UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: Parnassus Funds (811-04044) and Parnassus Income Funds (811-06673)

Parnassus Funds

Parnassus Income Funds

(Exact name of registrant as specified in charter)

1 Market Street, Suite 1600, San Francisco, California 94105

(Address of principal executive offices) (Zip code)

Marc C. Mahon

Parnassus Funds

Parnassus Income Funds

1 Market Street, Suite 1600, San Francisco, California 94105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (415) 778-0200

Date of fiscal year end: December 31

Date of reporting period: June 30, 2013

Item 1: Report to Shareholders

PARNASSUS FUNDS®

SEMIANNUAL REPORT ¡ JUNE 30, 2013

PARNASSUS FUNDS

| | |

| |

| Parnassus FundSM | | PARNX |

| |

| Parnassus Equity Income FundSM – Investor Shares | | PRBLX |

| |

| Parnassus Equity Income Fund – Institutional Shares | | PRILX |

| |

| Parnassus Mid-Cap FundSM | | PARMX |

| |

| Parnassus Small-Cap FundSM | | PARSX |

| |

| Parnassus Workplace Fund® | | PARWX |

| |

| Parnassus Asia FundSM | | PAFSX |

| |

| Parnassus Fixed-Income FundSM | | PRFIX |

Table of Contents

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

August 2, 2013

Dear Shareholder:

Enclosed are the semiannual reports for all the Parnassus Funds. I think that you’ll find that they make for interesting reading, as they describe our investment strategy and the results for the quarter. They will also give you insights into the companies we invest in. Below is a photograph of a recent reunion of our interns.

Front Row (from left to right): Chi Tran-Brandli, Rachel Tan, Cina Loarie, Jerome Dodson, Thao Dodson, Rachel Chang, Madeline Lissner and Annie Lee. Middle Row: Lori Lai, Andrea Reichert, Hallie Marshall, Ben Allen, Katherine Loarie, Bryan Wong, Ian Sexsmith, Minh Bui, Matthew Gershuny, Robert Klaber, Fred Jones and Marie Lee. Back Row: Russ Caprio, Dan Beck, Josh Harrington, Iyassu Essayas, Ryan Wilsey, Peter Tsai, Gee Leung, Ben Hamlin, Billy Hwan and John Haskell.

Interns

We have eight terrific interns on our research team this summer. Ben Hamlin is an MBA candidate at the Haas School of Business at the University of California, Berkeley. Prior to business school, he spent four years in the equity capital markets division of Bank of America Merrill Lynch. He graduated with honors from Claremont McKenna College, with a degree in economics. Ben enjoys cooking, tennis, travelling, and serves on the board of a non-profit that assists microfinance recipients.

John Haskell earned an MBA from the Harvard Business School this past May. His experience includes stints at Boston Consulting Group, Eagle Capital Management and the Capital Group. John studied comparative literature and society at Columbia University, where he earned a bachelor’s degree with honors. He also studied in China on a Fulbright Grant and in Syria on a scholarship from the U.S. National Security Education Program. John’s favorite leisure activities are reading fiction and playing with his dachshund.

4

| | | | |

| | |

| Semiannual Report • 2013 | | | | PARNASSUS FUNDS |

Annie Lee is an MBA candidate at the Wharton School at the University of Pennsylvania. She holds a bachelor’s degree in business administration and a master’s degree in accounting from the University of Texas at Austin. She worked in Visa’s corporate finance group and the investment banking division of RBC Capital Markets. Annie is a founding board member of Nonprofit Investor, an organization that evaluates non-profits, and a board member of Leap, an arts education non-profit in San Francisco. In her free time, Annie enjoys traveling, playing piano and attending concerts.

Madeline Lissner is also an MBA candidate at the Wharton School. Previously, she was an investment banker in the New York offices of Centerview Partners and Citigroup. Madeline graduated magna cum laude from Harvard College, where she studied economics and served as Secretary of her class. At Wharton, Madeline has led character-development backpacking treks in locations such as Antarctica and Patagonia.

Bryan Wong is pursuing his MBA at the Haas School of Business at the University of California, Berkeley. Prior to business school, he was a senior associate at the David & Lucile Packard Foundation and an analyst at two hedge funds, Wohl Capital and Khan Capital Management. Bryan earned a bachelor’s degree from Yale University with distinction in political science and international studies. He is an avid San Francisco Giants fan and is looking forward to getting married in August.

The following three interns are helping our environmental, social and governance (ESG) research team this summer. Rachel Chang is a senior at the University of California, Berkeley, where she is pursuing a bachelor’s degree in business with a minor in energy and resources. She previously interned with a social impact consulting firm in Singapore and the Lawrence Berkeley National Laboratory’s Department of Energy Efficiency.

Emily Dwyer graduated from Smith College in May, where she double-majored in economics and environmental science and policy. While at Smith, Emily served as the Student Liaison and Intern for the Environmental Science & Policy department. During her junior year, she studied at the Graduate Institute of International and Developmental Studies in Geneva, Switzerland, and interned for the United Nations Environment Programme Finance Initiative (UNEP FI).

Cina Loarie earned a bachelor’s degree in biology from Duke University and a master’s degree in conservation from Scripps Institution of Oceanography at the University of California, San Diego. She worked as an analyst at the China Greentech Initiative in Beijing and as a project manager at the California Ocean Protection Council in Oakland. Cina holds a 100-ton captain’s license from the U.S. Coast Guard, making her the first certified skipper to intern at Parnassus Investments. Cina plans to pursue her master’s degree in sustainable business administration from the Presidio Graduate School in San Francisco this coming fall.

In other personnel news, Amy Phan has accepted an offer to join Parnassus Investments as a full-time Marketing Associate in August, upon completion of her current internship with the firm. Amy graduated in May from the University of California, Berkeley as a quadruple major, with bachelor’s degrees in environmental economics and policy, media studies, political economy and sociology. She was on the leadership team of MarketingCamp San Francisco 2013 and is a strong advocate for the LGBTQIA community.

Andrew Saeta is currently interning on our sales and marketing team. He graduated from Stanford University in May with a bachelor’s degree in science, technology and society. As a member of the varsity swim team, Andrew earned four NCAA All-American honors, three PAC-12 First Team Academic All-American honors and competed in the 2008 and 2012 U.S. Olympic Trials. Andrew’s interests outside of the pool include designing and distributing custom t-shirts and playing guitar.

Flora Dai is a software engineer intern, working on improving the user experience on our website. She is working towards a bachelor’s degree in electrical engineering and computer science at the University of California, Berkeley. She is a music enthusiast and during her spare time, enjoys playing the piano.

Greg Owyang is an information technology intern, working to support our technology infrastructure. He is working towards a bachelor’s degree in mechanical engineering at the California State Polytechnic University, Pomona. He enjoys snowboarding and playing video games in his spare time.

5

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

Downey Blount is a Compliance Project Manager, who will be handling special projects over the next three months. Downey brings a wealth of experience, as her prior positions include Mutual Fund Administration Manager at Montgomery Asset Management and Chief Compliance Officer at Matthews International Capital Management. She has a bachelor’s degree from the University of California, Santa Barbara, and attended law school at the University of San Francisco. Downey is fluent in Spanish and spent a year living in Spain.

Yours truly,

Jerome L. Dodson

President

6

| | | | |

| | |

| Semiannual Report • 2013 | | | | PARNASSUS FUNDS |

PARNASSUS FUND

Ticker: PARNX

As of June 30, 2013, the net asset value per share (“NAV”) of the Parnassus Fund was $45.81, so the total return for the quarter was 6.61%. This compares favorably to 2.91% for the S&P 500 Index (“S&P 500”) and 2.57% for the Lipper Multi-Cap Core Average, which represents the average return of the multi-cap core funds followed by Lipper (“Lipper average”). For the quarter, we beat the S&P 500 by 3.7 percentage points and the Lipper average by 4.04 percentage points. Although we lagged our benchmarks by quite a bit at the end of the first quarter, we bounced back nicely in the second quarter, so that now we’re only a little over a percentage point behind the S&P 500 for the year-to-date: 12.78% vs. 13.82%; and only about half a percentage point behind the Lipper average: 12.78% vs. 13.34%. As you’ll see in the Company Analysis section, technology and telecommunications stocks helped us the most in this comeback quarter, but we also had help from financial stocks and a consumer-products company.

Below is a table comparing the Parnassus Fund with the S&P 500 and the Lipper average over the past one-, three-, five- and ten-year periods ended June 30, 2013. We’re ahead of both benchmarks for all periods except for the ten-year period, where we’re slightly behind both the S&P 500 and the Lipper average.

| | | | | | | | | | | | | | | | | | | | | | | | |

| Parnassus Fund | | | | | | | |

Average Annual

Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended

June 30, 2013 | | | | | | |

| | | | | | | |

| Parnassus Fund | | | 27.16 | | | | 19.28 | | | | 10.57 | | | | 7.20 | | | | 0.90 | | | | 0.90 | |

| | | | | | | |

| S&P 500 Index | | | 20.60 | | | | 18.45 | | | | 7.01 | | | | 7.29 | | | | NA | | | | NA | |

| | | | | | | |

| Lipper Multi-Cap Core Average | | | 21.87 | | | | 16.24 | | | | 5.79 | | | | 7.38 | | | | NA | | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 Composite Stock Index (also known as the S&P 500) is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Prior to May 1, 2004, the Parnassus Fund charged a sales load (maximum of 3.5%), which is not reflected in the total return calculations.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website, or by calling (800) 999-3505.

Company Analysis

Six companies helped us the most during the quarter, with each one adding 20¢ or more to the NAV. No company took as much as 20¢ off the value of each fund share. The one that hurt us the most was Autodesk, which subtracted 19¢ from each Parnassus Fund share, as it fell from $41.24 to $33.94 – a decline of 17.7%. The company provides software for architects, engineers and designers. Weak demand in Europe caused the company to miss earnings expectations, and the company lowered revenue guidance for the full year. Despite the weak start to the year, Autodesk saw encouraging signs of demand in the commercial construction and manufacturing markets in North America, so we expect the stock to rebound, as economic activity picks up later in the year.

The Fund’s strongest performer was Ciena, a maker of optical equipment used in telecommunications networks. The stock soared 21.3% from $16.01 to $19.42 for a gain of 51¢ for each fund share. The large telecommunications service providers have delayed capital expenditures over the past several years because of the weak economy. This has put a big strain on the networks as they tried to handle an ever-increasing amount of data. The telecommunications companies are finally purchasing a lot more equipment. AT&T, Ciena’s largest customer, recently announced plans to increase capital expenditures by 15% per year over the next three years. Ciena recently gave guidance to analysts, projecting substantial increases in revenue over the coming year.

7

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

Like Ciena, Finisar makes optical equipment for telecommunications networks, and during the quarter, its stock rose 28.5% from $13.19 to $16.95, adding 46¢ to the NAV. The company’s data-communications division generates almost 65% of the firm’s revenue, and customers of this division are rapidly upgrading the servers within their data centers to handle increased Internet traffic, so demand for Finisar’s equipment should remain strong.

Credit card issuer Capital One climbed 14.3% from $54.95 to $62.81, adding 29¢ to each fund share. Last year, the company’s quarterly earnings were very volatile, as Capital One integrated its recent acquisitions of online bank ING Direct and HSBC’s private label credit card portfolio. Earnings in the most recent quarter exceeded expectations, as the benefits of the acquisitions are becoming apparent.

Coach, the big retailer of handbags and accessories, rose 14.2% from $49.99 to $57.09, adding 27¢ to each fund share. The company posted better-than-expected results for its March quarter, led by solid sales in China and strong demand for men’s accessories in North America. While Coach faces more competition from newer entrants such as Michael Kors and Tory Burch, we believe the company’s reputation for high-quality handbags and accessories combined with its expansion in Asia will pave the way for healthy profits ahead.

Applied Materials is the world’s largest maker of equipment used in manufacturing semiconductors, and its stock climbed 10.6% during the quarter from $13.48 to $14.91, contributing 27¢ to each fund share. Rising demand for smartphones and tablets means that memory chipmakers and flat-panel display manufacturers have to buy more equipment from Applied Materials to meet this demand. Semiconductors are finding their way into more and more products, and Applied is one of only a few companies with the technology and the scale to provide equipment. The company’s president, Gary Dickerson, recently restructured Applied to increase efficiency and profitability.

Charles Schwab, the San Francisco-based bank and brokerage firm, jumped 20.0% from $17.69 to $21.23, while boosting the NAV by 24¢. Because of expectations for an increase in interest rates, the stock is now up an amazing 47.8% for the year-to-date. With higher rates, Schwab can earn much more on their banking assets, money market products and margin loans to brokerage clients. In February, the company told investors that if interest rates returned to their pre-crisis levels of the second quarter of 2008, Schwab’s earnings would be almost triple their current quarterly earnings of 15¢ per share. We’re holding onto most of our Schwab shares, even after the big move up, because we think there’s still more room for the stock to go higher.

| | |

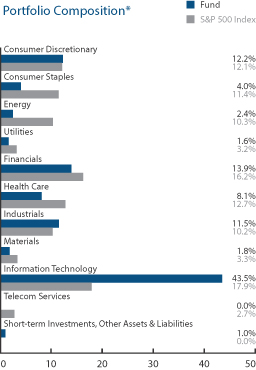

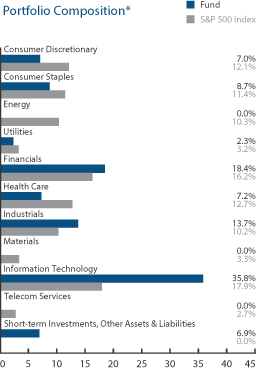

Parnassus Fund Sector Weightings as of June 30, 2013 (percentage of net assets) |

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

Top 10 Holdings

(percentage of net assets)

| | | | |

| |

| Ciena Corp. | | | 6.6% | |

| |

| Applied Materials Inc. | | | 5.6% | |

| |

| Riverbed Technology Inc. | | | 5.3% | |

| |

| Capital One Financial Corp. | | | 4.8% | |

| |

| Finisar Corp. | | | 4.7% | |

| |

| Coach Inc. | | | 3.6% | |

| |

| EZchip Semiconductor Ltd. | | | 3.4% | |

| |

| C.H. Robinson Worldwide Inc. | | | 3.2% | |

| |

| Charles Schwab Corp. | | | 3.1% | |

| |

| QUALCOMM Inc. | | | 3.1% | |

Portfolio characteristics and holdings are subject to change periodically.

8

| | | | |

| | |

| Semiannual Report • 2013 | | | | PARNASSUS FUNDS |

Outlook and Strategy

Note: This section represents my thoughts and applies to two of the funds that I manage: the Parnassus Fund and the Parnassus Workplace Fund, which are managed as a pair. The outlook and strategy for the Parnassus Small-Cap Fund appears in that Fund’s section and was written by myself and Portfolio Manager, Ryan Wilsey. There is no outlook and strategy section for the new Parnassus Asia Fund, since that section already contains general thoughts about the ideas behind the Asia Fund.

The economy continues to grow at a slow pace with modest increases in job creation. Normally after a recession, the economy starts to grow at a rapid clip, with new job creation sometimes exceeding 300,000 or 400,000 per month. Since 2009, the economy has expanded slowly with job creation hovering in the range of 100,000 to, at most, 200,000. Looked at in one way, this slow growth is frustrating, because the unemployment rate remains high, and there are concerns that the economy may fall into a recession again.

Looked at another way, the slow growth phenomenon may not be all bad. The measured pace of growth may prevent the economy from overheating. The stock market seems to like the slow and steady rate of growth, as it has moved sharply higher this year with a gain of 13.82% for the S&P 500 for the first six months of the year.

Many economists and top government officials, including Federal Reserve Chairman Ben Bernanke, are concerned that the rate of growth is so slow, that the economy could fall back into a recession. In fact, Chairman Bernanke has had the Fed purchase $85 billion of securities per month, mostly in mortgage securities, to stimulate the economy.

Although I agree with the Bernanke policy, I think it’s highly unlikely that the economy will fall back into a recession, even if the Fed tapers off its purchase of securities and reduces the economic stimulus. The reason for my optimism is the state of the housing market. As many of you know, I’m convinced that almost without exception, the housing market is what drives the economy into a recession and pulls the economy out of a recession. It was clearly speculation in the housing market and abuse of subprime mortgages that drove us into the great recession of 2008. The crash of the housing market is what drove us to the brink of financial meltdown in 2008 and has kept the economy on its knees for so long.

Housing is now driving the economy forward. Existing home sales grew 12.9% in May, and home prices in the twenty largest American cities jumped 12.1% in April; the largest increase since 2006. At first glance, these numbers might cause concern that the housing market may be overheating again, but remember that these increases are from low bases. Lenders are more disciplined than they were in the 2006-2007 period, so it’s unlikely that things will get out of hand in the housing market – at least not right away. Also, for most of the country, housing prices are still far below their peaks of 2007-2008.

As home prices recover and construction picks up, bricklayers, carpenters, plumbers and electricians have more work. People will buy more furniture, home appliances, pots and pans, dishes, drapes and rugs, and so on throughout the economy. This is a force that is not easy to stop, so the economy should keep growing. Interest rates will rise slowly, but this should not choke off the expansion, since they remain low compared to historic levels.

Our portfolio is positioned to take advantage of this growth in the economy, as evidenced by our continuing position in homebuilders and our holdings in telecommunications and technology stocks. Even with the big move up in the stock market this year, stocks don’t appear to be overvalued. Volatility will continue, and may have big moves down when there are concerns that interest rates are moving higher. For us, though, this will be a good time to buy.

Yours truly,

Jerome L. Dodson

Portfolio Manager

9

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

PARNASSUS EQUITY INCOME FUND

Ticker: Investor Shares - PRBLX

Ticker: Institutional Shares - PRILX

As of June 30, 2013, the NAV of the Parnassus Equity Income Fund-Investor Shares was $33.17. After taking dividends into account, the total return for the second quarter was 1.40%. This compares to increases of 2.91% for the S&P 500 Index (“S&P 500”) and 2.17% for the Lipper Equity Income Fund Average, which represents the average return of the equity income funds followed by Lipper (“Lipper average”). For the first half of 2013, the Fund posted a return of 14.28%, which compares favorably to gains of 13.82% for the S&P 500 and 13.01% for the Lipper average.

| | | | | | | | | | | | | | | | | | | | | | | | |

| Parnassus Equity Income Fund | |

Average Annual Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Ten

Years | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended

June 30, 2013 | | | | | | |

| | | | | | | |

| Parnassus Equity Income Fund Investor Shares | | | 23.76 | | | | 17.04 | | | | 8.88 | | | | 8.74 | | | | 0.90 | | | | 0.90 | |

| | | | | | | |

| Parnassus Equity Income Fund Institutional Shares | | | 23.90 | | | | 17.25 | | | | 9.09 | | | | 8.88 | | | | 0.68 | | | | 0.68 | |

| | | | | | | |

| S&P 500 Index | | | 20.60 | | | | 18.45 | | | | 7.01 | | | | 7.29 | | | | NA | | | | NA | |

| | | | | | | |

| Lipper Equity Income Fund Average | | | 19.18 | | | | 17.06 | | | | 6.71 | | | | 7.83 | | | | NA | | | | NA | |

The total return for the Parnassus Equity Income Fund-Institutional Shares from commencement (April 28, 2006) was 8.75%. Performance shown prior to the inception of the Institutional Shares reflects the performance of the Parnassus Equity Income Fund-Investor Shares and includes expenses that are not applicable to and are higher than those of the Institutional Shares. The performance of Institutional Shares differs from that shown for the Investor Shares to the extent that the classes do not have the same expenses. Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted, and current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The S&P 500 is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. On March 31, 1998, the Fund changed its investment objective from a balanced portfolio to an equity income portfolio.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website, or by calling (800) 999-3505.

To the left is a table that summarizes the performance of the Fund, the S&P 500 and the Lipper average. The returns are for the one-, three-, five- and ten-year periods ended June 30, 2013. Our goal is to beat our benchmarks over a full market cycle, so we’re not overly concerned about our slight underperformance for the three-year bull market period. More important to us are the five- and ten-year periods, because these reflect the Fund’s performance in positive return years, as well as bearish periods such as 2008 and early 2009.

Second Quarter Review

Stock prices surged in April and May, building on the previous quarter’s rally. The S&P 500 subsequently retreated 3.8% from a new record close set in May, but still managed to post a solid 2.9% gain for the quarter. The index faded in late June, after Federal Reserve Chairman Ben Bernanke said that he expects a tapering of central bank purchases of government and mortgage bonds later this year. Since a key goal of the Fed’s recent policy has been to boost asset prices, it’s not surprising that stocks dropped after Bernanke’s speech. On the bright side, the chairman emphasized that any reduction in Fed support of financial markets would be contingent upon further improvement in economic fundamentals.

The Fund trailed the S&P 500 this quarter by 151 basis points (one basis point equals 0.01%). For the period, our portfolio held far fewer financial and consumer discretionary stocks than the index. These allocation decisions reduced our return relative to the S&P 500 by a combined 0.8%, because these were the best two performing sectors in the index. The rest of our underperformance was due to individual stock selection.

Company Analysis

Iron Mountain, the nation’s largest document storage company, was the Fund’s biggest loser;

10

| | | | |

| | |

| Semiannual Report • 2013 | | | | PARNASSUS FUNDS |

it dropped 26.7% from $36.31 to $26.61, slicing 25¢ off the Fund’s NAV. In June, Iron Mountain’s management announced that the IRS had put on hold the company’s application to become a real estate investment trust (REIT), and that the agency was “tentatively adverse” to the application before doing so. One silver lining is that the halt was not specific to Iron Mountain, but rather, applied to a large number of other applicants as well. Since a REIT structure would drastically reduce Iron Mountain’s tax bill and increase its dividend, the stock fell sharply on the news.

In response to the “tentatively adverse” feedback, a team from Iron Mountain met with the IRS to press their case. Management thinks that the meeting went well and still expects to convert the company to a REIT. If this happens, the stock will move significantly higher. If it doesn’t, we don’t think there is much further downside from the current price. Since we still like Iron Mountain’s long-term business prospects, we bought more of the stock after the price drop in June.

Teleflex, a medical company that makes single-use products such as catheters, declined 8.3% to $77.49 from $84.51, and reduced the NAV by 8¢. The stock dropped after management reported weaker-than-expected revenue growth for the most recent quarter. In addition, the company has to pay a new medical device tax, which will trim earnings starting this year. Despite the sub-par quarter, we still think that Teleflex is well-positioned to grow profits and cash flow for the long-term, as it increases its portfolio of critical care products through acquisitions and R&D.

C.H. Robinson, a logistics brokerage company with an emphasis on trucking, trimmed the NAV by 5¢, as the stock fell 5.3% from $59.46 to $56.31. While this is a relatively modest impact, we offer a detailed account of the investment, because C.H. Robinson was the Fund’s largest holding as of June 30. The stock dropped this quarter because the company’s net revenue margin fell below expectations. Weak margins have been plaguing the company since early 2010, primarily for two reasons. The first is that C.H. Robinson has been brokering more low-margin, predictable shipments versus high-margin, rush deliveries, as compared to their historical mix. This is a result of the economy’s subdued recovery from the 2008-2009 recession. Simply put, when consumer demand is tepid, retailers don’t require as many rush deliveries to refill their shelves. The second issue is that some large competitors have decided to aggressively pursue market share gains by accepting lower brokerage margins.

We think that these problems will prove to be temporary, though it’s impossible to predict exactly when they will be resolved. We also believe that the stock price adequately reflects the margin-related concerns. Over the last two years, C.H. Robinson has dropped 31% from its all-time high of $81 to its quarter-end price of $56, which is one dollar less than our average cost and well below our intrinsic value estimate.

Charles Schwab, the San Francisco-based bank and brokerage firm, jumped 20.0% from $17.69 to $21.23 during the quarter, adding 18¢ to the Fund’s NAV. The stock is now up an amazing 47.8% for the year-to-date, mostly due to expectations of a continued rise in interest rates. With higher rates, Schwab can earn much more on their banking assets, money market products and margin loans to brokerage clients than they do today. In February, the company told investors that if interest rates returned to their pre-credit crisis levels of the second quarter of 2008,

| | |

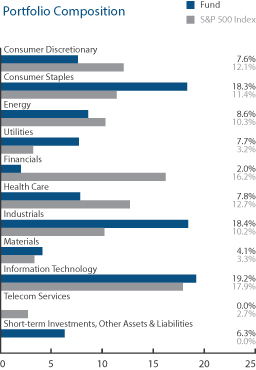

Parnassus Equity Income Fund Sector Weightings as of June 30, 2013 (percentage of net assets) |

Top 10 Holdings

(percentage of net assets)

| | | | |

| |

| C.H. Robinson Worldwide Inc. | | | 4.4% | |

| |

| Applied Materials Inc. | | | 4.1% | |

| |

| Procter & Gamble Co. | | | 4.1% | |

| |

| Apple Inc. | | | 3.9% | |

| |

| Mondelez International Inc. | | | 3.1% | |

| |

| National Oilwell Varco Inc. | | | 3.1% | |

| |

| Questar Corp. | | | 3.0% | |

| |

| Waste Management Inc. | | | 3.0% | |

| |

| PepsiCo Inc. | | | 2.9% | |

| |

| Pentair Ltd. | | | 2.9% | |

Portfolio characteristics and holdings are subject to change periodically.

11

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

Schwab’s earnings would be almost triple their current 15¢ quarterly rate. We trimmed our Schwab position in response to the big move up, but still held some stock at quarter-end.

Applied Materials, the manufacturer of semiconductor capital equipment, climbed 10.6% to $14.91 from $13.48 and increased the NAV by 14¢. The company’s customers are steadily increasing their capacity to build chips for computing devices, such as smartphones and tablets. Importantly for an equipment maker like Applied Materials, as the technical specifications for these chips evolve, they become more difficult and expensive to manufacture. This trend should continue for many years, and the company is well-positioned to profit from it. Another positive is that Applied Materials’ management team has significantly improved over the past 18 months, with the promotion of Gary Dickerson to President and the addition of Bob Halliday as Chief Financial Officer. These executives have already reshaped the company’s culture, with a focus on innovation, cost control and anticipating customer needs.

Google climbed 10.9% to $880.37 from $794.03 and added 13¢ to the NAV. The company reported excellent first quarter results in April, with revenues 31% higher than last year. Google’s mobile advertising sales are surging, and the company has done an excellent job at monetizing its non-search services, such as YouTube. We trimmed our Google position at an average price of $908 during the quarter, because we expect more modest investment returns given the current valuation.

Outlook and Strategy

Our overall strategy is basically unchanged from last quarter. We still think there are pockets of fragility in the global economy, but are encouraged by the fact that the housing market in the United States has roared back to life. According to the latest Case-Shiller report, national home prices rose at an average annual rate of 12.1% in April and were up a record 2.5% as compared to the previous month. This real estate recovery has increased the wealth of millions of American homeowners and encouraged new home construction. Since a homebuilding recovery usually precedes a broader economic expansion, it’s a great sign that builders sought permits in May at the highest rate since the spring of 2008.

Federal Reserve Chairman Ben Bernanke has taken note of the strength in the real estate market and the overall economy. On June 19, he announced that if the economy keeps improving as he expects, the central bank would soon reduce the size of its quantitative easing (QE) program, which is designed to boost asset prices and keep interest rates low. Bernanke specified that by year-end the Fed would ratchet down its monthly bond purchases from the current pace of $85 billion and likely end the program in 2014. Since the Fed has played a major role in propping up debt markets, we expect bonds to display increased volatility as QE tapers off and eventually expires. We wouldn’t be surprised to see turbulence in the stock market as well, since changes in the value of credit securities normally impact equity prices.

We’re still paying close attention to events overseas that could potentially impair the value of our portfolio companies. Europe’s persistent economic contraction and fragile credit system top our list of global concerns. Amazingly, the 17 nations that comprise the Eurozone are, in aggregate, enduring their sixth consecutive quarter of recession. This is the longest recession for the region since records began in 1995. We think that Europe’s banking system is still vulnerable to a credit shock, so the Fund didn’t own any financial firms with significant exposure to Europe as of quarter-end.

The market surge that culminated in the S&P 500’s record high in May lifted many of our stocks close to their intrinsic values. Two stocks, Nike and Valeant Pharmaceuticals, actually exceeded our fair value assessment, so we no longer own them as of quarter-end. In addition to these outright sales, we trimmed a handful of other positions in the Fund. We reinvested the sales proceeds into existing portfolio companies, as well as three new holdings: Apple, Thomson Reuters and National Oilwell Varco. These are terrific businesses with stocks that we think offer asymmetric payoffs, with far more potentially to gain than to lose. We hope to write about these stocks in detail as Fund winners in future reports.

Thank you for your trust and investment with us,

| | | | |

| |  | | |

| | |

| Todd C. Ahlsten | | Benjamin E. Allen | | |

| Lead Portfolio Manager | | Portfolio Manager | | |

12

| | | | |

| | |

| Semiannual Report • 2013 | | | | PARNASSUS FUNDS |

PARNASSUS MID-CAP FUND

Ticker: PARMX

As of June 30, 2013, the NAV of the Parnassus Mid-Cap Fund was $22.50, so the total return for the quarter was 1.08%. This compares to 2.21% for the Russell Midcap Index (“Russell”) and 2.57% for the Lipper Multi-Cap Core Average, which represents the average return of the multi-cap core funds followed by Lipper (“Lipper average”).

For the year-to-date, we are behind both the Russell and the Lipper average, as we have gained 11.00%, compared to 15.45% for the Russell and 13.34% for the Lipper average. Normally, we’d be thrilled with an 11% return for six-months, but it’s hard to celebrate when we’re trailing our benchmarks by such a large margin.

Our strategy of owning high-quality businesses at good prices should continue to generate shareholder wealth over the long-term. Since we began managing the Fund on September 30, 2008, the Fund’s annualized return is 12.03%, ahead of the Russell’s 11.94% and the Lipper average’s 8.77%. We’re also proud of our five-year return, which is well ahead of both the Russell and Lipper averages. Our three-year return is slightly behind the Russell but well ahead of the Lipper average, which we consider to be adequate considering the Fund’s relatively low risk profile.

Below is a table comparing the Parnassus Mid-Cap Fund with the Russell and the Lipper average for the one-, three- and five-year periods ended June 30, 2013, and for the period since inception on April 29, 2005.

| | | | | | | | | | | | | | | | | | | | | | | | |

| Parnassus Mid-Cap Fund | | | | | | | |

Average Annual

Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception on

4/29/05 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended

June 30, 2013 | | | | | | |

| | | | | | | |

| Parnassus Mid-Cap Fund | | | 19.22 | | | | 18.44 | | | | 11.14 | | | | 8.10 | | | | 1.23 | | | | 1.20 | |

| | | | | | | |

| Russell Midcap Index | | | 25.41 | | | | 19.53 | | | | 8.28 | | | | 8.53 | | | | NA | | | | NA | |

| | | | | | | |

| Lipper Multi-Cap Core Average | | | 21.87 | | | | 16.24 | | | | 5.79 | | | | 6.02 | | | | NA | | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell Midcap Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Mid-cap companies can be more sensitive to changing economic conditions and have fewer financial resources than large-cap companies.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website, or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2013, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.20% of net assets, exclusive of acquired fund fees, until May 1, 2014. This agreement will not be terminated prior to May 1, 2014, and may be continued indefinitely by the Adviser on a year-to-year basis.

Second Quarter Review

Mid-Cap stocks fell 2.9% to start the quarter, after the Labor Department reported that 88,000 jobs were created in March versus expectations of 200,000. The Russell then surged 9.4% to an all-time high by May 21st, when Federal Reserve policy makers expressed growing confidence in the economic recovery. Investor optimism didn’t last long though, as mid-cap stocks retreated 4.2% after Federal Reserve Chairman Ben Bernanke opened the door to curtailing the Fed’s stimulus program. When all was said and done, mid-cap stocks ended the turbulent quarter with a 2.2% gain.

The Fund trailed the Russell by 113 basis points (one basis point equals 0.01%) and the Lipper average by 149 basis points. During the quarter, we held fewer consumer discretionary stocks than the index, which cost us 71 basis points. We underweighted the sector relative to the index, but unfortunately, the sector outperformed the overall index. Making matters worse, the consumer discretionary stocks we owned underperformed their sector peers.

As usual, stock selection had a greater influence on the Fund’s return than sector allocation. We’ll get into specifics in the Company Analysis section, but our stock picks in the healthcare and information technology sector hurt us the most, reducing performance by almost two percentage points. Good stock picking in the financial and energy sectors helped make up some of the difference, by adding almost one percentage point to our performance.

13

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

Company Analysis

Three stocks reduced the Fund’s NAV by 5¢ or more in the quarter, while three stocks added at least 7¢. The stock that hurt us the most was Iron Mountain, the nation’s largest document management company. The stock sank 26.7% to $36.31 from $26.61, slicing 17¢ from the NAV. In June, Iron Mountain’s management announced that the IRS had put on hold the company’s application to become a real estate investment trust (REIT), and that the agency was “tentatively adverse” to the application before doing so. One silver lining is that the halt was not specific to Iron Mountain, but applied to a large number of other applicants as well. Since a REIT structure would drastically reduce Iron Mountain’s tax bill and increase its dividend, the stock fell sharply on the news.

In response to the “tentatively adverse” feedback, a team from Iron Mountain met with the IRS to press their case. Management thinks that the meeting went well and still expects to convert the company to a REIT. If this happens, the stock will move significantly higher. If it doesn’t, we don’t think there is much further downside from the current price. Since we still like Iron Mountain’s long-term business prospects, we bought more of the stock after the price drop in June.

Concho Resources, a Texas-based oil and gas producer, declined 14.1% from $97.43 to $83.72, cutting 5¢ from the NAV. Natural gas prices slumped from $4.02 to $3.56 per million British Thermal Unit (Btu) during the quarter, which hurt Concho’s profits. We believe Concho’s deep inventory of oil and gas assets in West Texas creates a long runway for robust earnings growth ahead.

Medical equipment manufacturer Teleflex dropped 8.3%, from $84.51 to $77.49, reducing each fund share by 5¢. When the stock was close to its all-time high of $87 per share in early April, we trimmed our position. The stock proceeded to drop, after the company reported weaker-than-expected sales results. We are holding our remaining shares, because we believe Teleflex is well-positioned to deliver strong profits and cash flow in the coming years, as it expands its portfolio of critical care products through acquisitions and R&D.

Our biggest winner this quarter was Charles Schwab, the brokerage firm and bank. The stock soared 20.0% during the quarter to $21.23 from $17.69, adding 10¢ to the Fund’s NAV. The stock is up 47.8% for the year-to-date, primarily due to expectations of a continued rise in interest rates, which will allow Schwab to earn much more on their banking assets, money market products and margin loans to brokerage clients. In February, the company told investors that if interest rates returned to their pre-credit crisis levels of the second quarter of 2008, Schwab’s earnings would be almost triple their current 15¢ quarterly rate. We trimmed our Schwab position in response to the big move up and its large-cap size, but still held a position at quarter end.

Pentair, a water and energy industrial product manufacturer, added 8¢ to the Fund’s NAV, as its stock rose 9.4% to $57.69 from $52.75. The stock jumped during the quarter, because management reaffirmed its longer-term performance targets, given the rebounding U.S. residential construction market. We’re holding onto the stock, because we think the company can realize greater-than-expected efficiencies from its recent merger with Tyco Flow Control.

| | |

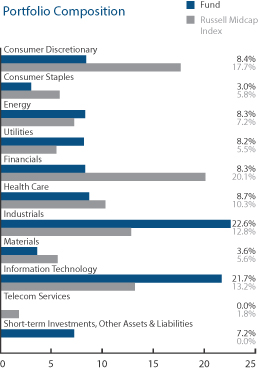

Parnassus Mid-Cap Fund Sector Weightings as of June 30, 2013 (percentage of net assets) |

Top 10 Holdings

(percentage of net assets)

| | | | |

| |

| Pentair Ltd. | | | 3.7% | |

| |

| C.H. Robinson Worldwide Inc. | | | 3.6% | |

| |

| Shaw Communications Inc. | | | 3.5% | |

| |

| Expeditors International of Washington Inc. | | | 3.3% | |

| |

| Waste Management Inc. | | | 3.2% | |

| |

| Insperity Inc. | | | 3.2% | |

| |

| Sysco Corp. | | | 3.0% | |

| |

| Questar Corp. | | | 2.9% | |

| |

| Applied Materials Inc. | | | 2.8% | |

| |

| MDU Resources Group Inc. | | | 2.8% | |

Portfolio characteristics and holdings are subject to change periodically.

14

| | | | |

| | |

| Semiannual Report • 2013 | | | | PARNASSUS FUNDS |

Spectra Energy, a leading natural gas pipeline and storage company, added 7¢ to each Fund share, as its stock jumped 12.1% from $30.75 to $34.46. Strong distribution segment results, which saw higher customer usage due to colder weather, drove better than expected earnings results. Investor sentiment moved higher after the company announced plans to move its U.S. transmission and storage assets into a tax-advantaged master-limited partnership subsidiary.

Outlook and Strategy

Years of government stimulus, including near-zero inter-bank borrowing rates and over a trillion dollars of bond-buying, have driven mid-cap stocks up almost 200% from their March of 2009 lows. Investors now see easy Fed policy as a sign to buy stocks. So when the Fed recently signaled that it will probably wind down its $85 billion a month bond buying program next year, the markets sold off.

The stimulus of the past few years has helped get the country back on track. GDP has grown for the past fifteen quarters, consumer confidence hit a high in June, and the housing market is thriving, with home prices in multiple U.S. cities reaching record highs. The unemployment rate is also down to 7.6%, well below the 10% rate at recession peak.

We don’t think investors should fear the end of stimulus. We expect the Fed to proceed slowly, in a way that encourages continued economic growth. The economy will eventually become self-sustaining, and this should drive further stock market gains. In the meantime, we are using the market turbulence to buy the best businesses we can.

Our process of finding undervalued companies is always on a stock-by-stock basis. We currently own more technology and industrial companies than our benchmarks, because we’re finding especially good bargains in these sectors. Most of our holdings in these areas also have secular growth drivers, robust free cash flow and significant cash balances, which help mitigate downside risk.

During the quarter, we initiated a few sizeable positions. Autodesk is the market leader in 3D design and engineering software, which is used to design everything from Nike sneakers to San Francisco’s new Bay Bridge. Designers, architects and manufacturers are trained to use the company’s quality software early in their careers, so it’s difficult for them to switch to competing products. This in turn allows Autodesk to consistently raise prices with little resistance from clients.

Autodesk’s sluggish European growth recently disappointed investors, but the company has opportunities to expand its business in North America, Latin America and Asia. The recovery in the manufacturing and construction sectors, particularly in the U.S., should boost demand for Autodesk’s engineering design software. Since we believe Autodesk is a great business, we bought the stock when the price dropped and the valuation became attractive.

Another new position is Intuit. You probably know Intuit for its user-friendly TurboTax software. What is less appreciated by investors is its small business software segment, which offers products that simplify small businesses’ day-to-day tasks. The company has over five million users of its QuickBooks accounting software. Like Autodesk, Intuit’s widespread adoption creates high switching costs. The company’s competitive advantage is reflected in its impressive returns on capital, averaging 23.5% over the past ten years. We think management is top notch, and so is the company’s workplace, which Fortune magazine recognized in 2012 in its Top 100 Best Places to Work survey.

We also bought Cardinal Health, a leading pharmaceutical distributor in the United States. Cardinal is poised to benefit from greater health care spending on prescription drugs, driven by an aging population and expansion of health care insurance. Similar to Patterson Companies, another leading medical distributor, which we own in the Fund, we believe Cardinal is a wide-moat franchise with good growth prospects, solid free cash flow generation and a reasonable valuation.

15

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

We remain committed to generating market-beating returns over the long-run, by focusing on our process of investing in attractively-valued, well-managed companies with strong growth prospects and competitive advantages.

Thank you for your investment in the Parnassus Mid-Cap Fund.

| | | | |

| |  | | |

| Matthew D. Gershuny | | Lori A. Keith | | |

| Lead Portfolio Manager | | Portfolio Manager | | |

16

| | | | |

| | |

| Semiannual Report • 2013 | | | | PARNASSUS FUNDS |

PARNASSUS SMALL-CAP FUND

Ticker: PARSX

As of June 30, 2013, the NAV of the Parnassus Small-Cap Fund was $25.63, so the total return for the second quarter was a gain of 2.81%. By comparison, the Russell 2000 Index of smaller companies (“Russell 2000”) had a gain of 3.08%, and the Lipper Small-Cap Core Average, which represents the average return of the small-cap core funds followed by Lipper (“Lipper average”), had a gain of 2.44%. For the quarter, we underperformed the Russell 2000, but were slightly ahead of the Lipper average.

Year-to-date, the Fund is trailing both indices, up 7.83%, compared to 15.86% for the Russell 2000 and 14.78% for the Lipper average. Below is a table comparing the Parnassus Small-Cap Fund with the Russell 2000 and the Lipper average over the past one-, three- and five-year periods ended June 30, 2013 and the period since inception. Although our one- and three-year performance has been subpar, our longer-term five-year and since inception performance exceeded both benchmarks. Since our investment process (identifying high-quality businesses that are temporarily out-of-favor) remains the same, we expect to return to outperformance in the future.

| | | | | | | | | | | | | | | | | | | | | | | | |

| Parnassus Small-Cap Fund | | | | | | | |

Average Annual

Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception on

4/29/05 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended

June 30, 2013 | | | | | | |

| | | | | | | |

| Parnassus Small-Cap Fund | | | 17.54 | | | | 13.40 | | | | 9.84 | | | | 8.82 | | | | 1.23 | | | | 1.20 | |

| | | | | | | |

| Russell 2000 Index | | | 24.21 | | | | 18.67 | | | | 8.77 | | | | 8.05 | | | | NA | | | | NA | |

| | | | | | | |

| Lipper Small-Cap Core Average | | | 23.93 | | | | 17.59 | | | | 8.14 | | | | 7.67 | | | | NA | | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell 2000 Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Small-cap companies can be particularly sensitive to changing economic conditions and have fewer financial resources than large-cap companies.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website, or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2013, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.20% of net assets, exclusive of acquired fund fees, until May 1, 2014. This agreement will not be terminated prior to May 1, 2014, and may be continued indefinitely by the Adviser on a year-to-year basis.

Company Analysis

Three companies slashed 11¢ or more from each fund share. The company that hurt us the most was Iron Mountain, a document storage company whose stock dove 26.7% from $36.31 to $26.61, carving 14¢ off the Fund’s NAV. The IRS delayed action on the company’s application to convert to a real estate investment trust (REIT), because it needed further time to determine whether the company qualifies. Since a REIT structure would drastically reduce Iron Mountain’s tax bill, the stock fell sharply on this news. We bought more shares after the drop, because we think the stock is attractively priced, even if the company isn’t allowed to become a REIT. Of course, if the IRS ends up ruling in Iron Mountain’s favor, the stock should move much higher.

Ceragon Networks, a manufacturer of wireless communication equipment, sank 27.3% from $4.32 to $3.14, slicing 12¢ off the NAV. Ceragon reported weak earnings because Asian and European customers delayed large projects due to the weak economy. However, wireless data demand is growing rapidly because of increased smartphone and tablet usage, which should eventually force Ceragon’s customers to upgrade their networks.

Blount International, the leading manufacturer of chainsaw cutting chains, slumped 11.7% from $13.38 to $11.82, knocking 11¢ off the NAV. Husqvarna, a large chainsaw manufacturer, announced that it will begin manufacturing its own cutting chains rather than sole-sourcing from Blount. Although this will negatively impact Blount, it will take Husqvarna two years to build a factory and another year to fine-tune the

17

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

manufacturing process. Additionally, most of Blount’s sales are replacement chains sold to end customers, where its Oregon brand has excellent name recognition.

Three companies helped the Fund the most, two optical-communications equipment-manufacturers and a pharmaceutical company: each contributed 15¢ or more to the NAV. Finisar, a manufacturer of optical components used in data centers and communications networks, provided the biggest gain, adding 26¢ to each fund share as its stock rocketed up 28.5%, from $13.19 to $16.95. Finisar benefited from Internet data growth, as its customers added data center servers to meet demand. Finisar’s products connect servers within the data center, allowing very rapid data transfer. As the number of data center servers increases, demand for Finisar’s equipment should remain strong.

Ciena, a manufacturer of high-speed optical routers used in communications networks, jumped 21.3%, from $16.01 to $19.42, increasing the NAV by 23¢. Ciena also benefited from Internet data growth, which finally forced telecommunications carriers to upgrade to faster networks. Ciena’s focus on next-generation technology is paying off, because it is winning new orders and gaining market share.

Salix Pharmaceuticals, a pharmaceutical company focused on treatments for gastrointestinal disorders, soared 29.2% from $51.18 to $66.15, boosting each fund share by 15¢. The stock rose as Apriso, Salix’s treatment for irritable bowel disease, grew 50% as it benefited from a competitor’s stumble. Additionally, Salix’s largest drug, Xifaxan, a treatment for liver failure and traveler’s diarrhea, has significant room to grow because its results appear to be superior to alternative treatments.

Outlook and Strategy

Given the market’s strong run-up so far this year, we expect a temporary pullback as investors digest recent stock gains, higher interest rates and contemplate a world with less Federal Reserve stimulus. However, we remain bullish longer-term, because the economy is healing. GDP grew 1.8% in the first quarter, the fifteenth consecutive quarter of growth, while consumer confidence hit a five-year high in June. Additionally, the unemployment rate declined to 7.6% in May, down from 8.2% one year ago and 10% at the peak of the recession. We expect the economy to improve and interest rates to move higher, but not enough to derail the economic recovery. Therefore, we have positioned the Fund to benefit from four opportunities: a sustained housing recovery, higher interest rates, increased demand for faster Internet and competitively advantaged businesses with company-specific drivers.

The U.S. housing market has begun a substantial, long-term recovery. Existing home sales grew 12.9% in May, and home prices in the twenty largest U.S. cities jumped 12.1% in April, the largest increase since 2006. In fact, in our hometown of San Francisco, housing prices jumped an amazing 23.9% in April, thanks to an influx of technology companies and their employees moving into the city. We don’t expect these eye-popping gains to continue, but we do expect housing sales to grow over time because prices remain very affordable in most parts of the country. This growth helps our homebuilder investments PulteGroup and Toll Brothers, as well as our title insurer investment, First American Financial.

|

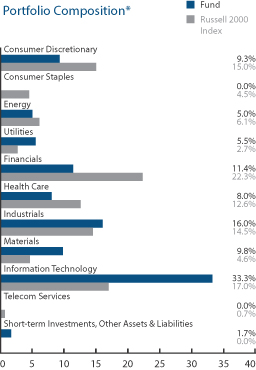

Parnassus Small-Cap Fund Sector Weightings as of June 30, 2013 (percentage of net assets) |

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

Top 10 Holdings

(percentage of net assets)

| | | | |

| |

| Ciena Corp. | | | 5.3% | |

| |

| Finisar Corp. | | | 4.7% | |

| |

| VCA Antech Inc. | | | 4.2% | |

| |

| Riverbed Technology Inc. | | | 3.9% | |

| |

| UTi Worldwide Inc. | | | 3.8% | |

| |

| First Horizon National Corp. | | | 3.7% | |

| |

| First American Financial Corp. | | | 3.7% | |

| |

| Gentex Corp. | | | 3.6% | |

| |

| MICROS Systems Inc. | | | 3.6% | |

| |

| EZchip Semiconductor Ltd. | | | 3.5% | |

Portfolio characteristics and holdings are subject to change periodically.

18

| | | | |

| | |

| Semiannual Report • 2013 | | | | PARNASSUS FUNDS |

Interest rates have begun to rise, with the 10-year Treasury jumping from 1.6% at the beginning of May to 2.5% at the end of June, and we have positioned our portfolio to benefit. Our bank investments in First Horizon National, Pinnacle Financial Partners and TCF Financial benefit from increasing rates because they earn a higher return on their loans. Additionally, Insperity benefits because the company collects payroll cash from employers in advance of paying employees and can invest this cash in short-term investments. Recently, short-term investments have yielded very little, but as rates increase, this cash will generate meaningful earnings for Insperity.

Consumers and businesses continue to demand ever-faster Internet speeds. As carriers deploy faster networks, consumers have quickly found new ways to consume data, such as streaming their favorite television shows and sporting events. Finisar and Ciena make high-speed optical networking-equipment that moves enormous amounts of data very quickly. As carriers compete to attract and retain customers, we expect significant reinvestment in their networks, which will benefit both Finisar and Ciena.

Thanks to faster Internet speeds, business software is transitioning to a Software-as-a-Service (SaaS) model, where the software is hosted at a central data center and employees access it via high-speed Internet service. Our Riverbed Technology investment benefits from this transition, because it offers technology that accelerates data-transfer across the Internet. Using Riverbed, employees can access SaaS without any annoying delays.

We also own a collection of businesses that benefit from company-specific trends. For example, thanks to its superior technology, Gentex supplies nine out of ten auto-dimming rearview car mirrors around the world. Gentex will benefit for many years as this safety feature trickles down from luxury cars to mid- and lower-priced cars. Another example is our most recent investment, MRC Global, the largest distributor of pipes and valves to the energy sector. The company benefits from the rapid expansion of shale drilling in the U.S., which requires significant amounts of pipes and valves.

The Small-Cap Fund invests in high-quality businesses that are temporarily out-of-favor. We have positioned the Fund to benefit from a sustained housing recovery, higher interest rates, increased demand for faster Internet and competitively advantaged businesses with specific drivers. Our investment process remains the same since inception, so we expect to return to outperformance in the future. We thank you for investing in the Parnassus Small-Cap Fund.

| | |

Yours truly, Jerome L. Dodson Lead Portfolio Manager | |

Ryan Wilsey Portfolio Manager |

19

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

PARNASSUS WORKPLACE FUND

Ticker: PARWX

As of June 30, 2013, the NAV of the Parnassus Workplace Fund was $25.15, so the total return for the quarter was 4.75%. This compares favorably to 2.91% for the S&P 500 Index (“S&P 500”) and 2.65% for the Lipper Large-Cap Core Average, which represents the average return of the large-cap core funds followed by Lipper (“Lipper average”). Although we lagged the S&P 500 by more than two percentage points in the first quarter of the year, we’ve now practically closed the gap. For the year-to-date, we’re up 13.44%, compared to 13.82% for the S&P 500 and 13.19% for the Lipper average.

Below is a table comparing the Parnassus Workplace Fund with the S&P 500 and the Lipper average for the past one-, three- and five-year periods ended June 30, 2013, and for the period since inception. As you can see from the table, we’re ahead of all the benchmarks for all periods.

Company Analysis

Four companies each contributed 12¢ or more to the NAV of the Parnassus Workplace Fund. Only one company knocked 12¢ or more off the price of each fund share, and that was Autodesk, which sliced 15¢ off the NAV, as its stock sank 17.7% from $41.24 to $33.94. The company provides software for architects, engineers and designers, and weak demand in Europe caused the company to miss earnings expectations and lower revenue guidance for the full-year. Despite the weak start to the

| | | | | | | | | | | | | | | | | | | | | | | | |

| Parnassus Workplace Fund | |

Average Annual

Total Returns (%) | | One

Year | | | Three

Years | | | Five

Years | | | Since

Inception

on

4/29/05 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended

June 30, 2013 | | | | | | |

| | | | | | | |

| Parnassus Workplace Fund | | | 26.69 | | | | 19.33 | | | | 13.36 | | | | 10.11 | | | | 1.14 | | | | 1.14 | |

| | | | | | | |

| S&P 500 Index | | | 20.60 | | | | 18.45 | | | | 7.01 | | | | 6.31 | | | | NA | | | | NA | |

| | | | | | | |

| Lipper Large-Cap Core Average | | | 20.42 | | | | 16.64 | | | | 5.84 | | | | 5.74 | | | | NA | | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The Russell 2000 Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. Small-cap companies can be particularly sensitive to changing economic conditions and have fewer financial resources than large-cap companies.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website, or by calling (800) 999-3505.

year, Autodesk saw encouraging signs of demand in the commercial construction and manufacturing markets in North America, so we expect the stock to rebound, as economic activity picks up later in the year.

The stock that contributed the most to our second quarter performance was Charles Schwab, which added 20¢ to the value of each fund share. The stock soared 20.0% during the quarter from $17.69 to $21.23. Because of expectations for an increase in interest rates, the stock is now up an amazing 47.8% for the year-to-date. With higher rates, Schwab can earn much more on their banking assets, money market products and margin loans to brokerage clients. In February, the company told investors that if interest rates returned to their pre-crisis levels of the second quarter of 2008, Schwab’s earnings would be almost triple their current quarterly earnings of 15¢ per share. We’re holding onto most of our Schwab shares, even after the big move up, because we think there’s still more room for the stock to move higher.

Credit card issuer Capital One climbed 14.3% from $54.95 to $62.81, adding 16¢ to each fund share. Last year, the company’s quarterly earnings were very volatile, as Capital One integrated its recent acquisitions of online bank ING Direct and HSBC’s private label credit card portfolio. Earnings in the most recent quarter exceeded expectations, as the benefits of the acquisitions are becoming apparent.

20

| | | | |

| | |

| Semiannual Report • 2013 | | | | PARNASSUS FUNDS |

Applied Materials, the big maker of equipment used in semiconductor-manufacturing, saw its stock climb 10.6% from $13.48 to $14.91 for a gain of 13¢ on the NAV. Rising demand for smartphones and tablets means that memory-chipmakers and flat-panel display manufacturers have to buy more equipment from Applied Materials. Semiconductors are finding their way into more and more products, and Applied is one of only a few companies with the technology and the scale to provide equipment to meet this demand. Also, the company’s president, Gary Dickerson, has restructured Applied to increase efficiency and profitability.

Cisco Systems makes switches, routers and other networking equipment, and its stock jumped 16.3% during the quarter from $20.91 to $24.31, while adding 12¢ to the Fund’s NAV. Robust demand from telecommunications service providers for routers and video products, along with higher sales of its data center products, drove improved results during the quarter. After several years of losing market share in its core networking segment to Hewlett-Packard and Juniper Networks, Cisco regained share with its innovative networking products. A coming introduction of new cloud-computing and mobile-products along with improving gross margins should move the stock higher.

Yours truly,

Jerome L. Dodson

Portfolio Manager

| | |

Parnassus Workplace Fund Sector Weightings as of June 30, 2013 (percentage of net assets) |

* For purposes of categorizing securities for diversification requirements under the Investment Company Act, the Fund uses industry classifications that are more specific than those used for the chart.

Top 10 Holdings

(percentage of net assets)

| | | | |

| |

| Applied Materials Inc. | | | 5.0% | |

| |

| Capital One Financial Corp. | | | 4.8% | |

| |

| Expeditors International of Washington Inc. | | | 4.8% | |

| |

| Riverbed Technology Inc. | | | 4.6% | |

| |

| Intuit Inc. | | | 4.3% | |

| |

| Charles Schwab Corp. | | | 4.1% | |

| |

| C.H. Robinson Worldwide Inc. | | | 4.1% | |

| |

| Intel Corp. | | | 3.9% | |

| |

| First Horizon National Corp. | | | 3.7% | |

| |

| Wells Fargo & Co. | | | 3.7% | |

Portfolio characteristics and holdings are subject to change periodically.

21

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

PARNASSUS ASIA FUND

Ticker: PAFSX

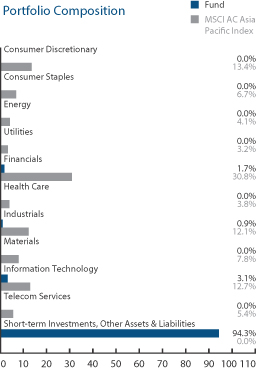

As of June 30, 2013, the NAV of the Parnassus Asia Fund was $14.95, so the total return since inception on April 30, 2013 was a loss of 0.33%. This compares favorably to a loss of 7.52% for the MSCI AC Asia Pacific Index (“MSCI Index”) and a loss of 7.95% for the Lipper Pacific Region Average, which represents the average return of the Asia Pacific Region funds followed by Lipper (“Lipper average”). Below you will find a table comparing the Asia Fund with the MSCI Index and the Lipper average for the period since inception.

As you can see, we are well ahead of both of our benchmarks, but I cannot credit my brilliance in stock-picking for these terrific results. As shown in the portfolio report, we have less than 6% of the Fund’s assets in stocks with the rest in cash. The reason we have been able to beat the benchmarks by so much is that we held most of our assets in cash, while the Asian markets had big moves down after the big run-up over the past year. So we were lucky to be in cash instead of Asian stocks over the past two months.

Why did we have so much cash on hand? The Fund invests principally in stocks of Asian companies that we believe are financially sound and have good prospects for the future. The companies in which the Fund invests must, in our opinion, be undervalued, but they must also have good prospects for long-term capital appreciation over the course of the expected holding period. As we invest the initial assets of the Fund, we are being very careful and deliberate in making investment decisions. We will continue to have cash holdings where we believe that such cash holdings, given the risks and characteristics of the available securities in which the Fund may invest, are more beneficial to shareholders than investments in such securities.

| | | | | | | | | | | | |

| Parnassus Asia Fund | |

Average Annual Total Returns (%) | | Since

Inception

on

4/30/13 | | | Gross

Expense

Ratio | | | Net

Expense

Ratio | |

for periods ended June 30, 2013 | | | |

| | | | |

| Parnassus Asia Fund | | | -0.33 | | | | 5.00 | | | | 1.45 | |

| | | | |

| MSCI AC Asia Pacific Index | | | -7.52 | | | | NA | | | | NA | |

| | | | |

| Lipper Pacific Region Average | | | -7.95 | | | | NA | | | | NA | |

Performance data quoted represent past performance and are no guarantee of future returns. Current performance may be lower or higher than the performance data quoted. Current performance information to the most recent month-end is available on the Parnassus website (www.parnassus.com). Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original principal cost. Returns shown in the table do not reflect the deduction of taxes a shareholder may pay on fund distributions or redemption of shares. The MSCI AC Asia Pacific Index is an unmanaged index of common stocks, and it is not possible to invest directly in an index. Index figures do not take any expenses, fees or taxes into account, but mutual fund returns do. This fund invests primarily in non-U.S. securities. Foreign markets can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market or economic developments and can perform differently from the U.S. market.

Before investing, an investor should carefully consider the investment objectives, risks, charges and expenses of the Fund and should carefully read the prospectus or summary prospectus, which contain this and other information. The prospectus or summary prospectus can be obtained on the Parnassus website, or by calling (800) 999-3505. As described in the Fund’s current prospectus dated May 1, 2013, Parnassus Investments has contractually agreed to limit the total operating expenses to 1.45% of net assets, exclusive of acquired fund fees, until May 1, 2014. This agreement will not be terminated prior to May 1, 2014, and may be continued indefinitely by the Adviser on a year-to-year basis.

The ESG factors (environmental, social and governance) of our companies are taking particular time to consider. Unfortunately, information on ESG criteria is not as available for Asian companies as it is for U.S. companies. Also, the ESG record of many Asian companies is not as good as that of U.S. companies, in general. This forces us to take extra time to assemble information and to put it into context per company. Both slow the investment process.

Making decisions on ESG factors is also a very subjective matter. No company, of course is perfect. We have to make decisions based upon available information about a company’s intentions and its record. We have been pleasantly surprised with the responsiveness of some companies to our ESG questions. So, while we do have more good companies to choose from for the U.S. funds, we are building a base of good Asian companies as well.

Given these difficulties, why are we starting an Asia Fund? The short answer is that economies within the region are very dynamic and creative. The region is growing at a fast pace, and we expect that growth to continue. It contains the world’s fastest growing middle class, and it is the scene of much technological innovation. Asia is also a region with a lot of entrepreneurship, as well as political and financial reform. For all these reasons, we believe it makes sense to invest in Asia ahead of future positive developments.

22

| | | | |

| | |

| Semiannual Report • 2013 | | | | PARNASSUS FUNDS |

We do have some important assets in managing the Parnassus Asia Fund. We have almost 30 years of successful experience in making investments, which will guide us going forward. Also, we have a great staff member, helping me as a senior analyst. Billy Hwan is a graduate of Stanford University and holds an MBA from the University of California at Berkeley. He also speaks Mandarin and Japanese. Previously, he worked as an analyst at Dodge & Cox, a large mutual fund company based here in San Francisco. Billy also interned at Matthews Asia Funds, the biggest mutual fund company specializing in Asian stocks. Billy and I spent three weeks in Asia in May, visiting thirty companies in Thailand, Singapore, Indonesia, Hong Kong, Taiwan and Japan. This has given us a lot of intellectual capital to use in making investment decisions for the Fund.

We are actively seeking to be fully invested, as soon as possible, within the mandates of the Fund’s investment strategy, and we plan to watch for opportunities to buy stocks at low prices, should there be another downward correction in the Asian stock markets.

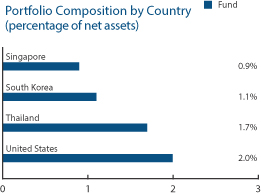

There are only four stocks in the portfolio right now, but they will give you an idea of the strategy we’re pursuing. Keppel Corporation is based in Singapore and does infrastructure and offshore rig construction. Thanachart Capital is a fast-growing bank in Thailand. Samsung Electronics is a South Korean semiconductor company that also has a large business in smartphones. Applied Materials is a U.S.-based company that makes equipment for use in manufacturing semiconductors, but almost half of its business is in Asia, where most semiconductors are now produced.

We hope you are as excited about the new fund as we are.

Yours truly,

Jerome L. Dodson

Portfolio Manager

| | |

Parnassus Asia Fund Sector Weightings as of June 30, 2013 (percentage of net assets) |

Fund Holdings

(percentage of net assets)

| | | | |

| |

| Applied Materials Inc. | | | 2.0% | |

| |

| Thanachart Capital PCL | | | 1.7% | |

| |

| Samsung Electronics Co. Ltd. | | | 1.1% | |

| |

| Keppel Corp. Ltd. | | | 0.9% | |

Portfolio characteristics and holdings are subject to change periodically.

23

| | | | |

| | |

| PARNASSUS FUNDS | | | | Semiannual Report • 2013 |

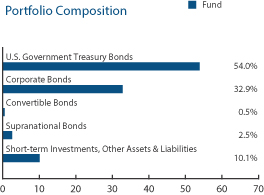

PARNASSUS FIXED-INCOME FUND

Ticker: PRFIX