UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-5344

William Blair Funds

(Exact name of registrant as specified in charter)

| | |

| 222 West Adams Street, Chicago, IL | | 60606 |

| (Address of principal executive offices) | | (Zip Code) |

Michelle R. Seitz

William Blair Funds

222 West Adams Street, Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: 312-236-1600

Date of fiscal year end: December 31

Date of reporting period: June 30, 2007

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A Registrant is not required to respond to the collection of information contained in Form N-CSR unless the form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimates and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. (ss) 3507.

June 30, 2007 Semi-Annual Reports transmitted to shareholders.

Table of Contents

This report is submitted for the general information of the shareholders of the William Blair Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by a prospectus of the William Blair Funds. Please carefully consider the Funds’ investment objectives, risks, charges, and expenses before investing. This and other information is contained in the Funds’ prospectus, which you may obtain by calling 1-800-742-7272. Read it carefully before you invest or send money.

June 30, 2007 | William Blair Funds 1 |

PERFORMANCE AS OF JUNE 30, 2007—CLASS N SHARES (unaudited)

| | | | | | | | | | | | | | |

| | | Year to

Date | | 1 Yr. | | 3 Yr. | | 5 Yr. | | 10 Yr.

(or since

inception) | | Inception

Date | | Overall Morningstar Rating |

| | | | | | | | | | | | | | | |

Growth Fund | | 7.88 | | 18.45 | | 12.66 | | 9.06 | | 5.71 | | 3/20/1946 | | ««« |

Morningstar Large Growth | | 8.13 | | 17.17 | | 9.27 | | 8.96 | | 5.47 | | | | Among 1,426 |

Russell 3000® Growth | | 8.22 | | 18.84 | | 8.97 | | 9.58 | | 4.42 | | | | large growth funds |

Standard & Poor’s 500 | | 6.96 | | 20.59 | | 11.68 | | 10.71 | | 7.13 | | | | |

| | | | | | | |

Tax-Managed Growth Fund | | | | | | | | | | | | | | ««« |

Return before Taxes | | 7.40 | | 14.52 | | 11.40 | | 9.02 | | 2.16 | | 12/27/1999 | | Among 1,426 |

After Taxes on Distributions | | 7.40 | | 14.52 | | 11.40 | | 9.02 | | 2.16 | | | | large growth funds |

After Taxes on distributions and Sale of | | | | | | | | | | | | | | |

Fund Shares | | 4.81 | | 9.44 | | 9.83 | | 7.85 | | 1.86 | | | | |

Morningstar Large Growth | | 8.13 | | 17.17 | | 9.27 | | 8.96 | | — | | | | |

Russell 3000® Growth | | 8.22 | | 18.84 | | 8.97 | | 9.58 | | -3.09 | | | | |

| | | | | | | |

Large Cap Growth Fund | | 5.81 | | 13.57 | | 7.38 | | 6.08 | | -4.13 | | 12/27/1999 | | «« |

Morningstar Large Growth | | 8.13 | | 17.17 | | 9.27 | | 8.96 | | — | | | | Among 1,426 |

Russell 1000® Growth | | 8.13 | | 19.04 | | 8.70 | | 9.28 | | -3.48 | | | | large growth funds |

| | | | | | | |

Small Cap Growth Fund | | 8.97 | | 17.49 | | 12.80 | | 17.52 | | 18.88 | | 12/27/1999 | | ««« « |

Morningstar Small Growth | | 10.49 | | 16.28 | | 11.54 | | 12.08 | | — | | | | Among 645 |

Russell 2000® Growth | | 9.33 | | 16.83 | | 11.76 | | 13.08 | | 1.66 | | | | small growth funds |

Russell 2000® | | 6.45 | | 16.43 | | 13.45 | | 13.88 | | 8.83 | | | | |

| The Small Cap Growth Fund’s Performance during 2000 was primarily attributable to investments in initial public offerings (IPOs) during a rising market. Since then, IPOs have had an insignificant effect on the Fund’s performance. | | | | | | |

| | | | | | | |

Mid Cap Growth Fund | | 12.91 | | 18.46 | | — | | — | | 12.51 | | 2/1/2006 | | Not rated. |

Russell Mid Cap Growth® | | 10.97 | | 19.73 | | — | | — | | 10.89 | | | | |

| | | | | | | |

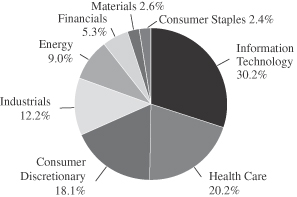

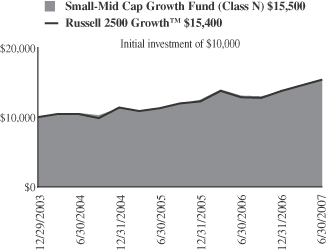

Small-Mid Cap Growth Fund | | 13.27 | | 18.23 | | 13.40 | | — | | 13.31 | | 12/29/2003 | | ««« |

Morningstar Mid-Cap Growth | | 12.33 | | 19.00 | | 13.26 | | — | | — | | | | Among 814 |

Russell 2500™ Growth | | 11.30 | | 19.03 | | 13.60 | | — | | 13.06 | | | | mid cap growth funds |

| | | | | | | |

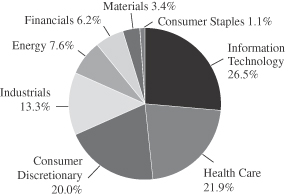

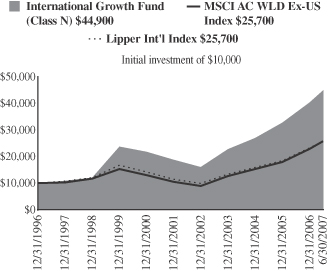

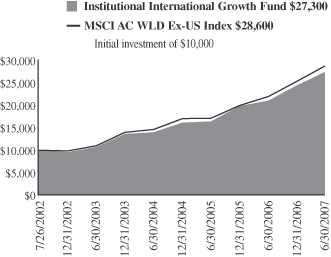

International Growth Fund | | 11.66 | | 29.69 | | 24.37 | | 18.80 | | 14.55 | | 10/1/1992 | | ««««« |

Morningstar Foreign Large Growth | | 10.65 | | 27.19 | | 21.09 | | 15.80 | | 7.02 | | | | Among 183 |

MSCI All Country World Ex-US | | 12.58 | | 30.15 | | 25.03 | | 19.93 | | 8.58 | | | | foreign large growth funds |

| | | | | | | |

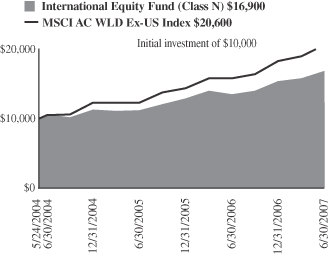

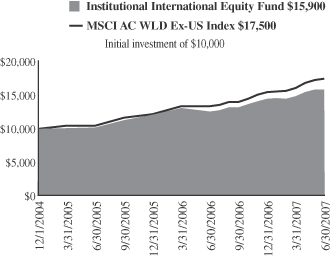

International Equity Fund | | 9.47 | | 25.47 | | 16.94 | | — | | 18.34 | | 5/24/2004 | | « |

Morningstar Foreign Large Growth | | 10.65 | | 27.19 | | 21.09 | | — | | — | | | | Among 183 |

MSCI All Country World Ex-US | | 12.58 | | 30.15 | | 25.03 | | — | | 25.95 | | | | foreign large growth funds |

| | | | | | | |

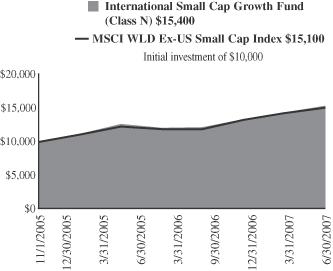

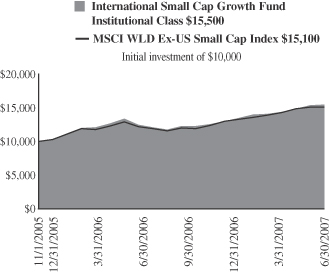

International Small Cap Growth Fund | | 14.36 | | 26.81 | | — | | — | | 29.38 | | 11/1/2005 | | Not rated. |

Morningstar Foreign Small/Mid Growth | | 14.91 | | 32.70 | | — | | — | | — | | | | |

MSCI World Small Cap ex-US | | 13.06 | | 26.54 | | — | | — | | 27.54 | | | | |

Please see the next page for important disclosure information.

See accompanying Notes to Financial Statements.

2 Semi-Annual Report | June 30, 2007 |

PERFORMANCE AS OF JUNE 30, 2007—CLASS N SHARES—CONTINUED (unaudited)

| | | | | | | | | | | | | | |

| | | Year to

Date | | 1 Yr. | | 3 Yr. | | 5 Yr. | | 10 Yr.

(or since

inception) | | Inception

Date | | Overall Morningstar Rating |

| | | | | | | | | | | | | | | |

| | | | | | | |

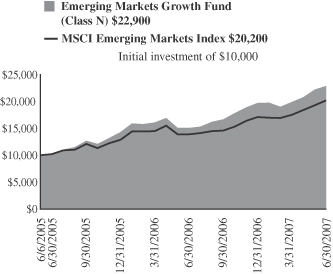

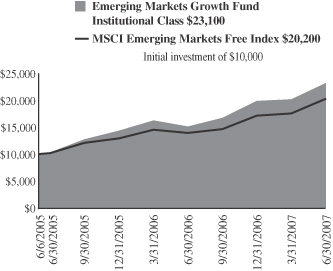

Emerging Markets Growth Fund | | 16.53 | | 51.80 | | — | | — | | 49.14 | | 6/6/2005 | | Not rated. |

Morningstar Diversified Emerging Markets | | 17.73 | | 45.91 | | — | | — | | — | | | | |

MSCI Emerging Markets | | 17.75 | | 45.45 | | — | | — | | 40.31 | | | | |

| | | | | | | |

| A portion of the Emerging Markets Growth Fund’s performance since inception is attributable to an investment in an initial public offering. (IPO) | | | | | | | | | | | | | | |

| | | | | | | |

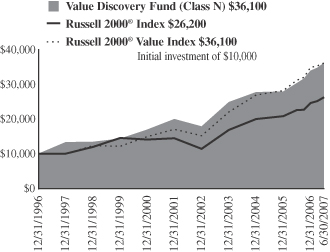

Value Discovery Fund | | 6.45 | | 19.41 | | 11.52 | | 10.11 | | 12.52 | | 12/23/1996 | | «« |

Morningstar Small Value | | 7.07 | | 16.39 | | 13.83 | | 14.11 | | 11.46 | | | | Among 305 small value funds |

Russell 2000® | | 6.45 | | 16.43 | | 13.45 | | 13.88 | | 9.06 | | | |

Russell 2000® Value | | 3.80 | | 16.05 | | 15.02 | | 14.62 | | 12.14 | | | | |

| | | | | | | |

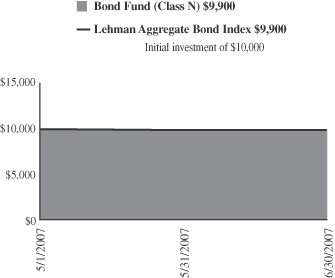

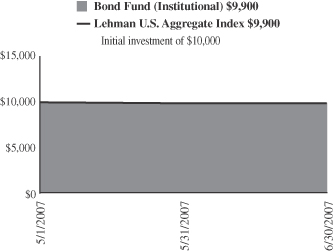

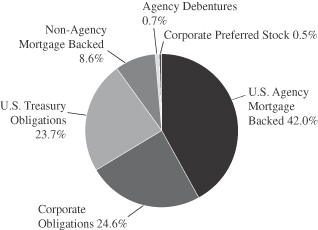

Bond Fund | | — | | — | | — | | — | | -1.15 | | 5/1/2007 | | Not rated. |

Morningstar Short-term Bond | | — | | — | | — | | — | | — | | | | |

Lehman Aggregate Bond Index | | — | | — | | — | | — | | -1.00 | | | | |

| | | | | | | |

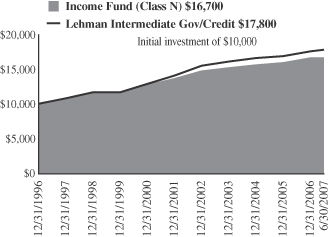

Income Fund | | 0.45 | | 4.48 | | 3.16 | | 3.46 | | 4.96 | | 10/1/1990 | | «««« |

Morningstar Short-term Bond | | 1.72 | | 4.96 | | 2.90 | | 3.05 | | 4.47 | | | | Among 364 short-term bond funds |

Lehman Intermediate Govt./Credit Bond Index | | 1.45 | | 5.76 | | 3.41 | | 4.14 | | 5.66 | | | |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Returns shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or a loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment advisor may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Investing in smaller companies involves special risks, including higher volatility and lower liquidity. International and emerging markets investing involves special risk considerations, including currency fluctuations, lower liquidity, economic and political risk. As interest rates rise, bond prices will fall and bond funds become more volatile. From time to time, the investment advisor may waive fees or reimburse expenses for certain Funds. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load.

Tax-Managed Growth Fund’s after-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Actual after-tax returns depend on the investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown only for Class N and the after-tax returns for Class N shares will vary.

Morningstar RatingsTM are as of 6/30/07 and are subject to change every month. The ratings are based on a risk-adjusted return measure that accounts for variation in a fund’s monthly performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each Category receive 5 stars, the next 22.5% receive 4 stars, the middle 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a fund is derived from a weighted-average of the performance figures associated with its three-, five- and ten-year (if applicable) Morningstar Rating metrics. The 3/5/10 year Morningstar ratings were as follows: Growth Fund ««««/«««/« ««, Tax-Managed Growth Fund ««««/«««/NA, and Large Cap Growth Fund «««/« «/NA, out of 1,426/1,151/471 large growth funds; Small Cap Growth Fund «««/ «««««/NA out of 645/533/NA small growth funds; Small-Mid Cap Growth Fund «««/NA/NA out of 814/NA/NA mid cap growth funds; Value Discovery Fund ««/«/««« out of 305/239/76 small value funds; International Growth Fund ««««/««««/««««« and International Equity Fund «/NA/NA out of 183/155/60 foreign large growth funds; Income Fund «««/ ««««/«««« out of 304/261/158 short-term bond funds.

Please carefully consider the Funds’ investment objectives, risks, charges, and expenses before investing. This and other information is contained in the Funds’ prospectus, which you may obtain by calling 1-800-742-7272. Read it carefully before you invest or send money.

See accompanying Notes to Financial Statements.

June 30, 2007 | William Blair Funds 3 |

David C. Fording

John F. Jostrand

GROWTH FUND

The Growth Fund invests primarily in common stocks of domestic growth companies that the Advisor expects to have sustainable, above-average growth from one business cycle to the next.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform over the first half of the year? How did the Fund’s performance compare to its benchmark?

The Growth Fund posted a 7.88% increase on a total return basis (Class N Shares) for the six month period ended June 30, 2007. By comparison, the Fund’s benchmark, the Russell 3000® Growth Index, posted a gain of 8.22% during the same period.

What were the most significant factors impacting Fund performance?

For the first six months of 2007, domestic equity markets experienced strong gains across the board. As measured by the Russell indices, Midcap growth stocks led the charge, appreciating over 10% during the period. Small Caps and Large Caps trailed behind, respectively, but still posted strong results during the period. Growth overtook value as style leader when the Federal Reserve paused with its interest rate hikes in August of 2006, and the lead was extended in the latter half of the year-to-date period.

There were several noteworthy trends that affected performance, many of which were more prevalent during the last months of the second quarter, which drove most of the performance of the entire period. The credit concerns that arose with respect to subprime lending in February re-emerged later in the period, putting significant pressure on financial stocks, particularly REITs and smaller capitalization banks. Second, although U.S. earnings growth is moderating, growth rates for international companies remains strong. In the first quarter of 2007, stocks with larger non-US exposure experienced twice as much year-over-year earnings growth relative to companies with less significant portions of non-US revenues. Generally speaking, most of these companies, with larger non-U.S. exposure, are ones with larger market capitalizations. Third, liquidity in the market continues to be significant, fueling continued merger and acquisition activity as well as sizeable share-buy backs. The impact of these “liquidity events” is causing price appreciation among primary and ancillary stocks that are moving on speculation that they may be a next candidate. Lastly, higher quality stocks (as measured by S&P quality ratings) continue to under-perform. Typically, higher quality stocks begin to out-perform in periods when earnings growth slows. Although earnings growth has slowed significantly over the last several quarters, overall growth is still at elevated levels compared to historical trends. Investors may not pursue higher quality stocks until earnings growth slows significantly below double-digit levels.

On the positive side, our portfolio does not have any exposure to REITs or banks, and our financial stocks performed well during the period. Conversely, due to our high quality philosophy, our stocks did not benefit significantly from some of these trends. Although larger capitalization stocks generally fared well during the period, ours were not quite as strong. But our stock selection among the smallest cap stocks overcame slight weakness in the other capitalization buckets.

Which sectors enhanced the Fund’s return? What were among the best performing investments for the Fund?

In the first half of 2007, the portfolio benefited the most from stock selection in Information Technology. WebEx Communications Inc. experienced strong price appreciation early in the quarter when the company reported continued robust growth in sales as well as improving margins for its on-line collaboration tools. Toward the end of the period, the company reached an agreement to be acquired by Cisco Systems, causing the stock price to climb

4 Semi-Annual Report | June 30, 2007 |

further. The performance of this stock in particular caused our smallest capitalization sector to have the greatest impact on relative returns. Similarly, j2 Global Communications, Inc., appreciated significantly during the period. The company provides outsourced, value-added messaging and communications services to individuals and businesses. During the last quarter, j2 Global Communications implemented a significant price increase to eFax customers, which is progressing on schedule. In addition, the company has multiple growth initiatives: international growth, expansion of voice services and faster adoption of digital fax services by large enterprises.

Stocks in the Energy sector were also strong contributors during the period, with Smith International Inc. being one of the top performers in the broad portfolio. During May, the company reported an excellent quarter and announced upbeat guidance. Consumer Discretionary placed third in terms of relative contribution for the six months. In January, Laureate Education announced a management-led buyout at a premium to the level at which the stock was trading, which was the basis for significant stock appreciation. Auto components and HVAC systems producer Johnson Controls experienced strong price appreciation as investors began to revalue the underlying earnings power of the company.

Were there any investment strategies or themes that did not measure up to your expectations?

Industrials were the largest detractor from relative performance, due in part to extremely strong performance by Russell 3000® Growth stocks in this sector. Corporate Executive Board stock fell during the period, mainly due to disappointing guidance for 2007 results and concerns about current and future subscriber rates. During February, Danaher Corp. reported an in-line quarter which disappointed overly enthusiastic investors. Following strong price appreciation in 2006, the stock was likely due for a pause to consolidate its recent gains.

Health Care stocks in the portfolio were also relatively weak during the period. Both Amgen Inc. and Genentech Inc. in the biotechnology area suffered, although for different reasons. Amgen has had a significant overhang around its Aranesp franchise, and recent studies show that prospects for its pipeline products are likely less robust than originally thought. As a result the Fund liquidated its position in this holding. For Genentech, although there are some concerns about the growth rate of its core Avastin product, the pipeline is promising and the market, in our view, has overly discounted growth prospects for the company. ResMed, Inc., which manufactures and distributes medical equipment, primarily for treating, diagnosing and managing sleep-disordered breathing, had a significant setback in April as the company initiated a recall of its S8 flow generator product. Although a third party was hired to handle the bulk of this job, we believe that the company’s sales representatives spent more time than expected handling customer issues related to the recall, which led to lost selling time. As a result, investors have lowered revenue and earnings projections for the current quarter, which has negatively affected the stock price.

Although Technology stocks overall contributed to performance, it was in fact a tale of two sides; there were several stocks in this sector that offered disappointing results. Network Appliance Inc. announced weak guidance for the coming quarter as a result of a bookings slowdown. Investors have placed premium valuation on the growth of this company, and the stock has recently struggled to meet expectations. Cognizant Technology Solutions Corp., an offshore provider of application development and management services, modestly raised its utilization rates which in turned reduced its year-end hiring goal. Investors interpreted this lower hiring goal as a sign of decreased demand, although we believe that demand remains solid and that there were other, less concerning factors at play.

What is your current strategy? How is the Fund Positioned?

Impact of credit quality on the broader market, and concerns about the health of the consumer given flat to eroding housing prices and rising fuel costs are looming over the market. Despite these overhangs, significant amounts of global liquidity continue to bolster prices of financial instruments. Merger and acquisition activity is continuing at record levels, and numerous corporate share buybacks have had a sizeable impact on stocks. Additionally, stock valuations remain in a reasonable range, providing additional support for prices. Regardless of the macro issues on the market, we continue to find high quality stocks that offer growth opportunities.

June 30, 2007 | William Blair Funds 5 |

Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 6/30/2007

| | | | | | | | | | | | | | | | | | | | |

| | | Year to

Date | | | 1 Year | | | 3 Year | | | 5 Year | | | 10 Year | | | Since Inception | | | |

Growth Fund Class N | | 7.88 | % | | 18.45 | % | | 12.66 | % | | 9.06 | % | | 5.71 | % | | — | % | | |

Growth Fund

Class I | | 8.15 | | | 18.83 | | | 12.98 | | | 9.34 | | | — | | | 3.18 | | | |

Russell 3000® Growth Index | | 8.22 | | | 18.84 | | | 8.97 | | | 9.58 | | | 4.42 | | | (.20 | )(a) | | |

S&P 500 Index | | 6.96 | | | 20.59 | | | 11.68 | | | 10.71 | | | 7.13 | | | 3.72 | (a) | | |

| | (a) | | For the period from October 1, 1999 to June 30, 2007. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company L.L.C. without a sales load or distribution (12b-1) or service fees.

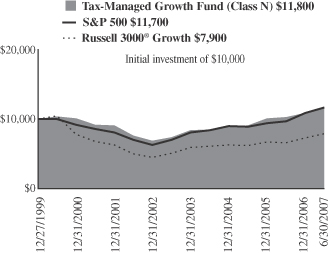

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 3000® Growth Index consists of large, medium, and small capitalization companies with above average price-to-book ratios and forecasted growth rates. The index is weighted by market capitalization and large/medium/small companies make up approximately 80%/15%/5% of the index.

The S&P 500 Index indicates broad larger capitalization equity market performance.

This report identifies the Fund’s investments on June 30, 2007. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

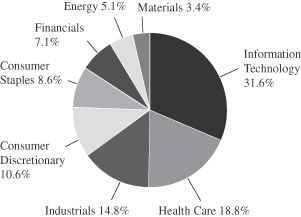

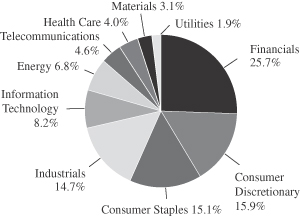

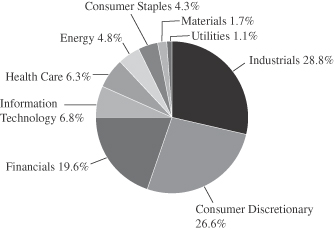

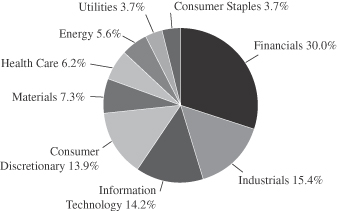

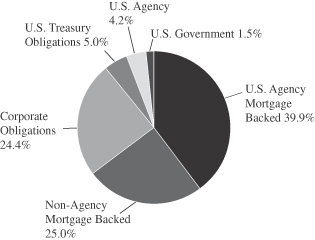

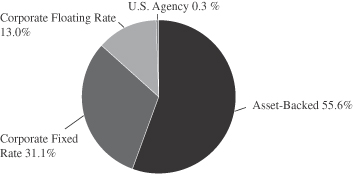

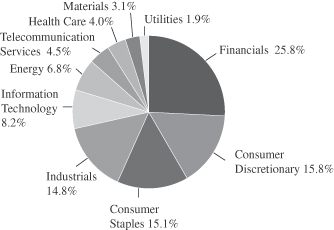

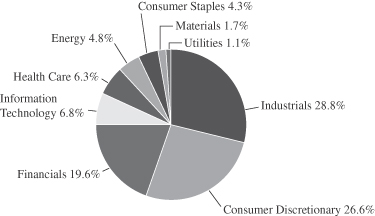

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

6 Semi-Annual Report | June 30, 2007 |

Growth Fund

Portfolio of Investments, June 30, 2007 (all dollar amounts in thousands) (unaudited)

| | | | | |

Issuer | |

Shares | | Value |

| | |

Common Stocks | | | | | |

Information Technology—30.6% | | | | | |

*Activision, Inc. | | 297,365 | | $ | 5,552 |

*Adobe Systems Incorporated | | 164,385 | | | 6,600 |

Arm Holding plc—ADR | | 501,615 | | | 4,389 |

*Cognizant Technology Solutions Corporation | | 86,105 | | | 6,466 |

*EMC Corporation | | 346,385 | | | 6,270 |

*Euronet Worldwide, Inc. | | 141,655 | | | 4,131 |

*FLIR Systems, Inc. | | 105,205 | | | 4,866 |

*j2 Global Communications, Inc. | | 234,870 | | | 8,197 |

*Network Appliance, Inc. | | 205,250 | | | 5,993 |

*Nuance Communications, Inc. | | 233,900 | | | 3,913 |

Paychex, Inc. | | 218,050 | | | 8,530 |

Qualcomm Incorporated | | 155,695 | | | 6,756 |

*Silicon Laboratories Inc. | | 113,950 | | | 3,944 |

Taiwan Semiconductor Mfg. Co. Ltd.—ADR | | 678,751 | | | 7,555 |

*Verisign Inc. | | 111,450 | | | 3,536 |

*Vistaprint Limited | | 121,528 | | | 4,648 |

*Yahoo!, Inc. | | 242,235 | | | 6,572 |

| | | | | |

| | | | | 97,918 |

| | | | | |

Health Care—18.2% | | | | | |

C.R. Bard, Inc. | | 71,975 | | | 5,947 |

*Genentech, Inc. | | 102,740 | | | 7,773 |

*Gilead Sciences, Inc. | | 224,030 | | | 8,686 |

*Healthways, Inc. | | 136,595 | | | 6,470 |

*Integra Lifesciences Holding Corporation | | 100,745 | | | 4,979 |

*Kyphon, Inc. | | 132,760 | | | 6,392 |

Medtronic, Inc. | | 111,335 | | | 5,774 |

Pharmaceutical Product Development Inc. | | 203,955 | | | 7,805 |

ResMed, Inc. | | 104,740 | | | 4,322 |

| | | | | |

| | | | | 58,148 |

| | | | | |

Industrials & Services—14.3% | | | | | |

Danaher Corporation | | 171,546 | | | 12,952 |

Fastenal Company | | 185,525 | | | 7,766 |

Graco, Inc. | | 115,190 | | | 4,640 |

*InnerWorkings, Inc. | | 270,540 | | | 4,334 |

Knight Transportation, Inc. | | 183,530 | | | 3,557 |

Rockwell Automation, Inc. | | 67,285 | | | 4,672 |

Rockwell Collins, Inc. | | 109,785 | | | 7,755 |

| | | | | |

| | | | | 45,676 |

| | | | | |

Consumer Discretionary—10.2% | | | | | |

*Coinstar, Inc. | | 170,730 | | | 5,375 |

Johnson Controls, Inc. | | 72,917 | | | 8,442 |

*McCormick & Schmick’s Seafood Restaurants, Inc. | | 126,105 | | | 3,271 |

Staples, Inc. | | 293,315 | | | 6,960 |

*Starbucks Corporation | | 151,240 | | | 3,968 |

*Tractor Supply Company | | 89,235 | | | 4,645 |

| | | | | |

| | | | | 32,661 |

| | | | | |

*Non-income producing securities

ADR = American Depository Receipt

† = U.S. listed foreign security

VRN = Variable Rate Note

| | | | | | | |

Issuer | | Shares or

Principal

Amount | | Value | |

| | |

Common Stocks—(continued) | | | | | | | |

Consumer Staples—8.3% | | | | | | | |

PepsiCo, Inc. | | | 243,530 | | $ | 15,793 | |

Wal Mart De Mexico—ADR | | | 126,225 | | | 4,752 | |

Walgreen Co. | | | 139,960 | | | 6,094 | |

| | | | | | | |

| | | | | | 26,639 | |

| | | | | | | |

Financials—6.9% | | | | | | | |

Charles Schwab & Co., Inc. | | | 369,990 | | | 7,592 | |

Goldman Sachs Group, Inc. | | | 44,150 | | | 9,570 | |

*IntercontinentalExchange Inc. | | | 33,580 | | | 4,965 | |

| | | | | | | |

| | | | | | 22,127 | |

| | | | | | | |

Energy—5.0% | | | | | | | |

Smith International, Inc. | | | 157,695 | | | 9,247 | |

Suncor Energy, Inc.† | | | 73,035 | | | 6,567 | |

| | | | | | | |

| | | | | | 15,814 | |

| | | | | | | |

Materials—3.3% | | | | | | | |

Praxair, Inc. | | | 145,130 | | | 10,448 | |

| | | | | | | |

Total Common Stock—96.8%

(cost $240,951) | | | 309,431 | |

| | | | | | | |

| | |

Investment in Affiliate | | | | | | | |

William Blair Ready Reserves Fund | | | 2,634,785 | | | 2,635 | |

| | | | | | | |

Total Investment in Affiliate—0.8%

(cost $2,635) | | | 2,635 | |

| | | | | | | |

| | |

Short-Term Investment | | | | | | | |

Prudential Funding Demand Note,

VRN 5.305%, due 07/02/07 | | $ | 4,330,000 | | | 4,330 | |

| | | | | | | |

Total Short-Term Investment—1.4%

(cost $4,330) | | | 4,330 | |

| | | | | | | |

| | |

Repurchase Agreement | | | | | | | |

Investors Bank & Trust Company,

4.50% dated 6/29/2007, due 7/02/2007, repurchase price $4,204, collateralized by SBA Pool # 506131 | | $ | 4,202,129 | | | 4,202 | |

| | | | | | | |

Total Repurchase Agreement—1.3%

(cost $4,202) | | | 4,202 | |

| | | | | | | |

Total Investments—100.3%

(cost $252,118) | | | 320,598 | |

Liabilities, plus cash and other assets—(0.3)% | | | (1,051 | ) |

| | | | | | | |

Net assets—100.0% | | $ | 319,547 | |

| | | | | | | |

See accompanying Notes to Financial Statements.

June 30, 2007 | William Blair Funds 7 |

Mark A. Fuller III

Gregory J. Pusinelli

TAX-MANAGED GROWTH FUND

The Tax-Managed Growth Fund invests primarily in common stocks of large, medium and small domestic growth companies that the Advisor expects will have sustainable, above-average growth from one business cycle to the next.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform over the first half of the year? How did the Fund’s performance compare to its benchmark?

The Tax-Managed Growth Fund posted a 7.40% gain on a total return basis (Class N Shares) for the six-months ended June 30, 2007. By comparison, the Fund’s benchmark, the Russell 3000® Growth Index rose 8.22% while the Standard & Poor’s 500 Stock Index increased 6.96%.

What were the most significant market factors impacting Fund performance?

Although the year started off on a positive note, investors awakened the morning of February 27th to learn that many Asian markets had plummeted overnight, an amounts as great as 9%. This precipitated a decline in global stock markets as markets around the world opened, finally culminating in a sharp slide in U.S. equity prices. Weakness in the U.S. markets was exacerbated by concerns over a series of bankruptcies by issuers of sub-prime mortgage loans. Equity prices finally staged a rally in the final weeks of the first quarter to bring prices off their lows.

Following a relatively flat first quarter, and in spite of some setbacks along the way, the stock market forged ahead in the second quarter to a strong mid-year finish.

Facing strong headwinds from rising interest rates, a slump in housing prices and rising energy prices, the Standard & Poor’s 500-Stock Index set a record high in late May and gained 6.28% in the second quarter.

Boosting the market’s performance was a strong flow of private equity acquisitions, a pickup in manufacturing activity and signs that inflation has moderated.

Our stock selection in the Financials and Consumer Discretionary sectors contributed to the Fund’s strong performance in the first half of the year. On the other hand, the Information Technology (IT) and Health Care sectors were a drag on Fund performance.

What were among the best performing investments for the Fund?

All three of our top-performing investments were involved in acquisitions, which we believe lends credibility to our quality growth philosophy of investing in high quality companies with strong management and durable business franchises.

The best-performing investment, in terms of contribution to the Fund’s return, was Investors Financial Services Company. State Street Bank and Trust Company announced in February it had reached a definitive agreement to acquire Investors Financial Services Company. Investors Financial was up 46.9% for the Fund.

8 Semi-Annual Report | June 30, 2007 |

MedImmune was the second-best performing investment for the Fund, in terms of contribution, up 75.5%. In late April, European drug manufacturer AstraZeneca announced it had entered into a definitive agreement to acquire MedImmune.

The third best-performing investment in terms of contribution to the Fund’s return was WebEx Communications. Cisco Systems announced it would be acquiring WebEx Communications during the first quarter, and WebEx was up 63.1% for the Fund.

What were among the weakest performing investments for the Fund?

The three worst-performing investments, in terms of contribution to return were Network Appliance, Resmed and Santarus.

Network Appliance sells hardware, software, and services for customers to store and manage critical data across their networks. Although Network Appliance’s fourth quarter earnings figures were in line with expectations, the company lowered guidance on earnings for the first quarter. The company experienced weak sales in March and said that many of its customers had put off making capital expenditures until the second quarter. Although April sales rebounded, Network Appliance was down 25.7% for the Fund.

ResMed, Inc., whose major focus is solutions for sleep-disordered breathing, missed its earnings estimates during the first quarter. A rival competitor launched a new product during the period and flooded the market with free product offers. ResMed, which was down 16.2% was a fairly large holding for the Fund, at 2.59%, and was the second worst performer in terms of contribution to return.

Santarus, a pharmaceutical company that makes less expensive versions of drugs made by large cap drug companies to treat gastrointestinal diseases and disorders, was down 34.0% for the Fund. Santarus missed its quarterly earnings due to lower revenues during the March-April period.

What is your current strategy? How is the Fund positioned?

We believe that in the months ahead growth in overseas economies will outpace that of the U.S. One of our current investment themes is to search for companies with a global “footprint,” that do a considerable amount of business outside the U.S. In particular, we are looking at industrial-oriented companies that are well positioned to capitalize on growth in the global economy.

Johnson Controls is a company that epitomizes this investment theme. Johnson Controls operates three distinct business segments: automotive interiors, vehicle batteries, and building controls and services. We chose this well-managed company in part to increase our exposure to the Industrial sector. The company’s interiors segment has experienced strong demand for its products in emerging markets countries.

Starbucks, a recent addition to the Fund’s portfolio, meets the profile of a company with a strong global brand. The company shows potential for good profit growth with a significant “runway” for further growth internationally, in spite of a somewhat slower rate of expansion in the U.S.

Another new addition to the Fund���s portfolio of investments was Allergan, a company we have owned before, and were able to purchase at what we believe was an attractive share price point. Allergan is one of the largest specialty pharmaceutical firms in the world and the maker of Botox. Roughly half of the company’s sales come from its eye care pharmaceutical

June 30, 2007 | William Blair Funds 9 |

division, but last year the company acquired Inamed, and increased its exposure to the cosmetic surgical market, as it now sells breast implants, dermal fillers, and products to treat obesity.

Silicon Laboratories, a designer of integrated circuits and semiconductor chips used in various markets such as communications, industrial, consumer, medical, and power management, was also added to the Fund.

We continue to be selective investors in the Consumer Discretionary sector. The slump in the housing sector and recent problems in the sub-prime lending market are negative factors overhanging the market, and could eventually impact consumer spending.

We believe the environment remains favorable for corporate profit growth in 2007. And we are encouraged by the earnings growth potential of the companies in the Fund’s portfolio, despite what we expect to be a year of tempered economic growth. In such an environment, security selection becomes even more important. We think our high quality growth approach paid off during the first half of the year, and we believe our focus on quality franchise businesses and respect for downside risk is the appropriate time-tested approach as the year progresses.

10 Semi-Annual Report | June 30, 2007 |

Tax-Managed Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 6/30/2007

| | | | | | | | | | | | | | | |

| | | Year to

Date | | | 1

Year | | | 3

Year | | | 5

Year | | | Since Inception(a) | |

Tax-Managed Growth Fund

Class N | | 7.40 | % | | 14.52 | % | | 11.40 | % | | 9.02 | % | | 2.16 | % |

Tax-Managed Growth Fund

Class I | | 7.53 | | | 14.85 | | | 11.67 | | | 9.32 | | | 2.44 | |

Russell 3000®

Growth Index | | 8.22 | | | 18.84 | | | 8.97 | | | 9.58 | | | (3.09 | ) |

S&P 500 Index | | 6.96 | | | 20.59 | | | 11.68 | | | 10.71 | | | 2.06 | |

| | (a) | | For the period from December 27, 1999 to June 30, 2007. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment advisor may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 3000® Growth Index consists of large, medium, and small-capitalization companies with above average price-to-book ratios and forecasted growth rates. The index is weighted by market capitalization and large/medium/small companies make up approximately 80%/15%/5% of the index.

The S&P 500 Index indicates broad larger capitalization equity market performance.

This report identifies the Fund’s investments on June 30, 2007. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

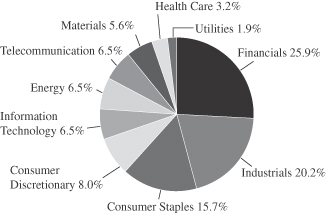

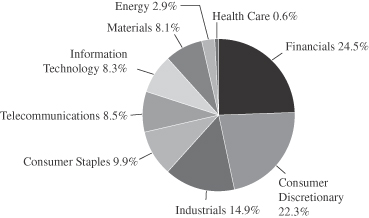

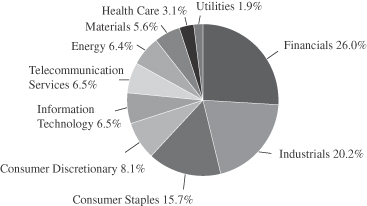

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

June 30, 2007 | William Blair Funds 11 |

Tax-Managed Growth Fund

Portfolio of Investments, June 30, 2007 (all dollar amounts in thousands) (unaudited)

| | | | | |

Issuer | |

Shares | | Value |

| | |

Common Stocks | | | | | |

Information Technology—27.3% | | | | | |

*Activision, Inc. | | 8,453 | | $ | 158 |

*Adobe Systems Incorporated | | 6,160 | | | 247 |

*Alliance Data Systems Corporation | | 1,610 | | | 124 |

Arm Holdings plc—ADR | | 11,960 | | | 105 |

*Electronic Arts Inc. | | 2,950 | | | 140 |

*EMC Corporation | | 14,140 | | | 256 |

*Euronet Worldwide, Inc. | | 3,770 | | | 110 |

*F5 Networks, Inc. | | 2,580 | | | 208 |

Jabil Circuit Inc. | | 12,590 | | | 278 |

Microchip Technology Incorporated | | 5,250 | | | 194 |

*Network Appliance, Inc. | | 5,650 | | | 165 |

Paychex, Inc. | | 5,950 | | | 233 |

Qualcomm Incorporated | | 5,100 | | | 221 |

*Silicon Laboratories Inc. | | 3,300 | | | 114 |

Taiwan Semiconductor Mfg. Co. Ltd.—ADR | | 10,719 | | | 119 |

*Yahoo!, Inc. | | 6,450 | | | 175 |

| | | | | |

| | | | | 2,847 |

| | | | | |

Health Care—22.8% | | | | | |

Allergan Inc. | | 2,600 | | | 150 |

C.R.Bard, Inc. | | 1,710 | | | 141 |

*Genzyme Corporation | | 1,500 | | | 97 |

*Gilead Sciences, Inc. | | 3,080 | | | 119 |

*Healthways, Inc. | | 5,710 | | | 271 |

IMS Health, Inc. | | 8,820 | | | 283 |

*Kyphon, Inc. | | 2,740 | | | 132 |

Medtronic, Inc. | | 2,730 | | | 142 |

Pharmaceutical Product Development, Inc. | | 5,970 | | | 228 |

*Psychiatric Solutions, Inc. | | 4,820 | | | 175 |

*ResMed, Inc. | | 5,534 | | | 228 |

*Santarus, Inc. | | 36,800 | | | 190 |

Stryker Corporation | | 3,600 | | | 227 |

| | | | | |

| | | | | 2,383 |

| | | | | |

Industrials—12.1% | | | | | |

Danaher Corporation | | 3,810 | | | 288 |

Fastenal Company | | 6,350 | | | 266 |

General Electric Company | | 6,985 | | | 267 |

Knight Transportation, Inc. | | 7,832 | | | 152 |

Rockwell Collins, Inc. | | 4,110 | | | 290 |

| | | | | |

| | | | | 1,263 |

| | | | | |

Consumer Staples—8.6% | | | | | |

Colgate-Palmolive Company | | 3,020 | | | 196 |

CVS/Caremark Corporation | | 3,774 | | | 138 |

PepsiCo, Inc. | | 4,595 | | | 298 |

Wal Mart De Mexico—ADR | | 3,810 | | | 143 |

Walgreen Co. | | 2,975 | | | 130 |

| | | | | |

| | | | | 905 |

| | | | | |

*Non-income producing securities

ADR = American Depository Receipt

† = U.S. listed foreign security

VRN = Variable Rate Note

| | | | | | | |

Issuer | | Shares or

Principal

Amount | | Value | |

| | |

Common Stocks—(continued) | | | | | | | |

Consumer Discretionary—8.5% | | | | | | | |

*CarMax, Inc. | | | 6,840 | | $ | 174 | |

International Game Technology | | | 3,800 | | | 151 | |

Johnson Controls, Inc. | | | 1,890 | | | 219 | |

McGraw-Hill Companies, Inc. | | | 1,460 | | | 99 | |

*Starbucks Corporation | | | 5,190 | | | 136 | |

*Tractor Supply Company | | | 2,030 | | | 106 | |

| | | | | | | |

| | | | | | 885 | |

| | | | | | | |

Financials—6.3% | | | | | | | |

*Affiliated Managers Group, Inc. | | | 1,040 | | | 134 | |

American International Group | | | 2,780 | | | 195 | |

*IntercontinentalExchange, Inc. | | | 930 | | | 138 | |

Moody’s Corporation | | | 3,060 | | | 190 | |

| | | | | | | |

| | | | | | 657 | |

| | | | | | | |

Energy—5.6% | | | | | | | |

Smith International, Inc. | | | 4,360 | | | 256 | |

Suncor Energy, Inc.† | | | 3,630 | | | 326 | |

| | | | | | | |

| | | | | | 582 | |

| | | | | | | |

Materials—5.5% | | | | | | | |

Airgas, Inc. | | | 4,870 | | | 233 | |

Praxair, Inc. | | | 4,750 | | | 342 | |

| | | | | | | |

| | | | | | 575 | |

| | | | | | | |

Total Common Stock—96.7%

(cost $7,816) | | | 10,097 | |

| | | | | | | |

| | |

Investment in Affiliate | | | | | | | |

William Blair Ready Reserves Fund | | | 6,413 | | | 6 | |

| | | | | | | |

Total Investment in Affiliate—0.1%

(cost $6) | | | 6 | |

| | | | | | | |

| | |

Short-Term Investment | | | | | | | |

Prudential Funding Demand Note, VRN 5.305%, due 7/2/07 | | $ | 210,000 | | | 210 | |

| | | | | | | |

Total Short-Term Investment—2.0%

(cost $210) | | | 210 | |

| | | | | | | |

| | |

Repurchase Agreement | | | | | | | |

Investors Bank & Trust Company,

4.50% dated 6/29/2007, due 7/2/2007, repurchase price $141, collateralized by SBA Pool # 505283 | | $ | 140,850 | | | 141 | |

| | | | | | | |

Total Repurchase Agreement—1.3%

(cost $141) | | | 141 | |

| | | | | | | |

Total Investments—100.1%

(cost $8,173) | | | 10,454 | |

Liabilities, plus cash and other assets—( 0.1)% | | | (12 | ) |

| | | | | | | |

Net assets—100.0% | | $ | 10,442 | |

| | | | | | | |

See accompanying Notes to Financial Statements.

12 Semi-Annual Report | June 30, 2007 |

James S. Golan

John F. Jostrand

LARGE CAP GROWTH FUND

The Large Cap Growth Fund invests primarily in common stocks of large domestic growth companies of high quality that the Advisor believes have demonstrated sustained growth over a long period of time.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform over the first half of the year? How did the Fund’s performance compare to its benchmark?

The Large Cap Growth Fund posted a 5.81% increase on a total return basis (Class N Shares) for the six-month period ended June 30, 2007. During the same period, the Fund’s benchmark, the Russell 1000 Growth® Index, gained 8.13%.

What were the most significant factors impacting Fund performance?

For the first six months of 2007, domestic equity markets experienced strong gains across the board. As measured by the Russell indices, Midcap growth stocks led the charge, appreciating over 10% during the period. Small Caps and Large Caps trailed behind, respectively, but still posted strong results during the period. Growth overtook value as style leader when the Federal Reserve paused its interest rate hikes in August of 2006, and the lead was extended in the latter half of the year-to-date period.

There were several noteworthy trends that affected performance, many of which were more prevalent during the last months of the second quarter, which drove most of the performance of the entire period. The credit concerns that arose with respect to sub-prime lending in February re-emerged later in the period, putting significant pressure on financial stocks, particularly REITs and smaller capitalization banks. Second, although U.S. earnings growth is moderating, growth rates for international companies remain strong. In the first quarter of 2007, stocks with larger non-US exposure experienced twice as much year-over-year earnings growth relative to companies with less significant portions of non-US revenues. Generally speaking, most of these companies, with larger non-US exposure, are ones with larger market capitalizations. Third, liquidity in the market continues to be significant, fueling continued merger and acquisition activity as well as sizeable share-buy backs. The impact of these “liquidity events” is causing price appreciation among primary and ancillary stocks that are moving on speculation that they may be a next candidate. Lastly, higher quality stocks (as measured by S&P quality ratings) continue to under-perform. Typically, higher quality stocks begin to out-perform in periods when earnings growth slows. Although earnings growth has slowed significantly over the last several quarters, overall growth is still at elevated levels compared to historical trends. Investors may not pursue higher quality stocks until earnings growth slows significantly below double-digit levels.

On the positive side, our portfolio does not have any exposure to REITs or banks, and our financial stocks performed well during the period. Conversely, due to our high quality philosophy, our stocks did not benefit significantly from these trends.

Which sectors enhanced the Fund’s return? What were among the best performing investments for the Fund?

Financials provided the strongest benefit to relative returns during the first half of the year. The portfolio did not have any direct exposure to the highly interest-rate sensitive companies such as smaller cap banks and REITs, which pulled back in relation to concerns about the subprime lending market and related defaults. Charles Schwab Inc. fared well during the

June 30, 2007 | William Blair Funds 13 |

period, as it continues to grow the asset-based part of its business. Additionally, the company announced a new initiative with respect to gaining additional assets. Similarly, Franklin Resources showed strong asset growth during the period, resulting in a stronger revenue outlook.

Energy stocks provided the second largest contribution to returns during the period. With rising oil prices, most stocks in this sector did well. Companies that produce oilfield services fared particularly well, as the oil companies are seeking to expand production. Schlumberger Ltd. provides project management and information solutions to the oil and gas industry. While the current global demand for oil has benefited Schlumberger tremendously, the company has also experienced strong earnings growth from Eastern Hemisphere markets as well as services from its seismic division. Similarly, Praxair Inc., a company that produces and delivers a variety of gasses for industrial uses, enjoyed strong price appreciation during the quarter. The company continues to exhibit strong earnings growth, not only from its excellence of product and services, but from the strength in the Energy and Industrials areas as well.

Were there any investment strategies or themes that did not measure up to your expectations?

Although Information Technology stocks were the greatest contributors in terms of contribution to portfolio return, this sector was the largest detractor from performance relative to the benchmark during the six months. In part, this was due to the strength in these companies in the Russell 1000® Growth Index, which in aggregate were up nearly 10%. A couple of stocks in the portfolio that had disappointing results during the period include Jabil Circuit Inc. and Network Appliance Inc. Jabil is one of the largest global suppliers of electronic manufacturing services (EMS) used in the communication products, computer peripherals, and automobile industries. Shares sold off after the company announced disappointing revenue guidance during the quarter. Additionally, Jabil lost a contract from one of its biggest customers due to aggressive pricing from an Asian competitor, further eroding growth prospects for the company. Network Appliance Inc. sells data management and storage solutions to corporate customers. Although Network Appliance, Inc. has continued to gain traction and market share in the storage space, the company announced weak guidance for the coming quarter as a result of a bookings slowdown. Investors have placed premium valuation on the growth of this company, and the stock has recently struggled to meet expectations.

Health Care stocks in the portfolio were also relatively weak during the period. Both Amgen Inc. and Genentech Inc. in the biotechnology area suffered, although for different reasons. Amgen has had a significant cloud regarding its Aranesp franchise, and recent studies show that prospects for its pipeline products are likely less robust than originally thought. For Genentech, although there are some concerns about the growth rate of its core Avastin product, the pipeline is promising and the market, in our view, has overly discounted growth prospects for the company.

What is your current strategy? How is the Fund Positioned?

Impact of credit quality on the broader market, and concerns about the health of the consumer given flat to eroding housing prices and rising fuel costs are looming over the market. Despite these overhangs, significant amounts of global liquidity continue to bolster prices of financial instruments. Merger and acquisition activity is continuing at record levels, and numerous corporate share buybacks have had a sizeable impact on stocks. Additionally, stock valuations remain in a reasonable range, providing additional support for prices. Regardless of the macro issues on the market, we continue to find high quality stocks that offer growth opportunities. Although it sounds paradoxical, growth stocks, particularly high quality growth stocks, tend to perform well in a slowing economy, as investors will commonly pay a premium for companies that can sustain earnings during this time. We believe that as overall earnings growth decelerates, investors will pay more attention to earnings multiples, and reward stocks with longer, more sustainable earnings trends.

14 Semi-Annual Report | June 30, 2007 |

Large Cap Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 6/30/2007

| | | | | | | | | | | | | | | |

| | | Year to

Date | | | 1

Year | | | 3

Year | | | 5

Year | | | Since

Inception(a) | |

Large Cap Growth Fund Class N | | 5.81 | % | | 13.57 | % | | 7.38 | % | | 6.08 | % | | (4.13 | )% |

Large Cap Growth Fund Class I | | 5.72 | | | 13.69 | | | 7.55 | | | 6.28 | | | (3.93 | ) |

Russell 1000®

Growth Index | | 8.13 | | | 19.04 | | | 8.70 | | | 9.28 | | | -3.48 | |

| | (a) | | For the period from December 27, 1999 to June 30, 2007. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment advisor may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

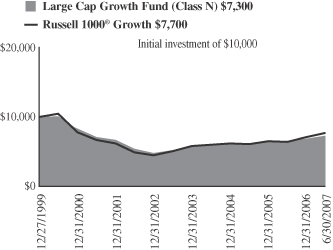

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 1000® Growth Index consists of large capitalization companies with above average price-to-book ratios and forecasted growth rates.

This report identifies the Fund’s investments on June 30, 2007. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

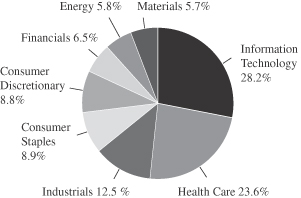

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

June 30, 2007 | William Blair Funds 15 |

Large Cap Growth Fund

Portfolio of Investments, June 30, 2007 (all dollar amounts in thousands) (unaudited)

| | | | | |

Issuer | | Shares | | Value |

| | |

Common Stocks | | | | | |

Information Technology—28.5% | | | | | |

*Adobe Systems Incorporated | | 21,115 | | $ | 848 |

*Cisco Systems Incorporated | | 47,729 | | | 1,329 |

*Corning Incorporated | | 22,170 | | | 566 |

*EMC Corporation | | 47,675 | | | 863 |

Infosys Technologies Ltd.—ADR | | 7,985 | | | 402 |

*Network Appliance, Inc. | | 14,380 | | | 420 |

Paychex, Inc. | | 27,325 | | | 1,069 |

Qualcomm Incorporated | | 18,735 | | | 813 |

Taiwan Semiconductor Mfg. Co. Ltd.—ADR | | 59,726 | | | 665 |

*Verisign, Inc. | | 9,700 | | | 308 |

*Yahoo!, Inc. | | 23,925 | | | 649 |

| | | | | |

| | | | | 7,932 |

| | | | | |

Industrials—13.0% | | | | | |

ABB LTD—ADR | | 27,640 | | | 625 |

Danaher Corporation | | 21,237 | | | 1,603 |

Rockwell Automation, Inc. | | 5,990 | | | 416 |

Rockwell Collins, Inc. | | 13,825 | | | 977 |

| | | | | |

| | | | | 3,621 |

| | | | | |

Financials—10.8% | | | | | |

Charles Schwab & Co, Inc. | | 38,205 | | | 784 |

Franklin Resources, Inc. | | 5,835 | | | 773 |

Goldman Sachs Group, Inc. | | 4,740 | | | 1,027 |

*IntercontinentalExchange, Inc. | | 2,920 | | | 432 |

| | | | | |

| | | | | 3,016 |

| | | | | |

Consumer Discretionary—10.7% | | | | | |

*Coach, Inc. | | 8,720 | | | 413 |

Johnson Controls, Inc. | | 8,545 | | | 989 |

Marriott International, Inc., Class “A” | | 11,469 | | | 496 |

Staples, Inc. | | 31,390 | | | 745 |

*Starbucks Corporation | | 13,230 | | | 347 |

| | | | | |

| | | | | 2,990 |

| | | | | |

Consumer Staples—10.5% | | | | | |

PepsiCo, Inc. | | 24,105 | | | 1,563 |

Wal Mart De Mexico—ADR | | 11,160 | | | 420 |

Walgreen Co. | | 21,575 | | | 939 |

| | | | | |

| | | | | 2,922 |

| | | | | |

*Non-income producing securities

ADR = American Depository Receipt

† = U.S. listed foreign security

VRN = Variable Rate Note

| | | | | | | |

Issuer | | Shares or

Principal

Amount | | Value | |

| | |

Common Stocks—(continued) | | | | | | | |

Health Care—10.2% | | | | | | | |

Allergan, Inc. | | | 9,700 | | $ | 559 | |

C. R. Bard, Inc. | | | 6,425 | | | 531 | |

*Genentech, Inc. | | | 12,570 | | | 951 | |

*Gilead Sciences, Inc. | | | 20,310 | | | 787 | |

| | | | | | | |

| | | | | | 2,828 | |

| | | | | | | |

Energy—7.4% | | | | | | | |

Apache Corporation | | | 5,050 | | | 412 | |

Schlumberger Limited† | | | 11,375 | | | 966 | |

Suncor Energy, Inc.† | | | 7,595 | | | 683 | |

| | | | | | | |

| | | | | | 2,061 | |

| | | | | | | |

Materials—4.2% | | | | | | | |

Praxair, Inc. | | | 16,150 | | | 1,163 | |

| | | | | | | |

Total Common Stock—95.3%

(cost $22,800) | | | 26,533 | |

| | | | | | | |

| | |

Investment in Affiliate | | | | | | | |

William Blair Ready Reserves Fund | | | 238,607 | | | 239 | |

| | | | | | | |

Total Investment in Affiliate—0.9%

(cost $239) | | | 239 | |

| | | | | | | |

| | |

Short-Term Investment | | | | | | | |

Prudential Funding Demand Note, VRN 5.305%, due 7/2/07 | | $ | 1,040,000 | | | 1,040 | |

| | | | | | | |

Total Short-Term Investment—3.7%

(cost $1,040) | | | 1,040 | |

| | | | | | | |

| | |

Repurchase Agreement | | | | | | | |

IBT Repurchase Agreement, 4.50% dated 6/29/2007, due 7/2/2007, repurchase price $557, collateralized

by SBA Pool # 503694 | | $ | 556,652 | | | 557 | |

| | | | | | | |

Total Repurchase Agreement—2.0%

(cost $557) | | | 557 | |

| | | | | | | |

Total Investments—101.9%

(cost $24,636) | | | 28,369 | |

Liabilities, plus cash and other assets—(1.9)% | | | (530 | ) |

| | | | | | | |

Net assets—100.0% | | $ | 27,839 | |

| | | | | | | |

See accompanying Notes to Financial Statements.

16 Semi-Annual Report | June 30, 2007 |

Karl W. Brewer

Colin J. Williams

SMALL CAP GROWTH FUND

The Small Cap Growth Fund invests primarily in common stocks of small domestic growth companies that the Advisor expects to have solid growth in earnings.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform in the first six months of 2007? How did the Fund’s performance compare to its benchmark?

The William Blair Small Cap Growth Fund gained 8.97% on a total return basis (Class N shares) during the first six months of 2007. By comparison the Fund’s benchmark, the Russell 2000® Growth Index, increased 9.33%.

What were the most significant factors impacting Fund performance? What factors were behind the Fund’s performance versus the benchmark?

The domestic equity market posted a sizeable return during the first half of 2007. Small caps finished just behind mid caps as the strongest group along the market cap spectrum. Within the small cap market spectrum, while the entire small cap growth universe performed well, the largest quintile of market cap companies performed significantly better than the rest of the space. From a style perspective within the small cap space, growth stocks have outperformed their value peers by over 5% thus far in 2007. This style dynamic has been maintained since the Federal Reserve stopped raising interest rates in August of 2006.

Although the market turned in positive results during the first quarter, the bulk of the year’s return came during the second quarter. The year began relatively slow during January and February as many companies guided Wall Street to lower earnings growth expectations for the coming year. This brief skittishness culminated in a short lived market sell-off prompted by rising sub-prime mortgage defaults, a fall off in housing starts and a correction in the Chinese stock market that made investors question the strength in the global economy and financial markets. However, the domestic market sell-off was relatively modest and short-lived as the market rebounded in March and maintained that momentum throughout the second quarter. This momentum was helped by increasingly encouraging data points about the global economy and the US industrial economy outside of residential real estate. The market strength was also aided by a continued robust environment for mergers and acquisitions and corporate stock repurchase programs.

The Small Cap Growth Fund narrowly underperformed the Russell 2000® Growth Index during the first half of 2007. One of the main reasons for the Fund’s benchmark-like performance was its smaller average market capitalization than the benchmark. We discussed earlier that larger was better within small capitalization stocks. As we have said in the past, we often like to find under-followed and misunderstood companies in our quality growth research process. This typically positions us overweight the smallest market cap quintile within the Russell 2000® Growth Index, and underweight the largest market cap quintile – both of which detracted from relative performance. From a sector perspective, negative stock selection in the Consumer Discretionary and Industrials sectors were the leading detractors. Strong stock selection in the Financials and Consumer Staples sectors was the largest positive contributor to relative performance.

What were among the best performing investments for the Fund?

Two of the best performing stocks during the period were Laureate Education and WebEx Communications.

June 30, 2007 | William Blair Funds 17 |

Laureate Education is a leader in the post secondary education market. The company operates online and campus-based institutions both in the US and abroad. During January, Laureate announced that it would be taken private at a premium to its then current stock price by a consortium of investors led by their CEO, Doug Becker, and several private equity firms.

WebEx is the leading web collaboration services company. The stock experienced two legs of appreciation during the early part of 2007. First, the company released an impressive earnings report in early February and, at the same time, increased forward revenue and earnings expectations. However, the main driver of the stock’s solid first quarter return was Cisco Systems’ announcement that they would be acquiring the company.

What were among the weakest performing investments for the Fund?

Two of the worst performing stocks during the period were Rackable Systems and Santarus.

Rackable Systems sells computer servers and data storage systems to corporate customers. During the quarter, the company pre-announced that revenues and earnings would come in below expectations. This was mainly due to a large competitor in the server market undercutting Rackable on price which caused the company to lose one of their largest customers. We sold the position due to the significant change in the company’s growth outlook.

Santarus is a specialty pharmaceutical company primarily focused on the treatment of acid reflux disease and the associated ailments. Although the number of prescriptions written for their main drug, Zegerid, was encouraging, pricing was worse than expected. Revenue was therefore lower than anticipated and the stock moved lower on the uncertainty of pricing going forward. We continue to own the stock and feel that management’s investment in their direct sales force should improve sales as we look forward a few quarters.

What is your current outlook?

In May as the economy seemed to be stronger than most expected, interest rates began to move higher on fears that the Federal Reserve may have to move interest rates higher to preempt any pick up in inflation. The relatively flat market returns experienced during June would suggest investors are still concerned about the potential inflationary effects of the current economic strength. However, core inflation remains at a reasonable level and we remain—as we have for the past few quarters—in a balance of healthy economic activity and moderate inflation. The consumer remains arguably the largest risk to the economy and equity markets. With higher energy prices, continued weakness in housing activity and rising defaults in the sub-prime mortgage market, pressure on consumer spending remains significant. Fortunately, employment trends remain solid and should help offset weakness related to housing for now. Regardless of the macro issues facing the market, we continue to find high quality stocks that offer attractive growth opportunities. We believe that as overall earnings growth becomes less broad-based, investors will rotate to stocks with more company specific and sustainable growth initiatives.

Is there any other news with respect to the Fund?

With respect to illiquid securities in the Fund, there are five companies for which we hold illiquid securities or warrants. These securities amounted to roughly 2.2% of the Fund as of June 30, 2007. The Fund holds common stock and warrants to buy common stock of Motorcar Parts of America, an auto parts company. The common shares and those shares underlying the warrants are expected to become freely tradable by the end of 2007. Likewise, the Fund’s shares of BancTec are expected to become freely tradable by the end of the year. BancTec provides automation solutions to the retail banking industry. Shares of Kona Grill, a restaurant company, were purchased in two private transactions during 2006 and remain illiquid. The Fund’s Pricing Committee and Valuation Committee are currently pricing these securities at fair value.

18 Semi-Annual Report | June 30, 2007 |

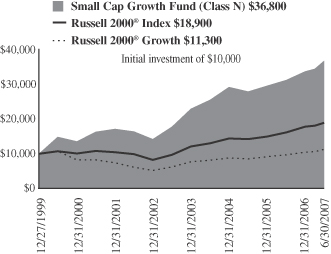

Small Cap Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 6/30/2007

| | | | | | | | | | | | | | |

| | | Year

to Date | | | 1 Year | | | 3

Year | | | 5

Year | | | Since Inception(a) |

Small Cap Growth Fund Class N | | 8.97 | % | | 17.49 | % | | 12.80 | % | | 17.52 | % 18.88% | | |

Small Cap Growth Fund Class I | | 9.14 | | | 17.85 | | | 13.12 | | | 17.82 | | | 19.17 |

Russell 2000®

Growth Index | | 9.33 | | | 16.83 | | | 11.76 | | | 13.08 | | | 1.66 |

Russell 2000® Index | | 6.45 | | | 16.43 | | | 13.45 | | | 13.88 | | | 8.83 |

| | (a) | | For the period from December 27, 1999 to June 30, 2007. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. Investing in smaller companies involves special risks, including higher volatility and lower liquidity. From time to time, the investment advisor may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 2000® Growth Index consists of small-capitalization companies with above average price-to-book ratios and forecasted growth rates.

The Russell 2000® Index is an unmanaged composite of the smallest 2000 stocks of the Russell 3000® Index.

This report identifies the Fund’s investments on June 30, 2007. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

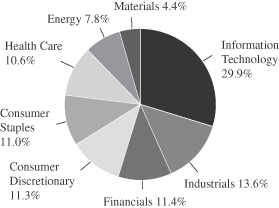

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

June 30, 2007 | William Blair Funds 19 |

Small Cap Growth Fund

Portfolio of Investments, June 30, 2007 (all dollar amounts in thousands)

| | | | | |

Issuer | | Shares | | Value |

| | |

Common Stocks | | | | | |

Information Technology—29.4% | | | | | |

*Access Integrated Technologies, Inc. | | 2,213,981 | | $ | 17,911 |

*CyberSource Corporation | | 480,100 | | | 5,790 |

*DTS, Inc. | | 956,740 | | | 20,828 |

*EarthLink, Inc. | | 2,053,038 | | | 15,336 |

*Euronet Worldwide, Inc. | | 1,278,782 | | | 37,289 |

*GigaMedia Limited† | | 2,030,547 | | | 27,372 |

*j2 Global Communications, Inc. | | 952,847 | | | 33,254 |

*MathStar, Inc. | | 2,708,904 | | | 4,172 |

*Miva, Inc. | | 1,141,513 | | | 7,420 |

*Monolithic Power Systems | | 744,248 | | | 12,987 |

*Nuance Communications, Inc. | | 1,149,944 | | | 19,238 |

*Optimal Group, Inc.† | | 2,859,908 | | | 21,592 |

Patni Computer Systems Limited—ADR | | 151,453 | | | 3,818 |

*PDF Solutions, Inc. | | 1,283,793 | | | 15,187 |

*Silicon Laboratories, Inc. | | 604,091 | | | 20,908 |

*Skillsoft, plc—ADR | | 1,883,815 | | | 17,501 |

*Think Partnership, Inc. | | 4,626,270 | | | 13,833 |

*Transaction Systems Architect, Inc. | | 416,619 | | | 14,023 |

*Ultimate Software Group, Inc. | | 519,585 | | | 15,032 |

*VistaPrint Limited† | | 250,805 | | | 9,593 |

*Volterra Semiconductor Corporation | | 1,856,618 | | | 26,364 |

*Website Pros, Inc. | | 1,331,800 | | | 12,546 |

*WNS Holdings Limited—ADR | | 773,079 | | | 22,002 |

*Xyratex Ltd† | | 599,973 | | | 13,337 |

| | | | | |

| | | | | 407,333 |

| | | | | |

Health Care—27.3% | | | | | |

*Air Methods Corporation | | 983,803 | | | 36,076 |

*American Medical Systems Holdings, Inc. | | 1,166,917 | | | 21,051 |

*Axcan Pharma, Inc.† | | 1,587,690 | | | 30,690 |

*Capital Senior Living Corporation | | 1,247,946 | | | 11,756 |

*DJO, Inc. | | 360,358 | | | 14,872 |

*Healthways, Inc. | | 506,540 | | | 23,995 |

*Hythiam, Inc. | | 1,802,434 | | | 15,591 |

*Integra Lifesciences Holdings Corporation | | 563,254 | | | 27,836 |

*Iris International, Inc. | | 482,281 | | | 8,122 |

*Kensey Nash Corporation | | 305,400 | | | 8,188 |

*Kyphon, Inc. | | 378,536 | | | 18,226 |

*LifeCell Corporation | | 534,477 | | | 16,323 |

*Lifecore Biomedical, Inc. | | 1,095,112 | | | 17,379 |

*Providence Service Corporation | | 821,861 | | | 21,960 |

*PSS World Medical, Inc. | | 629,099 | | | 11,462 |

*Psychiatric Solutions, Inc. | | 430,078 | | | 15,595 |

*Sangamo Biosciences, Inc. | | 918,074 | | | 7,455 |

*Santarus, Inc. | | 3,631,472 | | | 18,775 |

*Surmodics, Inc. | | 601,437 | | | 30,072 |

*Trinity Biotech plc—ADR | | 1,142,849 | | | 13,268 |

*Zila, Inc. | | 7,237,388 | | | 10,060 |

| | | | | |

| | | | | 378,752 |

| | | | | |

Consumer Discretionary—19.2% | | | | | |

*4 Kids Entertainment, Inc. | | 702,478 | | | 10,537 |

*BUCA, Inc. | | 220,429 | | | 772 |

*Century Casinos, Inc. | | 1,566,233 | | | 14,080 |

*Coinstar, Inc. | | 722,124 | | | 22,732 |

*DG Fastchannel, Inc | | 1,126,830 | | | 22,965 |

*Duckwall-ALCO Stores, Inc. | | 405,838 | | | 15,138 |

*Granite City Food & Brewery Ltd. | | 1,372,423 | | | 7,480 |

*Jarden Corporation | | 568,715 | | | 24,460 |

| | | | | |

Issuer | | Shares | | Value |

| | |

Common Stocks—(continued) | | | | | |

Consumer Discretionary—(continued) | | | | | |

*Jos. A. Bank Clothiers, Inc. | | 304,412 | | $ | 12,624 |

*Kona Grill, Inc. | | 322,795 | | | 5,885 |

*Kona Grill, Inc.** (restricted) | | 435,134 | | | 6,417 |

*Laureate Education, Inc. | | 364,253 | | | 22,460 |

*Lions Gate Entertainment Corporation† | | 1,263,532 | | | 13,937 |

*Mertiage Homes Corporation | | 196,244 | | | 5,250 |

*Motorcar Parts of America,

Inc.** (restricted) | | 743,836 | | | 9,086 |

*Select Comfort Corporation | | 839,318 | | | 13,614 |

*Shuffle Master, Inc. | | 694,768 | | | 11,533 |

*Smith & Wesson Holdings | | 344,725 | | | 5,774 |

Standard Pacific Corporation | | 598,403 | | | 10,490 |

Strayer Education, Inc. | | 116,506 | | | 15,345 |

*ValueVision Media, Inc., Class “A” | | 1,444,377 | | | 16,350 |

| | | | | |

| | | | | 266,929 |

| | | | | |

Industrials—9.2% | | | | | |

*American Reprographics Company | | 433,384 | | | 13,344 |

Frozen Food Express Industries, Inc. | | 902,303 | | | 9,149 |

*GEO Group, Inc. | | 921,246 | | | 26,808 |

*Hudson Highland Group, Inc. | | 301,635 | | | 6,452 |

*InnerWorkings, Inc. | | 1,679,752 | | | 26,910 |

*Kforce, Inc. | | 1,219,650 | | | 19,490 |

*Mobile Mini, Inc. | | 450,564 | | | 13,156 |

*NCI Building Systems, Inc. | | 254,908 | | | 12,575 |

| | | | | |

| | | | | 127,884 |

| | | | | |

Financials—7.7% | | | | | |

*Banctec, Inc.** (restricted) | | 1,809,982 | | | 14,480 |

*First Cash Financial Services, Inc. | | 569,889 | | | 13,358 |

*FirstService Corporation† | | 545,721 | | | 19,657 |

*Marlin Business Services Corporation | | 832,213 | | | 17,734 |

National Financials Partners Corporation | | 468,450 | | | 21,694 |

*Signature Bank New York | | 601,373 | | | 20,507 |

| | | | | |

| | | | | 107,430 |

| | | | | |

Energy—4.4% | | | | | |

*Carrizo Oil & Gas, Inc. | | 86,397 | | | 3,583 |

*Edge Petroleum Corporation | | 699,054 | | | 9,794 |

*Oil States International, Inc. | | 422,192 | | | 17,453 |

*Petrohawk Energy Corporation | | 1,877,867 | | | 29,783 |

| | | | | |

| | | | | 60,613 |

| | | | | |

Consumer Staples—0.9% | | | | | |

*Overhill Farms, Inc. | | 1,903,720 | | | 10,699 |

*Physicians Formula Holdings, Inc. | | 132,220 | | | 2,079 |

| | | | | |

| | | | | 12,778 |

| | | | | |

Total Common Stock—98.1%

(Total Cost $1,169,503) | | | 1,361,719 |

| | | | | |

| | |

Investment in Warrants | | | | | |

*Motorcar Parts of America, Inc.** | | 111,575 | | | — |

*Think Partnership, Inc., 2011, $2.50** | | 1,424,000 | | | 698 |

*Think Partnership, Inc., 2011, $3.05** | | 448,409 | | | — |

*Think Partnership, Inc., 2011, $4.00** | | 224,205 | | | — |

*Zila, Inc., 2011, $2.21** | | 2,271,528 | | | — |

| | | | | |

Total Investment in Warrants—0.1%

(cost $0) | | | 698 |

| | | | | |

See accompanying Notes to Financial Statements.

20 Semi-Annual Report | June 30, 2007 |

Small Cap Growth Fund

Portfolio of Investments, June 30, 2007 (all dollar amounts in thousands) (unaudited)

| | | | | | |

Issuer | | Shares or

Principal

Amount | | Value |

| | |

Investment in Affiliate | | | | | | |

William Blair Ready Reserves Fund | | | 5,496,989 | | $ | 5,497 |

| | | | | | |

Total Investment in Affiliate—0.4%

(cost $5,497) | | | 5,497 |

| | | | | | |

| | |

Short-Term Investments | | | | | | |

American Express Demand Note, VRN

5.170%, due 7/2/07 | | $ | 3,110,000 | | | 3,110 |

Prudential Funding Demand Note, VRN

5.305%, due 7/2/07 | | | 2,702,000 | | | 2,702 |

| | | | | | |

Total Short-Term Investments—0.4%

(cost $5,812) | | | 5,812 |

| | | | | | |

*Non-income producing securities

ADR = American Depository Receipt

† = U.S. listed foreign security

VRN = Variable Rate Note

** = Fair valued pursuant to Valuation Procedures adopted by the Board of Trustees. The holdings represents 2.2% of the Fund’s net assets at June 30, 2007. These securities were also deemed illiquid pursuant to Liquidity Procedures approved by Board of Trustees.

| | | | | | |

Issuer | |

Principal

Amount | | Value |

| | |

Repurchase Agreement | | | | | | |

Investors Bank & Trust Company, 4.50% dated 6/29/2007, due 7/02/2007, repurchase price $8,645, collateralized by SBA Pool #506485 | | $ | 8,641,962 | | $ | 8,642 |

| | | | | | |

Total Repurchase Agreement—0.6%

(cost $8,642) | | | 8,642 |

| | | | | | |

Total Investments—99.6%

(cost $1,189,454) | | | 1,382,368 |

Cash and other assets, less liabilities—0.4% | | | 5,678 |

| | | | | | |

Net assets—100.0% | | $ | 1,388,046 |

| | | | | | |

If a Fund’s portfolio holding represents ownership of 5% or more of the voting securities of a company, the company is deemed to be an affiliate as defined in the Investment Company Act of 1940. The Small Cap Growth Fund had the following transactions during the period ended June 30, 2007 with affiliated companies:

| | | | | | | | | | | | | | |

| | | Share Activity | | Period Ended

June 30, 2007 |

| | | | | | | | | | | (in thousands) |

Security Name | | Balance

12/31/2006 | | Purchases | | Sales | | Balance

6/30/2007 | | Value | | Dividends

Included

in Income |

4 Kids Entertainment, Inc. | | 696,575 | | 23,800 | | 17,897 | | 702,478 | | $ | 10,537 | | $ | — |

Access Integrated Technologies, Inc. | | 1,530,387 | | 740,427 | | 56,833 | | 2,213,981 | | | 17,911 | | | — |

Century Casinos, Inc. | | 1,546,133 | | 75,400 | | 56,300 | | 1,565,233 | | | 14,080 | | | — |

DG Fastchannel, Inc | | 971,150 | | 555,237 | | 399,557 | | 1,126,830 | | | 22,965 | | | — |

Duckwall-ALCO Stores, Inc. | | 325,133 | | 80,705 | | — | | 405,838 | | | 15,138 | | | — |

Frozen Food Express Industries, Inc. | | 894,816 | | 30,400 | | 22,913 | | 902,303 | | | 9,149 | | | 28 |

Granite City Food & Brewery, Ltd. | | — | | 1,372,423 | | — | | 1,372,423 | | | 7,480 | | | — |

Kona Grill, Inc. | | 764,729 | | — | | 6,800 | | 757,929 | | | 12,302 | | | — |

Lifecore Biomedical, Inc. | | 1,117,713 | | 29,700 | | 52,301 | | 1,095,112 | | | 17,379 | | | — |

Marlin Business Services Corp. | | 756,915 | | 96,400 | | 21,102 | | 832,213 | | | 17,734 | | | — |

Optimal Group, Inc. | | 2,150,379 | | 780,542 | | 71,013 | | 2,859,908 | | | 21,592 | | | — |

Overhill Farms, Inc. | | 1,903,720 | | — | | — | | 1,903,720 | | | 10,699 | | | — |