| | |

| UNITED STATES

SECURITIES AND EXCHANGE COMMISSION |

| | |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | |

| Investment Company Act file number: | (811-00058) |

| | |

| Exact name of registrant as specified in charter: | The George Putnam Fund of Boston |

| | |

| Address of principal executive offices: | One Post Office Square, Boston, Massachusetts 02109 |

| | |

| Name and address of agent for service: | Robert T. Burns, Vice President

One Post Office Square

Boston, Massachusetts 02109 |

| | |

| Copy to: | John W. Gerstmayr, Esq.

Ropes & Gray LLP

800 Boylston Street

Boston, Massachusetts 02199-3600 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: | July 31, 2014 |

| | |

| Date of reporting period: | August 1, 2013 — January 31, 2014 |

| | |

|

Item 1. Report to Stockholders: | |

| | |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |

George Putnam

Balanced

Fund

Semiannual report

1 | 31 | 14

| | |

| Message from the Trustees | 1 | |

| |

| About the fund | 2 | |

| |

| Performance snapshot | 4 | |

| |

| Interview with your fund’s portfolio managers | 5 | |

| |

| Your fund’s performance | 11 | |

| |

| Your fund’s expenses | 14 | |

| |

| Terms and definitions | 16 | |

| |

| Other information for shareholders | 17 | |

| |

| Trustee approval of management contract | 18 | |

| |

| Financial statements | 25 | |

| |

| Shareholder meeting results | 59 | |

| |

Consider these risks before investing: Investments in small and/or midsize companies increase the risk of greater price fluctuations. Value stocks may fail to rebound, and the market may not favor value-style investing. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Risks associated with derivatives include increased investment exposure (which may be considered leverage) and, in the case of over-the-counter instruments, the potential inability to terminate or sell derivatives positions and the potential failure of the other party to the instrument to meet its obligations. Unlike bonds, funds that invest in bonds have fees and expenses. Stock and bond prices may fall or fail to rise over time for several reasons, including general financial market conditions and factors related to a specific issuer or industry. You can lose money by investing in the fund.

Message from the Trustees

Dear Fellow Shareholder:

In early 2014, stock prices fluctuated while most bond markets advanced, reversing the trends that dominated the two asset classes during 2013. Although the economic recovery appears to remain intact and previous market forces may re-emerge, the shift in short-term trends reminds investors once again about the value of portfolio diversification.

In this environment, we believe Putnam’s commitment to active fundamental research and taking a proactive view about risk is well suited to uncovering attractive investment opportunities.

We are pleased to report that this focus continues to earn Putnam high marks among industry peers. In 2013 — and for the third time in five years — Barron’s ranked Putnam one of the top two mutual fund families based on total returns across asset classes.

Lastly, for guidance on today’s markets, we also believe that you are well served by consulting with your financial advisor, who can help you assess your individual needs, time horizon, and risk tolerance — crucial for guiding you toward your investment goals.

As always, thank you for investing with Putnam.

About the fund

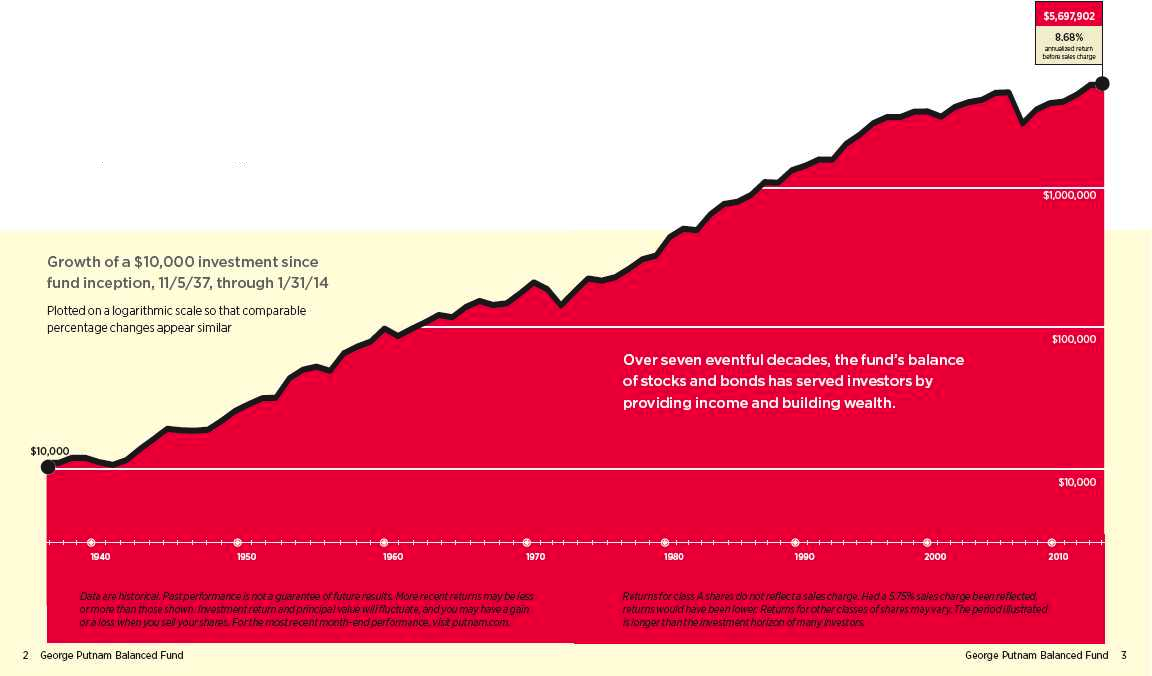

Providing the benefits of balanced investing since 1937

The fund launched in 1937 when George Putnam, a Boston investment manager, decided to introduce an innovative approach — a balance of stocks to seek capital growth and bonds to help provide current income. The original portfolio featured industrial stocks and railroad bonds.

This balanced approach made sense then, and we believe it continues to make sense now. In the late 1930s, the stock market experienced dramatic swings as businesses struggled to recover from the Great Depression and the shadow of war began to spread across Europe and Asia. Today, economic uncertainties continue to challenge investors.

Although the fund has experienced volatility at times, its balanced approach has kept it on course. When stocks were weak, the fund’s bonds helped results. Similarly, stocks often performed better when bonds were hurt by rising interest rates or inflation.

In a letter to shareholders dated July 12, 1938, George Putnam articulated the strategy this way: “Successful investing calls not so much for some clairvoyant ability to read the future as for the courage to stick to tested, commonsense policies in the face of the unreliable emotional stresses and strains that constantly sweep the market place.” Today, Putnam remains committed to this prudent approach.

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 5.75%; had they, returns would have been lower. See pages 2–3 and 11–13 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

* The fund’s benchmarks (Russell 1000 Value Index and George Putnam Blended Index) were introduced on 12/31/78 and its Lipper group (Balanced Funds) was introduced on 12/31/59; they all post-date the inception of the fund’s class A shares.

† Returns for the six-month period are not annualized, but cumulative.

George Putnam Blended Index is an unmanaged index administered by Putnam Management, 60% of which is the Russell 1000 Value Index and 40% of which is the Barclays U.S. Aggregate Bond Index.

| |

| 4 | George Putnam Balanced Fund |

Interview with your fund’s portfolio managers

What was the market environment like during the six months ended January 31, 2014?

David: During the semiannual period, investors who took on risk were generally rewarded. The period was not without volatility, however. For example, the market advance slowed in October as a result of the congressional budget debate, which led to a 16-day partial shutdown of the federal government. In January, the period’s final month, there was a small correction in U.S. equities, with the S&P 500 Index, a broad measure of U.S. stocks, declining more than 3.5%, due in part to year-end profit taking and some weaker macroeconomic data.

During the period, the Federal Reserve did a good job of communicating its intentions to eventually draw down its $85-billion-a-month purchase of bonds. Although the actual first $10 billion reduction did not take place until January 2014, this announcement of its intent to reduce bond buying affected the more interest-rate-sensitive areas of the fixed-income market.

How would you characterize the bond market environment during the period?

Kevin: Through the fourth quarter of 2013 and into 2014, the bond market continued to be a favorable environment for taking credit and liquidity risk. The central bank’s December decision to modestly reduce its bond-buying

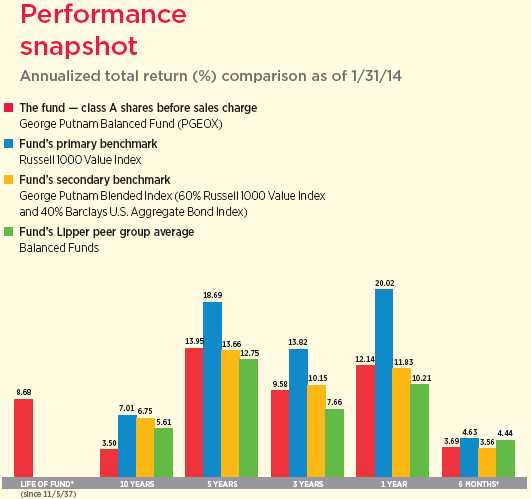

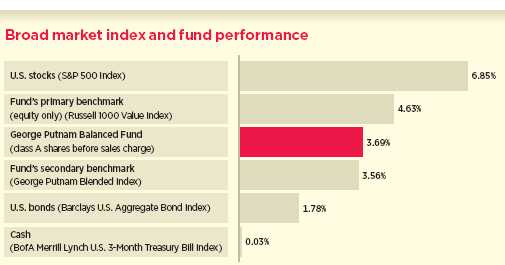

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 1/31/14. See pages 2–4 and 11–13 for additional fund performance information. Index descriptions can be found on pages 16–17.

| |

| George Putnam Balanced Fund | 5 |

program offered a degree of confirmation that the economy has continued to heal and growth was on track. Bond yields spiked on the news as the first reduction in the bond-buying program was somewhat earlier than the market was anticipating. Additionally, Japan’s economy strongly rebounded, while core European economies performed better than expected. All told, a supportive global economic backdrop encouraged investors to put capital to work in the credit markets.

How did the fund’s fixed-income portfolio fare during the period?

During the period, the fund’s fixed-income portfolio consisted primarily of U.S. Treasuries, agency securities, and high-grade corporate bonds. We’ve continued to de-emphasize interest-rate risk, reducing Treasuries and agencies in favor of the more attractive yield spreads of high-quality corporates. Overall, we also trimmed more of our bond exposure, elevating our cash position. While this cash exposure offered negligible returns and was a drag on performance versus the secondary benchmark, the George Putnam Blended Index, the lower bond exposure gave us a relative boost.

How did the fund’s stock portfolio perform for the period?

David: The fund’s stock portfolio returned 3.69% during the period, underperforming its benchmark, the Russell 1000 Value Index, which returned 4.63%. Our relatively underweight position in financials aided fund performance, while an overweight position in consumer staples detracted. We continued to see solid performance from individual stocks, which aided absolute performance.

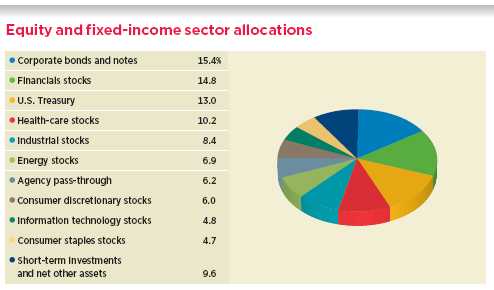

Allocations are shown as a percentage of the fund’s net assets as of 1/31/14. Short-term investments and net other assets, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, the exclusion of as-of trades, if any, and the use of different classifications of securities for presentation purposes. Holdings and allocations may vary over time.

| |

| 6 | George Putnam Balanced Fund |

How would you characterize the equity market environment you were investing in during the period?

David: As is usually the case, the overall market environment was dictated both by the actual and the forecasted movements in interest rates and company earnings. Prior to the period, interest rates had risen on expectations that the Fed would soon taper its monthly bond buying. As the period progressed, interest rates stabilized and overall economic growth remained tepid. With the postponement of Fed tapering, the market rally continued through the fourth quarter, pushing U.S. equities to their best annual performance since the 1990s.

Today, however, one of the interesting features of the U.S. equity market is that valuations are at an unusual level of parity. Rarely do we see equities with more homogeneity. To put it simply, most stocks are trading at a price-earnings ratio of around 15x earnings, meaning that valuations are essentially the same across all market sectors. Stocks are not overly expensive nor are they particularly cheap at this point in the cycle. This signals an environment in which fundamental research and bottom-up stock selection become more critical, and suggests that investors should pay closer attention to growth potential than to valuation.

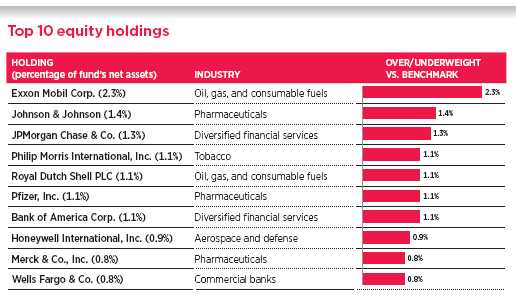

This table shows the fund’s top 10 holdings by percentage of the fund’s net assets as of 1/31/14. Short-term holdings and derivatives, if any, are excluded. Holdings may vary over time.

| |

| George Putnam Balanced Fund | 7 |

Which individual holdings contributed to performance versus the Russell 1000 Value Index, the equity-only benchmark, for the period?

David: The biggest contributor was our decision to underweight energy giant Chevron, which saw its fourth-quarter profit fall 32% on lower global production and weaker refined products margins.

We also benefited by overweighting media and technology company Comcast and hotel operator Marriott International. We believed both were solid franchises with growing cash flows and were reasonably priced at the beginning of the period. Ultimately, these two holdings benefited the fund’s performance.

Which individual holdings detracted from performance?

David: As was the case during the last period, an overweight position in multinational tobacco distributor Philip Morris International hurt performance, with the company suffering from negative earnings revisions due to weakening international markets and currencies. At today’s prices, however, we still believe the stock represents excellent value.

Another overweight position in domestic merchandiser Bed Bath & Beyond also detracted from performance. Overall weak consumer demand generally hurt retailers during the period, and earnings estimates for Bed Bath & Beyond were lowered. That said, we still believe the stock represents solid value in the current environment.

The fund changed its distribution rate during the period. Could you comment on the reasons for the change?

Kevin: The fund increased its dividend rate from $0.050 per share to $0.053 per share, an increase of 6.00% effective November 2013.

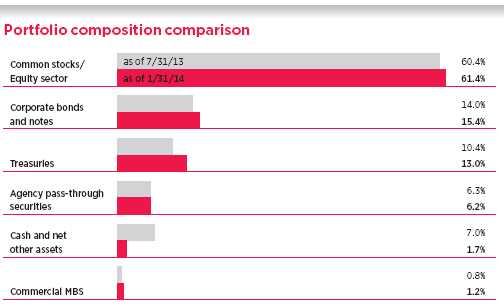

This chart shows how the fund’s top weightings have changed over the past six months. Allocations are shown as a percentage of the fund’s net assets. Current period summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, the exclusion of as-of trades, if any, and the use of different classifications of securities for presentation purposes. Holdings and allocations may vary over time.

| |

| 8 | George Putnam Balanced Fund |

This was the result of an increase in distributable income due to an increase in interest income earned in the fund.

What is your outlook for stocks over the next six months, and how are you positioning the fund in response?

David: When we consider the combination of valuation, fundamentals, and sentiment in today’s environment, we believe the 2013 run-up in the stock market was rational. However, by historical standards, this performance was exceedingly strong, and our outlook is more tempered for 2014. We believe equity valuations are at the middle of their historical range. With stocks at what we believe are average valuations, our expectation is for average returns. While we remain constructive on the current market, given how far we have risen, we are investing with a bit more caution than six months ago.

What is your outlook for the bond market for the coming months, and how are you positioning the fund?

Kevin: We are focused on several key risks. First, the Fed is faced with a delicate balancing act as it seeks to communicate further reductions in its bond-buying program without destabilizing the financial markets or the U.S. economy. This will bear watching as economic data unfold in the coming months.

The second area we are looking at is wage inflation. Generally speaking, investors believe wage inflation could become problematic at higher levels of employment. As the unemployment rate moves downward, if wage inflation develops earlier than the Fed is anticipating, we could see the Fed reducing its stimulus efforts much earlier than the markets are currently forecasting.

Lastly, it is possible that economic growth could be stronger in 2014 than forecast, particularly during the second half of the year. If that occurs, real interest rates [prevailing interest rate minus the rate of inflation], which have been negative since 2008, could significantly rise. In our opinion, however, rates are unlikely to rise so quickly that they undermine the markets.

In terms of positioning, given the prospect of higher interest rates, we have de-emphasized interest-rate risk and will continue to seek attractive opportunities for capitalizing on credit and liquidity spreads.

Thank you, David and Kevin, for bringing us up to date on the fund.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Portfolio Manager David M. Calabro holds a B.A. from Williams College. David joined Putnam in 2008 and has been in the investment industry since 1982.

Portfolio Manager Kevin F. Murphy holds a B.S. from Columbia University. He joined Putnam in 1999 and has been in the investment industry since 1988.

| |

| George Putnam Balanced Fund | 9 |

IN THE NEWS

The U.S. federal deficit this year will dip to its lowest level since 2007, but the trend may be short-lived. The Congressional Budget Office (CBO) has projected that the U.S. deficit will fall to $514 billion by the end of the current fiscal year on September 30, 2014, down from $680 billion last fiscal year and the recent peak of $1.4 trillion in 2009. Government spending cuts, tax hikes, and the overall economic expansion all helped to lower the deficit, which has been the focus of intense political debate in Washington. However, in coming years as baby boomers age, spending will accelerate on such government programs as Medicare and Social Security, widening the deficit. Without more robust economic growth, spending for Social Security, Medicare (including offsetting receipts), Medicaid, the Children’s Health Insurance Program, and subsidies for health insurance purchased through exchanges will rise from 9.7% of GDP in 2014 to 11.7% in 2024, the CBO estimates.

| |

| 10 | George Putnam Balanced Fund |

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended January 31, 2014, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance information as of the most recent calendar quarter-end and expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class R, R5, R6, and Y shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 1/31/14

| | | | | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R5 | Class R6 | Class Y |

| (inception dates) | (11/5/37) | (4/27/92) | (7/26/99) | (12/1/94) | (1/21/03) | (12/2/13) | (12/2/13) | (3/31/94) |

|

| | Before | After | | | | | Before | After | Net | Net | Net | Net |

| | sales | sales | Before | After | Before | After | sales | sales | asset | asset | asset | asset |

| | charge | charge | CDSC | CDSC | CDSC | CDSC | charge | charge | value | value | value | value |

|

| Annual average | | | | | | | | | | | | |

| (life of fund) | 8.68% | 8.59% | 8.56% | 8.56% | 7.86% | 7.86% | 7.95% | 7.90% | 8.41% | 8.75% | 8.75% | 8.75% |

|

| 10 years | 41.01 | 32.90 | 32.55 | 32.55 | 30.81 | 30.81 | 34.17 | 29.47 | 37.56 | 44.55 | 44.64 | 44.55 |

| Annual average | 3.50 | 2.89 | 2.86 | 2.86 | 2.72 | 2.72 | 2.98 | 2.62 | 3.24 | 3.75 | 3.76 | 3.75 |

|

| 5 years | 92.10 | 81.05 | 84.90 | 82.90 | 85.11 | 85.11 | 87.44 | 80.88 | 89.77 | 94.45 | 94.57 | 94.45 |

| Annual average | 13.95 | 12.61 | 13.08 | 12.83 | 13.11 | 13.11 | 13.39 | 12.58 | 13.67 | 14.22 | 14.24 | 14.22 |

|

| 3 years | 31.57 | 24.01 | 28.52 | 25.52 | 28.57 | 28.57 | 29.57 | 25.03 | 30.49 | 32.44 | 32.52 | 32.44 |

| Annual average | 9.58 | 7.44 | 8.72 | 7.87 | 8.74 | 8.74 | 9.02 | 7.73 | 9.28 | 9.82 | 9.84 | 9.82 |

|

| 1 year | 12.14 | 5.70 | 11.29 | 6.29 | 11.26 | 10.26 | 11.60 | 7.70 | 11.83 | 12.46 | 12.53 | 12.46 |

|

| 6 months | 3.69 | –2.28 | 3.26 | –1.74 | 3.26 | 2.26 | 3.40 | –0.21 | 3.51 | 3.81 | 3.87 | 3.81 |

|

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 5.75% and 3.50% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class R, R5, R6, and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares, except for class Y shares, for which 12b-1 fees are not applicable. Performance for class R5 and R6 shares prior to their inception is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R5 and R6 shares; had it, returns would have been higher.

Class B share performance reflects conversion to class A shares after eight years.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

| |

| George Putnam Balanced Fund | 11 |

Comparative index returns For periods ended 1/31/14

| | | | |

| | | Barclays | | Lipper |

| | Russell 1000 | U.S. Aggregate | George Putnam | Balanced Funds |

| | Value Index | Bond Index | Blended Index† | category average‡ |

|

| Annual average (life of fund) | —* | —* | —* | —* |

|

| 10 years | 96.89% | 57.03% | 92.09% | 73.49% |

| Annual average | 7.01 | 4.62 | 6.75 | 5.61 |

|

| 5 years | 135.55 | 27.23 | 89.66 | 82.74 |

| Annual average | 18.69 | 4.93 | 13.66 | 12.75 |

|

| 3 years | 47.45 | 11.61 | 33.64 | 24.92 |

| Annual average | 13.82 | 3.73 | 10.15 | 7.66 |

|

| 1 year | 20.02 | 0.12 | 11.83 | 10.21 |

|

| 6 months | 4.63 | 1.78 | 3.56 | 4.44 |

|

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

* The fund’s benchmarks (Russell 1000 Value Index and George Putnam Blended Index) were introduced on 12/31/78. The Barclays U.S. Aggregate Bond Index was introduced on 12/31/75, and the fund’s Lipper group (Balanced Funds) was introduced on 12/31/59. They all post-date the inception of the fund’s class A shares.

† George Putnam Blended Index is an unmanaged index administered by Putnam Management, 60% of which is the Russell 1000 Value Index and 40% of which is the Barclays U.S. Aggregate Bond Index.

‡ Over the 6-month, 1-year, 3-year, 5-year, and 10-year periods ended 1/31/14, there were 703, 687, 636, 601, and 328 funds, respectively, in this Lipper category.

Fund performance as of most recent calendar quarter

Total return for periods ended 12/31/13

| | | | | | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R5 | Class R6 | Class Y |

| (inception dates) | (11/5/37) | (4/27/92) | (7/26/99) | (12/1/94) | (1/21/03) | (12/2/13) | (12/2/13) | (3/31/94) |

|

| | Before | After | | | | | Before | After | Net | Net | Net | Net |

| | sales | sales | Before | After | Before | After | sales | sales | asset | asset | asset | asset |

| | charge | charge | CDSC | CDSC | CDSC | CDSC | charge | charge | value | value | value | value |

|

| Annual average | | | | | | | | | | | | |

| (life of fund) | 8.71% | 8.63% | 8.59% | 8.59% | 7.89% | 7.89% | 7.98% | 7.93% | 8.44% | 8.78% | 8.78% | 8.78% |

|

| 10 years | 44.83 | 36.50 | 36.14 | 36.14 | 34.38 | 34.38 | 37.76 | 32.93 | 41.46 | 48.53 | 48.53 | 48.53 |

| Annual average | 3.77 | 3.16 | 3.13 | 3.13 | 3.00 | 3.00 | 3.25 | 2.89 | 3.53 | 4.04 | 4.04 | 4.04 |

|

| 5 years | 90.03 | 79.11 | 82.80 | 80.80 | 83.02 | 83.02 | 85.20 | 78.72 | 87.64 | 92.36 | 92.36 | 92.36 |

| Annual average | 13.70 | 12.36 | 12.82 | 12.57 | 12.85 | 12.85 | 13.12 | 12.31 | 13.41 | 13.98 | 13.98 | 13.98 |

|

| 3 years | 35.91 | 28.09 | 32.89 | 29.89 | 32.81 | 32.81 | 33.78 | 29.10 | 34.89 | 36.90 | 36.90 | 36.90 |

| Annual average | 10.77 | 8.60 | 9.94 | 9.11 | 9.92 | 9.92 | 10.19 | 8.89 | 10.49 | 11.04 | 11.04 | 11.04 |

|

| 1 year | 17.76 | 10.99 | 16.92 | 11.92 | 16.85 | 15.85 | 17.18 | 13.08 | 17.44 | 18.08 | 18.08 | 18.08 |

|

| 6 months | 8.78 | 2.52 | 8.38 | 3.38 | 8.35 | 7.35 | 8.47 | 4.68 | 8.68 | 8.88 | 8.88 | 8.88 |

|

See the discussion following the Fund performance table on page 11 for information about the calculation of fund performance.

| |

| 12 | George Putnam Balanced Fund |

Fund price and distribution information For the six-month period ended 1/31/14

| | | | | | | | | | |

| Distributions | Class A | Class B | Class C | Class M | Class R | Class R5 | Class R6 | Class Y |

|

| Number | 2 | 2 | 2 | 2 | 2 | 0 | 0 | 2 |

|

| Income | $0.103 | $0.047 | $0.048 | $0.066 | $0.086 | — | — | $0.122 |

|

| Capital gains | — | — | — | — | — | — | — | — |

|

| Total | $0.103 | $0.047 | $0.048 | $0.066 | $0.086 | — | — | $0.122 |

|

| | Before | After | Net | Net | Before | After | Net | Net | Net | Net |

| | sales | sales | asset | asset | sales | sales | asset | asset | asset | asset |

| Share value | charge | charge | value | value | charge | charge | value | value | value | value |

|

| 7/31/13 | $14.81 | $15.71 | $14.65 | $14.72 | $14.62 | $15.15 | $14.77 | — | — | $14.86 |

|

| 12/2/13* | — | — | — | — | — | — | — | $15.28 | $15.28 | — |

|

| 1/31/14 | 15.25 | 16.18 | 15.08 | 15.15 | 15.05 | 15.60 | 15.20 | 15.30 | 15.31 | 15.30 |

|

| | Before | After | Net | Net | Before | After | Net | Net | Net | Net |

| Current rate | sales | sales | asset | asset | sales | sales | asset | asset | asset | asset |

| (end of period) | charge | charge | value | value | charge | charge | value | value | value | value |

|

| Current dividend | | | | | | | | | | |

| rate 1 | 1.39% | 1.31% | 0.66% | 0.69% | 0.93% | 0.90% | 1.16% | N/A | N/A | 1.62% |

|

| Current 30-day SEC | | | | | | | | | | |

| yield 2 | N/A | 1.24 | 0.57 | 0.57 | N/A | 0.79 | 1.07 | N/A | N/A | 1.57 |

|

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (5.75% for class A shares and 3.50% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

* Inception date of class R5 and R6 shares.

1 Most recent distribution, including any return of capital and excluding capital gains, annualized and divided by share price before or after sales charge at period-end.

2 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

| |

| George Putnam Balanced Fund | 13 |

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

| | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R5 | Class R6 | Class Y |

|

| Total annual operating expenses for | | | | | | | | |

| the fiscal year ended 7/31/13 | 1.01% | 1.76% | 1.76% | 1.51% | 1.26% | 0.73%* | 0.63%* | 0.76% |

|

| Annualized expense ratio for the six | | | | | | | | |

| month period ended 1/31/14† | 0.99% | 1.74% | 1.74% | 1.49% | 1.24% | 0.73% | 0.63% | 0.74% |

|

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report. Expenses are shown as a percentage of average net assets.

* Expenses for class R5 and R6 shares are based on the other expenses of class A shares for the fund’s last fiscal year, adjusted to reflect the lower investor servicing fees applicable to class R5 and R6 shares.

† For the fund’s most recent fiscal half year or, in the case of class R5 and R6 shares, for the period from 12/2/13 (commencement of operations) to 1/31/14.

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in the fund from August 1, 2013 (or, in the case of class R5 and R6 shares, from December 2, 2013 (commencement of operations)) to January 31, 2014. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R5 | Class R6 | Class Y |

|

| Expenses paid per $1,000*† | $5.08 | $8.91 | $8.91 | $7.64 | $6.36 | $1.22‡ | $1.05‡ | $3.80 |

|

| Ending value (after expenses) | $1,036.90 | $1,032.60 | $1,032.60 | $1,034.00 | $1,035.10 | $1,001.30 | $1,002.00 | $1,038.10 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 1/31/14 (or, in the case of class R5 and R6 shares, the period from 12/2/13 (commencement of operations) to 1/31/14). The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

‡ Had expenses for class R5 and R6 shares been shown for the entire period from 8/1/13 to 1/31/14, they would have been higher.

| |

| 14 | George Putnam Balanced Fund |

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended January 31, 2014, use the following calculation method. To find the value of your investment on August 1, 2013, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R5 | Class R6 | Class Y |

|

| Expenses paid per $1,000*† | $5.04 | $8.84 | $8.84 | $7.58 | $6.31 | $3.72 | $3.21 | $3.77 |

|

| Ending value (after expenses) | $1,020.21 | $1,016.43 | $1,016.43 | $1,017.69 | $1,018.95 | $1,021.53 | $1,022.03 | $1,021.48 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 1/31/14 (or, in the case of class R5 and R6 shares, the period from 12/2/13 (commencement of operations) to 1/31/14). The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the six-month period; then multiplying the result by the number of days in the six-month period; and then dividing that result by the number of days in the year.

| |

| George Putnam Balanced Fund | 15 |

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Before sales charge, or net asset value, is the price, or value, of one share of a mutual fund, without a sales charge. Before-sales-charge figures fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

After sales charge is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. After-sales-charge performance figures shown here assume the 5.75% maximum sales charge for class A shares and 3.50% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Current rate is the annual rate of return earned from dividends or interest of an investment. Current rate is expressed as a percentage of the price of a security, fund share, or principal investment.

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class R shares are not subject to an initial sales charge or CDSC and are available only to certain employer-sponsored retirement plans.

Class R5 shares and class R6 shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are only available to employer-sponsored retirement plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Comparative indexes

Barclays U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

George Putnam Blended Index is an unmanaged index administered by Putnam Management, LLC, 60% of which is the Russell 1000 Value Index and 40% of which is the Barclays U.S. Aggregate Bond Index.

Russell 1000 Value Index is an unmanaged index of those companies in the large-cap Russell 1000 Index chosen for their value orientation.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a

| |

| 16 | George Putnam Balanced Fund |

fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2013, are available in the Individual Investors section of putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of January 31, 2014, Putnam employees had approximately $433,000,000 and the Trustees had approximately $105,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

| |

| George Putnam Balanced Fund | 17 |

Trustee approval of management contract

Putnam Investment Management (“Putnam Management”) serves as investment manager to your fund under a management contract. In addition, Putnam Management’s affiliate, Putnam Investments Limited (“PIL”), provides services to your fund under a sub-management contract between Putnam Management and PIL. Putnam Management is majority owned (directly and indirectly) by Power Corporation of Canada, a diversified international management and holding company with interests in companies in the financial services, communications and other business sectors. Until his death on October 8, 2013, The Honourable Paul G. Desmarais, both directly and through holding companies, controlled a majority of the voting shares of Power Corporation of Canada. Upon his death, Mr. Desmarais’ voting control of shares of Power Corporation of Canada was transferred to The Desmarais Family Residuary Trust (the “Transfer”). As a technical matter, the Transfer may have constituted an “assignment” within the meaning of the Investment Company Act of 1940, as amended (the “1940 Act”), causing your fund’s existing management and sub-management contracts to terminate automatically. On October 18, 2013, the Trustees, including all of the Trustees who are not “interested persons” (as this term is defined in the 1940 Act) of the Putnam funds (the “Independent Trustees”), approved interim management contracts between the Putnam funds and Putnam Management and the continuance of your fund’s sub-management contract to address this possibility and to avoid disruption of investment advisory and other services provided to the Putnam funds. At a subsequent meeting on November 22, 2013, the Trustees, including all of the Independent Trustees, approved new definitive management contracts between the Putnam funds and Putnam Management and determined to recommend their approval to the shareholders of the Putnam funds at a shareholder meeting called for February 27, 2014. The Trustees also approved new sub-management contracts, to be effective at the same time as the new definitive management contracts. The fund’s shareholders approved your fund’s new management contract at a special meeting on February 27, 2014.

In considering whether to approve your fund’s interim management contract and the continuance of your fund’s sub-management contract in October, and in considering whether to approve your fund’s new definitive management contract and its new sub-management contract in November, the Trustees took into account that they had recently approved the continuation (through June 30, 2014) of the fund’s previous management and sub-management contracts at their meeting in June 2013. The Trustees considered that the terms of the interim management contract and new definitive management contract were identical to those of the previous management contract, except for the effective dates and initial terms and for certain non-substantive changes. They also considered that the terms of the sub-management contract were identical to those of the previous sub-management contract, except for the effective dates and initial terms. In light of the substantial similarity between the proposed contracts and the previous versions of these contracts approved by the Trustees at their June 2013 meeting, the Trustees relied to a considerable extent on their review of these contracts in connection with their June meeting. In addition, the Trustees considered a number other factors relating to the Transfer, including, but not limited to, the following:

• Information about the operations of The Desmarais Family Residuary Trust, including that Paul Desmarais, Jr. and André Desmarais,

| |

| 18 | George Putnam Balanced Fund |

Mr. Desmarais’ sons, were expected to exercise, jointly, voting control over the Power Corporation of Canada shares controlled by The Desmarais Family Residuary Trust.

• That Paul Desmarais, Jr. and André Desmarais had been playing active managerial roles at Power Corporation of Canada, with responsibility for the oversight of Power Corporation of Canada’s subsidiaries, including Putnam Investments, since Power Corporation of Canada had acquired Putnam Investments in 2007, including serving as Directors of Putnam Investments, and that the Transfer would not affect their responsibilities as officers of Power Corporation of Canada.

• The intention expressed by representatives of Power Corporation of Canada and its subsidiaries, Power Financial Corporation and Great-West Lifeco, that there would be no change to the operations or management of Putnam Investments, to Putnam Management’s management of the funds or to investment, advisory and other services provided to the funds by Putnam Management and its affiliates as a result of the Transfer.

• Putnam Management’s assurances that, following the Transfer, Putnam Management would continue to provide the same level of services to each fund and that the Transfer will not have an adverse impact on the ability of Putnam Management and its affiliates to continue to provide high quality investment advisory and other services to the funds.

• Putnam Management’s assurances that there are no current plans to make any changes to the operations of the funds, existing management fees, expense limitations, distribution arrangements, or the quality of any services provided to the funds or their shareholders, as a result of the Transfer.

• The benefits that the funds have received and may potentially receive as a result of Putnam Management being a member of the Power Corporation of Canada group of companies, which promotes the stability of the Putnam organization.

• Putnam Investments’ commitment to bear a reasonable share of the expenses incurred by the Putnam Funds in connection with the Transfer.

General conclusions in connection with the Trustees’ June 2013 approval of the fund’s management and sub-management contracts

As noted above, in connection with their deliberations in October and November 2013, in addition to the factors described above, the Trustees considered their recent approval of your fund’s management and sub-management contracts in June 2013. The Board oversees the management of each fund and, as required by law, determines annually whether to approve the continuance of your fund’s management and sub-management contracts. The Board, with the assistance of its Contract Committee, requests and evaluates all information it deems reasonably necessary under the circumstances in connection with its annual contract review. The Contract Committee consists solely of Independent Trustees.

At the outset of the review process, members of the Board’s independent staff and independent legal counsel met with representatives of Putnam Management to review the annual contract review materials furnished to the Contract Committee during the course of the previous year’s review and to discuss possible changes in these materials that might be necessary or desirable for the coming year. Following these discussions and in consultation with the Contract Committee, the Independent Trustees’ independent legal counsel requested that Putnam Management furnish specified information, together with any additional information that Putnam Management considered relevant, to the Contract Committee. Over the

| |

| George Putnam Balanced Fund | 19 |

course of several months ending in June 2013, the Contract Committee met on a number of occasions with representatives of Putnam Management, and separately in executive session, to consider the information that Putnam Management provided. Throughout this process, the Contract Committee was assisted by the members of the Board’s independent staff and by independent legal counsel for the Putnam funds and the Independent Trustees.

In May 2013, the Contract Committee met in executive session to discuss and consider its preliminary recommendations with respect to the continuance of the contracts. At the Trustees’ June 20, 2013 meeting, the Contract Committee met in executive session with the other Independent Trustees to review a summary of the key financial data that the Contract Committee considered in the course of its review. The Contract Committee then presented its written report, which summarized the key factors that the Committee had considered and set forth its final recommendations. The Contract Committee then recommended, and the Independent Trustees approved, the continuance of your fund’s management and sub-management contracts, effective July 1, 2013, subject to certain changes in the sub-management contract noted below. (Because PIL is an affiliate of Putnam Management and Putnam Management remains fully responsible for all services provided by PIL, the Trustees have not evaluated PIL as a separate entity, and all subsequent references to Putnam Management below should be deemed to include reference to PIL as necessary or appropriate in the context.)

The Independent Trustees’ June 2013 approval was based on the following conclusions:

• That the fee schedule in effect for your fund represented reasonable compensation in light of the nature and quality of the services being provided to the fund, the fees paid by competitive funds, and the costs incurred by Putnam Management in providing services to the fund, and

• That the fee schedule represented an appropriate sharing between fund shareholders and Putnam Management of such economies of scale as may exist in the management of the fund at current asset levels.

These conclusions were based on a comprehensive consideration of all information provided to the Trustees and were not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations and how the Trustees considered these factors are described below, although individual Trustees may have evaluated the information presented differently, giving different weights to various factors. It is also important to recognize that the management arrangements for your fund and the other Putnam funds are the result of many years of review and discussion between the Independent Trustees and Putnam Management, that some aspects of the arrangements may receive greater scrutiny in some years than others, and that the Trustees’ conclusions may be based, in part, on their consideration of fee arrangements in previous years. For example, with some minor exceptions, the current fee arrangements in the management contracts for the Putnam funds were implemented at the beginning of 2010 following extensive review and discussion by the Trustees, as well as approval by shareholders.

As noted above, the Trustees considered administrative revisions to your fund’s sub-management contract. Putnam Management recommended that the sub-management contract be revised to reduce the sub-management fee that Putnam Management pays to PIL with respect to the portion of the portfolios of certain funds, but not your fund, that may be allocated to PIL from time to time. The Independent Trustees’ approval of this recommendation was based on their conclusion that these changes would have no practical

|

| 20 George Putnam Balanced Fund |

effect on Putnam Management’s continued responsibility for the management of these funds or the costs borne by fund shareholders and would not result in any reduction in the nature and quality of services provided to the funds.

Management fee schedules and total expenses

The Trustees reviewed the management fee schedules in effect for all Putnam funds, including fee levels and breakpoints. The Trustees also reviewed the total expenses of each Putnam fund, recognizing that in most cases management fees represented the major, but not the sole, determinant of total costs to shareholders.

In reviewing fees and expenses, the Trustees generally focus their attention on material changes in circumstances — for example, changes in assets under management, changes in a fund’s investment style, changes in Putnam Management’s operating costs or profitability, or changes in competitive practices in the mutual fund industry — that suggest that consideration of fee changes might be warranted. The Trustees concluded that the circumstances did not warrant changes to the management fee structure of your fund.

Under its management contract, your fund has the benefit of breakpoints in its management fee schedule that provide shareholders with economies of scale in the form of reduced fee levels as assets under management in the Putnam family of funds increase. The Trustees concluded that the fee schedule in effect for your fund represented an appropriate sharing of economies of scale between fund shareholders and Putnam Management.

As in the past, the Trustees also focused on the competitiveness of each fund’s total expense ratio. In order to ensure that expenses of the Putnam funds continue to meet competitive standards, the Trustees and Putnam Management have implemented certain expense limitations. These expense limitations were: (i) a contractual expense limitation applicable to all retail open-end funds of 32 basis points on investor servicing fees and expenses and (ii) a contractual expense limitation applicable to all open-end funds of 20 basis points on so-called “other expenses” (i.e., all expenses exclusive of management fees, investor servicing fees, distribution fees, investment-related expenses, interest, taxes, brokerage commissions, extraordinary expenses and acquired fund fees and expenses). These expense limitations serve in particular to maintain competitive expense levels for funds with large numbers of small shareholder accounts and funds with relatively small net assets. Most funds, including your fund, had sufficiently low expenses that these expense limitations did not apply. Putnam Management’s support for these expense limitations was an important factor in the Trustees’ decision to approve the continuance of your fund’s management and sub-management contracts.

The Trustees reviewed comparative fee and expense information for a custom group of competitive funds selected by Lipper Inc. This comparative information included your fund’s percentile ranking for effective management fees and total expenses (excluding any applicable 12b-1 fee), which provides a general indication of your fund’s relative standing. In the custom peer group, your fund ranked in the second quintile in effective management fees (determined for your fund and the other funds in the custom peer group based on fund asset size and the applicable contractual management fee schedule) and in the second quintile in total expenses (excluding any applicable 12b-1 fees) as of December 31, 2012 (the first quintile representing the least expensive funds and the fifth quintile the most expensive funds). The fee and expense data reported by Lipper as of December 31, 2012 reflected the most recent fiscal year-end data available in Lipper’s database at that time.

| |

| George Putnam Balanced Fund | 21 |

In connection with their review of the management fees and total expenses of the Putnam funds, the Trustees also reviewed the costs of the services provided and the profits realized by Putnam Management and its affiliates from their contractual relationships with the funds. This information included trends in revenues, expenses and profitability of Putnam Management and its affiliates relating to the investment management, investor servicing and distribution services provided to the funds. In this regard, the Trustees also reviewed an analysis of Putnam Management’s revenues, expenses and profitability, allocated on a fund-by-fund basis, with respect to the funds’ management, distribution, and investor servicing contracts. For each fund, the analysis presented information about revenues, expenses and profitability for each of the agreements separately and for the agreements taken together on a combined basis. The Trustees concluded that, at current asset levels, the fee schedules in place represented reasonable compensation for the services being provided and represented an appropriate sharing of such economies of scale as may exist in the management of the Putnam funds at that time.

The information examined by the Trustees as part of their annual contract review for the Putnam funds has included for many years information regarding fees charged by Putnam Management and its affiliates to institutional clients such as defined benefit pension plans, college endowments, and the like. This information included comparisons of those fees with fees charged to the funds, as well as an assessment of the differences in the services provided to these different types of clients. The Trustees observed that the differences in fee rates between institutional clients and mutual funds are by no means uniform when examined by individual asset sectors, suggesting that differences in the pricing of investment management services to these types of clients may reflect historical competitive forces operating in separate markets. The Trustees considered the fact that in many cases fee rates across different asset classes are higher on average for mutual funds than for institutional clients, as well as the differences between the services that Putnam Management provides to the Putnam funds and those that it provides to its institutional clients. The Trustees did not rely on these comparisons to any significant extent in concluding that the management fees paid by your fund are reasonable.

Investment performance

The quality of the investment process provided by Putnam Management represented a major factor in the Trustees’ evaluation of the quality of services provided by Putnam Management under your fund’s management contract. The Trustees were assisted in their review of the Putnam funds’ investment process and performance by the work of the investment oversight committees of the Trustees, which meet on a regular basis with the funds’ portfolio teams and with the Chief Investment Officer and other senior members of Putnam Management’s Investment Division throughout the year. The Trustees concluded that Putnam Management generally provides a high-quality investment process — based on the experience and skills of the individuals assigned to the management of fund portfolios, the resources made available to them, and in general Putnam Management’s ability to attract and retain high-quality personnel — but also recognized that this does not guarantee favorable investment results for every fund in every time period.

The Trustees considered that 2012 was a year of strong competitive performance for many of the Putnam funds, with only a relatively small number of exceptions. They noted that this strong performance was exemplified by the fact that the Putnam funds were recognized by Barron’s as the best performing mutual fund complex for 2012 — the second time in four years that Putnam Management has achieved

|

| 22 George Putnam Balanced Fund |

this distinction for the Putnam funds. They also noted, however, the disappointing investment performance of some funds for periods ended December 31, 2012 and considered information provided by Putnam Management regarding the factors contributing to the underperformance and actions being taken to improve the performance of these particular funds. The Trustees indicated their intention to continue to monitor performance trends to assess the effectiveness of these efforts and to evaluate whether additional actions to address areas of underperformance are warranted.

For purposes of evaluating investment performance, the Trustees generally focus on competitive industry rankings for the one-year, three-year, and five-year periods. For a number of Putnam funds with relatively unique investment mandates, the Trustees evaluated performance based on comparisons of their total returns with the returns of selected investment benchmarks or targeted returns. In the case of your fund, the Trustees considered that its class A share cumulative total return performance at net asset value was in the following quartiles of its Lipper Inc. peer group (Lipper Balanced Funds) for the one-year, three-year and five-year periods ended December 31, 2012 (the first quartile representing the best-performing funds and the fourth quartile the worst-performing funds):

| |

| One-year period | 2nd |

|

| Three-year period | 1st |

|

| Five-year period | 4th |

|

Over the one-year, three-year and five-year periods ended December 31, 2012, there were 674, 645 and 607 funds, respectively, in your fund’s Lipper peer group. (When considering performance information, shareholders should be mindful that past performance is not a guarantee of future results.) The Trustees, while noting that your fund’s investment performance over the one- and three-year periods ended December 31, 2012 had been favorable, expressed concern about your fund’s fourth quartile performance over the five-year period then ended and considered the circumstances that may have contributed to this disappointing performance. The Trustees considered Putnam Management’s observation that the fund’s underperformance over this period was due in significant part to the fund’s particularly weak performance 2008, which was largely due to the fund’s exposure to mortgage-backed securities and collateralized mortgage obligations.

The Trustees considered steps that Putnam Management had taken to support improved performance, noting in particular that, in November 2008, a new portfolio manager replaced the three individuals on the portfolio management team with responsibility for the fund’s equity investments, and that the fund’s relative performance has improved under this portfolio manager, with the fund ranking in the second quartile for the one-year period ended December 31, 2012 and in the first quartile for the three-year period then ended. The Trustees also considered a number of other changes that Putnam Management had made in recent years in efforts to support and improve fund performance generally. These changes included Putnam Management’s efforts to increase accountability and to reduce complexity in the portfolio management process for the Putnam equity funds by moving generally from a portfolio management team structure to a decision-making process that vests full authority and responsibility with individual portfolio managers and by affirming its commitment to a fundamental-driven approach to investing. The Trustees noted that Putnam Management had also worked to strengthen its fundamental research capabilities by adding new investment personnel to the large-cap equities research team and by bringing U.S. and international research under common leadership. In addition, the Trustees recognized that Putnam Management has adjusted the compensation

| |

| George Putnam Balanced Fund | 23 |

structure for portfolio managers and research analysts so that only those who achieve top-quartile returns over a rolling three-year basis are eligible for full bonuses.

As a general matter, the Trustees believe that cooperative efforts between the Trustees and Putnam Management represent the most effective way to address investment performance issues that may arise from time to time. The Trustees noted that investors in the Putnam funds have, in effect, placed their trust in the Putnam organization, under the oversight of the funds’ Trustees, to make appropriate decisions regarding the management of the funds. Based on past responsiveness of Putnam Management to Trustee concerns about investment performance, the Trustees concluded that it is preferable to seek change within Putnam Management to address performance shortcomings. In the Trustees’ view, the alternative of engaging a new investment adviser for an underperforming fund would entail significant disruptions and would not provide any greater assurance of improved investment performance.

Brokerage and soft-dollar allocations; investor servicing

The Trustees considered various potential ben-efits that Putnam Management may receive in connection with the services it provides under the management contract with your fund. These include benefits related to brokerage allocation and the use of soft dollars, whereby a portion of the commissions paid by a fund for brokerage may be used to acquire research services that are expected to be useful to Putnam Management in managing the assets of the fund and of other clients. Subject to pol icies established by the Trustees, soft dollars generated by these means are used primar ily to acquire brokerage and research services that enhance Putnam Management’s invest ment capabilities and supplement Putnam Management’s internal research efforts. How ever, the Trustees noted that a portion of available soft dollars continues to be used to pay fund expenses. The Trustees indicated their continued intent to monitor regulatory and industry developments in this area with the assistance of their Brokerage Committee and also indicated their continued intent to monitor the allocation of the Putnam funds’ brokerage in order to ensure that the principle of seeking best price and execution remains paramount in the portfolio trading process.

Putnam Management may also receive benefits from payments that the funds make to Putnam Management’s affiliates for investor or distri bution services. In conjunction with the annual review of your fund’s management and sub management contracts, the Trustees reviewed your fund’s investor servicing agreement with Putnam Investor Services, Inc. (“PSERV”) and its distributor’s contracts and distribution plans with Putnam Retail Management Limited Part nership (“PRM”), both of which are affiliates of Putnam Management. The Trustees concluded that the fees payable by the funds to PSERV and PRM, as applicable, for such services are reasonable in relation to the nature and quality of such services, the fees paid by competitive funds, and the costs incurred by PSERV and PRM, as applicable, in providing such services.

|

| 24 George Putnam Balanced Fund |

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

| |

| George Putnam Balanced Fund | 25 |

The fund’s portfolio 1/31/14 (Unaudited)

| | |

| COMMON STOCKS (57.7%)* | Shares | Value |

|

| Banking (7.5%) | | |

| Bank of America Corp. | 813,800 | $13,631,150 |

|

| Bank of New York Mellon Corp. (The) | 188,200 | 6,014,872 |

|

| Barclays PLC ADR (United Kingdom) | 111,400 | 1,994,060 |

|

| BB&T Corp. | 63,900 | 2,390,499 |

|

| Capital One Financial Corp. | 73,700 | 5,203,957 |

|

| Citigroup, Inc. | 204,550 | 9,701,807 |

|

| City National Corp. | 28,200 | 2,040,270 |

|

| Fifth Third Bancorp | 167,500 | 3,520,850 |

|

| JPMorgan Chase & Co. | 286,800 | 15,877,248 |

|

| PNC Financial Services Group, Inc. | 29,600 | 2,364,448 |

|

| Regions Financial Corp. | 310,500 | 3,157,785 |

|

| State Street Corp. | 125,000 | 8,368,750 |

|

| U.S. Bancorp | 228,700 | 9,086,251 |

|

| Wells Fargo & Co. | 230,000 | 10,428,200 |

|

| | | 93,780,147 |

| Basic materials (1.5%) | | |

| Agrium, Inc. (Canada) | 37,300 | 3,248,830 |

|

| Alcoa, Inc. | 76,900 | 885,119 |

|

| Dow Chemical Co. (The) | 102,948 | 4,685,163 |

|

| E.I. du Pont de Nemours & Co. | 28,400 | 1,732,684 |

|

| Freeport-McMoRan Copper & Gold, Inc. (Indonesia) | 72,200 | 2,340,002 |

|

| International Paper Co. | 59,600 | 2,845,304 |

|

| Nucor Corp. | 46,400 | 2,243,440 |

|

| PPG Industries, Inc. | 8,700 | 1,586,532 |

|

| | | 19,567,074 |

| Capital goods (3.4%) | | |

| Caterpillar, Inc. | 27,200 | 2,554,352 |

|

| Eaton Corp PLC | 72,300 | 5,284,407 |

|

| Emerson Electric Co. | 22,000 | 1,450,680 |

|

| General Dynamics Corp. | 64,200 | 6,504,102 |

|

| Illinois Tool Works, Inc. | 52,700 | 4,156,449 |

|

| Ingersoll-Rand PLC | 21,500 | 1,263,985 |

|

| Northrop Grumman Corp. | 35,100 | 4,055,805 |

|

| Parker Hannifin Corp. | 16,000 | 1,813,920 |

|

| Raytheon Co. | 72,100 | 6,854,547 |

|

| Schneider Electric SA (France) | 19,144 | 1,546,330 |

|

| Staples, Inc. | 28,500 | 375,060 |

|

| United Technologies Corp. | 58,300 | 6,647,366 |

|

| | | 42,507,003 |

| Communication services (1.5%) | | |

| AT&T, Inc. | 97,982 | 3,264,760 |

|

| Comcast Corp. Class A | 148,200 | 8,069,490 |

|

| Juniper Networks, Inc. † | 38,400 | 1,021,824 |

|

| Verizon Communications, Inc. | 134,800 | 6,473,096 |

|

| | | 18,829,170 |

| Conglomerates (1.5%) | | |

| 3M Co. | 12,900 | 1,653,651 |

|

| General Electric Co. | 301,500 | 7,576,695 |

|

|

| 26 George Putnam Balanced Fund |

| | |

| COMMON STOCKS (57.7%)* cont. | Shares | Value |

|

| Conglomerates cont. | | |

| Siemens AG ADR (Germany) † | 13,100 | $1,654,399 |

|

| Tyco International, Ltd. | 201,000 | 8,138,490 |

|

| | | 19,023,235 |

| Consumer cyclicals (5.2%) | | |

| ADT Corp. (The) | 42,450 | 1,275,198 |

|

| Bed Bath & Beyond, Inc. † | 87,100 | 5,561,335 |

|

| CBS Corp. Class B (non-voting shares) | 112,900 | 6,629,487 |

|

| D.R. Horton, Inc. † | 119,800 | 2,812,904 |

|

| Ford Motor Co. | 194,200 | 2,905,232 |

|

| Gaming and Leisure Properties, Inc. † R | 41,700 | 1,446,990 |

|

| General Motors Co. † | 82,900 | 2,991,032 |

|

| Hasbro, Inc. | 15,900 | 781,008 |

|

| Hilton Worldwide Holdings, Inc. † | 89,563 | 1,939,039 |

|

| Home Depot, Inc. (The) | 16,600 | 1,275,710 |

|

| Johnson Controls, Inc. | 148,300 | 6,839,595 |

|

| Macy’s, Inc. | 14,900 | 792,680 |

|

| Marriott International, Inc. Class A | 112,720 | 5,557,096 |

|

| Owens Corning, Inc. † | 53,000 | 2,021,950 |

|

| Penn National Gaming, Inc. † | 86,700 | 1,016,991 |

|

| PulteGroup, Inc. | 153,300 | 3,115,056 |

|

| Target Corp. | 20,400 | 1,155,456 |

|

| Time Warner, Inc. | 120,700 | 7,583,581 |

|

| TJX Cos., Inc. (The) | 28,700 | 1,646,232 |

|

| Viacom, Inc. Class B | 51,700 | 4,244,570 |

|

| Walt Disney Co. (The) | 55,600 | 4,037,116 |

|

| | | 65,628,258 |

| Consumer finance (0.2%) | | |

| American Express Co. | 37,500 | 3,188,250 |

|

| | | 3,188,250 |

| Consumer staples (4.6%) | | |

| Altria Group, Inc. | 98,000 | 3,451,560 |

|

| Coca-Cola Co. (The) | 41,300 | 1,561,966 |

|

| Coca-Cola Enterprises, Inc. | 86,500 | 3,744,585 |

|

| Colgate-Palmolive Co. | 27,400 | 1,677,702 |

|

| Coty, Inc. Class A | 269,300 | 3,632,857 |

|

| CVS Caremark Corp. | 120,800 | 8,180,576 |

|

| Dr. Pepper Snapple Group, Inc. | 47,400 | 2,269,512 |

|

| General Mills, Inc. | 64,500 | 3,097,290 |

|

| Kellogg Co. | 69,300 | 4,018,014 |

|

| Lorillard, Inc. | 21,000 | 1,033,620 |

|

| McDonald’s Corp. | 25,500 | 2,401,335 |

|

| PepsiCo, Inc. | 23,900 | 1,920,603 |

|

| Philip Morris International, Inc. | 180,400 | 14,096,456 |

|

| Procter & Gamble Co. (The) | 74,300 | 5,692,866 |

|

| Walgreen Co. | 26,900 | 1,542,715 |

|

| | | 58,321,657 |

| Energy (6.6%) | | |

| Anadarko Petroleum Corp. | 56,600 | 4,567,054 |

|

| Chevron Corp. | 55,400 | 6,184,302 |

|

| ConocoPhillips | 46,700 | 3,033,164 |

|

| |

| George Putnam Balanced Fund | 27 |

| | |

| COMMON STOCKS (57.7%)* cont. | Shares | Value |

|

| Energy cont. | | |

| Exxon Mobil Corp. | 310,600 | $28,624,896 |

|

| Halliburton Co. | 94,600 | 4,636,346 |

|

| Marathon Oil Corp. | 191,500 | 6,279,285 |

|

| Noble Corp. PLC | 48,500 | 1,504,955 |

|

| Occidental Petroleum Corp. | 26,100 | 2,285,577 |

|

| Phillips 66 | 18,300 | 1,337,547 |

|

| QEP Resources, Inc. | 67,200 | 2,075,808 |

|

| Royal Dutch Shell PLC ADR (United Kingdom) | 203,356 | 14,051,900 |

|

| Southwestern Energy Co. † | 54,900 | 2,233,881 |

|

| Suncor Energy, Inc. (Canada) | 117,100 | 3,844,393 |

|

| Total SA ADR (France) | 34,200 | 1,955,214 |

|

| | | 82,614,322 |

| Financial (0.8%) | | |

| Carlyle Group LP (The) (Partnership shares) | 149,200 | 5,193,652 |

|

| CME Group, Inc. | 70,900 | 5,300,484 |

|

| | | 10,494,136 |

| Health care (10.0%) | | |

| AstraZeneca PLC ADR (United Kingdom) | 61,500 | 3,905,250 |

|

| Baxter International, Inc. | 111,100 | 7,588,130 |

|

| Bristol-Myers Squibb Co. | 51,200 | 2,558,464 |

|

| CIGNA Corp. | 38,200 | 3,297,042 |

|

| Covidien PLC | 76,812 | 5,241,651 |

|

| Eli Lilly & Co. | 83,700 | 4,520,637 |

|

| GlaxoSmithKline PLC ADR (United Kingdom) | 107,400 | 5,535,396 |

|

| Johnson & Johnson | 196,000 | 17,340,120 |

|

| Medtronic, Inc. | 69,600 | 3,936,576 |

|

| Merck & Co., Inc. | 201,600 | 10,678,752 |

|

| Novartis AG ADR (Switzerland) | 27,300 | 2,158,610 |

|

| Pfizer, Inc. | 453,694 | 13,792,298 |

|

| Quest Diagnostics, Inc. | 40,300 | 2,115,750 |

|

| Sanofi ADR (France) | 96,200 | 4,704,180 |

|

| St. Jude Medical, Inc. | 68,900 | 4,184,297 |

|

| Stryker Corp. | 56,000 | 4,345,600 |

|

| Teva Pharmaceutical Industries, Ltd. ADR (Israel) | 97,200 | 4,338,036 |

|

| Thermo Fisher Scientific, Inc. | 62,900 | 7,242,306 |

|

| UnitedHealth Group, Inc. | 86,500 | 6,252,220 |

|

| Ventas, Inc. R | 46,000 | 2,869,940 |

|

| Zimmer Holdings, Inc. | 68,000 | 6,389,960 |

|

| Zoetis, Inc. | 76,205 | 2,313,584 |

|

| | | 125,308,799 |

| Insurance (3.5%) | | |

| Aflac, Inc. | 25,300 | 1,588,334 |

|

| American International Group, Inc. | 142,900 | 6,853,484 |

|

| Chubb Corp. (The) | 38,600 | 3,263,244 |

|

| Hartford Financial Services Group, Inc. (The) | 214,000 | 7,115,500 |

|

| Marsh & McLennan Cos., Inc. | 85,300 | 3,899,063 |

|

| MetLife, Inc. | 150,700 | 7,391,835 |

|

| Prudential Financial, Inc. | 69,100 | 5,831,349 |

|

|

| 28 George Putnam Balanced Fund |

| | |

| COMMON STOCKS (57.7%)* cont. | Shares | Value |

|

| Insurance cont. | | |

| Sun Life Financial, Inc. (Canada) | 57,300 | $1,888,035 |

|

| Travelers Cos., Inc. (The) | 74,400 | 6,047,232 |

|

| | | 43,878,076 |

| Investment banking/Brokerage (1.1%) | | |

| Charles Schwab Corp. (The) | 178,600 | 4,432,852 |

|

| Goldman Sachs Group, Inc. (The) | 50,010 | 8,207,641 |

|

| Morgan Stanley | 49,940 | 1,473,729 |

|

| | | 14,114,222 |

| Real estate (0.4%) | | |

| AvalonBay Communities, Inc. R | 22,800 | 2,815,800 |

|

| Public Storage R | 14,700 | 2,316,573 |

|

| | | 5,132,373 |

| Technology (6.1%) | | |

| Apple, Inc. | 10,400 | 5,206,240 |

|

| Cisco Systems, Inc. | 368,400 | 8,071,644 |

|

| eBay, Inc. † | 39,500 | 2,101,400 |

|

| EMC Corp. | 214,100 | 5,189,784 |

|

| Google, Inc. Class A † | 4,779 | 5,643,855 |

|