UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07062 | |||||||

| ||||||||

PACIFIC GLOBAL FUND INC. D/B/A PACIFIC ADVISORS FUND INC. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CALIFORNIA |

| 91203 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

GEORGE A. HENNING 101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CA 91203 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 818-242-6693 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | December 31, 2013 |

| ||||||

Item 1. Report to Shareholders

annual report

december 31, 2013

government securities fund

income and equity fund

balanced fund

large cap value fund

mid cap value fund

small cap value fund

Pacific Advisors

table of contents

Message from the Chairman | 1 | ||||||

Government Securities Fund | 5 | ||||||

Income and Equity Fund | 11 | ||||||

Balanced Fund | 17 | ||||||

Large Cap Value Fund | 23 | ||||||

Mid Cap Value Fund | 28 | ||||||

Small Cap Value Fund | 33 | ||||||

Schedule of Investments | 40 | ||||||

Statement of Assets and Liabilities | 62 | ||||||

Statement of Operations | 64 | ||||||

Statement of Changes in Net Assets | 66 | ||||||

Financial Highlights | 70 | ||||||

Notes to Financial Statements | 77 | ||||||

| Report of Independent Registered Public Accounting Firm | 87 | ||||||

| Disclosure Regarding the Board's Approval of the Funds' Advisory Contracts | 88 | ||||||

Directors and Officers | 92 | ||||||

Additional Tax Information | 94 | ||||||

This Report is submitted for the general information of the shareholders of Pacific Advisors Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by the Funds' current prospectus, which contains information concerning the investment policies of the Funds as well as other pertinent information.

This Report is for informational purposes only and is not a solicitation or recommendation that any particular investor should purchase or sell any particular security. The statements in the Chairman's Letter and the discussions of the Funds' performance are the opinions and beliefs expressed at the time of this commentary and are not intended to represent opinions and beliefs at any other time. These opinions are subject to change at any time based on market or other conditions and are not meant as a market forecast. All economic and performance information referenced is historical. Past performance does not guarantee future results.

For more information on the Pacific Advisors Funds, including information on charges, expenses and other classes offered, please obtain a copy of the prospectus by calling (800) 989-6693. Please read the prospectus and consider carefully the investment risks, objectives, charges and expenses before you invest or send money. Shares of the Pacific Advisors Funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

Message

from the chairman

Dear Shareholders,

2013: The Year of the Bull. The impressive fourth quarter growth enabled the equities markets to end the year on a high note; each of the major indices recorded 2013 returns in excess of 25%. The Pacific Advisors Funds posted impressive results; in particular Class A shares of the Small Cap Value, Government Securities, Balanced and Income & Equity Funds were all top performers for 2013 in their respective Lipper Categories. Further information about their success and a discussion with each of the portfolio managers follows my letter.

Lipper Rank (# of Funds) as of 12/31/13 Based on Total Return

2013 | Small Cap Value Fund (A) | Balanced Fund (A) | Income and Equity Fund (A) | Government Securities Fund (A) | |||||||||||||||

| Small Cap Core Category Kings | Mixed Asset Target Allocation Growth Category | Mixed Asset Target Allocation Conservative Category | General US Government Category | ||||||||||||||||

| 1 Year | 1 | (718) | 6 | (563) | 6 | (357) | 3 | (115) | |||||||||||

| 3 Year | 2 | (622) | 66 | (502) | 63 | (296) | 109 | (110) | |||||||||||

| 5 Year | 21 | (573) | 326 | (467) | 183 | (272) | 98 | (104) | |||||||||||

| 10 Year | 1 | (350) | 241 | (287) | 105 | (121) | 81 | (82) | |||||||||||

The impressive performance in the equity markets resulted principally from the underlying strength of the global economy and the impact of accommodative monetary policies that were introduced by the central banks in the U.S., Europe, China and Japan. Significantly, low interest rates encouraged merger and acquisitions activity; business expansions; stock buybacks; higher dividend rates; and increased confidence by both business owners and consumers. The growth strategies that many companies initiated during the post-recession years progressed at a measured pace. Investors rewarded other companies on their emerging market growth opportunities which should bear fruit as the world economy improves. Also, many investors who had long-remained on the sidelines became more confident in the economy; stocks gained as they migrated into equities.

The U.S. continued to grow slowly yet steadily as the unemployment picture improved and inflation remained subdued. The resurgent housing industry created important spillover benefits for consumer confidence, construction, furniture sales and other retail activities. Also, the boom in shale oil and gas production provided welcome growth while also contributing to the country's energy needs. Abroad, both Japan and China implemented growth initiatives: Japan's new Prime Minister Abe introduced an aggressive monetary policy to finally shake the world's third largest economy out of its decade-long doldrums; in China, newly-installed President Xi Jinping laid the groundwork for important financial and social reforms to aid the country's growing middle class. And, perhaps most crucially, the euro zone emerged from recession following 31/2 years of debt-crisis-induced drama. By the end of the year, the world's four major economies, which account for over 60% of global GDP, were expanding in synchrony.

Over the past five years, events including fiscal crises in the euro zone and legislative impasses in Washington unsettled consumers, investors and businesses. Yet, 2013 ended without cliffhangers. During this period, the Federal Reserve maintained an unwavering commitment to accommodative monetary policies. The eventual unwinding (or "tapering") of the Fed's extraordinary policies had obsessed the markets since May when Chairman Bernanke first announced the Fed's intentions to begin tapering. In mid-December, the Fed revealed its highly-anticipated decision to begin tapering in January. The markets surged on the news as the Fed confirmed that its monetary policies would remain highly accommodative even as the economy showed signs of improvement. Investors, having accepted the inevitability of the policy change, appeared to agree with the Fed's timing. The relief rally also seemed to acknowledge the economy's underlying strength. And, Congress negotiated a budget agreement that should fund the government for another two years.

A confluence of factors created a market environment that enabled equities to advance at a measured pace. The ebbs and flows of the slow economic recovery have, not surprisingly, tempered expectations. Consumers paid down debt and gradually increased spending as they became more confident in their job security and as their homes and investment portfolios gained in value. The combination of low interest rates, a stabilizing world economy and successful company growth initiatives propelled the equity markets higher; investors took on more risk in search of higher investment returns as they gained confidence in the markets.

1

Message

from the chairman continued

Many other investors, however, remained on the sidelines while they awaited an entry point following an anticipated major correction. Market skeptics helped to keep valuations in check, but these investors also seemed to ignore the extraordinary incentives for risk-taking in the central banks' easy money policies.

Companies continued to allocate capital to growth initiatives. Low interest rates encouraged shareholder-friendly actions such as higher dividends and stock buybacks while still maintaining significant cash reserves. Stock prices, which had been heavily discounted during the recession, had recovered; by year-end, the markets were more representative of actual business conditions. And, unlike recent years, the markets avoided broad selloffs during which stock prices declined regardless of the performance of individual businesses. Such reasonable behavior from companies and investors bodes well for equities. A continuation of slow but steady economic growth will enable companies to execute disciplined strategies without the excesses often seen during periods of rapid economic expansion. These conditions may enable equity markets to advance for some time.

Market Review

Volatility was somewhat subdued as the markets enjoyed the welcomed absence of major disruptions. During the year, the S&P 500® Index rose 32.36%, the Dow Jones Industrial Average rose 26.50%, and the technology-heavy NASDAQ rose 38.32%. Smaller companies enjoyed strong performance as well: the Russell Midcap® Index gained 34.76%, while the Russell 2000® Index of small companies gained 38.82%. Within the small cap universe, value slightly outperformed growth: the Russell 2000® Value Index grew 34.52% compared to the 43.30% increase in the Russell 2000® Growth Index.1

Fixed income markets, on the other hand, had a more challenging year; rising investor confidence and strong equity market performance encouraged the migration from "safe havens" to potentially more rewarding investments. Also, the Fed's tapering discussions prompted more investors to flee bonds; in response, the yield on the 10-year U.S. Treasury Note edged higher to close the year above 3% for the first time in 21/2 years.

Equity Investment Review

Many areas of the market performed well; in particular, investors' enthusiasm for risk led to strong performance in economically-sensitive stocks such as Consumer Discretionary holdings which benefit from increased consumer spending. Similarly, Industrials stocks, which also tend to offer better growth opportunities along with more volatility and greater exposure to economic developments, performed well. The Energy industry continued its strong performance as oil and gas exploration in shale and off shore areas has transformed the U.S. from a net importer to an exporter of petroleum products. This important development has created U.S. jobs and reduced the economic threat of geopolitical events in the Middle East, Africa and other less politically stable countries.

Financial companies also responded to the economic recovery as lending activity increased, reserves for loan losses shrank along with the improved economy, and the impact of the "Great Recession's" banking crisis faded. Residential and commercial construction, an important growth catalyst, also grew. The U.S. economy continues to expand at a modest pace while many companies have grown their operations considerably faster. Often, these businesses identified opportunities to expand in well-performing areas of the economy; frequently, they were able to recognize and respond to growth opportunities when their weaker competitors could not.

The slow rate of economic growth has motivated companies to improve efficiencies and expand selectively after identifying the best opportunities in their particular markets. The current economic climate also requires investors be more selective in evaluating companies to select those with the management and financial strength to operate and grow successfully.

Market Review – December 31, 2013

Index1 | Close | YTD Return | |||||||||

Dow Jones Industrial Avg | 16,576.66 | 26.50 | % | ||||||||

S&P 500® | 1,848.36 | 32.36 | % | ||||||||

NASDAQ | 4,176.59 | 38.32 | % | ||||||||

Russell Midcap® | 1,491.75 | 34.76 | % | ||||||||

Russell 2000® (small cap) | 1,163.64 | 38.82 | % | ||||||||

12/31/13 | 12/31/12 | ||||||||||

| 10-Year T-Note Yield | 3.04 | % | 1.78 | % | |||||||

Data: Bloomberg; Federal Reserve

2

Fixed Income Investment Review

News surrounding the Fed dominated headlines in the fixed income markets during this past year. In December, the central bank cited an improved economic outlook in announcing a reduction in its monthly bond-buying program from $85 billion to $75 billion in January. The Fed continued to stress that tapering does not mean a tightening of monetary policy; the bank reemphasized its commitment to keeping short-term interest rates exceptionally low. Furthermore, the confirmation of Janet Yellen as the new Fed Chair (following Ben Bernanke's late-January departure) should ensure the near-term continuation of the central bank's easy monetary policies.

During the latter part of the year, interest rates for longer-term bonds rose in response to falling demand. Many investors who had remained in long-duration bonds took steps to protect principal as rising interest rates resulted in lost principal; increasingly, investors migrated to shorter-term bonds, foreign bonds or equities.

Our fixed income strategies continued to focus on investment-grade bonds with shorter durations. We utilized this approach as we anticipated that interest rates would continue to rise from historically low levels as the economy improves and the Fed's stimulus programs wind down.

We expect interest rates to remain somewhat volatile while maintaining an upward bias in response to the slow growth of the U.S. economy and Fed policies.

Looking Ahead

A rising tide lifts all boats; 2013 was definitely a year of rising tides. The relative stability of economies around the world set the stage for markets to advance. At home, discretionary spending increased as job security improved. Growing consumer confidence led to the resurgence in the housing market; in turn, rising home valuations and investment returns bolstered outlooks. Meanwhile, the strategic growth initiatives undertaken by leading companies during the past few years started to pay off; indeed, many are still in the early growth stages.

The market advances this year have been stellar but not euphoric; stock prices are not dramatically overpriced. Some skeptics suggest that the market is overdue for a correction. Much of this market psychology is a remnant of the upheaval created by the "Great Recession" and the subsequent global strife. This market reticence has been, and will likely remain, a factor which will act to moderate the markets' upward trend. Investors should view any correction as a healthy market rebalancing rather than a signal of perilous times. A market decline of 10% to 20% is typical for a correction; while often lasting only a few weeks or months, they nevertheless prevent overheating. Corrections are usually transition periods rather than turning points.

Looking out into 2014, we believe that the improving global economy may well position the equity markets for continued growth. With the world's economies connected now as never before, the potential benefits of synchronized global growth are enormous. Economic growth in Europe will be particularly important for many companies. The euro zone has been mired in a deep recession for several years; the region's deferred spending, even if somewhat constrained, will nevertheless be a growth catalyst for many companies. Still, unforeseen global events are always a potential threat. Even so, well-disciplined yet adaptive investment strategies remain critical in navigating the ups and downs of the markets.

Within the U.S., investment opportunities in industries related to the ongoing housing recovery and non-residential construction are compelling. Also, energy companies, including energy infrastructure and offshore drilling services, will continue to drive the economy. And, financial institutions should benefit as interest rates rise. Finally, mergers and acquisitions activity will likely accelerate as businesses take advantage of low cost financing. We believe that attractive investment opportunities remain in proven companies that are well positioned for further expansion in the New Year. Therefore, we anticipate the equity markets to continue their upward momentum in 2014.

3

Message

from the chairman continued

I encourage you to read the interviews with each of our Fund portfolio managers to gain more insight into the investment strategies being employed by each Fund. This past year was a very good year and we believe that in the coming year the markets will continue to improve.

Sincerely,

George A. Henning

1 The Dow Jones Industrial Average is an unmanaged, price weighted measure of 30 U.S. stocks selected by the Averages Committee to represent the performance of all U.S. stocks outside the Transportation and Utilities sectors. The S&P 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. The NASDAQ Composite Index is an unmanaged, market capitalization weighted measure of all domestic and international common stocks (currently over 3,000 stocks) listed on The Nasdaq Stock Market. The Russell 2000® Index is an unmanaged, market-weighted measure of the 2,000 smallest publicly traded companies of the Russell 3000® Index. The Russell Midcap® Index is an unmanaged, weighted measure of the 800 smallest companies within the Russell 1000® Index based on a combination of their market cap and current index membership. The Russell 2000® Growth Index includes those Russell 2000® Index companies with higher price-to-value ratios and higher forecasted growth values; the Russell 2000® Value Index includes those Russell 2000® Index companies with lower price-to-book ratios and lower forecasted growth values. These indices are not available for direct investment. Index returns assume the reinvestment of dividends.

Economic and performance information referenced is historical and past performance does not guarantee future results. Rankings shown are for Class A shares and do not take into account the maximum sales charge of 4.75% on the Government Securities and Income and Equity Funds or 5.75% on the Balanced and Small Cap Value Funds. Rankings for other share classes may differ. The principal value and return of an investment will fluctuate so that an investor's shares may be worth less than the original cost when redeemed. For more information on the Pacific Advisors Funds, including information on charges, expenses and other classes offered, please obtain a copy of the prospectus by calling (800) 989-6693. Please read the prospectus and consider carefully the investment risks, objectives, charges and expenses before you invest or send money.

Shares of the Funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested. The views expressed represent the opinions and beliefs at the time of this commentary and are not meant as a market forecast. These views are subject to change at any time based on market or other conditions. This information may not be relied on as investment advice or as an indication of trading intent on behalf of any Fund. Fund investments may change at any time.

4

Pacific Advisors

Government Securities Fund

Fund Objective: High current income, preservation of capital, and rising future income consistent with prudent investment risk.

Investment Invests at least 80% of its assets in U.S. Government fixed income securities. These

Strategy: include securities issued or guaranteed by the U.S. Treasury; issued by a U.S. Government agency; or issued by a Government-Sponsored Enterprise (GSE). May also invest in high quality dividend-paying common stocks.

Investor Profile: Conservative. Income-focused; capital preservation aim.

TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||||||||||||||

For the year ended December 31, 2013 | Current (For the year ended 12/31/13) | Prospectus (For the year ended 12/31/12) | |||||||||||||||||||||||||

Net | Gross | Net | Gross | ||||||||||||||||||||||||

Class A | 0.77 | % | Class A | 3.39 | % | 6.09 | % | 3.12 | % | 5.44 | % | ||||||||||||||||

Class C | 0.00 | % | Class C | 4.16 | % | 6.82 | % | 3.85 | % | 6.29 | % | ||||||||||||||||

Barclays Capital U.S. Int T-Bond Index1 | – 1.25 | % | |||||||||||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Rankings shown are for Class A shares; rankings for other share classes may be different. Returns and rankings do not take into account the maximum 4.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's board, but is expected to continue at current levels. Please see the Notes to Financial Statements in this report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Manager February 24, 2014

Jingjing Yan, CFA

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review

as well as the Manager's general market outlook.

Pacific Advisors Government Securities Fund (A) | |||||||

| Lipper General US Government Category Rank (# of funds) as of 12/31/13 based on total return | |||||||

| 1 Year | 3 | (115) | |||||

| 3 Year | 109 | (110) | |||||

| 5 Year | 98 | (104) | |||||

| 10 Year | 81 | (82) | |||||

1 The Barclays Capital U.S. Intermediate Treasury Bond Index is an unmanaged index of U.S. government securities with one to ten years to maturity. It is not possible to invest directly in the Index.

5

Pacific Advisors

Government Securities Fund continued

Fund Performance

For the year, Class A shares of the Fund returned 0.77% compared to -1.25% for its benchmark, the Barclays Capital U.S. Intermediate T-Bond Index. The Fund's strategy proved effective as the Fund was one of only two funds in its Lipper category that ended 2013 with positive performance; it ranked #3 in its Lipper category. In response to the slow but steady economic recovery and the upward trend of interest rates, the Fund's fixed income investments remained concentrated in short to intermediate-term bonds. This strategy provided price stability during periods of interest rate volatility and enabled the Fund to protect principal as interest rates rose.

During the period, the Fund maintained an average duration of approximately 0.5 years; in contrast, the benchmark's average duration was 3.7 years. Duration measures a portfolio's sensitivity to interest rate movements; when interest rates increase by 1%, a portfolio with a 4-year duration would decline by approximately 4%. The Fund's short average duration reflected our commitment to minimize the impact of rising interest rates.

In the second half of the year, interest rates rose erratically but significantly in response to the recovering global economy. GDP growth, declining unemployment and the highly-anticipated reduction of the Federal Reserve's bond-buying program placed upward pressure on rates. The Fund's approach anticipated the decline in demand for U.S. government securities resulting from strengthened investor sentiment and the Fed's monetary policy. Investors continued to migrate capital from "safe havens," including U.S. Treasuries, into more rewarding alternatives. This rotation caused the benchmark 10-year U.S. Treasury Note to rise from 2.52% on June 30th to 3.04% by year-end; the upward movement of rates forced investors to acknowledge that long-term bonds, including U.S. government bonds, are not "low-risk" investments when interest rates rise.

The Fund's strategy of holding shorter-term bonds in expectation of higher interest rates proved successful and resulted in positive performance for the year. In contrast to the Fund's investment approach, alternative investment strategies sought to maximize returns by investing in longer-term bonds or other higher-risk strategies. Such an approach, however, exposed investors to the risk of sudden interest rate increases. During 2013, the prices for these higher-yielding securities became depressed in the absence of interested buyers; investors were forced to sell long-term holdings at significant losses.

The Fund's small allocation to common stocks provided dividend income and price appreciation which supported total return in the historically low interest rate environment. These high-quality, dividend-paying common stocks helped manage volatility by counterbalancing price movements in U.S. government securities holdings.

Market Overview

Interest rates in the second half of the year were volatile: the rate on the 10-year U.S. Treasury Note rose and fell in July only to rise again in late August and early September as the markets anticipated an imminent start to the Fed's tapering program. Rates reached an interim high of 2.98% in early September. The central bank's decision in mid-September to delay reducing bond purchases sent shockwaves through the markets; the rate fell back to 2.51% in October. Continuing positive economic data then boosted investor confidence; speculation that the Fed would begin tapering sooner rather than later again put upward pressure on rates; investors had seemingly come to accept the inevitability of tapering. When the central bank formally announced in mid-December that it would begin gradually reducing its bond-buying program in January, the market seemed unphased. The Fed cited an improved economic outlook while stressing its commitment to keeping short-term interest rates exceptionally low. The gradual upward movement in the 10-year rate in November and December suggested that investors accepted the Fed's timing and finally gave credit to the strength of the underlying fundamentals. At year-end, the rate on the 10-year hit 3.04%.

As interest rates increased, bonds with longer durations, including U.S. government securities, incurred additional principal losses. During the extended period of historically low interest rates, many fixed income investors placed significant amounts of capital in longer-term and higher-yield bonds in search of greater

6

returns. The rise in interest rates impacted investor sentiment; the outflow from bonds and bond funds that began in the first half of 2013 continued with full force as investors fled these positions. By year-end, annual net bond fund redemptions hit a record of $83.4 billion.

These developments in the fixed income markets underscore the importance of positioning a portfolio for events beyond the immediate time horizon. As demonstrated by recent events, long-term bonds are not risk-free. Many bond portfolios were unable to quickly change their investment strategies as interest rates increased; consequently, investors who may have anticipated a longer period to unwind riskier positions suffered as the rapid rise in rates triggered a tide of redemptions. In sharp contrast, the Fund had, for some time, been positioned to manage a transitioning interest rate environment by remaining in short-term bonds.

Fund Strategy

Fixed Income Strategy

The supply of attractive, risk-appropriate fixed income investments remained limited. Shorter-term bonds provided limited yield whereas longer-term bonds carried a higher risk of principal loss. The Fund maintained its strategy of utilizing bonds with a duration of less than one year and callable "step-up" government agency bonds. The yield on a "step-up" bond increases at fixed intervals over its lifetime. Since these bonds are more likely to be called back by the issuing agencies, their durations, which are determined by the earlier of maturity dates or likely call dates, are relatively short. In addition, as interest rates rise, these bonds, with their higher rates, will preserve their value better than fixed-rate government securities with comparable maturities. Step-up bonds also provide the flexibility to adapt to the current interest rates and reinvest as more attractive opportunities arise. By the end of the year, however, these types of bonds became difficult to find as other managers, who opted to employ strategies similar to the Fund's further constrained supply. Consequently, as holdings matured, we invested in standard, short-term government securities.

The Fund does not employ higher-risk strategies to enhance return. For example, the Fund does not purchase bonds with extended durations, utilize leverage strategies or invest in mortgage-backed securities. The avoidance of these riskier investment approaches was critical in the Fund's ability to generate positive returns during the year.

Equity Positioning

The Fund invests a minor portion of its portfolio in high-quality, dividend-paying common stocks. Equity holdings focus on stocks that are relatively less sensitive to economic developments and have attractive dividends and appreciation potential. These blue-chip securities help provide stability by offsetting price movements in the fixed income markets without significantly increasing the Fund's risk exposure.

During the period, we took advantage of the equity market rally to trim positions in companies such as Microsoft, General Mills and McDonald's.2 We also added Pepsi and Unilever to the portfolio; these multinational companies have opportunities for revenue growth in emerging markets as these regions participate in the global economic recovery. Consumer Staples holdings, including Safeway and Kimberly Clark, enjoyed strong gains during the period; also, 3M and Johnson & Johnson performed well as these stocks benefitted from increased consumer spending and global economic growth.

The equity positions in the Fund are, at less than 17%, a small percentage of the portfolio; nonetheless, these holdings provided important price appreciation to offset the low interest rates on short to intermediate-term U.S. government securities. We believe that the Fund's strategy of investing in high-quality common stocks is less risky than alternative strategies such as leveraging, options or investing in mortgage-backed securities when interest rates have an upward bias. We anticipate that the Fund's allocation to equities may be reduced as interest rates rise and the Fund increases its investments in longer-term U.S. government securities.

2 For detailed information on Fund holdings, please see the Fund's Schedule of Investments in this Report.

7

Pacific Advisors

Government Securities Fund continued

Looking Ahead

In 2013, rising interest rates and volatility pressured investors to alter their investment approaches. Investors who bought longer-term bonds in search of higher yields suffered real losses as rates increased. Now, many investors are employing a strategy similar to that of the Fund; they are buying shorter-term bonds to reduce the potential for further losses as interest rates increase. This strategic shift will further constrain the supply of short-term government securities.

We believe the markets will continue the transition from a low interest rate environment to one in which rates gradually increase. Several factors, including improving domestic and global economic conditions, the Fed's tapering, and the prospect of rising inflation will pressure rates to rise. Market developments, and Fed policies, will determine the speed and the extent to which rates rise. Our investment strategy will monitor changing market conditions. As rates increase, we expect to migrate the Fund's investments toward longer-term U.S. government securities to capture higher yields. The Fund's adaptive strategy provides the flexibility to adapt portfolio holdings according to market conditions while keeping the current bias of increasing interest rates in mind.

8

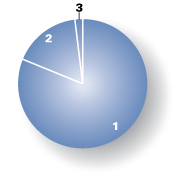

Portfolio Holdings as of 12/31/13 (Based on Total Investments)

| 1. | U.S. Government Securities | 81.23 | % | ||||||||

| 2. | Equities | 16.84 | % | ||||||||

| 3. | Cash and Cash Equivalents | 1.93 | % | ||||||||

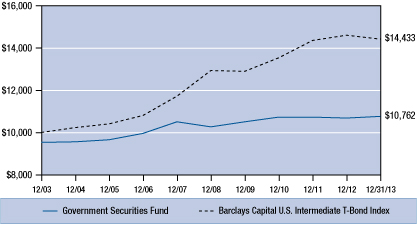

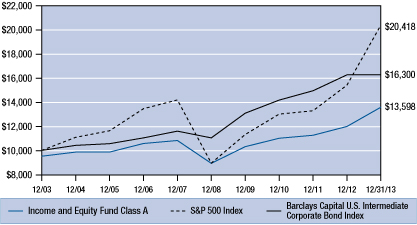

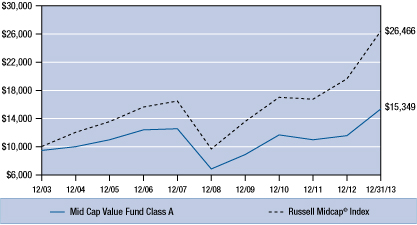

Change in Value of $10,000 Investment1

This chart compares the growth of a $10,000 investment in Class A shares of the Government Securities Fund for the period January 1, 2004 through December 31, 2013 with the same investment in the Barclays Capital U.S. Intermediate Treasury Bond Index2.

Average Annual Compounded Return as of December 31, 2013

Class A | Class C | ||||||||||

One Year | – 3.98 | % | – 1.00 | % | |||||||

Five Year | – 0.04 | % | 0.23 | % | |||||||

Ten Year | 0.74 | % | 0.49 | % | |||||||

Past performance does not guarantee future results. Performance quoted represents past performance. Current performance may be higher or lower than the performance data quoted. Returns include reinvested dividends and capital gains. Returns for Class A shares reflect a maximum front-end sales charge of 4.75%; and returns for Class C shares reflect the deduction of a contingent deferred sales charge of 1% on shares sold within the first year of purchase. Returns do not take into account individual taxes which may reduce actual returns when shares are sold. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Call (800) 989-6693 for the most recent month-end performance.

1 Fund results are shown for Class A shares and reflect deduction of the maximum front-end sales charge of 4.75% on the $10,000 investment for a net amount invested of $9,525. At the end of the same period, a $10,000 investment in Class C shares would have been valued at $10,500, and no contingent deferred sales charges would apply. Performance of the share classes will vary based on the difference in charges and expenses. The inception date is 02/08/93 for Class A shares and 04/01/98 for Class C shares. It is not possible to invest directly in the Index. Unlike the Fund's results, the results for the Index do not reflect sales charges, fees or expenses.

2 The Barclays Capital U.S. Intermediate Treasury Bond Index is an unmanaged index of U.S. government securities with one to ten years to maturity.

9

Pacific Advisors

Government Securities Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2013 through December 31, 2013.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 07/01/13 | Ending Account Value 12/31/13 | Expense Paid During Period 07/01/13 – 12/31/13 | |||||||||||||

Government Secs Fund Class A | |||||||||||||||

Actual | $ | 1,000.00 | $ | 1,000.00 | $ | 17.09 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,008.12 | $ | 17.16 | |||||||||

Government Secs Fund Class C | |||||||||||||||

Actual | $ | 1,000.00 | $ | 995.50 | $ | 20.92 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,004.23 | $ | 21.02 | |||||||||

3 Expenses are equal to the Fund's annualized expense ratio, net of expense waivers, of 3.39% for Class A shares and 4.16% for Class C shares, multiplied by the average account value over the period, multiplied by 184/365 days to reflect the one-half year period.

10

Pacific Advisors

Income and Equity Fund

Fund Objective: Current income and, secondarily, long-term capital appreciation.

Investment Invests primarily in investment grade U.S. corporate bonds and in dividend-paying

Strategy: stocks.

Investor Profile: Conservative. Some current income required; capital preservation aim.

TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||||||||||||||

For the year ended December 31, 2013 | Current (For the year ended 12/31/13) | Prospectus (For the year ended 12/31/12) | |||||||||||||||||||||||||

Net | Gross | Net | Gross | ||||||||||||||||||||||||

Class A | 13.40 | % | Class A | 2.23 | % | 3.03 | % | 2.68 | % | 3.42 | % | ||||||||||||||||

Class C | 12.55 | % | Class C | 2.98 | % | 3.78 | % | 3.45 | % | 4.20 | % | ||||||||||||||||

Barclays Capital U.S. Int Corp Bond Index1 | 0.08 | % | |||||||||||||||||||||||||

S&P 500® Index2 | 32.36 | % | |||||||||||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Rankings are shown for Class A shares; rankings for other share classes may be different. Returns and rankings do not take into account the maximum 4.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's board, but is expected to continue at current levels. Please see the Notes to Financial Statements in this report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Managers February 24, 2014

Charles Suh, CFA

Jingjing Yan, CFA

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review

as well as the Manager's general market outlook.

Pacific Advisors Income and Equity Fund (A) | |||||||

| Lipper Mixed Asset Target Allocation Conservative Category Rank (# of funds) as of 12/31/13 based on total return | |||||||

| 1 Year | 6 | (357) | |||||

| 3 Year | 63 | (296) | |||||

| 5 Year | 183 | (272) | |||||

| 10 Year | 105 | (121) | |||||

1 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity. It is not possible to invest directly in the Index.

2 The S&P 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses. It is not possible to invest directly in the Index.

11

Pacific Advisors

Income and Equity Fund continued

Fund Performance

The Fund's conservative investment approach proved successful in 2013 as the fixed income market entered a transition phase. For the period, Class A shares gained 13.40%. Notably, the Fund generated these returns with substantially less risk than the broader market as demonstrated by the Fund's one-year beta of 0.413, as of December 31st, versus the S&P 500® Index. Class A shares of the Fund ranked #6 in its Lipper category, as of December 31st. The Fund's fixed income strategy anticipated the stronger economic conditions which set the stage for interest rates to move higher. The Fund's bond holdings focused on shorter-term investment grade bonds; these conservative bonds provided important protection against price volatility. In addition, these holdings added to Fund performance by maintaining their valuations as interest rates rose. Also, the appreciation of the Fund's equity holdings added significantly to performance.

The average maturity of the Fund's fixed income holdings, at 3.3 years, was significantly shorter than the Barclays Capital U.S. Intermediate Corporate Bond Index's average maturity of 4.4 years. The difference reflects the Fund's strategy of maintaining shorter maturities versus the benchmark's unmanaged bond portfolio.

The Fund's equity portfolio benefitted from impressive performance of individual stocks as well as the strong stock market. Equity holdings remained concentrated in 30 to 40 high-quality, dividend-paying stocks with stable growth patterns and low volatility; in contrast, the Fund's equity benchmark, the S&P 500® Index includes companies with a broad range of size, quality, risk factors, and volatility.

Fund Strategy

The Fund's fixed income holdings in short-to-intermediate-term investment grade corporate bonds provided both principal protection as interest rates rose and the opportunity to reinvest at higher rates. For the equity portfolio, the Fund has selected diverse holdings in blue-chip, dividend-paying stocks to compensate for historically low interest rates. This equity approach has been critical to the Fund's performance during the extended period of low interest rates as the dividend rates for portfolio stocks were often higher than the corporate bond rates on those same companies.

In the second half of the year, interest rates rose erratically but significantly in response to the recovering global economy. GDP growth, declining unemployment and the highly-anticipated reduction of the Federal Reserve's bond-buying program placed upward pressure on rates. These factors drove investors to migrate capital from "safe haven" U.S. Treasuries and corporate bonds into more rewarding alternatives. Much of this capital flowed to the U.S. equity markets as investors sought blue-chip stocks with higher dividend rates along with the potential for price appreciation.

Investors were seemingly caught off guard when interest rates began to rise toward the end of the second quarter; later, as rates continued to rise, bond investors faced the consequence of holding longer-term bonds. Prices became depressed as the demand for bonds with longer maturities fell. Bond fund redemptions accelerated; by year-end, annual net redemptions hit a record of $83.4 billion.

The Fund actively managed the allocation between fixed income and equity securities to find the most attractive, risk-appropriate opportunities for income and growth. The Fund maintained its corporate bond holdings at approximately 50% through the end of the year; the equity portion decreased from approximately 49% to over 45% during the period. We anticipate that the equity allocation may decrease further as interest rates continue to rise and we reinvest capital in higher-yielding bonds.

Fixed Income Strategy

The Fund's fixed income strategy sought to protect principal by investing in shorter maturities; these holdings also offered the flexibility to identify timely investment opportunities in the transitioning fixed income market. By the end of the year, short-term bonds enjoyed extraordinary demand as other bond

3 "Beta" measures volatility relative to the stock market or an alternative benchmark. A beta less than 1.0 indicates lower risk than the market or the benchmark; a beta greater than 1.0 indicates higher risk than the market or the benchmark.

12

fund managers altered their strategies in favor of bonds with shorter maturities. This shift constrained the supply of attractive fixed income securities. As of December 31st, the average yield on 5-year investment grade corporate bonds was 2.6%; in this relatively low-yield, limited-supply environment, the Fund also sought to enhance returns by identifying investment grade corporate bonds with risk-appropriate special situations.

The Fund's strategy often utilizes callable bonds. Callable bonds are securities that can be bought back, or "called," by the issuer prior to maturity at predefined prices and dates. These types of bonds generally have higher yields due to their call features; the issuer also typically pays a premium to the bondholder when the bond is called. We purchase callable bonds to seek potentially higher returns while preserving capital. For example, in September, we bought a 4-year callable bond issued by Petrohawk Energy at an attractive price.4 We anticipate that the bond will be called; if so, we will be able to reinvest the capital in higher-yielding securities. If, on the other hand, the bond is not bought back, we may have the opportunity to generate higher returns as the bond's yield increases.

The Fund also purchased high-quality bonds at discounted prices due to company-specific issues or economic conditions. For example, Air Lease, an aircraft leasing company, was pressured by slow industry growth and economic uncertainty; consequently, investors seemed to overlook this company's bond offerings. Our analysis concluded that the company's financials have been improving, and will likely continue to improve as the airline industry's fundamentals strengthen. In September, we purchased an Air Lease bond maturing in 3.5 years. Since then, the price of the bond appreciated as the company's financial condition improved and investor concerns subsided.

Equity Strategy

The Fund's equity holdings offer an important complement to corporate bonds especially during periods of historically low interest rates. Our equity strategy focuses on total return by investing in high-quality, well-established large cap companies from a wide range of industries. During the period, we increased our allocation to Consumer Discretionary holdings; these cyclical stocks generally provide better opportunities for growth during periods of global economic expansion.

We also continued to favor blue-chip stocks with attractive dividends. Lately, companies have tended not to increase dividend rates; even so, the depressed price valuations that lingered since the recession had the effect of increasing yields. Companies took advantage of interest rates to borrow or refinance at extremely low rates; as a result, the difference between a company's bond yield and its dividend yield may have narrowed. In some cases, the dividend yields of portfolio holdings even surpassed the yields of the companies' corresponding debt offerings. For example, as of December 31st, AT&T's dividend yield of 5.23% significantly exceeded the approximate 2% yield of the company's corporate bond maturing in November 2018.

The weighted average yield for the Fund's equity holdings is 3.11% which is notably higher than the 2.6% average yield for 5-year investment grade corporate bonds. Stocks with a dividend yield over 4.5% included AT&T and Duke Energy while companies with a dividend over 3.5% included Public Services Enterprise Group, Verizon, Vodafone, Xcel Energy and ConocoPhillips.

The extended period of low interest rates called attention to the importance of the Fund's equity strategy. Central banks around the world have utilized low interest rates to spur growth which, in turn, set the stage for interest rates to rise. We anticipate that, as the global economy continues to improve and rates gradually trend upward, our strategy of managing risk while generating meaningful investment returns will adjust. We expect to further reduce the Fund's equity position as interest rates increase.

Looking Ahead

2013 was an exceptional year for equities; investors, including the Fund, certainly benefitted from the equity market's performance. 2014 may provide opportunities in fixed income as interest rates transition

4 For detailed information on Fund holdings, please see the Fund's Schedule of Investments in this Report.

13

Pacific Advisors

Income and Equity Fund continued

to a more normal environment. The Fed will likely continue tapering its bond-buying program as the domestic economic outlook improves further. The strengthening global economy will eventually push rates higher and spur inflation. Yet, the overall market conditions will determine how high, and how fast, interest rates will increase. The changing interest rate environment will challenge even the most conservative investors to reevaluate their fixed income strategies; 2013 should have reinforced the message that long-term bonds are not a "safe haven" when interest rates rise.

The Fund's adaptive fixed income strategy should perform well even in a more measured equity market environment. The Fund is well-positioned to successfully navigate the transition from extremely low interest rates to rising rates. The Fund will then be able to reinvest capital at the prevailing higher rates as the Fund's bond holdings mature.

The Fund's adaptive strategy helps manage the risk of higher interest rates; the approach also enables the Fund to gradually increase yield and generate total return. Furthermore, the flexibility allows us to proactively adjust to changing market environments while acknowledging the upward bias of interest rates. We believe that the Fund is well-positioned for developing economic and market conditions regardless of how high and how quickly interest rates rise.

14

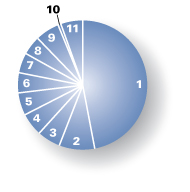

Portfolio Holdings as of 12/31/13 (Based on Total Investments)

| 1. | Corporate Bonds | 48.86 | % | ||||||||

Equities | 45.32 | % | |||||||||

| 2. | Consumer Staples | 8.54 | % | ||||||||

| 3. | Consumer Discretionary | 5.72 | % | ||||||||

| 4. | Utilities | 5.54 | % | ||||||||

| 5. | Industrials | 5.40 | % | ||||||||

| 6. | Telecommunication Services | 4.94 | % | ||||||||

| 7. | Health Care | 4.72 | % | ||||||||

| 8. | Information Technology | 4.54 | % | ||||||||

| 9. | Others | 5.92 | % | ||||||||

| 10. | Preferred Stock | 0.66 | % | ||||||||

| 11. | Cash and Cash Equivalents | 5.16 | % | ||||||||

Change in Value of $10,000 Investment1

This chart compares the growth of a $10,000 investment in Class A shares of the Income and Equity Fund for the period January 1, 2004 through December 31, 2013 with the same investment in the S&P 500 Index2 and the Barclays Capital U.S. Intermediate Corporate Bond Index3.

Average Annual Compounded Returns as of December 31, 2013

Class A | Class C | ||||||||||

One Year | 8.05 | % | 11.55 | % | |||||||

Five Year | 7.72 | % | 7.96 | % | |||||||

Ten Year | 3.12 | % | 2.86 | % | |||||||

Past performance does not guarantee future results. Performance quoted represents past performance. Current performance may be higher or lower than the performance data quoted. Returns include reinvested dividends and capital gains. Returns for Class A shares reflect a maximum front-end sales charge of 4.75%; and returns for Class C shares reflect the deduction of a contingent deferred sales charge of 1% on shares sold within the first year of purchase. Returns do not take into account individual taxes which may reduce actual returns when shares are sold. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Call (800) 989-6693 for the most recent month-end performance.

1 Fund results are shown for Class A shares and reflect deduction of the maximum front-end sales charge of 4.75% on the $10,000 investment for a net amount invested of $9,525. At the end of the same period, a $10,000 investment in Class C shares would have been valued at $13,256, and no contingent deferred sales charges would apply. Performance of the share classes will vary based on the difference in charges and expenses. The inception date is 02/08/93 for Class A shares and 04/01/98 for Class C shares. It is not possible to invest directly in either Index. Index results assume reinvestment of dividends, but, unlike the Fund's results, do not reflect sales charges, fees or expenses.

2 The Standard & Poor's 500 Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy.

3 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity.

15

Pacific Advisors

Income and Equity Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2013 through December 31, 2013.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 07/01/13 | Ending Account Value 12/31/13 | Expense Paid During Period 07/01/13 – 12/31/13 | |||||||||||||

Income & Equity Fund Class A | |||||||||||||||

Actual | $ | 1,000.00 | $ | 1,060.70 | $ | 11.58 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,013.96 | $ | 11.32 | |||||||||

Income & Equity Fund Class C | |||||||||||||||

Actual | $ | 1,000.00 | $ | 1,057.70 | $ | 15.72 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,009.93 | $ | 15.35 | |||||||||

4 Expenses are equal to the Fund's annualized expense ratio, net of expense waivers, of 2.23% for Class A shares and 3.03% for Class C shares, multiplied by the average account value over the period, multiplied by 184/365 days to reflect the one-half year period.

16

Pacific Advisors

Balanced Fund

Fund Objective: Long-term capital appreciation and income consistent with reduced risk.

Investment Invests primarily in large cap common stocks and investment grade

Strategy: U.S. corporate bonds. Invests at least 25% of its assets in fixed income securities and preferred stocks and at least 25% in equities.

Investor Profile: Moderately conservative. Seeks combination of long-term growth, income, liquidity and reduced risk of price fluctuations.

TOTAL RETURNS | EXPENSE RATIOS | ||||||||||||||||||

For the year ended December 31, 2013 | Current (For the year ended 12/31/13) | Prospectus (For the year ended 12/31/12) | |||||||||||||||||

Class A | 26.68 | % | Class A | 3.07 | % | 3.30 | % | ||||||||||||

Class C | 27.75 | % | Class C | 3.86 | % | 4.02 | % | ||||||||||||

S&P 500® Index1 | 32.36 | % | |||||||||||||||||

Barclays Capital U.S. Int Corp Bond Index2 | 0.08 | % | |||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Rankings are shown for Class A shares; rankings for other share classes may be different. Returns and rankings do not take into account the maximum 5.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

Discussion with Portfolio Manager February 24, 2014

Charles Suh, CFA

Jingjing Yan, CFA

Samuel C. Coquillard

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review as well as the Manager's general market outlook.

Pacific Advisors Balanced Fund (A) | |||||||

| Lipper Mixed Asset Target Allocation Growth Category Rank (# of funds) as of 12/31/13 based on total return | |||||||

| 1 Year | 6 | (563) | |||||

| 3 Year | 66 | (502) | |||||

| 5 Year | 326 | (467) | |||||

| 10 Year | 241 | (287) | |||||

1 The S&P 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses. It is not possible to invest directly in the Index.

2 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity. It is not possible to invest directly in the Index.

17

Pacific Advisors

Balanced Fund continued

Fund Performance

2013 was an excellent year for the Fund: Class A shares ranked #6 in the Fund's Lipper category. Class A shares of the Fund returned 28.68%; in comparison, the Fund's equity benchmark, the S&P 500® Index, gained 32.36% while the Fund's fixed income benchmark, the Barclays Capital U.S. Int. Corp Bond Index, was essentially flat for the year with a 0.08% increase. The Fund's blend of equity and fixed income securities suggests that its performance would be best viewed against a blend of its equity and fixed income benchmarks. Importantly, the Fund achieved its performance with less volatility than the market as evidenced by its one-year beta3 of 0.82, as of December 31st, versus to the S&P 500® Index.

The Fund's impressive gain highlights the combined benefits of its "all cap" equity strategy and total return approach to fixed income investing. Equity holdings accounted for the majority of the Fund's gains; mid-cap stocks, in particular, performed well. Active portfolio positioning toward economically-sensitive areas of the market, including Industrials and Consumer Discretionary, also contributed to the Fund's strong equity returns. The Fund's strategy concentrated fixed income holdings in shorter-term (maturing in 3 to 5 years) investment grade corporate bonds; these conservative bonds provided important protection against price volatility. In addition, these holdings added to Fund performance by maintaining their valuations as interest rates rose.

Fund Strategy

The Fund is designed for conservative investors who want to participate in the equity markets with reduced risk. The Fund's strategy combines high-quality, dividend-paying stocks across all market capitalizations with investment grade corporate bonds that provide additional income and appreciation potential. We manage the Fund's asset allocation based on our identification of risk-appropriate investments in the context of the overall economic and market outlook. This approach enables the Fund to take advantage of specific growth opportunities while reducing price volatility.

During 2013, the global economy steadily improved while the fixed income markets remained challenged. Accordingly, the Fund's equity allocation remained at approximately 71%, near the high end of its historical range. Notably, interest rates rose meaningfully during the year in response to the Federal Reserve's decision to initiate "tapering" its bond-buying program. The resulting price declines for long-term fixed income securities affirmed our decision to remain weighted towards equities.

Equity Strategy

The Fund's "all cap" equity strategy diversifies investments among high-quality, well-managed companies with proven growth track records. Large cap stocks, which accounted for approximately 45% of the equity holdings, favor dominant global franchises that offer stability with moderate growth potential. Mid-cap holdings, which represented approximately the same equity allocation, feature industry leaders benefitting from broad sector or economic trends. Small cap holdings focus on established companies with long-term growth prospects. Importantly, the Fund's mid and small cap holdings have contributed to performance without significantly increasing volatility; the Fund's one-year beta remained at just 0.82, as of December 31st.

Strong performance by the Fund's mid-cap holdings in the second half of 2013 reflects our strategy to identify companies at the forefront of growth trends. Engineering and construction firm Chicago Bridge & Iron announced a steady stream of contract awards which underscored the company's prime position in the global energy and power infrastructure market.4 Truck manufacturer Navistar began to recapture lost market share following a failed 2011 engine strategy. Train parts supplier Wabtec benefitted from improved growth in rail transportation. The company continues to develop its international presence in attractive growth markets such as Europe, Russia, and China. Specialty retailer Conn's enjoyed stellar sales, particularly in new product areas such as furniture and bedding. More importantly, at just 70 locations

3 "Beta" measures volatility relative to the stock market or an alternative benchmark. A beta less than 1.0 indicates lower risk than the market or the benchmark and a beta greater than 1.0 indicates higher risk than the market or the benchmark.

4 For detailed information on Fund holdings, please see the Fund's Schedule of Investments in this Report.

18

nationwide, Conn's has outstanding growth potential with increased store locations; the company's primary competition is rent-to-own stores which have a greater location density.

Large cap holdings also performed well with broad-based gains across various sectors and industries. Within Industrials, truck engine maker Cummins and railroad operator CSX led the way. Energy services giant Halliburton gained on improved performance in key North American markets and improved outlooks for 2014. Walt Disney profited from solid advertising sales across its television networks and strong performance in its parks and resorts division. Technology company Qualcomm benefitted from the increasing use of mobile chips in smartphones and tablet computers as sales of these devices strengthened throughout the year. And, CVS Caremark rose on investor expectations that the company will benefit not only from gradual population aging but also new business resulting from the Affordable Care Act.

Small cap holdings also enjoyed impressive gains. Industrial parts and services distributor, DXP Enterprises, reported strong earnings results and announced several highly profitable acquisitions that broadened the company's product portfolio and geographic presence. Just two years ago, DXP operated only in the U.S.; today, its reach extends to Canada, the Middle East and Africa. TAL International leases shipping containers to the world's largest vessel operators. Shares of this industry-leading company climbed as signs of a recovery in Europe improved expectations for ocean-going trade activity. Moreover, the recent rise in interest rates bodes well for container lease pricing which is tied to prevailing borrowing costs.

In the second half of 2013, the Fund added one position, mid-cap stock MRC Global. MRC, a leading distributor of pipes, valves and fittings to the global oil and gas industry, stands to profit from two developing Energy trends: unconventional onshore oil production and the development of deepwater offshore oil fields. Management's strategy is to use its broad geographic network to secure long-term global supply agreements with major oil producers, such as British Petroleum. MRC continues to expand through acquisitions; its most recent acquisition establishes a leading position in the North Sea, the world's largest offshore market.

Fixed Income Strategy

The Fund's "total return" approach actively manages fixed income holdings in response to current interest rate trends. During periods of historically low interest rates, the Fund seeks to protect principal value by limiting the impact of rising rates. The Fund's investments have continued to focus on shorter-term bonds that are less sensitive to interest rate changes. The Fund also avoids higher risk investments such as high yield, or "junk," bonds. The low interest rate environment and our expectation for higher interest rates contributed to our decision to maintain the Fund's fixed income allocation near the lower end of its historical range.

Interest rates rose erratically but significantly in the second half of the year; the yield on the U.S. 10-year Treasury Note ended 2013 at 3.04% compared to 2.52% at the end of June and 1.78% at the end of 2012. The increase primarily resulted from the Fed's decision to begin "tapering" its bond-buying program. In response, investors began moving assets out of longer-term fixed income holdings. The Fund's high-quality, shorter-term corporate bonds effectively managed the risk of principal loss as interest rates rose. Importantly, shorter-term bonds also enabled the Fund to reinvest proceeds at higher yields as interest rates increased.

Looking Ahead