Table of Contents

PARNASSUS INCOME FUNDS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06673

Parnassus Income Funds

(Exact name of registrant as specified in charter)

1 Market Street, Suite 1600, San Francisco, California 94105

(Address of principal executive offices) (Zip code)

Marc C. Mahon

Parnassus Income Funds

1 Market Street, Suite 1600, San Francisco, California 94105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (415) 778-0200

Date of fiscal year end: December 31

Date of reporting period: June 30, 2009

Table of Contents

Item 1: Report to Shareholders

THE PARNASSUS FUNDSSM

Semiannual Report June 30, 2009

Parnassus Fund

Parnassus Equity Income Fund

Parnassus Mid-Cap Fund

Parnassus Small-Cap Fund

Parnassus Workplace Fund

Parnassus Fixed-Income Fund

Table of Contents

Parnassus Fund | (PARNX | ) | |

Parnassus Equity Income Fund–Investor Shares | (PRBLX | ) | |

Parnassus Equity Income Fund–Institutional Shares | (PRILX | ) | |

Parnassus Mid-Cap Fund | (PARMX | ) | |

Parnassus Small-Cap Fund | (PARSX | ) | |

Parnassus Workplace Fund | (PARWX | ) | |

Parnassus Fixed-Income Fund | (PRFIX | ) |

| 1 | ||

Fund Performance | ||

| 3 | ||

| 7 | ||

| 11 | ||

| 14 | ||

| 16 | ||

| 18 | ||

| 20 | ||

| 22 | ||

Portfolios of Investments | ||

| 23 | ||

| 25 | ||

| 28 | ||

| 30 | ||

| 32 | ||

| 33 | ||

| 36 | ||

| 43 | ||

| 48 | ||

| 52 |

Table of Contents

August 7, 2009

DEAR SHAREHOLDER:

Enclosed you will find the semiannual reports for all six Parnassus Funds. We had another good quarter, and I’m happy to report that four of our five equity funds beat both their primary stock market indices and their respective Lipper categories for both the quarter and the year-to-date. For the one-year and three-year periods, all five equity funds outperformed all their benchmarks.

The best-performing fund for the quarter was the Parnassus Workplace Fund, which gained 26.65% compared to 15.93% for the S&P 500 Index and 17.77% for the average multi-cap core fund followed by Lipper Inc. For the year-to-date, the Workplace Fund is up 26.02% compared to 3.16% for the S&P 500 and 7.32% for the Lipper Multi-Cap Core Average. The Workplace Fund is also ahead of all its benchmarks for the one- and three-year periods and for the period since inception. It seems to show that companies with good workplaces can have excellent investment returns.

On November 19 of this year, we will be celebrating the 25th anniversary of Parnassus Investments. The celebration will be held at the Palace Hotel in San Francisco from 5:00 pm to 9:00 pm and all of you are invited to attend. Shareholders holding accounts directly with the Parnassus Funds will receive a formal invitation at a later date, but be sure to mark your calendars now.

As I was thinking about our 25 years of history, I received a letter from one of our original shareholders, Ruth Gottstein, founder of Volcano Press, a small, high-quality publisher. Now located in Volcano, California in the foothills of our state, Ruth used to work out of her house in the Haight-Ashbury district of San Francisco. When Parnassus Investments was founded, I also used to work out of my house in the Haight-Ashbury district right near Parnassus Avenue. At the time we were founded, we started with only $330,000 in assets distributed among 30 original shareholders. I was so happy to get Ruth as an original shareholder, that I personally walked down the street to pick up her check. Since that time, we’ve become friends and she has remained a loyal shareholder through ups and downs.

Ruth and I share a passion for San Francisco history, so she recently sent me a beautifully illustrated book published by Volcano Press about the famous San Francisco landmark, Coit Tower. Masha Zakheim, Ruth’s sister, is the author of the book, and it features the murals of Coit Tower painted by Bernard Zakheim, the father of Ruth and Masha. (If you’re interested in purchasing the book, go to Volcanopress.com.)

Ruth’s letter got me thinking about how much we’ve grown over the years. We now have almost $2.2 billion in assets under management and we have more than 100,000 shareholders. I’m really fortunate to have had this great history with Parnassus.

Four New Interns

We have four excellent interns working with us this summer. Katherine Loarie is a recent graduate of the Tuck School of Business at Dartmouth where she earned her MBA. She is also a graduate of the University of California at Berkeley, where she majored in economics and mass communication and played on the varsity women’s water polo team. Her previous experience includes three years with Morgan Stanley working in private wealth management.

Ian Sexsmith is an MBA candidate at the Haas School of Business at the University of California at Berkeley, where he is a Haas Merit Scholar. He also graduated from the University of Manitoba in Winnipeg, Canada and played for the Elmwood Giants in the Manitoba Junior Baseball League. For four years, Ian worked at Scotia Capital in Toronto, where he was an analyst in the investment banking division and also worked in institutional equity trading.

| The Parnassus Funds | 1 |

Table of Contents

Samantha Seto graduated cum laude from Choate Rosemary Hall School in Connecticut and is now a junior at Columbia College where she is majoring in economics and East Asia Studies. She also studied one summer at Fudan University in Shanghai and has worked at ChinaVest, a venture capital firm in Shanghai. Samantha is also the founder of Caring Soles, a non-profit that collects shoes from local clubs, gyms and schools and donates them to San Francisco homeless centers.

Also joining us this summer for his second time as an intern is Ryan Wilsey, who first interned with us in the summer of 1998 when he was an undergraduate at Princeton. He graduated from Harvard Business School in 2006 and most recently worked as an analyst for Scout Capital, a hedge fund in New York. Ryan has decided to return home to the San Francisco Bay Area and will intern with us while he looks for a permanent investment management role.

Below you will find a picture of attendees at the Parnassus Intern Reunion Dinner on June 13, 2009.

Seated in the front row (left to right): Samantha Seto, Andrea Reichert, Christine Song, Jeanine Cotter, Jerome Dodson, Vivian Wang, Lori Keith, Pearle Lee and Elina Sheykh-Zade. Standing in the back row (left to right): Daniel Conrad, Russell Caprio, Peter Tsai, Ian Sexsmith, Brendan Simon, Todd Ahlsten, Ben Allen, Minh Bui, Matt Gershuny, Ryan Wilsey, Michael Fernandez, Yanik Jayaram, Andrew Livingston and Marie Lee.

Yours truly,

Jerome L. Dodson

President

Parnassus Investments

| 2 | The Parnassus Funds |

Table of Contents

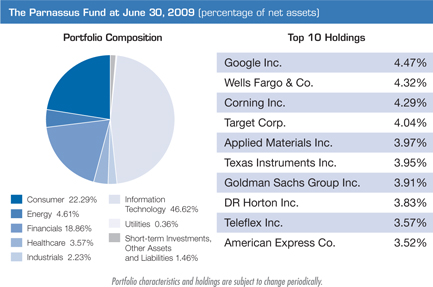

As of June 30, 2009, the net asset value per share (“NAV”) of the Parnassus Fund was $27.65, so the total return for the quarter was 18.67%. This compares to 15.93% for the S&P 500 Index (“S&P 500”), 17.77% for the average multi-cap core fund followed by Lipper Inc. (“Lipper average”) and 20.34% for the Nasdaq Composite Index (“Nasdaq”). For the quarter, then, we beat the S&P 500 and the Lipper average, but we lagged slightly behind the Nasdaq.

For the year-to-date as of June 30, we are ahead of all our benchmarks with a gain of 17.21%, compared to 3.16% for the S&P 500, 7.32% for the Lipper average and 16.98% for the Nasdaq. Below is a table comparing the Parnassus Fund with the S&P 500, the Lipper Multi-Cap Core Average and the Nasdaq over the past one-, three-, five- and ten-year periods. You’ll notice that we’re ahead of all the benchmarks for all time periods. We’re very proud of this record. Of special note is the ten-year period, where we actually show a positive return of 1.61% per year compared to negative returns for the S&P 500 and the Nasdaq. You’ll notice that if you have been a shareholder of the Parnassus Fund for the past ten years, you have earned almost 4% more per year than the S&P 500 returned during that time period.

Average Annual Total Returns

for periods ended June 30, 2009

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

THE PARNASSUS FUND | -16.89 | % | -2.62 | % | -0.14 | % | 1.61 | % | 1.02 | % | 0.99 | % | ||||||

S&P 500 Index | -26.21 | % | -8.22 | % | -2.24 | % | -2.22 | % | NA | NA | ||||||||

Lipper Multi-Cap Core Average | -26.35 | % | -8.33 | % | -1.74 | % | 0.17 | % | NA | NA | ||||||||

Nasdaq Composite Index | -19.13 | % | -4.64 | % | -1.37 | % | -3.17 | % | NA | NA |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 Index and the Nasdaq Composite Index are unmanaged indices of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Prior to May 1, 2004, the Parnassus Fund charged a sales load (maximum of 3.5%), which is not reflected in the total return calculations. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2009, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.99% of net assets, exclusive of acquired fund fees, until May 1, 2010. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

Company Analysis

Only two companies in the portfolio had a substantial negative impact on the Fund during the quarter. The one that hurt us the most was homebuilder Pulte Homes; it cut 19¢ off the NAV, as its shares sank 19.2%, going from $10.93 to $8.83 by the end of June. In the March quarter, the homebuilders helped us quite a bit, but difficult conditions in the housing industry pulled their shares back down in the June quarter. Declining orders and write-offs on land depressed earnings for all the homebuilders, pushing their stock prices lower. For the most part, these declines in share prices did not affect the Fund too much, but Pulte was a special case. Pulte is buying rival Centex, and investors usually don’t like mergers, because they normally have a negative financial impact on the companies in question. Most of the time, I’m in the camp that dislikes mergers, so I would normally sell the stock of a company making a big acquisition. In the case of Pulte, though, the stock price is down so low that I regard it as a very good value.

Refiner Valero Energy cost the Fund 10¢ for each fund share, as its stock declined from $17.90 to $16.89 for a loss of 5.6%. The company temporarily shut down several of its refineries during the quarter due to depressed demand for gasoline. Earnings were hurt because of lower margins or reduced “crack spread” (the difference between the price of oil and the price of gasoline). We expect refining margins to recover as the economy picks up, so we’re hanging on to the stock, since we think it’s very undervalued.

| The Parnassus Funds | 3 |

Table of Contents

Seven companies each contributed 21¢ or more to the NAV during the quarter. The star was Wells Fargo, which added 46¢ to each Parnassus share, as its stock soared an amazing 70.4% from $14.24 to $24.26. The stock moved higher because the company reported better than expected earnings, with higher mortgage banking and trading revenues offsetting credit losses.

American Express contributed almost as much to the NAV as Wells Fargo, adding 42¢ to each fund share, as its stock rocketed up 70.5% from $13.63 to $23.24. The stock had been trading at very depressed levels because of investor concerns about the possibility of big losses in the company’s credit card portfolio. As it turned out, earnings came in better than expected because of good expense control and lower funding costs due to low interest rates. The balance sheet of American Express also looks in reasonably good shape, as the company obtained permission in June to repay the U.S. Treasury the $3.4 billion in TARP money it had received; the company paid it all back before the end of the quarter.

Goldman Sachs added 34¢ to each Parnassus share, climbing from $106 to $147 for a gain of 39.1%. The company reported earnings well in excess of expectations, with the big money-makers being commodities, currency and fixed-income trading. Goldman enjoyed higher trading margins because of less competition as weaker players were forced out of the market. It also demonstrated its financial strength during the quarter by paying back the $10 billion in TARP funds it received from the U.S. Treasury.

Semiconductor-maker Texas Instruments moved the NAV higher by 26¢, as its stock rose 29.0% from $16.51 to $21.30. The company reported higher orders, increased revenue and better earnings, driven by demand from China’s 3G build-out and improving conditions in the handset, notebook and LCD TV end-markets.

Seagate Technology makes hard disk-drives used for electronic storage and its stock rose 74.0% during the quarter from $6.01 to $10.46 for a gain of 25¢ on the NAV. Late in the quarter, the company said demand was increasing and it was able to get better pricing for its products. It also raised guidance for revenue in the next quarter from an average of $2.05 billion to an average of $2.25 billion. Analysts from ten brokerage firms raised their forecasts for Seagate.

Google also added 22¢ to the NAV, as its stock climbed 21.1% from $348 to $422. The company’s earnings were better than expected because of strong financial controls and lower discretionary spending. Revenue declined from the previous quarter due to general softness in the economy, but was still up 10% year-over-year, as Google continues to dominate the online search market.

After seeing its stock lose 57.8% in the first quarter because of investment losses and slowing sales, insurer AFLAC rebounded in the second quarter, contributing 21¢ to each fund share, as its stock soared 84.5% from $19.36 to $35.72 where we sold it during the quarter. Financial results gave investors a positive surprise, as sales in Japan and the US held up better than expected and investment losses were not as bad as feared. Standard & Poor’s removed AFLAC from its credit watch list, indicating that no downgrade was imminent. The Parnassus Fund sold this stock, because we thought it became fully-valued after the run-up, and we had better uses for the money.

| 4 | The Parnassus Funds |

Table of Contents

Outlook And Strategy

This section represents my thoughts and applies to the three funds that I manage: the Parnassus Fund, the Small-Cap Fund and the Workplace Fund. The other portfolio managers will discuss their thoughts in their respective sections.

The market made a strong comeback in the second quarter with technology and small-cap companies leading the way. The Dow Jones Industrial Average was up 11.96% for the quarter and the S&P 500 was up 15.93%, so these big-company indices had substantial gains, but they were overshadowed by the technology-heavy Nasdaq which was up 20.34% and the Russell 2000 Index of smaller companies that was up 20.69%. Coming out of a recession, small-cap stocks tend to do better than large-cap stocks, and this past quarter has followed that pattern. There’s no mystery as to why this happens. When the stock market falls before and during a recession, small-cap and technology names fall more than large-cap names, because the former are riskier than the latter. Just before the economy comes out of a recession, small-cap and technology stocks make substantial moves upward, outshining their large-cap brethren. Since the small-cap and technology names fell further, they moved higher and sooner than the big companies in their effort to return to non-recession levels.

I think the market action of the second quarter signaled an end to the recession fairly soon— probably by the end of the year. Given this situation, stocks should continue to move higher. There will, however, continue to be periods of volatility with strong moves higher followed by major moves downward. Despite these stomach-churning dips, the market should be substantially higher by the end of the year. I plan to keep all three funds fully-invested to take advantage of this move upward.

When markets go down, they can go down very quickly, but the corollary is that when they go up, they can go up very quickly. For example, from the market bottom on March 9 until June 30, the Parnassus Fund gained 45.5%. During the same time period of less than four months, the Small-Cap Fund gained an astounding 55.2%, while the Workplace Fund gained an even more astounding 57.0%. Because of the possibility of these sharp upward moves, it’s prudent to keep all three funds fully invested.

Although the Parnassus Fund, the Small-Cap Fund and the Workplace Fund are all up substantially since the market hit bottom on March 9, all three are still substantially below the levels they reached when the market peaked on October 9 of 2007. Since that time, the Parnassus Fund is down 30.72%, the Small-Cap Fund is down 24.72% and the Workplace Fund is down 17.64%, so we still have a lot of work to do. However, all three funds have dropped far less than the S&P 500 which is down 38.6% from its high point.

The Small-Cap Fund did well for the quarter, gaining 23.21% compared to 20.69% for the Russell 2000, so the Fund beat the index by 2.52%. For the year-to-date, however, the Fund is almost 13 percentage points ahead of the Russell 2000—a much more substantial margin. The reason for this is that the Small-Cap Fund dropped only 6.18% for the first quarter compared to 14.95% for the Russell 2000. In choosing companies for the Small-Cap portfolio, I try to choose firms that have relatively unique characteristics, and this normally helps to keep their stocks from falling as much as the Russell 2000.

For the Parnassus Fund, I plan to put more emphasis on technology and some smaller-cap names, although that fund will continue to hold a lot of large-cap and mid-cap stocks as well. The Parnassus Fund earned 18.67% for the quarter compared to 15.93% for the S&P 500 so it finished 2.74% ahead. However, for the year-to-date, the Parnassus Fund is up 17.21% compared to only 3.16% for the S&P. Here again, the reason for the big lead for the year-to-date is because the Parnassus Fund did not go down much in the first quarter—only 1.23% compared to 11.01% for the S&P 500.

| The Parnassus Funds | 5 |

Table of Contents

Not all large-cap companies lose out to small-cap names when the economy is coming out of a recession. The Workplace Fund has mostly large-cap names in its portfolio, but it was up 26.65% for the quarter, substantially outperforming the S&P 500’s gain of 15.93%. For the year-to-date, the Workplace Fund is up 26.02% compared to a gain of 3.16% for the S&P 500. This performance is truly amazing, so I’m sure there’s some amount of luck involved, but I think it also shows that companies that treat their employees well can have excellent stock-market performance.

Yours truly,

Jerome L. Dodson

President

Parnassus Investments

| 6 | The Parnassus Funds |

Table of Contents

THE PARNASSUS EQUITY INCOME FUND

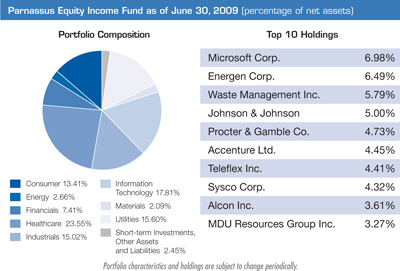

As of June 30, 2009, the net asset value per share (“NAV”) of the Equity Income Fund – Investor Shares was $20.04, so after taking dividends into account, the total return for the second quarter was 17.67%. This compares to a gain of 15.93% for the S&P 500 and a return of 15.50% for the average equity income fund followed by Lipper Inc. The Fund had a good quarter as it outperformed the S&P 500 during a strong market rally. We were able to beat the market due to strong gains in energy, healthcare and technology stocks.

For the first half of 2009, the Fund is also doing well versus the market and its peers. Since the beginning of the year, the Fund is up 4.79% versus a gain of 3.16% for the S&P 500 and a return of 1.23% for the Lipper Equity Income Fund Average. Most importantly, we are proud that the Fund’s strategy of buying good businesses at undervalued prices has generated solid long-term results. The Fund’s one-, three-, five- and ten-year returns beat both the S&P 500 and the Lipper Average for all periods. In fact, our 10-year average annual return of 5.48% far exceeds the 2% average annual loss for the S&P 500.

Below is a table that compares the performance of the Fund with that of the S&P 500 and the average equity income fund followed by Lipper. Average annual total returns are for the one-, three-, five- and ten-year periods.

Average Annual Total Returns

for periods ended June 30, 2009

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

PARNASSUS EQUITY INCOME FUND– | ||||||||||||||||||

Investor Shares | -15.92 | % | 0.46 | % | 2.88 | % | 5.48 | % | 1.02 | % | 1.01 | % | ||||||

Institutional Shares | -15.73 | % | 0.68 | % | 3.04 | % | 5.55 | % | 0.81 | % | 0.80 | % | ||||||

S&P 500 Index | -26.21 | % | -8.22 | % | -2.24 | % | -2.22 | % | NA | NA | ||||||||

Lipper Equity Income | ||||||||||||||||||

Fund Average | -24.52 | % | -7.84 | % | -0.92 | % | 0.38 | % | NA | NA |

The performance of Institutional Shares differs from that shown for the Investor Shares to the extent that the Classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500, is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. On March 31, 1998, the Fund changed its investment objective from a balanced portfolio to an equity income portfolio. Before investing, an investor should carefully consider the investment objectives, risk, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is on the Parnassus website, or you can obtain one by calling (800) 999-3505. As described in the Fund’s current prospectus dated, May 1, 2009, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.99% and 0.78% of net assets, exclusive of acquired fund fees, through May 31, 2010 for the Investor Shares and Institutional Shares, respectively. These limitations may be continued indefinitely by the Adviser on a year-to-year basis. Parnassus Equity Income Fund – Institutional Shares incepted on April 28, 2006. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Equity Income Fund – Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares.

Second Quarter Review

The stock market had a huge rally during the second quarter, as the prospect of an economic recovery fueled a wave of investor optimism. I was especially pleased that the Fund beat the S&P 500 in spite of being underweighted relative to the index in finance stocks, which surged 37% during the quarter.

The big driver of our outperformance was the energy-utilities sector, which added 3.6% to our gain compared to the S&P 500. We spent much of early 2009 buying stock in energy companies with low-cost operations and long-lived reserves. Our energy investments did well in the quarter for short-and long-term factors. Near-term, the earnings picture looks better as oil prices jumped more than 40% during the quarter in anticipation of economic recovery. This will help many of our energy companies post strong earnings for the second half of 2009. The long-term factor affecting energy stocks is the expectation of increased inflation. Quite simply, it’s much easier to print U.S. dollars than it is to find oil. As our government keeps interest rates artificially low and runs record deficits, it increases the chances that we will experience higher inflation.

| The Parnassus Funds | 7 |

Table of Contents

Strong stock-picking in the healthcare sector added almost 1% to our lead versus the S&P 500. Despite the uncertainty caused by looming healthcare reform in Washington, all six of our healthcare investments added to the Fund’s NAV during the quarter. Finally, our technology stocks, led by a resurgent Microsoft, added nearly half a percent to our return versus the S&P 500.

While it was nice to generate strong gains during the second quarter, we still have quite a ways to go before our NAV returns to past levels. The Fund is down “only” 19.4% from its all-time high, versus an incredible decline of 38.6% for the S&P 500 from its peak. Our team continues to work hard to identify good businesses that meet our strict investment criteria. Companies in the portfolio must have wide competitive moats in growth industries and be run by good people.

Company Analysis

Given the strong stock market, the Fund didn’t have any investments that significantly hurt our NAV during the second quarter. In contrast, we were fortunate to have many winners, with six companies adding 13¢ or more to the NAV. Our biggest gainer was Energen Corporation, a Birmingham, Alabama-based energy company that runs a utility and produces natural gas and oil. The stock jumped an amazing 37.0% during the quarter from $29.13 to $39.90, adding 38¢ to the Fund’s NAV.

We like Energen because it owns long-lived, low-cost energy reserves. The management team, led by CEO James McManus, is also top notch. During late February, I met with him at Energen’s headquarters in Alabama and was impressed by his ability to grow the company in a relatively low-risk way. For instance, during the oil bubble of 2008, McManus pre-sold a major portion of the company’s 2009 and 2010 production at high prices to lock in revenues. This move protected short-term earnings and provided cash flow to pay down the company’s debt.

Longer-term, Energen has over 18 years worth of proven reserves at current production rates, and vast unproven opportunities. This means that the company has major long-term earnings potential. While other investors focused on temporary factors such as depressed oil and gas prices, we significantly increased our position in the first half of 2009. We have owned this stock since 1996 and are now the company’s second largest shareholder.

The Fund’s second largest winner was Microsoft, which jumped 29.4% during the quarter from $18.37 per share to $23.77 and boosted our NAV by 35¢. Despite the recession, the company’s prospects brightened during the second quarter. Anticipation of Microsoft’s Windows 7 launch, scheduled for this fall, was a major catalyst that boosted investor optimism. In addition, the outlook for computer sales seemed to improve, which pushed the stock higher. I owe thanks to Parnassus Mid-Cap Fund Portfolio Manager and Senior Research Analyst, Lori Keith, who has done an outstanding job researching Microsoft. Her conviction and investment insight contributed to making Microsoft the largest holding of the Fund.

AFLAC, the insurance company represented by the famous duck, was a big winner during the second quarter. The stock jumped 60.6% from $19.36 to $31.09 and added 18¢ to the NAV. While it was a nice pop, the move was from a very depressed level. The stock had plunged during the first quarter of 2009 due to concerns about the company’s investment portfolio. While we acknowledge the risks to some of their assets, we feel that the expected losses could be absorbed by the company’s otherwise healthy balance sheet. In addition, we continue to like the AFLAC insurance business long-term. As a result, we added significantly to our position during early 2009.

| 8 | The Parnassus Funds |

Table of Contents

By May, the stock began bouncing back, as fears about the company’s investment portfolio started to subside. Around this time, Parnassus Fixed-Income Fund Portfolio Manager Minh Bui and I attended AFLAC’s analyst day in New York. During a dinner meeting, CEO Daniel Amos spoke about AFLAC’s great track record, strong capital position and commitment to social responsibility. In a humorous moment of candor, he admitted that during the volatile early months of 2009, he slept “just like a baby—I would get up and cry every hour.” We remain bullish on the long-term prospects of AFLAC, and trust that Mr. Amos is getting better sleep these days.

Alcon, the Swiss-based pharmaceutical company focused on eye care, had a strong quarter. The stock jumped 27.7% from $90.91 to $116.12 and boosted the NAV by 18¢. Alcon’s eye care products have been relatively recession-resistant, allowing the company to report strong first quarter results. In a rare act these days, the company even boosted its dividend by an impressive 50% during the quarter. Our healthcare analyst, Pearle Lee, has done a superb job researching this investment.

Accenture, the global consulting, technology services and outsourcing firm, added 15¢ to the Fund’s NAV as the stock climbed 21.7% to $33.46 from $27.49. Despite softening demand for consulting services due to the global recession, Accenture has defended its bottom line by aggressively cutting costs. The company also booked a healthy $6.4 billion worth of business during the quarter, as clients looked to save money by outsourcing non-core business functions. In addition, the company generated almost a billion dollars of free cash flow during the quarter. This boosted Accenture’s already large cash position and underscored its ability to increase stock buybacks and dividends over time. Matt Gershuny, one of our Parnassus Mid-Cap Fund portfolio managers, made a significant contribution by convincing me to make Accenture a top five holding during April.

Our final winner was W&T Offshore, a Houston, Texas-based producer of oil and natural gas. Like Energen, the stock fell during early 2009 only to bounce back strong as oil prices recovered. In the past quarter, the stock soared 58.4% from $6.15 per share to $9.74 and added 12¢ to the NAV. During a February meeting in Houston with CEO Tracy Krohn, Parnassus Director of Research Ben Allen and I were impressed with the company’s long-term opportunities. In essence, the recession is hurting weaker drillers in the Gulf of Mexico, and Mr. Krohn has the capital to scoop up assets at attractive prices. He is a true entrepreneur, and we are excited to watch him take advantage of uncertainty and grow the company.

Outlook And Strategy

We draw great comfort that our investment process has yielded consistency and strong, long-term results. The cornerstone of this process is to own businesses that have long-term competitive advantages in secular growth markets. Furthermore, we want to invest with managers who are ethical and treat shareholders as true partners. That is why I write so much in these reports about meeting executives directly. This is a critical factor in an era when too many executives put their interests before those of their shareholders.

Despite the S&P 500’s 37% rally since March 9th, there remains a lot of uncertainty for the economy and stock market, and we think the key factor to monitor is jobs. Unemployment is a significant concern because jobs produce wages, wages fuel consumption, and consumer spending represents almost 70% of our entire economy. The U.S. lost 467,000 jobs in June, according to the Department of Labor, which brings the total job losses since the start of 2008 to 6.5 million—a truly staggering sum. While many argue that the economy typically improves before the job market grows, we think it could be different this time. In fact, we try to stay a few steps ahead of other investors precisely by analyzing how things could be different this time.

One key difference is that both the government and the consumers have massive debts that need to be paid down. At all levels of our society, starting with households, extending to cities, counties, states and the Federal government, we are consuming more than we produce. In most previous recessions, we had the option of increasing total debt to solve economic slumps, even before the job market improved. It may not be that easy this time. As a result, while we think the economy could stabilize this year, we don’t anticipate a “V-shaped” recovery.

| The Parnassus Funds | 9 |

Table of Contents

Another source of uncertainty is the potential for major government reform in the healthcare and energy sectors. Almost every day, I read about the predicted costs and promised benefits of these reforms. While I trust our lawmakers’ good intentions, I worry that their plans could be more expensive than they think, and that the range of possible outcomes is less certain than they admit.

One of my favorite authors, Nassim Taleb, argues in his book The Black Swan that “the policies we need to make decisions on should depend far more on the range of possible outcomes than on the expected number.” As an investor, I take this approach to heart, and I hope that our representatives in Washington do too. In short, while I hope that any new government reforms yield positive results for our economy, so far the biggest effect has been a widening of the range of outcomes and an increase in uncertainty. We expect that uncertainly will benefit us because of our disciplined investment approach. When uncertainty causes stock price volatility, we’ll use temporary drops in stock prices to buy larger stakes in companies we like for the long-term.

From a sector perspective, our two largest overweight positions relative to the index are energy-utilities and healthcare. We expect the energy sector to perform well due to shrinking supply, growing global demand and potential inflation. Despite looming healthcare reform, companies that offer low-cost solutions that improve healthcare should also do well.

The Fund remains underweighted relative to the index in financial services. Despite the second quarter rally, we still see significant risks of loan write-offs and other balance sheet concerns. The four financial stocks we own have either paid the TARP money back or didn’t accept it in the first place. We think this demonstrates their relative strength and will allow our portfolio companies to operate with fewer restrictions going forward. Given our concerns about jobs, we’re still significantly underweighted relative to the index in the consumer discretionary sector.

Thank you for your trust and investment in the Fund.

| Yours truly, |

|

| Todd C. Ahlsten |

| Chief Investment Officer |

| 10 | The Parnassus Funds |

Table of Contents

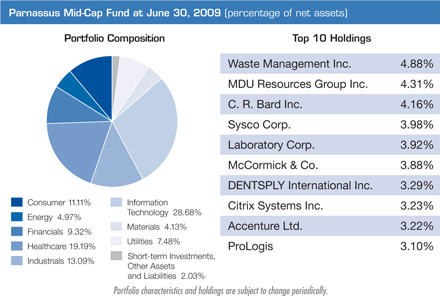

As of June 30, 2009, the net asset value per share (“NAV”) of the Parnassus Mid-Cap Fund was $13.08, so the total return for the quarter was a gain of 18.26%. This compares to a gain of 20.80% for the Russell Midcap Index and a gain of 19.07% for the average mid-cap core fund followed by Lipper Inc. Although the Fund fell short of its benchmarks for the quarter, we are pleased to have made such a large gain.

For the first half of 2009, the Fund is slightly behind the benchmark and its peers. Since the beginning of the year, the Fund is up 9.00% versus a gain of 9.96% for the Russell Index and a return of 9.21% for the Lipper Average. The Fund’s one- and three-year returns and its record since inception beat both the Russell Midcap Index and Lipper Mid-Cap Core Average for all periods. We are proud that the Fund’s strategy of buying good businesses at undervalued prices has generated solid longer-term results.

Below is a table comparing the Parnassus Mid-Cap Fund with the Russell Index and the Lipper average for the one- and three-year periods, for the period since September 30, 2005 when we first had most of the Fund’s assets invested in stock and for the period since inception on April 29, 2005.

Average Annual Total Returns

for periods ended June 30, 2009

| One Year | Three Years | Since September 30, 2005 | Since Inception April 29, 2005 | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

PARNASSUS MID-CAP FUND | -15.97 | % | -4.44 | % | -1.54 | % | -1.56 | % | 2.26 | % | 1.21 | % | ||||||

Russell Midcap Index | -30.36 | % | -9.25 | % | -5.72 | % | -2.14 | % | NA | NA | ||||||||

Lipper Mid-Cap Core Average | -29.09 | % | -8.86 | % | -5.48 | % | -2.14 | % | NA | NA |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information up to the most recent month-end is on the Parnassus Investments website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell Midcap Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Mid-cap companies can be more sensitive to changing economic conditions and have fewer financial resources than large-cap companies. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus Investments website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2009, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.40% of net assets, exclusive of acquired fund fees, until May 1, 2010. Effective with the year ending December 31, 2008, Parnassus Investments has agreed to further reduce the total operating expenses to 1.20% of net assets, exclusive of acquired fund fees. These limitations may be continued indefinitely by the Adviser on a year-to-year basis.

Second Quarter Review

This quarter, the Russell Midcap Index surged an amazing 20.8%, far outpacing most major market indices. The climb was fueled by the prospects of an economic recovery and by the magnitude of the recent market correction. Despite the Fund’s impressive 18.3% gain in the quarter, we trailed our index.

Two key factors caused the under-performance. First, the Fund was invested primarily in higher-quality companies. This quality bias helped us weather the storm when the stock market dropped, but it held us back somewhat in the rebound. Second, we owned fewer consumer and financial stocks than our benchmark, and these sectors led the market recovery from the early March nadir. Though we are still underweighted relative to the index in the consumer and financial sectors, during the quarter we doubled positions at very favorable prices in quality retailer Coach and insurance company AFLAC. These investments added significantly to Fund NAV.

| The Parnassus Funds | 11 |

Table of Contents

Company Analysis

The biggest positive contributor by far was AFLAC, which gained a whopping 60.6%, adding 24¢ to the NAV. While we are happy to report this gain, it’s important to note that AFLAC was coming off a major swoon in the first quarter on concerns about the company’s investment portfolio. The stock rebounded as investors became more optimistic that the company wouldn’t need to raise additional capital. First quarter financial results also surprised investors to the upside, as sales in the U.S. and Japan held up better than expected, and investment losses were mostly lower than expectations. Fortunately, we had strong enough conviction in the stock and the businesses’ long-term health to double the position at low levels.

Another winner was Citrix Systems, which gained 40.9%, increasing the NAV by 15¢. Demand for Citrix’s unique virtualization software remains steady, and customers continue to renew their licenses for Citrix’s products. This enabled the company to report better than expected financial results during the quarter. Aside from strong demand for Citrix’s products, we also like the company’s healthy balance sheet, which should help fund growth and innovation.

Our third largest positive contributor was retailer Coach, which rose 61.0% during the quarter adding 11¢ to the Fund’s NAV. The company boosted its sales by releasing a moderately priced handbag line appealing to more price sensitive consumers. Despite the big move, we still like the stock and expect further outperformance as the company continues executing its international expansion plan.

Our only significant loser was oil refiner Sunoco, which dropped 12.4%, knocking 4¢ from the NAV. Utilization at Sunoco’s refineries was down to 74% during the quarter in response to weak demand for refined products. The company’s chemicals division also reported poor quarterly results, reflecting lower margins for its polypropylene and phenol products. We expect margins to recover as the economy moves out of recession and demand for refined products picks up. In the meantime, we think the stock is undervalued, and we plan to hold on to our shares.

| 12 | The Parnassus Funds |

Table of Contents

Outlook And Strategy

While there are signs of economic stabilization, we believe the recent market rally has been a bit hasty. We are still concerned about unemployment, corporate bankruptcies, consumer spending and housing. As a result, we have invested the Fund’s assets in high-quality companies that we think will better weather the recession than their weaker competitors.

The Fund continues to be heavily weighted toward technology and healthcare companies. Despite lower corporate spending, we like the positive long-term, secular growth trends in our technology investments. We’re trying to look past the uncertainty surrounding potential healthcare reform by focusing on top-notch franchises. Our companies offer necessary and cost-effective solutions. Since last quarter, we have increased our utilities and energy sector holdings, believing that limited supply, growing global demand, and long-term inflationary pressures will drive earnings for these companies.

In response to the market’s tremendous move, we further reduced our exposure to consumer stocks during the quarter, believing that stocks in this sector have moved too far too fast. Our most meaningful underweight position relative to the index continues to be the financial sector. We continue to believe that a sustained recovery path is not yet visible for most companies in this sector.

For further detail on our investment strategy, please refer to the strategy section prepared by our Chief Investment Officer, Todd Ahlsten. This can be found at the end of the report he has prepared for the Parnassus Equity Income Fund.

Thank you for your investment with us.

Yours truly,

|  |  | ||

| Benjamin E. Allen | Matthew D. Gershuny | Lori A. Keith | ||

| Portfolio Manager | Portfolio Manager | Portfolio Manager |

| The Parnassus Funds | 13 |

Table of Contents

THE PARNASSUS SMALL - CAP FUND

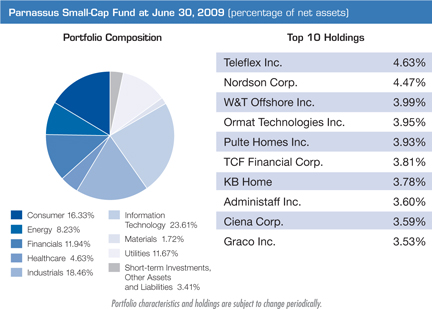

As of June 30, 2009, the net asset value per share (“NAV”) of the Parnassus Small-Cap Fund was $14.60, so the total return for the quarter was 23.21%. By comparison, the Russell 2000 Index (“Russell”) of smaller companies gained 20.69%, and the average small-cap core fund followed by Lipper Inc. gained 21.57%. For the quarter, then, we beat the Russell and the Lipper average.

For the year-to-date as of June 30, we’re substantially ahead of all the benchmarks, with the Fund up 15.60%, the Russell up 2.64% and the Lipper average up 6.29%.

Below is a table comparing the performance of the Small-Cap Fund with that of the Russell 2000 and the Lipper Small-Cap Core Average. Besides the one- and three-year numbers, we’ve also included the period since inception and the return since September 30, 2005, since that is the approximate date when the Fund first had most of its assets invested in stocks. As you can see from the table, the Fund beat all the benchmarks for all time periods.

Average Annual Total Returns

for periods ended June 30, 2009

| One Year | Three Years | Since September 30, 2005 | Since Inception April 29, 2005 | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

PARNASSUS SMALL-CAP FUND | -14.71 | % | -4.02 | % | 1.10 | % | 1.50 | % | 1.88 | % | 1.21 | % | ||||||

Russell 2000 Index | -25.01 | % | -9.89 | % | -5.75 | % | -1.78 | % | .NA | NA | ||||||||

Lipper Small-Cap Core Average | -25.42 | % | -10.09 | % | -6.24 | % | -2.39 | % | .NA | NA |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell 2000 Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Small-cap companies can be particularly sensitive to changing economic conditions and have fewer financial resources than large-cap companies. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is on the Parnassus website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2009, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.40% of net assets, exclusive of acquired fund fees, until May 1, 2010. Effective with the year ending December 31, 2008, Parnassus Investments has agreed to further reduce the total operating expenses to 1.20% of net assets, exclusive of acquired fund fees. These limitations may be continued indefinitely by the Adviser on a year-to-year basis.

Company Analysis

Only one company made a substantial dent in the NAV of the Small-Cap Fund. Pulte Homes dropped 19.2% from $10.93 to $8.83, slicing 13¢ off the value of each fund share. In the March quarter, the homebuilders helped us quite a bit, but difficult conditions in the housing industry pulled their shares back down to earth in the June quarter. Declining orders and write-offs on land depressed earnings for all the homebuilders, pushing their stock prices lower. For the most part, though, these declines in share prices did not affect the Fund too much, but Pulte was a special case. Pulte is buying rival Centex, and investors usually don’t like mergers, because they normally have a negative financial impact on the companies in question. Most of the time, I’m in the camp that dislikes mergers, so I would normally sell the stock of a company making a big acquisition. In the case of Pulte, though, the stock price is down so low that I regard it as a good value.

Six companies made substantial contributions to the Fund’s share price in the quarter, each one adding 14¢ or more. The big winner was Baldor Electric, the maker of energy-efficient motors based in Ft. Smith, Arkansas. The company’s stock motored up 64.2% from $14.49 to $23.79 for a gain of 22¢ for each fund share. Financial results for the last quarter were stronger than expected and analysts raised estimates for the company. Baldor was also able to renegotiate terms of its major credit agreement, thereby ensuring access to the financing it needs to operate effectively.

| 14 | The Parnassus Funds |

Table of Contents

W&T Offshore saw its stock price rebound 58.4% from $6.15 to $9.74 during the quarter, adding 19¢ to the NAV. Rising energy prices helped this oil-producer’s earnings, while service and drilling costs have come down, which greatly improves the economics of the company’s drilling program.

Ormat Technologies contributed 17¢ to the NAV during the quarter, as its stock climbed 46.8% from $27.46 to $40.31. Ormat is a renewable energy company that develops, owns and operates geothermal power plants. Increased revenue and better margins contributed to strong financial results.

Nordson is a leading manufacturer of precision dispensing equipment that applies adhesives, sealants and coatings for consumer goods and industrial products. During the quarter, Nordson contributed 15¢ to each fund share, with its stock price increasing by 36.0% from $28.43 to $38.66. Revenue has held up better than expected in the packaging and non-woven markets, while orders and sales have improved in all business segments, especially in electronic assembly and life sciences.

Ciena Corporation makes products for optical networks used in telecommunications. The stock had been trading at depressed levels because phone companies have cut back on capital spending. During the second quarter, the stock added 14¢ to the NAV, as it climbed 33.0% from $7.78 to $10.35. Investors anticipate that orders from telecommunications providers will pick up soon, and Ciena has already received a number of orders for its excellent products.

The price of Energen shares surged 37.0% in the second quarter from $29.13 to $39.90 for a gain of 14¢ on the NAV. The firm is a diversified energy holding company that has a natural gas utility and also develops and produces oil and natural gas. Crude oil prices moved from the low forties to about $70 per barrel during the quarter, benefitting Energen’s exploration and production businesses.

| Yours truly, |

|

Jerome L. Dodson President Parnassus Investments |

| The Parnassus Funds | 15 |

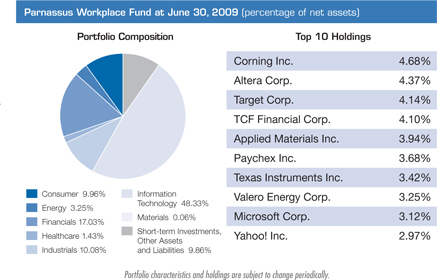

Table of Contents

As of June 30, 2009, the net asset value per share (“NAV”) of the Parnassus Workplace Fund was $15.40, so the total return for the quarter was 26.65%. This compares to a return of 15.93% for the S&P 500 and 17.77% for the average multi-cap core fund followed by Lipper Inc. It was an outstanding quarter for the Workplace Fund, as we beat both benchmarks by a substantial amount.

For the year-to-date, the Workplace Fund is even further ahead of its benchmarks, gaining 26.02% as of June 30, compared to 3.16% for the S&P 500 and 7.32% for the Lipper average. The Workplace Fund was the best-performing of all the Parnassus Funds for the quarter and the year-to-date.

Below is a table comparing the Workplace Fund with the S&P 500 and the Lipper Multi-Cap Core Average. Besides the one- and three-year numbers, we’ve also included the period since inception and the return since September 30, 2005, since that is the approximate date when the Fund first had most of its assets invested in stocks. You’ll notice that the Fund has a very substantial lead over all the indices for all time periods. It seems as if the Fund’s strategy of investing in companies that provide their workers with great workplaces is succeeding in providing solid returns to its shareholders.

Average Annual Total Returns

for periods ended June 30, 2009

| One Year | Three Years | Since September 30, 2005 | Since Inception April 29, 2005 | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

PARNASSUS WORKPLACE FUND | -5.42 | % | 1.54 | % | 2.56 | % | 2.53 | % | 2.34 | % | 1.21 | % | ||||||

S&P 500 Index | -26.21 | % | -8.22 | % | -5.44 | % | -3.34 | % | NA | NA | ||||||||

Lipper Multi-Cap Core Average | -26.35 | % | -8.33 | % | -5.32 | % | -2.59 | % | NA | NA |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2009, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.20% of net assets, exclusive of acquired fund fees, until May 1, 2010. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

Company Analysis

Only one stock in the Workplace Fund portfolio had a substantial negative impact on the Fund’s NAV. Refiner Valero Energy sliced 10¢ off the NAV, with its shares declining 5.6% from $17.90 to $16.89 at the end of the quarter. The company temporarily shut down several of its refineries during the quarter due to depressed demand for gasoline. Earnings were hurt because of lower margins or reduced “crack spreads” (the difference between the price of oil and the price of gasoline.) We expect refining margins to recover as the economy picks up, so we’re hanging on to the stock, since we think it’s very undervalued.

Seven companies made substantial contributions, each one boosting the NAV by 14¢ or more. The big winner for the quarter was Wells Fargo, with its stock soaring 70.4% from $14.24 to $24.26 for a gain of 22¢ for each fund share. The stock moved higher, because the company reported earnings that were much better than expected, with higher mortgage banking and trading revenues offsetting credit losses.

American Express also made a major contribution to the Fund’s strong second quarter performance, as its stock climbed 70.5% from $13.63 to $23.24 for a gain of 19¢. The stock had been trading at very depressed levels because of investor concerns about the possibility of big losses in the company’s credit card portfolio. As it turned out, earnings came in better than expected because of good expense control and lower funding costs courtesy of low interest rates. The balance sheet of American Express also looks reasonably healthy, as the company obtained permission in June to repay the U.S. Treasury the $3.4 billion in TARP money it had received; the company paid it all back before the end of the quarter.

| 16 | The Parnassus Funds |

Table of Contents

Baldor Electric, the maker of energy-efficient motors, added 17¢ to the NAV, as its stock soared 64.2% from $14.49 to $23.79. Financial results for the last quarter were stronger than expected and analysts raised estimates for the company. Baldor was also able to renegotiate terms of its major credit agreement, thereby ensuring access to the financing it needs to operate effectively.

Semiconductor-maker Texas Instruments contributed 16¢ to the shares of the Workplace Fund, as its stock climbed 29.0% from $16.51 to $21.30. The company reported higher orders, increased revenue and better earnings, driven by demand from China’s 3G build-out and improving conditions in the handset, notebook and LCD TV end-markets.

Seagate Technology makes hard disk-drives used for electronic storage and its stock rose 74.0% during the quarter from $6.01 to $10.46 for a gain of 15¢ on the NAV. Late in the quarter, the company said demand was increasing and it was able to get better pricing for its products. It also raised guidance for revenue in the next quarter from an average of $2.05 billion to an average of $2.25 billion. Analysts from ten brokerage firms raised their forecasts for Seagate.

After seeing its stock lose 57.8% in the first quarter, because of investments losses and slowing sales, insurer AFLAC rebounded in the second quarter, contributing 14¢ to each fund share, as its stock soared 60.6% from $19.36 to $31.09. Financial results gave investors a positive surprise, as sales in Japan and the US held up better than expected and investment losses were not as bad as feared. Standard & Poor’s removed AFLAC from its credit watch list, indicating that no downgrade was imminent.

Microsoft boosted the Workplace Fund by 14¢ per share, with its stock rising 29.4% from $18.37 to $23.77. Expectations for the company increased on the release of Bing, its new search engine and the announcement that a new operating system, Windows 7, is on track to launch this fall.

Yours truly, |

|

| Jerome L. Dodson |

| President |

| Parnassus Investments |

| The Parnassus Funds | 17 |

Table of Contents

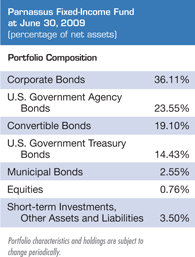

THE PARNASSUS FIXED - INCOME FUND

As of June 30, 2009, the net asset value per share (“NAV”) of the Parnassus Fixed-Income Fund was $16.41, producing a total return for the quarter of 2.93% (including dividends). This compares to a gain of 6.36% for the average A-rated bond fund followed by Lipper Inc. and a gain of 1.85% for the Barclays Capital U.S. Government/Credit Bond Index. Since the beginning of the year, the total return for the Fund was 2.73% compared to a gain of 0.55% for the Barclays Capital U.S. Government/ Credit Bond Index and a gain of 6.56% for the average A-rated bond fund followed by Lipper Inc.

Below is a table comparing the performance of the Fund with that of the Barclays Capital U.S Government/Credit Bond Index and the average A-rated bond fund followed by Lipper. Average annual total returns are for the one-, three-, five- and ten-year periods. The 30-day SEC yield for the Fund for June 2009 was 2.96%. We’re pleased to report that our returns are better than the Lipper average for each of the one-, three-, five- and ten-year periods as of the end of the year.

Average Annual Total Returns

for periods ended June 30, 2009

| One Year | Three Years | Five Years | Ten Years | Gross Expense Ratio | Net Expense Ratio | |||||||||||||

PARNASSUS FIXED-INCOME FUND | 4.60 | % | 5.25 | % | 4.68 | % | 5.52 | % | 0.90 | % | 0.77 | % | ||||||

Lipper A-rated Bond Fund Average | 0.42 | % | 2.98 | % | 2.78 | % | 4.58 | % | NA | NA | ||||||||

Barclays Capital U.S. Government/Credit Bond Index | 5.26 | % | 6.16 | % | 4.80 | % | 5.95 | % | NA | NA |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent-month end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns shown in the table do not reflect the deduction of taxes a shareholder would pay in fund distributions or redemption of shares. The Barclays Capital U.S. Government/Credit Bond Index is an unmanaged index of bonds, and it is not possible to invest directly in an index. An index does not take expenses into account, but mutual fund returns do. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should read the prospectus, which contains this and other information. The prospectus is on the Parnassus Investments website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2009, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.87% of net assets, exclusive of acquired fund fees, until May 1, 2010. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

Second Quarter Review

The appetite for risk came roaring back during the second quarter, as financial markets erased most of the losses incurred earlier in the year. Equity markets were up on average more than 40% from their lows in March, while U.S. corporate bonds returned 10% during the quarter, according to the Barclays Capital U.S. Credit Index. Animal spirits got a jolt of life after several indicators of economic activity showed some signs of stabilization. Fueled by a slower rate of decline in these economic data, investors started to see green shoots at every corner and quickly concluded than an economic recovery was on the way.

The U.S. Treasury market suffered from all this excitement. The reason is that a robust economic turnaround would imply higher inflation, and in turn make the equity market a better investment alternative. Consequently, yields backed up across the curve, most notably in the long end, where the yield on the 30-year increased by 80 basis points to 4.33% during the quarter, and the 10-year increased from 2.66% to 3.53%. Interest rates at the front end of the curve went up less, with the 3-year ending at 1.62%, up 50 basis points and the 2-year up 31 basis points to 1.11%.

The Fund’s performance in the quarter trailed the average A-rated bond fund followed by Lipper, because we don’t invest in commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS). CMBS are bonds that represent a claim on the cash flows from commercial property loans, while ABS are bonds backed by a pool of assets such as credit card and auto loans. During the quarter, these securities returned more than 10%, as the perceived default risk on the underlying assets declined with the improving economic data. While these bonds offer much higher yields than

| 18 | The Parnassus Funds |

Table of Contents

investment-grade corporate bonds, they come with much higher risk profiles and complexity. We are willing to give up some of these riskier returns, as our investment strategy emphasizes safety and risk management. Even though we underperformed for the quarter, our longer-term performance is substantially better than the Lipper average as illustrated in the table.

On the other hand, the Fund performed much better for the quarter compared to the Barclays Capital U.S. Government/Credit Bond Index. The reason is that we had less exposure to the declining Treasury market. The decision during the last quarter to increase the Fund’s holdings in corporate and convertible bonds also contributed to our quarterly performance. The investments in corporate bonds contributed the most, adding 30¢ per share to the NAV. Convertible bonds added about 19¢ per share due to their sensitivity to the soaring equity market. Finally, agency bonds were unchanged during the quarter, while the Treasury holdings negatively impacted the Fund by 2¢ per share.

Outlook And Strategy

During the second quarter, the market has been looking for signs of economic stabilization. Going forward, however, investors will likely pay more attention to the prospects for growth in consumer demand, so employment and consumer data will have increasing importance. If investors are to take on more risk, there needs to be rapid improvements in labor market indicators, as well as sustainable evidence of recovery in consumer confidence and spending. Indeed, without a recovery in these drivers of demand, profit margins will stay compressed and corporate credit quality will deteriorate.

The current labor market is unlike previous cycles because of the permanency of job losses. With roughly 75% of the workers that were fired over the last 12 months on a permanent, not temporary, basis, there are now a relatively low number of temporary layoffs and a high number of involuntary part-time workers. This means that employment growth will be tepid, when the economy starts to expand again and a jobless recovery would be more likely. In turn, this implies that the next economic expansion is going to be more fragile and more volatile than in the past cycles.

In light of the above, the portfolio is positioned for a slow and volatile economic recovery. I added a few investment-grade corporate bonds during the quarter as they still offer an attractive risk/return profile. Even though the yield differential between corporate and Treasury bonds has decreased from its peak in January, it remains wider than during past crises. In addition, the Fund remains flexible and also provides safety in cases of a sharp increase in risk aversion or a sudden surge in inflation expectations. The investments in agency and Treasury bonds would outperform with lower interest rates, while convertible bonds and the relative short duration of the portfolio lowers its sensitivity to rising interest rates.

Thank you for investing in the Parnassus Fixed-Income Fund.

Yours truly, |

|

| Minh T. Bui |

| Portfolio Manager |

| The Parnassus Funds | 19 |

Table of Contents

by Jerome L. Dodson and Milton Moskowitz

The Obama Administration has created an Office of Social Innovation to promote the idea of social entrepreneurship. The First Lady, Michelle Obama, announced that plans call for the office to be funded with a $50 million appropriation in the 2010 budget. Heading up the office is Sonal Shah, who designed a development strategy for Google.org and an environmental strategy for Goldman Sachs.

Applied Materials takes a pro-active stance on environmental issues. In late June, after the U.S. House of Representatives passed a climate security act that includes a cap-and-trade component, Applied’s CEO, Mike Splinter, fired off a message urging the Senate to follow suit to show “the world that we want to be leaders when it comes to saving our climate.” Long the leading supplier of equipment used to make semiconductors, Applied also has a hand in solar energy, supplying products used to make silicon solar panels. Its SunFab Thin Line makes possible the world’s largest solar panels...Adobe Foundation, philanthropic arm of Adobe Systems, convened a three-day digital immersion event for 100 students and educators from around the world. The goal: “to empower youth to create media for social change.” More than 60 students, ages 14 to 19, came from more than 16 countries to participate in workshops led by Adobe employees. “Now more than ever, youths need to be able to relate to other cultures and ideas and to express themselves in digital media,” said Michelle Mann, executive director of the Adobe Foundation. The summit took place at Stanford University...In the July issue of The Costco Connection, the monthly magazine sent to 53 million cardholders, Costco Wholesale featured 13 members who are doing something to change the world, ranging from Russell Jackson, an ex-firefighter who started a foundation, Kid One, which transports impoverished children from poor rural communities in Alabama to metropolitan hospitals, to Lucy Summer, a retired school teacher who set up a nonprofit, The Magic Penny, to help rural communities in West Africa. The magazine ended its report with the message, “Now it’s your turn,” listing places where they could find help to launch their own humanitarian projects...Paychex, which handles payroll services for more than half a million businesses across the country, was recognized by the National Business Group on Health as one of the nation’s best employers for its healthy lifestyles. Paychex’s Active Health programs include on-site health screenings, online health risk assessments, healthy cooking classes and unlimited access to preventive medical care at no cost to employees. Eighty-seven percent of Paychex employees participated in these programs in 2008...Pulte Homes, one of the nation’s largest home builders, was recognized by the Department of Energy for building more energy-efficient homes than any

| 20 | The Parnassus Funds |

Table of Contents

other builder. During 2008, Pulte completed 649 homes which had scores of 70 or better on the DOE’s EnergySmart Home Scale... Mentor Graphics came to the aid of unemployed engineers and designers with a Displaced Worker Program that offers free training courses. Classroom instruction takes place at the company’s training centers — in Austin, Boston, Chicago, Minneapolis, Dallas, Denver, Portland and San Jose — but the courses are also offered online...Intel, the world’s largest maker of microprocessors, has invested over $23 million in energy efficiency and conservation since 2001, resulting in savings of more than $50 million. The company is now the nation’s largest purchaser of green power. Intel ties a portion of employee compensation to environmental metrics...Whole Foods Market was the first national retailer to offer 100 percent recycled paper bags at its checkouts, and last year it banned plastic bags from its checkouts. Now it has gone one step further by using recycled paper bags certified by the Forest Stewardship Council, which means the paper has been traced through the supply chain to ensure zero impact on virgin forests. Shoppers who bring their own bags get refunds of five or 10 cents at the checkouts...Women hold top jobs at the Tennessee-based bank holding company, First Horizon, accounting for 67% of managers and supervisors and 18% of senior managers and top executives. As a result, the bank has been named to the list of the Top 50 Companies for Executive Women by the National Association for Female Executives. Two of the top female officers are Christine Munson, executive vice president-corporate banking, and Kim Cherry, executive vice president-corporate communications...Institutional Investor has named AFLAC chairman Dan Amos the best CEO in the life insurance field, the fourth time he has earned this designation...Johnson & Johnson, a healthcare company, reports on the health of its employee force: 4% are smokers, down from 5% in 2005, 6% have high blood pressure, down from 10% in 2005, 7% have high cholesterol, down from 8% in 2005, and 36% do little or no exercise, down from 38% in 2005...The University of Michigan’s American Customer Satisfaction Industry ranked FedEx Corp. number one in customer satisfaction in the Express Delivery industry...Coach, provider of luxury leatherware, has been impacted by the recession but it signaled how strong its financial condition is by paying a cash dividend to shareholders on June 29. It’s the first dividend in its history. The company promotes a Global Business Integrity Program, imposing ethical standards on its vendors. China is becoming one of its major markets — and the leader of this push is Andre Cohen, who joined Coach in 2008 after six years at Timberland, a shoe maker widely known for its social responsibility programs.

| The Parnassus Funds | 21 |

Table of Contents

As a shareholder of the funds, you incur ongoing costs, which include portfolio management fees, administrative fees, shareholder reports, and other fund expenses. The funds do not charge transaction fees, so you do not incur transaction costs such as sales charges (loads) on purchase payments, reinvested dividends, or other distributions, redemption fees, and exchange fees. The information on this page is intended to help you understand your ongoing costs of investing in the funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The following example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the period of January 1, 2009 through June 30, 2009.

Actual Expenses

In the example below, the first line for each fund provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of each fund provides information about hypothetical account values and hypothetical expenses based on the fund’s expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. You may compare the ongoing costs of investing in the fund with other mutual funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Please note that the expenses shown in the table are meant to highlight only your ongoing costs in these funds. Therefore, the second line of each fund is useful in comparing only ongoing costs and will not help you determine the relative total costs of owning other mutual funds, which may include transactional costs such as loads.

| Beginning Account Value January 1, 2009 | Ending Account Value June 30, 2009 | Expenses Paid During Period* | |||||||

Parnassus Fund: Actual | $ | 1,000.00 | $ | 1,172.11 | $ | 5.33 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,019.89 | $ | 4.96 | |||

Parnassus Equity Income Fund – Investor Shares: Actual | $ | 1,000.00 | $ | 1,047.91 | $ | 5.03 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,019.89 | $ | 4.96 | |||

Parnassus Equity Income Fund – Institutional Shares: Actual | $ | 1,000.00 | $ | 1,048.86 | $ | 3.96 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,020.93 | $ | 3.91 | |||

Parnassus Mid-Cap Fund: Actual | $ | 1,000.00 | $ | 1,090.00 | $ | 6.22 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,018.84 | $ | 6.01 | |||

Parnassus Small-Cap Fund: Actual | $ | 1,000.00 | $ | 1,155.98 | $ | 6.41 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,018.84 | $ | 6.01 | |||

Parnassus Workplace Fund: Actual | $ | 1,000.00 | $ | 1,260.23 | $ | 6.72 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,018.84 | $ | 6.01 | |||

Parnassus Fixed-Income Fund: Actual | $ | 1,000.00 | $ | 1,027.33 | $ | 4.37 | |||

Hypothetical (5% before expenses) | $ | 1,000.00 | $ | 1,020.48 | $ | 4.36 | |||

| * | Expenses are equal to the fund’s annualized expense ratio of 0.99%, 0.99%, 0.78%, 1.20%, 1.20%, 1.20% and 0.87% for the Parnassus Fund, Equity Income Fund – Investor Shares, Equity Income Fund – Institutional Shares, Mid-Cap Fund, Small-Cap Fund, Workplace Fund and Fixed-Income Fund respectively, multiplied by the average account value over the period, multiplied by the ratio of days in the period. The ratio of days in the period is 181/365 (to reflect the one-half year). |

| 22 | The Parnassus Funds |

Table of Contents

Portfolio of Investments as of

June 30, 2009 (unaudited)

Shares | Equities | Percent of Net Assets | Market Value | |||||

| Building Materials | ||||||||

| 25,000 | Simpson Manufacturing Co., Inc. | 0.2 | % | $ | 540,500 | |||

| Computer Peripherals | ||||||||

| 530,000 | Seagate Technology | 2.1 | % | $ | 5,543,800 | |||

| Consulting Services | ||||||||

| 200,000 | Accenture Ltd. | 2.5 | % | $ | 6,692,000 | |||

| Data Processing | ||||||||

| 10,000 | Fiserv Inc.1 | 0.2 | % | $ | 457,000 | |||

| Financial Services | ||||||||

| 400,000 | American Express Co. | $ | 9,296,000 | |||||

| 25,000 | Charles Schwab Corp. | 438,500 | ||||||

| 450,000 | First Horizon National Corp.1 | 5,400,000 | ||||||

| 70,000 | Goldman Sachs Group Inc. | 10,320,800 | ||||||

| 15,000 | JPMorgan Chase & Co. | 511,650 | ||||||

| 67,604 | Paychex Inc. | 1,703,620 | ||||||

| 320,000 | TCF Financial Corp. | 4,278,400 | ||||||

| 470,000 | Wells Fargo & Co. | 11,402,200 | ||||||

| 16.4 | % | $ | 43,351,170 | |||||

Food Products | ||||||||

| 40,000 | Sysco Corp. | 0.3 | % | $ | 899,200 | |||

Home Builders | ||||||||

| 1,080,000 | DR Horton Inc. | $ | 10,108,800 | |||||

| 510,000 | KB Home | 6,976,800 | ||||||

| 940,000 | Pulte Homes Inc.1 | 8,300,200 | ||||||

| 360,000 | Toll Brothers Inc.1 | 6,109,200 | ||||||

| 11.9 | % | $ | 31,495,000 | |||||

Home Products | ||||||||

| 60,000 | WD-40 Co. | 0.7 | % | $ | 1,740,000 | |||

Industrial Manufacturing | ||||||||

| 210,000 | Teleflex Inc. | 3.6 | % | $ | 9,414,300 | |||

Insurance | ||||||||

| 205,000 | Tower Group Inc. | 1.9 | % | $ | 5,079,900 | |||

Internet | ||||||||