PARNASSUS INCOME FUNDS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06673

Parnassus Income Funds

(Exact name of registrant as specified in charter)

1 Market Street, Suite 1600, San Francisco, California 94105

(Address of principal executive offices) (Zip code)

Marc C. Mahon

Parnassus Income Funds

1 Market Street, Suite 1600, San Francisco, California 94105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (415) 778-0200

Date of fiscal year end: December 31

Date of reporting period: December 31, 2010

| Item 1: | Report to Shareholders |

P A R N A S S U S F U N D S ®

ANNUAL REPORT DECEMBER 31, 2010

PARNASSUS FUNDS

Parnassus FundSM PARNX Parnassus Equity Income FundSM– Investor Shares PRBLX Parnassus Equity Income Fund – Institutional Shares PRILX Parnassus Mid-Cap FundSM PARMX Parnassus Small-Cap FundSM PARSX Parnassus Workplace Fund® PARWX Parnassus Fixed-Income FundSM PRFIX

Table of Contents

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

February 8, 2011

Dear Shareholder:

2010 was quite a year! The market started off reasonably well, then moved sharply lower into the summer before finishing strongly. All our funds participated in this year’s attractive returns, but the standout was the Parnassus Small-Cap Fund, which returned 37.37%. The Parnassus Fund and the Parnassus Mid-Cap Fund beat both the S&P 500 Index and the Lipper Multi-Cap Core Average. Both the Parnassus Workplace Fund and the Parnassus Equity Income Fund underperformed for 2010, but have excellent market-beating long-term performances. Read the enclosed fund reports for the details.

As many of you know, I personally manage three of the six Parnassus Funds. I am now 67 years old, but I am very healthy, in excellent physical condition and love my job, so I plan to keep working well into my 70’s. As time goes on, though, I’m looking for more help in managing the funds. Right now, Parnassus Investments has an excellent staff of analysts overseen by Benjamin Allen, our Director of Research. Ben and his team have done a great job and they have helped a lot in managing my three funds. They will continue to provide me with research assistance of a very high quality, but Todd Ahlsten, our Chief Investment Officer, and I are also looking to add co-managers for my three funds. There is no timetable for adding co-managers, since it’s not easy to find the right person. Over time, I will make announcements when co-managers are found.

The first announcement is that effective May 2, 2011, Ryan Wilsey will become co-manager of the Parnassus Small-Cap Fund. Ryan interned with us in 1998 while he was an undergraduate at Princeton University. After college, he went to work for Opsware (aka Loudcloud), then served as an analyst at Summit Partners, an investment firm in Palo Alto, California. After graduating from Harvard Business School in 2006, he worked as an associate at Greylock Partners, a venture capital firm, then as an analyst at Scout Capital, a hedge fund in New York. Ryan began his second internship with us in the summer of 2009, then joined the staff as a senior analyst in November of that year. Ryan has done an excellent job as a senior analyst, and will make an even bigger contribution as co-manager.

New Team Member

I’m also happy to announce that Valerie Tan has joined us and will help the firm in both accounting and compliance. Valerie is an accounting graduate of San Francisco State University, and she has previously worked for other mutual fund companies in the San Francisco Bay Area. In her spare time, she likes to swim, play tennis and listen to music.

Yours truly,

Jerome L. Dodson, President

Parnassus Investments

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

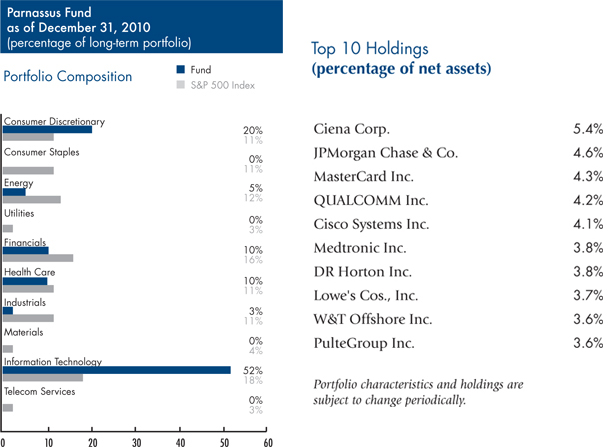

PARNASSUS FUND

Ticker: PARNX

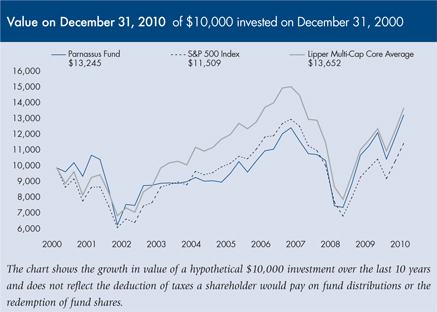

As of December 31, 2010, the net asset value per share (“NAV”) of the Parnassus Fund was $40.49, so after taking dividends into account, the total return for the quarter was 11.64%. This compares to 10.76% for the S&P 500 Index (“S&P 500”) and 10.93% for the Lipper Multi-Cap Core Average, which represents the average multi-cap core fund followed by Lipper (“Lipper average”). For the quarter, we beat both of our benchmarks by modest amounts.

Below are a table and a graph comparing the Parnassus Fund with the S&P 500 and the Lipper average over the past one-, three-, five- and ten-year periods. With one exception, you’ll notice that we’re ahead of both our benchmarks for all time periods. The exception is the ten-year number for the Lipper average, where the Fund trailed that index by a small amount. However, we are ahead of the S&P 500 by a substantial amount for the ten-year period.

I’m happy that we’ve been able to give our shareholders solid returns. The one I’m most proud of is the three-year number, where the Fund has a positive return of over 4% per year, while the two benchmarks are down an average of more than 2% per year.

Parnassus Fund

| | | | | | | | | | | | | | | | | | | | | | | | |

Average Annual Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended 12/31/2010 | | | | | | |

Parnassus Fund | | | 16.71 | | | | 4.39 | | | | 6.52 | | | | 2.85 | | | | 1.00 | | | | 0.99 | |

S&P 500 Index | | | 15.08 | | | | -2.84 | | | | 2.29 | | | | 1.42 | | | | NA | | | | NA | |

Lipper Multi-Cap Core Average | | | 15.91 | | | | -2.35 | | | | 2.42 | | | | 2.91 | | | | NA | | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 Composite Stock Index (also known as the S&P 500) is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Prior to May 1, 2004, the Parnassus Fund charged a sales load (maximum of 3.5%), which is not reflected in the total return calculations. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2010, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.99% of net assets, exclusive of acquired fund fees, until May 1, 2011. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

Company Analysis

The Parnassus Fund had eight winners, each contributing 32¢ or more to the NAV. Only one company sliced more than 32¢ off each Parnassus share. Homebuilder Pulte Group cost the Fund 33¢ per share for the year, as its stock sank 25% from $10.00 to $7.52 per share. Pulte surprised investors when it set aside $272 million to cover construction defects from homes built in the 2005-2006 period and also wrote down $655 million in assets related to its 2009 acquisition of Centex. Despite difficult conditions in the housing market, we’re holding onto the stock, since it’s trading at very depressed levels and should move higher if the housing market picks up in 2011.

Our biggest winner was Ciena, maker of products used in optical networks for telecommunications. Its stock soared 94% from $10.84 to $21.05, adding $1.05 to each Parnassus share. Surging demand for video and smartphone bandwidth has put pressure on telecommunications carriers to buy more equipment. Because the company bought the optical equipment assets of Nortel networks last year, sales have increased 90%, and this will enable Ciena to spread its costs over a higher volume of sales which will eventually lead to higher earnings. The company has also indicated that it has been gaining market share.

Our second biggest winner was W&T Offshore, an oil and natural gas producer. At the beginning of the year, energy prices were much lower than they are now, and we thought there was a possibility that they would move much higher later in the year. We had invested in W&T a couple of years ago, and we added substantially to our position

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

in early 2010. As oil prices increased during the year and the company acquired valuable assets, the stock moved from $11.70 to $17.87 for an increase of 53% and a gain of 61¢ for each fund share.

Genzyme, a biotechnology company that produces drugs for patients born with rare genetic diseases, saw its stock climb 45% from $49.01 to $71.20 by the end of the year, for a gain of 53¢ for each Parnassus Fund share. The company received a buyout offer from French pharmaceutical company, Sanofi-Aventis. We’re holding onto the shares because we think the ultimate buyout price could be even higher. Genzyme has also made significant operational improvements to its business.

Verisign manages the “.com” domain name server, enabling people to surf the internet. In May, the company sold its non-core security business to focus on growing its “.com” business, then returned the proceeds to shareholders in the form of a $3 dividend and a $1.1 billion share repurchase program. The stock climbed 35%, going from $24.24 to $32.67 for a gain of 51¢ on the NAV.

Autodesk, the leading producer of construction design software, added 41¢ to each fund share, as its stock price surged 50% from $25.41 to $38.20. The stock had been trading at depressed levels early in the year because of weak demand for its software. The shares moved higher in the second half of the year in anticipation of increased construction activity. Big customer orders came in late in the year, pushing the stock even higher.

Administaff provides personnel services and employee benefits such as health insurance to small- and medium-sized businesses including Parnassus Investments. The stock moved 25% lower during the year, because of concern about the higher cost of benefi ts and the lower number of covered employees. What investors didn’t understand was that the lower number of covered employees and the medical cost issue were temporary phenomena. The stock moved higher as the number of covered employees increased and insurance costs declined. Administaff contributed 39¢ to each Parnassus share, as its stock rose 64% from $17.85, where we bought it during the year, to $29.30.

Finisar, a provider of optical equipment used in telecommunications, rocketed up an incredible 233% from $8.92 to $29.69 for a gain of 32¢ to the NAV. Sales of its higher-speed products have been especially strong, such as the ROADM, a device that allows firms to reconfigure wavelength remotely to address bandwidth needs. Even after all the price appreciation, we’re still hanging onto the stock, because demand for bandwidth continues to grow from smartphones and other electronic devices.

Tractor-maker Deere & Co. saw a 54% increase in its stock price during the year, rising from $54.09 to $83.05 for a gain of 32¢ for each Parnassus share. The company reported stronger than expected sales of tractors and combines, as much higher prices for corn and other agricultural products meant higher income for farmers. Sales in Russia and Brazil have been especially strong, and Deere has moved to strengthen operations in those high-growth countries; for example, improving financing terms for customers.

Outlook and Strategy

This section represents my thoughts and applies to the funds I manage: the Parnassus Fund, Parnassus Small-Cap Fund, and the Parnassus Workplace Fund. The other portfolio managers will discuss their thoughts in their respective reports. Also, I’ll be writing a separate piece in the Parnassus Small-Cap Fund section.

.

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

Someone reading this report might be surprised to see that the annual return of one fund was so different than those of the other two funds, even though all three funds have the same portfolio manager. The Parnassus Fund gained 16.71% for the year, which was about 1.6 percentage points above the 15.08% return for the S&P 500, and the Parnassus Workplace Fund returned 12.96%, which was about two percentage points below the S&P 500, so they were both relatively close to that index. On the other hand, the Parnassus Small-Cap Fund had an annual return of 37.37%, far above the S&P 500.

One reason for the vast difference in returns is the nature of the companies in the portfolios. The Parnassus Fund and the Parnassus Workplace Fund both emphasize large-cap companies, while the Parnassus Small-Cap Fund, as its name implies, emphasizes smaller companies such as those that make up the Russell 2000 Index. While the S&P 500 returned 15.08%, the Russell 2000 returned 26.85%—a big difference. So, one reason for differences in fund performance is the size of the companies in the portfolio. Small-cap companies just had a great year in 2010.

In the Parnassus Small-Cap Fund section on Outlook and Strategy, I tell shareholders that the Parnassus Small-Cap Fund is unlikely to repeat such a performance in future years, because at some point, small-cap companies will stop outperforming larger-cap companies. It’s impossible to know when this will happen. My own opinion is that this will happen sometime late in 2011, but that’s just a guess. Sometimes, trends go on for years.

The message in this Outlook section is the same. At some point, larger companies will start to perform better than smaller-cap companies on a relative basis. While I’m telling shareholders in the Parnassus Small-Cap Fund to lower their expectations for the future, I’m telling shareholders in the Parnassus Fund and the Parnassus Workplace Fund that those funds might do better relative to smaller companies sometime in the future.

Right now, the valuations of the stocks in the Parnassus Small-Cap Fund are much higher than those in my other two funds. For this reason, there might be more potential upside in those funds. Of course, there are a lot of variables, so nothing is guaranteed, but that’s my observation as of early 2011.

Overall, I’m still optimistic for all three funds. We’re out of the recession now, and as I write this report in January of 2011, the economy appears to be improving. We’re again seeing job growth after losing millions of jobs during the recession. I think companies will continue to hire as orders keep growing for businesses. More jobs should also help the housing market and the homebuilding companies that are in the Parnassus Fund portfolio.

For 2011, I expect the market to be strong again. Small-cap stocks will continue to do well, but at some point late in the year, the larger-cap issues should start catching up with the small-cap stocks. Both the Parnassus Fund and the Parnassus Workplace Fund should benefit from this trend. Given this outlook, I plan to stay fully invested in good companies trading at reasonable prices.

Yours truly,

Jerome L. Dodson

Portfolio Manager

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

PARNASSUS EQUITY INCOME FUND

Ticker: Investor Shares - PRBLX

Ticker: Institutional Shares - PRILX

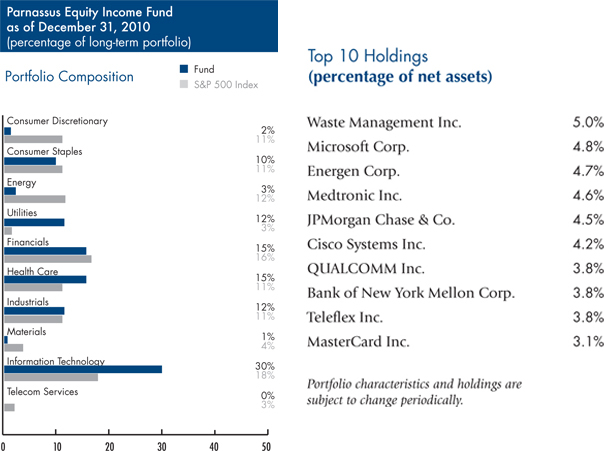

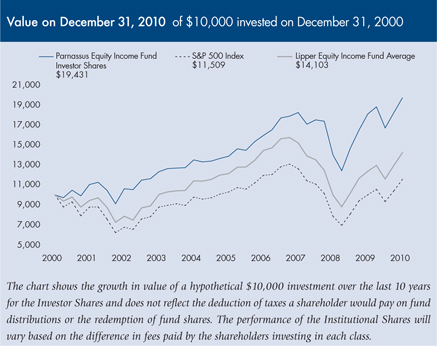

As of December 31, 2010, the NAV of the Parnassus Equity Income Fund-Investor Shares was $26.31. After taking dividends into account, the total return for 2010 was a gain of 8.89%. This compares to an increase of 15.08% for the S&P 500 Index (“S&P 500”) and 15.03% for the Lipper Equity Income Fund Average, which represents the average equity income fund followed by Lipper (“Lipper average”). For the fourth quarter, the Fund rose 8.01% versus 10.76% for the S&P 500 and 9.26% for the Lipper average.

Parnassus Equity Income Fund

| | | | | | | | | | | | | | | | | | | | | | | | |

Average Annual Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended 12/31/2010 | | | | | | |

Parnassus Equity Income Fund Investor Shares | | | 8.89 | | | | 2.60 | | | | 7.17 | | | | 6.87 | | | | 1.00 | | | | 1.00 | |

Parnassus Equity Income Fund Institutional Shares | | | 9.07 | | | | 2.82 | | | | 7.38 | | | | 6.97 | | | | 0.78 | | | | 0.78 | |

S&P 500 Index | | | 15.08 | | | | -2.84 | | | | 2.29 | | | | 1.42 | | | | NA | | | | NA | |

Lipper Equity Income Fund Average | | | 15.03 | | | | -2.07 | | | | 3.08 | | | | 3.48 | | | | NA | | | | NA | |

The total return for the Parnassus Equity Income Fund-Institutional Shares from commencement (April 28, 2006) was 6.39%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Equity Income Fund-Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not refl ect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. On March 31, 1998, the Fund changed its investment objective from a balanced portfolio to an equity income portfolio. Before investing, an investor should carefully consider the investment objectives, risk, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is on the Parnassus website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated, May 1, 2010, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.99% and 0.78% of net assets, exclusive of acquired fund fees, through May 1, 2011 for the Investor Shares and Institutional Shares, respectively. These limitations may be continued indefinitely by the Adviser on a year-to-year basis.

While we underperformed during 2010, our long-term record remains outstanding. Our three-, five- and ten-year trailing returns beat the S&P 500 by substantial margins for every period.

Below are a table and a graph that compare the performance of the Fund with that of the S&P 500 and the Lipper average. Average annual total returns are for the one-, three-, five- and ten-year periods.

2010 Review

The S&P 500 finished 2010 with an impressive 15% return, but it was a bumpy ride to get there. The index shot up nearly 10% by late April, before plunging more than 15% to its early July low. The market swooned because the U.S. economy showed signs of decelerating growth and, at the same time, concerns grew about a European Union sovereign debt crisis. But at the end of August, the market started shooting up again. The reasons for this rally include Fed Chairman Ben Bernanke’s second round of quantitative easing, improved economic data and corporate earnings, and an agreement between President Obama and Congress to extend the Bush-era tax cuts.

Unfortunately, the Fund’s returns fell short of the index for 2010. Our goal is to outperform the S&P 500 over the long haul. During the past decade, we’ve done this by limiting losses in bear markets and gaining almost as much as the index during bull markets. This formula has enabled the Fund to post a positive return from the S&P 500’s October 2007 peak, despite the fact that the index is still nearly 20% below its all-time high. Nevertheless, I’m disappointed with the Fund’s underperformance for 2010.

The biggest negative impact on our performance came from our technology investments, which hurt us by 2.2% versus the index. Despite sturdy competitive moats and growing sales, our large investments in Microsoft, Cisco and Hewlett-

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

Packard didn’t participate in the stock market rally of 2010. In contrast, investors flocked to higher growth technology businesses not in the portfolio, such as Apple, Amazon.com and Salesforce.com.

I’m confident that our technology investments will generate strong returns for our shareholders over time, because of the companies’ positive business prospects. Just as important, these securities offer relatively limited downside, because their franchises are stable and the stocks are currently trading at just 8-to-12 times next year’s earnings.

The second biggest drag on our performance was our energy and utility investments, which cost us 1.5% versus the S&P 500. During 2010, the Fund was overweight in natural gas producers, which underperformed oil-producing companies, due to depressed natural gas prices. While there is currently an oversupply of natural gas due to new discoveries and weak industrial demand, I like the long-term prospects for the fuel. Gas burns cleaner than coal and the U.S. has an abundant supply, which means we don’t have to rely on imports as we do for crude oil. Since several natural gas producers are currently shifting their focus to oil production, the gas market should return to equilibrium soon, boosting the price of that commodity and our gas-related stocks.

Finally, while our cash position averaged only 5.3% during the year, it reduced our return against the S&P 500 by 1.5%. Our cash position is a byproduct of our stock-specific buying and selling decisions, and it typically varies over the course of a year. Unfortunately, during 2010 our cash position happened to be relatively high during periods when the stock market rallied sharply.

While our return for 2010 was disappointing, our process is based on a three-year investment horizon. Over the last twelve months, almost all of our portfolio companies increased their intrinsic values, but some were not rewarded with proportionately higher share prices. As a result, I expect the Fund to perform well in 2011, as the market prices for our investments approach their intrinsic values.

Company Analysis

The Fund had only one stock that meaningfully reduced the NAV in 2010. Gilead Sciences, a leading pharmaceutical company focused on HIV drug therapies, fell 16% from our initial average cost of $39.41 per share to $33.22, the price where we sold a portion of our position. This decline cost the Fund 13¢ per share.

Gilead’s stock took a turn for the worse in April, when management announced that health care reform would reduce the company’s revenue by $200 million in 2010. This news caused the stock to drop from $48 per share in February to $40 in April, at which price I thought Gilead was undervalued. Unfortunately, the company faced additional headwinds during the summer, when several European countries cut prices for Gilead’s HIV drugs due to state budget pressures. In addition, investors became more concerned about looming competition, even though Gilead was promising new molecules for HIV treatment in clinical studies.

My mistake with regard to Gilead was buying the stock too quickly after it dropped on the April news. As part of our due diligence process, members of my team and I met with Chief Operating Officer John Milligan at Gilead’s corporate headquarters. I left the meeting impressed with management’s strategy to defend and grow its extremely valuable HIV franchise. Unfortunately, I didn’t anticipate the above-mentioned short-term challenges that drove the stock down after our purchase.

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

Four stocks added 17¢ or more to the Fund’s NAV during 2010. Cooper Industries, a maker of electrical products such as lighting, wiring devices, transformers and fuses, was the co-champion along with Nike for our stock-of-the-year in 2010. Both companies benefitted from strong company-specific drivers. Cooper rose 37% to $58.29 per share from $42.64 and increased the Fund’s NAV by 21¢. The company’s energy-efficient lighting and electrical products had strong sales as the economy recovered in 2010. In addition, CEO Kirk Hachigan successfully grew international sales and formed a joint venture with Danaher to enhance the profitability of Cooper’s tools business.

Parnassus Senior Analyst Matt Gershuny, who has done an outstanding job managing our Cooper investment, thinks the company’s long-term business prospects are fantastic. Cooper’s products play an important role in modernizing our electrical infrastructure and improving energy efficiency.

Nike, the athletic footwear and apparel giant, jumped 29% to $85.42 per share from $66.07, increasing the NAV by 21¢. Parnassus Director of Research Ben Allen recommended this stock to me, because he considers Nike to be one of the few consumer-discretionary businesses with a defensible competitive moat. The company’s scale, innovation, marketing and prime shelf space allow it to dominate the global athletic footwear and apparel market. This attractive competitive position allows Nike to profit from the global growth of sports, as evidenced by the company’s most recently reported annual sales growth of 11%. Even more impressive were Nike’s Chinese and emerging markets businesses, which grew 18% and 15%, respectively, last quarter.

Gen-Probe, a San Diego-based company that makes molecular diagnostic products used to diagnose diseases and screen blood, rose 36% in 2010 from $42.90 to $58.35 and boosted our NAV by 19¢. Matt Gershuny and I researched Gen-Probe, and decided to buy the stock in the summer of 2009 after short-term issues pushed the shares down. The stock moved higher in 2010, because investors started attributing value to certain positive developments at the company, including new tests for Human Papilloma virus and prostate cancer, and the introduction of Panther, a blood diagnostic machine aimed at small laboratory customers.

The Fund’s largest investment, Waste Management, increased 9% to $36.87 from $33.81 and boosted the NAV by 17¢. The company’s collection and disposal businesses are recovering from the recession, and the prices Waste Management charges for its environmental services are growing above inflation. This pricing power, combined with cost control and stable volumes, should bode well for the company in 2011. Waste Management is a stable, recurring revenue company that produces an attractive 3.5% dividend yield, and owns valuable assets that represent a repository of value. The company also has exciting growth opportunities in its waste-to-energy and recycling businesses.

Outlook and Strategy

While the long-term impacts of quantitative easing and record deficit spending are unknown, in the short-term these policies seem to have helped the economy in late 2010. The Institute for Supply Management’s index for the services sector reached 57 for December, indicating that this important sector of the economy is growing again. In addition, holiday retail sales strengthened in 2010, demonstrating that consumers are confident enough to increase their spending compared to last year. These positive economic factors should provide a boost to corporate earnings for at least the first half of 2011.

As for short-term risk, we’re keeping a close eye on the European sovereign debt market, rising oil and food prices and a potential jump in historically low U.S. interest rates. Each of these factors could create problems for the stock market in 2011. More importantly, any number of unforeseen issues could trip up the still fragile economy and stock market. Because of this, we routinely stress test each of our investments, to understand how their businesses would withstand negative events.

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

Even after last year’s gains, high-quality large-cap stocks still look attractive, especially in contrast to more speculative issues. As a result, the Fund is well-positioned for 2011, because of our focus on secular growth, competitive moats and top-notch management. As discussed earlier, technology titans such as Microsoft, Cisco Systems and Hewlett-Packard all trade at P/E multiples significantly below the market average, despite having good business prospects. In addition, we own energy and utility companies whose stock prices lagged the market average in 2010, but nevertheless increased their intrinsic values.

Since our last report, we’ve increased our holdings in well-managed financial service companies, such as Bank of New York, JPMorgan Chase and Royal Bank of Canada. We think these companies are undervalued and well positioned to increase earnings, due to their strong capital structures and wide moat businesses.

As the global economy and financial markets become more complex, our investment process remains clear and consistent. Our strategy is to own undervalued companies with increasingly relevant products or services and long-term competitive advantages. We are confident that our time-tested process will generate attractive returns for shareholders.

Thank you for your trust and investment in the Parnassus Equity Income Fund.

Highest regards,

Todd C. Ahlsten

Portfolio Manager

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

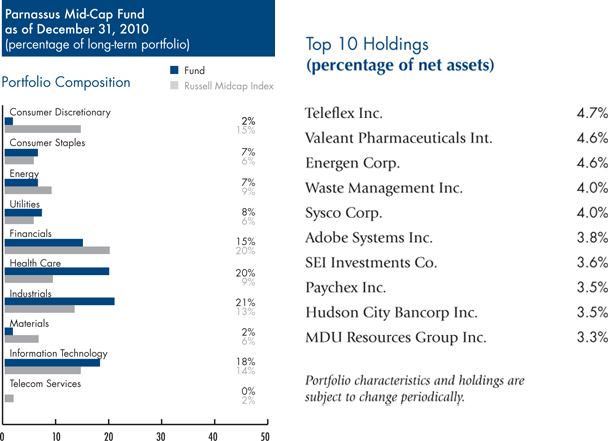

PARNASSUS MID-CAP FUND

Ticker: PARMX

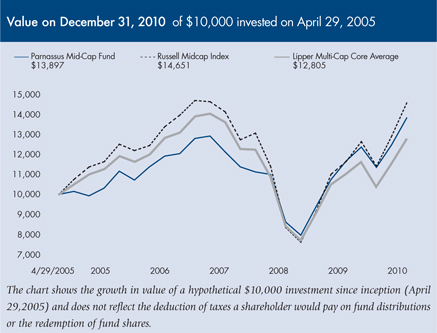

As of December 31, 2010, the NAV of the Parnassus Mid-Cap Fund was $18.25, so after taking dividends into account, the total return for 2010 was a gain of 18.70%. This compares to a gain of 25.48% for the Russell Midcap Index (the “Russell”) and a gain of 15.91% for the Lipper Multi-Cap Core Average, which represents the average multi-cap core fund followed by Lipper (“Lipper average”). While we trailed the Russell for the year, we are pleased with the Fund’s performance relative to its peers.

For the fourth quarter, the Fund was up 10.93%, compared to a gain of 13.07% for the Russell and 10.93% for the Lipper average. While the Fund’s double-digit return matched the Lipper average’s performance during the quarter, it wasn’t enough to keep up with the surging Russell.

Our strategy of buying high-quality businesses at attractive prices has enabled the Fund to beat both the Russell and the Lipper average over the long-term. Our three-year annualized gain is 4.53%, considerably better than the 1.05% gain for the Russell and the 2.35% loss for the Lipper average. The Fund’s five-year annualized return also compares favorably to our benchmarks.

Below is a table comparing the Parnassus Mid-Cap Fund with the Russell and the Lipper average for the one-, three- and five-year periods and for the period since inception on April 29, 2005.

Parnassus Mid-Cap Fund

| | | | | | | | | | | | | | | | | | | | | | | | |

Average Annual Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception

4/29/05 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended 12/31/2010 | | | | | | |

| | | | | | |

Parnassus Mid-Cap Fund | | | 18.70 | | | | 4.53 | | | | 6.13 | | | | 5.98 | | | | 1.73 | | | | 1.20 | |

Russell Midcap Index | | | 25.48 | | | | 1.05 | | | | 4.66 | | | | 6.97 | | | | NA | | | | NA | |

Lipper Multi-Cap Core Average | | | 15.91 | | | | -2.35 | | | | 2.42 | | | | 4.34 | | | | NA | | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is on the Parnassus website (www. parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell Midcap Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Mid-cap companies can be more sensitive to changing economic conditions and have fewer financial resources than large-cap companies. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2010, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.20% of net assets, exclusive of acquired fund fees, until May 1, 2011. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

2010 Review

Following a volatile year, the market wound up with an excellent overall return for 2010. After a quick 15% jump through April, the Russell was down for the year by the end of August, due to concerns over economic growth and European sovereign debt. Sentiment changed by year-end, in light of robust corporate earnings and the Fed’s second round of quantitative easing. As a result, the Russell finished the year up over 25%. Astonishingly, the Russell is up 126% from its March 2009 trough, and is only 10% below its all-time high, which it reached in July 2007.

For 2010, we beat our Lipper peers by almost three percentage points, but came up short against the Russell. The index’s rally has its roots in the sharp market drop of 2008 and early 2009. We attribute our relative underperformance since then to the fact that the Russell generated a larger loss in 2008 than the Fund, and therefore had more to gain in the recovery. While we’re disappointed that we didn’t perform better against the Russell over the last year, we’re confident that our investment strategy will provide long-term outperformance.

We underperformed our index this year because we invested in larger and higher-quality stocks, as compared to the Russell. This strategy served us well in 2008, because it helped limit losses in the dramatic bear market, but it has held us

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

back since then. Another interesting attribute of the 2010 rally in mid-cap stocks is that stocks with relatively high price-to-earnings (P/E) ratios handily outperformed low P/E stocks. Since we prefer to own inexpensively priced issues, this factor hurt us in 2010.

Company Analysis

Six stocks added at least 15¢ to the Fund’s NAV in 2010, and only one significantly reduced the Fund’s value. Valeant Pharmaceuticals, a developer of neurology, dermatology and generic drugs, was the Fund’s biggest positive contributor. The stock jumped 37% from our average cost of $20.58 to $28.29, adding 36¢ to the Fund’s NAV. Following the company’s merger with Biovail, a Canadian specialty pharmaceutical company, management provided better than expected revenue and earnings growth projections, driving the stock higher.

Cooper Industries, an electrical products manufacturer, added 24¢ to the Fund’s NAV, as its stock rose 37% from $42.64 to $58.29. Demand for the company’s product suite, which includes energy efficient-lighting and other electrical products, was strong as the economy recovered. Management also created value by combining its tools business with Danaher’s in a joint venture.

Gen-Probe, a molecular diagnostics company, rose 36% during the year from $42.90 to $58.35, boosting the Fund’s NAV by 19¢. The stock moved higher when investors realized the great potential in the company’s pipeline, which includes tests for detecting Human Papilloma virus and prostate cancer, as well as Panther, a diagnostic machine for small laboratories.

SEI, an asset manager and investment technology solutions provider, rose 36% from $17.52 to $23.79, to add 16¢ to the Fund’s NAV. Most of the company’s revenue is based on fees earned from assets under management and administration, so the stock went up during the year along with rising equity and debt markets. The company also benefited from aggressive cost reductions and an investment in a new technology platform.

Deere, the farm equipment manufacturer, rose 36% from $54.09 to $73.66 where we sold the stock, contributing 16¢ to the Fund’s NAV. Positive farming trends in the U.S., Brazil and Russia drove demand for the company’s products. Despite the good news, we sold the position, as the company is now too large to be considered a mid-cap stock.

McCormick, the spice company, added 16¢ to the NAV, as its stock rose 29% during the year from $36.13 to $46.53. McCormick had successful new product introductions last year and is benefiting from a trend to more at-home eating. The stock also got a boost when Wal-Mart decided to continue carrying its brands.

The Fund’s biggest disappointment was Noble Corporation, an offshore oil and gas services company. The stock dropped 12% during the year from $40.70 to $35.77, slicing 12¢ from the NAV, after the U.S. imposed a ban on offshore drilling in the Gulf of Mexico, where Noble has significant operations. The stock stayed low, because many of the company’s rigs are not back to work due to the slow permitting process for Gulf drilling. Despite the near-term weakness, we’re holding onto the stock because we believe the company has bright prospects with its deep backlog of projects and strong safety and environmental records.

Outlook and Strategy

There’s little question that fiscal and monetary stimulus measures provided a strong boost to the economy in 2010. Record deficit spending, tax-cut extensions, low interest rates and quantitative easing, combined with sub-

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

par 2009 results, allowed many corporations to post amazing improvements in earnings in 2010. As a result, the stock market averages moved significantly higher for the second year in a row.

While concerns remain about the recovery’s trajectory, we think that fundamental improvements will continue, and we’ll avoid a double-dip recession. At the same time, we don’t expect the recovery to be consistently robust. The economic data posted in the third quarter were lackluster and unemployment remains high.

We’ve positioned the portfolio to perform well regardless of the economic environment. Throughout the year, we added to our financial issues, buying high-quality banks, which should perform well as foreclosures abate and financial markets improve. We also reduced our technology exposure because of high valuations from that fast rising segment of the stock market. We remain overweighted in the industrial and health care sectors, owning businesses that are well-positioned to capture increasing share in attractively growing end-markets. We remain underweighted in the consumer discretionary sector, where very few companies meet our valuation and competitive moat criteria.

We believe larger, less expensive stocks will perform well in 2011. This is based on a reversion to the mean following the Russell’s tremendous 2009 and 2010 performance, which was led by smaller, expensively-priced companies.

Our core strategy for long-term outperformance remains the same: participate as much as possible in rising markets, while protecting shareholder’s capital in declining markets. We aim to achieve this by investing in attractively-valued businesses with secular growth opportunities, competitive advantages and high-quality management teams.

Thank you for your investment.

Yours truly,

| | | | |

| |  | |  |

| | |

| Benjamin E. Allen | | Matthew D. Gershuny | | Lori A. Keith |

| Portfolio Manager | | Portfolio Manager | | Portfolio Manager |

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

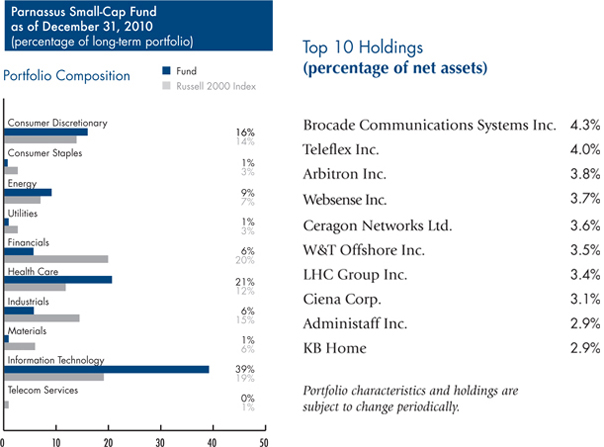

PARNASSUS SMALL-CAP FUND

Ticker: PARSX

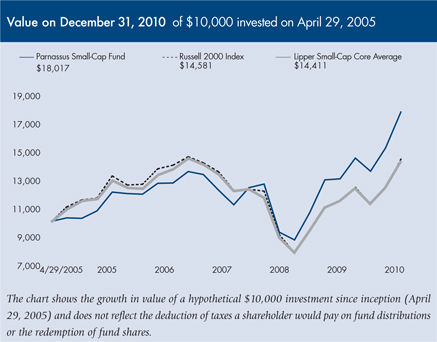

As of December 31, 2010, the NAV of the Parnassus Small-Cap Fund was $23.95, so after taking dividends into account, the total return for the fourth quarter was 17.05%. This compares to a return of 16.25% for the Russell 2000 Index (“Russell 2000”) of smaller companies and 15.59% for the Lipper Small-Cap Core Average, which represents the average small-cap core fund followed by Lipper (“Lipper average”), so we beat both benchmarks for the quarter. Below are a table and a graph, comparing the performance of the Parnassus Small-Cap Fund with that of the Russell 2000 and the Lipper average over the past one-, three- and five-year periods and for the period since inception. As you can see from the table, the Fund beat all its benchmarks for all time periods by substantial amounts.

Parnassus Small-Cap Fund

| | | | | | | | | | | | | | | | | | | | | | | | |

Average Annual Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception

4/29/05 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended 12/31/2010 | | | | | | |

Parnassus Small-Cap Fund | | | 37.37 | | | | 13.61 | | | | 10.85 | | | | 10.94 | | | | 1.47 | | | | 1.20 | |

Russell 2000 Index | | | 26.85 | | | | 2.22 | | | | 4.47 | | | | 6.88 | | | | NA | | | | NA | |

Lipper Small-Cap Core Average | | | 25.23 | | | | 2.04 | | | | 4.08 | | | | 6.50 | | | | NA | | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell 2000 Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Small-cap companies can be particularly sensitive to changing economic conditions and have fewer financial resources than large-cap companies. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2010, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.20% of net assets, exclusive of acquired fund fees, until May 1, 2011. This limitation may be continued indefinitely by the Adviser on a year-to year basis.

Although I’m happy that the Fund has been able to provide shareholders with such attractive returns over the past five years, I’m a little concerned that expectations for the future may be too high. Last year, we earned over 37% and beat the Russell 2000 by more than ten percentage points. Over the past three years, we have on average beat the Russell by over 11 percentage points per year. It’s unlikely that we will be able to continue doing this in the future.

For one thing, the Fund has grown substantially over the past year. At the end of 2009, the Fund had about $115 million in assets, but in January of 2011, we were approaching $500 million in assets, or almost five times as much as a year ago. As the Fund grows, it will be harder to make those kinds of returns.

Also, as our stocks and the market climb higher, it will be more difficult to achieve the kind of performance we’ve had over the past few years. For those of you expecting a repeat performance, you’re probably in the wrong fund. Remember that past performance is no guarantee of future returns.

Nevertheless, I’m still keeping a lot of my money in the Parnassus Small-Cap Fund, and I’ve been adding to my stake all along. I have yet to redeem any of my shares. The goal is still to beat the Russell 2000 over the long term. While I can’t promise a given outcome, I can promise to work hard and continue to apply the principles of the Parnassus Small-Cap Fund in a disciplined manner.

Since we have so many new shareholders, I think it makes sense to repeat those principles again in this report. First, we try to find companies that have unique characteristics, or a “moat” that defends a company’s castle from invasion by competitors. Of course, all companies face competition, but some are better equipped than others to handle that competition and we try to invest in those firms. We try to find companies that provide a product or service that meets an important need and has the potential to grow faster than the economy.

Second, we try to determine a company’s intrinsic value, and if the market price is far below the value of the company, it is a candidate for investment. Valuation is very important, as it gives us a margin of safety and provides some downside protection in falling markets.

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

Third, size and financial strength are important. At the time we buy them, almost all of our companies have market valuations below $3 billion, so we’re investing in smaller companies. However, we try to invest in companies that are in the higher end of that range and in firms that have strong balance sheets. We think size and financial strength give us an investing edge.

A fourth element is environmental, social and governance issues (ESG). Investing in companies with good ESG characteristics protects us from many negative forces such as labor problems, fines and lawsuits over environmental issues and faulty accounting. Companies that treat their employees well will have greater internal harmony and their workers are likely to be more productive.

Company Analysis

Seven companies in the portfolio each accounted for an increase of 37¢ or more for each fund share during the year. No stocks in the portfolio accounted for a loss of that much, so there were no significant losers. (The stock that lost the most only accounted for a loss of 14¢ on the NAV.) The seven winners accounted for most of the Fund’s gain during the year, and those stocks reflected three separate portfolio strategies. The first strategy was to invest in telecommunications equipment providers, anticipating that telecom service providers would have to increase their investments to upgrade their networks. Many Parnassus Funds shareholders may have noticed that they have experienced “dead spaces” and dropped calls while using their cell phones. The networks have been unable to keep up with the growing demand. My view was that service providers would have to buy more equipment to maintain service, so the equipment makers would benefit. Network investments did increase during the year, although not as much as I expected. Those equities went up anyhow, as investors bought the stocks, anticipating much higher investments in late 2011 and 2012. The stock market is a discounting mechanism, so securities trade more on future projections than on past results.

The stock that helped us the most was Finisar Corporation, a provider of optical equipment used in telecommunications. It rocketed up an incredible 233% from $8.92 to $29.69 for a gain of 75¢ for each fund share. Sales of its higher-speed products, such as ROADM, have been especially strong. ROADM is a device allowing firms to reconfigure wavelength remotely to address bandwidth needs. Even after all the price appreciation, we’re still hanging onto the stock because demand for bandwidth continues to grow from smartphones and other electronic devices.

Ciena Corporation also makes products for optical networks used in telecommunications, and its stock soared 94% from $10.84 to $21.05 while adding 56¢ to the NAV. Surging demand for video and smartphone bandwidth has put pressure on telecommunications carriers to buy more equipment. Because the company bought the optical equipment assets of Nortel Networks last year, sales have increased 90%, and this will enable Ciena to spread its costs over a higher volume of sales, which will eventually lead to higher earnings. The company has also indicated that it has been gaining market share.

The third telecom company that helped the Fund was Ceragon Networks, a provider of microwave equipment for wireless backhaul, which connects cellular telephone towers to the main communications network. The stock collapsed during the spring, sinking from $12 to $7, because the Indian government implemented security measures that temporarily prevented vendors from selling into this huge market. We took advantage of this opportunity by purchasing shares at the end of April at an average cost of $9.64. The government has now opened up the market again, the

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

company’s orders from India have bounced back and the stock ended the year at $13.18, an increase of 37% over our cost. Ceragon contributed 39¢ to the NAV.

The second strategy that paid off for us during the year was investing in companies that were selling at low prices because they were misunderstood by the investing public. Once new information emerged about these stocks, the prices went higher. The three companies in this category are Arbitron, Cyberonics and Administaff.

Arbitron is the industry standard radio ratings agency used in every top 50 U.S. market to determine listener audience, and hence, advertising rates. The misperceptions that radio is a declining medium, that competition would hurt the company and there was little innovation coming that would drive sales. As it turned out, people still listen to the radio and there was no major competitive threat. The latter became evident when Clear Channel Radio, Arbitron’s largest customer, signed a six-year contract extension, which alleviated customer concerns. As far as innovation goes, Arbitron came out with a Portable People Meter that gives exact measurements of what station someone listens to, as opposed to the traditional diary method, where survey participants write down which station they listened to. The company has been able to charge more for this innovation because the data are more exact and reliable. Arbitron contributed 54¢ to each fund share, as its stock climbed from $27.02 where we bought it during the year to $41.52 by year’s end for an increase of 54%.

Cyberonics makes implantable medical devices, and when we bought the stock during the year, it was unclear how successful its products would be, since some earlier products had not done well. As it turned out, its product for vagus nerve stimulation worked well to control epilepsy in patients for whom medicine was not effective. The product has been very effective, and new patient growth has been strong, especially in Japan, which is a large potential market. We bought the stock at $19.34 a share during the year, and it ended the year at $31.02 for an increase of 60% and a contribution of 43¢ to the NAV.

Administaff provides personnel services and employee benefits such as health insurance to small- and medium-sized businesses including Parnassus Investments. The stock moved 25% lower during the year, because of concern about the higher cost of benefits and the lower number of covered employees. What investors didn’t understand was that the lower number of covered employees and the medical cost issue were temporary phenomena. The stock moved higher as the number of covered employees increased and insurance costs declined. Administaff added 37¢ to each fund share, as its stock rose 24% from $23.59 to $29.30.

The third and final strategy that paid off for us during the year was a hedge against any possible increase in energy prices. At the beginning of the year, energy prices were much lower, and we thought there was a possibility that they would move higher in 2010. We had invested in oil- and natural gas-producer W&T Offshore a couple of years ago, and we added substantially to our position in early 2010 since the stock was trading at very depressed levels. As oil prices increased during the year, and the company acquired some valuable assets, the stock moved from $11.70 to $17.87 for an increase of 53% and a contribution of 62¢ to the NAV.

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

Outlook and Strategy

Beginning in early 2008, we had a lot of undervalued, small-cap stocks to choose from. Even six months ago, I had no trouble finding good companies selling at bargain prices. With the run-up in small-cap stocks this year, that situation has changed dramatically. Of course, most stocks have run up in 2010, but small-cap stocks have appreciated much more than large-cap ones. For example, the Russell 2000 index of smaller companies gained 26.85% during year, while the S&P 500 Index of large companies gained only 15.08%. In fact, an article in the Wall Street Journal pointed out that prices of small-cap stocks were relatively at their highest level in recent memory compared to large-cap valuations. At some point, this trend will reverse itself, and large-cap stocks will start to do better than small-cap stocks. It’s impossible to know when this will happen, and sometimes these trends go on for years. My guess, though, is that sometime late this year, large-cap issues will start to have better returns than small-cap stocks.

Since at some point small-cap issues will underperform large-cap stocks, and since I’m finding it difficult to find undervalued small-cap companies, some shareholders might consider taking their money out of the Fund. Personally, I’m keeping all my shares in my personal account and even adding to my stake in the Fund. Here’s why. First, stock market trends have a history of going on much longer than anyone thinks, and small-cap stocks usually do very well for several years after the economy comes out of a recession. Second, even though many small-cap stocks may be overvalued, I carefully watch the stocks in our portfolio with an eye toward avoiding overvalued issues and investing in companies only when they’re below our estimate of intrinsic value. Third, I think our strategy of investing in undervalued stocks with unique characteristics is a sound one and should do relatively well in all market environments. Fourth, the economy looks as if it’s starting to have solid, sustained growth again, and in this environment, the stock market should move higher, so even if small-cap stocks don’t do as well as large-cap stocks, we should still do pretty well. We probably won’t have the sizzling performance we’ve had the last three years, but chances are that we’ll do reasonably well.

Yours truly,

Jerome L. Dodson

Portfolio Manager

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

PARNASSUS WORKPLACE FUND

Ticker: PARWX

As of December 31, 2010, the NAV of the Parnassus Workplace Fund was $20.81, so after taking dividends into account, the total return for the quarter was 10.40%. This compares to 10.76% for the S&P 500 and 10.41% for the Lipper Large-Cap Core Average, which represents the average large-cap core fund followed by Lipper (“Lipper average”). (Note: As of the last quarter, Lipper has changed the category of the Parnassus Workplace Fund from multi-cap core to large-cap core, because according to Lipper’s guidelines, the Parnassus Workplace Fund had primarily large-cap companies in its portfolio.) For the quarter, the Fund was slightly behind both benchmarks.

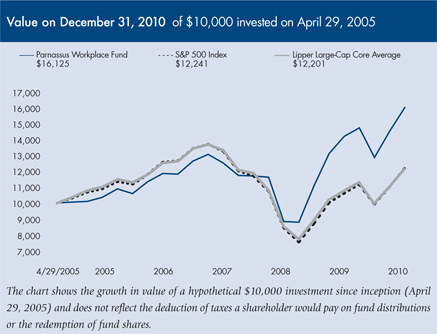

Below are a table and a graph that compare the Parnassus Workplace Fund with the S&P 500 and the Lipper average for the one-, three- and fi ve-year periods as well as the period since inception on April 29, 2005. While we’re behind the S&P 500 and the Lipper average for the one-year period, we’re far ahead of our benchmarks for all other time periods. The most striking comparison is for the three-year period, when the benchmarks showed negative returns, but the Parnassus Workplace Fund had a positive average return of over 8% per year.

Company Analysis

The Parnassus Workplace Fund had six stocks that each contributed 18¢ or more to the NAV and only one that cut that much off the value of the fund shares. That one was Gilead Sciences, whose stock fell 16% from $39.02 where we originally bought it to $32.68 where we sold it during the year. The Fund bought the stock because Gilead makes the world’s most prescribed AIDS drug, but we became concerned when early–stage clinical studies from competitors presented a threat to the company’s franchise. We also noticed that fiscal pressures in Europe caused governments to lower the prices they were willing to pay for Gilead’s drugs.

Parnassus Workplace Fund

| | | | | | | | | | | | | | | | | | | | | | | | |

Average Annual Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception

4/29/05 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended 12/31/2010 | | | | | | |

Parnassus Workplace Fund | | | 12.96 | | | | 8.66 | | | | 9.25 | | | | 8.79 | | | | 1.36 | | | | 1.20 | |

S&P 500 Index | | | 15.08 | | | | -2.84 | | | | 2.29 | | | | 3.63 | | | | NA | | | | NA | |

Lipper Large-Cap Core Average | | | 12.94 | | | | -3.23 | | | | 1.93 | | | | 3.49 | | | | NA | | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is available on the Parnassus website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2010, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.20% of net assets, exclusive of acquired fund fees, until May 1, 2011. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

The stock that helped the Parnassus Workplace Fund the most was Genzyme, a biotechnology company that produces drugs for patients born with rare genetic diseases. Its stock soared 45% from $49.01 to $71.20 for a gain of 37¢��per fund share. The company received a buyout offer from French pharmaceutical company Sanofi -Aventis. We’re holding our shares because we think the ultimate buyout price could be even higher. Genzyme has also made significant operational improvements to its business, which have increased its value.

Tractor-maker Deere & Co. saw a 54% increase in its stock price during the year, rising from $54.09 to $83.05 for a gain of 30¢ for each fund share. The company reported stronger than expected sales of tractors and combines, as much higher prices for corn and other agricultural products mean higher income for farmers. Sales in Russia and Brazil have been especially strong, and Deere has moved to strengthen operations in those high-growth countries including improving financing terms for customers.

Qualcomm, a provider of software and semiconductors used in cellular telephone handsets, had a rollercoaster year. The stock fell 35% in the fi rst half of the year, as investors feared that price declines for cell phones would continue and have a heavy impact on the

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

company. After this drop, we added to our position, making Qualcomm the largest position in the portfolio. The stock made a full recovery in the second half and added 23¢ to the NAV, as the shares went from $46.26 at the beginning of the year to $49.49 at the end. Our average cost, though, is only $39.79 because we bought on dips.

SEI is an asset-manager and also provides services and support to other asset-managers. The stock rose 36% during the year from $17.52 to $23.79 for a gain of 20¢ on the NAV. Most of the company’s revenue comes from fees earned from assets under management and administration, so the stock went up during the year along with the equity markets.

The stock of eBay climbed 18% during the year from $23.54 to $27.83, adding 20¢ to the NAV. While eBay’s core Marketplace business struggled in early 2010, the company made significant improvements to its auction website, evidenced by improving internet traffic and more listings. The company’s PayPal business posted impressive financial results because of market share gains and strong trends in e-commerce.

Autodesk, the leading producer of construction design software, added 18¢ to each fund share, as its stock price surged 50% from $25.41 to $38.20. The stock had been trading at depressed levels early in the year because of weak demand for its software. The shares moved higher in the second half of the year in anticipation of increased construction activity. Big customer orders came in late in the year, pushing the stock even higher.

Yours truly,

Jerome L. Dodson

Portfolio Manager

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

PARNASSUS FIXED-INCOME FUND

Ticker: PRFIX

As of December 31, 2010, the NAV of the Parnassus Fixed-Income Fund was $16.90, producing a total return for the year of 6.61% (including dividends). This compares to a gain of 6.59% for the Barclays Capital U.S. Government/Credit Bond Index (“Barclays Capital Index”) and a gain of 7.51% for the Lipper A-Rated Bond Fund Average, which represents the average return of all A-rated bond funds followed by Lipper (“Lipper average”). For the fourth quarter, the Fund was down 2.06% compared to a loss of 2.17% for the Barclays Capital Index and a loss of 1.09% for the Lipper average.

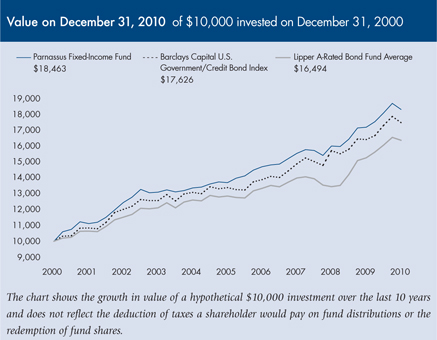

Below is a table comparing the performance of the Fund with that of the Barclays Capital Index and the Lipper average. Average annual total returns are for the one-, three-, five- and ten-year periods. The 30-day subsidized SEC yield for the Fund for December 2010 was 1.25%. We’re pleased to report that our long-term returns are better than the Lipper average and the Barclays Capital Index for the three-, five- and ten-year periods as of the end of the year.

2010 Review

Through the beginning of November, the U.S. Treasury market enjoyed an impressive rally. Investors sought safety in U.S. Treasuries amid weaker than expected economic data, European sovereign debt concerns, a slowdown in the Chinese economy and the anticipation of another round of government bond purchases by the Federal Reserve.

The middle of the yield curve, 5-year to 7-year maturities, benefited the most from this flight to safety. The yield on the 5-year bond reached a low of 1.01% in early November compared to 2.68% at the end of 2009. Meanwhile, the 7-year bond yield troughed at 1.69% in early November after ending 2009 at 3.38%.

Parnassus Fixed-Income Fund

| | | | | | | | | | | | | | | | | | | | | | | | |

Average Annual Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended 12/31/2010 | | | | | | |

Parnassus Fixed-Income Fund | | | 6.61 | | | | 5.67 | | | | 6.05 | | | | 6.32 | | | | 0.88 | | | | 0.76 | |

Barclays Capital U.S. Government/Credit Bond Index | | | 6.59 | | | | 5.60 | | | | 5.56 | | | | 5.83 | | | | NA | | | | NA | |

Lipper A-Rated Bond Fund Average | | | 7.51 | | | | 5.19 | | | | 4.78 | | | | 5.24 | | | | NA | | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Returns shown in the table do not reflect the deduction of taxes a shareholder would pay in fund distributions or redemption of shares. The Barclays Capital U.S. Government/Credit Bond Index is an unmanaged index of bonds, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees, or taxes into account, but mutual fund returns do. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is on the Parnassus website, or one can be obtained by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2010, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.75% of net assets, exclusive of acquired fund fees, until May 1, 2011. This limitation may be continued indefinitely by the Adviser on a year-to-year basis.

The holiday season ended up being not very festive for bond investors. The final months of 2010 saw a speculative burst following the Federal Reserve’s announcement of another round of quantitative easing to support the economic recovery. This jolt of optimism pushed investors back into the stock market. As a result, the Treasury market experienced an abrupt reversal, with a dramatic rise in yields. The middle of the yield curve saw the largest increases, because it had reached very low levels compared to other maturities. For example, between November and December, the 5-year bond yield doubled from its low of 1.01% to end the year at 2.00%.

The Fund’s performance during the fourth quarter was therefore disappointing, with a loss of 2.06%. The loss resulted primarily from the Fund’s sensitivity to the middle of the yield curve, as bond prices move inversely to interest rates. The Fund was down 11 basis points (a “basis point” is 1/100th of a percentage point) less than the Barclays Capital Index, because we had less exposure to the underperforming Treasury market.

However, we underperformed the Lipper average by 97 basis points, because we owned more Treasury bonds than most of our peers. This underperformance is especially frustrating, because it more than erased the lead over the Lipper average that the Fund had accumulated through the end of the third quarter.

Despite this fourth quarter setback, the Fund

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

returned 6.61% for the year. This is roughly in line with the Barclays Capital Index, but behind the Lipper average by 90 basis points. For the year, all asset classes in the portfolio contributed positively to the NAV. Our corporate bonds were the biggest winners, adding 46¢ to the NAV. U.S. government bonds, which include U.S. Treasuries and U.S. agencies, increased the NAV by 45¢ and our convertible bonds added 22¢.

Outlook and Strategy

Having a skeptical view on the sustainability and strength of the economic recovery played out well last year. Contrary to most forecasts, interest rates moved lower across the yield curve and pushed bond prices higher during most of 2010. However, with the dramatic increase in yields in the past few months, the challenge is whether this rise will persist in 2011.

While many factors influence interest rates, it’s safe to assume that the improved U.S. economic outlook played an important role in the recent increase. Indeed, starting in December, several coincident and leading economic indicators have improved notably. Hence, the direction for interest rates is likely tied to the path of economic improvements. How much more progress is there then?

The answer is not straightforward. The arguments for and against further economic improvements seem to be equally convincing. On the one hand, recent economic indicators, such as jobless claims and retail sales, are encouraging. Also, the economy should get a temporary boost from new fiscal measures, such as the extensions of the Bush-era tax cuts and unemployment benefits, as well as a reduction in payroll tax. Moreover, U.S. companies are flush with cash, with a ratio of cash to total assets of about 7.4%, the highest since 1960. In turn, this should bode well for mergers and acquisitions, dividend payouts, and stock buybacks.

| | | | |

Parnassus Fixed-Income Fund as of December 31, 2010 | | | |

| (percentage of long-term portfolio) | | | |

| |

Portfolio Composition | | | | |

| |

U.S. Government Treasury Bonds | | | 63 | % |

Corporate Bonds | | | 32 | % |

Convertible Bonds | | | 5 | % |

| | | | |

| | | 100 | % |

Portfolio characteristics and holdings are subject to change periodically.

On the other hand, the housing market, which has historically led U.S. economic recoveries, is still missing in action. The S&P/Case-Shiller Home Price Index has started to go down in recent months. The employment market also remains weak, with a stubbornly high unemployment rate over 9%. In addition, state and local governments are facing substantial budget deficits. This means that we’ll likely see tax hikes and public sector layoffs. Finally, rising oil prices will start to create economic headwinds, if they remain at the current elevated level of $90 per barrel.

All things considered, I think that the risk of further significant increases in interest rates is relatively low for now. As mentioned above, there are still major hurdles before strong economic growth resumes and translates into high inflation. Moreover, the Federal Reserve will likely ensure that higher bond yields do not destabilize the financial system and the broader economy.

As of the end of 2010, the Fund is positioned for moderate economic improvement, but hedged for the possibility of renewed economic weaknesses. Of our total net assets, 36% is invested in high quality corporate bonds and convertible bonds, which would perform well with a slowly growing economy. The Fund would also benefit in case of disappointing economic data with 60% of the total net assets invested in Treasury bonds.

Thank you for your confidence and investments in the Parnassus Fixed-Income Fund.

Yours truly,

Minh T. Bui

Portfolio Manager

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

Responsible Investing Notes

By Milton Moskowitz and Jerome Dodson

2010 was marked by the largest oil spill in the history of the petroleum industry, caused by a wellhead blowout at a Gulf of Mexico deepwater rig operated by BP. Oil fl owed into the Gulf waters for three months before the wellhead was capped in July. Eleven workers on the rig were killed in the initial explosion. The spill was at least 10 times greater than the Exxon Valdez spill in Alaska in 1989. Thanks to the initiative of the late Joan Bavaria, the Exxon Valdez spill sparked the launch of the Coalition for Environmentally Responsible Economies (CERES), which has become the principal force in getting companies to address sustainability challenges and climate change. It’s not clear yet whether the BP spill will result in comparable actions. One of the troubling concerns is that of all the companies in the petroleum industry, BP was widely regarded as the most sensitive to environmental issues and the need to tap alternative sources of energy. Its shares have never appeared in Parnassus Funds portfolios, but they were considered acceptable by other responsible investment funds. Our current portfolios include nine energy companies: Energen, Ultra Petroleum, Spectra Energy, Southwestern Energy, W&T Offshore, AGL Resources, Devon Energy, MDU Resources and SM Energy. They are heavily weighted on the natural gas side.

MDU Resources, which is engaged in construction and utility operations in addition to oil and gas production, issued its 2010 Sustainability Report, showing sharp improvements in safety and health practices. The company had a recordable incidence rate of 3.4 in 2009, a 10.5% reduction from 2008 and 32% better than the industry average. (Recordable incident rates are computed by multiplying the number of injuries and accidents by employee hours worked.) MDU accepts the responsibility of providing “a safe work environment,” and its safety policy begins with this statement: “All injuries can be prevented.”… No country has propelled more women into top positions than Norway, where there is now a law mandating that at least 40% of board seats in corporations be reserved for women. However, one of our portfolio companies, the wholesale food distributor Sysco, comes close to meeting that standard. Of the 12 people on its board of directors, four are women: Judith B. Craven, retired CEO of Corus Entertainment; Nancy C. Newcombe, retired risk management officer at Citibank; Phyllis S. Sewell, retired senior vice president, Federated Department Stores; and Jackie M. Ward, founder of Computer Generation, now a part of Intec Telecom Systems…Wells Fargo, the nation’s third largest bank, opened 27 Home Preservation Centers in distressed markets impacted by foreclosures. It then met face-to-face with more than 15,000 home loan customers seeking modifications in their mortgages. Workshops were held in 15 cities across the country. Wells said that it had added 10,600 jobs to deal with the foreclosure crisis — and that it now had more than 16,000 team members “focused on home preservation.”

Lowe’s Companies, which grew from a small hardware store in North Carolina into the nation’s second largest home improvement chain (behind Home Depot), issues annually one of the best social responsibility reports. Its latest report focuses on global sourcing. The average Lowe’s store stocks 40,000 products, which come from more than 900 factories in 19 countries. Lowe’s uses factory certifications, random social compliance audits, product tests and pre-shipment inspections to insure that its suppliers do not use child labor and “operate safe and ethical factory environments.” In 2009, the company carried out more than 900 factory certifications and more than 2,100 random social compliance audits… According to a report in FastCompany.com, Procter & Gamble will soon require its suppliers to fill out a scorecard showing their ratings in energy and water use, waste and greenhouse gas emissions. The consumer products giant has some 75,000 suppliers across the world.

| | |

Annual Report · 2010 | | PARNASSUS FUNDS |

Companies in Parnassus Funds portfolios did well in the latest ranking of homebuilders, based on their green sensibilities. The ranking was done by Calvert Asset Management, which listed the following as the Top 10: KB Home, Pulte Homes, Meritage Homes, Toll Brothers, Lennar, DR Horton, Standard Pacific, NVR, Ryland Group and MDC Holdings. Three of the Top Five — KB Home, Pulte Group and Toll Brothers — are Parnassus Holdings, as is No. 6, DR Horton. Calvert noted that KB Home is the only homebuilder to issue a comprehensive sustainability report.

Social responsibility activists celebrated last November 13 when the military junta in Myanmar released pro-democracy leader Aung San Suu Kyi from the house arrest she has been under for most of the past 20 years. A Nobel Peace laureate, Suu Kyi has been a lightning rod for human rights groups trying to effect change in the country that used to be called Burma. They have urged boycotts of companies active in Myanmar. Among the major companies operating there are Total, the French oil company, Suzuki of Japan, Daewoo of South Korea and Union Oil, a subsidiary of Chevron. “Her dignity and courage in the face of injustice has been an inspiration to many people around the world,” said UN Secretary-General Ban Kimoon.

And one final note: Alex Edmans, assistant professor of finance at the University of Pennsylvania’s Wharton School, has written a paper exploring why the stock market does not fully value intangibles like employee satisfaction. His studies have shown that companies on the 100 Best Companies to Work for list have consistently beaten all the averages, yet the market pays little or no heed to this phenomenon. The big news is that his paper has been accepted by the Journal of Financial Economics. It will mark the first time that a leading academic journal has published a paper that is positive about responsible investing. Hallelujah!

| | |

PARNASSUS FUNDS | | Annual Report · 2010 |

Fund Expenses (unaudited)