UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-06279 |

|

Harris Associates Investment Trust |

(Exact name of registrant as specified in charter) |

|

Two North La Salle Street, Suite 500

Chicago, Illinois | | 60602-3790 |

(Address of principal executive offices) | | (Zip code) |

|

John R. Raitt Harris Associates L.P. Two North La Salle Street, #500 Chicago, Illinois 60602 | Cameron S. Avery Bell, Boyd & Lloyd LLP Three First National Plaza, #3100 Chicago, Illinois 60602 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (312) 621-0600 | |

|

Date of fiscal year end: | 9/30/08 | |

|

Date of reporting period: | 3/31/08 | |

| | | | | | | | |

Item 1. Reports to Shareholders.

SEMI-ANNUAL REPORT

MARCH 31, 2008

Advised by Harris Associates L.P.

THE OAKMARK FUNDS

2008 Semi-Annual Report

| President's Letter | | | 1 | | |

|

| Summary Information | | | 2 | | |

|

| Fund Expenses | | | 4 | | |

|

| Commentary on The Oakmark and Oakmark Select Funds | | | 6 | | |

|

| The Oakmark Fund | |

|

| Letter from the Portfolio Managers | | | 8 | | |

|

| Schedule of Investments | | | 9 | | |

|

| The Oakmark Select Fund | |

|

| Letter from the Portfolio Managers | | | 13 | | |

|

| Schedule of Investments | | | 14 | | |

|

| The Oakmark Equity and Income Fund | |

|

| Letter from the Portfolio Managers | | | 16 | | |

|

| Schedule of Investments | | | 18 | | |

|

| The Oakmark Global Fund | |

|

| Letter from the Portfolio Managers | | | 24 | | |

|

| Global Diversification Chart | | | 26 | | |

|

| Schedule of Investments | | | 27 | | |

|

| The Oakmark Global Select Fund | |

|

| Letter from the Portfolio Managers | | | 31 | | |

|

| Global Diversification Chart | | | 33 | | |

|

| Schedule of Investments | | | 34 | | |

|

| Commentary on The International and International Small Cap Funds | | | 37 | | |

|

| The Oakmark International Fund | |

|

| Letter from the Portfolio Manager | | | 38 | | |

|

| Global Diversification Chart | | | 40 | | |

|

| Schedule of Investments | | | 41 | | |

|

| The Oakmark International Small Cap Fund | |

|

| Letter from the Portfolio Managers | | | 46 | | |

|

| Global Diversification Chart | | | 48 | | |

|

| Schedule of Investments | | | 49 | | |

|

| Financial Statements | |

|

| Statements of Assets and Liabilities | | | 54 | | |

|

| Statements of Operations | | | 56 | | |

|

| Statements of Changes in Net Assets | | | 58 | | |

|

| Notes to Financial Statements | | | 65 | | |

|

| Disclosure Regarding Investment Advisory Contract Approval | | | 82 | | |

|

| Oakmark Philosophy and Process | | | 87 | | |

|

| The Oakmark Glossary | | | 88 | | |

|

| Trustees and Officers | | | 89 | | |

|

FORWARD-LOOKING STATEMENT DISCLOSURE

One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered "forward-looking statements". Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as "estimate", "may", "will", "expect", "believe", "plan" and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

President's Letter

Dear Fellow Shareholders,

The first quarter proved to be difficult for equity investors. Domestic and international stock markets fell sharply during the quarter. Broader equity market indexes around the world registered declines in the 8-10% range, due to concerns about economic growth and unsettled credit markets. While we are not pleased with recent performance, we still remain intently focused on future prospects for our investments and on helping our clients build long-term wealth.

Credit Market Developments and the Economy

The credit correction that began last spring continued to deepen during the first quarter. What started last year as a reversal in the mortgage market now has expanded to almost every corner of the lending marketplace. Tighter credit has brought a predictable slowing of economic growth, and these abrupt shifts in the markets have created several instances of severe financial stress. Significant setbacks recently hit the markets in rapid succession. Large increases in mortgage foreclosures, major loan write-offs at banks that forced substantial capital infusions, money market liquidity runs, the dramatic failure and rescue of Bear Stearns and the plummeting value of the dollar have all shaken investor confidence.

The sharp contrast between today's market conditions and those of only a year ago is remarkable and instructive. Lenders and equity investors have gone from being confident and aggressive to fearful and tentative. Credit has gone from being plentiful to scarce. Lastly, with the shift in the availability of capital, equity and fixed income markets have become less liquid and more volatile. In fact, equity market volatility reached its highest level in seventy years in the first quarter, with broader U.S. market indexes changing by over 1% on more than half of the quarter's trading days. Stock prices today seem much more a function of a stock's liquidity than the fundamentals of its underlying business and business value.

Maintaining Investment Discipline and Adhering to a Long-Term Plan

At times like this it can be difficult for investors to maintain a proper perspective in making investment decisions. Recent economic events are worrisome, and the sharp market declines are unnerving. Moreover, the constant barrage of negative news and the herd-like behavior of the media make it easy to decide to head for the investment sidelines.

Once again, however, we reiterate our belief that when market conditions are difficult, it is especially important to maintain a consistent investment discipline, removing emotion from the investment decision process, and buying stocks when they are weak and out of favor. While we anticipate that the remainder of 2008 will be challenging for the economy—and for financial firms in particular—past experience has shown us that times like these can play to the strengths of our value philosophy. We believe that the impetuous and often extreme sentiments surrounding the market today can actually create greater investment opportunity. Volatile prices, illiquidity, emotional investors, and broad market declines are all factors that provide us opportunities to execute upon our value investing discipline—and acquire stocks at substantial discounts to underlying business value and at prices that prove to be very attractive over time.

Thank you for your continued investment and confidence in The Oakmark Funds. We welcome your comments and questions. You can reach us via e-mail at ContactOakmark@oakmark.com.

John R. Raitt

President and CEO of The Oakmark Funds

President and CEO of Harris Associates L.P.

March 31, 2008

1

THE OAKMARK FUNDS

Summary Information

Performance for Periods

Ended March 31, 20081 | | The Oakmark

Fund—Class I

(OAKMX) | | The Oakmark

Select Fund—Class I

(OAKLX) | | The Oakmark

Equity and Income

Fund—Class I

(OAKBX) | | The Oakmark

Global Fund—Class I

(OAKGX) | |

| 3 Months* | | | -7.36 | % | | | -7.62 | % | | | 0.97 | % | | | -8.42 | % | |

| 1 Year | | | -10.49 | % | | | -18.87 | % | | | 9.54 | % | | | -6.38 | % | |

Average Annual Total

Return for: | |

| 3 Year | | | 2.13 | % | | | -1.88 | % | | | 11.05 | % | | | 11.17 | % | |

| 5 Year | | | 8.75 | % | | | 6.12 | % | | | 13.62 | % | | | 21.63 | % | |

| 10 Year | | | 3.38 | % | | | 8.11 | % | | | 11.08 | % | | | N/A | | |

| Since inception | | | 13.55%

(8/5/91) | | | | 13.81%

(11/1/96) | | | | 13.17%

(11/1/95) | | | | 14.53%

(8/4/99) | | |

Top Five Equity

Holdings as of

March 31, 20082

Company and % of Total

Net Assets | | | Yum! Brands, Inc. 3.5%

Viacom, Inc.-

Class B 2.7%

H&R Block, Inc. 2.7%

Wal-Mart Stores,

Inc. 2.5%

Capital One

Financial

Corporation 2.5% | | | | Yum! Brands, Inc. 8.7%

H&R Block, Inc. 8.6%

Discovery Holding

Company,

Class A 6.2%

Washington

Mutual, Inc. 6.2%

Viacom, Inc.

Class B 5.0% | | | | XTO Energy, Inc. 5.7%

Nestle SA 3.4%

Apache Corporation 3.2%

CVS Caremark

Corporation 3.1%

Newfield Exploration

Company 2.7% | | | | Neopost SA 4.5%

XTO Energy, Inc. 4.5%

Daiwa Securities

Group Inc. 4.2%

Snap-on

Incorporated 3.8%

Credit Suisse Group 3.8% | | |

Sector

Allocation as of

March 31, 2008

Sector and %

of Market Value | | | Consumer

Discretionary 39.3%

Financials 16.2%

Information

Technology 15.8%

Consumer Staples 14.0%

Health Care 8.7%

Industrials 3.5%

Telecommunication

Services 1.5%

Energy 1.0% | | | | Consumer

Discretionary 57.1%

Financials 19.8%

Information

Technology 18.6%

Health Care 4.5% | | | | U.S. Government

Securities 39.1%

Energy 14.9%

Consumer Staples 13.7%

Consumer

Discretionary 10.0%

Industrials 9.0%

Health Care 5.7%

Foreign Government

Securities 3.8%

Financials 2.5%

Information

Technology 1.2%

Materials 0.1% | | | | Consumer

Discretionary 24.4%

Information

Technology 22.7%

Health Care 17.5%

Financials 16.7%

Energy 7.8%

Industrials 7.3%

Consumer Staples 3.6% | | |

The performance data quoted represents past performance. The above performance information for the Funds does not reflect the imposition of a 2% redemption fee on shares of all Funds, other than The Oakmark Equity & Income Fund, held for 90 days or less to deter market timers. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain current month end performance data, visit oakmark.com.

* Not annualized

THE OAKMARK FUNDS

2

Performance for Periods

Ended March 31, 20081 | | The Oakmark

Global Select

Fund—Class I

(OAKWX) | | The Oakmark

International

Fund—Class I

(OAKIX) | | The Oakmark

International

Small Cap Fund—Class I

(OAKEX) | |

| 3 Months* | | | -10.98 | % | | | -11.03 | % | | | -8.08 | % | |

| 1 Year | | | -15.16 | % | | | -15.63 | % | | | -20.37 | % | |

Average Annual Total

Return for: | |

| 3 Year | | N/A | | | 8.91 | % | | | 9.34 | % | |

| 5 Year | | N/A | | | 19.69 | % | | | 25.29 | % | |

| 10 Year | | N/A | | | 9.16 | % | | | 14.13 | % | |

| Since inception | | -3.41%

(10/2/06) | | | 11.66%

(9/30/92) | | | | 12.44%

(11/1/95) | | |

Top Five Equity

Holdings as of

March 31, 20082

Company and % of Total

Net Assets | | Adecco SA 7.6%

Daiwa Securities

Group Inc. 6.0%

Schroders PLC 5.6%

Societe Television

Francaise 1 5.5%

Credit Suisse Group 5.3% | | | Credit Suisse Group 4.7%

Daiwa Securities

Group Inc. 3.7%

GlaxoSmithKline plc 3.6%

Adecco SA 3.4%

Publicis Groupe 3.4% | | | | Neopost SA 5.1%

MLP AG 4.3%

Orbotech, Ltd. 3.1%

Duerr AG 3.1%

USS Co., Ltd. 2.9% | | |

Sector

Allocation as of

March 31, 2008

Sector and %

of Market Value | | Consumer

Discretionary 37.9%

Financials 25.5%

Information

Technology 14.6%

Health Care 14.0%

Industrials 8.0% | | | Financials 33.2%

Consumer

Discretionary 32.5%

Information

Technology 14.3%

Industrials 9.8%

Health Care 7.2%

Consumer Staples 3.0% | | | | Consumer

Discretionary 29.5%

Industrials 28.6%

Information

Technology 17.0%

Financials 14.9%

Consumer Staples 5.7%

Health Care 2.2%

Materials 2.1% | | |

As of 9/30/07, the expense ratio for Class I shares was 1.01% for The Oakmark Fund, 0.97% for The Oakmark Select Fund, 0.83% for The Oakmark Equity and Income Fund, 1.13% for The Oakmark Global Fund, 1.31% for The Oakmark Global Select Fund, 1.05% for The Oakmark International Fund and 1.34% for The Oakmark International Small Cap Fund.

THE OAKMARK FUNDS

3

FUND EXPENSES

A shareholder of each Fund incurs two types of costs: (1) transaction costs, such as redemption fees, and (2) ongoing costs, including investment advisory fees, transfer agent fees, and other fund expenses. The examples below are intended to help shareholders understand the ongoing cost (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other funds.

Actual Expenses

The following table provides information about actual account values and actual fund expenses for Class I of each Fund. The table shows the expenses a Class I shareholder would have paid on a $1,000 investment in each Fund from October 1, 2007, to March 31, 2008, as well as how much a $1,000 investment would be worth at the close of the period, assuming actual fund returns and expenses. Class I shareholders can estimate expenses incurred for the period by dividing their account value at March 31, 2008, by $1,000 and multiplying the result by the number in the Expenses Paid During Period row as shown below.

Certain accounts invested for 90 days or less may be charged a 2% redemption fee. Please consult the Funds' prospectus at oakmark.com for more information.

| | | The Oakmark Fund | | The Oakmark Select Fund | | The Oakmark Equity and Income Fund | | The Oakmark Global Fund | | The Oakmark Global Select Fund | | The Oakmark International Fund | | The Oakmark International Small Cap Fund | |

Beginning

Account

Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | |

Ending

Account

Value | | $ | 867.10 | | | $ | 804.50 | | | $ | 1,020.50 | | | $ | 884.70 | | | $ | 817.00 | | | $ | 847.20 | | | $ | 831.60 | | |

Expenses

Paid

During

Period* | | $ | 5.09 | | | $ | 4.87 | | | $ | 4.14 | | | $ | 5.56 | | | $ | 6.13 | | | $ | 5.17 | | | $ | 6.69 | | |

Annualized

Expense

Ratio | | | 1.09 | % | | | 1.08 | % | | | 0.82 | % | | | 1.18 | % | | | 1.35 | % | | | 1.12 | % | | | 1.46 | % | |

* Expenses are equal to each Fund's annualized expense ratio for Class I, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year divided by 366 (to reflect the one-half year period).

THE OAKMARK FUNDS

4

Hypothetical Example for Comparison Purposes

The following table provides information about hypothetical account values and hypothetical expenses for Class I of each Fund based on actual expense ratios and an assumed rate of return of 5% per year before expenses, which are not the Funds' actual returns. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses shareholders paid for the period. Shareholders may use this information to compare the ongoing costs of investing in a Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as redemption fees. Therefore, the third line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, the total costs would have been higher.

| | | The Oakmark Fund | | The Oakmark Select Fund | | The Oakmark Equity and Income Fund | | The Oakmark Global Fund | | The Oakmark Global Select Fund | | The Oakmark International Fund | | The Oakmark International Small Cap Fund | |

Beginning

Account

Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | |

Ending

Account

Value | | $ | 1,019.55 | | | $ | 1,019.60 | | | $ | 1,020.90 | | | $ | 1,019.10 | | | $ | 1,018.25 | | | $ | 1,019.40 | | | $ | 1,017.70 | | |

Expenses

Paid

During

Period* | | $ | 5.50 | | | $ | 5.45 | | | $ | 4.14 | | | $ | 5.96 | | | $ | 6.81 | | | $ | 5.65 | | | $ | 7.36 | | |

Annualized

Expense

Ratio | | | 1.09 | % | | | 1.08 | % | | | 0.82 | % | | | 1.18 | % | | | 1.35 | % | | | 1.12 | % | | | 1.46 | % | |

* Expenses are equal to each Fund's annualized expense ratio for Class I, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year divided by 366 (to reflect the one-half year period).

THE OAKMARK FUNDS

5

THE OAKMARK AND OAKMARK SELECT FUNDS

At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close.

"More than any time in history, mankind faces a crossroads. One path leads to total despair and utter hopelessness. The other, to total extinction. Let us pray we have the wisdom to choose correctly."

"More than any time in history, mankind faces a crossroads. One path leads to total despair and utter hopelessness. The other, to total extinction. Let us pray we have the wisdom to choose correctly."

Woody Allen

"My Speech to the Graduates"

August 10, 1979, New York Times

I guess Woody Allen wouldn't be an uplifting commencement speaker. But his view of the world, almost thirty years later, seems to be the dominant view in today's commodity and credit markets. If prices in those markets reflect fundamentals, then we are facing a future of materials shortages and unprecedented bankruptcies. If one looks at Main Street instead of Wall Street, the picture, though far from perfect, looks much brighter. Businesses are profitable, unemployment is low and consumer spending remains at reasonable levels. Is it possible that market forecasts could be that far off the mark?

As large shareholders in JP Morgan, we took more than a passing interest in its agreement to purchase Bear Stearns. Bear opened its doors in 1923, survived the Great Depression and grew into one of the world's leading securities firms. Like many other financial services firms, Bear had heavy exposure to home mortgages because those securities historically had very low default rates. Like many of its peers, Bear's 2007 earnings were nearly erased by mortgage losses, and its stock price was cut in half, closing the year at $88. By Thursday, March 13, Bear stock had fallen to $57. Up to that point, you could have substituted quite a few financial company names for "Bear Stearns," and the story would have hardly changed. On Friday, March 14, however, Bear's story sharply diverged from the others. Rumors that Bear had a liquidity problem caused customers to search for safety and move their funds to other firms. The stock price was again cut in ha lf to $30. In that one day, Bear's liquidity problems sharply increased as it needed to sell assets to fund withdrawals. The downward spiral had gone too far to be reversed. On Sunday, JP Morgan agreed to rescue Bear Stearns for $2 per share. A run on the bank had virtually wiped out the stockholders. Did the short sellers profit from being quick to identify a fire raging out of control, or had they spotted a spark and thrown gasoline on it? The answer to that question will be an important one to those calling for more regulation. To the stockholders, whether or not Bear was insolvent on Thursday had become irrelevant. On Sunday it was. Fearful investors had forced the outcome. At least it was one of our companies, JP Morgan, that was positioned to take advantage of an amazing bargain (even at the revised price of $10 per share).

There is a tremendous amount of fear in today's markets. Some portion is due to real economic events. The future for home prices is clearly not the straight upward march it used to be. With average home prices already down 10% from their peak and many homeowners having borrowed as much as their banks would allow, credit losses are certainly increasing. But are loss rates really going to be as high as the bond market is predicting? We normally like to use market prices as estimates for macro variables such as bond default rates, future inflation rates, or energy costs. We assume that those markets incorporate their specific experts' best thinking and that our time would be more productively spent analyzing individual companies. However, the magnitude of gaps we now see between price and value across many markets has made it imprudent to simply use current market prices for our forecasts.

In his New York Times column last month, Ben Stein argued that today's economy is not in such bad shape, but rather, "the new part is the hedge funds and the changing of Wall Street from a financing entity to a market manipulation entity."3 In its cover story "Guess Who's Behind the Commodities Boom,"4 Barron's argued that the increase in mo st commodity prices had less to do with changes in supply and demand than it did with increased investment by institutions who now consider commodities an asset class deserving of a higher portfolio allocation. Barron's states that most long positions are held by speculators and most shorts are held by suppliers. This implies that if commodity market participants were limited to producers and consumers, prices would almost certainly be much lower. A recent article in the Wall Street Journal5 examined the role short sellers play in stock price declines. In July of last year the short sale rules were changed to make it easier to sel l short stocks that were already falling. The article quoted legendary fund manager Marty Whitman, who said "In my 58 years in the market it has never been easier to conduct bear raids." As these articles suggest, there are numerous examples of large pools of new capital whose investment rationale is unrelated to estimates of intrinsic value. In the long run, the resulting higher price volatility should improve the opportunities for investors like us, but in the short run it requires more suspicion of the assumption that any given day's market price reflects long-term fundamental reality.

THE OAKMARK AND OAKMARK SELECT FUNDS

6

As shown by Bear Stearns, the market today is extracting a large toll from forced sellers. Though we always discourage short-term investing, we believe that such advice is especially important now. The gaps between price and value in a fearful market can become very large. If you have to sell stocks by a certain date, the risk is high that you might not get full intrinsic value for those shares. As always, we believe that equity investors, including those in mutual funds, should only invest capital that can remain invested for at least five years. We also don't ever want an Oakmark fund to be a forced seller. That's why we keep a percentage of each of our mutual fund's assets in cash equivalents. Some argue that funds should invest every last dollar to prevent cash from being a drag, but we believe that by holding some cash we not only avoid the cost of forced selling, but we are positioned to benefit when other sellers become desperate.

The financial media is painting a picture that is similar to the Woody Allen quote at the beginning of this report: If the Fed acts aggressively then we are doomed to a future of hyper-inflation and a permanently declining dollar. If the Fed doesn't act, then there is no bottom to the housing market and we are headed toward a depression. We hope they have the wisdom to choose correctly! As you might guess, our view is not so dire, and is in fact quite positive. We find it encouraging that the Fed is thinking outside the box and directly targeting the problem of financial market illiquidity. More importantly, we believe that the dividend yield of the S&P 5006 now equaling the five-year Treasury yield is a significant sign of undervaluation. When the front page news is so negative, there is a high probability that the reality won't be as bad as feared. In 1995, the financial author John Train wrote The Craft of Investing. Five years ago I cited a section from his book that described a typical market bottom. I think it is worth revisiting:

"At a major bottom, current business news is usually terrible and many authorities feel that things are likely to get even worse. There are several spectacular bankruptcies, of international importance. Unemployment is usually up. There is usually some grave unresolved national problem that is bothering everybody. The brokerage business itself is likely to be in the dumps, with many bankruptcies. Big "producers" of the up years have to cut back on their lifestyles. Wall Street's own desperation reinforces the syndrome. When in a market collapse everything finally caves in during a few catastrophic days and weeks, there is an almost audible flushing effect. Stocks are hurled into the abyss, like the cargo of a sinking ship that the crew is desperately trying to save. Value means nothing."7

To me, the Bear Stearns collapse was "an almost audible flushing effect." There is, of course, no guarantee that things won't get worse, but this environment seems to closely parallel Train's description of a bottom. Time to buy?

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

oaklx@oakmark.com

March 31, 2008

THE OAKMARK AND OAKMARK SELECT FUNDS

7

THE OAKMARK FUND

Report from Bill Nygren and Kevin Grant, Portfolio Managers

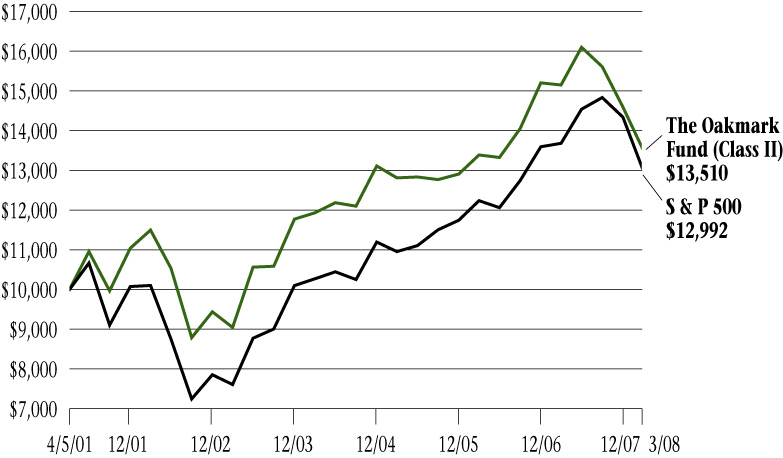

THE VALUE OF A $10,000 INVESTMENT IN THE OAKMARK FUND FROM ITS INCEPTION (8/5/91) TO PRESENT (3/31/08) AS COMPARED TO THE STANDARD & POOR'S 500 INDEX6 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 3/31/08) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(8/5/91) | |

| Oakmark Fund (Class I) | | | -7.36 | % | | | -10.49 | % | | | 8.75 | % | | | 3.38 | % | | | 13.55 | % | |

| S&P 500 | | | -9.44 | % | | | -5.08 | % | | | 11.32 | % | | | 3.50 | % | | | 9.85 | % | |

| Dow Jones Average8 | | | -7.00 | % | | | 1.58 | % | | | 11.44 | % | | | 5.49 | % | | | 11.32 | % | |

Lipper Large Cap

Value Index9 | | | -9.53 | % | | | -7.99 | % | | | 11.92 | % | | | 3.93 | % | | | 9.60 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Expense Ratio for Class I shares as of 9/30/07 was 1.01%.

The performance data quoted represents past performance. The above performance information for the Fund does not reflect the imposition of a 2% redemption fee on shares held for 90 days or less to deter market timers. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

The Oakmark Fund declined in value 7% last quarter. The sting of another down quarter was somewhat softened by comparison to the larger 9% loss for the S&P 500. The Fund's top performers were H&R Block and Pulte Homes. We applaud Block's new management for exiting its mortgage business and refocusing the company on its successful tax preparation business. We sold our position in Pulte following its significant price rebound. On the negative side, Sprint declined due to continued defections of its Nextel subscribers, and Schering–Plough declined following release of a study claiming poor efficacy for its Vytorin and Zetia drugs. We continue to hold both stocks because we believe their prices reflect worst case scenarios, which we believe are unlikely.

During the quarter we eliminated six holdings. Baxter, Honeywell, and Raytheon achieved our targets. Abbott performed significantly better than other healthcare companies, and even though it had not quite reached our sell target, we sold it to fund an investment in a related business, which we judged to be much more undervalued. We also sold two stocks that have been disappointments: Masco and Pulte Homes. Both businesses have been hard hit by the collapse in new home construction. Though both traded well below our sell targets, we captured tax-losses and re-invested in financial stocks that we judged to be more undervalued.

We have five new holdings. We bought positions in the technology leader Cisco Systems, pharmaceutical company GlaxoSmithKline, and brokerage firms Merrill Lynch and Morgan Stanley. Our purchase rationale for each is provided on our website, Oakmark.com. We also received shares of Liberty Media Entertainment (LMDIA - $23) when it was spun-off to holders of Liberty Capital. We believed Liberty Capital was undervalued prior to the spin-off, and now we believe that both Liberty Capital and Liberty Entertainment are attractive. Liberty Entertainment's most important asset is its 41% stake in DirecTV (DTV - $25). DirecTV is the leading provider of satellite TV service in the U.S. Each share of Liberty Entertainment effectively owns about seven-eighths of a DirecTV share. Liberty currently trades for just the market value of its DirecTV, before giving any credit to its ownership of Starz/Encore, its regional sports channels, or the net cash on its balance sheet. We believe that combining Liberty Entertainment and DirecTV would be synergistic, and if it happens, Liberty's value would increase and its discount would be eliminated.

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com | | Kevin G. Grant, CFA

Portfolio Manager

oakmx@oakmark.com | |

|

March 31, 2008

THE OAKMARK FUND

8

THE OAKMARK FUND

Schedule of Investments—March 31, 2008 (Unaudited)

| Name | | Shares Held | | Market Value | |

| Common Stocks—94.9% | |

| Apparel Retail—1.9% | |

| Limited Brands | | | 4,628,047 | | | $ | 79,139,603 | | |

| Broadcasting & Cable TV—4.7% | |

| Liberty Media Corp. - Entertainment (a) | | | 3,798,680 | | | $ | 86,002,115 | | |

| Comcast Corporation, Class A | | | 4,000,000 | | | | 75,880,000 | | |

| Discovery Holding Company, Class A (a) | | | 1,540,140 | | | | 32,681,771 | | |

| | | | 194,563,886 | | |

| Catalog Retail—1.4% | |

| Liberty Media Holding Corporation - Interactive, Class A (a) | | | 3,699,850 | | | $ | 59,715,579 | | |

| Computer & Electronics Retail—2.4% | |

| Best Buy Co., Inc. | | | 2,419,400 | | | $ | 100,308,324 | | |

| Department Stores—2.2% | |

| Kohl's Corporation (a) | | | 2,076,900 | | | $ | 89,078,241 | | |

| Home Improvement Retail—2.2% | |

| The Home Depot, Inc. | | | 3,181,500 | | | $ | 88,986,555 | | |

| Household Appliances—2.2% | |

| The Black & Decker Corporation | | | 1,350,000 | | | $ | 89,235,000 | | |

| Housewares & Specialties—2.3% | |

| Fortune Brands, Inc. | | | 1,350,000 | | | $ | 93,825,000 | | |

| Motorcycle Manufacturers—1.8% | |

| Harley-Davidson, Inc. | | | 2,000,000 | | | $ | 75,000,000 | | |

| Movies & Entertainment—7.6% | |

| Viacom, Inc., Class B (a) | | | 2,839,745 | | | $ | 112,510,697 | | |

| The Walt Disney Company | | | 3,300,000 | | | | 103,554,000 | | |

| Time Warner, Inc. | | | 7,147,700 | | | | 100,210,754 | | |

| | | | 316,275,451 | | |

| Restaurants—5.9% | |

| Yum! Brands, Inc. | | | 3,864,000 | | | $ | 143,779,440 | | |

| McDonald's Corporation | | | 1,794,000 | | | | 100,051,380 | | |

| | | | 243,830,820 | | |

| Specialized Consumer Services—2.7% | |

| H&R Block, Inc. | | | 5,358,600 | | | $ | 111,244,536 | | |

THE OAKMARK FUND

9

THE OAKMARK FUND

Schedule of Investments—March 31, 2008 (Unaudited) cont.

| Name | | Shares Held | | Market Value | |

| Common Stocks—94.9% (cont.) | |

| Brewers—4.3% | |

| InBev NV (b) | | | 1,000,000 | | | $ | 87,999,457 | | |

| Anheuser-Busch Companies, Inc. | | | 1,850,000 | | | | 87,782,500 | | |

| | | | 175,781,957 | | |

| Distillers & Vintners—2.0% | |

| Diageo Plc (c) | | | 1,021,000 | | | $ | 83,027,720 | | |

| Hypermarkets & Super Centers—2.5% | |

| Wal-Mart Stores, Inc. | | | 2,000,000 | | | $ | 105,360,000 | | |

| Packaged Foods & Meats—4.5% | |

| General Mills, Inc. | | | 1,556,000 | | | $ | 93,173,280 | | |

| H.J. Heinz Company | | | 1,950,000 | | | | 91,591,500 | | |

| | | | 184,764,780 | | |

| Integrated Oil & Gas—0.9% | |

| ConocoPhillips | | | 500,373 | | | $ | 38,133,426 | | |

| Asset Management & Custody Banks—1.9% | |

| Bank of New York Mellon Corporation | | | 1,839,630 | | | $ | 76,767,760 | | |

| Consumer Finance—2.5% | |

| Capital One Financial Corporation | | | 2,128,000 | | | $ | 104,740,160 | | |

| Diversified Banks—2.1% | |

| U.S. Bancorp | | | 2,650,000 | | | $ | 85,754,000 | | |

| Investment Banking & Brokerage—2.1% | |

| Morgan Stanley | | | 1,100,000 | | | $ | 50,270,000 | | |

| Merrill Lynch & Co., Inc. | | | 900,000 | | | | 36,666,000 | | |

| | | | 86,936,000 | | |

| Life & Health Insurance—0.7% | |

| AFLAC Incorporated | | | 467,000 | | | $ | 30,331,650 | | |

| Multi-Sector Holdings—0.4% | |

| Liberty Media Holding Corporation - Capital, Class A (a) | | | 949,670 | | | $ | 14,947,806 | | |

| Other Diversified Financial Services—4.1% | |

| JPMorgan Chase & Co. | | | 2,400,000 | | | $ | 103,080,000 | | |

| Citigroup, Inc. | | | 3,100,000 | | | | 66,402,000 | | |

| | | | 169,482,000 | | |

| Thrifts & Mortgage Finance—1.6% | |

| Washington Mutual, Inc. | | | 6,637,300 | | | $ | 68,364,190 | | |

THE OAKMARK FUND

10

THE OAKMARK FUND

Schedule of Investments—March 31, 2008 (Unaudited) cont.

| Name | | Shares Held | | Market Value | |

| Common Stocks—94.9% (cont.) | |

| Health Care Equipment—2.8% | |

| Medtronic, Inc. | | | 1,850,000 | | | $ | 89,484,500 | | |

| Covidien Limited | | | 639,500 | | | | 28,297,875 | | |

| | | | 117,782,375 | | |

| Pharmaceuticals—5.4% | |

| GlaxoSmithKline plc (c) | | | 2,000,000 | | | $ | 84,860,000 | | |

| Bristol-Myers Squibb Company | | | 3,600,000 | | | | 76,680,000 | | |

| Schering-Plough Corporation | | | 4,260,200 | | | | 61,389,482 | | |

| | | | 222,929,482 | | |

| Air Freight & Logistics—2.2% | |

| FedEx Corp. | | | 950,000 | | | $ | 88,036,500 | | |

| Industrial Conglomerates—1.2% | |

| Tyco International, Ltd. | | | 1,139,500 | | | $ | 50,194,975 | | |

| Communications Equipment—1.2% | |

| Cisco Systems, Inc. (a) | | | 2,000,000 | | | $ | 48,180,000 | | |

| Computer Hardware—5.2% | |

| Dell Inc. (a) | | | 4,100,000 | | | $ | 81,672,000 | | |

| Hewlett-Packard Company | | | 1,725,000 | | | | 78,763,500 | | |

| Sun Microsystems, Inc. (a) | | | 3,442,500 | | | | 53,462,025 | | |

| | | | 213,897,525 | | |

| Data Processing & Outsourced Services—1.3% | |

| Western Union Company | | | 2,575,000 | | | $ | 54,770,250 | | |

| Electronic Manufacturing Services—0.5% | |

| Tyco Electronics, Ltd. | | | 639,500 | | | $ | 21,947,640 | | |

| Office Electronics—1.9% | |

| Xerox Corporation | | | 5,272,400 | | | $ | 78,927,828 | | |

| Semiconductors—4.9% | |

| Texas Instruments Incorporated | | | 3,700,000 | | | $ | 104,599,000 | | |

| Intel Corporation | | | 4,700,000 | | | | 99,546,000 | | |

| | | | 204,145,000 | | |

| Wireless Telecommunication Services—1.4% | |

| Sprint Nextel Corporation | | | 8,903,000 | | | $ | 59,561,071 | | |

| Total Common Stocks (Cost: $3,429,444,244) | | | | | | | 3,925,967,090 | | |

THE OAKMARK FUND

11

THE OAKMARK FUND

Schedule of Investments—March 31, 2008 (Unaudited) cont.

| Name | | Par Value | | Market Value | |

| Short Term Investment—5.1% | |

| Repurchase Agreement—5.1% | |

Fixed Income Clearing Corp. Repurchase Agreement,

2.25% dated 3/31/2008 due 4/1/2008, repurchase price

$211,564,821, collateralized by Federal Home Loan

Mortgage Corp. Bonds, with rates from 3.550% - 7.000%,

with maturities from 2/12/2010 - 9/15/2011, and with an

aggregate market value plus accrued interest of

$112,382,556, and by a Federal National Mortgage

Association Bond, with a rate of 5.125%, with a maturity

of 4/15/2011, and with an aggregate market value plus

accrued interest of $109,750,000 | | $ | 211,551,599 | | | $ | 211,551,599 | | |

| Total Repurchase Agreement (Cost: $211,551,599) | | | | | 211,551,599 | | |

| Total Investments (Cost: $3,640,995,843)—100.0% | | | | $ | 4,137,518,689 | | |

| Other Assets In Excess of Liabilities—0.0% | | | | | 47,988 | | |

| Total Net Assets—100% | | | | $ | 4,137,566,677 | | |

(a) Non income-producing security.

(b) Represents a foreign domiciled corporation.

(c) Represents an American Depositary Receipt.

See accompanying Notes to Financial Statements.

THE OAKMARK FUND

12

THE OAKMARK SELECT FUND

Report from Bill Nygren and Henry Berghoef, Portfolio Managers

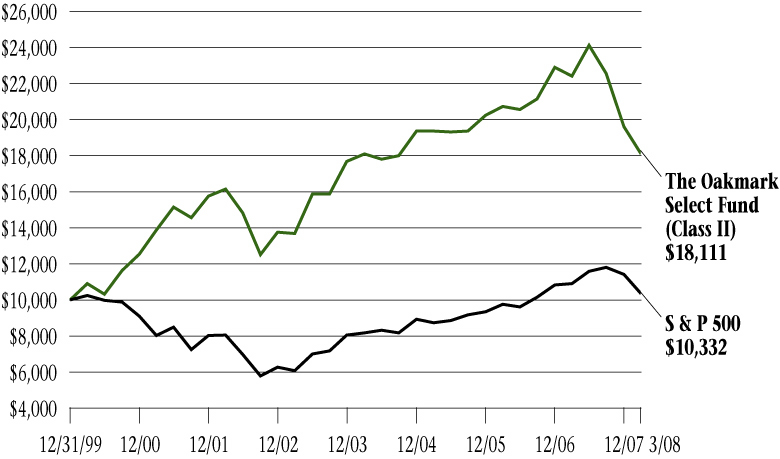

THE VALUE OF A $10,000 INVESTMENT IN THE OAKMARK SELECT FUND FROM ITS INCEPTION (11/1/96) TO PRESENT (3/31/08) AS COMPARED TO THE STANDARD & POOR'S 500 INDEX6 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 3/31/08) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(11/1/96) | |

Oakmark Select Fund

(Class I) | | | -7.62 | % | | | -18.87 | % | | | 6.12 | % | | | 8.11 | % | | | 13.81 | % | |

| S&P 500 | | | -9.44 | % | | | -5.08 | % | | | 11.32 | % | | | 3.50 | % | | | 7.43 | % | |

Lipper Multi-Cap

Value Index10 | | | -10.04 | % | | | -11.70 | % | | | 12.03 | % | | | 4.59 | % | | | 7.79 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Expense Ratio for Class I shares as of 9/30/07 was 0.97%.

The performance data quoted represents past performance. The above performance information for the Fund does not reflect the imposition of a 2% redemption fee on shares held for 90 days or less to deter market timers. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

The Oakmark Select Fund declined 8% last quarter. We take small comfort that the decline was less than the 9% decline in the S&P 500. Our focus is more on absolute returns, and even our relative performance recouped only a fraction of last year's underperformance. Our best performing stocks, both achieving double-digit increases, were H&R Block and Capital One. The market breathed a sigh of relief when Block exited its sub-prime mortgage business without requiring further write-downs. Capital One was a new purchase for the Fund and immediately helped results. The turmoil in the asset-backed debt markets allowed us to purchase it at an attractive price. Our third most positive contributor was another new purchase, Morgan Stanley. Although the stock actually declined fractionally, the quarter-end price was up significantly from both our purchase price and the low it reached following the Bear Stearns take over. On the negative side, Wa shington Mutual was hurt by continued declines in the mortgage market, Discovery Holdings suffered a partial reversal of its strong 2007 performance, and Intel and Dell were part of a weak technology market. For both the positive and negative outliers, we continue to believe these stocks are attractive.

We sold two holdings during the quarter, Dun & Bradstreet and IMS International. D&B was the last of Select's original holdings. Shares we purchased in 1996, adjusted for their Moody's spin-off, had a cost below $10 and were among Select's most successful investments. IMS had been a profitable investment for us. However, operating results were below what we anticipated, and we believed that financial services companies had become more undervalued.

In our last report we noted our belief that many financial stocks had become attractive, but we hadn't added to Washington Mutual because of increased company-specific risk. Our two sales this quarter were non-financial companies, and our two purchases were both financials. We believed, due to unsettled capital markets, that it was prudent to increase the number of financial holdings rather than the weighting of one holding. Because each company has somewhat different exposure, portfolio risk is lowered by spreading our investment across multiple companies. Note that we do not believe that company-specific risk has increased for non-financial businesses, and we are very comfortable with the combined 24% portfolio weighting in our three largest positions, YUM Brands, H&R Block and Discovery Holdings.

William C. Nygren, CFA

Portfolio Manager

oaklx@oakmark.com | | Henry R. Berghoef, CFA

Portfolio Manager

oaklx@oakmark.com | |

|

March 31, 2008

THE OAKMARK SELECT FUND

13

THE OAKMARK SELECT FUND

Schedule of Investments—March 31, 2008 (Unaudited)

| Name | | Shares Held | | Market Value | |

| Common Stocks—94.2% | |

| Apparel Retail—4.6% | |

| Limited Brands | | | 9,180,981 | | | $ | 156,994,775 | | |

| Broadcasting & Cable TV—10.5% | |

| Discovery Holding Company, Class A (a) | | | 10,009,500 | | | $ | 212,401,590 | | |

| Comcast Corporation, Class A | | | 7,600,000 | | | | 144,172,000 | | |

| | | | 356,573,590 | | |

| Catalog Retail—4.9% | |

| Liberty Media Holding Corporation - Interactive, Class A (a) | | | 10,350,000 | | | $ | 167,049,000 | | |

| Home Improvement Retail—3.0% | |

| The Home Depot, Inc. | | | 3,700,000 | | | $ | 103,489,000 | | |

| Movies & Entertainment—9.4% | |

| Viacom, Inc., Class B (a) | | | 4,275,000 | | | $ | 169,375,500 | | |

| Time Warner, Inc. | | | 10,817,000 | | | | 151,654,340 | | |

| | | | 321,029,840 | | |

| Restaurants—12.7% | |

| Yum! Brands, Inc. | | | 7,965,000 | | | $ | 296,377,650 | | |

| McDonald's Corporation | | | 2,428,000 | | | | 135,409,560 | | |

| | | | 431,787,210 | | |

| Specialized Consumer Services—8.7% | |

| H&R Block, Inc. | | | 14,169,600 | | | $ | 294,160,896 | | |

| Consumer Finance—4.0% | |

| Capital One Financial Corporation | | | 2,810,600 | | | $ | 138,337,732 | | |

| Investment Banking & Brokerage—3.9% | |

| Morgan Stanley | | | 2,900,000 | | | $ | 132,530,000 | | |

| Other Diversified Financial Services—4.5% | |

| JPMorgan Chase & Co. | | | 3,544,000 | | | $ | 152,214,800 | | |

| Thrifts & Mortgage Finance—6.2% | |

| Washington Mutual, Inc. | | | 20,417,400 | | | $ | 210,299,220 | | |

| Pharmaceuticals—4.2% | |

| Bristol-Myers Squibb Company | | | 6,760,200 | | | $ | 143,992,260 | | |

| Computer Hardware—4.4% | |

| Dell Inc. (a) | | | 7,513,000 | | | $ | 149,658,960 | | |

THE OAKMARK SELECT FUND

14

THE OAKMARK SELECT FUND

Schedule of Investments—March 31, 2008 (Unaudited) cont.

| Name | | Shares Held/

Par Value | | Market Value | |

| Common Stocks—94.2% (cont.) | |

| Data Processing & Outsourced Services—4.5% | |

| Western Union Company | | | 7,165,400 | | | $ | 152,408,058 | | |

| Office Electronics—4.0% | |

| Xerox Corporation | | | 9,146,400 | | | $ | 136,921,608 | | |

| Semiconductors—4.7% | |

| Intel Corporation | | | 7,447,000 | | | $ | 157,727,460 | | |

| Total Common Stocks (Cost: $2,886,112,825) | | | | | | | 3,205,174,409 | | |

| Short Term Investment—5.4% | |

| Repurchase Agreement—5.4% | |

Fixed Income Clearing Corp. Repurchase Agreement,

2.25% dated 3/31/2008 due 4/1/2008, repurchase price

$183,545,292, collateralized a by Federal Home Loan

Mortgage Corp. Bond, with a rate of 5.500%, with a

maturity of 9/15/2011, and with an aggregate market

value plus accrued interest of $111,912,500, and by a

Federal Home Loan Bank Bond, with a rate of 4.875%,

with a maturity of 10/5/2011, and with an aggregate

market value plus accrued interest of $80,802,075 | | $ | 183,533,821 | | | $ | 183,533,821 | | |

| Total Repurchase Agreement (Cost: $183,533,821) | | | | | | | 183,533,821 | | |

| Total Short Term Investment (Cost: $183,533,821) | | | | | | | 183,533,821 | | |

| Total Investments (Cost: $3,069,646,646)—99.6% | | | | | | $ | 3,388,708,230 | | |

| Other Assets In Excess of Liabilities—0.4% | | | | | | | 14,441,505 | | |

| Total Net Assets—100% | | | | | | $ | 3,403,149,735 | | |

(a) Non income-producing security.

See accompanying Notes to Financial Statements.

THE OAKMARK SELECT FUND

15

THE OAKMARK EQUITY AND INCOME FUND

Report from Clyde S. McGregor and Edward A. Studzinski, Portfolio Managers

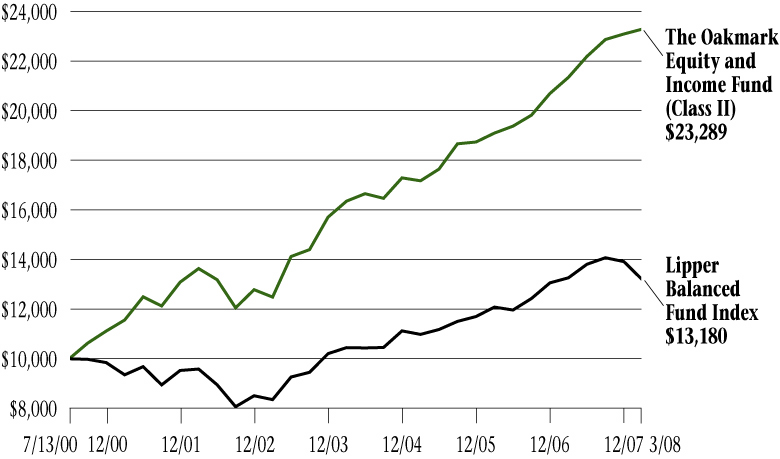

THE VALUE OF A $10,000 INVESTMENT IN THE OAKMARK EQUITY AND INCOME FUND FROM ITS INCEPTION (11/1/95) TO PRESENT (3/31/08) AS COMPARED TO THE LIPPER BALANCED FUND INDEX11 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 3/31/08) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(11/1/95) | |

Oakmark Equity &

Income Fund (Class I) | | | 0.97 | % | | | 9.54 | % | | | 13.62 | % | | | 11.08 | % | | | 13.17 | % | |

Lipper Balanced

Fund Index | | | -5.29 | % | | | -0.64 | % | | | 9.55 | % | | | 4.76 | % | | | 7.44 | % | |

| S&P 5006 | | | -9.44 | % | | | -5.08 | % | | | 11.32 | % | | | 3.50 | % | | | 8.62 | % | |

Lehman Govt./

Corp. Bond12 | | | 2.53 | % | | | 8.35 | % | | | 4.62 | % | | | 6.12 | % | | | 6.30 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Expense Ratio for Class I shares as of 9/30/07 was 0.83%.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

Quarter Review

In a quarter remarkable for its volatility (by one measure the most volatile for equities in seventy years!) the Equity and Income Fund managed to eke out a positive return of 1%. This contrasts to the -5% that Lipper reported for its Balanced Funds Index. For the six-month fiscal year-to-date, the Fund returned 2%, while the Index reported -6%. We are pleased to report returns that best the benchmark in this difficult time period. But more important to us is the generation of positive returns. We know that our co-investors can survive mediocre positive returns, but negative returns—no matter how strong they may be in relative terms—can create actual hardship. This is especially true for the Equity and Income Fund because many investors use the Fund as a complete investment program. As always, we are most happy to report that the compound annualized rate of return since inception for the Fund is 13%.

The lead article in the March 26 edition of the Wall Street Journal was titled "Stocks Tarnished By 'Lost Decade.'"13 E.S. Browning, the author of the piece, described in unpleasant detail the stock market's lack of returns in the new millennium. The article goes further to describe historical market cycles, investing manias, etc. The article's focus on stock market averages is understandable, but misleading from the standpoint of fundamental value investors. We do not invest the Equity and Income Fund in "the market" as represented by indices and averages. Rather, for the equity portion of the Fund, we attempt to take advantage of the stock market's propensity to create a constant flow of undervalued equities even in the most unsavory environment. Since the beginning of 2000, the Equity and Income Fund has produced a compound annualized rate of return of just over 12%. For the past five years, which excludes the Fund's one down year of the decade (2002), the Fund's compound rate of return is 14%. Your managers' job now is to try to figure out how to do the same (or better) in the future.

In terms of equities, our portfolio activity was rather modest in the quarter. We initiated positions in Advanced Medical Optics, Dish Network, Kirby, and Pentair, and we eliminated the holdings of CBS Class A and International Rectifier. Investors often ask us if our investing is thematic. For our new purchases the best theme we can come up with is water: Kirby is an inland waterway barge company and Pentair makes water filters and pumps. Of course, the real theme is value: buying strong, growing businesses that are selling at a discount to their intrinsic value and that have management teams that treat their shareholders as partners. We were more active in the fixed income segment of the portfolio, and we will devote the remainder of the report to that discussion.

THE OAKMARK EQUITY AND INCOME FUND

16

The Airbag

A recent James Altucher column in the Financial Times newspaper was titled "Forget the stock crash—grab an airbag."14 This piece brought back memories of the days when previous Oakmark Funds group Chairman Victor Morgenstern referred to the Equity and Income Fund as "the Oakmark Fund with an airbag." When your writer mentioned Vic's description in an earlier quarterly report, your writer also took pains to explain that the airbag referred to the Fund's fixed income allocation and not the writer/portfolio managers. To this date, few have accepted this explanation.

In any event, the recent quarter helped to illustrate how the fixed income portion of the portfolio can dampen volatility. We began the quarter with roughly 39% of the Fund invested in fixed income investments. U.S. Treasury notes and bonds comprised nearly two-thirds of the 39%. Inflation-indexed Treasury notes were another one-fourth of the fixed income allocation, and government agencies made up nearly all of the rest.

You will note that the Fund did not have any mortgage-backed securities (RMBS, CMO's, CDO's, CDS's, etc.). We have historically avoided investing in the vast array of mortgage-backed securities because of what our industry terms "negative convexity," a term which basically means that in order to win conditions can never change. This idea is simpler than the jargon makes it sound. Think about how mortgages normally work. If a home-owner with a mortgage spies an opportunity to refinance at a desirable (lower) interest rate, he/she will do so and pay off the higher rate mortgage. As an owner of a mortgage-backed security, I would find that my principal was being returned to me prematurely at a time when interest rates had fallen, forcing me to reinvest at a lower rate, which is less desirable to me as a security holder. Conversely, if mortgage interest rates rise, home-owners do not refinance, and I am stuck with an investment that does not yie ld as much as current opportunities.

The past few years have introduced many other reasons for not owning these securities. As is now well known, lending standards declined over the decade. For example, obtaining a mortgage historically required documentation of income and financial assets. As the current decade matured, however, mortgage originators became increasingly lenient. By 2006 low-documentation loans made up almost half of new mortgage originations. Another example of the evolution of lending standards was the emergence of mortgages that did not require down payments. No-down-payment mortgages made up more than one-fourth of 2006 mortgage originations. As long as housing prices continued to climb, a virtuous circle prevailed whereby even mortgages written with the loosest standards could be packaged into securities, taken off the balance sheet of the originator, and sold to investors. Declining home prices, however, broke the circle.

During the housing boom, investment bankers became increasingly creative when constructing new types of securities out of pools of mortgages. Besides negative convexity, your managers have many natural aversions. One such aversion is to complexity. If we cannot explain a potential investment to our clients in a few simple declarative sentences, the investment is probably a bad idea. We also have an aversion to anything that smart salespeople are trying hard to sell to us. Mortgage-backed securities presented us with both complexity and the hard sell, and given our temperament, this made them easy for us to avoid.

While avoiding the pitfalls of mortgage-backed securities, we were active in the fixed income portion of the portfolio. We reestablished a position in Canadian Government debt, which increased overall portfolio yield and allowed us to invest in a country that is benefiting from the current resource boom. We also increased the position in U.S. Treasury inflation-indexed securities, generally called TIPS. We have often written about TIPS, but for the purposes of this report the reader must only understand that TIPS provide returns both through a conventional interest rate coupon and through a periodic adjustment in principal value based on actual inflation. Oddly, all of this activity had no meaningful effect on portfolio duration (a measure of sensitivity to changes in interest rates), while increasing the portfolio's fixed income allocation to 41%.

The bond market's move toward greater risk aversion in the quarter both enhanced the value of our TIPS and created a quandary for your managers. At the nadir for equity investing sentiment in the quarter, the "flight to quality" caused some TIPS prices to reach levels which implied a zero or negative yield—that is, the only investing return would come from the inflation-indexing factor. Yield compression (very low income generation at current bond prices) is probably the single greatest challenge facing the Fund's managers at present. While we will continue to seek out opportunities to enhance portfolio income, we will do so while remembering that the function of the bond portfolio is to be "the airbag" for the portfolio. In closing this section your writer should note that Mr. Altucher's column actually discussed a European company which manufactures airbags.

As always, we thank you for being our shareholders and invite your comments and questions.

Clyde S. McGregor, CFA

Portfolio Manager

oakbx@oakmark.com | | Edward A. Studzinski, CFA

Portfolio Manager

oakbx@oakmark.com | |

|

March 31, 2008

THE OAKMARK EQUITY AND INCOME FUND

17

THE OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2008 (Unaudited)

| Name | | Shares Held | | Market Value | |

| Equity and Equivalents—53.8% | |

| Common Stocks—53.8% | |

| Apparel Retail—1.3% | |

| The TJX Companies, Inc. | | | 2,813,000 | | | $ | 93,025,910 | | |

| Foot Locker, Inc. | | | 7,050,000 | | | | 82,978,500 | | |

| | | | 176,004,410 | | |

| Apparel, Accessories & Luxury Goods—0.1% | |

| Carter's, Inc. (a) | | | 1,033,500 | | | $ | 16,691,025 | | |

| Automobile Manufacturers—0.4% | |

| Thor Industries, Inc. | | | 2,000,000 | | | $ | 59,540,000 | | |

| Broadcasting & Cable TV—3.5% | |

| The E.W. Scripps Company, Class A | | | 6,208,000 | | | $ | 260,798,080 | | |

| DISH Network Corp. (a) | | | 8,002,500 | | | | 229,911,825 | | |

| | | | 490,709,905 | | |

| Home Furnishings—1.2% | |

| Mohawk Industries, Inc. (a) | | | 2,314,100 | | | $ | 165,712,701 | | |

| Movies & Entertainment—1.3% | |

| News Corporation, Class B | | | 9,405,100 | | | $ | 179,073,104 | | |

| Publishing—1.6% | |

| The Washington Post Company, Class B | | | 315,200 | | | $ | 208,504,800 | | |

| Idearc, Inc. | | | 5,200,000 | | | | 18,928,000 | | |

| Primedia, Inc. | | | 572,300 | | | | 4,206,405 | | |

| | | | 231,639,205 | | |

| Brewers—1.4% | |

| InBev NV (b) | | | 2,279,000 | | | $ | 200,550,762 | | |

| Distillers & Vintners—2.3% | |

| Diageo Plc (c) | | | 3,977,000 | | | $ | 323,409,640 | | |

| Drug Retail—3.1% | |

| CVS Caremark Corporation | | | 10,670,000 | | | $ | 432,241,700 | | |

| Packaged Foods & Meats—3.4% | |

| Nestle SA (c) (d) | | | 3,783,000 | | | $ | 472,587,492 | | |

| Personal Products—1.6% | |

| Avon Products, Inc. | | | 5,548,500 | | | $ | 219,387,690 | | |

| Tobacco—1.1% | |

| UST, Inc. | | | 2,969,625 | | | $ | 161,903,955 | | |

THE OAKMARK EQUITY AND INCOME FUND

18

THE OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2008 (Unaudited) cont.

| Name | | Shares Held | | Market Value | |

| Equity and Equivalents—53.8% (cont.) | |

| Oil & Gas Exploration & Production—14.1% | |

| XTO Energy, Inc. | | | 12,805,572 | | | $ | 792,152,684 | | |

| Apache Corporation | | | 3,734,500 | | | | 451,202,290 | | |

| Newfield Exploration Co. (a) (e) | | | 7,203,000 | | | | 380,678,550 | | |

| EnCana Corp. (b) | | | 4,500,000 | | | | 340,875,000 | | |

| | | | 1,964,908,524 | | |

| Property & Casualty Insurance—1.6% | |

| SAFECO Corporation | | | 3,880,000 | | | $ | 170,254,400 | | |

| First American Corporation | | | 1,406,500 | | | | 47,736,610 | | |

| | | | 217,991,010 | | |

| Reinsurance—0.8% | |

| PartnerRe, Ltd. (b) | | | 1,500,000 | | | $ | 114,450,000 | | |

| Health Care Distributors—0.2% | |

| Advanced Medical Optics, Inc. (a) | | | 1,310,090 | | | $ | 26,594,827 | | |

| Health Care Equipment—3.8% | |

| Medtronic, Inc. | | | 6,693,000 | | | $ | 323,740,410 | | |

| Hospira, Inc. (a) | | | 4,850,000 | | | | 207,434,500 | | |

| | | | 531,174,910 | | |

| Health Care Services—0.8% | |

| Express Scripts, Inc. (a) | | | 1,800,000 | | | $ | 115,776,000 | | |

| Life Sciences Tools & Services—0.6% | |

| Varian, Inc. (a) (e) | | | 1,459,400 | | | $ | 84,528,448 | | |

| Aerospace & Defense—5.1% | |

| General Dynamics Corporation | | | 4,559,000 | | | $ | 380,083,830 | | |

| Raytheon Company | | | 3,200,000 | | | | 206,752,000 | | |

| Alliant Techsystems, Inc. (a) | | | 1,285,200 | | | | 133,056,756 | | |

| | | | 719,892,586 | | |

| Industrial Conglomerates—1.1% | |

| Walter Industries, Inc. | | | 2,425,700 | | | $ | 151,921,591 | | |

| Industrial Machinery—2.2% | |

| Ingersoll-Rand Co., Class A | | | 5,111,478 | | | $ | 227,869,689 | | |

| Mueller Water Products, Inc., Class B (e) | | | 6,000,000 | | | | 47,280,000 | | |

| Pentair, Inc. | | | 1,058,142 | | | | 33,754,730 | | |

| | | | 308,904,419 | | |

| Marine—0.1% | |

| Kirby Corporation (a) | | | 150,000 | | | $ | 8,550,000 | | |

THE OAKMARK EQUITY AND INCOME FUND

19

THE OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2008 (Unaudited) cont.

| Name | | Shares Held/

Par Value | | Market Value | |

| Equity and Equivalents—53.8% (cont.) | |

| Application Software—0.2% | |

| Mentor Graphics Corporation (a) | | | 3,189,718 | | | $ | 28,165,210 | | |

| Communications Equipment—0.7% | |

| EchoStar Corp. (a) | | | 3,158,557 | | | $ | 93,303,774 | | |

| Computer Hardware—0.2% | |

| Teradata Corporation (a) | | | 1,557,600 | | | $ | 34,360,656 | | |

| Total Common Stocks (Cost: $5,497,996,430) | | | | | | | 7,529,973,544 | | |

| Total Equity and Equivalents (Cost: $5,497,996,430) | | | | | | | 7,529,973,544 | | |

| Fixed Income—40.5% | |

| Corporate Bonds—0.1% | |

| Paper Packaging—0.1% | |

| Sealed Air Corporation, 144A, 5.625%, due 7/15/2013 (f) | | $ | 19,400,000 | | | $ | 20,281,866 | | |

| Total Corporate Bonds (Cost: $19,552,362) | | | | | | | 20,281,866 | | |

| Government and Agency Securities—40.4% | |

| Canadian Government Bonds—3.0% | |

| Canadian Government, 3.75%, due 6/1/2012 | | CAD | 250,000,000 | | | $ | 251,546,593 | | |

| Canadian Government, 4.25%, due 9/1/2008 | | CAD | 125,000,000 | | | | 122,661,844 | | |

| Canadian Government, 4.25%, due 9/1/2009 | | CAD | 50,000,000 | | | | 49,796,385 | | |

| | | | 424,004,822 | | |

| France Government Bonds—0.5% | |

France Government, 3.00%, due 7/25/2012,

Inflation Indexed | | EUR | 44,099,692 | | | $ | 74,433,238 | | |

| U.S. Government Agencies—4.1% | |

| Federal Farm Credit Bank, 2.489%, due 2/22/2012 (g) | | | 97,000,000 | | | $ | 96,727,236 | | |

| Tennessee Valley Authority, 6.79%, due 5/23/2012 | | | 58,730,000 | | | | 66,552,073 | | |

| Federal Farm Credit Bank, 2.25%, due 7/1/2010 | | | 50,000,000 | | | | 49,880,500 | | |

Federal National Mortgage Association, 5.00%,

due 10/15/2010 | | | 48,500,000 | | | | 49,176,575 | | |

Federal National Mortgage Association, 5.30%,

due 8/6/2009 | | | 48,500,000 | | | | 48,947,994 | | |

| Federal Home Loan Bank, 4.75%, due 12/12/2014 | | | 25,000,000 | | | | 26,583,925 | | |

| Federal Home Loan Bank, 3.50%, due 11/3/2009 | | | 25,000,000 | | | | 25,475,400 | | |

| Federal Home Loan Bank, 4.50%, due 6/9/2010 | | | 24,250,000 | | | | 25,364,675 | | |

Federal Home Loan Mortgage Corp., 5.05%,

due 10/15/2010 | | | 24,250,000 | | | | 24,593,428 | | |

THE OAKMARK EQUITY AND INCOME FUND

20

THE OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2008 (Unaudited) cont.

| Name | | Par Value | | Market Value | |

| Fixed Income—40.5% (cont.) | |

| U.S. Government Agencies—4.1% (cont.) | |

| Federal Farm Credit Bank, 4.92%, due 1/11/2010 | | $ | 19,400,000 | | | $ | 20,299,656 | | |

| Federal Home Loan Bank, 4.50%, due 5/12/2010 | | | 14,550,000 | | | | 15,205,492 | | |

| Federal National Mortgage Association, 5.75%, due 6/9/2011 | | | 14,140,000 | | | | 14,220,018 | | |

| Federal Farm Credit Bank, 5.15%, due 7/20/2009 | | | 10,216,000 | | | | 10,594,779 | | |

| Federal Farm Credit Bank, 5.25%, due 7/16/2010 | | | 9,700,000 | | | | 10,317,715 | | |

| Federal Home Loan Bank, 4.54%, due 7/6/2010 | | | 9,700,000 | | | | 10,163,088 | | |

| Tennessee Valley Authority, 5.625%, due 1/18/2011 | | | 8,721,000 | | | | 9,410,430 | | |

| Federal Farm Credit Bank, 5.28%, due 8/16/2013 | | | 7,500,000 | | | | 8,182,043 | | |

| Federal Farm Credit Bank, 4.85%, due 12/16/2009 | | | 6,305,000 | | | | 6,570,794 | | |

| Federal Farm Credit Bank, 5.125%, due 6/6/2011 | | | 5,435,000 | | | | 5,818,787 | | |

| Federal Home Loan Bank, 5.25%, due 9/12/2014 | | | 5,000,000 | | | | 5,460,125 | | |

| Federal Farm Credit Bank, 5.10%, due 8/9/2011 | | | 4,850,000 | | | | 5,203,812 | | |

| Federal Farm Credit Bank, 4.75%, due 5/7/2010 | | | 4,850,000 | | | | 5,092,141 | | |

| Federal Home Loan Bank, 4.75%, due 12/11/2009 | | | 4,850,000 | | | | 5,049,675 | | |

| Federal Farm Credit Bank, 4.90%, due 9/2/2009 | | | 4,850,000 | | | | 5,029,916 | | |

| Federal Farm Credit Bank, 4.125%, due 7/17/2009 | | | 4,850,000 | | | | 4,965,580 | | |

| Federal Farm Credit Bank, 2.534%, due 7/29/2009 (g) | | | 4,850,000 | | | | 4,848,118 | | |

| Federal Farm Credit Bank, 4.85%, due 3/9/2011 | | | 4,322,000 | | | | 4,578,831 | | |

| Federal Farm Credit Bank, 5.05%, due 5/25/2011 | | | 3,880,000 | | | | 4,143,157 | | |

| Federal Farm Credit Bank, 4.50%, due 8/8/2011 | | | 2,910,000 | | | | 3,043,537 | | |

| Federal Farm Credit Bank, 4.82%, due 10/12/2012 | | | 2,425,000 | | | | 2,590,967 | | |

| | | | 574,090,467 | | |

| U.S. Government Bonds—4.1% | |

U.S. Treasury Bond, 2.375%, due 4/15/2011,

Inflation Indexed | | $ | 531,640,000 | | | $ | 571,180,725 | | |

| U.S. Government Notes—28.7% | |

United States Treasury Notes, 0.875%, due 4/15/2010,

Inflation Indexed | | $ | 556,508,691 | | | $ | 569,508,178 | | |

United States Treasury Notes, 2.00%, due 4/15/2012,

Inflation Indexed | | | 519,551,982 | | | | 559,370,965 | | |

| United States Treasury Notes, 4.875%, due 2/15/2012 | | | 485,000,000 | | | | 534,977,795 | | |

| United States Treasury Notes, 5.125%, due 6/30/2011 | | | 485,000,000 | | | | 533,992,760 | | |

| United States Treasury Notes, 4.875%, due 5/15/2009 | | | 477,500,000 | | | | 494,958,355 | | |

| United States Treasury Notes, 5.125%, due 5/15/2016 | | | 250,000,000 | | | | 284,804,750 | | |

| United States Treasury Notes, 5.00%, due 8/15/2011 | | | 242,500,000 | | | | 266,731,085 | | |

| United States Treasury Notes, 4.75%, due 3/31/2011 | | | 242,500,000 | | | | 263,112,500 | | |

| United States Treasury Notes, 4.00%, due 4/15/2010 | | | 242,500,000 | | | | 253,980,920 | | |

| United States Treasury Notes, 4.875%, due 8/15/2009 | | | 242,500,000 | | | | 253,374,670 | | |

| | | | 4,014,811,978 | | |

THE OAKMARK EQUITY AND INCOME FUND

21

THE OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2008 (Unaudited) cont.

| Name | | Par Value | | Market Value | |

| Fixed Income—40.5% (cont.) | |

| U.S. Government Notes—28.7% (cont.) | |

Total Government and Agency Securities

(Cost: $5,359,715,540) | | | | | | $ | 5,658,521,230 | | |

| Total Fixed Income (Cost: $5,379,267,902) | | | | | | | 5,678,803,096 | | |

| Short Term Investments—5.1% | |

| U.S. Government Agencies—1.2% | |

Federal National Mortgage Association, 4.12%,

due 4/11/2008 | | $ | 100,000,000 | | | $ | 99,885,555 | | |

| Federal Home Loan Bank, 2.93% - 3.00%, due 3/4/2009 | | | 48,845,000 | | | | 48,845,000 | | |

Federal Agricultural Mortgage Corp., 0.00%,

due 4/22/2008 (h) | | | 10,000,000 | | | | 9,986,350 | | |

| Federal Home Loan Mortgage Corp., 3.56%, due 4/25/2008 | | | 5,000,000 | | | | 5,003,307 | | |

| Federal Home Loan Bank, 0.00%, due 4/18/2008 (h) | | | 5,000,000 | | | | 4,988,125 | | |

| Total U.S. Government Agencies (Cost: $168,708,337) | | | | | | | 168,708,337 | | |

| Repurchase Agreement—3.9% | |

Fixed Income Clearing Corp. Repurchase Agreement,

2.25% dated 3/31/2008 due 4/1/2008, repurchase price

$542,703,747, collateralized by a Federal Home Loan

Bank Bond, with a rate of 4.400%, with a maturity of

5/5/2008, and with an aggregate market value plus

accrued interest of $86,340,600, and by Federal Home

Loan Mortgage Corp. Bonds, with rates of

3.550% - 6.625%, with maturities from

9/15/2009 - 6/27/2016, and with an aggregate market

value plus accrued interest of $202,142,219, and by

Federal National Mortgage Association Bonds, with

rates of 2.750% - 6.375%, with maturities from

6/30/2008 - 1/22/2018, and with an aggregate market

value plus accrued interest of $281,329,994 | | $ | 542,669,830 | | | $ | 542,669,830 | | |

| Total Repurchase Agreement (Cost: $542,669,830) | | | | | | | 542,669,830 | | |

| Total Short Term Investments (Cost: $711,378,167) | | | | | | | 711,378,167 | | |

| Total Investments (Cost: $11,588,642,499)—99.4% | | | | | | $ | 13,920,154,807 | | |

| Other Assets In Excess of Liabilities—0.6% | | | | | | | 81,830,910 | | |

| Total Net Assets—100% | | | | | | $ | 14,001,985,717 | | |

THE OAKMARK EQUITY AND INCOME FUND

22

THE OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2008 (Unaudited) cont.

(a) Non income-producing security.

(b) Represents a foreign domiciled corporation.

(c) Represents an American Depositary Receipt.

(d) Market value is determined in accordance with procedures established in good faith by the Board of Trustees.

(e) See footnote number five in the Notes to the Financial Statements regarding investments in affiliated issuers.

(f) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

(g) Floating Rate Note. Rate shown is as of March 31, 2008.

(h) Zero Coupon Bond.

Key to abbreviations:

CAD: Canadian Dollar

EUR: Euro Dollar

See accompanying Notes to Financial Statements.

THE OAKMARK EQUITY AND INCOME FUND

23

THE OAKMARK GLOBAL FUND

Report from Clyde S. McGregor and Robert A. Taylor, Portfolio Managers

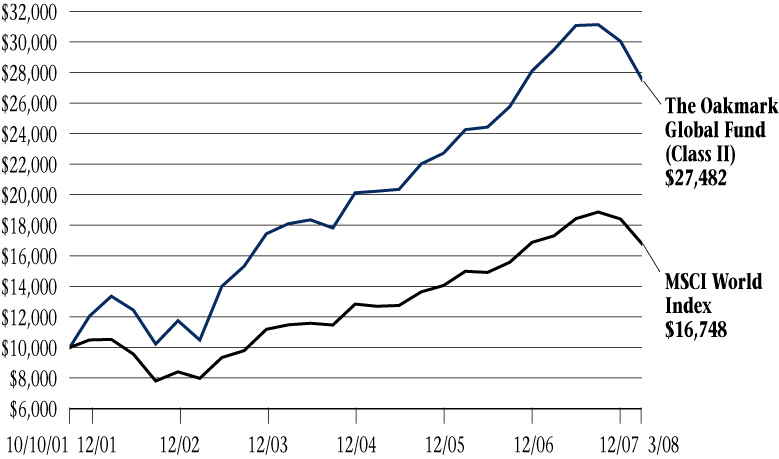

THE VALUE OF A $10,000 INVESTMENT IN THE OAKMARK GLOBAL FUND FROM ITS INCEPTION (8/4/99) TO PRESENT (3/31/08) AS COMPARED TO THE MSCI WORLD INDEX15 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 3/31/08) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | Since

Inception

(8/4/99) | |

| Oakmark Global Fund (Class I) | | | -8.42 | % | | | -6.38 | % | | | 21.63 | % | | | 14.53 | % | |

| MSCI World | | | -9.06 | % | | | -3.25 | % | | | 15.96 | % | | | 3.48 | % | |

| Lipper Global Fund Index16 | | | -8.45 | % | | | -2.43 | % | | | 16.65 | % | | | 5.24 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Expense Ratio for Class I shares as of 9/30/07 was 1.13%.

The performance data quoted represents past performance. The above performance information for the Fund does not reflect the imposition of a 2% redemption fee on shares held for 90 days or less to deter market timers. If reflected, the fee would reduce the performance quoted. Past performance does not guarantee future results. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Average annual total return measures annualized change, while total return measures aggregate change. To obtain most recent month-end performance data, visit oakmark.com.

* Not annualized

Quarter Review

The Oakmark Global Fund registered a decline of 8% for the quarter ended March 31. The MSCI World Index, the benchmark for global funds, lost 9% for the quarter, and the Lipper Global Fund Index, which measures the outcomes of mutual funds similar to Oakmark Global, reported an 8% drop. We are not "benchmark investors," so we derive little satisfaction from returns that are competitive with indices that are probably at best an obscure abstraction to many of our shareholder/partners. Companies with declining stocks varied from Swiss financials to Japanese semiconductor manufacturers to U.S. media concerns. Countries where the Fund enjoyed strong relative performance included the U.S., South Korea, and France, while Switzerland, Japan, and the United Kingdom produced the worst relative outcomes. For the 2008 fiscal year-to-date, returns are also negative with the Fund reporting a drop of 12%, while the MSCI World Index declined 11% and the Lip per Global Fund Index declined 10%.

"Stocks Tarnished by 'Lost Decade' "proclaimed the headline of a March 26 Wall Street Journal article.13 The article, written by E.S. Browning, described in harrowing detail the minimal returns stocks had managed over the past ten years. While written from the perspective of a U.S. investor focused on U.S. stocks, the story is much the same for internationally diversified investors. Beginning January 1, 2000, the MSCI World Index, our usual standard of comparison, has returned a mere 2% per year. We are pleased to be able to report that the Global Fund, despite the recent poor quarter, has returned more than 15% annualized over that same 8.2 5 year period. Expressed in dollar terms, a dollar invested in the Fund as of January 1, 2000, would now be worth $3.24.

All Financials Are Not Created Equal

JPMorgan Chase, helped by emergency funding from the Federal Reserve Bank, is acquiring Bear Stearns. Even after the eye-popping $2/share bid was increased to $10/share, the total amount paid is little more than the value of Bear Stearns's Madison Avenue headquarters. Given this property value, along with a solid prime brokerage business that earned over $500 million in operating profits in 2007, why was Bear Stearns sold for such a cheap price? The answer is liquidity.

While there is no doubt Bear Stearns had troubled assets on its books, the real reason the company needed to be saved was due to a traditional bank run. Hedge fund clients no longer wanted to do prime brokerage business with Bear Stearns, and lenders no longer wanted to extend credit to

THE OAKMARK GLOBAL FUND

24

such a leveraged firm. This net impact resulted in Bear Stearns losing $17 billion in liquidity in a mere two days. Without JPMorgan Chase and the Fed, bankruptcy was highly probable.

Since UBS was the Fund's largest detractor and is, like Bear Stearns, an investment bank, it seemed appropriate to highlight the reasons why UBS is not facing the same issues that affected Bear Stearns:

1. Bear Stearns is heavily involved in investment banking activities, which include prime brokerage, proprietary trading and underwriting—all of which require short-term funding and leverage. These activities comprise 85% of Bear Stearns's revenues, compared to less than 50% of UBS's revenues.

2. Bear Stearns makes very little money from its private banking/asset management franchise. These businesses generate less than 5% of total profits at Bear Stearns compared to over 50% of the profits at UBS. Private banking and asset management businesses require very little capital and generate strong, stable cashflows. These cashflows provide UBS with steady income that it can use for liquidity needs at the investment bank.

3. The Swiss banking regulator is very conservative, requiring banks to maintain some of the highest capital and liquidity ratios in the world.

Investment banks have been negatively affected by the mortgage bubble in the U.S., and the subsequent liquidity crisis has hurt all financial securities. Despite this, the private banking franchise at UBS has yet to be materially harmed. We know this because UBS's private banking continues to attract net inflows. Although we overestimated the value of UBS's investment bank, our assessment of the private bank remains unchanged. Private banking is an excellent business due to its sticky asset base, steady growth and limited capital needs. We are now buying UBS for just the value of the private bank while getting the investment bank, asset management business and Swiss commercial bank for less than zero. Because of this, we continue to hold and add to this position.

Astute followers of our holdings will notice the weight in UBS has decreased since December 31, 2007, while the weight in Credit Suisse has increased. This trade was done to capture the short-term losses incurred in our UBS position while maintaining our exposure to the attractive private banking business. This tax trade is similar to the one done in the Oakmark Global Select portfolio last quarter. This is in line with our strategy to maximize the after-tax returns for our shareholders.