Exhibit (17)(b)(ii)

A n n u a l R e p o r t S e p t e m b e r 3 0 , 2 0 0 7

EATON VANCE NATIONAL MUNICIPALS

FUND

| | IMPORTANT NOTICES REGARDING PRIVACY,

DELIVERY OF SHAREHOLDER DOCUMENTS,

PORTFOLIO HOLDINGS AND PROXY VOTING |

Privacy. The Eaton Vance organization is committed to ensuring your financial privacy. Each of the financial institutions identified below has in effect the following policy (“Privacy Policy”) with respect to nonpublic personal information about its customers:

- Only such information received from you, through application forms or otherwise, and information about your Eaton Vance fund transactions will be collected. This may include information such as name, address, social security number, tax status, account balances and transactions.

- None of such information about you (or former customers) will be disclosed to anyone, except as permitted by law (which includes disclosure to employees necessary to service your account). In the normal course of servicing a customer’s account, Eaton Vance may share information with unaffiliated third parties that perform various required services such as transfer agents, custodians and broker/dealers.

- Policies and procedures (including physical, electronic and procedural safeguards) are in place that are designed to protect the confidentiality of such information.

- We reserve the right to change our Privacy Policy at any time upon proper notification to you. Customers may want to review our Policy periodically for changes by accessing the link on our homepage: www.eatonvance.com.

Our pledge of privacy applies to the following entities within the Eaton Vance organization: the Eaton Vance Family of Funds, Eaton Vance Management, Eaton Vance Investment Counsel, Boston Management and Research, and Eaton Vance Distributors, Inc.

In addition, our Privacy Policy only applies to those Eaton Vance customers who are individuals and who have a direct relationship with us. If a customer’s account (i.e. fund shares) is held in the name of a third-party financial adviser/ broker-dealer, it is likely that only such adviser’s privacy policies apply to the customer. This notice supersedes all previously issued privacy disclosures.

For more information about Eaton Vance’s Privacy Policy, please call 1-800-262-1122.

Delivery of Shareholder Documents. The Securities and Exchange Commission (the “SEC”) permits funds to deliver only one copy of shareholder documents, including prospectuses, proxy statements and shareholder reports, to fund investors with multiple accounts at the same residential or post office box address. This practice is often called “householding” and it helps eliminate duplicate mailings to shareholders.

Eaton Vance, or your financial adviser, may household the mailing of your documents indefinitely unless you instruct Eaton Vance, or your financial adviser, otherwise.

If you would prefer that your Eaton Vance documents not be householded, please contact Eaton Vance at 1-800-262-1122, or contact your financial adviser.

Your instructions that householding not apply to delivery of your Eaton Vance documents will be effective within 30 days of receipt by Eaton Vance or your financial adviser.

Portfolio Holdings. Each Eaton Vance Fund and its underlying Portfolio (if applicable) will file a schedule of its portfolio holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. The Form N-Q will be available on the Eaton Vance website www.eatonvance.com, by calling Eaton Vance at 1-800-262-1122 or in the EDGAR database on the SEC’s website at www.sec.gov. Form N-Q may also be reviewed and copied at the SEC’s public reference room in Washington, D.C. (call 1-800-732-0330 for information on the operation of the public reference room).

Proxy Voting. From time to time, funds are required to vote proxies related to the securities held by the funds. The Eaton Vance Funds or their underlying Portfolios (if applicable) vote proxies according to a set of policies and procedures approved by the Funds’ and Portfolios’ Boards. You may obtain a description of these policies and procedures and information on how the Funds or Portfolios voted proxies relating to Portfolio securities during the most recent 12 month period ended June 30, without charge, upon request, by calling 1-800-262-1122. This description is also available on the SEC’s website at www.sec.gov.

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

M A N A G E M E N T ' S D I S C U S S I O N O F F U N D P E R F O R M A N C E |

Eaton Vance National Municipals Fund (the “Fund”) is designed to provide current income exempt from regular federal income tax. The Fund invests primarily in investment-grade municipal obligations but also invests in lower-rated municipal obligations.

Economic and Market Conditions

Third quarter economic growth rose 3.1%, following the 3.8% growth rate achieved in the second quarter of 2007, according to preliminary Commerce Department data. During the third quarter ended September 30, 2007, the housing sector continued to struggle, as market concerns related to subprime mortgages caused a number of mortgage lenders to file for bankruptcy protection and others to limit new mortgage originations. Building permits and housing starts have both fallen significantly from their highs in early 2006, while sales of new and existing homes are down from their 2005 peaks. However, the weaker dollar is having a stimulative effect on economic growth in export-related industries and on U.S.-based multinational companies whose foreign profits are translated into more dollars. Overall, we believe the economy appears to be slowing, but in a somewhat controlled manner.

According to the Federal Reserve’s (the “Fed”) preferred inflation indicator, the Personal Consumption Expenditure (PCE) price deflator, both absolute and core (excludes food and energy) inflation is fairly well contained within the upper end of the Fed’s comfort zone. In an unscheduled August 17, 2007 meeting, the Fed lowered its Discount Rate – the rate charged to banks borrowing directly from the Fed – to 5.75% from 6.25% . The move was aimed at providing liquidity during a period of increased uncertainty and tighter credit conditions that surfaced rapidly in mid-August. On September 18, 2007, the Fed lowered its Federal Funds Rate to 4.75% from 5.25% – its first rate cut since the Fed stopped raising rates in June 2006 – and lowered the Discount Rate again to 5.25% from 5.75% .

Municipal market supply rose to record levels in the first half of 2007, resulting in underperformance of the municipal sector. On September 30, 2007, long-term AAA-rated municipal bonds yielded 93.9% of U.S. Treasury bonds with similar maturities.1

For the year ended September 30, 2007, the Lehman Brothers Municipal Bond Index2 (the “Index”), an unmanaged index of municipal bonds, posted a gain of 3.10% . For more information about the Fund’s performance and that of funds in the same Lipper Classification,2 see the Performance Information and Portfolio Composition pages that follow.

Management Discussion

The Fund invests primarily in bonds with stated maturities of 10 years or longer at the time of investment, as longer-maturity bonds historically have provided greater tax-exempt income for investors than shorter-maturity bonds.

The Fund underperformed its benchmark Index during the year ended September 30, 2007. Much of the under-performance can be attributed to the broader-based credit scare that took hold of the fixed-income markets in late August 2007. Yields on some municipal bonds reached 105% of U.S. Treasury yields. We believe that the ratio was not the result of any fundamental problems within the municipal market, but rather reflected the extreme dislocation in the fixed-income marketplace caused by the subprime fears, hedge fund problems, the decentralized municipal marketplace and illiquidity across a range of markets. The Fund's exposure to more liquid, higher-credit quality bonds actually hurt performance as hedge funds and other non-traditional municipal market participants sold large positions of their most liquid bonds in order to raise cash.

Historically, there have been only a few instances of municipals trading at the cheap levels seen in August 2007, and it has generally been a short-term phenomenon. During September 2007, municipals outperformed Treasury bonds, as municipal yields reverted to their more historic relationship to Treasuries. Overall, liquidity has returned to the fixed-income marketplace, with a more rational view of the market and risk assessment.

| 1 | Source: Bloomberg L.P. Yields are a compilation of a representative variety of general obligations and are not necessarily representative of the Fund’s yield. |

| |

| 2 | It is not possible to invest directly in an Index or a Lipper Classification. The Index’s total return does not reflect expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. |

| |

| | Past performance is no guarantee of future results. |

| |

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

The views expressed throughout this report are those of the portfolio manager and are current only through the end of the period of the report as stated on the cover. These views are subject to change at any time based upon market or other conditions, and the investment adviser disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund are based on many factors, may not be relied on as an indication of trading intent on behalf of any Eaton Vance fund.

1

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

P E R F O R M A N C E I N F O R M A T I O N A N D P O R T F O L I O C O M P O S I T I O N |

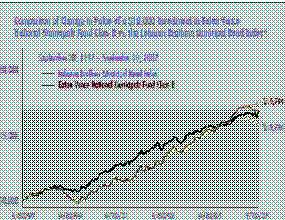

The line graph and table set forth below provide information about the Fund’s performance. The line graph compares the performance of Class B of the Fund with that of the Lehman Brothers Municipal Bond Index, an unmanaged index of municipal bonds. The lines on the graph represent the total returns of a hypothetical investment of $10,000 in each of Class B and the Lehman Brothers Municipal Bond Index. The table includes the total returns of each Class of the Fund at net asset value and maximum public offering price. The performance presented below does not reflect the deduction of taxes, if any, that a shareholder would pay on distributions or redemptions of Fund shares.

| Fund Performance1 As of 9/30/07 | | Class A | | Class B | | Class C | | Class I |

| Share Class Symbol | | EANAX | | EVHMX | | ECHMX | | EIHMX |

|

| Average Annual Total Returns (at net asset value) | | | | | | | | |

|

| One Year | | 1.95% | | 1.20% | | 1.20% | | 2.20% |

| Five Years | | 6.47 | | 5.85 | | 5.71 | | 6.74 |

| Ten Years | | 5.94 | | 5.32 | | 5.13 | | N.A. |

| Life of Fund† | | 7.05 | | 6.59 | | 5.33 | | 6.74 |

| | | | |

| | | | |

| SEC Average Annual Total Returns (including sales charge or applicable CDSC) | | | | |

|

| One Year | | -2.92% | | -3.68% | | 0.22% | | 2.20% |

| Five Years | | 5.45 | | 5.53 | | 5.71 | | 6.74 |

| Ten Years | | 5.43 | | 5.32 | | 5.13 | | N.A. |

| Life of Fund† | | 6.66 | | 6.59 | | 5.33 | | 6.74 |

†Inception Dates – Class A: 4/5/94; Class B: 12/19/85; Class C: 12/3/93; Class I: 7/1/99

| Total Annual | | | | | | | | |

| Operating Expenses2 | | Class A | | Class B | | Class C | | Class I |

|

| Expense Ratio | | 1.33% | | 2.08% | | 2.08% | | 1.08% |

| |

| Distribution Rates/Yields | | Class A | | Class B | | Class C | | Class I |

|

| |

| Distribution Rate3 | | 4.53% | | 3.78% | | 3.78% | | 4.79% |

| Taxable-Equivalent Dist. Rate3,4 | | 6.97 | | 5.82 | | 5.82 | | 7.37 |

| SEC 30-day Yield5 | | 4.16 | | 3.62 | | 3.62 | | 4.63 |

| Taxable-Equivalent SEC 30-day Yield4,5 | | 6.40 | | 5.57 | | 5.57 | | 7.12 |

| | | | | | | | |

| Index Performance6 | | | | | | | | |

|

| Lehman Brothers Municipal Bond Index – Average Annual Total Returns |

|

| One Year | | 3.10% | | | | |

| Five Years | | 4.02 | | | | |

| Ten Years | | 5.32 | | | | |

| | | | | | | | |

| Lipper Averages7 | | | | | | | | |

|

| Lipper General Municipal Debt Funds Classification – Average Annual Total Returns |

|

| One Year | | 1.78% | | | | |

| Five Years | | 3.33 | | | | |

| Ten Years | | 4.33 | | | | |

Portfolio Manager: Thomas M. Metzold, CFA

*Sources: Thomson Financial; Lipper, Inc.

A $10,000 hypothetical investment at net asset value in Class A and Class C on 9/30/97 and Class I on 7/1/99 (commencement of operations), respectively, would have been valued at $17,814 ($16,968 at the maximum offering price), $16,500 and $17,132, respectively, on 9/30/07. It is not possible to invest directly in an Index. The Index’s total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or offering price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

1 Average annual total returns do not include the 4.75% maximum sales charge for Class A shares or the applicable contingent deferred sales charges (CDSC) for Class B and Class C shares. If sales charges were deducted, returns would be lower. SEC Average Annual Total Returns for Class A reflect the maximum 4.75% sales charge. SEC Average Annual Total Returns for Class B reflect the applicable CDSC based on the following schedule: 5% - 1st and 2nd years; 4% - 3rd year; 3% - 4th year; 2% - 5th year; 1% - 6th year. SEC Average Annual Total Returns for Class C reflect a 1% CDSC for the first year. Class I shares are not subject to a sales charge. 2 Source: Prospectus dated 2/1/07, as revised 6/27/07. Includes interest expense of 0.61% relating to the Fund's liability with respect to floating-rate notes held by third parties in conjunction with inverse floater securities transactions by the Fund. The Fund also records offsetting interest income re lating to the municipal obligations underlying such transactions, and, as a result, net asset value and performance have not been affected by this expense. 3 The Fund's distribution rate represents actual distributions paid to shareholders and is calculated by dividing the last distribution per share (annualized) by the net asset value. 4 Taxable-equivalent figure assumes a maximum 35.00% federal income tax rate. A lower tax rate would result in lower tax-equivalent figures. 5 The Fund's SEC yield is calculated by dividing the net investment income per share for the 30-day period by the offering price at the end of the period and annualizing the result. 6 It is not possible to invest directly in an Index. The Index's total return does not reflect the expenses that would have been incurred if an investor individually purchased or sold the securities represented in the Index. Index performance is available as of month end only. 7 The Lipper Averages are the average annual total returns, at net asset value, of the funds that are in the same Lipper Classification as the Fund. It is not possible to invest in a Lipper Classification. Lipper Classifications may include insured and uninsured funds, as well as leveraged and unleveraged funds. The Lipper General Municipal Debt Funds Classification contained 236, 212 and 138 funds for the 1-year, 5-year and 10-year periods, respectively. Lipper Averages are available as of month end only.

2

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

P E R F O R M A N C E I N F O R M A T I O N A N D P O R T F O L I O C O M P O S I T I O N |

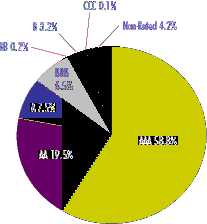

Rating Distribution*1,2

By total investments

*The rating distribution presented above includes the ratings of securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 11 to the Fund's financial statements. Absent such securities, the Fund's rating distribution at Septemer 30, 2007, is as follows, and the average rating is AA:

| AAA | | 59.6% | | BB | | 0.3% |

| AA | | 14.7% | | B | | 3.6% |

| A | | 8.4% | | CCC | | 0.1% |

| BBB | | 7.5% | | Non-Rated | | 5.8% |

Fund Statistics2,3

| • Number of Issues: | | 271 |

| • Average Maturity: | | 27.6 years |

| • Average Effective Maturity: | | 21.9 years |

| • Average Call Protection: | | 11.4 years |

| • Average Dollar Price: | | $93.13 |

1 Rating Distribution is determined by dividing the total market value of the issues by the total investments of the Fund. 2 As of 9/30/07. Portfolio information may not be representative of the Fund's current or future investments and may change due to active management. 3 Portfolio holdings information excludes securities held by special purpose vehicles in which the Fund holds a residual interest. See Note 1I to the Fund’s financial statements.

| Morningstar RatingsTM3 | | | | | | | | |

|

| |

| NATIONAL MUNICIPALS FUND – CLASS A | | OVERALL | | 3-YEARR | | 5-YEAR | | 10-YEAR |

| | | ***** | | ***** | | ***** | | ***** |

| Load waived | | ***** | | ***** | | ***** | | ***** |

| MUNI NATIONAL LONG CATEGORY | | 256 FUNDS | | 256 FUNDS | | 245 FUNDS | | 189 FUNDS |

|

3Based on risk-adjusted returns. Eaton Vance offers other mutual funds that are not listed here and that do not have similar performance records.

The Overall Morningstar Rating™ for a fund is derived from a weighted average of the performance figures associated with its 3-, 5- and 10-year (if applicable) Morningstar Rating™ metrics.

©2007 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers is responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. For each fund with at least a three-year history, Morningstar calculates a Morningstar Rating™ based on how a fund ranks on a Morningstar Risk-Adjusted Return measure against other funds in the same category. This measure takes into account variations in a fund’s monthly performance after adjusting for sales loads (except for load-waived A shares), redemption fees, and the risk-free rate, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each category receive 5 stars; the next 22.5% receive 4 stars; the next 35% receive 3 stars; the next 22.5% receive 2 stars, and the bottom 10% receive 1 star.

Load-waived A share star ratings do not include any front-end sales load and are intended for those investors who have access to such purchase terms (e.g., plan participants of a defined contribution plan). Not all A share mutual funds for which Morningstar calculates a load-waived A share star rating may actually waive their front-end load. Therefore, Morningstar strongly encourages investors to contact their investment professional to determine whether they are eligible to purchase the A share without paying the front load. The Morningstar Rating may differ among share classes of a mutual fund as a result of different sales loads and/or expense structure.

As interest rates rise, the value of fixed-income securities is likely to decrease. Fluctuations in the value of securities may not affect interest income on existing securities, but will be reflected in the funds’ net asset values. A portion of income may be subject to federal alternative minimum tax. Please see the Fund’s prospectus for more information. Consult tax/legal advisor before making any tax-related investment decisions.

3

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

F U N D E X P E N S E S |

Example: As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchases and redemption fees (if applicable); and (2) ongoing costs, including management fees; distribution or service fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (April 1, 2007 – September 30, 2007).

Actual Expenses: The first section of the table below provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes: The second section of the table below provides information about hypothetical account values and hypothetical expenses based on the actual Fund expense ratio and an assumed rate of return of 5% per year (before expenses), which is not the actual return of the Fund. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption fees (if applicable). Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Eaton Vance National Municipals Fund | | |

| |

| | | Beginning Account Value | | Ending Account Value | | Expenses Paid During Period* |

| | | (4/1/07) | | (9/30/07) | | (4/1/07 – 9/30/07) |

|

| |

| Actual | | | | | | |

| Class A | | $1,000.00 | | $988.30 | | $6.03 |

| Class B | | $1,000.00 | | $984.60 | | $9.75 |

| Class C | | $1,000.00 | | $984.60 | | $9.75 |

| Class I | | $1,000.00 | | $989.50 | | $4.79 |

|

| |

| |

| Hypothetical | | | | | | |

| (5% return per year before expenses) | | | | | | |

| Class A | | $1,000.00 | | $1,019.00 | | $6.12 |

| Class B | | $1,000.00 | | $1,015.20 | | $9.90 |

| Class C | | $1,000.00 | | $1,015.20 | | $9.90 |

| Class I | | $1,000.00 | | $1,020.30 | | $4.86 |

| * | Expenses are equal to the Fund’s annualized expense ratio of 1.21% for Class A shares, 1.96% for Class B shares, 1.96% for Class C shares, and 0.96% for Class I shares multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). The Example assumes that the $1,000 was invested at the net asset value per share determined at the close of business on March 31, 2007. |

| |

4

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

P O R T F O L I O O F I N V E S T M E N T S |

| Ta x - E x e m p t I n v e s t m e n t s — 1 1 0 . 9 % | | |

| |

| Principal Amount | | | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Cogeneration — 0.9% | | | | |

|

| $ 22,150 | | Maryland Energy Cogeneration, (AES Warrior Run), | | |

| | | (AMT), 7.40%, 9/1/19 | | $ 22,208,254 |

| 6,100 | | Pennsylvania Economic Development Financing Authority, | | |

| | | (Northampton Generating), (AMT), 6.50%, 1/1/13 | | 6,180,337 |

| 21,950 | | Pennsylvania Economic Development Financing Authority, | | |

| | | (Northampton Generating), (AMT), 6.60%, 1/1/19 | | 22,045,921 |

| 4,200 | | Pennsylvania Economic Development Financing Authority, | | |

| | | (Northampton Generating), Junior Liens, (AMT), | | |

| | | 6.875%, 1/1/11 | | | | 4,191,180 |

| 5,000 | | Pennsylvania Economic Development Financing Authority, | | |

| | | (Northampton Generating), Junior Liens, (AMT), | | |

| | | 6.95%, 1/1/21 | | | | 4,955,800 |

|

| | | | | $ 59,581,492 |

|

| |

| Education — 2.6% | | | | |

|

| $ 12,390 | | California Educational Facilities Authority, (Stanford | | |

| | | University), 5.35%, 6/1/27(1) | | $ 12,543,471 |

| 32,055 | | Houston, TX, Higher Education Finance Corp., | | |

| | | 4.50%, 11/15/37 | | | | 30,970,579 |

| 31,200 | | Houston, TX, Higher Education Finance Corp., | | |

| | | 4.50%, 5/15/42 | | | | 29,696,472 |

| 22,035 | | Massachusetts Development Finance Agency, | | |

| | | (Smith College), 5.00%, 7/1/35(1) | | | | 22,668,286 |

| 50,475 | | New Jersey Educational Facilities Authority, | | | | |

| | | (Princeton University), 4.50%, 7/1/37 | | | | 50,340,232 |

| 5,725 | | New York Dormitory Authority, (Vassar College), | | |

| | | 4.25%, 7/1/32 | | | | 5,427,930 |

| 15,265 | | New York Dormitory Authority, (Vassar College), | | |

| | | 4.25%, 7/1/39 | | | | 14,246,367 |

|

| | | | | $ 165,893,337 |

|

| |

| Electric Utilities — 2.0% | | | | |

|

| $ 13,000 | | Brazos River Authority, TX, (Reliant Energy, Inc.), | | |

| | | 7.75%, 12/1/18 | | $ 13,487,630 |

| 9,260 | | Brazos River Authority, TX, PCR, (Texas Energy Co.), | | |

| | | (AMT), 5.40%, 5/1/29 | | | | 8,603,466 |

| 2,000 | | Matagorda County, TX, Navigation District No.1, | | |

| | | (Reliant Energy), 8.00%, 5/1/29 | | | | 2,069,280 |

| 5,000 | | Matagorda County, TX, Navigation District No.1, | | |

| | | (Reliant Energy), (AMT), 5.95%, 5/1/30 | | | | 5,092,800 |

| 8,000 | | North Carolina Municipal Power Agency, (Catawba), | | |

| | | 6.50%, 1/1/20 | | | | 8,501,200 |

| 42,000 | | Salt River Project, AZ, Agricultural Improvements and | | |

| | | Power District, 5.00%, 1/1/31(1) | | | | 43,087,212 |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Electric Utilities (continued) | | |

|

| $ 42,000 | | Salt River Project, AZ, Agricultural Improvements and | | |

| | | Power District, 5.00%, 1/1/31(1) | | $ 43,087,212 |

|

| | | | | $ 123,928,800 |

|

| |

| Escrowed / Prerefunded — 5.3% | | |

|

| $ 3,000 | | ABAG Finance Authority, CA, (Civic Center Drive Apartments), | | |

| | | (AMT), Prerefunded to 9/1/09, 6.375%, 9/1/32 | | $ 3,170,430 |

| 2,400 | | Bexar County, TX, Health Facilities, (St. Luke’s Lutheran), | | |

| | | Escrowed to Maturity, 7.00%, 5/1/21 | | 3,054,456 |

| 1,500 | | Capital Trust Agency, FL, (Seminole Tribe Convention), | | |

| | | Prerefunded to 10/1/12, 8.95%, 10/1/33(2) | | 1,839,255 |

| 11,195 | | Colorado Health Facilities Authority, (Liberty Heights), | | |

| | | Escrowed to Maturity, 0.00%, 7/15/22 | | 5,711,577 |

| 215,825 | | Dawson Ridge, CO, Metropolitan District #1, Series A, | | |

| | | Escrowed to Maturity, 0.00%, 10/1/22 | | 109,060,689 |

| 11,175 | | Dawson Ridge, CO, Metropolitan District #1, Series B, | | |

| | | Escrowed to Maturity, 0.00%, 10/1/22 | | 5,646,951 |

| 101,555 | | Illinois Development Finance Authority, (Regency Park), | | |

| | | Escrowed to Maturity, 0.00%, 7/15/23 | | 48,976,930 |

| 5,690 | | Louisiana Public Facilities Authority, (Southern Baptist | | |

| | | Hospitals, Inc.), Escrowed to Maturity, 8.00%, 5/15/12 | | 6,273,737 |

| 5,675 | | Maricopa County, AZ, Industrial Development Authority, | | |

| | | (Place Five and The Greenery), Escrowed to Maturity, | | |

| | | 6.625%, 1/1/27 | | 6,098,355 |

| 100,000 | | Mississippi Housing Finance Corp., Single Family, | | |

| | | Escrowed to Maturity, 0.00%, 6/1/15 | | 73,655,000 |

| 1,190 | | New York, NY, Prerefunded to | | |

| | | 6/1/13, 5.25%, 6/1/28(1) | | 1,290,681 |

| 11,435 | | North Miami, FL, Health Care Facilities Authority, | | |

| | | (Imperial Club), Prerefunded to 1/1/09, 6.75%, 1/1/33 | | 12,135,051 |

| 10,885 | | Tobacco Settlement Financing Corp., NY, Prerefunded to | | |

| | | 6/1/13, 6.75%, 6/1/39 | | 12,572,719 |

| 36,000 | | Tobacco Settlement Financing Corp., VA, Prerefunded to | | |

| | | 6/1/15, 5.625%, 6/1/37(1) | | 40,328,640 |

| 3,655 | | Wisconsin Health and Educational Facilities Authority, | | |

| | | (Wisconsin Illinois Senior Housing), Prerefunded to | | |

| | | 8/1/09, 7.00%, 8/1/29 | | 3,902,261 |

|

| | | | | $ 333,716,732 |

|

| |

| General Obligations — 7.9% | | |

|

| $ 35,000 | | California, 4.75%, 6/1/35 | | $ 34,651,750 |

| 57,575 | | California, 4.75%, 9/1/35 | | 57,001,553 |

| 20,050 | | California, 5.00%, 6/1/37 | | 20,410,499 |

| 16,000 | | California, 5.25%, 11/1/29 | | 16,732,160 |

| 19,930 | | California, 5.25%, 2/1/30 | | 20,969,549 |

| 9,875 | | California, 5.50%, 11/1/33 | | 10,463,056 |

| 41,130 | | Cypress-Fairbanks, TX, Independent School District, | | |

| | | 4.50%, 2/15/28 | | 40,454,234 |

S e e n o t e s t o f i n a n c i a l s t a t e m e n t s

5

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

P O R T F O L I O O F I N V E S T M E N T S C O N T ’ D |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| |

| General Obligations (continued) | | |

|

| 34,500 | | Georgia, 1.00%, 3/1/26 | | $ 19,460,760 |

| 88,410 | | Judson, TX, Independent School District, 4.50%, 2/1/35 | | 85,646,303 |

| 13,015 | | New York, NY, 5.25%, 6/1/28(1) | | 13,549,993 |

| 15,000 | | North Carolina, 3.00%, 3/1/28 | | 11,817,600 |

| 37,500 | | San Francisco, CA, Bay Area Rapid Transit District, | | |

| | | 4.75%, 8/1/37 | | 37,806,000 |

| 10,750 | | South Carolina, 3.00%, 8/1/21 | | 9,257,362 |

| 10,000 | | South Carolina, 3.00%, 8/1/22 | | 8,490,500 |

| 115,000 | | Texas (Transportation Commission-Mobility Fund), | | |

| | | 4.50%, 4/1/33 | | 111,852,450 |

|

| | | | | $ 498,563,769 |

|

| |

| Health Care-Miscellaneous — 0.1% | | |

|

| 1,840 | | Tax Revenue Exempt Securities Trust, Community Health | | |

| | | Provider, (Pooled Loan Program Various States Trust | | |

| | | Certificates), 5.50%, 12/1/36(2) | | $ 1,879,011 |

| 1,971 | | Tax Revenue Exempt Securities Trust, Community Health | | |

| | | Provider, (Pooled Loan Program Various States Trust | | |

| | | Certificates), 5.875%, 12/1/36(2) | | 2,016,997 |

|

| | | | | $ 3,896,008 |

|

| |

| Hospital — 11.5% | | |

|

| 34,260 | | Alabama Special Care Facilities Financing Authority, | | |

| | | (Ascension Health), 5.00%, 11/15/39(1) | | $ 34,485,316 |

| 14,000 | | Brevard County, FL, Health Facilities Authority, | | |

| | | (Health First, Inc.), 5.00%, 4/1/36 | | 13,936,720 |

| 30,500 | | California Health Facilities Financing Authority, | | |

| | | (Cedars-Sinai Medical Center), 5.00%, 11/15/34 | | 30,568,930 |

| 13,000 | | California Statewide Communities Development Authority, | | |

| | | (Huntington Memorial Hospital), 5.00%, 7/1/35 | | 13,077,870 |

| 17,295 | | California Statewide Communities Development Authority, | | |

| | | (John Muir Health), 5.00%, 8/15/36 | | 17,312,468 |

| 45,500 | | California Statewide Communities Development Authority, | | |

| | | (Kaiser Permanente), 5.00%, 3/1/41 | | 45,096,415 |

| 77,500 | | California Statewide Communities Development Authority, | | |

| | | (Kaiser Permanente), 5.25%, 3/1/45 | | 78,470,300 |

| 7,100 | | Camden County, NJ, Improvement Authority, | | |

| | | (Cooper Health System), 5.00%, 2/15/25 | | 7,006,351 |

| 13,475 | | Camden County, NJ, Improvement Authority, | | |

| | | (Cooper Health System), 5.00%, 2/15/35 | | 12,846,795 |

| 14,320 | | Camden County, NJ, Improvement Authority, | | |

| | | (Cooper Health System), 5.25%, 2/15/27 | | 14,393,032 |

| 31,520 | | Colorado Health Facilities Authority, | | |

| | | (Catholic Health Initiatives), 4.50%, 9/1/38 | | 29,167,978 |

| 4,000 | | Erie County, OH, Hospital Facilities, (Firelands | | |

| | | Regional Medical Center), 5.00%, 8/15/36 | | 3,981,600 |

| 9,500 | | Erie County, OH, Hospital Facilities, (Firelands | | |

| | | Regional Medical Center), 5.25%, 8/15/46 | | 9,598,800 |

| Principal Amount | | | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Hospital (continued) | | | | |

|

| $ 27,775 | | Highlands County, FL, Health Facilities Authority, | | | | |

| | | (Adventist Health System), 5.00%, 11/15/35 | | $ 27,800,831 |

| 67,700 | | Indiana Health and Educational Facilities Authority, | | | | |

| | | (Ascension Health), 5.00%, 11/15/36 | | | | 68,165,099 |

| 39,025 | | Maryland Health and Higher Educational Facilities Authority, | | | | |

| | | (Medstar Health), 4.75%, 5/15/42 | | | | 35,663,386 |

| 3,660 | | Maryland Health and Higher Educational Facilities Authority, | | | | |

| | | (Peninsula Regional Medical Center), 5.00%, 7/1/36 | | | | 3,663,587 |

| 26,730 | | Michigan Hospital Finance Authority, (McLaren Healthcare), | | | | |

| | | 5.00%, 8/1/35 | | | | 26,857,235 |

| 44,055 | | New York Dormitory Authority, (Memorial Sloan-Kettering | | | | |

| | | Cancer Center), 4.75%, 7/1/28(1) | | | | 44,762,376 |

| 4,000 | | Oneida County, NY, Industrial Development Agency, | | | | |

| | | (Elizabeth Medical Center), 6.00%, 12/1/29 | | | | 4,030,360 |

| 25,000 | | Rochester, MN, Health Care Facilities, (Mayo Clinic), | | | | |

| | | 5.50%, 11/15/27(1) | | | | 25,490,875 |

| 48,205 | | South Miami, FL, Health Facilities Authority, (Baptist | | | | |

| | | Health), 5.00%, 8/15/37 | | | | 48,482,661 |

| 75,725 | | South Miami, FL, Health Facilities Authority, (Baptist | | | | |

| | | Health), 5.00%, 8/15/42 | | | | 75,534,173 |

| 52,400 | | Tarrant County, TX, Cultural Education Facilities Finance Corp., | | |

| | | (Texas Health Resources), 5.00%, 2/15/36 | | | | 52,728,548 |

| 1,365 | | University of Kansas Hospital Authority, 4.50%, 9/1/32 | | | | 1,237,618 |

|

| | | | | $ 724,359,324 |

|

| |

| Housing — 2.1% | | | | |

|

| $ 6,970 | | Arkansas Development Finance Authority, MFMR, | | | | |

| | | (Park Apartments), (AMT), 5.95%, 12/1/28 | | $ 5,708,012 |

| 7,610 | | California Department of Veterans Affairs, Home Purchase | | | | |

| | | Revenue, 5.20%, 12/1/28 | | | | 7,613,348 |

| 16,000 | | Charter Mac Equity Trust, TN, (AMT), | | | | |

| | | 6.625%, 6/30/09(2) | | | | 16,610,080 |

| 9,100 | | Lake Creek, CO, (Affordable Housing Corp.), Multifamily | | | | |

| | | Housing, 6.25%, 12/1/23 | | | | 9,458,267 |

| 14,835 | | New Hampshire Housing Finance Authority, Multifamily | | | | |

| | | Housing, (AMT), 6.20%, 7/1/36 | | | | 15,046,695 |

| 10,640 | | Texas Student Housing Corp., (University of Northern Texas), | | | | |

| | | 6.85%, 7/1/31 | | | | 10,165,243 |

| 65,720 | | Virginia Housing Development Authority, Series A, | | | | |

| | | Subseries A-2, (AMT), 5.10%, 10/1/35 | | | | 65,187,011 |

|

| | | | | $ 129,788,656 |

|

| |

| Housing-Multifamily — 0.2% | | | | |

|

| $ 10,770 | | Florida Capital Projects Finance Authority, Student Housing | | | | |

| Revenue, (Florida University), Prerefunded to 8/15/10, |

| | | 7.85%, 8/15/31 | | $ 12,214,257 |

|

| | | | | $ 12,214,257 |

|

S e e n o t e s t o f i n a n c i a l s t a t e m e n t s

6

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

P O R T F O L I O O F I N V E S T M E N T S C O N T ’ D |

| Principal Amount | | | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Industrial Development Revenue — 11.6% | | |

|

| |

| 6,850 | | Austin, TX, (Cargoport Development LLC), (AMT), | | | | |

| | | 8.30%, 10/1/21 | | $ 7,472,322 |

| 10,260 | | Bedford County, VA, Industrial Development Authority, | | | | |

| | | (Nekoosa Packaging), (AMT), 6.55%, 12/1/25 | | | | 10,396,663 |

| 2,250 | | Calhoun County, AR, Solid Waste Disposal Revenue, | | | | |

| | | (Georgia-Pacific Corp.), (AMT), 6.375%, 11/1/26 | | | | 2,261,947 |

| 6,050 | | Carbon County, UT, (Laidlaw Environmental), (AMT), | | | | |

| | | 7.50%, 2/1/10 | | | | 6,092,532 |

| 4,000 | | Courtland, AL, Solid Waste Disposal, (Champion | | | | |

| | | International Corp.), (AMT), 6.70%, 11/1/29 | | | | 4,152,760 |

| 29,090 | | Denver, CO, City and County Special Facilities, | | | | |

| | | (United Airlines), (AMT), 5.25%, 10/1/32 | | | | 26,890,505 |

| 23,590 | | Denver, CO, City and County Special Facilities, | | | | |

| | | (United Airlines), (AMT), 5.75%, 10/1/32 | | | | 23,389,013 |

| 3,500 | | Effingham County, GA, Industrial Development Authority, | | | | |

| | | PCR, (Georgia Pacific Corp.), 6.50%, 6/1/31 | | | | 3,558,660 |

| 13,290 | | Effingham County, GA, Solid Waste Disposal, | | | | |

| | | (Fort James Project), (AMT), 5.625%, 7/1/18 | | | | 12,918,279 |

| 5,905 | | Hardeman County, TN, (Correctional Facilities Corp.), | | | | |

| | | 7.75%, 8/1/17 | | | | 6,028,651 |

| 30,000 | | Houston, TX, Airport System, (Continental Airlines), (AMT), | | | | |

| | | 6.75%, 7/1/29 | | | | 31,242,600 |

| 42,000 | | Liberty, NY, Development Corp., (Goldman Sachs | | | | |

| | | Group, Inc.), 5.25%, 10/1/35(1) | | | | 44,860,760 |

| 98,100 | | Liberty, NY, Development Corp., (Goldman Sachs | | | | |

| | | Group, Inc.), 5.25%, 10/1/35(1) | | | | 104,781,918 |

| 115,730 | | Liberty, NY, Development Corp., (Goldman Sachs | | | | |

| | | Group, Inc.), 5.50%, 10/1/37(3) | | | | 129,235,691 |

| 5,000 | | McMinn County, TN, (Calhoun Newsprint - Bowater, Inc.), | | | | |

| | | (AMT), 7.40%, 12/1/22 | | | | 5,029,850 |

| 10,000 | | Michigan Strategic Fund, (S.D. Warren), (AMT), Series A, | | | | |

| | | 7.375%, 1/15/22 | | | | 10,112,800 |

| 15,000 | | Michigan Strategic Fund, (S.D. Warren), (AMT), Series B, | | | | |

| | | 7.375%, 1/15/22 | | | | 15,169,050 |

| 3,500 | | Michigan Strategic Fund, (S.D. Warren), (AMT), Series C, | | | | |

| | | 7.375%, 1/15/22 | | | | 3,539,445 |

| 5,025 | | New Jersey Economic Development Authority, | | | | |

| | | (American Airlines), (AMT), 7.10%, 11/1/31 | | | | 5,028,266 |

| 18,820 | | New Jersey Economic Development Authority, | | | | |

| | | (Continental Airlines), (AMT), 6.25%, 9/15/29 | | | | 19,122,249 |

| 4,950 | | New Jersey Economic Development Authority, | | | | |

| | | (Continental Airlines), (AMT), 9.00%, 6/1/33 | | | | 5,723,636 |

| 7,000 | | New York City, NY, Industrial Development Agency, | | | | |

| | | (American Airlines, Inc.), (AMT), 7.50%, 8/1/16 | | | | 7,839,020 |

| 15,000 | | New York City, NY, Industrial Development Agency, | | | | |

| | | (American Airlines, Inc.), (AMT), 7.75%, 8/1/31 | | | | 17,157,150 |

| 29,000 | | New York City, NY, Industrial Development Agency, | | | | |

| (American Airlines, Inc. - JFK International Airport), (AMT), |

| | | 7.625%, 8/1/25 | | | | 32,921,670 |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Industrial Development Revenue (continued) |

|

| $ 10,000 | | New York City, NY, Industrial Development Agency, | | |

| (American Airlines, Inc. - JFK International Airport), (AMT), |

| | | 8.00%, 8/1/12 | | $ 11,026,600 |

| 12,500 | | New York City, NY, Industrial Development Agency, | | |

| | | (JFK International Airport), (AMT), 8.50%, 8/1/28 | | 14,073,375 |

| 2,567 | | Savannah, GA, Economic Development Authority, | | |

| | | (Intercat-Savannah), (AMT), 9.00%, 1/1/15 | | 2,572,529 |

| 904 | | Savannah, GA, Economic Development Authority, | | |

| | | (Intercat-Savannah), (AMT), 9.75%, 7/1/10 | | 908,820 |

| 5,000 | | Skowhegan, ME, (S.D. Warren), (AMT), | | |

| | | 6.65%, 10/15/15 | | 5,103,900 |

| 160,425 | | St. John Baptist Parish, LA, (Marathon Oil Corp.), | | |

| | | 5.125%, 6/1/37 | | 160,267,784 |

|

| | | | | $ 728,878,445 |

|

| |

| Insured-Education — 2.0% | | |

|

| $ 4,905 | | Alabama State Board of Education, (Jefferson | | |

| | | State Community College), (MBIA), 4.625%, 10/1/32 | | $ 4,883,369 |

| 43,060 | | Baldwin County, AL, Board of Education, (AMBAC), | | |

| | | 4.50%, 7/1/37 | | 41,517,591 |

| 15,045 | | Broward County, FL, Educational Facilities Authority, | | |

| | | (Nova Southeastern University), (AGC), 4.50%, 4/1/36 | | 13,984,027 |

| 28,695 | | Pennsylvania Higher Educational Facilities Authority, | | |

| | | (Temple University), (MBIA), 4.50%, 4/1/36 | | 27,908,470 |

| 22,675 | | University of California, (MBIA), 4.75%, 5/15/33 | | 22,821,254 |

| 12,720 | | University of California, (MBIA), 4.75%, 5/15/37 | | 12,773,170 |

|

| | | | | $ 123,887,881 |

|

| |

| Insured-Electric Utilities — 3.9% | | |

|

| $ 7,500 | | Burlington, KS, PCR, (Kansas Gas & Electric Co.), (MBIA), | | |

| | | 5.30%, 6/1/31 | | $ 7,873,425 |

| 57,090 | | Hawaii Department of Budget and Finance, (Hawaiian | | |

| | | Electric Company), (FGIC), (AMT), 4.60%, 5/1/26 | | 55,135,238 |

| 27,900 | | Hawaii Department of Budget and Finance, (Hawaiian | | |

| | | Electric Company), (FGIC), (AMT), 4.65%, 3/1/37 | | 26,129,466 |

| 20,000 | | Los Angeles, CA, Department of Water and Power, (FSA), | | |

| | | 4.625%, 7/1/37 | | 19,807,000 |

| 38,190 | | Matagorda County ,TX, Navigation District No.1, | | |

| | | (AEP Texas Central Co.), (MBIA), 5.20%, 5/1/30 | | 39,340,283 |

| 78,990 | | Missouri Joint Municipal Electric Utility Commission, | | |

| | | Series A, (AMBAC), 4.50%, 1/1/37 | | 76,547,629 |

| 18,000 | | Sacramento, CA, Municipal Electric Utility District, (FSA), | | |

| | | 5.00%, 8/15/28(1) | | 18,456,960 |

|

| | | | | $ 243,290,001 |

|

S e e n o t e s t o f i n a n c i a l s t a t e m e n t s

7

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

P O R T F O L I O O F I N V E S T M E N T S C O N T ’ D |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Insured-Escrowed / Prerefunded — 2.7% | | |

|

| $ 18,450 | | California Infrastructure and Economic Development, | | |

| | | (Bay Area Toll Bridges), (AMBAC), Prerefunded to | | |

| | | 1/1/28, 5.00%, 7/1/33(1) | | $ 19,987,624 |

| 78,360 | | California Infrastructure and Economic Development, | | |

| | | (Bay Area Toll Bridges), (AMBAC), Prerefunded to | | |

| | | 1/1/28, 5.00%, 7/1/36(1) | | 84,890,522 |

| 19,000 | | Massachusetts Turnpike Authority, (FGIC), Escrowed to | | |

| | | Maturity, 5.00%, 1/1/20(1) | | 20,344,250 |

| 41,010 | | Massachusetts Turnpike Authority, (FGIC), Escrowed to | | |

| | | Maturity, 5.125%, 1/1/23(1) | | 44,987,765 |

|

| | | | | $ 170,210,161 |

|

| |

| Insured-General Obligations — 9.1% | | |

|

| $ 17,670 | | Beaverton, OR, School District, (FSA), 4.125%, 6/1/25 | | $ 16,914,961 |

| 10,085 | | Beaverton, OR, School District, (FSA), 4.125%, 6/1/26 | | 9,557,555 |

| 34,995 | | California, (AMBAC), 5.00%, 2/1/28(1) | | 37,968,875 |

| 9,900 | | California, (AMBAC), Variable Rate, | | |

| | | 8.75%, 5/1/26(2)(4) | | 11,771,298 |

| 49,000 | | California, (FSA), 4.50%, 9/1/36 | | 47,105,170 |

| 12,000 | | California, (MBIA), 4.75%, 3/1/31 | | 12,066,360 |

| 16,980 | | Chicago, IL, Board of Education, (FGIC), 0.00%, 12/1/25 | | 7,363,717 |

| 50,985 | | Detroit, MI, School District, (FSA), 5.25%, 5/1/32 | | 56,595,389 |

| 104,360 | | District of Columbia, (FGIC), 4.50%, 6/1/37 | | 100,901,510 |

| 26,340 | | District of Columbia, (FGIC), Variable Rate, | | |

| | | 6.123%, 6/1/33(2)(4) | | 26,645,544 |

| 26,125 | | Florida Board of Education, Capital Outlay, | | |

| | | (Public Education), Series G, (MBIA), 4.75%, 6/1/37 | | 26,102,794 |

| 12,250 | | Frisco, TX, Independent School District, Series A, (FSA), | | |

| | | 3.75%, 8/15/38(5) | | 10,215,030 |

| 15,380 | | Frisco, TX, Independent School District, Series A, (FSA), | | |

| | | 4.75%, 8/15/35(5) | | 15,397,226 |

| 4,450 | | Geary County, KS, Unified School District #475, (MBIA), | | |

| | | 3.00%, 9/1/26 | | 3,554,171 |

| 8,500 | | Georgia, (MBIA), 2.00%, 9/1/24 | | 6,004,400 |

| 51,625 | | Los Angeles, CA, Unified School District, 4.75%, 7/1/32 | | 52,245,016 |

| 10,000 | | Montgomery County, TX, (Municipal Utility District No. 46 | | |

| | | Waterworks and Sewer), (AMBAC), 4.00%, 3/1/30 | | 9,046,100 |

| 32,340 | | Puerto Rico, (AGC), 5.50%, 7/1/29(1) | | 36,917,188 |

| 90,790 | | Texas (Transportation Commission-Mobility Fund), (FGIC), | | |

| | | 4.50%, 4/1/35 | | 88,070,840 |

|

| | | | | $ 574,443,144 |

|

| |

| Insured-Hospital — 0.7% | | |

|

| $ 15,210 | | Maryland Health and Higher Educational Facilities | | |

| | | Authority, (Medlantic), (AMBAC), 5.25%, 8/15/38(1) | | $ 16,683,950 |

| 7,835 | | Tyler, TX, Health Facility Development Corp., (East Texas | | |

| | | Medical Center), (FSA), 5.375%, 11/1/27 | | 8,122,231 |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Insured-Hospital (continued) | | |

|

| $ 4,195 | | Washington Health Care Facilities Authority, (Providence | | |

| | | Health Care), (FGIC), 4.50%, 10/1/35 | | $ 3,968,260 |

| 7,500 | | Washington Health Care Facilities Authority, (Providence | | |

| | | Health Care), (FGIC), 4.625%, 10/1/34 | | 7,274,850 |

| 5,000 | | Wisconsin Health and Educational Facilities Authority, | | |

| | | (Ministry Health Care), (MBIA), 5.125%, 2/15/22 | | 5,165,700 |

|

| | | | | $ 41,214,991 |

|

| |

| Insured-Housing — 0.7% | | |

|

| $ 40,496 | | Virginia Housing Development Authority, (MBIA), | | |

| | | 5.375%, 7/1/36(1) | | $ 41,473,733 |

|

| | | | | $ 41,473,733 |

|

| |

| Insured-Lease Revenue / Certificates of | | |

| Participation — 1.8% | | |

|

| $ 83,200 | | Hudson, NY, Infrastructure Corp., (MBIA), | | |

| | | 4.50%, 2/15/47 | | $ 80,007,616 |

| 19,715 | | Jackson County, MO, (Harry S. Truman Sports Complex), | | |

| | | (AMBAC), 4.50%, 12/1/31 | | 19,405,475 |

| 6,350 | | Western Regional Jail Authority, VA, (MBIA), | | |

| | | 4.25%, 6/1/34 | | 5,873,179 |

| 8,020 | | Western Regional Jail Authority, VA, (MBIA), | | |

| | | 4.25%, 6/1/39 | | 7,303,894 |

|

| | | | | $ 112,590,164 |

|

| |

| Insured-Other Revenue — 2.7% | | |

|

| $ 71,985 | | Golden State Tobacco Securitization Corp., CA, (AGC), | | |

| | | 5.00%, 6/1/45 | | $ 73,102,927 |

| 25,000 | | Harris County-Houston, TX, Sports Authority, (MBIA), | | |

| | | 0.00%, 11/15/41 | | 3,923,250 |

| 25,470 | | New York City, NY, Industrial Development Agency, | | |

| | | (Queens Baseball Stadium), (AMBAC), 4.75%, 1/1/42 | | 25,477,641 |

| 14,715 | | New York City, NY, Industrial Development Agency, | | |

| | | (Yankee Stadium), (FGIC), 4.50%, 3/1/39 | | 14,406,574 |

| 55,475 | | New York City, NY, Industrial Development Agency, | | |

| | | (Yankee Stadium), (MBIA), 4.75%, 3/1/46 | | 55,036,748 |

|

| | | | | $ 171,947,140 |

|

| |

| Insured-Ports — 0.5% | | |

|

| $ 37,115 | | Alabama State Dock Authority, (MBIA), (AMT), | | |

| | | 4.50%, 10/1/36 | | $ 34,396,326 |

|

| | | | | $ 34,396,326 |

|

S e e n o t e s t o f i n a n c i a l s t a t e m e n t s

8

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

P O R T F O L I O O F I N V E S T M E N T S C O N T ’ D |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Insured-Special Tax Revenue — 7.9% | | |

|

| $ 13,305 | | Illinois Sports Facility Authority, (AMBAC), | | |

| | | 0.00%, 6/15/23 | | $ 6,520,914 |

| 31,010 | | Illinois Sports Facility Authority, (AMBAC), | | |

| | | 0.00%, 6/15/24 | | 14,476,708 |

| 10,000 | | Illinois Sports Facility Authority, (AMBAC), | | |

| | | 0.00%, 6/15/25 | | 4,437,300 |

| 43,225 | | Louisiana Gas and Fuels Tax, (FGIC), | | |

| | | 4.50%, 5/1/41 | | 41,488,220 |

| 72,275 | | Louisiana Gas and Fuels Tax, (FSA), | | |

| | | 4.75%, 5/1/39 | | 72,398,590 |

| 20,000 | | Massachusetts School Building Authority, | | |

| | | (AMBAC), 4.50%, 8/15/35 | | 19,426,400 |

| 49,570 | | New York City, NY, Transitional Finance Authority, (FGIC), | | |

| | | 4.25%, 1/15/34 | | 46,697,914 |

| 29,200 | | New York Convention Center Development Corp., | | |

| | | Hotel Occupancy Tax, (AMBAC), 4.75%, 11/15/45 | | 29,075,900 |

| 1,406,680 | | Puerto Rico Sales Tax Financing, (AMBAC), | | |

| | | 0.00%, 8/1/54 | | 138,529,846 |

| 156,320 | | Puerto Rico Sales Tax Financing, (MBIA), | | |

| | | 0.00%, 8/1/44 | | 25,802,179 |

| 310,060 | | Puerto Rico Sales Tax Financing, (MBIA), | | |

| | | 0.00%, 8/1/45 | | 48,682,521 |

| 247,755 | | Puerto Rico Sales Tax Financing, (MBIA), | | |

| | | 0.00%, 8/1/46 | | 36,957,613 |

| 9,185 | | Regional Transportation Authority, LA, (FGIC), | | |

| | | 0.00%, 12/1/15 | | 6,273,079 |

| 9,500 | | Regional Transportation Authority, LA, (FGIC), | | |

| | | 0.00%, 12/1/21 | | 4,656,520 |

|

| | | | | $ 495,423,704 |

|

| |

| Insured-Student Loan — 0.8% | | |

|

| $ 52,030 | | Massachusetts Educational Financing Authority, (AMBAC), | | |

| | | 4.70%, 1/1/33 | | $ 49,600,199 |

|

| | | | | $ 49,600,199 |

|

| |

| Insured-Transportation — 13.8% | | |

|

| $ 29,800 | | Central, TX, Regional Mobility Authority, (FGIC), | | |

| | | 5.00%, 1/1/45 | | $ 30,388,252 |

| 10,000 | | Chicago, IL, O’Hare International Airport, (AMBAC), | | |

| | | (AMT), 5.375%, 1/1/32 | | 10,209,400 |

| 45,355 | | Clark County, NV, Airport Authority, (FGIC), | | |

| | | 5.00%, 7/1/36(6) | | 46,355,531 |

| 2,500 | | Dallas Fort Worth, TX, International Airport Facility | | |

| | | Improvements Corp., (FGIC), (AMT), 5.50%, 11/1/20 | | 2,605,175 |

| 5,000 | | Dallas Fort Worth, TX, International Airport Facility | | |

| | | Improvements Corp., (FGIC), (AMT), 5.625%, 11/1/21 | | 5,239,250 |

| 10,000 | | Dallas Fort Worth, TX, International Airport Facility | | |

| | | Improvements Corp., (FSA), (AMT), 5.50%, 11/1/17(1) | | 10,595,798 |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Insured-Transportation (continued) | | |

|

| $ 12,000 | | Dallas Fort Worth, TX, International Airport Facility | | |

| | | Improvements Corp., (MBIA), (AMT), | | |

| | | 5.50%, 11/1/19(1) | | $ 12,694,880 |

| 10,000 | | E-470 Public Highway Authority, CO, (MBIA), | | |

| | | 0.00%, 9/1/37 | | 2,228,600 |

| 25,720 | | E-470 Public Highway Authority, CO, (MBIA), | | |

| | | 0.00%, 9/1/38 | | 5,451,611 |

| 33,060 | | Harris County, TX, Transportation Project, (MBIA), | | |

| | | 4.75%, 8/15/32 | | 33,174,718 |

| 75,300 | | Indianapolis, IN, Local Public Improvement Bond Bank, | | |

| | | (Indianapolis Airport Authority), (AMBAC), (AMT), | | |

| | | 5.00%, 1/1/36(1) | | 75,772,131 |

| 40,525 | | Maryland Transportation Authority, (FSA), 4.50%, 7/1/41 | | 39,257,378 |

| 17,635 | | Metropolitan Transportation Authority, NY, (FGIC), | | |

| | | 4.75%, 11/15/37 | | 17,739,752 |

| 151,030 | | Minneapolis and St. Paul, MN, Metropolitan Airport | | |

| | | Commission, (AMBAC), 4.50%, 1/1/32 | | 146,633,517 |

| 19,750 | | New Jersey Transportation Trust Fund Authority, (AMBAC), | | |

| | | Variable Rate, 6.835%, 12/15/37(2)(4) | | 20,413,205 |

| 7,410 | | North Texas Tollway Authority, (FSA), 4.50%, 1/1/38 | | 7,131,014 |

| 81,940 | | Orlando and Orange County, FL, Expressway Authority, (FSA), | | |

| | | 4.50%, 7/1/35 | | 78,915,595 |

| 63,145 | | Port Authority of New York and New Jersey, (CIFG), (AMT), | | |

| | | 4.50%, 9/1/35 | | 58,687,594 |

| 29,975 | | Port Authority of New York and New Jersey, (FSA), (AMT), | | |

| | | 4.50%, 12/1/36 | | 27,837,183 |

| 20,995 | | Port Authority of New York and New Jersey, (FSA), (AMT), | | |

| | | 4.25%, 12/1/32 | | 18,769,530 |

| 62,000 | | Puerto Rico Commonwealth Highway and Transportation | | |

| | | Authority, (AGC), 5.25%, 7/1/36 | | 68,439,940 |

| 24,100 | | Regional Transportation Authority, IL, (MBIA), | | |

| | | 4.50%, 7/1/35 | | 23,304,459 |

| 10,000 | | San Francisco, CA, City and County Airport Commission, | | |

| International Airport Revenue, (FGIC), (AMT), Variable Rate, |

| | | 6.876%, 5/1/30(2)(4) | | 10,140,400 |

| 70,950 | | San Jose, CA, Airport Revenue, (AMBAC), (AMT), Series A, | | |

| | | 5.00%, 3/1/37 | | 71,531,081 |

| 15,270 | | Tampa-Hillsborough County, FL, Expressway Authority, | | |

| | | (AMBAC), 4.00%, 7/1/34 | | 13,439,432 |

| 50,000 | | Texas Turnpike Authority, (AMBAC), 0.00%, 8/15/22 | | 25,599,000 |

| 8,735 | | Tri-County, OR, Metropolitan Transportation District, (MBIA), | | |

| | | 4.25%, 9/1/31 | | 8,196,313 |

|

| | | | | $ 870,750,739 |

|

| |

| Insured-Water and Sewer — 5.7% | | |

|

| $ 11,915 | | Atlanta, GA, Water and Wastewater, (FGIC), | | |

| | | 5.00%, 11/1/38 | | $ 12,013,775 |

| 97,765 | | Birmingham, AL, Waterworks and Sewer Board, (AMBAC), | | |

| | | 4.50%, 1/1/39 | | 94,199,510 |

S e e n o t e s t o f i n a n c i a l s t a t e m e n t s

9

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

P O R T F O L I O O F I N V E S T M E N T S C O N T ’ D |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Insured-Water and Sewer (continued) | | |

|

| $ 29,865 | | Birmingham, AL, Waterworks and Sewer Board, (AMBAC), | | |

| | | 4.50%, 1/1/43 | | $ 28,458,956 |

| 10,445 | | Castaic Lake, CA, Water Agency Certificates of | | |

| | | Participation, (Water System Improvements), (AMBAC), | | |

| | | 0.00%, 8/1/21 | | 5,672,157 |

| 22,560 | | East Baton Rouge, LA, Sewer Commission, (FSA), | | |

| | | 4.50%, 2/1/31 | | 22,218,893 |

| 15,480 | | East Baton Rouge, LA, Sewer Commission, (FSA), | | |

| | | 4.50%, 2/1/36 | | 15,089,285 |

| 8,175 | | Fort Lauderdale, FL, Water and Sewer, (MBIA), | | |

| | | 4.25%, 9/1/33 | | 7,494,840 |

| 55,655 | | Honolulu, HI, City and County Wastewater System, (MBIA), | | |

| | | 4.50%, 7/1/37 | | 54,269,191 |

| 8,375 | | Houston, TX, Water and Sewer System, (FSA), | | |

| | | 0.00%, 12/1/28 | | 3,061,146 |

| 2,215 | | King County, WA, Sewer Revenue, (MBIA), | | |

| | | 4.50%, 1/1/32 | | 2,155,527 |

| 12,915 | | Los Angeles, CA, Wastewater System, (MBIA), | | |

| | | 4.50%, 6/1/29 | | 12,820,591 |

| 60,665 | | New York City, NY, Municipal Finance Authority, (FSA), | | |

| | | 4.25%, 6/15/39 | | 56,752,714 |

| 31,360 | | San Francisco, CA, City and County Public Utilities | | |

| | | Commission, Water Revenue, (FSA), 4.25%, 11/1/33 | | 29,316,896 |

| 20,805 | | Spartanburg, SC, Sanitation Sewer District, (MBIA), | | |

| | | 4.00%, 3/1/40 | | 18,267,414 |

|

| | | | | $ 361,790,895 |

|

| |

| Lease Revenue / Certificates of Participation — 0.1% |

|

| $ 10,000 | | Orange County, VA, Economic Development Authority, | | |

| | | (Various Projects), 4.50%, 2/1/34 | | $ 9,618,700 |

|

| | | | | $ 9,618,700 |

|

| |

| Nursing Home — 0.9% | | |

|

| $ 4,455 | | Delaware County, PA, Industrial Development Authority, | | |

| | | (Care Institute, Inc.), 9.00%, 8/1/31 | | $ 3,502,744 |

| 9,270 | | Hillsborough County, FL, Industrial Development Authority, | | |

| | | (Tampa Bay Retirement Center), 7.50%, 6/1/25 | | 9,471,344 |

| 2,150 | | Lackawanna County, PA, Industrial Development Authority, | | |

| | | (Edella Street Associates), 8.875%, 9/1/14 | | 2,154,193 |

| 12,965 | | Massachusetts Industrial Finance Agency, (Age Institute of | | |

| | | Massachusetts), 8.05%, 11/1/25 | | 13,226,763 |

| 11,315 | | Mississippi Business Finance Corp., (Magnolia Healthcare), | | |

| | | 7.99%, 7/1/25 | | 11,056,452 |

| 10,375 | | Montgomery, PA, Industrial Development Authority, | | |

| | | (Advancement of Geriatric Health Care Institute), | | |

| | | 8.375%, 7/1/23 | | 10,391,808 |

| 3,500 | | Orange County, FL, Health Facilities Authority, | | |

| | | (Westminster Community Care), 6.75%, 4/1/34 | | 3,598,805 |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Nursing Home (continued) | | |

|

| $ 2,125 | | Westmoreland, PA, (Highland Health Systems, Inc.), | | |

| | | 9.25%, 6/1/22 | | $ 2,129,611 |

|

| | | | | $ 55,531,720 |

|

| |

| Other Revenue — 5.1% | | |

|

| $ 20,000 | | Golden State Tobacco Securitization Corp., CA, | | |

| | | 5.50%, 6/1/33(1) | | $ 21,928,300 |

| 21,900 | | Golden State Tobacco Securitization Corp., CA, | | |

| | | 5.50%, 6/1/43(1) | | 24,011,489 |

| 22,600 | | Golden State Tobacco Securitization Corp., CA, | | |

| | | 5.625%, 6/1/38(1) | | 24,922,828 |

| 91,335 | | Golden State Tobacco Securitization Corp., CA, | | |

| | | 5.75%, 6/1/47 | | 87,157,337 |

| 10,000 | | Main Street National Gas Inc., GA, Series A, | | |

| | | 5.50%, 9/15/28(5) | | 10,531,100 |

| 31,700 | | Michigan Tobacco Settlement Finance Authority, | | |

| | | 6.00%, 6/1/48 | | 31,692,075 |

| 12,000 | | Non-Profit Preferred Funding Trust, Various States, | | |

| | | Series B, 4.47%, 9/15/37(2) | | 11,824,320 |

| 19,000 | | Non-Profit Preferred Funding Trust, Various States, | | |

| | | Series C, 4.72%, 9/15/37(2) | | 18,336,710 |

| 21,350 | | Northern Tobacco Securitization Corp., AK, | | |

| | | 0.00%, 6/1/46 | | 1,647,366 |

| 23,300 | | Silicon Valley Tobacco Securitization Authority, CA, | | |

| | | 0.00%, 6/1/36 | | 3,555,114 |

| 15,000 | | Silicon Valley Tobacco Securitization Authority, CA, | | |

| | | 0.00%, 6/1/41 | | 1,611,900 |

| 27,555 | | Silicon Valley Tobacco Securitization Authority, CA, Class A, | | |

| | | 0.00%, 6/1/47 | | 1,990,022 |

| 14,000 | | Silicon Valley Tobacco Securitization Authority, CA, Class B, | | |

| | | 0.00%, 6/1/47 | | 973,000 |

| 10,000 | | Texas Municipal Gas Acquisition and Supply Corp., Class I, | | |

| | | Variable Rate, 3.384%, 12/15/17(2)(4) | | 8,727,500 |

| 13,000 | | Texas Municipal Gas Acquisition and Supply Corp., Class I, | | |

| | | Variable Rate, 3.384%, 12/15/17(2)(4) | | 11,345,750 |

| 115,180 | | Tobacco Settlement Financing Corp., NJ, 0.00%, 6/1/41 | | 12,912,830 |

| 37,685 | | Tobacco Settlement Financing Corp., NJ, 4.75%, 6/1/34 | | 31,387,460 |

| 102,710 | | Tobacco Settlement Financing Corp., VA, 0.00%, 6/1/47 | | 7,978,513 |

| 2,275 | | Willacy County, TX, Local Government Corp., | | |

| | | 6.00%, 3/1/09 | | 2,325,915 |

| 3,745 | | Willacy County, TX, Local Government Corp., | | |

| | | 6.00%, 9/1/10 | | 3,816,043 |

|

| | | | | $ 318,675,572 |

|

| |

| Pooled Loans — 0.4% | | |

|

| $ 25,530 | | Rickenbacker Port Authority, OH, Oasbo Expanded Asset | | |

| | | Pool Loan, 5.375%, 1/1/32(1) | | $ 27,181,706 |

|

| | | | | $ 27,181,706 |

|

S e e n o t e s t o f i n a n c i a l s t a t e m e n t s

10

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

P O R T F O L I O O F I N V E S T M E N T S C O N T ’ D |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| |

| Senior Living / Life Care — 1.0% | | |

|

| $ 9,380 | | Albuquerque, NM, Retirement Facilities, (La Vida Liena | | |

| | | Retirement Center), 6.60%, 12/15/28 | | $ 9,696,856 |

| 6,035 | | Arizona Health Facilities Authority, (Care Institute, | | |

| | | Inc. - Mesa), 7.625%, 1/1/26(7) | | 5,759,683 |

| 6,680 | | Glen Cove, NY, Industrial Development Agency, | | |

| | | (The Regency at Glen Cove), 9.50%, 7/1/12(7) | | 6,054,552 |

| 600 | | Kansas City, MO, Industrial Development Authority, | | |

| | | (Kingswood United Methodist Manor), | | |

| | | 5.375%, 11/15/09 | | 595,446 |

| 9,345 | | New Jersey Economic Development Authority, (Forsgate), | | |

| | | (AMT), 8.625%, 6/1/25(7) | | 7,932,223 |

| 12,590 | | North Miami, FL, Health Care Facilities Revenue, | | |

| | | (Imperial Club), 6.125%, 1/1/42 | | 12,143,810 |

| 7,915 | | Roseville, MN, Elder Care Facility, (Care Institute, | | |

| | | Inc. - Roseville), 7.75%, 11/1/23(7) | | 7,382,241 |

| 12,140 | | St. Paul, MN, Housing and Redevelopment Authority, | | |

| | | (Care Institute, Inc. - Highland), 8.75%, 11/1/24(7) | | 11,904,848 |

|

| | | | | $ 61,469,659 |

|

| |

| Special Tax Revenue — 1.0% | | |

|

| $ 6,000 | | New Jersey Economic Development Authority, | | |

| | | (Cigarette Tax), 5.50%, 6/15/24 | | $ 6,148,140 |

| 10,000 | | New Jersey Economic Development Authority, | | |

| | | (Cigarette Tax), 5.75%, 6/15/29 | | 10,471,800 |

| 1,815 | | New Jersey Economic Development Authority, | | |

| | | (Cigarette Tax), 5.75%, 6/15/34 | | 1,906,984 |

| 463,895 | | Puerto Rico Sales Tax Financing, Series A, | | |

| | | 0.00%, 8/1/56 | | 37,440,965 |

| 4,045 | | University Square, FL, Community Development District, | | |

| | | 6.75%, 5/1/20 | | 4,198,427 |

|

| | | | | $ 60,166,316 |

|

| |

| Transportation — 2.0% | | |

|

| $ 101,500 | | Port Authority of New York and New Jersey, | | |

| | | 4.75%, 4/15/37(1) | | $ 98,825,475 |

| 30,345 | | Port Authority of New York and New Jersey, (AMT), | | |

| | | 4.75%, 12/1/34 | | 29,538,733 |

|

| | | | | $ 128,364,208 |

|

| |

| Water and Sewer — 3.9% | | |

|

| $ 27,660 | | Massachusetts Water Resources Authority, | | |

| | | 4.00%, 8/1/46 | | $ 23,865,601 |

| 16,000 | | New York City, NY, Municipal Water Finance Authority, | | |

| | | 4.25%, 6/15/33 | | 15,021,920 |

| 64,280 | | New York City, NY, Municipal Water Finance Authority, | | |

| | | (Water and Sewer System), 4.50%, 6/15/37 | | 62,378,598 |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| Water and Sewer (continued) | | |

|

| $ 121,150 | | New York City, NY, Municipal Water Finance Authority, | | |

| | | (Water and Sewer System), 4.75%, 6/15/33(1) | | $ 121,700,021 |

| 23,625 | | New York City, NY, Municipal Water Finance Authority, | | |

| | | (Water and Sewer System), 4.75%, 6/15/38 | | 23,681,936 |

|

| | | | | $ 246,648,076 |

|

| |

| Total Tax-Exempt Investments | | |

| (identified cost $6,873,542,972) | | $6,979,495,855 |

|

| |

| S h o r t - Te r m I n v e s t m e n t s — 0 . 3 % | | |

| |

| Principal Amount | | |

| (000’s omitted) | | Security | | Value |

|

| $ 18,125 | | Massachusetts Development Finance Agency, | | |

| | | (Wentworth Institute), Variable Rate, 6.00%, 10/1/33(8) | | $ 18,125,000 |

|

| |

| Total Short-Term Investments | | |

| (identified cost $18,125,000) | | $ 18,125,000 |

|

| |

| Total Investments — 111.2% | | |

| (identified cost $6,891,667,972) | | $6,997,620,855 |

|

| |

| Other Assets, Less Liabilities — (11.2)% | | $ (703,912,933) |

|

| |

| Net Assets — 100.0% | | $6,293,707,922 |

|

AGC - Assured Guaranty Corp.

AMBAC - AMBAC Financial Group, Inc.

AMT - Interest earned from these securities may be considered a tax preference item for purposes of the Federal Alternative Minimum Tax.

CIFG - CIFG Assurance North America, Inc.

FGIC - Financial Guaranty Insurance Company

FSA - Financial Security Assurance, Inc.

MBIA - Municipal Bond Insurance Association

At September 30, 2007, the concentration of the Fund’s investments in the various states, determined as a percentage of net assets, is as follows:

| New York | | 18.7% |

| California | | 18.0% |

| Texas | | 12.1% |

| Others, representing less than 10% individually | | 62.4% |

S e e n o t e s t o f i n a n c i a l s t a t e m e n t s

11

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

P O R T F O L I O O F I N V E S T M E N T S C O N T ’ D |

The Fund invests primarily in debt securities issued by municipalities. The ability of the issuers of the debt securities to meet their obligations may be affected by economic developments in a specific industry or municipality. In order to reduce the risk associated with such economic developments, at September 30, 2007, 47.0% of total investments are backed by bond insurance of various financial institutions and financial guaranty assurance agencies. The aggregate percentage insured by an individual financial institution ranged from 0.8% to 15.7% of total investments.

| (1) | Security represents the underlying municipal obligation of an inverse floating rate obligation held by the Fund. |

| |

| (2) | Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in transactions exempt from registration, normally to qualified institutional buyers. At September 30, 2007, the aggregate value of the securities is $141,550,070 or 2.2% of the Fund’s net assets. |

| |

| (3) | Security (or a portion thereof) has been segregated to cover payable for when-issued securities. |

| |

| (4) | Security has been issued as a leveraged inverse floater bond. The stated interest rate represents the rate in effect at September 30, 2007. |

| |

| (5) | When-issued security. |

| |

| (6) | Security (or a portion thereof) has been segregated to cover margin requirements on open financial futures contracts. |

| |

| (7) | Security is in default with respect to scheduled principal payments. |

| |

| (8) | Variable rate demand obligation. The stated interest rate represents the rate in effect at September 30, 2007. |

| |

S e e n o t e s t o f i n a n c i a l s t a t e m e n t s

12

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

F I N A N C I A L S T A T E M E N T S |

| S t a t e m e n t o f A s s e t s a n d L i a b i l i t i e s | | |

| |

| As of September 30, 2007 | | | | |

| Assets | | | | |

|

| Investments, at value (identified cost, $6,891,667,972) | | $6,997,620,855 |

| Cash | | | | 810,960 |

| Receivable for investments sold | | | | 64,092,106 |

| Receivable for Fund shares sold | | | | 22,300,660 |

| Interest receivable | | | | 81,023,555 |

| Receivable for open interest rate swap contracts | | | | 2,777,133 |

|

| |

| Total assets | | $7,168,625,269 |

|

| |

| Liabilities | | | | |

|

| Payable for floating rate notes issued | | $ 763,890,950 |

| Payable for investments purchased | | | | 30,605,356 |

| Payable for when-issued securities | | | | 35,421,826 |

| Payable for Fund shares redeemed | | | | 15,268,185 |

| Interest expense and fees payable | | | | 8,594,757 |

| Dividends payable | | | | 8,563,351 |

| Payable for open interest rate swap contracts | | | | 109,884 |

| Payable for closed interest rate swap contracts | | | | 5,991,117 |

| Payable to affiliate for distribution and service fees | | | | 4,145,155 |

| Payable to affiliate for investment advisory fee | | | | 1,593,815 |

| Accrued expenses | | | | 732,951 |

|

| |

| Total liabilities | | $ 874,917,347 |

|

| |

| Net assets | | $6,293,707,922 |

|

| |

| Sources of Net Assets | | | | |

|

| Paid-in capital | | $6,161,072,330 |

| Accumulated undistributed net realized gain | | | | |

| (computed on the basis of identified cost) | | | | 12,130,016 |

| Accumulated undistributed net investment income | | | | 7,463,123 |

| Net unrealized appreciation (computed on the basis of identified cost) | | | | 113,042,453 |

|

| |

| Total | | $6,293,707,922 |

|

| |

| Class A Shares | | | | |

|

| Net Assets | | $4,647,177,131 |

| Shares Outstanding | | | | 404,537,014 |

| Net Asset Value and Redemption Price Per Share | | | | |

| (net assets ÷ shares of beneficial interest outstanding) | | $ 11.49 |

| Maximum Offering Price Per Share | | | | |

| (100 ÷ 95.25 of $11.49) | | $ 12.06 |

|

| |

| Class B Shares | | | | |

|

| Net Assets | | $ 173,175,768 |

| Shares Outstanding | | | | 15,078,003 |

| Net Asset Value and Offering Price Per Share* | | | | |

| (net assets ÷ shares of beneficial interest outstanding) | | $ 11.49 |

|

| |

| Class C Shares | | | | |

|

| Net Assets | | $1,334,054,048 |

| Shares Outstanding | | | | 116,150,637 |

| Net Asset Value and Offering Price Per Share* | | | | |

| (net assets ÷ shares of beneficial interest outstanding) | | $ 11.49 |

|

| |

| Class I Shares | | | | |

|

| Net Assets | | $ 139,300,975 |

| Shares Outstanding | | | | 12,123,471 |

| Net Asset Value, Offering Price and Redemption Price Per Share | | | | |

| (net assets ÷ shares of beneficial interest outstanding) | | $ 11.49 |

|

On sales of $25,000 or more, the offering price of Class A shares is reduced.

* Redemption price per share is equal to the net asset value less any applicable contingent deferred sales charge.

| S t a t e m e n t o f O p e r a t i o n s | | |

| |

| For the Year Ended | | |

| September 30, 2007 | | |

| | |

| Investment Income | | |

|

| Interest | | $ 315,838,164 |

|

| Total investment income | | $ 315,838,164 |

|

| |

| |

| Expenses | | |

|

| Investment adviser fee | | $ 17,648,068 |

| Trustees’ fees and expenses | | 33,013 |

| Distribution and service fees | | |

| Class A | | 10,307,515 |

| Class B | | 1,637,307 |

| Class C | | 11,342,789 |

| Interest expense and fees | | 34,697,607 |

| Transfer and dividend disbursing agent fees | | 1,905,936 |

| Custodian fee | | 827,009 |

| Registration fees | | 367,915 |

| Printing and postage | | 301,386 |

| Legal and accounting services | | 219,836 |

| Miscellaneous | | 164,743 |

|

| Total expenses | | $ 79,453,124 |

|

| Deduct — | | |

| Reduction of custodian fee | | $ 344,590 |

| Allocation of expenses to investment adviser | | 22,477 |

|

| Total expense reductions | | $ 367,067 |

|

| |

| Net expenses | | $ 79,086,057 |

|

| |

| Net investment income | | $ 236,752,107 |

|

| |

| |

| Realized and Unrealized Gain (Loss) | | |

|

| Net realized gain (loss) — | | |

| Investment transactions (identified cost basis) | | $ (27,997,819) |

| Financial futures contracts | | 27,938,831 |

| Interest rate swap contracts | | (10,090,784) |

|

| Net realized loss | | $ (10,149,772) |

|

| Change in unrealized appreciation (depreciation) — | | |

| Investments (identified cost basis) | | $(195,145,880) |

| Financial futures contracts | | 23,790,071 |

| Interest rate swap contracts | | 2,667,249 |

|

| Net change in unrealized appreciation (depreciation) | | $(168,688,560) |

|

| |

| Net realized and unrealized loss | | $(178,838,332) |

|

| |

| Net increase in net assets from operations | | $ 57,913,775 |

|

S e e n o t e s t o f i n a n c i a l s t a t e m e n t s

13

Eaton Vance National Municipals Fund a s o f S e p t e m b e r 3 0 , 2 0 0 7

F I N A N C I A L S T A T E M E N T S C O N T ’ D |

| S t a t e m e n t s o f C h a n g e s i n N e t A s s e t s | | |

| |

| |

| Increase (Decrease) | | Year Ended | | Year Ended |

| in Net Assets | | September 30, 2007 | | September 30, 2006 |

|

| From operations — | | | | | | |

| Net investment income | | $ 236,752,107 | | $ 155,263,037 |

| Net realized gain (loss) | | | | | | |

| from investment transactions, | | | | | | |

| financial futures contracts and | | | | | | |

| interest rate swap contracts | | (10,149,772) | | | | 70,533,392 |

| Net change in unrealized | | | | | | |

| appreciation (depreciation) | | | | | | |

| from investments, financial | | | | | | |

| futures contracts and | | | | | | |

| interest rate swap contracts | | (168,688,560) | | | | 73,862,460 |

|

| |

| Net increase in net assets from operations | | $ 57,913,775 | | $ 299,658,889 |

|

| Distributions to shareholders — | | | | | | |

| From net investment income | | | | | | |

| Class A | | $ (182,156,469) | | $ (118,051,895) |

| Class B | | (6,042,672) | | | | (4,320,365) |

| Class C | | (41,801,397) | | | | (20,894,988) |

| Class I | | (6,290,466) | | | | (2,101,962) |

|

| |

| Total distributions to shareholders | | $ (236,291,004) | | $ (145,369,210) |

|

| Transactions in shares of beneficial interest — | | | | | | |

| Proceeds from sale of shares | | | | | | |

| Class A | | $2,233,505,164 | | $1,268,188,085 |

| Class B | | 56,490,915 | | | | 61,402,718 |

| Class C | | 766,113,589 | | | | 420,877,219 |

| Class I | | 153,566,977 | | | | 71,850,088 |

| Net asset value of shares issued to | | | | | | |

| shareholders in payment of | | | | | | |

| distributions declared | | | | | | |

| Class A | | 111,268,215 | | | | 64,304,849 |

| Class B | | 3,456,739 | | | | 2,334,782 |

| Class C | | 23,191,417 | | | | 10,889,973 |

| Class I | | 5,032,964 | | | | 1,617,446 |

| Cost of shares redeemed | | | | | | |

| Class A | | (830,456,403) | | | | (342,257,371) |

| Class B | | (20,291,846) | | | | (10,711,188) |

| Class C | | (199,151,037) | | | | (63,309,338) |

| Class I | | (96,464,039) | | | | (8,201,000) |

| Net asset value of shares exchanged | | | | | | |

| Class A | | 2,291,497 | | | | 1,388,451 |

| Class B | | (2,291,497) | | | | (1,388,451) |

|

| |

| Net increase in net assets from Fund | | | | | | |

| share transactions | | $2,206,262,655 | | $1,476,986,263 |

|

| |

| |

| Net increase in net assets | | $2,027,885,426 | | $1,631,275,942 |

|

| | | Year Ended | | Year Ended |

| Net Assets | | September 30, 2007 | | September 30, 2006 |