PARNASSUS INCOME FUNDS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06673

Parnassus Income Funds

(Exact name of registrant as specified in charter)

One Market—Steuart Tower #1600, San Francisco, California 94105

(Address of principal executive offices) (Zip code)

Marc C. Mahon

Parnassus Income Funds

One Market—Steuart Tower #1600, San Francisco, California 94105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (415) 778-0200

Date of fiscal year end: December 31

Date of reporting period: December 31, 2007

| Item 1: | Report to Shareholders |

THE PARNASSUS FUNDS

Annual Report December 31, 2007

Parnassus Fund Parnassus Small-Cap Fund Parnassus Equity Income Fund Parnassus Workplace Fund Parnassus Mid-Cap Fund Parnassus Fixed-Income Fund

| | | |

Parnassus Fund | | (PARNX | ) |

Parnassus Equity Income Fund–Investor Shares | | (PRBLX | ) |

Parnassus Equity Income Fund–Institutional Shares | | (PRILX | ) |

Parnassus Mid-Cap Fund | | (PARMX | ) |

Parnassus Small-Cap Fund | | (PARSX | ) |

Parnassus Workplace Fund | | (PARWX | ) |

Parnassus Fixed-Income Fund | | (PRFIX | ) |

TABLE OF CONTENTS

THE PARNASSUS FUNDS

February 11, 2008

DEAR SHAREHOLDER:

It was quite a ride for stocks in 2007. They rose at a healthy clip in the first half of the year, reflecting a relatively resilient economy, but the market deteriorated in the second half as investors became concerned about the mortgage crisis and the condition of the economy overall. Despite the cut in interest rates by the Federal Reserve, we saw the unemployment rate rise to 5% by year-end. The Parnassus Equity Income Fund had a great year, returning 14.1% versus 5.5% for the S&P 500. In this report, you’ll find out more about how each of our funds performed, as well as our outlook and strategy. We have combined the information on all of our funds into one report to make them easier for shareholders to read and also to save paper.

Shareholder Communication Awards

We believe an essential part of our job in serving you, the shareholder, is to communicate how we’ve performed for you and how we invest in general. We try to use plain language and explain things in a straightforward way. We try to talk about our mistakes as well as our successes. We take pride in these reports, but until now, you’ve had to take our word for it that these reports are among the best in the mutual fund world. Now we’re proud to say that we have some confirmation. In October, the Mutual Fund Education Alliance (MFEA) awarded Parnassus with their STAR award for the best Annual Report to Shareholders for a small fund group. The MFEA is a mutual fund industry trade group that gives annual awards to fund groups for various categories in shareholder communication. We also won the award for the best retail website, also for the small fund category. We believe our website is a great tool to provide our shareholders with current and historical information on their investment with Parnassus. We won’t let these awards go to our head, though. We’ll keep working hard to write informative, clearly-written reports; we’ll also keep improving our website.

Thank you for being an investor with Parnassus.

| | |

| |  |

| |

| Jerome L. Dodson | | Stephen J. Dodson |

| President | | Executive Vice President and |

| | Chief Operating Officer |

THE PARNASSUS FUND

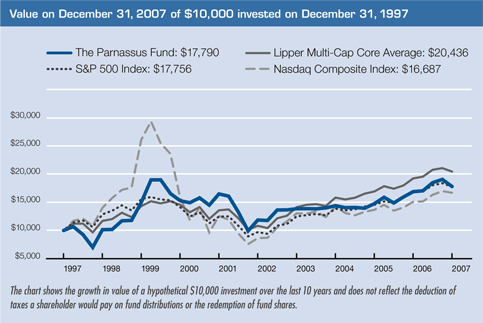

As of December 31, 2007, the net asset value per share (NAV) of the Parnassus Fund was $36.66, so after taking dividends into account, the total return for the year was 5.43%. This compares to 5.49% for the S&P 500 Index (“S&P 500”), 6.43% for the Lipper Multi-Cap Core Average and 10.66% for the Nasdaq Composite Index (“Nasdaq”). We finished the year with about the same return as the S&P 500, but we lagged behind both the Nasdaq and the Lipper average.

Although we finished the year in line with the S&P 500, the results were disappointing, considering that year-to-date figures at the end of the September quarter showed that we were 3.7 percentage points ahead of the S&P 500, 3.42 percentage points ahead of the Lipper average and 0.35 percentage points ahead of the Nasdaq. The Fund had a difficult fourth quarter, as we dropped 6.56% compared to a decline of only 3.33% for the S&P 500 and 2.88% for the Lipper average. We’ll discuss what happened in the Analysis.

For the longer term (ten-year period), the Fund is slightly ahead of the S&P 500 and the Nasdaq, but somewhat behind the Lipper average. Below are a table and a graph comparing the Parnassus Fund with the S&P 500, the Nasdaq and the Lipper Multi-Cap Core Average over the past one-, three-, five- and ten-year periods.

Average Annual Total Returns

for periods ended December 31, 2007

| | | | | | | | | | | | | | | | | | |

| | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

PARNASSUS FUND | | 5.43 | % | | 7.33 | % | | 8.46 | % | | 5.93 | % | | 1.02 | % | | 1.00 | % |

S&P 500 Index | | 5.49 | % | | 8.62 | % | | 12.82 | % | | 5.91 | % | | NA | | | NA | |

Lipper Multi-Cap Core Average | | 6.43 | % | | 8.73 | % | | 13.33 | % | | 7.07 | % | | NA | | | NA | |

Nasdaq Composite Index | | 10.66 | % | | 7.65 | % | | 15.46 | % | | 5.90 | % | | NA | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Standard and Poor’s 500 Composite Stock Price Index, also known as the S&P 500 Index and the Nasdaq Composite Index are unmanaged indices of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. Prior to May 1, 2004, the Parnassus Fund charged a sales load (maximum of 3.5%), which is not reflected in the total return calculations. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is on the Parnassus website, or you can get one by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2007, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.99% of net assets, exclusive of acquired fund fees, through April 30, 2008.

Analysis

Before I analyze the Fund’s annual performance, I would like to explain the reasons for the shortfall in the fourth quarter. As I indicated earlier, at the end of the third quarter, we were ahead of the S&P 500 by over three percentage points, but the Fund lost 6.56% in the fourth quarter, compared to a loss of 3.33% for the S&P or a difference of 3.23 percentage points. The losses from just three companies in the portfolio accounted for a 3.47% decline in the NAV during the quarter, or enough to mean the difference between a substantial edge over the S&P, and falling slightly short of that benchmark for the year.

The stock having the biggest impact for the quarter was the SLM Corporation, better known as Sallie Mae, a provider of student loans for higher education. SLM began the fourth quarter trading at $49.67 a share, but ended the year at $20.14 for an incredible drop of 59% or 78¢ for each Parnassus share. The company had accepted a buyout offer of $60 per share from J.C. Flowers & Co., backed by J.P. Morgan Chase and the Bank of America. After the buyout offer was announced, the stock climbed into the 50’s, but then the Flowers Group withdrew the offer, citing the reduced federal subsidy for student loans and difficult conditions in the credit markets. We sold some shares in the $55-$56 range, but we held onto most of our shares when the stock dropped into the 40s. SLM management indicated that the deal would go through, and there was also a provision that the Flowers Group would have to pay a $900 million break-up fee if they did not complete the transaction. In the end, Flowers reneged on the deal and refused to pay the break-up fee, claiming that conditions had changed. SLM is now suing the Flowers Group.

Much to my surprise, the stock plunged into the 20’s, far below my assessment of its intrinsic value. We’re holding the stock, because we think it’s worth far more that its current quotation.

Powerwave Technologies, a maker of infrastructure products for cellular telephone networks, dropped 35% during the quarter, sinking from $6.16 to $4.03 for a loss of 35¢ for each Parnassus share. Disappointing earnings including a loss for the year, combined with a negative forecast by the company for the immediate future, sent the shares lower. We’re holding the stock, since we think it’s trading at bargain-basement levels, and we think the shares will move higher as wireless phone companies increase capital budgets to build out pending 3G networks.

The third company was Tuesday Morning, a home-furnishings retailer, whose stock dropped 44% from $8.99 to $5.07 for a loss of 29¢ on the NAV for the quarter. The company’s earnings fell far short of expectations because of the weak home-furnishings market, which caused heavy discounting and very low margins.

Because their losses were so great in the fourth quarter, these three companies also accounted for the three biggest losses for the Fund on an annual basis, with each costing the Fund more than 32¢ on the NAV. For the year, SLM dropped 59%, going from $48.77 to $20.14 for a loss of 52¢ for each Parnassus share. Tuesday Morning sank 67% from $15.55 to $5.07, slicing 48¢ off the NAV. Powerwave lost 38%, sliding from $6.45 to $4.03, depressing the NAV by 33¢ for the year.

Fortunately, those three were the only ones that cost us 32¢ or more on the NAV. By contrast, seven companies each added 32¢ or more to each Parnassus share for the year. The big winner was Invitrogen, a company that provides research tools in kit form along with other research products and services to government agencies, corporations and universities involved in molecular biology research. For the year, Invitrogen boosted the NAV by an awesome 72¢ for each Parnassus share, with its stock soaring 65% from $56.59 to $93.41. A restructuring of its product line and redirection of its sales force resulted in higher revenue.

Apache Corporation saw a 62% increase in its stock price, rocketing up from $66.51 to $107.54 for a gain of 63¢ for each Parnassus share. The company searches for and produces oil and natural gas, and the high price of energy has helped the company’s earnings. Also important are new discoveries and increasing output from its natural gas fields in Egypt and increased output from its fields in Australia.

Intel’s share price rose 32% from $20.25 to $26.66 for an increase of 56¢ on the NAV. Intel’s technology leadership and manufacturing advantage over AMD moved the stock higher, as did strong PC and notebook sales, particularly in Europe and Asia.

Citrix Systems climbed 41% during the year from $27.05 to $38.01, adding 53¢ to the NAV. Demand for the company’s core product, PresentationServer, increased substantially, as customers from locations around the world used it to connect their computers to the applications and databases at corporate headquarters. Citrix also saw strong demand for products that control the flow and speed of data delivery within the Internet network.

Ciena makes optical network products for telecommunications providers. Its stock climbed 23% during the year from $27.71 to $34.11 for an increase of 44¢ per fund share. Telecommunications providers have increased capital spending to cope with higher demand for bandwidth. Ciena has been able to increase its operating margins from zero to 16% and revenue is growing at well over 20%.

Texas Instruments contributed 34¢ to each Parnassus share, as its stock went from $28.80 to $33.40 for an increase of 16%. The stock price was depressed at the beginning of the year because of excess inventory. These levels dropped during the first half of 2007, as sales increased for telecommunications semiconductors and a wide range of other products.

Headset-maker Plantronics added 32¢ to each fund share, as the stock climbed 23% from $21.20 to $26.00 by the end of the year. Sales to offices and call centers continue to be strong, and prices are stable, partially because of a competitor’s weakness.

Outlook and Strategy

With this annual report, we have combined all six Parnassus Funds into one report. Each portfolio manager will write his own Outlook and Strategy section. This analysis in the Parnassus Fund section applies to all four funds that I manage: the Parnassus Fund, the Workplace Fund, the Small-Cap Fund and the Mid-Cap Fund.

As this report is being written in mid-January, the economy looks weak. The sub-prime mortgage crisis has made the weak housing market even weaker, and home prices have dropped more than we’ve seen in decades. (There are, of course, a few exceptions to this pattern of falling home prices. Here in my hometown of San Francisco, prices have, on balance, remained firm.) Consumer spending has also been weak across the country either because of the housing crisis, because of high gasoline prices, or for both reasons. This weakness is also reflected in the job market, as the unemployment rate for December climbed from 4.7% to 5.0%—a large increase.

The housing and sub-prime mortgage crises have also changed the debt markets. For years now, there has been an abundant supply of low-cost debt for both speculative and non-speculative purposes. It is now very difficult to borrow for speculative purposes, whether for sub-prime mortgages or highly-leveraged buyout deals.

The stock market fell in the fourth quarter of 2007, and it continues to fall even more in January. The November to April period is normally the strongest time of the year, and the stock market usually goes higher. This unusual decline reflects economic uncertainty.

Although a slight majority of economists are saying that we will avoid a recession, a substantial minority are predicting one in 2008. I’m not sure if we’ll have a recession, but slow-growth and no-growth often feel the same. Regardless of what you call it, the economy will be weak.

On the positive side, if there is a recession, I expect it to be a mild one. The Federal Reserve has done a good job handling this economic weakness—not only by lowering interest rates, but also by making credit more readily available in the banking system and by coordinating with the central banks of other developed nations, so that credit will be readily available overseas. Interest rates are quite low right now, and this should help us to weather the economic storm.

There still won’t be funds available for speculative borrowing such as sub-prime lending and the more highly-leveraged buyouts, but in my opinion, that’s a positive. There’s ample credit available for more constructive economic purposes.

I’m finding a lot of bargain-priced stocks in the market today. It’s possible that shares will go down further, but eventually prices will bounce back.

My current strategy is to stay fully invested, even with the present economic uncertainty. Right now, we have almost half the portfolio in technology stocks, because in my judgment, these stocks have the potential to go a lot higher. Although stocks may fall further, when they come back, they come back quickly, and I don’t want to be on the sidelines.

| | |

| | Yours truly, |

| |

| | |

| |

| | Jerome L. Dodson |

| | President |

THE PARNASSUS EQUITY INCOME FUND

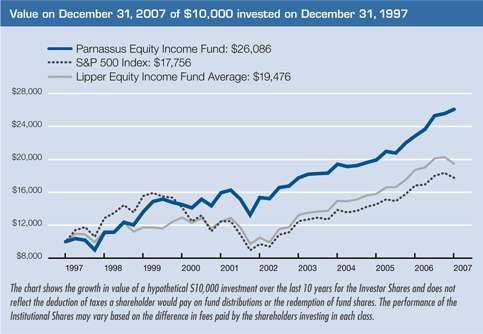

As of December 31, 2007, the net asset value per share (NAV) of the Equity Income Fund – Investor Shares was $25.31, so after taking dividends into account, the total return for 2007 was 14.13%. This compares to a return of 5.49% for the S&P 500 index (“S&P 500”) and a gain of 4.00% for the average equity income fund followed by Lipper, Inc. The Fund had a great year, as our research team avoided stocks linked to the housing downturn and generated strong gains in the energy, technology, healthcare and insurance sectors. This portfolio strategy proved especially valuable during the volatile fourth quarter of 2007. The Fund was up 2.04% versus a loss of 3.33% for the S&P 500 and a decline of 3.96% for the Lipper index.

While 2007 was a great year, our investment philosophy of engaging in rigorous research to find good businesses at undervalued prices has generated solid long-term results. Despite volatile markets, the Fund has generated average annual returns of more than 10% for the one-, three-, five- and ten-year periods. We are especially pleased that our 10-year average annual return of 10.07% is ahead of the S&P 500’s average annual gain by over 4% per year.

Below are a table and a graph that compare the performance of the Fund with that of the S&P 500 and the average equity income fund followed by Lipper. Average annual total returns are for the one-, three-, five- and ten-year periods.

Average Annual Total Returns

for periods ended December 31, 2007

| | | | | | | | | | | | | | | | | | |

| | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

EQUITY INCOME FUND– | | | | | | | | | | | | | | | | | | |

Investor Shares | | 14.13 | % | | 10.34 | % | | 11.18 | % | | 10.07 | % | | 1.07 | % | | 1.00 | % |

Institutional Shares | | 14.35 | % | | NA | | | NA | | | NA | | | 0.86 | % | | 0.79 | % |

S&P 500 Index | | 5.49 | % | | 8.62 | % | | 12.82 | % | | 5.91 | % | | NA | | | NA | |

Lipper Equity Income | | | | | | | | | | | | | | | | | | |

Fund Average | | 4.00 | % | | 9.20 | % | | 13.05 | % | | 6.66 | % | | NA | | | NA | |

The total return for the Equity Income Fund-Institutional Shares from commencement (April 28, 2006) was 13.12%. The performance of Institutional Shares differ from that shown for the Investor Shares to the extent that the Classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Standard and Poor’s 500 Composite Stock Index, also known as the S&P 500 is an unmanaged index of common stock, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. On March 31,1998, the Fund changed its investment objective from a balanced portfolio to an equity income portfolio. Before investing, an investor should carefully consider the investment objectives, risk, charges and expenses of the Fund and should carefully read the prospectus which contains this and other information. The prospectus is on the Parnassus website or you can get one by calling (800) 999–3505. As described in the Fund’s current prospectus dated, May 1, 2007, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.99% and 0.78% of net assets, exclusive of acquired fund fees, through April 30, 2008 for the Investor Shares and Institutional Shares, respectively.

Review of 2007

The Fund had a terrific year in 2007, as our return of 14.13% far exceeded the 5.49% return for the S&P 500 and the 4.00% return for the Lipper Average. Going into 2007, many of my most trusted analysts, advisors and contacts were telling me to avoid stocks linked to the housing and mortgage market. I was even getting a few calls from my mother in Sonoma County, telling me home prices were starting to fall in the beautiful wine country. I agreed with my team’s advice, and the biggest driver of our 2007 performance was avoiding bank stocks and finding profitable investments in financial companies not linked to sub-prime mortgages.

As the year unfolded, our theory about the housing market proved correct. Dominating the news were near daily reports of falling real estate prices, delinquent mortgages and home foreclosures. The severity and frequency of the bad news accelerated during 2007, and as the year reached a close, the average financial stock in the S&P 500 had declined a whopping 18.6% for the year. As a result, our decision to underweight the financial sector in the portfolio added 2.0% to our lead versus the S&P 500 during 2007.

While the strategy of sidestepping mortgage companies proved to be correct, it was our stock-picking within the financials sector that added the most to our performance in 2007. While the average financial stock in the S&P 500 plunged over 18%, ours rose 7.2% for 2007. We posted large investment gains in stable, growing insurance companies such as AFLAC and the Tower Group. As these companies reported strong earnings, they attracted investors fleeing the troubled home finance sector. This positive stock picking in the financial sector boosted our return by an amazing 3.5% for the year versus the S&P 500. As a result, due to some superb research by my analysts, the final scoreboard showed the financial sector accounting for 5.5% of the Fund’s 8.64% outperformance relative to the S&P 500 for 2007.

Healthcare was the second-largest contributor to our performance in 2007, as good stock-picking and an overweight position added 2.18% to our return versus the S&P 500. Analysts Pearle Lee, Ben Allen and Matt Gershuny all did a great job identifying healthcare stocks that could grow earnings despite a slowing economy.

The Fund also did very well in energy as the industry added 1.34% to our lead versus the S&P 500. We entered the year very bullish on the prospects for oil prices and had profitable investments across exploration, pipelines and refiners.

Finally, our technology exposure, lead by senior analyst Lori Keith, had a strong year, boosting our return by 1.17% versus the S&P 500. She did an outstanding job finding stocks with strong catalysts, trading at undervalued prices.

While I am very pleased with the Fund’s results, rest assured our team is working harder than ever to maintain our strong long-term performance. Over the past three years, we have hired five very talented analysts who are making significant contributions to the Fund. I am honored to work with this team.

Company Analysis

Tuesday Morning, the closeout retailer of home goods, was the Fund’s biggest disappointment this year. The stock dropped 67%, from $15.55 to $5.07, reducing the NAV by 33¢. This investment has suffered from the twin evils of being associated with housing and retail. Like Pier 1 and Restoration Hardware, Tuesday Morning saw store traffic drop dramatically from the levels of a few years ago. This resulted in industry-wide discounting, which greatly reduced earnings.

The Fund’s biggest winner of 2007 was oil and gas exploration company Apache. Based on record-high oil prices and strong production growth, the stock soared 62% during 2007 from $66.51 to $107.54, which increased the NAV by a whopping 57¢. I met with management during 2007 in Boston, Houston and New Orleans and remain very impressed with their business. Not only does Apache do a great job finding oil and gas around the globe, they also operate with responsible business ethics. The company is utilizing cutting-edge carbon-dioxide injection technology in Canada that helps reduce greenhouse gases. In addition, Apache is building dozens of schools for young girls in Egypt.

Microsoft was a big contributor to the Fund, adding 30¢ to the NAV, as the stock gained 20% from our cost of $29.57 to $35.60. This is a new investment for the Fund, as Parnassus has avoided Microsoft in the past, due to concerns about the company’s aggressive business practices and anti-trust lawsuits. However, as of 2006, many of Microsoft’s largest class action lawsuits were resolved. This prompted a social review at Parnassus, during which we concluded that Microsoft was eligible for investment. We were especially impressed that Microsoft leads the way in establishing common labor standards for electronics suppliers, provides terrific employee benefits and is dedicated to maintaining a diversified workplace.

Once Microsoft passed our social screen, Senior Analyst Lori Keith led the fundamental research efforts. She convinced me that the company’s leadership in desktop software and its rich pipeline of new products for mobile devices, servers and desktops, made the investment attractive. I believe that these positive attributes will support the stock, even if the economy slows down. This is why Microsoft was the largest position in the portfolio at year-end.

Google was up 51% from our average cost of $458 to $691 at year-end, adding 28¢ to the NAV. The company continues to win market share in the high-growth online-advertising industry. As of last November, according to industry analysis firm ComScore, Google enjoyed a 59% market share of Internet searches in the United States and a 70% share internationally. This share should increase throughout 2008.

Back in October, Senior Analysts Ben Allen and Lori Keith attended Google’s annual analyst day. They reported that the company’s core Internet search business should continue to outpace industry growth. They also were excited about the company’s other growth opportunities, like YouTube and non-Internet advertising. It is because of these exciting growth opportunities that the Fund still has a sizeable position in Google.

Chemed was our big winner in healthcare this year, as the stock was up 51% from $36.98 to $55.88, adding 26¢ to the NAV. As you may recall from previous reports, Chemed is the parent company of VITAS, the leader in the hospice industry, and Roto-Rooter, the leader in plumbing and drain-cleaning services. The stock was up this year because both business lines performed well, allowing the company to achieve earnings higher than expected. Even more impressive to me than these earnings is the consistent cash-flow that the company generates. As analyst Ben Allen reminds me, Chemed’s cash-flow generation and predictable businesses should support the stock even if the economy gets rocky. This is why I have increased my holdings in Chemed since the third quarter.

Insurance company AFLAC had a great year, boosting the NAV by 21¢ as the stock soared 36% from $46 to $62.63 per share. The company began 2007 plagued by investor pessimism about the challenging life insurance market in Japan and the company’s turnaround initiatives. Throughout 2007, however, AFLAC has demonstrated that the turnaround in Japan sales has made solid progress and the momentum in the U.S. business remains strong. In addition, as a testament to the company’s superior franchise, AFLAC has been selected by the Japan Post Office to be the exclusive provider of cancer insurance through the nationwide postal office network. Finally, the general flight to quality financial companies that followed the debacle of financial stocks has contributed to

renewed interests in a company that is benefiting from significant exposure to non-U.S. operations and can deliver consistent double-digit earnings growth.

Valero, the large refinery company, had a great year as its stock jumped 37% to $70.03 from $51.16, boosting the NAV by 20¢. Based on strong demand for petroleum products and limited refining capacity in the U.S., Valero’s profit margins hit record levels of over $20 a barrel during 2007. We remain bullish on Valero’s long-term prospects. It is now the largest oil refiner in North America and it has been 30 years since a new refinery has been built in the United States. While the company still has room for improvement, Valero has been doing a much better job in recent years in improving its environmental record.

Strategy For 2008

For 2008, we will continue to play defense as the economic picture looks weak. While the U.S. economy grew at a robust 4.9% in the third quarter of 2007, the fourth quarter growth will likely show a significant slowdown with an estimated real GDP growth of only 1.0%. The fallout from the bursting of interconnected bubbles in the housing and credit markets has put the U.S. economy on a challenging path for the year ahead. Since our last quarterly report, housing deflation has intensified with home prices down even more than during the early 1990s correction. From peak to trough, home prices were down 6.7% during 1989-1991, as measured by the S&P/Case-Shiller index, while the current decline stands at 7.3% since the high in June 2006. Meanwhile, the unemployment rate increased to 5% from 4.7% last quarter, oil finished the year at $95.98 compared to $60.50 last year, and consumer confidence at the end of 2007 was at its lowest level of the year.

Amid these weak economic conditions, the Federal Reserve stimulated the economy by cutting the federal funds rate by another 50 basis points during the fourth quarter to 4.25%. As we mentioned in the last report, this stimulus is unlikely to eliminate the downside risk to the economy, though it may shorten the length of a potential economic slowdown. So far, the efforts of the Fed have produced only marginally positive effects in an environment where risk aversion prevails and doubts about financial institutions’ capital adequacy still linger. In fact, since the Fed first cut rates on September 18th until the end of the year, the stock market fell almost 5%.

Until recently, one could argue that as long as the job market grew, supporting income growth, the U.S. consumer would keep on spending. However, there is now increasing evidence that the employment picture has deteriorated. The latest employment report shows that only 18,000 jobs were created (the lowest increase since August 2003), private payrolls were down 13,000, and the unemployment rate was up to 5%. In addition, after three consecutive months of negative real wage growth, we will likely see continued economic weakness as food and oil price inflation offsets gain in salary increase. This negative real income trend combined with falling home values, declining consumer confidence and record oil prices, is pointing to weak consumer spending over the next few quarters. This theory is the cornerstone of our defensive posture for the Fund.

Homebuilding should also remain sluggish. In the short term, homebuilders face two problems: excess inventory, with more than 10 months worth of supply, and a lack of affordability. In addition, longer term, demand for houses will be significantly lower than during the 1995-2005 period as the home ownership rate continues to fall. This rate peaked in 2004 at 69.2% and has since dropped by a full percentage point to 68.2%. According to a Goldman Sachs report, two fundamental factors underlie this trend and are likely to continue. First, rising foreclosures mean that some homeowners are involuntarily becoming renters. Second, because of tightening mortgage credit standards and reduced availability of high loan-to-value mortgages, the home ownership rate among the next group of young households will likely be much lower than during the boom period. As a result of this long-term structural over-supply and lack of affordability, we are not tempted to buy homebuilding stocks.

Even after enduring a massive correction in 2007, the financial sector still looks vulnerable to the ongoing credit crisis. The lack of transparency among financial institutions, and the ensuing loss of trust, have left investors with little confidence in the reported earnings of most bank stocks. In order to regain investors’ faith, banks will need to show that they have disclosed all their losses and, more importantly, that the peak in credit losses is past. Although progress has been made on the first point, the complexity of new financial instruments makes it hard even for experts to determine the scope of the losses. The second issue might prove to be the most lengthy and difficult to resolve. One emerging concern is that the trend in defaults that affected the mortgage market will spread into the corporate world, producing a second wave of losses that could potentially rival sub-prime losses. Citigroup estimates that U.S. leveraged corporate defaults will rise from 1.3% last year to 5.5% at the start of 2009 – and this assumes no recession. It appears that the same laxity that caused the sub-prime mess may have extended into some segments of corporate loans. Consequently, we continue to avoid the sector because we think the current financial stocks’ downturn will take more time to work through than most people think.

Finally, current market expectations for both the consumer discretionary and financial sectors’ earnings growth rates appear to be too high. According to estimates from Standard & Poor’s, the operating earnings of the consumer discretionary sector will grow 23.1% in 2008 after declining 12.7% in 2007. Meanwhile, earnings in the financial sector are expected to increase 18.5% in 2008 compared to a drop of 18.9% in 2007. It is interesting to note that both of these 2008 growth estimates exceed the ones achieved in 2006, when the economy was growing at 2.9%, compared to an estimated 2.2% for this year. In essence, investors are expecting big earnings growth despite a slower economy, which doesn’t make sense. Accordingly, we see continued weak performance of these two sectors relative to the market.

Against this backdrop, we are maintaining our investment themes from 2007 with only slight modifications. We remain underweight in the consumer discretionary and financial sectors, due to our economic views. The Fund is also underweight in industrial stocks, since we feel a slowing economy increases risk for that sector. Our biggest overweight position remains in the healthcare industry, because we have found many companies there that can grow earnings, even in the current economic climate. The Fund also remains overweight technology and energy stocks, but has scaled back our exposure in each sector a bit, due to higher valuations and concerns about a slowing economy. We have used the proceeds from these sales to build our cash position to 8% of Fund assets. While the economic outlook is challenging, I feel we own a collection of great businesses in the portfolio and will look to add more during market corrections in 2008.

| | |

| | Yours truly, |

| |

| |  |

| |

| | Todd C. Ahlsten |

| | Portfolio Manager |

THE PARNASSUS MID - CAP FUND

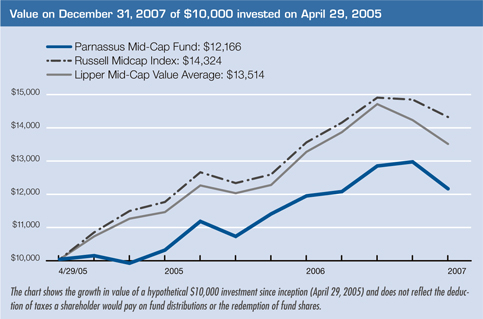

As of December 31, 2007, the net asset value per share (NAV) of the Parnassus Mid-Cap Fund was $17.39, so after taking dividends into account, the total return for the year was 1.81%. This compares to 1.98% for the Lipper Mid-Cap Value Index and 5.60% for the Russell Midcap Index. The reason for the disparity is that “growth stocks” were responsible for the rise in the Russell Index, while “value stocks” did not do as well, as reflected in both the Fund’s performance and the Lipper Index. For the fourth quarter, the Mid-Cap Fund dropped 6.24% compared to a loss of 5.05% for the Lipper average and a decline of 3.55% for the Russell Midcap Index.

Below are a table and a graph that compare the performance of the Mid-Cap Fund with that of the Russell Midcap Index and the Lipper Mid-Cap Value Average. For the period since September 30, 2005, when the Fund first had most of its assets in stocks instead of cash, the Mid-Cap Fund lagged the Russell Midcap Index, but outperformed the Lipper Mid-Cap Value Average.

As you can see from the table, the Mid-Cap Fund is about one percentage point ahead of the Lipper Mid-Cap Value Average for the period since September 30, 2005, when the Fund first had most of its assets invested in stocks.

Average Annual Total Returns

for periods ended December 31, 2007

| | | | | | | | | | | | | | | |

| | | One

Year | | | Since

September 30,

2005 | | | Since

Inception

April 29, 2005 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

MID-CAP FUND | | 1.81 | % | | 9.46 | % | | 7.62 | % | | 5.31 | % | | 1.42 | % |

Russell Midcap Index | | 5.60 | % | | 10.26 | % | | 14.03 | % | | NA | | | NA | |

Lipper Mid-Cap Value Average | | 1.98 | % | | 8.44 | % | | 11.87 | % | | NA | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell Midcap Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. Mid-cap companies can be more sensitive to changing economic conditions and have fewer financial resources than large-cap companies. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is on the Parnassus website, or you can get one by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2007, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.40% of net assets, exclusive of acquired fund fees, through April 30, 2008.

Analysis

Three companies depressed the Fund’s return by 20¢ or more per share. The one that hurt us the most was Micron Technology, which knocked 38¢ off the NAV, as its stock sank 48% from $13.96 to $7.25. The company makes memory chips, which were oversupplied in 2007, causing prices to fall.

SLM Corporation, better known as Sallie Mae, cost the Mid-Cap Fund 36¢ per share, as its stock fell 59% from $48.77 to $20.14 by the end of the year. See the SLM discussion in the Parnassus Fund section for the reasons for the decline.

First Horizon dropped 57% for the year, falling from $41.78 to $18.15 for a decline of 34¢ on the NAV. See the Parnassus Workplace Fund discussion for details.

The big winner for the year was Invitrogen, the maker of supplies for molecular biology research. The stock rose 65% from $56.59 to $93.41 for a gain of 32¢ for each fund share. See the Parnassus Fund discussion for the details.

Citrix Systems contributed 20¢ to each fund share, as its stock climbed 41% from $27.05 to $38.01. See the Parnassus Fund section for more information.

At the present time, almost half the Mid-Cap portfolio is in technology stocks. In my view, technology shares have a lot of upside potential, especially mid-cap companies, so we’re expecting a good year in 2008.

Yours truly,

|

|

|

| Jerome L. Dodson |

| President |

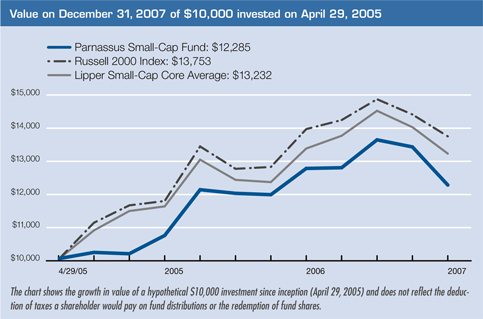

THE PARNASSUS SMALL - CAP FUND

As of December 31, 2007, the net asset value per share (NAV) of the Parnassus Small-Cap Fund was $16.91, so after taking dividends into account, the total return for the year was a loss of 3.92%. This compares to a loss of 1.57% for the Russell 2000 Index and a loss of 1.00% for the Lipper Small-Cap Core Average. As with the Parnassus Fund and the Workplace Fund, this finish was disappointing, because the Small-Cap Fund was well ahead of both indices for the year-to-date as of September 30.

The fourth quarter was very difficult for almost all small-cap stocks, but especially difficult for the Parnassus Small-Cap Fund which lost 8.56% during the quarter, compared to a loss of 4.58% for the Russell 2000 and a loss of 5.69% for the Lipper average.

Below are a table and a graph that compare the performance of the Small-Cap Fund with that of the Russell 2000 and the Lipper Small-Cap Core Average. You will notice that despite our weak performance for the quarter, the Fund is still ahead of the Russell 2000 Index and the Lipper Small-Cap Core Average for the period since September 30, 2005, which is when the Fund first became substantially invested. (From inception on April 29, 2005 until then, the Fund had the majority of its assets in cash.)

Average Annual Total Returns

for periods ended December 31, 2007

| | | | | | | | | | | | | | | |

| | | One

Year | | | Since

September 30,

2005 | | | Since

Inception

April 29, 2005 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

SMALL-CAP FUND | | (3.92 | %) | | 8.55 | % | | 8.01 | % | | 3.05 | % | | 1.42 | % |

Russell 2000 Index | | (1.57 | %) | | 7.57 | % | | 12.37 | % | | NA | | | NA | |

Lipper Small-Cap Core Average | | (1.00 | %) | | 6.54 | % | | 11.18 | % | | NA | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell 2000 Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. Small-cap companies can be particularly sensitive to changing economic conditions and have fewer financial resources than large-cap companies. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is on the Parnassus website, or you can get one by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2007, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.40% of net assets, exclusive of acquired fund fees, through April 30, 2008.

Analysis

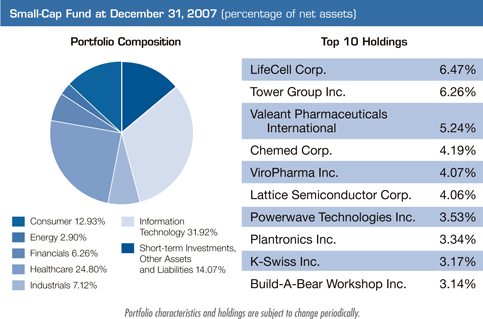

Four companies in the Small-Cap portfolio each accounted for losses of 23¢ or more per fund share, while three companies accounted for gains of 23¢ or more each. The one that hurt us the most was Tuesday Morning, the home-furnishings retailer, whose stock sank 67% from $15.55 to $5.07, subtracting 51¢ from the NAV. This 51¢ loss depressed the Fund’s return by 2.8%, or more than the 2.35 percentage points by which the Fund underperformed the Russell 2000 Index for the year. The company’s earnings fell far short of expectations because of the weak home-furnishings market.

Powerwave Technologies, a maker of infrastructure products for cellular telephone networks, dropped 35% during the quarter, sinking from $6.16 to $4.03 for a loss of 26¢ on the NAV. A loss for the year plus the company’s bleak forecast for the immediate future, sent the shares lower. We’re holding onto the stock, since we think it’s trading at bargain-basement levels and will move higher as wireless phone companies increase capital budgets to build out pending 3G networks.

ACI Worldwide is an electronics payment software and service provider, whose shares dropped 15% from $22.32 where we bought it late in the third quarter of the year to $19.04 by year’s end, slicing 28¢ off the NAV. Earnings have been weak, as customers have delayed upgrading to the company’s latest software release.

RadiSys cost the Fund 25¢ per share, as its stock dropped 23% from $16.67 at the first of the year to $12.89, where we sold it in the middle of the year. Our original motivation for investing was development of the Promentum, a 10-gigabit switch for wireless base stations to help digital packets of information move through the network. Unfortunately, the product was not widely adopted and we lost confidence in management.

Looking on the bright side, we had three companies that did very well for us. LifeCell added 54¢ to the NAV as its stock soared 79% from $24.14 to $43.11. The company provides tissue regeneration and cell preservation products such as tissue graft AlloDerm used in the treatment of third-degree burns and reconstructive surgery. The stock had been trading at depressed levels early in the year, because of investor concern about competing products, but as it turned out, LifeCell had the best product, and the shares moved higher.

Invitrogen, the maker of research products for molecular biology, boosted the NAV by 41¢, as its stock rocketed up 65% from $56.59 to $93.41. A restructuring of its product line and redirection of its sales force resulted in higher revenue.

Ciena added 23¢ to each fund share, with its stock climbing 23% for the year from $27.71 to $34.11. Telecommunications providers have increased capital spending for the company’s optical network products.

Right now, there is a lot of economic uncertainty and for that reason, we have a somewhat defensive position in the Small-Cap Fund including keeping 14% of net assets in cash.

| | |

| | Yours truly, |

| |

| | |

| |

| | Jerome L. Dodson |

| | President |

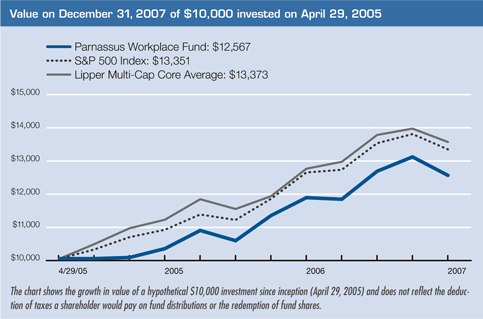

THE PARNASSUS WORKPLACE FUND

As of December 31, 2007, the net asset value per share (NAV) of the Parnassus Workplace Fund was $17.60, so after taking dividends into account, the total return for the year was 5.64%. This compares to 5.49% for the S&P 500 and 6.43% for the Lipper Multi-Cap Core Average, so we slightly outperformed the S&P 500, but lagged the Lipper average. As with the Parnassus Fund, this finish was disappointing, because the Workplace Fund was up 10.32% year-to-date as of September 30, compared to 9.13% for the S&P 500 and 9.41% for the Lipper average. In the fourth quarter, the Fund dropped 4.24%, compared to a decline of 2.88% for the Lipper average and a loss of 3.33% for the S&P 500.

Below are a table and a graph comparing the Parnassus Workplace Fund with the S&P 500 and the Lipper Multi-Cap Core Average. The Fund first became substantially invested around September 30, 2005, and since that time the Fund is up about the same as the S&P 500, but ahead of the Lipper average. (For the period from April 29, 2005 until September 30, 2005, the Fund had the majority of its assets in cash.)

Average Annual Total Returns

for periods ended December 31, 2007

| | | | | | | | | | | | | | | |

| | | One

Year | | | Since

September 30,

2005 | | | Since Inception

April 29, 2005 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

WORKPLACE FUND | | 5.64 | % | | 10.24 | % | | 8.94 | % | | 4.05 | % | | 1.21 | % |

S&P 500 Index | | 5.49 | % | | 10.30 | % | | 11.42 | % | | NA | | | NA | |

Lipper Multi-Cap Core Average | | 6.43 | % | | 9.79 | % | | 12.00 | % | | NA | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Standard and Poor’s 500 Composite Stock Price Index, also known as the S&P 500 Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus, which contains this and other information. The prospectus is on the Parnassus website, or you can get one by calling (800) 999–3505. As described in the Fund’s current prospectus dated May 1, 2007, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.20% of net assets, exclusive of acquired fund fees, through April 30, 2008.

Analysis

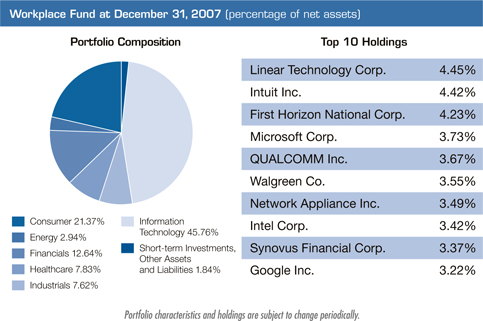

As with the Parnassus Fund, the fourth quarter of the Workplace Fund was somewhat disappointing. Although we did manage to beat the S&P 500 for the year by a small amount, we lagged the annual return for the Lipper average. By contrast, we were ahead of both benchmarks going into the fourth quarter. For the fourth quarter, the fund lost 4.24% compared to a loss of 3.33% for the S&P and a loss of 2.88% for the Lipper average, so we underperformed the S&P by 0.91 percentage point and we underperformed the Lipper by 1.36 percentage points. One company caused a loss of 2.74% to the NAV. In other words, had we not suffered that loss, we would have beaten both the benchmarks for the quarter and the year.

That company was a regional bank based in Tennessee called First Horizon. The company was #46 last year on Fortune’s list of the “100 Best Companies to Work For” and it has been on the list for the last ten years. The company is well managed and has a reputation for being a good employer which helps it attract talent.

Unfortunately, the company has been caught up in the housing meltdown. Although First Horizon does not have a lot of sub-prime exposure, it does have a lot of construction and home equity loans that may go bad. The company announced a $150 million write-down for the fourth quarter, which will probably mean a loss for 2007.

For the quarter, the stock sank from $26.66 to $18.15 for a loss of 32% and drop of 28¢ on the NAV. For the year, the stock fell 57% from $41.78 to $18.15 for a loss of 51¢ for each fund share.

I’m still holding onto the stock, since I think its price will be much higher by the end of 2008. There are some real concerns regarding construction loans and mortgage lending, but the share price is far below the company’s intrinsic value.

Fortunately, First Horizon was the only stock in the portfolio to lose more than 15¢ per fund share for the year. On the positive side, six companies accounted for gains of more than 15¢ on the NAV.

Refiner Valero Energy Corporation contributed the most for the year with a 27¢ addition to the NAV, as its shares climbed 37% from $51.16 to $70.03. The company is an efficient operator and the United States has a limited amount of refining capacity, since it’s been years since a new refinery was built in this country. The spread between crude oil and gasoline remains high, so earnings are strong. On the social side, the company is on Fortune’s list of the “100 Best Companies to Work For,” and it is investing more capital to reduce the emissions coming from its refineries.

Intel climbed 32% from $20.25 to $26.66, adding 23¢ to each fund share. The company’s technology leadership and manufacturing advantage over AMD moved the stock higher, as did strong PC and notebook sales, particularly in Europe and Asia.

Google also contributed 23¢ to the NAV on a 44% increase in its stock price from an average cost of $479 where we bought it early in the year to $691 by year’s end. The company’s revenue is growing around 50% per year, as it dominates the Internet search business with a 59% market share in the United States and 70% internationally. Google has become a powerful advertising medium as a result of its dominant position in Internet search.

Texas Instruments added 17¢ to each share of the Workplace Fund this year, as its stock rose 16% from $28.80 to $33.40. Excess inventory at the start of the year depressed the stock price, but these levels declined with increased spending for telecommunications, and the shares moved higher.

Microsoft’s stock climbed 22% from our cost of $29.24, where we bought it in the third quarter of the year, to $35.60, where it ended the year. This accounted for a gain of 16¢ per fund share. Sales and earnings moved higher on the release of Office 2007 and increased use of its new Vista operating system.

AFLAC contributed 16¢ to the NAV on a 36% gain in its stock price from $46.00 to $62.63. Earnings increased through the year on higher sales in Japan because of new product offerings and new sales initiatives, strong sales in the United States and lower operating expenses.

| | |

| | Yours truly, |

| |

| | |

| |

| | Jerome L. Dodson |

| | President |

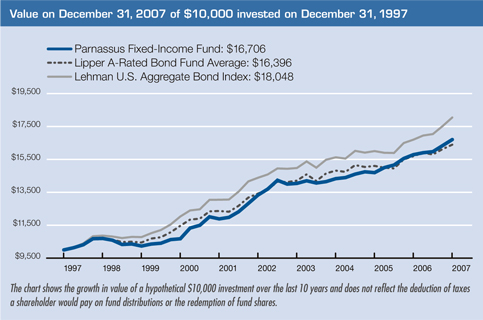

THE PARNASSUS FIXED - INCOME FUND

As of December 31, 2007, the net asset value per share (NAV) of the Fixed-Income Fund was $16.29, yielding a total return for the year of 5.81% (including dividends). This compares to a gain of 4.47% for the average A-rated bond fund followed by Lipper, Inc. and a gain of 6.97% for the Lehman U.S. Aggregate Bond Index. We’re pleased that our performance this year helped us rank 40 out of 172 of the A-rated bond funds tracked by Lipper, Inc.*

Below are a table and a graph comparing the performance of the Fund with that of the Lehman U.S. Aggregate Bond Index and the average A-rated bond fund followed by Lipper. Average annual total returns are for the one-, three-, five- and ten-year periods. We’re proud to report that for each of these periods, the Fund has outperformed the Lipper average. The 30-day SEC yield for the Fund for December 2007 was 3.73%.

Average Annual Total Returns

for periods ended December 31, 2007

| | | | | | | | | | | | | | | | | | |

| | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

FIXED-INCOME FUND | | 5.81 | % | | 5.25 | % | | 4.61 | % | | 5.27 | % | | 0.93 | % | | 0.88 | % |

Lipper A-rated Bond Fund Average* | | 4.47 | % | | 3.40 | % | | 4.11 | % | | 5.08 | % | | NA | | | NA | |

Lehman U.S. Aggregate Bond Index | | 6.97 | % | | 4.56 | % | | 4.42 | % | | 5.97 | % | | NA | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month-end is on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Lehman U.S. Aggregate Bond Index is an unmanaged index of bonds, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns may. Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus which contains this and other information. The prospectus is on the Parnassus website or you can also get one by calling (800) 999 – 3505. As described in the Fund’s current prospectus dated May 1, 2007, Parnassus Investments has contractually agreed to limit the total operating expenses to 0.87% of net assets, exclusive of acquired fund fees, through April 30, 2008.

| * | For the one-, three-, five- and ten-year periods ended December 31, 2007 based on the Lipper A-Rated Bond Fund Average the Parnassus Fixed-Income Fund placed #40 out of 172 funds, #5 out of 155 funds, #36 out of 132 funds and #25 out of 60 funds, respectively. |

Analysis for 2007

We’re pleased to report that in 2007 we beat our Lipper peers by more than 100 basis points, and that our one-, three-, five- and ten-year returns are all above the Lipper average. Our 5.81% return for 2007 is especially satisfying because last year the credit markets were rocked when the housing market bubble burst.

While markets typically react to changes in return expectations, sharp drops in the fixed income market are normally caused by increased perceptions of risk. The specific cause for the credit crisis of 2007 was the most basic one faced by lenders: repayment risk. In this case, holders of sub-prime mortgages suddenly realized that they might not receive payment from borrowers who put no money down, and never documented their income. After an unprecedented period of lax lending standards, the chickens finally came home to roost in 2007.

Fortunately for our shareholders, we anticipated trouble in the residential real estate market and, as a result, avoided bonds backed by sub-prime mortgages. In fact, our overall stance throughout the year was that the extra return offered by most non-government-backed bonds simply wasn’t high enough to justify the added risk. As of the end of the year, 60% of our portfolio is still in bonds backed by the Federal government or one of its agencies. This defensive stance was one factor that helped us outpace our Lipper peers.

The other interesting story from 2007 is the change in the yield curve. This curve describes the relative returns offered by equivalent risk bonds of different maturities. Entering 2007, the yield curve was essentially flat, meaning that there was little difference between the returns of a 2-year versus a 10-year U.S. Treasury bond, for example. By the end of the year, the 10-year bond yielded almost a full percentage point more than the 2-year bond (4.04% versus 3.05%).

This “steepening” happened because the 2-year yield dropped 177 basis points, which was much more than the 67 basis point drop in the 10-year yield. The primary reason why short-maturity bonds have gone up in price, and seen their yields drop precipitously, is that the Federal Open Market Committee led by Ben Bernanke has been cutting short-term interest rates. More importantly, the market expects the Fed to continue cutting rates for at least the next few quarters.

Strategy

Given these market conditions, we own a high concentration of relatively short-maturity bonds. We think there is a high probability that the Fed will continue to cut the Fed Funds rate, in an effort to dampen the impact of an economic slowdown. We think this rate, which currently stands at 4.25%, will eventually reach 3% by the time the Fed is done cutting. If this happens, our relatively short-maturity bonds should perform well.

As for long-term rates, we think that the 10-year Treasury will be higher in a year’s time. At its current price, there simply isn’t much return offered to a bond investor. This is especially true if one takes into consideration the effects of inflation, which any fixed-income investor must do.

On an inflation-adjusted basis, the 10-year Treasury offered a return of only 1.73% at the end of 2007, as measured by the Fed’s Treasury inflation protected securities, or TIPS. This is down from 2.41% at the end of 2006, and is near the low end of the range over the last five years. Since we think long-term rates will increase, we have positioned the portfolio with an average duration of 4.1 years, slightly lower than the 4.4 year duration of the Lehman U.S. Aggregate Bond Index.

We haven’t made any changes to our convertible bond holdings since last quarter. As always, we will continue to look for attractive opportunities in the convertible bond market to increase the returns of the Fund.

Thank you for investing in the Parnassus Fixed-Income Fund.

Yours truly,

| | |

| |  |

| |

Todd C. Ahlsten | | Ben Allen |

Portfolio Manager | | Co-Portfolio Manager |

SOCIAL NOTES

Each day, approximately 450 trucks rumble up a tree-lined drive to deposit waste at the Atascacita Landfill just outside of Houston, Texas. This is one of 283 active disposal sites operated by Waste Management, the country’s largest waste and recycling company, and a new Parnassus portfolio company. On a company visit to Houston, Parnassus analysts Ben Allen and Andrea Reichert experienced why communities often don’t want landfills in their backyards: the waste smells bad, the machinery is loud, and the circling vultures are ominous. More troubling are the unseen, potential environmental impacts, such as water contamination and air pollution. After completing our rigorous research process on the company, including an examination of these issues, we concluded that Waste Management is making critical improvements to the way waste is handled, and meets our environmental, social and governance criteria.

Under the leadership of Dave Steiner, who became CEO in 2004, Waste Management has made a dramatic turnaround from the 1990s, when the company was rocked by accounting scandals and numerous serious environmental violations. Helping Steiner with this governance transition is an unusually strong, independent board. Leadership at Waste Management is keenly focused on corporate-wide personnel development, long-term strategic planning, and risk mitigation. Steiner also leads the company’s efforts to be more environmentally friendly, an initiative summarized by the company’s motto, “Think Green.”

While the environmental aspects of the waste business are highly regulated, it is important to us that our companies do more than meet minimum standards. That’s why we’re pleased that Waste Management leads its peers with green initiatives, like the conversion of waste into energy. The company currently generates enough waste-based energy to satisfy the needs of one million homes, a number it plans to double over the next twelve years. As the country’s largest recycler, Waste Management diverts eight million tons of waste from landfills every year. Diversion is crucial to making waste services more sustainable. Waste Management has been exploring ways to reduce the amount of material on its way to a landfill or incinerator, and improve profitability at the same time. These efforts include recovering scrap metal, expanding single-stream sorting for recyclables and in the part of Texas where sand and gravel are scarce, reselling demolition concrete. In addition, the company was a founding member of the Chicago Climate Exchange, pledging to reduce greenhouse gas emissions. More recently, the company committed to expand the number of acres it sets aside for wildlife habitat to roughly 25,000 by the year 2020.

While we’d like to see more women and minorities in senior management and a company-wide focus on lowering employee turnover, the company’s workplace record is satisfactory and improving. In certain areas, such as injury and auto accident rates, the improvements are enormous. In fact, over the last four years, employee injuries have dropped 70%. We don’t think it’s coincidental that this period roughly correlates with Dave Steiner’s tenure as CEO.

While we’re pleased with many attributes of Waste Management, we recognize that the company isn’t perfect. However, we think Waste Management’s leadership has embraced corporate responsibility under growing public demand for environmentally sensitive waste services. Waste Management has indicated that it is willing to engage with shareholders to explore new reporting metrics regarding environmental and workplace concerns, a strong signal that this company is moving in the right direction.

Invitrogen, a California-based manufacturer of tools for life sciences research, makes drug discovery and health breakthroughs possible. The company donates their products to non-profit and educational organizations, and is particularly strong on the environmental front, actively participating in the cleanup of hazardous waste sites acquired when the company bought the Dexter Corporation in 2000. In addition, Invitrogen sponsors employee volunteer cleanup days, and has put an environmental management system (EMS) in place at their facilities nationwide, with performance measured by internal and third-party audits.

Microsoft is a new investment for Parnassus, as we have avoided it in the past due to concerns about the company’s aggressive business practices and anti-trust lawsuits. However, as of 2006 many of Microsoft’s largest class action lawsuits with consumers and large competitors were resolved. This prompted a recent social review at Parnassus, during which we concluded that Microsoft was eligible for investment in our funds. We were especially impressed that Microsoft leads the way in establishing common labor standards for electronics suppliers, provides terrific employee benefits and is dedicated to maintaining a diversified workplace.

Texas Instruments’ educational products business provides classroom tools and professional development resources to help students and teachers explore math and science interactively. The company has a history of strong philanthropic support for education, has taken a leadership role in establishing the Center for Environmentally Benign Semiconductor Manufacturing, and in 2007, was included on Fortune magazine’s annual list of the “100 Best Companies to Work For” for the fifth consecutive year.

| | |

| | Yours truly, |

| |

| | |

| |

| | Todd C. Ahlsten |

| | Portfolio Manager |

FUND EXPENSES (UNAUDITED)

As a shareholder of the funds, you incur ongoing costs, which include portfolio management fees, administrative fees, shareholder reports, and other fund expenses. The funds do not charge transaction fees, so you do not incur transaction costs such as sales charges (loads) on purchase payments, reinvested dividends, or other distributions, redemption fees and exchange fees. The information on this page is intended to help you understand your ongoing costs of investing in the funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The following example is based on an investment of $1,000 invested at the beginning of the most recent six-month period and held for the period of July 1, 2007 through December 31, 2007.

Actual Expenses

In the example below, the first line for each fund provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of each fund provides information about hypothetical account values and hypothetical expenses based on the fund’s expense ratio and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. You may compare the ongoing costs of investing in the fund with other mutual funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Please note that the expenses shown in the table are meant to highlight only your ongoing costs in these funds. Therefore, the second line of each fund is useful in comparing only ongoing costs and will not help you determine the relative total costs of owning other mutual funds, which may include transactional costs such as loads.

| | | | | | | | | |

| | | Beginning

Account Value

July 1, 2007 | | Ending

Account Value

December 31, 2007 | | Expenses

Paid During

Period* |

Parnassus Fund: Actual | | $ | 1,000.00 | | $ | 963.10 | | $ | 4.90 |

Hypothetical (5% before expenses) | | $ | 1,000.00 | | $ | 1,020.21 | | $ | 5.04 |

| | | |

Equity Income Fund – Investor Shares: Actual | | $ | 1,000.00 | | $ | 1,030.49 | | $ | 5.07 |

Hypothetical (5% before expenses) | | $ | 1,000.00 | | $ | 1,020.21 | | $ | 5.04 |

| | | |

Equity Income Fund – Institutional Shares: Actual | | $ | 1,000.00 | | $ | 1,031.45 | | $ | 3.99 |

Hypothetical (5% before expenses) | | $ | 1,000.00 | | $ | 1,021.27 | | $ | 3.97 |

| | | |

Mid-Cap Fund: Actual | | $ | 1,000.00 | | $ | 946.67 | | $ | 6.87 |

Hypothetical (5% before expenses) | | $ | 1,000.00 | | $ | 1,018.15 | | $ | 7.12 |

| | | |

Small-Cap Fund: Actual | | $ | 1,000.00 | | $ | 900.10 | | $ | 6.71 |

Hypothetical (5% before expenses) | | $ | 1,000.00 | | $ | 1,018.15 | | $ | 7.12 |

| | | |

Workplace Fund: Actual | | $ | 1,000.00 | | $ | 990.20 | | $ | 6.02 |

Hypothetical (5% before expenses) | | $ | 1,000.00 | | $ | 1,019.16 | | $ | 6.11 |

| | | |

Fixed-Income Fund: Actual | | $ | 1,000.00 | | $ | 1,046.01 | | $ | 4.49 |

Hypothetical (5% before expenses) | | $ | 1,000.00 | | $ | 1,020.82 | | $ | 4.43 |

| * | Expenses are equal to the fund’s annualized expense ratio of 0.99%, 0.99%, 0.78%, 1.40%, 1.40%, 1.20% and 0.87% for the Parnassus Fund, Equity Income Fund – Investor Shares, Equity Income Fund – Institutional Shares, Mid-Cap Fund, Small-Cap Fund, Workplace Fund and Fixed-Income Fund respectively, multiplied by the average account value over the period, multiplied by the ratio of days in the period. The ratio of days in the period is 184/365 (to reflect the one-half year period). |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and Board of Trustees of the Parnassus Funds and the Parnassus Income Funds

San Francisco, California

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments, of the Parnassus Funds (comprised of Parnassus Fund, Parnassus Mid-Cap Fund, Parnassus Small-Cap Fund and Parnassus Workplace Fund) and the Parnassus Income Funds (comprised of Parnassus Equity Income Fund and Parnassus Fixed-Income Fund) (collectively, the “Trusts”) as of December 31, 2007, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the periods presented. These financial statements and financial highlights are the responsibility of the Trusts’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Trusts are not required to have, nor were we engaged to perform, an audit of their internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Trusts’ internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2007, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, such financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of each of the funds constituting the Parnassus Funds and the Parnassus Income Funds as of December 31, 2007, the results of their operations for the year then ended, the changes in their net assets for each of the two years in the period then ended, and the financial highlights for each of the periods presented, in conformity with accounting principles generally accepted in the United States of America.

|

|

| San Francisco, California |

February 1, 2008 |

THE PARNASSUS FUND

Portfolio of Investments as of

December 31, 2007

| | | | | | | | |

| Shares | | Equities | | Percent of

Net Assets | | | Market Value |

| | Biotechnology | | | | | | |

| 80,000 | | Genentech Inc.1 | | | | | $ | 5,365,600 |

| 30,000 | | Invitrogen Corp.1, 2 | | | | | | 2,802,300 |

| | | | | | | | |

| | | | 2.9 | % | | $ | 8,167,900 |

| | | | | | | | |

| | Childcare Services | | | | | | |

| 50,000 | | Bright Horizons | | | | | | |

| | Family Solutions Inc.1, 2 | | 0.6 | % | | $ | 1,727,000 |

| | | | | | | | |

| | Communications Equipment | | | | | | |

| 175,000 | | QUALCOMM Inc. | | 2.5 | % | | $ | 6,886,250 |

| | | | | | | | |

| | Computer Peripherals | | | | | | |

| 70,000 | | Avocent Corp.1 | | 0.6 | % | | $ | 1,631,700 |

| | | | | | | | |

| | Consulting Services | | | | | | |

| 60,000 | | Cognizant Technology Solutions Corp.1 | | 0.7 | % | | $ | 2,036,400 |

| | | | | | | | |

| | Data Storage | | | | | | |

| 200,000 | | Network Appliance Inc.1 | | 1.8 | % | | $ | 4,992,000 |

| | | | | | | | |

| | Electronics | | | | | | |

| 60,000 | | Plantronics Inc.2 | | 0.6 | % | | $ | 1,560,000 |

| | | | | | | | |

| | Financial Services | | | | | | |

| 280,000 | | First Horizon National Corp.2 | | | | | $ | 5,082,000 |

| 60,000 | | Freddie Mac | | | | | | 2,044,200 |

| 200,000 | | SLM Corp. | | | | | | 4,028,000 |

| 10,000 | | Wells Fargo & Co. | | | | | | 301,900 |

| | | | | | | | |

| | | | 4.1 | % | | $ | 11,456,100 |

| | | | | | | | |

| | Healthcare Products | | | | | | |

| 65,000 | | Johnson & Johnson | | 1.5 | % | | $ | 4,335,500 |

| | | | | | | | |

| | Healthcare Services | | | | | | |

| 135,000 | | Chemed Corp.2 | | | | | $ | 7,543,800 |

| 50,000 | | Lincare Holdings Inc.1, 2 | | | | | | 1,758,000 |

| | | | | | | | |

| | | | 3.3 | % | | $ | 9,301,800 |

| | | | | | | | |

| | Home Builders | | | | | | |

| 300,000 | | DR Horton Inc.2 | | | | | $ | 3,951,000 |

| 370,000 | | Pulte Homes Inc.2 | | | | | | 3,899,800 |

| | | | | | | | |

| | | | 2.8 | % | | $ | 7,850,800 |

| | | | | | | | |

| | Insurance | | | | | | |

| 290,000 | | Tower Group Inc.2 | | | | | $ | 9,686,000 |

| 80,000 | | WR Berkley Corp. | | | | | | 2,384,800 |

| | | | | | | | |

| | | | 4.3 | % | | $ | 12,070,800 |

| | | | | | | | |

| | Machinery | | | | | | |

| 50,000 | | Graco Inc.2 | | 0.7 | % | | $ | 1,863,000 |

| | | | | | | | |

| | Networking Products | | | | | | |

| 325,000 | | Cisco Systems Inc.1 | | 3.1 | % | | $ | 8,797,750 |

| | | | | | | | |

| | Oil & Gas | | | | | | |

| 90,000 | | Apache Corp. | | | | | $ | 9,678,600 |

| 50,000 | | Ultra Petroleum Corp.1 | | | | | | 3,575,000 |

| 90,000 | | Valero Energy Corp. | | | | | | 6,302,700 |

| 160,000 | | W&T Offshore Inc.2 | | | | | | 4,793,600 |

| | | | | | | | |

| | | | 8.7 | % | | $ | 24,349,900 |

| | | | | | | | |

| | Pharmaceuticals | | | | | | |

| 75,000 | | Barr Pharmaceuticals Inc.1 | | | | | $ | 3,982,500 |

| 100,000 | | Cardinal Health Inc. | | | | | | 5,775,000 |

| 180,000 | | Forest Laboratories Inc.1 | | | | | | 6,561,000 |

| 80,000 | | Pfizer Inc. | | | | | | 1,818,400 |

| 60,000 | | Pharmaceutical Product Development Inc. | | | | | | 2,422,200 |

| 450,000 | | Valeant Pharmaceuticals International1, 2 | | | | | | 5,386,500 |

| 360,000 | | Viropharma Inc.1, 2 | | | | | | 2,858,400 |

| | | | | | | | |

| | | | 10.3 | % | | $ | 28,804,000 |

| | | | | | | | |

| | Real Estate Investment Trust | | | | | | |

| 90,000 | | ProLogis | | 2.0 | % | | $ | 5,704,200 |

| | | | | | | | |

| | Retail | | | | | | |

| 80,000 | | Bed Bath & Beyond Inc.1, 2 | | | | | $ | 2,351,200 |

| 55,000 | | Best Buy Co., Inc.2 | | | | | | 2,895,750 |

| 220,000 | | Lowe’s Cos., Inc. | | | | | | 4,976,400 |

| 50,000 | | Nordstrom Inc.2 | | | | | | 1,836,500 |

| 100,000 | | Target Corp. | | | | | | 5,000,000 |

| 510,000 | | Tuesday Morning Corp.2 | | | | | | 2,585,700 |

| 130,000 | | Walgreen Co. | | | | | | 4,950,400 |

| 240,000 | | Whole Foods Market Inc.2 | | | | | | 9,792,000 |

| | | | | | | | |

| | | | 12.3 | % | | $ | 34,387,950 |

| | | | | | | | |

| | | | |

| 24 | | The accompanying notes are an integral part of these financial statements. | | |

| | | | | | | | |

Shares | | Equities | | Percent of

Net Assets | | | Market Value |

| | Semiconductor Capital Equipment | | | | | | |

| 80,000 | | Applied Materials Inc. | | | | | $ | 1,420,800 |

| 40,000 | | Cognex Corp.2 | | | | | | 806,000 |