UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-06247 | |||||

| AMERICAN CENTURY WORLD MUTUAL FUNDS, INC. | ||||||

| (Exact name of registrant as specified in charter) | ||||||

| 4500 MAIN STREET, KANSAS CITY, MISSOURI | 64111 | |||||

| (Address of principal executive offices) | (Zip Code) | |||||

CHARLES A. ETHERINGTON 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 | ||||||

| (Name and address of agent for service) | ||||||

| Registrant’s telephone number, including area code: | 816-531-5575 | |||||

| Date of fiscal year end: | 11-30 | |||||

| Date of reporting period: | 11-30-2012 | |||||

ITEM 1. REPORTS TO STOCKHOLDERS.

ANNUAL REPORT NOVEMBER 30, 2012

| Emerging Markets Fund |

| President’s Letter | 2 |

| Independent Chairman’s Letter | 3 |

| Market Perspective | 4 |

| Performance | 5 |

| Portfolio Commentary | 7 |

| Fund Characteristics | 9 |

| Shareholder Fee Example | 10 |

| Schedule of Investments | 12 |

| Statement of Assets and Liabilities | 15 |

| Statement of Operations | 16 |

| Statement of Changes in Net Assets | 17 |

| Notes to Financial Statements | 18 |

| Financial Highlights | 24 |

| Report of Independent Registered Public Accounting Firm | 26 |

| Management | 27 |

| Approval of Management Agreement | 30 |

| Additional Information | 35 |

Any opinions expressed in this report reflect those of the author as of the date of the report, and do not necessarily represent the opinions of American Century Investments® or any other person in the American Century Investments organization. Any such opinions are subject to change at any time based upon market or other conditions and American Century Investments disclaims any responsibility to update such opinions. These opinions may not be relied upon as investment advice and, because investment decisions made by American Century Investments funds are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any American Century Investments fund. Security examples are used for representational purposes only and are not intended as recommendations to purchase or sell securities. Performance information for comparative indices and securities is provided to American Century Investments by third party vendors. To the best of American Century Investments’ knowledge, such information is accurate at the time of printing.

Dear Investor:

Thank you for reviewing this annual report for the 12 months ended November 30, 2012. It offers investment performance, market analysis, and portfolio information, presented with the expert perspective of our portfolio management team.

Annual reports remain important vehicles for conveying information about fund returns, including key factors that affected fund performance. For additional, updated investment and market insights, we encourage you to visit our website, americancentury.com.

Favorable Fiscal-Year Returns for Most Major Stock and Bond Benchmarks

Despite a global economic slowdown, continued concerns about European financial system stability, and uncertainty about U.S. political and fiscal conditions in 2013, 12-month stock and bond returns were generally favorable, particularly for U.S. value stocks and high-yield bonds.

U.S. value stock indices outpaced the S&P 500 Index’s 16.13% return for the period, as did U.S. corporate and municipal high-yield benchmarks. U.S. growth and international index returns were generally lower, but still solid—the MSCI EAFE Index, for example, returned 12.61%.

With the exception of high-yield bond sectors, stocks generally outperformed bonds for the period, though bonds benefitted from economic stagnation, reduced inflation pressures, and low interest rates. The 10-year U.S. Treasury yield declined from 2.07% to 1.62% during the period, and the Barclays U.S. Aggregate Bond Index returned 5.51%. Related global bond indices also returned in roughly the mid-single digits.

Bucking the global trend, the U.S. economy showed signs of improvement during the fiscal year, particularly the long-depressed housing market. However, the outlook for 2013 remains guarded, as the fragile recovery remains vulnerable to fiscal and financial factors that could trigger further slowdowns and market volatility.

Under these conditions, we continue to believe in a disciplined, diversified, long-term investment approach, using both stocks and bonds—as appropriate—for meeting financial goals. We appreciate your continued trust in us in this challenging environment.

Sincerely,

Jonathan Thomas

President and Chief Executive Officer

American Century Investments

2

Dear Fellow Shareholders,

The board has once again completed its annual review of the advisory contract between the American Century Investments mutual funds overseen by the board and the funds’ advisor, American Century Investment Management, Inc. This process, often referred to as the 15(c) review, involves the independent directors considering all of the material monitored throughout the year and evaluating a wide range of factors to determine whether the management fee paid by each fund to the advisor is reasonable.

The independent directors’ rationale for this decision is provided in detail in this, or in a previous, report. However, there are several highlights that should be of interest to all shareholders.

| • | Fund performance and client service continue to be rated among the industry’s best. |

| • | Target date and other asset allocation products continue to successfully gather assets and industry acclaim. |

| • | Compliance programs continue to function successfully with no issues impacting shareholder interests. |

| • | Fees were found to be within an acceptable competitive range, with minor fee waivers being negotiated on five funds. |

Knowing that most shareholders are long term investors, the board was particularly pleased with our succession planning review. Talented professionals are being added within portfolio management and experienced managers have been added to the senior management team.

Overall it was a very positive review for the American Century Investments mutual funds during a challenging market environment.

Best personal regards,

Don Pratt

3

By Mark Kopinski, Chief Investment Officer, Global and Non-U.S. Equity

Central Bank Action Drove Global Stocks Higher

Despite a backdrop of weaker global economic growth and mounting sovereign debt problems in Europe and the United States, most global stock benchmarks advanced strongly for the 12-month period ended November 30, 2012. Investors generally overlooked the lackluster economic data, recession fears (which eventually turned to reality for Europe), and the instability of the eurozone’s banking system and currency. Instead, they focused on the optimism inspired by unprecedented central bank intervention.

In particular, the European Central Bank (ECB) launched several programs to help the eurozone’s troubled banks shore up their balance sheets and finance ongoing operations. The ECB also agreed to purchase the sovereign debt of financially strapped member nations that conform to the ECB’s fiscal reform measures. Meanwhile, in response to sluggish economic growth and high unemployment, the U.S. Federal Reserve (the Fed) announced its third—and most aggressive—quantitative easing program to date. The Bank of Japan also took action with an asset purchase program, while the People’s Bank of China eased its reserve requirements for commercial lenders.

Overall, developed markets outperformed emerging markets for the 12-month period, even as the emerging economies generally enjoyed higher absolute levels of growth, albeit slower growth than in previous periods. Strong stock market performance in Europe and the United States, where central bank stimulus was the greatest, primarily drove the better relative results in the developed markets.

Valuations, Stock Selection Remain Key Factors

Even though economic growth and corporate earnings in aggregate have been slowing, and sovereign debt issues have yet to be resolved, there are some positive factors at work for global equity investors. Stock valuations around the globe appear attractive relative to historical averages. Similarly, equity earnings yields are also compelling when measured against long-term averages and current bond yields. Most important, we believe through our rigorous, bottom-up stock selection process it’s still possible to find individual companies growing earnings, either from a new product launch, market share gains, secular changes, or

beneficial acquisitions.

| International Equity Total Returns | ||||

| For the 12 months ended November 30, 2012 (in U.S. dollars) | ||||

| MSCI EAFE Index | 12.61% | MSCI Europe Index | 14.07% | |

| MSCI EAFE Growth Index | 12.66% | MSCI World Index | 13.62% | |

| MSCI EAFE Value Index | 12.45% | MSCI Japan Index | 3.59% | |

| MSCI Emerging Markets Index | 11.35% | |||

4

| Total Returns as of November 30, 2012 | ||||||

| Average Annual Returns | ||||||

Ticker Symbol | 1 year | 5 years | 10 years | Since Inception | Inception Date | |

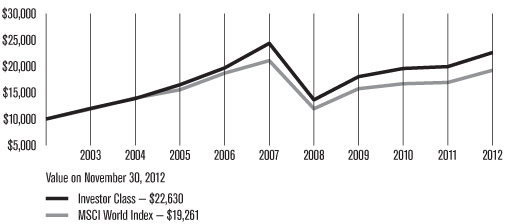

| Investor Class | TWMIX | 13.28% | -5.54% | 14.22% | 7.10% | 9/30/97 |

| MSCI Emerging Markets Growth Index | — | 14.21% | -2.76% | 13.88% | N/A(1) | — |

| Institutional Class | AMKIX | 13.43% | -5.37% | 14.43% | 11.09% | 1/28/99 |

A Class(2) No sales charge* With sales charge* | AEMMX | 12.99% 6.45% | -5.76% -6.87% | 13.94% 13.26% | 8.66% 8.19% | 5/12/99 |

| C Class | ACECX | 12.13% | -6.49% | 13.10% | 10.19% | 12/18/01 |

| R Class | AEMRX | 12.74% | -6.01% | — | -5.03% | 9/28/07 |

| * | Sales charges include initial sales charges and contingent deferred sales charges (CDSCs), as applicable. A Class shares have a 5.75% maximum initial sales charge and may be subject to a maximum CDSC of 1.00%. C Class shares redeemed within 12 months of purchase are subject to a maximum CDSC of 1.00%. The SEC requires that mutual funds provide performance information net of maximum sales charges in all cases where charges could be applied. |

| (1) | Benchmark data first available January 2001. |

| (2) | Prior to September 4, 2007, the A Class was referred to as the Advisor Class and did not have a front-end sales charge. Performance prior to that date has been adjusted to reflect this charge. |

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

5

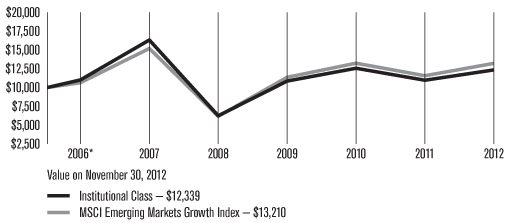

| Growth of $10,000 Over 10 Years |

| $10,000 investment made November 30, 2002 |

| Total Annual Fund Operating Expenses | ||||

| Investor Class | Institutional Class | A Class | C Class | R Class |

| 1.72% | 1.52% | 1.97% | 2.72% | 2.22% |

The total annual fund operating expenses shown is as stated in the fund’s prospectus current as of the date of this report. The prospectus may vary from the expense ratio shown elsewhere in this report because it is based on a different time period, includes acquired fund fees and expenses, and, if applicable, does not include fee waivers or expense reimbursements.

Data presented reflect past performance. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment return and principal value will fluctuate, and redemption value may be more or less than original cost. To obtain performance data current to the most recent month end, please call 1-800-345-2021 or visit americancentury.com. International investing involves special risks, such as political instability and currency fluctuations. Investing in emerging markets may accentuate these risks.

Unless otherwise indicated, performance reflects Investor Class shares; performance for other share classes will vary due to differences in fee structure. For information about other share classes available, please consult the prospectus. Data assumes reinvestment of dividends and capital gains, and none of the charts reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the index are provided for comparison. The fund’s total returns include operating expenses (such as transaction costs and management fees) that reduce returns, while the total returns of the index do not.

6

| Portfolio Commentary |

Portfolio Managers: Patricia Ribeiro and Anthony Han

Performance Summary

Emerging Markets gained 13.28%* for the 12 months ended November 30, 2012, compared with its benchmark, the MSCI Emerging Markets Growth Index, which advanced 14.21%.

Emerging market growth stocks generally demonstrated robust performance during the 12-month period, even as key countries, including China and Brazil, experienced slowdowns in their economic growth rates. Unprecedented central bank intervention, particularly in Europe, the United States, and Japan, helped drive overall global stock market optimism. In general, emerging market stocks slightly lagged their developed market counterparts. But, in the growth stock universe, emerging market stocks outpaced developed market stocks.

The portfolio underperformed its benchmark for the period, primarily due to sector allocations, including an underweight position in health care and an overweight position in information technology. Overall, stock selection was a strong contributor, with holdings in the materials, consumer discretionary, and industrials sectors driving results. Stock selection was a detractor only in the information technology and energy sectors.

China Handset Maker was a Leading Detractor

From a regional perspective, stock selection hurt relative performance in China, which was among the portfolio’s largest performance detractors on a country basis. An overweight position in ZTE Corp., a cellular handset manufacturer, was among the top individual detractors. In October, the company reported its first quarterly loss, as weak sales drove margins to record lows. Mounting competition, revenue accounting changes, delayed orders in Africa, and a strategy of chasing market share in Europe through low-margin contracts accounted for the disappointing results. In addition, a U.S. Congressional committee named the company a potential security threat, a charge ZTE denied.

Another prominent China-based detractor included a position in Baidu, an Internet search provider. Late in the period, the company forecast its fourth-quarter revenue growth would slow to its weakest level in three years, which was below analysts’ expectations. In addition, reluctance from advertisers to purchase space on the company’s search pages for mobile phones, a slowdown in search revenue, and an analyst downgrade weighed on the company’s shares.

Mando, a South Korea-based parts supplier to automakers, also was among the portfolio’s leading individual detractors. The stock tumbled early in the period, as South Korean officials acknowledged the lackluster European economy hindered the country’s growth rate. Yet, the Bank of Korea refrained from lowering its key lending rate, citing inflationary concerns.

*All fund returns referenced in this commentary are for Investor Class shares.

7

Mexican Conglomerate was a Top Contributor

In terms of the portfolio’s favorable regional exposure, Mexico was among the top contributors for the 12-month period, driven by strong stock selection. In fact, one of the portfolio’s top individual contributors was Mexico’s Alfa SAB de CV, an industrial conglomerate operating in the petrochemical, food processing, automotive and telecommunication industries. The company reported strong quarterly results and favorable industry conditions and operating improvements in most of its business lines throughout the period. In addition, the company announced a 10-for-1 stock split in August to boost its market liquidity, sending its share prices to record highs.

South Africa also was among the portfolio’s top-performing countries, driven by strong stock selection. In particular, an overweight position in retailer Mr Price Group was among the portfolio’s top individual contributors for the period. During the second quarter of 2012, the company reported a 50% jump in full-year profits, as its total sales grew 12.9% during the fiscal period. Additionally, the company boosted its margins by slowing its store expansion efforts and tightening inventory controls. Then, in November, the company said it posted a 34% jump in first-half profit, aided by lower tax liabilities and debt-fuelled consumer spending. Overall, Mr Price and other South African retailers benefited from continued consumer spending due to above-inflation wage increases, low-cost borrowing, and government grants.

Stock selection in Indonesia also contributed favorably to portfolio performance, with cement producer Semen Gresik among the portfolio’s leading performance contributors. The company’s stock benefited from the booming cement demand in Indonesia’s property construction sector. The islands of Java and Sumatra account for nearly 85% of domestic demand. The company also maintained better-than-anticipated pricing.

Outlook

Looking ahead, the world’s macroeconomic landscape remains undermined by financial market, recession, and sovereign debt challenges in Europe and economic sluggishness in the U.S. and China. As a result, stock markets continued to be susceptible to bouts of volatility. Against this backdrop, our investment approach remained focused on companies located in emerging economies around the world that we believe are benefitting from secular tailwinds and not reliant upon broader economic developments.

8

| NOVEMBER 30, 2012 | |

| Top Ten Holdings | % of net assets |

| Samsung Electronics Co. Ltd. | 9.0% |

| Taiwan Semiconductor Manufacturing Co. Ltd. | 4.9% |

| Tencent Holdings Ltd. | 2.4% |

| China Overseas Land & Investment Ltd. | 2.0% |

| iShares MSCI Emerging Markets Index Fund | 2.0% |

| Ping An Insurance Group Co. H Shares | 1.8% |

| ITC Ltd. | 1.7% |

| CNOOC Ltd. | 1.7% |

| Hon Hai Precision Industry Co. Ltd. | 1.7% |

| Kunlun Energy Co. Ltd. | 1.6% |

| Types of Investments in Portfolio | % of net assets |

| Foreign Common Stocks | 96.5% |

| Exchange-Traded Funds | 2.0% |

| Total Equity Exposure | 98.5% |

| Temporary Cash Investments | 3.4% |

| Other Assets and Liabilities | (1.9)% |

| Investments by Country | % of net assets |

| China | 17.9% |

| South Korea | 15.2% |

| Brazil | 10.5% |

| Taiwan | 8.7% |

| Russia | 5.9% |

| India | 5.6% |

| Mexico | 5.2% |

| South Africa | 5.0% |

| Thailand | 4.2% |

| Turkey | 4.1% |

| Indonesia | 4.0% |

| United Kingdom | 2.2% |

| Peru | 2.0% |

| United States | 2.0% |

| Other Countries | 6.0% |

| Cash and Equivalents* | 1.5% |

*Includes temporary cash investments and other assets and liabilities.

9

Fund shareholders may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and redemption/exchange fees; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees; and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in your fund and to compare these costs with the ongoing cost of investing in other mutual funds.

The example is based on an investment of $1,000 made at the beginning of the period and held for the entire period from June 1, 2012 to November 30, 2012.

Actual Expenses

The table provides information about actual account values and actual expenses for each class. You may use the information, together with the amount you invested, to estimate the expenses that you paid over the period. First, identify the share class you own. Then simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

If you hold Investor Class shares of any American Century Investments fund, or Institutional Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not a financial intermediary or retirement plan account), American Century Investments may charge you a $12.50 semiannual account maintenance fee if the value of those shares is less than $10,000. We will redeem shares automatically in one of your accounts to pay the $12.50 fee. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments Brokerage accounts) registered under your Social Security number. Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts and IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments Brokerage accounts, you are currently not subject to this fee. If you are subject to the Account Maintenance Fee, your account value could be reduced by the fee amount.

Hypothetical Example for Comparison Purposes

The table also provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio of each class of your fund and an assumed rate of return of 5% per year before expenses, which is not the actual return of a fund’s share class. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

10

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or redemption/exchange fees. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Beginning Account Value 6/1/12 | Ending Account Value 11/30/12 | Expenses Paid During Period(1) 6/1/12 – 11/30/12 | Annualized Expense Ratio(1) | |

| Actual | ||||

| Investor Class | $1,000 | $1,146.80 | $9.34 | 1.74% |

| Institutional Class | $1,000 | $1,147.50 | $8.27 | 1.54% |

| A Class | $1,000 | $1,144.30 | $10.67 | 1.99% |

| C Class | $1,000 | $1,139.70 | $14.66 | 2.74% |

| R Class | $1,000 | $1,143.10 | $12.00 | 2.24% |

| Hypothetical | ||||

| Investor Class | $1,000 | $1,016.30 | $8.77 | 1.74% |

| Institutional Class | $1,000 | $1,017.30 | $7.77 | 1.54% |

| A Class | $1,000 | $1,015.05 | $10.02 | 1.99% |

| C Class | $1,000 | $1,011.30 | $13.78 | 2.74% |

| R Class | $1,000 | $1,013.80 | $11.28 | 2.24% |

| (1) | Expenses are equal to the class’s annualized expense ratio listed in the table above, multiplied by the average account value over the period, multiplied by 183, the number of days in the most recent fiscal half-year, divided by 366, to reflect the one-half year period. |

11

NOVEMBER 30, 2012

| Shares | Value | |

| Common Stocks — 96.5% | ||

| BRAZIL — 10.5% | ||

| Anhanguera Educacional Participacoes SA | 167,700 | $ 2,532,609 |

| BR Malls Participacoes SA | 487,800 | 6,266,431 |

| BR Properties SA | 560,600 | 6,611,344 |

| Brazil Pharma SA | 420,000 | 2,604,362 |

| CCR SA | 447,200 | 3,842,471 |

| Cia de Bebidas das Americas Preference Shares ADR | 142,190 | 5,916,526 |

| Cia de Saneamento de Minas Gerais-COPASA | 151,967 | 3,200,353 |

| Grupo BTG Pactual | 170,500 | 2,393,766 |

Hypermarcas SA(1) | 339,000 | 2,443,186 |

| Klabin SA Preference Shares | 703,100 | 3,961,683 |

| Marcopolo SA Preference Shares | 465,400 | 2,735,597 |

| MRV Engenharia e Participacoes SA | 482,800 | 2,555,442 |

| Vale SA Preference Shares | 427,800 | 7,347,557 |

| 52,411,327 | ||

| CANADA — 0.4% | ||

| Pacific Rubiales Energy Corp. | 100,047 | 2,182,532 |

| CHILE — 1.3% | ||

| SACI Falabella | 396,411 | 3,964,522 |

| Sociedad Quimica y Minera de Chile SA ADR | 42,187 | 2,387,784 |

| 6,352,306 | ||

| CHINA — 17.9% | ||

| Belle International Holdings Ltd. | 2,075,000 | 4,358,726 |

Brilliance China Automotive Holdings Ltd.(1) | 3,674,000 | 4,470,313 |

| China Communications Construction Co. Ltd. H Shares | 5,023,000 | 4,575,673 |

| China Minsheng Banking Corp. Ltd. H Shares | 3,100,000 | 3,039,922 |

| China Overseas Land & Investment Ltd. | 3,356,000 | 9,937,834 |

| China Railway Construction Corp. Ltd. H Shares | 5,672,500 | 6,323,759 |

| China Shenhua Energy Co. Ltd. H Shares | 1,186,000 | 4,858,649 |

| CNOOC Ltd. | 3,964,000 | 8,480,184 |

| Focus Media Holding Ltd. ADR | 131,982 | 3,205,843 |

Haier Electronics Group Co. Ltd.(1) | 2,538,000 | 3,484,338 |

| Hengan International Group Co. Ltd. | 305,500 | 2,759,284 |

| Industrial & Commercial Bank of China Ltd. H Shares | 7,313,645 | 4,935,403 |

| Kunlun Energy Co. Ltd. | 3,864,000 | 7,867,400 |

| Ping An Insurance Group Co. H Shares | 1,155,000 | 8,740,516 |

| Tencent Holdings Ltd. | 372,500 | 12,169,621 |

| 89,207,465 | ||

| COLOMBIA — 0.6% | ||

| Almacenes Exito SA | 144,215 | 2,860,148 |

| HONG KONG — 0.7% | ||

| AAC Technologies Holdings, Inc. | 957,500 | 3,595,165 |

| INDIA — 5.6% | ||

| HDFC Bank Ltd. | 515,619 | 6,672,856 |

| ICICI Bank Ltd. ADR | 128,848 | 5,281,480 |

| ITC Ltd. | 1,573,194 | 8,633,117 |

| Tata Global Beverages Ltd. | 1,001,074 | 3,054,108 |

| Tata Motors Ltd. | 827,765 | 4,161,271 |

| 27,802,832 | ||

| INDONESIA — 4.0% | ||

| PT AKR Corporindo Tbk | 9,856,000 | 4,417,658 |

| PT Astra International Tbk | 4,153,000 | 3,138,505 |

| PT Bank Rakyat Indonesia (Persero) Tbk | 3,535,000 | 2,597,774 |

| PT Media Nusantara Citra Tbk | 7,818,500 | 2,180,069 |

| PT Semen Gresik (Persero) Tbk | 3,152,500 | 4,863,397 |

| PT XL Axiata Tbk | 4,780,500 | 2,566,277 |

| 19,763,680 | ||

| MALAYSIA — 1.3% | ||

| Axiata Group Bhd | 3,203,600 | 6,239,103 |

| MEXICO — 5.2% | ||

| Alfa SAB de CV, Series A | 2,831,910 | 5,896,597 |

Cemex SAB de CV ADR(1) | 318,501 | 2,834,659 |

| Fomento Economico Mexicano SAB de CV ADR | 43,549 | 4,271,286 |

| Grupo Aeroportuario del Sureste SAB de CV B Shares | 139,854 | 1,427,363 |

| Grupo Financiero Banorte SAB de CV | 687,568 | 3,923,887 |

| Mexichem SAB de CV | 923,598 | 4,784,575 |

| Wal-Mart de Mexico SAB de CV | 877,718 | 2,754,607 |

| 25,892,974 | ||

12

| Shares | Value |

| PERU — 2.0% | ||

| Credicorp Ltd. | 37,267 | $ 5,213,653 |

| Southern Copper Corp. | 136,513 | 4,955,422 |

| 10,169,075 | ||

| POLAND — 1.0% | ||

| Eurocash SA | 232,485 | 3,238,538 |

| Powszechny Zaklad Ubezpieczen SA | 11,821 | 1,480,509 |

| 4,719,047 | ||

| RUSSIA — 5.9% | ||

| Eurasia Drilling Co. Ltd. GDR | 109,175 | 3,553,646 |

| Magnit OJSC GDR | 201,161 | 7,096,960 |

| Mail.ru Group Ltd. GDR | 91,525 | 3,020,325 |

| Mobile Telesystems OJSC ADR | 194,641 | 3,392,593 |

| NovaTek OAO GDR | 43,692 | 4,793,012 |

| Sberbank of Russia | 2,540,543 | 7,469,197 |

| 29,325,733 | ||

| SOUTH AFRICA — 5.0% | ||

| Aspen Pharmacare Holdings Ltd. | 293,078 | 5,158,139 |

| Clicks Group Ltd. | 639,457 | 4,531,381 |

| Discovery Holdings Ltd. | 708,526 | 4,447,813 |

| Exxaro Resources Ltd. | 107,587 | 1,869,074 |

| Mr Price Group Ltd. | 153,306 | 2,293,451 |

| Naspers Ltd. N Shares | 111,153 | 6,863,920 |

| 25,163,778 | ||

| SOUTH KOREA — 15.2% | ||

| Hyundai Glovis Co. Ltd. | 25,814 | 5,625,991 |

| Hyundai Motor Co. | 7,349 | 1,530,405 |

| Hyundai Wia Corp. | 22,569 | 3,793,284 |

| LG Chem Ltd. | 9,657 | 2,782,457 |

LG Display Co. Ltd.(1) | 101,540 | 3,244,479 |

| LG Household & Health Care Ltd. | 8,716 | 5,199,738 |

| Orion Corp. | 6,247 | 6,478,627 |

| Paradise Co. Ltd. | 144,676 | 2,505,125 |

| Samsung Electronics Co. Ltd. | 34,452 | 44,733,354 |

| 75,893,460 | ||

| TAIWAN — 8.7% | ||

| Chailease Holding Co. Ltd. | 2,800,910 | 5,697,452 |

| Hon Hai Precision Industry Co. Ltd. | 2,631,232 | 8,440,518 |

| MediaTek, Inc. | 287,000 | 3,264,731 |

| Taiwan Semiconductor Manufacturing Co. Ltd. | 7,208,939 | 24,489,650 |

| TPK Holding Co. Ltd. | 99,000 | 1,581,056 |

| 43,473,407 | ||

| THAILAND — 4.2% | ||

| CP ALL PCL | 4,943,600 | 6,362,730 |

| Kasikornbank PCL NVDR | 914,100 | 5,569,785 |

| Minor International PCL | 5,728,900 | 3,602,730 |

| Siam Cement PCL NVDR | 423,200 | 5,446,856 |

| 20,982,101 | ||

| TURKEY — 4.1% | ||

| BIM Birlesik Magazalar AS | 56,317 | 2,560,795 |

| Koza Altin Isletmeleri AS | 163,210 | 4,073,742 |

TAV Havalimanlari Holding AS(1) | 683,560 | 3,397,047 |

| Tofas Turk Otomobil Fabrikasi | 516,049 | 3,147,961 |

| Turkiye Garanti Bankasi AS | 846,950 | 4,019,440 |

| Turkiye Halk Bankasi AS | 354,895 | 3,436,037 |

| 20,635,022 | ||

| TURKMENISTAN — 0.7% | ||

| Dragon Oil plc | 377,660 | 3,358,129 |

| UNITED KINGDOM — 2.2% | ||

| Antofagasta plc | 179,190 | 3,697,711 |

| Petrofac Ltd. | 171,716 | 4,478,845 |

| Tullow Oil plc | 132,450 | 2,922,061 |

| 11,098,617 | ||

TOTAL COMMON STOCKS (Cost $352,818,199) | 481,125,901 | |

| Exchange-Traded Funds — 2.0% | ||

| iShares MSCI Emerging Markets Index Fund (Cost $9,828,862) | 235,066 | 9,825,759 |

| Temporary Cash Investments — 3.4% | ||

| SSgA U.S. Government Money Market Fund (Cost $17,094,329) | 17,094,329 | 17,094,329 |

TOTAL INVESTMENT SECURITIES — 101.9% (Cost $379,741,390) | 508,045,989 | |

| OTHER ASSETS AND LIABILITIES — (1.9)% | (9,232,647) | |

| TOTAL NET ASSETS — 100.0% | $498,813,342 | |

13

| Market Sector Diversification | |

| (as a % of net assets) | |

| Information Technology | 20.9% |

| Financials | 19.6% |

| Consumer Staples | 13.2% |

| Consumer Discretionary | 12.4% |

| Materials | 10.0% |

| Energy | 8.6% |

| Industrials | 7.7% |

| Telecommunication Services | 2.5% |

| Diversified | 2.0% |

| Health Care | 1.0% |

| Utilities | 0.6% |

| Cash and Equivalents* | 1.5% |

*Includes temporary cash investments and other assets and liabilities.

Notes to Schedule of Investments

ADR = American Depositary Receipt

GDR = Global Depositary Receipt

MSCI = Morgan Stanley Capital International

NVDR = Non-Voting Depositary Receipt

OJSC = Open Joint Stock Company

| (1) | Non-income producing. |

See Notes to Financial Statements.

14

| NOVEMBER 30, 2012 | |||

| Assets | |||

| Investment securities, at value (cost of $379,741,390) | $508,045,989 | ||

| Receivable for capital shares sold | 1,340,336 | ||

| Dividends and interest receivable | 149,816 | ||

| 509,536,141 | |||

| Liabilities | |||

| Payable for investments purchased | 9,828,863 | ||

| Payable for capital shares redeemed | 203,204 | ||

| Accrued management fees | 684,871 | ||

| Distribution and service fees payable | 5,861 | ||

| 10,722,799 | |||

| Net Assets | $498,813,342 | ||

| Net Assets Consist of: | |||

| Capital (par value and paid-in surplus) | $502,805,816 | ||

| Undistributed net investment income | 757,588 | ||

| Accumulated net realized loss | (133,051,346 | ) | |

| Net unrealized appreciation | 128,301,284 | ||

| $498,813,342 | |||

| Net assets | Shares outstanding | Net asset value per share | |

| Investor Class, $0.01 Par Value | $452,331,427 | 54,109,568 | $8.36 |

| Institutional Class, $0.01 Par Value | $28,536,428 | 3,332,607 | $8.56 |

| A Class, $0.01 Par Value | $13,745,155 | 1,698,488 | $8.09* |

| C Class, $0.01 Par Value | $3,376,132 | 439,943 | $7.67 |

| R Class, $0.01 Par Value | $824,200 | 100,138 | $8.23 |

*Maximum offering price $8.58 (net asset value divided by 0.9425).

See Notes to Financial Statements.

15

| YEAR ENDED NOVEMBER 30, 2012 | |||

| Investment Income (Loss) | |||

| Income: | |||

| Dividends (net of foreign taxes withheld of $1,020,529) | $9,870,147 | ||

| Interest (net of foreign taxes withheld of $5,414) | 31,588 | ||

| 9,901,735 | |||

| Expenses: | |||

| Management fees | 8,400,410 | ||

| Distribution and service fees: | |||

| A Class | 35,475 | ||

| C Class | 36,775 | ||

| R Class | 3,757 | ||

| Directors’ fees and expenses | 17,635 | ||

| Other expenses | 10,195 | ||

| 8,504,247 | |||

| Net investment income (loss) | 1,397,488 | ||

| Realized and Unrealized Gain (Loss) | |||

| Net realized gain (loss) on: | |||

| Investment transactions | 14,209,069 | ||

| Foreign currency transactions | (675,478 | ) | |

| 13,533,591 | |||

| Change in net unrealized appreciation (depreciation) on: | |||

| Investments | 46,214,547 | ||

| Translation of assets and liabilities in foreign currencies | 19,489 | ||

| 46,234,036 | |||

| Net realized and unrealized gain (loss) | 59,767,627 | ||

| Net Increase (Decrease) in Net Assets Resulting from Operations | $61,165,115 | ||

See Notes to Financial Statements.

16

| YEARS ENDED NOVEMBER 30, 2012 AND NOVEMBER 30, 2011 | |||||||

| Increase (Decrease) in Net Assets | November 30, 2012 | November 30, 2011 | |||||

| Operations | |||||||

| Net investment income (loss) | $1,397,488 | $938,130 | |||||

| Net realized gain (loss) | 13,533,591 | 49,355,393 | |||||

| Change in net unrealized appreciation (depreciation) | 46,234,036 | (120,227,565 | ) | ||||

| Net increase (decrease) in net assets resulting from operations | 61,165,115 | (69,934,042 | ) | ||||

| Distributions to Shareholders | |||||||

| From net investment income: | |||||||

| Institutional Class | (51,371 | ) | — | ||||

| Capital Share Transactions | |||||||

| Net increase (decrease) in net assets from capital share transactions | (46,952,076 | ) | (106,484,925 | ) | |||

| Redemption Fees | |||||||

| Increase in net assets from redemption fees | 11,993 | 144,876 | |||||

| Net increase (decrease) in net assets | 14,173,661 | (176,274,091 | ) | ||||

| Net Assets | |||||||

| Beginning of period | 484,639,681 | 660,913,772 | |||||

| End of period | $498,813,342 | $484,639,681 | |||||

| Undistributed net investment income | $757,588 | $86,949 | |||||

See Notes to Financial Statements.

17

1. Organization

American Century World Mutual Funds, Inc. (the corporation) is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company and is organized as a Maryland corporation. Emerging Markets Fund (the fund) is one fund in a series issued by the corporation. The fund is diversified as defined under the 1940 Act. The fund’s investment objective is to seek capital growth. The fund pursues its objective by investing at least 80% of its assets in equity securities of companies located in emerging market countries.

The fund offers the Investor Class, the Institutional Class, the A Class, the C Class and the R Class. The A Class may incur an initial sales charge. The A Class and C Class may be subject to a contingent deferred sales charge. The share classes differ principally in their respective sales charges and distribution and shareholder servicing expenses and arrangements. The Institutional Class is made available to institutional shareholders or through financial intermediaries whose clients do not require the same level of shareholder and administrative services as shareholders of other classes. As a result, the Institutional Class is charged a lower unified management fee. On October 21, 2011, all outstanding B Class shares were converted to A Class shares and the fund discontinued offering the B Class.

2. Significant Accounting Policies

The following is a summary of significant accounting policies consistently followed by the fund in preparation of its financial statements. The financial statements are prepared in conformity with accounting principles generally accepted in the United States of America, which may require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from these estimates.

Investment Valuations — The fund determines the fair value of its investments and computes its net asset value per share as of the close of regular trading (usually 4 p.m. Eastern time) on the New York Stock Exchange (NYSE) on each day the NYSE is open.

Equity securities that are listed or traded on a domestic securities exchange are valued at the last reported sales price or at the official closing price as provided by the exchange. Equity securities traded on foreign securities exchanges are typically valued at the closing price on the exchange where primarily traded or as of the close of the NYSE, if that is earlier. If no last sales price is reported, or if local convention or regulation so provides, the mean of the latest bid and asked prices is used. Depending on local convention or regulation, securities traded over-the-counter are valued at the mean of the latest bid and asked prices, the last sales price, or the official closing price. In its determination of fair value, the fund may review several factors including: market information specific to a security; news developments in U.S. and foreign markets; the performance of particular U.S. and foreign securities, indices, comparable securities, American Depositary Receipts, Exchange-Traded Funds, and other relevant market indicators.

Debt securities maturing within 60 days at the time of purchase may be valued at cost, plus or minus any amortized discount or premium or at the evaluated mean as provided by an independent pricing service. Evaluated mean prices are commonly derived through utilization of market models, which may consider, among other factors, trade data, quotations from dealers and active market makers, relevant yield curve and spread data, related sector levels, creditworthiness, and other relevant market information on the same or comparable securities.

Investments in open-end management investment companies are valued at the reported net asset value per share. Repurchase agreements are valued at cost.

The value of investments initially expressed in foreign currencies is translated into U.S. dollars at prevailing exchange rates.

18

If the fund determines that the market price for a portfolio security is not readily available or the valuation methods mentioned above do not reflect a security’s fair value, such security is valued as determined in good faith by the Board of Directors or its designee, in accordance with procedures adopted by the Board of Directors. Circumstances that may cause the fund to use these procedures to value a security include, but are not limited to: a security has been declared in default; trading in a security has been halted during the trading day; there is a foreign market holiday and no trading occurred; or an event occurred between the close of a foreign exchange and the NYSE that may affect the value of a security.

Security Transactions — Security transactions are accounted for as of the trade date. Net realized gains and losses are determined on the identified cost basis, which is also used for federal income tax purposes.

Investment Income — Dividend income less foreign taxes withheld, if any, is recorded as of the ex-dividend date. Distributions received on securities that represent a return of capital or capital gain are recorded as a reduction of cost of investments and/or as a realized gain. The fund estimates the components of distributions received that may be considered nontaxable distributions or capital gain distributions for income tax purposes. Interest income less foreign taxes withheld, if any, is recorded on the accrual basis and includes accretion of discounts and amortization of premiums.

Foreign Currency Translations — All assets and liabilities initially expressed in foreign currencies are translated into U.S. dollars at prevailing exchange rates at period end. The fund may enter into spot foreign currency exchange contracts to facilitate transactions denominated in a foreign currency. Purchases and sales of investment securities, dividend and interest income, spot foreign currency exchange contracts, and expenses are translated at the rates of exchange prevailing on the respective dates of such transactions. Net realized and unrealized foreign currency exchange gains or losses related to investment securities are a component of net realized gain (loss) on investment transactions and change in net unrealized appreciation (depreciation) on investments, respectively.

Repurchase Agreements — The fund may enter into repurchase agreements with institutions that American Century Investment Management, Inc. (ACIM) (the investment advisor) has determined are creditworthy pursuant to criteria adopted by the Board of Directors. The fund requires that the collateral, represented by securities, received in a repurchase transaction be transferred to the custodian in a manner sufficient to enable the fund to obtain those securities in the event of a default under the repurchase agreement. ACIM monitors, on a daily basis, the securities transferred to ensure the value, including accrued interest, of the securities under each repurchase agreement is equal to or greater than amounts owed to the fund under each repurchase agreement.

Joint Trading Account — Pursuant to an Exemptive Order issued by the Securities and Exchange Commission, the fund, along with certain other funds in the American Century Investments family of funds, may transfer uninvested cash balances into a joint trading account. These balances are invested in one or more repurchase agreements that are collateralized by U.S. Treasury or Agency obligations.

Income Tax Status — It is the fund’s policy to distribute substantially all net investment income and net realized gains to shareholders and to otherwise qualify as a regulated investment company under provisions of the Internal Revenue Code. The fund is no longer subject to examination by tax authorities for years prior to 2009. Additionally, non-U.S. tax returns filed by the fund due to investments in certain foreign securities remain subject to examination by the relevant taxing authority for seven years from the date of filing. At this time, management believes there are no uncertain tax positions which, based on their technical merit, would not be sustained upon examination and for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months. Accordingly, no provision has been made for federal or state income taxes.

19

Multiple Class — All shares of the fund represent an equal pro rata interest in the net assets of the class to which such shares belong, and have identical voting, dividend, liquidation and other rights and the same terms and conditions, except for class specific expenses and exclusive rights to vote on matters affecting only individual classes. Income, non-class specific expenses, and realized and unrealized capital gains and losses of the fund are allocated to each class of shares based on their relative net assets.

Distributions to Shareholders — Distributions from net investment income and net realized gains, if any, are generally declared and paid annually. The fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code, in all events in a manner consistent with provisions of the 1940 Act.

Redemption — The fund may impose a 2.00% redemption fee on shares held less than 60 days. The fee may not be applicable to all classes. The redemption fee is retained by the fund and helps cover transaction costs that long-term investors may bear when the fund sells securities to meet investor redemptions. Prior to November 14, 2011, the redemption fee applied to shares held less than 180 days.

Indemnifications — Under the corporation’s organizational documents, its officers and directors are indemnified against certain liabilities arising out of the performance of their duties to the fund. In addition, in the normal course of business, the fund enters into contracts that provide general indemnifications. The maximum exposure under these arrangements is unknown as this would involve future claims that may be made against a fund. The risk of material loss from such claims is considered by management to be remote.

3. Fees and Transactions with Related Parties

Management Fees — The corporation has entered into a management agreement with ACIM, under which ACIM provides the fund with investment advisory and management services in exchange for a single, unified management fee (the fee) per class. The agreement provides that all expenses of managing and operating the fund, except distribution and service fees, brokerage expenses, taxes, interest, fees and expenses of the independent directors (including legal counsel fees), and extraordinary expenses, will be paid by ACIM. The fee is computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The rate of the fee is determined by applying a fee rate calculation formula. This formula takes into account the fund’s assets as well as certain assets, if any, of other clients of the investment advisor outside the American Century Investments family of funds (such as subadvised funds and separate accounts) that have very similar investment teams and investment strategies (strategy assets). The strategy assets of the fund include the assets of NT Emerging Markets Fund, one fund in a series issued by the corporation. The annual management fee schedule ranges from 1.25% to 1.85% for the Investor Class, A Class, C Class and R Class. The Institutional Class is 0.20% less at each point within the range. The effective annual management fee for each class for the year ended November 30, 2012 was 1.74% for the Investor Class, A Class, C Class and R Class and 1.54% for the Institutional Class.

Distribution and Service Fees — The Board of Directors has adopted a separate Master Distribution and Individual Shareholder Services Plan for each of the A Class, C Class and R Class (collectively the plans), pursuant to Rule 12b-1 of the 1940 Act. The plans provide that the A Class will pay American Century Investment Services, Inc. (ACIS) an annual distribution and service fee of 0.25%. The plans provide that the C Class will pay ACIS an annual distribution and service fee of 1.00%, of which 0.25% is paid for individual shareholder services and 0.75% is paid for distribution services. The plans provide that the R Class will pay ACIS an annual distribution and service fee of 0.50%. The fees are computed and accrued daily based on each class’s daily net assets and paid monthly in arrears. The fees are used to pay financial intermediaries for distribution and individual shareholder services. Fees incurred under the plans during the year ended November 30, 2012 are detailed in the Statement of Operations.

20

Related Parties — Certain officers and directors of the corporation are also officers and/or directors of American Century Companies, Inc., the parent of the corporation’s investment advisor, ACIM, the distributor of the corporation, ACIS, and the corporation’s transfer agent, American Century Services, LLC. Various funds issued by American Century Asset Allocation Portfolios, Inc. and American Century Strategic Asset Allocations, Inc. own, in aggregate, 20% of the shares of the fund. These funds do not invest in the fund for the purpose of exercising management or control.

4. Investment Transactions

Purchases and sales of investment securities, excluding short-term investments, for the year ended November 30, 2012 were $413,704,500 and $465,628,752, respectively.

5. Capital Share Transactions

Transactions in shares of the fund were as follows:

| Year ended November 30, 2012 | Year ended November 30, 2011 | ||||||||||||||

| Shares | Amount | Shares | Amount | ||||||||||||

| Investor Class/Shares Authorized | 235,000,000 | 235,000,000 | |||||||||||||

| Sold | 6,929,950 | $53,455,116 | 6,538,088 | $55,636,956 | |||||||||||

| Redeemed | (11,776,977 | ) | (91,432,663 | ) | (16,579,314 | ) | (141,943,249 | ) | |||||||

| (4,847,027 | ) | (37,977,547 | ) | (10,041,226 | ) | (86,306,293 | ) | ||||||||

| Institutional Class/Shares Authorized | 40,000,000 | 40,000,000 | |||||||||||||

| Sold | 765,815 | 6,099,475 | 814,282 | 7,001,115 | |||||||||||

| Issued in reinvestment of distributions | 6,334 | 51,366 | — | — | |||||||||||

| Redeemed | (1,368,338 | ) | (10,963,145 | ) | (1,621,034 | ) | (14,518,773 | ) | |||||||

| (596,189 | ) | (4,812,304 | ) | (806,752 | ) | (7,517,658 | ) | ||||||||

| A Class/Shares Authorized | 40,000,000 | 40,000,000 | |||||||||||||

| Sold | 275,763 | 2,115,216 | 2,314,402 | 20,284,532 | |||||||||||

| Redeemed | (718,945 | ) | (5,450,958 | ) | (3,764,042 | ) | (31,735,094 | ) | |||||||

| (443,182 | ) | (3,335,742 | ) | (1,449,640 | ) | (11,450,562 | ) | ||||||||

| B Class/Shares Authorized | N/A | 10,000,000 | |||||||||||||

| Sold | 2,549 | 21,664 | |||||||||||||

| Redeemed | (39,638 | ) | (294,160 | ) | |||||||||||

| (37,089 | ) | (272,496 | ) | ||||||||||||

| C Class/Shares Authorized | 5,000,000 | 5,000,000 | |||||||||||||

| Sold | 48,215 | 346,043 | 99,057 | 738,536 | |||||||||||

| Redeemed | (177,535 | ) | (1,274,469 | ) | (193,003 | ) | (1,533,169 | ) | |||||||

| (129,320 | ) | (928,426 | ) | (93,946 | ) | (794,633 | ) | ||||||||

| R Class/Shares Authorized | 10,000,000 | 10,000,000 | |||||||||||||

| Sold | 36,789 | 282,556 | 42,747 | 331,354 | |||||||||||

| Redeemed | (23,118 | ) | (180,613 | ) | (54,656 | ) | (474,637 | ) | |||||||

| 13,671 | 101,943 | (11,909 | ) | (143,283 | ) | ||||||||||

| Net increase (decrease) | (6,002,047 | ) | $(46,952,076 | ) | (12,440,562 | ) | $(106,484,925 | ) | |||||||

21

6. Fair Value Measurements

The fund’s securities valuation process is based on several considerations and may use multiple inputs to determine the fair value of the positions held by the fund. In conformity with accounting principles generally accepted in the United States of America, the inputs used to determine a valuation are classified into three broad levels as follows:

| • | Level 1 valuation inputs consist of unadjusted quoted prices in an active market for identical securities; |

| • | Level 2 valuation inputs consist of direct or indirect observable market data (including quoted prices for similar securities, evaluations of subsequent market events, interest rates, prepayment speeds, credit risk, etc.); or |

| • | Level 3 valuation inputs consist of unobservable data (including a fund’s own assumptions). |

The level classification is based on the lowest level input that is significant to the fair valuation measurement. The valuation inputs are not necessarily an indication of the risks associated with investing in these securities or other financial instruments.

The following is a summary of the level classifications as of period end. The Schedule of Investments provides additional information on the fund’s portfolio holdings.

| Level 1 | Level 2 | Level 3 | |

| Investment Securities | |||

| Foreign Common Stocks | $37,459,246 | $443,666,655 | — |

| Exchange-Traded Funds | 9,825,759 | — | — |

| Temporary Cash Investments | 17,094,329 | — | — |

| Total Value of Investment Securities | $64,379,334 | $443,666,655 | — |

7. Risk Factors

There are certain risks involved in investing in foreign securities. These risks include those resulting from future adverse political, social and economic developments, fluctuations in currency exchange rates, the possible imposition of exchange controls, and other foreign laws or restrictions. Investing in emerging markets may accentuate these risks.

22

8. Federal Tax Information

The tax character of distributions paid during the years ended November 30, 2012 and November 30, 2011 were as follows:

| 2012 | 2011 | |

| Distributions Paid From | ||

| Ordinary income | $51,371 | — |

| Long-term capital gains | — | — |

The book-basis character of distributions made during the year from net investment income or net realized gains may differ from their ultimate characterization for federal income tax purposes. These differences reflect the differing character of certain income items and net realized gains and losses for financial statement and tax purposes, and may result in reclassification among certain capital accounts on the financial statements.

As of November 30, 2012, the federal tax cost of investments and the components of distributable earnings on a tax-basis were as follows:

| Federal tax cost of investments | $382,600,625 |

| Gross tax appreciation of investments | $128,524,862 |

| Gross tax depreciation of investments | (3,079,498) |

| Net tax appreciation (depreciation) of investments | $125,445,364 |

| Net tax appreciation (depreciation) on translation of assets and liabilities in foreign currencies | $(3,315) |

| Net tax appreciation (depreciation) | $125,442,049 |

| Undistributed ordinary income | $778,609 |

| Accumulated short-term capital losses | $(129,636,164) |

| Post-October capital loss deferral | $(576,968) |

The difference between book-basis and tax-basis cost and unrealized appreciation (depreciation) is attributable primarily to the tax deferral of losses on wash sales and the realization to ordinary income for tax purposes of unrealized gains on investments in passive foreign investment companies.

Accumulated capital losses represent net capital loss carryovers that may be used to offset future realized capital gains for federal income tax purposes. Future capital loss carryover utilization in any given year may be subject to Internal Revenue Code limitations. Capital loss carryovers of $(12,429,763) and $(117,206,401) expire in 2016 and 2017, respectively.

Loss deferrals represent certain qualified losses that the fund has elected to treat as having been incurred in the following fiscal year for federal income tax purposes.

23

| For a Share Outstanding Throughout the Years Ended November 30 (except as noted) | ||||||||||||||

| Per-Share Data | Ratios and Supplemental Data | |||||||||||||

| Income From Investment Operations: | Distributions From: | Ratio to Average Net Assets of: | ||||||||||||

Net Asset Value, Beginning of Period | Net Investment Income (Loss)(1) | Net Realized and Unrealized Gain (Loss) | Total From Investment Operations | Net Investment Income | Net Realized Gains | Total Distributions | Redemption Fees(1) | Net Asset Value, End of Period | Total Return(2) | Operating Expenses | Net Investment Income (Loss) | Portfolio Turnover Rate | Net Assets, End of Period (in thousands) | |

| Investor Class | ||||||||||||||

| 2012 | $7.38 | 0.02 | 0.96 | 0.98 | — | — | — | —(3) | $8.36 | 13.28% | 1.74% | 0.29% | 85% | $452,331 |

| 2011 | $8.46 | 0.01 | (1.09) | (1.08) | — | — | — | —(3) | $7.38 | (12.77)% | 1.71% | 0.17% | 71% | $435,079 |

| 2010 | $7.28 | —(3) | 1.18 | 1.18 | — | — | — | —(3) | $8.46 | 16.21% | 1.72% | (0.02)% | 87% | $583,978 |

| 2009 | $4.17 | 0.01 | 3.13 | 3.14 | (0.03) | — | (0.03) | —(3) | $7.28 | 75.36% | 1.78% | 0.11% | 126% | $567,248 |

| 2008 | $12.69 | 0.09 | (7.21) | (7.12) | (0.10) | (1.31) | (1.41) | 0.01 | $4.17 | (62.66)% | 1.66% | 1.06% | 121% | $316,695 |

| Institutional Class | ||||||||||||||

| 2012 | $7.56 | 0.04 | 0.97 | 1.01 | (0.01) | — | (0.01) | —(3) | $8.56 | 13.43% | 1.54% | 0.49% | 85% | $28,536 |

| 2011 | $8.65 | 0.03 | (1.12) | (1.09) | — | — | — | —(3) | $7.56 | (12.60)% | 1.51% | 0.37% | 71% | $29,695 |

| 2010 | $7.43 | 0.02 | 1.20 | 1.22 | — | — | — | —(3) | $8.65 | 16.42% | 1.52% | 0.18% | 87% | $40,969 |

| 2009 | $4.26 | 0.02 | 3.18 | 3.20 | (0.03) | — | (0.03) | —(3) | $7.43 | 75.92% | 1.58% | 0.31% | 126% | $27,787 |

| 2008 | $12.92 | 0.12 | (7.35) | (7.23) | (0.13) | (1.31) | (1.44) | 0.01 | $4.26 | (62.63)% | 1.46% | 1.26% | 121% | $27,235 |

| A Class | ||||||||||||||

| 2012 | $7.16 | —(3) | 0.93 | 0.93 | — | — | — | —(3) | $8.09 | 12.99% | 1.99% | 0.04% | 85% | $13,745 |

| 2011 | $8.23 | (0.01) | (1.06) | (1.07) | — | — | — | —(3) | $7.16 | (13.00)% | 1.96% | (0.08)% | 71% | $15,339 |

| 2010 | $7.10 | (0.02) | 1.15 | 1.13 | — | — | — | —(3) | $8.23 | 15.92% | 1.97% | (0.27)% | 87% | $29,572 |

| 2009 | $4.07 | (0.01) | 3.06 | 3.05 | (0.02) | — | (0.02) | —(3) | $7.10 | 75.24% | 2.03% | (0.14)% | 126% | $23,260 |

| 2008 | $12.40 | 0.07 | (7.03) | (6.96) | (0.07) | (1.31) | (1.38) | 0.01 | $4.07 | (62.78)% | 1.91% | 0.81% | 121% | $17,105 |

24

| For a Share Outstanding Throughout the Years Ended November 30 (except as noted) | ||||||||||||||

| Per-Share Data | Ratios and Supplemental Data | |||||||||||||

| Income From Investment Operations: | Distributions From: | Ratio to Average Net Assets of: | ||||||||||||

Net Asset Value, Beginning of Period | Net Investment Income (Loss)(1) | Net Realized and Unrealized Gain (Loss) | Total From Investment Operations | Net Investment Income | Net Realized Gains | Total Distributions | Redemption Fees(1) | Net Asset Value, End of Period | Total Return(2) | Operating Expenses | Net Investment Income (Loss) | Portfolio Turnover Rate | Net Assets, End of Period (in thousands) | |

| C Class | ||||||||||||||

| 2012 | $6.84 | (0.05) | 0.88 | 0.83 | — | — | — | —(3) | $7.67 | 12.13% | 2.74% | (0.71)% | 85% | $3,376 |

| 2011 | $7.93 | (0.07) | (1.02) | (1.09) | — | — | — | —(3) | $6.84 | (13.75)% | 2.71% | (0.83)% | 71% | $3,896 |

| 2010 | $6.89 | (0.07) | 1.11 | 1.04 | — | — | — | —(3) | $7.93 | 15.09% | 2.72% | (1.02)% | 87% | $5,257 |

| 2009 | $3.96 | (0.05) | 2.98 | 2.93 | — | — | — | —(3) | $6.89 | 73.99% | 2.78% | (0.89)% | 126% | $5,372 |

| 2008 | $12.10 | 0.01 | (6.87) | (6.86) | — | (1.29) | (1.29) | 0.01 | $3.96 | (63.09)% | 2.66% | 0.06% | 121% | $3,217 |

| R Class | ||||||||||||||

| 2012 | $7.30 | (0.02) | 0.95 | 0.93 | — | — | — | —(3) | $8.23 | 12.74% | 2.24% | (0.21)% | 85% | $824 |

| 2011 | $8.42 | (0.03) | (1.09) | (1.12) | — | — | — | —(3) | $7.30 | (13.30)% | 2.21% | (0.33)% | 71% | $631 |

| 2010 | $7.28 | (0.04) | 1.18 | 1.14 | — | — | — | —(3) | $8.42 | 15.66% | 2.22% | (0.52)% | 87% | $828 |

| 2009 | $4.17 | (0.02) | 3.14 | 3.12 | (0.01) | — | (0.01) | —(3) | $7.28 | 74.94% | 2.28% | (0.39)% | 126% | $516 |

| 2008 | $12.68 | 0.05 | (7.22) | (7.17) | (0.04) | (1.31) | (1.35) | 0.01 | $4.17 | (62.92)% | 2.19% | 0.53% | 121% | $144 |

Notes to Financial Highlights

| (1) | Computed using average shares outstanding throughout the period. |

| (2) | Total returns are calculated based on the net asset value of the last business day and do not reflect applicable sales charges, if any. Total returns for periods less than one year are not annualized. |

| (3) | Per-share amount was less than $0.005. |

See Notes to Financial Statements.

25

The Board of Directors and Shareholders of

American Century World Mutual Funds, Inc.:

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Emerging Markets Fund, one of the funds constituting American Century World Mutual Funds, Inc. (the “Corporation”) as of November 30, 2012, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Corporation’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Corporation is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Corporation’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of November 30, 2012, by correspondence with the custodian and brokers; where replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Emerging Markets Fund of American Century World Mutual Funds, Inc., as of November 30, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Deloitte & Touche LLP

Kansas City, Missouri

January 17, 2013

26

The Board of Directors

The individuals listed below serve as directors of the funds. Each director will continue to serve in this capacity until death, retirement, resignation or removal from office. The mandatory retirement age for directors who are not “interested persons,” as that term is defined in the Investment Company Act (independent directors), is 72. However, the mandatory retirement age for an individual director may be extended with the approval of the remaining independent directors.

Mr. Thomas is an “interested person” because he currently serves as President and Chief Executive Officer of American Century Companies, Inc. (ACC), the parent company of American Century Investment Management, Inc. (ACIM or the advisor). Mr. Fink is an “interested person” because he currently serves as Executive Vice President of ACC.

The other directors (more than three-fourths of the total number) are independent; that is, they have never been employees, directors or officers of, and have no financial interest in, ACC or any of its wholly owned, direct or indirect, subsidiaries, including ACIM, American Century Investment Services, Inc. (ACIS) and American Century Services, LLC (ACS). The directors serve in this capacity for seven (in the case of Mr. Thomas, 15) registered investment companies in the American Century Investments family of funds.

The following table presents additional information about the directors. The mailing address for each director is 4500 Main Street, Kansas City, Missouri 64111.

Name (Year of Birth) | Position(s) Held with Funds | Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of American Century Portfolios Overseen by Director | Other Directorships Held During Past 5 Years | |

| Independent Directors | ||||||

Thomas A. Brown (1940) | Director | Since 1980 | Managing Member, Associated Investments, LLC (real estate investment company); Brown Cascade Properties, LLC (real estate investment company) (2001 to 2009) | 66 | None | |

Andrea C. Hall (1945) | Director | Since 1997 | Retired | 66 | None | |

Jan M. Lewis (1957) | Director | Since 2011 | President and Chief Executive Officer, Catholic Charities of Northeast Kansas (human services organization) | 66 | None | |

James A. Olson (1942) | Director | Since 2007 | Member, Plaza Belmont LLC (private equity fund manager) | 66 | Saia, Inc. (2002 to 2012) and Entertainment Properties Trust | |

Donald H. Pratt (1937) | Director and Chairman of the Board | Since 1995 (Chairman since 2005) | Chairman and Chief Executive Officer, Western Investments, Inc. (real estate company) | 66 | None | |

27

Name (Year of Birth) | Position(s) Held with Funds | Length of Time Served | Principal Occupation(s) During Past 5 Years | Number of American Century Portfolios Overseen by Director | Other Directorships Held During Past 5 Years | |

| Independent Directors | ||||||

M. Jeannine Strandjord (1945) | Director | Since 1994 | Retired | 66 | Euronet Worldwide Inc.; Charming Shoppes, Inc. (2006 to 2010); and DST Systems Inc. (1996 to 2012) | |

John R. Whitten (1946) | Director | Since 2008 | Retired | 66 | Rudolph Technologies, Inc. | |

Stephen E. Yates (1948) | Director | Since 2012 | Retired; Executive Vice President, Technology & Operations, KeyCorp. (computer services) (2004 to 2010) | 66 | Applied Industrial Technologies, Inc. (2001 to 2010) | |

| Interested Directors | ||||||

Barry Fink (1955) | Director and Executive Vice President | Since 2012 (Executive Vice President since 2007) | Executive Vice President, ACC (September 2007 to present); President, ACS (October 2007 to present); Chief Operating Officer, ACC (September 2007 to November 2012). Also serves as Manager, ACS | 66 | None | |

Jonathan S. Thomas (1963) | Director and President | Since 2007 | President and Chief Executive Officer, ACC (March 2007 to present). Also serves as Chief Executive Officer and Manager, ACS; Executive Vice President, ACIM; Director, ACC, ACIM and other ACC subsidiaries | 108 | None | |

28

Officers

The following table presents certain information about the executive officers of the funds. Each officer serves as an officer for each of the 15 investment companies in the American Century family of funds, unless otherwise noted. No officer is compensated for his or her service as an officer of the funds. The listed officers are interested persons of the funds and are appointed or re-appointed on an annual basis. The mailing address for each officer listed below is 4500 Main Street, Kansas City, Missouri 64111.

Name (Year of Birth) | Offices with the Funds | Principal Occupation(s) During the Past Five Years | |

Jonathan S. Thomas (1963) | Director and President since 2007 | President and Chief Executive Officer, ACC (March 2007 to present). Also serves as Chief Executive Officer and Manager, ACS; Executive Vice President, ACIM; Director, ACC, ACIM and other ACC subsidiaries | |

Barry Fink (1955) | Director since 2012 and Executive Vice President since 2007 | Executive Vice President, ACC (September 2007 to present); President, ACS (October 2007 to present); Chief Operating Officer, ACC (September 2007 to November 2012). Also serves as Manager, ACS | |

Maryanne L. Roepke (1956) | Chief Compliance Officer since 2006 and Senior Vice President since 2000 | Chief Compliance Officer, American Century funds, ACIM and ACS (August 2006 to present). Also serves as Senior Vice President, ACS | |

Charles A. Etherington (1957) | General Counsel since 2007 and Senior Vice President since 2006 | Attorney, ACC (February 1994 to present); Vice President, ACC (November 2005 to present), General Counsel, ACC (March 2007 to present). Also serves as General Counsel, ACIM, ACS, ACIS and other ACC subsidiaries; and Senior Vice President, ACIM and ACS | |

C. Jean Wade (1964) | Vice President, Treasurer and Chief Financial Officer since 2012 | Vice President, ACS (February 2000 to present) | |

Robert J. Leach (1966) | Vice President since 2006 and Assistant Treasurer since 2012 | Vice President, ACS (February 2000 to present) | |

David H. Reinmiller (1963) | Vice President since 2000 | Attorney, ACC (January 1994 to present); Associate General Counsel, ACC (January 2001 to present). Also serves as Vice President, ACIM and ACS | |

Ward D. Stauffer (1960) | Secretary since 2005 | Attorney, ACC (June 2003 to present) |

The Statement of Additional Information has additional information about the fund’s directors and is available without charge, upon request, by calling 1-800-345-2021.

29

At a meeting held on June 21, 2012, the Fund’s Board of Directors unanimously approved the renewal of the management agreement pursuant to which American Century Investment Management, Inc. (the “Advisor”) acts as the investment advisor for the Fund. Under Section 15(c) of the Investment Company Act, contracts for investment advisory services are required to be reviewed, evaluated, and approved by a majority of a fund’s independent directors (the “Directors”) each year.

As a part of the approval process, the Board requested and reviewed extensive data and information compiled by the Advisor and certain independent providers of evaluation data concerning the Fund and the services provided to the Fund by the Advisor. This review was in addition to the oversight and evaluation undertaken by the Board and its committees on a continuous basis throughout the year and included, but was not limited to the following:

| • | the nature, extent, and quality of investment management, shareholder services, and other services provided by the Advisor to the Fund; |

| • | the wide range of other programs and services the Advisor provides to the Fund and its shareholders on a routine and non-routine basis; |

| • | the investment performance of the fund, including data comparing the Fund’s performance to appropriate benchmarks and/or a peer group of other mutual funds with similar investment objectives and strategies; |

| • | data comparing the cost of owning the Fund to the cost of owning similar funds; |

| • | the Advisor’s compliance policies, procedures, and regulatory experience; |

| • | financial data showing the cost of services provided to the Fund, the profitability of the Fund to the Advisor, and the overall profitability of the Advisor; |

| • | data comparing services provided and charges to other investment management clients of the Advisor; and |

| • | consideration of collateral benefits derived by the Advisor from the management of the Fund and any potential economies of scale relating thereto. |

In keeping with its practice, the Board held two in-person meetings and one telephonic meeting to review and discuss the information provided. The Directors also had the benefit of the advice of independent counsel throughout the period.

Factors Considered

The Directors considered all of the information provided by the Advisor, the independent data providers, and independent counsel, and evaluated such information for the Fund. In connection with their review, the Directors did not identify any single factor as being all-important or controlling, and each Director may have attributed different levels of importance to different factors. In deciding to renew the management agreement, the Board based its decision on a number of factors, including the following:

30

Nature, Extent and Quality of Services — Generally. Under the management agreement, the Advisor is responsible for providing or arranging for all services necessary for the operation of the Fund. The Board noted that under the management agreement, the Advisor provides or arranges at its own expense a wide variety of services including:

| • | constructing and designing the Fund |

| • | portfolio research and security selection |

| • | initial capitalization/funding |

| • | securities trading |

| • | Fund administration |

| • | custody of Fund assets |

| • | daily valuation of the Fund’s portfolio |

| • | shareholder servicing and transfer agency, including shareholder confirmations, recordkeeping, and communications |

| • | legal services |

| • | regulatory and portfolio compliance |

| • | financial reporting |

| • | marketing and distribution |

The Board noted that many of these services have expanded over time both in terms of quantity and complexity in response to shareholder demands, competition in the industry, changing distribution channels, and the changing regulatory environment.

Investment Management Services. The nature of the investment management services provided to the Fund is quite complex and allows Fund shareholders access to professional money management, instant diversification of their investments within an asset class, the opportunity to easily diversify among asset classes by investing in or exchanging among various American Century Investments funds, and liquidity. In evaluating investment performance, the Board expects the Advisor to manage the Fund in accordance with its investment objectives and approved strategies. Further, the Directors recognize that the Advisor has an obligation to monitor trading activities, and in particular to seek the best execution of fund trades, and to evaluate the use of and payment for research. In providing these services, the Advisor utilizes teams of investment professionals (portfolio managers, analysts, research assistants, and securities traders) who require extensive information technology, research, training, compliance and other systems to conduct their business. The Board, directly and through its Fund Performance Review Committee, regularly reviews investment performance information for the Fund, together with comparative information for appropriate benchmarks and/or peer groups of similarly-managed funds, over different time horizons.

31

The Directors also review detailed performance information during the management agreement approval process. If performance concerns are identified, the Fund receives special reviews until performance improves, during which the Board discusses with the Advisor the reasons for such results (e.g., market conditions, security selection) and any efforts being undertaken to improve performance. Taking all these factors into consideration, the Board found the investment management services provided by the Advisor to the Fund to meet or exceed industry standards. More detailed information about the Fund’s performance can be found in the Performance and Portfolio Commentary sections of this report.