Table of Contents

PARNASSUS INCOME FUNDS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06673

Parnassus Income Funds

(Exact name of registrant as specified in charter)

1 Market Street, Suite 1600, San Francisco, California 94105

(Address of principal executive offices) (Zip code)

Marc C. Mahon

Parnassus Income Funds

1 Market Street, Suite 1600, San Francisco, California 94105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (415) 778-0200

Date of fiscal year end: December 31

Date of reporting period: June 30, 2008

Table of Contents

| Item 1: | Report to Shareholders |

THE PARNASSUS FUNDSSM

Semiannual Report June 30, 2008

Parnassus Fund Parnassus Small-Cap Fund

Parnassus Equity Income Fund Parnassus Workplace Fund

Parnassus Mid-Cap Fund Parnassus Fixed-Income Fund

Table of Contents

Parnassus Fund | (PARNX | ) | |||||

Parnassus Equity Income Fund–Investor Shares | (PRBLX | ) | |||||

Parnassus Equity Income Fund–Institutional Shares | (PRILX | ) | |||||

Parnassus Mid-Cap Fund | (PARMX | ) | |||||

Parnassus Small-Cap Fund | (PARSX | ) | |||||

Parnassus Workplace Fund | (PARWX | ) | |||||

Parnassus Fixed-Income Fund | (PRFIX | ) |

| 1 | ||

Fund Performance | ||

| 2 | ||

| 6 | ||

| 11 | ||

| 13 | ||

| 16 | ||

| 18 | ||

| 20 | ||

| 21 | ||

Portfolios of Investments | ||

| 22 | ||

| 24 | ||

| 28 | ||

| 30 | ||

| 32 | ||

| 33 | ||

| 36 | ||

| 43 | ||

| 48 | ||

| 52 | ||

Table of Contents

August 4, 2008

Dear Shareholder:

There was a lot of volatility in the capital markets during the second quarter of 2008, and most of the major market indices were down. We’re happy to report, though, that our funds have weathered the storms pretty well. Five of our six funds outperformed their Lipper peer groups for both the second quarter and the year-to-date, and although the Mid-Cap Fund underperformed its Lipper peer group for the second quarter, it outperformed that benchmark for the year-to-date. The Equity Income Fund and the Small-Cap Fund have done especially well this year, with both funds having a positive return for this difficult second quarter.

Although there are a lot of economic clouds on the horizon, the good news is that we’re finding many bargains. The intrinsic value of an individual company is, roughly speaking, the present value of its future earnings, and an investment in its stock is an ownership claim on those earnings. Therefore, over the very long term, the returns of the stock market will reflect the total earnings of public companies. The tricky part is that in the short term, the psychology of investors gets in the way of this fundamental relationship. Investors are people, and can be influenced by emotion and other things unrelated to fundamental value. Year-to-year, the market may have large swings, but over the long term, stocks stay around their intrinsic value.

As a steward of your money, it’s our job to find companies with the ability to earn a lot compared to the amount of capital invested regardless of where the market is. We’re happy to report that, overall, the companies in our portfolio have continued to perform well despite a weak economy, and our returns relative to the market reflect that. We’d also like to note that a major benefit of a down market is that companies that we have always admired, but couldn’t own because they were too expensive, are now a lot more attractive. We’ll be keeping our eyes open for great opportunities.

Personnel Matters

We’re fortunate to have three very good interns with us this summer. All of them are undergraduates at the University of California, Berkeley. Yanik Jayaram is a senior at Berkeley studying economics and also pursuing a minor in music. He’s a drummer in the UC Jazz Big Band. We won’t be able to offer Yanik much opportunity to hone his music skills, but hopefully, he leaves here with a better sense of economics than he did coming in.

Abdullah Nezami is a senior majoring in business administration at UC Berkeley’s Haas School of Business. Abdullah was born in Afghanistan and grew up in Fremont, California. He’s a member of the National Society of Collegiate Scholars honor society at Berkeley and initiated its student scholarship program.

Elina Sheykh-Zade is a senior at UC Berkeley studying economics. At Berkeley, she has volunteered for the school’s Habitat for Humanity chapter and also works as a tour guide on the Berkeley campus. Elina was born in Russia and lived there until the age of 9.

Enclosed you’ll find the reports for the six Parnassus Funds. As always, thank you for being an investor with Parnassus.

|  | |||

| Jerome L. Dodson | Stephen J. Dodson | |||

| Chairman and Chief Executive | President | |||

| Parnassus Investments | Parnassus Investments | |||

The Parnassus Funds 1

Table of Contents

Dear Shareholder:

As of June 30, 2008, the net asset value (“NAV”) per share of the Parnassus Fund was $34.06, so the total return for the second quarter was a loss of 0.50%. This compares to a loss of 2.73% for the S&P 500 Index (“S&P 500”), a loss of 0.81% for the average multi-cap core fund followed by Lipper Inc. (“Lipper average”), and a gain of 0.82% for the NASDAQ Composite Index (“NASDAQ”). For the quarter, then, we beat the S&P by over two percentage points, beat the Lipper average by a small margin and underperformed the NASDAQ.

For the year-to-date, the Fund is down 7.09% compared to a loss of 11.91% for the S&P, a loss of 10.62% for the Lipper average and a loss of 13.18% for the NASDAQ. Although we’re down for the year-to-date, we’re substantially ahead of all our benchmarks.

Below is a table comparing the Parnassus Fund with the S&P 500, the Lipper Multi-Cap Core Average and the NASDAQ over the past one-, three-, five- and ten-year periods. The Fund is ahead of all the indices for all periods, except for the five-year term.

Analysis

Although the Fund’s loss for the quarter was a modest half of one percent, six companies each accounted for a loss of 23¢ or more for each fund share. Two were homebuilders. As most of you know, homebuilders are one of the two industries suffering the most from the subprime mortgage problem and the resulting impact on credit markets. As the economy slows, fewer people are qualified to buy homes, resulting in too many houses on the market. With weak demand, the credit problems and the oversupply of houses, homebuilders are in trouble. Given this situation, you might wonder why I’m putting some of the Fund’s assets into homebuilders. As I explained in the March quarterly report, previous cycles have shown that homebuilder stocks hit bottom about 12-18 months before the fundamentals of the business start to improve. In my view, conditions for the homebuilders will start to improve sometime in the middle of 2009, or about a year from now. In previous cycles, homebuilder stocks have increased more than 100% from the bottom. Psychologically, it’s very hard to buy a stock at the bottom, but if you can control your emotions, it’s a great time to invest.

Average Annual Total Returns

for periods ended June 30, 2008

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

PARNASSUS FUND | (10.52 | %) | 5.49 | % | 3.94 | % | 5.96 | % | 1.00 | % | 0.99 | % | ||||||

S&P 500 Index | (13.12 | %) | 4.41 | % | 7.58 | % | 2.88 | % | NA | NA | ||||||||

Lipper Multi-Cap Core Average | (11.88 | %) | 4.82 | % | 8.27 | % | 4.52 | % | NA | NA | ||||||||

NASDAQ Composite Index | (11.19 | %) | 4.51 | % | 7.90 | % | 2.45 | % | NA | NA |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 Index and the NASDAQ Composite Index are unmanaged indices of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. Prior to May 1, 2004, the Parnassus Fund charged a sales load (maximum of 3.5%), which is not reflected in the total return calculations. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus website, or you can obtain one by calling (800) 999–3505. As described in the Fund’s current prospectus dated May 1, 2008, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.99% of net assets, exclusive of acquired fund fees, until May 1, 2009. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

2 The Parnassus Funds

Table of Contents

What was really surprising during the first quarter of this year was that homebuilder stocks increased on average between 20% and 40%. Pulte Homes climbed 38%, DH Horton rose 20% and Toll Brothers ran up 25%. I had mixed emotions about this surge. On the one hand, I was happy because it helped the Fund’s first quarter return; on the other, I was a little disappointed that I didn’t have a chance to build a bigger position in these issues.

I also had mixed emotions when the homebuilding companies lost all that gain in the second quarter. I was disappointed because it hurt our second quarter return, but I was happy that it gave me another chance to build a bigger position. I believe our homebuilder stocks will do well over the next two years. We’ve invested in companies with strong balance sheets that will be able to weather the current economic storm. They should also be able to increase market share over the next 18 months, as smaller homebuilders go out of business.

For the quarter, Pulte Homes sliced 32¢ off the NAV, as its stock fell 33.8% from $14.55 to $9.63, and DH Horton dropped 31.1% from $15.75 to $10.85, for a loss of 26¢ on the NAV.

Refiner Valero Energy cost the Fund 30¢ per share, as its stock declined 16.2% from $49.11 to $41.18. One would think that with record-high oil prices, an energy company would be hitting all-time highs. The difficulty is that Valero produces no oil – it only refines it into gasoline. Oil is a cost for Valero, so the higher price means more expensive raw materials. What really determines profits for Valero is the difference between the price of oil and the price of gasoline or the so-called “crack spread.” In June of 2007, the “crack spread” was around $27.88 per barrel, while in June of 2008, the margin was only about $9.24 per barrel. We’re hanging onto Valero, because we think the stock price will come back when margins return. Since no new refineries are being constructed in the United States, margins will definitely return at some point. We also like the company because it’s a great place to work, appearing regularly on the Fortune list of best places to work.

First Horizon, the holding company for First Tennessee Bank, sank an incredible 47.0% during the quarter, going from $14.01 to $7.43 per share for a loss of 26¢ on the NAV. The company had real estate loans that soured, and it also financed small and medium-sized homebuilders who are having difficulties. The stock is now trading at a fraction of its book value, even after taking huge reserves for bad loans. I think there’s still a lot of value in the banking franchise, so I’ll continue to hold the stock.

Ciena Corporation cost the NAV 26¢, as its stock dropped 24.9% from $30.83 to $23.17. The company makes optical network products for telecommunications, and investors perceive that the demand for these products is declining. I think demand will pick up late this year or early in 2009.

Freddie Mac, the big federally-sponsored, but privately-owned purchaser of home mortgages, dropped 35.2% from $25.32 to $16.40, because of concerns about mortgage foreclosures. There is also concern about dilution, since the company plans to increase its capital base by selling more stock.

Fortunately, we had four companies in the portfolio that each added 23¢ or more to the NAV, virtually balancing out the losses. The big winner for the quarter was W&T Offshore, which contributed an amazing 61¢ to each fund share, as its stock soared 71.5% from $34.11 to $58.51. Part of the reason for the dramatic increase, of course, was the big jump in oil prices, which helped all companies that own and operate oil wells. However, W&T has been especially successful in exploration, having found oil in 12 of 14 wells drilled since the first of the year. The company also has been environmentally responsible in its oil operations. None of its wells in the Gulf of Mexico leaked while Hurricane Katrina raged offshore. W&T also has a very good safety record.

The Parnassus Funds 3

Table of Contents

Some socially responsible investors have asked us what we think about investing in oil companies. We reply that it depends on the company. We probably wouldn’t invest in most of them, but we’re proud of our position in W&T. Of course, I’m in favor of moving away from petroleum products and finding renewable resources such as solar, wind, geothermal and biomass. In the meantime, however, virtually all of us use petroleum products in some form, and we’ll probably continue to do so for the rest of our lifetimes.

Powerwave Technologies, a manufacturer and distributor of products for wireless telephone networks, saw its stock climb 66.7% during the quarter from $2.55 to $4.25 for a gain of 33¢ per fund share. Demand for improved wireless coverage and more data capacity is driving carriers to buy more products from Powerwave. The company also showed progress in reducing costs.

Valeant Pharmaceuticals rose 33.4% during the quarter from $12.83 to $17.11 for a gain of 27¢ on the NAV. The company’s epilepsy drug successfully completed Phase 3 clinical studies and its second-generation hepatitis drug released a favorable side-effect profile. Valeant also announced a $100 million stock buyback program.

Mentor Graphics contributed 24¢ to each Parnassus share, as its stock rose 74.2% from $8.83 at the beginning of the quarter to $15.38 where we sold it. The company makes software for use in designing semi-conductors, and it received a hostile takeover bid of $16 per share from competitor Cadence Design. We decided to sell our stock, even though the merger might go through at $16.00, because Mentor’s management opposed the deal. If the merger were called off, the stock might have dropped down below $10. We decided not to be greedy and accepted $15.38 in the open market.

4 The Parnassus Funds

Table of Contents

Outlook and Strategy

This section represents my thoughts and applies to the four funds that I manage: the Parnassus Fund, the Mid-Cap Fund, the Small-Cap Fund and the Workplace Fund. Portfolio manager Todd Ahlsten will cover the outlook and strategy for the Equity Income Fund and the Fixed-Income Fund in those sections. Although we share the same investment philosophy, we manage different funds and our views may differ.

The most important factor in the current economic weakness has been the collapse of the housing market, which induced the subprime mortgage crisis, which in turn induced the financial crisis in the credit markets. Homebuilders and financial institutions have suffered the most from the crisis. The trouble in the housing and credit markets has affected the entire economy, and the huge jump in oil prices has cast a pall over consumer confidence and dampened economic activity. To me, though, the striking thing is that these factors have not created an economic crisis – at least not yet. The economy is down, but not out. Unemployment jumped from around 4.0% to the current 5.5%, but even that is relatively low. (By comparison, France and Germany have unemployment rates closer to 10%) Manufacturing has held up reasonably well, primarily because exchange rates have pushed down the value of the dollar, making our manufactured goods cheaper in international markets, while making foreign products more expensive in U.S. markets. This has reduced our trade deficit and given a boost to the economy. All in all, the American economy has been pretty resilient, given all the negative factors it has had to deal with.

No one knows if things will get worse or how long the current economic weakness will last. In general, though, recessions and other bouts of economic weakness rarely last longer than 12-16 months. If what’s past is prologue and the economic weakness started early this year, then the current recession or quasi-recession should be over in the first half of 2009. That, however, doesn’t mean that the stock market will continue dropping until then. The stock market is a leading indicator and foretells economic developments that lie ahead. It can lead events by 6-18 months. That means that the stock market will likely hit bottom very soon, if it hasn’t done so already. My view is that the market should be headed upward by late this fall.

My goal is to keep the funds that I manage fully-invested. I’ve been finding a lot of stocks trading at low valuations, so I’m doing a lot of bargain-hunting. I expect these stocks to be trading at much higher prices a year from now.

| Yours truly, |

|

| Jerome L. Dodson |

| Chairman and Chief Executive |

| Parnassus Investments |

The Parnassus Funds 5

Table of Contents

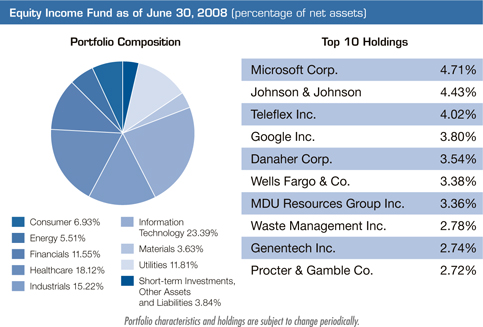

THE PARNASSUS EQUITY INCOME FUND

As of June 30, 2008, the NAV of the Parnassus Equity Income Fund – Investor Shares was $24.19, so after taking dividends into account, the total return for the second quarter was 2.55%. This compares to a loss of 2.73% for the S&P 500 and a decline of 3.86% for the average equity income fund followed by Lipper Inc. We had a great quarter as the Fund had a positive return in an extremely difficult environment. We were able to do this because the Fund owned few bank and large industrial stocks that suffered major price declines. In contrast, the Fund was over-weight in technology, healthcare and energy stocks, which moved higher during the quarter.

For the first half of 2008, the Fund kept losses modest and is doing very well versus the market and its peers. Since the beginning of the year, the Fund has declined only 3.97% compared with a loss of 11.91% for the S&P and a drop of 11.41% for the Lipper average. We are also pleased that our strategy of buying good businesses at undervalued prices has generated solid long-term results. The Fund’s one-, three-, five- and ten-year returns beat both the S&P 500 and Lipper averages for all periods. In fact, our ten-year return of 9.42% is over triple the 2.88% annual gain for the S&P 500.

Below is a table that compares the performance of the Fund with that of the S&P 500 and the average equity income fund followed by Lipper. Average annual total returns are for the one-, three-, five- and ten-year periods.

Second Quarter Recap

I am happy to report that the Fund was up 2.55% during a volatile and negative quarter for the S&P 500. The quarter started with a big rally as the S&P 500 soared 8.15% from March 31 to May 19. Fueled by persistent rate-cutting by the Federal Reserve, many investors bet that the financial, housing and inflationary crises were being well managed, and that an economic recovery was on the horizon. The Fund participated in the rally, outperforming the S&P 500. Our research team, however, was cautious. The Fund’s positioning reflected our concern that the aforementioned crises were being underestimated and would likely overpower the Fed’s monetary policy actions.

Average Annual Total Returns

for periods ended June 30, 2008

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

EQUITY INCOME FUND– | ||||||||||||||||||

Investor Shares | (1.05 | %) | 9.18 | % | 8.60 | % | 9.42 | % | 1.04 | % | 1.00 | % | ||||||

Institutional Shares | (0.81 | %) | NA | NA | NA | 0.83 | % | 0.79 | % | |||||||||

S&P 500 Index | (13.12 | %) | 4.41 | % | 7.58 | % | 2.88 | % | NA | NA | ||||||||

Lipper Equity Income Fund Average | (14.15 | %) | 4.31 | % | 8.10 | % | 4.32 | % | NA | NA |

The total return for the Equity Income Fund-Institutional Shares from commencement (April 28, 2006) was 7.99%. The performance of Institutional Shares differs from that shown for the Investor Shares to the extent that the Classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end can be found on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 is an unmanaged index of common stock, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. On March 31, 1998, the Fund changed its investment objective from a balanced portfolio to an equity income portfolio. Before investing, an investor should carefully consider the investment objectives, risk, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus website, and can also be obtained by calling (800) 999–3505. As described in the Fund’s current prospectus dated May 1, 2008, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.99% and 0.78% of net assets, exclusive of acquired fund fees, until May 1, 2009 for the Investor Shares and Institutional Shares, respectively. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

As we expected, the rally was fleeting and stock prices began a major decline on May 20th. Headlines citing record oil prices, accelerating inflation, falling home prices and weakening employment took turns atop the Wall Street Journal’s front page. Rising inflation was, perhaps, the most damaging to the market’s upward momentum, since it signaled an end to the Federal Reserve’s rate-cutting trend. Furthermore, the dramatic rise in oil prices delivered a blow to consumer spending. By June 30, the S&P 500 had

6 The Parnassus Funds

Table of Contents

plunged 10.1% from its mid-May highs and ended the quarter down 2.73%. In light of this volatility and severe late quarter market decline, I am proud that we were able to generate a gain of 2.55% for the quarter.

It was not easy to make money during the second quarter, but here is how we did it: Our stock-picking in the industrials area was the biggest contributor to our gain for the second quarter, adding 2.18% versus the S&P 500. Amazingly, not owning General Electric (“GE”) stock, which fell over 27% during the quarter, helped the Fund by almost 1% versus the S&P 500. While GE doesn’t meet our social responsibility requirements due to defense contracting, nuclear power and a troubled long-term environmental record, from a business standpoint, we have long been concerned about its financial services exposure. That business, in combination with weak orders, crushed GE’s stock during the first quarter. In contrast, we owned large stakes in smaller industrial companies with good secular growth trends, such as Danaher and Teleflex, which actually rose during the quarter.

The second-largest contributor to performance was our long-standing decision to underweight financial stocks. This position added 1.62% to our lead versus the S&P 500 during the second quarter. Finally, our overweight positions in technology and healthcare boosted our results versus the S&P 500 by 0.84% and 0.47%, respectively. We have identified many companies in both sectors that are positioned to grow their earnings and intrinsic values during 2008 despite the significant economic slowdown.

Looking back on the current cycle, I am pleased to report that the Fund is down only 3.68% versus a 16.42% drop for the S&P 500 since the stock market peaked on October 11, 2007. Our strategy of owning good companies, with time-tested management teams and sustainable business models, at reasonable prices has provided downside protection during this market cycle. I am very proud of our team for their dedication to rigorous research.

Company Analysis

The Fund had only one stock that hurt the NAV by more than 10¢ per share. Wells Fargo, the large financial services firm, fell 18.4% from $29.10 to $23.75 and reduced the NAV by 17¢ per share. For the most part, Wells Fargo maintained responsible lending standards during the housing boom. Unfortunately, its large home equity portfolio and mortgage businesses are not immune to falling home prices and a weakening economy. After the stock had fallen over 25% from its 2008 highs, I started adding to our position in May, thinking the company could weather this downturn and gain major share long-term. It appears I was a bit early, and, as credit losses are expected to increase significantly over the next year, we might have a long turnaround time on this investment. However, I am willing to accept the risk, as I feel there is limited chance of permanent capital loss. Longer-term, I feel the position will boost the Fund’s return. I am encouraged by the fact that the company’s largest shareholder is Warren Buffet. Wells Fargo is the only U.S. bank awarded the highest (AAA) rating by S&P.

I spent an hour with CEO John Stumpf at the Wells Fargo headquarters here in San Francisco during late May and I left the meeting confident the company will survive this credit crisis and thrive following it. He is an excellent CEO — confident but humble, and focused on the long-term franchise. Mr. Stumpf enjoys an admirable combination of financial acumen and the common sense and virtues of being raised in a small, central Minnesota town.

The housing market may not begin recovery until spring of 2010, but a significant portion of the bad news is finally starting to get priced into financial stocks. Stock prices of massive companies such as Citigroup and Wachovia have declined over 70% from their all-time highs, so it is no longer a secret that the U.S. banking system has challenges. At the same time, subprime poster child Countrywide Financial saw its stock fall over 90% before it was bought by Bank of America. Washington Mutual, another significant subprime lender, has witnessed its shares plunge almost 85% from their peak. At some point, the strong banks will bounce back in anticipation of stabilizing home prices and economic recovery while the weak ones will vanish. I feel the “easy” part of being underweight

The Parnassus Funds 7

Table of Contents

financials, due to our expectation of large bank losses, is coming to a conclusion, and that the tricky part, timing the up-cycle, is just beginning. In the meantime, outside of Wells Fargo and J.P. Morgan, we have not bought any other bank stocks and are being prudent and rigorous with our research in the sector.

The Fund had five stocks that added 10¢ to the NAV, and four of them were energy stocks. Our largest contributor to performance was MDU Resources, a Bismarck, North Dakota-based energy company which soared 42.0% during the quarter to $34.86 from $24.55 and added 25¢ to the NAV. The company not only reported big profits from oil and gas production, but also announced that it found significant new reserves in the Bakken Shale of North Dakota. In addition, MDU’s pipeline and natural gas utilities generated strong profits, which more than offset weakness at the company’s construction materials business. MDU has excellent management as the company has increased dividends 13 straight years. This was confirmed after I had a great, two-hour meeting with Terry Hildestat, the CEO of MDU, at their Bismarck offices last October. He is a talented CEO, who demonstrated a combination of calm demeanor with a laser focus on the company’s long-term strategy. They also have a good environmental track record and are investing to build a 20-megawatt wind farm this year. While I was a long way from home, it was truly worth the trip, as after the meeting I was able to enjoy a big meal and a couple of days with my 86-year-old grandmother Ella Ahlsten, a lifetime resident of northern Minnesota.

Our second biggest winner this quarter was Internet search firm Google, which increased 19.5% from $440 to $526, increasing the Fund’s NAV by 16¢. This positive move stands in contrast to the stock’s weakness in the first quarter, when the market overreacted to a report hinting at slower growth for Google. After analyzing this report with my colleague, Ben Allen, I decided to triple the amount of Google shares owned by the Fund by the start of the second quarter. This move paid off when the company reported its results in mid-April, and the stock jumped about 20% in one day. Even after this increase, I still think Google is a good investment, which is why the stock was a top holding for the Fund at quarter-end.

W&T Offshore, a Houston-based oil and gas producer in the Gulf of Mexico, jumped 71.5% from $34.11 to $58.51 and boosted the NAV by 15¢. While the company benefited from high oil and gas prices, W&T is doing a good job finding more reserves in the Gulf. As I wrote last quarter, CEO Tracy Krohn is an outstanding executive who cares about environmentally-responsible drilling and the safety of his employees. I have met Tracy Krohn three times and can say without exception that few executives match his passion for running a business. He is a petroleum engineer running an oil company, not an accountant.

Smith International, another Houston-based company that sells drill bits and completion fluid systems for oil and gas wells, rose 29.4% during the quarter to $83.14 from $64.23 and added 11¢ to the NAV. While high energy prices help Smith’s earnings as firms have more incentive to find more oil and gas, the company sells an extensive line of products that help make drilling wells more environmentally friendly. As a result, Smith is experiencing tremendous demand for its fluid completion systems, which keep areas around wells clean. In February, I visited Smith’s headquarters in Houston

8 The Parnassus Funds

Table of Contents

and, in true Parnassus form, pulled up to the security gate driving a Toyota Prius. After about 90 minutes speaking with CFO Margaret Dorman, I could really see why many investors consider her a top executive in the oil and gas business. She is a great business partner to CEO Douglas Rock, and I am excited about the long-term secular trends for Smith International.

Another winner for the Fund was Apache Corporation, a company that seems to make our leader board on a regular basis. Apache’s stock jumped 15.1% during the period from $120.82 per share to $139.00 and boosted the NAV by 10¢. Clearly, high energy prices are helping Apache’s profits. However, the company continues to do a great job finding oil and gas responsibly in the U.S., Canada, Argentina, Australia, Egypt and the North Sea. I enjoyed the annual Apache dinner with CEO Stephen Farris at the Howard Weil Energy Conference in New Orleans during early April. While energy prices could pull back over the near-term, I remain impressed with Mr. Farris’ plan to grow production for many years to come. In addition, he remains committed to Apache’s Project SpringBoard to help build schools for underprivileged Egyptian girls.

Strategy

We have been increasingly concerned about the fallout of the financial crisis on the broader economy, and have positioned the portfolio with defensive stocks that could provide not only upside participation but also downside protection in a volatile market. While we understand that the equity market is a discounting mechanism, we expect few positive economic developments over the next few quarters that would justify a sustainable recovery. Therefore, at this point, we plan on maintaining our defensive stance for the rest of the year. Since the Federal Reserve first cut interest rates on September 18 of last year, the economy hasn’t shown much improvement. The Case-Shiller home price index has slumped 14%, employment payrolls have declined for six consecutive months, earnings for the S&P 500 have fallen for three straight quarters and are estimated to have dropped about 10% in the second quarter. In addition, soaring oil prices and other commodities have brought American consumer confidence to the lowest level since February 1992 and raised serious concerns about inflation.

The investment themes that we have discussed in previous reports still prevail in this challenging economic environment. We continue to expect the financial and consumer discretionary sectors to underperform relative to the market.

Since last summer, financial institutions have recognized between $200 and $250 billion of losses on subprime mortgage securities. According to reports from the Bank of International Settlements and Goldman Sachs, these announced and discounted losses may be a reasonable estimate of the losses that will eventually occur. Therefore, at an aggregate level, the subprime crisis is probably mostly over as far as investors are concerned. However, banks have only recognized about $50 billion of losses on residential mortgages other than securitized subprime debt (Alt-A, HELOCs, home equity loans, prime mortgages). These losses could spike fivefold to reach $250 billion or more according to Goldman Sachs. In essence, now is time for the “prime” mortgage shoe to drop. There is mounting evidence that loan delinquencies are rising as the economy slows. In its latest report, the American Bankers Association (“ABA”) reported that delinquent home-equity accounts are at the highest level in 11 years and have increased at the fastest pace since the ABA began collecting data in 1987. Increased recognition of these losses is likely to weigh on balance sheets, especially among smaller regional banks with large portfolios of home equity loans. Consequently, we see few compelling investment opportunities in banks at this time.

After more than a decade of relentless consumer spending fueled by easy access to credit and high asset valuations, we see a structural shift in households’ consumption-savings behavior that will dampen discretionary spending over the next few years. While we have explained how banks are in the midst of de-leveraging by raising capital and shrinking their balance sheets, the same process is at play with household balance sheets. The substantial rise in household debt-to-income and the fall in saving rates over the last 10-15 years have left consumer balance sheets extremely stretched.

The Parnassus Funds 9

Table of Contents

Given a significant fall in house prices and reduced access to credit, the only way the gap between income and consumption growth can be filled is through increased savings which means people need to spend less. The need to rebuild savings will also be reinforced as the baby boomers intensify their retirement-planning efforts. Finally, in the short-term, the U.S. consumer is facing rising unemployment, falling home prices, soaring food and energy costs and stagnant wage growth. As a result, these trends will negatively affect the business outlook for firms in consumer-driven sectors.

Given our current expectations, the Fund remains underweight the financial sector and doesn’t own any consumer discretionary stocks. While we have a significant position in energy-utilities, we have reduced exposure as oil soared 38% during the quarter to close at $140 a barrel. Healthcare and technology remain our largest overweight positions, because we expect companies in those sectors to be able to weather a slowing economy better than the ones in the other sectors. Finally, with the market down more than 10% year-to-date, we are starting to see investment opportunities emerge and have slightly increased our industrial exposure. However, we remain disciplined and focused on our research process and are only selectively adding companies that meet our requirements. We prefer companies that can benefit from secular industry trends and become more relevant businesses over the next two to three years. Despite these challenging times, I feel we own a portfolio of good businesses with time-tested executives. We expect to find some great investment opportunities, as this economic slowdown eventually nears an inevitable recovery.

| Yours truly, |

|

| Todd C. Ahlsten |

| Chief Investment Officer |

| Parnassus Investments |

10 The Parnassus Funds

Table of Contents

As of June 30, 2008, the NAV of the Parnassus Mid-Cap Fund was $15.93, so the total return for the quarter was a loss of 2.27%. This compares to a gain of 2.67% for the Russell Midcap Index (the “Russell”) and a return of 0.0% for the average mid-cap value fund followed by Lipper Inc. (“Lipper average”), so we trailed both indices for the quarter. For the year-to-date, the Fund was down 8.40% compared to a loss of 7.57% for the Russell and a loss of 9.36% for the Lipper average, so we underperformed the Russell, but beat the Lipper average.

Below is a table comparing the Parnassus Mid-Cap Fund with the Russell index and the Lipper average for the one- and three-year periods, for the period since September 30, 2005 when we first had most of the Fund’s assets invested in stock and for the period since inception on April 29, 2005.

Average Annual Total Returns

for periods ended June 30, 2008

| One Year | Three Years | Since September 30, 2005 | Since Inception April 29, 2005 | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

MID-CAP FUND | (13.28 | %) | 3.16 | % | 4.30 | % | 3.48 | % | 2.05 | % | 1.41 | % | ||||||

Russell Midcap Index | (11.19 | %) | 6.84 | % | 5.26 | % | 8.96 | % | NA | NA | ||||||||

Lipper Mid-Cap Value Average | (16.89 | %) | 4.46 | % | 3.05 | % | 6.54 | % | NA | NA |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell Midcap Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. Mid-cap companies can be more sensitive to changing economic conditions and have fewer financial resources than large-cap companies. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus website, or you can obtain one by calling (800) 999–3505. As described in the Fund’s current prospectus dated May 1, 2008, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.40% of net assets, exclusive of acquired fund fees, until May 1, 2009. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

Analysis

Four companies in the Mid-Cap Fund’s portfolio hurt us the most, each accounting for a loss of 11¢ or more on the NAV. The one with the largest impact was First Horizon, holding company for First Tennessee Bank, which sank 47.0% during the quarter, dropping from $14.01 to $7.43 for a loss of 30¢ per fund share. The bank financed many of the small- and medium-sized homebuilders that are having trouble now and a lot of its real estate loans have soured. The stock is now trading at a fraction of its book value, even after taking huge write-downs for bad loans. I think there’s still a lot of value in this banking franchise, however, so I’m holding onto the stock.

Two homebuilders also hurt the performance of the Fund in the second quarter. Pulte homes sliced 27¢ off the NAV, as its stock plunged 33.8% from $14.55 to $9.63. DH Horton dropped 31.1% from $15.75 to $10.85, depressing the NAV by 19¢. Home-building stocks ran up quite a bit in the first quarter, then came back down in the second quarter. I’ve used the drop in stock prices to add more of these issues to our portfolio. Please read the discussion on homebuilders in the Parnassus Fund section for more information on my thoughts and our strategy with these stocks.

Oil-refiner Sunoco threw the NAV for a loss of 11¢, with its shares sinking 22.5% from $52.47 to $40.69. As oil prices climbed higher, the company had to pay more for its raw material, but was unable to pass along all the increases in the prices it charges for gasoline. A year ago, refining margins were around $27.88 per barrel, while current refining margins are around $9.24 per barrel.

The Parnassus Funds 11

Table of Contents

Three companies made positive contributions of 11¢ each or more to each fund share. Ultra Petroleum added 12¢, as its stock went from $77.50 to $98.20 for a gain of 26.7%. Earnings were up because of higher energy prices, and the company increased its natural gas production by 31%.

Cognizant Technology also contributed 12¢ to the NAV, with its stock price rising 12.8% from $28.83 to $32.51. This company provides high-quality information technology services at very low prices. Cognizant reported strong earnings and a positive full-year outlook because companies are increasingly focusing on lowering costs.

MDU Resources owns a utility serving Montana and North Dakota, explores for oil and runs a natural gas pipeline. Its stock added 11¢ to each fund share, rising an amazing 42.0% from $24.55 to $34.86. First quarter earnings rose 70% to a record high, as all its businesses posted strong results.

| Yours truly, |

|

| Jerome L. Dodson |

| Chairman and Chief Executive |

| Parnassus Investments |

12 The Parnassus Funds

Table of Contents

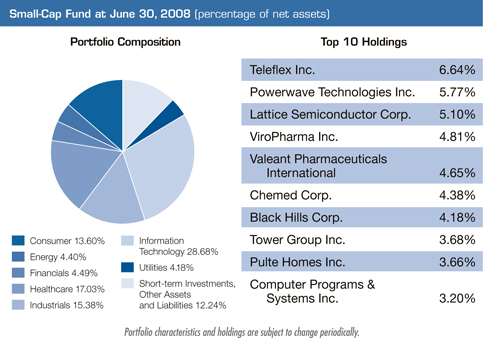

As of June 30, 2008, the NAV of the Parnassus Small-Cap Fund was $17.17, so the total return for the quarter was 11.21%, compared to 0.58% for the Russell 2000 Index (“Russell 2000”) and 0.72% for the average small-cap core fund followed by Lipper Inc. (“Lipper average”). The Small-Cap Fund performed exceptionally well this quarter, beating each of its benchmarks by more than 10 percentage points.

For the year-to-date, the Fund is up 1.54%, compared to a loss of 9.37% for the Russell 2000 and a loss of 9.19% for the Lipper average. We believe this is a remarkable performance in a year when all the major indices had big losses.

Below is a table comparing the performance of the Small-Cap Fund with that of the Russell 2000 and the Lipper average for the one- and three-year periods, for the period since September 30, 2005, when we first had most of the Fund’s assets in stock, and for the period since inception on April 29, 2005. Looking at the table, you’ll see that the Fund is ahead of all its benchmarks for all time periods, in most cases by substantial margins. The one exception is the period since inception on April 29, 2005, where the Fund’s lead over the indices is more modest. The reason for the discrepancy is that the Fund’s assets over the period from inception until September 30, 2005 were mostly in cash, and small stocks moved sharply higher while we were on the sidelines. From inception on April 29 of 2005 until September 30 of 2005, the Fund gained only 2.13% compared to 16.73% for the Russell 2000, which meant that we were over 14 percentage points behind because of our high cash position. Our intentions were good, since we wanted to invest our assets slowly and carefully, but our timing was unfortunate. Since that time, however, we’ve more than closed the gap, and the performance since the third quarter of 2005 has been remarkable.

Average Annual Total Returns

for periods ended June 30, 2008

| One Year | Three Years | Since September 30, 2005 | Since Inception April 29, 2005 | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

SMALL-CAP FUND | (8.61 | %) | 6.75 | % | 7.54 | % | 7.22 | % | 2.08 | % | 1.42 | % | ||||||

Russell 2000 Index | (16.19 | %) | 3.79 | % | 2.42 | % | 6.94 | % | NA | NA | ||||||||

Lipper Small-Cap Core Average | (16.99 | %) | 3.40 | % | 1.71 | % | 6.05 | % | NA | NA |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell 2000 Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. Small-cap companies can be particularly sensitive to changing economic conditions and have fewer financial resources than large-cap companies. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is on the Parnassus website, or you can obtain one by calling (800) 999–3505. As described in the Fund’s current prospectus dated May 1, 2008, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.40% of net assets, exclusive of acquired fund fees, until May 1, 2009. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

I hasten to add that the Small-Cap Fund is not for everyone. It’s much more volatile than, say, the Parnassus Equity Income Fund. The Small-Cap Fund has had its ups and downs, and it went through some difficult times last year. The best use of the Fund is for money that you don’t need any time soon, and for which you can take a longer-term perspective. However, for money you may need in, say, less than two or three years, it may not be the right choice. In any case, I don’t think most shareholders will mind a few bumps in the road, as long as we get to the right destination.

The Parnassus Funds 13

Table of Contents

Analysis

Seven stocks contributed at least 13¢ each to the value of each fund share during the quarter, but even more remarkable was the fact that no stock accounted for a loss of 13¢ or more on the NAV. The big winner for the quarter was Mentor Graphics, which added 44¢ to each fund share, as the stock rose 70.4% from $8.83 at the beginning of the quarter to $15.05 where we sold it during the period. The company makes software for use in designing semiconductors, and it received a hostile takeover bid of $16 per share from competitor Cadence Design. We decided to sell our stock, even though the merger might go through at $16.00, since Mentor’s management opposed the deal. If the merger were to be called off, the stock might drop below $10. We decided not to be greedy and accepted the $15.05 in the open market.

W&T Offshore boosted the NAV by 42¢, as its stock soared 71.5% from $34.11 to $58.51. The company drills for oil and operates wells, so part of the reason for the dramatic increase in the value of its stock was the big jump in oil prices. The other part is that W&T has been especially successful in exploration, having found oil in 12 of 14 wells drilled since the first of the year. The company has been environmentally responsible in its oil operations. None of its wells in the Gulf of Mexico leaked while Hurricane Katrina raged offshore. W&T also has a good safety record.

Powerwave Technologies, a manufacturer and distributor of products for wireless telephone networks, saw its stock climb 66.7% from $2.55 to $4.25 for a gain of 41¢ for each fund share. Demand for improved wireless coverage and more data capacity is driving carriers to buy more products from Powerwave. The company also showed progress in reducing costs.

Valeant Pharmaceuticals climbed 33.4% during the quarter from $12.83 to $17.11 for a gain of 22¢ for each fund share. The company’s epilepsy drug successfully completed Phase III clinical studies, and its second-generation hepatitis drug released a favorable side-effects profile. Valeant also announced a $100 million stock buyback program.

Nordson designs, manufactures and markets equipment that applies adhesives, sealants and coatings to consumer and industrial products as part of the manufacturing process. The stock added 20¢ to the NAV, as it climbed 35.4% from $53.85 to $72.89. Despite economic weakness in the United States, orders were strong for Nordson’s pumps and dispensers, as it gained market share in the industrial sector. Orders from Asia were up 31% in the first quarter.

14 The Parnassus Funds

Table of Contents

ViroPharma shares rose 23.7% from $8.94 to $11.06, while pushing each fund share 17¢ higher. A recent decision by an FDA panel will probably mean that it will be harder for generic companies to copy Vancocin, the company’s main drug. Phase II trials for the company’s new Camvia drug indicated that it was working well for patients that had bone marrow transplants.

LifeCell added 13¢ to the NAV, as its stock went up 12.7% from $42.03 to $47.38, which was the average price where we sold it during the quarter. The stock moved higher on a takeout offer from Kinetic Concepts.

One factor that helped performance is a focus on companies that have unique characteristics. This doesn’t mean they don’t have competition; it does mean they have expertise in a specific area that helps them weather economic storms in bad times and do very well in good times. To give you a better idea of what I mean, let me give examples from the seven companies we’ve discussed in this report.

Mentor Graphics has a software tool called Calibre, used for designing semiconductors of very small sizes. It is the best in its field for ensuring that a computer drawing can be transformed into a chip that can actually be manufactured. W&T Offshore specializes in drilling and exploration only in the Gulf of Mexico, and unlike many big oil companies, W&T has a CEO who is a petroleum engineer with a remarkable record in finding oil.

Powerwave provides almost all the equipment a carrier would need to build out a wireless network. Valeant Pharmaceuticals is on the verge of receiving approval for a new epilepsy drug that can help many patients who receive no benefit from medicines currently available. Nordson has a product line so broad that its equipment can be used to apply virtually all kinds of adhesives, sealants and coatings.

ViroPharma makes Vancocin, the only antibiotic approved to treat significant bacterial infection of the lower digestive tract, and if its new Camvia drug receives approval, it would be the only one that fights the cytomegalovirus in bone marrow transplant patients without having toxic effects on the kidney. LifeCell makes a unique artificial skin used for third-degree burns and in reconstructive surgery.

| Yours truly, |

|

| Jerome L. Dodson |

| Chairman and Chief Executive |

| Parnassus Investments |

The Parnassus Funds 15

Table of Contents

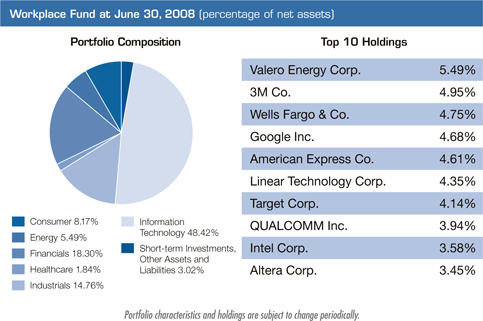

As of June 30, 2008, the NAV of the Parnassus Workplace Fund was $16.43, so the total return for the quarter was a loss of 0.30%. This compares to a loss of 2.73% for the S&P 500 and a loss of 0.81% for the average multi-cap core fund followed by Lipper Inc. (“Lipper average”). Although we lost a small amount of money in the second quarter, we beat both of our benchmarks. For the year-to-date, the Fund lost 6.65%, compared to a loss of 11.91% for the S&P 500 and a loss of 10.62% for the Lipper average, so we were ahead of both indices.

Below is a table comparing the Parnassus Workplace Fund with the S&P 500 and the Lipper Multi-Cap Core average for the one- and three-year periods, for the period since September 30, 2005 when we first had most of the Fund’s assets in stock, and the period since inception on April 29, 2005. You will notice that the Fund is ahead of both its benchmarks for all periods, except the period since inception when its return lagged the Lipper average and was slightly below the S&P 500. The reason for the discrepancy is that from April 29 of 2005 until September 30 of that year, the Fund had most of its assets in cash, and stocks moved higher while we were on the sidelines. The S&P 500 gained over six percentage points on the Fund. Our idea was to invest slowly and carefully, but the timing was unfortunate. Since September 30 of 2005, the Fund has performed substantially better than the benchmarks, essentially closing the gap with the S&P 500.

The premise on which the Workplace Fund was founded was that companies that are good places to work should be better investments than the average company in the S&P 500. At least since September 30 of 2005, that has been the case. It certainly has been with the companies in our portfolio.

Average Annual Total Returns

for periods ended June 30, 2008

| One Year | Three Years | Since September 30, 2005 | Since Inception April 29, 2005 | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

WORKPLACE FUND | (7.56 | %) | 5.26 | % | 5.62 | % | 5.17 | % | 2.65 | % | 1.21 | % | ||||||

S&P 500 Index | (13.12 | %) | 4.41 | % | 3.47 | % | 5.24 | % | NA | NA | ||||||||

Lipper Multi-Cap Core Average | (11.88 | %) | 4.82 | % | 3.60 | % | 6.20 | % | NA | NA |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus website, or you can obtain one by calling (800) 999–3505. As described in the Fund’s current prospectus dated May 1, 2008, Parnassus Investments has contractually agreed to limit total operating expenses to 1.20% of net assets, exclusive of acquired fund fees, until May 1, 2009. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

Analysis

Four stocks accounted for losses of 11¢ or more on the NAV. There were also four that accounted for gains of 11¢ or more per fund share. First Horizon hurt the Fund the most. This holding company for First Tennessee Bank dropped an astounding 47.0%, sinking from $14.01 to $7.43 for a loss of 27¢ on the NAV. The bank made real estate and construction loans all over the country, moving beyond its base in Tennessee. Many of these loans have gone bad. First Horizon has recently written off these bad loans and shrunk the size of its footprint, retreating to its base in Tennessee. I’m hanging onto the stock, since there’s a lot of value in the banking franchise and it’s trading at a fraction of its book value.

16 The Parnassus Funds

Table of Contents

Refiner Valero Energy sliced 24¢ off the NAV, as its stock fell 16.2% from $49.11 to $41.18. The company doesn’t produce oil, but refines it into gasoline, so as oil prices climb, Valero’s costs increase. A year ago, the margin between the price of crude oil and the price of gasoline was $27.88 a barrel, but last month the spread was only $9.24 per barrel and the result was much lower earnings.

Wells Fargo saw its stock price decline 18.4% from $29.10 to $23.75 for a loss of 14¢ per fund share. Although Wells Fargo has weathered the financial crisis better than most banks, investors are concerned and have depressed the price of virtually all banking shares. When the crisis is over, Wells Fargo should make a strong comeback.

American Express saw its stock drop 13.8% during the quarter from $43.72 to $37.67 for a decline of 12¢ per fund share. Financial concerns and fear that cardholders will not pay their bills caused the decline. We think American Express will weather the storm and its share price will bounce back.

Turning to the winners, Nordson was the company that helped us the most, climbing 35.4% from $53.85 to $72.89 while boosting the NAV by 17¢. The company makes industrial equipment for applying adhesives, sealants and coatings, and orders were strong in the first quarter despite the economic weakness; orders in Asia grew 31%. Nordson has an excellent CEO in Ed Campbell, who is able to focus R&D spending to come up with excellent products, while at the same time controlling costs and motivating an effective sales force.

Google contributed 13¢ to each fund share, as its stock rose 19.5% from $440 to $526. Shareholders may remember that the company’s stock dropped over 36% in the first quarter, because data-analysis firm comScore reported that Google had fewer “paid clicks” than expected in January and February. As it turned out, “paid clicks” were fine, search revenue continues to be strong and the stock bounced back.

Daycare-provider Bright Horizons added 11¢ to the NAV, as it climbed from $43.04 to $48.20 for a gain of 12%. The company received and accepted a buyout offer from a private equity firm.

Baldor Electric rose 24.9% from $28.00 to $34.98 for an increase of 11¢ on the NAV. Despite the weak economy, sales increased 19% and earnings 11% in the first quarter. Its energy-efficient Super-E motors continue to sell well.

| Yours truly, |

|

| Jerome L. Dodson |

| Chairman and Chief Executive Parnassus Investments |

The Parnassus Funds 17

Table of Contents

THE PARNASSUS FIXED-INCOME FUND

As of June 30, 2008, the NAV of the Fixed-Income Fund was $16.22, so the total return for the quarter was a loss of 0.34% (including dividends). This compares to a loss of 0.89% for the average A-rated bond fund followed by Lipper Inc. and a loss of 1.02% for the Lehman U.S. Aggregate Bond Index. Since the beginning of the year, our gain of 1.14% is in line with the 1.13% return for the Lehman Index, and is considerably better than the loss of 0.72% registered by our Lipper peer group. We’re very proud to report that our returns are better than the Lipper average for each of the one-, three-, five- and ten-year periods as of the end of the quarter.

Below is a table comparing the performance of the Fund with that of the Lehman U.S. Aggregate Bond Index and the average A-rated bond fund followed by Lipper. Average annual total returns are for the one-, three-, five- and ten-year periods. The 30-day SEC yield for the Fund for June 2008 was 2.49%.

Average Annual Total Returns

for periods ended June 30, 2008

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

FIXED-INCOME FUND | 5.80 | % | 4.98 | % | 3.49 | % | 5.06 | % | 0.88 | % | 0.76 | % | ||||||

Lipper A-rated Bond Fund Average* | 3.06 | % | 2.37 | % | 2.89 | % | 4.65 | % | NA | NA | ||||||||

Lehman U.S. Aggregate Bond Index | 7.12 | % | 4.09 | % | 3.85 | % | 5.68 | % | NA | NA |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns shown in the table do not reflect the deduction of taxes a shareholder would pay in fund distributions or redemption of shares. The Lehman U.S. Aggregate Bond Index is an unmanaged index of bonds, and it is not possible to invest directly in an index. An index doesn’t take expenses, fees or taxes into account, but mutual fund returns do. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should read the prospectus which contains this and other information. The prospectus is available on the Parnassus website, or you can obtain one by calling (800) 999–3505. As described in Fund’s current prospectus dated May 1, 2008, Parnassus Investments has contractually agreed to limit total operating expenses to 0.87% of net assets, exclusive of acquired fund fees, until May 1, 2009. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

Second Quarter Review

The Fund’s strong relative performance in the quarter was due to our decision to position the portfolio for rising interest rates. During the quarter, we held a lot of short-term bonds that were able to maintain their value better than the longer-term bonds held by many of our peers. The yield on the 10-year Treasury note was just 3.41% at the end of the first quarter, and it jumped to 3.97% by the end of June. Considering that the latest annual inflation reading for May was 4.2%, we still think long-term rates are too low. In essence, “real” interest rates are negative right now. As a result, long-term bonds are not great investments given current conditions.

Here is why negative real interest rates make bond values unattractive. Imagine a basket of goods that costs $100 today. If we assume that inflation will run at the current 4.2% rate for the next 10 years, this same basket of goods will cost $151 in 2018. Now, let’s say we decide to buy $100 of 10-year Treasuries at a rate of 4.0%. If we reinvest the coupons at the same 4.0% rate, then our original $100 investment would be worth $148.

18 The Parnassus Funds

Table of Contents

The difference between the $151 future cost of our basket of goods and the $148 that we would end up with by buying Treasuries represents a reduction in our purchasing power of about 2% over this 10-year period. And this is even before taxes are factored in! Our objective is to preserve value and generate stable income. We feel that short-term bonds give us the best combination of short duration and current yield to meet this goal.

In order to avoid a reduction in purchasing power, either one of two things would have to happen. First, inflation could go down, which would make that future basket of goods less expensive. The second option would be for long-term interest rates to go up. We think the second option is more likely, and we’ve based our strategy on this assumption.

Fixed-Income Fund at June 30, 2008 (percentage of net assets) | |||

Portfolio Composition | |||

Long-term: | |||

Consumer | 0.45 | % | |

Long-term U.S. Government and Agency Securities | 24.81 | ||

Financials | 12.37 | % | |

Healthcare | 3.14 | % | |

Information Technology | 5.67 | % | |

Utilities | 1.54 | % | |

Telecommunication Services | 1.03 | % | |

Short-term: | |||

Short-term U.S. Government Agency Securities | 44.25 | % | |

Other Short-term Investments and Assets and Liabilities | 6.74 | % | |

Portfolio characteristics and holdings are subject to change periodically.

Strategy

We think that higher than normal inflation is likely to persist in the short term, especially given the global supply-demand dynamics for food and energy, which are pushing up prices of both of those critical household items. An additional and significant cause of elevated inflation is the weakening of the dollar. A weaker dollar means that imported goods will go up in price. Since we think inflation will remain high, it follows that we expect interest rates to keep climbing.

Because of this expectation, we’ve positioned the portfolio with a lower-than-average duration. At quarter-end, the Fund’s average duration was 2.8 years, significantly below the Lehman index, which currently has a 4.7-year duration. Duration is important because it measures how sensitive a bond’s price is to changes in interest rates.

At the end of the quarter, about 5% of the portfolio was invested in convertible bonds. We think these securities will increase in value over time, as the stocks of the issuing companies rise. Our convertible bond strategy will depend in large part on the stock market, which has recently seen a rather dramatic move downward, as you can read about in other parts of this report. A lower stock market generally makes convertible bonds more attractively priced, so we are actively searching for appropriate convertible bonds to boost the returns to the portfolio.

Thank you for investing in the Parnassus Fixed-Income Fund.

Yours truly, | ||||

|  |  | ||

| Todd C. Ahlsten | Ben Allen | Minh Bui | ||

Portfolio Manager and Chief Investment Officer | Co-Portfolio Manager | Co-Portfolio Manager | ||

The Parnassus Funds 19

Table of Contents

(This section was written by Milton Moskowitz, a consultant to Parnassus Investments who helps with the Parnassus Workplace Fund. Mr. Moskowitz has been a “corporation-watcher” for over 40 years and also co-authors the annual Fortune survey, “The 100 Best Companies To Work For.”)

All the Parnassus funds take social and environmental factors into consideration before investing in companies. We are proud of the steps taken by our portfolio companies in these areas.

Aflac became the first publicly-traded company to give shareholders a say on executive compensation. At the annual meeting on May 5, 2008, 93% of shareholders voted to approve the pay given to top officers. Only 2.5% said “no.” CEO Daniel Amos said that if the majority vote had been negative, the compensation plan would have been revised. His pay in 2007: $11.9 million…Microsoft has been a fixture on Fortune’s 100 Best Workplaces since inception of the survey in 1998 and now it is beginning to repeat that performance in Europe. In employee surveys conducted by the Great Place to Work Institute, the software company made the best workplace lists in 14 countries: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Netherlands, Norway, Portugal, Spain and Sweden. No other company came close to that multi-country ranking… Swiss pharmaceutical giant Novartis has pledged to pay at least a living wage to every employee throughout the world.…3M matches employee contributions to higher education and public broadcasting on a dollar-for-dollar basis. Effective this year, it raised the maximum match from $5,000 to $10,000…Target has its roots in the old Dayton department store of Minneapolis, which was an early promoter of the 5% Club in which member companies agreed to donate 5% of pretax profits to charitable causes. Target continues to adhere to that policy. It gives away $3 million a week to education, the arts and social services…Valero, the nation’s largest oil refiner, invested $600 million in environmental protection in 2007 and plans another $1.9 billion over the next three years. State-of-the-art scrubbers have reduced emissions of sulfur dioxide by more than 95%...Corning, worldwide leader in specialty glass and ceramics, has a support group for everyone. Among the affinity groups sponsored by the company are the following: Black Growth Council, Black Women’s Forum, Corning Chinese Association, Council of Indigenous People, Corning Latino Association, Corning Professionals Network, Corning Professional Women’s Forum, Ethnic Diversity Group of Employees, MTE Asian & Latin American Group, Society of Black Professionals, Southern Tier Indian Cultural Association, SPECTRA (Lesbian, Gay, Bisexual, Transgender Employee Resource Group), Society of Women Engineers, Women’s Leadership Forum, Women’s Quality Improvement Team…Intel invests heavily in education. Its Teach Program has trained five million teachers in more than 40 countries on how to effectively integrate technology into their classrooms. In 2007, it awarded more than $4 million in prizes and scholarships to 1,500 high school students who were finalists in the Intel International Science and Engineering Fair…IBM is piloting a new initiative, enabling employees to contribute up to $1,000 a year to an interest-bearing account. The company matches half of this contribution and the funds are then available to each staff member for educational courses of the employee’s choosing. IBM invests close to $700 million a year in employee education and training. More than 30,000 online courses are available to employees…In 2007, Best Buy increased the number of female general managers in its stores by 40%, female sales managers by 100% and female district managers by 200%.

20 The Parnassus Funds

Table of Contents

As a shareholder of the Funds, you incur ongoing costs, which include portfolio management fees, administrative fees, the production of shareholder reports, and other fund expenses. The Funds do not charge transaction fees, so you do not incur transaction costs such as sales charges (loads) on purchases, reinvested dividends, or other distributions, redemptions, and exchanges. The information on this page is intended to help you understand your ongoing costs of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The following example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the period of January 1, 2008 through June 30, 2008.

Actual Expenses

In the example below, the first line for each fund provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of each fund provides information about hypothetical account values and hypothetical expenses based on the fund’s expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. You may compare the ongoing costs of investing in the Fund with other mutual funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Please note that the expenses shown in the table are meant to highlight only your ongoing costs in these funds. Therefore, the second line of each fund is useful in comparing only ongoing costs and will not help you determine the relative total costs of owning other mutual funds, which may include transactional costs such as loads.

| Beginning Account Value January 1, 2008 | Ending Account Value June 30, 2008 | Expenses Paid During Period* | |||||||

Parnassus Fund: Actual | $ | 1,000.00 | $ | 929.08 | $ | 4.75 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,019.94 | $ | 4.97 | |||

Equity Income Fund – Investor Shares: Actual | $ | 1,000.00 | $ | 960.27 | $ | 4.83 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,019.94 | $ | 4.97 | |||

Equity Income Fund – Institutional Shares: Actual | $ | 1,000.00 | $ | 961.64 | $ | 3.80 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,020.98 | $ | 3.92 | |||

Mid-Cap Fund: Actual | $ | 1,000.00 | $ | 916.04 | $ | 6.67 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,017.90 | $ | 7.02 | |||

Small-Cap Fund: Actual | $ | 1,000.00 | $ | 1,015.38 | $ | 7.02 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,017.90 | $ | 7.02 | |||

Workplace Fund: Actual | $ | 1,000.00 | $ | 933.52 | $ | 5.77 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,018.90 | $ | 6.02 | |||

Fixed-Income Fund: Actual | $ | 1,000.00 | $ | 1,011.43 | $ | 4.35 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,020.54 | $ | 4.37 | |||

| * | Expenses are equal to the fund’s annualized expense ratio of 0.99%, 0.99%, 0.78%, 1.40%, 1.40%, 1.20% and 0.87% for the Parnassus Fund, Equity Income Fund – Investor Shares, Equity Income Fund – Institutional Shares, Mid-Cap Fund, Small-Cap Fund, Workplace Fund and Fixed-Income Fund respectively, multiplied by the average account value over the period, multiplied by the ratio of days in the period. The ratio of days in the period is 182/366 (to reflect the one-half year period). |

The Parnassus Funds 21

Table of Contents

Portfolio of Investments

as of June 30, 2008 (unaudited)

Shares | Equities | Percent of Net Assets | Market Value | |||||

| Communications Equipment | ||||||||

| 150,000 | QUALCOMM Inc. | 2.6 | % | $ | 6,655,500 | |||

| Computer Peripherals | ||||||||

| 100,000 | Seagate Technology | 0.8 | % | $ | 1,913,000 | |||

| Data Storage | ||||||||

| 240,000 | NetApp Inc.1 | 2.1 | % | $ | 5,198,400 | |||

| Electronics | ||||||||

| 100,000 | Vishay Intertechnology1 | 10.4 | % | $ | $887,000 | |||

| Financial Services | ||||||||

| 110,000 | American Express Co. | $ | 4,143,700 | |||||

| 60,000 | Fannie Mae | 1,170,600 | ||||||

| 330,000 | First Horizon National Corp. | 2,451,900 | ||||||

| 230,000 | Freddie Mac | 3,772,000 | ||||||

| 7,000 | Goldman Sachs Group Inc. | 1,224,300 | ||||||

| 120,000 | JPMorgan Chase & Co. | 4,117,200 | ||||||

| 15,000 | Paychex Inc. | 469,200 | ||||||

| 335,000 | SLM Corp.1 | 6,482,250 | ||||||

| 355,000 | Wells Fargo & Co. | 8,431,250 | ||||||

| 12.7 | % | $ | 32,262,400 | |||||

| Food Products | ||||||||

| 70,000 | Sysco Corp. | 0.8 | % | $ | 1,925,700 | |||

| Healthcare Services | ||||||||

| 169,400 | Chemed Corp. 2 | 2.5 | % | $ | 6,201,734 | |||

| Home Builders | ||||||||

| 560,000 | DR Horton Inc. 2 | $ | 6,076,000 | |||||

| 70,000 | KB Home 2 | 1,185,100 | ||||||

| 600,000 | Pulte Homes Inc. 2 | 5,778,000 | ||||||

| 175,000 | Toll Brothers Inc.1, 2 | 3,277,750 | ||||||

| 6.5 | % | $ | 16,316,850 | |||||

| Home Products | ||||||||

| 66,000 | WD-40 Co. 2 | 0.8 | % | $ | 1,930,500 | |||

| Industrial Manufacturing | ||||||||

| 15,000 | 3M Co. | $ | 1,043,850 | |||||

| 10,000 | Cooper Industries Ltd. | 395,000 | ||||||

| 10,000 | Illinois Tool Works Inc. | 475,100 | ||||||

| 210,000 | Teleflex Inc. | 11,673,900 | ||||||

| 5.4 | % | $ | 13,587,850 | |||||

| Insurance | ||||||||

| 295,000 | Tower Group Inc. 2 | 2.5 | % | $ | 6,251,050 | |||

| Internet | ||||||||

| 16,000 | Google Inc.1 | 3.3 | % | $ | 8,422,720 | |||

| Machinery | ||||||||

| 80,000 | Graco Inc. 2 | 1.2 | % | $ | 3,045,600 | |||

| Networking Products | ||||||||

| 325,000 | Cisco Systems Inc.1 | 3.0 | % | $ | 7,559,500 | |||

| Oil & Gas | ||||||||

| 30,000 | Ultra Petroleum Corp.1 | $ | 2,946,000 | |||||

| 230,000 | Valero Energy Corp. | 9,471,400 | ||||||

| 90,000 | W&T Offshore Inc. | 5,265,900 | ||||||

| 7.0 | % | $ | 17,683,300 | |||||

| Pharmaceuticals | ||||||||

| 110,000 | Barr Pharmaceuticals Inc.1 | $ | 4,958,800 | |||||

| 90,000 | Cardinal Health Inc. | 4,642,200 | ||||||

| 150,000 | Forest Laboratories Inc.1 | 5,211,000 | ||||||

| 475,000 | Valeant Pharmaceuticals International 1, 2 | 8,127,250 | ||||||

| 360,000 | ViroPharma Inc.1, 2 | 3,981,600 | ||||||

| 10.6 | % | $ | 26,920,850 | |||||

| Real Estate Investment Trusts | ||||||||

| 80,000 | ProLogis | 1.7 | % | $ | 4,348,000 | |||

| Retail | ||||||||

| 80,000 | Best Buy Co., Inc. 2 | $ | 3,168,000 | |||||

| 240,000 | Lowe’s Cos., Inc. | 4,980,000 | ||||||

| 130,000 | Target Corp. | 6,043,700 | ||||||

| 130,000 | Walgreen Co. | 4,226,300 | ||||||

| 7.3 | % | $ | 18,418,000 | |||||

| Semiconductor Capital Equipment | ||||||||

| 90,000 | Applied Materials Inc. | $ | 1,718,100 | |||||

| 120,000 | Cognex Corp. 2 | 2,766,000 | ||||||

| 100,000 | Cymer Inc.1, 2 | 2,688,000 | ||||||

| 140,000 | Lam Research Corp.1 | 5,061,000 | ||||||

| 4.8 | % | $ | 12,233,100 | |||||

| Semiconductors | ||||||||