Item 1. Reports to Stockholders

| | |

| Annual report | | |

| |

| October 31, 2015 | | |

| |

| U.S. equities | | U.S. fixed income |

The Large-Cap Value Equity Portfolio | | The High-Yield Bond Portfolio |

The Select 20 Portfolio | | The Core Plus Fixed Income Portfolio |

The Large-Cap Growth Equity Portfolio | | |

The Focus Smid-Cap Growth Equity Portfolio | | |

| | International equities |

| | The International Equity Portfolio |

| | The Labor Select International Equity Portfolio |

| | The Emerging Markets Portfolio |

| | The Emerging Markets Portfolio II |

This page intentionally left blank.

Delaware Pooled® Trust

Delaware Pooled Trust, based in Philadelphia, is a registered investment company that offers no-load, open-end equity and fixed income mutual funds to institutional and high net worth individual investors.

Delaware Management Company, a series of Delaware Management Business Trust (DMBT), serves as investment advisor for the Portfolios. Mondrian Investment Partners Limited serves as investment sub-advisor for The International Equity Portfolio,* The Labor Select International Equity Portfolio, and The Emerging Markets Portfolio.* Jackson Square Partners, LLC, serves as investment sub-advisor for The Select 20 Portfolio, The Large-Cap Growth Equity Portfolio, and The Focus-Smid Cap Growth Equity Portfolio.

The performance quoted in this report represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 800 231-8002 or visiting delawareinvestments.com/dpt/performance. Carefully consider the Portfolios’ investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Portfolios’ prospectus and, if available, their summary prospectuses, which may be obtained by visiting delawareinvestments.com or calling 800 231-8002. Investors should read the prospectus and, if available, the summary prospectus carefully before investing. Performance includes reinvestment of all distributions.

Portfolios are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested. Mutual fund advisory services are provided by Delaware Management Company, a series of DMBT, which is a registered investment advisor.

Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Portfolios’ distributor, Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

Neither Delaware Investments nor its affiliates noted in this document are authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia). The obligations of these entities do not represent deposits or other liabilities of Macquarie Bank Limited (MBL). MBL does not guarantee or otherwise provide assurance in respect of these entities, unless noted otherwise.

*Closed to new investors.

©2015 Delaware Management Holdings, Inc.

All third-party marks cited are the property of their respective owners.

Portfolio objectives and strategies

The Large-Cap Value Equity Portfolio seeks long-term capital appreciation. The Portfolio invests primarily in securities of large-capitalization companies that we believe have long-term capital appreciation potential. The Portfolio currently defines large-capitalization stocks as those with market capitalizations of $5 billion or greater at the time of purchase. Typically, we seek to select securities that we believe are undervalued in relation to their intrinsic value as indicated by multiple factors.

The Select 20 Portfolio seeks long-term capital appreciation. The Portfolio seeks to achieve its objective by investing in a portfolio of twenty (20) securities, primarily common stocks of companies that the Portfolio’s sub-advisor, Jackson Square Partners, LLC believes have long-term capital appreciation potential and are expected to grow faster than the U.S. economy.

The Large-Cap Growth Equity Portfolio seeks capital appreciation. The Portfolio invests primarily in common stocks of growth-oriented companies that the Portfolio’s sub-advisor, Jackson Square Partners, LLC (“JSP”), believes have long-term capital appreciation potential and expects to grow faster than the U.S. economy. For purposes of the Portfolio, JSP generally considers large-capitalization companies to be those that, at the time of purchase, have total market capitalizations within the range of market capitalizations of companies in the Russell 1000® Growth Index.

The Focus Smid-Cap Growth Equity Portfolio seeks long-term capital appreciation. The Portfolio invests primarily in common stocks of growth-oriented companies that the Portfolio’s sub-advisor, Jackson Square Partners, LLC believes have long-term capital appreciation potential and expects to grow faster than the U.S. economy. For purposes of this Portfolio, small-market capitalization companies are those companies whose market capitalization is similar to the market capitalization of companies in the Russell 2000® Growth Index, and mid-market capitalization companies are those companies whose market capitalization is similar to the market capitalization of companies in the Russell Midcap® Growth Index. The two indices listed above are for purposes of determining range and not for targeting portfolio management.

The High-Yield Bond Portfolio seeks high total return. The Portfolio will primarily invest its assets at the time of purchase in: (1) corporate bonds rated BB or lower by Standard & Poor’s (S&P) or similarly rated by another nationally recognized statistical rating organization; (2) securities issued or guaranteed by the U.S. government, its agencies, or instrumentalities; or (3) commercial paper of companies rated A-1 or A-2 by S&P, rated P-1 or P-2 by Moody’s Investors Service, Inc. (Moody’s), or unrated but considered to be of comparable quality.

The Core Plus Fixed Income Portfolio seeks maximum long-term total return, consistent with reasonable risk. The Portfolio allocates its investments principally among three sectors of the fixed income securities markets: U.S. investment grade sector, U.S. high yield sector, and international sector.

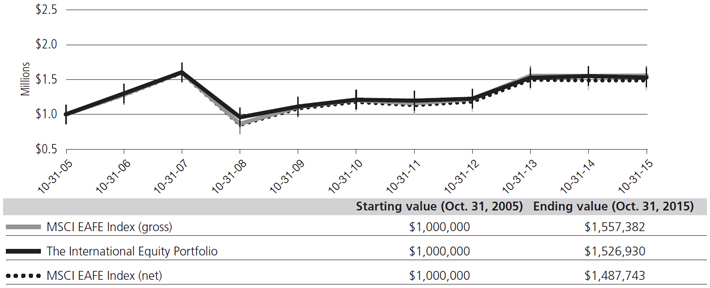

The International Equity Portfolio seeks maximum long-term total return. The Portfolio invests primarily in equity securities of companies that are organized, have a majority of their assets, or derive most of their operating income outside the United States, and that, in the opinion of Mondrian Investment Partners Limited, the Portfolio’s sub-advisor, are undervalued at the time of purchase based on the sub-advisor’s fundamental analysis. Investments will be made mainly in marketable securities of companies in developed countries. The International Equity Portfolio is presently closed to new investors.

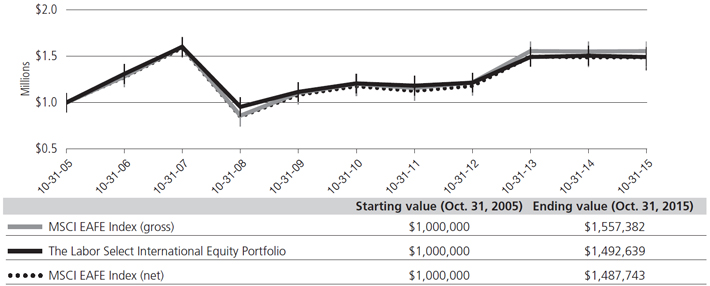

The Labor Select International Equity Portfolio seeks maximum long-term total return. The Portfolio invests primarily in equity securities of companies that are organized, have a majority of their assets, or derive most of their operating income outside of the United States, and that, in the opinion of Mondrian Investment Partners Limited (“Mondrian”), the Portfolio’s sub-advisor, are undervalued at the time of purchase based on the rigorous fundamental analysis that the sub-advisor employs. In addition to following these quantitative guidelines, Mondrian will select securities of issuers that present certain characteristics that are compatible or operate in accordance with certain investment policies or restrictions followed by organized labor.

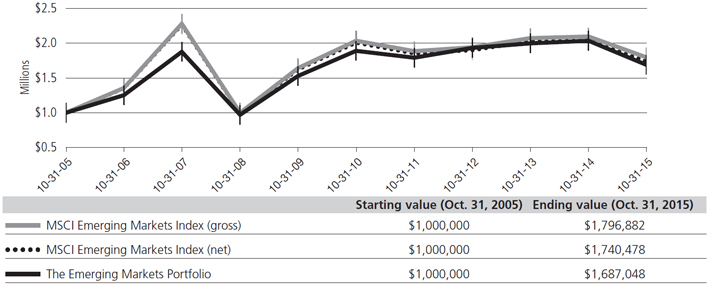

The Emerging Markets Portfolio seeks long-term capital appreciation. The Portfolio generally invests in equity securities of companies that are organized in, have a majority of their assets in, or derive a majority of their operating income from emerging countries. The Emerging Markets Portfolio is presently closed to new investors.

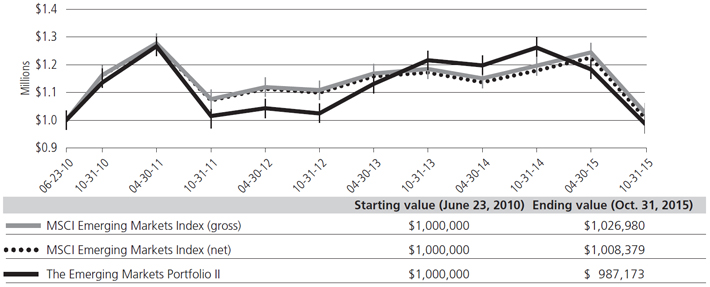

The Emerging Markets Portfolio II seeks long-term capital appreciation. The Portfolio invests primarily in a broad range of equity securities of companies located in emerging market countries. The Portfolio may invest in companies of any size. The portfolio manager believes that although market price and intrinsic business value are positively correlated in the long run, short-term divergences can emerge. The Portfolio seeks to take advantage of these divergences through a fundamental, bottom-up approach. The Portfolio invests in securities of companies with sustainable franchises when they are trading at a discount to the portfolio manager’s intrinsic value estimate for that security.

2

Carefully consider the Portfolios’ investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Portfolios’ prospectus and, if available, its summary prospectus, which may be obtained by visiting delawareinvestments.com or calling 800 231-8002. Investors should read the applicable prospectus and, if available, the applicable summary prospectus carefully before investing.

The Portfolios of Delaware Pooled® Trust (DPT) are designed exclusively for institutional investors and high net worth individuals.

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations. Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

Narrowly focused investments may exhibit higher volatility than investments in multiple industry sectors.

The Portfolios’ share prices and yields will fluctuate in response to movements in stock prices.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Portfolios may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Portfolios may be prepaid prior to maturity, potentially forcing the Portfolios to reinvest that money at a lower interest rate.

Securities in the lowest of the rating categories considered to be investment grade (that is, Baa or BBB) have some speculative characteristics.

High yielding, noninvestment grade bonds (junk bonds) involve higher risk than investment grade bonds.

The high yield secondary market is particularly susceptible to liquidity problems when institutional investors, such as mutual funds and certain other financial institutions, temporarily stop buying bonds for regulatory, financial, or other reasons. In addition, a less liquid secondary market makes it more difficult for a Portfolio to obtain precise valuations of the high yield securities in its portfolio.

Certain Portfolios expect to hold a concentrated portfolio of a limited number of securities; those Portfolios’ risk is increased because each investment has a greater effect on that Portfolio’s overall performance.

The Select 20 Portfolio is considered “nondiversified” as defined in the Investment Company Act of 1940. “Nondiversified” Portfolios may allocate more of their net assets to investments in single securities than “diversified” Portfolios. Resulting adverse effects may subject this Portfolio to greater risks and volatility.

3

Portfolio management review

Delaware Pooled® Trust — The Large-Cap Value Equity Portfolio

October 31, 2015

For the fiscal year ended Oct. 31, 2015, Delaware Pooled Trust — The Large-Cap Value Equity Portfolio, returned +3.18% at net asset value (NAV) with all distributions reinvested. This result outpaced the Portfolio’s benchmark, the Russell 1000® Value Index, which returned +0.53% for the same period. Complete annualized performance for The Large-Cap Value Equity Portfolio is shown on the table on page 6.

Stock prices failed to gather much momentum over the Portfolio’s fiscal year, reflecting the U.S. economy’s slow but steady growth. The country’s gross domestic product (GDP) — a measure of economic activity — rose 2.1% in the fourth quarter of 2014, followed by a slight gain of 0.6% in the first three months of 2015. Growth picked up in the second quarter of 2015, with GDP expanding 3.9% before falling back to 1.5% in the subsequent quarter.

Relative to the benchmark, the Portfolio benefited from its defensive positioning. In other words, we emphasized stocks with what we viewed as having stronger business fundamentals, many of which were in traditionally defensive sectors, such as consumer staples, which tend to maintain more price stability in a down market. Our security selection was especially favorable in this group. Also, when we did invest in more typically economically sensitive sectors, we tended to focus on companies that in our opinion had more conservative characteristics.

Within consumer staples, the Portfolio benefited the most from food products companies Kraft Heinz and Mondelez International. We originally invested in Kraft Foods, the predecessor of Kraft Heinz, for what we viewed as its strong collection of brands and reasonably valued stock. We were also attracted to the company’s solid dividend and potential to further improve its financial strength. Heinz appeared to notice these characteristics as well, agreeing to merge with Kraft in March 2015, a move that resulted in a sharply higher share price.

Meanwhile, shares of Mondelez — which was spun off from Kraft several years ago — benefited from the company’s success in managing expenses and expanding its business footprint. Its stock was up by roughly one-third for the fiscal year, while Kraft Heinz saw its shares gain close to three-quarters of its value overall.

Stock selection in industrials also contributed to the Portfolio’s outperformance, especially its position in defense contractor Northrop Grumman. The company produced strong financial results despite cutbacks in U.S. military spending that seemed to concern many investors. Late in the fiscal year, Northrop Grumman further benefited from news that the company won a significant contract to build the U.S. Air Force’s next-generation Long Range Strike Bomber (LRS-B); the stock went up 10% on the news.

Other notable relative contributors included Broadcom, a maker of semiconductors for communications applications, and Lowe’s, a retailer of home improvement products. Shares of Broadcom gained

sharply after the company agreed to be acquired by Avago at a significant premium. This put the company’s stock near our price target, and we ultimately sold the Portfolio’s position. Meanwhile, Lowe’s continued to benefit from the steady recovery in the housing market, and from the company’s efforts to improve its merchandising, which helped lift its sales and earnings.

On the negative side, security selection was poor in the energy sector, where continued weakness in commodity prices hampered most companies. By far, the Portfolio’s largest detractor in the group was Marathon Oil, whose relatively high exposure to U.S. shale markets was a significant negative, as was its elevated debt level and smaller size relative to other large-cap operators. A position in Halliburton hurt performance, as reduced energy exploration activity across the industry cut into the company’s revenues and earnings. Weak market prices of crude oil and natural gas also hurt two other Portfolio holdings, Chevron and ConocoPhillips. We continue to closely monitor the Portfolio’s energy stocks for signs of lasting financial stress. It’s possible that a bottoming process in oil prices is starting to take shape and our longer term view on global oil demand remains positive.

Elsewhere, a stake in Xerox, a provider of document management and other business services, produced disappointing results. The company continued to face various business challenges that led to narrower profit margins, lower earnings, and reduced revenues. Despite recent execution challenges, Xerox has the potential to benefit from its transformation to a services-oriented business model, in our view.

We made relatively few changes to the Portfolio during the fiscal year. With the sale of Broadcom in June, we used the proceeds to establish a new position in pharmacy benefits manager Express Scripts Holding, which we viewed as a high-quality growth opportunity with an unusually attractive valuation. Another meaningful purchase was of CA, which we acquired in March 2015. The company’s recent business challenges left its stock with what we saw as a favorable risk-reward tradeoff.

We sold the Portfolio’s holding in Baxter International, which spun off its global pharmaceutical business, Baxalta. The new company will build on its strengths in hematology and immunology. With the proceeds of the sale, we added to our stake in Baxalta, which we think has an attractive valuation relative to its growth potential.

At fiscal year end, it remained difficult for us to identify attractive new purchase candidates in light of relatively high valuations. At the end of the period, we were closing in on a few favorable opportunities in the consumer discretionary sector, and we were also considering some longer-range ideas in the consumer staples, financials, and industrials sectors. We are also taking a fresh look at

the Portfolio’s exposure to the energy sector and where energy prices might be going in the next three to five years.

That said, we do not anticipate large adjustments to the Portfolio anytime soon. Regardless of market conditions, our approach remains consistent. We will continue to look for companies available for purchase at what we view as attractive valuations because of temporary fundamental challenges and negative investor sentiment, adhering to our process of searching for what we believe are favorable relative values in the marketplace.

The views expressed are current as of the date of this report and subject to change.

5

Performance summary

Delaware Pooled® Trust — The Large-Cap Value Equity Portfolio

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 231-8002 or visiting our website at delawareinvestments.com.

Carefully consider the Portfolio’s investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Portfolio’s prospectus and, if available, its summary prospectus, which may be obtained by visiting delawareinvestments.com or calling 800 231-8002. Investors should read the prospectus and, if available, the summary prospectus carefully before investing.

| | | | | | | | | | |

| Portfolio and benchmark performance | | | | | | | | | | |

| Average annual total returns | | | | | | | | | | |

| Periods ended Oct. 31, 2015 | | 1 year | | 3 years | | 5 years | | 10 years | | Lifetime |

| | | | | |

| | | | | | | | | | |

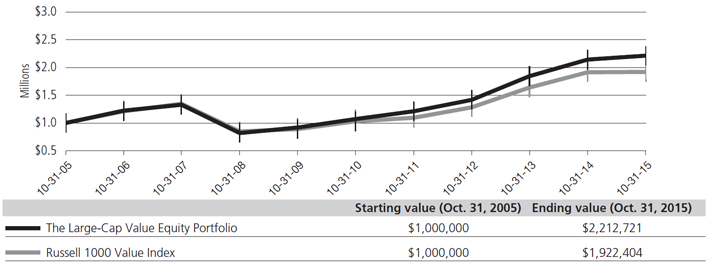

The Large-Cap Value Equity Portfolio | | +3.18% | | +15.97% | | +15.59% | | +8.27% | | +9.96% |

Russell 1000 Value Index | | +0.53% | | +14.52% | | +13.26% | | +6.75% | | +9.95% |

| | |

| |

| Portfolio profile | | |

| Oct. 31, 2015 | | |

| | |

Total net assets | | Number of holdings |

$214.7 million | | 33 |

| | |

Inception date | | |

Feb. 3, 1992 | | |

Growth of $1,000,000

The performance graph assumes $1 million invested on Oct. 31, 2005, and includes reinvestment of all distributions. The performance graph does not reflect the deduction of taxes the shareholder would pay on Portfolio distributions or redemptions of Portfolio shares.

Total return assumes reinvestment of dividends and capital gains, but does not reflect reductions for taxes. Returns and share values will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The most recent prospectus disclosed the Portfolio’s total operating expenses as 0.68%. Management has contractually agreed to reimburse certain expenses and/or waive its management fees from Nov. 1, 2014, through Oct. 31, 2015,* in order to prevent total annual Portfolio

operating expenses (with certain exclusions) from exceeding, in an aggregate amount, 0.70% of the Portfolio’s average daily net assets, as described in the most recent prospectus.

Expense limitations were in effect during the period shown. Performance would have been lower had the expense limitations not been in effect.

The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values.

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Investing involves risk, including the possible loss of principal.

Past performance is not a guarantee of future results.

* The contractual waiver period is from Feb. 27, 2014 through Feb. 29, 2016.

7

Portfolio management review

Delaware Pooled® Trust — The Select 20 Portfolio

October 31, 2015

For the fiscal year ended Oct. 31, 2015, Delaware Pooled Trust — The Select 20 Portfolio, returned +10.60% at net asset value (NAV) with all distributions reinvested. This result outpaced the Portfolio’s benchmark, the Russell 3000® Growth Index, which returned +8.72% for the same period. Complete annualized performance for The Select 20 Portfolio is shown in the table on page 10.

The U.S. economy hit several rough patches in late summer and early fall as a China-led global slowdown rocked the financial world. An eleventh-hour rebound in October helped domestic stocks climb back to pre-correction levels, enabling the broad-based stock market, as measured by the S&P 500® Index, to gain a moderate 5.20% during the 12-month period.

Oil prices were a recurring theme as the price per barrel fell precipitously throughout the fiscal year, eventually bottoming out at a six-year low. Despite a drop in consumption brought on primarily by the slowdown in China, major oil producers like the Organization of the Petroleum-Exporting Countries (OPEC) maintained production levels in an effort to remain competitive with U.S. shale oil producers. The resulting dramatic supply-demand imbalance led many U.S. producers to cut back or close rigs late in the period. (Source: Bloomberg.)

The once reliable Chinese growth engine sputtered amid a combination of excess manufacturing capacity and a slowing growth rate. In mid-August, the Chinese government surprised investors by devaluing its currency by roughly 2% relative to the U.S. dollar. As the cost of Chinese goods fell in foreign markets, fears about the stability of other Asian nations resulted in emerging markets being among the weakest performers during the period.

The European Union (EU) continued to struggle with the management of Greece’s ongoing debt crisis. The EU also shared concerns about the Chinese economy, volatility amid faltering energy stocks, and apprehension about a potential rate increase by the U.S. Federal Reserve. The European Central Bank advised that it would continue its easing of monetary policy. All of these factors led to dramatic market swings that left international equity market performance, as measured by the MSCI EAFE Index, essentially flat for the fiscal year.

U.S. investors spent a majority of the year trying to predict when the Fed would reverse its seven-year-old, zero interest-rate policy. Though the Fed hinted throughout the year that a rate hike was just around the corner, uncertain economic data repeatedly pushed the Fed off that path. An October delay in the rate hike led to a widespread market rally, with U.S. equities — in particular large-cap growth equities — posting outsized gains for the month.

At fiscal year end, despite recent market gains, uncertainty remained about China’s economic future, the long-term trajectory of oil prices, and the timeline for Fed rate hikes.

The Portfolio’s strong relative performance in the healthcare and financial services sectors was partially offset by weak relative performance in the technology and consumer discretionary sectors.

Electronic Arts, a global interactive entertainment software company, was a contributor to performance during the period. The company reported relatively strong financial results driven in part by several individual game titles, cost controls, and growth in digital game sales. Additionally, we believe the company had a particularly strong showing at this year’s Electronic Entertainment Expo (E3) after its upcoming game Star Wars Battlefront received an overall positive initial response. We believe the company should continue to benefit from upcoming and established game franchises and its growth within the digital-downloads and mobile-phone gaming channels, which we think will be increasingly important for the company’s growth going forward.

Visa was also a contributor to performance during the period. The company continued to report strong financial results and had several positive developments during the period. The market reacted favorably to the proposed acquisition between Visa and Visa Europe (the latter is a former subsidiary of Visa that has been an independent entity since 2007). Additionally, Visa invested in an online digital-payment company, Stripe, giving Visa immediate access to the digital-payment space. While there are some concerns over disintermediating technologies, such as alternative mobile-payment services, we believe Visa has attempted to take aggressive initiatives through technology upgrades and strategic partnerships. We continue to believe the company is well positioned to benefit from the secular global trend of payment transactions moving from paper-based currency to electronic transactions.

Qualcomm was a detractor from performance during the period. The stock experienced weakness over concerns related to fears of increased competition and more pricing pressure than expected. We believe these issues are transitory and do not threaten our long-term thesis on the company. A positive development was a settlement of the antimonopoly suit with the Chinese government that had added to downward pressure on the stock. We believe that Qualcomm continues to benefit from its unique intellectual property and patent position in the semiconductor industry as well as its technology applications targeted at the explosive growth and proliferation of wireless devices. Further, we believe that new management at the company appears more willing than its predecessors to consider meaningful capital allocation actions that could potentially create significant value for shareholders.

VeriFone Systems was also a detractor from performance during the period. Investors may have become concerned about future financial guidance and the impact of global currency fluctuations, given that more than half of the company’s revenues are generated outside the United States. The company also faces increased

competition within the digital-payment space. Despite these concerns, we believe the company’s capital investment in next-generation products should help create a more complete and integrated product offering suite to clients and consumers. We believe this technology will allow the company to effectively compete with existing technology offered by Square and Apple Pay. We continue to believe the company is well positioned to benefit from the secular trend to electronic forms of payments.

Regardless of the economic outcome, we remain consistent in our long-term investment philosophy: We want to own what we view as strong secular-growth companies with solid business models and competitive positions that we believe can grow market share and have the potential to deliver shareholder value in a variety of market environments.

The views expressed are current as of the date of this report and subject to change.

9

Performance summary

Delaware Pooled® Trust — The Select 20 Portfolio

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 231-8002 or visiting our website at delawareinvestments.com.

Carefully consider the Portfolio’s investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Portfolio’s prospectus and, if available, its summary prospectus, which may be obtained by visiting delawareinvestments.com or calling 800 231-8002. Investors should read the prospectus and, if available, the summary prospectus carefully before investing.

Portfolio and benchmark performance

| | | | | | | | | | |

| Average annual total returns | | | | | | | | | | |

| Periods ended Oct. 31, 2015 | | 1 year | | 3 years | | 5 years | | 10 years | | Lifetime |

| | | | | |

| | | | | | | | | | |

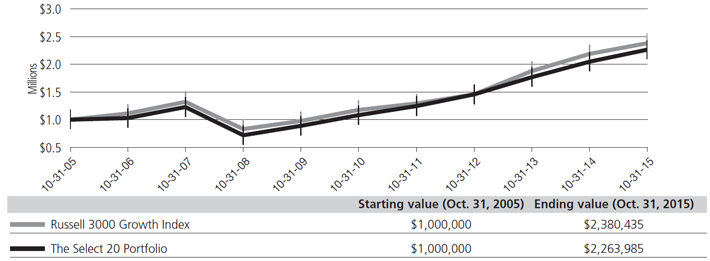

The Select 20 Portfolio | | +10.60% | | +15.76% | | +15.90% | | +8.51% | | +2.59% |

Russell 3000 Growth Index | | +8.72% | | +17.79% | | +15.16% | | +9.06% | | +2.22% |

| | |

| |

| Portfolio profile | | |

| Oct. 31, 2015 | | |

| | |

Total net assets | | Number of holdings |

$93.6 million | | 21 |

| | |

Inception date | | |

March 31, 2000 | | |

Growth of $1,000,000

The performance graph assumes $1 million invested on Oct. 31, 2005, and includes reinvestment of all distributions. The performance graph does not reflect the deduction of taxes the shareholder would pay on Portfolio distributions or redemptions of Portfolio shares.

Total return assumes reinvestment of dividends and capital gains, but does not reflect reductions for taxes. Returns and share values will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The most recent prospectus disclosed the Portfolio’s total operating expenses as 0.87%. Management has contractually agreed to reimburse certain expenses and/or waive its management fees from Nov. 1, 2014, through Oct. 31, 2015,* in order to prevent total annual Portfolio

operating expenses (with certain exceptions) from exceeding, in an aggregate amount, 0.89% of the Portfolio’s average daily net assets, as described in the most recent prospectus.

Expense limitations were in effect during the period shown. Performance would have been lower had the expense limitations not been in effect.

The Russell 3000 Growth Index measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 3000 companies with higher price-to-book ratios and higher forecasted growth values.

The S&P 500 Index, mentioned on page 8, measures the performance of 500 mostly large-cap stocks weighted by market value, and is often used to represent performance of the U.S. stock market.

The MSCI EAFE (Europe, Australasia, Far East) Index, mentioned on page 8, is a free float-adjusted market capitalization weighted index designed to measure equity market performance of developed markets, excluding the United States and Canada. Index “net” return approximates the minimum possible dividend reinvestment, after deduction of withholding tax at the highest possible rate.

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Investing involves risk, including the possible loss of principal.

Past performance is not a guarantee of future results.

Because the Portfolio expects to hold a concentrated portfolio of a limited number of securities, the Portfolio’s risk is increased because each investment has a greater effect on the Portfolio’s overall performance.

Investments in small and/or medium-sized companies typically exhibit greater risk and higher volatility than larger, more established companies.

“Nondiversified” Portfolios may allocate more of their net assets to investments in single securities than “diversified” Portfolios. Resulting adverse effects may subject these Portfolios to greater risks and volatility.

On Feb. 28, 2008, the Portfolio changed its investment strategy to limit its investments to no less than 15 securities and no more than 25 securities. The performance prior to Feb. 28, 2008 is that of the Portfolio’s predecessor, The All-Cap Growth Equity Portfolio.

* The contractual waiver period is from Feb. 27, 2014 through Feb. 29, 2016.

11

Portfolio management review

Delaware Pooled® Trust — The Large-Cap Growth Equity Portfolio

October 31, 2015

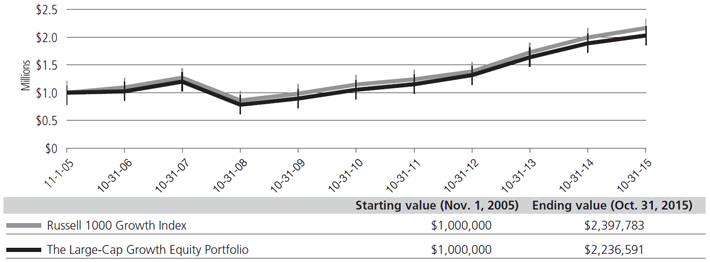

For the fiscal year ended Oct. 31, 2015, Delaware Pooled Trust — The Large-Cap Growth Equity Portfolio, returned +8.06% at net asset value (NAV) with all distributions reinvested. For the same period, the Portfolio’s benchmark, the Russell 1000® Growth Index, returned +9.18%. Complete annualized performance for The Large-Cap Growth Equity Portfolio is shown on the table on page 14.

The U.S. economy hit several rough patches in late summer and early fall as a China-led global slowdown rocked the financial world. An eleventh-hour rebound in October helped domestic stocks climb back to pre-correction levels, enabling the broad-based stock market, as measured by the S&P 500® Index, to gain a moderate 5.20% during the 12-month period.

Oil prices were a recurring theme as the price per barrel fell precipitously throughout the fiscal year, eventually bottoming out at a six-year low. Despite a demand in consumption brought on primarily by the slowdown in China, major oil producers like the Organization of the Petroleum-Exporting Countries (OPEC) maintained production levels in an effort to remain competitive with U.S. shale oil producers. The resulting supply-demand imbalance led many U.S. producers to cut back or close rigs late in the period. (Source: Bloomberg.)

The once reliable Chinese growth engine sputtered amid a combination of excess manufacturing capacity and a slowing growth rate. In mid-August, the Chinese government surprised investors by devaluing its currency by roughly 2% relative to the U.S. dollar. As the cost of Chinese goods fell in foreign markets, fears about the stability of other Asian nations resulted in emerging markets’ being among the weakest performers during the period.

The European Union (EU) continued to struggle with the management of Greece’s ongoing debt crisis. The EU also shared concerns about the Chinese economy, volatility amid faltering energy stocks, and apprehension about a potential rate increase by the U.S. Federal Reserve. The European Central Bank advised that it would continue its easing of monetary policy. All of these factors led to dramatic market swings that left international equity market performance, as measured by the MSCI EAFE Index, essentially flat for the fiscal year.

U.S. investors spent most of the year trying to predict when the Fed would reverse its seven-year-old, zero interest-rate policy. Though the Fed hinted throughout the year that a rate hike was just around the corner, uncertain economic data repeatedly pushed it off that path. An October delay in the rate hike led to a widespread market rally, with U.S. equities — in particular large-cap growth equities — posting outsized gains for the month.

At fiscal year end, despite recent market gains, uncertainty remained about China’s economic future, the long-term trajectory of oil prices, and the timeline for Fed rate hikes.

The Portfolio’s strong relative performance in the financial services and producer durables sectors was unable to overcome weak relative performance in the consumer discretionary and technology sectors.

Equinix was a contributor to performance during the period. The company reported relatively strong financial results and received a favorable real estate investment trust (REIT) status ruling from the Internal Revenue Service. Additionally, the company is pursuing several strategic acquisitions that should further strengthen its global presence. The company continues to benefit from significant opportunities associated with cloud computing and its disruption of the information technology supply chain. Increased globalization and the robust need for a secure and accessible network to meet the needs of a dispersed user base are creating significant demand. We believe the company’s innovative product offerings make it well positioned in a technology-spending environment that is focused on addressing the needs of enterprises struggling to maintain the highest level of network performance and quality of service for global users.

Electronic Arts, a global interactive entertainment software company, was also a contributor to performance during the period. The company reported relatively strong financial results driven in part by several individual game titles, cost controls, and growth in digital-game sales. Additionally, we believe the company had a particularly strong showing at this year’s Electronic Entertainment Expo (E3) after its upcoming game Star Wars Battlefront received an overall positive initial response. We believe the company should continue to benefit from upcoming and established game franchises and its growth within the digital-downloads and mobile-phone gaming channels, which we think will be increasingly important for the company’s growth going forward.

Valeant Pharmaceuticals International was a detractor from performance during the period. The company was hit hard by allegations of wrongdoing at its specialty pharmacy partner, Philidor. Investors’ lack of familiarity with this relationship left the stock vulnerable when questions were raised, and a short-seller’s analogy to Enron put incremental pressure on the stock and raised investor scrutiny. Our best assessment at this point is that Philidor is a relatively small part of Valeant’s total business. Further, third-quarter cash generation was positive and would indicate the company is what we thought it was: a cash-generating business with solid medium-term growth prospects. It is now trading at a very high free-cash-flow yield on our 2016 projections, despite our having applied a very substantial haircut to those projections. We also note that the shareholder base and board include large owners with an interest in reaching an economic outcome we believe could be beneficial. Considering both risk and reward, as well as the remaining unknowns, we have maintained exposure to the stock in the midrange of our portfolio weights.

Qualcomm was also a detractor from performance during the period. The stock experienced weakness over concerns related to fears of increased competition and more pricing pressure than expected. We believe these issues are transitory and do not threaten our long-term thesis on the company. A positive development was a settlement of the antimonopoly suit with the Chinese government that had added to downward pressure on the stock. We believe that Qualcomm continues to benefit from its unique intellectual property and patent position in the semiconductor industry as well as its technology applications targeted at the explosive growth and proliferation of wireless devices. Further, we believe that new management at the company appears more willing than its predecessors to consider meaningful capital allocation actions that could potentially create significant value for shareholders.

Regardless of the economic outcome, we remain consistent in our long-term investment philosophy: We want to own what we view as strong secular-growth companies with solid business models and competitive positions that we believe can grow market share and have the potential to deliver shareholder value in a variety of market environments.

The views expressed are current as of the date of this report and subject to change.

13

Performance summary

Delaware Pooled® Trust — The Large-Cap Growth Equity Portfolio

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 231-8002 or visiting our website at delawareinvestments.com.

Carefully consider the Portfolio’s investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Portfolio’s prospectus and, if available, its summary prospectus, which may be obtained by visiting delawareinvestments.com or calling 800 231-8002. Investors should read the prospectus and, if available, the summary prospectus carefully before investing.

| | | | | | | | |

| Portfolio and benchmark performance | | | | | | | | |

| Average annual total returns | | | | | | | | |

| Periods ended Oct. 31, 2015 | | 1 year | | 3 years | | 5 years | | Lifetime |

| | | | |

| | | | | | | | |

The Large-Cap Growth Equity Portfolio | | +8.06% | | +17.40% | | +15.98% | | +8.38% |

Russell 1000 Growth Index | | +9.18% | | +17.94% | | +15.30% | | +9.09% |

| | | | |

| | |

| Portfolio profile | | | | |

| Oct. 31, 2015 | | | | |

| | | | |

Total net assets | | | | Number of holdings |

$313.5 million | | | | 30 |

| | | | |

Inception date | | | | |

Nov. 1, 2005 | | | | |

Growth of $1,000,000

The performance graph assumes $1 million invested on Nov. 1, 2005, and includes reinvestment of all distributions. The performance graph does not reflect the deduction of taxes the shareholder would pay on Portfolio distributions or redemptions of Portfolio shares.

Total return assumes reinvestment of dividends and capital gains, but does not reflect reductions for taxes. Returns and share values will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The most recent prospectus disclosed the Portfolio’s total operating expenses as 0.64%. Management has contractually agreed to reimburse certain expenses and/or waive its management fees from Nov. 1, 2014, through Oct. 31, 2015,* in order to prevent total annual Portfolio

operating expenses (with certain exceptions) from exceeding, in an aggregate amount, 0.65% of the Portfolio’s average daily net assets, as described in the most recent prospectus.

Expense limitations were in effect during the period shown. Performance would have been lower had the expense limitations not been in effect.

The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

The S&P 500 Index, mentioned on page 12, measures the performance of 500 mostly large-cap stocks weighted by market value, and is often used to represent performance of the U.S. stock market.

The MSCI EAFE (Europe, Australasia, Far East) Index, mentioned on page 12, is a free float-adjusted market capitalization weighted index designed to measure equity market performance of developed markets, excluding the United States and Canada. Index “net” return approximates the minimum possible dividend reinvestment, after deduction of withholding tax at the highest possible rate.

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Investing involves risk, including the possible loss of principal.

Past performance is not a guarantee of future results.

Because the Portfolio expects to hold a concentrated portfolio of a limited number of securities, the Portfolio’s risk is increased because each investment has a greater effect on the Portfolio’s overall performance.

*The contractual waiver period is from Feb. 27, 2014 through Feb. 29, 2016.

15

Portfolio management review

Delaware Pooled® Trust — The Focus Smid-Cap Growth Equity Portfolio

October 31, 2015

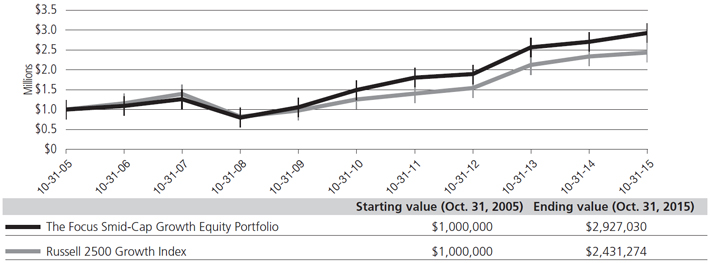

For the fiscal year ended Oct. 31, 2015, Delaware Pooled Trust — The Focus Smid-Cap Growth Equity Portfolio, returned +8.30% at net asset value (NAV) with all distributions reinvested. This result outpaced the Portfolio’s benchmark, the Russell 2500™ Growth Index, which returned +4.17% for the same period. Complete annualized performance for The Focus Smid-Cap Growth Equity Portfolio is shown in the table on page 18.

The U.S. economy hit several rough patches during the fiscal year, most notably in late summer and early fall as a China-led global slowdown rocked the financial world. An eleventh-hour rebound in October helped domestic stocks climb back to pre-correction levels, enabling the broad-based stock market, as measured by the S&P 500® Index, to gain a moderate 5.20% during the 12-month period.

Oil prices were a recurring theme as the price per barrel fell precipitously throughout the period, eventually bottoming out at a six-year low. Despite a drop in consumption brought on primarily by the slowdown in China, major oil producers like the Organization of the Petroleum-Exporting Countries (OPEC) maintained production levels in an effort to remain competitive with U.S. shale oil producers. The resulting supply-demand imbalance led many U.S. producers to cut back or close rigs late in the period. (Source: Bloomberg.)

The once reliable Chinese growth engine sputtered amid a combination of excess manufacturing capacity and a slowing growth rate. In mid-August, the Chinese government surprised investors by devaluing its currency by roughly 2% relative to the U.S. dollar. As the cost of Chinese goods fell in foreign markets, fears about the stability of other Asian nations resulted in emerging markets’ being among the weakest performers during the period.

The European Union (EU) continued to struggle with the management of Greece’s ongoing debt crisis. The EU also shared concerns about the Chinese economy, volatility amid faltering energy stocks, and apprehension about a potential rate increase by the U.S. Federal Reserve. The European Central Bank advised that it would continue its easing of monetary policy. All of these factors led to dramatic market swings that left international equity market performance, as measured by the MSCI EAFE Index, essentially flat for the fiscal year.

Within the United States, investors spent a majority of the year trying to predict when the Federal Reserve would reverse its seven-year-old, zero interest-rate policy. Though the Fed hinted throughout the year that a rate hike was just around the corner, uncertain economic data repeatedly pushed it off that path. An October delay in the rate hike led to a widespread market rally, with U.S. equities — in particular large-cap growth equities — posting outsized gains for the month.

At fiscal year end, despite recent market gains, uncertainty remained about China’s economic future, the long-term trajectory of oil prices, and the timeline for Fed rate hikes.

The Portfolio’s strong relative performance in the financial services and utilities sectors was partially offset by weak relative performance in the consumer discretionary sector.

Abiomed was a contributor to performance during the period. The company continued to experience strong growth in its Impella (heart pump) product line and also received positive regulatory approval for several new heart-pump devices. Additionally, the U.S. Department of Justice announced it had closed an investigation into the company’s marketing and labeling practices associated with its Impella 2.5 device without taking any enforcement action. We believe these developments should further enhance the company’s ability to increase shareholder value.

Heartland Payment Systems was also a contributor to performance during the period. There has been some concern over the past few years about the effect of the company’s acquisition strategy and heavy capital investment on financials over the near-to-intermediate term. However, we feel we are already seeing some benefits as evidenced by the company’s strong organic growth rates in both card and non-card business segments and its margin expansion. Overall, we believe the company is well-positioned to benefit from the secular global trend of payment transactions moving from paper-based currency to electronic transactions.

Shutterstock, a provider of digital image and sound licensing services, was a detractor from performance during the period. The stock experienced weakness amid increasing concerns that Adobe, among other competitors, is aggressively pursuing the space. We continue to believe that Shutterstock provides an attractive alternative to traditional licensed digital image and sound providers by providing a pure-pricing model and relatively transparent terms at a significantly lower cost compared to existing companies. Image and sound licensing has historically been very expensive, often with excessively complex terms. Therefore we feel Shutterstock should be able to gain considerable market share. Despite Shutterstock’s being a new entrant to the market, we believe recent acquisitions should help the company further strengthen its competitive position.

Sally Beauty Holdings was also a detractor from performance during the period. Relatively new management has introduced several marketing initiatives and promotional activity that have hurt margins, but we anticipate promotional spending will drive increased growth over the intermediate to long term. We continue to believe that this beauty-supply retailer is a relatively steady growth business due to aging demographics and the relatively low level of discretionary income required of its target customer base.

16

Regardless of the economic outcome, we remain consistent in our long-term investment philosophy: We want to own what we view as strong secular-growth companies with solid business models and competitive positions that we believe can grow market share and have the potential to deliver shareholder value in a variety of market environments.

The views expressed are current as of the date of this report and subject to change.

17

Performance summary

Delaware Pooled® Trust — The Focus Smid-Cap Growth Equity Portfolio

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 231-8002 or visiting our website at delawareinvestments.com.

Carefully consider the Portfolio’s investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Portfolio’s prospectus and, if available, its summary prospectus, which may be obtained by visiting delawareinvestments.com or calling 800 231-8002. Investors should read the prospectus and, if available, the summary prospectus carefully before investing.

| | | | | | | | | | | | | | | | | | | | |

| Portfolio and benchmark performance | | | | | | | | | | | | | | | | | | | | |

Average annual total returns | | | | | | | | | | | | | | | | | | | | |

Periods ended Oct. 31, 2015 | | 1 year | | | 3 years | | | 5 years | | | 10 years | | | Lifetime | |

The Focus Smid-Cap Growth Equity Portfolio | | | +8.30% | | | | +15.70% | | | | +14.53% | | | | +11.34% | | | | +10.42% | |

Russell 2500 Growth Index | | | +4.17% | | | | +16.48% | | | | +14.25% | | | | +9.29% | | | | +9.16% | |

Portfolio profile | | | | | | | | | | | | | | | | | | | | |

Oct. 31, 2015 | | | | | | | | | | | | | | | | | | | | |

Total net assets | | | | | | | Number of holdings | | | | | |

$51.4 million | | | | | | | 41 | | | | | | | | | | | | | |

Inception date | | | | | | | | | | | | | | | | | | | | |

Dec. 1, 2003 | | | | | | | | | | | | | | | | | | | | |

Growth of $1,000,000

The performance graph assumes $1 million invested on Oct. 31, 2005, and includes reinvestment of all distributions. The performance graph does not reflect the deduction of taxes the shareholder would pay on Portfolio distributions or redemptions of Portfolio shares.

Total return assumes reinvestment of dividends and capital gains, but does not reflect reductions for taxes. Returns and share values will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The most recent prospectus disclosed the Portfolio’s total operating expenses as 0.91%. Management has contractually agreed to reimburse certain expenses and/or waive its management fees from Nov. 1, 2014, through Oct. 31, 2015,* in order to prevent total annual Portfolio

18

operating expenses (with certain exclusions) from exceeding, in an aggregate amount, 0.92% of the Portfolio’s average daily net assets, as described in the most recent prospectus.

Expense limitations were in effect during the period shown. Performance would have been lower had the expense limitations not been in effect.

The Russell 2500 Growth Index measures the performance of the small- to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500 companies with higher price-to-book ratios and higher forecasted growth values.

The S&P 500 Index, mentioned on page 16, measures the performance of 500 mostly large-cap stocks weighted by market value, and is often used to represent performance of the U.S. stock market.

The MSCI EAFE (Europe, Australasia, Far East) Index, mentioned on page 16, is a free float-adjusted market capitalization weighted index designed to measure equity market performance of developed markets, excluding the United States and Canada. Index “net” return approximates the minimum possible dividend reinvestment, after deduction of withholding tax at the highest possible rate.

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Past performance is not a guarantee of future results.

Because the Portfolio expects to hold a concentrated portfolio of a limited number of securities, the Portfolio’s risk is increased because each investment has a greater effect on the Portfolio’s overall performance.

Investments in small and/or medium-sized companies typically exhibit greater risk and higher volatility than larger, more established companies.

*The contractual waiver period is from Feb. 27, 2014 through Feb. 29, 2016.

Portfolio management review

Delaware Pooled® Trust — The High-Yield Bond Portfolio

October 31, 2015

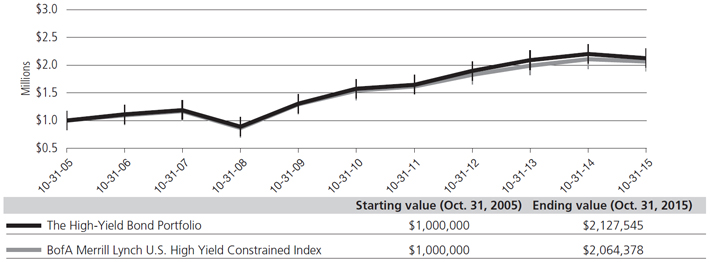

For the fiscal year ended Oct. 31, 2015, Delaware Pooled Trust — The High-Yield Bond Portfolio returned -3.41% at net asset value (NAV) with all distributions reinvested. For the same period, the Portfolio’s benchmark, the BofA Merrill Lynch U.S. High Yield Constrained Index, returned -2.03%. Complete annualized performance for The High-Yield Bond Portfolio is shown in the table on page 22.

Despite stable benchmark interest rates, modest economic growth, and clear signs of recovery in the U.S. labor market, high yield bonds experienced a volatile 12 months through Oct. 31, 2015, ending in negative territory for the year. The main culprit was the 50% drop in oil prices during the Portfolio’s fiscal year. That triggered rising defaults and a subsequent selloff in the energy sector, which accounts for 20% of the $1.5 trillion high yield market (source: JPMorgan Chase). The result was an asset class sharply bifurcated along mostly cyclical lines: The energy, metals-and-mining, and basic industry groups underperformed, while more stable, higher-quality sectors like cable, healthcare, and food and beverages outperformed the benchmark.

Throughout the fiscal period, the story in high yield revolved around energy. Though oil prices still hovered near $100 a barrel during the summer of 2014, an economic slowdown in China — combined with geopolitical instability in Europe and an unwillingness among the Organization of the Petroleum Exporting Countries (OPEC) members to cut production — caused prices to drop to around $50 a barrel by December 2014, and to the mid-$40 range at the end of October 2015. At that level, many energy companies are unprofitable, and those with the highest amounts of leverage are most at risk. So, while defaults within all nonenergy sectors of the high yield market were just 2.2% for the 12 months ended Oct. 31, 2015, the default rate within the energy and metals-and-mining groups rose to nearly 5% over the same period, a 13-year high for the sector.

With the plunge in energy debt prices making for unnerving headlines — and dragging the Portfolio’s benchmark lower as well — selling pressure spiked in October and December 2014. This increased selling exposed liquidity shortfalls in the high yield market, as financial regulations (Dodd-Frank) have reduced the incentive for dealers to hold as much inventory of certain securities as they did previously. Though bargain hunters eventually stepped in to support bond prices, weakness reappeared late in the Portfolio’s fiscal year, as another Greece-related crisis in the euro zone compounded unresolved concerns over Chinese economic growth and overcapacity in the energy sector.

As the fiscal year began, the Portfolio’s weighting in the energy sector was roughly in line with the benchmark. Within a few months, we reduced this to an underweight position. Still, two of the Portfolio’s three weakest- performing individual issues over the fiscal

period were from the energy group. Though we sold the Portfolio’s entire position in exploration and development company MidStates Petroleum, it nonetheless cost the Portfolio 0.26 percentage points of relative performance. When an attempted asset sale failed to close, MidStates Petroleum bonds reacted negatively and we exited the position given concerns about tighter liquidity.

Similarly, holdings in Halcon Resources cost the Portfolio 0.21 percentage points in return relative to the benchmark before we closed the position. Halcon, an independent exploration and production company, suffered a steep drop in earnings as the prices of oil and natural gas plunged. The Portfolio’s largest performance shortfall resulted from its position in Intelsat, the largest global communications satellite operator. Intelsat has experienced a difficult pricing environment and declining government revenues at the same time that it needs to refinance large near-term maturities. Against the backdrop of a volatile high yield market, the Portfolio’s position in Intelsat negatively affected performance by 0.77 percentage points.

On the positive side, the Portfolio’s holdings in the 7.5% bonds of Gray Television, an operator of 50 local-market TV stations, contributed 0.11 percentage points to performance as a result of strong operating metrics during the year.

Similarly, the Portfolio’s position in Landry’s added 0.09 percentage points of relative return. Investors were attracted to Landry’s high coupon and terms, a 9.375% issue that was callable in September 2015 (but is still outstanding). The Portfolio’s position in the 6% bonds of MGM Resorts International, a casino operator, contributed 0.08 percentage points of outperformance as a result of good operating performance and investor demand for higher-quality high yield issues during times of market stress. Notably, each outperforming security in the Portfolio had similar characteristics: above-average coupons, acceptable performance, and operations outside the energy and metals-and-mining industries.

The Portfolio had minimal exposure to derivatives, briefly holding futures contracts and credit default swaps in amounts equal to about 2% of the notional value of assets. Neither position had a material effect (that is, greater than 0.50 percentage points) on total Portfolio performance, and there were no derivative positions outstanding as of the end of the fiscal year.

Portfolio holdings reflect our view that the U.S. Federal Reserve may soon raise short-term interest rates off the zero-to-0.25% floor, where they have languished since the days of the financial crisis in December 2008. Though high yield bonds generally are considered less interest rate sensitive than other fixed income market sectors, the group’s response to rate changes varies. For example, in our view, the lower-rated credit tiers often are the least vulnerable to rate hikes if, as now, the rationale for tightening monetary policy is accelerating economic growth and not accelerating inflation.

20

Accordingly, we have overweighted CCC-rated credits, maintained a market weighting to BB-rated bonds, and underweighted the B-rated segment. With regard to industry groups, the Portfolio ended the fiscal year with a significant underweight to the energy sector, given the murky (and largely unfavorable) outlook for oil and gas prices. In general, the Portfolio is also overweight higher-coupon securities in sectors that we view as more stable and lower risk than the benchmark. As always, we maintain a broadly diversified approach to investing in the sector, with the average position size of the Portfolio’s approximately 200 holdings being just 0.50% of Portfolio net assets at the end of the fiscal year.

The views expressed are current as of the date of this report and subject to change.

Performance summary

Delaware Pooled® Trust — The High-Yield Bond Portfolio

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 231-8002 or visiting our website at delawareinvestments.com.

Carefully consider the Portfolio’s investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Portfolio’s prospectus and, if available, its summary prospectus, which may be obtained by visiting delawareinvestments.com or calling 800 231-8002. Investors should read the prospectus and, if available, the summary prospectus carefully before investing.

| | | | | | | | | | | | | | | | | | | | |

| Portfolio and benchmark performance | | | | | | | | | | | | | | | | | | | | |

| Average annual total returns | | | | | | | | | | | | | | | | | | | | |

Periods ended Oct. 31, 2015 | | 1 year | | | 3 years | | | 5 years | | | 10 years | | | Lifetime | |

The High-Yield Bond Portfolio | | | –3.41% | | | | +3.87% | | | | +6.19% | | | | +7.84% | | | | +7.70% | |

BofA Merrill Lynch U.S. High Yield Constrained Index | | | –2.03% | | | | +4.11% | | | | +6.00% | | | | +7.52% | | | | +6.83% | |

Portfolio profile | | | | | | | | | | | | | | | | | | | | |

Oct. 31, 2015 | | | | | | | | | | | | | | | | | | | | |

Total net assets | | | | | | | Number of holdings | | | | | |

$206.1 million | | | | | | | 260 | | | | | | | | | | | | | |

Inception date | | | | | | | | | | | | | | | | | | | | |

Dec. 2, 1996 | | | | | | | | | | | | | | | | | | | | |

Growth of $1,000,000

The performance graph assumes $1 million invested on Oct. 31, 2005, and includes reinvestment of all distributions. The performance graph does not reflect the deduction of taxes the shareholder would pay on Portfolio distributions or redemptions of Portfolio shares.

Total return assumes reinvestment of dividends and capital gains, but does not reflect reductions for taxes. Returns and share values will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The most recent prospectus disclosed the Portfolio’s total operating expenses as 0.57%. Management has contractually agreed to reimburse certain expenses and/or waive its management fees from Nov. 1, 2014, through Oct. 31, 2015,* in order to prevent total annual Portfolio

22

operating expenses (with certain exceptions) from exceeding, in an aggregate amount, 0.59% of the Portfolio’s average daily net assets, as described in the most recent prospectus.

Expense limitations were in effect during the period shown. Performance would have been lower had the expense limitations not been in effect.

The BofA Merrill Lynch U.S. High Yield Constrained Index tracks the performance of U.S. dollar–denominated high yield corporate debt publicly issued in the U.S. domestic market, but caps individual issuer exposure at 2% of the benchmark. Qualifying securities must have, among other things, a below-investment-grade rating (based on an average of Moody’s, Standard & Poor’s, and Fitch), an investment grade issuing country (based on an average of Moody’s, Standard & Poor’s, and Fitch foreign currency long-term sovereign debt ratings), and maturities of one year or more.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Investing involves risk, including the possible loss of principal.

Past performance is not a guarantee of future results.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Portfolio may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Portfolio may be prepaid prior to maturity, potentially forcing the Portfolio to reinvest that money at a lower interest rate.

The Portfolio may be invested in foreign corporate bonds, which have special risks not ordinarily associated with domestic investments, such as currency fluctuations, economic and political change, and different accounting standards.

High yielding, noninvestment grade bonds (junk bonds) involve higher risk than investment grade bonds.

The high yield secondary market is particularly susceptible to liquidity problems when institutional investors, such as mutual funds and certain other financial institutions, temporarily stop buying bonds for regulatory, financial, or other reasons. In addition, a less liquid secondary market makes it more difficult for the Portfolio to obtain precise valuations of the high yield securities in its portfolio.

The Portfolio may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

Per Standard & Poor’s credit rating agency, bonds rated below AAA, including A, are more susceptible to the adverse effects of changes in circumstances and economic conditions than those in higher-rated categories, but the obligor’s capacity to meet its financial commitment on the obligation is still strong. Bonds rated BBB exhibit adequate protection parameters, although adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity of the obligor to meet its financial commitments. Bonds rated BB, B, and CCC are regarded as having significant speculative characteristics with BB indicating the least degree of speculation.

Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

*The contractual waiver period is from Feb. 27, 2014 through Feb. 29, 2016.

23

Portfolio management review

Delaware Pooled® Trust — The Core Plus Fixed Income Portfolio

October 31, 2015

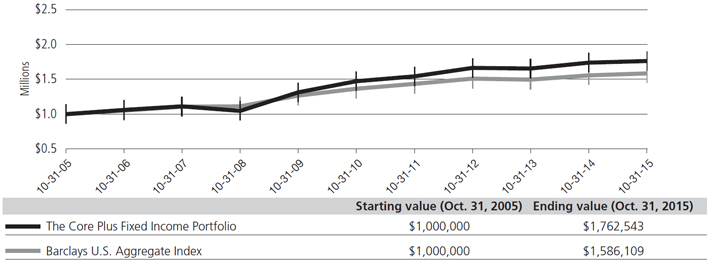

For the fiscal year ended Oct. 31, 2015, Delaware Pooled Trust — The Core Plus Fixed Income Portfolio returned +1.29% at net asset value (NAV) with all distributions reinvested. The Portfolio’s benchmark, the Barclays U.S. Aggregate Index, returned +1.96% for the same period. Complete annualized performance for The Core Plus Fixed Income Portfolio is shown in the table on page 25.

A key development during the fiscal year was the divergence in central bank policies. As the European Central Bank launched its quantitative easing program, the U.S. Federal Reserve signaled a potential rate hike. This had a profound effect on the market, particularly in currencies, driving the U.S. dollar higher relative to many other currencies. That contributed to deterioration in emerging-market economies and held back revenue growth for U.S.-based multinational companies.

The strong U.S. dollar cut significantly into global sales and net earnings of many U.S. corporations. Not only did it make U.S. exports more expensive for consumers in other countries, but currency conversions into U.S. dollars became highly unfavorable for many large U.S. companies. This, in turn, affected investment-grade corporate credit, leading us to reduce the Portfolio’s credit overweight during the fiscal year.

Slowdowns in global growth and global trade were among the macroeconomic factors affecting the markets. Of particular concern were continued indications of slowing Chinese growth and the collapse in commodity prices. China’s decelerating economic growth rate is expected to keep commodity prices under pressure, while weighing on many emerging-market nations and Asian countries that have grown dependent on Chinese demand. (Source: Bloomberg.)

The Portfolio’s overweight to investment grade corporate credit was a key contributor to performance versus the Barclays U.S. Aggregate Index. As the fiscal year progressed, however, we reduced that position. The Portfolio’s below-investment-grade holdings detracted from performance along with its overall exposure to high yield credit and emerging markets. Security selection within commodities was also negative. Disappointing holdings included FMG Resources, a metals and mining company, and Pacific Exploration and Production.

Security selection within industrials was a slight negative, hurt by energy holdings. In particular, the Portfolio’s exposure to mid-stream assets, such as pipeline companies, was costly. Enbridge Energy Partners and Williams Partners were weak performers. During the fiscal year, we moved to a slightly more conservative position, including an allocation to electric utilities, and the Portfolio benefited from owning National Rural Utilities bonds also.

Generally, security selection in investment grade corporate credit was positive for performance. The Portfolio’s holdings largely did well. Financials, utilities, and noncorporates outperformed their benchmark

sectors and the benchmark overall. The Portfolio’s holdings in industrials outperformed the benchmark.

The Portfolio’s performance was hurt by its significant underweight to U.S. Treasurys, as they outperformed credit and both high yield and emerging market bonds. The Portfolio’s overweight to asset-backed securities (ABS) detracted from performance. Security selection was weak, and the Portfolio trailed the benchmark’s ABS component. However, the Portfolio’s exposure to commercial mortgage-backed securities (CMBS) was positive, helped by security selection and asset allocation. Our primary focus was on seasoned multifamily- and conduit-loan securitizations.

The Portfolio’s strongest-performing sector was financials. Wells Fargo and Bank of America were among the better individual contributors. Because the Portfolio had minimal exposure to asset managers that had negative absolute returns, they had little effect on overall performance.

The Portfolio had a slight underweight to mortgage-backed securities (MBS), with minimal effect. The Portfolio held a barbell position — that is, combining long-term bonds and short-term bonds in an attempt to seek better risk-adjusted returns in the process — in MBS, balanced between current coupons and seasoned high-coupon securities. An out-of-benchmark position in municipals, one of the strongest-performing asset classes, was beneficial. These included Golden State Tobacco Securitization bonds and City of New York general obligation bonds.

In assessing market risks, credit risk remains paramount. In 2015, we’ve seen a significant rise in security-specific risk, and we believe this should continue. Furthermore, fundamentals have also been under pressure. Issuers have taken advantage of relaxed underwriting standards, leading to an abundance of new issuance, particularly in investment grade corporate credit. We have also seen a significant rise in debt-financed share buybacks and debt-financed mergers and acquisitions, which can be detrimental to bond investors because they increase the companies’ leverage profile.

We believe that slower global growth may continue to weigh on commodities; accordingly, we have taken steps designed to reduce the Portfolio’s exposure to these issuers in both high yield and investment grade corporate credit, while allocating more to U.S. Treasurys and structured product, primarily MBS.

The Portfolio used derivatives during the fiscal year, but they did not have a material effect on performance (that is, more than 50 basis points). The Portfolio used U.S. Treasury futures, euro-bond futures, and credit derivatives. The credit protection hedges had minimal effect on performance and exposure to U.S. Treasury futures was positive, helping to manage duration risk. Overall, derivatives contributed fewer than 20 basis points to Portfolio performance.

|

| The views expressed are current as of the date of this report and subject to change. |

24

Performance summary

Delaware Pooled® Trust — The Core Plus Fixed Income Portfolio

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 231-8002 or visiting our website at delawareinvestments.com.

Carefully consider the Portfolio’s investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Portfolio’s prospectus and, if available, its summary prospectus, which may be obtained by visiting delawareinvestments.com or calling 800 231-8002. Investors should read the prospectus and, if available, the summary prospectus carefully before investing.

| | | | | | | | | | | | | | | | | | | | |

| Portfolio and benchmark performance | | | | | | | | | | | | | | | | | | | | |

| Average annual total returns | | | | | | | | | | | | | | | | | | | | |

Periods ended Oct. 31, 2015 | | | 1 year | | | | 3 years | | | | 5 years | | | | 10 years | | | | Lifetime | |

The Core Plus Fixed Income Portfolio | | | +1.29% | | | | +1.89% | | | | +3.66% | | | | +5.83% | | | | +6.01% | |

Barclays U.S. Aggregate Index | | | +1.96% | | | | +1.65% | | | | +3.03% | | | | +4.72% | | | | +4.75% | |

Portfolio profile | | | | | | | | | | | | | | | | | | | | |

Oct. 31, 2015 | | | | | | | | | | | | | | | | | | | | |

Total net assets | | | | | | | Number of holdings | | | | | |

$128.1 million | | | | | | | 744 | | | | | | | | | | | | | |

Inception date | | | | | | | | | | | | | | | | | | | | |

June 28, 2002 | | | | | | | | | | | | | | | | | | | | |

Growth of $1,000,000

The performance graph assumes $1 million invested on Oct. 31, 2005, and includes reinvestment of all distributions. The performance graph does not reflect the deduction of taxes the shareholder would pay on Portfolio distributions or redemptions of Portfolio shares.

Total return assumes reinvestment of dividends and capital gains, but does not reflect reductions for taxes. Returns and share values will fluctuate so that shares, when redeemed, may be worth more or less than their original cost.

The most recent prospectus disclosed the Portfolio’s total operating expenses as 0.65%. Management has contractually agreed to reimburse certain expenses and/or waive its management fees from Nov. 1, 2014, through Oct. 31, 2015,* in order to prevent total annual Portfolio

Performance summary

Delaware Pooled® Trust — The Core Plus Fixed Income Portfolio