UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-06279 |

|

Harris Associates Investment Trust |

(Exact name of registrant as specified in charter) |

|

Two North La Salle Street, Suite 500 Chicago, Illinois | | 60602-3790 |

(Address of principal executive offices) | | (Zip code) |

|

| | | |

John R. Raitt | | Paulita A. Pike |

Harris Associates L.P. | | K&L Gates LLP |

Two North La Salle Street, #500 | | Three First National Plaza, #3100 |

Chicago, Illinois 60602 | | Chicago, Illinois 60602 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (312) 621-0600 | |

|

Date of fiscal year end: | 9/30/10 | |

|

Date of reporting period: | 3/31/10 | |

| | | | | |

Item 1. Reports to Shareholders.

SEMI-ANNUAL REPORT

MARCH 31, 2010

oakmark.com

Advised by Harris Associates L.P.

THE OAKMARK FUNDS

2010 Semi-Annual Report

| President's Letter | | | 1 | | |

|

| Summary Information | | | 2 | | |

|

| Fund Expenses | | | 4 | | |

|

| Commentary on Oakmark and Oakmark Select Funds | | | 6 | | |

|

| Oakmark Fund | |

|

| Letter from the Portfolio Managers | | | 8 | | |

|

| Schedule of Investments | | | 9 | | |

|

| Oakmark Select Fund | |

|

| Letter from the Portfolio Managers | | | 13 | | |

|

| Schedule of Investments | | | 14 | | |

|

| Oakmark Equity and Income Fund | |

|

| Letter from the Portfolio Managers | | | 16 | | |

|

| Schedule of Investments | | | 18 | | |

|

| Oakmark Global Fund | |

|

| Letter from the Portfolio Managers | | | 25 | | |

|

| Global Diversification Chart | | | 28 | | |

|

| Schedule of Investments | | | 29 | | |

|

| Oakmark Global Select Fund | |

|

| Letter from the Portfolio Managers | | | 34 | | |

|

| Global Diversification Chart | | | 36 | | |

|

| Schedule of Investments | | | 37 | | |

|

| Oakmark International Fund | |

|

| Letter from the Portfolio Managers | | | 40 | | |

|

| Global Diversification Chart | | | 42 | | |

|

| Schedule of Investments | | | 43 | | |

|

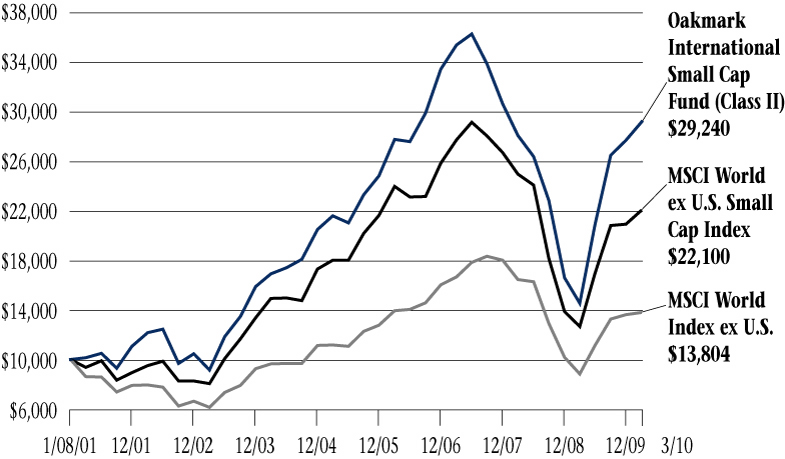

| Oakmark International Small Cap Fund | |

|

| Letter from the Portfolio Manager | | | 49 | | |

|

| Global Diversification Chart | | | 51 | | |

|

| Schedule of Investments | | | 52 | | |

|

| Financial Statements | |

|

| Statements of Assets and Liabilities | | | 60 | | |

|

| Statements of Operations | | | 62 | | |

|

| Statements of Changes in Net Assets | | | 64 | | |

|

| Notes to Financial Statements | | | 71 | | |

|

| Financial Highlights | | | 83 | | |

|

| Disclosure Regarding Investment Advisory Contract Approval | | | 91 | | |

|

| Oakmark Glossary | | | 96 | | |

|

| Trustees and Officers | | | 99 | | |

|

FORWARD-LOOKING STATEMENT DISCLOSURE

One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered "forward-looking statements". Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as "estimate", "may", "will", "expect", "believe", "plan" and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

IMPORTANT MESSAGE ABOUT

OAKMARK QUARTERLY REPORT MAILINGS

Kindly be advised that we will no longer print and mail our first and third quarter reports. These reports will only be available online at oakmark.com.

If you wish to receive an e-mail each quarter letting you know when the quarterly reports are posted, please visit our website and sign up for e-mail updates.

To sign up, simply enter your e-mail address in the appropriate box on the right-hand side of the home page and click Join.

(This page has been intentionally left blank.)

President's Letter

Dear Fellow Shareholders,

The Oakmark Funds performed well in the first half of fiscal year 2010. Stock markets around the world continued to rise, driven by stronger corporate earnings and the unfolding economic recovery. Each one of the Oakmark Funds significantly grew shareholder capital for the fiscal year-to-date and the most recent quarter, extending the strong long-term record of outperformance for all of our Funds.

Economic Recovery and Market Valuation

The worldwide economic expansion continued to gain momentum in the recent quarter. Signs of economic strength are now wide-spread. International trade is up, and U.S. exports are growing at a rate of more than 25%. Housing price indexes are also improving. Capital markets, which were completely frozen only a year ago, are active again, and issuance of corporate debt, equity and even mortgage-backed securities is robust. Finally, employment, which is typically one of the last areas to recover after a downturn, is now rising around the world. We believe that the U.S and world economies will continue to grow for the foreseeable future, but we admit to being concerned about the growing size of the U.S. budget deficit and its potential long-term impact on interest rates and the health of the U.S. economy.

World stock markets have rebounded strongly from their lows of a year ago. While the valuation gap has narrowed from the extreme levels at the height of the market panic, we believe that stocks are still undervalued. Bonds—and U.S. government bonds in particular—present a different case, however. The Federal Reserve has provided immense amounts of liquidity to the markets over the past two years to support the economy. With the economy steadily regaining its health, the need for aggressive stimulus is receding. In fact, we believe the Fed will ultimately need to tighten monetary policy in order to prevent the economy from overheating and to avoid triggering inflation. The combination of: 1) the massive borrowings needed to fund the growing federal deficit; 2) the typical rebound in corporate and individual borrowings in an economic recovery; and 3) tighter monetary policy suggest to us that interest rates will rise over the next fe w years. Because bond prices fall when interest rates rise, we believe that U.S. government bonds hold significant risk today. Since stocks currently offer healthy dividend yields and will benefit from a stronger economy, we also believe that the typical risk hierarchy has been reversed and that stocks are actually less risky than bonds in today's market.

Many investors decreased their equity holdings after last year's stock market decline, choosing instead the "safety" of bonds. While we see the attraction of safety after the roller coaster ride equity investors have experienced over the last few years, we believe that chasing what has "worked" (high quality bonds) is a mistake. With this in mind, we take the opportunity to remind investors of the value of adopting and adhering to a long-term investment plan, which includes target asset weightings. We believe emotions can often lead investors in the wrong direction, but sticking to a long-term plan can ensure that you maintain your exposure to equities, especially when they are attractively valued, as we believe they are now.

Minding the Details

Investment advisors frequently discuss the power of compound growth and the ability to multiply wealth over long periods of time, even at average rates of return. A corollary to this truth is that small changes in returns can have a very significant impact on long-term wealth accumulation.

Mutual fund returns are a function of both investment returns and fund expenses. While fund expenses are typically small relative to investment returns, higher fund expenses can create a significant drag on results. Thus, while we believe that it is important to choose a fund run by talented investors, it is also important to choose a fund that watches clients' pennies when making investment decisions.

Morningstar, Inc., one of the mutual fund industry's most respected commentators, recently published a study of mutual fund industry trading costs. Granted, this is a complicated subject, and brokerage commissions can vary across funds for many reasons, but the Morningstar study does allow us to draw some broad conclusions. The study found that an average equity mutual fund incurs commission expense (as a percent of average net assets) in the range of 30 basis points (0.30%) annually. At Oakmark, we watch expenses like brokerage commissions closely. Therefore, we are pleased to report that average brokerage commission expense for every one of our Funds was less than half of the 2009 Morningstar peer group average, with several Funds running at substantially less than half of the average. Clearly, our attention to details like trading costs is paying off for our shareholders.

Thank you for your continued investment and confidence in The Oakmark Funds. We welcome your comments and questions. You can reach us via e-mail at ContactOakmark@oakmark.com.

John R. Raitt

President and CEO of The Oakmark Funds

President and CEO of Harris Associates L.P.

March 31, 2010

1

THE OAKMARK FUNDS

Summary Information

Performance for Period

Ended March 31, 20101 | | Oakmark

Fund—Class I

(OAKMX) | | Oakmark

Select Fund—Class I

(OAKLX) | | Oakmark

Equity and Income

Fund—Class I

(OAKBX) | | Oakmark

Global Fund—Class I

(OAKGX) | |

| 3 Months* | | | 6.21 | % | | | 6.34 | % | | | 4.70 | % | | | 6.67 | % | |

| 1 Year | | | 70.07 | % | | | 72.95 | % | | | 33.52 | % | | | 73.29 | % | |

Average Annual Total

Return for: | |

| 3 Year | | | 0.04 | % | | | -3.16 | % | | | 4.49 | % | | | -2.18 | % | |

| 5 Year | | | 3.57 | % | | | 1.12 | % | | | 7.36 | % | | | 6.55 | % | |

| 10 Year | | | 7.33 | % | | | 6.68 | % | | | 9.84 | % | | | 12.38 | % | |

| Since inception | | | 12.69%

(8/5/91) | | | | 12.58%

(11/1/96) | | | | 11.55%

(11/1/95) | | | | 11.64%

(8/4/99) | | |

Top Five Equity

Holdings as of

March 31, 20102

Company and % of Total

Net Assets | | | Intel Corp. 2.4%

DIRECTV, Class A 2.3%

Medtronic, Inc. 2.3%

Comcast Corp. 2.2%

Liberty Media

Holding Corp.

- Interactive,

Class A 2.1% | | | | Discovery

Communications Inc.

Class C 10.1%

DIRECTV, Class A 7.0%

Liberty Media

Holding Corp.

- Interactive,

Class A 5.5%

Bristol-Myers

Squibb Co. 4.5%

H&R Block, Inc. 4.4% | | | | General Dynamics

Corp. 3.3%

Wal-Mart Stores,

Inc. 3.0%

Covidien Plc. 2.8%

Avon Products, Inc. 2.8%

Cenovus Energy, Inc. 2.6% | | | | Snap-on Inc. 4.4%

Oracle Corp. 4.0%

Laboratory Corp. of

America Holdings 4.0%

Daiwa Securities

Group Inc. 3.9%

Square Enix

Holdings Co., Ltd. 3.7% | | |

Sector

Allocation as of

March 31, 2010

Sector and % of

Market Value | | | Consumer

Discretionary 31.7%

Information

Technology 25.3%

Financials 13.5%

Health Care 11.3%

Industrials 8.3%

Consumer Staples 7.3%

Energy 2.6% | | | | Consumer

Discretionary 44.7%

Information

Technology 24.5%

Financials 12.6%

Health Care 9.4%

Energy 8.8% | | | | U.S. Government

Securities 24.1%

Consumer Staples 20.3%

Industrials 13.6%

Energy 12.3%

Health Care 12.1%

Consumer

Discretionary 7.5%

Materials 2.7%

Information

Technology 2.7%

Foreign Government

Securities 2.6%

Financials 2.1% | | | | Information

Technology 27.7%

Consumer

Discretionary 20.0%

Industrials 18.4%

Financials 14.8%

Health Care 8.3%

Consumer Staples 6.2%

Materials 2.4%

Energy 2.2% | | |

The performance data quoted represents past performance. The above performance information for the Funds does not reflect the imposition of a 2% redemption fee on shares of all Funds, other than Oakmark Equity & Income Fund, redeemed within 90 days, in order to deter market timers. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain current month end performance data, visit oakmark. com.

* Not annualized

THE OAKMARK FUNDS

2

Performance for Period

Ended March 31, 20101 | | Oakmark

Global Select

Fund—Class I

(OAKWX) | | Oakmark

International

Fund—Class I

(OAKIX) | | Oakmark

International

Small Cap Fund—Class I

(OAKEX) | |

| 3 Months* | | | 6.41 | % | | | 5.70 | % | | | 5.38 | % | |

| 1 Year | | | 70.74 | % | | | 82.17 | % | | | 101.36 | % | |

Average Annual Total

Return for: | |

| 3 Year | | | 1.69 | % | | | -2.62 | % | | | -6.02 | % | |

| 5 Year | | | N/A | | | | 7.17 | % | | | 6.38 | % | |

| 10 Year | | | N/A | | | | 8.80 | % | | | 11.24 | % | |

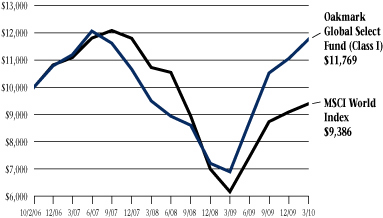

| Since inception | | | 4.77%

(10/2/06) | | | | 10.83%

(9/30/92) | | | | 10.94%

(11/1/95) | | |

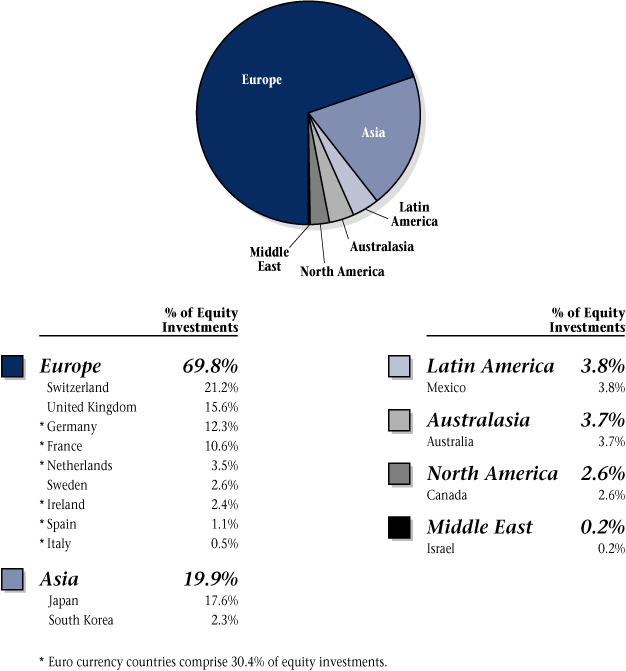

Top Five Equity

Holdings as of

March 31, 20102

Company and % of Total

Net Assets | | | Adecco SA 6.7%

Societe Television

Francaise 1 6.1%

ROHM Company

Ltd. 6.1%

Compagnie Financiere

Richemont SA 6.0%

UBS AG 5.3% | | | | Credit Suisse Group 3.5%

Daiwa Securities

Group Inc. 3.4%

Allianz SE 3.1%

Daimler AG 3.0%

Adecco SA 3.0% | | | | Julius Baer Group,

Ltd. 3.7%

Sperian Protection 3.3%

Square Enix

Holdings Co., Ltd. 3.2%

BBA Aviation PLC 3.1%

Interpump Group

SpA 3.0% | | |

Sector

Allocation as of

March 31, 2010

Sector and % of

Market Value | | | Consumer

Discretionary 39.7%

Information

Technology 24.8%

Financials 19.3%

Industrials 7.1%

Energy 4.9%

Health Care 4.2% | | | | Consumer

Discretionary 34.6%

Financials 22.0%

Industrials 14.8%

Information

Technology 11.7%

Consumer Staples 10.0%

Health Care 4.0%

Materials 2.4%

Energy 0.5% | | | | Industrials 35.3%

Consumer

Discretionary 17.9%

Information

Technology 16.3%

Financials 12.4%

Consumer Staples 8.3%

Materials 5.6%

Health Care 4.2% | | |

As of 9/30/09, the expense ratio for Class I shares was 1.23% for Oakmark Fund, 1.19% for Oakmark Select Fund, 0.85% for Oakmark Equity and Income Fund, 1.23% for Oakmark Global Fund, 1.43% for Oakmark Global Select Fund, 1.17% for Oakmark International Fund and 1.54% for Oakmark International Small Cap Fund.

THE OAKMARK FUNDS

3

FUND EXPENSES

A shareholder of each Fund incurs two types of costs: (1) transaction costs, such as redemption fees, and (2) ongoing costs, including investment advisory fees, transfer agent fees, and other fund expenses. The examples below are intended to help shareholders understand the ongoing cost (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other funds.

Actual Expenses

The following table provides information about actual account values and actual fund expenses for Class I of each Fund. The table shows the expenses a Class I shareholder would have paid on a $1,000 investment in each Fund from October 1, 2009 to March 31, 2010, as well as how much a $1,000 investment would be worth at the close of the period, assuming actual fund returns and expenses. A Class I shareholder can estimate expenses incurred for the period by dividing the account value at March 31, 2010, by $1,000 and multiplying the result by the number in the Expenses Paid During Period row as shown below.

Shares of all Funds, other than Oakmark Equity and Income Fund, invested for 90 days or less may be charged a 2% redemption fee. Please consult the Funds' prospectus at oakmark.com for more information.

| | | Oakmark Fund | | Oakmark Select Fund | | Oakmark Equity and Income Fund | | Oakmark Global Fund | | Oakmark Global Select Fund | | Oakmark International Fund | | Oakmark International Small Cap Fund | |

Beginning

Account

Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | |

Ending

Account

Value | | $ | 1,145.90 | | | $ | 1,142.30 | | | $ | 1,094.30 | | | $ | 1,106.10 | | | $ | 1,118.60 | | | $ | 1,103.10 | | | $ | 1,103.90 | | |

Expenses

Paid

During

Period* | | $ | 5.99 | | | $ | 5.82 | | | $ | 4.12 | | | $ | 6.04 | | | $ | 6.71 | | | $ | 5.66 | | | $ | 7.19 | | |

Annualized

Expense

Ratio | | | 1.12 | % | | | 1.09 | % | | | 0.79 | % | | | 1.15 | % | | | 1.27 | % | | | 1.08 | % | | | 1.37 | % | |

* Expenses are equal to each Fund's annualized expense ratio for Class I, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year divided by 365 (to reflect the one-half year period).

THE OAKMARK FUNDS

4

Hypothetical Example for Comparison Purposes

The following table provides information about hypothetical account values and hypothetical expenses for Class I of each Fund based on actual expense ratios and an assumed rate of return of 5% per year before expenses, which are not the Funds' actual returns. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses shareholders paid for the period. Shareholders may use this information to compare the ongoing costs of investing in a Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as redemption fees. Therefore, the third line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, the total costs would have been higher.

| | | Oakmark Fund | | Oakmark Select Fund | | Oakmark Equity and Income Fund | | Oakmark Global Fund | | Oakmark Global Select Fund | | Oakmark International Fund | | Oakmark International Small Cap Fund | |

Beginning

Account

Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | |

Ending

Account

Value | | $ | 1,019.35 | | | $ | 1,019.50 | | | $ | 1,020.99 | | | $ | 1,019.20 | | | $ | 1,018.60 | | | $ | 1,019.55 | | | $ | 1,018.10 | | |

Expenses

Paid

During

Period* | | $ | 5.64 | | | $ | 5.49 | | | $ | 3.98 | | | $ | 5.79 | | | $ | 6.39 | | | $ | 5.44 | | | $ | 6.89 | | |

Annualized

Expense

Ratio | | | 1.12 | % | | | 1.09 | % | | | 0.79 | % | | | 1.15 | % | | | 1.27 | % | | | 1.08 | % | | | 1.37 | % | |

* Expenses are equal to each Fund's annualized expense ratio for Class I, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year divided by 365 (to reflect the one-half year period).

THE OAKMARK FUNDS

5

OAKMARK AND OAKMARK SELECT FUNDS

At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close.

"It was then late 2008. By then there was a long and growing list of pundits who claimed they predicted the catastrophe, but a far shorter list who actually did."

"It was then late 2008. By then there was a long and growing list of pundits who claimed they predicted the catastrophe, but a far shorter list who actually did."

Michael Lewis, The Big Short

Michael Lewis has been on quite a roll. His 1989 best seller, Liar's Poker, provided an early insight into how life was changing inside investment banking firms. His 2003 best seller, Moneyball, about the economics of baseball salaries, changed the way teams are managed. Last year, The Blind Side, his 2006 book about the emergence of the left tackle as one of the highest paid positions in the NFL, was turned into a feel-good movie that was both a box office hit and an Oscar winner. Last month he r eleased another best seller, The Big Short, which explores the sub-prime mortgage collapse through the eyes of a handful of investors who saw it coming. (As one who didn't, I can tell you the book didn't make me feel very smart!) The quote at the top of the page was his well-deserved shot at those in the financial community who are now behaving like politicians, re-inventing history in an attempt to make themselves appear smarter than they really were. We see the spin machines rolling as CEOs quote pro-forma earnings that exclude losses from mistakes they know will recur, money managers advertise short-term performance numbers they know aren't sustainable, and the financial media tout retirement plan recovery schemes they know are destined to fail.

As one considers the plusses and minuses of various investments, I think one of the most overlooked positives of mutual funds is the vast amount of information that becomes permanent public record. Though past performance is no guarantee of future results, daily performance of every mutual fund is public record. There is no way to spin past performance to make it look better than it was—no representative account, no carefully selected endpoints for performance measurement, and no performance numbers that hide the cost of management fees. A mutual fund is also required to send reports to shareholders semi-annually, which explain its investment performance. (Oakmark voluntarily writes these reports every quarter and posts each one on its website Oakmark.com.) These reports highlight the stocks that most significantly affected a fund's performance and often give rationales for important holdings. Additionally, a mutual fund is required to file a full list of its portfolio holdings quarterly with the SEC. If a fund owns a given stock at the end of a quarter, there's no way to get around disclosing it. Although these reports are available to anyone through the SEC's website, they can often be tricky to find. Again, we put all our reports on Oakmark.com as a convenience to our investors and potential investors and to save them the trouble of searching for the reports on the SEC's website. It amazes me that more investors don't take advantage of this resource. Investors are eager to hear a fund manager's thoughts on the market and specific stocks, but most don't do the research to develop a historical perspective for evaluating a manager's current commentary.

So, with Kevin Grant and me recently passing the ten-year mark as managers of The Oakmark Fund, I thought it would be interesting to re-visit the first report we wrote to shareholders in March of 2000.

"It is important to us that our investors understand that we will continue to employ the same value philosophy that has been responsible for [Oakmark's historically strong] results. We will only buy a stock when it is selling below 60% of what we believe the business is worth today. We will sell it when it is priced at more than 90% of estimated value, or when we believe we have made a mistake analyzing the company. In addition, we will seek to identify companies where value grows as time passes and where managements have economic interests that are well aligned with their shareholders. When we identify these stocks, we will buy them in meaningful size. While most mutual funds own over 100 different stocks, we expect to usually have only 40-50 stocks. We are confident that this approach will continue to deliver excellent long-term returns, and we have both made substantial personal investments in The Oakmark Fund since being named the new ma nagers."

About the only change we'd make if we wrote that paragraph today would be that we own about 55 stocks, compared to the average equity fund, which is now up to 166. We still believe that stock picking is our most important skill, and we want to maximize its effect without taking excessive risk in any individual position. Our investment philosophy, the long-term goals, and investing side-by-side with the shareholders all remain the same—not just for The Oakmark Fund, but for all of Oakmark's Funds.

"We are well aware that recent results have been disappointing, and the quarter just ended was no exception.... We are not satisfied with recent performance and are energized by the challenge of restoring The Oakmark Fund to the position of the premier diversified value fund."

OAKMARK AND OAKMARK SELECT FUNDS

6

Candor in shareholder communication has always been important to us, whether we are communicating to our shareholders or whether a management team is communicating to us. If things aren't going well, we want a management team to be upfront about it.

"In addition to having a portfolio full of great values, we inherit a very favorable tax position. It is unlikely that we will have to make any capital gains distributions for at least a couple of years. We will only pay capital gains taxes after the portfolio appreciates substantially from current levels and that will be welcomed by all of us!"

We have always managed our portfolios with the goal of maximizing long-term after-tax returns. We won't enter into transactions that hurt our tax-free holders, but by actively managing our tax situation—selling our highest cost shares first, tax-trading loss positions, and taking mostly long-term gains—our shareholders have kept a very high percentage of their pre-tax gains.

"We are seeing an increased level of acquisition activity that we believe will benefit the Fund. Additionally, our companies continue to repurchase large quantities of their own stocks, which we believe adds significant value to the remaining shares. The price-to-earnings ratio of The Oakmark Fund stands at 11.5 (using estimated 2000 eps3) compared to 26 for the S&P 5004. That means that each share of The Oakmark Fund that you purchase for $24.76 represents $2.16 of current earnings. If you invested enough money in the S&P 500 to create that same $2.16 of earnings, it would cost $57 or 130% more than in The Oakmark Fund."

Merger activity has significantly contributed to our returns and served as confirmation that we have been identifying undervalued businesses. Of the 44 stocks we owned in Oakmark ten years ago, 13 were subsequently acquired. We continue to like managers who use excess capital to repurchase their company's shares when their stock is undervalued. Most managers today understand that they need to maximize value. Those who embrace the goal of maximizing per-share value, rather than total value, continue to be our preferred managers. Last, we remain focused on undeserved valuation gaps. That valuation gap in 2000 was the single largest contributor to our outperformance over the past decade. Today the valuation gap is much smaller, but the good news is that the market itself sells at a markedly lower price-to-earnings ratio than it did then, and competing bond yields are substantially lower. I'm almost certain we won't outperform the market by as m uch in this decade as we did in the past decade, but I also expect that the market will provide a tailwind (as it usually does) rather than a headwind.

The 2000 report closed with a look at our largest holdings: Fortune Brands, Washington Mutual, Dun & Bradstreet, Brunswick and AC Nielsen. The average performance of that list was a gain of 74% during our ownership. AC Nielsen was acquired by VNU soon after that report was written. Dun & Bradstreet split into two companies, and we sold both pieces after nice increases. Brunswick was also sold after a good gain. We still own Fortune Brands along with Heinz, H&R Block and YUM! Brands. Our business value estimates for all four have grown substantially, and we continue to believe they are undervalued despite an average total return of just over 200% for the decade. Finally, Washington Mutual—the mistake I'd love to exclude by using pro-forma numbers. We sold the stock, down 80% in price, after being proven dead wrong about the company's participation in bad sub-prime mortgage underwriting. But even with an error of this magnitud e, after including dividend income, the stock only lost 12% during our ownership. Anyone who says dividends don't matter clearly hasn't looked at the numbers.

Before we invest your assets in new companies, we read through their old annual reports to see if the management team and the company goals have been consistent. It also gives us a chance to evaluate how management has reacted to their successes and failures. Next time you are trying to figure out if the guy who says he can double your money in three years is legit or not (he's not), remember the advantages inherent in mutual fund transparency. Before you invest your money in another fund, consider investing some time to read its old reports. Even if it only confirms your decision to purchase, gaining the perspective of history can make it a lot easier to confidently stay the course in uncertain times. And now with Oakmark's historical context in place, here's what we are thinking today. We still believe stocks are undervalued, though not nearly to the degree they were a year ago. Despite the strong rally, investors continue to pour money in to bond funds, not equity funds, and skepticism remains very high. We've never liked being on the side with the crowd, and most investors remain underinvested in equities. We believe they are still making a mistake.

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

oaklx@oakmark.com

March 31, 2010

OAKMARK AND OAKMARK SELECT FUNDS

7

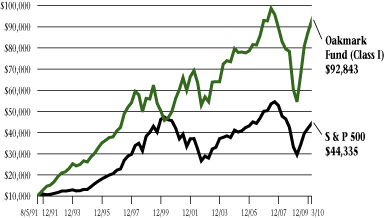

OAKMARK FUND

Report from Bill Nygren and Kevin Grant, Portfolio Managers

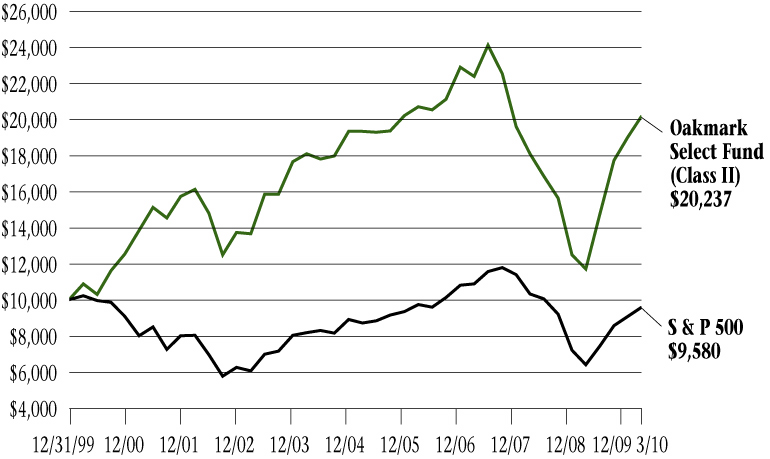

THE VALUE OF A $10,000 INVESTMENT IN OAKMARK FUND FROM ITS INCEPTION (8/5/91) TO PRESENT (3/31/10) AS COMPARED TO THE STANDARD & POOR'S 500 INDEX4 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 3/31/10) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(8/5/91) | |

| Oakmark Fund (Class I) | | | 6.21 | % | | | 70.07 | % | | | 3.57 | % | | | 7.33 | % | | | 12.69 | % | |

| S&P 500 | | | 5.39 | % | | | 49.77 | % | | | 1.92 | % | | | -0.65 | % | | | 8.31 | % | |

| Dow Jones Average5 | | | 4.82 | % | | | 46.93 | % | | | 3.34 | % | | | 2.26 | % | | | 9.67 | % | |

Lipper Large Cap

Value Index6 | | | 5.74 | % | | | 49.73 | % | | | 1.57 | % | | | 1.40 | % | | | 8.05 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The expense ratio for Class I shares as of 9/30/09 was 1.23%.

The performance data quoted represents past performance. The above performance information for the Fund does not reflect the imposition of a 2% redemption fee on shares redeemed within 90 days. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

The Oakmark Fund increased in value by 6% for the quarter compared to a 5% gain for the S&P 500. The stock market has now been up for four consecutive quarters, and the S&P 500 has returned 50% for the trailing twelve months. The Oakmark Fund has performed even better, gaining 70% over that same time period. As mentioned in the introductory letter, we passed the ten-year mark last month as your Fund's co-managers. The S&P 500 performed poorly for the decade ended March 31, losing 6% of its value. We are pleased to report that for that same decade The Oakmark Fund gained 103%.

The Fund's biggest gainers in the quarter were its Liberty Media investments: Liberty Capital up 52% and Liberty Interactive up 41%. About a year ago Liberty Capital made an investment in Sirius XM Radio debt, which allowed Sirius to avoid bankruptcy. That debt has been repaid with generous interest. In addition, at the market value of Sirius stock, the warrants that Liberty received are now worth more than $21 per Liberty share. Liberty Interactive's primary business, QVC, is recovering from the recession much more rapidly than investors had expected. The stock that most hurt our quarterly performance was H&R Block, down 21%. Block reported a larger than expected decline in early season tax filers. We believe that the recession caused many of Block's lower income customers not to file returns for 2009. When that headwind reverses, we expect Block's customer count will recover. During the quarter we eliminated our position in Limited Bra nds, because the stock responded strongly to some improvement at its Victoria's Secret chain, and we purchased Allstate.

Allstate Corp (ALL - $32)

Allstate is the second largest auto insurer in the United States. Additionally, the company offers homeowners and life insurance. Like many financial companies, Allstate's investment portfolio suffered when the markets fell in 2008. Unlike many financial companies, Allstate neither required government assistance nor diluted shareholders by raising additional capital. At the end of 2006, Allstate's book value peaked at $35. At the end of 2009, including mark-to-market hits on its investments, book value had declined only to $31. For that, the market slashed the company's stock price in half. The stock now sells at 8 times estimated earnings and yields 3%. Put differently, we are buying the high-return auto insurance business at a meaningful discount to our estimate of fair value, and we are getting the homeowners and life insurance operations for free. At this price, we believe our investment is in good hands with Allstate.

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com | | Kevin G. Grant, CFA

Portfolio Manager

oakmx@oakmark.com | |

|

March 31, 2010

OAKMARK FUND

8

OAKMARK FUND

Schedule of Investments—March 31, 2010 (Unaudited)

Name | |

Shares Held | |

Value | |

| Common Stocks—94.6% | |

| Advertising—1.5% | |

| Omnicom Group, Inc. | | | 1,316,254 | | | $ | 51,083,818 | | |

| Aerospace & Defense—2.0% | |

| The Boeing Co. | | | 975,000 | | | | 70,794,750 | | |

| Air Freight & Logistics—1.0% | |

| FedEx Corp. | | | 390,000 | | | | 36,426,000 | | |

| Asset Management & Custody Banks—4.1% | |

| Bank of New York Mellon Corp. | | | 2,389,630 | | | | 73,791,775 | | |

| State Street Corp. | | | 1,560,000 | | | | 70,418,400 | | |

| | | | 144,210,175 | | |

| Broadcasting—1.3% | |

| Discovery Communications, Inc., Class C (a) | | | 1,500,140 | | | | 44,119,117 | | |

| Cable & Satellite—4.5% | |

| DIRECTV, Class A (a) | | | 2,399,155 | | | | 81,115,431 | | |

| Comcast Corp., Class A | | | 4,320,000 | | | | 77,630,400 | | |

| | | | 158,745,831 | | |

| Catalog Retail—2.1% | |

| Liberty Media Corp. - Interactive, Class A (a) | | | 4,905,000 | | �� | | 75,095,550 | | |

| Communications Equipment—1.8% | |

| Cisco Systems, Inc. (a) | | | 2,450,000 | | | | 63,773,500 | | |

| Computer & Electronics Retail—2.1% | |

| Best Buy Co., Inc. | | | 1,760,000 | | | | 74,870,400 | | |

| Computer Hardware—5.3% | |

| Hewlett-Packard Co. | | | 1,370,000 | | | | 72,815,500 | | |

| Dell, Inc. (a) | | | 3,820,000 | | | | 57,338,200 | | |

| Apple, Inc. (a) | | | 240,000 | | | | 56,383,200 | | |

| | | | 186,536,900 | | |

| Consumer Finance—3.0% | |

| Capital One Financial Corp. | | | 1,694,800 | | | | 70,181,668 | | |

| American Express Co. | | | 850,000 | | | | 35,071,000 | | |

| | | | 105,252,668 | | |

| Data Processing & Outsourced Services—2.8% | |

| Automatic Data Processing, Inc. | | | 1,275,000 | | | | 56,699,250 | | |

| Western Union Co. | | | 2,490,000 | | | | 42,230,400 | | |

| | | | 98,929,650 | | |

| Department Stores—1.0% | |

| Kohl's Corp. (a) | | | 611,900 | | | | 33,519,882 | | |

OAKMARK FUND

9

OAKMARK FUND

Schedule of Investments—March 31, 2010 (Unaudited) cont.

Name | |

Shares Held | |

Value | |

| Common Stocks—94.6% (cont.) | |

| Distillers & Vintners—1.7% | |

| Diageo PLC (b) | | | 896,000 | | | $ | 60,435,200 | | |

| Diversified Banks—1.6% | |

| Wells Fargo & Co. | | | 1,800,000 | | | | 56,016,000 | | |

| Drug Retail—1.8% | |

| Walgreen Co. | | | 1,665,000 | | | | 61,754,850 | | |

| Electronic Manufacturing Services—2.1% | |

| Tyco Electronics, Ltd. (c) | | | 2,729,500 | | | | 75,006,660 | | |

| Health Care Equipment—3.5% | |

| Medtronic, Inc. | | | 1,800,000 | | | | 81,054,000 | | |

| Covidien PLC (c) | | | 840,000 | | | | 42,235,200 | | |

| | | | 123,289,200 | | |

| Home Improvement Retail—2.1% | |

| The Home Depot, Inc. | | | 2,231,500 | | | | 72,189,025 | | |

| Housewares & Specialties—1.8% | |

| Fortune Brands, Inc. | | | 1,320,000 | | | | 64,033,200 | | |

| Hypermarkets & Super Centers—2.0% | |

| Wal-Mart Stores, Inc. | | | 1,270,000 | | | | 70,612,000 | | |

| Industrial Conglomerates—3.3% | |

| Tyco International, Ltd. (c) | | | 1,860,000 | | | | 71,145,000 | | |

| 3M Co. | | | 540,000 | | | | 45,127,800 | | |

| | | | 116,272,800 | | |

| Industrial Machinery—1.5% | |

| Illinois Tool Works, Inc. | | | 1,075,000 | | | | 50,912,000 | | |

| Integrated Oil & Gas—1.5% | |

| Cenovus Energy, Inc. (c) | | | 1,930,000 | | | | 50,585,300 | | |

| Internet Software & Services—1.8% | |

| eBay, Inc. (a) | | | 2,340,000 | | | | 63,063,000 | | |

| Motorcycle Manufacturers—1.8% | |

| Harley-Davidson, Inc. | | | 2,212,000 | | | | 62,090,840 | | |

| Movies & Entertainment—7.0% | |

| Viacom, Inc., Class B (a) | | | 2,039,745 | | | | 70,126,433 | | |

OAKMARK FUND

10

OAKMARK FUND

Schedule of Investments—March 31, 2010 (Unaudited) cont.

Name | |

Shares Held | |

Value | |

| Common Stocks—94.6% (cont.) | |

| Movies & Entertainment—7.0% (cont.) | |

| The Walt Disney Co. | | | 1,950,000 | | | $ | 68,074,500 | | |

| Time Warner, Inc. | | | 1,942,566 | | | | 60,744,039 | | |

| Liberty Media Holding Corp. - Capital, Class A (a) | | | 1,320,836 | | | | 48,038,805 | | |

| | | | 246,983,777 | | |

| Oil & Gas Exploration & Production—1.0% | |

| EnCana Corp. (c) | | | 1,140,000 | | | | 35,374,200 | | |

| Other Diversified Financial Services—3.1% | |

| Bank of America Corp. | | | 3,271,000 | | | | 58,387,350 | | |

| JPMorgan Chase & Co. | | | 1,130,000 | | | | 50,567,500 | | |

| | | | 108,954,850 | | |

| Packaged Foods & Meats—1.4% | |

| H.J. Heinz Co. | | | 1,100,000 | | | | 50,171,000 | | |

| Pharmaceuticals—7.2% | |

| Bristol-Myers Squibb Co. | | | 2,650,000 | | | | 70,755,000 | | |

| Johnson & Johnson | | | 980,000 | | | | 63,896,000 | | |

| GlaxoSmithKline PLC (b) | | | 1,565,000 | | | | 60,283,800 | | |

| Merck & Co., Inc. | | | 1,571,535 | | | | 58,696,832 | | |

| | | | 253,631,632 | | |

| Property & Casualty Insurance—0.9% | |

| Allstate Corp. | | | 1,000,000 | | | | 32,310,000 | | |

| Restaurants—3.3% | |

| McDonald's Corp. | | | 869,000 | | | | 57,979,680 | | |

| Yum! Brands, Inc. | | | 1,484,000 | | | | 56,881,720 | | |

| | | | 114,861,400 | | |

| Semiconductor Equipment—1.9% | |

| Applied Materials, Inc. | | | 5,050,000 | | | | 68,074,000 | | |

| Semiconductors—4.4% | |

| Intel Corp. | | | 3,850,000 | | | | 85,701,000 | | |

| Texas Instruments, Inc. | | | 2,750,000 | | | | 67,292,500 | | |

| | | | 152,993,500 | | |

| Specialized Consumer Services—1.6% | |

| H&R Block, Inc. | | | 3,128,600 | | | | 55,689,080 | | |

| Systems Software—3.8% | |

| Oracle Corp. | | | 2,750,000 | | | | 70,647,500 | | |

| Microsoft Corp. | | | 2,150,000 | | | | 62,930,500 | | |

| | | | 133,578,000 | | |

| Total Common Stocks (Cost: $2,144,598,163) | | | | | | $ | 3,322,239,755 | | |

OAKMARK FUND

11

OAKMARK FUND

Schedule of Investments—March 31, 2010 (Unaudited) cont.

Name | |

Par Value | |

Value | |

| Short Term Investment—2.9% | |

| Repurchase Agreement—2.9% | |

Fixed Income Clearing Corp. Repurchase

Agreement, 0.00% dated 3/31/2010 due 4/1/2010,

repurchase price $101,231,632, collateralized by

a Federal Home Loan Bank Bond, with a rate of

2.330%, with a maturity of 5/23/2013, and with

a market value plus accrued interest of $45,795,913,

and by Federal Home Loan Mortgage Corp. Bonds,

with rates from 2.000% - 2.250%, with maturities

from 8/24/2012 - 3/29/2013, and with an aggregate

market value plus accrued interest of $11,916,319,

and by Federal National Mortgage Association Bonds,

with a rate of 1.750%, with maturities from

3/23/2011 - 5/7/2013, and with an aggregate

market value plus accrued interest of $45,544,563

(Cost: $101,231,632) | | $ | 101,231,632 | | | $ | 101,231,632 | | |

| Total Short Term Investment (Cost: $101,231,632) | | | | $ | 101,231,632 | | |

| Total Investments (Cost: $2,245,829,795)—97.5% | | | | | 3,423,471,387 | | |

| Other Assets In Excess of Liabilities—2.5% | | | | | 89,273,855 | | |

| Total Net Assets—100% | | | | $ | 3,512,745,242 | | |

(a) Non income-producing security.

(b) Represents a Sponsored American Depositary Receipt.

(c) Represents a foreign domiciled corporation.

See accompanying Notes to Financial Statements.

OAKMARK FUND

12

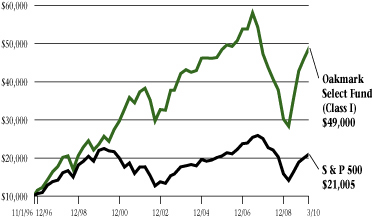

OAKMARK SELECT FUND

Report from Bill Nygren and Henry Berghoef, Portfolio Managers

THE VALUE OF A $10,000 INVESTMENT IN OAKMARK SELECT FUND FROM ITS INCEPTION (11/1/96) TO PRESENT (3/31/10) AS COMPARED TO THE STANDARD & POOR'S 500 INDEX4 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 3/31/10) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(11/1/96) | |

Oakmark Select Fund

(Class I) | | | 6.34 | % | | | 72.95 | % | | | 1.12 | % | | | 6.68 | % | | | 12.58 | % | |

| S&P 500 | | | 5.39 | % | | | 49.77 | % | | | 1.92 | % | | | -0.65 | % | | | 5.69 | % | |

Lipper Multi-Cap

Value Index7 | | | 6.18 | % | | | 51.98 | % | | | 0.85 | % | | | 3.70 | % | | | 6.04 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The expense ratio for Class I shares as of 9/30/09 was 1.19%.

The performance data quoted represents past performance. The above performance information for the Fund does not reflect the imposition of a 2% redemption fee on shares redeemed within 90 days. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

The Oakmark Select Fund increased in value by 6% for the quarter compared to a 5% gain for the S&P 500. The stock market has now been up for four consecutive quarters, and the S&P 500 has returned 50% for the trailing twelve months. The Oakmark Select Fund has performed significantly better, gaining 73% over that same time period. Though we view gains of that magnitude as unsustainable, we continue to believe that long-term returns from stocks are likely to be meaningfully higher than returns for either bonds or cash.

During the past quarter, our biggest contributors were Liberty Interactive, up 41%, Bank of America, up 19%, and Discovery Communications, up 11%. Liberty Interactive's primary business is QVC. QVC, remembered by many as a peddler of cubic zirconium jewelry, is now an on-air and on-line department store. We view QVC's quick recovery from the recession as a testament to its competitive advantages over its brick and mortar department store competition. Bank of America is benefiting from an apparent peak in loan charge-offs. As investors gain the confidence to look forward to normalized losses, we think they'll like the earnings outlook for Bank of America. Discovery continued to demonstrate its ability to grow its viewership and thus its attractiveness to advertisers. If you enjoyed the Planet Earth series, make sure you see Life. Its debut set a new high for Discovery Channel's ratings, giving viewers some of the best HD nature photography ever seen on TV.

The biggest detractors for the quarter were H&R Block, down 21%, Western Union, down 10%, and Texas Instruments, down 6%. Importantly, these were the only stocks in the portfolio that declined. Block reported a larger than expected decline in early season tax filers. Investors are concerned that the decline is secular, as a growing number of individuals prepare their own returns using tax preparation software. We believe the problem is mostly cyclical, with the recession causing many of Block's lower income customers not to file returns for 2009. When employment recovers, we expect that headwind to become a tailwind and that Block's customer counts will recover. Western Union's money transfer business also reported weak results, and again, our expectation is that this will reverse as employment recovers. Texas Instruments, despite a strong sales and earnings rebound, left some investors disappointed that its margins weren't improving eve n more rapidly. We remain pleased with the company's investments in future growth, and we continue to believe that the stock is quite undervalued. No positions were eliminated during the quarter, and no new positions were added.

William C. Nygren, CFA

Portfolio Manager

oaklx@oakmark.com | | Henry R. Berghoef, CFA

Portfolio Manager

oaklx@oakmark.com | |

|

March 31, 2010

OAKMARK SELECT FUND

13

OAKMARK SELECT FUND

Schedule of Investments—March 31, 2010 (Unaudited)

Name | |

Shares Held | |

Value | |

| Common Stocks—95.0% | |

| Broadcasting—10.1% | |

| Discovery Communications, Inc., Class C (a) | | | 8,709,500 | | | $ | 256,146,395 | | |

| Cable & Satellite—11.0% | |

| DIRECTV, Class A (a) | | | 5,247,949 | | | | 177,433,156 | | |

| Comcast Corp., Class A | | | 5,750,000 | | | | 103,327,500 | | |

| | | | 280,760,656 | | |

| Catalog Retail—5.5% | |

| Liberty Media Corp. - Interactive, Class A (a) | | | 9,100,000 | | | | 139,321,000 | | |

| Computer & Electronics Retail—4.3% | |

| Best Buy Co., Inc. | | | 2,550,000 | | | | 108,477,000 | | |

| Computer Hardware—3.3% | |

| Dell, Inc. (a) | | | 5,613,000 | | | | 84,251,130 | | |

| Consumer Finance—3.9% | |

| Capital One Financial Corp. | | | 2,410,600 | | | | 99,822,946 | | |

| Data Processing & Outsourced Services—3.4% | |

| Western Union Co. | | | 5,165,400 | | | | 87,605,184 | | |

| Electronic Manufacturing Services—4.4% | |

| Tyco Electronics, Ltd. (b) | | | 4,067,838 | | | | 111,784,188 | | |

| Health Care Equipment—4.4% | |

| Medtronic, Inc. | | | 2,500,000 | | | | 112,575,000 | | |

| Integrated Oil & Gas—4.0% | |

| Cenovus Energy, Inc. (b) | | | 3,924,800 | | | | 102,869,008 | | |

| Internet Software & Services—4.0% | |

| eBay, Inc. (a) | | | 3,800,000 | | | | 102,410,000 | | |

| Movies & Entertainment—4.0% | |

| Time Warner, Inc. | | | 3,210,666 | | | | 100,397,526 | | |

| Oil & Gas Exploration & Production—4.3% | |

| Newfield Exploration Co. (a) | | | 2,100,000 | | | | 109,305,000 | | |

OAKMARK SELECT FUND

14

OAKMARK SELECT FUND

Schedule of Investments—March 31, 2010 (Unaudited) cont.

Name | | Shares Held/

Par Value | |

Value | |

| Common Stocks—95.0% (cont.) | |

| Other Diversified Financial Services—8.0% | |

| Bank of America Corp. | | | 6,195,100 | | | $ | 110,582,535 | | |

| JPMorgan Chase & Co. | | | 2,094,000 | | | | 93,706,500 | | |

| | | | 204,289,035 | | |

| Pharmaceuticals—4.5% | |

| Bristol-Myers Squibb Co. | | | 4,310,200 | | | | 115,082,340 | | |

| Restaurants—3.3% | |

| Yum! Brands, Inc. | | | 2,215,000 | | | | 84,900,950 | | |

| Semiconductors—8.1% | |

| Intel Corp. | | | 5,047,000 | | | | 112,346,220 | | |

| Texas Instruments, Inc. | | | 3,875,000 | | | | 94,821,250 | | |

| | | | 207,167,470 | | |

| Specialized Consumer Services—4.5% | |

| H&R Block, Inc. | | | 6,369,600 | | | | 113,378,880 | | |

| Total Common Stocks (Cost: $1,697,647,719) | | | | | | $ | 2,420,543,708 | | |

| Short Term Investment—5.0% | |

| Repurchase Agreement—5.0% | |

Fixed Income Clearing Corp. Repurchase

Agreement, 0.00% dated 3/31/2010 due 4/1/2010,

repurchase price $126,701,474, collateralized by

a Federal Home Loan Bank Bond, with a rate of

2.330%, with a maturity of 5/23/2013, and with

a market value plus accrued interest of $4,579,088,

and by Federal Home Loan Mortgage Corp. Bonds,

with rates from 2.125% - 4.000%, with maturities

from 6/12/2013 - 6/18/2013, and with an aggregate

market value plus accrued interest of

$124,660,000 (Cost: $126,701,474) | | $ | 126,701,474 | | | $ | 126,701,474 | | |

| Total Short Term Investment (Cost: $126,701,474) | | | | | | $ | 126,701,474 | | |

| Total Investments (Cost: $1,824,349,193)—100.0% | | | | | | | 2,547,245,182 | | |

| Other Assets In Excess of Liabilities—0.0% | | | | | | | 1,106,428 | | |

| Total Net Assets—100% | | | | | | $ | 2,548,351,610 | | |

(a) Non income-producing security.

(b) Represents a foreign domiciled corporation.

See accompanying Notes to Financial Statements.

OAKMARK SELECT FUND

15

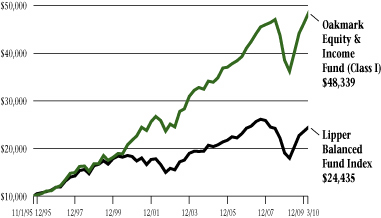

OAKMARK EQUITY AND INCOME FUND

Report from Clyde S. McGregor and Edward A. Studzinski, Portfolio Managers

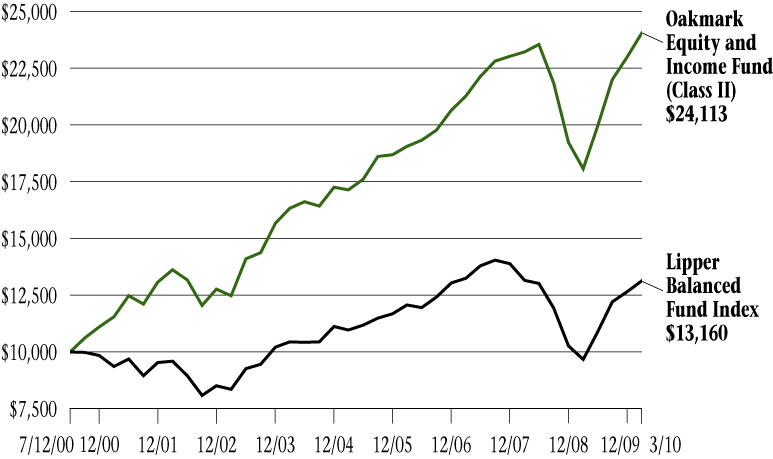

THE VALUE OF A $10,000 INVESTMENT IN OAKMARK EQUITY AND INCOME FUND FROM ITS INCEPTION (11/1/95) TO PRESENT (3/31/10) AS COMPARED TO THE LIPPER BALANCED FUND INDEX8 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 3/31/10) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(11/1/95) | |

Oakmark Equity &

Income Fund (Class I) | | | 4.70 | % | | | 33.52 | % | | | 7.36 | % | | | 9.84 | % | | | 11.55 | % | |

Lipper Balanced

Fund Index | | | 3.84 | % | | | 36.03 | % | | | 3.68 | % | | | 2.88 | % | | | 6.40 | % | |

| S&P 5004 | | | 5.39 | % | | | 49.77 | % | | | 1.92 | % | | | -0.65 | % | | | 6.82 | % | |

Barclays Capital

U.S. Govt./Credit9 | | | 1.55 | % | | | 7.51 | % | | | 5.17 | % | | | 6.22 | % | | | 6.07 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The expense ratio for Class I shares as of 9/30/09 was 0.85%.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

Quarter Review

We are happy to report the fourth consecutive quarter of positive returns to the Equity and Income Fund. In the March quarter the Fund gained nearly 5%, slightly besting the 4% return that Lipper Analytics reports for its Balanced Fund Index. The Fund's equities contributed nearly all of the total return, earning over 7% in the period while the fixed income segment generated only a fractional percentage return. For the first six months of the Fund's fiscal year, the returns are 9% for the Fund versus 8% for the Lipper Balanced Fund Index. The annualized rate of return from the Fund's inception date is 12% compared to the Lipper Balanced Fund Index return of 6%.

During the past quarter the leading contributors to the Fund's return were General Dynamics, Walter Energy, Varian Medical Systems, Rockwell Collins, and Hospira. Fund holdings that declined in price included: H&R Block (disappointing preliminary tax season results), Unilever (unexpected management changes along with euro weakness), Alliant Techsystems (adverse changes in NASA's budget), Martin Marietta Materials (disappointing economic stimulus derived sales), and Diageo (some trade-down to cheaper liquor brands). Our discussion of net equity purchases later in this letter will make it clear why we continued to increase the portfolio's equity allocation to 65%. Appreciation, however, also contributed to the growth in equity commitment. We reduced the fixed income portfolio duration to 2 1/4 years.

Sharp-eyed readers may have already noted that this quarter's winner's list is populated with companies from politically challenged industries. General Dynamics and Rockwell Collins both have significant private aviation product lines, Walter Energy is a coal company, and Varian Medical and Hospira are health care concerns. The stock market seems to have come around to our viewpoint that the environment is not really as negative for these companies and their industries as was feared. General aviation is an industry that the U.S. dominates, its employees are highly compensated, and it generates significant export volumes. As well, General Dynamics participates in the U.S. cyber-defense effort, while Rockwell Collins benefits from an improving production outlook for Boeing and Airbus. Although Walter Energy mines coal, its coal is primarily metallurgical quality, meaning that it is used in steel production. And, exports to emerging markets countries take up much of Walter's output. The Fund's health care holdings' share prices moved upward as the health care bill's details hardened. In this case, certainty seems to have relieved investors. Several smaller health care holdings also enjoyed strong share price advances in the quarter: Kinetic Concepts, Steris, PerkinElmer, and Omnicare. Finally, we should note that the Fund's retail holdings gained strength. Three months ago we wrote somewhat skeptically about the consumer's role in

OAKMARK EQUITY AND INCOME FUND

16

the economic recovery, titling one of our paragraphs "Consumer to the Rescue?" While consumers may not have been particularly ebullient in the March quarter, retailers' stocks were, as evidenced by Fund holdings Foot Locker, TJX, Home Depot, CVS, and Tractor Supply.

Transaction Activity

Although our equity transaction activity had been fairly quiet as calendar 2009 ended, the March quarter proved rather busy. We initiated six new equity holdings while eliminating four. Beginning with the eliminations, Precision Cast Parts, Varian, and Williams were all successful holdings for the Fund. Precision Cast Parts hit our price target very quickly, and Varian is being acquired. We chose to exit the Williams position because of concerns regarding management strategy and so that we could redeploy the proceeds to more attractive opportunities. The fourth sale, Mueller Water, was not a successful holding for the Fund, but it was through our involvement with Mueller that we began to develop our position in Walter Energy, a stock that has proven extremely rewarding.

Addressing the new names alphabetically, Concho Resources is an independent exploration and production company with particular strengths in older onshore North American oilfields. The company's management team has demonstrated entrepreneurial success at predecessor firms. At Home Depot, new management appears to be revitalizing the company just as the environment for home improvement retailing improves. The stock also sports a superior dividend yield. Omnicare returns to the Fund after a seven-year absence. Interestingly, we began this round of share purchases at almost exactly the same share price at which we last sold the stock in 2003. Omnicare is an institutional pharmacy company, primarily solving the pharmaceutical needs of long-term care patients. Of the six new purchases, Teledyne Technologies has the smallest market capitalization, but it participates in a wide variety of capital goods markets, in particular defense electronics and instrumentation. Transocean Limited is the world's largest offshore drilling contractor with particular expertise in deepwater drilling. As oil exploration activity continues to migrate to deeper waters, we believe Transocean should benefit. Last but not least, Weight Watchers is a major beneficiary of what our security analyst calls the "corpulence wave." The company has suffered somewhat from the recession, but we believe that management's efforts to reignite growth, including a significant internet effort, make the stock attractive.

Is Greek Tragedy Too Much Drama?

"Should the woes of a country with fewer people than metropolitan Los Angeles really roil the massive U.S. financial markets?" asked Tom Lauricella in a February 8 Wall Street Journal article10. (This section's title is also borrowed from that article.) Although U.S. markets have stabilized and rebounded since the article was written, it remains unclear which force is stronger: over-indebted smaller nations' ability to spawn financial contagion or multinational agencies' ability to contain this contagion. Before 2007, investors would not have worried about such issues, but the extreme correlations experienced in the recent bear market have c hanged attitudes.

We believe that the answer to the question in the previous paragraph is "no," but that does not mean that Greece's problems (as well as those in Portugal, Ireland, Italy, Spain, etc.) are irrelevant to our management of the Equity and Income Fund. From our vantage point these issues have the greatest impact on our fixed income activity, both long-term and short-term. History teaches that problems such as Greece's tend to be handled by accelerating inflation and currency debasement, both of which work to make debt less onerous to the debtor. Although Europe's common currency (the euro) complicates the situation, we still expect that the policy answer will be the same. Accordingly, we have attempted to protect the Fund's fixed income portfolio by avoiding euro-denominated debt in this period.

Of course, it can well be asked, as Michael Gordon did in the January 7th Financial Times, "Should [any] government bonds still be viewed as risk free?"11 Greece's bonds have been downgraded, but they are a tiny, albeit rapidly growing, factor in the total debt market. Of far greater import was Moody's warning that the U.S. could lose its triple-A bond rating unless the federal budget deficit declines or the economy recovers sufficiently. Adding to the fiscal stress, the government admitted that the Social Security program went into a deficit position in 2009, seven years before this was expected to occur. The cause was the high unemployment level (which reduces tax payments to the "trust fund") combined with a surfeit of individuals filing for benefits sooner than anticipated. Finally, Am erican states' fiscal problems (e.g. California and Illinois) have become well-known.

We come to the conclusion that for now bonds are more likely than stocks to produce losses and that we should take an extremely risk-averse fixed income posture. As noted above, we have reduced the fixed income duration down to near two years. Remember that the duration number tells you how much your principal value would change if the entire yield curve would shift by 1%. A more typical duration for the portfolio has been four years, so we have halved the exposure to a shift in the term structure of interest rates. We have also diversified the long-term fixed income portfolio into Canadian government bonds and the short-term portfolio into Canadian and Australian Treasury bills. Finally, we have increased the Fund's equity percentage to its historic zenith, believing that equities that have growing income and dividend streams are a safer investment under current conditions.

Of course, we do not claim to be able to predict the future given the very difficult choices investors face today. What we can attempt is to protect our investors' capital while positioning the Fund to benefit from many likely scenarios. Once again, we thank you for being our shareholders and invite your questions and comments.

Clyde S. McGregor, CFA

Portfolio Manager

oakbx@oakmark.com | | Edward A. Studzinski, CFA

Portfolio Manager

oakbx@oakmark.com | |

|

March 31, 2010

OAKMARK EQUITY AND INCOME FUND

17

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2010 (Unaudited)

Name | |

Shares Held | |

Value | |

| Common Stocks—64.9% | |

| Aerospace & Defense—9.6% | |

| General Dynamics Corp. | | | 8,000,000 | | | $ | 617,600,000 | | |

| L-3 Communications Holdings, Inc. | | | 4,410,625 | | | | 404,145,569 | | |

| Rockwell Collins, Inc. | | | 6,279,000 | | | | 393,002,610 | | |

| Goodrich Corp. | | | 4,293,700 | | | | 302,791,724 | | |

| Alliant Techsystems, Inc. (a) | | | 1,000,000 | | | | 81,300,000 | | |

| Teledyne Technologies, Inc. (a) | | | 191,210 | | | | 7,891,237 | | |

| | | | 1,806,731,140 | | |

| Apparel Retail—1.8% | |

| The TJX Cos., Inc. | | | 6,000,000 | | | | 255,120,000 | | |

| Foot Locker, Inc. | | | 4,830,000 | | | | 72,643,200 | | |

| | | | 327,763,200 | | |

| Application Software—0.1% | |

| Mentor Graphics Corp. (a) | | | 3,081,318 | | | | 24,712,170 | | |

| Cable & Satellite—1.7% | |

| Scripps Networks Interactive, Inc., Class A | | | 7,000,000 | | | | 310,450,000 | | |

| Communications Equipment—0.6% | |

| Cisco Systems, Inc. (a) | | | 4,000,000 | | | | 104,120,000 | | |

| Computer Hardware—0.2% | |

| Diebold, Inc. | | | 1,250,000 | | | | 39,700,000 | | |

| Construction Materials—0.8% | |

| Martin Marietta Materials, Inc. | | | 1,900,000 | | | | 158,745,000 | | |

| Data Processing & Outsourced Services—0.5% | |

| Broadridge Financial Solutions, Inc. | | | 4,343,300 | | | | 92,859,754 | | |

| Distillers & Vintners—2.0% | |

| Diageo PLC (b) | | | 5,683,300 | | | | 383,338,585 | | |

| Diversified Metals & Mining—1.5% | |

| Walter Energy, Inc. (c) | | | 3,000,000 | | | | 276,810,000 | | |

| Drug Retail—1.4% | |

| CVS Caremark Corp. | | | 7,000,000 | | | | 255,920,000 | | |

| Electrical Components & Equipment—1.1% | |

| Rockwell Automation Inc. | | | 3,609,600 | | | | 203,437,056 | | |

OAKMARK EQUITY AND INCOME FUND

18

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2010 (Unaudited) cont.

Name | |

Shares Held | |

Value | |

| Common Stocks—64.9% (cont.) | |

| Electronic Manufacturing Services—1.0% | |

| Tyco Electronics, Ltd. (d) | | | 6,500,000 | | | $ | 178,620,000 | | |

| Health Care Equipment—7.8% | |

| Covidien PLC (d) | | | 10,600,000 | | | | 532,968,000 | | |

| Hospira, Inc. (a) | | | 7,728,000 | | | | 437,791,200 | | |

| Varian Medical Systems, Inc. (a) | | | 5,700,000 | | | | 315,381,000 | | |

| Steris Corp. | | | 2,873,300 | | | | 96,715,278 | | |

| Kinetic Concepts, Inc. (a) | | | 1,800,000 | | | | 86,058,000 | | |

| | | | 1,468,913,478 | | |

| Health Care Services—2.5% | |

| Laboratory Corp. of America Holdings (a) | | | 4,935,000 | | | | 373,628,850 | | |

| Omnicare, Inc. | | | 3,300,000 | | | | 93,357,000 | | |

| | | | 466,985,850 | | |

| Home Furnishings—1.1% | |

| Mohawk Industries, Inc. (a) | | | 3,420,000 | | | | 185,979,600 | | |

| Leggett & Platt, Inc. | | | 1,327,656 | | | | 28,730,476 | | |

| | | | 214,710,076 | | |

| Home Improvement Retail—1.1% | |

| The Home Depot, Inc. | | | 6,425,500 | | | | 207,864,925 | | |

| Hypermarkets & Super Centers—5.0% | |

| Wal-Mart Stores, Inc. | | | 10,000,000 | | | | 556,000,000 | | |

| Costco Wholesale Corp. | | | 6,426,400 | | | | 383,720,344 | | |

| | | | 939,720,344 | | |

| Industrial Machinery—0.8% | |

| Pentair, Inc. | | | 4,200,000 | | | | 149,604,000 | | |

| Integrated Oil & Gas—2.6% | |

| Cenovus Energy, Inc. (d) | | | 18,500,000 | | | | 484,885,000 | | |

| Life Sciences Tools & Services—0.4% | |

| PerkinElmer, Inc. | | | 3,500,000 | | | | 83,650,000 | | |

| Marine—0.6% | |

| Kirby Corp. (a) (c) | | | 2,809,900 | | | | 107,197,685 | | |

| Oil & Gas Drilling—1.4% | |

| Transocean, Ltd. (a) (d) | | | 3,000,000 | | | | 259,140,000 | | |

OAKMARK EQUITY AND INCOME FUND

19

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2010 (Unaudited) cont.

Name | | Shares Held/

Par Value | |

Value | |

| Common Stocks—64.9% (cont.) | |

| Oil & Gas Exploration & Production—7.0% | |

| XTO Energy, Inc. | | | 10,000,000 | | | $ | 471,800,000 | | |

| Apache Corp. | | | 4,000,000 | | | | 406,000,000 | | |

| EnCana Corp. (d) | | | 8,250,000 | | | | 255,997,500 | | |

| Concho Resources, Inc. (a) | | | 3,500,000 | | | | 176,260,000 | | |

| | | | 1,310,057,500 | | |

| Packaged Foods & Meats—6.8% | |

| Nestle SA (b) (e) | | | 9,136,000 | | | | 467,891,104 | | |

| ConAgra Foods, Inc. | | | 17,500,000 | | | | 438,725,000 | | |

| Unilever PLC (b) | | | 8,500,000 | | | | 248,880,000 | | |

| Unilever NV (b) | | | 4,000,000 | | | | 120,640,000 | | |

| | | | 1,276,136,104 | | |

| Personal Products—2.8% | |

| Avon Products, Inc. | | | 15,500,000 | | | | 524,985,000 | | |

| Real Estate Investment Trusts—0.1% | |

| Walter Investment Management Corp. (c) | | | 1,093,695 | | | | 17,499,120 | | |

| Reinsurance—1.7% | |

| PartnerRe, Ltd. (d) | | | 3,900,000 | | | | 310,908,000 | | |

| Specialized Consumer Services—0.5% | |

| H&R Block, Inc. | | | 3,300,000 | | | | 58,740,000 | | |

| Weight Watchers International, Inc. | | | 1,085,000 | | | | 27,700,050 | | |

| | | | 86,440,050 | | |

| Specialty Stores—0.4% | |

| Tractor Supply Co. | | | 1,367,300 | | | | 79,371,765 | | |

| Total Common Stocks (Cost: $9,191,271,101) | | | | | | $ | 12,151,275,802 | | |

| Fixed Income—24.0% | |

| Corporate Bonds—0.4% | |

| Leisure Facilities—0.1% | |

| Vail Resorts, Inc., 6.75%, due 2/15/2014 | | $ | 14,897,000 | | | $ | 14,952,864 | | |

| Paper Packaging—0.1% | |

| Sealed Air Corp., 144A, 5.625%, due 7/15/2013 (f) | | | 18,740,000 | | | | 19,804,619 | | |

| Property & Casualty Insurance—0.1% | |

| Fund American Cos., Inc., 5.875%, due 5/15/2013 | | | 20,498,000 | | | | 21,096,890 | | |

OAKMARK EQUITY AND INCOME FUND

20

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2010 (Unaudited) cont.

Name | |

Par Value | |

Value | |

| Fixed Income—24.0% (cont.) | |

| Semiconductor Equipment—0.1% | |

| ASML Holding NV, 5.75%, due 6/13/2017 | | EUR | 9,660,000 | | | $ | 13,569,175 | | |

| Total Corporate Bonds (Cost: $57,103,093) | | | | | | $ | 69,423,548 | | |

| Government and Agency Securities—23.6% | |

| Canadian Government Bonds—2.1% | |

| Canadian Government Bond, 4.00%, due 6/1/2016 | | CAD | 97,735,000 | | | | 100,960,597 | | |

| Canadian Government Bond, 3.00%, due 6/1/2014 | | CAD | 98,870,000 | | | | 98,465,038 | | |

| Canadian Government Bond, 3.50%, due 6/1/2013 | | CAD | 96,600,000 | | | | 98,337,687 | | |

| Canadian Government Bond, 1.25%, due 6/1/2011 | | CAD | 98,870,000 | | | | 97,489,626 | | |

| | | | 395,252,948 | | |

| Swedish Government Bonds—0.1% | |

| Swedish Government Bond, 3.00%, due 7/12/2016 | | SEK | 200,000,000 | | | | 28,177,437 | | |

| U.S. Government Agencies—4.0% | |

| Federal Farm Credit Bank, 3.50%, due 10/3/2011 | | $ | 96,600,000 | | | | 100,368,946 | | |

| Federal Farm Credit Bank, 0.13%, due 2/22/2012 (g) | | | 93,700,000 | | | | 93,450,758 | | |

| Tennessee Valley Authority, 6.79%, due 5/23/2012 | | | 56,735,000 | | | | 63,240,178 | | |

| Tennessee Valley Authority, 5.50%, due 7/18/2017 | | | 56,515,000 | | | | 62,954,489 | | |

| Federal Farm Credit Bank, 3.875%, due 11/13/2012 | | | 38,645,000 | | | | 40,849,427 | | |

Federal Home Loan Mortgage Corp., 0.75%,

due 2/19/2013 (h) | | | 22,500,000 | | | | 22,493,835 | | |

| Federal Home Loan Bank, 1.30%, due 1/25/2013 (h) | | | 20,000,000 | | | | 20,013,020 | | |

| Federal Home Loan Bank, 1.00%, due 3/15/2013 (h) | | | 20,000,000 | | | | 19,973,860 | | |

Federal National Mortgage Association, 1.00%,

due 3/15/2013 (h) | | | 20,000,000 | | | | 19,945,900 | | |

Federal National Mortgage Association, 1.00%,

due 2/11/2013 (h) | | | 18,500,000 | | | | 18,508,972 | | |

| Federal Farm Credit Bank, 4.50%, due 10/17/2012 | | | 15,215,000 | | | | 16,320,522 | | |

| Federal Farm Credit Bank, 5.125%, due 8/25/2016 | | | 14,130,000 | | | | 15,659,926 | | |

| Federal Home Loan Bank, 0.75%, due 12/11/2012 (h) | | | 15,000,000 | | | | 15,006,855 | | |

| Federal Farm Credit Bank, 3.875%, due 8/25/2011 | | | 14,005,000 | | | | 14,602,271 | | |

| Federal Home Loan Bank, 1.25%, due 3/30/2015 (h) | | | 12,200,000 | | | | 12,153,799 | | |

| Tennessee Valley Authority, 4.375%, due 6/15/2015 | | | 9,660,000 | | | | 10,274,675 | | |

| Federal Farm Credit Bank, 3.85%, due 2/11/2015 | | | 9,415,000 | | | | 9,898,545 | | |

| Federal Farm Credit Bank, 0.278%, due 6/8/2011 (g) | | | 9,885,000 | | | | 9,892,967 | | |

Federal National Mortgage Association, 3.10%,

due 8/18/2015 | | | 9,500,000 | | | | 9,480,981 | | |

Federal National Mortgage Association, 1.00%,

due 9/18/2012 (h) | | | 9,500,000 | | | | 9,463,691 | | |

| Federal Home Loan Bank, 1.00%, due 12/10/2014 (h) | | | 9,450,000 | | | | 9,458,590 | | |

| Federal Home Loan Bank, 1.00%, due 6/8/2012 (h) | | | 9,390,000 | | | | 9,400,075 | | |

Federal Home Loan Mortgage Corp., 3.00%,

due 6/30/2014 (h) | | | 8,780,000 | | | | 8,843,541 | | |

OAKMARK EQUITY AND INCOME FUND

21

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2010 (Unaudited) cont.

Name | |

Par Value | |

Value | |

| Fixed Income—24.0% (cont.) | |

| U.S. Government Agencies—4.0% (cont.) | |

| Federal Farm Credit Bank, 5.28%, due 8/16/2013 | | $ | 7,245,000 | | | $ | 7,999,422 | | |

| Federal Home Loan Bank, 2.10%, due 12/17/2014 (h) | | | 6,970,000 | | | | 6,938,558 | | |

| Federal Farm Credit Bank, 5.20%, due 11/28/2016 | | | 5,650,000 | | | | 6,229,176 | | |

| Federal Farm Credit Bank, 5.125%, due 6/6/2011 | | | 5,250,000 | | | | 5,523,730 | | |

| Federal Home Loan Bank, 2.00%, due 12/24/2014 (h) | | | 5,500,000 | | | | 5,506,105 | | |

| Federal Farm Credit Bank, 4.875%, due 12/16/2015 | | | 4,710,000 | | | | 5,155,858 | | |

| Federal Farm Credit Bank, 4.92%, due 8/26/2013 | | | 4,710,000 | | | | 5,147,074 | | |

Federal National Mortgage Association, 1.50%,

due 1/12/2015 (h) | | | 5,000,000 | | | | 5,017,735 | | |

Federal National Mortgage Association, 1.25%,

due 11/10/2014 (h) | | | 5,000,000 | | | | 5,004,520 | | |

| Federal Farm Credit Bank, 5.10%, due 8/9/2011 | | | 4,685,000 | | | | 4,957,302 | | |

Federal Home Loan Mortgage Corp., 1.25%,

due 3/16/2015 (h) | | | 4,800,000 | | | | 4,813,474 | | |

Federal National Mortgage Association, 1.125%,

due 12/30/2014 (h) | | | 4,750,000 | | | | 4,779,749 | | |

Federal National Mortgage Association, 1.50%,

due 1/20/2015 (h) | | | 4,750,000 | | | | 4,758,949 | | |

Federal Home Loan Mortgage Corp., 1.00%,

due 3/15/2013 (h) | | | 4,750,000 | | | | 4,750,869 | | |

Federal National Mortgage Association, 1.00%,

due 3/15/2013 (h) | | | 4,750,000 | | | | 4,732,354 | | |

Federal National Mortgage Association, 2.25%,

due 12/15/2014 (h) | | | 4,750,000 | | | | 4,710,523 | | |

Federal National Mortgage Association, 1.00%,

due 9/30/2013 (h) | | | 4,700,000 | | | | 4,685,289 | | |

| Federal Home Loan Bank, 1.375%, due 9/16/2013 (h) | | | 4,700,000 | | | | 4,681,035 | | |

Federal National Mortgage Association, 2.00%,

due 3/30/2016 (h) | | | 4,700,000 | | | | 4,668,656 | | |

| Federal Home Loan Bank, 2.00%, due 9/16/2015 (h) | | | 4,700,000 | | | | 4,665,666 | | |

| Federal Home Loan Bank, 0.625%, due 11/12/2013 (h) | | | 4,650,000 | | | | 4,652,916 | | |

Federal National Mortgage Association, 1.25%,

due 2/25/2015 (h) | | | 4,650,000 | | | | 4,641,918 | | |

Federal National Mortgage Association, 1.00%,

due 3/15/2013 (h) | | | 4,650,000 | | | | 4,619,966 | | |

Federal National Mortgage Association, 2.00%,

due 3/26/2015 (h) | | | 4,600,000 | | | | 4,565,882 | | |

Federal National Mortgage Association, 1.25%,

due 12/30/2014 (h) | | | 4,500,000 | | | | 4,534,173 | | |

| Federal Farm Credit Bank, 5.05%, due 5/25/2011 | | | 3,746,000 | | | | 3,933,884 | | |

| Federal Farm Credit Bank, 4.50%, due 8/8/2011 | | | 2,815,000 | | | | 2,955,660 | | |

| Federal Farm Credit Bank, 4.82%, due 10/12/2012 | | | 2,345,000 | | | | 2,533,015 | | |

| | | | 749,419,281 | | |

OAKMARK EQUITY AND INCOME FUND

22

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2010 (Unaudited) cont.

Name | |

Par Value | |

Value | |

| Fixed Income—24.0% (cont.) | |

| U.S. Government Notes—17.4% | |

United States Treasury Note, 1.375%, due 7/15/2018,

Inflation Indexed | | $ | 502,375,000 | | | $ | 502,728,170 | | |

| United States Treasury Note, 2.875%, due 1/31/2013 | | | 483,005,000 | | | | 501,646,095 | | |

| United States Treasury Note, 3.25%, due 5/31/2016 | | | 494,340,000 | | | | 500,557,808 | | |

| United States Treasury Note, 0.875%, due 1/31/2012 | | | 500,000,000 | | | | 499,414,000 | | |

| United States Treasury Note, 0.75%, due 11/30/2011 | | | 500,000,000 | | | | 499,316,500 | | |

| United States Treasury Note, 1.375%, due 9/15/2012 | | | 250,000,000 | | | | 250,547,000 | | |

| United States Treasury Note, 1.375%, due 10/15/2012 | | | 250,000,000 | | | | 250,312,500 | | |

| United States Treasury Note, 1.125%, due 12/15/2012 | | | 250,000,000 | | | | 247,832,000 | | |

| | | | 3,252,354,073 | | |

Total Government and Agency Securities

(Cost: $4,320,036,059) | | | | | | $ | 4,425,203,739 | | |

| Total Fixed Income (Cost: $4,377,139,152) | | | | | | $ | 4,494,627,287 | | |

| Short Term Investments—11.4% | |

| Australian Government Bills—0.2% | |

Australian Treasury Bills, 3.76% - 3.85%,

due 4/23/2010 - 6/11/2010 (i) (Cost: $36,681,011) | | AUD | 41,000,000 | | | $ | 37,483,611 | | |

| Canadian Treasury Bills—1.8% | |

Canadian Treasury Bills, 0.45% - 0.84%,

due 4/15/2010 - 3/17/2011 (i) (Cost: $323,290,470) | | CAD | 349,145,000 | | | | 342,694,332 | | |

| Commercial Paper—2.5% | |

American Honda Finance Corp., 0.13% - 0.18%,

due 4/13/2010 - 5/4/2010 (i) | | $ | 96,000,000 | | | | 95,986,063 | | |

Johnson & Johnson, 144A, 0.09% - 0.17%,

due 4/12/2010 - 5/3/2010 (f) (i) | | | 75,000,000 | | | | 74,995,905 | | |

Medtronic, Inc., 144A, 0.13% - 0.16%,

due 4/5/2010 - 4/21/2010 (f) (i) | | | 50,000,000 | | | | 49,997,788 | | |

Microsoft Corp., 144A, 0.10% - 0.18%,