| OMB APPROVAL |

OMB Number: 3235-0570 Expires: January 31, 2017 Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-05685 | |

| Williamsburg Investment Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

W. Lee H. Dunham, Esq.

| Sullivan & Worcester LLP One Post Office Square Boston, Massachusetts 02109 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (513) 587-3400 | |

| Date of fiscal year end: | March 31 | |

| | | |

| Date of reporting period: | September 30, 2015 | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

SEMI-ANNUAL REPORT September 30, 2015

(Unaudited) |

THE DAVENPORT FUNDS

LETTER TO SHAREHOLDERS | November 3, 2015 |

Dear Shareholders,

Equity markets experienced a significant selloff during the third quarter. The S&P 500 Index (“S&P 500”) declined 6.44% while the Russell 2000 Index (“Russell”) was down 11.92%. Year-to-date, domestic equity markets ended the period firmly in negative territory with the S&P 500 and Russell down 5.29% and 7.73%, respectively. The S&P 500 was over 10% off its recent high. While one down quarter doesn’t necessarily come as a surprise, recent volatility has been unsettling nonetheless. Many stocks are down much more than the indices would lead one to believe, with shares of more cyclical companies exhibiting pronounced weakness.

So why the sharp pullback? For one, we think there may have been some buyer exhaustion after a period of extended gains. We had not seen a 10% correction in nearly four years and have witnessed extraordinary gains off the 2009 lows. The primary trigger, however, has been signs of global economic strain. Many economies outside the U.S. appear to be slowing and signaling a threat of deflation. This is best evidenced by plummeting commodity prices. China has been at the epicenter of this story with decelerating GDP growth and a recent stock market implosion. Unfortunately, these signs of “global cooling” have emerged just as our Federal Reserve (the “Fed”) is attempting to raise interest rates for the first time in a decade, thereby creating concern that “tighter” monetary policy could be ill-timed.

We also think the domestic economy may need time to catch up to the stock market. From 2012-2014, U.S. GDP growth averaged roughly 2% and earnings growth for the S&P 500 averaged approximately 5.5%. Meanwhile, the total return for the S&P 500 averaged nearly 21%. Such returns were clearly driven more by an upward “re-rating” (i.e. valuation expansion) than profit improvement; hence, it makes sense for the market to bide time while we wait for more meaningful economic and earnings growth. It doesn’t appear as though growth this year will provide the fuel, with GDP expected to grow 2.5% in 2015 and S&P 500 earnings actually expected to decline slightly.

So what will the Fed do? This is still a subject of intense debate after the Fed decided to once again delay raising rates at its mid-September meeting. On one hand, the domestic economy is no longer in crisis mode; hence, zero percent interest rate policy seems unwarranted. On the other hand, interest rate hikes normally occur alongside accelerating economic growth and inflation. Nominal GDP is expanding at roughly half the pace it was when the 2004-2006 rate increase cycle commenced. Not to mention corporate profits are barely growing, commodity prices have collapsed and the rest of the world looks to be slowing. While a 25 basis point (0.25%) hike appears imminent, we expect the Fed will refrain from going too far too fast, and we look for accommodative monetary policy to persist. Of note, we also point out that markets have historically traded higher a year after the first rate hike.

In addition to Fed policy remaining supportive, there are some other positives to consider. For one, the U.S. consumer appears healthy. The job market continues to improve, home prices have recovered to a large extent, fuel prices are cheaper and consumer debt levels are down markedly from pre-crisis levels. These factors should allow for improving consumer demand for goods and services. Two, stock valuations are not unreasonable. At 15.2x earnings estimates for next year,

1

the S&P 500 is more richly valued than a couple years ago, but not far above historical averages despite ultra-low interest rates. Lastly, we note that investor sentiment doesn’t appear overly positive. Famed investor Sir John Templeton once said: “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” We are having a hard time finding investors who feel euphoric at the moment, which leads us to believe we may continue to “climb a wall of worry.”

All told, we think it’s sensible for the market to take a timeout as prior years’ returns seem to have borrowed from the future a bit. We don’t know what the near term will bring, but are sticking to our view that returns in coming years will be more moderate. That said, we don’t perceive there to be a stock market “bubble” given prevailing valuations and sentiment and are finding some attractively valued companies in the wake of recent weakness.

Please read on for a discussion of fund themes and ideas. We thank you for your trust and look forward to reporting back to you.

Davenport Core Fund

The following chart represents Davenport Core Fund (the “Core Fund”) performance and the performance of the S&P 500 Index*, the Core Fund’s primary benchmark, for the periods ended September 30, 2015.

| Q3 2015 | 1 Year | 3 Years** | 5 Years** | 10 Years** | Since Inception** 1/15/98 | Fiscal Year 2015 Expense Ratio |

Core Fund | -6.20% | 2.06% | 12.38% | 12.84% | 7.17% | 5.99% | 0.93% |

S&P 500 Index* | -6.44% | -0.61% | 12.40% | 13.34% | 6.80% | 6.00% | — |

30-Day SEC Yield: 0.63%

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

* | The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

The Core Fund fell by 6.20% in the third quarter, holding up a little better than the S&P 500 Index’s 6.44% decline. The quarter’s weakness has dragged year-to-date returns into negative territory, with the fund down 4.14%, outpacing the 5.29% decline in the S&P 500. While certainly a challenging quarter for investors of all stripes, we are pleased with the fund’s relative resilience.

As mentioned above, the market has increasingly narrowed, further favoring growth stocks that have already been “working.” Our ownership of growth names such as Google (GOOG), Priceline (PCLN), Amazon (AMZN), Starbucks (SBUX) and Visa (V) all fall into this camp and benefitted performance during the quarter. During the quarter, Baxter International (BAX) spun off its biopharmaceutical business Baxalta (BXLT). We elected to sell our legacy BAX position

2

and use the proceeds to add to Baxalta (BXLT) given its modest valuation and higher growth profile, with a promising pipeline of new products in targeting hemophilia and oncology. Shortly thereafter, the stock made a 10%+ one day move after Shire PLC announced a takeover offer. We elected to sell BXLT as this announcement brought forward gains, and we saw downside risk if the transaction was unable to close, as has been the case with other announced transactions in the health care sector recently. Importantly, while we were able to participate in the upside for high quality growth names, we sidestepped some of the carnage in more aggressive momentum names in the healthcare/biotechnology and information technology sectors. We didn’t entirely escape the selloff, however, with key detractors Capital One (COF) and Brookfield Asset Management (BAM) in the financials sector and Range Resources (RRC) and Schlumberger (SLB) in the energy sector, with the former negatively impacted by the Fed’s choice to wait on a rate hike and the latter continuing to suffer alongside commodity prices.

We took advantage of volatility in the quarter to further strengthen the quality and risk-adjusted return profile of the Core Fund. In some cases, this meant bottom fishing in depressed sectors, and in other cases, this meant adding to strong companies with reasonable valuations. The ability for a company to weather more difficult times and participate in economic upside, should it occur, was a common thread among investments that we initiated or added to. We moved away from companies attempting to execute a turnaround in what is proving to be an increasingly difficult economic environment. This approach can be illustrated through our transactions in cyclical stocks during the quarter: we sold United Technologies (UTX), a company undergoing management changes and upheaval in business lines, and added to Union Pacific Corporation (UNP), Schlumberger (SLB) and ExxonMobil (XOM), all companies that earn some of the highest returns on capital in their sector, that are well positioned to strengthen their economic moats during this down cycle and ultimately emerge stronger on the other side, while generating free cash flow for investors in the meantime.

During the quarter, we also chose to add to high quality names that aren’t as far off from their highs as the aforementioned stocks. Danaher (DHR) and Visa (V) are two examples. Danaher’s capital allocation track record is unmatched in the industrial sector, and we added to the position ahead of its split into two companies by the end of 2016. We think both pieces will be attractive investments, as the life sciences & technology piece benefits from a high organic growth rate and the industrial business should be able to continue its rollup strategy with more needle-moving transactions, given the smaller capital base. Turning to Visa, we continue to view its business model as one of the best in the world. Combine this with double-digit growth rates in payment volumes and we think the stock’s premium multiple is justified.

Ultimately, we like the Core Fund’s positioning at present. The Fund has a strong roster of companies, many of which are capable of generating organic growth even in a difficult macroeconomic environment. The remainder of the Fund is balanced with businesses that have seen their share prices cut along with growth prospects, and could offer a meaningful snap back should economic growth pick up. We think this combination continues to set up an attractive risk/reward profile for the Fund in the currently volatile investment landscape.

The following are transactions performed in the Core Fund for the quarter ended September 30, 2015.

3

Recent Purchases

Baxalta, Inc. (BXLT) After Baxter International (BAX) elected to split into two companies, we elected to sell our legacy BAX position and use the proceeds to add to Baxalta (BXLT) given its modest valuation and higher growth profile, with a promising pipeline of new products in targeting hemophilia and oncology.

Danaher Corporation (DHR) With a capital allocation track record unmatched in the industrial sector, we added to the position ahead of its split into two companies anticipated by the end of 2016.

Exxon Mobil Corporation (XOM) Following broad based energy sector weakness, we elected to add to XOM due to the defensive qualities of the business, strong balance sheet and solid dividend yield.

Johnson & Johnson (JNJ) Based on balance sheet, yield and below market multiple, we elected to add to JNJ as the share price weakened alongside the broader market.

Liberty Broadband Corporation (LBRDK) We added to our position feeling the company is well positioned to participate in the consolidation of the cable industry through its 26% stake in Charter Communications.

Merck & Company, Inc. (MRK) Following a strong Q2 which reaffirmed our outlook for this company, we added to the position on weakness as the product pipeline and business prospects continue to look favorable.

Schlumberger Ltd. (SLB) We added to SLB on general market weakness, as this company appears to be navigating the current down-cycle in energy and looks poised to emerge stronger on the other side.

The Priceline Group, Inc. (PCLN) With Euro zone and Chinese market concerns weighing on the stock, we added to this dominant franchise which continues to provide a great long term growth opportunity.

Union Pacific Corporation (UNP) With the transport sector under considerable pressure, we purchased UNP due to its significant competitive advantages and compelling long term outlook.

Visa, Inc. (V) We added to V as it trades at a very reasonable multiple while operating one of the best business models in the world. Payment volumes continue to grow at double digit rates.

Recent Sales

Alcoa, Inc. (AA) With significant exposure to a weakening commodity sector alongside our view that a rebound in aluminum prices may already be ‘in’ the stock, we elected to move out of AA at this time.

Baxalta, Inc. (BXLT) We elected to sell the stock after a 10%+ one day move after Shire PLC announced a takeover offer. This announcement brought forward gains, and we saw downside risk if the transaction was unable to close, as has been the case with other announced transactions in the healthcare sector recently.

Baxter International, Inc. (BAX) We sold Baxter after it spun off its crown jewel Baxalta (BXLT). The remaining Baxter is a lower-growth biosciences and medical products company, with less upside potential, in our view.

4

General Motors Company (GM) Given recent weakness in the stock and our concerns the domestic auto cycle may be peaking, we sold the position and deployed funds into opportunities with a better risk return profile.

QUALCOMM, Inc. (QCOM) Facing customer losses and royalty rate headwinds, we chose to sell this relatively small position in the portfolio in favor of situations showing a better long term outlook.

United Technologies Corporation (UTX) Faced with internal management issues and a challenging industrial backdrop, we elected to sell and move proceeds to higher conviction ideas.

Davenport Value & Income Fund

The following chart represents Davenport Value & Income Fund (the “Value & Income Fund”) performance and the performance of the S&P 500 Index, the Value & Income Fund’s primary benchmark, and the Lipper Equity Income Index for the periods ended September 30, 2015.

| Q3 2015 | 1 Year | 3 Years** | Since Inception** 12/31/2010 | Fiscal

Year 2015 Expense Ratio |

Value & Income Fund | -7.97% | -0.45% | 11.09% | 11.90% | 0.95% |

S&P 500 Index* | -6.44% | -0.61% | 12.40% | 11.67% | — |

Lipper Equity Income Index* | -7.25% | -4.24% | 9.74% | 9.41% | — |

30-Day SEC Yield: 2.73%

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

* | The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. The Lipper Equity Income Index is an unmanaged index of the 30 largest funds in the Lipper Equity Income fund category. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

The Value & Income Fund declined 7.97% during the third quarter, lagging the 6.44% decline for the S&P 500 and the 7.25% decline for the Lipper Equity Income Index. Year-to-date as of September 30, 2015, the Value & Income Fund is down 6.54%, relative to the declines of the 5.29% for the S&P 500 and the 7.83% for the Lipper Equity Income Index. After struggling to start the year, income oriented equities dug in somewhat as global growth concerns pushed out investor expectations regarding the timing of an eventual interest rate hike from the Federal Reserve. What did not change, however, was the continued outperformance of growth stocks versus value stocks, which have struggled mightily since the beginning of the year.

Manufactured housing REITS, Sun Communities (SUI) and Equity Lifestyle Holdings (ELS), were two of the Value & Income Fund’s top performers during the quarter. In addition to benefitting from a shift in interest rate expectations mentioned above, these two companies stand out versus the rest of the REIT sector due to recent momentum in operating results, which reflect

5

their above average growth potential, pricing power and favorable demographic tailwinds. Other key contributors included Altria (MO) and Dominion (D), each of which has a strong history of dividend increases and predictable cash flows. The Fund’s biggest detractor during the quarter was Las Vegas Sands (LVS), which weakened alongside heightened investor angst surrounding declining Macau revenue. The financials sector was also a source of weakness as bank holdings such as JPMorgan (JPM) and Capital One Financial (COF), both of which should be beneficiaries of higher interest rates, reacted to yet another delay in the “lift-off” decision from the Fed. Though near term action has been disappointing, we continue to believe the banking sector looks attractive given solid balance sheets, improving profitability and cheap valuations.

The Value & Income Fund’s underweight stance in the energy sector has been a significant contributor to relative performance since the price of crude oil began its slide in mid-2014. Following a slight rebound in Q2, crude prices fell to new lows during the third quarter and many stocks in the sector followed suit. Though the industry continues to face clear challenges on both the supply and demand sides of the equation, we believe weakness in the sector has created some attractive opportunities. While we remain underweight, we have begun to add exposure to the energy space. On one hand, we added to defensive holdings such as Occidental Petroleum (OXY) and Exxon Mobil (XOM), which can use their strong balance sheets to maintain their dividends (yields of 4.5% and 3.9%, respectively) and make opportunistic acquisitions if weakness persists. On the other hand, we initiated a position in independent power producer NRG Energy (NRG). Though admittedly more of an aggressive play given the company’s leverage, we note free cash flow at NRG should ramp dramatically in coming years as capital expenditures fall off, enabling debt repayment, increases to the dividend (yields 3.9%) and share repurchases. Finally, we note the company could see significant upside in the event natural gas prices increase given the fact that power prices are tied to natural gas. Ultimately, we felt the risk/reward profile was compelling.

We elected to add to our position in Lamar Advertising (LAMR) during the quarter. LAMR has been a solid performer since our initial purchase, however, the company had recently come under pressure after Q2 results showed a slowdown in organic revenue trends. Of particular concern for investors was a decline in “same board” revenue trends on digital boards, which appear to be in a digestion phase after significant new builds in prior years. While new supply of digital boards may take a little time to absorb, we do not feel this is the beginning of a trend and note that the company remains on track to deliver the 10% Funds from Operations (growth it originally forecasted at the beginning of the year. Furthermore, pricing has picked up across the industry and key verticals such as real estate are improving. We point out that billboards generate fairly stable growth and prodigious amounts of free cash flow given modest capital requirements. They are also much less vulnerable to secular trends (i.e. “cord-cutting”) that currently haunt the cable and TV advertising industries. Ultimately, we felt recent weakness provided an attractive opportunity to gain exposure to a steady business with a growing dividend (yields 5.3%) and attractive reinvestment opportunities.

In summary, Q3 returns were a bit disappointing, but we are still comfortable with where we stand on a year- to-date basis. Moreover, we feel that recent actions taken amid significant volatility have improved the risk/reward profile of the entire Value & Income Fund. Though we have begun to lean against the wind in the depressed energy sector following significant declines, our primary focus remains on quality businesses with attractive payouts that can grow. Given this mix, we feel confident in the Value & Income Fund’s ability to deliver an element of defensiveness and income (yield is 3.5%), while also participating in potential market upside.

6

The following are transactions performed in the Value & Income Fund for the quarter ended September 30, 2015.

Recent Purchases

Exxon Mobil Corporation (XOM) We added to the name on weakness as the defensive qualities of the business, strong balance sheet and solid dividend yield should prove to be supportive in the time ahead.

Kinder Morgan, Inc. (KMI) The stock sold off alongside the broader energy sector, and we chose to add to the name given its critical infrastructure assets backed by long term contracts with producers and consumers.

Lamar Advertising Company (LAMR) With a growing dividend yield and attractive reinvestment opportunities, we added to LAMR, which looks to be entering a digestion phase following its digital board build out.

Las Vegas Sands Corporation (LVS) We added to our position following the stock’s resiliency to worse than expected numbers out of Macau and our belief that gaming numbers appear to be bottoming.

NRG Energy, Inc. (NRG) With natural gas and wholesale power prices on the decline, we felt this was an opportune time to buy shares of the nation’s largest competitive power generation company.

Occidental Petroleum Corporation (OXY) Given the share repurchase program, high quality balance sheet and solid dividend yield, we elected to add to this name which has traded in tandem with the Exploration & Production sector.

Regions Financial Corporation (RF) Improving profitability, a shareholder focus and large portfolio of variable rate loans led us to purchase this company, which is well positioned for an eventual rate hike.

Recent Sales

Chemours Company (CC) A recent spin out of DuPont, we elected to sell Chemours Co given its limited liquidity, business prospects and small position size in the portfolio.

Deutsche X-trackers Harvest CSI 300 China A-Shares ETF (ASHR) Following a period of solid performance, we sold our position due to increasing volatility in the shares and belief that the valuation tailwind is largely behind us.

iShares China Large- Cap ETF (FXI) A strong performer since inception, recent deteriorating economic visibility and increased government intervention led us to sell the position and move to the sidelines.

Markel Corporation (MKL) With the stock up nearly 30% YTD and trading near all time highs, we elected to chip and reallocate proceeds to more timely situations from a risk/reward perspective.

Waddell & Reed Financial, Inc. (WDR) We sold the stock as fund outflows have remained a significant factor in the wake of manager turnover and underperformance of its flagship Asset Strategy Fund.

7

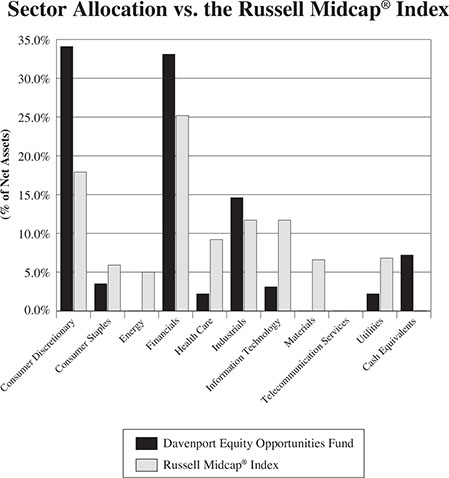

Davenport Equity Opportunities Fund

The following chart represents Davenport Equity Opportunities Fund (the “Equity Opportunities Fund”) performance and the performance of the Russell Midcap Index, the Fund’s primary benchmark, and the S&P 500 Index for the periods ended September 30, 2015.

| Q3 2015 | 1 Year | 3 Years** | Since Inception** 12/31/2010 | Fiscal

Year 2015 Expense Ratio |

Equity Opportunities Fund | -12.47% | 2.43% | 13.75% | 12.98% | 1.02% |

Russell Midcap Index* | -8.01% | -0.25% | 13.91% | 11.25% | — |

S&P 500 Index* | -6.44% | -0.61% | 12.40% | 11.67% | — |

30-Day SEC Yield: 0.32%

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

* | The Russell Midcap Index measures the performance of the 800 smallest companies in the Russell 1000, which represent approximately 25% of the total market capitalization of the Russell 1000. The S&P 500 Index is comprised of 500 U.S. stocks and is an indicator of the performance of the overall U.S. stock market. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

The Equity Opportunities Fund experienced a challenging third quarter. The Fund declined 12.47% as compared to losses of 8.01% and 6.44%, respectively, for the Russell Midcap Index (“Russell Midcap”) and S&P 500. Year-to-date, the Fund ended the period down 6.81% versus declines of 5.84% and 5.29% for the Russell Midcap and S&P 500. A period of relative underperformance wasn’t totally surprising after three consecutive quarters of relative gains, but was still frustrating. Unfortunately, a handful of positions conspired against us with above-average declines. Over time, we have demonstrated better returns during tougher market environments. While this wasn’t the case recently, we don’t put too much emphasis on one quarter’s results.

Colfax (CFX) and Discovery Communications (DISCK) were our biggest drags during the quarter. Shares of both companies have appeared bottomless with relentless declines. In the case of Colfax, which traded in the low $70s just over a year ago and is now roughly $30/share, the company is plagued by exposure to both emerging markets and customers in the downtrodden energy sector. Its welding business also appears to be losing share as management implements an operational turnaround. Admittedly, we feel a bit silly for building this position too early in the face of stiff headwinds and a deteriorating earnings outlook. However, at current prices the stock’s risk/reward profile seems very attractive and upside could be significant if earnings just stabilize.

In terms of Discovery, which is currently our largest position, the shares continue to be haunted by fears of “cord-cutting.” Put simply, “cord-cutting” is the concept of people abandoning traditional cable/TV in favor of alternatives like Netflix, Hulu and Amazon Prime. Talk of the looming demise of leading cable networks seems greatly exaggerated and the anti-media trade is overwhelmingly popular right now. At its recent investor day, management reiterated its domestic media business

8

would continue to grow even in tougher times due to rising affiliate fees (payments from cable and satellite TV operators) and a rising share of total advertising dollars. Furthermore, the company projects high-single digit revenue growth from its international business, which is now roughly 50% of revenue. All told, management expects to generate double-digit free cash flow growth over the next few years and to produce $10 billion of excess capital that could be used for acquisitions, content investment or share buybacks. We are particularly excited about Discovery’s investment in foreign sports content and opportunity to create the “ESPN of Europe”. Given the company’s growth profile and investment opportunities, we have a hard time understanding the stock’s depressed valuation.

We added to both of these positions in the face of extremely negative sentiment. As we’ve noted in the past, part of our modus operandi is to buy good businesses at attractive prices. This oftentimes means buying shares of companies facing well-documented headwinds. We aren’t “value” investors per se, but are drawn to stocks that are depressed and therefore appear to offer above-average long-term returns. This approach has been unrewarding of late as investors have fled anything with headwinds and crowded into the few stocks that are working. Unfortunately, anything that has looked “cheap” has only become cheaper in following weeks/months as Wall Street has become increasingly myopic. We think investors are currently taking excess risk by paying too much of a premium for momentum stories. In the meantime, we continue to build positions in durable companies that have fallen out of favor.

Continuing that theme, we’ve also established a new position in Genesee & Wyoming (GWR), which is a short line railroad operator. Shares of GWR have retreated from a high of $105 to a recent price in the low $60s as investors fret about the company’s exposure to commodity markets. Indeed, part of its business is transporting commodities like coal and iron ore that have seen softening demand. While we generally aren’t attracted to commodity companies given unpredictable results and sometimes inferior returns on capital, this is a high quality business model that has been deemed guilty by association. Even with volumes depressed, the company could earn roughly $4.00/share, and incremental earnings on improved volumes could be substantial. We also note GWR has better free cash flow dynamics than Class I rail operators given lower capital requirements and has a sizeable acquisition opportunity due to an abundance of independently owned short line railroads. Given these factors and its wide competitive moat (the threat of new railroads is minimal), GWR has traditionally commanded a premium multiple. After its recent swoon, the stock appears to offer a compelling value.

In closing, we would have liked to have held up better during the third quarter. Over time, we hope to generate above-average returns and dampen risk by focusing on timely purchases and companies that can manage through challenging economic cycles. While Q3 performance was disappointing, many of our top holdings seem to now offer very attractive risk/reward profiles and we are excited to be adding to these names. Hence, we think the Fund’s overall timeliness and risk/reward profile is the best it’s been in recent memory.

9

The following are transactions performed in the Equity Opportunities Fund for the quarter ended September 30, 2015.

Recent Purchases

Capital One Financial Corporation (COF) Given a number of one-time items which led Q2 results below expectations, we took the ‘longer view’ and added to our position at what we consider attractive levels.

Colfax Corporation (CFX) We added to our position in this well managed entity as shares have come under significant pressure alongside currency headwinds and weakness in key end-markets such as oil and gas.

Discovery Communications, Inc. (DISCK) We elected to add to shares in this name, which had weakened substantially alongside a broader shift in investor sentiment within the space.

Dollar Tree, Inc. (DLTR) A lack of near term guidance surrounding the recent Family Dollar acquisition led to weakness in the shares (an over-reaction in our view), which we used to add to the position.

Genesee & Wyoming, Inc. (GWR) Shares in the nation’s largest short line railroad operator are well off their highs as demand and volumes are down for bulk commodities, presenting an attractive entry point.

Hanesbrands, Inc. (HBI) Recent one-time events put downward pressure on the stock, providing an opportunity to increase our position in this well managed, shareholder friendly company.

Las Vegas Sands Corporation (LVS) We initiated a position during the quarter in this global developer of resort properties across Asia and the United States.

NRG Energy, Inc. (NRG) We elected to add to this name as supply demand factors have weighed on the company and the energy/utility sector as a whole, moving the shares into favorable risk-reward territory.

Recent Sales

Alcoa, Inc. (AA) With significant exposure to a weakening commodity sector alongside our view that a rebound in aluminum prices may already be ‘in’ the stock, we elected to move out of AA at this time.

Cabela’s, Inc. (CAB) While the company’s strong brand should lead to growth of the store-base, ongoing competitive pressures and management’s underestimation of these trends led us to exit the position.

Markel Corporation (MKL) The epitome of a long-term compounding growth situation, we chipped this core holding due to recent strength in the shares (up ~30% YTD at time of sale) and resulting size in the portfolio.

Morgan Stanley China A Share Fund, Inc. (CAF) With increased Chinese government intervention and resulting volatility in the shares, we elected to chip on two occasions and ultimately sell this name during the quarter.

Penn National Gaming, Inc. (PENN) We elected to chip this position on strength and move to more favorable risk return opportunities as regional gaming trends have improved along with investor sentiment.

10

Davenport Small Cap Focus Fund

The following chart represents Davenport Small Cap Focus Fund (the “Small Cap Focus Fund”) performance and the performance of the Russell 2000 Index, the Small Cap Focus Fund’s primary benchmark, for the periods ended September 30, 2015.

| Q3 2015 | Since Inception** 12/31/2014 | Fiscal

Year 2015 Gross Expense Ratio | Fiscal

Year 2015 Net Expense Ratio |

Small Cap Focus Fund | -12.94% | -9.11% | 1.44% | 1.27%1 |

Russell 2000 Index* | -11.92% | -7.73% | — | — |

Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance data, current to the most recent month end, may be obtained by calling 1-800-281-3217.

* | The Russell 2000 Index measures the performance of the 2000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

1 | Davenport & Company LLC (the “Advisor”) has contractually agreed, until August 1, 2016, to reduce Management Fees and to reimburse Other Expenses to the extent necessary to limit Total Annual Fund Operating Expenses (excluding Acquired Fund Fees and Expenses) to an amount not exceeding 1.25% of the Fund’s average daily net assets. Total Annual Fund Operating Expenses exclude brokerage costs, taxes, interest, costs to organize the Fund and extraordinary expenses. For additional details please request a prospectus. |

The Davenport Small Cap Focus Fund (DSCPX) struggled alongside broader market weakness during the third quarter, posting a 12.94% decline versus an 11.92% slide for the Russell 2000 Index. Year- to- date, the strategy is down 9.11%, relative to the 7.73% decline for the Russell 2000. Small capitalization stocks have significantly underperformed large caps year-to-date, as evidenced by the S&P 500’s more manageable decline of 5.29%. As such, we believe valuations are much more reasonable across the asset class and note that the Fund’s domestic bias should serve as a buffer against many of the issues plaguing the global economy.

Commodity and commodity-related stocks have been our primary detractors. Such stocks don’t comprise a huge portion of the Fund, but having moderate exposure to a few names suffering steep declines has been a problem. Over time, we expect to generally be underweight commodities and materials as we don’t like being dependent on commodity prices and often question the long-term returns on capital for these businesses. However, the group was broadly out of favor as we started the year (and started the Small Cap Focus Fund) and appeared to offer some value. Unfortunately, commodity/commodity-related stocks have continued their fall and we were clearly early to a few names.

We’ve recently emphasized some companies that aren’t commodity producers, but have been found guilty by association. One example is Genesee & Wyoming (GWR), which is a short line railroad operator. Shares of GWR have retreated from a high of $105 to a recent price in the mid $60s as investors fret about the company’s exposure to commodity markets. Indeed, part of its business is transporting commodities like coal and iron ore that have seen softening demand. Even with volumes depressed, the company could earn roughly $4.00/share, and incremental

11

earnings on improved volumes could be substantial. We also note GWR has better free cash flow dynamics than Class I rail operators given lower capital requirements and has a sizeable acquisition opportunity due to an abundance of independently owned short line railroads. Given these factors and its wide competitive moat (the threat of new railroads is minimal), GWR has traditionally commanded a premium multiple. After its recent swoon, the stock appears to offer a compelling value.

Significant exposure to the consumer sector has generally helped performance this year. We’ve continued to add to a few consumer stocks that seem to have the potential for years of compounding growth. One instance is Monarch Casino & Resort (MCRI). Monarch is a little known casino operator with a flagship property based in Reno, Nevada. With no new casino supply and a flourishing local economy, we expect MCRI’s property to generate solid results for years to come. What’s more, the company has purchased a second property in Black Hawk, CO and is in the midst of a sizeable expansion. Black Hawk caters to the under-penetrated Denver market and we believe this project will generate attractive returns on capital. At current prices, the stock looks very cheap relative to potential free cash flow generation in a couple years. We also point out that CEO John Farahi currently owns 17% of the company and clearly has substantial “skin in the game.”

In the health care arena, we’ve been adding to animal hospital and reference lab operator, VCA Antech (WOOF). The animal health industry is experiencing significant growth due to rising pet ownership rates, the “humanization of pets” and the emergence of specialty medicine and diagnostics. Both the hospital and reference lab businesses sport strong organic growth rates (mid-single digits) and boast very attractive incremental margins (~15% and 60+% respectively). Over its 30 year history, WOOF has acquired significant scale in this business allowing the company to recycle its strong cash generation into accretive acquisitions and share repurchases. This combination of organic growth, operating leverage and capital allocation should lead to relatively predictable high teens EPS growth over the next few years.

In our opinion, the most exciting aspect of small cap investing is the potential to find uncommon value in companies that are off the beaten path. We feel like we are currently finding such names and “stocking the pond” with companies that seem to have very good risk/reward profiles. You won’t hear about these companies at cocktail parties or on Fast Money, but they could deliver us solid returns over the next few years.

We thank you for your trust and look forward to reporting back as we proceed through the year.

Sincerely,

John P. Ackerly, IV

President, The Davenport Funds

12

DAVENPORT CORE FUND

PERFORMANCE INFORMATION (Unaudited)

| | Average Annual Total Returns(a)

(for periods ended September 30, 2015) |

| | 1 Year | 5 Years | 10 Years |

Davenport Core Fund | 2.06% | 12.84% | 7.17% |

Standard & Poor’s 500® Index | (0.61%) | 13.34% | 6.80% |

(a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

13

DAVENPORT VALUE & INCOME FUND

PERFORMANCE INFORMATION (Unaudited)

| | Average Annual Total Returns(a)

(for periods ended September 30, 2015) |

| | 1 Year | Since Inception(b) |

Davenport Value & Income Fund | (0.45%) | 11.90% |

Standard & Poor’s 500® Index | (0.61%) | 11.67% |

Lipper Equity Income Index | (4.25%) | 9.41% |

(a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(b) | Commencement of operations was December 31, 2010. |

14

DAVENPORT EQUITY OPPORTUNITIES FUND

PERFORMANCE INFORMATION (Unaudited)

| | Average Annual Total Returns(a)

(for periods ended September 30, 2015) |

| | 1 Year | Since Inception(b) |

Davenport Equity Opportunities Fund | 2.43% | 12.98% |

Russell Midcap® Index | (0.25%) | 11.25% |

(a) | The total returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(b) | Commencement of operations was December 31, 2010. |

15

DAVENPORT SMALL CAP FOCUS FUND

PERFORMANCE INFORMATION (Unaudited)

| | Total Returns(a)

(for period ended September 30, 2015) |

| | Since Inception(b) |

Davenport Small Cap Focus Fund | (9.11%) |

Russell 2000® Index | (7.73%) |

(a) | The total return shown does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(b) | Commencement of operations was December 31, 2014. |

16

DAVENPORT CORE FUND

PORTFOLIO INFORMATION

September 30, 2015 (Unaudited)

Top Ten Equity Holdings

Security Description | % of Net Assets |

Markel Corporation | 3.4% |

Brookfield Asset Management, Inc. - Class A | 3.3% |

Danaher Corporation | 3.2% |

Capital One Financial Corporation | 2.9% |

American Tower Corporation | 2.6% |

Citigroup, Inc. | 2.6% |

Nestlé SA - ADR | 2.6% |

Accenture plc - Class A | 2.5% |

CarMax, Inc. | 2.5% |

Berkshire Hathaway, Inc. - Class B | 2.5% |

17

DAVENPORT VALUE & INCOME FUND

PORTFOLIO INFORMATION

September 30, 2015 (Unaudited)

Top Ten Equity Holdings

Security Description | % of Net Assets |

Markel Corporation | 2.9% |

JPMorgan Chase & Company | 2.8% |

Capital One Financial Corporation | 2.7% |

Wells Fargo & Company | 2.7% |

SPDR EURO STOXX 50 ETF | 2.7% |

W.P. Carey, Inc. | 2.7% |

Watsco, Inc. | 2.6% |

Johnson & Johnson | 2.4% |

Equity LifeStyle Porperties, Inc. | 2.3% |

General Electric Company | 2.3% |

18

DAVENPORT EQUITY OPPORTUNITIES FUND

PORTFOLIO INFORMATION

September 30, 2015 (Unaudited)

Top Ten Equity Holdings

Security Description | % of Net Assets |

Markel Corporation | 5.7% |

Discovery Communications, Inc. - Series C | 5.5% |

Capital One Financial Corporation | 5.3% |

Brookfield Asset Management, Inc. - Class A | 5.1% |

Gaming and Leisure Properties, Inc. | 5.1% |

CarMax, Inc. | 4.2% |

American Tower Corporation | 4.1% |

Colfax Corporation | 3.9% |

Dollar Tree, Inc. | 3.8% |

Amazon.com, Inc. | 3.6% |

19

DAVENPORT SMALL CAP FOCUS FUND

PORTFOLIO INFORMATION

September 30, 2015 (Unaudited)

Top Ten Equity Holdings

Security Description | % of Net Assets |

Stewart Information Services Corporation | 3.4% |

Monarch Casino & Resort, Inc. | 3.3% |

Boston Beer Company, Inc. (The) - Class A | 3.2% |

VWR Corporation | 3.0% |

Genesee & Wyoming, Inc. - Class A | 2.9% |

Encore Capital Group, Inc. | 2.9% |

Outfront Media, Inc. | 2.8% |

Liberty Broadband Corporation - Series C | 2.8% |

Live Nation Entertainment, Inc. | 2.8% |

TowneBank | 2.7% |

20

DAVENPORT CORE FUND

SCHEDULE OF INVESTMENTS

September 30, 2015 (Unaudited) | |

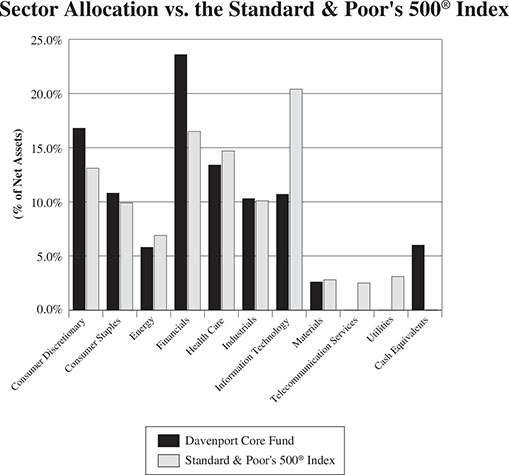

COMMON STOCKS — 94.1% | | Shares | | | Value | |

Consumer Discretionary — 16.8% | | | | | | |

Amazon.com, Inc. (a) | | | 13,525 | | | $ | 6,923,312 | |

CarMax, Inc. (a) | | | 135,754 | | | | 8,052,927 | |

DISH Network Corporation - Class A (a) | | | 68,710 | | | | 4,008,542 | |

Liberty Broadband Corporation - Series A (a) | | | 10,584 | | | | 544,441 | |

Liberty Broadband Corporation - Series C (a) | | | 49,854 | | | | 2,551,029 | |

Liberty Media Corporation - Series A (a) | | | 42,337 | | | | 1,512,278 | |

Liberty Media Corporation - Series C (a) | | | 131,829 | | | | 4,542,827 | |

Priceline Group, Inc. (The) (a) | | | 5,692 | | | | 7,040,207 | |

PVH Corporation | | | 65,338 | | | | 6,660,556 | |

Starbucks Corporation | | | 108,705 | | | | 6,178,792 | |

Walt Disney Company (The) | | | 51,531 | | | | 5,266,468 | |

| | | | | | | | 53,281,379 | |

Consumer Staples — 10.8% | | | | | | | | |

Anheuser-Busch InBev SA/NV - ADR | | | 39,920 | | | | 4,244,294 | |

Hershey Company (The) | | | 48,065 | | | | 4,416,212 | |

J.M. Smucker Company (The) | | | 56,957 | | | | 6,498,224 | |

Mondelēz International, Inc. - Class A | | | 135,520 | | | | 5,674,222 | |

Nestlé SA - ADR | | | 108,802 | | | | 8,186,263 | |

PepsiCo, Inc. | | | 54,796 | | | | 5,167,263 | |

| | | | | | | | 34,186,478 | |

Energy — 5.9% | | | | | | | | |

Chevron Corporation | | | 42,157 | | | | 3,325,344 | |

Exxon Mobil Corporation | | | 86,462 | | | | 6,428,450 | |

Range Resources Corporation | | | 96,407 | | | | 3,096,593 | |

Schlumberger Ltd. | | | 83,140 | | | | 5,734,166 | |

| | | | | | | | 18,584,553 | |

Financials — 23.6% | | | | | | | | |

American Tower Corporation (b) | | | 93,792 | | | | 8,251,820 | |

Berkshire Hathaway, Inc. - Class B (a) | | | 60,361 | | | | 7,871,074 | |

Brookfield Asset Management, Inc. - Class A | | | 329,959 | | | | 10,373,911 | |

Capital One Financial Corporation | | | 127,036 | | | | 9,212,651 | |

Citigroup, Inc. | | | 165,742 | | | | 8,222,461 | |

CME Group, Inc. | | | 81,011 | | | | 7,512,960 | |

JPMorgan Chase & Company | | | 114,578 | | | | 6,985,821 | |

Markel Corporation (a) | | | 13,588 | | | | 10,895,674 | |

Wells Fargo & Company | | | 111,829 | | | | 5,742,419 | |

| | | | | | | | 75,068,791 | |

Health Care — 13.4% | | | | | | | | |

AmerisourceBergen Corporation | | | 66,695 | | | | 6,335,358 | |

Amgen, Inc. | | | 29,511 | | | | 4,081,962 | |

Anthem, Inc. | | | 28,788 | | | | 4,030,320 | |

Celgene Corporation (a) | | | 66,513 | | | | 7,194,711 | |

Express Scripts Holding Company (a) | | | 55,426 | | | | 4,487,289 | |

21

DAVENPORT CORE FUND

SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 94.1% (Continued) | | Shares | | | Value | |

Health Care — 13.4% (Continued) | | | | | | |

Johnson & Johnson | | | 72,113 | | | $ | 6,731,749 | |

Merck & Company, Inc. | | | 112,855 | | | | 5,573,908 | |

Valeant Pharmaceuticals International, Inc. (a) | | | 23,787 | | | | 4,243,125 | |

| | | | | | | | 42,678,422 | |

Industrials — 10.3% | | | | | | | | |

American Airlines Group, Inc. | | | 135,720 | | | | 5,270,008 | |

Cummins, Inc. | | | 28,709 | | | | 3,117,223 | |

Danaher Corporation | | | 118,422 | | | | 10,090,739 | |

General Electric Company | | | 156,250 | | | | 3,940,625 | |

Parker-Hannifin Corporation | | | 40,430 | | | | 3,933,839 | |

Union Pacific Corporation | | | 72,299 | | | | 6,391,954 | |

| | | | | | | | 32,744,388 | |

Information Technology — 10.7% | | | | | | | | |

Accenture plc - Class A | | | 82,336 | | | | 8,090,335 | |

Apple, Inc. | | | 52,695 | | | | 5,812,258 | |

Cisco Systems, Inc. | | | 173,988 | | | | 4,567,185 | |

Google, Inc. - Class A (a) | | | 7,045 | | | | 4,497,317 | |

Google, Inc. - Class C (a) | | | 6,387 | | | | 3,885,979 | |

Visa, Inc. - Class A | | | 103,926 | | | | 7,239,485 | |

| | | | | | | | 34,092,559 | |

Materials — 2.6% | | | | | | | | |

Monsanto Company | | | 49,140 | | | | 4,193,607 | |

Praxair, Inc. | | | 40,658 | | | | 4,141,424 | |

| | | | | | | | 8,335,031 | |

| | | | | | | | | |

Total Common Stocks (Cost $230,715,873) | | | | | | $ | 298,971,601 | |

MONEY MARKET FUNDS — 1.8% | | Shares | | | Value | |

First American Treasury Obligations Fund - Class Z, 0.00% (c) (Cost $5,895,704) | | | 5,895,704 | | | $ | 5,895,704 | |

| | | | | | | | | |

Total Investments at Value — 95.9% (Cost $236,611,580) | | | | | | $ | 304,867,305 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 4.1% | | | | | | | 12,940,066 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 317,807,371 | |

ADR - American Depositary Receipt.

(a) | Non-income producing security. |

(b) | Real estate investment trust (REIT). |

(c) | The rate shown is the 7-day effective yield as of September 30, 2015. |

See accompanying notes to financial statements.

22

DAVENPORT VALUE & INCOME FUND

SCHEDULE OF INVESTMENTS

September 30, 2015 (Unaudited) | |

COMMON STOCKS — 93.4% | | Shares | | | Value | |

Consumer Discretionary — 8.0% | | | | | | |

Las Vegas Sands Corporation | | | 155,800 | | | $ | 5,915,726 | |

McDonald's Corporation | | | 89,705 | | | | 8,838,633 | |

Ralph Lauren Corporation | | | 47,255 | | | | 5,583,651 | |

Six Flags Entertainment Corporation | | | 147,600 | | | | 6,757,128 | |

Time Warner, Inc. | | | 74,765 | | | | 5,140,094 | |

| | | | | | | | 32,235,232 | |

Consumer Staples — 15.7% | | | | | | | | |

Altria Group, Inc. | | | 130,026 | | | | 7,073,415 | |

Anheuser-Busch InBev SA/NV - ADR | | | 60,295 | | | | 6,410,565 | |

Archer-Daniels-Midland Company | | | 152,590 | | | | 6,324,856 | |

Coca-Cola Company (The) | | | 213,350 | | | | 8,559,602 | |

Diageo plc - ADR | | | 71,485 | | | | 7,705,368 | |

PepsiCo, Inc. | | | 82,120 | | | | 7,743,916 | |

Philip Morris International, Inc. | | | 97,380 | | | | 7,725,155 | |

Procter & Gamble Company (The) | | | 81,845 | | | | 5,887,929 | |

Wal-Mart Stores, Inc. | | | 88,967 | | | | 5,768,620 | |

| | | | | | | | 63,199,426 | |

Energy — 6.6% | | | | | | | | |

Chevron Corporation | | | 58,171 | | | | 4,588,528 | |

Exxon Mobil Corporation | | | 100,510 | | | | 7,472,918 | |

Kinder Morgan, Inc. | | | 219,195 | | | | 6,067,318 | |

Occidental Petroleum Corporation | | | 124,365 | | | | 8,226,745 | |

| | | | | | | | 26,355,509 | |

Financials — 28.7% | | | | | | | | |

Capital One Financial Corporation | | | 152,035 | | | | 11,025,578 | |

Citigroup, Inc. | | | 160,730 | | | | 7,973,816 | |

Equity LifeStyle Properties, Inc. (b) | | | 157,955 | | | | 9,251,425 | |

FNF Group | | | 240,445 | | | | 8,528,584 | |

Gaming and Leisure Properties, Inc. (b) | | | 301,649 | | | | 8,958,975 | |

JPMorgan Chase & Company | | | 186,070 | | | | 11,344,688 | |

Lamar Advertising Company - Class A (b) | | | 156,540 | | | | 8,168,257 | |

Markel Corporation (a) | | | 14,529 | | | | 11,650,224 | |

Regions Financial Corporation | | | 848,530 | | | | 7,645,255 | |

Sun Communities, Inc. (b) | | | 127,805 | | | | 8,660,067 | |

W.P. Carey, Inc. (b) | | | 189,304 | | | | 10,943,664 | |

Wells Fargo & Company | | | 213,815 | | | | 10,979,400 | |

| | | | | | | | 115,129,933 | |

Health Care — 8.4% | | | | | | | | |

Johnson & Johnson | | | 103,945 | | | | 9,703,266 | |

Merck & Company, Inc. | | | 144,640 | | | | 7,143,770 | |

Sanofi - ADR | | | 168,960 | | | | 8,020,531 | |

Teva Pharmaceutical Industries Ltd. - ADR | | | 156,290 | | | | 8,824,133 | |

| | | | | | | | 33,691,700 | |

23

DAVENPORT VALUE & INCOME FUND

SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 93.4% (Continued) | | Shares | | | Value | |

Industrials — 11.2% | | | | | | |

3M Company | | | 51,695 | | | $ | 7,328,800 | |

Eaton Corporation plc | | | 106,907 | | | | 5,484,329 | |

General Electric Company | | | 366,035 | | | | 9,231,403 | |

Illinois Tool Works, Inc. | | | 68,990 | | | | 5,678,567 | |

Raytheon Company | | | 59,836 | | | | 6,537,681 | |

Watsco, Inc. | | | 89,245 | | | | 10,573,748 | |

| | | | | | | | 44,834,528 | |

Information Technology — 3.2% | | | | | | | | |

Cisco Systems, Inc. | | | 236,840 | | | | 6,217,050 | |

Microsoft Corporation | | | 146,393 | | | | 6,479,354 | |

| | | | | | | | 12,696,404 | |

Materials — 5.1% | | | | | | | | |

E.I. du Pont de Nemours and Company | | | 93,680 | | | | 4,515,376 | |

Eastman Chemical Company | | | 124,015 | | | | 8,026,251 | |

Nucor Corporation | | | 113,845 | | | | 4,274,880 | |

Potash Corporation of Saskatchewan, Inc. | | | 177,930 | | | | 3,656,461 | |

| | | | | | | | 20,472,968 | |

Telecommunication Services — 3.4% | | | | | | | | |

TELUS Corporation | | | 225,560 | | | | 7,114,162 | |

Verizon Communications, Inc. | | | 155,460 | | | | 6,764,065 | |

| | | | | | | | 13,878,227 | |

Utilities — 3.1% | | | | | | | | |

Dominion Resources, Inc. | | | 109,775 | | | | 7,725,965 | |

NRG Energy, Inc. | | | 309,025 | | | | 4,589,021 | |

| | | | | | | | 12,314,986 | |

| | | | | | | | | |

Total Common Stocks (Cost $357,636,014) | | | | | | $ | 374,808,913 | |

EXCHANGE-TRADED FUNDS — 2.7% | | Shares | | | Value | |

SPDR EURO STOXX 50 ETF (Cost $11,296,518) | | | 323,770 | | | $ | 10,959,614 | |

24

DAVENPORT VALUE & INCOME FUND

SCHEDULE OF INVESTMENTS (Continued) | |

MONEY MARKET FUNDS — 2.9% | | Shares | | | Value | |

First American Treasury Obligations Fund - Class Z, 0.00% (c) (Cost $11,585,942) | | | 11,585,942 | | | $ | 11,585,942 | |

| | | | | | | | | |

Total Investments at Value — 99.0% (Cost $380,518,474) | | | | | | $ | 397,354,469 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 1.0% | | | | | | | 4,056,079 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 401,410,548 | |

ADR - American Depositary Receipt.

(a) | Non-income producing security. |

(b) | Real estate investment trust (REIT). |

(c) | The rate shown is the 7-day effective yield as of September 30, 2015. |

See accompanying notes to financial statements.

25

DAVENPORT EQUITY OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS

September 30, 2015 (Unaudited) | |

COMMON STOCKS — 92.8% | | Shares | | | Value | |

Consumer Discretionary — 34.1% | | | | | | |

Amazon.com, Inc. (a) | | | 20,240 | | | $ | 10,360,654 | |

CarMax, Inc. (a) | | | 204,210 | | | | 12,113,737 | |

Discovery Communications, Inc. - Series A (a) | | | 116,935 | | | | 3,043,818 | |

Discovery Communications, Inc. - Series C (a) | | | 665,066 | | | | 16,154,453 | |

Dollar Tree, Inc. (a) | | | 165,766 | | | | 11,049,962 | |

Hanesbrands, Inc. | | | 353,445 | | | | 10,228,698 | |

Las Vegas Sands Corporation | | | 119,918 | | | | 4,553,287 | |

Liberty Broadband Corporation - Series C (a) | | | 191,090 | | | | 9,778,075 | |

Live Nation Entertainment, Inc. (a) | | | 311,200 | | | | 7,481,248 | |

LKQ Corporation (a) | | | 319,691 | | | | 9,066,437 | |

Penn National Gaming, Inc. (a) | | | 338,457 | | | | 5,679,308 | |

| | | | | | | | 99,509,677 | |

Consumer Staples — 3.5% | | | | | | | | |

Church & Dwight Company, Inc. | | | 122,335 | | | | 10,263,907 | |

| | | | | | | | | |

Financials — 33.1% | | | | | | | | |

American Tower Corporation (b) | | | 137,155 | | | | 12,066,897 | |

Brookfield Asset Management, Inc. - Class A | | | 476,012 | | | | 14,965,817 | |

Capital One Financial Corporation | | | 212,249 | | | | 15,392,297 | |

Fairfax Financial Holdings Ltd. | | | 18,913 | | | | 8,616,385 | |

FNF Group | | | 162,250 | | | | 5,755,007 | |

Gaming and Leisure Properties, Inc. (b) | | | 500,089 | | | | 14,852,643 | |

Markel Corporation (a) | | | 20,802 | | | | 16,680,292 | |

PRA Group, Inc. (a) | | | 156,355 | | | | 8,274,307 | |

| | | | | | | | 96,603,645 | |

Health Care — 2.2% | | | | | | | | |

Henry Schein, Inc. (a) | | | 48,615 | | | | 6,452,183 | |

| | | | | | | | | |

Industrials — 14.6% | | | | | | | | |

American Airlines Group, Inc. | | | 207,510 | | | | 8,057,613 | |

Colfax Corporation (a) | | | 379,201 | | | | 11,341,902 | |

Genesee & Wyoming, Inc. - Class A (a) | | | 137,195 | | | | 8,105,481 | |

WABCO Holdings, Inc. (a) | | | 89,615 | | | | 9,394,340 | |

Watsco, Inc. | | | 48,740 | | | | 5,774,715 | |

| | | | | | | | 42,674,051 | |

Information Technology — 3.1% | | | | | | | | |

Intuit, Inc. | | | 101,350 | | | | 8,994,813 | |

| | | | | | | | | |

Utilities — 2.2% | | | | | | | | |

NRG Energy, Inc. | | | 428,105 | | | | 6,357,359 | |

| | | | | | | | | |

Total Common Stocks (Cost $271,057,784) | | | | | | $ | 270,855,635 | |

26

DAVENPORT EQUITY OPPORTUNITIES FUND

SCHEDULE OF INVESTMENTS (Continued) | |

MONEY MARKET FUNDS — 2.8% | | Shares | | | Value | |

First American Treasury Obligations Fund - Class Z, 0.00% (c) (Cost $8,151,436) | | | 8,151,436 | | | $ | 8,151,436 | |

| | | | | | | | | |

Total Investments at Value — 95.6% (Cost $279,209,220) | | | | | | $ | 279,007,071 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 4.4% | | | | | | | 12,773,937 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 291,781,008 | |

(a) | Non-income producing security. |

(b) | Real estate investment trust (REIT). |

(c) | The rate shown is the 7-day effective yield as of September 30, 2015. |

See accompanying notes to financial statements.

27

DAVENPORT SMALL CAP FOCUS FUND

SCHEDULE OF INVESTMENTS

September 30, 2015 (Unaudited) | |

COMMON STOCKS — 91.3% | | Shares | | | Value | |

Consumer Discretionary — 22.2% | | | | | | |

Cable One, Inc. (a) | | | 1,500 | | | $ | 629,130 | |

Core-Mark Holding Company, Inc. | | | 16,071 | | | | 1,051,847 | |

J. Alexander's Holdings, Inc. (a) | | | 8,382 | | | | 83,569 | |

Liberty Broadband Corporation - Series C (a) | | | 21,918 | | | | 1,121,544 | |

Lions Gate Entertainment Corporation | | | 24,000 | | | | 883,200 | |

Live Nation Entertainment, Inc. (a) | | | 46,179 | | | | 1,110,143 | |

Monarch Casino & Resort, Inc. (a) | | | 73,778 | | | | 1,325,791 | |

Pinnacle Entertainment, Inc. (a) | | | 20,256 | | | | 685,463 | |

Pool Corporation | | | 11,457 | | | | 828,341 | |

Scripps Networks Interactive, Inc. - Class A | | | 16,500 | | | | 811,635 | |

Unifi, Inc. (a) | | | 11,107 | | | | 331,100 | |

| | | | | | | | 8,861,763 | |

Consumer Staples — 7.2% | | | | | | | | |

Boston Beer Company, Inc. (The) - Class A (a) | | | 6,100 | | | | 1,284,721 | |

Seaboard Corporation (a) | | | 275 | | | | 846,725 | |

Snyder's-Lance, Inc. | | | 21,617 | | | | 729,141 | |

| | | | | | | | 2,860,587 | |

Energy — 8.8% | | | | | | | | |

CNX Coal Resources LP (a) | | | 55,500 | | | | 624,375 | |

Fission Uranium Corporation (a) | | | 241,484 | | | | 114,898 | |

Peyto Exploration & Development Corporation | | | 42,051 | | | | 874,241 | |

Sunoco LP | | | 23,652 | | | | 800,620 | |

Westmoreland Coal Company (a) | | | 76,047 | | | | 1,071,502 | |

| | | | | | | | 3,485,636 | |

Financials — 22.3% | | | | | | | | |

Diamond Hill Investment Group, Inc. | | | 3,644 | | | | 677,930 | |

Encore Capital Group, Inc. (a) | | | 31,579 | | | | 1,168,423 | |

FNFV Group (a) | | | 48,530 | | | | 568,772 | |

FRP Holdings, Inc. (a) | | | 21,893 | | | | 659,855 | |

Gaming and Leisure Properties, Inc. (b) | | | 26,198 | | | | 778,081 | |

Lamar Advertising Company - Class A | | | 14,500 | | | | 756,610 | |

Outfront Media, Inc.(b) | | | 54,289 | | | | 1,129,211 | |

PRA Group, Inc. (a) | | | 13,302 | | | | 703,942 | |

Stewart Information Services Corporation | | | 33,529 | | | | 1,371,671 | |

TowneBank | | | 57,359 | | | | 1,081,217 | |

| | | | | | | | 8,895,712 | |

Health Care — 5.3% | | | | | | | | |

VCA, Inc. (a) | | | 17,155 | | | | 903,211 | |

VWR Corporation (a) | | | 46,361 | | | | 1,191,014 | |

| | | | | | | | 2,094,225 | |

Industrials — 14.4% | | | | | | | | |

Colfax Corporation (a) | | | 35,014 | | | | 1,047,269 | |

Covenant Transportation Group, Inc. - Class A (a) | | | 45,557 | | | | 818,659 | |

28

DAVENPORT SMALL CAP FOCUS FUND

SCHEDULE OF INVESTMENTS (Continued) | |

COMMON STOCKS — 91.3% (Continued) | | Shares | | | Value | |

Industrials — 14.4% (Continued) | | | | | | |

Genesee & Wyoming, Inc. - Class A (a) | | | 19,870 | | | $ | 1,173,920 | |

Marten Transport Ltd. | | | 55,178 | | | | 892,228 | |

Mistras Group, Inc. (a) | | | 63,033 | | | | 809,974 | |

Watsco, Inc. | | | 8,558 | | | | 1,013,952 | |

| | | | | | | | 5,756,002 | |

Information Technology — 3.4% | | | | | | | | |

Black Knight Financial Services, Inc. - Class A (a) | | | 21,000 | | | | 683,550 | |

EchoStar Corporation - Class A (a) | | | 15,559 | | | | 669,504 | |

| | | | | | | | 1,353,054 | |

Materials — 3.3% | | | | | | | | |

Fortuna Silver Mines, Inc. (a) | | | 385,580 | | | | 840,564 | |

NewMarket Corporation | | | 1,336 | | | | 476,952 | |

| | | | | | | | 1,317,516 | |

Telecommunication Services — 2.3% | | | | | | | | |

Iridium Communications, Inc. (a) | | | 79,227 | | | | 487,246 | |

United States Cellular Corporation (a) | | | 12,236 | | | | 433,522 | |

| | | | | | | | 920,768 | |

Utilities — 2.1% | | | | | | | | |

Dynegy, Inc. (a) | | | 39,753 | | | | 821,694 | |

| | | | | | | | | |

Total Common Stocks (Cost $40,799,130) | | | | | | $ | 36,366,957 | |

MONEY MARKET FUNDS — 8.6% | | Shares | | | Value | |

First American Treasury Obligations Fund - Class Z, 0.00% (c) (Cost $3,432,577) | | | 3,432,577 | | | $ | 3,432,577 | |

| | | | | | | | | |

Total Investments at Value — 99.9% (Cost $44,231,707) | | | | | | $ | 39,799,534 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 0.1% | | | | | | | 40,881 | |

| | | | | | | | | |

Net Assets — 100.0% | | | | | | $ | 39,840,415 | |

(a) | Non-income producing security. |

(b) | Real estate investment trust (REIT). |

(c) | The rate shown is the 7-day effective yield as of September 30, 2015. |

See accompanying notes to financial statements.

29

THE DAVENPORT FUNDS

STATEMENTS OF ASSETS AND LIABILITIES

September 30, 2015 (Unaudited) | |

| | Davenport

Core

Fund | | | Davenport Value & Income

Fund | |

ASSETS | | | | | | |

Investments in securities: | | | | | | |

At acquisition cost | | $ | 236,611,580 | | | $ | 380,518,474 | |

At market value (Note 2) | | $ | 304,867,305 | | | $ | 397,354,469 | |

Cash | | | 12,967,423 | | | | 2,136,424 | |

Dividends receivable | | | 199,767 | | | | 1,229,773 | |

Receivable for capital shares sold | | | 209,892 | | | | 1,369,266 | |

Other assets | | | 25,854 | | | | 29,443 | |

TOTAL ASSETS | | | 318,270,241 | | | | 402,119,375 | |

| | | | | | | | | |

LIABILITIES | | | | | | | | |

Payable for capital shares redeemed | | | 222,439 | | | | 407,704 | |

Accrued investment advisory fees (Note 4) | | | 199,978 | | | | 249,516 | |

Payable to administrator (Note 4) | | | 34,450 | | | | 41,500 | |

Other accrued expenses | | | 6,003 | | | | 10,107 | |

TOTAL LIABILITIES | | | 462,870 | | | | 708,827 | |

| | | | | | | | | |

NET ASSETS | | $ | 317,807,371 | | | $ | 401,410,548 | |

| | | | | | | | | |

Net assets consist of: | | | | | | | | |

Paid-in capital | | $ | 239,598,276 | | | $ | 375,069,110 | |

Accumulated net investment income | | | 28,331 | | | | 373,779 | |

Accumulated net realized gains from security transactions | | | 9,925,039 | | | | 9,131,664 | |

Net unrealized appreciation on investments | | | 68,255,725 | | | | 16,835,995 | |

Net assets | | $ | 317,807,371 | | | $ | 401,410,548 | |

| | | | | | | | | |

Shares of beneficial interest outstanding (unlimited number of shares authorized, $0.01 par value) | | | 17,290,384 | | | | 29,336,310 | |

| | | | | | | | | |

Net asset value, offering price and redemption price per share (Note 2) | | $ | 18.38 | | | $ | 13.68 | |

See accompanying notes to financial statements.

30

THE DAVENPORT FUNDS

STATEMENTS OF ASSETS AND LIABILITIES (Continued)

September 30, 2015 (Unaudited) | |

| | Davenport Equity Opportunities Fund | | | Davenport Small Cap Focus

Fund | |

ASSETS | | | | | | |

Investments in securities: | | | | | | |

At acquisition cost | | $ | 279,209,220 | | | $ | 44,231,707 | |

At market value (Note 2) | | $ | 279,007,071 | | | $ | 39,799,534 | |

Cash | | | 12,626,377 | | | | — | |

Dividends receivable | | | 63,091 | | | | 13,859 | |

Receivable for capital shares sold | | | 372,299 | | | | 93,500 | |

Other assets | | | 25,738 | | | | 17,970 | |

TOTAL ASSETS | | | 292,094,576 | | | | 39,924,863 | |

| | | | | | | | | |

LIABILITIES | | | | | | | | |

Payable for investment securities purchased | | | — | | | | 8,625 | |

Payable for capital shares redeemed | | | 83,562 | | | | 41,204 | |

Accrued investment advisory fees (Note 4) | | | 185,125 | | | | 25,483 | |

Payable to administrator (Note 4) | | | 33,500 | | | | 6,200 | |

Other accrued expenses and liabilities | | | 11,381 | | | | 2,936 | |

TOTAL LIABILITIES | | | 313,568 | | | | 84,448 | |

| | | | | | | | | |

NET ASSETS | | $ | 291,781,008 | | | $ | 39,840,415 | |

| | | | | | | | | |

Net assets consist of: | | | | | | | | |

Paid-in capital | | $ | 284,112,714 | | | $ | 44,404,476 | |

Accumulated net investment income (loss) | | | 100,506 | | | | (34,864 | ) |

Accumulated net realized gains (losses) from security transactions | | | 7,769,937 | | | | (97,024 | ) |

Net unrealized depreciation on investments | | | (202,149 | ) | | | (4,432,173 | ) |

Net assets | | $ | 291,781,008 | | | $ | 39,840,415 | |

| | | | | | | | | |

Shares of beneficial interest outstanding (unlimited number of shares authorized, $0.01 par value) | | | 20,270,237 | | | | 4,387,612 | |

| | | | | | | | | |

Net asset value, offering price and redemption price per share (Note 2) | | $ | 14.39 | | | $ | 9.08 | |

See accompanying notes to financial statements.

31

THE DAVENPORT FUNDS

STATEMENTS OF OPERATIONS

Six Months Ended September 30, 2015 (Unaudited) | |

| | Davenport

Core

Fund | | | Davenport Value & Income

Fund | |

INVESTMENT INCOME | | | | | | |

Dividends | | $ | 2,513,064 | | | $ | 6,585,531 | |

Foreign withholding taxes on dividends | | | (51,282 | ) | | | (165,202 | ) |

TOTAL INVESTMENT INCOME | | | 2,461,782 | | | | 6,420,329 | |

| | | | | | | | | |

EXPENSES | | | | | | | | |

Investment advisory fees (Note 4) | | | 1,264,359 | | | | 1,587,538 | |

Administration fees (Note 4) | | | 200,212 | | | | 242,542 | |

Registration and filing fees | | | 13,526 | | | | 18,368 | |

Compliance service fees (Note 4) | | | 13,051 | | | | 15,727 | |

Custodian and bank service fees | | | 12,371 | | | | 16,019 | |

Professional fees | | | 12,668 | | | | 13,718 | |

Printing of shareholder reports | | | 6,440 | | | | 7,542 | |

Insurance expense | | | 5,382 | | | | 6,548 | |

Trustees’ fees and expenses (Note 4) | | | 5,120 | | | | 5,120 | |

Postage and supplies | | | 3,250 | | | | 3,568 | |

Other expenses | | | 4,567 | | | | 4,398 | |

TOTAL EXPENSES | | | 1,540,946 | | | | 1,921,088 | |

| | | | | | | | | |

NET INVESTMENT INCOME | | | 920,836 | | | | 4,499,241 | |

| | | | | | | | | |

REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS | | | | | | | | |

Net realized gains from security transactions | | | 9,937,866 | | | | 9,132,233 | |

Net change in unrealized appreciation/depreciation on investments | | | (31,875,342 | ) | | | (49,235,001 | ) |

| | | | | | | | | |

NET REALIZED AND UNREALIZED LOSSES ON INVESTMENTS | | | (21,937,476 | ) | | | (40,102,768 | ) |

| | | | | | | | | |

NET DECREASE IN NET ASSETS FROM OPERATIONS | | $ | (21,016,640 | ) | | $ | (35,603,527 | ) |

See accompanying notes to financial statements.

32

THE DAVENPORT FUNDS

STATEMENTS OF OPERATIONS (Continued)

Six Months Ended September 30, 2015 (Unaudited) | |

| | Davenport Equity Opportunities Fund | | | Davenport Small Cap Focus

Fund | |

INVESTMENT INCOME | | | | | | |

Dividends | | $ | 1,537,593 | | | $ | 196,035 | |

Foreign withholding taxes on dividends | | | (16,506 | ) | | | (4,721 | ) |

TOTAL INVESTMENT INCOME | | | 1,521,087 | | | | 191,314 | |

| | | | | | | | | |

EXPENSES | | | | | | | | |

Investment advisory fees (Note 4) | | | 1,147,955 | | | | 158,871 | (a) |

Administration fees (Note 4) | | | 191,553 | | | | 32,816 | |

Registration and filing fees | | | 19,510 | | | | 11,986 | |

Professional fees | | | 11,978 | | | | 8,578 | |

Custodian and bank service fees | | | 12,486 | | | | 4,075 | |

Compliance service fees (Note 4) | | | 12,156 | | | | 3,731 | |

Trustees’ fees and expenses (Note 4) | | | 5,120 | | | | 5,120 | |

Printing of shareholder reports | | | 6,571 | | | | 2,884 | |

Insurance expense | | | 4,707 | | | | 744 | |

Postage and supplies | | | 3,651 | | | | 1,790 | |

Other expenses | | | 4,894 | | | | 2,410 | |

TOTAL EXPENSES | | | 1,420,581 | | | | 233,005 | |

| | | | | | | | | |

NET INVESTMENT INCOME (LOSS) | | | 100,506 | | | | (41,691 | ) |

| | | | | | | | | |

REALIZED AND UNREALIZED GAINS

(LOSSES) ON INVESTMENTS | | | | | | | | |

Net realized gains (losses) from security transactions | | | 7,770,631 | | | | (97,008 | ) |

Net change in unrealized appreciation/depreciation on investments | | | (46,679,240 | ) | | | (5,567,101 | ) |

| | | | | | | | | |

NET REALIZED AND UNREALIZED LOSSES ON INVESTMENTS | | | (38,908,609 | ) | | | (5,664,109 | ) |

| | | | | | | | | |

NET DECREASE IN NET ASSETS FROM OPERATIONS | | $ | (38,808,103 | ) | | $ | (5,705,800 | ) |

(a) | Includes previously waived investment advisory fees recouped by the Adviser of $10,744 (Note 4). |

See accompanying notes to financial statements.

33

DAVENPORT CORE FUND

STATEMENTS OF CHANGES IN NET ASSETS | |

| | Six Months

Ended

September 30,

2015

(Unaudited) | | | Year

Ended

March 31,

2015 | |

FROM OPERATIONS | | | | | | |

Net investment income | | $ | 920,836 | | | $ | 1,488,043 | |

Net realized gains from security transactions | | | 9,937,866 | | | | 14,551,320 | |

Net change in unrealized appreciation/depreciation on investments | | | (31,875,342 | ) | | | 19,717,017 | |

Net increase (decrease) in net assets from operations | | | (21,016,640 | ) | | | 35,756,380 | |

| | | | | | | | | |

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | | | | | | | | |

From net investment income | | | (892,505 | ) | | | (1,509,705 | ) |

From net realized gains from security transactions | | | (6,233,547 | ) | | | (22,409,339 | ) |

Decrease in net assets from distributions to shareholders | | | (7,126,052 | ) | | | (23,919,044 | ) |

| | | | | | | | | |

FROM CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Proceeds from shares sold | | | 20,586,323 | | | | 43,532,772 | |

Net asset value of shares issued in reinvestment of distributions to shareholders | | | 6,895,742 | | | | 23,153,291 | |

Payments for shares redeemed | | | (12,218,656 | ) | | | (29,067,963 | ) |

Net increase in net assets from capital share transactions | | | 15,263,409 | | | | 37,618,100 | |

| | | | | | | | | |

TOTAL INCREASE (DECREASE) IN NET ASSETS | | | (12,879,283 | ) | | | 49,455,436 | |

| | | | | | | | | |

NET ASSETS | | | | | | | | |

Beginning of period | | | 330,686,654 | | | | 281,231,218 | |

End of period | | $ | 317,807,371 | | | $ | 330,686,654 | |

| | | | | | | | | |

ACCUMULATED NET INVESTMENT INCOME | | $ | 28,331 | | | $ | — | |

| | | | | | | | | |

CAPITAL SHARE ACTIVITY | | | | | | | | |

Shares sold | | | 1,036,004 | | | | 2,233,700 | |

Shares reinvested | | | 347,892 | | | | 1,207,808 | |

Shares redeemed | | | (612,755 | ) | | | (1,495,763 | ) |

Net increase in shares outstanding | | | 771,141 | | | | 1,945,745 | |

Shares outstanding at beginning of period | | | 16,519,243 | | | | 14,573,498 | |

Shares outstanding at end of period | | | 17,290,384 | | | | 16,519,243 | |

See accompanying notes to financial statements.

34

DAVENPORT VALUE & INCOME FUND

STATEMENTS OF CHANGES IN NET ASSETS | |

| | Six Months

Ended

September 30,

2015

(Unaudited) | | | Year

Ended

March 31,

2015 | |

FROM OPERATIONS | | | | | | |

Net investment income | | $ | 4,499,241 | | | $ | 5,877,403 | |

Net realized gains from security transactions | | | 9,132,233 | | | | 18,731,719 | |

Net change in unrealized appreciation/depreciation on investments | | | (49,235,001 | ) | | | 14,874,206 | |

Net increase (decrease) in net assets from operations | | | (35,603,527 | ) | | | 39,483,328 | |

| | | | | | | | | |

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | | | | | | | | |

From net investment income | | | (4,379,582 | ) | | | (5,878,113 | ) |

From net realized gains from security transactions | | | (11,144,935 | ) | | | (15,874,061 | ) |

Decrease in net assets from distributions to shareholders | | | (15,524,517 | ) | | | (21,752,174 | ) |

| | | | | | | | | |

FROM CAPITAL SHARE TRANSACTIONS | | | | | | | | |

Proceeds from shares sold | | | 44,496,126 | | | | 93,258,289 | |

Net asset value of shares issued in reinvestment of distributions to shareholders | | | 14,368,942 | | | | 20,026,663 | |

Payments for shares redeemed | | | (14,103,272 | ) | | | (27,526,918 | ) |

Net increase in net assets from capital share transactions | | | 44,761,796 | | | | 85,758,034 | |

| | | | | | | | | |

TOTAL INCREASE (DECREASE) IN NET ASSETS | | | (6,366,248 | ) | | | 103,489,188 | |

| | | | | | | | | |

NET ASSETS | | | | | | | | |

Beginning of period | | | 407,776,796 | | | | 304,287,608 | |

End of period | | $ | 401,410,548 | | | $ | 407,776,796 | |

| | | | | | | | | |

ACCUMULATED NET INVESTMENT INCOME | | $ | 373,779 | | | $ | 254,321 | |

| | | | | | | | | |

CAPITAL SHARE ACTIVITY | | | | | | | | |

Shares sold | | | 2,933,664 | | | | 6,192,254 | |

Shares reinvested | | | 961,488 | | | | 1,332,807 | |

Shares redeemed | | | (941,343 | ) | | | (1,830,740 | ) |

Net increase in shares outstanding | | | 2,953,809 | | | | 5,694,321 | |

Shares outstanding at beginning of period | | | 26,382,501 | | | | 20,688,180 | |

Shares outstanding at end of period | | | 29,336,310 | | | | 26,382,501 | |

See accompanying notes to financial statements.

35

DAVENPORT EQUITY OPPORTUNITIES FUND

STATEMENTS OF CHANGES IN NET ASSETS | |

| | Six Months

Ended

September 30,

2015

(Unaudited) | | | Year

Ended

March 31,

2015 | |

FROM OPERATIONS | | | | | | |

Net investment income | | $ | 100,506 | | | $ | 730,888 | |

Net realized gains from security transactions | | | 7,770,631 | | | | 15,756,298 | |

Net change in unrealized appreciation/depreciation on investments | | | (46,679,240 | ) | | | 18,256,256 | |