UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number: 811-06431 |

MANAGERS TRUST II

|

| (Exact name of registrant as specified in charter) |

| | |

| 800 Connecticut Avenue, Norwalk, Connecticut | | 06854 |

| (Address of principal executive offices) | | (Zip code) |

Managers Investment Group LLC

800 Connecticut Avenue, Norwalk, Connecticut 06854

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (203) 299-3500

Date of fiscal year end: MARCH 31

Date of reporting period: APRIL 1, 2006 – MARCH 31, 2007

(Annual Shareholder Report)

| Item 1. | Reports to Shareholders |

ANNUAL REPORT

Managers Funds

March 31, 2007

| • | | Managers Short Duration Government Fund |

| • | | Managers Intermediate Duration Government Fund |

Managers Short Duration Government Fund

Managers Intermediate Duration Government Fund

Annual Report – March 31, 2007

TABLE OF CONTENTS

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of The Managers Funds or any fund presented within this report. Such offering is made only by Prospectus, which includes details as to offering price and other material information.

Letter to Shareholders

Dear Fellow Shareholder,

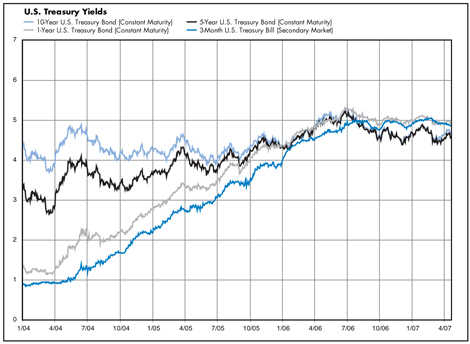

WE WOULD LIKE TO THANK OUR INVESTORS for their commitment to the Managers Short Duration Government and Managers Intermediate Duration Government Funds. Both of these Funds performed well over the fiscal year ended March 31, 2007, in an environment which finally saw the Federal Open Market Committee (FOMC) pause its methodical rate increases in August, after raising its key federal funds rate 17 consecutive times. Throughout the rest of the fiscal year, the Fed left its target rate unchanged at 5.25%, as inflation fears diminished and the prospects of slower economic growth became a higher probability. The bond market reacted in agreement with the Fed’s economic assessment by inverting the yield curve even more than it had been — a signal that moderating inflation and a slowing economy were anticipated (see chart on page 2).

In assessing the yield curve, it is important to consider that the U.S. economy and interest rates are more linked to the global economy and asset flows than ever before. Hence, the inverted yield curve is not a pure reflection of U.S. economic, interest rate, and inflation expectations, but also factors in the effect that foreign demand for U.S. Treasuries has on long-term rates — in this case, it holds rates down.

The Managers Short Duration Government Fund, a very high quality portfolio that invests mainly in U.S. Government and agency issues, and limits overall interest rate risk to match a portfolio of six-month U.S. Treasuries, returned 5.05% for the fiscal year ended March 31, 2007. Over this same time period, the Managers Intermediate Duration Government Fund, a high quality U.S. Government- and agency-dominated portfolio that keeps interest rate risk similar to three- to five-year U.S. Treasuries, returned 6.30%. Smith Breeden Associates, Inc., the manager of both of these Funds, has done an excellent job of consistently executing their investment strategy of seeking the best relative value available while maintaining high credit quality and focused risk controls.

ONE OF OUR FOREMOST GOALS AT MANAGERS INVESTMENT GROUP (“Managers”) is to structure and manage mutual funds that will help our shareholders and clients become more successful in reaching their investment goals and objectives. Each of our Funds is geared to provide you with exposure to a specific asset class or segment of the market. Investors tend to use our Funds as part of their overall asset allocation in order to structure a well-diversified portfolio intended to meet individual needs. Most of our Funds, therefore, are designed to be building blocks.

At Managers we appreciate the privilege of being part of your investment plan. If you are curious about how you can better diversify your investment program, visit the Knowledge Center on our Web site at www.managerinvest.com and view our articles in the investment strategies section. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit. Thank you again for entrusting your assets to Managers.

|

| Respectfully, |

|

|

| John H. Streur |

| Senior Managing Partner |

| Managers Investment Group LLC |

1

Letter to Shareholders (continued)

2

About Your Fund’s Expenses

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, redemption fees; and exchange fees; and (2) ongoing costs, including management fees and other Fund expenses. These Funds incur only ongoing costs. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | |

Six Months Ended March 31, 2007 | | Beginning

Account Value

10/1/2006 | | Ending

Account Value

3/31/2007 | | Expenses

Paid During

the Period* |

Short Duration Government Fund | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,026 | | $ | 4.24 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,021 | | $ | 4.23 |

Intermediate Duration Government Fund | | | | | | | | | |

Based on Actual Fund Return | | $ | 1,000 | | $ | 1,027 | | $ | 4.30 |

Based on Hypothetical 5% Annual Return | | $ | 1,000 | | $ | 1,021 | | $ | 4.28 |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (182), then divided by 365. |

3

Managers Short Duration Government Fund

Portfolio Manager’s Comments

The Managers Short Duration Government Bond Fund (“the Fund”) seeks to provide investors with a high level of current income, consistent with a low volatility of net asset value.

The Fund seeks to achieve its objective by matching the duration, or interest-rate risk, of a portfolio that invests exclusively in Six-Month U.S. Treasury securities on a constant maturity basis. Under normal circumstances, the Fund will invest at least 80% of its assets in debt securities issued by the U.S. Government or its agencies and instrumentalities and synthetic instruments or derivatives having economic characteristics similar to such debt securities.

The Fund typically employs hedging techniques using instruments such as interest rate futures, options, floors, caps, and swaps, designed to reduce the interest-rate risk of its fixed-income securities. The Fund’s benchmark is the Six-Month T-Bill.

The Portfolio Manager

Smith Breeden Associates, Inc.

Smith Breeden Associates, Inc. (“Smith Breeden”) is the subadvisor for the Fund. Smith Breeden, located at 100 Europa Drive, Suite 200, Chapel Hill, NC., was founded in 1982. Smith Breeden is a money management and consulting firm involved in money management for separate accounts such as pensions and endowments, financial institution consulting and investment advice, and equity investments. The firm specializes in high credit quality fixed-income investments, interest rate risk management, and the application of option pricing to banking and investments. As of March 31, 2007, Smith Breeden advised or managed assets of approximately $32 billion.

Smith Breeden believes that innovative research provides critical insights into the fixed-income market. The firm’s experienced investment professionals apply these research insights to the management of investment portfolios designed to achieve their clients’ objectives. The key tenets of this market-tested investment philosophy are:

| | • | | Over a market cycle, a portfolio of fixed-income securities with wide risk-adjusted spreads produces an attractive total return in comparison to the market return. |

| | • | | The incremental return available from security selection and sector allocation, based on careful relative-value analysis, quantitative research, and experienced market judgment, is more consistent than the incremental return from predicting the direction of interest rates. |

| | • | | Within the investment grade fixed-income market, the spread sectors i.e., corporate bonds, mortgage-backed securities (MBS), commercial MBS (CMBS), and asset-backed securities (ABS) will tend to outperform Treasury securities over a market cycle. The mortgage, corporate, CMBS, and ABS sectors also offer the greatest active management opportunity for adding value through security selection. |

The portfolio management team at Smith Breeden Associates, Inc. specializes in analyzing and investing in mortgage securities. Through careful analysis and comparison of the characteristics of these securities, such as type of issuer, coupon, maturity, geographic structure, and prepayment rates, the portfolio manager seeks to structure

4

Managers Short Duration Government Fund

Portfolio Manager’s Comments (continued)

a portfolio with similar risk characteristics to six-month U.S. Treasury securities and slightly higher returns. Because there is less certainty about the timing of principal payments to individual mortgage securities than for U.S. Treasury securities, they tend to carry a slightly higher yield. A properly structured portfolio of mortgage securities, however, can have a highly predictable cash flow while maintaining a yield advantage over Treasuries. Although the portfolio management team often purchases securities with maturities longer than six months, it does not attempt to increase returns by actively positioning the interest rate sensitivity of the portfolio. Instead the team typically manages the weighted average duration of the Portfolio so that it remains close to six months.

The ideal investment exhibits many of the following traits:

| | • | | Yield advantage over Treasuries |

| | • | | Very high quality (AAA or Government) |

| | • | | Attractive value relative to other MBS opportunities |

The portfolio:

| | • | | Seeks to optimize return per unit of risk |

| | • | | Minimal exposure to credit risk and interest rate risk |

| | • | | Consists of high quality MBS, CMBS, and ABS securities |

| | • | | Will tend to have an interest-rate sensitivity similar to a Six-month Treasury Bill |

The investment team will make a sell decision when:

| | • | | They no longer view the bonds as attractive |

| | • | | They deem it necessary to reallocate the Portfolio |

| | • | | To maintain the Portfolio’s target duration |

The Year in Review

During the 12 months ended March 31, 2007, the Fund returned +5.05% compared to +5.10% for its benchmark, the Six-Month T-Bill.

The Federal Open Market Committee (FOMC) ended its campaign of policy rate hikes during the summer of 2006 as the yield curve continued to flatten, and even invert. All told, the FOMC raised short-term rates a total of 17 times before finally halting. The FOMC actions continued to provide better yields for very short-term instruments such as Treasury Bills. Meanwhile, the market has revealed that its concern about the possibility of economic weakness outweighs the threat of inflation and has anticipated FOMC rate cuts in the near future. Thus, the treasury yield curve for maturities beyond three years has dropped over the past several months and regained an upward slope. Now, the FOMC is left with the task of balancing inflation concerns and concerns about U.S. economic growth in deciding its next move with respect to interest rates.

The investment team at Smith Breeden has focused almost exclusively on the securitized portions of the bond market in subadvising this Fund. This has included the

5

Managers Short Duration Government Fund

Portfolio Manager’s Comments (continued)

mortgage-backed securities (MBS), asset-backed securities (ABS), and commercial mortgage-backed securities (CMBS) sectors. As noted in its investment philosophy, Smith Breeden believes these instruments should offer a yield advantage over Treasuries given their added risks. That said, the yield spreads available within these sectors over the past year have been very narrow on average, leading Smith Breeden to maintain the Portfolio’s interest rate sensitivity (duration) and sensitivity to overall changes in yield spreads (spread duration) at minimal levels; the duration of the Fund has been less than six months for most of the year, and the spread duration remains close to zero. Hence, the Fund’s returns have been very closely aligned with the six-month Treasury Bill. While it is often tempting for portfolio managers to extend risk and reach for returns, it takes discipline to remain patient and accept what the environment offers. The portfolio management team has limited itself to adding value through individual security selection and pockets of investment opportunities within the securitized market.

The Fund lagged its benchmark very modestly throughout most of the fiscal year and then made up most of the ground in the final months. One of the pockets where the investment team had positioned the Portfolio throughout the year was in 15-year mortgage pools. The steepening of the yield curve (beyond three-years) helped 15-year MBS outperform 30-year issues and benefited higher coupon relative to lower coupon securities. In addition, the steepening of the yield curve combined with a weak housing market boosted returns of hedged interest-only strips (IOs) in which Smith Breeden had built a modest position. Finally, the Fund’s significant position in adjustable rate mortgages (ARMs) performed well over the last few months as ARMs were scheduled to be added to the Lehman Mortgage Index beginning April 1, 2007.

Looking Forward

The positioning of the Fund as of the end of the first quarter of 2007 looks similar to the positioning throughout the course of the past year. Smith Breeden maintains a core portfolio of mortgage pools, while maintaining a limited position in IO mortgage securities along with high-quality CMBS. The bulk of the Fund, however, remains in conventional fixed-rate mortgage pools, with a significant percentage in ARMs. As ARMs became more expensive throughout the first quarter 2007, the portfolio managers did opportunistically sell certain positions into the strength. The Fund maintains a sensitivity to overall changes in yield spreads (spread duration) to a minimum, although the rise in volatility in the first quarter of 2007 potentially foreshadows an opportunity to raise spread duration exposure as spreads begin to expand.

6

Managers Short Duration Government Fund

Portfolio Manager’s Comments (continued)

Cumulative Total Return Performance

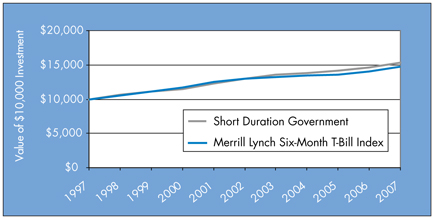

Managers Short Duration Government Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all distributions were reinvested. The Merrill Lynch Six-Month T-Bill Index is an unmanaged index that measures returns of six-month treasury bills. Unlike the Fund, the Merrill Lynch Six-Month T-Bill Index is unmanaged, is not available for investment, and does not incur expenses. The chart illustrates the performance of a hypothetical $10,000 investment made in the Fund on March 31, 1997 to a $10,000 investment made in the Merrill Lynch Six-Month T-Bill Index for the same time periods. Figures include reinvestment of capital gains and dividends. The listed returns for the Fund are net of expenses and the returns for the indices exclude expenses. Total returns for the Fund would have been lower had certain expenses not been reduced.

The table below shows the average annualized total returns for the Managers Short Duration Government Fund and the Merrill Lynch Six-Month T-Bill Index for the 1, 5 and 10 year periods ended March 31, 2007.

| | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS: | | One

Year | | | Five

Years | | | Ten

Years | |

Short Duration Government | | 5.05 | % | | 3.28 | % | | 4.35 | % |

Merrill Lynch Six-Month T-Bill Index | | 5.10 | % | | 2.68 | % | | 3.99 | % |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and the principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end please call (800) 835-3879 or visit our Web site at www.managersinvest.com.

Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed-income securities to fall.

7

Managers Short Duration Government Fund

Portfolio Manager’s Comments (continued)

The Fund may use derivative instruments for hedging purposes or as part of its investment strategy. There is also a risk that a derivative intended as a hedge may not perform as expected. The main risk with derivatives is that some types can amplify a gain or loss, potentially earning or losing substantially more money than the actual cost of the derivative or that the counterparty may fail to honor its contract terms, causing a loss for the Fund. Use of these instruments may involve certain costs and risks such as liquidity risk, interest rate risk, market risk, credit risk, management risk and the risk that a fund could not close out a position when it would be most advantageous to do so.

The Merrill Lynch Six-Month T-Bill Index is an unmanaged index that measures returns of six-month Treasury Bills. Unlike the Funds, the Merrill Lynch Six-Month T-Bill Index and the Citigroup Mortgage Index are unmanaged, not available for investment, and do not incur expenses.

Not FDIC insured, nor bank guaranteed. May lose value.

8

Managers Short Duration Government Fund

Fund Snapshots

March 31, 2007

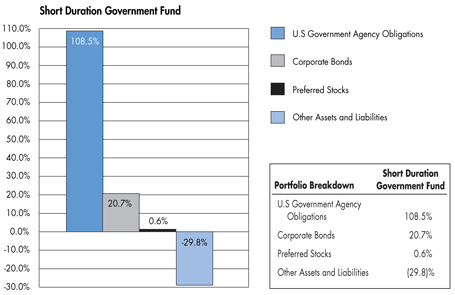

Portfolio Breakdown (as a % of net assets)

Short Duration Government Fund

Top Ten Holdings

| | | |

Top Ten Holdings (out of 190 securities) | | % of

Net Assets | |

FHLMC, 5.570%, 06/15/35* | | 5.4 | % |

FHLMC Gold Pool, 6.000%, TBA | | 5.1 | |

GMAC, 7.724%, 03/15/33* | | 4.3 | |

FHLMC Gold Pool, 6.000%, 10/01/21 | | 3.9 | |

FNMA Whole Loan, 5.520%, 05/25/35* | | 3.8 | |

FNMA, 6.500%, TBA | | 3.4 | |

FHLMC, 6.000%, 02/01/22 | | 3.3 | |

FNMA, 5.720%, 07/25/44* | | 3.2 | |

GNMA, 4.500%, 07/20/35* | | 3.1 | |

FHLMC Gold Pool, 4.000%, 12/01/20 | | 2.7 | |

| | | |

Top Ten as a Group | | 38.2 | % |

| | | |

| * | Top Ten Holding at September 30, 2006. |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security.

9

Managers Short Duration Government Fund

Schedule of Portfolio Investments

March 31, 2007

| | | | | | |

| | | Principal Amount | | Value |

U.S. Government and Agency Obligations – 108.5%1 | | | | | | |

Federal Home Association/Veteran’s Association – 0.5% | | | | | | |

FHA/VA, 5.750%, 08/20/23, (10/01/07) 2 | | $ | 143,151 | | $ | 144,424 |

FHA/VA, 6.125%, 10/20/17 to 12/20/25, (01/01/08) 2,9 | | | 736,096 | | | 745,354 |

Total Federal Home Association/Veteran’s Association | | | | | | 889,778 |

Federal Home Loan Mortgage Corporation – 34.4% | | | | | | |

FHLMC, 2.783%, 07/01/34, (06/01/07) 2,9 | | | 1,602,156 | | | 1,598,720 |

FHLMC, 3.036%, 05/01/34, (06/01/07) 2,9 | | | 872,514 | | | 869,098 |

FHLMC, 5.000%, 06/01/09 to 05/01/18 9 | | | 4,642,057 | | | 4,588,958 |

FHLMC, 5.500%, 11/01/17 to 09/01/19 | | | 2,542,861 | | | 2,552,796 |

FHLMC, 5.500%, TBA | | | 1,150,000 | | | 1,152,155 |

FHLMC, 5.570%, 06/15/35, (04/15/07) 2,9 | | | 9,777,884 | | | 9,717,481 |

FHLMC, 6.000%, 09/01/17 to 05/01/35 | | | 12,357,014 | | | 12,553,983 |

FHLMC, 7.500%, 04/01/15 | | | 645,973 | | | 668,745 |

FHLMC Gold Pool, 4.000%, 12/01/20 9 | | | 5,062,765 | | | 4,780,851 |

FHLMC Gold Pool, 5.000%, 04/01/19 to 08/01/19 | | | 932,600 | | | 921,144 |

FHLMC Gold Pool, 6.000%, 09/01/17 to 11/01/21 | | | 11,797,521 | | | 11,994,924 |

FHLMC Gold Pool, 6.000%, TBA | | | 9,000,000 | | | 9,146,250 |

FHLMC Gold Pool, 7.500%, 04/01/15 to 04/01/29 | | | 304,496 | | | 317,044 |

FHLMC Gold Pool, 8.500%, 12/01/25 9 | | | 94,254 | | | 101,129 |

FHLMC Structured Pass Through Securities, 4.391%, 11/25/38 | | | 468,792 | | | 464,348 |

FHLMC Structured Pass Through Securities, 7.500%, 02/25/42 | | | 186,885 | | | 194,596 |

FHLMC Structured Pass Through Securities, 7.500%, 08/25/42 11 | | | 306,896 | | | 317,829 |

Total Federal Home Loan Mortgage Corporation | | | | | | 61,940,051 |

Federal National Mortgage Association – 52.0% | | | | | | |

FNMA, 3.180%, 07/25/44 | | | 10,502 | | | 10,460 |

FNMA, 4.568%, 01/01/33, (12/01/07) 2 | | | 691,526 | | | 694,757 |

FNMA, 5.000%, 07/01/18 to 01/01/19 9 | | | 4,402,449 | | | 4,349,497 |

FNMA, 5.250%, 04/15/07 | | | 60,000 | | | 59,997 |

FNMA, 5.430%, 09/26/33, (04/26/07) 2 | | | 38,648 | | | 38,654 |

FNMA, 5.460%, 10/25/33, (04/25/07) 2 | | | 540,240 | | | 540,915 |

FNMA, 5.480%, 06/25/35, (04/25/07) 2,9 | | | 1,613,714 | | | 1,616,025 |

The accompanying notes are an integral part of these financial statements.

10

Managers Short Duration Government Fund

Schedule of Portfolio Investments (continued)

| | | | | | |

| | | Principal Amount | | Value |

Federal National Mortgage Association - 52.0% (continued) | | | | | | |

FNMA, 5.500%, 12/01/18 to 05/01/21 9 | | $ | 21,954,619 | | $ | 22,010,847 |

FNMA, 5.500%, TBA | | | 600,000 | | | 593,625 |

FNMA, 5.507%, 05/01/36, (05/01/11) 2 | | | 945,791 | | | 951,898 |

FNMA, 5.568%, 05/01/36, (05/01/11) 2 | | | 1,801,765 | | | 1,816,163 |

FNMA, 5.640%, 11/25/30, (04/25/07) 2,9 | | | 3,906,404 | | | 3,911,056 |

FNMA, 5.662%, 09/01/33, (09/01/07) 2,9 | | | 1,654,920 | | | 1,673,498 |

FNMA, 5.700%, 07/01/09 | | | 917,368 | | | 914,512 |

FNMA, 5.720%, 03/25/35 to 07/25/44, (04/25/07) 2,9 | | | 13,340,824 | | | 13,389,089 |

FNMA, 5.730%, 11/01/08 | | | 266,484 | | | 266,915 |

FNMA, 6.000%, 03/01/17 to 08/01/17 | | | 1,002,407 | | | 1,020,332 |

FNMA, 6.000%, TBA | | | 5,400,000 | | | 5,456,939 |

FNMA, 6.010%, 12/01/08 9 | | | 4,348,297 | | | 4,371,622 |

FNMA, 6.040%, 10/01/08 9 | | | 1,138,323 | | | 1,142,420 |

FNMA, 6.305%, 02/01/08 | | | 10,323 | | | 10,296 |

FNMA, 6.473%, 10/25/31 12 | | | 254,064 | | | 253,114 |

FNMA, 6.500%, 04/01/17 9 | | | 1,075,946 | | | 1,102,240 |

FNMA, 6.500%, TBA | | | 6,000,000 | | | 6,120,000 |

FNMA, 6.510%, 01/01/08 | | | 145,450 | | | 145,355 |

FNMA, 6.620%, 01/01/08 to 11/01/07 9 | | | 1,822,406 | | | 1,819,065 |

FNMA, 6.740%, 06/01/09 | | | 908,104 | | | 905,611 |

FNMA, 6.750%, 08/01/07 9 | | | 1,753,112 | | | 1,748,314 |

FNMA, 6.825%, 09/01/07 9 | | | 2,238,080 | | | 2,232,093 |

FNMA, 7.500%, 10/01/15 to 12/25/42 9 | | | 3,888,930 | | | 4,047,833 |

FNMA Grantor Trust, 5.470%, 01/25/35, (04/25/07) 2,9 | | | 833,436 | | | 834,035 |

FNMA Grantor Trust, 5.560%, 05/25/32, (04/25/07) 2 | | | 877,247 | | | 877,247 |

FNMA Grantor Trust, 5.600%, 03/25/33, (04/25/07) 2 | | | 394,826 | | | 394,828 |

FNMA Whole Loan, 5.520%, 05/25/35, (04/25/07) 2,9 | | | 6,901,167 | | | 6,922,971 |

FNMA Whole Loan, 5.770%, 02/25/47, (04/25/07) 2 | | | 1,412,511 | | | 1,421,119 |

Total Federal National Mortgage Association | | | | | | 93,663,342 |

Government National Mortgage Association – 17.2% | | | | | | |

GNMA, 4.500%, 07/20/35 to 09/20/35, (10/01/07) 2 | | | 10,306,116 | | | 10,260,471 |

GNMA, 4.750%, 01/20/32, (04/01/08) 2 | | | 397,221 | | | 398,355 |

The accompanying notes are an integral part of these financial statements.

11

Managers Short Duration Government Fund

Schedule of Portfolio Investments (continued)

| | | | | | |

| | | Principal Amount | | Value |

Government National Mortgage Association - 17.2% (continued) | | | | | | |

GNMA, 5.000%, 03/20/35 to 09/20/35, (07/01/07 to 04/01/08) 2 | | $ | 3,758,279 | | $ | 3,781,925 |

GNMA, 5.250%, 01/20/28, (04/01/08) 2 | | | 160,034 | | | 161,203 |

GNMA, 5.375%, 03/20/21 to 05/20/33, (07/01/07 to 04/01/08) 2 | | | 3,171,825 | | | 3,203,456 |

GNMA, 5.500%, 08/20/32 to 10/20/34, (10/01/07 to 04/01/08) 2 | | | 10,341,649 | | | 10,420,888 |

GNMA, 5.750%, 07/20/18 to 08/20/26, (10/01/07) 2 | | | 549,605 | | | 555,214 |

GNMA, 6.000%, 07/20/28 9 | | | 168,060 | | | 167,751 |

GNMA, 6.000%, 10/20/32, (01/01/08) 2 | | | 798,488 | | | 807,140 |

GNMA, 6.125%, 11/20/17 to 11/20/27, (01/01/08) 2 | | | 1,086,927 | | | 1,099,553 |

GNMA, 9.500%, 07/15/09 to 12/15/17 | | | 30,094 | | | 32,271 |

Total Government National Mortgage Association | | | | | | 30,888,227 |

Interest Only Strips – 2.2% | | | | | | |

FHLMC IO Strip, 1.780%, 11/15/30, (04/15/07) 2 | | | 411,422 | | | 18,352 |

FHLMC IO Strip, 4.500%, 08/15/35 to 09/15/35 | | | 996,235 | | | 237,617 |

FHLMC IO Strip, 5.000%, 05/15/18 to 08/01/35 | | | 7,333,876 | | | 1,624,109 |

FHLMC IO Strip, 7.500%, 10/01/27 | | | 75,409 | | | 17,901 |

FHLMC IO Strip, 8.000%, 06/01/31 | | | 18,213 | | | 4,429 |

FNMA IO Strip, 1.906%, 01/25/24, (04/25/07) 2 | | | 135,808 | | | 8,706 |

FNMA IO Strip, 2.500%, 10/01/36 | | | 581,323 | | | 139,728 |

FNMA IO Strip, 5.000%, 02/01/35 to 12/01/35 | | | 8,069,299 | | | 1,882,353 |

FNMA IO Strip, 7.500%, 11/18/14 | | | 180,809 | | | 21,584 |

FNMA IO Strip, 8.000%, 08/25/22 to 05/01/30 | | | 284,269 | | | 63,791 |

FNMA IO Strip, 9.000%, 12/15/16 | | | 71,073 | | | 17,331 |

Total Interest Only Strips | | | | | | 4,035,901 |

U.S. Treasury Notes- 2.2% | | | | | | |

USTN, 2.375%, 04/15/11 9 | | | 2,639,744 | | | 2,674,082 |

USTN, 2.625%, 05/15/08 7 | | | 1,260,000 | | | 1,229,731 |

Total U.S. Treasury Notes | | | | | | 3,903,813 |

Total U.S. Government and Agency Obligations (cost $195,264,133) | | | | | | 195,321,112 |

The accompanying notes are an integral part of these financial statements.

12

Managers Short Duration Government Fund

Schedule of Portfolio Investments (continued)

| | | | | | |

| | | Principal Amount | | Value |

Corporate Bonds – 20.7% | | | | | | |

Asset-Backed Securities – 20.4% | | | | | | |

Asset Securitization Corp., 7.040%, 11/13/29 | | $ | 476,664 | | $ | 479,706 |

Countrywide Home Loans, 5.820%, 02/25/35, (04/25/07) 2,9 | | | 2,727,039 | | | 2,741,480 |

Deutsche Alt-A Securities Inc. Mortgage Loan, 6.250%, 07/25/36 11 | | | 1,038,576 | | | 1,040,077 |

DLJ Commercial Mortgage Corp., 6.410%, 06/10/31 | | | 1,226,640 | | | 1,236,181 |

FNMA Grantor Trust Pass Through, Series 2004-T1, Class 1A2, 6.500%, 01/25/44 | | | 1,124,751 | | | 1,154,237 |

First Franklin Mortgage Loan Asset Backed Certificates, Series | | | | | | |

2005-FF10, Class A4, 5.640%, 11/25/35, (04/25/07) 2 | | | 1,800,000 | | | 1,801,542 |

GE Capital Commercial Mortgage Corporation, 6.496%, 01/15/33 | | | 525,000 | | | 546,374 |

GMAC, 6.957%, 09/15/35 | | | 1,570,000 | | | 1,657,109 |

GMAC, 7.724%, 03/15/33 9 | | | 7,338,580 | | | 7,733,579 |

GMAC, Series 2000-C2, Class A2, 7.455%, 08/16/33 | | | 1,055,433 | | | 1,115,954 |

Greenwich Capital Commercial Funding Corp., Class A2, Series 2005-GG3, 4.305%, 08/10/42 | | | 1,754,000 | | | 1,720,172 |

Harborview Mortgage Loan Trust, 5.730%, 11/19/34, (04/19/07) 2 | | | 3,017,047 | | | 3,025,360 |

Lehman Brothers Mortgage Trust, 6.000%, 08/25/21 | | | 2,812,758 | | | 2,854,235 |

Merrill Lynch Mortgage Investors, Inc., 7.560%, 11/15/31 | | | 2,513,068 | | | 2,613,107 |

PNC Mortgage Acceptance, 7.300%, 10/12/33 | | | 2,318,310 | | | 2,434,722 |

Salomon Brothers Mortgage, 7.455%, 07/18/33 | | | 313,042 | | | 328,926 |

Structured Asset Investment Loan Trust, 5.860%, 12/25/34, (04/25/07) 2,9 | | | 2,652,492 | | | 2,658,570 |

Washington Mutual, Class 2A3, Series 2005-AR2, 5.670%, 01/25/45, (04/25/07) 2 | | | 1,665,642 | | | 1,667,864 |

Total Asset-Backed Securities | | | | | | 36,809,195 |

Asset-Backed Interest Only Strips – 0.3% | | | | | | |

Bank of America-First Union IO Strip, Series 2001-3, Class XC, 0.474%, 04/11/37 3,11 | | | 4,967,521 | | | 205,974 |

CS First Boston Mortgage IO Strip, 0.552%, 12/15/35 3,11 | | | 1,674,378 | | | 66,168 |

CS First Boston Mortgage Sec. Corp. IO Strip, Series 1998-C1, Class AX, 0.983%, 05/17/40 11 | | | 3,193,750 | | | 78,242 |

The accompanying notes are an integral part of these financial statements.

13

Managers Short Duration Government Fund

Schedule of Portfolio Investments (continued)

| | | | | | | |

| | | Principal Amount | | Value | |

Asset-Backed Interest Only Strips - 0.3% (continued) | | | | | | | |

GMAC, Series 1999-C1 IO Strip, Class X, 0.586%, 05/15/33 11 | | $ | 9,751,603 | | $ | 123,393 | |

Total Asset-Backed Interest Only Strips | | | | | | 473,777 | |

Total Corporate Bonds (cost $38,885,791) | | | | | | 37,282,972 | |

| | |

| | | Shares | | | |

Preferred Stock – 0.6%3 | | | | | | | |

Home Ownership Funding Corp., 1.000% (cost $1,457,704) | | | 7,300 | | | 1,082,086 | |

Short-Term Investments – 4.2% | | | | | | | |

Other Investment Companies – 4.0%4 | | | | | | | |

Bank of New York Institutional Cash Reserves Fund, 5.34% 8 | | | 1,269,868 | | | 1,269,868 | |

JPMorgan Prime Money Market Fund, Institutional Class Shares, 5.19% | | | 5,899,183 | | | 5,899,183 | |

Total Other Investment Companies | | | | | | 7,169,051 | |

| | |

| | | Principal Amount | | | |

U.S. Government Agency Discount Notes - 0.2%5,6 | | | | | | | |

FHLMC Discount Notes, 5.104%, 11/09/07 10 | | $ | 350,000 | | | 339,322 | |

Total Short-Term Investments (cost $7,508,162) | | | | | | 7,508,373 | |

Total Investments - 134.0% (cost $243,115,790) | | | | | | 241,194,543 | |

Other Assets, less Liabilities - (34.0)% | | | | | | (61,210,400 | ) |

Net Assets - 100.0% | | | | | $ | 179,984,143 | |

The accompanying notes are an integral part of these financial statements.

14

Managers Intermediate Duration Government Fund

Portfolio Manager’s Comments

The Managers Intermediate Duration Government Fund’s objective is to achieve total return in excess of the total return of the major market indexes for mortgage-backed securities.

The Managers Intermediate Duration Government Fund seeks to achieve its objective by matching the duration, or interest-rate risk, of a portfolio that invests exclusively in mortgage-backed securities, as weighted in the major market indexes for mortgage-backed securities. These indexes currently include the Citigroup Mortgage Index and the Lehman Brothers Mortgage Index, each of which includes all outstanding government sponsored fixed-rate mortgage-backed securities, weighted in proportion to their current market capitalization. The duration of these indexes is generally similar to that of intermediate-term U.S. Treasury Notes, and typically will range between three and five years.

Under normal circumstances, the Fund will invest at least 80% of its assets in debt securities issued by the U.S. Government, its agencies and instrumentalities, and synthetic instruments or derivatives, or securities having economic characteristics similar to such debt securities. The Fund’s benchmark is the Citigroup Mortgage Index.

The Portfolio Manager

Smith Breeden Associates, Inc.

Smith Breeden Associates, Inc. (“Smith Breeden”) is the subadvisor for the Managers Intermediate Duration Government Bond Fund. Smith Breeden, located at 100 Europa Drive, Suite 200, Chapel Hill, NC., was founded in 1982. Smith Breeden is a money management and consulting firm involved in money management for separate accounts such as pensions and endowments, financial institution consulting and investment advice, and equity investments. The firm specializes in high credit quality fixed-income investments, interest rate risk management, and the application of option pricing to banking and investments. As of March 31, 2007, Smith Breeden advised or managed assets of approximately $32 billion.

Smith Breeden believes that innovative research provides critical insights into the fixed-income market. The firm’s experienced investment professionals apply these research insights to the management of investment portfolios designed to achieve our clients’ objectives. The key tenets of this market-tested investment philosophy are:

| | • | | Over a market cycle, a portfolio of fixed-income securities with wide risk-adjusted spreads produces an attractive total return in comparison to the market return. |

| | • | | The incremental return available from security selection and sector allocation, based on careful relative-value analysis, quantitative research, and experienced market judgment, is more consistent than the incremental return from predicting the direction of interest rates. |

| | • | | Within the investment grade fixed-income market, the spread sectors i.e., corporate bonds, mortgage-backed securities (MBS), commercial MBS (CMBS), and asset-backed securities (ABS) will tend to outperform Treasury securities over a market cycle. The mortgage, corporate, CMBS, and ABS sectors also offer the greatest active management opportunity for adding value through security selection. |

15

Managers Intermediate Duration Government Fund

Portfolio Manager’s Comments (continued)

The portfolio management team at Smith Breeden Associates specializes in analyzing and investing in mortgage-backed securities. Through careful analysis and comparison of the characteristics of these securities, such as type of issuer, coupon, maturity, geographic structure, and historic and prospective prepayment rates, the team seeks to structure a portfolio that will outperform the Citigroup Mortgage Index. While the portfolio managers will purchase securities of any maturity or duration, they do not attempt to add value by actively positioning the interest rate sensitivity of the portfolio. Instead, they typically manage the weighted average duration of the portfolio so that it is similar to that of the duration of the Citigroup Mortgage Index.

The ideal investment exhibits many of the following traits:

| | • | | Very high quality (AAA or Government) |

| | • | | Attractive value relative to other MBS opportunities |

The portfolio managers limit purchases to securities from the following asset classes:

| | • | | Securities issued directly or guaranteed by the U.S. Government or its agencies or instrumentalities |

| | • | | Mortgage-backed securities rated AAA Standard & Poor’s Corporation (“S&P”) or Aaa by Moody’s Investors Service, Inc. (“Moody’s”) |

| | • | | Securities fully collateralized by assets in either of the above classes |

| | • | | Assets which would qualify as liquidity items under federal regulations (which may change from time to time) if held by a commercial bank or savings institution; and hedge instruments |

| | • | | Stripped mortgage-backed securities, which may only be used for risk management purposes |

The investment team will make a sell decision when:

| | • | | They no longer view the bonds as attractive |

| | • | | To maintain the portfolio’s target duration |

| | • | | For portfolio allocation purposes |

The Year in Review

During the 12 months ended March 31, 2007, the Fund returned +6.30% compared to +6.97% for its benchmark, the Citigroup Mortgage Index (“Citi Mortgage”).

The Federal Open Market Committee (FOMC) ended its campaign of policy rate hikes during the summer of 2006 as the yield curve continued to flatten, and even invert. All told, the FOMC raised short-term rates a total of 17 times before finally halting. The FOMC actions continued to provide better yields for very short-term instruments such as Treasury bills. Meanwhile, the market has revealed that its concern about the possibility of economic weakness outweighs the threat of inflation and has anticipated FOMC rate cuts in the near future. Thus, the treasury yield curve for maturities beyond three years has dropped over the past several months and regained an upward slope. Now,

16

Managers Intermediate Duration Government Fund

Portfolio Manager’s Comments (continued)

the FOMC is left with the task of balancing inflation concerns and concerns about U.S. economic growth in deciding their next move with respect to interest rates.

The investment team at Smith Breeden has focused almost exclusively on the securitized portions of the bond market in subadvising this Fund. This has included the mortgage-backed securities (MBS), asset-backed securities (ABS), and commercial mortgage-backed securities (CMBS) sectors. However, the yield spreads available within these sectors over the past year have been very narrow on average, leading Smith Breeden to maintain the Portfolio’s interest rate sensitivity (duration) and sensitivity to overall changes in yield spreads (spread duration) at levels closely aligned with the Citigroup Mortgage Index. Hence, the Fund’s returns have been very closely aligned with the benchmark. While it is often tempting for portfolio managers to extend risk and reach for returns, it takes discipline to remain patient and accept what the environment offers. The portfolio management team has limited itself to adding value through individual security selection and pockets of investment opportunities within the securitized market.

The Fund lagged its benchmark very modestly throughout most of the fiscal year and made up some ground in the final month. Over recent years mortgage benchmark indexes have been difficult to outperform on a consistent basis. This is because many of the securities included in MBS benchmarks are “seasoned” bonds that have very little liquidity, and are thus difficult for portfolio managers to obtain with any consistency. Because they are so thinly traded, they may offer yields that are higher than those typically available in the marketplace. Within the set of available securities, the portfolio managers were able to add value. One of the pockets where the investment team had positioned the Portfolio throughout the year was in 15-year mortgage pools. The steepening of the yield curve (beyond three years) over the last few months helped 15-year MBS outperform 30-year issues and benefited higher coupon securities relative to lower coupon securities. In addition, the steepening of the yield curve combined with a weak housing market boosted returns of hedged interest-only strips (IOs) in which Smith Breeden had built a modest position. Finally, the Fund’s significant position in adjustable rate mortgages (ARMs) performed well over the last few months as ARMs were scheduled to be added to the Lehman Mortgage Index beginning April 1, 2007.

Looking Forward

The positioning of the Fund as of the end of March 2007 looks similar to the positioning throughout the course of the past year. Smith Breeden continues to maintain a core portfolio of mortgage pools, while maintaining a limited position in IO mortgage securities along with high quality CMBS. Smith Breeden reduced exposure over the last three months to 30-year FNMA 6.5% coupons in favor of FNMA 5.5% and 6.0% coupons. The bulk of the Fund remains in conventional fixed-rate mortgage pools, with a significant percentage in ARMs. As ARMs became more expensive throughout the course of the first quarter, the portfolio managers did opportunistically sell certain positions into the strength. The management team has kept the Fund’s sensitivity to overall changes in yield spreads (spread duration) closely in line with the benchmark, although the rise in volatility in the first quarter of 2007 could foreshadow an opportunity to raise spread duration exposure as spreads begin to expand.

17

Managers Intermediate Duration Government Fund

Portfolio Manager’s Comments (continued)

Cumulative Total Return Performance

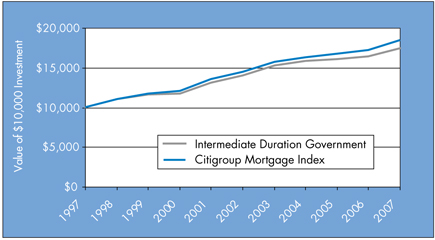

Managers Intermediate Duration Government Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all distributions were reinvested. Unlike the Fund, the Citigroup Mortgage Index is unmanaged, is not available for investment, and does not incur expenses. The chart illustrates the performance of a hypothetical $10,000 investment made in the Fund on March 31, 1997 to a $10,000 investment made in the Citigroup Mortgage Index for the same time periods. Figures include reinvestment of capital gains and dividends. The listed returns for the Fund are net of expenses and the returns for the indices exclude expenses. Total returns for the Fund would have been lower had certain expenses not been reduced.

The table below shows the average annualized total returns for the Managers Intermediate Duration Government Fund and the Citigroup Mortgage Index for the 1, 5 and 10 year periods ended March 31, 2007.

| | | | | | | | | |

AVERAGE ANNUAL TOTAL RETURNS: | | One

Year | | | Five

Years | | | Ten

Years | |

Intermediate Duration Government | | 6.30 | % | | 4.50 | % | | 5.78 | % |

Citigroup Mortgage Index | | 6.97 | % | | 5.01 | % | | 6.33 | % |

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and the principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. For performance information through the most recent month end please call (800) 835-3879 or visit our Web site at www.managersinvest.com.

Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed-income securities to fall.

18

Managers Intermediate Duration Government Fund

Portfolio Manager’s Comments (continued)

The Fund may use derivative instruments for hedging purposes or as part of its investment strategy. There is also a risk that a derivative intended as a hedge may not perform as expected. The main risk with derivatives is that some types can amplify a gain or loss, potentially earning or losing substantially more money than the actual cost of the derivative or that the counterparty may fail to honor its contract terms, causing a loss for the Fund. Use of these instruments may involve certain costs and risks such as liquidity risk, interest rate risk, market risk, credit risk, management risk and the risk that a fund could not close out a position when it would be most advantageous to do so.

Not FDIC insured, nor bank guaranteed. May lose value.

19

Managers Intermediate Duration Government Fund

Fund Snapshots

March 31, 2007

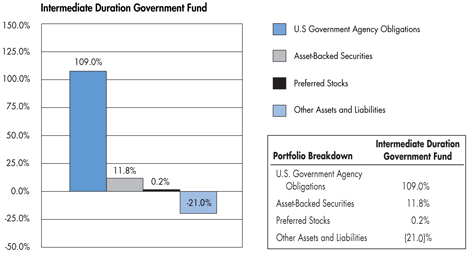

Portfolio Breakdown (as a % of net assets)

Intermediate Duration Government Fund

Top Ten Holdings

| | | |

Top Ten Holdings (out of 163 securities) | | % of

Net Assets | |

FHLMC Gold Pool, 5.500%, 02/01/35* | | 6.4 | % |

FNMA, 5.500%, TBA | | 6.3 | |

FHLMC, 5.628%, 01/01/36* | | 6.3 | |

FNMA, 6.500%, TBA | | 5.9 | |

FHLMC Gold Pool, 5.500%, 06/01/35* | | 5.7 | |

FNMA, 5.500%, TBA | | 5.5 | |

FHLMC, 5.000%, TBA | | 5.3 | |

FHLMC, 6.000%, 10/01/21 | | 4.9 | |

FHLMC Gold Pool, 5.500%, 01/01/35* | | 4.4 | |

FNMA, 4.500%, 09/01/35 | | 2.9 | |

| | | |

Top Ten as a Group | | 53.6 | % |

| | | |

| | * | Top Ten Holding at September 30, 2006. |

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security.

20

Managers Intermediate Duration Government Fund

Schedule of Portfolio Investments

March 31, 2007

| | | | | | |

| | | Principal Amount | | Value |

U.S. Government and Agency Obligations – 109.0%1 | | | | | | |

Federal Home Loan Mortgage Corporation – 60.0% | | | | | | |

FHLMC, 4.500%, 04/01/35 | | $ | 789,490 | | $ | 743,167 |

FHLMC, 5.000%, 05/01/18 to 07/01/35 | | | 968,332 | | | 1,398,659 |

FHLMC, 5.000%, TBA | | | 10,000,000 | | | 9,662,500 |

FHLMC, 5.500%, 11/01/17 to 05/01/34 9 | | | 5,905,331 | | | 5,884,202 |

FHLMC, 5.628%, 01/01/36, (01/01/13) 2,9 | | | 11,480,310 | | | 11,499,153 |

FHLMC, 6.000%, 09/01/17 to 07/01/35 | | | 21,384,138 | | | 21,716,912 |

FHLMC, 6.000%, TBA | | | 2,000,000 | | | 2,032,500 |

FHLMC, 7.500%, 01/01/31 | | | 95,202 | | | 99,752 |

FHLMC Gold Pool, 4.000%, 12/01/20 | | | 1,066,431 | | | 1,007,048 |

FHLMC Gold Pool, 4.500%, 05/01/34 to 01/01/36 9 | | | 24,532,084 | | | 23,483,318 |

FHLMC Gold Pool, 5.000%, 04/01/19 to 08/01/19 | | | 3,968,336 | | | 3,748,826 |

FHLMC Gold Pool, 5.500%, 10/01/33 to 06/01/35 9 | | | 28,076,737 | | | 27,827,409 |

FHLMC, Series 2186, Class PG, 6.000%, 07/15/28 | | | 56,316 | | | 56,376 |

FHLMC Structured Pass Through Securities, 7.500%, 08/25/42 11 | | | 429,655 | | | 444,961 |

Total Federal Home Loan Mortgage Corporation | | | | | | 109,604,783 |

Federal National Mortgage Association – 43.7% | | | | | | |

FNMA, 4.500%, 03/01/35 to 10/01/35 9 | | | 12,353,184 | | | 11,614,916 |

FNMA, 5.000%, 06/01/18 to 01/01/20 9 | | | 5,160,359 | | | 5,098,491 |

FNMA, 5.000%, TBA | | | 600,000 | | | 591,563 |

FNMA, 5.500%, 03/01/17 to 02/01/35 9 | | | 17,300,236 | | | 17,302,039 |

FNMA, 5.500%, TBA | | | 21,700,000 | | | 21,597,568 |

FNMA, 5.590%, 02/01/36, (01/01/11) 2 | | | 500,115 | | | 502,725 |

FNMA, 5.640%, 11/25/30, (04/25/07) 2,9 | | | 3,906,404 | | | 3,911,056 |

FNMA, 5.720%, 03/25/35, (04/25/07) 2,9 | | | 2,922,001 | | | 2,923,897 |

FNMA, 6.000%, 08/01/17 | | | 593,471 | | | 604,041 |

FNMA, 6.000%, TBA | | | 1,000,000 | | | 1,016,250 |

FNMA, 6.500%, 11/01/28 to 07/01/32 | | | 779,200 | | | 798,004 |

FNMA, 6.500%, TBA | | | 10,500,000 | | | 10,710,000 |

FNMA, 7.000%, 03/25/24 9 | | | 2,750,000 | | | 2,872,165 |

The accompanying notes are an integral part of these financial statements.

21

Managers Intermediate Duration Government Fund

Schedule of Portfolio Investments (continued)

| | | | | | |

| | | Principal Amount | | Value |

Federal National Mortgage Association - 43.7% (continued) | | | | | | |

FNMA, 7.500%, 10/25/42 | | $ | 259,251 | | $ | 269,743 |

Total Federal National Mortgage Association | | | | | | 79,812,458 |

Government National Mortgage Association – 0.5% | | | | | | |

GNMA, 5.375%, 03/20/16 to 05/20/21, (07/01/07 to 04/01/08) 2 | | | 187,743 | | | 189,513 |

GNMA, 5.750%, 08/20/17 to 08/20/18, (10/01/07) 2 | | | 228,478 | | | 230,719 |

GNMA, 6.125%, 11/20/17 to 12/20/17, (01/01/08) 2 | | | 453,328 | | | 458,513 |

GNMA, 7.500%, 09/15/28 to 11/15/31 | | | 144,992 | | | 151,466 |

Total Government National Mortgage Association | | | | | | 1,030,211 |

Interest/Principal Only Strips – 3.6% | | | | | | |

FHLMC IO Strip, 1.380%, 11/15/18, (04/15/07) 2 | | | 912,116 | | | 42,210 |

FHLMC IO Strip, 1.780%, 11/15/30, (04/15/07) 2 | | | 334,160 | | | 14,905 |

FHLMC IO Strip, 2.330%, 09/15/16 to 10/15/16, (04/15/07) 2 | | | 750,617 | | | 35,009 |

FHLMC IO Strip, 2.580%, 06/15/31, (04/15/07) 2 | | | 119,330 | | | 11,912 |

FHLMC IO Strip, 4.500%, 04/15/22 to 09/15/35 | | | 1,881,319 | | | 410,225 |

FHLMC IO Strip, 5.000%, 05/15/17 9 | | | 10,977,683 | | | 2,472,793 |

FHLMC IO Strip, 6.000%, 05/01/31 | | | 14,531 | | | 3,118 |

FNMA IO Strip, 2.500%, 10/01/36 | | | 290,661 | | | 69,534 |

FNMA IO Strip, 4.000%, 09/01/33 to 09/01/34 | | | 1,844,563 | | | 243,770 |

FNMA IO Strip, 4.500%, 07/25/19 to 09/01/33 | | | 679,954 | | | 127,108 |

FNMA IO Strip, 5.000%, 11/01/33 to 12/01/35 | | | 11,414,734 | | | 2,640,265 |

FNMA IO Strip, 7.000%, 04/01/23 to 06/01/23 | | | 519,926 | | | 113,016 |

FNMA PO Strip, 5.462%, 07/01/33 5,10 | | | 549,755 | | | 407,511 |

Total Interest/Principal Only Strips | | | | | | 6,591,376 |

U.S. Treasury Notes – 1.2% | | | | | | |

USTN, 2.375%, 04/15/11 | | | 2,122,807 | | | 2,150,421 |

Total U.S. Government and Agency Obligations

(cost $199,827,759) | | | | | | 199,189,249 |

Asset-Backed Securities – 11.8% | | | | | | |

AHMA, Series 2005-1, Class 1A1, 6.030%, 11/25/35 11 | | | 548,088 | | | 557,351 |

American Home Loan Investment Trust,

5.294%, 06/25/45, (03/25/10) 2 | | | 3,204,901 | | | 3,207,398 |

The accompanying notes are an integral part of these financial statements.

22

Managers Intermediate Duration Government Fund

Schedule of Portfolio Investments (continued)

| | | | | | |

| | | Principal Amount | | Value |

Asset-Backed Securities - 11.8% (continued) | | | | | | |

American Home Mortgage Investment Trust, 3.280%, 04/25/44, (02/25/09) 2 | | $ | 350,587 | | $ | 341,306 |

American Home Mortgage Investment Trust, 4.390%, 02/25/45, (11/25/09) 2 | | | 1,585,725 | | | 1,564,116 |

American Home Mortgage Investment Trust, 5.001%, 06/25/45, (03/25/08) 2 | | | 383,795 | | | 381,957 |

Bank of America Funding Corp., 3.969%, 12/20/34 11 | | | 806,915 | | | 820,865 |

Bear Stearns Alt-A Trust, 4.917%, 04/25/35 11 | | | 585,725 | | | 581,761 |

Countrywide Alternative Loan Trust, 5.500%, 05/25/35, (04/25/07) 2 | | | 1,067,596 | | | 1,058,537 |

Countrywide Alternative Loan Trust, 6.000%, 06/25/34 | | | 783,354 | | | 790,587 |

Countrywide Home Loans, Inc., 4.501%, 05/20/35 11 | | | 355,690 | | | 352,967 |

Countrywide Home Loans, Inc., Series 2005-HYB8, Class 1A1, 5.047%, 12/20/35 11 | | | 335,591 | | | 339,858 |

Countrywide Home Loans, Inc., Series 2004-R2, Class 1AF1, 5.740%, 11/25/34, (04/25/07) 2,3 | | | 624,498 | | | 628,571 |

DLJ Commercial Mortgage Corp., 6.410%, 06/10/31 | | | 190,472 | | | 191,954 |

GSMPS Mortgage Loan Trust, 5.670%, 03/25/35, (04/25/07) 2,3 | | | 484,432 | | | 483,149 |

GSR Mortgage Loan Trust, 3.685%, 05/25/34, (04/25/07) 2 | | | 457,489 | | | 458,054 |

Harborview Mortgage Loan Trust, 3.749%, 11/19/34 11 | | | 549,443 | | | 553,828 |

Master Alternative Loans Trust, 6.000%, 01/25/35 9 | | | 1,738,208 | | | 1,743,909 |

Morgan Stanley Mortgage Loan Trust, 6.168%, 08/25/35 11 | | | 2,041,243 | | | 2,056,234 |

Merrill Lynch Mortgage Investors, Inc., 7.560%, 11/15/31 | | | 1,839,275 | | | 1,912,491 |

Structured Asset Securities Corp., Series 2005-RF1, Class A, 5.670%, 03/25/35, (04/25/07) 2,3 | | | 601,805 | | | 598,343 |

Washington Mutual Mortgage Pass-Through Certificates, 6.000%, 10/25/35 | | | 2,930,482 | | | 2,943,467 |

Total Asset-Backed Securities (cost $21,772,814) | | | | | | 21,566,703 |

| | |

| | | Shares | | |

Preferred Stocks - 0.2%3 | | | | | | |

Home Ownership Funding Corp., 1.000% | | | 1,500 | | | 222,347 |

Home Ownership Funding Corp. 2, 1.000% | | | 1,500 | | | 222,347 |

Total Preferred Stocks (cost $402,591) | | | | | | 444,694 |

The accompanying notes are an integral part of these financial statements.

23

Managers Intermediate Duration Government Fund

Schedule of Portfolio Investments (continued)

| | | | | | | |

| | | Shares | | Value | |

Short-Term Investments – 6.2% | | | | | | | |

Other Investment Companies – 5.8%4 | | | | | | | |

JPMorgan Prime Money Market Fund, Institutional Class Shares, 5.19% | | | 10,549,538 | | $ | 10,549,538 | |

| | |

| | | Principal

Amount | | | |

U.S. Government Agency Discount Notes - 0.4%5,6 | | | | | | | |

FHLMC Discount Notes, 5.104%, 11/09/07 10 | | $ | 750,000 | | | 727,118 | |

Total Short-Term Investments (cost $11,276,205) | | | | | | 11,276,656 | |

Total Investments - 127.2% (cost $233,279,369) | | | | | | 232,477,302 | |

Other Assets, less Liabilities – (27.2)% | | | | | | (49,705,835 | ) |

Net Assets - 100.0% | | | | | $ | 182,771,467 | |

The accompanying notes are an integral part of these financial statements.

24

The Managers Funds

Notes to Schedules of Portfolio Investments

The following footnotes and abbreviations are to be read in conjunction with the Schedules of Portfolio Investments previously presented in this report.

At March 31, 2007, the cost of securities for Federal income tax purposes and the gross aggregate unrealized appreciation and/or depreciation based on tax cost were approximately as follows:

| | | | | | | | | | | | |

Fund | | Cost | | Appreciation | | Depreciation | | | Net | |

Short Duration | | $ | 243,119,888 | | $ | 1,126,363 | | ($3,051,708) | | | ($1,925,345) | |

Intermediate Duration | | | 233,291,730 | | | 1,073,076 | | (1,887,504 | ) | | (814,428 | ) |

| | 1 | Mortgage-backed obligations and other assets are subject to principal paydowns as a result of prepayments or refinancing of the underlying mortgage instruments. As a result, the average life may be substantially less than the original maturity. The interest rate shown is the rate in effect at March 31, 2007. |

| | 2 | Floating Rate Security. The rate listed is as of March 31, 2007. Date in parenthesis represents the security’s next coupon rate reset. |

| | 3 | Security is exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration, normally to qualified buyers. At March 31, 2007, the value of these securities amounted to the following: |

| | | | | | |

Fund | | Market

Value | | % of

Net

Assets | |

Short Duration | | $ | 1,354,228 | | 0.8 | % |

Intermediate Duration | | | 2,154,757 | | 1.2 | % |

| | 4 | Yield shown for an investment company represents the March 31, 2007, seven-day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

| | 6 | Security pledged to cover margin requirements for open futures positions at March 31, 2007. |

| | 7 | Some or all of these securities were out on loan to various brokers as of March 31, 2007, amounting to $1,242,161 representing 0.7% of net assets for Short Duration. |

| | 8 | Collateral received from brokers for securities lending was invested in this short-term investment. |

| | 9 | All or part of security has been segregated for delayed delivery transactions and reverse repurchase agreements. |

| | 10 | Indicates yield to maturity at March 31, 2007. |

| | 11 | Variable Rate Security. The rate listed is as of March 31, 2007 and is periodically reset subject to terms and conditions set forth in the debenture. |

25

The Managers Funds

Notes to Schedules of Portfolio Investments (continued)

Investments Abbreviations:

| | |

| AHMA: | | American Home Mortgage Assets. |

| DLJ: | | Donaldson, Lufkin & Jenrette Securities Corp. |

| FHA/VA: | | Federal Home Association/Veteran’s Association |

| FHLMC: | | Federal Home Loan Mortgage Corp. |

| FNMA: | | Federal National Mortgage Association |

| GMAC: | | General Motors Acceptance Corp. |

| GNMA: | | Government National Mortgage Association |

| GSMPS: | | Goldman Sachs Mortgage Participating Security |

| GSR: | | Goldman Sachs REMIC |

| IO: | | Interest Only |

| PO: | | Principal Only |

| TBA: | | To Be Announced |

| USTN: | | United States Treasury Note |

Security Ratings (unaudited):

The composition of debt holdings as a percentage of portfolio assets is as follows:

| | | | | | | | | | | | | | | | | | |

S&P/Moody’s Ratings | | Gov’t/AAA | | | AA | | | A | | | BBB | | | BB | | | Not Rated | |

Short Duration | | 97.9 | % | | 0.5 | % | | 0.0 | % | | 0.0 | % | | 0.0 | % | | 1.6 | % |

Intermediate Duration | | 99.8 | % | | 0.2 | % | | 0.0 | % | | 0.0 | % | | 0.0 | % | | 0.0 | % |

26

The Managers Funds

Statements of Assets and Liabilities

March 31, 2007

| | | | | | | | |

| | | Managers Short Duration

Government Fund | | | Managers

Intermediate Duration

Government Fund | |

Assets: | | | | | | | | |

Investments at value (including securities on loan valued at $1,242,161 and $0, respectively)* | | $ | 241,194,543 | | | $ | 232,477,302 | |

Receivable for investments sold | | | 16,287,479 | | | | 10,144,309 | |

Receivable for TBA sale commitment | | | 14,625,539 | | | | — | |

Receivable for Fund shares sold | | | 655,170 | | | | 1,268,562 | |

Dividends, interest and other receivables | | | 1,049,555 | | | | 1,018,069 | |

Receivable for variation margin on futures | | | 49,486 | | | | 875 | |

Prepaid expenses | | | 20,029 | | | | 14,176 | |

| | | | | | | | |

Total assets | | | 273,881,801 | | | | 244,923,293 | |

| | | | | | | | |

Liabilities: | | | | | | | | |

Payable to custodian | | | 1,047,545 | | | | 863,952 | |

Payable upon return of securities loaned | | | 1,269,868 | | | | — | |

Payable for investments purchased | | | 17,293,615 | | | | 9,820,220 | |

Payable for investments purchased on a when-issued basis | | | 21,325,063 | | | | 45,893,062 | |

Payable for Fund shares repurchased | | | 137,604 | | | | 529,242 | |

Payable for TBA sale commitment | | | 14,591,882 | | | | — | |

Reverse repurchase agreements (proceeds $37,898,000 and $4,830,000, respectively) | | | 37,971,669 | | | | 4,839,261 | |

Payable for variation margin on futures | | | 57,398 | | | | 6,663 | |

Investment advisory and management fee payable | | | 107,927 | | | | 107,983 | |

Other accrued expenses | | | 95,087 | | | | 91,443 | |

| | | | | | | | |

Total liabilities | | | 93,897,658 | | | | 62,151,826 | |

| | | | | | | | |

Net Assets | | $ | 179,984,143 | | | $ | 182,771,467 | |

| | | | | | | | |

Shares outstanding | | | 18,594,521 | | | | 17,344,426 | |

Net asset value, offering and redemption price per share | | $ | 9.68 | | | $ | 10.54 | |

Net Assets Represent: | | | | | | | | |

Paid-in capital | | $ | 184,975,642 | | | $ | 184,916,221 | |

Undistributed net investment income | | | 727,076 | | | | 51,348 | |

Accumulated net realized loss from investments, options, futures contracts and TBA sale commitments | | | (3,881,338 | ) | | | (1,421,215 | ) |

Net unrealized depreciation of investments, options, futures contracts and TBA sale commitments | | | (1,837,237 | ) | | | (774,887 | ) |

| | | | | | | | |

Net Assets | | $ | 179,984,143 | | | $ | 182,771,467 | |

| | | | | | | | |

*Investments at cost | | $ | 243,115,790 | | | $ | 233,279,369 | |

The accompanying notes are an integral part of these financial statements.

27

The Managers Funds

Statements of Operations

For the fiscal year ended March 31, 2007

| | | | | | | | |

| | | Managers

Short Duration

Government Fund | | | Managers

Intermediate Duration

Government Fund | |

Investment Income: | | | | | | | | |

Interest income | | $ | 10,916,088 | | | $ | 8,822,868 | |

Dividend income | | | 334,154 | | | | 725,158 | |

Securities lending fees | | | 7,384 | | | | 341 | |

| | | | | | | | |

Total investment income | | | 11,257,626 | | | | 9,548,367 | |

| | | | | | | | |

Expenses: | | | | | | | | |

Investment advisory and management fees | | | 1,432,104 | | | | 1,244,823 | |

Interest expense | | | 1,074,853 | | | | 66,510 | |

Custodian | | | 76,141 | | | | 68,656 | |

Transfer agent | | | 55,840 | | | | 57,556 | |

Professional fees | | | 51,746 | | | | 55,064 | |

Registration fees | | | 30,093 | | | | 32,742 | |

Shareholder reports | | | 27,001 | | | | 29,820 | |

Trustees fees and expenses | | | 13,253 | | | | 8,815 | |

Miscellaneous | | | 13,500 | | | | 19,428 | |

| | | | | | | | |

Total expenses before offsets | | | 2,774,531 | | | | 1,583,414 | |

| | | | | | | | |

Expense recoupment | | | — | | | | 30,594 | |

Expense reductions | | | (592 | ) | | | (48 | ) |

| | | | | | | | |

Net expenses | | | 2,773,939 | | | | 1,613,960 | |

| | | | | | | | |

Net investment income | | | 8,483,687 | | | | 7,934,407 | |

| | | | | | | | |

Net Realized and Unrealized Gain (Loss): | | | | | | | | |

Net realized gain (loss) on investments and TBA sales commitments | | | 197,805 | | | | (129,988 | ) |

Net realized gain (loss) on options and futures contracts | | | 524,141 | | | | (218,425 | ) |

Net unrealized appreciation of investments and TBA sales commitments | | | 2,055,450 | | | | 2,819,332 | |

Net unrealized appreciation (depreciation) of options and futures contracts | | | (1,273,441 | ) | | | 161,608 | |

| | | | | | | | |

Net realized and unrealized gain | | | 1,503,955 | | | | 2,632,527 | |

| | | | | | | | |

Net Increase in Net Assets Resulting from Operations | | $ | 9,987,642 | | | $ | 10,566,934 | |

| | | | | | | | |

The accompanying notes are an integral part of these financial statements.

28

Managers Short Duration Government Fund

Statement of Changes in Net Assets

For the fiscal year ended March 31,

| | | | | | | | |

| | | 2007 | | | 2006 | |

Increase (Decrease) in Net Assets From Operations: | | | | | | | | |

Net investment income | | $ | 8,483,687 | | | $ | 8,260,207 | |

Net realized gain on investments, options and futures | | | 721,946 | | | | 437,028 | |

Net unrealized appreciation (depreciation) of investments, options and futures | | | 782,009 | | | | (1,627,812 | ) |

| | | | | | | | |

Net increase in net assets resulting from operations | | | 9,987,642 | | | | 7,069,423 | |

| | | | | | | | |

Distributions to Shareholders: | | | | | | | | |

From net investment income | | | (8,566,062 | ) | | | (8,321,069 | ) |

| | | | | | | | |

Total distributions to shareholders | | | (8,566,062 | ) | | | (8,321,069 | ) |

| | | | | | | | |

From Capital Share Transactions: | | | | | | | | |

Proceeds from sale of shares | | | 123,190,502 | | | | 160,082,951 | |

Net asset value of shares issued in connection with reinvestment of dividends | | | 8,136,268 | | | | 7,882,937 | |

Cost of shares repurchased | | | (159,287,605 | ) | | | (198,090,359 | ) |

| | | | | | | | |

Net decrease from capital share transactions | | | (27,960,835 | ) | | | (30,124,471 | ) |

| | | | | | | | |

Total decrease in net assets | | | (26,539,255 | ) | | | (31,376,117 | ) |

Net Assets: | | | | | | | | |

Beginning of year | | | 206,523,398 | | | | 237,899,515 | |

| | | | | | | | |

End of year | | $ | 179,984,143 | | | $ | 206,523,398 | |

| | | | | | | | |

End of year undistributed net investment income | | $ | 727,076 | | | $ | 727,076 | |

Share Transactions: | | | | | | | | |

Sale of shares | | | 12,771,423 | | | | 16,712,702 | |

Shares issued in connection with reinvestment of dividends | | | 844,943 | | | | 820,082 | |

Shares repurchased | | | (16,513,626 | ) | | | (20,675,431 | ) |

| | | | | | | | |

Net decrease in shares | | | (2,897,260 | ) | | | (3,142,647 | ) |

| | | | | | | | |

The accompanying notes are an integral part of these financial statements.

29

Managers Intermediate Duration Government Fund

Statement of Changes in Net Assets

For the fiscal year ended March 31,

| | | | | | | | |

| | | 2007 | | | 2006 | |

Increase (Decrease) in Net Assets From Operations: | | | | | | | | |

Net investment income | | $ | 7,934,407 | | | $ | 7,098,787 | |

Net realized loss on investments, options and futures | | | (348,413 | ) | | | (730,620 | ) |

Net unrealized appreciation (depreciation) of investments, options and futures | | | 2,980,940 | | | | (2,548,969 | ) |

| | | | | | | | |

Net increase in net assets resulting from operations | | | 10,566,934 | | | | 3,819,198 | |

| | | | | | | | |

Distributions to Shareholders: | | | | | | | | |

From net investment income | | | (7,937,857 | ) | | | (7,085,544 | ) |

| | | | | | | | |

Total distributions to shareholders | | | (7,937,857 | ) | | | (7,085,544 | ) |

| | | | | | | | |

From Capital Share Transactions: | | | | | | | | |

Proceeds from sale of shares | | | 66,087,961 | | | | 101,429,509 | |

Net asset value of shares issued in connection with reinvestment of dividends and distributions | | | 7,038,492 | | | | 6,437,795 | |

Cost of shares repurchased | | | (87,529,430 | ) | | | (96,081,215 | ) |

| | | | | | | | |

Net increase (decrease) from capital share transactions | | | (14,402,977 | ) | | | 11,786,089 | |

| | | | | | | | |

Total increase (decrease) in net assets | | | (11,773,900 | ) | | | 8,519,743 | |

Net Assets: | | | | | | | | |

Beginning of year | | | 194,545,367 | | | | 186,025,624 | |

| | | | | | | | |

End of year | | $ | 182,771,467 | | | $ | 194,545,367 | |

| | | | | | | | |

End of year undistributed net investment income | | $ | 51,348 | | | $ | 54,798 | |

Share Transactions: | | | | | | | | |

Sale of shares | | | 6,314,692 | | | | 9,591,937 | |

Shares issued in connection with reinvestment of dividends and distributions | | | 675,812 | | | | 611,895 | |

Shares repurchased | | | (8,405,912 | ) | | | (9,109,886 | ) |

| | | | | | | | |

Net increase (decrease) in shares | | | (1,415,408 | ) | | | 1,093,946 | |

| | | | | | | | |

The accompanying notes are an integral part of these financial statements.

30

Managers Short Duration Government Fund

Financial Highlights

For a share outstanding throughout each fiscal year ended March 31,

| | | | | | | | | | | | | | | | | | | | |

| | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

Net Asset Value, Beginning of Year | | $ | 9.61 | | | $ | 9.66 | | | $ | 9.69 | | | $ | 9.74 | | | $ | 9.72 | |

| | | | | | | | | | | | | | | | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.42 | | | | 0.34 | | | | 0.27 | | | | 0.25 | | | | 0.30 | |

Net realized and unrealized gain (loss) on investments | | | 0.06 | | | | (0.05 | ) | | | (0.02 | ) | | | (0.06 | ) | | | 0.06 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 0.48 | | | | 0.29 | | | | 0.25 | | | | 0.19 | | | | 0.36 | |

| | | | | | | | | | | | | | | | | | | | |

Less Distributions to Shareholders from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.41 | ) | | | (0.34 | ) | | | (0.28 | ) | | | (0.24 | ) | | | (0.32 | ) |

Return of capital | | | — | | | | — | | | | — | | | | — | | | | (0.02 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total distributions to shareholders | | | (0.41 | ) | | | (0.34 | ) | | | (0.28 | ) | | | (0.24 | ) | | | (0.34 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net Asset Value, End of Year | | $ | 9.68 | | | $ | 9.61 | | | $ | 9.66 | | | $ | 9.69 | | | $ | 9.74 | |

| | | | | | | | | | | | | | | | | | | | |

Total Return 1 | | | 5.05 | % | | | 3.00 | % | | | 2.62 | % | | | 2.00 | % | | | 3.76 | % |

| | | | | | | | | | | | | | | | | | | | |

Ratio of net operating expenses to average net assets 1,2 | | | 0.83 | % | | | 0.83 | % | | | 0.78 | % | | | 0.78 | % | | | 0.78 | % |

Ratio of total expenses to average net assets 3 | | | 1.36 | % | | | 1.08 | % | | | 1.00 | % | | | 0.95 | % | | | 0.93 | % |

Ratio of net investment income to average net assets 1,2 | | | 4.15 | % | | | 3.41 | % | | | 2.90 | % | | | 2.59 | % | | | 2.74 | % |

Portfolio turnover | | | 230 | % | | | 315 | % | | | 341 | % | | | 349 | % | | | 418 | % |

Net assets at end of year (000’s omitted) | | $ | 179,984 | | | $ | 206,523 | | | $ | 237,900 | | | $ | 198,726 | | | $ | 160,710 | |

| | | | | | | | | | | | | | | | | | | | |

1 | Total returns and net investment income would have been lower had certain expenses not been reduced. |

2 | After expense offsets excluding interest expense. (See Note 1(c) of “Notes to Financial Statements.”) |

3 | Includes interest expense for the fiscal years ended March 31, 2007, 2006, 2005, 2004 and 2003 of 0.53%, 0.23%, 0.16%, 0.03% and 0.01%, respectively. (See Note 1(c) of “Notes to Financial Statements.”) |

31

Managers Intermediate Duration Government Fund

Financial Highlights

For a share outstanding throughout each fiscal year ended March 31,

| | | | | | | | | | | | | | | | | | | | |

| | | 2007 | | | 2006 | | | 2005 | | | 2004 | | | 2003 | |

Net Asset Value, Beginning of Year | | $ | 10.37 | | | $ | 10.53 | | | $ | 10.74 | | | $ | 10.61 | | | $ | 10.16 | |

| | | | | | | | | | | | | | | | | | | | |

Income from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | 0.47 | | | | 0.37 | | | | 0.26 | | | | 0.23 | | | | 0.40 | |

Net realized and unrealized gain (loss) on investments | | | 0.17 | | | | (0.16 | ) | | | (0.06 | ) | | | 0.20 | | | | 0.45 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 0.64 | | | | 0.21 | | | | 0.20 | | | | 0.43 | | | | 0.85 | |

| | | | | | | | | | | | | | | | | | | | |

Less Distributions to Shareholders from: | | | | | | | | | | | | | | | | | | | | |

Net investment income | | | (0.47 | ) | | | (0.37 | ) | | | (0.26 | ) | | | (0.23 | ) | | | (0.40 | ) |

Net realized gain on investments | | | — | | | | — | | | | (0.15 | ) | | | (0.07 | ) | | | 0.00 | |

| | | | | | | | | | | | | | | | | | | | |

Total distributions to shareholders | | | (0.47 | ) | | | (0.37 | ) | | | (0.41 | ) | | | (0.30 | ) | | | (0.40 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net Asset Value, End of Year | | $ | 10.54 | | | $ | 10.37 | | | $ | 10.53 | | | $ | 10.74 | | | $ | 10.61 | |

| | | | | | | | | | | | | | | | | | | | |

Total Return 1 | | | 6.30 | % | | | 2.02 | % | | | 1.78 | % | | | 4.07 | % | | | 8.48 | % |

| | | | | | | | | | | | | | | | | | | | |

Ratio of net operating expenses to average net assets 1,2 | | | 0.87 | % | | | 0.88 | % | | | 0.88 | % | | | 0.88 | % | | | 0.88 | % |

Ratio of total expenses to average net assets 3 | | | 0.89 | % | | | 0.88 | % | | | 0.89 | % | | | 0.93 | % | | | 1.06 | % |

Ratio of net investment income to average net assets 1,2 | | | 4.46 | % | | | 3.53 | % | | | 2.45 | % | | | 2.09 | % | | | 3.75 | % |

Portfolio turnover | | | 445 | % | | | 672 | % | | | 851 | % | | | 667 | % | | | 578 | % |

Net assets at end of year (000’s omitted) | | $ | 182,771 | | | $ | 194,545 | | | $ | 186,026 | | | $ | 123,826 | | | $ | 71,342 | |

| | | | | | | | | | | | | | | | | | | | |

1 | Total returns and net investment income would have been lower had certain expenses not been reduced. |

2 | After expense offsets excluding interest expense. (See Note 1(c) of “Notes to Financial Statements.”) |

3 | Includes interest expense for the fiscal years ended March 31, 2007, 2005, 2004 and 2003 of 0.04%, 0.01%, 0.00%, 0.03%, respectively. (See Note 1(c) of “Notes to Financial Statements.”) |

32

The Managers Funds

Notes to Financial Statements

March 31, 2007

| 1. | Summary of Significant Accounting Policies |

Managers Trust II (“Trust II”) is an open-end management investment company organized as a Massachusetts business trust and registered under the Investment Company Act of 1940, as amended (the “1940 Act”). Included in this report are two series of Trust II: Managers Short Duration Government Fund (“Short Duration”) and Managers Intermediate Duration Government Fund (“Intermediate Duration”). The financial statements of Short Duration and Intermediate Duration (each a “Fund” and collectively, the “Funds”) are prepared in accordance with accounting principles generally accepted in the United States of America which require management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting periods. Actual results could differ from those estimates. The following is a summary of significant accounting policies followed by the Funds in the preparation of their financial statements.

| a. | Valuation of Investments |