UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06431

MANAGERS TRUST II

(Exact name of registrant as specified in charter)

| | |

| 800 Connecticut Avenue, Norwalk, Connecticut | | 06854 |

| |

| (Address of principal executive offices) | | (Zip code) |

Managers Investment Group LLC

800 Connecticut Avenue,

Norwalk, Connecticut 06854

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203) 299-3500

Date of fiscal year end: DECEMBER 31

Date of reporting period: JANUARY 1, 2005 - DECEMBER 31, 2005 (Semi-Annual Shareholder Report)

| Item 1. | Reports to Shareholders |

ANNUAL REPORT

Managers Funds

December 31, 2005

Table of Contents

| | |

Letter to Shareholders | | 1 |

Fund Performance | | 2 |

Performance table for the Funds as of December 31, 2005 | | |

About Your Fund’s Expenses | | 4 |

Investment Managers’ Comments and Schedules of Portfolio Investments | | |

Managers 20 Fund | | 6 |

Managers Mid-Cap Fund | | 10 |

Managers Balanced Fund | | 15 |

Managers High Yield Fund | | 22 |

Managers Fixed Income Fund | | 30 |

Notes to Schedules of Portfolio Investments | | 37 |

Financial Statements | | |

Statements of Assets and Liabilities | | 38 |

Funds’ balance sheets, net asset value (NAV) per share computations and cumulative undistributed amounts | | |

Statements of Operations | | 39 |

Detail of sources of income, Fund expenses, and realized and unrealized gains (losses) during the year | | |

Statements of Changes in Net Assets | | 40 |

Detail of changes in Fund assets for the past two years | | |

| |

Financial Highlights | | 41 |

Historical net asset values per share, distributions, total returns, expense ratios, turnover ratios and net assets for each Fund | | |

| |

Notes to Financial Statements | | 47 |

Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and description of certain investment risks | | |

| |

Report of Independent Registered Public Accounting Firm | | 55 |

| |

Trustees and Officers | | 56 |

Nothing contained herein is to be considered an offer, sale, or solicitation of an offer to buy shares of Managers Funds. Such offering is made only by Prospectus, which includes details as to offering price and other material information.

Letter to Shareholders

Dear Fellow Shareholder:

Over the past 12 months the markets have been beset with a number of difficult and unpredictable challenges, including recovery from a massive tsunami in Southeast Asia; continuing strife in the Middle East; numerous terrorist incidents; multiple hurricanes in the Gulf of Mexico; and a significant rise in energy prices. We are fortunate that the financial markets have continued to perform so well under these circumstances.

These events serve to remind us that no one can predict the events that are going to shape the markets in coming months. This reinforces our belief that to invest successfully in an uncertain world you have to diversify your investments and be patient.

Most people think of diversification as holding different types of stocks and bonds, but we believe that there is another type of diversification that receives too little notice, and that is diversification by investment manager and holdings. Simply put, no single approach is going to succeed in every kind of market—some growth stock managers will be successful in a rising market, and some will be more successful in a stagnant market. This can be an issue with some investment firms that adhere to only one method of looking at the markets.

That is a major benefit that we bring you at Managers Funds—since we hire subadvisors (affiliates and non-affiliates) to run our portfolios, we offer you a wide selection of very different investment styles to choose from, sometimes within the same asset class. Invest in multiple Managers Funds, and you can get managers with very different approaches and holdings, helping you reduce the risks created by changing economic conditions and natural and man-made events, such as those of the past 12 months.

We also believe that once you have made your manager selection, you must be patient. On the home page of our Web site at www.managersinvest.com, you will find a short article entitled “Stay Invested for the Long Term” that highlights how important it is to consistently stay in the market rather than trying to time the market. We think the implication is clear: to be successful in the market over the long term, select a wide variety of investments giving you good diversification, invest regularly, and stick with your investment plan no matter what events dominate the news.

We invite you to visit our Web site on an ongoing basis to stay in tune with your Managers Funds holdings. The Web site provides detailed profiles of our subadvisors and their investment styles, as well as quarterly commentary on each Fund. If you have any questions, please do call us at 800.835.3879. Thank you for investing with Managers Funds.

Sincerely,

| | | | |

| | | |

|

| Peter M. Lebovitz | | | | Thomas G. Hoffman, CFA |

| President | | | | Chief Investment Officer |

| Managers Funds | | | | Managers Investment Group LLC |

1

Fund Performance

All periods ended December 31, 2005

Managers Funds Performance (unaudited)

All periods ended December 31, 2005

| | | | | | | | | | | | | | | | | | |

| | | | | | | Average Annual Total Returns (1) |

| | | | | | | 1 Year | | | 3

Years | | | 5

Years | | | Since

Inception | | | Inception

Date |

Managers Funds: | | | | | | | | | | | | | | | | | | |

Equity Funds: | | | | | | | | | | | | | | | | | | |

20 Fund | | -Class A | | No Load | | (5.19 | )% | | 11.99 | % | | (15.96 | )% | | (4.69 | )% | | Jan-98 |

| | -Class A | | With Load | | (10.69 | )% | | 9.84 | % | | (16.95 | )% | | (5.40 | )% | | Jan-98 |

| | -Class B | | No Load | | (5.82 | )% | | 11.43 | % | | (16.39 | )% | | (6.65 | )% | | Feb-98 |

| | -Class B | | With Load | | (10.53 | )% | | 10.62 | % | | (16.73 | )% | | (6.65 | )% | | Feb-98 |

| | -Class C | | No Load | | (5.80 | )% | | 11.37 | % | | (16.38 | )% | | (7.29 | )% | | Mar-98 |

| | -Class C | | With Load | | (7.67 | )% | | 11.04 | % | | (16.55 | )% | | (7.41 | )% | | Mar-98 |

| | -Inst. Class | | No Load | | (4.92 | )% | | 12.45 | % | | (15.57 | )% | | (7.10 | )% | | Apr-98 |

| | | | | | | |

Mid-Cap | | -Class A | | No Load | | 11.32 | % | | 21.12 | % | | 6.44 | % | | 13.82 | % | | Jan-97 |

| | -Class A | | With Load | | 4.91 | % | | 18.77 | % | | 5.19 | % | | 13.08 | % | | Jan-97 |

| | -Class B | | No Load | | 10.61 | % | | 20.48 | % | | 5.89 | % | | 12.26 | % | | Jan-97 |

| | -Class B | | With Load | | 5.61 | % | | 19.79 | % | | 5.57 | % | | 12.26 | % | | Jan-97 |

| | -Class C | | No Load | | 10.60 | % | | 20.46 | % | | 5.91 | % | | 11.34 | % | | Feb-98 |

| | -Class C | | With Load | | 8.48 | % | | 20.08 | % | | 5.69 | % | | 11.20 | % | | Feb-98 |

| | -Inst. Class | | No Load | | 11.74 | % | | 21.69 | % | | 6.96 | % | | 14.40 | % | | Jan-97 |

| | | | | | | |

Hybrid Fund: | | | | | | | | | | | | | | | | | | |

Balanced | | -Class A | | No Load | | 4.24 | % | | 12.22 | % | | 2.98 | % | | 8.72 | % | | Jan-97 |

| | -Class A | | With Load | | (1.79 | )% | | 10.01 | % | | 1.76 | % | | 8.00 | % | | Jan-97 |

| | -Class B | | No Load | | 3.53 | % | | 11.64 | % | | 2.47 | % | | 6.63 | % | | Feb-98 |

| | -Class B | | With Load | | (1.47 | )% | | 10.83 | % | | 2.10 | % | | 6.63 | % | | Feb-98 |

| | -Class C | | No Load | | 3.49 | % | | 11.61 | % | | 2.44 | % | | 6.54 | % | | Feb-98 |

| | -Class C | | With Load | | 1.49 | % | | 11.22 | % | | 2.24 | % | | 6.41 | % | | Feb-98 |

| | -Inst. Class | | No Load | | 4.57 | % | | 12.74 | % | | 3.18 | % | | 9.25 | % | | Jan-97 |

| | | |

| | | | | | | Average Annual Total Returns (1) |

| | | | | | | 1 Year | | | 3

Years | | | 5

Years | | | Since

Inception | | | Inception

Date |

Income Funds: | | | | | | | | | | | | | | | | | | |

High Yield | | -Class A | | No Load | | 2.37 | % | | 13.68 | % | | 9.41 | % | | 6.27 | % | | Jan-98 |

| | -Class A | | With Load | | (3.53 | )% | | 11.47 | % | | 8.12 | % | | 5.48 | % | | Jan-98 |

| | -Class B | | No Load | | 1.59 | % | | 12.99 | % | | 8.81 | % | | 5.16 | % | | Feb-98 |

| | -Class B | | With Load | | (3.19 | )% | | 12.20 | % | | 8.52 | % | | 5.16 | % | | Feb-98 |

| | -Class C | | No Load | | 1.60 | % | | 13.01 | % | | 8.82 | % | | 5.15 | % | | Feb-98 |

| | -Class C | | With Load | | (0.40 | )% | | 12.64 | % | | 8.61 | % | | 5.01 | % | | Feb-98 |

| | -Inst. Class | | No Load | | 2.60 | % | | 14.15 | % | | 9.93 | % | | 6.21 | % | | Mar-98 |

| | | | | | | |

Fixed Income | | -Class A | | No Load | | 2.68 | % | | 6.21 | % | | 6.47 | % | | 6.48 | % | | Jan-97 |

| | -Class A | | With Load | | (2.46 | )% | | 4.41 | % | | 5.39 | % | | 5.87 | % | | Jan-97 |

| | -Class B | | No Load | | 2.01 | % | | 5.61 | % | | 5.92 | % | | 5.60 | % | | Mar-98 |

| | -Class B | | With Load | | (2.87 | )% | | 4.71 | % | | 5.60 | % | | 5.60 | % | | Mar-98 |

| | -Class C | | No Load | | 1.90 | % | | 5.56 | % | | 5.92 | % | | 5.75 | % | | Mar-98 |

| | -Class C | | With Load | | (0.11 | )% | | 5.22 | % | | 5.71 | % | | 5.62 | % | | Mar-98 |

| | -Inst. Class | | No Load | | 2.91 | % | | 6.64 | % | | 6.97 | % | | 7.05 | % | | Jan-97 |

2

Fund Performance (continued)

Notes to the Performance Table

Performance differences among the share classes are due to differences in sales charge structures and class expenses. Returns shown reflect maximum sales charge of 5.75% on Class A (5.00% maximum for Managers Fixed Income Fund), as well as the applicable contingent deferred sales charge (CDSC) on both Class B and C shares. The Class B shares’ CDSC declines annually between years 1 through 6 according to the following schedule: 5, 4, 3, 3, 2, 1%. No sales charge is assessed after year six. Class C shares held for less than one year are subject to a 1% CDSC.

The Fund share classes differ with regard to sales charges and Fund expenses. In choosing a Fund and class(es), investors should consider the amount they plan to invest, their investment objectives, the Fund’s investment objectives, risks, charges and expenses carefully before investing, and how long they intend to keep their money invested in the Fund and class(es). Each Fund’s prospectus contains information concerning the Fund’s investment objective, risk, charges and expenses and other information. Additional risks are associated with investing in high yield bonds, and such securities may be considered speculative.

There are also risks associated with investing in small-cap companies, such as increased volatility, and bonds, such as rising interest rates. More specifically, the value of debt instruments held in bond funds declines when interest rates rise and longer-term bonds are more vulnerable to interest rate risk. To obtain a prospectus, please call (800) 835-3879 or visit our website at www.managersinvest.com. Please read the Prospectus carefully before you invest in a Fund or send money. Investors should discuss their goals and choices with a registered financial professional in order to determine which share class is appropriate for them. Distributed by Managers Distributors, Inc., member NASD.

| (1) | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the Prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and the principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end please call (800) 835-3879 or visit our Web site at www.managersinvest.com.

3

About Your Fund’s Expenses

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments; reinvested dividends or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-l) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Fund return

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | |

Six Months Ended December 31, 2005 | | Beginning

Account

Value

7/1/2005 | | Ending

Account

Value

12/31/2005 | | Expenses

Paid

During

Period* |

Managers 20 Fund Class A | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,058 | | $ | 7.78 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,018 | | $ | 7.63 |

| | | |

Managers 20 Fund Class B | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,054 | | $ | 11.65 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,014 | | $ | 11.42 |

| | | |

Managers 20 Fund Class C | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,054 | | $ | 11.65 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,014 | | $ | 11.42 |

| | | |

Managers 20 Fund Institutional Class | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,057 | | $ | 6.48 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,019 | | $ | 6.36 |

| | | |

Six Months Ended December 31, 2005 | | Beginning

Account

Value

7/1/2005 | | Ending

Account

Value

12/31/2005 | | Expenses

Paid

During

Period* |

Managers Mid-Cap Fund Class A | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,071 | | $ | 6.52 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,019 | | $ | 6.36 |

| | | |

Managers Mid-Cap Fund Class B | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,067 | | $ | 10.42 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,015 | | $ | 10.16 |

| | | |

Managers Mid-Cap Fund Class C | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,067 | | $ | 10.42 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,015 | | $ | 10.16 |

| | | |

Managers Mid-Cap Fund Institutional Class | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,073 | | $ | 5.22 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,020 | | $ | 5.09 |

4

About Your Fund’s Expenses (continued)

| | | | | | | | | |

Six Months Ended December 31 , 2005 | | Beginning

Account

Value

7/1/2005 | | Ending

Account

Value

12/31/2005 | | Expenses

Paid

During

Period* |

Managers Balanced Fund Class A | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,030 | | $ | 6.39 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,019 | | $ | 6.36 |

| | | |

Managers Balanced Fund Class B | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,025 | | $ | 10.21 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,015 | | $ | 10.16 |

| | | |

Managers Balanced Fund Class C | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,025 | | $ | 10.21 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,015 | | $ | 10.16 |

| | | |

Managers Balanced Fund Institutional Class | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,031 | | $ | 5.12 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,020 | | $ | 5.09 |

| | | |

Six Months Ended December 31, 2005 | | Beginning

Account

Value

7/1/2005 | | Ending

Account

Value

12/31/2005 | | Expenses

Paid

During

Period* |

Managers High Yield Fund Class A | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,012 | | $ | 5.83 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,019 | | $ | 5.85 |

| | | |

Managers High Yield Fund Class B | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,007 | | $ | 9.61 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,016 | | $ | 9.65 |

| | | |

Managers High Yield Fund Class C | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,007 | | $ | 9.61 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,016 | | $ | 9.65 |

| | | |

Managers High Yield Fund Institutional Class | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,012 | | $ | 4.56 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,021 | | $ | 4.58 |

| | | |

Six Months Ended December 31, 2005 | | Beginning

Account

Value

7/1/2005 | | Ending

Account

Value 12/31/2005 | | Expenses

Paid

During

Period* |

Managers Fixed Income Fund Class A | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,007 | | $ | 3.74 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,021 | | $ | 3.77 |

| | | |

Managers Fixed Income Fund Class B | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,003 | | $ | 7.52 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,018 | | $ | 7.58 |

| | | |

Managers Fixed Income Fund Class C | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,002 | | $ | 7.52 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,018 | | $ | 7.58 |

| | | |

Managers Fixed Income Fund Institutional Class | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,008 | | $ | 2.48 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,023 | | $ | 2.50 |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 365. |

5

Managers 20 Fund

Portfolio Manager Comments

The Managers 20 Fund’s (the “Fund”) objective is to achieve capital appreciation through a non-diversified portfolio of equity securities.

The Managers 20 Fund invests in a non-diversified portfolio consisting of the common stocks of 15 to 25 U.S. and foreign companies of any size, which offer strong growth potential. The Fund management selects securities based on a global economic outlook, with a particular focus on investments in specific industries, and seeks companies in out-of-favor situations at attractive prices. In addition to common stocks, the Fund may invest from time to time in any or all of the following: preferred stocks, convertible securities, warrants and bonds and other fixed-income securities. The S&P 500 Index is the benchmark for the Fund.

The Fund currently employs a subadvisor, Oak Associates, ltd. (“Oak”), to manage the assets of the Fund. Oak believes that macroeconomic analysis is the best way to start their process of finding industries where the most attractive secular growth opportunities reside. Oak’s investment team begins its investment process with the overall outlook for the economy. They assess the overall economic background, including an analysis of fiscal policies, monetary polices, inflation, interest rates, exchange rates, and evolving relationships of economic sectors.

The investment team follows securities from favored industries. When researching a potential security, the analysts look at the company growth rate and valuation in absolute terms, relative to the market as a whole, and relative to each security’s historical valuation.

The ideal investment exhibits the following traits:

| | • | | Impressive growth potential |

Portfolio management:

| | • | | Builds the portfolio stock by stock and actively manages the Fund |

| | • | | Begins by analyzing key global economic factors, then determines which specific sectors will benefit from emerging trends |

| | • | | Employs qualitative analysis based on the fundamental characteristics of individual securities |

| | • | | Visits company locations and has discussions with company management |

| | • | | Buys securities generally with a long-term time horizon, resulting in relatively low portfolio turnover |

| | • | | Concentrates in their best ideas and remains focused on core growth discipline |

Sell Discipline

Generally, Oak does not make many weight adjustments to reflect changes in sentiment about a holding. If their opinion changes for the worse, they will tend to sell the holding completely. There are times when they will add to a stock if its weight has declined due to relative underperformance that they feel is unjustified. Their sell decision is based on three criteria:

| | • | | As a concentrated investment manager, a stock may be sold based on relative opportunity. This occurs when a better investment idea presents itself. |

| | • | | Valuation is considered if the stock price reflects the best potential outcome. |

| | • | | Oak may sell if their long-term investment thesis for that company has deteriorated. If so, they first assess whether it is salvageable: Is it a company-specific issue? Did they simply make a mistake? |

These criteria are often combined with factors such as changes in the competitive landscape, product commoditization, or relative market opportunity. Downward revisions in earnings estimates, changes in long-term earnings projections, analyst contacts, valuation, and balance sheet issues are all considerations that may help Oak determine if a stock should be sold. Portfolio turnover is low - the typical holding period for securities is three-to-five years.

The Year in Review

For the year 2005, the Managers 20 Fund Institutional Class Shares returned -4.92% compared with a gain of 4.91% for the S&P 500 Index. In the U.S., the broad market (using for example, the Russell 3000, Wilshire 5000, and S&P 500 indices) rose about 6% for the year.

Mid-cap and small-cap stocks rose more than large-caps for the year as measured by the S&P indices. From a style standpoint, the S&P 500/Citigroup Value Index outperformed its counterpart for the sixth consecutive year. Low price-to-earnings stocks were leaders throughout the year, but much of this also coincides with the strong energy sector that has a lower P/E.

Despite strong corporate earnings, 2005 got off to a rocky start. The markets were down about 4% after the first four months of the year, but one sector continued to rise. The energy sector was the story of 2005, up over 30%. As oil and gas prices continued to rise throughout the summer, oil rose to over $69 per barrel finishing the year at $61, while gold ended the year at $517/oz. The higher fuel and commodity prices combined with devastating hurricanes to the Gulf Coast region,

6

Managers 20 Fund

Portfolio Manager Comments (continued)

and continued increases in short-term interest rates could not slow down the economy. GDP continued to grow and core CPI inflation was kept to low levels. Markets rallied in the fourth quarter as the industrials and materials sectors climbed and energy stocks declined. While the holiday shopping season was far from a boom, neither was it the bust that some analysts had anticipated due to higher energy prices.

Since the Fund concentrates on high growth opportunities, the lack of energy holdings hurt from an attribution standpoint. The Fund is positioned with nearly half its holdings in the technology sector which performed poorly over the year. Of the fifteen technology positions held over the course of 2005, only 4 posted positive returns, and one of them was the late addition of Google. Dell, Symantec and Cisco were all large detractors. Dell, EMC and Microsoft were all liquidated throughout the year.

Over the course of the year, the healthcare sector has become increasingly larger. Oak added Teva Pharmaceuticals and built up its position in all other heathcare stocks, with the exception of Pfizer. Despite the negative contribution by Pfizer this sector was the largest positive contributor during 2005. Affymetrix, Amgen, Medtronic and Teva Pharmaceuticals all posted double digit gains for the year.

The financials sector was pared down with the sale of MBNA, following its acquisition by Bank of America, while consumer discretionary has added Amazon.com.

Looking Forward

The portfolio manager has constructed a portfolio that should benefit from continued strong earnings. Expecting the end of the Fed tightening, Oak is looking for stock valuations to catch up with the strong earnings of the past year. Oak’s comments as we progress into 2006:

The housing market, which was so hot in 2005, should continue to cool (price appreciation and sales slowing). This could be exacerbated by tighter lending standards. The strength in housing has helped to drive consumer spending, but the effect of the cooling market should not be too dramatic, as real pay per worker climbs. As a result, we think the economy should remain relatively healthy. One thing to watch though is the temperature in the north and the already high price of natural gas; high heating bills could impact spending. In spite of rising energy costs, inflation continues to be restrained by globalization, competition, and productivity. This is positive for the market.

With strong cash flow from operations in recent years, corporations’ balance sheets are in great shape, which means merger activity, stock buybacks and dividend increases should continue. Capital spending could also pick up. Chief Investment Strategist Ed Yardeni’s CIO poll indicates IT budgets are expected to rise 8% this year - technology companies would be beneficiaries.

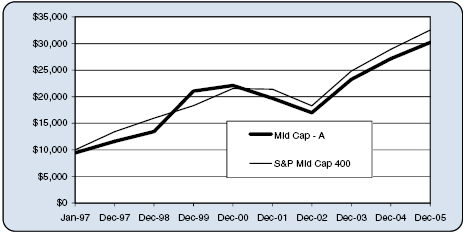

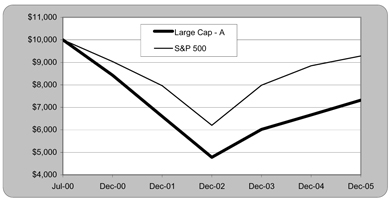

Cumulative Total Return Performance

Managers 20 Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. The S&P 500 Index is an unmanaged capitalization weighted index of 500 commonly traded stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of those stocks. Unlike the Fund, the S&P 500 Index is unmanaged, is not available for investment, and does not incur expenses. The chart illustrates the performance of a hypothetical $10,000 investment made in the Fund’s Class A shares on January 2, 1998 to a $10,000 investment made in the S&P 500 Index for the same time periods. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. Performance for periods longer than one year is annualized. Figures include reinvestment of capital gains and dividends. The listed returns for the Fund are net of expenses and the returns for the indices exclude expenses. Total returns for the Fund would have been lower had certain expenses not been reduced.

7

Managers 20 Fund

Portfolio Manager Comments (continued)

The table below shows the average annualized total returns for the 20 Fund - Class A Shares (with load) and the S&P 500 Index since inception through December 31, 2005.

| | | | | | | | | |

Average Annual Total Returns: | | 1 Year | | | 5 Years | | | Since Inception* | |

20 Fund – A Shares | | (10.69 | )% | | (16.95 | )% | | (5.40 | )% |

S&P 500 | | 4.91 | % | | 0.54 | % | | 4.73 | % |

| * | Commencement of operations was January 2, 1998. |

The table below displays a full breakdown of the sector allocation of the Fund as well as the top ten positions as of December 31, 2005.

| | | | | | | | | | | |

Top Ten Holdings (out of 25 securities) | | Managers 20 Fund

% Fund | | | Portfolio Breakdown | | % Fund | | | S&P 500 | |

QUALCOMM, Inc. | | 5.8 | % | | Financials | | 9.8 | % | | 21.3 | % |

eBay, Inc.* | | 5.7 | | | Information Technology | | 50.2 | | | 15.1 | |

Teva Pharmaceutical Industries, Ltd., Sponsored ADR | | 5.4 | | | Health Care | | 22.2 | | | 13.3 | |

Caterpillar, Inc. | | 5.3 | | | Industrials | | 8.2 | | | 11.3 | |

Citigroup, Inc. | | 5.0 | | | Consumer Discretionary | | 10.8 | | | 10.8 | |

Linear Technology Corp. | | 5.0 | | | Consumer Staples | | 0.0 | | | 9.5 | |

Cisco Systems, Inc.* | | 4.9 | | | Energy | | 0.0 | | | 9.3 | |

Applied Materials, Inc. | | 4.9 | | | Utilities | | 0.0 | | | 3.4 | |

Schwab (Charles) Corp.* | | 4.7 | | | Telecommunication Services | | 0.0 | | | 3.0 | |

Amgen, Inc.* | | 4.7 | | | Materials | | 0.0 | | | 3.0 | |

| | | | | | | | | | | |

Top Ten as a Group | | 51.4 | % | | Other Assets and Liabilities | | (1.2 | ) | | 0.0 | |

| | | | | | | | | | | |

| | | | | | | 100.0 | % | | 100.0 | % |

| | | | | | | | | | | |

| * | Top Ten Holding at June 30, 2005 |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or a solicitation to sell that security.

8

Managers 20 Fund

Schedule of Portfolio Investments

December 31, 2005

| | | | | | | |

Security Description | | Shares | | | Value | |

Common Stocks - 101.2% | | | | | | | |

Consumer Discretionary - 10.8% | | | | | | | |

Amazon.Com, Inc.* | | 16,600 | | | $ | 782,690 | |

eBay, Inc.* | | 29,100 | 2 | | | 1,258,575 | |

Harman International Industries, Inc. | | 3,700 | 2 | | | 362,045 | |

Total Consumer Discretionary | | | | | | 2,403,310 | |

Financials - 9.8% | | | | | | | |

Citigroup, Inc. | | 23,000 | | | | 1,116,190 | |

Schwab (Charles) Corp. | | 71,700 | 2 | | | 1,051,839 | |

Total Financials | | | | | | 2,168,029 | |

Health Care - 22.2% | | | | | | | |

Affymetrix, Inc.* | | 18,400 | 2 | | | 878,600 | |

Amgen, Inc.* | | 13,300 | | | | 1,048,838 | |

Medtronic, Inc. | | 17,400 | | | | 1,001,718 | |

Pfizer, Inc. | | 33,900 | | | | 790,548 | |

Teva Pharmaceutical Industries, Ltd., Sponsored ADR | | 28,000 | 2 | | | 1,204,280 | |

Total Health Care | | | | | | 4,923,984 | |

Industrials - 8.2% | | | | | | | |

Caterpillar, Inc. | | 20,500 | 2 | | | 1,184,285 | |

Rockwell Automation, Inc. | | 11,000 | 2 | | | 650,760 | |

Total Industrials | | | | | | 1,835,045 | |

Information Technology - 50.2% | | | | | | | |

Applied Materials, Inc. | | 60,200 | 2 | | | 1,079,988 | |

Avid Technology, Inc.* | | 14,600 | 2 | | | 799,496 | |

Cisco Systems, Inc.* | | 64,000 | | | | 1,095,680 | |

Cognizant Technology Solutions Corp.* | | 18,127 | 2 | | $ | 912,694 | |

Electronic Arts, Inc.* | | 18,900 | 2 | | | 988,659 | |

Google Inc.* | | 2,000 | | | | 829,720 | |

Juniper Networks, Inc.* | | 43,100 | | | | 961,130 | |

Linear Technology Corp. | | 30,600 | | | | 1,103,742 | |

Maxim Integrated Products, Inc. | | 24,600 | | | | 891,504 | |

QUALCOMM, Inc. | | 29,900 | | | | 1,288,092 | |

Symantec Corp.* | | 41,700 | | | | 729,750 | |

Symbol Technologies, Inc. | | 36,500 | | | | 467,930 | |

Total Information Technology | | | | | | 11,148,385 | |

Total Common Stocks

(cost $23,215,817) | | | | | | 22,478,753 | |

Other Investment Companies – 27.4%1 | | | | | | | |

Bank of New York Institutional Cash Reserves Fund, 4.30%3 | | 6,076,726 | | | | 6,076,726 | |

JPMorgan Prime Money Market Fund, Institutional Class Shares, 4.14% | | 49,038 | | | | 49,038 | |

Total Other Investment Companies

(cost $6,125,764) | | | | | | 6,125,764 | |

Total Investments – 128.6%

(cost $29,341,581) | | | | | | 28,604,517 | |

Other Assets, less Liabilities – (28.6)% | | | | | | (6,387,432 | ) |

Net Assets - 100.0% | | | | | $ | 22,217,085 | |

The accompanying notes are an integral part of these financial statements.

9

Managers Mid-Cap Fund

Portfolio Manager Comments

The Managers Mid-Cap Fund’s (the “Fund”) objective is to provide a high total return, consistent with the preservation of capital and a prudent level of risk.

The Managers Mid-Cap Fund seeks to achieve its investment objective by investing in a diversified portfolio consisting of the common stocks of medium-sized companies which will generally be listed on the New York or American stock exchanges or on NASDAQ and be widely held among a large number of investors.

The Fund invests at least 80% of its assets in companies that, at the time of purchase, have market capitalizations between $1 billion and $12 billion. The Fund may also invest in other U.S. and foreign securities, including foreign securities and warrants. The Fund’s benchmark is the S&P MidCap 400 Index.

The Fund currently employs a sub-advisor, Chicago Equity Partners (“CEP”), to manage the assets of the Fund. The investment team at CEP believes that fundamentals drive stock prices – that companies with favorable valuations and earnings expectations will outperform their peers. CEP employs a disciplined investment strategy utilizing a proprietary multi-factor model, which includes momentum, value and quality factors, to select securities. The process focuses on security selection while remaining neutral to industry, sector, style and capitalization benchmarks. CEP seeks to consistently apply an objective, quantitative, fundamental investment approach that identifies undervalued and overvalued securities within industry sectors.

CEP utilizes a systematic ranking system to identify attractive stocks and construct its portfolios through a disciplined process that minimizes portfolio risks like sector, capitalization and style exposures. Every day the investment team at CEP uses its proprietary model to evaluate the expectations, valuation and quality attributes of 3,000 stocks.

The ideal investment exhibits the following traits:

| | • | | Favorable valuation ratios relative to peers |

| | • | | Corporate profits growth is expected to be above average compared to peers |

Portfolio Management:

| | • | | Utilizes a systematic ranking system to identify attractive stocks |

| | • | | Follows a disciplined portfolio construction process that minimizes portfolio risks like sector, capitalization and style exposures |

| | • | | Constructs portfolios that neutralize risk elements that are not consistently rewarded, such as style tilts, industry weightings and market capitalization |

| | • | | Reviews and confirms the model’s daily rankings, paying special attention to any changes in rank |

| | • | | Each analyst follows a specific sector focusing on: |

| | • | | The timing and nature of earnings releases |

| | • | | Legal and regulatory exposures of companies |

| | • | | Any other factors the model may not capture |

| | • | | The analysts use an objective, systematic approach to choose the best risk-adjusted stocks within their sector |

Sell Discipline

CEP has a structured sell discipline: a stock is sold if it is lowly ranked and if there is a viable alternative within its industry, based upon risk/return. This is applied consistently across the universe and over time. The team format assures decisions are being made that are consistent with the Fund’s objectives.

The Year in Review

For the year 2005, the Managers Mid-Cap Fund Institutional Class returned 11.74% compared with a gain of 12.56% for the S&P Mid Cap 400 Index. In the U.S., the broad market (using for example, the Russell 3000, Wilshire 5000, and S&P 500 indices) rose about 6% for the year. Please note that this Fund has multiple classes. Performance for all classes can be found on the Fund’s summary page and at www.managersinvest.com.

Mid-cap and small-cap stocks rose more than large-caps for the year as measured by the S&P indices. From a style standpoint, the S&P 400/Citigroup Growth Index outperformed its value counterpart. Much of this difference stemmed from energy stocks that belonged to one index and not the other. Coal companies Arch Coal and Peabody Energy accounted for over 1.5% contribution to the S&P 400/Citigroup Growth Index, almost the entire outperformance.

Despite strong corporate earnings, 2005 got off to a rocky start. The broad markets were down about 4% after the first four months of the year, but mid-caps declined less than other market cap groups. Much like the broad markets, the energy sector was the story of 2005, up over 50%. As oil and gas prices continued to rise throughout the summer, oil rose to over $69 per barrel during the summer, finishing at $61, while gold ended the year at $517/oz. The higher fuel and commodity prices combined with devastating hurricanes to the Gulf Coast region, and continued increases in short-term interest rates could not slow down the economy. GDP continued to grow and core CPI inflation was kept to low levels. Markets rallied in the fourth quarter as the industrials and materials sectors climbed and energy stocks declined. While the holiday shopping season was far from a boom, neither was it the bust that some analysts had anticipated due to higher energy prices.

10

Managers Mid-Cap Fund

Portfolio Manager Comments (continued)

CEP matches sectors with the S&P Mid Cap to immunize the Fund against sector allocation effects relative to the benchmark. The Fund was successful in this regard, as sector weights were closely aligned throughout the year. In fact, the Fund was in pace with the Index after the first three quarters of the year. However, during a decline in October, the Fund fell behind the Index by over 200 basis points (bps). It was within the energy, utilities and health care sectors that the holdings performed poorly during October. However, over the next two months, the Fund outperformed the Index by over 150 bps, led by the technology, industrials, financials and consumer discretionary sectors.

As the Fund’s sector weights are closely aligned with those of the Index, it is essentially by definition that stock selection drives the Fund’s relative returns. Stock selection in the consumer discretionary and utilities sectors were the greatest contributors to the Fund this year. Increased production and higher commodity prices drove the utility sector, just as they did the energy sector. Questar and Energen, up 51% and 25% respectively, were among the Fund’s top holdings and largest contributors, despite a poor fourth quarter. Retailers Chico’s, Abercrombie & Fitch, Payless Shoes and Claire’s Stores were all top performers. Chico’s, a retailer of exclusively designed private label women’s clothing, has seen 106 consecutive months of positive same store sales, while Abercrombie & Fitch saw sales increase 37% over last year.

On the downside were the consumer staples and industrial sectors. A large position in Tyson Foods (-6%) hurt the Fund, as well as the decline in NBTY (-32%), a manufacturer, marketer and retailer of nutritional supplements, which realized weak sales over 2005. The industrials sector greatly underperformed the benchmark despite strong performance from Joy Global (+110%), Precision Castparts (+58%) and Thomas & Betts (+36%). Underperformance from YRC Worldwide, formerly Yellow Corp., J.B. Hunt Transport Services and Grace all were a drag on Fund performance. All three have been liquidated from the portfolio.

Looking Forward

The portfolio manager continues to add value through security selection. This process will immunize the portfolio against sector swings by matching sectors to the benchmark, regardless of the current economic environment. CEP models still emphasize valuation, expectation and quality attributes to select the best risk adjusted stocks within each sector.

Cumulative Total Return Performance

Mid-Cap’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. The S&P Mid Cap 400 Index is an unmanaged capitalization weighted index of 400 commonly traded stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of those stocks. Unlike the Fund, the S&P Mid Cap 400 Index is unmanaged, is not available for investment, and does not incur expenses. The chart illustrates the performance of a hypothetical $10,000 investment made in the Fund’s Class A Shares on January 2, 1997 to a $10,000 investment made in the S&P Mid Cap 400 Index for the same time periods. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. Performance for periods longer than one year is annualized. Figures include reinvestment capital gains and dividends. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns for the Fund would have been lower had certain expenses not been reduced.

11

Managers Mid-Cap Fund

Portfolio Manager Comments (continued)

The table below shows the average annualized total returns for the Mid-Cap Fund - Class A Shares (with load) and the S&P Mid Cap 400 Index since inception through December 31, 2005.

| | | | | | | | | |

Average Annual Total Returns: | | 1 Year | | | 5 Years | | | Since Inception* | |

Mid-Cap – A Shares | | 4.91 | % | | 5.19 | % | | 13.08 | % |

S&P Mid Cap 400 | | 12.56 | % | | 8.60 | % | | 14.01 | % |

| * | Commencement of operations was January 2, 1997. |

The table below displays a full breakdown of the sector allocation of the Fund as well as the top ten positions as of December 31, 2005

| | | | | | | | | | | |

Top Ten Holdings (out of 105 securities) | | Managers Mid-Cap Fund

% Fund | | | Portfolio Breakdown | | %

Fund | | | S&P Mid Cap 400 | |

Questar Corp. | | 3.1 | % | | Financials | | 18.0 | % | | 18.7 | % |

Joy Global, Inc. | | 2.7 | | | Consumer Discretionary | | 14.6 | | | 16.2 | |

American Financial Group, Inc.* | | 2.5 | | | Information Technology | | 16.1 | | | 15.6 | |

Patterson-UTI Energy, Inc. | | 2.4 | | | Industrials | | 12.0 | | | 13.3 | |

Newfield Exploration Co. | | 2.3 | | | Health Care | | 11.8 | | | 11.5 | |

Martin Marietta Materials, Inc. | | 2.2 | | | Energy | | 9.3 | | | 9.6 | |

Energen Corp. | | 2.0 | | | Utilities | | 7.1 | | | 7.4 | |

Highwoods Properties, Inc. | | 2.0 | | | Materials | | 7.4 | | | 4.0 | |

Humana, Inc.* | | 1.8 | | | Consumer Staples | | 2.3 | | | 3.3 | |

Western Digital Corp. | | 1.8 | | | Telecommunications | | 0.4 | | | 0.4 | |

| | | | | | | | | | | |

Top Ten as a Group | | 22.8 | % | | U. S. Government Obligations | | 0.1 | | | 0.0 | |

| | | | | | | | | | | |

| | | | | Other Assets and Liabilities | | 0.9 | | | 0.0 | |

| | | | | | | | | | | |

| | | | | | | 100.0 | % | | 100.0 | % |

| | | | | | | | | | | |

| * | Top Ten Holding at June 30, 2005 |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or a solicitation to sell that security.

12

Managers Mid-Cap Fund

Schedule of Portfolio Investments

December 31, 2005

| | | | | | |

Security Description | | Shares | | | Value |

| Common Stocks - 99.0% | | | | | | |

Consumer Discretionary - 14.6% | | | | | | |

Abercrombie & Fitch Co. | | 22,700 | 2 | | $ | 1,479,586 |

Advance Auto Parts, Inc.* | | 15,400 | | | | 669,284 |

American Greetings Corp., Class A | | 17,100 | 2 | | | 375,687 |

Autoliv, Inc. | | 14,000 | 2 | | | 635,880 |

Barnes & Noble, Inc. | | 14,200 | 2 | | | 605,914 |

Brinker International, Inc. | | 19,000 | | | | 734,540 |

Brunswick Corp. | | 12,700 | 2 | | | 516,382 |

Catalina Marketing Corp.* | | 23,200 | 2 | | | 588,120 |

Chico’s FAS, Inc.* | | 26,500 | | | | 1,164,145 |

Claire’s Stores, Inc. | | 33,400 | | | | 975,948 |

Darden Restaurants, Inc. | | 38,300 | | | | 1,489,104 |

Dillard’s, Inc., Class A | | 38,100 | 2 | | | 945,642 |

Goodyear Tire & Rubber Co.* | | 29,800 | 2 | | | 517,924 |

NVR, Inc.* | | 1,325 | 2 | | | 930,150 |

Payless ShoeSource, Inc.* | | 40,400 | 2 | | | 1,014,040 |

Rent-A-Center, Inc.* | | 12,200 | | | | 230,092 |

Timberland Co.* | | 14,100 | 2 | | | 458,955 |

Tupperware Corp. | | 25,300 | | | | 566,720 |

Washington Post Co., The | | 410 | | | | 313,650 |

Total Consumer Discretionary | | | | | | 14,211,763 |

Consumer Staples - 2.3% | | | | | | |

Energizer Holdings, Inc.* | | 6,900 | | | | 343,551 |

Hormel Foods Corp. | | 6,400 | | | | 209,152 |

PepsiAmericas, Inc. | | 12,200 | 2 | | | 283,772 |

Pilgrim’s Pride Corp., Class B | | 29,600 | 2 | | | 981,536 |

SUPERVALU, Inc. | | 14,300 | | | | 464,464 |

Total Consumer Staples | | | | | | 2,282,475 |

Energy - 9.3% | | | | | | |

Diamond Offshore Drilling, Inc. | | 24,800 | 2 | | | 1,725,087 |

Newfield Exploration Co.* | | 44,800 | | | | 2,243,136 |

Overseas Shipholding Group, Inc. | | 25,800 | 2 | | | 1,300,062 |

Patterson-UTI Energy, Inc. | | 71,700 | | | | 2,362,515 |

Tesoro Corp. | | 23,900 | | | | 1,471,045 |

Total Energy | | | | | | 9,101,845 |

Financials - 18.0% | | | | | | |

A.G. Edwards, Inc. | | 20,200 | 2 | | | 946,572 |

American Capital Strategies Ltd. | | 29,900 | 2 | | | 1,082,679 |

American Financial Group, Inc. | | 63,600 | | | | 2,436,516 |

CBL & Associates Properties, Inc. | | 37,900 | 2 | | | 1,497,429 |

Commerce Bancshares, Inc. | | 7,980 | 2 | | | 415,918 |

Compass Bancshares, Inc. | | 14,200 | | | | 685,717 |

Downey Financial Corp. | | 9,900 | | | | 677,061 |

First American Corp. | | 29,200 | | | | 1,322,760 |

Highwoods Properties, Inc. | | 68,900 | 2 | | | 1,960,205 |

Indymac Mortgage Holdings, Inc. | | 38,400 | 2 | | | 1,498,368 |

Janus Capital Group, Inc. | | 33,300 | 2 | | | 620,379 |

Mercantile Bankshares Corp. | | 23,600 | | | | 1,331,984 |

Nationwide Financial Services, Inc. | | 13,800 | 2 | | | 607,200 |

Radian Group, Inc. | | 28,700 | | | | 1,681,533 |

Wilmington Trust Corp. | | 9,400 | | | | 365,754 |

Zions Bancorporation | | 6,400 | | | | 483,584 |

Total Financials | | | | | | 17,613,659 |

Health Care - 11.8% | | | | | | |

Barr Laboratories, Inc.* | | 6,700 | | | | 417,343 |

Bausch & Lomb, Inc. | | 7,900 | 2 | | | 536,410 |

C.R. Bard, Inc. | | 11,600 | | | | 764,672 |

Cerner Corp.* | | 7,300 | 2 | | | 663,643 |

Charles River Laboratories International, Inc.* | | 22,600 | | | | 957,562 |

Coventry Health Care, Inc.* | | 25,325 | | | | 1,442,512 |

Endo Pharmaceuticals Holdings, Inc.* | | 30,400 | | | | 919,904 |

Humana, Inc.* | | 33,200 | | | | 1,803,756 |

Intuitive Surgical, Inc.* | | 8,200 | | | | 961,614 |

Lincare Holdings, Inc.* | | 6,500 | | | | 272,415 |

Renal Care Group, Inc.* | | 6,650 | | | | 314,612 |

STERIS Corp. | | 31,000 | | | | 775,620 |

Techne Corp.* | | 25,770 | 2 | | | 1,446,986 |

Watson Pharmaceuticals, Inc.* | | 7,300 | 2 | | | 237,323 |

Total Health Care | | | | | | 11,514,372 |

Industrials - 12.0% | | | | | | |

Alaska Airgroup, Inc.* | | 14,500 | 2 | | | 517,940 |

Banta Corp | | 14,600 | | | | 727,080 |

Cummins, Inc. | | 16,700 | 2 | | | 1,498,491 |

Equifax, Inc. | | 27,900 | 2 | | | 1,060,758 |

GATX Corp. | | 28,400 | 2 | | | 1,024,672 |

Hubbell, Inc. | | 6,600 | | | | 297,792 |

ITT Educational Services, Inc.* | | 11,500 | | | | 679,765 |

Joy Global, Inc. | | 64,800 | | | | 2,592,000 |

Precision Castparts Corp. | | 18,400 | 2 | | | 953,304 |

Republic Services, Inc. | | 41,600 | 2 | | | 1,562,080 |

Thomas & Betts Corp.* | | 18,300 | | | | 767,868 |

Total Industrials | | | | | | 11,681,750 |

Information Technology - 16.1% | | | | | | |

Avnet, Inc.* | | 31,500 | 2 | | | 754,110 |

Cognizant Technology Solutions Corp.* | | 12,000 | | | | 604,200 |

CommScope, Inc.* | | 24,800 | 2 | | | 499,224 |

DST Systems, Inc.* | | 14,700 | | | | 880,677 |

Factset Research Systems, Inc. | | 13,750 | 2 | | | 565,950 |

Fair Isaac Corp. | | 18,100 | 2 | | | 799,477 |

Harris Corp. | | 22,800 | | �� | | 980,628 |

Imation Corp. | | 13,300 | | | | 612,731 |

Ingram Micro, Inc., Class A* | | 44,200 | | | | 880,906 |

Integrated Device Technology, Inc.* | | 87,400 | | | | 1,151,932 |

The accompanying notes are an integral part of these financial statements.

13

Managers Mid-Cap Fund

Schedule of Portfolio Investments (continued)

| | | | | | | | |

Security Description | | Shares | | | Value | |

Information Technology (continued) | | | | | | | | |

Intersil Corp., Class A | | | 34,500 | | | $ | 858,360 | |

Lam Research Corp.* | | | 18,900 | 2 | | | 674,352 | |

McAfee, Inc.* | | | 15,000 | 2 | | | 406,950 | |

MEMC Electronic Materials, Inc.* | | | 10,700 | | | | 237,219 | |

MoneyGram International, Inc. | | | 14,500 | 2 | | | 378,160 | |

Omnivision Technologies, Inc.* | | | 26,400 | 2 | | | 526,944 | |

Sabre Holdings Corp. | | | 49,900 | 2 | | | 1,203,089 | |

Sybase, Inc.* | | | 31,500 | | | | 688,590 | |

Transaction Systems Architects, Inc.* | | | 18,800 | | | | 541,252 | |

United Online, Inc. | | | 32,200 | 2 | | | 457,884 | |

Varian, Inc.* | | | 7,400 | | | | 294,446 | |

Western Digital Corp.* | | | 93,100 | 2 | | | 1,732,591 | |

Total Information Technology | | | | | | | 15,729,672 | |

Materials - 7.4% | | | | | | | | |

Ashland, Inc. | | | 11,300 | 2 | | | 654,270 | |

FMC Corp.* | | | 22,500 | | | | 1,196,325 | |

Georgia Gulf Corp. | | | 17,100 | 2 | | | 520,182 | |

Louisana-Pacific Corp. | | | 54,500 | 2 | | | 1,497,115 | |

Martin Marietta Materials, Inc. | | | 27,400 | | | | 2,102,128 | |

Peabody Energy Corp. | | | 11,000 | | | | 906,620 | |

United States Steel Corp. | | | 7,200 | 2 | | | 346,104 | |

Total Materials | | | | | | | 7,222,744 | |

Telecommunication Services - 0.4% | | | | | | | | |

NII Holdings, Inc., Class B* | | | 9,800 | 2 | | | 428,064 | |

Utilities - 7.1% | | | | | | | | |

CMS Energy Corp.* | | | 20,000 | 2 | | | 290,200 | |

Energen Corp. | | | 54,000 | | | | 1,961,280 | |

NRG Energy, Inc.* | | | 34,100 | 2 | | | 1,606,792 | |

Questar Corp. | | | 40,500 | | | | 3,065,850 | |

Total Utilities | | | | | | | 6,924,122 | |

Total Common Stocks

(cost $79,757,225) | | | | | | | 96,710,466 | |

| | |

Security Description | | Principal Amount | | | Value | |

U.S. Government Obligations – 0.1%6 | | | | | | | | |

United States Treasury Bonds – 0.0% | | | | | | | | |

U.S. Treasury Bonds, | | | | | | | | |

8.750%, 08/15/20 | | $ | 4,398 | | | $ | 6,471 | |

United States Treasury Notes – 0.1% | | | | | | | | |

U.S. Treasury Notes, | | | | | | | | |

4.000%, 06/15/09 | | | 13,620 | | | | 13,478 | |

U.S. Treasury Inflation Indexed Notes, | | | | | | | | |

1.875%, 07/15/13 | | | 23,089 | | | | 24,907 | |

Total United States Treasury Notes | | | | | | | 38,385 | |

Total U.S. Government Obligations

(cost $44,856) | | | | | | | 44,856 | |

| | |

| | | Shares | | | | |

Other Investment Companies – 28.2%1 | | | | | | | | |

Bank of New York Institutional Cash Reserves Fund, 4.30%3 | | | 26,957,222 | | | | 26,957,222 | |

JPMorgan Prime Money Market Fund, Institutional Class Shares, 4.14% | | | 657,564 | | | | 657,564 | |

Total Other Investment Companies

(cost $27,614,786) | | | | | | | 27,614,786 | |

Total Investments – 127.3%

(cost $107,416,867) | | | | | | | 124,370,108 | |

Other Assets, less Liabilities – (27.3)% | | | | | | | (26,730,589 | ) |

Net Assets - 100.0% | | | | | | $ | 97,639,519 | |

The accompanying notes are an integral part of these financial statements.

14

Managers Balanced Fund

Portfolio Manager Comments

The Managers Balanced Fund’s (the “Fund”) investment objective is to achieve a high total investment return, consistent with the preservation of capital and prudent investment risk.

The Managers Balanced Fund seeks to achieve its investment objective by investing approximately 50-65% of its total assets in equity securities and investing the remainder in bonds and other fixed-income securities, as well as cash or cash equivalents. The equity portion of the Fund is invested primarily in a diversified portfolio of U.S. common stocks, as well as other U.S. and foreign securities, including convertible securities and warrants. Normally, the equity portion of the Fund will focus on large and medium-sized companies which will generally be listed on the New York, American or NASDAQ exchanges and be widely held among a large number of investors.

The Fund will generally invest at least 25 % of the Fund’s total assets in a range of fixed income securities, including domestic and foreign fixed-income securities and non-U.S. dollar securities. The Fund may also invest up to 25% of the Fund’s total assets in below-investment grade securities (those rated Bal/BB+ or lower by Moody’s/Standard & Poor’s). The Fund’s benchmark is an equal blend of the S&P 500 Index and the Lehman Brothers Aggregate Bond Index.

The Portfolio Managers

The Fund employs multiple portfolio managers who specialize in distinct investment approaches. This “intelligence diversification” not only serves to manage risk, but also helps us tap the markets’ full potential by focusing different analytical insights on each class of investment. Fund management strives to achieve this performance and diversification while ensuring that the Fund operates within the framework of its investment objective and principal investment strategies.

Chicago Equity Partners, LLC

The investment team at Chicago Equity Partners (“CEP”) believes that fundamentals drive stock prices – that companies with favorable valuations and earnings expectations will outperform their peers. CEP employs a disciplined investment strategy utilizing a proprietary multi-factor model, which includes momentum, value and quality factors, to select securities. The process focuses on security selection while remaining neutral to industry, sector, style and capitalization benchmarks. CEP seeks to consistently apply an objective, quantitative, fundamental investment approach that identifies undervalued and overvalued securities within industry sectors.

Chicago Equity Partners, LLC utilizes a systematic ranking system to identify attractive stocks and construct its portfolios through a disciplined process that minimizes portfolio risks like sector, capitalization and style exposures. Every day the investment team at CEP uses its proprietary model to evaluate the expectations, valuation and quality attributes of 3,000 stocks.

The ideal investment exhibits the following traits:

| | • | | Favorable valuation ratios relative to peers |

| | • | | Corporate profits growth is expected to be above average compared to peers |

Portfolio management:

| | • | | Utilizes a systematic ranking system to identify attractive stocks |

| | • | | Follows a disciplined portfolio construction process that minimizes portfolio risks like sector, capitalization and style exposures |

| | • | | Constructs portfolios that neutralize risk elements that are not consistently rewarded, such as style tilts, industry weightings and market capitalization |

| | • | | Reviews and confirms the model’s daily rankings, paying special attention to any changes in rank |

| | • | | Each analyst follows a specific sector focusing on: |

| | • | | The timing and nature of earnings releases |

| | • | | Legal and regulatory exposures of companies |

| | • | | Any other factors the model may not capture |

| | • | | The analysts use an objective, systematic approach to choose the best risk-adjusted stocks within their sector |

The Portfolio:

| | • | | Typically holds 100 to 200 securities that the investment team believes will generate solid excess returns over the S&P 500 at a moderate risk |

Sell Discipline

CEP has a structured sell discipline: a stock is sold if it is lowly ranked and if there is a viable alternative within its industry, based upon risk/return. This is applied consistently across the universe and over time. The team format assures decisions are being made that are consistent with the Fund’s objectives.

Loomis, Sayles & Company, L.P.

Loomis utilizes a team approach in managing the fixed income portion of the Balanced Fund’s portfolio. The investment team utilizes a contrarian bond investment philosophy, focusing on individual issues which are expected to provide the highest return over long periods of time.

15

Managers Balanced Fund

Portfolio Manager Comments (continued)

The team of credit analysts research debt offerings in the same way equity analysts research stocks, looking for undervalued bonds where they see either a yield premium, the potential for price appreciation, or both. They analyze the company’s financial condition in detail, as well as the terms of specific bond offerings. Price appreciation can come from a variety of catalysts including improving company fundamentals which would lead to credit upgrades, changing market supply and demand forces, improving sector or economic trends.

Portfolio manager John Hyll and his team of credit analysts at Loomis Sayles & Company, L.P. research debt offerings in the same way equity analysts research stocks, looking for undervalued bonds where they see a yield premium, the potential for price appreciation, or both. They analyze the company’s financial condition in detail, as well as the terms of specific bond offerings. They believe price appreciation can come from a variety of catalysts, including improving company fundamentals which would lead to credit upgrades, changing market supply and demand forces, improving sector or economic trends.

The ideal investment typically exhibits some of the following traits:

| | • | | An attractive yield, both absolute and relative to Loomis’ credit research expectations |

| | • | | Good call protection, particularly when prevailing rates are low |

| | • | | Stable or improving fundamentals (for corporate bonds) |

| | • | | Non-market relatedness to counter the impact of systematic risk |

Portfolio management:

| | • | | Targets bond investments on issue-specific credit considerations |

| | • | | Utilizes broad investment opportunities: U.S. and non-U.S. Government and corporate issues |

| | • | | Maintains long-term orientation for currency exposure and security selection |

| | • | | Employs exposure limitations |

The investment team may make a sell decision when:

| | • | | There is a change in sovereign, industry, or company fundamentals |

| | • | | The issuer is downgraded by Loomis research |

| | • | | Relative valuation is not consistent with its expected rating category |

| | • | | Other securities or sectors offer greater total return potential |

The Year in Review

Managers Balanced Fund (Institutional Class) returned 4.57% during 2005, compared to a return of 3.81% for the hypothetical benchmark consisting of 50% S&P 500 and 50% Lehman Brothers Aggregate Bond Index (“the “Index”). Please note that this Fund has multiple classes. Performance for all classes can be found on the Fund’s summary page and at www.managersinvest.com.

U.S. stocks rose moderately and in a fairly narrow band during 2005. Within this broad market, large-cap stocks (as measured by the Russell 1000 Index) outperformed small-cap stocks (as measured by the Russell 2000 Index) by a margin of +6.3% versus +4.6%. Similarly, the Russell 3000 Value Index gained +6.9% compared to +5.2% for its growth counterpart. The 1.7% return differentials between these slices of the market are very narrow by historical standards. Digging into the market indexes further reveals one significant attributable factor: for 2005 as a whole, energy stocks rose 33% and accounted for about one-third of the market’s total gain. The rise in energy prices clearly had an impact on this sector’s performance. Besides energy, only utilities stocks (a rather small portion of the market) rose by more than 10% on average. The range of 2005 total returns from the other sectors was -4% to +8%.

With regard to the bond market, longer-term interest rates changed little during 2005. Although a strong economy and aggressive rate hikes by the Federal Open Market Committee (FOMC) will typically cause long-term rates to rise, there was enough demand for dollar based assets by foreign investors and a lack of more broadly measurable inflation to keep these rates in check. Thus, the yield on the 10-year Treasury rose by only 18 basis points to a still low 4.4%. As longer-term interest rates inched higher, the return for bonds (as measured by the Lehman Brothers Aggregate Bond Index) was more modest than in recent years. This was the third-lowest annual return for the index over the past 20 years and the lowest since 1999. Within the broad bond market, corporate bonds lagged Treasuries during 2005. Again, this came in the face of good corporate profits and creditworthiness. However, corporate bonds (especially high-yield bonds) had performed extremely well over the prior few years and thus offered less compelling valuations (typically measured by yield spreads over Treasury yields) heading into the year. Additionally, the high-profile downgrades of GM and Ford (deserved as they were) startled many investors.

16

Managers Balanced Fund

Portfolio Manager Comments (continued)

The Fund’s equity-centric allocation was beneficial to performance as stocks moderately outperformed bonds. We had noted in last year’s Annual Report that the investment outlook favored equities over bonds. Thus, we generally maintained an allocation of 70% equities versus 30% bonds throughout the year (compared to a neutral allocation of 60% equities and 40% bonds).

Within this broad allocation, the Fund’s managers performed reasonably well during 2005. The manager of the equity portion, Chicago Equity Partners, produced returns that were moderately ahead of the S&P 500 Index. As the managers investment philosophy is intended to immunize the Fund’s sector exposure, this outperformance came from good security selection within sectors. For instance, the Fund’s utilities holdings surged 37%, on average, compared to a 17% increase for the utilities securities within the S&P 500. Similarly the Fund’s consumer staples holdings rose almost 10% on average compared to a near 4% increase for the consumer staples stocks within the S&P 500.

Meanwhile the Fund’s fixed income portion, managed by John Hyll of Loomis Sayles, performed about in line with the Lehman Brothers Aggregate Bond Index. The Funds longer-than market duration was generally advantageous as the long end of the curve contributed positively to the return of the portfolio (given the lack of a material rise in rates). In terms of quality, the Fund held approximately 40% in Government/Agency issues followed by over 26% in BAA issues. High yield holdings comprised just over 12% of the Fund with minimal impact on performance as high yield returns were very similar to Investment Grade returns for the year. With almost the entire portfolio allocated to US Dollars, the portfolio was largely unaffected by foreign currency exposure.

Looking Forward

The Asset Allocation Committee of Managers Investment Group continues to view stocks as having generally better current risk/reward prospects than bonds. Thus, the Fund’s overall allocation remains weighted towards stocks versus bonds. Within those allocations, neither manager has made any significant changes to his strategy.

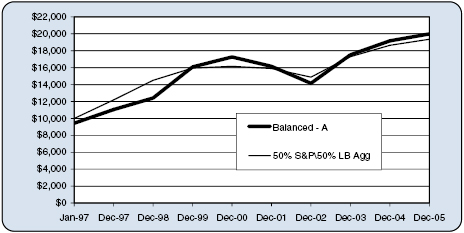

Cumulative Total Return Performance

Managers Balanced Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. The benchmark is a combination of the S&P 500 Index and the Lehman Brothers U.S. Aggregate Index, each comprising half of the benchmark. The S&P 500 Index is an unmanaged capitalization weighted index of 500 commonly traded stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of those stocks. The Lehman Brothers U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with 6,434 government and corporate securities, mortgage pass-through securities, and asset-backed securities. Unlike the Fund, the S&P 500 Index and the Lehman Brothers U.S. Aggregate Index are unmanaged, are not available for investment, and do not incur expenses. The chart illustrates the performance of a hypothetical $10,000 investment made in the Fund’s Class A Shares on January 2,1997, to a $10,000 investment made in the benchmark for the same time periods. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. Performance for periods longer than one year is annualized. The listed returns for the Fund are net of expenses and the returns for the indices exclude expenses. Total returns for the Fund would have been lower had certain expenses not been reduced.

17

Managers Balanced Fund

Portfolio Manager Comments (continued)

The table below shows the average annualized total returns for the Balanced Fund - Class A Shares (with load) and the 50% S&P 500 / 50% Lehman Brothers U.S. Aggregate Index since inception through December 31, 2005.

| | | | | | | | | |

Average Annual Total Returns: | | 1 Year | | | 5 Years | | | Since Inception* | |

Balanced – A Shares | | (1.79 | )% | | 1.76 | % | | 8.00 | % |

50% S&P 500 | | | | | | | | | |

50% Lehman Brothers U.S. Aggregate | | 3.81 | % | | 3.67 | % | | 7.62 | % |

| * | Commencement of operations was January 2, 1997. |

The table below displays a full breakdown of the sector allocation of the Fund as well as the top ten positions as of December 31, 2005

Managers Balanced Fund

| | | | | | | | |

Top Ten Holdings (out of 158 securities) | | %

Fund | | | Portfolio Breakdown | | %

Fund | |

USTB, 3.875%, 05/15/09* | | 3.7 | % | | Industrials | | 20.9 | % |

Johnson & Johnson Co.* | | 2.5 | | | Financials | | 20.2 | |

Bank of America Corp.* | | 2.4 | | | U. S. Government Obligations | | 13.1 | |

USTN, 2.250%, 02/15/07* | | 2.1 | | | Information Technology | | 10.0 | |

Wachovia Corp.* | | 2.0 | | | Health Care | | 8.7 | |

USTB, 5.250%, 11/15/28 | | 1.8 | | | Consumer Discretionary | | 7.1 | |

USTN, 2.375%, 08/15/06* | | 1.8 | | | Consumer Staples | | 5.2 | |

Intel Corp.* | | 1.8 | | | Energy | | 5.1 | |

USTN, 2.500%, 10/31/06 | | 1.7 | | | Utilities | | 2.7 | |

BellSouth Corp. | | 1.7 | | | Materials | | 2.1 | |

| | | | | | | | |

Top Ten as a Group | | 21.5 | % | | Telecommunications Services | | 1.7 | |

| | | | | | | | |

| | | | | Other Assets and Liabilities | | 1.3 | |

| | | | | Asset-Backed Securities | | 1.1 | |

| | | | | Foreign Government | | 0.8 | |

| | | | | | | | |

| | | | | | | 100.0 | % |

| | | | | | | | |

| * | Top Ten Holding at June 30, 2005 |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or a solicitation to sell that security.

18

Managers Balanced Fund

Schedule of Portfolio Investments

December 31, 2005

| | | | | | |

Security Description | | Shares | | | Value |

Common Stocks - 64.3% | | | | | | |

Consumer Discretionary - 7.1% | | | | | | |

Abercrombie & Fitch Co. | | 1,600 | 2 | | $ | 104,288 |

Coach, Inc.* | | 2,000 | | | | 66,680 |

Dillard’s, Inc., Class A | | 2,300 | 2 | | | 57,086 |

Federated Department Stores, Inc. | | 3,100 | 2 | | | 205,623 |

Goodyear Tire & Rubber Co.* | | 4,400 | 2 | | | 76,472 |

Home Depot, Inc. | | 4,370 | | | | 176,898 |

J.C. Penney Co., Inc., Holding Co. | | 2,300 | 2 | | | 127,880 |

McDonald’s Corp. | | 8,000 | | | | 269,760 |

McGraw-Hill Companies, Inc., The | | 1,700 | | | | 87,771 |

Rent-A-Center, Inc.* | | 2,200 | | | | 41,492 |

Time Warner Co., Inc. | | 14,860 | | | | 259,158 |

Viacom, Inc., Class B* | | 2,300 | | | | 74,980 |

Walt Disney Co., The* | | 6,000 | | | | 143,820 |

Total Consumer Discretionary | | | | | | 1,691,908 |

Consumer Staples - 5.2% | | | | | | |

Altria Group, Inc. | | 2,820 | 2 | | | 210,710 |

PepsiCo, Inc. | | 4,900 | | | | 289,492 |

Pilgrim’s Pride Corp., Class B | | 4,700 | 2 | | | 155,852 |

Procter & Gamble Co. | | 6,612 | 2 | | | 382,703 |

Reynolds American, Inc. | | 700 | 2 | | | 66,731 |

SUPERVALU, Inc. | | 4,400 | | | | 142,912 |

Total Consumer Staples | | | | | | 1,248,400 |

Energy - 5.1% | | | | | | |

ConocoPhillips Co. | | 4,400 | | | | 255,992 |

Devon Energy Corp. | | 1,900 | | | | 118,826 |

Exxon Mobil Corp. | | 3,820 | | | | 214,569 |

Marathon Oil Corp. | | 5,200 | 2 | | | 317,044 |

Unit Corp.* | | 2,600 | 2 | | | 143,078 |

Valero Energy Corp. | | 3,600 | | | | 185,760 |

Total Energy | | | | | | 1,235,269 |

Financials - 15.1% | | | | | | |

Allstate Corp., The | | 2,800 | | | | 151,396 |

Assurant, Inc. | | 1,200 | | | | 52,188 |

AvalonBay Communities, Inc. | | 800 | | | | 71,400 |

Bank of America Corp. | | 12,400 | | | | 572,260 |

CBL & Associates Properties, Inc. | | 5,000 | 2 | | | 197,550 |

CIT Group, Inc. | | 5,400 | | | | 279,612 |

Conseco, Inc.* | | 9,600 | 2 | | | 222,432 |

Goldman Sachs Group, Inc. | | 500 | 2 | | | 63,855 |

JPMorgan Chase & Co. | | 5,948 | | | | 236,076 |

Lehman Brothers Holdings, Inc. | | 800 | | | | 102,536 |

Merrill Lynch & Co., Inc. | | 2,000 | | | | 135,460 |

Moody’s Corp. | | 5,700 | 2 | | | 350,094 |

PMI Group, Inc. | | 800 | 2 | | | 32,856 |

Principal Financial Group | | 2,500 | 2 | | | 118,575 |

Prudential Financial, Inc. | | 2,500 | | | | 182,975 |

Radian Group, Inc. | | 600 | 2 | | | 35,154 |

UnumProvident Corp. | | 1,700 | | | | 38,675 |

Wachovia Corp. | | 9,000 | | | | 475,740 |

Washington Mutual, Inc. | | 6,808 | 2 | | | 296,148 |

Total Financials | | | | | | 3,614,982 |

Health Care - 8.7% | | | | | | |

AmerisourceBergen Corp. | | 2,400 | | | | 99,360 |

Amgen, Inc.* | | 4,100 | | | | 323,326 |

Becton, Dickinson & Co. | | 1,800 | | | | 108,144 |

CIGNA Corp. | | 2,100 | | | | 234,570 |

Coventry Health Care, Inc.* | | 3,525 | | | | 200,784 |

Johnson & Johnson Co. | | 9,780 | | | | 587,778 |

King Pharmaceuticals Inc* | | 7,900 | | | | 133,668 |

Merck & Co., Inc. | | 5,100 | 2 | | | 162,231 |

Pfizer, Inc. | | 8,840 | | | | 206,149 |

Wyeth Co. | | 600 | | | | 27,642 |

Total Health Care | | | | | | 2,083,652 |

Industrials - 6.8% | | | | | | |

CNF, Inc. | | 1,300 | | | | 72,657 |

CSX Corp. | | 3,100 | | | | 157,387 |

Cummins, Inc. | | 2,000 | 2 | | | 179,460 |

Florida Rock Industries, Inc. | | 3,100 | | | | 152,086 |

General Electric Co. | | 6,000 | | | | 210,300 |

Honeywell International, Inc. | | 7,200 | | | | 268,200 |

Northrop Grumman Corp. | | 4,900 | 2 | | | 294,539 |

Textron, Inc. | | 3,000 | | | | 230,940 |

West Corp.* | | 1,800 | 2 | | | 75,870 |

Total Industrials | | | | | | 1,641,439 |

Information Technology - 10.0% | | | | | | |

Adobe Systems, Inc. | | 5,400 | 2 | | | 199,584 |

Apple Computer, Inc.* | | 1,500 | | | | 107,835 |

Avnet, Inc.* | | 2,100 | 2 | | | 50,274 |

Cisco Systems, Inc.* | | 13,140 | | | | 224,957 |

Computer Sciences Corp.* | | 2,200 | | | | 111,408 |

Google Inc.* | | 300 | | | | 124,458 |

Hewlett-Packard Co. | | 7,200 | | | | 206,136 |

Intel Corp. | | 16,960 | | | | 423,322 |

International Business Machines Corp. | | 2,200 | | | | 180,840 |

MEMC Electronic Materials, Inc.* | | 2,700 | | | | 59,859 |

Microsoft Corp. | | 7,600 | | | | 198,740 |

Motorola, Inc. | | 8,200 | | | | 185,237 |

Oracle Corp.* | | 18,600 | | | | 227,106 |

Western Digital Corp.* | | 4,500 | 2 | | | 83,745 |

Total Information Technology | | | | | | 2,383,501 |

Materials - 2.1% | | | | | | |

Dow Chemical Co. | | 2,100 | | | | 92,022 |

The accompanying notes are an integral part of these financial statements.

19

Managers Balanced Fund

Schedule of Portfolio Investments (continued)

| | | | | | | |

Security Description | | Shares | | | Value |

Materials (continued) | | | | | | | |

Sigma-Aldrich Corp. | | | 1,300 | 2 | | $ | 82,277 |

United States Steel Corp. | | | 6,900 | 2 | | | 331,683 |

Total Materials | | | | | | | 505,982 |

Telecommunication Services - 1.7% | | | | | | | |

BellSouth Corp. | | | 15,000 | 2 | | | 406,500 |

Utilities - 2.5% | | | | | | | |

PG&E Corp. | | | 9,300 | 2 | | | 345,216 |

Questar Corp. | | | 3,300 | | | | 249,810 |

Total Utilities | | | | | | | 595,026 |

Total Common Stocks

(cost $13,430,404) | | | | | | | 15,406,659 |

| | |

| | | Principal

Amount | | | |

Corporate Bonds - 20.5% | | | | | | | |

Asset-Backed Securities – 1.1% | | | | | | | |

First Union National Bank Commercial Mortgage, Series 1999-C4, Class A1,

7.184%, 12/15/31 | | $ | 57,423 | | | | 58,429 |

Greenwich Capital Commercial Funding Corp., Series 2005-GG5, Class A2,

5.117%, 04/10/37 | | | 90,000 | | | | 90,275 |

GS Mortgage Securities Corp. II Series 2005-GG4,

4.751%, 07/10/39 | | | 50,000 | | | | 48,547 |

Morgan Stanley Capital I, Series 2005-T19,

4.890%, 06/12/47 | | | 75,000 | | | | 73,574 |

Total Asset-Backed Securities | | | | | | | 270,825 |

Finance – 5.1% | | | | | | | |

Boeing Capital Corp., | | | | | | | |

4.750%, 08/25/08 | | | 25,000 | | | | 24,948 |

Carramerica Realty Corp., | | | | | | | |

3.625%, 04/01/09 | | | 165,000 | | | | 157,968 |

CIT Group Inc., | | | | | | | |

5.500%, 12/01/14 | | | 50,000 | | | | 88,851 |

Developers Diversified Realty, | | | | | | | |

5.375%, 10/15/12 | | | 90,000 | | | | 88,766 |

Health Care, Inc., | | | | | | | |

7.500%, 08/15/07 | | | 38,000 | | | | 39,215 |

Hospitality Properties Trust, | | | | | | | |

6.750%, 02/15/13 | | | 150,000 | | | | 160,035 |

Host Marriott, LP, | | | | | | | |