UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04323

Natixis Funds Trust I

(Exact name of Registrant as specified in charter)

399 Boylston Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Russell L. Kane, Esq.

NGAM Distribution, L.P.

399 Boylston Street

Boston, Massachusetts 02116

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 449-2822

Date of fiscal year end: December 31

Date of reporting period: December 31, 2016

Item 1. Reports to Stockholders.

The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

ANNUAL REPORT

December 31, 2016

Mirova Global Sustainable Equity Fund

Natixis Oakmark Fund

Natixis Oakmark International Fund

Vaughan Nelson Small Cap Value Fund

Vaughan Nelson Value Opportunity Fund

TABLE OF CONTENTS

Portfolio Review page 1

Portfolio of Investments page 29

Financial Statements page 51

Notes to Financial Statements page 77

MIROVA GLOBAL SUSTAINABLE EQUITY FUND

| | |

| Managers | | Symbols |

| Jens Peers, CFA® | | Class A ESGMX |

| Suzanne Senellart | | Class C ESGCX |

| Hua Cheng, CFA®, PhD | | Class Y ESGYX |

| Natixis Asset Management U.S., LLC (“Natixis AM US”) | | |

Investment Goal

The Fund seeks long-term capital appreciation.

Market Conditions

2016 was another positive year for equity markets, especially as a sentiment driven year-end rally after the U.S. elections boosted returns significantly. On a relative basis, it turned out to be a rather negative year for ESG (Environmental, Social and Governance) investors though as traditional style biases, typical for ESG investing, were out of favor: Growth and Quality underperformed, while Value outperformed.

The year was clearly dominated by political news: Brexit and the U.S. elections. They turned out to be typical cases of buy on the rumor, sell on the news, as markets retracted before both events, but rebounded strongly (and more) after.

The macro-economic picture was generally positive with U.S. economic growth stronger than expected, leading to increased interest rates. There were also signs of a European economic recovery as construction activity picked up and unemployment numbers improved.

Performance Results

The Mirova Global Sustainable Equity Fund was launched on March 31, 2016. For the nine months ended December 31, 2016, Class A shares of Mirova Global Sustainable Equity Fund returned -0.85% at net asset value. The Fund underperformed its benchmark, the MSCI World Index (Net), which returned 7.89% over the same period. It is important to note that there are material differences between the Fund and this benchmark.

Explanation of Fund Performance

In terms of sector performance, we saw a reversal of 2015 trends. The best performing sector in the broader market was energy (oil and gas), followed by financials as interest rates increased. The fund does not invest in oil and gas companies, and invests less than its benchmark in financials, which explains a large part of its underperformance. The market experienced a strong sector rotation from IT to financials after the summer. Even though long-term growth prospects may be lower, the market clearly preferred the low valuation levels in both sectors, and the election of Donald Trump to become the next U.S. president helped the performance of these sectors even more. The same was true for the materials sector where mining companies such as Rio Tinto and BHP Billiton posted strong returns but the fund does not hold any mining companies. Meanwhile, health care was one of the

1 |

worst performing sectors, due to profit taking, uncertainty about the potential U.S. health care reform and general pricing pressure on pharma products.

Relative to its benchmark, the Fund had a much larger position in health care, as we like the long-term fundamental growth drivers such as an aging population and the increased use of technology in finding solutions for insufficiently treated diseases.

The performance difference between the best performing and the worst performing stocks in the portfolio was larger than we would have anticipated. Danish companies Novo Nordisk (diabetes drugs) and Novozymes (biological enzymes) both issued profit warnings due to pressure on their profit margins. Ingenico, a French specialist in payment terminals, also reduced their growth expectations as the U.S. move to chipcards is slower than had been anticipated. Their poor performance could not be fully offset by the strong performance of stocks such as KBC (Belgian retail bank), A.O. Smith (energy-efficient water boilers) and Amazon.com (e-retail and cloud computing).

Outlook

We expect 2017 to be a relatively positive, but volatile year for equity market performance.

Valuations are relatively high on average but still attractive compared to bonds. Valuation support may be absent in the context of rising interest rates. Markets will therefore be relying more on earnings growth to generate returns. However, earnings growth expectations are flat in the United States before a potential tax reform impact. We therefore expect companies whose growth is supported by long-term demographic, environmental and technological megatrends to perform well in this low-growth environment. This should be more visible after first or second quarter results as it may become clear by then that some of the election promises may not be translated into corporate earnings growth. We like exposure to the U.S. market because of the tax reform and the strong dollar. This goes for U.S. companies with domestic exposure but also for non-U.S. companies selling into the United States. European equities should benefit from continued central bank support, lower valuations and improving economic numbers. Political uncertainty remains however and should lead to increased volatility (elections in France, the Netherlands and Germany).

| 2

MIROVA GLOBAL SUSTAINABLE EQUITY FUND

Growth of $10,000 Investment in Class A Shares3

March 31, 2016 (inception) through December 31, 2016

Top Ten Holdings as of December 31, 2016

| | | | | | |

| Security name | | % of

net assets | |

| 1 | | Alphabet, Inc. | | | 4.94 | % |

| 2 | | Thermo Fisher Scientific, Inc. | | | 4.71 | |

| 3 | | Visa, Inc. | | | 4.58 | |

| 4 | | Roper Technologies, Inc. | | | 4.16 | |

| 5 | | Microsoft Corp. | | | 3.67 | |

| 6 | | KBC Groep NV | | | 3.65 | |

| 7 | | Danaher Corp. | | | 3.63 | |

| 8 | | Essilor International S.A. | | | 3.45 | |

| 9 | | Novo Nordisk AS | | | 2.99 | |

| 10 | | Amazon.com, Inc. | | | 2.87 | |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced.

3 |

Total Returns — December 31, 20163

| | | | | | | | | | | | |

| | | |

| | | | | | Expense Ratios4 | |

| | | Life of Fund | | | Gross | | | Net | |

| | | | |

| Class A (Inception 3/31/16) | | | | | | | | | | | | |

| NAV | | | -0.85 | % | | | 1.88 | % | | | 1.30 | % |

| With 5.75% Maximum Sales Charge | | | -6.55 | | | | | | | | | |

| | | | |

| Class C (Inception 3/31/16) | | | | | | | | | | | | |

| NAV | | | -1.39 | | | | 2.63 | | | | 2.05 | |

| With CDSC1 | | | -2.37 | | | | | | | | | |

| | | | |

| Class Y (Inception 3/31/16) | | | | | | | | | | | | |

| NAV | | | -0.70 | | | | 1.63 | | | | 1.05 | |

| | | | |

| Comparative Performance | | | | | | | | | | | | |

| MSCI World Index (Net)2 | | | 7.89 | | | | | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit ngam.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Performance for Class C shares assumes a 1.00% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase. |

| 2 | MSCI World Index (Net) is an unmanaged index that is designed to measure the equity market performance of developed markets. It is composed of common stocks of companies representative of the market structure of 22 developed market countries in North America, Europe, and the Asia/Pacific Region. The index is calculated without dividends, with net or with gross dividends reinvested, in both U.S. dollars and local currencies. You may not invest directly in an index. |

| 3 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 4 | As of the most recent prospectus, the investment advisor has contractually agreed to waive fees and/or reimburse expenses (with certain exceptions) once the expense cap of the Fund has been exceeded. This arrangement is set to expire on 4/30/17. When an expense cap has not been exceeded, the fund may have similar expense ratios. |

| 4

NATIXIS OAKMARK FUND

| | |

| Managers | | Symbols |

| William C. Nygren, CFA® | | Class A NEFOX |

| Kevin G. Grant, CFA® | | Class C NECOX |

| M. Colin Hudson, CFA® | | Class Y NEOYX |

| Michael J. Mangan, CFA® | | |

| Harris Associates L.P. | | |

Investment Goal

The Fund seeks long-term capital appreciation.

Market Conditions

The year began on a sour note in 2016, as stock prices stumbled meaningfully in January across major global markets. As the year progressed, we saw instances of recovery offset by periodic events that prompted large declines (e.g. depressed commodity prices, the Brexit vote and ineffective central bank strategies to increase inflation in certain geographies).

At the conclusion of the year, major global market movements were largely influenced by the results of the U.S. presidential election in November. Although futures for the Dow Jones Industrial Average dropped nearly 900 points in the immediate aftermath of the election, investors surprisingly absorbed the implications of this political sea change. Subsequently, key indexes rebounded, and the Dow went on to close at a record high level on November 10, 2016 and finish up for the year. Financials led the advance, first benefiting from investors’ hopes that the new Republican administration would roll back industry regulations and second from the Federal Reserve’s decision to raise short-term interest rates for the first time in 2016. Citing signs that the economy has improved, the Fed also stated it intends to raise rates three times in 2017.

Elsewhere, the European Central Bank and the Bank of England both maintained key interest rates in December. The Bank of Japan (BOJ) opted to maintain its yield-curve and asset-purchasing programs. In addition, the BOJ pledged to further expand the monetary base in its continued efforts to lift inflation above 2%. In the weeks following the U.S. election, the Japanese yen sank over 10% against the dollar, which some investors expect will boost Japanese exports.

Meanwhile, members of the Organization of the Petroleum Exporting Countries (OPEC) reached an agreement with non-members to further reduce oil production. As a result of the deal, an additional 600,000 barrels per day will be removed from the market on top of the 1.2 million barrels per day cut agreed upon by OPEC in November. When all was said and done, Brent crude finished up approximately 52% for the year.

As value investors, we feel that our key task is to see through the haze generated by market pundits who are overly influenced by geopolitical events such as referendums and elections. Instead, we focus on the fundamental drivers of long-term cash flows. We seek to make investment decisions based on a company’s ability to generate and sustain a growing cash

5 |

flow stream. While the market chased stable stocks in the face of uncertainty, we felt the attractive valuations in financials and cyclically-exposed areas of the market provided more safety. As is often the case, share price declines from the macro events of 2016 afforded us the opportunity to act on our convictions and reward our patient shareholders.

Performance Results

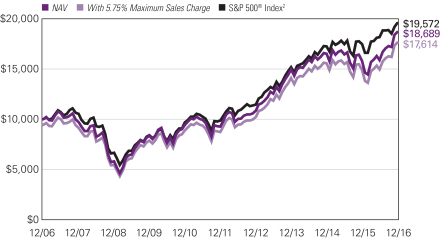

For the 12 months ended December 31, 2016, Class A shares of Natixis Oakmark Fund returned 18.37% at net asset value. The Fund outperformed its benchmark, the S&P 500® Index, which returned 11.96%.

Explanation of Fund Performance

As value investors with an emphasis on individual stock selection, our sector weights are a byproduct of our bottom-up process. On an absolute-return basis, shares in the energy sector gained the most value, while holdings in the consumer staples sector posted the largest negative return for calendar 2016.

The leading contributors to fund performance for the year were Apache and Cummins. Apache, a global oil and gas exploration company, was a beneficiary of the oil price rebound in 2016 after a volatile stretch. Apache has specifically benefitted from solid quarterly results that have demonstrated improved capital efficiency, including a 45% decline in North American well costs compared to 2014 levels. This year, the company also announced the discovery of a new resource play in the Permian Basin called “Alpine High.” Initial results indicate that Apache has discovered a high quality resource at a low cost. This increased our estimate of intrinsic value and also increased our confidence in management. In our view, Apache has the balance sheet and asset quality to survive continued volatility in oil and gas prices, and we like how the management team is preserving and growing per share value during the commodity price downturn. Cummins issued fiscal third-quarter results that indicated the company is on track to meet its full-year guidance. Although organic revenues declined, its decremental earnings margin (excluding the warranty charge) reached -23%, which is better than management’s full-year expectation of -25%. This positive outcome was a benefit of ongoing restructuring and cost reduction initiatives that helped buffer the impact from weak underlying end markets. From a segment perspective, Cummins’ components segment was a relative standout, as revenue growth of 7% internationally (+37% in China) partially offset the revenue decline in North America. Conversely, the power systems segment remains very weak globally, as the lack of infrastructure spending in developing markets and sluggish oil and gas/mining demand pressured results. Even so, the company repurchased about 7 million shares in 2016 through the third quarter, and Cummins’ management team reiterated its expectation for earnings per share of roughly $8 for the full year.

Liberty Interactive QVC and American Express were the largest detractors to Fund performance for the calendar year. After a long period of rather stable but low single-digit growth, Liberty Interactive QVC announced that sales fell by a mid-to-upper single digit amount in June, and these trends continued through July. The management team cited numerous company-specific reasons for the decline and noted they were taking action accordingly. In our estimation, the company’s underlying value was only modestly affected,

| 6

NATIXIS OAKMARK FUND

relative to the decline in its share price. However, QVC CEO Mike George indicated at a conference in September that the trend from June and July had persisted through August. Despite this, investors were pleased with the results from the company’s third quarter, helping its share price to recoup some of the losses incurred earlier in 2016. Given that QVC also continues to buy back more stock, we remain confident that the company will reward shareholders over the long term. American Express was another large detractor to fund performance in the calendar year. News in January 2016 that Fidelity Investments had ended its 12-year partnership with American Express negatively affected the latter. This is in addition to the skepticism lingering from the 2015 announcement that Costco would not renew its co-brand partnership with American Express. We believe these factors will cause earnings growth to slow in the short term while American Express invests in marketing efforts to replace these customers, but we believe the company’s financial fundamentals remain very healthy. Despite what we believe is favorable secular growth and superior economics, American Express is trading at a large discount to the market. Our long-term view allows us to look past the short-term disappointment of the Costco and Fidelity announcements, and see the potential lucrative long-term value of American Express’ global payment network and growing customer base.

Outlook

Improving market conditions have prompted investors to realize the earnings potential of some otherwise overlooked companies. We appreciate when the market begins to recognize our perception of the intrinsic values of our holdings. Yet, our approach remains steadfast even when market sentiment turns pessimistic. We know that several policy-related issues are in flux over the coming year, and the outcomes of these could have large economic effects that move markets. Therefore, we remain prepared to capitalize on the opportunities that these events provide for the benefit of our investors.

7 |

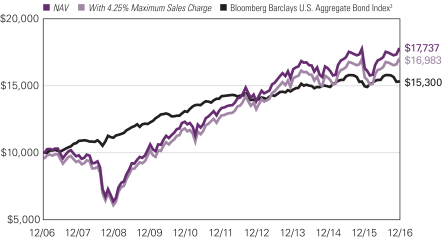

Growth of $10,000 Investment in Class A Shares3

December 31, 2006 through December 31, 2016

See notes to chart on page 9.

Top Ten Holdings as of December 31, 2016

| | | | | | |

| Security name | | % of

net assets | |

| 1 | | Citigroup, Inc. | | | 3.54 | % |

| 2 | | Alphabet, Inc., Class A | | | 3.11 | |

| 3 | | Bank of America Corp. | | | 2.91 | |

| 4 | | American International Group, Inc. | | | 2.82 | |

| 5 | | General Electric Co. | | | 2.75 | |

| 6 | | Apache Corp. | | | 2.72 | |

| 7 | | JPMorgan Chase & Co. | | | 2.69 | |

| 8 | | Visa, Inc., Class A | | | 2.45 | |

| 9 | | MasterCard, Inc., Class A | | | 2.41 | |

| 10 | | Capital One Financial Corp. | | | 2.39 | |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced.

| 8

NATIXIS OAKMARK FUND

Average Annual Total Returns — December 31, 20163

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | Expense Ratios4 | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | Gross | | | Net | |

| | | | | | |

| Class A (Inception 5/6/31) | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 18.37 | % | | | 15.05 | % | | | 6.45 | % | | | 1.14 | % | | | 1.14 | % |

| With 5.75% Maximum Sales Charge | | | 11.55 | | | | 13.69 | | | | 5.81 | | | | | | | | | |

| | | | | | |

| Class C (Inception 5/1/95) | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 17.45 | | | | 14.19 | | | | 5.65 | | | | 1.89 | | | | 1.89 | |

| With CDSC1 | | | 16.45 | | | | 14.19 | | | | 5.65 | | | | | | | | | |

| | | | | | |

| Class Y (Inception 11/18/98) | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 18.69 | | | | 15.34 | | | | 6.75 | | | | 0.89 | | | | 0.89 | |

| | | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | | | | | |

| S&P 500® Index2 | | | 11.96 | | | | 14.66 | | | | 6.95 | | | | | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit ngam.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Performance for Class C shares assumes a 1.00% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase. |

| 2 | S&P 500® Index is a widely recognized measure of U.S. stock market performance. It is an unmanaged index of 500 common stocks chosen for market size, liquidity, and industry group representation, among other factors. |

| 3 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 4 | As of the most recent prospectus, the investment advisor has contractually agreed to waive fees and/or reimburse expenses (with certain exceptions) once the expense cap of the Fund has been exceeded. This arrangement is set to expire on 4/30/17. When an expense cap has not been exceeded, the fund may have similar expense ratios. |

9 |

NATIXIS OAKMARK INTERNATIONAL FUND

| | |

| Managers | | Symbols |

| David G. Herro, CFA® | | Class A NOIAX |

| Michael L. Manelli, CFA® | | Class C NOICX |

| Harris Associates L.P. | | |

Investment Goal

The Fund seeks long-term capital appreciation.

Market Conditions

Major global market movements in the fourth quarter of 2016 were largely influenced by the results of the U.S. presidential election in November. Although futures for the Dow Jones Industrial Average dropped nearly 900 points in the immediate aftermath of the election, investors surprisingly absorbed the implications of this political sea change. Subsequently, key indexes rebounded, and the Dow went on to close at a record high level on November 10, 2016 and finish up for the quarter. Financials led the advance, benefiting from investors’ hopes that the new Republican administration would roll back industry regulations and from the Federal Reserve’s decision to raise short-term interest rates for the first time in 2016. Citing signs that the economy has improved, the Fed also stated it intends to raise rates three times in 2017.

Elsewhere, the European Central Bank and the Bank of England both maintained key interest rates in December. The Bank of Japan (BOJ) opted to maintain its yield-curve and asset-purchasing programs. In addition, the BOJ pledged to further expand the monetary base in its continued efforts to lift inflation above 2%. In the weeks following the U.S. election, the Japanese yen sank over 10% against the dollar, which some investors expect will boost Japanese exports.

Meanwhile, non-members of the Organization of the Petroleum Exporting Countries (OPEC) reached an agreement with OPEC members to further reduce oil production. As a result of the deal, an additional 600,000 barrels per day will be removed from the market in addition to the 1.2 million barrels per day cut agreed upon by OPEC last month. When all was said and done, Brent crude finished up 52% for the year.

As value investors, we feel that our key task is to see through the haze generated by market pundits who are overly influenced by geopolitical events such as referendums and elections. Instead, we focus on the fundamental drivers of long-term cash flows. We seek to make investment decisions based on a company’s ability to generate and sustain a growing cash flow stream. While the market chased stable stocks in the face of uncertainty, we felt the attractive valuations in financials and cyclically exposed areas of the market provided more safety. As is often the case, share price declines from the macro events of 2016 afforded us the opportunity to act on our convictions and reward our patient shareholders.

| 10

NATIXIS OAKMARK INTERNATIONAL FUND

Performance Results

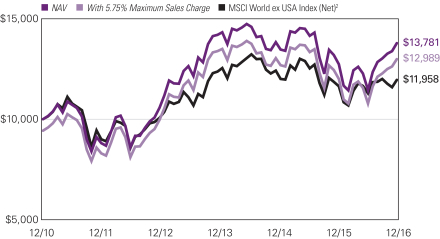

For the 12 months ended December 31, 2016, Class A shares of Natixis Oakmark International Fund returned 8.19% at net asset value. The Fund outperformed its benchmark, the MSCI World ex USA Index (Net), which returned 2.75%.

Explanation of Fund Performance

Geographically, we ended the quarter with 76% of our holdings in Europe, 9% in Japan and 4% in Australia. The remaining positions are in China, the United States, Indonesia, Mexico, Hong Kong, South Korea, India, Taiwan and Israel. As value investors with an emphasis on individual stock selection, our country and sector weights are a by-product of our bottom-up process.

On an absolute-return basis, shares in the materials sector produced the best collective return. Holdings in the financials sector declined the most during the year.

The top contributors to the yearly return were Glencore and CNH Industrial. In 2016, Glencore’s share price reacted positively to a rebound in commodity prices, the successful execution of its debt reduction plan and the election of Donald Trump as U.S. President. During the fourth quarter, Glencore completed its sale of non-core assets and raised a total of $6.3 billion in proceeds from all asset disposals, which puts the company on pace to meet its targeted net debt level of $16.5-$17.5 billion. Furthermore, management reinstated its dividend policy and plans to return at least $1 billion to shareholders starting in 2017. We believe management is working to enhance shareholder value, and our investment thesis remains intact. CNH Industrial received a boost early in 2016 following an analyst report that cited an increase in the price of corn and in the demand for agriculture equipment as potential drivers of CNH’s future share price recovery. We met with the company’s CEO Richard Tobin and CFO Max Chiara during the second quarter and discussed the performance status of each business segment. We were pleased to learn of progress in the agricultural business where inventory and manufacturing have been rightsized. The commercial vehicle and construction businesses also have targeted improvement plans in place. In the fourth quarter, CNH Industrial’s share price was boosted by the election of Donald Trump and the perceived benefits to the industrials sector. In addition, news that industry peer Deere delivered fiscal fourth-quarter earnings results that handily beat market expectations drove CNH’s share price higher, on hopes that the latter would follow suit. As previously mentioned, non-members of the Organization of the Petroleum Exporting Countries (OPEC) reached an agreement with OPEC members to further reduce oil production. As a result of the deal, an additional 600,000 barrels per day will be removed from the market in addition to the 1.2 million barrels per day cut agreed upon by OPEC earlier in the quarter. In conjunction with the recovery in oil prices during the fourth quarter, we find that the company continues to be undervalued relative to its normalized earnings power.

The largest detractors from return were Credit Suisse Group and BMW. Although Credit Suisse Group’s CEO Tidjane Thiam warned that fiscal fourth-quarter earnings would be weak, some one-off expenses related to litigation, pension true-up charges and write-downs on certain credit assets were negative surprises during the period. However, this caused the

11 |

management team to accelerate the restructuring and reduction of non-core investment banking lines of businesses. The goal is to emphasize the wealth management business that has very good secular growth trends, is fee-based and requires little capital. Credit Suisse shares were also negatively impacted by the U.K.’s decision to leave the European Union. We believe it is important to remember that the bank derives minimal revenues (2%) from the U.K., while 13% of its costs are denominated in pound sterling currency, the net result of which may be somewhat positive for profitability. Later in the year, investor sentiment improved due to Credit Suisse Group’s Investor Day during the fourth quarter. The company indicated that it was lowering its target operating cost base from CHF 18 billion to CHF 17 billion and increasing its total net cost savings target from CHF 3.2 billion to greater than CHF 4.2 billion in 2018. In addition, Credit Suisse Group’s fiscal nine-month results benefited from effective cost controls that offset weaker revenues; lower operating expenses helped total net income to marginally exceed our projections. We were pleased that improvements in Global Markets drove core operating expenses to be roughly 5% better than we estimated. Credit Suisse’s capital ratios increased, and the bank finished the third quarter with a common equity Tier 1 ratio of 12%, which reflects a 180 basis point advance from a year ago. BMW’s share price experienced volatility in the first half of 2016, even though fiscal year 2015 fourth-quarter and fiscal year 2016 first-quarter earnings results were largely in line with our expectations. Despite this, we were disappointed in BMW’s capital allocation and significant cash position. We had hoped to discuss our concerns with management, but management refused to hear our thoughts on the topic. Given our concerns about capital allocation and management’s unwillingness to meet with us, we decided to sell our shares in June. However, we once again initiated a position in the company following a meeting with management in November. As a result of the meeting, we believe BMW’s motivations are in the right place and appreciate reaffirmation of management’s intention to increase the company’s payout ratio closer to 40%. Furthermore, the outlook for long-term auto demand is quite optimistic given emerging market growth, a revived U.S. market and potential for an auto sales rebound in Europe off of a 20-year low. In addition, we think that growth of premium auto brands will be faster than the overall market, as luxury goods sales have been robust even in a challenging economy. The company has expanded its product lines by introducing variations of several models, which has resulted in market share gains and constantly attractive product cycles. Overall, we believe BMW is a solid investment that will reward shareholders into the future.

Outlook

Again this year, macro and geopolitical events dominated the news. However, we believe it is a mistake to focus on these happenings when making investment decisions. We find that these events rarely impact long-term business value in a meaningful way. In fact, these events should be used to exploit short-term mispricing, as they enable investors to buy into businesses at low entry prices. We recognize that our job is to measure and determine intrinsic value, to buy when stock prices are low and to sell when stock prices are high. It is our belief that by focusing on this, rather than the exogenous events mentioned above, we will earn acceptable rates of return over time for those who entrust their funds with us.

| 12

NATIXIS OAKMARK INTERNATIONAL FUND

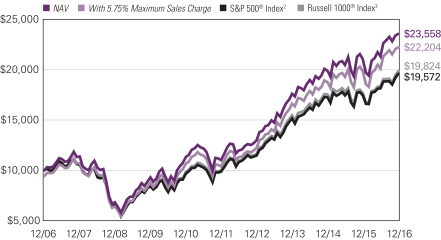

Growth of $10,000 Investment in Class A Shares3

December 15, 2010 (inception) through December 31, 2016

Top Ten Holdings as of December 31, 2016

| | | | | | |

| Security name | | % of

net assets | |

| 1 | | Glencore PLC | | | 4.33 | % |

| 2 | | Lloyds Banking Group PLC | | | 3.92 | |

| 3 | | BNP Paribas S.A. | | | 3.59 | |

| 4 | | Intesa Sanpaolo SpA | | | 3.53 | |

| 5 | | Allianz SE, (Registered) | | | 3.46 | |

| 6 | | Credit Suisse Group AG, (Registered) | | | 3.44 | |

| 7 | | Daimler AG, (Registered) | | | 3.36 | |

| 8 | | CNH Industrial NV | | | 3.30 | |

| 9 | | Honda Motor Co. Ltd. | | | 2.48 | |

| 10 | | EXOR | | | 2.42 | |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced.

13 |

Average Annual Total Returns — December 31, 20163

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | Expense Ratios4 | |

| | | 1 Year | | | 5 Years | | | Life of Fund | | | Gross | | | Net | |

| | | | | | |

| Class A (Inception 12/15/10) | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 8.19 | % | | | 9.68 | % | | | 5.45 | % | | | 1.31 | % | | | 1.31 | % |

| With 5.75% Maximum Sales Charge | | | 1.97 | | | | 8.39 | | | | 4.43 | | | | | | | | | |

| | | | | | |

| Class C (Inception 12/15/10) | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 7.36 | | | | 8.89 | | | | 4.68 | | | | 2.06 | | | | 2.06 | |

| With CDSC1 | | | 6.36 | | | | 8.89 | | | | 4.68 | | | | | | | | | |

| | | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | | | | | |

| MSCI World ex USA Index (Net)2 | | | 2.75 | | | | 6.07 | | | | 3.00 | | | | | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit ngam.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Performance for Class C shares assumes a 1.00% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase. |

| 2 | MSCI World ex USA Index (Net) is an unmanaged index that is designed to measure the equity market performance of developed markets, excluding the United States. The index calculates reinvested dividends net of withholding taxes using Luxembourg tax rates. |

| 3 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 4 | As of the most recent prospectus, the investment advisor has contractually agreed to waive fees and/or reimburse expenses (with certain exceptions) once the expense cap of the Fund has been exceeded. This arrangement is set to expire on 4/30/17. When an expense cap has not been exceeded, the fund may have similar expense ratios. |

| 14

VAUGHAN NELSON SMALL CAP VALUE FUND

| | |

| Managers | | Symbols |

| Dennis G. Alff, CFA® | | Class A NEFJX |

| Chad D. Fargason | | Class C NEJCX |

| Chris D. Wallis, CFA® | | Class Y NEJYX |

| Scott J. Weber, CFA® | | |

| Vaughan Nelson Investment Management, L.P. |

Effective July 31, 2009, the fund was closed to new investors.

Investment Goal

The Fund seeks capital appreciation.

Market Conditions

During the year, volatility remained elevated as the market digested the United Kingdom’s vote to leave the European Union (“Brexit”), Donald Trump’s successful campaign for President of the United States, and the Federal Reserve’s ability to raise interest rates. However, equity markets appreciated despite declining earnings expectations and deteriorating international economic conditions. We believe the incremental multiple expansion was driven by easy monetary conditions globally, by modest improvement in economic growth expectations throughout the year, and by foreign investors increasing portfolio allocations to U.S. equities post-Brexit.

Despite attractive gains in 2016, we believe equity markets might be in a state of unstable equilibrium given the significant structural changes that are occurring with central banks’ monetary policies and with U.S. government deficits in addition to the escalating number of earnings headwinds including: higher interest rates, a stronger U.S. dollar, rising health care costs, and wage inflation pressures. In fact, corporate earnings expectations declined for the fourth quarter of 2016 and for the full-year 2017, resulting in even richer valuation multiples as equity markets set new highs.

Performance Results

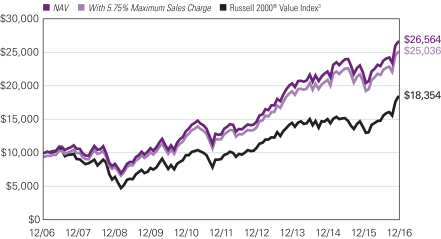

For the twelve months ended December 31, 2016, Class A shares of Vaughan Nelson Small Cap Value Fund returned 20.24% at net asset value. The Fund underperformed its benchmark, the Russell 2000® Value Index, which returned 31.74%.

Explanation of Fund Performance

While the Fund’s absolute performance was strong for the year, the Fund underperformed the benchmark primarily due to stock selection within materials, information technology, consumer discretionary, industrials, and financials. In addition, the Fund was also overweight health care during the year, which detracted from performance as the sector underperformed the market. The Fund was positioned more defensively during the year as valuations become more expensive, which hurt relative performance as more cyclical sectors such as materials outperformed. Financials, industrials, energy, utilities and information technology were the biggest contributors to absolute performance, while consumer discretionary, materials and real estate detracted from performance.

15 |

Stock selection within the materials sector detracted the most from relative performance. This was primarily due to the Fund’s overweight in paper and packaging stocks, which as a group are more defensive and performed worse than the higher beta industries within the materials sector, such as metals and mining. Kapstone Paper and Packaging, Multi Packaging Solutions International, Silgan, and Graphic Packaging detracted the most from relative performance. Kapstone was hurt by concerns about product pricing and inventory levels in its end markets. Multi Packaging Solutions suffered from poor execution and weak end market volumes within its consumer products end markets. Silgan and Graphic Packaging underperformed primarily due to their defensive nature as noted above.

Stock selection within the information technology sector detracted from relative performance with RingCentral and Verint as the primary detractors. RingCentral performed poorly due to market concerns around its customer concentration, while Verint faced headwinds from its exposure to weak Emerging Market economies, as well as a strong U.S. dollar. In addition, the Fund was overweight IT services stocks, a more defensive industry, which did not perform as well as more cyclical industries such as semiconductors.

The industrials sector also detracted from performance on a relative basis as the portfolio was positioned in more defensive, less cyclical companies in industries such as commercial services and supplies. The Fund’s industrial holdings performed well on an absolute basis, but lagged in performance relative to the Fund’s benchmark.

The consumer discretionary sector detracted from performance on both an absolute and relative basis due to stock selection within auto component manufacturers, homebuilders, and retail. Vista Outdoor, CalAtlantic, Tenneco, and Tailored Brands detracted the most from performance. Vista Outdoor was negatively impacted by a customer bankruptcy that resulted in excess inventory in its sales channels. CalAtlantic saw order weakness in its Texas markets, driven by weak oil prices, and also faced a headwind from potentially higher mortgage rates going forward. Tenneco was negatively impacted by its exposure to China early in the year, as well as investor concerns that auto production levels may have peaked in the U.S. Tailored Brands continued to struggle with the integration of the Jos. A. Bank business with its Men’s Wearhouse business.

The Fund’s financial sector holdings performed well on an absolute basis, but underperformed on a relative basis driven by stock selection. The portfolio was overweight insurance due to its more defensive characteristics but insurance stocks did not perform as well as other interest rate sensitive names as the yield curve backed up following the election. Insurance holdings such as RenaissanceRe, First American Financial, and Aspen Insurance performed well on an absolute basis, while American Equity Life performed poorly due to regulatory headwinds and a continued low rate environment. American Equity Life was sold early in the year and did not benefit from the post-election rebound in interest rate sensitive stocks.

Sector selection drove the relative underperformance in health care. The Fund was overweight health care during the year due to the secular growth opportunities given the aging population and reasonable valuations. However, following Trump’s successful bid for the White House, health care stocks underperformed as the chances of repealing or replacing the Affordable Care Act increased. VWR, Civitas, Envision Healthcare, and

| 16

VAUGHAN NELSON SMALL CAP VALUE FUND

Surgery Partners were the largest underperformers for the Fund. VWR performed poorly due to a headwind from a stronger U.S. dollar as well as concerns around National Institutes of Health funding levels. Civitas was negatively impacted by a reduction in funding levels at its largest customer, as well as a headwind from higher labor costs. Envision Healthcare was impacted by volatility around the Company’s merger with AmSurg. Surgery Partners saw weaker than expected surgery volumes late in the year.

The energy sector contributed the most to performance during the year due to strong stock selection. The Fund was also overweight energy and it was one of the best performing sectors for the year. Laredo Petroleum, Forum Energy, and Superior Energy Services contributed most to the sector’s results as all benefited from higher oil prices as the year progressed. Laredo, an E&P company, also performed very well on a company specific basis as it continued to increase the efficiency of its operations.

Other notable performers during the year included Prosperity Bancshares, CACI International, and First Financial Bancorp. Prosperity Bancshares and First Financial Bancorp are interest rate sensitive names that benefited from an increase in rate expectations and a steepening yield curve during the year, particularly after the election. CACI is a government IT services company that produced strong results through the year, and performed particularly well after the election on the prospect of higher fiscal spending by the U.S. Government.

Outlook

The U.S. presidential election has not caused us to change our view regarding portfolio positioning or the opportunity set. We still believe that there is little room for profit margins to improve and that interest rates cannot move materially higher without negative consequences. While we welcome a business friendly administration, corporate tax reform, and more fiscal spending, we think that these conditions are necessary to hit next year’s earnings estimates anyway. For example, earnings for the S&P 500® Index are estimated to grow approximately 20% in 2017, which seems unrealistic at this point in the business and corporate margin cycle. From here, the biggest fundamental impact to the economy and to asset prices is likely a renewal of animal spirits.

With corporate margins near all-time highs, labor markets tight, and benefit costs on the rise, we do not believe top line growth will be sufficient to prevent further margin pressure. With monetary stimulus nearly exhausted, we believe fiscal stimulus will be necessary not only in the United States but internationally so that the macro imbalances can continue to adjust without creating excessive volatility. Our outlook remains balanced, stock-specific, and not reflective of opportunities in specific industries, regions of the world, or broader market indices.

As it relates to the intermediate to long-term outlook, we believe we are entering the final stages of rebalancing the monetary bubble that has been building in our financial markets for several decades. While the financial crisis was effective at eliminating excesses within our regulated banking systems, it pushed imbalances into the unregulated financial system and accentuated the imbalances that exist in international markets.

We continue to seek investments in companies that have better pricing power, lower earnings variability, higher profitability, and stronger balance sheets than the broader

17 |

investment universe. We still do not favor any single industry or sector, and continue to look for companies with the characteristics noted above that trade at attractive valuations.

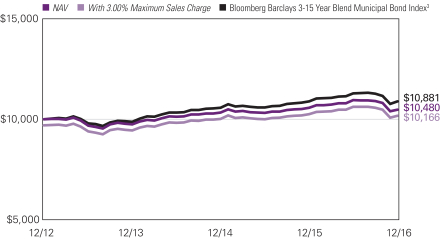

Growth of $10,000 Investment in Class A Shares4

December 31, 2006 through December 31, 2016

See notes to chart on page 19.

Top Ten Holdings as of December 31, 2016

| | | | | | |

| Security name | | % of

net assets | |

| 1 | | iShares® Russell 2000 Value Index ETF | | | 5.13 | % |

| 2 | | Prosperity Bancshares, Inc. | | | 3.25 | |

| 3 | | Brown & Brown, Inc. | | | 2.32 | |

| 4 | | Hillenbrand, Inc. | | | 2.23 | |

| 5 | | RenaissanceRe Holdings Ltd. | | | 2.21 | |

| 6 | | First Financial Bancorp | | | 2.12 | |

| 7 | | First American Financial Corp. | | | 2.12 | |

| 8 | | Envision Healthcare Corp. | | | 2.10 | |

| 9 | | First Merchants Corp. | | | 2.06 | |

| 10 | | Union Bankshares Corp. | | | 2.01 | |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced.

| 18

VAUGHAN NELSON SMALL CAP VALUE FUND

Average Annual Total Returns — December 31, 20163

| | | | | | | | | | | | | | | | | | | | |

| | | | | |

| | | | | | | | | | | | Expense Ratios4 | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | Gross | | | Net | |

| | | | | | |

| Class A (Inception 12/31/96) | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 20.24 | % | | | 15.82 | % | | | 10.27 | % | | | 1.45 | % | | | 1.45 | % |

| With 5.75% Maximum Sales Charge | | | 13.34 | | | | 14.46 | | | | 9.62 | | | | | | | | | |

| | | | | | |

| Class C (Inception 12/31/96) | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 19.32 | | | | 14.95 | | | | 9.44 | | | | 2.20 | | | | 2.20 | |

| With CDSC1 | | | 18.32 | | | | 14.95 | | | | 9.44 | | | | | | | | | |

| | | | | | |

| Class Y (Inception 8/31/06) | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 20.53 | | | | 16.10 | | | | 10.55 | | | | 1.20 | | | | 1.20 | |

| | | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | | | | | |

| Russell 2000® Value Index2 | | | 31.74 | | | | 15.07 | | | | 6.26 | | | | | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit ngam.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Performance for Class C shares assumes a 1.00% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase. |

| 2 | Russell 2000® Value Index is an unmanaged index that measures the performance of the small-cap value segment of the U.S. equity universe. It includes those Russell 2000® companies with lower price-to-book ratios and lower forecasted growth values. |

| 3 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 4 | As of the most recent prospectus, the investment advisor has contractually agreed to waive fees and/or reimburse expenses (with certain exceptions) once the expense cap of the Fund has been exceeded. This arrangement is set to expire on 4/30/17. When an expense cap has not been exceeded, the fund may have similar expense ratios. |

19 |

VAUGHAN NELSON VALUE OPPORTUNITY FUND

| | |

| Managers | | Symbols |

| Dennis G. Alff, CFA® | | Class A VNVAX |

| Chad D. Fargason | | Class C VNVCX |

| Chris D. Wallis, CFA® | | Class N VNVNX |

| Scott J. Weber, CFA® | | Class Y VNVYX |

| Vaughan Nelson Investment Management, L.P. |

Investment Goal

The Fund seeks long-term capital appreciation.

Market Conditions

During the year, volatility remained elevated as the market digested the United Kingdom’s vote to leave the European Union (“Brexit”), Donald Trump’s successful campaign for President of the United States, and the Federal Reserve’s ability to raise interest rates. However, equity markets appreciated despite declining earnings expectations and deteriorating international economic conditions. We believe the incremental multiple expansion was driven by easy monetary conditions globally, by modest improvement in economic growth expectations throughout the year, and by foreign investors increasing portfolio allocations to U.S. equities post Brexit.

Despite attractive gains in 2016, we believe equity markets might be in a state of unstable equilibrium given the significant structural changes that are occurring with central banks’ monetary policies and with U.S. government deficits in addition to the escalating number of earnings headwinds including: higher interest rates, a stronger U.S. dollar, rising health care costs, and wage inflation pressures. In fact, corporate earnings expectations declined for the fourth quarter of 2016 and for the full-year 2017, resulting in even richer valuation multiples as equity markets set new highs.

Performance Results

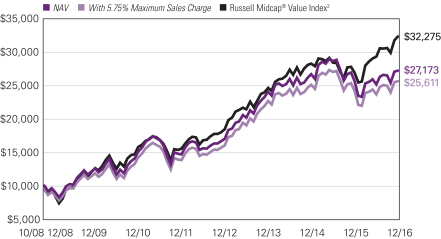

For the 12 months ended December 31, 2016, Class A shares of Vaughan Nelson Value Opportunity Fund returned 5.85% at net asset value. The fund underperformed its benchmark, the Russell Midcap® Value Index, which returned 20.00%.

Explanation of Fund Performance

While the Fund’s absolute performance was positive for the year, the Fund underperformed the benchmark primarily due to stock selection within information technology, materials, health care, consumer discretionary, and industrials. In addition, the Fund was overweight health care and consumer discretionary stocks during the year, which detracted from performance since both sectors underperformed the market. The Fund was positioned more defensively during the year as valuations become more expensive, which hurt relative performance as more cyclical sectors such as energy and industrials outperformed. Financials, technology, consumer discretionary, and energy were the biggest contributors to absolute performance, while health care detracted from performance.

| 20

VAUGHAN NELSON VALUE OPPORTUNITY FUND

The information technology sector weighed on relative performance due to stock selection, with First Data and RingCentral detracting the most. First Data completed its initial public offering during the year and the stock performed poorly after management elected not to provide guidance. While the stock was only down modestly for the year, the technology sector was one of the best performing sectors, thus magnifying relative underperformance. RingCentral performed poorly due to market concerns related to its customer concentration. Last, the Fund was overweight IT services stocks, a more defensive industry with recurring revenues, which did not perform as well as cyclical industries such as semiconductors.

The materials sector also hampered relative performance due to stock selection. Constellium and Caesarstone detracted the most from performance. Constellium traded lower due to concerns about its acquisition of Wise Metals and fears of a slowdown in two of its primary end markets, aerospace and automotive. Caesarstone performed poorly during the year as its market share growth in the U.S. continued to suffer from increased competition while at the same time the company is expanding capacity. The Fund was also overweight paper and packaging stocks, which as a group are more defensive and performed worse than the higher beta industries within the materials sector, such as construction materials and metals and mining.

Sector selection and stock selection drove the relative underperformance in the health care sector. The Fund was overweight health care due to the secular growth opportunities given the aging population and due to reasonable valuations. However, following Trump’s successful bid for the White House, health care stocks underperformed as the chances of repealing or replacing the Affordable Care Act increased. Endo International, Community Health Systems, and Envision Healthcare detracted the most from performance. Endo International, a branded and generic pharmaceutical company, experienced pricing pressures in the generics business and litigation charges stemming from its mesh business. Community Health suffered from industry wide volume problems and from poor cost control. Envision Healthcare was impacted by volatility related to the Company’s merger with AmSurg, which is now complete.

The consumer discretionary sector detracted from relative performance due to stock and sector selection. The Fund was overweight consumer discretionary stocks relative to the benchmark, and the sector did not perform as well as the benchmark. H&R Block, Signet Jewelers, Delphi Automotive, and HSN, Inc. were the biggest detractors. H&R Block was negatively impacted by sluggish tax return volume growth. Delphi declined due to investor concerns that auto production levels may have peaked in the U.S. Signet and HSN continued to struggle with the challenging consumer retail environment.

The industrials sector also detracted from relative performance due to stock and sector selection. The Fund’s industrials holdings performed well on an absolute basis, but lagged relative to the benchmark. Also, the Fund was underweight industrials for the year and the industrials sector turned out to be one of the best performing sectors, partially driven by Donald Trump’s infrastructure spending plans. On a relative basis, the portfolio was positioned in more defensive, less cyclical companies rather than the more cyclical industries such as airlines, which performed the best. Hertz Global detracted the most

21 |

from performance. Hertz was hurt by higher depreciation expenses on fleet vehicles as residual car values began to decline during the year.

The Fund’s underweight in energy detracted from relative performance. The energy sector was one of the best performers for the year benefitting from a recovery in oil prices. The Fund was concentrated in exploration and production companies, which performed better than energy equipment and services companies. WPX Energy and Continental Resources contributed the most to the Fund’s results as both companies benefited from higher oil prices as the year progressed.

Despite lagging the benchmark, the Fund had many notable outperformers during the year including Grand Canyon Education, New Residential Investment, Reinsurance Group of America, Chemical Financial, and NCR Corporation. As disappointing as 2016 was, the portfolio looks attractive relative to the benchmark going into 2017. Since inception we have tracked the PEG ratio of the strategy and as of December 31, 2016, the strategy is trading at about a 60% discount to the index. Further, the earnings growth for the portfolio is 12% versus 8% for the index and the Fund’s P/E ratio is 14x versus 16x for the index.

Outlook

The U.S. presidential election has not caused us to change our view regarding portfolio positioning or the opportunity set. We still believe that there is little room for profit margins to improve and that interest rates cannot move materially higher without negative consequences. While we welcome a business-friendly administration, corporate tax reform, and more fiscal spending, we think that these conditions are necessary to hit next year’s earnings estimates anyway. For example, earnings for the S&P 500® Index are estimated to grow approximately 20% in 2017, which seems unrealistic at this point in the business and corporate margin cycle. From here, the biggest fundamental impact to the economy and to asset prices is likely a renewal of animal spirits.

With corporate margins near all-time highs, labor markets tight, and benefit costs on the rise, we do not believe top line growth will be sufficient to prevent further margin pressure. With monetary stimulus nearly exhausted, we believe fiscal stimulus will be necessary not only in the United States but internationally so that the macro imbalances can continue to adjust without creating excessive volatility. Our outlook remains balanced, stock-specific, and not reflective of opportunities in specific industries, regions of the world, or broader market indices.

As it relates to the intermediate to long-term outlook, we believe we are entering the final stages of rebalancing the monetary bubble that has been building in our financial markets for several decades. While the financial crisis was effective at eliminating excesses within our regulated banking systems, it pushed imbalances into the unregulated financial system and accentuated the imbalances that exist in international markets.

We continue to seek investments in companies that have better pricing power, lower earnings variability, higher profitability, and stronger balance sheets than the broader investment universe. We still do not favor any single industry or sector, and continue to look for companies with the characteristics noted above that trade at attractive valuations.

| 22

VAUGHAN NELSON VALUE OPPORTUNITY FUND

Growth of $10,000 Investment in Class A Shares3

October 31, 2008 (inception) through December 31, 2016

Top Ten Holdings as of December 31, 2016

| | | | | | |

| Security name | | % of

net assets | |

| 1 | | Ares Capital Corp. | | | 2.83 | % |

| 2 | | Arthur J. Gallagher & Co. | | | 2.81 | |

| 3 | | Fidelity National Information Services, Inc. | | | 2.77 | |

| 4 | | New Residential Investment Corp. | | | 2.68 | |

| 5 | | Synchrony Financial | | | 2.51 | |

| 6 | | Envision Healthcare Corp. | | | 2.50 | |

| 7 | | Newell Brands, Inc. | | | 2.42 | |

| 8 | | Grand Canyon Education, Inc. | | | 2.28 | |

| 9 | | Reinsurance Group of America, Inc., Class A | | | 2.27 | |

| 10 | | Chemical Financial Corp. | | | 2.26 | |

The portfolio is actively managed and holdings are subject to change. There is no guarantee the Fund continues to invest in the securities referenced.

23 |

Average Annual Total Returns — December 31, 20163

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | | | | | | | | | | | Expense Ratios4 | |

| | | 1 Year | | | 5 Years | | | Life of Class | | | Gross | | | Net | |

| | | | | | | |

| Class A (Inception 10/31/08) | | | | | | | | | | | Class A/C/Y | | | | Class N | | | | | | | | | |

| NAV | | | 5.85 | % | | | 13.12 | % | | | 13.02 | % | | | — | % | | | | | | | | |

| With 5.75% Maximum Sales Charge | | | -0.22 | | | | 11.79 | | | | 12.20 | | | | — | | | | 1.45 | % | | | 1.45 | % |

| | | | | | | |

| Class C (Inception 10/31/08) | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 5.03 | | | | 12.27 | | | | 12.18 | | | | — | | | | 2.20 | | | | 2.20 | |

| With CDSC1 | | | 4.03 | | | | 12.27 | | | | 12.18 | | | | — | | | | | | | | | |

| | | | | | | |

| Class N (Inception 5/1/13) | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 6.21 | | | | — | | | | — | | | | 10.11 | | | | 1.11 | | | | 1.11 | |

| | | | | | | |

| Class Y (Inception 10/31/08) | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 6.14 | | | | 13.40 | | | | 13.30 | | | | — | | | | 1.20 | | | | 1.20 | |

| | | | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | | | | | | | | | |

| Russell Midcap® Value Index2 | | | 20.00 | | | | 15.70 | | | | 15.44 | | | | 12.38 | | | | | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit ngam.natixis.com/performance. Performance for other share classes will be greater or less than shown based on differences in fees and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Performance for Class C shares assumes a 1.00% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase. |

| 2 | Russell Midcap® Value Index is an unmanaged index that measures the performance of the mid-cap value segment of the U.S. equity universe. It includes those Russell Midcap® Index companies with lower price-to-book ratios and lower forecasted growth values. |

| 3 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 4 | As of the most recent prospectus, the investment advisor has contractually agreed to waive fees and/or reimburse expenses (with certain exceptions) once the expense cap of the Fund has been exceeded. This arrangement is set to expire on 4/30/17. When an expense cap has not been exceeded, the fund may have similar expense ratios. |

| 24

ADDITIONAL INFORMATION

The views expressed in this report reflect those of the portfolio managers as of the dates indicated. The managers’ views are subject to change at any time without notice based on changes in market or other conditions. References to specific securities or industries should not be regarded as investment advice. Because the Funds are actively managed, there is no assurance that they will continue to invest in the securities or industries mentioned.

All investing involves risk, including the risk of loss. There is no assurance that any investment will meet its performance objectives or that losses will be avoided.

ADDITIONAL INDEX INFORMATION

This document may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Natixis Global Asset Management or any of its related or affiliated companies (collectively “NGAM”) and does not sponsor, endorse or participate in the provision of any NGAM services, funds or other financial products.

The index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

PROXY VOTING INFORMATION

A description of the Natixis Funds’ proxy voting policies and procedures is available without charge, upon request, by calling Natixis Funds at 800-225-5478; on Natixis Funds’ website at ngam.natixis.com; and on the Securities and Exchange Commission’s (SEC) website at www.sec.gov. Information regarding how Natixis Funds voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available from Natixis Funds’ website and the SEC’s website.

QUARTERLY PORTFOLIO SCHEDULES

Natixis Funds file a complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Forms N-Q are available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public

Reference Room may be obtained by calling 800-SEC-0330.

25 |

UNDERSTANDING FUND EXPENSES

As a mutual fund shareholder, you incur different costs: transaction costs, including sales charges (loads) on purchases and contingent deferred sales charges on redemptions, and ongoing costs, including management fees, distribution and/or service fees (12b-1 fees), and other fund expenses. Certain exemptions may apply. These costs are described in more detail in the Funds’ prospectus. The following examples are intended to help you understand the ongoing costs of investing in the Funds and help you compare these with the ongoing costs of investing in other mutual funds.

The first line in the table of each class of Fund shares shows the actual account values and actual Fund expenses you would have paid on a $1,000 investment in the Fund from July 1, 2016 through December 31, 2016. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example $8,600 account value divided by $1,000 = 8.60) and multiply the result by the number in the Expenses Paid During Period column as shown for your class.

The second line in the table for each class of fund shares provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid on your investment for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown reflect ongoing costs only, and do not include any transaction costs, such as sales charges. Therefore, the second line in the table of each fund is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. If transaction costs were included, total costs would be higher.

| | | | | | | | | | | | |

MIROVA GLOBAL SUSTAINABLE EQUITY

FUND | | BEGINNING

ACCOUNT VALUE

7/1/2016 | | | ENDING

ACCOUNT VALUE

12/31/2016 | | | EXPENSES PAID

DURING PERIOD*

7/1/2016 – 12/31/2016 | |

| Class A | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,001.50 | | | | $6.54 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,018.60 | | | | $6.60 | |

| Class C | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $998.10 | | | | $10.30 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,014.83 | | | | $10.38 | |

| Class Y | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,002.00 | | | | $5.28 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,019.86 | | | | $5.33 | |

| * | Expenses are equal to the Fund’s annualized expense ratio (after waiver/reimbursement): 1.30%, 2.05% and 1.05% for Class A, C and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), divided by 366 (to reflect the half-year period). |

| 26

| | | | | | | | | | | | |

| NATIXIS OAKMARK FUND | | BEGINNING

ACCOUNT VALUE

7/1/2016 | | | ENDING

ACCOUNT VALUE

12/31/2016 | | | EXPENSES PAID

DURING PERIOD*

7/1/2016 – 12/31/2016 | |

| Class A | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,178.00 | | | | $6.41 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,019.26 | | | | $5.94 | |

| Class C | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,173.00 | | | | $10.49 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,015.48 | | | | $9.73 | |

| Class Y | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,179.60 | | | | $5.04 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,020.51 | | | | $4.67 | |

| * | Expenses are equal to the Fund’s annualized expense ratio: 1.17%, 1.92% and 0.92% for Class A, C and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), divided by 366 (to reflect the half-year period). |

| | | | | | | | | | | | |

| NATIXIS OAKMARK INTERNATIONAL FUND | | BEGINNING

ACCOUNT VALUE

7/1/2016 | | | ENDING

ACCOUNT VALUE

12/31/2016 | | | EXPENSES PAID

DURING PERIOD*

7/1/2016 – 12/31/2016 | |

| Class A | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,204.40 | | | | $7.43 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,018.40 | | | | $6.80 | |

| Class C | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,200.90 | | | | $11.56 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,014.63 | | | | $10.58 | |

| * | Expenses are equal to the Fund’s annualized expense ratio: 1.34% and 2.09% for Class A and C, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), divided by 366 (to reflect the half-year period). |

27 |

| | | | | | | | | | | | |

| VAUGHAN NELSON SMALL CAP VALUE FUND | | BEGINNING

ACCOUNT VALUE

7/1/2016 | | | ENDING

ACCOUNT VALUE

12/31/2016 | | | EXPENSES PAID

DURING PERIOD*

7/1/2016 – 12/31/2016 | |

| Class A | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,158.40 | | | | $7.27 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,018.40 | | | | $6.80 | |

| Class C | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,153.80 | | | | $11.32 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,014.63 | | | | $10.58 | |

| Class Y | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,159.20 | | | | $5.92 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,019.66 | | | | $5.53 | |

| * | Expenses are equal to the Fund’s annualized expense ratio: 1.34%, 2.09% and 1.09% for Class A, C and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), divided by 366 (to reflect the half-year period). |

| | | | | | | | | | | | |

| VAUGHAN NELSON VALUE OPPORTUNITY FUND | | BEGINNING

ACCOUNT VALUE

7/1/2016 | | | ENDING

ACCOUNT VALUE

12/31/2016 | | | EXPENSES PAID

DURING PERIOD*

7/1/2016 – 12/31/2016 | |

| Class A | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,081.70 | | | | $6.38 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,019.00 | | | | $6.19 | |

| Class C | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,077.30 | | | | $10.29 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,015.23 | | | | $9.98 | |

| Class N | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,082.90 | | | | $4.61 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,020.71 | | | | $4.47 | |

| Class Y | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,082.70 | | | | $5.08 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,020.26 | | | | $4.93 | |

| * | Expenses are equal to the Fund’s annualized expense ratio: 1.22%, 1.97%, 0.88% and 0.97% for Class A, C, N and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), divided by 366 (to reflect the half-year period). |

| 28

Portfolio of Investments – as of December 31, 2016

Mirova Global Sustainable Equity Fund

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

| | Common Stocks — 94.1% of Net Assets | |

| | | | Belgium — 3.7% | | | | |

| | 29,353 | | | KBC Groep NV | | $ | 1,813,657 | |

| | | | | | | | |

| | | | Canada — 1.1% | | | | |

| | 21,332 | | | AltaGas Ltd. | | | 538,603 | |

| | | | | | | | |

| | | | Denmark — 7.0% | | | | |

| | 8,800 | | | Chr. Hansen Holding AS | | | 486,687 | |

| | 5,826 | | | Coloplast AS, Series B | | | 392,431 | |

| | 41,389 | | | Novo Nordisk AS, Class B | | | 1,484,713 | |

| | 10,116 | | | Novozymes AS | | | 348,111 | |

| | 11,569 | | | Vestas Wind Systems AS | | | 749,261 | |

| | | | | | | | |

| | | | | | | 3,461,203 | |

| | | | | | | | |

| | | | France — 7.1% | | | | |

| | 15,221 | | | Essilor International S.A. | | | 1,717,358 | |

| | 2,371 | | | Ingenico Group S.A. | | | 189,172 | |

| | 4,658 | | | L’Oreal S.A. | | | 848,992 | |

| | 13,492 | | | Valeo S.A. | | | 774,546 | |

| | | | | | | | |

| | | | | | | 3,530,068 | |

| | | | | | | | |

| | | | Germany — 5.2% | | | | |

| | 3,720 | | | Allianz SE, (Registered) | | | 613,941 | |

| | 61,274 | | | Deutsche Telekom AG | | | 1,051,290 | |

| | 15,055 | | | Symrise AG | | | 914,708 | |

| | | | | | | | |

| | | | | | | 2,579,939 | |

| | | | | | | | |

| | | | Hong Kong — 1.9% | | | | |

| | 80,737 | | | AIA Group Ltd. | | | 452,276 | |

| | 21,000 | | | Tencent Holdings Ltd. | | | 509,189 | |

| | | | | | | | |

| | | | | | | 961,465 | |

| | | | | | | | |

| | | | Ireland — 3.5% | | | | |

| | 17,500 | | | Eaton Corp. PLC | | | 1,174,075 | |

| | 8,100 | | | Medtronic PLC | | | 576,963 | |

| | | | | | | | |

| | | | | | | 1,751,038 | |

| | | | | | | | |

| | | | Japan — 3.0% | | | | |

| | 4,100 | | | Rinnai Corp. | | | 329,901 | |

| | 19,700 | | | Toyota Motor Corp. | | | 1,154,979 | |

| | | | | | | | |

| | | | | | | 1,484,880 | |

| | | | | | | | |

| | | | Netherlands — 3.8% | | | | |

| | 7,332 | | | ASML Holding NV | | | 821,700 | |

| | 26,392 | | | Unilever NV | | | 1,084,152 | |

| | | | | | | | |

| | | | | | | 1,905,852 | |

| | | | | | | | |

| | | | Singapore — 1.5% | | | | |

| | 768,700 | | | Raffles Medical Group Ltd. | | | 758,429 | |

| | | | | | | | |

| | | | Spain — 1.1% | | | | |

| | 21,397 | | | Enagas S.A. | | | 542,269 | |

| | | | | | | | |

See accompanying notes to financial statements.

29 |

Portfolio of Investments – as of December 31, 2016

Mirova Global Sustainable Equity Fund – (continued)

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

| | | | Switzerland — 1.5% | | | | |

| | 11,471 | | | Cie Financiere Richemont S.A., (Registered) | | $ | 758,124 | |

| | | | | | | | |

| | | | United Kingdom — 4.2% | | | | |

| | 303,943 | | | Legal & General Group PLC | | | 925,924 | |

| | 59,345 | | | Prudential PLC | | | 1,184,376 | |

| | | | | | | | |

| | | | | | | 2,110,300 | |

| | | | | | | | |

| | | | United States — 49.5% | | | | |

| | 16,200 | | | A.O. Smith Corp. | | | 767,070 | |

| | 2,100 | | | Alexion Pharmaceuticals, Inc.(b) | | | 256,935 | |

| | 3,101 | | | Alphabet, Inc., Class A(b) | | | 2,457,387 | |

| | 1,900 | | | Amazon.com, Inc.(b) | | | 1,424,753 | |

| | 10,174 | | | American Water Works Co., Inc. | | | 736,191 | |

| | 10,600 | | | Criteo S.A., Sponsored ADR(b) | | | 435,448 | |

| | 23,187 | | | Danaher Corp. | | | 1,804,876 | |

| | 16,500 | | | Delphi Automotive PLC | | | 1,111,275 | |

| | 9,000 | | | Ecolab, Inc. | | | 1,054,980 | |

| | 13,200 | | | Ellie Mae, Inc.(b) | | | 1,104,576 | |

| | 8,400 | | | Facebook, Inc., Class A(b) | | | 966,420 | |

| | 8,400 | | | Gilead Sciences, Inc. | | | 601,524 | |

| | 3,400 | | | Illumina, Inc.(b) | | | 435,336 | |

| | 4,100 | | | International Flavors & Fragrances, Inc. | | | 483,103 | |

| | 13,700 | | | MasterCard, Inc., Class A | | | 1,414,525 | |

| | 29,363 | | | Microsoft Corp. | | | 1,824,617 | |

| | 6,296 | | | NextEra Energy, Inc. | | | 752,120 | |

| | 11,300 | | | Roper Technologies, Inc. | | | 2,068,804 | |

| | 16,600 | | | Thermo Fisher Scientific, Inc. | | | 2,342,260 | |

| | 5,800 | | | United Natural Foods, Inc.(b) | | | 276,776 | |

| | 29,200 | | | Visa, Inc., Class A | | | 2,278,184 | |

| | | | | | | | |

| | | | | | | 24,597,160 | |

| | | | | | | | |

| | | | Total Common Stocks