| OMB APPROVAL |

OMB Number: 3235-0570 Expires: January 31, 2014 Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05685

Williamsburg Investment Trust

(Exact name of registrant as specified in charter)

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

W. Lee H. Dunham, Esq.

Sullivan & Worcester LLP One Post Office Square Boston, Massachusetts 02109

(Name and address of agent for service)

Registrant's telephone number, including area code: (513) 587-3400

Date of fiscal year end: March 31, 2014

Date of reporting period: September 30, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

SEMI-ANNUAL REPORT

September 30, 2013 (Unaudited) |

THE DAVENPORT FUNDS LETTER TO SHAREHOLDERS | |

Dear Shareholders,

Equity markets enjoyed very strong returns during the third quarter. The S&P 500 and Russell 2000 indices advanced 5.24% and 10.21%, respectively. On a year-to-date basis, the S&P 500 and Russell 2000 finished the period up 19.79% and 27.69%. When we started 2013, we suggested stocks should have some more “gas in the tank,” but suggested returns would be more subdued than in 2012. To some, even that forecast seemed optimistic given a period of great returns and the potential headwinds of fiscal restraint and higher interest rates. Well, here we are nine months into the year and the market is exceeding expectations once again. CNBC recently referred to it as the “zombie market…a staggering, stumbling, somnambulant thing of macabre beauty that sustains slings, arrows and shotgun blasts but still marches forward.” This description seems appropriate as equities have indeed shrugged off every potential threat.

The Federal Reserve System’s (the “Fed”) “taper” plans continue to dominate headlines. Recently coined by financial news outlets, so-called “tapering” involves a reduction in the bond buying plan that has helped suppress interest rates in recent years. The prevailing fear is that interest rates will move higher and bring an end to the “cheap money” environment that has supported stocks and many other asset classes.

We think the 2012 bottom of roughly 1.40% on the 10-year Treasury yield may have indeed marked an inflection point comparable to the NASDAQ hitting 5,000 in year 2000 (13 years later it stands at 3,600). In other words, longer-dated Treasuries may be due for a sustained period of underperformance following a long period of outperformance (BCA Research notes that Treasuries have outperformed the S&P 500 by 70 percentage points since the tech bubble peaked — for more information visit www.bcaresearch.com). However, we don’t expect yields to skyrocket in the near term given tepid economic growth and limited inflationary pressure.

Apparently, the Fed also perceives economic growth to be fairly lackluster. Recently, the Fed surprised investors and pundits by deciding to delay the tapering process, which most expected would commence in September. Now, some have accused the Fed of sending mixed messages and being “chicken.” Many, including us, would prefer to see a world less dependent on an accommodative Fed policy. Chairman Bernanke’s remarks suggested employment growth wasn’t yet strong enough to warrant a reduction of monetary stimulus. He and his colleagues also seem to fear actions on Capitol Hill (i.e., higher taxes and reduced government spending) could restrain the economy.

While tapering has temporarily been put on hold, it’s likely something we’ll contend with in coming months. Many investors wonder how stocks will fare if rates continue to rise. BCA Research points out that there have been 21 instances over the past 68 years where 10-year Treasury yields have increased by at least 100 basis points and during those instances stocks have risen three times as often as they’ve fallen and have generated a median Compound Annual Growth Rate (CAGR) of 7%. The S&P 500’s CAGR over that time frame also equals roughly 7%, “making returns during periods of rising real rates indistinguishable from returns across the entire postwar period.” (BCA)

Taper talk aside, we’ve become less bullish as the market has enjoyed a solid rally this year. We don’t consider ourselves bearish, but we recognize that much of the market’s upside has been multiple driven (i.e., higher valuations rather than higher earnings). Over time, stocks should appreciate at a rate commensurate with earnings growth. Clearly, they’ve accomplished much more than this during 2013 and we suspect the market’s “re-rating” likely won’t continue at its recent pace. If one believes 7%-9% Earnings Per Share (EPS) growth is attainable as the economy improves, this would seem to be a reasonable target for equity market returns. Hopefully, we can add a little to these returns by identifying companies that are growing at an above average pace and paying reasonable prices for them. We thank you for your trust and look forward to reporting back to you at year-end.

Davenport Core Fund

The following chart represents Davenport Core Fund (the “Core Fund”) performance and the performance of the S&P 500 Index*, the Core Fund’s primary benchmark, for the periods ended September 30, 2013.

| | | | | | Since Inception** 1/15/1998 | |

| Core Fund | 6.51% | 21.89% | 16.25% | 10.15% | 7.94% | 5.75% | 0.94% |

| S&P 500 Index* | 5.24% | 19.34% | 16.27% | 10.02% | 7.57% | 5.61% | — |

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

| * | The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

The Core Fund advanced 6.51% during the third quarter, nicely outpacing the 5.24% gain for the S&P 500 Index. The Core Fund is up 20.12% year-to-date, ahead of the 19.79% rise for the S&P 500 Index.

Biotechnology holdings Celgene (CELG) and Amgen (AMGN) surged during the period alongside solid results at the former and a major acquisition announcement at the latter. Announcements such as these drove significant gains across the sector, benefitting our holdings in the iShares Nasdaq Biotechnology Index Fund (IBB), which posted a 20%+ return during the quarter. Exxon (XOM) was the biggest laggard during the quarter, followed by International Business Machines (IBM). Though we have decided to stick with our position in XOM due to its high-quality assets and strong track record of shareholder returns, we sold our position in IBM given a lack of conviction in the company’s ability to reinvigorate organic growth.

The Information Technology sector saw a lot of activity during the quarter. In addition to the sale of IBM mentioned above, we elected to use price strength created by the announcement of CEO Steve Ballmer’s resignation to take profits in Microsoft (MSFT). With the funds, we elected to increase our position in Google (GOOG) and purchase a new position in Facebook (FB). While GOOG and FB are certainly more expensive relative to current earnings, we feel each company has proven an ability to monetize mobile internet traffic and are poised to profit from the evolution

of technology and consumer preferences. Ultimately, we feel comfortable having moved away from two mature franchises fighting secular declines while adding exposure to more innovative companies that are better positioned for the future.

We initiated a position in iconic global beverage and food products retailer Starbucks (SBUX) during the quarter. CEO Howard Schultz has done an incredible job turning a small Seattle coffee store chain into a global juggernaut, changing the consumption patterns of people across the globe. While SBUX is often viewed solely as a collection of coffee stores, the company has numerous levers at its disposal to grow moving forward. Ultimately, we believe the company’s new product innovation, groundbreaking leadership in social media and large international opportunity could allow it to achieve and surpass its goals for 15%-20% earnings growth over time. Furthermore, we note the company’s significant cash generation provides more than enough capital to fuel its growth objectives, which could translate into increased buybacks and dividends over time.

Near quarter end, we purchased a position in leading satellite TV provider, DIRECTV (DTV). The company’s domestic operations have high recurring revenues and generate strong free cash flow, much of which is being redeployed into the company’s quickly growing Latin American operations that carry very attractive returns. While the company faces competitive challenges domestically, we feel there is a long runway for growth in Latin America given low penetration rates, less competition and lower Subscriber Acquisition Costs (SAC). Finally, we note the company has repurchased roughly 60% of its shares outstanding since 2005. Going forward, we expect the company to continue to aggressively repurchase stock with excess cash flow.

In sum, we are encouraged by such strong performance in light of the robust market conditions as of late. Though “deals” are increasingly harder to come by as the market plows ahead, we are still seeing opportunities to invest in quality franchises at reasonable prices.

New Positions

Chicago Bridge & Iron Company (CBI) We purchased a position in this engineering and construction company which is well positioned to capitalize on increasing energy project spending due to the oil and gas shale revolution.

DIRECTV (DTV) We purchased a position in this leading satellite provider in the Americas as we were attracted to the company’s strong cash generation and inexpensive value.

Facebook, Inc. – Class A (FB) We purchased a position in the world’s largest social network as the company is in the early stages of monetizing its membership base through advertisements.

Monsanto Company (MON) We purchased a position in this leading agricultural products provider as we are attracted to its strong competitive position and favorable exposure to increasing global food consumption.

Starbucks Corporation (SBUX) We purchased a position in this premier coffee purveyor given its long runway for growth across the globe in a variety of product channels, including packaged products, tea, juice and new food offerings.

Increased Positions

American Tower Corporation (AMT) We added to this wireless tower owner and operator as weakness across the real estate investment trust (REIT) sector provided an attractive entry point to this quality, high-growth story.

Google, Inc. – Class A (GOOG) We added to our position as we believe the company’s constant innovation makes it one of the most attractive ways to play increased internet and mobile consumption.

Decreased Positions

Visa, Inc. – Class A (V) We chipped our position in this leading payment network provider following the stock’s strong run and some concern over increasing regulatory/legal headwinds.

Positions Sold

Brookfield Property Partners LP (BPY) After receiving them via a spin-off, we sold our shares as a matter of housekeeping.

CSTBrands, Inc. (CST) After receiving them via a spin-off, we sold our shares as a matter of housekeeping.

International Business Machines Corporation (IBM) We sold our position in this technology bellwether as we are concerned sluggish revenue trends will continue into the foreseeable future.

Microsoft Corporation (MSFT) We sold our position in this mature technology player as part of our shift towards dominant franchises with strong growth potential.

News Corporation – Class A (NWSA) After receiving the shares as a result of the breakup of News Corporation (NWS), we sold our position as a matter of housekeeping.

Procter & Gamble Company (PG) We sold our position in this large consumer products company given slow revenue growth and a great run in the stock which has left the valuation full.

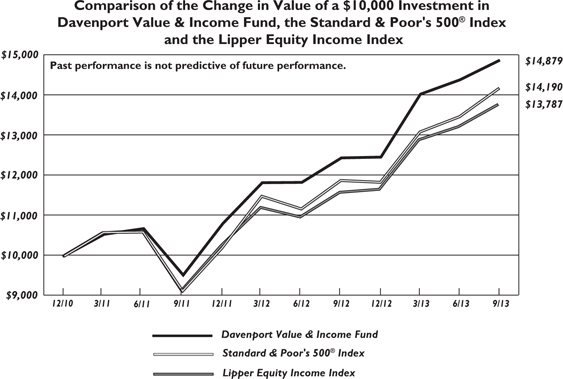

Davenport Value & Income Fund

The following chart represents Davenport Value & Income Fund (the “Value & Income Fund”) performance and the performance of the S&P 500 Index*, the Value & Income Fund’s primary benchmark, and the Lipper Equity Income Index for the periods ended September 30, 2013.

| | | Since Inception** 12/31/2010 | | |

| Value & Income Fund | 3.39% | 19.58% | 15.56% | 0.94% | 1.51% |

| S&P 500 Index* | 5.24% | 19.34% | 13.58% | — | — |

| Lipper Equity Income Index* | 4.16% | 18.88% | 12.39% | — | — |

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

| * | The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. The Lipper Equity Income Fund Index is an unmanaged index of the 30 largest funds, based on total year-end net asset value, in the Lipper Equity Income Fund Index. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

The Value & Income Fund gained 3.39% during the quarter, lagging gains of 5.24% and 4.16%, respectively, for the S&P 500 Index and Lipper Equity Income Index. Year-to-date, the Value & Income Fund is up 19.39% versus gains of 19.79% and 18.11%, respectively, for the S&P 500 Index and Lipper Equity Income Index. Dividend stocks continued to underperform broader market averages during the quarter; however, they still managed nice absolute gains despite fears of rising interest rates. At quarter end, the Value & Income Fund’s 30-day SEC yield was 1.51%.

Walgreen (WAG) was the Value & Income Fund’s top performer during the quarter, gaining over 20% in response to improved results and greater visibility into the benefits of recent strategic partnerships with Alliance Boots and AmerisourceBergen (ABC). The SPDR EURO STOXX 50 ETF (FEZ) produced substantial gains given improving sentiment (and data) coming out of the Eurozone. Vodafone (VOD) was also a key contributor, as the long awaited sale of its stake in Verizon Wireless back to Verizon (VZ) finally came to fruition. We elected to take profits on strength given a lack of confidence in management’s ability to elevate returns. Key detractors during the quarter were LinnCo (LNCO) and Sun Communities (SUI). Though we decided to part ways with our position in LNCO, we used weakness as an opportunity to add to our position in SUI.

After a blistering start to the year, shares of SUI tumbled alongside other high yielding REITs. While we would admit that the stock’s high of almost $58 in late May was probably an overshot, we feel its subsequent underperformance has also been a bit too extreme. Following SUI’s 25% decline from its high, the shares now yield near 6.0% and trade at less than 12x Funds From Operations (FFO) estimates for next year. This compares to apartment and self storage REITs that trade at almost 20x FFO and nearly half the yield in some cases. Though we do not expect the stock’s discount to peers to go away completely, we feel the current disparity is excessive given the company’s strong underlying fundamentals coupled with the attractive characteristics of the manufactured housing industry (i.e., low capex and stable and predictable cash flows). Furthermore, we feel the company is in a great position to start raising its dividend and can sustain meaningful dividend growth into the future as earnings improve alongside increasing occupancy, new site additions and rate increases.

At the end of the second quarter, we initiated a position in Canada’s second largest telecommunications operator, Telus (TU). The shares had weakened substantially in response to speculation that VZ is attempting to enter the Canadian market via the acquisition of a smaller competitor. While increased competition is never a welcome sight in such a rationally competitive environment, we felt the stock’s reaction provided us a great entry point into a company that has been gaining share, improving profitability and growing its dividend at an attractive rate. Since our purchase, VZ announced the acquisition of VOD’s stake in Verizon Wireless, while also indicating that it has abandoned its strategy of making a push into Canada. Though this prompted a rally in TU, we are still attracted to the company’s growth prospects and ability to increase the dividend at a 10% pace through 2016.

Near quarter end, we initiated a position in diversified theme park operator Six Flags (SIX). After emerging from bankruptcy in 2010 with a new management team, low debt levels and almost $1.0 billion of Net Operating Losses (NOLs), SIX has gone on to be a great stock alongside improving operating metrics that have allowed for significant return of capital to shareholders. More recently, however, the shares have weakened as a tragic accident at one of the company’s Texas parks and unfavorable weather trends have compounded general weakness among dividend

paying stocks. We feel this weakness has presented a buying opportunity in a well-run company that generates strong cash flows, has sizable barriers to entry and pays an attractive dividend (yields over 5%) that can grow.

In summary, we are pleased with the Value & Income Fund’s performance and continue to find exciting investment opportunities. At the risk of sounding like a broken record, we feel dividends (especially growing dividends) will continue to be a meaningful component of total returns despite headwinds created by rising interest rates. There is no guarantee that a company will continue to pay a dividend.

New Positions

Kinder Morgan, Inc. (KMI) We purchased a position in this holding company that owns a plethora of hydrocarbon transportation assets and has a strong growth outlook driven by the need for additional pipelines to connect new oil and gas production to demand centers. Current yield: 4.5%

Six Flags Entertainment Corporation (SIX) We purchased a position in this diversified theme park operator given its attractive yield and high barriers to entry. Current yield: 5.3%

Teva Pharmaceutical Industries Ltd. - ADR (TEVA) We purchased a position in this Israel-based generic and branded pharmaceutical company as we were attracted to its strong franchise, hefty cash flow and inexpensive share price. Current yield: 3.2%

Increased Positions

Marathon Petroleum Corporation (MPC) We added to our position in this refining company given our belief that the company will continue to benefit from increasing domestic oil production. Current yield: 2.6%

Sun Communities, Inc. (SUI) We added to our position in this manufactured housing REIT as weakness across the REIT complex provided an attractive entry point. Current yield: 5.9%

Positions Sold

Cracker Barrel Old Country Store, Inc. (CBRL) We sold our position in this owner and operator of themed restaurants, electing to take profits in the name following strong performance which resulted in the shares being more fairly valued.

LinnCo, LLC (LNCO) We sold our position in this Master Limited Partnership investment vehicle as a short attack and subsequent ongoing SEC investigation raised this risk profile above our comfort level.

Microsoft Corporation (MSFT) We sold our position in this mature technology player as part of our shift towards dominant franchises with strong growth potential.

Vodafone Group plc - ADR (VOD) We sold our position in this European telecom, taking profits after the company announced a deal to sell its stake in Verizon Wireless which drove the stock higher.

WisdomTree Japan Hedged Equity Fund (DXJ) We sold our position in this Japanese ETF after enjoying outsized returns and growing concern that their market had become somewhat disconnected from economic fundamentals.

Davenport Equity Opportunities Fund

The following chart represents Davenport Equity Opportunities Fund (the “Equity Opportunties Fund”) performance and the performance of the Russell Midcap Index*, the Equity Opportunity Fund’s primary benchmark, and the S&P 500 Index for the periods ended September 30, 2013.

| | | Since Inception** 12/31/2010 | |

| Equity Opportunities Fund | 6.44% | 27.63% | 17.23% | 0.98% |

| Russell Midcap Index* | 7.70% | 27.91% | 14.06% | — |

| S&P 500 Index* | 5.24% | 19.34% | 13.58% | — |

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

| * | The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000, which represent approximately 25% of the total market capitalization of the Russell 1000. The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

The Equity Opportunities Fund enjoyed a very strong third quarter. The Fund advanced 6.44% as a number of its holdings posted sizeable gains. This compared to gains of 5.24% and 7.70%, respectively, for the S&P 500 and Russell Midcap indices. Year-to-date, the Equity Opportunities Fund was up 20.83% at quarter-end versus gains of 19.79% and 24.34% for the S&P 500 and Russell Midcap, respectively. In our last letter, we noted it might be difficult to sustain the positive momentum we witnessed in the first half of the year. Fortunately, we’ve been wrong thus far.

A few of our holdings in the consumer arena were standouts during the quarter. Shares of CarMax (KMX), Hanesbrands (HBI), Dollar Tree (DLTR) and O’Reilly Automotive (ORLY) were among our top performers. Each company continues to exhibit solid organic growth while also wisely deploying excess free cash flow into store openings, acquisitions and/or share buybacks. Aon (AON), which is one of our larger holdings in the Financials sector, was another bright spot. The stock continued to hit new highs as enthusiasm built around the company’s blossoming health care exchange business. We chipped our position modestly given outsized gains this year, but think momentum in the core insurance brokerage business, coupled with a newfound contribution from the exchange business, will drive further upside. We also sold our position in Rockwell Collins (COL). Shares of the defense/aerospace company shrugged off sequestration fears and marched to new highs, where they seemed fully valued.

As we’ve mentioned in the past, we are a fan of companies that own durable brands. In a rapidly changing world, such brands tend to stand the test of time and steadily grow more valuable. To that end, we recently added to a position in Church & Dwight (CHD) and bought a new position in Beam (BEAM). Many have never heard the name Church & Dwight, but may recognize household brands such as Arm & Hammer, Nair, OxiClean and Orajel. Over time, this nimble company has innovated new products while also acquiring and improving existing brands. With a market capitalization just over $8 billion (compared to Procter & Gamble (PG) at $210 billion),

there’s ample room for growth and recent weakness in the stock afforded us an opportunity. In the case of BEAM, the company is best known for its flagship Jim Beam brand, but has a stable of well-known spirits. The company continues to deliver steady growth and could be a takeout candidate for larger global players with broader distribution capabilities.

While the bulk of the Equity Opportunities Fund is focused on compounding growth stories, occasionally we’ll look at distressed situations where the odds seemed stacked in our favor. One recent example is Ultra Petroleum (UPL). UPL is a natural gas producer with a well regarded management team and low-cost, long-lived dry natural gas assets in Wyoming and Pennsylvania. The company’s shares, which traded near $50 just over two years ago versus $20.50 currently, are deeply out of favor given the poor price environment for natural gas. We think natural gas prices could move higher in coming years as supply growth flattens and demand improves alongside the construction of gas-dependent petrochemical plants, exports of liquefied natural gas and more stringent emission standards from the U.S. Environmental Protection Agency (EPA) (favoring gas over coal). Management has shown capital discipline during a tough time and has stuck to the company’s dry gas roots; hence, UPL is one of few remaining dry gas pure plays and could exhibit material upside in a better environment. While we acknowledge we could be early, we think UPL is a compelling contrarian investment opportunity.

On a final note, we were pleased to recently spend time with management of Brookfield Asset Management (BAM). CEO Bruce Flatt is sometimes called the Warren Buffett of Canada given his track record as a value investor. He and his team’s interests are clearly aligned with ours as 20% of the stock is owned by management and directors. As a reminder, BAM owns hard assets such as hydroelectric power facilities, rails, electric transmission lines and commercial real estate, all of which generate toll booth-like cash flows. Following some recent asset sales, the company finds itself loaded with liquidity and ready to pounce on new opportunities. Perhaps even more exciting, the company has a flourishing asset management franchise that invests in hard assets on behalf of other investors and could see significant fee growth in coming years. We came away from our meeting happier than ever to count BAM as one of our largest positions and are very confident in management’s ability to grow the company’s intrinsic value at a double-digit rate over time. Hopefully, by owning BAM and other top shelf companies, we’ll also do pretty well.

New Positions

Beam, Inc. (BEAM) We purchased a position in this global spirits company which manufactures and markets such popular brands as Pinnacle vodka, Sauza tequila, Skinnygirl cocktails and the fastest growing North American whiskey brand, Jim Beam.

Krispy Kreme Doughnuts, Inc. (KKD) We purchased a position in this well-known doughnut restaurant company due to the company’s industry leading returns on new stores and immense growth opportunities domestically and abroad.

Pinnacle Entertainment, Inc. (PNK) We purchased a position in this regional gaming operator. We are encouraged by the company’s new, operationally-focused management and the recent acquisition of Ameristar Casinos (ASCA), which we view as a transformational deal.

Ultra Petroleum Corporation (UPL) We purchased a position in this natural gas producer as the outlook for natural gas prices is more constructive over the next several years due to rising demand and moderating supply growth.

Increased Positions

Brookfield Asset Management, Inc. – Class A (BAM) We added to our position in this premier global infrastructure asset manager; penalized by fears of rising interest rates, we felt the stock’s underperformance provided an opportunity in this well-run company.

Church & Dwight Company, Inc. (CHD) One of our longest standing positions, this well-run company owns a collection of “power” brands including OxiClean, Orajel and flagship brand, Arm & Hammer; we added to our position following weakness in the stock which left the shares trading as cheaply as we have seen in some time.

Penn National Gaming, Inc. (PENN) We added to our position in this regional gaming operator as recent weakness provided an opportunity to gain exposure to an entity with a top notch management team whose pending conversion to a REIT could unlock significant value for shareholders.

Decreased Positions

Albemarle Corporation (ALB) We chipped our position in this specialty chemicals developer, manufacturer and marketer given our belief that near-term upside is limited amidst sluggish demand.

Aon plc (AON) We chipped our position in this insurance brokerage and human resources outsourcing provider as the stock appeared more fairly valued following strong performance.

Safety Insurance Group, Inc. (SAFT) We chipped our position in this auto and homeowners insurance provider as strong performance provided the ability to take profits in the name.

Positions Sold

Lamar Advertising Company – Class A (LAMR) We sold our position in this outdoor advertising firm as the stock seemed more fairly valued.

Rockwell Collins, Inc. (COL) We sold our position in this avionics systems provider following strong year-to-date performance resulting in a seemingly fair valuation.

Sincerely,

John P. Ackerly, IV

President, The Davenport Funds

DAVENPORT CORE FUND

PERFORMANCE INFORMATION (Unaudited)

| | Average Annual Total Returns(a) (for periods ended September 30, 2013) |

| | | | |

| Davenport Core Fund | 21.89% | 10.15% | 7.94% |

Standard & Poor’s 500® Index | 19.34% | 10.02% | 7.57% |

| (a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

DAVENPORT VALUE & INCOME FUND

PERFORMANCE INFORMATION (Unaudited)

| | Average Annual Total Returns(a) (for periods ended September 30, 2013) |

| | | |

| Davenport Value & Income Fund | 19.58% | 15.56% |

Standard & Poor’s 500® Index | 19.34% | 13.58% |

| Lipper Equity Income Index | 18.88% | 12.40% |

| (a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| | |

| (b) | Commencement of operations was December 31, 2010. |

DAVENPORT EQUITY OPPORTUNITIES FUND

PERFORMANCE INFORMATION (Unaudited)

| | Average Annual Total Returns(a) (for periods ended September 30, 2013) |

| | | |

| Davenport Equity Opportunities Fund | 27.63% | 17.23% |

Russell Midcap® Index | 27.91% | 14.06% |

| (a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| | |

| (b) | Commencement of operations was December 31, 2010. |

DAVENPORT CORE FUND

PORTFOLIO INFORMATION

September 30, 2013 (Unaudited)

Top Ten Equity Holdings

| Security Description | % of Net Assets |

| CarMax, Inc. | 3.1% |

| Johnson & Johnson | 2.9% |

| Capital One Financial Corporation | 2.8% |

| Markel Corporation | 2.6% |

| Berkshire Hathaway, Inc. - Class B | 2.5% |

| Danaher Corporation | 2.5% |

| iShares Nasdaq Biotechnology Index Fund | 2.4% |

| Brookfield Asset Management, Inc. - Class A | 2.4% |

| Wells Fargo & Company | 2.3% |

| Google, Inc. - Class A | 2.2% |

DAVENPORT VALUE & INCOME FUND

PORTFOLIO INFORMATION

September 30, 2013 (Unaudited)

Top Ten Equity Holdings

| Security Description | % of Net Assets |

| JPMorgan Chase & Company | 2.8% |

| Walgreen Company | 2.7% |

SPDR EURO STOXX 50® ETF | 2.6% |

| Johnson & Johnson | 2.5% |

| GlaxoSmithKline plc - ADR | 2.5% |

| Wells Fargo & Company | 2.5% |

| General Electric Company | 2.5% |

| Travelers Companies, Inc. (The) | 2.4% |

| Sun Communities, Inc. | 2.4% |

| Capital One Financial Corporation | 2.3% |

DAVENPORT EQUITY OPPORTUNITIES FUND

PORTFOLIO INFORMATION

September 30, 2013 (Unaudited)

Top Ten Equity Holdings

| Security Description | % of Net Assets |

| Penn National Gaming, Inc. | 7.4% |

| CarMax, Inc. | 5.7% |

| Markel Corporation | 5.2% |

| Brookfield Asset Management, Inc. - Class A | 4.8% |

| O'Reilly Automotive, Inc. | 4.6% |

| Intuit, Inc. | 3.7% |

| American Tower Corporation | 3.7% |

| Capital One Financial Corporation | 3.6% |

| Dollar Tree, Inc. | 3.6% |

| Hanesbrands, Inc. | 3.4% |

DAVENPORT CORE FUND

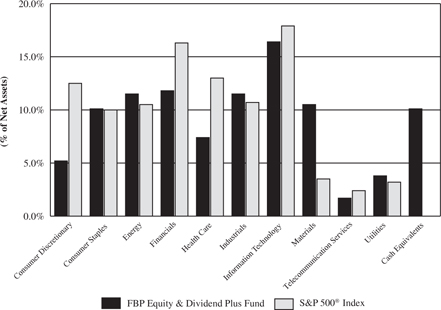

SCHEDULE OF INVESTMENTS

September 30, 2013 (Unaudited)

| | | | | | |

| Consumer Discretionary — 17.4% | | | | | | |

Amazon.com, Inc. (a) | | | 15,343 | | | $ | 4,796,836 | |

CarMax, Inc. (a) | | | 153,012 | | | | 7,416,492 | |

DIRECTV (a) | | | 58,515 | | | | 3,496,271 | |

General Motors Company (a) | | | 128,555 | | | | 4,624,123 | |

| Lowe's Companies, Inc. | | | 96,006 | | | | 4,570,846 | |

| McDonald's Corporation | | | 43,220 | | | | 4,158,196 | |

News Corporation - Class A (a) | | | 1 | | | | 16 | |

| Starbucks Corporation | | | 49,290 | | | | 3,793,851 | |

| Twenty-First Century Fox, Inc. - Class A | | | 131,566 | | | | 4,407,461 | |

| Walt Disney Company (The) | | | 72,218 | | | | 4,657,339 | |

| | | | | | | | 41,921,431 | |

| Consumer Staples — 10.7% | | | | | | | | |

| Anheuser-Busch InBev SA/NV - ADR | | | 34,645 | | | | 3,436,784 | |

| J.M. Smucker Company (The) | | | 49,837 | | | | 5,234,879 | |

| Nestle SA - ADR | | | 66,177 | | | | 4,605,919 | |

| PepsiCo, Inc. | | | 48,106 | | | | 3,824,427 | |

| Walgreen Company | | | 83,485 | | | | 4,491,493 | |

| Wal-Mart Stores, Inc. | | | 55,682 | | | | 4,118,241 | |

| | | | | | | | 25,711,743 | |

| Energy — 9.1% | | | | | | | | |

| Chevron Corporation | | | 37,137 | | | | 4,512,146 | |

| Exxon Mobil Corporation | | | 55,692 | | | | 4,791,740 | |

| National Oilwell Varco, Inc. | | | 55,340 | | | | 4,322,607 | |

| Occidental Petroleum Corporation | | | 41,499 | | | | 3,881,816 | |

| Valero Energy Corporation | | | 129,461 | | | | 4,421,093 | |

| | | | | | | | 21,929,402 | |

| Financials — 20.3% | | | | | | | | |

American Tower Corporation (b) | | | 72,543 | | | | 5,377,613 | |

| Aon plc | | | 71,210 | | | | 5,300,872 | |

Berkshire Hathaway, Inc. - Class B (a) | | | 53,556 | | | | 6,079,142 | |

| Brookfield Asset Management, Inc. - Class A | | | 152,289 | | | | 5,695,609 | |

| Capital One Financial Corporation | | | 97,892 | | | | 6,729,096 | |

| Goldman Sachs Group, Inc. (The) | | | 26,225 | | | | 4,149,057 | |

| JPMorgan Chase & Company | | | 69,728 | | | | 3,604,240 | |

Markel Corporation (a) | | | 12,218 | | | | 6,326,114 | |

| Wells Fargo & Company | | | 137,044 | | | | 5,662,658 | |

| | | | | | | | 48,924,401 | |

| Health Care — 9.9% | | | | | | | | |

| AmerisourceBergen Corporation | | | 80,870 | | | | 4,941,157 | |

| Amgen, Inc. | | | 33,320 | | | | 3,729,841 | |

Celgene Corporation (a) | | | 26,962 | | | | 4,150,260 | |

| Johnson & Johnson | | | 79,913 | | | | 6,927,658 | |

DAVENPORT CORE FUND

SCHEDULE OF INVESTMENTS (Continued)

COMMON STOCKS — 93.9% (Continued) | | | | | | |

| Health Care — 9.9% (Continued) | | | | | | |

| WellPoint, Inc. | | | 50,390 | | | $ | 4,213,108 | |

| | | | | | | | 23,962,024 | |

| Industrials — 10.3% | | | | | | | | |

| Chicago Bridge & Iron Company NV | | | 55,008 | | | | 3,727,892 | |

| Danaher Corporation | | | 85,872 | | | | 5,952,647 | |

| General Electric Company | | | 132,645 | | | | 3,168,889 | |

| Parker Hannifin Corporation | | | 35,710 | | | | 3,882,391 | |

| Stanley Black & Decker, Inc. | | | 39,738 | | | | 3,599,071 | |

| United Technologies Corporation | | | 42,694 | | | | 4,603,267 | |

| | | | | | | | 24,934,157 | |

| Information Technology — 11.5% | | | | | | | | |

| Accenture plc - Class A | | | 57,314 | | | | 4,220,603 | |

| Apple, Inc. | | | 6,920 | | | | 3,299,110 | |

| Automatic Data Processing, Inc. | | | 49,175 | | | | 3,559,286 | |

Facebook, Inc. - Class A (a) | | | 88,440 | | | | 4,443,226 | |

Google, Inc. - Class A (a) | | | 6,205 | | | | 5,435,022 | |

| QUALCOMM, Inc. | | | 49,890 | | | | 3,360,590 | |

| Visa, Inc. - Class A | | | 18,669 | | | | 3,567,646 | |

| | | | | | | | 27,885,483 | |

| Materials — 4.7% | | | | | | | | |

| Albemarle Corporation | | | 55,483 | | | | 3,492,100 | |

| Monsanto Company | | | 33,426 | | | | 3,488,671 | |

| Praxair, Inc. | | | 37,208 | | | | 4,472,774 | |

| | | | | | | | 11,453,545 | |

| | | | | | | | | |

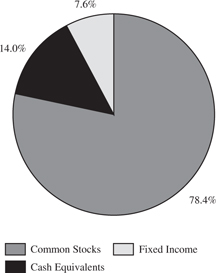

Total Common Stocks (Cost $155,922,543) | | | | | | $ | 226,722,186 | |

EXCHANGE-TRADED FUNDS — 2.4% | | | | | | |

| iShares Nasdaq Biotechnology Index Fund (Cost $4,014,106) | | | 28,182 | | | $ | 5,906,947 | |

DAVENPORT CORE FUND

SCHEDULE OF INVESTMENTS (Continued)

MONEY MARKET FUNDS — 1.9% | | | | | | |

First American Treasury Obligations Fund - Class Z, 0.00% (c) (Cost $4,571,006) | | | 4,571,006 | | | $ | 4,571,006 | |

| | | | | | | | | |

Total Investments at Value — 98.2% (Cost $164,507,655) | | | | | | $ | 237,200,139 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 1.8% | | | | | | | 4,374,421 | |

| | | | | | | | | |

| Net Assets — 100.0% | | | | | | $ | 241,574,560 | |

ADR - American Depositary Receipt.

| (a) | Non-income producing security. |

| (b) | Real estate investment trust (REIT). |

| (c) | The rate shown is the 7-day effective yield as of September 30, 2013. |

See accompanying notes to financial statements.

DAVENPORT VALUE & INCOME FUND

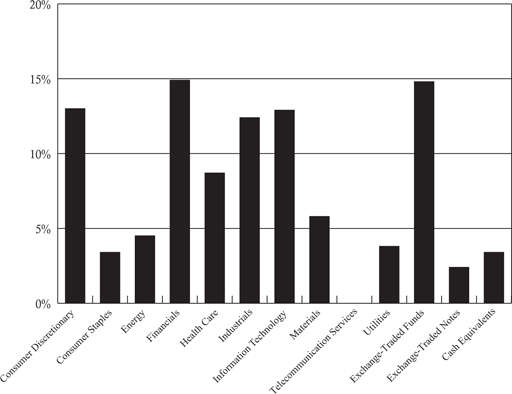

SCHEDULE OF INVESTMENTS

September 30, 2013 (Unaudited)

| | | | | | |

| Consumer Discretionary — 6.3% | | | | | | |

| Darden Restaurants, Inc. | | | 55,990 | | | $ | 2,591,777 | |

| McDonald's Corporation | | | 44,715 | | | | 4,302,030 | |

Penn National Gaming, Inc. (a) | | | 86,455 | | | | 4,786,149 | |

| Six Flags Entertainment Corporation | | | 103,330 | | | | 3,491,521 | |

| | | | | | | | 15,171,477 | |

| Consumer Staples — 15.6% | | | | | | | | |

| Altria Group, Inc. | | | 89,166 | | | | 3,062,852 | |

| Anheuser-Busch InBev SA/NV - ADR | | | 41,340 | | | | 4,100,928 | |

| Archer-Daniels-Midland Company | | | 106,430 | | | | 3,920,881 | |

| Coca-Cola Company (The) | | | 106,960 | | | | 4,051,645 | |

| Diageo plc - ADR | | | 26,195 | | | | 3,328,861 | |

| PepsiCo, Inc. | | | 56,290 | | | | 4,475,055 | |

| Philip Morris International, Inc. | | | 44,450 | | | | 3,848,925 | |

| Walgreen Company | | | 121,780 | | | | 6,551,764 | |

| Wal-Mart Stores, Inc. | | | 61,052 | | | | 4,515,406 | |

| | | | | | | | 37,856,317 | |

| Energy — 10.8% | | | | | | | | |

| BP plc - ADR | | | 105,900 | | | | 4,450,977 | |

| Chevron Corporation | | | 39,886 | | | | 4,846,149 | |

| Exxon Mobil Corporation | | | 50,470 | | | | 4,342,439 | |

| Kinder Morgan, Inc. | | | 122,925 | | | | 4,372,442 | |

| Marathon Petroleum Corporation | | | 69,580 | | | | 4,475,385 | |

| TransCanada Corporation | | | 86,520 | | | | 3,801,689 | |

| | | | | | | | 26,289,081 | |

| Financials — 24.0% | | | | | | | | |

| Aflac, Inc. | | | 84,340 | | | | 5,228,237 | |

| Capital One Financial Corporation | | | 81,430 | | | | 5,597,498 | |

| Fidelity National Financial, Inc. - Class A | | | 163,450 | | | | 4,347,770 | |

| Hartford Financial Services Group, Inc. | | | 178,005 | | | | 5,539,516 | |

| JPMorgan Chase & Company | | | 129,320 | | | | 6,684,551 | |

Markel Corporation (a) | | | 6,615 | | | | 3,425,048 | |

Sun Communities, Inc. (b) | | | 136,823 | | | | 5,831,396 | |

| Travelers Companies, Inc. (The) | | | 69,390 | | | | 5,882,190 | |

W.P. Carey, Inc. (b) | | | 82,354 | | | | 5,328,304 | |

| Wells Fargo & Company | | | 146,650 | | | | 6,059,578 | |

Weyerhaeuser Company (b) | | | 147,839 | | | | 4,232,631 | |

| | | | | | | | 58,156,719 | |

| Health Care — 10.3% | | | | | | | | |

| GlaxoSmithKline plc - ADR | | | 121,405 | | | | 6,090,889 | |

| Johnson & Johnson | | | 71,240 | | | | 6,175,796 | |

| Merck & Company, Inc. | | | 80,305 | | | | 3,823,321 | |

| Teva Pharmaceutical Industries Ltd. - ADR | | | 113,235 | | | | 4,278,018 | |

DAVENPORT VALUE & INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

COMMON STOCKS — 88.8% (Continued) | | | | | | |

| Health Care — 10.3% (Continued) | | | | | | |

| WellPoint, Inc. | | | 54,705 | | | $ | 4,573,885 | |

| | | | | | | | 24,941,909 | |

| Industrials — 13.3% | | | | | | | | |

| 3M Company | | | 35,455 | | | | 4,233,681 | |

| Eaton Corporation plc | | | 73,357 | | | | 5,049,896 | |

| General Electric Company | | | 250,965 | | | | 5,995,554 | |

| Illinois Tool Works, Inc. | | | 47,295 | | | | 3,607,190 | |

| Norfolk Southern Corporation | | | 51,130 | | | | 3,954,905 | |

| Raytheon Company | | | 65,356 | | | | 5,036,987 | |

| Watsco, Inc. | | | 46,570 | | | | 4,390,154 | |

| | | | | | | | 32,268,367 | |

| Information Technology — 2.0% | | | | | | | | |

| Automatic Data Processing, Inc. | | | 65,950 | | | | 4,773,461 | |

| | | | | | | | | |

| Materials — 3.1% | | | | | | | | |

| E.I. du Pont de Nemours and Company | | | 64,230 | | | | 3,761,309 | |

| Eastman Chemical Company | | | 47,230 | | | | 3,679,217 | |

| | | | | | | | 7,440,526 | |

| Telecommunication Services — 1.5% | | | | | | | | |

| TELUS Corporation | | | 107,085 | | | | 3,546,655 | |

| | | | | | | | | |

| Utilities — 1.9% | | | | | | | | |

| Dominion Resources, Inc. | | | 75,540 | | | | 4,719,739 | |

| | | | | | | | | |

Total Common Stocks (Cost $182,675,098) | | | | | | $ | 215,164,251 | |

EXCHANGE-TRADED FUNDS — 2.6% | | | | | | |

SPDR EURO STOXX 50 ® ETF (Cost $5,205,354) | | | 166,360 | | | $ | 6,384,897 | |

| | | | | | |

| Tortoise Energy Infrastructure Corporation (Cost $1,641,240) | | | 39,355 | | | $ | 1,806,395 | |

DAVENPORT VALUE & INCOME FUND

SCHEDULE OF INVESTMENTS (Continued)

MONEY MARKET FUNDS — 2.8% | | | | | | |

First American Treasury Obligations Fund - Class Z, 0.00% (c) (Cost $6,792,005) | | | 6,792,005 | | | $ | 6,792,005 | |

| | | | | | | | | |

Total Investments at Value — 95.0% (Cost $196,313,697) | | | | | | $ | 230,147,548 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 5.0% | | | | | | | 12,184,761 | |

| | | | | | | | | |

| Net Assets — 100.0% | | | | | | $ | 242,332,309 | |

ADR - American Depositary Receipt.

| (a) | Non-income producing security. |

| (b) | Real estate investment trust (REIT). |

| (c) | The rate shown is the 7-day effective yield as of September 30, 2013. |

See accompanying notes to financial statements.

DAVENPORT EQUITY OPPORTUNITIES FUND

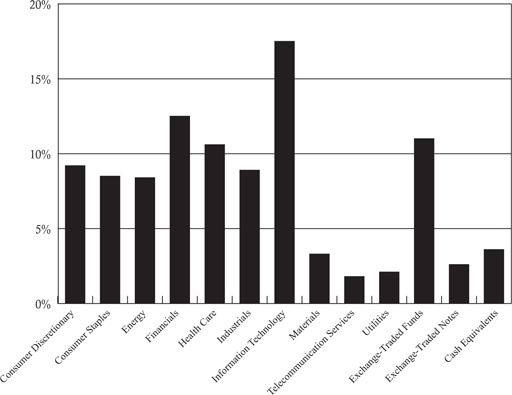

SCHEDULE OF INVESTMENTS

September 30, 2013 (Unaudited)

| | | | | | |

| Consumer Discretionary — 31.7% | | | | | | |

Cabela's, Inc. - Class A (a) | | | 28,865 | | | $ | 1,819,361 | |

CarMax, Inc. (a) | | | 154,975 | | | | 7,511,638 | |

| CST Brands, Inc. | | | 87,922 | | | | 2,620,076 | |

Dollar Tree, Inc. (a) | | | 83,220 | | | | 4,756,855 | |

| Hanesbrands, Inc. | | | 70,825 | | | | 4,413,106 | |

Krispy Kreme Doughnuts, Inc. (a) | | | 97,050 | | | | 1,876,947 | |

O'Reilly Automotive, Inc. (a) | | | 47,070 | | | | 6,005,661 | |

Penn National Gaming, Inc. (a) | | | 175,055 | | | | 9,691,045 | |

Pinnacle Entertainment, Inc. (a) | | | 118,160 | | | | 2,959,908 | |

| | | | | | | | 41,654,597 | |

| Consumer Staples — 10.3% | | | | | | | | |

| Beam, Inc. | | | 39,255 | | | | 2,537,836 | |

| Church & Dwight Company, Inc. | | | 65,770 | | | | 3,949,488 | |

| J.M. Smucker Company (The) | | | 36,850 | | | | 3,870,724 | |

| Walgreen Company | | | 58,930 | | | | 3,170,434 | |

| | | | | | | | 13,528,482 | |

| Energy — 5.8% | | | | | | | | |

| National Oilwell Varco, Inc. | | | 33,375 | | | | 2,606,922 | |

Ultra Petroleum Corporation (a) | | | 158,100 | | | | 3,252,117 | |

| Valero Energy Corporation | | | 52,815 | | | | 1,803,632 | |

| | | | | | | | 7,662,671 | |

| Financials — 28.8% | | | | | | | | |

| American International Group, Inc. | | | 58,665 | | | | 2,852,879 | |

American Tower Corporation (b) | | | 65,815 | | | | 4,878,866 | |

| Aon plc | | | 55,255 | | | | 4,113,182 | |

| Brookfield Asset Management, Inc. - Class A | | | 170,110 | | | | 6,362,114 | |

| Brookfield Property Partners L.P. | | | 6,543 | | | | 126,803 | |

| Capital One Financial Corporation | | | 69,721 | | | | 4,792,621 | |

| Fidelity National Financial, Inc. - Class A | | | 86,995 | | | | 2,314,067 | |

Markel Corporation (a) | | | 13,100 | | | | 6,782,787 | |

| Safety Insurance Group, Inc. | | | 34,375 | | | | 1,820,844 | |

Sun Communities, Inc. (b) | | | 90,667 | | | | 3,864,228 | |

| | | | | | | | 37,908,391 | |

| Health Care — 2.1% | | | | | | | | |

Henry Schein, Inc. (a) | | | 26,060 | | | | 2,702,422 | |

| | | | | | | | | |

| Industrials — 8.4% | | | | | | | | |

Colfax Corporation (a) | | | 49,310 | | | | 2,785,522 | |

| Delta Air Lines, Inc. | | | 133,360 | | | | 3,145,962 | |

| Pall Corporation | | | 34,375 | | | | 2,648,250 | |

| Watsco, Inc. | | | 26,125 | | | | 2,462,804 | |

| | | | | | | | 11,042,538 | |

DAVENPORT EQUITY OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS (Continued)

COMMON STOCKS — 95.4% (Continued) | | | | | | |

| Information Technology — 3.7% | | | | | | |

| Intuit, Inc. | | | 74,300 | | | $ | 4,926,833 | |

| | | | | | | | | |

| Materials — 1.8% | | | | | | | | |

| Albemarle Corporation | | | 38,270 | | | | 2,408,714 | |

| | | | | | | | | |

| Utilities — 2.8% | | | | | | | | |

| ITC Holdings Corporation | | | 39,790 | | | | 3,734,689 | |

| | | | | | | | | |

Total Common Stocks (Cost $101,205,394) | | | | | | $ | 125,569,337 | |

MONEY MARKET FUNDS — 2.9% | | | | | | |

First American Treasury Obligations Fund - Class Z, 0.00% (c) (Cost $3,800,594) | | | 3,800,594 | | | $ | 3,800,594 | |

| | | | | | | | | |

Total Investments at Value — 98.3% (Cost $105,005,988) | | | | | | $ | 129,369,931 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities — 1.7% | | | | | | | 2,221,277 | |

| | | | | | | | | |

| Net Assets — 100.0% | | | | | | $ | 131,591,208 | |

| (a) | Non-income producing security. |

| (b) | Real estate investment trust (REIT). |

| (c) | The rate shown is the 7-day effective yield as of September 30, 2013. |

See accompanying notes to financial statements.

THE DAVENPORT FUNDS

STATEMENTS OF ASSETS AND LIABILITIES

September 30, 2013 (Unaudited)

| | | | | Davenport Value & Income Fund | | | Davenport Equity Opportunities Fund | |

| ASSETS | | | | | | | | | |

| Investments in securities: | | | | | | | | | |

| At acquisition cost | | $ | 164,507,655 | | | $ | 196,313,697 | | | $ | 105,005,988 | |

| At market value (Note 2) | | $ | 237,200,139 | | | $ | 230,147,548 | | | $ | 129,369,931 | |

| Cash | | | 4,481,615 | | | | 10,062,248 | | | | 1,980,950 | |

| Dividends receivable | | | 125,373 | | | | 672,182 | | | | 90,228 | |

| Receivable for capital shares sold | | | 320,605 | | | | 1,841,612 | | | | 462,410 | |

| Other assets | | | 24,392 | | | | 25,959 | | | | 18,234 | |

| TOTAL ASSETS | | | 242,152,124 | | | | 242,749,549 | | | | 131,921,753 | |

| | | | | | | | | | | | | |

| LIABILITIES | | | | | | | | | | | | |

| Payable for capital shares redeemed | | | 383,846 | | | | 232,739 | | | | 224,326 | |

| Accrued investment advisory fees (Note 4) | | | 164,650 | | | | 153,017 | | | | 86,070 | |

| Payable to administrator (Note 4) | | | 27,500 | | | | 27,600 | | | | 16,200 | |

| Other accrued expenses and liabilities | | | 1,568 | | | | 3,884 | | | | 3,949 | |

| TOTAL LIABILITIES | | | 577,564 | | | | 417,240 | | | | 330,545 | |

| | | | | | | | | | | | | |

| NET ASSETS | | $ | 241,574,560 | | | $ | 242,332,309 | | | $ | 131,591,208 | |

| | | | | | | | | | | | | |

| Net assets consist of: | | | | | | | | | | | | |

| Paid-in capital | | $ | 162,181,741 | | | $ | 202,879,988 | | | $ | 103,919,166 | |

| Accumulated net investment income | | | 28,017 | | | | 215,307 | | | | 169,714 | |

Accumulated net realized gains

from security transactions | | | 6,672,318 | | | | 5,403,163 | | | | 3,138,385 | |

| Net unrealized appreciation on investments | | | 72,692,484 | | | | 33,833,851 | | | | 24,363,943 | |

| Net assets | | $ | 241,574,560 | | | $ | 242,332,309 | | | $ | 131,591,208 | |

| | | | | | | | | | | | | |

Shares of beneficial interest outstanding

(unlimited number of shares authorized,

$0.01 par value) | | | 13,262,715 | | | | 17,764,084 | | | | 8,941,446 | |

| | | | | | | | | | | | | |

Net asset value, offering price and

redemption price per share (Note 2) | | $ | 18.21 | | | $ | 13.64 | | | $ | 14.72 | |

See accompanying notes to financial statements.

THE DAVENPORT FUNDS

STATEMENTS OF OPERATIONS

Six Months Ended September 30, 2013 (Unaudited)

| | | | | Davenport Value & Income Fund | | | Davenport Equity Opportunities Fund | |

| INVESTMENT INCOME | | | | | | | | | |

| Dividends | | $ | 2,052,024 | | | $ | 3,450,314 | | | $ | 771,947 | |

| Foreign withholding taxes on dividends | | | (56,150 | ) | | | (29,502 | ) | | | (27,143 | ) |

| TOTAL INVESTMENT INCOME | | | 1,995,874 | | | | 3,420,812 | | | | 744,804 | |

| | | | | | | | | | | | | |

| EXPENSES | | | | | | | | | | | | |

| Investment advisory fees (Note 4) | | | 853,995 | | | | 839,388 | | | | 439,436 | |

| Administration fees (Note 4) | | | 147,486 | | | | 145,766 | | | | 83,260 | |

| Professional fees | | | 16,413 | | | | 15,863 | | | | 12,213 | |

| Compliance service fees (Note 4) | | | 12,650 | | | | 12,580 | | | | 8,071 | |

| Custodian and bank service fees | | | 10,213 | | | | 11,410 | | | | 6,842 | |

| Registration and filing fees | | | 8,763 | | | | 9,207 | | | | 7,968 | |

| Printing of shareholder reports | | | 7,623 | | | | 7,213 | | | | 5,246 | |

| Insurance expense | | | 5,672 | | | | 5,264 | | | | 3,060 | |

| Trustees’ fees and expenses (Note 4) | | | 3,956 | | | | 3,956 | | | | 3,956 | |

| Postage and supplies | | | 3,054 | | | | 2,941 | | | | 2,178 | |

| Other expenses | | | 978 | | | | 2,310 | | | | 2,860 | |

| TOTAL EXPENSES | | | 1,070,803 | | | | 1,055,898 | | | | 575,090 | |

| | | | | | | | | | | | | |

| NET INVESTMENT INCOME | | | 925,071 | | | | 2,364,914 | | | | 169,714 | |

| | | | | | | | | | | | | |

REALIZED AND UNREALIZED

GAINS ON INVESTMENTS | | | | | | | | | | | | |

| Net realized gains from security transactions | | | 7,004,743 | | | | 5,404,427 | | | | 3,191,678 | |

Net change in unrealized appreciation/

depreciation on investments | | | 13,350,027 | | | | 4,764,819 | | | | 6,189,656 | |

| | | | | | | | | | | | | |

NET REALIZED AND UNREALIZED

GAINS ON INVESTMENTS | | | 20,354,770 | | | | 10,169,246 | | | | 9,381,334 | |

| | | | | | | | | | | | | |

NET INCREASE IN NET ASSETS

FROM OPERATIONS | | $ | 21,279,841 | | | $ | 12,534,160 | | | $ | 9,551,048 | |

See accompanying notes to financial statements.

DAVENPORT CORE FUND

STATEMENTS OF CHANGES IN NET ASSETS

| | Six Months Ended September 30, 2013 (Unaudited) | | | | |

| FROM OPERATIONS | | | | | | |

| Net investment income | | $ | 925,071 | | | $ | 1,307,207 | |

| Net realized gains from security transactions | | | 7,004,743 | | | | 9,676,207 | |

Net change in unrealized appreciation/

depreciation on investments | | | 13,350,027 | | | | 12,010,397 | |

| Net increase in net assets from operations | | | 21,279,841 | | | | 22,993,811 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| From net investment income | | | (908,702 | ) | | | (1,315,956 | ) |

| From net realized gains from security transactions | | | (1,456,213 | ) | | | — | |

| Decrease in net assets from distributions to shareholders | | | (2,364,915 | ) | | | (1,315,956 | ) |

| | | | | | | | | |

| FROM CAPITAL SHARE TRANSACTIONS | | | | | | | | |

| Proceeds from shares sold | | | 19,215,267 | | | | 32,795,331 | |

Net asset value of shares issued in reinvestment

of distributions to shareholders | | | 2,275,693 | | | | 1,246,351 | |

| Payments for shares redeemed | | | (9,730,331 | ) | | | (19,718,238 | ) |

| Net increase in net assets from capital share transactions | | | 11,760,629 | | | | 14,323,444 | |

| | | | | | | | | |

| TOTAL INCREASE IN NET ASSETS | | | 30,675,555 | | | | 36,001,299 | |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

| Beginning of period | | | 210,899,005 | | | | 174,897,706 | |

| End of period | | $ | 241,574,560 | | | $ | 210,899,005 | |

| | | | | | | | | |

| ACCUMULATED NET INVESTMENT INCOME | | $ | 28,017 | | | $ | 11,648 | |

| | | | | | | | | |

| CAPITAL SHARE ACTIVITY | | | | | | | | |

| Shares sold | | | 1,090,139 | | | | 2,156,214 | |

| Shares reinvested | | | 130,061 | | | | 82,322 | |

| Shares redeemed | | | (552,013 | ) | | | (1,300,040 | ) |

| Net increase in shares outstanding | | | 668,187 | | | | 938,496 | |

| Shares outstanding at beginning of period | | | 12,594,528 | | | | 11,656,032 | |

| Shares outstanding at end of period | | | 13,262,715 | | | | 12,594,528 | |

See accompanying notes to financial statements.

DAVENPORT VALUE & INCOME FUND

STATEMENTS OF CHANGES IN NET ASSETS

| | Six Months Ended September 30, 2013 (Unaudited) | | | | |

| FROM OPERATIONS | | | | | | |

| Net investment income | | $ | 2,364,914 | | | $ | 3,299,446 | |

| Net realized gains from security transactions | | | 5,404,427 | | | | 6,183,266 | |

Net change in unrealized appreciation/

depreciation on investments | | | 4,764,819 | | | | 18,460,679 | |

| Net increase in net assets from operations | | | 12,534,160 | | | | 27,943,391 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| From net investment income | | | (2,152,728 | ) | | | (3,316,928 | ) |

| From net realized gains from security transactions | | | (3,232,544 | ) | | | (1,962,920 | ) |

| Decrease in net assets from distributions to shareholders | | | (5,385,272 | ) | | | (5,279,848 | ) |

| | | | | | | | | |

| FROM CAPITAL SHARE TRANSACTIONS | | | | | | | | |

| Proceeds from shares sold | | | 44,250,965 | | | | 85,076,371 | |

Net asset value of shares issued in reinvestment

of distributions to shareholders | | | 4,923,703 | | | | 4,722,338 | |

| Payments for shares redeemed | | | (10,881,118 | ) | | | (14,329,788 | ) |

| Net increase in net assets from capital share transactions | | | 38,293,550 | | | | 75,468,921 | |

| | | | | | | | | |

| TOTAL INCREASE IN NET ASSETS | | | 45,442,438 | | | | 98,132,464 | |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

| Beginning of period | | | 196,889,871 | | | | 98,757,407 | |

| End of period | | $ | 242,332,309 | | | $ | 196,889,871 | |

| | | | | | | | | |

| ACCUMULATED NET INVESTMENT INCOME | | $ | 215,307 | | | $ | 3,121 | |

| | | | | | | | | |

| CAPITAL SHARE ACTIVITY | | | | | | | | |

| Shares sold | | | 3,257,346 | | | | 7,171,909 | |

| Shares reinvested | | | 365,649 | | | | 398,116 | |

| Shares redeemed | | | (795,548 | ) | | | (1,212,247 | ) |

| Net increase in shares outstanding | | | 2,827,447 | | | | 6,357,778 | |

| Shares outstanding at beginning of period | | | 14,936,637 | | | | 8,578,859 | |

| Shares outstanding at end of period | | | 17,764,084 | | | | 14,936,637 | |

See accompanying notes to financial statements.

DAVENPORT EQUITY OPPORTUNITIES FUND

STATEMENTS OF CHANGES IN NET ASSETS

| | Six Months Ended September 30, 2013 (Unaudited) | | | | |

| FROM OPERATIONS | | | | | | |

| Net investment income | | $ | 169,714 | | | $ | 164,908 | |

| Net realized gains from security transactions | | | 3,191,678 | | | | 4,578,353 | |

Net change in unrealized appreciation/

depreciation on investments | | | 6,189,656 | | | | 10,165,302 | |

| Net increase in net assets from operations | | | 9,551,048 | | | | 14,908,563 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | | |

| From net investment income | | | (25,889 | ) | | | (139,019 | ) |

| From net realized gains from security transactions | | | (2,415,824 | ) | | | (1,731,142 | ) |

| Decrease in net assets from distributions to shareholders | | | (2,441,713 | ) | | | (1,870,161 | ) |

| | | | | | | | | |

| FROM CAPITAL SHARE TRANSACTIONS | | | | | | | | |

| Proceeds from shares sold | | | 23,807,584 | | | | 33,820,160 | |

Net asset value of shares issued in reinvestment

of distributions to shareholders | | | 2,363,209 | | | | 1,800,189 | |

| Payments for shares redeemed | | | (4,367,915 | ) | | | (5,114,447 | ) |

| Net increase in net assets from capital share transactions | | | 21,802,878 | | | | 30,505,902 | |

| | | | | | | | | |

| TOTAL INCREASE IN NET ASSETS | | | 28,912,213 | | | | 43,544,304 | |

| | | | | | | | | |

| NET ASSETS | | | | | | | | |

| Beginning of period | | | 102,678,995 | | | | 59,134,691 | |

| End of period | | $ | 131,591,208 | | | $ | 102,678,995 | |

| | | | | | | | | |

| ACCUMULATED NET INVESTMENT INCOME | | $ | 169,714 | | | $ | 25,889 | |

| | | | | | | | | |

| CAPITAL SHARE ACTIVITY | | | | | | | | |

| Shares sold | | | 1,667,890 | | | | 2,737,625 | |

| Shares reinvested | | | 169,284 | | | | 145,972 | |

| Shares redeemed | | | (304,829 | ) | | | (419,552 | ) |

| Net increase in shares outstanding | | | 1,532,345 | | | | 2,464,045 | |

| Shares outstanding at beginning of period | | | 7,409,101 | | | | 4,945,056 | |

| Shares outstanding at end of period | | | 8,941,446 | | | | 7,409,101 | |

See accompanying notes to financial statements.

DAVENPORT CORE FUND

FINANCIAL HIGHLIGHTS

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Period

| | | Six Months Ended Sept. 30, 2013 | | | | |

| | | | | | | | | | | | | | | | | | | |

Net asset value at

beginning of period | | $ | 16.75 | | | $ | 15.00 | | | $ | 13.73 | | | $ | 12.05 | | | $ | 8.36 | | | $ | 13.82 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Income (loss) from

investment operations: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.07 | | | | 0.11 | | | | 0.09 | | | | 0.07 | | | | 0.08 | | | | 0.11 | |

| Net realized and unrealized gains (losses) on investments | | 1.57 | | | | 1.75 | | | | 1.27 | | | | 1.68 | | | | 3.69 | | | | (5.17 | ) |

| Total from investment operations | | | 1.64 | | | | 1.86 | | | | 1.36 | | | | 1.75 | | | | 3.77 | | | | (5.06 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends from net

investment income | | | (0.07 | ) | | | (0.11 | ) | | | (0.09 | ) | | | (0.07 | ) | | | (0.08 | ) | | | (0.11 | ) |

Distributions from net

realized gains | | | (0.11 | ) | | | — | | | | — | | | | — | | | | — | | | | (0.29 | ) |

| Total distributions | | | (0.18 | ) | | | (0.11 | ) | | | (0.09 | ) | | | (0.07 | ) | | | (0.08 | ) | | | (0.40 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net asset value at end of period | | $ | 18.21 | | | $ | 16.75 | | | $ | 15.00 | | | $ | 13.73 | | | $ | 12.05 | | | $ | 8.36 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Total return (a) | | | 9.86% | (b) | | | 12.47% | | | | 9.99% | | | | 14.61% | | | | 45.20% | | | | (36.85% | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets at end of period (000’s) | $ | 241,575 | | | $ | 210,899 | | | $ | 174,898 | | | $ | 159,894 | | | $ | 132,662 | | | $ | 92,358 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Ratio of total expenses to

average net assets | | | 0.94% | (c) | | | 0.95% | | | | 0.96% | | | | 0.99% | | | | 1.00% | | | | 1.00% | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Ratio of net investment income

to average net assets | | | 0.81% | (c) | | | 0.71% | | | | 0.66% | | | | 0.58% | | | | 0.75% | | | | 0.98% | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Portfolio turnover rate | | | 11% | (b) | | | 26% | | | | 19% | | | | 34% | | | | 25% | | | | 39% | |

| (a) | Total return is a measure of the change in value of an investment in the Fund over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

See accompanying notes to financial statements.

DAVENPORT VALUE & INCOME FUND

FINANCIAL HIGHLIGHTS

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Period

| | Six Months Ended Sept. 30, 2013 (Unaudited) | | | | | | | | | Period Ended March 31, 2011 (a) | |

| Net asset value at beginning of period | | $ | 13.18 | | | $ | 11.51 | | | $ | 10.50 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | |

| Income from investment operations: | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.14 | | | | 0.28 | | | | 0.23 | | | | 0.04 | |

| Net realized and unrealized gains on investments | | | 0.65 | | | | 1.81 | | | | 1.02 | | | | 0.49 | |

| Total from investment operations | | | 0.79 | | | | 2.09 | | | | 1.25 | | | | 0.53 | |

| | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.13 | ) | | | (0.27 | ) | | | (0.23 | ) | | | (0.03 | ) |

| Distributions from net realized gains | | | (0.20 | ) | | | (0.15 | ) | | | (0.01 | ) | | | — | |

| Total distributions | | | (0.33 | ) | | | (0.42 | ) | | | (0.24 | ) | | | (0.03 | ) |

| | | | | | | | | | | | | | | | | |

| Net asset value at end of period | | $ | 13.64 | | | $ | 13.18 | | | $ | 11.51 | | | $ | 10.50 | |

| | | | | | | | | | | | | | | | | |

Total return (b) | | | 6.03% | (c) | | | 18.69% | | | | 12.23% | | | | 5.35% | (c) |

| | | | | | | | | | | | | | | | | |

| Net assets at end of period (000’s) | | $ | 242,332 | | | $ | 196,890 | | | $ | 98,757 | | | $ | 48,831 | |

| | | | | | | | | | | | | | | | | |

| Ratio of total expenses to average net assets | | | 0.94% | (d) | | | 0.96% | | | | 1.04% | | | | 1.25% | (d) |

| | | | | | | | | | | | | | | | | |

| Ratio of net investment income to average net assets | | | 2.11% | (d) | | | 2.37% | | | | 2.30% | | | | 1.99% | (d) |

| | | | | | | | | | | | | | | | | |

| Portfolio turnover rate | | | 18% | (c) | | | 29% | | | | 27% | | | | 10% | (c) |

| (a) | Represents the period from commencement of operations (December 31, 2010) through March 31, 2011. |

| (b) | Total return is a measure of the change in value of an investment in the Fund over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

See accompanying notes to financial statements.

DAVENPORT EQUITY OPPORTUNITIES FUND

FINANCIAL HIGHLIGHTS

Selected Per Share Data and Ratios for a Share Outstanding Throughout Each Period

| | Six Months Ended Sept. 30, 2013 (Unaudited) | | | | | | | | | Period Ended March 31, 2011 (a) | |

| Net asset value at beginning of period | | $ | 13.86 | | | $ | 11.96 | | | $ | 10.72 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | |

| Income (loss) from investment operations: | | | | | | | | | | | | | | | | |

| Net investment income (loss) | | | 0.02 | | | | 0.03 | | | | (0.02 | ) | | | (0.01 | ) |

| Net realized and unrealized gains on investments | | | 1.15 | | | | 2.17 | | | | 1.30 | | | | 0.73 | |

| Total from investment operations | | | 1.17 | | | | 2.20 | | | | 1.28 | | | | 0.72 | |

| | | | | | | | | | | | | | | | | |

| Less distributions: | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.01 | ) | | | (0.02 | ) | | | — | | | | — | |

| Distributions from net realized gains | | | (0.30 | ) | | | (0.28 | ) | | | (0.04 | ) | | | — | |

| Total distributions | | | (0.31 | ) | | | (0.30 | ) | | | (0.04 | ) | | | — | |

| | | | | | | | | | | | | | | | | |

| Net asset value at end of period | | $ | 14.72 | | | $ | 13.86 | | | $ | 11.96 | | | $ | 10.72 | |

| | | | | | | | | | | | | | | | | |

Total return (b) | | | 8.54% | (c) | | | 18.77% | | | | 12.00% | | | | 7.20% | (c) |

| | | | | | | | | | | | | | | | | |

| Net assets at end of period (000’s) | | $ | 131,591 | | | $ | 102,679 | | | $ | 59,135 | | | $ | 34,375 | |

| | | | | | | | | | | | | | | | | |

| Ratio of total expenses to average net assets | | | 0.98% | (d) | | | 1.01% | | | | 1.10% | | | | 1.25% | (d) |

| | | | | | | | | | | | | | | | | |

Ratio of net investment income (loss)

to average net assets | | | 0.29% | (d) | | | 0.23% | | | | (0.22% | ) | | | (0.40% | )(d) |

| | | | | | | | | | | | | | | | | |

| Portfolio turnover rate | | | 18% | (c) | | | 41% | | | | 35% | | | | 6% | (c) |

| (a) | Represents the period from commencement of operations (December 31, 2010) through March 31, 2011. |

| (b) | Total return is a measure of the change in value of an investment in the Fund over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

See accompanying notes to financial statements.

THE DAVENPORT FUNDS

NOTES TO FINANCIAL STATEMENTS

September 30, 2013 (Unaudited)

1. Organization

Davenport Core Fund, Davenport Value & Income Fund and Davenport Equity Opportunities Fund (individually, a “Fund,” and, collectively, the “Funds”) are each a no-load, diversified series of the Williamsburg Investment Trust (the “Trust”), an open-end management investment company registered under the Investment Company Act of 1940. The Trust was organized as a Massachusetts business trust on July 18, 1988. Other series of the Trust are not incorporated in this report. Davenport Core Fund began operations on January 15, 1998. Davenport Value & Income Fund and Davenport Equity Opportunities Fund each began operations on December 31, 2010.

Davenport Core Fund’s investment objective is long term growth of capital.

Davenport Value & Income Fund’s investment objective is to achieve long term growth while generating current income through dividend payments on portfolio securities.

Davenport Equity Opportunities Fund’s investment objective is long term capital appreciation.

2. Significant Accounting Policies

The following is a summary of the Funds’ significant accounting policies. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

Securities valuation — The Funds’ portfolio securities are valued as of the close of business of the regular session of the New York Stock Exchange (normally 4:00 p.m., Eastern time). Securities traded on a national stock exchange are valued based upon the closing price on the principal exchange where the security is traded. Securities which are quoted by NASDAQ are valued at the NASDAQ Official Closing Price. Securities which are traded over-the-counter are valued at the last sales price, if available, otherwise, at the last quoted bid price. Fixed income securities will ordinarily be traded in the over-the-counter market and common stocks will ordinarily be traded on a national securities exchange, but may also be traded in the over-the-counter market.

When market quotations are not readily available, securities may be valued on the basis of prices provided by an independent pricing service. The prices provided by the pricing service are determined with consideration given to institutional bid and last sale prices and take into account securities prices, yields, maturities, call features, ratings, institutional trading in similar groups of securities and developments related to specific securities. If a pricing service cannot provide a valuation or the investment adviser believes the price received from the pricing service is not indicative of fair value, securities will be valued in good faith at fair value using methods consistent with those determined by the Board of Trustees and will be classified as Level 2 or 3 within the fair value hierarchy (see below), depending on the inputs used. Such methods of fair valuation may include, but are not limited to: multiple of earnings, multiple of book value, discount from market of a similar freely traded security, purchase price of the security, subsequent private transactions in the security or related securities, or a combination of these and other factors.

THE DAVENPORT FUNDS

NOTES TO FINANCIAL STATEMENTS (Continued)

Short-term instruments (those with remaining maturities of 60 days or less) may be valued at amortized cost, which approximates market value. Money market funds have been determined to be represented at amortized cost which approximates fair value, absent unusual circumstances.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the Funds’ investments. These inputs are summarized in the three broad levels listed below:

• Level 1 – quoted prices in active markets for identical securities

• Level 2 – other significant observable inputs

• Level 3 – significant unobservable inputs

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Funds’ investments as of September 30, 2013 by security type:

| | | | | | | | | | | | |

| Common Stocks | | $ | 226,722,186 | | | $ | — | | | $ | — | | | $ | 226,722,186 | |

| Exchange-Traded Funds | | | 5,906,947 | | | | — | | | | — | | | | 5,906,947 | |

| Money Market Funds | | | 4,571,006 | | | | — | | | | — | | | | 4,571,006 | |

| Total | | $ | 237,200,139 | | | $ | — | | | $ | — | | | $ | 237,200,139 | |

Davenport Value & Income Fund | | | | | | | | | | | | |

| Common Stocks | | $ | 215,164,251 | | | $ | — | | | $ | — | | | $ | 215,164,251 | |

| Exchange-Traded Funds | | | 6,384,897 | | | | — | | | | — | | | | 6,384,897 | |

| Closed-End Funds | | | 1,806,395 | | | | — | | | | — | | | | 1,806,395 | |

| Money Market Funds | | | 6,792,005 | | | | — | | | | — | | | | 6,792,005 | |

| Total | | $ | 230,147,548 | | | $ | — | | | $ | — | | | $ | 230,147,548 | |

Davenport Equity Opportunities Fund | | | | | | | | | | | | |

| Common Stocks | | $ | 125,569,337 | | | $ | — | | | $ | — | | | $ | 125,569,337 | |

| Money Market Funds | | | 3,800,594 | | | | — | | | | — | | | | 3,800,594 | |

| Total | | $ | 129,369,931 | | | $ | — | | | $ | — | | | $ | 129,369,931 | |

THE DAVENPORT FUNDS

NOTES TO FINANCIAL STATEMENTS (Continued)

Refer to each Fund’s Schedule of Investments for a listing of the securities valued by sector type. As of September 30, 2013, the Funds did not have any transfers in and out of any Level. There were no Level 2 or Level 3 securities or derivative instruments held by the Funds as of September 30, 2013. It is the Funds’ policy to recognize transfers into and out of any Level at the end of the reporting period.

Share valuation — The net asset value per share of each Fund is calculated daily by dividing the total value of its assets, less liabilities, by the number of shares outstanding. The offering price and redemption price per share of each Fund is equal to the net asset value per share.

Investment income — Interest income is accrued as earned. Dividend income is recorded on the ex-dividend date. Discounts and premiums on fixed-income securities purchased are amortized using the interest method.

Security transactions — Security transactions are accounted for on trade date for financial reporting purposes. Gains and losses on securities sold are determined on a specific identification basis.

Common expenses — Common expenses of the Trust are allocated among the funds within the Trust based on relative net assets of each fund or the nature of the services performed and the relative applicability to each fund.

Distributions to shareholders — Dividends arising from net investment income, if any, are declared and paid quarterly to shareholders of Davenport Core Fund and Davenport Value & Income Fund; and declared and paid annually to shareholders of Davenport Equity Opportunities Fund. Net realized short-term capital gains, if any, may be distributed throughout the year and net realized long-term capital gains, if any, are distributed at least once each year. The amount of distributions from net investment income and net realized gains are determined in accordance with federal income tax regulations which may differ from GAAP. Dividends and distributions are recorded on the ex-dividend date.

The tax character of distributions paid during the periods ended September 30, 2013 and March 31, 2013 is as follows:

| | | | | | | | | | |

| Davenport Core Fund | 9/30/13 | | $ | 908,702 | | | $ | 1,456,213 | | | $ | 2,364,915 | |

| | 3/31/13 | | $ | 1,315,956 | | | $ | — | | | $ | 1,315,956 | |

| Davenport Value & Income Fund | 9/30/13 | | $ | 2,726,686 | | | $ | 2,658,586 | | | $ | 5,385,272 | |

| | 3/31/13 | | $ | 3,316,928 | | | $ | 1,962,920 | | | $ | 5,279,848 | |

| Davenport Equity Opportunities Fund | 9/30/13 | | $ | 36,859 | | | $ | 2,404,854 | | | $ | 2,441,713 | |

| | 3/31/13 | | $ | 505,327 | | | $ | 1,364,834 | | | $ | 1,870,161 | |

THE DAVENPORT FUNDS

NOTES TO FINANCIAL STATEMENTS (Continued)

Estimates — The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Federal income tax — It is each Fund’s policy to comply with the special provisions of Subchapter M of the Internal Revenue Code applicable to regulated investment companies. As provided therein, in any fiscal year in which a Fund so qualifies and distributes at least 90% of its taxable net income, the Fund (but not the shareholders) will be relieved of federal income tax on the income distributed. Accordingly, no provision for income taxes has been made.