144A 2.539% 11/15/19 # | | | 165,000 | | | | 169,217 | |

8.00% 1/15/24 | | | 100,000 | | | | 134,463 | |

International Paper 5.15% 5/15/46 | | | 145,000 | | | | 168,225 | |

INVISTA Finance 144A 4.25% 10/15/19 # | | | 120,000 | | | | 119,690 | |

NOVA Chemicals 144A 5.00% 5/1/25 # | | | 60,000 | | | | 61,050 | |

OCP 144A 4.50% 10/22/25 # | | | 200,000 | | | | 201,562 | |

Rio Tinto Finance USA 3.75% 6/15/25 | | | 185,000 | | | | 199,094 | |

Vale Overseas 5.875% 6/10/21 | | | 50,000 | | | | 51,875 | |

WR Grace & Co-Conn 144A 5.125% 10/1/21 # | | | 60,000 | | | | 63,600 | |

| | | | | | | | |

| | | | | | | 2,621,626 | |

| | | | | | | | |

Brokerage – 0.23% | | | | | | | | |

Jefferies Group | | | | | | | | |

6.45% 6/8/27 | | | 60,000 | | | | 67,162 | |

6.50% 1/20/43 | | | 50,000 | | | | 51,967 | |

Lazard Group | | | | | | | | |

3.75% 2/13/25 | | | 125,000 | | | | 126,466 | |

6.85% 6/15/17 | | | 64,000 | | | | 66,860 | |

| | | | | | | | |

| | | | | | | 312,455 | |

| | | | | | | | |

Capital Goods – 1.16% | | | | | | | | |

Ball 5.00% 3/15/22 | | | 315,000 | | | | 338,625 | |

Cemex 144A 7.75% 4/16/26 # | | | 200,000 | | | | 222,500 | |

Fortive 144A 3.15% 6/15/26 # | | | 150,000 | | | | 159,025 | |

Fortune Brands Home & Security 3.00% 6/15/20 | | | 70,000 | | | | 72,200 | |

General Electric 2.10% 12/11/19 | | | 65,000 | | | | 67,289 | |

Lockheed Martin 3.55% 1/15/26 | | | 105,000 | | | | 115,854 | |

Masco 3.50% 4/1/21 | | | 175,000 | | | | 182,661 | |

Parker-Hannifin 3.30% 11/21/24 | | | 10,000 | | | | 10,819 | |

United Rentals North America 5.875% 9/15/26 | | | 340,000 | | | | 354,875 | |

Waste Management 2.40% 5/15/23 | | | 70,000 | | | | 71,389 | |

| | | | | | | | |

| | | | | | | 1,595,237 | |

| | | | | | | | |

Communications – 4.60% | | | | | | | | |

21st Century Fox America 4.95% 10/15/45 | | | 180,000 | | | | 214,368 | |

American Tower | | | | | | | | |

4.00% 6/1/25 | | | 150,000 | | | | 163,381 | |

4.40% 2/15/26 | | | 95,000 | | | | 105,426 | |

American Tower Trust I 144A 3.07% 3/15/23 # | | | 210,000 | | | | 217,326 | |

AT&T | | | | | | | | |

3.60% 2/17/23 | | | 110,000 | | | | 117,004 | |

20

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Communications (continued) | | | | | | | | |

AT&T | | | | | | | | |

4.35% 6/15/45 | | | 95,000 | | | $ | 95,513 | |

5.65% 2/15/47 | | | 230,000 | | | | 275,187 | |

CC Holdings GS V 3.849% 4/15/23 | | | 100,000 | | | | 108,219 | |

Charter Communications Operating 144A | | | | | | | | |

4.908% 7/23/25 # | | | 605,000 | | | | 669,212 | |

Columbus International 144A 7.375% 3/30/21 # | | | 200,000 | | | | 214,192 | |

Comcast 2.35% 1/15/27 | | | 580,000 | | | | 581,491 | |

Crown Castle International 5.25% 1/15/23 | | | 150,000 | | | | 172,261 | |

Crown Castle Towers 144A 4.883% 8/15/20 # | | | 505,000 | | | | 551,751 | |

CSC Holdings 5.25% 6/1/24 | | | 525,000 | | | | 501,055 | |

DISH DBS 144A 7.75% 7/1/26 # | | | 255,000 | | | | 265,041 | |

Frontier Communications | | | | | | | | |

10.50% 9/15/22 | | | 80,000 | | | | 86,700 | |

11.00% 9/15/25 | | | 175,000 | | | | 187,469 | |

GTP Acquisition Partners I 144A 2.35% 6/15/20 # | | | 100,000 | | | | 99,653 | |

SBA Tower Trust 144A 2.24% 4/16/18 # | | | 160,000 | | | | 160,320 | |

Sky 144A 3.75% 9/16/24 # | | | 355,000 | | | | 377,549 | |

Sprint Communications 144A 7.00% 3/1/20 # | | | 230,000 | | | | 245,237 | |

Time Warner Cable 7.30% 7/1/38 | | | 145,000 | | | | 189,837 | |

Verizon Communications | | | | | | | | |

1.75% 8/15/21 | | | 270,000 | | | | 270,270 | |

4.125% 8/15/46 | | | 205,000 | | | | 207,965 | |

4.522% 9/15/48 | | | 135,000 | | | | 144,697 | |

4.862% 8/21/46 | | | 60,000 | | | | 67,625 | |

WPP Finance 2010 5.625% 11/15/43 | | | 45,000 | | | | 54,355 | |

| | | | | | | | |

| | | | | | | 6,343,104 | |

| | | | | | | | |

Consumer Cyclical – 2.86% | | | | | | | | |

BMW U.S. Capital | | | | | | | | |

144A 2.00% 4/11/21 # | | | 265,000 | | | | 269,606 | |

144A 2.80% 4/11/26 # | | | 120,000 | | | | 124,871 | |

CVS Health 5.00% 12/1/24 | | | 555,000 | | | | 646,599 | |

Ford Motor Credit 3.096% 5/4/23 | | | 200,000 | | | | 204,385 | |

General Motors Financial | | | | | | | | |

3.45% 4/10/22 | | | 155,000 | | | | 158,318 | |

3.70% 5/9/23 | | | 105,000 | | | | 107,408 | |

5.25% 3/1/26 | | | 65,000 | | | | 72,711 | |

Goodyear Tire & Rubber 5.00% 5/31/26 | | | 325,000 | | | | 343,281 | |

Home Depot 3.00% 4/1/26 | | | 65,000 | | | | 70,065 | |

Hyundai Capital America | | | | | | | | |

144A 2.125% 10/2/17 # | | | 130,000 | | | | 131,178 | |

144A 3.00% 3/18/21 # | | | 70,000 | | | | 72,640 | |

21

Schedule of investments

Delaware Core Plus Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Consumer Cyclical (continued) | | | | | | | | |

Lowe’s | | | | | | | | |

2.50% 4/15/26 | | | 95,000 | | | $ | 97,525 | |

3.375% 9/15/25 | | | 100,000 | | | | 110,369 | |

3.70% 4/15/46 | | | 150,000 | | | | 158,716 | |

Marriott International 3.125% 6/15/26 | | | 145,000 | | | | 148,277 | |

MGM Resorts International 6.00% 3/15/23 | | | 180,000 | | | | 195,188 | |

O’Reilly Automotive 3.55% 3/15/26 | | | 70,000 | | | | 75,103 | |

Starbucks 2.45% 6/15/26 | | | 80,000 | | | | 82,636 | |

Starwood Hotels & Resorts Worldwide | | | | | | | | |

3.75% 3/15/25 @ | | | 140,000 | | | | 148,538 | |

4.50% 10/1/34 @ | | | 20,000 | | | | 20,972 | |

Target 3.625% 4/15/46 | | | 80,000 | | | | 83,683 | |

Walgreens Boots Alliance | | | | | | | | |

3.10% 6/1/23 | | | 355,000 | | | | 367,246 | |

3.45% 6/1/26 | | | 200,000 | | | | 209,884 | |

4.80% 11/18/44 | | | 40,000 | | | | 45,448 | |

| | | | | | | | |

| | | | | | | 3,944,647 | |

| | | | | | | | |

Consumer Non-Cyclical – 5.41% | | | | | | | | |

AbbVie | | | | | | | | |

3.20% 5/14/26 | | | 215,000 | | | | 220,967 | |

4.45% 5/14/46 | | | 125,000 | | | | 133,515 | |

Anheuser-Busch InBev Finance 3.65% 2/1/26 | | | 740,000 | | | | 796,092 | |

AstraZeneca 3.375% 11/16/25 | | | 180,000 | | | | 193,284 | |

Becton Dickinson 6.375% 8/1/19 | | | 185,000 | | | | 211,305 | |

Biogen | | | | | | | | |

4.05% 9/15/25 | | | 40,000 | | | | 43,870 | |

5.20% 9/15/45 | | | 125,000 | | | | 150,409 | |

Celgene | | | | | | | | |

3.25% 8/15/22 | | | 80,000 | | | | 84,050 | |

3.875% 8/15/25 | | | 145,000 | | | | 157,605 | |

JB y Cia 144A 3.75% 5/13/25 # | | | 150,000 | | | | 155,414 | |

Kraft Heinz Foods 144A 3.00% 6/1/26 # | | | 260,000 | | | | 266,386 | |

LifePoint Health 144A 5.375% 5/1/24 # | | | 402,000 | | | | 412,050 | |

Molson Coors Brewing | | | | | | | | |

2.10% 7/15/21 | | | 35,000 | | | | 35,506 | |

3.00% 7/15/26 | | | 100,000 | | | | 102,340 | |

4.20% 7/15/46 | | | 280,000 | | | | 296,309 | |

Mylan | | | | | | | | |

144A 3.15% 6/15/21 # | | | 50,000 | | | | 51,624 | |

144A 3.95% 6/15/26 # | | | 540,000 | | | | 563,457 | |

New York & Presbyterian Hospital 4.063% 8/1/56 | | | 130,000 | | | | 144,771 | |

22

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Consumer Non-Cyclical (continued) | | | | | | | | |

Pernod Ricard | | | | | | | | |

144A 3.25% 6/8/26 # | | | 310,000 | | | $ | 321,071 | |

144A 4.45% 1/15/22 # | | | 300,000 | | | | 332,034 | |

Reynolds American | | | | | | | | |

4.00% 6/12/22 | | | 155,000 | | | | 170,223 | |

4.45% 6/12/25 | | | 315,000 | | | | 356,287 | |

St. Jude Medical 2.80% 9/15/20 | | | 75,000 | | | | 77,835 | |

Sysco 3.30% 7/15/26 | | | 400,000 | | | | 423,571 | |

Tempur Sealy International 144A 5.50% 6/15/26 # | | | 330,000 | | | | 334,745 | |

Teva Pharmaceutical Finance Netherlands III | | | | | | | | |

2.20% 7/21/21 | | | 125,000 | | | | 125,777 | |

2.80% 7/21/23 | | | 475,000 | | | | 484,001 | |

3.15% 10/1/26 | | | 80,000 | | | | 81,931 | |

Thermo Fisher Scientific 3.00% 4/15/23 | | | 560,000 | | | | 578,640 | |

Zimmer Biomet Holdings 4.45% 8/15/45 | | | 140,000 | | | | 150,270 | |

| | | | | | | | |

| | | | | | | 7,455,339 | |

| | | | | | | | |

Electric – 6.20% | | | | | | | | |

AES 5.50% 4/15/25 | | | 135,000 | | | | 138,881 | |

AES Gener 144A 5.00% 7/14/25 # | | | 200,000 | | | | 213,889 | |

Alabama Power 4.30% 1/2/46 | | | 105,000 | | | | 122,004 | |

Ameren 3.65% 2/15/26 | | | 110,000 | | | | 119,630 | |

Ameren Illinois 9.75% 11/15/18 | | | 389,000 | | | | 460,303 | |

American Transmission Systems 144A 5.25% 1/15/22 # | | | 100,000 | | | | 114,705 | |

Appalachian Power | | | | | | | | |

3.40% 6/1/25 | | | 270,000 | | | | 290,242 | |

4.45% 6/1/45 | | | 80,000 | | | | 89,002 | |

Black Hills 3.95% 1/15/26 | | | 40,000 | | | | 43,011 | |

Cleveland Electric Illuminating 5.50% 8/15/24 | | | 230,000 | | | | 276,497 | |

CMS Energy 6.25% 2/1/20 | | | 190,000 | | | | 218,018 | |

ComEd Financing III 6.35% 3/15/33 @ | | | 190,000 | | | | 201,739 | |

Commonwealth Edison | | | | | | | | |

3.65% 6/15/46 | | | 5,000 | | | | 5,272 | |

4.35% 11/15/45 | | | 130,000 | | | | 152,859 | |

Consumers Energy 4.10% 11/15/45 | | | 35,000 | | | | 40,405 | |

Dominion Resources 3.90% 10/1/25 | | | 195,000 | | | | 212,417 | |

DTE Energy 3.30% 6/15/22 | | | 115,000 | | | | 121,916 | |

Duke Energy 4.80% 12/15/45 | | | 70,000 | | | | 84,492 | |

Duke Energy Carolinas 3.875% 3/15/46 | | | 95,000 | | | | 105,495 | |

Electricite de France 144A 5.25% 1/29/49 #• | | | 125,000 | | | | 122,344 | |

Emera 6.75% 6/15/76 • | | | 205,000 | | | | 222,018 | |

Emera US Finance 144A 4.75% 6/15/46 # | | | 195,000 | | | | 215,638 | |

Enel 144A 8.75% 9/24/73 #• | | | 200,000 | | | | 232,250 | |

23

Schedule of investments

Delaware Core Plus Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Electric (continued) | | | | | | | | |

Enel Finance International 144A 6.00% 10/7/39 # | | | 100,000 | | | $ | 121,541 | |

Entergy 4.00% 7/15/22 | | | 285,000 | | | | 309,518 | |

Entergy Arkansas 3.50% 4/1/26 | | | 50,000 | | | | 54,969 | |

Entergy Louisiana 4.95% 1/15/45 | | | 55,000 | | | | 59,076 | |

Entergy Mississippi 2.85% 6/1/28 | | | 105,000 | | | | 108,776 | |

Exelon 3.95% 6/15/25 | | | 90,000 | | | | 98,117 | |

Indiana Michigan Power 4.55% 3/15/46 | | | 65,000 | | | | 75,310 | |

IPALCO Enterprises 3.45% 7/15/20 | | | 125,000 | | | | 129,063 | |

ITC Holdings | | | | | | | | |

3.25% 6/30/26 | | | 75,000 | | | | 76,673 | |

3.65% 6/15/24 | | | 70,000 | | | | 73,588 | |

Kansas City Power & Light 3.65% 8/15/25 | | | 255,000 | | | | 273,518 | |

LG&E & KU Energy 4.375% 10/1/21 | | | 380,000 | | | | 419,892 | |

Louisville Gas & Electric 4.375% 10/1/45 | | | 40,000 | | | | 47,781 | |

Metropolitan Edison 144A 4.00% 4/15/25 # | | | 50,000 | | | | 52,832 | |

MidAmerican Energy 4.25% 5/1/46 | | | 210,000 | | | | 248,234 | |

National Rural Utilities Cooperative Finance | | | | | | | | |

2.30% 11/1/20 | | | 20,000 | | | | 20,734 | |

2.70% 2/15/23 | | | 170,000 | | | | 177,461 | |

4.75% 4/30/43 • | | | 190,000 | | | | 191,055 | |

5.25% 4/20/46 • | | | 60,000 | | | | 63,474 | |

NextEra Energy Capital Holdings | | | | | | | | |

2.40% 9/15/19 | | | 265,000 | | | | 270,459 | |

3.625% 6/15/23 | | | 60,000 | | | | 63,803 | |

NV Energy 6.25% 11/15/20 | | | 100,000 | | | | 118,776 | |

Pennsylvania Electric 5.20% 4/1/20 | | | 175,000 | | | | 190,226 | |

SCANA 4.125% 2/1/22 | | | 85,000 | | | | 89,692 | |

South Carolina Electric & Gas 4.10% 6/15/46 | | | 125,000 | | | | 136,381 | |

Southern | | | | | | | | |

2.75% 6/15/20 | | | 395,000 | | | | 410,355 | |

3.25% 7/1/26 | | | 170,000 | | | | 178,155 | |

4.40% 7/1/46 | | | 160,000 | | | | 178,019 | |

Trans-Allegheny Interstate Line 144A 3.85% 6/1/25 # | | | 115,000 | | | | 123,437 | |

WEC Energy Group 3.55% 6/15/25 | | | 55,000 | | | | 60,151 | |

Wisconsin Electric Power 4.30% 12/15/45 | | | 75,000 | | | | 87,982 | |

Xcel Energy 3.30% 6/1/25 | | | 230,000 | | | | 245,832 | |

| | | | | | | | |

| | | | | | | 8,557,907 | |

| | | | | | | | |

Energy – 1.91% | | | | | | | | |

CNOOC Finance 2015 Australia 2.625% 5/5/20 | | | 200,000 | | | | 204,077 | |

ConocoPhillips 4.95% 3/15/26 | | | 180,000 | | | | 200,559 | |

Dominion Gas Holdings 4.60% 12/15/44 | | | 90,000 | | | | 97,995 | |

24

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Energy (continued) | | | | | | | | |

Energy Transfer Partners | | | | | | | | |

4.75% 1/15/26 | | | 55,000 | | | $ | 56,310 | |

6.125% 12/15/45 | | | 90,000 | | | | 94,603 | |

9.70% 3/15/19 | | | 127,000 | | | | 146,578 | |

EnLink Midstream Partners | | | | | | | | |

2.70% 4/1/19 | | | 75,000 | | | | 73,520 | |

4.85% 7/15/26 | | | 65,000 | | | | 63,304 | |

Enterprise Products Operating | | | | | | | | |

3.95% 2/15/27 | | | 135,000 | | | | 142,539 | |

7.034% 1/15/68 • | | | 30,000 | | | | 31,655 | |

Noble Energy 5.05% 11/15/44 | | | 90,000 | | | | 89,600 | |

Petrobras Global Finance 8.375% 5/23/21 | | | 50,000 | | | | 52,988 | |

Petroleos Mexicanos | | | | | | | | |

6.625% 6/15/35 | | | 20,000 | | | | 20,779 | |

144A 6.875% 8/4/26 # | | | 55,000 | | | | 61,875 | |

Petronas Global Sukuk 144A 2.707% 3/18/20 # | | | 200,000 | | | | 203,336 | |

Plains All American Pipeline 8.75% 5/1/19 | | | 195,000 | | | | 225,985 | |

Regency Energy Partners 5.875% 3/1/22 | | | 155,000 | | | | 169,246 | |

Shell International Finance | | | | | | | | |

2.875% 5/10/26 | | | 95,000 | | | | 96,995 | |

4.00% 5/10/46 | | | 235,000 | | | | 242,362 | |

Sunoco Logistics Partners Operations 3.90% 7/15/26 | | | 140,000 | | | | 139,427 | |

Woodside Finance | | | | | | | | |

144A 3.65% 3/5/25 # | | | 70,000 | | | | 69,870 | |

144A 8.75% 3/1/19 # | | | 125,000 | | | | 145,361 | |

| | | | | | | | |

| | | | | | | 2,628,964 | |

| | | | | | | | |

Finance Companies – 0.86% | | | | | | | | |

AerCap Ireland Capital 3.95% 2/1/22 | | | 450,000 | | | | 472,356 | |

Affiliated Managers Group 3.50% 8/1/25 | | | 110,000 | | | | 110,829 | |

Aviation Capital Group | | | | | | | | |

144A 2.875% 9/17/18 # | | | 10,000 | | | | 10,162 | |

144A 4.875% 10/1/25 # | | | 80,000 | | | | 83,572 | |

144A 6.75% 4/6/21 # | | | 90,000 | | | | 105,277 | |

Peachtree Corners Funding Trust 144A 3.976% 2/15/25 # | | | 200,000 | | | | 203,487 | |

SMBC Aviation Capital Finance 144A 2.65% 7/15/21 # | | | 200,000 | | | | 201,418 | |

| | | | | | | | |

| | | | | | | 1,187,101 | |

| | | | | | | | |

Insurance – 1.42% | | | | | | | | |

Berkshire Hathaway | | | | | | | | |

2.75% 3/15/23 | | | 85,000 | | | | 88,781 | |

3.125% 3/15/26 | | | 255,000 | | | | 271,740 | |

Highmark 144A 6.125% 5/15/41 #@ | | | 30,000 | | | | 30,169 | |

MetLife 5.25% 12/29/49 • | | | 145,000 | | | | 145,478 | |

25

Schedule of investments

Delaware Core Plus Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Insurance (continued) | | | | | | | | |

Principal Life Global Funding II 144A 3.00% 4/18/26 # | | | 105,000 | | | $ | 109,045 | |

Prudential Financial | | | | | | | | |

4.50% 11/15/20 | | | 50,000 | | | | 55,125 | |

5.375% 5/15/45 • | | | 95,000 | | | | 98,919 | |

5.625% 6/15/43 • | | | 95,000 | | | | 101,840 | |

5.875% 9/15/42 • | | | 225,000 | | | | 249,637 | |

TIAA Asset Management Finance | | | | | | | | |

144A 2.95% 11/1/19 # | | | 95,000 | | | | 97,557 | |

144A 4.125% 11/1/24 # | | | 425,000 | | | | 449,873 | |

XLIT | | | | | | | | |

4.45% 3/31/25 | | | 85,000 | | | | 86,367 | |

5.50% 3/31/45 | | | 115,000 | | | | 115,621 | |

6.50% 10/29/49 • | | | 80,000 | | | | 55,400 | |

| | | | | | | | |

| | | | | | | 1,955,552 | |

| | | | | | | | |

Natural Gas – 0.07% | | | | | | | | |

Southern Gas Capital 3.25% 6/15/26 | | | 90,000 | | | | 93,647 | |

| | | | | | | | |

| | | | | | | 93,647 | |

| | | | | | | | |

REITs – 1.28% | | | | | | | | |

Alexandria Real Estate Equities 3.95% 1/15/27 | | | 45,000 | | | | 47,135 | |

AvalonBay Communities 2.95% 5/11/26 | | | 195,000 | | | | 198,630 | |

Corporate Office Properties | | | | | | | | |

3.60% 5/15/23 | | | 150,000 | | | | 149,275 | |

5.25% 2/15/24 | | | 85,000 | | | | 92,300 | |

DDR 7.875% 9/1/20 | | | 90,000 | | | | 109,027 | |

Education Realty Operating Partnership 4.60% 12/1/24 | | | 115,000 | | | | 120,854 | |

Hospitality Properties Trust 4.50% 3/15/25 | | | 100,000 | | | | 101,803 | |

Host Hotels & Resorts | | | | | | | | |

3.75% 10/15/23 | | | 135,000 | | | | 137,973 | |

4.50% 2/1/26 | | | 5,000 | | | | 5,345 | |

Kimco Realty 3.40% 11/1/22 | | | 25,000 | | | | 26,349 | |

PLA Administradora Industrial 144A 5.25% 11/10/22 # | | | 200,000 | | | | 207,200 | |

Regency Centers 5.875% 6/15/17 | | | 71,000 | | | | 73,548 | |

Simon Property Group 2.50% 7/15/21 | | | 45,000 | | | | 46,625 | |

Sovran Acquisition 3.50% 7/1/26 | | | 95,000 | | | | 96,361 | |

Trust F/1401 144A 5.25% 1/30/26 # | | | 200,000 | | | | 211,250 | |

UDR 4.00% 10/1/25 | | | 40,000 | | | | 43,745 | |

WP Carey 4.60% 4/1/24 | | | 90,000 | | | | 93,754 | |

| | | | | | | | |

| | | | | | | 1,761,174 | |

| | | | | | | | |

Technology – 1.65% | | | | | | | | |

Apple | | | | | | | | |

2.45% 8/4/26 | | | 80,000 | | | | 80,250 | |

3.85% 8/4/46 | | | 150,000 | | | | 150,950 | |

26

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Corporate Bonds (continued) | | | | | | | | |

| |

Technology (continued) | | | | | | | | |

CDK Global 4.50% 10/15/24 | | | 105,000 | | | $ | 106,507 | |

Diamond 1 Finance 144A 6.02% 6/15/26 # | | | 425,000 | | | | 456,146 | |

Fidelity National Information Services 5.00% 10/15/25 | | | 250,000 | | | | 289,847 | |

NXP 144A 4.625% 6/1/23 # | | | 330,000 | | | | 342,583 | |

Oracle | | | | | | | | |

2.40% 9/15/23 | | | 305,000 | | | | 308,318 | |

4.00% 7/15/46 | | | 130,000 | | | | 134,997 | |

Samsung Electronics America 144A 1.75% 4/10/17 # | | | 200,000 | | | | 200,708 | |

Tencent Holdings 144A 3.375% 5/2/19 # | | | 200,000 | | | | 207,604 | |

| | | | | | | | |

| | | | | | | 2,277,910 | |

| | | | | | | | |

Transportation – 1.26% | | | | | | | | |

Air Canada 2015-1 Class A Pass Through Trust 144A | | | | | | | | |

3.60% 3/15/27 # ¿ | | | 68,906 | | | | 71,317 | |

American Airlines 2014-1 Class A Pass Through Trust | | | | | | | | |

3.70% 10/1/26 ¿ | | | 50,237 | | | | 52,874 | |

American Airlines 2015-1 Class A Pass Through Trust | | | | | | | | |

3.375% 5/1/27 ¿ | | | 85,906 | | | | 89,020 | |

American Airlines 2015-2 Class AA Pass Through Trust | | | | | | | | |

3.60% 9/22/27 ¿ | | | 25,000 | | | | 26,909 | |

American Airlines 2016-1 Class AA Pass Through Trust | | | | | | | | |

3.575% 1/15/28 ¿ | | | 59,853 | | | | 64,417 | |

Burlington Northern Santa Fe 4.70% 9/1/45 | | | 275,000 | | | | 336,448 | |

Canadian National Railway 3.20% 8/2/46 | | | 135,000 | | | | 134,917 | |

ERAC USA Finance 144A 3.30% 12/1/26 # | | | 230,000 | | | | 237,855 | |

Norfolk Southern 2.90% 6/15/26 | | | 170,000 | | | | 176,879 | |

Penske Truck Leasing | | | | | | | | |

144A 3.30% 4/1/21 # | | | 115,000 | | | | 118,993 | |

144A 3.375% 2/1/22 # | | | 215,000 | | | | 219,635 | |

United Airlines 2014-1 Class A Pass Through Trust | | | | | | | | |

4.00% 4/11/26 ¿ | | | 42,423 | | | | 45,684 | |

United Airlines 2014-2 Class A Pass Through Trust | | | | | | | | |

3.75% 9/3/26 ¿ | | | 97,090 | | | | 103,523 | |

United Airlines 2016-1 Class AA Pass Through Trust | | | | | | | | |

3.10% 7/7/28 ¿ | | | 55,000 | | | | 57,269 | |

| | | | | | | | |

| | | | | | | 1,735,740 | |

| | | | | | | | |

| | |

Total Corporate Bonds (cost $50,146,320) | | | | | | | 52,557,554 | |

| | | | | | | | |

27

Schedule of investments

Delaware Core Plus Bond Fund

| | | | | | | | |

| | | Principal amount° | | | Value (U.S. $) | |

| |

Municipal Bonds – 1.10% | | | | | | | | |

| |

Bay Area Toll Authority | | | | | | | | |

(Build America Bond) Series S-3 6.907% 10/1/50 | | | 170,000 | | | $ | 284,225 | |

California State | | | | | | | | |

(Build America Bond) 7.55% 4/1/39 | | | 135,000 | | | | 223,345 | |

(Various Purpose) 5.00% 9/1/26 | | | 90,000 | | | | 118,730 | |

Commonwealth of Massachusetts | | | | | | | | |

Series B 5.00% 7/1/26 | | | 35,000 | | | | 46,047 | |

Series D 5.00% 4/1/26 | | | 35,000 | | | | 45,853 | |

Dallas, Texas Area Rapid Transit | | | | | | | | |

Series A 5.00% 12/1/46 | | | 140,000 | | | | 170,288 | |

New Jersey Turnpike Authority | | | | | | | | |

Series A 7.102% 1/1/41 | | | 90,000 | | | | 140,928 | |

(Build America Bonds) | | | | | | | | |

Series E 5.00% 1/1/45 | | | 140,000 | | | | 166,547 | |

Series F 7.414% 1/1/40 | | | 45,000 | | | | 72,701 | |

New York City, New York | | | | | | | | |

Series C 5.00% 8/1/26 | | | 65,000 | | | | 84,200 | |

Series C 5.00% 8/1/27 | | | 35,000 | | | | 44,969 | |

South Carolina Public Service Authority | | | | | | | | |

Series D 4.77% 12/1/45 | | | 55,000 | | | | 65,393 | |

Texas Water Development Board | | | | | | | | |

Series A 5.00% 10/15/45 | | | 45,000 | | | | 54,990 | |

| | | | | | | | |

Total Municipal Bonds (cost $1,453,160) | | | | | | | 1,518,216 | |

| | | | | | | | |

| | | | | | | | |

| |

Non-Agency Asset-Backed Securities – 6.65% | | | | | | | | |

| |

AEP Texas Central Transition Funding II | | | | | | | | |

Series 2006-A A4 5.17% 1/1/18 | | | 52,899 | | | | 54,743 | |

Ally Master Owner Trust | | | | | | | | |

Series 2012-5 A 1.54% 9/15/19 | | | 365,000 | | | | 366,002 | |

Series 2014-4 A2 1.43% 6/17/19 | | | 180,000 | | | | 180,231 | |

American Express Credit Account Master Trust | | | | | | | | |

Series 2014-1 A 0.851% 12/15/21 • | | | 1,200,000 | | | | 1,200,672 | |

Series 2014-3 A 1.49% 4/15/20 | | | 100,000 | | | | 100,554 | |

ARI Fleet Lease Trust | | | | | | | | |

Series 2015-A A2 144A 1.11% 11/15/18 # | | | 69,203 | | | | 69,082 | |

Avis Budget Rental Car Funding AESOP | | | | | | | | |

Series 2013-1A A 144A 1.92% 9/20/19 # | | | 120,000 | | | | 120,049 | |

Series 2014-1A A 144A 2.46% 7/20/20 # | | | 200,000 | | | | 202,096 | |

Bank of America Credit Card Trust | | | | | | | | |

Series 2014-A3 A 0.771% 1/15/20 • | | | 265,000 | | | | 265,280 | |