UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-04615

HARTFORD HLS SERIES FUND II, INC.

(Exact name of registrant as specified in charter)

690 Lee Road, Wayne, Pennsylvania 19087

(Address of Principal Executive Offices) (Zip Code)

Thomas R. Phillips, Esquire

Hartford Funds Management Company, LLC

690 Lee Road

Wayne, Pennsylvania 19087

(Name and Address of Agent for Service)

Copy to:

John V. O’Hanlon, Esquire

Dechert LLP

One International Place, 40th Floor

100 Oliver Street

Boston, Massachusetts 02110-2605

Registrant’s telephone number, including area code: (610) 386-4068

Date of fiscal year end: December 31

Date of reporting period: December 31, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

(a)

Hartford HLS Funds

Annual Report

December 31, 2022

| ■ Hartford Balanced HLS Fund |

| ■ Hartford Capital Appreciation HLS Fund |

| ■ Hartford Disciplined Equity HLS Fund |

| ■ Hartford Dividend and Growth HLS Fund |

| ■ Hartford Healthcare HLS Fund |

| ■ Hartford International Opportunities HLS Fund |

| ■ Hartford MidCap HLS Fund |

| ■ Hartford Small Cap Growth HLS Fund |

| ■ Hartford Small Company HLS Fund |

| ■ Hartford Stock HLS Fund |

| ■ Hartford Total Return Bond HLS Fund |

| ■ Hartford Ultrashort Bond HLS Fund |

A MESSAGE FROM THE PRESIDENT

Dear Shareholders:

Thank you for investing in Hartford HLS Funds. The following is the Funds’ Annual Report covering the period from January 1, 2022 to December 31, 2022.

Market Review

During the 12 months ended December 31, 2022, U.S. stocks, as measured by the S&P 500 Index,1 lost 18.11%. Markets disappointed most investors in 2022 as both equity and fixed-income indices struggled against relentless inflationary pressures, interest-rate hikes from the US Federal Reserve (Fed), geopolitical instability abroad, and mounting fears of a pending recession.

It’s hard to believe that on January 3, 2022, the S&P 500 Index set a new record close at 4,796.56. Roughly one year later, on the final trading day of the year, the S&P 500 Index closed at 3,839.50, bringing an end to the worst-performing year since 2008. Bondholders fared little better, as the Bloomberg US Aggregate Bond Index2 posted its largest loss ever at -13.01% for the period.

There appeared to be few safe harbors for investors during the period as the Fed began the year signaling its determination to combat rising prices—beginning with a quarter-percent increase in the federal funds rate in March 2022. In subsequent months, as inflation skyrocketed to a 9.1% peak annual rate in June 2022, the Fed responded with four three-quarter-percent hikes between June and November 2022.

At various times during the period, markets attempted to rally in response to even the slightest hint that moderating inflation might provide the Fed with a reason to pause its rate-hike campaign. This was especially the case during the mid-summer months when stocks briefly surged from their June 2022 lows—only to see those gains erased after statements from Fed chair Jerome Powell making it clear that rates would instead keep on rising higher for longer.

Another important challenge to markets earlier in the period came in February 2022 when Russia invaded Ukraine, a decision that continues to threaten global security and strain worldwide food and energy supplies. The soaring gasoline prices spurred by the invasion were a major contributor to the inflationary spiral that peaked in the summer months.

In spite of the year-long economic turbulence, the nation’s employment picture remained surprisingly strong as labor shortages in key economic sectors continued to prop up job and wage growth. By the end of the period, the continued strength in labor markets provided something of a conundrum for Fed policymakers, who had hoped their interest-rate hiking campaign would have had a more measurable impact on inflation. The apparent resilience of the economy continued to underscore the risks for the Fed’s goal of bringing inflation to heel without sparking a recession sometime

in 2023.

As the new year unfolds, recession concerns are likely to grow while corporate earnings will likely be carefully scrutinized. With market volatility likely to persist, it’s more important than ever to maintain a strong relationship with your financial professional.

Thank you again for investing in Hartford HLS Funds. For the most up-to-date information on our funds, please take advantage of all the resources available at hartfordfunds.com.

James Davey

President

Hartford HLS Funds

| 1 | S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks. The index is unmanaged and not available

for direct investment. Past performance does not guarantee future results. |

| 2 | Bloomberg US Aggregate Bond Index is composed of securities that cover the US investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. The index is unmanaged and not available for direct investment. Past performance does not guarantee future results. |

Table of Contents

The views expressed in each Fund’s Manager Discussion contained in the Fund Overview section are views of that Fund’s portfolio Manager(s) through the end of the period and are subject to change based on market and other conditions, and we disclaim any responsibility to update the views contained herein. These views may contain statements that are “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements. Each Fund’s Manager Discussion is for informational purposes only and does not represent an offer, recommendation or solicitation to buy, hold or sell any security. The specific securities identified and described, if any, do not represent all of the securities purchased or sold and you should not assume that investments in the securities identified and discussed will be profitable. Holdings and characteristics are subject to change. Fund performance reflected in each Fund’s Manager Discussion reflects the returns of such Fund’s Class IA shares. Returns for such Fund’s other classes differ only to the extent that the classes do not have the same expenses.

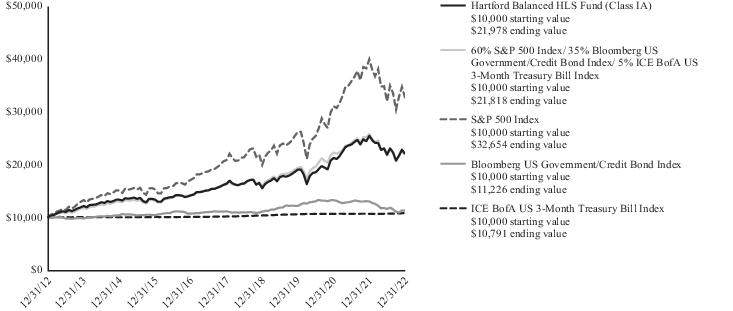

Hartford Balanced HLS Fund

Fund Overview

December 31, 2022 (Unaudited)

Inception 03/31/1983

Sub-advised by Wellington Management Company LLP | Investment objective – The Fund seeks long-term total return. |

Comparison of Change in Value of $10,000 Investment (12/31/2012 - 12/31/2022)

The chart above represents the hypothetical growth of a $10,000 investment in Class IA shares. Returns for Class IB shares differ only to the extent that Class IA shares and Class IB shares do not have the same expenses.

| Average Annual Total Returns |

| for the Periods Ended 12/31/2022 |

| | 1 Year | 5 Years | 10 Years |

| Class IA | -13.42% | 6.11% | 8.19% |

| Class IB | -13.66% | 5.84% | 7.92% |

| 60% S&P 500 Index/ 35% Bloomberg US Government/Credit Bond Index/5% ICE BofA US 3-Month Treasury Bill Index1 | -15.29% | 6.10% | 8.11% |

| S&P 500 Index | -18.11% | 9.42% | 12.56% |

| Bloomberg US Government/Credit Bond Index | -13.58% | 0.21% | 1.16% |

| ICE BofA US 3-Month Treasury Bill Index | 1.45% | 1.26% | 0.76% |

| 1 | Calculated by Hartford Funds Management Company, LLC |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable contract level or by a qualified pension or retirement plan. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the applicable class' net asset value available to shareholders for sale or redemption of Fund shares on 12/31/2022, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses. The total returns presented in the Financial Highlights section of the report are calculated in the same manner, but also take into account certain adjustments that are necessary under generally accepted accounting principles. As a result, the total returns in the Financial Highlights section may differ from the total returns presented above.

You cannot invest directly in an index.

See "Benchmark Glossary" for benchmark descriptions.

Performance information may reflect expense waivers/reimbursements without which performance would have been lower.

As shown in the Fund’s current prospectus, the total annual fund operating expense ratios for Class IA shares and Class IB shares were 0.65% and 0.90%, respectively. Gross and net expenses are the same. Actual expenses may be higher or lower. Please see the accompanying Financial Highlights for expense ratios for the period ended 12/31/2022.

Class IA shares and Class IB shares of the Fund are closed to certain qualified pension and retirement plans. For more information, please see the Fund’s statutory prospectus.

Hartford Balanced HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

Portfolio Managers

Adam H. Illfelder, CFA

Senior Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

Loren L. Moran, CFA

Senior Managing Director and Fixed Income Portfolio Manager

Wellington Management Company LLP

Matthew C. Hand, CFA

Senior Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

Manager Discussion

How did the Fund perform during the period?

The Class IA shares of Hartford Balanced HLS Fund returned -13.42% for the twelve-month period ended December 31, 2022, outperforming the Fund’s blended benchmark, which is comprised of 60% S&P 500 Index/ 35% Bloomberg US Government/Credit Bond Index/ 5% ICE BofA US 3-Month Treasury Bill Index, which returned -15.29% for the same period. Individually, the S&P 500 Index, Bloomberg US Government/Credit Bond Index, and ICE BofA US 3-Month Treasury Bill Index returned -18.11%, -13.58%, and 1.45%, respectively, during the period. For the same period, the Class IA shares of the Fund also outperformed the -15.30% average return of the Lipper Mixed-Asset Target Allocation Growth Funds peer group, a group of funds that hold between 60%-80% in equity securities, with the remainder invested in bonds, cash, and cash equivalents.

Why did the Fund perform this way?

United States (U.S.) equities, as measured by the S&P 500 Index, fell during the twelve-month period ended December 31, 2022 amid rampant inflation, surging borrowing costs, uncertainty about corporate earnings, and an increased probability of recession. U.S. equities fell during the first quarter of 2022, registering their first quarterly loss since the quarter ended March 2020. Fears about the economic implications of Russia’s large-scale military attack on Ukraine and the prospect of aggressive monetary policy tightening by the U.S. Federal Reserve (Fed) drove the S&P 500 Index into correction territory in February 2022. President Joe Biden signed into law a massive $1.5 trillion spending bill, which included substantial increases in domestic and national security programs and $13.6 billion of aid to Ukraine. U.S. equities continued to fall during a volatile second quarter of 2022. Growth stocks significantly underperformed their value counterparts as surging Treasury yields and disappointing earnings results from some of the largest technology companies drove the Nasdaq Composite Index to its largest quarterly loss since September 2001. The housing market was pressured by soaring mortgage rates, slowing demand, and elevated home prices. U.S. equities fell in the third quarter of 2022 as risk sentiment deteriorated on fears that aggressive interest-rate increases and tighter financial conditions would constrict economic growth and drive the U.S. to recession. U.S. equities rallied in the fourth quarter of 2022 following three straight quarterly declines. Greater optimism that the Fed would

begin to scale back its aggressive pace of interest-rate increases, along with outsized short position covering and hedging, helped to fuel a sharp rebound in stocks in October 2022 and November 2022 before risk sentiment waned in December 2022 amid recession fears, macroeconomic challenges, and downside earnings risks in the coming quarters. In December, the Fed raised interest rates by 0.50%, snapping a streak of four consecutive increases of 0.75%.

During the twelve-month period, two of the eleven sectors within the S&P 500 Index ― the Energy (+66%) and Utilities (+2%) sectors posted positive results; conversely, the Communication Services (-40%), Consumer Discretionary (-37%), and Information Technology (-28%) sectors performed the worst.

Broad fixed-income markets largely generated negative total returns over the trailing twelve-month period, driven by rising U.S. Treasury yields.

Government bond yields moved sharply higher following ongoing monetary policy tightening intentions in response to persistent inflation pressures. U.S. labor-market strength persisted while housing market resilience was tested by surging mortgage rates, lack of inventory, and home-price appreciation. Central banks across most developed markets reinforced their intentions to tighten monetary policy and expressed a willingness to keep policy in restrictive territory, even in the face of slower economic growth and weaker labor markets.

During the period, asset allocation decisions detracted from the Fund’s performance relative to the blended benchmark. The Fund was generally overweight equities and underweight fixed income and cash relative to the blended benchmark. The equity portion of the Fund outperformed the S&P 500 Index, while the fixed-income portion of the Fund underperformed the Bloomberg US Government/Credit Bond Index.

Equity outperformance versus the S&P 500 Index was driven by security selection during the period. Strong selection within the Consumer Discretionary, Financials, and Healthcare sectors was partially offset by weak selection in the Materials and Energy sectors. Sector allocation, a result of our bottom-up stock selection process, also contributed positively to relative performance due to the Fund’s underweight allocations to the Consumer Discretionary and

Hartford Balanced HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

Information Technology sectors, along with an overweight to the Healthcare sector. This was partially offset by the Fund’s underweights to the Energy and Consumer Staples sectors.

From a security perspective, within the equity portion of the Fund, not holding benchmark constituents Amazon.com (Consumer Discretionary) and Tesla (Consumer Discretionary), as well as an overweight position in Eli Lilly (Healthcare), were the top contributors to relative performance during the period. Shares of Amazon.com fell over the period after the company reported disappointing quarterly results that showed a slowing in both its core online retailing business and advertising unit. Tesla’s stock declined due to lower-than-expected production and delivery numbers. Eli Lilly’s shares rose as the company reported notable pipeline achievements, including U.S. Food and Drug Administration (FDA) approval for Tirzepatide, a type II diabetes treatment. In addition, Eli Lilly's competitors reported breakthrough trial results for their Alzheimer’s drug, fueling optimism over Eli Lilly’s drug Donanemab, which also targets removing the amyloid beta protein to slow disease progression.

Top detractors from relative performance within the equity portion of the Fund during the period included Meta Platforms (Communication Services) and not holding benchmark constituents Exxon Mobil (Energy) and Chevron (Energy). Meta Platforms, along with other social media stocks, faced challenges to its growth stemming from a decline in digital advertising spending and a more stringent regulatory environment. Meta’s announced decision to maintain exceptionally high spending on the Metaverse with an increase in forecasted operating losses in 2023 also furthered concerns around the company’s capital discipline and governance oversight. Both Exxon Mobil and Chevron’s stocks benefited from strong momentum within the Energy sector as oil prices spiked due to a steep supply/demand imbalance.

The fixed-income portion of the Fund underperformed the Bloomberg US Government/Credit Bond Index during the period. Security selection within investment-grade corporate credit was the primary driver of relative underperformance, particularly on account of issuers within the Industrials and Financials sectors. An overweight to and security selection within the Utilities sector was additive to performance over the period. Within non-corporate credit, an overweight to and security selection within taxable municipal bonds detracted from relative performance over the period. Additionally, out-of-benchmark allocations to commercial mortgage-backed securities (CMBS), asset-backed securities (ABS), and non-agency residential mortgage-backed securities (RMBS) had a negative impact on relative performance. Conversely, an out-of-benchmark exposure to agency mortgage-backed securities (agency MBS) contributed positively to relative performance during the period. Duration and yield curve positioning had a positive impact on relative performance over the period.

Derivatives were not used in a significant manner in the Fund during the period and did not have a material impact on performance during the period.

What is the outlook as of the end of the period?

Our aim is to consistently mitigate downside risk for the Fund over a market cycle. As of the end of the period, we have been trimming back and eliminating some exposures that have outperformed in favor of more reasonably valued opportunities elsewhere. We stress-test the Fund even in the best of times, and continue to stress-test extreme scenarios and remain vigilant around any balance-sheet risks.

In the equity allocation of the Fund, as of the end of the period, we continue to focus on seeking high-quality businesses that we believe have attractive valuation and capital returns. We take a balanced approach to portfolio construction—not leaning too heavily on any one scenario—and we always strive to upgrade the quality of the positions within the Fund. Within equities, the Fund ended the period with its largest overweight in the Financials sector and the largest underweight in the Energy sector.

On the fixed-income side, we believe credit fundamentals are strong but have likely peaked. While financial conditions tightened meaningfully in 2022, we believe their impacts are only beginning to be felt. We believe corporate fundamentals are likely to deteriorate in the quarters ahead as sustained inflation pressures margins and if/when demand wanes. We expect the evolving macroeconomic landscape will result in more fundamental and performance dispersion, which we believe may create better security selection opportunities. As of the end of the period, our primary focus on fundamentals is the impact of persistent cost inflation (particularly labor) on free cash flow generation. As of the end of the period, we have reduced exposure to more cyclical issuers that we feel will have difficulty generating positive free cash flow in a recessionary environment, as well as to issuers operating with more levered balance sheets that we believe will be more substantially impacted by higher borrowing costs. We have also been more cautious on companies that we believe are mostly directly exposed to commodity cost inflation. From a sector perspective, as of the end of the period, we have increased our positions in the Utilities sector and in some parts of the Insurance sector where we view valuations as attractive. In terms of non-corporate credit, we remain positive on taxable municipals as we think this sector still provides diversification and a broad selection of high-quality issuers that have benefited from fiscal support, although we are more cautious on the not-for-profit hospital sector given continued operating challenges. On a rating basis, we have reduced the Fund’s exposure to the BBB rated cohort of the market as of the end of the period and remain focused on investing in companies with defensive operating profiles and balance sheets that we believe will be able to weather a more difficult operating environment in 2023.

As of the end of the period, the Fund holds a slight out-of-benchmark allocation to agency MBS as we believe it may serve as a source of liquidity to rotate the Fund’s portfolio into credit when the opportunities present themselves. As of the end of the period, the Fund also holds out-of-benchmark allocations to high-quality securitized sectors such as ABS, CMBS, and non-agency RMBS. We are more cautious on certain securitized sectors, and this has been an area of reduced exposure during the period as the Fund has focused on more liquid areas of the fixed-income markets.

Hartford Balanced HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

Important Risks

Investing involves risk, including the possible loss of principal. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies. • Fixed income security risks include credit, liquidity, call, duration, event, and interest-rate risk. As interest rates rise, bond prices generally fall. • Foreign investments may be more volatile and less liquid than U.S. investments and are subject to the risk of currency fluctuations and adverse political, economic and regulatory developments. • Obligations of U.S. Government agencies are supported by varying degrees of credit but are generally not backed by the full faith and credit of the U.S. Government. • Mortgage-related and asset-backed securities’ risks include credit, interest-rate, prepayment, and extension risk. • To the extent the Fund focuses on one or more sectors, the Fund may be subject to increased volatility and risk of loss if adverse developments occur.

| Composition by Security Type(1) |

| as of 12/31/2022 |

| Category | Percentage of

Net Assets |

| Equity Securities | |

| Common Stocks | 64.6% |

| Fixed Income Securities | |

| Asset & Commercial Mortgage-Backed Securities | 1.2% |

| Corporate Bonds | 12.3 |

| Foreign Government Obligations | 0.1 |

| Municipal Bonds | 0.7 |

| U.S. Government Agencies(2) | 0.9 |

| U.S. Government Securities | 19.0 |

| Total | 34.2% |

| Short-Term Investments | 0.9 |

| Other Assets & Liabilities | 0.3 |

| Total | 100.0% |

| (1) | For Fund compliance purposes, the Fund may not use the same classification system. These classifications are used for financial reporting purposes. |

| (2) | All, or a portion of the securities categorized as U.S. Government Agencies, were agency mortgage-backed securities as of December 31, 2022. |

Hartford Capital Appreciation HLS Fund

Fund Overview

December 31, 2022 (Unaudited)

Inception 04/02/1984

Sub-advised by Wellington Management Company LLP | Investment objective – The Fund seeks growth of capital. |

Comparison of Change in Value of $10,000 Investment (12/31/2012 - 12/31/2022)

The chart above represents the hypothetical growth of a $10,000 investment in Class IA shares. Returns for the Fund’s other classes differ only to the extent that the classes do not have the same expenses.

| Average Annual Total Returns |

| for the Periods Ended 12/31/2022 |

| | 1 Year | 5 Years | 10 Years |

| Class IA | -15.30% | 7.68% | 10.89% |

| Class IB | -15.50% | 7.41% | 10.62% |

| Class IC | -15.71% | 7.15% | 10.34% |

| Russell 3000 Index | -19.21% | 8.79% | 12.13% |

| S&P 500 Index | -18.11% | 9.42% | 12.56% |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable contract level or by a qualified pension or retirement plan. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the applicable class' net asset value available to shareholders for sale or redemption of Fund shares on 12/31/2022, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses. The total returns presented in the Financial Highlights section of the report are calculated in the same manner, but also take into account certain adjustments that are necessary under generally accepted accounting principles. As a result, the total returns in the Financial Highlights section may differ from the total returns presented above.

Class IC shares commenced operations on 04/30/2014. Class IC shares performance prior to that date reflects Class IA shares performance adjusted to reflect the 12b-1 fee of 0.25% and the administrative services fee of 0.25% applicable to Class IC shares. The performance after such date reflects actual Class IC shares performance.

You cannot invest directly in an index.

See "Benchmark Glossary" for benchmark descriptions.

As shown in the Fund’s current prospectus, the total annual fund operating expense ratios for Class IA shares, Class IB shares and Class IC shares were 0.67%, 0.92% and 1.17%, respectively. Gross and net expenses are the same. Actual expenses may be higher or lower. Please see the accompanying Financial Highlights for expense ratios for the period ended 12/31/2022.

Class IA shares and IB shares of the Fund are closed to certain qualified pension and retirement plans. For more information, please see the Fund’s statutory prospectus.

Hartford Capital Appreciation HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

Portfolio Managers

Gregg R. Thomas, CFA

Senior Managing Director and Director, Investment Strategy

Wellington Management Company LLP

Thomas S. Simon, CFA, FRM

Senior Managing Director and Portfolio Manager

Wellington Management Company LLP

Manager Discussion

How did the Fund perform during the period?

The Class IA shares of Hartford Capital Appreciation HLS Fund returned -15.30% for the twelve-month period ended December 31, 2022, outperforming its primary benchmark, the Russell 3000 Index, which returned -19.21% for the same period, and its secondary benchmark, the S&P 500 Index, which returned -18.11% for the same period. For the same period, the Class IA shares of the Fund outperformed the -18.04% average return of the Lipper Multi-Cap Core Funds peer group, a group of funds with investment strategies similar to those of the Fund.

Why did the Fund perform this way?

United States (U.S.) equities, as measured by the Russell 3000 Index, posted negative results over the trailing twelve-month period ended December 31, 2022. In the first quarter of 2022, U.S. equities registered their first quarterly loss since the quarter ended March 2020. Fears about the economic implications of Russia’s large-scale military attack on Ukraine and the prospect of aggressive monetary policy tightening by the U.S. Federal Reserve (Fed) drove the S&P 500 Index into correction territory in February 2022. In March 2022, the Fed raised interest rates by 0.25%, lifted its 2022 core inflation forecast to 4.1%, and cut its 2022 gross domestic product (GDP) growth forecast to 2.8%.

In the second quarter of 2022, U.S. equities fell sharply during a volatile quarter. Rampant inflation and tighter financial conditions negatively affected risk sentiment and increased the probability of recession. Growth stocks significantly underperformed their value counterparts, as surging Treasury yields and disappointing earnings results from some of the largest technology companies drove the Nasdaq Composite Index to its biggest quarterly loss since September 2001. The Fed responded to the larger-than-expected increase in prices by accelerating its pace of interest-rate increases to 0.75% in June 2022, following an increase of 0.50% in May 2022.

In the third quarter of 2022, U.S. equities fell as risk sentiment deteriorated on fears that aggressive interest-rate increases and tighter financial conditions would constrict economic growth and drive the U.S. to recession. Stocks suffered steep losses in September 2022 after a larger-than-expected rise in core consumer prices showed that inflation continued to mount across broad areas of the economy. As expected, the Fed raised interest rates by 0.75% in September 2022— the third straight increase of this magnitude.

U.S. equities rallied in the fourth quarter of 2022. Greater optimism that the Fed would begin to scale back its aggressive pace of interest-rate increases, along with outsized short position covering and hedging, helped to fuel a sharp rebound in stocks in October 2022 and November 2022 before risk sentiment waned in December 2022 amid recession fears, macroeconomic challenges, and downside earnings risks in the coming quarters. In December, the Fed raised interest rates by 0.50%, snapping a streak of four consecutive increases of 0.75%. However, the Fed’s Summary of Economic Projections in December 2022 indicated that outlook was more inclined to tighter monetary conditions when compared to its September 2022 forecast.

Returns varied by market cap during the period; mid-cap equities, as measured by the S&P MidCap 400 Index, outperformed large-cap equities, as measured by the S&P 500 Index, while small-cap equities, as measured by the Russell 2000 Index, underperformed large-cap equities, as measured by the S&P 500 Index. Nine of eleven sectors in the Russell 3000 Index had negative returns during the period. The Communication Services (-40%), Consumer Discretionary (-36%), and Information Technology (-30%) sectors were the worst performers.

Security selection was the driver of the Fund’s outperformance relative to the Russell 3000 Index during the period. Strong stock selection in the Consumer Discretionary, Industrials, Financials, and Consumer Staples sectors was only partially offset by weaker selection in the Healthcare and Information Technology sectors during the period. Sector allocation, a residual of the bottom-up security selection process, was a modest detractor from relative performance during the period. An underweight exposure to the Energy sector detracted most from Fund performance and was only partially offset by an underweight exposure to the Information Technology sector, which contributed positively during the period.

Our investment process includes the use of factor-based strategies, which involve targeting certain company characteristics, or factors, that we believe impact returns across asset classes. Factor exposures detracted marginally from performance during the period, driven by the Fund’s underweight exposure to value names and higher momentum names and its positive exposure to names with higher residual volatility relative to the Russell 3000 Index. This was partially offset by the positive impact of the Fund’s underweight exposure to higher-beta names and its overweight exposure to mid-cap names relative to the Russell 3000 Index.

The largest contributors to performance over the period relative to the Russell 3000 Index were an underweight exposure to Tesla (Consumer Discretionary), and the overweight exposures to Chubb (Financials)

Hartford Capital Appreciation HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

and Northrop Grumman (Industrials). Tesla is an American multinational automotive and clean energy company. The stock declined over the period, with growing pains from executive turnover, logistical challenges, and rising commodity prices negatively impacting the company. During the period, we reduced the position in the Fund and the Fund became underweight relative to the benchmark.

Chubb is an American property and casualty insurance company. Shares of Chubb rose during the period on a series of strong earnings announcements. Shares performed particularly well late in the period, as the company announced third-quarter earnings that were above expectations. We maintained the Fund’s overweight position relative to the Russell 3000 Index as of the end of the period.

Northrop Grumman is an American aerospace and defense technology company. The company’s shares ended the period higher along with other defense stocks in response to the Ukraine-Russia conflict. The stock was also bolstered by Germany’s announcement of its plans to increase military strength for the first time in decades by almost doubling its military spending and plans to buy fighter planes made in the U.S. We maintained the Fund’s overweight position relative to the Russell 3000 Index as of the end of the period.

Schlumberger (Energy) and TJX Companies (Consumer Discretionary) were the top contributors to absolute performance for the period.

The largest detractors from performance relative to the Russell 3000 Index during the period were the decision to not hold Exxon Mobil (Energy) and Chevron (Energy), and an out-of-benchmark exposure to Roku (Communication Services). Exxon Mobil and Chevron are both American multinational oil and gas corporations. Shares of both companies rose over the year along with other oil and gas stocks after the U.S. indicated it would ban oil imports from Russia in response to the invasion of Ukraine. Crude oil prices increased on supply fears as concerns arose that U.S. shale may not be enough to offset the loss of Russian barrels; additionally, the industry is dealing with equipment and labor bottlenecks that may lead to supply-cost inflation. Later in the year, both companies benefited following the Organization of the Petroleum-Exporting Countries and its allies (OPEC+) reducing production by 2 million barrels per day in October 2022 while later increasing the quantity in December 2022 by 150,000 barrels per day. The Fund continued to not hold Exxon Mobil and Chevron as of the end of the period.

Roku is an American company that provides digital media players for video streaming. Shares of Roku declined during the period after the company reported weaker earnings results and guidance than expected and saw multiple downgrades. The Fund maintained the out-of-benchmark position as of the end of the period.

Meta Platforms (Communication Services) and Alphabet (Communication Services) were the top absolute detractors from performance during the period.

During the period, the Fund, at times, used derivative instruments such as equity index futures to equitize cash or hedge market risk. During the period, the use of equity index futures detracted from relative performance.

What is the outlook as of the end of the period?

Macroeconomic and geopolitical uncertainties continued to weigh on markets as of the end of the period, and we expect this volatility to persist in 2023. As ever, we remain mindful of the evolving risks facing different equity factors, and seek to create a portfolio of diversified styles and philosophies.

As of the end of the period, the Fund maintained structural exposure to sleeve managers that use a “quality” approach by investing in companies with stable businesses. This is intended to provide a defensive position for the portfolio to seek to offset the risk profiles of growth and value sleeves as the volatility of those factors increases.

Within the growth universe, we are cognizant of the outsized downside risk to areas of heightened speculation. While the Fund saw these speculative companies underperform in 2022, our research shows that risks remain elevated relative to history. We look to the fundamental growth sleeve managers' security selection processes to seek to differentiate companies with strong long-term fundamentals from those that have been caught up in excessive speculation.

In evaluating the value universe, we are aware that the lower-volatility profile value achieved in 2022 is outsized relative to the universe's historical experience, and we do not expect the pattern to continue going forward. Therefore, the Fund is focused on potential risks to value, including the influence of macroeconomic factors like interest rates and energy prices, and we look to the value sleeve managers to seek out companies with the potential for fundamental mean-reversion (e.g. low valuations relative to fundamentals). As allocators, there is a keen focus on risk management, and we seek to balance risks in the portfolio across value, growth, and quality sleeve managers such that security selection drives results.

At the end of the period, the Fund’s largest overweights were to the Consumer Discretionary and Healthcare sectors, while the largest underweights were to the Information Technology and Energy sectors, relative to the Russell 3000 Index.

Important Risks

Investing involves risk, including the possible loss of principal. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies. The Fund’s strategy for allocating assets among portfolio management teams may not work as intended. • Mid-cap securities can have greater risks and volatility than large-cap securities. • Foreign investments may be more volatile and less liquid than U.S. investments and are subject to the risk of currency fluctuations and adverse political, economic and regulatory developments. These risks are generally greater for investments in emerging markets. • To the extent the Fund focuses on one or more sectors, the Fund may be subject to increased volatility and risk of loss if adverse developments occur.

Hartford Capital Appreciation HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

| Composition by Sector(1) |

| as of 12/31/2022 |

| Sector | Percentage

of Net Assets |

| Equity Securities | |

| Communication Services | 6.1% |

| Consumer Discretionary | 12.0 |

| Consumer Staples | 7.0 |

| Energy | 3.4 |

| Financials | 13.4 |

| Health Care | 17.5 |

| Industrials | 10.4 |

| Information Technology | 18.6 |

| Materials | 4.9 |

| Real Estate | 2.6 |

| Utilities | 2.3 |

| Total | 98.2% |

| Short-Term Investments | 0.9 |

| Other Assets & Liabilities | 0.9 |

| Total | 100.0% |

| (1) | A sector may be comprised of several industries. For Fund compliance purposes, the Fund may not use the same classification system. These sector classifications are used for financial reporting purposes. |

Hartford Disciplined Equity HLS Fund

Fund Overview

December 31, 2022 (Unaudited)

Inception 05/29/1998

Sub-advised by Wellington Management Company LLP | Investment objective – The Fund seeks growth of capital. |

Comparison of Change in Value of $10,000 Investment (12/31/2012 - 12/31/2022)

The chart above represents the hypothetical growth of a $10,000 investment in Class IA shares. Returns for the Fund’s other classes differ only to the extent that the classes do not have the same expenses.

| Average Annual Total Returns |

| for the Periods Ended 12/31/2022 |

| | 1 Year | 5 Years | 10 Years |

| Class IA | -18.96% | 9.56% | 13.12% |

| Class IB | -19.20% | 9.28% | 12.83% |

| Class IC | -19.40% | 9.01% | 12.56% |

| S&P 500 Index | -18.11% | 9.42% | 12.56% |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable contract level or by a qualified pension or retirement plan. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the applicable class' net asset value available to shareholders for sale or redemption of Fund shares on 12/31/2022, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses. The total returns presented in the Financial Highlights section of the report are calculated in the same manner, but also take into account certain adjustments that are necessary under generally accepted accounting principles. As a result, the total returns in the Financial Highlights section may differ from the total returns presented above.

Class IC shares commenced operations on 09/18/2020. Class IC shares performance prior to that date reflects Class IA shares performance adjusted to reflect the 12b-1 fee of 0.25% and the administrative services fee of 0.25% applicable to Class IC shares. The performance after such date reflects actual Class IC shares performance.

You cannot invest directly in an index.

See "Benchmark Glossary" for benchmark descriptions.

As shown in the Fund’s current prospectus, the total annual fund operating expense ratios for Class IA shares, Class IB shares and Class IC shares were 0.60%, 0.85% and 1.10%, respectively. Gross and net expenses are the same. Actual expenses may be higher or lower. Please see the accompanying Financial Highlights for expense ratios for the period ended 12/31/2022.

Class IA shares and Class IB shares of the Fund are closed to certain qualified pension and retirement plans. For more information, please see the Fund’s statutory prospectus.

Hartford Disciplined Equity HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

Portfolio Managers

Mammen Chally, CFA

Senior Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

David A. Siegle, CFA

Managing Director and Equity Research Analyst

Wellington Management Company LLP

Douglas W. McLane, CFA

Senior Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

Manager Discussion

How did the Fund perform during the period?

The Class IA shares of the Hartford Disciplined Equity HLS Fund returned -18.96% for the twelve-month period ended December 31, 2022, underperforming its benchmark, the S&P 500 Index, which returned -18.11% for the same period. For the same period, the Class IA shares of the Fund underperformed the -18.20% average return of the Lipper Large-Cap Core Funds peer group, a group of funds with investment strategies similar to those of the Fund.

Why did the Fund perform this way?

United States (U.S.) equities, as measured by the S&P 500 Index, fell during the twelve-month period ended December 31, 2022 amid rampant inflation, surging borrowing costs, uncertainty about corporate earnings, and an increased probability of recession. U.S. equities opened the year lower as they registered their first quarterly loss since the quarter ended March 2020. Fears about the economic implications of Russia’s large-scale military attack on Ukraine and the prospect of aggressive monetary policy tightening by the U.S. Federal Reserve (Fed) drove the S&P 500 Index into correction territory in February 2022. President Joe Biden signed into law a massive $1.5 trillion spending bill, which included substantial increases in domestic and national security programs and $13.6 billion of aid to Ukraine. U.S. equities continued to fall during a volatile second quarter of 2022. Growth stocks significantly underperformed their value counterparts as surging Treasury yields and disappointing earnings results from some of the largest technology companies drove the Nasdaq Composite Index to its largest quarterly loss since September 2001. The housing market was pressured by soaring mortgage rates, slowing demand, and elevated home prices.

U.S. equities fell in the third quarter of 2022 as risk sentiment deteriorated on fears that aggressive interest-rate increases and tighter financial conditions would constrict economic growth and drive the U.S. to recession. U.S. equities rallied in the fourth quarter of 2022 following three straight quarterly declines. Greater optimism that the Fed would begin to scale back its aggressive pace of interest-rate increases, along with outsized short position covering and hedging, helped to fuel a sharp rebound in stocks in October 2022 and November 2022 before risk sentiment waned in December 2022 amid

recession fears, macroeconomic challenges, and downside earnings risks in the coming quarters. In December, the Fed raised interest rates by 0.50%, snapping a streak of four consecutive increases of 0.75%.

Returns varied by market cap, as large-cap stocks, as measured by the S&P 500 Index, underperformed mid-cap stocks, as measured by the S&P MidCap 400 Index, and outperformed small-cap stocks, as measured by the Russell 2000 Index. During the twelve-month period, nine out of eleven sectors within the S&P 500 Index fell, with the Communication Services (-40%), Consumer Discretionary (-37%), and Information Technology (-28%) sectors performing worst. Energy (+66%) was the top-performing sector during the period.

Security selection was the primary driver of the Fund’s performance relative to the S&P 500 Index. Selection within the Communication Services, Real Estate, and Materials sectors detracted most from performance, while selection within the Consumer Discretionary, Information Technology, and Industrials sectors were the largest contributors to performance. Sector allocation, which is a residual of our bottom-up security selection process, contributed positively to relative performance during the period. The Fund’s overweight positions in the Healthcare and Industrials sectors as well as an underweight position in the Consumer Discretionary sector were the largest contributors. This was partially offset by underweight allocations to both the Energy and Materials sectors.

Top detractors from performance relative to the S&P 500 Index over the period were not owning benchmark constituents Exxon Mobil (Energy) and Chevron (Energy), as well as poor timing in holding Netflix (Communication Services). Shares of Exxon Mobil advanced during the period following the Organization of the Petroleum-Exporting Countries and its allies (OPEC+) reducing production by 2 million barrels per day in October 2022 while later increasing the quantity in December 2022 by 150,000 barrels per day. Exxon Mobil also reported record profits for the third quarter, boosted by the surge in oil and natural gas prices. Shares of Chevron rose over the period after reporting higher-than-expected third-quarter earnings. Chevron’s liquefied natural gas business was strong. Elevated oil and natural gas prices were also a key factor in Exxon Mobil's and Chevron's performance. The share price of Netflix declined over the period after the company announced first-quarter earnings where it saw a loss of 200,000 subscribers, marking the first

Hartford Disciplined Equity HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

time it had lost subscribers since 2011. The company also warned that it expected to lose 2 million subscribers in the second quarter of 2023 as new passwords sharing restrictions are introduced. We eliminated the Fund’s position in Netflix during the period.

The largest contributors to relative performance over the period were an overweight holding in EOG Resources (Energy), an underweight holding in Tesla (Consumer Discretionary), and an overweight holding in Eli Lilly (Healthcare). Shares of EOG Resources rose along with other oil stocks after OPEC+ announced plans to cut production by 2 million barrels per day, marking the biggest cut since late 2019. Shares of Tesla fell over the period after the company reported lower-than-expected third-quarter production and delivery numbers. Tesla reported 343,000 total deliveries and 365,000 vehicles produced during the quarter. The company also announced a 20% output cut of the Model Y at their Shanghai plant along with growing pains from executive turnover, logistical challenges, and rising commodity prices. Eli Lilly shares rose after Eisai and Biogen reported breakthrough trial results for their Alzheimer’s drugs. The news about these trials was welcome for Eli Lilly’s drug donanemab, which also targets removing the amyloid beta protein to slow disease progression. Donanemab’s readout is slated for the second quarter of 2023. The U.S. Food and Drug Administration (FDA) also approved the company's oral lung cancer drug, Retevmo, for certain adult patients with solid tumors with a specific genetic makeup.

Derivatives were not used in the Fund during the period.

What is the outlook as of the end of the period?

U.S. equity markets ended a tumultuous year with positive performance at the end of the period. As we look ahead, we believe the macroeconomic environment continues to have an outsized influence on market behavior. We anticipate volatility will remain high, exaggerated by the next macroeconomic datapoint, interest-rate signal, or geopolitical event. As bottom-up investors, we remain disciplined regarding our philosophy. We continue to try to minimize downside risks while seeking longer-term upside potential.

At the end of the period, the Fund’s largest overweights were to the Healthcare, Industrials, and Utilities sectors, while the Fund’s largest underweights were to the Communication Services, Materials, and Energy sectors, relative to the S&P 500 Index.

Important Risks

Investing involves risk, including the possible loss of principal. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies.

| Composition by Sector(1) |

| as of 12/31/2022 |

| Sector | Percentage

of Net Assets |

| Equity Securities | |

| Communication Services | 5.4% |

| Consumer Discretionary | 9.3 |

| Consumer Staples | 7.6 |

| Energy | 3.8 |

| Financials | 12.0 |

| Health Care | 18.5 |

| Industrials | 10.5 |

| Information Technology | 25.3 |

| Materials | 1.1 |

| Real Estate | 1.7 |

| Utilities | 3.7 |

| Total | 98.9% |

| Short-Term Investments | 0.5 |

| Other Assets & Liabilities | 0.6 |

| Total | 100.0% |

| (1) | A sector may be comprised of several industries. For Fund compliance purposes, the Fund may not use the same classification system. These sector classifications are used for financial reporting purposes. |

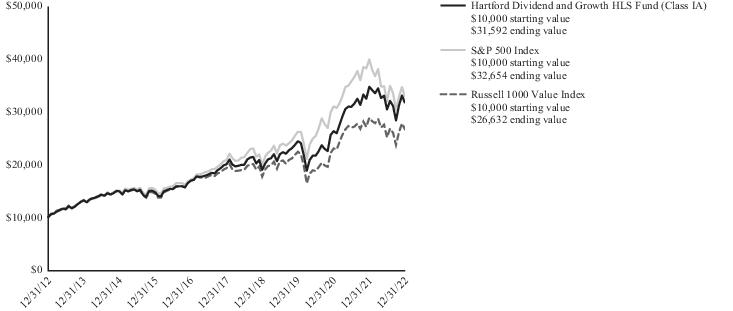

Hartford Dividend and Growth HLS Fund

Fund Overview

December 31, 2022 (Unaudited)

Inception 03/09/1994

Sub-advised by Wellington Management Company LLP | Investment objective – The Fund seeks a high level of current income consistent with growth of capital. |

Comparison of Change in Value of $10,000 Investment (12/31/2012 - 12/31/2022)

The chart above represents the hypothetical growth of a $10,000 investment in Class IA shares. Returns for Class IB shares differ only to the extent that Class IA shares and Class IB shares do not have the same expenses.

| Average Annual Total Returns |

| for the Periods Ended 12/31/2022 |

| | 1 Year | 5 Years | 10 Years |

| Class IA | -8.93% | 9.54% | 12.19% |

| Class IB | -9.15% | 9.27% | 11.91% |

| S&P 500 Index | -18.11% | 9.42% | 12.56% |

| Russell 1000 Value Index | -7.54% | 6.67% | 10.29% |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable contract level or by a qualified pension or retirement plan. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the applicable class' net asset value available to shareholders for sale or redemption of Fund shares on 12/31/2022, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses. The total returns presented in the Financial Highlights section of the report are calculated in the same manner, but also take into account certain adjustments that are necessary under generally accepted accounting principles. As a result, the total returns in the Financial Highlights section may differ from the total returns presented above.

You cannot invest directly in an index.

See "Benchmark Glossary" for benchmark descriptions.

As shown in the Fund’s current prospectus, the total annual fund operating expense ratios for Class IA shares and Class IB shares were 0.66% and 0.91%, respectively. Gross and net expenses are the same. Actual expenses may be higher or lower. Please see the accompanying Financial Highlights for expense ratios for the period ended 12/31/2022.

Class IA shares and Class IB shares of the Fund are closed to certain qualified pension and retirement plans. For more information, please see the Fund’s statutory prospectus.

Hartford Dividend and Growth HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

Portfolio Managers

Matthew G. Baker

Senior Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

Nataliya Kofman

Managing Director and Equity Portfolio Manager

Wellington Management Company LLP

Manager Discussion

How did the Fund perform during the period?

The Class IA shares of Hartford Dividend and Growth HLS Fund returned -8.93% for the twelve-month period ended December 31, 2022, outperforming its primary benchmark, the S&P 500 Index, which returned -18.11% for the same period, and underperforming its secondary benchmark, the Russell 1000 Value Index, which returned -7.54% for the same period. For the same period, the Fund underperformed the -7.41% average return of the Lipper Equity Income Funds peer group, a group of funds with investment strategies similar to those of the Fund.

Why did the Fund perform this way?

In the first quarter of 2022, United States (U.S.) equities, as measured by the S&P 500 Index, registered their first quarterly loss since the quarter ended March 2020. Fears about the economic implications of Russia’s large-scale military attack on Ukraine and the prospect of aggressive monetary policy tightening by the U.S. Federal Reserve (Fed) drove the S&P 500 Index into correction territory in February 2022. In March 2022, the Fed raised interest rates by 0.25%, lifted its 2022 core inflation forecast to 4.1%, and cut its 2022 gross domestic product (GDP) growth forecast to 2.8%.

In the second quarter of 2022, U.S. equities fell sharply during a volatile quarter. Rampant inflation and tighter financial conditions negatively affected risk sentiment and increased the probability of recession. Growth stocks significantly underperformed their value counterparts, as surging Treasury yields and disappointing earnings results from some of the largest technology companies drove the Nasdaq Composite Index to its biggest quarterly loss since September 2001. The Fed responded to the larger-than-expected increase in prices by accelerating its pace of interest-rate increases to 0.75% in June 2022, following an increase of 0.50% in May 2022.

In the third quarter of 2022, U.S. equities fell as risk sentiment deteriorated on fears that aggressive interest-rate increases and tighter financial conditions would constrict economic growth and drive the U.S. to recession. Stocks suffered steep losses in September 2022 after a larger-than-expected rise in core consumer prices showed that inflation continued to mount across broad areas of the economy. As expected, the Fed raised interest rates by 0.75% in September 2022— the third straight increase of this magnitude.

U.S. equities rallied in the fourth quarter of 2022. Greater optimism that the Fed would begin to scale back its aggressive pace of interest-rate increases, along with outsized short position covering and

hedging, helped to fuel a sharp rebound in stocks in October 2022 and November 2022 before risk sentiment waned in December 2022 amid recession fears, macroeconomic challenges, and downside earnings risks in the coming quarters. In December, the Fed raised interest rates by 0.50%, snapping a streak of four consecutive increases of 0.75%. However, the Fed’s Summary of Economic Projections in December 2022 indicated that outlook was more inclined to tighter monetary conditions when compared to its September 2022 forecast.

Returns varied by market cap, as mid-cap stocks, measured by the S&P MidCap 400 Index, outperformed large-cap and small-cap stocks, as measured by the S&P 500 Index and Russell 2000 Index, respectively. During the twelve-month period, nine out of eleven sectors within the S&P 500 Index posted negative returns, led by the Communication Services (-40%), Consumer Discretionary (-37%), and Information Technology (-28%) sectors. Conversely, the Energy (66%) and Utilities (2%) sectors performed best.

Security selection was the primary driver of the Fund’s outperformance relative to the S&P 500 Index over the period. Strong selection within the Consumer Discretionary, Financials, and Communication Services sectors was partially offset by weaker selection within the Energy, Materials, and Consumer Staples sectors during the period. Sector allocation, a result of the bottom-up stock selection process, also added to relative returns during the period. Underweight allocations to the Consumer Discretionary and Information Technology sectors as well as an overweight to the Financials sector contributed positively to relative performance but was marginally offset by an overweight to the Real Estate sector.

Top contributors to performance relative to the S&P 500 Index over the period included lack of exposure to benchmark constituents Amazon.com (Consumer Discretionary), Tesla (Consumer Discretionary), and Meta Platforms (Communications Services). Shares of Amazon.com ended the period lower after the e-commerce giant reported third-quarter results that missed consensus estimates and issued a disappointing fourth-quarter revenue forecast. The company is confronting soaring inflation, rising interest rates and a slowdown in its core retail business as customers return to stores. Shares of Tesla fell over the period after the company reported lower-than-expected third-quarter production and delivery numbers. Tesla reported 343,000 total deliveries and 365,000 vehicles produced during the quarter. The company also announced a 20% output cut of the Model Y at their Shanghai plant along with growing pains from executive turnover, logistical challenges, and rising commodity prices. The share price of Meta Platforms, a U.S.-based social networking operator, fell after management released disappointing third quarter

Hartford Dividend and Growth HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

2022 results and weak near-term guidance. The company reported a decline in quarterly revenues for the second consecutive quarter with the most recent figure down more than 4% year over year. Additionally, the company’s overall net income fell 52% to $4.4 billion.

The Fund’s top detractor from performance relative to S&P 500 Index during the period was the lack of allocation to benchmark constituent Exxon Mobil (Energy). Returns relative to the S&P 500 Index were also held back by the overweights to Fidelity National Information Services (Information Technology) and Baxter International (Healthcare). Shares of Exxon Mobil advanced during the period following Organization of the Petroleum-Exporting Countries and its allies (OPEC+) reducing production by 2 million barrels per day in October 2022 while later increasing the quantity in December 2022 by 150,000 barrels per day. Exxon Mobil also reported record profits for the third quarter, boosted by the surge in oil and natural gas prices. Shares of payments company Fidelity National Information Services (FIS) fell during the period. The company reported third-quarter results that missed expectations and management cut its full-year forecast. FIS announced a cost-cutting program as it cut full-year revenue and profit guidance to reflect changes in the macroeconomic environment. The Fund maintained an overweight position in FIS as of the end of the period. Shares of Baxter International declined during the period. Management continued to emphasize the uncertainties Baxter faces due to COVID. Baxter is a U.S. based Healthcare products company with global reach. The Fund initiated a position in Baxter over the period and continued to build the position through the year as valuations came down, driven by increasing input costs and supply-chain challenges.

The Fund did not utilize derivatives during the period.

What is the outlook as of the end of the period?

Market volatility persisted as of the end of the period; however, U.S. equities ended the period higher as a perceived pivot in Fed policy boosted investor sentiment and consumer confidence. Despite recent market strength, we do not anticipate that the Fed will reverse its policy stance in the near term, nor are we ruling out the potential for additional meaningful interest-rate increases. In our view, market volatility continues to be driven by a steady state of macroeconomic cross-currents ranging from supply chain bottlenecks to Russia’s invasion of Ukraine. In the current environment, we are seeking to avoid taking undue risk by focusing on long-term value creation potential and predictable ranges of outcomes.

We continue to anticipate negative impacts from inflationary pressures and restrictive monetary policy as of the end of the period. The Fund remains positioned for persistent inflation and decelerating growth by focusing on companies that we believe have balance-sheet strength, sustainable and growing cash flows, and high-quality management teams. Earnings have come down over the last year but remain elevated compared to long-term averages, in our view. We expect companies to struggle to maintain margins in a contracting economy; therefore, most of the Fund’s portfolio is invested in companies that play a more defensive role in the portfolio and that we believe may help mitigate downside risk in the event of a potential recession.

Important Risks

Investing involves risk, including the possible loss of principal. Security prices fluctuate in value depending on general market and economic conditions and the prospects of individual companies. • For dividend-paying stocks, dividends are not guaranteed and may decrease without notice. • Foreign investments may be more volatile and less liquid than U.S. investments and are subject to the risk of currency fluctuations and adverse political, economic and regulatory developments. • To the extent the Fund focuses on one or more sectors, the Fund may be subject to increased volatility and risk of loss if adverse developments occur. • Integration of environmental, social, and/or governance (ESG) characteristics into the investment process may not work as intended.

| Composition by Sector(1) |

| as of 12/31/2022 |

| Sector | Percentage

of Net Assets |

| Equity Securities | |

| Communication Services | 7.8% |

| Consumer Discretionary | 5.7 |

| Consumer Staples | 6.4 |

| Energy | 5.5 |

| Financials | 17.8 |

| Health Care | 18.2 |

| Industrials | 7.5 |

| Information Technology | 17.4 |

| Materials | 3.6 |

| Real Estate | 3.8 |

| Utilities | 4.8 |

| Total | 98.5% |

| Short-Term Investments | 0.6 |

| Other Assets & Liabilities | 0.9 |

| Total | 100.0% |

| (1) | A sector may be comprised of several industries. For Fund compliance purposes, the Fund may not use the same classification system. These sector classifications are used for financial reporting purposes. |

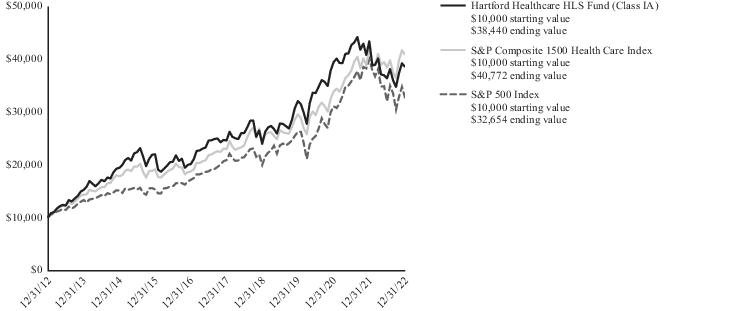

Hartford Healthcare HLS Fund

Fund Overview

December 31, 2022 (Unaudited)

Inception 05/01/2000

Sub-advised by Wellington Management Company LLP | Investment objective – The Fund seeks long-term capital appreciation. |

Comparison of Change in Value of $10,000 Investment (12/31/2012 - 12/31/2022)

The chart above represents the hypothetical growth of a $10,000 investment in Class IA shares. Returns for Class IB shares differ only to the extent that Class IA shares and Class IB shares do not have the same expenses.

| Average Annual Total Returns |

| for the Periods Ended 12/31/2022 |

| | 1 Year | 5 Years | 10 Years |

| Class IA | -11.24% | 9.40% | 14.41% |

| Class IB | -11.47% | 9.13% | 14.13% |

| S&P Composite 1500 Health Care Index | -3.31% | 12.27% | 15.09% |

| S&P 500 Index | -18.11% | 9.42% | 12.56% |

PERFORMANCE DATA QUOTED REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The investment return and principal value of the investment will fluctuate so that investors’ shares, when redeemed, may be worth more or less than their original cost. The chart and table do not reflect the deductions of taxes, sales charges or other fees which may be applied at the variable contract level or by a qualified pension or retirement plan. Any such additional sales charges or other fees or expenses would lower the contract’s or plan’s performance. Current performance may be lower or higher than the performance data quoted. To obtain performance data current to the most recent month-end, please visit our website hartfordfunds.com.

Total returns presented above were calculated using the applicable class' net asset value available to shareholders for sale or redemption of Fund shares on 12/31/2022, which may exclude investment transactions as of this date. All share class returns assume the reinvestment of all distributions at net asset value and the deduction of all fund expenses. The total returns presented in the Financial Highlights section of the report are calculated in the same manner, but also take into account certain adjustments that are necessary under generally accepted accounting principles. As a result, the total returns in the Financial Highlights section may differ from the total returns presented above.

You cannot invest directly in an index.

See "Benchmark Glossary" for benchmark descriptions.

As shown in the Fund’s current prospectus, the total annual fund operating expense ratios for Class IA shares and Class IB shares were 0.92% and 1.17%, respectively. Gross and net expenses are the same. Actual expenses may be higher or lower. Please see the accompanying Financial Highlights for expense ratios for the period ended 12/31/2022.

Class IA shares and Class IB shares of the Fund are closed to certain qualified pension and retirement plans. For more information, please see the Fund’s statutory prospectus.

Hartford Healthcare HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

Portfolio Managers

Ann C. Gallo*

Senior Managing Director and Global Industry Analyst

Wellington Management Company LLP

Rebecca D. Sykes, CFA

Senior Managing Director and Global Industry Analyst

Wellington Management Company LLP

Wen Shi, CFA, PhD

Managing Director and Global Industry Analyst

Wellington Management Company LLP

David M. Khtikian, CFA

Managing Director and Global Industry Analyst

Wellington Management Company LLP

Fayyaz Mujtaba

Managing Director and Global Industry Analyst

Wellington Management Company LLP

| * | Effective February 28, 2023, Ms. Gallo will no longer serve as a portfolio manager to the Fund. Ms. Gallo will transition her portfolio management responsibilities for the Fund to Messrs. Khtikian and Mujtaba. |

Manager Discussion

How did the Fund perform during the period?

The Class IA shares of Hartford Healthcare HLS Fund returned -11.24% for the twelve-month period ended December 31, 2022, underperforming the S&P Composite 1500 Health Care Index, which returned -3.31% for the same period, while outperforming the S&P 500 Index, which returned -18.11% for the same period. For the same period, the Class IA shares of the Fund outperformed the -12.95% average return of the Lipper Global Health and Biotechnology peer group, a group of funds with investment strategies similar to those of the Fund.

Why did the Fund perform this way?

United States (U.S.) healthcare equities returned -3.31% for the period as measured by the S&P Composite 1500 Health Care Index, outperforming both the broader U.S. equity market, which returned -18.11% as measured by the S&P 500 Index, and the global equity market, which returned -17.73% during the period, as measured by the MSCI World Index. Within the S&P Composite 1500 Health Care Index, small-cap biopharma returned -34%, medical technology returned -22%, mid-cap biopharma returned 1%, healthcare services returned 2%, and large-cap biopharma returned 12% during the period.

The Fund underperformed the S& P Composite 1500 Health Care Index over the period, which was due primarily to unfavorable security selection decisions. Security selection was weakest in healthcare services, mid-cap biopharma, and large-cap biopharma, while selection in small-cap biopharma was strongest. Sector allocation also detracted from the Fund’s performance relative to the S&P Composite 1500 Health Care Index. The Fund’s underweight to large-cap

biopharma and overweight to small-cap biopharma detracted from relative results during the period. This was partially offset by positive results from an underweight to medical technology and overweight to mid-cap biopharma.

Merck & Co. (large-cap biopharma), AbbVie (large-cap biopharma), and Syneos Health (healthcare services) were the top detractors from performance relative to the S&P Composite 1500 Health Care Index over the period. Not holding a position in Merck & Co. for most of the period weighed on performance as shares rose on the back of management delivering solid earnings results that beat expectations early in the year and raising guidance around their key oncology products, Keytruda and Gardasil. More recently, the company announced positive phase 3 data for sotatercept, a drug for pulmonary arterial hypertension that was added to Merck’s pipeline through its acquisition of Acceleron Pharma. The study achieved its primary endpoint of showing significant improvement in exercise capacity, as measured by six-minute walk distance. Not owning AbbVie, a constituent of the S&P Composite 1500 Health Care Index, detracted from relative performance, as shares continued to rise through the first quarter of 2022 on the back of the U.S. Food and Drug Administration (FDA) approval of RINVOQ for the treatment of adults with active psoriatic arthritis who have had an inadequate response or intolerance to one or more TNF inhibitors. AbbVie's launches have done well in the marketplace, allaying some of the concerns about the upcoming biosimilar competition for its largest franchise, Humira. Additionally, in an environment with rising interest rates, heightened geopolitical risk, and fears around slowing a global growth rate, large-cap pharma was seen as a safe haven for investors and lack of ownership in some of these mega-cap names, including Merck and AbbVie, weighed on relative results. Shares of Syneos Health declined after reporting disappointing quarterly results throughout the period, driven by

Hartford Healthcare HLS Fund

Fund Overview – (continued)

December 31, 2022 (Unaudited)

weaker-than-expected net new business and book-to-bill ratios. The company cited macroeconomic driven challenges including decision delays, slowdown in awards from small/mid-cap companies, and a decline in repeat business. Edwards Lifesciences, Zoetis, and Syneos Health were the top absolute detractors from the Fund’s performance during the period.

Eli Lilly (large-cap biopharma), Abbott Laboratories (medical technology), and Thermo Fisher Scientific (medical technology) contributed positively to results relative to the S&P Composite 1500 Health Care Index over the period. Shares of Eli Lilly rose after the company reported strong first-quarter earnings results, but more importantly received FDA approval for its drug, tirzepatide, for the treatment of type 2 diabetes. Compelling pivotal data in the setting of non-diabetic obesity during the second quarter also underscored the long-term value of this drug. More recently, Eli Lilly's stock benefited from positive results in Eisai’s Alzheimer’s phase 3 trial, which raised hopes for other anti-amyloid drugs including Eli Lilly’s drug donanemab. Not owning Abbott Laboratories for the majority of the period was a positive contributor to performance, as shares underperformed during the period. Shares of Abbott Laboratories have been pressured as the company has faced short-term challenges, including declines in COVID-19 testing demand as well as a voluntarily recall of several baby powder formulas in February, including various Similac, Alimentum, and EleCare branded product. We initiated the Fund’s position in Abbott Laboratories in October 2022. Not owning Thermo Fisher Scientific contributed positively to performance as shares underperformed during the period. Despite reporting solid earnings throughout the year, shares of Thermo Fisher Scientific fell on concerns of fading COVID-19 testing volumes. Top absolute contributors to performance during the period included Eli Lilly, Bristol-Myers Squibb, and UnitedHealth Group.

Derivatives were not used in the Fund during the period.

What is the outlook as of the end of the period?

As of the end of the period, we have a positive outlook across the Healthcare opportunity set. Groundbreaking innovation, supportive valuations, and business models that are positioned to show resilience through the cycle may benefit long-term investors in this sector, in our view.

Within biopharma, we continue to find what we consider to be a rich environment for innovation. We anticipate continued developments in disease areas such as Alzheimer’s disease, metabolic diseases, and cancer, as well as for companies discovering drugs using new modalities such as messenger RNA, RNA interference, and gene therapy. Aside from groundbreaking innovation, we expect the fundamental backdrop and resilient earnings of large-cap biopharma to be supportive in a potential recessionary environment. Furthermore, we believe valuations remain attractive relative to history, and key clinical readouts in the year ahead could create an abundance of opportunities.

We are just as enthusiastic about medical technology, where we observe that innovative pipelines have never been stronger, in our view. We expect more attractive medical device categories will see growth accelerate at a faster pace over the next decade. These