UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-4840

The Tocqueville Trust

(Exact name of registrant as specified in charter)

The Tocqueville Trust

40 W. 57th St., 19th Floor

New York, NY 10019

(Address of principal executive offices) (Zip code)

Robert W. Kleinschmidt

The Tocqueville Trust

40 W. 57th St., 19th Floor

New York, NY 10019

(Name and address of agent for service)

(212) 698-0800

Registrant’s telephone number, including area code

Date of fiscal year end: October 31

Date of reporting period: October 31, 2014

Item 1. Reports to Stockholders.

ANNUAL REPORT

October 31, 2014

The Tocqueville Trust

Mutual Funds

The Tocqueville Fund

The Tocqueville Opportunity Fund

The Tocqueville International Value Fund

The Tocqueville Gold Fund

The Delafield Fund

The Tocqueville Select Fund

The Tocqueville Alternative Strategies Fund

This report is not authorized for distribution to prospective investors unless preceded or accompanied by a currently effective prospectus of The Tocqueville Trust. Please call 1-800-697-FUND (3863) for a free prospectus. Read it carefully before you invest.

You are invited to visit our website @ www.tocqueville.com/mutual-funds

Dear Fellow Shareholder,

According to the National Bureau of Economic Research Business Cycle Dating Committee, there have been seven economic recessions in the United States since 1969. Paradoxically, the stock market crash of Monday October 19, 1987, when the Dow Jones Industrial Average dropped almost 23% in one day, does not appear on that list. The reason is that even though the market decline was both violent and global, no economic recession ensued. The Federal Reserve managed to convince the banks to continue lending to each other: liquidity was preserved and the economy continued to operate normally.

It is very likely, however, that this scary episode deeply influenced Alan Greenspan, who had only become the Federal Reserve Chairman three months earlier. His whole tenure at the “Fed” (1987-2006) was marked by the tacit promise (the Greenspan Put) that the Fed would intervene to provide ample liquidity to the financial system as soon as the stock market declined significantly and threatened to destabilize the whole economy.

The recessions I remember, since 1969, followed a similar pattern. Central Banks, the U.S. Federal Reserve for example, tended to intervene towards the end of recessions by injecting free or very low-cost reserves into their banking system. Since this took place during a recession, when banks were still leery of lending and potential borrowers were scarce, commercial banks would invest most of these low-cost funds into Treasury securities. There was little immediate effect on economic activity, but this action allowed the banks to make a small but positive margin at zero risk, which offset the charges incurred from writing-off the bad loans extended during the previous boom. When bank balance sheets had been repaired and credit demand from the private sector eventually recovered, banks would be ready to lend anew.

The basic pattern has not changed materially in more recent years, but the Greenspan Put first, and then ZIRP (Zero Interest Rate Policy) and various stages of QE (Quantitative Easing) under Fed Chairman Ben Bernanke have institutionalized the role of the Fed as protector of the investment community. Some observers have claimed that, by tacitly eliminating the risk of large losses from the stock markets, the Fed and other central banks have contributed to the buildup of the next bubble, as they did with dot-com stocks in the late 1990s and sub-prime mortgages in the mid-2000s. History will tell, but one thing is sure: This is the way investors have played the game since 2009.

Economies have recovered in Europe, Japan and most emerging markets, but at very disappointing rates. The U.S. recovery has been more dynamic but still uneven. As a result, there exists ample unused capacity around the world and inflationary pressures have, so far, been feeble enough to give comfort to the major western Central Banks that their stimulus policies are appropriate; some European politicians actually are agitating for more. For the economies, that is. But since there is widespread concern in the public that, when the economies recover in earnest, the financial markets may suffer a withdrawal syndrome from the closure of the monetary floodgates, the new pattern for stock markets, has been to weaken when the economies accelerate and to recover in earnest as soon as economic activity seems to stumble—with faith that central banks’ monetary stimulus would then resume.

Of course, there has never been a precise correlation between economic activity and the stock market, except over the very long term. Nevertheless, the kind of (historically) perverse reasoning that has recently prevailed sounds like it deserves to be regarded with caution. Mostly because one cannot tell how long the game can be played, but for sure it is not forever because inflation and higher interest rates are sure to return one day as a result of the massive amount of money that has been injected into the world’s banking systems.

Fortunately, not all markets have been as buoyant as those for large-capitalization U.S. stocks. Many smaller companies as well as equities of emerging-markets have been moving toward more conservative valuations, while a relatively small sample of large companies or “trendy” sectors kept up the momentum of major indexes.

Opportunity in selectivity should be a challenging but favorable environment for discipline-oriented managers like the ones at Tocqueville.

Respectfully,

François Sicart

Chairman

| Annual Report | 1 |

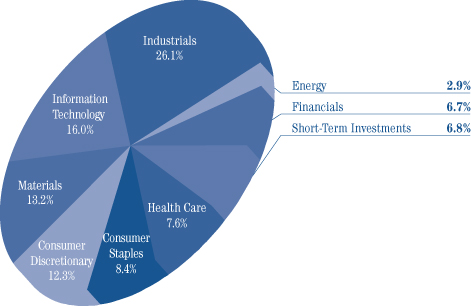

The Tocqueville Fund

Dear Fellow Shareholder,

The Tocqueville Fund’s fiscal year that ended October 31, 2014 was full of surprises. Equity markets continued their upward trajectory throughout the year, overcoming several brief but sharp corrections that tested investor resolve before eventually returning to near record levels as the year came to a close. The bull market that some have argued has gone on too long ploughed right through a variety of macroeconomic and geopolitical concerns, any one of which might have been enough to turn the tide of investor sentiment, including multiple conflicts in the Middle East, a Russian incursion into the Ukraine, sharp price declines across the commodity complex, economic uncertainty in China and malaise in Europe, not to mention the Ebola scare in the U.S. That the market withstood these forces was indeed surprising perhaps but the biggest surprise (to most, though not us) was that interest rates failed to rise despite the “tapering” of the Fed’s quantitative easing initiative.

Over the past year, the Fund returned 13.43% while the S&P 500, the index against which the Fund is most often compared, gained 17.27%. This result is mildly disappointing when compared to the benchmark, and due largely to the performance of the positions in the energy sector, but it is better than we would have expected following last year’s strong results and the various headwinds described above.

The top performing sectors of the Fund in the past year were information technology, healthcare and industrials. while energy, materials and telecommunications were the laggards. The top individual contributors to portfolio performance were the pharmaceutical companies Allergan, which is the subject of an ongoing contested takeover, Isis Pharmaceuticals and Alkermes, two small capitalization, relatively early stage biotechnology companies, along with large cap technology stalwarts Microsoft and Xerox; while the largest detractors from performance were the energy companies Bill Barret Corporation, Energy XXI, and Frank’s International, along with Goldcorp, and surprisingly Ford.

As we see it, two of the fundamental forces that move risk markets are the cost of capital and the rate of economic growth. The cost of capital is tied to interest rates and, as the bull market marched onward in spite of the Fed’s plans to reduce its intervention into fixed income markets. Many investors believed that interest rates were set to rise once the Fed ended its bond purchases and began to shrink its balance sheet, increasing the cost of doing business for net borrowers and the discount rate for investors, and positioned their portfolios accordingly. That has certainly been one of the root causes of the brief bouts of volatility the market has seen over the past year.

The other driver of these corrections has been repeated scares that the global economy was weakening sufficiently to cause growth problems here at home. We too have been worried that double digit returns on equities would seem hard to support indefinitely on 2% GDP growth. U.S. dollar strength, export demand weakness and falling commodity prices have added to the concern that corporate profits might be topping out after several years of profit growth which has been driven by margin expansion rather than material improvement in top line revenues. Recent poor performance of energy and other commodity driven companies as well as those of multinationals, particularly industrials, is testimony to that concern. But, it is also true that lower commodity prices, particularly lower energy prices represent a significant cost reduction to most developed countries and companies. The markets seem to be missing this obvious long-term positive factor.

Despite the end of quantitative easing, the Fed is unlikely to change its key rates until things stabilize both here and abroad. With $18 trillion in public sector debt at the Federal level, the Fed has to be wary of what higher interests rates would do to the Federal fiscal landscape and, might better wait until the Federal government gets its fiscal house in order before adding to the burden of carrying all this debt. Also, offsetting the Fed’s taper have been a reduced supply of new Treasuries as budget deficits have shrunk as well as the actions of just about every other central bank around the globe which seem intent to devalue their own currencies to gain export advantage and stimulate their own economies. Low rates abroad and geopolitical uncertainty is driving foreign investors to step up their purchasing of Treasuries just as the Fed steps away.

While we could be wrong and the oft cited bond vigilantes could come out of the woodwork at any time and sooner rather than later, it does seem that rates and the cost of capital component of the risk market debate are likely to remain accommodating for some time.

| 2 | October 31, 2014 |

This leaves the growth component of the valuation equation as the determining factor. There are a few positive influences that lead us to conclude that growth may be better than expected and help us remain optimistic about equities despite the various concerns mentioned above. One of these is that we appear to be entering a period of lower energy prices driven by an increase in supply coming from new extraction technologies and soft demand in a slow global growth environment. While this isn’t great for those highly levered exploration and production companies, it is, as noted, a real tailwind for many businesses and consumers. An improvement in real wages and disposable income is the fuel that drives the consumption component of the economy. The vast middle class hasn’t experienced much of that during the post financial crisis period, but lower energy prices, coupled with restrained labor costs and continued low costs of capital, will contribute to improving the competitiveness of domestically sited manufacturing. This, in turn, and in due course, should have a salutary impact on consumer’s budgets.

Another positive factor for the economy is that bank loan growth is starting to expand. Many investors have been expecting inflation as a byproduct of the Fed’s balance sheet expansion and loose monetary policy (and as the hidden means to address the U.S. Government’s debt and fixed entitlement obligations). For the most part this hasn’t happened, as banks have been forced to retain greater capital, exit so-called “risk” businesses, and increase legal reserves, in an effort to repair their balance sheets and respond to greater regulation. If bank loan growth does pick up sustainably, economic growth could be greater than widely expected, at least nominally.

The global economic outlook may also be more gloomy than warranted. The European Central Bank continues to make incremental progress in recovering from its financial crisis, and may step up its stimulative efforts. Were that to occur, it might further improve that regions prospects. Japan has recently taken surprising steps to weaken the Yen even further to improve export demand. China, while targeting lower growth than in recent history and combating graft and consumer excesses, is also still working on stimulus programs.

Lastly, while it would be naive to expect any real progress, there is some prospect that the highly anticipated Republican victory in mid-term elections might lead to economically helpful legislation. If the President and Congress cancould set aside their differences, they might well be able to fashion some bi-partisan solutions to some well recognized problems. Corporate tax reform would be a favorite for investors, particularly more globally competitive tax rates and the elimination of the unitary tax provision which punishes U.S. companies for repatriating already taxed foreign income. Immigration reform might also be a boon to certain businesses and a way to offset declines in labor force participation, or at least that portion of it caused by demographics. Changes in energy policy, if they can be accomplished in a way that doesn’t hurt domestic consumers, could stabilize the current glut in that sector and open up new markets for domestically produced oil. That is a wish list perhaps, but hardly fanciful.

On balance, it is these forces and possibilities that lead us to remain constructive on U.S. equities, particularly in relation to fixed income assets which we expect to be range bound for some time. Even after a multi-year bull market there are sectors and companies that fall out of favor. We will continue to search for these opportunities to purchase quality businesses at a substantial discount to intrinsic value.

Thank you for your continued support,

Sincerely,

Robert W. Kleinschmidt

Portfolio Manager

| Annual Report | 3 |

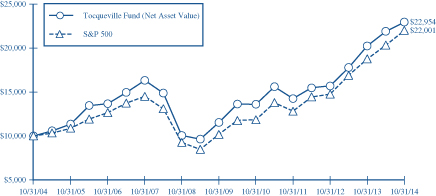

The Tocqueville Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/04. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held for 90 days or less.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns assume the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2014

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

The Tocqueville Fund | 13.43% | 17.24% | 14.77% | 8.66% | ||||||||||||

Standard & Poor’s 500 Stock Index | 17.27% | 19.77% | 16.69% | 8.20% | ||||||||||||

| 4 | October 31, 2014 |

The Tocqueville Opportunity Fund

Dear Fellow Shareholder,

We are pleased to provide this review of the Tocqueville Opportunity Fund’s performance for the fiscal year ended October 31, 2014. The Fund out performed its SMID cap (small/midcap) growth benchmark (the Russell 2500 Growth Index) for the fiscal year with a gain of 12.55% versus the benchmark return of 10.24%. Through the calendar year to date ended October 2014, the Fund also out performed with a gain of 6.10% versus the benchmark increase of 3.98%. The past fiscal year has been a bit of an unusual period for SMID cap stocks as headway has been difficult to establish given price volatility and rapid changes in sentiment.

The Fund experienced seven corrections of significance (10% or greater) since I assumed oversight of the Fund in the summer of 2010—with the average correction occurring every 6-7 months. In all of the prior cases, the corrections proved to be short lived, and the Fund moved to newer highs. Almost like clockwork, another correction hit the SMID cap (and the large cap) indices in early September. This most recent and last correction of nearly 11% was one month in duration, and once again provided plenty of fodder for market timers and bears, but sellers were severely whipsawed as SMID caps roared back and the Fund gained nearly 14% in just the last two weeks of the fiscal period! Corrections are unsettling, but they have continued to present numerous opportunities to increase the Fund’s investments in innovative companies that are achieving milestones and flawless execution. Sentiment driven corrections are generally driven by short-term oriented traders who are preoccupied with macroeconomic and political events and are not focused on investment fundamentals. Over the past year there have been five price swings of 10% or more—3 ups and 2 downs—which have allowed valuations to compress against prices and earnings growth, and proven to be excellent times for us to increase our investments in the strongest core positions.

We have continued to increase investments in the Healthcare and Technology sectors during the past twelve months. Most of the allocation to these sectors has come from a reduction in the economy sensitive sectors—particularly Basic Materials, Producer Durables, and Energy. A year ago, economy sensitive investments represented the largest collective sector based holdings for the Fund and reflected a positive view on the pace of the economic recovery. Economy sensitive sector allocations have been reduced from nearly 42% to 30% over the past year with decreases concentrated in automobile supply, housing, and European exposed manufacturing firms. Also, Energy investments have been reduced over the past year based on an ongoing view that technological advances would ultimately lead to imbalances in the global equilibrium in oil demand and supply—at the period’s end, the Fund had less than 1% of its holdings invested in Energy. For the first time in our lifetimes, the prospect of real competition driven by technology, conservation, alternative energy, and failing collusion could completely change the paradigm for investments in this sector. Healthcare sector investments comprised the largest single sector commitments in the Fund as of the end of the fourth quarter at 31% versus 23% last year—this increase was driven most significantly by appreciation of existing holdings—Healthcare investment returns were the leading contributors to both the Fund and the benchmark during the year. On a stand-alone basis, the Consumer and Technology sectors were #2 and #3 respectively at 19.5% and 19% of the Fund’s holdings. Over the past year, Technology investments were increased by nearly one-half with a particular emphasis on software companies which are providing new and disruptive services—these investments were significantly increased during the sentiment driven sell off in Technology holding in March and April this year, and Technology investments were the second leading contributors to the Fund’s performance for the year.

The Fund’s sector level investments provided relative out performance in 9 of the 11 measured sectors (Energy and Oils combined). Aside from the leading contributions of Healthcare and Technology investments, the Fund’s low allocation to Energy led to significant value added relative to the benchmark. Automobile, Transportation and Consumer investments accounted for additional positive relative performance. As we wrote in our semi-annual letter, we have maintained a very constructive view on the airline industry—this view was temporarily shaken by recent, ill- timed capacity expansions and the Ebola crisis, but appeared to be back on track at period end. The Fund’s performance was negatively impacted by its Utilities and Basic Materials exposures—or rather the lack of these exposures; the Fund held no Utility investments during the period, and was under weighted in certain Materials investments which appreciated significantly.

| Annual Report | 5 |

Eleven of the Fund’s top 15 contributors to performance were Healthcare investments, including: Forest Laboratories (acquired) and Actavis (acquirer) and Alnylam (the leading contributor). During the period, Algeta was acquired and Allergan was a named target by Valeant Pharmaceutical. The three Technology investments included: Manhattan Associates, Palo Alto Networks and Concur Technologies—Concur is being acquired by SAP. The investment in Delta Air Lines was the second leading contributor to the Fund’s relative performance. On the flip side, the Fund had several meaningful disappointments despite its diversification strategy—Intercept Pharmaceuticals and Aegerion Pharmaceuticals accounted for nearly 1% drag; and the Fund did not own Intermune which was acquired in the late summer. On an absolute basis, the Fund had 34 investments (common stock) which appreciated 50% or more during the period versus 6 which declined 50% or more. The leaders included Regulus Therapeutics, Puma Biotechnology, and Skyworks Solutions and three takeovers - Forest Labs, Hillshire and OpenTable. Of the six losers, five were Healthcare names and included the aforementioned Intercept and Aegerion as well as Sarepta Therapeutics, Dicerna Pharmaceuticals and Sangamo Biosciences.

As noted above, the past year’s volatility has provided several great shots to increase investments in the Fund’s leading companies. The top 50 holdings at the end of the fiscal year comprised over 52% of the Fund versus 37.5% one year ago. While we have continued to diversify the Fund against single issue risks, the Fund is very actively managed vis-à-vis its benchmark—of the top 50 positions weighting of 52%, less than 9.5% overlaps with the benchmark itself. For the Fund in total, the overlap with the benchmark at the period’s end was less than 37% - the Fund is very diversified, but very actively invested. We continue to employ fundamental research in a classically driven effort to identify and to invest in the leading companies and the companies which we expect to be tomorrow’s leaders. We want to own companies which innovate and reinvent, gain market share, set prices, expand and invest—companies which sustain competitive advantage and capital returns. We continue to be very optimistic with regard to investment opportunities and the appreciation potential within the SMID cap category, and we particularly appreciate your ongoing confidence in our efforts on behalf of the Fund and its shareholders.

Sincerely,

Thomas R. Vandeventer

Portfolio Manager

| 6 | October 31, 2014 |

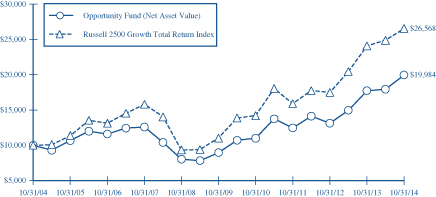

The Tocqueville Opportunity Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/04. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held for 90 days or less.

The chart and table primarily reflect The Opportunity Fund’s performance achieved prior to the changes effected in 2010 to its investment strategy.

The Russell 2500 Growth Total Return Index is an unmanaged index that measures the performance of the small to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500 companies with higher price-to-book ratios and higher forcasted growth values. Returns assume the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2014

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

The Tocqueville Opportunity Fund | 12.55% | 17.00% | 17.34% | 7.17% | ||||||||||||

Russell 2500 Growth Total Return Index | 10.24% | 18.64% | 19.20% | 10.26% | ||||||||||||

| Annual Report | 7 |

The Tocqueville International Value Fund

Dear Fellow Shareholder,

For the fiscal year ended October 31, 2014, the Tocqueville International Value Fund’s total U.S. dollar return was -0.04%. In the same period, the Morgan Stanley EAFE Index Net, the index against which we are most often compared, had a net total U.S. dollar loss of -0.60%. For the 10 year period ended October 31, 2014, the Tocqueville International Value Fund’s total U.S. dollar return was 93.61%. In the same period, the Morgan Stanley EAFE Index Net had a net total U.S. dollar return of 75.84%.

During the year, global equity markets had mixed results, as investors grappled with the potential impact of the end of quantitative easing in the U.S., weaker than expected manufacturing data from China and core Europe, the implications of geopolitical unrest in Ukraine and the Middle East, an outbreak of the Ebola virus, and renewed concerns about deflation and peripheral Europe. Markets in the U.S. and Japan had gains in local currency terms, driven by improving corporate earnings coupled with persistent low interest rates, while markets in Europe had losses on the back of disappointing economic data. Index results were generally flattered by a narrow group of large cap stocks, while the broader markets fared less well. With the U.S. economy growing at a healthy pace relative to most developed nations, and quantitative easing in the U.S. nearing its end, the U.S. dollar strengthened meaningfully against most currencies, resulting in flat to down returns in U.S. dollar terms in most non-U.S. markets. China and certain Asian emerging markets were notable exceptions, while emerging markets in Eastern Europe and Latin America were hard hit. In the context of increasing volatility and a growth scare, large caps fared better than smaller companies, and economically sensitive companies fared poorly, particularly in Europe. Commodity prices generally declined, as did the share prices of commodity producing companies. In terms of sectors, declines in Europe were led by auto related, building materials and food retail shares, and in Japan by marine transport, pulp & paper and energy.

While the Fund’s positions in Japan and Asia performed well during the period and it avoided problems in emerging markets, the results were hurt by the Fund’s exposure to economically sensitive stocks in core Europe. Notable contributors to gains include Japanese optical glass maker Hoya, U.K. emergency home repair insurer Homeserve, Singapore mail and logistics company Singapore Post, subject of a strategic investment by Chinese online retailing giant Alibaba, Hong Kong based outdoor advertising concern Clear Media, and Japanese imaging technology company Fujifilm. The Fund had meaningful losses in UK food retailer Tesco, Italian auto parts maker Sogefi, French oil country tubular goods maker Vallourec, French wire and cable producer Nexans, French marketing research concern Ipsos, and Dutch textile technology company Royal Ten Cate.

During the period, the Fund exited its positions in Telecom Italia, Dutch logistics concern TNT Express, Japanese athletic footwear maker Asics, French design software concern Dassault Systemes, oil service company Schlumberger, Japanese industrial automation concern Omron, and Japanese test and measurement maker Horiba, as they approached our estimates of intrinsic value. Fugro was sold when a new senior management team announced a large capital expenditure program, undercutting the central tenet of the investment thesis, which was based on harvesting free cash flow from prior investments. Also sold was Itau Unibanco, as we came to believe that our fundamental thesis will be overshadowed by deteriorating political circumstances in advance of Brazil’s Presidential election. The Fund exited its position in uranium producer Cameco, when the Japanese government extended the timetable for the reintroduction of nuclear power generation capacity. Tesco was sold when it became evident that the management has used aggressive accounting methods to inflate earnings.

The Fund took new positions in Canadian fuel distribution and chemical concern Superior Plus, a strong franchise where cost reductions under a new management team and the completion of a capital expenditure program should yield a substantial expansion in free cash flow; in Hong Kong real estate concern Hopewell Holdings, which trades at a meaningful discount to net asset value; in Korean consumer electronics maker Samsung Electronics, which is temporarily depressed due to investor concerns about competition in its smartphone business, trades at a single digit multiple of free cash flow and has an unrecognized asset in its memory chip business, an industry where pricing is benefitting from consolidation. The Fund took a new position in Japanese time recording equipment maker Amano, which is generally

| 8 | October 31, 2014 |

unknown to non-Japanese investors but has dominant market shares in Japan and Asia, strong free cash flow generation, excess cash and an investor friendly management team. Another new position was French market research firm Ipsos, a cash generative franchise in which the Fund has previously invested, which had declined recently in connection with market concerns about accelerating competition from social media and other digital means of data collection. In our view the concerns are overdone, the stock trades at a steep discount to its takeover value, and an eventual sale of the company is likely. A new position was initiated in Ireland domiciled Actavis, an emerging drug giant that trades at a low valuation of free cash flow pro forma for its recent acquisition of Forest Labs, and where management generally has a stellar track record of value enhancing acquisitions. Another new position is in Japanese motion picture producer and distributor Toho, which has net cash and real estate equal to the value of the shares. Positions in Misumi, Disco, Incitec Pivot, Kao, Sanofi, CRH, Akzo Nobel, Vallourec, Saint Gobain, Nexans, and Sogefi, inter alia were increased.

During the period, there was a decrease in the Fund’s exposure to Europe and Latin America and an increase in exposures to Japan and Asia. The Fund began the period with approximately 6% in cash reserves and finished the period with 7% in cash reserves.

The baseline macro scenario is: Europe experiences a gradual recovery, but it remains a growth challenged region in need of deep structural reforms; China averts a hard landing and consumer led growth settles at a lower but still healthy level; the U.S. continues to grow, though below potential; Japan achieves mild reflation and consumer sentiment there improves; inflation is more probable in light of serial monetary easing; the Yen is likely to decline in value against the Pound, Euro and U.S. dollar as the government there pursues an aggressive policy of devaluation.

In the U.S., we continue to be concerned about high corporate profit margins and the fact that equity valuations have been abetted by financial and tax engineering, in addition to lax monetary policy. For developed markets generally, certain emerging markets heretofore presumed to be a source of growth for multinationals have become a headwind, due both to slowing growth and to the declining value of currencies. In Europe, tensions in the Middle East and sanctions on Russia are having a direct impact on some businesses and, perhaps more importantly, a depressing effect on business sentiment, while a moderation of growth in China is affecting the German export machine.

In this context, we continue to focus our research efforts on idiosyncratic situations, particularly where activists are involved or we believe are likely to get involved. The Fund is also focusing more attention on Europe, where as noted weak economic data and geopolitical tensions have produced a sharp pullback in cyclical stocks. In Japan, there continue to be opportunities in companies that export to the global marketplace and companies where new and younger management teams are focused on improving profitability and capital allocation.

To protect and grow your capital, we continue to seek out companies that have defensible business franchises, pricing power, limited financial leverage and the ability to return cash to shareholders, and which trade at a discount to intrinsic value based on future cash flows in a conservative economic growth scenario.

Respectfully,

|

James Hunt

Portfolio Manager

| Annual Report | 9 |

The Tocqueville International Value Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/04. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

The MSCI EAFE Index is an unmanaged market-capitalization-weighted index composed of companies representative of the market structure of 21 Developed Market Countries in Europe, Australia, Asia and the Far East.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2014

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

The Tocqueville International Value Fund | -0.04% | 7.91% | 7.90% | 6.83% | ||||||||||||

MSCI EAFE Net Index | -0.60% | 9.68% | 6.52% | 5.81% | ||||||||||||

MSCI EAFE Gross Index | -0.17% | 10.17% | 7.00% | 6.29% | ||||||||||||

| 10 | October 31, 2014 |

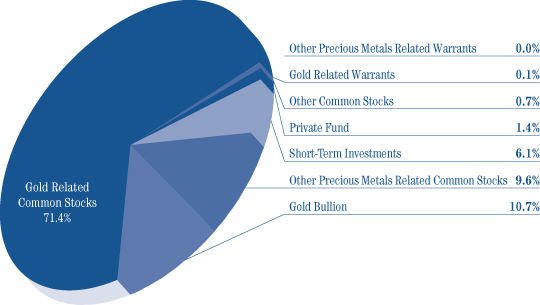

The Tocqueville Gold Fund

Dear Fellow Shareholder,

The Tocqueville Gold Fund declined 20.07% during the fiscal year ended October 2014, while the Philadelphia Gold and Silver Index, declined -30.89%, the Standard & Poor’s 500 Index increased 17.27% and the gold price fell 11.49% to finish the period at $1,171.60 per ounce. The top three performers in the Fund over this period included Anthem United Inc., GoGold Resources Inc. and Barisan Gold Corp. which appreciated by 141.5%, 47.0% and 41.4%, respectively. The bottom three performers were Ivanhoe Mines Ltd., East Asia Minerals Corp. and IAMGOLD Corp. which declined by 68.8%, 63.0% and 62.9%, respectively.

During the first quarter of the fiscal year, as the gold price put in a bottom for 2013, gold equity investors sold positions into market weakness to capture tax losses. However, by the turn of the calendar year, markets reassessed the overdone correction in gold and gold equities, as an opportunity. Gold prices and gold mining stocks turned up quickly with the start of the new calendar year. The value observed by gold stock investors was not lost on gold mining companies either. Goldcorp initiated a hostile bid in January for one of the Fund’s largest equity positions, Osisko Mining, which was wrapping up some of the start-up challenges of operating its newly built Malartic mine and beginning to settle in to more steady state production and cash flow generation. Osisko Mining was ultimately taken over with a friendly offer from Agnico Eagle Mines Limited and Yamana Gold Inc., both prominent positions in the Fund prior to their combined cash and stock offer for Osisko Mining. Even though Goldcorp was not successful with its bid, it did attract a broader interest in the sector’s low valuations, as investors sought out other potential take-out candidates. Detour Gold, also in the Fund, was one that became the subject of market commentary as a potential target and its stock rose in response, which added to the contribution Osisko Mining’s performance made to the Fund during the first nine months of fiscal 2014.

The middle of the fiscal year—February through July—continued to see a renewed interest in gold and gold stocks, with robust enthusiasm during the first few months and then more reluctantly, as general equity and bond markets attempted to factor in sluggish global economic growth and the U.S. Federal Reserve’s future interest rate policy. During this period, precious metal equities did outperform broader markets by a large margin and investors seemed to prefer exposure through royalty companies such as Franco Nevada Corporation, Royal Gold Inc. and Silver Wheaton Corp. Through most of the year those companies represented about 10% to 15% of the Fund’s overall investment in the precious metals equity sector. The royalty companies enjoy a business model that participates directly in metal production and revenues with less direct exposure to the operating risks and costs that precious metal mining companies are exposed to. Additionally, royalty companies have more flexibility and are more disciplined with their allocation of capital. Along with their diverse exposure to various sources of gold production or royalties, and reduced risk exposure, they tend to receive a much better valuation. The weighting exposure to the royalty companies and their performance made a considerable difference to the Fund’s returns throughout the year but especially during the middle of the year.

While the first nine months of the fiscal year showed impressive gains for the Fund’s precious metal equities positions, outperforming the S&P 500 during that time-frame; those strong gains were confronted with a bout of weakness for gold which began in late August and coincided with the breakdown of the Yen and the Euro vs. the U.S. dollar. Commentators from all quarters became aggressively negative on gold and increasingly on gold stocks with a chorus that seemed unanimously bearish during the last three months into late October. Meanwhile, investors seemed more committed to the performance in U.S. equity and bond markets as they left gold behind. The Fund’s weighting in gold bullion, the Fund’s largest investment position, tempered the decline in precious metal mining stock performance during the final fiscal quarter. Gold prices fell about a quarter of what gold equities corrected, offering a degree of stability in a sector that moved quickly from strong outperformer to underperformer as markets witnessed weaker Yen and Euros relative to the U.S. dollar.

As we start a new fiscal year, we have become more enthusiastic about values in the gold sector, and are witnessing more asset sales and signs of mergers and acquisitions. The lower gold price will make it more difficult for some of the higher cost producers to carry on, which will likely result in consolidation, usually a healthy development for a beaten up industry. M&A activity tends to attract capital and along with that higher valuations, in addition to a new commitment to profitability.

| Annual Report | 11 |

We continue to seek investments for the Fund in well managed companies with strong balance sheets and assets, which are able to create value independently of gold price action. Value creation comes about in numerous ways, whether it’s progress in the construction of new mines, or successful exploration or M&A activity. We believe that during 2015, cost cutting, capital allocation and M&A activity will likely be some of the main topics precious metal stock investors and market speculators will focus on. We continue to believe that investing in the securities of well managed precious metal mining and royalty companies, with sound balance sheets, offers the most dynamic and reliable exposure to the upside potential in the gold price. Our research activity and portfolio selection is based on emphasizing the value creators in the sector and avoiding the value destroyers.

Best regards,

|

| |

| John C. Hathaway | Douglas B. Groh | |

| Portfolio Manager | Portfolio Manager |

| 12 | October 31, 2014 |

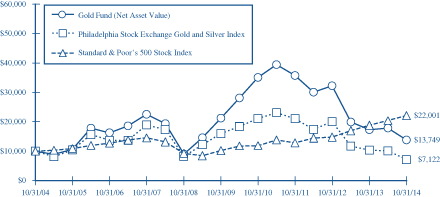

The Tocqueville Gold Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/04. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

In 2006, 2009, and 2010 the performance of The Tocqueville Gold Fund was achieved during a period of unusually favorable market conditions. Such performance may not be sustainable.

The Philadelphia Stock Exchange Gold and Silver Index is an unmanaged capitalization-weighted index which includes the leading companies involved in the mining of gold and silver. Returns include the reinvestment of all dividends.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2014

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

The Tocqueville Gold Fund | -20.07% | -27.11% | -8.21% | 3.24% | ||||||||||||

Philadelphia Stock Exchange Gold and Silver Index | -30.89% | -30.18% | -14.87% | -3.32% | ||||||||||||

Standard & Poor’s 500 Stock Index | 17.27% | 19.77% | 16.69% | 8.20% | ||||||||||||

| Annual Report | 13 |

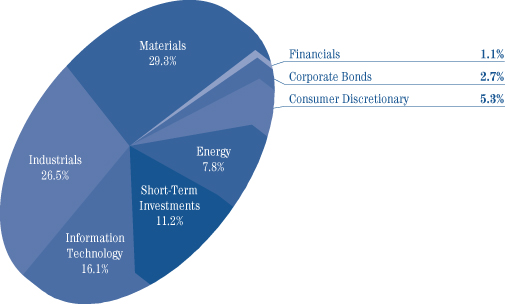

The Delafield Fund

Dear Fellow Shareholder,

Markets exhibited extraordinary resiliency early in the fiscal year, shrugging off the government shutdown in October 2013 and advancing to near all-time-highs despite ongoing concerns about the tapering of the Fed’s quantitative easing program, only modest improvement in labor data, and mixed signals from the housing market. Broadly speaking, investors remained favorably disposed to equities for the balance of the fiscal year, though episodic sell-offs seemed to reveal an underlying nervousness among investors. For example, solid corporate earnings results in February convinced investors that concurrent weak retail and housing data were only temporary and weather driven, and so markets rose across the board. However, in March, a lack of favorable data points seemed to trigger profit taking, and markets began to come under pressure, which continued into April with the release of weaker than expected first quarter domestic economic data. Then, as temperatures began to rise, both economic activity and the stock market began to rebound. Specifically, improved consumer confidence, jobs and housing reports during the latter part of the second calendar quarter seemed to be the tonic for a jittery market, and most major indices experienced solid gains despite renewed geopolitical flare-ups in the Middle East and Ukraine. The next selloff occurred in July, after the Federal Reserve’s meeting commentary caused investor anticipation of a near term interest rate hike. The volatile situation in both the Middle East and Ukraine also seemed to weigh on the markets. Mostly favorable domestic economic data released throughout August offered a respite, albeit only temporarily, as September brought with it renewed worries over slowing growth in foreign economies, particularly Europe and China, as well as reduced corporate earnings expectations heading into earnings season. These concerns then faded to close out the year, with the market rebounding in October.

The Fund’s performance, which had been satisfactory through the midpoint of the period, deteriorated in the latter half and resulted in a disappointing fiscal year. For the twelve months ended October 31, 2014, The Delafield Fund’s net asset value increased 1.58% to $36.40 per share. During the same twelve months, on a total return basis, the Russell 2000 Index (“Russell 2000”) posted an 8.06% increase, while the Standard & Poor’s 500 Index (“S&P 500”) increased 17.27%. Owing to the smaller average market capitalization of companies in the Russell 2000, we view it as the more appropriately comparative index to the Fund.

During the year, exposure to the energy sector was increased after identifying a number of compelling investment opportunities in the equipment and services and oil/gas consumable fuels industries. However, our timing proved to be early. Several of the energy companies have progressed somewhat more slowly on their turnarounds than we had anticipated and experienced earnings related disappointments. Later in the fiscal year, a global decline in oil prices further pressured all energy sector stocks, though the shares of the smaller capitalization energy names in which the Fund was invested were particularly impacted. In aggregate, the Fund’s energy holdings were responsible for nearly 300 basis points of negative absolute performance and roughly 165 basis points of relative underperformance when compared to the Russell 2000. One energy sector stock, Energy XXI Ltd. was the largest individual detractor from the fiscal year performance. Shares were initially purchased believing that its anticipated acquisition of EPL Oil & Gas would consolidate its position in the Gulf Coast shelf leading to efficiencies of operation and substantial free cash flow. However, due to some unexpected operating inefficiencies, the decline in the price of oil referenced earlier, and then late in the fiscal year, tax loss selling, the shares declined radically.

Performance in the specialty retail and metals and mining industries were also detrimental to the absolute and relative return this year (about 225 and 250 basis points, respectively). In specialty retail, Ascena Retail Group Inc. was the primary culprit, with the shares off on weaker than expected near-term results in a challenging retail environment. However, our thesis on this stock remains intact, and the position was opportunistically added to. The disappointing metal and mining performance was largely driven by Molycorp Inc. Considerable time was spent visiting Molycorp’s operations and with management, and we continue to believe that eventually Molycorp will be successful at operating the Mountain Pass mine efficiently and become a low cost, profitable supplier of rare earths. Unfortunately, however, the capital needed to achieve this result has increased dramatically and has stretched their balance sheet to the breaking point and therefore, we came to the difficult decision to sell the holding.

| 14 | October 31, 2014 |

Despite the disappointments highlighted above, the Fund did experience a number of successful outcomes as well. The chemicals industry, which represented about 15% of portfolio during the year, strongly outperformed the Russell 2000. The chemicals stocks in the Fund, led by LyondellBasell Industries, Minerals Technologies Inc. and PolyOne Corporation, generated better than a 12% aggregate return during the year compared to less than a 2% return in the Russell 2000 chemical industry components. Similarly, the electronic equipment instruments and components investments, together totaling almost 9% of the portfolio, increased about 23% during the year as compared to a 7% return from the comparable Russell 2000 stocks. Flextronics International Ltd. was the standout here, with the shares benefiting from consistently solid earnings results; strong free cash flow generation; and, meaningful share repurchase activity. And there were winning stocks even within sectors which hurt the portfolio the most this past year. For example, the Fund exited its investment in Finish Line, Inc. during the year, after the shares generated close to a 28% increase for the year.

To sum up, while not satisfied with last year’s results, we remain confident in our approach. We continued to actively search for companies that we believed were selling at prices which seemed modest in relation to the company’s intrinsic value and where something could change to alter that company’s future for the better. In general, we believe the companies in which the Fund is already invested in are doing well both fiscally and operationally. Some may be impacted in the near term by declining commodity prices, especially if energy exposed, and by the strengthening dollar. However, we continue to like the portfolio of special situation and value stocks and believe that over time the market will reflect the true value of these holdings. In retrospect, we should have taken more profits than we did earlier in the year, but since we believed the investments were making solid progress we were loath to do so. And, while the sharp decline in share prices over the past few months has reduced valuations we are paradoxically beginning to feel more bullish.

Sincerely,

|  | |

| J. Dennis Delafield | Vincent Sellecchia | |

| Portfolio Manager | Portfolio Manager | |

| Annual Report | 15 |

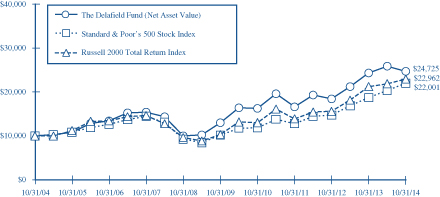

The Delafield Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/04. Since the Delafield Fund did not commence operations until 9/28/09, returns prior to that date are those of the Predecessor Fund. The Delafield Fund assumed the net asset value and performance history of the Predecessor Fund (See Footnote 1 to the Financial Statements). Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns include the reinvestment of all dividends.

The Russell 2000 Total Return Index is an unmanaged index that measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represent approximately 10% of the total market capitalization of the Russell 3000 Index. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2014

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

The Delafield Fund | 1.58% | 14.18% | 13.69% | 9.47% | ||||||||||||

Standard & Poor’s 500 Stock Index | 17.27% | 19.77% | 16.69% | 8.20% | ||||||||||||

Russell 2000 Total Return Index | 8.06% | 18.18% | 17.39% | 8.67% | ||||||||||||

| 16 | October 31, 2014 |

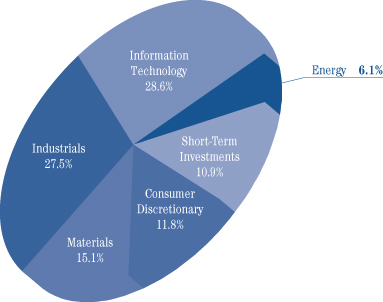

The Tocqueville Select Fund

Dear Fellow Shareholder,

Markets exhibited extraordinary resiliency early in the fiscal year, shrugging off the government shutdown in October 2013 and advancing to near all-time-highs despite ongoing concerns about the tapering of the Fed’s quantitative easing program, only modest improvement in labor data, and mixed signals from the housing market. Broadly speaking, investors remained favorably disposed to equities for the balance of the fiscal year, though episodic sell-offs seemed to reveal an underlying nervousness among investors. For example, solid corporate earnings results in February convinced investors that concurrent weak retail and housing data were only temporary and weather driven, and so markets rose across the board. However, in March, a lack of favorable data points seemed to trigger profit taking, and markets began to come under pressure, which continued into April with the release of weaker than expected first quarter domestic economic data. Then, as temperatures began to rise, both economic activity and the stock market began to rebound. Specifically, improved consumer confidence, jobs and housing reports during the latter part of the second calendar quarter seemed to be the tonic for a jittery market, and most major indices experienced solid gains despite renewed geopolitical flare-ups in the Middle East and Ukraine. The next selloff occurred in July, after the Federal Reserve’s meeting commentary caused investor anticipation of a near term interest rate hike. The volatile situation in both the Middle East and Ukraine also seemed to weigh on the markets. Mostly favorable domestic economic data released throughout August offered a respite, albeit only temporarily, as September brought with it renewed worries over slowing growth in foreign economies, particularly Europe and China, as well as reduced corporate earnings expectations heading into earnings season. These concerns then faded to close out the year, with the market rebounding in October.

Unfortunately, the portfolio was at times out of sync with the market and did not manage to keep stride for the fiscal year. For the twelve months ended October 31, 2014, The Tocqueville Select Fund’s net asset value increased 6.14% to $14.90 per share. During the same twelve months, on a total return basis, the Russell 2500 Index (“Russell 2500”) posted a 10.23% increase, while the Russell 2000 Index (“Russell 2000”), the Fund’s benchmarks, increased 8.06%.

Stock selection was in aggregate, favorable to the Fund’s relative return for the fiscal year. However, the performance of the holdings in the specialty retail and containers and packaging industries was subpar. Positions in both industries detracted from the absolute performance for the year, and, owing to their large weighting in the Fund (about 16% combined), adversely impacted the performance relative to the Russell 2500 by more than 400 basis points. In specialty retail, Ascena Retail Group Inc. was the primary culprit and also the largest single detractor to the Fund for the year. The shares were off on weaker than expected near-term results in a challenging retail environment. However, our thesis on this stock remains intact, and we opportunistically added to the position. Staples, Inc., also a specialty retail name, experienced a difficult twelve months, though the stock did rebound somewhat towards the end of the period. Owens-Illinois, Inc. was the biggest disappointment in the containers and packaging industry, with the stock off almost 19% on disappointing earnings driven by sluggish end market trends in certain geographies as well as operating inefficiencies in some manufacturing facilities.

Performance was also tempered somewhat by the size of the reserves, which approached 15% of the Fund’s net assets for the year and accounted for close to 160 basis points of underperformance. That said, holding cash was by no means an asset allocation strategy on our part. Rather, the level of reserves was an indication of the challenge we faced finding attractive investment opportunities in a market that generally appeared fully valued to us, in particular during the first half of the fiscal year. We were content to use the cash as a hedge against volatility in the near term and ultimately, we will employ these cash reserves to seize upon attractive and appropriately priced investment opportunities as we uncover them.

With respect to positive highlights for the year, the chemicals industry, which represented about 7% of our portfolio, strongly outperformed the Russell 2500. The chemicals stocks, led by Minerals Technologies Inc. and Ashland Inc. generated better than a 28% aggregate return during the year compared to just above a 9% return in the Russell 2500 chemical industry components. Similarly, the internet software and services investments, together totaling more than 5% of the portfolio, increased about 15% during the year as compared to a loss of close to 5% from the comparable Russell

| Annual Report | 17 |

2500 stocks. Conversant Inc. was the standout here, with the shares up sharply after agreeing to a takeover by Alliance Data Systems Corp.

While we are not satisfied with last year’s end results, we remain confident in our approach. Our investment strategy utilizes a strictly bottom-up approach whereby we search for companies that we believe are selling at prices which seem modest in relation to the company’s intrinsic value and where something may change which will alter that company’s future for the better. We continued to actively search for companies that we believed were selling at prices which seemed modest in relation to the company’s intrinsic value and where something could change to alter that company’s future for the better. In general, we believe the companies in which the Fund has already invested in are doing well both fiscally and operationally. Some may be impacted in the near term by declining commodity prices, especially if energy exposed, and by the strengthening dollar. However, we continue to like the portfolio of special situation and value stocks and believe that over time the market will reflect the true value of these holdings.

Sincerely,

| ||||

| |  | ||

| J. Dennis Delafield | Vincent Sellecchia | Donald Wang | ||

| Portfolio Manager | Portfolio Manager | Portfolio Manager |

| 18 | October 31, 2014 |

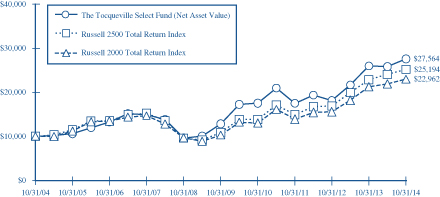

The Tocqueville Select Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on 10/31/04. Since The Tocqueville Select Fund did not commence operations until 9/28/09, returns from the period from September 29, 2008 to September 27, 2009 are those of the Class Y Shares of the Predecessor Fund (See Footnote 1 to the Financial Statements). Prior to that period, returns shown are those of a limited partnership managed by the adviser. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held 90 days or less.

In 2013 the performance of The Tocqueville Select Fund was achieved during a period of unusually favorable market conditions. Such performance may not be sustainable.

The Russel 2500 Total Return Index is an unmanaged index that measures the performance of the 2,500 smallest companies in the Russell 3000 Index. Returns include the reinvestment of all dividends.

The Russell 2000 Total Return Index is an unmanaged index that measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index. Returns include the reinvestment of all dividends.

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2014

| 1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

The Tocqueville Select Fund | 6.14% | 16.35% | 16.53% | 10.67% | ||||||||||||

Russell 2500 Total Return Index | 10.23% | 19.03% | 18.40% | 9.68% | ||||||||||||

Russell 2000 Total Return Index | 8.06% | 18.18% | 17.39% | 8.67% | ||||||||||||

| Annual Report | 19 |

The Tocqueville Alternative Strategies Fund

Dear Fellow Shareholder,

I am pleased to be writing this first annual letter to you as portfolio manager of the Tocqueville Alternative Strategies Fund. This Fund, previously managed by me as the CIO of Bridgehampton Capital Management, was reorganized into a series of The Tocqueville Trust and, simultaneously, my team and I became affiliated with Tocqueville Asset Management. The focus throughout the process was to find a home for the Fund that would provide the best platform from which to generate strong results for shareholders. The move to Tocqueville has enhanced absolutely every aspect of our business, including research, operations, marketing support, compliance and trading, among other things. The official transition date was June 30, 2014, and I could not be more pleased with the deep resources that have been added to our efforts as we have sought both continuity and continuous process improvement.

In this context, I would like to take a moment to review the investment objectives: the Fund seeks higher returns and lower volatility than the S&P 500 Index over a three to five year time horizon. Over shorter time periods, some Fund investors like to compare it to the HFRX North America (HFRXNA) Index. Parsing this a little bit, it should be made clear that we are not expecting to do better than the S&P 500 Index in every market condition or every part of the market cycle. Instead, through the use of the alternative strategies we deploy, the Fund seeks to generate absolute returns in a 1-2 year period with strategies that have modest, low or negative correlations to the broad indexes. We believe, but cannot guarantee, that the result will be an attractive return profile resulting in better risk-adjusted returns in aggregate than the S&P 500 Index over the entire cycle.

Over the twelve month period ending October 31, 2014, the Fund generated a total return of 3.14%1 versus a total return of 17.27% for the S&P 500 (the Fund’s benchmark) and a loss of -1.03% for the HFRXNA and. Since the inception of the predecessor fund, June 29, 2012, the Fund has had an annualized return of 7.84%1 versus 20.83% for the S&P 500 and 6.17% for the HFRXNA.

Of the 314 basis points (or 3.14 percentage points) the Fund made in the fiscal year, more than half can be accounted for by gains in Blackberry (BBRY), a special situations trade which has consistently been in the top holdings over the last few quarters. We have a high degree of confidence that the new CEO, John Chen, and his team can capitalize on the security, messaging and software assets that were underutilized by the prior hardware-focused management. BBRY’s enterprise software solutions support iphones, android and Windows phones. We believe that the company is widely misunderstood by investors and that this investment can work in any market environment. As such, BBRY remains a high conviction position, although the position size has been aggressively reduced to lock in gains, and BBRY is strongly positive for shareholders since the position was initiated in 2012. Hallador Energy (HNRG), a coal and gas company, and ISIS Pharmaceuticals, a biotechnology firm, also contributed positively on the equity front. In fixed income and converts, returns were generally muted, but our largest positive contributor was a hedged position in JC Penney Bonds (JCP 7.65% 2016), which contributed approximately +37 basis points in the period.

There were a handful of poorly performing positions, including a position in Corinthian Colleges (COCO) which went to its risk management limit as investors, including the Fund, lost confidence in the company’s ability to meet its financial obligations. The largest losing position in a fixed income security was a position in NII Holdings, a distressed bond position which was exited at a loss. The company’s liquidity position deteriorated to the point that we felt it prudent to take losses and move on, rather than wait for a default or restructuring event.

Overall, however, returns were muted across strategies. The four main strategy classifications, Convertible Arbitrage, Fixed Income, Special Situations and Long Equity contributed approximately +55 basis points, -57 basis points, +253 basis points and +261 basis points, respectively. In addition, the portfolio was adversely impacted by approximately -195 basis points in its portfolio hedges, primarily as a result of index hedges hurting the portfolio as stock markets rallied strongly, although the Fund also experienced losses in interest rate hedges.

With the depth of Tocqueville research, our idea generation tools, an experienced team and the ability to go anywhere in the capital structure, we believe we have a sustainable process that will serve the Fund well in any market environment, including today’s. Thank you for investing with the Tocqueville Alternative Strategies Fund.

| 20 | October 31, 2014 |

We hope to work for you for many years to come!

Sincerely,

| ||||

| ||||

| Kenneth Lee | ||||

| Portfolio Manager | ||||

| 1 | The performance information provided prior to June 30, 2014 is historical information for the Bridgehampton Value Strategies Fund (the “Predecessor Fund”), which was reorganized into the Tocqueville Alternative Strategies Fund on June 30, 2014. The Predecessor Fund was managed by Bridgehampton Capital Management LLC and has the same portfolio managers, investment objectives and investment strategies as the Tocqueville Alternative Strategies Fund. |

| Annual Report | 21 |

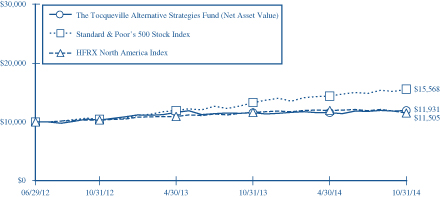

The Tocqueville Alternative Strategies Fund

(Unaudited)

This chart assumes an initial gross investment of $10,000 made on June 29, 2012. Since the Tocqueville Alternative Strategies Fund did not commence operations until June 30, 2014, returns prior to that date are those of the Predecessor Fund (See Footnote 1 to the Financial Statements). Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Performance reflects fee waivers in effect. In the absence of fee waivers, total return would be reduced. Returns shown include the reinvestment of all dividends and other distributions. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The Fund imposes a 2% redemption fee on shares held for 90 days or less.

The Standard & Poor’s 500 Stock Index (S&P 500) is a capital-weighted index, representing the aggregate market value of the common equity of 500 stocks primarily traded on the New York Stock Exchange. Returns include the reinvestment of all dividends.

The HFRX North America Index is designed to reflect the performance of the North American region of the hedge fund universe. Regional Investment Focus is designed to reflect the primary focus of the Fund’s strategic exposure, over various market cycles, independent of the investment manager’s physical location or the domiciled registration location of the fund. Fund investing in North America typically have greater than 50% exposure in North America. Returns include the reinvestment of all dividends

AVERAGE ANNUAL RATE OF RETURN (%)

FOR PERIODS ENDED OCTOBER 31, 2014

| 1 Year | Inception(1) | |||||||

The Tocqueville Alternative Strategies Fund | 3.14% | 7.84% | ||||||

Standard & Poor’s 500 Stock Index | 17.27% | 20.83% | ||||||

HFRX North America Index | –1.03% | 6.17% | ||||||

| (1) | Inception of the Predecessor Fund was June 29, 2012. |

| 22 | October 31, 2014 |

Expense Example—October 31, 2014 (Unaudited)

As a shareholder of The Tocqueville Trust (the “Funds”), you incur ongoing costs, including management fees; distribution fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held the entire period (May 1, 2014-October 31, 2014).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Annual Report | 23 |

Expense Example Tables (Unaudited)

| The Tocqueville Fund | Beginning Account Value May 1, 2014 | Ending Account Value October 31, 2014 | Expenses Paid During Period* May 1, 2014 - October 31, 2014 | |||||||||

Actual | $ | 1,000.00 | $ | 1,048.10 | $ | 6.40 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.95 | 6.31 | |||||||||

| The Tocqueville Opportunity Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 1,112.80 | $ | 6.98 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.60 | 6.67 | |||||||||

| The Tocqueville International Value Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 932.40 | $ | 6.09 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.90 | 6.36 | |||||||||

| The Tocqueville Gold Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 771.80 | $ | 5.94 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.50 | 6.77 | |||||||||

| The Delafield Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 954.90 | $ | 6.01 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,019.06 | 6.21 | |||||||||

| The Tocqueville Select Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 1,067.30 | $ | 6.93 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,018.50 | 6.77 | |||||||||

| The Tocqueville Alternative Strategies Fund | ||||||||||||

Actual | $ | 1,000.00 | $ | 1,030.20 | $ | 13.15 | ||||||

Hypothetical (5% return before expenses) | 1,000.00 | 1,012.25 | 13.03 | |||||||||

| * | Expenses are equal to the Fund’s annualized six-month expense ratio (including extraordinary expenses) of 1.24%, 1.31%, 1.25%, 1.33%, 1.22%, 1.33% and 2.57% for The Tocqueville Fund, Opportunity Fund, International Value Fund, Gold Fund, Delafield Fund, Select Fund, and Alternative Strategies Fund respectively, multiplied by the average account value over the period, multiplied by 184/365 to reflect the one-half year period. |

| 24 | October 31, 2014 |

The Tocqueville Fund

Financial Highlights

| Per share operating performance (For a share outstanding throughout the year) | Years Ended October 31, | |||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

Net asset value, beginning of year | $ | 30.67 | $ | 24.11 | $ | 22.23 | $ | 21.53 | $ | 18.47 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operations: | ||||||||||||||||||||

Net investment income (1) | 0.28 | 0.40 | 0.40 | 0.23 | 0.32 | |||||||||||||||

Net realized and unrealized gain | 3.78 | 6.51 | 1.81 | 0.80 | 2.97 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations * | 4.06 | 6.91 | 2.21 | 1.03 | 3.29 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | (0.30 | ) | (0.35 | ) | (0.33 | ) | (0.33 | ) | (0.23 | ) | ||||||||||

Distributions from net realized gains | (0.25 | ) | — | — | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total distributions | (0.55 | ) | (0.35 | ) | (0.33 | ) | (0.33 | ) | (0.23 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Change in net asset value for the year | 3.51 | 6.56 | 1.88 | 0.70 | 3.06 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value, end of year | $ | 34.18 | $ | 30.67 | $ | 24.11 | $ | 22.23 | $ | 21.53 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

* Includes redemption fees per share of | 0.00 | (2) | 0.00 | (2) | 0.00 | (2) | 0.00 | (2) | 0.00 | (2) | ||||||||||

Total Return | 13.4 | % | 29.0 | % | 10.1 | % | 4.8 | % | 18.0 | % | ||||||||||

Ratios/supplemental data | ||||||||||||||||||||

Net assets, end of year (000) | $ | 380,561 | $ | 348,269 | $ | 366,025 | $ | 491,541 | $ | 489,670 | ||||||||||

Ratio to average net assets: | ||||||||||||||||||||

Expenses before waiver/reimbursement | 1.25 | % | 1.28 | % | 1.29 | % | 1.26 | % | 1.26 | % | ||||||||||

Expenses after waiver/reimbursement | 1.24 | % | 1.26 | %(3) | 1.26 | %(3) | 1.25 | % | 1.25 | % | ||||||||||

Net investment income before waiver/reimbursement | 0.84 | % | 1.33 | % | 1.30 | % | 0.97 | % | 1.65 | % | ||||||||||

Net investment income after waiver/reimbursement | 0.85 | % | 1.35 | % | 1.33 | % | 0.98 | % | 1.66 | % | ||||||||||

Portfolio turnover rate | 19 | % | 16 | % | 17 | % | 28 | % | 23 | % | ||||||||||

| (1) | Net investment income per share is calculated using the ending balance prior to consideration or adjustment for permanent book-to-tax differences. |

| (2) | Represents less than $0.01. |

| (3) | Includes 0.01% of interest expense which is not included in the Fund’s operating expense cap. |

The Accompanying Notes are an Integral Part of these Financial Statements.

| Annual Report | 25 |

The Tocqueville Opportunity Fund

Financial Highlights

| Per share operating performance (For a share outstanding throughout the year) | Years Ended October 31, | |||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

Net asset value, beginning of year | $ | 21.29 | $ | 15.76 | $ | 14.96 | $ | 13.20 | $ | 10.78 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Operations: | ||||||||||||||||||||

Net investment loss (1) | (0.22 | ) | (0.13 | ) | (0.11 | ) | (0.13 | ) | (0.12 | ) | ||||||||||

Net realized and unrealized gain | 2.80 | 5.66 | 0.91 | 1.89 | 2.54 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from investment operations * | 2.58 | 5.53 | 0.80 | 1.76 | 2.42 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Distributions to shareholders: | ||||||||||||||||||||

Dividends from net investment income | — | — | — | — | — | |||||||||||||||

Distributions from net realized gains | (1.09 | ) | — | — | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total distributions | (1.09 | ) | — | — | — | — | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Change in net asset value for the year | 1.49 | 5.53 | 0.80 | 1.76 | 2.42 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net asset value, end of year | $ | 22.78 | $ | 21.29 | $ | 15.76 | $ | 14.96 | $ | 13.20 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

* Includes redemption fees per share of | 0.00 | (2) | 0.00 | (2) | 0.00 | (2) | 0.00 | (2) | 0.00 | (2) | ||||||||||

Total Return | 12.6 | % | 35.1 | % | 5.4 | % | 13.3 | % | 22.6 | % | ||||||||||

Ratios/supplemental data | �� | |||||||||||||||||||

Net assets, end of year (000) | $ | 80,324 | $ | 80,609 | $ | 65,455 | $ | 46,963 | $ | 32,863 | ||||||||||

Ratio to average net assets: | ||||||||||||||||||||

Expense | 1.30 | % | 1.30 | % | 1.32 | % | 1.36 | % | 1.41 | % | ||||||||||

Net investment loss | (0.90 | )% | (0.64 | )% | (0.76 | )% | (1.04 | )% | (1.08 | )% | ||||||||||

Portfolio turnover rate | 92 | % | 100 | % | 77 | % | 110 | % | 104 | % | ||||||||||

| (1) | Net investment loss per share is calculated using the ending balance prior to consideration or adjustment for permanent book-to-tax differences. |