|

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| WASHINGTON, D.C. 20549 |

| -------- |

| |

| FORM N-CSR |

| -------- |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT |

| INVESTMENT COMPANIES |

| |

| INVESTMENT COMPANY ACT FILE NUMBER 811-4325 |

FIRST INVESTORS LIFE SERIES FUNDS

(Exact name of registrant as specified in charter)

40 Wall Street

New York, NY 10005

(Address of principal executive offices) (Zip code)

Joseph I. Benedek

Foresters Investment Management Company, Inc.

Raritan Plaza I

Edison, NJ 08837-3620

(Name and address of agent for service)

REGISTRANT'S TELEPHONE NUMBER, INCLUDING AREA CODE:

1-212-858-8000

DATE OF FISCAL YEAR END: DECEMBER 31

DATE OF REPORTING PERIOD: DECEMBER 31, 2016

Item 1. Reports to Stockholders

|

| The annual report to stockholders follows |

This report is for the information of the shareholders of the Funds. It is the policy of each Fund described in this report to mail only one copy of a Fund’s prospectus, annual report, semi-annual report and proxy statements to all shareholders who share the same mailing address and share the same last name and have invested in a Fund covered by the same document. You are deemed to consent to this policy unless you specifically revoke this policy and request that separate copies of such documents be mailed to you. In such case, you will begin to receive your own copies within 30 days after our receipt of the revocation. You may request that separate copies of these disclosure documents be mailed to you by writing to us at: Foresters Investor Services, Inc., Raritan Plaza I, Edison, NJ 08837-3620 or calling us at 1-800-423-4026.

The views expressed in the portfolio manager letters reflect those views of the portfolio managers only through the end or the period covered. Any such views are subject to change at any time based upon market or other conditions and we disclaim any responsibility to update such views. These views may not be relied on as investment advice.

You may obtain a free prospectus for any of the Funds by contacting your representative, calling 1-800-423-4026, writing to us at the following address: Foresters Financial Services, Inc., 40 Wall Street, New York, NY 10005, or by visiting our website at www.foresters.com. You should consider the investment objectives, risks, charges and expenses of a Fund carefully before investing. The prospectus contains this and other information about the Fund, and should be read carefully before investing.

An investment in a Fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. Although the Cash Management Fund* seeks to preserve a net asset value at $1.00 per share, it is possible to lose money by investing in it, just as it is possible to lose money by investing in any of the other Funds. Past performance is no guarantee of future results.

A Statement of Additional Information (“SAI”) for any of the Funds may also be obtained, without charge, upon request by calling 1-800-423-4026, writing to us at our address or by visiting our website listed above. The SAI contains more detailed information about the Funds, including information about their Trustees.

*Effective October 3, 2016, the Cash Management Fund changed its name to the Government Cash Management Fund.

Foresters Financial™ and Foresters™ are the trade names and trademarks of The Independent Order of Foresters (Foresters), a fraternal benefit society, 789 Don Mills Road, Toronto, Canada M3C 1T9 and its subsidiaries.

Portfolio Managers’ Letter

BALANCED INCOME FUND

Dear Investor:

This is the annual report for the First Investors Life Balanced Income Fund for the year ended December 31, 2016. The Fund’s return on a net asset value basis was 6.71%.

Market and Economic Overview

The majority of equity and fixed income markets around the world generated positive returns during the 12 months ended December 31, 2016. However, the trajectory of these returns was very uneven as market sentiment changed several times during the year. U.S. economic growth was also uneven, continuing the post-recession trend of subdued but positive growth.

The year began with a 10% correction in the stock market and a rally in the bond market as weakness in the Chinese economy and stock market, first quarter U.S. growth of only 0.8%, and falling commodity prices created recession and deflation fears. Markets stabilized and the stock market recovered through the summer until Brexit—Great Britain’s unexpected decision to leave the European Union. Stock prices fell, but quickly stabilized as central banks made clear that they would do whatever was necessary to stabilize economic growth. Reacting to very accommodative monetary policy, interest rates fell to historical lows across developed country bond markets. A pickup in U.S. growth in the third quarter to 3.5%, the best quarterly rate in two years, pushed interest rates somewhat higher, while stock prices traded in a range. Following Donald Trump’s unexpected victory in the U.S. Presidential election, the stock market rallied and interest rates increased sharply as markets focused on Trump’s pro-growth agenda. The Federal Reserve (“the Fed”) rate increase in December, the only hike in 2016, had no impact on the markets. Notably, the Fed cited improving labor market indicators as a reason for raising interest rates as the U.S. unemployment rate fell to levels preceding the Great Recession.

Divergence in monetary policies and market expectations of central bank actions was a dominant factor affecting markets throughout the review period. While the Fed tightened its monetary policy, major international central banks continued easing their monetary policies. In particular, the European Central Bank cut its deposit rate to a negative 0.4% rate, expanded its bond-buying program to include corporate bonds, and extended its bond-buying stimulus program by nine months. These moves contributed to the decline in interest rates globally. Yields for many international bonds fell into negative territory, which resulted in higher demand from overseas investors for positive yielding U.S. fixed income and strengthened the U.S. dollar.

Portfolio Managers’ Letter (continued)

BALANCED INCOME FUND

The Equity Market

Overall, U.S. equities (measured by the S&P 500 Index) posted a strong return of 11.96% for the 12 months ended December 31, 2016. However, stocks had one of the worst starts to the beginning of the year on record, plunging 10.27% by February 11, amid worries about China, global growth and falling oil prices. Most of those fears subsided by mid-February as China’s markets stabilized, oil producers talked about decreasing supply, and Janet Yellen implied there would be fewer rate hikes than expected. Markets subsequently rebounded, gaining almost 17% by the June 23rd Brexit vote. Momentum paused as markets lost over 5% in the two days following the Brexit vote, followed by another strong rally which lasted until mid-July. Markets declined ahead of the U.S. presidential election, but reacted positively to Donald Trump’s unexpected win, focusing on the pro-growth aspects of his agenda.

While all market cap segments posted double-digit returns for the year, small-cap stocks (Russell 2000 Index) had the best performance, returning 21.31%, followed by mid-caps (S&P MidCap 400 Index) at 20.74%. Small-cap stocks in particular benefited from the post-election rally and President-elect Trump’s domestically centered policies. Value stocks outperformed growth stocks, supported by strong performance from Financials at the end of the year.

10 out of 11 S&P 500 sectors were positive in 2016, but with several sector rotations during the period. Energy was the strongest sector at 27.36%. It was weak during the beginning of the year, but recovered during the second half due to rising oil prices. The Healthcare sector, which had performed well for the past several years, was the weakest sector, down 2.69%. Higher yielding stocks, including Utilities and REITs, held up well during the first half of the year, supported by the low yielding environment and lack of other higher yielding options, but were negative during the second half.

International equities experienced wide swings during the review period. Developed markets (MSCI EAFE Index) finished the review period up 5.88% in local currencies and 1.51% in U.S. dollar terms as an appreciating dollar reduced returns for U.S. investors. Emerging markets (MSCI EM Index) had a difficult fourth quarter in 2016, but outperformed developed markets for the year with returns of 10.11% in local currencies and 11.60% in U.S. dollars. For most of the year, negative yields on many international bonds increased demand for emerging market assets. Select emerging markets also benefited from recovering commodity and oil prices.

The Bond Market

The broad U.S. bond market returned 2.61% for the year, according to the Bank of America Merrill Lynch US Broad Market Index, notably higher than the 0.60% return delivered in 2015. The benchmark 10-year Treasury note interest rate began the year at 2.27%, fell to an all-time low of 1.36% in July, rose as high as 2.60% following the U.S. election, and closed the year at 2.45%. The two-year Treasury note interest rate moved higher in anticipation of the Fed rate hike, ending the year at 1.19% versus 2015’s closing level of 1.05%. Bond prices move in the opposite direction of interest rates.

The U.S. Treasury market returned 1.14% for the year. The market returned 5.66% during the first half of the year, but lost 3.96% during the fourth quarter selloff.

Investment grade corporate bonds ended the year up 5.96%. The market returned 9.42% between January and August, as many overseas fixed income investors turned to U.S. markets due to low global interest rates. In addition, investment grade corporate bonds benefited from corporate bond buying programs from both the Bank of England and the European Central Bank.

Mortgage-backed bonds returned 1.67%. The sector was buoyed by its additional yield compared to Treasury securities but higher interest rates and prepayments resulted in negative returns on a price basis.

The high yield bond market was the strongest fixed income sector in 2016, returning 17.34%. The sector attracted domestic and overseas investors searching for income. High yield bonds benefited from the rebound in the Energy sector, which comprises the largest sector of the market. The lowest rated high yield bonds (CCC-rated) had the best performance, gaining 37.46%.

Municipal bonds were the weakest fixed income sector in 2016, returning 0.44% for the year. Despite elevated issuance, municipal bonds returned 4.59% between January and August, supported by strong demand. However, this gain was reversed due to record supply in September and October, and—following the elections—concern about lower tax rates under the Trump presidency.

There was wide dispersion among individual international fixed income market returns, depending on their sovereign bond markets and currencies. Overall, international fixed income as measured by the Citi World Government ex U.S. Bond Index was up 1.81%. Although the Index returned 13.50% during the first half of the year, it lost 10.84% during the fourth quarter, as the U.S. dollar rallied strongly in the aftermath of Trump’s victory and interest rates, in general, rose.

Portfolio Managers’ Letter (continued)

BALANCED INCOME FUND

The Fund — Fixed Income

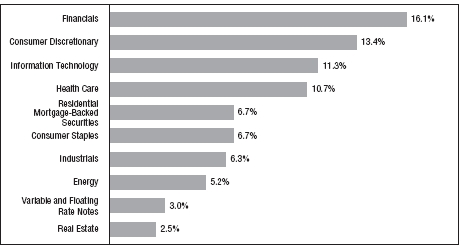

For 2016, the Fund had an average asset allocation of 53.2% in fixed income, 38.4% in equities, and 8.5% in money market instruments. With respect to the fixed income allocation, as a percent of total fund assets, the Fund had an average allocation of 32.5% in investment grade corporate bonds, 10.2% in agency mortgage-backed securities, 8.2% in U.S. Government securities, and 2.3% in high yield bonds. The substantial allocation to corporate bonds reflects the income objective of the Fund.

The fixed income holdings returned 4.66%, compared to 2.61% for its benchmark, the Bank of America Merrill Lynch US Broad Market Index. The Fund benefited from its overweight in corporate bonds versus the benchmark as corporate bonds, as measured by the Bank of America Merrill Lynch U.S. Corporate Bond Index, returned 5.96%. The Fund also benefited from the use of Treasury futures to hedge interest rate risk. Given the rise in interest rates and decline in bond prices, particularly in the second half of the year, the interest rate hedge accounted for approximately half of the Fund’s outperformance versus the benchmark. Lastly, the Fund’s exposure to high yield bonds, although a small allocation, provided a boost to returns as the allocation returned 13.4%.

The Fund — Equities

Both absolute and relative performance was positive, reflecting the strength of the Fund’s strategy during the period under review. The Fund’s equity segment, which represented 38.1% of the Fund’s assets as of period end, posted a strong +15.3% total return. The Fund emphasizes high dividend yield as the key determinant in stock selection, and follows a disciplined growth-at-a-reasonable price, catalyst-focused investment process seeking out exceptional long-term total return. As of period end, the Fund’s investments reflected a 3.4% dividend yield, well above the 2% yield of the S&P 500 Index. This strategy benefited the Fund’s returns during the past year. Overall stock selection was strong, with sector allocations also providing some upside. Among key sectors, Technology represented the bright spot for the Fund contributing most to return. Investments in the Financials, Utilities, Materials and Telecommunications sectors also contributed. Among the laggards, shares within the Consumer Discretionary and Healthcare sectors hurt performance. Among market capitalization segments, the Fund’s large-cap stocks outperformed the market, while the small-cap and mid-cap segments underperformed. The Fund had allocated 66% of its equity holdings to large-cap stocks, 18% to mid-cap stocks and 16% to small-cap stocks (ranges defined by Lipper) as of December 31, 2016.

Among top performing individual investments, within Technology: Semiconductor equipment provider Applied Materials, which returned +72%, was the Fund’s best overall individual stock. The shares benefited from increasing customer spending outlooks in its memory and display businesses. Shares of telecommunications chipmaker Qualcomm also boosted returns, up +35%, on resolved licensing disputes with Chinese service providers and strong market share gains on new smartphone platforms. Among Financials, bank stocks in particular saw strong gains after the November election on increased hopes for economic expansion, higher interest rate spreads and reduced regulatory pressures. This buoyed Fund holding and bellwether JPMorgan Chase, which returned +35% amidst solid execution and reduced legal and regulatory headwinds, and Discover Financial Services which returned +37% in the year due, in part, to healthy loan growth and steady operational execution. Certain sectors benefited from strong demand for higher-yielding equities—a result of persistent low interest rates. Among Utilities, shares of Black Hills Corporation rallied 32%, and electricity and gas provider Excelon Corporation was up 28%. Within Telecom, service provider giants AT&T and Verizon gained 24% and 15% for the fiscal year, respectively.

Thank you for placing your trust in Foresters Financial. As always, we appreciate the opportunity to serve your investment needs.

Understanding Your Fund’s Expenses (unaudited)

FIRST INVESTORS LIFE SERIES FUNDS

As a mutual fund shareholder, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including advisory fees and other expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 in each Fund at the beginning of the period, July 1, 2016, and held for the entire six-month period ended December 31, 2016. The calculations assume that no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

Actual Expense Example:

These amounts help you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the “Expenses Paid During Period” shows the dollar amount that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid during the period.

To estimate the expenses you paid on your account during this period simply divide your ending account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60), then multiply the result by the number given for your Fund under the heading “Expenses Paid During Period”.

Hypothetical Expense Example:

These amounts provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight and help you compare your ongoing costs only and do not reflect any transactional costs. Therefore, the hypothetical expense example is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Fund Expenses (unaudited)

BALANCED INCOME FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 6 for a detailed explanation of the information presented in these examples.

| | | |

| | | | |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (7/1/16) | (12/31/16) | (7/1/16–12/31/16)* |

| Expense Examples | | | |

| Actual | $1,000.00 | $1,013.52 | $8.65 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,016.54 | $8.67 |

| |

| * | Expenses are equal to the annualized expense ratio of 1.71%, multiplied by the average account |

| value over the period, multiplied by 184/366 (to reflect the one-half year period). Expenses paid |

| during the period are net of expenses waived. |

Portfolio Composition

TOP TEN SECTORS

|

| Portfolio holdings and allocations are subject to change. Percentages are as of December 31, 2016, |

| and are based on the total value of investments. |

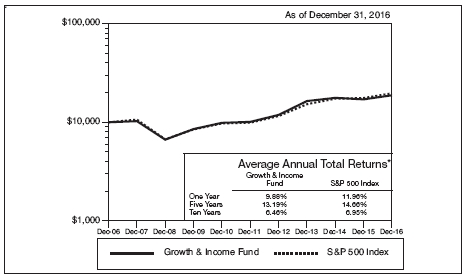

Cumulative Performance Information (unaudited)

BALANCED INCOME FUND

Comparison of change in value of $10,000 investment in the First Investors Life Series Balanced Income Fund, the Bank of America (“BofA”) Merrill Lynch U.S. Corporate, Government & Mortgage Index and the Standard & Poor’s 500 Index.

The graph compares a $10,000 investment in the First Investors Life Series Balanced Income Fund beginning 11/2/15 (commencement of operations) with theoretical investments in the BofA Merrill Lynch U.S. Corporate, Government & Mortgage Index and the Standard & Poor’s 500 Index (the “Indices”). The BofA Merrill Lynch U.S. Corporate, Government & Mortgage Index tracks the performance of U.S. dollar denominated investment grade debt publicly issued in the US domestic market, including U.S. Treasuries, quasi-government securities, corporates, covered bonds and residential mortgage pass-through securities. The Standard & Poor’s 500 Index is an unmanaged capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of such stocks, which represent all major industries. It is not possible to invest directly in these Indices. In addition, the Indices do not reflect fees and expenses associated with the active management of a mutual fund portfolio. For purposes of the graph and the accompanying table it is assumed that all dividends and distributions were reinvested.

* Average Annual Total Return figures are for the periods ended 12/31/16. During the periods shown, some of the expenses of the Fund were waived. If such expenses had been paid by the Fund, the Average Annual Total Returns for One Year and Since Inception would have been 6.55% and 4.02%, respectively.

The returns shown do not reflect any sales charges, since the Fund sells its shares solely to variable annuity and/or variable life insurance subaccounts at net asset value. The returns do not reflect the fees and charges that an individual would pay in connection with an investment in a variable annuity or life contract or policy. Results represent past performance and do not indicate future results. The graph and the returns shown do not reflect the deduction of taxes that an investor would pay on distributions or the redemption of fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. BofA Merrill Lynch U.S. Corporate, Government & Mortgage Index figures are from Bank of America Merrill Lynch & Co. and Standard & Poor’s 500 Index figures are from Standard & Poor’s and all other figures are from Foresters Investment Management Company, Inc.

Portfolio of Investments

BALANCED INCOME FUND

December 31, 2016

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| Shares | | Security | | Value |

| | | COMMON STOCKS—38.1% | | |

| | | Consumer Discretionary—4.4% | | |

| 84 | * | Adient, PLC | | $ 4,922 |

| 800 | | American Eagle Outfitters, Inc. | | 12,136 |

| 1,500 | | DSW, Inc. – Class “A” | | 33,975 |

| 1,700 | | Ford Motor Company | | 20,621 |

| 942 | | Johnson Controls International, PLC | | 38,801 |

| 700 | | L Brands, Inc. | | 46,088 |

| 1,000 | | Newell Brands, Inc. | | 44,650 |

| 700 | | Nordstrom, Inc. | | 33,551 |

| 400 | | Penske Automotive Group, Inc. | | 20,736 |

| 900 | | Regal Entertainment Group – Class “A” | | 18,540 |

| 2,600 | | Stein Mart, Inc. | | 14,248 |

| 750 | | Tupperware Brands Corporation | | 39,465 |

| 100 | | Whirlpool Corporation | | 18,177 |

| 400 | | Wyndham Worldwide Corporation | | 30,548 |

| | | | | 376,458 |

| | | Consumer Staples—5.8% | | |

| 1,350 | | Altria Group, Inc. | | 91,287 |

| 1,200 | | B&G Foods, Inc. | | 52,560 |

| 900 | | Coca-Cola Company | | 37,314 |

| 1,576 | | Koninklijke Ahold Delhaize NV (ADR) | | 33,080 |

| 500 | | Nu Skin Enterprises, Inc. – Class “A” | | 23,890 |

| 700 | | PepsiCo, Inc. | | 73,241 |

| 950 | | Philip Morris International, Inc. | | 86,916 |

| 350 | | Procter & Gamble Company | | 29,428 |

| 600 | | Sysco Corporation | | 33,222 |

| 650 | | Wal-Mart Stores, Inc. | | 44,928 |

| | | | | 505,866 |

| | | Energy—1.7% | | |

| 100 | | Chevron Corporation | | 11,770 |

| 250 | | ExxonMobil Corporation | | 22,565 |

| 350 | | Marathon Petroleum Corporation | | 17,623 |

| 100 | | Occidental Petroleum Corporation | | 7,123 |

| 700 | | PBF Energy, Inc. – Class “A” | | 19,516 |

| 150 | | Phillips 66 | | 12,962 |

| 400 | | Royal Dutch Shell, PLC – Class “A” (ADR) | | 21,752 |

| 150 | | Schlumberger, Ltd. | | 12,593 |

| 600 | | Suncor Energy, Inc. | | 19,614 |

| | | | | 145,518 |

Portfolio of Investments (continued)

BALANCED INCOME FUND

December 31, 2016

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| Shares | | Security | | Value |

| | | Financials—4.7% | | |

| 450 | | Ameriprise Financial, Inc. | | $ 49,923 |

| 600 | | Berkshire Hills Bancorp, Inc. | | 22,110 |

| 300 | | Chubb, Ltd. | | 39,636 |

| 800 | | Discover Financial Services | | 57,672 |

| 600 | | JPMorgan Chase & Company | | 51,774 |

| 700 | | MetLife, Inc. | | 37,723 |

| 350 | | PNC Financial Services Group, Inc. | | 40,936 |

| 900 | | U.S. Bancorp | | 46,233 |

| 1,550 | | Waddell & Reed Financial, Inc. – Class “A” | | 30,241 |

| 550 | | Wells Fargo & Company | | 30,311 |

| | | | | 406,559 |

| | | Health Care—4.2% | | |

| 1,150 | | Abbott Laboratories | | 44,171 |

| 1,100 | | AbbVie, Inc. | | 68,882 |

| 1,300 | | GlaxoSmithKline, PLC (ADR) | | 50,063 |

| 600 | | Johnson & Johnson | | 69,126 |

| 850 | | Merck & Company, Inc. | | 50,040 |

| 2,400 | | Pfizer, Inc. | | 77,952 |

| | | | | 360,234 |

| | | Industrials—4.3% | | |

| 400 | | 3M Company | | 71,428 |

| 1,400 | | General Electric Company | | 44,240 |

| 400 | | Honeywell International, Inc. | | 46,340 |

| 1,200 | | Koninklijke Philips NV (ADR) | | 36,684 |

| 300 | | Lockheed Martin Corporation | | 74,982 |

| 900 | | Mobile Mini, Inc. | | 27,225 |

| 500 | | Textainer Group Holdings, Ltd. | | 3,725 |

| 2,400 | | Triton International, Ltd. | | 37,920 |

| 250 | | United Technologies Corporation | | 27,405 |

| | | | | 369,949 |

| | | Information Technology—6.2% | | |

| 800 | | Apple, Inc. | | 92,656 |

| 1,950 | | Cisco Systems, Inc. | | 58,929 |

| 1,000 | | Intel Corporation | | 36,270 |

| 250 | | International Business Machines Corporation | | 41,497 |

| 1,200 | | Maxim Integrated Products, Inc. | | 46,284 |

| 1,450 | | Microsoft Corporation | | 90,103 |

| 1,000 | | QUALCOMM, Inc. | | 65,200 |

| | | | |

| | | | | |

| | | | | |

| Shares or | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | Information Technology (continued) | | |

| 1,400 | | Symantec Corporation | | $ 33,446 |

| 1,750 | | Travelport Worldwide, Ltd. | | 24,675 |

| 700 | | Western Digital Corporation | | 47,565 |

| | | | | 536,625 |

| | | Materials—.9% | | |

| 500 | | International Paper Company | | 26,530 |

| 250 | | Praxair, Inc. | | 29,298 |

| 400 | | RPM International, Inc. | | 21,532 |

| | | | | 77,360 |

| | | Real Estate—2.0% | | |

| 1,500 | | Brixmor Property Group, Inc. (REIT) | | 36,630 |

| 950 | | Chesapeake Lodging Trust (REIT) | | 24,567 |

| 2,950 | | FelCor Lodging Trust, Inc. (REIT) | | 23,629 |

| 1,900 | | Sunstone Hotel Investors, Inc. (REIT) | | 28,975 |

| 1,000 | | Tanger Factory Outlet Centers, Inc. (REIT) | | 35,780 |

| 1,000 | | Urstadt Biddle Properties, Inc. – Class “A” (REIT) | | 24,110 |

| | | | | 173,691 |

| | | Telecommunication Services—1.5% | | |

| 1,750 | | AT&T, Inc. | | 74,427 |

| 1,100 | | Verizon Communications, Inc. | | 58,718 |

| | | | | 133,145 |

| | | Utilities—2.4% | | |

| 500 | | Black Hills Corporation | | 30,670 |

| 600 | | Duke Energy Corporation | | 46,572 |

| 850 | | Exelon Corporation | | 30,166 |

| 1,200 | | NiSource, Inc. | | 26,568 |

| 550 | | SCANA Corporation | | 40,304 |

| 500 | | WEC Energy Group, Inc. | | 29,325 |

| | | | | 203,605 |

| Total Value of Common Stocks (cost $3,051,965) | | 3,289,010 |

| | | CORPORATE BONDS—35.2% | | |

| | | Automotive—.6% | | |

| $ 50M | | O’Reilly Automotive, Inc., 3.55%, 3/15/2026 | | 49,770 |

| | | Chemicals—.6% | | |

| 50M | | Dow Chemical Co., 4.25%, 11/15/2020 | | 53,001 |

Portfolio of Investments (continued)

BALANCED INCOME FUND

December 31, 2016

| | | | |

| | | | | |

| | | | | |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | Energy—.6% | | |

| $ 50M | | Magellan Midstream Partners, LP, 5%, 3/1/2026 | | $ 54,928 |

| | | Financial Services—3.8% | | |

| 100M | | American International Group, Inc., 3.75%, 7/10/2025 | | 100,823 |

| 50M | | Ameriprise Financial, Inc., 5.3%, 3/15/2020 | | 54,220 |

| 50M | | Berkshire Hathaway, Inc., 3.4%, 1/31/2022 | | 52,222 |

| | | General Electric Capital Corp.: | | |

| 50M | | 3.1%, 1/9/2023 | | 50,715 |

| 50M | | 6.75%, 3/15/2032 | | 66,660 |

| | | | | 324,640 |

| | | Financials—10.0% | | |

| 100M | | Bank of America Corp., 5.875%, 2/7/2042 | | 121,294 |

| 100M | | Capital One Financial Corp., 3.75%, 4/24/2024 | | 101,461 |

| 50M | | Citigroup, Inc., 4.5%, 1/14/2022 | | 53,369 |

| 50M | | Deutsche Bank AG, 3.7%, 5/30/2024 | | 48,699 |

| 100M | | General Motors Financial Co., 5.25%, 3/1/2026 | | 105,236 |

| 50M | | Goldman Sachs Group, Inc., 3.625%, 1/22/2023 | | 51,140 |

| 50M | | JPMorgan Chase & Co., 4.5%, 1/24/2022 | | 53,958 |

| | | Morgan Stanley: | | |

| 50M | | 5.5%, 7/28/2021 | | 55,463 |

| 50M | | 7.25%, 4/1/2032 | | 67,917 |

| 50M | | U.S. Bancorp, 3.6%, 9/11/2024 | | 51,004 |

| 50M | | Visa, Inc., 3.15%, 12/14/2025 | | 50,276 |

| | | Wells Fargo & Co.: | | |

| 50M | | 5.606%, 1/15/2044 | | 56,777 |

| 50M | | 3.9%, 5/1/2045 | | 47,544 |

| | | | | 864,138 |

| | | Food/Beverage/Tobacco—1.8% | | |

| | | Anheuser-Busch InBev Finance, Inc.: | | |

| 100M | | 4.7%, 2/1/2036 | | 105,516 |

| 50M | | 4.9%, 2/1/2046 | | 54,258 |

| | | | | 159,774 |

| | | Food/Drug—1.2% | | |

| 100M | | CVS Health Corp., 3.875%, 7/20/2025 | | 103,342 |

| | | Health Care—1.2% | | |

| 100M | | Gilead Sciences, Inc., 3.65%, 3/1/2026 | | 101,509 |

| | | | |

| | | | | |

| | | | | |

| | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | Information Technology—2.2% | | |

| $ 50M | | Apple, Inc., 2.5%, 2/9/2025 | | $ 48,098 |

| 100M | | Microsoft Corp., 3.7%, 8/8/2046 | | 94,394 |

| 50M | | Oracle Corp., 2.95%, 5/15/2025 | | 49,068 |

| | | | | 191,560 |

| | | Manufacturing—.6% | | |

| 50M | | Johnson Controls International, PLC, 5%, 3/30/2020 | | 53,837 |

| | | Media-Broadcasting—1.8% | | |

| 150M | | Comcast Corp., 4.25%, 1/15/2033 | | 156,373 |

| | | Real Estate—2.2% | | |

| 50M | | AvalonBay Communities, Inc., 3.5%, 11/15/2024 | | 50,471 |

| 100M | | Boston Properties, LP, 2.75%, 10/1/2026 | | 91,625 |

| 50M | | Simon Property Group, LP, 3.375%, 10/1/2024 | | 50,516 |

| | | | | 192,612 |

| | | Retail-General Merchandise—2.1% | | |

| 50M | | Amazon.com, Inc., 4.8%, 12/5/2034 | | 55,199 |

| 100M | | Home Depot, Inc., 5.875%, 12/16/2036 | | 126,577 |

| | | | | 181,776 |

| | | Telecommunications—1.2% | | |

| 50M | | AT&T, Inc., 3.8%, 3/15/2022 | | 51,317 |

| 50M | | Verizon Communications, Inc., 5.15%, 9/15/2023 | | 55,366 |

| | | | | 106,683 |

| | | Transportation—2.3% | | |

| 75M | | Burlington North Santa Fe, LLC, 5.15%, 9/1/2043 | | 86,329 |

| 100M | | Cummins, Inc., 4.875%, 10/1/2043 | | 111,511 |

| | | | | 197,840 |

| | | Utilities—3.0% | | |

| 50M | | Dominion Resources, Inc., 3.9%, 10/1/2025 | | 51,139 |

| 100M | | Duke Energy Progress, Inc., 4.15%, 12/1/2044 | | 99,596 |

| 50M | | Ohio Power Co., 5.375%, 10/1/2021 | | 55,916 |

| 50M | | Oklahoma Gas & Electric Co., 4%, 12/15/2044 | | 49,462 |

| | | | | 256,113 |

| Total Value of Corporate Bonds (cost $3,102,431) | | 3,047,896 |

Portfolio of Investments (continued)

BALANCED INCOME FUND

December 31, 2016

| | | | | |

| | | | | | |

| | | | | | |

| Principal | | | | | |

| Amount or | | | | | |

| Shares | | Security | | | Value |

| | | RESIDENTIAL MORTGAGE-BACKED | | |

| | | SECURITIES—7.3% | | | |

| | | Fannie Mae: | | | |

| $144M | | 3%, 4/1/2046 – 6/1/2046 | | | $ 143,120 |

| 307M | | 3.5%, 11/1/2045 – 6/1/2046 | | | 315,053 |

| 115M | | 4%, 10/1/2035 – 7/1/2046 | | | 121,432 |

| 50M | | 4.5%, 1/18/2047 (a) | | | 53,787 |

| Total Value of Residential Mortgage-Backed Securities (cost $646,080) | | 633,392 |

| | | VARIABLE AND FLOATING RATE NOTES†—5.2% | | |

| | | Municipal Bond | | | |

| 300M | | Illinois St. Fin. Auth. Rev., 0.7%, 7/1/2038 | | | 300,000 |

| 150M | | Valdez, AK Marine Term. Rev., 0.67%, 12/1/2033 | | 150,000 |

| Total Value of Variable and Floating Rate Notes (cost $450,000) | | 450,000 |

| | | U.S. GOVERNMENT OBLIGATIONS—4.9% | | |

| 425M | | U.S. Treasury Notes, 0.8278%, 1/31/2018 (cost $425,626) † | | 426,289 |

| | | EXCHANGE TRADED FUNDS—2.4% | | | |

| 2,350 | | ishares iBoxx USD High Yield Corporate Bond ETF (ETF) | | |

| | | (cost $193,522) | | | 203,392 |

| | | SHORT-TERM U.S. GOVERNMENT AGENCY | | |

| | | OBLIGATIONS—5.8% | | | |

| | | Federal Home Loan Bank: | | | |

| $300M | | 0.45%, 2/1/2017 | | | 299,882 |

| 200M | | 0.47%, 2/7/2017 | | | 199,905 |

| Total Value of Short-Term U.S. Government Agency Obligations (cost $499,787) | | 499,787 |

| Total Value of Investments (cost $8,369,411) | 98.9 | % | 8,549,766 |

| Other Assets, Less Liabilities | 1.1 | | 99,024 |

| Net Assets | | | 100.0 | % | $8,648,790 |

| |

| * | Non-income producing |

| |

| (a) | A portion or all of the security purchased on a when-issued or delayed delivery basis |

| (see Note 1G). |

| |

| † | Interest rates on adjustable rate bonds are determined and reset periodically. The interest rates |

| shown are the rates in effect of December 31, 2016. |

| | |

| Summary of Abbreviations: |

| ADR | American Depositary Receipts |

| ETF | Exchange Traded Fund |

| REIT | Real Estate Investment Trust |

| USD | United States Dollar |

Futures contracts outstanding at December 31, 2016:

| | | | | | | | | | | | | |

| | | | | | | | Value at | | | | | |

| Number of | | | Value at | | December 31, | | Unrealized | | |

| Contracts | Type | Expiration | Trade Date | | 2016 | | Appreciation | | |

| 1 | | 5 Year U.S. | Mar. 2017 | $117,812 | | $117,948 | | | $ 135 | | |

| | | Treasury Note | | | | | | | | | | | |

| 5 | | 10 Year U.S. | Mar. 2017 | 622,813 | | 624,155 | | | 1,342 | | |

| | | Treasury Note | | | | | | | | | | | |

| 2 | | U.S. Treasury | Mar. 2017 | 302,891 | | 304,444 | | | 1,552 | | |

| | | Long Bond | | | | | | | | | | | |

| | | | | | | | | | | | $3,029 | | |

The Fund’s assets and liabilities are classified into the following three levels based on the inputs used to value the assets or liabilities:

| Level 1 — Unadjusted quoted prices in active markets for identical securities that the Fund has the ability to access. |

| Level 2 — Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| Level 3 — Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumption about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, U.S. Government securities are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market.

Portfolio of Investments (continued)

BALANCED INCOME FUND

December 31, 2016

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of December 31, 2016:

| | | | | | | | | | | | |

| | | | Level 1 | | | Level 2 | | | Level 3 | | | Total |

| Common Stocks | | $ | 3,289,010 | | $ | — | | $ | — | | $ | 3,289,010 |

| Corporate Bonds | | | — | | | 3,047,896 | | | — | | | 3,047,896 |

| Residential Mortgage-Backed | | | | | | | | | | | | |

| Securities | | | — | | | 633,392 | | | — | | | 633,392 |

| Variable and Floating Rate Notes | | | — | | | 450,000 | | | — | | | 450,000 |

| U.S. Government Obligations | | | — | | | 426,289 | | | — | | | 426,289 |

| Exchange Traded Funds | | | — | | | 203,392 | | | — | | | 203,392 |

| Short-Term U.S. Government | | | | | | | | | | | | |

| Agency Obligations | | | — | | | 499,787 | | | — | | | 499,787 |

| Total Investments in Securities* | | $ | 3,289,010 | | $ | 5,260,756 | | $ | — | | $ | 8,549,766 |

| |

| Other Assets | | | | | | | | | | | | |

| Futures Contracts | | $ | 3,131 | | $ | — | | $ | — | | $ | 3,131 |

| |

| * | The Portfolio of Investments provides information on the industry categorization for common stocks |

| and corporate bonds. |

| |

| There were no transfers into or from Level 1 and Level 2 by the Fund for the year ended December 31, |

| 2016. Transfers, if any, between Levels are recognized at the end of the reporting period. |

| | |

| 16 | See notes to financial statements | |

Portfolio Managers’ Letter

COVERED CALL STRATEGY FUND

Dear Investor:

This is the annual report for the First Investors Life Series Covered Call Strategy Fund for the year ended December 31, 2016. The Fund’s return from May 2, 2016 (commencement of operations) through year-end on a net asset value basis was 5.30%.

Market Overview

The U.S. Presidential election results created an equity market with increasing stock dispersion, with Financials, Energy and Industrials outperforming bond-proxy and consumer stocks. Interest rates increased across the yield curve as inflation expectations accelerated. The equity market rally resulted in valuations becoming less attractive based on trailing earnings. However, the prospect for reduced government regulations and lower tax rates could boost earnings for U.S. corporations in 2017. News cycles will likely ebb and flow based on the details of policy changes, which will likely create pockets of market volatility. Given this investment environment, we positioned the portfolio toward stocks likely to benefit from less government regulation, lower corporate tax rates, overseas cash repatriation and the Industrial/Energy/ Manufacturing recovery that has been gaining momentum. The call options, which provide income and downside protection, can help stabilize portfolio returns, with the overall goal of producing a better risk-adjusted total return versus the S&P 500 Index. This strategy should be viewed as a core equity strategy, and can serve as a foundation for investors’ equity allocations. It can be used to reduce the volatility of an overall equity allocation or to allow more optimistic investors to allocate to more aggressive equity strategies in a so-called “barbell” approach.

The Fund

During both the quarter and the year-to-date periods, the Fund outperformed the S&P 500 Index on a return-per-unit-of-risk basis. For example, year-to-date since inception, the Fund returned 6.6% with a standard deviation of 6.7%. The S&P 500 Index returned 9.2% with a standard deviation of 10.9%, an inferior risk-adjusted return versus the Fund.

The Fund’s higher quality equity holdings and downside protection from the call options were the keys to producing a higher return-per-unit-of-risk and reducing risk by more than one third compared to the S&P 500 Index. Due to the income and risk-reducing characteristics of the call options, the Fund produced a superior Sharpe ratio relative to the S&P 500 Index both quarter-to-date and year-to-date. Put another way, the Fund captured 72% of the return of the S&P 500, but only 62% of the risk of the S&P 500 year-to-date. Compared to the CBOE S&P 500 BuyWrite Index (“BXM”) during the inception year-to-date period, the Fund returned 6.6% versus 6.8% for the BXM Index. The Fund captured 97% of the BXM’s return and 96%

Portfolio Managers’ Letter (continued)

COVERED CALL STRATEGY FUND

of the risk, resulting in a slightly higher Sharpe ratio for the Fund versus the BXM, since inception.

In terms of the equity-only attribution since inception on May 2, 2016, the stocks in the Fund outperformed the stocks in the S&P 500 by 116 basis points. The Fund was positively impacted by stock selection during both the year and the quarter. The Fund’s underweight to the Healthcare sector, due to worries over drug price regulation, contributed positively to returns as it was one of the worst performing sectors during the inception-to-date period. Stock selection was strong in Consumer Discretionary but detracted from returns in Consumer Staples. The portfolio changes following the election positively impacted performance, as the Fund’s stocks continued to outperform the S&P 500 after the election. The call options detracted from returns in the Financial sector, which returned 21% during the fourth quarter, but made a positive contribution in Consumer Staples.

Outlook

Given the dispersion in sector performance, active management of option positions created a wide range for strike price selection in recent months. For more stable names, we have kept strike prices closer to current stock prices, seeking to maximize call premium at the expense of upside capture. With momentum stocks, we sold calls higher in price, seeking upside potential. Such a strategy is likely to continue into 2017 as news from Washington could create sector or company specific price volatility. While the S&P 500’s valuation (trailing P/E = 21.0) may appear to be a head-wind to stock appreciation, that view is offset by regulatory and tax policy changes that could boost earnings, thereby bringing P/E ratios back toward more average levels. That being said, valuation is an important part of our process. For example, the ten largest “low volatility” U.S. equity funds have an average trailing price/earnings (P/E) ratio of 22.9 versus the S&P 500 at 21.0 and our portfolio at 18.4 as of December 31, 2016. We continue to believe reasonably priced large-cap stocks offer the best risk/reward potential going forward, especially when combined with call premiums that can help stabilize returns and provide downside protection.

Thank you for placing your trust in Foresters Financial. As always, we appreciate the opportunity to serve your investment needs.

Fund Expenses (unaudited)

COVERED CALL STRATEGY FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 6 for a detailed explanation of the information presented in these examples.

| | | |

| | | | |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (7/1/16) | (12/31/16) | (7/1/16–12/31/16)* |

| Expense Examples | | | |

| Actual | $1,000.00 | $1,053.00 | $8.62 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,016.74 | $8.47 |

| |

| * | Expenses are equal to the annualized expense ratio of 1.67%, multiplied by the average account |

| value over the period, multiplied by 184/366 (to reflect the one-half year period). Expenses paid |

| during the period are net of expenses waived. |

Portfolio Composition

BY SECTOR

|

| Portfolio holdings and allocations are subject to change. Percentages are as of December 31, 2016, |

| and are based on the total value of investments. |

Portfolio of Investments

COVERED CALL STRATEGY FUND

December 31, 2016

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| Shares | | Security | | Value |

| | | COMMON STOCKS—99.7% | | |

| | | Consumer Discretionary—11.2% | | |

| 300 | * | AutoZone, Inc. | | $ 236,937 |

| 3,400 | | CBS Corporation – Class “B” | | 216,308 |

| 1,600 | | Home Depot, Inc. | | 214,528 |

| 1,900 | | Walt Disney Company | | 198,018 |

| 1,500 | | Whirlpool Corporation | | 272,655 |

| | | | | 1,138,446 |

| | | Consumer Staples—5.0% | | |

| 800 | | Kimberly-Clark Corporation | | 91,296 |

| 4,000 | | PepsiCo, Inc. | | 418,520 |

| | | | | 509,816 |

| | | Energy—9.9% | | |

| 2,700 | | Chevron Corporation | | 317,790 |

| 6,500 | | Halliburton Company | | 351,585 |

| 5,000 | | Valero Energy Corporation | | 341,600 |

| | | | | 1,010,975 |

| | | Financials—20.7% | | |

| 3,500 | | American Express Company | | 259,280 |

| 16,500 | | Bank of America Corporation | | 364,650 |

| 800 | | BlackRock, Inc. | | 304,432 |

| 1,600 | | Goldman Sachs Group, Inc. | | 383,120 |

| 5,100 | | JPMorgan Chase & Company | | 440,079 |

| 7,000 | | U.S. Bancorp | | 359,590 |

| | | | | 2,111,151 |

| | | Health Care—17.5% | | |

| 1,400 | * | Allergan, PLC | | 294,014 |

| 1,800 | | Amgen, Inc. | | 263,178 |

| 3,100 | | Cardinal Health, Inc. | | 223,107 |

| 2,900 | * | Express Scripts Holding Company | | 199,491 |

| 3,000 | | Johnson & Johnson | | 345,630 |

| 10,700 | | Pfizer, Inc. | | 347,536 |

| 1,100 | | Zimmer Biomet Holdings, Inc. | | 113,520 |

| | | | | 1,786,476 |

| | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| Shares | | Security | | | Value |

| | | Industrials—13.7% | | | |

| 6,900 | | General Electric Company | | | $ 218,040 |

| 3,400 | | Honeywell International, Inc. | | | 393,890 |

| 800 | | Lockheed Martin Corporation | | | 199,952 |

| 2,600 | | Raytheon Company | | | 369,200 |

| 2,100 | | Union Pacific Corporation | | | 217,728 |

| | | | | | 1,398,810 |

| | | Information Technology—16.2% | | | |

| 3,600 | | Apple, Inc. | | | 416,952 |

| 12,500 | | Cisco Systems, Inc. | | | 377,750 |

| 1,300 | | International Business Machines Corporation | | | 215,787 |

| 8,000 | | Oracle Corporation | | | 307,600 |

| 5,200 | | QUALCOMM, Inc. | | | 339,040 |

| | | | | | 1,657,129 |

| | | Materials—3.5% | | | |

| 6,300 | | Dow Chemical Company | | | 360,486 |

| | | Telecommunication Services—2.0% | | | |

| 3,900 | | Verizon Communications, Inc. | | | 208,182 |

| Total Value of Common Stocks (cost $9,601,881) | 99.7 | % | 10,181,471 |

| Other Assets, Less Liabilities | .3 | | 26,535 |

| Net Assets | | | 100.0 | % | $10,208,006 |

Portfolio of Investments (continued)

COVERED CALL STRATEGY FUND

December 31, 2016

| | | | |

| | | | | |

| | Expiration | Exercise | | |

| CALL OPTIONS WRITTEN—1.8% | Date | Price | Contracts | Value |

| Allergan, PLC | 2/17/17 | $205.00 | 1 | $ 1,340 |

| Allergan, PLC | 2/17/17 | 210.00 | 13 | 13,650 |

| American Express Company | 1/20/17 | 67.50 | 2 | 1,340 |

| American Express Company | 1/20/17 | 75.00 | 33 | 4,191 |

| Amgen, Inc. | 2/17/17 | 155.00 | 17 | 3,230 |

| Apple, Inc. | 2/17/17 | 120.00 | 36 | 7,020 |

| AutoZone, Inc. | 1/20/17 | 800.00 | 3 | 2,685 |

| Bank of America Corporation | 2/17/17 | 24.00 | 165 | 5,115 |

| BlackRock, Inc. | 4/21/17 | 410.00 | 8 | 5,680 |

| Cardinal Health, Inc. | 3/17/17 | 72.50 | 31 | 9,765 |

| CBS Corporation | 3/17/17 | 67.50 | 34 | 4,760 |

| Chevron Corporation. | 2/17/17 | 115.00 | 24 | 11,640 |

| Chevron Corporation. | 2/17/17 | 120.00 | 3 | 615 |

| Cisco Systems, Inc. | 2/17/17 | 32.00 | 125 | 2,750 |

| Dow Chemical Company | 3/17/17 | 60.00 | 63 | 7,497 |

| Express Scripts Holding Company | 3/17/17 | 75.00 | 1 | 129 |

| General Electric Company | 1/20/17 | 32.00 | 69 | 2,484 |

| Goldman Sachs Group, Inc. | 1/20/17 | 245.00 | 16 | 6,672 |

| Halliburton Company | 1/20/17 | 57.50 | 65 | 1,690 |

| Home Depot, Inc. | 1/20/17 | 130.00 | 14 | 7,224 |

| Home Depot, Inc. | 1/20/17 | 135.00 | 2 | 402 |

| Honeywell International, Inc. | 3/17/17 | 120.00 | 34 | 7,070 |

| International Business Machines | | | | |

| Corporation | 2/17/17 | 175.00 | 13 | 1,846 |

| Johnson & Johnson | 1/20/17 | 115.00 | 24 | 4,128 |

| Johnson & Johnson | 1/20/17 | 117.00 | 6 | 432 |

| JPMorgan Chase & Company | 2/17/17 | 90.00 | 51 | 6,069 |

| Kimberly-Clark Corporation | 1/20/17 | 115.00 | 8 | 1,016 |

| Lockheed Martin Corporation | 2/17/17 | 255.00 | 1 | 500 |

| Lockheed Martin Corporation | 3/17/17 | 280.00 | 7 | 560 |

| Oracle Corporation | 1/20/17 | 41.00 | 37 | 74 |

| Oracle Corporation | 3/17/17 | 40.00 | 43 | 2,795 |

| PepsiCo, Inc. | 1/20/17 | 105.00 | 40 | 4,280 |

| Pfizer, Inc. | 1/20/17 | 35.00 | 2 | 6 |

| Pfizer, Inc. | 2/17/17 | 33.00 | 105 | 6,090 |

| QUALCOMM, Inc. | 1/20/17 | 70.00 | 52 | 624 |

| Raytheon Company | 1/20/17 | 150.00 | 1 | 25 |

| Raytheon Company | 2/17/17 | 145.00 | 3 | 894 |

| Raytheon Company | 5/19/17 | 160.00 | 22 | 3,190 |

| U.S. Bancorp | 3/17/17 | 55.00 | 70 | 3,780 |

| Union Pacific Corporation | 1/20/17 | 100.00 | 21 | 10,689 |

| | | | |

| | | | | |

| | Expiration | Exercise | | |

| CALL OPTIONS WRITTEN (continued) | Date | Price | Contracts | Value |

| Valero Energy Corporation | 1/20/17 | $70.00 | 21 | $ 2,100 |

| Valero Energy Corporation | 1/20/17 | 72.50 | 29 | 1,247 |

| Verizon Communications, Inc | 6/16/17 | 52.50 | 39 | 9,828 |

| Walt Disney Company | 1/27/17 | 107.00 | 19 | 1,216 |

| Whirlpool Corporation | 3/17/17 | 185.00 | 14 | 10,920 |

| Whirlpool Corporation | 3/17/17 | 190.00 | 1 | 520 |

| Zimmer Biomet Holdings, Inc. | 3/17/17 | 105.00 | 2 | 800 |

| Zimmer Biomet Holdings, Inc. | 3/17/17 | 110.00 | 9 | 1,719 |

| Total Value of Call Options Written (premium received $209,302) | | $182,297 |

The Fund’s assets and liabilities are classified into the following three levels based on the inputs used to value the assets and liabilities:

| Level 1 — Unadjusted quoted prices in active markets for identical securities that the Fund has the ability to access. |

| Level 2 — Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| Level 3 — Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumption about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

The inputs methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, U.S. Government securities are reflected as Level 2 because the inputs used to determine fair value may not always be quoted prices in an active market.

The following is a summary, by category of Level, of inputs used to value the Fund’s investments as of December 31, 2016:

| | | | | | | | | | | | |

| | | | Level 1 | | | Level 2 | | | Level 3 | | | Total |

| Assets | | | | | | | | | | | | |

| Common Stocks* | | $ | 10,181,471 | | $ | — | | $ | — | | $ | 10,181,471 |

| Liabilities | | | | | | | | | | | | |

| Call Options Written | | $ | (182,297) | | $ | — | | $ | — | | $ | (182,297) |

| |

| * | The Portfolio of Investments provides information on the industry categorization for common stocks. |

| |

| There were no transfers into or from Level 1 and Level 2 by the Fund for the year ended December 31, |

| 2016. Transfers, if any, between Levels are recognized at the end of the reporting period. |

| | |

| See notes to financial statements | 23 |

Portfolio Manager’s Letter

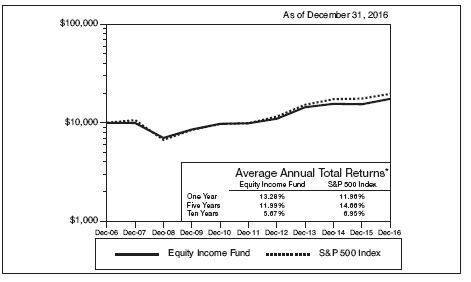

EQUITY INCOME FUND

Dear Investor:

This is the annual report for First Investors Life Equity Income Fund for the year ended December 31, 2016. The Fund’s return on a net asset value basis was 13.28%, including dividends of $0.40 cents per share and capital gains of $0.70 cents per share.

Market and Economic Overview

The majority of equity and fixed income markets around the world generated positive returns during the 12 months ended December 31, 2016. However, the trajectory of these returns was very uneven as market sentiment changed several times during the year. U.S. economic growth was also uneven, continuing the post-recession trend of subdued but positive growth.

The year began with a 10% correction in the stock market and a rally in the bond market as weakness in the Chinese economy and stock market, first quarter U.S. growth of only 0.8%, and falling commodity prices created recession and deflation fears. Markets stabilized and the stock market recovered through the summer until Brexit—Great Britain’s unexpected decision to leave the European Union. Stock prices fell, but quickly stabilized as central banks made clear that they would do whatever was necessary to stabilize economic growth. Reacting to very accommodative monetary policy, interest rates fell to historical lows across developed country bond markets. A pickup in U.S. growth in the third quarter to 3.5%, the best quarterly rate in two years, pushed interest rates somewhat higher, while stock prices traded in a range. Following Donald Trump’s unexpected victory in the U.S. Presidential election, the stock market rallied and interest rates increased sharply as markets focused on Trump’s pro-growth agenda. The Federal Reserve (“the Fed”) rate increase in December, the only hike in 2016, had no impact on the markets. Notably, the Fed cited improving labor market indicators as a reason for raising interest rates as the U.S. unemployment rate fell to levels preceding the Great Recession.

Divergence in monetary policies and market expectations of central bank actions was a dominant factor affecting markets throughout the review period. While the Fed tightened its monetary policy, major international central banks continued easing their monetary policies. In particular, the European Central Bank cut its deposit rate to a negative 0.4% rate, expanded its bond-buying program to include corporate bonds, and extended its bond-buying stimulus program by nine months. These moves contributed to the decline in interest rates globally. Yields for many international bonds fell into negative territory, which resulted in higher demand from overseas investors for positive yielding U.S. fixed income and strengthened the U.S. dollar.

The Equity Market

Overall, U.S. equities (measured by the S&P 500 Index) posted a strong return of 11.96% for the 12 months ending December 31, 2016. However, stocks had one of

the worst starts to the beginning of the year on record, plunging 10.27% by February 11, amid worries about China, global growth and falling oil prices. Most of those fears subsided by mid-February as China’s markets stabilized, oil producers talked about decreasing supply, and Janet Yellen implied there would be fewer rate hikes than expected. Markets subsequently rebounded, gaining almost 17% by the June 23rd Brexit vote. Momentum paused as markets lost over 5% in the two days following the Brexit vote, followed by another strong rally which lasted until mid-July. Markets declined ahead of the U.S. presidential election, but reacted positively to Donald Trump’s unexpected win, focusing on the pro-growth aspects of his agenda.

While all market cap segments posted double-digit returns for the year, small-cap stocks (Russell 2000 Index) had the best performance, returning 21.31%, followed by mid-caps (S&P MidCap 400 Index) at 20.74%. Small-cap stocks in particular benefited from the post-election rally and President-elect Trump’s domestically centered policies. Value stocks outperformed growth stocks, supported by strong performance from Financials at the end of the year.

10 out of 11 S&P 500 sectors were positive in 2016, but with several sector rotations during the period. Energy was the strongest sector at 27.36%. It was weak during the beginning of the year, but recovered during the second half due to rising oil prices. The Healthcare sector, which had performed well for the past several years, was the weakest sector, down 2.69%. Higher yielding stocks, including Utilities and REITs, held up well during the first half of the year, supported by the low yielding environment and lack of other higher yielding options, but were negative during the second half.

International equities experienced wide swings during the review period. Developed markets (MSCI EAFE Index) finished the review period up 5.88% in local currencies and 1.51% in U.S. dollar terms as an appreciating dollar reduced returns for U.S. investors. Emerging markets (MSCI EM Index) had a difficult fourth quarter in 2016, but outperformed developed markets for the year with returns of 10.11% in local currencies and 11.60% in U.S. dollars. For most of the year, negative yields on many international bonds increased demand for emerging market assets. Select emerging markets also benefited from recovering commodity and oil prices.

The Fund

The Fund primarily invests in dividend-paying stocks and this year, with increased interest rate volatility, the Fund’s dividend-paying stocks performed very well. In 2016, we saw the yield on the 10-year Treasury go from 2.30% in January to a low of 1.31% in July only to rally to 2.62% by the end of December 2016 after the Fed rate increase of 25 basis points. Disappointing GDP numbers started to come out in the beginning of 2016 and the market began to sell off, investors started buying the safety of Treasuries and forced the yield back below 2%. By July, the yield on the 10-year Treasury reached a low of 1.31%. High dividend paying stocks rose as

Portfolio Manager’s Letter (continued)

EQUITY INCOME FUND

rates collapsed in late spring. By the end of the summer—with GDP and job growth showing signs of improvement—the Fed began to signal its intention to raise rates by the end of 2016 and the yield on the 10-year Treasury started to rise in anticipation of the rate hike.

The significance of these moves plays a role in the direction of dividend-paying stocks. When interest rates fell over the past few years, fixed income investors looked to dividend-paying equities to supplement their income when money market accounts and CDs no longer offered compelling returns. When interest rates rise and those fixed income products become more competitive with higher yields, investors will likely return to fixed income as they offer lower volatility compared to equities. Investors who could not find adequate yield in fixed income securities bid up higher yielding equities to a point, one could argue, where they were overvalued. Typically, companies with higher yields have much slower earnings growth and such companies offer higher yield as an incentive to invest. The only way to get meaningful stock appreciation is through earnings growth or multiple expansions. We have seen this expansion of multiples mainly in the Utilities, Staples and REIT sectors.

When interest rates rise, the ability of banks to grow earnings also rises. The spread on which banks borrow money and, in turn, lend out to customers widens and banks become more profitable. Sterling Bancorp a small-cap regional bank in the New York area has appreciated over 40% this year. Investors are anticipating stronger loan growth and increased earnings going forward. The Fund’s other regional banks have all outperformed the market significantly: Berkshire Hills, a small Massachusetts bank was up over 30% this year; Prosperity Bankshare, a small bank based in Houston, Texas also benefited from the price of oil recovering from the lows to increase their earning potential; Chubb, a stock we wrote about in last year’s letter played out much as we thought. ACE acquired Chubb last year and assumed Chubb’s name. Earnings have been strong, pricing has been good and the cost cuts have come in at a higher level than expected. The stock is up over 15% in the past 12 months and is one of our biggest financial holdings. We continue to see the benefits of this combination playing out over the coming years especially in a rising interest rate environment.

The Fund’s Healthcare holdings had strong returns this past year, led by our large-cap pharmaceutical holdings. Merck has had a good year, with the stock rising over 15%. Earnings have been strong but Merck’s pipeline has been garnering all the attention lately. Merck recently presented Phase 3 data on Keytruda, their first line lung cancer drug and results were very strong. It is widely believed that Keytruda will become the dominant drug used in the treatment of lung cancer because the data showed superior effectiveness over chemotherapy. This drug, by some estimates, could see sales of over $8 billion in the coming years. Merck’s biggest competitor in the lung cancer space came out with disappointing results solidifying Merck’s dominance for the next few years. Baxalta was a name the Fund owned after it was spun off from our holding in Baxter. Baxalta specializes in hematology, immunology and oncology and was

showing nice earnings growth. Shire PLC offered to buy them for $32 billion at the beginning of the year.

A relatively new holding, Applied Materials, was purchased back in March and the stock price is up over 100% from where we made our initial investment. We were able to correctly identify a new spending cycle for semiconductor equipment for two main areas, 3D NAND and the adoption of OLED (organic light emitting diode) display for mobile devices and television. 3D NAND is the next generation for memory chips that will allow for both faster and greater capacity for flash storage. OLED is widely recognized as the best display for both mobile devices and televisions. It is expected that Apple will adopt OLED for its next generation iPhone and Samsung is currently using OLED in their mobile devices. When capacity comes on, and manufacturing yields improve, we will likely see a large adoption of OLED televisions in the coming years. The new wild card is demand from China. Historically, China has not been a player in semiconductor manufacturing, but they are spending heavily to become a factor in global foundry production. With this new market, earnings should be higher than any point in their past.

The Fund also added a new strategy in the past year that we hope will enhance performance in the coming years. We are now selling covered calls on securities we own and are looking to sell at specific prices. Selling covered calls allows the Fund to take in cash for securities we would otherwise be selling in the marketplace and that cash is added to the total return of the security.

As we look forward, we believe dividend-paying stocks should be a focus for any investor. Dividend-paying stocks tend to outperform non-dividend-paying stocks when interest rates are either rising or falling. If we look at stock returns since the 1970s, dividend-paying stocks have outperformed the S&P 500 Index. The Fund is focused on finding those stocks that not only provide yield and stability, but provide dividend growth and appreciation.

Thank you for placing your trust in Foresters Financial. As always, we appreciate the opportunity to serve your investment needs.

Fund Expenses (unaudited)

EQUITY INCOME FUND

The examples below show the ongoing costs (in dollars) of investing in your Fund and will help you in comparing these costs with costs of other mutual funds. Please refer to page 6 for a detailed explanation of the information presented in these examples.

| | | |

| | | | |

| | Beginning | Ending | |

| | Account | Account | Expenses Paid |

| | Value | Value | During Period |

| | (7/1/16) | (12/31/16) | (7/1/16–12/31/16)* |

| Expense Examples | | | |

| Actual | $1,000.00 | $1,076.61 | $4.18 |

| Hypothetical | | | |

| (5% annual return before expenses) | $1,000.00 | $1,021.12 | $4.06 |

| |

| * | Expenses are equal to the annualized expense ratio of .80%, multiplied by the average account |

| value over the period, multiplied by 184/366 (to reflect the one-half year period). |

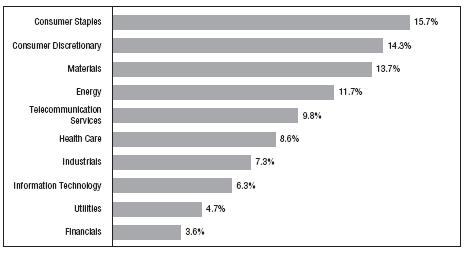

Portfolio Composition

TOP TEN SECTORS

|

| Portfolio holdings and allocations are subject to change. Percentages are as of December 31, 2016, |

| and are based on the total value of investments. |

Cumulative Performance Information (unaudited)

EQUITY INCOME FUND

Comparison of change in value of $10,000 investment in the First Investors Life Series Equity Income Fund and the Standard & Poor’s 500 Index.

The graph compares a $10,000 investment in the First Investors Life Series Equity Income Fund beginning 12/31/06 with a theoretical investment in the Standard & Poor’s 500 Index (the “Index”). The Index is an unmanaged capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of such stocks, which represent all major industries. It is not possible to invest directly in this Index. In addition, the Index does not reflect fees and expenses associated with the active management of a mutual fund portfolio. For purposes of the graph and the accompanying table it is assumed that all dividends and distributions were reinvested.

* The Average Annual Total Return figures are for the periods ended 12/31/16.

The returns shown do not reflect any sales charges, since the Fund sells its shares solely to variable annuity and/or variable life insurance subaccounts at net asset value. The returns do not reflect the fees and charges that an individual would pay in connection with an investment in a variable annuity or life contract or policy. Results represent past performance and do not indicate future results. The graph and the returns shown do not reflect the deduction of taxes that an investor would pay on distributions or the redemption of fund shares. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Index figures are from Standard & Poor’s and all other figures are from Foresters Investment Management Company, Inc.

Portfolio of Investments

EQUITY INCOME FUND

December 31, 2016

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| Shares | | Security | | Value |

| | | COMMON STOCKS—93.2% | | |

| | | Consumer Discretionary—9.4% | | |

| 17,000 | * | Acushnet Holdings Corporation | | $ 335,070 |

| 13,200 | | American Eagle Outfitters, Inc. | | 200,244 |

| 8,687 | | CBS Corporation – Class “B” | | 552,667 |

| 17,650 | | Comcast Corporation – Special Shares “A” | | 1,218,732 |

| 4,800 | | Delphi Automotive, PLC | | 323,280 |

| 52,450 | | Ford Motor Company | | 636,218 |

| 2,150 | | Harman International Industries, Inc. | | 238,994 |

| 8,950 | | Home Depot, Inc. | | 1,200,016 |

| 21,734 | | Johnson Controls International, PLC | | 895,223 |

| 4,500 | | L Brands, Inc. | | 296,280 |

| 6,900 | | McDonald’s Corporation | | 839,868 |

| 16,837 | | Newell Brands, Inc. | | 751,772 |

| 4,800 | | Oxford Industries, Inc. | | 288,624 |

| 23,300 | | Regal Entertainment Group – Class “A” | | 479,980 |

| 11,016 | | Time Warner, Inc. | | 1,063,375 |

| 6,500 | | Tupperware Brands Corporation | | 342,030 |

| 4,300 | | Walt Disney Company | | 448,146 |

| 2,300 | | Whirlpool Corporation | | 418,071 |

| 5,300 | | Wyndham Worldwide Corporation | | 404,761 |

| | | | | 10,933,351 |

| | | Consumer Staples—8.6% | | |

| 4,900 | | AdvancePierre Foods Holdings, Inc. | | 145,922 |

| 23,800 | | Altria Group, Inc. | | 1,609,356 |

| 17,600 | | Coca-Cola Company | | 729,696 |

| 11,700 | | CVS Health Corporation | | 923,247 |

| 3,850 | | Dr. Pepper Snapple Group, Inc. | | 349,079 |

| 3,600 | | Kimberly-Clark Corporation | | 410,832 |

| 20,782 | | Koninklijke Ahold Delhaize NV (ADR) | | 436,214 |

| 3,666 | | Kraft Heinz Company | | 320,115 |

| 3,400 | | Molson Coors Brewing Company | | 330,854 |

| 12,000 | | PepsiCo, Inc. | | 1,255,560 |

| 16,200 | | Philip Morris International, Inc. | | 1,482,138 |

| 15,300 | | Procter & Gamble Company | | 1,286,424 |

| 10,200 | | Wal-Mart Stores, Inc. | | 705,024 |

| | | | | 9,984,461 |

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| Shares | | Security | | Value |

| | | Energy—8.0% | | |

| 17,200 | | Chevron Corporation | | $ 2,024,440 |

| 15,250 | | ConocoPhillips | | 764,635 |

| 13,500 | | Devon Energy Corporation | | 616,545 |

| 14,500 | | ExxonMobil Corporation | | 1,308,770 |

| 8,400 | | Halliburton Company | | 454,356 |

| 13,400 | | Marathon Petroleum Corporation | | 674,690 |

| 15,500 | | Occidental Petroleum Corporation | | 1,104,065 |

| 15,800 | | PBF Energy, Inc. – Class “A” | | 440,504 |

| 14,400 | | Royal Dutch Shell, PLC – Class “A” (ADR) | | 783,072 |

| 6,400 | | Schlumberger, Ltd. | | 537,280 |

| 20,400 | | Suncor Energy, Inc. | | 666,876 |

| | | | | 9,375,233 |

| | | Financials—17.7% | | |

| 28,800 | | AllianceBernstein Holding, LP (MLP) | | 675,360 |

| 8,550 | | American Express Company | | 633,384 |

| 11,500 | | American International Group, Inc. | | 751,065 |

| 4,050 | | Ameriprise Financial, Inc. | | 449,307 |

| 22,100 | | Bank of New York Mellon Corporation | | 1,047,098 |

| 23,650 | | Berkshire Hills Bancorp, Inc. | | 871,502 |

| 13,567 | | Chubb, Ltd. | | 1,792,472 |

| 26,300 | | Citizens Financial Group, Inc. | | 937,069 |

| 14,350 | | Discover Financial Services | | 1,034,491 |

| 28,270 | | Financial Select Sector SPDR Fund (ETF) | | 657,278 |

| 13,900 | | Invesco, Ltd. | | 421,726 |

| 18,100 | | iShares S&P U.S. Preferred Stock Index Fund (ETF) | | 673,501 |

| 25,300 | | JPMorgan Chase & Company | | 2,183,137 |

| 22,800 | | MetLife, Inc. | | 1,228,692 |

| 9,000 | | PNC Financial Services Group, Inc. | | 1,052,640 |

| 5,400 | | Prosperity Bancshares, Inc. | | 387,612 |

| 14,500 | | SPDR S&P Regional Banking (ETF) | | 805,765 |

| 32,200 | | Sterling Bancorp | | 753,480 |

| 5,400 | | Travelers Companies, Inc. | | 661,068 |

| 20,600 | | U.S. Bancorp | | 1,058,222 |

| 17,100 | | Waddell & Reed Financial, Inc. – Class “A” | | 333,621 |

| 40,850 | | Wells Fargo & Company | | 2,251,244 |

| | | | | 20,659,734 |

Portfolio of Investments (continued)

EQUITY INCOME FUND

December 31, 2016

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| Shares | | Security | | Value |

| | | Health Care—10.3% | | |

| 20,400 | | Abbott Laboratories | | $ 783,564 |

| 18,300 | | AbbVie, Inc. | | 1,145,946 |

| 8,292 | | Baxter International, Inc. | | 367,667 |

| 6,700 | | Gilead Sciences, Inc. | | 479,787 |

| 10,050 | | GlaxoSmithKline, PLC (ADR) | | 387,026 |

| 20,450 | | Johnson & Johnson | | 2,356,045 |

| 10,412 | | Medtronic, PLC | | 741,647 |

| 34,020 | | Merck & Company, Inc. | | 2,002,757 |

| 74,585 | | Pfizer, Inc. | | 2,422,521 |

| 16,300 | | Phibro Animal Health Corporation – Class “A” | | 477,590 |

| 3,050 | | Thermo Fisher Scientific, Inc. | | 430,355 |

| 8,490 | | Zoetis, Inc. | | 454,470 |

| | | | | 12,049,375 |

| | | Industrials—10.6% | | |

| 5,400 | | 3M Company | | 964,278 |

| 5,600 | | A.O. Smith Corporation | | 265,160 |

| 12,400 | | Eaton Corporation, PLC | | 831,916 |

| 2,500 | | General Dynamics Corporation | | 431,650 |

| 64,930 | | General Electric Company | | 2,051,788 |

| 11,800 | | Honeywell International, Inc. | | 1,367,030 |

| 13,300 | | Industrial Select Sector SPDR Fund (ETF) | | 827,526 |

| 7,800 | | Ingersoll-Rand, PLC | | 585,312 |

| 12,550 | | ITT, Inc. | | 484,054 |

| 19,100 | | Koninklijke Philips NV (ADR) | | 583,887 |

| 3,680 | | Lockheed Martin Corporation | | 919,779 |

| 13,300 | | Nielsen Holdings, PLC | | 557,935 |

| 4,350 | | Snap-On, Inc. | | 745,025 |

| 8,200 | | United Parcel Service, Inc. – Class “B” | | 940,048 |

| 7,900 | | United Technologies Corporation | | 865,998 |

| | | | | 12,421,386 |

| | | Information Technology—13.8% | | |

| 9,690 | | Apple, Inc. | | 1,122,296 |

| 26,000 | | Applied Materials, Inc. | | 839,020 |

| 5,450 | | Automatic Data Processing, Inc. | | 560,151 |

| 4,300 | | Broadcom, Ltd. | | 760,111 |

| 65,200 | | Cisco Systems, Inc. | | 1,970,344 |

| 25,700 | | HP Enterprise Company | | 594,698 |

| 26,800 | | HP, Inc. | | 397,712 |

| 33,300 | | Intel Corporation | | 1,207,791 |

| | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| Shares | | Security | | Value |

| | | Information Technology (continued) | | |

| 13,400 | | Juniper Networks, Inc. | | $ 378,684 |

| 6,450 | | Lam Research Corporation | | 681,959 |

| 9,000 | | Microchip Technology, Inc. | | 577,350 |

| 43,250 | | Microsoft Corporation | | 2,687,555 |

| 19,300 | | QUALCOMM, Inc. | | 1,258,360 |

| 14,400 | | Silicon Motion Technology Corporation (ADR) | | 611,712 |

| 22,700 | | Symantec Corporation | | 542,303 |

| 7,500 | | TE Connectivity, Ltd. | | 519,600 |

| 10,900 | | Technology Select Sector SPDR Fund (ETF) | | 527,124 |

| 13,200 | | Western Digital Corporation | | 896,940 |

| | | | | 16,133,710 |

| | | Materials—4.1% | | |

| 16,450 | | Dow Chemical Company | | 941,269 |

| 10,990 | | DuPont (E.I.) de Nemours & Company | | 806,666 |

| 25,100 | * | Ferro Corporation | | 359,683 |

| 10,700 | | International Paper Company | | 567,742 |

| 9,600 | | LyondellBasell Industries NV – Class “A” | | 823,488 |

| 4,300 | | Praxair, Inc. | | 503,917 |

| 8,200 | | Sealed Air Corporation | | 371,788 |

| 3,200 | | Steel Dynamics, Inc. | | 113,856 |

| 6,090 | | WestRock Company | | 309,189 |

| | | | | 4,797,598 |

| | | Real Estate—3.2% | | |

| 27,800 | | Brixmor Property Group, Inc. (REIT) | | 678,876 |

| 20,000 | | Chesapeake Lodging Trust (REIT) | | 517,200 |

| 2,700 | | Federal Realty Investment Trust (REIT) | | 383,697 |

| 8,850 | | iShares U.S. Real Estate ETF (ETF) | | 680,919 |

| 17,700 | | Sunstone Hotel Investors, Inc. (REIT) | | 269,925 |

| 15,400 | | Tanger Factory Outlet Centers, Inc. (REIT) | | 551,012 |

| 28,900 | | Urstadt Biddle Properties, Inc. – Class “A” (REIT) | | 696,779 |

| | | | | 3,778,408 |

| | | Telecommunication Services—3.8% | | |

| 49,760 | | AT&T, Inc. | | 2,116,293 |

| 42,600 | | Verizon Communications, Inc. | | 2,273,988 |

| | | | | 4,390,281 |

Portfolio of Investments (continued)

EQUITY INCOME FUND

December 31, 2016

| | | | |

| | | | | |

| | | | | |

| Shares or | | | | |

| Principal | | | | |

| Amount | | Security | | Value |

| | | Utilities—3.7% | | |

| 7,350 | | American Electric Power Company, Inc. | $ 462,756 |

| 19,200 | | CenterPoint Energy, Inc. | | 473,088 |

| 6,750 | | Dominion Resources, Inc. | | 516,982 |

| 6,900 | | Duke Energy Corporation | | 535,578 |

| 21,700 | | Exelon Corporation | | 770,133 |

| 3,400 | | NextEra Energy, Inc. | | 406,164 |

| 19,900 | | PPL Corporation | | 677,595 |

| 8,300 | | Vectren Corporation | | 432,845 |

| | | | | 4,275,141 |

| Total Value of Common Stocks (cost $76,636,919) | | 108,798,678 |

| | | PREFERRED STOCKS—1.6% | | |

| | | Financials—.6% | | |

| 200 | | Citizens Financial Group, Inc., Series A, 5.5%, 2049 | | 199,000 |

| 21,200 | | JPMorgan Chase & Co., Series Y, 6.125%, 2020 | | 537,420 |

| | | | | 736,420 |

| | | Health Care—.3% | | |

| 500 | | Allergan, PLC, Series A, 5.5%, 2018 | | 381,230 |

| | | Real Estate—.7% | | |

| 11,400 | | Digital Realty Trust, Inc., Series G (REIT), 5.875%, 2049 | | 272,802 |

| | | Urstadt Biddle Properties, Inc., (REIT): | | |

| 9,000 | | 7.125%, 2049 – Series F | | 229,500 |

| 11,000 | | 6.75%, 2049 – Series G | | 283,360 |

| | | | | 785,662 |

| Total Value of Preferred Stocks (cost $2,019,492) | | 1,903,312 |

| | | SHORT-TERM U.S. GOVERNMENT AGENCY | | |

| | | OBLIGATIONS—2.6% | | |

| | | Federal Home Loan Bank: | | |

| $2,000M | | 0.39%, 1/12/2017 | | 1,999,814 |