Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-06431

AMG Funds II

(Exact name of registrant as specified in charter)

600 Steamboat Road, Suite 300, Greenwich, Connecticut 06830

(Address of principal executive offices) (Zip code)

AMG Funds LLC

600 Steamboat Road, Suite 300, Greenwich, Connecticut 06830

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203)299-3500

Date of fiscal year end: DECEMBER 31

Date of reporting period: JANUARY 1, 2018 – DECEMBER 31, 2018

(Annual Shareholder Report)

Table of Contents

| Item 1. | Reports to Shareholders |

Table of Contents

|

| ANNUAL REPORT |

| AMG Funds | ||||||||||||||

| December 31, 2018 | ||||||||||||||

AMG Chicago Equity Partners Balanced Fund

|

| |||||||||||||

Class N: MBEAX

|

| Class I: MBESX

| Class Z: MBEYX | |||||||||||

AMG Managers Amundi Intermediate Government Fund

|

| |||||||||||||

| Class N: MGIDX | Class I: MADIX | Class Z: MAMZX | ||||||||||||

AMG Managers Amundi Short Duration Government Fund

|

| |||||||||||||

| Class N: MGSDX | Class I: MANIX | Class Z: MATZX | ||||||||||||

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Funds’ website (https://www.amgfunds.com/resources/order_literature.html), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically at any time by contacting your financial intermediary or, if you invest directly with the Funds, by logging into your account at www.amgfunds.com.

You may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Funds, you can call1-800-548-4539 to inform the Funds that you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds in the AMG Funds Family of Funds held in your account if you invest through your financial intermediary or all funds in the AMG Funds Family of Funds held with the fund complex if you invest directly with the Funds.

amgfunds.com

|

123118 AR002

|

Table of Contents

Table of Contents

AMG Funds Annual Report — December 31, 2018 |

TABLE OF CONTENTS

| PAGE

| |||||

| ||||||

| 2 | |||||

| 3 | ||||||

| PORTFOLIO MANAGER’S COMMENTS, FUND SNAPSHOTS AND SCHEDULES OF PORTFOLIO INVESTMENTS | ||||||

| 4 | ||||||

| 21 | ||||||

| 29 | ||||||

FINANCIAL STATEMENTS | ||||||

| 38 | ||||||

Balance sheets, net asset value (NAV) per share computations and cumulative distributable earnings (loss) | ||||||

| 40 | ||||||

Detail of sources of income, expenses, and realized and unrealized gains (losses) during the fiscal year | ||||||

| 41 | ||||||

Detail of changes in assets for the past two fiscal years | ||||||

| 42 | ||||||

Historical net asset values per share, distributions, total returns, income and expense ratios, turnover ratios and net assets | ||||||

| 51 | ||||||

Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | ||||||

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | 60 | |||||

| 61 | ||||||

| 62 | ||||||

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the AMG Funds family of mutual funds. Such offering is made only by prospectus, which includes details as to offering price and other material information.

Table of Contents

Dear Shareholder:

It was a difficult year for financial markets in 2018. Strong domestic economic growth fueled equity returns for the majority of the year, but a pullback in the fourth quarter reversed returns, leaving indices across market caps firmly in negative territory. Investors were driven by signs of deceleration in growth across the globe combined with political uncertainty and tighter monetary policy. The S&P 500® Index, a widely followed barometer of the U.S. equity market, returned +9.9% in the first three quarters of the year before a period of heightened volatility resulted in a fourth quarter return of-13.5% and a-4.4% return for the full fiscal year.

In 2018, there was wide performance dispersion across the eleven economic sectors of the S&P 500® Index. Despite a weak fourth quarter, health care, utilities, information technology, and consumer discretionary sectors ended the year on a positive note with returns of +6.4%, +4.1%, +3.4% and +1.9%, respectively. Corporate earnings are expected to continue growing at double digits for the fifth consecutive quarter. According to FactSet, fourth quarter earnings growth for S&P 500® companies is +10.9% (as of January 25, 2019). Growth stocks outperformed value for the first three quarters of the year until the fourth quarter’s risk off environment reversed the trend. Full year returns for the Russell 1000® Growth and Russell 1000® Value Indexes were-1.5% and-8.3%, respectively.

Despite skittish investor sentiment, the U.S. economy continued to show signs of growth, albeit at a slower pace with third quarter GDP growth ringing in at 3.4%. The Federal Reserve raised short-term interest rates four times over the course of the year to end the year at a target rate of 2.25%–2.50%. Higher interest rates eroded the performance of bonds in the first three quarters of the year and a risk off fourth quarter resulted in mixed results. The Bloomberg Barclays U.S. Aggregate Bond Index, a broad measure of U.S. bond market performance, ended the year where it began with a 0.0% return for 2018. The yield on the10-year U.S. Treasury note crossed above 3% at the end of September but fell dramatically as investors sought to insulate themselves from market volatility. During the past year, the short end of the yield curve has risen faster than the longer end, resulting in the 2–10 year Treasury spread of 0.21%. As expected, high yield bonds held up in the rising interest rate environment but struggled in the fourth quarter as investors removed risk from their portfolios. As a result, spreads between investment grade and high yield corporate debt climbed past 300 bps. In 2018, the Bloomberg Barclays U.S. Aggregate Credit Index and Bloomberg Barclays U.S. Corporate High Yield Bond Index returned-2.1% and-2.1%, respectively.

Economic conditions outside the U.S. started the year with strong growth indicators but finished with signs of deceleration. At the European Central Bank’s most recent monetary policy meeting, the governing council issued guidance that quantitative easing measures would continue and interest rates would remain at their present levels through summer of 2019. This is a departure from guidance earlier in the year which indicated the asset repurchase program would come to an end in December 2018 and rates would rise in 2019. The Bank of England increased its target rate in August for the first time since 2009, but deceleration in growth and increased downside risks, including a disorderly Brexit, have halted discussion of additional hikes in the near future.

International equities and emerging markets demonstrated significantly weaker returns, with the MSCI EAFE and MSCI Emerging Markets Index returning-13.8% and-14.6%, respectively, in the 12 months ending December 31, 2018. In a recent speech at the Hudson Institute, Vice President Mike Pence acknowledged China’s

aggressive actions toward the United States and highlighted a dramatic shift in U.S foreign policy with China: “We seek a relationship grounded in fairness, reciprocity and respect for sovereignty, and we have taken strong and swift action to achieve that goal.” This new tone combined with two rounds of new U.S. tariffs for Chinese imports and signs of a slowing economy acted as a drag on the largest economy within the MSCI Emerging Markets Index. Concurrently, the U.S. Dollar strengthened against most major global currencies, particularly in emerging markets, where those with large current account deficits faced significant pressure, adding to the drag on performance for emerging markets.

AMG Funds appreciates the privilege of providing investment tools to you and your clients. Our foremost goal is to provide investment solutions that help our shareholders successfully reach their long-term investment goals. AMG Funds provides access to a distinctive array of actively managed return-oriented investment strategies. We thank you for your continued confidence and investment in AMG Funds. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

Respectfully,

Keitha Kinne

President

AMG Funds

Average Annual Total Returns | | Periods ended December 31, 2018* | | |||||||||||

Stocks: | 1 Year | 3 Years | 5 Years | |||||||||||

Large Caps | (S&P 500® Index) | (4.38 | )% | 9.26% | 8.49% | |||||||||

Small Caps | (Russell 2000® Index) | (11.01 | )% | 7.36% | 4.41% | |||||||||

International | (MSCI All Country World Index ex USA) | (14.20 | )% | 4.48% | 0.68% | |||||||||

Bonds: | ||||||||||||||

Investment Grade | (Bloomberg Barclays U.S. Aggregate Bond Index) | 0.01 | % | 2.06% | 2.52% | |||||||||

High Yield | (Bloomberg Barclays U.S. Corporate High Yield Bond Index) | (2.08 | )% | 7.23% | 3.83% | |||||||||

Tax-exempt | (Bloomberg Barclays Municipal Bond Index) | 1.28 | % | 2.30% | 3.82% | |||||||||

Treasury Bills | (ICE BofAML U.S.6-Month Treasury Bill Index) | 1.92 | % | 1.18% | 0.78% | |||||||||

*Source: FactSet. Past performance is no guarantee of future results.

| 2 |

Table of Contents

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution(12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below.

ACTUAL EXPENSES

The first line of the following table provides information about the actual account values and | actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES

The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s | actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. |

| Six Months Ended December 31, 2018 | Expense Ratio for the Period | Beginning Account Value 07/01/18 | Ending Account Value 12/31/18 | Expenses Paid During the Period* | ||||||

AMG Chicago Equity Partners Balanced Fund |

| |||||||||

Based on Actual Fund Return | ||||||||||

Class N | 1.09% | $1,000 | $943 | $5.34 | ||||||

Class I | 0.93% | $1,000 | $943 | $4.56 | ||||||

Class Z | 0.84% | $1,000 | $944 | $4.12 | ||||||

Based on Hypothetical 5% Annual Return |

| |||||||||

Class N | 1.09% | $1,000 | $1,020 | $5.55 | ||||||

Class I | 0.93% | $1,000 | $1,021 | $4.74 | ||||||

Class Z | 0.84% | $1,000 | $1,021 | $4.28 | ||||||

AMG Managers Amundi Intermediate Government Fund |

| |||||||||

Based on Actual Fund Return | ||||||||||

Class N | 0.84% | $1,000 | $1,013 | $4.26 | ||||||

Class I | 0.75% | $1,000 | $1,013 | $3.80 | ||||||

Class Z | 0.69% | $1,000 | $1,013 | $3.50 | ||||||

Based on Hypothetical 5% Annual Return |

| |||||||||

Class N | 0.84% | $1,000 | $1,021 | $4.28 | ||||||

Class I | 0.75% | $1,000 | $1,021 | $3.82 | ||||||

Class Z | 0.69% | $1,000 | $1,022 | $3.52 | ||||||

| Six Months Ended December 31, 2018 | Expense Ratio for the Period | Beginning Account Value 07/01/18 | Ending Account Value 12/31/18 | Expenses Paid During the Period* | ||||||

AMG Managers Amundi Short Duration Government Fund |

| |||||||||

Based on Actual Fund Return | ||||||||||

Class N | 0.72% | $1,000 | $1,002 | $3.63 | ||||||

Class I | 0.62% | $1,000 | $1,003 | $3.13 | ||||||

Class Z | 0.57% | $1,000 | $1,003 | $2.88 | ||||||

Based on Hypothetical 5% Annual Return |

| |||||||||

Class N | 0.72% | $1,000 | $1,022 | $3.67 | ||||||

Class I | 0.62% | $1,000 | $1,022 | $3.16 | ||||||

Class Z | 0.57% | $1,000 | $1,022 | $2.91 | ||||||

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 365. |

| 3 |

Table of Contents

THE YEAR IN REVIEW

For the year ended December 31, 2018, the AMG Chicago Equity Partners Balanced Fund (Class N shares) (the “Fund”) returned-2.89%, compared to the-2.53% return for its benchmark, which consists of 60% the return of the Russell 1000® Index and 40% the return of the Bloomberg Barclays U.S. Aggregate Bond Index.

After hitting new highs in the third quarter, stocks declined sharply, resulting in negative returns across size and style indices in 2018. The S&P 500® Index posted its first negative total return year since the global financial crisis (2008). As stocks went down, volatility shot up, and the VIX was up 130% in 2018. A mix of early performers—technology and health care—joined utilities as the best-performing sectors of 2018. The stock market finished the year with the worst December since the Great Depression due to uncertainty over trade, rising rates, and declining earnings expectations for 2019. The Fed raised rates in the fourth quarter for the fourth time in 2018, with two more hikes slated for 2019. Corporate spreads widened in the year and the slope of the yield curve continued to flatten. The move in rates and spreads largely reflected growing concern over the impact of tighter monetary policy from the Federal Reserve on future economic growth. While parts of the U.S. economy remain strong (2018 GDP expected at just under 3%, unemployment under 4%, strong consumer spending), business confidence declined, as uncertainty over trade weighs on expectations. | The Fund was overweight equities (65/35) in the first three quarters of the year, when stocks (Russell 1000® Index) outperformed bonds (Bloomberg Barclays U.S. Aggregate Bond Index) by more than 12% (+10.5% vs.-1.6%, respectively). This contributed to performance during the first three quarters of the year. In October, we moved to a neutral asset allocation (60/40) due to weaker signals for the Expansion regime in our Market Phase Identification Model. The timing was right, as bonds outperformed equities in the fourth quarter by more than 15% (1.6% vs.-13.8%, respectively).

The equity portfolio added more than 100 bps of excess return relative to the Russell 1000® Index for the year. Our tilt toward secular growth stocks in 2018 contributed to excess returns as growth style stocks (Russell 1000® Growth Index) outperformed value (Russell 1000® Value Index) by nearly 7%(-1.5% vs.-8.3%) in large caps, despite a reversal in the fourth quarter. The equity portfolio’s factor emphasis also added value throughout the year. Momentum demonstrated positive performance across most sectors, particularly in the more cyclical sectors emphasized. The avoidance of value factors also helped, as they experienced their second worst year in three decades (in U.S. large caps).

In 2018, the fixed income sleeve of the portfolio slightly detracted approximately-30 bps from excess return relative to the Bloomberg Barclays U.S. Aggregate Bond Index, all of which came in the fourth quarter. Taking advantage of some volatility | and spread widening, the portfolio increased exposure to corporate bonds throughout the year, which can be a good hedge in periods of rising interest rates. This hurt relative performance in the fourth quarter, when corporate spreads widened.

Our research has shown that constructing a well-diversified portfolio of companies with attractive valuation ratios, quality balance sheets, and positive growth and momentum expectations built through a disciplined, risk-controlled process offers the potential to deliver consistent excess returns for the equity portion of the Fund. For the fixed income sleeve, we will continue to use our disciplined approach to investing to provide principal preservation, income, diversification, and risk control. We will continue to monitor inputs to our investment process for indications of improving conditions and opportunity but believe our positioning is in line with our stated objectives. Overall, our philosophy will not change based on short-term trends or conditions in the market. We will continue to use our disciplined approach to provide added value at controlled levels of risk.

This commentary reflects the viewpoints of the portfolio manager, Chicago Equity Partners, LLC, as of December 31, 2018, is not intended as a forecast or guarantee of future results, and is subject to change without notice. |

| 4 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Portfolio Manager’s Comments(continued) |

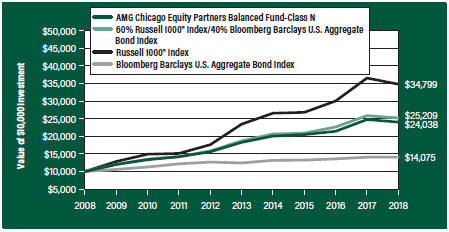

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG Chicago Equity Partners Balanced Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in the AMG Chicago Equity Partners Balanced Fund’s Class N shares on December 31, 2008, to a $10,000 investment made in the 60% Russell 1000® Index/40% Bloomberg Barclays U.S. Aggregate Bond Index, Russell 1000® Index and the Bloomberg Barclays U.S. Aggregate Bond Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG Chicago Equity Partners Balanced Fund, the 60% Russell 1000® Index/40% Bloomberg Barclays U.S. Aggregate Bond Index, the Russell 1000® Index and the Bloomberg Barclays U.S. Aggregate Bond Index for the same time periods ended December 31, 2018.

| Average Annual Total Returns1 | One Year | Five Years | Ten Years | Since Inception | Inception Date | |||||||||||||||||

AMG Chicago Equity Partners Balanced Fund2,3, 4, 5, 6, 7

|

| |||||||||||||||||||||

Class N | (2.89% | ) | 5.64% | 9.17% | 7.53% | 01/02/97 | ||||||||||||||||

Class I | (2.77% | ) | 5.80% | — | 7.48% | 11/30/12 | ||||||||||||||||

Class Z | (2.68% | ) | 5.90% | 9.45% | 7.90% | 01/02/97 | ||||||||||||||||

60% Russell 1000® Index8/40% Bloomberg Barclays U.S. Aggregate Bond Index9 | (2.53% | ) | 6.16% | 9.69% | 7.23% | 01/02/97 | † | |||||||||||||||

Russell 1000® Index8 | (4.78% | ) | 8.21% | 13.28% | 7.87% | 01/02/97 | † | |||||||||||||||

Bloomberg Barclays U.S. Aggregate Bond Index9 | 0.01% | 2.52% | 3.48% | 4.98% | 01/02/97 | † | ||||||||||||||||

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.835.3879 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

† Date reflects inception date of the Fund, not the index.

1 Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of December 31, 2018. All returns are in U.S. dollars ($).

2 From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns.

3 To the extent that the Fund invests in asset-backed or mortgage-backed securities, its exposure to prepayment and extension risks may be greater than investments in other fixed income securities.

4 The Fund is subject to the risks associated with investments in debt securities, such as default risk and fluctuations in the perception of the debtor’s ability to pay its creditors. Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed income securities to fall.

5 Investments in international securities are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuations.

6 The Fund is subject to risks associated with investments inmid-capitalization companies such as greater price volatility, lower trading volume, and less liquidity than the stocks of larger, more established companies.

7 The Fund invests in value stocks, which may perform differently from the market as a whole and may be undervalued by the market for a long period of time.

8 The Russell 1000® Index measures the performance of approximately 1,000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000® represents approximately 92% of the U.S. market. Unlike the Fund, the Russell 1000® Index is unmanaged, is not available for investment, and does not incur expenses.

9 The Bloomberg Barclays U.S. Aggregate Bond Index represents securities that are Securities and Exchange Commission-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Unlike the Fund, the Bloomberg Barclays U.S. Aggregate Bond Index is unmanaged, is not available for investment, and does not incur expenses. |

| 5 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Portfolio Manager’s Comments(continued) |

The Russell 1000® Index is a trademark of the London Stock Exchange Group companies.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its | affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent | allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Not FDIC insured, nor bank guaranteed. May lose value. |

| 6 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Fund Snapshots(unaudited) December 31, 2018 |

PORTFOLIO BREAKDOWN

| Sector | % of Net Assets | |||

U.S. Government and Agency Obligations | 28.9 | |||

Industrials | 14.8 | |||

Information Technology | 13.5 | |||

Financials | 9.6 | |||

Health Care | 8.2 | |||

Consumer Discretionary | 7.1 | |||

Consumer Staples | 4.1 | |||

Communication Services | 3.9 | |||

Utilities | 2.4 | |||

Real Estate | 2.0 | |||

Energy | 2.0 | |||

Materials | 1.6 | |||

Short-Term Investments | 1.9 | |||

Other Assets Less Liabilities | 0.01 | |||

| 1 | Less than 0.05% |

| Rating | % of Market Value1 | |||

U.S. Government and Agency Obligations | 69.2 | |||

Aaa | 0.1 | |||

Aa | 2.2 | |||

A | 14.6 | |||

Baa | 13.9 | |||

| 1 | Includes market value of long-term fixed-income securities only. |

TOP TEN HOLDINGS

| Security Name | % of Net Assets | |

Microsoft Corp.

| 2.4

| |

Amazon.com, Inc.

| 2.1

| |

Apple, Inc.

| 2.0

| |

U.S. Treasury Notes, 1.500%, 01/31/22

| 1.5

| |

Alphabet, Inc., Class A

| 1.5

| |

U.S. Treasury Notes, 2.625%, 06/15/21

| 1.1

| |

U.S. Treasury Notes, 1.375%, 08/31/20

| 0.9

| |

U.S. Treasury Notes, 1.625%, 07/31/20

| 0.8

| |

U.S. Treasury Notes, 1.125%, 07/31/21

| 0.8

| |

Facebook, Inc., Class A

| 0.8

| |

| ||

Top Ten as a Group

| 13.9

| |

| ||

Credit quality ratings shown above reflect the highest rating assigned by either Standard & Poor’s (“S&P”) or Moody’s Investors Service, Inc. (“Moody’s”). These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change.

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

| 7 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments December 31, 2018 |

| Shares | Value | |||||||

Common Stocks - 56.3% |

| |||||||

Communication Services - 3.9% |

| |||||||

Alphabet, Inc., Class A* | 3,615 | $3,777,530 | ||||||

AT&T, Inc. | 18,134 | 517,544 | ||||||

Borussia Dortmund GmbH & Co. KGaA (Germany) | 1,800 | 16,499 | ||||||

Cable One, Inc.1 | 230 | 188,623 | ||||||

Capcom Co., Ltd. (Japan) | 2,500 | 49,569 | ||||||

Comcast Corp., Class A | 24,005 | 817,370 | ||||||

CTS Eventim AG & Co. KGaA (Germany) | 1,200 | 44,813 | ||||||

GungHo Online Entertainment, Inc. (Japan)* | 14,000 | 25,623 | ||||||

HKBN, Ltd. (Hong Kong) | 29,000 | 43,965 | ||||||

Infrastrutture Wireless Italiane S.P.A. (Italy)2 | 1,300 | 8,899 | ||||||

KCOM Group PLC (United Kingdom) | 11,200 | 10,421 | ||||||

Live Nation Entertainment, Inc.*,1 | 2,860 | 140,855 | ||||||

Match Group, Inc. | 8,050 | 344,299 | ||||||

Netflix, Inc.* | 3,140 | 840,452 | ||||||

Nine Entertainment Co. Holdings, Ltd. (Australia) | 33,290 | 32,390 | ||||||

Proto Corp. (Japan) | 800 | 10,190 | ||||||

Rightmove PLC (United Kingdom) | 1,400 | 7,716 | ||||||

Sirius XM Holdings, Inc.1 | 36,585 | 208,900 | ||||||

SKY Perfect JSAT Holdings, Inc. (Japan) | 11,900 | 50,789 | ||||||

SmarTone Telecommunications Holdings, Ltd. (Hong Kong) | 20,100 | 22,289 | ||||||

Take-Two Interactive Software, Inc.* | 5,745 | 591,390 | ||||||

Telephone & Data Systems, Inc. | 8,040 | 261,622 | ||||||

T-Mobile US, Inc.* | 1,875 | 119,269 | ||||||

TripAdvisor, Inc.* | 8,240 | 444,466 | ||||||

Twenty-First Century Fox, Inc., Class A | 3,930 | 189,112 | ||||||

United States Cellular Corp.* | 1,790 | 93,026 | ||||||

Verizon Communications, Inc. | 12,610 | 708,934 | ||||||

Viacom, Inc., Class B | 13,240 | 340,268 | ||||||

Total Communication Services | 9,906,823 | |||||||

Consumer Discretionary - 7.1% | ||||||||

888 Holdings PLC (Gibraltar) | 23,400 | 52,195 | ||||||

Accent Group, Ltd. (Australia) | 93,300 | 78,889 | ||||||

Amazon.com, Inc.* | 3,470 | 5,211,836 | ||||||

AMC Networks, Inc., Class A*,1 | 1,700 | 93,296 | ||||||

Aptiv PLC (Ireland) | 5,050 | 310,929 | ||||||

Beneteau, S.A. (France) | 3,300 | 43,399 | ||||||

Best Buy Co., Inc. | 5,360 | 283,866 | ||||||

boohoo Group PLC (United Kingdom)* | 700 | 1,444 | ||||||

BorgWarner, Inc. | 6,870 | 238,664 | ||||||

Burlington Stores, Inc.*,1 | 4,260 | 692,974 | ||||||

| Shares | Value | |||||||

Capri Holdings, Ltd. (United Kingdom)* | 3,970 | $150,542 | ||||||

Chipotle Mexican Grill, Inc.* | 840 | 362,704 | ||||||

Choice Hotels International, Inc. | 1,840 | 131,707 | ||||||

Columbia Sportswear Co. | 6,350 | 533,972 | ||||||

De’ Longhi S.P.A. (Italy) | 500 | 12,667 | ||||||

DFS Furniture PLC (United Kingdom) | 12,100 | 28,038 | ||||||

Discovery, Inc., Class A*,1 | 4,520 | 111,825 | ||||||

Domino’s Pizza Group PLC (United Kingdom) | 2,800 | 8,322 | ||||||

Domino’s Pizza, Inc.1 | 2,465 | 611,295 | ||||||

Dunkin’ Brands Group, Inc.1 | 5,620 | 360,354 | ||||||

Exedy Corp. (Japan) | 3,200 | 78,165 | ||||||

Fujibo Holdings, Inc. (Japan) | 300 | 6,766 | ||||||

Garrett Motion, Inc. (Switzerland)* | 1 | 12 | ||||||

Harley-Davidson, Inc.1 | 6,470 | 220,756 | ||||||

Hilton Grand Vacations, Inc.*,1 | 2,825 | 74,552 | ||||||

HIS Co., Ltd. (Japan) | 400 | 14,544 | ||||||

The Home Depot, Inc. | 6,625 | 1,138,307 | ||||||

Hyatt Hotels Corp., Class A | 7,355 | 497,198 | ||||||

IDP Education, Ltd. (Australia) | 8,900 | 61,899 | ||||||

The Interpublic Group of Cos., Inc. | 22,360 | 461,287 | ||||||

Kindred Group PLC, SDR (Malta) | 3,100 | 28,497 | ||||||

Kohl’s Corp. | 2,920 | 193,713 | ||||||

Lifestyle International Holdings, Ltd. (Hong Kong) | 26,500 | 40,173 | ||||||

Lululemon Athletica, Inc. (Canada)*,1 | 2,860 | 347,805 | ||||||

Macy’s, Inc.1 | 4,925 | 146,667 | ||||||

Marriott International, Inc., Class A | 1,640 | 178,038 | ||||||

Matas A/S (Denmark) | 2,600 | 23,175 | ||||||

Moneysupermarket.com Group PLC (United Kingdom) | 5,400 | 18,959 | ||||||

NetEnt AB (Sweden) | 7,700 | 31,700 | ||||||

NIKE, Inc., Class B | 1,920 | 142,349 | ||||||

Nishimatsuya Chain Co., Ltd. (Japan) | 2,800 | 22,677 | ||||||

Nobia AB (Sweden) | 1,500 | 8,362 | ||||||

Ocado Group PLC (United Kingdom)* | 3,000 | 30,239 | ||||||

Omnicom Group, Inc. | 6,540 | 478,990 | ||||||

On the Beach Group PLC (United Kingdom)2 | 2,800 | 12,001 | ||||||

Pool Corp.1 | 4,775 | 709,804 | ||||||

Ralph Lauren Corp. | 3,565 | 368,835 | ||||||

Ross Stores, Inc. | 7,595 | 631,904 | ||||||

Sa Sa International Holdings, Ltd. (Hong Kong)1 | 40,000 | 15,109 | ||||||

Seiko Holdings Corp. (Japan) | 1,200 | 23,040 | ||||||

SSP Group PLC (United Kingdom) | 2,387 | 19,704 | ||||||

Thule Group AB (Sweden)2 | 800 | 14,642 | ||||||

| The accompanying notes are an integral part of these financial statements. |

| 8 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments(continued) |

| Shares | Value | |||||||

Consumer Discretionary - 7.1%(continued) | ||||||||

The TJX Cos., Inc. | 13,380 | $598,621 | ||||||

Tokai Rika Co., Ltd. (Japan) | 1,800 | 29,722 | ||||||

Tractor Supply Co. | 5,260 | 438,894 | ||||||

Trade Me Group, Ltd. (New Zealand) | 2,300 | 9,805 | ||||||

Urban Outfitters, Inc.* | 4,420 | 146,744 | ||||||

VF Corp. | 4,020 | 286,787 | ||||||

The Walt Disney Co. | 2,540 | 278,511 | ||||||

Xinyi Glass Holdings, Ltd. (Hong Kong) | 11,900 | 13,145 | ||||||

Yum! Brands, Inc. | 5,520 | 507,398 | ||||||

Total Consumer Discretionary |

| 17,668,414 | ||||||

Consumer Staples - 4.1% | ||||||||

Altria Group, Inc. | 14,595 | 720,847 | ||||||

Archer-Daniels-Midland Co. | 10,305 | 422,196 | ||||||

Austevoll Seafood A.S.A. (Norway) | 2,200 | 27,158 | ||||||

Axfood AB (Sweden) | 1,700 | 29,077 | ||||||

Bakkafrost P/F (Faroe Islands) | 300 | 14,683 | ||||||

Best World International, Ltd. (Singapore) | 30,700 | 59,199 | ||||||

C&C Group PLC (Ireland) | 11,500 | 35,905 | ||||||

The Coca-Cola Co. | 11,785 | 558,020 | ||||||

Constellation Brands, Inc., Class A | 1,120 | 180,118 | ||||||

Costco Wholesale Corp. | 2,600 | 529,646 | ||||||

Edgewell Personal Care Co.*,1 | 5,205 | 194,407 | ||||||

The Estee Lauder Cos., Inc., Class A | 4,930 | 641,393 | ||||||

Flowers Foods, Inc.1 | 12,750 | 235,493 | ||||||

Herbalife Nutrition, Ltd.*,1 | 9,900 | 583,605 | ||||||

Kimberly-Clark Corp. | 9,610 | 1,094,963 | ||||||

The Kroger Co. | 9,930 | 273,075 | ||||||

La Doria S.P.A. (Italy) | 1,400 | 12,719 | ||||||

Lamb Weston Holdings, Inc. | 1,355 | 99,674 | ||||||

McCormick & Co., Inc.,Non-Voting Shares | 320 | 44,557 | ||||||

Monster Beverage Corp.* | 11,440 | 563,077 | ||||||

Oriflame Holding AG (Switzerland) | 400 | 8,997 | ||||||

Origin Enterprises PLC (Ireland) | 8,300 | 54,403 | ||||||

PepsiCo, Inc. | 6,320 | 698,234 | ||||||

Philip Morris International, Inc. | 5,760 | 384,538 | ||||||

The Procter & Gamble Co. | 7,930 | 728,926 | ||||||

Rallye, S.A. (France)1 | 2,000 | 20,644 | ||||||

Rami Levy Chain Stores Hashikma Marketing 2006, Ltd. (Israel) | 650 | 33,455 | ||||||

Royal Unibrew A/S (Denmark) | 450 | 31,092 | ||||||

Salmar A.S.A. (Norway) | 2,000 | 99,198 | ||||||

Sysco Corp. | 14,870 | 931,754 | ||||||

| Shares | Value | |||||||

Tate & Lyle PLC (United Kingdom) | 4,800 | $40,391 | ||||||

TreeHouse Foods, Inc.*,1 | 7,910 | 401,116 | ||||||

US Foods Holding Corp.* | 4,460 | 141,114 | ||||||

Walmart, Inc. | 3,910 | 364,216 | ||||||

Total Consumer Staples |

| 10,257,890 | ||||||

Energy - 2.0% | ||||||||

Anadarko Petroleum Corp. | 2,800 | 122,752 | ||||||

Apache Corp.1 | 8,770 | 230,213 | ||||||

Baker Hughes, a GE Co. | 3,650 | 78,475 | ||||||

Cabot Oil & Gas Corp.1 | 5,680 | 126,948 | ||||||

Cheniere Energy, Inc.*,1 | 2,620 | 155,078 | ||||||

Chevron Corp. | 5,905 | 642,405 | ||||||

CNX Resources Corp.*,1 | 16,420 | 187,516 | ||||||

ConocoPhillips | 6,775 | 422,421 | ||||||

Continental Resources, Inc.* | 5,890 | 236,719 | ||||||

Devon Energy Corp. | 8,060 | 181,672 | ||||||

EOG Resources, Inc. | 1,020 | 88,954 | ||||||

Exxon Mobil Corp. | 12,965 | 884,083 | ||||||

Gaztransport Et Technigaz, S.A. (France) | 1,050 | 80,745 | ||||||

Gulf Keystone Petroleum, Ltd. (United Kingdom)* | 5,400 | 12,371 | ||||||

Japan Petroleum Exploration Co., Ltd. (Japan) | 600 | 10,637 | ||||||

Kosmos Energy, Ltd.*,1 | 27,050 | 110,094 | ||||||

Marathon Oil Corp. | 7,770 | 111,422 | ||||||

Modec, Inc. (Japan) | 1,400 | 28,918 | ||||||

Naphtha Israel Petroleum Corp., Ltd. (Israel)* | 5,800 | 37,033 | ||||||

National Oilwell Varco, Inc. | 5,790 | 148,803 | ||||||

Occidental Petroleum Corp. | 3,280 | 201,326 | ||||||

ONEOK, Inc. | 7,670 | 413,797 | ||||||

PBF Energy, Inc., Class A1 | 1,985 | 64,850 | ||||||

Petrofac, Ltd. (United Kingdom) | 7,500 | 45,526 | ||||||

Pioneer Natural Resources Co. | 745 | 97,982 | ||||||

TGS NOPEC Geophysical Co., A.S.A. (Norway) | 400 | 9,665 | ||||||

Washington H Soul Pattinson & Co., Ltd. (Australia) | 3,500 | 61,379 | ||||||

Whitehaven Coal, Ltd. (Australia) | 19,800 | 60,339 | ||||||

Whiting Petroleum Corp.*,1 | 3,000 | 68,070 | ||||||

Total Energy |

| 4,920,193 | ||||||

Financials - 6.2% | ||||||||

The Allstate Corp. | 4,430 | 366,051 | ||||||

Ameriprise Financial, Inc. | 6,330 | 660,662 | ||||||

Aspen Insurance Holdings, Ltd. (Bermuda) | 3,880 | 162,921 | ||||||

Assured Guaranty, Ltd. (Bermuda) | 5,480 | 209,774 | ||||||

Bank of America Corp. | 29,195 | 719,365 | ||||||

| The accompanying notes are an integral part of these financial statements. |

| 9 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments(continued) |

| Shares | Value | |||||||

Financials - 6.2%(continued) |

| |||||||

Bank of Georgia Group PLC (Georgia) | 1,500 | $26,350 | ||||||

Berkshire Hathaway, Inc., Class B* | 5,490 | 1,120,948 | ||||||

BlackRock, Inc. | 420 | 164,984 | ||||||

Burford Capital, Ltd. | 600 | 12,657 | ||||||

Cembra Money Bank AG (Switzerland) | 800 | 63,476 | ||||||

Citizens Financial Group, Inc. | 4,220 | 125,461 | ||||||

CME Group, Inc. | 3,390 | 637,727 | ||||||

Comerica, Inc. | 2,630 | 180,655 | ||||||

Commerce Bancshares, Inc.1 | 4,297 | 242,222 | ||||||

Credit Acceptance Corp.* | 1,160 | 442,842 | ||||||

Cullen/Frost Bankers, Inc. | 1,420 | 124,875 | ||||||

Dah Sing Financial Holdings, Ltd. (Hong Kong) | 10,400 | 51,418 | ||||||

Deutsche Pfandbriefbank AG (Germany)2 | 2,700 | 26,998 | ||||||

E*TRADE Financial Corp. | 3,700 | 162,356 | ||||||

Fifth Third Bancorp | 9,920 | 233,418 | ||||||

FinecoBank Banca Fineco S.P.A. (Italy) | 900 | 9,055 | ||||||

Franklin Resources, Inc. | 10,885 | 322,849 | ||||||

Israel Discount Bank, Ltd., Class A (Israel) | 16,500 | 50,913 | ||||||

JPMorgan Chase & Co. | 11,958 | 1,167,340 | ||||||

Just Group PLC (United Kingdom) | 1,500 | 1,753 | ||||||

kabu.com Securities Co., Ltd. (Japan) | 13,400 | 45,999 | ||||||

Legg Mason, Inc. | 7,020 | 179,080 | ||||||

Lincoln National Corp. | 5,210 | 267,325 | ||||||

LPL Financial Holdings, Inc. | 1,880 | 114,830 | ||||||

M&T Bank Corp. | 3,790 | 542,463 | ||||||

Marusan Securities Co., Ltd. (Japan) | 10,700 | 74,687 | ||||||

MetLife, Inc. | 5,750 | 236,095 | ||||||

Navient Corp.1 | 12,920 | 113,825 | ||||||

nib holdings, Ltd. (Australia) | 3,200 | 11,732 | ||||||

Northern Trust Corp. | 6,780 | 566,740 | ||||||

Okasan Securities Group, Inc. (Japan) | 3,800 | 16,855 | ||||||

Plus500, Ltd. (Israel)1 | 6,500 | 113,502 | ||||||

ProAssurance Corp. | 2,110 | 85,582 | ||||||

The Progressive Corp. | 27,050 | 1,631,927 | ||||||

Prudential Financial, Inc. | 1,770 | 144,344 | ||||||

Regions Financial Corp. | 13,780 | 184,376 | ||||||

S&P Global, Inc. | 5,050 | 858,197 | ||||||

Santander Consumer USA Holdings, Inc.1 | 43,370 | 762,878 | ||||||

SEI Investments Co. | 3,620 | 167,244 | ||||||

SpareBank 1 Nord Norge (Norway) | 7,500 | 54,433 | ||||||

State Street Corp. | 1,590 | 100,281 | ||||||

Storebrand A.S.A. (Norway) | 200 | 1,427 | ||||||

| Shares | Value | |||||||

SunTrust Banks, Inc. | 3,225 | $162,669 | ||||||

SVB Financial Group* | 1,745 | 331,410 | ||||||

Swissquote Group Holding, S.A. (Switzerland) | 650 | 30,075 | ||||||

T Rowe Price Group, Inc. | 950 | 87,704 | ||||||

TD Ameritrade Holding Corp. | 2,270 | 111,139 | ||||||

TOC Co., Ltd. (Japan) | 8,100 | 54,091 | ||||||

Tokai Tokyo Financial Holdings, Inc. (Japan) | 3,100 | 13,234 | ||||||

Topdanmark A/S (Denmark) | 2,100 | 98,005 | ||||||

Torchmark Corp. | 1,480 | 110,304 | ||||||

U.S. Bancorp | 6,675 | 305,048 | ||||||

Waddell & Reed Financial, Inc., Class A | 12,580 | 227,446 | ||||||

Wells Fargo & Co. | 10,220 | 470,938 | ||||||

White Mountains Insurance Group, Ltd. | 2 | 1,715 | ||||||

Total Financials |

| 15,564,670 | ||||||

Health Care - 8.2% | ||||||||

AbbVie, Inc. | 5,805 | 535,163 | ||||||

ABIOMED, Inc.* | 560 | 182,022 | ||||||

Alexion Pharmaceuticals, Inc.* | 9,170 | 892,791 | ||||||

Almirall, S.A. (Spain) | 300 | 4,593 | ||||||

Amgen, Inc. | 3,355 | 653,118 | ||||||

Baxter International, Inc. | 2,040 | 134,273 | ||||||

BioGaia AB, Class B (Sweden) | 1,300 | 46,562 | ||||||

Biogen, Inc.* | 1,900 | 571,748 | ||||||

Bio-Rad Laboratories, Inc., Class A* | 580 | 134,688 | ||||||

Bristol-Myers Squibb Co. | 7,090 | 368,538 | ||||||

Bruker Corp. | 9,015 | 268,377 | ||||||

Celgene Corp.* | 1,460 | 93,571 | ||||||

Chemed Corp. | 2,000 | 566,560 | ||||||

Cigna Corp. | 1,479 | 280,892 | ||||||

CVS Health Corp. | 1,155 | 75,676 | ||||||

Eli Lilly & Co. | 5,570 | 644,560 | ||||||

EMIS Group PLC (United Kingdom) | 5,500 | 64,004 | ||||||

Exelixis, Inc.* | 30,660 | 603,082 | ||||||

Galenica AG (Switzerland)2 | 350 | 15,417 | ||||||

Gilead Sciences, Inc. | 4,115 | 257,393 | ||||||

GN Store Nord A/S (Denmark) | 200 | 7,494 | ||||||

HCA Healthcare, Inc. | 1,760 | 219,032 | ||||||

Henry Schein, Inc.*,1 | 2,620 | 205,722 | ||||||

Humana, Inc. | 2,410 | 690,417 | ||||||

IDEXX Laboratories, Inc.* | 4,740 | 881,735 | ||||||

Illumina, Inc.* | 2,620 | 785,817 | ||||||

Intuitive Surgical, Inc.* | 1,940 | 929,105 | ||||||

Johnson & Johnson | 5,445 | 702,677 | ||||||

| The accompanying notes are an integral part of these financial statements. |

| 10 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments(continued) |

| Shares | Value | |||||||

Health Care - 8.2%(continued) |

| |||||||

Kaken Pharmaceutical Co., Ltd. (Japan) | 1,200 | $53,282 | ||||||

KYORIN Holdings, Inc. (Japan) | 2,700 | 58,980 | ||||||

McKesson Corp. | 2,510 | 277,280 | ||||||

Medtronic PLC (Ireland) | 7,425 | 675,378 | ||||||

Merck & Co., Inc. | 19,725 | 1,507,187 | ||||||

Molina Healthcare, Inc.*,1 | 4,850 | 563,667 | ||||||

Paramount Bed Holdings Co., Ltd. (Japan) | 400 | 16,495 | ||||||

Perrigo Co. PLC (Ireland) | 4,515 | 174,956 | ||||||

Pfizer, Inc. | 26,157 | 1,141,753 | ||||||

Regeneron Pharmaceuticals, Inc.* | 1,340 | 500,490 | ||||||

ResMed, Inc. | 8,540 | 972,450 | ||||||

Seikagaku Corp. (Japan) | 2,400 | 27,208 | ||||||

STADA Arzneimittel AG (Germany) | 50 | 4,612 | ||||||

Toho Holdings Co., Ltd. (Japan) | 3,300 | 80,715 | ||||||

UnitedHealth Group, Inc. | 5,340 | 1,330,301 | ||||||

Varian Medical Systems, Inc.* | 4,025 | 456,073 | ||||||

Veeva Systems, Inc., Class A* | 6,540 | 584,153 | ||||||

Vertex Pharmaceuticals, Inc.* | 2,085 | 345,505 | ||||||

Waters Corp.* | 1,400 | 264,110 | ||||||

WellCare Health Plans, Inc.* | 1,315 | 310,458 | ||||||

ZERIA Pharmaceutical Co., Ltd. (Japan) | 1,100 | 19,758 | ||||||

Zimmer Biomet Holdings, Inc. | 2,350 | 243,742 | ||||||

Total Health Care | 20,423,580 | |||||||

Industrials - 6.3% |

| |||||||

Aeon Delight Co., Ltd. (Japan) | 100 | 3,336 | ||||||

Aida Engineering, Ltd. (Japan) | 9,900 | 64,835 | ||||||

Allegion PLC (Ireland)1 | 2,120 | 168,985 | ||||||

Allison Transmission Holdings, Inc. | 23,305 | 1,023,323 | ||||||

Amadeus Fire AG (Germany) | 500 | 46,763 | ||||||

Armstrong World Industries, Inc. | 12,150 | 707,251 | ||||||

The Boeing Co. | 5,330 | 1,718,925 | ||||||

Caterpillar, Inc. | 9,425 | 1,197,635 | ||||||

Cintas Corp. | 1,000 | 167,990 | ||||||

CIR-Compagnie Industriali Riunite S.P.A. (Italy) | 32,100 | 34,282 | ||||||

Copart, Inc.*,1 | 2,120 | 101,294 | ||||||

Costain Group PLC (United Kingdom) | 5,300 | 21,313 | ||||||

CoStar Group, Inc.* | 1,665 | 561,671 | ||||||

CSX Corp. | 12,810 | 795,885 | ||||||

Cummins, Inc. | 920 | 122,949 | ||||||

Daiseki Co., Ltd. (Japan) | 300 | 6,195 | ||||||

Dart Group PLC (United Kingdom) | 2,900 | 28,569 | ||||||

Delta Air Lines, Inc. | 2,180 | 108,782 | ||||||

| Shares | Value | |||||||

Diploma PLC (United Kingdom) | 200 | $3,087 | ||||||

Dover Corp. | 7,420 | 526,449 | ||||||

Enav S.P.A. (Italy)2 | 800 | 3,894 | ||||||

Expeditors International of Washington, Inc. | 15,870 | 1,080,588 | ||||||

Fudo Tetra Corp. (Japan) | 2,070 | 31,974 | ||||||

Galliford Try PLC (United Kingdom) | 1,700 | 13,506 | ||||||

TheGo-Ahead Group PLC (United Kingdom) | 4,500 | 87,643 | ||||||

Harris Corp. | 780 | 105,027 | ||||||

HEICO Corp. | 1 | 77 | ||||||

Huber + Suhner AG (Switzerland) | 350 | 23,381 | ||||||

Huntington Ingalls Industries, Inc. | 875 | 166,521 | ||||||

Intertrust, N.V. (Netherlands)2 | 300 | 5,036 | ||||||

Irish Continental Group PLC (Ireland) | 5,700 | 27,756 | ||||||

Italmobiliare S.P.A. (Italy) | 800 | 16,847 | ||||||

Itoki Corp. (Japan) | 6,500 | 35,245 | ||||||

Kanematsu Corp. (Japan) | 2,900 | 35,121 | ||||||

Kardex AG (Switzerland) | 390 | 45,096 | ||||||

Kokuyo Co., Ltd. (Japan) | 1,100 | 16,067 | ||||||

Komori Corp. (Japan) | 9,100 | 91,407 | ||||||

Kyodo Printing Co., Ltd. (Japan) | 900 | 20,113 | ||||||

Landstar System, Inc. | 4,540 | 434,342 | ||||||

Lockheed Martin Corp. | 3,620 | 947,861 | ||||||

Meitec Corp. (Japan) | 300 | 12,174 | ||||||

Mersen, S.A. (France) | 1,100 | 29,545 | ||||||

Morgan Advanced Materials PLC (United Kingdom) | 19,500 | 65,418 | ||||||

Nibe Industrier AB, Class B (Sweden) | 4,000 | 41,118 | ||||||

Nissin Electric Co., Ltd. (Japan) | 600 | 4,364 | ||||||

Norfolk Southern Corp. | 1,100 | 164,494 | ||||||

Okumura Corp. (Japan) | 1,800 | 52,447 | ||||||

Old Dominion Freight Line, Inc. | 2,310 | 285,262 | ||||||

PACCAR, Inc. | 3,785 | 216,275 | ||||||

QinetiQ Group PLC (United Kingdom) | 16,000 | 58,432 | ||||||

Raytheon Co. | 860 | 131,881 | ||||||

Redde PLC (United Kingdom) | 4,100 | 8,860 | ||||||

Robert Half International, Inc. | 16,410 | 938,652 | ||||||

Rockwell Automation, Inc. | 5,035 | 757,667 | ||||||

Rockwool International A/S, Class B (Denmark) | 110 | 28,765 | ||||||

Sanki Engineering Co., Ltd. (Japan) | 5,600 | 58,108 | ||||||

Signify, N.V. (Netherlands)2 | 100 | 2,339 | ||||||

Sodick Co., Ltd. (Japan) | 1,900 | 11,903 | ||||||

Sojitz Corp. (Japan) | 19,800 | 68,561 | ||||||

Southwest Airlines Co. | 1,970 | 91,566 | ||||||

| The accompanying notes are an integral part of these financial statements. |

| 11 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments(continued) |

| Shares | Value | |||||||

Industrials - 6.3%(continued) |

| |||||||

Stagecoach Group PLC (United Kingdom) | 14,000 | $23,644 | ||||||

Star Micronics Co., Ltd. (Japan) | 2,500 | 33,888 | ||||||

Tokyu Construction Co., Ltd. (Japan) | 9,100 | 82,217 | ||||||

Toshiba Plant Systems & Services Corp. (Japan) | 400 | 7,362 | ||||||

Toyo Construction Co., Ltd. (Japan) | 5,200 | 17,887 | ||||||

TransUnion | 2,340 | 132,912 | ||||||

Union Pacific Corp. | 620 | 85,703 | ||||||

United Rentals, Inc.* | 6,315 | 647,477 | ||||||

Waste Management, Inc. | 1,290 | 114,797 | ||||||

WW Grainger, Inc.1 | 2,730 | 770,843 | ||||||

XPO Logistics, Inc.*,1 | 2,840 | 161,994 | ||||||

Total Industrials | 15,703,576 | |||||||

Information Technology - 13.5% |

| |||||||

Accenture PLC, Class A (Ireland) | 9,850 | 1,388,948 | ||||||

Adobe, Inc.* | 4,420 | 999,981 | ||||||

Advanced Micro Devices, Inc.* | 8,150 | 150,449 | ||||||

Akamai Technologies, Inc.* | 1,120 | 68,410 | ||||||

Amphenol Corp., Class A | 985 | 79,805 | ||||||

Apple, Inc. | 31,050 | 4,897,827 | ||||||

Arista Networks, Inc.* | 1,100 | 231,770 | ||||||

Atlassian Corp. PLC, Class A (Australia)* | 1,380 | 122,792 | ||||||

Automatic Data Processing, Inc. | 2,740 | 359,269 | ||||||

Azbil Corp. (Japan) | 1,000 | 19,764 | ||||||

BE Semiconductor Industries, N.V. (Netherlands) | 300 | 6,324 | ||||||

Booz Allen Hamilton Holding Corp. | 4,330 | 195,153 | ||||||

Broadridge Financial Solutions, Inc. | 3,060 | 294,525 | ||||||

CDW Corp. | 15,320 | 1,241,686 | ||||||

Cisco Systems, Inc. | 11,925 | 516,710 | ||||||

Citizen Watch Co., Ltd. (Japan) | 6,500 | 32,011 | ||||||

Citrix Systems, Inc. | 11,460 | 1,174,192 | ||||||

Conduent, Inc.* | 9,120 | 96,946 | ||||||

CyberArk Software, Ltd. (Israel)* | 150 | 11,121 | ||||||

Electrocomponents PLC (United Kingdom) | 3,100 | 20,024 | ||||||

F5 Networks, Inc.* | 3,900 | 631,917 | ||||||

Facebook, Inc., Class A* | 14,625 | 1,917,191 | ||||||

Fortinet, Inc.* | 6,180 | 435,257 | ||||||

Halma PLC (United Kingdom) | 1,300 | 22,647 | ||||||

Hewlett Packard Enterprise Co. | 24,780 | 327,344 | ||||||

HP, Inc. | 7,350 | 150,381 | ||||||

Ines Corp. (Japan) | 4,400 | 45,575 | ||||||

Intel Corp. | 3,040 | 142,667 | ||||||

Intuit, Inc. | 4,400 | 866,140 | ||||||

| Shares | Value | |||||||

Juniper Networks, Inc. | 10,830 | $291,435 | ||||||

Kainos Group PLC (United Kingdom) | 6,900 | 35,027 | ||||||

KLA-Tencor Corp. | 2,720 | 243,413 | ||||||

Logitech International, S.A. (Switzerland) | 600 | 18,953 | ||||||

Manhattan Associates, Inc.*,1 | 16,500 | 699,105 | ||||||

Mastercard, Inc., Class A | 9,810 | 1,850,656 | ||||||

Maxim Integrated Products, Inc. | 3,690 | 187,637 | ||||||

Micron Technology, Inc.* | 13,220 | 419,471 | ||||||

Microsoft Corp. | 58,635 | 5,955,557 | ||||||

National Instruments Corp. | 12,000 | 544,560 | ||||||

Nemetschek SE (Germany) | 60 | 6,601 | ||||||

Neopost, S.A. (France) | 900 | 24,568 | ||||||

NetApp, Inc. | 6,170 | 368,164 | ||||||

NSD Co., Ltd. (Japan) | 1,900 | 36,566 | ||||||

NVIDIA Corp. | 3,980 | 531,330 | ||||||

Okta, Inc.* | 2,060 | 131,428 | ||||||

Paycom Software, Inc.*,1 | 1,260 | 154,287 | ||||||

PayPal Holdings, Inc.* | 4,730 | 397,746 | ||||||

Pure Storage, Inc., Class A* | 18,630 | 299,570 | ||||||

QUALCOMM, Inc. | 7,355 | 418,573 | ||||||

Red Hat, Inc.* | 650 | 114,166 | ||||||

Riso Kagaku Corp. (Japan) | 3,700 | 56,944 | ||||||

Shinko Electric Industries Co., Ltd. (Japan) | 5,200 | 33,132 | ||||||

Siltronic AG (Germany) | 560 | 46,593 | ||||||

Skyworks Solutions, Inc. | 1,865 | 124,992 | ||||||

Softcat PLC (United Kingdom) | 5,500 | 41,274 | ||||||

Square, Inc., Class A* | 1,530 | 85,818 | ||||||

SS&C Technologies Holdings, Inc. | 2,970 | 133,977 | ||||||

Texas Instruments, Inc. | 11,530 | 1,089,585 | ||||||

TIS, Inc. (Japan) | 800 | 31,498 | ||||||

Total System Services, Inc. | 980 | 79,664 | ||||||

Twitter, Inc.* | 9,540 | 274,180 | ||||||

Visa, Inc., Class A | 12,350 | 1,629,459 | ||||||

VTech Holdings, Ltd. (Hong Kong) | 600 | 4,977 | ||||||

WEX, Inc.* | 1,080 | 151,265 | ||||||

Worldpay, Inc., Class A* | 2,140 | 163,560 | ||||||

Xilinx, Inc. | 1,980 | 168,637 | ||||||

Zebra Technologies Corp., Class A* | 2,780 | 442,659 | ||||||

Total Information Technology | 33,733,853 | |||||||

Materials - 1.6% |

| |||||||

Altri SGPS, S.A. (Portugal) | 6,300 | 41,980 | ||||||

Avery Dennison Corp. | 1,850 | 166,186 | ||||||

Cabot Corp. | 1,285 | 55,178 | ||||||

| The accompanying notes are an integral part of these financial statements. |

| 12 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments(continued) |

| Shares | Value | |||||||

Materials - 1.6%(continued) | ||||||||

Celanese Corp.1 | 3,840 | $345,485 | ||||||

CF Industries Holdings, Inc. | 1,360 | 59,174 | ||||||

The Chemours Co. | 4,960 | 139,971 | ||||||

Domtar Corp. | 10,090 | 354,462 | ||||||

DowDuPont, Inc. | 1,355 | 72,465 | ||||||

Ence Energia y Celulosa, S.A. (Spain) | 6,000 | 37,705 | ||||||

Evraz PLC (Russia) | 2,100 | 12,859 | ||||||

Ferrexpo PLC (Switzerland) | 3,500 | 8,683 | ||||||

Freeport-McMoRan, Inc. | 16,845 | 173,672 | ||||||

Fujimi, Inc. (Japan) | 900 | 17,223 | ||||||

LyondellBasell Industries, N.V., Class A | 6,540 | 543,866 | ||||||

Metsa Board OYJ (Finland) | 4,200 | 24,670 | ||||||

The Navigator Co., S.A. (Portugal) | 100 | 413 | ||||||

NOF Corp. (Japan) | 400 | 13,619 | ||||||

PPG Industries, Inc. | 2,235 | 228,484 | ||||||

Reliance Steel & Aluminum Co. | 2,740 | 195,006 | ||||||

Royal Gold, Inc. | 3,845 | 329,324 | ||||||

Sealed Air Corp. | 9,080 | 316,347 | ||||||

Southern Copper Corp. (Peru) | 16,190 | 498,166 | ||||||

Svenska Cellulosa AB SCA, Class B (Sweden) | 6,400 | 49,732 | ||||||

Toagosei Co., Ltd. (Japan) | 600 | 6,613 | ||||||

Toyo Ink SC Holdings Co., Ltd. (Japan) | 600 | 13,274 | ||||||

Westlake Chemical Corp.1 | 3,160 | 209,097 | ||||||

Yodogawa Steel Works, Ltd. (Japan) | 200 | 3,972 | ||||||

Total Materials |

| 3,917,626 | ||||||

Real Estate - 2.0% | ||||||||

Alexandria Real Estate Equities, Inc., REIT | 1,210 | 139,440 | ||||||

alstria officeREIT-AG, REIT (Germany) | 600 | 8,400 | ||||||

Bayside Land Corp. (Israel) | 30 | 12,777 | ||||||

CapitaLand Retail China Trust, REIT (Singapore) | 7,500 | 7,486 | ||||||

CBRE Group, Inc., Class A* | 3,420 | 136,937 | ||||||

CoreSite Realty Corp., REIT | 2,250 | 196,268 | ||||||

Corporate Office Properties Trust, REIT | 5,940 | 124,918 | ||||||

Crown Castle International Corp., REIT | 860 | 93,422 | ||||||

Digital Realty Trust, Inc., REIT | 1,780 | 189,659 | ||||||

Equinix, Inc., REIT | 320 | 112,819 | ||||||

Equity Residential, REIT | 3,455 | 228,065 | ||||||

Eurocommercial Properties, N.V. (Netherlands) | 600 | 18,519 | ||||||

Fabege AB (Sweden) | 3,700 | 49,454 | ||||||

First Real Estate Investment Trust, REIT (Singapore) | 33,400 | 24,130 | ||||||

GDI Property Group, REIT (Australia) | 46,500 | 44,218 | ||||||

| Shares | Value | |||||||

Great Portland Estates PLC, REIT (United Kingdom) | 8,800 | $73,973 | ||||||

Hemfosa Fastigheter AB (Sweden) | 5,700 | 44,980 | ||||||

Intervest Offices & Warehouses, N.V., REIT (Belgium) | 2,100 | 49,558 | ||||||

Jones Lang LaSalle, Inc. | 400 | 50,640 | ||||||

Kungsleden AB (Sweden) | 9,500 | 67,569 | ||||||

Lamar Advertising Co., Class A, REIT | 6,090 | 421,306 | ||||||

Life Storage, Inc., REIT | 5,630 | 523,534 | ||||||

LondonMetric Property PLC, REIT (United Kingdom) | 5,500 | 12,194 | ||||||

The Macerich Co., REIT | 2,710 | 117,289 | ||||||

Mori Trust Sogo Reit, Inc., REIT (Japan) | 40 | 58,242 | ||||||

NSI, N.V., REIT (Netherlands) | 100 | 3,907 | ||||||

Nyfosa AB (Sweden)* | 4,600 | 22,191 | ||||||

OUE Hospitality Trust (Singapore) | 31,700 | 15,580 | ||||||

Park Hotels & Resorts, Inc., REIT | 12,670 | 329,167 | ||||||

Piedmont Office Realty Trust, Inc., Class A, REIT1 | 16,810 | 286,442 | ||||||

Prologis, Inc., REIT | 3,350 | 196,712 | ||||||

Raysum Co., Ltd. (Japan) | 1,400 | 12,403 | ||||||

RDI REIT PLC, REIT (United Kingdom) | 8,000 | 2,923 | ||||||

Retail Value, Inc., REIT | 1,382 | 35,365 | ||||||

SBA Communications Corp., REIT* | 3,765 | 609,516 | ||||||

Selvaag Bolig A.S.A. (Norway) | 1,900 | 8,895 | ||||||

Senior Housing Properties Trust, REIT | 11,990 | 140,523 | ||||||

SITE Centers Corp., REIT | 14,940 | 165,386 | ||||||

Soilbuild Business Space REIT, REIT (Singapore) | 215,700 | 91,791 | ||||||

Spirit Realty Capital, Inc., REIT | 3,816 | 134,514 | ||||||

Takara Leben Co., Ltd. (Japan) | 1,300 | 3,579 | ||||||

Tanger Factory Outlet Centers, Inc., REIT 1 | 6,480 | 131,026 | ||||||

Taubman Centers, Inc., REIT | 2,280 | 103,717 | ||||||

Vastned Retail, N.V., REIT (Netherlands) | 100 | 3,585 | ||||||

Total Real Estate |

| 5,103,019 | ||||||

Utilities - 1.4% | ||||||||

American Electric Power Co., Inc. | 2,920 | 218,241 | ||||||

American Water Works Co., Inc. | 4,965 | 450,673 | ||||||

Atmos Energy Corp. | 4,870 | 451,547 | ||||||

CenterPoint Energy, Inc. | 12,345 | 348,499 | ||||||

Consolidated Edison, Inc. | 4,170 | 318,838 | ||||||

Eversource Energy | 3,610 | 234,794 | ||||||

FirstEnergy Corp. | 4,420 | 165,971 | ||||||

Italgas S.P.A. (Italy) | 5,000 | 28,673 | ||||||

Kenon Holdings, Ltd. (Singapore) | 3,900 | 58,662 | ||||||

NRG Energy, Inc. | 6,445 | 255,222 | ||||||

| The accompanying notes are an integral part of these financial statements. |

| 13 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments(continued) |

Shares | Value | |||||||

Utilities - 1.4%(continued) | ||||||||

OGE Energy Corp. | 6,290 | $246,505 | ||||||

Pinnacle West Capital Corp. | 3,460 | 294,792 | ||||||

PPL Corp.1 | 9,910 | 280,750 | ||||||

REN - Redes Energeticas Nacionais SGPS, S.A. (Portugal) | 11,100 | 31,007 | ||||||

Xcel Energy, Inc. | 3,780 | 186,241 | ||||||

Total Utilities |

| 3,570,415 | ||||||

Total Common Stocks | ||||||||

(Cost $141,951,269) | 140,770,059 | |||||||

| Principal Amount | ||||||||

Corporate Bonds and Notes - 12.9% |

| |||||||

Financials - 3.4% |

| |||||||

Aflac, Inc. | $30,000 | 27,752 | ||||||

The Allstate Corp. | 30,000 | 29,993 | ||||||

American Express Co. | 435,000 | 431,365 | ||||||

4.050%, 12/03/421 | 250,000 | 236,450 | ||||||

American Financial Group, Inc. | 25,000 | 22,518 | ||||||

Aon Corp. | 20,000 | 20,592 | ||||||

Bank of America Corp., GMTN | 1,150,000 | 1,091,753 | ||||||

Brown & Brown, Inc. | 25,000 | 24,889 | ||||||

Capital One Financial Corp. | 210,000 | 194,439 | ||||||

CBRE Services, Inc. | 210,000 | 219,040 | ||||||

EPR Properties | 25,000 | 24,769 | ||||||

The Goldman Sachs Group, Inc. | ||||||||

(3 month LIBOR + 1.510%), 3.691%, 06/05/283 | 125,000 | 116,295 | ||||||

3.850%, 01/26/27 | 700,000 | 659,126 | ||||||

Hospitality Properties Trust | 245,000 | 247,889 | ||||||

Host Hotels & Resorts, LP | ||||||||

Series F, 4.500%, 02/01/26 | 255,000 | 253,660 | ||||||

Series C, 4.750%, 03/01/23 | 170,000 | 173,843 | ||||||

JPMorgan Chase & Co. | 490,000 | 452,991 | ||||||

3.200%, 01/25/23 | 820,000 | 808,510 | ||||||

Kemper Corp. | 25,000 | 24,712 | ||||||

Principal Amount | Value | |||||||

Lazard Group LLC | $340,000 | $320,319 | ||||||

3.750%, 02/13/25 | 25,000 | 24,281 | ||||||

Mastercard, Inc. | 30,000 | 29,049 | ||||||

Mercury General Corp. | 530,000 | 513,450 | ||||||

MetLife, Inc. | 40,000 | 39,512 | ||||||

Morgan Stanley | ||||||||

(3 month LIBOR + 1.340%) 3.591%, 07/22/283 | 355,000 | 336,019 | ||||||

Old Republic International Corp. | 540,000 | 516,476 | ||||||

Omega Healthcare Investors, Inc. | 540,000 | 550,280 | ||||||

The Progressive Corp. | 330,000 | 300,796 | ||||||

4.350%, 04/25/44 | 205,000 | 209,458 | ||||||

SunTrust Bank, BKNT | 30,000 | 29,432 | ||||||

TD Ameritrade Holding Corp. | 25,000 | 24,743 | ||||||

Visa, Inc. | 210,000 | 199,107 | ||||||

2.800%, 12/14/22 | 40,000 | 39,520 | ||||||

4.150%, 12/14/35 | 240,000 | 248,655 | ||||||

Total Financials |

| 8,441,683 | ||||||

Industrials - 8.5% | ||||||||

3M Co., MTN | 20,000 | 19,431 | ||||||

AbbVie, Inc. | 700,000 | 617,746 | ||||||

Advance Auto Parts, Inc. | 25,000 | 25,614 | ||||||

Aetna, Inc. | 520,000 | 484,428 | ||||||

Agilent Technologies, Inc. | 30,000 | 30,316 | ||||||

Altria Group, Inc. | 645,000 | 522,015 | ||||||

Amazon.com, Inc. | 45,000 | 43,594 | ||||||

AmerisourceBergen Corp. | 30,000 | 25,812 | ||||||

Amgen, Inc. | 40,000 | 40,554 | ||||||

Anthem, Inc. | 40,000 | 38,691 | ||||||

Apple, Inc. | 100,000 | 94,917 | ||||||

| The accompanying notes are an integral part of these financial statements. |

| 14 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments(continued) |

Principal Amount | Value | |||||||

Industrials - 8.5%(continued) | ||||||||

Aptiv PLC (Ireland) | $25,000 | $24,357 | ||||||

AstraZeneca PLC (United Kingdom) | 35,000 | 33,600 | ||||||

AT&T, Inc. | 190,000 | 183,042 | ||||||

5.200%, 03/15/20 | 100,000 | 102,193 | ||||||

Automatic Data Processing, Inc. | 20,000 | 19,895 | ||||||

Baxter International, Inc. | 30,000 | 24,872 | ||||||

Becton Dickinson and Co. | 25,000 | 24,551 | ||||||

Best Buy Co., Inc. | 520,000 | 496,951 | ||||||

5.500%, 03/15/21 | 25,000 | 25,790 | ||||||

Biogen, Inc. | 30,000 | 31,088 | ||||||

The Boeing Co. | 275,000 | 260,800 | ||||||

2.800%, 03/01/27 | 325,000 | 310,076 | ||||||

Boston Scientific Corp. | 350,000 | 355,308 | ||||||

BP Capital Markets PLC (United Kingdom) | 55,000 | 53,254 | ||||||

3.994%, 09/26/23 | 295,000 | 301,448 | ||||||

Broadridge Financial Solutions, Inc. | 25,000 | 23,824 | ||||||

CA, Inc. | 25,000 | 23,746 | ||||||

Caterpillar Financial Services Corp., MTN | 440,000 | 428,295 | ||||||

Celanese US Holdings LLC | 25,000 | 25,719 | ||||||

Cisco Systems, Inc. | 45,000 | 44,134 | ||||||

Citrix Systems, Inc. | 530,000 | 507,494 | ||||||

Comcast Corp. | 450,000 | 423,127 | ||||||

ConocoPhillips Co. | 465,000 | 498,056 | ||||||

Costco Wholesale Corp. | 30,000 | 29,694 | ||||||

CSX Corp. | 25,000 | 24,999 | ||||||

3.700%, 10/30/20 | 495,000 | 500,403 | ||||||

Danaher Corp. | 20,000 | 19,822 | ||||||

Principal Amount | Value | |||||||

Darden Restaurants, Inc. | $30,000 | $27,678 | ||||||

Delta Air Lines, Inc. | 10,000 | 9,793 | ||||||

4.375%, 04/19/28 | 15,000 | 14,402 | ||||||

Devon Energy Corp. | 315,000 | 299,614 | ||||||

Dollar General Corp. | 235,000 | 228,152 | ||||||

DXC Technology Co. | 25,000 | 25,130 | ||||||

Eastman Chemical Co. | 25,000 | 23,117 | ||||||

Emerson Electric Co. | 30,000 | 29,601 | ||||||

Enable Midstream Partners, LP | 25,000 | 23,709 | ||||||

The Estee Lauder Cos., Inc. | 300,000 | 291,877 | ||||||

Express Scripts Holding Co. | 230,000 | 213,734 | ||||||

4.800%, 07/15/46 | 440,000 | 423,392 | ||||||

Fibria Overseas Finance, Ltd. (Brazil) | 280,000 | 285,012 | ||||||

Fidelity National Information Services, Inc. | 185,000 | 170,478 | ||||||

4.500%, 08/15/461 | 30,000 | 27,387 | ||||||

Fiserv, Inc. | 30,000 | 29,819 | ||||||

Fluor Corp. | 25,000 | 24,402 | ||||||

Gilead Sciences, Inc. | 645,000 | 601,127 | ||||||

3.250%, 09/01/221 | 50,000 | 49,908 | ||||||

Hess Corp. | 475,000 | 435,996 | ||||||

Hewlett Packard Enterprise Co. | 495,000 | 499,584 | ||||||

HollyFrontier Corp. | 430,000 | 435,308 | ||||||

The Home Depot, Inc. | 50,000 | 49,512 | ||||||

Honeywell International, Inc. | 10,000 | 9,363 | ||||||

HP, Inc. | 30,000 | 30,373 | ||||||

4.050%, 09/15/221 | 350,000 | 355,180 | ||||||

Hyatt Hotels Corp. | 25,000 | 24,635 | ||||||

Intel Corp. | 40,000 | 43,547 | ||||||

| The accompanying notes are an integral part of these financial statements. |

| 15 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments(continued) |

Principal Amount | Value | |||||||

Industrials - 8.5%(continued) |

| |||||||

International Paper Co. | $40,000 | $36,475 | ||||||

The Interpublic Group of Cos., Inc. | 10,000 | 9,504 | ||||||

John Deere Capital Corp., MTN | 40,000 | 39,638 | ||||||

3.050%, 01/06/28 | 530,000 | 504,568 | ||||||

Kerr-McGee Corp. | 30,000 | 33,484 | ||||||

Keysight Technologies, Inc. | 25,000 | 25,137 | ||||||

Kinder Morgan, Inc. | 50,000 | 49,028 | ||||||

KLA-Tencor Corp. | 25,000 | 25,419 | ||||||

Kohl’s Corp. | 485,000 | 479,262 | ||||||

The Kroger Co. | 290,000 | 295,596 | ||||||

Lockheed Martin Corp. | 40,000 | 39,753 | ||||||

Lowe’s Cos., Inc. | 35,000 | 33,161 | ||||||

LYB International Finance BV (Netherlands) | 225,000 | 215,224 | ||||||

LYB International Finance II BV (Netherlands) | 200,000 | 182,381 | ||||||

Macy’s Retail Holdings, Inc. | 510,000 | 472,668 | ||||||

Marathon Oil Corp. | 15,000 | 14,278 | ||||||

McDonald’s Corp., MTN | 40,000 | 41,110 | ||||||

Merck & Co., Inc. | 35,000 | 34,550 | ||||||

3.600%, 09/15/42 | 210,000 | 198,826 | ||||||

Micron Technology, Inc. | 335,000 | 329,556 | ||||||

Microsoft Corp. | 85,000 | 84,282 | ||||||

NetApp, Inc. | 180,000 | 171,583 | ||||||

3.375%, 06/15/21 | 25,000 | 24,920 | ||||||

NIKE, Inc. | 30,000 | 27,778 | ||||||

Nordstrom, Inc. | 30,000 | 28,383 | ||||||

Norfolk Southern Corp. | 20,000 | 19,675 | ||||||

3.850%, 01/15/24 | 170,000 | 172,267 | ||||||

Principal Amount | Value | |||||||

Norfolk Southern Corp. | $15,000 | $15,594 | ||||||

Occidental Petroleum Corp. | 235,000 | 233,845 | ||||||

ONEOK Partners, LP | 30,000 | 30,062 | ||||||

6.125%, 02/01/41 | 235,000 | 242,851 | ||||||

Oracle Corp. | 80,000 | 77,247 | ||||||

O’Reilly Automotive, Inc. | 30,000 | 29,930 | ||||||

Pfizer, Inc. | 50,000 | 48,328 | ||||||

Philip Morris International, Inc. | 45,000 | 43,313 | ||||||

4.375%, 11/15/41 | 610,000 | 555,906 | ||||||

Phillips 66 | 25,000 | 24,484 | ||||||

Praxair, Inc. | 30,000 | 30,037 | ||||||

QUALCOMM, Inc. | 605,000 | 577,525 | ||||||

Ralph Lauren Corp. | 25,000 | 24,737 | ||||||

Raytheon Co. | 30,000 | 30,452 | ||||||

Reliance Steel & Aluminum Co. | 25,000 | 25,302 | ||||||

S&P Global, Inc. | 30,000 | 30,070 | ||||||

Shell International Finance BV (Netherlands) | 60,000 | 57,736 | ||||||

2.500%, 09/12/26 | 660,000 | 613,268 | ||||||

The Sherwin-Williams Co. | 35,000 | 29,533 | ||||||

Shire Acquisitions Investments Ireland DAC (Ireland) | 40,000 | 36,257 | ||||||

Spirit AeroSystems, Inc. | 25,000 | 23,030 | ||||||

Stanley Black & Decker, Inc. | 15,000 | 16,400 | ||||||

Target Corp. | 300,000 | 280,357 | ||||||

4.000%, 07/01/42 | 235,000 | 222,111 | ||||||

The TJX Cos., Inc. | 30,000 | 27,247 | ||||||

Total System Services, Inc. | 25,000 | 25,232 | ||||||

Toyota Motor Credit Corp., MTN | 400,000 | 411,439 | ||||||

| The accompanying notes are an integral part of these financial statements. |

| 16 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments(continued) |

Principal Amount | Value | |||||||

Industrials - 8.5%(continued) |

| |||||||

Union Pacific Corp. | $10,000 | $10,057 | ||||||

4.000%, 04/15/47 | 250,000 | 233,961 | ||||||

United Technologies Corp. | 50,000 | 46,265 | ||||||

UnitedHealth Group, Inc. | 55,000 | 54,646 | ||||||

Vale Overseas, Ltd. (Brazil) | 525,000 | 568,312 | ||||||

Verisk Analytics, Inc. | 25,000 | 25,394 | ||||||

Verizon Communications, Inc. | 855,000 | 800,820 | ||||||

4.750%, 11/01/41 | 100,000 | 97,287 | ||||||

VF Corp. | 25,000 | 25,214 | ||||||

VMware, Inc. | 30,000 | 26,658 | ||||||

Walmart, Inc. | 35,000 | 34,461 | ||||||

4.000%, 04/11/431 | 25,000 | 24,928 | ||||||

Waste Management, Inc. | 30,000 | 30,711 | ||||||

Westlake Chemical Corp. | 25,000 | 22,909 | ||||||

WW Grainger, Inc. | 450,000 | 463,383 | ||||||

Zoetis, Inc. | 30,000 | 30,096 | ||||||

Total Industrials |

| 21,267,387 | ||||||

Utilities - 1.0% | ||||||||

BP Capital Markets America, Inc. | 245,000 | 246,133 | ||||||

Commonwealth Edison Co. | ||||||||

Series 122 2.950%, 08/15/27 | 485,000 | 466,884 | ||||||

Enterprise Products Operating LLC | 20,000 | 20,192 | ||||||

Exelon Generation Co. LLC | 245,000 | 244,550 | ||||||

Florida Power & Light Co. | 40,000 | 39,169 | ||||||

Georgia Power Co. | ||||||||

Series10-C 4.750%, 09/01/40 | 285,000 | 282,740 | ||||||

IPALCO Enterprises, Inc. | 25,000 | 24,362 | ||||||

National Fuel Gas Co. | 425,000 | 419,962 | ||||||

Principal Amount | Value | |||||||

NextEra Energy Capital Holdings, Inc. | $460,000 | $439,733 | ||||||

PacifiCorp | 280,000 | 272,496 | ||||||

Plains All American Pipeline, LP / PAA Finance Corp. | 35,000 | 33,768 | ||||||

Total Utilities | 2,489,989 | |||||||

Total Corporate Bonds and Notes | ||||||||

(Cost $32,634,134) | 32,199,059 | |||||||

U.S. Government and AgencyObligations - 28.9% |

| |||||||

Fannie Mae - 3.5% |

| |||||||

Federal National Mortgage Association | 510,000 | 494,867 | ||||||

1.625%, 01/21/20 | 425,000 | 420,814 | ||||||

2.625%, 09/06/24 | 345,000 | 344,069 | ||||||

FNMA | 48,620 | 47,514 | ||||||

2.500%, 04/01/28 to 05/01/43 | 1,543,232 | 1,485,001 | ||||||

3.000%, 03/01/42 to 01/01/47 | 1,394,882 | 1,364,824 | ||||||

3.500%, 11/01/25 to 08/01/48 | 2,411,036 | 2,420,489 | ||||||

4.000%, 12/01/21 to 07/01/48 | 1,261,129 | 1,288,000 | ||||||

4.500%, 06/01/39 to 09/01/43 | 598,643 | 627,265 | ||||||

5.000%, 09/01/33 to 10/01/41 | 254,893 | 270,728 | ||||||

5.500%, 02/01/35 to 05/01/39 | 119,729 | 128,336 | ||||||

Total Fannie Mae |

| 8,891,907 | ||||||

Freddie Mac - 8.0% | ||||||||

Federal Home Loan Mortgage Corp. 1.375%, 05/01/20 | 170,000 | 167,397 | ||||||

2.375%, 01/13/22 | 490,000 | 488,261 | ||||||

FHLMC Gold Pool | 1,180,025 | 1,134,977 | ||||||

3.000%, 01/01/29 to 01/01/48 | 6,221,198 | 6,108,316 | ||||||

3.500%, 03/01/42 to 09/01/48 | 6,536,296 | 6,553,039 | ||||||

4.000%, 03/01/44 to 09/01/48 | 3,978,479 | 4,063,679 | ||||||

4.500%, 02/01/39 to 04/01/44 | 731,136 | 761,302 | ||||||

5.000%, 07/01/35 to 07/01/41 | 580,777 | 615,968 | ||||||

5.500%, 04/01/38 to 01/01/39 | 35,170 | 37,853 | ||||||

Total Freddie Mac |

| 19,930,792 | ||||||

U.S. Treasury Obligations - 17.4% |

| |||||||

U.S. Treasury Notes | 2,065,000 | 1,995,790 | ||||||

1.375%, 05/31/20 to 08/31/20 | 3,915,000 | 3,846,522 | ||||||

1.500%, 01/31/22 | 3,900,000 | 3,789,551 | ||||||

1.625%, 07/31/20 to 10/31/23 | 5,765,000 | 5,599,031 | ||||||

1.750%, 11/15/20 to 06/30/22 | 3,390,000 | 3,320,973 | ||||||

1.875%, 06/30/20 to 11/30/21 | 2,950,000 | 2,910,146 | ||||||

2.000%, 02/28/21 to 02/15/25 | 3,905,000 | 3,821,893 | ||||||

2.125%, 12/31/21 | 1,310,000 | 1,297,412 | ||||||

2.250%, 03/31/20 to 11/15/25 | 3,035,000 | 2,995,837 | ||||||

2.375%, 08/15/24 | 1,145,000 | 1,134,847 | ||||||

2.500%, 06/30/20 to 05/15/24 | 4,360,000 | 4,356,602 | ||||||

2.625%, 06/15/21 | 2,850,000 | 2,860,187 | ||||||

| The accompanying notes are an integral part of these financial statements. |

| 17 |

Table of Contents

AMG Chicago Equity Partners Balanced Fund Schedule of Portfolio Investments(continued) |

Principal Amount | Value | |||||||

U.S. Treasury Obligations - 17.4% |

| |||||||

U.S. Treasury Bonds | $1,330,000 | $1,260,019 | ||||||

3.000%, 11/15/45 to 02/15/48 | 2,845,000 | 2,834,772 | ||||||

3.125%, 05/15/48 | 1,510,000 | 1,539,109 | ||||||

Total U.S. Treasury Obligations |

| 43,562,691 | ||||||

Total U.S. Government and Agency Obligations | ||||||||

(Cost $72,793,789) | 72,385,390 | |||||||

| Shares | ||||||||

Preferred Stock - 0.0%# |

| |||||||

Industrials - 0.0%# | ||||||||

Sixt SE (Germany) | 150 | 8,260 | ||||||

| Principal Amount | ||||||||

Short-Term Investments - 1.9% |

| |||||||

Joint Repurchase Agreements - 0.9%4 |

| |||||||

Cantor Fitzgerald Securities, Inc., dated 12/31/18, due 01/02/19, 3.350% total to be received $1,000,186 (collateralized by various U.S. Government Agency Obligations and U.S. Treasuries, 0.000% - 10.000%, 01/25/19 -10/20/68, totaling $1,020,000) | $1,000,000 | 1,000,000 | ||||||

Deutsche Bank Securities, Inc., dated 12/31/18, due 01/02/19, 2.950% total to be received $307,905 (collateralized by U.S. Government Agency Obligation, 4.125%, 03/13/20, totaling $314,019) | 307,855 | 307,855 | ||||||

Principal Amount | Value | |||||||

RBC Dominion Securities, Inc., dated 12/31/18, due 01/02/19, 3.020% total to be received $1,000,168 (collateralized by various U.S. Government Agency Obligations, 3.000%- 7.000%, 10/01/25 - 10/20/48, totaling $1,020,000) | $1,000,000 | $1,000,000 | ||||||

Total Joint Repurchase Agreements |

| 2,307,855 | ||||||

| Shares | ||||||||

Other Investment Companies - 1.0% |

| |||||||

Dreyfus Government Cash Management Fund, Institutional Shares, 2.29%5 | 835,172 | 835,172 | ||||||

Dreyfus Institutional Preferred Government Money Market Fund, Institutional Shares, 2.40%5 | 835,172 | 835,172 | ||||||

JPMorgan U.S. Government Money Market Fund, IM Shares, 2.36%5 | 860,480 | 860,480 | ||||||

Total Other Investment Companies | 2,530,824 | |||||||

Total Short-Term Investments | ||||||||

(Cost $4,838,679) | 4,838,679 | |||||||

Total Investments - 100.0% |

| 250,201,447 | ||||||

Other Assets, less Liabilities - 0.0%# |

| 52,038 | ||||||

Net Assets - 100.0% | $250,253,485 | |||||||

| * | Non-income producing security. |

| # | Less than 0.05%. |

| 1 | Some or all of these securities, amounting to $12,415,179 or 5.0% of net assets, were out on loan to various brokers and are collateralized by cash and various U.S. Treasury Obligations. See Note 4 of Notes to Financial Statements. |

| 2 | Security exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions exempt from registration, normally to qualified buyers. At December 31, 2018, the value of these securities amounted to $89,226 or less than 0.1% of net assets. |

| 3 | Variable rate security. The rate shown is based on the latest available information as of December 31, 2018. |

| 4 | Cash collateral received from brokers for securities lending was invested in these joint repurchase agreements. |

| 5 | Yield shown represents the December 31, 2018, seven day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |