UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

Investment Company Act file number | | 811-04367 |

Columbia Funds Series Trust I

|

| (Exact name of registrant as specified in charter) |

| | |

| One Financial Center, Boston, Massachusetts | | 02111 |

| (Address of principal executive offices) | | (Zip code) |

James R. Bordewick, Jr., Esq.

Columbia Management Advisors, LLC

One Financial Center

Boston, MA 02111

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: 1-617-426-3750

Date of fiscal year end: April 30

Date of reporting period: April 30, 2009

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

Annual Report

April 30, 2009

Columbia Core Bond Fund

| | |

| NOT FDIC INSURED | | May Lose Value |

| NOT BANK ISSUED | | No Bank Guarantee |

Table of contents

The views expressed in this report reflect the current views of the respective parties. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict, so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Fund. References to specific securities should not be construed as a recommendation or investment advice.

President’s Message

Dear Shareholder:

Recent events have shown great volatility in the markets and uncertainty in the economy. During these challenging times, it becomes even more important to focus on long-term horizons and key investment tools that can help manage volatility. This may be the time to reflect on your investment goals and evaluate your portfolio to ensure you are positioned for any potential market rebound.

A long-term financial plan can serve as a road map and guide you through the necessary steps designed to meet your financial goals. Your financial plan should take into account your investment goals, time horizon, overall financial situation, risk tolerance and willingness to ride out market volatility. Your investment professional can be a key resource as you work through this process. The knowledge and experience of an investment professional can help as you create or reevaluate your investment strategy.

The importance of diversification

Although diversification does not ensure a profit or guarantee against loss, a diversified portfolio can be a strategy for successful long-term investing. Diversification refers to the mix of investments within a portfolio. A mutual fund can contribute to portfolio diversification given that a mutual fund’s portfolio represents several investments. Additionally, the way you allocate your money among stocks, bonds and cash, and geographically between foreign and domestic investments, can help to reduce risks. Diversification can result in multiple investments where the positive performance of certain holdings can offset any negative performance from other holdings. Having a diversified portfolio doesn’t mean that the value of the portfolio will never go down, but rather helps strike a balance between risk and reward.

Reevaluate your strategy

An annual review of your investments is a key opportunity to determine if your investment needs have changed or if you need minor adjustments to rebalance your portfolio. Life events like a birth, marriage, home improvement, or change in employment can have a major effect on your spending and goals. Ask yourself how your spending or goals have changed and factor this into your financial plan. Are you using automated investments or payroll deductions to help keep your savings on track? Are you able to set aside additional savings or increase your 401(k) plan contributions? If during your review you find that your investments in any one category (e.g., stocks, bonds or cash) have grown too large based on your diversification plan, you may want to consider redirecting future investments to get back on track.

History has shown that the U.S. stock market has been remarkably resilient¹. Volatility can lead to opportunity. Patience and a commitment to your long-term financial plan may position you to potentially benefit over your investment horizon. We appreciate your business and continued support of Columbia Funds.

Sincerely,

J. Kevin Connaughton

President, Columbia Funds

The board of trustees elected J. Kevin Connaughton president of Columbia Funds on January 16, 2009.

| 1 | The Dow Jones Industrial Average is the most widely used indicator of the overall condition of the stock market. The Dow Jones Industrial Average Index is a price-weighted average of 30 actively traded blue-chip stocks as selected by the editors of the Wall Street Journal. Indices are not investments, do not incur fees or expenses and are not professionally managed. It is not possible to invest directly in an index. |

Fund Profile – Columbia Core Bond Fund

Summary

| n | | For the 12-month period that ended April 30, 2009, the fund’s Class A shares returned 1.48% without sales charge. |

n | | The fund underperformed its benchmark, the Barclays Capital U.S. Aggregate Bond Index1, because it had more exposure to securitized asset classes, which lagged Treasury securities. |

n | | The fund’s relatively conservative security selection enabled it to outperform its peer group, the Lipper Corporate Debt Funds A Rated Classification2. |

Portfolio Management

Alexander D. Powers has co-managed the fund since December 2007 and has been associated with the advisor or its predecessors since 1996.

Jonathan P. Carlson has co-managed the fund since December 2007 and has been associated with the advisor or its predecessors since 2007.

Michael Zazzarino has co-managed the fund since December 2007 and has been associated with the advisor or its predecessors since 2005.

Carl Pappo has co-managed the fund since March 2008 and has been associated with the advisor or its predecessors since 1993.

1 | The Barclays Capital U.S. Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs and total return performance of fixed-rate, publicly placed, dollar-denominated and non-convertible investment grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity. Indices are not available for investment and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index. |

2 | Lipper Inc., a widely respected data provider in the industry, calculates an average total return (assuming reinvestment of distributions) for mutual funds with investment objectives similar to those of the fund. Lipper makes no adjustment for the effect of sales loads. |

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

Summary

1-year return as of 04/30/09

| | |

| |

| | +1.48% Class A shares |

| | (without sales charge) |

| |

| | +3.84% Barclays Capital U.S. Aggregate Bond Index |

|

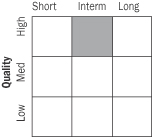

Morningstar Style Box™ |

|

Fixed Income Maturity |

|

The Morningstar Style Box™ reveals a fund’s investment strategy. For fixed-income funds, the vertical axis shows the average credit quality of the bonds owned, and the horizontal axis shows interest rate sensitivity as measured by a bond’s duration (short, intermediate or long). Information shown is based on the most recent data provided by Morningstar.

1

Economic Update – Columbia Core Bond Fund

Summary

For the 12-month period that ended April 30, 2009

| | n | | Despite volatility, the Barclays Capital U.S. Aggregate Bond Index delivered a modest gain. High-yield bonds lost ground, as measured by the Merrill Lynch U.S. High Yield, Cash Pay Index. | |

| | |

| Barclays Aggregate Index | | Merrill Lynch Index |

| |

| |

|

3.84% | | –14.48% |

| | n | | The broad U.S. stock market, as measured by the S&P 500 Index, returned negative 35.31%. Stock markets outside the United States returned negative 42.76%, as measured (in U.S. dollars) by the MSCI EAFE Index. | |

| | |

| S&P Index | | MSCI Index |

| |

| |

|

–35.31% | | –42.76% |

Economic growth ground to a halt during the 12-month period that began May 1, 2008 and ended April 30, 2009. The National Bureau of Economic Research reported that the U.S. economy had slipped into recession late in 2007, and the downturn worsened as the period wore on. Gross domestic product, a common measure of economic growth, declined 6.3% in the fourth quarter of 2008 and 6.1% in the first quarter of 2009.

A host of factors weighed on consumers and businesses alike. The most severe housing downturn in decades showed few signs of abating as inventories of homes for sale rose, home prices declined and tighter credit standards, the result of continued turmoil in the subprime mortgage market, made it more difficult for homebuyers to qualify for loans. In addition, home mortgage foreclosure rates soared in March and April.

Consumers bore the brunt of the recession on more than one front. In addition to housing woes, the labor market continued to contract throughout the period, driving the unemployment rate to 8.9%. More than 5.5 million jobs have been lost since the recession commenced late in 2007, although the April decline was smaller than it had been in the prior five months. An increase in chain store sales in the early months of 2009 raised hopes that this severe recession may not be intensifying. However, overall retail sales continued to lose ground, as consumers remained reluctant to spend, especially on higher-end goods.

A weakening economy and turmoil in the financial markets took a toll on consumer confidence, which set new all-time lows during the period. However, the monthly Conference Board gauge was nearly unchanged in March and actually rose in April. Another bright spot during this period of relative uncertainty: energy and commodity prices declined. Gasoline prices came down from $4 per gallon or more last summer to just above $2 per gallon. The price of oil fell below $40 per barrel in December before rising just above $50 at the end of April.

In an effort to restore confidence in the capital markets, loosen the reins on credit and shore up economic growth, the Federal Reserve Board (the Fed) brought a key short-term rate — the federal funds rate — down from 2.00% to a target between zero and 0.25% during the 12-month period — a record low.

Bonds outperformed stocks

The U.S. bond market seesawed during the 12-month period, but many sectors delivered positive returns. As the economy faltered and stock market volatility increased, the benchmark 10-year U.S. Treasury yield declined from 3.8% to 3.1% and Treasury prices rose. High quality corporate bonds had a poor showing in 2008, but they rebounded early in 2009. The Barclays Capital U.S. Aggregate Bond Index (formerly the Lehman Brothers U.S. Aggregate Bond Index) returned 3.84%. High-yield bond prices fell sharply as economic prospects weakened and default fears rose. The Merrill Lynch U.S. High Yield, Cash Pay Index1 returned negative 14.48% despite a modest comeback in the final months of the period. The Barclays Capital Municipal Bond Index2 returned 3.11% for the 12-month period.

2

Economic Update (continued) – Columbia Core Bond Fund

After sharp retreat, stocks regain some ground

Against a weakening economic backdrop, the U.S. stock market lost 35.31% for the 12-month period, as measured by the S&P 500 Index.3 Losses affected the stocks of companies of all sizes and investment style categories, although growth stocks held up better than value stocks, as measured by their respective Russell indices.4 Stock markets outside the U.S. suffered even greater losses. The MSCI EAFE Index,5 a broad gauge of stock market performance in foreign developed markets, lost 42.76% (in U.S. dollars) for the period. Emerging stock markets, which generally have had a strong run over the past several years, were also caught in the downdraft. As investors backed away from risk, the MSCI Emerging Markets Index6 returned negative 42.90% (in U.S. dollars).

Past performance is no guarantee of future results.

1 | The Merrill Lynch U.S. High Yield, Cash Pay Index tracks the performance of non-investment-grade corporate bonds. As of 01/01/2009, Merrill Lynch & Co., Inc. is a wholly-owned subsidiary of Bank of America Corporation and an affiliate of Columbia Management. |

2 | The Barclays Capital Municipal Bond Index is considered representative of the broad market for investment-grade, tax-exempt bonds with maturities of at least one year. |

3 | The Standard & Poor’s (S&P) 500 Index tracks the performance of 500 widely held, large-capitalization U.S. stocks. |

4 | The Russell 1000® Index measures the performance of 1,000 of the largest U.S. companies, based on market capitalization. The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000 Index, as ranked by total market capitalization. The Russell 2000 Index measures the performance of the 2,000 smallest of the 3,000 largest U.S. companies, based on market capitalization. The Russell 1000 Growth Index measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 1000 Value Index measures the performance of those companies in the Russell 1000 Index with lower price-to-book ratios and lower forecasted growth values. The Russell 2000 Growth Index measures the performance of those Russell 2000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2000 Value Index measures the performance of those Russell 2000 Index companies with lower price-to-book ratios and lower forecasted growth values. The Russell 3000 Growth Index measures the performance of those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Russell 3000 Value Index measures the performance of those Russell 3000 Index companies with lower price-to-book ratios and lower forecasted growth values. The Russell Midcap Growth Index measures the performance of those Russell Midcap companies with higher price-to-book ratios and higher forecasted growth values. The Russell Midcap Value Index measures the performance of those Russell Midcap Index companies with lower price-to-book ratios and lower forecasted growth values. |

5 | The Morgan Stanley Capital International (MSCI) Europe, Australasia, Far East (EAFE) Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance, excluding the U.S. and Canada. |

6 | The Morgan Stanley Capital International (MSCI) Emerging Markets Index is a widely accepted index composed of a sample of companies from 25 countries representing the global emerging stock markets. |

Indicesare not available for investment, and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index.

3

Performance Information – Columbia Core Bond Fund

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

| | |

| Annual operating expense ratio (%)* |

Class A | | 0.88 |

Class B | | 1.63 |

Class C | | 1.63 |

Class T | | 0.78 |

Class Z | | 0.63 |

| | |

Annual operating expense ratio

after contractual waivers (%)* |

Class A | | 0.70 |

Class B | | 1.45 |

Class C | | 1.45 |

Class T | | 0.60 |

Class Z | | 0.45 |

| * | The annual operating expense ratio and annual operating expense ratio after contractual waivers are as stated in the fund’s prospectus that is current as of the date of this report. The contractual waiver expires 08/31/09. Differences in expense ratios disclosed elsewhere in this report may result from including fee waivers and expense reimbursements as well as different time periods used in calculating the ratios. |

|

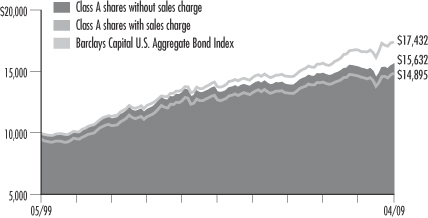

| Performance of a $10,000 investment 05/01/99 – 04/30/09 |

The chart above shows the change in value of a hypothetical $10,000 investment in Class A shares of Columbia Core Bond Fund during the stated time period, and does not reflect the deduction of taxes a shareholder may pay on fund distributions or on the redemption of fund shares. The Barclays Capital U.S. Aggregate Bond Index is a market value weighted index that tracks the daily price, coupon, pay-downs and total return performance of fixed-rate, publicly placed, dollar denominated non-convertible investment grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity. Indices are not available for investment, and do not reflect sales charges, fees, brokerage commissions, taxes or other expenses of investing. Securities in the fund may not match those in an index.

| | | | |

| Performance of a $10,000 investment 05/01/99 – 04/30/09 ($) |

| Sales charge | | without | | with |

Class A | | 15,632 | | 14,895 |

Class B | | 14,535 | | 14,535 |

Class C | | 14,671 | | 14,671 |

Class T | | 15,725 | | 14,984 |

Class Z | | 16,009 | | n/a |

| | | | | | | | | | | | | | | | | | |

| Average annual total return as of 04/30/09 (%) |

| Share class | | A | | B | | C | | T | | Z |

| Inception | | 11/01/98 | | 11/01/98 | | 11/25/02 | | 12/14/90 | | 12/14/90 |

| Sales charge | | without | | with | | without | | with | | without | | with | | without | | with | | without |

1-year | | 1.48 | | –3.33 | | 0.72 | | –4.13 | | 0.87 | | –0.10 | | 1.58 | | –3.24 | | 1.73 |

5-year | | 3.17 | | 2.16 | | 2.41 | | 2.07 | | 2.55 | | 2.55 | | 3.28 | | 2.27 | | 3.43 |

10-year | | 4.57 | | 4.06 | | 3.81 | | 3.81 | | 3.91 | | 3.91 | | 4.63 | | 4.13 | | 4.82 |

| Average annual total return as of 03/31/09 (%) |

| Share class | | A | | B | | C | | T | | Z |

| Sales charge | | without | | with | | without | | with | | without | | with | | without | | with | | without |

1-year | | 0.14 | | –4.58 | | –0.61 | | –5.39 | | –0.46 | | –1.42 | | 0.24 | | –4.48 | | 0.39 |

5-year | | 2.37 | | 1.38 | | 1.61 | | 1.27 | | 1.76 | | 1.76 | | 2.47 | | 1.49 | | 2.63 |

10-year | | 4.48 | | 3.97 | | 3.72 | | 3.72 | | 3.81 | | 3.81 | | 4.54 | | 4.03 | | 4.73 |

The “with sales charge” returns include the maximum initial sales charge of 4.75% for Class A and T shares, the applicable contingent deferred sales charge of 5.00% in the first year, declining to 1.00% in the sixth year and eliminated thereafter for Class B shares and 1.00% for Class C shares for the first year only. The “without sales charge” returns do not include the effect of sales charges. If they had, returns would be lower.

All results shown assume reinvestment of distributions. Class Z shares are sold at net asset value with no distribution and service (Rule 12b-1) fees. Class Z shares have limited eligibility and the investment minimum requirements may vary. Please see the fund’s prospectus for details. Performance for different share classes will vary based on differences in sales charges and fees associated with each class.

Performance results reflect any fee waivers or reimbursements of fund expenses by the investment advisor and/or any of its affiliates. Absent these fee waivers or expense reimbursement arrangements, performance results would have been lower.

The tables do not reflect the deduction of taxes that a shareholder may pay on fund distributions or on the redemption of fund shares.

Class A, Class B, Class C, Class T and Class Z share performance information includes returns of Prime A shares (for Class A shares), Prime B shares (for Class B and Class C shares), Retail A shares (for Class T shares) and Trust shares (for Class Z shares) of Galaxy Quality Plus Bond Fund, the predecessor to the fund and a series of The Galaxy Fund (the “Predecessor Fund”), for periods prior to November 25, 2002, the date on which Class A, Class B, Class C, Class T and Class Z shares were initially offered by the fund. The returns shown for all share classes reflect any differences in sales charges, but have not been restated to reflect any differences in expenses between the Predecessor Fund share classes and the corresponding newer share classes. If differences in expenses had been reflected, the returns shown for periods prior to November 25, 2002 would be lower for Class C and Class T shares.

4

Understanding Your Expenses – Columbia Core Bond Fund

Estimating your actual expenses

To estimate the expenses that you paid over the period, first you will need your account balance at the end of the period:

| | n | | For shareholders who receive their account statements from Columbia Management Services, Inc., your account balance is available online at www.columbiafunds.com or by calling Shareholder Services at 800.345.6611. | |

| | n | | For shareholders who receive their account statements from their financial intermediary, contact your financial intermediary to obtain your account balance. | |

| | 1. | Divide your ending account balance by $1,000. For example, if an account balance was $8,600 at the end of the period, the result would be 8.6. | |

| | 2. | In the section of the table below titled “Expenses paid during the period,” locate the amount for your share class. You will find this number in the column labeled “Actual.” Multiply this number by the result from step 1. Your answer is an estimate of the expenses you paid on your account during the period. | |

If the value of your account falls below the minimum initial investment requirement applicable to you, your account generally will be subject to a $20 annual fee. This fee is not included in the accompanying table. If you are subject to the fee, keep it in mind when you are estimating the ongoing expenses of investing in the fund and when comparing the expenses of this fund with other funds.

As a fund shareholder, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption fees or exchange fees. There are also ongoing costs, which generally include investment advisory fees, distribution and service (Rule 12b-1) fees and other fund expenses. The information on this page is intended to help you understand the ongoing costs of investing in the fund and to compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your fund’s expenses by share class

To illustrate these ongoing costs, we have provided an example and calculated the expenses paid by investors in each share class during the period. The information in the following table is based on an initial investment of $1,000, which is invested at the beginning of the period and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the “Actual” column is calculated using the fund’s actual operating expenses and total return for the period. The amount listed in the “Hypothetical” column for each share class assumes that the return each year is 5% before expenses and is calculated based on the fund’s actual operating expenses. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during this period.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the fund with other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the ongoing costs of investing in a fund and do not reflect any transaction costs, such as sales charges, redemption fees or exchange fees.

| | | | | | | | | | | | | | |

| 11/01/08 – 04/30/09 |

| | | | |

| | | Account value at the

beginning of the period ($) | | Account value at the

end of the period ($) | | Expenses paid

during the period ($) | | Fund’s annualized

expense ratio (%) |

| | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual |

Class A | | 1,000.00 | | 1,000.00 | | 1,077.01 | | 1,021.32 | | 3.60 | | 3.51 | | 0.70 |

Class B | | 1,000.00 | | 1,000.00 | | 1,073.00 | | 1,017.60 | | 7.45 | | 7.25 | | 1.45 |

Class C | | 1,000.00 | | 1,000.00 | | 1,073.79 | | 1,018.35 | | 6.68 | | 6.51 | | 1.30 |

Class T | | 1,000.00 | | 1,000.00 | | 1,077.61 | | 1,021.82 | | 3.09 | | 3.01 | | 0.60 |

Class Z | | 1,000.00 | | 1,000.00 | | 1,078.30 | | 1,022.56 | | 2.32 | | 2.26 | | 0.45 |

Expenses paid during the period are equal to the annualized expense ratio for the share class, multiplied by the average account value over the period, then multiplied by the number of days in the fund’s most recent fiscal half-year and divided by 365.

Had the investment advisor and/or any of its affiliates not waived fees or reimbursed a portion of expenses, account value at the end of the period would have been reduced.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the fund and do not reflect any transaction costs, such as sales charges, redemption fees or exchange fees. Therefore, the hypothetical examples provided may not help you determine the relative total costs of owning shares of different funds. If these transaction costs were included, your costs would have been higher.

5

Portfolio Managers’ Report – Columbia Core Bond Fund

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Please visit www.columbiafunds.com for daily and most recent month-end performance updates.

| | |

| Net asset value per share |

| |

as of 04/30/09 ($) | | |

Class A | | 10.13 |

Class B | | 10.13 |

Class C | | 10.13 |

Class T | | 10.13 |

Class Z | | 10.13 |

| | |

| Distributions declared per share |

| |

05/01/08 – 04/30/09 ($) | | |

Class A | | 0.45 |

Class B | | 0.38 |

Class C | | 0.39 |

Class T | | 0.46 |

Class Z | | 0.48 |

| | |

| |

as of 04/30/09 (%) | | |

Class A | | 4.11 |

Class B | | 3.57 |

Class C | | 3.72 |

Class T | | 4.20 |

Class Z | | 4.56 |

The 30-day SEC yields reflect the fund’s earning power net of expenses, expressed as an annualized percentage of the public offering price per share at the end of the period. Had the investment advisor not waived fees or reimbursed a portion of expenses, the 30-day SEC yields would have been lower.

For the 12-month period that ended April 30, 2008, the fund’s Class A shares returned 1.48% without sales charge. The fund’s Class Z shares returned 1.73%. By comparison, the fund’s benchmark, the Barclays Capital U.S. Aggregate Bond Index (formerly the Lehman Brothers U.S. Aggregate Bond Index), returned 3.84%. The average return of the fund’s peer group, the Lipper Corporate Debt Funds A Rated Classification, was negative 4.47%. In a risk-averse environment, performance was almost entirely determined by credit quality and risk orientation.

Overweights in CMBS and ABS hampered performance

The fund underperformed its benchmark generally because it had more exposure to commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS). A slowdown in the housing market, a faltering national economy and a lack of confidence in a wide range of securitized investments induced a flight to quality among investors. Against this backdrop of economic uncertainty and investor fear, Treasury securities were the instruments of choice. Investor demand pushed long-term Treasury yields to all-time lows in late 2008, and short-term rates ended just above zero following a series of interventions by the Federal Reserve Board. For the 12 months as a whole, Treasury securities outperformed virtually all other fixed-income asset classes, in some cases by a significant margin.

Conservative security selection aided performance versus peer group

Although the fund underperformed the index, it held up significantly better than many of its peers because we hedged our asset-allocation decisions with conservative security selections. Our CMBS selections were almost exclusively seasoned securities at the high end of the credit tier, minimizing the fund’s exposure to the lax credit standards that have plagued more recent issues. A concentration in high quality agency mortgages paid off when the federal government assumed control over the operations of Fannie Mae and Freddie Mac in the summer of 2008. In the months that followed, the government announced a series of recovery-oriented plans (notably the Troubled Asset Relief Plan, or TARP, and the Term Asset-Backed Securities Loan Facility, or TALF), and we positioned the fund to potentially benefit from these capital infusions. We reintroduced some banks into the fund’s corporate bond holdings following the passage of TARP, and these positions were additive to performance for the period. In addition, some of the fund’s ABS positions rallied nicely as a result of the TALF legislation, and we took some profits in this group in the last months of the period. The overall impact of security selection was sufficiently positive that the fund easily outperformed its peer group average for the period.

6

Portfolio Managers’ Report (continued) – Columbia Core Bond Fund

| | |

| Portfolio structure |

|

as of 04/30/09 (%) |

Mortgage-Backed Securities | | 46.6 |

Corporate Fixed-Income Bonds & Notes | | 21.7 |

Government & Agency Obligations | | 12.5 |

Commercial Mortgage-Backed Securities | | 9.3 |

Asset-Backed Securities | | 8.1 |

Collateralized Mortgage Obligations | | 0.5 |

Short-Term Obligation | | 7.9 |

The fund is actively managed and the composition of its portfolio will change over time. Portfolio structure is calculated as a percentage of total net assets.

| | |

| Maturity breakdown | | |

| |

as of 04/30/09 (%) | | |

0-1 year | | 5.2 |

1-5 years | | 64.8 |

5-10 years | | 23.0 |

10-20 years | | 2.4 |

20 years and over | | 4.6 |

Maturity breakdown is based on weighted average life and calculated as a percentage of total investments. Swaps are not calculated in maturity years.

| | |

| Quality breakdown | | |

| |

as of 04/30/09 (%) | | |

AAA | | 18.4 |

AA | | 6.1 |

A | | 8.4 |

BBB | | 9.0 |

BB | | 0.1 |

Treasury | | 6.4 |

Agency | | 50.6 |

Cash and Equivalents | | 0.9 |

Other | | 0.1 |

Quality breakdown is calculated as a percentage of total investments.

Ratings shown in the quality breakdown represent the rating assigned to a particular bond by one of the following nationally-recognized rating agencies: Standard & Poor’s, a division of The McGraw-Hill Companies, Inc., Moody’s Investors Service, Inc. or Fitch Ratings Ltd. Ratings are relative and subjective and are not absolute standards of quality. The fund’s credit quality does not remove market risk.

Looking ahead

We plan to continue to focus on the areas of the market under active sponsorship by the federal government, hedging our decisions by investing in high quality assets. Implicit in this strategy is a vigilance that helps us separate short-term beneficiaries of the Treasury’s largesse from those issues that make attractive long-term investments in their own right. We have been cautiously optimistic that the government’s efforts will prove successful over time, and we note the market enters the new reporting period having shed at least some of the rampant pessimism that prevailed in 2008.

Investing in fixed-income securities may involve certain risks, including the credit quality of individual issuers, possible prepayments, market or economic developments and yield and share price fluctuations due to changes in interest rates. Investing in foreign fixed-income markets carries additional risks associated with foreign political and economic developments and changes in currency exchange rates. When interest rates go up, bond prices typically drop, and vice versa.

7

Investment Portfolio – Columbia Core Bond Fund

April 30, 2009

Mortgage-Backed Securities – 46.6%

| | | | |

| | | Par ($) | | Value ($) |

| Federal Home Loan Mortgage Corp. | | |

5.000% 08/01/35 | | 2,423,219 | | 2,495,394 |

5.000% 10/01/35 | | 21,528,638 | | 22,169,858 |

5.000% 12/01/36 | | 10,897,589 | | 11,217,060 |

5.000% 03/01/37 | | 2,860,197 | | 2,942,991 |

5.500% 01/01/37 | | 116,978,094 | | 121,159,935 |

7.000% 12/01/10 | | 14,423 | | 14,919 |

7.000% 12/01/14 | | 38,350 | | 40,604 |

7.000% 11/01/25 | | 4,099 | | 4,474 |

7.000% 03/01/27 | | 3,539 | | 3,824 |

7.000% 10/01/31 | | 28,944 | | 31,047 |

7.500% 09/01/25 | | 1,839 | | 2,014 |

7.500% 10/01/29 | | 87,377 | | 95,181 |

8.000% 06/01/26 | | 2,212 | | 2,435 |

9.500% 09/01/10 | | 1,071 | | 1,093 |

9.500% 04/01/11 | | 160 | | 171 |

9.500% 09/01/16 | | 861 | | 959 |

10.000% 05/01/11 | | 2,128 | | 2,256 |

| |

| Federal National Mortgage Association | | |

4.000% 03/01/39 | | 44,019,510 | | 43,930,585 |

4.500% 02/01/39 | | 65,647,530 | | 66,872,761 |

4.852% 04/01/38 (a) | | 8,734,169 | | 9,005,003 |

4.901% 04/01/38 (a) | | 9,563,822 | | 9,845,888 |

5.000% 03/01/37 | | 29,425,531 | | 30,301,955 |

5.000% 05/01/37 | | 7,414,615 | | 7,633,879 |

5.000% 03/01/38 | | 22,032,653 | | 22,684,202 |

5.199% 08/01/36 (a) | | 119,074 | | 121,408 |

5.240% 09/01/12 | | 2,336,410 | | 2,461,709 |

5.500% 02/01/37 | | 7,974,429 | | 8,270,506 |

5.765% 09/01/37 (a) | | 7,940,512 | | 8,277,747 |

6.500% 09/01/36 | | 7,110,182 | | 7,543,574 |

6.500% 09/01/37 | | 15,250,733 | | 16,179,463 |

6.500% 10/01/37 | | 8,003,713 | | 8,491,119 |

6.500% 12/01/37 | | 18,378,119 | | 19,497,299 |

6.500% 03/01/38 | | 7,655,597 | | 8,121,803 |

7.000% 06/01/32 | | 12,607 | | 13,592 |

7.500% 10/01/15 | | 23,031 | | 24,342 |

7.500% 01/01/30 | | 12,163 | | 13,261 |

7.500% 03/01/30 | | 19,123 | | 20,821 |

7.785% 02/01/19 | | 1,745,617 | | 1,882,324 |

8.000% 12/01/09 | | 1 | | 1 |

8.000% 12/01/29 | | 249,205 | | 272,726 |

8.000% 02/01/30 | | 18,286 | | 20,023 |

8.000% 03/01/30 | | 59,709 | | 65,261 |

8.000% 04/01/30 | | 67,621 | | 73,908 |

8.000% 05/01/30 | | 5,214 | | 5,699 |

8.500% 08/01/17 | | 1,159 | | 1,251 |

10.000% 10/01/20 | | 71,078 | | 78,396 |

| | | | |

| | | Par ($) | | Value ($) |

10.000% 12/01/20 | | 151,827 | | 166,955 |

TBA | | | | |

6.000% 05/01/39 (b) | | 204,000,000 | | 213,243,648 |

| |

| Government National Mortgage Association | | |

4.625% 07/20/21 (a) | | 46,596 | | 47,163 |

4.625% 07/20/22 (a) | | 53,679 | | 54,210 |

5.000% 05/19/09 (b) | | 57,800,000 | | 59,851,028 |

5.375% 04/20/22 (a) | | 223,770 | | 230,058 |

7.000% 05/15/12 | | 26,854 | | 28,405 |

7.000% 09/15/13 | | 29,122 | | 30,842 |

7.000% 11/15/22 | | 51,990 | | 55,688 |

7.000% 10/15/23 | | 25,503 | | 27,272 |

7.000% 06/15/26 | | 172,434 | | 184,820 |

7.000% 10/15/27 | | 19,632 | | 21,051 |

7.000% 05/15/28 | | 39,942 | | 42,842 |

7.000% 06/15/28 | | 7,425 | | 7,965 |

7.000% 12/15/28 | | 37,624 | | 40,356 |

7.000% 08/15/29 | | 20,437 | | 21,957 |

7.000% 02/15/30 | | 4,503 | | 4,840 |

7.000% 05/15/32 | | 148,295 | | 158,338 |

7.500% 04/15/26 | | 124,557 | | 134,569 |

7.500% 02/15/27 | | 13,941 | | 15,072 |

7.500% 09/15/29 | | 449,657 | | 486,472 |

7.500% 03/15/30 | | 81,693 | | 88,147 |

8.000% 06/15/25 | | 3,827 | | 4,166 |

8.000% 10/15/25 | | 17,613 | | 19,171 |

8.000% 01/15/26 | | 11,681 | | 12,725 |

8.000% 02/15/26 | | 2,270 | | 2,473 |

8.000% 05/15/26 | | 2,144 | | 2,335 |

8.000% 06/15/26 | | 10,695 | | 11,642 |

8.000% 03/15/27 | | 18,425 | | 20,066 |

9.000% 11/15/17 | | 40,328 | | 43,617 |

9.500% 08/15/20 | | 1,837 | | 2,023 |

9.500% 12/15/20 | | 1,262 | | 1,390 |

10.000% 05/15/16 | | 2,771 | | 3,036 |

10.000% 07/15/17 | | 14,681 | | 16,034 |

10.000% 08/15/17 | | 3,857 | | 4,213 |

10.000% 08/15/18 | | 35 | | 38 |

11.500% 06/15/13 | | 16,262 | | 18,063 |

| | | | |

Total Mortgage-Backed Securities

(cost of $690,137,271) | | 706,997,411 |

See Accompanying Notes to Financial Statements.

8

Columbia Core Bond Fund

April 30, 2009

Corporate Fixed-Income Bonds & Notes – 21.7%

| | | | |

| | | Par ($) | | Value ($) |

| Basic Materials – 0.5% | | | | |

| Chemicals – 0.2% | | | | |

| Dow Chemical Co. | | | | |

5.700% 05/15/18 | | 2,485,000 | | 2,105,329 |

| | |

| Lubrizol Corp. | | | | |

6.500% 10/01/34 | | 1,000,000 | | 767,842 |

| | | | |

Chemicals Total | | | | 2,873,171 |

| | |

| Iron/Steel – 0.3% | | | | |

| Nucor Corp. | | | | |

5.000% 06/01/13 | | 2,575,000 | | 2,686,541 |

5.850% 06/01/18 | | 1,575,000 | | 1,600,394 |

| | | | |

Iron/Steel Total | | | | 4,286,935 |

| | | | |

Basic Materials Total | | | | 7,160,106 |

| | | | |

| Communications – 2.1% | | | | |

| Media – 0.8% | | | | |

| Comcast Corp. | | | | |

5.700% 05/15/18 | | 1,680,000 | | 1,642,482 |

6.300% 11/15/17 | | 770,000 | | 783,991 |

6.950% 08/15/37 | | 1,635,000 | | 1,614,440 |

| | |

| Time Warner Cable, Inc. | | | | |

7.300% 07/01/38 | | 2,630,000 | | 2,628,998 |

| | |

| Time Warner, Inc. | | | | |

6.875% 05/01/12 | | 3,435,000 | | 3,612,624 |

| | |

| Viacom, Inc. | | | | |

5.750% 04/30/11 | | 1,635,000 | | 1,634,231 |

6.875% 04/30/36 | | 250,000 | | 203,870 |

| | | | |

Media Total | | | | 12,120,636 |

| |

Telecommunication Services – 1.3% | | |

| AT&T, Inc. | | | | |

5.625% 06/15/16 | | 2,275,000 | | 2,314,956 |

6.550% 02/15/39 | | 2,535,000 | | 2,437,953 |

| | |

| BellSouth Corp. | | | | |

5.200% 09/15/14 | | 765,000 | | 792,388 |

| |

| British Telecommunications PLC | | |

5.150% 01/15/13 | | 565,000 | | 531,757 |

| |

| Telefonica Emisiones SAU | | |

6.221% 07/03/17 | | 1,325,000 | | 1,371,698 |

6.421% 06/20/16 | | 2,500,000 | | 2,615,445 |

| |

| Verizon Wireless Capital LLC | | |

5.550% 02/01/14 (c) | | 6,010,000 | | 6,304,658 |

8.500% 11/15/18 (c) | | 2,450,000 | | 2,934,127 |

|

Telecommunication Services Total | | 19,302,982 |

| | | | |

Communications Total | | 31,423,618 |

| | | | |

| | | Par ($) | | Value ($) |

| Consumer Cyclical – 0.8% | | | | |

| Airlines – 0.0% | | | | |

| Continental Airlines, Inc. | | |

7.461% 04/01/15 | | 665,228 | | 485,617 |

|

Airlines Total | | 485,617 |

| | |

| Home Builders – 0.0% | | | | |

| D.R. Horton, Inc. | | |

5.625% 09/15/14 | | 365,000 | | 308,425 |

|

Home Builders Total | | 308,425 |

| | |

| Restaurants – 0.2% | | | | |

| McDonald’s Corp. | | |

5.000% 02/01/19 | | 510,000 | | 517,019 |

5.700% 02/01/39 | | 1,900,000 | | 1,808,492 |

|

Restaurants Total | | 2,325,511 |

| | |

| Retail – 0.6% | | | | |

| Best Buy Co., Inc. | | |

6.750% 07/15/13 | | 2,745,000 | | 2,711,258 |

| |

| CVS Pass-Through Trust | | |

5.298% 01/11/27 (c) | | 771,448 | | 559,912 |

6.036% 12/10/28 (c) | | 3,308,636 | | 2,452,129 |

| |

| Macy’s Retail Holdings, Inc. | | |

5.350% 03/15/12 | | 455,000 | | 415,245 |

| |

| Starbucks Corp. | | |

6.250% 08/15/17 | | 2,710,000 | | 2,500,352 |

|

Retail Total | | 8,638,896 |

| | | | |

Consumer Cyclical Total | | 11,758,449 |

| | | | |

| Consumer Non-cyclical – 2.4% |

| Beverages – 0.8% | | | | |

| Anheuser-Busch InBev Worldwide, Inc. | | |

7.750% 01/15/19 (c)(d) | | 3,660,000 | | 3,831,910 |

8.200% 01/15/39 (c) | | 930,000 | | 931,872 |

| |

| Bottling Group LLC | | |

5.125% 01/15/19 | | 1,700,000 | | 1,726,501 |

| |

| PepsiCo, Inc. | | |

7.900% 11/01/18 | | 2,530,000 | | 3,053,389 |

| |

| SABMiller PLC | | |

6.200% 07/01/11 (c) | | 2,755,000 | | 2,773,395 |

|

Beverages Total | | 12,317,067 |

| | |

| Food – 0.7% | | | | |

| Campbell Soup Co. | | |

4.500% 02/15/19 | | 2,470,000 | | 2,437,082 |

| |

| ConAgra Foods, Inc. | | |

7.000% 10/01/28 | | 3,160,000 | | 3,062,135 |

| |

| Kraft Foods, Inc. | | |

6.500% 08/11/17 | | 1,405,000 | | 1,457,504 |

See Accompanying Notes to Financial Statements.

9

Columbia Core Bond Fund

April 30, 2009

Corporate Fixed-Income Bonds & Notes (continued)

| | | | |

| | | Par ($) | | Value ($) |

| Consumer Non-cyclical (continued) |

| Kroger Co. | | |

8.000% 09/15/29 | | 2,260,000 | | 2,446,226 |

|

Food Total | | 9,402,947 |

| |

| Healthcare Services – 0.1% | | |

| WellPoint, Inc. | | |

7.000% 02/15/19 | | 1,700,000 | | 1,733,413 |

|

Healthcare Services Total | | 1,733,413 |

| |

| Household Products/Wares – 0.3% | | |

| Clorox Co. | | |

5.950% 10/15/17 | | 900,000 | | 910,671 |

| |

| Fortune Brands, Inc. | | |

5.125% 01/15/11 | | 3,815,000 | | 3,816,412 |

|

Household Products/Wares Total | | 4,727,083 |

| |

| Pharmaceuticals – 0.5% | | |

| Novartis Securities Investment Ltd. | | |

5.125% 02/10/19 | | 3,640,000 | | 3,727,091 |

| |

| Wyeth | | |

5.500% 02/15/16 | | 3,680,000 | | 3,774,138 |

|

Pharmaceuticals Total | | 7,501,229 |

| | | | |

Consumer Non-cyclical Total | | 35,681,739 |

| | | | |

| Energy – 2.8% | | | | |

| Oil & Gas – 1.3% | | | | |

| Canadian Natural Resources Ltd. | | |

6.250% 03/15/38 | | 1,445,000 | | 1,174,999 |

| | |

| Devon Energy Corp. | | | | |

6.300% 01/15/19 | | 1,230,000 | | 1,273,129 |

| | |

| Gazprom International SA | | | | |

7.201% 02/01/20 | | 176,498 | | 158,848 |

| | |

| Hess Corp. | | | | |

7.300% 08/15/31 | | 1,980,000 | | 1,789,286 |

| | |

| Marathon Oil Corp. | | | | |

6.000% 07/01/12 | | 3,065,000 | | 3,119,686 |

7.500% 02/15/19 | | 1,160,000 | | 1,215,454 |

| | |

| Nexen, Inc. | | | | |

5.875% 03/10/35 | | 1,995,000 | | 1,380,304 |

| | |

| Qatar Petroleum | | | | |

5.579% 05/30/11 (c) | | 1,552,902 | | 1,576,893 |

|

| Ras Laffan Liquefied Natural Gas Co., Ltd. III |

5.832% 09/30/16 (c) | | 2,130,000 | | 2,072,660 |

| | |

| Talisman Energy, Inc. | | | | |

5.850% 02/01/37 | | 2,145,000 | | 1,450,994 |

| | | | |

| | | Par ($) | | Value ($) |

| Valero Energy Corp. | | | | |

6.625% 06/15/37 | | 2,235,000 | | 1,769,584 |

6.875% 04/15/12 | | 2,547,000 | | 2,605,540 |

| | | | |

Oil & Gas Total | | | | 19,587,377 |

| | |

| Oil & Gas Services – 0.6% | | | | |

| Halliburton Co. | | | | |

5.900% 09/15/18 | | 2,040,000 | | 2,118,581 |

| | |

| Smith International, Inc. | | | | |

9.750% 03/15/19 | | 1,855,000 | | 1,960,503 |

| | |

| Weatherford International Ltd. | | | | |

5.150% 03/15/13 | | 4,500,000 | | 4,225,527 |

7.000% 03/15/38 | | 1,090,000 | | 806,131 |

| | | | |

Oil & Gas Services Total | | 9,110,742 |

|

| Pipelines – 0.9% |

| Enbridge Energy Partners LP |

7.500% 04/15/38 | | 1,060,000 | | 837,332 |

| | |

| Energy Transfer Partners LP | | | | |

6.000% 07/01/13 | | 3,195,000 | | 3,166,993 |

8.500% 04/15/14 | | 2,175,000 | | 2,347,636 |

| |

| Kinder Morgan Energy Partners LP | | |

6.950% 01/15/38 | | 1,945,000 | | 1,691,061 |

| | |

| ONEOK Partners LP | | | | |

6.850% 10/15/37 | | 835,000 | | 628,139 |

| | |

| Plains All American Pipeline LP | | | | |

6.500% 05/01/18 | | 635,000 | | 568,386 |

| | |

| TEPPCO Partners LP | | | | |

7.625% 02/15/12 | | 1,311,000 | | 1,294,758 |

| | |

| TransCanada Pipelines Ltd. | | | | |

6.350% 05/15/67 (a) | | 5,160,000 | | 3,302,400 |

| | | | |

Pipelines Total | | | | 13,836,705 |

| | | | |

Energy Total | | | | 42,534,824 |

| | | | |

| Financials – 8.7% | | | | |

| Banks – 5.5% | | | | |

| American Express Centurion Bank | | |

4.375% 07/30/09 | | 1,265,000 | | 1,265,230 |

| | |

| ANZ National International Ltd. | | | | |

6.200% 07/19/13 (c) | | 5,490,000 | | 5,481,150 |

| | |

| Bank of New York Mellon Corp. | | | | |

4.500% 04/01/13 (d) | | 2,100,000 | | 2,130,912 |

5.125% 08/27/13 | | 1,125,000 | | 1,165,900 |

| | |

| Capital One Capital IV | | | | |

6.745% 02/17/37 (a) | | 3,185,000 | | 1,353,335 |

| | |

| Capital One Financial Corp. | | | | |

5.700% 09/15/11 | | 4,485,000 | | 4,285,072 |

See Accompanying Notes to Financial Statements.

10

Columbia Core Bond Fund

April 30, 2009

Corporate Fixed-Income Bonds & Notes (continued)

| | | | |

| | | Par ($) | | Value ($) |

| Financials (continued) | | | | |

| Citigroup, Inc. | | | | |

6.500% 08/19/13 | | 8,265,000 | | 7,542,680 |

| | |

| Comerica Bank | | | | |

5.200% 08/22/17 | | 2,425,000 | | 1,649,677 |

5.750% 11/21/16 | | 545,000 | | 403,489 |

| | |

| Deutsche Bank AG | | | | |

4.875% 05/20/13 | | 5,880,000 | | 5,839,158 |

| | |

| HSBC Bank USA | | | | |

3.875% 09/15/09 | | 4,145,000 | | 4,106,941 |

| | |

| JPMorgan Chase & Co. | | | | |

6.300% 04/23/19 | | 7,125,000 | | 7,011,306 |

| | |

| JPMorgan Chase Capital XXII | | | | |

6.450% 02/02/37 | | 1,930,000 | | 1,375,548 |

| | |

| KeyBank NA | | | | |

5.800% 07/01/14 | | 1,770,000 | | 1,500,250 |

| | |

| Keycorp | | | | |

6.500% 05/14/13 | | 5,850,000 | | 5,558,243 |

| | |

| Lloyds TSB Group PLC | | | | |

6.267% 12/31/49 (a)(c) | | 1,425,000 | | 406,125 |

| | |

| M&I Marshall & Ilsley Bank | | | | |

5.300% 09/08/11 | | 2,490,000 | | 2,255,708 |

| | |

| Merrill Lynch & Co., Inc. | | | | |

6.050% 08/15/12 (e) | | 645,000 | | 593,260 |

6.150% 04/25/13 (e) | | 2,200,000 | | 2,022,680 |

5.700% 05/02/17 (e) | | 3,850,000 | | 2,524,029 |

7.750% 05/14/38 (e) | | 2,075,000 | | 1,417,161 |

| | |

| National Australia Bank Ltd. | | | | |

5.350% 06/12/13 (c) | | 3,530,000 | | 3,473,647 |

| | |

| National City Bank of Cleveland | | | | |

6.200% 12/15/11 | | 715,000 | | 708,340 |

| | |

| National City Bank of Kentucky | | | | |

6.300% 02/15/11 | | 1,275,000 | | 1,252,527 |

| | |

| National City Corp. | | | | |

4.900% 01/15/15 | | 655,000 | | 587,653 |

6.875% 05/15/19 | | 2,135,000 | | 1,823,907 |

| | |

| Northern Trust Co. | | | | |

6.500% 08/15/18 | | 1,620,000 | | 1,680,301 |

| | |

| Northern Trust Corp. | | | | |

5.500% 08/15/13 | | 1,865,000 | | 1,919,846 |

| | |

| Regions Financing Trust II | | | | |

6.625% 05/15/47 (a) | | 1,075,000 | | 367,515 |

| | | | |

| | | Par ($) | | Value ($) |

| Scotland International Finance No. 2 | | |

4.250% 05/23/13 (c) | | 1,700,000 | | 1,257,898 |

| | |

| Union Planters Corp. | | | | |

4.375% 12/01/10 | | 1,665,000 | | 1,574,805 |

| | |

| USB Capital IX | | | | |

6.189% 04/15/42 (a) | | 2,965,000 | | 1,645,575 |

| | |

| Wachovia Corp. | | | | |

5.500% 05/01/13 | | 2,975,000 | | 2,916,636 |

5.750% 02/01/18 | | 3,700,000 | | 3,385,615 |

| | | | |

Banks Total | | | | 82,482,119 |

| | | | |

| Diversified Financial Services – 0.9% | | |

| Eaton Vance Corp. | | | | |

6.500% 10/02/17 | | 1,970,000 | | 1,715,716 |

| | |

| General Electric Capital Corp. | | | | |

5.450% 01/15/13 | | 3,015,000 | | 3,039,639 |

6.875% 01/10/39 | | 6,520,000 | | 5,108,668 |

| | |

| International Lease Finance Corp. | | | | |

4.750% 07/01/09 | | 630,000 | | 615,793 |

4.875% 09/01/10 | | 2,095,000 | | 1,826,796 |

| | |

| Lehman Brothers Holdings, Inc. | | | | |

5.625% 01/24/13 (f)(g) | | 6,620,000 | | 943,350 |

6.875% 05/02/18 (f)(g) | | 505,000 | | 71,962 |

| | | | |

Diversified Financial Services Total | | 13,321,924 |

| | |

| Insurance – 1.8% | | | | |

| Hartford Life Global Funding Trusts | | |

1.490% 09/15/09 (a) | | 3,530,000 | | 3,368,361 |

| | |

| ING Groep NV | | | | |

5.775% 12/29/49 (a) | | 2,845,000 | | 1,052,650 |

| | |

| Liberty Mutual Group, Inc. | | | | |

7.500% 08/15/36 (c) | | 4,615,000 | | 2,906,135 |

| | |

| MetLife, Inc. | | | | |

7.717% 02/15/19 | | 3,610,000 | | 3,620,877 |

| |

| Metropolitan Life Global Funding I | | |

5.125% 04/10/13 (c) | | 5,650,000 | | 5,401,005 |

| | |

| New York Life Global Funding | | | | |

4.650% 05/09/13 (c) | | 6,080,000 | | 6,018,203 |

| |

| Principal Life Income Funding Trusts | | |

5.300% 04/24/13 | | 5,930,000 | | 5,587,821 |

| | | | |

Insurance Total | | | | 27,955,052 |

| | | | |

| Real Estate Investment Trusts (REITs) – 0.2% |

| Camden Property Trust | | | | |

5.375% 12/15/13 | | 1,744,000 | | 1,374,369 |

See Accompanying Notes to Financial Statements.

11

Columbia Core Bond Fund

April 30, 2009

Corporate Fixed-Income Bonds & Notes (continued)

| | | | |

| | | Par ($) | | Value ($) |

| Financials (continued) | | | | |

| Highwoods Properties, Inc. | | | | |

5.850% 03/15/17 | | 995,000 | | 662,872 |

| | |

| Hospitality Properties Trust | | | | |

5.625% 03/15/17 | | 2,140,000 | | 1,421,812 |

| | | | |

Real Estate Investment Trusts (REITs) Total | | 3,459,053 |

| | |

| Savings & Loans – 0.3% | | | | |

| World Savings Bank | | | | |

4.125% 12/15/09 | | 3,905,000 | | 3,937,076 |

4.500% 06/15/09 | | 630,000 | | 629,821 |

| | | | |

Savings & Loans Total | | | | 4,566,897 |

| | | | |

Financials Total | | | | 131,785,045 |

| | | | |

| Industrials – 1.5% | | | | |

| Aerospace & Defense – 0.3% | | | | |

| Boeing Co. | | | | |

6.000% 03/15/19 | | 1,660,000 | | 1,745,610 |

| | |

| Raytheon Co. | | | | |

7.200% 08/15/27 | | 2,595,000 | | 2,846,424 |

| | |

| United Technologies Corp. | | | | |

6.125% 02/01/19 | | 355,000 | | 382,242 |

| | | | |

Aerospace & Defense Total | | | | 4,974,276 |

| | |

Machinery – 0.5% | | | | |

| Caterpillar Financial Services Corp. | | |

4.250% 02/08/13 | | 2,830,000 | | 2,754,083 |

5.450% 04/15/18 | | 1,485,000 | | 1,265,680 |

6.200% 09/30/13 | | 300,000 | | 308,280 |

| | |

| Caterpillar, Inc. | | | | |

8.250% 12/15/38 | | 2,040,000 | | 2,207,757 |

| | |

| John Deere Capital Corp. | | | | |

4.950% 12/17/12 | | 1,035,000 | | 1,056,158 |

| | | | |

Machinery Total | | | | 7,591,958 |

| | |

Transportation – 0.7% | | | | |

| BNSF Funding Trust I | | | | |

6.613% 12/15/55 (a) | | 800,000 | | 592,000 |

| |

| Burlington Northern Santa Fe Corp. | | |

6.200% 08/15/36 | | 785,000 | | 724,991 |

7.950% 08/15/30 | | 1,260,000 | | 1,383,810 |

| | |

| Union Pacific Corp. | | | | |

5.700% 08/15/18 | | 1,835,000 | | 1,762,061 |

6.650% 01/15/11 | | 5,550,000 | | 5,850,194 |

| | | | |

Transportation Total | | | | 10,313,056 |

| | | | |

Industrials Total | | | | 22,879,290 |

| | | | |

| | | Par ($) | | Value ($) |

| Technology – 0.6% | | | | |

| Networking & Telecom Equipment – 0.2% | | |

| Cisco Systems, Inc. | | | | |

5.900% 02/15/39 | | 2,900,000 | | 2,744,598 |

| | | | |

Networking & Telecom Equipment Total | | 2,744,598 |

| | |

Software – 0.4% | | | | |

| Oracle Corp. | | | | |

5.000% 01/15/11 | | 2,455,000 | | 2,586,851 |

6.500% 04/15/38 | | 3,995,000 | | 4,073,717 |

| | | | |

Software Total | | | | 6,660,568 |

| | | | |

Technology Total | | | | 9,405,166 |

| | | | |

| Utilities – 2.3% |

| Electric – 1.8% |

| American Electric Power Co., Inc. | | |

5.250% 06/01/15 | | 1,465,000 | | 1,422,442 |

| | |

| Carolina Power & Light Co. | | | | |

5.125% 09/15/13 | | 2,545,000 | | 2,690,650 |

| | |

| Commonwealth Edison Co. | | | | |

4.700% 04/15/15 | | 1,250,000 | | 1,162,373 |

5.900% 03/15/36 | | 790,000 | | 656,327 |

5.950% 08/15/16 | | 2,825,000 | | 2,775,079 |

6.150% 09/15/17 | | 1,200,000 | | 1,182,668 |

6.950% 07/15/18 | | 1,575,000 | | 1,530,743 |

| |

| Consolidated Edison Co. of New York, Inc. | | |

6.750% 04/01/38 | | 2,710,000 | | 2,761,233 |

| | |

| Duke Energy Corp. | | | �� | |

5.300% 10/01/15 | | 2,400,000 | | 2,455,560 |

| | |

| Exelon Generation Co. LLC | | | | |

6.200% 10/01/17 | | 1,000,000 | | 927,327 |

| | |

| FPL Energy National Wind LLC | | | | |

5.608% 03/10/24 (c) | | 773,480 | | 619,047 |

| | |

| Hydro Quebec | | | | |

8.500% 12/01/29 | | 1,195,000 | | 1,605,754 |

| |

| MidAmerican Energy Holdings Co. | | |

5.875% 10/01/12 | | 2,855,000 | | 2,951,039 |

| | |

| Oncor Electric Delivery Co. | | | | |

5.950% 09/01/13 (c) | | 2,370,000 | | 2,384,007 |

| | |

| Southern California Edison Co. | | | | |

5.000% 01/15/16 | | 2,500,000 | | 2,531,877 |

| | |

| Southern Power Co. | | | | |

6.375% 11/15/36 | | 850,000 | | 697,081 |

| | | | |

Electric Total | | | | 28,353,207 |

See Accompanying Notes to Financial Statements.

12

Columbia Core Bond Fund

April 30, 2009

Corporate Fixed-Income Bonds & Notes (continued)

| | | | |

| | | Par ($) | | Value ($) |

| Utilities (continued) |

| Gas – 0.5% |

| Atmos Energy Corp. | | | | |

6.350% 06/15/17 | | 1,760,000 | | 1,626,013 |

8.500% 03/15/19 | | 2,220,000 | | 2,352,760 |

| | |

| Nakilat, Inc. | | | | |

6.067% 12/31/33 (c) | | 1,895,000 | | 1,276,908 |

| | |

| Southern California Gas Co. | | | | |

1.431% 12/01/09 (a) | | 2,080,000 | | 2,073,513 |

| | | | |

Gas Total | | | | 7,329,194 |

| | | | |

Utilities Total | | | | 35,682,401 |

| | | | |

Total Corporate Fixed-Income Bonds & Notes

(cost of $354,407,958) | | 328,310,638 |

|

Commercial Mortgage-Backed Securities – 9.3% |

| Bear Stearns Commercial Mortgage Securities |

4.740% 03/13/40 | | 14,889,000 | | 13,879,986 |

4.933% 02/13/42 (a) | | 2,707,000 | | 2,379,384 |

5.145% 01/12/45 | | 6,748,055 | | 6,593,046 |

5.588% 09/11/42 | | 9,635,000 | | 8,232,432 |

5.742% 09/11/42 (a) | | 2,540,000 | | 2,093,346 |

|

| Chase Commercial Mortgage Securities Corp. |

6.484% 02/12/16 (a)(c) | | 12,585,000 | | 12,735,724 |

|

| Citigroup Commercial Mortgage Trust |

4.733% 10/15/41 | | 3,765,000 | | 3,213,513 |

|

| Citigroup/Deutsche Bank Commercial Mortgage Trust |

5.399% 07/15/44 (a) | | 8,510,000 | | 7,418,948 |

|

| JPMorgan Chase Commercial Mortgage Securities Corp. |

4.878% 01/15/42 | | 2,000,000 | | 1,688,290 |

5.255% 07/12/37 (a) | | 3,875,000 | | 3,740,806 |

5.440% 06/12/47 | | 4,710,000 | | 3,571,638 |

|

| LB-UBS Commercial Mortgage Trust |

4.853% 09/15/31 | | 7,150,000 | | 6,848,348 |

5.124% 11/15/32 (a) | | 6,865,000 | | 6,325,242 |

5.611% 04/15/41 | | 3,360,909 | | 3,415,494 |

6.462% 03/15/31 | | 6,825,000 | | 6,934,418 |

|

| Merrill Lynch Mortgage Investors, Inc. |

I.O., | | | | |

0.583% 12/15/30 (a) | | 3,917,967 | | 59,948 |

|

| Merrill Lynch Mortgage Trust |

4.747% 06/12/43 (a) | | 7,500,000 | | 6,412,346 |

|

| Morgan Stanley Capital I |

4.970% 12/15/41 | | 7,949,000 | | 7,214,885 |

4.989% 08/13/42 | | 3,940,000 | | 3,394,726 |

| | | | |

| | | Par ($) | | Value ($) |

5.328% 11/12/41 | | 6,000,000 | | 4,918,202 |

5.378% 11/14/42 (a) | | 3,495,000 | | 3,090,706 |

|

| Morgan Stanley Dean Witter Capital I |

4.920% 03/12/35 | | 6,335,000 | | 6,000,667 |

5.980% 01/15/39 | | 7,730,000 | | 7,718,652 |

|

| Wachovia Bank Commercial Mortgage Trust |

5.037% 03/15/42 | | 5,560,000 | | 5,426,560 |

5.609% 03/15/45 (a) | | 5,052,000 | | 2,596,934 |

5.726% 06/15/45 | | 3,484,789 | | 3,485,846 |

5.997% 06/15/45 | | 2,610,000 | | 2,348,418 |

| | | | |

Total Commercial Mortgage-Backed Securities (cost of $148,379,610) | | 141,738,505 |

|

Government & Agency Obligations – 12.5% |

| | | | |

| Foreign Government Obligations – 2.3% |

| European Investment Bank |

3.000% 04/08/14 | | 3,295,000 | | 3,251,681 |

5.125% 05/30/17 | | 5,935,000 | | 6,297,266 |

|

| Export-Import Bank of Korea |

5.500% 10/17/12 | | 700,000 | | 694,031 |

|

International Bank for Reconstruction &

Development |

5.000% 04/01/16 | | 10,570,000 | | 11,413,169 |

|

| Kreditanstalt fuer Wiederaufbau |

4.500% 07/16/18 | | 1,695,000 | | 1,698,192 |

|

| Pemex Project Funding Master Trust |

5.750% 03/01/18 | | 5,765,000 | | 5,217,325 |

|

| Province of Quebec |

4.625% 05/14/18 | | 6,395,000 | | 6,189,049 |

| | | | |

Foreign Government Obligations Total | | 34,760,713 |

|

| U.S. Government Agency – 3.9% |

| Federal National Mortgage Association |

3.625% 08/15/11 | | 45,000,000 | | 47,218,410 |

|

| Resolution Funding Corp., STRIPS |

(h) 01/15/21 | | 19,755,000 | | 11,573,072 |

| | | | |

U.S. Government Agency Total | | 58,791,482 |

|

| U.S. Government Obligations – 6.3% |

| U.S. Treasury Bonds |

4.500% 05/15/38 (i) | | 7,370,000 | | 7,930,813 |

6.125% 11/15/27 | | 10,000,000 | | 12,639,060 |

|

| U.S. Treasury Inflation-Indexed Notes |

1.625% 01/15/18 | | 20,780,604 | | 20,676,701 |

3.000% 07/15/12 | | 3,038,423 | | 3,207,435 |

See Accompanying Notes to Financial Statements.

13

Columbia Core Bond Fund

April 30, 2009

Government & Agency Obligations (continued)

| | | | |

| | | Par ($) | | Value ($) |

| U.S. Government Obligations (continued) |

| U.S. Treasury Notes |

1.875% 02/28/14 | | 7,185,000 | | 7,148,500 |

2.375% 03/31/16 | | 25,000,000 | | 24,554,700 |

2.625% 02/29/16 | | 20,000,000 | | 20,006,240 |

|

U.S. Government Obligations Total | | 96,163,449 |

| | | | |

Total Government & Agency Obligations

(cost of $190,252,220) | | 189,715,644 |

| |

Asset-Backed Securities – 8.1% | | |

| AmeriCredit Automobile Receivables Trust | | |

3.930% 10/06/11 | | 1,442,748 | | 1,382,707 |

4.730% 07/06/10 | | 335,946 | | 335,903 |

| |

| Bay View Auto Trust | | |

5.310% 06/25/14 | | 2,550,000 | | 2,295,402 |

|

| Bombardier Capital Mortgage Securitization Corp. |

6.230% 04/15/28 | | 2,469 | | 2,014 |

| |

| Capital Auto Receivables Asset Trust | | |

5.500% 04/20/10 (c) | | 1,850,000 | | 1,841,472 |

5.730% 03/15/11 | | 4,000,000 | | 2,800,656 |

| |

| Capital One Multi-Asset Execution Trust | | |

0.431% 08/15/12 (a) | | 7,505,000 | | 7,435,062 |

4.850% 11/15/13 | | 3,675,000 | | 3,692,879 |

4.850% 02/18/14 | | 9,330,000 | | 9,260,255 |

4.950% 08/15/12 | | 6,215,000 | | 6,274,503 |

| |

| Capital One Prime Auto Receivables Trust | | |

4.890% 01/15/12 | | 5,300,914 | | 5,359,060 |

| |

| Chase Issuance Trust | | |

4.260% 05/15/13 | | 6,990,000 | | 7,075,559 |

| |

| Citibank Credit Card Issuance Trust | | |

1.241% 05/21/12 (a) | | 2,405,000 | | 2,353,836 |

| |

| CitiFinancial Mortgage Securities, Inc. | | |

2.645% 04/25/34 | | 387,069 | | 353,327 |

| |

| Citigroup Mortgage Loan Trust, Inc. | | |

5.517% 08/25/35 | | 2,800,000 | | 271,823 |

5.666% 08/25/35 | | 1,885,000 | | 116,075 |

| |

| Daimler Chrysler Auto Trust | | |

4.940% 02/08/12 | | 7,891,000 | | 7,716,129 |

| |

| Discover Card Master Trust | | |

5.100% 10/15/13 | | 6,640,000 | | 6,696,139 |

| |

| Equity One ABS, Inc. | | |

0.778% 07/25/34 (a) | | 416,020 | | 157,944 |

| |

| First Plus Home Loan Trust | | |

7.720% 05/10/24 | | 14,810 | | 14,756 |

| | | | |

| | | Par ($) | | Value ($) |

| Ford Credit Auto Owner Trust | | |

5.150% 11/15/11 | | 6,525,000 | | 6,671,269 |

5.160% 04/15/13 | | 9,405,000 | | 9,097,983 |

5.680% 06/15/12 | | 2,300,000 | | 1,822,854 |

| |

| Franklin Auto Trust | | |

5.360% 05/20/16 | | 4,980,000 | | 4,843,313 |

| |

| GE Capital Credit Card Master Note Trust | | |

4.130% 06/15/13 | | 3,966,000 | | 3,924,907 |

| |

| GE Equipment Small Ticket LLC | | |

4.620% 12/22/14 (c) | | 243,868 | | 239,674 |

5.120% 06/22/15 (c) | | 1,197,688 | | 1,111,272 |

| |

| Green Tree Financial Corp. | | |

8.250% 07/15/27 (a) | | 402,118 | | 348,005 |

| |

| GS Auto Loan Trust | | |

4.980% 11/15/13 | | 19,028 | | 18,983 |

| |

| GSAA Trust | | |

4.316% 11/25/34 (a) | | 1,177,843 | | 903,259 |

| |

| Honda Auto Receivables Owner Trust | | |

4.470% 01/18/12 | | 7,020,000 | | 7,132,390 |

| |

| Long Beach Auto Receivables Trust | | |

4.522% 06/15/12 | | 1,672,798 | | 1,624,181 |

| |

| Oakwood Mortgage Investors, Inc. | | |

7.100% 08/15/27 | | 182,282 | | 174,173 |

| |

| Origen Manufactured Housing | | |

4.490% 05/15/18 | | 311,508 | | 296,263 |

|

| Residential Funding Mortgage Securities II, Inc. |

4.700% 08/25/34 | | 412,899 | | 379,966 |

| |

| USAA Auto Owner Trust | | |

4.280% 10/15/12 | | 5,295,000 | | 5,410,365 |

4.900% 02/15/12 | | 6,967,910 | | 7,068,491 |

| |

| Wachovia Auto Loan Owner Trust | | |

5.650% 02/20/13 | | 5,000,000 | | 2,210,375 |

| |

| WFS Financial Owner Trust | | |

4.620% 11/19/12 | | 3,500,000 | | 3,453,862 |

| | | | |

Total Asset-Backed Securities

(cost of $132,205,609) | | 122,167,086 |

|

Collateralized Mortgage Obligations – 0.5% |

| | | | |

| Agency – 0.5% | | | | |

| Federal Home Loan Mortgage Corp. | | |

I.O., | | | | |

5.500% 05/15/27 | | 366,765 | | 3,244 |

See Accompanying Notes to Financial Statements.

14

Columbia Core Bond Fund

April 30, 2009

Collateralized Mortgage Obligations (continued)

| | | | | |

| | | Par ($) | | Value ($) | |

| Federal National Mortgage Association | | | |

4.717% 08/25/12 | | 3,713,154 | | 3,867,154 | |

5.500% 09/25/35 | | 3,707,718 | | 3,749,007 | |

| |

| Vendee Mortgage Trust | | | |

I.O., | | | |

0.300% 03/15/29 (a) | | 7,462,931 | | 37,736 | |

0.439% 03/15/28 (a) | | 5,727,588 | | 91,528 | |

| | | | | |

Agency Total | | 7,748,669 | |

| | | | | |

| Non-agency – 0.0% | | | | | |

| Countrywide Alternative Loan Trust | | | |

5.500% 09/25/35 | | 4,698,367 | | 367,385 | |

| | | | | |

Non-Agency Total | | 367,385 | |

| | | | | |

Total Collateralized Mortgage Obligations (cost of $12,042,748) | | 8,116,054 | |

| |

Short-Term Obligation – 7.9% | | | |

Repurchase agreement with Fixed Income Clearing Corp., dated 04/30/09, due 05/01/09, at 0.120%, collateralized by U.S. Government Agency Obligations with various maturities to 07/14/28, market value $121,427,713 (repurchase proceeds $119,046,397) | | 119,046,000 | | 119,046,000 | |

| | | | | |

Total Short-Term Obligation (cost of $119,046,000) | | 119,046,000 | |

| | | | | |

Total Investments – 106.6%

(cost of $1,646,471,416) (j) | | 1,616,091,338 | |

| | | | | |

Other Assets & Liabilities, Net – (6.6)% | | (99,575,305 | ) |

| | | | | |

Net Assets – 100.0% | | 1,516,516,033 | |

Notes to Investment Portfolio:

| (a) | The interest rate shown on floating rate or variable rate securities reflects the rate at April 30, 2009. |

| (b) | Security purchased on a delayed delivery basis. |

| (c) | Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At April 30, 2009, these securities, which are not illiquid, except for the following, amounted to $68,589,823, which represents 4.5% of net assets. |

| | | | | | | | | | | |

Security | | Acquisition

Date | | Par/Unit | | Cost | | Value |

Qatar Petroleum 5.579%, 05/30/11 | | 05/19/06 | | $ | 1,552,902 | | $ | 1,552,902 | | $ | 1,576,893 |

| (d) | A portion of this security is pledged as collateral for credit default swaps. At April 30, 2009, the total market value of securities pledged amounted to $2,331,535. |

| (e) | Investments in affiliates during the year ended April 30, 2009: Security name: Merrill Lynch & Co., Inc., 6.050%, 08/15/12 |

| | | |

Par as of 04/30/08: | | $ | 645,000 |

Par purchased: | | $ | — |

Par sold: | | $ | — |

Par as of 04/30/09: | | $ | 645,000 |

Net realized gain (loss): | | $ | — |

Interest income earned: | | $ | 39,023 |

Value at end of period: | | $ | 593,260 |

| | Security name: Merrill Lynch & Co., Inc., 6.150%, 04/25/13 |

| | | | |

Par as of 04/30/08: | | $ | 2,685,000 | |

Par purchased: | | $ | — | |

Par sold: | | $ | (485,000 | ) |

Par as of 04/30/09: | | $ | 2,200,000 | |

Net realized loss: | | $ | (22,460 | ) |

Interest income earned: | | $ | 145,408 | |

Value at end of period: | | $ | 2,022,680 | |

| | Security name: Merrill Lynch & Co., Inc., 5.700%, 05/02/17 |

| | | |

Par as of 04/30/08: | | $ | 3,850,000 |

Par purchased: | | $ | — |

Par sold: | | $ | — |

Par as of 04/30/09: | | $ | 3,850,000 |

Net realized gain (loss): | | $ | — |

Interest income earned: | | $ | 219,450 |

Value at end of period: | | $ | 2,524,029 |

| | Security name: Merrill Lynch & Co., Inc., 7.750%, 05/14/38 |

| | | | |

Par as of 04/30/08: | | $ | — | |

Par purchased: | | $ | 2,280,000 | |

Par sold: | | $ | (745,000 | ) |

Par as of 04/30/09: | | $ | 2,075,000 | |

Net realized loss: | | $ | (12,859 | ) |

Interest income earned: | | $ | 155,807 | |

Value at end of period: | | $ | 1,417,161 | |

As of 01/01/2009, Merrill Lynch & Co., Inc. is a wholly owned subsidiary of Bank of America Corporation and an affiliate of Columbia Management.

| (f) | The issuer has filed for bankruptcy protection under Chapter 11 and is in default of certain debt covenants. Income is not being accrued. At April 30, 2009, the value of these securities amounted to $1,015,312, which represents 0.1% of net assets. |

| (g) | Represents fair value as determined in good faith under procedures approved by the Board of Trustees. At April 30, 2009, the value of these securities amounted to $1,015,312, which represents 0.1% of net assets. |

| (i) | A portion of this security is pledged as collateral for open futures contracts. At April 30, 2009, the market value of this security pledged amounted to $2,582,626. |

| (j) | Cost for federal income tax purposes is $1,646,345,388. |

See Accompanying Notes to Financial Statements.

15

Columbia Core Bond Fund

April 30, 2009

The following table summarizes the inputs used, as of April 30, 2009, in valuing the Fund’s assets:

| | | | | | | |

Valuation Inputs | | Investments in

Securities | | Other Financial

Instruments* | |

Level 1 – Quoted Prices | | $ | 309,407,097 | | $ | 139,866 | |

Level 2 – Other Significant Observable Inputs | | | 1,306,198,624 | | | (413,925 | ) |

Level 3 – Significant Unobservable Inputs | | | 485,617 | | | — | |

| | | | | | | |

Total | | $ | 1,616,091,338 | | $ | (274,059 | ) |

| | | | | | | |

* Other financial instruments consist of futures contracts and credit default swap contracts which are not included in the investment portfolio.

The following table reconciles asset balances for the year ended April 30, 2009, in which significant unobservable inputs (Level 3) were used in determining value:

| | | | | | | |

| | | Investments in

Securities | | | Other Financial

Instruments |

Balance as of April 30, 2008 | | $ | 653,291 | | | $ | — |

Accretion of discounts/Amortization of premiums | | | — | | | | — |

Realized gain | | | 2,999 | | | | — |

Change in unrealized depreciation | | | (552,981 | ) | | | — |

Net purchases | | | 11,528,696 | | | | — |

Transfers out of Level 3 | | | (11,146,388 | ) | | | — |

| | | | | | | |

Balance as of April 30, 2009 | | $ | 485,617 | | | $ | — |

| | | | | | | |

The change in unrealized losses attributable to securities owned at April 30, 2009 which were valued using significant unobservable inputs (Level 3) amounted to $552,981. This amount is included in net change in unrealized depreciation on the Statement of Changes in Net Assets

The information in the above reconciliation represents fiscal year to date activity for any securities identified as using Level 3 inputs at either the beginning or the end of the current fiscal period.

For more information on valuation inputs, and their aggregation into the levels used in the tables above, please refer to the Security Valuation section in the accompanying Notes to Financial Statements.

At April 30, 2009, the Fund held the following open long futures contracts:

| | | | | | | | | | | | | | |

Type | | Number of

Contracts | | Value | | Aggregate

Face Value | | Expiration

Date | | Unrealized

Appreciation

(Depreciation) | |

5-Year U.S. Treasury Notes | | 470 | | $ | 55,056,094 | | $ | 54,903,403 | | Jun-2009 | | $ | 152,691 | |

10-Year U.S. Treasury Notes | | 100 | | | 12,093,750 | | | 12,106,575 | | Jun-2009 | | | (12,825 | ) |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | $ | 139,866 | |

| | | | | | | | | | | | | | |

At April 30, 2009, the Fund had entered into the following credit default swap contracts:

| | | | | | | | | | | | | | | | |

Swap

Counterparty | | Referenced

Obligation | | Receive

Buy/Sell

Protection | | Fixed

Rate | | | Expiration

Date | | Notional

Amount | | Value of

Contract | |

Morgan Stanley | | Limited Brands, Inc.

6.125% 12/01/12 | | Buy | | 5.270 | % | | 12/20/13 | | $ | 500,000 | | $ | (58,905 | ) |

Barclays Capital | | Limited Brands, Inc.

6.125% 12/01/12 | | Buy | | 6.150 | % | | 03/20/14 | | | 500,000 | | | (81,341 | ) |

JPMorgan | | Macy’s, Inc.

7.450% 07/15/17 | | Buy | | 3.600 | % | | 12/20/13 | | | 5,070,000 | | | (273,679 | ) |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | $ | (413,925 | ) |

| | | | | | | | | | | | | | | | |

At April 30, 2009, the asset allocation of the Fund is as follows:

| | | |

Asset Allocation (Unaudited) | | % of

Net Assets | |

Mortgage-Backed Securities | | 46.6 | |

Corporate Fixed-Income Bonds & Notes | | 21.7 | |

Government & Agency Obligations | | 12.5 | |

Commercial Mortgage-Backed Securities | | 9.3 | |

Asset-Backed Securities | | 8.1 | |

Collateralized Mortgage Obligations | | 0.5 | |

| | | |

| | 98.7 | |

Short-Term Obligation | | 7.9 | |

Other Assets & Liabilities, Net | | (6.6 | ) |

| | | |

| | 100.0 | |

| | | |

| | |

Acronym | | Name |

| I.O. | | Interest Only |

| TBA | | To Be Announced |

| STRIPS | | Separate Trading of Registered Interest and Principal of Securities |

See Accompanying Notes to Financial Statements.

16

Statement of Assets and Liabilities – Columbia Core Bond Fund

April 30, 2009

| | | | | |

| | | | | ($) | |

| Assets | | Unaffiliated investments, at cost | | 1,637,737,942 | |

| | Affiliated investments, at cost | | 8,733,474 | |

| | | | | |

| | Total investments, at cost | | 1,646,471,416 | |

| | Unaffiliated investments, at value | | 1,609,534,208 | |

| | Affiliated investments, at value | | 6,557,130 | |

| | | | | |

| | Total investments, at value | | 1,616,091,338 | |

| | |

| | Cash | | 725 | |

| | Receivable for: | | | |

| | Investments sold | | 54,976,022 | |

| | Investments sold on a delayed delivery basis | | 113,371,741 | |

| | Fund shares sold | | 2,774,306 | |

| | Interest | | 10,379,741 | |

| | Securities lending | | 19,477 | |

| | Expense reimbursement due from investment advisor | | 270,687 | |

| | Trustees’ deferred compensation plan | | 65,332 | |

| | Other assets | | 39,648 | |

| | | |

| | Total Assets | | 1,797,989,017 | |

| | |

| Liabilities | | Open credit default swap contracts | | 413,925 | |

| | Payable for: | | | |

| | Investments purchased | | 399,900 | |

| | Investments purchased on a delayed delivery basis | | 274,012,375 | |

| | Fund shares repurchased | | 2,214,800 | |

| | Futures variation margin | | 26,094 | |

| | Distributions | | 3,362,283 | |

| | Investment advisory fee | | 544,169 | |

| | Administration fee | | 83,347 | |

| | Transfer agent fee | | 140,645 | |

| | Trustees’ fees | | 42,749 | |