UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4840

The Tocqueville Trust

(Exact name of registrant as specified in charter)

The Tocqueville Trust

40 W. 57th St., 19th Floor

New York, NY 10019

(Address of principal executive offices) (Zip code)

Robert W. Kleinschmidt

The Tocqueville Trust

40 W. 57th St., 19th Floor

New York, NY 10019

(Name and address of agent for service)

(212) 698-0800

Registrant’s telephone number, including area code

Date of fiscal year end: October 31

Date of reporting period: October 31, 2012

Item 1. Reports to Stockholders.

ANNUAL REPORT

October 31, 2012

The Tocqueville Trust

Mutual Funds

The Tocqueville Fund

The Tocqueville Opportunity Fund

The Tocqueville International Value Fund

The Tocqueville Gold Fund

The Delafield Fund

The Tocqueville Select Fund

This report is not authorized for distribution to prospective investors unless preceded or accompanied by a currently effective prospectus of The Tocqueville Trust. Please call 1-800-697-FUND (3863) for a free prospectus. Read it carefully before you invest.

You are invited to visit our website @ www.tocqueville.com/mutual-funds

Dear Fellow Shareholder,

From an investment perspective, the declines of global stock markets in 2007-2009 were a watershed event. This is not so much because the declines were so deep or so protracted, but because they discredited most historically-successful investment disciplines. That short-term traders or momentum followers got caught in the big reversal was not a novel surprise. The real shock was that some of the best value investors, including some iconic ones, who typically resisted bear markets better than the majority of participants, also got caught in the downward spiral.

As bottom-up investors, our view had always been that our time is better spent on the analysis of company-specific fundamentals and valuations than on trying to forecast macro-economic or “market” developments. In retrospect, however, no strategy or discipline would have been better, going into that bear market, than staying out of the markets altogether. That lesson was learned by many market participants and was reinforced during the subsequent recoveries by a compression of valuations and a tendency by most equity investments to move more or less in unison. Avoidance of macro or market risk became the accepted wisdom.

To cap this trend, several studies and articles proclaimed something like the famous magazine cover on the eve of the preceding, long boom—the “death of equities”. Going further, other sources suggested, like CNBC, that: “the days of stock picking may be coming to an end”.

These are normal human reactions, but probably misguided.

There have been great global traumas, even in recent history. But seldom has the world been faced with a broader set of uncertainties—political (regional wars and uprisings everywhere; even tensions between major powers such as China and Japan); economic (global, seemingly irrepressible sea of debt; the threat of implosion of a major economic bloc such as Europe; a tricky change of economic locomotives in Asia); even a climatic threat to the planet (global warming; famine-threatening droughts).

To some degree, global stock markets have reflected these uncertainties for some time and, from a purely contrarian point of view, it would be time to try and adopt a more optimistic tack. The principal remaining problem is that, historically, company valuations in the stock markets have become much more reasonable than in 2007, for example, but not as deeply undervalued as they have been on the eves of past, secular bull markets.

One safe assumption, however, is that we have not seen the end of stock picking, for this is the nature of both human and crowd psychology, and the very essence of stock market investing. At Tocqueville, we will refrain from assuming that the most recent bear market reflects a new paradigm, a “new normal”, and, instead, intensify our search for individual stock opportunities.

Respectfully,

François Sicart

Chairman

| Annual Report | 1 |

The Tocqueville Fund

Dear Fellow Shareholder,

Your Fund finished its fiscal year on October 31, 2012, just days before the voters spoke and returned the President and most of the Congress back to Washington for another two, four or six years, depending upon the office. So, notwithstanding all the talk about a dysfunctional government during the campaign, it appears that voters, in the aggregate, prefer divided government. The Founders of the U.S., who constructed a government full of checks and balances, meant to move slowly and to prevent abuses, would be proud. (So would Alexis de Tocqueville, our namesake, who worried about the tyranny of majorities). From an investment point of view, the return of the partisan combatants seems to have sparked the realization among the politicians that compromise, that dirty word, is a necessary component of governing. (Who knew?) This could well prove to be the best of all possible outcomes. Politics is, after all, the art of the possible, and what is possible when you have divided government and strongly held and conflicting points of view on both sides, is compromise. Investors would greet such a compromise favorably, in our view, if only for the temporary elimination of uncertainty, and this could well set the stage for a better tone in the markets next year. We live in hope.

This year, the markets enjoyed a modest rally, but it was not one that generated much enthusiasm. The S&P 500 gained 15.21% while your Fund recorded a 10.08% gain. (The Dow Jones Index was up 12.56% in the same twelve month period). The underperformance of the Fund relative to the S&P 500 was due to several factors, most significantly the absence of Apple in our holdings. Apple is such a large component in the indices and performed so remarkably well that it had an outsized impact on the Standard and Poor index. (Apple isn’t in the Dow). Why didn’t we own Apple? On the metrics we favor, it was certainly cheap enough to own, but we were troubled by the universal enthusiasm for the company and its products and feared that there was no room for disappointments, notwithstanding the valuation. (In fact, some of our caution was rewarded late in the fiscal year as the stock sold off rather sharply with some disappointment in its latest phone and tablet offerings, and, taking advantage of the sell-off, early in the new fiscal year we initiated a small position). The next largest driver of the underperformance was our positioning in the materials sector, specifically Newmont Mining and Cliffs Natural Resources. As a gold producer, Newmont is leveraged to the price of the underlying metal (of which we maintain a favorable long-term view) and the shares are inexpensive on traditional value metrics; however, its price has lagged as production problems, higher energy costs and fears of increased regional taxes weighed on sentiment. Cliffs Natural Resources, which we had trimmed at significantly higher prices, was also a significant detractor as recessionary concerns, particularly in China, impacted demand for iron ore and metallurgical coal even as we continue to believe this major domestic resource has strategic value well in excess of its fiscal year end price.

On a positive note, it is worth mentioning the contribution we had from the financial sector. This is an area in which we are typically underweight because we have had a hard time making a long-term investment case for large, money center, “too big to fail” banks. While we acknowledge there have been trading opportunities in names like Goldman Sachs, Citibank, J.P. Morgan, Bank of America, et al, we believe these institutions have been transformed into quasi- government entities or highly regulated utilities, taking orders from politicians rather than shareholders. Given the tight but uncertain regulations that Dodd-Frank imposes upon them, and the political interference of grandstanding politicians, traditional financial analysis on which we base our investment criteria is not very helpful; so we have chosen to avoid them altogether. Rather, we have focused our attention on more transparent ways to invest in the recovery of credit and housing markets such as transaction processors, title insurers, financial advisors and timber REITs. Still the banks are large companies and when they rally, as they have somewhat this year, they can have an outsized impact on market averages. So be it; we prefer to invest in what we can understand.

That the markets could rally at all, what with the cross currents of negative news out of Europe, slowing Chinese growth and the looming prospect of the fiscal cliff, all combined with the uncertainty of the U.S. elections, is something of a minor miracle and a testament to the underlying resiliency of the American economy. It is also due, in no small part, to the ministrations of the Federal Reserve, combined with fortuitously low inflation rates and concomitant interest rates. How long these happy circumstances can persist is anybody’s guess. Ours is “not very long.” But the markets are not priced as if the current level of interest rates will last forever, so we do not expect an immediate sell-off once interest and inflation rates do begin their inevitable and inexorable climb, perhaps as early as the next fiscal year.

| 2 | October 31, 2012 |

No comment on the markets would be complete without referring to the remarkable rebirth of the oil and gas industry in the United States, despite, it seems at times, the best efforts of the federal and some state governments to stifle it. After billions in government subsidies to promote “alternative” energy fantasies, with little to show for it, it is the traditional energy industry which has come roaring back, so much so that recent estimates put the U.S. as the largest oil and gas producer in the world in the not too distant future. If true, the salutary impact on the U.S. economy, as well as on the geopolitical environment, can scarcely be over-emphasized. Notwithstanding all the problems the country faces with the combination of an enormous federal debt and deficit, and an entitlement system not built for the realities of today’s demographics, the outlook for the domestic economy is considerably enhanced by this revolution in energy production. While staying within our discipline, we have taken several positions that seek to take advantage of our home grown energy resurgence.

Regardless of what the markets may or may not do, we continue to believe that high quality common stocks represent good value and the best way to preserve wealth for the long term in an uncertain world. Our proprietary research continues to uncover overlooked, unloved and undervalued stocks across the capitalization spectrum, and we will continue to buy and own these names so long as they remain at a discount to their intrinsic value. This is a strategy that has served us well over the years. As ever, we thank you for your interest and support.

Respectfully,

Robert W. Kleinschmidt

Portfolio Manager

| Annual Report | 3 |

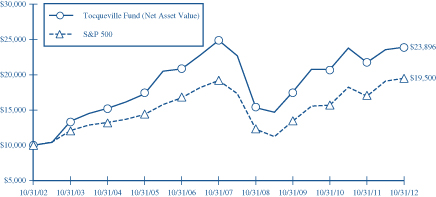

The Tocqueville Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/02. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held for 90 days or less.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns assume the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2012

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

Tocqueville Fund | 10.08% | 10.80% | -0.79% | 9.10% | ||||||||||||

Standard & Poor’s 500 Stock Index | 15.21% | 13.21% | 0.36% | 6.91% | ||||||||||||

| 4 | October 31, 2012 |

The Tocqueville Opportunity Fund

Dear Fellow Shareholder,

We are pleased to provide this review of the Opportunity Fund’s performance for the fiscal year ended October 31, 2012. While the Fund and major indices provided positive returns over the past twelve months, performance was less favorable for small and mid-capitalization issues and growth stocks in particular. The trend favoring value and large capitalization issues persisted throughout the period, but there was a distinct bias away from the small growth asset class during the past six months—macro risk dominated investor concerns and included the ongoing issues with the European Union, U.S. political uncertainty in front of the Presidential election, and the threat of a U.S. recession upon the expiration of current fiscal stimulus at the end of 2012. For the fiscal period, the Fund returned 5.35% versus the Russell 2500 Growth Index return of 10.08%. While the Fund solidly outperformed its benchmark during the first half of the fiscal year, selling off many of the Fund’s over weighted winners intensified during the post-Labor Day period through the end of October. Despite a majority of these companies having exceeded earnings expectations, muted corporate earnings guidance for the remainder of 2012 and the first half of 2013 appears to be providing an incentive for short-term oriented traders to sell in order to lock in profits. Moreover a dimming economic view framed by political uncertainty and a potential recession, may push investors concerned with a potential increase in the capital gains tax rate in 2013 to sell early.

Rapid fire rotations and profit taking have impacted several of the Fund’s larger holdings, which had performed excellently including Apple, Tractor Supply, priceline.com, LinkedIn and Hain Celestial. All reported positive earnings surprises during the last fiscal quarter and we are confident that all continue to be superbly positioned. The Fund’s biotechnology investments are perhaps the best example of the increased volatility of stock performance over the past several months—after having led all industry sectors over the first nine months of the fiscal year in relative and absolute returns, biotechnology was the worst performing group over the last three months of the fiscal year—despite terrific sales outlooks and new therapeutic approvals, shorter term oriented investors raced to sell ahead of the election, higher tax rates and each other!

The technology, consumer discretionary and healthcare sectors comprised the Fund’s dominant investment allocations at the fiscal year end—23.0%, 21.4%, and 19.2% respectively. Over the past year the commitment to the healthcare sector has increased markedly through appreciation of existing holdings and new investments. Four of the Fund’s top 5 performers for the year were biotech issues, including: Pharamasset, Alnylam Pharmaceuticals, Pharmacyclics, and Onyx Pharmaceuticals. The healthcare and financial services sectors provided the lead contributions to absolute returns over the past fiscal year. We increased investments in financials significantly. Several of the Fund’s technology holdings were among the top 10 performers including Equinix, Ultimate Software, Netsuite, and Cirrus Logic, which was the top performer for the fiscal year. Technology takeovers included: Kenexa (IBM), Success Factors (SAP), and Taleo (Oracle). We reduced investments in energy to less than 5% of the Fund. While energy investments provided a slight positive relative performance during the year, the overall energy sector return was negative and the worst performing sector for both the Fund and the benchmark. Oil prices would certainly benefit from increased risk to supply due to increased tensions in the Middle East, but absent this cyclical, geopolitical risk we see little reason to increase exposure.

New names among the top 10 included LinkedIn, salesforce.com, Portfolio Recovery Associates, Hain Celestial, Pharmacyclics and Fresh Market. The top 10 and top 25 holdings comprised 16.3% and 31.2% respectively of the Fund versus 17.8% and 34.0% a year ago—the Fund continues to be well diversified. At the beginning of the year, Facebook had been a top holding. Facebook was among the top 5 relative performers in the first half of the fiscal year, but was the third worst in the second half. Among one of the more controversial IPO’s in memory, Facebook delivered surprisingly strong growth in revenues and key metrics this past quarter—we continue to believe that Facebook is developing a dominant internet business with a massive daily audience. Over the past fiscal year, 11 of the Fund’s holdings were takeover targets; during the second half Medicis Pharmaceuticals, Peet’s Coffee and Tea, Robbins and Myers and Kenexa were sold as a result of takeover offers.

| Annual Report | 5 |

We believe it is important to emphasize that our fundamental approach is primarily oriented to identify and to invest in long-term investments in leading companies which are positioned to continue to innovate successfully, to gain market share in expanding markets, and to sustain competitive advantage and high returns on investment. We have been surprised by intense recent price volatility in many of our holdings, but we are confident that our investment principles will deliver competitive returns over the long run. While we do not subscribe to the tax tail wagging the dog maxim with regard to a focus on after-tax returns, our objective of investing in high return and high reinvestment companies is by consequence an investment approach with a longer time horizon than many of today’s prevailing market participants. Over a long investment career, there have been plenty of difficult markets but time has provided a perspective on the irrational behavior which grips investors at peaks of elation and the depths of despair. We expect there is a very high probability that companies will take advantage of their strong balance sheets and low prices to announce increased stock repurchases and/or to provide special dividends.

We appreciate your ongoing confidence in our efforts on behalf of the Opportunity Fund.

Sincerely,

Thomas R. Vandeventer

Portfolio Manager

| 6 | October 31, 2012 |

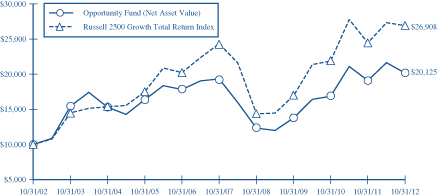

The Tocqueville Opportunity Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/02. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held for 90 days or less.

The Russell 2500 Growth Total Return Index is an unmanaged index that measures the performance of the small to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500 companies with higher price-to-book ratios and higher forcasted growth values. Returns assume the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2012

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

Tocqueville Opportunity Fund | 5.35% | 13.53% | 0.85% | 7.24% | ||||||||||||

Russell 2500 Growth Total Return Index | 10.08% | 16.62% | 2.04% | 10.40% | ||||||||||||

| Annual Report | 7 |

The Tocqueville International Value Fund

Dear Fellow Shareholder,

For the fiscal year ended October 31, 2012, the Tocqueville International Value Fund’s total U.S. dollar return was a loss of 1.60%. In the same period, the Morgan Stanley EAFE Index, the index against which we are most often compared, had a total U.S. dollar gain of 5.15%. For the 10 year period ended October 31, 2012, the Tocqueville International Value Fund’s cumulative total U.S. dollar return was 174.4%. In the same period, the Morgan Stanley EAFE Index had a total U.S. dollar return of 120.17%.

During the fiscal year, global equity markets were driven to an unusually large extent by macroeconomic forces and changes in Central Bank policy. Equity markets advanced early in the period as the European Central Bank’s Long Term Refinancing Operations (“LTRO”) reduced credit spreads and created a false sense of security regarding Europe’s debt crisis. Then in April markets declined as the palliative of Europe’s LTRO program wore off and investors focused once more on the deterioration of bank and government finances in Europe, the possibility of a sharp slowdown in China, and the prospect of a fiscal cliff in the U.S. Markets recovered beginning in July after the ECB stated its determination to recapitalize Europe’s faltering banks and move toward fiscal integration and a common banking system, and the U.S. Fed promised to maintain low interest rates until unemployment comes down.

Over the course of the fiscal year, on a total return basis the European BE 500 Index increased by 14.1% in local currency terms, the Japanese Nikkei 225 Index increased by 1.4% in local currency terms, and the MSCI Asia Pacific ex- Japan Index increased by 4.3%. The Euro declined against the U.S. dollar as shaky bank and sovereign finances undercut confidence in the currency, and the Yen remained at historically high levels in U.S. dollar terms. Among equity sectors, gains were dominated by traditionally defensive groups like tobacco products, health care and food and beverage, as well as financials, while steel, energy, telecom and utilities performed poorly.

Due to the bottom up nature of our investment approach, which has served us well for many years, there may be times when our performance is out of step with the overall market. This fiscal year was clearly one of those times. Gains in the developed international markets were concentrated in mega cap consumer stocks and in financials, both areas where we are underrepresented by virtue of our contrarian value investment discipline. The consumer stocks, which were fairly valued at the outset of the period in our judgment, were revalued upward by investors placing a premium on certainty of cash flows and high dividend yields. The financials did represent a sector that might appeal to a contrarian and eventually the stocks recovered from valuation levels that reflected some probability of a banking system meltdown as the ECB and other central banks took actions to calm investor nerves. However, financial institutions are by their nature structurally leveraged and operate opaque business models and, in the current circumstances, depend on some measure of government largesse. For these reasons, they generally do not meet our standards regarding margin of safety for our investors. On the other hand, our investment process led us to industrial and materials companies, where we have a large weighting, and smaller capitalization companies, that were overlooked or revalued downward despite cheap valuations and attractive long-term business fundamentals. With time, fundamentals are normally recognized by the market, value realized, and our positioning rewarded.

Significant contributors to the Fund’s profits during the year included: French logistics-focused holding company Bollore, Australian business services concern Spotless Group, subject of a takeover offer, Hong Kong broadcast television concern Television Broadcasts, UK auto parts retailer Halfords Group, French pharmaceutical concern Sanofi, Dutch lighting and healthcare conglomerate Philips, and Japanese performance athletic shoe maker Asics. We had meaningful losses in the shares of Japanese exporting companies, including precision equipment concern Canon and auto parts maker Takata, that declined due to Yen strength and related investor concerns regarding the competitiveness and profitability of their businesses. We believe these stocks represent some of the most compelling values in our portfolio today. We also had losses in certain economically sensitive names in Europe, including German steel distributor Kloeckner, Italian auto parts maker Sogefi, and French wire and cable producer Nexans.

During the fiscal year, we exited positions in UK credit scoring concern Experian, Mexican beverage producer FEMSA, Italian hydraulic equipment maker Interpump, and UK business and construction services concern Interserve,

| 8 | October 31, 2012 |

which, following strong performance, approached our estimates of intrinsic value. We tendered our shares of Spotless Group into the takeover offer, the terms of which we considered to be adequate. We sold French integrated oil producer Total after a gas leak in the North Sea created an unquantifiable liability for the company. We also sold Mobistar, where our investment thesis was undercut by a change in competitive conditions that had a negative impact on pricing and profit margins, French drug maker Ipsen, where management failed to meet certain of its execution milestones, and Spanish IT services provider Indra Sistemas, where weakening payment terms from government customers undercut our thesis regarding free cash generation. We took new positions in French television broadcaster M6, which generates a double digit free cash flow yield in a tepid economic environment; in drug maker Novartis, which has a high free cash yield based on its existing pharma portfolio and where we were not paying much for an attractive pipeline of new products and the eyecare franchise; in German chipmaker Infineon, which has a market leading position in analog chips for power management and auto applications and trades at a mid-single digit multiple of mid-cycle cash flow; in Hong Kong real estate and investment conglomerate Guoco Group, which in our judgment trades at a 50% discount to its net asset value; and in Japanese company Disco, the global leader in chip dicing and wafer grinding equipment and related consumables which was depressed due to worries about the global IT cycle. We also added to several existing positions when prices were under pressure, including Siemens, Halfords Group, Groupe Bruxelles Lambert, Statoil, Hoya, Takata and SMC.

The macro backdrop contains much uncertainty. While Europe has articulated a reasonable prescription to address its banking and fiscal issues, implementation is subject to political forces. Further, while the plan may address the problem in financial markets, Europe still needs structural reform in labor markets and entitlements in order to improve its growth potential. Also, the U.S. is drawing nearer to the so-called fiscal cliff, which, if allowed to occur, will have a negative impact on growth in the U.S. On a more positive note, China’s economy, which slowed predictably during this year of political transition, appears to be firming. Too, Japan’s government has called for elections that are likely to result in growth oriented economic policies. All that being said, as part of our discipline, when we analyze and value companies and evaluate opportunity and risk in individual stocks, we do so on the basis of conservative macro assumptions.

We continue to employ our investment discipline, seeking to discover fundamentally attractive companies that are out of favor and undervalued, and to provide our shareholders with above average returns with below average risk over the course of an economic cycle.

Respectfully,

|

James Hunt |

| Portfolio Manager |

| Annual Report | 9 |

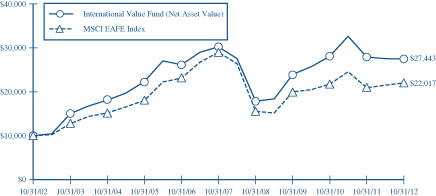

The Tocqueville International Value Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/02. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

The MSCI EAFE Index is an unmanaged market-capitalization-weighted index composed of companies representative of the market structure of 20 Developed Market Countries in Europe, Australia, Asia and the Far East.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2012

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

Tocqueville International Value Fund | -1.60% | 4.63% | -1.90% | 10.62% | ||||||||||||

MSCI EAFE Index | 5.15% | 3.31% | -5.35% | 8.21% | ||||||||||||

| 10 | October 31, 2012 |

The Tocqueville Gold Fund

Dear Fellow Shareholder,

The past year was one of consolidation in the gold price as well as mining shares, following the run up to historic highs in the bullion price in August of 2011. Over the past fiscal year, the Tocqueville Gold Fund returned -9.53% vs. -4.84% for the Philadelphia Stock Exchange Gold and Silver Index benchmark and 15.21% for the S&P 500.

The gold price spent most of the year consolidating its 2011 run up to the all-time high of $1921/oz. The 2011 run up was driven by investor worries about a credit downgrade of the U.S. as well as a possible shutdown of the U.S. government because of the deadlock over raising the ceiling on the national debt. Those fears receded with the last minute compromise over tax and fiscal issues. However, those same issues remain unresolved and a replay of last year’s drama still seems to be in the cards as 2012 comes to a close. The ongoing euro zone currency crisis has also heightened investor worries as to the safety of paper currency. The prospect of widespread monetary debasement seems stronger today than in August of 2011, and for this reason, we believe that the bull market in gold is far from over.

The corrective action of the past twelve months has, in our opinion, served to stabilize an overbought market and to create sufficient doubt in the minds of investors as to validity of the investment rationale for gold and precious metals. We believe that all of this, while frustrating, is a necessary precursor for a dynamic move higher in the entire sector.

Gold mining shares remain exceptionally cheap in our opinion. Our XAU benchmark traded at 9% of the spot gold price in May of 2012, approximately the same level as October 2008, which was followed by a rally of 155% in the subsequent twelve months. Gold shares have rallied relative to the bullion price since the low of 141 (XAU) in mid-2012 with a rise of 34% through the end of our fiscal year vs. a rise of 13% in the gold price.

Market sentiment on mining stocks relative to physical gold appears to be at a negative extreme comparable to the low of 2008. We believe that the negative issues raised by skeptics such as rising costs of mining, political risk, competition from ETFs, and poor capital allocation decisions by senior management are well known and already discounted in the current low valuations of mining stocks. This negative view will change, in our opinion, should gold trade at new highs over the coming twelve months. From a contrarian and from a valuation point of view, we believe gold mining stocks are poised to outperform the metal in the coming year. Should the bull market in gold resume in earnest, as we expect, gold and silver mining equities are well positioned to deliver satisfactory returns.

Our investment approach remains consistent with our practice of the past ten years. We have a strong research group consisting of five full time research professionals committed to extensive due diligence on all aspects of the business of mining for gold and silver. This includes extensive travel to remote locations to visit mine sites, local mine management, and in many cases, officials of host countries in order to assess political risk. Our low turnover is based on the idea that in order to capture value in excess of whatever return is provided by the gold price, we must identify those companies which in turn understand how best to create shareholder value through exploration for new ore bodies, and developing those assets through mine building activity into cash generators.

For the fiscal year, the top contributors to the Fund over this period included Franco-Nevada, Yamana Gold, and Primero Mining which appreciated 46.6%, 36.9%, and 163.4% respectively. Notable among these was the performance by Primero Mining, which received a favorable tax ruling. The Fund also had its fair share of disappointments, which included Turquoise Hill, International Tower Hill, and Alacer Gold which declined by 58.0%, 52.0% and 52.6% respectively. We continue to view these holdings as companies which fit well with our aforementioned investment approach.

Thank you for your continued support.

Sincerely,

|  | |

| John C. Hathaway | Douglas B. Groh | |

| Portfolio Manager | Portfolio Manager | |

| Annual Report | 11 |

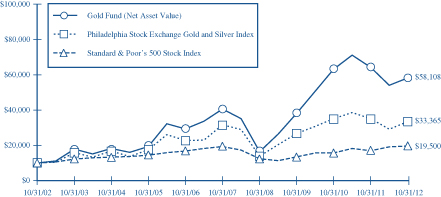

The Tocqueville Gold Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/02. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

In 2003, 2006, 2009, and 2010 the performance of The Tocqueville Gold Fund was achieved during a period of unusually favorable market conditions. Such performance may not be sustainable.

The Philadelphia Stock Exchange Gold and Silver Index is an unmanaged capitalization-weighted index which includes the leading companies involved in the mining of gold and silver. Returns include the reinvestment of all dividends.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2012

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

Tocqueville Gold Fund | -9.53% | 15.03% | 7.46% | 19.24% | ||||||||||||

Philadelphia Stock Exchange Gold and Silver Index | -4.84% | 7.72% | 1.15% | 12.79% | ||||||||||||

Standard & Poor’s 500 Stock Index | 15.21% | 13.21% | 0.36% | 6.91% | ||||||||||||

| 12 | October 31, 2012 |

The Delafield Fund

Dear Fellow Shareholder,

For the twelve months ended October 31, 2012, the Fund returned 10.96%. This compares to a 15.21% increase in the Standard & Poor’s 500 Index (“S&P 500”) and an increase of 12.08% for the more representative Russell 2000 Index (“Russell 2000”), both on a total return basis. The Fund’s net asset value as of October 31, 2012 was $29.79 per share. The net asset value amounted to $1,346,273,436, of which 79.5% was invested in equities and the balance held in cash reserves.

Fiscal 2012, much like the prior fiscal year, was a tale of two halves. Equities experienced a strong recovery for almost the entire first half of the fiscal year. Investors responded enthusiastically to modest improvement in U.S. economic indicators and to solid corporate earnings. A pause in negative Eurozone related headlines during this period also seemed to calm investors’ nerves and helped drive the market’s upturn. Through the first six months of the fiscal year ending April 30, 2012, the Fund was up 16.25% versus total returns of 12.77% and 11.02% for the S&P 500 and Russell 2000, respectively.

In the second half of the fiscal year, investors took a decidedly less optimistic view of the domestic political and economic landscape, including the persistently high unemployment rate and the outcome of the Presidential election. The rapid approach of the January 2013 “fiscal cliff” and the possible repercussions also became more in focus. Outside the U.S., Europe continued to suffer, Chinese economic growth further decelerated, and rising nationalism and mounting religious intolerance contributed to global unease. The Fund declined 4.55% during the final six months of the fiscal year, while the S&P 500 managed a 2.16% gain and the Russell 2000 increased 0.95%, both on a total return basis.

While stock selection was generally favorable to our performance this year, several of our holdings experienced outsized declines on weak financial results, particularly in the information technology sector. In contrast, our consumer discretionary and energy holdings exhibited very strong performance during the year, but owing to their modest aggregate position size in the portfolio, they made only a small contribution. Our heavy exposure to the industrials and materials sectors benefited our return for the year as a whole, but negatively impacted our second half performance due to their more cyclical nature. Our large cash position was also a negative factor with respect to our performance, although we remain content to use the cash reserves as a hedge against volatility and as “dry powder” to allow us to seize upon attractive investment opportunities as we uncover them.

Eastman Chemical Company was the largest contributor to our performance during the year, with the shares showing steady gains on strong earnings and the smooth integration of the Solutia acquisition. In contrast, Checkpoint Systems, Inc. and Acco Brands Corp. were the largest detractors, negatively impacting our return by nearly 200 basis points in total. Both stocks fell on the heels of disappointing earnings.

We believe that our portfolio is generally composed of companies where managements are taking actions to position their businesses for a bright long-term future which could allow them to outperform expectations in a difficult environment. Additionally, virtually all of our holdings exhibit substantial free cash flow and strong or improving balance sheets. Due to the company specific nature of our investment approach, our performance is not likely to correlate closely to any of the market indices, nor can we control the volatility of market prices, which can sometimes gyrate significantly. However, we continue to expect that over time, the market will accurately reflect the true value of a business. Therefore, our focus remains on employing our long-standing strategy to protect your capital and to enhance its growth.

Sincerely,

|  | |

| J. Dennis Delafield | Vincent Sellecchia | |

| Portfolio Manager | Portfolio Manager | |

| Annual Report | 13 |

The Delafield Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/02. Since the Delafield Fund did not commence operations until 9/28/09, returns prior to that date are those of the Predecessor Fund. The Delafield Fund assumed the net asset value and performance history of the Predecessor Fund (See Footnote 1 to the Financial Statements). Returns shown does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee wiaviers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns include the reinvestment of all dividends.

The Russell 2000 Total Return Index is an unmanaged index that measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represent approximately 8% of the total market capitalization of the Russell 3000 Index. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2012

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

The Delafield Fund | 10.96% | 12.28% | 3.61% | 11.67% | ||||||||||||

Standard & Poor’s 500 Stock Index | 15.21% | 13.21% | 0.36% | 6.91% | ||||||||||||

Russell 2000 Total Return Index | 12.08% | 14.82% | 1.19% | 9.58% | ||||||||||||

| 14 | October 31, 2012 |

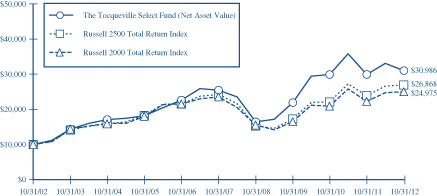

The Tocqueville Select Fund

Dear Fellow Shareholder,

For the twelve months ended October 31, 2012, the Fund returned 3.66% versus an increase of 13.00% for the Russell 2500 Index (“Russell 2500”) and 12.08% for the Russell 2000 Index (“Russell 2000”), each on a total return basis. The Fund’s net asset value as of October 31, 2012 was $11.35 per share. The net asset value amounted to $84,548,513, of which 89.3% was invested in equities and the balance held in cash reserves.

Fiscal 2012, much like the prior fiscal year, was a tale of two halves. Equities experienced a strong recovery for almost the entire first half of the fiscal year. Investors responded enthusiastically to modest improvement in U.S. economic indicators and to solid corporate earnings. A pause in negative Eurozone related headlines during this period also seemed to calm investors’ nerves and helped drive the market’s upturn. Through the first six months of the fiscal year ending April 30, 2012, the Fund was up 10.60% versus total returns of 12.03% and 11.02% for the Russell 2500 and Russell 2000, respectively.

In the second half of the fiscal year, investors took a decidedly less optimistic view of the domestic political and economic landscape, including the persistently high unemployment rate and the outcome of the Presidential election. The rapid approach of the January 2013 “fiscal cliff” and the possible repercussions also became more in focus. Outside the U.S., Europe continued to suffer, Chinese economic growth further decelerated, and rising nationalism and mounting religious intolerance contributed to global unease. The Fund declined 6.28% during the final six months of the fiscal year, while the Russell 2500 gained 0.87% and the Russell 2000 increased 0.95%, both on a total return basis.

Our performance during the year, particularly in the second half, was disappointing. Several of our investments suffered outsized declines, and owing to the relatively concentrated nature of the Fund, their impact on total performance was magnified. Summer Infant, Inc. was the most substantial detractor to our performance, representing about 400 basis points of negative return. During the year, the company struggled with issues related to its cost structure, an overly promotional sales environment and undisciplined pricing. We continue to own the stock because we believe that management will successfully navigate the company through these challenges and that the current valuation does not adequately reflect the potential operating margin and earnings power of the business. Our holdings in Checkpoint Systems, Inc. and Ferro Corporation were also substantial drags on our performance, negatively impacting our return by nearly 250 basis points in total. Both stocks fell on the heels of disappointing earnings, and we have exited our position in Ferro. In contrast, our heavy exposure to the industrials and materials sectors benefited our return for the year. Our position in Solutia Inc. was particularly beneficial, with the shares contributing nearly 200 basis points to performance after the announcement of a deal to be acquired by Eastman Chemical Company.

Despite our challenging 2012, we continue to believe that our portfolio is well positioned. In general, our investments have solid balance sheets, strong free cash flow and excellent management teams, which should position them to prosper over time.

Sincerely,

| ||||

| |  | ||

| J. Dennis Delafield | Vincent Sellecchia | Donald Wang | ||

| Portfolio Manager | Portfolio Manager | Portfolio Manager | ||

| Annual Report | 15 |

The Tocqueville Select Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/02. Since The Tocqueville Select Fund did not commence operations until 9/28/09, returns from the period from September 29, 2008 to September 27, 2009 are those of the Class Y Shares of the Predecessor Fund (See Footnote 1 to the Financial Statements). Prior to that period, returns shown are those of a limited partnership managed by the adviser. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

The Russel 2500 Total Return Index is an unmanaged index that measures the performance of the 2,500 smallest companies in the Russell 3000 Index. Returns include the reinvestment of all dividends.

The Russell 2000 Total Return Index is an unmanaged index that measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2012

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

The Tocqueville Select Fund | 3.66% | 12.24% | 4.03% | 11.97% | ||||||||||||

Russell 2500 Total Return Index | 13.00% | 15.95% | 2.06% | 10.39% | ||||||||||||

Russell 2000 Total Return Index | 12.08% | 14.82% | 1.19% | 9.58% | ||||||||||||

| 16 | October 31, 2012 |

Expense Example—October 31, 2012 (Unaudited)

As a shareholder of The Tocqueville Trust (the “Funds”), you incur ongoing costs, including management fees; distribution fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held the entire period (May 1, 2012-October 31, 2012).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Annual Report | 17 |

Expense Example Tables (Unaudited)

| The Tocqueville Fund | Beginning Account Value May 1, 2012 | Ending Account Value October 31, 2012 | Expenses Paid During Period* May 1, 2012 - October 31, 2012 | |||||||||

Actual | $ | 1,000.00 | $ | 1,014.30 | $ | 6.33 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.85 | 6.34 | |||||||||

| The Tocqueville Opportunity Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 929.80 | $ | 6.50 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.40 | 6.80 | |||||||||

| The Tocqueville International Value Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 995.70 | $ | 7.88 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,017.24 | 7.96 | |||||||||

| The Tocqueville Gold Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 1,075.80 | $ | 6.73 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.65 | 6.55 | |||||||||

| The Delafield Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 954.50 | $ | 6.04 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.95 | 6.24 | |||||||||

| The Tocqueville Select Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 937.20 | $ | 6.72 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.20 | 7.00 | |||||||||

| * | Expenses are equal to the Fund’s annualized six-month expense ratio of 1.25%, 1.34%, 1.57%, 1.29%, 1.23% and 1.38% for The Tocqueville Fund, Opportunity Fund, International Value Fund, Gold Fund, Delafield Fund, and Select Fund, respectively, multiplied by the average account value over the period, multiplied by 184/366 to reflect the one-half year period. |

| 18 | October 31, 2012 |

The Tocqueville Fund

Financial Highlights

Per share operating performance (For a share outstanding throughout the year) | Years Ended October 31, | |||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

Net asset value, beginning of year | $ | 22.23 | $ | 21.53 | $ | 18.47 | $ | 16.39 | $ | 28.93 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operations: | ||||||||||||||||||||

Net investment income (1) | 0.40 | 0.23 | 0.32 | 0.28 | 0.24 | |||||||||||||||

Net realized and unrealized gain (loss) | 1.81 | 0.80 | 2.97 | 2.09 | (10.56 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations (2) | 2.21 | 1.03 | 3.29 | 2.37 | (10.32 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | (0.33 | ) | (0.33 | ) | (0.23 | ) | (0.29 | ) | (0.19 | ) | ||||||||||

Distributions from net realized gains | — | — | — | — | (2.03 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total distributions | (0.33 | ) | (0.33 | ) | (0.23 | ) | (0.29 | ) | (2.22 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Change in net asset value for the year | 1.88 | 0.70 | 3.06 | 2.08 | (12.54 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value, end of year | $ | 24.11 | $ | 22.23 | $ | 21.53 | $ | 18.47 | $ | 16.39 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total Return | 10.1 | % | 4.8 | % | 18.0 | % | 14.8 | % | (38.5 | )% | ||||||||||

Ratios/supplemental data | ||||||||||||||||||||

Net assets, end of year (000) | $ | 366,025 | $ | 491,541 | $ | 489,670 | $ | 383,470 | $ | 328,609 | ||||||||||

Ratio to average net assets: | ||||||||||||||||||||

Expense (3) | 1.26 | %(4) | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | ||||||||||

Net investment income (3) | 1.33 | % | 0.98 | % | 1.66 | % | 1.68 | % | 0.94 | % | ||||||||||

Portfolio turnover rate | 17 | % | 28 | % | 23 | % | 32 | % | 51 | % | ||||||||||

| (1) | Net investment income per share is calculated using the ending balances prior to consideration or adjustment for permanent book-to-tax differences. |

| (2) | Total from investment operations per share includes redemption fees of $0.002, $0.002, $0.002, $0.004, and $0.009 per share for the fiscal years ended October 31, 2012, 2011, 2010, 2009, and 2008, respectively. |

| (3) | Net of fees waived amounting to 0.03%, 0.01%, 0.01%, 0.08%, and 0.04% of average net assets for the fiscal years ended October 31, 2012, 2011, 2010, 2009, and 2008, respectively. |

| (4) | Includes 0.01% of interest expense which is not included in the Fund’s operating expense cap. |

The Accompanying Notes are an Integral Part of these Financial Statements.

| Annual Report | 19 |

The Tocqueville Opportunity Fund

Financial Highlights

Per share operating performance (For a share outstanding throughout the year) | Years Ended October 31, | |||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

Net asset value, beginning of year | $ | 14.96 | $ | 13.20 | $ | 10.78 | $ | 9.77 | $ | 17.24 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operations: | ||||||||||||||||||||

Net investment income (loss) (1) | (0.11 | ) | (0.13 | ) | (0.12 | ) | (0.11 | ) | 0.02 | |||||||||||

Net realized and unrealized gain (loss) | 0.91 | 1.89 | 2.54 | 1.23 | (5.67 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations (2) | 0.80 | 1.76 | 2.42 | 1.12 | (5.65 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | — | — | — | (0.01 | ) | (0.12 | ) | |||||||||||||

Distributions from net realized gains | — | — | — | (0.10 | ) | (1.70 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total distributions | — | — | — | (0.11 | ) | (1.82 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Change in net asset value for the year | 0.80 | 1.76 | 2.42 | 1.01 | (7.47 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value, end of year | $ | 15.76 | $ | 14.96 | $ | 13.20 | $ | 10.78 | $ | 9.77 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total Return | 5.4 | % | 13.3 | % | 22.6 | % | 11.7 | % | (36.2 | )% | ||||||||||

Ratios/supplemental data | ||||||||||||||||||||

Net assets, end of year (000) | $ | 65,455 | $ | 46,963 | $ | 32,863 | $ | 30,498 | $ | 36,429 | ||||||||||

Ratio to average net assets: | ||||||||||||||||||||

Expense | 1.32 | % | 1.36 | % | 1.41 | % | 1.41 | % | 1.35 | % | ||||||||||

Net investment income (loss) | (0.76 | )% | (1.04 | )% | (1.08 | )% | (0.97 | )% | 0.12 | % | ||||||||||

Portfolio turnover rate | 77 | % | 110 | % | 104 | % | 62 | % | 169 | % | ||||||||||

| (1) | Net investment income (loss) per share is calculated using the ending balances prior to consideration or adjustment for permanent book-to-tax differences. |

| (2) | Total from investment operations per share includes redemption fees of $0.004, $0.001, and $0.005 for the fiscal years ended October 31, 2012, 2009, and 2008, respectively and less than $0.001 for the fiscal years ended October 31, 2011 and 2010. |

The Accompanying Notes are an Integral Part of these Financial Statements.

| 20 | October 31, 2012 |

The Tocqueville International Value Fund

Financial Highlights

Per share operating performance (For a share outstanding throughout the year) | Years Ended October 31, | |||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

Net asset value, beginning of year | $ | 12.00 | $ | 12.12 | $ | 10.48 | $ | 8.49 | $ | 16.48 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operations: | ||||||||||||||||||||

Net investment income (1) | 0.17 | 0.11 | 0.11 | 0.10 | 0.13 | |||||||||||||||

Net realized and unrealized gain (loss) | (0.37 | ) | (0.16 | ) | 1.65 | 2.59 | (6.09 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations (2) | (0.20 | ) | (0.05 | ) | 1.76 | 2.69 | (5.96 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | (0.12 | ) | (0.07 | ) | (0.12 | ) | (0.20 | ) | (0.10 | ) | ||||||||||

Distributions from net realized gains | — | — | — | (0.50 | ) | (1.93 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total distributions | (0.12 | ) | (0.07 | ) | (0.12 | ) | (0.70 | ) | (2.03 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Change in net asset value for the year | (0.32 | ) | (0.12 | ) | 1.64 | 1.99 | (7.99 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value, end of year | $ | 11.68 | $ | 12.00 | $ | 12.12 | $ | 10.48 | $ | 8.49 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total Return | (1.6 | )% | (0.5 | )% | 17.0 | % | 34.0 | % | (40.8 | )% | ||||||||||

Ratios/supplemental data | ||||||||||||||||||||

Net assets, end of year (000) | $ | 218,793 | $ | 199,848 | $ | 150,103 | $ | 131,613 | $ | 118,189 | ||||||||||

Ratio to average net assets: | ||||||||||||||||||||

Expense | 1.56 | % | 1.56 | % | 1.56 | % | 1.62 | % | 1.56 | % | ||||||||||

Net investment income | 1.53 | % | 0.99 | % | 1.03 | % | 0.96 | % | 1.07 | % | ||||||||||

Portfolio turnover rate | 38 | % | 30 | % | 27 | % | 27 | % | 63 | % | ||||||||||

| (1) | Net investment income per share is calculated using the ending balances prior to consideration or adjustment for permanent book-to-tax differences. |

| (2) | Total from investment operations per share includes redemption fees of $0.001, $0.010, $0.002, $0.001, and $0.001 for the fiscal years ended October 31, 2012, 2011, 2010, 2009, and 2008, respectively. |

The Accompanying Notes are an Integral Part of these Financial Statements.

| Annual Report | 21 |

The Tocqueville Gold Fund

Financial Highlights

Per share operating performance (For a share outstanding throughout the year) | Years Ended October 31, | |||||||||||||||||||

| 2012 | 2011 | 2010 | 2009 | 2008 | ||||||||||||||||

Net asset value, beginning of year | $ | 81.97 | $ | 82.00 | $ | 49.71 | $ | 21.77 | $ | 64.36 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operations: | ||||||||||||||||||||

Net investment loss (1) | (0.35 | ) | (0.67 | ) | (0.58 | ) | (0.45 | ) | (0.57 | ) | ||||||||||

Net realized and unrealized gain (loss) | (7.47 | ) | 2.25 | 32.96 | 29.28 | (33.24 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations (2) | (7.82 | ) | 1.58 | 32.38 | 28.83 | (33.81 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | — | — | — | — | (0.46 | ) | ||||||||||||||

Distributions from net realized gains | (1.33 | ) | (1.61 | ) | (0.09 | ) | (0.89 | ) | (8.32 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total distributions | (1.33 | ) | (1.61 | ) | (0.09 | ) | (0.89 | ) | (8.78 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Change in net asset value for the year | (9.15 | ) | (0.03 | ) | 32.29 | 27.94 | (42.59 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value, end of year | $ | 72.82 | $ | 81.97 | $ | 82.00 | $ | 49.71 | $ | 21.77 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total Return | (9.5 | )% | 1.8 | % | 65.2 | % | 135.2 | % | (60.0 | )% | ||||||||||

Ratios/supplemental data | ||||||||||||||||||||

Net assets, end of year (000) | $ | 2,445,913 | $ | 2,647,078 | $ | 2,199,603 | $ | 937,492 | $ | 410,857 | ||||||||||

Ratio to average net assets: | ||||||||||||||||||||

Expense | 1.28 | % | 1.25 | % | 1.34 | % | 1.50 | % | 1.43 | % | ||||||||||

Net investment loss | (0.56 | )% | (0.86 | )% | (1.11 | )% | (1.25 | )% | (1.07 | )% | ||||||||||

Portfolio turnover rate | 11 | % | 3 | % | 9 | % | 9 | % | 28 | % | ||||||||||

| (1) | Net investment loss per share is calculated using the ending balances prior to consideration or adjustment for permanent book-to-tax differences. |

| (2) | Total from investment operations per share includes redemption fees of $0.021, $0.102, $0.056, $0.025, and $0.027 for the fiscal years ended October 31, 2012, 2011, 2010, 2009, and 2008, respectively. |

The Accompanying Notes are an Integral Part of these Financial Statements.

| 22 | October 31, 2012 |

The Delafield Fund

Financial Highlights

Per share operating performance (For a share outstanding throughout | Years Ended October 31, | January 1, 2009 through October 31, 2009 | Years Ended December 31, | |||||||||||||||||||||

| 2012 | 2011 | 2010 | 2008 | 2007 | ||||||||||||||||||||

Net asset value, beginning of period | $ | 27.21 | $ | 26.65 | $ | 21.35 | $ | 15.10 | $ | 24.33 | $ | 25.64 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Operations: | ||||||||||||||||||||||||

Net investment income (loss) (1) | (0.04 | ) | (0.08 | ) | (0.00 | )(3) | 0.03 | 0.07 | 0.17 | |||||||||||||||

Net realized and unrealized gain (loss) | 2.99 | 0.64 | 5.32 | 6.25 | (9.23 | ) | 1.10 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total from investment operations (2) | 2.95 | 0.56 | 5.32 | 6.28 | (9.16 | ) | 1.27 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Distributions to shareholders: | ||||||||||||||||||||||||

Dividends from net investment income | — | — | — | (0.03 | ) | (0.07 | ) | (0.16 | ) | |||||||||||||||

Distributions from net realized gains | (0.37 | ) | — | — | — | (0.00 | )(3) | (2.42 | ) | |||||||||||||||

Return of capital | — | — | (0.02 | ) | (0.00 | )(3) | (0.00 | )(3) | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total distributions | (0.37 | ) | — | (0.02 | ) | (0.03 | ) | (0.07 | ) | (2.58 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Change in net asset value for the period | 2.58 | 0.56 | 5.30 | 6.25 | (9.23 | ) | (1.31 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Net asset value, end of period | $ | 29.79 | $ | 27.21 | $ | 26.65 | $ | 21.35 | $ | 15.10 | $ | 24.33 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total Return | 11.0 | % | 2.1 | % | 25.0 | % | 41.6 | %(4) | (37.6 | )% | 4.9 | % | ||||||||||||

Ratios/supplemental data | ||||||||||||||||||||||||

Net assets, end of period (000) | $ | 1,346,273 | $ | 1,262,876 | $ | 933,674 | $ | 636,548 | $ | 404,860 | $ | 656,999 | ||||||||||||

Ratio to average net assets: | ||||||||||||||||||||||||

Expense | 1.23 | % | 1.23 | % | 1.27 | % | 1.38 | %(5) | 1.34 | %(6) | 1.28 | %(6) | ||||||||||||

Net investment income (loss) | (0.13 | )% | (0.30 | )% | (0.02 | )% | 0.21 | %(5) | 0.35 | %(6) | 0.57 | %(6) | ||||||||||||

Portfolio turnover rate | 49 | % | 38 | % | 30 | % | 46 | %(4) | 81 | % | 61 | % | ||||||||||||

| (1) | Net investment income (loss) per share is calculated using the ending balances prior to consideration or adjustment for permanent book-to-tax differences. |

| (2) | Total from investment operations per share includes redemption fees of $0.003, $0.006, and $0.006 for the fiscal years ended October 31, 2012, 2011, and 2010, $0.008 per share for the period ended October 31, 2009, less than $0.01 for the fiscal year ended December 31, 2008 and $0.01 for the fiscal year ended December 31, 2007. |

| (3) | Represents less than $0.01. |

| (4) | Not Annualized. |

| (5) | Annualized. |

| (6) | Net of fees waived amounting to 0.06% and 0.05% for the fiscal years ended December 31, 2008, and 2007, respectively. |

The Accompanying Notes are an Integral Part of these Financial Statements.

| Annual Report | 23 |

The Tocqueville Select Fund

Financial Highlights

Per share operating performance (For a share outstanding throughout the | Years Ended October 31, | January 1, 2009 through October 31, 2009 | Period from September 2008 (3) through December 31, 2008 | |||||||||||||||||

| 2012 | 2011 | 2010 | ||||||||||||||||||

Net asset value, beginning of period | $ | 11.06 | $ | 11.54 | $ | 8.46 | $ | 5.77 | $ | 8.74 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operations: | ||||||||||||||||||||

Net investment income (loss) (1) | (0.04 | ) | (0.07 | ) | (0.03 | ) | (0.00 | )(4) | 0.01 | |||||||||||

Net realized and unrealized gain (loss) | 0.44 | 0.12 | 3.12 | 2.70 | (2.97 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations (2) | 0.40 | 0.05 | 3.09 | 2.70 | (2.96 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | — | — | (0.01 | ) | (0.00 | )(4) | (0.01 | ) | ||||||||||||

Distributions from net realized gains | (0.11 | ) | (0.53 | ) | — | — | — | |||||||||||||

Return of capital | — | — | — | (0.01 | ) | | — | | ||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total distributions | (0.11 | ) | (0.53 | ) | (0.01 | ) | (0.01 | ) | (0.01 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Change in net asset value for the period | 0.29 | (0.48 | ) | 3.08 | 2.69 | (2.97 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value, end of period | $ | 11.35 | $ | 11.06 | $ | 11.54 | $ | 8.46 | $ | 5.77 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total Return | 3.7 | % | (0.1 | )% | 36.6 | % | 46.7 | %(5) | (33.9 | )%(5) | ||||||||||

Ratios/supplemental data | ||||||||||||||||||||

Net assets, end of period (000) | $ | 84,549 | $ | 71,554 | $ | 41,788 | $ | 24,681 | $ | 9,226 | ||||||||||

Ratio to average net assets: | ||||||||||||||||||||

Expense | 1.37 | % | 1.36 | % | 1.38 | % | 1.26 | %(6)(7) | 1.15 | %(6)(7) | ||||||||||

Net investment income (loss) | (0.36 | )% | (0.67 | )% | (0.43 | )% | (0.16 | )%(6)(7) | 0.29 | %(6)(7) | ||||||||||

Portfolio turnover rate | 31 | % | 28 | % | 40 | % | 24 | %(5) | 29 | %(5) | ||||||||||

| (1) | Net investment income (loss) per share is calculated using the ending balances prior to consideration or adjustment for permanent book-to-tax differences. |

| (2) | Total from investment operations per share includes redemption fees of $0.002, $0.008 and $0.007 for the fiscal years ended October 31, 2012, 2011, and 2010, respectively. |

| (3) | Inception of Fund. |

| (4) | Represents less than $0.01. |

| (5) | Not Annualized. |

| (6) | Annualized. |

| (7) | Net of fees waived amounting to 0.77% and 2.32% for the fiscal periods ended October 31, 2009 and December 31, 2008, respectively. |

The Accompanying Notes are an Integral Part of these Financial Statements.

| 24 | October 31, 2012 |

The Tocqueville Fund

Schedule of Investments as of October 31, 2012

| Common Stocks—99.3% | Shares | Value | ||||||

Automobiles & Components—2.3% |

| |||||||

Ford Motor Co. | 748,000 | $ | 8,347,680 | |||||

Banks—0.9% | ||||||||

Mitsubishi UFJ Financial Group, Inc.—ADR | 750,000 | 3,367,500 | ||||||

Capital Goods—7.4% | ||||||||

General Electric Co. | 750,000 | 15,795,000 | ||||||

Illinois Tool Works, Inc. | 100,000 | 6,133,000 | ||||||

The Boeing Co. | 75,000 | 5,283,000 | ||||||

| 27,211,000 | ||||||||

Commercial & Professional Services—1.9% |

| |||||||

Steelcase, Inc. | 700,000 | 7,007,000 | ||||||

Couriers and Messengers—0.8% |

| |||||||

FedEx Corp. | 30,000 | 2,759,700 | ||||||

Credit Intermediation and Related Activities—0.3% |

| |||||||

M&T Bank Corp. | 11,000 | 1,145,100 | ||||||

Diversified Financials—2.8% | ||||||||

Lazard Ltd.(a) | 100,000 | 2,946,000 | ||||||

The Bank of New York Mellon Corp. | 300,000 | 7,413,000 | ||||||

| 10,359,000 | ||||||||

Educational Services—0.7% | ||||||||

DeVry, Inc. | 100,000 | 2,626,000 | ||||||

Energy—13.1% | ||||||||

Cameco Corp.(a) | 171,400 | 3,316,590 | ||||||

Chesapeake Energy Corp. | 300,000 | 6,078,000 | ||||||

Endeavour International Corp.(b) | 125,000 | 907,500 | ||||||

Energen Corp. | 100,000 | 4,665,000 | ||||||

Exxon Mobil Corp. | 150,000 | 13,675,500 | ||||||

Murphy Oil Corp. | 150,000 | 9,000,000 | ||||||

Schlumberger Ltd.(a) | 150,000 | 10,429,500 | ||||||

| 48,072,090 | ||||||||

Food & Staples Retailing—2.1% |

| |||||||

Wal-Mart Stores, Inc. | 100,000 | 7,502,000 | ||||||

Food, Beverage & Tobacco—5.1% |

| |||||||

Campbell Soup Co. | 225,000 | 7,935,750 | ||||||

PepsiCo, Inc. | 50,000 | 3,462,000 | ||||||

The Coca-Cola Co. | 200,000 | 7,436,000 | ||||||

| 18,833,750 | ||||||||

Household & Personal Products—4.3% |

| |||||||

Colgate-Palmolive Co. | 50,000 | 5,248,000 | ||||||

The Procter & Gamble Co. | 150,000 | 10,386,000 | ||||||

| 15,634,000 | ||||||||

| Common Stocks (continued) | Shares | Value | ||||||

Insurance—4.7% | ||||||||

Aflac, Inc. | 171,500 | $ | 8,537,270 | |||||

Fidelity National Financial, Inc. | 200,000 | 4,282,000 | ||||||

XL Group PLC(a) | 171,000 | 4,230,540 | ||||||

| 17,049,810 | ||||||||

Materials—10.0% | ||||||||

BHP Billiton Ltd.—ADR | 63,900 | 4,520,286 | ||||||

Cliffs Natural Resources, Inc. | 75,000 | 2,720,250 | ||||||

EI du Pont de Nemours & Co. | 250,000 | 11,130,000 | ||||||

Newmont Mining Corp. | 250,000 | 13,637,500 | ||||||

Sonoco Products Co. | 150,000 | 4,669,500 | ||||||

| 36,677,536 | ||||||||

Pharmaceuticals, Biotechnology & Life Sciences—9.9% |

| |||||||

Alkermes PLC(a)(b) | 250,000 | 4,632,500 | ||||||

Isis Pharmaceuticals, Inc.(b) | 200,000 | 1,730,000 | ||||||

Johnson & Johnson | 150,000 | 10,623,000 | ||||||

Merck & Co., Inc. | 150,000 | 6,844,500 | ||||||

Pfizer, Inc. | 500,000 | 12,435,000 | ||||||

| 36,265,000 | ||||||||

Real Estate—3.0% | ||||||||

Weyerhaeuser Co. | 400,000 | 11,076,000 | ||||||

Retailing—1.3% | ||||||||

Lowe’s Companies, Inc. | 150,000 | 4,857,000 | ||||||

Semiconductors & Semiconductor Equipment—4.4% |

| |||||||

Applied Materials, Inc. | 700,000 | 7,420,000 | ||||||

Intel Corp. | 400,000 | 8,650,000 | ||||||

| 16,070,000 | ||||||||

Software & Services—12.2% | ||||||||

Adobe Systems, Inc.(b) | 150,000 | 5,100,000 | ||||||

Automatic Data Processing, Inc. | 100,000 | 5,779,000 | ||||||

Google, Inc.(b) | 15,000 | 10,196,550 | ||||||

Mastercard, Inc. | 20,000 | 9,218,600 | ||||||

Microsoft Corp. | 500,000 | 14,267,500 | ||||||

| 44,561,650 | ||||||||

Technology Hardware & Equipment—7.2% |

| |||||||

Bio-key International, Inc.(b)(c)(d)(e) | 47,090 | — | ||||||

Cisco Systems, Inc. | 420,000 | 7,198,800 | ||||||

EMC Corp.(b) | 125,000 | 3,052,500 | ||||||

Hitachi Ltd.—ADR | 150,000 | 7,869,000 | ||||||

Plexus Corp.(b) | 125,000 | 3,363,750 | ||||||

Xerox Corp. | 750,000 | 4,830,000 | ||||||

| 26,314,050 | ||||||||

Telecommunication Services—1.5% |

| |||||||

Verizon Communications, Inc. | 125,000 | 5,580,000 | ||||||

The Accompanying Footnotes are an Integral Part of these Financial Statements.

| Annual Report | 25 |

The Tocqueville Fund

Schedule of Investments as of October 31, 2012

| Common Stocks (continued) | Shares | Value | ||||||

Utilities—3.4% | ||||||||

NextEra Energy, Inc. | 175,000 | $ | 12,260,500 | |||||

Total Common Stocks | 363,576,366 | |||||||

Warrant—0.0% | ||||||||

Technology Hardware & Equipment—0.0% |

| |||||||

EMCORE Corp. | ||||||||

Expiration: 02/19/13, | 9,844 | — | ||||||

Total Warrant | — | |||||||

| Short-Term Investments—0.5% | Principal Amount | |||||||

Repurchase Agreement—0.5% | ||||||||

Repurchase Agreement with U.S. Bank, N.A., 0.01% dated 10/31/2012, due 11/01/2012, collateralized by: Freddie Mac Conventional 15 Year Fixed (Pool #E99837) valued at $62,234. Repurchase proceeds of $60,975. Fannie Mae Conventional Level Pay 15 Year Fixed (Pool #254919) valued at $1,868,550. Repurchase proceeds of $1,832,026. | $ | 1,893,000 | 1,893,000 | |||||

Total Short-Term Investments | 1,893,000 | |||||||

Total Investments |

| 365,469,366 | ||||||

Other Assets in Excess of Liabilities—0.2% |

| 555,222 | ||||||

Total Net Assets—100.0% | $ | 366,024,588 | ||||||

|

| |||||||

Percentages are stated as a percent of net assets.

ADR—American Depository Receipt

| (a) | Foreign issued security. Foreign concentration (including ADRs) was as follows: Australia 1.2%; Bermuda 0.8%; Canada 0.9%; Ireland 2.4%; Japan 3.1%; Netherlands Antilles 2.8%; |

| (b) | Non-income producing security. |

| (c) | Denotes a security is either fully or partially restricted to resale. The aggregate value of restricted securities at October 31, 2012 was $0 which represented 0.0% of net assets. |

| (d) | Fair valued security.The aggregate value of fair valued securities as of October 31, 2012 was $0 which represented 0.0% of net assets. |

| (e) | Security is considered illiquid and may be difficult to sell. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”).GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bancorp Fund Services, LLC.

The Accompanying Footnotes are an Integral Part of these Financial Statements.

| 26 | October 31, 2012 |

The Tocqueville Opportunity Fund

Schedule of Investments as of October 31, 2012

| Common Stocks—99.8% | Shares | Value | ||||||

Automobiles & Components—0.7% | ||||||||

BorgWarner, Inc.(a) | 4,200 | $ | 276,444 | |||||

The Goodyear Tire & Rubber Co.(a) | 17,000 | 193,970 | ||||||

| 470,414 | ||||||||

Banks—3.5% | ||||||||

BankUnited, Inc. | 19,000 | 450,490 | ||||||

Pinnacle Financial Partners, Inc.(a) | 34,000 | 664,700 | ||||||

SCBT Financial Corp. | 6,900 | 273,792 | ||||||

Signature Bank(a) | 9,900 | 705,276 | ||||||

Texas Capital Bancshares, Inc.(a) | 3,800 | 180,386 | ||||||

| 2,274,644 | ||||||||

Capital Goods—7.6% | ||||||||

Acuity Brands, Inc. | 4,200 | 271,740 | ||||||

AMETEK, Inc. | 13,950 | 495,922 | ||||||

AO Smith Corp. | 11,700 | 711,009 | ||||||