UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-5344

William Blair Funds

(Exact name of registrant as specified in charter)

| | |

| 222 West Adams Street, Chicago, IL | | 60606 |

| (Address of principal executive offices) | | (Zip Code) |

Marco Hanig

William Blair Funds

222 West Adams Street, Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: 312-236-1600

Date of fiscal year end: December 31

Date of reporting period: December 31, 2005

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A Registrant is not required to respond to the collection of information contained in Form N-CSR unless the form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimates and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. (ss) 3507.

| Item 1. | December 31, 2005 Annual Reports transmitted to shareholders. |

Table of Contents

This report is submitted for the general information of the shareholders of the William Blair Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by a prospectus of the William Blair Funds. Please carefully consider the Funds’ investment objectives, risks, charges, and expenses before investing. This and other information is contained in the Funds’ prospectus, which you may obtain by calling 1-800-742-7272. Read it carefully before you invest or send money.

December 31, 2005 | William Blair Funds 1 |

Marco Hanig

A LETTER FROM THE PRESIDENT

Dear Shareholders:

In 2005, the U.S. stock market prolonged its rally into a third year, but with moderate growth. The Standard & Poor’s 500 Index of large cap stocks posted a 4.91% return, and the Russell 2000® Index of small cap stocks was up 4.55%. Despite the rise in interest rates, bonds had positive returns, with the Lehman Aggregate Bond Index increasing 2.44%. Abroad, returns were higher, with the MSCI All Country World Free Ex-US Index of foreign stocks up 17.11%

After the bursting of the technology bubble in 2000-2002, the market rebounded sharply in 2003, then began to slow down to low double-digit growth in 2004, and in 2005 leveled off further to a modest single-digit growth rate. The economy is growing quite nicely, but growth in stock prices has been dampened by high energy prices and the continuing efforts by the Fed to keep the economy from overheating by raising interest rates.

The big story was the out-performance of mid-cap stocks, which did better than both small and large-caps. Beginning in 2003, small caps had done much better than mid- and large-caps, and it had been widely expected that eventually this trend would reverse. This is beginning to happen, as leadership shifted from small-caps to mid-caps. It remains to be seen whether, as expected, this trend will continue and result in large-caps having their day in the sun in the coming year.

The differences between value and growth were very modest, with value just edging out growth one more year, continuing a five-year winning streak. This trend is also widely expected to reverse, and the fact that it didn’t happen in 2005 was a bit of a surprise.

Total Returns by Russell Style Index

January 1 through December 31, 2005

| | | | | | | | | |

| | | Value

| | | Blend

| | | Growth

| |

Large Cap (Russell 1000) | | 7.05 | % | | 6.27 | % | | 5.26 | % |

Mid Cap (Russell MidCap) | | 12.65 | % | | 12.65 | % | | 12.10 | % |

Small Cap (Russell 2000) | | 4.71 | % | | 4.55 | % | | 4.15 | % |

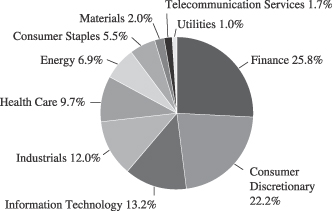

The best news for our shareholders is that each and every one of our funds had positive absolute returns in 2005. In terms of relative performance, the top performer was the newly launched Emerging Markets Growth Fund, which beat the MSCI Emerging Markets benchmark by a wide margin (42.52% vs. 29.26%) in the first seven months of its existence, due in significant part to participation in the IPO of Baidu, the Google of China. The Tax-Managed Growth Fund and the Growth Fund also did quite well, with returns of 12.46% and 9.75% respectively versus 5.17% for the Russell 3000 Growth Index. The International Growth Fund, with returns of 21.65% versus 17.11% for the MSCI World ex-US Index rounds out the list of strong relative performers. Funds that struggled in relative terms during the year were Value Discovery Fund, which posted a 0.49% return vs. 4.71% for the Russell 2000 Value Index, and the International Equity Fund, with a 13.50% return vs. 17.11% for the MSCI All Country World Free ex-US Index. The Fund managers’ letters discuss in greater detail the reasons for their over- or under-performance.

As always, thank you for investing with us!

Marco Hanig

As always, we thank you for investing with us!

Marco Hanig

Please see page 4 for important performance disclosure information.

2 Annual Report | December 31, 2005 |

PERFORMANCE AS OF DECEMBER 31, 2005—CLASS N SHARES

| | | | | | | | | | | | |

| | | 1 Yr

| | 3 Yr

| | 5 Yr

| | 10 Yr (or since

inception)

| | Inception

Date

| | Overall Morningstar Rating

|

Growth Fund | | 9.75 | | 13.36 | | -1.35 | | 6.45 | | 3/20/46 | | ««« |

Morningstar Large Growth | | 6.46 | | 13.88 | | -3.36 | | 6.95 | | | | Among 1,353 large growth funds |

Russell 3000® Growth | | 5.17 | | 13.78 | | -3.15 | | 6.48 | | | |

Standard & Poor’s 500 | | 4.91 | | 14.39 | | 0.54 | | 9.07 | | | | |

| | | | | | |

Tax-Managed Growth Fund | | | | | | | | | | | | «««« |

Return before Taxes | | 12.46 | | 13.80 | | 0.06 | | 0.18 | | 12/27/99 | | Among 1,353 large growth funds |

After Taxes on Distributions | | 12.46 | | 13.80 | | 0.06 | | 0.18 | | | |

After Taxes on Distributions and Sale of Fund Shares | | 8.10 | | 11.94 | | 0.05 | | 0.15 | | | | |

Morningstar Large Growth | | 6.46 | | 13.88 | | -3.36 | | — | | | | |

Russell 3000® Growth | | 5.17 | | 13.78 | | -3.15 | | -6.45 | | | | |

| | | | | | |

Large Cap Growth Fund | | 3.69 | | 10.46 | | -5.20 | | -6.96 | | 12/27/99 | | «« |

Morningstar Large Growth | | 6.46 | | 13.88 | | -3.36 | | — | | | | Among 1,353 large growth funds |

Russell 1000® Growth | | 5.26 | | 13.23 | | -3.58 | | -6.85 | | | |

| | | | | | |

Small Cap Growth Fund | | 1.18 | | 27.73 | | 16.79 | | 19.68 | | 12/27/99 | | ««««« |

Morningstar Small Growth | | 5.74 | | 19.56 | | 2.17 | | — | | | | Among 650 small growth funds |

Russell 2000® Growth | | 4.15 | | 20.93 | | 2.28 | | -1.37 | | | |

| The Small Cap Growth Fund’s performance during 2000 was primarily attributable to investments in initial public offerings (IPOs) during a rising market. Since then, IPOs have had an insignificant effect on the Fund’s performance. | | | | | | |

| | | | | | |

Small-Mid Cap Growth Fund | | 10.72 | | — | | — | | 11.64 | | 12/29/03 | | Not rated. |

Morningstar Mid-Cap Growth | | 9.70 | | — | | — | | — | | | | |

Russell 2500TM Growth | | 8.17 | | — | | — | | 11.75 | | | | |

| | | | | | |

International Growth Fund | | 21.65 | | 27.03 | | 8.46 | | 13.68 | | 10/1/92 | | ««««« |

Morningstar Foreign Large Growth | | 15.27 | | 21.66 | | 2.15 | | 5.69 | | | | Among 196 foreign large growth funds |

MSCI All Country World Free Ex-US | | 17.11 | | 26.20 | | 6.66 | | 6.70 | | | |

| | | | | | |

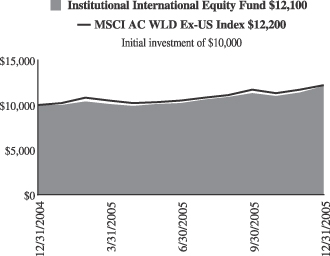

International Equity Fund | | 13.50 | | — | | — | | 16.85 | | 5/24/04 | | Not rated. |

Morningstar Foreign Large Growth | | 15.27 | | — | | — | | — | | | | |

MSCI All Country World Free Ex-US | | 17.11 | | — | | — | | 25.10 | | | | |

| | | | | | |

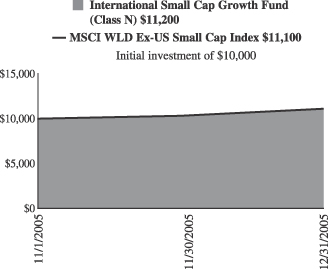

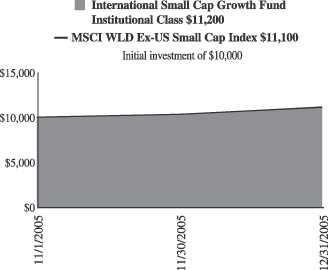

International Small Cap Growth | | — | | — | | — | | 11.60 | | 11/1/05 | | Not rated. |

MSCI All Country World Free Small Cap Ex-US | | — | | — | | — | | 10.68 | | | | |

| | | | | | |

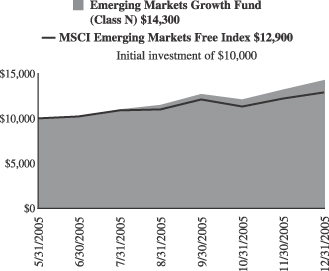

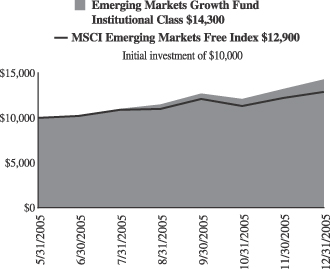

Emerging Markets Growth Fund | | — | | — | | — | | 42.52 | | 6/6/05 | | Not rated. |

MSCI Emerging Markets Free | | — | | — | | — | | 29.26 | | | | |

| A portion of the Emerging Markets Growth Funds performance since inception was attributable to an investment in an initial public offering (IPO). | | | | | | |

| | | | | | |

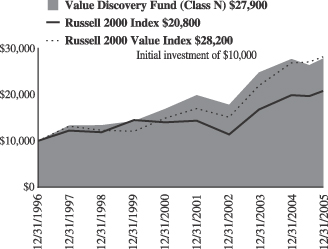

Value Discovery Fund | | 0.49 | | 16.19 | | 10.46 | | 11.98 | | 12/23/96 | | «« |

Morningstar Small Value | | 6.13 | | 22.30 | | 13.50 | | — | | | | Among 276 small value funds |

Russell 2000® | | 4.55 | | 22.13 | | 8.22 | | 8.64 | | | |

Russell 2000® Value | | 4.71 | | 23.18 | | 13.55 | | 12.31 | | | | |

| | | | | | |

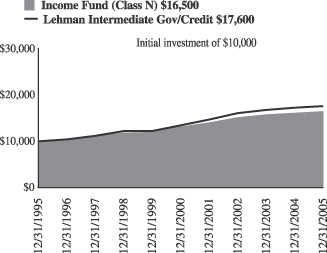

Income Fund | | 1.71 | | 2.66 | | 4.59 | | 5.11 | | 10/1/90 | | «««« |

Morningstar Short-Term Bond | | 1.43 | | 1.96 | | 3.82 | | 4.63 | | | | Among 317 short-term bond funds |

Lehman Intermediate Govt./Credit Bond Index | | 1.57 | | 2.96 | | 5.49 | | 5.80 | | | |

Please see the next page for important disclosure information.

December 31, 2005 | William Blair Funds 3 |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher that the data quoted. Returns shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or a loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. Investing in smaller companies involves special risks, including higher volatility and lower liquidity. International and emerging markets investing involves special risk considerations, including currency fluctuations, lower liquidity, economic and political risk. As interest rates rise, bond prices will fall and bond funds become more volatile. From time to time, the investment advisor may waive fees or reimburse expenses for certain Funds. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load.

Tax-Managed Growth Fund’s after-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Actual after-tax returns depend on the investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown only for Class N and the after-tax returns for Class N shares will vary.

Morningstar RatingsTM are as of 12/31/05 and are subject to change every month. The ratings are based on a risk-adjusted return measure that accounts for variation in a fund’s monthly performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each Category receive 5 stars, the next 22.5% receive 4 stars, the middle 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a fund is derived from a weighted-average of the performance figures associated with its three-, five- and ten-year (if applicable) Morningstar Rating metrics. The 3/5/10 year Morningstar ratings were as follows: Growth Fund «««/«««/«««, Tax-Managed Growth Fund «««/««««/NA, and Large Cap Growth Fund ««/««/NA, out of 1,353/1,065/370 large growth funds; Small Cap Growth Fund «««««/«««««/NA out of 650/507/NA small growth funds; Value Discovery Fund «/««/NA out of 276/192/NA small value funds; International Growth Fund ««««/«««««/««««« out of 196/151/62 foreign large growth funds; Income Fund ««««/««««/«««« out of 317/227/131 short-term bond funds.

Please carefully consider the Funds’ investment objectives, risks, charges, and expenses before investing. This and other information is contained in the Funds’ prospectus, which you may obtain by calling 1-800-742-7272. Read it carefully before you invest or send money. William Blair & Company, L.L.C., distributor. 02/06.

4 Annual Report | December 31, 2005 |

John F. Jostrand

GROWTH FUND

The Growth Fund invests primarily in common stocks of domestic growth companies that the Advisor expects to have sustainable, above-average growth from one business cycle to the next.

AN OVERVIEW FROM THE PORTFOLIO MANAGER

How did the Fund perform over the last year? How did the Fund’s performance compare to its benchmark?

The Growth Fund posted a 9.75% increase on a total return basis (Class N Shares) for the 12 months ended December 31, 2005. By comparison, the Fund’s benchmarks, the Russell 3000® Growth Index gained 5.17%, while the Standard & Poor’s 500 Index rose 4.91%.

What were the most significant factors impacting Fund performance?

Stock selection was the strongest factor with respect to the Fund’s overall out-performance relative to the benchmark for the year. The Fund’s overweight position to stocks with the smallest capitalizations (below $2 billion), along with particularly strong stock selection in this area, provided the largest benefit to absolute and relative returns.

Which sectors enhanced the Fund’s return? What were among the best performing investments for the Fund?

The strongest contributing sector to the Fund and Russell 3000® Growth Index returns during the year was Health Care. Our extremely strong stock selection allowed the Fund to significantly outpace the Russell 3000® Growth Index in this area. Health Care Equipment and Supplies offered the largest benefit to absolute and relative returns. Alcon, Inc. in the eye care area, received approval for its ReStor Lens for cataract surgery, and Medicare approved funding of the procedure; these proved to be catalysts for stock appreciation. Kyphon, Inc. a provider of groundbreaking product and technique in spine restoration surgery, also experienced strong growth during the year. The Health Care Providers and Services industry provided the second best returns within health care for the portfolio, with UnitedHealth Group, Express Scripts, Inc. and American Healthways, Inc. posting positive stock price gains.

Information Technology stocks were the second largest contributors to Fund returns, on both an absolute and relative basis. A large benefit came from the software area, where the Fund showed positive results while the Russell 3000® Growth Index had negative returns. Nuance Communications, Inc., providing imaging services, with a focus on voice-oriented command services, scan-to-digital and fax-to-digital services, saw strong stock price gains during the year. Adobe Inc. also had excellent results, particularly in the fourth quarter.

Were there any investment strategies or themes that did not measure up to your expectations?

Consumer stocks were soft during the year, taking the brunt of rising interest rates and higher oil prices. In the Fund, our stocks within the Retail sector were particularly disappointing. Kohl’s Corporation was anticipated to achieve promising results after some significant management changes, remerchandising of products, and adding several items to higher

December 31, 2005 | William Blair Funds 5 |

margin personal care and beauty lines. The softness in consumer stocks in general, combined with discount pricing and unseasonable weather contributed to the stock’s weakness. In a similar vein, Bed, Bath and Beyond, Inc. had an optimistic outlook with respect to their new larger “box” stores, their strong competitive position, and their roll out of Christmas Tree Stores. The company experienced modest sales results during the year, which disappointed investors who anticipated much better growth. In the last quarter, the company announced that financial results were likely to be at the lower end of the expected range, news which further pressured the stock.

Dell Inc. was the largest detractor from returns, both on an absolute and relative basis. Despite meeting earnings estimates during the year, the stock experienced some weakness in revenues driven by aggressive pricing strategies to stave off the recently rejuvenated Hewlett-Packard Co. Additionally, the stock experienced significant Price/Earnings multiple compression.

We were slightly underweight in Energy stock during the year. Although our stock selection significantly outpaced the Russell 3000® Growth Index, our underweight caused a modest drag to relative performance.

What is your current strategy? How is the Fund positioned?

We continue to seek interesting opportunities for sustainable growth in the Information Technology and Health Care areas. We are cautious in the consumer area, particularly to stocks that are heavily reliant on the lower-end customer, and have not found compelling growth opportunities in the consumer staples area.

Compared to historic ratios, valuations are relatively compressed, resulting in no significant differentiation between higher and lower quality companies. As the economy slows, we believe the higher quality companies will be able to differentiate themselves from those of average quality due to superior business models that will likely generate above average growth, and be rewarded with higher earnings multiples.

6 Annual Report | December 31, 2005 |

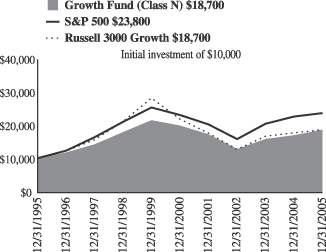

Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 12/31/2005

| | | | | | | | | | | | | | | | | |

| | | 1 Year

| | | 3 Year

| | | 5 Year

| | | 10 Year

| | | Since Inception(a)

| | | |

Growth Fund Class N | | 9.75 | % | | 13.36 | % | | (1.35 | )% | | 6.45 | % | | — | | | |

Growth Fund Class I | | 10.08 | | | 13.69 | | | (1.10 | ) | | — | | | 0.73 | | | |

Russell 3000® Growth Index | | 5.17 | | | 13.78 | | | (3.15 | ) | | 6.48 | | | (2.91 | ) | | |

S&P 500 Index | | 4.91 | | | 14.39 | | | 0.54 | | | 9.07 | | | 1.13 | | | |

| | (a) | | For the period from October 1, 1999 to December 31, 2005. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company L.L.C. without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 3000® Growth Index consists of large, medium, and small-capitalization companies with above average price-to-book ratios and forecasted growth rates. The index is weighted by market capitalization and large/medium/small companies make up approximately 80%/15%/5% of the index.

The S&P 500 Index indicates broad larger capitalization equity market performance.

This report identifies the Fund’s investments on December 31, 2005. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

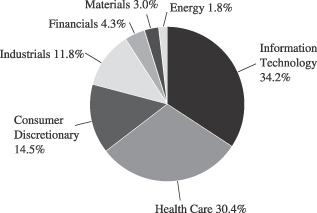

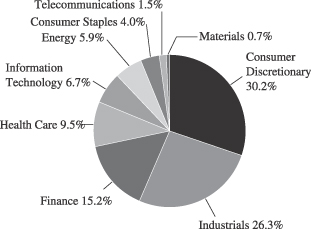

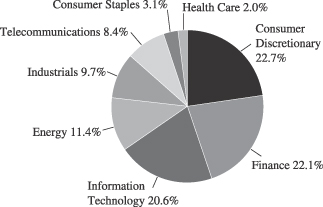

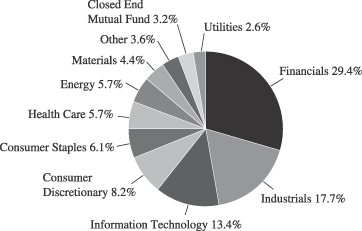

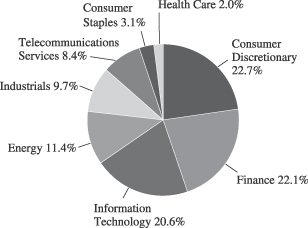

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

December 31, 2005 | William Blair Funds 7 |

Growth Fund

Portfolio of Investments, December 31, 2005 (all dollar amounts in thousands)

| | | | | |

Issuer

| | Shares

| | Value

|

| | |

Common Stocks | | | | | |

Information Technology—33.4% | | | | | |

*Adobe Systems Incorporated | | 174,860 | | $ | 6,463 |

Arm Holding plc—ADR | | 749,885 | | | 4,657 |

*Cognizant Technology Solutions Corporation | | 64,565 | | | 3,251 |

*Dell, Inc. | | 255,425 | | | 7,660 |

*EMC Corporation | | 544,550 | | | 7,417 |

First Data Corporation | | 125,230 | | | 5,386 |

*J2 Global Communications, Inc. | | 106,415 | | | 4,548 |

*Jabil Circuit, Inc. | | 169,205 | | | 6,276 |

Linear Technology Corporation | | 97,420 | | | 3,514 |

Microchip Technology, Inc. | | 83,560 | | | 2,686 |

*Network Appliance, Inc. | | 109,780 | | | 2,964 |

*Nuance Communications, Inc. | | 737,765 | | | 5,629 |

Paychex, Inc. | | 163,200 | | | 6,221 |

*PDF Solutions, Inc. | | 82,870 | | | 1,347 |

Taiwan Semiconductor Mfg. Co. Ltd.—ADR | | 774,470 | | | 7,675 |

*ValueClick, Inc. | | 284,980 | | | 5,161 |

*WebEx Communications, Inc. | | 174,285 | | | 3,770 |

| | | | |

|

|

| | | | | | 84,625 |

| | | | |

|

|

Health Care—29.7% | | | | | |

Allergan, Inc. | | 35,440 | | | 3,826 |

*Amgen, Inc. | | 144,735 | | | 11,414 |

*Axcan Pharma, Inc.† | | 249,540 | | | 3,778 |

*IDEXX Laboratories, Inc. | | 59,090 | | | 4,253 |

*Integra Lifesciences Holding Corporation | | 143,470 | | | 5,088 |

*Kyphon, Inc. | | 77,510 | | | 3,165 |

*MedImmune, Inc. | | 94,065 | | | 3,294 |

Medtronic, Inc. | | 207,085 | | | 11,922 |

*ResMed, Inc. | | 81,830 | | | 3,135 |

Sanofi-Aventis—ADR | | 167,595 | | | 7,357 |

Schering-Plough Corporation | | 295,815 | | | 6,168 |

UnitedHealth Group, Inc. | | 163,435 | | | 10,156 |

Valeant Pharmaceuticals International | | 104,115 | | | 1,882 |

| | | | |

|

|

| | | | | | 75,438 |

| | | | |

|

|

Consumer Discretionary—14.2% | | | | | |

*Bed, Bath & Beyond, Inc. | | 174,480 | | | 6,307 |

*CarMax, Inc. | | 101,335 | | | 2,805 |

*Education Management Corporation | | 138,960 | | | 4,657 |

Johnson Controls, Inc. | | 52,855 | | | 3,854 |

*Kohl’s Corporation | | 118,190 | | | 5,744 |

*Laureate Education, Inc. | | 87,030 | | | 4,570 |

*Shuffle Master, Inc. | | 113,455 | | | 2,852 |

*Non-income producing securities

ADR = American Depository Receipt

† = U.S. listed foreign security

VRN = Variable Rate Note

| | | | | | |

Issuer

| | Shares or

Principal

Amount

| | Value

|

| | |

Common Stocks—(continued) | | | | | | |

Consumer Discretionary—(continued) | | | | | | |

*Williams-Sonoma, Inc. | | | 120,840 | | $ | 5,214 |

| | | | | |

|

|

| | | | | | | 36,003 |

| | | | | |

|

|

Industrials—11.5% | | | | | | |

*Coinstar, Inc. | | | 194,020 | | | 4,429 |

Corporate Executive Board Company | | | 44,780 | | | 4,017 |

Danaher Corporation | | | 185,946 | | | 10,372 |

Graco, Inc. | | | 111,730 | | | 4,076 |

Knight Transportation, Inc. | | | 300,900 | | | 6,238 |

| | | | | |

|

|

| | | | | | | 29,132 |

| | | | | |

|

|

Financials—4.2% | | | | | | |

Goldman Sachs Group, Inc. | | | 42,595 | | | 5,440 |

SLM Corporation | | | 94,295 | | | 5,194 |

| | | | | |

|

|

| | | | | | | 10,634 |

| | | | | |

|

|

Materials—2.9% | | | | | | |

Praxair, Inc. | | | 141,165 | | | 7,476 |

| | | | | |

|

|

Energy—1.8% | | | | | | |

Suncor Energy, Inc.† | | | 71,095 | | | 4,488 |

| | | | | |

|

|

Total Common Stock—97.7%

(cost $184,148) | | | 247,796 |

| | | | | |

|

|

| | |

Investment in Affiliate | | | | | | |

William Blair Ready Reserves | | | 724,307 | | | 724 |

| | | | | |

|

|

Total Investment in Affiliate—0.3%

(cost $724) | | | 724 |

| | | | | |

|

|

| | |

Short-Term Investment | | | | | | |

Prudential Funding Demand Note, VRN

3.93%, due 1/03/06 | | $ | 3,868,000 | | | 3,868 |

| | | | | |

|

|

Total Short-Term Investment—1.5%

(cost $3,868) | | | 3,868 |

| | | | | |

|

|

Total Investments—99.5%

(cost $188,740) | | | 252,388 |

Cash and other assets, less liabilities—0.5% | | | 1,171 |

| | | | | |

|

|

Net assets—100.0% | | $ | 253,559 |

| | | | | |

|

|

See accompanying Notes to Financial Statements.

8 Annual Report | December 31, 2005 |

Mark A. Fuller III

Gregory J. Pusinelli

TAX-MANAGED GROWTH FUND

The Tax-Managed Growth Fund invests primarily in common stocks of large, medium and small domestic growth companies that the Advisor expects will have sustainable, above-average growth from one business cycle to the next.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform over the last year? How did the Fund’s performance compare to its benchmark?

The Tax-Managed Growth Fund posted a strong 12.46% gain on a total return basis (Class N Shares) for the 12 months ended December 31, 2005. By comparison, the Fund’s primary benchmark, the Russell 3000® Growth Index increased 5.17% and the Standard & Poor’s 500 Stock Index gained 4.91%.

What were the most significant market factors impacting Fund performance?

The stock market, as represented by the Standard & Poor’s 500 Index, finished the year in positive territory. In spite of this showing, the equity markets were restrained in 2005 by high energy prices, an ongoing Federal Reserve campaign to raise short-term interest rates, and a flat interest rate yield curve, which many interpreted as a signal that slower economic growth might be on the horizon.

Concerns that rising energy prices could dampen economic growth weighed on the equity markets for a good part of the year. In addition, indications early in the year that inflationary pressures had the potential to increase had an unsettling effect on equity market participants.

Investors also worried about the potential for slowing corporate profits, although optimism during the second quarter earnings reporting period seemed to provide some underlying support to the market.

Lastly, investors were troubled by the Federal Reserve’s eight interest rate increases during 2005. Investors grew increasingly concerned that the Fed was being overly cautious—and perhaps too restrictive—with its monetary policy.

What were among the best performing investments for the Fund?

Health Care was the strongest performing sector for the Tax-Managed Growth Fund in 2005, followed by Energy and Industrials. Four of the top five performing stocks were Health Care names.

ExpressScripts, Inc., which was up over 119%, was the best performing stock in the Fund’s portfolio. ExpressScripts provides pharmacy-benefit management services to managed-care firms, third-party administrators, large employers, and union-sponsored benefit plans, representing more than 50 million members. ExpressScripts continued to experience strong growth in their business throughout the course of the year.

We trimmed our position in ExpressScripts during the fourth quarter, mainly taking profits in view of our belief that the stock had achieved fairly full valuation.

December 31, 2005 | William Blair Funds 9 |

Suncor Energy, Inc. was the second-best performing investment for the Fund in 2005, rising over 79%. Suncor Energy produces and refines oil from the Alberta oil sands in Canada and is a pioneer in oil sands production.

Genentech, Inc. was the third strongest contributor for the Fund in 2005, and was up over 69%. Genentech’s cancer products—and their crossover use for different types of cancers—look promising. Increased earnings estimates for the company, especially during the second quarter, reinforced our enthusiasm for this company. We especially favor this company because Genentech has an entire portfolio of products, compared to other biotechnology companies which may only have one drug either in test trials or to market. Valuation of this stock, however, seems “rich” in our view.

What were among the weakest performing investments for the Fund?

Valeant Pharmaceuticals International was the worst-performing investment for the Fund for the year. Valeant markets more than 400 health-care products worldwide. As we reported earlier this year, concerns about the company’s ability to get certain new drugs approved by the FDA hurt this stock. We nonetheless believe in this company and their strong new management team that has joined the firm from many of the world’s top pharmaceutical companies. We should also note that we “tax-traded” Valeant, harvesting a tax-loss by selling the stock in November and then buying it back in late December. This strategy was one example of our efforts to manage the Fund in a tax-efficient manner. We are willing to withstand the short-term fluctuations in the company’s share price because of this management, and because of Valeant’s promising portfolio of products which is in various stages of testing.

Investors Financial Services Corp., was the second worst-performing stock for the Fund last year. Investors’ earnings have suffered from the flattening interest rate yield curve resulting from the Federal Reserve’s short-term interest rate hikes, as higher short-term rates impact margins.

Pfizer, Inc., was the third worst-performing investment for the Fund in 2005, in terms of impacting the Fund’s return. With an insufficient lineup of new drugs coming down the pipeline, and competitive pressures to its cholesterol-lowering drug Lipitor, we sold the stock in December, believing the company was unlikely to meet our long-term minimum growth objectives.

What is your current strategy? How is the Fund positioned?

During the fourth quarter we added four new names to the Fund’s portfolio of investments: DR Horton, Inc., Johnson Controls, Inc., MedImmune, Inc., and Network Appliance, Inc.

DR Horton is the largest homebuilder in the country based on homes sold, and operates in about 75 major markets across 25 states. Although some investors are nervous about the prospects for the housing market in an environment of gradually rising interest rates, we like this company’s solid management team and long uninterrupted track record of growth. We took advantage of price weakness in the stock to add this company to the Fund’s portfolio.

Johnson Controls operates three distinct business segments: automotive interiors, vehicle batteries, and building controls and services. We chose this well-managed company in part to increase our exposure to the Industrial sector.

MedImmune, Inc., is a biotechnology company with a very interesting pipeline of new drugs and expectations for a strong earnings growth rate over the next several years.

10 Annual Report | December 31, 2005 |

Network Appliance, an information technology company, sells hardware, software, and services for customers to store and manage critical data across their networks. Network Appliance was an early pioneer in building storage hardware that could easily attach to a customer’s existing network as a simple “storage appliance.” In an era of ever-increasing information flow, we believe this company should benefit from the demand for its products, and its ability to take market share from its competitors.

After several years of “value” stocks outperforming their “growth” stock counterparts, sometime during 2005 the pendulum swung back towards growth. This strength in growth stocks is reflected in the performance of the Fund’s Russell 3000 Growth Index benchmark. With this trend seeming to now move in our favor, we are optimistic that the cycle may continue, as it has historically, for an extended period.

Regardless of whether this trend may continue, with the potential for higher interest rates and slower growth in the economy in 2006—and subsequently lower forecasted corporate profits growth—we are encouraged by the earnings growth potential of the companies in the Fund’s portfolio. In such an environment, security selection becomes even more important. We believe our focus on quality franchise businesses and a respect for downside risk should serve us well as we begin the new year.

December 31, 2005 | William Blair Funds 11 |

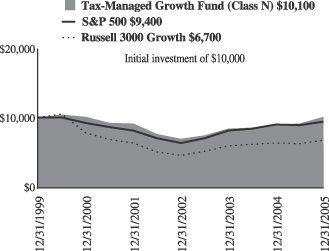

Tax-Managed Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 12/31/2005

| | | | | | | | | | | | |

| | | 1

Year

| | | 3

Year

| | | 5

Year

| | | Since Inception(a)

| |

Tax-Managed Growth

Fund Class N | | 12.46 | % | | 13.80 | % | | 0.06 | % | | 0.18 | % |

Tax-Managed Growth

Fund Class I | | 12.86 | | | 14.07 | | | 0.31 | | | 0.44 | |

Russell 3000®

Growth Index | | 5.17 | | | 13.78 | | | (3.15 | ) | | (6.45 | ) |

S&P 500 Index | | 4.91 | | | 14.39 | | | 0.54 | | | (1.00 | ) |

| | (a) | | For the period from December 27, 1999 to December 31, 2005. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment adviser may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 3000® Growth Index consists of large, medium, and small-capitalization companies with above average price-to-book ratios and forecasted growth rates. The index is weighted by market capitalization and large/medium/small companies make up approximately 80%/15%/5% of the index.

The S&P 500 Index indicates broad larger capitalization equity market performance.

This report identifies the Fund’s investments on December 31, 2005. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

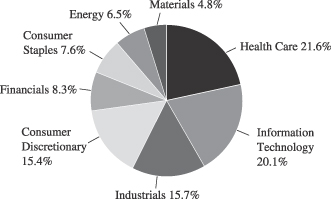

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

12 Annual Report | December 31, 2005 |

Tax-Managed Growth Fund

Portfolio of Investments, December 31, 2005 (all dollar amounts in thousands)

| | | | | |

Issuer

| | Shares

| | Value

|

| | |

Common Stocks | | | | | |

Health Care—20.0% | | | | | |

Alcon, Inc.† | | 965 | | $ | 125 |

*Amgen, Inc. | | 2,625 | | | 207 |

*Express Scripts, Inc., Class “A” | | 1,420 | | | 119 |

*Genentech, Inc. | | 1,940 | | | 180 |

IMS Health, Inc. | | 5,110 | | | 127 |

*MedImmune, Inc. | | 2,080 | | | 73 |

*ResMed, Inc. | | 4,734 | | | 181 |

Sanofi-Aventis—ADR | | 2,480 | | | 109 |

*St. Jude Medical, Inc. | | 2,550 | | | 128 |

Stryker Corporation | | 1,330 | | | 59 |

Valeant Pharmaceuticals International | | 6,450 | | | 117 |

*Zimmer Holdings, Inc. | | 2,060 | | | 139 |

| | | | |

|

|

| | | | | | 1,564 |

| | | | |

|

|

Information Technology—18.6% | | | | | |

*Activision, Inc. | | 4,283 | | | 59 |

*Adobe Systems Incorporated | | 3,470 | | | 128 |

Arm Holdings plc—ADR | | 9,500 | | | 59 |

*CACI International, Inc., Class “A” | | 1,470 | | | 84 |

CDW Corporation | | 1,750 | | | 101 |

*EMC Corporation | | 7,110 | | | 97 |

First Data Corporation | | 3,130 | | | 135 |

*Intuit, Inc. | | 2,645 | | | 141 |

*Jabil Circuit, Inc. | | 3,825 | | | 142 |

Microchip Technology, Inc. | | 4,500 | | | 145 |

*Network Appliance, Inc. | | 2,550 | | | 69 |

Paychex, Inc. | | 3,660 | | | 139 |

*ScanSource, Inc. | | 1,330 | | | 73 |

Taiwan Semiconductor Mfg. Co. Ltd.—ADR | | 8,220 | | | 81 |

| | | | |

|

|

| | | | | | 1,453 |

| | | | |

|

|

Industrials—14.5% | | | | | |

C.H. Robinson Worldwide, Inc. | | 5,040 | | | 187 |

Danaher Corporation | | 3,260 | | | 182 |

Expeditors International of Washington | | 2,425 | | | 164 |

Fastenal Company | | 5,440 | | | 213 |

General Electric Company | | 3,615 | | | 127 |

Knight Transportation, Inc. | | 5,273 | | | 109 |

Pentair, Inc. | | 4,410 | | | 152 |

| | | | |

|

|

| | | | | | 1,134 |

| | | | |

|

|

Consumer Discretionary—14.2% | | | | | |

*Bed, Bath & Beyond, Inc. | | 2,230 | | | 81 |

*CarMax, Inc. | | 2,920 | | | 81 |

D. R. Horton, Inc. | | 2,230 | | | 80 |

Dollar General Corporation | | 4,560 | | | 87 |

*eBAY, Inc. | | 1,850 | | | 80 |

Johnson Controls, Inc. | | 1,580 | | | 115 |

*Laureate Education, Inc. | | 2,830 | | | 148 |

Lowe’s Companies, Inc. | | 1,875 | | | 125 |

Time Warner, Inc. | | 4,890 | | | 85 |

*Non-income producing securities

ADR = American Depository Receipt

† = U.S. listed foreign security

VRN = Variable Rate Note

| | | | | | |

Issuer

| | Shares or

Principal

Amount

| | Value

|

| | |

Common Stocks—(continued) | | | | | | |

Consumer Discretionary—(continued) | | | | | | |

*Univision Communications, Inc. | | | 1,960 | | $ | 57 |

*Williams-Sonoma, Inc. | | | 3,935 | | | 170 |

| | | | | |

|

|

| | | | | | | 1,109 |

| | | | | |

|

|

Financials—7.7% | | | | | | |

AFLAC, Inc. | | | 1,500 | | | 70 |

Ambac Financial Group, Inc. | | | 1,560 | | | 120 |

American International Group | | | 2,380 | | | 162 |

Investors Financial Service Corporation | | | 2,420 | | | 89 |

Moody’s Corporation | | | 2,620 | | | 161 |

| | | | | |

|

|

| | | | | | | 602 |

| | | | | |

|

|

Consumer Staples—7.0% | | | | | | |

Colgate-Palmolive Company | | | 2,590 | | | 142 |

PepsiCo, Inc. | | | 3,045 | | | 180 |

Walgreen Co. | | | 2,555 | | | 113 |

Whole Foods Market, Inc. | | | 1,460 | | | 113 |

| | | | | |

|

|

| | | | | | | 548 |

| | | | | |

|

|

Energy—6.0% | | | | | | |

EOG Resources, Inc. | | | 1,010 | | | 74 |

Smith International, Inc. | | | 2,050 | | | 76 |

Suncor Energy, Inc.† | | | 5,010 | | | 316 |

| | | | | |

|

|

| | | | | | | 466 |

| | | | | |

|

|

Materials—4.5% | | | | | | |

Airgas, Inc. | | | 5,990 | | | 197 |

Praxair, Inc. | | | 2,870 | | | 152 |

| | | | | |

|

|

| | | | | | | 349 |

| | | | | |

|

|

Total Common Stock—92.5%

(cost $5,112) | | | 7,225 |

| | | | | |

|

|

| | |

Investment in Affiliate | | | | | | |

William Blair Ready Reserves | | | 362,919 | | | 363 |

| | | | | |

|

|

Total Investment in Affiliate—4.6%

(cost $363) | | | 363 |

| | | | | |

|

|

| | |

Short-Term Investment | | | | | | |

Prudential Funding Demand Note, VRN

3.93%, due 1/03/06 | | $ | 165,000 | | | 165 |

| | | | | |

|

|

Total Short-Term Investment—2.1%

(cost $165) | | | 165 |

| | | | | |

|

|

Total Investments—99.2%

(cost $5,640) | | | 7,753 |

Cash and other assets, less liabilities—0.8% | | | 62 |

| | | | | |

|

|

Net assets—100.0% | | $ | 7,815 |

| | | | | |

|

|

See accompanying Notes to Financial Statements.

December 31, 2005 | William Blair Funds 13 |

James W. Golan

John F. Jostrand

Norbert W. Truderung

LARGE CAP GROWTH FUND

The Large Cap Growth Fund invests primarily in common stocks of large domestic growth companies of high quality that the Advisor believes have demonstrated sustained growth over a long period of time.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform over the last year? How did the Fund’s performance compare to its benchmark?

The Large Cap Growth Fund posted a 3.69% increase on a total return basis (Class N Shares) for the 12 months ended December 31, 2005. By comparison, the Fund’s benchmark, the Russell 1000 Growth® Index, gained 5.26%.

What were the most significant factors impacting Fund performance?

The Large Cap Growth strategy underperformed the Russell 1000 Growth® Index, facing two significant headwinds during the year: the considerable out-performance of the smaller capitalization stocks within the benchmark and relative under-performance by higher quality stocks. In the Russell 1000 Growth® Index, the smallest stocks (under $8 billion market capitalization) contributed nearly half of the Index’s returns for the year. Since we are required to invest at least 80% of the Fund’s net assets in stocks of companies with market capitalizations of at least $8 billion, we had little representation in that area. As a result, our portfolio underperformed the benchmark in the below $8 billion market cap range. That said, we were able to find some compelling quality growth stocks at the high end of the large cap range; in particular: UnitedHealth Group, Inc., Amgen, Inc., and Goldman Sachs Group, Inc. These stocks provided significant relative out-performance against names with market capitalizations above $50 billion held in the benchmark.

Higher quality stocks continued to give ground to lower quality counterparts during the year, a trend that began three years ago with the earnings acceleration at the beginning of the economic recovery. In 2005, using return on equity (ROE) as a proxy for quality, the stocks in the Russell 1000 Index with the highest ROEs returned an average of 3%, while the stocks with the lowest ROEs returned roughly 11%. Our philosophy leads us to invest in higher quality companies, which we believe tend to outperform over the long-term. While performance of our highest quality stocks was more than double those in the index, our lack of significant investment in lower quality issues has been a relative drag on the portfolio.

Which sectors enhanced the Fund’s return? What were among the best performing investments for the Fund?

With respect to sectors and stocks, Health Care stocks offered the strongest benefit to Fund performance during the year. UnitedHealth, Amgen and Alcon were three of the top performing stocks in the Fund. We were underweight large cap pharmaceuticals due to concerns about pricing, pipeline issues, and significant legal and regulatory problems, which was also a benefit to overall returns.

Our extremely strong stock selection allowed the Fund to significantly outpace the benchmark in the Health Care sector. Health care equipment and supplies offered the largest benefit to absolute and relative returns. Alcon, in the eye care area, received approval for its ReStor Lens for cataract surgery, and Medicare approved funding of the procedure; these proved to be catalysts for stock appreciation. Medtronic, Inc., a leader in devices and techniques for treating

14 Annual Report | December 31, 2005 |

chronic care patients, also achieved positive results during the year. The health care providers and services industry provided the second best returns within the Health Care sector of the Fund, with both UnitedHealth Group and Caremark posting positive stock price gains.

Financial stocks did well in the portfolio for the year as well. Goldman Sachs strengthened during the year as the company’s investment banking activity continued to be strong, and bodes well for the coming year. SLM Corp., the student loan processing company, overcame concerns regarding the significant regulatory and governmental issues facing other agencies, and posted modestly positive results for the year

Were there any investment strategies or themes that did not measure up to your expectations?

Consumer stocks were soft during the year, taking the brunt of rising interest rates and higher oil prices. In the portfolio, our stocks within the retail section were particularly disappointing. Kohl’s Corporation was anticipated to achieve promising results after some significant management changes, remerchandising of products, and adding several items to higher margin personal care and beauty lines. The softness in consumer stocks in general, combined with discount pricing and unseasonable weather contributed to the stock’s weakness. In a similar vein, Bed, Bath and Beyond, Inc. had an optimistic outlook with respect to their new larger “box” stores, their strong competitive position, and their roll out of Christmas Tree Stores. The company experienced modest sales results during the year, which disappointed investors who anticipated much better growth. In the last quarter, the company announced that financial results were likely to be at the lower end of the expected range, news which further pressured the stock.

Technology stocks offered a mixed bag during the year. Taiwan Semiconductor Mfg Co. Ltd. and Adobe Systems Incorporated both provided positive contribution to the Fund’s return. Conversely, Dell, Inc. was the largest detractor from returns, both on an absolute and relative basis. Despite meeting earnings estimates during the year, the stock experienced some weakness in revenues driven by aggressive pricing strategies to stave off the recently rejuvenated Hewlett-Packard Co. Additionally, the stock experienced significant Price/Earnings multiple compression.

What is your current strategy? How is the Fund positioned?

We continue to find the best opportunities for quality growth investments in the Technology and Health Care sectors. Although we did not hold many financial stocks in 2005 due to lack of compelling growth opportunities, we are now finding a few new investments in this area. Given that price-to-earnings ratios (P/Es) are at relatively low levels (20x currently versus 24x average over 16 years), we are seeking compelling growth stories at good valuations in the large cap area. We believe that the moderating growth environment that analysts anticipate for 2006 may tend to favor higher quality growth stocks.

December 31, 2005 | William Blair Funds 15 |

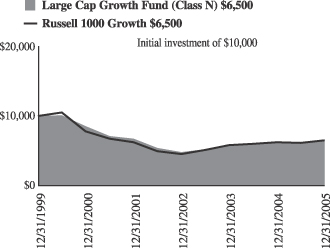

Large Cap Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 12/31/2005

| | | | | | | | | | | | |

| | | 1

Year

| | | 3

Year

| | | 5

Year

| | | Since

Inception(a)

| |

Large Cap Growth Fund Class N | | 3.69 | % | | 10.46 | % | | (5.20 | )% | | (6.96 | )% |

Large Cap Growth Fund Class I | | 3.96 | | | 10.82 | | | (4.98 | ) | | (6.74 | ) |

Russell 1000®

Growth Index | | 5.26 | | | 13.23 | | | (3.58 | ) | | (6.85 | ) |

| | (a) | | For the period from December 27, 1999 to December 31, 2005. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment adviser may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 1000® Growth Index consists of large-capitalization companies with above average-to-book ratios and forecasted growth rates.

This report identifies the Fund’s investments on December 31, 2005. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

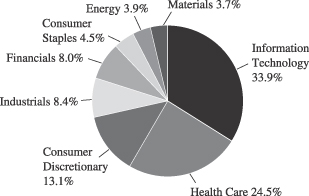

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

16 Annual Report | December 31, 2005 |

Large Cap Growth Fund

Portfolio of Investments, December 31, 2005 (all dollar amounts in thousands)

| | | | | |

Issuer

| | Shares

| | Value

|

| | |

Common Stocks | | | | | |

Information Technology—32.7% | | | | | |

Accenture, Ltd.† | | 10,395 | | $ | 300 |

*Adobe Systems Incorporated | | 11,520 | | | 426 |

*Corning Incorporated | | 19,045 | | | 374 |

*Dell, Inc. | | 22,475 | | | 674 |

*EMC Corporation | | 32,560 | | | 444 |

First Data Corporation | | 10,025 | | | 431 |

Infosys Technologies Ltd.—ADR | | 2,720 | | | 220 |

Linear Technology Corporation | | 10,800 | | | 390 |

*Network Appliance, Inc. | | 7,120 | | | 192 |

Paychex, Inc. | | 11,300 | | | 431 |

Qualcomm Incorporated | | 7,970 | | | 343 |

SAP AG—ADR | | 3,625 | | | 163 |

Taiwan Semiconductor Mfg. Co. Ltd.—ADR | | 58,517 | | | 580 |

*Yahoo!, Inc. | | 14,235 | | | 558 |

| | | | |

|

|

| | | | | | 5,526 |

| | | | |

|

|

Health Care—23.6% | | | | | |

Allergan, Inc. | | 3,075 | | | 332 |

*Amgen, Inc. | | 7,640 | | | 602 |

*Caremark Rx, Inc. | | 6,375 | | | 330 |

*MedImmune, Inc. | | 6,325 | | | 222 |

Medtronic, Inc. | | 16,970 | | | 977 |

Sanofi-Aventis—ADR | | 11,355 | | | 498 |

Schering-Plough Corporation | | 15,015 | | | 313 |

UnitedHealth Group, Inc. | | 11,375 | | | 707 |

| | | | |

|

|

| | | | | | 3,981 |

| | | | |

|

|

Consumer Discretionary—12.6% | | | | | |

*Apollo Group, Inc., Class “A” | | 4,340 | | | 262 |

*Bed, Bath & Beyond, Inc. | | 11,470 | | | 415 |

Johnson Controls, Inc. | | 3,500 | | | 255 |

*Kohl’s Corporation | | 11,263 | | | 547 |

Nike, Inc., Class “B” | | 5,570 | | | 484 |

Staples, Inc. | | 7,350 | | | 167 |

| | | | |

|

|

| | | | | | 2,130 |

| | | | |

|

|

Industrials—8.1% | | | | | |

3M Company | | 4,230 | | | 328 |

Danaher Corporation | | 14,197 | | | 792 |

General Electric Company | | 7,155 | | | 251 |

| | | | |

|

|

| | | | | | 1,371 |

| | | | |

|

|

*Non-income producing securities

ADR = American Depository Receipt

† = U.S. listed foreign security

| | | | | |

Issuer

| | Shares

| | Value

|

| | |

Common Stocks—(continued) | | | | | |

Financials—7.7% | | | | | |

Capital One Financial Corporation | | 1,990 | | $ | 172 |

Goldman Sachs Group, Inc. | | 4,110 | | | 525 |

Schwab (Charles) Corporation | | 12,820 | | | 188 |

SLM Corporation | | 7,655 | | | 422 |

| | | | |

|

|

| | | | | | 1,307 |

| | | | |

|

|

Consumer Staples—4.4% | | | | | |

PepsiCo, Inc. | | 7,470 | | | 441 |

Walgreen Co. | | 6,675 | | | 296 |

| | | | |

|

|

| | | | | | 737 |

| | | | |

|

|

Energy—3.8% | | | | | |

Schlumberger Limited† | | 3,245 | | | 315 |

Suncor Energy, Inc.† | | 5,050 | | | 319 |

| | | | |

|

|

| | | | | | 634 |

| | | | |

|

|

Materials—3.5% | | | | | |

Praxair, Inc. | | 11,355 | | | 601 |

| | | | |

|

|

Total Common Stock—96.4%

(cost $14,585) | | | 16,287 |

| | | | |

|

|

| | |

Investment in Affiliate | | | | | |

William Blair Ready Reserves | | 424,078 | | | 424 |

| | | | |

|

|

Total Investment in Affiliate—2.5%

(cost $424) | | | 424 |

| | | | |

|

|

Total Investments—98.9%

(cost $15,009) | | | 16,711 |

Cash plus other assets less liabilities—1.1% | | | 177 |

| | | | |

|

|

Net assets—100.0% | | $ | 16,888 |

| | | | |

|

|

See accompanying Notes to Financial Statements.

December 31, 2005 | William Blair Funds 17 |

Karl W. Brewer

SMALL CAP GROWTH FUND

The Small Cap Growth Fund invests primarily in common stocks of small domestic growth companies that the Advisor expects to have solid growth in earnings.

AN OVERVIEW FROM THE PORTFOLIO MANAGER

How did the Fund perform over the last year? How did the Fund’s performance compare to its benchmark?

The Small Cap Growth Fund posted a 1.18% increase on a total return basis (Class N Shares) for the 12 months ended December 31, 2005. By comparison, the Fund’s benchmark, the Russell 2000 Growth® Index, gained 4.15% during the period, while the Russell 2000® Index rose 4.55%.

What were the most significant factors impacting Fund performance? What factors were behind the Fund’s performance versus the benchmark?

With respect to the Fund’s performance compared to the Russell 2000® Growth Index benchmark, stock selection in Health Care was the biggest detractor from relative performance while stock selection in the Consumer Discretionary and Energy sectors also detracted. Strong stock selection within the Information Technology sector was the main contributor toward relative performance.

While there was not a large disparity in returns from a style perspective, value narrowly outperformed growth during 2005 (and as evidenced by the Russell 2000 Value Index’s increase of 4.71%, compared to the Russell 2000 Growth Index’s gain of 4.15%). Growth outperformed value in the fourth quarter (with the Russell 2000 Growth Index up 1.61%, versus the Russell 2000 Value Index’s gain of 0.66%). From a market capitalization perspective, mid-cap stocks once again outperformed their small and large cap counterparts during the fourth quarter as they did for 2005 as a whole.

Within the Russell 2000 Growth Index during 2005, Energy was the sector of the year. Over half of the return for the index came from Energy stocks (roughly 2.8% of the 4.15% return of the index). The Health Care and Industrial sectors were also mildly outperforming sectors compared to the rest of the market. Within the small cap health care space, we saw a large disparity between the poor relative performance of pharmaceutical and biotechnology stocks as compared to both healthcare providers and healthcare equipment stocks. Information Technology finished the year down in absolute terms and was therefore an underperforming sector. Within the sector, the market preferred computer software and services over computer hardware and semiconductors. The small cap Financials sector, due to the many regional banks that were adversely affected by the flattening of the yield curve, and the Consumer Discretionary sector joined Information Technology as the major sectors that underperformed the broader small cap market.

What were among the best performing investments for the Fund?

Two specific stocks that helped the portfolio during 2005 were Nuance Communications, Inc. and ValueClick, Inc. Nuance Communications was a top contributor for the Fund in the fourth quarter and for 2005 as a whole. ScanSoft and Nuance merged during the year and the new entity kept the name Nuance. This merger of two industry leaders, the continued evolution of speech recognition technology and increased coverage of the stock by Wall

18 Annual Report | December 31, 2005 |

Street helped drive growth in the stock price during 2005. ValueClick was one of the top performers for the Fund for 2005 as well. The company is focused on the online advertising market. The stock price appreciated over the year as management executed and grew the business, made a strategic acquisition, and as Wall Street increasingly discovered the company.

What were among the weakest performing investments for the Fund?

Two of the Fund’s worst performing stocks were TRM Corp and Cell Therapeutics. TRM Corp, an owner and operator of ATM networks, was a poor performer for the Fund in both the fourth quarter and for 2005. The company announced disappointing earnings in November in part due to higher than expected expenses related to operating their expanding network of ATM’s. The company should have realized cost savings and scale as they built their network, but, this did not happen and as a result we liquidated the position. Cell Therapeutics, a biotechnology stock, was also one of the largest detractors from performance for 2005. We liquidated the position during the second quarter after they announced a series of negative data points relating to prospective pipeline drugs.

What is your current outlook?

As we look at 2006, there are a number of dynamics that could affect the equity markets. Ben Bernanke takes over for Alan Greenspan as the Chairman of the Federal Reserve in the first quarter of 2006. His efforts to tame inflation and keep the economy on track will be watched closely. A possible housing market slowdown, high heating bills and any implications of an inverted yield curve are the ubiquitously discussed headwinds in the marketplace. However, we are still seeing healthy levels of economic and corporate earnings growth, contained inflation, and signs of business spending picking up after the past couple years of record earnings growth have left companies flush with cash. A possible reversal of the multi-year trend of value outperforming growth, after growth’s outperformance in the second half of the 2005, could create another tailwind for our quality growth style of investing. Regardless of the macro environment, we will continue to look for durable businesses whose stocks have favorable risk reward profiles.

Is there any other news with respect to the Fund?

Also, with respect to illiquid securities in the Fund, Overhill Farms Inc. is a portfolio holding that we acquired through a Private Investment in Public Equity (PIPE) transaction in late December. Overhill Farms is a food distribution company whose customers include restaurants and airlines. We were able to purchase shares in the transaction at a discount to market prices and we expect these shares to become freely tradable within 120 days of the transaction. The Fund’s Pricing Committee and Valuation Committee is currently pricing the security at fair value.

December 31, 2005 | William Blair Funds 19 |

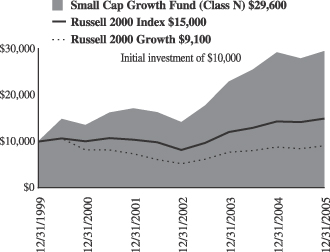

Small Cap Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 12/31/2005

| | | | | | | | | | | | |

| | | 1

Year

| | | 3

Year

| | | 5

Year

| | | Since Inception(a)

| |

Small Cap Growth Fund Class N | | 1.18 | % | | 27.73 | % | | 16.79 | % | | 19.68 | % |

Small Cap Growth Fund Class I | | 1.48 | | | 28.03 | | | 17.09 | | | 19.97 | |

Russell 2000®

Growth Index | | 4.15 | | | 20.93 | | | 2.28 | | | (1.37 | ) |

Russell 2000® Index | | 4.55 | | | 22.13 | | | 8.22 | | | 7.03 | |

| | (a) | | For the period from December 27, 1999 to December 31, 2005. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. Investing in smaller companies involves special risks, including higher volatility and lower liquidity. From time to time, the investment advisor may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 2000® Growth Index consists of small-capitalization companies with above average price-to-book ratios and forecasted growth rates.

The Russell 2000® Index is an unmanaged composite of the smallest 2000 stocks of the Russell 3000® Index.

This report identifies the Fund’s investments on December 31, 2005. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

20 Annual Report | December 31, 2005 |

Small Cap Growth Fund

Portfolio of Investments, December 31, 2005 (all dollar amounts in thousands)

| | | | | |

Issuer

| | Shares

| | Value

|

| | |

Common Stocks | | | | | |

Information Technology—31.3% | | | | | |

*Access Integrated Technologies, Inc. | | 444,977 | | $ | 4,619 |

*AMIS Holdings, Inc. | | 1,093,370 | | | 11,644 |

ARM Holdings, plc—ADR | | 670,962 | | | 4,167 |

*BISYS Group, Inc. (The) | | 30,400 | | | 426 |

*eCollege.com, Inc. | | 528,451 | | | 9,528 |

*Electronic Clearing House | | 652,297 | | | 6,503 |

*Euronet Worldwide, Inc. | | 269,342 | | | 7,488 |

*Heartland Payment Systems, Inc. | | 420,061 | | | 9,099 |

*Internet Capital Group, Inc. | | 1,547,474 | | | 12,720 |

*Intrado, Inc. | | 459,813 | | | 10,585 |

*J2 Global Communications, Inc. | | 272,164 | | | 11,632 |

*Kanbay International, Inc. | | 816,719 | | | 12,978 |

*Lionbridge Technologies, Inc. | | 1,184,467 | | | 8,315 |

*Nuance Communications, Inc. | | 2,834,256 | | | 21,625 |

*OPNET Technologies, Inc. | | 924,040 | | | 8,492 |

*Optimal Group, Inc.† | | 782,973 | | | 15,863 |

*Patni Computer Systems—ADR | | 32,800 | | | 760 |

*PDF Solutions, Inc. | | 1,035,312 | | | 16,824 |

*Skillsoft, plc—ADR | | 1,251,567 | | | 6,884 |

*TNS, Inc. | | 714,969 | | | 13,713 |

*Ultimate Software Group, Inc. | | 534,336 | | | 10,190 |

*ValueClick, Inc. | | 840,728 | | | 15,226 |

*Volterra Semiconductor Corporation | | 1,466,807 | | | 22,002 |

*WebEx Communications, Inc. | | 606,862 | | | 13,126 |

*Workstream, Inc.† | | 3,661,887 | | | 6,038 |

| | | | |

|

|

| | | | | | 260,447 |

| | | | |

|

|

Consumer Discretionary—21.4% | | | | | |

*4 Kids Entertainment, Inc. | | 466,935 | | | 7,326 |

*Century Casinos, Inc. | | 956,611 | | | 8,227 |

*Cumulus Media, Inc., Class “A” | | 918,476 | | | 11,398 |

*DeVry, Inc. | | 142,190 | | | 2,844 |

*Dick’s Sporting Goods, Inc. | | 326,915 | | | 10,866 |

*Jarden Corporation | | 593,687 | | | 17,900 |

*Laureate Education, Inc. | | 464,237 | | | 24,377 |

*Lions Gate Entertainment Corporation† | | 2,018,315 | | | 15,501 |

*Meritage Homes Corporation | | 141,540 | | | 8,906 |

*Mikohn Gaming Corporation | | 652,260 | | | 6,438 |

Nautilus Group, Inc. | | 623,177 | | | 11,628 |

*Nevada Gold and Casinos, Inc. | | 507,589 | | | 5,274 |

*Shuffle Master, Inc. | | 483,154 | | | 12,146 |

Strayer Education, Inc. | | 154,064 | | | 14,436 |

*ValueVision Media, Inc., Class “A” | | 1,047,885 | | | 13,203 |

*WMS Industries, Inc. | | 283,170 | | | 7,105 |

| | | | |

|

|

| | | | | | 177,575 |

| | | | |

|

|

Industrials—14.7% | | | | | |

*Coinstar, Inc. | | 454,275 | | | 10,371 |

Comfort Systems USA, Inc. | | 1,399,760 | | | 12,878 |

*Corrections Corporation of America | | 267,820 | | | 12,044 |

*CRA International, Inc. | | 199,420 | | | 9,510 |

*FirstService Corporation† | | 523,250 | | | 13,421 |

*Frozen Food Express Industries, Inc. | | 483,765 | | | 5,336 |

*Hudson Highland Group, Inc. | | 178,684 | | | 3,102 |

| | | | | |

Issuer

| | Shares

| | Value

|

| | |

Common Stocks—(continued) | | | | | |

Industrials—(continued) | | | | | |

*Huron Consulting Group, Inc. | | 352,527 | | $ | 8,457 |

*Kforce, Inc. | | 1,375,450 | | | 15,350 |

*Labor Ready, Inc. | | 560,035 | | | 11,660 |

*Marten Transport, Ltd. | | 480,115 | | | 8,748 |

*SIRVA, Inc. | | 1,430,630 | | | 11,445 |

| | | | |

|

|

| | | | | | 122,322 |

| | | | |

|

|

Health Care—11.4% | | | | | |

*Axcan Pharma, Inc.† | | 692,964 | | | 10,491 |

*Encore Medical Corporation | | 1,739,235 | | | 8,609 |

*Integra Lifesciences Holdings Corporation | | 387,449 | | | 13,739 |

*Lifecore Biomedical, Inc. | | 319,389 | | | 5,184 |

*Matria Healthcare, Inc. | | 239,815 | | | 9,295 |

*Nuvasive, Inc. | | 489,168 | | | 8,854 |

*PSS World Medical, Inc. | | 304,390 | | | 4,517 |

*Psychiatric Solutions, Inc. | | 161,196 | | | 9,469 |

*Sangamo Biosciences, Inc. | | 609,818 | | | 2,458 |

*Santarus, Inc. | | 974,738 | | | 5,341 |

*Telik, Inc. | | 560,033 | | | 9,515 |

*Zila, Inc. | | 1,965,922 | | | 7,569 |

| | | | |

|

|

| | | | | | 95,041 |

| | | | |

|

|

Financials—7.4% | | | | | |

*Affiliated Managers Group, Inc. | | 168,242 | | | 13,501 |

American Equity Investment Life Holding Co. | | 511,500 | | | 6,675 |

East West Bancorp, Inc. | | 248,557 | | | 9,070 |

*First Cash Financial Services, Inc. | | 527,424 | | | 15,380 |

Highland Hospitality Corporation | | 632,260 | | | 6,986 |

National Financial Partners Corporation | | 191,639 | | | 10,071 |

| | | | |

|

|

| | | | | | 61,683 |

| | | | |

|

|

Energy—6.8% | | | | | |

*ATP Oil and Gas Corporation | | 195,422 | | | 7,233 |

*Gasco Energy Inc. | | 860,817 | | | 5,621 |

*Grey Wolf, Inc. | | 1,658,622 | | | 12,821 |

*Hornbeck Offshore Services, Inc. | | 351,044 | | | 11,479 |

*Petrohawk Energy Corporation | | 876,596 | | | 11,589 |

*Toreador Resources Corporation | | 349,696 | | | 7,368 |

| | | | |

|

|

| | | | | | 56,111 |

| | | | |

|

|

Materials—1.6% | | | | | |

Airgas, Inc. | | 415,618 | | | 13,674 |

| | | | |

|

|

Consumer Staples—0.5% | | | | | |

*Overhill Farms, Inc.** | | 1,684,600 | | | 4,348 |

| | | | |

|

|

Total Common Stock—95.1%

(cost $670,756) | | | 791,201 |

| | |

|

|

| | |

Investment in Affiliate | | | | | |

William Blair Ready Reserves | | 11,002,174 | | | 11,002 |

| | | | |

|

|

Total Investment in Affiliate—1.3%

(cost $11,002) | | | 11,002 |

| | |

|

|

See accompanying Notes to Financial Statements.

December 31, 2005 | William Blair Funds 21 |

Small Cap Growth Fund

Portfolio of Investments, December 31, 2005 (all dollar amounts in thousands)

| | | | | | |

Issuer

| | Principal

Amount

| | Value

|

| | |

Short-Term Investments | | | | | | |

American Express Demand Note, VRN 4.235%, due 1/3/06 | | $ | 8,413,000 | | $ | 8,413 |

Prudential Funding Demand Note, VRN 3.930%, due 1/3/06 | | $ | 13,176,000 | | | 13,176 |

| | | | | |

|

|

Total Short-Term Investments—2.6%

(cost $21,589) | | | 21,589 |

| | | | | |

|

|

Total Investments—99.0%

(cost $703,347) | | | 823,792 |

Cash and other assets, less liabilities—1.0% | | | 7,946 |

| | | | | |

|

|

Net assets—100.0% | | $ | 831,738 |

| | | | | |

|

|

*Non-income producing securities

ADR = American Depository Receipt

† = U.S. listed foreign security

VRN = Variable Rate Note

**Fair Valued pursuant to Valuation Procedures adopted by the Board of Trustees. The holding represents 0.52% of the Fund’s net assets at December 31, 2005. This security was also deemed illiquid pursuant to Liquidity Procedures approved by the Board of Trustees.

See accompanying Notes to Financial Statements.

22 Annual Report | December 31, 2005 |

Karl W. Brewer

Harvey H. Bundy, III

Robert C. Lanphier, IV

SMALL-MID CAP GROWTH FUND

The Small-Mid Cap Growth Fund primarily invests in a diversified portfolio of common stocks of small and medium-sized domestic growth companies that the Advisor expects to experience solid growth in earnings.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform over the last year? How did the Fund’s performance compare to its benchmark?

The Small-Mid Cap Growth Fund posted a 10.72% total return (Class N Shares) for the year ended December 31, 2005. By comparison, the Fund’s benchmark, the Russell 2500 Growth® Index, returned 8.17% during the period.

What were the most significant factors impacting Fund performance? What factors were behind the Fund’s performance versus the benchmark?

There was no significant disparity in returns from a style perspective during the year. Measured by most broad-based indexes, value narrowly outperformed growth during 2005. However, within the small to mid cap space as represented by the Russell 2500 Indexes, growth edged value for 2005 (Russell 2500 Growth® Index +8.17%; Russell 2500 Value® Index +7.74%) as it did in the fourth quarter specifically. From a market capitalization perspective, mid-cap stocks once again outperformed their small and large cap counterparts during the fourth quarter as they did for 2005 as a whole.

Within the Russell 2500 Growth Index, energy stocks were by far the best performers during 2005. Small to mid cap industrial names turned in the second strongest results among the six major sectors. The Consumer Discretionary, Financials, Health Care and Information Technology sectors all underperformed the broader market. Within the small to mid cap health care space, we saw a large disparity between the poor relative performance of pharmaceutical and biotechnology stocks as compared to both healthcare providers and healthcare equipment stocks. Within the Information Technology sector, computer software and services outperformed computer hardware and semiconductor stocks. The small to mid cap Financials sector underperformed during the year mostly due to the many regional banks that were adversely affected by the flattening of the yield curve.

Relative to the benchmark, strong stock selection within the Information Technology sector was the main contributor toward the Fund’s relative outperformance. Stock selection and our overweight position in the Industrials sector also contributed to the Fund’s relative outperformance during 2005. Also, our higher average market capitalization was modestly advantageous toward relative performance. Stock selection in the Energy sector was a detractor from relative performance. This was mostly due to our stocks not keeping pace with the roughly 57% average return for energy stocks in the benchmark.

What were among the weakest performing investments for the Fund?

Two of the weakest performing issues in the Fund in 2005 were Cell Therapeutics and AMIS Holdings. Cell Therapeutics is a biotechnology stock in the Health Care sector. We liquidated the position during the second quarter after they announced a series of negative data points relating to prospective pipeline drugs. AMIS Holdings, a semiconductor holding within the information technology sector, detracted from the Fund’s performance for 2005 as well. The

December 31, 2005 | William Blair Funds 23 |

company’s design capabilities are used for various applications in the automotive, industrial and medical fields and represent attractive growth catalysts for the stock. However, the level of earnings growth investors were expecting for 2005 did not come to fruition and the stock price suffered accordingly.

What were among the best performing investments for the Fund?

Among the strongest performing issues for the Fund were ValueClick, Inc. and Fastenal Company. ValueClick is focused on the online advertising market. The stock price appreciated over the year as management executed and grew the business, made a strategic acquisition, and as Wall Street increasingly discovered the company. Fastenal, a distributor of various industrial supplies, was a strong contributor to the Fund’s performance for the fourth quarter and the full year 2005. The company continues to drive earnings growth organically through store growth and efficient management of the business. Fastenal, as did many of our industrial holdings, also benefited from the realization by the market that we are more likely in the earlier part of this capital goods cycle.

What is your current outlook?

As we look at 2006, there are a number of dynamics that could affect the equity markets. Ben Bernanke takes over for Alan Greenspan as the Chairman of the Federal Reserve in the first quarter of 2006. His efforts to tame inflation and keep the economy on track will be watched closely. A possible housing market slowdown, high heating bills and any implications of an inverted yield curve are the ubiquitously discussed headwinds in the marketplace. However, we are still seeing healthy levels of economic and corporate earnings growth, contained inflation, and signs of business spending picking up after the past couple years of record earnings growth have left companies flush with cash. A possible reversal of the multi-year trend of value outperforming growth, after growth’s outperformance in the second half of the 2005, could create another tailwind for our quality growth style of investing. Regardless of the macro environment, we will continue to look for durable businesses whose stocks have favorable risk reward profiles.

24 Annual Report | December 31, 2005 |

Small-Mid Cap Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 12/31/2005

| | | | | | |

| | | 1 Year

| | | Since Inception(a)

| |

Small-Mid Cap Growth Fund

Class N | | 10.72 | % | | 11.64 | % |

Small-Mid Cap Growth Fund

Class I | | 11.05 | | | 11.90 | |

Russell 2500® Growth Index | | 8.17 | | | 11.75 | |

| | (a) | | For the period from December 29, 2003 to December 31, 2005. | |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. Investing in smaller companies involves special risks, including higher volatility and lower liquidity. From time to time, the investment advisor may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 2500™ Growth Index measures the performance of those Russell 2500 companies with above average price-to-book ratios and forecasted growth rates.