UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4840

The Tocqueville Trust

(Exact name of registrant as specified in charter)

The Tocqueville Trust

40 W. 57th Street, 19th Floor

New York, NY 10019

(Address of principal executive offices) (Zip code)

Robert W. Kleinschmidt, President

The Tocqueville Trust

40 W. 57th Street, 19th Floor

New York, NY 10019

(Name and address of agent for service)

212-698-0800

Registrant’s telephone number, including area code

Date of fiscal year end: October 31

Date of reporting period: October 31, 2010

| Item 1. | Report to Stockholders. |

ANNUAL REPORT

October 31, 2010

The Tocqueville Trust

Mutual Funds

The Tocqueville Fund

The Tocqueville Opportunity Fund

The Tocqueville International Value Fund

The Tocqueville Gold Fund

The Delafield Fund

The Select Fund

This report is not authorized for distribution to prospective investors unless preceded or accompanied by a currently effective prospectus of The Tocqueville Trust. Please call 1-800-697-FUND (3863) for a free prospectus. Read it carefully before you invest.

You are invited to visit our website @ www.tocquevillefunds.com

Dear Fellow Shareholder,

The markets have been generally good to investors for the past year and, in their wake, the major economies have given some signs of revival or, at least, stabilization. The more dynamic emerging economies have even weathered the financial crisis and continued to grow strongly.

Nevertheless, the global economic backdrop continues to follow a path that has been characteristic of the aftermaths of financial crises, as documented in last year’s opus by professors Carmen Reinhart and Kenneth Rogoff: This Time Is Different: Eight Centuries of Financial Folly (Princeton University Press). What this means, essentially, is that even if the worst is behind us, we may not yet be close to resuming pre-crisis rates of economic growth.

If history according to the authors is any guide, we could expect the following to continue for another few years:

Rising, or at least stubborn, unemployment in the major, developed economies; weak industrial commodities prices; continued weakness in housing activity and prices; and, altogether, historically sub-par economic growth. This does not mean that there will not be phases of growth acceleration, but these should be followed, in shorter order than usual, by slowdowns and hesitancies. More importantly, in the aftermath of financial crises, governments’ debts have always continued to rise even as economic activity began to recover and, according to Reinhart and Rogoff, this was not principally due to governments’ stimulus initiatives but, simply, to the fact that the sub-par rates of economic growth produced disappointing tax revenues.

Finally, convalescence from major financial crises are typically interrupted by aftershocks—often in the currency or sovereign credit areas. In other words, it will be prudent not to extrapolate too fast and too far every sign of reacceleration in economic growth.

One additional reason to be patient in awaiting the next great Bull Run is that share valuations across markets, while they have fallen back toward their historical averages, have not yet declined enough to qualify as a prelude to a significant expansion of multiples. This is especially true in view of near record-low interest rates. Without another major collapse in stock prices, which we neither wish nor expect, the resolution of this valuation problem would be for stock prices to mark time while corporate profits continue to recover.

In all this, I see a somewhat paradoxical silver lining. In recent weeks, some leading individual stocks have experienced air pockets (declines of 25%-30% in a few days) on news that were somewhat disappointing for the near-term but not necessarily devastating in a fundamental or longer-term perspective. Such declines, if not fully warranted (subject, of course, to further analyses), may have brought the individual stocks in question much closer to bottom-like valuation levels. If this trend persists, it may become a kind of rolling bottom that would not necessitate a deep correction of the broad market. What I find encouraging is that, while it has been difficult, since 2008, for investors to outperform without making macro-decisions (to be in or out of the “market”), such a development would usher a new golden period for stock-picking investors.

Wishing everyone a happy and prosperous New Year,

Respectfully,

François Sicart

Chairman

| Annual Report | 1 |

The Tocqueville Fund

Dear Fellow Shareholder,

Our fiscal year ended just prior to an important so-called “wave” election that dramatically altered the power structure in Washington, D.C., at least according to the pundits. Whether the results will really change anything remains to be seen, but the rally in the markets leading up to the election suggests that investors expect, at the very least, to see a slowdown, if not a reversal, in the rash of new government programs, regulations, and taxes that have spooked the economy. While hopeful, we’re not so sure. Both national political parties have been complicit in the steady growth in the size, power, and scope of the federal government over the past several decades, and it is almost too much to ask of the mere mortals recently elected to begin the long process of voluntary reduction.

It is the natural tendency of governments to broaden their prerogatives, and the historical record is bereft of peaceful diminishments. The only exception in the past century was the collapse of communism in Eastern Europe. Fortunately, our situation is not yet so dire that we can or need contemplate a similar fate for our own government. But the signs do not auger well. Throughout what used to be called the developed world, sovereign debt and public finances are in a state of extreme disrepair, but not yet at crisis levels except in such places as Greece, Ireland, and, arguably, California. It will take a crisis, I suspect—and one more severe than what we experienced in 2008 and 2009—before U.S. politicians of either stripe feel the sense of urgency required to scale back the size of the State. Until that time (and it is not to be wished for), it is against precedent to expect a solution to our budgetary woes, regardless of who is in power. As a result, it is unlikely that the markets will continue a rally based upon that particular note of optimism.

Nor do we expect corporate profits, which have rebounded very smartly from their recession lows, to continue their torrid pace. Profitability has been restored in large part by cost-cutting and inventory restocking, and it seems likely that there is little momentum left in either of those two drivers. This leaves us where we have been for most of the past decade: in a stock-picker’s market. Individual companies selling at depressed levels and at a discount from their intrinsic long-term value are attractive purchase candidates in just about any macroeconomic or political scenario, and that is precisely what our “contrarian-value” approach endeavors to identify. Increasingly, we also look for companies whose internal dynamics offer opportunity for either reassessment by the consensus or the possibility of a “corporate event,” such as a merger or recapitalization, to surface submerged value.

In the fiscal year just ended, in which the Tocqueville Fund returned 17.95 percent compared with a 16.52 percent return for the S&P 500 Index, stocks involved in corporate actions were important contributors to our results. Smith International, Mariner Energy, King Pharmaceuticals, Genzyme, Weyerhaeuser, and East West Bancorp were all involved in various corporate actions that benefited shareholders. In the coming year we will continue to look for companies similarly positioned to take actions to enhance the value of their stock.

Our major winners in the year just past, however, were material companies that gained from their exposure to higher commodity prices; the result, no doubt, of the inflationary fears engendered by the aforementioned budgetary crisis in the U.S., Europe, and Japan, as well as by soaring demand from China. Cliffs Natural Resources, an iron-ore producer; Newmont Mining, a leading gold company; and DuPont de Nemours, a chemical and agricultural giant, generated more than 20 percent of our total return for the year.

On the other side of the equation, losing positions were modest, with financial names Wilmington Trust (the subject of a “take-under” bid), Bank of New York, and Mitsubishi Financial Group being among the largest negative contributors to our results. As is usually the case in a strong year, it was the relatively few losing positions and their lack of severity that was most beneficial to our returns. Of the 87 positions held in the fund at one time or another over the course of the year, only 16 contributed negatively to performance; the largest of these cost fewer than 40 basis points. Avoiding losers by managing price risk remains a key focus of our value strategy.

“Bull markets climb a wall of worry” is an old Wall Street adage, and there are plenty of bricks in that wall at present. So we cannot rule out a continuation of the rally that began in earnest in March of ‘09 and resumed in the two

| 2 | October 31, 2010 |

months before the recent election. But, as I said before, we are not counting on it; nor are we investing in names that would particularly profit from market momentum. If we are incorrect in our assessment, our shareholders will certainly benefit from an updraft, though likely at a slower pace than the overall market. That is a price we are willing to pay in order to manage our downside risk in this uncertain world.

As the fund’s portfolio manager and one of its largest shareholders, let me take this opportunity to thank you for your continued support.

Respectfully,

Robert W. Kleinschmidt

Portfolio Manager

| Annual Report | 3 |

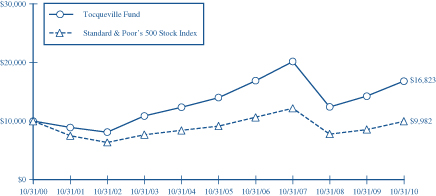

The Tocqueville Fund

This chart assumes an initial gross investment of $10,000 made on 10/31/00. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held for 120 days or less.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns assume the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2010

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

Tocqueville Fund | 17.95% | -5.90% | 3.70% | 5.34% | ||||||||||||

Standard & Poor’s 500 Stock Index | 16.52% | -6.49% | 1.73% | -0.02% | ||||||||||||

| 4 | October 31, 2010 |

The Tocqueville Opportunity Fund

Dear Fellow Shareholder,

We are pleased to provide a review of the Fund’s performance and strategy for the fiscal year ended 10/31/10. For the fiscal year, the Fund performance was +22.56%, the Russell 2500 Growth Index rose 28.76% and the Russell 2000 Index rose +26.58%. The Fund was managed in the Contrarian value style for the bulk of the fiscal year, and slightly outperformed the respective small capitalization Russell 2000 Value index which increased +24.43%. On July 1, 2010 a new portfolio management team assumed management of the Fund, and on October 12, 2010 the Fund was renamed The Tocqueville Opportunity Fund. Over the last four months of the fiscal year, the Fund’s value increased +18.92% under the new portfolio management team versus the Russell 2000 Index which increased +15.84%.

During the fiscal year, the portfolio team proceeded to shift investments toward a more pro-cyclical, economy sensitive bias as our confidence in a sustained economic recovery strengthened. Investments in the Healthcare and Consumer Staples sectors were reduced, and commitments to the Technology and Consumer Discretionary sectors were increased. While investments in the Energy sector were reduced significantly, the sector’s overall investment profile was diversified by adding exposure to U.S. based oil production and offshore drilling equipment suppliers. In a notable shift over the past year, the Fund’s holdings at the end of the fiscal year included a 5% holding in ADRs which were predominantly comprised of investments in China based companies in the Internet, Industrial, Travel and Lodging industries.

The Fund’s name has been changed to reflect an expanded investment strategy which will include small and mid capitalization stocks which may be categorized as either value or growth stocks. The investment strategy is built around a stock selection methodology in which valuation, growth, stability, return on capital, and management execution are assessed through fundamental based research. This effort includes meeting with the managements of the companies in which we are invested. Cyclical recovery and restructuring themes have frequently been investment targets for the Fund. As a result of a broadened investment approach, the Fund will also be increasingly tilted toward investment opportunities which have demonstrated superior and steady growth in operating earnings. At its core, the strategy is focused on a search for better than average growth investments while maintaining a valuation discipline which we deem “growth at a reasonable price” versus “growth at any price”.

The universe of stocks in the small and mid cap space is immense at more than 5000 issues, and the team applies a proprietary selection methodology which reduces the universe to less than 400 issues which should be considered as premier candidates. This universe is subsequently further refined and ranked . The team’s approach includes the evaluation of young, emerging companies which may have limited operating track records and therefore may provide limitations with regard to historical analysis—these kinds of investments may present a significant investment opportunity for the Fund and may be made during the initial public offer or shortly thereafter. The Fund recently invested in the initial sale of shares in NetSpend Holdings and in the shares of RealD which went public in July 2010. Our investment approach does not specify investment in companies with any targeted holding period, however there is a preference for strategic and long term investments in companies which are positioned to continue to gain market share in a dynamic and expanding underlying business. In selecting issues for the portfolio, there are several standards which are critical in addition to valuation levels and expected growth, including:

| 1) | a differentiated model and potentially disruptive technology, product or service |

| 2) | a powerful and innovative R&D platform |

| 3) | a leadership position in a growth market |

| 4) | a competitive advantage and high barriers to competition |

| 5) | a visionary management and high insider ownership |

Unlike many investment approaches which emphasize concentrated portfolio holdings of 25 to 50 issues, we anticipate that the Fund will average 75 to 100 issues. Against a benchmark comprised of 2500 issues, the Russell 2500

| Annual Report | 5 |

Growth Index, even 100 issues should provide plenty of concentration but enough diversification to mitigate risks experienced by smaller companies—competitor innovation, financing, single product, key management, obsolescence. A wider lens for investment than the Fund historically allowed should allow for strategic footholds in strong, emerging investment opportunities which can be increased over time as evidence of success is achieved—often it is the surviving pawn which claims the victory from the standing King in the game of chess. The strategy allows a prospective winner a spot on the field. And we expect the diversified portfolio to provide a measured level of protection against any single issue’s risk.

During the past year, strong performance attribution was provided by investments in TIBCO Software, Ultratech and Silicon Images in Technology, and Thoratec, Alkermes and IMS Health in the Healthcare sector. These investments were reduced during the fiscal period in order to fund new investments. Portfolio performance was negatively impacted by investments in Energy Solutions and Telecommunications Systems. From the end of June 30, 2010, new investments which have contributed significantly to Fund performance include: Priceline; Dril-Quip; Plains Exploration; Chipotle Mexican Grill; Real D; Northern Oil and Gas, Brigham Exploration ; and Pride International. As a group, the Chinese ADRs also provided a good lift to performance: Ctrip Intl, VanceInfo Technologies, Home Inns and Hotels and Baidu.

The past year has proven once again the difficulty of forecasting. A year ago, investment strategists were seized with fears of inflation, a valueless dollar, double dips and an earnings peak. One year later, the market is higher, deflation is a primary concern, the dollar still stands, and earnings have grown strongly. Ironically, while companies have exceeded both revenue and earnings expectations every quarter, investors refuse to believe the good news can continue. We have continued to maintain that valuation multiples are attractive on an historical basis and are significantly discounted relative to potentially improved news over the next several quarters with regard to the pace of economic growth, the unemployment level, and a resumption of capital spending by private enterprise. Moreover, we find many examples of companies in the USA which grew right through the recession and have continued to grow by leaps and bounds—disproving the argument that investors need to move to emerging markets to find growth. Finally, strict attention to costs should positioned companies to experience significant profitability if revenues accelerate with a decent economy.

The Opportunity Fund team appreciates your confidence in our efforts and looks forward to the coming year.

Sincerely,

Thomas R. Vandeventer

Portfolio Manager

| 6 | October 31, 2010 |

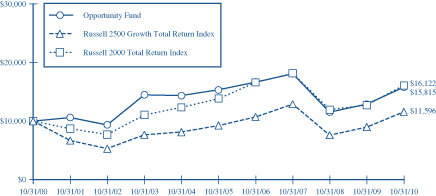

The Tocqueville Opportunity Fund

This chart assumes an initial gross investment of $10,000 made on 10/31/00. On July 1, 2010, a new portfolio management team assumed management of The Tocqueville Small Cap Fund and the Fund’s name and investment strategy changed as of October 12, 2010 (See Footnote 1 to the Financial Statements). Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held for 120 days or less.

The Russell 2500 Growth Total Return Index* is an unmanaged index that measures the performance of the small to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500 companies with higher price-to-book ratios and higher forcasted growth values. Returns assume the reinvestment of all dividends.

The Russell 2000 Total Return Index is an unmanaged index that measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index. Returns assume the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2010

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

Tocqueville Opportunity Fund | 22.56% | -4.40% | 0.61% | 4.69% | ||||||||||||

Russell 2500 Growth Total Return Index | 28.76% | -3.52% | 4.55% | 1.49% | ||||||||||||

Russell 2000 Total Return Index | 26.58% | -3.91% | 3.07% | 4.89% | ||||||||||||

| * | As a result of the Fund’s change in investment strategy, the Fund is changing its primary benchmark to the Russell 2500 Growth Total Return Index. Management feels that this index more accurately compares to the Fund in its broader scope of market capitalization than that of the Russell 2000 Total Return Index and focus on companies with growth characteristics. |

| Annual Report | 7 |

The Tocqueville International Value Fund

Dear Fellow Shareholder,

For the fiscal year ended October 31, 2010, the Tocqueville International Value Fund’s total U.S. dollar return was 16.96%. In the same period, the Morgan Stanley EAFE Index, the index against which we are most often compared, had a total U.S. dollar return of 8.82%.

During the first part of the year, global equity markets continued the recovery begun in March 2009, as credit spreads tightened further, an inventory cycle took hold and helped fuel growth, and improving corporate cash flows and business confidence fueled an increase in mergers and acquisitions activity. Markets suffered a sharp setback mid-year when investors were unnerved by a host of issues including European fiscal problems, the possibility of tightening measures in China, the as yet unresolved oil spill in the Gulf of Mexico, a growing lack of faith in the economic policies of the Obama administration, and the possibility of deflation and a “double dip” economic scenario. However, markets began to rally in late summer as these worries were allayed by an apparently benign outcome to European bank stress tests, better than expected macroeconomic data, strong corporate earnings, and the recognition that the U.S. Federal Reserve stood ready to implement additional quantitative easing.

Over the course of the fiscal year, on a total return basis the European BE 500 Index increased by 16.66% in local currency terms, the Japanese Nikkei 225 Index decreased by 6.80% in local currency terms, and the MSCI Asia Pacific ex- Japan Index increased by 11.29%. The Euro declined against the U.S. dollar as shaky bank and sovereign finances raised the specter of weak economic growth and a challenge to the integrity of Europe’s economic unit. The Japanese Yen strengthened further as local investors repatriated cash and deflation produced acceptable real interest rates. Elsewhere, the currencies of well-capitalized sovereigns with positive current accounts, like Australia, Brazil, Malaysia and Thailand, increased against the US dollar while currencies of indebted nations in Eastern Europe and elsewhere, flagged. The CRB RIND Index of commodities increased by 23.34% and gold continued its ascent as money printing undercut the credibility of paper currencies and tepid economic performance in developed economies raised the specter of competitive devaluations. In equities, the greatest gains were experienced in frontier markets in Africa and Asia like Bangladesh, Philippines and Kenya, and in markets whose economies are linked with commodities, like Indonesia and Chile. In terms of sectors, the greatest gains were experienced in real estate, auto parts, metals and mining, and industrial products, while banks and construction materials were laggards.

Our Fund produced a meaningful absolute return during the fiscal year and finished well ahead of its benchmark largely due to security selection: most of our positions produced gains, we avoided substantial losses, and we generated substantial profits in Japan, notwithstanding the fact that the overall markets was up marginally in U.S. dollar terms. Standout contributors to profits during the year included: Belgian steel wire and cord producer Bekaert, which continued to benefit from growing car production in emerging markets; German compact equipment maker Wacker Neuson, where effective business management and export demand helped the company generate strong cash flow despite a tepid demand environment in Europe; Thai broadcast television company BEC World, whose leading market position in a recovering advertising market combined to produce strong free cash generation; and Japanese industrial automation concern Omron, a beneficiary of increased industrial activity in Asia and globally. Our only notable loss was in Brazilian oil giant Petrobras, whose shares declined in anticipation of a large equity financing, the proceeds of which will be used to develop the company’s plentiful reserves.

We believe the global economy will continue along a path of uneven recovery, where fortunes will be mixed among countries and companies that are well capitalized and those that are not. Europe will likely muddle through as the leading European nations have too much invested in the Euro project to allow it to fail. Growth in developed economies will likely underwhelm. Moreover, it is reasonable to think that China’s growth has been fueled in part by government directed investment in unneeded real estate projects and excess production capacity, giving rise to the possibility of a slowdown there. Further, while bank finances have improved, the financial system is still not healthy. In sum, it remains a stock picker’s market. And in the face of multiple macro uncertainties, our approach is to be ever more strict in applying our discipline of purchasing stocks at a substantial discount to intrinsic value and selling them when they are fairly valued.

| 8 | October 31, 2010 |

During the year, we exited positions in BEC World, in Japanese robotics maker Fanuc, in Swiss technology firm Kudelski, and in French outdoor advertising concern JC Decaux as they reached our valuations objectives.

We continue to seek and find exceptional values in companies with strong business franchises. A few notable additions to the portfolio during the year include: UK telecom operator Vodafone, whose minority stake in Verizon Wireless is ascribed little value by the market and where we see events unfolding that will cause that value to be realized; Japanese conglomerate Hitachi, which trades at a substantial discount to the value of its parts and where a new management team has undertaken shareholder friendly restructuring initiatives and a program of improving the returns of underperforming business units; UK private equity concern 3i, which trades at a steep discount to net asset value; Hong Kong Electric, a highly cash generative utility that stands to benefit from growth in demand and price inflation; German steel distributor Kloeckner, which remains a well-capitalized leader in a consolidating industry; Belgian holding company Groupe Bruxelles Lambert, which trades at a substantial discount to the net asset value of its holdings, several of which are in turn undervalued; Interserve, a UK-based facilities management company with operations in the Middle East whose business produces a double digit cash flow yield in spite of currently depressed business conditions; and Makita, a leading global producer of power tools with large exposure to emerging markets in Asia that trades at a modest multiple of operating cash flow.

One question that is often posed to us by investors and potential investors in our Fund is our target exposure to emerging markets stocks. Our response is that we have no preconceived notions about an appropriate level of exposure. We have at times had a very substantial exposure to emerging markets stocks and at times quite limited exposure. Our holdings are a byproduct of our contrarian value discipline and our investment dollars flow to the most attractive risk reward propositions wherever they might exist. Today, it may be the case that economic growth fundamentals in emerging markets are generally more attractive than those in developed economies, and the risk profile of some emerging markets is improving with better fiscal management, improved disclosure etc. It is also the case, in our view, that with the consensus of investors favorably disposed to emerging markets, it is more difficult to uncover compelling values in emerging markets stocks. On the other hand, there are plenty of companies in developed markets that derive a significant portion of their cash flows from emerging economies, a fact which may not be reflected in their valuations. So there are times, and in our view today is one, when the best way to get exposure to emerging market economic growth is through developed market stocks. This abstract notion is brought to life in a number of our current portfolio holdings, such as Makita, which derives some 40% of its revenues from emerging markets, Bekaert, which derives roughly 50% of its operating earnings from China, Italian auto parts maker Sogefi, which derives approximately 40% of its operating earnings from Mercosur, or even Unilever, which has very substantial businesses in Indonesia and India, inter alia. We aim to buy good businesses, part of the definition of which is having a strong market position in healthy end markets, including the growth attendant in emerging markets exposure, but we also buy good businesses when they are out of favor and cheap in order to ensure a margin of safety for our investors.

We continue to employ our investment discipline, seeking to discover fundamentally attractive companies that are out of favor and undervalued, and to provide our shareholders with above average returns with below average risk over the course of an economic cycle.

Respectfully,

/s/ James Hunt | /s/ | |||

| James Hunt | Francois Sicart | |||

| Portfolio Manager | Portfolio Manager | |||

| Annual Report | 9 |

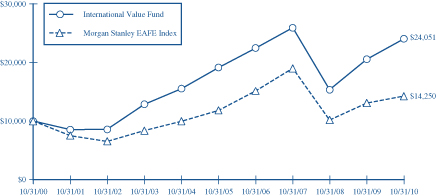

The Tocqueville International Value Fund

This chart assumes an initial gross investment of $10,000 made on 10/31/00. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 120 days or less.

The Morgan Stanley EAFE Index is an unmanaged market-capitalization-weighted index composed of companies representative of the market structure of 20 Developed Market Countries in Europe, Australia, Asia and the Far East.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2010

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

Tocqueville International Value Fund | 16.96% | -2.47% | 4.66% | 9.17% | ||||||||||||

Morgan Stanley EAFE Index | 8.82% | -9.15% | 3.79% | 3.61% | ||||||||||||

| 10 | October 31, 2010 |

The Tocqueville Gold Fund

Dear Fellow Shareholder,

During fiscal 2010, the Tocqueville Gold Fund returned 65.22% and over the past ten years the cumulative return has been 1187.84%. For the same respective time periods, this compares to 31.46% and 425.37% for the Philadelphia Stock Exchange Gold and Silver Index (“XAU Index”); 30.04% and 412.49% for the gold price; and, 16.52% and -0.17% for the S&P 500 Index.

Two significant developments boosted the gold price in 2010. First the Greek debt crisis in the spring contributed to doubts as to the safety of the euro. In our opinion, many investors who took refuge in the euro to escape from the US dollar learned a tough lesson—that no paper currency deserves safe haven status. As investors dumped their euro holdings, the dollar appreciated and gave the appearance of strength. Dollar strength has usually been associated with a weak gold price. However, in this instance, the gold price rallied both in US dollar and euro terms. More important, gold broke out to an all time high in euro terms. As a side note, it is remarkable but unsurprising that the European sovereign debt crisis remains unresolved. At the moment, finance ministers in Europe are scrambling to rescue Ireland, while spreads for Greek sovereign debt have widened to levels that exceed those when Greece was front page news in May. In our opinion, permanent resolution of the credit woes afflicting the weaker European economies (PIIGS-Portugal, Italy, Ireland, Greece, and Spain) will remain elusive. Bailouts and rescues resolve nothing and have only bought time while potentially fueling inflation by further undermining confidence in the euro.

The second key development was the launch of a second round of quantitative easing (QE 2) by the Federal Reserve. While economists debate whether additional money printing by the Fed was necessary or will have a positive effect on economic activity, the rationale put forth by Chairman Bernanke and other Fed officials was quite disturbing to foreign holders of US dollars. That rationale unequivocally stated that the purpose of QE 2 was to create inflation. Such statements coincided with a new upward leg in the gold price, which rose from $1,308.35 at the end of September to an all time high of $1,387.35 on October 14, 2010. On the day after the Fed officially announced that it would proceed with QE 2, the gold price rallied 3% in a single day. The action was met with a storm of criticism from academia, former Fed officials, and ministries of our trading partners claiming Fed actions would result in dollar debasement.

While many observers feel that the gold rally has been over done, is too crowded, resembles a bubble or whatever, the simple fact remains that central banks of the Western democracies appear on course to debase paper currencies. On the one hand, currency debasement is the path of least resistance to grapple with the seemingly intractable fiscal issues of record deficits and unchecked growth in entitlements. On the other hand, persistent economic weakness translates into political pressure for central banks to pursue extremely lax monetary policies. Under these circumstances, it is hard to argue against the notion that some exposure to gold offers protection against monetary damage still to come.

Our investment strategy in managing the Tocqueville Gold Fund portfolio remains consistent with practices since the inception date of 6/30/98. Our research team has travelled over 500,000 miles since 2003, to remote sites around the world to visit the mining and exploration activities of smaller companies. We seek to invest in companies at an early stage of development which can generate growth through exploration success or new mine construction. In this way, we have invested earlier than most of our peers and well before investment banks and brokerage firms commenced research coverage. This strategy is reflected in the fact that our average market cap is 60% of our peer group average. It is also exhibited in our low turnover of less than 10% in 2010. The success of our approach is manifest in having numerous acquisitions of our positions by large cap mining companies. Two notable examples of this in the past year were the acquisition of Red Back by Kinross and the acquisition of Andean Resources by Gold Corp.

Other examples of the our strategy contributing to the outperformance of the Fund over the past year were Andean Resources, Osisko Mining and Ivanhoe Mines, which were up 211.8%, 105.8%, and 123.5% respectively. Overall, many of the positions in the portfolio performed well but there were also some that did not meet our expectations. However, these were few and far between and did not significantly impact the overall performance of the Fund. Among this group were Wits Gold, Ivanhoe Australia, and Minefinders which were down -31.2%, -2.6%, and -6.9% respectively.

| Annual Report | 11 |

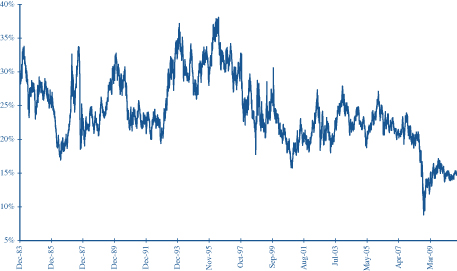

We believe that mining stocks remain cheap relative to gold bullion. As evidence, we point to the chart below which depicts our benchmark, the XAU Index, as a fraction of the gold price. At its level on 10/31/10 of 15%, it remains well below its historical norm of 20%-25%. What investors seem to be forgetting is that the business of producing gold has suddenly become a quite healthy, unlike the lean years leading up to 2008. This is reflected in strong earnings reports, much improved returns on capital, and a multitude of dividend increases. Unlike gold bullion, successful gold mining companies are capable of generating internal growth, returning capital to shareholders in the form of dividends, and participating in potentially accretive merger activity. We believe that investment in gold mining shares, given the current level of profitability, is capable of producing acceptable investment returns even if the price of gold were to hypothetically remain range bound for a period of a few years.

XAU (PHLX Gold/Silver Sector Index) as a Ratio of Spot Gold ($/oz)

(Dec. 19, 1983 – Oct. 29, 2010)

Finally, I am pleased to report that the Tocqueville Gold Fund was cited in the Wall Street Journal (10/01/10) as one of the top four “Ten Year Best Performers” as of 9/30/10. This designation was not only in comparison to other precious metals funds, but against the entire Lipper universe of equity mutual funds. Furthermore, the Fund’s performance was in the top 1% of all mutual funds in the Morningstar universe for the 1-, 3-, 5-, 10-year periods ended 9/30/10. Lastly, the Fund is the only fund in Morningstar’s Equity Precious Metals Funds Category with top quartile performance for the 1-, 3-, 5- and 10-year periods ended 9/30/10 and below average risk for its category.

With best wishes for a prosperous 2011,

Sincerely,

/s/ John C. Hathaway

John C. Hathaway

Portfolio Manager

| 12 | October 31, 2010 |

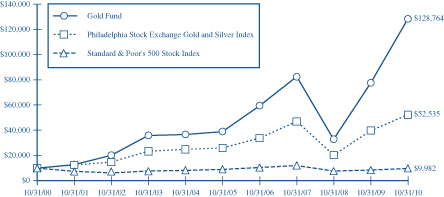

The Tocqueville Gold Fund

This chart assumes an initial gross investment of $10,000 made on 10/31/00. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 120 days or less.

In 2003, 2006, 2009, and 2010 the performance of The Tocqueville Gold Fund was achieved during a period of unusually favorable market conditions. Such performance may not be sustainable.

The Philadelphia Stock Exchange Gold and Silver Index is an unmanaged capitalization-weighted index which includes the leading companies involved in the mining of gold and silver. Returns include the reinvestment of all dividends.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2010

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

Tocqueville Gold Fund | 65.22% | 15.87% | 26.84% | 29.12% | ||||||||||||

Philadelphia Stock Exchange Gold and Silver Index | 31.46% | 3.64% | 15.02% | 18.04% | ||||||||||||

Standard & Poor’s 500 Stock Index | 16.52% | -6.49% | 1.73% | -0.02% | ||||||||||||

| Annual Report | 13 |

The Delafield Fund

Dear Fellow Shareholder,

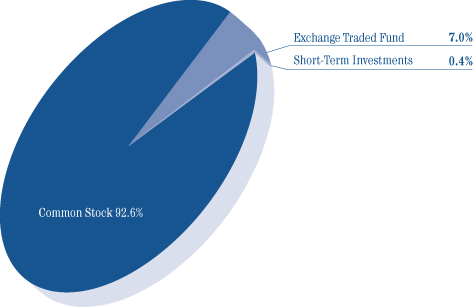

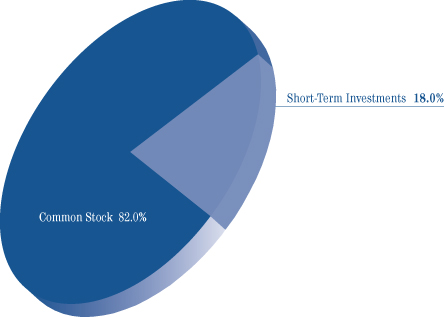

For the twelve months ended October 31, 2010, the Fund’s net asset value increased 24.96% versus an increase of 16.52% for the Standard & Poor’s 500 Index (“S&P 500”) and 26.58% for the Russell 2000 Index (“Russell 2000”), each on a total return basis. The Fund’s net asset value as of October 31, 2010 was $26.65 per share. The net asset value amounted to $933,673,585, of which 81.0% was invested in equities, 2.7% in fixed income, and the balance held in cash reserve.

The largest contributors to our twelve month performance were Ferro Corporation, Checkpoint Systems, Inc. and Vishay Intertechnology, Inc. On the negative side, Collective Brands, Inc., School Specialty, Inc. and Harsco Corporation were among the largest detractors. While the portfolio is not constructed with Sector/Industry allocation targets, the portfolio was relatively overweight in the materials and industrials sectors throughout the year, which benefited performance. In contrast, we were relatively underweight in the consumer discretionary sector, which was among the top performing sectors in the Russell 2000 for the fiscal year.

Share price volatility remains high and the stock market, which went on an unabated upward tear through the first six months of the year, waffled over the last six months. At the end of the year, the S&P 500 was almost flat relative to its closing price on April 30th, while the Russell 2000 trailed its second fiscal quarter close by a modest amount. The debate between inflation and deflation continues to rage. Moderate growth is generally expected in the U.S. and Europe, while strength continues in Latin America and Asia. To some extent, the emerging markets are supporting the rest of the world.

The situation of the American consumer remains mixed. Unemployment remains high, foreclosures continue and during the second calendar quarter of 2010, the consumers’ net worth declined modestly. A further drop in interest rates has allowed some homeowners to refinance at more attractive rates, increasing disposable income and enabling our savings rate to increase.

The financial system is slowly deleveraging. Corporate balance sheets, in general, remain strong. Companies are able to borrow with relative ease at rates which seem very attractive compared to recent years. As a corollary, with rates down, pension fund obligations, which have increased meaningfully, will have to be satisfied with substantial capital additions.

It seems worth reiterating the strategy which we employ in attempting to protect your capital and to enhance its growth. This approach has resulted in above average returns for many years. We believe it is logical and we will continue to seek to provide attractive returns in the years ahead.

1. We search for companies that we believe are selling at prices which seem modest in relationship to the company’s intrinsic value.

2. We meet with management, visit plants, talk to their competitors, consider the makeup of the Board of Directors and make a judgment as to whether we wish to be in business with the management. In other words, we try to understand the business of the companies in which we invest and the individuals who direct the company’s future.

3. We search for companies wherein something may change which will alter that company’s future for the better. These can be simple matters ranging from a change in the management or management’s attitude toward how they run the business, to a change in control, to a change in business opportunity, or to a change in the dynamics of a company’s cash flow and its use.

4. If we perform our analysis correctly, the value added we bring to you is an earlier and better understanding of the companies in our portfolio than that of other investors. Then, if the companies begin to improve, their earnings should increase and they should be valued at a higher price earnings multiple.

5. We have never worried about the profits that we did not make. We worry much more about what we might lose. We believe that stock selection is much more relevant to successful investing than total commitment to equities. In the volatile markets which have developed over the last 15 to 20 years, we have come to believe that the long-term

| 14 | October 31, 2010 |

investors’ best hedge against volatility is to have cash with which to invest in companies when prices seem unduly depressed.

While it is nice to be able to report that we have recovered substantially the wealth which we had lost since June 2007, the mixed signals we observed during the year and continue to monitor currently keep us cautious.

Sincerely,

/s/ |  /s/ | |

| J. Dennis Delafield | Vincent Sellecchia | |

| Portfolio Manager | Portfolio Manager | |

| Annual Report | 15 |

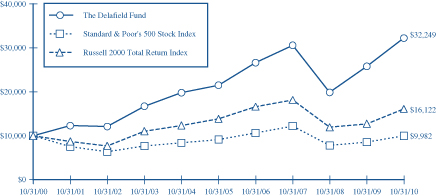

The Delafield Fund

This chart assumes an initial gross investment of $10,000 made on 10/31/00. Since the Delafield Fund did not commence operations until 9/28/09, returns prior to that date are those of the Predecessor Fund. The Delafield Fund assumed the net asset value and performance history of the Predecessor Fund (See Footnote 1 to the Financial Statements). Returns shown does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee wiaviers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 120 days or less.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns include the reinvestment of all dividends.

The Russell 2000 Total Return Index is an unmanaged index that measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represent approximately 8% of the total market capitalization of the Russell 3000 Index. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2010

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

The Delafield Fund | 24.96% | 1.77% | 8.44% | 12.42% | ||||||||||||

Standard & Poor’s 500 Stock Index | 16.52% | -6.49% | 1.73% | -0.02% | ||||||||||||

Russell 2000 Total Return Index | 26.58% | -3.91% | 3.07% | 4.89% | ||||||||||||

| 16 | October 31, 2010 |

The Select Fund

Dear Fellow Shareholder,

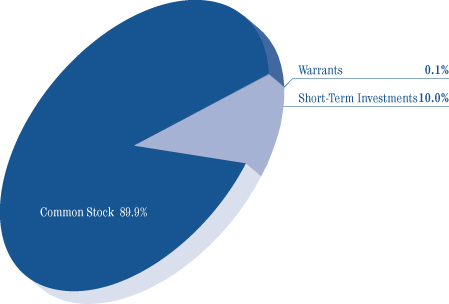

For the twelve months ended October 31, 2010, the Fund’s net asset value increased 36.55% versus an increase of 27.76% for the Russell 2500 Index (“Russell 2500”) and 26.58% for the Russell 2000 Index (“Russell 2000”), each on a total return basis. The Fund’s net asset value as of October 31, 2010 was $11.54 per share. The net asset value amounted to $41,788,138, of which 81.7% was invested in equities and the balance held in cash reserve.

The largest contributors to our twelve month performance were Trimas Corporation, Vishay Intertechnology, Inc., and Maidenform Brands, Inc. On the negative side, Tier Technologies, Inc. and Collective Brands, Inc. were among the largest detractors. While the portfolio is not constructed with Sector/Industry allocation targets, the portfolio was relatively overweight in the industrials sectors throughout the year, which benefited performance.

Share price volatility remains high and the stock market, which went on an unabated upward tear through the first six months of the year, waffled over the last six months. At the end of the fiscal year, the Standard & Poor’s 500 was almost flat relative to its closing price on April 30th, while the Russell 2000 trailed its second fiscal quarter close by a modest amount. The debate between inflation and deflation continues to rage. Moderate growth is generally expected in the U.S. and Europe, while strength continues in Latin America and Asia. To some extent, the emerging markets are supporting the rest of the world.

The situation of the American consumer remains mixed. Unemployment remains high, foreclosures continue and during the second calendar quarter of 2010, the consumers’ net worth declined modestly. A further drop in interest rates has allowed some homeowners to refinance at more attractive rates, increasing disposable income and enabling our savings rate to increase.

The financial system is slowly deleveraging. Corporate balance sheets, in general, remain strong. Companies are able to borrow with relative ease at rates which seem very attractive compared to recent years. As a corollary, with rates down, pension fund obligations, which have increased meaningfully, will have to be satisfied with substantial capital additions.

It seems worth reiterating the strategy which we employ in attempting to protect your capital and to enhance its growth. This approach has resulted in above average returns for many years. We believe it is logical and we will continue to seek to provide attractive returns in the years ahead.

1. We search for companies that we believe are selling at prices which seem modest in relationship to the company’s intrinsic value.

2. We meet with management, visit plants, talk to their competitors, consider the makeup of the Board of Directors and make a judgment as to whether we wish to be in business with the management. In other words, we try to understand the business of the companies in which we invest and the individuals who direct the company’s future.

3. We search for companies wherein something may change which will alter that company’s future for the better. These can be simple matters ranging from a change in the management or management’s attitude toward how they run the business, to a change in control, to a change in business opportunity, or to a change in the dynamics of a company’s cash flow and its use.

4. We will typically invest in a focused group of 12 to 25 common stocks issued primarily by small- to mid- sized domestic companies.

5. If we perform our analysis correctly, the value added we bring to you is an earlier and better understanding of the companies in our portfolio than that of other investors. Then, if the companies begin to improve, their earnings should increase and they should be valued at a higher price earnings multiple.

6. We have never worried about the profits that we did not make. We worry much more about what we might lose. We believe that stock selection is much more relevant to successful investing than total commitment to equities.

| Annual Report | 17 |

In the volatile markets which have developed over the last 15 to 20 years, we have come to believe that the long-term investors’ best hedge against volatility is to have cash with which to invest in companies when prices seem unduly depressed.

While it is nice to be able to report that we have recovered substantially the wealth which we had lost since June 2007, the mixed signals we observed during the year and continue to monitor currently keep us cautious.

| Sincerely, | ||||

/s/ | |  /s/ | ||

| J. Dennis Delafield | Vincent Sellecchia | Donald Wang | ||

| Portfolio Manager | Portfolio Manager | Portfolio Manager | ||

| 18 | October 31, 2010 |

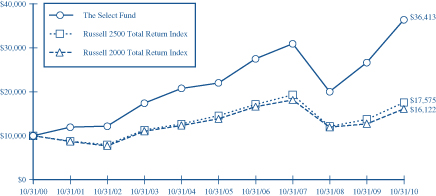

The Select Fund

This chart assumes an initial gross investment of $10,000 made on 10/31/00. Since The Select Fund did not commence operations until 9/28/09, returns from the period from September 29, 2008 to September 27, 2009 are those of the Class Y Shares of the Predecessor Fund (See Footnote 1 to the Financial Statements). Prior to that period, returns shown are those of a limited partnership managed by the adviser. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 120 days or less.

The Russel 2500 Total Return Index is an unmanaged index that measures the performance of the 2,500 smallest companies in the Russell 3000 Index. Returns include the reinvestment of all dividends.

The Russell 2000 Total Return Index is an unmanaged index that measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2010

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

The Select Fund | 36.55% | 5.58% | 10.56% | 13.80% | ||||||||||||

Russell 2500 Total Return Index | 27.76% | -3.17% | 3.78% | 5.80% | ||||||||||||

Russell 2000 Total Return Index | 26.58% | -3.91% | 3.07% | 4.89% | ||||||||||||

| Annual Report | 19 |

Expense Example—October 31, 2010

As a shareholder of The Tocqueville Trust (the “Funds”), you incur ongoing costs, including management fees; distribution fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held the entire period (May 1, 2010-October 31, 2010).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| 20 | October 31, 2010 |

Expense Example Tables

The Tocqueville Fund

| Beginning Account Value May 1, 2010 | Ending Account Value October 31, 2010 | Expenses Paid During Period* May 1, 2010 - October 31, 2010 | ||||||||||

Actual | $ | 1,000.00 | $ | 998.10 | $ | 6.30 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.90 | 6.36 | |||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio of 1.25%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

The Tocqueville Opportunity Fund

| Beginning Account Value May 1, 2010 | Ending Account Value October 31, 2010 | Expenses Paid During Period* May 1, 2010 - October 31, 2010 | ||||||||||

Actual | $ | 1,000.00 | $ | 1,026.40 | $ | 7.46 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,017.85 | 7.43 | |||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio of 1.46%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

The Tocqueville International Value Fund

| Beginning Account Value May 1, 2010 | Ending Account Value October 31, 2010 | Expenses Paid During Period* May 1, 2010 - October 31, 2010 | ||||||||||

Actual | $ | 1,000.00 | $ | 1,088.00 | $ | 8.21 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,017.34 | 7.93 | |||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio of 1.56%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

The Tocqueville Gold Fund

| Beginning Account Value May 1, 2010 | Ending Account Value October 31, 2010 | Expenses Paid During Period* May 1, 2010 - October 31, 2010 | ||||||||||

Actual | $ | 1,000.00 | $ | 1,246.20 | $ | 7.53 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.50 | 6.77 | |||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio of 1.33%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

The Delafield Fund

| Beginning Account Value May 1, 2010 | Ending Account Value October 31, 2010 | Expenses Paid During Period* May 1, 2010 - October 31, 2010 | ||||||||||

Actual | $ | 1,000.00 | $ | 992.20 | $ | 6.43 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.75 | 6.51 | |||||||||

| * | Expense are equal to the Fund’s annualized expense ratio of 1.28%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

| Annual Report | 21 |

The Select Fund

| Beginning Account Value May 1, 2010 | Ending Account Value October 31, 2010 | Expenses Paid During Period* May 1, 2010 - October 31, 2010 | ||||||||||

Actual | $ | 1,000.00 | $ | 1,015.80 | $ | 7.11 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.15 | 7.12 | |||||||||

| * | Expense are equal to the Fund’s annualized expense ratio of 1.40%, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

| 22 | October 31, 2010 |

The Tocqueville Fund

Financial Highlights

Per share operating performance (For a share outstanding throughout the year) | Years Ended October 31, | |||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

Net asset value, beginning of year | $ | 18.47 | $ | 16.39 | $ | 28.93 | $ | 24.25 | $ | 22.17 | ||||||||||

Operations: | ||||||||||||||||||||

Net investment income | 0.32 | 0.28 | 0.24 | 0.18 | 0.14 | |||||||||||||||

Net realized and unrealized gain (loss) | 2.97 | 2.09 | (10.56 | ) | 4.53 | 4.33 | ||||||||||||||

Total from investment operations (1) | 3.29 | 2.37 | (10.32 | ) | 4.71 | 4.47 | ||||||||||||||

Dividends and distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | (0.23 | ) | (0.29 | ) | (0.19 | ) | (0.03 | ) | (0.22 | ) | ||||||||||

Distributions from net realized gains | — | — | (2.03 | ) | — | (2.17 | ) | |||||||||||||

Total dividends and distributions | (0.23 | ) | (0.29 | ) | (2.22 | ) | (0.03 | ) | (2.39 | ) | ||||||||||

Change in net asset value for the year | 3.06 | 2.08 | (12.54 | ) | 4.68 | 2.08 | ||||||||||||||

Net asset value, end of year | $ | 21.53 | $ | 18.47 | $ | 16.39 | $ | 28.93 | $ | 24.25 | ||||||||||

Total return | 18.0 | % | 14.8 | % | (38.5 | )% | 19.4 | % | 20.5 | % | ||||||||||

Ratios/supplemental data | ||||||||||||||||||||

Net assets, end of year (000) | $ | 489,670 | $ | 383,470 | $ | 328,609 | $ | 523,878 | $ | 392,495 | ||||||||||

Ratio to average net assets: | ||||||||||||||||||||

Expenses | 1.25 | %(2) | 1.25 | %(2) | 1.25 | %(2) | 1.25 | %(2) | 1.30 | % | ||||||||||

Net investment income | 1.66 | %(2) | 1.68 | %(2) | 0.94 | %(2) | 0.69 | %(2) | 0.68 | % | ||||||||||

Portfolio turnover rate | 23 | % | 32 | % | 51 | % | 39 | % | 32 | % | ||||||||||

| (1) | Total from investment operations per share includes redemption fees of $0.002, $0.004, $0.009, $ 0.002 and $0.002 per share for the five years ended October 31, 2010, 2009, 2008, 2007 and 2006, respectively. |

| (2) | Net of fees waived amounting to 0.01%, 0.08%, 0.04%, and 0.01% of average net assets for the four years ended October 31, 2010, 2009, 2008 and 2007, respectively. |

The accompanying notes are an integral part of these financial statements.

| Annual Report | 23 |

The Tocqueville Opportunity Fund

Financial Highlights

Per share operating performance (For a share outstanding throughout the year) | Years Ended October 31, | |||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

Net asset value, beginning of year | $ | 10.78 | $ | 9.77 | $ | 17.24 | $ | 18.04 | $ | 16.58 | ||||||||||

Operations: | ||||||||||||||||||||

Net investment income (loss) | (0.12 | ) | (0.11 | ) | 0.02 | 0.11 | (0.07 | ) | ||||||||||||

Net realized and unrealized gain (loss) | 2.54 | 1.23 | (5.67 | ) | 1.26 | 1.53 | ||||||||||||||

Total from investment operations (1) | 2.42 | 1.12 | (5.65 | ) | 1.37 | 1.46 | ||||||||||||||

Distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | — | (0.01 | ) | (0.12 | ) | — | — | |||||||||||||

Distributions from net realized gains | — | (0.10 | ) | (1.70 | ) | (2.17 | ) | — | ||||||||||||

Total distributions | — | (0.11 | ) | (1.82 | ) | (2.17 | ) | — | ||||||||||||

Change in net asset value for the year | 2.42 | 1.01 | (7.47 | ) | (0.80 | ) | 1.46 | |||||||||||||

Net asset value, end of year | $ | 13.20 | $ | 10.78 | $ | 9.77 | $ | 17.24 | $ | 18.04 | ||||||||||

Total return | 22.6 | % | 11.7 | % | (36.2 | )% | 8.4 | % | 8.8 | % | ||||||||||

Ratios/supplemental data | ||||||||||||||||||||

Net assets, end of year (000) | $ | 32,863 | $ | 30,498 | $ | 36,429 | $ | 49,543 | $ | 52,701 | ||||||||||

Ratio to average net assets: | ||||||||||||||||||||

Expenses | 1.41 | % | 1.41 | % | 1.35 | % | 1.32 | % | 1.34 | % | ||||||||||

Net investment income (loss) | (1.08 | )% | (0.97 | )% | 0.12 | % | 0.63 | % | (0.38 | )% | ||||||||||

Portfolio turnover rate | 104 | % | 62 | % | 169 | % | 90 | % | 45 | % | ||||||||||

| (1) | Total from investment operations per share includes redemption fees of less than $0.001, $0.001, $0.005, $ 0.001 and $0.015 per share for the five years ended October 31, 2010, 2009, 2008, 2007 and 2006, respectively. |

The accompanying notes are an integral part of these financial statements.

| 24 | October 31, 2010 |

The Tocqueville International Value Fund

Financial Highlights

Per share operating performance | Years Ended October 31, | |||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

Net asset value, beginning of year | $ | 10.48 | $ | 8.49 | $ | 16.48 | $ | 16.72 | $ | 16.06 | ||||||||||

Operations: | ||||||||||||||||||||

Net investment income | 0.11 | 0.10 | 0.13 | 0.08 | 0.27 | |||||||||||||||

Net realized and unrealized gain (loss) | 1.65 | 2.59 | (6.09 | ) | 2.25 | 2.30 | ||||||||||||||

Total from investment operations (1) | 1.76 | 2.69 | (5.96 | ) | 2.33 | 2.57 | ||||||||||||||

Dividends and distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | (0.12 | ) | (0.20 | ) | (0.10 | ) | (0.27 | ) | (0.05 | ) | ||||||||||

Distributions from net realized gains | — | (0.50 | ) | (1.93 | ) | (2.30 | ) | (1.86 | ) | |||||||||||

Total dividends and distributions | (0.12 | ) | (0.70 | ) | (2.03 | ) | (2.57 | ) | (1.91 | ) | ||||||||||

Change in net asset value for the year | 1.64 | 1.99 | (7.99 | ) | (0.24 | ) | 0.66 | |||||||||||||

Net asset value, end of year | $ | 12.12 | $ | 10.48 | $ | 8.49 | $ | 16.48 | $ | 16.72 | ||||||||||

Total return | 17.0 | % | 34.0 | % | (40.8 | )% | 15.3 | % | 17.4 | % | ||||||||||

Ratios/supplemental data | ||||||||||||||||||||

Net assets, end of year (000) | $ | 150,103 | $ | 131,613 | $ | 118,189 | $ | 219,220 | $ | 225,234 | ||||||||||

Ratio to average net assets: | ||||||||||||||||||||

Expenses | 1.56 | % | 1.62 | % | 1.56 | % | 1.59 | % | 1.61 | % | ||||||||||

Net investment income | 1.03 | % | 0.96 | % | 1.07 | % | 0.49 | % | 1.49 | % | ||||||||||

Portfolio turnover rate | 27 | % | 27 | % | 63 | % | 49 | % | 39 | % | ||||||||||

| (1) | Total from investment operations per share includes redemption fees of $0.002, $0.001, $0.001, $0.002 and $0.011 per share for the five years ended October 31, 2010, 2009, 2008, 2007 and 2006, respectively. |

The accompanying notes are an integral part of these financial statements.

| Annual Report | 25 |

The Tocqueville Gold Fund

Financial Highlights

| Per share operating performance (For a share outstanding throughout the year) | Years Ended October 31, | |||||||||||||||||||

| 2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

Net asset value, beginning of year | $ | 49.71 | $ | 21.77 | $ | 64.36 | $ | 51.41 | $ | 35.51 | ||||||||||

Operations: | ||||||||||||||||||||

Net investment loss | (0.58 | ) | (0.45 | ) | (0.57 | ) | (0.30 | ) | (0.22 | ) | ||||||||||

Net realized and unrealized gain (loss) | 32.96 | 29.28 | (33.24 | ) | 18.52 | 18.21 | ||||||||||||||

Total from investment operations (1) | 32.38 | 28.83 | (33.81 | ) | 18.22 | 17.99 | ||||||||||||||

Dividends and distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | — | — | (0.46 | ) | (0.22 | ) | — | |||||||||||||

Dividends from net realized gains | (0.09 | ) | (0.89 | ) | (8.32 | ) | (5.05 | ) | (2.09 | ) | ||||||||||

Total distributions | (0.09 | ) | (0.89 | ) | (8.78 | ) | (5.27 | ) | (2.09 | ) | ||||||||||

Change in net asset value for the year | 32.29 | 27.94 | (42.59 | ) | 12.95 | 15.90 | ||||||||||||||

Net asset value, end of year | $ | 82.00 | $ | 49.71 | $ | 21.77 | $ | 64.36 | $ | 51.41 | ||||||||||

Total return | 65.2 | % | 135.2 | % | (60.0 | )% | 38.4 | % | 52.5 | % | ||||||||||

Ratios/supplemental data | ||||||||||||||||||||

Net assets, end of year (000) | $ | 2,199,603 | $ | 937,492 | $ | 410,857 | $ | 1,231,475 | $ | 833,254 | ||||||||||

Ratios to average net assets: | ||||||||||||||||||||

Expenses | 1.34 | % | 1.50 | % | 1.43 | % | 1.42 | % | 1.50 | % | ||||||||||

Net investment loss | (1.11 | )% | (1.25 | )% | (1.07 | )% | (0.81 | )% | (0.51 | )% | ||||||||||

Portfolio turnover rate | 9 | % | 9 | % | 28 | % | 26 | % | 30 | % | ||||||||||

| (1) | Total from investment operations per share includes redemption fees of $0.056, $0.025, $0.027, $0.028, and $0.060 per share for the five years ended October 31, 2010, 2009, 2008, 2007 and 2006, respectively. |

The accompanying notes are an integral part of these financial statements.

| 26 | October 31, 2010 |

The Delafield Fund

Financial Highlights

| Year Ended October 31, 2010 | January 1, 2009 through October 31, 2009 | Years Ended December 31, | ||||||||||||||||||||||

| Per share operating performance (For a share outstanding throughout the period) | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||||||

Net asset value, beginning of period | $ | 21.35 | $ | 15.10 | $ | 24.33 | $ | 25.64 | $ | 23.63 | $ | 25.21 | ||||||||||||

Operations: | ||||||||||||||||||||||||

Net investment income (loss) | (0.00 | )(2) | 0.03 | 0.07 | 0.17 | 0.19 | 0.03 | |||||||||||||||||

Net realized and unrealized gain (loss) | 5.32 | 6.25 | (9.23 | ) | 1.10 | 4.64 | 1.49 | |||||||||||||||||

Total from investment operations (1) | 5.32 | 6.28 | (9.16 | ) | 1.27 | 4.83 | 1.52 | |||||||||||||||||

Dividends and distributions to shareholders: | ||||||||||||||||||||||||

Dividends from net investment income | — | (0.03 | ) | (0.07 | ) | (0.16 | ) | (0.19 | ) | (0.03 | ) | |||||||||||||

Dividends from net realized gains | — | — | (0.00 | )(2) | (2.42 | ) | (2.63 | ) | (3.07 | ) | ||||||||||||||

Return of capital | (0.02 | ) | (0.00 | )(2) | (0.00 | )(2) | — | — | — | |||||||||||||||

Total distributions | (0.02 | ) | (0.03 | ) | (0.07 | ) | (2.58 | ) | (2.82 | ) | (3.10 | ) | ||||||||||||

Change in net asset value for the period | 5.30 | 6.25 | (9.23 | ) | (1.31 | ) | 2.01 | (1.58 | ) | |||||||||||||||

Net asset value, end of period | $ | 26.65 | $ | 21.35 | $ | 15.10 | $ | 24.33 | $ | 25.64 | $ | 23.63 | ||||||||||||

Total return | 25.0 | % | 41.6 | %(3) | (37.6 | )% | 4.9 | % | 20.4 | % | 6.0 | % | ||||||||||||

Ratios / supplemental data | ||||||||||||||||||||||||

Net assets, end of period (000) | $ | 933,674 | $ | 636,548 | $ | 404,860 | $ | 656,999 | $ | 532,108 | $ | 372,467 | ||||||||||||

Ratios to average net assets: | ||||||||||||||||||||||||

Expenses | 1.27 | % | 1.38 | %(4) | 1.34 | %(5) | 1.28 | %(5) | 1.32 | %(5) | 1.33 | % | ||||||||||||

Net investment income (loss) | (0.02 | )% | 0.21 | %(4) | 0.35 | %(5) | 0.57 | %(5) | 0.82 | %(5) | 0.11 | % | ||||||||||||

Portfolio turnover rate | 30 | % | 46 | %(3) | 81 | % | 61 | % | 72 | % | 71 | % | ||||||||||||

| (1) | Total from investment operations per share includes redemption fees of $0.006 per share for the year ended October 31, 2010, $0.008 per share for the period ended October 31, 2009, $0.01 per share for the fiscal year ended December 31, 2007 and less than $0.01 per share for the fiscal years ended December 31, 2008, 2006 and 2005. |

| (2) | Represents less than $0.01. |

| (3) | Not Annualized. |

| (4) | Annualized. |

| (5) | Net of fees waived amounting to 0.06%, 0.05%, 0.08%, and 0.11% for the fiscal years ended December 31, 2008, 2007, 2006, and 2005, respectively. |

The accompanying notes are an integral part of these financial statements.

| Annual Report | 27 |

The Select Fund

Financial Highlights

| Year Ended October 31, 2010 | January 1, 2009 through October 31, 2009 | Period from September 29, 2008 (2) through December 31, 2008 | ||||||||||

Per share operating performance (For a share outstanding throughout the period) | ||||||||||||

Net asset value, beginning of period | $ | 8.46 | $ | 5.77 | $ | 8.74 | ||||||

Operations: | ||||||||||||

Net investment income (loss) | (0.03 | ) | (0.00 | )(3) | 0.01 | |||||||

Net realized and unrealized gain (loss) | 3.12 | 2.70 | (2.97 | ) | ||||||||

Total from investment operations (1) | 3.09 | 2.70 | (2.96 | ) | ||||||||

Dividends and distributions to shareholders: | ||||||||||||

Dividends from net investment income | (0.01 | ) | (0.00 | )(3) | (0.01 | ) | ||||||

Dividends from net realized gains | — | — | — | |||||||||

Return of capital | — | (0.01 | ) | — | ||||||||

Total distributions | (0.01 | ) | (0.01 | ) | (0.01 | ) | ||||||

Change in net asset value for the period | 3.08 | 2.69 | (2.97 | ) | ||||||||

Net asset value, end of period | $ | 11.54 | $ | 8.46 | $ | 5.77 | ||||||

Total return | 36.6 | % | 46.7 | %(4) | (33.9 | )%(4) | ||||||

Ratios/supplemental data | ||||||||||||

Net assets, end of period (000) | $ | 41,788 | $ | 24,681 | $ | 9,226 | ||||||

Ratios to average net assets: | ||||||||||||

Expenses | 1.38 | % | 1.26 | %(5)(6) | 1.15 | %(5)(6) | ||||||

Net investment income (loss) | (0.43 | )% | (0.16 | )%(5)(6) | 0.29 | %(5)(6) | ||||||

Portfolio turnover rate | 40 | % | 24 | %(4) | 29 | %(4) | ||||||

| (1) | Total from investment operations per share includes redemption fees of $0.007 per share for the year ended October 31, 2010. |

| (2) | Inception of Fund. |

| (3) | Represents less than $0.01 per share. |

| (4) | Not Annualized. |

| (5) | Annualized. |

| (6) | Net of fees waived amounting to 0.77% and 2.32% for the periods ended October 31, 2009 and December 31, 2008, respectively. |

The accompanying notes are an integral part of these financial statements.

| 28 | October 31, 2010 |

The Tocqueville Fund

Schedule of Investments as of October 31, 2010

| Common Stocks—100.0% | Shares | Value | ||||||

Automobiles & Components—1.1% |

| |||||||

Toyota Motor Corp.—ADR | 75,000 | $ | 5,311,500 | |||||

Banks—3.2% | ||||||||

Banco Santander SA—ADR | 300,000 | 3,843,000 | ||||||

East West Bancorp, Inc. | 250,000 | 4,407,500 | ||||||

Mitsubishi UFJ Financial Group, Inc.—ADR | 1,000,000 | 4,660,000 | ||||||

Wilmington Trust Corp. | 400,000 | 2,844,000 | ||||||

| 15,754,500 | ||||||||

Capital Goods—10.4% | ||||||||

3M Co. | 50,000 | 4,211,000 | ||||||

The Boeing Co. | 75,000 | 5,298,000 | ||||||

General Electric Co. | 1,000,000 | 16,020,000 | ||||||

Illinois Tool Works, Inc. | 150,000 | 6,855,000 | ||||||

Masco Corp. | 400,000 | 4,264,000 | ||||||

Northrop Grumman Corp. | 75,000 | 4,740,750 | ||||||

Rockwell Automation, Inc. | 75,000 | 4,677,750 | ||||||

Tyco International Ltd.(a) | 125,000 | 4,785,000 | ||||||

| 50,851,500 | ||||||||

Commercial & Professional Services—1.7% |

| |||||||

Steelcase, Inc. | 1,000,000 | 8,410,000 | ||||||

Consumer Services—1.0% | ||||||||

Yum! Brands, Inc. | 100,000 | 4,956,000 | ||||||

Diversified Financials—2.8% | ||||||||

American Express Co. | 150,000 | 6,219,000 | ||||||

The Bank of New York Mellon Corp. | 300,000 | 7,518,000 | ||||||

| 13,737,000 | ||||||||

Energy—8.6% | ||||||||

Anadarko Petroleum Corp. | 50,000 | 3,078,500 | ||||||

Chesapeake Energy Corp. | 250,000 | 5,425,000 | ||||||

Exxon Mobil Corp. | 200,000 | 13,294,000 | ||||||

Murphy Oil Corp. | 150,000 | 9,774,000 | ||||||

Schlumberger Ltd.(a) | 150,000 | 10,483,500 | ||||||

| 42,055,000 | ||||||||

Food, Beverage & Tobacco—7.0% |

| |||||||

Campbell Soup Co. | 225,000 | 8,156,250 | ||||||

The Coca-Cola Co. | 150,000 | 9,198,000 | ||||||

Kraft Foods, Inc. | 300,000 | 9,681,000 | ||||||

Unilever NV—ADR | 100,000 | 2,969,000 | ||||||

Zhongpin, Inc.(a)(b) | 200,000 | 4,044,000 | ||||||

| 34,048,250 | ||||||||

Health Care Equipment & Services—1.0% |

| |||||||

St. Jude Medical, Inc.(b) | 125,000 | 4,787,500 | ||||||

Household & Personal Products—3.5% |

| |||||||

Colgate-Palmolive Co. | 100,000 | 7,712,000 | ||||||

Kimberly-Clark Corp. | 150,000 | 9,501,000 | ||||||

| 17,213,000 | ||||||||

| Common Stocks (continued) | Shares | Value | ||||||

Insurance—2.7% | ||||||||

Aflac, Inc. | 75,000 | $ | 4,191,750 | |||||

The Allstate Corp. | 125,000 | 3,811,250 | ||||||

Fidelity National Financial, Inc. | 400,000 | 5,356,000 | ||||||

| 13,359,000 | ||||||||

Materials—14.2% | ||||||||

BHP Billiton Ltd.—ADR | 75,000 | 6,194,250 | ||||||

Cliffs Natural Resources, Inc. | 150,000 | 9,780,000 | ||||||

EI du Pont de Nemours & Co. | 300,000 | 14,184,000 | ||||||

Minefinders Corp.(a)(b) | 90,000 | 792,900 | ||||||

Newmont Mining Corp. | 300,000 | 18,261,000 | ||||||

Owens-Illinois, Inc.(b) | 250,000 | 7,007,500 | ||||||

Sonoco Products Co. | 200,000 | 6,700,000 | ||||||

W.R. Grace & Co.(b) | 200,000 | 6,412,000 | ||||||

| 69,331,650 | ||||||||

Media—1.0% | ||||||||

The Washington Post Co. | 12,500 | 5,026,875 | ||||||

Pharmaceuticals, Biotechnology & Life Sciences—8.3% |

| |||||||

Genzyme Corp.(b) | 75,000 | 5,409,750 | ||||||

Isis Pharmaceuticals, Inc.(b) | 300,000 | 2,742,000 | ||||||

Johnson & Johnson | 150,000 | 9,550,500 | ||||||

King Pharmaceuticals, Inc.(b) | 250,000 | 3,535,000 | ||||||

Myriad Genetics, Inc.(b) | 200,000 | 3,986,000 | ||||||

Pfizer, Inc. | 900,000 | 15,660,000 | ||||||

| 40,883,250 | ||||||||

Real Estate—1.7% | ||||||||

CB Richard Ellis Group, Inc.(b) | 200,000 | 3,670,000 | ||||||

Weyerhaeuser Co. | 300,000 | 4,866,000 | ||||||

| 8,536,000 | ||||||||

Retailing—1.3% | ||||||||

Home Depot, Inc. | 200,000 | 6,176,000 | ||||||

Semiconductors & Semiconductor Equipment—4.5% |

| |||||||

Applied Materials, Inc. | 750,000 | 9,270,000 | ||||||

Intel Corp. | 500,000 | 10,035,000 | ||||||

LSI Corp.(b) | 500,000 | 2,620,000 | ||||||

| 21,925,000 | ||||||||

Software & Services—10.9% | ||||||||

Adobe Systems, Inc.(b) | 150,000 | 4,222,500 | ||||||

Automatic Data Processing, Inc. | 150,000 | 6,663,000 | ||||||

Bio-key International, Inc.(b)(c)(d)(e) | 47,090 | — | ||||||

Google, Inc.(b) | 16,000 | 9,807,840 | ||||||

Mastercard, Inc. | 20,000 | 4,801,200 | ||||||

Microsoft Corp. | 600,000 | 15,984,000 | ||||||

Symantec Corp.(b) | 450,000 | 7,281,000 | ||||||

Total System Services, Inc. | 300,000 | 4,683,000 | ||||||

| 53,442,540 | ||||||||

The accompanying footnotes are an integral part of these Schedules of Investments

| Annual Report | 29 |

The Tocqueville Fund

Schedule of Investments as of October 31, 2010

| Common Stocks (continued) | Shares | Value | ||||||

Technology Hardware & Equipment—6.4% |

| |||||||

Canon, Inc.—ADR | 60,000 | $ | 2,760,000 | |||||

Cisco Systems, Inc.(b) | 500,000 | 11,415,000 | ||||||

Corning, Inc. | 450,000 | 8,226,000 | ||||||