UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04323

Natixis Funds Trust I

(Exact name of Registrant as specified in charter)

888 Boylston Street, Suite 800

Boston, Massachusetts 02199-8197

(Address of principal executive offices) (Zip code)

Russell L. Kane, Esq.

Natixis Distribution, L.P.

888 Boylston Street, Suite 800

Boston, Massachusetts 02199-8197

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 449-2822

Date of fiscal year end: September 30

Date of reporting period: September 30, 2017

Item 1. Reports to Stockholders.

The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

ANNUAL REPORT

September 30, 2017

Loomis Sayles Core Plus Bond Fund

TABLE OF CONTENTS

Portfolio Review page 1

Portfolio of Investments page 14

Financial Statements page 33

Notes to Financial Statements page 41

Shareholder Supplement enclosed

(previously posted to the Fund’s website)

LOOMIS SAYLES CORE PLUS BOND FUND

| | | | |

| Managers | | Symbols | | |

| Peter W. Palfrey, CFA® | | Class A | | NEFRX |

| Richard G. Raczkowski | | Class C | | NECRX |

| Loomis, Sayles & Company, L.P. | | Class N | | NERNX |

| | Class Y | | NERYX |

Investment Goal

The Fund seeks high total investment return through a combination of current income and capital appreciation.

Market Conditions

Following the November 2016 US presidential election, investors expected less accommodative US monetary policy and pro-business reform. These expectations drove the US dollar and equities higher, and weighed on many fixed income assets as the US Treasury yield curve steepened (a curve that shows the relationship among bond yields across the maturity spectrum). The Federal Reserve (Fed) raised interest rates on December 14, 2016, March 15, 2017 and June 14, 2017; investors took the increases in stride as a number of developments supported fixed income market performance through the rest of the period. The yield curve flattened out, the US dollar declined, global growth strengthened and corporate profits rebounded. Government bond yields remained low, driving investors into riskier assets like high yield credit and emerging markets. As a result, nearly all asset classes posted positive returns for the full period.

Despite an early rise, US inflation stayed largely range-bound for most of the period, hovering just below the Fed’s 2% target. Europe and Japan also struggled to meet inflation targets, while emerging markets saw steep declines. The spread between developed market and emerging market inflation reached its lowest point in 30 years.

All US Treasury yields rose during the 12-month period. However, much of the rise in longer-maturity yields took place shortly after the US presidential election while the two-year yield rose steadily over the entire period. Despite increasing overall, longer-term US Treasury yields declined from the start of 2017 until early September, when expectations for new and expansionary US fiscal policy and inflation began to rise.

Overall, investment grade corporate bonds generated positive return and outperformed duration-matched Treasuries (duration refers to a security’s price sensitivity to interest rate changes). The sector’s longer duration was beneficial as investors moved to the long end of the yield curve. High yield credit was a leading asset class throughout the period, benefiting from the “risk-on” environment and the search for yield. Improving corporate profits around the globe provided an additional tailwind to the sector.

Securitized credit assets generated positive total returns and outperformed duration-matched Treasuries. In September 2017, volatility remained muted after the Fed announced it would start tapering mortgage-backed security (MBS) reinvestments in October 2017; the move had been well telegraphed and was largely expected.

1 |

Emerging market bonds struggled at the beginning of the period, hurt by uncertainties related to global trade, the incoming US administration and geopolitics. But as 2017 progressed, sentiment shifted, emerging market bonds rallied and the asset class posted broadly positive returns for the full period. The sector benefited from the weakening US dollar, a rebound in corporate profits, and improving emerging market GDP growth.

Performance Results

For the 12 months ended September 30, 2017, Class Y shares of the Loomis Sayles Core Plus Bond Fund returned 2.10% at net asset value. The Fund outperformed its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index, which returned 0.07%.

Explanation of Fund Performance

Out-of-benchmark exposure to high yield corporate securities, particularly within industrials and financials, generated positive absolute and relative results. Selected energy, basic industry, wireless and finance company names were among the greatest positive contributors to the Fund’s relative performance.

The Fund maintained a meaningful underweight to US Treasuries. This positioning aided performance, as the period proved more beneficial for riskier assets. The Fund maintained an allocation to US Treasury inflation protected securities (TIPS), comprising 1-, 10- and 30-year TIPS. TIPS exposure benefited total and relative performance as TIPS outperformed nominal US Treasuries.

The Fund’s investment grade corporate holdings aided absolute and relative performance. Security selection among industrial names was the largest contributor to excess return, as selected basic industry and technology issues posted positive results.

Non-US-dollar exposure, particularly to the Mexican peso, boosted absolute and relative performance. After hitting a 14-year high during the fourth quarter of 2016, the US dollar steadily weakened through the rest of the period as risk appetite remained strong and fears about China’s economy and the potential for a US trade war waned.

A small out-of-benchmark allocation to emerging market issues, primarily Yankee bonds (US dollar-denominated bonds issued by a non-US entity), aided absolute and relative performance. The weaker US dollar fueled currency rallies in many emerging and developed overseas markets. Emerging markets also benefited from the search for yield, positive risk sentiment and improving fundamentals.

Security selection within our government-related exposure was positive; in particular, government-related sovereigns and oil-related Yankee bonds performed well.

Our longer-than-benchmark nominal duration was the largest detractor from performance. Over the period, we reduced this overweight from approximately 0.7 years longer to approximately 0.1 years longer than the benchmark.

Within investment grade corporates, the Fund’s financial holdings dragged on relative performance, primarily due to security selection. An underweight allocation to utility names also diminished excess return. The Fund maintained a small out-of-benchmark bank loan allocation, which had a neutral impact on relative return.

| 2

LOOMIS SAYLES CORE PLUS BOND FUND

Outlook

We believe that the Fed will tighten monetary conditions in a gradual and measured way as aggregate demand remains healthy, with the third hike of 2017 coming in December. The Fed began balance sheet reductions in October. We expect the market reaction to this activity to remain contained, given the well-telegraphed taper “caps” on both US Treasuries and MBS.

Corporate fundamentals have continued to indicate the US is in the late expansion phase of the credit cycle,1 with slowing margin growth, increased mergers and acquisitions, and rising leverage. Our view is that the cycle will continue to evolve slowly. The Trump administration may implement fiscal programs and tax reforms that could support asset classes like credit, although any impact is likely a 2018 event. Any reductions in corporate borrowing may preserve balance sheet health, promoting tighter credit spreads (the difference in yield between non-Treasury and Treasury yields of similar maturity) and lower default rates. While valuations may not be as attractive as they were last year, we continue to favor high yield relative to investment grade securities. We believe the primary risks to the credit markets include the pace of global growth, the timing of Fed tightening, shareholder-friendly activity and commodity price volatility.

While portfolio positioning became more defensive during the second half of 2016, the Fund remains oriented toward reflation. We maintain a broad underweight to the government sectors and a broad overweight to sectors offering a yield advantage over Treasuries.

We continued to overweight high-quality asset-backed securities (ABS), commercial mortgage-backed securities (CMBS) and high yield, though we have reduced our high yield allocation from nearly 20% during the summer of 2016 to approximately 10% at present. We also have a modest underweight to investment grade credit and continue to underweight the more interest-rate-sensitive government sectors, including US Treasuries, agencies and agency MBS, as we believe these sectors are fully valued.

While we do not believe the broad investment grade corporate market offers compelling value, we see selected opportunities in lower-quality investment grade companies, particularly outside the US.

Despite lower default rates and significant spread tightening in high yield over the past year, we are maintaining our reduced out-of-benchmark allocation to high yield and continue to search for selected issues with attractive yield and carry. Our allocation is primarily in higher-quality, shorter-maturity high yield names, which we believe offer better protection than lower-quality, longer-maturity names.

We believe bank loans offer front-end yield and can help protect against rising rates; we currently view secured better-quality high yield loans as the most attractive.

In April, we added a 5% position in one-year TIPS, bringing our total TIPS position to about 14% of the portfolio. We also continue to find breakeven inflation levels (the difference between yields on nominal Treasuries and TIPS of the same maturity) on

| 1 | A credit cycle is a cyclical pattern that follows credit availability and corporate health. |

3 |

10- and 30-year TIPS attractive relative to historical levels and versus our inflation and rates expectations. We expect TIPS to provide an attractive alternative to long-dated US Treasuries going forward.

Our relative portfolio duration is approximately 0.1 years longer than the benchmark on a nominal basis, but we expect it to behave about 1 year shorter because of our TIPS and other out-of-benchmark positions. Approximately 30% of the portfolio total duration contribution comes from TIPS, which we believe may provide incremental protection from rising inflation pressures.

Our non-US dollar exposure is slightly over 2% of total market value, composed primarily of the Mexican peso and a small allocation to the Uruguayan peso. Our focus has been on more pro-cyclical economies and foreign currencies tied to the improving global growth story.

Overall, we remain underweight agency mortgages, but recently opportunistically reduced our underweight from 15% to just 10%. We have also been adding to our agency CMBS exposure as a source of high-quality, 7- to 9-year spread in the government space. We continue to view home-equity conversion mortgages (HECMs) as an attractive alternative to 15-year agency MBS exposure given more stable duration and option-adjusted spreads.

We believe our yield advantage over the benchmark, in combination with our underweight to the government sector, should help reduce interest rate risk.

We may opportunistically add exposure back to investment grade and high yield credit and emerging market debt and currencies in the coming months, as valuations permit. Given our belief that we remain in the late expansion phase of the credit cycle, we are unlikely to return to the levels of overall credit exposure that we carried in recent years without a significant repricing of credit markets or a more significant improvement in the US and global economic outlook.

During periods in which the US dollar appreciates relative to foreign currencies, funds that hold non-US-dollar-denominated bonds may realize currency losses in connection with the maturity or sale of certain bonds. These losses impact a fund’s ordinary income distributions (to the extent that losses are not offset by realized currency gains within the fund’s fiscal year). A recognized currency loss, in accordance with federal tax rules, decreases the amount of ordinary income a fund has available to distribute, even though these bonds continue to generate coupon income.

Fund officers have analyzed the fund’s current portfolio of investments, schedule of maturities and the corresponding amounts of unrealized currency losses that may become realized in the fiscal year ending on September 30, 2018. Based on this analysis, fund officers believe that realized currency losses may have less of an impact on this fund’s distributions in the 2018 fiscal year. This analysis is based on certain assumptions, including but not limited to the level of foreign currency exchange rates, security prices, interest rates, fund advisors’ ability to manage realized currency losses and the net asset level of the fund. Changes to these assumptions could materially impact the analysis and the amounts of future fund distributions. Fund officers will continue to monitor on a regular basis and take the necessary actions required to manage the fund’s distributions to address realized currency losses while seeking to avoid a return of capital distribution.

| 4

LOOMIS SAYLES CORE PLUS BOND FUND

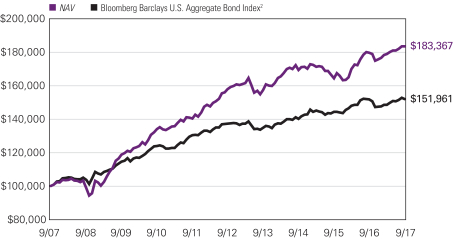

Hypothetical Growth of $100,000 Investment in Class Y Shares3

September 30, 2007 to September 30, 2017

See notes to chart on page 6.

5 |

Average Annual Total Returns — September 30, 20173

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | Expense Ratios4 | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | Life of Class N | | | Gross | | | Net | |

| | | | | | | |

| Class Y (Inception 12/30/94) | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 2.10 | % | | | 3.04 | % | | | 6.25 | % | | | — | % | | | 0.48 | % | | | 0.48 | % |

| | | | | | | |

| Class A (Inception 11/7/73) | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 1.86 | | | | 2.79 | | | | 5.98 | | | | — | | | | 0.73 | | | | 0.73 | |

| With 4.25% Maximum Sales Charge | | | -2.47 | | | | 1.90 | | | | 5.52 | | | | — | | | | | | | | | |

| | | | | | | |

| Class C (Inception 12/30/94) | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 1.08 | | | | 2.01 | | | | 5.19 | | | | — | | | | 1.48 | | | | 1.48 | |

| With CDSC1 | | | 0.09 | | | | 2.01 | | | | 5.19 | | | | | | | | | | | | | |

| | | | | | | |

| Class N (Inception 2/1/13) | | | | | | | | | | | | | | | | | | | | | | | | |

| NAV | | | 2.12 | | | | — | | | | — | | | | 2.97 | | | | 0.39 | | | | 0.39 | |

| | | | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | | | | | | | | | |

| Bloomberg Barclays U.S. Aggregate Bond Index2 | | | 0.07 | | | | 2.06 | | | | 4.27 | | | | 2.35 | | | | | | | | | |

Performance data shown represents past performance and is no guarantee of, and not necessarily indicative of, future results. Total return and value will vary, and you may have a gain or loss when shares are sold. Current performance may be lower or higher than quoted. For most recent month-end performance, visit im.natixis.com. Performance for other share classes will be greater or less than shown based on differences and sales charges. You may not invest directly in an index. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

| 1 | Class C shares performance assumes a 1% CDSC applied when you sell shares within one year of purchase. |

| 2 | The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS. The Bloomberg Barclays U.S. Aggregate Bond Index rolls up into other Bloomberg Barclays flagship indices, such as the multi-currency Bloomberg Barclays Global Aggregate Bond Index and the Bloomberg Barclays U.S. Universal Index, which includes high yield and emerging markets debt. The Bloomberg Barclays U.S. Aggregate Bond Index was created in 1986, with index history backfilled to January 1, 1976. You may not invest directly in an index. |

| 3 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 4 | Expense ratios are as shown in the Fund’s prospectus in effect as of the date of this report. The expense ratios for the current reporting period can be found in the Financial Highlights section of this report under Ratios to Average Net Assets. Net expenses reflect contractual expense caps set to expire on 1/31/18. When a Fund’s expenses are below the cap, gross and net expense ratios will be the same. See Note 6 of the Notes to Financial Statements for more information about the Fund’s expense caps. |

| 6

ADDITIONAL INFORMATION

The views expressed in this report reflect those of the portfolio managers as of the dates indicated. The managers’ views are subject to change at any time without notice based on changes in market or other conditions. References to specific securities or industries should not be regarded as investment advice. Because the Fund is actively managed, there is no assurance that it will continue to invest in the securities or industries mentioned.

All investing involves risk, including the risk of loss. There is no assurance that any investment will meet its performance objectives or that losses will be avoided.

ADDITIONAL INDEX INFORMATION

This document may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Natixis Investment Managers or any of its related or affiliated companies (collectively “Natixis Affiliates”) and does not sponsor, endorse or participate in the provision of any Natixis Affiliates services, funds or other financial products.

The index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

PROXY VOTING INFORMATION

A description of the Natixis Funds’ proxy voting policies and procedures is available without charge, upon request, by calling Natixis Funds at 800-225-5478; on the Fund’s website at im.natixis.com; and on the Securities and Exchange Commission’s (“SEC’s”) website at www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities the most recent 12-month period ended June 30 is available from the Fund’s website and the SEC’s website.

QUARTERLY PORTFOLIO SCHEDULES

The Natixis Funds file complete schedules of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 800-SEC-0330.

7 |

UNDERSTANDING FUND EXPENSES

As a mutual fund shareholder, you incur different costs: transaction costs, including sales charges (loads) on purchases and contingent deferred sales charges on redemptions; and ongoing costs, including management fees, distribution and/or service fees (12b-1 fees), and other fund expenses. Certain exemptions may apply. These costs are described in more detail in the Fund’s prospectuses. The following examples are intended to help you understand the ongoing costs of investing in the Fund and help you compare these with the ongoing costs of investing in other mutual funds.

The first line in the table of each class of Fund shares shows the actual account values and actual fund expenses you would have paid on a $1,000 investment in the Fund from April 1, 2017 through September 30, 2017. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example $8,600 account value divided by $1,000 = 8.6) and multiply the result by the number in the Expenses Paid During Period column as shown below for your class.

The second line in the table of each class of Fund shares provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid on your investment for the period. You may use this information to compare the ongoing costs of investing in the Fund to other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown reflect ongoing costs only, and do not include any transaction costs, such as sales charges. Therefore, the second line in the table of each fund is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. If transaction costs were included, total costs would be higher.

| | | | | | | | | | | | |

| LOOMIS SAYLES CORE PLUS BOND FUND | | BEGINNING

ACCOUNT VALUE

4/1/2017 | | | ENDING

ACCOUNT VALUE

9/30/2017 | | | EXPENSES PAID

DURING PERIOD*

4/1/2017 – 9/30/2017 | |

| Class A | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,024.00 | | | | $3.65 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,021.46 | | | | $3.65 | |

| Class C | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,020.20 | | | | $7.44 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,017.70 | | | | $7.44 | |

| Class N | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,025.60 | | | | $1.98 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,023.11 | | | | $1.98 | |

| Class Y | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,025.10 | | | | $2.39 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,022.71 | | | | $2.38 | |

| * | Hypothetical expenses are equal to the Fund’s annualized expense ratio: 0.72%, 1.47%, 0.39% and 0.47% for Class A, C, N and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (183), divided by 365 (to reflect the half-year period). |

| 8

BOARD APPROVAL OF THE EXISTING ADVISORY AGREEMENTS

The Board of Trustees of the Trust (the “Board”), including the Independent Trustees, considers matters bearing on the Fund’s advisory agreement and the Fund’s Advisory Administration Agreement (collectively, the “Agreements”) at most of its meetings throughout the year. Each year, usually in the spring, the Contract Review Committee of the Board meets to review the Agreements to determine whether to recommend that the full Board approve the continuation of the Agreements, typically for an additional one-year period. After the Contract Review Committee has made its recommendation, the full Board, including the Independent Trustees, determines whether to approve the continuation of the Agreements.

In connection with these meetings, the Trustees receive materials that the Fund’s investment adviser (the “Adviser”) believes to be reasonably necessary for the Trustees to evaluate the Agreements. These materials generally include, among other items, (i) information on the investment performance of the Fund and the performance of a peer group of funds and the Fund’s performance benchmarks, (ii) information on the Fund’s advisory fees and other expenses, including information comparing the Fund’s expenses to the fees charged to institutional accounts with similar strategies managed by the Adviser, if any, and to those of a peer group of funds and information about any applicable expense caps and/or fee “breakpoints,” (iii) sales and redemption data in respect of the Fund, (iv) information about the profitability of the Agreements to the Adviser and (v) information obtained through the completion by the Adviser of a questionnaire distributed on behalf of the Trustees. The Board, including the Independent Trustees, also considers other matters such as (i) the Adviser’s financial results and financial condition, (ii) the Fund’s investment objective and strategies and the size, education and experience of the Adviser’s investment staff and its use of technology, external research and trading cost measurement tools, (iii) arrangements in respect of the distribution of the Fund’s shares and the related costs, (iv) the allocation of the Fund’s brokerage, if any, including, if applicable, allocations to brokers affiliated with the Adviser and the use of “soft” commission dollars to pay Fund expenses and to pay for research and other similar services, (v) the resources devoted to, and the record of compliance with, the Fund’s investment policies and restrictions, policies on personal securities transactions and other compliance policies, (vi) the Adviser’s policies and procedures relating to, among other things, compliance, trading and best execution, proxy voting and valuation, (vii) information about amounts invested by the Fund’s portfolio managers in the Fund or in similar accounts that they manage and (viii) the general economic outlook with particular emphasis on the mutual fund industry. Throughout the process, the Trustees are afforded the opportunity to ask questions of and request additional materials from the Adviser.

In addition to the materials requested by the Trustees in connection with their annual consideration of the continuation of the Agreements, the Trustees receive materials in advance of each regular quarterly meeting of the Board that provide detailed information about the Fund’s investment performance and the fees charged to the Fund for advisory and other services. This information generally includes, among other things, an internal

9 |

performance rating for the Fund based on agreed-upon criteria, graphs showing the Fund’s performance and fee differentials against the Fund’s peer group/category, performance ratings provided by a third-party, total return information for various periods, and third-party performance rankings for various periods comparing the Fund against similarly categorized funds. The portfolio management team for the Fund or other representatives of the Adviser make periodic presentations to the Contract Review Committee and/or the full Board, and if the Fund is identified as presenting possible performance concerns it may be subject to more frequent board presentations and reviews. In addition, each quarter the Trustees are provided with detailed statistical information about the Fund’s portfolio. The Trustees also receive periodic updates between meetings.

The Board most recently approved the continuation of the Agreements at its meeting held in June 2017. The Agreements were continued for a one-year period for the Fund. In considering whether to approve the continuation of the Agreements, the Board, including the Independent Trustees, did not identify any single factor as determinative. Individual Trustees may have evaluated the information presented differently from one another, giving different weights to various factors. Matters considered by the Trustees, including the Independent Trustees, in connection with their approval of the Agreements included, but were not limited to, the factors listed below.

The nature, extent and quality of the services provided to the Fund under the Agreements. The Trustees considered the nature, extent and quality of the services provided by the Adviser and its affiliates to the Fund and the resources dedicated to the Fund by the Adviser and its affiliates.

The Trustees considered not only the advisory services provided by the Adviser to the Fund, but also the monitoring and oversight services provided by Natixis Advisors, L.P. (“Natixis Advisors”). They also considered the administrative services provided by Natixis Advisors and its affiliates to the Fund.

The Trustees also considered the benefits to shareholders of investing in a mutual fund that is part of a family of funds that offers shareholders the right to exchange shares of one type of fund for shares of another type of fund, and provides a variety of fund and shareholder services.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding the Agreements, that the nature, extent and quality of services provided supported the renewal of the Agreements.

Investment performance of the Fund and the Adviser. As noted above, the Trustees received information about the performance of the Fund over various time periods, including information that compared the performance of the Fund to the performance of a peer group and category of funds and the Fund’s performance benchmark. In addition, the Trustees also reviewed data prepared by an independent third party that analyzed the performance of the Fund using a variety of performance metrics, including metrics that also measured the performance of the Fund on a risk adjusted basis.

The Board noted that, through December 31, 2016, the Fund’s one- and three-year performance stated as percentile rankings within categories selected by the independent

| 10

third-party data provider was as follows (where the best performance would be in the first percentile of its category):

| | | | | | | | |

| | | One-Year | | | Three-Year | |

Loomis Sayles Core Plus Bond Fund | | | 2 | % | | | 39 | % |

The Trustees also considered the Adviser’s performance and reputation generally, the performance of the fund family generally, and the historical responsiveness of the Adviser to Trustee concerns about performance and the willingness of the Adviser to take steps intended to improve performance.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding the Agreements, that the performance of the Fund and the Adviser and/or other relevant factors supported the renewal of the Agreements.

The costs of the services to be provided and profits to be realized by the Adviser and its affiliates from their respective relationships with the Fund. The Trustees considered the fees charged to the Fund for advisory services as well as the total expense level of the Fund. This information included comparisons (provided both by management and also by an independent third party) of the Fund’s advisory fee and total expense level to those of its peer group and information about the advisory fees charged by the Adviser to comparable accounts (such as institutional separate accounts), as well as information about differences in such fees and the reasons for any such differences. In considering the fees charged to comparable accounts, the Trustees considered, among other things, management’s representations about the differences between managing mutual funds as compared to other types of accounts, including the additional resources required to effectively manage mutual fund assets and the greater regulatory costs associated with the management of such assets. In evaluating the Fund’s advisory fee, the Trustees also took into account the demands, complexity and quality of the investment management of the Fund, as well as the need for the Adviser to offer competitive compensation and the potential need to expend additional resources to the extent the Fund grows in size. The Trustees considered that over the past several years, management had made recommendations regarding reductions in advisory fee rates, implementation of advisory fee breakpoints and the institution of advisory fee waivers and expense caps for various funds in the fund family. The Trustees noted that the Fund currently has an expense cap in place, and that the current expenses are below the cap.

The Trustees also considered the compensation directly or indirectly received by the Adviser and its affiliates from their relationships with the Fund. The Trustees reviewed information provided by management as to the profitability of the Adviser’s and its affiliates’ relationships with the Fund, and information about the allocation of expenses used to calculate profitability. They also reviewed information provided by management about the effect of distribution costs and changes in asset levels on Adviser profitability, including information regarding resources spent on distribution activities. When reviewing profitability, the Trustees also considered information about court cases in which adviser compensation or profitability were issues, the performance of the Fund, the expense levels of the Fund, and whether the Adviser had implemented breakpoints and/or expense caps. The Trustees also noted management’s history of proposing additional advisory fee breakpoints as the Fund grew to substantially larger scale.

11 |

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding the Agreement, that the advisory fee charged to the Fund was fair and reasonable, and that the costs of these services generally and the related profitability of the Adviser and its affiliates in respect of their relationships with the Fund supported the renewal of the Agreements.

Economies of Scale. The Trustees considered the existence of any economies of scale in the provision of services by the Adviser and whether those economies are shared with the Fund through breakpoints in its investment advisory fee or other means, such as expense waivers or caps. The Trustees also discussed with management the factors considered with respect to the implementation of breakpoints in investment advisory fees or expense waivers or caps for certain funds. Management explained that a number of factors are taken into account in considering the possible implementation of breakpoints or an expense cap for a fund, including, among other things, factors such as a fund’s assets, the projected growth of a fund, projected profitability and a fund’s fees and performance. With respect to economies of scale, the Trustees noted that the Fund’s management fee and overall net expense ratio were below the median compared to a peer group of funds and that the Fund was subject to an expense cap or waiver, as well as breakpoints in the fees payable under the Agreements. In considering these issues, the Trustees also took note of the costs of the services provided (both on an absolute and on a relative basis) and the profitability to the Adviser and its affiliates of their relationships with the Fund, as discussed above.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding the Agreements, that the extent to which economies of scale were shared with the Fund supported the renewal of the Agreements.

The Trustees also considered other factors, which included but were not limited to the following:

| · | | The effect of recent market and economic events on the performance, asset levels and expense ratios of the Fund. |

| · | | Whether the Fund has operated in accordance with its investment objective and the Fund’s record of compliance with its investment restrictions, and the compliance programs of the Fund and the Adviser. They also considered the compliance-related resources the Adviser and its affiliates were providing to the Fund. |

| · | | The nature, quality, cost and extent of administrative and shareholder services performed by the Adviser and its affiliates under the Agreements. |

| · | | So-called “fallout benefits” to the Adviser, such as the engagement of affiliates of the Adviser to provide distribution, administrative and brokerage services to the Fund, and the benefits of research made available to the Adviser by reason of brokerage commissions (if any) generated by the Fund’s securities transactions. The Trustees also considered the benefits to the parent company of Natixis Advisors from the retention of the Adviser. The Trustees considered the possible conflicts of interest associated with these fallout and other benefits, and the reporting, disclosure and other processes in place to disclose and monitor such possible conflicts of interest. |

| 12

| · | | The Trustees’ review and discussion of the Fund’s advisory arrangements in prior years, and management’s record of responding to Trustee concerns raised during the year and in prior years. |

Based on their evaluation of all factors that they deemed to be material, including those factors described above, and assisted by the advice of independent counsel, the Trustees, including the Independent Trustees, concluded that the existing Agreements should be continued through June 30, 2018.

13 |

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | Bonds and Notes — 92.1% of Net Assets | |

| | | | ABS Car Loan — 3.0% | | | | |

| $ | 3,060,000 | | | AmeriCredit Automobile Receivables Trust, Series 2014-2, Class C, 2.180%, 6/08/2020 | | $ | 3,068,624 | |

| | 1,553,774 | | | AmeriCredit Automobile Receivables Trust, Series 2014-3, Class B, 1.920%, 11/08/2019 | | | 1,554,545 | |

| | 4,262,000 | | | AmeriCredit Automobile Receivables Trust, Series 2014-3, Class C, 2.580%, 9/08/2020 | | | 4,290,090 | |

| | 2,438,000 | | | AmeriCredit Automobile Receivables Trust, Series 2014-4, Class C, 2.470%, 11/09/2020 | | | 2,453,815 | |

| | 16,421,000 | | | AmeriCredit Automobile Receivables Trust, Series 2015-1, Class C, 2.510%, 1/08/2021 | | | 16,536,922 | |

| | 7,135,000 | | | AmeriCredit Automobile Receivables Trust, Series 2015-4, Class B, 2.110%, 1/08/2021 | | | 7,149,164 | |

| | 4,495,000 | | | AmeriCredit Automobile Receivables Trust, Series 2015-4, Class C, 2.880%,��7/08/2021 | | | 4,536,421 | |

| | 485,000 | | | AmeriCredit Automobile Receivables Trust, Series 2017-1, Class A3, 1.870%, 8/18/2021 | | | 484,821 | |

| | 1,950,000 | | | Avis Budget Rental Car Funding AESOP LLC, Series 2012-3A, Class A, 2.100%, 3/20/2019, 144A | | | 1,951,936 | |

| | 1,535,000 | | | Avis Budget Rental Car Funding AESOP LLC, Series 2013-1A, Class B, 2.620%, 9/20/2019, 144A | | | 1,538,716 | |

| | 3,900,000 | | | Avis Budget Rental Car Funding AESOP LLC, Series 2013-2A, Class A, 2.970%, 2/20/2020, 144A | | | 3,936,324 | |

| | 2,000,000 | | | Avis Budget Rental Car Funding AESOP LLC, Series 2015-1A, Class A, 2.500%, 7/20/2021, 144A | | | 1,997,010 | |

| | 11,955,000 | | | Avis Budget Rental Car Funding AESOP LLC, Series 2016-1A, Class A, 2.990%, 6/20/2022, 144A | | | 12,060,969 | |

| | 15,005,000 | | | Avis Budget Rental Car Funding AESOP LLC, Series 2016-2A, Class A, 2.720%, 11/20/2022, 144A | | | 15,005,059 | |

| | 10,350,000 | | | Avis Budget Rental Car Funding AESOP LLC, Series 2017-1A, Class A, 3.070%, 9/20/2023, 144A | | | 10,433,239 | |

| | 2,602,681 | | | CPS Auto Receivables Trust, Series 2015-A, Class A, 1.530%, 7/15/2019, 144A | | | 2,601,870 | |

| | 2,910,984 | | | CPS Auto Receivables Trust, Series 2015-B, Class A, 1.650%, 11/15/2019, 144A | | | 2,910,995 | |

| | 14,384,000 | | | CPS Auto Receivables Trust, Series 2015-C, Class C, 3.420%, 8/16/2021, 144A | | | 14,502,664 | |

| | 6,754,034 | | | Credit Acceptance Auto Loan Trust, Series 2014-2A, Class B, 2.670%, 9/15/2022, 144A | | | 6,755,776 | |

| | 354,617 | | | Credit Acceptance Auto Loan Trust, Series 2015-1A, Class A, 2.000%, 7/15/2022, 144A | | | 354,678 | |

| | 7,515,000 | | | Credit Acceptance Auto Loan Trust, Series 2016-2A, Class A, 2.420%, 11/15/2023, 144A | | | 7,550,819 | |

| | 8,230,000 | | | Credit Acceptance Auto Loan Trust, Series 2016-3A, Class A, 2.150%, 4/15/2024, 144A | | | 8,209,523 | |

| | 3,600,000 | | | Credit Acceptance Auto Loan Trust, Series 2017-1A, Class A, 2.560%, 10/15/2025, 144A | | | 3,610,498 | |

See accompanying notes to financial statements.

| 14

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund – (continued)

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | | | ABS Car Loan — continued | | | | |

| $ | 2,982,041 | | | Drive Auto Receivables Trust, Series 2016-BA, Class B, 2.560%, 6/15/2020, 144A | | $ | 2,989,243 | |

| | 7,260,000 | | | Drive Auto Receivables Trust, Series 2016-BA, Class C, 3.190%, 7/15/2022, 144A | | | 7,333,685 | |

| | 3,185,000 | | | Drive Auto Receivables Trust, Series 2017-1, Class B, 2.360%, 3/15/2021 | | | 3,190,533 | |

| | 2,595,000 | | | Drive Auto Receivables Trust, Series 2017-AA, Class B, 2.510%, 1/15/2021, 144A | | | 2,608,662 | |

| | 3,625,000 | | | Drive Auto Receivables Trust, Series 2017-AA, Class C, 2.980%, 1/18/2022, 144A | | | 3,663,497 | |

| | 1,325,000 | | | Drive Auto Receivables Trust, Series 2017-BA, Class B, 2.200%, 5/15/2020, 144A | | | 1,327,746 | |

| | 2,353,180 | | | DT Auto Owner Trust, Series 2014-3A, Class C, 3.040%, 9/15/2020, 144A | | | 2,357,890 | |

| | 2,489,245 | | | DT Auto Owner Trust, Series 2017-1A, Class A, 1.560%, 6/15/2020, 144A | | | 2,487,677 | |

| | 3,270,193 | | | DT Auto Owner Trust, Series 2017-2A, Class A, 1.720%, 5/15/2020, 144A | | | 3,270,497 | |

| | 1,417,206 | | | Exeter Automobile Receivables Trust, Series 2014-3A, Class B, 2.770%, 11/15/2019, 144A | | | 1,419,600 | |

| | 1,368,415 | | | Exeter Automobile Receivables Trust, Series 2016-1A, Class A, 2.350%, 7/15/2020, 144A | | | 1,369,614 | |

| | 3,348,015 | | | Exeter Automobile Receivables Trust, Series 2017-1A, Class A, 1.960%, 3/15/2021, 144A | | | 3,341,350 | |

| | 2,606,172 | | | First Investors Auto Owner Trust, Series 2014-3A, Class A3, 1.670%, 11/16/2020, 144A | | | 2,606,271 | |

| | 1,738,810 | | | First Investors Auto Owner Trust, Series 2017-1A, Class A1, 1.690%, 4/15/2021, 144A | | | 1,736,342 | |

| | 52,851 | | | Flagship Credit Auto Trust, Series 2014-2, Class A, 1.430%, 12/16/2019, 144A | | | 52,852 | |

| | 5,672,863 | | | Flagship Credit Auto Trust, Series 2016-1, Class A, 2.770%, 12/15/2020, 144A | | | 5,708,402 | |

| | 5,336,413 | | | Santander Drive Auto Receivables Trust, Series 2014-2, Class C, 2.330%, 11/15/2019 | | | 5,348,505 | |

| | 1,229,607 | | | Santander Drive Auto Receivables Trust, Series 2014-3, Class C, 2.130%, 8/17/2020 | | | 1,231,556 | |

| | 2,292,433 | | | Santander Drive Auto Receivables Trust, Series 2014-4, Class C, 2.600%, 11/16/2020 | | | 2,300,985 | |

| | 6,190,900 | | | Santander Drive Auto Receivables Trust, Series 2014-5, Class C, 2.460%, 6/15/2020 | | | 6,214,891 | |

| | 4,440,000 | | | Santander Drive Auto Receivables Trust, Series 2017-2, Class B, 2.210%, 10/15/2021 | | | 4,446,897 | |

| | | | | | | | |

| | | | | | | 198,501,173 | |

| | | | | | | | |

| | | | ABS Credit Card — 0.4% | | | | |

| | 463,000 | | | World Financial Network Credit Card Master Trust, Series 2012-A, Class A, 3.140%, 1/17/2023 | | | 471,497 | |

| | 11,115,000 | | | World Financial Network Credit Card Master Trust, Series 2016-A, Class A, 2.030%, 4/15/2025 | | | 10,986,604 | |

| | 12,265,000 | | | World Financial Network Credit Card Master Trust, Series 2016-C, Class A, 1.720%, 8/15/2023 | | | 12,188,408 | |

| | | | | | | | |

| | | | | | | 23,646,509 | |

| | | | | | | | |

See accompanying notes to financial statements.

15 |

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund – (continued)

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | | | ABS Home Equity — 1.6% | | | | |

| $ | 5,338,683 | | | Bayview Opportunity Master Fund IVa Trust, Series 2016-SPL1, Class A, 4.000%, 4/28/2055, 144A | | $ | 5,528,446 | |

| | 2,891,833 | | | Bayview Opportunity Master Fund IVa Trust, Series 2017-RT1, Class A1, 3.000%, 3/28/2057, 144A(a) | | | 2,923,530 | |

| | 7,434,850 | | | Bayview Opportunity Master Fund IVa Trust, Series 2017-SPL1, Class A, 4.000%, 10/28/2064, 144A(a) | | | 7,748,637 | |

| | 3,149,719 | | | Bayview Opportunity Master Fund IVb Trust, Series 2017-SPL2, Class A, 4.000%, 6/28/2054, 144A(a) | | | 3,282,162 | |

| | 3,501,241 | | | Bayview Opportunity Master Fund IVb Trust, Series 2017-SPL3, Class A, 4.000%, 11/28/2053, 144A(a) | | | 3,645,584 | |

| | 17,225,950 | | | Colony American Finance Ltd., Series 2015-1, Class A, 2.896%, 10/15/2047, 144A | | | 17,328,675 | |

| | 4,003,237 | | | Colony American Homes, Series 2014-1A, Class A, 1-month LIBOR + 1.150%, 2.384%, 5/17/2031, 144A(m) | | | 4,019,989 | |

| | 99,775 | | | Countrywide Asset-Backed Certificates, Series 2004-S1, Class A3, 5.115%, 2/25/2035(a) | | | 100,812 | |

| | 10,310,350 | | | Home Partners of America Trust, Series 2016-1, Class A, 1-month LIBOR + 1.650%, 2.884%, 3/17/2033, 144A(m) | | | 10,419,953 | |

| | 6,156,480 | | | Mill City Mortgage Trust, Series 2015-2, Class A1, 3.000%, 9/25/2057, 144A(a) | | | 6,182,512 | |

| | 4,693,633 | | | Mill City Mortgage Trust, Series 2016-1, Class A1, 2.500%, 4/25/2057, 144A(a) | | | 4,691,175 | |

| | 2,890,000 | | | Sequoia Mortgage Trust, Series 2017-CH1, Class A1, 4.000%, 10/25/2047, 144A(a)(b) | | | 2,967,183 | |

| | 1,454,000 | | | Towd Point Mortgage Trust, Series 2015-1, Class A5, 3.521%, 10/25/2053, 144A(a) | | | 1,502,690 | |

| | 13,331,956 | | | Towd Point Mortgage Trust, Series 2015-2, Class 1AE2, 2.750%, 11/25/2060, 144A(a) | | | 13,390,580 | |

| | 5,018,000 | | | Towd Point Mortgage Trust, Series 2015-4, Class M2, 3.750%, 4/25/2055, 144A(a) | | | 5,115,995 | |

| | 9,655,785 | | | Towd Point Mortgage Trust, Series 2016-2, Class A1A, 2.750%, 8/25/2055, 144A(a) | | | 9,698,598 | |

| | 6,017,000 | | | Towd Point Mortgage Trust, Series 2016-2, Class M2, 3.000%, 8/25/2055, 144A(a) | | | 5,645,207 | |

| | 2,726,000 | | | Towd Point Mortgage Trust, Series 2016-3, Class M1, 3.500%, 4/25/2056, 144A(a) | | | 2,749,667 | |

| | | | | | | | |

| | | | | | | 106,941,395 | |

| | | | | | | | |

| | | | ABS Other — 1.0% | | | | |

| | 9,092,850 | | | DB Master Finance LLC, Series 2015-1A, Class A2I, 3.262%, 2/20/2045, 144A | | | 9,107,126 | |

| | 205,292 | | | OneMain Financial Issuance Trust, Series 2014-2A, Class A, 2.470%, 9/18/2024, 144A | | | 205,526 | |

| | 19,255,000 | | | OneMain Financial Issuance Trust, Series 2015-1A, Class A, 3.190%, 3/18/2026, 144A | | | 19,443,397 | |

| | 13,980,000 | | | OneMain Financial Issuance Trust, Series 2016-1A, Class A, 3.660%, 2/20/2029, 144A | | | 14,310,628 | |

| | 15,600,000 | | | OneMain Financial Issuance Trust, Series 2016-2A, Class A, 4.100%, 3/20/2028, 144A | | | 15,870,939 | |

See accompanying notes to financial statements.

| 16

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund – (continued)

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | | | ABS Other — continued | | | | |

| $ | 6,209,200 | | | TAL Advantage V LLC, Series 2014-3A, Class A, 3.270%, 11/21/2039, 144A | | $ | 6,177,623 | |

| | | | | | | | |

| | | | | | | 65,115,239 | |

| | | | | | | | |

| | | | ABS Student Loan — 0.0% | | | | |

| | 604,865 | | | SoFi Professional Loan Program LLC, Series 2014-A, Class A2, 3.020%, 10/25/2027, 144A | | | 611,379 | |

| | 1,953,239 | | | SoFi Professional Loan Program LLC, Series 2014-B, Class A2, 2.550%, 8/27/2029, 144A | | | 1,960,903 | |

| | | | | | | | |

| | | | | | | 2,572,282 | |

| | | | | | | | |

| | | | Aerospace & Defense — 0.2% | | | | |

| | 921,000 | | | Bombardier, Inc., 5.750%, 3/15/2022, 144A | | | 891,068 | |

| | 12,842,000 | | | Embraer Netherlands Finance BV, 5.050%, 6/15/2025 | | | 13,628,572 | |

| | | | | | | | |

| | | | | | | 14,519,640 | |

| | | | | | | | |

| | | | Agency Commercial Mortgage-Backed Securities — 1.9% | | | | |

| | 15,165,000 | | | Federal National Mortgage Association, Series 2015-M15, Class A2, 2.923%, 10/25/2025(a) | | | 15,330,567 | |

| | 6,750,000 | | | Federal National Mortgage Association, Series 2015-M17, Class A2, 3.038%, 11/25/2025(a) | | | 6,866,932 | |

| | 10,975,000 | | | Federal National Mortgage Association, Series 2016-M4, Class A2, 2.576%, 3/25/2026 | | | 10,792,807 | |

| | 7,591,000 | | | Federal National Mortgage Association, Series 2017-M3, Class A2, 2.569%, 12/25/2026(a) | | | 7,387,999 | |

| | 7,200,000 | | | FHLMC Multifamily Structured Pass Through Certificates, Series K050, Class A2, 3.334%, 8/25/2025(a) | | | 7,531,819 | |

| | 5,580,000 | | | FHLMC Multifamily Structured Pass Through Certificates, Series K051, Class A2, 3.308%, 9/25/2025 | | | 5,828,164 | |

| | 8,680,450 | | | FHLMC Multifamily Structured Pass Through Certificates, Series K052, Class A2, 3.151%, 11/25/2025 | | | 8,964,254 | |

| | 5,810,000 | | | FHLMC Multifamily Structured Pass Through Certificates, Series K053, Class A2, 2.995%, 12/25/2025 | | | 5,930,670 | |

| | 11,220,000 | | | FHLMC Multifamily Structured Pass Through Certificates, Series K057, Class A2, 2.570%, 7/25/2026 | | | 11,056,493 | |

| | 2,770,000 | | | FHLMC Multifamily Structured Pass Through Certificates, Series K058, Class A2, 2.653%, 8/25/2026 | | | 2,742,126 | |

| | 6,195,000 | | | FHLMC Multifamily Structured Pass Through Certificates, Series K061, Class A2, 3.347%, 11/25/2026(a) | | | 6,453,509 | |

| | 6,995,000 | | | FHLMC Multifamily Structured Pass Through Certificates, Series K062, Class A2, 3.413%, 12/25/2026 | | | 7,318,725 | |

| | 5,105,490 | | | FHLMC Multifamily Structured Pass Through Certificates, Series K063, Class A2, 3.430%, 1/25/2027(a) | | | 5,348,632 | |

| | 11,410,000 | | | FHLMC Multifamily Structured Pass Through Certificates, Series K727, Class A2, 2.946%, 7/25/2024 | | | 11,675,923 | |

| | 7,760,000 | | | FHLMC Multifamily Structured Pass Through Certificates, Series KPLB, Class A, 2.770%, 5/25/2025 | | | 7,793,879 | |

| | | | | | | | |

| | | | | | | 121,022,499 | |

| | | | | | | | |

See accompanying notes to financial statements.

17 |

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund – (continued)

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | | | Airlines — 0.1% | | | | |

| $ | 2,607,566 | | | Continental Airlines Pass Through Certificates, Series 2012-2, Class A, 4.000%, 4/29/2026 | | $ | 2,720,082 | |

| | 728,004 | | | Continental Airlines Pass Through Trust, Series 2010-1, Class A, 4.750%, 7/12/2022 | | | 773,141 | |

| | | | | | | | |

| | | | | | | 3,493,223 | |

| | | | | | | | |

| | | | Automotive — 2.0% | | | | |

| | 642,000 | | | American Axle & Manufacturing, Inc., 5.125%, 2/15/2019 | | | 642,803 | |

| | 1,285,000 | | | Ford Motor Credit Co. LLC, 2.375%, 1/16/2018 | | | 1,287,736 | |

| | 4,742,000 | | | Ford Motor Credit Co. LLC, 2.375%, 3/12/2019 | | | 4,765,516 | |

| | 12,010,000 | | | Ford Motor Credit Co. LLC, 3.336%, 3/18/2021 | | | 12,282,784 | |

| | 7,612,000 | | | Ford Motor Credit Co. LLC, 5.000%, 5/15/2018 | | | 7,763,393 | |

| | 27,688,000 | | | Ford Motor Credit Co. LLC, 5.750%, 2/01/2021 | | | 30,362,304 | |

| | 16,412,000 | | | Ford Motor Credit Co. LLC, 5.875%, 8/02/2021 | | | 18,255,169 | |

| | 16,051,000 | | | General Motors Co., 5.000%, 4/01/2035 | | | 16,381,209 | |

| | 14,829,000 | | | General Motors Co., 6.250%, 10/02/2043 | | | 16,947,186 | |

| | 22,752,000 | | | Hyundai Capital America, 3.000%, 10/30/2020, 144A | | | 22,875,535 | |

| | | | | | | | |

| | | | | | | 131,563,635 | |

| | | | | | | | |

| | | | Banking — 7.2% | | | | |

| | 17,853,000 | | | Ally Financial, Inc., 3.750%, 11/18/2019 | | | 18,245,766 | |

| | 16,016,000 | | | Banco Santander Chile, 3.875%, 9/20/2022, 144A | | | 16,825,005 | |

| | 7,967,000 | | | Bangkok Bank PCL, 2.750%, 3/27/2018, 144A | | | 7,986,918 | |

| | 34,130,000 | | | Bangkok Bank PCL, 3.300%, 10/03/2018, 144A | | | 34,516,693 | |

| | 6,608,000 | | | Bank of America Corp., 2.650%, 4/01/2019 | | | 6,667,471 | |

| | 2,370,000 | | | Bank of America Corp., 5.625%, 7/01/2020 | | | 2,581,263 | |

| | 5,715,000 | | | Bank of America Corp., GMTN, 2.625%, 4/19/2021 | | | 5,754,291 | |

| | 47,520,000 | | | Bank of America Corp., MTN, 5.000%, 5/13/2021(c) | | | 51,706,376 | |

| | 4,199,000 | | | Bank of America Corp., MTN, 6.875%, 4/25/2018 | | | 4,319,864 | |

| | 45,518,000 | | | Barclays PLC, 2.875%, 6/08/2020 | | | 45,976,366 | |

| | 7,058,000 | | | Barclays PLC, 3.200%, 8/10/2021 | | | 7,166,411 | |

| | 25,327,000 | | | BBVA Banco Continental S.A., 3.250%, 4/08/2018, 144A | | | 25,509,354 | |

| | 15,481,000 | | | Citigroup, Inc., 2.500%, 9/26/2018 | | | 15,583,984 | |

| | 5,780,000 | | | Citigroup, Inc., 2.650%, 10/26/2020 | | | 5,839,405 | |

| | 27,055,000 | | | Citigroup, Inc., 4.050%, 7/30/2022 | | | 28,321,470 | |

| | 5,780,000 | | | Goldman Sachs Group, Inc. (The), 2.600%, 4/23/2020 | | | 5,832,106 | |

| | 9,636,000 | | | Goldman Sachs Group, Inc. (The), 3.625%, 1/22/2023 | | | 9,983,962 | |

| | 14,867,000 | | | Goldman Sachs Group, Inc. (The), 5.750%, 1/24/2022 | | | 16,662,968 | |

| | 13,448,000 | | | Goldman Sachs Group, Inc. (The), 6.750%, 10/01/2037 | | | 17,741,832 | |

| | 3,205,000 | | | JPMorgan Chase & Co., 2.550%, 3/01/2021 | | | 3,237,044 | |

| | 8,819,000 | | | JPMorgan Chase & Co., 3.200%, 1/25/2023 | | | 9,044,585 | |

| | 1,785,000 | | | JPMorgan Chase & Co., 4.250%, 10/15/2020 | | | 1,889,851 | |

| | 10,223,000 | | | JPMorgan Chase & Co., 4.350%, 8/15/2021 | | | 10,952,765 | |

| | 23,597,000 | | | JPMorgan Chase & Co., 4.500%, 1/24/2022 | | | 25,567,598 | |

| | 3,235,000 | | | Lloyds Banking Group PLC, 3.000%, 1/11/2022 | | | 3,261,783 | |

| | 3,955,000 | | | Lloyds Banking Group PLC, 3.100%, 7/06/2021 | | | 4,021,450 | |

| | 7,690,000 | | | Morgan Stanley, 2.800%, 6/16/2020 | | | 7,818,267 | |

| | 3,381,000 | | | Morgan Stanley, 3.700%, 10/23/2024 | | | 3,502,627 | |

See accompanying notes to financial statements.

| 18

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund – (continued)

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | | | Banking — continued | | | | |

| $ | 19,598,000 | | | Morgan Stanley, 5.750%, 1/25/2021 | | $ | 21,639,429 | |

| | 12,550,000 | | | Morgan Stanley, GMTN, 5.500%, 7/28/2021 | | | 13,920,882 | |

| | 21,770,000 | | | Morgan Stanley, Series F, 3.875%, 4/29/2024 | | | 22,782,558 | |

| | 4,977,000 | | | Morgan Stanley, Series F, GMTN, 6.625%, 4/01/2018 | | | 5,098,637 | |

| | 9,123,000 | | | Santander UK Group Holdings PLC, 5.625%, 9/15/2045, 144A | | | 10,582,169 | |

| | | | | | | | |

| | | | | | | 470,541,150 | |

| | | | | | | | |

| | | | Building Materials — 0.1% | | | | |

| | 8,563,000 | | | Owens Corning, 4.200%, 12/01/2024 | | | 9,019,030 | |

| | | | | | | | |

| | | | Cable Satellite — 0.5% | | | | |

| | 14,275,000 | | | Time Warner Cable LLC, 4.500%, 9/15/2042 | | | 13,529,082 | |

| | 3,939,000 | | | Time Warner Cable LLC, 5.500%, 9/01/2041 | | | 4,089,964 | |

| | 2,648,000 | | | Time Warner Cable LLC, 5.875%, 11/15/2040 | | | 2,905,820 | |

| | 8,447,000 | | | Time Warner Cable LLC, 6.550%, 5/01/2037 | | | 9,921,417 | |

| | 2,013,000 | | | Time Warner Cable LLC, 6.750%, 6/15/2039 | | | 2,415,280 | |

| | | | | | | | |

| | | | | | | 32,861,563 | |

| | | | | | | | |

| | | | Chemicals — 1.3% | | | | |

| | 26,749,000 | | | Braskem America Finance Co., 7.125%, 7/22/2041, 144A | | | 30,360,115 | |

| | 3,680,000 | | | Koppers, Inc., 6.000%, 2/15/2025, 144A | | | 3,956,000 | |

| | 3,566,000 | | | Methanex Corp., 3.250%, 12/15/2019 | | | 3,598,805 | |

| | 14,107,000 | | | Methanex Corp., 5.250%, 3/01/2022 | | | 14,862,857 | |

| | 7,727,000 | | | Mexichem SAB de CV, 5.875%, 9/17/2044, 144A | | | 8,016,762 | |

| | 11,165,000 | | | Mexichem SAB de CV, 6.750%, 9/19/2042, 144A(c) | | | 12,616,450 | |

| | 4,402,000 | | | RPM International, Inc., 3.450%, 11/15/2022 | | | 4,599,725 | |

| | 3,558,000 | | | RPM International, Inc., 6.125%, 10/15/2019 | | | 3,847,515 | |

| | 4,155,000 | | | Venator Finance S.a.r.l/Venator Materials LLC, 5.750%, 7/15/2025, 144A | | | 4,321,200 | |

| | | | | | | | |

| | | | | | | 86,179,429 | |

| | | | | | | | |

| | | | Collateralized Mortgage Obligations — 2.1% | | | | |

| | 5,000,000 | | | Federal Home Loan Mortgage Corp., REMIC, Series 3654, Class DC, 5.000%, 4/15/2030 | | | 5,628,313 | |

| | 33,656,455 | | | Federal Home Loan Mortgage Corp., Series 277, Class 30, 3.000%, 9/15/2042 | | | 34,041,931 | |

| | 3,402,996 | | | Federal Home Loan Mortgage Corp., Series 353, Class 300, 3.000%, 12/15/2046 | | | 3,427,528 | |

| | 620,741 | | | Government National Mortgage Association, Series 2010-H20, Class AF, 1-month LIBOR + 0.330%, 1.561%, 10/20/2060(m) | | | 616,563 | |

| | 481,632 | | | Government National Mortgage Association, Series 2010-H24, Class FA, 1-month LIBOR + 0.350%, 1.581%, 10/20/2060(m) | | | 478,507 | |

| | 426,977 | | | Government National Mortgage Association, Series 2011-H06, Class FA, 1-month LIBOR + 0.450%, 1.681%, 2/20/2061(m) | | | 426,417 | |

| | 4,770,495 | | | Government National Mortgage Association, Series 2012-H12, Class FA, 1-month LIBOR + 0.550%, 1.781%, 4/20/2062(m) | | | 4,778,453 | |

| | 634,727 | | | Government National Mortgage Association, Series 2012-H18, Class NA, 1-month LIBOR + 0.520%, 1.751%, 8/20/2062(m) | | | 634,508 | |

| | 5,193,297 | | | Government National Mortgage Association, Series 2012-H27, Class FA, 1-month LIBOR + 0.400%, 1.631%, 10/20/2062(m) | | | 5,178,550 | |

| | 2,846,852 | | | Government National Mortgage Association, Series 2013-H01, Class FA, 1.650%, 1/20/2063 | | | 2,828,243 | |

See accompanying notes to financial statements.

19 |

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund – (continued)

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | | | Collateralized Mortgage Obligations — continued | | | | |

| $ | 4,538,624 | | | Government National Mortgage Association, Series 2013-H03, Class HA, 1.750%, 12/20/2062 | | $ | 4,515,927 | |

| | 6,489,674 | | | Government National Mortgage Association, Series 2013-H04, Class BA, 1.650%, 2/20/2063 | | | 6,447,792 | |

| | 16,627,274 | | | Government National Mortgage Association, Series 2013-H07, Class DA, 2.500%, 3/20/2063 | | | 16,738,186 | |

| | 23,115,095 | | | Government National Mortgage Association, Series 2013-H10, Class PA, 2.500%, 4/20/2063 | | | 23,129,854 | |

| | 22,173,885 | | | Government National Mortgage Association, Series 2015-H10, Class JA, 2.250%, 4/20/2065 | | | 21,723,083 | |

| | 3,298,227 | | | Government National Mortgage Association, Series 2015-H13, Class FL, 1-month LIBOR + 0.280%, 1.511%, 5/20/2063(m) | | | 3,297,232 | |

| | | | | | | | |

| | | | | | | 133,891,087 | |

| | | | | | | | |

| | | | Construction Machinery — 0.1% | | | | |

| | 8,705,000 | | | CNH Industrial Capital LLC, 4.375%, 4/05/2022 | | | 9,140,250 | |

| | | | | | | | |

| | | | Consumer Cyclical Services — 0.4% | | | | |

| | 26,745,000 | | | Amazon.com, Inc., 4.250%, 8/22/2057, 144A | | | 27,442,105 | |

| | | | | | | | |

| | | | Consumer Products — 0.1% | | | | |

| | 3,495,000 | | | Whirlpool Corp., MTN, 4.850%, 6/15/2021 | | | 3,783,689 | |

| | | | | | | | |

| | | | Diversified Manufacturing — 0.5% | | | | |

| | 1,158,000 | | | Crane Co., 6.550%, 11/15/2036 | | | 1,417,164 | |

| | 32,127,000 | | | Votorantim Cimentos S.A., 7.250%, 4/05/2041, 144A | | | 34,014,461 | |

| | | | | | | | |

| | | | | | | 35,431,625 | |

| | | | | | | | |

| | | | Electric — 0.6% | | | | |

| | 3,315,000 | | | Enel Americas S.A., 4.000%, 10/25/2026 | | | 3,393,598 | |

| | 3,364,000 | | | Enel Generacion Chile S.A., 4.250%, 4/15/2024 | | | 3,530,723 | |

| | 17,247,000 | | | National Rural Utilities Cooperative Finance Corp., (fixed rate to 4/30/2023, variable rate thereafter), 4.750%, 4/30/2043 | | | 17,905,258 | |

| | 8,413,000 | | | Transelec S.A., 4.250%, 1/14/2025, 144A | | | 8,745,492 | |

| | 4,380,000 | | | Transelec S.A., 4.625%, 7/26/2023, 144A | | | 4,684,178 | |

| | | | | | | | |

| | | | | | | 38,259,249 | |

| | | | | | | | |

| | | | Finance Companies — 2.2% | | | | |

| | 16,922,000 | | | AerCap Ireland Capital DAC/AerCap Global Aviation Trust, 3.750%, 5/15/2019 | | | 17,315,776 | |

| | 18,154,000 | | | International Lease Finance Corp., 5.875%, 4/01/2019 | | | 19,123,399 | |

| | 3,910,000 | | | International Lease Finance Corp., 5.875%, 8/15/2022 | | | 4,378,131 | |

| | 16,190,000 | | | International Lease Finance Corp., 6.250%, 5/15/2019 | | | 17,208,117 | |

| | 16,195,000 | | | iStar, Inc., 6.500%, 7/01/2021 | | | 16,923,775 | |

| | 14,547,000 | | | Navient LLC, MTN, 8.000%, 3/25/2020 | | | 16,038,068 | |

| | 13,509,000 | | | Quicken Loans, Inc., 5.750%, 5/01/2025, 144A | | | 14,184,450 | |

| | 39,143,000 | | | Springleaf Finance Corp., 5.250%, 12/15/2019 | | | 40,747,863 | |

| | | | | | | | |

| | | | | | | 145,919,579 | |

| | | | | | | | |

| | | | Financial Other — 0.2% | | | | |

| | 15,649,000 | | | Cielo S.A./Cielo USA, Inc., 3.750%, 11/16/2022, 144A | | | 15,453,387 | |

| | | | | | | | |

See accompanying notes to financial statements.

| 20

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund – (continued)

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | | | Food & Beverage — 0.1% | | | | |

| $ | 3,490,000 | | | Gruma SAB de CV, 4.875%, 12/01/2024, 144A | | $ | 3,791,012 | |

| | 1,230,000 | | | Sigma Alimentos S.A. de CV, 6.875%, 12/16/2019, 144A | | | 1,357,613 | |

| | | | | | | | |

| | | | | | | 5,148,625 | |

| | | | | | | | |

| | | | Government Owned – No Guarantee — 2.9% | | | | |

| | 2,355,000 | | | Abu Dhabi National Energy Co. PJSC, 2.500%, 1/12/2018, 144A | | | 2,355,316 | |

| | 7,757,000 | | | CNPC General Capital Ltd., 3.950%, 4/19/2022, 144A | | | 8,136,985 | |

| | 17,981,000 | | | Dolphin Energy Ltd., 5.500%, 12/15/2021, 144A | | | 19,774,209 | |

| | 18,213,000 | | | OCP S.A., 5.625%, 4/25/2024, 144A | | | 19,620,865 | |

| | 7,355,000 | | | Ooredoo International Finance Ltd., 3.250%, 2/21/2023, 144A | | | 7,346,042 | |

| | 9,385,000 | | | Ooredoo International Finance Ltd., 3.875%, 1/31/2028, 144A | | | 9,446,322 | |

| | 2,862,000 | | | Ooredoo International Finance Ltd., 7.875%, 6/10/2019, 144A | | | 3,115,573 | |

| | 22,772,000 | | | Pertamina Persero PT, 5.625%, 5/20/2043, 144A | | | 24,511,348 | |

| | 10,497,000 | | | Petrobras Global Finance BV, 5.625%, 5/20/2043 | | | 9,368,572 | |

| | 27,590,000 | | | Petrobras Global Finance BV, 6.850%, 6/05/2115 | | | 26,313,962 | |

| | 24,068,000 | | | Tennessee Valley Authority, 4.250%, 9/15/2065 | | | 27,396,003 | |

| | 6,160,000 | | | Tennessee Valley Authority, 4.625%, 9/15/2060 | | | 7,465,864 | |

| | 6,401,000 | | | Tennessee Valley Authority, 4.875%, 1/15/2048 | | | 8,090,448 | |

| | 10,957,000 | | | Tennessee Valley Authority, 5.250%, 9/15/2039 | | | 14,368,298 | |

| | | | | | | | |

| | | | | | | 187,309,807 | |

| | | | | | | | |

| | | | Healthcare — 0.8% | | | | |

| | 16,635,000 | | | CHS/Community Health Systems, Inc., 6.250%, 3/31/2023 | | | 16,343,888 | |

| | 16,381,000 | | | Kindred Healthcare, Inc., 8.000%, 1/15/2020 | | | 16,089,254 | |

| | 3,089,000 | | | PerkinElmer, Inc., 5.000%, 11/15/2021 | | | 3,348,279 | |

| | 7,682,000 | | | Universal Health Services, Inc., 3.750%, 8/01/2019, 144A | | | 7,854,845 | |

| | 10,364,000 | | | Universal Health Services, Inc., 4.750%, 8/01/2022, 144A | | | 10,726,740 | |

| | | | | | | | |

| | | | | | | 54,363,006 | |

| | | | | | | | |

| | | | Hybrid ARMs — 0.0% | | | | |

| | 64,992 | | | FNMA, 6-month LIBOR + 1.504%, 2.952%, 2/01/2037(m) | | | 67,069 | |

| | | | | | | | |

| | | | Independent Energy — 1.6% | | | | |

| | 4,885,000 | | | MEG Energy Corp., 7.000%, 3/31/2024, 144A | | | 4,188,888 | |

| | 8,160,000 | | | Newfield Exploration Co., 5.375%, 1/01/2026 | | | 8,578,200 | |

| | 10,499,000 | | | Newfield Exploration Co., 5.750%, 1/30/2022 | | | 11,207,682 | |

| | 13,888,000 | | | Pan American Energy LLC/Argentine Branch, 7.875%, 5/07/2021, 144A | | | 14,987,513 | |

| | 13,612,000 | | | QEP Resources, Inc., 5.250%, 5/01/2023 | | | 13,237,670 | |

| | 6,862,000 | | | QEP Resources, Inc., 5.375%, 10/01/2022 | | | 6,741,915 | |

| | 10,701,000 | | | Range Resources Corp., 5.000%, 8/15/2022, 144A | | | 10,687,624 | |

| | 9,158,000 | | | SM Energy Co., 5.000%, 1/15/2024 | | | 8,631,415 | |

| | 775,000 | | | SM Energy Co., 5.625%, 6/01/2025 | | | 736,250 | |

| | 16,166,000 | | | SM Energy Co., 6.125%, 11/15/2022 | | | 16,206,415 | |

| | 1,096,000 | | | SM Energy Co., 6.500%, 11/15/2021 | | | 1,106,960 | |

| | 4,851,000 | | | SM Energy Co., 6.500%, 1/01/2023 | | | 4,887,382 | |

| | 1,045,000 | | | SM Energy Co., 6.750%, 9/15/2026 | | | 1,045,000 | |

| | | | | | | | |

| | | | | | | 102,242,914 | |

| | | | | | | | |

| | | | Industrial Other — 0.6% | | | | |

| | 5,919,000 | | | Briggs & Stratton Corp., 6.875%, 12/15/2020 | | | 6,525,698 | |

| | 7,035,000 | | | CBRE Services, Inc., 5.000%, 3/15/2023 | | | 7,289,302 | |

See accompanying notes to financial statements.

21 |

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund – (continued)

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | | | Industrial Other — continued | | | | |

| $ | 9,275,000 | | | CK Hutchison International 16 Ltd., 2.750%, 10/03/2026, 144A | | $ | 8,929,457 | |

| | 5,859,000 | | | Ferreycorp SAA, 4.875%, 4/26/2020, 144A | | | 5,932,238 | |

| | 9,650,000 | | | President and Fellows of Harvard College, 3.300%, 7/15/2056 | | | 9,237,982 | |

| | | | | | | | |

| | | | | | | 37,914,677 | |

| | | | | | | | |

| | | | Media Entertainment — 1.3% | | | | |

| | 7,430,000 | | | AMC Networks, Inc., 4.750%, 8/01/2025 | | | 7,504,300 | |

| | 8,660,000 | | | Discovery Communications LLC, 5.000%, 9/20/2037 | | | 8,793,462 | |

| | 8,685,000 | | | Discovery Communications LLC, 5.200%, 9/20/2047 | | | 8,813,158 | |

| | 2,405,000 | | | EW Scripps Co. (The), 5.125%, 5/15/2025, 144A | | | 2,453,100 | |

| | 63,720,000 | | | Grupo Televisa SAB, EMTN, 7.250%, 5/14/2043, (MXN) | | | 2,757,704 | |

| | 15,635,000 | | | Myriad International Holdings BV, 4.850%, 7/06/2027, 144A | | | 16,150,799 | |

| | 32,599,000 | | | Myriad International Holdings BV, 6.000%, 7/18/2020, 144A | | | 35,173,017 | |

| | 5,638,000 | | | Viacom, Inc., 5.250%, 4/01/2044 | | | 5,399,604 | |

| | | | | | | | |

| | | | | | | 87,045,144 | |

| | | | | | | | |

| | | | Metals & Mining — 1.3% | | | | |

| | 12,381,000 | | | ArcelorMittal, 7.250%, 3/01/2041 | | | 14,656,009 | |

| | 4,470,000 | | | ArcelorMittal, 7.500%, 10/15/2039 | | | 5,364,000 | |

| | 14,896,000 | | | Freeport-McMoRan, Inc., 2.375%, 3/15/2018 | | | 14,896,000 | |

| | 12,627,000 | | | Freeport-McMoRan, Inc., 3.550%, 3/01/2022 | | | 12,433,681 | |

| | 5,097,000 | | | Freeport-McMoRan, Inc., 6.875%, 2/15/2023 | | | 5,555,730 | |

| | 11,203,000 | | | Goldcorp, Inc., 2.125%, 3/15/2018 | | | 11,214,258 | |

| | 18,444,000 | | | Southern Copper Corp., 5.875%, 4/23/2045 | | | 21,005,508 | |

| | | | | | | | |

| | | | | | | 85,125,186 | |

| | | | | | | | |

| | | | Midstream — 1.2% | | | | |

| | 1,600,000 | | | AmeriGas Partners LP/AmeriGas Finance Corp., 5.500%, 5/20/2025 | | | 1,644,000 | |

| | 670,000 | | | Energy Transfer LP, 5.150%, 2/01/2043 | | | 653,519 | |

| | 6,959,000 | | | Energy Transfer LP, 5.950%, 10/01/2043 | | | 7,451,073 | |

| | 10,082,000 | | | Energy Transfer LP, 6.500%, 2/01/2042 | | | 11,406,824 | |

| | 1,578,000 | | | Energy Transfer LP, 6.625%, 10/15/2036 | | | 1,795,044 | |

| | 13,236,000 | | | Energy Transfer LP/Regency Energy Finance Corp., 5.000%, 10/01/2022 | | | 14,296,193 | |

| | 331,000 | | | Energy Transfer LP/Regency Energy Finance Corp., 5.500%, 4/15/2023 | | | 340,599 | |

| | 2,745,000 | | | Energy Transfer LP/Regency Energy Finance Corp., 5.875%, 3/01/2022 | | | 3,038,359 | |

| | 2,555,000 | | | Kinder Morgan Energy Partners LP, 4.150%, 2/01/2024 | | | 2,648,419 | |

| | 10,668,000 | | | Kinder Morgan Energy Partners LP, 4.300%, 5/01/2024 | | | 11,101,257 | |

| | 4,861,000 | | | Kinder Morgan, Inc., 5.000%, 2/15/2021, 144A | | | 5,215,227 | |

| | 17,979,000 | | | Kinder Morgan, Inc., 5.625%, 11/15/2023, 144A | | | 20,025,603 | |

| | | | | | | | |

| | | | | | | 79,616,117 | |

| | | | | | | | |

| | | | Mortgage Related — 17.9% | | | | |

| | 26,956,958 | | | FHLMC, 3.000%, with various maturities from 2042 to 2046(d) | | | 27,100,369 | |

| | 50,439,743 | | | FHLMC, 3.500%, with various maturities from 2043 to 2047(d) | | | 52,257,912 | |

| | 21,311,626 | | | FHLMC, 4.000%, with various maturities from 2044 to 2046(d) | | | 22,540,269 | |

| | 20,616,017 | | | FHLMC, 4.500%, with various maturities from 2041 to 2047(d) | | | 22,342,218 | |

| | 4,441 | | | FHLMC, 5.500%, 12/01/2018 | | | 4,511 | |

| | 15,033 | | | FHLMC, 6.000%, 6/01/2035 | | | 17,075 | |

| | 100,938,335 | | | FNMA, 2.500%, with various maturities in 2046(d) | | | 97,772,878 | |

See accompanying notes to financial statements.

| 22

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund – (continued)

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | | | Mortgage Related — continued | | | | |

| $ | 86,093,480 | | | FNMA, 3.000%, with various maturities from 2045 to 2047(d) | | $ | 86,567,469 | |

| | 131,899,121 | | | FNMA, 3.500%, with various maturities from 2042 to 2047(d) | | | 136,541,083 | |

| | 98,350,916 | | | FNMA, 4.000%, with various maturities from 2041 to 2047(d) | | | 104,041,962 | |

| | 33,669,827 | | | FNMA, 4.500%, with various maturities from 2043 to 2047(d) | | | 36,349,720 | |

| | 224,582 | | | FNMA, 6.000%, with various maturities from 2034 to 2037(d) | | | 256,493 | |

| | 22,698 | | | FNMA, 6.500%, with various maturities from 2029 to 2031(d) | | | 25,431 | |

| | 45,533 | | | FNMA, 7.000%, with various maturities in 2030(d) | | | 49,946 | |

| | 32,062 | | | FNMA, 7.500%, with various maturities from 2024 to 2032(d) | | | 36,113 | |

| | 14,740,000 | | | FNMA (TBA), 3.000%, 11/01/2047(e) | | | 14,765,334 | |

| | 344,635,000 | | | FNMA (TBA), 4.000%, 11/01/2047(e) | | | 362,324,460 | |

| | 654,847 | | | GNMA, 1-month LIBOR + 1.952, 3.172%, 9/20/2063(m) | | | 690,433 | |

| | 154,918 | | | GNMA, 4.131%, 1/20/2063(a) | | | 161,140 | |

| | 144,627 | | | GNMA, 4.300%, 5/20/2063(a) | | | 150,861 | |

| | 10,405,010 | | | GNMA, 4.376%, 12/20/2066(a) | | | 11,383,092 | |

| | 3,006,565 | | | GNMA, 4.412%, 10/20/2066(a) | | | 3,287,124 | |

| | 187,094 | | | GNMA, 4.421%, 7/20/2063(a) | | | 196,182 | |

| | 5,261,633 | | | GNMA, 4.425%, 11/20/2066(a) | | | 5,736,894 | |

| | 4,452,888 | | | GNMA, 4.478%, 10/20/2062(a) | | | 4,607,911 | |

| | 896,114 | | | GNMA, 4.495%, 12/20/2062(a) | | | 928,537 | |

| | 641,938 | | | GNMA, 4.499%, 7/20/2063(a) | | | 673,374 | |

| | 5,240,012 | | | GNMA, 4.500%, 2/20/2066(a) | | | 5,703,915 | |

| | 14,166,746 | | | GNMA, 4.520%, 12/20/2061(a)(c) | | | 14,497,271 | |

| | 9,816,072 | | | GNMA, 4.528%, with various maturities from 2063 to 2064(a)(d) | | | 10,591,394 | |

| | 6,065,715 | | | GNMA, 4.529%, with various maturities from 2062 to 2066(a)(d) | | | 6,586,537 | |

| | 872,852 | | | GNMA, 4.532%, 8/20/2062(a) | | | 903,162 | |

| | 9,782,241 | | | GNMA, 4.537%, with various maturities from 2062 to 2063(a)(d) | | | 10,219,066 | |

| | 3,623,182 | | | GNMA, 4.538%, 6/20/2066(a) | | | 3,980,970 | |

| | 3,126,236 | | | GNMA, 4.539%, 9/20/2066(a) | | | 3,437,766 | |

| | 4,651,714 | | | GNMA, 4.542%, 1/20/2065(a) | | | 5,037,806 | |

| | 2,637,812 | | | GNMA, 4.545%, 2/20/2066(a) | | | 2,883,312 | |

| | 12,852,778 | | | GNMA, 4.547%, 11/20/2062(a) | | | 13,324,828 | |

| | 15,349,497 | | | GNMA, 4.549%, with various maturities in 2066(a)(d) | | | 16,903,024 | |

| | 3,088,799 | | | GNMA, 4.550%, 1/20/2065(a) | | | 3,344,622 | |

| | 4,878,901 | | | GNMA, 4.565%, 2/20/2065(a) | | | 5,237,072 | |

| | 2,121,913 | | | GNMA, 4.580%, 6/20/2062(a) | | | 2,188,554 | |

| | 2,578,880 | | | GNMA, 4.581%, 4/20/2066(a) | | | 2,824,162 | |

| | 1,135,237 | | | GNMA, 4.583%, 6/20/2061(a) | | | 1,158,057 | |

| | 6,342,288 | | | GNMA, 4.586%, 10/20/2064(a) | | | 6,869,912 | |

| | 367,414 | | | GNMA, 4.592%, 8/20/2061(a) | | | 375,552 | |

| | 7,840,392 | | | GNMA, 4.595%, 12/20/2064(a) | | | 8,499,303 | |

| | 6,780,272 | | | GNMA, 4.598%, 2/20/2065(a) | | | 7,359,898 | |

| | 1,235,530 | | | GNMA, 4.613%, 7/20/2062(a) | | | 1,279,015 | |

| | 5,479,695 | | | GNMA, 4.615%, 3/20/2066(a) | | | 6,026,183 | |

| | 5,699,071 | | | GNMA, 4.616%, with various maturities from 2062 to 2065(a)(d) | | | 6,076,170 | |

| | 931,596 | | | GNMA, 4.631%, 1/20/2064(a) | | | 999,986 | |

| | 3,727,503 | | | GNMA, 4.644%, 1/20/2064(a) | | | 4,002,926 | |

| | 5,482,325 | | | GNMA, 4.648%, 5/20/2062(a) | | | 5,635,316 | |

See accompanying notes to financial statements.

23 |

Portfolio of Investments – as of September 30, 2017

Loomis Sayles Core Plus Bond Fund – (continued)

| | | | | | | | |

Principal

Amount (‡) | | | Description | | Value (†) | |

| | | | Mortgage Related — continued | | | | |

| $ | 2,849,494 | | | GNMA, 4.650%, 1/20/2061(a) | | $ | 2,907,220 | |

| | 603,044 | | | GNMA, 4.657%, 5/20/2062(a) | | | 620,176 | |

| | 5,930,184 | | | GNMA, 4.663%, 6/20/2064(a) | | | 6,403,522 | |

| | 6,721,500 | | | GNMA, 4.673%, 4/20/2062(a) | | | 6,914,225 | |

| | 248,268 | | | GNMA, 4.682%, 3/20/2062(a) | | | 255,531 | |

| | 902,007 | | | GNMA, 4.700%, with various maturities in 2061(a)(d) | | | 919,252 | |

| | 4,043,440 | | | GNMA, 4.708%, 1/20/2064(a) | | | 4,362,381 | |

| | 382,288 | | | GNMA, 5.500%, 4/15/2038 | | | 426,525 | |

| | 71,512 | | | GNMA, 6.000%, with various maturities from 2029 to 2038(d) | | | 81,115 | |

| | 59,498 | | | GNMA, 6.500%, with various maturities from 2029 to 2032(d) | | | 65,833 | |

| | 76,732 | | | GNMA, 7.000%, with various maturities from 2025 to 2029(d) | | | 80,228 | |

| | 17,713 | | | GNMA, 7.500%, with various maturities from 2025 to 2030(d) | | | 19,303 | |

| | 11,607 | | | GNMA, 8.500%, with various maturities from 2020 to 2023(d) | | | 11,658 | |

| | | | | | | | |

| | | | | | | 1,169,821,539 | |

| | | | | | | | |

| | | | Non-Agency Commercial Mortgage-Backed Securities — 1.2% | | | | |

| | 1,476,136 | | | Barclays Commercial Mortgage Securities, Series 2015-SLP, Class A, 1-month LIBOR + 1.110%, 2.344%, 2/15/2028, 144A(m) | | | 1,476,190 | |

| | 63,027 | | | Citigroup Commercial Mortgage Trust, Series 2008-C7, Class A4, 6.427%, 12/10/2049(a) | | | 62,995 | |

| | 1,025,000 | | | Commercial Mortgage Trust, Series 2010-C1, Class D, 6.324%, 7/10/2046, 144A(a) | | | 1,085,391 | |