UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-05309

Nuveen Investment Funds, Inc.

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: December 31

Date of reporting period: December 31, 2015

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

| | |

| | |  |

| Mutual Funds | |

| | | | | | |

| | | | | | | Annual Report December 31, 2015 |

| | | | | | | | | | | | | | | | |

| | | | | | | Share Class / Ticker Symbol | | |

| | | Fund Name | | | | Class A | | Class C | | Class R3 | | Class R6 | | Class I | | |

| | |

| | Nuveen Global Infrastructure Fund | | | | FGIAX | | FGNCX | | FGNRX | | — | | FGIYX | | |

| | Nuveen Real Asset Income Fund | | | | NRIAX | | NRICX | | — | | — | | NRIIX | | |

| | Nuveen Real Estate Securities Fund | | | | FREAX | | FRLCX | | FRSSX | | FREGX | | FARCX | | |

| | | | | | | | | | | | |

| | | | | | |

| | | | |

| | | | | | | | |

| | |

| | Life is Complex. | | |

| | |

| | Nuveen makes things e-simple. | | |

| | |

| | It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish. | | |

| | | | |

| | | | | | Free e-Reports right to your e-mail! | | |

| | | |

| | | | | | www.investordelivery.com If you receive your Nuveen Fund distributions and statements from your

financial advisor or brokerage account. |

| | | | |

| | | | or | | www.nuveen.com/accountaccess If you receive your Nuveen Fund distributions and statements directly from Nuveen. Must be preceded by or accompanied by a prospectus. NOT FDIC INSURED MAY LOSE VALUE

NO BANK GUARANTEE | | |

| | | | | | | | | | |

| | | | | | | | | | | | | |

Table

of Contents

Chairman’s Letter

to Shareholders

Dear Shareholders,

For better or for worse, the financial markets spent most of the past year waiting for the U.S. Federal Reserve (Fed) to end its accommodative monetary policy. The policy has propped up stock and bond markets since the Great Recession, but the question remains: how will markets behave without its influence? This uncertainty was a considerable source of volatility for stock and bond prices for much of 2015, despite the Fed carefully conveying its intention to raise rates slowly and only when the economy shows evidence of readiness.

As was widely expected, the long-awaited Fed rate hike materialized in mid-December. While the move was interpreted as a vote of confidence on the U.S. economy’s underlying strength, the Fed emphasized that future rate increases will be gradual and guided by its ongoing assessment of financial conditions. Headwinds including rising borrowing costs, softer commodity prices, low inflation, a strong U.S. dollar and a stagnant global economy could necessitate keeping monetary conditions accommodative for longer. Meanwhile, policy makers in Europe and Japan are deploying their available tools to try to bolster their economies’ fragile growth, while Chinese authorities have stepped up efforts to manage China’s slowdown.

Although the new year began with a more pessimistic tone to investor sentiment and elevated volatility in the markets, we caution investors from making long-term decisions based on short-term news. In times like these, you can look to a professional investment manager with the experience and discipline to maintain the proper perspective on short-term events. And if the daily headlines do concern you, I encourage you to reach out to your financial advisor. Your financial advisor can help you evaluate your investment strategies in light of current events, your time horizon and risk tolerance.

On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

William J. Schneider

Chairman of the Board

February 22, 2016

Portfolio Managers’

Comments

Nuveen Global Infrastructure Fund

Nuveen Real Asset Income Fund

Nuveen Real Estate Securities Fund

These Funds feature portfolio management by Nuveen Asset Management, LLC, an affiliate of Nuveen Investments, Inc. For the Nuveen Global Infrastructure Fund, Jay L. Rosenberg has been the lead portfolio manager since its inception in 2007 and Tryg T. Sarsland has been the co-portfolio manager since 2012. For the Nuveen Real Asset Income Fund, Jay L. Rosenberg has been the lead portfolio manager and Jeffrey T. Schmitz, CFA, has been a co-manager since the Fund’s inception in 2011. Effective April 30, 2015, Brenda A. Langenfeld, CFA, and Tryg T. Sarsland were added as co-managers. For the Nuveen Real Estate Securities Fund, Jay L. Rosenberg has served as a portfolio manager since he joined the Fund’s management team in 2005, while Scott C. Sedlak joined the team as a co-portfolio manager in 2011. Effective April 30, 2015, John G. Wenker is no longer a co-manager of the three Funds, but continues to lead the Real Assets Team at Nuveen Asset Management.

On the following pages, the portfolio management teams for the Funds discuss economic and market conditions, key investment strategies and the Funds’ performance for the twelve-month reporting period ended December 31, 2015.

What factors affected the U.S. economy and financial markets during the twelve-month reporting period ended December 31, 2015?

The U.S. economy grew at an overall moderate pace during the twelve-month reporting period. Harsh winter weather and a West coast port strike weighed on growth in the first quarter of 2015, but those factors proved temporary. Rebounding economic activity in the second quarter was followed by a mediocre advance in the latter half of the year. Real gross domestic product (GDP), which is the value of the goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes, increased at an annual rate of 0.7% in the fourth quarter of 2015, as reported by the “advance” estimate of the Bureau of Economic Analysis, down from 2.0% in the third quarter.

The labor and housing markets were among the bright spots in the economy during the reporting period, as both showed steady improvement. As reported by the Bureau of Labor Statistics, the unemployment rate fell to 5.0% in December from 5.7% in January 2015, and job gains averaged slightly above 200,000 per month for the past twelve months. The S&P/Case-Shiller U.S. National Home Price Index, which covers all nine U.S. census divisions, recorded a 5.1% annual gain in November 2015 (most recent data available at the time this report was prepared). The 10-City and 20-City Composites reported year-over-year increases of 5.3% and 5.8%, respectively.

With GDP growth averaging around 2% for the previous four quarters, the U.S. economic recovery continued to underwhelm. Consumers, whose purchases comprise the largest component of the U.S. economy, benefited from lower gasoline prices and an improving jobs market but didn’t necessarily spend more. Pessimism about the economy’s future and lackluster wage growth likely contributed to consumers’ somewhat muted spending. The sharp decline in energy prices and tepid wage growth kept inflation subdued during this reporting period. The Consumer Price Index CPI declined 0.1% in December on a seasonally adjusted basis, as reported by the U.S. Bureau of Labor Statistics. The core CPI (which excludes food and energy) increased 0.1% during the same period, below the Fed’s unofficial longer term inflation objective of 2.0%.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Portfolio Managers’ Comments (continued)

Business investment was also rather restrained. Corporate earnings growth slowed during 2015, reflecting an array of factors ranging from weakening demand amid sluggish U.S. and global growth to the impact of falling commodity prices and a strong U.S. dollar. Energy, materials and industrials companies were hit particularly hard by the downturn in natural resource prices, as well as the expectation of rising interest rates, which would make their debts more costly to service. With demand waning, companies, especially in the health care and technology sectors, looked to consolidations with rivals as a way to boost revenues. Merger and acquisition deals, both in the U.S. and globally, reached record levels in the calendar year 2015.

Although the current expansion continued to look subpar relative to past recoveries, the U.S. Federal Reserve (Fed) believed the economy was strong enough to begin the withdrawal of its stimulus policies. After winding down its bond buying program, known as quantitative easing, in October 2014, the Fed began telegraphing its intention to raise the target federal funds rate some time in 2015. The Fed had held the fed funds rate near zero since December 2008. However, the timing of its first rate hike was uncertain, particularly as the inflation rate stayed stubbornly low and signs of global economic weakness, notably from China, merited caution. After delaying the rate change at each prior meeting in 2015, the Fed announced in December 2015 that it would raise its main policy interest rate by 0.25%. The news had a relatively muted impact on the financial markets, as the move was widely expected.

Meanwhile, a number of issues weighed on economies across the globe including geopolitical turmoil, weak growth overseas and sharply falling oil prices, which were caused by the faltering global economy, a global supply glut and the Organization of the Petroleum Exporting Countries (OPEC’s) decision to maintain its production levels. Falling oil prices propelled significant appreciation in the U.S. dollar, which hit a multi-year high versus a basket of other major currencies, supported by the confident Fed and weaker data coming out of Europe, Japan and China. In an effort to improve their economic growth, countries across the globe maintained extraordinarily accommodative monetary policies. The European Central Bank (ECB) launched a massive quantitative easing program via a government bond-buying program that pumped more than 1 trillion euros into the weak eurozone economy, while other central banks around the world enacted more than 30 policy easing actions during the first few months of 2015.

Political drama also dominated the news, including the escalating tensions over Greece’s debt issues and aggressive policy intervention by the Chinese government to deflate the country’s stock market bubble. In late June, Greece took front and center in world market headlines with defaults on its payments to the International Monetary Fund and threats of a potential exit from the European Monetary Union (EMU). However, by mid-July, Greece had agreed to austerity measures in return for more bailout funds. Meanwhile, after skyrocketing for nearly a year, China’s stock market suddenly shifted gears in June and embarked on a massive sell-off that quickly spilled over to the rest of the world. Investors pulled money out of Chinese stocks despite efforts by China’s government to stem the tide, including further rate cuts, a 1 trillion yuan bond for infrastructure build-out, new regulations surrounding equity purchases and redemptions and the unexpected devaluation of the yuan currency in mid-August. A number of factors helped fuel the sell-off, including weak Chinese economic data and falling commodity prices.

As the reporting period progressed, the U.S. economy continued to show resilience, but China remained a key area of focus with the country showing markedly slower manufacturing activity and uncertainty surrounding actual levels of consumption. Slower Chinese production and the ongoing weakness across emerging markets led to renewed volatility and weakness in commodity prices across the board. Oil prices sold off sharply into year-end to a decade-low level of below $36-per-barrel level for West Texas Intermediate crude in December.

In light of the uncertain backdrop, global volatility spiked across all asset classes during the reporting period. Oil and gas shares, other energy-related stocks and petrocurrencies were hit hard around the world due to dramatically falling commodity prices. In overseas stock markets, news of widespread monetary policy moves across the globe gave equities a boost through May; however, in the summer months, renewed fears over China and uncertainty about the Fed’s next move hit markets, spurring a massive global sell-off in August. Overall for the reporting period, international equity markets were collectively weaker than the U.S. market and ended with flat to negative returns. For example, the MSCI EAFE Index returned -0.39% for the reporting period. Emerging market stocks experienced even greater headwinds from the strong U.S. dollar, weak Chinese data, the commodity sell-off and Fed uncertainty, significantly underperforming developed market peers. As measured by the MSCI Emerging Markets Index, this segment ended the period with a -14.60% return.

In the U.S., equities experienced a correction in August, dipped again in late September, and then rose back to mid-2015 levels before selling off in the final days of the period. The S&P 500® Index ended up posting a return of 1.38% for the reporting period.

However, the positive overall index results masked the more than 30% spread between the return of the best-performing sector, consumer discretionary, and the worst-performing sector, energy, which fell by more than 21%. Larger, more established companies outperformed riskier, smaller-cap stocks, which continued to be hampered by heightened risk aversion and the pending Fed rate tightening, which will remove liquidity from the market. The small-cap segment produced a -4.41% return as measured by the Russell 2000® Index versus a 0.92% return for the large-cap Russell 1000® Index. Across the capitalization spectrum, growth stocks significantly outperformed value stocks.

Nuveen Global Infrastructure Fund

How did the Fund perform during the twelve-month reporting period ended December 31, 2015?

The table in the Fund Performance and Expense Ratios section of this report provides total returns for the Fund for the one-year, five-year and since inception periods ended December 31, 2015. Comparative performance information is provided for the Fund’s Class A Shares at net asset value (NAV). The Fund’s Class A Shares at NAV outperformed the S&P Global Infrastructure Index and the Lipper classification average during the twelve-month reporting period.

What strategies were used to manage the Fund during the reporting period and how did these strategies influence performance?

The Fund seeks to provide capital appreciation and income potential by investing primarily in equity securities issued by U.S. and non-U.S. companies that typically derive the majority of their value from owned or operated infrastructure assets. During the reporting period, our strategy for managing the Fund remained consistent as we focused on buying global infrastructure companies that own and operate long life assets that have visible cash flows, strong balance sheets, manageable amounts of leverage and inelastic demand characteristics. We believe these types of companies will have ongoing access to capital and the best chances for producing sustainable and growing cash flow. The Fund is structured using a number of core infrastructure companies that we believe should provide long-term outperformance versus the market, combined with more opportunistic holdings that we believe are undervalued by the market in the short term. We have exposure around the globe to a mixture of holdings that represent significant value, as well as positions in companies that may prove to be more stable in a slowly growing global economy.

During the twelve-month reporting period, the global infrastructure sector posted a -11.46% return as measured by the S&P Global Infrastructure Index, significantly below the broad U.S. equity market return of 1.38% as measured by the S&P 500® Index. The sector also fell short of the global markets (MSCI ACWI Index -1.68%) by almost 10%. The utility and energy sectors, both large components of the S&P Global Infrastructure Index, were responsible for the bulk of the downside as the decline in the price of oil put pressure on pipeline and master limited partnership (MLP) companies, while fear about potential interest rate increases hampered the utility names.

The Fund significantly outperformed its benchmark during the reporting period, benefiting from favorable results in the pipeline, technology infrastructure, electric utilities and water utilities sectors. The airport and alternative energy sectors were the only notable detractors versus the S&P Global Infrastructure Index during the reporting period.

Although the Fund has a sizeable underweight to pipelines relative to the benchmark, the sector still represented the second largest overall weight in its portfolio. Therefore, due to the dramatic sell-off in energy-related companies, the sector was the main reason for the Fund’s underperformance relative to broader equity indices. However, our stock selection within the group, as well as the lower-than-benchmark weight overall, contributed the most to the Fund’s relative outperformance versus the benchmark during the reporting period. In general, pipelines continued to be under pressure as the lower price of oil impacted the outlook for future growth in the space and hence share prices. While the continued underweight generally helped the Fund, an even larger portion of its outperformance came from positive selection effect. The Fund’s significant underweight in Kinder Morgan Inc., which persisted throughout the reporting period, was again the leading positive contributor. Kinder Morgan shares were under continued pressure from the declines in oil prices and the company’s nearly 75% dividend cut in December, which it made in order to conserve capital to service a significant debt load. The dividend cut led to even more concern about Kinder Morgan’s future growth opportunities and to further share price weakness.

Portfolio Managers’ Comments (continued)

Technology infrastructure, a sector not represented in the benchmark, was also beneficial in terms of the Fund’s relative performance. Collectively, the holdings in our portfolio advanced strongly during the reporting period, far surpassing the infrastructure sector’s negative return. U.S.-based cellular tower and data center companies performed exceptionally well, which provided nearly all of the sector’s positive attribution. The cell tower space continued to enjoy strong fundamentals, given the seemingly insatiable demand for data on behalf of smart phone users, while data centers were supported by corporations needing to store data or provide cloud-computing capacity. These trends provided a boost to data center companies in an environment that has seen a significant increase in demand for space where there were previously some oversupply concerns.

Stock selection in electric utilities also benefited the Fund, mainly due to what we didn’t own in the sector. The Fund benefited from no exposure to benchmark constituents such as German companies E.ON SE and RWE Group as well as a significant underweight to U.S. firm Exelon Corporation. Generally speaking, our exposure in this sector is focused on regulated utilities rather than integrated utilities that have substantial exposure to power generation. Integrated utilities remained under pressure for much of the reporting period due to weakness in commodity prices. Additionally, the German integrated names were negatively affected by weakened demand for energy in Europe’s tepid economic growth environment as well as a regulatory overhang because these companies are required to provide a significant amount of power from renewable sources. (As noted in the previous shareholder report, RWE was removed from the S&P Global Infrastructure Index during the reporting period.) At the same time, the Fund benefited from positions in a number of out-of-index U.S. utilities.

The water utilities sector was another contributor to the Fund’s relative outperformance versus the benchmark. In general, we believe this sector is underrepresented in the benchmark and our portfolio maintained a substantial overweight to the area throughout the reporting period. Given the essential service nature of this sector, water utilities held up much better during the global equity market decline. The two largest weights in our portfolio, American Water Works Company and United Utilities Group PLC, were responsible for most of the outperformance and are not represented in the benchmark. American Water Works, the largest regulated water company in the U.S., operates high quality assets and possesses a strong management team. The company has traded at a relative discount to competitors in the space, which has led us to be constructive on its valuation, while we also believe it has one of the highest potential growth rates in the sector. These attributes, combined with operations located in favorable regulatory jurisdictions, are the reasons for our strong conviction in the name. The market also seemed to recognize value in American Water Works as its shares advanced strongly in the midst of the broader market sell-off. Also, U.K.-based United Utilities contributed strongly to relative returns in the water utilities sector. We added significantly to this position during the reporting period because one of its competitors was rumored to be a takeover candidate and was performing very well. We anticipated the potential merger and acquisition activity would be a positive catalyst for U.K. companies in general, while we also believed United Utilities was trading at a very attractive valuation versus its peer group. Although the company still underperformed some of its peers, it solidly outperformed the benchmark return.

The Fund’s largest detractor was the result of an underweight position in the airport sector. Although global economic data was tepid, total freight rail volumes were down and the amounts of cargo passing through seaports was less than compelling, airports seemed much less affected as underlying fundamentals have remained quite good. Some of the underperformance was the Fund’s underweight to Mexican airports, which are significant benchmark constituents. The group was bolstered by robust traffic growth at Mexican airports and the expected acceleration in traffic growth for some airports that experienced depressed revenues after last year’s hurricane. At the same time, a favorable ruling from the Mexican Supreme Court regarding a shareholder dispute removed an overhang from the group. Also, an underweight position in Japan Airport Terminal Co. Ltd. detracted. The company, which manages the passenger terminal and airport facilities at Haneda Airport in Tokyo, has been a key beneficiary of the Japan’s increase in inbound tourism as well as the expansion of arrival and departure slots at the airport. Our position in Japan Airport Terminal is approximately half of the benchmark’s weight due to the stock’s modest liquidity and limited investor communication from the company’s management team. Finally, the Fund’s significant underweight to newcomer Aena SA, a Spanish airport company that came to market in 2015, was another detractor. We did participate in Aena’s IPO in February and the stock has performed very well; however, we believe it represents an overly large part of the benchmark as the biggest weight in the airport sector. Given the concentration of the company’s assets in a single geography and the lofty valuation it now trades at, we maintained an underweight in the stock and will likely continue to going forward.

Stock selection in the alternative energy sector was also a modest detractor. The sector represented just slightly more than 1% of the Fund, but has no representation in the benchmark. The holdings we own in the alternative energy space are yield companies, which

are companies that have been created as subsidiaries of parent companies or conglomerates that segregate their renewable energy assets and list them as distinct entities. The future growth we expected to see in the space was to be from the parent company dropping down assets into the yield company, which would increase the size of its asset base and hence the earnings from operations. However, as the reporting period progressed, the marketplace began to question the short-term viability of the yield company model. As yield company stock prices fell, it became more expensive to fund those asset purchases and therefore the future growth as their cost of equity issuance continued to climb. Because this became a vicious cycle, we dramatically reduced the Fund’s exposure to the area. While the Fund’s total exposure to the area was quite small, it still had a noticeable negative impact because of the significant share price weakness across holdings.

Toward the end of the reporting period, we began to reduce the Fund’s underweight to pipelines, most of which occurred in late November through December. We are beginning to see value in select companies, given the precipitous fall in share prices resulting from a very weak oil market. We added only to high quality companies in the space that we believe can make it through a sustained period of low oil prices. By the end of the year, however, the Fund still had a nearly 3% underweight to the pipeline group. We also added just under 1% to MLPs, again focusing on quality within the space. We currently prefer to own MLPs that are unencumbered by incentive distribution rights agreements, which require a percentage of their cash flows to flow up to a general partner or parent company, and those that have low leverage ratios resulting in lower interest expense. We reduced the Fund’s weight to the technology infrastructure sector by nearly 2% based on relative strength. We reallocated the capital to areas where we believed there were better valuations, specifically in energy infrastructure and toll roads. Toll roads continue to perform well bolstered by strong underlying fundamentals, primarily traffic growth, which has led to higher revenues. Because we currently believe this trend will continue in 2016, we have narrowed the Fund’s previous toll road underweight and moved closer to a neutral position relative to the benchmark weight.

Nuveen Real Asset Income Fund

How did the Fund perform during the twelve-month reporting period ended December 31, 2015?

The table in the Fund Performance and Expense Ratios section of this report provides total returns for the Fund for the one-year and since inception periods ended December 31, 2015. Comparative performance information is provided for the Fund’s Class A Shares at net asset value (NAV). The Fund’s Class A Shares at NAV outperformed the new Real Asset Income Blend benchmark, the Barclays U.S. Corporate High Yield Bond Index and the Lipper classification average during the twelve-month reporting period. The Fund underperformed its old Real Asset Income Blend benchmark.

Effective December 31, 2015, the Real Asset Income Blend Index constituents were changed to the following: 28% S&P Global Infrastructure Index, 21% FTSE EPRA/NAREIT Developed Index, 18% Wells Fargo Hybrid & Preferred Securities REIT Index, 15% Barclays Global Capital Securities Index and 18% Barclays U.S. Corporate High Yield Bond Index. The benchmark change was made for three primary reasons. First, the management team believes the new benchmark better approximates what the Fund’s expected weighted average exposures to real estate and infrastructure common equity, preferred securities and debt are likely to look like over time. Second, the new benchmark should reduce the Fund’s performance differential as a result of country/currency exposures (the former benchmark had a U.S. bias versus the more global universe of securities from which the Fund is constructed). Third, the management team believes the new benchmark more accurately reflects the types of securities held by the Fund. There was no change to the Fund’s Barclays benchmark or its Lipper peer group.

Until December 31, 2015, the Real Asset Income Blend Index constituents were as follows: 33% S&P Global Infrastructure Index, 12% BofA/Merrill Lynch Preferred Fixed Rate Index, 15% MSCI U.S. REIT Index, 20% BofA/Merrill Lynch REIT Preferred Index and 20% Barclays U.S. Corporate High Yield Bond Index.

What strategies were used to manage the Fund during the reporting period and how did these strategies influence performance?

The Fund seeks to provide a high level of current income and the potential for capital appreciation by investing in a global portfolio of infrastructure and commercial real estate related securities (i.e. real assets) across the capital markets. These securities include a combination of infrastructure and real estate common stock, infrastructure and real estate preferred stock, and infrastructure and real estate related debt. Our goal is to combine these securities into a portfolio that provides investors with an attractive level of income and dampens levels of risk versus the broader equity market. We continued to select securities using an investment process that

Portfolio Managers’ Comments (continued)

screens for companies and assets across the real assets market that provide higher yields. From the group of securities providing significant yields, we focus on owning those companies and securities with the highest total return potential in the Fund. Our process places a premium on finding securities whose revenues come from tangible assets with long-term concessions, contracts or leases and are therefore capable of producing steady, predictable and recurring cash flows. The Fund’s management team employs a bottom-up, fundamental approach to security selection and portfolio construction. We look for stable companies that demonstrate consistent and growing cash flow, strong balance sheets and histories of being good stewards of shareholder capital.

With the backdrop of heightened volatility across global equity and fixed income markets, four of the five “real asset” categories represented in the new Real Asset Income Blend Index produced negative absolute returns during the twelve-month reporting period. Only the real estate investment trust (REIT) preferred segment boasted a positive return of 6.13%, as measured by the Wells Fargo Hybrid & Preferred Securities REIT Index. The global infrastructure sector, as measured by the S&P Global Infrastructure Index, was the worst performer on an absolute basis with a -11.46% return. The sector remained under significant downward pressure due to plunging oil prices throughout the reporting period, falling well below both the U.S. stock market and the global equity markets. In the high yield bond segment, spreads continued to widen during the reporting period’s increasingly “risk-off” environment due to the sustained downward movement in the price of oil and the flight to quality that ensued. The overall high yield market, as measured by the Barclays U.S. Corporate High Yield Bond Index, produced a -4.47% return during the reporting period. The public commercial REIT sector produced a return of -0.79% (FTSE EPRA/NAREIT Developed Index) mostly due to elevated levels of volatility in the real estate market earlier in the year as a result of higher interest rates and fears they would continue to rise in the second half of the year. Meanwhile, the infrastructure preferred segment, as measured by the Barclays Global Capital Securities Index, returned -2.85% during the reporting period.

The Fund continued to generate a consistent gross yield that remained well above our overall yield hurdle, while producing a total return ahead of its new Real Asset Income Blend Index. We attempt to add value versus the benchmark in two ways: by re-allocating money among five main security types when we see pockets of value at differing times and, more importantly, through individual security selection. The Fund’s outperformance relative to the blended benchmark was driven by the infrastructure common equity and high yield debt segments, while results in the other three segments, REIT common equity, REIT preferred and infrastructure preferred, detracted modestly on a relative basis.

The bulk of the Fund’s outperformance of its blended benchmark was driven by strong security selection in the infrastructure common equity space. As noted above, this asset class posted sharply negative returns and significantly underperformed broader global equity indices. While the global infrastructure equity benchmark was down more than 11% during the reporting period, the Fund’s infrastructure equity holdings declined less than 3%. The most significant contributor to our favorable relative performance in the segment was the Fund’s substantial underweight to pipeline companies, which represent a large part of the benchmark. We remained bearish on energy infrastructure for the entire year, maintaining an underweight position because we believed the midstream energy names would be adversely affected by the continuing weakness in the price of oil. Our thesis proved correct, particularly in the second half of the reporting period. Instead, we favored non-U.S. pipeline companies over domestic companies, which performed better on a relative basis. Security selection within the electric utility area also contributed strongly to the relative outperformance within the global infrastructure equity portfolio. We prefer to own more regulated utility companies with less sensitivity to commodity prices. The Fund’s emphasis on these types of companies benefited results because utilities with higher amounts of commodity price exposure performed poorly in light of the weakness in commodity prices across the globe.

Relative to the Fund’s benchmark, the high yield portion of the portfolio was also beneficial to returns. Security selection within the group, along with an underweight versus the benchmark, contributed positively. With spreads widening during the reporting period and the high yield benchmark return down more than 4%, our approximately 200 basis point underweight to the sector helped. Also, our significant underweight and stock selection within the more economically sensitive industrial sector benefited results because the sector traded off much more than the benchmark return.

The two real estate sectors lagged on a relative basis during the reporting period, with the REIT common equity segment detracting slightly more than REIT preferreds. Because of the Fund’s primary objective to produce income, we place more emphasis on higher dividend-paying REIT equities. However, this stance hurt relative returns during the reporting period as many real estate and generalist investors alike were concerned about the possibility of rising interest rates. During the reporting period, the REIT sectors with lower payout ratios and, therefore higher expected growth rates, were the outperformers. The lower growth/higher dividend names we generally held in the Fund were out of favor, which detracted from returns relative to the benchmark. On an absolute basis, the

Fund’s REIT preferred holdings contributed the most in terms of positive performance because it was the only sector with strongly positive returns, as noted earlier. However, relative to the benchmark, the Fund’s REIT preferred holdings detracted. The Fund owned a higher percentage of non-rated securities, which we believed would perform better in a rising rate environment. While these non-rated holdings advanced approximately 5%, higher quality securities outperformed them, despite the outlook for higher rates, due to credit spread widening and investors’ preference for quality as the widening occurred.

As the reporting period progressed, we reduced the Fund’s U.S. exposure to 61%, which is approximately 9% less than where it started and roughly in line with what we expect the weight to be over the long term. The change in geography was mostly due to our mix within the regulated utility sector, where we continued to find more value in European companies relative to their domestic U.S. counterpart. Growth rates were not demonstrably different between the two regions, however, given the continued easy monetary policy from the European Central Bank, we believed interest rate risk would be a little lower abroad.

Where possible, we continued to shift the portfolio higher up the quality spectrum within the investable universe and slightly down the yield ladder as a result. This, however, did not significantly affect the overall yield of the Fund. As spreads widened, we moved into securities where we were more confident about balance sheet dynamics without sacrificing much by way of the income generated in the portfolio relative to historic levels.

In terms of sector weights, the Fund’s overall allocation to common equities ended the year at roughly 45%; with both infrastructure equities and REIT equities at slight underweight positions. Within common equity, we continued to have very few energy and electric utility holdings. However, we did add approximately 150 basis points of exposure within the master limited partnership (MLP) equity area based on valuation, given how far their prices had fallen. We will, however, remain extremely selective within the space, owning only those companies in which we have the highest levels of confidence. While real estate fundamentals remained strong and many REITs were trading at discounts, we believe technical pressures due to interest rate fears may continue to weigh on the sector domestically. As a result, we continued to find more opportunities outside of the REIT equity space and more opportunities within the preferred universe. Preferred exposures totaled approximately 36% of the portfolio, with slightly more than half in REIT preferreds and the remainder in infrastructure preferreds.

The Fund’s high yield fixed income exposure ended the year at 16% of the portfolio, a slight underweight and a reduction of about 4% from the beginning of the reporting period. Our largest absolute exposure remained in pipeline companies whose credits are much more stable than their equity securities and offer substantially more income. However, after holding up quite well in the first eight months of the year, these issues, along with independent power producers, did trade down during the final months due to the continued weakness in oil and natural gas prices. We will continue to monitor all positions within these two sectors closely.

During the reporting period, the Fund shorted short-term U.S. Treasury futures contracts to hedge against potential increases in interest rates. The effect of these positions on performance was negative during this reporting period.

Nuveen Real Estate Securities Fund

How did the Fund perform during the twelve-month reporting period ended December 31, 2015?

The table in the Fund Performance and Expense Ratios section of this report provides total returns for the Fund for the one-year, five-year and ten-year periods ended December 31, 2015. Comparative performance information is provided for the Fund’s Class A Shares at net asset value (NAV). The Fund’s Class A Shares at NAV outperformed the MSCI U.S. REIT Index and the Lipper classification average during the twelve-month reporting period.

What strategies were used to manage the Fund during the reporting period and how did these strategies influence performance?

The Fund seeks to provide above average income potential and long-term capital appreciation by investing in income producing common stocks of publicly traded companies engaged in the real estate industry. During the reporting period, we continued to implement the Fund’s strategy of investing on a relative value basis with a focus on individual stocks rather than economic or market cycles. We also continued to invest the Fund in a fairly sector neutral manner (with a couple of notable exceptions within the health care and net lease sectors) with a goal of providing a well-diversified portfolio of public real estate stocks to our shareholders. A

Portfolio Managers’ Comments (continued)

sector neutral approach reduces the impact of any one property type on performance. Additionally, we continued to invest in a broader universe of stocks than our benchmark index to access more dynamic parts of the commercial real estate cycle.

During the twelve-month reporting period, the public commercial real estate sector returned 2.52% as measure by the MSCI U.S. REIT Index, amidst an environment that produced elevated levels of volatility in the real estate market. Most of the volatility was a direct result of higher interest rates and fears surrounding the timing of the first Fed rate hike, which was finally enacted in December. While real estate investment trusts (REITs) are generally thought to be more interest rate sensitive than the broader equity market, the segment actually outperformed U.S. equities as measured by the S&P 500® Index, by slightly more than 1% during the reporting period. REIT fundamentals remained stable and the bulk of the headwind effects of higher rates may have been priced in during the first half of the reporting period when REITs struggled relative to broader markets. Most REITs continued to have solid balance sheets and growing dividend yields, while the underperformance they experienced also had made their valuations more compelling. Relative to historic averages, REITs still enjoy a very low cost of capital and the outlook for operating fundamentals is still positive, but more mixed than it has been over the last several years. Continued strength in economic growth and job growth will be important moving forward. Net operating income projections for 2016 remain above long-term averages. At the underlying asset level, many property owners continue to have pricing power and have increased rents due to high occupancy rates. The pace of these rent gains, however, could slow given that many sectors are operating at or very near all-time peaks in occupancy rates. Returns on new property development, which have remained reasonably well contained in most sectors, are expected to earn a premium over where existing assets are currently trading, thus providing additional growth potential for those companies that are able to take advantage. However, markets where development is taking place will require robust economic activity in order to absorb the new inventory. Property values have already more than doubled since the nadir of the financial crisis and we are more than seven years into the recovery, which may temper the pace of future gains for commercial real estate.

The Fund benefited from strong results in several sectors, including health care REITs, diversified, self-storage and net lease. Outperformance in health care was driven primarily by security selection within the space, as well as a modest benefit from an underweight in the sector. While the Fund has generally been sector neutral in health care over the long term, it maintained an underweight to the sector during this reporting period. Because of the longer duration of lease structures within the sector, somewhat muted growth opportunities, along with supply concerns specifically within the long-term care industry, we continued to believe the sector had limited upside relative to other commercial real estate sectors. The largest single contributor in the sector was HCP, Inc., the third largest weight in the benchmark within the sector and the Fund’s largest active underweight position. We continued to underweight HCP due to the company’s less favorable and concentrated tenant exposure and weaker external growth prospects. Also, the company’s largest tenant has had trouble growing cash flow fast enough to keep up with its rent obligations, causing HCP to cut rent in the middle of the reporting period to retain the tenant. As a result of these headwinds, we anticipated that HCP’s earnings and guidance expectations still needed to come down from where the street had them. That thesis played out with HCP posting returns significantly lower than the REIT sector overall and also lower than most of its peers.

Stock selection within the diversified sector was the second largest contributor to relative performance. Within the diversified sector, which represents less than 2% of the benchmark weight, the Fund held less than half of the total benchmark exposure and did not own the two largest constituents, Iron Mountain Inc. and NorthStar Realty Finance Corp. Both the underweight generally and the selection within the group contributed to the relative outperformance. The diversified sector was the second worst performer from an absolute return standpoint, while the two aforementioned names were the worst performers within the group. With the expectation of higher interest rates domestically, the Fund has been biased toward companies and sectors that we believe should demonstrate better cash-flow growth to try to offset the impact of higher rates. Ongoing concerns around future growth for Iron Mountain combined with foreign currency exposure led to our zero weight position. Regarding NorthStar, the company seems to have lost the confidence of the market and continues to get pushed down in spite of a share buyback and modest deleveraging. We also continue to be concerned about a potential conflict of interest due to the externally-advised nature of the company.

Within the self-storage group, the Fund’s substantial overweight to Public Storage, Inc. was the primary driver of outperformance within the group. As discussed above, we positioned the Fund with a bias toward companies and sectors that have historically demonstrated less sensitivity to rate increases. Given the short duration of leases within self-storage, we believed an overweight to the sector was warranted and was expressed primarily via our overweight to Public Storage. We believe Public Storage is well positioned relative to its peers because the company possesses modest balance sheet leverage and a very low cost of capital, which gives it a potential advantage in terms of growth as consolidation continues in the space. The company also operates very efficiently

and is likely to take advantage of its economies of scale. On an absolute basis as well, self-storage was the best performing property type in the REIT universe by a significant margin during the reporting period.

The net lease sector also contributed favorably to relative performance versus the benchmark. Over the long term, the Fund has generally been sector neutral in net lease relative to the benchmark weight. However, we maintained the Fund’s large underweight to net lease companies as a result of our defensive positioning due to the interest rate risk inherent in the sector. Because of the longer duration of lease structures within the sector and somewhat muted growth opportunities, we continued to believe it had limited upside relative to other commercial real estate sectors. This underweight proved helpful during the reporting period as net lease underperformed many of the other sub-property groups. We also saw widespread outperformance from security selection because we maintained underweight positions in most of the benchmark constituents. This strategy worked well as very few of our holdings detracted from relative performance, while the majority of our positions were either positive or neutral.

While the Fund had relatively few areas that detracted in any meaningful way, the office and hotel C-corp sectors were modest laggards. The office sector was the leading detractor of relative performance. Our overweight positions in Brandywine Realty Trust, Liberty Property Trust and SL Green Realty Corp. were responsible for much of the shortfall within the space. Shares of Brandywine Realty underperformed this year on the heels of an expected earnings dilution from additional asset sales that were not originally factored into the company’s guidance. While these asset sales may be dilutive to earnings in the near term, we believe it makes sense for Brandywine Realty to capitalize on the strong pricing environment to sell the assets. A lull in the company’s acquisition activity and a lack of incremental leasing in its development pipeline have also weighed on the stock price. Liberty Property Trust continued to dispose of lower quality assets, which we believed was an appropriate strategy. However, the market punished the stock on a relative basis due to the cash-flow dilution that resulted from a higher-than-expected number of transactions. We believe there is value in Liberty’s shares, especially in light of the recent underperformance, and want to own the company for the long term. SL Green Realty Corporation also modestly underperformed the group; therefore, our overweight to the name negatively impacted relative performance. Earlier in the reporting period, SL Green underperformed due to the market’s surprise about its announced Manhattan property acquisition. The company was going to fund the purchase with asset sales that the market believed would likely be cash flow dilutive. However, the company eventually received higher-than-anticipated prices for its asset sales to fund the vast majority of the purchase. Also, SL Green employs more leverage than most of its competitors, which may have contributed to its underperformance due to uncertainty about rising rates and how that would impact the company’s cost structure. We continue to believe in management’s ability to dispose of additional assets to de-lever its balance sheet and to execute on its business plan.

Within the hotel C-corp sector, which is not represented in the benchmark, our modest position in Hilton Worldwide Holdings Inc. was responsible for the underperformance. Hotels in general are more economically sensitive than most other REIT sectors. Therefore, Hilton Worldwide, along with nearly all of the hotel REIT names, suffered as concerns about slowing global growth accelerated as the reporting period progressed. Weak economic data out of China and other developing markets caused worries about the overall health of the global economy, which could lead to potential slowdowns in travel and hotel demand. While the REIT sector as a whole produced a positive return, all but three of the Fund’s hotel C-corp and hotel REIT names were sharply negative.

In terms of changes, we continued to maintain slight biases to large cap over small cap and high quality over lower quality, which was reflected in the Fund’s focus on core/high-conviction names. We continued to favor companies that operate under shorter lease terms as well. That positioning is reflected in the Fund’s continued underweights to the health care REIT and net lease sectors, a slight overweight to apartments and a continued overweight to the self-storage sector, which we believe still possesses the potential for superior net operating income growth relative to most other sectors. This positioning is also reflective of the interest rate environment and our belief that domestic interest rates are likely biased in the upward direction.

Risk Considerations

and Dividend Information

Risk Considerations

Nuveen Global Infrastructure Fund

Mutual fund investing involves risk; principal loss is possible. Concentration in infrastructure-related securities involves sector risk and concentration risk, particularly greater exposure to adverse economic, regulatory, political, legal, liquidity, and tax risks associated with MLPs and REITS. Foreign investments involve additional risks including currency fluctuations and economic and political instability. These risks are magnified in emerging markets. Common stocks are subject to market risk or the risk of decline. Small- and mid-cap stocks are subject to greater price volatility. The use of derivatives involves substantial financial risks and transaction costs. The Fund’s potential investment in other investment companies means shareholders bear their proportionate share of fund expenses and indirectly, the expenses of other investment companies. Fund investments in ETFs may involve tracking error. Preferred securities may involve greater credit risk than other debt instruments.

Nuveen Real Asset Income Fund

Mutual fund investing involves risk; principal loss is possible. Equity investments such as those held by the Fund, are subject to market risk, call risk, derivatives risk, other investment companies risk, common stock risk, and tax risks associated with MLPs. Concentration in specific sectors may involve greater risk and volatility than more diversified investments: real estate sector involves the risk of exposure to economic downturns and changes in real estate values, rents, property taxes, interest rates and tax laws; infrastructure-related securities may involve greater exposure to adverse economic, regulatory, political, legal, and other changes affecting such securities. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity, and differing legal and accounting standards. These risks are magnified in emerging markets. Investments in small- and mid-cap companies are subject to greater volatility. In addition, the fund will bear its proportionate share of any fees and expenses paid by the ETFs in which it invests.

Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk and income risk. As interest rates rise, bond prices fall. Below investment grade or high yield debt securities are subject to liquidity risk and heightened credit risk. Preferred securities are subordinated to bonds and other debt instruments in a company’s capital structure and therefore are subject to greater credit risk. Asset-backed and mortgage-backed securities are subject to additional risks such as prepayment risk, liquidity risk, default risk and adverse economic developments.

Nuveen Real Estate Securities Fund

Mutual fund investing involves risk; principal loss is possible. Common stocks and REITs such as those held in the Fund involve market risk, concentration risk, sector risk, and non-diversification risk. The real estate industry is greatly affected by economic downturns that may persist as well as changes in property values, taxes, and regulatory developments. Foreign investments involve additional risks including currency fluctuations, and economic or political instability. These risks are magnified in emerging markets. The use of derivatives involves substantial financial risks and transaction costs. Small cap stocks may experience more volatility than large cap stocks.

Dividend Information

Regular dividends are declared and distributed annually for Nuveen Global Infrastructure Fund, declared and distributed monthly for Nuveen Real Asset Income Fund and declared and distributed quarterly for Nuveen Real Estate Securities Fund. To permit a Fund to maintain a more stable dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net investment income it actually earned during the period. If the Fund has cumulatively earned more than it has paid in dividends, it will hold the excess in reserve as undistributed net investment income (UNII) as part of the Fund’s NAV. Conversely, if the Fund has cumulatively paid out dividends more than it has earned, the excess will constitute negative UNII that will likewise be reflected in the Fund’s NAV. Each Fund will, over time, pay all of its net investment income as dividends to shareholders.

In certain instances, a portion of each Fund’s distributions may be paid from sources or comprised of elements other than ordinary income, including capital gains and/or a return of capital. This is generally due to the fact that the tax character of Fund distributions for a fiscal year is dependent upon the amount and tax character of distributions received from securities held in the Fund’s portfolio. Distributions received from certain securities in which the Fund invests, most notably REIT securities, may be characterized for tax purposes as ordinary income, long-term capital gain and/or a return of capital. The issuer of a security typically reports the tax character of its distributions only once per year, generally during the first two months of the following calendar year. The full amount of the distributions received from such securities is included in the Fund’s ordinary income during the course of the year until such

time the Fund is notified by the issuer of the actual tax character. To the extent that at the time of a particular distribution the Fund estimates that a portion of that distribution is attributable to a source or sources other than ordinary income, the Fund would send shareholders a notice to that effect. The final determination of the sources and tax character of all distributions for the fiscal year is made after the end of the fiscal year. The sources for and per share amounts of each Fund’s distributions for the reporting period are respectively presented in the Statement of Changes in Net Assets and Financial Highlights (for financial reporting purposes), and are also reflected in Note 6 – Income Tax Information within the accompany Notes to Financial Statements (for income tax purposes), later in this report.

Additional Dividend Information for Nuveen Real Asset Income Fund and Nuveen Real Estate Securities Fund

Nuveen Real Asset Income Fund and Nuveen Real Estate Securities Fund seek to pay regular dividends at a rate that reflects the cash flow received from each Fund’s investment in securities, less fund expenses. Fund distributions are not intended to include expected portfolio appreciation; however, the Fund invests in securities that make payments which ultimately may be fully or partially characterized for tax purposes by the securities’ issuers as gains or return of capital. This tax treatment will generally “flow through” to the Fund’s distributions, but the specific tax treatment is often not known with certainty until after the end of the Fund’s tax year. As a result, certain portions of the regular distributions by these two Funds throughout the year were later re-characterized for tax purposes as either long-term gains (both realized and unrealized), or as a non-taxable return of capital, as set forth in each Fund’s table below.

Nuveen Real Asset Income Fund

| | | | | | | | | | | | |

| | | Share Class | |

| Fiscal Year (Calendar Year) Ended December 31, 2015 | | Class A | | | Class C | | | Class I | |

Regular monthly per share distribution | | | | | | | | | | | | |

From net investment income | | $ | 1.0754 | | | $ | 0.8954 | | | $ | 1.1354 | |

From net realized capital gains | | $ | 0.0131 | | | $ | 0.0131 | | | $ | 0.0131 | |

Return of capital | | $ | 0.1015 | | | $ | 0.1015 | | | $ | 0.1015 | |

Total per share distribution | | $ | 1.1900 | | | $ | 1.0100 | | | $ | 1.2500 | |

Yields1,2,3 | | | | | | | | | | | | |

Dividend Yield | | | 5.12% | | | | 4.66% | | | | 5.68% | |

SEC 30-Day Yield – Subsidized | | | 5.00% | | | | 4.56% | | | | 5.56% | |

SEC 30-Day Yield – Unsubsidized | | | 5.00% | | | | 4.55% | | | | 5.56% | |

Nuveen Real Estate Securities Fund

| | | | | | | | | | | | | | | | | | | | |

| | | Share Class | |

| Fiscal Year (Calendar Year) Ended December 31, 2015 | | Class A | | | Class C | | | Class R3 | | | Class R6 | | | Class I | |

Regular quarterly per share distribution | | | | | | | | | | | | | | | | | | | | |

From net investment income | | $ | 0.3748 | | | $ | 0.1848 | | | $ | 0.3248 | | | $ | 0.4448 | | | $ | 0.4448 | |

From net realized capital gains | | $ | 1.4552 | | | $ | 1.4552 | | | $ | 1.4552 | | | $ | 1.4552 | | | $ | 1.4552 | |

Total per share distribution | | $ | 1.8300 | | | $ | 1.6400 | | | $ | 1.7800 | | | $ | 1.9000 | | | $ | 1.9000 | |

Yields1,2,3 | | | | | | | | | | | | | | | | | | | | |

Dividend Yield | | | 2.82% | | | | 2.22% | | | | 2.73% | | | | 3.25% | | | | 3.25% | |

SEC 30-Day Yield – Subsidized | | | 1.99% | | | | 1.36% | | | | 1.86% | | | | 2.51% | | | | 2.36% | |

SEC 30-Day Yield – Unsubsidized | | | 1.99% | | | | 1.36% | | | | 1.86% | | | | 2.51% | | | | 2.36% | |

| 1 | Dividend Yield is the most recent dividend per share (annualized) divided by the offering price per share. |

| 2 | The SEC 30-Day Yield is a standardized measure of a fund’s yield that accounts for the future amortization of premiums or discounts of bonds held in the Fund’s portfolio. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. Subsidized yields reflect fee waivers and/or expense reimbursements from the investment adviser during the period. If any such waivers and/or reimbursements had not been in place, yields would have been reduced. Unsubsidized yields do not reflect waivers and/or reimbursements from the investment adviser during the period. Refer to the Fund Performance and Expense Ratios page for further details on the investment adviser’s most recent agreement with the Fund to waive fees and/or reimburse expenses, where applicable. Dividend Yield may differ from the SEC 30-Day Yield because the fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 3 | The SEC Yield for Class A Shares quoted in the table reflects the maximum sales load. Investors paying a reduced load because of volume discounts, investors paying no load because they qualify for one of the several exclusions from the load, and existing shareholders who previously paid a load but would like to know the SEC Yield applicable to their shares on a going-forward basis, should understand that the SEC Yield effectively applicable to them would be higher than the figure quoted in the table. |

THIS PAGE INTENTIONALLY LEFT BLANK

Fund Performance

and Expense Ratios

The Fund Performance and Expense Ratios for each Fund are shown within this section of the report.

Returns quoted represent past performance, which is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Returns may reflect fee waivers and/or expense reimbursements by the investment adviser during the periods presented. If any such waivers and/or reimbursements had not been in place, returns would have been reduced. See Notes to Financial Statements, Note 7—Management Fees and Other Transactions with Affiliates for more information. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees, and assume reinvestment of dividends and capital gains.

Comparative index and Lipper return information is provided for Class A Shares at net asset value (NAV) only.

The expense ratios shown reflect total operating expenses (before fee waivers and/or expense reimbursements, if any) as shown in the most recent prospectus. The expense ratios include management fees and other fees and expenses.

Fund Performance and Expense Ratios (continued)

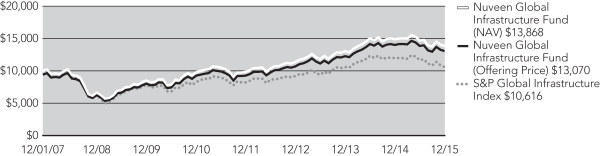

Nuveen Global Infrastructure Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance

Average Annual Total Returns as of December 31, 2015

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | Since

Inception | |

Class A Shares at NAV | | | (6.89)% | | | | 7.11% | | | | 4.15% | |

Class A Shares at maximum Offering Price | | | (12.25)% | | | | 5.86% | | | | 3.39% | |

S&P Global Infrastructure Index | | | (11.46)% | | | | 5.09% | | | | 0.75% | |

Lipper Specialty/Miscellaneous Funds Classification Average | | | (10.13)% | | | | 5.59% | | | | 0.94% | |

| | | |

Class C Shares | | | (7.50)% | | | | 6.35% | | | | 10.41% | |

Class R3 Shares | | | (7.10)% | | | | 6.76% | | | | 10.88% | |

Class I Shares | | | (6.67)% | | | | 7.39% | | | | 4.41% | |

Since inception returns for Class A Shares and Class I Shares, and for the comparative index and Lipper classification average, are from 12/17/07; since inception returns for Class C Shares and Class R3 Shares are from 11/03/08. Indexes and Lipper averages are not available for direct investment.

Class A Shares have a maximum 5.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within twelve months of purchase. Such CDSC will be equal to 1.00% for any shares purchased on or after November 1, 2015 if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are only available for purchase by eligible retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | Class A | | | Class C | | | Class R3 | | | Class I | |

Gross Expense Ratios | | | 1.42% | | | | 2.17% | | | | 1.67% | | | | 1.17% | |

Net Expense Ratios | | | 1.22% | | | | 1.97% | | | | 1.47% | | | | 0.97% | |

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through September 30, 2016 so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, acquired fund fees and expenses, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 1.00% of the average daily net assets of any class of Fund shares. The expense limitation may be terminated or modified prior to that date only with the approval of the Board of Directors of the Fund.

Growth of an Assumed $10,000 Investment as of December 31, 2015 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

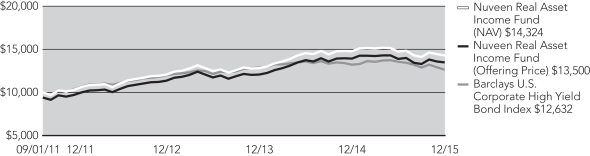

Nuveen Real Asset Income Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance

Average Annual Total Returns as of December 31, 2015

| | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | Since

Inception | |

Class A Shares at NAV | | | (3.19)% | | | | 8.71% | |

Class A Shares at maximum Offering Price | | | (8.75)% | | | | 7.22% | |

Barclays U.S. Corporate High Yield Bond Index | | | (4.47)% | | | | 5.59% | |

Real Asset Income Blend Index (New Comparative Benchmark) | | | (3.47)% | | | | 7.98% | |

Real Asset Income Blend Index (Old Comparative Benchmark) | | | (1.56)% | | | | 8.24% | |

Lipper Global Flexible Portfolio Funds Classification Average | | | (4.70)% | | | | 5.59% | |

| | |

Class C Shares | | | (3.88)% | | | | 7.92% | |

Class I Shares | | | (2.90)% | | | | 8.99% | |

As previously noted in the Portfolio Managers’ Comments section of this report, effective December 31, 2015, the Custom Blended Benchmark constituents were changed. The changes were made for three primary reasons. First, the management team believes the new benchmark better approximates what the Fund’s expected weighted average exposures to real estate and infrastructure common equity, preferred securities and debt are likely to look like over time. Second, the new benchmark should reduce the Fund’s performance differential as a result of country/currency exposures (the former Custom Blended Benchmark had a U.S. bias versus the more global universe of securities from which the Fund is constructed). Third, the management team believes the new Custom Blended Benchmark more accurately reflects the types of securities held by the Fund.

Since inception returns are from 9/13/11. Indexes and Lipper averages are not available for direct investment.

Class A Shares have a maximum 5.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within twelve months of purchase. Such CDSC will be equal to 1.00% for any shares purchased on or after November 1, 2015 if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | | | | | |

| | | Share Class | |

| | | Class A | | | Class C | | | Class I | |

Gross Expense Ratios | | | 1.23% | | | | 1.98% | | | | 0.97% | |

Net Expense Ratios | | | 1.17% | | | | 1.92% | | | | 0.92% | |

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse expenses through September 30, 2016 so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, acquired fund fees and expenses, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 0.95% of the average daily net assets of any class of Fund shares. The expense limitation may be terminated or modified prior to that date only with the approval of the Board of Directors of the Fund.

Growth of an Assumed $10,000 Investment as of December 31, 2015 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Fund Performance and Expense Ratios (continued)

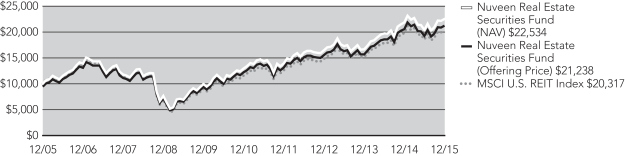

Nuveen Real Estate Securities Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance

Average Annual Total Returns as of December 31, 2015

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares at NAV | | | 3.22% | | | | 11.67% | | | | 8.47% | |

Class A Shares at maximum Offering Price | | | (2.71)% | | | | 10.35% | | | | 7.82% | |

MSCI U.S. REIT Index | | | 2.52% | | | | 11.88% | | | | 7.35% | |

Lipper Real Estate Funds Classification Average | | | 2.17% | | | | 11.03% | | | | 6.61% | |

| | | |

Class C Shares | | | 2.45% | | | | 10.83% | | | | 7.66% | |

Class R3 Shares | | | 2.95% | | | | 11.39% | | | | 8.20% | |

Class I Shares | | | 3.48% | | | | 11.95% | | | | 8.74% | |

| | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | Since

Inception | |

Class R6 Shares | | | 3.60% | | | | 7.54% | |

Since inception return for Class R6 Shares is from 4/30/13. Indexes and Lipper averages are not available for direct investment.

Class A Shares have a maximum 5.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within twelve months of purchase. Such CDSC will be equal to 1.00% for any shares purchased on or after November 1, 2015 if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are only available for purchase by eligible retirement plans. Class R6 Shares have no sales charge and are available only to certain limited categories of investors as described in the prospectus. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | Class A | | | Class C | | | Class R3 | | | Class R6 | | | Class I | |

Expense Ratios | | | 1.30% | | | | 2.05% | | | | 1.55% | | | | 0.89% | | | | 1.05% | |

Growth of an Assumed $10,000 Investment as of December 31, 2015 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

Holding

Summaries as of December 31, 2015

This data relates to the securities held in each Fund’s portfolio of investments as of the end of this reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Nuveen Global Infrastructure Fund

Portfolio Allocation

(% of net assets)

| | | | |

Common Stocks | | | 97.0% | |

Real Estate Investment Trust (REIT) Common Stocks | | | 2.0% | |

Investment Companies | | | 0.7% | |

Repurchase Agreements | | | 0.6% | |

Other Assets Less Liabilities | | | (0.3)% | |

Net Assets | | | 100% | |

Top Five Common Stock & REIT Common Stock Holdings

(% of net assets)

| | | | |

Transurban Group | | | 4.9% | |

NextEra Energy Inc. | | | 4.0% | |

Atlantia SpA | | | 3.6% | |

Enbridge Inc. | | | 2.8% | |

Groupe Eurotunnel SA | | | 2.7% | |

Portfolio Composition

(% of net assets)

| | | | |

Transportation Infrastructure | | | 29.8% | |

Electric Utilities | | | 15.1% | |

Multi-Utilities | | | 13.6% | |

Oil, Gas & Consumable Fuels | | | 11.6% | |

Gas Utilities | | | 6.4% | |

Water Utilities | | | 4.5% | |

Other | | | 18.7% | |

Repurchase Agreements | | | 0.6% | |

Other Assets Less Liabilities | | | (0.3)% | |

Net Assets | | | 100% | |

Country Allocation

(% of net assets)

| | | | |

United States | | | 36.0% | |

Australia | | | 9.9% | |

Italy | | | 7.5% | |

France | | | 7.3% | |

Canada | | | 5.3% | |

United Kingdom | | | 4.8% | |

Japan | | | 4.8% | |

Spain | | | 4.7% | |

Hong Kong | | | 4.6% | |

New Zealand | | | 2.8% | |

Singapore | | | 2.3% | |

Other | | | 10.3% | |

Other Assets Less Liabilities | | | (0.3)% | |

Net Assets | | | 100% | |

Nuveen Real Asset Income Fund

Portfolio Allocation

(% of net assets)

| | | | |

Common Stocks | | | 26.5% | |

Real Estate Investment Trust (REIT) Common Stocks | | | 18.1% | |

Convertible Preferred Securities | | | 8.5% | |

$25 Par (or similar) Retail Preferred | | | 21.9% | |

Corporate Bonds | | | 16.3% | |