UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT

COMPANIES

Investment Company Act file number 811-05201

Thornburg Investment Trust

(Exact name of registrant as specified in charter)

c/o Thornburg Investment Management, Inc.

2300 North Ridgetop Road, Santa Fe, New Mexico 87506

(Address of principal executive offices) (Zip code)

Garrett Thornburg, 2300 North Ridgetop Road, Santa Fe, New Mexico 87506

(Name and address of agent for service)

Registrant’s telephone number, including area code: 505-984-0200

Date of fiscal year end: September 30, 2014

Date of reporting period: March 31, 2014

Item 1. Reports to Stockholders

The following annual reports are attached hereto, in order:

Thornburg Low Duration Municipal Fund

Thornburg Limited Term Municipal Fund

Thornburg Intermediate Municipal Fund

Thornburg Strategic Municipal Income Fund

Thornburg California Limited Term Municipal Fund

Thornburg New Mexico Intermediate Municipal Fund

Thornburg New York Intermediate Municipal Fund

Thornburg Low Duration Income Fund

Thornburg Limited Term Income Funds

Thornburg Strategic Income Fund

Thornburg Value Fund

Thornburg International Value Fund

Thornburg Core Growth Fund

Thornburg International Growth Fund

Thornburg Investment Income Builder Fund

Thornburg Global Opportunities Fund

Thornburg Developing World Fund

2 This page is not part of the Semi-Annual Report

IMPORTANT INFORMATION

The information presented on the following pages is current as of March 31, 2014. The managers’ views, portfolio holdings, and sector diversification are provided for the general information of the Fund’s shareholders; to the extent this information is historical, it should not be considered predictive of future circumstances. This material should not be deemed a recommendation to buy or sell any of the securities mentioned.

Investments in the Fund carry risks, including possible loss of principal. Bond funds have the same interest rate, inflation, and credit risks that are associated with the underlying bonds. The principal value of bonds will fluctuate relative to changes in interest rates, decreasing when interest rates rise. Unlike bonds, bond funds have ongoing fees and expenses. Please see the Fund’s Prospectus for a discussion of the risks associated with an investment in the Fund. Investments in the Fund are not FDIC insured, nor are they deposits of or guaranteed by a bank or any other entity. There is no guarantee that the Fund will meet its investment objectives. Diversification does not assure or guarantee better performance and cannot eliminate the risk of investment losses. The laddering strategy does not assure or guarantee better performance and cannot eliminate the risk of investment losses.

Performance data given at net asset value (NAV) does not take into account applicable sales charges. If the sales charges had been included, the performance would have been lower.

Minimum investments for Class I shares are higher than those for other classes. Class I shares may not be available to all investors.

| | | | |

Share Class | | NASDAQ Symbol | | CUSIP |

Class A | | TLMAX | | 885-216-788 |

Class I | | TLMIX | | 885-216-770 |

Glossary

Bloomberg Economic Evaluation of States (BEES) Index – A survey, updated quarterly, that examines the pace of states’ growth following the 18-month recession that officially ended in June 2009.

Bloomberg State Stock Indices – Capitalization-weighted indices consisting of equities domiciled in each state.

BofA Merrill Lynch 1-3 Year Municipal Securities Index – An index that is a subset of the BofA Merrill Lynch U.S. Municipal Securities Index including all securities with a remaining term to final maturity less than 3 years.

Consumer Price Index (CPI) – Index that measures prices of a fixed basket of goods bought by a typical consumer, including food, transportation, shelter, utilities, clothing, medical care, entertainment and other items. The CPI, published by the Bureau of Labor Statistics in the Department of Labor, is based at 100 in 1982 and is released monthly. It is widely used as a cost-of-living benchmark to adjust Social Security payments and other payment schedules, union contracts and tax brackets. Also known as the cost-of-living index.

Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. Investors may not make direct investments into any index.

Annualized Distribution Yield – The distribution yield reflects actual distributions made to shareholders. The annualized distribution yield is calculated by summing the last 30 days of income at a given month end and annualizing to a 360-day year. The result is divided by the ending maximum offering price.

Barbell Structure – A bond investment strategy that concentrates holdings in shorter-term and longer-term maturities, forming a structure that resembles a barbell.

Basis Point (bp) – A unit equal to 1/100th of 1%. 1% = 100 basis points (bps).

Bond Credit Ratings – A bond credit rating assesses the financial ability of a debt issuer to make timely payments of principal and interest. Ratings of AAA (the highest), AA, A, and BBB are investment-grade quality. Ratings of BB, B, CCC, CC, C, and D (the lowest) are considered below investment grade, speculative grade, or junk bonds. Unless otherwise noted, the ratings listed are from Municipal Market Data and are a combination of ratings from Standard and Poor’s, Moody’s Investors Service, and Fitch Ratings.

Bullet Structure – A bond investment strategy that concentrates holdings in intermediate-term maturities and avoids shorter-term or longer-term maturities.

Credit Spread/Quality Spread – The difference between the yields of securities with different credit qualities.

Duration – A bond’s sensitivity to interest rates. Bonds with longer durations experience greater price volatility than bonds with shorter durations.

Effective Duration – A bond’s sensitivity to interest rates, incorporating the embedded option features, such as call provisions. Bonds with longer durations experience greater price volatility than bonds with shorter durations.

Fed Funds Rate – The interest rate at which a depository institution lends immediately available funds (balances at the Federal Reserve) to another depository institution overnight.

General Obligation Bond – A municipal bond backed by the credit and “taxing power” of the issuing jurisdiction rather than the revenue from a given project.

Gross Domestic Product (GDP) – A country’s income minus foreign investments: the total value of all goods and services produced within a country in a year, minus net income from investments in other countries.

Participation Rate – The number of people who are either employed or are actively looking for work. The people who are no longer actively searching for work would not be included in the participation rate. During an economic recession, many workers often get discouraged and stop looking for employment, as a result, the participation rate decreases.

Quantitative Easing – The Federal Reserve’s monetary policy intended to stimulate the U.S. economy following the recession that began in 2007/08.

Quantitative Easing 3 (QE3) – The third round of the Federal Reserve’s monetary policy intended to stimulate the U.S. economy following the recession that began in 2007/08. Announced in September 2012 and revised in December 2012, December 2013, and January 2014, the Fed intends to buy $65 billion in mortgage-backed securities and Treasuries each month until the economy improves.

SEC Yield – SEC yield is computed in accordance with SEC standards measuring the net investment income per share over a specified 30-day period expressed as a percentage of the maximum offering price of the Fund’s shares at the end of the period.

Yield Curve – A line that plots the interest rates, at a set point in time, of bonds having equal credit quality, but differing maturity dates.

This page is not part of the Semi-Annual Report 3

THORNBURG LOW DURATION MUNICIPAL FUND

Laddering – an All Weather Strategy

The newest addition to Thornburg’s municipal fund line-up is Thornburg Low Duration Municipal Fund. The Fund pursues its primary goal by investing principally in a laddered maturity portfolio of municipal obligations issued by states and state agencies, local governments and their agencies and by certain United States territories and possessions. Thornburg Investment Management actively manages the Fund’s portfolio.

In our opinion, current market conditions have created an ideal situation in which to launch this strategy. Because the magnitude of changes in value of interest-bearing obligations is greater for obligations with longer durations, given an equivalent change in interest rates, the Fund seeks to reduce changes in its share value compared to longer duration fixed income portfolios by maintaining a portfolio of investments with a dollar-weighted average duration of normally no more than three years. The Fund also attempts to reduce changes in its share value through credit analysis, selection, and diversification.

At Thornburg, our approach to management of the Fund is based on the premise that investors in the Fund seek preservation of capital along with an attractive, relatively stable yield. While aggressive bond strategies may generate stronger returns when the market is turning a blind eye towards risk, they often fail to stack up over longer periods of time.

We apply these techniques to manage risk and pursue attractive returns:

| | • | | Building a laddered portfolio. Laddering has been shown over time to mitigate reinvestment and interest rate risk. |

| | • | | Conducting in-depth fundamental research on each issue and actively monitoring positions for subsequent credit events. |

| | • | | Diversifying among a large number of generally high-quality bonds. |

| | • | | Investing on a cash-only basis without using leverage. |

Portfolio Managers

Josh Gonze Chris Ryon, CFA

Objectives

The Fund seeks current income exempt from federal income taxes, consistent with preservation of capital.

Average Annual Total returns

For Periods Ended March 31, 2014

| | | | | | | | | | | | | | | | | | | | |

| | | 1 Yr | | | 3 Yrs | | | 5 Yrs | | | 10 Yrs | | | Since

Inception | |

A Shares (Incep: 12/30/13) | | | | | | | | | | | | | | | | | | | | |

Without sales charge | | | — | | | | — | | | | — | | | | — | | | | 0.06 | % |

With sales charge | | | — | | | | — | | | | — | | | | — | | | | -1.46 | % |

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate so shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than quoted. For performance current to the most recent month end, visit thornburg.com or call 800.847.0200.

The maximum sales charge for the Fund’s Class A shares is 1.50%. The total annual fund operating expense of Class A shares is 1.73%, as disclosed in the most recent Prospectus. Thornburg Investment Management and Thornburg Securities Corporation have contractually agreed to waive fees and reimburse expenses until at least February 1, 2015, so that actual expenses for Class A shares do not exceed 0.70%.

30-Day Yields, A Shares

As of March 31, 2014

| | | | |

Annualized Distribution Yield | | | 0.18 | % |

SEC Yield | | | 0.42 | % |

Without fee waivers and expense reimbursements, the 30-day SEC Yield would have been negative 1.58% and the Annualized Distribution Yield would have been negative 1.81%.

Key Portfolio Attributes

As of March 31, 2014

| | | | |

Number of Bonds | | | 38 | |

| |

Effective Duration | | | 1.5Yrs | |

| |

Average Maturity | | | 1.6Yrs | |

See the entire portfolio in the Schedule of Investments beginning on page 11.

4 This page is not part of the Semi-Annual Report

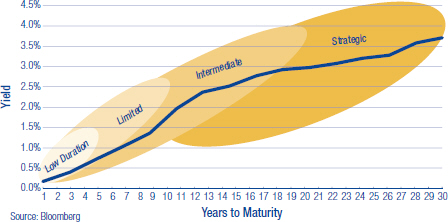

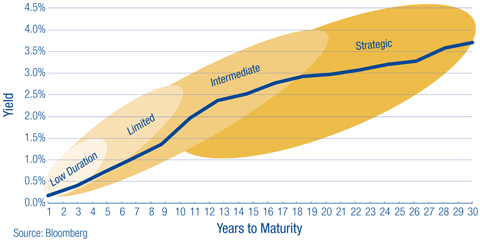

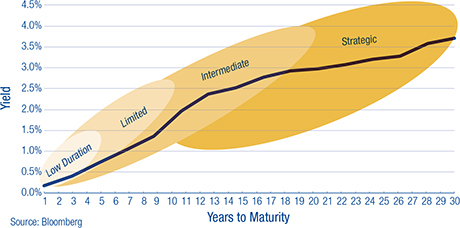

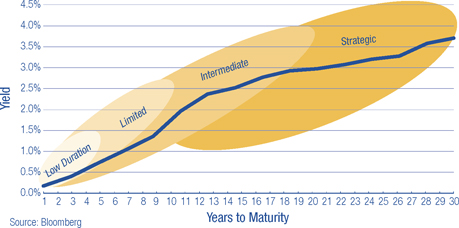

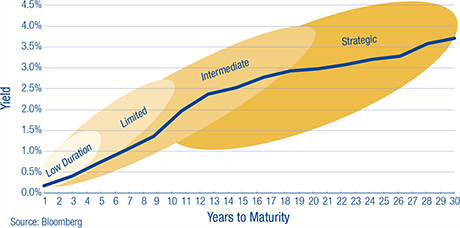

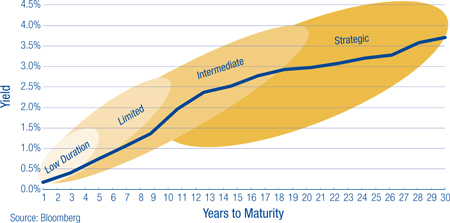

THORNBURG’S SUITE OF MUNICIPAL FUNDS

Municipal Funds for a Range of Interest-Rate Scenarios

At Thornburg, we often say that predicting interest rates is a fool’s game. And with the Federal Reserve still heavily involved in the markets, it’s even more difficult to forecast how rates may rise than when they may rise. Will long rates rise first and short rates follow? Will long and short rates climb simultaneously?

A traditional strategy to protect oneself against interest-rate risk is to move into shorter-duration bond strategies. But the seemingly counterintuitive response of moving to longer-duration strategies can sometimes yield better results.

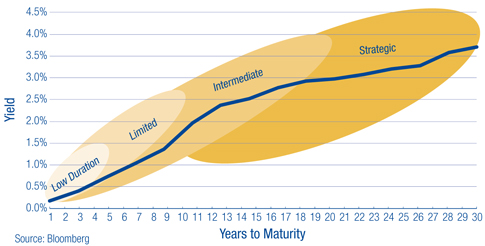

Diversify Across the Yield Curve

This uncertainty points to why it’s important for investors to match their investment horizon to the duration of the strategy in which they’re invested, and to diversify assets across the yield curve.

For any interest-rate scenario, Thornburg’s comprehensive suite of municipal funds gives prudent investors the ability to diversify across the yield curve.

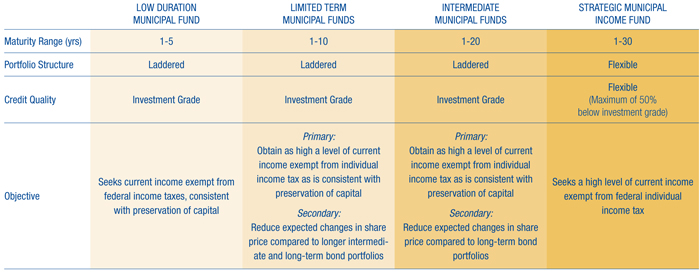

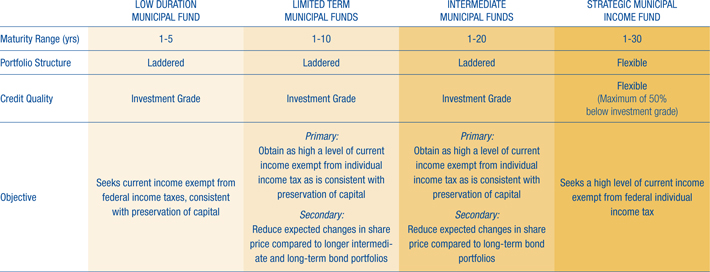

Diversify Across the Yield Curve with Thornburg Municipal Funds

AAA General Obligation Municipal Yield Curve, as of April 2, 2014

| | | | | | | | |

| | | Low Duration

Municipal Fund | | Limited Term

Municipal Funds | | Intermediate

Municipal Funds | | Strategic Municipal

Income Fund |

Maturity Range (yrs) | | 1-5 | | 1-10 | | 1-20 | | 1-30 |

| | | | |

Portfolio Structure | | Laddered | | Laddered | | Laddered | | Flexible |

| | | | |

Credit Quality | | Investment Grade | | Investment Grade | | Investment Grade | | Flexible

(Maximum of 50%

below investment grade) |

| | | | |

Objective | | Seeks current income

exempt from federal

income taxes,

consistent with

preservation of

capital | | Primary:

Obtain as high a level of current

income exempt from individual

income tax as is consistent with

preservation of capital Secondary: Reduce expected changes in

share price compared to longer

intermediate and long-term

bond portfolios | | Primary:

Obtain as high a level of current

income exempt from individual

income tax as is consistent with

preservation of capital Secondary: Reduce expected changes in

share price compared to long-

term bond portfolios | | Seeks a high level of current

income exempt from federal

individual income tax |

This page is not part of the Semi-Annual Report 5

Thornburg Low Duration Municipal Fund –

March 31, 2014

This report is certified under the Sarbanes-Oxley Act of 2002, which requires that public companies, including mutual funds, affirm that the information provided in their annual and semiannual shareholder reports fully and fairly represents their financial position and the results of their operations for the period presented.

6 Certified Semi-Annual Report

LETTER TO SHAREHOLDERS

April 15, 2014

Dear Fellow Shareholder:

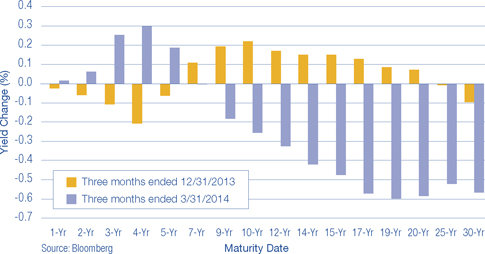

We are pleased to present the semi-annual report for the Thornburg Low Duration Municipal Fund. The fund commenced operations on December 30, 2013. Therefore this “semi-annual” report will reference the first three months of operations. The net asset value (NAV) of the Class A shares remained $12.31 per share during the three months ended March 31, 2014. If you were with us for the entire period, you received dividends of 0.0799 cents per share. If you reinvested your dividends, you received 0.0800 cents per share. Dividends were higher for Class I shares to account for varying class-specific expenses. The Class A shares of your Fund underperformed the index with a total return of 0.06% at NAV for the three months ended March 31, 2014, compared to the 0.25% total return for the BofA Merrill Lynch 1-3 Year Municipal Securities Index (BAML 1-3 Year Municipal Index). The Fund generated 0.85% more price return and 1.04% less income than the index.

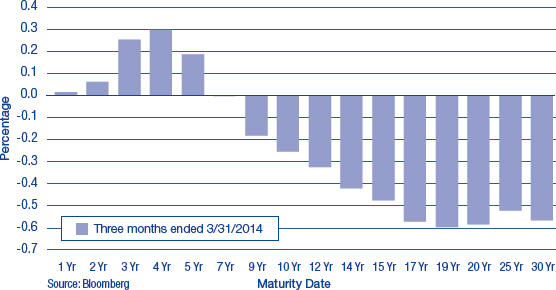

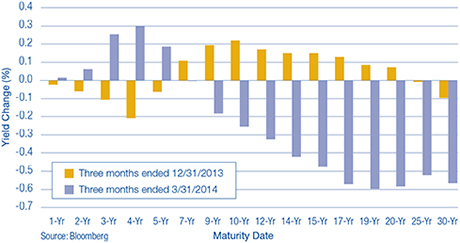

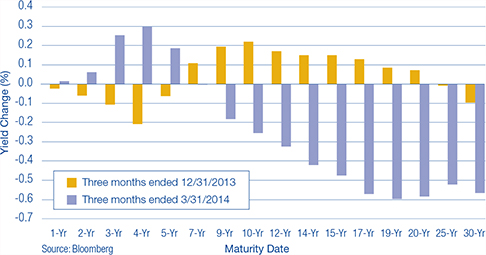

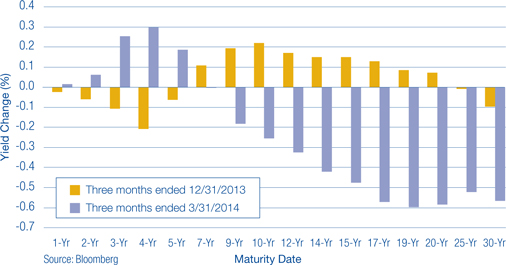

The first three months of fiscal 2014 were very interesting, as interest-rate changes went in various directions, depending on the maturity discussed. This period certainly highlighted that interest rates do not change uniformly across the entire maturity spectrum (the yield curve).

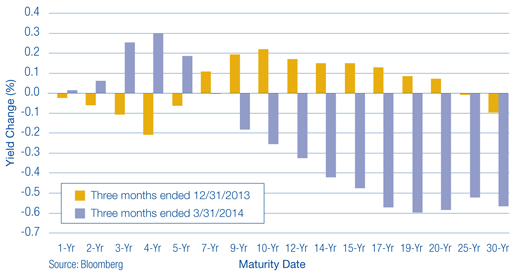

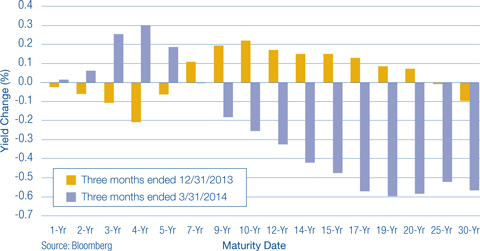

Chart I illustrates how yields changed during the period. It is good to remember the tone of the market at the end of 2013. Most market commentators believed the stock market and yields were going in the same direction: up. The blue bars show the yield changes from December 31, 2013 through March 31, 2014. Those commentators were only partially correct: the only yields to increase were those for the shortest-maturity segment of the municipal bond market. Again, yield changes were not uniform across the yield curve. This time, after new U.S. Federal Reserve Chair Janet Yellen hinted that short-term interest rates may eventually need to increase, short-term yields increased and long-term yields decreased.

Investors may wonder how best to protect themselves from these changes. One way to hedge this risk is to own securities or mutual funds that spread their investments across the different segments of the yield curve. In our opinion, that would mean owning some of our new Thornburg Low Duration Municipal Fund and our Limited Term Municipal, Intermediate Municipal, and Strategic Municipal Income Funds. The percentage ownership of each would depend on levels of risk tolerance.

Chart I: Changes in AAA General-Obligation Municipal Yield Curve

The Economy and the Federal Reserve

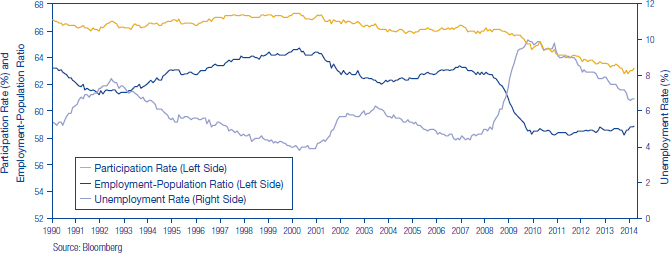

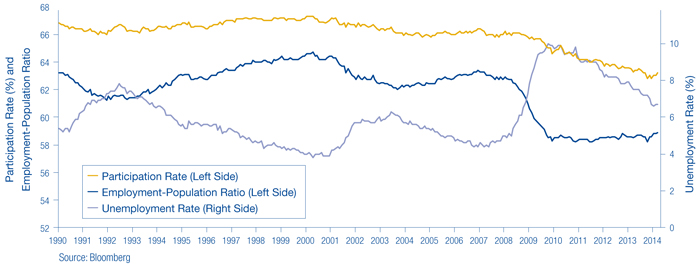

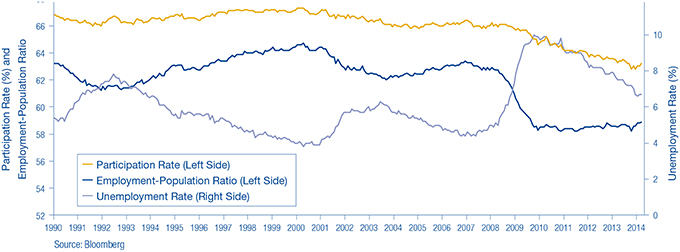

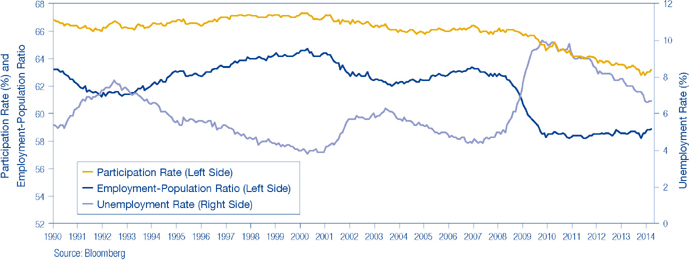

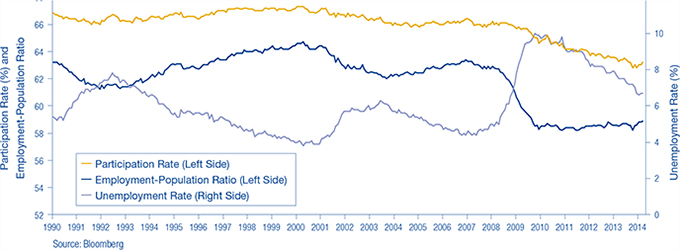

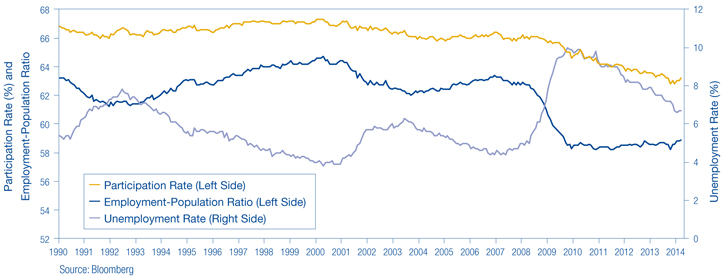

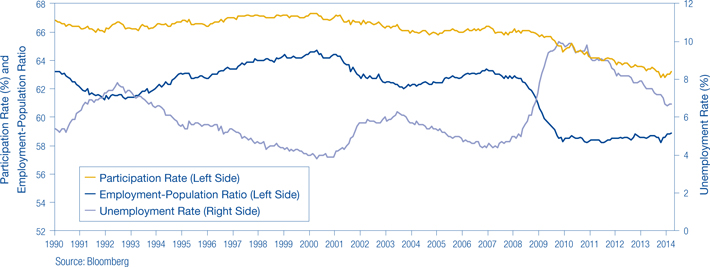

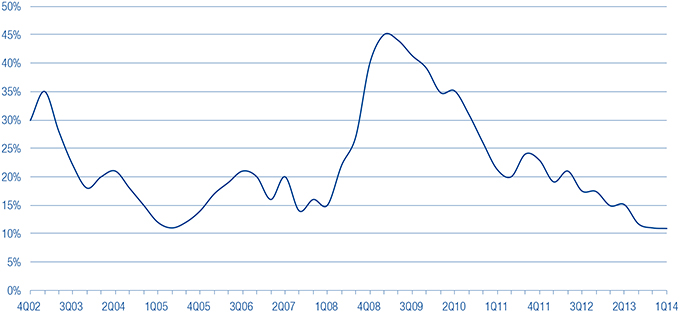

Gross domestic product (GDP) for the year ended December 31, 2013 came in at 2.6%, around its long-term average (to March 1990) of 2.5%. Additions to non-farm payroll employment have averaged about 178,000 per month for the three months ended March 31, 2014. The unemployment rate declined to 6.7%, but it has been clouded by a declining labor participation rate. The percentage of the U.S. population that is employed declined to 58.9% as of March 31, 2014, from 63.3% on March 31, 2007. The retirement of the “baby boomer” generation has certainly contributed to this decline but does not account for all of it. Chart II illustrates each of these trends from 1990.

Certified Semi-Annual Report 7

| | |

| LETTER TO SHAREHOLDERS, | | |

| |

CONTINUED | | |

Chart II: Labor Market Indicators

2/28/1990 – 3/31/2014

Inflation, the bondholder’s worst enemy, has remained well controlled in the last three months. The year-over-year change in the Consumer Price Index increased (CPI) increased to 1.5% as of March 31, 2014 from 1.2% as of December 30, 2013. Subtracting the food and energy components to arrive at the core measure presents a picture of a well-behaved, unchanged 1.7%. The economic backdrop is one of mild expansion with low inflation. The $64,000 question is, “How long can it last?”

In January 2014, Janet Yellen replaced Ben Bernanke as Fed Chair. Her appointment assured a continuation of current Fed policies. Last year, Bernanke roiled the fixed income markets by alluding to the prospect of a decrease in the Fed’s monthly purchases of Treasury and mortgage-backed securities, the tapering of QE3. Rates went up! This year, the tapering started in actuality with the Fed reducing its purchases by $10.0 billion per meeting. Rates went down! Go figure!

Chair Yellen learned that in her new position (to borrow an old E.F. Hutton advertisement tag line), “When she speaks, markets listen.” At her first news conference, Ms. Yellen tried to clarify what “for a considerable time” meant from the last Fed Statement: “This is the kind of term it’s hard to define,” Yellen said. “Probably means something on the order of six months, or that type of thing” [after QE3 tapering ends]. This sent the debt markets, especially the short-term debt markets, lower in price and higher in yield. The results can be seen in Chart I.

8 Certified Semi-Annual Report

LETTER TO SHAREHOLDERS,

CONTINUED

The Municipal Market

The long end of the municipal market has performed very well over the last three months. The short end, those maturities of five years or less, has not been so fortunate. Even with the increase in interest rates in the short end of the market, the NAV of the Thornburg Low Duration Municipal Fund did not change. Low NAV volatility is a key feature of the Fund.

Monthly outflows from municipal bond mutual funds have abated. The Investment Company Institute (ICI), an industry trade group, reported that for the last three months of calendar year 2013, municipal bond mutual funds lost an average of $6.6 billion per month. For the first three months of calendar year 2014, municipal bond mutual funds experienced $1.1 billion of inflows per month. This is not a significant amount, but at least it is positive.

These cash flows would normally not support a significantly positive return environment but when coupled with a decline in new issuance of municipal bonds, a clearer picture presents itself. The supply of new municipal bonds was down 26% for the first three months of 2014. So muted demand was met with reduce supply yielding positive results.

The overall economic health of the municipal bond market is improving, albeit unevenly. We arrive at this judgment in part through the use of the Bloomberg Economic Evaluation of States Index, which includes:

| | • | | Mortgage delinquencies – from the Mortgage Bankers Association |

| | • | | State personal income – from the Bureau of Economic Analysis |

| | • | | Tax revenue – from the U.S. Census Bureau |

| | • | | Employment – from the Bureau of Labor Statistics |

| | • | | Home prices – from the Federal Housing Finance Agency |

| | • | | Bloomberg State Stock Index |

From the fourth quarter of 2012 through the last quarter of 2013 (latest data available), the index increased on average 2.8%, ranging from a high of 8.8% to a low of negative 7.5%. For the comparable prior year period, the average was an increase of 0.2%, with a range from 9.9% to negative 4.1%. Nonetheless, state pension funds are still wrestling with some issues. The median funding level has declined from 82.6% in 2007 to 68.6% in 2012 (the Pew Center on the States suggests a funding level of 80% is adequate).

Two municipal bond market credit stories (Detroit and Puerto Rico) continue to grab headlines. In Detroit’s case, some significant settlements have been announced, but they are short on specifics, including where the new cash came from, and are dependent upon state approval. As in most Chapter 9 proceedings, one should read very little into early reports because the final results may prove very different. For example, a settlement was announced between insured bondholders and the city for a recovery of about 74% of par (a bond’s original face value); a second component of the settlement was reached with several unions for 100% of existing pension obligations and a reduction in cost-of-living adjustments. The original opening offer for these parties was 20% of par for the bondholders, and between 75% and 95% of outstanding pension obligations. It appears to us that these compromises do not address the root problems.

Puerto Rico made the news in March 2014 by successfully coming to market with the largest “junk” bond deal in municipal market history. Puerto Rico, which is now rated BB, pulled off a $3.5 billion offering, which was purchased by non-traditional market participants, i.e. hedge funds. It was a 21-year maturity bond that was priced at $93.00 to yield 8.73%. We looked at the issue very closely as a potential addition to the Thornburg Strategic Municipal Income Fund and decided not to purchase it. The deal initially traded up to around $97.00, but as of this writing (close of business April 15th) it is trading at a dollar price of $87.50, a loss of almost 6.00% from the original offering price. Thornburg Funds are among the 30% of U.S. municipal mutual funds that do not own any debt from the Commonwealth of Puerto Rico.

Certified Semi-Annual Report 9

LETTER TO SHAREHOLDERS,

CONTINUED

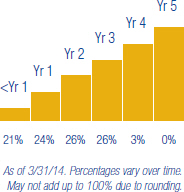

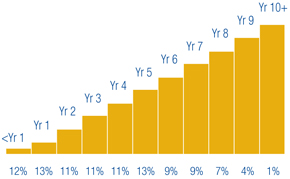

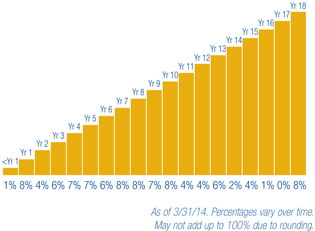

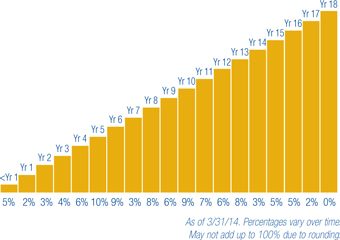

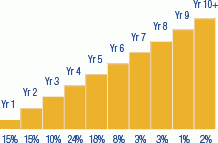

Chart III: Percent of Portfolio Maturing

Conclusion

Your Thornburg Low Duration Municipal Fund maintains a laddered portfolio structure, which was comprised of 38 municipal obligors as of March 31, 2014. We believe that this structure tends to maximize an investor’s income. In our opinion, a laddered portfolio outperforms the other structures (bullet and barbell) two-thirds of the time.1 It effectively manages a portfolio’s yield-curve exposure by owning a roughly equal weighting of each maturity, thereby minimizing a major risk factor.

We diversify our holdings across the Fund’s investment universe. Chart I illustrates that yield changes are not uniform across the Fund’s investment universe. Laddering also reduces reinvestment risk by ensuring that a portion of the portfolio matures each year so it can be reinvested. More importantly, it frees the team to concentrate on higher value-added tasks, such as fundamental, bottom-up credit research. It is just this type of research has allowed us to avoid the two largest, headline-grabbing credit issues in the municipal bond market.

This year has gotten off to a strong start. We thank you for the trust you have placed in us and will keep that foremost in our minds.

Sincerely,

| | |

| |  |

| Christopher Ryon, CFA | | Josh Gonze |

| Portfolio Manager | | Portfolio Manager |

| Managing Director | | Managing Director |

| 1 | For a copy of the study, go to www.thornburg.com/whyladder |

The matters discussed in this report may constitute forward-looking statements made pursuant to the safe harbor provisions of the Securities Litigation Reform Act of 1995. These include any advisor or portfolio manager prediction, assessment, analysis or outlook for individual securities, industries, investment styles, market sectors and/or markets. These statements involve risks and uncertainties. In addition to the general risks described for each fund in its current prospectus, other factors bearing on these reports include the accuracy of the advisor’s or portfolio manager’s forecasts and predictions, the appropriateness of the investment strategies designed by the advisor or portfolio manager and the ability of the advisor or portfolio manager to implement their strategies efficiently and successfully. Any one or more of these factors, as well as other risks affecting the securities markets generally, could cause the actual results of any fund to differ materially as compared to its benchmarks.

10 Certified Semi-Annual Report

| | |

| SCHEDULE OF INVESTMENTS | | |

| |

Thornburg Low Duration Municipal Fund | | March 31, 2014 (Unaudited) |

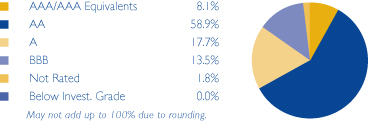

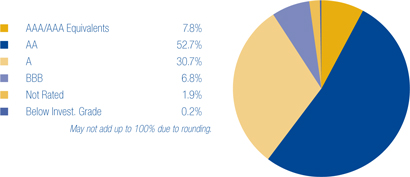

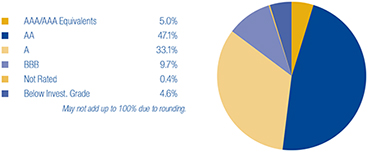

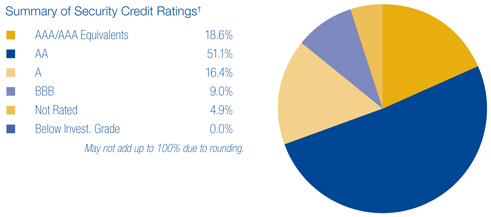

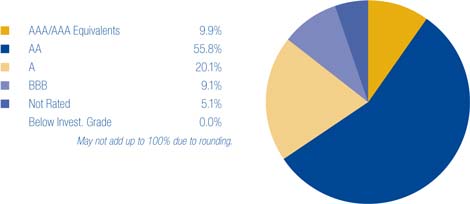

SUMMARY OF SECURITY CREDIT RATINGS†

We have used ratings from Standard & Poor’s (S&P). Where S&P ratings are not available, we have used Moody’s Investors Service. Where neither rating is available, we have used ratings from Fitch Ratings. The category of investments identified as “AAA” in this graph includes investments which are pre-refunded or escrowed to maturity. Such investments are backed by an escrow or trust containing sufficient U.S. Government or U.S. Government agency securities to satisfy the timely payment of principal and interest and, therefore, are normally deemed to be equivalent to AAA-rated securities.

| | | | | | | | | | |

Issuer-Description | | Credit Rating†

S&P/ Moody’s | | Principal

Amount | | | Value | |

ARIZONA — 3.93% | | | | | | | | | | |

Pima County COP, 3.00% due 12/1/2014 (Sewer System & Fleet Services Facilities) | | A+/NR | | $ | 200,000 | | | $ | 203,736 | |

a State of Arizona COP, 5.00% due 10/1/2014 (Lease-Purchases-Various State Agency Properties; Insured: AGM) | | AA/A1 | | | 200,000 | | | | 204,724 | |

| | | |

ARKANSAS — 2.00% | | | | | | | | | | |

Jefferson County, 4.00% due 6/1/2015 (Jefferson Regional Medical Center; Insured: AGM) | | AA/NR | | | 200,000 | | | | 207,566 | |

| | | |

CALIFORNIA — 6.79% | | | | | | | | | | |

a California HFFA, 4.00% due 7/1/2016 (Children’s Hospital; Insured: AGM) | | AA/A2 | | | 200,000 | | | | 212,208 | |

California Statewide Communities Development Authority, 5.25% due 7/1/2017 (St. Joseph Health System; Insured: AGM) | | AA/A1 | | | 100,000 | | | | 112,835 | |

San Diego Redevelopment Agency, 5.00% due 9/1/2016 (Centre City Redevelopment; Insured: AMBAC) | | NR/Baa3 | | | 50,000 | | | | 53,544 | |

b Successor Agency to the Richmond County Redevelopment Agency, 4.00% due 9/1/2017 (Insured: BAM) | | AA/NR | | | 300,000 | | | | 326,622 | |

| | | |

COLORADO — 5.16% | | | | | | | | | | |

City & County of Denver Airport System, 0.28% due 11/15/2025 put 4/1/2014 (Denver International Airport; Insured: AGM; SPA: Morgan Stanley Bank) (daily demand notes) | | AA/A1 | | | 200,000 | | | | 200,000 | |

City & County of Denver GO, 3.00% due 8/1/2015 (Civic Facilities and Denver Zoological Gardens Improvements) | | AAA/Aaa | | | 200,000 | | | | 207,580 | |

Denver Convention Center Hotel Authority, 5.25% due 12/1/2014 (Insured: Syncora) | | BBB-/Baa3 | | | 125,000 | | | | 128,569 | |

| | | |

DISTRICT OF COLUMBIA — 2.10% | | | | | | | | | | |

District of Columbia, 5.00% due 4/1/2016 (National Public Radio) (ETM) | | AA-/Aa3 | | | 200,000 | | | | 217,994 | |

| | | |

FLORIDA — 4.22% | | | | | | | | | | |

Florida Higher Educational Facilities Financing Authority, 5.00% due 4/1/2015 (Nova Southeastern University) | | BBB/Baa1 | | | 200,000 | | | | 207,594 | |

Hillsborough County IDA, 5.65% due 5/15/2018 (Tampa Electric Co.) | | BBB+/A2 | | | 200,000 | | | | 230,612 | |

| | | |

GEORGIA — 2.12% | | | | | | | | | | |

City of Atlanta, 5.25% due 12/1/2016 (Atlantic Station Project; Insured: AGM) | | AA/A3 | | | 200,000 | | | | 220,570 | |

| | | |

ILLINOIS — 5.32% | | | | | | | | | | |

City of Chicago, 0.29% due 1/1/2034 put 4/1/2014 (Liquidity Facility; SPA: JPMorgan Chase Bank) (daily demand notes) | | AAA/Baa1 | | | 200,000 | | | | 200,000 | |

a Illinois Finance Authority, 4.30% due 6/1/2035 put 6/1/2016 (Peoples Gas Light & Coke Co.; Insured: AMBAC) | | A/Aa3 | | | 200,000 | | | | 214,480 | |

Town of Cicero Cook County GO, 5.00% due 1/1/2018 (Insured: AGM) | | AA/A2 | | | 125,000 | | | | 137,907 | |

| | | |

INDIANA — 4.11% | | | | | | | | | | |

b Hammond Multi-School Building Corp., 4.00% due 7/15/2017 (School City of Hammond Educational Facilities) (State Aid Withholding) | | AA+/NR | | | 300,000 | | | | 327,216 | |

Indiana Finance Authority, 0.08% due 2/1/2037 put 4/1/2014 (Stadium Project; SPA: JPMorgan Chase Bank) (dailydemand notes) | | AA+/Aa2 | | | 100,000 | | | | 100,000 | |

| | | |

IOWA — 2.00% | | | | | | | | | | |

Iowa Finance Authority, 5.00% due 2/15/2015 (Iowa Health System; Insured: AGM) | | NR/Aa3 | | | 200,000 | | | | 207,836 | |

Certified Semi-Annual Report 11

| | |

| SCHEDULE OF INVESTMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | March 31, 2014 (Unaudited) |

| | | | | | | | | | |

Issuer-Description | | Credit Rating†

S&p/ Moody’s | | Principal

Amount | | | Value | |

MICHIGAN — 4.24% | | | | | | | | | | |

Michigan State Hospital Finance Authority, 5.00% due 11/15/2016 (Ascension Health) | | AA+/Aa2 | | $ | 200,000 | | | $ | 222,292 | |

Michigan State Hospital Finance Authority, 5.75% due 12/1/2034 put 12/1/2015 (Trinity Health) | | AA-/Aa2 | | | 200,000 | | | | 217,650 | |

| | | |

NEVADA — 3.68% | | | | | | | | | | |

a Carson City, 4.00% due 9/1/2016 (Carson Tahoe Regional Healthcare Project) | | BBB+/NR | | | 200,000 | | | | 211,852 | |

Washoe County School District GO, 5.25% due 6/1/2017 (School Improvements; Insured: AGM) | | AA/Aa3 | | | 150,000 | | | | 169,997 | |

| | | |

NEW YORK — 2.14% | | | | | | | | | | |

Lake Placid Central School District GO, 5.00% due 6/15/2017 (Elementary, Middle/High School Projects; Insured: Natl-Re) (State Aid Withholding) | | NR/A1 | | | 200,000 | | | | 222,402 | |

| | | |

NORTH DAKOTA — 2.06% | | | | | | | | | | |

North Dakota Building Authority, 4.25% due 12/1/2015 (Various State Agency Capital Projects; Insured: Natl-Re) | | AA+/Aa2 | | | 200,000 | | | | 213,412 | |

| | | |

OHIO — 6.76% | | | | | | | | | | |

City of Cleveland, 3.00% due 10/1/2016 (Public Facilities) | | AA/A1 | | | 200,000 | | | | 211,634 | |

a County of Franklin, 4.00% due 11/15/2033 put 8/1/2016 (OhioHealth Corp. Hospital Facilities) | | AA+/Aa2 | | | 200,000 | | | | 215,166 | |

University of Toledo, 3.50% due 6/1/2016 (University Facilities Improvements) | | A+/A1 | | | 260,000 | | | | 275,192 | |

| | | |

PENNSYLVANIA — 9.11% | | | | | | | | | | |

City of Philadelphia Gas Works, 5.00% due 10/1/2017 (Insured: AMBAC) | | BBB+/Baa2 | | | 200,000 | | | | 222,872 | |

b East Allegheny School District GO, 2.00% due 4/1/2017 (Insured: BAM) (State Aid Withholding) | | AA/A3 | | | 300,000 | | | | 306,117 | |

Pennsylvania Economic Development Financing Authority, 3.375% due 12/1/2040 put 7/1/2015 (Shippingport Project) | | BBB-/NR | | | 200,000 | | | | 203,524 | |

Wilson School District GO, 3.00% due 6/1/2017 (State Aid WIthholding) | | AA/NR | | | 200,000 | | | | 212,984 | |

| | | |

TEXAS — 4.93% | | | | | | | | | | |

Brazos River Authority, 4.90% due 10/1/2015 (Center Point Energy; Insured:

Natl-Re) | | AA-/Baa1 | | | 200,000 | | | | 210,676 | |

Harris County Health Facilities Development Corp., 0.07% due 10/1/2041 put 4/1/2014 (Texas Children’s Hospital; SPA: Wells Fargo Bank N.A.) (daily demand notes) | | AA/Aa2 | | | 100,000 | | | | 100,000 | |

a State of Texas, 2.00% due 8/28/2014 (General Revenue Fund-Cash Flow Management) | | SP-1+/Mig1 | | | 200,000 | | | | 201,552 | |

| | | |

VIRGINIA — 2.04% | | | | | | | | | | |

Fairfax County GO, 4.00% due 10/1/2015 (Public Facilities and Improvements) (State Aid Withholding) | | AAA/Aaa | | | 200,000 | | | | 211,438 | |

| | | |

WASHINGTON — 2.09% | | | | | | | | | | |

Seattle Municipal Light & Power, 5.00% due 2/1/2016 | | AA/Aa2 | | | 200,000 | | | | 216,824 | |

| | | | | | | | | | |

TOTAL INVESTMENTS — 74.80% (Cost $7,764,817) | | | | | | | | $ | 7,767,177 | |

OTHER ASSETS LESS LIABILITIES — 25.20% | | | | | | | | | 2,616,932 | |

| | | | | | | | | | |

NET ASSETS — 100.00% | | | | | | | | $ | 10,384,109 | |

| | | | | | | | | | |

12 Certified Semi-Annual Report

| | |

| SCHEDULE OF INVESTMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | March 31, 2014 (Unaudited) |

Footnote Legend

| † | Credit ratings are unaudited. Rating changes may have occurred subsequent to the reporting period end. Bonds issued with a maturity of one year or less are assigned Moody’s ratings from MIG-1 to MIG-4 and Standard and Poor’s ratings from SP-1+ to SP-3 with MIG-1 and SP-1+ being the strongest ratings. |

| a | Segregated as collateral for a when-issued security. |

Portfolio Abbreviations

To simplify the listings of securities, abbreviations are used per the table below:

| | |

| AGM | | Insured by Assured Guaranty Municipal Corp. |

| AMBAC | | Insured by American Municipal Bond Assurance Corp. |

| BAM | | Build America Mutual Insurance Co. |

| COP | | Certificates of Participation |

| ETM | | Escrowed to Maturity |

| GO | | General Obligation |

| HFFA | | Health Facilities Financing Authority |

| IDA | | Industrial Development Authority |

| Natl-Re | | Insured by National Public Finance Guarantee Corp. |

| SPA | | Stand-by Purchase Agreement |

| Syncora | | Insured by Syncora Guarantee Inc. |

See notes to financial statements.

Certified Semi-Annual Report 13

| | |

| STATEMENT OF ASSETS AND LIABILITIES | | |

| |

Thornburg Low Duration Municipal Fund | | March 31, 2014 (Unaudited) |

| | | | |

ASSETS | | | | |

Investments at value (cost $7,764,817) (Note 2) | | $ | 7,767,177 | |

Cash | | | 3,328,833 | |

Receivable for investments sold | | | 100,000 | |

Receivable from investment advisor | | | 7,123 | |

Interest receivable | | | 81,373 | |

Prepaid expenses and other assets | | | 58,546 | |

| | | | |

Total Assets | | | 11,343,052 | |

| | | | |

| |

LIABILITIES | | | | |

Payable for investments purchased | | | 958,905 | |

Dividends payable | | | 38 | |

| | | | |

Total Liabilities | | | 958,943 | |

| | | | |

| |

NET ASSETS | | $ | 10,384,109 | |

| | | | |

NET ASSETS CONSIST OF | | | | |

Net unrealized appreciation on investments | | $ | 2,360 | |

Net capital paid in on shares of beneficial interest | | | 10,381,749 | |

| | | | |

| | $ | 10,384,109 | |

| | | | |

NET ASSET VALUE | | | | |

Class A Shares: | | | | |

Net asset value and redemption price per share ($2,679,462 applicable to 217,600 shares of beneficial interest outstanding - Note 4) | | $ | 12.31 | |

Maximum sales charge, 1.50% of offering price | | | 0.19 | |

| | | | |

Maximum offering price per share | | $ | 12.50 | |

| | | | |

| |

Class I Shares: | | | | |

Net asset value, offering and redemption price per share ($7,704,647 applicable to 625,714 shares of beneficial interest outstanding - Note 4) | | $ | 12.31 | |

| | | | |

See notes to financial statements.

14 Certified Semi-Annual Report

| | |

| STATEMENT OF OPERATIONS | | |

| |

Thornburg Low Duration Municipal Fund | | Period ended March 31, 2014 (Unaudited)* |

| | | | |

INVESTMENT INCOME | | | | |

Interest income (net of premium amortized of $40,323) | | $ | 15,915 | |

| | | | |

| |

EXPENSES | | | | |

Investment advisory fees (Note 3) | | | 7,102 | |

Administration fees (Note 3) | | | | |

Class A Shares | | | 793 | |

Class I Shares | | | 571 | |

Distribution and service fees (Note 3) | | | | |

Class A Shares | | | 1,282 | |

Transfer agent fees | | | | |

Class A Shares | | | 920 | |

Class I Shares | | | 920 | |

Registration and filing fees | | | | |

Class A Shares | | | 4,600 | |

Class I Shares | | | 4,600 | |

Custodian fees (Note 3) | | | 4,622 | |

Professional fees | | | 6,992 | |

Accounting fees | | | 92 | |

Trustee fees | | | 92 | |

Other expenses | | | 7,081 | |

| | | | |

Total Expenses | | | 39,667 | |

Less: | | | | |

Expenses reimbursed by investment advisor (Note 3) | | | (12,771 | ) |

Investment advisory fees waived by investment advisor (Note 3) | | | (17,630 | ) |

Fees paid indirectly (Note 3) | | | (22 | ) |

| | | | |

Net Expenses | | | 9,244 | |

| | | | |

Net Investment Income | | | 6,671 | |

| | | | |

REALIZED AND UNREALIZED GAIN (LOSS) | | | | |

Net change in unrealized appreciation (depreciation) of investments | | | 2,360 | |

| | | | |

Net Realized and Unrealized Gain | | | 2,360 | |

| | | | |

Net Increase in Net Assets Resulting from Operations | | $ | 9,031 | |

| | | | |

| * | For the period from commencement of operations on December 30, 2013 through March 31, 2014. |

See notes to financial statements.

Certified Semi-Annual Report 15

| | |

| STATEMENT OF CHANGES IN NET ASSETS | | |

| |

Thornburg Low Duration Municipal Fund | | |

| | | | |

| | | Period Ended*

March 31, 2014 | |

INCREASE (DECREASE) IN NET ASSETS FROM | | | | |

| |

OPERATIONS | | | | |

Net investment income | | $ | 6,671 | |

Net unrealized appreciation (depreciation) on investments | | | 2,360 | |

| | | | |

| |

Net Increase (Decrease) in Net Assets Resulting from Operations | | | 9,031 | |

| |

DIVIDENDS TO SHAREHOLDERS | | | | |

From net investment income | | | | |

Class A Shares | | | (1,649 | ) |

Class I Shares | | | (5,022 | ) |

| |

FUND SHARE TRANSACTIONS (NOTE 4) | | | | |

Class A Shares | | | 2,678,714 | |

Class I Shares | | | 7,703,035 | |

| | | | |

Net Increase in Net Assets | | | 10,384,109 | |

| |

NET ASSETS | | | | |

Beginning of Period | | | — | |

| | | | |

| |

End of Period | | $ | 10,384,109 | |

| | | | |

| * | For the unaudited period from commencement of operations on December 30, 2013 through March 31, 2014. |

See notes to financial statements.

16 Certified Semi-Annual Report

| | |

| NOTES TO FINANCIAL STATEMENTS | | |

| |

Thornburg Low Duration Municipal Fund | | March 31, 2014 (Unaudited) |

NOTE 1 – ORGANIZATION

Thornburg Low Duration Municipal Fund (the “Fund”) is a diversified series of Thornburg Investment Trust (the “Trust”). The Trust is organized as a Massachusetts business trust under a Declaration of Trust dated June 3, 1987 and is registered as a diversified, open-end management investment company under the Investment Company Act of 1940, as amended. The Fund is currently one of eighteen separate series of the Trust. Each series is considered to be a separate entity for financial reporting and tax purposes and bears expenses directly attributable to it. The Fund’s investment objective is to seek current income exempt from federal income tax consistent with preservation of capital.

The Fund currently offers two classes of shares of beneficial interest outstanding: Class A and Institutional Class (“Class I”). Each class of shares of the Fund represents an interest in the same portfolio of investments, except that (i) Class A shares are sold subject to a front-end sales charge collected at the time the shares are purchased and bear a service fee, (ii) Class I shares are sold at net asset value without a sales charge at the time of purchase and may be subject to a service fee, and (iii) the respective classes may have different reinvestment privileges and conversion rights. Additionally, the Fund may allocate among its classes certain expenses, to the extent allocable to specific classes, including transfer agent fees, government registration fees, certain printing and postage costs, and administrative and legal expenses. Currently, class specific expenses of the Fund are limited to service and distribution fees, administration fees, and certain registration and transfer agent expenses.

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

Significant accounting policies of the Trust are as follows:

Valuation Policy and Procedures: The Fund’s Trustees of the Trust (the “Trustees”) have authorized employees of the Fund’s investment advisor, acting as the Valuation and Pricing Committee (the “Committee”), to make certain valuation determinations, subject to oversight and review by the Trustees and the Audit Committee of the Trustees. The Committee and other employees of the Fund’s investment advisor administer and implement the valuation process. The Committee regularly reviews its own fair value decisions, as well as valuations, valuation techniques and services furnished by pricing services, considers circumstances in the markets which may require valuation determinations by the Committee and reviews previous valuation determinations. The Committee also reports on its activities, the performance of the pricing services and other matters to the Trustees and the Audit Committee of the Trustees.

In determining a fair value for a portfolio investment, the Committee seeks to determine the price that the Fund would reasonably expect to receive upon a sale of the investment in an orderly transaction between market participants at the measurement date. Typically, the fair value process employs standing instructions to use quoted prices in active markets or the use of independent pricing services. Less frequently, the Committee may make a fair value determination using other methods. However, because fair value prices are estimated prices, the determination of fair value for an investment may differ from the value that would be realized by the Fund upon a sale of the investment, and that difference could be material to the Fund’s financial statements. The Committee’s determination of fair value for an investment may also differ from the prices obtained by other persons (including other mutual funds) for the investment.

Valuation of Investments: Debt obligations held by the Fund have a primary over-the-counter market and are valued by an independent pricing service approved by the Trustees. The pricing service ordinarily values debt obligations at quoted bid prices. When quotations are not available, debt obligations held by the Fund are valued at evaluated prices determined by the pricing service using methods which include consideration of yields or prices of debt obligations of comparable quality, type of issue, coupon, maturity and rating, and indications as to value from dealers and general market conditions. Short-term obligations having remaining maturities of 60 days or less are ordinarily valued at amortized cost, which approximates market value.

In any case when a pricing service fails to provide a price for a debt obligation held by the Fund, the Committee determines a fair value for the debt obligation using procedures in accordance with a policy approved by the Trustees, which may include the use of a price obtained from a different independent pricing service. Additionally, in any case when management believes that a price provided by a pricing service for a debt obligation held by the Fund may be unreliable, the Committee decides whether or not to use the pricing service’s valuation or to use an alternative method to determine a fair value for the debt obligation.

Valuation Measurements: The Fund categorizes its investments based upon the inputs used in valuing those investments, according to a three-level hierarchy established by guidance from the Financial Accounting Standards Board (the “FASB”). Categorization of investments using this hierarchy is intended by the FASB to maximize the use of observable inputs and minimize the use of unobservable inputs by prioritizing that the most observable input be used when available. Observable inputs are those that market participants would use in valuing an investment based on available market data. Unobservable inputs are those that reflect assumptions about the information market participants would use in valuing an investment. An investment’s level within the hierarchy is based on the lowest level input that is deemed significant to the fair value measurement. The methodologies and relative inputs used to value investments are not necessarily indications of the risk or liquidity associated with investing in those investments.

Certified Semi-Annual Report 17

| | |

| NOTES TO FINANCIAL STATEMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | March 31, 2014 (Unaudited) |

Various inputs are used in determining the fair value measurement of the Fund’s investments. These inputs are generally summarized according to the three-level hierarchy below:

Level 1: Quoted prices in active markets for identical investments.

Level 2: Other direct or indirect significant observable inputs (including quoted prices for similar investments in active markets and other observable inputs, such as interest rates, prepayment rates, credit risk, etc.).

Level 3: Significant unobservable inputs, (including the Committee’s own assumptions in determining the fair value of investments), are generally applicable to investments fair valued with single broker quotes and other investments.

Portfolio investments with minimal, if any, market activity are characterized as Level 3 and are valued using significant unobservable inputs, typically including single broker quotes, which may be adjusted or unadjusted, related or comparable investments, last available transactions, and other relevant information. Valuations may also be based upon current market prices of securities that are comparable in coupon, rating, maturity and industry. An income based valuation approach would consider discounted anticipated future cash flows of the investment. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investment. The derived value of a Level 3 investment may not represent the value which is received upon disposition.

The following table displays a summary of the fair value hierarchy measurements of the Fund’s investments as of March 31, 2014. In any instance when valuation inputs from more than one level are used to determine the fair value of a specific investment, the investment is placed in the level of the table based upon the lowest level input that is significant in determining the fair value of the investment:

| | | | | | | | | | | | | | | | |

| | | Fair Value Measurements at March 31, 2014 | |

| | | Total | | | Level 1 | | | Level 2 | | | Level 3 | |

Assets | | | | | | | | | | | | | | | | |

Investments in Securities | | | | | | | | | | | | | | | | |

Municipal Bonds | | $ | 7,767,177 | | | $ | — | | | $ | 7,767,177 | | | $ | — | |

| | | | | | | | | | | | | | | | |

Total Investments in Securities | | $ | 7,767,177 | | | $ | — | | | $ | 7,767,177 | | | $ | — | |

In accordance with the guidance prescribed in Accounting Standards Update No. 2011-04, it is the policy of the Fund to recognize transfers between levels and those underlying events which caused the movement. The Fund recognized no transfers between levels for the period ended March 31, 2014.

Federal Income Taxes: It is the policy of the Trust to comply with the provisions of the Internal Revenue Code applicable to “regulated investment companies” and to distribute to shareholders substantially all taxable (if any) and tax exempt income of the Fund. Therefore, no provision for federal income tax is required.

Management reviews each uncertain tax position believed to be material to the preparation of the Fund’s financial statements, to assess if it is more likely than not that the position would be sustained upon examination, based upon the technical merits of the position. As of March 31, 2014, management has not identified any such position for which an asset or liability must be reflected in the Statement of Assets and Liabilities. The Fund’s tax returns remain subject to examination for three years after filing.

When-Issued and Delayed Delivery Transactions: The Fund may engage in when-issued or delayed delivery transactions. To the extent the Fund engages in such transactions, it will do so for the purpose of acquiring portfolio investments consistent with the Fund’s investment objectives and not for the purpose of investment leverage or to speculate on interest rate and/or market changes. At the time the Fund makes a commitment to purchase an investment on a when-issued or delayed delivery basis, the Fund will record the transaction and reflect the value in determining its net asset value. When effecting such transactions, assets of an amount sufficient to make payment for the portfolio investments to be purchased will be segregated on the Fund’s records on the trade date. Investments purchased on a when-issued or delayed delivery basis do not earn interest until the settlement date.

Dividends: Net investment income of the Fund is declared daily as a dividend on shares for which the Fund has received payment. Dividends are paid monthly and are reinvested in additional shares of the Fund at net asset value per share at the close of business on the dividend payment date, or at the shareholder’s option, paid in cash. Net realized capital gains, to the extent available, will be distributed at least annually.

18 Certified Semi-Annual Report

| | |

| NOTES TO FINANCIAL STATEMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | March 31, 2014 (Unaudited) |

General: Investment transactions are accounted for on a trade date basis. Interest income is accrued as earned. Premiums and discounts on investments purchased are amortized to call dates or maturity dates of the respective investments. Realized gains and losses from the sale of investments are recorded on an identified cost basis. Net investment income (other than class specific expenses) and realized and unrealized gains and losses are allocated daily to each class of shares based upon the relative net asset value of outstanding shares (or the value of the dividend-eligible shares, as appropriate) of each class of shares at the beginning of the day (after adjusting for the current capital shares activity of the respective class). Expenses common to all Funds are allocated among the Funds comprising the Trust based upon their relative net asset values or other appropriate allocation methods.

Guarantees and Indemnifications: Under the Trust’s organizational documents (and under separate agreements with the independent Trustees), its officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. Additionally, in the normal course of business the Trust enters into contracts with service providers that contain general indemnification clauses. The Trust’s maximum exposure under these arrangements is unknown. However, based on experience, the Trust expects the risk of loss to be remote.

Use of Estimates: The preparation of financial statements, in conformity with United States generally accepted accounting principles, requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual amounts could differ from those estimates.

NOTE 3 – INVESTMENT ADVISORY FEE AND OTHER TRANSACTIONS WITH AFFILIATES

Pursuant to an investment advisory agreement, Thornburg Investment Management, Inc. (the “Advisor”) serves as the investment advisor and performs services for the Fund for which the fees are payable at the end of each month. For the period ended March 31, 2014, these fees were payable at annual rates ranging from .40 of 1% to .225 of 1% per annum of the average daily net assets of the Fund depending on the Fund’s asset size. The Trust also has entered into administrative services agreements with the Advisor, whereby the Advisor will perform certain administrative services for the shareholders of each class of the Fund’s shares, and for which fees will be payable at an annual rate of up to .125 of 1% per annum of the average daily net assets attributable to each class of shares.

The Trust has an underwriting agreement with Thornburg Securities Corporation (the “Distributor,” an affiliate of the Advisor), which acts as the distributor of the Fund’s shares. For the period ended March 31, 2014, the Distributor has advised the Fund that it earned net commissions aggregating $25 from the sale of Class A shares of the Fund.

Pursuant to a service plan under Rule 12b-1 of the Investment Company Act of 1940, the Fund may reimburse to the Advisor an amount not to exceed .20 of 1% per annum of the average daily net assets attributable to each Class of shares of the Fund for payments made by the Advisor to securities dealers and other financial institutions to obtain various shareholder and distribution related services. For the period ended March 31, 2014, there were no 12b-1 service plan fees charged for Class I shares. The Advisor may pay out of its own resources additional expenses for distribution of the Fund’s shares.

The Advisor and Distributor have contractually agreed to waive fees and reimburse expenses incurred by the Fund so that actual expenses of certain share classes do not exceed specified levels. The agreement may be terminated by the Fund at any time, but may not be terminated by the Advisor or Distributor before February 1, 2015, unless the Advisor ceases to be the investment advisor to the Fund or the Distributor ceases to be the distributor of the Fund prior to that date. The Advisor and Distributor retain the right to be repaid by the Fund for fee waivers and expense reimbursements if expenses fall below the contractual limit prior to the end of the fiscal year.

For the period ended March 31, 2014, the Advisor contractually reimbursed certain class specific expenses and administrative fees of $6,681 for Class A shares and $6,090 for Class I shares, and voluntarily waived investment advisory fees of $17,630.

The Trust has an agreement with the custodian bank to indirectly pay a portion of the custodian’s fees through credits earned by the Fund’s cash on deposit with the bank. This deposit agreement is an alternative to overnight investments. Custodial fees are adjusted to reflect amounts that would have been paid without this agreement, with a corresponding adjustment reflected as fees paid indirectly in the Statement of Operations. For the period ended March 31, 2014, fees paid indirectly were $22.

Certain officers and Trustees of the Trust are also officers or directors of the Advisor and Distributor. The compensation of independent Trustees is borne by the Trust.

Certified Semi-Annual Report 19

| | |

| NOTES TO FINANCIAL STATEMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | March 31, 2014 (Unaudited) |

NOTE 4 – SHARES OF BENEFICIAL INTEREST

At March 31, 2014, there were an unlimited number of shares of beneficial interest authorized. Transactions in shares of beneficial interest were as follows:

| | | | | | | | |

| | | Period Ended*

March 31, 2014 | |

| | | Shares | | | Amount | |

Class A Shares | | | | | | | | |

Shares sold | | | 217,467 | | | $ | 2,677,069 | |

Shares issued to shareholders in reinvestment of dividends | | | 133 | | | | 1,645 | |

Shares repurchased | | | — | | | | — | |

| | | | | | | | |

| | |

Net increase (decrease) | | | 217,600 | | | $ | 2,678,714 | |

| | | | | | | | |

| | |

Class I Shares | | | | | | | | |

Shares sold | | | 625,309 | | | $ | 7,698,050 | |

Shares issued to shareholders in reinvestment of dividends | | | 405 | | | | 4,985 | |

Shares repurchased | | | — | | | | — | |

| | | | | | | | |

| | |

Net increase (decrease) | | | 625,714 | | | $ | 7,703,035 | |

| | | | | | | | |

| * | Fund commenced operations on December 30, 2013. |

NOTE 5 – INVESTMENT TRANSACTIONS

For the period ended March 31, 2014, the Fund had purchase and sale transactions of investments (excluding short-term investments) of $7,205,141 and $0, respectively.

NOTE 6 – INCOME TAXES

At March 31, 2014, information on the tax components of capital was as follows:

| | | | |

Cost of investments for tax purposes | | $ | 7,764,817 | |

| | | | |

Gross unrealized appreciation on a tax basis | | $ | 11,161 | |

Gross unrealized depreciation on a tax basis | | | (8,801 | ) |

| | | | |

Net unrealized appreciation (depreciation) on investments (tax basis) | | $ | 2,360 | |

| | | | |

OTHER NOTES

Risks: The Fund’s investments subject it to risks including, but not limited to, credit risk, interest rate risk, management risk, market and economic risk, and liquidity risk. Please see the Fund’s prospectus for a discussion of the risks associated with an investment in the Fund.

Subsequent Events: Fund management believes no events have occurred between March 31, 2014 and the date of issuance of the financial statements that require adjustment to or disclosure in the accompanying financial statements.

20 Certified Semi-Annual Report

This page intentionally left blank.

Certified Semi-Annual Report 21

FINANCIAL HIGHLIGHTS

Thornburg Low Duration Municipal Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | PER SHARE PERFORMANCE (for a share outstanding throughout the

Period)+ | | RATIOS TO AVERAGE NET ASSETS | | | SUPPLEMENTAL DATA | |

Unless

Otherwise

Noted,

Periods are Fiscal Years Ended Sept. 30, | | Net Asset

Value

Beginning

of Period | | | Net

Investment

Income

(Loss) | | Net

Realized

&

Unrealized

Gain (Loss)

on

Investments | | | Total from

Investment

Operations | | Dividends

from Net

Investment

Income | | | Dividends

from Net

Realized

Gains | | Total

Dividends | | | Net

Asset

Value

End of

Period | | Net

Investment

Income

(Loss)

(%) | | | Expenses,

After

Expense

Reductions

(%) | | | Expenses,

After

Expense

Reductions

and

Net of

Custody

Credits

(%) | | | Expenses,

Before

Expense

Reductions

(%) | | | Total

Return

(%)(a) | | Portfolio

Turnover

Rate (%)(a) | | Net

Assets

at End

of

Period

(Thousands) | |

Class A Shares | |

2014(b)(c)(d) | | $ | 12.31 | | | 0.01 | | | — | | | 0.01 | | | (0.01 | ) | | — | | | (0.01 | ) | | $12.31 | | | 0.26 | (e) | | | 0.63 | (e) | | | 0.63 | (e) | | | 2.68 | (e) | | 0.06 | | — | | $ | 2,679 | |

Class I Shares | |

2014(b)(d) | | $ | 12.31 | | | 0.01 | | | — | | | 0.01 | | | (0.01 | ) | | — | | | (0.01 | ) | | $12.31 | | | 0.44 | (e) | | | 0.46 | (e) | | | 0.46 | (e) | | | 1.99 | (e) | | 0.11 | | — | | $ | 7,705 | |

| (a) | Not annualized for periods less than one year. |

| (b) | Fund commenced operations on December 30, 2013. |

| (c) | Sales loads are not reflected in computing total return. |

| (d) | Unaudited Period Ended March 31. |

| + | Based on weighted average shares outstanding, except for Dividends from Net Investment Income and Net Realized Gains, which are actual amounts per share. |

See notes to financial statements.

| | | | |

| 22 Certified Semi-Annual Report | | | | Certified Semi-Annual Report 23 |

| | |

| EXPENSE EXAMPLE | | |

| |

Thornburg Low Duration Municipal Fund | | March 31, 2014 (Unaudited) |

As a shareholder of the Fund, you incur two types of costs:

| | (1) | transaction costs, including |

(a) sales charges (loads) on purchase payments, for Class A shares;

(b) a deferred sales charge on redemptions of any part or all of a purchase of $1 million of Class A shares within 12 months of purchase;

| | (2) | ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. |

This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on a $1,000 investment beginning on October 1, 2013, and held until March 31, 2014.

| | | | | | | | | | | | |

| | | Beginning

Account Value

10/1/13 | | | Ending

Account Value

3/31/14 | | | Expenses Paid

During Period†

10/1/13–3/31/14 | |

Class A Shares | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,000.60 | | | $ | 3.14 | |

Hypothetical* | | $ | 1,000.00 | | | $ | 1,021.79 | | | $ | 3.17 | |

Class I Shares | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,001.10 | | | $ | 2.30 | |

Hypothetical* | | $ | 1,000.00 | | | $ | 1,022.64 | | | $ | 2.32 | |

| † | Expenses are equal to the annualized expense ratio for each class (A: 0.63%; I: 0.46%) multiplied by the average account value over the period, multiplied by 182/365 to reflect the one-half year period. |

| * | Hypothetical assumes a rate of return of 5% per year before expenses. |

ACTUAL EXPENSES

For each class of shares, the first line of the accompanying table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line for your class of shares under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES

For each class of shares, the second line of the accompanying table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table for each class of shares is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

24 Certified Semi-Annual Report

| | |

| OTHER INFORMATION | | |

| |

Thornburg Low Duration Municipal Fund | | March 31, 2014 (Unaudited) |

PORTFOLIO PROXY VOTING

Policies and Procedures:

The Trust has delegated to Thornburg Investment Management, Inc. (the “Advisor”) voting decisions respecting proxies for the Fund’s voting securities. The Advisor makes voting decisions in accordance with its Proxy Voting Policy. A description of the Policy is available (i) without charge, upon request, by calling the Advisor toll-free at 1-800-847-0200, (ii) on the Thornburg website at www.thornburg. com, and (iii) on the Securities and Exchange Commission’s website at www.sec.gov.

No proxy voting information is currently available because the Fund commenced operations on December 30, 2013. The Fund expects to begin making annual proxy voting information available in accordance with applicable regulations commencing on or before August 31, 2014. This information is available (i) without charge, upon request by calling the Advisor toll-free at 1-800-847-0200, (ii) on the Thornburg website at www.thornburg.com, and (iii) on the Securities and Exchange Commission’s website at www.sec.gov.

AVAILABILITY OF QUARTERLY PORTFOLIO SCHEDULE

The Fund files with the Securities and Exchange Commission schedules of its portfolio holdings on Form N-Q for the first and third quarters of each fiscal year. The Fund’s Forms N-Q are available on the Commission’s website at www.sec.gov, or may be reviewed and copied at the Commission’s Public Reference Room in Washington, D.C. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. The Fund also makes this information available on its website at www.thornburg. com/download or upon request by calling 1-800-847-0200.

Certified Semi-Annual Report 25

TRUSTEES’ STATEMENT TO SHAREHOLDERS

Not part of the Certified Semi-Annual Report

Reissued September 15, 2013

The Trustees believe current and prospective shareholders should know how we discharge our responsibilities in supervising the Funds’ investment advisor and in reviewing the advisor’s contract for renewal. Since 2005, we have issued a statement which sets out clearly the three principal guidelines that we follow in supervising the Trust’s investment advisor on your behalf. In accordance with our customary practice, in September of this year we again reviewed our statement and concluded we should reissue this statement outlining the principal features of our supervision of the advisor’s performance of investment management services for the Funds.

We begin with the premise that each shareholder selected his or her Fund because its investments are managed by the investment advisor identified in the prospectus and in accordance with the objective and policies described in the prospectus. We realize, as each of you do, that if you believe that your Fund’s stated objective and policies no longer serve your personal investment goals, you can sell your shares and leave the Fund.

Therefore, we believe that our primary supervisory task – our principal obligation to you – is to assess the nature and quality of the advisor’s services, and to confirm that the advisor actively and competently pursues the Fund’s objective, in accordance with the policies set out in the prospectus. To do this, we meet regularly with management to review your Fund’s portfolio and to discuss the advisor’s specific actions and judgments in pursuing the Fund’s objective. We do not substitute our own judgment for the advisor’s decisions in selecting investments; the advisor is paid to exercise its informed judgment on investment decisions, and we seek to confirm, in reviewing the advisor’s performance, that the advisor is doing just that.

Second, while we are conscious of costs and the effect that costs have on shareholders’ returns, we do not seek the lowest fees or expense ratio as our sole or primary objective. We try to make sure that your Fund’s fees and costs are reasonable in relationship to the services rendered and that they are generally in line with those charged by other expert investment advisors, consistent with our belief that the Fund’s investors searched for and expect that expertise and attention and have decided to pay a reasonable price for it. We do not put the management contract “out to bid” as a matter of course, and we would not do so unless we had concluded that the advisor materially had failed to pursue the Fund’s objectives in accordance with its policies, or for other equally important reasons. We believe that any other approach would be inconsistent with your interests and contrary to your expectations when you bought shares of the Fund in the first place.

Finally, because we believe that most Thornburg Fund shareholders have invested with a long-term perspective, we try not to focus too much on the fashions of the moment and on short-term performance. The market will not favor any specific investment objective or set of policies at all times and under all economic circumstances. A fund will experience periods of both high and low returns relative to other funds and other investments. Even if one of our Funds is not favored by the market at a particular time, we believe that the advisor is nonetheless obliged to remain true to the Fund’s objective and policies, and we watch to see that it does so.

26 This page is not part of the Semi-Annual Report

RETIREMENT AND EDUCATION ACCOUNTS

Thornburg Investment Management offers retirement and education savings accounts that can help you meet a variety of planning challenges. For account applications or further information on any of the accounts below, please call 1-800-847-0200 or go to www.thornburg.com/ira. Your financial advisor can help you determine which plan is right for you.

Individual Retirement Accounts

Individual Retirement Accounts (IRAs) provide a tax-advantaged means to save money for the future. For a detailed outline of the difference between retirement accounts, see www.thornburg.com/ira. Rollovers are available. Call 1-800-847-0200 for more information.

Traditional IRAs – Contributions to Traditional IRAs are tax deductible for eligible individuals, and withdrawals are taxed as additional ordinary income. You may contribute to an IRA if you receive compensation and are under 70 1/2, even if you are covered by an employer retirement plan. Deductible contributions are subject to certain qualifications. Please consult your tax advisor.

Roth IRAs – Under a Roth IRA, there is no tax deduction for contributions, but there is no income tax on qualified withdrawals. For a more detailed comparison of Traditional and Roth IRAs, please see our website at www.thornburg. com/ira.

SEP IRAs – Simplified Employee Pension (SEP) IRAs are established by employers. The employer is allowed a tax deduction for contributions made to the SEP Plan and makes contributions to each eligible employee’s SEP IRA on a discretionary basis.

SIMPLE IRAs – Savings Incentive Match Plan for Employees of Small Employers (SIMPLE) is designed to give small business owners a simplified method to establish and contribute to a retirement plan for employees. The employer is allowed a tax deduction for contributions and makes either matching or non-elective contributions to each eligible employee’s SIMPLE IRA. Employees may make salary deferral contributions.

Coverdell Education Savings Account

These savings accounts are designed to provide a way to save money for higher education expenses. In an Education Savings Account, earnings and interest grow tax-free, and qualified withdrawals used to pay for eligible higher-education expenses are tax- and penalty-free.

Funds Available

The following funds are available in the accounts listed above:

| | • | | Thornburg Core Growth Fund |

| | • | | Thornburg International Value Fund |

| | • | | Thornburg International Growth Fund |

| | • | | Thornburg Developing World Fund |

| | • | | Thornburg Investment Income Builder Fund |

| | • | | Thornburg Global Opportunities Fund |

| | • | | Thornburg Low Duration Income Fund |

| | • | | Thornburg Limited Term U.S. Government Fund |

| | • | | Thornburg Limited Term Income Fund |

| | • | | Thornburg Strategic Income Fund |

This page is not part of the Semi-Annual Report 27

28 This page is not part of the Semi-Annual Report

THORNBURG FUND FAMILY

Thornburg Equity Funds

Thornburg’s equity research uses a fundamentally driven, bottom-up, comprehensive analytical approach. Thornburg equity funds generally focus on a limited number of securities so that each holding can impact performance. The team searches for firms believed to have a promising future and seeks to buy shares of those companies at a discount to their intrinsic or long-term value.

| | • | | Thornburg Core Growth Fund |

| | • | | Thornburg International Value Fund |

| | • | | Thornburg International Growth Fund |

| | • | | Thornburg Developing World Fund |

| | • | | Thornburg Investment Income Builder Fund |

| | • | | Thornburg Global Opportunities Fund |

Thornburg Bond Funds

Thornburg Investment Management applies a disciplined philosophy to fixed-income management. Since the launch of our first fixed-income fund over 25 years ago, we have been conducting fundamental, bottom-up research in an effort to identify bonds which we believe provide the best return for a given level of risk. We avoid leverage or complex strategies which could backfire in periods of market uncertainty.

| | • | | Thornburg Low Duration Income Fund |

| | • | | Thornburg Limited Term U.S. Government Fund |

| | • | | Thornburg Limited Term Income Fund |

| | • | | Thornburg Strategic Income Fund |

| | • | | Thornburg Low Duration Municipal Fund |

| | • | | Thornburg Limited Term Municipal Fund |

| | • | | Thornburg Intermediate Municipal Fund |

| | • | | Thornburg California Limited Term Municipal Fund |

| | • | | Thornburg New Mexico Intermediate Municipal Fund |

| | • | | Thornburg New York Intermediate Municipal Fund |

| | • | | Thornburg Strategic Municipal Income Fund |

Before investing, carefully consider the Fund’s investment goals, risks, charges, and expenses. For a prospectus or summary prospectus containing this and other information, contact your financial advisor or visit thornburg.com. Read it carefully before investing.

For additional information, please visit thornburg.com

Thornburg Investment Management, Inc. 2300 North Ridgetop Road, Santa Fe, NM 87506

This page is not part of the Semi-Annual Report 29

This page intentionally left blank.

30 This page is not part of the Semi-Annual Report

This page intentionally left blank.

This page is not part of the Semi-Annual Report 31

2 This page is not part of the Semi-Annual Report

IMPORTANT INFORMATION

Best Short-Intermediate Municipal Debt Fund

Lipper Fund Awards are granted annually to the fund in each Lipper classification that consistently delivered the strongest risk-adjusted performance (calculated with dividends reinvested). In 2014, Class I shares won for the ten-year period ended 11/30/2013 among 29 funds. The Fund did not win the award for other time periods.

The information presented on the following pages is current as of March 31, 2014. The managers’ views, portfolio holdings, and sector diversification are provided for the general information of the Fund’s shareholders; to the extent this information is historical, it should not be considered predictive of future circumstances. This material should not be deemed a recommendation to buy or sell any of the securities mentioned.