UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-05629

Voya Investors Trust

(Exact name of registrant as specified in charter)

| 7337 East Doubletree Ranch Road, Suite 100, Scottsdale, AZ | 85258 |

| (Address of principal executive offices) | (Zip code) |

CT Corporation System, 101 Federal Street, Boston, MA 02110

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-366-0066

Date of fiscal year end: December 31

Date of reporting period: December 31, 2020

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Annual Report

December 31, 2020

Classes ADV, I, R6, S and S2

Voya Investors Trust | | ■ | VY® Morgan Stanley Global Franchise Portfolio |

| ■ | | Voya Government Liquid Assets Portfolio | | ■ | VY® T. Rowe Price Capital Appreciation Portfolio |

| ■ | | VY® Clarion Global Real Estate Portfolio | | ■ | VY® T. Rowe Price Equity Income Portfolio |

| ■ | | VY® Invesco Growth and Income Portfolio | | ■ | VY® T. Rowe Price International Stock Portfolio |

| ■ | | VY® JPMorgan Emerging Markets Equity Portfolio | | | |

As permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of each Portfolio’s annual and semi-annual shareholder reports, like this annual report, are not sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on a website and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you need not take any action. You may elect to receive shareholder reports and other communications from your insurance carrier electronically by contacting them directly.

You may elect to receive all future reports in paper free of charge. If you received this document in the mail, please follow the instructions provided to elect to continue receiving paper copies of your shareholder reports. You can inform us that you wish to continue receiving paper copies by calling 1-800-283-3427. Your election to receive reports in paper will apply to all the funds in which you invest. |

| This report is submitted for general information to shareholders of the Voya mutual funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully. |

INVESTMENT MANAGEMENT

voyainvestments.com |  |

TABLE OF CONTENTS

| | 1 | |

| | 3 | |

| | 19 | |

| | 21 | |

| | 22 | |

| | 26 | |

| | 28 | |

| | 32 | |

| | 37 | |

| | 56 | |

| | 93 | |

| | 95 | |

| | 99 | |

PROXY VOTING INFORMATION

A description of the policies and procedures that the Portfolios use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the Portfolios’ website at www.voyainvestments.com; and (3) on the U.S. Securities and Exchange Commission’s (“SEC’s”) website at www.sec.gov. Information regarding how the Portfolios voted proxies related to portfolio securities during the most recent 12-month year ended June 30 is available without charge on the Portfolios’ website at www.voyainvestments.com and on the SEC’s website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Portfolios file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form NPORT-P. This report contains a summary portfolio of investments for the Portfolios. The Portfolios’ Forms NPORT-P are available on the SEC’s website at www.sec.gov. Each Portfolio’s complete schedule of portfolio holdings is available at: www.voyainvestments.com and without charge upon request from the Portfolio by calling Shareholder Services toll-free at (800) 992-0180. Voya Government Liquid Assets Portfolio does not file on Form N-PORT.

The Voya Government Liquid Assets Portfolio files its complete schedule of portfolio holdings with the SEC monthly on Form N-MFP. The Portfolio’s Form N-MFP is available on the SEC’s website at www.sec.gov or the monthly schedule of portfolio holdings are also available at: www.voyainvestments.com and without charge upon request from the Portfolio by calling Shareholder Services toll-free at (800) 992-0180.

(THIS PAGE INTENTIONALLY LEFT BLANK)

Beyond the Headlines, a Glimpse of Global Economic Recovery

Beyond the Headlines, a Glimpse of Global Economic RecoveryDear Shareholder,

For those of us hoping that 2021 would bring more encouraging headlines, it has been a rough start to the year: political turmoil, surging COVID-19 cases and a new, more virulent strain of the coronavirus. On the surface, economic news also has seemed disappointing: labor markets have cooled, manufacturing and services activity has slowed and consumer sentiment has dropped. Yet, the financial markets continue to march higher, begging the question: Where are the markets getting their news?

Voya investment strategists have written about the uneven pressures that have created a “two-speed” or “K-shaped” economic recovery. Consumers on the higher end of the income distribution have largely kept their jobs and adapted to the pandemic by working from home. By contrast, jobs in lower paying segments of the labor market such as leisure, lodging and retail have been eliminated or furloughed and have yet to return. For lower income consumers, the good news is that the fiscal response to help offset job losses has been enormous — and fiscal relief is expected to grow under a Democratic-controlled government. The initial rollout of the coronavirus vaccines, while slower than many had hoped, still represents a significant milestone as vaccines are the bridge that are expected to allow the economy to reopen fully.

In addition to fiscal support, the response from central banks has been extraordinary. The U.S. Federal Reserve Board (“Fed”) has adjusted its policy framework in ways that make the Fed more likely to remain accommodative longer than might otherwise be expected during economic recovery phases, a game changer for financial assets. We believe that analogous developments across the world should help reignite global economic growth in 2021 and breathe new life into struggling sectors. Despite today’s negative headlines, the data is telling us that the future is likely to be better. Looking broadly at the economic picture, in our opinion, it appears that a global synchronous expansion is underway.

Of course there are still risks, and we believe that one should not overlook the potential for episodic market stresses connected to the vaccine rollout or other global factors. As always, we glimpse the future “through a glass darkly,” and must allow for contingencies we can’t foresee. For this reason, we maintain that staying fully invested and broadly diversified is the most likely way to achieve one’s long-term investment goals. Should your goals change, discuss them thoroughly with your investment advisor before making any changes to your portfolio.

We remain humble and realistic in the face of the challenges ahead, but well prepared for and fully committed to serving our clients without disruption. We appreciate your continued confidence in us, and we look forward to serving your investment needs in the future.

Dina Santoro

President

Voya Family of Funds

January 22, 2021

The views expressed in the President’s Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and the Voya mutual funds disclaim any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for a Voya mutual fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any Voya mutual fund. Reference to specific company securities should not be construed as recommendations or investment advice.

International investing poses special risks including currency fluctuation, economic and political risks not found in investments that are solely domestic.

1

BENCHMARK DESCRIPTIONS

| Index | | Description |

|---|

| Bloomberg Barclays U.S. Aggregate Bond Index | | An index of publicly issued investment grade U.S. government, mortgage-backed, asset-backed and corporate debt securities. |

| Bloomberg Barclays U.S. Government/Credit Index | | An index made up of the Barclays Government and Credit indices, including securities issued by the U.S. government and its agencies and publicly issued U.S. corporate and foreign debentures and secured notes that meet specified maturity, liquidity and quality requirements. |

| FTSE EPRA Nareit Developed Index | | The index is designed to track the performance of listed real estate companies and real-estate investment trusts (REITs) worldwide. Relevant activities are defined as the ownership, disposal and development of income-producing real estate. Constituents are classified into distinct property sectors based on gross invested book assets, as disclosed in the latest published financial statement. Index constituents are free-float adjusted, liquidity, size and revenue screened. |

| iMoneyNet Government Institutional Index | | The average return for a category of money market funds that includes all government institutional funds: Treasury Institutional, Treasury and Repo Institutional and Government and Agencies Institutional. |

MSCI All Country World (ex-US) IndexSM | | A free float-adjusted market capitalization index that is designed to measure equity market performance in global developed and emerging markets, excluding the U.S. It includes the reinvestment of dividends net of withholding taxes, but does not reflect fees, brokerage commissions or other expenses of investing. |

MSCI Emerging Markets IndexSM | | An index that measures the performance of securities listed on exchanges in developing nations throughout the world. It includes the reinvestment of dividends and distributions net of withholding taxes, but does not reflect fees, brokerage commissions or other expenses of investing. |

MSCI World IndexSM | | An index that measures the performance of over 1,600 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. |

| Russell 1000® Value Index | | An index that measures the performance of those Russell 1000® securities with lower price-to-book ratios and lower forecasted growth values. |

| S&P 500® Index | | An index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets. |

2

PORTFOLIO MANAGERS’ REPORT | VOYA GOVERNMENT LIQUID ASSETS PORTFOLIO

|

Voya Government Liquid Assets Portfolio (the “Portfolio”) seeks a high level of current income consistent with the preservation of capital and liquidity. The Portfolio is managed by David S. Yealy, Portfolio Manager of Voya Investment Management Co. LLC (“Voya IM”) — the Sub-Adviser.

Performance*: For the year ended December 31, 2020, the Portfolio’s Class S shares provided a total return of 0.24% compared to the iMoneyNet Government Institutional Index, which returned 0.31% for the same period.

The Portfolio has waived fees in order to maintain a zero or positive yield, as have other money market funds. The Portfolio was able to realize some capital gains by primarily buying longer-term new issue T-Bills, and selling them after yields declined to market levels over time. These gains were distributed to the shareholders and allowed the Portfolio to increase the total return over the yield of the fund. The Portfolio continued to maintain an exposure to floating rate money market securities, shifting out of floaters tied to 3-month London inter-bank offered rate (“LIBOR”) or 1-month LIBOR, and into floaters tied to 1-day secured overnight financing rate (“SOFR”), as the market prepares for LIBOR to be replaced by SOFR.

Portfolio Specifics: The year ended December 31, 2020, can be summed up by the COVID-19 pandemic and the Federal Open Market Committee (“FOMC”), the U.S. Federal Reserve Board (the “Fed”), the U.S. Treasury and U.S. government’s response to the impact that the coronavirus had on the markets and the economy. On March 3, prior to their regularly scheduled meeting on March 15, the FOMC lowered the federal funds rate by 0.50% to a range of 1.00% to 1.25%. They took that action in light of the risks posed to economic activity by the coronavirus despite the current strong economy and low level of unemployment. The FOMC again lowered the federal funds rate another 1% at the March 15 meeting, lowering it to a range of 0% to 0.25%. The FOMC indicated that global financial conditions had been significantly affected by the coronavirus. In addition, the Fed also agreed to purchase $500 billion of U.S. Treasury securities and $200 billion of mortgage-backed securities (“MBS”), and expand overnight and term repurchase agreement operations. The Fed and U.S. Treasury were forced to institute various programs in order to stabilize the markets, provide liquidity and support the smooth operations of the various markets. The U.S. government instituted a stimulus program to lessen the impact from the coronavirus on the U.S. economy. The federal funds rate has remained at the 0% to 0.25% range, and the Fed continues to purchase U.S. Treasury securities and MBS, as well as reinvest maturities and paydowns on a monthly basis as the coronavirus continued to have a major impact on the U.S. economy and global economies. Money market rates of securities purchased by the Portfolio as well as other money market funds declined in direct response to the FOMC actions.

Top Ten Holdings

as of December 31, 2020

(as a percentage of net assets) |

| United States Treasury Bill, 0.070%, 01/28/21 | | 26.9 | % |

| United States Cash Management Bill, 0.080%, 03/30/21 | | 14.0 | % |

| Fannie Mae, 0.210%, 03/16/21 | | 11.1 | % |

| Deutsche Bank Repurchase Agreement dated 12/31/2020, 0.070%, due 1/4/2021, $81,392,633 to be received upon repurchase (Collateralized by $83,044,000, Bill, 0.00%, Market Value plus accrued interest $83,019,938 due 2/9/2021-8/12/2021) | | 8.4 | % |

Deutsche Bank Repurchase Agreement dated 12/31/2020, 0.070%, due 1/4/2021, $55,000,428 to be received upon repurchase (Collateralized by $53,311,300, Note, 2.125-2.875%, Market Value plus accrued interest $56,100,064 due 5/31/21-

11/30/2023) | | 5.7 | % |

| United States Treasury Bill, 0.070%, 02/09/21 | | 5.5 | % |

| Federal Home Loan Banks, 0.125%, 12/10/21 | | 5.2 | % |

| United States Treasury Bill, 0.070%, 01/12/21 | | 4.0 | % |

| United States Cash Management Bill, 0.080%, 03/23/21 | | 2.8 | % |

| United States Treasury Bill, 0.090%, 03/25/21 | | 2.8 | % |

Portfolio holdings are subject to change daily. |

Current Strategy and Outlook: Looking ahead we believe that the U.S. economy and employment will take a significant amount of time to fully recover as the effects from the coronavirus will continue well into 2021, the vaccine rollout takes time and additional stimulus is needed to bridge the gap. The FOMC has indicated that they expect to hold rates at the current level till at least 2023, based on their dot plot estimates of the federal funds rate. We do not envision a scenario where the FOMC will be in a position to raise rates in the upcoming year. Any increases in short-term money market rates would be viewed by us as temporary and as an opportunity to add a few basis points of yield or the ability to capture some capital gains. We will otherwise maintain a shorter weighted average maturity, an exposure to floating rate securities and look to take advantage of any market dislocations due to temporary supply and demand imbalances for short-term U.S. Treasury and agency securities.

| |

| * | | Please see Note 5 for more information regarding the contractual waiver in place to reimburse certain expenses of the Portfolio to the extent necessary to assist the Portfolio in maintaining a yield of not less than zero. |

You could lose money by investing in the Portfolio. Although the Portfolio seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. An investment in the Portfolio is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Portfolio’s sponsor has no legal obligation to provide financial support to the Portfolio, and you should not expect that the sponsor will provide financial support to the Portfolio at any time.

The views expressed in this commentary are informed opinions. They should not be considered promises or advice. The views expressed reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. Portfolio holdings are subject to change daily. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements. The Portfolio’s performance returns shown reflect applicable fee waivers and/or expense limits in effect during this period. Absent such fee waivers/expense limitations, if any, performance would have been lower. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

3

| VY® CLARION GLOBAL REAL ESTATE PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Geographic Diversification

as of December 31, 2020

(as a percentage of net assets) |

| United States | | 52.5 | % |

| Japan | | 10.9 | % |

| Germany | | 7.8 | % |

| Hong Kong | | 6.5 | % |

| United Kingdom | | 3.8 | % |

| Australia | | 3.7 | % |

| Singapore | | 3.5 | % |

| Canada | | 2.8 | % |

| Sweden | | 1.8 | % |

| Belgium | | 1.3 | % |

| Countries between 0.3%–1.0%ˆ | | 2.8 | % |

| Assets in Excess of Other Liabilities* | | 2.6 | % |

| Net Assets | | 100.0 | % |

| * Includes short-term investments. |

| ** Includes 4 countries, which each represents 0.3%-1.0% of net assets. |

Portfolio holdings are subject to change daily. |

VY® Clarion Global Real Estate Portfolio (the “Portfolio”) seeks high total return consisting of capital appreciation and current income. The Portfolio is managed* by T. Ritson Ferguson, CFA, Chief Executive Officer and Global Chief Investment Officer, Joseph P. Smith, CFA, President and Co-Chief Investment Officer and Christopher S. Reich, CFA, Senior Global Portfolio Manager, Portfolio Managers of CBRE Clarion Securities LLC — the Sub-Adviser.

Performance: For the year ended December 31, 2020, the Portfolio’s Class S shares provided a total return of -5.04% compared to the FTSE EPRA Nareit Developed Index and S&P 500® Index, which returned -9.04% and 18.40%, respectively, for the same period.

Portfolio Specifics: Global real estate stocks rallied materially in the fourth quarter but were down for the year. In our opinion, real estate stocks may have “bounced,” but the stocks have not “recovered.” Global real estate stocks rebounded powerfully in the fourth quarter in response to positive developments concerning the availability of effective COVID-19 vaccines as well as the U.S. Presidential Election outcome. Despite rallying in the fourth quarter, global real estate stocks were down -9.0% for the year, materially underperforming many asset classes including the S&P 500® Index, the Bloomberg Barclays U.S. Aggregate Bond Index, and the MSCI World IndexSM. Global real estate stocks still have tremendous ground to make up versus broader market indices.

Since bottoming in early May, real estate stocks have performed well when news was announced about either improving economic conditions or positive news about a vaccine to fight the COVID-19 virus. We believe real estate stocks will outperform when investors become more certain about the timing and scale of an “economic re-opening.” In our opinion, this will help catalyze the realization of the good relative value, improving earnings growth, and attractive dividend yields in the current low yield environment, in our view.

We believe a moderate and controlled re-opening of the global economy will occur in 2021 and may act as a further catalyst for good absolute and relative performance of real estate securities. As a result, we estimate earnings for global real estate stocks will grow in the mid-single-digit range in 2021 and 2022 assuming the vaccines and health policies are effective to minimize the pandemic and that the global economy can re-open in 2021.

The Portfolio outperformed the FTSE EPRA Nareit Developed Index during the period as value was added in each of the three major geographic regions. Stock selection was the main driver of relative outperformance and sector allocation decisions also added value during the period. The Americas region was the top contributor to performance, followed closely by outperformance in the Asia-Pacific region. The European region was a modest contributor as stock selection was mostly offset by sector allocation decisions.

Top Ten Holdings

as of December 31, 2020

(as a percentage of net assets) |

| ProLogis, Inc. | | 5.4 | % |

| Simon Property Group, Inc. | | 4.5 | % |

| Duke Realty Corp. | | 2.8 | % |

| Invitation Homes, Inc. | | 2.7 | % |

| Vonovia SE | | 2.6 | % |

| VEREIT, Inc. | | 2.5 | % |

| Alexandria Real Estate Equities, Inc. | | 2.4 | % |

| Link REIT | | 2.1 | % |

| Life Storage, Inc. | | 2.1 | % |

| STORE Capital Corp. | | 2.0 | % |

Portfolio holdings are subject to change daily. |

In the Americas, positioning in the U.S. and Canada was positive. Notable contributors included stock selection in the U.S. healthcare, mall and industrial sectors. Sector allocation decisions in the U.S. tower, mall and hotel sectors also benefited relative performance. Meanwhile, sector allocation in the U.S. residential sector detracted from relative performance. In the Asia-Pacific region, stock selection was positive in all markets within the region and was led by good stock selection in Japan and Hong Kong. Sector allocation was essentially flat during the period. In Europe, positive stock selection on the Continent was somewhat offset by sub-par stock selection in the U.K. Sector allocation was a modest detractor from relative performance for the year.

Current Strategy and Outlook: We believe that long-term investors have a unique opportunity to invest in high-quality real estate assets at very attractive valuations. Based on our proprietary analytical tools, we believe that global real estate securities are cheap relative to the private real estate market, the fixed income market, and the broader stock market. We also believe investors committing capital to listed real estate at this time have the potential to earn above average absolute and relative long-term total returns.

We own a well-balanced portfolio of securities, in our view, that have been screened for their growth prospects in combination with the quality of their business models, assets, balance sheets, and management teams. We are positive on property types, regions, and stocks that offer these qualities at reasonable valuations. In the U.S., we favor towers, net lease, industrial, gaming, retail, and storage sectors. Since the beginning of the fourth quarter, we have added to the portfolio “over-sold” stocks that represent what we believe to be “great value” in the net lease, mall, and grocery-anchored shopping center sectors and we have funded these purchases by selling YTD outperforming stocks, particularly in the data center sector.

4

| PORTFOLIO MANAGERS’ REPORT | VY® CLARION GLOBAL REAL ESTATE PORTFOLIO |

In Japan, we prefer mid-cap office stocks that are providing earnings resiliency at what we see as a very attractive relative valuation, and we continue to overweight select larger diversified real estate companies that have committed to improving their corporate governance. In Hong Kong, we are overweight residential companies, diversified companies with a residential bias, non-discretionary retail, and decentralized office. In Australia, we prefer residential companies and a few select diversified companies.

In the U.K., we favor the storage, industrial, and residential sectors, and companies with, in our view, superior balance sheets and the management acumen to create value in times of uncertainty. In continental Europe, we own German residential companies and we continue to prefer property companies in markets with a positive earnings growth profile, which favors mid to small cap stocks in Germany, the Nordics and Switzerland.

| * | | Effective January 1, 2020, Mr. Steven D. Burton retired as a portfolio manager to the Portfolio and Christopher S. Reich has been added as a portfolio manager to the Portfolio. |

The views expressed in this commentary are informed opinions. They should not be considered promises or advice. The views expressed reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. Portfolio holdings are subject to change daily. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements. The Portfolio’s performance returns shown reflect applicable fee waivers and/or expense limits in effect during this period. Absent such fee waivers/expense limitations, if any, performance would have been lower. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

5

| VY® CLARION GLOBAL REAL ESTATE PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

| | Average Annual Total Returns for the Periods Ended December 31, 2020 | |

| | | | | | 1 Year | | 5 Year | | 10 Year | |

|---|

| | Class ADV | | | | | –5.37 | % | | | 3.33 | % | | | 4.80 | % | |

| | Class I | | | | | –4.83 | % | | | 3.95 | % | | | 5.43 | % | |

| | Class S | | | | | –5.04 | % | | | 3.68 | % | | | 5.17 | % | |

| | Class S2 | | | | | –5.19 | % | | | 3.54 | % | | | 5.01 | % | |

| | FTSE EPRA Nareit Developed Index | | | | | –9.04 | % | | | 3.74 | % | | | 5.44 | % | |

| | S&P 500® Index | | | | | 18.40 | % | | | 15.22 | % | | | 13.88 | % | |

Based on a $10,000 initial investment the graph and table above illustrate the total return of VY® Clarion Global Real Estate Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in the index.

The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your variable annuity contract or variable life insurance policy. Total returns would have been lower if such expenses or charges were included.

The graph and performance table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown includes, if applicable, the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other

service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract or a variable life insurance policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.voyainvestments.com or call (800) 366-0066 to get performance through the most recent month end.

Portfolio holdings are subject to change daily.

6

PORTFOLIO MANAGERS’ REPORT | VY® INVESCO GROWTH AND INCOME PORTFOLIO |

Sector Diversification

as of December 31, 2020

(as a percentage of net assets) |

| Financials | | 22.6 | % |

| Health Care | | 15.7 | % |

| Information Technology | | 13.3 | % |

| Industrials | | 11.6 | % |

| Consumer Discretionary | | 7.5 | % |

| Consumer Staples | | 5.9 | % |

| Communication Services | | 5.9 | % |

| Materials | | 5.4 | % |

| Energy | | 5.3 | % |

| Utilities | | 2.7 | % |

| Real Estate | | 2.2 | % |

| Assets in Excess of Other Liabilities* | | 1.9 | % |

| Net Assets | | 100.0 | % |

| * Includes short-term investments. |

Portfolio holdings are subject to change daily. |

VY® Invesco Growth and Income Portfolio (the “Portfolio”) seeks long-term growth of capital and income. The Portfolio is managed by Brian Jurkash, Co-lead Portfolio Manager, Matthew Titus, Co-lead Portfolio Manager and Sergio Marcheli, Portfolio Manager, of Invesco Advisers, Inc. — the Sub-Adviser.

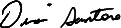

Performance: For the year ended December 31, 2020, the Portfolio’s Class S shares provided a total return of 2.90%, compared to the Russell 1000® Value Index, which returned 2.80%, for the same period.

Portfolio Specifics: For the year ended December 31, 2020, the Portfolio outperformed the Russell 1000 Value® Index.

Stock selection and an overweight in the information technology (“IT”) sector was the largest contributor to the Portfolio’s relative performance for the year. Within the sector, Apple, Qualcomm and Cognizant Technology Solutions were the largest contributors, benefitting from a strong rally in the sector that began in the second quarter of 2020.

Stock selection and an underweight in real estate also helped relative performance as the sector underperformed, posting a decline for the year.

Security selection in the financials sector also contributed to the Portfolio’s relative performance. Large banks and capital markets firms benefited from a rise in yields during the quarter and these stocks performed well amid a broader rally in cyclical stocks.

Security selection in the consumer discretionary sector was the largest detractor from the Portfolio’s relative performance for the year. Within the sector, Carnival and Capri Holdings were significant detractors, driven in large part by the pandemic-related sell-off in early 2020.

Security selection and an overweight in energy also detracted from relative performance, as oil prices declined sharply due to an ongoing supply/demand imbalance, exacerbated by the sharp deceleration in demand due to COVID-19 pandemic. Key detractors from relative performance included Royal Dutch Shell and Marathon Oil.

Security selection in and underweight in consumer staples also detracted from the Portfolio’s relative performance. Restaurant supplier US Foods was a key detractor from Portfolio performance as demand declined sharply due to COVID-19-related restaurant closures.

Top Ten Holdings

as of December 31, 2020

(as a percentage of net assets) |

| General Motors Co. | | 3.4 | % |

| Cognizant Technology Solutions Corp. | | 3.1 | % |

| Morgan Stanley | | 2.7 | % |

| Philip Morris International, Inc. | | 2.7 | % |

| Wells Fargo & Co. | | 2.6 | % |

| Goldman Sachs Group, Inc. | | 2.5 | % |

| Corteva, Inc. | | 2.3 | % |

| Anthem, Inc. | | 2.2 | % |

| American International Group, Inc. | | 2.2 | % |

| CSX Corp. | | 2.2 | % |

Portfolio holdings are subject to change daily. |

The Portfolio held currency forward contracts during the fiscal year for the purpose of hedging currency exposure of non-U.S.-based companies held in the Portfolio. These derivatives were not for speculative purposes or leverage, and these positions had a small negative impact on the Portfolio’s relative performance for the year.

Current Strategy and Outlook: During the fiscal year, the team reduced the Portfolio’s relative overweight exposure to the financials and energy sectors, and increased exposure to the industrials, communication services, IT and real estate sectors. At the end of the fiscal year, the Portfolio’s largest overweight exposures were in the financials, IT and health care sectors, while the largest underweight exposures were to the communication services, utilities and real estate sectors.

The views expressed in this commentary are informed opinions. They should not be considered promises or advice. The views expressed reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. Portfolio holdings are subject to change daily. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements. The Portfolio’s performance returns shown reflect applicable fee waivers and/or expense limits in effect during this period. Absent such fee waivers/expense limitations, if any, performance would have been lower. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

7

| VY® INVESCO GROWTHAND INCOME PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

| | Average Annual Total Returns for the Periods Ended December 31, 2020 | |

| | | | | | 1 Year | | 5 Year | | 10 Year | |

|---|

| | Class ADV | | | | | 2.55 | % | | | 8.28 | % | | | 8.90 | % | |

| | Class I | | | | | 3.22 | % | | | 8.94 | % | | | 9.56 | % | |

| | Class S | | | | | 2.90 | % | | | 8.66 | % | | | 9.28 | % | |

| | Class S2 | | | | | 2.77 | % | | | 8.50 | % | | | 9.12 | % | |

| | Russell 1000® Value Index | | | | | 2.80 | % | | | 9.74 | % | | | 10.50 | % | |

| | | | | | | | | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of VY® Invesco Growth and Income Portfolio against the index indicated. The index is unmanaged and has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your variable annuity contract or variable life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown includes, if applicable, the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other

service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract or a variable life insurance policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.voyainvestments.com or call (800) 366-0066 to get performance through the most recent month end.

Portfolio holdings are subject to change daily.

8

PORTFOLIO MANAGERS’ REPORT | VY® JPMORGAN EMERGING

MARKETS EQUITY PORTFOLIO |

Geographic Diversification

as of December 31, 2020

(as a percentage of net assets) |

| China | | 38.6 | % |

| India | | 18.0 | % |

| Taiwan | | 7.6 | % |

| South Korea | | 6.9 | % |

| Brazil | | 6.2 | % |

| Hong Kong | | 5.7 | % |

| Singapore | | 3.3 | % |

| Argentina | | 3.0 | % |

| United States | | 2.6 | % |

| Indonesia | | 2.0 | % |

| Countries between 0.3%–1.8%ˆ | | 7.8 | % |

| Liabilities in Excess of Other Assets* | | (1.7 | )% |

| Net Assets | | 100.0 | % |

| * Includes short-term investments. |

| ** Includes 9 countries, which each represents 0.3%–1.8% of net assets. |

Portfolio holdings are subject to change daily. |

VY® JPMorgan Emerging Markets Equity Portfolio (the “Portfolio”) seeks capital appreciation. The Portfolio is managed by Austin Forey, Managing Director, Leon Eidelman, CFA and Managing Director, and Amit Mehta, CFA and Executive Director; each a Portfolio Manager of J.P. Morgan Investment Management Inc. — the Sub-Adviser.

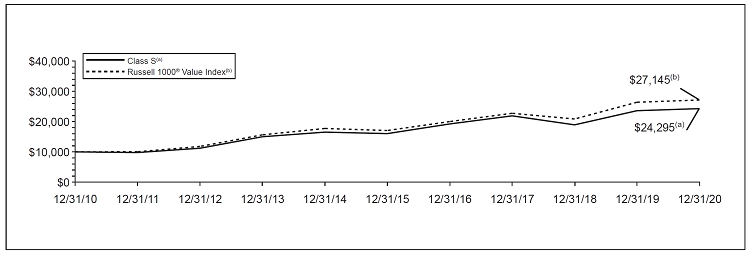

Performance: For the year ended December 31, 2020, the Portfolio’s Class S Shares provided a total return of 33.23% compared to the MSCI Emerging Markets IndexSM (“MSCI EM IndexSM”), which returned 18.31% for the same period.

Portfolio Specifics: The Portfolio outperformed MSCI EM IndexSM for the year ended December 31, 2020, as stock selection and country allocation contributed to returns.

Stock selection in China was the leading contributor to performance. The Portfolio’s position in Techtronic Industries, which manufactures power tools, was a top contributor in China during the period. The company has delivered solid revenue growth, with the majority of their distributors deemed essential services and permitted to remain open in many countries. At the same time, demand for DIY home improvement and maintenance equipment, such as lawnmowers, saw relatively significant growth.

The Portfolio’s off- benchmark exposure to Singapore, the result of stock selection, also boosted relative returns. Specifically, exposure to Sea Limited, an ASEAN e-commerce and gaming business listed in Singapore, was among the top performers. In our opinion, Sea Limited is an example of a strong business that has benefitted from the shift to online consumption in 2020, which was accelerated by the breakout of the COVID-19 pandemic. During the period, the company consistently reported strong results, growing e-commerce and gaming revenues substantially. The company’s fintech platform and digital entertainment services group both experienced significant new user growth in 2020.

On the downside, stock selection in India weighed on relative returns during the period, most notably led by exposure to IndusInd Bank. The stock fell 42.1% (in USD terms) on the back of concerns over its asset quality during the reporting period.

The Portfolio’s underweight to South Korea, the result of stock selection, also weighed on relative performance. Relatively better control of the pandemic by South Korea relative to other countries in the West and a heavier tilt towards the tech hardware sector buoyed South Korean equities in the year.

Top Ten Holdings

as of December 31, 2020

(as a percentage of net assets) |

| Samsung Electronics Co., Ltd. | | 5.5 | % |

| Taiwan Semiconductor Manufacturing Co., Ltd. ADR | | 4.8 | % |

| HDFC Bank Ltd. ADR | | 4.1 | % |

| Tencent Holdings Ltd. | | 3.9 | % |

| Housing Development Finance Corp. | | 3.7 | % |

| Sea Ltd. ADR | | 3.3 | % |

| MercadoLibre, Inc. | | 3.0 | % |

| Wuxi Biologics Cayman, Inc. | | 2.9 | % |

| Alibaba Group Holding Ltd. ADR | | 2.8 | % |

| Taiwan Semiconductor Manufacturing Co., Ltd. | | 2.8 | % |

| Portfolio holdings are subject to change daily. |

Current Strategy and Outlook: How long the COVID-19 pandemic persists as a health risk is crucial for economies and financial markets. Medical developments could mean a path to normalcy is possible in 2021, in our opinion. A growing list of developed market and emerging market (“EM”) economies appear to be discussing vaccination plans. However, speeds of vaccine rollouts differ greatly and uncertainties still remain, especially in the near term.

The path of U.S. fiscal stimulus now has the chance to be larger than the base case prior to January given Democratic control of the U.S. government following the special elections in Georgia. For EM equities, protectionism has already re-emerged in 2021 and we will watch how the U.S.-China relationship evolves.

Valuations are slightly above average, but earnings revisions are turning positive across a broader range of sectors. We believe that the path of the dollar will be key, as it has weakened considerably over the past quarter. In our view, further weakness would provide support to EM equities.

The views expressed in this commentary are informed opinions. They should not be considered promises or advice. The views expressed reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. Portfolio holdings are subject to change daily. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements. The Portfolio’s performance returns shown reflect applicable fee waivers and/or expense limits in effect during this period. Absent such fee waivers/expense limitations, if any, performance would have been lower. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

9

VY® JPMORGAN EMERGING

MARKETS EQUITY PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

| | Average Annual Total Returns for the Periods Ended December 31, 2020 | |

| | | | | | 1 Year | | 5 Year | | 10 Year | |

| | Class ADV | | | | | 32.71 | % | | | 18.35 | % | | | 5.92 | % | |

| | Class I | | | | | 33.52 | % | | | 19.07 | % | | | 6.56 | % | |

| | Class S | | | | | 33.23 | % | | | 18.77 | % | | | 6.30 | % | |

| | Class S2 | | | | | 33.03 | % | | | 18.58 | % | | | 6.13 | % | |

| | MSCI EM IndexSM | | | | | 18.31 | % | | | 12.81 | % | | | 3.63 | % | |

| | | | | | | | | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of the VY® JPMorgan Emerging Markets Equity Portfolio against the index indicated. The index is unmanaged and has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your variable annuity contract or variable life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown includes, if applicable, the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other

service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract or a variable life insurance policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.voyainvestments.com or call (800) 366-0066 to get performance through the most recent month end.

Portfolio holdings are subject to change daily.

10

| PORTFOLIO MANAGERS’ REPORT | VY® MORGAN STANLEY GLOBAL

FRANCHISE PORTFOLIO |

Geographic Diversification

as of December 31, 2020

(as a percentage of net assets) |

| United States | | 68.7 | % |

| United Kingdom | | 15.9 | % |

| France | | 5.8 | % |

| Germany | | 4.4 | % |

| Netherlands | | 2.3 | % |

| Italy | | 0.5 | % |

| Assets in Excess of Other Liabilities* | | 2.4 | % |

| Net Assets | | 100.0 | % |

| * Includes short-term investments. |

| Portfolio holdings are subject to change daily. |

VY® Morgan Stanley Global Franchise Portfolio (the “Portfolio”) seeks long-term capital appreciation. The Portfolio is managed by William D. Lock, Managing Director, Bruno Paulson, Managing Director, Nic Sochovsky, Managing Director, Vladimir A. Demine, Executive Director, Dirk Hoffmann-Becking, Executive Director, Marcus Watson, Executive Director, Alex Gabriele, Executive Director, Nathan Wong, Executive Director, and Richard Perrott, Executive Director, Portfolio Managers* of Morgan Stanley Investment Management Inc.— the Sub-Adviser.

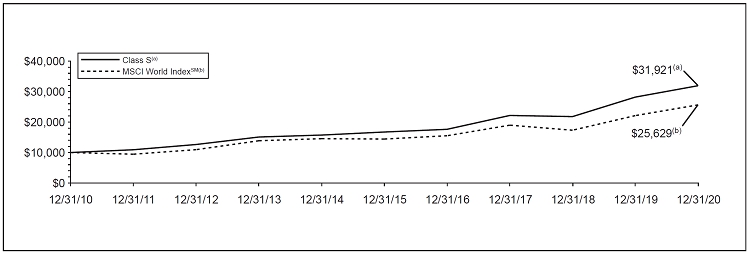

Performance: For the year ended December 31, 2020, the Portfolio’s Class S shares provided a total return of 13.28% compared to the MSCI World IndexSM (the “Index”), which returned 15.90% for the same period.

Portfolio Specifics: For the one-year period, sector allocation was positive, but stock selection was negative. The overweight in information technology helped a great deal with sector allocation, as did the underweight in financials and the lack of energy stocks, despite the two sectors’ strong performance in the fourth quarter. These positive effects were significantly larger than the negative impacts of the consumer staples overweight and consumer discretionary underweight. The underperformance in information technology was the main driver of the negative stock selection. Communication services also underperformed for 2020 as a whole, while health care and financials outperformed.

Top Ten Holdings

as of December 31, 2020

(as a percentage of net assets) |

| Microsoft Corp. | | 8.6 | % |

| Reckitt Benckiser Group PLC | | 7.9 | % |

| Philip Morris International, Inc. | | 7.8 | % |

| Visa, Inc.—Class A | | 5.6 | % |

| Accenture PLC | | 4.8 | % |

| Procter & Gamble Co. | | 4.7 | % |

| SAP SE | | 4.4 | % |

| Baxter International, Inc. | | 4.0 | % |

| Danaher Corp. | | 4.0 | % |

| Automatic Data Processing, Inc. | | 3.9 | % |

| Portfolio holdings are subject to change daily. |

Current Strategy and Outlook: We believe, there are only two ways of losing money in equities: either the earnings go away or the valuation goes away. Our quality-obsessed investment philosophy looks to minimize the former, and the rise in the Portfolio’s 2020 earnings has provided further evidence of market resilience, despite some of the idiosyncratic headwinds the COVID-19 pandemic has produced. We have also looked to reduce the risk of the latter. The Portfolio’s shift to cheaper stocks has been to the detriment of performance, given the continued progress for growthier names, but we believe should support the Portfolio’s resilience in the future.

We do not claim that the Portfolio is cheap in absolute terms. Now more than ever, we believe it is time to focus on keeping the lights on, rather than attempting to shoot them out, and it is our opinion that reasonably priced compounders seem a reasonable way of avoiding a plunge into darkness.

| |

| * | | Effective March 31, 2021, Dirk Hoffmann-Becking will retire and will no longer serve as a portfolio manager of the Portfolio. |

The views expressed in this commentary are informed opinions. They should not be considered promises or advice. The views expressed reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. Portfolio holdings are subject to change daily. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements. The Portfolio’s performance returns shown reflect applicable fee waivers and/or expense limits in effect during this period. Absent such fee waivers/expense limitations, if any, performance would have been lower. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

11

VY® MORGAN STANLEY GLOBAL

FRANCHISE PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

| | Average Annual Total Returns for the Periods Ended December 31, 2020 | |

| | | | | | 1 Year | | 5 Year | | 10 Year | |

| | Class ADV | | | | | 12.87 | % | | | 13.41 | % | | | 11.92 | % | |

| | Class R6(1) | | | | | 13.55 | % | | | 14.07 | % | | | 12.44 | % | |

| | Class S | | | | | 13.28 | % | | | 13.80 | % | | | 12.30 | % | |

| | Class S2 | | | | | 13.06 | % | | | 13.62 | % | | | 12.13 | % | |

| | MSCI World IndexSM | | | | | 15.90 | % | | | 12.19 | % | | | 9.87 | % | |

| | | | | | | | | | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of VY® Morgan Stanley Global Franchise Portfolio against the index indicated. The index is unmanaged and has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your variable annuity contract or variable life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown includes, if applicable, the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract or a variable life insurance policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.voyainvestments.com or call (800) 366-0066 to get performance through the most recent month end.

Portfolio holdings are subject to change daily.

| (1) | | Class R6 incepted on May 3, 2016. The Class R6 shares performance shown for the period prior to their inception date is the performance of Class S shares without adjustment for any differences in the expenses between the two classes. If adjusted for such differences, returns would be different. |

12

| PORTFOLIO MANAGERS’ REPORT | VY® T. ROWE PRICE CAPITAL

APPRECIATION PORTFOLIO |

Investment Type Allocation

as of December 31, 2020

(as a percentage of net assets) |

| Common Stock | | | | | 68.0 | % |

| Bank Loans | | | | | 11.3 | % |

| Corporate Bonds/Notes | | | | | 9.3 | % |

| Preferred Stock | | | | | 2.8 | % |

| Asset-Backed Securities | | | | | 0.3 | % |

| Convertible Bonds/Notes** | | | | | 0.0 | % |

| Assets in Excess of Other Liabilities* | | | | | 8.3 | % |

| Net Assets | | | | | 100.0 | % |

| * Includes short-term investments. | |

| ** Amount is less than 0.05% |

| Portfolio holdings are subject to change daily. |

VY® T. Rowe Price Capital Appreciation Portfolio (the “Portfolio”) seeks, over the long-term, a high total investment return, consistent with the preservation of capital and with prudent investment risk. The Portfolio is managed by David R. Giroux, CFA and Vice President of T. Rowe Price Associates, Inc. — the Sub-Adviser.

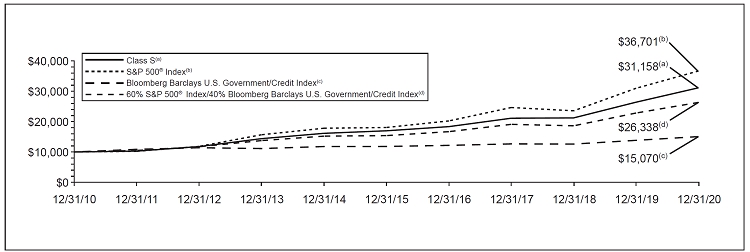

Performance: For the year ended December 31, 2020, the Portfolio’s Class S shares provided a total return of 17.97%. By comparison, the S&P 500® Index, the Bloomberg Barclays U.S. Government/Credit Index, and the 60% S&P 500® Index/40% Bloomberg Barclays U.S. Government/Credit Index returned 18.40%, 8.93% and 15.30%, respectively, for the same period.

Portfolio Specifics: In 2020, the Portfolio posted a positive return and outperformed the S&P 500® Index, before fees and expenses. The Portfolio performed well versus its peers, ranking in the top decile of both its Morningstar and Lipper peer groups. The Portfolio’s equity holdings posted a strongly positive return, outpacing its S&P 500® Index benchmark. The Portfolio’s fixed income holdings posted a positive return during the one-year period, slightly outperforming its benchmark, the Bloomberg Barclays U.S. Government/Credit Index.

Our overall fixed income weight declined from the prior year, as we trimmed our allocations in high yield bonds and investment-grade corporates. Our largest exposure in fixed income is in bank loans, where we have found select issues that at current levels offer compelling risk-adjusted return profiles.

Within equities, the financials sector contributed to relative returns due to stock picks, such as Intercontinental Exchange, and a beneficial underweight. Intercontinental Exchange, a data service provider and global operator of exchanges, benefited from growth in data revenue throughout the year as well as from its less cyclical business model relative to many banks and capital markets companies. Health care further aided results due to stock choices such as Danaher. Diversified medical equipment and supplies conglomerate Danaher benefited from growing demand for diagnostic tools needed to test for the coronavirus, as well as from organic growth and margins from recently acquired Cytiva, formerly GE Healthcare Life Sciences. An underweight allocation to the energy sector further aided relative results. Conversely, the information technology sector weighed on relative results due to security selection, led by Fiserv. Fiserv lagged within the very strong-performing information technology sector on significant disruption to its merchant acceptance business due to the coronavirus pandemic. An unexpected announcement in early May that the company’s CEO would retire in mid-2020 also raised some investor concern amid a challenging market environment. An overweight allocation to the utilities sector further hindered relative results. Utilities lagged the broader market’s strong one-year return as investors mostly favored areas of the market with exposure to such things as e-commerce and the broader digitalization of the economy due to the circumstances that were caused by the coronavirus pandemic.

Top Ten Holdings

as of December 31, 2020*

(as a percentage of net assets) |

| Microsoft Corp. | | 5.3 | % |

| Amazon.com, Inc. | | 3.7 | % |

| General Electric Co. | | 3.6 | % |

| PNC Financial Services Group, Inc. | | 3.4 | % |

| Alphabet, Inc. — Class C | | 3.4 | % |

| Marsh & McLennan Cos., Inc. | | 3.0 | % |

| Fiserv, Inc. | | 3.0 | % |

| American Electric Power Co., Inc. | | 2.9 | % |

| Visa, Inc. — Class A | | 2.8 | % |

| Humana, Inc. | | 2.7 | % |

| * Excludes short-term investments. |

| Portfolio holdings are subject to change daily. |

During the reporting period, the covered call strategy represented, on average, 8.33% of the overall Portfolio and generated a return of approximately 7.68%. The covered call strategy’s estimated contribution to the Portfolio’s total return was 1.30%. The estimated return impact from employing options was -18 basis points (-0.18%) for the reporting period December 31, 2020.

Current Strategy and Outlook: After a year dominated by the devastating impacts of the coronavirus pandemic, optimism has risen that the successful development of vaccines and their subsequent distribution will bring an end to economic harm the virus has left in its wake. This optimism has, however, broadened a market rally that had been more narrowly concentrated in perceived “COVID winners” earlier in 2020, leaving valuations constrained and compelling opportunities harder to come by, in our view. After initial expectations for a divided government, Democrats ultimately won control of both chambers of Congress as well as the White House, giving rise to hopes for additional economic relief. While further stimulus may provide a tailwind for markets, we believe it will likely be short-lived. Taking a longer view, it is our opinion that markets already appear expensive with an optimistic outlook for growth priced-in, and the potential for regulatory and tax policy reform merits caution. We have a balanced view of the current market and have positioned the Portfolio accordingly. We remain focused on identifying high-quality businesses with strong fundamentals that we believe can deliver solid earnings and the potential for growth over the long term.

The views expressed in this commentary are informed opinions. They should not be considered promises or advice. The views expressed reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. Portfolio holdings are subject to change daily. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements. The Portfolio’s performance returns shown reflect applicable fee waivers and/or expense limits in effect during this period. Absent such fee waivers/expense limitations, if any, performance would have been lower. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

13

VY® T. ROWE PRICE CAPITAL

APPRECIATION PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

| | Average Annual Total Returns for the Periods Ended December 31, 2020 | |

| | | | 1 Year | | 5 Year | | 10 Year | |

|---|

| | Class ADV | | | 17.54 | % | | | 12.50 | % | | | 11.65 | % | |

| | Class I | | | 18.28 | % | | | 13.18 | % | | | 12.32 | % | |

| | Class R6(1) | | | 18.27 | % | | | 13.18 | % | | | 13.32 | % | |

| | Class S | | | 17.97 | % | | | 12.89 | % | | | 11.03 | % | |

| | Class S2 | | | 17.82 | % | | | 12.73 | % | | | 11.87 | % | |

| | S&P 500® Index | | | 18.40 | % | | | 15.22 | % | | | 13.88 | % | |

| | Bloomberg Barclays U.S. Government/Credit Index | | | 8.93 | % | | | 4.98 | % | | | 4.19 | % | |

| | 60% S&P 500® Index/40% Bloomberg Barclays U.S. Government/Credit Index | | | 15.30 | % | | | 11.34 | % | | | 10.17 | % | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of VY® T. Rowe Price Capital Appreciation Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your variable annuity contract or variable life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown includes, if applicable, the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract or a variable life insurance policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.voyainvestments.com or call (800) 366-0066 to get performance through the most recent month end.

Portfolio holdings are subject to change daily.

| (1) | | Class R6 incepted on May 3, 2016. The Class R6 shares performance shown for the period prior to their inception date is the performance of Class I shares without adjustment for any differences in the expenses between the two classes. If adjusted for such differences, returns would be different. |

14

| PORTFOLIO MANAGERS’ REPORT | VY® T. ROWE PRICE EQUITY INCOME PORTFOLIO |

Sector Diversification

as of December 31, 2020

(as a percentage of net assets) |

| Financials | | 21.0 | % |

| Health Care | | 13.2 | % |

| Industrials | | 12.1 | % |

| Information Technology | | 9.5 | % |

| Utilities | | 9.0 | % |

| Consumer Staples | | 7.4 | % |

| Energy | | 6.5 | % |

| Materials | | 6.1 | % |

| Communication Services | | 5.4 | % |

| Real Estate | | 4.5 | % |

| Consumer Discretionary | | 4.1 | % |

| Assets in Excess of Other Liabilities* | | 1.2 | % |

| Net Assets | | 100.0 | % |

| * Includes short-term investments. |

| Portfolio holdings are subject to change daily. |

VY® T. Rowe Price Equity Income Portfolio (the “Portfolio”) seeks a high level of dividend income as well as long-term growth of capital primarily through investments in stocks. The Portfolio is managed by John Linehan, CFA, Head of U.S. Equity and Portfolio Manager of T. Rowe Price Associates, Inc. — the Sub-Adviser.

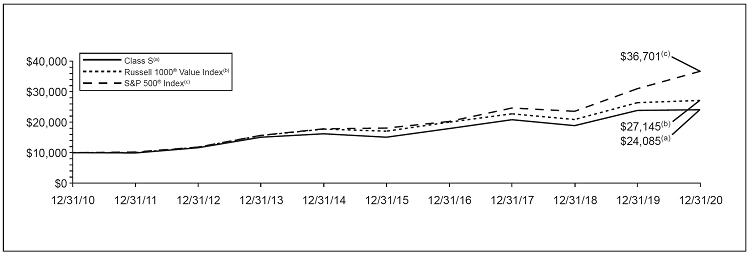

Performance: For the year ended December 31, 2020, the Portfolio’s Class S shares provided a total return of 0.95% compared to the Russell 1000® Value Index and the S&P 500® Index, which returned 2.80% and 18.40%, respectively, for the same period.

Portfolio Specifics: The Portfolio underperformed its benchmark, the Russell 1000® Value Index due to stock selection in the health care sector detracted from relative results. CVS Health traded lower throughout the year amid short-term concerns over a potential decline in demand due to coronavirus lockdowns.

Stock choices in the consumer staples sector hindered relative returns. During the first half of the year, shares of Tyson Foods lagged the broader market as the company grappled with uncertainty stemming from the coronavirus outbreak and a shift from commercial to residential consumption. Additionally, shares were pressured due to reports of coronavirus outbreaks at numerous plants. In the fourth quarter, the company came under fire after reports surfaced of management’s actions related to the coronavirus.

Within industrials and business services, stock choices and an unfavorable overweight allocation detracted from relative performance. Despite finishing lower for the one-year period, shares of Boeing significantly rebounded from March lows. Boeing shares began trending upward late in the first half of the year as airlines began rescheduling more flights. Additionally, late in the fourth quarter, shares trended upward following the recertification of the 737 MAX but ultimately remained well below the level we saw early in the year.

In contrast, stock selection in information technology contributed to relative returns for the 12-month period. Shares of Qualcomm regained from the first-quarter sell-off and were up considerably for the one-year period, stemming from favorable earnings reports (which exceeded market expectations) and the unveiling of the company’s new Snapdragon 888 5G mobile platform.

Top Ten Holdings

as of December 31, 2020

(as a percentage of net assets) |

| Qualcomm, Inc. | | 3.1 | % |

| Wells Fargo & Co. | | 2.8 | % |

| Southern Co. | | 2.7 | % |

| General Electric Co. | | 2.6 | % |

| DuPont de Nemours, Inc. | | 2.5 | % |

| Chubb Ltd. | | 2.3 | % |

| United Parcel Service, Inc. — Class B | | 2.3 | % |

| Morgan Stanley | | 2.1 | % |

| Metlife, Inc. | | 2.0 | % |

| Total SE ADR | | 1.9 | % |

| Portfolio holdings are subject to change daily. |

Stock selection in energy also contributed to relative results, led by TC Energy. However, the impact was partially offset by an unfavorable overweight position in the sector.

Current Strategy and Outlook: Given market performance in 2020, in our view we are beginning to see signs of exuberance, with narrow leadership, high index concentration, and increased special purpose acquisition company and initial public offering activity. Considering this, we believe 2021 will present a stock pickers’ market, where more tempered returns may remind investors of the importance of dividends. Additionally, in the event of an economic recovery, we believe this may be an environment where we could see inflation, as consumers and businesses have capital to deploy while household net worth is at an all-time high. Ultimately, there may be a recoupling between the market and the economy, which might benefit areas of the market that were left behind over the course of 2020, in our opinion.

The views expressed in this commentary are informed opinions. They should not be considered promises or advice. The views expressed reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. Portfolio holdings are subject to change daily. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. This report contains statements that may be “forward-looking“ statements. Actual results may differ materially from those projected in the “forward-looking“ statements. The Portfolio’s performance returns shown reflect applicable fee waivers and/or expense limits in effect during this period. Absent such fee waivers/expense limitations, if any, performance would have been lower. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

15

| VY® T. ROWE PRICE EQUITY INCOME PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

| | Average Annual Total Returns for the Periods Ended December 31, 2020 | |

| | | | 1 Year | | 5 Year | | 10 Year | |

|---|

| | Class ADV | | | 0.64 | % | | | 9.43 | % | | | 8.80 | % | |

| | Class I | | | 1.27 | % | | | 10.09 | % | | | 9.46 | % | |

| | Class S | | | 0.95 | % | | | 9.82 | % | | | 9.19 | % | |

| | Class S2 | | | 0.85 | % | | | 9.65 | % | | | 9.03 | % | |

| | Russell 1000® Value Index | | | 2.80 | % | | | 9.74 | % | | | 10.50 | % | |

| | S&P 500® Index | | | 18.40 | % | | | 15.22 | % | | | 13.88 | % | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of VY® T. Rowe Price Equity Income Portfolio against the indices indicated. An index is unmanaged and has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your variable annuity contract or variable life insurance policy. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown includes, if applicable, the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract or a variable life insurance policy. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.voyainvestments.com or call (800) 366-0066 to get performance through the most recent month end.

Portfolio holdings are subject to change daily.

Effective May 25, 2018, the Portfolio changed its benchmark from the S&P 500® Index to the Russell 1000® Value Index because the Russell 1000® Value Index is considered by the Sub-Adviser to be a more appropriate benchmark that better aligns with the Portfolio’s value-focused investment style.

16

| PORTFOLIO MANAGERS’ REPORT | VY® T. ROWE PRICE INTERNATIONAL

STOCK PORTFOLIO |

Geographic Diversification

as of December 31, 2020

(as a percentage of net assets) |

| Japan | | 15.2 | % |

| United Kingdom | | 8.8 | % |

| China | | 8.2 | % |

| Netherlands | | 7.9 | % |

| France | | 6.9 | % |

| Switzerland | | 6.8 | % |

| South Korea | | 5.7 | % |

| India | | 4.5 | % |

| Germany | | 4.3 | % |

| Canada | | 3.8 | % |

| Countries between 0.0%-3.4%ˆ | | 24.7 | % |

| Assets in Excess of Other Liabilities* | | 3.2 | % |

| Net Assets | | 100.0 | % |

| * Includes short-term investments. |

| ** Includes 19 countries, which each represents 0.0%–3.4% of net assets. |

| Portfolio holdings are subject to change daily. |

VY® T. Rowe Price International Stock Portfolio (the “Portfolio”) seeks long-term growth of capital. The Portfolio is managed by Richard N. Clattenburg, CFA and Vice President, Portfolio Manager of T. Rowe Price Associates, Inc. — the Sub-Adviser.

Performance: For the year ended December 31, 2020, the Portfolio’s Class I shares provided a total return of 14.74% compared to the MSCI All Country World (ex-U.S.) IndexSM (“MSCI ACWI ex-U.S.”), which returned 10.65% for the same period.

Portfolio Specifics: The Portfolio outperformed its benchmark, the MSCI ACWI ex-U.S., for the reporting period. Broadly speaking, sector allocation aided relative performance. At the sector level, communication services was the largest contributor due to security selection. Financials aided relative returns due to stock selection and a favorable underweight. Energy also boosted relative results with a favorable underweight position. In contrast, holdings within industrials and business services detracted. Health care also hindered relative performance due to stock choices.

Regionally, the Portfolio found relative success in developed Europe — particularly the United Kingdom — due to beneficial security selection. No regions detracted from relative performance.

Within the communication services sector, NAVER was one of the top relative contributors to the Portfolio in 2020. The company reported in-line results in late July that showed core revenues growing steadily as the investments made over the last three years pay off. That was reinforced in October’s earnings, where NAVER beat consensus estimates for revenue and noted that it continued to invest in new e-commerce, fintech, and cloud initiatives.

Top Ten Holdings

as of December 31, 2020*

(as a percentage of net assets) |

| Taiwan Semiconductor Manufacturing Co., Ltd. | | 3.4 | % |

| Samsung Electronics Co., Ltd. | | 2.7 | % |

| Alibaba Group Holding Ltd. ADR | | 2.6 | % |

| Naspers Ltd. | | 2.5 | % |

| NAVER Corp. | | 2.3 | % |

| Thales S.A. | | 2.2 | % |

| Unilever PLC | | 2.1 | % |

| AIA Group Ltd. | | 2.0 | % |

| Housing Development Finance Corp. | | 1.9 | % |

| Prosus NV | | 1.8 | % |

| * Excludes short-term investments. |

| Portfolio holdings are subject to change daily. |

The Portfolio’s weakness in the industrials and business services sector was largely explained by Thales, a global aerospace and defense company that specializes in electrical systems. The near-complete halting of air travel due to the coronavirus pandemic, and fears for what that means for aircraft suppliers like Thales, sent shares sharply lower. However, earnings in late July showed in-line performance at the group level, with the headwinds in the aerospace segments offset somewhat by good results in other areas. Earnings in October again met expectations and showed business was returning to normal, a very welcome sign.

Current Strategy and Outlook: The historically extraordinary divide between growth and value stocks persisted in the final quarter of 2020 even as the coronavirus pandemic spiraled in many countries. We believe a value snapback lasting more than a few days is likely at some point in a post-pandemic recovery and could be violent, consistent with past value rallies. However, the timing of a value-driven rally is impossible to predict. Our focus remains on leveraging the strengths of our fundamental research platform and investing in companies that we think reflect the most compelling trade-off between valuation and fundamentals. Near term, we believe that massive and frequent virus testing is key to a recovery before vaccines become widely available. We expect a strong recovery in travel demand as more people get vaccinated. However, it is our opinion that international travel will take longer to rebound than domestic travel, and business travel may not fully return to pre-pandemic levels as videoconferencing replaces in-person meetings in the near term.

The views expressed in this commentary are informed opinions. They should not be considered promises or advice. The views expressed reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. Portfolio holdings are subject to change daily. The outlook for this Portfolio may differ from that presented for other Voya mutual funds. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements. The Portfolio’s performance returns shown reflect applicable fee waivers and/or expense limits in effect during this period. Absent such fee waivers/expense limitations, if any, performance would have been lower. Performance for the different classes of shares will vary based on differences in fees associated with each class. An index has no cash in its portfolio and imposes no sales charges. An investor cannot invest directly in an index.

17

VY® T. ROWE PRICE INTERNATIONAL

STOCK PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

| | Average Annual Total Returns for the Periods Ended December 31, 2020 | |

| | | | | | 1 Year | | 5 Year | | 10 Year | |

|---|

| | Class ADV | | | | | 14.11 | % | | | 9.96 | % | | | 6.29 | % | |

| | Class I | | | | | 14.74 | % | | | 10.61 | % | | | 6.94 | % | |

| | Class S | | | | | 14.49 | % | | | 10.33 | % | | | 6.67 | % | |

| | MSCI ACWI ex-U.S. | | | | | 10.65 | % | | | 8.93 | % | | | 4.92 | % | |