UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-04604 | ||||||||

| |||||||||

CREDIT SUISSE CAPITAL FUNDS | |||||||||

(Exact name of registrant as specified in charter) | |||||||||

| |||||||||

Eleven Madison Avenue, New York, New York |

| 10010 | |||||||

(Address of principal executive offices) |

| (Zip code) | |||||||

| |||||||||

J. Kevin Gao, Esq. | |||||||||

(Name and address of agent for service) | |||||||||

| |||||||||

Registrant’s telephone number, including area code: | (212) 325-2000 |

| |||||||

| |||||||||

Date of fiscal year end: | October 31 |

| |||||||

| |||||||||

Date of reporting period: | November 1, 2007 to April 30, 2008 |

| |||||||

Item 1. Reports to Stockholders.

CREDIT SUISSE FUNDS

Semiannual Report

April 30, 2008

(unaudited)

n CREDIT SUISSE

ABSOLUTE RETURN FUND

The Fund's investment objectives, risks, charges and expenses (which should be considered carefully before investing), and more complete information about the Fund, are provided in the Prospectus, which should be read carefully before investing. You may obtain additional copies by calling 800-927-2874 or by writing to Credit Suisse Funds, P.O. Box 55030, Boston, MA 02205-5030.

Credit Suisse Asset Management Securities, Inc., Distributor, is located at Eleven Madison Avenue, New York, NY 10010. Credit Suisse Funds are advised by Credit Suisse Asset Management, LLC.

Investors in the Credit Suisse Funds should be aware that they may be eligible to purchase Common Class and/or Advisor Class shares (where offered) directly or through certain intermediaries. Such shares are not subject to a sales charge but may be subject to an ongoing service and distribution fee of up to 0.50% of average daily net assets. Investors in the Credit Suisse Funds should also be aware that they may be eligible for a reduction or waiver of the sales charge with respect to Class A, B or C shares (where offered). For more information, please review the relevant prospectuses or consult your financial representative.

The views of the Fund's management are as of the date of the letter and the Fund holdings described in this document are as of April 30, 2008; these views and Fund holdings may have changed subsequent to these dates. Nothing in this document is a recommendation to purchase or sell securities.

Fund shares are not deposits or other obligations of Credit Suisse Asset Management, LLC ("Credit Suisse") or any affiliate, are not FDIC-insured and are not guaranteed by Credit Suisse or any affiliate. Fund investments are subject to investment risks, including loss of your investment.

Credit Suisse Absolute Return Fund

Semiannual Investment Adviser's Report

April 30, 2008 (unaudited)

June 16, 2008

Dear Shareholder:

Performance Summary

11/01/07 – 04/30/08

| Fund & Benchmark | Performance | ||||||

| Common1 | (2.28 | )% | |||||

| Class A1,2 | (2.43 | )% | |||||

| Class C1,2 | (2.74 | )% | |||||

| LIBOR + 350 bps3 | 4.19 | % | |||||

| Merrill Lynch US Treasury Notes & Bonds 0-1 Year Index4 | 2.40 | % | |||||

Performance for the Fund's Class A and Class C shares is without the maximum sales charge of 4.00% and 1.00%, respectively.2

Market Review: The credit crunch has widespread repercussions

The six-month period ended April 30, 2008 was a volatile one for global equity markets. Heightened fears of a U.S. recession with possible stagflation and concerns of systemic risk in the financial system drove the increase in volatility.

The negative news began to flow in January with fears of credit downgrades for the monoline bond insurers, weak economic U.S. data, and the revelation of Societe Generale's rogue trader. The unwinding of Societe Generale's long positions and subsequent €4.9 billion loss was thought to be largely behind the sharp fall in global equity markets on January 21. Additionally, the U.S. Federal Reserve's 0.75% emergency rate cut helped sentiment, but many developed and emerging markets still suffered double digit falls in January.

Global equities staged a partial recovery through February, with a decoupling of the United States from the rest of the world. For example, in Europe, business surveys were surprisingly stronger than forecast, while in the United States, weakening consumer confidence was compounded by a softening labor market. Emerging markets and Asia ex Japan outperformed, with China's market staging a recovery. Additionally, positive political developments in Taiwan and Thailand helped these countries to outperform their regional peers.

In March, equity market volatility reached its highest point in more than five years as the increased risk of default led to a vicious spiral of illiquidity and distressed selling that triggered the crisis at Bear Stearns and undermined the global financial system. Uncertainty drove some commodity prices to new highs — oil hit $111 and gold went above $1,000. Additionally, as investors shunned stocks even remotely linked to the consumer cycle, the blue chips were

1

Credit Suisse Absolute Return Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

among the biggest casualties, ironic because of their greater liquidity. The Fed's rapid response calmed some of the fears and caused global equity markets to stage a modest rally, led by the financials, going into quarter end.

The Bear Stearns rescue in mid-March increasingly appears to be a key watershed as it signaled the willingness of central banks to underwrite the debt and counterparty obligations of key financial institutions and find more effective means to channel liquidity to banks and brokers.

The banking sector has also made a more concerted effort to separate their good and bad assets, and buyers are now making acceptable bids for some of the bad assets. In addition, we have started to see the first moves to rebuild balance sheets through raising new capital via equity, which does relieve some of the strains in the credit markets. There is still more to do but the actions so far have reduced the risk of an even deeper financial crisis, as evidenced by credit derivatives and equities rising from their lows.

Despite the Federal Reserve's latest initiatives, banking and credit problems remain. However, there is still a risk of an overshoot for commodities and currencies driven by investors looking for a hedge against inflation and an alternative to equities. In fact, some have now risen beyond fundamentally justifiable values. Government bonds are overbought with negative real rates in the U.S., while in equity, long-term valuations are more attractive.

Risk aversion led to a further unwinding of the 'carry trade' with Sterling and the U.S. Dollar at a record low versus the Euro and the Japanese Yen (up 11.5% year to date).

The global economy is showing divergent trends, for example, the sharp slowdown in the United States and the countries most closely linked to it (e.g., Canada and Mexico) as compared to emerging countries, where domestic demand remains robust with the strength of infrastructure spending and export growth also solid.

In Europe, growth has softened, but there is growing dispersion across the Euro region — Germany and France remain firm, while Spain and Italy are weakening. The European Central Bank, however, is unlikely to cut rates anytime soon. Additionally, there are risks for Eastern Europe given their strong links within the Euro area. And, in the UK, the slowdown in the housing market has accelerated as both the availability and cost of credit have risen.

In Japan, domestic demand weakened as household spending stagnated. Housing starts have recovered, albeit from a low base, and exports are still providing some stimulus despite the stronger currency.

2

Credit Suisse Absolute Return Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

In some emerging markets, the combination of higher inflation and sharply rising grain prices poses a serious dichotomy for policymakers. With inflation in China reaching an 11 year high (8.7%), fears of further austerity measures have grown, though the resource based markets, Brazil and Russia, have continued to outperform.

Strategic Review: We remain positive on stocks

Main contributors to performance included U.S. stocks and Hong Kong equities (held from March on) and the use of tactical allocation with commodities. Conversely, primary detractors from performance included all stocks held from October until the beginning of February.

Currently, we are still positive for stocks, as the markets are currently discounting negative profit growth and we believe this is too pessimistic. Our expectation going forward is for weak, but not negative, profit growth. Should this materialize, it would have a positive impact on stocks due to the current attractive valuation. With equities, valuations have become even more attractive and the sentiment factor is now increasing its positive stance given more signs of capitulation. Within equities, emerging markets and Canada remain our preferred regions. Additionally, given the problems in Japan (collapsing sentiment indicators combined with a slowdown), this equity market remains our least attractive market

From a valuation perspective, Canadian stocks look attractive compared to Canadian bonds. We have a positive view on commodities and the Canadian stock market is highly exposed to that asset class.

There has still been surprisingly strong growth in emerging market equities despite the U.S. slowdown. This is the "decoupling" discussion in the markets, which refers to the capability of countries to insulate themselves from a slowdown in the United States. Additionally, we like Hong Kong due to its surprising growth and very positive earnings revisions.

With our expectation for slow growth, we chose to invest in less cyclical markets like the U.S. as opposed to European stocks. As soon as the economy starts to pick up (3rd and 4th quarters in our expectations), we might shift into the more cyclical European markets.

In fixed income markets, sentiment is growing more extreme and we do not see any value in long-term bonds, particularly government issues. We therefore remain in the short duration space.

3

Credit Suisse Absolute Return Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

Market Outlook: Expecting growth to pick up by year-end

The financial markets remain fraught with great uncertainty. In our opinion, the greatest unrest concerns the consequences of the immense leverage in the bond markets and fears of an uncontrolled sell-off. A persistent stream of bad news in recent weeks has pushed the markets to test new lows and we believe volatility is likely to remain high. Nonetheless, this scenario also opens opportunities for medium-term investors, since the equity markets are discounting a much gloomier scenario than our evaluation of the global economy would warrant.

After the stellar growth rates of the last few years (at levels not seen since the 1960s), the world economy has clearly been slowing down over the past year or so. At the same time, however, there has been a real shift in momentum. While the G4 countries — the U.S., Europe, the UK and Japan — are experiencing a severe slowdown, emerging markets, particularly China and India, continue to move ahead and are compensating in some part.

The U.S. economy is still slowing down with indicators negative in the aggregate. However, the aggregate is only mildly negative. The main problem in the U.S. remains the housing market and the impact it will have on the consumer. GDP growth for the first half of this year came in close to zero, with the consumer and housing sectors being the main drags. Falls in equity markets and home prices, combined with rising energy and utility prices, have generated a sharp fall in consumer confidence. Home prices are already lower and expected to fall further, while jobs data have also been weak, suggesting that labor income, the key support factor for private consumption growth, is deteriorating sharply. In our opinion, this implies that a significant slowdown is underway in the U.S. domestic economy on top of the housing contraction (which has been ongoing for almost two years). Employment growth has not been as strong as in previous cycles and thu s the downside, in terms of job cuts as the economy slows, seems to be more limited. Additionally, the overall balance sheet health of the non-financial corporate sector, together with an inventory build-up that seems to have been (apart from housing) lower than in the past, also speaks in favor of a more limited downside. We still believe the fiscal stimulus package will be able to boost growth in the months to come but this does depend on consumer sentiment and willingness to actually spend the money.

There are clearly downside risks to our expectation that growth will pick up again later this year. The Fed has cut interest rates drastically, but the easing has been partly offset. Interest rates for mortgages and other areas of credit for private households have increased since the cuts. This could imply that the Fed will have to do more and it might continue to act swiftly.

4

Credit Suisse Absolute Return Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

In Europe, the picture is a bit more encouraging. Although the Eurozone economies are also slowing down, the region is still expected to have positive growth of between 0.5-1% this year. An important positive is that activity in the main economies of France and Germany is surprising on the upside. In fact, German export growth accelerated again in January to above 9% year over year, and there appears to be room for improvement of consumer spending following the strong employment growth and potentially stronger wage gains this year. It is the Spanish and Italian economies that are in the worst shape. Consider that, even though the European consumer and producer sentiment data have been deteriorating and overall growth has slowed down, exports have remained surprisingly resilient given the strength of the Euro.

As for the UK, we expect a situation similar to that of the U.S. (i.e., a housing market led slowdown). In fact, house prices in the UK are already showing negative growth month-on-month and will soon be negative year-on-year.

Of the major economies, Japan remains a big concern in our opinion. The Tankan survey, which measures business sentiment, continues to trend lower, while the country's economy is also suffering from a demand-led slowdown, with consumer confidence at very weak levels.

As for emerging markets, we continue to argue in favor of the decoupling scenario, which seems to have been confirmed by recent history. For the emerging markets world, the credit shock related to credit market problems has been much less pronounced or even nonexistent. In fact, new trade patterns with strong increases of trade between emerging markets seem to have led to a declining importance of the U.S.

Recently, commodity prices have been strong almost across the board. Oil has firmly established itself above the $100 per barrel level and the gold price continues to enter uncharted territory, trading for the first time at above $1,000 per ounce. The price of gold has been pushed higher based on structural factors as well as by the weak U.S. dollar. And as long as U.S. economic data remain poor, we believe the price of gold will remain high. This is because the dollar will weaken more due to further expectations of interest rate cuts, and because of an interest rate differential that is not in favor of the dollar. Investors are thus buying gold as a safe-haven alternative to the U.S. dollar. Overall, the medium- to longer-term arguments, such as a growing affluent population fuelling demand and supply side constraints, remain intact and we are likely to see further upside. In the short term (the next three months), we believe commodity mark ets remain vulnerable to profit taking and an unwinding of the speculative positions that have been built-up over recent weeks and months.

5

Credit Suisse Absolute Return Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

One of the key characteristics of the bond markets has been the steepening in all of the major markets with the exception of Japan, where the short end of the term structure is firmly anchored at very low levels. Nevertheless, even in Japan, the worst performing part of the curve in yield terms has been the long end. This is understandable considering the increased inflation risk that needs to be priced in. At the same time, most of the major yield curves have been flat between 10 years and 30 years, if not inverted. We believe this is nothing more than a return to a so-called "normal" shape. The main question that remains is how much further this trend could go. With the Fed still firmly in easing mode and the market anticipating rate cuts by the other main central banks, we believe that the curve steepening could go further. In fact, because of the overall low level of interest rates, the phenomenon could even surpass previous top levels.

Christine Gaelzer

Portfolio Manager

There is no guarantee that the Fund's absolute return will be achieved, and there may be negative returns at any given time. In addition, investments in the Fund are subject to a number of risks, including, but not limited to, asset class risk, issuer risk, credit risk, derivatives risk and foreign securities risk.

In addition to historical information, this report contains forward-looking statements that may concern, among other things, domestic and foreign market, industry and economic trends and developments and government regulation and their potential impact on the Fund's investments. These statements are subject to risks and uncertainties and actual trends, developments and regulations in the future, and their impact on the Fund could be materially different from those projected, anticipated or implied. The Fund has no obligation to update or revise forward-looking statements.

6

Credit Suisse Absolute Return Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

Average Annual Returns as of March 31, 20081

| One Year | Since Inception | Inception Date | |||||||||||||

| Common Class | 3.15 | % | 4.18 | % | 12/29/06 | ||||||||||

| Class A Without Sales Charge | 2.91 | % | 3.93 | % | 12/29/06 | ||||||||||

| Class A With Maximum Sales Charge | (1.20 | )% | (0.25 | )% | 12/29/06 | ||||||||||

| Class C Without CDSC | 2.12 | % | 2.94 | % | 12/29/06 | ||||||||||

| Class C With CDSC | 1.15 | % | 2.94 | % | 12/29/06 | ||||||||||

Average Annual Returns as of April 30, 20081

| One Year | Since Inception | Inception Date | |||||||||||||

| Common Class | 4.83 | % | 6.61 | % | 12/29/06 | ||||||||||

| Class A Without Sales Charge | 4.58 | % | 6.25 | % | 12/29/06 | ||||||||||

| Class A With Maximum Sales Charge | 0.43 | % | 1.97 | % | 12/29/06 | ||||||||||

| Class C Without CDSC | 3.79 | % | 5.24 | % | 12/29/06 | ||||||||||

| Class C With CDSC | 2.79 | % | 5.24 | % | 12/29/06 | ||||||||||

Returns represent past performance and include change in share price and reinvestment of dividends and capital gains. Past performance cannot guarantee future results. The current performance of the Fund may be lower or higher than the figures shown. Returns and share price will fluctuate, and redemption value may be more or less than original cost. The performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance information current to the most recent month-end is available at www.credit-suisse.com/us.

1 Fee waivers and/or expense reimbursements may reduce expenses for the Fund, without which performance would be lower. Waivers and/or reimbursements may be discontinued at any time.

2 Total return for the Fund's Class A shares for the reporting period, based on offering price (including maximum sales charge of 4.00%), was –6.30%. Total return for the Fund's Class C shares for the reporting period, based on redemption value (including a maximum contingent deferred sales charge of 1.00%) was –3.67%.

3 Over a three to five-year economic cycle, the Fund aims to achieve an aggregate positive absolute return of 3-month LIBOR + 350 basis points, gross of fees. The Fund is not designed to achieve consistent annual returns, and the return in any year may be lower than the three- to five-year aggregate return the Fund seeks.

4 The Merrill Lynch US Treasury Notes & Bonds 0-1 Year Index tracks the performance of all outstanding US Treasury Notes and Bonds having less than one year remaining term to maturity and a minimum amount outstanding of $1 billion. The Index is rebalanced daily to take account of issues that are maturing and new additions. Bonds are "purchased" into the Index basket on the day they fall below one year to maturity and are removed on the day they mature. Additional sub-indices are available that segment the Index into quarterly maturity ranges. Investors cannot invest directly in an index.

7

Credit Suisse Absolute Return Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

Information About Your Fund's Expenses

As an investor of the Fund, you incur two types of costs: ongoing expenses and transaction costs. Ongoing expenses include management fees, distribution and service (12b-1) fees and other Fund expenses. Examples of transaction costs include sales charges (loads), redemption fees and account maintenance fees, which are not shown in this section and which would result in higher total expenses. The following table is intended to help you understand your ongoing expenses of investing in the Fund and to help you compare these expenses with the ongoing expenses of investing in other mutual funds. The table is based on an investment of $1,000 made at the beginning of the six month period ended April 30, 2008.

The table illustrates your Fund's expenses in two ways:

• Actual Fund Return. This helps you estimate the actual dollar amount of ongoing expenses paid on a $1,000 investment in the Fund using the Fund's actual return during the period. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the "Expenses Paid per $1,000" line under the share class you hold.

• Hypothetical 5% Fund Return. This helps you to compare your Fund's ongoing expenses with those of other mutual funds using the Fund's actual expense ratio and a hypothetical rate of return of 5% per year before expenses. Examples using a 5% hypothetical fund return may be found in the shareholder reports of other mutual funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Please note that the expenses shown in these tables are meant to highlight your ongoing expenses only and do not reflect any transaction costs, such as sales charges (loads) or redemption fees. If these transaction costs had been included, your costs would have been higher. The "Expenses Paid per $1,000" line of the tables is useful in comparing ongoing expenses only and will not help you determine the relative total expenses of owning different funds.

8

Credit Suisse Absolute Return Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

Expenses and Value of a $1,000 Investment

for the six month period ended April 30, 2008

| Actual Fund Return | Common Class | Class A | Class C | ||||||||||||

| Beginning Account Value 11/1/07 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | |||||||||

| Ending Account Value 4/30/08 | $ | 977.20 | $ | 975.70 | $ | 972.60 | |||||||||

| Expenses Paid per $1,000* | $ | 4.92 | $ | 6.14 | $ | 9.81 | |||||||||

| Hypothetical 5% Fund Return | |||||||||||||||

| Beginning Account Value 11/1/07 | $ | 1,000.00 | $ | 1,000.00 | $ | 1,000.00 | |||||||||

| Ending Account Value 4/30/08 | $ | 1,019.89 | $ | 1,018.65 | $ | 1,014.92 | |||||||||

| Expenses Paid per $1,000* | $ | 5.02 | $ | 6.27 | $ | 10.02 | |||||||||

| Common Class | Class A | Class C | |||||||||||||

| Annualized Expense Ratios* | 1.00 | % | 1.25 | % | 2.00 | % | |||||||||

* Expenses are equal to the Fund's annualized expense ratio for each share class, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year period, then divided by 366.

The "Expenses Paid per $1,000" and the "Annualized Expense Ratios" in the tables are based on actual expenses paid by the Fund during the period, net of fee waivers and/or expense reimbursements. If those fee waivers and/or expense reimbursements had not been in effect, the Fund's actual expenses would have been higher.

For more information, please refer to the Fund's prospectus.

9

Credit Suisse Absolute Return Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

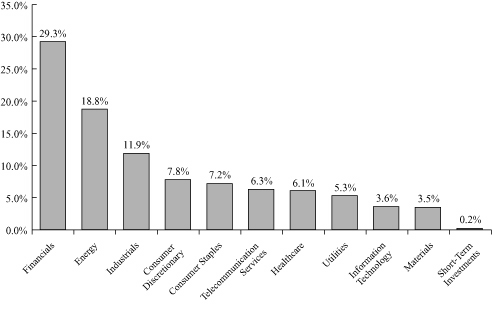

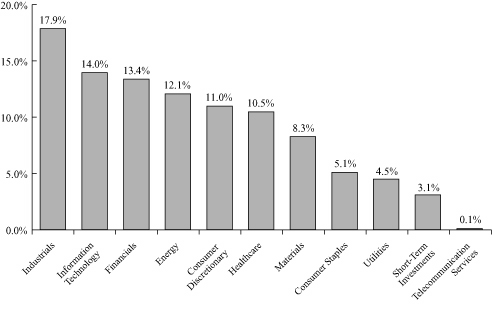

| Sector Breakdown* | |||||||

| Commingled Funds | 55.9 | % | |||||

| United States Agency Obligations | 44.1 | % | |||||

| Total | 100.0 | % | |||||

* Expressed as a percentage of total investments (excluding security lending collateral) and may vary over time.

10

Credit Suisse Absolute Return Fund

Schedule of Investments

April 30, 2008 (unaudited)

| Number of Shares | Value | ||||||||||

| COMMON STOCKS (56.2%) | |||||||||||

| Commingled Funds (56.2%) | |||||||||||

| iPATH Dow Jones-AIG Commodity Index Total Return ETN* | 7,050 | $ | 452,116 | ||||||||

| iShares Lehman 7-10 Year Treasury Bond Fund§ | 12,710 | 1,133,351 | |||||||||

| iShares MSCI Australia Index Fund§ | 10,910 | 303,080 | |||||||||

| iShares MSCI Canada Index Fund | 12,080 | 392,117 | |||||||||

| iShares MSCI Emerging Markets Index§ | 8,391 | 1,230,624 | |||||||||

| iShares MSCI Hong Kong Index Fund | 12,800 | 248,960 | |||||||||

| iShares S&P 500 Index Fund | 4,900 | 679,091 | |||||||||

| TOTAL COMMON STOCKS (Cost $4,196,344) | 4,439,339 | ||||||||||

| Par (000) | Ratings† (S&P/Moody's) | Maturity | Rate% | ||||||||||||||||||||

| UNITED STATES AGENCY OBLIGATIONS (44.2%) | |||||||||||||||||||||||

| $ | 500 | Fannie Mae Discount Notes(a) | (AAA, Aaa) | 05/07/08 | 2.030 | 499,777 | |||||||||||||||||

| 520 | Federal Home Loan Discount Notes(a) | (AAA, Aaa) | 05/21/08 | 1.918 | 519,357 | ||||||||||||||||||

| 500 | Freddie Mac Discount Notes(a) | (AAA, Aaa) | 05/12/08 | 1.875 | 499,594 | ||||||||||||||||||

| 450 | Freddie Mac Discount Notes(a) | (AAA, Aaa) | 05/19/08 | 2.081 | 449,393 | ||||||||||||||||||

| 600 | Freddie Mac Discount Notes | (AAA, Aaa) | 01/18/11 | 4.750 | 626,518 | ||||||||||||||||||

| 500 | United States Treasury Notes | (AAA, Aaa) | 05/15/08 | 2.625 | 500,352 | ||||||||||||||||||

| 400 | United States Treasury Notes | (AAA, Aaa) | 06/30/08 | 5.125 | 402,656 | ||||||||||||||||||

| TOTAL UNITED STATES AGENCY OBLIGATIONS (Cost $3,479,723) | 3,497,647 | ||||||||||||||||||||||

| Number of Shares | |||||||||||

| SHORT-TERM INVESTMENT (28.8%) | |||||||||||

| State Street Navigator Prime Portfolio§§ (Cost $2,278,991) | 2,278,991 | 2,278,991 | |||||||||

| TOTAL INVESTMENTS AT VALUE (129.2%) (Cost $9,955,058) | 10,215,977 | ||||||||||

| LIABILITIES IN EXCESS OF OTHER ASSETS (-29.2%) | (2,308,870 | ) | |||||||||

| NET ASSETS (100.0%) | $ | 7,907,107 | |||||||||

INVESTMENT ABBREVIATION

ETN = Exchange Traded Note

† Credit ratings given by the Standard & Poor's Division of The McGraw-Hill Companies, Inc. ("S&P") and Moody's Investors Service, Inc. ("Moody's") are unaudited.

(a) Zero-coupon bond. Rate represents annualized yield at date of purchase.

* Non-income producing security.

§ Security or portion thereof is out on loan.

§§ Represents security purchased with cash collateral received for securities on loan.

See Accompanying Notes to Financial Statements.

11

Credit Suisse Absolute Return Fund

Statement of Assets and Liabilities

April 30, 2008 (unaudited)

| Assets | |||||||

| Investments at value, including collateral for securities on loan of $2,278,991 (Cost $9,955,058) (Note 2) | $ | 10,215,9771 | |||||

| Cash | 71,318 | ||||||

| Interest receivable | 21,083 | ||||||

| Receivable for fund shares sold | 20,893 | ||||||

| Receivable from investment adviser (Note 3) | 5,654 | ||||||

| Prepaid expenses and other assets | 34,004 | ||||||

| Total Assets | 10,368,929 | ||||||

| Liabilities | |||||||

| Distribution fee payable (Note 3) | 848 | ||||||

| Payable upon return of securities loaned (Note 2) | 2,278,991 | ||||||

| Offering Costs payable (Note 3) | 159,381 | ||||||

| Trustees' fee payable | 13,043 | ||||||

| Other accrued expenses payable | 9,559 | ||||||

| Total Liabilities | 2,461,822 | ||||||

| Net Assets | |||||||

| Capital stock, $.001 par value (Note 6) | 784 | ||||||

| Paid-in capital (Note 6) | 7,660,569 | ||||||

| Undistributed net investment income | 43,352 | ||||||

| Accumulated net realized loss on investments | (58,517 | ) | |||||

| Net unrealized appreciation from investments | 260,919 | ||||||

| Net Assets | $ | 7,907,107 | |||||

| Common Shares | |||||||

| Net assets | $ | 5,092,000 | |||||

| Shares outstanding | 505,208 | ||||||

| Net asset value, offering price, and redemption price per share | $ | 10.08 | |||||

| A Shares | |||||||

| Net assets | $ | 2,336,608 | |||||

| Shares outstanding | 231,561 | ||||||

| Net asset value and redemption price per share | $ | 10.09 | |||||

| Maximum offering price per share (net asset value/ (1-4.00%)) | $ | 10.51 | |||||

| C Shares | |||||||

| Net assets | $ | 478,499 | |||||

| Shares outstanding | 47,535 | ||||||

| Net asset value and offering price per share | $ | 10.07 | |||||

1 Including $2,230,932 of securities on loan.

See Accompanying Notes to Financial Statements.

12

Credit Suisse Absolute Return Fund

Statement of Operations

For the Six Months Ended April 30, 2008 (unaudited)

| Investment Income (Note 2) | |||||||

| Interest | $ | 63,300 | |||||

| Dividends | 62,777 | ||||||

| Securities lending | 12,735 | ||||||

| Total investment income | 138,812 | ||||||

| Expenses | |||||||

| Investment advisory fees (Note 3) | 27,822 | ||||||

| Administrative services fees (Note 3) | 4,414 | ||||||

| Distribution fees (Note 3) | |||||||

| Class A | 2,440 | ||||||

| Class C | 1,916 | ||||||

| Offering costs (Note 3) | 27,510 | ||||||

| Trustees' fees | 13,373 | ||||||

| Audit and tax fees | 12,572 | ||||||

| Legal fees | 8,927 | ||||||

| Printing fees (Note 3) | 5,073 | ||||||

| Registration fees | 3,029 | ||||||

| Insurance expense | 103 | ||||||

| Interest expense (Note 4) | 55 | ||||||

| Commitment fees (Note 4) | 31 | ||||||

| Total expenses | 107,265 | ||||||

| Less: fees waived and expenses reimbursed (Note 3) | (65,812 | ) | |||||

| Net expenses | 41,453 | ||||||

| Net investment income | 97,359 | ||||||

| Net Realized and Unrealized (Loss) from Investments | |||||||

| Net realized loss from investments | (33,615 | ) | |||||

| Net change in unrealized appreciation (depreciation) from investments | (219,685 | ) | |||||

| Net realized and unrealized loss from investments | �� | (253,300 | ) | ||||

| Net decrease in net assets resulting from operations | $ | (155,941 | ) | ||||

See Accompanying Notes to Financial Statements.

13

Credit Suisse Absolute Return Fund

Statements of Changes in Net Assets

| For the Six Months Ended April 30, 2008 (unaudited) | For the Period Ended October 31, 20071 | ||||||||||

| From Operations | |||||||||||

| Net investment income | $ | 97,359 | $ | 163,712 | |||||||

| Net realized gain (loss) from investments | (33,615 | ) | 32,289 | ||||||||

| Net change in unrealized appreciation (depreciation) from investments | (219,685 | ) | 480,604 | ||||||||

| Net increase (decrease) in net assets resulting from operations | (155,941 | ) | 676,605 | ||||||||

| From Dividends and Distributions | |||||||||||

| Dividends from net investment income | |||||||||||

| Common Class shares | (251,406 | ) | — | ||||||||

| Class A shares | (81,581 | ) | — | ||||||||

| Class C shares | (16,603 | ) | — | ||||||||

| Distributions from net realized gains | |||||||||||

| Common Class shares | (40,951 | ) | — | ||||||||

| Class A shares | (14,197 | ) | — | ||||||||

| Class C shares | (2,043 | ) | — | ||||||||

| Net decrease in net assets resulting from dividends and distributions | (406,781 | ) | — | ||||||||

| From Capital Share Transactions (Note 6) | |||||||||||

| Proceeds from sale of shares | 1,601,480 | 1,347,944 | |||||||||

| Reinvestment of dividends and distributions | 110,617 | — | |||||||||

| Net asset value of shares redeemed | (216,068 | ) | (5,050,749 | ) | |||||||

| Net increase (decrease) in net assets from capital share transactions | 1,496,029 | (3,702,805 | ) | ||||||||

| Net increase (decrease) in net assets | 933,307 | (3,026,200 | ) | ||||||||

| Net Assets | |||||||||||

| Beginning of period | 6,973,800 | 10,000,0002 | |||||||||

| End of period | $ | 7,907,107 | $ | 6,973,800 | |||||||

| Undistributed net investment income | $ | 43,352 | $ | 295,583 | |||||||

1 For the period December 29, 2006 (commencement of operations) through October 31, 2007.

2 The Fund was seeded on December 29, 2006.

See Accompanying Notes to Financial Statements.

14

Credit Suisse Absolute Return Fund

Financial Highlights

(For a Common Class Share of the Fund Outstanding Throughout Each Period)

| For the Six Months Ended April 30, 2008 (unaudited) | For the Period Ended October 31, 20071 | ||||||||||

| Per share data | |||||||||||

| Net asset value, beginning of period | $ | 10.91 | $ | 10.00 | |||||||

| INVESTMENT OPERATIONS | |||||||||||

| Net investment income2 | 0.14 | 0.19 | |||||||||

| Net gain (loss) on investments (both realized and unrealized) | (0.39 | ) | 0.72 | ||||||||

| Total from investment operations | (0.25 | ) | 0.91 | ||||||||

| LESS DIVIDENDS AND DISTRIBUTIONS | |||||||||||

| Dividends from net investment income | (0.50 | ) | — | ||||||||

| Distributions from net realized gains | (0.08 | ) | — | ||||||||

| Total dividends and distributions | (0.58 | ) | — | ||||||||

| Net asset value, end of period | $ | 10.08 | $ | 10.91 | |||||||

| Total return3 | (2.28 | )% | 9.10 | % | |||||||

| RATIOS AND SUPPLEMENTAL DATA | |||||||||||

| Net assets, end of period (000s omitted) | $ | 5,092 | $ | 5,511 | |||||||

| Ratio of expenses to average net assets4 | 1.00 | % | 1.00 | % | |||||||

| Ratio of net investment income to average net assets4 | 2.76 | % | 2.21 | % | |||||||

| Decrease reflected in above operating expense ratios due to waivers/reimbursements4 | 1.84 | % | 3.29 | % | |||||||

| Portfolio turnover rate | 39 | % | 206 | % | |||||||

1 For the period December 29, 2006 (commencement of operations) through October 31, 2007.

2 Per share information is calculated using the average shares outstanding method.

3 Total returns are historical and assume changes in share price and reinvestment of all dividends and distributions. Had certain expenses not been reduced during the periods shown, total returns would have been lower. Total returns for periods less than one year are not annualized.

4 Annualized.

See Accompanying Notes to Financial Statements.

15

Credit Suisse Absolute Return Fund

Financial Highlights

(For a Class A Share of the Fund Outstanding Throughout Each Period)

| For the Six Months Ended April 30, 2008 (unaudited) | For the Period Ended October 31, 20071 | ||||||||||

| Per share data | |||||||||||

| Net asset value, beginning of period | $ | 10.89 | $ | 10.00 | |||||||

| INVESTMENT OPERATIONS | |||||||||||

| Net investment income2 | 0.12 | 0.17 | |||||||||

| Net gain (loss) on investments (both realized and unrealized) | (0.39 | ) | 0.72 | ||||||||

| Total from investment operations | (0.27 | ) | 0.89 | ||||||||

| LESS DIVIDENDS AND DISTRIBUTIONS | |||||||||||

| Dividends from net investment income | (0.45 | ) | — | ||||||||

| Distributions from net realized gains | (0.08 | ) | — | ||||||||

| Total dividends and distributions | (0.53 | ) | — | ||||||||

| Net asset value, end of period | $ | 10.09 | $ | 10.89 | |||||||

| Total return3 | (2.43 | )% | 8.90 | % | |||||||

| RATIOS AND SUPPLEMENTAL DATA | |||||||||||

| Net assets, end of period (000s omitted) | $ | 2,337 | $ | 1,345 | |||||||

| Ratio of expenses to average net assets4 | 1.25 | % | 1.25 | % | |||||||

| Ratio of net investment income to average net assets4 | 2.41 | % | 1.90 | % | |||||||

| Decrease reflected in above operating expense ratios due to waivers/reimbursements4 | 1.66 | % | 3.33 | % | |||||||

| Portfolio turnover rate | 39 | % | 206 | % | |||||||

1 For the period December 29, 2006 (commencement of operations) through October 31, 2007.

2 Per share information is calculated using the average shares outstanding method.

3 Total returns are historical and assume changes in share price, reinvestment of all dividends and distributions and no sales charge. Had certain expenses not been reduced during the periods shown, total returns would have been lower. Total returns for periods less than one year are not annualized.

4 Annualized.

See Accompanying Notes to Financial Statements.

16

Credit Suisse Absolute Return Fund

Financial Highlights

(For a Class C Share of the Fund Outstanding Throughout Each Period)

| For the Six Months Ended April 30, 2008 (unaudited) | For the Period Ended October 31, 20071 | ||||||||||

| Per share data | |||||||||||

| Net asset value, beginning of period | $ | 10.82 | $ | 10.00 | |||||||

| INVESTMENT OPERATIONS | |||||||||||

| Net investment income2 | 0.09 | 0.10 | |||||||||

| Net gain (loss) on investments (both realized and unrealized) | (0.39 | ) | 0.72 | ||||||||

| Total from investment operations | (0.30 | ) | 0.82 | ||||||||

| LESS DIVIDENDS AND DISTRIBUTIONS | |||||||||||

| Dividends from net investment income | (0.37 | ) | — | ||||||||

| Distributions from net realized gains | (0.08 | ) | — | ||||||||

| Total dividends and distributions | (0.45 | ) | — | ||||||||

| Net asset value, end of period | $ | 10.07 | $ | 10.82 | |||||||

| Total return3 | (2.74 | )% | 8.20 | % | |||||||

| RATIOS AND SUPPLEMENTAL DATA | |||||||||||

| Net assets, end of period (000s omitted) | $ | 478 | $ | 118 | |||||||

| Ratio of expenses to average net assets4 | 2.00 | % | 2.00 | % | |||||||

| Ratio of net investment income to average net assets4 | 1.88 | % | 1.15 | % | |||||||

| Decrease reflected in above operating expense ratios due to waivers/reimbursements4 | 1.52 | % | 3.37 | % | |||||||

| Portfolio turnover rate | 39 | % | 206 | % | |||||||

1 For the period December 29, 2006 (commencement of operations) through October 31, 2007.

2 Per share information is calculated using the average shares outstanding method.

3 Total returns are historical and assume changes in share price, reinvestment of all dividends and distributions and no sales charge. Had certain expenses not been reduced during the periods shown, total returns would have been lower. Total returns for periods less than one year are not annualized.

4 Annualized.

See Accompanying Notes to Financial Statements.

17

Credit Suisse Absolute Return Fund

Notes to Financial Statements

April 30, 2008 (unaudited)

Note 1. Organization

The Credit Suisse Capital Funds (the "Trust") covered in this report is the Absolute Return Fund (the "Fund"). The Trust is registered under the Investment Company Act of 1940, as amended (the "1940 Act") as an open-end management investment company. The Trust was organized under the laws of the Commonwealth of Massachusetts as a business trust on November 26, 1985. The Fund is a diversified, open-end management investment company that seeks to achieve a positive absolute return over a three to five year economic cycle.

The Fund is authorized to offer three classes of shares: Common Class shares, Class A shares, and Class C shares. Each class of shares in the Fund represents an equal pro rata interest in the Fund, except that they bear different expenses which reflect the differences in the range of services provided to them. Class A shares are sold subject to a front-end sales charge of up to 4.00%. Class C shares are sold subject to a contingent deferred sales charge of 1.00% if redeemed within the first year of purchase.

Note 2. Significant Accounting Policies

A) SECURITY VALUATION — The net asset value of the Fund is determined daily as of the close of regular trading on The New York Stock Exchange, Inc. (the "Exchange") on each day the Exchange is open for business. Equity investments are valued at market value, which is generally, determined using the closing price on the exchange or market on which the security is primarily traded at the time of valuation (the "Valuation Time"). If no sales are reported, equity investments are generally valued at the most recent bid quotation as of the Valuation Time or at the lowest asked quotation in the case of a short sale of securities. Debt securities with a remaining maturity greater than 60 days are valued in accordance with the price supplied by a pricing service, which may use a matrix, formula or other objective method that takes into consideration market indices, yield curves and other specific adjustments. Debt obligations that will mature in 60 days or less are valued on the basis of amortized cost, which approximates market value, unless it is determined that using this method would not represent fair value. Investments in mutual funds are valued at the mutual fund's closing net asset value per share on the day of valuation. Securities and other assets for which market quotations are not readily available, or whose values have been materially affected by events occurring before the Fund's Valuation Time but after the close of the securities' primary markets, are valued at fair value as determined in good faith by, or under the direction of, the Board of Trustees under procedures established by the Board of Trustees. The Fund may utilize a service provided by an

18

Credit Suisse Absolute Return Fund

Notes to Financial Statements (continued)

April 30, 2008 (unaudited)

Note 2. Significant Accounting Policies

independent third party which has been approved by the Board of Trustees to fair value certain securities. When fair-value pricing is employed, the prices of securities used by a fund to calculate its net asset value may differ from quoted or published prices for the same securities.

B) SECURITY TRANSACTIONS AND INVESTMENT INCOME — Security transactions are accounted for on a trade date basis. Interest income is recorded on the accrual basis. Dividends are recorded on the ex-dividend date. Certain expenses are class specific expenses and vary by class. Income, expenses (excluding class-specific expenses) and realized/unrealized gains/losses are allocated proportionately to each class of shares based upon the relative net asset value of outstanding shares of that class. The cost of investments sold is determined by use of the specific identification method for both financial reporting and income tax purposes.

C) DIVIDENDS AND DISTRIBUTIONS TO SHAREHOLDERS — Dividends from net investment income and distributions of net realized capital gains, if any, are declared and paid at least annually. However, to the extent that a net realized capital gain can be reduced by a capital loss carryforward, such gain will not be distributed. Income and capital gain distributions are determined in accordance with federal income tax regulations, which may differ from accounting principles generally accepted in the United States of America ("GAAP").

D) FEDERAL INCOME TAXES — No provision is made for federal taxes as it is the Fund's intention to continue to qualify for and elect the tax treatment applicable to regulated investment companies under the Internal Revenue Code of 1986, as amended, and to make the requisite distributions to its shareholders, which will be sufficient to relieve it from federal income and excise taxes.

E) USE OF ESTIMATES — The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from these estimates.

F) SHORT-TERM INVESTMENTS — The Fund, together with other funds/portfolios advised by Credit Suisse Asset Management, LLC ("Credit Suisse"), an indirect, wholly-owned subsidiary of Credit Suisse Group, pools available cash into either a short-term variable rate time deposit issued by State Street Bank and Trust Company ("SSB"), the Fund's custodian, or a

19

Credit Suisse Absolute Return Fund

Notes to Financial Statements (continued)

April 30, 2008 (unaudited)

Note 2. Significant Accounting Policies

money market fund advised by Credit Suisse. The short-term time deposit issued by SSB is a variable rate account classified as a short-term investment.

G) SECURITIES LENDING — Loans of securities are required at all times to be secured by collateral at least equal to 102% of the market value of domestic securities on loan (including any accrued interest thereon) and 105% of the market value of foreign securities on loan (including any accrued interest thereon). Cash collateral received by the Fund in connection with securities lending activity may be pooled together with cash collateral for other funds/portfolios advised by Credit Suisse and may be invested in a variety of investments, including certain Credit Suisse-advised funds, funds advised by SSB, the Fund's securities lending agent, or money market instruments. However, in the event of default or bankruptcy by the other party to the agreement, realization and/or retention of the collateral may be subject to legal proceedings.

SSB has been engaged by the Fund to act as the Fund's securities lending agent. The Fund's securities lending arrangement provides that the Fund and SSB will share the net income earned from securities lending activities. During the six months ended April 30, 2008, total earnings from the Fund's investment in cash collateral received in connection with securities lending arrangements was $36,621, of which $20,731 was rebated to borrowers (brokers). The Fund retained $12,735 in income from the cash collateral investment, and SSB, as lending agent, was paid $3,155. The Fund may also be entitled to certain minimum amounts of income from its securities lending activities. Securities lending income is accrued as earned.

Note 3. Transactions with Affiliates and Related Parties

Credit Suisse serves as investment adviser for the Fund. For its investment advisory services, Credit Suisse is entitled to receive a fee from the Fund at an annual rate of 0.75% of the Fund's average daily net assets. For the six months ended April 30, 2008, investment advisory fees earned, voluntarily waived and expenses reimbursed were as follows:

| Gross Advisory Fee | Waiver | Net Advisory Fee | Expense Reimbursement | ||||||||||||

| $ | 27,822 | $ | (27,822 | ) | $ | — | $ | (37,990 | ) | ||||||

Fee waivers and reimbursements are voluntary and may be discontinued by Credit Suisse at any time.

20

Credit Suisse Absolute Return Fund

Notes to Financial Statements (continued)

April 30, 2008 (unaudited)

Note 3. Transactions with Affiliates and Related Parties

Credit Suisse Asset Management Securities, Inc. ("CSAMSI"), an affiliate of Credit Suisse, and SSB serve as co-administrators to the Fund. For its co-administrative services, CSAMSI currently receives a fee calculated at an annual rate of 0.09% of the Fund's average daily net assets. For the six months ended April 30, 2008, co-administrative services fees earned by CSAMSI were $3,338.

For its co-administrative services, SSB receives a fee, exclusive of out-of-pocket expenses, calculated in total for all the Credit Suisse funds/portfolios co-administered by SSB and allocated based upon relative average net assets of each fund/portfolio, subject to an annual minimum fee. For the six months ended April 30, 2008, co-administrative services fees earned by SSB (including out-of-pocket expenses) were $1,076.

In addition to serving as the Fund's co-administrator, CSAMSI currently serves as distributor of the Fund's shares. Pursuant to distribution plans adopted by the Fund pursuant to Rule 12b-1 under the 1940 Act, CSAMSI receives fees for its distribution services. For Class A shares the fees are calculated at an annual rate of 0.25% of the average daily net assets. For Class C shares of the Fund, the fees are calculated at an annual rate of 1.00% of the average daily net assets. Common Class shares do not bear distribution fees.

For the six months ended April 30, 2008, Credit Suisse and its affiliates advised the Fund that they retained $323 from commissions earned on the sale of the Fund's Class A shares.

Merrill Corporation ("Merrill"), an affiliate of Credit Suisse, has been engaged by the Fund to provide certain financial printing and fulfillment services. For the six months ended April 30, 2008, Merrill was paid $5,073 for its services to the Fund.

The Fund will reimburse Credit Suisse for offering costs in the amount of $159,381 that have been paid by Credit Suisse. Offering costs, including initial registration costs, were deferred and will be charged to expenses during the Fund's first year of operation. For the six months ended April 30, 2008, $27,510 has been expensed to the Fund.

Note 4. Line of Credit

The Fund, together with other funds/portfolios advised by Credit Suisse (collectively, the "Participating Funds"), participates in a $50 million committed, unsecured line of credit facility ("Credit Facility") for temporary or emergency purposes with Deutsche Bank, A.G. as administrative agent and

21

Credit Suisse Absolute Return Fund

Notes to Financial Statements (continued)

April 30, 2008 (unaudited)

Note 4. Line of Credit

syndication agent and SSB as operations agent. Under the terms of the Credit Facility, the Participating Funds pay an aggregate commitment fee at a rate of 0.10% per annum on the average unused amount of the Credit Facility, which is allocated among the Participating Funds in such manner as is determined by the governing Boards of the Participating Funds. In addition, the Participating Funds pay interest on borrowing at the Federal Funds rate plus 0.50%. Effective June 2008, Deutsche Bank, A.G. will no longer serve as administrative agent and syndication agent to the credit facility. At April 30, 2008, the Fund had no borrowing under the Credit Facility. During the six months ended April 30, 2008, the Fund had borrowings under the Credit Facility as follows:

| Average Daily Loan Balance | Weighted Average Interest Rate% | Maximum Daily Loan Outstanding | |||||||||

| $ | 197,000 | 3.343 | % | $ | 201,000 | ||||||

Note 5. Purchases and Sales of Securities

For the six months ended April 30, 2008, purchases and sales of investment securities (excluding short-term investments) were $3,877,940 and $2,149,993, respectively.

At April 30, 2008, the identified cost for federal income tax purposes, as well as the gross unrealized appreciation from investments for those securities having an excess of value over cost, gross unrealized depreciation from investments for those securities having an excess of cost over value and the net unrealized appreciation from investments were $9,955,058, $324,916, $(63,997) and $260,919, respectively.

Note 6. Capital Share Transactions

The Fund is authorized to issue an unlimited number of full and fractional shares of capital stock, $.001 par value per share, of which an unlimited number are classified as Common class shares, Class A shares, and Class C shares. Transactions in capital shares for each class of the fund were as follows:

| Common Class | |||||||||||||||||||

| For the Six Months Ended April 30, 2008 (unaudited) | For the Period Ended October 31, 20071,2 | ||||||||||||||||||

| Shares | Value | Shares | Value | ||||||||||||||||

| Shares sold | 30 | $ | 300 | 991,922 | $ | 9,919,740 | |||||||||||||

| Shares issued in reinvestment of dividends and distributions | 111 | 1,127 | — | — | |||||||||||||||

| Shares redeemed | — | — | (486,855 | ) | (5,000,000 | ) | |||||||||||||

| Net increase | 141 | $ | 1,427 | 505,067 | $ | 4,919,740 | |||||||||||||

22

Credit Suisse Absolute Return Fund

Notes to Financial Statements (continued)

April 30, 2008 (unaudited)

Note 6. Capital Share Transactions

| Class A | |||||||||||||||||||

| For the Six Months Ended April 30, 2008 (unaudited) | For the Period Ended October 31, 20071,3 | ||||||||||||||||||

| Shares | Value | Shares | Value | ||||||||||||||||

| Shares sold | 120,764 | $ | 1,236,673 | 128,409 | $ | 1,318,204 | |||||||||||||

| Shares issued in reinvestment of dividends and distributions | 9,197 | 93,111 | — | — | |||||||||||||||

| Shares redeemed | (21,912 | ) | (216,068 | ) | (4,897 | ) | (50,749 | ) | |||||||||||

| Net increase | 108,049 | $ | 1,113,716 | 123,512 | $ | 1,267,455 | |||||||||||||

| Class C | |||||||||||||||||||

| For the Six Months Ended April 30, 2008 (unaudited) | For the Period Ended October 31, 20071,3 | ||||||||||||||||||

| Shares | Value | Shares | Value | ||||||||||||||||

| Shares sold | 34,996 | $ | 364,507 | 10,917 | $ | 110,000 | |||||||||||||

| Shares issued in reinvestment of dividends and distributions | 1,622 | 16,379 | — | — | |||||||||||||||

| Net increase | 36,618 | $ | 380,886 | 10,917 | $ | 110,000 | |||||||||||||

1 For the period December 29, 2006 (commencement of operations) through October 31, 2007.

2 The Class was seeded on December 29, 2006 with initial capital of $9,900,000 and 990,000 shares.

3 The Classes were seeded on December 29, 2006 with initial capital of $50,000 and 5,000 shares.

On April 30, 2008 the number of shareholders that held 5% or more of the outstanding shares of each class of the Fund was as follows:

| Number of Shareholders | Approximate Percentage of Outstanding Shares | ||||||||||

| Common Class | 1 | 99 | % | ||||||||

| Class A | 2 | 88 | % | ||||||||

| Class C | 1 | 90 | % | ||||||||

Some of the shareholders are omnibus accounts, which hold shares on behalf of individual shareholders.

Note 7. Contingencies

In the normal course of business, the Fund may provide general indemnifications pursuant to certain contracts and organizational documents. The Fund's maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be estimated; however, based on experience, the risk of loss from such claims is considered remote.

23

Credit Suisse Absolute Return Fund

Notes to Financial Statements (continued)

April 30, 2008 (unaudited)

Note 8. Recent Accounting Pronouncements

During June 2006, the Financial Accounting Standards Board ("FASB") issued FASB Interpretation 48 ("FIN 48" or the "Interpretation"), Accounting for Uncertainty in Income Taxes — an interpretation of FASB statement 109. FIN 48 supplements FASB Statement 109, Accounting for Income Taxes, by defining the confidence level that a tax position must meet in order to be recognized in the financial statements. FIN 48 prescribes a comprehensive model for how a fund should recognize, measure, present, and disclose in its financial statements uncertain tax positions that the fund has taken or expects to take on a tax return. FIN 48 requires that the t ax effects of a position be recognized only if it is "more likely than not" to be sustained based solely on its technical merits. Management must be able to conclude that the tax law, regulations, case law, and other objective information regarding the technical merits sufficiently support the position's sustainability with a likelihood of more than 50 percent. During the period ended April 30, 2008, Management has adopted FIN 48. There was no material impact to the financial statements or disclosures thereto as a result of the adoption of this pronouncement.

On September 20, 2006, the FASB released Statement of Financial Accounting Standards No. 157 "Fair Value Measurements" ("FAS 157"). FAS 157 establishes an authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair-value measurements. The application of FAS 157 is required for fiscal years, beginning after November 15, 2007 and interim periods within those fiscal years. As of April 30, 2008, management does not believe the adoption of FAS 157 will impact the amounts reported in the financial statements, however, additional disclosures will be required in subsequent reports.

In March 2008, FASB issued Statement of Financial Accounting Standards No. 161, Disclosures about Derivative Instruments and Hedging Activities ("FAS 161"), an amendment of FASB Statement No. 133. FAS 161 requires enhanced disclosures about (a) how and why an entity uses derivative instruments, (b) how derivative instruments and hedging activities are accounted for, and (c) how derivative instruments and related hedging activities affect a fund's financial position, financial performance, and cash flows. Management of the Funds does not believe the adoption of FAS 161 will materially impact the financial statement amounts, but will require additional disclosures. This will include qualitative and quantitative disclosures on derivative positions existing at period end and the effect of using de rivatives during the reporting period. FAS 161 is effective for financial statements issued for fiscal years and interim periods beginning after November 15, 2008.

24

Credit Suisse Absolute Return Fund

Privacy Policy Notice (unaudited)

Important Privacy Choices for Consumers

We are committed to maintaining the privacy of every current and prospective customer. We recognize that you entrust important personal information to us, and we wish to assure you that we take seriously our responsibilities in protecting and safeguarding this information.

In connection with making available investment products and services to current and potential customers, we may obtain nonpublic personal information about you. This information may include your name, address, e-mail address, social security number, account number, assets, income, financial situation, transaction history and other personal information.

We may collect nonpublic information about you from the following sources:

• Information we receive on applications, forms, questionnaires, web sites, agreements or in the course of establishing or maintaining a customer relationship; and

• Information about your transactions with us, our affiliates, or others.

We do not disclose any nonpublic personal information about our customers or former customers to anyone, except with your consent or as otherwise permitted by law.

In cases where we believe that additional products and services may be of interest to you, we may share the information described above with our affiliates.

We may also disclose this information to firms that perform services on our behalf. These agents and service providers are required to treat the information confidentially and use it only for the purpose for which it is provided.

We restrict access to nonpublic personal information about you to those employees, agents or other parties who need to know that information to provide products or services to you or in connection with your investments with or through us. We maintain physical, electronic and procedural safeguards that comply with federal standards to guard your nonpublic personal information.

Note: This Notice is provided to clients and prospective clients of Credit Suisse Asset Management, LLC ("Credit Suisse"), and Credit Suisse Asset Management Securities, Inc., and shareholders and prospective shareholders in Credit Suisse sponsored and advised investment companies, including Credit Suisse Funds, and other consumers and customers, as applicable. This Notice is not intended to be incorporated in any offering materials but is merely a statement of our current Privacy Policy, and may be amended from time to time upon notice to you. This Notice is dated as of May 13, 2008.

25

Credit Suisse Absolute Return Fund

Proxy Voting and Portfolio Holdings Information (unaudited)

Information regarding how the Fund voted proxies related to its portfolio securities during the 12 month period ended June 30 of each year, as well as the policies and procedures that the Fund uses to determine how to vote proxies relating to its portfolio securities are available:

• By calling 1-800-927-2874

• On the Fund's website, www.credit-suisse.com/us

• On the website of the Securities and Exchange Commission, www.sec.gov.

The Fund files a complete schedule of its portfolio holdings for the first and third quarters of its fiscal year with the SEC on Form N-Q. The Fund's Forms N-Q are available on the SEC's website at www.sec.gov and may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information on the operation of the SEC's Public Reference Room may be obtained by calling 1-202-551-8090.

26

This page intentionally left blank

This page intentionally left blank

P.O. BOX 55030, BOSTON, MA 02205-5030

800-927-2874 n www.credit-suisse.com/us

CREDIT SUISSE ASSET MANAGEMENT SECURITIES, INC., DISTRIBUTOR. AR-SAR-0408

CREDIT SUISSE FUNDS

Semiannual Report

April 30, 2008

(unaudited)

n CREDIT SUISSE

LARGE CAP VALUE FUND

n CREDIT SUISSE

SMALL CAP CORE FUND

The Funds' investment objectives, risks, charges and expenses (which should be considered carefully before investing), and more complete information about the Funds, are provided in the Prospectus, which should be read carefully before investing. You may obtain additional copies by calling 800-927-2874 or by writing to Credit Suisse Funds, P.O. Box 55030, Boston, MA 02205-5030.

Credit Suisse Asset Management Securities, Inc., Distributor, is located at Eleven Madison Avenue, New York, NY 10010. Credit Suisse Funds are advised by Credit Suisse Asset Management, LLC.

Investors in the Credit Suisse Funds should be aware that they may be eligible to purchase Common Class and/or Advisor Class shares (where offered) directly or through certain intermediaries. Such shares are not subject to a sales charge but may be subject to an ongoing service and distribution fee of up to 0.50% of average daily net assets. Investors in the Credit Suisse Funds should also be aware that they may be eligible for a reduction or waiver of the sales charge with respect to Class A, B or C shares (where offered). For more information, please review the relevant prospectuses or consult your financial representative.

The views of the Funds' management are as of the date of the letter and the Fund holdings described in this document are as of April 30, 2008; these views and Fund holdings may have changed subsequent to these dates. Nothing in this document is a recommendation to purchase or sell securities.

Fund shares are not deposits or other obligations of Credit Suisse Asset Management, LLC ("Credit Suisse") or any affiliate, are not FDIC-insured and are not guaranteed by Credit Suisse or any affiliate. Fund investments are subject to investment risks, including loss of your investment.

Credit Suisse Large Cap Value Fund

Semiannual Investment Adviser's Report

April 30, 2008 (unaudited)

June 11, 2008

Dear Shareholder:

Performance Summary

11/01/07 – 04/30/08

| Fund and Benchmark | Performance | ||||||

| Common Class1 | (11.33 | %) | |||||

| Advisor Class1 | (11.45 | %) | |||||

| Class A1,2 | (11.49 | %) | |||||

| Class B1,2 | (11.81 | %) | |||||

| Class C1,2 | (11.84 | %) | |||||

| Russell 1000® Value Index3 | (9.84 | %) | |||||

Performance for the Fund's Class A, Class B and Class C Shares is without the maximum sales charge of 5.75%, 4.00% and 1.00%, respectively.2

Market Review: Housing and the dollar continue to weaken

The six-month period ended April 30, 2008 was a volatile one for U.S. equities, with the benchmark Russell 1000 Value Index falling –9.84% and the bellwether S&P 500 Index losing –9.64% in total return. In fact, nine out of the ten economic sectors in the large-cap S&P 500 Index fell during the period.

The weak dollar and elevated commodity prices buoyed the energy sector, which was up 5.6%. And, as the credit crunch intensified in the first quarter of 2008, the greatest laggards in the large-cap space were the financial (-21.3%) and information technology (-15.6%) sectors.

During the period, the U.S. Federal Reserve cut the Federal Funds rate five times, for a total of 250 basis points. The last cut of 25 basis points, on April 30, 2008, brought the rate down to the 2% level. At that time, the Fed said "substantial" easing should promote growth, but to date, economic activity "remains weak."

The U.S. housing sector has continued to weaken in 2008. In fact, since January 2007, the S&P/Case Shiller U.S. Home Price Index (a measure of home prices in 20 U.S. metropolitan areas) has fallen every month. Additionally, the number of homes entering foreclosure jumped more than 100% in the first three months of the year as compared to the same quarter in 2007. According to RealtyTrac, one in every 194 homes received a foreclosure filing. In fact, foreclosure activity rose in 46 of the 50 states and in 90 of the 100 largest metropolitan areas.

1

Credit Suisse Large Cap Value Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

Gross Domestic Product rose only a scant 0.6% in both Q4'07 and Q1'08, compared to being up 4.9% in Q3'07, as housing and the credit crunch put the breaks on economic growth. Inflation appears to be well contained.

The labor market has weakened considerably in 2008. Non-farm payrolls fell by 260,000 in the first four months of 2008, as compared to an increase of 374,000 in the same period of 2007. Additionally, the household unemployment rate measured 5.0% in April, up from 4.7% in November of 2007.

Additionally, while the U.S. dollar falls, crude oil continues to rise. During the six-month period ended April 30, 2008, crude rose from $88 to $113 per barrel.

Strategic Review and Outlook: Expect the market to remain volatile over the short term

Stock selection in four sectors produced positive performance, while six sectors underperformed during the six-month period. The largest contributors to performance relative to the benchmark came primarily from stock selection within the telecomm services sector followed by the consumer discretionary and information technology sectors. Conversely, stock selection in the consumer staples, healthcare and industrials groups was the largest detractor to performnce.

As of April 30, 2008, the Fund's largest overweights against the Russell 1000 Value Index were in the energy (+1.79%) and healthcare (+1.61%) sectors, while the largest underweights were in the consumer discretionary (-1.09%) and materials (-0.99%) sectors.

The Federal Reserve believes that the substantial easing thus far, in combination with ongoing measures to foster market liquidity, should help to promote moderate growth over time while mitigating the risks to economic activity. In addition, though the outlook is uncertain, inflation is expected to moderate in coming quarters, but will need to be carefully monitored.

The Federal Open Market Committee's next interest rate meeting is scheduled for June 25, 2008. Based on interest-rate futures as of May 6, 2008, traders are expecting the Fed to leave its target rate at the current level of 2.00%.

The near-term outlook for the U.S. housing market remains bleak. In fact, Federal Reserve Chairman Ben Bernanke urged the government and mortgage lenders to intensify their efforts to avoid home foreclosures in a speech given in New York on May 5, 2008. Additionally, the outlook for merger and acquisition activity is unlikely to improve in upcoming quarters as the Federal Reserve said the proportion of U.S. banks making it tougher for companies to borrow approached a record high in the past three months as the credit crunch deepened.

2

Credit Suisse Large Cap Value Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

Further, expectations for U.S. stock market volatility remain high on a historical basis, though they have been significantly reduced since hitting a multi-year high in mid-March.

Now that the Fed appears to be done easing, we expect our Valuation and Capital Use factors — and the companies we choose based on them — to rebound as contributing factors to performance. From a sector perspective, we are favorable toward energy, industrials, and financials, while we are currently underweight healthcare, consumer staples, and consumer services.

Jordan Low

Portfolio Manager

The value of investments generally will fluctuate in response to market movements and the Fund's performance will largely depend on the performance of value stocks, which may be more volatile than the overall market.

In addition to historical information, this report contains forward-looking statements that may concern, among other things, domestic and foreign market, industry and economic trends and developments and government regulation and their potential impact on the Fund's investments. These statements are subject to risks and uncertainties and actual trends, developments and regulations in the future, and their impact on the Fund could be materially different from those projected, anticipated or implied. The Fund has no obligation to update or revise forward-looking statements.

The Fund adopted new investment strategies effective December 1, 2006 so that its holdings are selected using quantitative stock selection models rather than a more traditional fundamental analysis approach. Investors should be aware that performance information for periods prior to December 1, 2006 does not reflect the current investment strategies.

3

Credit Suisse Large Cap Value Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

Average Annual Returns as of March 31, 20081

| 1 Year | 5 Years | 10 Years | Since Inception | Inception Date | |||||||||||||||||||

| Common Class | (9.87 | )% | 11.30 | % | — | 5.02 | % | 08/01/00 | |||||||||||||||

| Advisor Class | (10.15 | )% | — | — | 8.21 | % | 06/06/03 | ||||||||||||||||

| Class A Without Sales Charge | (10.08 | )% | 11.13 | % | 5.08 | % | — | ||||||||||||||||

| Class A With Maximum Sales Charge | (15.25 | )% | 9.82 | % | 4.45 | % | — | ||||||||||||||||

| Class B Without CDSC | (10.74 | )% | 10.29 | % | 4.31 | % | — | 02/28/96 | |||||||||||||||

| Class B With CDSC | (13.66 | )% | 10.29 | % | 4.31 | % | — | 02/28/96 | |||||||||||||||

| Class C Without CDSC | (10.82 | )% | 10.28 | % | — | 4.67 | % | 02/28/00 | |||||||||||||||

| Class C With CDSC | (11.54 | )% | 10.28 | % | — | 4.67 | % | 02/28/00 | |||||||||||||||

Average Annual Returns as of April 30, 20081

| 1 Year | 5 Years | 10 Years | Since Inception | Inception Date | |||||||||||||||||||

| Common Class | (9.93 | )% | 10.75 | % | — | 5.51 | % | 08/01/00 | |||||||||||||||

| Advisor Class | (10.28 | )% | — | — | 8.92 | % | 06/06/03 | ||||||||||||||||

| Class A Without Sales Charge | (10.21 | )% | 10.57 | % | 5.52 | % | — | ||||||||||||||||

| Class A With Maximum Sales Charge | (15.39 | )% | 9.27 | % | 4.90 | % | — | ||||||||||||||||

| Class B Without CDSC | (10.89 | )% | 9.73 | % | 4.75 | % | — | 02/28/96 | |||||||||||||||

| Class B With CDSC | (13.80 | )% | 9.73 | % | 4.75 | % | — | 02/28/96 | |||||||||||||||

| Class C Without CDSC | (10.91 | )% | 9.74 | % | — | 5.12 | % | 02/28/00 | |||||||||||||||

| Class C With CDSC | (11.64 | )% | 9.74 | % | — | 5.12 | % | 02/28/00 | |||||||||||||||

Returns represent past performance and include change in share price and reinvestment of dividends and capital gains. Past performance cannot guarantee future results. The current performance of the Fund may be lower or higher than the figures shown. Returns and share price will fluctuate, and redemption value may be more or less than original cost. The performance results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance information current to the most recent month-end is available at www.credit-suisse.com/us

1 Fee waivers and/or expense reimbursements may reduce expenses for the Fund, without which performance would be lower. Waivers and/or reimbursements may be discontinued at any time.

2 Total return for the Fund's Class A Shares for the reporting period, based on offering price (including maximum sales charge of 5.75%), was -16.60%. Total return for the Fund's Class B Shares for the reporting period, based on redemption value (including maximum contingent deferred sales charge of 4.00%), was -14.70%. Total return for the Fund's Class C Shares for the reporting period, based on redemption value (including maximum contingent deferred sales charge of 1.00%), was -12.56%.

3 The Russell 1000® Value Index measures the performance of those companies in the Russell 1000® Index with lower price-to-book ratios and lower forecasted growth values. It is an unmanaged index of common stocks that includes reinvestment of dividends and is compiled by Frank Russell Company. Investors cannot invest directly in an index.

4

Credit Suisse Large Cap Value Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

Information About Your Fund's Expenses

As an investor of the Fund, you incur two types of costs: ongoing expenses and transaction costs. Ongoing expenses include management fees, distribution and service (12b-1) fees and other Fund expenses. Examples of transaction costs include sales charges (loads), redemption fees and account maintenance fees, which are not shown in this section and which would result in higher total expenses. The following table is intended to help you understand your ongoing expenses of investing in the Fund and to help you compare these expenses with the ongoing expenses of investing in other mutual funds. The table is based on an investment of $1,000 made at the beginning of the six month period ended April 30, 2008.

The table illustrates your Fund's expenses in two ways:

• Actual Fund Return. This helps you estimate the actual dollar amount of ongoing expenses paid on a $1,000 investment in the Fund using the Fund's actual return during the period. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the "Expenses Paid per $1,000" line under the share class you hold.

• Hypothetical 5% Fund Return. This helps you to compare your Fund's ongoing expenses with those of other mutual funds using the Fund's actual expense ratio and a hypothetical rate of return of 5% per year before expenses. Examples using a 5% hypothetical fund return may be found in the shareholder reports of other mutual funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Please note that the expenses shown in these tables are meant to highlight your ongoing expenses only and do not reflect any transaction costs, such as sales charges (loads) or redemption fees. If these transaction costs had been included, your costs would have been higher. The "Expenses Paid per $1,000" line of the tables is useful in comparing ongoing expenses only and will not help you determine the relative total expenses of owning different funds.

5

Credit Suisse Large Cap Value Fund

Semiannual Investment Adviser's Report (continued)

April 30, 2008 (unaudited)

Expenses and Value of a $1,000 Investment

for the six month period ended April 30, 2008