UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04615

HARTFORD HLS SERIES FUND II, INC.

(Exact name of registrant as specified in charter)

690 Lee Road, Wayne, Pennsylvania 19087

(Address of Principal Executive Offices) (Zip Code)

Thomas R. Phillips, Esquire

Hartford Funds Management Company, LLC

690 Lee Road

Wayne, Pennsylvania 19087

(Name and Address of Agent for Service)

Copy to:

John V. O’Hanlon, Esquire

Dechert LLP

One International Place, 40th Floor

100 Oliver Street

Boston, Massachusetts 02110-2605

Registrant’s telephone number, including area code: (610) 386-4068

Date of fiscal year end: December 31

Date of reporting period: December 31, 2021

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

(a)

Hartford HLS Funds

Annual Report

December 31, 2021

| ■ Hartford Balanced HLS Fund |

| ■ Hartford Capital Appreciation HLS Fund |

| ■ Hartford Disciplined Equity HLS Fund |

| ■ Hartford Dividend and Growth HLS Fund |

| ■ Hartford Healthcare HLS Fund |

| ■ Hartford International Opportunities HLS Fund |

| ■ Hartford MidCap HLS Fund |

| ■ Hartford Small Cap Growth HLS Fund |

| ■ Hartford Small Company HLS Fund |

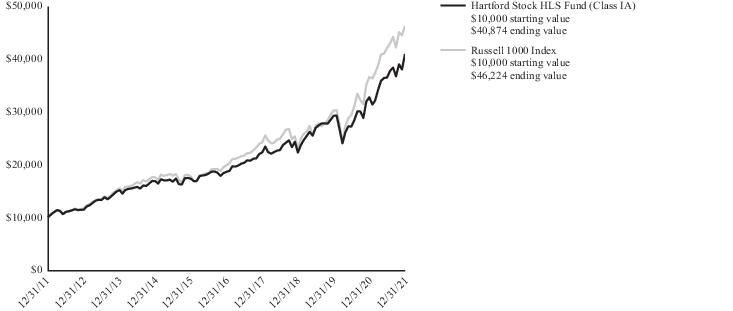

| ■ Hartford Stock HLS Fund |

| ■ Hartford Total Return Bond HLS Fund |

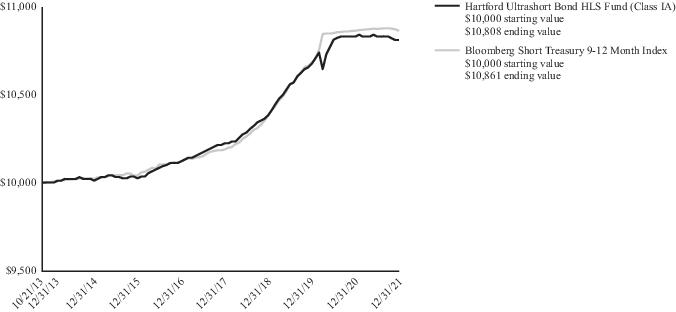

| ■ Hartford Ultrashort Bond HLS Fund |

A MESSAGE FROM THE PRESIDENT

Dear Shareholders:

Thank you for investing in Hartford HLS Funds. The following is the Funds’ Annual Report covering the period from January 1, 2021 to December 31, 2021.

Market Review

During the 12 months ended December 31, 2021, U.S. stocks, as measured by the S&P 500 Index,1 gained 28.71%. The strong performance was largely propelled by record corporate profits, a global economic rebound, timely fiscal stimulus, ongoing COVID-19 vaccination campaigns, and a flood of liquidity from central banks determined to keep interest rates near zero and supportive of the recovery for as long as possible.

While a long stretch of favorable economic trends helped bolster stock returns during the year, investors also endured bouts of market volatility spurred by some less-than-pleasant surprises: the sudden surge in inflation; the tightening of supply chains and labor markets; the stubborn persistence of new coronavirus variants; and a late-period decision by the U.S. Federal Reserve (Fed) to accelerate the winding down of asset purchases.

The period began with the inauguration of a new U.S. president and a nationwide vaccination rollout. Equity markets, already recovered from their March 2020 pandemic lows, were further lifted by congressional passage of a $1.9 trillion economic stimulus package designed to help families and businesses stay afloat. That was followed in August 2021 by approval for a $1 trillion package of infrastructure spending.

Inflation headlines dominated the rest of the year with the Fed’s preferred measure of inflation rising in November 2021 to levels not seen in 40 years.2 Supply-chain disruptions spawned in part by a surge in consumer demand helped drive up prices for gasoline, used cars, airfare tickets, durable goods, and a host of other items. In December 2021, the Consumer Price Index surged to an annual rate of 7%.

With inflation clearly trending upward toward the end of the period, the markets seemed well prepared when Fed chair Jerome Powell announced on December 15, 2021 the long-awaited implementation of the Fed’s plan to speed up its previously announced decision to taper its monthly $120 billion in asset purchases, in turn setting up expectations for interest rate increases in 2022. Markets responded positively to the move with a brief rally.

As millions were celebrating Thanksgiving, the new, highly transmissible COVID-19 Omicron variant unleashed yet another wave of global infections, casting a cloud over prospects for a more robust economic rebound. Adding to the uncertainty, proposals for additional fiscal stimulus were blocked by policy disagreements in Congress just as other previously enacted economic-support measures (i.e., extended child-tax credits and unemployment aid) began to expire.

As of the end of the period, the economic recovery still appears strong, with U.S. unemployment in December 2021 down to 3.9% compared with 14.8% in March 2020. Yet, inflation remains a wildcard, COVID-19 continues to disrupt daily life, and markets remain somewhat volatile. Nowadays, it’s more important than ever to maintain a strong relationship with your financial professional.

Thank you again for investing in Hartford HLS Funds. For the most up-to-date information on our funds, please take advantage of all the resources available at hartfordfunds.com.

James Davey

President

Hartford HLS Funds

| 1 | S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks. The index is unmanaged and not available for direct investment. Past performance does not guarantee future results. |

| 2 | The Personal Consumption Expenditures Price Index, which excludes food and energy prices, rose 5.7% in November 2021. Source: U.S. Bureau of Economic Analysis and the St. Louis Fed, as of November 2021. |

Table of Contents

The views expressed in each Fund’s Manager Discussion contained in the Fund Overview section are views of that Fund’s portfolio manager(s) through the end of the period and are subject to change based on market and other conditions, and we disclaim any responsibility to update the views contained herein. These views may contain statements that are “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements. Each Fund’s Manager Discussion is for informational purposes only and does not represent an offer, recommendation or solicitation to buy, hold or sell any security. The specific securities identified and described, if any, do not represent all of the securities purchased or sold and you should not assume that investments in the securities identified and discussed will be profitable. Holdings and characteristics are subject to change. Fund performance reflected in each Fund’s Manager Discussion reflects the returns of such Fund’s Class IA shares. Returns for such Fund’s other classes differ only to the extent that the classes do not have the same expenses.

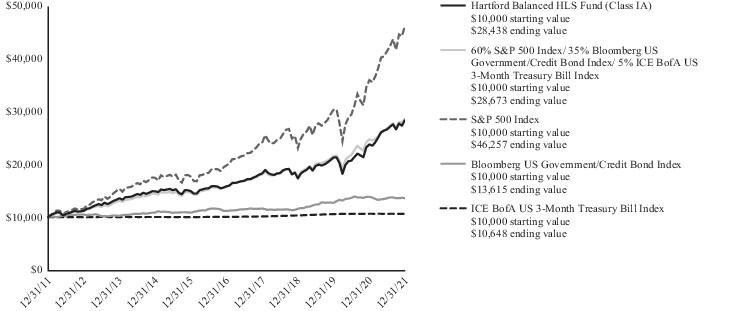

Hartford Balanced HLS Fund

Fund Overview

December 31, 2021 (Unaudited)

Inception 03/31/1983

Sub-advised by Wellington Management Company LLP | Investment objective – The Fund seeks long-term total return. |

Comparison of Change in Value of $10,000 Investment (12/31/2011 - 12/31/2021)

The chart above represents the hypothetical growth of a $10,000 investment in Class IA shares. Returns for Class IB shares differ only to the extent that Class IA shares and Class IB shares do not have the same expenses.

| Average Annual Total Returns |

| for the Periods Ended 12/31/2021 |

| | 1 Year | 5 Years | 10 Years |

| Class IA | 19.64% | 12.43% | 11.02% |

| Class IB | 19.37% | 12.14% | 10.74% |

| 60% S&P 500 Index/ 35% Bloomberg US Government/Credit Bond Index/5% ICE BofA US 3-Month Treasury Bill Index1 | 15.87% | 12.64% | 11.11% |

| S&P 500 Index | 28.71% | 18.47% | 16.55% |

| Bloomberg US Government/Credit Bond Index | -1.75% | 3.99% | 3.13% |

| ICE BofA US 3-Month Treasury Bill Index | 0.05% | 1.14% | 0.63% |

| 1 | Calculated by Hartford Funds Management Company, LLC |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable contract level or by a qualified pension or retirement plan. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the applicable class' net asset value available to shareholders for sale or redemption of Fund shares on 12/31/2021, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses. The total returns presented in the Financial Highlights section of the report are calculated in the same manner, but also take into account certain adjustments that are necessary under generally accepted accounting principles. As a result, the total returns in the Financial Highlights section may differ from the total returns presented above.

You cannot invest directly in an index.

See “Benchmark Glossary” for benchmark descriptions.

Performance information may reflect expense waivers/reimbursements without which performance would have been lower.

As shown in the Fund’s current prospectus, the total annual fund operating expense ratios for Class IA shares and Class IB shares were 0.67% and 0.92%, respectively. Gross and net expenses are the same. Actual expenses may be higher or lower. Please see the accompanying Financial Highlights for expense ratios for the period ended 12/31/2021.

Class IA shares and Class IB shares of the Fund are closed to certain qualified pension and retirement plans. For more information, please see the Fund’s statutory prospectus.

Hartford Balanced HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

Portfolio Managers

Adam H. Illfelder, CFA

Senior Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

Loren L. Moran, CFA

Senior Managing Director and Fixed Income Portfolio Manager

Wellington Management Company LLP

Matthew C. Hand, CFA

Senior Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

Manager Discussion

How did the Fund perform during the period?

The Class IA shares of Hartford Balanced HLS Fund returned 19.64% for the twelve-month period ended December 31, 2021, outperforming the Fund’s blended benchmark, which is comprised of 60% S&P 500 Index, 35% Bloomberg US Government/Credit Bond Index, and 5% ICE BofA US 3-Month Treasury Bill Index, which returned 15.87% for the same period. Individually, the S&P 500 Index, Bloomberg US Government/Credit Bond Index, and ICE BofA US 3-Month Treasury Bill Index returned 28.71%, -1.75%, and 0.05%, respectively, during the period. For the same period, the Class IA shares of the Fund also outperformed the 15.02% average return of the Lipper Mixed-Asset Target Allocation Growth Funds peer group, a group of funds that hold between 60%-80% in equity securities, with the remainder invested in bonds, cash, and cash equivalents.

Why did the Fund perform this way?

United States (U.S.) equities, as measured by the S&P 500 Index, advanced over the twelve-month period ended December 31, 2021, amid the accelerating global rollout of coronavirus vaccines, a favorable outlook for global economic growth, fiscal and monetary stimulus, and strong corporate earnings. However, markets contended with volatile coronavirus pandemic trends, fluctuating economic growth projections, and the imminent prospect of reduced quantitative easing and policy tightening. Inflation surged amid severe supply and labor shortages, rising energy prices, and heightened demand for goods and services. Fears that inflation could persist for longer than expected prompted the U.S. Federal Reserve (Fed) to announce an accelerated tapering of asset purchases.

U.S. President Joe Biden signed into law a roughly $1 trillion infrastructure bill, but as of the end of the period, the fate of the Democrats' $1.75 trillion spending and climate change plan was uncertain after U.S. Democratic Senator Joe Manchin withheld support due to concerns that it will exacerbate soaring inflation. The rapid spread of the Omicron variant of the coronavirus prompted a flurry of new restrictions and event cancellations to end the period.

During the twelve-month period, all eleven sectors within the S&P 500 Index posted positive returns, led by the Energy (+55%), Real Estate (+46%), and Financials (+35%) sectors, while the Utilities (+18%) and Consumer Staples (+19%) sectors performed the worst.

Most fixed-income sectors generated mixed total returns but positive excess returns compared to government bonds during the year as sovereign debt yields rose notably.

By the end of the period, central banks further progressed on their paths toward policy normalization as inflation broadened out across more goods and services. The Fed accelerated the timeline for tapering its large-scale asset purchase program and projected multiple interest-rate increases in both 2022 and 2023. The Bank of England (BOE) increased rates for the first time since the onset of the pandemic, citing persistent price pressures. While the European Central Bank (ECB) signaled an expectation to keep its policy rate on hold through the end of 2022, it announced it would conclude its purchases under the pandemic emergency purchase program by March 2022.

During the period, asset allocation decisions benefited the Fund’s performance relative to the blended benchmark. The Fund was generally overweight equities and underweight fixed income and cash relative to the blended benchmark. The equity portion of the Fund outperformed the S&P 500 Index, while the fixed-income portion of the Fund outperformed the Bloomberg US Government/Credit Bond Index.

Equity outperformance versus the S&P 500 Index was driven by security selection. Strong selection within the Industrials, Communication Services, and Healthcare sectors was partially offset by weak selection in the Information Technology, Materials, and Real Estate sectors. Sector allocation, a result of our bottom-up stock selection process, detracted from relative performance due to the Fund’s underweight allocations to the Energy and Real Estate sectors, along with an overweight to the Industrials sector. This was partially offset by the Fund’s overweight allocation to the Financials sector and underweights to the Consumer Staples and Utilities sectors.

From a security perspective, within the equity portion of the Fund, not holding benchmark constituent Amazon.com (Consumer Discretionary), along with the Fund’s overweight positions in Alphabet (Communication Services) and Pfizer (Healthcare) were the top contributors to performance. Alphabet beat earnings expectations, driven by strength in the company’s core search business and moderating losses in its cloud business. Pfizer’s share price rose during the period following the company’s announcement that its

Hartford Balanced HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

coronavirus booster shot was shown to provide protection against the Omicron variant of the coronavirus, and that the company had received the U.S. Food and Drug Administration’s Emergency Use Authorization for its oral antiviral for post-infection patients following positive phase 2 and 3 study results that showed it reduced the risk of hospitalization or death.

Top detractors from performance within the equity portion of the Fund included not holding benchmark constituent NVIDIA (Information Technology), as well as overweight positions in Global Payments (Information Technology) and Fidelity National Information Services (FIS, Information Technology). Shares of Global Payments fell during the period. Despite reporting third-quarter earnings that were slightly ahead of consensus expectations and raising the low end of full-year guidance, share prices were weighed down by expectations for slightly lower-than-expected fourth-quarter earnings and incremental pandemic-related challenges. In a similar vein, FIS fell sharply in sympathy with the broader payments complex on concerns around potential emerging competitive threats from new fintech companies, as well as the pace of the re-opening and its impact on consumer spending.

The fixed-income portion of the Fund outperformed the Bloomberg US Government/Credit Bond Index during the period. Security selection within investment-grade corporate credit was the biggest contributor to relative outperformance, with bonds in the Industrials, Financials and Utilities sectors all contributing positively to performance. Within non-corporate credit, an overweight to and security selection within taxable municipal bonds also contributed positively over the period. Additionally, out-of-benchmark allocations to commercial mortgage-backed securities (CMBS) and collateralized loan obligations (CLOs) made positive contributions to relative performance. Conversely, an out-of-benchmark allocation to agency mortgage-backed securities (agency MBS) slightly detracted from relative performance. Duration and yield curve positioning had a negligible impact on relative performance over the period.

Derivatives were not used in a significant manner in the Fund during the period and did not have a material impact on performance during the period.

What is the outlook as of the end of the period?

Our aim is to consistently mitigate downside risk for the Fund over a market cycle. Overall, we have been trimming back and eliminating some exposures that have outperformed in favor of more reasonably valued opportunities elsewhere. We stress-test the Fund even in the best of times, and continue to stress-test extreme scenarios and remain vigilant around any balance-sheet risks.

In the equity allocation of the Fund, as of the end of the period, we continue to focus on seeking high-quality businesses with attractive valuation and capital returns. We take a balanced approach to portfolio construction—not leaning too heavily on any one scenario—and we always strive to upgrade the quality of the positions within the Fund. Within equities, the Fund ended the period with its largest overweight in the Healthcare sector and the largest underweight in the Consumer Discretionary sector.

On the fixed-income side, we believe credit fundamentals remain strong, but the improvement in the fundamentals has peaked. Supply-chain disruptions and high labor/input costs are weighing on cash flows and corporate margins but are expected to wane throughout the year, in our view. We ended the twelve-month period with a neutral duration position in the Fund relative to the Bloomberg US Government/Credit Bond Index. As of the end of the period, we expect to continue to hold a largely benchmark-neutral duration position in the Fund but with a slight overweight to the five-year part of the yield curve given the attractive carry and our view that the market may have priced in too many interest-rate increases. Our expectation is that interest rates will move higher over the course of 2022 but not necessarily in a linear path. The pace and magnitude of interest-rate increases will primarily be determined by the impact on financial conditions and path of inflation, in our view. As of the end of the period, the fixed-income portion of the Fund is positioned with an underweight to corporate credit on a contribution-to-duration basis (calculated as the percentage weight of the bond within the total portfolio multiplied by the bond’s duration), as we view liquidity conditions as a driver of credit underperformance over the medium term. Investment-grade credit spreads remain in the bottom quartile relative to history, but we believe they could widen from current levels if volatility arises. On an industry basis, as of the end of the period, we positioned the Fund with an overweight to the less cyclical sectors such as Financials and Utilities while remaining cautious on more cyclical sectors such as Energy. As of the end of the period, the Fund holds a slight out-of-benchmark allocation to agency MBS as it may serve as a source of liquidity to rotate portfolios into credit when the opportunities present. As of the end of the period, the Fund holds out-of-benchmark allocations to securitized sectors such as asset-backed securities (ABS), CLOs, and CMBS, which we believe are supported by benign housing and consumer fundamentals.

At the end of the period, the Fund’s equity exposure was at 68.7% compared to 60% in its benchmark.

Important Risks

Investing involves risk, including the possible loss of principal. The Fund seeks to achieve its investment objective by allocating assets among different asset classes. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies. • Fixed income security risks include credit, liquidity, call, duration, event, and interest-rate risk. As interest rates rise, bond prices generally fall. • Foreign investments may be more volatile and less liquid than U.S. investments and are subject to the risk of currency fluctuations and adverse political, economic and regulatory developments. • Obligations of U.S. Government agencies are supported by varying degrees of credit but are generally not backed by the full faith and credit of the U.S. Government. • Mortgage-related and asset-backed securities’ risks include credit, interest-rate, prepayment, and extension risk.

Hartford Balanced HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

| Composition by Security Type(1) |

| as of 12/31/2021 |

| Category | Percentage of

Net Assets |

| Equity Securities | |

| Common Stocks | 68.7% |

| Fixed Income Securities | |

| Asset & Commercial Mortgage-Backed Securities | 2.8% |

| Corporate Bonds | 12.3 |

| Foreign Government Obligations | 0.3 |

| Municipal Bonds | 0.7 |

| U.S. Government Agencies(2) | 0.3 |

| U.S. Government Securities | 14.0 |

| Total | 30.4% |

| Short-Term Investments | 0.7 |

| Other Assets & Liabilities | 0.2 |

| Total | 100.0% |

| (1) | For Fund compliance purposes, the Fund may not use the same classification system. These classifications are used for financial reporting purposes. |

| (2) | All, or a portion of the securities categorized as U.S. Government Agencies, were agency mortgage-backed securities as of December 31, 2021. |

Hartford Capital Appreciation HLS Fund

Fund Overview

December 31, 2021 (Unaudited)

Inception 04/02/1984

Sub-advised by Wellington Management Company LLP | Investment objective – The Fund seeks growth of capital. |

Comparison of Change in Value of $10,000 Investment (12/31/2011 - 12/31/2021)

The chart above represents the hypothetical growth of a $10,000 investment in Class IA shares. Returns for the Fund’s other classes differ only to the extent that the classes do not have the same expenses.

| Average Annual Total Returns |

| for the Periods Ended 12/31/2021 |

| | 1 Year | 5 Years | 10 Years |

| Class IA | 14.76% | 15.86% | 14.67% |

| Class IB | 14.45% | 15.56% | 14.38% |

| Class IC | 14.18% | 15.28% | 14.10% |

| Russell 3000 Index | 25.66% | 17.97% | 16.30% |

| S&P 500 Index | 28.71% | 18.47% | 16.55% |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable contract level or by a qualified pension or retirement plan. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the applicable class' net asset value available to shareholders for sale or redemption of Fund shares on 12/31/2021, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses. The total returns presented in the Financial Highlights section of the report are calculated in the same manner, but also take into account certain adjustments that are necessary under generally accepted accounting principles. As a result, the total returns in the Financial Highlights section may differ from the total returns presented above.

Class IC shares commenced operations on 04/30/2014. Class IC shares performance prior to that date reflects Class IA shares performance adjusted to reflect the 12b-1 fee of 0.25% and the administrative services fee of 0.25% applicable to Class IC shares. The performance after such date reflects actual Class IC shares performance.

You cannot invest directly in an index.

See “Benchmark Glossary” for benchmark descriptions.

As shown in the Fund’s current prospectus, the total annual fund operating expense ratios for Class IA shares, Class IB shares and Class IC shares were 0.67%, 0.92% and 1.17%, respectively. Gross and net expenses are the same. Actual expenses may be higher or lower. Please see the accompanying Financial Highlights for expense ratios for the period ended 12/31/2021.

Class IA shares and IB shares of the Fund are closed to certain qualified pension and retirement plans. For more information, please see the Fund’s statutory prospectus.

Hartford Capital Appreciation HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

Portfolio Managers

Gregg R. Thomas, CFA

Senior Managing Director and Director, Investment Strategy

Wellington Management Company LLP

Thomas S. Simon, CFA, FRM

Senior Managing Director and Portfolio Manager

Wellington Management Company LLP

Manager Discussion

How did the Fund perform during the period?

The Class IA shares of Hartford Capital Appreciation HLS Fund returned 14.76% for the twelve-month period ended December 31, 2021, underperforming the Fund’s benchmarks, the Russell 3000 Index, which returned 25.66% for the same period, and the S& P 500 Index, which returned 28.71% for the same period. For the same period, the Class IA shares of the Fund also underperformed the 23.82% average return of the Lipper Multi-Cap Core Funds peer group, a group of funds with investment strategies similar to those of the Fund.

Why did the Fund perform this way?

United States (U.S.) equities, as measured by the Russell 3000 Index, posted positive results over the trailing twelve-month period ended December 31, 2021. In the first half of 2021, U.S. equities rallied, bolstered by an accelerating coronavirus vaccine rollout, substantial support from fiscal and monetary policy, and a broader reopening of the economy. Contributing to fiscal stimulus, U.S. President Biden signed into law a massive $1.9 trillion coronavirus relief bill and introduced an infrastructure package worth approximately $2.3 trillion, proposing to fund the initiative largely through higher corporate taxes. However, expectations for a strong rebound in the U.S. economy also sparked inflationary fears, contributing to a pro-cyclical rotation in the first quarter of 2021.

Inflation then rose sharply during the second quarter of 2021, as significant global supply-chain disruptions drove consumer and producer prices sharply higher. The U.S. Federal Reserve (Fed) maintained its view that elevated price pressures may prove transitory, but the Fed rattled markets by considerably raising its inflation forecast for 2021 and signaling the potential for interest-rate increases in 2022.

In the third quarter of 2021, U.S. equities declined as risk sentiment was pressured by anxiety about rising inflation, imminent policy normalization, moderating economic growth, and uncertainty about fiscal stimulus and the federal debt ceiling. Growth equities outperformed their value counterparts for the quarter; however, surging U.S. Treasury yields sparked a sharp sell-off in shares of large technology companies at the end of September, triggering a powerful rotation into value equities. Coronavirus cases fell sharply in September 2021, although the proliferation of the Delta variant in July and August 2021 weighed on consumer confidence and dampened reopening momentum. The Fed trimmed its 2021 gross domestic product (GDP) growth forecast to 5.9% from 7%.

U.S. equity markets surged in the fourth quarter of 2021, as risk sentiment was bolstered by robust equity inflows, strong corporate earnings, favorable economic data, and extremely accommodative financial conditions. Despite this optimism, risks persisted. The rapid spread of the Omicron variant of the coronavirus coincided with the largest increase in U.S. coronavirus cases since the onset of the pandemic, prompting a flurry of new restrictions and event cancellations. Inflation continued to surge against a backdrop of severe supply and labor shortages, rising energy prices, and high demand for goods and services, which resulted in the Fed coming under heightened scrutiny amid anxiety about a potential policy mistake. The Fed projected three interest-rate increases in 2022, up from its September 2021 forecast of one interest-rate increase.

Returns were positive across market capitalizations during the period. All eleven sectors in the Russell 3000 Index had positive returns during the period. Energy (+56.1%), Real Estate (+40.2%), and Financials (+34.7%) were the top-performing sectors.

Security selection detracted most from the Fund’s performance relative to the Russell 3000 Index during the period. Weak stock selection in the Information Technology, Healthcare, Consumer Discretionary, and Communication Services sectors was only partially offset by stronger selection in the Financials and Industrials sectors, which contributed positively. Sector allocation, a residual of our bottom-up security selection process, also slightly detracted from relative performance during the period. The Fund’s overweight exposure to the Consumer Staples sector and underweight exposure to the Energy sector detracted most from performance and was only partially offset by the Fund’s underweight exposure to the Utilities sector, which contributed positively.

Our investment process includes the use of factor-based strategies, which involve targeting certain company characteristics, or factors, that we believe impact returns across asset classes. Factor exposures detracted from performance during the period, driven by the Fund’s underweight exposure to higher-momentum names relative to the Russell 3000 Index. This was partially offset by the positive impact of the Fund’s smaller-cap footprint relative to the Russell 3000 Index.

The largest detractors from relative performance over the period were the Fund’s underweight exposures to Microsoft (Information Technology) and NVIDIA (Information Technology), as well as an overweight exposure to ChemoCentryx (Healthcare). Microsoft engages in the development and support of software, services, devices, and solutions. Shares of the company rose over the period, as the company consistently beat earnings estimates for multiple

Hartford Capital Appreciation HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

quarters. Shares rallied in the final quarter of 2021 after the company delivered strong results with balanced performance across the product set and good margin expansion in all three reporting segments. Windows, a Microsoft product, was a highlight due to strong growth in personal computer (PC) hardware manufacturers, even in the face of PC supply constraints. As of the end of the period, we maintained the Fund’s underweight position relative to the Russell 3000 Index.

NVIDIA engages in the design and manufacture of computer graphics processors, chipsets, and related multimedia software. Shares of NVIDIA rose during the period on a series of strong earnings announcements. Shares performed particularly well late in the period, as the company reported record revenue for the third quarter ended October 31, 2021, which was up 50% year-over-year on strength across the company’s Gaming, Data Center, and Professional Visualization market platforms. Shares were also aided by surging optimism around the metaverse concept. NVIDIA is at the forefront of the metaverse transformation due to its data center network and technology infrastructure. We initiated the Fund’s position during the period but remained underweight relative to the Russell 3000 Index as of the end of the period.

ChemoCentryx is a biopharmaceutical company focused on autoimmune diseases, inflammatory disorders, and cancer. The company’s shares fell sharply after the U.S. Food and Drug Administration (FDA) Arthritis Advisory Committee met to consider the new drug application for Avacopan, a candidate for the treatment of anti-neutrophil cytoplasmic autoantibody associated vasculitis. The FDA panel had a split vote on the question of whether the risk-benefit profile of Avacopan supports approval due to efficacy concerns. We eliminated the Fund’s position during the second quarter of 2021.

ChemoCentryx (Healthcare) and Allakos (Healthcare) were the top detractors from absolute performance during the period.

The largest contributors to the Fund’s performance relative to the Russell 3000 Index during the period were the Fund’s underweight exposure to Amazon (Consumer Discretionary), lack of exposure to PayPal (Information Technology) (a Russell 3000 Index constituent), and overweight exposure to Arista Networks (Information Technology). Amazon is an online retailer that offers a wide range of products. Shares of Amazon fell early in the period after the company announced that founder, Jeff Bezos, would step down as CEO to focus on new products and initiatives. The company stated that it planned for Bezos to remain with the company as executive chairman with Amazon Web Services (AWS) CEO Andy Jassy succeeding him as CEO. Amazon posted mostly strong earnings throughout the year, but shares were weighed by disappointing guidance, with management stating that sales growth was expected to slow over the next several quarters as consumers ventured outside of their homes and away from their coronavirus-induced online shopping habits. The company’s shares ended lower in the fourth quarter of 2021, driven by a regulatory fine of over 1 billion euros being imposed by the Italian Antitrust Authority, as well as an AWS outage that caused widespread issues for Amazon and its customers. We trimmed the Fund’s position throughout the period, increasing the Fund’s underweight exposure relative to the Russell 3000 Index.

PayPal is a technology platform with a focus on digital payments. Shares of PayPal declined over the second half of 2021, sparked by a negative reaction to the company’s interest in buying social media platform Pinterest, although the company eventually decided to back away from the deal. Shares fell further after the company announced a revenue forecast that came in well short of estimates. As of the end of the period, we continued not to hold this position within the Fund.

Arista Networks provides cloud networking solutions for data centers and computer environments. We initiated the Fund’s position in Arista Networks in the third quarter of 2021. Shares rose in the fourth quarter of 2021 after the company reported that it beat earnings estimates during the third quarter of 2021 and announced stronger-than-expected fourth-quarter guidance. The company forecasted that fiscal 2022 revenue growth would accelerate to 30% from 25% in 2021. Arista also expanded its stock buyback program by $1 billion and declared a four-for-one stock split. The Fund had an overweight position relative to the Russell 3000 Index as of the end of the period.

Alphabet (Communication Services) and Marsh & McLennan (Financials) were the top contributors to absolute performance during the period.

During the period, the Fund at times used derivative instruments, such as equity index futures to hedge the market risk. During the period, the use of equity index futures had a slight positive contribution to results.

What is the outlook as of the end of the period?

As of the end of the period, volatility continues to weigh on markets as investor exuberance gets muddled by increasing macro uncertainties. Despite positive news benefiting the equity market—such as strong company earnings data and the continued global rollout of vaccines—we believe that investor optimism has been diluted by increasing macroeconomic uncertainties, including the potential impact to company fundamentals as central banks begin to roll back stimulus programs, the possibility of an economic slowdown in China, and possible economic ramifications from the spread of coronavirus variants and the reemergence of pandemic-related restrictions in some regions. As ever, we remain vigilant in managing risks in the Fund and seek to deliver performance that is driven by security selection.

Looking across markets, we are mindful of the ever-evolving risks of different equity factors, and we seek to create a portfolio of diversified styles and philosophies. As of the end of the period, we maintained exposure in the Fund to cyclical areas of the market through our allocations to mean-reversion (e.g. value and contrarian) underlying portfolio managers. These underlying portfolio managers look to invest in undervalued names and use their security selection expertise to seek to identify companies with solid fundamentals and to avoid value traps that are unlikely to mean-revert in the future. We look to our trend-following (e.g. growth and momentum) underlying portfolio managers to seek to provide capital appreciation by investing in companies with favorable growth prospects. Within growth markets, we continue to watch speculative names that are at risk of whipsawing on evolving coronavirus news. We balance these exposures with risk-aversion (e.g. quality and low volatility) allocations, which seek to

Hartford Capital Appreciation HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

provide a defensive lever for the Fund by investing in companies with stable businesses. These equities, which continue to trade at low valuations relative to history and have attractive fundamentals in our view, are expected to add beneficial exposure to the Fund in the event of an unexpected shock to the economy or markets. We believe that the market backdrop will benefit fundamental portfolio managers who are able to differentiate between companies that can succeed in the current climate from those that cannot.

At the end of the period, the Fund’s largest overweights were to the Consumer Discretionary and Consumer Staples sectors, while the Fund’s largest underweights were to the Information Technology and Energy sectors, relative to the Russell 3000 Index.

Important Risks

Investing involves risk, including the possible loss of principal. The Fund’s strategy for allocating assets among portfolio management teams may not work as intended. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies. • Mid-cap securities can have greater risks and volatility than large-cap securities. • Foreign investments may be more volatile and less liquid than U.S. investments and are subject to the risk of currency fluctuations and adverse political, economic and regulatory developments. These risks are generally greater for investments in emerging markets. • To the extent the Fund focuses on one or more sectors, the Fund may be subject to increased volatility and risk of loss if adverse developments occur.

| Composition by Sector(1) |

| as of 12/31/2021 |

| Sector | Percentage

of Net Assets |

| Equity Securities | |

| Communication Services | 8.5% |

| Consumer Discretionary | 14.9 |

| Consumer Staples | 7.2 |

| Energy | 1.4 |

| Financials | 11.9 |

| Health Care | 14.2 |

| Industrials | 9.8 |

| Information Technology | 22.7 |

| Materials | 3.3 |

| Real Estate | 2.5 |

| Utilities | 2.0 |

| Total | 98.4% |

| Short-Term Investments | 1.8 |

| Other Assets & Liabilities | (0.2) |

| Total | 100.0% |

| (1) | A sector may be comprised of several industries. For Fund compliance purposes, the Fund may not use the same classification system. These sector classifications are used for financial reporting purposes. |

Hartford Disciplined Equity HLS Fund

Fund Overview

December 31, 2021 (Unaudited)

Inception 05/29/1998

Sub-advised by Wellington Management Company LLP | Investment objective – The Fund seeks growth of capital. |

Comparison of Change in Value of $10,000 Investment (12/31/2011 - 12/31/2021)

The chart above represents the hypothetical growth of a $10,000 investment in Class IA shares. Returns for the Fund’s other classes differ only to the extent that the classes do not have the same expenses.

| Average Annual Total Returns |

| for the Periods Ended 12/31/2021 |

| | 1 Year | 5 Years | 10 Years |

| Class IA | 25.52% | 18.88% | 17.41% |

| Class IB | 25.21% | 18.59% | 17.12% |

| Class IC | 24.92% | 18.30% | 16.83% |

| S&P 500 Index | 28.71% | 18.47% | 16.55% |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable contract level or by a qualified pension or retirement plan. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the applicable class' net asset value available to shareholders for sale or redemption of Fund shares on 12/31/2021, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses. The total returns presented in the Financial Highlights section of the report are calculated in the same manner, but also take into account certain adjustments that are necessary under generally accepted accounting principles. As a result, the total returns in the Financial Highlights section may differ from the total returns presented above.

Class IC shares commenced operations on 09/18/2020. Class IC shares performance prior to that date reflects Class IA shares performance adjusted to reflect the 12b-1 fee of 0.25% and the administrative services fee of 0.25% applicable to Class IC shares. The performance after such date reflects actual Class IC shares performance.

You cannot invest directly in an index.

See “Benchmark Glossary” for benchmark descriptions.

As shown in the Fund’s current prospectus, the total annual fund operating expense ratios for Class IA shares, Class IB shares and Class IC shares were 0.64%, 0.89% and 1.14%, respectively. Gross and net expenses are the same. Actual expenses may be higher or lower. Please see the accompanying Financial Highlights for expense ratios for the period ended 12/31/2021.

Class IA shares and Class IB shares of the Fund are closed to certain qualified pension and retirement plans. For more information, please see the Fund’s statutory prospectus.

Hartford Disciplined Equity HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

Portfolio Managers

Mammen Chally, CFA

Senior Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

David A. Siegle, CFA

Managing Director and Equity Research Analyst

Wellington Management Company LLP

Douglas W. McLane, CFA

Senior Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

Manager Discussion

How did the Fund perform during the period?

The Class IA shares of the Hartford Disciplined Equity HLS Fund returned 25.52% for the twelve-month period ended December 31, 2021, underperforming the Fund’s benchmark, the S&P 500 Index, which returned 28.71% for the same period. For the same period, the Class IA shares of the Fund underperformed the 26.49% average return of the Lipper Large-Cap Core Funds peer group, a group of funds with investment strategies similar to those of the Fund.

Why did the Fund perform this way?

United States (U.S.) equities, as measured by the S&P 500 Index, posted positive results over the trailing twelve-month period ended December 31, 2021. In the first quarter of 2021, U.S. equities rallied, bolstered by an accelerating coronavirus vaccine rollout, substantial support from fiscal and monetary policy, and upbeat forecasts for economic growth and earnings. Expectations for a strong rebound in the U.S. economy sparked inflationary fears, contributing to a pro-cyclical rotation. The U.S. Democratic Party secured slim majorities in both houses of Congress after winning control of the Senate, bolstering U.S. President Biden’s prospects of advancing his legislative agenda.

In the second quarter of 2021, U.S. equities rallied amid a backdrop of improving coronavirus vaccination rates, accelerating economic growth, and a broader reopening of the economy. Inflation rose sharply during the quarter, as robust demand for goods and services, along with significant global supply-chain disruptions, drove consumer and producer prices sharply higher.

During the third quarter of 2021, U.S. equities rose against a backdrop of accommodative monetary policy, robust corporate earnings, and strong demand for goods and services. Growth equities outperformed their value counterparts for the quarter; however, surging U.S. Treasury yields sparked a sharp sell-off in shares of large technology companies at the end of September 2021, triggering a powerful rotation into value equities.

U.S. equity markets surged in the fourth quarter of 2021, registering their seventh consecutive quarterly gain. Risk sentiment was bolstered by robust equity inflows, strong corporate earnings, favorable economic data, and extremely accommodative financial conditions.

The rapid spread of the Omicron variant of the coronavirus led to the largest increase in U.S. coronavirus cases since the onset of the pandemic, prompting a flurry of new restrictions and event cancellations. Inflation continued to surge against a backdrop of severe supply and labor shortages, rising energy prices, and high demand for goods and services, which resulted in the U.S. Federal Reserve (Fed) coming under heightened scrutiny amid anxiety about a potential policy mistake. In November, inflation accelerated to its highest level since 1982, as the Consumer Price Index rose 6.8% annually at the headline level and 4.9% at the core level. U.S. President Joe Biden signed into law a roughly $1 trillion infrastructure bill, but the fate of the Democrats' $1.75 trillion spending and climate change plan was uncertain as of the end of the period after U.S. Democratic Senator Joe Manchin withheld support for the current version of the plan due to concerns that it will exacerbate soaring inflation.

Returns varied by market capitalization during the period. Large-cap equities, as measured by the S&P 500 Index, outperformed mid-cap and small-cap equities, as measured by the S&P MidCap 400 Index and the Russell 2000 Index, respectively, during the period. During the twelve-month period, all eleven sectors within the S&P 500 Index rose, led by the Energy (+55%), Real Estate (46%), and Financials (+35%) sectors. Utilities was the worst-performing sector, up 18% during the period.

Sector allocation, which is a residual of our bottom-up security selection process, was the driver of the Fund’s underperformance relative to the S&P 500 Index during the period. The Fund’s underweights to the Energy, Consumer Staples and Communication Services sectors detracted the most from performance. This was partially offset by the Fund’s underweights to the Utilities and Materials sectors. Security selection also detracted from relative performance. Security selection within the Information Technology, Consumer Staples, and Utilities sectors detracted most during the period, but was partially offset by selection within the Healthcare, Communication Services, and Financials sectors.

Top detractors from the Fund’s performance relative to the S&P 500 Index during the period were an underweight holding in NVIDIA (Information Technology) and overweight holdings in Global Payments (Information Technology) and Walt Disney (Communication Services). Shares of NVIDIA, a leading producer of graphics processing units

Hartford Disciplined Equity HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

(GPUs), rose during the period as optimism around the metaverse concept surged. NVIDIA has been at the forefront of the metaverse transformation due to its data center network and technology infrastructure. Shares of financial technology company Global Payments lost ground during the period despite posting strong earnings that beat consensus estimates in November 2021. Rather than rewarding this positive news, market participants appeared to be more focused on increasing competition in the space, while also reacting skeptically to the company’s two announced acquisitions, causing the company’s share price to fall. Shares of Walt Disney fell during the period after reported earnings in November 2021 failed to meet consensus estimates on revenue, total subscribers, and segment operating income.

The largest contributors to the Fund’s performance relative to the S&P 500 Index over the period were an overweight holding in EOG Resources (Energy), not owning PayPal (Information Technology) (an S&P 500 Index constituent), and an overweight holding in Eli Lilly (Healthcare). Shares of oil and gas exploration and production company EOG Resources surged over the period after reporting both fourth-quarter and calendar-year 2020 earnings that beat consensus expectations. The company also saw an unusually tight supply-demand balance in European gas heading into the winter, which added further price pressure to a market already at record highs. At the same time, increased demand for crude oil continued to push prices higher, buoying the company’s share price. Shares of PayPal declined during the period after the payments company announced a revenue forecast that came in well short of estimates. Management cited consumer spending concerns in their merchant base, which was driven by global supply-chain shortages decreasing the amount of available goods, as well as by weaker consumer confidence and expectations of more people shopping in-person during the holidays. Investors had a more negative outlook on the stock in October 2021 when PayPal was in late-stage talks to acquire Pinterest, but the company later backed away from the deal. Shares of Eli Lilly rose during the period. The U.S. Food and Drug Administration (FDA) granted Breakthrough Therapy designation for Donanemab, an Alzheimer’s Disease treatment. Donanemab targets N3pG, a form of beta amyloid, and has exhibited positive safety and efficacy results. Eli Lilly began a rolling submission of a Biologics License Application in 2021. The company also reported strong full year 2020 results in January 2021, driven by initial sales of its new coronavirus antibody therapy.

Derivatives were not used in a significant manner in the Fund during the period and did not have a material impact on performance during the period.

What is the outlook as of the end of the period?

As of the end of the period, it appeared that negotiations on the large spending bill have resumed, and the U.S. Congress has extended the debt ceiling. Our expectation remains that the total package, which includes the bipartisan bill signed into law, will support growth in 2022.

Consistent with the last several months, we believe inflation expectations are a major concern, as companies struggle to offset costs with pricing and are seeing margin compression. The Fed has subtly changed its view on tightening monetary conditions over the

last few months, and we continue to monitor these developments very closely. Labor force participation rates are expected to continue increasing as stimulus effects wane, limiting the risk of runaway inflation. Additionally, we are encouraged thus far by the lower mortality rate in the face of the Omicron variant of the coronavirus. As confidence returns, we expect inflation will persist into 2022.

Outside of that, we believe little has changed from an outlook perspective. We believe geopolitical risks remain, the partisan divide within the U.S. is extreme, and the recovery in markets affected by the coronavirus pandemic remains uneven due to the uptake of vaccines and restrictions on travel. Still, we are encouraged that demand remains strong and supply chain disruptions are slowly getting resolved. Ultimately, as we start 2022, we view any potential increase in volatility as an opportunity for our approach, which is driven by stock selection.

We continue to focus on the long term. While we did make some changes in the Fund during the period, we continued to be incremental and mindful of the increased volatility at the end of the period.

At the end of the period, the Fund’s largest overweights were to the Communication Services, Industrials, and Healthcare sectors, while the largest underweights were to the Materials, Energy, and Real Estate sectors, relative to the S&P 500 Index.

Important Risks

Investing involves risk, including the possible loss of principal. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies.

| Composition by Sector(1) |

| as of 12/31/2021 |

| Sector | Percentage

of Net Assets |

| Equity Securities | |

| Communication Services | 11.8% |

| Consumer Discretionary | 11.8 |

| Consumer Staples | 6.3 |

| Energy | 1.3 |

| Financials | 11.8 |

| Health Care | 14.4 |

| Industrials | 9.1 |

| Information Technology | 28.1 |

| Materials | 1.1 |

| Real Estate | 1.7 |

| Utilities | 2.0 |

| Total | 99.4% |

| Short-Term Investments | 0.6 |

| Other Assets & Liabilities | 0.0 * |

| Total | 100.0% |

| * | Percentage rounds to zero. |

| (1) | A sector may be comprised of several industries. For Fund compliance purposes, the Fund may not use the same classification system. These sector classifications are used for financial reporting purposes. |

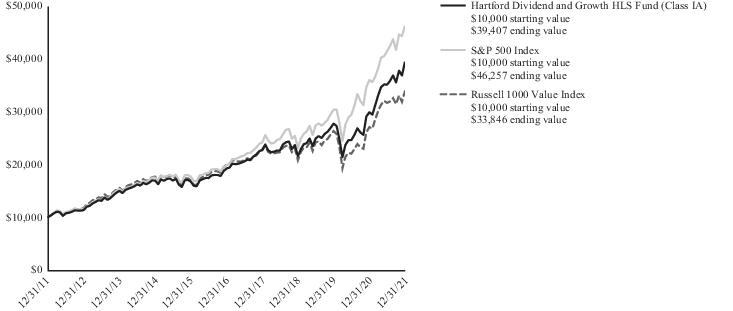

Hartford Dividend and Growth HLS Fund

Fund Overview

December 31, 2021 (Unaudited)

Inception 03/09/1994

Sub-advised by Wellington Management Company LLP | Investment objective – The Fund seeks a high level of current income consistent with growth of capital. |

Comparison of Change in Value of $10,000 Investment (12/31/2011 - 12/31/2021)

The chart above represents the hypothetical growth of a $10,000 investment in Class IA shares. Returns for Class IB shares differ only to the extent that Class IA shares and Class IB shares do not have the same expenses.

| Average Annual Total Returns |

| for the Periods Ended 12/31/2021 |

| | 1 Year | 5 Years | 10 Years |

| Class IA | 32.00% | 15.44% | 14.70% |

| Class IB | 31.68% | 15.15% | 14.41% |

| S&P 500 Index | 28.71% | 18.47% | 16.55% |

| Russell 1000 Value Index | 25.16% | 11.16% | 12.97% |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable contract level or by a qualified pension or retirement plan. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the applicable class' net asset value available to shareholders for sale or redemption of Fund shares on 12/31/2021, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses. The total returns presented in the Financial Highlights section of the report are calculated in the same manner, but also take into account certain adjustments that are necessary under generally accepted accounting principles. As a result, the total returns in the Financial Highlights section may differ from the total returns presented above.

You cannot invest directly in an index.

See “Benchmark Glossary” for benchmark descriptions.

As shown in the Fund’s current prospectus, the total annual fund operating expense ratios for Class IA shares and Class IB shares were 0.66% and 0.91%, respectively. Gross and net expenses are the same. Actual expenses may be higher or lower. Please see the accompanying Financial Highlights for expense ratios for the period ended 12/31/2021.

Class IA shares and Class IB shares of the Fund are closed to certain qualified pension and retirement plans. For more information, please see the Fund’s statutory prospectus.

Hartford Dividend and Growth HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

Portfolio Managers

Matthew G. Baker

Senior Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

Nataliya Kofman

Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

Manager Discussion

How did the Fund perform during the period?

The Class IA shares of Hartford Dividend and Growth HLS Fund returned 32.00% for the twelve-month period ended December 31, 2021, outperforming the Fund’s benchmarks, the S&P 500 Index, which returned 28.71% for the same period, and the Russell 1000 Value Index, which returned 25.16% for the same period. For the same period, the Class IA shares of the Fund outperformed the 25.00% average return of the Lipper Equity Income Funds peer group, a group of funds with investment strategies similar to those of the Fund.

Why did the Fund perform this way?

United States (U.S.) equities, as measured by the S&P 500 Index, posted positive results over the trailing twelve-month period ended December 31, 2021. In the first quarter of 2021, U.S. equities rallied, bolstered by an accelerating coronavirus vaccine rollout, substantial fiscal and monetary policy support, and upbeat forecasts for economic growth and earnings. Expectations for a strong rebound in the U.S. economy sparked inflationary fears, contributing to a pro-cyclical rotation. The U.S. Democratic Party secured slim majorities in both houses of Congress after winning control of the Senate, bolstering U.S. President Biden’s prospects of advancing his legislative agenda.

In the second quarter of 2021, U.S. equities rallied amid a backdrop of improving coronavirus vaccination rates, accelerating economic growth, and a broader reopening of the economy. Inflation rose sharply during the quarter, as robust demand for goods and services, along with significant global supply-chain disruptions, drove consumer and producer prices sharply higher.

During the third quarter of 2021, U.S. equities rose against a backdrop of accommodative monetary policy, robust corporate earnings, and strong demand for goods and services. Growth equities outperformed their value counterparts for the quarter; however, surging U.S. Treasury yields sparked a sharp sell-off in shares of large technology companies at the end of September 2021, triggering a powerful rotation into value equities.

U.S. equity markets surged in the fourth quarter of 2021, registering their seventh consecutive quarterly gain. Risk sentiment was bolstered by robust equity inflows, strong corporate earnings, favorable economic data, and extremely accommodative financial conditions. The rapid spread of the Omicron variant of the coronavirus led to the

largest increase in U.S. coronavirus cases since the onset of the pandemic, prompting a flurry of new restrictions and event cancellations.

Returns varied by market capitalization during the period. Large- and mid-cap equities, as measured by the S&P 500 Index and S&P MidCap 400 Index, respectively, outperformed small-cap equities, as measured by the Russell 2000 Index, during the period. During the twelve-month period, all eleven sectors within the S&P 500 Index posted positive returns, led by the Energy (+55%), Real Estate (+46%), and Financials (+35%) sectors. Conversely, the Utilities (18%), Consumer Staples (19%), and Industrials (21%) sectors lagged the broader S&P 500 Index.

Security selection was the primary driver of Fund’s outperformance relative to the S&P 500 Index over the period. Strong selection within the Industrials, Financials, and Consumer Discretionary sectors was partially offset by weaker selection within the Consumer Staples sector. Sector allocation, a result of our bottom-up stock selection process, also added to the Fund’s returns relative to the S&P 500 Index during the period. Overweights to the Financials and Energy sectors contributed positively to relative outperformance, but were partially offset by an underweight to the Information Technology sector.

Top contributors to performance relative to the S&P 500 Index over the period included Fund’s lack of exposure to Amazon.com (Consumer Discretionary) (a constituent in the S&P 500 Index) and overweight positions in Bank of America (Financials) and Pfizer (Healthcare). The share price of Amazon slightly rose over the period, but underperformed the broader S&P 500 Index. Shares of Bank of America (BAC) rose over the period, as the company consecutively reported earnings that beat consensus estimates. The share price of Pfizer rose during the period following the company’s announcement that its booster was shown to provide protection against the Omicron variant of the coronavirus and the Food and Drug Administration’s (FDA’s) Emergency Use Authorization issuance for its oral antiviral for post-infection coronavirus patients following positive phase 2 and 3 study results that showed it reduced the risk of hospitalization or death.

The Fund’s top detractor from performance relative to the S&P 500 Index was a lack of exposure to NVIDIA (Information Technology) (a S&P 500 constituent). Relative returns were also held back by our overweights to Verizon Communications (Communication Services) and Fidelity National Information Services (Information Technology). Shares of NVIDIA, a leading producer of graphics processing units

Hartford Dividend and Growth HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

(GPUs), rose during the period as optimism around the metaverse concept surged. Shares of Verizon ended the period lower despite consecutively reporting results that beat earnings expectations. The share price of Fidelity National Information Services (FIS) fell sharply after the company lowered profit projections for the year and booked a one-time charge tied to recalculating its deferred tax liability in the United Kingdom (UK) due to corporate tax changes in the country. We maintained an overweight position in FIS within the Fund as of the end of the period.

Derivatives were not used in a significant manner in the Fund during the period and did not have a material impact on performance during the period.

What is the outlook as of the end of the period?

Despite continued volatility driven by a number of issues including the Delta and Omicron variants of the coronavirus, inflation concerns, and interest-rate speculation, the market posted positive results for 2021. Despite high stock-price correlations within industries, we have observed meaningful dissent in the market regarding the economic outlook and the path of the recovery from here. Our view is that inflation is likely to remain going forward due to significant supply constraints and labor shortages. We believe that persistent inflation, which we have not seen for years, will put pressure on margins and likely lead to interest-rate increases.

Given this outlook, we favor equities with stability in downturns (e.g., the Healthcare, and Consumer Staples sectors as well as the defense industry) and pockets of value – such as equities that were oversold and have yet to recover (e.g., airlines). In the fourth quarter of 2021, we initiated new positions in the transportation industry and the Consumer Staples sector and increased the Fund’s exposure to the Healthcare and Utilities sectors. These adds were funded by trimming the Fund’s positions in banks and technology companies, particularly certain semiconductor holdings that outperformed over the period.

We remain focused on seeking to limit downside risk in the Fund and seek to avoid companies that we would expect to struggle in an inflationary environment with rising interest rates. Such companies include those with rich valuations amid increasing discount rates and those with margins that are vulnerable to inflation due to an inability to pass on price increases. As always, we remain focused on seeking to identify quality companies with positive risk/reward skew and a narrow range of outcomes.

Important Risks

Investing involves risk, including the possible loss of principal. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies. • For dividend-paying stocks, dividends are not guaranteed and may decrease without notice. • Foreign investments may be more volatile and less liquid than U.S. investments and are subject to the risk of currency fluctuations and adverse political, economic and regulatory developments. • To the extent the Fund focuses on one or more sectors, the Fund may be subject to increased volatility and risk of loss if adverse developments occur. • Integration of environmental, social, and/or governance (ESG) factors into the investment process may not work as intended.

| Composition by Sector(1) |

| as of 12/31/2021 |

| Sector | Percentage

of Net Assets |

| Equity Securities | |

| Communication Services | 7.5% |

| Consumer Discretionary | 6.2 |

| Consumer Staples | 6.0 |

| Energy | 3.9 |

| Financials | 18.3 |

| Health Care | 15.5 |

| Industrials | 8.9 |

| Information Technology | 20.2 |

| Materials | 3.6 |

| Real Estate | 3.2 |

| Utilities | 4.4 |

| Total | 97.7% |

| Short-Term Investments | 1.8 |

| Other Assets & Liabilities | 0.5 |

| Total | 100.0% |

| (1) | A sector may be comprised of several industries. For Fund compliance purposes, the Fund may not use the same classification system. These sector classifications are used for financial reporting purposes. |

Hartford Healthcare HLS Fund

Fund Overview

December 31, 2021 (Unaudited)

Inception 05/01/2000

Sub-advised by Wellington Management Company LLP | Investment objective – The Fund seeks long-term capital appreciation. |

Comparison of Change in Value of $10,000 Investment (12/31/2011 - 12/31/2021)

The chart above represents the hypothetical growth of a $10,000 investment in Class IA shares. Returns for Class IB shares differ only to the extent that Class IA shares and Class IB shares do not have the same expenses.

| Average Annual Total Returns |

| for the Periods Ended 12/31/2021 |

| | 1 Year | 5 Years | 10 Years |

| Class IA | 10.01% | 16.64% | 17.98% |

| Class IB | 9.76% | 16.35% | 17.68% |

| S&P Composite 1500 Health Care Index | 24.85% | 17.70% | 17.44% |

| S&P 500 Index | 28.71% | 18.47% | 16.55% |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable contract level or by a qualified pension or retirement plan. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the applicable class' net asset value available to shareholders for sale or redemption of Fund shares on 12/31/2021, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses. The total returns presented in the Financial Highlights section of the report are calculated in the same manner, but also take into account certain adjustments that are necessary under generally accepted accounting principles. As a result, the total returns in the Financial Highlights section may differ from the total returns presented above.

You cannot invest directly in an index.

See “Benchmark Glossary” for benchmark descriptions.

As shown in the Fund’s current prospectus, the total annual fund operating expense ratios for Class IA shares and Class IB shares were 0.91% and 1.16%, respectively. Gross and net expenses are the same. Actual expenses may be higher or lower. Please see the accompanying Financial Highlights for expense ratios for the period ended 12/31/2021.

Class IA shares and Class IB shares of the Fund are closed to certain qualified pension and retirement plans. For more information, please see the Fund’s statutory prospectus.

Hartford Healthcare HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

Portfolio Managers

Ann C. Gallo

Senior Managing Director and Global Industry Analyst

Wellington Management Company LLP

Robert L. Deresiewicz, MD*

Senior Managing Director and Global Industry Analyst

Wellington Management Company LLP

Rebecca D. Sykes

Senior Managing Director and Global Industry Analyst

Wellington Management Company LLP

Wen Shi, CFA, PhD**

Managing Director and Global Industry Analyst

Wellington Management Company LLP

| * | Robert L. Deresiewicz announced his plan to retire and withdraw from the partnership of Wellington Management Company LLP’s parent company, and effective June 30, 2022, he will no longer serve as a portfolio manager for the Fund. Robert Deresiewicz’s portfolio management responsibilities will transition to Wen Shi in the months leading up to his departure. |

**Effective July 22, 2021, Wen Shi, CFA, was added as a portfolio manager to the Fund.

Manager Discussion

How did the Fund perform during the period?

The Class IA shares of Hartford Healthcare HLS Fund returned 10.01% for the twelve-month period ended December 31, 2021, underperforming the Fund’s benchmarks, the S&P Composite 1500 Health Care Index, which returned 24.85% for the same period, and the S&P 500 Index, which returned 28.71% for the same period. For the same period, the Class IA shares of the Fund outperformed the 9.51% average return of the Lipper Global Health and Biotechnology peer group, a group of funds with investment strategies similar to those of the Fund.

Why did the Fund perform this way?

United States (U.S.) healthcare equities returned 24.85% for the period as measured by the S&P Composite 1500 Health Care Index, underperforming the broader U.S. equity market, which returned 28.71% as measured by the S&P 500 Index, but outperforming the global equity market, which returned 21.82% during the period, as measured by the MSCI World Index. Within the S&P Composite 1500 Health Care Index, healthcare services returned 37%, medical technology returned 24%, large-cap biopharma returned 22%, small-cap biopharma returned -2%, and mid-cap biopharma returned -8% during the period.

The Fund underperformed the S& P Composite 1500 Health Care Index over the period, which was due primarily to unfavorable security selection decisions. Security selection was weakest in medical technology, small-cap biopharma, and healthcare services, while selection in large-cap biopharma was strongest. Sector allocation also detracted from the Fund’s performance relative to the S&P Composite 1500 Health Care Index. The Fund’s overweight to mid- and small-cap biopharma detracted from relative results during the period. This was partially offset by positive results from an underweight to large-cap biopharma.

An underweight to Thermo Fisher Scientific (medical technology), along with out-of-benchmark positions in Zai Lab (mid-cap biopharma) and Daiichi Sankyo (large-cap biopharma) detracted most from relative performance over the period. Shares of Thermo Fisher Scientific rallied, and the Fund’s underweight position negatively affected relative performance. In February 2021, the company reported strong earnings, but expected fading COVID-19 testing volumes in the second quarter, which raised concerns around earnings growth potential. In April 2021, it was announced that Thermo Fisher intended to acquire contract research organization, PPD. After digesting the news of the acquisition, we grew concerned that such a large deal created additional integration risk, and in light of longer-term stock gains, decided it was most appropriate to trim back the Fund’s position. Since we pared back the position, the stock has rallied, and the Fund’s underweight position negatively affected relative performance. We eliminated the Fund’s position later in the period. Shares of Zai Lab declined nearly 50% throughout the year. From a stock specific perspective, the key asset Qinlock, via partnership with Deciphera Pharmaceuticals, failed its phase 3 study for the treatment of gastrointestinal stromal tumor (GIST). From a macro perspective, the stock was also weak due to rising concerns around heightened regulation from the Chinese government, much like we saw during the period across both the technology sector and after-school tutoring industry. Furthermore, Chinese biotech equities were weak after the Chinese Center for Drug Evaluation advocated that clinical trials replace placebos with best supportive care in the comparative arm for all cancer trials. While negatively received by the market, we viewed this development as a positive change that supports sustainable growth of truly innovative drugs over the long term. Shares of Daiichi Sankyo fell during the period. Fiscal-year 2020 revenue slightly declined due in part to the National Health Insurance market expansion rule, causing drug price revisions in Japan that negatively impacted the company as well as the termination of a vaccine partnership with Sanofi. The stock remained under pressure

Hartford Healthcare HLS Fund

Fund Overview – (continued)

December 31, 2021 (Unaudited)

as the country continues to battle a fourth wave of coronavirus infections. Zai Lab, Kodiak Sciences, and Gracell Biotech were top detractors from absolute performance during the period.