| OMB APPROVAL |

OMB Number: 3235-0570 Expires: January 31, 2014 Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05685

Williamsburg Investment Trust

(Exact name of registrant as specified in charter)

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

W. Lee H. Dunham, Esq.

Sullivan & Worcester LLP One Post Office Square Boston, Massachusetts 02109

(Name and address of agent for service)

Registrant's telephone number, including area code: (513) 587-3400

Date of fiscal year end: March 31, 2012

Date of reporting period: September 30, 2011

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

SEMI-ANNUAL REPORT September 30, 2011 (Unaudited) |

THE DAVENPORT FUNDS LETTER TO SHAREHOLDERS | October 20, 2011 |

Market Commentary

Equity investing hasn’t been very fun recently. In fact, we’ve just endured the toughest stretch for stocks since the 2008 financial crisis. Major stock indices declined during every month of the third quarter. The S&P 500 Index and Russell 2000 Index declined 13.9% and 21.9%, respectively, during the quarter ended September 30, 2011 and are now down 8.7% and 17.0%, respectively, on a year-to-date basis. Interestingly, the performance spread between large and small caps has become very noticeable during this tumultuous time. Perhaps most telling, the Dow Jones Industrial Average was down a more manageable 3.9% year-to-date. We entered the year thinking that large cap stocks should do well on a relative basis and that has proven to be the case thus far (although we’d rather it be under different circumstances).

We have a couple comments about performance. In terms of absolute performance, we think it’s important to put the market’s recent correction in perspective. Since March 2009 (the low point of the crisis), the S&P 500 has still gained over 60% through quarter end. Wide swings, including recent losses, have made for a bumpy and sometimes painful ride, but investors have nonetheless enjoyed a solid market recovery. Moving to relative performance, we note this has been a very tough year for active managers. In fact, J.P. Morgan recently reported this is the worst year for active managers since 1998 with nearly 50% of mutual funds under-performing their respective benchmarks by more than 2.5 percentage points. Stocks have been highly correlated, making it difficult for managers to differentiate themselves. We know relative performance doesn’t pay the bills, but are pleased that two of our three Funds are ahead of their benchmarks and the third isn’t far behind. Also, we sense a lot of investors have been whipsawed in this market and some have experienced big negative surprises. While we haven’t delivered big gains, we take pride in having stayed pretty consistent through turbulent times and not having delivered our shareholders any big surprises relative to how equity markets have behaved.

Clear signs of renewed economic weakness have emerged and have bolstered the case for a “double dip” recession. Unemployment remains elevated and the housing market continues to struggle. Furthermore, investor angst has been exacerbated by political discord out of Washington D.C. Politics in our country definitely seems to have hit a new low point and has eroded consumer, corporate and investor confidence. We also think market declines have taken on somewhat of a self-fulfilling nature. In other words, a prolonged downtrend has weighed on consumer and business demand, which in turn is weighing further on markets. While we have yet to see a broad based reduction of corporate earnings outlooks, we have seen some indications of weakness and the stock market is clearly saying there are more to follow. We definitely expect to hear some cautious commentary when companies report third quarter numbers in coming weeks.

We aren’t sure monetary policy can save us this time around. While current easy policy is expected to persist, there aren’t many more arrows in the Federal Reserve’s quiver. Recently, the Fed announced what was dubbed “Operation Twist.” Essentially, this entails shifting government bond purchases towards longer-dated notes with the intent of lowering long-term interest rates.

2

The Fed’s plans and a general flight to safety have driven up bond prices. A 10-year bond now yields less than 2% whereas a 30-year yields less than 3%. In theory, this would not only encourage borrowing, but would also entice investors to take on more risk in search of higher returns. Equities have performed quite poorly since the announcement as the marginal impact of these policy moves has been called into question. Meanwhile, commodity prices have plummeted giving rise to deflation worries (a significant change from six months ago when inflation was the focal point). Even Fed Chairman Ben Bernanke has noted that economic conditions are now more dependent on sound fiscal policy from Washington.

Unfortunately, government spending is needed at a time when governments can least afford to spend. Nations around the world are struggling beneath giant debt burdens following years of excess spending. Budget troubles are most evident in Europe, where the woes of specific nations such as Greece are threatening the vitality of the whole Eurozone and the viability of the Euro as a currency. The chickens also appear to be coming home to roost in the U.S., where spending cuts are at the heart of political rancor surrounding our record deficit. We recently noted it may be time to “take our medicine,” implying a long period of low growth alongside government austerity. This scenario is looking increasingly likely; however, it doesn’t mean economic growth will come to a halt. Furthermore, a period of government restraint and debt pay-down could ultimately sow the seeds for a stronger economy.

We are worried, but don’t believe we are in for a repeat of 2008. There’s no doubt that Europe’s problems will weigh on multinational companies and emerging markets are beginning to cool. Domestically, however, we aren’t coming off the same high as we were in ’08 and many industries are already operating at depressed levels. We think it currently makes sense to emphasize companies with a domestic bias. 2008 followed a period when many American individuals and companies did unwise things (mainly excessive borrowing) and growth was inflated. A financial/liquidity crisis, which we don’t expect to recur, prompted a period of more conservative behavior and repairing past mistakes. Now, companies generally are in good shape, many with little debt, large cash positions, lean cost structures and access to cheap capital. Corporate America is now much better suited to absorb any economic weakness.

Oftentimes, extreme levels of dread and uncertainty can lead to market gains as obstacles are overcome. We are hopeful that Eurozone leaders can arrange a comprehensive budget solution, even if it means slower growth in coming years. We are also hopeful that U.S. leadership will introduce constructive economic policy that instills confidence in businesses and consumers. Who knows, maybe the threat of not being re-elected in 2012 will drive more decisive action by many politicians? Market weakness has been very broad based and many companies are trading at low double-digit earnings multiples. It would appear that a lot of bad news is reflected in current stock prices. We continue to focus on companies we know and like best. In doing so, we believe we can lay the foundation for years of strong absolute and relative performance. We thank you for your trust and look forward to reporting back to you at year end.

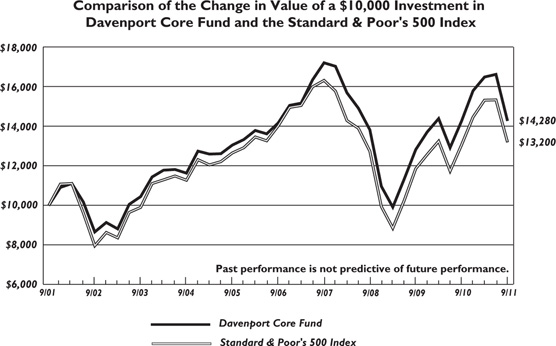

Davenport Core Fund

The following chart represents Davenport Core Fund (the “Fund”) performance and the performance of the S&P 500 Index*, the Fund’s primary benchmark, for the periods ended September 30, 2011.

3

Q3 | 1 Year | 3 Years** | 5 Years** | 10 Years** | Since Inception** (1/15/98) | Expense Ratio: | |

| DAVPX | -14.06 | 0.17 | 1.12 | 0.17 | 3.63 | 3.17 | 0.97% |

| S&P 500 | -13.87 | 1.14 | 1.23 | -1.18 | 2.82 | 3.09 |

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

| * | The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

| ** | Annualized. |

The Core Fund declined 14.06% during the third quarter, roughly in line with the S&P 500’s 13.87% tumble. Year to date, the Fund is down 9.54%, slightly trailing the 8.68% decline for the S&P 500. While large cap stocks fared better versus their smaller brethren, they were not spared from the global flight to safety (namely cash and U.S. Treasuries).

The combination of intense volatility and high correlations allowed few standouts in terms of absolute performance during the quarter. Ironically, after expressing our frustrations with large cap technology in our last letter, shares of Apple (AAPL) came to life, posting a gain in the mid teens. Other top performers included Dollar Tree (DLTR), McDonald’s (MCD) and American Tower (AMT), which all have the common thread of relatively insulated earnings streams. Smaller cap cyclical stocks such as CarMax (KMX) and Albemarle (ALB) were among the biggest detractors for the period. However, in each case, we are willing to look through near term volatility in results given a high level of confidence in longer term earnings power.

The Financials sector was the largest source of relative performance during the quarter as names such as Markel (MKL), Berkshire Hathaway (BRK/B) and Brookfield Asset Management (BAM) performed better than banks and other credit sensitive entities. While we have enjoyed our light exposure to banks, weakness provided a great opportunity to add to a credit sensitive name such as Capital One (COF). We believe 2012 earnings of $6.00+ seem achievable in light of credit and loan growth trends. Moreover, the company’s recent proposed acquisitions of ING Direct and HSBC’s credit card business should increase scale, improve profitability and generate significant cross selling opportunities down the road. We also added to our position in Berkshire Hathaway (BRK/B) at a slight premium to book value. Put simply, we thought the stock was too cheap given the company’s collection of above average businesses, immense cash flows and impressive history of capital allocation. While we realize “The Oracle” will not be around forever, we believe Mr. Buffett has built a valuable franchise capable of creating value long after he retires. Apparently, Mr. Buffet agrees as evidenced by the uncharacteristic share repurchase authorization the company announced near quarter end.

Excluding a strong quarter from recently purchased Dollar Tree (DLTR), the Consumer Discretionary sector had a rough go as troublesome economic data, European financial issues and market volatility pushed consumer confidence to new lows. As we enter a period likely

4

characterized by slow demand growth, we are attracted to capacity constrained industries that can maintain pricing power. As such, we sold our position in Ford Motor (F) and initiated a position in leading luxury hotel operator, Starwood Hotels (HOT). While we think auto demand will eventually recover, we are still concerned there may be overcapacity in the industry. On the other hand, hotel supply growth has been virtually dormant since the financial crisis. We believe that this phenomenon, coupled with an expectation for negligible supply growth over the next couple of years, provides a structural tailwind that should be supportive of occupancy, room rates and revenue per available room (RevPAR) for HOT. Given the company’s quality product offering, loyal customer base and meaningful operating leverage, we expect earnings to ramp significantly as the company captures these trends. Furthermore, we purchased the shares at valuation levels not seen since the beginning of 2009, which we think paves the way for significant upside as the aforementioned trends manifest and the stock’s multiple expands.

Near the end of the quarter, we initiated a position in the world’s largest food and beverage company, Nestlé (NSRGY). We think Nestlé is a great example of an all weather stock that can do well in a variety of market environments. For one, management has an impressive track record of value creation and the business produces returns on capital in the low 30% range. The company’s leading brands (Nestlé, Nescafé, Jenny Craig, Perrier, Pure Life, etc.) and unrivaled manufacturing scale create significant competitive advantages and enable pricing power with lead retailers. In addition to these defensive qualities, the company derives one third of its revenues from emerging markets, where it continues to invest in growth opportunities. Moreover, Nestlé has a rock solid balance sheet it can use to augment both top line growth through acquisitions and per share value through the repurchase of stock. We believe the combination of these characteristics pave the way for low risk, solid growth in revenues and earnings that should demand a premium valuation in today’s environment.

As we ponder recent results and survey the current market backdrop we continue to conclude that quality matters. Though the “dash to trash” following the meltdown of 2008-9 sent stocks of the lowest quality flying, we note that we are no longer dealing with an environment where companies are on the verge of collapse amid rampant leverage and frozen credit. Therefore, with different ingredients in place this time, we don’t expect junk to lead the market. In a low growth environment, large cap stocks should outperform given that they are generally cheap, have strong balance sheets and should be able to augment returns via buybacks and dividends. Furthermore, should things recover more quickly than expected; we don’t expect them to be left in the dust.

New Positions

Nestlé S.A. - ADR (NSRGY) Nestlé is the largest food and beverage company in the world with a diverse product portfolio that includes brands such as Nestlé, Nescafe, Jenny Craig, Perrier and Pure Life. Nestlé’s diverse product offering, manufacturing scale and global distribution network create significant competitive advantages. Moreover, the company’s leading brands and product breadth enable pricing power with lead retailers, protecting the company against rising input costs. In addition to its defensive qualities, the company has significant exposure to emerging markets where it continues to invest in growth opportunities. We believe the combination of these characteristics pave the way for low risk, solid growth in revenues and earnings over the next few years. Furthermore, we point out that the company has a massive cash position with which it can augment earnings growth via acquisitions or share buybacks. Though the shares trade at a slight premium to peers, we believe this is warranted due to the aforementioned factors.

5

Starwood Hotels & Resorts Worldwide, Inc. (HOT) Starwood is the largest operator of luxury and upscale hotels in the world. Company franchises including Sheraton, Westin, W Hotels, St. Regis and Aloft are well known throughout the world, enjoy a loyal customer base and have low levels of competition relative to others in the industry. In recent months the stock (alongside the lodging sector) has underperformed the market as investors have shed “risk” in the midst of slowing sector/economic data, European concerns and turmoil in the Middle East. With the stock off 30+% year-to-date, and now trading at valuation levels not seen since January of 2009, we think the risk reward profile is compelling. Despite an uncertain global economic backdrop and weak consumer demand expectations, a dearth of hotel supply growth should continue to support pricing across the industry over the next few years. This, in tandem with HOT’s high quality luxury brands, loyal customer base and meaningful exposure to business travel (corporations are still flush with cash), should support solid RevPAR (revenue per available room) growth. Given the significant operating leverage in the company’s business model, we believe results should continue to improve and could warrant an upward revision in the stock’s multiple. Put simply, we think this stock may have upside into the $60s while further downside should be limited.

Increased Positions

Berkshire Hathaway, Inc. - Class B (BRKB) Berkshire is a financial holding company with a wide variety of subsidiaries engaged in business activities ranging from insurance, manufacturing, retail, railroads, energy and finance. The stock is well off recent highs due to weak insurance results, anemic investment portfolio returns and concerns surrounding the company succession plan; however, at 1.1x book value we think the shares are a great deal. While BRK.B is a conglomerate by most standards, we believe it holds a portfolio of above average businesses, with sustainable competitive advantages and strong returns on capital that should have meaningful leverage to any cyclical recovery. Furthermore, should the economic backdrop worsen, the company has almost $30 billion for famed investor Warren Buffett to deploy as he sees fit. Though we realize he will not be around for much longer, we believe Mr. Buffett has built a valuable franchise that is capable of compounding value long after he retires. As such, we believe the risk reward profile is compelling at current levels.

Capital One Financial Corporation (COF) COF is the 5th largest U.S. credit card provider, with operations in auto lending, consumer installment lending, small business lending and deposit taking activities. The stock has been very weak alongside other credit sensitive financials amid recent market turmoil. We thought this was an opportune time to add to the position given the company’s improving credit profile, significant earnings power and ability to generate capital internally.

Caterpillar, Inc. (CAT) Caterpillar is the world’s largest manufacturer of earthmoving equipment, with a significant presence in the manufacture of construction equipment, material handling machinery, engines (diesel and natural gas) and turbines. We continue to believe CAT is one of the highest quality names in the Industrials space and point out that the company has emerged from the recent economic crisis a leaner entity with much greater earnings power. While various sectors of the economy are showing signs of slowing, CAT’s results have continued to press on. Ultimately, we think EPS power of $12-$14 per share is achievable as demand recovers and the company integrates its recent acquisition of Bucyrus.

6

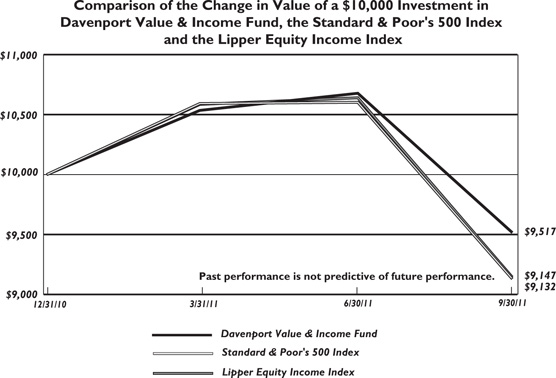

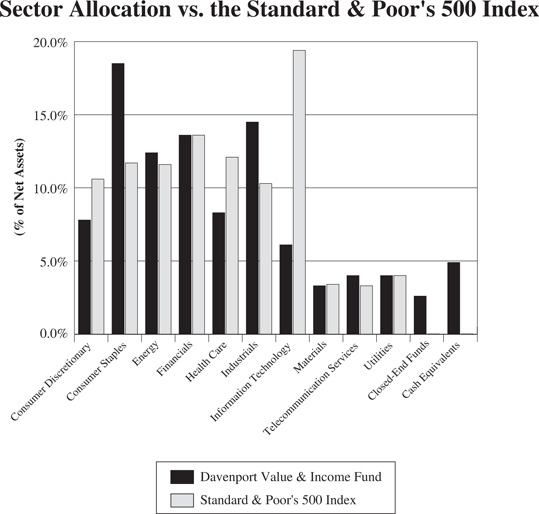

Davenport Value & Income Fund

The following chart represents Davenport Value & Income Fund (the “Fund”) performance and the performance of the S&P 500 Index*, the Fund’s primary benchmark, and the Lipper Equity Income Index* for the periods ended September 30, 2011.

Q3 2011 | Since Inception 12/31/2010 | Expense Ratio | |

| DVIPX | -10.86 | -4.83 | 1.09% |

| S&P 500 | -13.87 | -8.68 | |

| Lipper Equity Income Index | -14.04 | -8.53 |

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

| * | The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. The Lipper Equity Income Fund Index is an unmanaged index of the 30 largest funds, based on total year-end net asset value, in the Lipper Equity Income Fund Index. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

The Value & Income Fund had a rough quarter but held in well versus the market. The Fund was down 10.86%, outpacing the 13.87% decline for the S&P 500 Index and the 14.10% decline for the Lipper Equity Income Index. The Fund is now off 4.83% for the year, still well ahead of the 8.68% decline for the S&P 500 Index and the 8.53% decline for the Lipper Equity Income Index. Though we never enjoy reporting negative numbers, we are pleased with the way the Fund has behaved in such a difficult market.

For the second quarter in a row, the Fund’s’s Financials holdings generated strong relative performance. While much of this was due to lower exposure to the banking sector, we enjoyed another solid quarter of gains from Walter Investment Management (WAC). Given the elimination of the dividend and the company’s REIT status as a result of its merger with Green Tree, we used strength in the stock as an opportunity to exit our position in WAC. Other top performers during the period included Consumer Discretionary stocks VF Corp. (VFC) and McDonald’s (MCD). We decided to chip each of these holdings following recent strength; however, we are impressed by each company’s execution in the current consumer environment and remain encouraged by their longer term prospects. Due to problems plaguing the Euro Zone, international telecom holdings Vodafone (VOD) and Telefonica (TEF) underperformed their sectors. However, the Fund’s biggest detractors for the quarter were more cyclical holdings such as Encana (ECA) and Watsco (WSO).

Near the beginning of the quarter, we purchased a position in the world’s largest retailer, Wal-Mart (WMT). We think Wal-Mart is a great example of a large company that can still create significant value in a low growth environment. Though the company’s growth prospects are not what they used to be; we believe this classic growth story has morphed into an attractive value situation. Over the years the company has built a valuable competitive advantage through its low cost leadership and scalable distribution network. Domestic growth has stalled during the economic

7

downturn; however, the business continues to generate immense amounts of cash. Meanwhile the company is growing internationally with significant room for further expansion. Perhaps most importantly, management has gotten much more aggressive with capital management via increased share buybacks. Put simply, we think the company can buy back around 8% of its stock a year using internally generated cash flow. Assuming this level of buybacks alongside the 2.75% dividend yield, provides the potential for double digit returns on a per share basis.

We continue to emphasize quality in the Fund, adding to Travelers (TRV) and initiating a position in Southern Company (SO). Each of these companies is well respected in its industry, and has strong cash flows that should continue to support dividend growth. Travelers trades at a discount to book value and also appears cheap on a P/E basis. We thought this was attractive in light of the company’s solid balance sheet, focus on buybacks and solid dividend that yields 3.3%. Furthermore, it is hard to imagine things getting much worse for the company’s property & casuality insurance business given low interest rates (hurts investment income) and recent weather events. Southern is one of the largest regulated utilities in the U.S. While a bit more expensive, SO has a deep, highly regarded management team that has produced industry leading returns while being great proponents of shareholder value. The $1.89 dividend yields 4.5%, and has remained stable or increased for over 240 consecutive quarters (>60 years). Given its solid yield, high quality assets and attractive returns, we believe SO should perform well in the context of a slow growth economy and persistently low interest rates.

Though the Fund benefitted from a defensive bias throughout the quarter, we found that some of the best bargains were among the more cyclical names. While we can’t rule out a meaningful slowdown, we note that most companies’ cost structures are much improved and downside risk to earnings simply isn’t what it was headed into 2008. As such, we took advantage of what appeared to be great buying opportunity in Dow Chemical (DOW) which seems to be discounting a scenario in which earnings return to near 2008-2009 levels. Dow is the second largest chemical company in the world. While the company’s earnings are clearly cyclical, we are attracted to its diversified product mix and capital light approach to expansion. Given a sustainable dividend yielding 4.0%, a cheap valuation and long-term earnings tailwinds resulting from an abundance of cheap natural gas, we felt DOW was a solid fit for this Fund.

Low interest rates should continue to benefit income generating stocks for some time. At quarter end, the Fund’s yield stood at 3.6% versus the 10-year treasury at 1.9%. Though equities certainly contain more risk, the income component continues to be meaningful. As we look ahead, we feel the Fund is positioned to perform well as we enter what appears to be a period of persistently low interest rates and slower growth.

New Positions

Dow Chemical Company (The) (DOW) DOW is the second largest chemical company in the world, providing chemical, plastic and agricultural products and services to a diverse array of end markets. The stock has been pummeled in recent weeks alongside other cyclical names as economic concerns and fears surrounding global financial instability cascaded through markets. We viewed this as an opportunity to pick up some cyclical exposure in a depressed name at an attractive valuation with a solid yield (3.5%). Longer term, given an abundance of cheap, liquids-rich natural gas in the U.S., we think DOW’s cost advantage as a domestic producer of plastics (key feedstock for plastics is derived from natural gas liquids) distinguishes the company from other cyclical industrial commodity plays. Because of its defensive bias, the company has

8

performed very well recently relative to broader market indices. While we remain comfortable with our sector allocations in addition to the individual stocks we own, we believe some of the best bargains in the market are among the more cyclical names.

Southern Company (The) (SO) SO is one of the largest regulated utilities in the U.S., serving 4.4 million customers through its four electric utilities in Alabama, Georgia, Florida and Mississippi. The company is well positioned in stable/friendly regulatory environments that offer attractive demographics. SO has a deep, highly regarded management team that has produced industry leading returns while being great proponents of shareholder value. The $1.89 dividend yields 5.0%, and has remained stable or increased for over 240 consecutive quarters (>60 years). Given its solid yield, high quality assets and attractive returns, we believe SO should perform well in the context of a slow growth economy and persistently low interest rates.

Wal-Mart Stores, Inc. (WMT) WMT is the world’s largest retailer, with roughly 9,000 discount stores, superstores and warehouse centers located in 15 different countries. Like many large company growth stocks, WMT has seen earnings and dividends grow over the past ten years, yet the stock price has gone nowhere because of significant multiple contraction. Though we concede some multiple compression was warranted as the stock was overpriced at its peak and growth prospects are not what they used to be, we believe this classic growth story has morphed into an attractive value situation. Over the years the company has built a valuable competitive advantage through its low cost leadership and scalable distribution network. Domestic growth has stalled during the economic downturn; however, the business continues to generate immense amounts of cash. Meanwhile the company is growing internationally with significant room for further expansion. Perhaps most importantly, management has gotten much more aggressive with capital management (i.e. accelerated its buyback program) which should significantly magnify earnings and dividend growth (currently yields 2.7%) at the per share level. We feel that at 12x EPS, the shares inadequately reflect the potential value creation within the company.

Increased Positions

Fidelity National Financial, Inc. – Class A (FNF) After acquiring the bankrupt title operations of LandAmerica Financial in late 2008, FNF became the largest title insurer in the U.S. with roughly 44% market share of the $10 billion title premium market. Though housing has not shown many signs of recovery, it is difficult to imagine the environment getting much worse. Assuming the market is in the process of bottoming, we believe the risk/reward for FNF (and housing related stocks in general) is compelling given its cheap valuation and long term earnings power. As a reminder, we believe the long term EPS power of FNF is significant as housing transactions recover given their diligent cost focus and scale advantage resulting from the LandAmerica transaction. In the meantime, the company trades at a modest premium to book value and pays a solid dividend yielding ~3.0%.

Travelers Companies, Inc. (The) (TRV) Travelers is a leading provider of property and casualty insurance, with roughly one third of its business coming from personal lines and the balance generated through commercial lines. Following recent weakness, the stock trades at a discount to book value and also appears cheap on a P/E basis. We believe this is attractive in light of the company’s strong balance sheet, focus on share buybacks and a solid dividend that continues to grow. While recent results have suffered from anomalistic levels of catastrophic losses, we believe future pricing (and ultimately earnings) could benefit from these events. As such, we believe the risk-reward profile is compelling at current levels. The stock currently yields 3.2%.

9

Watsco, Inc. (WSO) Disappointing Q2 results and general market weakness have caused the shares to decline meaningfully from recent highs. Though economic uncertainty continues to delay a replacement cycle in HVAC equipment, we believe the company is executing well in a tough environment and still appears poised to deliver significant earnings growth as demand returns. The company’s strong balance sheet, attractive dividend yield and heavy insider ownership continue to support our excitement surrounding this attractive multi-year growth story. As such, we elected to use recent weakness as an opportunity to add to the position. the largest independent distributor of heating, ventilation, air conditioning (HVAC) and refrigeration equipment, parts, and supplies in the U.S. The stock currently yields 3.4%.

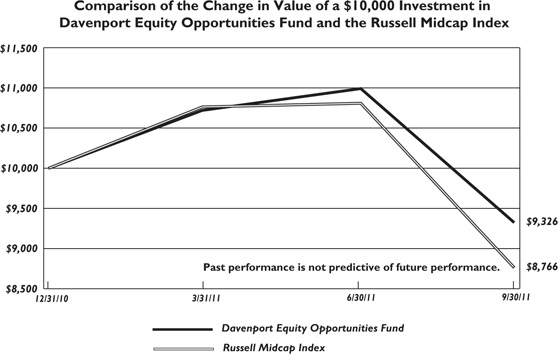

Davenport Equity Opportunities Fund

The following chart represents Davenport Equity Opportunities Fund (the “Fund”) performance and the performance of the Russell Midcap Index*, the Fund’s primary benchmark, and the S&P 500 Index* for the periods ended September 30, 2011.

Q3 2011 | Since Inception 12/31/2010 | Expense Ratio | |

| DEOPX | -15.14 | -6.74 | 1.15% |

| Russell Midcap Index | -18.90 | -12.34 | |

| S&P 500 Index | -13.87 | -8.68 |

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

| * | The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000, which represent approximately 25% of the total market capitalization of the Russell 1000. The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

The Equity Opportunities Fund declined 15.14% relative to an 18.90% decline for the Russell Midcap Index and a 13.87% drop for the S&P 500. Year-to-date, the Equity Opportunities Fund was down 6.74% at quarter end versus a 12.34% decline for the Russell Midcap and an 8.68% drop for the S&P 500. Perhaps most astonishing, the Russell 2000 declined a whopping 21.87% in Q3 and is now down 17.02% year-to-date. Suffice it to say, we don’t like reporting negative numbers and are unhappy to see solid gains be quickly erased. However, we do take some comfort in having held in relatively well versus the broader market, especially small and mid-cap indices.

As noted in our Market Commentary, this has been a very difficult year for managers to differentiate themselves given high correlations among stocks. Fortunately, we’ve been able to separate ourselves somewhat due to the solid performance of a few holdings. Companies with resilient earnings streams like Church & Dwight (CHD), ITC Holdings (ITC), American Tower (AMT) and O’Reilly (ORLY) actually managed small gains this past quarter. On the other hand, more cyclical consumer stocks such as CarMax (KMX) and Penn National (PENN) were big drags on performance. These two stocks are currently some of our largest holdings and we think the earnings streams of both companies will be more durable than currently expected. We were

10

also stung by our holdings in the Energy complex, namely Plains Exploration (PXP) and Ultra Petroleum (UPL). Fortunately, our small weighting in Energy stocks has helped limit downside versus the broader market as commodity prices have plummeted. The Financials sector has also been a source of positive relative performance for us. While our Financials holdings were down a bit, we have generally been light in credit sensitive areas (e.g. banks) that have been extremely weak.

In tough times, we think it’s important to have the conviction to add to favorite holdings. When the market swooned in early August, we bought more American Tower (AMT) and Brookfield Asset Management (BAM). We had been patiently waiting for an opportunity to own more of each and broad based market weakness gave us our chance. Both companies should be able to continue growing even in a tough environment and have held up relatively well since our recent purchases. Other additions involved more cyclical entities and were not quite as timely. For instance, we added to specialty chemical producer Albemarle (ALB) in early September after the stock had nosedived from over $70/share to roughly $48. Since then, the stock has dropped further into the high $30’s. We think the shares have now gone a long way towards discounting the likelihood of lower earnings next year. Even though we didn’t time the bottom, we expect to make money in the stock long-term. We also reduced a few positions at good prices. We chipped both Church & Dwight (CHD) and Fidelity National Financial (FNF) near 52-week highs and sold our position in Expedia (EXPE) not far from the stock’s high. We like the idea of recycling capital from these names into more depressed names with brighter outlooks.

We also like the idea of buying companies with embedded growth stories that aren’t solely dependent on the global economy. One example is International Game Technology (IGT) which is the world’s leading maker of slot machines and a name we have been familiar with for many years. We were able to establish a position just below $14/share. The stock peaked at nearly $50 a few years ago as new gaming jurisdictions were opening, a slot replacement cycle was booming, the company was taking market share and a buoyant economy was supporting participation games (machines where IGT takes a percent of daily win rather than sell the machine). Then, the replacement cycle came to a screeching halt, competitors started to regain their momentum and the economy cooled. As this was happening, IGT seemed to lose its creative edge and management lost some credibility. A couple years ago, IGT brought in new a CEO, who subsequently hired a new COO and new CTO (Chief Technology Officer). Since that time, the company has changed its focus and seems to be in the early stages of executing a successful turnaround. The company’s cost structure has been right-sized, new games seem to be gaining traction and the company’s market share is improving. Also, new management is very focused on returns on capital and value per share. The macro backdrop hasn’t improved much, but the company’s internal efforts, market share improvement and capital allocation practices seem to be ingredients for good share performance even in the absence of economic strength. At 12.5 times EPS estimates that should prove relatively sturdy, we feel like we’re getting a decent deal.

Another example is Colfax (CFX). Colfax is principally a pump manufacturer serving a variety of end markets including commercial marine, oil & gas and power generation. The company is in the process of acquiring Charter plc, which makes air and gas handling equipment as well as welding and cutting equipment. Colfax was capitalized by Mitch and Steve Rales, who are best known for their value creation at Danaher (DHR). The Rales own over 40% of Colfax and, while there is no way to insure a repeat of past success, we like having them as partners. CFX has weathered a very tough operating environment and posted impressive margin gains. Moreover, the

11

proposed acquisition of Charter could be transformational. While it entails taking on significant debt and increasing exposure to some markets that seem to be fragile at the moment (Europe and emerging markets), CFX has the opportunity to dramatically improve the profitability of an under-performing enterprise. While a global economic collapse could render our thesis irrelevant, this deal could yield multiple years of double-digit earnings growth even in a low growth environment.

In summary, our relative performance feels pretty good, but this clearly isn’t the year we were anticipating in terms of absolute performance. Some cooling off was to be expected after a big two year advance, but the degree of recent weakness has caught us off guard. Our main focus right now is continuing to optimize the Fund for future performance. This entails “high grading” the Fund by adding to favorite names, opportunistically seeking new opportunities and reducing exposure to areas where our conviction levels have waned. We feel like our recent moves have been steps in the right direction.

New Positions

Capital One Financial Corporation (COF) COF has been dragged down alongside other credit sensitive Financials and we think the risk/reward in the stock is very attractive right here. The yields on COF’s credit card portfolio are very attractive (especially when compared to bank assets) and the company has announced some sizeable acquisitions that could be very accretive. We think the company could be capable of earning $7.00/share and could ultimately trade to the $80 level. Also, we have benefitted from being light credit sensitive Financials in this Fund (we haven’t owned any banks). Now seems to be a good time to be looking at this depressed area, especially a unique growth story like COF.

Colfax, Inc. (CFX) Colfax is principally a pump manufacturer serving a variety of end markets including commercial marine, oil and gas, power generation, global navies and general industry. The company has a strong global presence with roughly 70% of sales outside of the U.S. The company is in the process of acquiring Charter plc which operates through two segments. The company’s ESAB segment supplies welding and cutting equipment and consumables. The company’s Howden segment designs and supplies air and gas handling equipment, particularly for the power generation industry.

International Game Technology (IGT) IGT is the world’s leading maker of slot machines. A couple years ago, IGT brought in new a CEO. Subsequently, the company hired a new COO and new CTO (Chief Technology Officer). Since that time, the company has changed its focus and seems to be in the early stages of executing a successful turnaround. The company’s cost structure has been right sized, new games seem to be gaining traction with casino operators and the company’s market share is improving. New management is very focused on returns on capital and value per share. Debt has been paid down and the company has started buying back stock. The macro backdrop hasn’t improved much, but the company’s internal efforts, market share improvement and capital allocation practices seem to be ingredients for good share performance even in the absence of economic strength.

Tessera Technologies, Inc. (TSRA) While an unusual story, the stock seems to have a very favorable risk/reward profile right here. In addition to a patent licensing business, TSRA has over $10/share of net cash (and growing). On a sum-of-the-parts basis, we think the stock should be worth more and believe downside should be cushioned by the company’s growing cash balance. The company lowered guidance last week and we are buying it near its lows.

12

Increased Positions

Albemarle Corporation (ALB) Albemarle is a specialty chemical company that operates in three segments: Polymer Solutions (includes flame retardants), Catalysts (refinery catalysts and others used in production of plastics) and Fine Chemistry (elemental bromine and third party services). While we are respectful of the risks to economic growth and the uncertainty surrounding demand in cyclical industries such as specialty chemicals, we believe the consensus has become overly pessimistic and that the selloff in the shares is overdone. Though exposed to cyclical factors, ALB participates in markets with attractive supply/demand characteristics that have continued to produce impressive results. Furthermore, the company has a credible management team that we believe has set an achievable goal of doubling EPS to >$9 by 2015. We elected to use recent weakness to add to this high quality situation with significant upside potential.

American Tower Corporation – Class A (AMT) AMT owns cell phone towers and leases space on those towers to wireless carriers. With the explosion of wireless devices, demand for new tower and space on existing tower continues to increase. Also, these are multi-year deals with annual price escalators, which provide some growth visibility. This business requires little capital and generates significant free cash flow. The company is now emulating its U.S. success abroad, having acquired towers in many other countries. The company is exceptionally well run, capable of growing even in a no/low growth environment, and very shareholder oriented. Also, the company will convert to a REIT at year end and begin paying a dividend, which should attract a broader shareholder base.

Brookfield Asset Management, Inc. (BAM) BAM owns and manages hard assets including hydroelectric power, electric transmission, timber and commercial real estate. Its assets have high barriers to entry, long lives and stable/predictable cash flows. The company also has significant excess liquidity and a proven track record of opportunistically buying assets. Lastly, it has a growing asset management business (investing third party capital) that is quickly scaling as hard assets become more appealing in a world where the value of many paper assets is being questioned. The company is exceptionally well run, capable of growing even in a no/low growth environment, and very shareholder oriented.

Lamar Advertising Company – Class A (LAMR) LAMR has been a big disappointment this year and one of our worst performing stocks. Lamar faces numerous headwinds including slowing local advertising growth, rising capital expenditure requirements and blossoming competition from mobile advertising. However, even in a flattish environment, this business will still generate significant free cash flow (perhaps $2.50/share), which can be used to de-lever and ultimately buy back stock. Also, the conversion to digital billboards creates an interesting re-investment opportunity for LAMR.

13

DAVENPORT CORE FUND

PERFORMANCE INFORMATION (Unaudited)

Average Annual Total Returns(a) (for periods ended September 30, 2011) | |||

| 1 Year | 5 Years | 10 Years | |

| Davenport Core Fund | 0.17% | 0.17% | 3.63% |

| Standard & Poor’s 500 Index | 1.14% | -1.18% | 2.82% |

| (a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

14

DAVENPORT VALUE & INCOME FUND

PERFORMANCE INFORMATION (Unaudited)

Total Returns(a) (for period ended September 30, 2011) | |

Since Inception(b) | |

| Davenport Value & Income Fund | -4.83% |

| Standard & Poor’s 500 Index | -8.68% |

| Lipper Equity Income Index | -8.53% |

| (a) | The total return shown does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (b) | Commencement of operations was December 31, 2010. |

15

DAVENPORT EQUITY OPPORTUNITIES FUND

PERFORMANCE INFORMATION (Unaudited)

Total Returns(a) (for period ended September 30, 2011) | |

Since Inception(b) | |

| Davenport Equity Opportunities Fund | -6.74% |

| Russell Midcap Index | -12.34% |

| (a) | The total return shown does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (b) | Commencement of operations was December 31, 2010. |

16

DAVENPORT CORE FUND

PORTFOLIO INFORMATION

September 30, 2011 (Unaudited)

Top Ten Equity Holdings

| Security Description | % of Net Assets |

| Exxon Mobil Corporation | 2.8% |

| International Business Machines Corporation | 2.6% |

| Apple, Inc. | 2.6% |

| Berkshire Hathaway, Inc. - Class B | 2.6% |

| QUALCOMM, Inc. | 2.5% |

| American Tower Corporation - Class A | 2.4% |

| Brookfield Asset Management, Inc. - Class A | 2.4% |

| Chevron Corporation | 2.3% |

| Markel Corporation | 2.3% |

| Millicom International Cellular S.A. | 2.2% |

17

DAVENPORT VALUE & INCOME FUND

PORTFOLIO INFORMATION

September 30, 2011 (Unaudited)

Top Ten Equity Holdings

| Security Description | % of Net Assets |

| Royal Dutch Shell plc - Class A - ADR | 2.8% |

| GlaxoSmithKline plc - ADR | 2.7% |

| Fidelity National Financial, Inc. - Class A | 2.6% |

| Altria Group, Inc. | 2.6% |

| Tortoise Energy Infrastructure Corporation | 2.6% |

| Dominion Resources, Inc. | 2.4% |

| Chevron Corporation | 2.4% |

| Coca-Cola Company (The) | 2.4% |

| Watsco, Inc. | 2.4% |

| Wells Fargo & Company | 2.3% |

18

DAVENPORT EQUITY OPPORTUNITIES FUND

PORTFOLIO INFORMATION

September 30, 2011 (Unaudited)

Top Ten Equity Holdings

| Security Description | % of Net Assets |

| Penn National Gaming, Inc. | 4.2% |

| Acacia Research Corporation | 4.1% |

| O'Reilly Automotive, Inc. | 3.9% |

| CarMax, Inc. | 3.9% |

| Millicom International Cellular S.A. | 3.8% |

| Markel Corporation | 3.6% |

| Hanesbrands, Inc. | 3.5% |

| NewMarket Corporation | 3.2% |

| American Tower Corporation - Class A | 3.1% |

| NCR Corporation | 3.0% |

19

DAVENPORT CORE FUND

SCHEDULE OF INVESTMENTS

September 30, 2011 (Unaudited)

COMMON STOCKS — 95.5% | Shares | Value | ||||||

| Consumer Discretionary — 12.9% | ||||||||

CarMax, Inc. (a) | 113,481 | $ | 2,706,522 | |||||

Discovery Communications, Inc. - Class C (a) | 66,909 | 2,351,851 | ||||||

Dollar Tree, Inc. (a) | 27,659 | 2,077,468 | ||||||

Lowe's Companies, Inc. | 119,617 | 2,313,393 | ||||||

McDonald's Corporation | 27,659 | 2,429,013 | ||||||

NVR, Inc. (a) | 3,024 | 1,826,436 | ||||||

| Starwood Hotels & Resorts Worldwide, Inc. | 50,910 | 1,976,326 | ||||||

Walt Disney Company (The) | 67,815 | 2,045,300 | ||||||

| 17,726,309 | ||||||||

| Consumer Staples — 8.6% | ||||||||

Anheuser-Busch InBev SA/NV - ADR | 34,245 | 1,814,300 | ||||||

Nestlé S.A. - ADR | 41,940 | 2,310,894 | ||||||

PepsiCo, Inc. | 43,938 | 2,719,762 | ||||||

Procter & Gamble Company (The) | 36,162 | 2,284,715 | ||||||

Wal-Mart Stores, Inc. | 52,305 | 2,714,630 | ||||||

| 11,844,301 | ||||||||

| Energy — 10.7% | ||||||||

Chevron Corporation | 34,782 | 3,218,031 | ||||||

EOG Resources, Inc. | 23,128 | 1,642,319 | ||||||

Exxon Mobil Corporation | 52,315 | 3,799,638 | ||||||

Occidental Petroleum Corporation | 27,648 | 1,976,832 | ||||||

Schlumberger Ltd. | 42,358 | 2,530,043 | ||||||

Transocean Ltd. | 30,894 | 1,474,880 | ||||||

| 14,641,743 | ||||||||

| Financials — 14.2% | ||||||||

Bank of America Corporation | 134,871 | 825,411 | ||||||

Berkshire Hathaway, Inc. - Class B (a) | 50,062 | 3,556,404 | ||||||

| Brookfield Asset Management, Inc. - Class A | 119,034 | 3,279,387 | ||||||

Capital One Financial Corporation | 67,274 | 2,666,069 | ||||||

JPMorgan Chase & Company | 51,714 | 1,557,626 | ||||||

Markel Corporation (a) | 8,956 | 3,198,456 | ||||||

T. Rowe Price Group, Inc. | 43,011 | 2,054,635 | ||||||

Wells Fargo & Company | 99,046 | 2,388,989 | ||||||

| 19,526,977 | ||||||||

| Health Care — 8.4% | ||||||||

Johnson & Johnson | 42,980 | 2,738,256 | ||||||

Laboratory Corporation of America Holdings (a) | 29,155 | 2,304,703 | ||||||

Merck & Company, Inc. | 63,484 | 2,076,562 | ||||||

Novo Nordisk A/S - ADR | 19,493 | 1,939,943 | ||||||

WellPoint, Inc. | 38,196 | 2,493,435 | ||||||

| 11,552,899 | ||||||||

| Industrials — 9.7% | ||||||||

Boeing Company (The) | 32,401 | 1,960,585 | ||||||

Caterpillar, Inc. | 27,964 | 2,064,862 | ||||||

20

DAVENPORT CORE FUND

SCHEDULE OF INVESTMENTS (Continued)

COMMON STOCKS — 95.5% (Continued) | Shares | Value | ||||||

| Industrials — 9.7% (Continued) | ||||||||

Danaher Corporation | 66,329 | $ | 2,781,838 | |||||

Illinois Tool Works, Inc. | 42,674 | 1,775,239 | ||||||

Stanley Black & Decker, Inc. | 37,932 | 1,862,461 | ||||||

United Technologies Corporation | 40,040 | 2,817,214 | ||||||

| 13,262,199 | ||||||||

| Information Technology — 21.6% | ||||||||

Accenture plc - Class A | 52,399 | 2,760,379 | ||||||

Apple, Inc. (a) | 9,336 | 3,558,696 | ||||||

Automatic Data Processing, Inc. | 47,057 | 2,218,738 | ||||||

Check Point Software Technologies Ltd. (a) | 51,103 | 2,696,194 | ||||||

Fiserv, Inc. (a) | 50,998 | 2,589,168 | ||||||

Google, Inc. - Class A (a) | 4,004 | 2,059,578 | ||||||

Intel Corporation | 104,588 | 2,230,862 | ||||||

| International Business Machines Corporation | 20,652 | 3,614,720 | ||||||

Microsoft Corporation | 98,603 | 2,454,229 | ||||||

QUALCOMM, Inc. | 70,070 | 3,407,504 | ||||||

Visa, Inc. - Class A | 25,288 | 2,167,687 | ||||||

| 29,757,755 | ||||||||

| Materials — 4.8% | ||||||||

Albemarle Corporation | 51,693 | 2,088,397 | ||||||

International Flavors & Fragrances, Inc. | 40,040 | 2,251,049 | ||||||

Praxair, Inc. | 24,719 | 2,310,732 | ||||||

| 6,650,178 | ||||||||

| Telecommunication Services — 4.6% | ||||||||

American Tower Corporation - Class A (a) | 62,346 | 3,354,215 | ||||||

Millicom International Cellular S.A. | 30,536 | 3,026,118 | ||||||

| 6,380,333 | ||||||||

Total Common Stocks (Cost $118,328,963) | $ | 131,342,694 | ||||||

MONEY MARKET FUNDS — 2.4% | Shares | Value | ||||||

First American Treasury Obligations Fund - Class Z, 0.00% (b) (Cost $3,262,917) | 3,262,917 | $ | 3,262,917 | |||||

Total Investments at Value — 97.9% (Cost $121,591,880) | $ | 134,605,611 | ||||||

| Other Assets in Excess of Liabilities — 2.1% | 2,913,532 | |||||||

Net Assets — 100.0% | $ | 137,519,143 | ||||||

ADR - American Depositary Receipt.

| (a) | Non-income producing security. |

| (b) | Variable rate security. The rate shown is the 7-day effective yield as of September 30, 2011. |

See accompanying notes to financial statements.

21

DAVENPORT VALUE & INCOME FUND

SCHEDULE OF INVESTMENTS

September 30, 2011 (Unaudited)

COMMON STOCKS — 92.5% | Shares | Value | ||||||

| Consumer Discretionary — 7.8% | ||||||||

Home Depot, Inc. (The) | 35,480 | $ | 1,166,228 | |||||

Leggett & Platt, Inc. | 51,955 | 1,028,189 | ||||||

McDonald's Corporation | 11,840 | 1,039,789 | ||||||

VF Corporation | 11,170 | 1,357,378 | ||||||

| 4,591,584 | ||||||||

| Consumer Staples — 18.5% | ||||||||

Altria Group, Inc. | 57,071 | 1,530,074 | ||||||

Anheuser-Busch InBev SA/NV - ADR | 22,675 | 1,201,321 | ||||||

Coca-Cola Company (The) | 20,865 | 1,409,639 | ||||||

Diageo plc - ADR | 15,945 | 1,210,704 | ||||||

H.J. Heinz Company | 17,515 | 884,157 | ||||||

Philip Morris International, Inc. | 21,750 | 1,356,765 | ||||||

Procter & Gamble Company (The) | 17,215 | 1,087,644 | ||||||

Sysco Corporation | 38,130 | 987,567 | ||||||

Wal-Mart Stores, Inc. | 23,820 | 1,236,258 | ||||||

| 10,904,129 | ||||||||

| Energy — 12.4% | ||||||||

Chevron Corporation | 15,506 | 1,434,615 | ||||||

ConocoPhillips | 16,575 | 1,049,529 | ||||||

Encana Corporation | 40,030 | 768,976 | ||||||

Exxon Mobil Corporation | 17,045 | 1,237,978 | ||||||

Royal Dutch Shell plc - Class A - ADR | 26,475 | 1,642,774 | ||||||

Spectra Energy Corporation | 47,560 | 1,166,647 | ||||||

| 7,300,519 | ||||||||

| Financials — 13.6% | ||||||||

Bank of America Corporation | 63,105 | 386,203 | ||||||

Fidelity National Financial, Inc. - Class A | 101,425 | 1,539,631 | ||||||

JPMorgan Chase & Company | 29,850 | 899,082 | ||||||

Plum Creek Timber Company, Inc. | 35,405 | 1,228,907 | ||||||

Travelers Companies, Inc. (The) | 26,445 | 1,288,665 | ||||||

Wells Fargo & Company | 57,225 | 1,380,267 | ||||||

Willis Group Holdings plc - ADR | 37,221 | 1,279,286 | ||||||

| 8,002,041 | ||||||||

| Health Care — 8.3% | ||||||||

Abbott Laboratories | 18,475 | 944,812 | ||||||

GlaxoSmithKline plc - ADR | 38,070 | 1,571,910 | ||||||

Johnson & Johnson | 20,875 | 1,329,946 | ||||||

Merck & Company, Inc. | 31,410 | 1,027,421 | ||||||

| 4,874,089 | ||||||||

| Industrials — 14.5% | ||||||||

3M Company | 13,835 | 993,215 | ||||||

General Dynamics Corporation | 18,305 | 1,041,371 | ||||||

General Electric Company | 68,520 | 1,044,245 | ||||||

Illinois Tool Works, Inc. | 18,470 | 768,352 | ||||||

22

DAVENPORT VALUE & INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

COMMON STOCKS — 92.5% (Continued) | Shares | Value | ||||||

| Industrials — 14.5% (Continued) | ||||||||

Norfolk Southern Corporation | 19,840 | $ | 1,210,637 | |||||

Raytheon Company | 25,505 | 1,042,389 | ||||||

Waste Management, Inc. | 31,745 | 1,033,617 | ||||||

Watsco, Inc. | 27,410 | 1,400,651 | ||||||

| 8,534,477 | ||||||||

| Information Technology — 6.1% | ||||||||

Automatic Data Processing, Inc. | 25,740 | 1,213,641 | ||||||

Intel Corporation | 58,035 | 1,237,887 | ||||||

Microsoft Corporation | 47,105 | 1,172,443 | ||||||

| 3,623,971 | ||||||||

| Materials — 3.3% | ||||||||

Dow Chemical Company (The) | 43,390 | 974,540 | ||||||

E.I. du Pont de Nemours and Company | 25,055 | 1,001,448 | ||||||

| 1,975,988 | ||||||||

| Telecommunication Services — 4.0% | ||||||||

Telefonica S.A. - ADR | 53,955 | 1,031,620 | ||||||

Vodafone Group plc - ADR | 51,020 | 1,308,663 | ||||||

| 2,340,283 | ||||||||

| Utilities — 4.0% | ||||||||

Dominion Resources, Inc. | 28,380 | 1,440,853 | ||||||

Southern Company (The) | 22,200 | 940,614 | ||||||

| 2,381,467 | ||||||||

Total Common Stocks (Cost $59,982,416) | $ | 54,528,548 | ||||||

CLOSED-END FUNDS — 2.6% | Shares | Value | ||||||

| Tortoise Energy Infrastructure Corporation (Cost $1,739,580) | 44,725 | $ | 1,517,519 | |||||

MONEY MARKET FUNDS — 2.9% | Shares | Value | ||||||

First American Treasury Obligations Fund - Class Z, 0.00% (a) (Cost $1,697,540) | 1,697,540 | $ | 1,697,540 | |||||

Total Investments at Value — 98.0% (Cost $63,419,536) | $ | 57,743,607 | ||||||

| Other Assets in Excess of Liabilities — 2.0% | 1,195,193 | |||||||

Net Assets — 100.0% | $ | 58,938,800 | ||||||

ADR - American Depositary Receipt.

| (a) | Variable rate security. The rate shown is the 7-day effective yield as of September 30, 2011. |

See accompanying notes to financial statements.

23

DAVENPORT EQUITY OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS

September 30, 2011 (Unaudited)

COMMON STOCKS — 95.1% | Shares | Value | ||||||

| Consumer Discretionary — 23.3% | ||||||||

Brookfield Residential Properties, Inc. (a) | 65,405 | $ | 434,943 | |||||

CarMax, Inc. (a) | 64,460 | 1,537,371 | ||||||

Hanesbrands, Inc. (a) | 56,045 | 1,401,686 | ||||||

International Game Technology | 58,610 | 851,603 | ||||||

Lamar Advertising Company - Class A (a) | 65,280 | 1,111,718 | ||||||

NVR, Inc. (a) | 1,142 | 689,745 | ||||||

O'Reilly Automotive, Inc. (a) | 23,334 | 1,554,745 | ||||||

Penn National Gaming, Inc. (a) | 50,095 | 1,667,663 | ||||||

| 9,249,474 | ||||||||

| Consumer Staples — 3.0% | ||||||||

Church & Dwight Company, Inc. | 19,180 | 847,756 | ||||||

Omega Protein Corporation (a) | 36,810 | 334,235 | ||||||

| 1,181,991 | ||||||||

| Energy — 3.0% | ||||||||

Plains Exploration & Production Company (a) | 27,295 | 619,869 | ||||||

Ultra Petroleum Corporation (a) | 20,005 | 554,539 | ||||||

| 1,174,408 | ||||||||

| Financials — 16.9% | ||||||||

| Brookfield Asset Management, Inc. - Class A | 37,525 | 1,033,814 | ||||||

Capital One Financial Corporation | 24,325 | 964,000 | ||||||

Fidelity National Financial, Inc. - Class A | 69,315 | 1,052,201 | ||||||

Markel Corporation (a) | 3,995 | 1,426,734 | ||||||

Safety Insurance Group, Inc. | 28,595 | 1,081,749 | ||||||

| Walter Investment Management Corporation | 49,900 | 1,144,207 | ||||||

| 6,702,705 | ||||||||

| Health Care — 3.7% | ||||||||

Henry Schein, Inc. (a) | 12,890 | 799,309 | ||||||

Laboratory Corporation of America Holdings (a) | 8,375 | 662,044 | ||||||

| 1,461,353 | ||||||||

| Industrials — 17.0% | ||||||||

Acacia Research Corporation (a) | 45,410 | 1,634,306 | ||||||

Babcock & Wilcox Company (a) | 32,214 | 629,784 | ||||||

Colfax Corporation (a) | 37,590 | 761,573 | ||||||

Cooper Industries plc - Class A | 15,925 | 734,461 | ||||||

Republic Services, Inc. | 32,165 | 902,550 | ||||||

Rockwell Collins, Inc. | 17,580 | 927,521 | ||||||

Watsco, Inc. | 23,195 | 1,185,264 | ||||||

| 6,775,459 | ||||||||

| Information Technology — 13.5% | ||||||||

Check Point Software Technologies Ltd. (a) | 18,115 | 955,747 | ||||||

CoreLogic, Inc. (a) | 60,455 | 645,055 | ||||||

Fiserv, Inc. (a) | 17,285 | 877,559 | ||||||

Intuit, Inc. (a) | 21,245 | 1,007,863 | ||||||

24

DAVENPORT EQUITY OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS (Continued)

COMMON STOCKS — 95.1% (Continued) | Shares | Value | ||||||

| Information Technology — 13.5% (Continued) | ||||||||

NCR Corporation (a) | 71,336 | $ | 1,204,865 | |||||

Tessera Technologies, Inc. (a) | 57,235 | 683,386 | ||||||

| 5,374,475 | ||||||||

| Materials — 5.3% | ||||||||

Albemarle Corporation | 21,515 | 869,206 | ||||||

NewMarket Corporation | 8,260 | 1,254,446 | ||||||

| 2,123,652 | ||||||||

| Telecommunication Services — 6.9% | ||||||||

American Tower Corporation - Class A (a) | 23,040 | 1,239,552 | ||||||

Millicom International Cellular S.A. | 15,355 | 1,521,681 | ||||||

| 2,761,233 | ||||||||

| Utilities — 2.5% | ||||||||

ITC Holdings Corporation | 12,970 | 1,004,267 | ||||||

Total Common Stocks (Cost $42,377,353) | $ | 37,809,017 | ||||||

MONEY MARKET FUNDS — 2.9% | Shares | Value | ||||||

First American Treasury Obligations Fund - Class Z, 0.00% (b) (Cost $1,138,924) | 1,138,924 | $ | 1,138,924 | |||||

Total Investments at Value — 98.0% (Cost $43,516,277) | $ | 38,947,941 | ||||||

| Other Assets in Excess of Liabilities — 2.0% | 810,363 | |||||||

Net Assets — 100.0% | $ | 39,758,304 | ||||||

| (a) | Non-income producing security. |

| (b) | Variable rate security. The rate shown is the 7-day effective yield as of September 30, 2011. |

See accompanying notes to financial statements.

25

THE DAVENPORT FUNDS

STATEMENTS OF ASSETS AND LIABILITIES

September 30, 2011 (Unaudited)

Davenport Core Fund | Davenport Value & Income Fund | Davenport Equity Opportunities Fund | ||||||||||

| ASSETS | ||||||||||||

| Investments in securities: | ||||||||||||

At acquisition cost | $ | 121,591,880 | $ | 63,419,536 | $ | 43,516,277 | ||||||

At market value (Note 2) | $ | 134,605,611 | $ | 57,743,607 | $ | 38,947,941 | ||||||

Cash | — | 686,065 | 585,269 | |||||||||

Dividends receivable | 102,335 | 186,157 | 34,906 | |||||||||

Receivable for investment securities sold | 2,699,501 | — | — | |||||||||

Receivable for capital shares sold | 323,950 | 386,551 | 230,733 | |||||||||

Other assets | 20,343 | 15,144 | 13,395 | |||||||||

TOTAL ASSETS | 137,751,740 | 59,017,524 | 39,812,244 | |||||||||

| LIABILITIES | ||||||||||||

Payable for capital shares redeemed | 101,824 | 19,570 | 12,613 | |||||||||

Accrued investment advisory fees (Note 4) | 102,670 | 37,161 | 26,535 | |||||||||

Payable to administrator (Note 4) | 17,750 | 8,200 | 6,125 | |||||||||

Other accrued expenses | 10,353 | 13,793 | 8,667 | |||||||||

TOTAL LIABILITIES | 232,597 | 78,724 | 53,940 | |||||||||

NET ASSETS | $ | 137,519,143 | $ | 58,938,800 | $ | 39,758,304 | ||||||

| Net assets consist of: | ||||||||||||

Paid-in capital | $ | 135,115,120 | $ | 64,374,092 | $ | 44,254,455 | ||||||

Accumulated net investment income (loss) | 1,748 | 1,986 | (65,050 | ) | ||||||||

Accumulated net realized gains (losses) from security transactions | (10,611,456 | ) | 238,651 | 137,235 | ||||||||

Net unrealized appreciation (depreciation) on investments | 13,013,731 | (5,675,929 | ) | (4,568,336 | ) | |||||||

Net assets | $ | 137,519,143 | $ | 58,938,800 | $ | 39,758,304 | ||||||

Shares of beneficial interest outstanding (unlimited number of shares authorized, $0.01 par value) | 11,595,520 | 6,289,818 | 4,279,639 | |||||||||

| Net asset value, offering price and redemption price per share (Note 2) | $ | 11.86 | $ | 9.37 | $ | 9.29 | ||||||

See accompanying notes to financial statements.

26

THE DAVENPORT FUNDS

STATEMENTS OF OPERATIONS

Six Months Ended September 30, 2011 (Unaudited)

Davenport Core Fund | Davenport Value & Income Fund | Davenport Equity Opportunities Fund | ||||||||||

| INVESTMENT INCOME | ||||||||||||

Dividends | $ | 1,223,672 | $ | 950,195 | $ | 167,294 | ||||||

Foreign withholding taxes on dividends | (12,957 | ) | (9,475 | ) | (4,552 | ) | ||||||

Interest | 25 | — | — | |||||||||

TOTAL INVESTMENT INCOME | 1,210,740 | 940,720 | 162,742 | |||||||||

| EXPENSES | ||||||||||||

Investment advisory fees (Note 4) | 587,787 | 211,952 | 148,825 | |||||||||

Administration fees (Note 4) | 107,339 | 42,888 | 31,601 | |||||||||

Professional fees | 9,405 | 8,405 | 8,405 | |||||||||

Custodian and bank service fees | 9,800 | 9,395 | 5,684 | |||||||||

Registration fees | 7,726 | 6,905 | 5,942 | |||||||||

Compliance service fees (Note 4) | 8,161 | 5,000 | 4,502 | |||||||||

Printing of shareholder reports | 9,066 | 3,919 | 3,383 | |||||||||

Trustees’ fees and expenses | 5,418 | 5,418 | 5,418 | |||||||||

Insurance expense | 5,836 | 2,108 | 1,587 | |||||||||

Postage and supplies | 707 | 468 | 449 | |||||||||

Other expenses | 9,224 | 11,900 | 11,996 | |||||||||

TOTAL EXPENSES | 760,469 | 308,358 | 227,792 | |||||||||

NET INVESTMENT INCOME (LOSS) | 450,271 | 632,362 | (65,050 | ) | ||||||||

REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS | ||||||||||||

Net realized gains from security transactions | 135,428 | 238,651 | 137,468 | |||||||||

| Net change in unrealized appreciation/ depreciation on investments | (21,868,177 | ) | (6,905,369 | ) | (5,898,980 | ) | ||||||

| NET REALIZED AND UNREALIZED LOSSES ON INVESTMENTS | (21,732,749 | ) | (6,666,718 | ) | (5,761,512 | ) | ||||||

NET DECREASE IN NET ASSETS FROM OPERATIONS | $ | (21,282,478 | ) | $ | (6,034,356 | ) | $ | (5,826,562 | ) | |||

See accompanying notes to financial statements.

27

DAVENPORT CORE FUND

STATEMENTS OF CHANGES IN NET ASSETS

Six Months Ended September 30, 2011 (Unaudited) | Year Ended March 31, 2011 | |||||||

| FROM OPERATIONS | ||||||||

Net investment income | $ | 450,271 | $ | 781,757 | ||||

Net realized gains from security transactions | 135,428 | 2,762,416 | ||||||

Net change in unrealized appreciation/ depreciation on investments | (21,868,177 | ) | 15,587,706 | |||||

Net increase (decrease) in net assets from operations | (21,282,478 | ) | 19,131,879 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

From net investment income | (470,333 | ) | (780,857 | ) | ||||

| FROM CAPITAL SHARE TRANSACTIONS | ||||||||

Proceeds from shares sold | 9,926,110 | 27,476,146 | ||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 441,253 | 741,331 | ||||||

Payments for shares redeemed | (10,989,857 | ) | (19,335,638 | ) | ||||

| Net increase (decrease) in net assets from capital share transactions | (622,494 | ) | 8,881,839 | |||||

TOTAL INCREASE (DECREASE) IN NET ASSETS | (22,375,305 | ) | 27,232,861 | |||||

| NET ASSETS | ||||||||

Beginning of period | 159,894,448 | 132,661,587 | ||||||

End of period | $ | 137,519,143 | $ | 159,894,448 | ||||

ACCUMULATED NET INVESTMENT INCOME | $ | 1,748 | $ | 21,810 | ||||

| CAPITAL SHARE ACTIVITY | ||||||||

Shares sold | 735,011 | 2,149,143 | ||||||

Shares reinvested | 33,989 | 61,329 | ||||||

Shares redeemed | (819,466 | ) | (1,570,298 | ) | ||||

Net increase (decrease) in shares outstanding | (50,466 | ) | 640,174 | |||||

Shares outstanding at beginning of period | 11,645,986 | 11,005,812 | ||||||

Shares outstanding at end of period | 11,595,520 | 11,645,986 | ||||||

See accompanying notes to financial statements.

28

DAVENPORT VALUE & INCOME FUND

STATEMENTS OF CHANGES IN NET ASSETS

Six Months Ended September 30, 2011 (Unaudited) | Period Ended March 31, 2011 (a) | |||||||

| FROM OPERATIONS | ||||||||

Net investment income | $ | 632,362 | $ | 140,872 | ||||

Net realized gains from security transactions | 238,651 | 71,734 | ||||||

Net change in unrealized appreciation/ depreciation on investments | (6,905,369 | ) | 1,229,440 | |||||

Net increase (decrease) in net assets from operations | (6,034,356 | ) | 1,442,046 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

From net investment income | (639,406 | ) | (131,842 | ) | ||||

From net realized gains from security transactions | (71,734 | ) | — | |||||

Decrease in net assets from distributions to shareholders | (711,140 | ) | (131,842 | ) | ||||

| FROM CAPITAL SHARE TRANSACTIONS | ||||||||

Proceeds from shares sold | 18,643,960 | 47,565,809 | ||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 608,068 | 110,894 | ||||||

Payments for shares redeemed | (2,398,262 | ) | (156,377 | ) | ||||

Net increase in net assets from capital share transactions | 16,853,766 | 47,520,326 | ||||||

TOTAL INCREASE IN NET ASSETS | 10,108,270 | 48,830,530 | ||||||

| NET ASSETS | ||||||||

Beginning of period | 48,830,530 | — | ||||||

End of period | $ | 58,938,800 | $ | 48,830,530 | ||||

ACCUMULATED NET INVESTMENT INCOME | $ | 1,986 | $ | 9,030 | ||||

| CAPITAL SHARE ACTIVITY | ||||||||

Shares sold | 1,813,380 | 4,655,581 | ||||||

Shares reinvested | 60,777 | 10,830 | ||||||

Shares redeemed | (235,893 | ) | (14,857 | ) | ||||

Net increase in shares outstanding | 1,638,264 | 4,651,554 | ||||||

Shares outstanding at beginning of period | 4,651,554 | — | ||||||

Shares outstanding at end of period | 6,289,818 | 4,651,554 | ||||||

| (a) | Represents the period from commencement of operations (December 31, 2010) through March 31, 2011. |

See accompanying notes to financial statements.

29

DAVENPORT EQUITY OPPORTUNITIES FUND

STATEMENTS OF CHANGES IN NET ASSETS

Six Months Ended September 30, 2011 (Unaudited) | Period Ended March 31, 2011 (a) | |||||||

| FROM OPERATIONS | ||||||||

Net investment loss | $ | (65,050 | ) | $ | (21,539 | ) | ||

Net realized gains from security transactions | 137,468 | 184,336 | ||||||

Net change in unrealized appreciation/ depreciation on investments | (5,898,980 | ) | 1,330,644 | |||||

Net increase (decrease) in net assets from operations | (5,826,562 | ) | 1,493,441 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

From net realized gains from security transactions | (163,030 | ) | — | |||||

| FROM CAPITAL SHARE TRANSACTIONS | ||||||||

Proceeds from shares sold | 12,809,226 | 34,425,550 | ||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 157,487 | — | ||||||

Payments for shares redeemed | (1,594,238 | ) | (1,543,570 | ) | ||||

Net increase in net assets from capital share transactions | 11,372,475 | 32,881,980 | ||||||

| TOTAL INCREASE IN NET ASSETS | 5,382,883 | 34,375,421 | ||||||

| NET ASSETS | ||||||||

Beginning of period | 34,375,421 | — | ||||||

End of period | $ | 39,758,304 | $ | 34,375,421 | ||||

ACCUMULATED NET INVESTMENT LOSS | $ | (65,050 | ) | $ | — | |||

| CAPITAL SHARE ACTIVITY | ||||||||

Shares sold | 1,209,724 | 3,357,207 | ||||||

Shares reinvested | 15,593 | — | ||||||

Shares redeemed | (153,373 | ) | (149,512 | ) | ||||

Net increase in shares outstanding | 1,071,944 | 3,207,695 | ||||||

Shares outstanding at beginning of period | 3,207,695 | — | ||||||

Shares outstanding at end of period | 4,279,639 | 3,207,695 | ||||||

| (a) | Represents the period from commencement of operations (December 31, 2010) through March 31, 2011. |

See accompanying notes to financial statements.

30

DAVENPORT CORE FUND

FINANCIAL HIGHLIGHTS

| Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Period | ||||||||||||||||||||||||

Six Months Ended Sept. 30, 2011 | Years Ended March 31, | |||||||||||||||||||||||

| (Unaudited) | 2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||||||||||

Net asset value at beginning of period | $ | 13.73 | $ | 12.05 | $ | 8.36 | $ | 13.82 | $ | 14.75 | $ | 13.99 | ||||||||||||

Income (loss) from investment operations: | ||||||||||||||||||||||||

Net investment income | 0.04 | 0.07 | 0.08 | 0.11 | 0.10 | 0.10 | ||||||||||||||||||

| Net realized and unrealized gains (losses) on investments | (1.87 | ) | 1.68 | 3.69 | (5.17 | ) | 0.53 | 1.28 | ||||||||||||||||

| Total from investment operations | (1.83 | ) | 1.75 | 3.77 | (5.06 | ) | 0.63 | 1.38 | ||||||||||||||||

| Less distributions: | ||||||||||||||||||||||||

Dividends from net investment income | (0.04 | ) | (0.07 | ) | (0.08 | ) | (0.11 | ) | (0.10 | ) | (0.10 | ) | ||||||||||||

Distributions from net realized gains | — | — | — | (0.29 | ) | (1.46 | ) | (0.52 | ) | |||||||||||||||

Total distributions | (0.04 | ) | (0.07 | ) | (0.08 | ) | (0.40 | ) | (1.56 | ) | (0.62 | ) | ||||||||||||

| Net asset value at end of period | $ | 11.86 | $ | 13.73 | $ | 12.05 | $ | 8.36 | $ | 13.82 | $ | 14.75 | ||||||||||||

Total return (a) | (13.35% | )(b) | 14.61% | 45.20% | (36.85% | ) | 3.44% | 10.02% | ||||||||||||||||

| Net assets at end of period (000’s) | $ | 137,519 | $ | 159,894 | $ | 132,662 | $ | 92,358 | $ | 155,799 | $ | 151,655 | ||||||||||||

Ratio of total expenses to average net assets | 0.97% | (c) | 0.99% | 1.00% | 1.00% | 0.96% | 0.98% | |||||||||||||||||

Ratio of net investment income to average net assets | 0.57% | (c) | 0.58% | 0.75% | 0.98% | 0.60% | 0.67% | |||||||||||||||||

Portfolio turnover rate | 11% | (b) | 34% | 25% | 39% | 37% | 26% | |||||||||||||||||

| (a) | Total return is a measure of the change in value of an investment in the Fund over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (b) | Not annualized. |

| (c) | Annualized. |

See accompanying notes to financial statements.

31

DAVENPORT VALUE & INCOME FUND

FINANCIAL HIGHLIGHTS

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Period | ||||||||

Six Months Ended September 30, 2011 (Unaudited) | Period Ended March 31, 2011 (a) | |||||||

| Net asset value at beginning of period | $ | 10.50 | $ | 10.00 | ||||

| Income (loss) from investment operations: | ||||||||

| Net investment income | 0.11 | 0.04 | ||||||

| Net realized and unrealized gains (losses) on investments | (1.12 | ) | 0.49 | |||||

| Total from investment operations | (1.01 | ) | 0.53 | |||||

| Less distributions: | ||||||||

| Dividends from net investment income | (0.11 | ) | (0.03 | ) | ||||

| Distributions from net realized gains | (0.01 | ) | — | |||||

| Total distributions | (0.12 | ) | (0.03 | ) | ||||

| Net asset value at end of period | $ | 9.37 | $ | 10.50 | ||||

Total return (b) (c) | (9.66% | ) | 5.35% | |||||

| Net assets at end of period (000’s) | $ | 58,939 | $ | 48,831 | ||||

Ratio of total expenses to average net assets (d) | 1.09% | 1.25% | ||||||

Ratio of net investment income to average net assets (d) | 2.24% | 1.99% | ||||||

Portfolio turnover rate (c) | 7% | 10% | ||||||

| (a) | Represents the period from commencement of operations (December 31, 2010) through March 31, 2011. |

| (b) | Total return is a measure of the change in value of an investment in the Fund over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (c) | Not annualized. |

| (d) | Annualized. |

See accompanying notes to financial statements.

32

DAVENPORT EQUITY OPPORTUNITIES FUND

FINANCIAL HIGHLIGHTS

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Period | ||||||||

Six Months Ended September 30, 2011 (Unaudited) | Period Ended March 31, 2011 (a) | |||||||

| Net asset value at beginning of period | $ | 10.72 | $ | 10.00 | ||||

| Income (loss) from investment operations: | ||||||||

| Net investment loss | (0.02 | ) | (0.01 | ) | ||||

| Net realized and unrealized gains (losses) on investments | (1.37 | ) | 0.73 | |||||

| Total from investment operations | (1.39 | ) | 0.72 | |||||

| Less distributions: | ||||||||

| Distributions from net realized gains | (0.04 | ) | — | |||||

| Net asset value at end of period | $ | 9.29 | $ | 10.72 | ||||

Total return (b) (c) | (13.00% | ) | 7.20% | |||||

| Net assets at end of period (000’s) | $ | 39,758 | $ | 34,375 | ||||

Ratio of total expenses to average net assets (d) | 1.15% | 1.25% | ||||||

Ratio of net investment loss to average net assets (d) | (0.33% | ) | (0.40% | ) | ||||

Portfolio turnover rate (c) | 19% | 6% | ||||||

| (a) | Represents the period from commencement of operations (December 31, 2010) through March 31, 2011. |