UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-06279 |

|

Harris Associates Investment Trust |

(Exact name of registrant as specified in charter) |

|

111 South Wacker Drive, Suite 4600 Chicago, Illinois | | 60606-4319 |

(Address of principal executive offices) | | (Zip code) |

|

Kristi L. Rowsell Harris Associates L.P. 111 South Wacker Drive, #4600 Chicago, Illinois 60606 | Alan P. Goldberg K&L Gates LLP Three First National Plaza, #3100 Chicago, Illinois 60602 |

(Name and address of agents for service) |

|

Registrant’s telephone number, including area code: | (312) 646-3600 | |

|

Date of fiscal year end: | 9/30/15 | |

|

Date of reporting period: | 3/31/15 | |

| | | | | | | | | |

Item 1. Reports to Shareholders.

OAKMARK FUNDS

SEMI-ANNUAL REPORT | MARCH 31, 2015

OAKMARK FUND

OAKMARK SELECT FUND

OAKMARK EQUITY AND INCOME FUND

OAKMARK GLOBAL FUND

OAKMARK GLOBAL SELECT FUND

OAKMARK INTERNATIONAL FUND

OAKMARK INTERNATIONAL SMALL CAP FUND

Oakmark Funds

2015 Semi-Annual Report

TABLE OF CONTENTS

Fund Expenses | | | 1 | | |

Commentary on Oakmark and Oakmark Select Funds | | | 2 | | |

Oakmark Fund (OAKMX) | |

Summary Information | | | 4 | | |

Portfolio Manager Commentary | | | 5 | | |

Schedule of Investments | | | 6 | | |

Oakmark Select Fund (OAKLX) | |

Summary Information | | | 8 | | |

Portfolio Manager Commentary | | | 9 | | |

Schedule of Investments | | | 10 | | |

Oakmark Equity and Income Fund (OAKBX) | |

Summary Information | | | 12 | | |

Portfolio Manager Commentary | | | 13 | | |

Schedule of Investments | | | 15 | | |

Oakmark Global Fund (OAKGX) | |

Summary Information | | | 20 | | |

Portfolio Manager Commentary | | | 21 | | |

Schedule of Investments | | | 23 | | |

Oakmark Global Select Fund (OAKWX) | |

Summary Information | | | 26 | | |

Portfolio Manager Commentary | | | 27 | | |

Schedule of Investments | | | 28 | | |

Oakmark International Fund (OAKIX) | |

Summary Information | | | 30 | | |

Portfolio Manager Commentary | | | 31 | | |

Schedule of Investments | | | 32 | | |

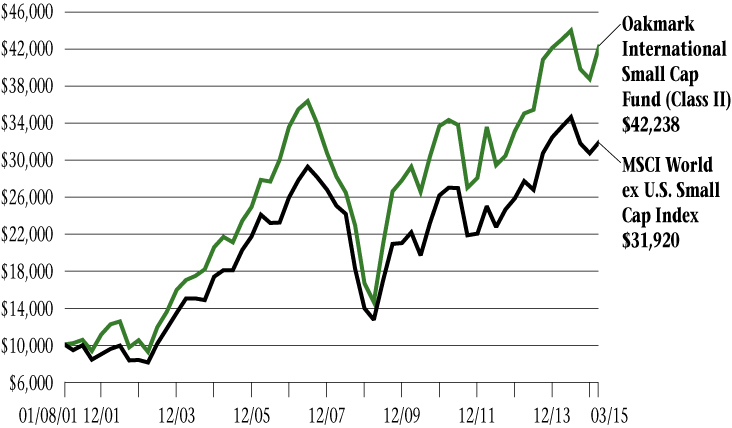

Oakmark International Small Cap Fund (OAKEX) | |

Summary Information | | | 34 | | |

Portfolio Manager Commentary | | | 35 | | |

Schedule of Investments | | | 36 | | |

Financial Statements | |

Statements of Assets and Liabilities | | | 38 | | |

Statements of Operations | | | 40 | | |

Statements of Changes in Net Assets | | | 42 | | |

Notes to Financial Statements | | | 49 | | |

Financial Highlights | | | 65 | | |

Disclosure Regarding Investment Advisory

Contract Approval | | | 72 | | |

Disclosures and Endnotes | | | 74 | | |

Trustees and Officers | | | 75 | | |

FORWARD-LOOKING STATEMENT DISCLOSURE

One of our most important responsibilities as mutual fund managers is to communicate with shareholders in an open and direct manner. Some of our comments in our letters to shareholders are based on current management expectations and are considered "forward-looking statements". Actual future results, however, may prove to be different from our expectations. You can identify forward-looking statements by words such as "estimate", "may", "will", "expect", "believe",

"plan" and other similar terms. We cannot promise future returns. Our opinions are a reflection of our best judgment at the time this report is compiled, and we disclaim any obligation to update or alter forward-looking statements as a result of new information, future events, or otherwise.

OAKMARK FUNDS

Fund Expenses (Unaudited)

A shareholder of each Fund incurs ongoing costs, including investment advisory fees, transfer agent fees and other Fund expenses. The examples below are intended to help shareholders understand the ongoing costs (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other funds.

The following table provides information about actual account values and actual Fund expenses as well as hypothetical account values and hypothetical fund expenses for shares of each Fund.

ACTUAL EXPENSES

The following table shows the expenses a shareholder would have paid on a $1,000 investment in each Fund from October 1, 2014 to March 31, 2015, as well as how much a $1,000 investment would be worth at the close of the period, assuming actual Fund returns and expenses. A shareholder can estimate expenses incurred for the period by dividing the account value at March 31, 2015, by $1,000 and multiplying the result by the number in the "Actual—Expenses Paid During Period" column shown below.

Shares of Oakmark International Small Cap Fund, invested for 90 days or less, may be charged a 2% redemption fee upon redemption. Please consult the Funds' prospectus at oakmark.com for more information.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES

The following table provides information about hypothetical account values and hypothetical expenses for shares of each Fund based on actual expense ratios and an assumed rate of return of 5% per year before expenses, which are not the Funds' actual returns. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or actual expenses shareholders paid for the period. Shareholders may use this information to compare the ongoing costs of investing in a Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs, such as redemption fees. Therefore, the "Hypothetical—Expenses Paid During Period" column of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. If these transaction costs were included, the total costs would have been higher.

| | | | | ACTUAL | | HYPOTHETICAL

(5% annual return

before expenses) | | | |

| | | Beginning

Account Value

(10/1/14) | | Ending

Account Value

(3/31/15) | | Expenses

Paid During

Period* | | Ending

Account Value

(3/31/15) | | Expenses

Paid During

Period* | | Annualized

Expense

Ratio | |

Oakmark Fund | |

Class I | | $ | 1,000.00 | | | $ | 1,030.50 | | | $ | 4.30 | | | $ | 1,020.69 | | | $ | 4.28 | | | | 0.85 | % | |

Class II | | $ | 1,000.00 | | | $ | 1,028.80 | | | $ | 6.07 | | | $ | 1,018.95 | | | $ | 6.04 | | | | 1.20 | % | |

Oakmark Select Fund | |

Class I | | $ | 1,000.00 | | | $ | 1,023.80 | | | $ | 4.79 | | | $ | 1,020.19 | | | $ | 4.78 | | | | 0.95 | % | |

Class II | | $ | 1,000.00 | | | $ | 1,022.30 | | | $ | 6.30 | | | $ | 1,018.70 | | | $ | 6.29 | | | | 1.25 | % | |

Oakmark Equity and Income Fund | |

Class I | | $ | 1,000.00 | | | $ | 1,046.90 | | | $ | 3.83 | | | $ | 1,021.19 | | | $ | 3.78 | | | | 0.75 | % | |

Class II | | $ | 1,000.00 | | | $ | 1,045.00 | | | $ | 5.51 | | | $ | 1,019.55 | | | $ | 5.44 | | | | 1.08 | % | |

Oakmark Global Fund | |

Class I | | $ | 1,000.00 | | | $ | 1,052.40 | | | $ | 5.73 | | | $ | 1,019.35 | | | $ | 5.64 | | | | 1.12 | % | |

Class II | | $ | 1,000.00 | | | $ | 1,050.10 | | | $ | 7.72 | | | $ | 1,017.40 | | | $ | 7.59 | | | | 1.51 | % | |

Oakmark Global Select Fund | |

Class I | | $ | 1,000.00 | | | $ | 1,043.10 | | | $ | 5.81 | | | $ | 1,019.25 | | | $ | 5.74 | | | | 1.14 | % | |

Oakmark International Fund | |

Class I | | $ | 1,000.00 | | | $ | 1,060.30 | | | $ | 4.88 | | | $ | 1,020.19 | | | $ | 4.78 | | | | 0.95 | % | |

Class II | | $ | 1,000.00 | | | $ | 1,058.70 | | | $ | 6.78 | | | $ | 1,018.35 | | | $ | 6.64 | | | | 1.32 | % | |

Oakmark International Small Cap Fund | |

Class I | | $ | 1,000.00 | | | $ | 1,063.10 | | | $ | 6.94 | | | $ | 1,018.20 | | | $ | 6.79 | | | | 1.35 | % | |

Class II | | $ | 1,000.00 | | | $ | 1,060.50 | | | $ | 8.89 | | | $ | 1,016.31 | | | $ | 8.70 | | | | 1.73 | % | |

* Expenses for each share class are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by the number of days in the most recent half-year divided by 365 (to reflect one-half year period)

oakmark.com 1

Oakmark and Oakmark Select Funds March 31, 2015

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close.

"Wall Street never changes, because human nature never changes."

-Jesse Livermore

Indexing is on a winning streak

Active managers had an unusually tough year in 2014. Only 10% of equity mutual funds outperformed the S&P 5001. There was blame assigned to the usual suspects—fund expenses, trading costs, and cash that earned next to nothing. Additionally last year, stocks of global companies headquartered outside the U.S. (think Nestle, Diageo and Unilever), yet owned in many mutual funds, performed much worse than their U.S.-based peers in the S&P 500. Also, some of the largest companies, like Apple and Microsoft, performed very well. Many mutual funds base their position sizes on perceived attractiveness rather than on capitalization, as the S&P 500 does. So even if a mutual fund owned these stocks, as Oakmark did, they likely added more to the performance of the S&P 500 than to the mutual fund's portfolio. All-in-all, the average equity mutual fund returned only 8% last year while the S&P 500 returned 14%. And unfortunately, the Oakmark Fund wasn't in the 10% of funds that performed better than the market.

For most mutual funds, performance wasn't disappointing just in 2014. As investors looked back at three-year performance, the average fund trailed the S&P 500 by seven percentage points, and over a five-year period, that gap increases to nine percentage points. Predictably, this has led many investors to question the rationale for active management, and they have increasingly shifted to index funds. So where does that leave Oakmark, whose Funds are not only active, but are quite concentrated compared to its peers?

For starters, we don't see anything wrong with passive strategies, such as owning index funds. We expect the global economy to achieve good long-term performance, and therefore we expect equities to continue delivering higher long-term returns than most other asset categories. At the same time, we don't see any reason that the investing environment we face today is materially different than what we've faced throughout our history, and our Funds' historical returns speak for themselves.

Why that won't change

How should we define success for active managers? A March article in The New York Times, titled "How Many Mutual Funds Routinely Rout the Market? Zero" defined success as having a top quartile return in each year since the market bottom in March 20092. By that standard, each of the 2,862 mutual funds they studied failed. Though predictable annual outperformance would be the holy grail, is that really the hurdle for claiming an active manager has failed?

Academics believe that risk and return correlate nearly perfectly. In their world, the only way to earn a return greater than the market is to take more risk, and likewise, the consequence of taking less risk than the market is earning a lower return. Were that the case, the only logical conclusion would be to own an index fund and use cash or debt to adjust the risk level to personal preferences. Success in this world—or proving the academics wrong—would be achieving a long-term return higher than the market without taking increased risk—or achieving the market return while reducing risk. What matters is the cumulative long-term return and the risk taken to achieve it, not the ranking in successive annual performance scorecards.

If you summed up the holdings of all active investors (both individual and professional), you'd end up owning the entire market portfolio. So no matter how each investor structures his or her portfolio, the average of active investors will be market performance. This means that net performance, after expenses, has to be worse than the market. That's just the unpleasant fact. No way around it—summing up all the results, as a class, active managers are destined to fail. That's why Vanguard's John Bogle preaches that most investors would be better off not trying to beat the market and instead should just purchase index funds.

Why Oakmark expects to keep winning

The only way investor A can succeed is to trade with investor B, who willingly takes the losing side. Think about that when you evaluate different managers—to succeed, they need to get investors to take the other side of their trades. When a manager says, "We buy growth at a reasonable price," does that mean the investors they sell to are saying, "We buy growth at an unreasonable price"?

At the beginning of each Oakmark commentary is the following statement: "At Oakmark, we are long-term investors. We attempt to identify growing businesses that are managed to benefit their shareholders. We will purchase stock in those businesses only when priced substantially below our estimate of intrinsic value. After purchase, we patiently wait for the gap between stock price and intrinsic value to close."

Are we dependent on finding investors who want to own shrinking businesses managed to the detriment of their shareholders? Of course not. We are generally purchasing stock from investors who appear to have overreacted to negative news that we believe will have little impact on long-term business value. Or if the other investors do share our assessment, they aren't prepared to wait for the stock price to reflect it. Purchasing from a fearful seller at a reduced price allows us the opportunity to earn a higher return and to also reduce our risk. To believe we have a chance to succeed, you must believe that other investors are impatient or emotional. I believe there is a tremendous amount of evidence that throughout history many—if not

2 OAKMARK FUNDS

Oakmark and Oakmark Select Funds March 31, 2015

Portfolio Manager Commentary (continued)

most—investors act emotionally or impatiently. In fact, I'd go so far as to say that's just human nature. In effect, then, our investment approach capitalizes on other investors not being able to suppress human nature. That's why I believe our historical success can be sustained.

As an aside, one might ask why I have such confidence in our long-term prospects when the Oakmark Fund has gained less than the S&P 500 in the past year. The biggest causes of our underperformance have been our heavy ownership of financials, especially banks, which have trailed the S&P 500, and our underweighting of healthcare stocks, many of which have exceeded our estimates of their intrinsic value. To anyone who has followed us, it should come as no surprise that we were early in selling a very strong sector and then used that capital to add to a less popular sector. That's the same thing we've been doing for more than twenty years. And we know from experience, it often doesn't start working immediately.

Why Oakmark concentrates

If you agree that stocks are likely to achieve good long-term returns and that a disciplined investor has the opportunity to outperform, then why concentrate? Again, the academics highlight diversification as a "free good" of which more is always better. That is the logical conclusion stemming from their belief that there is no way to select stocks, adjusting for risk, that will outperform the market. If stock selection can't add value, then concentrating into a smaller number of holdings won't increase expected return, but it will increase risk. And that's bad. Even among active managers, you can see how the "more is better" view of diversification has influenced portfolio construction: the average equity mutual fund holds 121 stocks.

Shortly after I started managing Oakmark Select, I was on a panel of investors discussing portfolio concentration. The manager seated next to me spoke glowingly of his process, which produced a portfolio that was invested in hundreds of stocks, and proudly stated, "This ensures that no single mistake can meaningfully hurt the portfolio." My response was not well-received: "If mistakes don't matter, doesn't that mean successes don't matter either?" (I've since learned that—despite the moderator's encouragement to speak up—investment panel decorum is to sit silently when others spout nonsense.) Active managers who widely diversify across hundreds of stocks have almost no chance of outperforming the market after deducting their fees and expenses. They are "closet indexing" with the goal of not underperforming by enough to get fired.

Our starting point is very different at Oakmark. We believe our disciplined long-term approach allows us to add value via stock selection. And since we believe that, we quickly get to the point that any benefit from reducing risk by adding more stocks to our portfolio is outweighed by the return lost from diluting our best ideas. We are trying to maximize our probability of outperforming by a meaningful amount. That's a very different goal than closet indexers have. That's why our Funds range from a low of 20 stocks to a high of about 60. Our most diversified portfolios have only half the positions of our average competitor.

Why over diversifying is a problem

Many well-intentioned mutual fund investors collect mutual funds for a hobby. They find an attractive fund and add it to their existing portfolio of funds. Eventually they own dozens of funds, each designed to have enough diversification to protect

an investor who puts all their equity assets in that one fund. Adding together all the funds they own, these investors often end up with a portfolio that doesn't look much different than the market, yet they are paying active management fees on the entire portfolio. The math suggests their likelihood of outperforming the market after fees becomes de minimis.

We realize that most Oakmark shareholders use our Funds for just part of their mutual fund portfolio. Since our investors are already taking steps to diversify their assets, we believe it is counterproductive if our portfolios are also heavily diversified. By concentrating our assets in our best ideas we are restoring our shareholders' opportunity to outperform.

We have great respect for the index funds we compete with. And we don't begrudge John Bogle's evangelic zeal for these products. In fact, he's probably right when he says that many investors won't put in the effort to identify attractive funds, and of those that do, many won't have the courage to stick with them when they encounter inevitable difficult times. So they really would be better off just buying index funds. But, for the disciplined investor who is willing to put in the effort—and who doesn't panic when times are tough—there is still as much opportunity as there has ever been for active management to add value. Human nature doesn't change.

oakmark.com 3

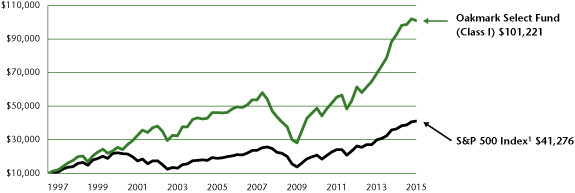

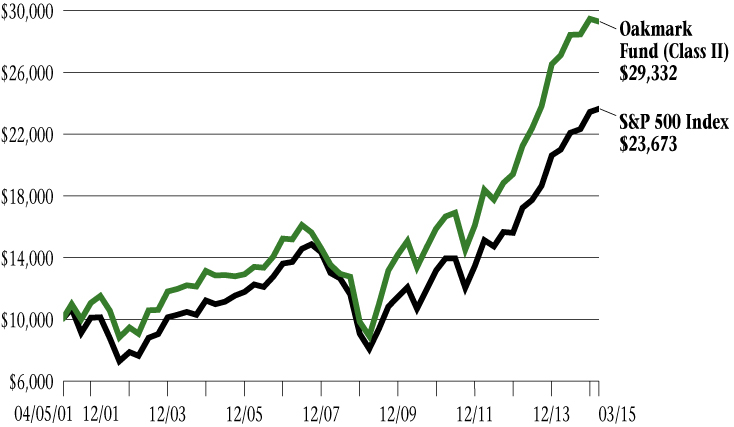

Oakmark Fund March 31, 2015

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 08/05/91 (Unaudited)

PERFORMANCE

| | | | Average Annual Total Returns (as of 03/31/15) | |

| (Unaudited) | | Total Return

Last 3 Months | | 1-year | | 3-year | | 5-year | | 10-year | | Since

Inception

(08/05/91) | |

Oakmark Fund (Class I) | | | -0.57 | % | | | 8.37 | % | | | 17.18 | % | | | 14.64 | % | | | 8.96 | % | | | 13.10 | % | |

S&P 500 Index | | | 0.95 | % | | | 12.73 | % | | | 16.11 | % | | | 14.47 | % | | | 8.01 | % | | | 9.58 | % | |

Dow Jones Industrial Average3 | | | 0.33 | % | | | 10.57 | % | | | 13.18 | % | | | 13.23 | % | | | 8.17 | % | | | 10.41 | % | |

Lipper Large Cap Value Funds Index4 | | | -0.07 | % | | | 8.43 | % | | | 15.29 | % | | | 12.36 | % | | | 6.83 | % | | | 8.95 | % | |

The graph and table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit oakmark.com.

TOP TEN EQUITY HOLDINGS5 | | % of Net Assets | |

Bank Of America Corp. | | | 3.0 | | |

Apache Corp. | | | 2.8 | | |

Amazon, Inc. | | | 2.5 | | |

MasterCard, Inc., Class A | | | 2.4 | | |

Google, Inc., Class A | | | 2.3 | | |

Citigroup, Inc. | | | 2.3 | | |

Oracle Corp. | | | 2.3 | | |

American International Group, Inc. | | | 2.2 | | |

Visa, Inc., Class A | | | 2.1 | | |

JPMorgan Chase & Co. | | | 2.1 | | |

FUND STATISTICS | |

Ticker | | OAKMX | |

Inception | | 08/05/91 | |

Number of Equity Holdings | | 58 | |

Net Assets | | $18.1 billion | |

Benchmark | | S&P 500 Index | |

Weighted Average Market Cap | | $111.4 billion | |

Median Market Cap | | $51.5 billion | |

Portfolio Turnover (for the 6-months ended 03/31/15) | | 12% | |

Expense Ratio - Class I (as of 09/30/14) | | 0.87% | |

SECTOR ALLOCATION | | % of Net Assets | |

Financials | | | 25.3 | | |

Information Technology | | | 24.0 | | |

Consumer Discretionary | | | 13.6 | | |

Industrials | | | 10.2 | | |

Energy | | | 6.0 | | |

Consumer Staples | | | 6.0 | | |

Health Care | | | 5.5 | | |

Materials | | | 2.4 | | |

Short-Term Investments and Other | | | 7.0 | | |

4 OAKMARK FUNDS

Oakmark Fund March 31, 2015

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oakmx@oakmark.com

Kevin Grant, CFA

Portfolio Manager

oakmx@oakmark.com

The Oakmark Fund declined 1% in the first quarter of 2015, and it lagged behind the 1% gain for the S&P 5001. Falling oil prices and the strengthening U.S. dollar captured investor attention and brought heightened volatility to company earnings and stock prices during the first quarter. With interest rates near multi-year lows, however, we feel that equities remain the most attractive asset class. We remain confident in the Oakmark Fund's long-term prospects, and our confidence is supported by the fact that a substantial portion of the recent underperformance has been driven by weakness in the financials sector, which is among the highest potential return sectors of the Fund.

The sectors that contributed the most to performance were consumer discretionary and healthcare, driven largely by Amazon and UnitedHealth Group, respectively. Amazon was up 20% after reporting stronger than expected revenue growth in the fourth quarter, and the company continues to invest heavily to support high-return future growth. UnitedHealth Group was up 17% due to strong fourth quarter results and continued momentum as concerns about healthcare reform wane. Our weakest sectors were financials and energy, and Bank of America and Chesapeake Energy were the worst performing securities. Despite the near-term weakness, we feel the financials and energy sectors remain undervalued, and the Oakmark Fund added to several positions in these sectors during the quarter.

We also initiated new positions in Caterpillar Inc. and Precision Castparts Corp., as discussed below. We eliminated the position in Walmart because its share price appreciated toward our estimate of intrinsic value. We also eliminated most of our position in Home Depot, which has performed well for several years and also reached our estimate of intrinsic value. We would like to commend Home Depot's former CEO Frank Blake and the entire Home Depot management team for their strong focus on maximizing returns and growing per-share value. Consistent with the message delivered in Bill Nygren's fourth quarter commentary, which discussed the Fund's desire to minimize tax consequences of our sales, we have maintained a small position in Home Depot shares that we have owned for less than one year. The Fund also captured a loss on some Halliburton shares when initiating a position in Baker Hughes, which Halliburton announced it plans to acquire.

Caterpillar Inc. (CAT-$81)

Caterpillar is the world's largest provider of construction equipment, diesel engines and industrial gas turbines. Caterpillar's products earn high marks, as do the quality and scope of its dealer network, but the company has considerable exposure to the highly cyclical and currently depressed oil and gas and mining segments. With substantial pressure from weak energy spending and the negative impact of the strong U.S. dollar,

Caterpillar's 2015 earnings will likely be down considerably from 2014 and toward the bottom end of their cyclical range. We prefer to value cyclical businesses on their earnings potential throughout the cycle, and we think that Caterpillar's mid-cycle earnings will be considerably higher than current levels. With the Caterpillar share price falling to multi-year lows, the business is now attractively valued at just 10x our forecast of mid-cycle earnings. When we combine this attractive valuation with a 3.4% dividend yield and a strong balance sheet, we find Caterpillar to be a compelling investment.

Precision Castparts Corp. (PCP-$212)

Precision Castparts Corp. (PCP) is a manufacturer of complex metal components and products, including castings, forgings, fasteners and aerostructures for aerospace, power generation and general industrial applications. Precision Castparts enjoys what we believe is an outstanding corporate culture and is led by a long-tenured CEO who is known for aggressively pursuing operating efficiencies. For many years, the company's stock traded at a significant premium to other aerospace and industrial peers, but recent weakness has brought the share price to attractive levels relative to these industry groups and the S&P 500. We believe the current valuation of less than 15x earnings is overly punitive, considering PCP's organic growth prospects and the company's ability to add value through acquisitions. PCP is providing more components on key new airplanes, which should allow the company to outgrow its end markets. In addition, management projects $4 billion-$6 billion of acquisition opportunities over the next couple of years with return characteristics similar to its existing business. Finally, the company's unique technical and process capabilities, coupled with its efficiently run operations, should allow it to continue to generate above-average margins. We are pleased to have the opportunity to add shares of what we consider a best-in-class company at a price that implies it is only average.

oakmark.com 5

Oakmark Fund March 31, 2015 (Unaudited)

Schedule of Investments (in thousands)

| | | Shares | | Value | |

COMMON STOCKS - 93.0% | |

FINANCIALS - 25.3% | |

DIVERSIFIED FINANCIALS - 9.4% | |

The Goldman Sachs Group, Inc.

Investment Banking & Brokerage | | | 1,740 | | | $ | 327,068 | | |

Capital One Financial Corp.

Consumer Finance | | | 4,113 | | | | 324,171 | | |

State Street Corp.

Asset Management & Custody Banks | | | 4,380 | | | | 322,061 | | |

Franklin Resources, Inc.

Asset Management & Custody Banks | | | 5,430 | | | | 278,668 | | |

Bank of New York Mellon Corp.

Asset Management & Custody Banks | | | 6,450 | | | | 259,533 | | |

T Rowe Price Group, Inc.

Asset Management & Custody Banks | | | 2,350 | | | | 190,303 | | |

| | | | | | 1,701,804 | | |

BANKS - 8.9% | |

Bank of America Corp.

Diversified Banks | | | 35,000 | | | | 538,650 | | |

Citigroup, Inc.

Diversified Banks | | | 8,130 | | | | 418,858 | | |

JPMorgan Chase & Co.

Diversified Banks | | | 6,140 | | | | 371,961 | | |

Wells Fargo & Co.

Diversified Banks | | | 5,290 | | | | 287,776 | | |

| | | | | | 1,617,245 | | |

INSURANCE - 7.0% | |

American International Group, Inc.

Multi-line Insurance | | | 7,305 | | | | 400,241 | | |

Aflac, Inc.

Life & Health Insurance | | | 5,070 | | | | 324,531 | | |

Aon PLC (b)

Insurance Brokers | | | 3,080 | | | | 296,049 | | |

Principal Financial Group, Inc.

Life & Health Insurance | | | 4,609 | | | | 236,780 | | |

| | | | | | 1,257,601 | | |

| | | | | | 4,576,650 | | |

INFORMATION TECHNOLOGY - 24.0% | |

SOFTWARE & SERVICES - 13.7% | |

MasterCard, Inc., Class A

Data Processing & Outsourced Services | | | 5,050 | | | | 436,269 | | |

Google, Inc., Class A (a)

Internet Software & Services | | | 762 | | | | 422,458 | | |

Oracle Corp.

Systems Software | | | 9,445 | | | | 407,552 | | |

Visa, Inc., Class A

Data Processing & Outsourced Services | | | 5,880 | | | | 384,611 | | |

Automatic Data Processing, Inc.

Data Processing & Outsourced Services | | | 4,220 | | | | 361,401 | | |

Microsoft Corp.

Systems Software | | | 6,650 | | | | 270,356 | | |

Accenture PLC, Class A (b)

IT Consulting & Other Services | | | 2,100 | | | | 196,749 | | |

| | | | | | 2,479,396 | | |

| | | Shares | �� | Value | |

TECHNOLOGY HARDWARE & EQUIPMENT - 5.6% | |

TE Connectivity, Ltd. (b)

Electronic Manufacturing Services | | | 5,036 | | | $ | 360,653 | | |

Apple, Inc.

Technology Hardware, Storage & Peripherals | | | 2,883 | | | | 358,732 | | |

QUALCOMM, Inc.

Communications Equipment | | | 4,245 | | | | 294,348 | | |

| | | | | | 1,013,733 | | |

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 4.7% | |

Intel Corp.

Semiconductors | | | 11,580 | | | | 362,107 | | |

Texas Instruments, Inc.

Semiconductors | | | 5,565 | | | | 318,234 | | |

Applied Materials, Inc.

Semiconductor Equipment | | | 7,260 | | | | 163,786 | | |

| | | | | | 844,127 | | |

| | | | | | 4,337,256 | | |

CONSUMER DISCRETIONARY - 13.6% | |

RETAILING - 4.7% | |

Amazon.com, Inc. (a)

Internet Retail | | | 1,219 | | | | 453,590 | | |

Liberty Interactive Corp., Class A (a)

Catalog Retail | | | 10,891 | | | | 317,905 | | |

The Home Depot, Inc.

Home Improvement Retail | | | 665 | | | | 75,551 | | |

| | | | | | 847,046 | | |

MEDIA - 4.5% | |

News Corp., Class A (a)

Publishing | | | 19,373 | | | | 310,166 | | |

Omnicom Group, Inc.

Advertising | | | 3,691 | | | | 287,844 | | |

Comcast Corp., Class A

Cable & Satellite | | | 3,940 | | | | 220,896 | | |

| | | | | | 818,906 | | |

AUTOMOBILES & COMPONENTS - 2.0% | |

General Motors Co.

Automobile Manufacturers | | | 7,850 | | | | 294,375 | | |

Harley-Davidson, Inc.

Motorcycle Manufacturers | | | 1,102 | | | | 66,936 | | |

| | | | | | 361,311 | | |

CONSUMER DURABLES & APPAREL - 1.2% | |

Whirlpool Corp.

Household Appliances | | | 1,100 | | | | 222,266 | | |

CONSUMER SERVICES - 1.2% | |

Las Vegas Sands Corp.

Casinos & Gaming | | | 3,800 | | | | 209,152 | | |

| | | | | | 2,458,681 | | |

See accompanying Notes to Financial Statements.

6 OAKMARK FUNDS

Oakmark Fund March 31, 2015 (Unaudited)

Schedule of Investments (in thousands) (continued)

| | | Shares | | Value | |

COMMON STOCKS - 93.0% (continued) | |

INDUSTRIALS - 10.2% | |

CAPITAL GOODS - 7.3% | |

General Electric Co.

Industrial Conglomerates | | | 14,500 | | | $ | 359,745 | | |

Illinois Tool Works, Inc.

Industrial Machinery | | | 3,115 | | | | 302,591 | | |

Parker-Hannifin Corp.

Industrial Machinery | | | 1,925 | | | | 228,651 | | |

Caterpillar, Inc.

Construction Machinery & Heavy Trucks | | | 2,730 | | | | 218,442 | | |

Precision Castparts Corp.

Aerospace & Defense | | | 1,000 | | | | 210,000 | | |

| | | | | | 1,319,429 | | |

TRANSPORTATION - 2.9% | |

FedEx Corp.

Air Freight & Logistics | | | 2,000 | | | | 330,900 | | |

Union Pacific Corp.

Railroads | | | 1,750 | | | | 189,543 | | |

| | | | | | 520,443 | | |

| | | | | | 1,839,872 | | |

ENERGY - 6.0% | |

Apache Corp.

Oil & Gas Exploration & Production | | | 8,275 | | | | 499,231 | | |

Halliburton Co.

Oil & Gas Equipment & Services | | | 4,500 | | | | 197,460 | | |

Chesapeake Energy Corp.

Oil & Gas Exploration & Production | | | 12,000 | | | | 169,920 | | |

National Oilwell Varco, Inc.

Oil & Gas Equipment & Services | | | 3,040 | | | | 151,969 | | |

Baker Hughes, Inc.

Oil & Gas Equipment & Services | | | 1,150 | | | | 73,117 | | |

| | | | | | 1,091,697 | | |

CONSUMER STAPLES - 6.0% | |

FOOD, BEVERAGE & TOBACCO - 6.0% | |

General Mills, Inc.

Packaged Foods & Meats | | | 5,820 | | | | 329,412 | | |

Nestle SA (b) (c)

Packaged Foods & Meats | | | 3,540 | | | | 266,281 | | |

Diageo PLC (b) (c)

Distillers & Vintners | | | 2,250 | | | | 248,783 | | |

Unilever PLC (b) (c)

Packaged Foods & Meats | | | 5,613 | | | | 234,118 | | |

| | | | | | 1,078,594 | | |

HEALTH CARE - 5.5% | |

HEALTH CARE EQUIPMENT & SERVICES - 3.9% | |

Medtronic PLC (b)

Health Care Equipment | | | 4,690 | | | | 365,773 | | |

UnitedHealth Group, Inc.

Managed Health Care | | | 2,890 | | | | 341,858 | | |

| | | | | | 707,631 | | |

| | | Shares | | Value | |

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 1.6% | |

Sanofi (b) (c)

Pharmaceuticals | | | 5,670 | | | $ | 280,325 | | |

| | | | | | 987,956 | | |

MATERIALS - 2.4% | |

Monsanto Co.

Fertilizers & Agricultural Chemicals | | | 2,450 | | | | 275,723 | | |

Glencore PLC (b)

Diversified Metals & Mining | | | 38,040 | | | | 161,330 | | |

| | | | | | 437,053 | | |

TOTAL COMMON STOCKS - 93.0%

(COST $12,497,636) | | | | | 16,807,759 | | |

| | | Par Value | | Value | |

SHORT TERM INVESTMENTS - 7.0% | |

REPURCHASE AGREEMENT - 3.6% | |

Fixed Income Clearing Corp. Repurchase

Agreement, 0.01% dated 03/31/15 due

04/01/15, repurchase price $654,132,

collateralized by a Federal National

Mortgage Association Bond, 2.635%,

due 09/13/23, value plus accrued

interest of $100,925, by United States

Treasury Notes, 1.750% - 2.000%,

due 10/31/21 - 05/15/23, aggregate

value plus accrued interest of $566,291

(Cost: $654,132) | | $ | 654,132 | | | | 654,132 | | |

U.S. GOVERNMENT BILLS - 2.0% | |

United States Treasury Bills,

0.05% - 0.11%, due 04/30/15 - 09/10/15 (d)

(Cost $349,943) | | | 350,000 | | | | 349,948 | | |

GOVERNMENT AND AGENCY SECURITIES - 1.4% | |

United States Treasury Floating Rate Note,

0.104%, due 04/30/16 (e)

(Cost $250,000) | | | 250,000 | | | | 250,021 | | |

TOTAL SHORT TERM INVESTMENTS - 7.0%

(COST $1,254,075) | | | | | 1,254,101 | | |

TOTAL INVESTMENTS - 100.0%

(COST $13,751,711) | | | | | 18,061,860 | | |

Other Assets In Excess of Liabilities - 0.0% (f) | | | | | 8,842 | | |

TOTAL NET ASSETS - 100.0% | | | | $ | 18,070,702 | | |

(a) Non-income producing security

(b) Foreign domiciled corporation

(c) Sponsored American Depositary Receipt

(d) The rate shown represents the annualized yield at the time of purchase; not a coupon rate.

(e) Floating Rate Note. Rate shown is as of March 31, 2015.

(f) Amount rounds to less than 0.1%.

See accompanying Notes to Financial Statements.

oakmark.com 7

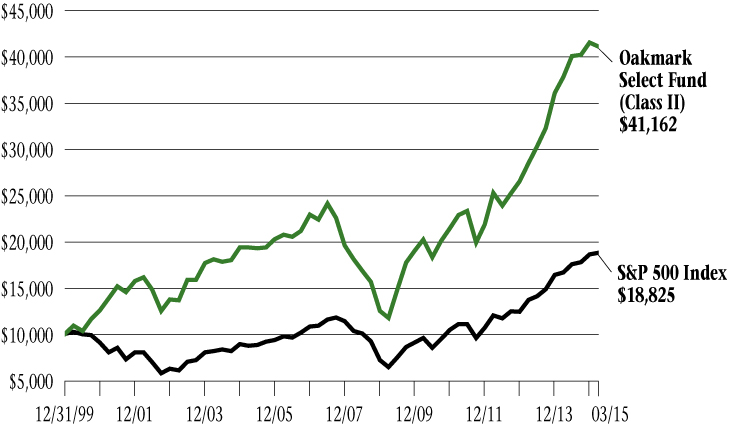

Oakmark Select Fund March 31, 2015

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 11/01/96 (Unaudited)

PERFORMANCE

| | | | Average Annual Total Returns (as of 03/31/15) | |

| (Unaudited) | | Total Return

Last 3 Months | | 1-year | | 3-year | | 5-year | | 10-year | | Since

Inception

(11/01/96) | |

Oakmark Select Fund (Class I) | | | -0.98 | % | | | 8.98 | % | | | 18.00 | % | | | 15.62 | % | | | 8.13 | % | | | 13.40 | % | |

S&P 500 Index | | | 0.95 | % | | | 12.73 | % | | | 16.11 | % | | | 14.47 | % | | | 8.01 | % | | | 8.00 | % | |

Lipper Multi-Cap Value Funds Index6 | | | 1.25 | % | | | 8.59 | % | | | 15.81 | % | | | 12.70 | % | | | 6.61 | % | | | 7.81 | % | |

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit oakmark.com.

TOP TEN EQUITY HOLDINGS5 | | % of Net Assets | |

MasterCard, Inc., Class A | | | 7.6 | | |

TE Connectivity, Ltd. | | | 6.0 | | |

Google, Inc., Class A | | | 5.6 | | |

American International Group, Inc. | | | 5.5 | | |

Apache Corp. | | | 5.5 | | |

CBRE Group, Inc. | | | 5.4 | | |

Amazon, Inc. | | | 5.3 | | |

Citigroup, Inc. | | | 5.2 | | |

Bank Of America Corp. | | | 5.0 | | |

JPMorgan Chase & Co. | | | 4.9 | | |

FUND STATISTICS | |

Ticker | | OAKLX | |

Inception | | 11/01/96 | |

Number of Equity Holdings | | 20 | |

Net Assets | | $6.5 billion | |

Benchmark | | S&P 500 Index | |

Weighted Average Market Cap | | $110.4 billion | |

Median Market Cap | | $87.6 billion | |

Portfolio Turnover (for the 6-months ended 03/31/15) | | 15% | |

Expense Ratio - Class I (as of 09/30/14) | | 0.95% | |

SECTOR ALLOCATION | | % of Net Assets | |

Financials | | | 38.3 | | |

Information Technology | | | 27.2 | | |

Energy | | | 9.5 | | |

Consumer Discretionary | | | 9.4 | | |

Industrials | | | 4.0 | | |

Health Care | | | 3.9 | | |

Utilities | | | 3.5 | | |

Short-Term Investments and Other | | | 4.2 | | |

8 OAKMARK FUNDS

Oakmark Select Fund March 31, 2015

Portfolio Manager Commentary

William C. Nygren, CFA

Portfolio Manager

oaklx@oakmark.com

Anthony P. Coniaris, CFA

Portfolio Manager

oaklx@oakmark.com

Win Murray

Portfolio Manager

oaklx@oakmark.com

For the quarter, the Oakmark Select Fund declined 1%, compared to a 1% gain in the S&P 500 Index1. The negative impact of our energy holdings coupled with our relatively large position in financials overwhelmed what otherwise was strong stock selection across our consumer discretionary and technology investments. While we are disappointed with the outcome, we have been through periods like this before and remain steadfast in our commitment to the same investment process that has delivered success since the Fund's inception.

Chesapeake Energy (–27%), Bank of America (–14%) and Intel (–13%) detracted the most from our performance. Chesapeake issued disappointing cash flow guidance for 2015 due primarily to legacy contracts, signed under the prior management regime, to market oil and gas. While the result is disappointing, we believe that the impact from these contracts is both manageable and temporary. Aside from this issue, the business's underlying performance has been as good, or better, than we expected on relevant metrics like production growth and operating costs. The company also announced a substantial share repurchase authorization to take advantage of the large disconnect between the share price and intrinsic value. So, we remain confident that Chesapeake's new management team can right the ship operationally and greatly improve capital allocation. Although this quarter's stock performance might indicate otherwise, Bank of America continues to march toward our estimate of normalized earnings power, despite headwinds from low interest rates, while improving the quality of its balance sheet. For these reasons, we remain confident in Bank of America and all of our large bank holdings.

Amazon (+20%), TE Connectivity (14%) and CBRE Group (13%) contributed the most to performance. In the short time we have owned it, Amazon has grown its share of retail sales considerably, as we expected. A surprisingly profitable fourth quarter gave investors a glimpse of what margins could be should management decide to more aggressively pull back on their ambitious growth investments. As long as Amazon continues to grow its online retail moat, we welcome either outcome.

During the quarter we added one new position (General Electric) and eliminated another (FedEx) from the Fund. We have always admired General Electric's (GE) collection of businesses, but we have questioned management's focus on returns when making capital allocation decisions. However, the appointment of a new CFO in mid-2013 ushered in significant changes. Since then, GE has, in our view, acquired assets cheaply (Alstom) and sold assets at good prices (Synchrony and its appliances division). In 2015, the company plans to totally revamp its variable compensation plan for thousands of employees, emphasizing factors that drive return on invested capital, which should boost future results. We believe there is substantial opportunity to improve gross margins, and the stock trades for just under a market multiple on 2016 earnings and offers a generous dividend yield of 3.7%. Some investors may have a stale opinion of

GE after the past 15 years of persistent underperformance, but we believe it's a good investment at the current price.

We eliminated our position in FedEx due to price. Management's renewed focus on costs and smart capital allocation was properly rewarded with a higher multiple, so we were able to redeploy those assets into more undervalued companies, such as GE.

Thank you for your continued investment in the Fund.

oakmark.com 9

Oakmark Select Fund March 31, 2015 (Unaudited)

Schedule of Investments (in thousands)

| | | Shares | | Value | |

COMMON STOCKS - 95.8% | |

FINANCIALS - 38.3% | |

BANKS - 15.1% | |

Citigroup, Inc.

Diversified Banks | | | 6,577 | | | $ | 338,847 | | |

Bank of America Corp.

Diversified Banks | | | 20,979 | | | | 322,861 | | |

JPMorgan Chase & Co.

Diversified Banks | | | 5,230 | | | | 316,833 | | |

| | | | | | 978,541 | | |

INSURANCE - 10.1% | |

American International Group, Inc.

Multi-line Insurance | | | 6,545 | | | | 358,612 | | |

FNF Group

Property & Casualty Insurance | | | 7,901 | | | | 290,448 | | |

| | | | | | 649,060 | | |

DIVERSIFIED FINANCIALS - 7.7% | |

Franklin Resources, Inc.

Asset Management & Custody Banks | | | 5,010 | | | | 257,113 | | |

Capital One Financial Corp.

Consumer Finance | | | 3,050 | | | | 240,401 | | |

| | | | | | 497,514 | | |

REAL ESTATE - 5.4% | |

CBRE Group, Inc., Class A (a)

Real Estate Services | | | 8,964 | | | | 346,996 | | |

| | | | | | 2,472,111 | | |

INFORMATION TECHNOLOGY - 27.2% | |

SOFTWARE & SERVICES - 18.1% | |

MasterCard, Inc., Class A

Data Processing & Outsourced Services | | | 5,720 | | | | 494,151 | | |

Google, Inc., Class A (a)

Internet Software & Services | | | 653 | | | | 362,219 | | |

Oracle Corp.

Systems Software | | | 7,240 | | | | 312,406 | | |

| | | | | | 1,168,776 | | |

TECHNOLOGY HARDWARE & EQUIPMENT - 6.0% | |

TE Connectivity, Ltd. (b)

Electronic Manufacturing Services | | | 5,394 | | | | 386,314 | | |

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT - 3.1% | |

Intel Corp.

Semiconductors | | | 6,447 | | | | 201,597 | | |

| | | | | | 1,756,687 | | |

ENERGY - 9.5% | |

Apache Corp.

Oil & Gas Exploration & Production | | | 5,860 | | | | 353,534 | | |

Chesapeake Energy Corp.

Oil & Gas Exploration & Production | | | 18,500 | | | | 261,960 | | |

| | | | | | 615,494 | | |

| | | Shares | | Value | |

CONSUMER DISCRETIONARY - 9.4% | |

RETAILING - 9.4% | |

Amazon.com, Inc. (a)

Internet Retail | | | 917 | | | $ | 341,216 | | |

Liberty Interactive Corp., Class A (a)

Catalog Retail | | | 9,214 | | | | 268,953 | | |

| | | | | | 610,169 | | |

INDUSTRIALS - 4.0% | |

CAPITAL GOODS - 4.0% | |

General Electric Co.

Industrial Conglomerates | | | 10,500 | | | | 260,505 | | |

HEALTH CARE - 3.9% | |

HEALTH CARE EQUIPMENT & SERVICES - 3.9% | |

Medtronic PLC (b)

Health Care Equipment | | | 3,200 | | | | 249,568 | | |

UTILITIES - 3.5% | |

Calpine Corp. (a)

Independent Power Producers & Energy Traders | | | 10,004 | | | | 228,801 | | |

TOTAL COMMON STOCKS - 95.8%

(COST $4,854,551) | | | | | 6,193,335 | | |

| | | Par Value | | Value | |

SHORT TERM INVESTMENTS - 4.3% | |

REPURCHASE AGREEMENT - 4.3% | |

Fixed Income Clearing Corp. Repurchase

Agreement, 0.01% dated 03/31/15 due

04/01/15, repurchase price $275,237,

collateralized by United States

Treasury Notes, 2.000% - 2.125%,

due 09/30/21- 10/31/21, aggregate

value plus accrued interest of

$280,745 (Cost: $275,237) | | $ | 275,237 | | | | 275,237 | | |

TOTAL SHORT TERM INVESTMENTS - 4.3%

(COST $275,237) | | | | | 275,237 | | |

TOTAL INVESTMENTS - 100.1%

(COST $5,129,788) | | | | | 6,468,572 | | |

Liabilities In Excess of Other Assets - (0.1)% | | | | | (4,292 | ) | |

TOTAL NET ASSETS - 100.0% | | | | $ | 6,464,280 | | |

(a) Non-income producing security

(b) Foreign domiciled corporation

See accompanying Notes to Financial Statements.

10 OAKMARK FUNDS

This page intentionally left blank.

oakmark.com 11

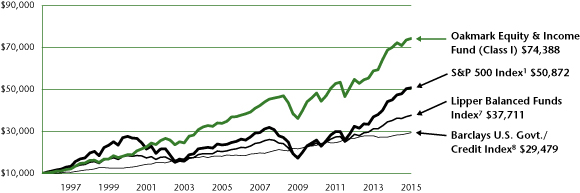

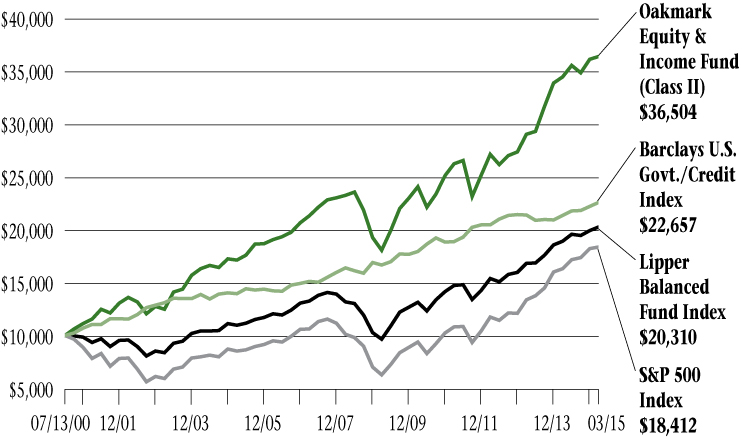

Oakmark Equity and Income Fund March 31, 2015

Summary Information

VALUE OF A $10,000 INVESTMENT

Since Inception - 11/01/95 (Unaudited)

PERFORMANCE

| | | | Average Annual Total Returns (as of 03/31/15) | |

| (Unaudited) | | Total Return

Last 3 Months | | 1-year | | 3-year | | 5-year | | 10-year | | Since

Inception

(11/01/95) | |

Oakmark Equity and Income Fund (Class I) | | | 0.91 | % | | | 6.02 | % | | | 10.65 | % | | | 9.00 | % | | | 8.18 | % | | | 10.89 | % | |

Lipper Balanced Funds Index | | | 1.78 | % | | | 7.17 | % | | | 9.64 | % | | | 9.07 | % | | | 6.34 | % | | | 7.08 | % | |

S&P 500 Index | | | 0.95 | % | | | 12.73 | % | | | 16.11 | % | | | 14.47 | % | | | 8.01 | % | | | 8.74 | % | |

Barclays U.S. Govt./Credit Index | | | 1.84 | % | | | 5.86 | % | | | 3.35 | % | | | 4.75 | % | | | 4.96 | % | | | 5.73 | % | |

The graph and table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. Total return includes change in share prices and, in each case, includes reinvestment of dividends and capital gain distributions. The investment return and principal value vary so that an investor's shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance, please visit oakmark.com.

TOP TEN EQUITY HOLDINGS5 | | % of Net Assets | |

Oracle Corp. | | | 3.7 | | |

General Motors Co. | | | 3.5 | | |

Bank Of America Corp. | | | 3.3 | | |

Nestle ADR | | | 3.1 | | |

TE Connectivity, Ltd. | | | 2.8 | | |

CVS Health Corp. | | | 2.6 | | |

Dover Corp. | | | 2.6 | | |

UnitedHealth Group, Inc. | | | 2.3 | | |

Foot Locker, Inc. | | | 2.2 | | |

Diageo ADR | | | 2.2 | | |

FUND STATISTICS | |

Ticker | | OAKBX | |

Inception | | 11/01/95 | |

Number of Equity Holdings | | 47 | |

Net Assets | | $20.7 billion | |

Benchmark | | Lipper Balanced Funds Index | |

Weighted Average Market Cap | | $71.4 billion | |

Median Market Cap | | $17.7 billion | |

Portfolio Turnover (for the 6-months ended 03/31/15) | | 13% | |

Expense Ratio - Class I (as of 09/30/14) | | 0.74% | |

SECTOR ALLOCATION | | % of Net Assets | |

Equity Investments | | | |

Financials | | | 14.4 | | |

Consumer Discretionary | | | 10.6 | | |

Industrials | | | 10.1 | | |

Consumer Staples | | | 9.8 | | |

Information Technology | | | 9.8 | | |

Health Care | | | 4.0 | | |

Energy | | | 3.6 | | |

Materials | | | 1.3 | | |

Total Equity Investments | | | 63.6 | | |

Fixed Income Investments | | | |

Government and Agency Securities | | | 8.1 | | |

Corporate Bonds | | | 5.9 | | |

Asset Backed Securities | | | 0.1 | | |

Total Fixed Income Investments | | | 14.1 | | |

Short-Term Investments and Other | | | 22.3 | | |

12 OAKMARK FUNDS

Oakmark Equity and Income Fund March 31, 2015

Portfolio Manager Commentary

Clyde S. McGregor, CFA

Portfolio Manager

oakbx@oakmark.com

M. Colin Hudson, CFA

Portfolio Manager

oakbx@oakmark.com

Matthew A. Logan, CFA

Portfolio Manager

oakbx@oakmark.com

Edward J. Wojciechowski, CFA

Portfolio Manager

oakbx@oakmark.com

Quarter Review

U.S. stocks showed little direction in the March quarter. In fact, in the second half of the quarter the market went 28 trading sessions without gains on back-to-back days, and this tied the record for that somewhat irrelevant statistic. The return for the Equity and Income Fund in the quarter was 1% while the Lipper Balanced Fund Index7, the Fund's performance benchmark, returned 2%. Our decision to keep the Fund's fixed income duration very short contributed to the Fund's shortfall versus the benchmark. For the fiscal year's six months, the Fund returned 5%, and the Lipper Balanced Funds Index return was 4%. The annualized compound rate of return since the Fund's inception in 1995 is 11% while the corresponding return to the Lipper Index is 7%.

Top contributors for the quarter were UnitedHealth Group, TE Connectivity, General Motors, Lear and Foot Locker. Bank of America, National Oilwell Varco, Union Pacific, Oracle and Glencore detracted most from return. For the first six months of the Fund's fiscal year, UnitedHealth Group, CVS Health, TE Connectivity, General Motors and Lear led the contributor list while National Oilwell Varco, Glencore, Bank of America, Dover and Ultra Petroleum detracted. Weak commodity prices have helped to pull down the shares of four of the five detractors.

Activist or Acquisition?

In the recent period, companies that have attracted activist attention as well as those that have announced significant acquisitions have both tended to outperform. This is a curious outcome for a couple of reasons. First, throughout our careers, we had grown accustomed to seeing the price of an acquirer drop following the announcement of a deal because investors often perceive acquisitions as diluting a company's value. Not only is it strange that acquiring companies now enjoy price lifts when they announce deals (e.g., UnitedHealth on the announcement of its deal to purchase Catamaran), but it's odder still that it comes at a time when activism is also causing prices to rise. Activists often agitate for the exact opposite of acquisitions: either an outright sale of the targeted company or divestment of business units, believing such actions can "unlock" value.

In a diversified portfolio of equities, like the equity portion of Equity and Income Fund, it is almost to be expected that there will be Fund holdings that demonstrate these factors. Two of the Fund's automotive industry holdings (General Motors and Lear) have attracted activists, and Bank of New York Mellon has added a representative of an activist firm to its board. General Motors recently responded to an activist group with a plan to return cash to shareholders through share repurchase, and Lear

had previously undertaken this action. Fund holdings have been less busy on the acquisition front, with the aforementioned UnitedHealth deal as the only recent example.

Obviously we like it when prevailing market currents carry along our holdings, but we worry that in an otherwise dull period investors are overreaching for investable concepts. Although the market's previously negative reactions to acquisition announcements was probably too extreme, today's judgment that acquisitions will almost always produce enhanced profitability seems too generous. Concerning activist investors, we welcome work that brings price and value together without impairing future value growth. Our job is to discriminate between activists who look to enhance long-term business value and those who seek merely to extract short-term profits.

Transaction Activity

During the quarter, the Fund initiated two new equity positions while eliminating three. The net effect of these transactions was to decrease the equity allocation by 1% with proceeds used to increase the corporate bond allocation.

We purchased shares of T. Rowe Price Group, the investment management company. As a significant player in our business, we have long admired T. Rowe but only recently perceived the share price to offer opportunity. Key to the franchise is the company's investment culture, which has sustainably generated commendable investment performance and enabled T. Rowe to establish a strong position in the defined contribution/401(k) market. In our view, the company has a solid balance sheet with over $3 billion in cash and investments with no debt. We also like that management has demonstrated good stewardship of capital through opportunistic share repurchases (i.e., during periods when the share price was weak and trading at a discount to our estimate of intrinsic value).

Our second new purchase was Precision Castparts Corp. (PCP), a manufacturer of complex metal components and products for aerospace, power generation, and general industrial applications. PCP's long-tenured CEO has helped to develop what we believe is an outstanding corporate culture that relentlessly pursues operating efficiencies. For many years, the company's stock traded at a significant premium to aerospace and industrial companies, but recent underperformance has caused it to sell at a discounted valuation. We believe the current valuation does not adequately reflect PCP's organic growth prospects and its ability to add value through acquisitions. PCP's unique technical and process capabilities coupled with its efficiently run operations should allow this best-in-class company to continue generating above-average margins.

oakmark.com 13

Oakmark Equity and Income Fund March 31, 2015

Portfolio Manager Commentary (continued)

Stock eliminations during the quarter were FedEx, Illinois Tool Works and Scripps Networks Interactive. We purchased shares of the first two companies in 2012, and both contributed to the Fund's returns. Scripps also contributed, but over a much longer 10-year holding period. During that time, which includes the financial crisis, much has happened at Scripps, including a corporate name change and several diversifying acquisitions. Through it all, the strength of the core cable television channel franchises was sufficient to grow shareholder value. With a rapidly changing media environment, however, we have begun to question if the increasing fragmentation of media viewership will limit future growth opportunities in this sector.

The Most Hated Rally in History

A Financial Times article on March 2 examined the post-financial crisis bull market and contained the phrase we have used to title this section9. The article discusses a theme we have often stated, "...that many investors have simply not believed in a stock market rally fueled by central banks' easy money policies." Or, according to Nicholas Colas, chief market strategist of Convergex, "There is a belief that the market rally has...not [been supported] by organic growth and rising revenues." The article also describes the difficulty investors have had in distinguishing themselves in this rally. The article notes that according to Standard & Poor's, dispersion among stocks reached a historic low in 2014, meaning that stocks have moved in tandem to an unprecedented degree.

We, too, would prefer an environment where market returns derive from economic improvement rather than cost cutting and financial engineering. But that is not the environment in which we currently operate. As one of Harris Associates' early partners often said, "The hardest time to invest is always right now," and it feels that way to us today. Though we do not love the investing landscape, the possibility of identifying attractive new opportunities remains. Our analyst teams, both domestic and international, continue to search the globe for mispriced securities. The search may or may not be harder today than at other times, but the challenge still inspires us. The late Herb Stein quipped, "If something cannot go on forever, it will stop," and, unfortunately, for quite some time we have felt that way about the Federal Reserve's suppression of short-term interest rates. We do not have any idea when the present unusual environment will evolve into something different, but however it evolves, we believe that our fundamental, value-based approach will produce the returns that our investors seek.

As always, we thank our shareholders for entrusting their assets to the Fund and welcome your questions and comments.

14 OAKMARK FUNDS

Oakmark Equity and Income Fund March 31, 2015 (Unaudited)

Schedule of Investments (in thousands)

| | | Shares | | Value | |

COMMON STOCKS - 63.6% | |

FINANCIALS - 14.4% | |

BANKS - 5.4% | |

Bank of America Corp.

Diversified Banks | | | 44,733 | | | $ | 688,438 | | |

Wells Fargo & Co.

Diversified Banks | | | 4,326 | | | | 235,334 | | |

U.S. Bancorp

Diversified Banks | | | 4,461 | | | | 194,805 | | |

| | | | | | 1,118,577 | | |

DIVERSIFIED FINANCIALS - 4.7% | |

TD Ameritrade Holding Corp.

Investment Banking & Brokerage | | | 12,006 | | | | 447,358 | | |

The Goldman Sachs Group, Inc.

Investment Banking & Brokerage | | | 1,208 | | | | 227,068 | | |

Bank of New York Mellon Corp.

Asset Management & Custody Banks | | | 5,340 | | | | 214,900 | | |

T Rowe Price Group, Inc.

Asset Management & Custody Banks | | | 608 | | | | 49,273 | | |

FNFV Group (a)

Multi-Sector Holdings | | | 2,202 | | | | 31,052 | | |

| | | | | | 969,651 | | |

INSURANCE - 4.3% | |

FNF Group

Property & Casualty Insurance | | | 7,689 | | | | 282,658 | | |

Principal Financial Group, Inc.

Life & Health Insurance | | | 5,061 | | | | 259,999 | | |

Reinsurance Group of America, Inc.

Reinsurance | | | 2,402 | | | | 223,852 | | |

Aflac, Inc.

Life & Health Insurance | | | 2,077 | | | | 132,936 | | |

| | | | | | 899,445 | | |

| | | | | | 2,987,673 | | |

CONSUMER DISCRETIONARY - 10.6% | |

AUTOMOBILES & COMPONENTS - 7.1% | |

General Motors Co.

Automobile Manufacturers | | | 19,469 | | | | 730,072 | | |

Lear Corp.

Auto Parts & Equipment | | | 3,387 | | | | 375,300 | | |

BorgWarner, Inc.

Auto Parts & Equipment | | | 5,699 | | | | 344,657 | | |

Remy International, Inc.

Auto Parts & Equipment | | | 394 | | | | 8,745 | | |

| | | | | | 1,458,774 | | |

RETAILING - 3.1% | |

Foot Locker, Inc. (b)

Apparel Retail | | | 7,348 | | | | 462,943 | | |

HSN, Inc.

Catalog Retail | | | 2,608 | | | | 177,974 | | |

| | | | | | 640,917 | | |

| | | Shares | | Value | |

CONSUMER DURABLES & APPAREL - 0.4% | |

Carter's, Inc.

Apparel, Accessories & Luxury Goods | | | 936 | | | $ | 86,506 | | |

| | | | | | 2,186,197 | | |

INDUSTRIALS - 10.1% | |

CAPITAL GOODS - 8.0% | |

Dover Corp.

Industrial Machinery | | | 7,713 | | | | 533,129 | | |

Flowserve Corp.

Industrial Machinery | | | 6,678 | | | | 377,229 | | |

Rockwell Automation, Inc.

Electrical Components & Equipment | | | 2,145 | | | | 248,799 | | |

Parker-Hannifin Corp.

Industrial Machinery | | | 1,638 | | | | 194,556 | | |

Precision Castparts Corp.

Aerospace & Defense | | | 794 | | | | 166,740 | | |

WESCO International, Inc. (a)

Trading Companies & Distributors | | | 1,522 | | | | 106,376 | | |

Blount International, Inc. (a)

Industrial Machinery | | | 2,263 | | | | 29,153 | | |

| | | | | | 1,655,982 | | |

TRANSPORTATION - 1.9% | |

Union Pacific Corp.

Railroads | | | 3,414 | | | | 369,759 | | |

Atlas Air Worldwide Holdings, Inc. (a)

Air Freight & Logistics | | | 647 | | | | 27,843 | | |

| | | | | | 397,602 | | |

COMMERCIAL & PROFESSIONAL SERVICES - 0.2% | |

Herman Miller, Inc.

Office Services & Supplies | | | 1,402 | | | | 38,908 | | |

| | | | | | 2,092,492 | | |

CONSUMER STAPLES - 9.8% | |

FOOD, BEVERAGE & TOBACCO - 7.2% | |

Nestle SA (c) (d)

Packaged Foods & Meats | | | 8,627 | | | | 648,958 | | |

Diageo PLC (c) (d)

Distillers & Vintners | | | 4,182 | | | | 462,393 | | |

Philip Morris International, Inc.

Tobacco | | | 5,060 | | | | 381,177 | | |

| | | | | | 1,492,528 | | |

FOOD & STAPLES RETAILING - 2.6% | |

CVS Health Corp.

Drug Retail | | | 5,285 | | | | 545,481 | | |

| | | | | | 2,038,009 | | |

See accompanying Notes to Financial Statements.

oakmark.com 15

Oakmark Equity and Income Fund March 31, 2015 (Unaudited)

Schedule of Investments (in thousands) (continued)

| | | Shares | | Value | |

COMMON STOCKS - 63.6% (continued) | |

INFORMATION TECHNOLOGY - 9.8% | |

SOFTWARE & SERVICES - 6.7% | |

Oracle Corp.

Systems Software | | | 17,795 | | | $ | 767,854 | | |

MasterCard, Inc., Class A

Data Processing & Outsourced Services | | | 4,832 | | | | 417,470 | | |

Broadridge Financial Solutions, Inc.

Data Processing & Outsourced Services | | | 3,578 | | | | 196,798 | | |

| | | | | | 1,382,122 | | |

TECHNOLOGY HARDWARE & EQUIPMENT - 3.1% | |

TE Connectivity, Ltd. (d)

Electronic Manufacturing Services | | | 8,052 | | | | 576,706 | | |

Knowles Corp. (a)

Electronic Components | | | 3,155 | | | | 60,805 | | |

| | | | | | 637,511 | | |

| | | | | | 2,019,633 | | |

HEALTH CARE - 4.0% | |

HEALTH CARE EQUIPMENT & SERVICES - 3.6% | |

UnitedHealth Group, Inc.

Managed Health Care | | | 4,090 | | | | 483,856 | | |

Omnicare, Inc.

Health Care Services | | | 3,406 | | | | 262,455 | | |

| | | | | | 746,311 | | |

PHARMACEUTICALS, BIOTECHNOLOGY & LIFE SCIENCES - 0.4% | |

Bruker Corp. (a)

Life Sciences Tools & Services | | | 4,814 | | | | 88,909 | | |

| | | | | | 835,220 | | |

ENERGY - 3.6% | |

National Oilwell Varco, Inc.

Oil & Gas Equipment & Services | | | 6,662 | | | | 333,046 | | |

Baker Hughes, Inc.

Oil & Gas Equipment & Services | | | 4,604 | | | | 292,737 | | |

Ultra Petroleum Corp. (a)

Oil & Gas Exploration & Production | | | 6,105 | | | | 95,413 | | |

Rowan Cos. PLC

Oil & Gas Drilling | | | 1,624 | | | | 28,755 | | |

| | | | | | 749,951 | | |

MATERIALS - 1.3% | |

Glencore PLC (d)

Diversified Metals & Mining | | | 60,533 | | | | 256,724 | | |

Southern Copper Corp.

Diversified Metals & Mining | | | 693 | | | | 20,225 | | |

| | | | | | 276,949 | | |

TOTAL COMMON STOCKS - 63.6%

(COST $8,545,988) | | | | | 13,186,124 | | |

| | | Par Value | | Value | |

FIXED INCOME - 14.1% | |

GOVERNMENT AND AGENCY SECURITIES - 8.1% | |

U.S. GOVERNMENT NOTES - 7.6% | |

1.25%, due 07/15/20, Inflation Indexed | | $ | 534,234 | | | $ | 579,101 | | |

1.375%, due 07/15/18, Inflation Indexed | | | 513,630 | | | | 549,664 | | |

2.125%, due 01/15/19, Inflation Indexed | | | 217,065 | | | | 238,958 | | |

1.00%, due 09/30/16 | | | 199,380 | | | | 201,093 | | |

| | | | | | 1,568,816 | | |

U.S. GOVERNMENT AGENCIES - 0.5% | |

Federal Home Loan Bank,

1.65%, due 07/18/19 | | | 29,550 | | | | 29,570 | | |

Federal National Mortgage Association,

1.25%, due 09/27/18 | | | 24,680 | | | | 24,711 | | |

Federal Home Loan Bank,

1.25%, due 02/27/18 | | | 24,585 | | | | 24,624 | | |

Federal Home Loan Mortgage Corp.,

1.40%, due 01/08/18 | | | 19,665 | | | | 19,669 | | |

Federal National Mortgage Association,

1.25%, due 01/30/20 | | | 9,525 | | | | 9,514 | | |

Federal Home Loan Bank,

1.00%, due 04/15/20 | | | 6,500 | | | | 6,502 | | |

| | | | | | 114,590 | | |

Total Government and Agency Securities

(Cost $1,588,958) | | | | | 1,683,406 | | |

CORPORATE BONDS - 5.9% | |

Kinetic Concepts, Inc.,

10.50%, due 11/01/18 | | | 47,940 | | | | 51,895 | | |

JPMorgan Chase & Co.,

3.15%, due 07/05/16 | | | 44,592 | | | | 45,749 | | |

General Motors Co.,

4.875%, due 10/02/23 | | | 41,400 | | | | 44,824 | | |

Mondelez International, Inc.,

4.125%, due 02/09/16 | | | 43,567 | | | | 44,741 | | |

The Manitowoc Co., Inc.,

8.50%, due 11/01/20 | | | 35,655 | | | | 38,151 | | |

The William Carter Co.,

5.25%, due 08/15/21 | | | 35,137 | | | | 36,367 | | |

Ultra Petroleum Corp., 144A,

5.75%, due 12/15/18 (e) | | | 37,809 | | | | 34,123 | | |

Credit Suisse Group AG, 144A,

7.50% (d) (e) (f) (g) | | | 30,000 | | | | 32,212 | | |

Omnicom Group, Inc.,

3.625%, due 05/01/22 | | | 30,425 | | | | 31,906 | | |

CVS Health Corp.,

4.00%, due 12/05/23 | | | 29,325 | | | | 31,788 | | |

Live Nation Entertainment, Inc., 144A,

7.00%, due 09/01/20 (e) | | | 28,930 | | | | 30,810 | | |

1011778 BC ULC / New Red

Finance Inc., 144A,

6.00%, due 04/01/22 (d) (e) | | | 29,500 | | | | 30,532 | | |

General Motors Co.,

3.50%, due 10/02/18 | | | 29,525 | | | | 30,250 | | |

Toyota Motor Credit Corp.,

1.45%, due 01/12/18 | | | 29,495 | | | | 29,684 | | |

CNO Financial Group, Inc., 144A,

6.375%, due 10/01/20 (e) | | | 26,060 | | | | 27,493 | | |

See accompanying Notes to Financial Statements.

16 OAKMARK FUNDS

Oakmark Equity and Income Fund March 31, 2015 (Unaudited)

Schedule of Investments (in thousands) (continued)

| | | Par Value | | Value | |

FIXED INCOME - 14.1% (continued) | |

CORPORATE BONDS - 5.9% (continued) | |

Credit Suisse New York,

1.75%, due 01/29/18 (d) | | $ | 24,700 | | | $ | 24,775 | | |

Penn National Gaming, Inc.,

5.875%, due 11/01/21 | | | 23,704 | | | | 23,526 | | |

Glencore Canada Corp.,

6.00%, due 10/15/15 (d) | | | 21,915 | | | | 22,474 | | |

Activision Blizzard, Inc., 144A,

5.625%, due 09/15/21 (e) | | | 20,965 | | | | 22,328 | | |

Lam Research Corp.,

2.75%, due 03/15/20 | | | 19,660 | | | | 19,770 | | |

JPMorgan Chase & Co.,

1.70%, due 03/01/18 | | | 19,665 | | | | 19,744 | | |

DIRECTV Holdings LLC / DIRECTV Financing Co., Inc.,

5.00%, due 03/01/21 | | | 16,710 | | | | 18,599 | | |

Scientific Games International, Inc., 144A,

10.00%, due 12/01/22 (e) | | | 19,665 | | | | 18,387 | | |

Dollar General Corp.,

4.125%, due 07/15/17 | | | 17,095 | | | | 17,982 | | |

Ultra Petroleum Corp., 144A,

6.125%, due 10/01/24 (e) | | | 19,665 | | | | 16,863 | | |

Valeant Pharmaceuticals International Inc, 144A,

5.625%, due 12/01/21 (d) (e) | | | 16,370 | | | | 16,616 | | |

Aon Corp.,

5.00%, due 09/30/20 | | | 14,745 | | | | 16,603 | | |

Anthem, Inc.,

5.875%, due 06/15/17 | | | 15,150 | | | | 16,572 | | |

Kinetic Concepts, Inc.,

12.50%, due 11/01/19 | | | 14,360 | | | | 15,688 | | |

Medtronic Inc., 144A,

3.15%, due 03/15/22 (d) (e) | | | 14,750 | | | | 15,316 | | |

Activision Blizzard, Inc., 144A,

6.125%, due 09/15/23 (e) | | | 13,615 | | | | 14,840 | | |

Zayo Group LLC / Zayo Capital Inc, 144A,

6.00%, due 04/01/23 (e) | | | 14,745 | | | | 14,819 | | |

Zimmer Holdings, Inc.,

1.45%, due 04/01/17 | | | 14,750 | | | | 14,779 | | |

Cleopatra Finance Ltd, 144A,

6.25%, due 02/15/22 (d) (e) | | | 14,800 | | | | 14,467 | | |

Cleopatra Finance Ltd, 144A,

6.50%, due 02/15/25 (d) (e) | | | 14,800 | | | | 14,282 | | |

Royal Caribbean Cruises, Ltd.,

7.25%, due 06/15/16 | | | 12,688 | | | | 13,481 | | |

Omega Healthcare Investors, Inc.,

5.875%, due 03/15/24 | | | 12,390 | | | | 13,195 | | |

GLP Capital, LP / GLP Financing II, Inc.,

5.375%, due 11/01/23 | | | 12,000 | | | | 12,405 | | |

BorgWarner, Inc.,

4.625%, due 09/15/20 | | | 10,810 | | | | 11,934 | | |

Bank of America Corp.,

5.25%, due 12/01/15 | | | 10,778 | | | | 11,068 | | |

Howard Hughes Corp., 144A,

6.875%, due 10/01/21 (e) | | | 10,000 | | | | 10,475 | | |

Omega Healthcare Investors, Inc.,

6.75%, due 10/15/22 | | | 9,865 | | | | 10,420 | | |

GLP Capital, LP / GLP Financing II, Inc.,

4.875%, due 11/01/20 | | | 10,000 | | | | 10,250 | | |

Six Flags Entertainment Corp., 144A,

5.25%, due 01/15/21 (e) | | | 9,970 | | | | 10,244 | | |

| | | Par Value | | Value | |

Kellogg Co.,

4.45%, due 05/30/16 | | $ | 9,835 | | | $ | 10,243 | | |

Valeant Pharmaceuticals International, 144A,

6.375%, due 10/15/20 (e) | | | 9,805 | | | | 10,185 | | |

Chevron Corp.,

1.365%, due 03/02/18 | | | 9,835 | | | | 9,883 | | |

Cleopatra Finance Ltd, 144A,

5.625%, due 02/15/20 (d) (e) | | | 9,800 | | | | 9,575 | | |

Tempur Sealy International, Inc.,

6.875%, due 12/15/20 | | | 8,819 | | | | 9,414 | | |

Sirius XM Radio Inc, 144A,

5.25%, due 08/15/22 (e) | | | 8,895 | | | | 9,384 | | |

Health Net, Inc.,

6.375%, due 06/01/17 | | | 8,680 | | | | 9,266 | | |

Glencore Funding LLC, 144A,

1.70%, due 05/27/16 (e) | | | 8,060 | | | | 8,094 | | |

E*TRADE Financial Corp.,

4.625%, due 09/15/23 | | | 7,865 | | | | 8,003 | | |

Quiksilver, Inc. / QS Wholesale, Inc., 144A,

7.875%, due 08/01/18 (e) | | | 8,630 | | | | 7,810 | | |

Quiksilver, Inc. / QS Wholesale, Inc.,

10.00%, due 08/01/20 | | | 10,810 | | | | 7,648 | | |

Omnicare, Inc.,

5.00%, due 12/01/24 | | | 6,880 | | | | 7,190 | | |

Omnicare, Inc.,

4.75%, due 12/01/22 | | | 6,880 | | | | 7,104 | | |

Whirlpool Corp.,

6.50%, due 06/15/16 | | | 6,610 | | | | 7,043 | | |

Scientific Games International, Inc., 144A,

7.00%, due 01/01/22 (e) | | | 6,885 | | | | 7,040 | | |

Concho Resources, Inc.,

5.50%, due 10/01/22 | | | 6,980 | | | | 7,032 | | |

Thermo Fisher Scientific, Inc.,

3.20%, due 03/01/16 | | | 6,839 | | | | 6,978 | | |

Credit Suisse Group AG, 144A,

6.25% (d) (e) (f) (g) | | | 7,000 | | | | 6,877 | | |

Quest Diagnostics, Inc.,

4.70%, due 04/01/21 | | | 5,128 | | | | 5,655 | | |

Bank of America Corp.,

5.625%, due 10/14/16 | | | 5,285 | | | | 5,627 | | |

Anadarko Petroleum Corp.,

5.95%, due 09/15/16 | | | 5,005 | | | | 5,339 | | |

CBRE Services, Inc.,

5.25%, due 03/15/25 | | | 4,915 | | | | 5,284 | | |

Serta Simmons Holdings LLC, 144A,

8.125%, due 10/01/20 (e) | | | 4,990 | | | | 5,252 | | |

E*TRADE Financial Corp.,

5.375%, due 11/15/22 | | | 4,910 | | | | 5,180 | | |

Foot Locker, Inc.,

8.50%, due 01/15/22 (b) | | | 4,340 | | | | 5,143 | | |

GLP Capital, LP / GLP Financing II, Inc.,

4.375%, due 11/01/18 | | | 5,000 | | | | 5,137 | | |

Scotiabank Peru SA, 144A,

4.50%, due 12/13/27 (d) (e) (f) | | | 5,000 | | | | 4,987 | | |

Zayo Group LLC / Zayo Capital, Inc.,

10.125%, due 07/01/20 | | | 3,445 | | | | 3,901 | | |

Omnicom Group, Inc.,

6.25%, due 07/15/19 | | | 2,950 | | | | 3,430 | | |

Family Tree Escrow LLC, 144A,

5.75%, due 03/01/23 (e) | | | 2,950 | | | | 3,105 | | |

Medtronic Inc., 144A,

1.50%, due 03/15/18 (d) (e) | | | 2,950 | | | | 2,963 | | |

See accompanying Notes to Financial Statements.

oakmark.com 17

Oakmark Equity and Income Fund March 31, 2015 (Unaudited)

Schedule of Investments (in thousands) (continued)

| | | Par Value | | Value | |

FIXED INCOME - 14.1% (continued) | |

CORPORATE BONDS - 5.9% (continued) | |

CVS Health Corp.,

2.25%, due 08/12/19 | | $ | 2,884 | | | $ | 2,929 | | |

Boston Scientific Corp.,

5.125%, due 01/12/17 | | | 2,546 | | | | 2,704 | | |

The Goldman Sachs Group, Inc.,

5.625%, due 01/15/17 | | | 2,095 | | | | 2,246 | | |

Live Nation Entertainment, Inc., 144A,

5.375%, due 06/15/22 (e) | | | 2,000 | | | | 2,040 | | |

Tyco Electronics Group SA,

6.55%, due 10/01/17 (d) | | | 1,385 | | | | 1,553 | | |

Family Tree Escrow LLC, 144A,

5.25%, due 03/01/20 (e) | | | 1,000 | | | | 1,048 | | |

Centene Corp.,

4.75%, due 05/15/22 | | | 1,000 | | | | 1,038 | | |

Post Holdings, Inc.,

7.375%, due 02/15/22 | | | 1,000 | | | | 1,035 | | |

Post Holdings, Inc., 144A,

6.75%, due 12/01/21 (e) | | | 1,000 | | | | 1,010 | | |

Ventas Realty, LP REIT,

3.50%, due 02/01/25 | | | 1,000 | | | | 1,004 | | |

The Goldman Sachs Group, Inc.,

2.55%, due 10/23/19 | | | 980 | | | | 994 | | |

VRX Escrow Corp, 144A,

5.875%, due 05/15/23 (d) (e) | | | 500 | | | | 513 | | |

VRX Escrow Corp, 144A,

5.375%, due 03/15/20 (d) (e) | | | 500 | | | | 504 | | |

Hologic, Inc.,

6.25%, due 08/01/20 | | | 250 | | | | 259 | | |

VRX Escrow Corp, 144A,

6.125%, due 04/15/25 (d) (e) | | | 250 | | | | 259 | | |

Total Corporate Bonds

(Cost $1,218,067) | | | | | 1,231,335 | | |

ASSET BACKED SECURITIES - 0.1% | |

Cabela's Master Credit Card Trust, 144A,

0.725%, due 10/15/19 (e) (f)

(Cost $11,450) | | | 11,450 | | | | 11,486 | | |

TOTAL FIXED INCOME - 14.1%

(COST $2,818,475) | | | | | 2,926,227 | | |

SHORT TERM INVESTMENTS - 22.2% | |

COMMERCIAL PAPER - 17.8% | |

Toyota Motor Credit Corp.,

0.08% - 0.17%,

due 04/14/15 - 06/23/15 (h) | | | 1,050,000 | | | | 1,049,854 | | |

MetLife Short Term Funding LLC, 144A,

0.11% - 0.15%,

due 04/01/15 - 05/28/15 (e) (h) | | | 500,076 | | | | 500,025 | | |

Philip Morris International, Inc., 144A,

0.07% - 0.13%,

due 04/20/15 - 05/26/15 (e) (h) | | | 442,924 | | | | 442,883 | | |

BMW US Capital LLC, 144A,

0.10% - 0.13%,

due 04/01/15 - 05/04/15 (e) (h) | | | 343,000 | | | | 342,979 | | |

American Honda Finance Corp.,

0.09% - 0.15%,

due 04/08/15 - 06/23/15 (h) | | | 257,000 | | | | 256,970 | | |

| | | Par Value | | Value | |

General Mills, Inc., 144A,

0.31% - 0.54%,

due 04/06/15 - 05/22/15 (e) (h) | | $ | 225,100 | | | $ | 225,045 | | |

State Street Corp.,

0.18%, due 05/11/15 - 06/17/15 (h) | | | 225,000 | | | | 224,930 | | |

Kellogg Co., 144A,

0.35% - 0.49%,

due 04/01/15 - 04/21/15 (e) (h) | | | 176,650 | | | | 176,622 | | |

Walgreens Boots,

0.50% - 0.56%,

due 04/08/15 - 04/17/15 (h) | | | 145,000 | | | | 144,978 | | |

Anthem, Inc., 144A,

0.30% - 0.38%,

due 04/01/15 - 04/15/15 (e) (h) | | | 125,000 | | | | 124,991 | | |

John Deere Capital Co., 144A,

0.11%, due 04/13/15 - 05/08/15 (e) (h) | | | 100,000 | | | | 99,993 | | |

J.P. Morgan Securities LLC,

0.21%, due 04/06/15 (h) | | | 50,000 | | | | 49,999 | | |

BP Capital Markets PLC, 144A,

0.60% - 0.63%,

due 10/16/15 - 11/02/15 (d) (e) (h) | | | 40,750 | | | | 40,643 | | |

Total Commercial Paper

(Cost $3,679,879) | | | | | 3,679,912 | | |

REPURCHASE AGREEMENT - 2.6% | |

Fixed Income Clearing Corp. Repurchase

Agreement, 0.01% dated 03/31/15 due

04/01/15, repurchase price $542,290,

collateralized by a United States Treasury

Note, 2.000%, due 10/31/21, value plus

accrued interest of $553,138

(Cost: $542,289) | | | 542,289 | | | | 542,289 | | |

CORPORATE BONDS - 1.8% | |

Kraft Foods Group, Inc.,

1.625%, due 06/04/15 | | | 39,971 | | | | 40,038 | | |

Bank of America Corp.,

4.50%, due 04/01/15 | | | 37,334 | | | | 37,334 | | |

ConAgra Foods, Inc.,

1.30%, due 01/25/16 | | | 33,563 | | | | 33,651 | | |

Capital One Financial Corp.,