UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-4676

Harbor Funds

(Exact name of Registrant as specified in charter)

111 South Wacker Drive, 34th Floor

Chicago, Illinois 60606-4302

Chicago, Illinois 60606-4302

(Address of principal executive offices) (Zip code)

| Charles F. McCain, Esq. HARBOR FUNDS 111 South Wacker Drive, 34th Floor Chicago, Illinois 60606-4302 | Christopher P. Harvey, Esq. DECHERT LLP One International Place – 40th Floor 100 Oliver Street Boston, MA 02110-2605 |

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 443-4400

Date of fiscal year end: October 31

Date of reporting period: October 31, 2020

ITEM 1 – REPORTS TO STOCKHOLDERS

The following are copies of reports transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30e-1):

Annual Report

October 31, 2020

Domestic Equity Funds

| Retirement Class | Institutional Class | Administrative Class | Investor Class | |

| Harbor Capital Appreciation Fund | HNACX | HACAX | HRCAX | HCAIX |

| Harbor Large Cap Value Fund | HNLVX | HAVLX | HRLVX | HILVX |

| Harbor Mid Cap Fund | HMCRX | HMCLX | HMCDX | HMCNX |

| Harbor Mid Cap Growth Fund | HNMGX | HAMGX | HRMGX | HIMGX |

| Harbor Mid Cap Value Fund | HNMVX | HAMVX | HRMVX | HIMVX |

| Harbor Small Cap Growth Fund | HNSGX | HASGX | HRSGX | HISGX |

| Harbor Small Cap Value Fund | HNVRX | HASCX | HSVRX | HISVX |

| Harbor Strategic Growth Fund | HNGSX | MVSGX | HSRGX | HISWX |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website (harborfunds.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a Fund electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you invest directly with Harbor Funds, by calling 800-422-1050.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary (such as a broker-dealer or bank), you can contact your financial intermediary to request that you continue to receive paper copies of the Funds’ shareholder reports. If you invest directly, you can call 800-422-1050 to request that you continue to receive paper copies of the Funds’ shareholder reports. Your election to receive reports in paper will apply to all Harbor Funds held in your account.

Table of Contents

This document must be preceded or accompanied by a Prospectus.

Letter from the Chairman

Charles F. McCain Chairman |

Dear Fellow Shareholder:

The 2020 fiscal year has been a historic period that will undoubtedly live on in our memories as much as we might like to forget the massive disruptions caused by the coronavirus pandemic and the toll it has taken on human lives.

The period began quietly in investment markets, extending a lengthy stretch of subdued volatility. That relative calm came to a dramatic end in late February when the extent of the pandemic became clear, sending shockwaves across global investment markets. Volatility spiked sharply higher, market liquidity became challenged, and government bond yields plunged in a flight to safety. From its peak on February 19 to its March 23 trough, the S&P 500 tumbled 33.8% for its fastest ever descent into bear-market territory. International markets followed suit, with the MSCI All Country World Ex. US (ND) Index falling 32.9% over the same period. Although U.S. Treasuries served as a ballast during the period, corporate bonds did not escape the sharp selloff, with both investment-grade and high-yield credit indexes experiencing double-digit losses.

Governments and central banks acted swiftly and forcefully to support the global economy with massive fiscal and monetary stimulus. This jolt of liquidity put a floor under markets and set the stage for a sharp rebound. Broad stock and bond indexes gained ground throughout much of the rest of the year, shrugging off concerns about the pandemic, inconsistent policy responses, uncertainty around the U.S. election, and escalating social tensions.

As time marched on, economic data has improved. We see GDP is growing again, unemployment appears to have bottomed, and many market measures ended the fiscal year in positive territory. However, economic and market recovery has been uneven. The re-emergence of volatility has brought about significant dispersion across markets. For example, the difference between the best and worst sectors reached its widest levels in many years. Similarly, growth stocks outperformed value stocks by the widest margin in more than 20 years.

This volatile environment, though challenging, has been welcome news for talented active managers, because it has provided them with more opportunities to add value and distance themselves from the pack. Our research shows that the difference between top performing and bottom performing managers in many categories is at its highest level in 20 years.

Harbor believes there are many ways to seek to reach long-term financial goals. Drawing upon experienced portfolio managers who stay true to a strategy grounded in enduring investment principles is one way we believe offers the potential to achieve positive outcomes over time. Even though volatility is likely to be with us for some time to come, we are confident that all our subadvisers continue to strive to skillfully execute their strategies to benefit shareholders over the long haul.

It is important to acknowledge that while market gyrations provide opportunities for skillful professional managers, they can pose behavioral challenges for the rest of us. The sharp selloff in the first quarter was enough to test the mettle of the calmest investor. However, those who stayed the course and stuck to their long-term plans likely benefitted from the sharp recovery that followed. We will look back on this period as a time that underscored the value of thoughtful active management and timeless investment principles such as diversification, discipline, and a long-term view.

I hope that you and your families continue to fare well during these ongoing challenging times. Thank you for your continued investment in Harbor Funds.

December 21, 2020

|

| Charles F. McCain |

| Chairman |

1

Harbor Capital Appreciation Fund

Manager’s Commentary (Unaudited)

Manager’s Commentary (Unaudited)

Subadviser

Jennison Associates LLC

466 Lexington Avenue

New York, NY 10017

New York, NY 10017

Portfolio Managers

Spiros “Sig” Segalas

Since 1990

Since 1990

Kathleen A. McCarragher

Since 2013

Since 2013

Blair A. Boyer

Since 2019

Since 2019

Natasha Kuhlkin, CFA

Since 2019

Since 2019

Jennison Associates has subadvised the Fund since 1990.

Investment Objective

The Fund seeks long-term growth of capital.

Spiros “Sig” Segalas

Kathleen A. McCarragher

Blair A. Boyer

Natasha Kuhlkin, CFA

Management’s Discussion of

Fund Performance

Fund Performance

MARKET REVIEW

Markets were extremely volatile in the period, unsettled by U.S.-China trade discord and the COVID-19 pandemic.

Stocks peaked at new highs in early 2020, then dropped dramatically as the viral outbreak spread around the globe, disrupting markets and life everywhere.

The realities of the pandemic dictated daily conduct for individuals, businesses, and governments around the world. Shelter-in-place and work-from-home became standard. Global infection and mortality rates reflected varying policy and social behaviors, with the number of infections and deaths highest in the U.S. Developing a vaccine became an overwhelming focus, with both human and capital resources deployed.

Markets rebounded rapidly in the period’s final months, but the pandemic’s economic damage continued to accumulate.

The effects of fiscal stimulus blunted the pandemic’s effect on employment and spending. Comprehensive monetary policy initiatives to bolster liquidity and stabilize asset prices contributed to record-low interest rates.

PERFORMANCE

Harbor Capital Appreciation Fund advanced 42.79% (Retirement Class), 42.68% (Institutional Class), 42.32% (Administrative Class), and 42.15% (Investor Class) in the fiscal year, while the Russell 1000® Growth Index rose 29.22%, and the broader market, as represented by the S&P 500 Index, climbed 9.71%.

In the growth benchmark, the Consumer Discretionary, Information Technology, and Communication Services sectors outperformed the overall index. Energy posted a double-digit decline. Industrials was the only other sector in the benchmark to lose ground.

Stock selection and sector weights benefited Fund performance relative to the growth benchmark. Holdings in Consumer Discretionary, Information Technology, and Communication Services – the Fund’s three biggest sectors – were especially strong contributors to outperformance as both stock selection and overweights were beneficial.

In Consumer Discretionary, Tesla continues to surge on a host of impressive financial results made possible by solid production, increased capacity, and strong execution. In our view, the company’s technology, scale, and low-cost advantage make it not only the breakaway leader in the electric-vehicle market but also position it to disrupt the overall automotive industry. Consumer businesses that have migrated to digital direct-to-consumer business models were notably strong performers. Amazon has operated in this mode for years, and its relevance and dominance became even more apparent. We believe that Amazon continues to benefit from economies of scale and its platform-based business model. The AWS web services business is a significant additional driver of revenue and profit for Amazon. Apparel retailer Lululemon Athletica benefited from less-seasonal offerings, strong brand, and a direct-to-consumer infrastructure that shields it from wholesale distribution backlogs and increased levels of price discounting.

In Information Technology, digital payments processors were strong performers. Adyen has developed a single, dynamic, reliable, and secure payment platform that supports omni-channel commerce with end-to-end gateway, risk management, and processing services. PayPal is the largest ecommerce payments enabler in the U.S. and many developing countries. We believe that PayPal can deepen and extend its services among global, consumer, and business clients. The importance of digital commerce in times of restricted personal mobility is also benefitting Shopify, which provides cloud-based, easy-to-use infrastructure tools to enable omni-channel ecommerce capability.

With millions of people around the world working from home, the advantage of housing mission-critical software applications and services on the cloud has emerged. In addition to a strong and stable enterprise business, Microsoft has a differentiated hybrid cloud strategy

2

Harbor Capital Appreciation Fund

Manager’s Commentary—Continued

Manager’s Commentary—Continued

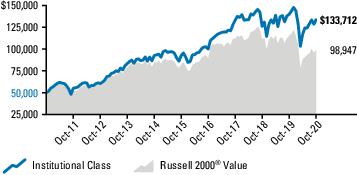

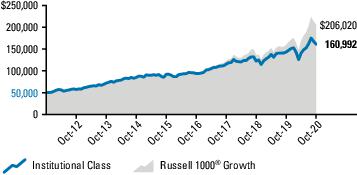

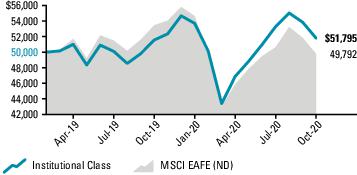

CHANGE IN A $50,000 INVESTMENT

For the period 11/01/2010 through 10/31/2020

The graph compares a $50,000 investment in the Institutional Class shares of the Fund with the performance of the Russell 1000® Growth Index and the S&P 500 Index. The Fund’s performance assumes the reinvestment of all dividend and capital gain distributions.

TOTAL RETURNS

For the periods ended 10/31/2020

| 1 Year | Annualized | |||||||

| 5 Years | 10 Years | |||||||

| Harbor Capital Appreciation Fund | ||||||||

Retirement Class1 | 42.79% | 18.43% | 17.10% | |||||

Institutional Class | 42.68 | 18.36 | 17.07 | |||||

Administrative Class | 42.32 | 18.06 | 16.78 | |||||

Investor Class | 42.15 | 17.92 | 16.64 | |||||

| Comparative Indices | ||||||||

Russell 1000® Growth | 29.22% | 17.32% | 16.31% | |||||

S&P 500 | 9.71 | 11.71 | 13.01 | |||||

As stated in the Fund’s prospectus dated March 1, 2020, the expense ratios were 0.59% (Net) and 0.64% (Gross) (Retirement Class); 0.67% (Net) and 0.72% (Gross) (Institutional Class); 0.92% (Net) and 0.97% (Gross) (Administrative Class); and 1.04% (Net) and 1.09% (Gross) (Investor Class). The net expense ratios reflect a contractual management fee waiver effective through 02/28/2021. The expense ratios in the prospectus may differ from the actual expense ratios for the period disclosed within this report. The expense ratios shown in the prospectus are based on the prior fiscal year, adjusted to reflect changes, if any, in contractual arrangements that occurred prior to the date of the prospectus (or supplement thereto, if applicable).

Performance data shown represents past performance and is no guarantee of future results. Past performance is net of management fees and expenses and reflects reinvested dividends and distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or upon the redemption of Fund shares. Past performance reflects the beneficial effect of any expense waivers or reimbursements, without which returns would have been lower. Investment returns and principal value will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Returns for periods less than one year are not annualized. Current performance may be higher or lower and is available through the most recent month end at harborfunds.com or by calling 800-422-1050.

that is leading to an increase in its share of technology capital spending. Its Azure cloud business hosts Microsoft software as well as hundreds of cloud-native applications that Microsoft customers or third parties create. The company’s Teams collaboration platform is also benefitting from increased work-from-home requirements. Adobe offers content creation and digital marketing applications and services that are transforming businesses operations. Salesforce remains at the forefront of migrating traditional customer records systems to comprehensive customer intelligence systems. Even in the face of unpredictable macroeconomic trends, in our view, enterprises are concluding that the financial benefits delivered by Salesforce offset the capital outlay required for software purchase and deployment.

The increased demand for cloud storage has led to robust data center spending by chipmaker Nvidia’s largest customers. Nvidia’s acquisition of Mellanox could enhance its functionality and potentially lead to further share gains in the data center space, in our view.

With its huge installed base, Apple has been benefiting from rapid growth in service business subscriptions, a key source of recurring revenue. In our view, the upcoming product cycle should provide robust revenue and profit growth.

In Communication Services, Netflix continues to enhance its long-term competitive position with the industry’s largest commitment of investment dollars in exclusive and original content. Given its still-low global penetration and the accelerating shift from linear TV, we believe that Netflix still has significant room for growth. The company’s secular growth profile looks even stronger in the current environment, as social-distancing and shelter-in-place directives are drawing renewed attention to the value, utility, and now, resilience, of video streaming business models.

Industrials positions detracted from performance. The longer-than-anticipated Boeing 737 Max 8 jet recertification process weighed on Boeing early in the period. With the COVID-19 outbreak severely restricting air travel and compromising the financial health of airlines, the position was eliminated. The position in Safran was closed based on the company’s exposure to the airline industry. Most of Safran’s revenue is generated by its aerospace propulsion business, which includes the company’s joint venture with General Electric, which makes 75% of the world’s narrow-body aircraft engines (including all of Boeing’s 737s and about half of Airbus’s A320s).

In Consumer Discretionary, the position in Adidas was eliminated based on the company’s softer-than-expected gross margin, COVID-19-related sporting event cancellations, and an anticipated back-up in wholesale inventories.

In Information Technology, the position in FleetCor Technologies, which provides specific-purpose charge cards and payment-processing services for commercial and government trucking fleets, was eliminated based on the impact of regulatory litigation related to the company’s marketing and fee practices, as well as on exposure to oil prices.

In Health Care, the position in Sage Therapeutics was closed as a Phase 3 clinical trial of its key developmental therapy to treat major depression (MDD) failed to meet the study’s primary endpoint. The MDD market opportunity was expected to be a key component of the company’s growth.

3

Harbor Capital Appreciation Fund

Manager’s Commentary—Continued

Manager’s Commentary—Continued

OUTLOOK & STRATEGY

The U.S. economy continues to recover from the worst effects of the pandemic, but the pace of the rebound appears to be moderating. Congress has so far failed to agree on additional stimulus to take up the slack from the massive, but now-largely-exhausted, programs approved in March.

Investors have demonstrated their preference for businesses that were thriving before COVID-19 and that have benefitted from pandemic-related tailwinds and enhanced competitive positions. The Fund holds many companies across the technology, consumer, and communications services industries in this category. In our view, prospects for these companies’ continued growth at above-average rates remain strong.

| 1 | Retirement Class shares commenced operations on March 1, 2016. The performance attributed to the Retirement Class shares prior to that date is that of the Institutional Class shares. Performance prior to March 1, 2016 has not been adjusted to reflect the lower expenses of Retirement Class shares. During this period, Retirement Class shares would have had returns similar to, but potentially higher than, Institutional Class shares due to the fact that Retirement Class shares represent interests in the same portfolio as Institutional Class shares but are subject to lower expenses. |

This report contains the current opinions of Jennison Associates LLC as of the date of this report and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Such opinions are subject to change without notice and securities described herein may no longer be included in, or may at any time be removed from, the Fund’s portfolio. This report is distributed for informational purposes only. Information contained herein has been obtained from sources believed reliable, but not guaranteed.

Equity securities, such as common stocks, are affected by company specific events and by movements in the overall stock markets in which those securities principally trade, among other factors. An adverse company specific event, or downturn in those stock markets, can depress the value of a particular company’s equity securities. For information on the different share classes and the risks associated with an investment in the Fund, please refer to the current prospectus.

4

Harbor Capital Appreciation Fund

Portfolio of Investments—October 31, 2020

Portfolio of Investments—October 31, 2020

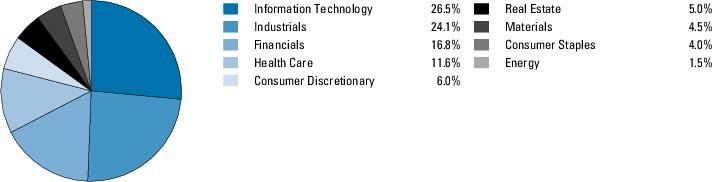

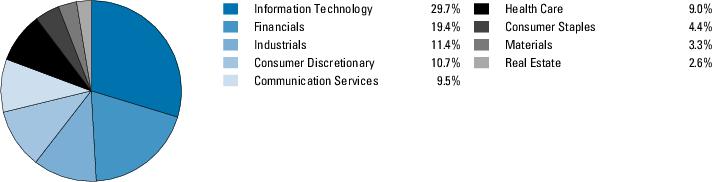

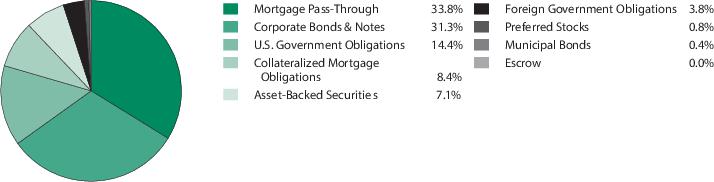

SECTOR ALLOCATION (% of investments) - Unaudited

Portfolio of Investments

Value, Cost, and Principal Amounts in Thousands

| COMMON STOCKS—99.4% | |||

| Shares | Value | ||

| AUTOMOBILES—6.5% | |||

| 6,203,769 | Tesla Inc.* | $ 2,407,311 | |

| BIOTECHNOLOGY—0.8% | |||

| 814,755 | Sarepta Therapeutics Inc.* | 110,734 | |

| 884,825 | Vertex Pharmaceuticals Inc.* | 184,362 | |

| 295,096 | |||

| CAPITAL MARKETS—1.2% | |||

| 195,417 | Goldman Sachs Group Inc. | 36,942 | |

| 1,269,823 | S&P Global Inc. | 409,810 | |

| 446,752 | |||

| ENTERTAINMENT—4.4% | |||

| 2,689,555 | Netflix Inc.* | 1,279,529 | |

| 1,468,988 | Spotify Technology SA (Sweden)* | 352,395 | |

| 1,631,924 | |||

| EQUITY REAL ESTATE INVESTMENT TRUSTS (REITs)—0.3% | |||

| 486,388 | American Tower Corp. | 111,699 | |

| FOOD & STAPLES RETAILING—1.6% | |||

| 1,615,235 | Costco Wholesale Corp. | 577,640 | |

| HEALTH CARE EQUIPMENT & SUPPLIES—2.0% | |||

| 1,439,002 | Danaher Corp. | 330,308 | |

| 826,700 | Dexcom Inc.* | 264,197 | |

| 231,299 | Intuitive Surgical Inc.* | 154,295 | |

| 748,800 | |||

| HEALTH CARE PROVIDERS & SERVICES—1.2% | |||

| 1,250,993 | Guardant Health Inc.* | 133,431 | |

| 747,746 | Humana Inc. | 298,560 | |

| 431,991 | |||

| HEALTH CARE TECHNOLOGY—1.0% | |||

| 1,888,314 | Teladoc Health Inc.* | 370,978 | |

| HOTELS, RESTAURANTS & LEISURE—1.4% | |||

| 434,813 | Chipotle Mexican Grill Inc.* | 522,419 | |

| INTERACTIVE MEDIA & SERVICES—11.3% | |||

| 454,450 | Alphabet Inc. Class A* | 734,441 | |

| 452,682 | Alphabet Inc. Class C* | 733,802 | |

| 6,150,128 | Facebook Inc.* | 1,618,160 | |

| COMMON STOCKS—Continued | |||

| Shares | Value | ||

| INTERACTIVE MEDIA & SERVICES—Continued | |||

| 5,236,778 | Match Group Inc.* | $ 611,551 | |

| 6,270,447 | Tencent Holdings Ltd. (China) | 479,098 | |

| 4,177,052 | |||

| INTERNET & DIRECT MARKETING RETAIL—9.7% | |||

| 1,867,071 | Alibaba Group Holding Ltd. ADR (China)*,1 | 568,878 | |

| 992,075 | Amazon.com Inc.* | 3,012,088 | |

| 3,580,966 | |||

| IT SERVICES—14.4% | |||

| 433,107 | Adyen NV (Netherlands)*,2 | 727,942 | |

| 2,336,484 | Mastercard Inc. | 674,403 | |

| 4,650,103 | PayPal Holdings Inc.* | 865,524 | |

| 996,565 | Shopify Inc. (Canada)* | 922,251 | |

| 1,726,075 | Square Inc.* | 267,334 | |

| 2,685,977 | Twilio Inc.* | 749,307 | |

| 6,003,738 | Visa Inc. | 1,090,939 | |

| 5,297,700 | |||

| LEISURE PRODUCTS—0.9% | |||

| 3,013,020 | Peloton Interactive Inc.* | 332,065 | |

| PERSONAL PRODUCTS—1.4% | |||

| 2,299,173 | Estée Lauder Companies Inc. | 505,036 | |

| PHARMACEUTICALS—1.2% | |||

| 8,458,724 | AstraZeneca plc ADR (United Kingdom)1 | 424,290 | |

| ROAD & RAIL—2.2% | |||

| 12,417,672 | Uber Technologies Inc.* | 414,874 | |

| 2,250,063 | Union Pacific Corp. | 398,689 | |

| 813,563 | |||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—4.4% | |||

| 2,998,476 | NVIDIA Corp. | 1,503,316 | |

| 1,433,825 | Taiwan Semiconductor Manufacturing Co. Ltd. ADR (Taiwan)1 | 120,255 | |

| 1,623,571 | |||

| SOFTWARE—19.2% | |||

| 2,507,554 | Adobe Inc.* | 1,121,127 | |

| 1,853,193 | Atlassian Corp. plc (Australia)* | 355,109 | |

| 1,352,814 | Coupa Software Inc.* | 362,148 | |

5

Harbor Capital Appreciation Fund

Portfolio of Investments—Continued

Portfolio of Investments—Continued

Value, Cost, and Principal Amounts in Thousands

| COMMON STOCKS—Continued | |||

| Shares | Value | ||

| SOFTWARE—Continued | |||

| 2,500,098 | CrowdStrike Holdings Inc.* | $ 309,612 | |

| 9,097,949 | Microsoft Corp. | 1,842,062 | |

| 1,079,996 | RingCentral Inc.* | 279,006 | |

| 4,667,131 | salesforce.com Inc.* | 1,084,034 | |

| 752,081 | ServiceNow Inc.* | 374,213 | |

| 2,591,142 | Splunk Inc.* | 513,150 | |

| 575,122 | Trade Desk Inc.* | 325,778 | |

| 1,527,878 | Workday Inc.* | 321,038 | |

| 360,968 | Zoom Video Communications Inc.* | 166,374 | |

| 7,053,651 | |||

| SPECIALTY RETAIL—2.2% | |||

| 1,323,142 | Carvana Co.* | 245,245 | |

| 2,180,733 | Home Depot Inc. | 581,623 | |

| 826,868 | |||

| TECHNOLOGY HARDWARE, STORAGE & PERIPHERALS—6.4% | |||

| 21,504,394 | Apple Inc. | 2,340,968 | |

| COMMON STOCKS—Continued | |||

| Shares | Value | ||

| TEXTILES, APPAREL & LUXURY GOODS—5.7% | |||

| 792,640 | Kering SA (France) | $ 479,005 | |

| 2,178,391 | Lululemon Athletica Inc. (Canada)* | 695,539 | |

| 528,509 | LVMH Moet Hennessy Louis Vuitton SE (France) | 247,737 | |

| 5,531,614 | NIKE Inc. | 664,236 | |

| 2,086,517 | |||

| TOTAL COMMON STOCKS | |||

(Cost $18,096,745) | 36,606,857 | ||

| TOTAL INVESTMENTS—99.4% | |||

(Cost $18,096,745) | 36,606,857 | ||

CASH AND OTHER ASSETS, LESS LIABILITIES—0.6% | 224,064 | ||

TOTAL NET ASSETS—100.0% | $36,830,921 | ||

FAIR VALUE MEASUREMENTS

At October 31, 2020, the investments in Tencent Holdings Ltd., Adyen NV, Kering SA, and LVMH Moet Hennessy Louis Vuitton SE (as disclosed in the preceding Portfolio of Investments) were classified as Level 2 and all other investments were classified as Level 1. There were no Level 3 investments at October 31, 2020 or 2019.

For more information on valuation inputs and their aggregation into the levels identified above, please refer to the Fair Value Measurements and Disclosures in Note 2 of the accompanying Notes to Financial Statements.

| * | Non-income producing security |

| 1 | Depositary receipts such as American Depositary Receipts (ADRs), Global Depositary Receipts (GDRs) and other country specific depositary receipts are certificates evidencing ownership of shares of a foreign issuer. These certificates are issued by depositary banks and generally trade on an established market in the U.S. or elsewhere. |

| 2 | Securities purchased in a transaction exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. The Fund has no right to demand registration of these securities. At October 31, 2020, the aggregate value of these securities was $727,942 or 2% of net assets. |

The accompanying notes are an integral part of the Financial Statements.

6

Harbor Large Cap Value Fund

Manager’s Commentary (Unaudited)

Manager’s Commentary (Unaudited)

Subadviser

Aristotle Capital Management, LLC

11100 Santa

Monica Boulevard

Suite 1700

Suite 1700

Los Angeles, CA 90025

Portfolio Manager

Howard Gleicher, CFA

Since 2012

Since 2012

Gregory D. Padilla, CFA

Since 2018

Aristotle has subadvised the Fund since 2012.

Investment Objective

The Fund seeks long-term total return.

Howard Gleicher, CFA

Gregory D. Padilla, CFA

Management’s Discussion of

Fund Performance

Fund Performance

Market Review

The new decade started with the world declaring war on COVID-19, the pandemic that has infected millions globally. Around the world, governments, central banks and corporations responded with a litany of actions aimed at containing the deadly virus and limiting its economic damage. Governments issued state-of-emergency declarations, announced shelter-in-place orders and passed trillions of dollars in relief packages for businesses and citizens. Central banks cut interest rates (to near zero in the U.S.), restarted quantitative easing programs and reintroduced an “alphabet soup” of crisis-era programs last seen in the Great Financial Crisis. Against this backdrop, the S&P 500 Index posted its worst quarterly performance since 2008 in the first quarter of 2020.

Throughout late spring and early summer, equity markets rebounded as many states initiated early phases of the reopening process. The worst-case scenario of the global pandemic crisis morphing into a liquidity crunch had thus been avoided as continued central bank support and improving economic data also provided some comfort to market participants despite a myriad of economic, social and political issues at hand.

The S&P 500 closed out the reporting period up after logging consecutive monthly declines in September and October. A resurgent COVID-19 pandemic, in Europe and the U.S., made for a downbeat backdrop as the market’s hopes for pre-election fiscal stimulus were dashed. U.S. technology stocks, which have benefited from the shift online caused by COVID-19 this year, also came under pressure throughout September and October, a reminder that the macroeconomic outlook remains uncertain and markets can still quickly become volatile. On a positive note, optimism around treatments and vaccine progress, have helped cushion the market somewhat amid darkening sentiment. Clearly, more positive news on this front could be optimistic for markets.

Performance

For the year ended October 31, 2020, Harbor Large Cap Value Fund posted a total return of 5.80% (Retirement Class), 5.72% (Institutional Class), 5.42% (Administrative Class) and 5.32% (Investor Class) outperforming the -7.57% return of the Russell 1000® Value Index.

The vast majority of the portfolio’s outperformance relative to the Russell 1000® Value Index during the year can be attributed to security selection, while sector allocation also contributed modestly. Security selection was positive in all but three sectors, with holdings in the Information Technology, Consumer Discretionary, and Energy sectors being the largest contributors to relative return. Conversely, security selection in the Consumer Staples and Industrials sectors coupled with an overweight position in the Consumer Discretionary sector detracted from relative return. (Relative weights are the result of bottom-up security selection.)

Digital media and digital experience software company, Adobe, was the top contributor to the Fund’s relative return during the period. The company reported strong results throughout the year despite the challenging macroeconomic environment, which we believe further demonstrates the resiliency of Adobe’s business model. In our view, the company has benefitted from its advantaged subscription business model and previous investments in products and services that allow customers to increase efficiency and productivity in normal work environments as well as the current remote work environment. Overall, we remain confident in management’s ability to continue to provide innovative solutions to its customers regardless of market environment, as the company’s migration from a license to subscription-based model continues to march on.

7

Harbor Large Cap Value Fund

Manager’s Commentary—Continued

Manager’s Commentary—Continued

CHANGE IN A $50,000 INVESTMENT

For the period 11/01/2010 through 10/31/2020

The graph compares a $50,000 investment in the Institutional Class shares of the Fund with the performance of the Russell 1000® Value Index. The Fund’s performance assumes the reinvestment of all dividend and capital gain distributions.

TOTAL RETURNS

For the periods ended 10/31/2020

| 1 Year | Annualized | |||||||

| 5 Years | 10 Years | |||||||

| Harbor Large Cap Value Fund | ||||||||

Retirement Class1 | 5.80% | 10.86% | 12.57% | |||||

Institutional Class | 5.72 | 10.79 | 12.53 | |||||

Administrative Class | 5.42 | 10.49 | 12.22 | |||||

Investor Class | 5.32 | 10.38 | 12.10 | |||||

| Comparative Index | ||||||||

Russell 1000® Value | -7.57% | 5.82% | 9.48% | |||||

As stated in the Fund’s prospectus dated March 1, 2020, the expense ratios were 0.61% (Net) and 0.65% (Gross) (Retirement Class); 0.69% (Net) and 0.73% (Gross) (Institutional Class); 0.94% (Net) and 0.98% (Gross) (Administrative Class); and 1.06% (Net) and 1.10% (Gross) (Investor Class). The net expense ratios reflect an expense limitation agreement (excluding interest expense, if any) effective through 02/28/2021. The expense ratios in the prospectus may differ from the actual expense ratios for the period disclosed within this report. The expense ratios shown in the prospectus are based on the prior fiscal year, adjusted to reflect changes, if any, in contractual arrangements that occurred prior to the date of the prospectus (or supplement thereto, if applicable).

Performance data shown represents past performance and is no guarantee of future results. Past performance is net of management fees and expenses and reflects reinvested dividends and distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or upon the redemption of Fund shares. Past performance reflects the beneficial effect of any expense waivers or reimbursements, without which returns would have been lower. Investment returns and principal value will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Returns for periods less than one year are not annualized. Current performance may be higher or lower and is available through the most recent month end at harborfunds.com or by calling 800-422-1050.

Diversified refiner, chemicals and midstream energy company Phillips 66 was the top detractor from the Fund’s relative return during the year. Shares of Phillips 66 fell as the company continues to combat industry-wide disruptions. Demand for the company’s refined products, such as gasoline, heating oil, and jet fuel, remained well below normal levels throughout the year with lockdown measures in place. Although these headwinds are likely to persist in the short run, we view the strong recoveries in countries that have not experienced a second wave and the initiation of operations at the South Texas Gateway Terminal and Gray Oak Pipeline as encouraging developments. Additionally, the company announced plans to reconfigure its San Francisco refinery to produce renewable fuels. We believe these developments will support Phillips 66’s ongoing diversification away from crude oil refining, a catalyst we previously identified.

Outlook & Strategy

As the pandemic continues to impact the world, and with U.S. elections front and center, there is no shortage of headlines. For Aristotle Capital, what is important to consider is whether such events are analyzable and meaningful for long-term investors or merely interesting conversation topics. Rather than attempting to reposition our portfolios based on an assumption of how the market may react to these events (e.g., election results, timing of a COVID-19 vaccine, size of the next stimulus package), we spend our time trying to identify what we consider to be high-quality companies that can succeed over the long term. Such long-term thinking, we believe, distinguishes us from our competitors and helps us identify companies that possess sustainable competitive advantages and appear poised to outperform their peers over a market cycle.

| 1 | Retirement Class shares commenced operations on March 1, 2016. The performance attributed to the Retirement Class shares prior to that date is that of the Institutional Class shares. Performance prior to March 1, 2016 has not been adjusted to reflect the lower expenses of Retirement Class shares. During this period, Retirement Class shares would have had returns similar to, but potentially higher than, Institutional Class shares due to the fact that Retirement Class shares represent interests in the same portfolio as Institutional Class shares but are subject to lower expenses. |

This report contains the current opinions of Aristotle Capital Management, LLC as of the date of this report and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Such opinions are subject to change without notice and securities described herein may no longer be included in, or may at any time be removed from, the Fund’s portfolio. This report is distributed for informational purposes only. Information contained herein has been obtained from sources believed reliable, but not guaranteed.

Equity securities, such as common stocks, are affected by company specific events and by movements in the overall stock markets in which those securities principally trade, among other factors. An adverse company specific event, or downturn in those stock markets, can depress the value of a particular company’s equity securities. For information on the different share classes and the risks associated with an investment in the Fund, please refer to the current prospectus.

8

Harbor Large Cap Value Fund

Portfolio of Investments—October 31, 2020

Portfolio of Investments—October 31, 2020

SECTOR ALLOCATION (% of investments) - Unaudited

Portfolio of Investments

Value, Cost, and Principal Amounts in Thousands

| COMMON STOCKS—95.9% | |||

| Shares | Value | ||

| AEROSPACE & DEFENSE—1.6% | |||

| 190,000 | General Dynamics Corp. | $ 24,953 | |

| BANKS—9.8% | |||

| 296,801 | Bank of America Corp. | 7,034 | |

| 177,284 | BOK Financial Corp. | 10,414 | |

| 370,000 | Commerce Bancshares Inc. | 23,032 | |

| 198,000 | Cullen/Frost Bankers Inc. | 13,913 | |

| 528,000 | East West Bancorp Inc. | 19,261 | |

| 340,000 | JPMorgan Chase & Co. | 33,334 | |

| 3,670,000 | Mitsubishi UFJ Financial Group Inc. ADR (Japan)1 | 14,460 | |

| 287,000 | PNC Financial Services Group Inc. | 32,110 | |

| 153,558 | |||

| BEVERAGES—2.4% | |||

| 800,000 | Coca-Cola Co. | 38,448 | |

| BIOTECHNOLOGY—2.9% | |||

| 209,000 | Amgen Inc. | 45,340 | |

| BUILDING PRODUCTS—4.4% | |||

| 345,000 | Allegion plc (Ireland) | 33,982 | |

| 850,000 | Johnson Controls International plc | 35,879 | |

| 69,861 | |||

| CAPITAL MARKETS—2.4% | |||

| 235,000 | Ameriprise Financial Inc. | 37,795 | |

| CHEMICALS—5.2% | |||

| 1,290,000 | Corteva Inc. | 42,544 | |

| 464,000 | RPM International Inc. | 39,287 | |

| 81,831 | |||

| CONSTRUCTION MATERIALS—2.5% | |||

| 148,000 | Martin Marietta Materials Inc. | 39,420 | |

| CONSUMER FINANCE—1.6% | |||

| 336,000 | Capital One Financial Corp. | 24,555 | |

| EQUITY REAL ESTATE INVESTMENT TRUSTS (REITs)—2.5% | |||

| 292,000 | Equity Lifestyle Properties Inc. | 17,283 | |

| 160,000 | Sun Communities Inc. | 22,021 | |

| 39,304 | |||

| COMMON STOCKS—Continued | |||

| Shares | Value | ||

| FOOD & STAPLES RETAILING—0.9% | |||

| 400,000 | Walgreens Boots Alliance Inc. | $ 13,616 | |

| FOOD PRODUCTS—1.6% | |||

| 445,000 | Tyson Foods Inc. | 25,467 | |

| HEALTH CARE EQUIPMENT & SUPPLIES—9.6% | |||

| 588,000 | Alcon Inc. (Switzerland)* | 33,422 | |

| 335,500 | Danaher Corp. | 77,011 | |

| 399,000 | Medtronic plc | 40,127 | |

| 150,560 | |||

| HOUSEHOLD DURABLES—5.9% | |||

| 599,000 | Lennar Corp. Class A | 42,068 | |

| 7,120 | Lennar Corp. Class B | 405 | |

| 603,000 | Sony Corp. ADR (Japan)1 | 50,447 | |

| 92,920 | |||

| HOUSEHOLD PRODUCTS—2.5% | |||

| 286,000 | Procter & Gamble Co. | 39,211 | |

| INSURANCE—2.7% | |||

| 206,000 | Chubb Ltd. (Switzerland) | 26,762 | |

| 221,591 | Cincinnati Financial Corp | 15,675 | |

| 42,437 | |||

| INTERACTIVE MEDIA & SERVICES—2.1% | |||

| 810,000 | Twitter Inc.* | 33,502 | |

| IT SERVICES—2.3% | |||

| 189,922 | PayPal Holdings Inc.* | 35,350 | |

| MACHINERY—6.9% | |||

| 460,000 | Oshkosh Corp. | 30,985 | |

| 188,600 | Parker-Hannifin Corp. | 39,297 | |

| 430,000 | Xylem Inc. | 37,470 | |

| 107,752 | |||

| OIL, GAS & CONSUMABLE FUELS—3.9% | |||

| 1,860,000 | Cabot Oil & Gas Corp. | 33,089 | |

| 365,000 | Phillips 66 | 17,031 | |

| 150,000 | Pioneer Natural Resources Co. | 11,934 | |

| �� | 62,054 | ||

9

Harbor Large Cap Value Fund

Portfolio of Investments—Continued

Portfolio of Investments—Continued

Value, Cost, and Principal Amounts in Thousands

| COMMON STOCKS—Continued | |||

| Shares | Value | ||

| PHARMACEUTICALS—4.1% | |||

| 1,190,000 | Elanco Animal Health Inc.* | $ 36,902 | |

| 359,000 | Novartis AG ADR (Switzerland)1 | 28,031 | |

| 64,933 | |||

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—5.9% | |||

| 433,000 | Microchip Technology Inc. | 45,499 | |

| 380,000 | QUALCOMM Inc. | 46,877 | |

| 92,376 | |||

| SOFTWARE—12.2% | |||

| 150,000 | Adobe Inc.* | 67,065 | |

| 192,500 | ANSYS Inc.* | 58,591 | |

| 324,000 | Microsoft Corp. | 65,601 | |

| 191,257 | |||

| TOTAL COMMON STOCKS | |||

(Cost $1,197,173) | 1,506,500 | ||

| TOTAL INVESTMENTS—95.9% | |||

(Cost $1,197,173) | 1,506,500 | ||

CASH AND OTHER ASSETS, LESS LIABILITIES—4.1% | 64,846 | ||

TOTAL NET ASSETS—100.0% | $1,571,346 | ||

FAIR VALUE MEASUREMENTS

All investments at October 31, 2020 (as disclosed in the preceding Portfolio of Investments) were classified as Level 1. There were no Level 3 investments at October 31, 2020 or 2019.

For more information on valuation inputs and their aggregation into the levels identified above, please refer to the Fair Value Measurements and Disclosures in Note 2 of the accompanying Notes to Financial Statements.

| * | Non-income producing security |

| 1 | Depositary receipts such as American Depositary Receipts (ADRs), Global Depositary Receipts (GDRs) and other country specific depositary receipts are certificates evidencing ownership of shares of a foreign issuer. These certificates are issued by depositary banks and generally trade on an established market in the U.S. or elsewhere. |

The accompanying notes are an integral part of the Financial Statements.

10

Harbor Mid Cap Fund

Manager’s Commentary (Unaudited)

Manager’s Commentary (Unaudited)

Subadviser

EARNEST Partners, LLC

1180 Peachtree St. NE

Suite 2300

Suite 2300

Atlanta, GA 30309

Portfolio Manager

Paul E. Viera

Since 2019

Since 2019

EARNEST Partners, LLC has subadvised the Fund since 2019.

Investment Objective

The Fund seeks long-term total return.

Paul E. Viera

Management’s Discussion of

Fund Performance

Fund Performance

MARKET REVIEW

The U.S. equity markets, represented by the S&P 500 Index were positive during the year ended October 31, 2020, posting nearly 10% return. However, the U.S. mid cap market, represented by the Russell Midcap® Index, ended the period lower, down 2% for the year ended October 31, 2020.

Capital markets continued to recover as investors received clarity on the economic impact from the coronavirus epidemic and began to look forward to how a post-COVID-19 environment would support future earnings growth. Many service and retail businesses adapted to the situation with standardized PPE requirements and social distancing standards, while white-collar businesses embraced a work-from-home environment, which enabled them to continue operations. Additionally, significant progress was made on vaccine candidates, several of which are currently being tested. Many areas of the economy saw a swift rebound in activity as the government’s stimulus measures supported renewed consumption of durable goods, and record low mortgage rates buoyed the housing market. With respect to monetary policy, the U.S. Federal Reserve’s (Fed) initial actions to curb the economic effects of the virus included a wide array of stimulative measures that included short-term rate reductions to near-zero and repurchases of U.S. Treasuries, mortgages and corporate debt, to include high-yield notes. In September, the Fed stated that it would hold rates near zero through at least 2022 and would continue to increase its fixed income holdings to provide liquidity to credit markets. These moves gave further confidence to equity and fixed income investors who understood that the Fed will continue to act as a lender-of-last resort and that stimulus measures were not a one-time deal. Additionally, the central bank projected a 6.5% contraction in GDP for 2020 and forecast a 5% gain next year followed by a 3.5% increase in 2022. After hitting a record high of 14.7% in April, unemployment fell to 7.9% in September. The Fed is projecting unemployment of 7.6% at the end of 2020, then falling to 5.5% and 4.6% in 2021 and 2022, respectively.

Performance

Harbor Mid Cap Fund posted modestly positive returns, 5.86% (Retirement Class), 5.75% (Institutional Class), and 5.42% (Investor Class) while the Russell Midcap® Index returned 0.53% for the period December 1, 2019 to October 31, 2020. The portfolio outperformed the benchmark, Russell Midcap® Index, during the period by a wide margin as investors began to refocus on company fundamentals after the sharp market downturn early in 2020 as a result of COVID-19. Stock selection continued to drive relative returns in the period. Stock selection was strongest in the Consumer Discretionary, Industrials and Materials sectors. Sector positioning also contributed to the strong results, as an overweight to Information Technology and an underweight to Energy boosted relative returns.

Contributing to performance for the period, D.R. Horton is one of the largest homebuilders in the U.S. Founded in 1978, The company’s footprint now spans across the United States and has a presence in 29 states, giving it both broad diversification and significant economies of scale. D.R. Horton’s brands include: D.R. Horton America’s Builder, Express Homes, Emerald Homes and Freedom Homes. D.R. Horton reported better-than-expected earnings driving shares up more than 35% during the period. Top line and margin improvement was driven by low mortgage rates and strong demand in entry level homes. August new home sales rose 43% year-over-year which translates to a 40% rise in sales from the pre-COVID-19 period. Targeting the entry-level and mid-level price point homes, we believe that the company is well positioned to continue to benefit from families’ demand for more space combined with a historically low interest rate environment that is expected to remain low in the foreseeable future.

11

Harbor Mid Cap Fund

Manager’s Commentary—Continued

Manager’s Commentary—Continued

CHANGE IN A $50,000 INVESTMENT

For the period 12/01/2019 through 10/31/2020

The graph compares a $50,000 investment in the Institutional Class shares of the Fund with the performance of the Russell Midcap® Index. The Fund’s performance assumes the reinvestment of all dividend and capital gain distributions.

TOTAL RETURNS

For the periods ended 10/31/2020

| 1 Year | 5 Years | Unannualized | ||||||

| Life of Fund | ||||||||

| Harbor Mid Cap Fund | ||||||||

Retirement Class1 | N/A | N/A | 5.86% | |||||

Institutional Class1 | N/A | N/A | 5.75 | |||||

Investor Class1 | N/A | N/A | 5.42 | |||||

| Comparative Index | ||||||||

Russell Midcap®1 | N/A | N/A | 0.53% | |||||

As stated in the Fund’s prospectus dated March 1, 2020, the expense ratios were 0.80% (Net) and 2.16% (Gross) (Retirement Class); 0.88% (Net) and 2.24% (Gross) (Institutional Class); 1.13% (Net) and 2.49% (Gross) (Administrative Class); and 1.25% (Net) and 2.61% (Gross) (Investor Class). The net expense ratios reflect an expense limitation agreement (excluding interest expense, if any) effective through 02/28/2021. The expense ratios in the prospectus may differ from the actual expense ratios for the period disclosed within this report. The expense ratios shown in the prospectus are based on the prior fiscal year, adjusted to reflect changes, if any, in contractual arrangements that occurred prior to the date of the prospectus (or supplement thereto, if applicable).

Performance data shown represents past performance and is no guarantee of future results. Past performance is net of management fees and expenses and reflects reinvested dividends and distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or upon the redemption of Fund shares. Past performance reflects the beneficial effect of any expense waivers or reimbursements, without which returns would have been lower. Investment returns and principal value will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Returns for periods less than one year are not annualized. Current performance may be higher or lower and is available through the most recent month end at harborfunds.com or by calling 800-422-1050.

Detracting from performance for the period, Boston Properties is a real estate investment trust whose portfolio is comprised primarily of first-class office space, hotels, residential properties, and retail properties which are concentrated in Boston, New York, San Francisco and Washington, DC. During the period, Boston Properties reported that a portion of its portfolio of properties was due for contract renewals. With uncertainty around the occupancy rate cycle and interest rates, market participants expressed concerns about the company’s ability to secure its existing contracts at advantageous rates and to grow new leasing of properties. Shares declined 45% during the period. We believe that Boston Properties has a strong balance sheet, experienced management team and an established track record of managing its portfolio of commercial office spaces. Additionally, the company’s properties are in the top end of the quality spectrum and are located in the high demand markets with a high-quality tenant base which we believe makes it a strong commercial real estate operator in the industry.

OUTLOOK & STRATEGY

As of October 31, 2020, the Fund had an overweight in the Industrials, Information Technology, and Financials sectors and an underweight in the Healthcare, Consumer Staples, Consumer Discretionary, and Utilities sectors. The Fund’s relative overweight and underweight positions are a result of where EARNEST Partners is finding attractive individual investment opportunities.

In managing the Harbor Mid Cap Fund, EARNEST Partners seeks companies with share prices that we believe do not fully reflect their earnings growth outlook. Going forward, we will continue to employ our three-step investment methodology: screen the broad universe to identify stocks that are best positioned to outperform, measure and manage downside risk to the benchmark, and perform in-depth, thorough, fundamental research to find what we believe are the best stocks to include in the Fund.

| 1 | The “Life of Fund” return as shown reflects the period 12/01/2019 through 10/31/2020. |

This report contains the current opinions of EARNEST Partners, LLC as of the date of this report and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Such opinions are subject to change without notice and securities described herein may no longer be included in, or may at any time be removed from, the Fund’s portfolio. This report is distributed for informational purposes only. Information contained herein has been obtained from sources believed reliable, but not guaranteed.

Stocks of mid cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Equity securities, such as common stocks, are affected by company specific events and by movements in the overall stock markets in which those securities principally trade, among other factors. An adverse company specific event, or downturn in those stock markets, can depress the value of a particular company’s equity securities. For information on the different share classes and the risks associated with an investment in the Fund, please refer to the current prospectus.

12

Harbor Mid Cap Fund

Portfolio of Investments—October 31, 2020

Portfolio of Investments—October 31, 2020

SECTOR ALLOCATION (% of investments) - Unaudited

Portfolio of Investments

Value, Cost, and Principal Amounts in Thousands

| COMMON STOCKS—97.6% | |||

| Shares | Value | ||

| AEROSPACE & DEFENSE—0.9% | |||

| 770 | General Dynamics Corp. | $ 101 | |

| BANKS—1.0% | |||

| 8,915 | KeyCorp | 116 | |

| BUILDING PRODUCTS—2.1% | |||

| 4,269 | Masco Corp* | 229 | |

| CAPITAL MARKETS—9.3% | |||

| 7,196 | Eaton Vance Corp. | 430 | |

| 2,889 | Intercontinental Exchange Inc. | 273 | |

| 2,151 | Raymond James Financial Inc. | 164 | |

| 2,644 | Stifel Financial Corp. | 155 | |

| 1,022 | |||

| CHEMICALS—4.0% | |||

| 1,460 | Albemarle Corp.* | 136 | |

| 1,614 | Eastman Chemical Co. | 130 | |

| 1,146 | Scotts Miracle-Gro Co. | 172 | |

| 438 | |||

| COMMERCIAL SERVICES & SUPPLIES—4.4% | |||

| 3,181 | Republic Services Inc* | 281 | |

| 3,228 | Stericycle Inc.* | 201 | |

| 482 | |||

| CONTAINERS & PACKAGING—2.4% | |||

| 1,249 | Packaging Corp. of America* | 143 | |

| 3,027 | Sealed Air Corp* | 120 | |

| 263 | |||

| ELECTRICAL EQUIPMENT—1.6% | |||

| 4,116 | Sensata Technologies Holding plc (United Kingdom)* | 180 | |

| ELECTRONIC EQUIPMENT, INSTRUMENTS & COMPONENTS—2.3% | |||

| 2,381 | Keysight Technologies Inc.* | 250 | |

| ENTERTAINMENT—2.1% | |||

| 3,104 | Activision Blizzard Inc.* | 235 | |

| EQUITY REAL ESTATE INVESTMENT TRUSTS (REITs)—4.5% | |||

| 5,621 | Americold Realty Trust* | 203 | |

| COMMON STOCKS—Continued | |||

| Shares | Value | ||

| EQUITY REAL ESTATE INVESTMENT TRUSTS (REITs)—Continued | |||

| 1,282 | Boston Properties Inc.* | $ 93 | |

| 675 | SBA Communications Corp.* | 196 | |

| 492 | |||

| FOOD & STAPLES RETAILING—1.3% | |||

| 2,564 | Sysco Corp.* | 142 | |

| HEALTH CARE EQUIPMENT & SUPPLIES—1.5% | |||

| 3,422 | Dentsply Sirona Inc.* | 161 | |

| HEALTH CARE PROVIDERS & SERVICES—2.5% | |||

| 1,333 | AmerisourceBergen Corp* | 128 | |

| 767 | Laboratory Corp. of America Holdings* | 153 | |

| 281 | |||

| HOTELS, RESTAURANTS & LEISURE—2.1% | |||

| 2,480 | Darden Restaurants Inc.* | 228 | |

| HOUSEHOLD DURABLES—2.8% | |||

| 4,558 | D.R. Horton Inc.* | 305 | |

| INSURANCE—4.8% | |||

| 1,391 | Reinsurance Group of America Inc. | 141 | |

| 788 | Renaissance Holdings Ltd. (Bermuda)* | 127 | |

| 2,876 | The Progressive Corp.* | 264 | |

| 532 | |||

| IT SERVICES—6.7% | |||

| 1,311 | Akamai Technologies Inc.* | 125 | |

| 1,398 | Arrow Electronics Inc.* | 109 | |

| 2,717 | Black Knight Inc.* | 239 | |

| 1,668 | Global Payments Inc.* | 263 | |

| 736 | |||

| LIFE SCIENCES TOOLS & SERVICES—5.9% | |||

| 2,220 | Agilent Technologies Inc. | 227 | |

| 485 | Bio-Rad Laboratories Inc.* | 284 | |

| 2,545 | Syneos Health Inc.* | 135 | |

| 646 | |||

| MACHINERY—6.1% | |||

| 924 | Cummins Inc. | 203 | |

| 1,384 | Dover Corp. | 153 | |

13

Harbor Mid Cap Fund

Portfolio of Investments—Continued

Portfolio of Investments—Continued

Value, Cost, and Principal Amounts in Thousands

| COMMON STOCKS—Continued | |||

| Shares | Value | ||

| MACHINERY—Continued | |||

| 1,051 | Snap-on Inc. | $ 166 | |

| 1,884 | Woodward Inc. | 150 | |

| 672 | |||

| MULTI-UTILITIES—1.9% | |||

| 2,118 | WEC Energy Group Inc. | 213 | |

| OIL, GAS & CONSUMABLE FUELS—1.6% | |||

| 3,857 | Cimarex Energy Co.* | 98 | |

| 6,505 | Continental Resources Inc.* | 78 | |

| 176 | |||

| REAL ESTATE MANAGEMENT & DEVELOPMENT—2.0% | |||

| 4,350 | CBRE Group Inc.* | 219 | |

| ROAD & RAIL—1.6% | |||

| 2,281 | CSX Corp* | 180 | |

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—9.1% | |||

| 3,995 | Applied Materials Inc. | 237 | |

| 1,208 | CMC Materials Inc. | 172 | |

| 2,297 | Skyworks Solutions Inc.* | 324 | |

| 2,286 | Xilinx Inc. | 271 | |

| 1,004 | |||

| COMMON STOCKS—Continued | |||

| Shares | Value | ||

| SOFTWARE—9.6% | |||

| 1,022 | ANSYS Inc.* | $ 311 | |

| 1,240 | Autodesk Inc.* | 292 | |

| 320 | Intuit Inc. | 101 | |

| 1,669 | Synopsys Inc.* | 357 | |

| 1,061 | |||

| SPECIALTY RETAIL—1.7% | |||

| 3,634 | TJX Companies Inc.* | 185 | |

| TRADING COMPANIES & DISTRIBUTORS—1.8% | |||

| 3,057 | Air Lease Corp. | 83 | |

| 1,775 | GATX Corp. | 121 | |

| 204 | |||

| TOTAL COMMON STOCKS | |||

(Cost $9,954) | 10,753 | ||

| TOTAL INVESTMENTS—97.6% | |||

(Cost $9,954) | 10,753 | ||

CASH AND OTHER ASSETS, LESS LIABILITIES—2.4% | 261 | ||

TOTAL NET ASSETS—100.0% | $11,014 | ||

FAIR VALUE MEASUREMENTS

All investments at October 31, 2020 (as disclosed in the preceding Portfolio of Investments) were classified as Level 1. There were no Level 3 investments at October 31, 2020 or December 1, 2019 (inception).

For more information on valuation inputs and their aggregation into the levels identified above, please refer to the Fair Value Measurements and Disclosures in Note 2 of the accompanying Notes to Financial Statements.

| * | Non-income producing security |

The accompanying notes are an integral part of the Financial Statements.

14

Harbor Mid Cap Growth Fund

Manager’s Commentary (Unaudited)

Manager’s Commentary (Unaudited)

Subadviser

Wellington Management Company LLP

280 Congress Street

Boston, MA 02210

Boston, MA 02210

Portfolio Managers

Stephen C. Mortimer

Since 2010

Since 2010

Mario E. Abularach, CFA, CMT

Since 2006

Since 2006

Wellington Management has subadvised the Fund since 2005.

Investment Objective

The Fund seeks long-term growth of capital.

Stephen C. Mortimer

Mario E. Abularach, CFA, CMT

Management’s Discussion of

Fund Performance

Fund Performance

MARKET REVIEW

U.S. equities, as measured by the S&P 500 Index, posted positive results over the trailing year ended October 31, 2020. Mid cap growth equities outperformed the broader market during this period. During the first quarter of 2020 equities ended sharply lower after achieving record highs in February following a strong fourth quarter as stocks benefitted from waning recession fears, improved trade sentiment, and accommodative U.S. Federal Reserve (Fed) policies. However, the markets fell sharply as COVID-19 spread rapidly throughout the country, causing unprecedented market disruptions and financial damage, and heightening fears of a severe economic downturn. Many states adopted extraordinary measures to fight the contagion, while companies shuttered stores and production, withdrew earnings guidance, and drew down credit lines at a record pace as borrowing costs soared. Volatility surged to extreme levels, and the S&P 500 Index suffered its fastest ever decline into a bear market. The unprecedented scale of fiscal and monetary stimulus implemented by Congress and the Fed in response to the pandemic drove the market’s rebound in the second quarter. Momentum carried into the third quarter bolstered by substantial monetary support from the Fed, a broadening U.S. economic recovery and promising trials for COVID-19 vaccines. However, the path to sustainable economic recovery was clouded by concerns about a resurgence in COVID-19 infections around the country, an undetermined timeline for vaccines, high unemployment, elevated debt burdens, and uncertainty about additional fiscal stimulus.

Performance

For the year ended October 31, 2020, Harbor Mid Cap Growth Fund outperformed the Russell Midcap® Growth Index. The Fund returned 46.03% (Retirement Class), 45.84% (Institutional Class), 45.42% (Administrative Class), 45.32% (Investor Class) for the year, while the Russell Midcap® Growth Index returned 21.14%.

Relative outperformance was driven by positive security selection, most notably within the Information Technology, Health Care, and Communication Services sectors. Unfavorable security selection within the Financials sector slightly offset positive returns. Sector allocation, a residual of the bottom-up stock selection process, also contributed to results. An overweight allocation to the Health Care sector and an underweight to the Industrials sector contributed most to performance. An overweight allocation to the Consumer Discretionary sector detracted, partially offsetting results.

Advanced Micro Devices, a semiconductor company, was the Fund’s most significant relative contributor during the period. The stock rose over the period after the Trump administration announced a phase one trade deal with China, removing a big obstacle for the company. The company has also introduced new products that were well received by customers. The company has further benefitted from Intel’s delay of its 7nm processors. We exited our position during the period as it grew beyond our market cap range for the portfolio. Other notable contributors during the period were exercise equipment and media company Peloton, mobile payment company Square, and medical devices provider Livongo Health.

Pinterest, a pinboard-style photo-sharing website, was the Fund’s most significant relative detractor during the period. Pinterest saw strong user growth in late 2019. However, the majority of new users came from international countries where users generate less revenue than those in the U.S. We eliminated the position from the portfolio during the period. Other notable detractors during the period were facilities, food and uniform service Aramark, property and casualty software provider Guidewire Software, and timeshare company Marriott Vacations.

15

Harbor Mid Cap Growth Fund

Manager’s Commentary—Continued

Manager’s Commentary—Continued

CHANGE IN A $50,000 INVESTMENT

For the period 11/01/2010 through 10/31/2020

The graph compares a $50,000 investment in the Institutional Class shares of the Fund with the performance of the Russell Midcap® Growth Index. The Fund’s performance assumes the reinvestment of all dividend and capital gain distributions.

TOTAL RETURNS

For the periods ended 10/31/2020

| 1 Year | Annualized | |||||||

| 5 Years | 10 Years | |||||||

| Harbor Mid Cap Growth Fund | ||||||||

Retirement Class1 | 46.03% | 20.07% | 16.10% | |||||

Institutional Class | 45.84 | 19.99 | 16.06 | |||||

Administrative Class | 45.42 | 19.68 | 15.76 | |||||

Investor Class | 45.32 | 19.54 | 15.62 | |||||

| Comparative Index | ||||||||

Russell Midcap® Growth | 21.14% | 14.15% | 14.13% | |||||

As stated in the Fund’s prospectus dated March 1, 2020, the expense ratios were 0.80% (Net) and 0.83% (Gross) (Retirement Class); 0.88% (Net) and 0.91% (Gross) (Institutional Class); 1.13% (Net) and 1.16% (Gross) (Administrative Class); and 1.25% (Net) and 1.28% (Gross) (Investor Class). The Adviser has contractually agreed to reduce the management fee to 0.72% through 02/28/2021. The expense ratios in the prospectus may differ from the actual expense ratios for the period disclosed within this report. The expense ratios shown in the prospectus are based on the prior fiscal year, adjusted to reflect changes, if any, in contractual arrangements that occurred prior to the date of the prospectus (or supplement thereto, if applicable).

Performance data shown represents past performance and is no guarantee of future results. Past performance is net of management fees and expenses and reflects reinvested dividends and distributions but does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or upon the redemption of Fund shares. Past performance reflects the beneficial effect of any expense waivers or reimbursements, without which returns would have been lower. Investment returns and principal value will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Returns for periods less than one year are not annualized. Current performance may be higher or lower and is available through the most recent month end at harborfunds.com or by calling 800-422-1050.

OUTLOOK & STRATEGY

Following a 30% rebound in the Russell Midcap® Growth Index in the second quarter of 2020 driven by cyclical sectors, mid cap U.S. equities continued on a positive trajectory in the third quarter. Investors largely remained risk-on despite COVID-19 continuing to affect large portions of the U.S., slowing the economic recovery and perpetuating market uncertainty. Cyclical sectors such as Communication Services and Consumer Discretionary led the index in the third quarter.

In terms of portfolio positioning, we continued to strive for more balance in the portfolio – an effort that we began in the second quarter as we trimmed our COVID-19 winners and deployed some of that capital into more cyclical growth names. Given the uncertainty of the current environment, we believe a barbell approach between cyclical growth and emerging and compounding growth names in the portfolio should help us protect on the downside if we see another severe wave of the virus that will slow down the recovery while also allowing us to participate on the upside if the market continues to anticipate a full reopening. Part of our barbell strategy is to find some COVID-19 losers that we believe will emerge stronger coming out of this crisis. Among the COVID-19 winners, we see them falling into two camps: those growth stocks which can build on their accelerated growth going forward and those which will likely revert to the mean. Importantly, we are evaluating how possible permanent or semi-permanent changes in consumer behavior will impact companies. The paradigm shifts going on now, whether sustainable or not, are mind boggling and non-linear, and we need to be more flexible in analyzing this new world than ever before.

While a lot of uncertainty remains including the trajectory of the virus and its impact on the economy as well as the upcoming U.S. presidential election, we are staying disciplined to our bottom-up stock selection process and are confident in our positioning heading into the end of the year. We continue to look for growth companies for which we have a differentiated view from consensus and have identified a higher upside potential relative to the downside.

| 1 | Retirement Class shares commenced operations on March 1, 2016. The performance attributed to the Retirement Class shares prior to that date is that of the Institutional Class shares. Performance prior to March 1, 2016 has not been adjusted to reflect the lower expenses of Retirement Class shares. During this period, Retirement Class shares would have had returns similar to, but potentially higher than, Institutional Class shares due to the fact that Retirement Class shares represent interests in the same portfolio as Institutional Class shares but are subject to lower expenses. |

This report contains the current opinions of Wellington Management Company LLP as of the date of this report and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Such opinions are subject to change without notice and securities described herein may no longer be included in, or may at any time be removed from, the Fund’s portfolio. This report is distributed for informational purposes only. Information contained herein has been obtained from sources believed reliable, but not guaranteed.

Stocks of mid cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Equity securities, such as common stocks, are affected by company specific events and by movements in the overall stock markets in which those securities principally trade, among other factors. An adverse company specific event, or downturn in those stock markets, can depress the value of a particular company’s equity securities. For information on the different share classes and the risks associated with an investment in the Fund, please refer to the current prospectus.

16

Harbor Mid Cap Growth Fund

Portfolio of Investments—October 31, 2020

Portfolio of Investments—October 31, 2020

SECTOR ALLOCATION (% of investments) - Unaudited

(Excludes short-term investments)

Portfolio of Investments

Value, Cost, and Principal Amounts in Thousands

| COMMON STOCKS—91.1% | |||

| Shares | Value | ||

| AUTOMOBILES—1.8% | |||

| 72,836 | Thor Industries Inc. | $ 6,160 | |

| BEVERAGES—4.0% | |||

| 5,288 | Boston Beer Co. Inc.* | 5,495 | |

| 105,300 | Monster Beverage Corp.* | 8,063 | |

| 13,558 | |||

| BIOTECHNOLOGY—7.1% | |||

| 34,945 | Apellis Pharmaceuticals Inc.* | 1,115 | |

| 16,393 | Ascendis Pharma AS ADR (Denmark)*,1 | 2,678 | |

| 89,596 | Exact Sciences Corp.* | 11,095 | |

| 30,127 | Galapagos NV (Belgium)* | 3,558 | |

| 1,736 | Galapagos NV ADR (Belgium)*,1 | 202 | |

| 29,414 | Kodiak Sciences Inc.* | 2,671 | |

| 17,724 | Seagen Inc.* | 2,956 | |

| 24,275 | |||

| CAPITAL MARKETS—2.7% | |||

| 57,202 | Blackstone Group Inc. | 2,884 | |

| 312,100 | Bowx Acquisition Corp.* | 3,115 | |

| 313,754 | Churchill Capital Corp. IV* | 3,081 | |

| 9,080 | |||

| COMMERCIAL SERVICES & SUPPLIES—1.6% | |||

| 50,468 | Copart Inc.* | 5,570 | |

| DIVERSIFIED CONSUMER SERVICES—2.5% | |||

| 115,178 | Chegg Inc.* | 8,459 | |

| ELECTRICAL EQUIPMENT—0.1% | |||

| 16,199 | Vontier Corp.* | 466 | |

| ENTERTAINMENT—3.4% | |||

| 17,141 | Roku Inc.* | 3,469 | |

| 33,564 | Spotify Technology SA (Sweden)* | 8,052 | |

| 11,521 | |||

| HEALTH CARE EQUIPMENT & SUPPLIES—13.5% | |||

| 27,877 | ABIOMED Inc.* | 7,022 | |

| 32,942 | Align Technology Inc.* | 14,036 | |

| 19,893 | Dexcom Inc.* | 6,357 | |

| 38,139 | Insulet Corp.* | 8,476 | |

| COMMON STOCKS—Continued | |||

| Shares | Value | ||

| HEALTH CARE EQUIPMENT & SUPPLIES—Continued | |||

| 22,372 | Novocure Ltd. (Jersey)* | $ 2,732 | |

| 68,975 | Tandem Diabetes Care Inc.* | 7,518 | |

| 46,141 | |||

| HEALTH CARE TECHNOLOGY—1.0% | |||

| 12,104 | Veeva Systems Inc.* | 3,269 | |

| HOTELS, RESTAURANTS & LEISURE—1.9% | |||

| 52,614 | Penn National Gaming Inc.* | 2,840 | |

| 63,840 | Planet Fitness Inc.* | 3,784 | |

| 6,624 | |||

| HOUSEHOLD DURABLES—1.8% | |||

| 88,041 | Lennar Corp. | 6,183 | |

| INTERACTIVE MEDIA & SERVICES—4.2% | |||

| 94,615 | Match Group Inc.* | 11,049 | |

| 80,878 | Twitter Inc.* | 3,345 | |

| 14,394 | |||

| IT SERVICES—5.9% | |||

| 104,219 | GoDaddy Inc.* | 7,373 | |

| 57,893 | Leidos Holdings Inc. | 4,805 | |

| 52,053 | Square Inc.* | 8,062 | |

| 20,240 | |||

| LEISURE PRODUCTS—6.3% | |||

| 196,797 | Draftkings Inc.* | 6,967 | |

| 94,985 | Peloton Interactive Inc.* | 10,468 | |

| 44,894 | Polaris Industries Inc. | 4,079 | |

| 21,514 | |||

| LIFE SCIENCES TOOLS & SERVICES—1.0% | |||

| 34,735 | Agilent Technologies Inc. | 3,546 | |

| MACHINERY—0.8% | |||

| 41,761 | Fortive Corp. | 2,572 | |

17

Harbor Mid Cap Growth Fund

Portfolio of Investments—Continued

Portfolio of Investments—Continued

Value, Cost, and Principal Amounts in Thousands

| COMMON STOCKS—Continued | |||

| Shares | Value | ||

| PHARMACEUTICALS—1.4% | |||

| 121,346 | Elanco Animal Health Inc.* | $ 3,763 | |

| 7,042 | Reata Pharmaceuticals Inc.* | 822 | |

| 4,585 | |||

| PROFESSIONAL SERVICES—3.2% | |||

| 13,305 | CoStar Group Inc.* | 10,958 | |

| SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT—1.7% | |||

| 149,440 | Marvell Technology Group Ltd. (Bermuda) | 5,605 | |

| SOFTWARE—19.0% | |||

| 88,032 | 2U Inc.* | 3,244 | |

| 14,449 | Fair Isaac Corp.* | 5,656 | |

| 79,664 | Guidewire Software Inc.* | 7,657 | |

| 398,218 | Multiplan Corp.* | 2,907 | |

| 18,304 | Paycom Software Inc.* | 6,664 | |

| 22,934 | RingCentral Inc.* | 5,925 | |

| 247,550 | Snap Inc.* | 9,751 | |

| 65,260 | Splunk Inc.* | 12,924 | |

| 47,817 | Workday Inc.* | 10,047 | |

| 64,775 | |||

| SPECIALTY RETAIL—6.2% | |||

| 48,591 | Burlington Stores Inc.* | 9,406 | |

| 49,052 | Five Below Inc.* | 6,541 | |

| 72,031 | Floor & Decor Holdings Inc.* | 5,258 | |

| 21,205 | |||

| TOTAL COMMON STOCKS | |||

(Cost $223,102) | 310,700 | ||

| EXCHANGE-TRADED FUNDS—4.8% | |||

| (Cost $16,028) | |||

| Shares | Value | ||

| CAPITAL MARKETS—4.8% | |||

| 95,009 | iShares Russell Mid-Cap Growth ETF | $ 16,444 | |

| SHORT-TERM INVESTMENTS—4.6% | |||

| (Cost $15,622) | |||

| Principal Amount | |||

| REPURCHASE AGREEMENTS—4.6% | |||

| $ | 15,622 | Repurchase agreement with Bank of America dated October 30, 2020 due November 02, 2020 at 0.060% collateralized by U.S. Treasury Notes (value $15,924) | 15,622 |

| TOTAL INVESTMENTS—100.5% | |||

(Cost $254,752) | 342,766 | ||

CASH AND OTHER ASSETS, LESS LIABILITIES—(0.5)% | (1,596) | ||

TOTAL NET ASSETS—100.0% | $341,170 | ||

FAIR VALUE MEASUREMENTS

At October 31, 2020, the repurchase agreement (as disclosed in the preceding Portfolio of Investments) was classified as Level 2 and all other investments were classified as Level 1. There were no Level 3 investments at October 31, 2020 or 2019.

For more information on valuation inputs and their aggregation into the levels identified above, please refer to the Fair Value Measurements and Disclosures in Note 2 of the accompanying Notes to Financial Statements.

| * | Non-income producing security |

| 1 | Depositary receipts such as American Depositary Receipts (ADRs), Global Depositary Receipts (GDRs) and other country specific depositary receipts are certificates evidencing ownership of shares of a foreign issuer. These certificates are issued by depositary banks and generally trade on an established market in the U.S. or elsewhere. |

The accompanying notes are an integral part of the Financial Statements.

18

Harbor Mid Cap Value Fund

Manager’s Commentary (Unaudited)

Manager’s Commentary (Unaudited)

Subadviser

LSV Asset Management

155 North Wacker Dr.

Suite 4600

Suite 4600

Chicago, IL 60606

Portfolio Managers

Josef Lakonishok, Ph.D.

Since 2004

Since 2004

Menno Vermeulen, CFA

Since 2004

Since 2004

Puneet Mansharamani, CFA

Since 2006

Greg Sleight

Since 2014

Since 2014

Guy Lakonishok, CFA

Since 2014

Since 2014

LSV has subadvised the Fund since 2004.

Investment Objective

The Fund seeks long-term total return.

Josef Lakonishok, Ph.D.

Menno Vermeulen, CFA

Puneet Mansharamani, CFA

Greg Sleight

Guy Lakonishok, CFA

Management’s Discussion of

Fund Performance

Fund Performance

Market Review

The broad U.S. equity market as measured by the S&P 500 Index finished up 9.71% for the twelve months ended October 31, 2020. However, equity markets took investors on a wild ride to the 9.71% return. Equities finished 2019 on a positive note but global equity markets plummeted in February and March 2020 as the COVID-19 outbreak shut down cities and economies around the globe. From mid-February to mid-March, the S&P 500 declined nearly 35%. Equity markets subsequently rebounded over the next several months in large part to massive monetary and fiscal stimulus measures.

While growth stocks have steadily outperformed value stocks since the global financial crisis, the gap in performance between growth and value stocks has reached extreme levels. Growth stocks outperformed value stocks by nearly 30% over the last twelve months as the Russell Midcap® Growth Index finished up 21.14% for the period while the Russell Midcap® Value Index was down 6.94%. The sell-off in February and March was particularly painful for value stocks as cyclical sectors of the market including Energy, Consumer Discretionary and Financial stocks were punished while defensive and growth-oriented stocks and sectors held up relatively well. While many value stocks subsequently staged a comeback, growth continued to outperform value as markets recovered in the second and third quarters. From a sector perspective, Health Care, Materials and Information Technology stocks led among mid cap value stocks while Energy, Real Estate and Financial stocks significantly lagged.

Performance