UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-06279 |

|

Harris Associates Investment Trust |

(Exact name of registrant as specified in charter) |

|

Two North La Salle Street, Suite 500 Chicago, Illinois | | 60602-3790 |

(Address of principal executive offices) | | (Zip code) |

|

Kristi L. Rowsell Harris Associates L.P. Two North La Salle Street, #500 Chicago, Illinois 60602 | Paulita A. Pike K&L Gates LLP Three First National Plaza, #3100 Chicago, Illinois 60602 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (312) 621-0600 | |

|

Date of fiscal year end: | 9/30/11 | |

|

Date of reporting period: | 3/31/11 | |

| | | | | | | | | |

Item 1. Reports to Shareholders.

SEMI-ANNUAL REPORT

MARCH 31, 2011

oakmark.com

Advised by Harris Associates L.P.

THE OAKMARK FUNDS

2011 Semi-Annual Report

| President's Letter | | | 1 | | |

|

| Summary Information | | | 2 | | |

|

| Fund Expenses | | | 4 | | |

|

| Commentary on Oakmark and Oakmark Select Funds | | | 6 | | |

|

| Oakmark Fund | |

|

| Letter from the Portfolio Managers | | | 8 | | |

|

| Schedule of Investments | | | 9 | | |

|

| Oakmark Select Fund | |

|

| Letter from the Portfolio Managers | | | 13 | | |

|

| Schedule of Investments | | | 14 | | |

|

| Oakmark Equity and Income Fund | |

|

| Letter from the Portfolio Managers | | | 16 | | |

|

| Schedule of Investments | | | 19 | | |

|

| Oakmark Global Fund | |

|

| Letter from the Portfolio Managers | | | 26 | | |

|

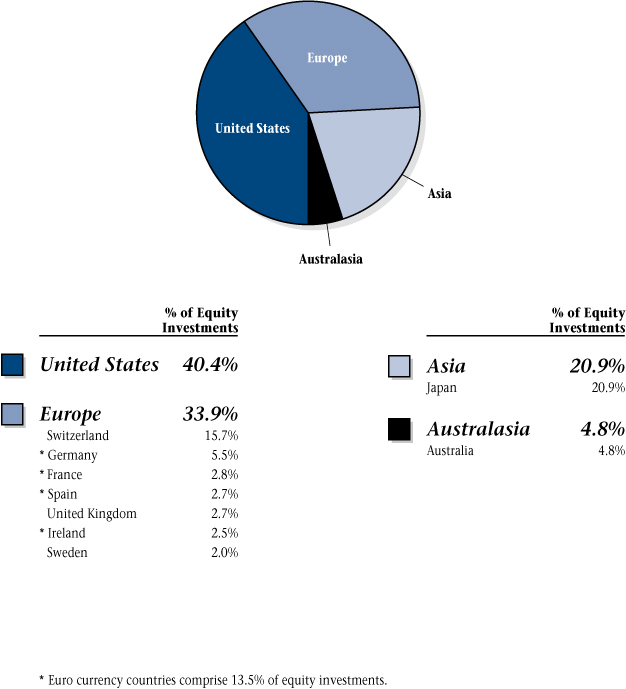

| Global Diversification Chart | | | 29 | | |

|

| Schedule of Investments | | | 30 | | |

|

| Oakmark Global Select Fund | |

|

| Letter from the Portfolio Managers | | | 35 | | |

|

| Global Diversification Chart | | | 37 | | |

|

| Schedule of Investments | | | 38 | | |

|

| Commentary on Oakmark International and International Small Cap Funds | | | 41 | | |

|

| Oakmark International Fund | |

|

| Letter from the Portfolio Managers | | | 43 | | |

|

| Global Diversification Chart | | | 45 | | |

|

| Schedule of Investments | | | 46 | | |

|

| Oakmark International Small Cap Fund | |

|

| Letter from the Portfolio Manager | | | 52 | | |

|

| Global Diversification Chart | | | 54 | | |

|

| Schedule of Investments | | | 55 | | |

|

| Financial Statements | |

|

| Statements of Assets and Liabilities | | | 62 | | |

|

| Statements of Operations | | | 64 | | |

|

| Statements of Changes in Net Assets | | | 66 | | |

|

| Notes to Financial Statements | | | 73 | | |

|

| Financial Highlights | | | 85 | | |

|

| Disclosure Regarding Investment Advisory Contract Approval | | | 93 | | |

|

| Oakmark Glossary | | | 98 | | |

|

| Trustees and Officers | | | 99 | | |

|

FORWARD-LOOKING STATEMENT DISCLOSURE

One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered "forward-looking statements". Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as "estimate", "may", "will", "expect", "believe", "plan" and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

IMPORTANT MESSAGE ABOUT

ELECTRONIC DELIVERY (E-DELIVERY) OF

OAKMARK REPORTS AND PROSPECTUSES

Kindly be advised that you may now sign up to receive email notification of reports and prospectuses at oakmark.com.

To enroll, please log into your account at oakmark.com and click "E-delivery Preferences" under the "My Account" tab.

You will receive notice to your email address that documents are available for viewing at oakmark.com. You will no longer receive paper versions of these documents.

(This page has been intentionally left blank.)

President's Letter

Dear Fellow Shareholders,

The Oakmark Funds posted strong returns this quarter, as the global markets continued their overall recovery. Four of our Funds have fully recovered their losses from the bear markets of 2008 and 2009 and have reached new highs in net asset value per share. Three Funds were within close reach of this mark as of the quarter end. As objective and disciplined investors, we achieved this by identifying what we saw as exceptional opportunities to buy high-quality companies at low valuations during this downturn while others may have stayed on the sidelines. Inflows to equity mutual funds are only now reaching more normal levels. Investors who reacted early should be quite happy.

As our Fund managers point out in their letters, the global macroeconomic environment is rarely tranquil, and current times are no exception. This past quarter was particularly troubled by turmoil in the Middle East and the horror of the earthquake, tsunami and potential nuclear disaster in Japan. Our managers address this situation in their commentaries, and we have also posted several relevant interviews and letters on our website, oakmark.com. We continue to emphasize our belief that superior long-term investment returns are best realized by focusing on a company's fundamentals. Nonetheless we also strive to determine how global events will affect a company's intrinsic business value and whether the market is pricing the company at a discount. Trusting this process requires discipline and patience, but we have found that market turmoil has often played to our strengths. We thank our shareholders for sharing this long-term perspective.

Kudos for Clyde McGregor

In March, Lipper named Clyde McGregor the inaugural winner of its Excellence in Fund Management Award. It is gratifying to see the mutual fund industry recognize what we know, as Oakmark shareholders, is a remarkable and consistent track record of successful investing. Clyde credits his co-managers and the research analysts at Harris Associates who identify—and also debate the merits of—each company in our portfolios. This collaboration between analysts and managers is yet another attribute of great leadership. Clyde is approaching his 30-year anniversary at Harris Associates, and he has served more than 15 years as an Oakmark fund manager. We congratulate him for this well-deserved honor.

E-Delivery of Reports is Available

Oakmark is pleased to announce that we will soon offer electronic delivery of shareholder reports and prospectuses as an alternative to sending booklets by mail. Starting in May, we will invite shareholders to come to Oakmark.com and select this feature for their accounts. When you log on to your account at Oakmark.com, you will see an invitation to register for e-mail notification to retrieve shareholder documents online. If you haven't already secured online access to your account, you may obtain this access by clicking the New User button under Account Access. In addition to the convenience of reviewing materials electronically, this feature will conserve environmental resources and deliver savings to the Funds by reducing print and mail expenses. E-Delivery will also help eliminate the delay that results from printing and mailing these materials. We endeavor to complete our reports as quickly as possible to inform you about your investments, and we hope you take advantage of this new service. We also encourage those who invest with us through financial intermediaries to register for E-Delivery; many intermediaries offer this feature to our clients.

Thank you for your continued investment and confidence in The Oakmark Funds. We welcome your comments and suggestions. You can reach us at ContactOakmark@Oakmark.com.

Kristi L. Rowsell

President of The Oakmark Funds

President of Harris Associates L.P.

March 31, 2011

1

THE OAKMARK FUNDS

Summary Information

Performance for Period

Ended March 31, 20111 | | Oakmark

Fund—Class I

(OAKMX) | | Oakmark

Select Fund—Class I

(OAKLX) | | Oakmark

Equity and Income

Fund—Class I

(OAKBX) | | Oakmark

Global Fund—Class I

(OAKGX) | |

| | 3 Months* | | | | 5.16 | % | | | 6.52 | % | | | 4.69 | % | | | 2.36 | % | |

| | 1 Year | | | | 11.07 | % | | | 13.43 | % | | | 9.49 | % | | | 11.07 | % | |

| Average Annual Total

Return for: | | | | | | | | | | | | | | | | | | |

| | 3 Year | | | | 7.50 | % | | | 8.28 | % | | | 4.48 | % | | | 3.55 | % | |

| | 5 Year | | | | 4.79 | % | | | 2.24 | % | | | 6.97 | % | | | 4.86 | % | |

| | 10 Year | | | | 5.51 | % | | | 5.41 | % | | | 8.87 | % | | | 12.08 | % | |

| | Since inception | | | 12.61%

(8/5/91) | | 12.64%

(11/1/96) | | 11.42%

(11/1/95) | | 11.59%

(8/4/99) | |

| Top Five Equity

Holdings as of

March 31, 20112

Company and % of Total

Net Assets | | | Comcast Corp.,

Class A 2.4%

Texas Instruments,

Inc. 2.2%

TE Connectivity, Ltd. 2.2%

Capital One

Financial Corp. 2.1%

Viacom, Inc.,

Class B 2.1% | | Discovery

Communications Inc.,

Class C 7.9%

TE Connectivity, Ltd. 6.1%

Liberty Media

Holding Corp. -

Interactive, Class A 6.0%

Comcast Corp.,

Class A 5.2%

Texas Instruments,

Inc. 4.9% | | Cenovus Energy, Inc. 4.1%

Nestle SA 3.1%

General Dynamics

Corp. 3.0%

Apache Corp. 2.9%

Diageo PLC 2.5% | | Snap-on, Inc. 4.8%

Oracle Corp. 4.5%

Laboratory Corp. of

America Holdings 4.2%

Daiwa Securities

Group, Inc. 3.8%

Square Enix

Holdings Co., Ltd. 3.5% | |

| Sector

Allocation as of

March 31, 2011

Sector and % of

Long-Term Investments at Fair Value | | | Consumer

Discretionary 26.9%

Information

Technology 24.8%

Financials 14.5%

Health Care 11.7%

Industrials 9.9%

Consumer Staples 7.6%

Energy 4.6% | | Consumer

Discretionary 36.2%

Information

Technology 28.1%

Financials 12.4%

Energy 9.8%

Health Care 8.6%

Utilities 4.9% | | U.S. Government

Securities 24.6%

Industrials 14.9%

Health Care 14.7%

Consumer Staples 13.2%

Energy 11.5%

Consumer

Discretionary 8.1%

Information

Technology 5.8%

Financials 4.0%

Materials 2.9%

Foreign Government

Securities 0.3% | | Information

Technology 34.0%

Industrials 16.8%

Financials 15.4%

Consumer

Discretionary 11.0%

Health Care 9.4%

Materials 5.5%

Consumer Staples 5.3%

Energy 2.6% | |

Past Performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. The performance of the Funds does not reflect the 2% redemption fee imposed on shares redeemed within 90 days of purchase with the exception of The Oakmark Equity & Income Fund which does not impose a redemption fee. To obtain the most recent month-end performance data, visit oakmark.com.

* Not annualized

THE OAKMARK FUNDS

2

Performance for Period

Ended March 31, 20111 | | Oakmark

Global Select

Fund—Class I

(OAKWX) | | Oakmark

International

Fund—Class I

(OAKIX) | | Oakmark

International

Small Cap Fund—Class I

(OAKEX) | |

| | 3 Months* | | | | 5.15 | % | | | 2.27 | % | | | 2.09 | % | |

| | 1 Year | | | | 9.75 | % | | | 12.44 | % | | | 17.73 | % | |

| Average Annual Total

Return for: | | | | | | | | | | | | | | |

| | 3 Year | | | | 10.80 | % | | | 7.16 | % | | | 7.06 | % | |

| | 5 Year | | | | N/A | | | | 5.25 | % | | | 4.51 | % | |

| | 10 Year | | | | N/A | | | | 9.77 | % | | | 13.19 | % | |

| | Since inception | | | 5.86%

(10/2/06) | | 10.91%

(9/30/92) | | 11.37%

(11/1/95) | |

| Top Five Equity

Holdings as of

March 31, 20112

Company and % of Total

Net Assets | | | ROHM Co., Ltd. 6.5%

Toyota Motor Corp. 6.3%

Diageo PLC 5.7%

G4S PLC 5.4%

SAP AG 5.2% | | Daiwa Securities

Group, Inc. 3.5%

Credit Suisse Group 3.3%

ROHM Co., Ltd. 3.0%

Toyota Motor Corp. 3.0%

Canon, Inc. 2.9% | | Julius Baer Group,

Ltd. 3.5%

Square Enix

Holdings Co., Ltd. 3.4%

Hirose Electric Co.,

Ltd. 3.0%

Goodman Fielder,

Ltd. 3.0%

Primary Health

Care, Ltd. 3.0% | |

| Sector

Allocation as of

March 31, 2011

Sector and % of

Long-Term Investments at Fair Value | | | Information

Technology 34.6%

Consumer

Discretionary 20.4%

Financials 14.4%

Consumer Staples 10.7%

Industrials 10.5%

Energy 5.0%

Health Care 4.4% | | Financials 23.3%

Consumer

Discretionary 17.7%

Industrials 17.0%

Consumer Staples 13.7%

Information

Technology 12.1%

Health Care 8.2%

Materials 8.0% | | Industrials 27.0%

Consumer

Discretionary 19.8%

Information

Technology 17.8%

Financials 11.9%

Consumer Staples 9.7%

Materials 8.1%

Health Care 5.7% | |

As of 9/30/10, the expense ratio for Class I shares was 1.11% for Oakmark Fund, 1.08% for Oakmark Select Fund, 0.79% for Oakmark Equity and Income Fund, 1.15% for Oakmark Global Fund, 1.29% for Oakmark Global Select Fund, 1.08% for Oakmark International Fund and 1.38% for Oakmark International Small Cap Fund.

THE OAKMARK FUNDS

3

FUND EXPENSES

A shareholder of each Fund incurs two types of costs: (1) transaction costs, such as redemption fees, and (2) ongoing costs, including investment advisory fees, transfer agent fees and other fund expenses. The examples below are intended to help shareholders understand the ongoing cost (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other funds.

Actual Expenses

The following table provides information about actual account values and actual fund expenses for Class I Shares of each Fund. The table shows the expenses a Class I shareholder would have paid on a $1,000 investment in each Fund from October 1, 2010 to March 31, 2011, as well as how much a $1,000 investment would be worth at the close of the period, assuming actual fund returns and expenses. A Class I shareholder can estimate expenses incurred for the period by dividing the account value at March 31, 2011, by $1,000 and multiplying the result by the number in the Expenses Paid During Period row as shown below.

Shares of all Funds, other than Oakmark Equity and Income Fund, invested for 90 days or less may be charged a 2% redemption fee. Please consult the Funds' prospectus at oakmark.com for more information.

| | | Oakmark Fund | | Oakmark Select Fund | | Oakmark Equity and Income Fund | | Oakmark Global Fund | | Oakmark Global Select Fund | | Oakmark International Fund | | Oakmark International Small Cap Fund | |

Beginning

Account

Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | |

Ending

Account

Value | | $ | 1,139.10 | | | $ | 1,142.80 | | | $ | 1,124.80 | | | $ | 1,133.00 | | | $ | 1,149.40 | | | $ | 1,100.90 | | | $ | 1,133.00 | | |

Expenses

Paid

During

Period* | | $ | 5.60 | | | $ | 5.72 | | | $ | 4.08 | | | $ | 6.01 | | | $ | 6.64 | | | $ | 5.39 | | | $ | 7.18 | | |

Annualized

Expense

Ratio | | | 1.05 | % | | | 1.07 | % | | | 0.77 | % | | | 1.13 | % | | | 1.24 | % | | | 1.03 | % | | | 1.35 | % | |

* Expenses are equal to each Fund's annualized expense ratio for Class I Shares, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year divided by 365 (to reflect the one-half year period).

THE OAKMARK FUNDS

4

Hypothetical Example for Comparison Purposes

The following table provides information about hypothetical account values and hypothetical expenses for Class I Shares of each Fund based on actual expense ratios and an assumed rate of return of 5% per year before expenses, which are not the Funds' actual returns. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses shareholders paid for the period. Shareholders may use this information to compare the ongoing costs of investing in a Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as redemption fees. Therefore, the third line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transaction costs were included, the total costs would have been higher.

| | | Oakmark Fund | | Oakmark Select Fund | | Oakmark Equity and Income Fund | | Oakmark Global Fund | | Oakmark Global Select Fund | | Oakmark International Fund | | Oakmark International Small Cap Fund | |

Beginning

Account

Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | |

Ending

Account

Value | | $ | 1,019.70 | | | $ | 1,019.60 | | | $ | 1,021.09 | | | $ | 1,019.30 | | | $ | 1,018.75 | | | $ | 1,019.80 | | | $ | 1,018.20 | | |

Expenses

Paid

During

Period* | | $ | 5.29 | | | $ | 5.39 | | | $ | 3.88 | | | $ | 5.69 | | | $ | 6.24 | | | $ | 5.19 | | | $ | 6.79 | | |

Annualized

Expense

Ratio | | | 1.05 | % | | | 1.07 | % | | | 0.77 | % | | | 1.13 | % | | | 1.24 | % | | | 1.03 | % | | | 1.35 | % | |

* Expenses are equal to each Fund's annualized expense ratio for Class I Shares, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year divided by 365 (to reflect the one-half year period).

THE OAKMARK FUNDS

5

OAKMARK AND OAKMARK SELECT FUNDS

At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close.

"Making mistakes was acceptable. Failure to learn from them was not."

"Making mistakes was acceptable. Failure to learn from them was not."

- Jonah Keri, The Extra 2%3

I enjoy reading books about successful organizations. I like to see how their methods overlap with ours and the companies we have investments in. I also like seeing what they do differently than we do to get ideas for how we can improve. While we have learned some things from studying other successful investment firms, I find we learn more from comparisons to non-investment companies. And given my non-work interests, I especially enjoy the comparisons to successful sports organizations. Several years ago I wrote about one such book, Moneyball by Michael Lewis, that examined how baseball's Oakland A's had applied a value-investing discipline to their investments in baseball players. Developing a better understanding of how some obscure statistics translated into runs scored allowed a small-market team like the A's to play competitively against teams that had payrolls multiples of their size.

Another successful small-market MLB team, the Tampa Bay Rays, is the subject of Jonah Keri's new book, The Extra 2%—How Wall Street Strategies Took a Major League Baseball Team from Worst to First. The book chronicles events leading up to Tampa Bay getting a major-league team in 1998. It then examines a decade of frustration as Tampa finished in last place in nine of its first 10 seasons. Following the sale of the franchise to new owners, the team went from last place in 2007 to American League champions in 2008, and in 2010 the team again beat the Yankees and Red Sox to win the AL East Division. Though the Rays were not as forthcoming with the baseball particulars that led to their success as the A's had been, I found the comments about organizational management to be especially insightful.

The original owner of the Tampa Bay Rays was a businessman who profited handsomely from leading several successful turnarounds of industrial companies. He made companies run much more efficiently by cutting expenses while boosting productivity. That skill proved less than helpful in launching a baseball team, which is effectively an entertainment company. In the Oakmark Fund we own ITW Industries, an industrial conglomerate. I think the management of ITW is as good as any industrial company management. We also own Discovery Communications, a cable-TV networks company. I think the Discovery management is as good as any management in the entertainment industry. However, if we switched the management teams and put the ITW managers in charge of Discovery and vice-versa, I'm not sure either management would succeed.

At various times, maximizing the value of a company might mean acquiring or disposing of business segments, improving profit margins, boosting sales or maximizing the value of the cash it generates. Often it is some combination. I think the failing of the original Tampa Bay management is a good reminder that when we refer to a company as having "good management," we really mean that we believe the managers have the skills needed for the challenges their specific company faces. For all of our holdings, we have made the judgment that the current management teams are suited to the current needs of each respective business.

After nearly a decade of disappointing results, Tampa Bay's team was sold to—and run by—a trio of ex-Wall Street guys who had no experience in managing professional sports teams. What they did have was an extensive background in statistical analysis. As Keri explains in The Extra 2%: "Sternberg, Silverman, and Friedman made a commitment from the start to track the effectiveness of their decision making. Draft picks would need to be scrutinized several years out, to see how the scouting staff could have done better. Ditto for trades, business partnerships, ticket sales strategies, and other decisions. Making mistakes was acceptable. Failure to learn from those mistakes was not." It is surprising to me how few companies rigorously analyze the results of their past decisions. Through that analysis, good companies can learn from their mistakes and constantly improve their processes. At Oakmark, we try to invest only with managements that we believe will be that self-reflective, and we strive to be equally thoughtful when we review our past investment decisions.

The Rays' new manager, Joe Maddon, was also key to the turnaround. Like his bosses, Maddon was a hard worker and an analyst of statistics. He toiled for 30 years as a minor-league manager and major-league assistant before getting the Rays prize. Given the track record of the Rays to that point, one wondered whether or not it was a prize worth winning. Maddon told the press, "When it comes down to individual effort, it takes absolutely zero talent, zero, to try hard and play hard every day. I'm okay with physical mistakes, with mental mistakes, I'm accepting of all that. The part I'm not accepting of is that part you can

OAKMARK AND OAKMARK SELECT FUNDS

6

control. And that's your effort. You just can't pick and choose when you put your effort out there. It has to be all the time." (I hope the Cubs' new manager demands the same!)

One of the reasons I enjoy comparing baseball to investing is because of their similarities. In baseball, the best teams lose more than a third of their games and endure extended losing streaks. The best hitters generate far more outs than hits. Applying high levels of talent and effort doesn't eliminate all the bad outcomes in baseball. Similar to the Rays, we always expect a high level of effort from our analysts, regardless of how the stock market is behaving. But that alone doesn't guarantee success. I've said before that investing is an endeavor where lack of effort or talent will eventually lead to disappointing results, but even consistently high levels of effort and talent will fail to produce consistently good short-term results. There is no magic formula that allows for winning every day. As I wrote in last quarter's report, despite achieving very good performance in the past decade, the Oakmark Fund either lost money or failed to outperform up markets by more than a percentage point in 80% of the quarters. We know what it's like to play the game hard but still go hitless.

In both baseball and investing, even the best performers experience bad short-term outcomes, and that invites second-guessing. And in both cases, long-term success requires having the discipline to stick with a good process even as it produces bad day-to-day results over a short period. The Rays' EVP of baseball operations, Andrew Friedman, said of the turnaround season, "People ask all the time what our expectations were. We don't get caught up in those things because we are so caught up in process. We believe, with the right process, good things will happen. I felt like we would score more runs than we allowed. What that meant, we weren't really sure." I think I've used almost those same words. "At Oakmark we believe we have a process in place that will result in us choosing more stocks that go up than down, and the magnitude of our winners should exceed that of our losers. What that means for any given quarter, I don't know."

The author Keri writes, "When self-confidence, an even-keeled personality, a nose for analysis, and job security come together, you get coaches and managers willing to make decisions that fly in the face of conventional wisdom." I believe that success in almost any endeavor requires having the freedom to think differently than others do. Like the Rays, we encourage unconventional thinking. "Trust the process," Maddon told himself, "and success will never be a surprise." At Oakmark we strive to maintain an environment where our investment professionals trust our process. Our analysts know that they won't be rewarded or penalized based just on short-term stock price movements, but rather on how well they followed our process. When we make mistakes, we try to identify them as quickly as possible in order to limit their damage and then we go back to see if we can improve our process to reduce the chance of a recurrence.

Just like the Tampa Bay Rays, we strive to get the right investment professionals on our team. We believe that self-confidence and an even-keeled personality are requirements for success in sports and in investing. So is passion. In investing, that passion has to be for analysis. We hire team-oriented individuals, and we especially like team-sports participants who didn't have the talent to fully quench their drive for success through sports. We believe the Oakmark process and our team of analysts give us an important competitive advantage. Several of our analysts compete quite successfully in fantasy baseball and football leagues. Our shareholders are fortunate that those analysts didn't have the talent to play those sports for real.

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

oaklx@oakmark.com

March 31, 2011

OAKMARK AND OAKMARK SELECT FUNDS

7

OAKMARK FUND

Report from Bill Nygren and Kevin Grant, Portfolio Managers

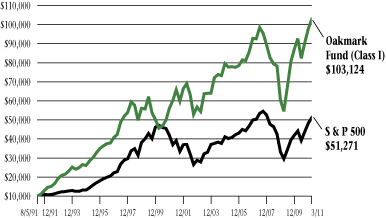

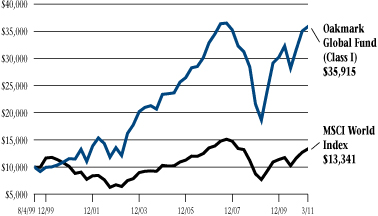

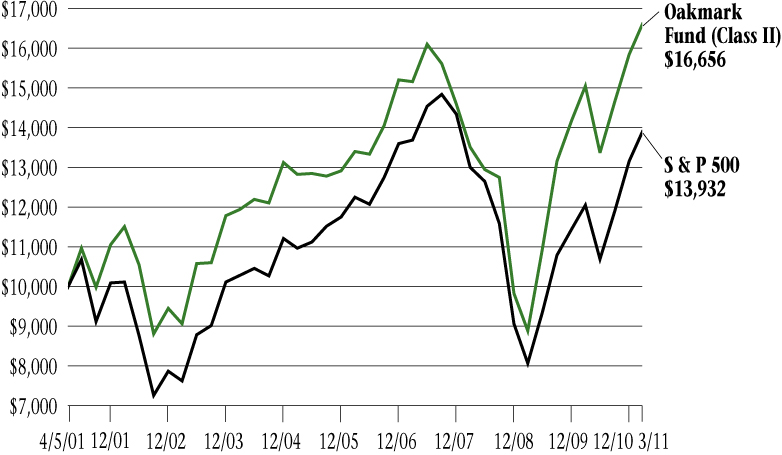

THE VALUE OF A $10,000 INVESTMENT IN OAKMARK FUND FROM ITS INCEPTION (8/5/91) TO PRESENT (3/31/11) AS COMPARED TO THE STANDARD & POOR'S 500 INDEX4 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 3/31/11) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(8/5/91) | |

| Oakmark Fund (Class I) | | | 5.16 | % | | | 11.07 | % | | | 4.79 | % | | | 5.51 | % | | | 12.61 | % | |

| S&P 500 Index | | | 5.92 | % | | | 15.65 | % | | | 2.62 | % | | | 3.29 | % | | | 8.67 | % | |

| Dow Jones Average5 | | | 7.07 | % | | | 16.51 | % | | | 4.87 | % | | | 4.73 | % | | | 10.00 | % | |

Lipper Large Cap

Value Index6 | | | 5.86 | % | | | 13.14 | % | | | 1.80 | % | | | 3.31 | % | | | 8.30 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The expense ratio for Class I shares as of 9/30/10 was 1.11%

Past Performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. The performance of the Fund does not reflect the 2% redemption fee imposed on shares redeemed within 90 days of purchase. To obtain the most recent month-end performance data, visit oakmark.com.

* Not annualized

The Oakmark Fund increased in value by 5% for the three months ended March 31, 2011. Though good as an absolute return, our return slightly trailed the S&P 500 gain of 6%.

The biggest reason we didn't quite keep up with the S&P was the strength of the energy sector. During the quarter, the price of oil increased by 17% (West Texas) or 24% (North Sea Brent), depending on which measure one uses. Commodity businesses, understandably, tend to perform quite well when the commodity they sell experiences such a price spike. For the quarter, the average energy stock increased two to three times as much as the S&P did, and our portfolio wasn't as heavily weighted in those stocks. We don't believe this higher price of oil reflects a long-term market-clearing price and, for that reason, we value oil stocks using an assumption that oil prices will fall. In our valuations, most oil companies are priced less attractively than other businesses are, and we are comfortable continuing to own just the few we have.

Returns of individual stocks in the portfolio followed the typical pattern for successful quarters—more winners than losers, and gains of greater magnitude than losses. The Fund had 18 double-digit gains and only two double-digit losses. The biggest losses were suffered by Cisco Systems (-15%) and Best Buy (-16%). Both reported disappointing operating results, and we are revisiting our long-term forecasts. In both cases, we believe that the stocks remain attractive.

On the positive side we had seven stocks that gained more than our largest loser lost: DirecTV (+17%), Viacom (+18%), Cenovus (+19%), EnCana (+19%), Capital One (+22%), Harley Davidson (+23%) and H&R Block (+42%). Block had been one of our weakest stocks in previous quarters, but snapped back nicely as early tax results exceeded expectations and lingering subprime mortgage losses remained trivial.

During the quarter, we neither added any new positions nor eliminated any positions that were owned at the end of 2010. However, we did receive one new security via corporate action: Huntington Ingalls Industries was spun off from Northrop Grumman. Our numbers showed Huntington trading at a substantial premium when comparing its total capitalization (including debt) to the pretax, pre-interest cash flow it generates. For that reason, we sold our shares in Huntington and used the proceeds to increase our Northrop position. In addition to Northrop, we also added substantially to our positions in Unilever, Aflac and FedEx.

Thank you for your continuing support.

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com | | Kevin G. Grant, CFA

Portfolio Manager

oakmx@oakmark.com | |

|

March 31, 2011

OAKMARK FUND

8

OAKMARK FUND

Schedule of Investments—March 31, 2011 (Unaudited)

Name | |

Shares Held | |

Value | |

| Common Stocks—94.7% | |

| Advertising—1.8% | |

| Omnicom Group, Inc. | | | 1,516,254 | | | $ | 74,387,421 | | |

| Aerospace & Defense—3.5% | |

| Northrop Grumman Corp. | | | 1,240,000 | | | | 77,760,400 | | |

| The Boeing Co. | | | 900,000 | | | | 66,537,000 | | |

| | | | 144,297,400 | | |

| Air Freight & Logistics—1.5% | |

| FedEx Corp. | | | 660,000 | | | | 61,743,000 | | |

| Asset Management & Custody Banks—3.6% | |

| State Street Corp. | | | 1,660,000 | | | | 74,600,400 | | |

| Bank of New York Mellon Corp. | | | 2,489,630 | | | | 74,365,248 | | |

| | | | 148,965,648 | | |

| Broadcasting—1.4% | |

| Discovery Communications, Inc., Class C (a) | | | 1,700,140 | | | | 59,861,930 | | |

| Cable & Satellite—4.1% | |

| Comcast Corp., Class A | | | 4,220,000 | | | | 97,988,400 | | |

| DIRECTV, Class A (a) | | | 1,499,155 | | | | 70,160,454 | | |

| | | | 168,148,854 | | |

| Catalog Retail—2.0% | |

| Liberty Media Corp. - Interactive, Class A (a) | | | 5,205,000 | | | | 83,488,200 | | |

| Communications Equipment—1.2% | |

| Cisco Systems, Inc. | | | 2,950,000 | | | | 50,592,500 | | |

| Computer & Electronics Retail—1.5% | |

| Best Buy Co., Inc. | | | 2,110,000 | | | | 60,599,200 | | |

| Computer Hardware—3.7% | |

| Apple, Inc. (a) | | | 220,000 | | | | 76,659,000 | | |

| Dell, Inc. (a) | | | 5,120,000 | | | | 74,291,200 | | |

| | | | 150,950,200 | | |

| Consumer Finance—2.1% | |

| Capital One Financial Corp. | | | 1,694,800 | | | | 88,061,808 | | |

| Data Processing & Outsourced Services—4.8% | |

| MasterCard, Inc., Class A | | | 300,000 | | | | 75,516,000 | | |

| Automatic Data Processing, Inc. | | | 1,275,000 | | | | 65,420,250 | | |

| Western Union Co. | | | 2,690,000 | | | | 55,871,300 | | |

| | | | 196,807,550 | | |

OAKMARK FUND

9

OAKMARK FUND

Schedule of Investments—March 31, 2011 (Unaudited) cont.

Name | |

Shares Held | |

Value | |

| Common Stocks—94.7% (cont.) | |

| Department Stores—1.6% | |

| Kohl's Corp. | | | 1,211,900 | | | $ | 64,279,176 | | |

| Distillers & Vintners—1.7% | |

| Diageo PLC (b) | | | 896,000 | | | | 68,293,120 | | |

| Diversified Banks—1.8% | |

| Wells Fargo & Co. | | | 2,400,000 | | | | 76,080,000 | | |

| Drug Retail—1.9% | |

| Walgreen Co. | | | 1,965,000 | | | | 78,875,100 | | |

| Electronic Manufacturing Services—2.2% | |

| TE Connectivity, Ltd. (c) | | | 2,629,500 | | | | 91,559,190 | | |

| Health Care Equipment—4.9% | |

| Medtronic, Inc. | | | 2,100,000 | | | | 82,635,000 | | |

| Covidien PLC (c) | | | 1,540,000 | | | | 79,987,600 | | |

| Baxter International, Inc. | | | 750,000 | | | | 40,327,500 | | |

| | | | 202,950,100 | | |

| Home Improvement Retail—1.9% | |

| The Home Depot, Inc. | | | 2,131,500 | | | | 78,993,390 | | |

| Housewares & Specialties—1.8% | |

| Fortune Brands, Inc. | | | 1,220,000 | | | | 75,505,800 | | |

| Hypermarkets & Super Centers—1.6% | |

| Wal-Mart Stores, Inc. | | | 1,270,000 | | | | 66,103,500 | | |

| Industrial Conglomerates—3.0% | |

| Tyco International, Ltd. (c) | | | 1,600,000 | | | | 71,632,000 | | |

| 3M Co. | | | 540,000 | | | | 50,490,000 | | |

| | | | 122,122,000 | | |

| Industrial Machinery—1.4% | |

| Illinois Tool Works, Inc. | | | 1,075,000 | | | | 57,749,000 | | |

| Integrated Oil & Gas—3.2% | |

| Cenovus Energy, Inc. (c) | | | 1,930,000 | | | | 76,003,400 | | |

| Exxon Mobil Corp. | | | 660,000 | | | | 55,525,800 | | |

| | | | 131,529,200 | | |

| Internet Software & Services—1.9% | |

| eBay, Inc. (a) | | | 2,540,000 | | | | 78,841,600 | | |

OAKMARK FUND

10

OAKMARK FUND

Schedule of Investments—March 31, 2011 (Unaudited) cont.

Name | |

Shares Held | |

Value | |

| Common Stocks—94.7% (cont.) | |

| Life & Health Insurance—1.5% | |

| Aflac, Inc. | | | 1,200,000 | | | $ | 63,336,000 | | |

| Motorcycle Manufacturers—1.8% | |

| Harley-Davidson, Inc. | | | 1,712,000 | | | | 72,742,880 | | |

| Movies & Entertainment—4.6% | |

| Viacom, Inc., Class B | | | 1,839,745 | | | | 85,584,938 | | |

| Time Warner, Inc. | | | 1,942,566 | | | | 69,349,606 | | |

| The Walt Disney Co. | | | 850,000 | | | | 36,626,500 | | |

| | | | 191,561,044 | | |

| Oil & Gas Exploration & Production—1.1% | |

| Encana Corp. (c) | | | 1,340,000 | | | | 46,270,200 | | |

| Other Diversified Financial Services—2.9% | |

| JPMorgan Chase & Co. | | | 1,630,000 | | | | 75,143,000 | | |

| Bank of America Corp. | | | 3,471,000 | | | | 46,268,430 | | |

| | | | 121,411,430 | | |

| Packaged Foods & Meats—2.0% | |

| Unilever PLC (b) | | | 2,100,000 | | | | 64,302,000 | | |

| H.J. Heinz Co. | | | 400,000 | | | | 19,528,000 | | |

| | | | 83,830,000 | | |

| Pharmaceuticals—6.2% | |

| Bristol-Myers Squibb Co. | | | 2,650,000 | | | | 70,039,500 | | |

| Merck & Co., Inc. | | | 2,071,535 | | | | 68,381,370 | | |

| GlaxoSmithKline PLC (b) | | | 1,565,000 | | | | 60,111,650 | | |

| Johnson & Johnson | | | 980,000 | | | | 58,065,000 | | |

| | | | 256,597,520 | | |

| Property & Casualty Insurance—1.7% | |

| Allstate Corp. | | | 2,200,000 | | | | 69,916,000 | | |

| Restaurants—1.6% | |

| McDonald's Corp. | | | 869,000 | | | | 66,122,210 | | |

| Semiconductor Equipment—2.1% | |

| Applied Materials, Inc. | | | 5,450,000 | | | | 85,129,000 | | |

| Semiconductors—4.1% | |

| Texas Instruments, Inc. | | | 2,650,000 | | | | 91,584,000 | | |

| Intel Corp. | | | 3,850,000 | | | | 77,654,500 | | |

| | | | 169,238,500 | | |

OAKMARK FUND

11

OAKMARK FUND

Schedule of Investments—March 31, 2011 (Unaudited) cont.

Name | | Shares Held/

Par Value | |

Value | |

| Common Stocks—94.7% (cont.) | |

| Specialized Consumer Services—1.4% | |

| H&R Block, Inc. | | | 3,428,600 | | | $ | 57,394,764 | | |

| Systems Software—3.6% | |

| Oracle Corp. | | | 2,450,000 | | | | 81,756,500 | | |

| Microsoft Corp. | | | 2,650,000 | | | | 67,204,000 | | |

| | | | 148,960,500 | | |

| Total Common Stocks (Cost: $2,617,659,879) | | | | $ | 3,913,294,935 | | |

| Short Term Investment—5.4% | |

| Repurchase Agreement—5.4% | |

Fixed Income Clearing Corp. Repurchase Agreement,

0.05% dated 3/31/2011 due 4/1/2011,

repurchase price $221,440,087, collateralized by

a Federal Home Loan Bank Bond, with

a rate of 1.375%, with a maturity of 6/8/2012, and

with a fair value plus accrued interest of $96,425,000,

and by Federal Home Loan Mortgage Corp. Bonds,

with rates from 1.750% - 5.125%, with maturities

from 6/15/2012 - 7/15/2012 and with an aggregate

fair value plus accrued interest of $87,946,688 and by

a Federal National Mortgage Association Bond,

with a rate of 0.500%, with a maturity of 10/30/2012,

and with a fair value plus accrued interest of $17,478,125,

and by a United States Treasury Note, with a rate of

0.750%, with a maturity of 5/31/2012, and with a

fair value plus accrued interest of $24,024,219

(Cost: $221,439,779) | | $ | 221,439,779 | | | | 221,439,779 | | |

| Total Short Term Investment (Cost: $221,439,779) | | | | $ | 221,439,779 | | |

| Total Investments (Cost: $2,839,099,658)—100.1% | | | | | 4,134,734,714 | | |

| Liabilities In Excess Of Other Assets—(0.1)% | | | | | (2,980,714 | ) | |

| Total Net Assets—100% | | | | $ | 4,131,754,000 | | |

(a) Non-income producing security.

(b) Represents a Sponsored American Depositary Receipt.

(c) Represents a foreign domiciled corporation.

See accompanying Notes to Financial Statements.

OAKMARK FUND

12

OAKMARK SELECT FUND

Report from Bill Nygren and Henry Berghoef, Portfolio Managers

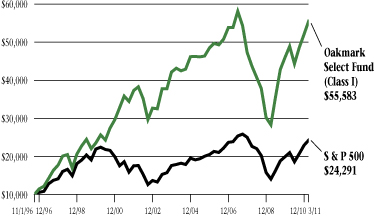

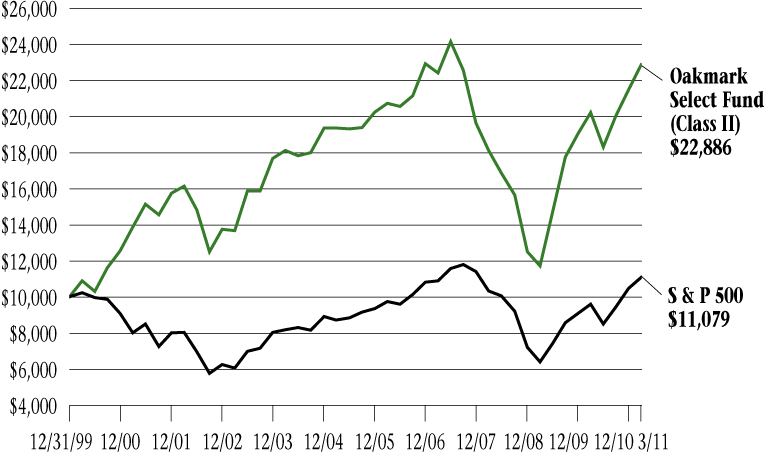

THE VALUE OF A $10,000 INVESTMENT IN OAKMARK SELECT FUND FROM ITS INCEPTION (11/1/96) TO PRESENT (3/31/11) AS COMPARED TO THE STANDARD & POOR'S 500 INDEX4 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 3/31/11) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(11/1/96) | |

Oakmark Select Fund

(Class I) | | | 6.52 | % | | | 13.43 | % | | | 2.24 | % | | | 5.41 | % | | | 12.64 | % | |

| S&P 500 Index | | | 5.92 | % | | | 15.65 | % | | | 2.62 | % | | | 3.29 | % | | | 6.35 | % | |

Lipper Multi-Cap

Value Index7 | | | 6.95 | % | | | 15.37 | % | | | 1.27 | % | | | 4.53 | % | | | 6.66 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The expense ratio for Class I shares as of 9/30/10 was 1.08%

Past Performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. The performance of the Fund does not reflect the 2% redemption fee imposed on shares redeemed within 90 days of purchase. To obtain the most recent month-end performance data, visit oakmark.com.

* Not annualized

The Oakmark Select Fund increased in value by 7% for the quarter ended March 31, 2011. That was a good return for just three months, and it also exceeded the 6% return achieved by the S&P 500.

Fourteen of the Fund's holdings increased by more than 5%, and only one lost that much. Best Buy was that one, falling 16% after also being one of our poor performers in the prior quarter. The company has strung together several months of disappointing sales. The bulls believe that the stock, now selling at eight to nine times projected earnings (compared to about 13 times for the S&P 500), has gone from undervalued to greatly undervalued. The bears believe Best Buy is a disadvantaged competitor to Wal-Mart and Amazon. We agree with the bulls and believe that even if Best Buy loses market share, it can use excess capital to repurchase shares, which would allow the company to achieve above-average per-share earnings growth.

On the positive side of the portfolio, we had five stocks that gained more than Best Buy lost: DirecTV (+17%), Calpine and Cenovus (+19% each), Capital One (+22%) and the best performer, H&R Block (+42%).

Block has appeared on our "Biggest Loser" list several times in the past year, but unlike the TV show, that's not the goal. Investors have been concerned about lingering liabilities from the Option One subprime mortgage business that Block shut down in 2007, as well as regulatory efforts to stop refund anticipation loans (RALs) and the growing trend of taxpayers preparing their returns online. We believe that online preparers are largely converts from pen-and-paper preparation, that RALs are a very small part of Block's income, and that the mortgage liabilities are not going to spiral out of control. One of the few positives in acknowledging that one is a subprime lender is that, unlike the so-called prime lenders, the buyers of Block's mortgages can't now come back claiming they were shocked to discover the loans were indeed subprime. During the quarter, Block reported good early-season tax results and also reported another quarter of relatively small mortgage losses. We think Block's new management is doing a terrific job.

During the quarter, we sold our Western Union shares to fund a purchase of MasterCard. We believe MasterCard, which has been achieving strong revenue and earnings growth, will continue to benefit from the global trend in spending toward using plastic instead of paper.

William C. Nygren, CFA

Portfolio Manager

oaklx@oakmark.com | | Henry R. Berghoef, CFA

Portfolio Manager

oaklx@oakmark.com | |

|

March 31, 2011

OAKMARK SELECT FUND

13

OAKMARK SELECT FUND

Schedule of Investments—March 31, 2011 (Unaudited)

Name | |

Shares Held | |

Value | |

| Common Stocks—95.0% | |

| Broadcasting—7.9% | |

| Discovery Communications, Inc., Class C (a) | | | 6,009,500 | | | $ | 211,594,495 | | |

| Cable & Satellite—9.2% | |

| Comcast Corp., Class A | | | 5,950,000 | | | | 138,159,000 | | |

| DIRECTV, Class A (a) | | | 2,297,949 | | | | 107,544,014 | | |

| | | | 245,703,014 | | |

| Catalog Retail—6.0% | |

| Liberty Media Corp. - Interactive, Class A (a) | | | 10,000,000 | | | | 160,400,000 | | |

| Computer & Electronics Retail—3.2% | |

| Best Buy Co., Inc. | | | 3,000,000 | | | | 86,160,000 | | |

| Computer Hardware—3.9% | |

| Dell, Inc. (a) | | | 7,113,000 | | | | 103,209,630 | | |

| Consumer Finance—4.4% | |

| Capital One Financial Corp. | | | 2,250,000 | | | | 116,910,000 | | |

| Data Processing & Outsourced Services—3.8% | |

| MasterCard, Inc., Class A | | | 400,000 | | | | 100,688,000 | | |

| Electronic Manufacturing Services—6.1% | |

| TE Connectivity, Ltd. (b) | | | 4,667,838 | | | | 162,534,119 | | |

| Health Care Equipment—4.1% | |

| Medtronic, Inc. | | | 2,800,000 | | | | 110,180,000 | | |

| Independent Power Producers & Energy Traders—4.7% | |

| Calpine Corp. (a) | | | 7,854,600 | | | | 124,652,502 | | |

| Integrated Oil & Gas—4.8% | |

| Cenovus Energy, Inc. (b) | | | 3,224,800 | | | | 126,992,624 | | |

| Internet Software & Services—4.2% | |

| eBay, Inc. (a) | | | 3,650,000 | | | | 113,296,000 | | |

| Movies & Entertainment—4.0% | |

| Time Warner, Inc. | | | 2,960,666 | | | | 105,695,776 | | |

| Oil & Gas Exploration & Production—4.5% | |

| Newfield Exploration Co. (a) | | | 1,580,000 | | | | 120,095,800 | | |

OAKMARK SELECT FUND

14

OAKMARK SELECT FUND

Schedule of Investments—March 31, 2011 (Unaudited) cont.

Name | | Shares Held/

Par Value | |

Value | |

| Common Stocks—95.0% (cont.) | |

| Other Diversified Financial Services—7.4% | |

| JPMorgan Chase & Co. | | | 2,494,000 | | | $ | 114,973,400 | | |

| Bank of America Corp. | | | 6,195,100 | | | | 82,580,683 | | |

| | | | 197,554,083 | | |

| Pharmaceuticals—4.1% | |

| Bristol-Myers Squibb Co. | | | 4,110,200 | | | | 108,632,586 | | |

| Semiconductors—8.7% | |

| Texas Instruments, Inc. | | | 3,800,000 | | | | 131,328,000 | | |

| Intel Corp. | | | 5,047,000 | | | | 101,797,990 | | |

| | | | 233,125,990 | | |

| Specialized Consumer Services—4.0% | |

| H&R Block, Inc. | | | 6,469,600 | | | | 108,301,104 | | |

| Total Common Stocks (Cost: $1,769,044,490) | | | | $ | 2,535,725,723 | | |

| Short Term Investment—4.4% | |

| Repurchase Agreement—4.4% | |

Fixed Income Clearing Corp. Repurchase

Agreement, 0.05% dated 3/31/2011 due 4/1/2011,

repurchase price $117,210,898, collateralized by

a Federal Home Loan Mortgage Corp. Bond, with

a rate of 4.500%, with a maturity of 7/15/2013,

and with a fair value plus accrued interest

of $119,558,106, (Cost: $117,210,735) | | $ | 117,210,735 | | | | 117,210,735 | | |

| Total Short Term Investment (Cost: $117,210,735) | | | | $ | 117,210,735 | | |

| Total Investments (Cost: $1,886,255,225)—99.4% | | | | | 2,652,936,458 | | |

| Other Assets In Excess Of Liabilities—0.6% | | | | | 16,068,287 | | |

| Total Net Assets—100% | | | | $ | 2,669,004,745 | | |

(a) Non-income producing security.

(b) Represents a foreign domiciled corporation.

See accompanying Notes to Financial Statements.

OAKMARK SELECT FUND

15

OAKMARK EQUITY AND INCOME FUND

Report from Clyde S. McGregor and Edward A. Studzinski, Portfolio Managers

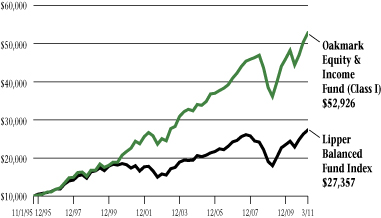

THE VALUE OF A $10,000 INVESTMENT IN OAKMARK EQUITY AND INCOME FUND FROM ITS INCEPTION (11/1/95) TO PRESENT (3/31/11) AS COMPARED TO THE LIPPER BALANCED FUND INDEX8 (UNAUDITED)

| | | | | Average Annual Total Returns

(as of 3/31/11) | |

| (Unaudited) | | Total Return

Last 3 Months* | | 1-year | | 5-year | | 10-year | | Since

Inception

(11/1/95) | |

Oakmark Equity &

Income Fund (Class I) | | | 4.69 | % | | | 9.49 | % | | | 6.97 | % | | | 8.87 | % | | | 11.42 | % | |

Lipper Balanced

Fund Index | | | 3.90 | % | | | 11.96 | % | | | 4.04 | % | | | 4.64 | % | | | 6.75 | % | |

| S&P 500 Index4 | | | 5.92 | % | | | 15.65 | % | | | 2.62 | % | | | 3.29 | % | | | 7.37 | % | |

Barclays Capital

U.S. Govt./Credit9 | | | 0.28 | % | | | 5.26 | % | | | 5.83 | % | | | 5.53 | % | | | 6.02 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

The expense ratio for Class I shares as of 9/30/10 was 0.79%

Past Performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance data, visit oakmark.com.

* Not annualized

Quarter Review

We are happy to report a return to the Equity and Income Fund in the March quarter almost identical to that which we reported last year at this time. Similar to one year ago, the Fund's 5% return slightly bested the 4% number that Lipper Analytics reported for its Balanced Fund Index. Once again, the Fund's equities provided the bulk of the return, gaining nearly 7% in the period. Fixed-income investments recorded positive but minimal returns. For the first six months of the Fund's fiscal year, the comparative numbers are 12% for the Fund and 10% for the Lipper Balanced Fund Index. Always of greatest importance is the comparison for the annualized rates of return since the Fund's inception in 1995: 11% for the Fund versus 7% for the Lipper Balanced Fund Index.

It is somewhat curious that investment outcomes have been so similar for the first quarters of the past two years. The problems that we highlighted in our letter to shareholders one year ago still persist, in particular the financial distress in countries on the European periphery (Portugal, Ireland, Greece and Spain). And, of course, all readers will be well aware of the March quarter's world-changing events. Despite the world's tragedies and problems, many businesses continue to add value, and increasing stock prices reflect this reality.

The recent quarter's leading contributors to the Fund's return were Cenovus Energy, Rockwell Automation, Concho Resources, United Health and ITT. While this is a more eclectic winner's list than often emerges, the one commonality is that two of the top three contributors are oil/gas exploration and development concerns. This probably does not surprise anyone who has purchased gasoline recently. As we have often written, when we buy shares of a commodity producer, we attempt to do so at a share price that gives us free optionality. What this means is that we wish to own the company's shares at a valuation that would be attractive if the price of the commodity it produces never changed from the moment of our purchase. The markets occasionally afford us such opportunities, and they often prove to be rewarding for our shareholders (examples of this include the Fund's previous history with Burlington Resources and XTO Energy).

Cenovus is one of the leading participants in what is probably the largest petrocarbon resource deposit located in a friendly, stable country. Extracting oil from Alberta, Canada's oil sands is expensive, so Cenovus' shares generally benefit more from rising oil prices than most other energy producers. In contrast, Concho Resources concentrates on exploiting old fields in the continental U.S. Techniques used decades ago in oil/gas exploration could only remove a modest percentage of the underground resource. Today's techniques allow for additional oil/gas recovery with considerably lessened dry-hole risk.

OAKMARK EQUITY AND INCOME FUND

16

Leaving energy, Rockwell Automation, which manufactures devices such as variable-speed motor controls and programmable logic controllers, and ITT, a diversified manufacturer of products for the water and defense industries, both appear to have benefited from the renaissance in U.S. industrial production. Finally, United Health's shares have risen as investors appear to be reassessing last year's health-care legislation. We always state that we will consider investing in any legal industry as long as the valuation opportunity is compelling. Heretofore we had avoided the managed-care industry, but share-price declines in the sector and uncertainty from 2010's health-care bill offered an attractive entry point for purchasing United Health shares.

The quarter's largest detractors were Cisco Systems, Microsoft, Nestle, Boston Scientific and Scripps Network Interactive. We clearly have covered ourselves with something other than glory with our investments in large-capitalization technology companies. Cisco continues to suffer profit-margin erosion because of price pressure from newly invigorated competitors. Microsoft's problems appear to be more strategic, and we exited the stock. The actual price declines for Nestle, Boston Scientific and Scripps were modest. The earthquakes in New Zealand and Japan have increased volatility in the shares of PartnerRe, a Bermuda-based reinsurance company. While the company will likely have to make significant payouts to its clients, the long-term impact on business value is less clear.

We kept the Fund's equity allocation fairly constant in the quarter, but we continued to reduce the fixed-income allocation. The biggest change was a reduction in inflation-indexed securities (TIPS), which resulted when we did not replace a significant January maturity. The fixed-income duration remained flat at just over two years, meaning that this portion of the portfolio should have little sensitivity to interest-rate movement. We continue to believe that fixed-income investments are riskier than normal. Some readers may be familiar with Pimco's Bill Gross and his critique of U.S. Treasury issues. We agree with Gross that unless entitlement spending patterns change substantially, the long-term outlook for government debt is unpleasant. Accordingly, we have oriented the Fund to an above-normal equity allocation and a below-normal fixed-income commitment.

Transaction Activity

Although we kept the equity allocation fairly constant during the quarter, we were quite active overall. We eliminated eight holdings, initiated two new positions and added to holdings that began the quarter with small position sizes.

Beginning with the sales, we have already discussed Microsoft, and Del Monte was bought out during the quarter. Diebold, Kirby, Rockwell Collins and Weight Watchers International either exceeded, met or approached our sell targets. We sold Unilever (Great Britain shares) to reduce the Fund's sensitivity to commodity prices. We sold Covidien to reduce our large weighting in health care. These holdings were all profitable for the Fund. Weight Watchers was a particularly outstanding holding, more than doubling in price in only one year's time.

Our two new purchases were Pepsico and Range Resources. Pepsico is probably well-known to most shareholders, although the fact that the company is more of a food business (Frito-Lay) than a beverage business is often overlooked. Sluggish beverage growth in North America has helped to constrain the share price for the past year. Rising commodity prices have also reduced investor enthusiasm for the company. We believe that the share price more than discounts the headwinds facing Pepsico. We also like what we view as management's shareholder-friendly orientation. Range Resources is an exploration and production company focused on natural gas, mostly in Appalachia and the Southwestern U.S. In our opinion, Range's operating and finding costs are well below average, and the company shows rapid growth in production as well as proven reserves. We believe that at our purchase price, the stock traded at a substantial discount to the company's asset value net of debt.

Risk On/Risk Off?

The Equity and Income Fund's managers have both worked in the investment industry for many decades, so we both should be at the point in our careers where dubious financial-industry innovations no longer surprise us. Such an assumption, however, would be incorrect.

For the past few quarters we have repeatedly read that the daily outcomes in the securities markets are the result of the "Risk On/Risk Off" trade, wherein investors (sic?) react to the most recent news by buying equities/selling bonds (Risk On) or the reverse (Risk Off). As value investors we think this is pure nonsense. A single day's events and data rarely affect the ability of a business to generate free-cash flow over the long term, and it is that sustained free-cash flow that we deem most important for investments. That said, we believe it is advantageous for us to have these Risk On/Risk Off traders in the market. They treat equities like commodities, using stocks to express a short-term belief about the market. It appears that their security selections have no foundation in fundamental business value. They are more than happy to sell when stocks are cheap or buy when they are expensive, as long as they can express their near-term market opinion. It is this sort of market action that makes it possible for value investors like us to prosper. If stock prices perfectly predicted the value of every business, value investors would be unemployed, so let's hear it for the Risk On/Risk Off trade!

The recent quarter has certainly demonstrated just how dangerous the world can be, and shareholders have expressed interest in the portfolio effects from these events. Turning first to the Middle East and North Africa, our work suggests that the portfolio has had little direct exposure to the turmoil there. One possible exception is our stake in Apache, the diversified energy company that has significant investments in western Egypt. However, this area has not seen any disruption to date. The widespread efforts to effect government change have also caused oil prices to increase. While a negative for economic activity in total, rising oil prices have helped the Fund's six energy-industry investments.

OAKMARK EQUITY AND INCOME FUND

17

In contrast, the impact from Japan's great earthquake will be felt across more companies and industries. The first Fund holding to disclose a problem was Texas Instruments, which has several Japanese factories. The company estimates that it could take approximately six months for its operations to return to normal there. We have already mentioned PartnerRe, the reinsurance company, in the opening section. TE Connectivity, the new name for Tyco Electronics, expects some setbacks in its sales pattern, especially in relation to the automotive industry. No doubt other companies will soon make similar announcements. We do not expect the cumulative economic effects from these events to significantly change our understanding of these companies' intrinsic values. We do send our best wishes and hopes for all who have been or remain in harm's way and look forward to more peaceful times.

We thank our shareholders for entrusting us with their assets. As always, we invite your questions and comments.

Clyde S. McGregor, CFA

Portfolio Manager

oakbx@oakmark.com | | Edward A. Studzinski, CFA

Portfolio Manager

oakbx@oakmark.com | |

|

March 31, 2011

OAKMARK EQUITY AND INCOME FUND

18

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2011 (Unaudited)

Name | |

Shares Held | |

Value | |

| Common Stocks—67.9% | |

| Aerospace & Defense—9.6% | |

| General Dynamics Corp. | | | 8,100,000 | | | $ | 620,136,000 | | |

| ITT Corp. | | | 8,000,000 | | | | 480,400,000 | | |

| L-3 Communications Holdings, Inc. | | | 5,400,000 | | | | 422,874,000 | | |

| Goodrich Corp. | | | 4,293,700 | | | | 367,240,161 | | |

| Teledyne Technologies, Inc. (a) | | | 1,097,314 | | | | 56,742,107 | | |

| | | | 1,947,392,268 | | |

| Apparel Retail—1.8% | |

| The TJX Cos., Inc. | | | 6,000,000 | | | | 298,380,000 | | |

| Foot Locker, Inc. | | | 3,000,000 | | | | 59,160,000 | | |

| | | | 357,540,000 | | |

| Application Software—0.2% | |

| Mentor Graphics Corp. (a) | | | 3,173,749 | | | | 46,431,948 | | |

| Broadcasting—1.7% | |

| Scripps Networks Interactive, Inc., Class A | | | 7,000,000 | | | | 350,630,000 | | |

| Catalog Retail—0.1% | |

| HSN, Inc. (a) | | | 724,470 | | | | 23,204,774 | | |

| Communications Equipment—0.7% | |

| Cisco Systems, Inc. | | | 8,100,000 | | | | 138,915,000 | | |

| Arris Group, Inc. (a) | | | 552,700 | | | | 7,041,398 | | |

| | | | 145,956,398 | | |

| Construction Materials—0.5% | |

| Martin Marietta Materials, Inc. | | | 1,215,528 | | | | 108,996,396 | | |

| Data Processing & Outsourced Services—1.8% | |

| MasterCard, Inc., Class A | | | 796,358 | | | | 200,459,236 | | |

| Broadridge Financial Solutions, Inc. (b) | | | 6,900,000 | | | | 156,561,000 | | |

| | | | 357,020,236 | | |

| Distillers & Vintners—2.5% | |

| Diageo PLC (c) | | | 6,665,100 | | | | 508,013,922 | | |

| Diversified Metals & Mining—2.0% | |

| Walter Energy, Inc. (b) | | | 3,000,000 | | | | 406,290,000 | | |

| Drug Retail—1.4% | |

| CVS Caremark Corp. | | | 8,500,000 | | | | 291,720,000 | | |

| Electrical Components & Equipment—1.7% | |

| Rockwell Automation Inc. | | | 3,609,600 | | | | 341,648,640 | | |

OAKMARK EQUITY AND INCOME FUND

19

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2011 (Unaudited) cont.

Name | |

Shares Held | |

Value | |

| Common Stocks—67.9% (cont.) | |

| Electronic Manufacturing Services—0.8% | |

| TE Connectivity, Ltd. (d) | | | 4,444,202 | | | $ | 154,747,113 | | |

| Health Care Distributors—0.1% | |

| PharMerica Corp. (a) (b) | | | 1,810,000 | | | | 20,706,400 | | |

| Health Care Equipment—7.7% | |

| Hospira, Inc. (a) | | | 8,000,000 | | | | 441,600,000 | | |

| Varian Medical Systems, Inc. (a) | | | 5,700,000 | | | | 385,548,000 | | |

| Boston Scientific Corp. (a) | | | 42,073,500 | | | | 302,508,465 | | |

| CR Bard, Inc. | | | 1,990,241 | | | | 197,650,834 | | |

| Kinetic Concepts, Inc. (a) | | | 2,500,000 | | | | 136,050,000 | | |

| Steris Corp. | | | 2,873,300 | | | | 99,243,782 | | |

| | | | 1,562,601,081 | | |

| Health Care Services—2.7% | |

| Laboratory Corp. of America Holdings (a) | | | 4,935,000 | | | | 454,661,550 | | |

| Omnicare, Inc. | | | 3,400,000 | | | | 101,966,000 | | |

| | | | 556,627,550 | | |

| Home Furnishings—0.9% | |

| Mohawk Industries, Inc. (a) | | | 2,500,000 | | | | 152,875,000 | | |

| Leggett & Platt, Inc. | | | 1,327,656 | | | | 32,527,572 | | |

| | | | 185,402,572 | | |

| Home Improvement Retail—2.1% | |

| The Home Depot, Inc. | | | 11,500,000 | | | | 426,190,000 | | |

| Industrial Machinery—2.2% | |

| Flowserve Corp. | | | 2,200,000 | | | | 283,360,000 | | |

| Pentair, Inc. | | | 4,200,000 | | | | 158,718,000 | | |

| | | | 442,078,000 | | |

| Integrated Oil & Gas—4.1% | |

| Cenovus Energy, Inc. (d) | | | 21,100,000 | | | | 830,918,000 | | |

| Life Sciences Tools & Services—0.4% | |

| PerkinElmer, Inc. | | | 3,500,000 | | | | 91,945,000 | | |

| Managed Health Care—2.2% | |

| UnitedHealth Group, Inc. | | | 10,000,000 | | | | 452,000,000 | | |

| Mortgage REITs—0.1% | |

| Walter Investment Management Corp. | | | 1,035,000 | | | | 16,694,550 | | |

| Office Services & Supplies—0.1% | |

| Mine Safety Appliances Co. | | | 300,000 | | | | 11,001,000 | | |

OAKMARK EQUITY AND INCOME FUND

20

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2011 (Unaudited) cont.

Name | | Shares Held/

Par Value | |

Value | |

| Common Stocks—67.9% (cont.) | |

| Oil & Gas Drilling—0.4% | |

| Patterson-UTI Energy, Inc. | | | 2,600,000 | | | $ | 76,414,000 | | |

| Oil & Gas Exploration & Production—6.0% | |

| Apache Corp. | | | 4,530,000 | | | | 593,067,600 | | |

| Concho Resources, Inc. (a) | | | 3,750,000 | | | | 402,375,000 | | |

| Range Resources Corp. | | | 2,480,000 | | | | 144,980,800 | | |

| Ultra Petroleum Corp. (a) | | | 1,775,000 | | | | 87,418,750 | | |

| | | | 1,227,842,150 | | |

| Packaged Foods & Meats—5.2% | |

| Nestle SA (c) (e) | | | 10,905,500 | | | | 625,125,071 | | |

| Sara Lee Corp. | | | 24,500,000 | | | | 432,915,000 | | |

| | | | 1,058,040,071 | | |

| Reinsurance—1.5% | |

| PartnerRe, Ltd. (b) (d) | | | 3,900,000 | | | | 309,036,000 | | |

| Semiconductors—1.7% | |

| Texas Instruments, Inc. | | | 10,300,000 | | | | 355,968,000 | | |

| Soft Drinks—1.2% | |

| PepsiCo., Inc. | | | 3,932,000 | | | | 253,260,120 | | |

| Specialized Finance—2.0% | |

| CME Group, Inc. | | | 1,323,677 | | | | 399,154,799 | | |

| Specialty Stores—0.8% | |

| Tractor Supply Co. | | | 2,734,600 | | | | 163,693,156 | | |

| Tobacco—1.7% | |

| Philip Morris International, Inc. | | | 5,150,000 | | | | 337,994,500 | | |

| Total Common Stocks (Cost: $9,883,340,823) | | | | $ | 13,817,158,644 | | |

| Fixed Income—23.3% | |

| Asset Backed Securities—0.1% | |

| Airlines—0.1% | |

Delta Air Lines Series 2001-1 Class A-2 Pass Through Trust,

7.111%, due 3/18/2013 | | $ | 14,160,000 | | | $ | 14,584,800 | | |

| Convertible Debt—0.3% | |

| Health Care Equipment—0.3% | |

| Medtronic, Inc., 1.50%, due 4/15/2011 | | | 52,493,000 | | | | 52,493,000 | | |

OAKMARK EQUITY AND INCOME FUND

21

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2011 (Unaudited) cont.

Name | | Par Value | |

Value | |

| Fixed Income—23.3% (cont.) | |

| Corporate Bonds—0.2% | |

| Paper Packaging—0.1% | |

| Sealed Air Corp., 144A, 5.625%, due 7/15/2013 (f) | | $ | 18,740,000 | | | $ | 19,642,631 | | |

| Property & Casualty Insurance—0.0%(g) | |

| OneBeacon US Holdings, Inc., 5.875%, due 5/15/2013 | | | 10,000,000 | | | | 10,750,000 | | |

| Semiconductor Equipment—0.1% | |

| ASML Holding NV, 5.75%, due 6/13/2017 | | EUR | 9,660,000 | | | | 14,377,939 | | |

| Total Corporate Bonds (Cost: $36,262,666) | | | | $ | 44,770,570 | | |

| Government and Agency Securities—22.7% | |

| Canadian Government Bonds—0.2% | |

| Canadian Government Bond, 4.25%, due 12/1/2021 | | CAD | 35,446,000 | | | $ | 49,051,122 | | |

| New Zealand Government Bonds—0.1% | |

New Zealand Government Bond, 6.00%,

due 11/15/2011 | | NZD | 20,000,000 | | | | 15,579,544 | | |

| U.S. Government Agencies—4.2% | |

Federal National Mortgage Association, 0.273%,

due 11/23/2012 (h) | | $ | 100,000,000 | | | | 100,039,600 | | |

Federal Home Loan Mortgage Corp., 0.27%,

due 10/12/2012 (h) | | | 95,400,000 | | | | 95,425,758 | | |

| Federal Farm Credit Bank, 0.144%, due 2/22/2012 (h) | | | 93,700,000 | | | | 93,645,841 | | |

Federal National Mortgage Association, 0.273%,

due 8/23/2012 (h) | | | 80,000,000 | | | | 80,040,480 | | |

| Federal Farm Credit Bank, 0.276%, due 10/12/2012 (h) | | | 78,500,000 | | | | 78,534,226 | | |

| Federal Farm Credit Bank, 0.28%, due 11/5/2012 (h) | | | 50,000,000 | | | | 50,020,900 | | |

| Federal Farm Credit Bank, 0.23%, due 8/20/2012 (h) | | | 47,700,000 | | | | 47,691,176 | | |

| Federal Farm Credit Bank, 0.308%, due 6/26/2013 (h) | | | 42,950,000 | | | | 42,984,360 | | |

| Federal Farm Credit Bank, 0.298%, due 4/26/2013 (h) | | | 42,900,000 | | | | 42,931,832 | | |

| Federal Farm Credit Bank, 3.875%, due 11/13/2012 | | | 38,645,000 | | | | 40,617,402 | | |

| Federal Farm Credit Bank, 0.31%, due 12/6/2013 (h) | | | 28,500,000 | | | | 28,499,145 | | |

Federal Home Loan Mortgage Corp., 0.13%,

due 1/13/2012 (h) | | | 23,850,000 | | | | 23,834,211 | | |

| Federal Farm Credit Bank, 0.266%, due 6/12/2013 (h) | | | 23,720,000 | | | | 23,713,762 | | |

| Federal Farm Credit Bank, 0.294%, due 12/20/2013 (h) | | | 18,500,000 | | | | 18,493,414 | | |

| Federal Home Loan Bank, 1.25%, due 3/30/2015 (i) | | | 12,200,000 | | | | 12,251,972 | | |

| Federal Farm Credit Bank, 0.252%, due 4/12/2012 (h) | | | 11,400,000 | | | | 11,401,835 | | |

| Federal Farm Credit Bank, 3.85%, due 2/11/2015 | | | 9,415,000 | | | | 10,095,563 | | |

OAKMARK EQUITY AND INCOME FUND

22

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2011 (Unaudited) cont.

Name | | Par Value | |

Value | |

| Fixed Income—23.3% (cont.) | |

| U.S. Government Agencies—4.2% (cont.) | |

Federal Home Loan Mortgage Corp., 0.75%,

due 7/29/2013 (i) | | $ | 9,500,000 | | | $ | 9,503,173 | | |

Federal National Mortgage Association, 0.65%,

due 8/16/2013 (i) | | | 9,500,000 | | | | 9,502,736 | | |

Federal National Mortgage Association, 1.25%,

due 8/10/2015 (i) | | | 9,500,000 | | | | 9,480,782 | | |

| Federal Home Loan Bank, 2.00%, due 12/24/2014 (i) | | | 5,500,000 | | | | 5,591,746 | | |

Federal National Mortgage Association, 1.00%,

due 8/25/2015 (i) | | | 5,000,000 | | | | 5,002,175 | | |

Federal National Mortgage Association, 1.00%,

due 8/25/2014 (i) | | | 5,000,000 | | | | 4,971,075 | | |

| Federal Home Loan Bank, 2.00%, due 9/16/2015 (i) | | | 4,700,000 | | | | 4,773,602 | | |

Federal National Mortgage Association, 2.00%,

due 3/30/2016 (i) | | | 4,700,000 | | | | 4,737,581 | | |

| Federal Home Loan Bank, 1.375%, due 9/16/2013 (i) | | | 4,700,000 | | | | 4,720,078 | | |

Federal National Mortgage Association, 2.00%,

due 3/26/2015 (i) | | | 4,600,000 | | | | 4,701,034 | | |

Federal National Mortgage Association, 1.25%,

due 8/6/2015 (i) | | | 4,500,000 | | | | 4,503,515 | | |

| | | | 867,708,974 | | |

| U.S. Government Bonds—0.6% | |

United States Treasury Bond, 2.50%, due 1/15/2029 ,

Inflation Indexed | | | 102,557,000 | | | | 116,169,801 | | |

| U.S. Government Notes—17.6% | |

United States Treasury Note, 1.375%, due 7/15/2018 ,

Inflation Indexed | | | 510,550,000 | | | | 543,616,281 | | |

United States Treasury Note, 1.25%, due 7/15/2020 ,

Inflation Indexed | | | 504,825,000 | | | | 521,349,942 | | |

| United States Treasury Note, 2.875%, due 1/31/2013 | | | 483,005,000 | | | | 502,381,712 | | |

United States Treasury Note, 2.125%, due 1/15/2019 ,

Inflation Indexed | | | 384,588,750 | | | | 429,146,818 | | |

| United States Treasury Note, 1.125%, due 6/15/2013 | | | 250,000,000 | | | | 251,230,000 | | |

| United States Treasury Note, 0.375%, due 8/31/2012 | | | 125,000,000 | | | | 124,790,000 | | |

| United States Treasury Note, 1.50%, due 7/15/2012 | | | 100,000,000 | | | | 101,367,200 | | |

| United States Treasury Note, 1.375%, due 10/15/2012 | | | 100,000,000 | | | | 101,226,600 | | |

| United States Treasury Note, 1.375%, due 11/15/2012 | | | 100,000,000 | | | | 101,226,600 | | |

| United States Treasury Note, 1.375%, due 9/15/2012 | | | 100,000,000 | | | | 101,222,700 | | |

| United States Treasury Note, 1.375%, due 5/15/2012 | | | 100,000,000 | | | | 101,113,300 | | |

| United States Treasury Note, 1.125%, due 12/15/2012 | | | 100,000,000 | | | | 100,789,100 | | |

| United States Treasury Note, 1.00%, due 4/30/2012 | | | 100,000,000 | | | | 100,691,000 | | |

| United States Treasury Note, 1.00%, due 3/31/2012 | | | 100,000,000 | | | | 100,668,000 | | |

OAKMARK EQUITY AND INCOME FUND

23

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2011 (Unaudited) cont.

Name | | Par Value | |

Value | |

| Fixed Income—23.3% (cont.) | |

| U.S. Government Notes—17.6% (cont.) | |

| United States Treasury Note, 1.00%, due 12/31/2011 | | $ | 100,000,000 | | | $ | 100,554,700 | | |

| United States Treasury Note, 0.875%, due 2/29/2012 | | | 100,000,000 | | | | 100,523,000 | | |

| United States Treasury Note, 0.875%, due 1/31/2012 | | | 100,000,000 | | | | 100,496,100 | | |

| United States Treasury Note, 0.625%, due 6/30/2012 | | | 100,000,000 | | | | 100,258,000 | | |

| | | | 3,582,651,053 | | |

Total Government and Agency Securities

(Cost: $4,544,683,700) | | | | $ | 4,631,160,494 | | |

| Total Fixed Income (Cost: $4,648,227,208) | | | | $ | 4,743,008,864 | | |

| Short Term Investments—9.5% | |

| Canadian Treasury Bills—2.9% | |

Canadian Treasury Bills, 1.12% - 1.42%,

due 6/9/2011 - 3/15/2012 (j) (Cost: $570,736,574) | | CAD | 575,000,000 | | | $ | 587,885,250 | | |

| Commercial Paper—1.7% | |

American Honda Finance Corp., 0.22%,

due 5/16/2011 (j) | | $ | 50,000,000 | | | | 49,983,965 | | |

BP Capital Markets PLC 144A, 0.23% - 0.24%,

due 5/27/2011 - 5/31/2011 (f) (j) | | | 66,500,000 | | | | 66,471,238 | | |

| Johnson & Johnson, 144A, 0.17%, due 4/21/2011 (f) (j) | | | 100,000,000 | | | | 99,991,830 | | |

| Toyota Motor Credit Corp., 0.16%, due 4/28/2011 (j) | | | 100,000,000 | | | | 99,988,000 | | |

Wellpoint, Inc. 144A, 0.26% - 0.32%,

due 4/12/2011 - 5/10/2011 (f) (j) | | | 30,000,000 | | | | 29,993,961 | | |

| Total Commercial Paper (Cost: $346,434,129) | | | | | 346,428,994 | | |

| U.S. Government Notes—1.5% | |

United States Treasury Notes, 0.28% - 0.32%,

due 9/30/2011 - 11/30/2011(j) | | | 300,000,000 | | | | 301,210,900 | | |

| Total U.S. Government Notes (Cost: $301,055,835) | | | | | 301,210,900 | | |

OAKMARK EQUITY AND INCOME FUND

24

OAKMARK EQUITY AND INCOME FUND

Schedule of Investments—March 31, 2011 (Unaudited) cont.

Name | | Par Value | |

Value | |

| Short Term Investments—9.5% (cont.) | |

| Repurchase Agreement—3.4% | |

Fixed Income Clearing Corp. Repurchase Agreement,

0.05% dated 3/31/2011 due 4/1/2011, repurchase

price $699,172,225, collateralized by a Federal

Home Loan Bank Bond, with a rate of 1.750%,

with a maturity of 12/14/2012, and with a fair

value plus accrued interest of $306,750,000 and by a

Federal Home Loan Mortgage Corp. Bond, with

a rate of 4.500%, with a maturity of 7/15/2013, and

with a fair value plus accrued interest of $1,672,825 and

by Federal National Mortgage Association Bonds,

with rates from 0.375% - 4.000%, with maturities from

10/30/2012 - 6/24/2013, and with an aggregate fair

value plus accrued interest of $404,733,006

(Cost: $699,171,254) | | $ | 699,171,254 | | | $ | 699,171,254 | | |

| Total Short Term Investments (Cost: $1,917,397,792) | | | | $ | 1,934,696,398 | | |

| Total Investments (Cost: $16,448,965,823)—100.7% | | | | | 20,494,863,906 | | |

| Liabilities In Excess Of Other Assets—(0.7)% | | | | | (136,160,600 | ) | |

| Total Net Assets—100% | | | | $ | 20,358,703,306 | | |

(a) Non-income producing security.

(b) See Note 5 in the Notes to the Financial Statements regarding investments in affiliated issuers.

(c) Represents a Sponsored American Depositary Receipt.

(d) Represents a foreign domiciled corporation.

(e) Fair value is determined in good faith in accordance with procedures established by the Board of Trustees.

(f) See Note 1 in the Notes to Financial Statements regarding restricted securities exempt from registration pursuant to Rule 144A under the Securities Act of 1933. These securities may be resold only in transactions exempt from registration, normally to qualified institutional buyers.

(g) Amount rounds to less than 0.1%

(h) Floating Rate Note. Rate shown is as of March 31, 2011.

(i) Step-Coupon.

(j) The rate shown represents the annualized yield at the time of purchase; not a coupon rate.

Key to abbreviations:

CAD: Canadian Dollar

EUR: Euro

NZD: New Zealand Dollar

See accompanying Notes to Financial Statements.

OAKMARK EQUITY AND INCOME FUND

25

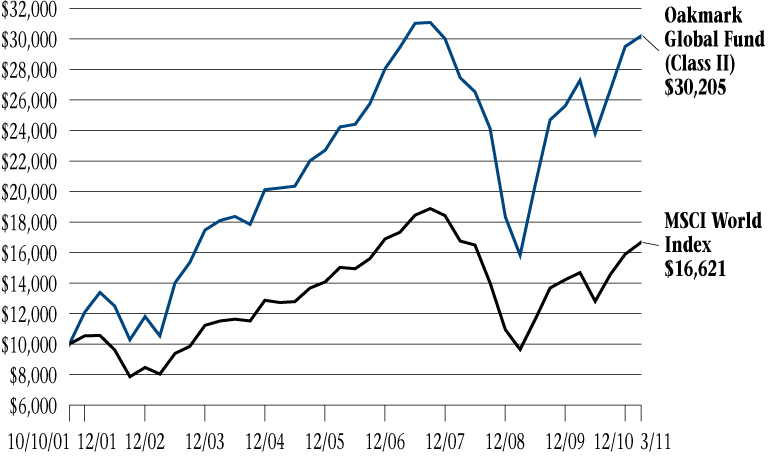

OAKMARK GLOBAL FUND

Report from Clyde S. McGregor and Robert A. Taylor, Portfolio Managers