UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-5344

William Blair Funds

(Exact name of registrant as specified in charter)

| | |

| 222 West Adams Street, Chicago, IL | | 60606 |

| (Address of principal executive offices) | | (Zip Code) |

Michelle R. Seitz

William Blair Funds

222 West Adams Street, Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: 312-236-1600

Date of fiscal year end: December 31

Date of reporting period: June 30, 2008

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A Registrant is not required to respond to the collection of information contained in Form N-CSR unless the form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimates and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. (ss) 3507.

| Item 1. | June 30, 2008 Semi Annual Reports transmitted to shareholders. |

Table of Contents

This report is submitted for the general information of the shareholders of the William Blair Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by a prospectus of the William Blair Funds. Please carefully consider the Funds’ investment objectives, risks, charges, and expenses before investing. This and other information is contained in the Funds’ prospectus, which you may obtain by calling 1-800-742-7272. Read it carefully before you invest or send money.

June 30, 2008 | William Blair Funds 1 |

PERFORMANCE AS OF JUNE 30, 2008—CLASS N SHARES (unaudited)

| | | | | | | | | | | | | | | | | | |

| | | Year to

Date | | | 1 Yr. | | | 3 Yr. | | | 5 Yr. | | 10 Yr

(or since

inception) | | | Inception

Date | | Overall

Morningstar

Rating |

Growth Fund | | (7.09 | ) | | (2.54 | ) | | 9.33 | | | 9.49 | | 2.86 | | | 3/20/1946 | | ««««

Among 1,488 large growth Funds |

Morningstar Large Growth | | (10.38 | ) | | (6.02 | ) | | 5.88 | | | 7.81 | | 2.61 | | | | |

Russell 3000® Growth | | (9.04 | ) | | (6.38 | ) | | 5.93 | | | 7.56 | | 1.08 | | | | |

Standard & Poor’s 500 | | (11.91 | ) | | (13.12 | ) | | 4.41 | | | 7.58 | | 2.88 | | | | | |

| | | | | | | |

Tax-Managed Growth Fund | | | | | | | | | | | | | | | | | | |

Return before Taxes | | (8.98 | ) | | (6.81 | ) | | 6.44 | | | 8.07 | | 1.07 | | | 12/27/1999 | | «««

Among 1,488 large growth Funds |

After Taxes on Distributions | | (8.98 | ) | | (6.81 | ) | | 6.44 | | | 8.07 | | 1.07 | | | | |

After Taxes on distributions and Sale of Fund Shares | | (5.84 | ) | | (4.43 | ) | | 5.52 | | | 7.00 | | 0.92 | | | | |

Morningstar Large Growth | | (10.38 | ) | | (6.02 | ) | | 5.88 | | | 7.81 | | — | | | | | |

Russell 3000® Growth | | (9.04 | ) | | (6.38 | ) | | 5.93 | | | 7.56 | | (3.48 | ) | | | | |

| | | | | | | |

Large Cap Growth Fund | | (8.51 | ) | | (5.49 | ) | | 3.92 | | | 5.60 | | (4.29 | ) | | 12/27/1999 | | ««

Among 1,488 large growth Funds |

Morningstar Large Growth | | (10.38 | ) | | (6.02 | ) | | 5.88 | | | 7.81 | | — | | | | |

Russell 1000® Growth | | (9.06 | ) | | (5.96 | ) | | 5.91 | | | 7.32 | | (3.77 | ) | | | |

| | | | | | | |

Small Cap Growth Fund | | (16.35 | ) | | (24.89 | ) | | (0.47 | ) | | 9.25 | | 12.65 | | | 12/27/1999 | | «««

Among 705 small growth Funds |

Morningstar Small Growth | | (11.63 | ) | | (13.94 | ) | | 4.10 | | | 9.24 | | — | | | | |

Russell 2000® Growth | | (8.93 | ) | | (10.83 | ) | | 6.08 | | | 10.37 | | 0.11 | | | | |

Russell 2000® | | (9.37 | ) | | (16.19 | ) | | 3.79 | | | 10.29 | | 5.54 | | | | | |

| The Small Cap Growth Fund’s Performance during 2000 was primarily attributable to investments in initial public offerings (IPOs) during a rising market. Since then, IPOs have had an insignificant effect on the Fund’s performance. | | | | | | | | | | |

| | | | | | | |

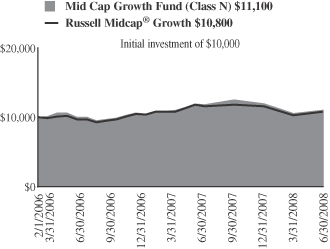

Mid Cap Growth Fund | | (7.49 | ) | | (6.09 | ) | | — | | | — | | 4.38 | | | 2/1/2006 | | Not rated. |

Morningstar Mid-Cap Growth | | (8.88 | ) | | (6.53 | ) | | — | | | — | | — | | | | | |

Russell Mid® Cap Growth | | (6.81 | ) | | (6.42 | ) | | — | | | — | | 3.35 | | | | | |

| | | | | | | |

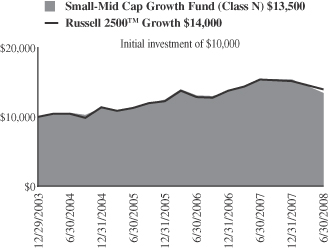

Small-Mid Cap Growth Fund | | (12.37 | ) | | (13.09 | ) | | 6.32 | | | — | | 6.84 | | | 12/29/2003 | | «««

Among 813 mid-cap growth funds |

Morningstar Mid-Cap Growth | | (8.88 | ) | | (6.53 | ) | | 7.85 | | | — | | — | | | | |

Russell 2500™ Growth | | (7.86 | ) | | (9.20 | ) | | 7.40 | | | — | | 7.69 | | | | |

| | | | | | | |

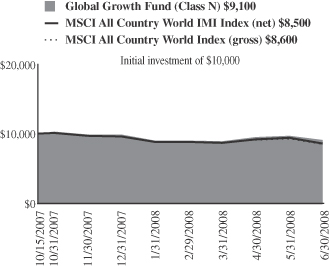

Global Growth Fund | | (7.79 | ) | | — | | | — | | | — | | (8.80 | ) | | 10/15/2007 | | Not rated. |

Morningstar World Stock | | (11.11 | ) | | — | | | — | | | — | | — | | | | | |

MSCI All Country World IMI (net) | | (10.62 | ) | | — | | | — | | | — | | (14.59 | ) | | | | |

MSCI All Country World (gross) | | (10.41 | ) | | — | | | — | | | — | | (14.08 | ) | | | | |

| | | | | | | |

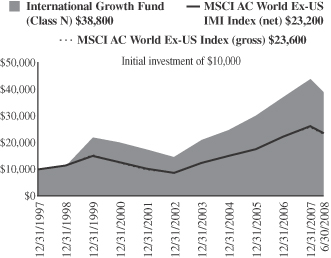

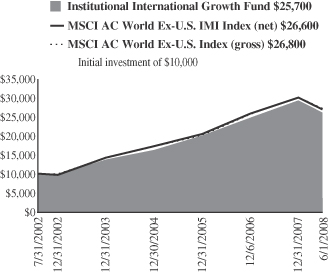

International Growth Fund | | (11.64 | ) | | (6.52 | ) | | 15.47 | | | 18.83 | | 12.93 | | | 10/1/1992 | | ««««

Among 182 foreign large growth funds |

Morningstar Foreign Large Growth | | (10.77 | ) | | (6.20 | ) | | 14.72 | | | 16.10 | | 5.54 | | | | |

MSCI All Country World Ex-U.S. IMI (net) | | (10.33 | ) | | (7.46 | ) | | 15.52 | | | 19.14 | | 7.65 | | | | |

MSCI All Country World Ex-U.S. (gross) | | (9.84 | ) | | (6.20 | ) | | 16.16 | | | 19.42 | | 7.73 | | | | | |

| | | | | | | |

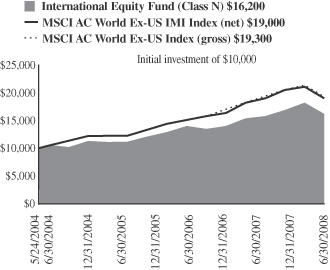

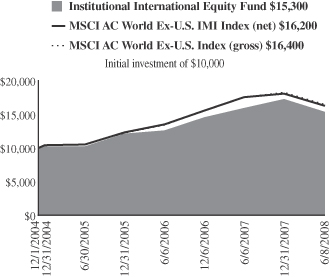

International Equity Fund | | (11.01 | ) | | (4.34 | ) | | 12.99 | | | — | | 12.36 | | | 5/24/2004 | | ««

Among 182 foreign large growth funds |

Morningstar Foreign Large Growth | | (10.77 | ) | | (6.20 | ) | | 14.72 | | | — | | — | | | | |

MSCI All Country World Ex-U.S. IMI (net) | | (10.33 | ) | | (7.46 | ) | | 15.52 | | | — | | 16.80 | | | | |

MSCI All Country World Ex-U.S. (gross) | | (9.84 | ) | | (6.20 | ) | | 16.16 | | | — | | 17.22 | | | | | |

Please see the next page for important disclosure information.

2 Semi-Annual Report | June 30, 2008 |

PERFORMANCE AS OF JUNE 30, 2008—CLASS N SHARES—CONTINUED (unaudited)

| | | | | | | | | | | | | | | | |

| | | Year to

Date | | | 1 Yr. | | | 3 Yr. | | 5 Yr. | | 10 Yr

(or since

inception) | | Inception

Date | | Overall

Morningstar

Rating |

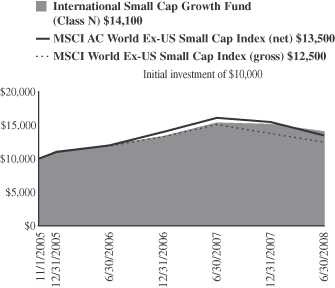

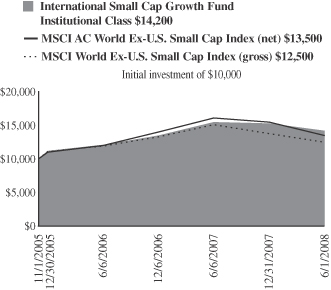

International Small Cap Growth Fund | | (7.30 | ) | | (8.35 | ) | | — | | — | | 13.66 | | 11/1/2005 | | Not rated. |

Morningstar Foreign Small/Mid Growth | | (10.72 | ) | | (12.45 | ) | | — | | — | | — | | | | |

MSCI All Country World Small Cap Ex-U.S. (net) | | (12.39 | ) | | (15.91 | ) | | — | | — | | 11.99 | | | | |

MSCI World Small Cap Ex-U.S. (gross) | | (9.50 | ) | | (17.04 | ) | | — | | — | | 8.52 | | | | |

| | | | | | | |

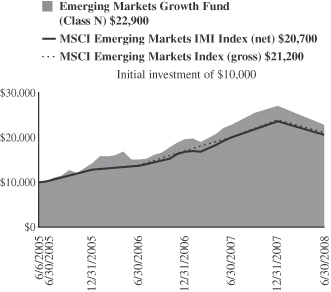

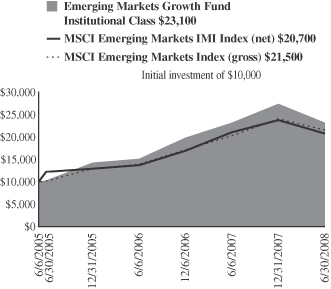

Emerging Markets Growth Fund | | (15.51 | ) | | (0.12 | ) | | 30.64 | | — | | 30.85 | | 6/6/2005 | | «««««

Among 217 diversified emerging

market funds |

Morningstar Diversified Emerging Markets | | (11.60 | ) | | 2.27 | | | 25.92 | | — | | — | | | |

MSCI Emerging Markets IMI (net) | | (12.75 | ) | | 2.76 | | | 26.50 | | — | | 26.55 | | | |

MSCI Emerging Markets (gross) | | (11.64 | ) | | 4.89 | | | 27.52 | | — | | 27.60 | | | |

| A portion of the Emerging Markets Growth Fund’s performance since inception is attributable to an investment in an initial public offering. (IPO) | | | | | | | | |

| | | | | | | |

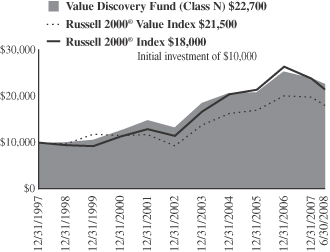

Value Discovery Fund | | (5.66 | ) | | (16.28 | ) | | 4.59 | | 8.87 | | 7.53 | | 12/23/1996 | | «««

Among 331 small value funds |

Morningstar Small Value | | (8.41 | ) | | (19.82 | ) | | 1.74 | | 9.75 | | 7.64 | | | |

Russell 2000® Value | | (9.84 | ) | | (21.63 | ) | | 1.39 | | 10.02 | | 7.47 | | | |

Russell 2000® | | (9.37 | ) | | (16.19 | ) | | 3.79 | | 10.29 | | 5.53 | | | | |

| | | | | | | |

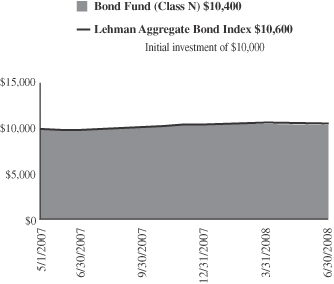

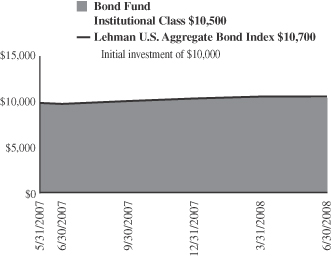

Bond Fund | | 0.86 | | | 5.48 | | | — | | — | | 3.65 | | 5/1/2007 | | Not rated. |

Morningstar Intermediate-Term Bond | | (0.73 | ) | | 3.38 | | | — | | — | | — | | | | |

Lehman Aggregate Bond Index | | 1.13 | | | 7.12 | | | — | | — | | 5.15 | | | | |

| | | | | | | |

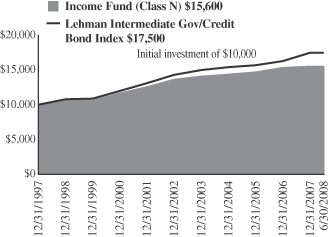

Income Fund | | (0.13 | ) | | 0.50 | | | 1.85 | | 2.03 | | 4.18 | | 10/1/1990 | | «««

Among 381 short-term bond funds |

Morningstar Short-term Bond | | (0.42 | ) | | 2.21 | | | 2.78 | | 2.26 | | 4.10 | | | |

Lehman Intermediate Govt./Credit | | 1.43 | | | 7.37 | | | 4.26 | | 3.48 | | 5.54 | | | |

Bond Index | | | | | | | | | | | | | | | | |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Returns shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or a loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment advisor may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Investing in smaller companies involves special risks, including higher volatility and lower liquidity. International and emerging markets investing involves special risk considerations, including currency fluctuations, lower liquidity, economic and political risk. As interest rates rise, bond prices will fall and bond funds become more volatile. Class N shares are available to the general public without a sales load. Emerging Leaders Growth Fund does not offer a Class N share.

Tax-Managed Growth Fund’s after-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Actual after-tax returns depend on the investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown only for Class N and the after-tax returns for Class N shares will vary.

Morningstar Ratings TM are as of 6/30/2008 and are subject to change every month. The ratings are based on a risk-adjusted return measure that accounts for variation in a fund’s monthly performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each Category receive 5 stars, the next 22.5% receive 4 stars, the middle 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a fund is derived from a weighted-average of the performance figures associated with its three-, five- and ten-year (if applicable) Morningstar Rating metrics. The 3/5/10 year Morningstar ratings were as follows: Growth Fund ««««/« «««/«««, Tax-Managed Growth Fund «««/«««/NA, and Large Cap Growth Fund «««/««/NA, out of 1,433/1,215/589 large growth funds; Small Cap Growth Fund ««/«««/NA out of 705/571/NA small growth funds; Small-Mid Cap Growth Fund «««/NA/NA out of 813/NA/NA mid cap growth funds; Value Discovery Fund «« ««/««/««« out of 331/265/108 small value funds; International Growth Fund «««/««««/««««« and International Equity Fund ««/NA/NA out of 182/157/75 foreign large growth funds; Income Fund ««/««/««« out of 381/303/164 short-term bond funds.

Please carefully consider the Funds’ investment objectives, risks, charges, and expenses before investing. This and other information is contained in the Funds’ prospectus, which you may obtain by calling 1-800-742-7272. Read it carefully before you invest or send money.

June 30, 2008 William Blair Funds 3 | |

David C. Fording

John F. Jostrand

GROWTH FUND

The Growth Fund invests primarily in common stocks of domestic growth companies that the Advisor expects to have sustainable, above-average growth from one business cycle to the next.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform over the first half of the year? How did the Fund’s performance compare to its benchmark?

In a difficult market environment, the Growth Fund declined but outperformed its Russell 3000® Growth Index benchmark in the first half of 2008. The Growth Fund (Class N Shares) had results of (7.09)% and the Russell 3000® Growth Index returned (9.04)% for the six-month period ended June 30, 2008.

What were the most significant factors impacting Fund performance?

So far in 2008, U.S. equity markets have been greatly challenged by much uncertainty and high volatility in response to the continued financial credit crisis and significant write-downs as well as continued consumer weakness with reports of rising gas and food costs, increasing unemployment, tightening lending standards and elevated levels of credit and mortgage delinquencies. In this environment, most broad equity markets indices traded near bear market levels (e.g. down 20% from recent highs); the most notable was the Dow Jones Industrial Average. For the period, the S&P 500 Index fell (11.91)%.

Also, impacting equity results were investors’ concerns which shifted from slowing economic growth to rising inflation. The price of oil surged to record levels of around $140 per barrel as demand remained high especially from emerging markets; also, supply issues surfaced and speculation from investors rose as many looked to oil as an inflationary hedge or an alternative to U.S. dollar investments or the risky credit markets. With high energy prices, consumers spend less on goods and services and products cost more due to higher input and transportation costs. So far, some oil demand destruction has occurred, but it has yet to impact the price of oil. Other commodities also saw new highs on supply issues including coal, with high emerging market demand, as well as corn and soy due to stormy weather conditions in the Midwest. As a result, inflation levels have risen globally and are expected to continue if commodity prices remain on their current trend. Some U.S. investors fear the current low interest rate levels—in place to stimulate the economy—may need to increase in order to curb inflation. Additionally, several countries outside the U.S., particularly emerging markets, have begun to raise interest rate levels in an attempt to slowdown inflation.

Another ongoing factor is U.S. economic growth which has slowed and is expected to remain slow into 2009 according to many pundits. GDP growth for the first quarter of 2008 was reported at 1.0% which was slightly higher than the fourth quarter 2007 at 0.6%. The Federal Reserve continued to cut rates into the second quarter in order to stimulate economic growth; the Federal Funds rate was cut 25 basis points to 2.0% in April followed by a pause at their June meeting. The Federal Reserve’s actions, such as lowering interest rates and liquidity injections, helped to prevent a collapse in the financial markets, but did little to promote growth and were more than offset by the substantial increases in energy, raw materials and food prices as well as rising credit spreads. Among experts it still remains debatable whether the U.S. economy will enter a recession in 2008; however, with oil trading at elevated levels, the risk of recession is on the rise in the U.S. and abroad.

4 Semi-Annual Report | June 30, 2008 |

For the first six months of the year, growth stocks held up better than value stocks; the Russell 3000® Growth Index was down (9.04)% while the Russell 3000® Value Index was down (13.28)%. A lower weighting in the Financial Services sector (which did poorly) and a larger weighting in Information Technology (which did well) assisted the Fund’s return relative to its benchmark. On market capitalization, mid-cap growth stocks did better on a relative basis than small- and large-cap growth stocks; the Russell Midcap® Growth Index fell (6.81)% while Russell 1000® Growth Index fell (9.06)% and Russell 2000® Growth Index fell (8.93)%. In regard to sectors on an absolute performance basis, there were only two positive groups in the Russell 3000® Growth Index—Energy and Materials; therefore, the opportunity for a well diversified portfolio, like ours, to be positive in the period was very difficult. The worst sectors were Financials and Consumer Discretionary as you might expect given the comments above.

Which sectors enhanced the Fund’s return? What were among the best performing investments for the Fund?

The portfolio was enhanced in the period by the Information Technology, Health Care and Consumer Staples sectors. Within Information Technology, our stock selection was strong in this relatively weak performing benchmark group. Visa, Inc. was the portfolio’s best performer as it performed well after its recent IPO offering and a strong quarterly report. This firm should benefit from the secular shift to electronic payment methods (credit and debit cards), both here and abroad. As a reminder Visa has no credit risk; rather its principal business is transactional processing. Also, Flir Systems, Inc. gained ground on strong first quarter results across all company segments: Government Systems, Commercial Vision Systems and Thermography. Importantly, they reported a substantial increase in their twelve month order backlog as a result of government spending.

Within Health Care, our stock selection was strong in this weak performing benchmark group. Gilead Sciences, Inc., the leading provider of drugs to treat HIV, gained ground on solid earnings and an announcement that a study on a competing medicine was halted on inferior efficacy and increased detrimental side effects. Pharmaceutical Product Development, Inc., a contract research organization, also did well on solid quarterly earnings. We continue to like this firm’s business in a growing marketplace, their strong management team and expanding product portfolio with the potential for increasing royalty revenue streams. Secondarily, the portfolio was also helped by lack of exposure to HMOs and pharmaceuticals which did poorly.

The third largest sector contributor to results on good stock selection was Consumer Staples. Wal-Mart de Mexico did well on solid sales in a difficult environment. Going forward, we believe this firm is well positioned with attractive square-footage growth, solid same-store transaction increases and efficiency initiatives. Additionally, the portfolio was helped by our lower exposure to weak performing beverage stocks. PepsiCo., Inc. was sold from the portfolio primarily due to relative valuation and growing input cost concerns; we felt there were better opportunities elsewhere.

Were there any investment strategies or themes that did not measure up to your expectations?

Weakness in the portfolio was seen in the Financials, Utilities and Telecommunications sectors. Beginning with Financials—the worst benchmark performer, the portfolio was helped by our underweight; however, our stock selection overshadowed this positive. MF Global fell on the announcement of an internal trading loss which reduced our confidence in the management team and its risk management policies. As a result, this stock was sold from the portfolio. Additionally, much of our exposure includes companies that are beneficiaries of volatility and not those that are credit or interest rate sensitive. In the fourth quarter, the portfolio was assisted significantly from this positioning as the credit crisis unfolded; however, in 2008, investors had concerns over slowing volume growth, potential regulation and took profits in names that had done well in the fourth quarter. As a result, the stock price for IntercontinentalExchange, Inc. came under pressure.

June 30, 2008 | William Blair Funds 5 |

Two other sectors, Utilities and Telecommunication Services, also detracted from results. Each benchmark groups had good relative performance but the portfolio does not own any positions in these small sectors due to a lack of quality growth in our view.

What is your current strategy? How is the Fund positioned?

Given the near bear market status, the broad equity markets have begun to discount current macro conditions in the financial, housing, consumer and commodities markets. However, it is difficult to predict whether additional downside risks remain or when sentiment will turn. While it is challenging to forecast economic events, we believe that growth is likely to remain subdued into 2009 as the financial system and consumer likely have a long work out period ahead.

Going forward, energy prices, global growth, the strength of U.S. financial markets, and the state of consumer confidence will be important issues to watch. Lower energy prices would positively impact consumer pocketbooks, company profit margins and relieve inflationary pressures for central banks; this could be a catalyst for stock market improvement. On global growth, we have seen economies outside the U.S. start to slow including emerging markets countries. However, the degree of slowing in emerging markets will be a critical factor to future global economic growth. Lastly, we will continue to look for repair in the U.S. financial markets and the consumer; positive developments in these groups can signal a change where early cyclical stocks could gain ground.

In this environment, we have not adopted a particularly defensive posture. Instead, we continue to rely on our quality growth investment philosophy and process to steer the portfolio through the current challenging market conditions. We continue to seek high quality growth stocks with attractive long term earnings growth, strong financial position and competitive and sustainable business models which we believe will outperform over time. This investment philosophy generally leads to companies that have somewhat more defensive characteristics during market conditions like those experienced recently, primarily due to more stable business models with better balance sheets. In our view, quality growth opportunities remain readily available and we are taking advantage of increasingly attractive valuation levels to buy stocks that we believe will produce superior long-term returns.

On a positive note, many investors have a significant amount of cash sitting on the sidelines, which could propel the market higher, if and when, the high level of risk aversion recedes. Also, growth continues to outperform value stocks. Large growth stocks have picked up substantial relative ground for the twelve month period ended June 30 2008; Russell 3000® Growth returned (6.38)% while Russell 3000® Value returned (19.02)%. Many investors would be surprised to note that growth stocks now surpass value stocks over the last three years by 2.60% annualized as measured by the Russell 3000® Indexes. With elevated levels of market volatility or a slow growth environment, we believe investors will continue to seek strong, high quality companies which become scarce and thus, more valuable in a challenging period.

6 Semi-Annual Report | June 30, 2008 |

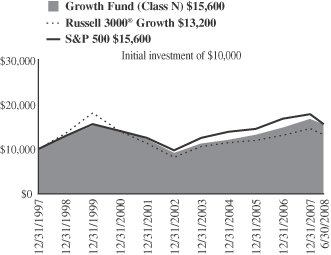

Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 6/30/2008

| | | | | | | | | | | | | | | | | | |

| | | Year to

Date | | | 1 Year | | | 3

Year | | | 5

Year | | | 10

Year | | | Since Inception | |

Growth Fund Class N | | (7.09 | )% | | (2.54 | )% | | 9.33 | % | | 9.49 | % | | 2.86 | % | | — | % |

Growth Fund

Class I | | (6.99 | ) | | (2.31 | ) | | 9.62 | | | 9.80 | | | — | | | 2.54 | (a) |

Russell 3000® Growth Index | | (9.04 | ) | | (6.38 | ) | | 5.93 | | | 7.56 | | | 1.08 | | | (0.93 | )(a) |

S&P 500 Index | | (11.91 | ) | | (13.12 | ) | | 4.41 | | | 7.58 | | | 2.88 | | | 1.65 | (a) |

| | (a) | | For the period from October 1, 1999 to June 30, 2008. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company L.L.C. without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 3000® Growth Index consists of large, medium, and small capitalization companies with above average price-to-book ratios and forecasted growth rates. The index is weighted by market capitalization and large/medium/small companies make up approximately 80%/15%/5% of the index.

The S&P 500 Index indicates broad larger capitalization equity market performance.

This report identifies the Fund’s investments on June 30, 2008. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

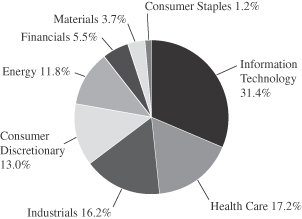

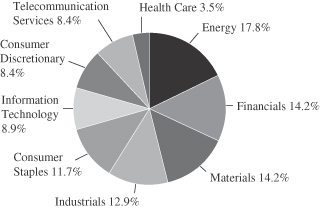

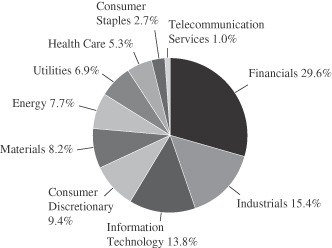

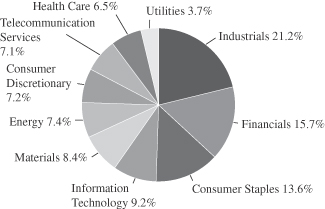

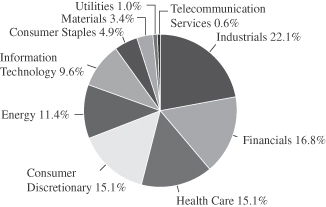

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

June 30, 2008 | William Blair Funds 7 |

Growth Fund

Portfolio of Investments, June 30, 2008 (all dollar amounts in thousands) (unaudited)

| | | | | |

Issuer | |

Shares | | Value |

| | |

Common Stocks | | | | | |

Information Technology—30.3% | | | | | |

Activision, Inc. | | 243,785 | | $ | 8,306 |

*Adobe Systems Incorporated | | 238,549 | | | 9,396 |

*Cisco Systems Inc. | | 636,550 | | | 14,806 |

*Citrix Systems, Inc. | | 124,675 | | | 3,667 |

*Cognizant Technology Solutions Corporation | | 223,790 | | | 7,275 |

*DTS, Inc. | | 96,149 | | | 3,011 |

*Euronet Worldwide, Inc. | | 267,075 | | | 4,514 |

*Flir Systems, Inc. | | 136,310 | | | 5,530 |

*Google Inc. | | 21,905 | | | 11,531 |

*Nuance Communications, Inc. | | 229,945 | | | 3,603 |

Qualcomm Incorporated † | | 277,940 | | | 12,332 |

*Silicon Laboratories, Inc. | | 178,075 | | | 6,427 |

*Visa Inc. | | 54,043 | | | 4,394 |

*VistaPrint Limited † | | 254,933 | | | 6,822 |

*WNS Holdings Limited—ADR | | 209,700 | | | 3,533 |

| | | | | |

| | | | | 105,147 |

| | | | | |

Health Care—16.6% | | | | | |

Allergan Inc. | | 123,900 | | | 6,449 |

*Genentech, Inc. | | 113,410 | | | 8,608 |

*Gilead Sciences, Inc. | | 189,815 | | | 10,051 |

*Healthways, Inc. | | 156,405 | | | 4,630 |

*Hologic, Inc. | | 240,960 | | | 5,253 |

*IDEXX Laboratories, Inc. | | 144,290 | | | 7,033 |

*Integra Lifesciences Holding Corporation | | 111,095 | | | 4,942 |

Pharmaceutical Product Development, Inc. | | 137,470 | | | 5,897 |

*Qiagen N.V. | | 229,290 | | | 4,616 |

| | | | | |

| | | | | 57,479 |

| | | | | |

Industrials & Services—15.6% | | | | | |

*ABB Ltd—ADR | | 309,395 | | | 8,762 |

Danaher Corporation | | 162,481 | | | 12,560 |

Expeditors International of Washington Inc. | | 118,330 | | | 5,088 |

Fastenal Company | | 171,439 | | | 7,399 |

*InnerWorkings, Inc. | | 430,910 | | | 5,154 |

Knight Transportation, Inc. | | 204,670 | | | 3,745 |

Rockwell Collins, Inc. | | 91,380 | | | 4,382 |

Roper Industries, Inc. | | 107,700 | | | 7,095 |

| | | | | |

| | | | | 54,185 |

| | | | | |

Consumer Discretionary—12.5% | | | | | |

*Coach, Inc. | | 124,260 | | | 3,589 |

*Coinstar, Inc. | | 155,690 | | | 5,093 |

DeVry Inc. | | 88,045 | | | 4,721 |

Johnson Controls, Inc. | | 241,931 | | | 6,939 |

*K12 Inc. | | 156,366 | | | 3,351 |

*Life Time Fitness, Inc. | | 170,205 | | | 5,030 |

*McCormick & Schmick’s Seafood Restaurants, Inc. | | 142,400 | | | 1,373 |

Omnicom Group Inc. | | 225,210 | | | 10,107 |

Phillips-Van Heusen Corporation | | 86,875 | | | 3,181 |

| | | | | |

| | | | | 43,384 |

| | | | | |

*Non-income producing securities

† = U.S. listed foreign security

ADR=American Depository Receipt

VRN=Variable Rate Note

**Fair value pursuant to Valuation Procedures approved by the Board of Trustees. This holding represents 1.20% of the Fund’s net assets at June 30, 2008.

| | | | | | |

Issuer | | Shares or

Principal

Amount | | Value |

| | |

Common Stocks—(continued) | | | | | | |

Energy—11.3% | | | | | | |

Apache Corporation | | | 72,685 | | $ | 10,103 |

*IHS Inc. | | | 116,665 | | | 8,120 |

Smith International, Inc. | | | 175,540 | | | 14,594 |

Suncor Energy, Inc.† | | | 112,180 | | | 6,520 |

| | | | | | |

| | | | | | 39,337 |

| | | | | | |

Financials—5.3% | | | | | | |

*Affiliated Managers Group, Inc. | | | 37,155 | | | 3,346 |

Charles Schwab & Co, Inc. | | | 393,875 | | | 8,090 |

CME Group Inc. | | | 9,055 | | | 3,470 |

*IntercontinentalExchange Inc. | | | 29,920 | | | 3,411 |

| | | | | | |

| | | | | | 18,317 |

| | | | | | |

Materials—3.6% | | | | | | |

Praxair, Inc. | | | 130,495 | | | 12,298 |

| | | | | | |

Consumer Staples—1.2% | | | | | | |

Wal Mart de Mexico—ADR** | | | 105,330 | | | 4,166 |

| | | | | | |

Total Common Stock—96.4% (cost $297,668) | | | 334,313 |

| | | | | | |

Investment in Affiliate | | | | | | |

William Blair Ready Reserves Fund | | | 4,723,401 | | | 4,723 |

| | | | | | |

Total Investment in Affiliate—1.3%

(cost $4,723) | | | 4,723 |

| | | | | | |

Short-Term Investment | | | | | | |

Prudential Funding Demand Note, VRN 2.430%, due 7/1/08 | | $ | 6,500 | | | 6,500 |

| | | | | | |

Total Short-Term Investment—1.9%

(cost $6,500) | | | 6,500 |

| | | | | | |

Repurchase Agreement

State Street Bank & Trust Company,

2.150% dated 6/30/08 due 7/1/08,

repurchase price $363, collateralized by

FNMA Note, 4.120%, due 5/6/13 | | $ | 363 | | | 363 |

| | | | | | |

Total Repurchase Agreement—0.1%

(cost $363) | | | 363 |

| | | | | | |

Total Investments—99.7%

(cost $309,254) | | | 345,899 |

Cash and other assets, less liabilities—0.3% | | | 1,000 |

| | | | | | |

Net assets—100.0% | | $ | 346,899 |

| | | | | | |

See accompanying Notes to Financial Statements.

8 Semi-Annual Report | June 30, 2008 |

Mark A. Fuller III

Gregory J. Pusinelli

TAX-MANAGED GROWTH FUND

The Tax-Managed Growth Fund invests primarily in common stocks of large, medium and small domestic growth companies that the Advisor expects will have sustainable, above-average growth from one business cycle to the next.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform over the first half of the year? How did the Fund’s performance compare to its benchmark?

The Tax-Managed Growth Fund posted an (8.98)% decrease on a total return basis (Class N Shares) for the six-months ended June 30, 2008. By comparison, the Fund’s benchmark, the Russell 3000® Growth Index declined (9.04)% while the Standard & Poor’s 500 Stock Index dropped (11.91)%.

What were the most significant market factors impacting Fund performance?

The first quarter of 2008 was the worst for the stock market in six years, and was marked by a number of significant events. During the quarter the Federal Reserve Board engineered a series of interest rate cuts in an effort to avert or soften a recession. The Fed lowered the federal funds rate from 4.25% to 2.25%, lowered the discount rate from 4.75% to 2.50%, opened the discount window to investment banks, and reduced the capital holding requirements for Fannie Mae and Freddie Mac, all in an effort to provide liquidity in order to encourage borrowing and lending without reigniting inflation.

In addition, an emergency financial stimulus package was passed by Congress in February in an attempt to reinvigorate consumer spending, and in turn accelerate the economy.

Finally, on March 13, executives at Bear Stearns informed financial regulators that the investment bank, one of Wall Street’s biggest, was facing imminent bankruptcy. After a weekend of round-the-clock negotiations, the Federal Reserve mediated a “fire sale” of Bear Stearns to JP Morgan Chase. The Fed’s efforts were widely seen as an effort on the part of the nation’s central bank to restore confidence to financial markets and encourage financial institutions to resume lending to one another.

The turmoil in the financial markets spilled into the second quarter, as the economy continued to deal with the worst credit crisis in nearly a generation and attempted to adjust to skyrocketing energy prices, higher food prices and weak consumer spending. Economic data had yet to confirm a recession was underway in spite of the fact that the markets behaved as though the economy was in one.

Following a 0.25% reduction in the federal funds rate in late April, Federal Reserve Chairman Ben Bernanke indicated an end to interest rate cuts in the Fed’s recent efforts to stimulate a slowing economy. For the time being the Federal Reserve appeared equally hesitant to raise interest rates, in spite of their concerns about inflationary pressures, to avoid the risk of choking economic growth.

Although the equity markets were strong during the months of April and May, the equity markets gave back all of their gains during the month of June.

The housing market remained in the doldrums, and the Consumer Discretionary, Financial and Healthcare sectors all remained weak.

June 30, 2008 | William Blair Funds 9 |

What factors were behind the Fund’s performance versus the benchmark?

The Fund outperformed its benchmark largely because of stock selection in the two sectors where the Fund has some of its largest weightings: Energy and Materials. Although our Energy weighting is in line with our benchmark, in the case of Materials our overweight position combined with our stock selection contributed to over a 6% outperformance in that sector relative to the Russell 3000® Growth Index.

What were the best performing sectors and investments for the Fund?

Energy and Materials were the two best performing sectors for the Fund during the second quarter, benefiting from strong pricing and increased exploration.

Although all of the Fund’s Energy holdings were strong performers during the first half of the year, two of the best performing investments in this sector were EnCana Corporation and Apache Corporation.

EnCana Corporation, a highly successful company in the very competitive North American natural gas business, experienced strong growth and was up 34.76% for the Fund.

Apache Corporation was up 29.71% for the Fund, after another excellent quarter for the company which reflected robust international growth and announced the successful completion of tests on three new oil wells.

Notable performers in the Materials sector included Airgas, Inc. the largest U.S. distributor of industrial, medical, and specialty gases and hardgoods, and Praxair, Inc. another of the largest industrial-gas companies in the Americas and one of the largest worldwide. As suppliers, both of these companies have exposure to the energy industry.

Among individual standouts, Gilead Sciences, Inc. in the Health Care sector was up 15.08% for the Fund. Gilead Sciences develops and produces drugs for life-threatening infectious diseases. The company currently has four products—Viread, Emtriva, combination pill Truvada, and triple combination Atripla—that are used for AIDS treatment regimens and which represent a sizable percentage of the company’s sales. The company also has three new promising products undergoing FDA review. We believe the potential for these drugs has yet to be reflected in the valuation of the company’s share price.

What were the weakest performing sectors and investments for the Fund?

The weakest performing sectors for the Fund were Consumer Discretionary and Financials. The Health Care sector also was a laggard.

The single largest detractor from the Fund’s return was Healthways, Inc. Healthways, which provides specialized health and care support for individuals, declined (49.35)% for the Fund. Healthways lowered 2008 guidance and attributed it to slow enrollment from a key health plan and customer conversion delays reflecting the deferral of a large contract. Healthways continues to be the industry leader in disease management and is currently moving into the international marketplace. We therefore believe this company has significant growth opportunities ahead of it.

We were underweight the Fund’s benchmark in the Consumer Discretionary sector and had sought to invest in companies that would outperform despite the weakness in the economy, but this has not been the case.

Within the Consumer Discretionary sector, International Game Technology declined (42.72)% for the Fund, while auto retailer CarMax, Inc. decreased (28.15)%.

10 Semi-Annual Report | June 30, 2008 |

International Game Technology designs and manufactures computerized gaming equipment, network systems, and licensing and services for the casino gaming industry. With the downturn in the economy, casinos are deferring the replacement of older equipment, pushing out the “replacement cycle,” for machines. However, we nonetheless expect International Game Technology to outperform over the long term, as the company is the first to offer server-based gaming—meaning games on machines can be reprogrammed from a central hub. This means that multiple choices can be offered throughout the gaming process, and games can be changed to those that are most popular without having to actually physically install new equipment.

CarMax, Inc. has struggled the past few quarters, partly due to the company having to fund higher loan losses in its credit division. The company also missed fourth quarter earnings in part because of a huge drop in the sales of sport utility vehicles (SUVs).

Lastly, in the Financials sector, insurer American International Group was down (54.16)% for the Fund, as it continues to experience pressure due to write-offs that have been caused by the stress in the financial markets. We believe, however, that the market is overestimating the amount of capital the company will need to raise to meet these challenges going forward.

What is your current strategy? How is the Fund positioned?

As we stated last period, we believe that the worst may not be over as far as the economy is concerned, and believe that corporate earnings will continue to deteriorate before the economy and market conditions begin to show signs of improvement. We do not look for the economy to reaccelerate until the second half of 2008 or early 2009.

We will continue to monitor our Financials holdings since we believe the equity markets will continue to come under pressure as a result of distress in the credit markets, a domestic economic slowdown, a residential real estate collapse and global political uncertainties.

We also continue to be cautious investors towards the Industrial and Consumer Discretionary sectors. The slump in the economy, housing market, and rising energy and food prices are negative factors overhanging the market, and have negatively impacted consumer spending and capital spending by companies. We continue to monitor these issues and any potential impact they may have on the Fund’s holdings.

We are also evaluating new “cyclical” names for the Fund’s portfolio which may benefit from the eventual strengthening of the economy.

June 30, 2008 | William Blair Funds 11 |

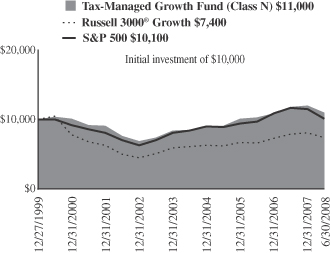

Tax-Managed Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 6/30/2008

| | | | | | | | | | | | | | | |

| | | Year to

Date | | | 1

Year | | | 3

Year | | | 5

Year | | | Since

Inception(a) | |

Tax-Managed Growth Fund

Class N | | (8.98 | )% | | (6.81 | )% | | 6.44 | % | | 8.07 | % | | 1.07 | % |

Tax-Managed Growth Fund

Class I | | (8.88 | ) | | (6.59 | ) | | 6.74 | | | 8.35 | | | 1.34 | |

Russell 3000®

Growth Index | | (9.04 | ) | | (6.38 | ) | | 5.93 | | | 7.56 | | | (3.48 | ) |

S&P 500 Index | | (11.91 | ) | | (13.12 | ) | | 4.41 | | | 7.58 | | | 0.16 | |

| | (a) | | For the period from December 27, 1999 to June 30, 2008. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment advisor may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 3000® Growth Index consists of large, medium, and small-capitalization companies with above average price-to-book ratios and forecasted growth rates. The index is weighted by market capitalization and large/medium/small companies make up approximately 80%/15%/5% of the index.

The S&P 500 Index indicates broad larger capitalization equity market performance.

This report identifies the Fund’s investments on June 30, 2008. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

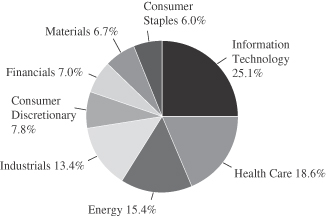

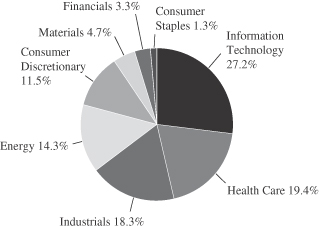

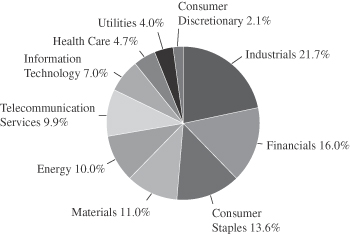

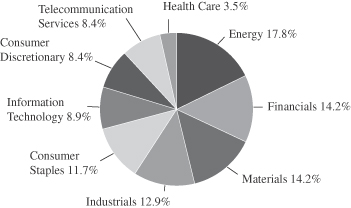

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

12 Semi-Annual Report | June 30, 2008 |

Tax-Managed Growth Fund

Portfolio of Investments, June 30, 2008 (all dollar amounts in thousands) (unaudited)

| | | | | |

Issuer | |

Shares | | Value |

| | |

Common Stocks | | | | | |

Information Technology—23.3% | | | | | |

Activision, Inc. | | 8,453 | | $ | 288 |

*Adobe Systems Incorporated | | 6,160 | | | 243 |

*Cisco Systems Inc. | | 7,180 | | | 167 |

*Citrix Systems, Inc. | | 3,670 | | | 108 |

*Cognizant Technology Solutions Corporation | | 5,350 | | | 174 |

*Dolby Laboratories, Inc. | | 2,690 | | | 108 |

*Electronic Arts Inc. | | 2,950 | | | 131 |

*Euronet Worldwide, Inc. | | 3,770 | | | 64 |

FactSet Research Systems Inc. | | 2,840 | | | 160 |

Microchip Technology, Inc. | | 5,250 | | | 160 |

Microsoft Corporation | | 5,070 | | | 139 |

*Nuance Communications, Inc. | | 5,420 | | | 85 |

Qualcomm Incorporated | | 5,100 | | | 226 |

*Silicon Laboratories, Inc. | | 3,300 | | | 119 |

Texas Instruments Incorporated | | 4,810 | | | 135 |

| | | | | |

| | | | | 2,307 |

| | | | | |

Health Care—17.2% | | | | | |

Allergan Inc. | | 4,090 | | | 213 |

C.R. Bard, Inc. | | 1,710 | | | 150 |

*Celgene Corporation | | 2,480 | | | 158 |

*Gilead Sciences, Inc. | | 5,770 | | | 306 |

*Healthways, Inc. | | 5,710 | | | 169 |

*Hologic, Inc. | | 6,720 | | | 147 |

Pharmaceutical Product Development, Inc. | | 3,620 | | | 155 |

*Psychiatric Solutions, Inc. | | 4,820 | | | 182 |

Stryker Corporation | | 3,600 | | | 226 |

| | | | | |

| | | | | 1,706 |

| | | | | |

Energy—14.3% | | | | | |

Apache Corporation | | 1,780 | | | 247 |

Encana Corporation† | | 2,370 | | | 216 |

*IHS Inc. | | 4,640 | | | 323 |

Schlumberger Limited† | | 1,460 | | | 157 |

Smith International, Inc. | | 2,280 | | | 190 |

Suncor Energy, Inc.† | | 4,960 | | | 288 |

| | | | | |

| | | | | 1,421 |

| | | | | |

Industrials—12.4% | | | | | |

*ABB Ltd.—ADR | | 6,650 | | | 188 |

*Corrections Corporation of America | | 9,020 | | | 248 |

Danaher Corporation | | 3,810 | | | 295 |

Expeditors International of Washington Inc. | | 3,500 | | | 151 |

General Electric Company | | 6,985 | | | 186 |

Roper Industries, Inc. | | 2,430 | | | 160 |

| | | | | |

| | | | | 1,228 |

| | | | | |

Consumer Discretionary—7.3% | | | | | |

*CarMax, Inc. | | 6,840 | | | 97 |

*GameStop Corp. | | 2,810 | | | 114 |

International Game Technology | | 5,420 | | | 135 |

*Non-income producing securities

† = U.S. listed foreign security

ADR=American Depository Receipt

VRN= Variable Rate Note

| | | | | | | |

Issuer | | Shares or

Principal

Amount | | Value | |

| | |

Common Stocks—(continued) | | | | | | | |

Consumer Discretionary—(continued) | | | | | | | |

Johnson Controls, Inc. | | | 5,670 | | $ | 163 | |

*Scientific Games Corporation | | | 3,590 | | | 106 | |

*Tractor Supply Company | | | 3,580 | | | 104 | |

| | | | | | | |

| | | | | | 719 | |

| | | | | | | |

Financials—6.5% | | | | | | | |

*Affiliated Managers Group, Inc. | | | 1,040 | | | 94 | |

American International Group | | | 2,780 | | | 74 | |

Charles Schwab & Co, Inc. | | | 9,720 | | | 200 | |

*IntercontinentalExchange Inc. | | | 930 | | | 106 | |

T. Rowe Price Group, Inc. | | | 2,990 | | | 169 | |

| | | | | | | |

| | | | | | 643 | |

| | | | | | | |

Materials—6.2% | | | | | | | |

Airgas, Inc. | | | 4,870 | | | 284 | |

Praxair, Inc. | | | 3,550 | | | 335 | |

| | | | | | | |

| | | | | | 619 | |

| | | | | | | |

Consumer Staples—5.6% | | | | | | | |

Colgate-Palmolive Company | | | 3,020 | | | 209 | |

CVS/Caremark Corporation | | | 3,774 | | | 149 | |

PepsiCo, Inc. | | | 3,095 | | | 197 | |

| | | | | | | |

| | | | | | 555 | |

| | | | | | | |

Total Common Stock—92.8%

(cost $8,032) | | | 9,198 | |

| | | | | | | |

| | |

Investment in Affiliate | | | | | | | |

William Blair Ready Reserves Fund | | | 231,948 | | | 232 | |

| | | | | | | |

Total Investment in Affiliate—2.3%

(cost $232) | | | 232 | |

| | | | | | | |

Short-Term Investment | | | | | | | |

Prudential Funding Demand Note, VRN 2.430%, due 7/1/08 | | $ | 240 | | | 240 | |

| | | | | | | |

Total Short-Term Investment—2.4%

(cost $240) | | | 240 | |

| | | | | | | |

Repurchase Agreement | | | | | | | |

State Street Bank & Trust Company, 2.150% dated 6/30/08 due 7/1/08, repurchase price $263, collateralized by FNMA Note, 4.120%, due 5/6/13 | | $ | 263 | | | 263 | |

| | | | | | | |

Total Repurchase Agreement—2.6%

(cost $263) | | | 263 | |

| | | | | | | |

Total Investments—100.1%

(cost $8,767) | | | 9,933 | |

Liabilities, plus cash and other assets—( 0.1)% | | | (14 | ) |

| | | | | | | |

Net assets—100.0% | | $ | 9,919 | |

| | | | | | | |

See accompanying Notes to Financial Statements.

June 30, 2008 | William Blair Funds 13 |

James S. Golan

John F. Jostrand

Tracy McCormick

LARGE CAP GROWTH FUND

The Large Cap Growth Fund invests primarily in common stocks of quality large domestic growth companies that the Advisor believes have demonstrated sustained growth over a long period of time.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform over the first half of the year? How did the Fund’s performance compare to its benchmark?

In a difficult market environment, the Large Cap Growth Fund (Class N Shares) declined but outperformed its Russell 1000® Growth Index benchmark in the first half of 2008. The Large Cap Growth Fund had results of (8.51)% and the Russell 1000® Growth Index returned (9.06)% for the six-month period ended June 30, 2008.

What were the most significant factors impacting Fund performance?

So far in 2008, U.S. equity markets have been greatly challenged by much uncertainty and high volatility in response to the continued financial credit crisis and significant write-downs as well as continued consumer weakness with reports of rising gas and food costs, increasing unemployment, tightening lending standards and elevated levels of credit and mortgage delinquencies. In this environment, most broad equity markets indices traded near bear market levels (e.g. down 20% from recent highs); the most notable was the Dow Jones Industrial Average. For the period, the S&P 500 Index fell (11.91)%.

Also, impacting equity results were investors’ concerns which shifted from slowing economic growth to rising inflation. The price of oil surged to record levels of around $140 per barrel as demand remained high especially from emerging markets; also, supply issues surfaced and speculation from investors rose as many looked to oil as an inflationary hedge or an alternative to U.S. dollar investments or the risky credit markets. With high energy prices, consumers spend less on goods and services and products cost more due to higher input and transportation costs. So far, some oil demand destruction has occurred, but it has yet to impact the price of oil. Other commodities also saw new highs on supply issues including coal, with high emerging market demand, as well as corn and soy due to stormy weather conditions in the Midwest. As a result, inflation levels have risen globally and are expected to continue if commodity prices remain on their current trend. Some U.S. investors fear the current low interest rate levels—in place to stimulate the economy—may need to increase in order to curb inflation. Additionally, several countries outside the U.S., particularly emerging markets, have begun to raise interest rate levels in an attempt to slowdown inflation.

Another ongoing factor is U.S. economic growth which has slowed and is expected to remain slow into 2009 according to many pundits. GDP growth for the first quarter 2008 was reported at 1.0% which was slightly higher than the fourth quarter 2007 at 0.6%. The Federal Reserve continued to cut rates into the second quarter in order to stimulate economic growth; the Federal Funds rate was cut 25 basis points to 2.0% in April followed by a pause at their June meeting. The Federal Reserve’s actions, such as lowering interest rates and liquidity injections, helped to prevent a collapse in the financial markets, but did little to promote growth and were more than offset by the substantial increases in energy, raw materials and food prices as well as rising credit spreads. Among experts it still remains debatable whether the U.S. economy will enter a recession in 2008; however, with oil trading at elevated levels, the risk of recession is on the rise in the U.S. and abroad.

14 Semi-Annual Report | June 30, 2008 |

For the first six months of the year, growth stocks held up better than value stocks; the Russell 1000® Growth Index was down (9.06)% while the Russell 1000® Value Index was down (13.57)%. A lower weighting in the Financial Services sector (which did poorly) and a larger weighting in Information Technology (which did well) assisted growth benchmark returns. In regard to sectors on an absolute performance basis, there were only two positive groups in the Russell 1000® Growth Index—Energy and Materials; therefore, the opportunity for a well diversified portfolio, like ours, to be positive in the period was very difficult. The worst sectors were Financials and Consumer Discretionary as you might expect given the comments above.

Which sectors enhanced the Fund’s return? What were among the best performing investments for the Fund?

The portfolio was assisted in the period by Health Care, Energy and Materials sectors. Within Health Care, our stock selection—especially in biotechnology—was strong in this weak performing benchmark group. One of the portfolio’s top overall performers was Gilead Sciences, Inc. the leading provider of drugs to treat HIV, gained ground on solid earnings and an announcement that a study on a competing medicine was halted on inferior efficacy and increased detrimental side effects. Genentech, Inc. also rose double digits on better-than-expected earnings guidance for the year as well as on the FDA approval of Avastin for the treatment of metastatic breast cancer, a $1 to $1.5 billion market. Secondarily, the portfolio was also helped by lack of exposure to HMOs and pharmaceuticals which did poorly.

As measured by the Russell 1000® Growth, the Energy sector results were up double digits for the period and were substantially higher than the next sector driven by the reasons discussed at length above. The portfolio benefited from an overweight and good stock selection especially in the oil gas and consumable fuels industry. Apache Corporation was best among all portfolio stocks as it rallied on attractive quarterly earnings reports driven by better price realizations and volumes. Going forward, we continue to favor this stock since it will benefit from the global tightening in the natural gas market and it is well positioned with significant future production from several large projects coming on-line over the next several years. Secondarily, Weatherford International Ltd. which provides equipment and services used for the selling, completion, and production of oil and natural gas wells was a strong contributor since its addition to the portfolio earlier in the year. Given its strong market position, Weatherford International should continue to experience attractive earning growth as a result of increased international projects and multi-year, major contract awards.

Lastly, Materials stocks helped overall results; the portfolio had a modest overweight in this positive benchmark group and good selection. Praxair, Inc. the largest portfolio position, performed well with strong quarterly earnings due to strength in all geographic areas with Asia and Latin America being the best. The firm continues to benefit from a substantial project backlog and bidding activity for new projects remains high.

Were there any investment strategies or themes that did not measure up to your expectations?

Weakness in the portfolio was seen in Financials, Consumer Staples and Industrials positions. Beginning with Financials—the worst benchmark performer, the portfolio was underweight this group which helped, but our stock selection detracted. Our exposure includes companies that are beneficiaries of volatility and not those that are credit or interest rate sensitive. In the fourth quarter, the portfolio was assisted significantly from this positioning as the credit crisis unfolded; however, in 2008, investors had concerns over slowing volume growth and took profits in names that had done well in the fourth quarter. As a result, IntercontinentalExchange, Inc. and CME Group, Inc. stock prices came under pressure.

On Consumer Staples, the portfolio was primarily hurt by our significant underweight in a group that held up relatively well in the down market. We believe the consumer will continue to remain under pressure and their spending habits will be curtailed. Also, rising input cost

June 30, 2008 | William Blair Funds 15 |

will likely plague many consumer product producers ultimately reducing earnings levels at firms. As a result, it is likely that we remain underweight here until the consumer and input cost outlook improves.

Also, Industrial stocks were a detractor due to stock selection. The weakest performer was Rockwell Automation, Inc., a firm that provides industrial automation power, control and information solutions globally. It declined after lowering its fiscal year 2008 earnings guidance citing less than favorable market conditions in the U.S. and Europe. While reporting solid earnings and raising their outlook for 2008, Rockwell Collins, Inc., an aerospace and defense firm, fell as investors had concerns about the health of the commercial aerospace business with rising jet fuel costs and declining orders. During the period, we sold Rockwell Collins based on the same concerns.

What is your current strategy? How is the Fund positioned?

Given the near bear market status, the broad equity markets have begun to discount current macro conditions in the financial, housing, consumer and commodities markets. However, it is difficult to predict whether additional downside risks remain or when sentiment will turn. While it is challenging to forecast economic events, we believe that growth is likely to remain subdued into 2009 as the financial system and consumer likely have a long work out period ahead.

Going forward, energy prices, global growth, the strength of U.S. financial markets, and the state of consumer confidence will be important issues to watch. Lower energy prices would positively impact consumer pocketbooks, company profit margins and relieve inflationary pressures for central banks; this could be a catalyst for stock market improvement. On global growth, we have seen economies outside the U.S. start to slow including emerging markets countries. However, the degree of slowing in emerging markets will be a critical factor to future global economic growth. Lastly, we will continue to look for repair in the U.S. financial markets and the consumer; positive developments in these groups can signal a change where early cyclical stocks could gain ground.

In this environment, we have not adopted a particularly defensive posture. Instead, we continue to rely on our quality growth investment philosophy and process to steer the portfolio through the current challenging market conditions. We continue to seek high quality growth stocks with attractive long term earnings growth, strong financial position and competitive and sustainable business models which we believe will outperform over time. This investment philosophy generally leads to companies that have somewhat more defensive characteristics during market conditions like those experienced recently, primarily due to more stable business models with better balance sheets. In our view, quality growth opportunities remain readily available and we are taking advantage of increasingly attractive valuation levels to buy stocks that we believe will produce superior long-term returns.

On a positive note, many investors have a significant amount of cash sitting on the sidelines, which could propel the market, if and when, the high level of risk aversion recedes. Also, growth continues to outperform value stocks. Large growth stocks have picked up substantial relative ground for the twelve month period ended June 30 2008; Russell 1000® Growth returned (5.96)% while Russell 1000® Value returned (18.78)%. Many investors would be surprised to note that growth stocks now surpass value stocks over the last three years by 2.40% annualized. With elevated levels of market volatility or a slow growth environment, we believe investors will continue to seek strong, high quality companies which become scarce and thus, more valuable in a challenging period.

16 Semi-Annual Report | June 30, 2008 |

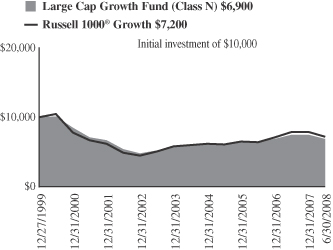

Large Cap Growth Fund

Performance Highlights (unaudited)

Average Annual Total Return at 6/30/2008

| | | | | | | | | | | | | | | |

| | | Year to

Date | | | 1

Year | | | 3

Year | | | 5

Year | | | Since

Inception(a) | |

Large Cap Growth Fund Class N | | (8.51 | )% | | (5.49 | )% | | 3.92 | % | | 5.60 | % | | (4.29 | )% |

Large Cap Growth Fund Class I | | (8.38 | ) | | (5.23 | ) | | 4.15 | | | 5.81 | | | (4.09 | ) |

Russell 1000®

Growth Index | | (9.06 | ) | | (5.96 | ) | | 5.91 | | | 7.32 | | | (3.77 | ) |

| | (a) | | For the period from December 27, 1999 to June 30, 2008. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment advisor may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 1000® Growth Index consists of large capitalization companies with above average price-to-book ratios and forecasted growth rates.

This report identifies the Fund’s investments on June 30, 2008. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

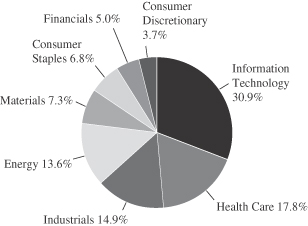

Sector Diversification (unaudited)

The sector diversification shown is based on the total investment portfolio.

June 30, 2008 | William Blair Funds 17 |

Large Cap Growth Fund

Portfolio of Investments, June 30, 2008 (all dollar amounts in thousands) (unaudited)

| | | | | |

Issuer | |

Shares | | Value |

| | |

Common Stocks | | | | | |

Information Technology—29.5% | | | | | |

*Adobe Systems Incorporated | | 24,795 | | $ | 977 |

*Apple Inc. | | 5,440 | | | 911 |

*Cisco Systems Inc. | | 63,594 | | | 1,479 |

Corning Incorporated | | 30,350 | | | 700 |

*Electronic Arts Inc. | | 10,350 | | | 460 |

*FLIR Systems, Inc. | | 8,710 | | | 353 |

*Google Inc. | | 1,905 | | | 1,003 |

Microsoft Corporation | | 43,735 | | | 1,203 |

Qualcomm Incorporated | | 24,495 | | | 1,087 |

*Salesforce.com, Inc. | | 5,070 | | | 346 |

*Verisign Inc. | | 16,445 | | | 622 |

| | | | | |

| | | | | 9,141 |

| | | | | |

Health Care—17.0% | | | | | |

Allergan Inc. | | 15,575 | | | 811 |

*Celgene Corporation | | 15,470 | | | 988 |

*Genentech, Inc. | | 10,190 | | | 773 |

*Gilead Sciences, Inc. | | 20,675 | | | 1,095 |

*Hologic, Inc. | | 20,920 | | | 456 |

*St. Jude Medical, Inc. | | 12,255 | | | 501 |

*Thermo Fisher Scientific Inc. | | 11,825 | | | 659 |

| | | | | |

| | | | | 5,283 |

| | | | | |

Industrials—14.3% | | | | | |

*ABB Ltd—ADR | | 26,385 | | | 747 |

Danaher Corporation | | 12,762 | | | 986 |

Expeditors International of Washington Inc. | | 10,875 | | | 468 |

Fastenal Company | | 12,630 | | | 545 |

Joy Global Inc. | | 6,470 | | | 491 |

Rockwell Automation, Inc. | | 9,515 | | | 416 |

Roper Industries, Inc. | | 11,850 | | | 781 |

| | | | | |

| | | | | 4,434 |

| | | | | |

Energy—13.0% | | | | | |

Apache Corporation | | 9,705 | | | 1,349 |

Schlumberger Limited† | | 11,540 | | | 1,240 |

Suncor Energy, Inc.† | | 11,390 | | | 662 |

*Weatherford International Ltd.† | | 15,770 | | | 782 |

| | | | | |

| | | | | 4,033 |

| | | | | |

Materials—7.0% | | | | | |

Monsanto Company | | 4,890 | | | 618 |

Praxair, Inc. | | 16,435 | | | 1,549 |

| | | | | |

| | | | | 2,167 |

| | | | | |

*Non-income producing securities

† = U.S. listed foreign security

ADR = American Depository Receipt

VRN = Variable Rate Note

**Fair valued pursuant to Valuation Procedures approved by the Board of Trustees. This holding represents 1.67% of the Fund’s net assets at June 30, 2008.

| | | | | | |

Issuer | | Shares or

Principal

Amount | | Value |

| | |

Common Stocks—(continued) | | | | | | |

Consumer Staples—6.5% | | | | | | |

Avon Products, Inc. | | | 15,605 | | $ | 562 |

Wal Mart de Mexico—ADR** | | | 13,095 | | | 518 |

Wal-Mart Stores, Inc. | | | 16,550 | | | 930 |

| | | | | | |

| | | | | | 2,010 |

| | | | | | |

Financials—4.8% | | | | | | |

CME Group Inc. | | | 775 | | | 297 |

*IntercontinentalExchange Inc. | | | 2,635 | | | 300 |

Charles Schwab & Co, Inc. | | | 42,865 | | | 880 |

| | | | | | |

| | | | | | 1,477 |

| | | | | | |

Consumer Discretionary—3.5% | | | | | | |

*Kohl’s Corporation | | | 12,550 | | | 502 |

Omnicom Group Inc. | | | 12,995 | | | 583 |

| | | | | | |

| | | | | | 1,085 |

| | | | | | |

Total Common Stock—95.6%

(cost $27,422) | | | 29,630 |

| | | | | | |

| | |

Investment in Affiliate | | | | | | |

William Blair Ready Reserves Fund | | | 337,591 | | | 338 |

| | | | | | |

Total Investment in Affiliate—1.1%

(cost $338) | | | 338 |

| | | | | | |

Short-Term Investments | | | | | | |

American Express Credit Corp. Demand Note, VRN 2.333%, due 7/1/08 | | $ | 220 | | | 220 |

Prudential Funding Demand Note, VRN 2.430%, due 7/1/08 | | | 220 | | | 220 |

| | | | | | |

Total Short-Term Investments—1.4%

(cost $440) | | | 440 |

| | | | | | |

Repurchase Agreement | | | | | | |

State Street Bank & Trust Company, 2.150% dated 6/30/08 due 7/1/08, repurchase price $393, collateralized by FNMA Note, 4.120%, due 5/6/13 | | $ | 393 | | | 393 |

| | | | | | |

Total Repurchase Agreement—1.3%

(cost $393) | | | 393 |

| | | | | | |

Total Investments—99.4%

(cost $28,593) | | | 30,801 |

Cash and other assets, less liabilities—0.6% | | | 190 |

| | | | | | |

Net assets—100.0% | | $ | 30,991 |

| | | | | | |

See accompanying Notes to Financial Statements.

18 Semi-Annual Report | June 30, 2008 |

Michael P. Balkin

Karl W. Brewer

Colin J. Williams

SMALL CAP GROWTH FUND

The Small Cap Growth Fund invests primarily in common stocks of small domestic growth companies that the Advisor expects to have solid growth in earnings.

AN OVERVIEW FROM THE PORTFOLIO MANAGERS

How did the Fund perform in the first six months of 2008? How did the Fund’s performance compare to its benchmark?

The William Blair Small Cap Growth Fund decreased (16.35)% on a total return basis (Class N shares) during the first six months of 2008. By comparison the Fund’s benchmark, the Russell 2000® Growth Index, declined (8.93)% for the same period.

What were the most significant factors impacting Fund performance? What factors were behind the Fund’s performance versus the benchmark?

The first half of 2008 was characterized by economic and financial system uncertainties that translated into elevated levels of stock market volatility. The market turned in one of its worst quarterly performances in decades during the first quarter as weakening data sparked more tangible recessionary concerns. Stocks digested data on continued housing market weakness, rising mortgage defaults, and fresh signs of the lingering credit crisis. In response, the Federal Reserve (the “Fed”) acted more aggressively in its interest rate easing campaign, and also introduced several credit-enhancement tools aimed at relieving the stresses in the short-term liquidity markets. In mid-March, the Fed backed JP Morgan Chase in its buyout of Bear Stearns, sending a signal to the market that it was unwilling to risk a major disruption to the financial system. This sent stocks on a two-month relief rally through mid-May; however, the rally was short-lived as inflationary fears intensified due to rising food prices and record-high energy prices. This was compounded by further debate about the strength of certain major financial institutions, which took its toll on investor confidence as well. In the end, the Russell 2000® Growth Index returned (8.93)% for the period. This was ahead of the Russell 2000® Value Index (9.84)% from a style perspective. Looking at performance by market cap through the Russell Growth Indexes, small caps (8.93)% finished ahead of large caps (9.06)% but trailed mid caps (6.81)% as measured by the Russell Indexes.

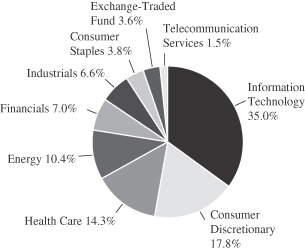

Energy was a key driver of the market for the first six months of the year. It was the only sector in the Russell 2000® Growth Index to finish in positive territory during that time period, and it did so with an impressive 46.27% return. The Industrials sector finished slightly in negative territory (1.47)%, but was the second best performing sector. On the other hand, with the challenging consumer environment, the Consumer Discretionary sector trailed all but one other sector, returning (18.44)%. The other typically growth-oriented sectors of Information Technology (16.13)% and Health Care (16.40)% turned in disappointing results as well. The small cap Financials sector underperformed the broader small cap market but beat many of the other sectors with a (12.48)% return.

The Small Cap Growth Fund underperformed its benchmark during the first half of the year with the vast majority of the underperformance coming in the second quarter. Stock selection in certain sectors detracted from relative performance and we will discuss some of those disappointing stocks below. There were also style factors that affected performance. We discussed in our 2007 review certain market dynamics that were prevalent after the onset of the credit crisis last August. Unfortunately, many of these dynamics continued into 2008, but from a historical perspective, we believe they are at unsustainable levels. First, the market has been narrowly focused on momentum-based stocks. Through the first six months of 2008, the

June 30, 2008 | William Blair Funds 19 |

highest quintile of momentum stocks returned 6%, while the quintile of stocks with the least amount of momentum finished (30)%. Given our investment discipline, this has been a meaningful detractor from relative performance. Second, another unsustainable dynamic in the current market is the lack of valuation sensitivity. Our valuation sensitivity, which should benefit the Fund over time, hurt performance in the first half of 2008, continuing the trend that began in 2007. Finally, the Fund’s bias of owning smaller, less-discovered companies was a sizable headwind, especially in the second quarter. For the six month period in total, the largest quintile of companies in the Russell 2000® Growth Index finished down (1.79)% while the smallest quintile of companies finished down (16.13)%. Since the Fund owns less of the largest quintile and more of the smallest quintile relative to the benchmark, this was meaningful. As we have said in the past, we do not expect these market dynamics to continue in perpetuity. The past tells us that the lack of valuation sensitivity and abundance of momentum in the market right now is unsustainable, but they are unfortunately driving material underperformance in the meantime.

What were among the weakest performing investments for the Fund?

Two of the worst performing stocks during the quarter were Euronet Worldwide, Inc. and VistaPrint Limited.

Euronet is an information technology company that processes electronic financial transactions. The company’s money transfer business, primarily the United States to Mexico corridor, has slowed for a variety of reasons and has been the main driver of the stock’s weak performance. However, we feel Euronet is uniquely positioned to use its existing relationships around the world to drive growth in its ATM network business, its money transfer business in a variety of corridors (including eastern Europe), and its pre-paid card business.

VistaPrint provides graphic design and printing services to small business and home office customers around the globe via the internet. The company’s products include business cards, brochures, invitations, letterheads, and many others. Weakening small business confidence and investors fear of a prolonged slowdown in small business spending weighed on the stock during the second quarter. However, we continue to feel the company has a distinguished business model in the highly fragmented printing industry and should produce solid earnings growth over the next several years.

What were among the best performing investments for the Fund?

Two of the best performing stocks during the quarter were Petrohawk Energy and Overhill Farms.

Petrohawk Energy Corporation engages in the acquisition, development and exploration of oil and natural gas in North America. The company’s strategy is one of a geographic focus on high quality and proven natural gas fields, with its two main assets being located on the Fayetteville Shale in Arkansas and the Haynesville Shale in Louisiana. In addition to rising energy prices, there was very encouraging data out during the second quarter regarding the productivity of the Haynesville Shale. The stock reacted favorably given the expectation of increased natural gas production from this asset.

Overhill Farms, Inc. produces custom prepared meals for a variety of customers including Jenny Craig, Panda Restaurant Group, Safeway, and American Airlines. After being one of the biggest detractors from the Fund’s return in the second half of 2007, Overhill Farms was the one of the top contributors to return during the first half of 2008. This strength was driven by a reacceleration in the company’s revenue and earnings growth, with solid earnings reports in both the first and second quarters. The company also turned down an offer by a pair of private equity firms, noting that the offer did not reflect the true value of the company. Given management’s confidence that this implied and the company’s business momentum, the stock turned in a stellar first half of the year.

20 Semi-Annual Report | June 30, 2008 |

What is your current outlook?

Looking forward, while we are cautious on the outlook for consumer spending broadly, we continue to find new growth ideas across economic sectors, including the consumer sector. As we discussed above, the momentum and valuation dynamics that have been prevalent in the market the last several months seem to be approaching unsustainable levels. If these were to reverse, we believe this should be positive for the Fund’s relative performance. Other positives for the market and economy are attractive stock valuations, lean business inventory levels, and an economy, ex-autos and housing, that has remained quite strong. As always, we do not focus on forecasting economic trends. Rather, we spend our time building the portfolio with companies that possess a differentiated growth outlook which should translate into superior long term investment results.

Is there any other news with respect to the Fund?

As we have previously announced, former co-manager of the Fund, Mike Balkin, returned to William Blair & Company on June 30, 2008, as co-manager of the Small Cap Growth Fund. Colin Williams, at his request, will transition into a senior research analyst role on October 1, 2008, and will cover technology services and business services. Colin will continue as co-manager of Small Cap Growth Fund until September 30, 2008. We also re-opened the Small Cap Growth Fund to new investors as of June 30, 2008.

June 30, 2008 | William Blair Funds 21 |

Small Cap Growth Fund

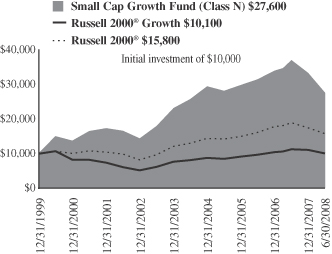

Performance Highlights (unaudited)

Average Annual Total Return at 6/30/2008

| | | | | | | | | | | | | | | |

| | | Year to

Date | | | 1

Year | | | 3

Year | | | 5

Year | | | Since

Inception(a) | |

Small Cap Growth Fund Class N | | (16.35 | )% | | (24.89 | )% | | (0.47 | )% | | 9.25 | % | | 12.65 | % |

Small Cap Growth Fund Class I | | (16.24 | ) | | 24.70 | | | (0.19 | ) | | 9.53 | | | 12.92 | |

Russell 2000® Growth Index | | (8.93 | ) | | (10.83 | ) | | 6.08 | | | 10.37 | | | 0.11 | |

Russell 2000® Index | | (9.37 | ) | | (16.19 | ) | | 3.79 | | | 10.29 | | | 5.54 | |

| | (a) | | For the period from December 27, 1999 to June 30, 2008. |