UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-5225

Oppenheimer Quest for Value Funds

(Exact name of registrant as specified in charter)

6803 South Tucson Way, Centennial, Colorado 80112-3924

(Address of principal executive offices) (Zip code)

Cynthia Lo Bessette

OFI Global Asset Management, Inc.

225 Liberty Street, New York, New York 10281-1008

(Name and address of agent for service)

Registrant’s telephone number, including area code: (303) 768-3200

Date of fiscal year end: October 31

Date of reporting period: 10/31/2017

Item 1. Reports to Stockholders.

Annual Report 10/31/2017 OppenheimerFunds® The Right Way to Invest Oppenheimer Global Allocation Fund

Table of Contents

Class A Shares

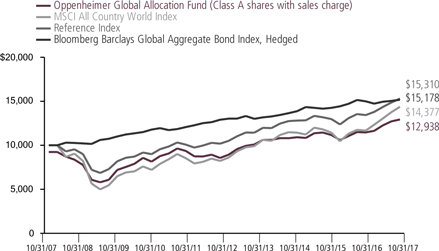

AVERAGE ANNUAL TOTAL RETURNS AT 10/31/17

| | | | | | | | | | | | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

| | | |

Class A Shares of the Fund without Sales Charge | | | 12.84 | % | | | 7.69 | % | | | 3.22% | |

| | | |

Class A Shares of the Fund with Sales Charge | | | 6.35 | | | | 6.42 | | | | 2.61 | |

| | | |

MSCI All Country World Index | | | 23.20 | | | | 10.80 | | | | 3.70 | |

| | | |

Bloomberg Barclays Global Aggregate Bond Index, Hedged | | | 1.23 | | | | 3.10 | | | | 4.26 | |

| | | |

Reference Index | | | 13.96 | | | | 7.82 | | | | 4.35 | |

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Fund returns include changes in share price, reinvested distributions, and a 5.75% maximum applicable sales charge except where “without sales charge” is indicated. Current performance may be lower or higher than the performance quoted. Returns do not consider capital gains or income taxes on an individual’s investment. Returns for periods of less than one year are cumulative and not annualized. For performance data current to the most recent month-end, visit oppenheimerfunds.com or call 1.800.CALL OPP (225.5677). See Fund prospectuses and summary prospectuses for more information on share classes and sales charges.

2 OPPENHEIMER GLOBAL ALLOCATION FUND

Fund Performance Discussion

The Fund’s Class A shares (without sales charge) produced a return of 12.84% during the reporting period. The Fund underperformed its Reference Index (the “Reference Index”), a customized weighted index currently comprised of 60% of the MSCI All Country World Index and 40% of the Bloomberg Barclays Global Aggregate Bond Index, Hedged, which returned 13.96%.

MARKET OVERVIEW

Shortly after the reporting period began, markets turned to “risk-on” mode after the surprise election of Donald Trump. Equities climbed and U.S. Treasury yields rose to levels not experienced since 2014. The 10-year yield opened the reporting period on November 1, 2016 at 1.38% and ended 2016 at 2.44%.

Global economic data continued to improve during the reporting period. Business and consumer confidence are at cyclical highs in many countries. Monetary policy in the United

States tightened during the reporting period, with the Federal Reserve (the “Fed”) raising its benchmark interest rate in December 2016, March 2017 and June 2017, each time by one-quarter of 1 percentage point. The Fed also announced the beginning of its plan to passively reduce the size of its balance sheet in September 2017. While we do not expect this process to have meaningful impact on bond markets, we are more cautious on the potential for tax cuts and the upcoming appointment of a new Fed chair.

COMPARISON OF CHANGE IN VALUE OF $10,000 HYPOTHETICAL INVESTMENTS IN:

3 OPPENHEIMER GLOBAL ALLOCATION FUND

Against this backdrop, equity markets throughout the globe produced positive absolute returns. Emerging market equities outperformed other international and U.S. counterparts, with the MSCI Emerging Markets Index up 26.45% for the one-year ended October 31, 2017, the MSCI All Country World Index up 23.20%, and the S&P 500 Index up 23.63%. Year to date in 2017, U.S. Treasury rates fell overall from the close of 2016 and ended the reporting period at 2.38%. In this environment, the Bloomberg Barclays U.S. Aggregate Bond Index produced a muted return of 0.90% for the one-year ended October 31, 2017.

FUND REVIEW

With respect to asset allocation at the end of the reporting period, the portfolio was slightly overweight equity-focused strategies versus the Reference Index, with a preference for the international and emerging markets. This benefited performance during the reporting period. Our macroeconomic tools and research indicate positive global economic growth that is making a new cyclical high. The new peak is being driven by strong data in the western hemisphere, the continued expansion in Europe, and a recovery in emerging markets that continues to gain widespread traction. In our view, this macro backdrop has justified an overweight equity exposure in our portfolio and we believe it will continue to support this positioning in the near-term. In particular, we have a relative

value tilt to European equities, where the Euro area expansion looks to be holding firm, which is funded through an underweight to U.S. equities. In Europe, we see cheaper valuations by a number of metrics and with the election of Emmanuel Macron in France, political risk is receding. We continue to have a preference for emerging market equities given cheaper valuations and an economic cycle that is younger in comparison to the developed world.

During the period, the security selection component of the Fund’s investment process was a positive contributor to relative performance, driven mostly by outperformance across international equity strategies. In an effort to manage our style exposure, we exited out of our global developed equity strategy to reduce the portfolio’s underweight to the value factor. We completed this transition on the back of very strong stock selection from the global equity strategy. Our developed international core and international growth equity strategies were contributors during the period. The emerging market equity strategy had positive stock selection in the Consumer Discretionary sector.

On the credit side, we continue to see warning signs that we are in late cycle stages.Specifically, growing corporate leverage and the resulting tighter lending standards could increase credit market vulnerability. As a

4 OPPENHEIMER GLOBAL ALLOCATION FUND

result, we have no exposure to certain areas of the credit markets, particularly high yield bonds. We do have a preference for bank loans, where we see comparable spreads for less interest rate and energy sector risk. Our exposure to bank loans benefited performance during the reporting period. We also view the current business cycle as very extended, a fact that is reflected in the expensive valuations of several asset classes as well as the build-up of leverage in the corporate sector. In the credit cycle, corporate leverage typically follows a cyclical pattern that precedes changes in credit conditions by several quarters and is followed by a re-pricing of credit spreads. Today, the non-financial corporate credit cycle has reached cyclical highs, surpassing the 2008 peak and approaching the peaks of 1989 and 2000. All three of these episodes coincided with recessions.

We are neutral duration and we continue to see attractive income and total return opportunities in emerging markets local debt, given attractive real yields, stable inflation and cheap currency valuations in most high-yielding markets. During the period, our allocation to emerging markets local debt was a positive contributor to relative performance. This asset class did well during the period, outperforming other fixed income assets. We see value in this asset class in comparison to developed market bonds that have low or negative real yields. In addition, many

emerging markets have room to cut rates as inflation declines and we believe this will provide some capital appreciation.

The largest detractor from relative performance was our allocation to alternatives. We hold event-linked bonds because we believe they offer strong potential for diversified income. With the recent string of natural disasters—notably the earthquake in Mexico and Hurricanes Harvey and Irma—this market had been under considerable stress. However, damage estimates have dropped considerably from those initial fears after Irma veered west of Miami and weakened from its peak strength. During the period, we added exposure to Master Limited Partnerships (“MLPs”) because of their cheap valuations and attractive yields. Despite a move higher in energy prices, MLPs struggled during the period and did not outperform the Reference Index. In our view, we started to see the excess supply of oil start to normalize, which should provide some upside and stability to prices. We continue to be bullish on MLPs due to the attractive yield relative to other income sources.

One of our key market views at the turn of the year was that the U.S. dollar, though already significantly overvalued, would continue to appreciate in light of a shifting U.S. policy landscape. A united Republican Congress and presidency had increased the odds of fiscal stimulus which, coupled with monetary

5 OPPENHEIMER GLOBAL ALLOCATION FUND

tightening already underway, created the potential for meaningful fiscal and monetary policy divergence between the United States and other major developed countries. As we explained at the time, such a policy mix was likely to boost the greenback against other major currencies. Throughout the year, the U.S. dollar has fallen on a trade-weighted basis. This has been a headwind to our currency positioning and has been a detractor during the period.

With a few setbacks to the current administration’s agenda and tax reform still an open question, we have reduced our U.S. dollar long position to neutral and continue to express relative relative-value views in high-yielding emerging market currencies such as the Turkish lira, Russian ruble and Indian rupee versus their developed-market peers. We have also added long exposure to Japanese yen as a means of balancing risk in this strategy.

The Fund’s return shaping strategies, which are designed to improve our overall risk profile, detracted from performance during the reporting period. Under normal circumstances, we expect return shaping strategies to cost money, like any insurance premium, and commensurately enhance returns or partially protect principal in environments of extreme market volatility. These strategies are also often used as an efficient way to access upside market participation, especially when we are running lower levels of risk. During

the period, we utilized downside hedges to reduce tail risk and layer in some downside mitigation in the event we had a risk-off environment. In the absence of volatility during the period, the premium spent for downside hedges was a small detractor.

STRATEGY & OUTLOOK

Overall, we are slightly overweight equities and have a neutral duration posture relative to the Reference Index. We have modest return expectations given valuations in most asset classes and prefer relative value opportunities rather than large directional tilts in the portfolio. We see an accelerating growth picture abroad as a potential tailwind to risk assets in the near term. We do have a relative value preference for European and emerging market equities versus the U.S. equity market, where we see cheaper valuations and earlier stages of the business cycle. With that said, we have increased our equity exposure to an overweight relative to the Reference Index and continue to prefer diversified income sources with attractive real yields. We do see increasing vulnerabilities in credit markets with non-financial corporate leverage nearing previous cyclical peaks, which causes us to prefer bank loans to high yield corporate debt.

As always, we continue to closely monitor the developments in the credit cycle as well as the political and policy landscape to assess risks to the macro outlook and financial markets.

6 OPPENHEIMER GLOBAL ALLOCATION FUND

While some fundamental risks have increased, the current macro backdrop is quite favorable to risk assets in the near term and we don’t see a clear catalyst for increased volatility.

Should we see deterioration in economic data, or volatility spread to equities and credit, we stand ready to adapt to a changing environment.

| | | | | | | | | | |

| |  | |

| |  |

| | Mark Hamilton Portfolio Manager | | | Benjamin Rockmuller, CFA Portfolio Manager |

| | | |

| |  | |

| |  |

| | Alessio de Longis, CFA Portfolio Manager | | | Dokyoung Lee, CFA Portfolio Manager |

7 OPPENHEIMER GLOBAL ALLOCATION FUND

Top Holdings and Allocations

TOP TEN COMMON STOCK HOLDINGS

| | | | |

Apple, Inc. | | | 1.3% | |

Alphabet, Inc., Cl. C | | | 1.1 | |

SAP SE | | | 0.7 | |

Facebook, Inc., Cl. A | | | 0.7 | |

Alibaba Group Holding Ltd., Sponsored ADR | | | 0.7 | |

Citigroup, Inc. | | | 0.7 | |

Infineon Technologies AG | | | 0.6 | |

Comcast Corp., Cl. A | | | 0.6 | |

UnitedHealth Group, Inc. | | | 0.6 | |

Nippon Telegraph & Telephone Corp. | | | 0.5 | |

Portfolio holdings and allocations are subject to change. Percentages are as of October 31, 2017, and are based on net assets. For more current Fund holdings, please visit oppenheimerfunds. com.

TOP TEN COMMON STOCK INDUSTRIES

| | | | |

Internet Software & Services | | | 3.8% | |

Oil, Gas & Consumable Fuels | | | 3.5 | |

Commercial Banks | | | 3.2 | |

Semiconductors & Semiconductor Equipment | | | 2.6 | |

Capital Markets | | | 2.0 | |

Hotels, Restaurants & Leisure | | | 2.0 | |

Food Products | | | 1.9 | |

Insurance | | | 1.9 | |

Beverages | | | 1.8 | |

Software | | | 1.8 | |

Portfolio holdings and allocations are subject to change. Percentages are as of October 31, 2017, and are based on net assets.

PORTFOLIO ALLOCATION

| | | | |

| Common Stocks | | | 62.0% | |

| Investment Companies | | | | |

Oppenheimer Institutional Government Money Market Fund | | | 11.0 | |

Oppenheimer Master Event- Linked Bond Fund, LLC | | | 4.3 | |

Oppenheimer Master Loan Fund, LLC | | | 7.4 | |

Oppenheimer Senior Floating Rate Fund | | | 2.2 | |

PowerShares Senior Loan Portfolio Exchange Traded Fund | | | 4.8 | |

| Foreign Government Obligations | | | 4.8 | |

| U.S. Government Obligations | | | 3.3 | |

| Preferred Stocks | | | 0.1 | |

| Short-Term Notes | | | 0.1 | |

| Over-the-Counter Options Purchased | | | —* | |

| Rights, Warrants and Certificates | | | —* | |

| Non-Convertible Corporate Bonds and Notes | | | —* | |

* Represents a value of less than 0.05%.

Portfolio holdings and allocations are subject to change. Percentages are as of October 31, 2017, and are based on the total market value of investments.

8 OPPENHEIMER GLOBAL ALLOCATION FUND

TOP TEN GEOGRAPHICAL HOLDINGS

| | | | |

United States | | | 59.5% | |

Japan | | | 5.7 | |

France | | | 5.1 | |

United Kingdom | | | 3.8 | |

Germany | | | 3.0 | |

China | | | 2.8 | |

Switzerland | | | 2.5 | |

Canada | | | 1.9 | |

India | | | 1.4 | |

Netherlands | | | 1.3 | |

Portfolio holdings and allocation are subject to change. Percentages are as of October 31, 2017, and are based on total market value of investments.

REGIONAL ALLOCATION

| | | | |

U.S./Canada | | | 61.4% | |

Europe | | | 18.1 | |

Asia | | | 14.6 | |

Latin & South America | | | 2.9 | |

Emerging Europe | | | 1.8 | |

Middle East/Africa | | | 1.2 | |

Portfolio holdings and allocation are subject to change. Percentages are as of October 31, 2017, and are based on total market value of investments.

9 OPPENHEIMER GLOBAL ALLOCATION FUND

Share Class Performance

AVERAGE ANNUAL TOTAL RETURNS WITHOUT SALES CHARGE AS OF 10/31/17

| | | | | | | | | | |

| | | Inception

Date | | 1-Year | | 5-Year | | 10-Year | | |

Class A (QVGIX) | | 11/1/91 | | 12.84% | | 7.69% | | 3.22% | | |

Class B (QGRBX) | | 9/1/93 | | 11.95 | | 6.83 | | 2.72 | | |

Class C (QGRCX) | | 9/1/93 | | 11.99 | | 6.89 | | 2.47 | | |

Class I (QGRIX) | | 2/28/12 | | 13.33 | | 8.17 | | 6.97* | | |

Class R (QGRNX) | | 3/1/01 | | 12.55 | | 7.42 | | 2.97 | | |

Class Y (QGRYX) | | 5/1/00 | | 13.13 | | 7.99 | | 3.56 | | |

AVERAGE ANNUAL TOTAL RETURNS WITH SALES CHARGE AS OF 10/31/17

| | | | | | | | | | |

| | | Inception Date | | 1-Year | | 5-Year | | 10-Year | | |

Class A (QVGIX) | | 11/1/91 | | 6.35% | | 6.42% | | 2.61% | | |

Class B (QGRBX) | | 9/1/93 | | 6.95 | | 6.52 | | 2.72 | | |

Class C (QGRCX) | | 9/1/93 | | 10.99 | | 6.89 | | 2.47 | | |

Class I (QGRIX) | | 2/28/12 | | 13.33 | | 8.17 | | 6.97* | | |

Class R (QGRNX) | | 3/1/01 | | 12.55 | | 7.42 | | 2.97 | | |

Class Y (QGRYX) | | 5/1/00 | | 13.13 | | 7.99 | | 3.56 | | |

| | | | |

| * Shows performance since inception. | | | | | | | | |

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the most recent month-end, visit oppenheimerfunds.com or call 1.800. CALL OPP (225.5677). Fund returns include changes in share price, reinvested distributions, and the applicable sales charge: for Class A shares, the current maximum initial sales charge of 5.75%; for Class B shares, the contingent deferred sales charge of 5% (1-year) and 2% (5-year); and for Class C shares, the contingent deferred sales charge (“CDSC”) of 1% for the 1-year period. There is no sales charge for Class I, Class R and Class Y shares. Because Class B shares convert to Class A shares 72 months after purchase, the 10-year return for Class B shares uses Class A performance for the period after conversion. Returns for periods of less than one year are cumulative and not annualized. See Fund prospectuses and summary prospectuses for more information on share classes and sales charges.

The Fund’s performance is compared to the performance of the MSCI All Country World Index, the S&P 500 Index, the Reference Index (60% MSCI All Country World Index / 40% Bloomberg Barclays Global Aggregate Bond Index, Hedged), and the Bloomberg Barclays Global Aggregate Bond Index, Hedged. The MSCI All Country World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The S&P 500 Index is a broad-based measure of domestic stock performance. The Bloomberg Barclays Global Aggregate Bond Index provides a broad-based measure of global investment grade fixed-rate debt markets.

10 OPPENHEIMER GLOBAL ALLOCATION FUND

The index is comprised of several other Bloomberg Barclays indexes that measure fixed income performance of regions around the world while hedging the currency back to the U.S. dollar. While index comparisons may be useful to provide a benchmark for the Fund’s performance, it must be noted that the Fund’s investments are not limited to the investments comprising the indices. Index performance includes reinvestment of income, but does not reflect transaction costs, fees, expenses or taxes. Index performance is shown for illustrative purposes only as a benchmark for the Fund’s performance, and does not predict or depict performance of the Fund. The Fund’s performance reflects the effects of the Fund’s business and operating expenses.

The Fund’s investment strategy and focus can change over time. The mention of specific fund holdings does not constitute a recommendation by OppenheimerFunds, Inc. or its affiliates.

Before investing in any of the Oppenheimer funds, investors should carefully consider a fund’s investment objectives, risks, charges and expenses. Fund prospectuses and summary prospectuses contain this and other information about the funds, and may be obtained by asking your financial advisor, visiting oppenheimerfunds.com, or calling 1.800.CALL OPP (225.5677). Read prospectuses and summary prospectuses carefully before investing.

Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested.

11 OPPENHEIMER GLOBAL ALLOCATION FUND

Fund Expenses

Fund Expenses. As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments and/or contingent deferred sales charges on redemptions; and (2) ongoing costs, including management fees; distribution and service fees; and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000.00 invested at the beginning of the period and held for the entire 6-month period ended October 31, 2017.

Actual Expenses. The first section of the table provides information about actual account values and actual expenses. You may use the information in this section for the class of shares you hold, together with the amount you invested, to estimate the expense that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600.00 account value divided by $1,000.00 = 8.60), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During 6 Months Ended October 31, 2017” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio for each class of shares, and an assumed rate of return of 5% per year for each class before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or contingent deferred sales charges (loads). Therefore, the “hypothetical” section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

12 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | | | | | | | | | | | | | | | | | |

| Actual | | Beginning Account Value May 1, 2017 | | | | | | Ending Account Value October 31, 2017 | | | Expenses Paid During 6 Months Ended

October 31, 2017 | |

Class A | | $ | 1,000.00 | | | | | | | $ | 1,055.20 | | | | | | | $ | 6.60 | | | | | |

Class B | | | 1,000.00 | | | | | | | | 1,051.20 | | | | | | | | 10.65 | | | | | |

Class C | | | 1,000.00 | | | | | | | | 1,051.20 | | | | | | | | 10.50 | | | | | |

Class I | | | 1,000.00 | | | | | | | | 1,057.40 | | | | | | | | 4.37 | | | | | |

Class R | | | 1,000.00 | | | | | | | | 1,053.90 | | | | | | | | 7.85 | | | | | |

Class Y | | | 1,000.00 | | | | | | | | 1,056.50 | | | | | | | | 5.30 | | | | | |

| | | | | | |

| Hypothetical | | | | | | | | | | | | | | | | | | | | | | | | |

(5% return before expenses) | | | | | | | | | | | | | | | | | | | | | | | | |

Class A | | | 1,000.00 | | | | | | | | 1,018.80 | | | | | | | | 6.48 | | | | | |

Class B | | | 1,000.00 | | | | | | | | 1,014.87 | | | | | | | | 10.46 | | | | | |

Class C | | | 1,000.00 | | | | | | | | 1,015.02 | | | | | | | | 10.31 | | | | | |

Class I | | | 1,000.00 | | | | | | | | 1,020.97 | | | | | | | | 4.29 | | | | | |

Class R | | | 1,000.00 | | | | | | | | 1,017.59 | | | | | | | | 7.71 | | | | | |

Class Y | | | 1,000.00 | | | | | | | | 1,020.06 | | | | | | | | 5.21 | | | | | |

Expenses are equal to the Fund’s annualized expense ratio for that class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). Those annualized expense ratios, excluding indirect expenses from affiliated funds, based on the 6-month period ended October 31, 2017 are as follows:

| | | | | | | | |

| Class | | Expense Ratios | | | | |

Class A | | | 1.27 | % | | | | |

Class B | | | 2.05 | | | | | |

Class C | | | 2.02 | | | | | |

Class I | | | 0.84 | | | | | |

Class R | | | 1.51 | | | | | |

Class Y | | | 1.02 | | | | | |

The expense ratios reflect voluntary and/or contractual waivers and/or reimbursements of expenses by the Fund’s Manager and Transfer Agent. Some of these undertakings may be modified or terminated at any time, as indicated in the Fund’s prospectus. The “Consolidated Financial Highlights” tables in the Fund’s financial statements, included in this report, also show the gross expense ratios, without such waivers or reimbursements and reduction to custodian expenses, if applicable.

13 OPPENHEIMER GLOBAL ALLOCATION FUND

CONSOLIDATED STATEMENT OF INVESTMENTS October 31, 2017

| | | | | | | | |

| | | Shares | | | Value | |

Common Stocks—61.6% | | | | | | | | |

Consumer Discretionary—9.8% | | | | | | | | |

Auto Components—1.4% | | | | | | | | |

Bridgestone Corp. | | | 101,600 | | | $ | 4,851,856 | |

Continental AG | | | 24,392 | | | | 6,191,234 | |

Delphi Automotive plc | | | 34,670 | | | | 3,445,505 | |

Koito Manufacturing Co. Ltd. | | | 41,000 | | | | 2,736,337 | |

Valeo SA | | | 81,727 | | | | 5,529,863 | |

| | | | | | | 22,754,795 | |

| | | | | | | | | |

Automobiles—0.6% | | | | | | | | |

Astra International Tbk PT | | | 1,435,000 | | | | 846,490 | |

Bayerische Motoren Werke AG | | | 17,542 | | | | 1,787,977 | |

Hero MotoCorp Ltd. | | | 57,543 | | | | 3,420,264 | |

Subaru Corp. | | | 62,500 | | | | 2,152,757 | |

Suzuki Motor Corp. | | | 37,200 | | | | 2,036,077 | |

| | | | | | | 10,243,565 | |

| | | | | | | | | |

Diversified Consumer Services—0.2% | | | | | | | | |

Dignity plc | | | 38,581 | | | | 1,241,949 | |

Estacio Participacoes SA | | | 53,800 | | | | 482,363 | |

New Oriental Education & Technology Group, Inc., Sponsored ADR | | | 9,220 | | | | 767,473 | |

| | | | | | | 2,491,785 | |

| | | | | | | | | |

Hotels, Restaurants & Leisure—2.0% | | | | | | | | |

Accor SA | | | 36,730 | | | | 1,833,250 | |

Carnival Corp. | | | 81,060 | | | | 5,381,573 | |

Cedar Fair LP1 | | | 16,418 | | | | 1,027,767 | |

China Lodging Group Ltd., Sponsored ADR2 | | | 15,548 | | | | 2,081,722 | |

Domino’s Pizza Group plc | | | 399,870 | | | | 1,783,850 | |

Galaxy Entertainment Group Ltd. | | | 323,000 | | | | 2,200,405 | |

Genting Bhd | | | 1,394,500 | | | | 2,981,118 | |

Genting Malaysia Bhd | | | 321,800 | | | | 382,349 | |

Jollibee Foods Corp. | | | 135,080 | | | | 651,538 | |

McDonald’s Corp. | | | 28,660 | | | | 4,783,641 | |

Sands China Ltd. | | | 900,800 | | | | 4,247,784 | |

Starbucks Corp. | | | 22,640 | | | | 1,241,578 | |

Whitbread plc | | | 28,301 | | | | 1,387,953 | |

Wyndham Worldwide Corp. | | | 7,960 | | | | 850,526 | |

Yum China Holdings, Inc.2 | | | 38,770 | | | | 1,564,369 | |

| | | | | | | 32,399,423 | |

| | | | | | | | | |

Household Durables—0.9% | | | | | | | | |

Newell Brands, Inc. | | | 11,460 | | | | 467,339 | |

SEB SA | | | 13,050 | | | | 2,432,754 | |

Sony Corp. | | | 160,300 | | | | 6,723,408 | |

Whirlpool Corp. | | | 26,690 | | | | 4,375,292 | |

| | | | | | | 13,998,793 | |

|

| 14 OPPENHEIMER GLOBAL ALLOCATION FUND |

| | | | | | | | |

| | | Shares | | | Value | |

Internet & Catalog Retail—0.5% | | | | | | | | |

Amazon.com, Inc.2 | | | 2,796 | | | $ | 3,090,363 | |

Ctrip.com International Ltd., ADR2 | | | 39,750 | | | | 1,903,627 | |

Priceline Group, Inc. (The)2 | | | 730 | | | | 1,395,731 | |

Rakuten, Inc. | | | 228,800 | | | | 2,435,422 | |

| | | | | | | 8,825,143 | |

| | | | | | | | | |

Leisure Products—0.3% | | | | | | | | |

Nintendo Co. Ltd. | | | 13,600 | | | | 5,296,918 | |

| | | | | | | | | |

Media—1.0% | | | | | | | | |

Comcast Corp., Cl. A | | | 257,014 | | | | 9,260,214 | |

DISH Network Corp., Cl. A2 | | | 11,880 | | | | 576,655 | |

ProSiebenSat.1 Media SE | | | 46,424 | | | | 1,619,355 | |

SES SA, Cl. A, FDR | | | 83,400 | | | | 1,356,372 | |

Technicolor SA | | | 264,210 | | | | 936,861 | |

Walt Disney Co. (The) | | | 6,840 | | | | 669,020 | |

Zee Entertainment Enterprises Ltd. | | | 209,371 | | | | 1,753,211 | |

| | | | | | | 16,171,688 | |

| | | | | | | | | |

Multiline Retail—0.2% | | | | | | | | |

Dollarama, Inc. | | | 25,902 | | | | 2,883,332 | |

Target Corp. | | | 17,660 | | | | 1,042,646 | |

| | | | | | | 3,925,978 | |

| | | | | | | | | |

Specialty Retail—1.2% | | | | | | | | |

AutoNation, Inc.2 | | | 30,200 | | | | 1,431,480 | |

AutoZone, Inc.2 | | | 7,820 | | | | 4,609,890 | |

Dufry AG2 | | | 15,316 | | | | 2,280,778 | |

Industria de Diseno Textil SA | | | 49,173 | | | | 1,838,070 | |

Lowe’s Cos., Inc. | | | 68,060 | | | | 5,441,397 | |

Nitori Holdings Co. Ltd. | | | 4,600 | | | | 666,124 | |

O’Reilly Automotive, Inc.2 | | | 6,240 | | | | 1,316,328 | |

Steinhoff International Holdings NV | | | 303,311 | | | | 1,319,610 | |

| | | | | | | 18,903,677 | |

| | | | | | | | | |

Textiles, Apparel & Luxury Goods—1.5% | | | | | | | | |

adidas AG | | | 5,261 | | | | 1,170,772 | |

Burberry Group plc | | | 21,688 | | | | 547,746 | |

Christian Dior SE | | | 4,810 | | | | 1,651,906 | |

Cie Financiere Richemont SA | | | 26,145 | | | | 2,413,251 | |

Hanesbrands, Inc. | | | 40,920 | | | | 920,700 | |

Hermes International | | | 4,771 | | | | 2,476,723 | |

Kering | | | 11,508 | | | | 5,276,613 | |

LVMH Moet Hennessy Louis Vuitton SE | | | 21,940 | | | | 6,547,795 | |

Pandora AS | | | 20,291 | | | | 1,918,209 | |

PRADA SpA | | | 367,500 | | | | 1,271,939 | |

Tapestry, Inc.2 | | | 16,390 | | | | 671,170 | |

| | | | | | | 24,866,824 | |

15 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| CONSOLIDATED STATEMENT OF INVESTMENTS Continued | | |

| | | |

| | | | | | | | |

| | | Shares | | | Value | |

Consumer Staples—5.5% | | | | | | | | |

Beverages—1.8% | | | | | | | | |

Anadolu Efes Biracilik Ve Malt Sanayii AS | | | 87,304 | | | $ | 505,601 | |

Anheuser-Busch InBev SA/NV | | | 12,409 | | | | 1,521,190 | |

Coca-Cola Co. (The) | | | 20,690 | | | | 951,326 | |

Coca-Cola European Partners plc | | | 67,140 | | | | 2,743,340 | |

Constellation Brands, Inc., Cl. A | | | 4,820 | | | | 1,056,014 | |

Dr Pepper Snapple Group, Inc. | | | 10,220 | | | | 875,445 | |

Fomento Economico Mexicano SAB de CV | | | 138,131 | | | | 1,205,888 | |

Fomento Economico Mexicano SAB de CV, Sponsored ADR | | | 6,910 | | | | 606,353 | |

Heineken NV | | | 28,086 | | | | 2,736,570 | |

Kweichow Moutai Co. Ltd., Cl. A | | | 12,269 | | | | 1,144,718 | |

Molson Coors Brewing Co., Cl. B | | | 11,750 | | | | 950,223 | |

Nigerian Breweries plc | | | 698,342 | | | | 291,521 | |

PepsiCo, Inc. | | | 65,070 | | | | 7,172,666 | |

Pernod Ricard SA | | | 50,040 | | | | 7,507,280 | |

| | | | | | | 29,268,135 | |

| | | | | | | | | |

Food & Staples Retailing—0.7% | | | | | | | | |

Alimentation Couche-Tard, Inc., Cl. B | | | 38,673 | | | | 1,813,293 | |

Atacadao Distribuicao Comercio e Industria Ltda2 | | | 140,300 | | | | 689,641 | |

BIM Birlesik Magazalar AS | | | 33,139 | | | | 676,399 | |

CP ALL PCL | | | 1,037,800 | | | | 2,187,393 | |

Jeronimo Martins SGPS SA | | | 4,913 | | | | 89,281 | |

Magnit PJSC | | | 15,693 | | | | 2,069,007 | |

Shoprite Holdings Ltd. | | | 43,599 | | | | 623,745 | |

SPAR Group Ltd. (The) | | | 118,131 | | | | 1,393,222 | |

Walgreens Boots Alliance, Inc. | | | 7,120 | | | | 471,842 | |

Wal-Mart Stores, Inc. | | | 19,180 | | | | 1,674,606 | |

| | | | | | | 11,688,429 | |

| | | | | | | | | |

Food Products—1.9% | | | | | | | | |

Barry Callebaut AG2 | | | 1,457 | | | | 2,274,791 | |

Danone SA | | | 68,310 | | | | 5,583,313 | |

Kraft Heinz Co. (The) | | | 63,250 | | | | 4,891,122 | |

Mondelez International, Inc., Cl. A | | | 103,610 | | | | 4,292,562 | |

Nestle SA | | | 62,787 | | | | 5,282,572 | |

Saputo, Inc. | | | 72,391 | | | | 2,613,730 | |

Unilever plc | | | 52,454 | | | | 2,975,036 | |

Vietnam Dairy Products JSC | | | 22,200 | | | | 147,600 | |

Want Want China Holdings Ltd. | | | 681,000 | | | | 557,123 | |

WH Group Ltd.3 | | | 2,338,000 | | | | 2,367,810 | |

| | | | | | | 30,985,659 | |

| | | | | | | | | |

Household Products—0.4% | | | | | | | | |

HRG Group, Inc.2 | | | 12,270 | | | | 199,019 | |

Kimberly-Clark de Mexico SAB de CV, Cl. A | | | 236,907 | | | | 407,908 | |

Procter & Gamble Co. (The) | | | 12,620 | | | | 1,089,611 | |

Reckitt Benckiser Group plc | | | 34,897 | | | | 3,121,153 | |

Spectrum Brands Holdings, Inc. | | | 7,120 | | | | 782,630 | |

16 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

Household Products (Continued) | | | | | | | | |

Weatherford International plc2 | | | 211,930 | | | $ | 735,397 | |

| | | | | | | 6,335,718 | |

| | | | | | | | | |

Personal Products—0.2% | | | | | | | | |

Amorepacific Corp. | | | 2,280 | | | | 640,010 | |

AMOREPACIFIC Group | | | 1,526 | | | | 195,152 | |

Beiersdorf AG | | | 6,943 | | | | 778,838 | |

LG Household & Health Care Ltd. | | | 2,314 | | | | 2,430,260 | |

Natura Cosmeticos SA | | | 7,600 | | | | 71,950 | |

| | | | | | | 4,116,210 | |

| | | | | | | | | |

Tobacco—0.5% | | | | | | | | |

Philip Morris International, Inc. | | | 54,710 | | | | 5,724,855 | |

Swedish Match AB | | | 46,610 | | | | 1,754,867 | |

| | | | | | | 7,479,722 | |

| | | | | | | | | |

Energy—3.8% | | | | | | | | |

Energy Equipment & Services—0.3% | | | | | | | | |

Halliburton Co. | | | 18,623 | | | | 795,947 | |

Schlumberger Ltd. | | | 60,860 | | | | 3,895,040 | |

TechnipFMC plc2 | | | 36,296 | | | | 987,302 | |

| | | | | | | 5,678,289 | |

| | | | | | | | | |

Oil, Gas & Consumable Fuels—3.5% | | | | | | | | |

Antero Midstream GP LP | | | 39,900 | | | | 746,529 | |

Buckeye Partners LP1 | | | 33,900 | | | | 1,800,429 | |

Chevron Corp. | | | 28,511 | | | | 3,304,140 | |

ConocoPhillips | | | 14,641 | | | | 748,887 | |

Enbridge, Inc. | | | 21,137 | | | | 812,929 | |

Energy Transfer Equity LP1 | | | 170,100 | | | | 3,019,275 | |

Energy Transfer Partners LP1 | | | 180,900 | | | | 3,149,469 | |

Enterprise Products Partners LP1 | | | 105,400 | | | | 2,582,300 | |

EQT Midstream Partners LP1 | | | 12,200 | | | | 891,332 | |

Genesis Energy LP1 | | | 22,600 | | | | 526,354 | |

Husky Energy, Inc.2 | | | 65,583 | | | | 849,971 | |

Koninklijke Vopak NV | | | 28,062 | | | | 1,214,858 | |

Magellan Midstream Partners LP1 | | | 120,530 | | | | 8,281,616 | |

MPLX LP1 | | | 65,000 | | | | 2,291,900 | |

Novatek PJSC, Sponsored GDR | | | 23,500 | | | | 2,682,450 | |

Phillips 66 | | | 6,539 | | | | 595,572 | |

Phillips 66 Partners LP1 | | | 18,700 | | | | 942,667 | |

Plains All American Pipeline LP1 | | | 36,500 | | | | 728,905 | |

Plains GP Holdings LP, Cl. A | | | 35,900 | | | | 732,360 | |

Rice Midstream Partners LP1 | | | 47,300 | | | | 981,002 | |

Suncor Energy, Inc. | | | 227,620 | | | | 7,729,975 | |

Tallgrass Energy GP LP, Cl. A | | | 57,600 | | | | 1,440,000 | |

Tallgrass Energy Partners LP1 | | | 6,700 | | | | 292,388 | |

Targa Resources Corp. | | | 49,400 | | | | 2,050,100 | |

TC PipeLines LP1 | | | 45,500 | | | | 2,424,695 | |

17 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| CONSOLIDATED STATEMENT OF INVESTMENTS Continued | | |

| | | |

| | | | | | | | |

| | | Shares | | | Value | |

Oil, Gas & Consumable Fuels (Continued) | | | | | | | | |

TOTAL SA | | | 57,610 | | | $ | 3,213,360 | |

Western Gas Partners LP1 | | | 14,200 | | | | 680,038 | |

Williams Cos., Inc. (The) | | | 26,500 | | | | 755,250 | |

Williams Partners LP1 | | | 40,800 | | | | 1,511,232 | |

| | | | | | | 56,979,983 | |

| | | | | | | | | |

Financials—9.7% | | | | | | | | |

Capital Markets—2.0% | | | | | | | | |

Ameriprise Financial, Inc. | | | 6,180 | | | | 967,417 | |

Bank of New York Mellon Corp. (The) | | | 85,390 | | | | 4,393,316 | |

BlackRock, Inc., Cl. A | | | 2,380 | | | | 1,120,575 | |

Charles Schwab Corp. (The) | | | 23,460 | | | | 1,051,946 | |

China International Capital Corp. Ltd., Cl. H3 | | | 172,000 | | | | 358,180 | |

CME Group, Inc., Cl. A | | | 33,910 | | | | 4,651,435 | |

Intercontinental Exchange, Inc. | | | 75,360 | | | | 4,981,296 | |

Morgan Stanley | | | 20,360 | | | | 1,018,000 | |

Nasdaq, Inc. | | | 20,910 | | | | 1,519,112 | |

NEX Group plc | | | 186,481 | | | | 1,570,814 | |

S&P Global, Inc. | | | 22,820 | | | | 3,570,645 | |

TP ICAP plc | | | 245,168 | | | | 1,772,759 | |

UBS Group AG2 | | | 347,743 | | | | 5,923,734 | |

| | | | | | | 32,899,229 | |

| | | | | | | | | |

Commercial Banks—3.2% | | | | | | | | |

Banco de Chile | | | 734,506 | | | | 112,671 | |

Banco Santander SA | | | 520,298 | | | | 3,530,965 | |

Bank Mandiri Persero Tbk PT | | | 1,396,000 | | | | 726,841 | |

Bank of America Corp. | | | 188,020 | | | | 5,149,868 | |

Bank of the Philippine Islands | | | 13,080 | | | | 24,848 | |

Bank Pekao SA | | | 4,257 | | | | 139,206 | |

Bank Rakyat Indonesia Persero Tbk PT | | | 408,000 | | | | 470,184 | |

Citigroup, Inc. | | | 144,030 | | | | 10,586,205 | |

Commercial International Bank Egypt SAE | | | 123,370 | | | | 551,420 | |

Credicorp Ltd. | | | 3,340 | | | | 699,530 | |

FirstRand Ltd. | | | 281,592 | | | | 1,020,747 | |

Grupo Aval Acciones y Valores SA, ADR | | | 83,160 | | | | 691,891 | |

Grupo Financiero Banorte SAB de CV, Cl. O | | | 55,350 | | | | 328,490 | |

Grupo Financiero Inbursa SAB de CV, Cl. O | | | 565,091 | | | | 971,207 | |

HSBC Holdings plc | | | 572,060 | | | | 5,578,311 | |

ICICI Bank Ltd., Sponsored ADR | | | 333,583 | | | | 3,052,284 | |

JPMorgan Chase & Co. | | | 46,520 | | | | 4,680,377 | |

KeyCorp | | | 65,940 | | | | 1,203,405 | |

Kotak Mahindra Bank Ltd. | | | 86,168 | | | | 1,363,668 | |

Lloyds Banking Group plc | | | 1,618,290 | | | | 1,467,480 | |

Sberbank of Russia PJSC, Sponsored ADR | | | 56,410 | | | | 809,324 | |

SunTrust Banks, Inc. | | | 45,590 | | | | 2,744,974 | |

US Bancorp | | | 66,840 | | | | 3,634,759 | |

Zenith Bank plc | | | 4,354,538 | | | | 308,652 | |

18 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

Commercial Banks (Continued) | | | | | | | | |

Zions Bancorporation | | | 32,780 | | | $ | 1,522,959 | |

| | | | | | | 51,370,266 | |

| | | | | | | | | |

Consumer Finance—0.6% | | | | | | | | |

American Express Co. | | | 56,950 | | | | 5,439,864 | |

Cholamandalam Investment & Finance Co. Ltd. | | | 15,348 | | | | 273,029 | |

Discover Financial Services | | | 35,500 | | | | 2,361,815 | |

Prosegur Cash SA2,3 | | | 575,614 | | | | 1,880,851 | |

| | | | | | | 9,955,559 | |

| | | | | | | | | |

Diversified Financial Services—1.1% | | | | | | | | |

Ayala Corp. | | | 11,470 | | | | 228,908 | |

B3 SA-Brasil Bolsa Balcao | | | 310,400 | | | | 2,267,771 | |

Berkshire Hathaway, Inc., Cl. B2 | | | 35,520 | | | | 6,640,109 | |

Grupo de Inversiones Suramericana SA | | | 40,892 | | | | 519,140 | |

Hong Kong Exchanges & Clearing Ltd. | | | 17,286 | | | | 481,412 | |

ING Groep NV | | | 208,737 | | | | 3,855,067 | |

Moscow Exchange (The) | | | 284,787 | | | | 575,941 | |

ORIX Corp. | | | 189,800 | | | | 3,270,092 | |

| | | | | | | 17,838,440 | |

| | | | | | | | | |

Insurance—1.9% | | | | | | | | |

AIA Group Ltd. | | | 377,000 | | | | 2,837,296 | |

American International Group, Inc. | | | 31,340 | | | | 2,024,877 | |

Aon plc | | | 7,990 | | | | 1,146,006 | |

Brighthouse Financial, Inc.2 | | | 4,952 | | | | 307,915 | |

Hartford Financial Services Group, Inc. (The) | | | 19,220 | | | | 1,058,061 | |

Marsh & McLennan Cos., Inc. | | | 35,510 | | | | 2,873,824 | |

MetLife, Inc. | | | 78,310 | | | | 4,195,850 | |

Ping An Insurance Group Co. of China Ltd., Cl. H | | | 322,500 | | | | 2,832,363 | |

Progressive Corp. (The) | | | 70,390 | | | | 3,424,474 | |

Prudential plc | | | 336,754 | | | | 8,289,356 | |

Sul America SA | | | 107,649 | | | | 590,024 | |

XL Group Ltd. | | | 31,070 | | | | 1,257,403 | |

| | | | | | | 30,837,449 | |

| | | | | | | | | |

Real Estate Investment Trusts (REITs)—0.4% | | | | | | | | |

Crown Castle International Corp. | | | 8,670 | | | | 928,384 | |

Digital Realty Trust, Inc. | | | 5,230 | | | | 619,441 | |

Invitation Homes, Inc. | | | 17,900 | | | | 404,003 | |

Mid-America Apartment Communities, Inc. | | | 22,660 | | | | 2,319,251 | |

Prologis, Inc. | | | 19,500 | | | | 1,259,310 | |

Ventas, Inc. | | | 21,880 | | | | 1,372,970 | |

| | | | | | | 6,903,359 | |

Real Estate Management & Development—0.2% | | | | | | | | |

Ayala Land, Inc. | | | 705,000 | | | | 589,723 | |

Emaar Properties PJSC | | | 255,089 | | | | 577,361 | |

Hang Lung Group Ltd. | | | 56,000 | | | | 196,690 | |

19 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| CONSOLIDATED STATEMENT OF INVESTMENTS Continued | | |

| | | |

| | | | | | | | |

| | | Shares | | | Value | |

Real Estate Management & Development (Continued) | | | | | | | | |

Scout24 AG3 | | | 37,771 | | | $ | 1,513,813 | |

SM Prime Holdings, Inc. | | | 1,532,103 | | | | 1,099,274 | |

| | | | | | | 3,976,861 | |

| | | | | | | | | |

Thrifts & Mortgage Finance—0.3% | | | | | | | | |

Housing Development Finance Corp. Ltd. | | | 167,921 | | | | 4,428,042 | |

| | | | | | | | | |

Health Care—5.6% | | | | | | | | |

Biotechnology—1.2% | | | | | | | | |

3SBio, Inc.2,3 | | | 210,000 | | | | 375,832 | |

Amgen, Inc. | | | 5,270 | | | | 923,409 | |

Biocon Ltd. | | | 46,917 | | | | 260,682 | |

Biogen, Inc.2 | | | 4,140 | | | | 1,290,272 | |

Celgene Corp.2 | | | 55,446 | | | | 5,598,383 | |

Celltrion Healthcare Co. Ltd.2 | | | 5,136 | | | | 270,413 | |

CSL Ltd. | | | 22,400 | | | | 2,389,030 | |

Galapagos NV2 | | | 2,723 | | | | 264,128 | |

Gilead Sciences, Inc. | | | 58,010 | | | | 4,348,430 | |

Grifols SA | | | 103,103 | | | | 3,228,549 | |

Wuxi Biologics Cayman, Inc.2,3 | | | 23,000 | | | | 130,398 | |

| | | | | | | 19,079,526 | |

| | | | | | | | | |

Health Care Equipment & Supplies—1.0% | | | | | | | | |

Boston Scientific Corp.2 | | | 76,660 | | | | 2,157,212 | |

Coloplast AS, Cl. B | | | 3,995 | | | | 351,293 | |

Danaher Corp. | | | 16,314 | | | | 1,505,293 | |

Essilor International SA | | | 17,134 | | | | 2,170,255 | |

Intuitive Surgical, Inc.2 | | | 1,980 | | | | 743,213 | |

Medtronic plc | | | 8,750 | | | | 704,550 | |

Sonova Holding AG | | | 12,045 | | | | 2,176,210 | |

Stryker Corp. | | | 21,620 | | | | 3,348,289 | |

William Demant Holding AS2 | | | 69,845 | | | | 2,017,901 | |

Zimmer Biomet Holdings, Inc. | | | 9,990 | | | | 1,214,984 | |

| | | | | | | 16,389,200 | |

| | | | | | | | | |

Health Care Providers & Services—1.1% | | | | | | | | |

Apollo Hospitals Enterprise Ltd. | | | 38,315 | | | | 614,347 | |

Express Scripts Holding Co.2 | | | 47,400 | | | | 2,905,146 | |

Humana, Inc. | | | 2,840 | | | | 725,194 | |

Laboratory Corp. of America Holdings2 | | | 7,030 | | | | 1,080,581 | |

Mediclinic International plc | | | 41,120 | | | | 317,639 | |

Sinopharm Group Co. Ltd., Cl. H | | | 444,600 | | | | 1,990,574 | |

Sonic Healthcare Ltd. | | | 33,848 | | | | 564,380 | |

UnitedHealth Group, Inc. | | | 43,780 | | | | 9,203,432 | |

| | | | | | | 17,401,293 | |

| | | | | | | | | |

Health Care Technology—0.3% | | | | | | | | |

Bharti Infratel Ltd. | | | 449,817 | | | | 3,077,180 | |

20 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

Health Care Technology (Continued) | | | | | | | | |

Cerner Corp.2 | | | 37,500 | | | $ | 2,532,000 | |

| | | | | | | 5,609,180 | |

| | | | | | | | | |

Life Sciences Tools & Services—0.4% | | | | | | | | |

Agilent Technologies, Inc. | | | 25,670 | | | | 1,746,330 | |

Lonza Group AG2 | | | 10,727 | | | | 2,852,206 | |

Samsung Biologics Co. Ltd.2,3 | | | 2,753 | | | | 951,813 | |

Thermo Fisher Scientific, Inc. | | | 4,170 | | | | 808,271 | |

| | | | | | | 6,358,620 | |

| | | | | | | | | |

Pharmaceuticals—1.6% | | | | | | | | |

Allergan plc | | | 5,560 | | | | 985,399 | |

Bayer AG | | | 29,359 | | | | 3,834,609 | |

Bristol-Myers Squibb Co. | | | 19,710 | | | | 1,215,319 | |

Celltrion, Inc.2 | | | 2,867 | | | | 446,235 | |

Dr. Reddy’s Laboratories Ltd. | | | 16,420 | | | | 615,062 | |

GlaxoSmithKline plc, Sponsored ADR | | | 26,730 | | | | 973,774 | |

Glenmark Pharmaceuticals Ltd. | | | 14,727 | | | | 140,764 | |

Hutchison China MediTech Ltd., ADR2 | | | 3,720 | | | | 113,274 | |

Jiangsu Hengrui Medicine Co. Ltd., Cl. A | | | 183,980 | | | | 1,865,325 | |

Merck & Co., Inc. | | | 129,670 | | | | 7,143,520 | |

Mylan NV2 | | | 47,480 | | | | 1,695,511 | |

Novo Nordisk AS, Cl. B | | | 56,384 | | | | 2,805,775 | |

Pfizer, Inc. | | | 59,630 | | | | 2,090,628 | |

Roche Holding AG | | | 8,623 | | | | 1,993,634 | |

Valeant Pharmaceuticals International, Inc.2 | | | 65,220 | | | | 762,422 | |

| | | | | | | 26,681,251 | |

| | | | | | | | | |

Industrials—8.8% | | | | | | | | |

Aerospace & Defense—1.0% | | | | | | | | |

Airbus SE | | | 75,630 | | | | 7,735,938 | |

Lockheed Martin Corp. | | | 22,146 | | | | 6,824,511 | |

MTU Aero Engines AG | | | 4,662 | | | | 787,245 | |

Spirit AeroSystems Holdings, Inc., Cl. A | | | 9,300 | | | | 744,930 | |

| | | | | | | 16,092,624 | |

| | | | | | | | | |

Air Freight & Couriers—0.1% | | | | | | | | |

FedEx Corp. | | | 2,410 | | | | 544,202 | |

XPO Logistics, Inc.2 | | | 15,470 | | | | 1,072,845 | |

ZTO Express Cayman, Inc., ADR2 | | | 24,880 | | | | 397,831 | |

| | | | | | | 2,014,878 | |

| | | | | | | | | |

Airlines—0.4% | | | | | | | | |

Alaska Air Group, Inc. | | | 21,140 | | | | 1,395,874 | |

Japan Airlines Co. Ltd. | | | 98,300 | | | | 3,365,561 | |

Southwest Airlines Co. | | | 9,200 | | | | 495,512 | |

Spirit Airlines, Inc.2 | | | 25,580 | | | | 948,762 | |

| | | | | | | 6,205,709 | |

21 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| CONSOLIDATED STATEMENT OF INVESTMENTS Continued | | |

| | | |

| | | | | | | | |

| | | Shares | | | Value | |

Building Products—0.3% | | | | | | | | |

SMC Corp. | | | 11,700 | | | $ | 4,489,400 | |

| | | | | | | | | |

Commercial Services & Supplies—0.7% | | | | | | | | |

Edenred | | | 68,380 | | | | 1,971,092 | |

Johnson Controls International plc | | | 72,509 | | | | 3,001,148 | |

KAR Auction Services, Inc. | | | 29,350 | | | | 1,389,135 | |

Prosegur Cia de Seguridad SA | | | 300,321 | | | | 2,291,643 | |

Republic Services, Inc., Cl. A | | | 10,850 | | | | 706,010 | |

Waste Connections, Inc. | | | 15,848 | | | | 1,119,978 | |

Waste Management, Inc. | | | 12,740 | | | | 1,046,846 | |

| | | | | | | 11,525,852 | |

| | | | | | | | | |

Construction & Engineering—0.7% | | | | | | | | |

Boskalis Westminster | | | 41,435 | | | | 1,481,216 | |

Ferrovial SA | | | 174,193 | | | | 3,785,398 | |

Vinci SA | | | 54,790 | | | | 5,366,466 | |

| | | | | | | 10,633,080 | |

Electrical Equipment—1.1% | | | | | | | | |

Legrand SA | | | 29,640 | | | | 2,202,578 | |

Mitsubishi Electric Corp. | | | 242,100 | | | | 4,158,772 | |

Nidec Corp. | | | 25,100 | | | | 3,322,443 | |

Philips Lighting NV3 | | | 120,243 | | | | 4,548,787 | |

Schneider Electric SE | | | 42,370 | | | | 3,716,632 | |

| | | | | | | 17,949,212 | |

| | | | | | | | | |

Industrial Conglomerates—0.7% | | | | | | | | |

General Electric Co. | | | 226,800 | | | | 4,572,288 | |

Jardine Strategic Holdings Ltd. | | | 42,572 | | | | 1,786,834 | |

Seibu Holdings, Inc. | | | 165,200 | | | | 2,955,986 | |

Siemens AG, Sponsored ADR | | | 9,140 | | | | 658,263 | |

SM Investments Corp. | | | 89,494 | | | | 1,657,929 | |

| | | | | | | 11,631,300 | |

| | | | | | | | | |

Machinery—0.8% | | | | | | | | |

Aalberts Industries NV | | | 49,695 | | | | 2,446,937 | |

Atlas Copco AB, Cl. A | | | 58,504 | | | | 2,559,395 | |

Caterpillar, Inc. | | | 10,790 | | | | 1,465,282 | |

Deere & Co. | | | 3,970 | | | | 527,534 | |

Kubota Corp. | | | 123,000 | | | | 2,318,662 | |

PACCAR, Inc. | | | 7,990 | | | | 573,123 | |

Parker-Hannifin Corp. | | | 7,630 | | | | 1,393,314 | |

Stanley Black & Decker, Inc. | | | 2,810 | | | | 453,956 | |

Wabtec Corp. | | | 11,580 | | | | 885,870 | |

Weir Group plc (The) | | | 32,753 | | | | 849,107 | |

| | | | | | | 13,473,180 | |

| | | | | | | | | |

Professional Services—1.1% | | | | | | | | |

Bureau Veritas SA | | | 101,990 | | | | 2,732,985 | |

22 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

Professional Services (Continued) | | | | | | | | |

Equifax, Inc. | | | 7,080 | | | $ | 768,392 | |

Experian plc | | | 78,858 | | | | 1,659,870 | |

Intertek Group plc | | | 28,580 | | | | 2,057,440 | |

Nielsen Holdings plc | | | 90,380 | | | | 3,350,387 | |

Recruit Holdings Co. Ltd. | | | 305,200 | | | | 7,471,578 | |

| | | | | | | 18,040,652 | |

| | | | | | | | | |

Road & Rail—0.4% | | | | | | | | |

Canadian National Railway Co. | | | 47,330 | | | | 3,809,592 | |

Canadian Pacific Railway Ltd. | | | 15,010 | | | | 2,603,334 | |

Kansas City Southern | | | 5,480 | | | | 571,126 | |

| | | | | | | 6,984,052 | |

| | | | | | | | | |

Trading Companies & Distributors—1.1% | | | | | | | | |

Brenntag AG | | | 75,567 | | | | 4,279,336 | |

Bunzl plc | | | 86,272 | | | | 2,688,421 | |

Fastenal Co. | | | 43,340 | | | | 2,035,680 | |

Ferguson plc | | | 16,343 | | | | 1,139,678 | |

ITOCHU Corp. | | | 280,900 | | | | 4,928,809 | |

Travis Perkins plc | | | 100,848 | | | | 2,036,308 | |

| | | | | | | 17,108,232 | |

| | | | | | | | | |

Transportation Infrastructure—0.4% | | | | | | | | |

Beijing Capital International Airport Co. Ltd., Cl. H | | | 2,156,000 | | | | 3,538,697 | |

DP World Ltd. | | | 67,925 | | | | 1,613,215 | |

Grupo Aeroportuario del Sureste SAB de CV, Cl. B | | | 33,044 | | | | 589,326 | |

Malaysia Airports Holdings Bhd | | | 530,300 | | | | 1,038,077 | |

| | | | | | | 6,779,315 | |

| | | | | | | | | |

Information Technology—12.8% | | | | | | | | |

Communications Equipment—0.4% | | | | | | | | |

Cisco Systems, Inc. | | | 85,410 | | | | 2,916,752 | |

Motorola Solutions, Inc. | | | 11,270 | | | | 1,020,386 | |

Nokia OYJ | | | 376,734 | | | | 1,850,221 | |

| | | | | | | 5,787,359 | |

| | | | | | | | | |

Electronic Equipment, Instruments, & Components—1.2% | | | | | | | | |

Hitachi Ltd. | | | 290,000 | | | | 2,307,631 | |

Hoya Corp. | | | 76,900 | | | | 4,156,360 | |

Keyence Corp. | | | 7,200 | | | | 3,983,483 | |

Spectris plc | | | 45,128 | | | | 1,534,588 | |

TDK Corp. | | | 34,800 | | | | 2,686,094 | |

TE Connectivity Ltd. | | | 35,050 | | | | 3,188,499 | |

Zebra Technologies Corp., Cl. A2 | | | 5,160 | | | | 598,508 | |

| | | | | | | 18,455,163 | |

| | | | | | | | | |

Internet Software & Services—3.8% | | | | | | | | |

Alibaba Group Holding Ltd., Sponsored ADR2 | | | 59,664 | | | | 11,031,277 | |

Alphabet, Inc., Cl. A2 | | | 730 | | | | 754,119 | |

23 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| CONSOLIDATED STATEMENT OF INVESTMENTS Continued | | |

| | | |

| | | | | | | | |

| | | Shares | | | Value | |

Internet Software & Services (Continued) | | | | | | | | |

Alphabet, Inc., Cl. C2 | | | 17,280 | | | $ | 17,567,539 | |

Baidu, Inc., Sponsored ADR2 | | | 28,480 | | | | 6,947,411 | |

China Literature Ltd.2 | | | 105 | | | | 740 | |

eBay, Inc.2 | | | 81,620 | | | | 3,072,177 | |

Facebook, Inc., Cl. A2 | | | 64,410 | | | | 11,597,665 | |

MercadoLibre, Inc. | | | 180 | | | | 43,256 | |

NAVER Corp. | | | 2,842 | | | | 2,276,429 | |

NetEase, Inc., ADR | | | 3,990 | | | | 1,124,861 | |

Tencent Holdings Ltd. | | | 131,885 | | | | 5,940,374 | |

United Internet AG | | | 29,641 | | | | 1,875,098 | |

| | | | | | | 62,230,946 | |

| | | | | | | | | |

IT Services—1.3% | | | | | | | | |

Amadeus IT Group SA | | | 28,705 | | | | 1,947,329 | |

Amdocs Ltd. | | | 58,570 | | | | 3,812,907 | |

Atos SE | | | 19,980 | | | | 3,105,628 | |

First Data Corp., Cl. A2 | | | 57,330 | | | | 1,021,047 | |

Infosys Ltd. | | | 83,370 | | | | 1,186,555 | |

Mastercard, Inc., Cl. A | | | 25,990 | | | | 3,866,532 | |

PayPal Holdings, Inc.2 | | | 77,640 | | | | 5,633,558 | |

Tata Consultancy Services Ltd. | | | 21,634 | | | | 877,288 | |

| | | | | | | 21,450,844 | |

| | | | | | | | | |

Semiconductors & Semiconductor Equipment—2.6% | | | | | | | | |

Applied Materials, Inc. | | | 66,080 | | | | 3,728,894 | |

ASML Holding NV | | | 17,606 | | | | 3,176,216 | |

Broadcom Ltd. | | | 9,077 | | | | 2,395,511 | |

Infineon Technologies AG | | | 362,521 | | | | 9,925,504 | |

Marvell Technology Group Ltd. | | | 71,700 | | | | 1,324,299 | |

Maxim Integrated Products, Inc. | | | 28,020 | | | | 1,472,171 | |

Renesas Electronics Corp.2 | | | 212,800 | | | | 2,747,721 | |

SK Hynix, Inc. | | | 43,679 | | | | 3,211,792 | |

STMicroelectronics NV | | | 143,950 | | | | 3,389,470 | |

Taiwan Semiconductor Manufacturing Co. Ltd. | | | 803,000 | | | | 6,485,973 | |

Texas Instruments, Inc. | | | 20,190 | | | | 1,952,171 | |

Tokyo Electron Ltd. | | | 16,200 | | | | 3,058,598 | |

| | | | | | | 42,868,320 | |

| | | | | | | | | |

Software—1.8% | | | | | | | | |

Activision Blizzard, Inc. | | | 14,410 | | | | 943,711 | |

Check Point Software Technologies Ltd.2 | | | 3,790 | | | | 446,121 | |

Dassault Systemes SE | | | 18,540 | | | | 1,969,360 | |

Microsoft Corp. | | | 77,440 | | | | 6,441,459 | |

Oracle Corp. | | | 28,470 | | | | 1,449,123 | |

SAP SE | | | 105,274 | | | | 11,975,867 | |

Snap, Inc., Cl. A2 | | | 70,550 | | | | 1,082,237 | |

Synopsys, Inc.2 | | | 14,730 | | | | 1,274,439 | |

24 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

Software (Continued) | | | | | | | | |

Temenos Group AG | | | 31,857 | | | $ | 3,679,881 | |

| | | | | | | 29,262,198 | |

| | | | | | | | | |

Technology Hardware, Storage & Peripherals—1.7% | | | | | | | | |

Apple, Inc. | | | 123,711 | | | | 20,912,107 | |

HP, Inc. | | | 49,480 | | | | 1,066,294 | |

Samsung Electronics Co. Ltd. | | | 1,404 | | | | 3,456,189 | |

Western Digital Corp. | | | 26,940 | | | | 2,404,934 | |

| | | | | | | 27,839,524 | |

| | | | | | | | | |

Materials—2.8% | | | | | | | | |

Chemicals—1.4% | | | | | | | | |

Air Liquide SA | | | 37,337 | | | | 4,755,530 | |

Akzo Nobel NV | | | 15,895 | | | | 1,439,203 | |

Albemarle Corp. | | | 3,710 | | | | 522,702 | |

DowDuPont, Inc. | | | 38,139 | | | | 2,757,831 | |

Eastman Chemical Co. | | | 16,900 | | | | 1,534,689 | |

Essentra plc | | | 176,040 | | | | 1,244,262 | |

Linde AG2 | | | 10,104 | | | | 2,169,665 | |

Novozymes AS, Cl. B | | | 43,017 | | | | 2,375,937 | |

PPG Industries, Inc. | | | 28,280 | | | | 3,287,267 | |

Sika AG | | | 263 | | | | 1,948,763 | |

Westlake Chemical Partners LP1 | | | 32,300 | | | | 718,675 | |

| | | | | | | 22,754,524 | |

| | | | | | | | | |

Construction Materials—0.3% | | | | | | | | |

Indocement Tunggal Prakarsa Tbk PT | | | 387,500 | | | | 643,327 | |

James Hardie Industries plc | | | 68,000 | | | | 1,038,850 | |

UltraTech Cement Ltd. | | | 13,428 | | | | 912,400 | |

Vulcan Materials Co. | | | 16,350 | | | | 1,990,613 | |

| | | | | | | 4,585,190 | |

| | | | | | | | | |

Containers & Packaging—0.2% | | | | | | | | |

CCL Industries, Inc., Cl. B | | | 58,378 | | | | 2,813,692 | |

WestRock Co. | | | 16,060 | | | | 984,960 | |

| | | | | | | 3,798,652 | |

| | | | | | | | | |

Metals & Mining—0.9% | | | | | | | | |

Agnico Eagle Mines Ltd. | | | 15,910 | | | | 710,063 | |

Alrosa PJSC | | | 462,362 | | | | 596,537 | |

Anglo American plc | | | 183,800 | | | | 3,463,080 | |

Compass Minerals International, Inc. | | | 7,550 | | | | 495,280 | |

Glencore plc2 | | | 549,320 | | | | 2,644,846 | |

Grupo Mexico SAB de CV | | | 318,773 | | | | 1,036,541 | |

Korea Zinc Co. Ltd. | | | 3,627 | | | | 1,659,591 | |

Newcrest Mining Ltd. | | | 113,700 | | | | 1,939,701 | |

Polyus PJSC, GDR3 | | | 6,900 | | | | 283,245 | |

Real Gold Mining Ltd.2,4 | | | 273,000 | | | | 350 | |

25 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| CONSOLIDATED STATEMENT OF INVESTMENTS Continued | | |

| | | |

| | | | | | | | |

| | | Shares | | | Value | |

Metals & Mining (Continued) | | | | | | | | |

Zhaojin Mining Industry Co. Ltd., Cl. H | | | 1,132,500 | | | $ | 922,580 | |

| | | | | | | 13,751,814 | |

| | | | | | | | | |

Telecommunication Services—1.9% | | | | | | | | |

Diversified Telecommunication Services—1.3% | | | | | | | | |

AT&T, Inc. | | | 36,040 | | | | 1,212,746 | |

BT Group plc, Cl. A | | | 281,702 | | | | 974,110 | |

Iliad SA | | | 7,340 | | | | 1,833,209 | |

Inmarsat plc | | | 119,800 | | | | 988,209 | |

Nippon Telegraph & Telephone Corp. | | | 180,000 | | | | 8,721,354 | |

Spark New Zealand Ltd. | | | 1,114,291 | | | | 2,806,921 | |

Verizon Communications, Inc. | | | 91,310 | | | | 4,371,010 | |

| | | | | | | 20,907,559 | |

| | | | | | | | | |

Wireless Telecommunication Services—0.6% | | | | | | | | |

China Mobile Ltd. | | | 104,500 | | | | 1,050,324 | |

Rogers Communications, Inc., Cl. B | | | 51,272 | | | | 2,660,373 | |

SK Telecom Co. Ltd. | | | 11,598 | | | | 2,733,821 | |

SoftBank Group Corp. | | | 22,000 | | | | 1,946,977 | |

Vodafone Group plc | | | 489,960 | | | | 1,401,812 | |

| | | | | | | 9,793,307 | |

| | | | | | | | | |

Utilities—0.9% | | | | | | | | |

Electric Utilities—0.6% | | | | | | | | |

Edison International | | | 31,310 | | | | 2,503,234 | |

Entergy Corp. | | | 12,660 | | | | 1,092,052 | |

NextEra Energy, Inc. | | | 2,971 | | | | 460,713 | |

PG&E Corp. | | | 102,880 | | | | 5,943,378 | |

| | | | | | | 9,999,377 | |

| | | | | | | | | |

Gas Utilities—0.1% | | | | | | | | |

AmeriGas Partners LP1 | | | 23,945 | | | | 1,083,511 | |

| | | | | | | | | |

Multi-Utilities—0.2% | | | | | | | | |

National Grid plc | | | 247,110 | | | | 2,973,793 | |

SCANA Corp. | | | 6,170 | | | | 266,174 | |

| | | | | | | 3,239,967 | |

Total Common Stocks (Cost $864,657,267) | | | | | | | 1,002,874,750 | |

| | | | | | | | |

Preferred Stocks—0.1% | | | | | | | | |

Lojas Americanas SA, Preference | | | 229,614 | | | | 1,233,948 | |

Zee Entertainment Enterprises Ltd., 6% Cum. Non-Cv. | | | 629,697 | | | | 96,344 | |

Total Preferred Stocks (Cost $1,246,203) | | | | | | | 1,330,292 | |

| | | | | | | | |

| | | Units | | | | |

Rights, Warrants and Certificates—0.0% | | | | | | | | |

Banco Santander SA Rts., Strike Price 1EUR, Exp. 11/15/172 | | | 520,298 | | | | 24,849 | |

Ferrovial SA Rts., Strike Price 1EUR, Exp. 11/13/172 | | | 174,193 | | | | 83,801 | |

Total Rights, Warrants and Certificates (Cost $106,336) | | | | | | | 108,650 | |

26 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | | | | | |

| | | | | | Principal Amount | | | Value | |

U.S. Government Obligations—3.3% | | | | | | | | | | | | |

United States Treasury Bonds, 2.875%, 8/15/45 | | | | | | $ | 17,022,000 | | | $ | 17,036,629 | |

United States Treasury Nts., 1.625%, 2/15/265,6 | | | | | | | 38,920,000 | | | | 36,882,021 | |

Total U.S. Government Obligations (Cost $55,663,093) | | | | | | | | | | | 53,918,650 | |

| | | | | | | | | | | | |

Foreign Government Obligations—4.7% | | | | | | | | | | | | |

Arab Republic of Egypt, 15.00% Unsec. Nts., 10/3/20 | | | EGP | | | | 4,250,000 | | | | 237,839 | |

Argentine Republic: | | | | | | | | | | | | |

16.00% Bonds, 10/17/23 | | | ARS | | | | 4,825,000 | | | | 277,979 | |

24.756% [BADLARPP+325] Sr. Unsec. Nts., 3/1/207 | | | ARS | | | | 16,346,000 | | | | 975,419 | |

27.146% [ARPP7DRR] Unsec. Nts., 6/21/207 | | | ARS | | | | 1,600,000 | | | | 97,144 | |

Federative Republic of Brazil: | | | | | | | | | | | | |

10.00% Unsec. Nts., 1/1/19 | | | BRL | | | | 9,420,000 | | | | 2,963,414 | |

10.00% Unsec. Nts., 1/1/21 | | | BRL | | | | 18,465,000 | | | | 5,793,617 | |

10.00% Unsec. Nts., 1/1/23 | | | BRL | | | | 3,930,000 | | | | 1,222,153 | |

17.517% Unsec. Nts., 5/15/458 | | | BRL | | | | 495,000 | | | | 502,523 | |

18.077% Unsec. Nts., 8/15/228 | | | BRL | | | | 1,200,000 | | | | 1,170,474 | |

Hungary: | | | | | | | | | | | | |

Series 20/A, 7.50% Bonds, 11/12/20 | | | HUF | | | | 116,700,000 | | | | 527,451 | |

Series 25/B, 5.50% Bonds, 6/24/25 | | | HUF | | | | 575,000,000 | | | | 2,663,000 | |

Series 27/A, 3.00% Bonds, 10/27/27 | | | HUF | | | | 70,000,000 | | | | 275,075 | |

Kingdom of Thailand, 1.875% Sr. Unsec. Nts., 6/17/22 | | | THB | | | | 80,500,000 | | | | 2,428,173 | |

Malaysia: | | | | | | | | | | | | |

3.26% Sr. Unsec. Nts., 3/1/18 | | | MYR | | | | 2,170,000 | | | | 513,027 | |

4.24% Sr. Unsec. Nts., 2/7/18 | | | MYR | | | | 1,660,000 | | | | 393,354 | |

4.378% Sr. Unsec. Nts., 11/29/19 | | | MYR | | | | 3,000,000 | | | | 723,530 | |

Oriental Republic of Uruguay, 9.875% Sr. Unsec. Nts., 6/20/223 | | | UYU | | | | 29,910,000 | | | | 1,094,505 | |

Republic of Chile: | | | | | | | | | | | | |

4.50% Unsec. Nts., 2/28/21 | | | CLP | | | | 1,220,000,000 | | | | 1,968,551 | |

4.50% Bonds, 3/1/26 | | | CLP | | | | 200,000,000 | | | | 316,123 | |

Republic of Colombia: | | | | | | | | | | | | |

Series B, 7.00% Bonds, 5/4/22 | | | COP | | | | 3,390,000,000 | | | | 1,164,413 | |

Series B, 7.50% Bonds, 8/26/26 | | | COP | | | | 3,650,000,000 | | | | 1,274,039 | |

Series B, 10.00% Bonds, 7/24/24 | | | COP | | | | 2,400,000,000 | | | | 946,062 | |

Republic of Indonesia: | | | | | | | | | | | | |

Series FR61, 7.00% Sr. Unsec. Nts., 5/15/22 | | | IDR | | | | 19,900,000,000 | | | | 1,500,207 | |

Series FR71, 9.00% Sr. Unsec. Nts., 3/15/29 | | | IDR | | | | 20,700,000,000 | | | | 1,739,945 | |

Series FR72, 8.25% Sr. Unsec. Nts., 5/15/36 | | | IDR | | | | 28,900,000,000 | | | | 2,323,839 | |

Series FR73, 8.75% Sr. Unsec. Nts., 5/15/31 | | | IDR | | | | 29,650,000,000 | | | | 2,459,447 | |

Republic of Peru: | | | | | | | | | | | | |

6.35% Sr. Unsec. Nts., 8/12/283 | | | PEN | | | | 5,945,000 | | | | 1,968,509 | |

6.95% Sr. Unsec. Nts., 8/12/313 | | | PEN | | | | 760,000 | | | | 262,877 | |

7.84% Sr. Unsec. Nts., 8/12/203 | | | PEN | | | | 2,180,000 | | | | 743,481 | |

8.20% Sr. Unsec. Nts., 8/12/263 | | | PEN | | | | 2,255,000 | | | | 851,693 | |

Republic of Poland: | | | | | | | | | | | | |

Series 0721, 1.75% Bonds, 7/25/21 | | | PLN | | | | 8,010,000 | | | | 2,155,908 | |

Series 0726, 2.50% Bonds, 7/25/26 | | | PLN | | | | 6,960,000 | | | | 1,789,888 | |

Series 0922, 5.75% Bonds, 9/23/22 | | | PLN | | | | 1,225,000 | | | | 383,750 | |

Republic of South Africa: | | | | | | | | | | | | |

Series 2023, 7.75% Bonds, 2/28/23 | | | ZAR | | | | 4,700,000 | | | | 323,164 | |

|

| 27 OPPENHEIMER GLOBAL ALLOCATION FUND |

CONSOLIDATED STATEMENT OF INVESTMENTS Continued

| | | | | | | | | | | | |

| | | | | | Principal Amount | | | Value | |

Foreign Government Obligations (Continued) | | | | | | | | | | | | |

Republic of South Africa: (Continued) | | | | | | | | | | | | |

Series 2030, 8.00% Bonds, 1/31/30 | | | ZAR | | | | 18,640,000 | | | $ | 1,167,649 | |

Series 2037, 8.50% Bonds, 1/31/37 | | | ZAR | | | | 16,550,000 | | | | 1,020,815 | |

Series R186, 10.50% Bonds, 12/21/26 | | | ZAR | | | | 16,975,000 | | | | 1,301,781 | |

Series R208, 6.75% Sr. Unsec. Nts., 3/31/21 | | | ZAR | | | | 42,700,000 | | | | 2,900,359 | |

Series R214, 6.50% Bonds, 2/28/41 | | | ZAR | | | | 9,140,000 | | | | 439,591 | |

Republic of Turkey: | | | | | | | | | | | | |

8.50% Bonds, 7/10/19 | | | TRY | | | | 1,165,000 | | | | 289,918 | |

8.80% Bonds, 11/14/18 | | | TRY | | | | 1,100,000 | | | | 280,397 | |

10.70% Bonds, 2/17/21 | | | TRY | | | | 2,670,000 | | | | 673,200 | |

11.00% Bonds, 2/24/27 | | | TRY | | | | 7,820,000 | | | | 2,003,675 | |

Romania, 5.95% Bonds, 6/11/21 | | | RON | | | | 5,640,000 | | | | 1,572,784 | |

Russian Federation: | | | | | | | | | | | | |

Series 6209, 7.60% Bonds, 7/20/22 | | | RUB | | | | 88,675,000 | | | | 1,535,027 | |

Series 6210, 6.80% Bonds, 12/11/19 | | | RUB | | | | 126,800,000 | | | | 2,147,794 | |

Series 6211, 7.00% Bonds, 1/25/23 | | | RUB | | | | 154,200,000 | | | | 2,602,494 | |

Series 6212, 7.05% Bonds, 1/19/28 | | | RUB | | | | 18,000,000 | | | | 298,796 | |

Series 6216, 6.70% Bonds, 5/15/19 | | | RUB | | | | 338,600,000 | | | | 5,740,220 | |

United Mexican States: | | | | | | | | | | | | |

Series M, 5.75% Bonds, 3/5/26 | | | MXN | | | | 45,000,000 | | | | 2,133,843 | |

Series M, 8.00% Bonds, 6/11/20 | | | MXN | | | | 10,000,000 | | | | 534,049 | |

Series M, 8.00% Sr. Unsec. Nts., 12/7/23 | | | MXN | | | | 3,800,000 | | | | 207,153 | |

Series M10, 8.50% Bonds, 12/13/18 | | | MXN | | | | 48,250,000 | | | | 2,555,657 | |

Series M20, 8.50% Sr. Unsec. Nts., 5/31/29 | | | MXN | | | | 17,020,000 | | | | 969,439 | |

Series M20, 10.00% Bonds, 12/5/24 | | | MXN | | | | 33,450,000 | | | | 2,025,268 | |

Series M30, 8.50% Sr. Unsec. Nts., 11/18/38 | | | MXN | | | | 5,880,000 | | | | 338,821 | |

Series M30, 10.00% Bonds, 11/20/36 | | | MXN | | | | 2,750,000 | | | | 179,855 | |

Total Foreign Government Obligations (Cost $76,652,403) | | | | | | | | | | | 76,949,158 | |

| | | | | | | | | | | | |

Non-Convertible Corporate Bond and Note—0.0% | | | | | | | | | | | | |

Omnicare, Inc., 4.75% Sr. Unsec. Nts., 12/1/22 (Cost $211,042) | | | | | | | 210,000 | | | | 224,753 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | Notional | | | | | | | | | |

| | | Counter- | | | | Exercise | | | | Expiration | | | | Amount | | | | Contracts | | | | | |

| | | party | | | | Price | | | | Date | | | | (000’s) | | | | (000’s) | | | | | |

Over-the-Counter Option Purchased—0.0% | | | | | | | | | | | | | | | | | | | | | | | | |

CLP Currency Put2 (Cost $24,039) | | | GSCO-OT | | | | CLP637.000 | | | | 1/12/18 | | | | CLP 5,096,000 | | | | CLP 1,130,000 | | | | 29,380 | |

| | | | | | | | | | | | |

| | | | | | Principal Amount | | | | |

Short-Term Notes—0.1% | | | | | | | | | | | | |

Arab Republic of Egypt Treasury Bills, 17.25%, 7/3/189 | | | EGP | | | | 16,000,000 | | | | 809,963 | |

Arab Republic of Egypt Treasury Bills, 17.946%, 4/3/189 | | | EGP | | | | 11,000,000 | | | | 582,117 | |

Argentine Republic Treasury Bills, 26.906%, 6/21/189 | | | ARS | | | | 6,100,000 | | | | 292,848 | |

Total Short-Term Notes (Cost $1,690,472) | | | | | | | | | | | 1,684,928 | |

| | | |

| | | | | | Shares | | | | |

Investment Companies—29.5% | | | | | | | | | | | | |

Oppenheimer Institutional Government Money Market Fund, Cl. E, 1.01%10,11 | | | | | | | 178,062,806 | | | | 178,062,806 | |

|

| 28 OPPENHEIMER GLOBAL ALLOCATION FUND |

| | | | | | | | | | | | |

| | | | | | | Shares | | | | Value | |

Investment Companies (Continued) | | | | | | | | | | | | |

Oppenheimer Master Event-Linked Bond Fund, LLC10 | | | | | | | 4,616,016 | | | $ | 68,756,417 | |

Oppenheimer Master Loan Fund, LLC10 | | | | | | | 7,213,775 | | | | 120,382,841 | |

Oppenheimer Senior Floating Rate Fund, Cl. I10 | | | | | | | 4,392,376 | | | | 35,534,323 | |

PowerShares Senior Loan Portfolio Exchange Traded Fund | | | | | | | 3,351,165 | | | | 77,478,935 | |

Total Investment Companies (Cost $487,651,277) | | | | | | | | | | | 480,215,322 | |

| | | | | | | | | | | | | |

Total Investments, at Value (Cost $1,487,902,132) | | | | | | | 99.3% | | | | 1,617,335,883 | |

Net Other Assets (Liabilities) | | | | | | | 0.7 | | | | 12,076,266 | |

Net Assets | | | | | | | 100.0% | | | $ | 1,629,412,149 | |

| | | | | | | | |

Footnotes to Consolidated Statement of Investments

1. Security is a Master Limited Partnership.

2. Non-income producing security.

3. Represents securities sold under Rule 144A, which are exempt from registration under the Securities Act of 1933, as amended. These securities have been determined to be liquid under guidelines established by the Board of Trustees. These securities amount to $17,331,794 or 1.06% of the Fund’s net assets at period end.

4. The value of this security was determined using significant unobservable inputs. See Note 3 of the accompanying

Consolidated Notes.

5. All or a portion of the security position is held in accounts at a futures clearing merchant and pledged to cover margin requirements on open futures contracts and written options on futures, if applicable. The aggregate market value of such securities is $7,757,354. See Note 6 of the accompanying Consolidated Notes.

6. All or a portion of the security position is held in segregated accounts and pledged to cover margin requirements under certain derivative contracts. The aggregate market value of such securities is $3,344,210. See Note 6 of the accompanying Consolidated Notes.

7. Represents the current interest rate for a variable or increasing rate security, determined as [Referenced Rate + Basis-point spread].

8. Denotes an inflation-indexed security: coupon or principal are indexed to a consumer price index.

9. Zero coupon bond reflects effective yield on the original acquisition date.

10. Is or was an affiliate, as defined in the Investment Company Act of 1940, as amended, at or during the reporting period, by virtue of the Fund owning at least 5% of the voting securities of the issuer or as a result of the Fund and the issuer having the same investment adviser. Transactions during the reporting period in which the issuer was an affiliate are as follows:

| | | | | | | | | | | | | | | | |

| | | Shares | | | Gross | | | Gross | | | Shares | |

| | | October 31, 2016 | | | Additions | | | Reductions | | | October 31, 2017 | |

| Oppenheimer Institutional Government Money Market Fund, Cl. E | | | 23,914,591 | | | | 528,837,739 | | | | 374,689,524 | | | | 178,062,806 | |

| Oppenheimer Master Event-Linked Bond Fund, LLC | | | 4,921,101 | | | | — | | | | 305,085 | | | | 4,616,016 | |

| Oppenheimer Master Loan Fund, LLC | | | 7,213,775 | | | | — | | | | — | | | | 7,213,775 | |

| Oppenheimer Senior Floating Rate Fund, Cl. I | | | 4,985,986 | | | | 194,466 | | | | 788,076 | | | | 4,392,376 | |

| | | | |

| | | | | | | | | | | | Change in | |

| | | | | | | | | Realized | | | Unrealized | |

| | | Value | | | Income | | | Gain (Loss) | | | Gain (Loss) | |

| Oppenheimer Institutional Government Money Market Fund, Cl. E | | $ | 178,062,806 | | | $ | 460,780 | | | $ | — | | | $ | — | |

29 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| CONSOLIDATED STATEMENT OF INVESTMENTS Continued | | |

| Footnotes to Consolidated Statement of Investments (Continued) | | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | Change in | |

| | | | | | | | Realized | | | Unrealized | |

| | | Value | | Income | | | Gain (Loss) | | | Gain (Loss) | |

| |

Oppenheimer Master Event-Linked Bond Fund, LLC | | $68,756,417 | | $ | 4,791,351 | a | | $ | (488,901 | )a | | $ | (9,079,810)a | |

Oppenheimer Master Loan Fund, LLC | | 120,382,841 | | | 7,008,693 | b | | | (85,233 | )b | | | (236,550)b | |

Oppenheimer Senior Floating Rate Fund, Cl. I | | 35,534,323 | | | 1,575,974 | | | | 149,734 | | | | 47,666 | |

| | | |

Total | | $ 402,736,387 | | $ | 13,836,798 | | | $ | (424,400) | | | $ | (9,268,694) | |

| | | |

a. Represents the amount allocated to the Fund from Oppenheimer Master Event-linked Bond Fund, LLC.

b. Represents the amount allocated to the Fund from Oppenheimer Master Loan Fund, LLC.

11. Rate shown is the 7-day yield at period end.

Distribution of investments representing geographic holdings, as a percentage of total investments at value, is as follows:

| | | | | | | | | | | | | | | | |

| Geographic Holdings (Unaudited) | | Value | | | | | | Percent | | | | |

United States | | $ | 962,991,671 | | | | | | | | 59.5% | | | | | |

Japan | | | 92,788,420 | | | | | | | | 5.7 | | | | | |

France | | | 81,905,763 | | | | | | | | 5.1 | | | | | |

United Kingdom | | | 60,897,006 | | | | | | | | 3.8 | | | | | |

Germany | | | 48,567,576 | | | | | | | | 3.0 | | | | | |

China | | | 44,961,781 | | | | | | | | 2.8 | | | | | |

Switzerland | | | 40,048,633 | | | | | | | | 2.5 | | | | | |

Canada | | | 30,420,263 | | | | | | | | 1.9 | | | | | |

India | | | 22,071,122 | | | | | | | | 1.4 | | | | | |

Netherlands | | | 20,898,854 | | | | | | | | 1.3 | | | | | |

Russia | | | 19,340,834 | | | | | | | | 1.2 | | | | | |

Spain | | | 18,611,454 | | | | | | | | 1.1 | | | | | |

South Korea | | | 18,271,705 | | | | | | | | 1.1 | | | | | |

Brazil | | | 16,987,880 | | | | | | | | 1.0 | | | | | |

Hong Kong | | | 14,231,504 | | | | | | | | 0.9 | | | | | |

Mexico | | | 14,089,797 | | | | | | | | 0.9 | | | | | |

South Africa | | | 11,828,322 | | | | | | | | 0.7 | | | | | |

Indonesia | | | 10,710,280 | | | | | | | | 0.7 | | | | | |

Denmark | | | 9,469,115 | | | | | | | | 0.6 | | | | | |

Taiwan | | | 6,485,973 | | | | | | | | 0.4 | | | | | |

Malaysia | | | 6,031,457 | | | | | | | | 0.4 | | | | | |

Australia | | | 4,893,111 | | | | | | | | 0.3 | | | | | |

Thailand | | | 4,615,565 | | | | | | | | 0.3 | | | | | |

Colombia | | | 4,595,545 | | | | | | | | 0.3 | | | | | |

Peru | | | 4,526,090 | | | | | | | | 0.3 | | | | | |

Poland | | | 4,468,751 | | | | | | | | 0.3 | | | | | |

Turkey | | | 4,429,190 | | | | | | | | 0.3 | | | | | |

Sweden | | | 4,314,263 | | | | | | | | 0.3 | | | | | |

Philippines | | | 4,252,219 | | | | | | | | 0.3 | | | | | |

Hungary | | | 3,465,526 | | | | | | | | 0.2 | | | | | |