Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-06431

AMG Funds II

(Exact name of registrant as specified in charter)

600 Steamboat Road, Suite 300,

Greenwich, Connecticut 06830

(Address of principal executive offices) (Zip code)

AMG Funds LLC

600 Steamboat Road, Suite 300,

Greenwich, Connecticut 06830

(Name and address of agent for service)

Registrant’s telephone number, including area code: (203) 299-3500

Date of fiscal year end: DECEMBER 31

Date of reporting period: JANUARY 1, 2017 – DECEMBER 31, 2017

(Annual Shareholder Report)

Table of Contents

Item 1. Reports to Shareholders

Table of Contents

| ANNUAL REPORT |

AMG Funds

December 31, 2017

AMG Chicago Equity Partners Balanced Fund

Class N: MBEAX | Class I: MBESX | Class Z: MBEYX

AMG Chicago Equity Partners Small Cap Value Fund

Class N: CESVX | Class I: CESSX | Class Z: CESIX

AMG Managers Amundi Intermediate Government Fund

Class N: MGIDX | Class I: MADIX | Class Z: MAMZX

AMG Managers Amundi Short Duration Government Fund

Class N: MGSDX | Class I: MANIX | Class Z: MATZX

| amgfunds.com | | 123117 AR009 |

Table of Contents

Table of Contents

AMG Funds

Annual Report—December 31, 2017

| PAGE | ||||

| 2 | ||||

| 3 | ||||

PORTFOLIO MANAGER’S COMMENTS, FUND SNAPSHOTS AND SCHEDULES OF PORTFOLIO INVESTMENTS | ||||

| 4 | ||||

| 16 | ||||

| 23 | ||||

| 31 | ||||

FINANCIAL STATEMENTS | ||||

| 41 | ||||

Balance sheets, net asset value (NAV) per share computations and cumulative undistributed amounts | ||||

| 43 | ||||

Detail of sources of income, expenses, and realized and unrealized gains (losses) during the fiscal year | ||||

| 44 | ||||

Detail of changes in assets for the past two fiscal years | ||||

| 46 | ||||

Historical net asset values per share, distributions, total returns, income and expense ratios, turnover ratios and net assets | ||||

| 58 | ||||

Accounting and distribution policies, details of agreements and transactions with Fund management and affiliates, and descriptions of certain investment risks | ||||

| 68 | ||||

| 69 | ||||

| 70 | ||||

Nothing contained herein is to be considered an offer, sale or solicitation of an offer to buy shares of any series of the AMG Funds family of mutual funds. Such offering is made only by prospectus, which includes details as to offering price and other material information.

Table of Contents

| | Letter to Shareholders |

Dear Shareholder:

The last 12 months was a strong period for equity markets as the health of the global economy improved and positive investor sentiment helped extend the U.S. bull market into its ninth year. The S&P 500® Index, a widely followed barometer of the U.S. equity market, returned 21.83% during the fiscal year ended December 31, 2017. By comparison, small cap stocks underperformed large caps with a 14.65% return for the small cap Russell 2000® Index.

The S&P 500 Index has notched positive performance in every month since the U.S. presidential election amidst the backdrop of strong corporate earnings, improving global economic growth and the passage of sweeping tax reform. 2017 also marked a turning point for the broader global economy as growth accelerated in a more coordinated fashion around the world, global trade improved and commodities recovered. U.S. equity market volatility remained extremely low despite saber rattling in North Korea and a devastating hurricane season. In fact, the S&P 500 Index has not seen a pullback greater than 5% since the summer of 2016.

In total, all but two sectors of the S&P 500 Index were positive during the last 12 months; however, there was significant dispersion in performance across sectors. Information technology and materials stocks led the Index with returns of 38.87% and 23.25%, respectively, while companies within the energy and telecommunication services sectors were the laggards with returns of (1.11)% and (1.49)%, respectively. Growth stocks outperformed value during all four quarters of the year and ended 2017 with returns of 30.2% and 13.7% for the Russell 1000® Growth and Russell 1000® Value Indexes, respectively. International equities outperformed domestic equities for the first time since 2012 as the global economy picked up and international returns were boosted by a weaker U.S. Dollar with the MSCI All Country World ex-USA Index returning 27.19% during the year. Meanwhile, emerging markets had their strongest year since 2009 with a 37.3% return for the MSCI Emerging Markets Index.

The U.S. bond market produced modestly positive returns for the year, as measured by the 3.54% return for the Bloomberg Barclays U.S. Aggregate Bond Index, a broad measure of U.S. bond market performance. The yield curve flattened as the U.S. Federal Reserve (the Fed) continued to normalize monetary policy and short-term interest rates rose more than longer-term rates. The 2-year U.S. Treasury note rose 69 basis points during the year to yield 1.89% while the 10-year U.S. Treasury note

ended 2017 at a 2.40% yield, five basis points lower than where it started. Investment grade corporates outperformed Treasuries and securitized credits with returns of 6.42%, 2.31% and 2.51%, respectively. Bond investors willing to accept more credit risk were rewarded with higher returns as high yield bonds performed strongly and credit spreads tightened. The Bloomberg Barclays U.S. Corporate High Yield Index ended the period with a 7.50% return.

AMG Funds appreciates the privilege of providing investment tools to you and your clients. Our foremost goal is to provide investment solutions that help our shareholders successfully reach their long-term investment goals. By partnering with AMG’s affiliated investment boutiques, AMG Funds provides access to a distinctive array of actively managed return-oriented investment strategies. Additionally, we oversee and distribute a number of complementary open-architecture mutual funds subadvised by unaffiliated investment managers. We thank you for your continued confidence and investment in AMG Funds. You can rest assured that under all market conditions our team is focused on delivering excellent investment management services for your benefit.

Respectfully,

Jeffery Cerutti

President

AMG Funds

| Periods ended December 31, 2017* | ||||||||||||||||

Average Annual Total Returns | 1 Year | 3 Years | 5 Years | |||||||||||||

Stocks: | ||||||||||||||||

Large Caps | (S&P 500® Index) | 21.83 | % | 11.41 | % | 15.79 | % | |||||||||

Small Caps | (Russell 2000® Index) | 14.65 | % | 9.96 | % | 14.12 | % | |||||||||

International | | (MSCI All Country World ex-USA Index) | | 27.19 | % | 7.83 | % | 6.80 | % | |||||||

Bonds: | ||||||||||||||||

Investment Grade | | (Bloomberg Barclays U.S. Aggregate Bond Index) | | 3.54 | % | 2.24 | % | 2.10 | % | |||||||

High Yield | | (Bloomberg Barclays U.S. Corporate High Yield Index) | | 7.50 | % | 6.35 | % | 5.78 | % | |||||||

Tax-exempt | | (Bloomberg Barclays Municipal Bond Index) | | 5.45 | % | 2.98 | % | 3.02 | % | |||||||

Treasury Bills | | (ICE BofAML 6-Month U.S. Treasury Bill Index) | | 0.95 | % | 0.62 | % | 0.43 | % | |||||||

| * | Source: Factset. Past performance is no guarantee of future results. |

2

Table of Contents

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on $1,000 invested at the beginning of the period and held for the entire period as indicated below.

ACTUAL EXPENSES

The first line of the following table provides information about the actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES

The second line of the following table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s

actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| Six Months Ended December 31, 2017 | Expense Ratio for the Period | Beginning Account Value 07/01/17 | Ending Account Value 12/31/17 | Expenses Paid During the Period* | ||||||||||||

AMG Chicago Equity Partners Balanced Fund | ||||||||||||||||

Based on Actual Fund Return | ||||||||||||||||

Class N | 1.09 | % | $ | 1,000 | $ | 1,080 | $ | 5.71 | ||||||||

Class I | .94 | % | $ | 1,000 | $ | 1,080 | $ | 4.93 | ||||||||

Class Z | .84 | % | $ | 1,000 | $ | 1,082 | $ | 4.41 | ||||||||

Based on Hypothetical 5% Annual Return | ||||||||||||||||

Class N | 1.09 | % | $ | 1,000 | $ | 1,020 | $ | 5.55 | ||||||||

Class I | .94 | % | $ | 1,000 | $ | 1,020 | $ | 4.79 | ||||||||

Class Z | .84 | % | $ | 1,000 | $ | 1,021 | $ | 4.28 | ||||||||

AMG Chicago Equity Partners Small Cap Value Fund | ||||||||||||||||

Based on Actual Fund Return | ||||||||||||||||

Class N | 1.35 | % | $ | 1,000 | $ | 1,069 | $ | 7.04 | ||||||||

Class I | 1.26 | % | $ | 1,000 | $ | 1,069 | $ | 6.57 | ||||||||

Class Z | .95 | % | $ | 1,000 | $ | 1,072 | $ | 4.96 | ||||||||

Based on Hypothetical 5% Annual Return | ||||||||||||||||

Class N | 1.35 | % | $ | 1,000 | $ | 1,018 | $ | 6.87 | ||||||||

Class I | 1.26 | % | $ | 1,000 | $ | 1,019 | $ | 6.41 | ||||||||

Class Z | .95 | % | $ | 1,000 | $ | 1,020 | $ | 4.84 | ||||||||

AMG Managers Amundi Intermediate Government Fund | ||||||||||||||||

Based on Actual Fund Return | ||||||||||||||||

Class N | .84 | % | $ | 1,000 | $ | 1,006 | $ | 4.25 | ||||||||

Class I | .73 | % | $ | 1,000 | $ | 1,006 | $ | 3.69 | ||||||||

Class Z | .69 | % | $ | 1,000 | $ | 1,007 | $ | 3.49 | ||||||||

Based on Hypothetical 5% Annual Return | ||||||||||||||||

Class N | .84 | % | $ | 1,000 | $ | 1,021 | $ | 4.28 | ||||||||

Class��I | .73 | % | $ | 1,000 | $ | 1,022 | $ | 3.72 | ||||||||

Class Z | .69 | % | $ | 1,000 | $ | 1,022 | $ | 3.52 | ||||||||

AMG Managers Amundi Short Duration Government Fund | ||||||||||||||||

Based on Actual Fund Return | ||||||||||||||||

Class N | .72 | % | $ | 1,000 | $ | 1,004 | $ | 3.64 | ||||||||

Class I | .63 | % | $ | 1,000 | $ | 1,004 | $ | 3.18 | ||||||||

Class Z | .57 | % | $ | 1,000 | $ | 1,005 | $ | 2.88 | ||||||||

Based on Hypothetical 5% Annual Return | ||||||||||||||||

Class N | .72 | % | $ | 1,000 | $ | 1,022 | $ | 3.67 | ||||||||

Class I | .63 | % | $ | 1,000 | $ | 1,022 | $ | 3.21 | ||||||||

Class Z | .57 | % | $ | 1,000 | $ | 1,022 | $ | 2.91 | ||||||||

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (184), then divided by 365. |

3

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Portfolio Manager’s Comments (unaudited)

THE YEAR IN REVIEW

For the year ended December 31, 2017, the AMG Chicago Equity Partners Balanced Fund (Class N shares) (the “Fund”) returned 15.54%, compared to the 14.17% return for its benchmark, which consists of 60% the return of the Russell 1000® Index and 40% the return of the Bloomberg Barclays U.S. Aggregate Bond Index.

The portfolio is managed to emphasize stock selection while also using our proprietary models to adjust size, style and allocation exposures. The Fund has had a strong year, beating the benchmark in three of the four quarters. A 65/35 asset allocation was maintained throughout the year and the overweight to equities helped returns relative to the 60/40 benchmark. The market phase identified by the firm’s proprietary model was in expansion all year, so the Fund maintained its preference for growth over value—this also helped relative returns as growth beat value in 2017. The equity portion of the Fund significantly outperformed the Russell 1000® Index, helped by the preference for growth over value and good performance from the alpha model. The fixed income portion of the Fund underperformed the Bloomberg Barclays Aggregate Index. The portfolio maintained its underweight to corporate bonds as well as its emphasis on higher quality issuers in this environment, which hurt relative performance.

The strong stock market of 2017 reflected not only multiple expansion, but also strong corporate earnings growth. Economic indicators in the U.S.

were generally strong in the fourth quarter and throughout 2017, with a solid job market, strong housing numbers, improved growth and earnings expectations, and moderate inflation. As such, the Federal Reserve raised rates three times in the year, with the targeted federal funds rate ending the year at 1.5%. Regarding fixed income markets, from a valuation standpoint, risk premiums are at cycle lows, demonstrated by the corporate option-adjusted spread (OAS) declining 30 basis points over the year to end at 93 basis points. Throughout the year, the yield curve flattened as short rates rose and longer rates declined. Additionally, we have seen an increase in risk overall, including in balance sheet leverage. The Federal Reserve’s intent is to continue to raise rates and reverse Quantitative Easing.

Given this backdrop, the fixed income portion of the Fund continues to focus on downside protection and the equity portion continues to follow its disciplined approach. Our research has shown that constructing a well-diversified portfolio of companies with attractive valuation ratios, quality balance sheets, and positive growth and momentum expectations built through a disciplined, risk-controlled process offers the potential to deliver consistent excess returns for the equity portion of the Fund. For the fixed income portion of the Fund, current circumstances support our strategy of maintaining a high quality bias. We believe the current environment demands an emphasis on downside protection in bond portfolios, and we are managing the portfolio in line with that belief. We will continue to monitor inputs to our investment process for indications of improving conditions and opportunity

but believe our positioning is prudent and in line with our stated objectives. Overall, our philosophy will not change based on short-term trends or conditions in the market. We will continue to use our disciplined approach to provide added value at controlled levels of risk.

This commentary reflects the viewpoints of the portfolio manager, Chicago Equity Partners, LLC, as of December 31, 2017 and is not intended as a forecast or guarantee of future results, and is subject to change without notice.

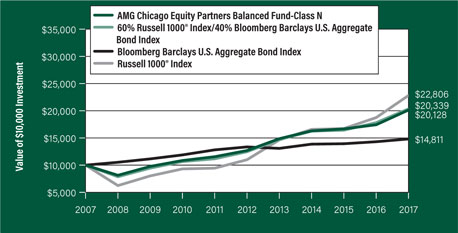

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG Chicago Equity Partners Balanced Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in the Fund’s Class N shares on December 31, 2007, to a $10,000 investment made in the 60% Russell 1000® Index/40% Bloomberg Barclays U.S. Aggregate Bond Index, Russell 1000® Index and the Bloomberg Barclays U.S. Aggregate Bond Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

4

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Portfolio Manager’s Comments (continued)

CUMULATIVE TOTAL RETURN PERFORMANCE (continued)

The table below shows the average annual total returns for the AMG Chicago Equity Partners Balanced Fund, the 60% Russell 1000® Index/40% Bloomberg Barclays U.S. Aggregate Bond Index, the Russell 1000® Index and the Bloomberg Barclays U.S. Aggregate Bond Index for the same time periods ended December 31, 2017.

| One | Five | Ten | Since | Inception | ||||||||||||||||

| Average Annual Total Returns1 | Year | Years | Years | Inception | Date | |||||||||||||||

AMG Chicago Equity Partners Balanced Fund2, 3, 4, 5, 6, 7, 8 | ||||||||||||||||||||

Class N | 15.54 | % | 9.67 | % | 7.25 | % | 8.05 | % | 01/02/97 | |||||||||||

Class I | 15.71 | % | 9.89 | % | — | 9.62 | % | 11/30/12 | ||||||||||||

Class Z | 15.90 | % | 9.96 | % | 7.53 | % | 8.43 | % | 01/02/97 | |||||||||||

60% Russell 1000® Index9 /40% Bloomberg Barclays U.S. Aggregate Bond Index10 | 14.17 | % | 10.29 | % | 7.36 | % | 7.72 | % | 01/02/97 | † | ||||||||||

Bloomberg Barclays U.S. Aggregate Bond Index10 | 3.54 | % | 2.10 | % | 4.01 | % | 5.22 | % | 01/02/97 | † | ||||||||||

Russell 1000® Index9 | 21.69 | % | 15.71 | % | 8.59 | % | 8.52 | % | 01/02/97 | † | ||||||||||

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.835.3879 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

† Date reflects inception date of the Fund, not the index.

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of December 31, 2017. All returns are in U.S. dollars ($). |

| 2 | From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. |

| 3 | To the extent that the Fund invests in asset-backed or mortgage-backed securities, its exposure to prepayment and extension risks may be greater than investments in other fixed income securities. |

| 4 | The Fund is subject to the risks associated with investments in debt securities, such as default risk and fluctuations in the perception of the debtor’s ability to pay its creditors. Changing interest rates may adversely affect the value of an investment. An increase in interest rates typically causes the value of bonds and other fixed income securities to fall. |

| 5 | Investments in international securities are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuations. These risks are magnified in emerging markets. |

| 6 | The Fund is subject to risks associated with investments in mid-capitalization companies such as greater price volatility, lower trading volume, and less liquidity than the stocks of larger, more established companies. |

| 7 | The Fund invests in value stocks, which may perform differently from the market as a whole and may be undervalued by the market for a long period of time. |

| 8 | Obligations of certain government agencies are not backed by the full faith and credit of the U.S. government. If one of these agencies defaulted on a loan, there is no guarantee that the U.S. government would provide financial support. Additionally, debt securities of the U.S. government may be affected by changing interest rates and subject to prepayment risk. |

| 9 | The Russell 1000® Index measures the performance of approximately 1,000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000® represents approximately 92% of the U.S. market. Unlike the Fund, the Russell 1000® Index is unmanaged, is not available for investment, and does not incur expenses. |

| 10 | The Bloomberg Barclays U.S. Aggregate Bond Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. Unlike the Fund, the Bloomberg Barclays U.S. Aggregate Bond Index is unmanaged, is not available for investment, and does not incur expenses. |

The Russell 1000® Index is a trademark of the London Stock Exchange Group companies.

Not FDIC insured, nor bank guaranteed. May lose value.

5

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Fund Snapshots (unaudited)

December 31, 2017

PORTFOLIO BREAKDOWN

Sector | % of Net Assets | |||

U.S. Government and Agency Obligations | 31.3 | |||

Information Technology | 17.2 | |||

Industrials | 10.4 | |||

Consumer Discretionary | 9.1 | |||

Financials | 8.9 | |||

Health Care | 8.0 | |||

Consumer Staples | 4.6 | |||

Energy | 2.4 | |||

Real Estate | 2.4 | |||

Materials | 2.2 | |||

Utilities | 1.7 | |||

Telecommunication Services | 0.7 | |||

Short-Term Investments* | 1.9 | |||

Other Assets Less Liabilities** | (0.8 | ) | ||

| * | Includes reinvestment of cash collateral into joint repurchase agreements on security lending transactions. |

| ** | Includes repayment of cash collateral on security lending transactions. |

TOP TEN HOLDINGS

Security Name | % of Net Assets | |||

Apple, Inc. | 2.9 | |||

U.S. Treasury Bonds, 2.750%, 08/15/42 | 2.4 | |||

Alphabet, Inc., Class A | 2.1 | |||

U.S. Treasury Notes, 2.250%, 11/15/24 | 2.0 | |||

U.S. Treasury Notes, 2.250%, 02/15/27 | 2.0 | |||

Microsoft Corp. | 1.5 | |||

Facebook, Inc., Class A | 1.4 | |||

Amazon.com, Inc. | 1.2 | |||

FHLMC Gold Pool, 3.500%, 01/01/46 | 1.1 | |||

U.S. Treasury Notes, 1.000%, 06/30/19 | 1.1 | |||

|

| |||

Top Ten as a Group | 17.7 | |||

|

| |||

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

6

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Schedule of Portfolio Investments

December 31, 2017

| Shares | Value | |||||||

Common Stocks - 63.8% | ||||||||

Consumer Discretionary - 9.1% | ||||||||

888 Holdings PLC (Gibraltar) | 21,500 | $ | 81,772 | |||||

Amazon.com, Inc.* | 2,020 | 2,362,329 | ||||||

Aoyama Trading Co., Ltd. (Japan) | 1,300 | 48,580 | ||||||

Bellway PLC (United Kingdom) | 300 | 14,382 | ||||||

Beneteau, S.A. (France) | 4,800 | 114,869 | ||||||

Best Buy Co., Inc. | 1,420 | 97,227 | ||||||

BorgWarner, Inc. | 5,780 | 295,300 | ||||||

Burlington Stores, Inc.* | 6,240 | 767,707 | ||||||

Cable One, Inc.1 | 390 | 274,307 | ||||||

Card Factory PLC (United Kingdom) | 29,400 | 117,138 | ||||||

CarMax, Inc.* | 3,480 | 223,172 | ||||||

Chipotle Mexican Grill, Inc.* | 195 | 56,361 | ||||||

Choice Hotels International, Inc. | 1,840 | 142,784 | ||||||

Comcast Corp., Class A | 34,675 | 1,388,734 | ||||||

CTS Eventim AG & Co. KGaA (Germany) | 1,200 | 55,790 | ||||||

De’ Longhi S.P.A. (Italy) | 100 | 3,027 | ||||||

Dollar Tree, Inc.* | 3,140 | 336,953 | ||||||

Domino’s Pizza, Inc. | 2,430 | 459,173 | ||||||

Dunkin’ Brands Group, Inc. | 2,590 | 166,977 | ||||||

EDION Corp. (Japan) | 5,500 | 63,946 | ||||||

Exedy Corp. (Japan) | 3,500 | 107,831 | ||||||

Harley-Davidson, Inc.1 | 2,360 | 120,077 | ||||||

Hilton Worldwide Holdings, Inc. | 9,285 | 741,500 | ||||||

The Home Depot, Inc. | 10,045 | 1,903,829 | ||||||

John Menzies PLC (United Kingdom) | 4,000 | 36,751 | ||||||

Kadokawa Dwango Corp. (Japan) | 4,500 | 55,486 | ||||||

Kindred Group PLC, SDR (Malta) | 3,100 | 44,264 | ||||||

Liberty Interactive Corp. QVC Group, Class A* | 28,355 | 692,429 | ||||||

Liberty Ventures* | 4,190 | 227,266 | ||||||

Macy’s, Inc.1 | 3,785 | 95,344 | ||||||

Marriott International, Inc., Class A | 4,440 | 602,641 | ||||||

McDonald’s Corp. | 5,400 | 929,448 | ||||||

Misawa Homes Co., Ltd. (Japan) | 12,000 | 105,424 | ||||||

N Brown Group PLC (United Kingdom) | 13,400 | 48,975 | ||||||

Netflix, Inc.* | 4,620 | 886,855 | ||||||

Nissan Shatai Co., Ltd. (Japan) | 3,100 | 31,642 | ||||||

Omnicom Group, Inc. | 2,300 | 167,509 | ||||||

Polaris Industries, Inc.1 | 3,305 | 409,787 | ||||||

Ralph Lauren Corp.1 | 2,115 | 219,304 | ||||||

Ross Stores, Inc. | 8,120 | 651,630 | ||||||

Royal Caribbean Cruises, Ltd. | 1,070 | 127,630 | ||||||

| Shares | Value | |||||||

Sanoma OYJ (Finland) | 8,600 | $ | 112,164 | |||||

Service Corp. International | 11,480 | 428,434 | ||||||

Sirius XM Holdings, Inc.1 | 36,585 | 196,096 | ||||||

SKY Perfect JSAT Holdings, Inc. (Japan) | 11,900 | 54,464 | ||||||

SSP Group PLC (United Kingdom) | 400 | 3,674 | ||||||

Target Corp. | 4,295 | 280,249 | ||||||

Thule Group AB (Sweden)2 | 2,000 | 45,054 | ||||||

Time Warner, Inc. | 1,910 | 174,708 | ||||||

Tokai Rika Co., Ltd. (Japan) | 1,800 | 37,771 | ||||||

Tupperware Brands Corp. | 4,875 | 305,662 | ||||||

VF Corp. | 7,620 | 563,880 | ||||||

Visteon Corp.* | 2,210 | 276,559 | ||||||

Wacoal Holdings Corp. (Japan) | 1,500 | 47,314 | ||||||

Total Consumer Discretionary | 17,802,179 | |||||||

Consumer Staples - 4.6% | ||||||||

a2 Milk Co., Ltd. (New Zealand)* | 18,100 | 103,518 | ||||||

Altria Group, Inc. | 7,625 | 544,501 | ||||||

Archer-Daniels-Midland Co. | 9,070 | 363,526 | ||||||

Brown-Forman Corp., Class B | 8,415 | 577,858 | ||||||

The Coca-Cola Co. | 11,535 | 529,226 | ||||||

Colgate-Palmolive Co. | 1,220 | 92,049 | ||||||

Conagra Brands, Inc. | 15,970 | 601,590 | ||||||

Constellation Brands, Inc., Class A | 3,650 | 834,281 | ||||||

CVS Health Corp. | 4,120 | 298,700 | ||||||

Edgewell Personal Care Co.* | 2,835 | 168,371 | ||||||

The Estee Lauder Cos., Inc., Class A | 8,055 | 1,024,918 | ||||||

Flowers Foods, Inc. | 7,530 | 145,404 | ||||||

Ingredion, Inc. | 2,780 | 388,644 | ||||||

La Doria S.P.A. (Italy) | 1,200 | 23,597 | ||||||

Lamb Weston Holdings, Inc. | 4,955 | 279,710 | ||||||

McCormick & Co., Inc., Non-Voting Shares | 1,080 | 110,063 | ||||||

Origin Enterprises PLC (Ireland) | 8,300 | 63,138 | ||||||

PepsiCo, Inc. | 5,970 | 715,922 | ||||||

Philip Morris International, Inc. | 1,660 | 175,379 | ||||||

Pilgrim’s Pride Corp.* | 11,040 | 342,902 | ||||||

The Procter & Gamble Co. | 9,800 | 900,424 | ||||||

Rami Levy Chain Stores Hashikma Marketing 2006, Ltd. (Israel) | 1,600 | 84,882 | ||||||

Salmar A.S.A. (Norway) | 3,100 | 93,135 | ||||||

Stock Spirits Group PLC (United Kingdom) | 27,200 | 98,696 | ||||||

The accompanying notes are an integral part of these financial statements.

7

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Schedule of Portfolio Investments (continued)

| Shares | Value | |||||||

Consumer Staples - 4.6% (continued) | ||||||||

Wal-Mart Stores, Inc. | 3,860 | $ | 381,175 | |||||

Total Consumer Staples | 8,941,609 | |||||||

Energy - 2.4% | ||||||||

Anadarko Petroleum Corp. | 2,800 | 150,192 | ||||||

Apache Corp. | 3,150 | 132,993 | ||||||

Baker Hughes, a GE company | 2,810 | 88,908 | ||||||

Cabot Oil & Gas Corp. | 4,870 | 139,282 | ||||||

Chevron Corp. | 5,335 | 667,889 | ||||||

CNX Resources Corp.* | 6,240 | 91,291 | ||||||

ConocoPhillips | 7,425 | 407,558 | ||||||

Devon Energy Corp. | 6,790 | 281,106 | ||||||

EOG Resources, Inc. | 920 | 99,277 | ||||||

EQT Corp. | 780 | 44,398 | ||||||

Exxon Mobil Corp. | 11,525 | 963,951 | ||||||

Japan Petroleum Exploration Co., Ltd. (Japan) | 2,800 | 74,013 | ||||||

National Oilwell Varco, Inc. | 3,300 | 118,866 | ||||||

Noble Corp. PLC (United Kingdom)*,1 | 16,620 | 75,122 | ||||||

Noble Energy, Inc. | 2,500 | 72,850 | ||||||

Occidental Petroleum Corp. | 1,420 | 104,597 | ||||||

Ocean Yield A.S.A. (Norway) | 2,700 | 22,855 | ||||||

Pioneer Natural Resources | 745 | 128,773 | ||||||

RPC, Inc.1 | 22,950 | 585,914 | ||||||

Sinanen Holdings Co., Ltd. (Japan) | 800 | 19,102 | ||||||

Subsea 7, S.A. (United Kingdom) | 3,000 | 44,946 | ||||||

Tethys Oil AB (Sweden) | 900 | 7,214 | ||||||

Valero Energy Corp. | 2,940 | 270,215 | ||||||

Whitehaven Coal, Ltd. (Australia) | 19,800 | 68,663 | ||||||

Whiting Petroleum Corp.* | 3,000 | 79,440 | ||||||

Total Energy | 4,739,415 | |||||||

Financials - 7.6% | ||||||||

The Allstate Corp. | 12,150 | 1,272,226 | ||||||

American Financial Group, Inc. | 640 | 69,466 | ||||||

Ameriprise Financial, Inc. | 3,870 | 655,849 | ||||||

Aspen Insurance Holdings, Ltd. (Bermuda) | 3,540 | 143,724 | ||||||

Associated Banc-Corp. | 7,100 | 180,340 | ||||||

Assurant, Inc. | 2,230 | 224,873 | ||||||

Assured Guaranty, Ltd. (Bermuda) | 6,240 | 211,349 | ||||||

Banca Mediolanum S.P.A. (Italy) | 1,300 | 11,254 | ||||||

Banca Popolare Di Sondrio SCARL (Italy) | 15,300 | 55,871 | ||||||

Bank of America Corp. | 28,255 | 834,087 | ||||||

Berkshire Hathaway, Inc., Class B* | 2,850 | 564,927 | ||||||

BlackRock, Inc. | 320 | 164,387 | ||||||

| Shares | Value | |||||||

Chesnara PLC (United Kingdom) | 1,500 | $ | 7,883 | |||||

Citizens Financial Group, Inc. | 3,520 | 147,770 | ||||||

CME Group, Inc. | 935 | 136,557 | ||||||

Comerica, Inc. | 2,330 | 202,267 | ||||||

Commerce Bancshares, Inc. | 4,043 | 225,761 | ||||||

Corp. Financiera Alba, S.A. (Spain) | 1,700 | 97,336 | ||||||

Cullen/Frost Bankers, Inc.1 | 1,120 | 106,008 | ||||||

Dah Sing Financial Holdings, Ltd. (Hong Kong) | 16,800 | 107,623 | ||||||

Deutsche Pfandbriefbank AG (Germany)2 | 7,100 | 113,420 | ||||||

Discover Financial Services | 855 | 65,767 | ||||||

Eaton Vance Corp. | 7,260 | 409,391 | ||||||

Erie Indemnity Co., Class A | 1,020 | 124,277 | ||||||

esure Group PLC (United Kingdom) | 30,900 | 103,673 | ||||||

Fifth Third Bancorp | 8,240 | 250,002 | ||||||

Franklin Resources, Inc. | 7,205 | 312,193 | ||||||

Genworth Mortgage Insurance Australia, Ltd. (Australia) | 2,300 | 5,372 | ||||||

Invesco, Ltd. | 4,150 | 151,641 | ||||||

Japan Securities Finance Co., Ltd. (Japan) | 19,700 | 111,365 | ||||||

JPMorgan Chase & Co. | 11,538 | 1,233,874 | ||||||

Lincoln National Corp. | 2,540 | 195,250 | ||||||

LPL Financial Holdings, Inc. | 1,880 | 107,423 | ||||||

M&T Bank Corp. | 1,130 | 193,219 | ||||||

Marusan Securities Co., Ltd. (Japan) | 11,500 | 102,888 | ||||||

MetLife, Inc. | 5,510 | 278,586 | ||||||

MFA Financial, Inc., REIT | 14,840 | 117,533 | ||||||

Moody’s Corp. | 2,735 | 403,713 | ||||||

Navient Corp. | 4,600 | 61,272 | ||||||

Northern Trust Corp. | 6,350 | 634,301 | ||||||

Plus500, Ltd. (Israel) | 8,400 | 102,881 | ||||||

The Progressive Corp. | 9,930 | 559,257 | ||||||

Prudential Financial, Inc. | 1,770 | 203,515 | ||||||

Regions Financial Corp. | 12,230 | 211,334 | ||||||

S&P Global, Inc. | 2,500 | 423,500 | ||||||

SEI Investments Co. | 2,890 | 207,675 | ||||||

SpareBank 1 Nord Norge (Norway) | 3,200 | 24,261 | ||||||

State Street Corp. | 3,680 | 359,205 | ||||||

SunTrust Banks, Inc. | 5,715 | 369,132 | ||||||

SVB Financial Group* | 960 | 224,419 | ||||||

T Rowe Price Group, Inc. | 950 | 99,683 | ||||||

TD Ameritrade Holding Corp. | 11,070 | 566,009 | ||||||

Torchmark Corp. | 1,480 | 134,251 | ||||||

The Travelers Cos., Inc. | 665 | 90,201 | ||||||

The accompanying notes are an integral part of these financial statements.

8

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Schedule of Portfolio Investments (continued)

| Shares | Value | |||||||

Financials - 7.6% (continued) | ||||||||

US Bancorp | 6,565 | $ | 351,753 | |||||

Waddell & Reed Financial, Inc., Class A1 | 10,210 | 228,091 | ||||||

Wells Fargo & Co. | 5,330 | 323,371 | ||||||

White Mountains Insurance Group, Ltd. | 110 | 93,641 | ||||||

Total Financials | 14,966,897 | |||||||

Health Care - 8.0% | ||||||||

AbbVie, Inc. | 2,760 | 266,920 | ||||||

ABIOMED, Inc.* | 1,560 | 292,360 | ||||||

ACADIA Pharmaceuticals, Inc.*,1 | 7,855 | 236,514 | ||||||

Aetna, Inc. | 1,775 | 320,192 | ||||||

Align Technology, Inc.* | 3,080 | 684,345 | ||||||

Amgen, Inc. | 415 | 72,168 | ||||||

Baxter International, Inc. | 22,633 | 1,462,997 | ||||||

Becton Dickinson & Co. | 224 | 47,818 | ||||||

BioGaia AB, Class B (Sweden) | 800 | 31,793 | ||||||

Bioverativ, Inc.* | 3,250 | 175,240 | ||||||

Bristol-Myers Squibb Co. | 2,980 | 182,614 | ||||||

Bruker Corp. | 15,465 | 530,759 | ||||||

Cardinal Health, Inc. | 750 | 45,952 | ||||||

Centene Corp.* | 2,490 | 251,191 | ||||||

Cigna Corp. | 810 | 164,503 | ||||||

COSMO Pharmaceuticals, N.V. (Ireland) | 100 | 15,024 | ||||||

Eli Lilly & Co. | 2,970 | 250,846 | ||||||

Exelixis, Inc.* | 16,450 | 500,080 | ||||||

Express Scripts Holding Co.* | 900 | 67,176 | ||||||

Gilead Sciences, Inc. | 4,915 | 352,111 | ||||||

Humana, Inc. | 1,410 | 349,779 | ||||||

IDEXX Laboratories, Inc.* | 4,390 | 686,508 | ||||||

Idorsia, Ltd. (Switzerland)* | 200 | 5,223 | ||||||

Indivior PLC (United Kingdom)* | 13,400 | 73,586 | ||||||

IQVIA Holdings, Inc.* | 2,870 | 280,973 | ||||||

Johnson & Johnson | 5,095 | 711,873 | ||||||

KYORIN Holdings, Inc. (Japan) | 4,800 | 89,573 | ||||||

McKesson Corp. | 690 | 107,605 | ||||||

Merck & Co., Inc. | 17,695 | 995,698 | ||||||

Mettler-Toledo International, Inc.* | 200 | 123,904 | ||||||

Neurocrine Biosciences, Inc.* | 10,225 | 793,358 | ||||||

Paramount Bed Holdings Co., Ltd. (Japan) | 1,500 | 74,124 | ||||||

Perrigo Co. PLC (Ireland) | 4,425 | 385,683 | ||||||

Pfizer, Inc. | 3,367 | 121,953 | ||||||

Regeneron Pharmaceuticals, Inc.* | 1,210 | 454,912 | ||||||

RHT Health Trust (Singapore) | 73,700 | 46,296 | ||||||

| Shares | Value | |||||||

Ship Healthcare Holdings, Inc. (Japan) | 1,400 | $ | 46,275 | |||||

Toho Holdings Co., Ltd. (Japan) | 5,200 | 117,220 | ||||||

UnitedHealth Group, Inc. | 7,060 | 1,556,448 | ||||||

Varian Medical Systems, Inc.* | 4,985 | 554,083 | ||||||

Veeva Systems, Inc., Class A* | 7,500 | 414,600 | ||||||

Vertex Pharmaceuticals, Inc.* | 1,055 | 158,102 | ||||||

WellCare Health Plans, Inc.* | 4,645 | 934,156 | ||||||

Zoetis, Inc. | 9,050 | 651,962 | ||||||

Total Health Care | 15,684,497 | |||||||

Industrials - 8.1% | ||||||||

3M Co. | 4,945 | 1,163,905 | ||||||

Aida Engineering, Ltd. (Japan) | 7,500 | 91,533 | ||||||

Air New Zealand, Ltd. (New Zealand) | 37,300 | 84,326 | ||||||

Allison Transmission Holdings, Inc. | 13,945 | 600,611 | ||||||

Amadeus Fire AG (Germany) | 500 | 46,320 | ||||||

Biesse S.P.A. (Italy) | 300 | 15,207 | ||||||

The Boeing Co. | 4,770 | 1,406,721 | ||||||

Caterpillar, Inc. | 11,555 | 1,820,837 | ||||||

Cintas Corp. | 2,140 | 333,476 | ||||||

Copa Holdings, S.A., Class A (Panama) | 950 | 127,357 | ||||||

Costain Group PLC (United Kingdom) | 14,700 | 92,835 | ||||||

Cummins, Inc. | 1,070 | 189,005 | ||||||

Eaton Corp. PLC | 870 | 68,739 | ||||||

Emerson Electric Co. | 2,910 | 202,798 | ||||||

Enav S.P.A. (Italy)2 | 5,100 | 27,599 | ||||||

Expeditors International of Washington, Inc. | 14,420 | 932,830 | ||||||

FACC AG (Austria)* | 4,800 | 99,664 | ||||||

Flowserve Corp. | 2,050 | 86,367 | ||||||

Fluor Corp. | 2,490 | 128,608 | ||||||

Fortive Corp. | 2,630 | 190,280 | ||||||

Galliford Try PLC (United Kingdom) | 1,700 | 29,517 | ||||||

GATX Corp.1 | 1,660 | 103,186 | ||||||

General Electric Co. | 10,300 | 179,735 | ||||||

Go-Ahead Group PLC (United Kingdom) | 2,100 | 42,218 | ||||||

HEICO Corp. | 1,990 | 187,756 | ||||||

Honeywell International, Inc. | 2,050 | 314,388 | ||||||

Hopewell Holdings, Ltd. (Hong Kong) | 22,700 | 83,764 | ||||||

Inabata & Co., Ltd. (Japan) | 600 | 9,077 | ||||||

Ingersoll-Rand PLC | 710 | 63,325 | ||||||

Itoki Corp. (Japan) | 6,500 | 48,034 | ||||||

Jacobs Engineering Group, Inc. | 2,980 | 196,561 | ||||||

Kanematsu Corp. (Japan) | 500 | 6,900 | ||||||

KAR Auction Services, Inc. | 2,370 | 119,709 | ||||||

The accompanying notes are an integral part of these financial statements.

9

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Schedule of Portfolio Investments (continued)

| Shares | Value | |||||||

Industrials - 8.1% (continued) |

| |||||||

Kirby Corp.* | 4,450 | $ | 297,260 | |||||

Komori Corp. (Japan) | 7,600 | 106,648 | ||||||

Kyodo Printing Co., Ltd. (Japan) | 3,400 | 109,336 | ||||||

Landstar System, Inc. | 4,820 | 501,762 | ||||||

Macquarie Atlas Roads Group (Australia) | 22,000 | 107,571 | ||||||

Mersen, S.A. (France) | 2,400 | 107,414 | ||||||

Morgan Advanced Materials | ||||||||

PLC (United Kingdom) | 4,200 | 19,127 | ||||||

Mota-Engil SGPS, S.A. (Portugal) | 26,000 | 114,271 | ||||||

Namura Shipbuilding Co., Ltd. (Japan) | 17,400 | 107,028 | ||||||

Northrop Grumman Corp. | 870 | 267,012 | ||||||

OC Oerlikon Corp. AG (Switzerland) | 3,200 | 54,015 | ||||||

Old Dominion Freight Line, Inc. | 3,930 | 516,991 | ||||||

Oshkosh Corp. | 980 | 89,072 | ||||||

Redde PLC (United Kingdom) | 17,000 | 40,224 | ||||||

Rheinmetall AG (Germany) | 100 | 12,646 | ||||||

Robert Half International, Inc. | 5,690 | 316,023 | ||||||

Rockwell Automation, Inc. | 4,775 | 937,571 | ||||||

SG Fleet Group, Ltd. (Australia) | 34,000 | 107,706 | ||||||

Sojitz Corp. (Japan) | 11,100 | 34,007 | ||||||

Spirit AeroSystems Holdings, Inc., Class A | 2,425 | 211,581 | ||||||

Sulzer AG (Switzerland) | 800 | 97,039 | ||||||

The Toro Co. | 770 | 50,227 | ||||||

TransUnion* | 15,480 | 850,781 | ||||||

Union Pacific Corp. | 620 | 83,142 | ||||||

United Rentals, Inc.* | 7,485 | 1,286,746 | ||||||

Valmont Industries, Inc. | 690 | 114,436 | ||||||

Waste Management, Inc. | 1,290 | 111,327 | ||||||

WW Grainger, Inc. | 1,020 | 240,975 | ||||||

Total Industrials | 15,985,126 | |||||||

Information Technology - 17.2% | ||||||||

Activision Blizzard, Inc. | 3,160 | 200,091 | ||||||

Adobe Systems, Inc.* | 2,790 | 488,920 | ||||||

Advanced Micro Devices, Inc.* | 11,890 | 122,229 | ||||||

Alphabet, Inc., Class A* | 3,945 | 4,155,663 | ||||||

Altium, Ltd. (Australia) | 900 | 9,303 | ||||||

Apple, Inc. | 33,810 | 5,721,666 | ||||||

Arista Networks, Inc.* | 3,665 | 863,401 | ||||||

Atea A.S.A. (Norway) | 4,700 | 66,116 | ||||||

Atlassian Corp. PLC, Class A (Australia)* | 2,180 | 99,234 | ||||||

Broadcom, Ltd. | 510 | 131,019 | ||||||

CDW Corp. | 18,100 | 1,257,769 | ||||||

| Shares | Value | |||||||

Cisco Systems, Inc. | 7,240 | $ | 277,292 | |||||

Dell Technologies, Inc., Class V* | 1,800 | 146,304 | ||||||

DXC Technology Co. | 2,800 | 265,720 | ||||||

Facebook, Inc., Class A* | 15,285 | 2,697,191 | ||||||

First Solar, Inc.* | 1,490 | 100,605 | ||||||

Fortinet, Inc.* | 22,450 | 980,840 | ||||||

Harris | 3,770 | 534,020 | ||||||

Hewlett Packard Enterprise Co. | 4,740 | 68,066 | ||||||

HP, Inc. | 19,450 | 408,644 | ||||||

IAC/InterActiveCorp* | 910 | 111,275 | ||||||

Ines Corp. (Japan) | 7,700 | 79,742 | ||||||

IPG Photonics Corp.* | 1,390 | 297,641 | ||||||

Jabil, Inc. | 6,740 | 176,925 | ||||||

Juniper Networks, Inc. | 10,970 | 312,645 | ||||||

Kainos Group PLC (United Kingdom) | 11,100 | 50,880 | ||||||

Leidos Holdings, Inc. | 13,110 | 846,513 | ||||||

LogMeIn, Inc. | 1,525 | 174,612 | ||||||

Mastercard, Inc., Class A | 5,930 | 897,565 | ||||||

Maxim Integrated Products, Inc. | 9,511 | 497,214 | ||||||

Micron Technology, Inc.* | 2,490 | 102,389 | ||||||

Microsoft Corp. | 35,365 | 3,025,122 | ||||||

Nemetschek SE (Germany) | 200 | 17,892 | ||||||

NVIDIA Corp. | 2,940 | 568,890 | ||||||

PayPal Holdings, Inc.* | 11,090 | 816,446 | ||||||

Red Hat, Inc.* | 880 | 105,688 | ||||||

Shinko Electric Industries Co., Ltd. (Japan) | 12,100 | 97,764 | ||||||

Siltronic AG (Germany)* | 400 | 57,829 | ||||||

Skyworks Solutions, Inc. | 6,700 | 636,165 | ||||||

Softcat PLC (United Kingdom) | 11,200 | 78,633 | ||||||

Square, Inc., Class A* | 17,240 | 597,711 | ||||||

Synopsys, Inc.* | 6,220 | 530,193 | ||||||

Take-Two Interactive Software, Inc.* | 5,215 | 572,503 | ||||||

Teradyne, Inc. | 2,635 | 110,327 | ||||||

Texas Instruments, Inc. | 13,290 | 1,388,008 | ||||||

Tower Semiconductor, Ltd. (Israel)* | 100 | 3,398 | ||||||

Toyo Corp./Chuo-ku (Japan) | 12,300 | 107,891 | ||||||

Universal Display Corp. | 1,260 | 217,539 | ||||||

Venture Corp., Ltd. (Singapore) | 5,300 | 80,916 | ||||||

Viavi Solutions, Inc.* | 20,960 | 183,190 | ||||||

Visa, Inc., Class A | 7,670 | 874,533 | ||||||

VMware, Inc., Class A*,1 | 650 | 81,458 | ||||||

Vtech Holdings (Hong Kong) | 3,700 | 48,392 | ||||||

Western Digital Corp. | 4,970 | 395,264 | ||||||

The accompanying notes are an integral part of these financial statements.

10

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Schedule of Portfolio Investments (continued)

| Shares | Value | |||||||

Information Technology - 17.2% (continued) |

| |||||||

Workday, Inc., Class A* | 2,540 | $ | 258,420 | |||||

Zebra Technologies Corp., Class A* | 7,160 | 743,208 | ||||||

Total Information Technology | 33,738,874 | |||||||

Materials - 2.2% | ||||||||

Air Products & Chemicals, Inc. | 1,855 | 304,368 | ||||||

Albemarle Corp. | 400 | 51,156 | ||||||

Avery Dennison Corp. | 1,850 | 212,491 | ||||||

Berry Global Group, Inc.* | 12,390 | 726,921 | ||||||

Cabot Corp. | 1,495 | 92,077 | ||||||

The Chemours Co. | 10,910 | 546,155 | ||||||

Domtar Corp. | 4,060 | 201,051 | ||||||

DowDuPont, Inc. | 5,427 | 386,511 | ||||||

DuluxGroup, Ltd. (Australia) | 12,400 | 73,893 | ||||||

Ence Energia y Celulosa, S.A. (Spain) | 7,200 | 47,514 | ||||||

FMC Corp. | 1,420 | 134,417 | ||||||

Freeport-McMoRan, Inc.* | 24,725 | 468,786 | ||||||

Huntsman Corp. | 4,950 | 164,785 | ||||||

Marshalls PLC (United Kingdom) | 17,200 | 105,639 | ||||||

Mitsubishi Steel Manufacturing Co., Ltd. (Japan) | 4,200 | 104,099 | ||||||

The Navigator Co., S.A. (Portugal) | 3,700 | 18,839 | ||||||

Newmont Mining Corp. | 3,755 | 140,888 | ||||||

Nippon Paper Industries Co., Ltd. (Japan) | 5,800 | 110,089 | ||||||

Nippon Soda Co., Ltd. (Japan) | 700 | 4,654 | ||||||

Owens-Illinois, Inc.* | 5,000 | 110,850 | ||||||

PPG Industries, Inc. | 585 | 68,340 | ||||||

Svenska Cellulosa AB SCA, Class B (Sweden) | 6,400 | 65,965 | ||||||

Toyo Ink SC Holdings Co., Ltd. (Japan) | 3,000 | 17,721 | ||||||

Vedanta Resources PLC (India) | 11,300 | 122,260 | ||||||

Westlake Chemical Corp. | 1,320 | 140,620 | ||||||

Total Materials | 4,420,089 | |||||||

Real Estate - 2.4% | ||||||||

Alexandria Real Estate Equities, Inc., REIT | 760 | 99,248 | ||||||

alstria office REIT-AG, REIT (Germany) | 3,000 | 46,362 | ||||||

Boston Properties, Inc., REIT | 1,530 | 198,946 | ||||||

CapitaLand Retail China Trust, REIT (Singapore) | 7,500 | 9,084 | ||||||

CBRE Group, Inc., Class A* | 11,950 | 517,554 | ||||||

Columbia Property Trust, Inc., REIT | 7,400 | 169,830 | ||||||

CoreSite Realty Corp., REIT | 4,990 | 568,361 | ||||||

Corporate Office Properties Trust, REIT | 4,180 | 122,056 | ||||||

DDR Corp., REIT | 23,260 | 208,410 | ||||||

Digital Realty Trust, Inc., REIT | 5,600 | 637,840 | ||||||

| Shares | Value | |||||||

Equity Residential, REIT | 3,475 | $ | 221,601 | |||||

Eurocommercial Properties, N.V. (Netherlands) | 600 | 26,140 | ||||||

Hemfosa Fastigheter AB (Sweden) | 2,800 | 37,520 | ||||||

Kungsleden AB (Sweden) | 15,500 | 112,399 | ||||||

Leopalace21 Corp. (Japan) | 1,100 | 8,542 | ||||||

The Macerich Co., REIT | 2,270 | 149,094 | ||||||

NSI, N.V., REIT (Netherlands) | 100 | 4,171 | ||||||

Outfront Media Inc., REIT | 10,125 | 234,900 | ||||||

Piedmont Office Realty Trust, Inc., Class A, REIT | 14,790 | 290,032 | ||||||

RDI REIT PLC, REIT (United Kingdom) | 215,200 | 106,380 | ||||||

Realty Income Corp., REIT | 740 | 42,195 | ||||||

Sabra Health Care REIT, Inc., REIT | 19,925 | 373,992 | ||||||

Savills PLC (United Kingdom) | 5,400 | 72,397 | ||||||

Senior Housing Properties Trust, REIT | 3,500 | 67,025 | ||||||

Soilbuild Business Space REIT, REIT (Singapore) | 215,700 | 108,056 | ||||||

Spirit Realty Capital, Inc., REIT | 16,000 | 137,292 | ||||||

Tanger Factory Outlet Centers, Inc., REIT 1 | 3,280 | 86,953 | ||||||

Vastned Retail, N.V., REIT (Netherlands) | 200 | 9,911 | ||||||

Total Real Estate | 4,666,291 | |||||||

Telecommunication Services - 0.7% | ||||||||

AT&T, Inc. | 20,490 | 796,651 | ||||||

B Communications, Ltd. (Israel)* | 6,200 | 113,419 | ||||||

DNA Oyj (Finland) | 700 | 13,144 | ||||||

Ei Towers S.P.A. (Italy) | 300 | 19,258 | ||||||

T-Mobile US, Inc.* | 4,445 | 282,302 | ||||||

Zayo Group Holdings, Inc.* | 4,510 | 165,968 | ||||||

Total Telecommunication Services | 1,390,742 | |||||||

Utilities - 1.5% | ||||||||

American Water Works Co., Inc. | 4,295 | 392,950 | ||||||

Atmos Energy Corp. | 3,300 | 283,437 | ||||||

CenterPoint Energy, Inc. | 9,475 | 268,711 | ||||||

Consolidated Edison, Inc. | 2,620 | 222,569 | ||||||

Entergy Corp. | 720 | 58,601 | ||||||

Eversource Energy | 1,770 | 111,829 | ||||||

Hokuriku Electric Power Co. (Japan) | 12,200 | 98,152 | ||||||

NRG Energy, Inc. | 20,855 | 593,950 | ||||||

OGE Energy Corp. | 4,240 | 139,538 | ||||||

Pinnacle West Capital Corp. | 2,530 | 215,505 | ||||||

PPL Corp. | 7,570 | 234,291 | ||||||

REN - Redes Energeticas Nacionais SGPS, | ||||||||

S.A. (Portugal) | 14,500 | 43,129 | ||||||

Vectren Corp. | 2,130 | 138,493 | ||||||

The accompanying notes are an integral part of these financial statements.

11

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Schedule of Portfolio Investments (continued)

| Shares | Value | |||||||

Utilities - 1.5% (continued) | ||||||||

Xcel Energy, Inc. | 2,650 | $ | 127,492 | |||||

Total Utilities | 2,928,647 | |||||||

Total Common Stocks | ||||||||

(Cost $103,058,322) | 125,264,366 | |||||||

| Principal Amount | ||||||||

Corporate Bonds and Notes - 3.8% |

| |||||||

Consumer Staples - 0.0%# |

| |||||||

Colgate-Palmolive Co., MTN 1.750%, 03/15/19 | $ | 105,000 | 104,703 | |||||

Financials - 1.3% |

| |||||||

American Express Credit Corp., MTN 2.250%, 05/05/21 | 160,000 | 158,813 | ||||||

Bank of America Corp., MTN 2.503%, 10/21/22 | 270,000 | 267,308 | ||||||

Bank of Montreal, MTN (Canada) 2.100%, 12/12/19 | 185,000 | 184,540 | ||||||

The Goldman Sachs Group, Inc. 2.350%, 11/15/21 | 320,000 | 315,438 | ||||||

JPMorgan Chase & Co., MTN 2.295%, 08/15/21 | 330,000 | 327,214 | ||||||

Morgan Stanley, MTN 2.625%, 11/17/21 | 295,000 | 293,817 | ||||||

The Toronto-Dominion Bank, MTN (Canada) 2.250%, 11/05/191 | 70,000 | 70,061 | ||||||

US Bancorp, MTN 2.200%, 04/25/19 | 175,000 | 175,527 | ||||||

Visa, Inc. 2.200%, 12/14/20 | 220,000 | 219,920 | ||||||

Wells Fargo & Co. 2.500%, 03/04/21 | 545,000 | 544,998 | ||||||

Total Financials | 2,557,636 | |||||||

Industrials - 2.3% | ||||||||

3M Co., MTN 2.000%, 06/26/22 | 130,000 | 127,788 | ||||||

Altria Group, Inc. 2.625%, 01/14/20 | 200,000 | 201,346 | ||||||

Apple, Inc. 2.300%, 05/11/22 | 310,000 | 308,023 | ||||||

AT&T, Inc. 4.100%, 02/15/282 | 370,000 | 371,972 | ||||||

BP Capital Markets PLC (United Kingdom) 1.676%, 05/03/19 | 225,000 | 223,860 | ||||||

Burlington Northern Santa Fe LLC 4.700%, 10/01/19 | 65,000 | 67,770 | ||||||

Cisco Systems, Inc. 1.400%, 02/28/18 | 200,000 | 199,900 | ||||||

| Principal Amount | Value | |||||||

Cisco Systems, Inc. 2.200%, 02/28/21 | $ | 160,000 | $ | 159,565 | ||||

Dr Pepper Snapple Group, Inc. 3.130%, 12/15/23 | 120,000 | 121,260 | ||||||

Exxon Mobil Corp. 1.708%, 03/01/19 | 95,000 | 94,794 | ||||||

Ford Motor Co. 4.346%, 12/08/26 | 120,000 | 125,336 | ||||||

General Electric Co. | ||||||||

Series A 6.750%, 03/15/32 | 45,000 | 61,737 | ||||||

The Home Depot, Inc. 2.250%, 09/10/18 | 210,000 | 210,620 | ||||||

Johnson & Johnson 5.150%, 07/15/18 | 90,000 | 91,678 | ||||||

Lockheed Martin Corp. 1.850%, 11/23/18 | 70,000 | 69,930 | ||||||

McDonald’s Corp., MTN 5.350%, 03/01/18 | 195,000 | 196,170 | ||||||

6.300%, 10/15/37 | 80,000 | 107,781 | ||||||

PepsiCo, Inc. 2.250%, 05/02/22 | 335,000 | 331,729 | ||||||

Pfizer, Inc. 1.700%, 12/15/19 | 230,000 | 228,619 | ||||||

Shell International Finance BV (Netherlands) 1.875%, 05/10/21 | 130,000 | 128,150 | ||||||

TransCanada PipeLines, Ltd. (Canada) 3.800%, 10/01/20 | 100,000 | 103,726 | ||||||

Tyson Foods, Inc. 2.650%, 08/15/19 | 200,000 | 201,039 | ||||||

Union Pacific Corp. 3.646%, 02/15/24 | 155,000 | 163,053 | ||||||

United Parcel Service, Inc. 6.200%, 01/15/38 | 120,000 | 165,483 | ||||||

Verizon Communications, Inc. 2.946%, 03/15/22 | 396,000 | 398,804 | ||||||

Total Industrials | 4,460,133 | |||||||

Utilities - 0.2% | ||||||||

Consolidated Edison Co. of New York, Inc. | ||||||||

Series 08-B 6.750%, 04/01/38 | 105,000 | 151,056 | ||||||

Dominion Energy, Inc. 4.450%, 03/15/21 | 75,000 | 79,254 | ||||||

Georgia Power Co. 5.400%, 06/01/40 | 65,000 | 78,288 | ||||||

PacifiCorp 6.000%, 01/15/39 | 85,000 | 114,448 | ||||||

Total Utilities | 423,046 | |||||||

Total Corporate Bonds and Notes | ||||||||

(Cost $7,480,385) | 7,545,518 | |||||||

The accompanying notes are an integral part of these financial statements.

12

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Schedule of Portfolio Investments (continued)

| Principal Amount | Value | |||||||

U.S. Government and Agency Obligations - 31.3% |

| |||||||

Fannie Mae - 2.8% | ||||||||

FNMA, 1.000%, 10/24/19 | $ | 360,000 | $ | 354,193 | ||||

1.375%, 10/07/211 | 170,000 | 165,419 | ||||||

1.875%, 02/19/19 | 440,000 | 440,163 | ||||||

2.000%, 01/01/30 | 57,355 | 56,470 | ||||||

2.500%, 04/01/28 to 05/01/43 | 1,742,100 | 1,713,683 | ||||||

2.625%, 09/06/24 | 305,000 | 309,344 | ||||||

3.000%, 03/01/42 to 08/01/43 | 575,059 | 578,309 | ||||||

3.500%, 11/01/25 to 07/01/43 | 301,315 | 311,195 | ||||||

4.000%, 12/01/21 to 11/01/44 | 320,064 | 335,667 | ||||||

4.500%, 06/01/39 to 09/01/43 | 740,615 | 792,613 | ||||||

5.000%, 09/01/33 to 10/01/41 | 308,405 | 333,389 | ||||||

5.500%, 02/01/35 to 05/01/39 | 147,372 | 162,702 | ||||||

Total Fannie Mae | 5,553,147 | |||||||

Freddie Mac - 9.1% | ||||||||

Federal Home Loan Mortgage Corp., 1.375%, 05/01/201 | 170,000 | 167,516 | ||||||

2.375%, 01/13/22 | 105,000 | 106,005 | ||||||

FHLMC Gold Pool, 2.500%, 07/01/28 to 09/01/46 | 1,329,454 | 1,307,587 | ||||||

3.000%, 01/01/29 to 11/01/47 | 5,012,021 | 5,043,795 | ||||||

3.500%, 03/01/42 to 10/01/47 | 5,650,900 | 5,814,298 | ||||||

4.000%, 03/01/44 to 11/01/45 | 3,414,220 | 3,572,354 | ||||||

4.500%, 02/01/39 to 04/01/44 | 874,010 | 931,285 | ||||||

5.000%, 07/01/35 to 07/01/41 | 706,236 | 767,911 | ||||||

5.500%, 04/01/38 to 01/01/39 | 42,493 | 47,122 | ||||||

Total Freddie Mac | 17,757,873 | |||||||

U.S. Treasury Obligations - 19.4% |

| |||||||

U.S. Treasury Bonds, | ||||||||

2.750%, 08/15/42 to 08/15/47 | 5,925,000 | 5,960,996 | ||||||

3.000%, 11/15/45 | 1,155,000 | 1,213,246 | ||||||

U.S. Treasury Notes, | ||||||||

0.875%, 07/31/19 | 840,000 | 827,400 | ||||||

1.000%, 06/30/19 to 11/30/19 | 3,930,000 | 3,875,554 | ||||||

1.125%, 07/31/21 | 1,555,000 | 1,503,977 | ||||||

1.375%, 05/31/20 to 08/31/20 | 3,155,000 | 3,111,510 | ||||||

1.500%, 02/28/19 to 01/31/22 | 1,955,000 | 1,928,023 | ||||||

1.625%, 07/31/20 to 05/15/26 | 3,185,000 | 3,074,984 | ||||||

1.750%, 05/15/22 to 06/30/22 | 2,175,000 | 2,138,001 | ||||||

1.875%, 11/30/21 | 1,670,000 | 1,656,660 | ||||||

2.000%, 02/15/25 | 725,000 | 708,843 | ||||||

2.250%, 11/15/24 to 02/15/27 | 8,845,000 | 8,766,406 | ||||||

2.500%, 08/15/23 to 05/15/24 | 3,255,000 | 3,295,206 | ||||||

Total U.S. Treasury Obligations | 38,060,806 | |||||||

|

| |||||||

Total U.S. Government and Agency Obligations | 61,371,826 | |||||||

|

| |||||||

| Shares | Value | |||||||

Rights - 0.0% | ||||||||

Health Care - 0.0% | ||||||||

Dyax Corp. CVR Expiration 12/31/19*,3,4 (Cost $0) | 670 | $ | 0 | |||||

| Principal Amount | ||||||||

Short-Term Investments - 1.9% |

| |||||||

Joint Repurchase Agreements - 1.3%5 |

| |||||||

Cantor Fitzgerald Securities, Inc., dated 12/29/17, due 01/02/18, 1.410% total to be received $1,000,157 (collateralized by various U.S. Government Agency Obligations, 0.000% - 8.500%, 01/31/18 - 06/20/63, totaling $1,020,000) | $ | 1,000,000 | 1,000,000 | |||||

Daiwa Capital Markets America, dated 12/29/17, due 01/02/18, 1.430% total to be received $448,828 (collateralized by various U.S. Government Agency Obligations, 0.000% - 6.500%, 01/11/18 - 12/01/51, totaling $457,732) | 448,757 | 448,757 | ||||||

State of Wisconsin Investment Board, dated 12/29/17, due 01/02/18, 1.630% total to be received $1,000,181 (collateralized by various U.S. Government Agency Obligations, 0.125% - 3.875%, 01/15/19 - 02/15/46, totaling $1,027,770) | 1,000,000 | 1,000,000 | ||||||

Total Joint Repurchase Agreements | 2,448,757 | |||||||

| Shares | ||||||||

Other Investment Companies - 0.6% |

| |||||||

Dreyfus Preferred Government Money Market Fund, Institutional Class Shares, 1.25%6 | 1,181,536 | 1,181,536 | ||||||

Total Short-Term Investments |

| 3,630,293 | ||||||

Total Investments - 100.8% | 197,812,003 | |||||||

Other Assets, less Liabilities - (0.8)% |

| (1,523,289 | ) | |||||

|

| |||||||

Net Assets - 100.0% | $ | 196,288,714 | ||||||

|

| |||||||

| # | Less than 0.05%. |

| * | Non-income producing security. |

| 1 | Some or all of these securities, amounting to $2,374,701 or 1.2% of net assets, were out on loan to various brokers. |

| 2 | Security exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions exempt from registration, normally to qualified buyers. At December 31, 2017, the value of these securities amounted to $558,045 or 0.3% of net assets. |

| 3 | Security’s value was determined by using significant unobservable inputs. |

The accompanying notes are an integral part of these financial statements.

13

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Schedule of Portfolio Investments (continued)

| 4 | This security is restricted and not available for re-sale. The security was received as part of a corporate action on January 22, 2016. |

| 5 | Collateral received from brokers for securities lending was invested in these joint repurchase agreements. |

| 6 | Yield shown represents the December 31, 2017, seven day average yield, which refers to the sum of the previous seven days’ dividends paid, expressed as an annual percentage. |

CVR Contingent Value Rights

FHLMC Freddie Mac

FNMA Fannie Mae

MTN Medium-Term Note

REIT Real Estate Investment Trust

SDR Sponsored Depositary Receipt

The following table summarizes the inputs used to value the Fund’s investments by the fair value hierarchy levels as of December 31, 2017:

| Level 1 | Level 2† | Level 3 | Total | |||||||||||||

Investments in Securities | ||||||||||||||||

Common Stocks | ||||||||||||||||

Information Technology | $ | 33,235,747 | $ | 503,127 | — | $ | 33,738,874 | |||||||||

Consumer Discretionary | 16,974,393 | 827,786 | — | 17,802,179 | ||||||||||||

Industrials | 15,064,347 | 920,779 | — | 15,985,126 | ||||||||||||

Health Care | 15,237,423 | 447,074 | — | 15,684,497 | ||||||||||||

Financials | 14,475,100 | 491,797 | — | 14,966,897 | ||||||||||||

Consumer Staples | 8,824,877 | 116,732 | — | 8,941,609 | ||||||||||||

Energy | 4,532,691 | 206,724 | — | 4,739,415 | ||||||||||||

Real Estate | 4,355,088 | 311,203 | — | 4,666,291 | ||||||||||||

Materials | 3,968,534 | 451,555 | — | 4,420,089 | ||||||||||||

Utilities | 2,830,495 | 98,152 | — | 2,928,647 | ||||||||||||

Telecommunication Services | 1,264,179 | 126,563 | — | 1,390,742 | ||||||||||||

Corporate Bonds and Notes†† | — | 7,545,518 | — | 7,545,518 | ||||||||||||

U.S. Government and Agency Obligations†† | — | 61,371,826 | — | 61,371,826 | ||||||||||||

Rights | — | — | $ | 0 | — | |||||||||||

Short-Term Investments | ||||||||||||||||

Joint Repurchase Agreements | — | 2,448,757 | — | 2,448,757 | ||||||||||||

Other Investment Companies | 1,181,536 | — | — | 1,181,536 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total Investments in Securities | $ | 121,944,410 | $ | 75,867,593 | $ | 0 | $ | 197,812,003 | ||||||||

|

|

|

|

|

|

|

| |||||||||

| † | As a result of the fair valuation policy utilized by the Fund, certain international equity securities may be level 2 and could result in transfers between level 1 to level 2. (See Note 1(a) in the Notes to Financial Statements.) |

| †† | All corporate bonds and notes and U.S. government and agency obligations held in the Fund are Level 2 securities. For a detailed breakout of corporate bonds and notes and U.S. government and agency obligations by major industry or agency classification, please refer to the Fund’s Schedule of Portfolio Investments. |

At December 31, 2017, the Level 3 securities are Rights received as a result of a corporate action. The security’s value was determined by using significant unobservable inputs which generated a change in unrealized depreciation of $7.

As of December 31, 2017, the Fund had no transfers between levels from the beginning of the reporting period.

The accompanying notes are an integral part of these financial statements.

14

Table of Contents

AMG Chicago Equity Partners Balanced Fund

Schedule of Portfolio Investments (continued)

Country | % of Long-Term Investments | |||

Australia | 0.2 | |||

Austria | 0.0 | # | ||

Bermuda | 0.2 | |||

Canada | 0.2 | |||

Finland | 0.1 | |||

France | 0.1 | |||

Germany | 0.2 | |||

Gibraltar | 0.0 | # | ||

Hong Kong | 0.1 | |||

India | 0.1 | |||

Ireland | 0.2 | |||

Israel | 0.2 | |||

Italy | 0.1 | |||

Japan | 1.2 | |||

Malta | 0.0 | # | ||

Netherlands | 0.1 | |||

New Zealand | 0.1 | |||

Norway | 0.1 | |||

Panama | 0.1 | |||

Portugal | 0.1 | |||

Singapore | 0.1 | |||

Spain | 0.1 | |||

Sweden | 0.1 | |||

Switzerland | 0.1 | |||

United Kingdom | 0.8 | |||

United States | 95.4 | |||

|

| |||

| 100.0 | ||||

|

| |||

| # | Less than 0.05%. |

The accompanying notes are an integral part of these financial statements.

15

Table of Contents

AMG Chicago Equity Partners Small Cap Value Fund

Portfolio Manager’s Comments (unaudited)

THE YEAR IN REVIEW

For the year ended December 31, 2017, the AMG Chicago Equity Partners Small Cap Value Fund (Class I shares) (the “Fund”) returned 5.35%, compared to the 7.84% return for its benchmark, the Russell 2000® Value Index.

The strong stock market of 2017 reflected not only multiple expansion, but also strong corporate earnings growth. Economic indicators in the U.S. were generally strong in the fourth quarter and throughout 2017, with a solid job market, strong housing numbers, improved growth and earnings expectations, and moderate inflation. As such, the Federal Reserve raised rates three times in the year, with the targeted federal funds rate ending the year at 1.5%.

While the Fund outperformed its benchmark in most months of 2017, weaker relative returns in March, May and December had the worst drag on relative performance for the year. In each of those months, at least two if not three factor groups detracted from returns. The Fund’s exposures to value and quality factors had weak performance, while momentum and growth were relatively strong. For the year, the spread between our top quintile-ranked and bottom quintile-ranked stocks was positive, but not as wide as the long-term average of our quantitative model.

Expectations for 2018 are for continued increased earnings as corporate tax reform is incorporated into expectations. It has been our experience that the market rewards a broad set of fundamental factors more often than not, which is why we consistently stick to our disciplined process.

The Fund is managed to emphasize stock selection while neutralizing size, style and sector exposure. Our research has shown that constructing a well-diversified portfolio of companies with attractive valuation ratios, quality balance sheets, and positive growth and momentum expectations built through a disciplined, risk-controlled process offers the potential to deliver consistent excess returns. Overall, our philosophy will not change based on short-term trends or conditions in the market. We will continue to use our disciplined approach to provide added value at controlled levels of risk.

This commentary reflects the viewpoints of the portfolio manager, Chicago Equity Partners, LLC, as of December 31, 2017 and is not intended as a forecast or guarantee of future results and is subject to change without notice.

16

Table of Contents

AMG Chicago Equity Partners Small Cap Value Fund

Portfolio Manager’s Comments (continued)

CUMULATIVE TOTAL RETURN PERFORMANCE

AMG Chicago Equity Partners Small Cap Value Fund’s cumulative total return is based on the daily change in net asset value (NAV), and assumes that all dividends and distributions were reinvested. This graph compares a hypothetical $10,000 investment made in the Fund’s Class I shares on December 31, 2014 (inception date), to a $10,000 investment made in the Russell 2000® Value Index for the same time period. The graph and table do not reflect the deduction of taxes that a shareholder would pay on a Fund distribution or redemption of shares. The listed returns for the Fund are net of expenses and the returns for the index exclude expenses. Total returns would have been lower had certain expenses not been reduced.

The table below shows the average annual total returns for the AMG Chicago Equity Partners Small Cap Value Fund and the Russell 2000® Value Index for the same time periods ended December 31, 2017.

| Average Annual Total Returns1 | One Year | Since Inception | Inception Date | |||||||||

AMG Chicago Equity Partners Small Cap Value Fund2, 3, 4, 5, 6, 7 | ||||||||||||

Class N | 5.18 | % | 8.41 | % | 12/31/14 | |||||||

Class I | 5.35 | % | 8.69 | % | 12/31/14 | |||||||

Class Z | 5.63 | % | 8.86 | % | 12/31/14 | |||||||

Russell 2000® Value Index8 | 7.84 | % | 9.55 | % | 12/31/14 | † | ||||||

The performance data shown represents past performance. Past performance is not a guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

Investors should carefully consider the Fund’s investment objectives, risks, charges and expenses before investing. For performance information through the most recent month end, current net asset values per share for the Fund and other information, please call 800.835.3879 or visit our website at amgfunds.com for a free prospectus. Read it carefully before investing or sending money.

Distributed by AMG Distributors, Inc., member FINRA/SIPC.

| † | Date reflects inception date of the Fund, not the index. |

| 1 | Total return equals income yield plus share price change and assumes reinvestment of all dividends and capital gain distributions. Returns are net of fees and may reflect offsets of Fund expenses as described in the prospectus. No adjustment has been made for taxes payable by shareholders on their reinvested dividends and capital gain distributions. Returns for periods greater than one year are annualized. The listed returns on the Fund are net of expenses and based on the published NAV as of December 31, 2017. All returns are in U.S. dollars ($). |

| 2 | From time to time, the Fund’s advisor has waived its fees and/or absorbed Fund expenses, which has resulted in higher returns. |

| 3 | The Fund is subject to risks associated with investments in small-capitalization companies, such as erratic earnings patterns, competitive conditions, limited earnings history and a reliance on one or a limited number of products. |

| 4 | Investments in international securities are subject to certain risks of overseas investing including currency fluctuations and changes in political and economic conditions, which could result in significant market fluctuations. |

| 5 | The Fund is subject to the risks associated with investments in emerging markets, such as erratic earnings patterns, economic and political instability, changing exchange controls, limitations on repatriation of foreign capital and changes in local governmental attitudes toward private investment, possibly leading to nationalization or confiscation of investor assets. |

| 6 | The Fund is subject to special risk considerations similar to those associated with the direct ownership of real estate. Real estate valuations may be subject to factors such as changing general and local economic, financial, competitive, and environmental conditions. |

| 7 | The Fund invests in value stocks, which may perform differently from the market as a whole and may be undervalued by the market for a long period of time. |

| 8 | The Russell 2000® Value Index is an unmanaged, market-value weighted, value-oriented index comprised of small stocks that have relatively low price-to-book ratios and lower forecasted growth values. Unlike the Fund, the Russell 2000® Value Index is unmanaged, is not available for investment and does not incur expenses. |

The Russell 2000® Value Index is a trademark of the London Stock Exchange Group companies.

Not FDIC insured, nor bank guaranteed. May lose value.

17

Table of Contents

AMG Chicago Equity Partners Small Cap Value Fund

Fund Snapshots (unaudited)

December 31, 2017

PORTFOLIO BREAKDOWN

Sector | %of Net Assets | |||

Financials | 31.2 | |||

Industrials | 15.5 | |||

Consumer Discretionary | 8.6 | |||

Information Technology | 8.6 | |||

Real Estate | 8.1 | |||

Utilities | 6.6 | |||

Health Care | 6.1 | |||

Energy | 5.4 | |||

Materials | 5.0 | |||

Consumer Staples | 2.7 | |||

Telecommunication Services | 0.7 | |||

Short-Term Investments* | 8.2 | |||

Other Assets Less Liabilities** | (6.7 | ) | ||

| * | Includes reinvestment of cash collateral into joint repurchase agreements on security lending transactions. |

| ** | Includes repayment of cash collateral on security lending transactions. |

TOP TEN HOLDINGS

| Security Name | %of Net Assets | |||

Wintrust Financial Corp. | 2.1 | |||

Cathay General Bancorp | 1.9 | |||

Vishay Intertechnology, Inc. | 1.7 | |||

MGIC Investment Corp. | 1.6 | |||

American Equity Investment Life Holding Co. | 1.6 | |||

Waddell & Reed Financial, Inc., Class A | 1.5 | |||

Invesco Mortgage Capital, Inc., 0.420% | 1.5 | |||

Xenia Hotels & Resorts, Inc., 0.275% | 1.5 | |||

Sunstone Hotel Investors, Inc., 0.580% | 1.4 | |||

Halyard Health, Inc. | 1.3 | |||

|

| |||

Top Ten as a Group | 16.1 | |||

|

| |||

Because a fund’s strategy may result in multiple investments in particular sectors of the economy, its performance may depend on the performance of those sectors and may fluctuate more widely than investments diversified across more sectors. For additional information on these and other risk considerations, please see the Fund’s prospectus.

Any sectors, industries, or securities discussed should not be perceived as investment recommendations. Mention of a specific security should not be considered a recommendation to buy or solicitation to sell that security. Specific securities mentioned in this report may have been sold from the Fund’s portfolio of investments by the time you receive this report.

18

Table of Contents

AMG Chicago Equity Partners Small Cap Value Fund

Schedule of Portfolio Investments

December 31, 2017

| Shares | Value | |||||||

Common Stocks - 98.5% | ||||||||

Consumer Discretionary - 8.6% | ||||||||

Beazer Homes USA, Inc.* | 540 | $ | 10,373 | |||||

Bridgepoint Education, Inc.* | 730 | 6,059 | ||||||

The Buckle, Inc.1 | 235 | 5,581 | ||||||

Callaway Golf Co. | 1,245 | 17,343 | ||||||

Career Education Corp.* | 605 | 7,308 | ||||||

Citi Trends, Inc. | 260 | 6,880 | ||||||

Conn’s, Inc.*,1 | 545 | 19,375 | ||||||

Cooper-Standard Holdings, Inc.* | 30 | 3,675 | ||||||

Dana, Inc. | 250 | 8,002 | ||||||

Deckers Outdoor Corp.* | 80 | 6,420 | ||||||

Flexsteel Industries, Inc. | 120 | 5,614 | ||||||

Group 1 Automotive, Inc. | 180 | 12,775 | ||||||

Johnson Outdoors, Inc., Class A | 320 | 19,869 | ||||||

KB Home | 255 | 8,147 | ||||||

Marriott Vacations Worldwide Corp. | 120 | 16,225 | ||||||

MDC Partners, Inc., Class A* | 1,560 | 15,210 | ||||||

MSG Networks, Inc., Class A* | 375 | 7,594 | ||||||

Office Depot, Inc. | 1,785 | 6,319 | ||||||

Oxford Industries, Inc. | 70 | 5,263 | ||||||

Stoneridge, Inc.* | 260 | 5,944 | ||||||

Tilly’s, Inc., Class A | 235 | 3,469 | ||||||

TopBuild Corp.* | 310 | 23,479 | ||||||

Tower International, Inc. | 205 | 6,263 | ||||||

tronc, Inc.* | 330 | 5,805 | ||||||

ZAGG, Inc.* | 225 | 4,151 | ||||||

Total Consumer Discretionary | 237,143 | |||||||

Consumer Staples - 2.7% | ||||||||

Cal-Maine Foods, Inc.* | 75 | 3,334 | ||||||

Central Garden & Pet Co., Class A* | 430 | 16,215 | ||||||

Ingles Markets, Inc., Class A | 10 | 346 | ||||||

Sanderson Farms, Inc. | 182 | 25,258 | ||||||

SpartanNash Co. | 55 | 1,467 | ||||||

SUPERVALU, Inc.*,1 | 615 | 13,284 | ||||||

United Natural Foods, Inc.* | 185 | 9,115 | ||||||

Village Super Market, Inc., Class A | 215 | 4,930 | ||||||

Total Consumer Staples | 73,949 | |||||||

Energy - 5.4% | ||||||||

C&J Energy Services, Inc.* | 495 | 16,568 | ||||||

Delek US Holdings, Inc. | 970 | 33,892 | ||||||

Exterran Corp.* | 450 | 14,148 | ||||||

McDermott International, Inc.* | 3,000 | 19,740 | ||||||

| Shares | Value | |||||||

Newpark Resources, Inc.* | 1,620 | $ | 13,932 | |||||

Oasis Petroleum, Inc.* | 755 | 6,349 | ||||||

Pacific Ethanol, Inc.* | 400 | 1,820 | ||||||

ProPetro Holding Corp.* | 735 | 14,818 | ||||||

Renewable Energy Group, Inc.* | 340 | 4,012 | ||||||

Unit Corp.* | 210 | 4,620 | ||||||

W&T Offshore, Inc.* | 5,545 | 18,354 | ||||||

Total Energy | 148,253 | |||||||

Financials - 31.2% | ||||||||

AG Mortgage Investment Trust, Inc., REIT | 635 | 12,071 | ||||||

American Equity Investment Life Holding Co. | 1,400 | 43,022 | ||||||

Anworth Mortgage Asset Corp., REIT | 2,275 | 12,376 | ||||||

Apollo Commercial Real Estate Finance, | 3 | 55 | ||||||

ARMOUR Residential REIT, Inc., REIT | 1,195 | 30,735 | ||||||

The Bancorp, Inc.* | 1,180 | 11,658 | ||||||

Bank of Commerce Holdings | 70 | 805 | ||||||

The Bank of NT Butterfield & Son, Ltd. (Bermuda) | 975 | 35,383 | ||||||

Cadence BanCorp* | 275 | 7,458 | ||||||

Cathay General Bancorp | 1,205 | 50,815 | ||||||

Chemical Financial Corp. | 240 | 12,833 | ||||||

City Holding Co. | 60 | 4,048 | ||||||

CNB Financial Corp. | 60 | 1,574 | ||||||

CoBiz Financial, Inc. | 390 | 7,796 | ||||||

Columbia Banking System, Inc. | 565 | 24,544 | ||||||

Evercore, Inc., Class A | 80 | 7,200 | ||||||

Farmers Capital Bank Corp. | 40 | 1,540 | ||||||

FB Financial Corp.* | 100 | 4,199 | ||||||

Federal Agricultural Mortgage Corp., Class C | 279 | 21,829 | ||||||

First American Financial Corp. | 245 | 13,730 | ||||||

First Commonwealth Financial Corp. | 575 | 8,234 | ||||||

First Community Bancshares, Inc. | 65 | 1,867 | ||||||

First Financial Bancorp | 1,224 | 32,252 | ||||||

Hancock Holding Co. | 495 | 24,503 | ||||||

Heritage Financial Corp. | 595 | 18,326 | ||||||

Hope Bancorp, Inc. | 715 | 13,049 | ||||||

Independent Bank Corp. | 570 | 12,740 | ||||||

Invesco Mortgage Capital, Inc., REIT | 2,330 | 41,544 | ||||||

Kearny Financial Corp. | 660 | 9,537 | ||||||

Kemper Corp. | 100 | 6,890 | ||||||

Lakeland Financial Corp. | 345 | 16,729 | ||||||

Macatawa Bank Corp. | 380 | 3,800 | ||||||

MBT Financial Corp. | 280 | 2,968 | ||||||

The accompanying notes are an integral part of these financial statements.

19

Table of Contents

AMG Chicago Equity Partners Small Cap Value Fund

Schedule of Portfolio Investments (continued)

| Shares | Value | |||||||

Financials - 31.2% (continued) | ||||||||