UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-04367 |

|

Columbia Funds Series Trust I |

(Exact name of registrant as specified in charter) |

|

One Financial Center, Boston, Massachusetts | | 02111 |

(Address of principal executive offices) | | (Zip code) |

|

James R. Bordewick, Jr., Esq. Columbia Management Advisors, LLC One Financial Center Boston, MA 02111 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-617-426-3750 | |

|

Date of fiscal year end: | May 31 | |

|

Date of reporting period: | May 31, 2009 | |

| | | | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Columbia Management®

Annual Report

May 31, 2009

Columbia Strategic Income Fund

| NOT FDIC INSURED | | May Lose Value | |

|

| NOT BANK ISSUED | | No Bank Guarantee | |

|

Table of contents

| Fund Profile | | | 1 | | |

|

| Economic Update | | | 2 | | |

|

| Performance Information | | | 3 | | |

|

| Understanding Your Expenses | | | 4 | | |

|

| Portfolio Managers' Report | | | 5 | | |

|

| Financial Statements | | | | | |

|

| Investment Portfolio | | | 7 | | |

|

Statement of Assets and

Liabilities | | | 24 | | |

|

| Statement of Operations | | | 26 | | |

|

Statement of Changes in

Net Assets | | | 27 | | |

|

| Financial Highlights | | | 29 | | |

|

| Notes to Financial Statements | | | 34 | | |

|

| Report of Independent Registered Public Accounting Firm | | | 45 | | |

|

| Fund Governance | | | 46 | | |

|

Important Information About

This Report | | | 53 | | |

|

The views expressed in this report reflect the current views of the respective parties. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict, so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Fund. References to specific securities should not be construed as a recommendation or investment advice.

President's Message

Dear Shareholder:

Recent events have shown great volatility in the markets and uncertainty in the economy. During these challenging times, it becomes even more important to focus on long-term horizons and key investment tools that can help manage volatility. This may be the time to reflect on your investment goals and evaluate your portfolio to ensure you are positioned for any potential market rebound.

A long-term financial plan can serve as a road map and guide you through the necessary steps designed to meet your financial goals. Your financial plan should take into account your investment goals, time horizon, overall financial situation, risk tolerance and willingness to ride out market volatility. Your investment professional can be a key resource as you work through this process. The knowledge and experience of an investment professional can help as you create or reevaluate your investment strategy.

The importance of diversification

Although diversification does not ensure a profit or guarantee against loss, a diversified portfolio can be a strategy for successful long-term investing. Diversification refers to the mix of investments within a portfolio. A mutual fund can contribute to portfolio diversification given that a mutual fund's portfolio represents several investments. Additionally, the way you allocate your money among stocks, bonds and cash, and geographically between foreign and domestic investments, can help to reduce risks. Diversification can result in multiple investments where the positive performance of certain holdings can offset any negative performance from other holdings. Having a diversified portfolio doesn't mean that the value of the portfolio will never go down, but rather helps strike a balance between risk and reward.

Reevaluate your strategy

An annual review of your investments is a key opportunity to determine if your investment needs have changed or if you need minor adjustments to rebalance your portfolio. Life events like a birth, marriage, home improvement, or change in employment can have a major effect on your spending and goals. Ask yourself how your spending or goals have changed and factor this into your financial plan. Are you using automated investments or payroll deductions to help keep your savings on track? Are you able to set aside additional savings or increase your 401(k) plan contributions? If during your review you find that your investments in any one category (e.g., stocks, bonds or cash) have grown too large based on your diversification plan, you may want to consider redirecting future investments to get back on track.

History has shown that the U.S. stock market has been remarkably resilient1. Volatility can lead to opportunity. Patience and a commitment to your long-term financial plan may position you to potentially benefit over your investment horizon. We appreciate your business and continued support of Columbia Funds.

Sincerely,

J. Kevin Connaughton

President, Columbia Funds

1The Dow Jones Industrial Average is the most widely used indicator of the overall condition of the stock market. The Dow Jones Industrial Average Index is a price-weighted average of 30 actively traded blue-chip stocks as selected by the editors of the Wall Street Journal. Indices are not investments, do not incur fees or expenses and are not professionally managed. It is not possible to invest directly in an index.

Fund Profile – Columbia Strategic Income Fund

Summary

g For the 12-month period that ended May 31, 2009, the fund's Class A shares returned negative 1.79% without sales charge.

g The fund came out behind its benchmark, the Barclays Capital U.S. Government/Credit Bond Index (formerly the Lehman Brothers U.S. Government/Credit Bond Index),1 but ahead of its peer group, the Lipper Multi-Sector Income Funds Classification.2

g High-yield debt and currency exposure hampered returns versus the fund's benchmark, while a high quality bias helped the fund outpace its peer group.

Portfolio Management

Laura A. Ostrander, lead manager of the fund, has managed or co-managed the fund since 2000 and has been associated with the advisor or its predecessors or affiliate organizations since 1996.

Kevin L. Cronk has co-managed the fund since 2005 and has been associated with the advisor or its predecessors or affiliate organizations since 1999.

1The Barclays Capital U.S. Government/Credit Bond Index is composed of high-quality, investment-grade U.S. Government and corporate fixed-income securities with maturities greater than one year. Indices are not available for investment, are not professionally managed and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index.

2Lipper Inc., a widely respected data provider in the industry, calculates an average total return (assuming reinvestment of distributions) for mutual funds with investment objectives similar to those of the fund. Lipper makes no adjustments for the effect of sales loads.

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

Summary

1-year return as of 05/31/09

| | | –1.79% | |

|

| |  | | | Class A shares

(without sales charge) | |

|

| | | +4.47% | |

|

| |  | | | Barclays Capital U.S. Government/Credit Bond Index | |

|

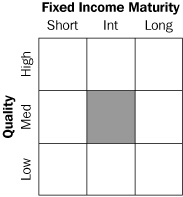

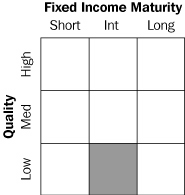

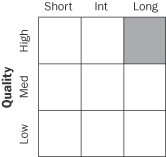

Morningstar Style BoxTM

The Morningstar Style BoxTM reveals a fund's investment strategy. For fixed-income funds, the vertical axis shows the average credit quality of the bonds owned, and the horizontal axis shows interest rate sensitivity as measured by a bond's duration (short, intermediate or long). Information shown is based on the most recent data provided by Morningstar.

1

Economic Update – Columbia Strategic Income Fund

Summary

For the 12-month period that ended May 31, 2009

g Despite volatility in many segments of the bond market, the Barclays Capital U.S. Aggregate Bond Index delivered positive results. High-yield bonds lost ground, as measured by the JPMorgan Global High Yield Index

Barclays

Aggregate

Index | | JPMorgan Global

High Yield

Index | |

|

| |  | |

|

g The broad U.S. stock market, as measured by the S&P 500 Index, returned negative 32.57%. Stock markets in foreign developed markets returned negative 36.61%, as measured (in U.S. dollars) by the MSCI EAFE Index.

| S&P Index | | MSCI Index | |

|

| |  | |

|

During the 12-month period that began June 1, 2008 and ended May 31, 2009, the U.S. economy struggled under the weight of the worst financial crisis since the Great Depression. Economic growth contracted by more than 6% in the second half of 2008. Although the decline for the first half of 2009 appears to have been less severe, hopes for a late 2009 recovery remain in doubt. The lapse from growth has resulted in the longest—and most severe—recession in nearly three decades.

The labor market shed millions of jobs between 2008 and 2009, raising the unemployment rate to 9.4% in May. Manufacturing activity slowed and consumer spending declined. The beleaguered housing market continued to lose ground as prices fell and inventories rose. However, mortgage purchase applications increased late in the period, buoyed by low interest rates and an $8,000 first-time home buyer tax credit. Late in 2008, consumer confidence, as measured by the Conference Board, plummeted to its lowest point ever. However, it stabilized in March and turned sharply higher in both April and May of 2009.

Troubles that began in the U.S. subprime mortgage market resulted in a meltdown within the U.S. financial sector that claimed several major institutions in 2008 and led others to seek bailouts, restructuring or both. New rigorous lending standards severely limited access to credit, further hampering economic growth. In this environment, a new administration sought to stabilize the financial system, address economic woes and introduce sweeping health care reform. Stimulus spending began to flow into the economy, raising hopes that growth would be restored in the second half of 2009. However, with much of the developed world in recession, any substantial improvement in economic conditions may be longer in coming. In December 2008, the Federal Reserve Board (the Fed) lowered a key short-term borrowing rate—the federal funds rate—to between zero and 0.25%—a record low. In light of protracted economic weakness, the Fed is unlikely to tighten its reins on money until the economy and the labor markets stabilize.

Bonds outperformed stocks

As investors sought refuge from a volatile stock market, the highest quality sectors of the U.S. bond market delivered modest gains. During the first half of the period, Treasury prices rose and yields declined sharply as the economy faltered and stock market volatility increased. As hopes for a recovery materialized in the second half of the period, yields rose and Treasuries lagged riskier segments of the bond market. The benchmark 10-year U.S. Treasury yield began the period at just over 4.0%, declined to 2.2% in December 2008 then rose to end the period at 3.4%. In this environment, the Barclays Capital U.S. Aggregate Bond Index1 returned 5.36%. High-yield bond prices fell sharply as economic prospects weakened and default fears rose in 2008, then rebounded strongly in 2009. For the 12-month period, the JPMorgan Global High Yield Index2 returned negative 9.53%. For the last six months of the period, the index gained 31.70%.

Stocks retreated, then rebounded

Against a weakening economic backdrop, the U.S. stock market lost 32.57% for the 12-month period, as measured by the S&P 500 Index.3 Losses affected the stocks of companies of all sizes and investment style categories, although growth stocks held up better than value stocks, as measured by their respective Russell indices.4 Stock markets outside the U.S. suffered even greater losses. The MSCI EAFE Index,5 a broad gauge of stock market performance in foreign developed markets, lost 36.61% (in U.S. dollars) for the period. Emerging stock markets, which generally have had a strong run over the past several years, were also caught in the downdraft. As investors backed away from risk, the MSCI Emerging Markets Index6 returned negative 34.36% (in U.S. dollars).

Past performance is no guarantee of future results.

1The Barclays Capital U.S. Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs and total return performance of fixed-rate, publicly placed, dollar-denominated and non-convertible investment-grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity.

2The JPMorgan Global High Yield Index is designed to mirror the investable universe of the U.S. dollar global high-yield corporate debt market, including domestic and international issues.

3The Standard & Poor's (S&P) 500 Index tracks the performance of 500 widely held, large-capitalization U.S. stocks.

4The Russell 1000 Growth Index measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000 Value Index measures the performance of those companies in the Russell 1000 Index with lower price-to-book ratios and lower forecasted growth values. The Russell 2000 Growth Index measures the performance of those Russell 2000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Value Index measures the performance of those Russell 2000 Index companies with lower price-to-book ratios and lower forecasted growth values. The Russell 3000 Growth Index measures the performance of those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 3000 Value Index measures the performance of those Russell 3000 Index companies with lower price-to-bo ok ratios and lower forecasted growth values. The Russell Midcap Growth Index measures the performance of those Russell Midcap companies with higher price-to-book ratios and higher forecasted growth values. The Russell Midcap Value Index measures the performance of those Russell Midcap Index companies with lower price-to-book ratios and lower forecasted growth values.

5The Morgan Stanley Capital International (MSCI) Europe, Australasia, Far East (EAFE) Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance excluding the U.S. and Canada.

6The MSCI Emerging Markets Index is composed of a sample of companies from 22 countries representing the global emerging stock markets.

Indices are not available for investment, are not professionally managed and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index.

2

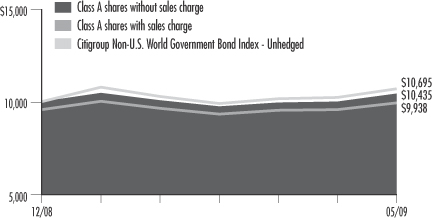

Performance Information – Columbia Strategic Income Fund

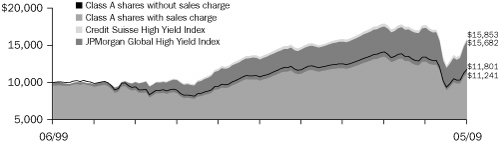

Performance of a $10,000 investment 06/01/99 – 05/31/09

The chart above shows the change in value of a hypothetical $10,000 investment in Class A shares of Columbia Strategic Income Fund during the stated time period, and does not reflect the deduction of taxes that a shareholder may pay on fund distributions or on the redemption of fund shares. The Barclays Capital U.S. Government/Credit Bond Index is composed of high-quality, investment-grade U.S. Government and corporate fixed-income securities with maturities greater than one year. Indices are not available for investment, are not professionally managed and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index.

Performance of a $10,000 investment 06/01/99 – 05/31/09 ($)

| Sales charge | | without | | with | |

| Class A | | | 16,761 | | | | 15,965 | | |

| Class B | | | 15,578 | | | | 15,578 | | |

| Class C | | | 15,835 | | | | 15,835 | | |

| Class J | | | 16,166 | | | | 15,681 | | |

| Class Z | | | 17,113 | | | | n/a | | |

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

Annual operating expense ratio (%)*

| Class A | | | 0.96 | | |

| Class B | | | 1.71 | | |

| Class C | | | 1.71 | | |

| Class J | | | 1.39 | | |

| Class Z | | | 0.71 | | |

* The annual operating expense ratio is as stated in the fund's prospectus that is current as of the date of this report. Differences in expense ratios disclosed elsewhere in this report may result from including fee waivers and expense reimbursements as well as different time periods used in calculating the ratios.

Average annual total return as of 05/31/09 (%)

| Share class | | A | | B | | C | | J | | Z | |

| Inception | | 04/21/77 | | 05/15/92 | | 07/01/97 | | 11/02/98 | | 01/29/99 | |

| Sales charge | | without | | with | | without | | with | | without | | with | | without | | with | | without | |

| 1-year | | | –1.79 | | | | –6.46 | | | | –2.52 | | | | –7.09 | | | | –2.21 | | | | –3.12 | | | | –2.22 | | | | –5.15 | | | | –1.38 | | |

| 5-year | | | 4.88 | | | | 3.87 | | | | 4.10 | | | | 3.80 | | | | 4.29 | | | | 4.29 | | | | 4.46 | | | | 3.83 | | | | 5.15 | | |

| 10-year | | | 5.30 | | | | 4.79 | | | | 4.53 | | | | 4.53 | | | | 4.70 | | | | 4.70 | | | | 4.92 | | | | 4.60 | | | | 5.52 | | |

Average annual total return as of 06/30/09 (%)

| Share class | | A | | B | | C | | J | | Z | |

| Sales charge | | without | | with | | without | | with | | without | | with | | without | | with | | without | |

| 1-year | | | 0.42 | | | | –4.35 | | | | –0.33 | | | | –5.01 | | | | –0.19 | | | | –1.13 | | | | –0.20 | | | | –3.20 | | | | 0.67 | | |

| 5-year | | | 4.92 | | | | 3.91 | | | | 4.14 | | | | 3.84 | | | | 4.29 | | | | 4.29 | | | | 4.46 | | | | 3.83 | | | | 5.19 | | |

| 10-year | | | 5.43 | | | | 4.92 | | | | 4.65 | | | | 4.65 | | | | 4.80 | | | | 4.80 | | | | 5.01 | | | | 4.69 | | | | 5.62 | | |

The "with sales charge" returns include the maximum initial sales charge of 4.75% for Class A shares and 3.00% for Class J shares and the applicable contingent deferred sales charge of 5.00% in the first year declining to 1.00% in the sixth year and eliminated thereafter for Class B shares and 1.00% for Class C shares for the first year only. The "without sales charge" returns do not include the effect of sales charges. If they had, returns would be lower.

Performance results reflect any fee waivers or reimbursements of fund expenses by the investment advisor and/or any of its affiliates. Absent these fee waivers or expense reimbursement arrangements, performance results would have been lower.

All results shown assume reinvestment of distributions. Class Z shares are sold at net asset value with no distribution and service (Rule 12b-1) fees. Class Z shares have limited eligibility and the investment minimum requirements may vary. Please see the fund's prospectus for details. Performance for different share classes will vary based on differences in sales charges and fees associated with each class.

The tables do not reflect the deduction of taxes that a shareholder may pay on fund distributions or on the redemption of fund shares.

3

Understanding Your Expenses – Columbia Strategic Income Fund

Estimating your actual expenses

To estimate the expenses that you paid over the period, first you will need your account balance at the end of the period:

g For shareholders who receive their account statements from Columbia Management Services, Inc., your account balance is available online at www.columbiafunds.com or by calling Shareholder Services at 800.345.6611.

g For shareholders who receive their account statements from their financial intermediary, contact your financial intermediary to obtain your account balance.

1. Divide your ending account balance by $1,000. For example, if an account balance was $8,600 at the end of the period, the result would be 8.6.

2. In the section of the table below titled "Expenses paid during the period," locate the amount for your share class. You will find this number in the column labeled "Actual." Multiply this number by the result from step 1. Your answer is an estimate of the expenses you paid on your account during the period.

If the value of your account falls below the minimum initial investment requirement applicable to you, your account generally will be subject to a $20 annual fee. This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

As a fund shareholder, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption fees or exchange fees. There are also ongoing costs, which generally include investment advisory fees, distribution and service (Rule 12b-1) fees and other fund expenses. The information on this page is intended to help you understand the ongoing costs of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your fund's expenses by share class

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in each share class during the period. The information in the following table is based on an initial investment of $1,000, which is invested at the beginning of the period and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "Actual" column is calculated using the fund's actual operating expenses and total return for the period. The amount listed in the "Hypothetical" column for each share class assumes that the return each year is 5% before expenses and is calculated based on the fund's actual operating expenses. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during this period.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the fund with other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing costs of investing in a fund and do not reflect any transaction costs, such as sales charges, redemption fees or exchange fees.

12/01/08 – 05/31/09

| | | Account value at the

beginning of the period ($) | | Account value at the

end of the period ($) | | Expenses paid

during the period ($) | | Fund's annualized

expense ratio (%) | |

| | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | |

| Class A | | | 1,000.00 | | | | 1,000.00 | | | | 1,114.59 | | | | 1,019.90 | | | | 5.32 | | | | 5.09 | | | | 1.01 | | |

| Class B | | | 1,000.00 | | | | 1,000.00 | | | | 1,110.50 | | | | 1,016.16 | | | | 9.26 | | | | 8.85 | | | | 1.76 | | |

| Class C | | | 1,000.00 | | | | 1,000.00 | | | | 1,113.29 | | | | 1,016.95 | | | | 8.43 | | | | 8.05 | | | | 1.60 | | |

| Class J | | | 1,000.00 | | | | 1,000.00 | | | | 1,112.69 | | | | 1,017.10 | | | | 8.27 | | | | 7.90 | | | | 1.57 | | |

| Class Z | | | 1,000.00 | | | | 1,000.00 | | | | 1,117.18 | | | | 1,021.14 | | | | 4.01 | | | | 3.83 | | | | 0.76 | | |

Expenses paid during the period are equal to the annualized expense ratio for the share class, multiplied by the average account value over the period, then multiplied by the number of days in the fund's most recent fiscal half-year and divided by 365.

Had the investment advisor and/or any of its affiliates not waived fees or reimbursed a portion of expenses for Class C shares, Class C share account value at the end of the period would have been reduced.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the fund and do not reflect any transaction costs, such as sales charges, redemption fees or exchange fees. Therefore, the hypothetical examples provided may not help you determine the relative total costs of owning shares of different funds. If these transaction costs were included, your costs would have been higher.

4

Portfolio Managers' Report – Columbia Strategic Income Fund

For the 12-month period that ended May 31, 2009, the fund's Class A shares returned negative 1.79% without sales charge. The fund held up better than the negative 6.05% average return of its peer group, the Lipper Multi-Sector Income Funds Classification.1 We believe the fund outperformed its peer group average because it had a larger allocation to higher quality, interest rate sensitive securities, such as U.S. Treasuries and developed country foreign bonds, and little exposure to commercial mortgage-backed securities (CMBS) or asset-backed securities (ABS) relative to many of its peers. The fund's performance lagged the 4.47% return of its benchmark, the Barclays Capital U.S. Government/Credit Bond Index,2 because of the fund's high-yield bond and currency exposure, neither of which are represented in the index.

Shifting market conditions

During the first half of the 12-month reporting period, an unfolding economic slowdown and worsening financial crisis dominated news headlines. Investors fled to higher quality assets, including U.S. and developed market foreign government debt, while the U.S. dollar and Japanese yen strengthened against most currencies. However, the tide shifted dramatically in 2009 as signs of an economic bottom encouraged investors to move out of Treasury bonds and into riskier assets. Massive new issuance also pushed Treasury yields up and their prices down. Sectors that had been laggards in the first half of the period—including high-yield and emerging market debt—became the winners in the second half, while the U.S. dollar and Japanese yen weakened against most other currencies. Despite this reversal, higher quality assets ended the year-long reporting period ahead of lower quality bonds with the 10-year Treasury bond returning 8 .5%, compared to a roughly 10% decline for the JPMorgan Global High Yield Index.3

Biggest gains from high quality bias

The fund benefited from having a larger stake than the Lipper peer group in higher quality assets, with over 30% of assets in U.S. government bonds and cash. Within the U.S. government bond sector, the fund owned U.S. Treasuries along with some government agency mortgage-backed securities. A sizable (18% or more) stake in developed market foreign government debt also helped, as the sector held up well versus lower quality bonds. The fund's non-U.S. developed market bond returns, with the notable exception of yen-denominated Japanese bonds, however, underperformed the sector due to currency exposure.

Negative impact from high-yield and currency exposure

Even though we selectively reduced high-yield exposure in the second half of 2008, the sector accounted for just over 30% of assets at the end of the period and, in a difficult environment for high yield, detracted from returns. Currency exposure further detracted from relative performance as the value of most currencies, except the

1Lipper Inc., a widely respected data provider in the industry, calculates an average total return (assuming reinvestment of distributions) for mutual funds with investment objectives similar to those of the fund. Lipper makes no adjustments for the effect of sales loads.

2The Barclays Capital U.S Government /Credit Bond Index is composed of high-quality, investment-grade U.S. Government and corporate fixed-income securities with maturities greater than one year.

3The JPMorgan Global High Yield Index, an unmanaged index that is designed to mirror the investable universe of the U.S. dollar global high yield corporate debt market, including domestic and international issues. Indices are not available for investment, are not professionally managed and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index.

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

Net asset value per share

as of 05/31/09 ($)

| Class A | | | 5.40 | | |

| Class B | | | 5.40 | | |

| Class C | | | 5.41 | | |

| Class J | | | 5.38 | | |

| Class Z | | | 5.35 | | |

Distributions declared per share

06/01/08 – 05/31/09 ($)

| Class A | | | 0.39 | | |

| Class B | | | 0.35 | | |

| Class C | | | 0.35 | | |

| Class J | | | 0.36 | | |

| Class Z | | | 0.40 | | |

30-day SEC yields

as of 05/31/09 (%)

| Class A | | | 5.29 | | |

| Class B | | | 4.80 | | |

| Class C | | | 4.95 | | |

| Class J | | | 4.51 | | |

| Class Z | | | 5.79 | | |

The 30-day SEC yields reflect the fund's earning power net of expenses, expressed as an annualized percentage of the public offering price per share at the end of the period.

5

Portfolio Managers' Report (continued) – Columbia Strategic Income Fund

Maturity breakdown

as of 05/31/09 (%)

| 0-1 year | | | 2.3 | | |

| 1-3 years | | | 16.2 | | |

| 3-5 years | | | 14.0 | | |

| 5-7 years | | | 23.6 | | |

| 7-10 years | | | 13.5 | | |

| 10-15 years | | | 5.3 | | |

| 15-20 years | | | 4.4 | | |

| 20-30 years | | | 12.2 | | |

| 30 years and over | | | 1.4 | | |

| Other | | | 7.1 | | |

Portfolio structure

as of 05/31/09 (%)

Corporate fixed-income

bonds & notes | | | 38.3 | | |

Foreign government

obligations | | | 31.4 | | |

U.S. government

obligations | | | 16.3 | | |

| Mortgage-backed securities | | | 7.1 | | |

| Asset-backed securities | | | 0.3 | | |

Commerical mortgage-backed

securities | | | 0.2 | | |

| Municipal bonds | | | 0.2 | | |

| U.S. government agencies | | | 0.2 | | |

| Convertible bond | | | 0.1 | | |

Collateralized mortgage

obligation | | | 0.0 | * | |

| Preferred stock | | | 0.0 | * | |

| Warrants | | | 0.0 | * | |

| Other | | | 5.9 | | |

*Round to less than 0.1%.

Quality breakdown

as of 05/31/09 (%)

| AAA | | | 44.4 | | |

| AA | | | 3.0 | | |

| A | | | 5.2 | | |

| BBB | | | 7.4 | | |

| BB | | | 16.0 | | |

| B | | | 14.0 | | |

| CCC | | | 6.2 | | |

| CC | | | 0.5 | | |

| D | | | 0.5 | | |

| Not Rated | | | 1.5 | | |

| Other | | | 1.3 | | |

The fund is actively managed and the composition of its portfolio will change over time. Maturity breakdown, portfolio structure and quality breakdown are calculated as a percentage of total investments excluding securities lending collateral. Ratings shown in the quality breakdown represent the rating assigned to a particular bond by one of the following nationally recognized rating agencies: Standard & Poor's, a division of The McGraw-Hill Companies, Inc., Moody's Investors Service, Inc. or Fitch Ratings Ltd. Ratings are relative and subjective and are not absolute standards of quality. The fund's credit quality does not remove market risk.

Japanese yen, declined against the U.S. dollar. We reduced currency exposure during the summer and fall, but still lost ground. The fund's 10%+ stake in emerging market debt posted modest gains but hampered returns versus the index as the sector underperformed higher quality issues.

Increased stake in more credit-sensitive sectors

In early 2009, we began shifting away from interest-rate sensitive sectors and toward credit-sensitive sectors. We trimmed exposure to U.S. and developed market foreign government bonds and increased investments in high-yield and emerging market debt. We also built a small position in investment-grade corporate bonds, whose prices seemed attractive relative to both U.S. Treasuries and high-yield bonds. In the foreign government bond sector, we reduced exposure to developed market debt and increased the fund's stake in emerging markets, adding exposure to markets such as Argentina, Venezuela and Indonesia.

Selective additions due to cautious outlook

Going forward, we plan to look for opportunities to add to high-yield and emerging market holdings. However, we expect to proceed with caution until we see signs that the economy has caught up with the technical forces driving the recent price increases in riskier assets. At period end, the yield difference between lower quality bonds and U.S. Treasuries had narrowed to levels indicating that economic recovery could be underway. In fact, we believe that a sustainable recovery will not occur until banks complete the task of cleaning up their balance sheets so that they are able to increase lending and consumers reduce their own debt exposure so that they can spend to fuel economic growth.

Portfolio holdings and characteristics are subject to change periodically and may not be representative of current holdings and characteristics. The outlook for the fund may differ from those presented for other Columbia Funds.

Investing in fixed-income securities may involve certain risks, including the credit quality of individual issuers, possible prepayments, market or economic developments and yield and share price fluctuations due to changes in interest rates. When interest rates go up, bond prices typically drop, and vice versa. Investing in foreign fixed-income markets carries additional risks associated with foreign political and economic developments and changes in currency exchange rates.

Investments in high-yield bonds (sometimes referred to as "junk" bonds) offer the potential for high current income and attractive total return but involve certain risks. Changes in economic conditions or other circumstances may adversely affect a junk bond issuer's ability to make principal and interest payments. Rising interest rates tend to lower the value of all bonds. High-yield bonds issued by foreign entities have greater potential risks, including less regulation, currency fluctuations, economic instability and political developments.

Investing in emerging markets may involve greater risks than investing in more developed countries. In addition, concentration of investments in a single region may result in greater volatility.

6

Investment Portfolio – Columbia Strategic Income Fund

May 31, 2009

| Government & Agency Obligations – 47.2% | |

| | | Par (a) | | Value ($) | |

| Foreign Government Obligations – 30.9% | |

| Aries Vermoegensverwaltungs GmbH | |

| 7.750% 10/25/09 (b) | | EUR | 2,750,000 | | | | 3,970,092 | | |

| 7.750% 10/25/09 | | EUR | 2,500,000 | | | | 3,609,174 | | |

| Banco Nacional de Desenvolvimento Economico e Social | |

| 6.369% 06/16/18 (b) | | | 2,850,000 | | | | 2,885,625 | | |

| Corp. Andina de Fomento | |

| 6.375% 06/18/09 | | EUR | 4,350,000 | | | | 6,140,306 | | |

| European Investment Bank | |

| 0.400% 09/21/11 (c) | | JPY | 2,715,000,000 | | | | 28,033,743 | | |

| 1.250% 09/20/12 | | JPY | 1,135,000,000 | | | | 11,997,622 | | |

| 1.400% 06/20/17 | | JPY | 1,457,000,000 | | | | 14,990,340 | | |

| 5.500% 12/07/11 | | GBP | 5,250,000 | | | | 9,196,616 | | |

| Federal Republic of Brazil | |

| 7.375% 02/03/15 | | EUR | 6,950,000 | | | | 10,955,109 | | |

| 8.250% 01/20/34 | | | 4,700,000 | | | | 5,522,500 | | |

| 8.750% 02/04/25 | | | 4,500,000 | | | | 5,445,000 | | |

| 11.000% 08/17/40 | | | 12,400,000 | | | | 16,182,000 | | |

| 12.500% 01/05/22 | | BRL | 10,275,000 | | | | 6,005,413 | | |

| Federal Republic of Germany | |

| 5.000% 07/04/12 | | EUR | 6,585,000 | | | | 10,143,501 | | |

| 6.000% 06/20/16 | | EUR | 21,500,000 | | | | 35,433,645 | | |

| Government of Canada | |

| 4.000% 06/01/16 | | CAD | 8,300,000 | | | | 8,120,201 | | |

| 8.000% 06/01/23 | | CAD | 8,215,000 | | | | 10,856,742 | | |

| 10.250% 03/15/14 | | CAD | 2,865,000 | | | | 3,540,424 | | |

| Government of Japan | |

| 1.400% 12/20/18 | | JPY | 975,000,000 | | | | 10,204,857 | | |

| Government of New Zealand | |

| 6.000% 11/15/11 | | NZD | 6,300,000 | | | | 4,264,886 | | |

| 6.000% 12/15/17 | | NZD | 1,900,000 | | | | 1,237,006 | | |

| Instituto de Credito Oficial | |

| 0.800% 09/28/09 | | JPY | 1,380,000,000 | | | | 14,491,361 | | |

| International Finance Corp. | |

| 7.500% 02/28/13 | | AUD | 9,245,000 | | | | 7,977,269 | | |

| Japan Finance Organization for Municipal Enterprises | |

| 1.900% 06/22/18 | | JPY | 910,000,000 | | | | 9,622,209 | | |

| Kingdom of Norway | |

| 4.250% 05/19/17 | | NOK | 97,185,000 | | | | 15,628,800 | | |

| 6.000% 05/16/11 | | NOK | 72,830,000 | | | | 12,426,264 | | |

| Kingdom of Sweden | |

| 6.750% 05/05/14 | | SEK | 55,300,000 | | | | 8,601,280 | | |

| Pemex Project Funding Master Trust | |

| 2.620% 06/15/10 (c) | | | 4,750,000 | | | | 4,702,500 | | |

| 5.750% 03/01/18 | | | 10,370,000 | | | | 9,747,800 | | |

| Province of British Columbia | |

| 5.700% 06/18/29 | | CAD | 4,710,000 | | | | 4,637,479 | | |

| 9.500% 01/09/12 | | CAD | 7,150,000 | | | | 7,821,154 | | |

| Province of Quebec | |

| 6.000% 10/01/12 | | CAD | 7,155,000 | | | | 7,310,388 | | |

| | | Par (a) | | Value ($) | |

| Queensland Treasury Corp. | |

| 6.500% 04/16/12 | | AUD | 8,425,000 | | | | 7,110,517 | | |

| Republic of Argentina | |

| 8.280% 12/31/33 | | | 9,777,374 | | | | 4,228,714 | | |

| Republic of Chile | |

| 7.125% 01/11/12 | | | 3,000,000 | | | | 3,296,700 | | |

| Republic of Colombia | |

| 2.654% 11/16/15 (c) | | | 600,000 | | | | 577,500 | | |

| 7.375% 03/18/19 | | | 6,150,000 | | | | 6,519,000 | | |

| 8.125% 05/21/24 | | | 8,525,000 | | | | 9,313,562 | | |

| 9.750% 04/09/11 | | | 2,312,428 | | | | 2,474,298 | | |

| Republic of Finland | |

| 4.250% 07/04/15 | | EUR | 3,275,000 | | | | 4,851,636 | | |

| Republic of France | |

| 4.000% 04/25/13 | | EUR | 9,100,000 | | | | 13,554,596 | | |

| 4.750% 10/25/12 | | EUR | 7,700,000 | | | | 11,755,997 | | |

| 5.500% 04/25/29 | | EUR | 7,000,000 | | | | 11,120,116 | | |

| Republic of Hungary | |

| 4.750% 02/03/15 | | | 2,435,000 | | | | 2,286,173 | | |

| Republic of Indonesia | |

| 10.375% 05/04/14 (b) | | EUR | 2,700,000 | | | | 3,098,250 | | |

| Republic of Italy | |

| 4.250% 02/01/15 | | EUR | 7,765,000 | | | | 11,339,629 | | |

| 5.250% 08/01/17 | | | 3,600,000 | | | | 5,494,275 | | |

| Republic of Panama | |

| 6.700% 01/26/36 | | | 9,300,000 | | | | 8,928,000 | | |

| 8.875% 09/30/27 | | | 7,270,000 | | | | 8,578,600 | | |

| Republic of Peru | |

| 7.350% 07/21/25 | | | 5,200,000 | | | | 5,571,800 | | |

| 8.375% 05/03/16 | | | 310,000 | | | | 357,430 | | |

| 9.875% 02/06/15 | | | 9,640,000 | | | | 11,809,000 | | |

| Republic of Philippines | |

| 8.875% 03/17/15 | | | 6,615,000 | | | | 7,656,862 | | |

| Republic of Poland | |

| 4.750% 04/25/12 | | PLN | 16,100,000 | | | | 4,921,148 | | |

| 5.625% 06/20/18 | | EUR | 4,280,000 | | | | 5,901,243 | | |

| 6.250% 10/24/15 | | PLN | 35,350,000 | | | | 11,240,685 | | |

| Republic of South Africa | |

| 6.500% 06/02/14 | | | 3,650,000 | | | | 3,777,750 | | |

| 6.875% 05/27/19 | | | 1,000,000 | | | | 1,005,000 | | |

| 13.000% 08/31/09 | | ZAR | 9,073,333 | | | | 1,157,852 | | |

| 13.000% 08/31/10 | | ZAR | 1,780,000 | | | | 240,043 | | |

| 13.000% 08/31/10 | | ZAR | 9,073,334 | | | | 1,227,871 | | |

| 13.000% 08/31/11 | | ZAR | 9,073,333 | | | | 1,293,009 | | |

| Republic of Turkey | |

| 7.000% 09/26/16 | | | 555,000 | | | | 560,550 | | |

| 7.375% 02/05/25 | | | 7,330,000 | | | | 7,348,325 | | |

| Republic of Uruguay | |

PIK,

7.875% 01/15/33 | | | 8,000,000 | | | | 7,920,000 | | |

See Accompanying Notes to Financial Statements.

7

Columbia Strategic Income Fund, May 31, 2009

| Government & Agency Obligations (continued) | |

| | | Par (a) | | Value ($) | |

| Republic of Venezuela | |

| 9.250% 09/15/27 | | | 20,225,000 | | | | 12,741,750 | | |

| Russian Federation | |

| 7.500% 03/31/30 | | | 26,121,600 | | | | 26,056,296 | | |

| 12.750% 06/24/28 | | | 7,430,000 | | | | 10,736,350 | | |

| State of Qatar | |

| 6.550% 04/09/19 (b) | | | 3,000,000 | | | | 3,112,500 | | |

| United Kingdom Treasury | |

| 5.000% 03/07/25 | | GBP | 4,680,000 | | | | 8,174,041 | | |

| 8.000% 09/27/13 | | GBP | 3,100,000 | | | | 6,113,649 | | |

| 9.000% 07/12/11 | | GBP | 5,350,000 | | | | 10,025,224 | | |

| United Mexican States | |

| 5.875% 02/17/14 | | | 5,000,000 | | | | 5,270,000 | | |

| 6.050% 01/11/40 | | | 5,350,000 | | | | 5,029,000 | | |

| 8.125% 12/30/19 | | | 11,020,000 | | | | 13,003,600 | | |

| 11.375% 09/15/16 | | | 7,590,000 | | | | 10,360,350 | | |

| Foreign Government Obligations Total | | | 608,840,197 | | |

| U.S. Government Agencies – 0.2% | |

| Federal Home Loan Mortgage Corp. | |

| 6.750% 03/15/31 (d) | | | 406,000 | | | | 500,981 | | |

| Federal National Mortgage Association | |

| 4.375% 07/17/13 (d) | | | 3,003,000 | | | | 3,217,129 | | |

| U.S. Government Agencies Total | | | 3,718,110 | | |

| U.S. Government Obligations – 16.1% | |

| U.S. Treasury Bonds | |

| 5.375% 02/15/31 (d) | | | 29,000,000 | | | | 33,100,774 | | |

| 7.500% 11/15/24 (d) | | | 18,400,000 | | | | 25,256,871 | | |

| 8.875% 02/15/19 (d) | | | 21,827,000 | | | | 31,212,610 | | |

| 10.625% 08/15/15 (d) | | | 29,415,000 | | | | 42,711,492 | | |

| 12.500% 08/15/14 (d) | | | 32,151,000 | | | | 32,942,204 | | |

| U.S. Treasury Notes | |

| 4.250% 09/30/12 (d) | | | 40,000,000 | | | | 43,525,000 | | |

| 5.000% 02/15/11 (d) | | | 47,600,000 | | | | 51,017,537 | | |

| 5.125% 05/15/16 | | | 46,000,000 | | | | 52,112,986 | | |

| U.S. Treasury STRIPS | |

| (e) 05/15/23 (d) | | | 4,550,000 | | | | 2,402,773 | | |

P.O.,

(e) 11/15/13 | | | 2,250,000 | | | | 2,025,423 | | |

| U.S. Government Obligations Total | | | 316,307,670 | | |

Total Government & Agency Obligations

(cost of $913,575,146) | | | 928,865,977 | | |

| Corporate Fixed-Income Bonds & Notes – 37.8% | |

| | | Par (a) | | Value ($) | |

| Basic Materials – 3.5% | |

| Chemicals – 0.8% | |

| Agricultural Chemicals – 0.1% | |

| Terra Capital, Inc. | |

| 7.000% 02/01/17 | | | 2,490,000 | | | | 2,328,150 | | |

| | | | 2,328,150 | | |

| Chemicals-Diversified – 0.6% | |

| Huntsman International LLC | |

| 6.875% 11/15/13 (b) | | EUR | 1,165,000 | | | | 1,029,350 | | |

| 7.875% 11/15/14 | | | 3,990,000 | | | | 2,733,150 | | |

| Ineos Group Holdings PLC | |

| 8.500% 02/15/16 (b) | | | 4,285,000 | | | | 1,328,350 | | |

| INVISTA | |

| 9.250% 05/01/12 (b) | | | 4,130,000 | | | | 3,861,550 | | |

| NOVA Chemicals Corp. | |

| 6.500% 01/15/12 | | | 3,050,000 | | | | 2,775,500 | | |

| | | | 11,727,900 | | |

| Chemicals-Specialty – 0.1% | |

| Chemtura Corp. | |

| 6.875% 06/01/16 (j) | | | 2,105,000 | | | | 1,473,500 | | |

| | | | 1,473,500 | | |

| Chemicals Total | | | 15,529,550 | | |

| Forest Products & Paper – 0.6% | |

| Paper & Related Products – 0.6% | |

| Cascades, Inc. | |

| 7.250% 02/15/13 | | | 2,250,000 | | | | 1,940,625 | | |

| Domtar Corp. | |

| 7.125% 08/15/15 | | | 1,915,000 | | | | 1,589,450 | | |

| Georgia-Pacific Corp. | |

| 8.000% 01/15/24 | | | 5,845,000 | | | | 4,968,250 | | |

| NewPage Corp. | |

| 10.000% 05/01/12 | | | 1,415,000 | | | | 792,400 | | |

| Westvaco Corp. | |

| 8.200% 01/15/30 | | | 2,195,000 | | | | 1,848,589 | | |

| | | | 11,139,314 | | |

| Forest Products & Paper Total | | | 11,139,314 | | |

| Iron/Steel – 0.6% | |

| Steel-Producers – 0.6% | |

| ArcelorMittal | |

| 9.850% 06/01/19 | | | 2,080,000 | | | | 2,136,135 | | |

| Nucor Corp. | |

| 5.000% 06/01/13 | | | 760,000 | | | | 782,143 | | |

See Accompanying Notes to Financial Statements.

8

Columbia Strategic Income Fund, May 31, 2009

| Corporate Fixed-Income Bonds & Notes (continued) | |

| | | Par (a) | | Value ($) | |

| Russel Metals, Inc. | |

| 6.375% 03/01/14 | | | 1,360,000 | | | | 1,098,200 | | |

| Steel Dynamics, Inc. | |

| 8.250% 04/15/16 (b) | | | 4,095,000 | | | | 3,490,988 | | |

| United States Steel Corp. | |

| 7.000% 02/01/18 | | | 5,160,000 | | | | 4,291,582 | | |

| | | | 11,799,048 | | |

| Iron/Steel Total | | | 11,799,048 | | |

| Metals & Mining – 1.5% | |

| Diversified Minerals – 0.5% | |

| FMG Finance Ltd. | |

| 10.625% 09/01/16 (b) | | | 4,265,000 | | | | 3,785,188 | | |

| Rio Tinto Finance USA Ltd. | |

| 8.950% 05/01/14 | | | 1,190,000 | | | | 1,278,905 | | |

| Teck Resources Ltd. | |

| 10.750% 05/15/19 (b) | | | 4,950,000 | | | | 5,092,312 | | |

| | | | 10,156,405 | | |

| Metal-Diversified – 0.5% | |

| Freeport-McMoRan Copper & Gold, Inc. | |

| 8.375% 04/01/17 | | | 10,435,000 | | | | 10,356,737 | | |

| | | | 10,356,737 | | |

| Mining Services – 0.1% | |

| Noranda Aluminium Holding Corp. | |

PIK,

7.163% 11/15/14 (c) | | | 2,357,546 | | | | 841,212 | | |

| | | | 841,212 | | |

| Non-Ferrous Metals – 0.4% | |

| Codelco, Inc. | |

| 5.500% 10/15/13 | | | 3,000,000 | | | | 3,161,544 | | |

| 7.500% 01/15/19 (b) | | | 4,500,000 | | | | 5,069,102 | | |

| | | | 8,230,646 | | |

| Metals & Mining Total | | | 29,585,000 | | |

| Basic Materials Total | | | 68,052,912 | | |

| Communications – 6.9% | |

| Advertising – 0.1% | |

| Advertising Agencies – 0.1% | |

| Interpublic Group of Companies, Inc. | |

| 7.250% 08/15/11 | | | 1,520,000 | | | | 1,428,800 | | |

| | | | 1,428,800 | | |

| Advertising Total | | | 1,428,800 | | |

| Media – 1.8% | |

| Cable TV – 1.4% | |

| Cablevision Systems Corp. | |

| 8.000% 04/15/12 | | | 3,299,000 | | | | 3,241,268 | | |

| | | Par (a) | | Value ($) | |

| Charter Communications Holdings II LLC | |

| 10.250% 09/15/10 (g) | | | 4,215,000 | | | | 4,080,442 | | |

| Charter Communications Operating LLC/Charter Communications Operating Capital | |

| 10.375% 04/30/14 (b)(g) | | | 4,010,000 | | | | 3,809,500 | | |

| Comcast Corp. | |

| 6.950% 08/15/37 | | | 1,330,000 | | | | 1,332,753 | | |

| CSC Holdings, Inc. | |

| 7.625% 04/01/11 | | | 2,365,000 | | | | 2,359,088 | | |

| 8.625% 02/15/19 (b) | | | 1,200,000 | | | | 1,177,500 | | |

| DirecTV Holdings LLC | |

| 6.375% 06/15/15 | | | 5,995,000 | | | | 5,455,450 | | |

| EchoStar DBS Corp. | |

| 6.625% 10/01/14 | | | 6,915,000 | | | | 6,275,362 | | |

| Time Warner Cable, Inc. | |

| 7.300% 07/01/38 | | | 745,000 | | | | 755,601 | | |

| | | | 28,486,964 | | |

| Multimedia – 0.1% | |

| News America, Inc. | |

| 6.400% 12/15/35 | | | 150,000 | | | | 124,019 | | |

| Time Warner, Inc. | |

| 6.875% 05/01/12 | | | 1,275,000 | | | | 1,342,296 | | |

| | | | 1,466,315 | | |

| Publishing-Books – 0.3% | |

| TL Acquisitions, Inc. | |

| 10.500% 01/15/15 (b) | | | 6,570,000 | | | | 5,124,600 | | |

| | | | 5,124,600 | | |

| Radio – 0.0% | |

| CMP Susquehanna Corp. | |

| 3.826% 05/15/14 (h) | | | 175,000 | | | | 78,750 | | |

| | | | 78,750 | | |

| Television – 0.0% | |

| Local TV Finance LLC | |

PIK,

9.250% 06/15/15 (b) | | | 1,885,000 | | | | 261,256 | | |

| | | | 261,256 | | |

| Media Total | | | 35,417,885 | | |

| Telecommunication Services – 5.0% | |

| Cellular Telecommunications – 1.5% | |

| Cricket Communications, Inc. | |

| 9.375% 11/01/14 | | | 4,970,000 | | | | 4,945,150 | | |

| Digicel Group Ltd. | |

| 8.875% 01/15/15 (b) | | | 6,860,000 | | | | 5,488,000 | | |

| MetroPCS Wireless, Inc. | |

| 9.250% 11/01/14 | | | 4,795,000 | | | | 4,812,981 | | |

| Nextel Communications, Inc. | |

| 7.375% 08/01/15 | | | 5,535,000 | | | | 4,386,488 | | |

See Accompanying Notes to Financial Statements.

9

Columbia Strategic Income Fund, May 31, 2009

| Corporate Fixed-Income Bonds & Notes (continued) | |

| | | Par (a) | | Value ($) | |

| Orascom Telecom Finance SCA | |

| 7.875% 02/08/14 (b) | | | 1,150,000 | | | | 943,000 | | |

| Verizon Wireless Capital LLC | |

| 5.550% 02/01/14 (b) | | | 2,280,000 | | | | 2,411,100 | | |

| 8.500% 11/15/18 (b) | | | 570,000 | | | | 691,541 | | |

| Wind Acquisition Finance SA | |

| 10.750% 12/01/15 (b) | | | 1,195,000 | | | | 1,254,750 | | |

PIK,

8.357% 12/21/11 (c)(i) | | | 4,904,087 | | | | 4,121,799 | | |

| | | | 29,054,809 | | |

| Media – 0.4% | |

| Nielsen Finance LLC/Nielsen Finance Co. | |

| 11.500% 05/01/16 (b) | | | 2,045,000 | | | | 1,942,750 | | |

| Quebecor Media, Inc. | |

| 7.750% 03/15/16 | | | 5,760,000 | | | | 5,112,000 | | |

| | | | 7,054,750 | | |

| Satellite Telecommunications – 0.7% | |

| Inmarsat Finance II PLC | |

| 10.375% 11/15/12 | | | 3,620,000 | | | | 3,737,650 | | |

| Inmarsat Finance PLC | |

| 7.625% 06/30/12 | | | 800,000 | | | | 781,000 | | |

| Intelsat Jackson Holdings Ltd. | |

| 11.250% 06/15/16 | | | 9,125,000 | | | | 9,353,125 | | |

| | | | 13,871,775 | | |

| Telecommunication Equipment – 0.2% | |

| Lucent Technologies, Inc. | |

| 6.450% 03/15/29 | | | 8,540,000 | | | | 4,867,800 | | |

| | | | 4,867,800 | | |

| Telecommunication Services – 0.6% | |

| Hellas Telecommunications Luxembourg II | |

| 6.881% 01/15/15 (b)(c) | | | 1,385,000 | | | | 263,150 | | |

| Nordic Telephone Co. Holdings ApS | |

| 8.250% 05/01/16 (b) | | EUR | 420,000 | | | | 575,941 | | |

| 8.875% 05/01/16 (b) | | | 3,115,000 | | | | 3,115,000 | | |

| Syniverse Technologies, Inc. | |

| 7.750% 08/15/13 | | | 2,415,000 | | | | 2,070,863 | | |

| Time Warner Telecom Holdings, Inc. | |

| 9.250% 02/15/14 | | | 2,705,000 | | | | 2,711,762 | | |

| West Corp. | |

| 11.000% 10/15/16 | | | 4,745,000 | | | | 4,033,250 | | |

| | | | 12,769,966 | | |

| Telephone-Integrated – 1.5% | |

| BellSouth Corp. | |

| 5.200% 09/15/14 | | | 2,205,000 | | | | 2,289,520 | | |

| Citizens Communications Co. | |

| 7.875% 01/15/27 | | | 5,105,000 | | | | 4,160,575 | | |

| | | Par (a) | | Value ($) | |

| Qwest Communications International, Inc. | |

| 7.500% 02/15/14 | | | 5,730,000 | | | | 5,271,600 | | |

| Qwest Corp. | |

| 7.500% 10/01/14 | | | 2,710,000 | | | | 2,588,050 | | |

| 7.500% 06/15/23 | | | 4,655,000 | | | | 3,700,725 | | |

| Telefonica Emisiones SAU | |

| 6.421% 06/20/16 | | | 925,000 | | | | 978,774 | | |

| Virgin Media Finance PLC | |

| 9.500% 08/15/16 | | EUR | 2,725,000 | | | | 2,673,906 | | |

| Windstream Corp. | |

| 8.625% 08/01/16 | | | 7,165,000 | | | | 7,039,613 | | |

| | | | 28,702,763 | | |

| Wireless Equipment – 0.1% | |

| Crown Castle International Corp. | |

| 9.000% 01/15/15 | | | 1,680,000 | | | | 1,696,800 | | |

| | | | 1,696,800 | | |

| Telecommunication Services Total | | | 98,018,663 | | |

| Communications Total | | | 134,865,348 | | |

| Consumer Cyclical – 3.4% | |

| Apparel – 0.2% | |

| Apparel Manufacturers – 0.2% | |

| Levi Strauss & Co. | |

| 9.750% 01/15/15 | | | 3,925,000 | | | | 3,787,625 | | |

| | | | 3,787,625 | | |

| Apparel Total | | | 3,787,625 | | |

| Auto Manufacturers – 0.0% | |

| Auto-Cars/Light Trucks – 0.0% | |

| General Motors Corp. | |

| 8.375% 07/15/33 (o) | | | 6,915,000 | | | | 622,350 | | |

| 7.200% 01/15/11 (o) | | | 2,775,000 | | | | 242,813 | | |

| | | | 865,163 | | |

| Auto Manufacturers Total | | | 865,163 | | |

| Auto Parts & Equipment – 0.4% | |

| Auto/Truck Parts & Equipment-Original – 0.1% | |

| Hayes Lemmerz Finance LLC - Luxembourg SCA | |

| 8.250% 06/15/15 (j) | | EUR | 2,050,000 | | | | 57,962 | | |

| TRW Automotive, Inc. | |

| 7.000% 03/15/14 (b) | | | 2,265,000 | | | | 1,664,775 | | |

| | | | 1,722,737 | | |

| Auto/Truck Parts & Equipment-Replacement – 0.1% | |

| Commercial Vehicle Group, Inc. | |

| 8.000% 07/01/13 | | | 2,380,000 | | | | 1,011,500 | | |

| | | | 1,011,500 | | |

See Accompanying Notes to Financial Statements.

10

Columbia Strategic Income Fund, May 31, 2009

| Corporate Fixed-Income Bonds & Notes (continued) | |

| | | Par (a) | | Value ($) | |

| Rubber-Tires – 0.2% | |

| Goodyear Tire & Rubber Co. | |

| 8.625% 12/01/11 | | | 560,000 | | | | 544,600 | | |

| 9.000% 07/01/15 | | | 3,865,000 | | | | 3,691,075 | | |

| 10.500% 05/15/16 | | | 1,045,000 | | | | 1,039,775 | | |

| | | | 5,275,450 | | |

| Auto Parts & Equipment Total | | | 8,009,687 | | |

| Entertainment – 0.2% | |

| Music – 0.2% | |

| WMG Acquisition Corp. | |

| 7.375% 04/15/14 | | | 2,465,000 | | | | 2,082,925 | | |

| 9.500% 06/15/16 (b) | | | 680,000 | | | | 679,150 | | |

| WMG Holdings Corp. | |

(k) 12/15/14

(9.500% 12/15/09) | | | 2,280,000 | | | | 1,812,600 | | |

| | | | 4,574,675 | | |

| Resorts/Theme Parks – 0.0% | |

| Six Flags, Inc. | |

| 9.625% 06/01/14 (p) | | | 1,557,000 | | | | 241,335 | | |

| | | | 241,335 | | |

| Entertainment Total | | | 4,816,010 | | |

| Home Builders – 0.5% | |

| Building-Residential/Commercial – 0.5% | |

| D.R. Horton, Inc. | |

| 5.625% 09/15/14 | | | 2,915,000 | | | | 2,477,750 | | |

| 5.625% 01/15/16 | | | 1,483,000 | | | | 1,216,060 | | |

| KB Home | |

| 5.875% 01/15/15 | | | 4,575,000 | | | | 3,911,625 | | |

| Ryland Group, Inc. | |

| 8.400% 05/15/17 | | | 1,400,000 | | | | 1,358,000 | | |

| | | | 8,963,435 | | |

| Home Builders Total | | | 8,963,435 | | |

| Home Furnishings – 0.0% | |

| Home Furnishings – 0.0% | |

| Simmons Co. | |

PIK,

8.224% 02/15/12 (c)(i) | | | 2,408,143 | | | | 24,883 | | |

| | | | 24,883 | | |

| Home Furnishings Total | | | 24,883 | | |

| Lodging – 0.9% | |

| Casino Hotels – 0.6% | |

| Boyd Gaming Corp. | |

| 6.750% 04/15/14 | | | 1,250,000 | | | | 975,000 | | |

| 7.125% 02/01/16 | | | 1,500,000 | | | | 1,065,000 | | |

| | | Par (a) | | Value ($) | |

| Harrah's Operating Co., Inc. | |

| 10.000% 12/15/18 (b) | | | 2,069,000 | | | | 1,381,057 | | |

| Jacobs Entertainment, Inc. | |

| 9.750% 06/15/14 | | | 2,165,000 | | | | 1,623,750 | | |

| Majestic Star LLC | |

| 9.750% 01/15/11 (f) | | | 2,740,000 | | | | 315,100 | | |

| MGM Mirage | |

| 7.500% 06/01/16 | | | 6,385,000 | | | | 4,150,250 | | |

| Snoqualmie Entertainment Authority | |

| 5.384% 02/01/14 (b)(c) | | | 375,000 | | | | 195,938 | | |

| 9.125% 02/01/15 (b) | | | 2,015,000 | | | | 1,078,025 | | |

| | | | 10,784,120 | | |

| Gambling (Non-Hotel) – 0.2% | |

| Mashantucket Western Pequot Tribe | |

| 8.500% 11/15/15 (b) | | | 4,265,000 | | | | 1,663,350 | | |

| Seminole Indian Tribe of Florida | |

| 7.804% 10/01/20 (b) | | | 3,215,000 | | | | 2,693,109 | | |

| | | | 4,356,459 | | |

| Hotels & Motels – 0.1% | |

| Starwood Hotels & Resorts Worldwide, Inc. | |

| 6.750% 05/15/18 | | | 3,305,000 | | | | 2,809,250 | | |

| | | | 2,809,250 | | |

| Lodging Total | | | 17,949,829 | | |

| Restaurants – 0.1% | |

| Retail-Restaurants – 0.1% | |

| McDonald's Corp. | |

| 5.700% 02/01/39 | | | 1,050,000 | | | | 1,023,501 | | |

| | | | 1,023,501 | | |

| Restaurants Total | | | 1,023,501 | | |

| Retail – 1.1% | |

| Retail-Apparel/Shoe – 0.2% | |

| Hanesbrands, Inc. | |

| 5.698% 12/15/14 (c) | | | 2,640,000 | | | | 2,125,200 | | |

| Phillips-Van Heusen Corp. | |

| 7.250% 02/15/11 | | | 725,000 | | | | 717,750 | | |

| 8.125% 05/01/13 | | | 1,760,000 | | | | 1,724,800 | | |

| | | | 4,567,750 | | |

| Retail-Computer Equipment – 0.1% | |

| GameStop Corp./GameStop, Inc. | |

| 8.000% 10/01/12 | | | 2,275,000 | | | | 2,283,531 | | |

| | | | 2,283,531 | | |

See Accompanying Notes to Financial Statements.

11

Columbia Strategic Income Fund, May 31, 2009

| Corporate Fixed-Income Bonds & Notes (continued) | |

| | | Par (a) | | Value ($) | |

| Retail-Discount – 0.2% | |

| Dollar General Corp. | |

PIK,

11.875% 07/15/17 | | | 4,445,000 | | | | 4,689,475 | | |

| | | | 4,689,475 | | |

| Retail-Drug Stores – 0.2% | |

| Rite Aid Corp. | |

| 9.500% 06/15/17 | | | 4,675,000 | | | | 3,038,750 | | |

| | | | 3,038,750 | | |

| Retail-Propane Distributors – 0.4% | |

| AmeriGas Partners LP | |

| 7.125% 05/20/16 | | | 2,910,000 | | | | 2,695,387 | | |

| 7.250% 05/20/15 | | | 1,335,000 | | | | 1,254,900 | | |

| Inergy LP/Inergy Finance Corp. | |

| 8.250% 03/01/16 | | | 1,365,000 | | | | 1,334,288 | | |

| 8.750% 03/01/15 (b) | | | 2,645,000 | | | | 2,618,550 | | |

| | | | 7,903,125 | | |

| Retail Total | | | 22,482,631 | | |

| Consumer Cyclical Total | | | 67,922,764 | | |

| Consumer Non-Cyclical – 5.7% | |

| Agriculture – 0.1% | |

| Tobacco – 0.1% | |

| Reynolds American, Inc. | |

| 7.625% 06/01/16 | | | 2,760,000 | | | | 2,709,180 | | |

| | | | 2,709,180 | | |

| Agriculture Total | | | 2,709,180 | | |

| Beverages – 0.4% | |

| Beverages-Non-Alcoholic – 0.1% | |

| Cott Beverages, Inc. | |

| 8.000% 12/15/11 | | | 2,305,000 | | | | 1,982,300 | | |

| PepsiCo, Inc. | |

| 7.900% 11/01/18 | | | 1,150,000 | | | | 1,376,940 | | |

| | | | 3,359,240 | | |

| Beverages-Wine/Spirits – 0.2% | |

| Constellation Brands, Inc. | |

| 8.125% 01/15/12 | | | 3,985,000 | | | | 3,965,075 | | |

| | | | 3,965,075 | | |

| Brewery – 0.1% | |

| Anheuser-Busch InBev Worldwide, Inc. | |

| 7.750% 01/15/19 (b) | | | 760,000 | | | | 817,492 | | |

| 8.000% 11/15/39 (b) | | | 645,000 | | | | 673,031 | | |

| | | | 1,490,523 | | |

| Beverages Total | | | 8,814,838 | | |

| | | Par (a) | | Value ($) | |

| Biotechnology – 0.2% | |

| Medical-Biomedical/Gene – 0.2% | |

| Bio-Rad Laboratories, Inc. | |

| 7.500% 08/15/13 | | | 2,625,000 | | | | 2,592,187 | | |

| 8.000% 09/15/16 (b) | | | 580,000 | | | | 581,450 | | |

| | | | 3,173,637 | | |

| Biotechnology Total | | | 3,173,637 | | |

| Commercial Services – 1.2% | |

| Commercial Services – 0.4% | |

| ARAMARK Corp. | |

| 8.500% 02/01/15 | | | 3,595,000 | | | | 3,428,731 | | |

| Iron Mountain, Inc. | |

| 8.000% 06/15/20 | | | 3,755,000 | | | | 3,473,375 | | |

| | | | 6,902,106 | | |

| Commercial Services-Finance – 0.0% | |

| ACE Cash Express, Inc. | |

| 10.250% 10/01/14 (b) | | | 1,550,000 | | | | 635,500 | | |

| | | | 635,500 | | |

| Funeral Services & Related Items – 0.2% | |

| Service Corp. International | |

| 6.750% 04/01/16 | | | 1,980,000 | | | | 1,821,600 | | |

| 7.000% 06/15/17 | | | 1,750,000 | | | | 1,596,875 | | |

| 7.375% 10/01/14 | | | 290,000 | | | | 279,125 | | |

| | | | 3,697,600 | | |

| Private Corrections – 0.3% | |

| Corrections Corp. of America | |

| 6.250% 03/15/13 | | | 2,355,000 | | | | 2,231,363 | | |

| GEO Group, Inc. | |

| 8.250% 07/15/13 | | | 2,865,000 | | | | 2,793,375 | | |

| | | | 5,024,738 | | |

| Rental Auto/Equipment – 0.3% | |

| Ashtead Holdings PLC | |

| 8.625% 08/01/15 (b) | | | 2,885,000 | | | | 2,163,750 | | |

| Rental Service Corp. | |

| 9.500% 12/01/14 | | | 2,800,000 | | | | 2,184,000 | | |

| United Rentals North America, Inc. | |

| 6.500% 02/15/12 | | | 2,650,000 | | | | 2,477,750 | | |

| | | | 6,825,500 | | |

| Commercial Services Total | | | 23,085,444 | | |

| Food – 0.9% | |

| Food-Meat Products – 0.3% | |

| JBS USA LLC/JBS USA Finance, Inc. | |

| 11.625% 05/01/14 (b) | | | 3,910,000 | | | | 3,753,600 | | |

See Accompanying Notes to Financial Statements.

12

Columbia Strategic Income Fund, May 31, 2009

| Corporate Fixed-Income Bonds & Notes (continued) | |

| | | Par (a) | | Value ($) | |

| Tyson Foods, Inc. | |

| 10.500% 03/01/14 (b) | | | 2,310,000 | | | | 2,448,600 | | |

| | | | 6,202,200 | | |

| Food-Miscellaneous/Diversified – 0.4% | |

| Campbell Soup Co. | |

| 4.500% 02/15/19 | | | 570,000 | | | | 553,795 | | |

| ConAgra Foods, Inc. | |

| 7.000% 10/01/28 | | | 855,000 | | | | 838,929 | | |

| Del Monte Corp. | |

| 6.750% 02/15/15 | | | 2,065,000 | | | | 1,956,588 | | |

| Pinnacle Foods Finance LLC | |

| 9.250% 04/01/15 | | | 4,500,000 | | | | 4,016,250 | | |

| Reddy Ice Holdings, Inc. | |

| 10.500% 11/01/12 | | | 1,875,000 | | | | 1,125,000 | | |

| | | | 8,490,562 | | |

| Food-Retail – 0.0% | |

| Kroger Co. | |

| 8.000% 09/15/29 | | | 480,000 | | | | 530,394 | | |

| | | | 530,394 | | |

| Retail-Hypermarkets – 0.2% | |

| New Albertsons, Inc. | |

| 8.000% 05/01/31 | | | 3,205,000 | | | | 2,756,300 | | |

| | | | 2,756,300 | | |

| Food Total | | | 17,979,456 | | |

| Healthcare Products – 0.4% | |

| Medical Products – 0.4% | |

| Biomet, Inc. | |

PIK,

10.375% 10/15/17 | | | 8,395,000 | | | | 7,975,250 | | |

| | | | 7,975,250 | | |

| Healthcare Products Total | | | 7,975,250 | | |

| Healthcare Services – 1.6% | |

| Dialysis Centers – 0.1% | |

| DaVita, Inc. | |

| 7.250% 03/15/15 | | | 2,460,000 | | | | 2,312,400 | | |

| | | | 2,312,400 | | |

| Medical-HMO – 0.1% | |

| Coventry Health Care, Inc. | |

| 5.875% 01/15/12 | | | 1,570,000 | | | | 1,455,558 | | |

| WellPoint, Inc. | |

| 7.000% 02/15/19 | | | 960,000 | | | | 982,894 | | |

| | | | 2,438,452 | | |

| Medical-Hospitals – 1.1% | |

| Community Health Systems, Inc. | |

| 8.875% 07/15/15 | | | 6,855,000 | | | | 6,777,881 | | |

| | | Par (a) | | Value ($) | |

| HCA, Inc. | |

| 9.250% 11/15/16 | | | 2,655,000 | | | | 2,608,538 | | |

PIK,

9.625% 11/15/16 | | | 13,400,000 | | | | 12,830,500 | | |

| | | | 22,216,919 | | |

| Physical Therapy/Rehab Centers – 0.1% | |

| Healthsouth Corp. | |

| 10.750% 06/15/16 | | | 1,825,000 | | | | 1,861,500 | | |

| | | | 1,861,500 | | |

| Physician Practice Management – 0.2% | |

| U.S. Oncology Holdings, Inc. | |

PIK,

6.904% 03/15/12 (c) | | | 1,857,000 | | | | 1,235,587 | | |

| US Oncology, Inc. | |

| 9.000% 08/15/12 | | | 1,585,000 | | | | 1,585,000 | | |

| | | | 2,820,587 | | |

| Healthcare Services Total | | | 31,649,858 | | |

| Household Products/Wares – 0.2% | |

| Consumer Products-Miscellaneous – 0.2% | |

| American Greetings Corp. | |

| 7.375% 06/01/16 | | | 2,365,000 | | | | 1,489,950 | | |

| Jostens IH Corp. | |

| 7.625% 10/01/12 | | | 2,250,000 | | | | 2,216,250 | | |

| | | | 3,706,200 | | |

| Household Products/Wares Total | | | 3,706,200 | | |

| Pharmaceuticals – 0.7% | |

| Medical-Drugs – 0.5% | |

| Elan Finance PLC | |

| 4.883% 11/15/11 (c) | | | 975,000 | | | | 843,375 | | |

| 8.875% 12/01/13 | | | 3,205,000 | | | | 2,756,300 | | |

| Novartis Securities Investment Ltd. | |

| 5.125% 02/10/19 | | | 950,000 | | | | 962,816 | | |

| Warner Chilcott Corp. | |

| 8.750% 02/01/15 | | | 3,765,000 | | | | 3,765,000 | | |

| Wyeth | |

| 5.500% 02/15/16 | | | 800,000 | | | | 828,098 | | |

| | | | 9,155,589 | | |

| Pharmacy Services – 0.2% | |

| Omnicare, Inc. | |

| 6.750% 12/15/13 | | | 3,480,000 | | | | 3,158,100 | | |

| 6.875% 12/15/15 | | | 650,000 | | | | 585,000 | | |

| | | | 3,743,100 | | |

| Pharmaceuticals Total | | | 12,898,689 | | |

| Consumer Non-Cyclical Total | | | 111,992,552 | | |

See Accompanying Notes to Financial Statements.

13

Columbia Strategic Income Fund, May 31, 2009

| Corporate Fixed-Income Bonds & Notes (continued) | |

| | | Par (a) | | Value ($) | |

| Energy – 5.6% | |

| Coal – 0.4% | |

| Coal – 0.4% | |

| Arch Western Finance LLC | |

| 6.750% 07/01/13 | | | 4,115,000 | | | | 3,744,650 | | |

| Massey Energy Co. | |

| 6.875% 12/15/13 | | | 5,585,000 | | | | 4,942,725 | | |

| | | | 8,687,375 | | |

| Coal Total | | | 8,687,375 | | |

| Energy-Alternate Sources – 0.1% | |

| Energy-Alternate Sources – 0.1% | |

| Power Sector Assets & Liabilities Management Corp. | |

| 7.250% 05/27/19 (b) | | | 2,500,000 | | | | 2,543,750 | | |

| | | | 2,543,750 | | |

| Energy-Alternate Sources Total | | | 2,543,750 | | |

| Oil & Gas – 2.9% | |

| Oil Companies-Exploration & Production – 2.3% | |

| Chesapeake Energy Corp. | |

| 6.375% 06/15/15 | | | 7,875,000 | | | | 6,752,812 | | |

| 9.500% 02/15/15 | | | 650,000 | | | | 641,875 | | |

| Cimarex Energy Co. | |

| 7.125% 05/01/17 | | | 2,675,000 | | | | 2,320,563 | | |

| Compton Petroleum Corp. | |

| 7.625% 12/01/13 | | | 2,875,000 | | | | 1,437,500 | | |

| KCS Energy, Inc. | |

| 7.125% 04/01/12 | | | 1,630,000 | | | | 1,519,975 | | |

| Newfield Exploration Co. | |

| 6.625% 04/15/16 | | | 5,680,000 | | | | 5,140,400 | | |

| Nexen, Inc. | |

| 5.875% 03/10/35 | | | 960,000 | | | | 761,944 | | |

| OPTI Canada, Inc. | |

| 8.250% 12/15/14 | | | 5,075,000 | | | | 3,501,750 | | |

| Pemex Finance Ltd. | |

| 9.150% 11/15/18 | | | 2,485,000 | | | | 2,591,603 | | |

| 10.610% 08/15/17 | | | 1,650,000 | | | | 1,827,309 | | |

| Pioneer Natural Resources Co. | |

| 5.875% 07/15/16 | | | 2,060,000 | | | | 1,792,200 | | |

| Quicksilver Resources, Inc. | |

| 7.125% 04/01/16 | | | 5,430,000 | | | | 3,963,900 | | |

| Range Resources Corp. | |

| 7.500% 05/15/16 | | | 4,110,000 | | | | 3,945,600 | | |

| Ras Laffan Liquefied Natural Gas Co., Ltd. III | |

| 5.832% 09/30/16 (b) | | | 4,200,000 | | | | 4,170,390 | | |

| Southwestern Energy Co. | |

| 7.500% 02/01/18 (b) | | | 4,185,000 | | | | 3,986,213 | | |

| XTO Energy, Inc. | |

| 7.500% 04/15/12 | | | 340,000 | | | | 356,603 | | |

| | | | 44,710,637 | | |

| | | Par (a) | | Value ($) | |

| Oil Company-Integrated – 0.0% | |

| Marathon Oil Corp. | |

| 7.500% 02/15/19 | | | 480,000 | | | | 506,301 | | |

| | | | 506,301 | | |

| Oil Refining & Marketing – 0.3% | |

| Frontier Oil Corp. | |

| 8.500% 09/15/16 | | | 1,840,000 | | | | 1,821,600 | | |

| Tesoro Corp. | |

| 6.625% 11/01/15 | | | 3,180,000 | | | | 2,706,975 | | |

| United Refining Co. | |

| 10.500% 08/15/12 | | | 2,145,000 | | | | 1,608,750 | | |

| Valero Energy Corp. | |

| 6.625% 06/15/37 | | | 960,000 | | | | 787,812 | | |

| | | | 6,925,137 | | |

| Oil-Field Services – 0.3% | |

| Gazprom International SA | |

| 7.201% 02/01/20 | | | 5,381,315 | | | | 5,044,983 | | |

| | | | 5,044,983 | | |

| Oil & Gas Total | | | 57,187,058 | | |

| Oil & Gas Services – 0.2% | |

| Oil-Field Services – 0.1% | |

| Halliburton Co. | |

| 5.900% 09/15/18 | | | 960,000 | | | | 1,003,864 | | |

| Smith International, Inc. | |

| 9.750% 03/15/19 | | | 315,000 | | | | 348,020 | | |

| Weatherford International Ltd. | |

| 5.150% 03/15/13 | | | 855,000 | | | | 820,681 | | |

| | | | 2,172,565 | | |

| Seismic Data Collection – 0.1% | |

| Seitel, Inc. | |

| 9.750% 02/15/14 | | | 1,530,000 | | | | 761,175 | | |

| | | | 761,175 | | |

| Oil & Gas Services Total | | | 2,933,740 | | |

| Oil, Gas & Consumable Fuels – 0.9% | |

| Oil Companies-Exploration & Production – 0.5% | |

| Forest Oil Corp. | |

| 8.500% 02/15/14 (b) | | | 4,010,000 | | | | 3,869,650 | | |

| PetroHawk Energy Corp. | |

| 7.875% 06/01/15 | | | 4,965,000 | | | | 4,605,038 | | |

| Talisman Energy, Inc. | |

| 7.750% 06/01/19 | | | 1,094,000 | | | | 1,146,909 | | |

| | | | 9,621,597 | | |

| Oil Company-Integrated – 0.4% | |

| Petrobras Energia SA | |

| 5.875% 05/15/17 (b) | | | 4,000,000 | | | | 3,560,000 | | |

See Accompanying Notes to Financial Statements.

14

Columbia Strategic Income Fund, May 31, 2009

| Corporate Fixed-Income Bonds & Notes (continued) | |

| | | Par (a) | | Value ($) | |

| Petrobras International Finance Co. | |

| 5.875% 03/01/18 | | | 4,150,000 | | | | 4,054,894 | | |

| | | | 7,614,894 | | |

| Oil, Gas & Consumable Fuels Total | | | 17,236,491 | | |

| Pipelines – 1.1% | |

| Pipelines – 1.1% | |

| Atlas Pipeline Partners LP | |

| 8.125% 12/15/15 | | | 3,125,000 | | | | 1,921,875 | | |

| El Paso Corp. | |

| 6.875% 06/15/14 | | | 2,970,000 | | | | 2,812,777 | | |

| 7.250% 06/01/18 | | | 3,035,000 | | | | 2,795,427 | | |

| Energy Transfer Partners LP | |

| 8.500% 04/15/14 | | | 1,700,000 | | | | 1,891,952 | | |

| Kinder Morgan Energy Partners LP | |

| 6.950% 01/15/38 | | | 670,000 | | | | 620,860 | | |

| Kinder Morgan Finance Co. ULC | |

| 5.700% 01/05/16 | | | 4,000,000 | | | | 3,420,000 | | |

| MarkWest Energy Partners LP | |

| 6.875% 11/01/14 | | | 2,800,000 | | | | 2,296,000 | | |

| 8.500% 07/15/16 | | | 1,905,000 | | | | 1,609,725 | | |

| Plains All American Pipeline LP | |

| 6.500% 05/01/18 | | | 1,520,000 | | | | 1,468,165 | | |

| TransCanada Pipelines Ltd. | |

| 6.350% 05/15/67 (c) | | | 950,000 | | | | 627,000 | | |

| 7.625% 01/15/39 | | | 575,000 | | | | 631,764 | | |

| Williams Companies, Inc. | |

| 7.625% 07/15/19 | | | 1,375,000 | | | | 1,340,625 | | |

| 7.875% 09/01/21 | | | 1,030,000 | | | | 999,100 | | |

| 8.125% 03/15/12 | | | 135,000 | | | | 138,059 | | |

| | | | 22,573,329 | | |

| Pipelines Total | | | 22,573,329 | | |

| Energy Total | | | 111,161,743 | | |

| Financials – 5.7% | |

| Banks – 2.5% | |

| Commercial Banks-Central US – 0.1% | |

| Northern Trust Co. | |

| 6.500% 08/15/18 | | | 1,500,000 | | | | 1,588,135 | | |

| | | | 1,588,135 | | |

| Commercial Banks-Non US – 0.2% | |

| ANZ National International Ltd. | |

| 6.200% 07/19/13 (b) | | | 3,200,000 | | | | 3,266,330 | | |

| | | | 3,266,330 | | |

| Commercial Banks-Western U.S. – 1.0% | |

| Citibank NA | |

| 1.875% 05/07/12 | | | 20,000,000 | | | | 20,046,420 | | |

| | | | 20,046,420 | | |

| | | Par (a) | | Value ($) | |

| Diversified Banking Institutional – 0.3% | |

| Citigroup, Inc. | |

| 6.500% 08/19/13 | | | 1,580,000 | | | | 1,565,741 | | |

| 8.500% 05/22/19 | | | 3,150,000 | | | | 3,261,478 | | |

| Goldman Sachs Group, Inc. | |

| 6.250% 09/01/17 | | | 665,000 | | | | 644,542 | | |

| | | | 5,471,761 | | |

| Diversified Financial Services – 0.0% | |

| JPMorgan Chase & Co. | |

| 6.300% 04/23/19 | | | 605,000 | | | | 601,920 | | |

| | | | 601,920 | | |

| Fiduciary Banks – 0.3% | |

| Bank of New York Mellon Corp. | |

| 5.450% 05/15/19 | | | 4,905,000 | | | | 4,914,330 | | |

| Northern Trust Corp. | |

| 5.500% 08/15/13 | | | 570,000 | | | | 594,988 | | |

| | | | 5,509,318 | | |

| Money Center Banks – 0.1% | |

| Comerica Bank | |

| 5.200% 08/22/17 | | | 500,000 | | | | 384,688 | | |

| Deutsche Bank AG London | |

| 4.875% 05/20/13 | | | 2,280,000 | | | | 2,304,366 | | |

| | | | 2,689,054 | | |

| Special Purpose Entity – 0.1% | |

| Goldman Sachs Capital II | |

| 5.793% 12/29/49 (c) | | | 1,335,000 | | | | 774,509 | | |

| JPMorgan Chase Capital XX | |

| 6.550% 09/29/36 | | | 950,000 | | | | 748,374 | | |

| | | | 1,522,883 | | |

| Super-Regional Banks-US – 0.4% | |

| Capital One Financial Corp. | |

| 5.700% 09/15/11 | | | 1,920,000 | | | | 1,951,133 | | |

| 7.375% 05/23/14 | | | 2,155,000 | | | | 2,220,391 | | |

| Keycorp | |

| 6.500% 05/14/13 | | | 1,780,000 | | | | 1,683,565 | | |

| National City Corp. | |

| 4.900% 01/15/15 | | | 1,440,000 | | | | 1,271,087 | | |

| USB Capital IX | |

| 6.189% 04/15/49 (c) | | | 775,000 | | | | 505,687 | | |

| Wachovia Capital Trust III | |

| 5.800% 03/15/42 (c) | | | 480,000 | | | | 292,800 | | |

| | | | 7,924,663 | | |

| Banks Total | | | 48,620,484 | | |

See Accompanying Notes to Financial Statements.

15

Columbia Strategic Income Fund, May 31, 2009

| Corporate Fixed-Income Bonds & Notes (continued) | |

| | | Par (a) | | Value ($) | |

| Diversified Financial Services – 2.2% | |

| Diversified Financial Services – 0.1% | |

| General Electric Capital Corp. | |

| 6.875% 01/10/39 | | | 1,260,000 | | | | 1,158,391 | | |

| 5.900% 05/13/14 | | | 1,215,000 | | | | 1,224,290 | | |

| | | | 2,382,681 | | |

| Finance-Auto Loans – 1.0% | |

| Ford Motor Credit Co. | |

| 8.000% 12/15/16 | | | 3,310,000 | | | | 2,658,069 | | |

| 7.800% 06/01/12 | | | 8,100,000 | | | | 6,916,954 | | |

| GMAC LLC | |

| 6.875% 09/15/11 (b) | | | 5,800,000 | | | | 5,191,000 | | |

| 8.000% 11/01/31 (b) | | | 6,853,000 | | | | 5,139,750 | | |

| | | | 19,905,773 | | |

| Finance-Consumer Loans – 0.3% | |

| Sears Roebuck Acceptance Corp. | |