UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

Investment Company Act file number | | 811-06241 |

Loomis Sayles Funds II

|

| (Exact name of registrant as specified in charter) |

| | |

| 399 Boylston Street, Boston, Massachusetts | | 02116 |

| (Address of principal executive offices) | | (Zip code) |

Coleen Downs Dinneen, Esq.

Natixis Distributors, L.P.

399 Boylston Street

Boston, Massachusetts 02116

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (617) 449-2810

Date of fiscal year end: September 30

Date of reporting period: March 31, 2009

| Item 1. | Reports to Stockholders. |

The Registrant’s semi-annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

INCOME FUNDS

SEMIANNUAL REPORT

March 31, 2009

Loomis Sayles Core Plus Bond Fund

Loomis Sayles High Income Fund

Loomis Sayles International Bond Fund

Loomis Sayles Limited Term Government and Agency Fund

Loomis Sayles Strategic Income Fund

TABLE OF CONTENTS

Management Discussion and Performancepage 1

Portfolio of Investmentspage 15

Financial Statementspage 65

LOOMIS SAYLES CORE PLUS BOND FUND

PORTFOLIO PROFILE

Objective:

Seeks a high level of current income consistent with what the fund considers reasonable risk

Strategy:

Invests primarily in U.S. corporate and U.S. government bonds

Fund Inception:

November 7, 1973

Managers:

Peter W. Palfrey, CFA

Richard G. Raczkowski

Loomis, Sayles & Company, L.P.

Symbols:

| | |

| Class A | | NEFRX |

| Class B | | NERBX |

| Class C | | NECRX |

| Class Y | | NERYX |

What You Should Know:

Fixed-income securities are subject to credit risk and interest rate risk; their value generally rises when prevailing interest rates fall and falls when rates rise.

The fund can invest a significant percentage of assets in debt securities that are rated below investment grade and the value of fund shares can be adversely affected by changes in economic conditions or other circumstances. Lower rated debt securities have speculative characteristics and may be subject to greater price volatility than higher rated investments. In addition, the secondary market for these securities may lack liquidity. The fund can also invest a significant percentage of assets in foreign securities and the value of the fund shares can be adversely affected by changes in currency exchange rates, political, and economic developments. In emerging markets, these risks can be significant. Fund shares should be viewed as a long-term investment.

Management Discussion

As Loomis Sayles Core Plus Bond Fund’s fiscal year got underway last fall, widespread concern about the world’s financial markets troubled investors, although the market’s risk tolerance appeared to increase modestly in March of 2009. For the six months ended March 31, 2009, the fund returned 3.80% based on the net asset value of Class A shares and $0.36 in reinvested dividends. The fund lagged its broad-based benchmark, Barclays Capital Aggregate Bond Index, which returned 4.70%, but its results were better than the -0.49% average return on the funds in its Morningstar Intermediate-Term Bond peer group. The fund’s 30-day SEC yield as of March 31, 2009 was 5.80%.

WHAT HELPED THE FUND OUTPERFORM ITS PEER GROUP?

As part of a gradual, tactical shift during the period, we capitalized on strength in certain high-yield assets and invested the proceeds in what we felt were attractive, investment-grade names, which did relatively well in December. We added to these positions primarily by investing in new issues that were brought to market at what we saw as significant discounts. In the first quarter of 2009 the fund benefited from rising valuations of higher-yielding, lower-quality issues as risk aversion began to diminish.

The fund’s holdings in U.S. government agency securities were positive after the Treasury announced targeted purchases. While commercial mortgage-backed securities (CMBS) modestly underperformed the broader market, our combination of well-seasoned, high-quality CMBS did relatively well. U.S. government agency securities also contributed to performance.

Generally speaking, our non-U.S. dollar allocations were positive for the fund during the past six months. We had a significant allocation to securities denominated in the Japanese yen as a defensive measure late in 2008, but we sold most of these positions at a profit later in the period and redeployed assets to securities denominated in Canadian and Australian dollars. These shifts proved to be opportune.

WHAT CAUSED THE FUND TO LAG ITS BENCHMARK?

Our allocation to mortgage-backed securities included 30-year, higher-quality issues in an effort to lengthen spread duration while keeping a lid on risk. Government support caused this sector to do well, but the fund was underweight in these issues relative to the benchmark, which limited its ability to benefit from the rally.

Treasury securities were the top performers during the final three months of 2008. However, this trend reversed in the first quarter of 2009 as interest rates rose and risk aversion diminished. The fund’s holdings in 20-year Treasury Inflation Protected Securities (TIPS) provided attractive returns in the first quarter of 2009, but this did not outweigh negative returns late in 2008. We recently reduced the fund’s TIPS exposure and redeployed the assets into a combination of shorter- and longer-maturity nominal (non-TIPS) Treasuries.

We took advantage of low prices late in 2008, adding to the fund’s position in financials. This strategy worked well in the closing quarter of 2008, although it detracted from performance early in 2009 as spreads (the price differential between lower- and higher-quality issues) narrowed. However, for the full six-month period, the fund’s overweight in financials was a net positive. Negative security selection among high-yield industrials made this the fund’s worst-performing group for the period.

WHAT NOW?

We plan to continue adding opportunistically to investment-grade corporate bonds, focusing on the new-issue market. We also plan to add to high-quality CMBS and cautiously extend the fund’s position in high-yielding securities if the credit markets show further signs of stabilizing. We are currently focusing on investment-grade, non-financial companies. Our goal is to build longer-term value while reducing interest rate sensitivity as the recovery in the financial markets gains traction.

1

LOOMIS SAYLES CORE PLUS BOND FUND

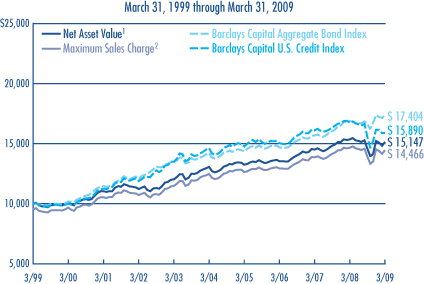

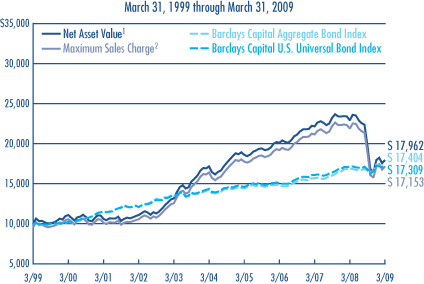

Investment Results through March 31, 2009

PERFORMANCE IN PERSPECTIVE

The charts comparing the fund’s performance to two indexes provide you with a general sense of how it performed. The fund’s total return for the period shown below appears with and without sales charges and includes fund expenses and fees. An index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged and does not have expenses that affect the results. It is not possible to invest directly in an index. Investors would incur transaction costs and other expenses if they purchased the securities necessary to match the index.

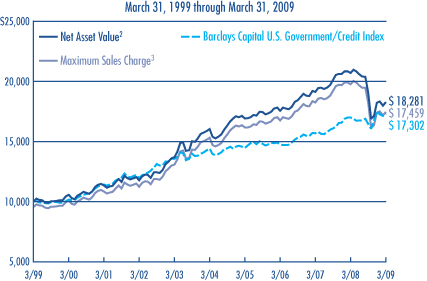

Growth of a $10,000 Investment in Class A Shares4

Average Annual Returns — March 31, 20094

| | | | | | | | | | | | |

| | | | | |

| | | 6 MONTHS | | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | |

CLASS A (Inception 11/7/73) | | | | | | | | | | | | |

Net Asset Value1 | | 3.80 | % | | -1.40 | % | | 3.01 | % | | 4.24 | % |

With Maximum Sales Charge2 | | -0.90 | | | -5.86 | | | 2.06 | | | 3.76 | |

| | | | | |

CLASS B (inception 9/13/93) | | | | | | | | | | | | |

Net Asset Value1 | | 3.40 | | | -2.15 | | | 2.26 | | | 3.48 | |

With CDSC3 | | -1.60 | | | -6.80 | | | 1.93 | | | 3.48 | |

| | | | | |

CLASS C (Inception 12/30/94) | | | | | | | | | | | | |

Net Asset Value1 | | 3.44 | | | -2.09 | | | 2.25 | | | 3.47 | |

With CDSC3 | | 2.44 | | | -3.01 | | | 2.25 | | | 3.47 | |

| | | | | |

CLASS Y (Inception 12/30/94) | | | | | | | | | | | | |

Net Asset Value1 | | 3.91 | | | -1.15 | | | 3.28 | | | 4.60 | |

| | | | | |

| COMPARATIVE PERFORMANCE | | 6 MONTHS | | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | |

Barclays Capital Aggregate Bond Index | | 4.70 | % | | 3.13 | % | | 4.13 | % | | 5.70 | % |

Barclays Capital U.S. Credit Index | | 2.18 | | | -5.21 | | | 1.62 | | | 4.74 | |

Morningstar Int.-Term Bond Fund Avg. | | -0.49 | | | -4.94 | | | 1.36 | | | 3.92 | |

See page 11 for a description of the indexes.

All returns represent past performance and do not guarantee future results. Periods of less than one year are not annualized. Share price and return will vary and you may have a gain or loss when you sell your shares. All results include reinvestment of any dividends and capital gains. Current returns may be higher or lower than those shown. For performance current to the most recent month-end, visit www.funds.natixis.com. Class Y shares are available to certain investors, as described in the prospectus.

The table and graph do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

PORTFOLIO FACTS

| | | | |

| |

| | | % of Net Assets as of |

| CREDIT QUALITY | | 3/31/09 | | 9/30/08 |

Aaa | | 48.2 | | 59.1 |

Aa | | 4.9 | | 5.6 |

A | | 11.2 | | 4.8 |

Baa | | 20.4 | | 14.6 |

Ba | | 5.0 | | 4.8 |

B | | 3.5 | | 5.7 |

Caa | | 0.8 | | 0.5 |

Ca | | 0.2 | | 0.3 |

Not Rated* | | 5.0 | | 3.8 |

Short-term and other | | 0.8 | | 0.8 |

Credit quality is based on ratings from Moody’s Investors Service.

* Securities that are not rated by Moody’s may be rated by another rating agency or by Loomis Sayles.

| | | | | | |

| |

| | | % of Net Assets as of | |

| EFFECTIVE DURATION | | 3/31/09 | | | 9/30/08 | |

1 year or less | | 5.0 | | | 8.8 | |

1-5 years | | 48.4 | | | 39.7 | |

5-10 years | | 34.7 | | | 40.0 | |

10+ years | | 11.9 | | | 11.5 | |

Average Effective Duration | | 5.4 | years | | 5.7 | years |

Portfolio characteristics will vary.

EXPENSE RATIOS AS STATED IN THE MOST RECENT PROSPECTUS

| | | | | | |

| Share Class | | Gross Expense Ratio5 | | | Net Expense Ratio6 | |

A | | 1.04 | % | | 0.90 | % |

B | | 1.80 | | | 1.65 | |

C | | 1.79 | | | 1.65 | |

Y | | 0.75 | | | 0.65 | |

NOTES TO CHARTS

1 | Does not include a sales charge. |

2 | Includes maximum sales charge of 4.50%. |

3 | Performance for Class B shares assumes a maximum 5% contingent deferred sales charge (“CDSC”) applied when you sell shares, which declines annually between years 1-6 according to the following schedule: 5, 4, 3, 3, 2, 1, 0%. Class C shares performance assumes a 1% CDSC applied when you sell shares within one year of purchase. |

4 | Fund performance has been increased by expense reductions and reimbursements, if any, without which performance would have been lower. |

5 | Before reductions and reimbursements. |

6 | After reductions and reimbursements. Expense reductions are contractual and are set to expire on 1/31/10. |

2

LOOMIS SAYLES HIGH INCOME FUND

PORTFOLIO PROFILE

Objective:

Seeks high current income plus the opportunity for capital appreciation to produce a high total return

Strategy:

Invests primarily in lower-quality fixed-income securities

Fund Inception:

February 22, 1984

Managers:

Matthew J. Eagan, CFA

Kathleen C. Gaffney, CFA

Elaine M. Stokes

Loomis, Sayles & Company, L.P.

Symbols:

| | |

| Class A | | NEFHX |

| Class B | | NEHBX |

| Class C | | NEHCX |

| Class Y | | NEHYX |

What You Should Know:

Fixed-income securities are subject to credit risk and interest rate risk; their value generally rises when prevailing interest rates fall and falls when rates rise.

The fund can invest a significant percentage of assets in debt securities that are rated below investment grade and the value of fund shares can be adversely affected by changes in economic conditions or other circumstances. Lower rated debt securities have speculative characteristics and may be subject to greater price volatility than higher rated investments. In addition, the secondary market for these securities may lack liquidity. The fund can also invest a significant percentage of assets in foreign securities and the value of the fund shares can be adversely affected by changes in currency exchange rates, political, and economic developments. In emerging markets, these risks can be significant. Fund shares should be viewed as a long-term investment.

Management Discussion

With the exception of U.S. government issues, bond markets suffered significant declines last fall, as credit markets remained frozen and the global economy continued to contract. However, conditions became more stable in December and for much of the first quarter of 2009. Massive government stimulus packages and loan programs brought a measure of reassurance, encouraging investors to move tentatively into corporate sectors.

For the six-month fiscal period ended March 31, 2009, the total return on Loomis Sayles High Income Fund was -12.25% based on the net asset value of Class A shares and $0.19 in reinvested dividends. Although these results are disappointing in absolute terms, the fund achieved a slim lead over its benchmark, Barclays Capital High Yield Composite Index, which returned -12.97% for the period, and outperformed the -15.47% average return on Morningstar’s High Yield Bond category. The fund’s 30-day SEC yield as of March 31, 2009 was 9.51%.

WHICH FACTORS WERE THE MOST HARMFUL?

Stretches of severe illiquidity that began last fall fueled investors’ risk aversion, as bond dealers were unwilling to take positions in the turbulent markets. The result was falling prices for corporate issues across all quality ranges, as nervous investors shifted assets into Treasury issues. The fund’s returns suffered from the marked weakness in holdings rated below investment grade, especially securities of companies burdened by heavy debt levels.

A combination of rising unemployment, recession and unwieldy debt loads also drove down the price of bonds that had been issued as part of leveraged buy-outs – corporate acquisitions that had been financed largely by borrowing when credit was abundant. Lower-rated holdings in the industrial and utilities sectors were especially hard hit as balance sheets weakened and defaults increased. Reduced consumer spending also drove down valuations on fund holdings in the consumer discretionary and staples sectors.

WHAT HELPED STABILIZE THE MARKETS?

A series of government measures in the past several months pumped large amounts of capital into the credit markets, allaying our concerns of a possible system-wide meltdown. We took advantage of the market’s improving tone to expand holdings of higher-quality banking issues selling at low prices. By the end of March 2009, this strategy had aided absolute and relative returns, as investment-grade issues staged a partial recovery.

The Federal Reserve introduced one program aimed at supporting the credit needs of households and small businesses and another designed to provide liquidity for banks with “toxic” assets on their balance sheets. These initiatives bolstered confidence in bonds backed by commercial mortgages and those secured by auto and student loans. We responded by increasing the fund’s exposure to AAA-rated Commercial Mortgage Backed Securities and Asset Backed Securities tied to credit card debt. This boosted both relative and absolute returns in the first three months of 2009, when investors began to take interest in better quality, high-yield issues – those rated BB – where default risks appeared lower. Unfortunately, this renewed interest was not enough to erase earlier declines.

WHAT DO YOU SEE AHEAD?

We believe high-yield issues will continue to be volatile, as defaults continue to increase over the course of the year. We remain underweight the CCC-rated portion of the market, as we believe most defaults will come from this space. We believe investment-grade credit continues to offer strong relative value, as spreads remain at relatively wide levels. As the markets grow more convinced the global recovery has taken hold, we eventually expect to see more demand for riskier assets, such as high-yield and investment-grade credit, as well as commodity currencies.

3

LOOMIS SAYLES HIGH INCOME FUND

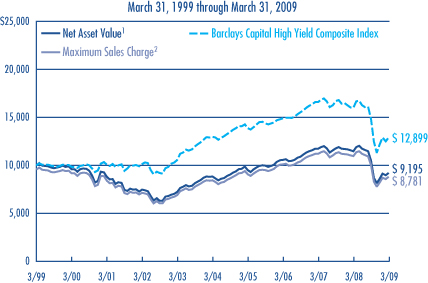

Investment Results through March 31, 2009

PERFORMANCE IN PERSPECTIVE

The charts comparing the fund’s performance to an index provide you with a general sense of how it performed. The fund’s total return for the period shown below appears with and without sales charges and includes fund expenses and fees. An index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged and does not have expenses that affect the results. It is not possible to invest directly in an index. Investors would incur transaction costs and other expenses if they purchased the securities necessary to match the index.

Growth of a $10,000 Investment in Class A Shares4

Average Annual Returns — March 31, 20094

| | | | | | | | | | | | | | | |

| | | | | | |

| | | 6 MONTHS | | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | SINCE

INCEPTION | |

CLASS A (Inception 2/22/84) | | | | | | | | | | | | | | | |

Net Asset Value1 | | -12.25 | % | | -19.85 | % | | 0.80 | % | | -0.83 | % | | — | |

With Maximum Sales Charge2 | | -16.21 | | | -23.51 | | | -0.12 | | | -1.29 | | | — | |

| | | | | | |

CLASS B (Inception 9/20/93) | | | | | | | | | | | | | | | |

Net Asset Value1 | | -12.81 | | | -20.65 | | | 0.02 | | | -1.59 | | | — | |

With CDSC3 | | -16.95 | | | -24.30 | | | -0.27 | | | -1.59 | | | — | |

| | | | | | |

CLASS C (Inception 3/2/98) | | | | | | | | | | | | | | | |

Net Asset Value1 | | -12.59 | | | -20.44 | | | 0.04 | | | -1.58 | | | — | |

With CDSC3 | | -13.42 | | | -21.17 | | | 0.04 | | | -1.58 | | | — | |

| | | | | | |

CLASS Y (Inception 2/29/08) | | | | | | | | | | | | | | | |

Net Asset Value1 | | -12.14 | | | -19.66 | | | — | | | — | | | -18.72 | % |

| | | | | | |

| COMPARATIVE PERFORMANCE | | 6 MONTHS | | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | SINCE

CLASS Y

INCEPTION7 | |

Barclays Capital High Yield Composite Index | | -12.97 | % | | -19.31 | % | | -0.10 | % | | 2.58 | % | | -18.22 | % |

Morningstar High Yield Bond Fund Avg. | | -15.47 | | | -20.97 | | | -1.42 | | | 0.99 | | | -19.77 | |

See page 11 for a description of the indexes.

All returns represent past performance and do not guarantee future results. Periods of less than one year are not annualized. Share price and return will vary and you may have a gain or loss when you sell your shares. All results include reinvestment of dividends and capital gains. Current returns may be higher or lower than those shown. For performance current to the most recent month-end, visit www.funds.natixis.com. Performance history includes periods from a predecessor fund. Class Y shares are available to certain investors, as described in the prospectus.

The table and graph do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

PORTFOLIO FACTS

| | | | |

| |

| | | % of Net Assets as of |

| CREDIT QUALITY | | 3/31/09 | | 9/30/08 |

Aaa | | 20.1 | | 17.3 |

Aa | | 1.2 | | 2.0 |

A | | 2.0 | | 1.0 |

Baa | | 7.2 | | 7.6 |

Ba | | 19.0 | | 14.9 |

B | | 26.4 | | 28.9 |

Caa | | 9.2 | | 16.4 |

Ca | | 1.3 | | 0.5 |

C | | 0.0 | | 0.0 |

Not Rated* | | 11.4 | | 10.1 |

Short-term and other | | 2.2 | | 1.3 |

Credit quality is based on ratings from Moody’s Investors Service.

* Securities that are not rated by Moody’s may be rated by another rating agency or by Loomis Sayles.

| | | | | | |

| |

| | | % of Net Assets as of | |

| EFFECTIVE MATURITY | | 3/31/09 | | | 9/30/08 | |

1 year or less | | 21.3 | | | 16.0 | |

1-5 years | | 24.4 | | | 25.7 | |

5-10 years | | 31.3 | | | 28.5 | |

10+ years | | 23.0 | | | 29.8 | |

Average Effective Maturity | | 7.8 | years | | 8.8 | years |

Portfolio characteristics will vary.

EXPENSE RATIOS AS STATED IN THE MOST RECENT PROSPECTUS

| | | | | | |

| Share Class | | Gross Expense Ratio5 | | | Net Expense Ratio6 | |

A | | 1.40 | % | | 1.15 | % |

B | | 2.15 | | | 1.90 | |

C | | 2.15 | | | 1.90 | |

Y | | 1.15 | | | 0.90 | |

NOTES TO CHARTS

1 | Does not include a sales charge. |

2 | Includes maximum sales charge of 4.50%. |

3 | Performance for Class B shares assumes a maximum 5% contingent deferred sales charge (“CDSC”) applied when you sell shares, which declines annually between years 1-6 according to the following schedule: 5, 4, 3, 3, 2, 1, 0%. Class C shares performance assumes a 1% CDSC applied when you sell shares within one year of purchase. |

4 | Fund performance has been increased by expense reductions and reimbursements, if any, without which performance would have been lower. |

5 | Before reductions and reimbursements. |

6 | After reductions and reimbursements. Expense reductions are contractual and are set to expire on 1/31/10. |

7 | The since-inception comparative performance figures shown for Class Y shares are calculated from 3/1/08. |

4

LOOMIS SAYLES INTERNATIONAL BOND FUND

PORTFOLIO PROFILE

Objective:

Seeks high total return through a combination of high current income and capital appreciation

Strategy:

Invests primarily in fixed-income securities located outside the U.S.

Fund Inception:

February 1, 2008

Managers:

Lynda L. Schweitzer, CFA

Kenneth M. Buntrock, CFA, CIC

David W. Rolley, CFA

Loomis, Sayles & Company, L.P.

Symbols:

| | |

| Class A | | LSIAX |

| Class C | | LSICX |

| Class Y | | LSIYX |

What You Should Know:

Fixed-income securities are subject to credit risk and interest rate risk; their value generally rises when prevailing interest rates fall and falls when rates rise. The fund may also invest in public or private debt obligations issued or guaranteed by U.S. or non-U.S. issuers. The fund can invest a significant percentage of assets in foreign securities and the value of the fund shares can be adversely affected by changes in currency exchange rates, political, and economic developments. In emerging markets these risks can be significant. The fund can invest a significant percentage of assets in debt securities that are rated below investment grade. Lower-rated debt securities have speculative characteristics and may be subject to greater price volatility than higher-rated investments. In addition, the secondary market for these securities may lack liquidity. Fund shares should be viewed as a long-term investment.

Management Discussion

Investors in capital markets around the world continued to be strongly risk averse as the credit crisis worsened and the global economy contracted during the six months ended March 31, 2009. Fixed-income securities with higher credit risk performed poorly throughout most of the period, while government bonds and other high-quality issues did relatively well. In the international currency markets, the U.S. dollar gained in strength against most foreign currencies, including the euro and the Japanese yen.

For the six months ended March 31, 2009, Class A shares of Loomis Sayles International Bond Fund returned -2.04% at net asset value, including $0.10 in dividends reinvested during the period. For the same six months, the fund’s benchmark, Barclays Capital Global Aggregate Bond ex-USD Index, returned -0.08%, while the average return on the funds in Morningstar’s World Bond category was -1.35%. The fund’s 30-day SEC yield as of March 31, 2009 was 3.95%.

WHAT CAUSED THE FUND TO LAG ITS BENCHMARK?

The fund’s emphasis on investment-grade corporate bonds and securities not represented in the benchmark detracted from results. Continuing reports of slowing worldwide economic activity during the period intensified risk aversion, causing the fund’s investment-grade holdings to become a drag on performance. The worst performers were investment-grade bonds issued by financial companies in the United Kingdom and Europe. Although high-yield corporate issues recovered somewhat in the March of 2009, the improvement was not enough to offset their poor results in October and November. The fund’s non-benchmark country position in U.S. dollar-denominated assets detracted from results when dollar-denominated bonds underperformed in foreign markets, despite strength in the dollar itself.

WHICH STRATEGIES PROVED SUPPORTIVE?

Despite disappointing results from some U.S. dollar-denominated assets, the fund’s overall currency strategy was positive. Our strategy of underweighting the euro and the Canadian dollar benefited the fund as those currencies weakened in value relative to the U.S. dollar. The fund’s non-benchmark exposure to the U.S. dollar also helped results, as did our de-emphasis of the Japanese market. As the yen weakened against the U.S. dollar in March, we reduced the fund’s exposure to Japan. Meanwhile, the fund had little or no exposure to such emerging-market currencies as the Korean won or the Polish zloty, which are represented in the benchmark.

WHAT CHANGED IN THE FIRST QUARTER OF 2009?

Even as some economic indicators in the United States and Japan appeared to worsen in the first three months of 2009, market attitudes about risk seemed to improve, as stock markets, high-yield bonds and currencies of commodity-rich countries all recovered. As a consequence, riskier assets began outperforming the higher-quality securities that had led the market since mid-2008. Meanwhile, long-duration U.S. Treasuries came under selling pressure as investors became concerned that inflationary pressures might begin to increase.

WHAT DO YOU SEE AHEAD?

Investor sentiment appears focused on the positives. In April, the Group of 20 (G-20) international policy makers agreed to pledge up to $1 trillion in emergency assistance to the global economy. This action seems to have further contributed to investors’ willingness to accept risk.

Consequently we have positioned the fund for the global economic recovery we see ahead by maintaining the fund’s underweight in the Japanese yen and continuing to emphasize investment-grade and high-yield corporate bonds. We think it is possible the market may pull back somewhat after the recent recovery by higher-risk securities. If this occurs, we intend to take advantage of the resulting lower prices to add to our positions in investments that we believe will benefit in an economic recovery. This would include increasing exposure to currencies linked to commodity prices, emerging-market bonds and high-yield corporate bonds.

5

LOOMIS SAYLES INTERNATIONAL BOND FUND

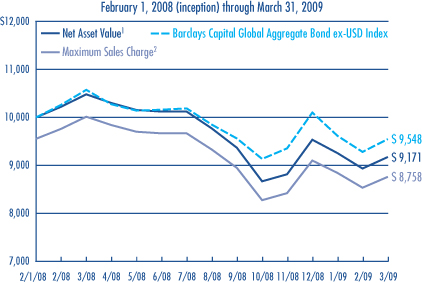

Investment Results through March 31, 2009

PERFORMANCE IN PERSPECTIVE

The charts comparing the fund’s performance to an index provide you with general sense of how it performed. The fund’s total return for the period shown below appears with and without sales charges and includes fund expenses and fees. An index measures the performance of a theoretical portfolio. Unlike a fund, an index is unmanaged and does not have expenses that affect the results. It is not possible to invest directly in an index. Investors would incur transaction costs and other expenses if they purchased the securities necessary to match the index.

Growth of $10,000 Investment in Class A Shares4

Average Annual Returns — March 31, 20094

| | | | | | | | | |

| | | | |

| | | 6 MONTHS | | | 1 YEAR | | | SINCE

INCEPTION | |

CLASS A (Inception 2/1/08) | | | | | | | | | |

Net Asset Value1 | | -2.04 | % | | -12.50 | % | | -7.17 | % |

With Maximum Sales Charge2 | | -6.42 | | | -16.42 | | | -10.77 | |

| | | | |

CLASS C (Inception 2/1/08) | | | | | | | | | |

Net Asset Value1 | | -2.41 | | | -13.30 | | | -7.96 | |

With CDSC3 | | -3.38 | | | -14.16 | | | -7.96 | |

| | | | |

CLASS Y (Inception 2/1/08) | | | | | | | | | |

Net Asset Value1 | | -1.82 | | | -12.33 | | | -7.01 | |

| | | | |

| COMPARATIVE PERFORMANCE | | 6 MONTHS | | | 1 YEAR | | | SINCE

INCEPTION | |

Barclays Capital Global Aggregate Bond ex-USD Index | | -0.08 | % | | -9.70 | % | | -3.89 | % |

Morningstar World Bond Fund Avg. | | -1.35 | | | -9.45 | | | -5.91 | |

See page 11 for a description of the indexes.

All returns represent past performance and do not guarantee future results. Periods of less than one year are not annualized. Share price and return will vary and you may have a gain or loss when you sell your shares. All results include reinvestment of dividends and capital gains. Current returns may be higher or lower than those shown. For performance current to the most recent month-end, visit www.funds.natixis.com. Class Y shares are available to certain investors, as described in the prospectus.

The table does not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

PORTFOLIO FACTS

| | | | |

| |

| | | % of Net Assets as of |

| CREDIT QUALITY | | 3/31/09 | | 9/30/08 |

Aaa | | 41.7 | | 54.2 |

Aa | | 16.8 | | 18.7 |

A | | 11.3 | | 8.3 |

Baa | | 15.4 | | 10.5 |

Ba | | 5.6 | | 3.1 |

B | | 1.4 | | 0.5 |

Caa | | 0.5 | | 0.7 |

Not Rated* | | 6.2 | | 2.3 |

Short-term and other | | 1.1 | | 1.7 |

Credit quality is based on ratings from Moody’s Investors Service.

* Securities that are not rated by Moody’s may be rated by another rating agency or by Loomis Sayles.

| | | | | | |

| |

| | | % of Net Assets as of | |

| EFFECTIVE MATURITY | | 3/31/09 | | | 9/30/08 | |

1 year or less | | 14.0 | | | 12.5 | |

1-5 years | | 24.5 | | | 18.4 | |

5-10 years | | 42.9 | | | 55.2 | |

10+ years | | 18.6 | | | 13.9 | |

Average Effective Maturity | | 8.0 | years | | 8.1 | years |

Portfolio characteristics will vary.

EXPENSE RATIOS AS STATED IN THE MOST RECENT PROSPECTUS

| | | | | | |

| Share Class | | Gross Expense Ratio5 | | | Net Expense Ratio6 | |

A | | 2.20 | % | | 1.10 | % |

C | | 2.93 | | | 1.85 | |

Y | | 1.83 | | | 0.85 | |

NOTES TO CHARTS

1 | Does not include a sales charge. |

2 | Includes maximum sales charge of 4.50%. |

3 | Class C shares performance assumes a 1% CDSC applied when you sell shares within one year of purchase. |

4 | Fund performance has been increased by expense reductions and reimbursements, if any, without which performance would have been lower. |

5 | Before reductions and reimbursements. |

6 | After reductions and reimbursements. Expense reductions are contractual and are set to expire on 1/31/10. |

6

LOOMIS SAYLES LIMITED TERM GOVERNMENTAND AGENCY FUND

PORTFOLIO PROFILE

Objective:

Seeks a high current return consistent with preservation of capital

Strategy:

Invests primarily in securities issued or guaranteed by the U.S. government, its agencies or instrumentalities

Fund Inception:

January 3, 1989

Managers:

John Hyll

Clifton V. Rowe, CFA

Loomis, Sayles & Company, L.P.

Symbols:

| | |

| Class A | | NEFLX |

| Class B | | NELBX |

| Class C | | NECLX |

| Class Y | | NELYX |

What You Should Know:

Fixed-income securities are subject to credit risk and interest rate risk; their value generally rises when prevailing interest rates fall and falls when rates rise. Securities issued by the U.S. government are guaranteed by the U.S. government if held to maturity; mutual funds that invest in these securities are not guaranteed. Securities issued by U.S. government agencies may not be government guaranteed.

Management Discussion

Government attempts to stabilize the financial system and reinvigorate the economy gradually worked to improve investors’ willingness to accept risk in the first half of Loomis Sayles Limited Term Government and Agency Fund’s fiscal year. Investors appear to believe that steps taken by global governments have, at a minimum, reduced the risk of an extended global depression. However, the staggering cost of this extensive government intervention is beginning to trouble investors.

During the six months ended March 31, 2009, the fund returned 3.79% based on the net asset value of Class A shares and $0.15 in dividends reinvested during the period. The fund lagged its benchmark, Barclays Capital 1-5 Year Government Bond Index, which returned 4.64% for the period, but came in ahead of the average 3.32% return on Morningstar’s Short Government category. The fund’s 30-day SEC yield was 2.41% at March 31, 2009.

WHAT WORKED WELL FOR THE FUND?

Mortgage-backed securities (MBS) backed by 30-year loans were the focus of the Federal Reserve’s purchase program, and the fund benefited from its emphasis on these securities during the period. Specifically, we focused on MBS issued by government-sponsored agencies, which have the advantage of indirect support from the U.S. government. High-quality, short duration, asset-backed securities (ABS), including those backed by automobile loans and credit card receivables, were another area of focus. These securities currently offer attractive yields and have strong credit quality due to their secured status and other credit enhancements. The fund’s position in Treasury inflation protected securities (TIPS) also performed well as deflation concerns eased during the period.

Relative to its benchmark, the fund is also overweight in commercial mortgage-backed securities (CMBS). In this sector, the fund holds senior securities backed by first mortgages on commercial properties. We see relatively little risk of rating downgrades in these holdings.

WHICH SECURITIES PROVED DISADVANTAGEOUS?

The worst performers during the period were MBS that were not issued by government-sponsored enterprises because they do not benefit from the implied government support. As the real estate markets continued to deteriorate, this weakness also spread into the corporate bond market and to non-residential mortgages, such as CMBS. Although the CMBS market recovered in the first quarter of 2009, it had lagged for the full period, and this contributed to the fund’s performance shortfall relative to the benchmark.

HOW DID YOU POSITION THE PORTFOLIO?

We increased the fund’s holdings in TIPS and CMBS, and reduced holdings in MBS issued by government-sponsored enterprises. We believe MBS will continue to benefit from the support of the U.S. government, given their critical function in the mortgage market, but we see limited additional upside potential.

High-quality CMBS have suffered as real estate concerns grew, so we used this as an opportunity to purchase the most senior securities – those we believe to have ample credit protection. We also added to the fund’s TIPS holdings because the sector had underperformed nominal (non-TIPS) Treasuries.

WHAT’S YOUR CURRENT OUTLOOK?

Near term, we are not expecting any changes in the Federal Funds rate, although we think longer-maturity interest rates will move modestly higher. Accordingly, we are more focused on identifying income opportunities than on looking for significant principal appreciation. U.S. Treasuries may do well near term, as the economy struggles along, but their yields are so low that any hint of a recovery or inflation could have a negative impact. We believe the income advantage offered by MBS holdings should make them perform well provided the interest rate environment remains relatively stable.

7

LOOMIS SAYLES LIMITED TERM GOVERNMENTAND AGENCY FUND

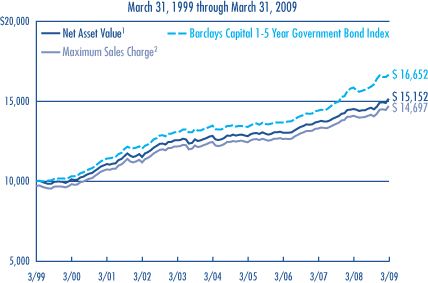

Investment Results through March 31, 2009

PERFORMANCE IN PERSPECTIVE

The charts comparing the fund’s performance to an index provide you with a general sense of how it performed. The fund’s total return for the period shown below appears with and without sales charges and includes fund expenses and fees. An index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged and does not have expenses that affect the results. It is not possible to invest directly in an index. Investors would incur transaction costs and other expenses if they purchased the securities necessary to match the index.

Growth of a $10,000 Investment in Class A Shares4

Average Annual Returns — March 31, 20094

| | | | | | | | | | | | |

| | | | | |

| | | 6 MONTHS | | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | |

CLASS A (Inception 1/3/89) | | | | | | | | | | | | |

Net Asset Value1 | | 3.79 | % | | 4.33 | % | | 3.35 | % | | 4.24 | % |

With Maximum Sales Charge2 | | 0.67 | | | 1.25 | | | 2.72 | | | 3.92 | |

| | | | | |

CLASS B (Inception 9/27/93) | | | | | | | | | | | | |

Net Asset Value1 | | 3.32 | | | 3.47 | | | 2.56 | | | 3.50 | |

With CDSC3 | | -1.68 | | | -1.53 | | | 2.21 | | | 3.50 | |

| | | | | |

CLASS C (Inception 12/30/94) | | | | | | | | | | | | |

Net Asset Value1 | | 3.32 | | | 3.57 | | | 2.57 | | | 3.51 | |

With CDSC3 | | 2.32 | | | 2.57 | | | 2.57 | | | 3.51 | |

| | | | | |

CLASS Y (Inception 3/31/94) | | | | | | | | | | | | |

Net Asset Value1 | | 3.91 | | | 4.59 | | | 3.59 | | | 4.57 | |

| | | | | |

| COMPARATIVE PERFORMANCE | | 6 MONTHS | | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | |

Barclays Capital 1-5 Yr Gov’t Bond Index | | 4.64 | % | | 4.97 | % | | 4.33 | % | | 5.23 | % |

Morningstar Short Gov’t Fund Avg. | | 3.32 | | | 3.51 | | | 3.30 | | | 4.22 | |

See page 11 for a description of the indexes.

All returns represent past performance and do not guarantee future results. Periods of less than one year are not annualized. Share price and return will vary and you may have a gain or loss when you sell your shares. All results include reinvestment of dividends and capital gains. Current returns may be higher or lower than those shown. For performance current to the most recent month-end, visit www.funds.natixis.com. Performance history includes periods from a predecessor fund. Class Y shares are available to certain investors, as described in the prospectus.

The table and graph do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

PORTFOLIO FACTS

| | | | | | |

| |

| | | % of Net Assets as of | |

| FUND COMPOSITION | | 3/31/09 | | | 9/30/08 | |

Mortgage Related | | 37.6 | | | 67.6 | |

Treasuries | | 21.7 | | | 4.6 | |

Government Sponsored | | 10.1 | | | — | |

Government Owned - No Guarantee | | 10.1 | | | — | |

Commercial Mortgage-Backed Securities | | 7.9 | | | — | |

ABS Credit Card | | 2.7 | | | 2.7 | |

Hybrid ARMs | | 2.0 | | | 1.6 | |

ABS Home Equity | | 1.1 | | | — | |

ABS Car Loan | | 1.1 | | | — | |

Collateralized Mortgage Obligations | | 0.5 | | | 0.1 | |

ABS Other | | 0.0 | | | — | |

Asset-Backed Securities | | — | | | 3.5 | |

Mortgage-Backed Securities | | — | | | 2.0 | |

Automotive | | — | | | 1.8 | |

Short-Term Investments & Other | | 5.2 | | | 13.1 | |

| |

| | | % of Net Assets as of | |

| EFFECTIVE MATURITY | | 3/31/09 | | | 9/30/08 | |

1 year or less | | 8.7 | | | 19.0 | |

1-5 years | | 78.9 | | | 74.5 | |

5-10 years | | 12.4 | | | 6.5 | |

10+ years | | n/a | | | n/a | |

Average Effective Maturity | | 3.2 | years | | 3.0 | years |

Portfolio characteristics will vary.

EXPENSE RATIOS AS STATED IN THE MOST RECENT PROSPECTUS

| | | | | | |

| Share Class | | Gross Expense Ratio5 | | | Net Expense Ratio6 | |

A | | 1.07 | % | | 0.90 | % |

B | | 1.82 | | | 1.65 | |

C | | 1.83 | | | 1.65 | |

Y | | 0.72 | | | 0.65 | |

NOTES TO CHARTS

1 | Does not include a sales charge. |

2 | Includes maximum sales charge of 3.00%. |

3 | Performance for Class B shares assumes a maximum 5% contingent deferred sales charge (“CDSC”) applied when you sell shares, which declines annually between years 1-6 according to the following schedule: 5, 4, 3, 3, 2, 1, 0%. Class C shares performance assumes a 1% CDSC applied when you sell shares within one year of purchase. |

4 | Fund performance has been increased by expense reductions and reimbursements, if any, without which performance would have been lower. |

5 | Before reductions and reimbursements. |

6 | After reductions and reimbursements. Expense reductions are contractual and are set to expire on 1/31/10. |

8

LOOMIS SAYLES STRATEGIC INCOME FUND

PORTFOLIO PROFILE

Objective:

Seeks high current income, with a secondary objective of capital growth

Strategy:

Invests primarily in income-producing securities in the U.S. and around the world

Fund Inception:

May 1, 1995

Managers:

Daniel J. Fuss, CFA, CIC

Kathleen C. Gaffney, CFA

Associate Managers:

Matthew J. Eagan, CFA

Elaine M. Stokes

Loomis, Sayles & Company, L.P.

Symbols:

| | |

| Class A | | NEFZX |

| Class B | | NEZBX |

| Class C | | NECZX |

| Class Y | | NEZYX |

What You Should Know:

Fixed-income securities are subject to credit risk and interest rate risk; their value generally rises when prevailing interest rates fall and falls when rates rise.

The fund can invest a significant percentage of assets in debt securities that are rated below investment grade and the value of fund shares can be adversely affected by changes in economic conditions or other circumstances. Lower rated debt securities have speculative characteristics and may be subject to greater price volatility than higher rated investments. In addition, the secondary market for these securities may lack liquidity. The fund can also invest a significant percentage of assets in foreign securities and the value of the fund shares can be adversely affected by changes in currency exchange rates, political, and economic developments. In emerging markets, these risks can be significant. Fund shares should be viewed as a long-term investment.

Management Discussion

With the exception of U.S. government issues, bond markets suffered significant declines last fall, as credit markets remained frozen and the global economy continued to contract. However, conditions became more stable in December and for much of the first quarter of 2009. Massive government stimulus packages and loan programs brought a measure of reassurance, encouraging investors to move tentatively into corporate sectors.

For the six months ended March 31, 2009, Class A shares of Loomis Sayles Strategic Income Fund provided a total return at net asset value of -9.47%, including $0.49 in dividends and $0.08 in capital gains reinvested during the period. The fund underperformed its benchmark, Barclays Capital Aggregate Bond Index, which returned 4.70% for the period. The fund also lagged Morningstar’s Multisector Bond category, which had an average return of -8.03%. The fund’s 30-day SEC yield at the end of March was 10.20%.

WHAT FACTORS WERE FAVORABLE FOR THE FUND?

The fund’s financial holdings rallied in response to the Treasury department’s lending programs. In the non-investment-grade arena, results got a boost when the financing arm of a major auto maker gained access to federal funding. Renewed confidence in the global financial system at the beginning of 2009 partially reversed losses incurred in the fourth quarter of 2008 across many sectors.

WHICH STRATEGIES HURT RETURNS?

At the sector level, the fund trailed its benchmark and Morningstar peers due to limited exposure to U.S. Treasury and agency securities – by far the period’s best performers. Investors poured money into these safe havens, siphoning assets from corporate bonds and driving down prices of investment-grade and high-yield segments where the fund held major stakes.

As the global economy weakened, demand for industrial products of all kinds declined. Fears grew that credit would become even tighter and companies carrying high levels of debt were especially hard hit. Fund holdings in telecommunications, healthcare and the troubled auto sector fell sharply. In December and January, prices firmed and spreads narrowed. However, this improved performance was not enough to offset losses incurred prior to December 2008. High-yield convertibles also held back performance, with losses only partially mitigated by improved market conditions in the first three months of 2009.

Falling commodity prices tied to shrinking global demand undercut the currencies of countries dependent on commodity exports. The U.S. dollar strengthened against many of these currencies as investors moved out of commodity-related areas and turned to the greenback for greater stability. As a result, the fund suffered declines in holdings denominated in the currencies of Canada, Indonesia, Brazil, Mexico and New Zealand. There were modest rebounds late in the period, but they were not able to recover losses sustained earlier.

WHAT DO YOU SEE AHEAD?

We believe high-yield issues will continue to be volatile, as defaults continue to increase over the course of the year. We remain underweight the CCC-rated portion of the market, as we believe most defaults will come from this space. We believe investment-grade credit continues to offer strong relative value, as spreads remain at relatively wide levels. As the markets grow more convinced the global recovery has taken hold, we eventually expect to see more demand for riskier assets, such as high-yield and investment-grade credit, as well as commodity currencies.

9

LOOMIS SAYLES STRATEGIC INCOME FUND

Investment Results through March 31, 2009

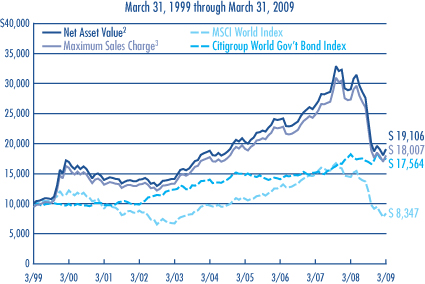

PERFORMANCE IN PERSPECTIVE

The charts comparing the fund’s performance to two indexes provide you with a general sense of how it performed. The fund’s total return for the period shown below appears with and without sales charges and includes fund expenses and fees. An index measures the performance of a theoretical portfolio. Unlike a fund, the index is unmanaged and does not have expenses that affect the results. It is not possible to invest directly in an index. Investors would incur transaction costs and other expenses if they purchased the securities necessary to match the index.

Growth of a $10,000 Investment in Class A Shares4

Average Annual Returns — March 31, 20094

| | | | | | | | | | | | | | | |

| | | | | | |

| | | 6 MONTHS | | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | SINCE

INCEPTION | |

CLASS A (Inception 5/1/95) | | | | | | | | | | | | | | | |

Net Asset Value1 | | -9.47 | % | | -21.58 | % | | 0.94 | % | | 6.03 | % | | — | |

With Maximum Sales Charge2 | | -13.54 | | | -25.10 | | | 0.02 | | | 5.55 | | | — | |

| | | | | | |

CLASS B (Inception 5/1/95) | | | | | | | | | | | | | | | |

Net Asset Value1 | | -9.86 | | | -22.22 | | | 0.17 | | | 5.23 | | | — | |

With CDSC3 | | -14.14 | | | -25.80 | | | -0.13 | | | 5.23 | | | — | |

| | | | | | |

CLASS C (Inception 5/1/95) | | | | | | | | | | | | | | | |

Net Asset Value1 | | -9.77 | | | -22.21 | | | 0.19 | | | 5.24 | | | — | |

With CDSC3 | | -10.63 | | | -22.92 | | | 0.19 | | | 5.24 | | | — | |

| | | | | | |

CLASS Y (Inception 12/1/99) | | | | | | | | | | | | | | | |

Net Asset Value1 | | -9.36 | | | -21.45 | | | 1.20 | | | — | | | 6.40 | % |

| | | | | | |

| COMPARATIVE PERFORMANCE | | 6 MONTHS | | | 1 YEAR | | | 5 YEARS | | | 10 YEARS | | | SINCE

CLASS Y

INCEPTION | |

Barclays Capital Aggregate Bond Index | | 4.70 | % | | 3.13 | % | | 4.13 | % | | 5.70 | % | | 6.10 | % |

Barclays Capital U.S. Universal Bond Index | | 3.12 | | | 1.10 | | | 3.83 | | | 5.64 | | | 5.99 | |

Morningstar Multisector Bond Fund Avg. | | -8.03 | | | -14.37 | | | 0.89 | | | 3.78 | | | 3.99 | |

See page 11 for a description of the indexes.

All returns represent past performance and do not guarantee future results. Periods of less than one year are not annualized. Share price and return will vary and you may have a gain or loss when you sell your shares. All results include reinvestment of dividends and capital gains. Current returns may be higher or lower than those shown. Performance history includes periods from a predecessor fund. For performance current to the most recent month-end, visit www.funds.natixis.com. Class Y shares are available to certain investors, as described in the prospectus.

The table and graph do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares.

PORTFOLIO FACTS

| | | | |

| |

| | | % of Net Assets as of |

| CREDIT QUALITY | | 3/31/09 | | 9/30/08 |

Aaa | | 14.1 | | 18.3 |

Aa | | 6.9 | | 4.1 |

A | | 7.7 | | 8.1 |

Baa | | 35.8 | | 32.0 |

Ba | | 10.4 | | 10.0 |

B | | 7.3 | | 10.3 |

Caa | | 5.2 | | 7.4 |

Ca | | 1.0 | | 0.8 |

C | | 0.1 | | 0.0 |

Not Rated* | | 8.3 | | 8.8 |

Short-term and other | | 3.2 | | 0.2 |

Credit quality is based on ratings from Moody’s Investors Service.

* Securities that are not rated by Moody’s may be rated by another rating agency or by Loomis Sayles.

| | | | | | |

| |

| | | % of Net Assets as of | |

| EFFECTIVE MATURITY | | 3/31/09 | | | 9/30/08 | |

1 year or less | | 6.8 | | | 8.6 | |

1-5 years | | 22.4 | | | 20.6 | |

5-10 years | | 29.5 | | | 28.2 | |

10+ years | | 41.3 | | | 42.6 | |

Average Effective Maturity | | 13.3 | years | | 13.8 | years |

Portfolio characteristics will vary.

EXPENSE RATIOS AS STATED IN THE MOST RECENT PROSPECTUS

| | | | | | |

| Share Class | | Gross Expense Ratio5 | | | Net Expense Ratio6 | |

A | | 0.98 | % | | 0.98 | % |

B | | 1.73 | | | 1.73 | |

C | | 1.73 | | | 1.73 | |

Y | | 0.73 | | | 0.73 | |

NOTES TO CHARTS

1 | Does not include a sales charge. |

2 | Includes maximum sales charge of 4.50%. |

3 | Performance for Class B shares assumes a maximum 5% contingent deferred sales charge (“CDSC”) applied when you sell shares, which declines annually between years 1-6 according to the following schedule: 5, 4, 3, 3, 2, 1, 0%. Class C share performance assumes a 1.00% CDSC applied when you sell shares within one year of purchase. |

4 | Fund performance has been increased by expense reductions and reimbursements, if any, without which performance would have been lower. |

5 | Before reductions and reimbursements. |

6 | After reductions and reimbursements. Expense reductions are contractual and are set to expire on 1/31/10. |

10

ADDITIONAL INFORMATION

The views expressed in this report reflect those of the portfolio managers as of the dates indicated. The managers’ views are subject to change at any time without notice based on changes in market or other conditions. References to specific securities or industries should not be regarded as investment advice. Because the funds are actively managed, there is no assurance that they will continue to invest in the securities or industries mentioned.

For more complete information on any Natixis Fund, contact your financial professional or call Natixis Funds and ask for a free prospectus, which contains more complete information including charges and other ongoing expenses. Investors should consider a fund’s objective, risks and expenses carefully before investing. This and other fund information can be found in the prospectus. Please read the prospectus carefully before investing.

INDEX/AVERAGE DESCRIPTIONS

Barclays Capital Aggregate Bond Index is an unmanaged index of investment-grade bonds with one- to ten-year maturities issued by the U.S. government, its agencies and U.S. corporations.

Barclays Capital Global Aggregate Bond ex-USD Index is an unmanaged index which provides a broad-based measure of the international investment-grade bond market.

Barclays Capital High Yield Composite Index is a market-weighted, unmanaged index of fixed-rate, non-investment grade debt.

Barclays Capital 1-5 Year Government Bond Index is an unmanaged, market-weighted index of bonds issued by the U.S. government and its agencies, with maturities between one and five years.

Barclays Capital U.S. Credit Index is an unmanaged index that includes all publicly issued, fixed-rate, nonconvertible, dollar-denominated, SEC-registered, U.S. investment-grade corporate debt, and foreign debt that meets specific maturity, liquidity and quality requirements.

Barclays Capital U.S. Universal Bond Index is an unmanaged index representing a blend of the Lehman Aggregate Bond Index, the High Yield Index, and the Emerging Market Index, among other indexes.

Morningstar Fund Averages are the average performance without sales charge of funds with similar investment objectives, as calculated by Morningstar, Inc.

PROXY VOTING INFORMATION

A description of the funds’ proxy voting policies and procedures is available without charge, upon request, by calling Natixis Funds at 800-225-5478; on the funds’ website at www.funds.natixis.com; and on the Securities and Exchange Commission’s (SEC’s) website at www.sec.gov. Information regarding how the funds voted proxies relating to portfolio securities during the 12-month period ended June 30, 2008 is available from the funds’ website and the SEC’s website.

QUARTERLY PORTFOLIO SCHEDULES

The funds file a complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The funds’ Forms N-Q are available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling

1-800-SEC-0330.

Effective November 3, 2008, the Lehman indices were rebranded to the Barclays Capital indices. There has been no change in the calculation or definition of the index data.

| | | | |

| NOT FDIC INSURED | | MAY LOSE VALUE | | NO BANK GUARANTEE |

11

UNDERSTANDING FUND EXPENSES

As a mutual fund shareholder, you incur different costs: transaction costs, including sales charges (loads) on purchases, redemption fees and certain exchange fees and ongoing costs, including management fees, distribution and/or service fees (12b-1 fees), and other fund expenses. In addition, each fund may assess a minimum balance fee of $20 on an annual basis for accounts that fall below the required minimum to establish an account. Certain exemptions may apply. These costs are described in more detail in the funds’ prospectuses. The examples below are intended to help you understand the ongoing costs of investing in the funds and help you compare these with the ongoing costs of investing in other mutual funds.

The first line in the table of each Class of fund shares shows the actual account values and actual fund expenses you would have paid on a $1,000 investment in the fund from October 1, 2008 through March 31, 2009. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example $8,600 account value divided by $1,000 = 8.60) and multiply the result by the number in the Expenses Paid During Period column as shown below for your Class.

The second line in the table of each Class of fund shares provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid on your investment for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown reflect ongoing costs only, and do not include any transaction costs such as sales charges, redemption fees, or exchange fees. Therefore, the second line in the table of each fund is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. If transaction costs were included, total costs would be higher.

| | | | | | |

| LOOMIS SAYLES CORE PLUS BOND FUND | | BEGINNING ACCOUNT VALUE

10/1/2008 | | ENDING ACCOUNT VALUE

3/31/2009 | | EXPENSES PAID DURING PERIOD*

10/1/2008 – 3/31/2009 |

CLASS A | | | | | | |

Actual | | $1,000.00 | | $1,038.00 | | $4.57 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,020.44 | | $4.53 |

CLASS B | | | | | | |

Actual | | $1,000.00 | | $1,034.00 | | $8.37 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,016.70 | | $8.30 |

CLASS C | | | | | | |

Actual | | $1,000.00 | | $1,034.40 | | $8.37 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,016.70 | | $8.30 |

CLASS Y | | | | | | |

Actual | | $1,000.00 | | $1,039.10 | | $3.30 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,021.69 | | $3.28 |

| * | Expenses are equal to the Fund’s annualized expense ratio (after fee reduction/reimbursement): 0.90%, 1.65%, 1.65% and 0.65% for Class A, B, C and Y respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, divided by 365 (to reflect the half-year period). |

12

UNDERSTANDING FUND EXPENSES

| | | | | | |

| LOOMIS SAYLES HIGH INCOME FUND | | BEGINNING ACCOUNT VALUE

10/1/2008 | | ENDING ACCOUNT VALUE

3/31/2009 | | EXPENSES PAID DURING PERIOD*

10/1/2008 – 3/31/2009 |

CLASS A | | | | | | |

Actual | | $1,000.00 | | $877.50 | | $5.38 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,019.20 | | $5.79 |

CLASS B | | | | | | |

Actual | | $1,000.00 | | $871.90 | | $8.87 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,015.46 | | $9.55 |

CLASS C | | | | | | |

Actual | | $1,000.00 | | $874.10 | | $8.88 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,015.46 | | $9.55 |

CLASS Y | | | | | | |

Actual | | $1,000.00 | | $878.60 | | $4.22 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,020.44 | | $4.53 |

| * | Expenses are equal to the Fund’s annualized expense ratio (after fee reduction/reimbursement): 1.15%, 1.90%, 1.90% and 0.90%, for Class A, B, C, and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, divided by 365 (to reflect the half-year period). |

| | | | | | |

| LOOMIS SAYLES INTERNATIONAL BOND FUND | | BEGINNING ACCOUNT VALUE

10/1/2008 | | ENDING ACCOUNT VALUE

3/31/2009 | | EXPENSES PAID DURING PERIOD*

10/1/2008 – 3/31/2009 |

CLASS A | | | | | | |

Actual | | $1,000.00 | | $979.60 | | $5.43 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,019.45 | | $5.54 |

CLASS C | | | | | | |

Actual | | $1,000.00 | | $975.90 | | $9.11 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,015.71 | | $9.30 |

CLASS Y | | | | | | |

Actual | | $1,000.00 | | $981.80 | | $4.20 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,020.69 | | $4.28 |

| * | Expenses are equal to the Fund’s annualized expense ratio (after fee reduction/reimbursement): 1.10%, 1.85% and 0.85%, for Class A, C and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, divided by 365 (to reflect the half-year period). |

13

UNDERSTANDING FUND EXPENSES

| | | | | | |

LOOMIS SAYLES LIMITED TERM GOVERNMENT AND

AGENCY FUND | | BEGINNING ACCOUNT VALUE

10/1/2008 | | ENDING ACCOUNT VALUE

3/31/2009 | | EXPENSES PAID DURING PERIOD*

10/1/2008 – 3/31/2009 |

CLASS A | | | �� | | | |

Actual | | $1,000.00 | | $1,037.90 | | $4.57 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,020.44 | | $4.53 |

CLASS B | | | | | | |

Actual | | $1,000.00 | | $1,033.20 | | $8.36 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,016.70 | | $8.30 |

CLASS C | | | | | | |

Actual | | $1,000.00 | | $1,033.20 | | $8.36 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,016.70 | | $8.30 |

CLASS Y | | | | | | |

Actual | | $1,000.00 | | $1,039.10 | | $3.30 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,021.69 | | $3.28 |

| * | Expenses are equal to the Fund’s annualized expense ratio (after fee reduction/reimbursement): 0.90%, 1.65%, 1.65% and 0.65% for Class A, B, C and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, divided by 365 (to reflect the half-year period). |

| | | | | | |

| LOOMIS SAYLES STRATEGIC INCOME FUND | | BEGINNING ACCOUNT VALUE

10/1/2008 | | ENDING ACCOUNT VALUE

3/31/2009 | | EXPENSES PAID DURING PERIOD*

10/1/2008 – 3/31/2009 |

CLASS A | | | | | | |

Actual | | $1,000.00 | | $905.30 | | $4.75 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,019.95 | | $5.04 |

CLASS B | | | | | | |

Actual | | $1,000.00 | | $901.40 | | $8.30 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,016.21 | | $8.80 |

CLASS C | | | | | | |

Actual | | $1,000.00 | | $902.30 | | $8.30 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,016.21 | | $8.80 |

CLASS Y | | | | | | |

Actual | | $1,000.00 | | $906.40 | | $3.52 |

Hypothetical (5% return before expenses) | | $1,000.00 | | $1,021.24 | | $3.73 |

| * | Expenses are equal to the Fund’s annualized expense ratio: 1.00%, 1.75%, 1.75% and 0.74% for Class A, B, C and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year, divided by 365 (to reflect the half-year period). |

14

LOOMIS SAYLES CORE PLUS BOND FUND — PORTFOLIOOF INVESTMENTS

Investments as of March 31, 2009 (Unaudited)

| | | | | | |

Principal

Amount (‡) | | Description | | Value (†) |

| | | | | | |

| | Bonds and Notes — 97.9% of Net Assets | | | |

| | | ABS Home Equity — 1.1% | | | |

| $ | 69,948 | | Countrywide Asset-Backed Certificates, Series 2004-S1, Class A2, 3.872%, 3/25/2020 | | $ | 68,153 |

| | 1,095,000 | | Countrywide Asset-Backed Certificates, Series 2004-S1, Class A3, 4.615%, 2/25/2035 | | | 661,057 |

| | 3,240,517 | | Countrywide Asset-Backed Certificates, Series 2006-S4, Class A3, 5.804%, 7/25/2034 | | | 816,286 |

| | 984,522 | | Residential Asset Securities Corp., Series 2003-KS10, Class AI4, 4.470%, 3/25/2032 | | | 700,223 |

| | | | | | |

| | | | | | 2,245,719 |

| | | | | | |

| | | Automotive — 0.7% | | | |

| | 955,000 | | Ford Motor Co., 7.450%, 7/16/2031 | | | 303,212 |

| | 865,000 | | Ford Motor Credit Co. LLC, 7.000%, 10/01/2013 | | | 578,393 |

| | 810,000 | | Ford Motor Credit Co. LLC, 8.000%, 12/15/2016 | | | 532,357 |

| | | | | | |

| | | | | | 1,413,962 |

| | | | | | |

| | | Banking — 6.8% | | | |

| | 970,000 | | Bank of America Corp., 5.750%, 12/01/2017 | | | 814,592 |

| | 1,365,000 | | Bear Stearns Cos., Inc. (The), 6.400%, 10/02/2017 | | | 1,328,481 |

| | 2,135,000 | | Citigroup, Inc., 6.500%, 8/19/2013 | | | 1,961,884 |

| | 625,000 | | Goldman Sachs Group, Inc. (The), 5.300%, 2/14/2012 | | | 603,076 |

| | 1,040,000 | | Goldman Sachs Group, Inc. (The), 6.150%, 4/01/2018 | | | 949,955 |

| | 2,160,000 | | Goldman Sachs Group, Inc. (The), 6.750%, 10/01/2037 | | | 1,460,897 |

| | 1,560,000 | | JPMorgan Chase & Co., 6.000%, 1/15/2018 | | | 1,575,729 |

| | 1,670,000 | | Merrill Lynch & Co., Inc., MTN, 6.875%, 4/25/2018 | | | 1,306,095 |

| | 1,230,000 | | Merrill Lynch & Co., Inc., Series C, MTN, 5.450%, 2/05/2013 | | | 1,008,305 |

| | 800,000 | | Morgan Stanley, 4.000%, 1/15/2010 | | | 794,357 |

| | 615,000 | | Morgan Stanley, 5.375%, 10/15/2015 | | | 555,603 |

| | 100,000 | | Morgan Stanley, 6.750%, 4/15/2011 | | | 100,077 |

| | 835,000 | | Morgan Stanley, Series F, GMTN, 6.625%, 4/01/2018 | | | 796,178 |

| | 515,000 | | Morgan Stanley, Series F, MTN, 5.550%, 4/27/2017 | | | 458,269 |

| | | | | | |

| | | | | | 13,713,498 |

| | | | | | |

| | | Building Materials — 0.4% | | | |

| | 815,000 | | Owens Corning, Inc., 7.000%, 12/01/2036 | | | 456,711 |

| | 795,000 | | USG Corp., 6.300%, 11/15/2016 | | | 421,350 |

| | | | | | |

| | | | | | 878,061 |

| | | | | | |

| | | | | | |

Principal

Amount (‡) | | Description | | Value (†) |

| | | | | | |

| | | Commercial Mortgage-Backed Securities — 7.4% | | | |

| $ | 795,000 | | Banc of America Commercial Mortgage, Inc., Series 2005-6, Class A2, 5.165%, 9/10/2047 | | $ | 730,085 |

| | 850,000 | | Banc of America Commercial Mortgage, Inc., Series 2006-1, Class A2, 5.334%, 9/10/2045 | | | 771,678 |

| | 1,305,000 | | Banc of America Commercial Mortgage, Inc., Series 2007-2, Class A2, 5.634%, 4/10/2049 | | | 1,065,845 |

| | 1,245,000 | | Bear Stearns Commercial Mortgage Securities, Inc., Series 2005-PW10, Class A2, 5.270%, 12/11/2040 | | | 1,148,070 |

| | 1,200,000 | | Bear Stearns Commercial Mortgage Securities, Inc., Series 2007-PW16, Class A2, 5.857%, 6/11/2040(b) | | | 1,002,517 |

| | 990,000 | | Bear Stearns Commercial Mortgage Securities, Series 2006-PW13, Class A4,

5.540%, 9/11/2041 | | | 821,762 |

| | 145,000 | | Bear Stearns Commercial Mortgage Securities, Series 2007-PW15, Class A4, 5.331%, 2/11/2044 | | | 105,692 |

| | 710,000 | | Citigroup/Deutsche Bank Commercial Mortgage Trust, Series 2006-CD2, Class A2, 5.408%, 1/15/2046 | | | 645,803 |

| | 960,000 | | Credit Suisse Mortgage Capital Certificates, Series 2008-C1, Class A3, 6.425%, 2/15/2041(b) | | | 657,514 |

| | 1,800,000 | | Greenwich Capital Commercial Funding Corp., Series 2005-GG5, Class A2, 5.117%, 4/10/2037 | | | 1,613,393 |

| | 900,000 | | Greenwich Capital Commercial Funding Corp., Series 2007-GG11, Class A4, 5.736%, 12/10/2049 | | | 647,404 |

| | 543,000 | | Greenwich Capital Commercial Funding Corp., Series 2007-GG9, Class A4, 5.444%, 3/10/2039 | | | 391,159 |

| | 1,500,000 | | GS Mortgage Securities Corp. II, Series 2005-GG4, Class A4A, 4.751%, 7/10/2039 | | | 1,109,583 |

| | 1,140,000 | | GS Mortgage Securities Corp. II, Series 2006-GG8, Class A4, 5.560%, 11/10/2039 | | | 855,980 |

| | 250,000 | | JP Morgan Chase Commercial Mortgage Securities Corp., Series 2007-LD11, Class A4, 6.007%, 6/15/2049(b) | | | 171,940 |

| | 375,000 | | JP Morgan Chase Commercial Mortgage Securities Corp., Series 2006-LDP7, Class A4,

6.065%, 4/15/2045(b) | | | 282,902 |

| | 1,710,000 | | LB-UBS Commercial Mortgage Trust, Series 2005-C3, Class A3, 4.647%, 7/15/2030 | | | 1,540,079 |

| | 900,000 | | Morgan Stanley Capital I, Series 2007-T27, Class A4, 5.803%, 6/11/2042(b) | | | 678,507 |

| | 775,000 | | Morgan Stanley Capital I, Series 2008-T29, Class A4, 6.458%, 1/11/2043(b) | | | 601,596 |

| | | | | | |

| | | | | | 14,841,509 |

| | | | | | |

| | | Construction Machinery — 0.5% | | | |

| | 220,000 | | Caterpillar Financial Service Corp., 5.450%, 4/15/2018 | | | 188,748 |

| | 830,000 | | Caterpillar Financial Services Corp., 7.150%, 2/15/2019 | | | 759,159 |

| | | | | | |

| | | | | | 947,907 |

| | | | | | |

See accompanying notes to financial statements.

15

LOOMIS SAYLES CORE PLUS BOND FUND — PORTFOLIOOF INVESTMENTS (continued)

Investments as of March 31, 2009 (Unaudited)

| | | | | | |

Principal

Amount (‡) | | Description | | Value (†) |

| | | | | | |

| | | Diversified Manufacturing — 1.4% | | | |

| $ | 1,200,000 | | Crane Co., 6.550%, 11/15/2036(c) | | $ | 895,217 |

| | 2,145,000 | | General Electric Co., 5.250%, 12/06/2017 | | | 1,983,717 |

| | | | | | |

| | | | | | 2,878,934 |

| | | | | | |

| | | Electric — 1.9% | | | |

| | 290,000 | | AES Corp. (The), 7.750%, 10/15/2015 | | | 253,025 |

| | 570,000 | | AES Corp. (The), 8.000%, 10/15/2017 | | | 488,775 |

| | 715,000 | | AES Corp. (The), 144A, 8.000%, 6/01/2020 | | | 579,150 |

| | 950,000 | | Enersis SA, Chile, 7.375%, 1/15/2014 | | | 986,412 |

| | 355,000 | | Florida Power & Light Co., 4.950%, 6/01/2035 | | | 311,581 |

| | 690,000 | | Ipalco Enterprises, Inc., 144A, 7.250%, 4/01/2016 | | | 610,650 |

| | 590,000 | | Southern California Edison Co., 7.625%, 1/15/2010 | | | 609,724 |

| | | | | | |

| | | | | | 3,839,317 |

| | | | | | |

| | | Entertainment — 0.9% | | | |

| | 1,760,000 | | Time Warner Cable, Inc., 8.250%, 4/01/2019 | | | 1,808,615 |

| | | | | | |

| | | Environmental — 0.3% | | | |

| | 545,000 | | Waste Management, Inc., 7.375%, 3/11/2019 | | | 555,859 |

| | | | | | |

| | | Financial Other — 0.8% | | | |

| | 1,430,000 | | HKCG Finance Ltd., 144A, 6.250%, 8/07/2018 | | | 1,518,586 |

| | | | | | |

| | | Food & Beverage — 1.9% | | | |

| | 560,000 | | Anheuser-Busch Cos., Inc., 4.500%, 4/01/2018 | | | 473,042 |

| | 805,000 | | Anheuser-Busch Cos., Inc., 6.450%, 9/01/2037 | | | 668,068 |

| | 815,000 | | Dr Pepper Snapple Group, Inc., 6.820%, 5/01/2018 | | | 769,206 |

| | 915,000 | | Kraft Foods, Inc., 6.125%, 8/23/2018 | | | 917,193 |

| | 925,000 | | Kraft Foods, Inc., 6.875%, 2/01/2038 | | | 908,384 |

| | | | | | |

| | | | | | 3,735,893 |

| | | | | | |

| | | Government Guaranteed — 1.9% | | | |

| | 74,000,000 | | Development Bank of Japan, 1.750%, 6/21/2010 (JPY) | | | 755,604 |

| | 910,000 | | JPMorgan Chase & Co., 2.125%, 6/22/2012 | | | 914,388 |

| | 210,000,000 | | Oesterreichische Kontrollbank AG, 1.800%, 3/22/2010 (JPY) | | | 2,130,370 |

| | | | | | |

| | | | | | 3,800,362 |

| | | | | | |

| | | Government Owned - No Guarantee — 4.7% | | | |

| | 1,280,000 | | Export-Import Bank of Korea, 8.125%, 1/21/2014 | | | 1,323,045 |

| | 5,617,000 | | Federal National Mortgage Association, 4.375%, 9/13/2010 | | | 5,874,253 |

| | | | | | |

Principal

Amount (‡) | | Description | | Value (†) |

| | | | | | |

| | | Government Owned - No Guarantee — continued | | | |

| $ | 2,139,000 | | Federal National Mortgage Association, 5.375%, 6/12/2017 | | $ | 2,387,986 |

| | | | | | |

| | | | | | 9,585,284 |

| | | | | | |

| | | Health Insurance — 0.7% | | | |

| | 1,470,000 | | WellPoint, Inc., 7.000%, 2/15/2019 | | | 1,470,792 |

| | | | | | |

| | | Healthcare — 1.3% | | | |

| | 575,000 | | HCA, Inc., 7.500%, 12/15/2023 | | | 304,653 |

| | 450,000 | | HCA, Inc., 9.125%, 11/15/2014 | | | 423,000 |

| | 485,000 | | Hospira, Inc., 6.050%, 3/30/2017 | | | 432,857 |

| | 680,000 | | McKesson Corp., 7.500%, 2/15/2019 | | | 721,750 |

| | 670,000 | | Medco Health Solutions, 7.250%, 8/15/2013 | | | 694,415 |

| | | | | | |

| | | | | | 2,576,675 |

| | | | | | |

| | | Hybrid ARMs — 1.5% | | | |

| | 1,368,872 | | FHLMC, 5.949%, 11/01/2036(b) | | | 1,413,833 |

| | 1,217,858 | | FNMA, 6.039%, 2/01/2037(b) | | | 1,265,740 |

| | 373,992 | | JPMorgan Mortgage Trust, Series 2006-A7, Class 1A3, 5.874%, 1/25/2037(b) | | | 273,762 |

| | | | | | |

| | | | | | 2,953,335 |

| | | | | | |

| | | Independent Energy — 1.0% | | | |

| | 290,000 | | Chesapeake Energy Corp., 6.500%, 8/15/2017 | | | 236,350 |

| | 385,000 | | Chesapeake Energy Corp., 6.875%, 11/15/2020 | | | 301,263 |

| | 1,735,000 | | XTO Energy, Inc., 6.375%, 6/15/2038 | | | 1,545,810 |

| | | | | | |

| | | | | | 2,083,423 |

| | | | | | |

| | | Media Cable — 2.5% | | | |

| | 590,000 | | Comcast Corp., 6.450%, 3/15/2037 | | | 515,453 |

| | 1,470,000 | | Comcast Corp., 6.950%, 8/15/2037 | | | 1,368,882 |

| | 755,000 | | Cox Communications, Inc., 6.750%, 3/15/2011 | | | 754,368 |

| | 1,085,000 | | CSC Holdings, Inc., Senior Note, Series B, 7.625%, 4/01/2011 | | | 1,076,862 |

| | 60,000 | | CSC Holdings, Inc., 7.875%, 2/15/2018 | | | 54,900 |

| | 105,000 | | CSC Holdings, Inc., 144A, 8.500%, 4/15/2014 | | | 103,425 |

| | 380,000 | | CSC Holdings, Inc., 144A, 8.625%, 2/15/2019 | | | 365,750 |

| | 873,000 | | Time Warner Cable, Inc., 6.550%, 5/01/2037 | | | 734,718 |

| | | | | | |

| | | | | | 4,974,358 |

| | | | | | |

| | | Metals & Mining — 0.9% | | | |

| | 655,000 | | Barrick Gold Corp., 6.950%, 4/01/2019 | | | 657,989 |

See accompanying notes to financial statements.

16

LOOMIS SAYLES CORE PLUS BOND FUND — PORTFOLIOOF INVESTMENTS (continued)

Investments as of March 31, 2009 (Unaudited)

| | | | | | |

Principal

Amount (‡) | | Description | | Value (†) |

| | | | | | |

| | | Metals & Mining — continued | | | |

| $ | 890,000 | | Steel Dynamics, Inc., 7.375%, 11/01/2012 | | $ | 694,200 |

| | 710,000 | | United States Steel Corp., 6.650%, 6/01/2037 | | | 400,071 |

| | | | | | |

| | | | | | 1,752,260 |

| | | | | | |

| | | Mortgage Related — 22.2% | | | |

| | 842,669 | | FHLMC, 4.000%, 7/01/2019 | | | 860,523 |

| | 1,594,204 | | FHLMC, 4.500%, 12/01/2034 | | | 1,630,852 |

| | 401,293 | | FHLMC, 5.000%, 11/01/2018 | | | 417,168 |

| | 1,122,203 | | FHLMC 5.500%, with various maturities in 2018(d) | | | 1,175,055 |

| | 165,997 | | FHLMC, 6.000%, 6/01/2035 | | | 174,331 |

| | 653,714 | | FNMA, 4.000%, 6/01/2019 | | | 668,382 |

| | 6,375,346 | | FNMA 4.500%, with various maturities from 2019 to 2035(d) | | | 6,559,896 |

| | 866,929 | | FNMA, 5.500%, 5/01/2018 | | | 909,119 |

| | 8,074,871 | | FNMA 6.000%, with various maturities from 2016 to 2039(d) | | | 8,451,151 |

| | 3,683,130 | | FNMA 6.500%, with various maturities from 2029 to 2037(d) | | | 3,887,640 |

| | 174,059 | | FNMA 7.000%, with various maturities in 2030(d) | | | 187,570 |

| | 197,125 | | FNMA 7.500%, with various maturities from 2024 to 2032(d) | | | 213,443 |

| | 5,572,003 | | GNMA 5.000%, with various maturities from 2035 to 2038(d) | | | 5,790,997 |

| | 8,468,164 | | GNMA 5.500%, with various maturities from 2034 to 2038(d) | | | 8,826,035 |

| | 3,471,416 | | GNMA 6.000%, with various maturities from 2029 to 2037(d) | | | 3,636,376 |

| | 612,690 | | GNMA 6.500%, with various maturities from 2028 to 2032(d) | | | 652,361 |

| | 298,811 | | GNMA 7.000%, with various maturities from 2025 to 2029(d) | | | 320,482 |

| | 111,268 | | GNMA 7.500%, with various maturities from 2025 to 2030(d) | | | 119,811 |

| | 59,675 | | GNMA, 8.000%, 11/15/2029 | | | 64,899 |

| | 100,263 | | GNMA 8.500%, with various maturities from 2017 to 2023(d) | | | 108,414 |

| | 19,592 | | GNMA 9.000%, with various maturities in 2016(d) | | | 21,135 |

| | 39,622 | | GNMA 11.500%, with various maturities from 2013 to 2015(d) | | | 44,713 |

| | | | | | |

| | | | | | 44,720,353 |

| | | | | | |

| | | Non-Captive Consumer — 0.8% | | | |

| | 735,000 | | HSBC Finance Corp.,

7.000%, 5/15/2012 | | | 589,985 |

| | 245,000 | | SLM Corp., MTN,

5.050%, 11/14/2014 | | | 129,691 |

| | 215,000 | | SLM Corp., Series A, MTN,

5.000%, 10/01/2013 | | | 114,330 |

| | | | | | |

Principal

Amount (‡) | | Description | | Value (†) |

| | | | | | |

| | | Non-Captive Consumer — continued | | | |

| $ | 120,000 | | SLM Corp., Series A, MTN, 5.000%, 6/15/2018 | | $ | 62,124 |

| | 35,000 | | SLM Corp., Series A, MTN, 5.375%, 5/15/2014 | | | 18,137 |

| | 420,000 | | SLM Corp., Series A, MTN, 5.625%, 8/01/2033 | | | 155,400 |

| | 1,135,000 | | SLM Corp., Series A, MTN, 8.450%, 6/15/2018 | | | 613,046 |

| | | | | | |

| | | | | | 1,682,713 |

| | | | | | |

| | | Non-Captive Diversified — 2.9% | | | |

| | 7,000 | | CIT Group, Inc., 5.400%, 2/13/2012 | | | 4,513 |

| | 63,000 | | CIT Group, Inc., 5.400%, 1/30/2016 | | | 37,760 |

| | 120,000 | | CIT Group, Inc., 5.800%, 10/01/2036 | | | 66,095 |

| | 11,000 | | CIT Group, Inc., 5.850%, 9/15/2016 | | | 6,221 |

| | 1,090,000 | | CIT Group, Inc., 144A, 12.000%, 12/18/2018 | | | 564,075 |

| | 109,000 | | CIT Group, Inc., GMTN, 5.000%, 2/13/2014 | | | 64,310 |

| | 103,000 | | CIT Group, Inc., GMTN, 5.000%, 2/01/2015 | | | 62,712 |

| | 35,000 | | CIT Group, Inc., MTN, 5.125%, 9/30/2014 | | | 21,157 |