UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06241

Loomis Sayles Funds II

(Exact name of Registrant as specified in charter)

399 Boylston Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Coleen Downs Dinneen, Esq.

NGAM Distribution, L.P.

399 Boylston Street

Boston, Massachusetts 02116

(Name and address of agent for service)

Registrant’s telephone number, including area code: (617) 449-2810

Date of fiscal year end: September 30

Date of reporting period: September 30, 2013

| Item 1. | Reports to Stockholders. |

The Registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

ANNUAL REPORT

September 30, 2013

Loomis Sayles Global Equity and Income Fund

Loomis Sayles Growth Fund

Loomis Sayles Mid Cap Growth Fund

Loomis Sayles Value Fund

TABLE OF CONTENTS

Portfolio Review page 1

Portfolio of Investments page 27

Financial Statements page 55

Notes to Financial Statements page 69

LOOMIS SAYLES GLOBAL EQUITY AND INCOME FUND

| | |

| Managers | | Symbols |

| Daniel J. Fuss, CFA, CIC | | Class A LGMAX |

| Warren N. Koontz, CFA, CIC* | | Class C LGMCX |

| Eileen N. Riley, CFA** | | Class Y LSWWX |

| David Rolley, CFA | | |

| Lee M. Rosenbaum** | | |

| Loomis, Sayles & Company, L.P. |

| * | Effective April 11, 2013, Warren N. Koontz no longer serves as a portfolio manager of the Fund. |

| ** | Eileen N. Riley, CFA and Lee M. Rosenbaum became portfolio managers of the Fund effective April 11, 2013. |

Objective

Seeks high total investment return through a combination of capital appreciation and current income

Strategy

Under normal circumstances, invests 80% of its net assets in equity and fixed-income securities of U.S. and foreign issuers, including securities of issuers located in emerging markets

Market Conditions

Developed equity markets rallied during the 12-month period, while fears of rising interest rates hurt many fixed-income markets. In the United States, the S&P 500 Index® trended higher on the back of rising consumer sentiment. European markets responded well to improving economic conditions despite slowing forecasts for corporate earnings. Although emerging market stocks generally rallied strongly in September 2013, earlier setbacks kept the year-to-date return negative and the 12-month return barely positive as of September 30, 2013.

Comments from the U.S. Federal Reserve (the Fed) and speculation about Fed policy, particularly in the second half of the reporting period, generally drove fixed-income performance for the 12-month period. The Fed introduced volatility and caution into the global fixed-income markets by hinting at a potential winding down of its program of monthly mortgage and Treasury security purchases, known as quantitative easing (QE). The magnitude of the resulting selloff and the overall disruption to risk markets tightened financial conditions significantly. Based on the Fed’s announcement, investors anticipated the Fed would begin tapering QE following the central bank’s September policy meeting. However, the Fed surprised markets and decided to delay the taper while softening its forward guidance. This announcement led to a rally in equities, emerging currencies and fixed-income markets.

1 |

Performance Results

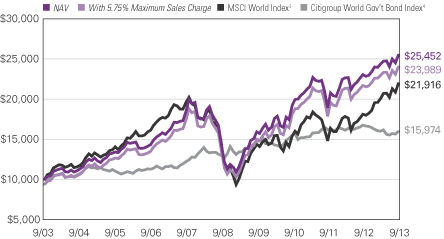

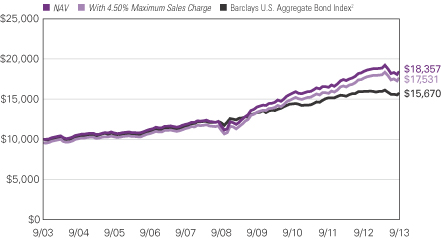

For the 12 months ended September 30, 2013, Class A shares of Loomis Sayles Global Equity and Income Fund returned 10.54% at net asset value. The fund underperformed its primary benchmark, the Morgan Stanley Capital International (MSCI) World Index, which returned 20.90%. The fund outpaced its secondary benchmark, the Citigroup World Government Bond Index, which returned -4.60%.

Explanation of Fund Performance

Weak performance from several out-of-benchmark emerging market equity holdings detracted from return. Although the fund’s fixed-income holdings posted positive results, the effect was not enough to offset the fund’s overall underperformance, as the fund maintains a larger overall weight in equities.

Within the fund’s equity component, an underweight position in the telecommunication sector and stock selection in the materials sector were the main detractors from results. Relative to the fund’s benchmark, stock selection in the energy, healthcare and utilities sectors was positive. However, these gains were largely offset by stock selection in consumer discretionary and financials stocks. We ended the period with overweight positions in the United States and United Kingdom and an underweight position in Japan. Throughout the period we increased exposure to North America and trimmed exposure to emerging markets — a result of our investment process, which continually looks for quality companies that trade at attractive valuations and have the ability to grow their intrinsic value.

In terms of individual stock holdings, Citigroup, a diversified financial services company, was the leading contributor, as positive industry data boosted many financial stocks during the first half of the year. We believe the company remains positioned for targeted growth and stability. In addition, a position in Priceline, an online travel service company, performed well due to rapid expansion in hotel listings and strong growth in its booking.com brand in the United States. A position in Roche, a Swiss pharmaceutical company, also was a top contributor. The company’s stock benefited from positive incremental data presented at the European Society for Medical Oncology (ESMO) as well as growing speculation about a deal with rival Novartis to sell its stake back to Roche.

Outperformance in the fund’s fixed-income component was due primarily to security selection in corporate bonds and favorable currency positioning. In particular, underweight positions in Australia’s dollar and Japan’s yen aided performance. Positioning in the industrials and financials sectors along with government securities also added to return.

Apple, the U.S.-based computer and electronic device maker, was the single largest individual performance detractor for the period. Throughout the summer, Apple faced product- and legal-related headwinds that muted returns overall. However, recent events have turned positive with the launch of the iPhone 5S and iPhone 5C and favorable resolutions to several legal issues. In addition, the fund’s holdings in Canada’s Potash Corporation of Saskatchewan, a producer of potash and other fertilizers, declined after OAO Uralkali, the world’s largest potash producer, ended its relationship with its distribution and trading organization. This change in market dynamics, and the heightened

| 2

LOOMIS SAYLES GLOBAL EQUITY AND INCOME FUND

risks to potash pricing, negatively influenced our downside view of the company, and we sold the stock. Elsewhere, U.K.-based mining company Antofagasta also detracted from performance, declining after the company warned copper and gold output would fall due to increased production costs. We sold the position.

In the fixed-income component, the fund’s bias toward U.S. local markets, combined with substantial underweight positions in European and Japanese local markets, detracted from performance. Issue selection within the utility sector and U.S. dollar yield curve (a curve that shows the relationship among bond yields across the maturity spectrum) positioning also detracted from relative performance.

Outlook

In the equity market, we continue to estimate earnings growth in the mid single-digit range this year and next. While margin expansion from recessionary lows has largely played out, the evidence tends to support our view that margins should remain healthy in an environment of moderate but steady gross domestic product growth. Dividends are expected to grow at a double-digit rate in 2013 and likely in 2014. The potential for dividend growth and moderately higher equity prices could provide equity investors with two opportunities over time. While the Fed has refrained from tapering QE for now, investors should prepare for an eventual return to a more normal interest rate environment with a federal funds rate above the zero lower bound. If yields gradually normalize on the basis of improved economic growth with contained inflation, equity investors should be able to adjust to the changing environment and use periodic average corrections as opportunities to add to favored positions.

We also believe the credit cycle is in the early stage of expansion. Bond yields should rise as the global economy continues to improve, but we expect the pace of growth to be inconsistent. Overall, this likely means corporate bonds will continue to outperform Treasuries. We remain comfortable with the fund’s overweight position in the corporate sector and will continue to look for companies with strong fundamentals and favorable risk/reward profiles. Among currencies, we continue to favor the U.S. dollar versus the euro or yen, as we see better relative growth opportunities in the United States. Due to our concerns about slow growth in China, we remain increasingly cautious toward non-Japan Asian currencies. Recent volatility in emerging markets has restored some value, but security selection remains critical in identifying promising long-term positions.

3 |

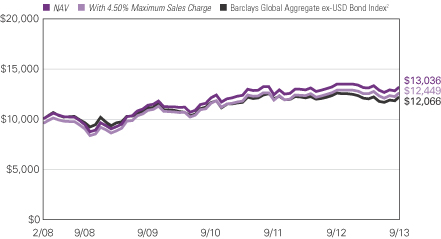

Growth of $10,000 Investment in Class A Shares1,5

September 30, 2003 through September 30, 2013

| 4

LOOMIS SAYLES GLOBAL EQUITY AND INCOME FUND

Average Annual Total Returns — September 30, 20135

| | | | | | | | | | | | |

| | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | |

| | | | |

| Class A (Inception 2/1/06)1 | | | | | | | | | | | | |

| NAV | | | 10.54 | % | | | 11.97 | % | | | 9.79 | % |

| With 5.75% Maximum Sales Charge | | | 4.20 | | | | 10.65 | | | | 9.14 | |

| | | | |

| Class C (Inception 2/1/06)1 | | | | | | | | | | | | |

| NAV | | | 9.77 | | | | 11.15 | | | | 8.98 | |

| With CDSC2 | | | 8.77 | | | | 11.15 | | | | 8.98 | |

| | | | |

| Class Y (Inception 5/1/96) | | | | | | | | | | | | |

| NAV | | | 10.90 | | | | 12.26 | | | | 10.07 | |

| | | | |

| Comparative Performance | | | | | | | | | | | | |

| MSCI World Index3 | | | 20.90 | | | | 8.46 | | | | 8.16 | |

| Citigroup World Government Bond Index4 | | | -4.60 | | | | 4.25 | | | | 4.79 | |

Past performance does not guarantee future results. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. Unlike a fund, an index is not managed and does not reflect fees and expenses.

NOTES TO CHARTS

| 1 | Prior to the inception of Class A and C shares (2/1/06), performance is that of Institutional Class shares, which were redesignated as Class Y shares, and restated to reflect the higher net expenses and sales loads of Class A and C shares. |

| 2 | Performance for Class C shares assumes a 1% contingent deferred sales charge (“CDSC”) applied when you sell shares within one year of purchase. |

| 3 | MSCI World Index is an unmanaged index that is designed to measure the equity market performance of developed markets. |

| 4 | Citigroup World Government Bond Index is an unmanaged index that includes the most significant and liquid government bond markets globally that carry at least an investment-grade rating. |

| 5 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

5 |

LOOMIS SAYLES GROWTH FUND

| | |

| Manager | | Symbols |

| Aziz Hamzaogullari, CFA | | Class A LGRRX |

| Loomis, Sayles & Company, L.P. | | Class B LGRBX |

| | Class C LGRCX |

| | Class N LGRNX |

| | Class Y LSGRX |

Objective

Long-term growth of capital

Strategy

Under normal circumstances invests primarily in equity securities, including common stocks, convertible securities, and warrants; focuses on stocks of large-capitalization companies, but may invest in companies of any size

Market Conditions

Equities generally performed well across the board in the third quarter. The Russell 1000® Growth Index returned more than 19% through September, surpassing expectations at the start of the year. Slow but steady economic growth in the United States, support from the Federal Reserve and more recently, signs of potentially better growth in Europe and Asia have been important positive catalysts.

Performance Results

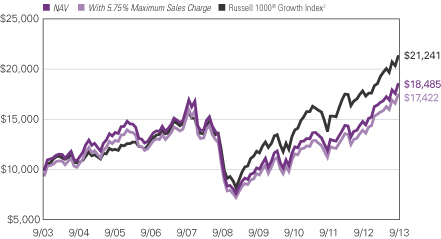

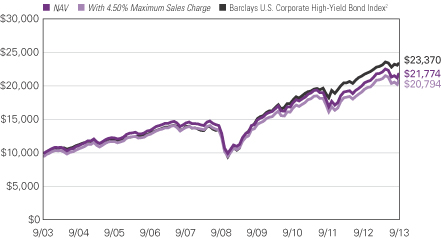

For the 12 months ended September 30, 2013, Class A shares of Loomis Sayles Growth Fund returned 25.23% at net asset value. The fund outperformed its benchmark, the Russell 1000® Growth Index, which returned 19.27%.

Explanation of Fund Performance

Stock selection in the information technology, financials and consumer staples sectors primarily accounted for the fund’s outperformance relative to its benchmark. Stock selection in the healthcare sector and our allocations to the industrials, consumer discretionary and energy sectors were the largest detractors from relative performance.

Facebook, a social networking provider and one of our top ten holdings, was the largest contributor to performance during the period. We first purchased Facebook in 2012 at the company’s initial public offering and have added to the fund’s position on price weakness. Facebook reported strong results, with all key metrics above consensus expectation. The company’s mobile platform was the primary driver of performance. Facebook also continued to show strong user growth, positive engagement trends, product innovation and good financials. In addition, a position in ARM Holdings, the leading supplier of semiconductor processor intellectual property, was a positive contributor to the fund’s return. ARM

| 6

LOOMIS SAYLES GROWTH FUND

Holdings has seen strong growth in its licensing business, which will drive future royalty revenue growth. Key product announcements from Apple and Samsung validated ARM’s next-generation products. Overall revenue increased with expansion in operating margins, driving even faster operating income growth. We believe ARM Holdings continues to trade at a discount to our estimate of intrinsic value based on our long-term fundamental analysis. The fund’s position in SEI Investments, a leading provider of investment management services and fully outsourced processing solutions to global financial institutions, also was a top performer. New sales were up 77% during the period, which is a positive indicator for revenue growth. All business segments reported growth, with new sales activity in the institutional investor category returning to pre-financial-crisis levels. SEI continues to offer an attractive reward-to-risk opportunity based on our estimate of intrinsic value.

A position in online jeweler Blue Nile was the largest performance detractor during the period. Blue Nile’s new management team has been shifting its strategic focus to the fashion-driven jewelry segment and away from its original core business, the diamond engagement market. We sold the fund’s position due to negative structural changes to our initial investment thesis, which resulted in a lower estimate of intrinsic value. A position in energy drink company Monster Beverage was an additional detractor. Monster, along with the entire energy drink industry, faced negative press regarding the safety of energy drinks, especially for children. This negative press spilled into European markets, softening consumption levels and weakening growth in international markets. We continue to believe Monster is well positioned in a fast-growing segment and in the long run should benefit from strong revenue growth and expanding profit margins. A position in Greenhill & Co., a boutique investment bank, also detracted from performance. Greenhill reported lower-than-expected earnings due to continued weakness in merger-and-acquisition activity and higher compensation due to new hires. We believe that Greenhill is thinking long term by taking advantage of ongoing industry weakness to add talent to its team. Although it compounded the company’s overall weak financial performance, we believe the hiring strategy should improve the company’s long-term opportunity.

Outlook

Our investment process is characterized by bottom-up, fundamental research and a long-term time horizon. The nature of the process creates a portfolio with lower turnover, in which sector positioning is derived from our fundamental research. This approach led to overweight positions in the financials, information technology and healthcare sectors and underweight positions in the industrials, consumer discretionary, energy and consumer staples sectors. We remain committed to our long-term investment approach.

7 |

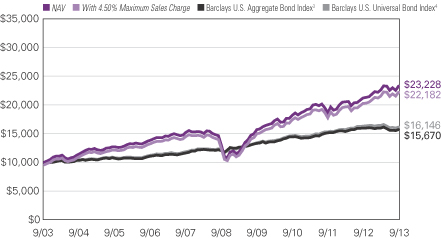

Growth of $10,000 Investment in Class A Shares3

September 30, 2003 through September 30, 2013

| 8

LOOMIS SAYLES GROWTH FUND

Average Annual Total Returns — September 30, 20133

| | | | | | | | | | | | | | | | |

| | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Class N

Inception | |

| | | | | |

| Class A (Inception 12/31/96) | | | | | | | | | | | | | | | | |

| NAV | | | 25.23 | % | | | 10.27 | % | | | 6.34 | % | | | — | % |

| With 5.75% Maximum Sales Charge | | | 17.97 | | | | 8.95 | | | | 5.71 | | | | — | |

| | | | | |

| Class B (Inception 9/12/03) | | | | | | | | | | | | | | | | |

| NAV | | | 24.14 | | | | 9.47 | | | | 5.54 | | | | — | |

| With CDSC1 | | | 19.14 | | | | 9.19 | | | | 5.54 | | | | — | |

| | | | | |

| Class C (Inception 9/12/03) | | | | | | | | | | | | | | | | |

| NAV | | | 24.21 | | | | 9.48 | | | | 5.54 | | | | — | |

| With CDSC1 | | | 23.21 | | | | 9.48 | | | | 5.54 | | | | — | |

| | | | | |

| Class N (Inception 2/1/13) | | | | | | | | | | | | | | | | |

| NAV | | | — | | | | — | | | | — | | | | 12.93 | |

| | | | | |

| Class Y (Inception 5/16/91) | | | | | | | | | | | | | | | | |

| NAV | | | 25.49 | | | | 10.65 | | | | 6.69 | | | | — | |

| | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | |

| Russell 1000® Growth Index2 | | | 19.27 | | | | 12.07 | | | | 7.82 | | | | 14.70 | |

Past performance does not guarantee future results. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. Unlike a fund, an index is not managed and does not reflect fees and expenses.

NOTES TO CHARTS

| 1 | Performance for Class B shares assumes a maximum of 5% contingent deferred sales charge (“CDSC”) applied when you sell shares, which declines annually between years 1-6 according to the following schedule: 5, 4, 3, 3, 2, 1, 0%. Class C shares performance assumes a 1% CDSC applied when you sell shares within one year of purchase. |

| 2 | Russell 1000® Growth Index is an unmanaged index that measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. |

| 3 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

9 |

LOOMIS SAYLES MID CAP GROWTH FUND

| | |

| Manager | | Symbols |

| Philip C. Fine, CFA | | Class A LAGRX |

| Loomis, Sayles & Company, L.P. | | Class C LSACX |

| | Class N LSANX |

| | Class Y LSAIX |

Objective

Long-term capital growth from investments in common stocks or similar securities

Strategy

Normally invests 80% of its net assets in common stocks or other equity securities; focuses on stocks of companies that fall within the capitalization range of the companies included in the Russell Midcap® Growth Index, but may invest the rest of its assets in companies of any size.

Market Conditions

Stocks started the period on a negative note, as equities sold off immediately following the November 2012 presidential election. Fears of the “fiscal cliff” — a combination of tax increases and spending cuts scheduled to take effect January 1, 2013 — drove the selloff. Ultimately, policymakers agreed to a deal to avert the worst of the fiscal cliff scenario, and stocks generally remained on an upswing for the remainder of the period.

Federal Reserve (Fed) Chairman Ben Bernanke rattled the financial markets in June 2013 by suggesting the Fed might begin to scale back its quantitative easing (QE) as early as September and perhaps terminate the program by mid 2014 should the economy and labor markets continue to improve. In response, investors rotated out of defensive stocks (utilities, healthcare, staples) that led the rally for much of the first half of 2013 and into more cyclical stocks (financials, technology). But, following its September policy meeting, the Fed shocked the financial markets when it said financial conditions were not strong enough to warrant a reduction in stimulus. Stocks rallied on the news the Fed would continue its $85 billion monthly bond purchases. In the final days of the quarter, the rally stalled, as failed federal budget negotiations gave way to an October 1 federal government shutdown.

Performance Results

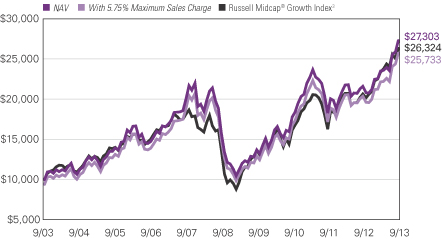

For the 12 months ended September 30, 2013, Class A shares of Loomis Sayles Mid Cap Growth Fund returned 26.39% at net asset value. The fund underperformed its benchmark, the Russell Midcap® Growth Index, which returned 27.54%.

Explanation of Fund Performance

The fund slightly lagged its benchmark during the 12-month period, primarily due to weakness from the overall allocation effect (sector weights, cash holdings, options hedges). By contrast, the fund benefited from strong stock selection, particularly within the information technology,

| 10

LOOMIS SAYLES MID CAP GROWTH FUND

energy and industrials sectors. Stock selection within healthcare, and to a lesser extent the consumer discretionary sector, created a drag on relative performance. The consumer discretionary sector made the largest contribution to the fund’s gains, led by positions in Lions Gate Entertainment, a leading independent film and television producer and distributor, and Melco Crown Entertainment (Melco), an operator of casinos in Macau. Lions Gate has posted several strong quarters, and expectations have been building for a strong fourth-quarter release schedule, paced by “Catching Fire,” the next installment of the “Hunger Games” franchise. For Melco, visitation to Macau has been robust, and the company has been gaining market share in the lucrative mass-market segment. It also entered into a joint venture to open a casino in the Philippines.

The technology and energy sectors made the greatest contributions to return relative to the benchmark. LinkedIn, the leading online professional network with more than 200 million members globally, was the largest contributor in technology. The company has increased user engagement by offering new features and functionality. It continued to report strong results, driven primarily by gains in its key talent solutions segment (licenses to corporate accounts). The fund’s strongest contributor in energy was Cabot Oil & Gas, a leading exploration and production company. The firm recently reported another strong quarter, split its stock for a second time, doubled its dividend and increased production guidance for 2013.

Corrections in the fund’s biotech holdings led to underperformance in the healthcare sector. In particular, several of 2012’s big winners, Alexion Pharmaceuticals and Medivation, began to sell off in late 2012. Alexion reported a disappointing third quarter 2012. While earnings modestly exceeded expectations, revenues were only in-line with expectations for the first time in several years. Medivation has transitioned from the clinical to commercial stage with the recent launch of a drug for metastatic prostate cancer that was approved for post-chemotherapy use. After a strong run-up prior to approval, the shares corrected as investors took profits ahead of the launch.

An overweight position in homebuilders triggered underperformance in the consumer discretionary sector. After a strong fourth quarter 2012, the fund’s homebuilders experienced a modest correction during the spring. A more severe selloff began in late June, when mortgage rates increased in response to the Fed’s potential tapering plans. In particular, D.R. Horton, the nation’s largest homebuilder, reported strong margins but disappointing orders. In the information technology sector, a position in Zillow, operator of a leading real estate information website, weighed on performance. The company has been the target of short sellers, who have questioned its business model and reticence to disclose key operating metrics. The firm issued disappointing fourth-quarter guidance with respect to revenues and margins.

The fund held several small derivatives positions for hedging purposes. In the fourth quarter of 2012, we held a Russell 2000 ETF put spread (a long position in an out-of-the-money put combined with a short position in a put with a lower strike price) to hedge against political and fiscal cliff risk during the post-election selloff and puts on the S&P Homebuilders sector ETF to hedge the fund’s large exposure to homebuilders. In the third quarter of 2013, we bought out-of-the-money puts on Medivation as a hedge against the risk of failure in a key clinical trial. We also bought calls on Cobalt International Energy to

11 |

gain investment exposure to several high impact exploratory drilling programs. While the fund’s derivative positions detracted modestly from return, all instruments behaved as expected, with the puts offering downside protection in a rising market. We continue to own the puts on Medivation and the calls on Cobalt.

Outlook

We continue to estimate earnings growth in the mid single-digit range this year and next. While margin expansion from recessionary lows has largely played out, the evidence tends to support our view that margins should remain healthy in an environment of moderate but steady gross domestic product growth. Dividends are expected to grow at a double-digit rate in 2013 and likely in 2014 as well. The potential for dividend growth and moderately higher equity prices could provide equity investors with two opportunities over time. While the Fed has refrained from tapering its monthly bond-buying purchases, known as QE for now, investors should prepare for an eventual return to a more normal interest rate environment with a federal funds rate above the zero lower bound. If yields normalize gradually, on the basis of improved economic growth with contained inflation, equity investors should be able to adjust to the changing environment and use periodic average corrections as opportunities to add to favored positions.

| 12

LOOMIS SAYLES MID CAP GROWTH FUND

Growth of $10,000 Investment in Class A Shares1,4

September 30, 2003 through September 30, 2013

13 |

Average Annual Total Returns — September 30, 20134

| | | | | | | | | | | | | | | | |

| | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | Since Class N

Inception | |

| | | | | |

| Class A (Inception 12/31/96)1 | | | | | | | | | | | | | | | | |

| NAV | | | 26.39 | % | | | 11.52 | % | | | 10.56 | % | | | — | % |

| With 5.75% Maximum Sales Charge | | | 19.12 | | | | 10.21 | | | | 9.91 | | | | — | |

| | | | | |

| Class C (Inception 2/2/09)1 | | | | | | | | | | | | | | | | |

| NAV | | | 25.46 | | | | 10.70 | | | | 9.71 | | | | — | |

| With CDSC2 | | | 24.46 | | | | 10.70 | | | | 9.71 | | | | — | |

| | | | | |

| Class N (Inception 2/1/13) | | | | | | | | | | | | | | | | |

| NAV | | | — | | | | — | | | | — | | | | 20.51 | |

| | | | | |

| Class Y (Inception 12/31/96) | | | | | | | | | | | | | | | | |

| NAV | | | 26.72 | | | | 11.82 | | | | 10.84 | | | | — | |

| | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | |

| Russell Midcap® Growth Index3 | | | 27.54 | | | | 13.92 | | | | 10.16 | | | | 16.97 | |

Past performance does not guarantee future results. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. Unlike a fund, an index is not managed and does not reflect fees and expenses.

NOTES TO CHARTS

| 1 | Prior to 2/1/09, performance of Class A shares is that of Retail Class shares, which were redesignated as Class A shares, restated to reflect the sales load of Class A shares. Prior to the inception of Class C shares (2/2/09), performance is that of Retail Class shares, restated to reflect the higher net expenses and sales loads of Class C shares. The fund revised its investment strategies on 2/1/07; performance may have been different had the current strategies been in place for all periods shown. |

| 2 | Class C shares performance assumes a 1% CDSC applied when you sell shares within one year of purchase. |

| 3 | Russell Midcap® Growth Index is an unmanaged index that measures the performance of the mid-cap growth segment of the U.S. equity universe. It includes those Russell Midcap Index companies with higher price-to-book ratios and higher forecasted growth values. |

| 4 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 14

LOOMIS SAYLES VALUE FUND

| | | | |

| Managers | | Symbols | | |

| Arthur Barry, CFA | | Class A | | LSVRX |

| James L. Carroll, CFA* | | Class B | | LSVBX |

| Warren N. Koontz, CFA, CIC | | Class C | | LSCVX |

| Loomis, Sayles & Company, L.P. | | Class N | | LSVNX |

| | Class Y | | LSGIX |

| | Admin Class | | LSAVX |

| * | Effective September 30, 2013, James L. Carroll no longer serves as a portfolio manager of the Fund. |

Objective

Long-term growth of capital and income

Strategy

Under normal conditions invests primarily in equity securities, including common stocks, convertible securities, and warrants.

Market Conditions

The U.S. stock market generated strong performance during the 12-month period. All major stock indexes continued to trend higher, while consumer sentiment improved worldwide. The U.S. equity market has returned to price-to-earnings valuation levels comparable to its 50-year average. Profit margins were healthy, and market consensus expects them to remain so going forward. As the period progressed, U.S. investors returned to equity mutual funds following a long stretch of net redemptions.

Performance Results

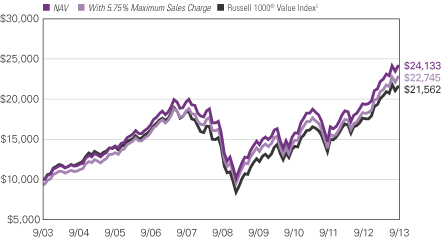

For the 12 months ended September 30, 2013, Class A shares of Loomis Sayles Value Fund returned 24.35% at net asset value. The fund outperformed its benchmark, the Russell 1000® Value Index, which returned 22.30% for the period.

Explanation of Fund Performance

The most significant driver of the fund’s outperformance was stock selection, particularly in the energy, financials, materials, industrials and telecommunication services sectors. An underweight in the utilities sector also boosted performance. Stock selection in the information technology sector was the primary detractor from relative performance, mostly due to owning Apple, the computer and electronic device maker.

State Street and JPMorgan were two of the top three performers for the fund. Strong fee revenues, robust share buybacks and market appreciation inflows have led to solid earnings for State Street Corporation. JPMorgan also recently reported better-than-expected earnings on the back of a larger reserve release and slightly better-than-expected investment

15 |

banking and trading revenue. Ameriprise was a solid performer throughout the period, primarily due to net new inflows and increased client activity. The company also continued to return capital to shareholders through share repurchases and dividends while maintaining a strong financial foundation. All three stocks were overweights relative to the index.

Although this past 12-month period was not Apple’s strongest, the company countered the skeptics with the arrival of the iPhone 5S and as a lower-end model, the 5C, in September. We think sales of these products, plus other potential catalysts, such as additional share buybacks, a dividend commitment and an agreement with China Mobile to sell iPhones, make the stock attractive at this level. In addition, an overweight position in FirstEnergy, a public utility company, weighed on fund performance. Data released in the summer indicated weak demand and excess generation supply will keep power prices low in certain areas for a long time. This led to weak stock performance for large electricity generators, including FirstEnergy. The fund’s exposure to Verizon, a telecommunication company, also detracted from performance. Concerns about discounting and increased competition from wireless peers pressured Verizon stock. Nevertheless, we believe the company remains attractive from a long-term perspective.

Outlook

As always, we will look for individual securities we believe offer attractive return potential by selling below our estimates of intrinsic value. We will seek to enter these stock positions when the downside risk seems limited or manageable.

| 16

LOOMIS SAYLES VALUE FUND

Growth of $10,000 Investment in Class A Shares1,4

September 30, 2003 through September 30, 2013

17 |

Average Annual Total Returns — September 30, 20134

| | | | | | | | | | | | | | | | |

| | | | | |

| | | 1 Year | | | 5 Years | | | 10 Years | | | Since

Class N Inception | |

| | | | | |

| Class A (Inception 6/30/06)1 | | | | | | | | | | | | | | | | |

| NAV | | | 24.35 | % | | | 8.71 | % | | | 9.21 | % | | | — | % |

| With 5.75% Maximum Sales Charge | | | 17.21 | | | | 7.44 | | | | 8.57 | | | | — | |

| | | | | |

| Class B (Inception 6/1/07)1 | | | | | | | | | | | | | | | | |

| NAV | | | 23.42 | | | | 7.91 | | | | 8.33 | | | | — | |

| With CDSC2 | | | 18.42 | | | | 7.61 | | | | 8.33 | | | | — | |

| | | | | |

| Class C (Inception 6/1/07)1 | | | | | | | | | | | | | | | | |

| NAV | | | 23.41 | | | | 7.91 | | | | 8.34 | | | | — | |

| With CDSC2 | | | 22.41 | | | | 7.91 | | | | 8.34 | | | | — | |

| | | | | |

| Class N (Inception 2/1/13) | | | | | | | | | | | | | | | | |

| NAV | | | — | | | | — | | | | — | | | | 13.55 | |

| | | | | |

| Class Y (Inception 5/13/91) | | | | | | | | | | | | | | | | |

| NAV | | | 24.65 | | | | 9.00 | | | | 9.52 | | | | — | |

| | | | | |

| Admin Class (Inception 2/1/10)1 | | | | | | | | | | | | | | | | |

| NAV | | | 24.08 | | | | 8.45 | | | | 8.92 | | | | — | |

| | | | | |

| Comparative Performance | | | | | | | | | | | | | | | | |

| Russell 1000® Value Index3 | | | 22.30 | | | | 8.86 | | | | 7.99 | | | | 12.07 | |

Past performance does not guarantee future results. The table(s) do not reflect taxes shareholders might owe on any fund distributions or when they redeem their shares. Performance for periods less than one year is cumulative, not annualized. Returns reflect changes in share price and reinvestment of dividends and capital gains, if any. Unlike a fund, an index is not managed and does not reflect fees and expenses.

NOTES TO CHARTS

| 1 | Prior to 6/1/07, performance of Class A shares is that of Retail Class shares, which were redesignated as Class A shares, restated to reflect the sales load of Class A shares. Prior to the inception of Retail Class shares (6/30/06), performance is that of Institutional Class shares, which were redesignated as Class Y shares, restated to reflect the higher net expenses and sales loads of Class A shares. Prior to the inception of Class B and C shares (6/1/07), performance is that of Institutional Class shares, restated to reflect the higher net expenses and sales loads of Class B and C shares. Prior to the inception of Admin Class shares (2/1/10), performance is that of Class A shares, restated to reflect the higher net expenses of Admin Class shares. |

| 2 | Performance for Class B shares assumes a maximum of 5% contingent deferred sales charge (“CDSC”) applied when you sell shares, which declines annually between years 1-6 according to the following schedule: 5, 4, 3, 3, 2, 1, 0%. Class C shares performance assumes a 1% CDSC applied when you sell shares within one year of purchase. |

| 3 | Russell 1000® Value Index is an unmanaged index that measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and higher forecasted growth values. |

| 4 | Fund performance has been increased by fee waivers and/or expense reimbursements, if any, without which performance would have been lower. |

| 18

ADDITIONAL INFORMATION

The views expressed in this report reflect those of the portfolio managers as of the dates indicated. The managers’ views are subject to change at any time without notice based on changes in market or other conditions. References to specific securities or industries should not be regarded as investment advice. Because these funds are actively managed, there is no assurance that they will continue to invest in the securities or industries mentioned.

ADDITIONAL INDEX INFORMATION

This document may contain references to third party copyrights, indexes, and trademarks, each of which is the property of its respective owner. Such owner is not affiliated with Natixis Global Asset Management or any of its related or affiliated companies (collectively “NGAM”) and does not sponsor, endorse or participate in the provision of any NGAM services, funds or other financial products.

The index information contained herein is derived from third parties and is provided on an “as is” basis. The user of this information assumes the entire risk of use of this information. Each of the third party entities involved in compiling, computing or creating index information disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to such information.

PROXY VOTING INFORMATION

A description of the funds’ proxy voting policies and procedures is available without charge, upon request, by calling Natixis Funds at 800-225-5478; on the funds’ website at ngam.natixis.com; and on the Securities and Exchange Commission’s website at www.sec.gov. Information regarding how the funds voted proxies relating to portfolio securities during the 12-month period ended June 30, 2013 is available from the funds’ website and the SEC’s website.

QUARTERLY PORTFOLIO SCHEDULES

The funds will file a complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The funds’ Forms N-Q are available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling

800-SEC-0330.

19 |

UNDERSTANDING FUND EXPENSES

As a mutual fund shareholder, you incur different types of costs: transaction costs, including sales charges (loads) on purchases and contingent deferred sales charges on redemptions, and ongoing costs, including management fees, distribution and/or service fees (12b-1 fees), and other fund expenses. These costs are described in more detail in the funds’ prospectus. The examples below are intended to help you understand the ongoing costs of investing in the funds and help you compare these with the ongoing costs of investing in other mutual funds.

The first line in the table for each class shows the actual amount of fund expenses you would have paid on a $1,000 investment in the fund from April 1, 2013 through September 30, 2013. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual fund returns and expenses. To estimate the expenses you paid over the period, simply divide your account value by $1,000 (for example, $8,600 account value divided by $1,000 = 8.6) and multiply the result by the number in the Expenses Paid During Period row as shown below for your class.

The second line in the table for each class provides information about hypothetical account values and hypothetical expenses based on the fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid on your investment for the period. You may use this information to compare the ongoing costs of investing in the fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown reflect ongoing costs only, and do not include any transaction costs, such as sales charges. Therefore, the second line in the table of each fund is useful in comparing ongoing costs only, and will not help you determine the relative costs of owning different funds. If transaction costs were included, total costs would be higher.

| | | | | | | | | | | | |

LOOMIS SAYLES GLOBAL EQUITY AND

INCOME FUND | | BEGINNING

ACCOUNT VALUE

4/1/2013 | | | ENDING

ACCOUNT VALUE

9/30/2013 | | | EXPENSES PAID

DURING PERIOD*

4/1/2013 – 9/30/2013 | |

| Class A | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,045.00 | | | $ | 6.05 | |

| Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,019.15 | | | $ | 5.97 | |

| Class C | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,041.40 | | | $ | 9.88 | |

| Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,015.39 | | | $ | 9.75 | |

| Class Y | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,046.50 | | | $ | 4.77 | |

| Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,020.41 | | | $ | 4.71 | |

| * | Expenses are equal to the Fund’s annualized expense ratio: 1.18%, 1.93% and 0.93% for Class A, C and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (183), divided by 365 (to reflect the half-year period). |

| 20

| | | | | | | | | | | | |

| LOOMIS SAYLES GROWTH FUND | | BEGINNING

ACCOUNT VALUE

4/1/2013 | | | ENDING

ACCOUNT VALUE

9/30/2013 | | | EXPENSES PAID

DURING PERIOD*

4/1/2013 – 9/30/2013 | |

| Class A | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,108.50 | | | | $5.34 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,020.00 | | | | $5.11 | |

| Class B | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,103.60 | | | | $9.28 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,016.24 | | | | $8.90 | |

| Class C | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,103.80 | | | | $9.28 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,016.24 | | | | $8.90 | |

| Class N | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,108.80 | | | | $5.02 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,020.31 | | | | $4.81 | |

| Class Y | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,110.10 | | | | $4.02 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,021.26 | | | | $3.85 | |

| * | Expenses are equal to the Fund’s annualized expense ratio (after waiver/reimbursement): 1.01%, 1.76%, 1.76%, 0.95% and 0.76% for Class A, B, C, N and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (183), divided by 365 (to reflect the half-year period). |

| | | | | | | | | | | | |

| LOOMIS SAYLES MID CAP GROWTH FUND | | BEGINNING

ACCOUNT VALUE

4/1/2013 | | | ENDING

ACCOUNT VALUE

9/30/2013 | | | EXPENSES PAID

DURING PERIOD*

4/1/2013 – 9/30/2013 | |

| Class A | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,161.90 | | | | $6.77 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,018.80 | | | | $6.33 | |

| Class C | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,157.70 | | | | $10.82 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,015.04 | | | | $10.10 | |

| Class N | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,163.80 | | | | $5.15 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,020.31 | | | | $4.81 | |

| Class Y | | | | | | | | | | | | |

| Actual | | | $1,000.00 | | | | $1,163.40 | | | | $5.42 | |

| Hypothetical (5% return before expenses) | | | $1,000.00 | | | | $1,020.05 | | | | $5.06 | |

| * | Expenses are equal to the Fund’s annualized expense ratio (after waiver/reimbursement): 1.25%, 2.00%, 0.95% and 1.00% for Class A, C, N and Y, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (183), divided by 365 (to reflect the half-year period). |

21 |

| | | | | | | | | | | | |

| LOOMIS SAYLES VALUE FUND | | BEGINNING

ACCOUNT VALUE

4/1/2013 | | | ENDING

ACCOUNT VALUE

9/30/2013 | | | EXPENSES PAID

DURING PERIOD*

4/1/2013 – 9/30/2013 | |

| Class A | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,087.50 | | | $ | 5.02 | |

| Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,020.26 | | | $ | 4.86 | |

| Class B | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,083.20 | | | $ | 8.93 | |

| Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,016.50 | | | $ | 8.64 | |

| Class C | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,083.40 | | | $ | 8.93 | |

| Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,016.50 | | | $ | 8.64 | |

| Class N | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,088.70 | | | $ | 2.98 | |

| Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,022.21 | | | $ | 2.89 | |

| Class Y | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,088.70 | | | $ | 3.72 | |

| Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,021.51 | | | $ | 3.60 | |

| Admin Class | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,086.50 | | | $ | 6.17 | |

| Hypothetical (5% return before expenses) | | $ | 1,000.00 | | | $ | 1,019.15 | | | $ | 5.97 | |

| * | Expenses are equal to the Fund’s annualized expense ratio: 0.96%, 1.71%, 1.71%, 0.57%, 0.71% and 1.18% for Class A, B, C, N, Y and Admin Class, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (183), divided by 365 (to reflect the half-year period). |

| 22

BOARD APPROVAL OF THE EXISTING ADVISORY AGREEMENTS

The Board of Trustees of the Trust (the “Board”), including the Independent Trustees, considers matters bearing on each Fund’s advisory agreement (collectively, the “Agreements”) at most of its meetings throughout the year. Each year, usually in the spring, the Contract Review and Governance Committee of the Board meets to review the Agreements to determine whether to recommend that the full Board approve the continuation of the Agreements, typically for an additional one-year period. After the Committee has made its recommendation, the full Board, including the Independent Trustees, determines whether to approve the continuation of the Agreements.

In connection with these meetings, the Trustees receive materials that the Funds’ investment adviser (the “Adviser”) believes to be reasonably necessary for the Trustees to evaluate the Agreements. These materials generally include, among other items, (i) information on the investment performance of the Funds and the performance of peer groups of funds and the Funds’ performance benchmarks, (ii) information on the Funds’ advisory fees and other expenses, including information comparing the Funds’ expenses to the fees charged to institutional accounts with similar strategies managed by the Adviser, if any, and to those of peer groups of funds and information about any applicable expense caps and fee “breakpoints,” (iii) sales and redemption data in respect of the Funds, (iv) information about the profitability of the Agreements to the Adviser and (v) information obtained through the completion by the Adviser of a questionnaire distributed on behalf of the Trustees. The Board, including the Independent Trustees, also consider other matters such as (i) the Adviser’s financial results and financial condition, (ii) each Fund’s investment objective and strategies and the size, education and experience of the Adviser’s investment staff and its use of technology, external research and trading cost measurement tools, (iii) arrangements in respect of the distribution of the Funds’ shares and the related costs, (iv) the procedures employed to determine the value of the Funds’ assets, (v) the allocation of the Funds’ brokerage, if any, including, if applicable, allocations to brokers affiliated with the Adviser and the use of “soft” commission dollars to pay Fund expenses and to pay for research and other similar services, (vi) the resources devoted to, and the record of compliance with, the Funds’ investment policies and restrictions, policies on personal securities transactions and other compliance policies, (vii) information about amounts invested by the Funds’ portfolio managers in the Funds or in similar accounts that they manage and (viii) the general economic outlook with particular emphasis on the mutual fund industry. Throughout the process, the Trustees are afforded the opportunity to ask questions of and request additional materials from the Adviser.

In addition to the materials requested by the Trustees in connection with their annual consideration of the continuation of the Agreements, the Trustees receive materials in advance of each regular quarterly meeting of the Board that provide detailed information about the Funds’ investment performance and the fees charged to the Funds for advisory and other services. This information generally includes, among other things, an internal performance rating for each Fund based on agreed-upon criteria, graphs showing each Fund’s performance and fee differentials against each Fund’s peer group/category, performance ratings provided by a third-party, total return information for various periods, and third-party performance rankings for various periods comparing a Fund against

23 |

similarly categorized funds. The portfolio management team for each Fund or other representatives of the Adviser make periodic presentations to the Contract Review and Governance Committee and/or the full Board, and Funds identified as presenting possible performance concerns may be subject to more frequent board presentations and reviews. In addition, each quarter the Trustees are provided with detailed statistical information about each Fund’s portfolio. The Trustees also receive periodic updates between meetings.

The Board most recently approved the continuation of the Agreements at their meeting held in June 2013. The Agreements were continued for a one-year period for the Funds. In considering whether to approve the continuation of the Agreements, the Board, including the Independent Trustees, did not identify any single factor as determinative. Individual Trustees may have evaluated the information presented differently from one another, giving different weights to various factors. Matters considered by the Trustees, including the Independent Trustees, in connection with their approval of the Agreements included, but were not limited to, the factors listed below.

The nature, extent and quality of the services provided to the Funds under the Agreements. The Trustees considered the nature, extent and quality of the services provided by the Adviser and its affiliates to the Funds and the resources dedicated to the Funds by the Adviser and its affiliates.

The Trustees considered not only the advisory services provided by the Adviser to the Funds, but also the administrative services provided by NGAM Advisors, L.P. (“NGAM Advisors”) and its affiliates to the Funds. For each Fund, the Trustees also considered the benefits to shareholders of investing in a mutual fund that is part of a family of funds that offers shareholders the right to exchange shares of one type of fund for shares of another type of fund, and provides a variety of fund and shareholder services.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding each of the Agreements, that the nature, extent and quality of services provided supported the renewal of the Agreements.

Investment performance of the Funds and the Adviser. As noted above, the Trustees received information about the performance of the Funds over various time periods, including information that compared the performance of the Funds to the performance of peer groups and categories of funds and the Funds’ respective performance benchmarks. In addition, the Trustees also reviewed data prepared by an independent third party that analyzed the performance of the Funds using a variety of performance metrics, including metrics that also measured the performance of the Funds on a risk adjusted basis.

With respect to each Fund, the Board concluded that the Fund’s performance or other relevant factors supported the renewal of the Agreement relating to that Fund. In the case of each Fund that had performance that lagged that of a relevant peer group median and/or category median for certain (although not necessarily all) periods, the Board concluded that other factors relevant to performance supported renewal of the Agreements. These factors included one or more of the following: (1) that the underperformance was attributable, to a significant extent, to investment decisions (such as security selection or sector allocation) by the Adviser that were reasonable and consistent with the Fund’s investment objective and policies; (2) that the Fund’s more recent performance was competitive when compared to its relevant performance benchmarks and peer group category; and (3) that the Fund’s performance, although lagging in certain recent periods, was stronger over the long term.

| 24

The Trustees also considered the Adviser’s performance and reputation generally, the performance of the fund family generally, and the historical responsiveness of the Adviser to Trustee concerns about performance and the willingness of the Adviser to take steps intended to improve performance.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding each of the Agreements, that the performance of the Funds and the Adviser supported the renewal of the Agreements.

The costs of the services to be provided and profits to be realized by the Adviser and its affiliates from their respective relationships with the Funds. The Trustees considered the fees charged to the Funds for advisory services as well as the total expense levels of the Funds. This information included comparisons (provided both by management and also by an independent third party) of the Funds’ advisory fees and total expense levels to those of their peer groups and information about the advisory fees charged by the Adviser to comparable accounts (such as institutional separate accounts), as well as information about differences in such fees and the reasons for any such differences. In considering the fees charged to comparable accounts, the Trustees considered, among other things, management’s representations about the differences between managing mutual funds as compared to other types of accounts, including the additional resources required to effectively manage and the greater regulatory costs associated with the management of mutual fund assets. In evaluating each Fund’s advisory fee, the Trustees also took into account the demands, complexity and quality of the investment management of such Fund and the need for the Adviser to offer competitive compensation. The Trustees considered that over the past several years, management had made recommendations regarding reductions in advisory fee rates, implementation of advisory fee breakpoints and the institution of advisory fee waivers and expense caps for various funds in the fund family. They noted that all four of the Funds included in this report have expense caps in place, and the Trustees considered the amounts waived or reimbursed by the Adviser under these caps for each Fund whose current expenses are above the cap.

The Trustees also considered the compensation directly or indirectly received by the Adviser and its affiliates from their relationships with the Funds. The Trustees reviewed information provided by management as to the profitability of the Adviser’s and its affiliates’ relationships with the Funds, and information about the allocation of expenses used to calculate profitability. They also reviewed information provided by management about the effect of distribution costs and changes in asset levels on Adviser profitability, including information regarding resources spent on distribution activities. When reviewing profitability, the Trustees also considered information about court cases in which adviser compensation or profitability were issues, the performance of the relevant Funds, the expense levels of the Funds, and whether the Adviser had implemented breakpoints and/or expense caps with respect to such Funds.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding each of the Agreements, that the advisory fee charged to each of the Funds was fair and reasonable, and that the costs of these services generally and the related profitability of the Adviser and its affiliates in respect of their relationships with the Funds supported the renewal of the Agreements.

25 |

Economies of Scale. The Trustees considered the existence of any economies of scale in the provision of services by the Adviser and whether those economies are shared with the Funds through breakpoints in their investment advisory fees or other means, such as expense waivers or caps. The Trustees also discussed with management the factors considered with respect to the implementation of breakpoints in investment advisory fees or expense waivers or caps for certain funds. Management explained that a number of factors are taken into account in considering the possible implementation of breakpoints or an expense cap for a fund, including, among other things, factors such as a fund’s assets, the projected growth of a fund, projected profitability and a fund’s fees and performance. With respect to economies of scale, the Trustees noted that each of the Funds was subject to an expense cap or waiver. In considering these issues, the Trustees also took note of the costs of the services provided (both on an absolute and a relative basis) and the profitability to the Adviser and its affiliates of their relationships with the Funds, as discussed above.

After reviewing these and related factors, the Trustees concluded, within the context of their overall conclusions regarding each of the Agreements, that the extent to which economies of scale were shared with the Funds supported the renewal of the Agreements.

The Trustees also considered other factors, which included but were not limited to the following:

| · | | The effect of recent market and economic events on the performance, asset levels and expense ratios of each Fund. |

| · | | Whether each Fund has operated in accordance with its investment objective and the Fund’s record of compliance with its investment restrictions, and the compliance programs of the Funds and the Adviser. They also considered the compliance-related resources the Adviser and its affiliates were providing to the Funds. |

| · | | The nature, quality, cost and extent of administrative and shareholder services performed by the Adviser and its affiliates, both under the Agreements and under separate agreements covering administrative services. |

| · | | So-called “fallout benefits” to the Adviser, such as the engagement of affiliates of the Adviser to provide distribution, administrative and brokerage services to the Funds, and the benefits of research made available to the Adviser by reason of brokerage commissions (if any) generated by the Funds’ securities transactions. The Trustees also considered the fact that NGAM Advisors’ parent company benefits from the retention of an affiliated Adviser. The Trustees considered the possible conflicts of interest associated with these fallout and other benefits, and the reporting, disclosure and other processes in place to disclose and monitor such possible conflicts of interest. |

| · | | The Trustees’ review and discussion of the Funds’ advisory arrangements in prior years, and management’s record of responding to Trustee concerns raised during the year and in prior years. |

Based on their evaluation of all factors that they deemed to be material, including those factors described above, and assisted by the advice of independent counsel, the Trustees, including the Independent Trustees, concluded that each of the existing Agreements should be continued through June 30, 2014.

| 26

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Global Equity and Income Fund

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

| | Common Stocks — 67.9% of Net Assets | | | | |

| | | | Belgium — 1.5% | | | | |

| | 177,107 | | | Anheuser-Busch InBev NV | | $ | 17,568,611 | |

| | | | | | | | |

| | | | Brazil — 0.6% | | | | |

| | 527,700 | | | Mills Estruturas e Servicos de Engenharia S.A. | | | 7,228,702 | |

| | | | | | | | |

| | | | Canada — 1.1% | | | | |

| | 348,600 | | | CGI Group, Inc., Class A(b) | | | 12,234,251 | |

| | | | | | | | |

| | | | Chile — 0.6% | | | | |

| | 759,310 | | | S.A.C.I. Falabella | | | 7,242,066 | |

| | | | | | | | |

| | | | China — 1.3% | | | | |

| | 1,300,000 | | | Hengan International Group Co. Ltd. | | | 15,212,973 | |

| | | | | | | | |

| | | | Germany — 3.9% | | | | |

| | 183,099 | | | Adidas AG | | | 19,861,052 | |

| | 109,467 | | | Bayer AG, (Registered) | | | 12,909,535 | |

| | 77,643 | | | Brenntag AG | | | 12,925,663 | |

| | | | | | | | |

| | | | | | | 45,696,250 | |

| | | | | | | | |

| | | | Japan — 1.2% | | | | |

| | 530,700 | | | Asahi Group Holdings Ltd. | | | 13,971,015 | |

| | | | | | | | |

| | | | Mexico — 1.3% | | | | |

| | 6,550,700 | | | Genomma Lab Internacional S.A. de CV, Class B(b) | | | 14,953,582 | |

| | | | | | | | |

| | | | Russia — 0.8% | | | | |

| | 240,740 | | | Mail.ru Group Ltd., GDR(c) | | | 9,184,231 | |

| | | | | | | | |

| | | | Sweden — 1.3% | | | | |

| | 527,029 | | | Atlas Copco AB, Class A | | | 15,439,069 | |

| | | | | | | | |

| | | | Switzerland — 2.1% | | | | |

| | 90,501 | | | Roche Holding AG | | | 24,423,811 | |

| | | | | | | | |

| | | | Thailand — 1.0% | | | | |

| | 900,400 | | | Bangkok Bank PCL | | | 5,674,613 | |

| | 413,700 | | | Siam Cement PCL | | | 5,694,338 | |

| | | | | | | | |

| | | | | | | 11,368,951 | |

| | | | | | | | |

| | | | Turkey — 0.6% | | | | |

| | 1,918,691 | | | Turkiye Garanti Bankasi AS | | | 7,568,843 | |

| | | | | | | | |

| | | | United Kingdom — 11.1% | | | | |

| | 1,887,092 | | | Aberdeen Asset Management PLC | | | 11,557,299 | |

| | 221,349 | | | British American Tobacco PLC | | | 11,649,440 | |

| | 347,695 | | | Burberry Group PLC | | | 9,200,427 | |

| | 732,984 | | | Diageo PLC | | | 23,299,668 | |

| | 388,891 | | | Hikma Pharmaceuticals PLC | | | 6,543,315 | |

| | 1,265,491 | | | HSBC Holdings PLC | | | 13,696,859 | |

| | 5,747,596 | | | Legal & General Group PLC | | | 18,238,010 | |

| | 438,776 | | | Shire PLC | | | 17,553,094 | |

| | 721,999 | | | Standard Chartered PLC | | | 17,297,454 | |

| | | | | | | | |

| | | | 129,035,566 | |

| | | | | | | | |

See accompanying notes to financial statements.

27 |

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Global Equity and Income Fund – (continued)

| | | | | | | | |

| Shares | | | Description | | Value (†) | |

| | | | United States — 39.5% | |

| | 182,362 | | | ACE Ltd. | | $ | 17,061,789 | |

| | 228,828 | | | American Express Co. | | | 17,281,091 | |

| | 39,095 | | | Apple, Inc. | | | 18,638,541 | |

| | 30,319 | | | AutoZone, Inc.(b) | | | 12,816,751 | |

| | 350,360 | | | Cabot Oil & Gas Corp. | | | 13,075,435 | |

| | 466,159 | | | Citigroup, Inc. | | | 22,613,373 | |

| | 46,194 | | | Core Laboratories NV | | | 7,816,487 | |

| | 136,771 | | | CVS Caremark Corp. | | | 7,761,754 | |

| | 177,583 | | | Deere & Co. | | | 14,453,480 | |

| | 87,118 | | | EOG Resources, Inc. | | | 14,747,335 | |

| | 180,180 | | | Genesee & Wyoming, Inc., Class A(b) | | | 16,751,335 | |

| | 103,803 | | | Gilead Sciences, Inc.(b) | | | 6,522,980 | |

| | 70,542 | | | Goldman Sachs Group, Inc. (The) | | | 11,160,450 | |

| | 25,701 | | | Google, Inc., Class A(b) | | | 22,511,763 | |

| | 146,257 | | | Gulfport Energy Corp.(b) | | | 9,410,175 | |

| | 955 | | | Hawaiian Telcom Holdco, Inc.(b) | | | 25,403 | |

| | 94,427 | | | Jones Lang LaSalle, Inc. | | | 8,243,477 | |

| | 358,557 | | | Lowe’s Cos., Inc. | | | 17,070,899 | |

| | 96,181 | | | M&T Bank Corp. | | | 10,764,577 | |

| | 119,826 | | | National Fuel Gas Co. | | | 8,239,236 | |

| | 129,071 | | | National Oilwell Varco, Inc. | | | 10,081,736 | |

| | 28,883 | | | NewMarket Corp. | | | 8,315,705 | |

| | 255,842 | | | Noble Energy, Inc. | | | 17,143,972 | |

| | 140,006 | | | Praxair, Inc. | | | 16,830,121 | |

| | 73,365 | | | Precision Castparts Corp. | | | 16,671,463 | |

| | 21,972 | | | priceline.com, Inc.(b) | | | 22,212,593 | |

| | 120,459 | | | QUALCOMM, Inc. | | | 8,114,118 | |

| | 181,009 | | | Schlumberger Ltd. | | | 15,993,955 | |

| | 166,200 | | | Signet Jewelers Ltd. | | | 11,908,230 | |

| | 402,196 | | | Texas Instruments, Inc. | | | 16,196,433 | |

| | 122,826 | | | TransDigm Group, Inc. | | | 17,035,966 | |

| | 152,180 | | | UnitedHealth Group, Inc. | | | 10,897,610 | |

| | 129,860 | | | Valspar Corp. (The) | | | 8,237,020 | |

| | 26,818 | | | Vertex Pharmaceuticals, Inc.(b) | | | 2,033,341 | |

| | 327,736 | | | Wyndham Worldwide Corp. | | | 19,982,064 | |

| | | | | | | | |

| | | | 458,620,658 | |

| | | | | | | | |

| | | | Total Common Stocks (Identified Cost $678,736,713) | | | 789,748,579 | |

| | | | | | | | |

Principal Amount (‡) | | | | | | |

| | Bonds and Notes — 27.8% | | | | |

| | Non-Convertible Bonds — 27.0% | | | | |

| | | | Argentina — 0.1% | |

| $ | 170,000 | | | Pan American Energy LLC/Argentine Branch, 7.875%, 5/07/2021, 144A | | | 170,000 | |

| | 500,000 | | | Transportadora de Gas del Sur S.A., 7.875%, 5/14/2017, 144A | | | 452,500 | |

| | | | | | | | |

| | | | 622,500 | |

| | | | | | | | |

See accompanying notes to financial statements.

| 28

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Global Equity and Income Fund – (continued)

| | | | | | | | |

Principal Amount (‡) | | | Description | | Value (†) | |

| | | | Australia — 0.4% | | | | |

| $ | 1,200,000 | | | Macquarie Bank Ltd., 5.000%, 2/22/2017, 144A | | $ | 1,308,720 | |

| | 500,000 | | | Macquarie Bank Ltd., 6.625%, 4/07/2021, 144A | | | 545,150 | |

| | 2,185,000 | | | New South Wales Treasury Corp., 6.000%, 2/01/2018, (AUD)(d) | | | 2,241,176 | |

| | 155,000 | | | Sydney Airport Finance Co., 5.125%, 2/22/2021, 144A | | | 162,930 | |

| | | | | | | | |

| | | | | | | 4,257,976 | |

| | | | | | | | |

| | | | Belgium — 0.1% | | | | |

| | 350,000 | | | Anheuser-Busch InBev NV, EMTN, 6.500%, 6/23/2017, (GBP) | | | 661,563 | |

| | | | | | | | |

| | | | Brazil — 1.8% | | | | |

| | 800,000 | | | Banco do Brasil S.A., 3.875%, 10/10/2022 | | | 692,000 | |

| | 1,100,000 | | | Banco Nacional de Desenvolvimento Economico e Social, 5.750%, 9/26/2023, 144A | | | 1,100,000 | |

| | 400,000 | | | Banco Santander Brasil S.A., 4.500%, 4/06/2015, 144A | | | 409,000 | |

| | 600,000 | | | Banco Santander Brasil S.A., 4.625%, 2/13/2017, 144A | | | 618,000 | |

| | 1,919,970 | | | Banco Votorantim S.A., 6.250%, 5/16/2016, 144A, (BRL) | | | 846,351 | |

| | 800,000 | | | Braskem Finance Ltd., 5.750%, 4/15/2021, 144A | | | 784,000 | |

| | 6,600,000 | | | Brazil Letras do Tesouro Nacional, Zero Coupon, 7/01/2016, (BRL) | | | 2,207,345 | |

| | 693,410(††) | | | Brazil Notas do Tesouro Nacional, Series B, 6.000%, 8/15/2014, (BRL) | | | 319,518 | |

| | 554,728(††) | | | Brazil Notas do Tesouro Nacional, Series B, 6.000%, 5/15/2015, (BRL) | | | 258,184 | |

| | 1,115(†††) | | | Brazil Notas do Tesouro Nacional, Series F, 10.000%, 1/01/2021, (BRL) | | | 464,847 | |

| | 2,250(†††) | | | Brazil Notas do Tesouro Nacional, Series F, 10.000%, 1/01/2019, (BRL) | | | 953,683 | |

| | 2,250,000 | | | Brazilian Government International Bond, 10.250%, 1/10/2028, (BRL) | | | 1,012,668 | |

| | 1,700,000 | | | BRF S.A., 3.950%, 5/22/2023, 144A | | | 1,462,000 | |

| | 600,000 | | | BRF S.A., 5.875%, 6/06/2022, 144A | | | 597,000 | |

| | 2,300,000 | | | BRF S.A., 7.750%, 5/22/2018, 144A, (BRL) | | | 822,429 | |

| | 1,075,000 | | | Caixa Economica Federal, 4.500%, 10/03/2018, 144A | | | 1,065,325 | |

| | 1,255,000 | | | Cielo S.A./Cielo USA, Inc., 3.750%, 11/16/2022, 144A | | | 1,079,300 | |

| | 400,000 | | | CSN Resources S.A., 6.500%, 7/21/2020, 144A | | | 399,000 | |

| | 450,000 | | | Fibria Overseas Finance Ltd., 6.750%, 3/03/2021, 144A | | | 480,150 | |

| | 800,000 | | | Gerdau Trade, Inc., 5.750%, 1/30/2021, 144A | | | 784,000 | |

| | 300,000 | | | Itau Unibanco Holding S.A., 6.200%, 12/21/2021, 144A | | | 300,000 | |

| | 100,000 | | | LPG International, Inc., 7.250%, 12/20/2015 | | | 109,970 | |

| | 185,000 | | | Odebrecht Drilling Norbe VIII/IX Ltd., 6.350%, 6/30/2021, 144A | | | 188,238 | |

| | 900,000 | | | Odebrecht Offshore Drilling Finance Ltd., 6.750%, 10/01/2022, 144A | | | 922,500 | |

| | 2,400,000 | | | Oi S.A., 9.750%, 9/15/2016, 144A, (BRL) | | | 948,391 | |

| | 320,000 | | | Petrobras International Finance Co., 5.375%, 1/27/2021 | | | 321,467 | |

| | 300,000 | | | Petrobras International Finance Co., 6.875%, 1/20/2040 | | | 294,703 | |

| | 800,000 | | | Samarco Mineracao S.A., 4.125%, 11/01/2022, 144A | | | 696,000 | |

| | 129,000 | | | Telemar Norte Leste S.A., 5.500%, 10/23/2020, 144A | | | 113,520 | |

| | 536,000 | | | Vale Overseas Ltd., 6.875%, 11/21/2036 | | | 543,608 | |

| | | | | | | | |

| | | | | | | 20,793,197 | |

| | | | | | | | |

| | | | Canada — 0.9% | | | | |

| | 1,085,000 | | | Air Canada, 7.625%, 10/01/2019, 144A, (CAD) | | | 1,055,980 | |

| | 1,570,000 | | | Bank of Nova Scotia, 1.375%, 12/18/2017 | | | 1,541,205 | |

| | 650,000 | | | Canadian Government, 1.000%, 8/01/2016, (CAD) | | | 623,995 | |

| | 2,880,000 | | | Canadian Government, 3.000%, 12/01/2015, (CAD)(d) | | | 2,901,193 | |

| | 2,695,000 | | | Canadian Government, 4.250%, 6/01/2018, (CAD)(d) | | | 2,900,569 | |

See accompanying notes to financial statements.

29 |

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Global Equity and Income Fund – (continued)

| | | | | | | | |

Principal Amount (‡) | | | Description | | Value (†) | |

| | | | Canada — continued | | | | |

| $ | 875,000 | | | Pacific Rubiales Energy Corp., 5.125%, 3/28/2023, 144A | | $ | 784,219 | |

| | 100,000 | | | Shaw Communications, Inc., 5.650%, 10/01/2019, (CAD) | | | 106,734 | |

| | 600,000 | | | Telus Corp., Series CG, 5.050%, 12/04/2019, (CAD) | | | 636,942 | |

| | | | | | | | |

| | | | | | | 10,550,837 | |

| | | | | | | | |

| | | | Chile — 0.4% | | | | |

| | 1,450,000 | | | Banco de Credito e Inversiones, 3.000%, 9/13/2017, 144A | | | 1,439,869 | |

| | 850,000,000 | | | Banco Santander Chile, 6.500%, 9/22/2020, 144A, (CLP) | | | 1,662,952 | |

| | 200,000 | | | Celulosa Arauco y Constitucion S.A., 4.750%, 1/11/2022 | | | 194,294 | |

| | 1,000,000 | | | Corp Nacional del Cobre de Chile, 4.500%, 8/13/2023, 144A | | | 1,008,103 | |

| | 250,000 | | | E.CL S.A., 5.625%, 1/15/2021, 144A | | | 255,482 | |

| | 800,000 | | | Inversiones CMPC S.A., 4.375%, 5/15/2023, 144A | | | 743,778 | |

| | | | | | | | |

| | | | | | | 5,304,478 | |

| | | | | | | | |

| | | | China — 0.3% | | | | |

| | 800,000 | | | Baidu, Inc., 2.250%, 11/28/2017 | | | 786,874 | |

| | 700,000 | | | Baidu, Inc., 3.250%, 8/06/2018 | | | 699,681 | |

| | 400,000 | | | China Resources Gas Group Ltd., 4.500%, 4/05/2022, 144A | | | 396,276 | |

| | 1,200,000 | | | CNOOC Finance 2013 Ltd., 3.000%, 5/09/2023 | | | 1,078,568 | |

| | 1,000,000 | | | Parkson Retail Group Ltd., 4.500%, 5/03/2018 | | | 920,000 | |

| | | | | | | | |

| | | | | | | 3,881,399 | |

| | | | | | | | |

| | | | Colombia — 0.4% | | | | |

| | 400,000 | | | Banco Davivienda S.A., 5.875%, 7/09/2022, 144A | | | 380,000 | |

| | 555,000 | | | Colombia Telecomunicaciones S.A., E.S.P., 5.375%, 9/27/2022, 144A | | | 510,600 | |

| | 1,180,000 | | | Ecopetrol S.A., 5.875%, 9/18/2023 | | | 1,227,200 | |

| | 1,265,000,000 | | | Emgesa S.A. E.S.P., 8.750%, 1/25/2021, 144A, (COP) | | | 704,669 | |

| | 2,140,000,000 | | | Empresas Publicas de Medellin E.S.P., 8.375%, 2/01/2021, 144A, (COP) | | | 1,169,299 | |

| | 200,000,000 | | | Republic of Colombia, 7.750%, 4/14/2021, (COP) | | | 118,576 | |

| | 40,000 | | | Republic of Colombia, 8.125%, 5/21/2024 | | | 51,650 | |

| | | | | | | | |

| | | | | | | 4,161,994 | |

| | | | | | | | |

| | | | Costa Rica — 0.1% | | | | |

| | 600,000 | | | Costa Rica Government International Bond, 4.250%, 1/26/2023, 144A | | | 537,000 | |

| | 800,000 | | | Costa Rica Government International Bond, 4.375%, 4/30/2025, 144A | | | 696,000 | |

| | | | | | | | |

| | | | | | | 1,233,000 | |

| | | | | | | | |

| | | | Czech Republic — 0.0% | | | | |

| | 400,000 | | | CEZ AS, 4.250%, 4/03/2022, 144A | | | 399,600 | |

| | | | | | | | |

| | | | Finland — 0.2% | | | | |

| | 1,435,000 | | | Finland Government Bond, 1.500%, 4/15/2023, 144A, (EUR) | | | 1,855,922 | |

| | | | | | | | |

| | | | France — 0.0% | | | | |

| | 200,000 | | | AXA S.A., 7.125%, 12/15/2020, (GBP) | | | 382,348 | |

| | | | | | | | |

| | | | Hong Kong — 0.1% | | | | |

| | 400,000 | | | Hutchison Whampoa International 11 Ltd., 3.500%, 1/13/2017, 144A | | | 417,774 | |

| | 400,000 | | | Noble Group Ltd., 6.750%, 1/29/2020, 144A | | | 412,000 | |

| | | | | | | | |

| | | | | | | 829,774 | |

| | | | | | | | |

See accompanying notes to financial statements.

| 30

Portfolio of Investments – as of September 30, 2013

Loomis Sayles Global Equity and Income Fund – (continued)

| | | | | | | | |

Principal Amount (‡) | | | Description | | Value (†) | |

| | | | Hungary — 0.0% | | | | |

| $ | 200,000 | | | Hungary Government International Bond, 6.375%, 3/29/2021 | | $ | 212,750 | |

| | | | | | | | |

| | | | Iceland — 0.1% | | | | |

| | 1,000,000 | | | Republic of Iceland, 5.875%, 5/11/2022, 144A | | | 1,027,500 | |

| | | | | | | | |

| | | | India — 0.2% | | | | |

| | 200,000 | | | Canara Bank Ltd., (fixed rate to 11/28/2016, variable rate thereafter), 6.365%, 11/28/2021 | | | 186,600 | |

| | 1,400,000 | | | ICICI Bank Ltd., (fixed rate to 4/30/2017, variable rate thereafter), 6.375%, 4/30/2022, 144A | | | 1,295,000 | |

| | 700,000 | | | State Bank of India/London, 4.125%, 8/01/2017, 144A | | | 694,719 | |

| | | | | | | | |

| | | | | | | 2,176,319 | |

| | | | | | | | |

| | | | Indonesia — 0.4% | | | | |