UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-07062 | |||||||

| ||||||||

PACIFIC GLOBAL FUND INC. D/B/A PACIFIC ADVISORS FUND INC. | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CALIFORNIA |

| 91203 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

GEORGE A. HENNING 101 NORTH BRAND BLVD., SUITE 1950 GLENDALE, CA 91203 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 818-242-6693 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31 |

| ||||||

| ||||||||

Date of reporting period: | December 31, 2015 |

| ||||||

Item 1. Report to Shareholders

Filed herewith.

annual report

december 31, 2015

government securities fund

income and equity fund

balanced fund

large cap value fund

mid cap value fund

small cap value fund

Pacific Advisors

table of contents

Message from the Chairman | 1 | ||||||

Government Securities Fund | 4 | ||||||

Income and Equity Fund | 9 | ||||||

Balanced Fund | 15 | ||||||

Large Cap Value Fund | 21 | ||||||

Mid Cap Value Fund | 26 | ||||||

Small Cap Value Fund | 32 | ||||||

Schedule of Investments | 39 | ||||||

Statement of Assets and Liabilities | 60 | ||||||

Statement of Operations | 62 | ||||||

Statement of Changes in Net Assets | 64 | ||||||

Financial Highlights | 68 | ||||||

Notes to Financial Statements | 75 | ||||||

| Report of Independent Registered Public Accounting Firm | 88 | ||||||

| Disclosure Regarding the Board's Approval of the Funds' Advisory Contracts | 89 | ||||||

Directors and Officers | 92 | ||||||

Additional Tax Information | 94 | ||||||

This Report is submitted for the general information of the shareholders of Pacific Advisors Funds. It is not authorized for distribution to prospective investors unless accompanied or preceded by the Funds' current prospectus, which contains information concerning the investment policies of the Funds as well as other pertinent information.

This Report is for informational purposes only and is not a solicitation or recommendation that any particular investor should purchase or sell any particular security. The statements in the Chairman's Letter and the discussions of the Funds' performance are the opinions and beliefs expressed at the time of this commentary and are not intended to represent opinions and beliefs at any other time. These opinions are subject to change at any time based on market or other conditions and are not meant as a market forecast. All economic and performance information referenced is historical. Past performance does not guarantee future results.

For more information on the Pacific Advisors Funds, including information on charges, expenses and other classes offered, please obtain a copy of the prospectus by calling (800) 989-6693. Please read the prospectus and consider carefully the investment risks, objectives, charges and expenses before you invest or send money. Shares of the Pacific Advisors Funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost.

Message

from the chairman

Dear Shareholders,

Volatility dominated the equity markets during the second half of the year; as the year ended, investors were left wondering, "What's next?" A selloff began in July after the Chinese stock market dropped 32% followed by an announcement in mid-August that China had devalued the yuan, long pegged to the U.S. dollar. China had, as we discussed in the semi-annual report, previously announced its ambition to have the yuan accepted as an international currency for trade; even so, the timing nevertheless caught investors by surprise and triggered speculation about a global economic slowdown. In response to the volatility in the international markets, the Federal Reserve chose not to initiate its first rate hike in September as many expected.

Following the August-to-September swoon, the S&P 500® Index, the Dow Jones Industrial Average, and the NASDAQ each rose over 6%; however, in the midst of ongoing market uncertainty, the gains were mostly limited to a handful of relatively "safe" large cap stocks, including Facebook, Amazon.com, Netflix, and Alphabet (formerly Google). For the year, however, approximately 35% of the stocks in the S&P 500® and 56% of the stocks in the Russell 2000® Index entered bear market territory with declines of 20% or more from their 52-week highs.

Despite market turmoil the major world economies provided reasons for optimism with Europe and Japan posting year-over-year growth; and yet investors remained cautious due to concerns of an economic slowdown in China, the Federal Reserve's interest rate liftoff, and falling oil prices. Selling pressure for many stocks increased as investors waited on the sidelines for a clearer view on the markets' near-term direction.

In October, China's leadership announced its five-year plan which calls for an annual growth rate of "around 6.5%" and an increased reliance on consumer-oriented activity. The transition to develop a consumer-driven economy is critical to reducing the country's dependence on exports and more closely aligning its economy to those of developed nations. In late November, the International Monetary Fund acknowledged China's economic reforms in approving the inclusion of the yuan, along with the dollar, the euro, the yen and the pound, as a world reserve currency.

During the second half of the year, interest rates trended higher in anticipation of the Fed's liftoff; the yield on the 10-year U.S. Treasury Note, which had risen to 2.35% as of June 30th, fell to 1.99% following the Fed's September meeting before drifting higher to close the year at 2.27%. The Fed's mid-December interest rate increase, while widely expected, nonetheless removed a significant cloud hanging over the market and signaled confidence in the U.S. economy. Still, stocks came under pressure as investors remained on the sidelines through year-end.

Meanwhile, U.S. crude oil prices fell 30% during the year due to the unrelenting supply/demand imbalance, and fears of a slowdown in demand, especially in China. As a result, the Energy sector fell 23.6%, only the sixth time since 1940 that a sector underperformed the S&P 500® Index by more than 20% for two years in a row. At current prices, most producers are operating at a loss while "petro-states" (i.e., countries which rely on oil for a significant portion of revenues) face staggering budget deficits. Economic adjustments are underway: nearly $400 billion of new energy projects have been deferred. And still, the world needs to replace 2.6 million barrels of oil per day to offset the natural depletion of existing wells, and add another 1.2 million barrels per day to meet estimated demand growth. Therefore, while oil prices may remain depressed in the near-term, the issue is not if but when oil prices will rise.

In December, Congress approved a $1.15 trillion pro-business spending package; the bill funded a five-year $305 billion transportation bill for road, bridge and mass transit projects, and ended the 40-year-old ban on crude oil exports. The removal of the export ban places the U.S. on an even playing field with global producers; shale oil, in particular, is now positioned as the world's most responsive source of supply to balance markets. OPEC's strategies, which first artificially maintained oil prices above $100 and, more recently, drove the price decline through its policy of overproduction, provided the economic incentive that led to shale technology; as oil prices recover, these outcomes will benefit the U.S. oil industry's position in the global marketplace.

1

Message

from the chairman continued

Market Review

Following the selloff in the third quarter, all major indices rebounded during the fourth quarter, but, with the exception of the NASDAQ, still ended the year in negative territory. For the year, the S&P 500® Index retreated 0.73% to snap three consecutive years of double digit returns; the Dow fell 2.23%, its first annual decline since 2008. The technology-heavy NASDAQ gained 5.73% and the Russell 2000® Index lost 5.71%. Growth outperformed Value, as value-oriented areas, including Energy and Industrials, fell to historically depressed levels while growth-oriented areas, such as Health Care and Information Technology, rose to near all-time highs. The disparity is reminiscent of the technology IPO boom in the late 1990s; then, investors focused single-mindedly on growth stocks while value stocks lagged in spite of deeply depressed valuations.

Equity Investment Review

Macro-related factors, including the downturn in energy markets, a reduction in U.S. industrial activity, and slowing growth in China, undermined market sentiment. The more conservative large cap blue chip stocks, and less volatile consumer product and food & beverage companies, outperformed. Growth stocks in Health Care and Technology sectors provided most of the gains for the year.

In contrast, the selloff in Energy-related stocks resulted in valuations that are now at or near all-time lows, in many cases falling well below the depths of the financial crisis. Shares of Industrials companies have also lagged due, in part, to concerns about the impact of the strengthening U.S. dollar on manufacturing activity. Investors seemed to overlook company fundamentals or positive news to instead focus on changes in oil prices as a barometer for the health of the global economies.

The underperformance of the Pacific Advisors equity Funds largely reflected investor preference, during this period of uncertainty, for growth over value. Looking ahead, we anticipate that renewed confidence in the global economy will provide a market catalyst. The selloff in value stocks, while certainly unwelcomed, has nevertheless provided an opportunity for the Funds to buy deeply discounted stocks in the Energy, Industrial and Consumer sectors at historically low prices. Further information on the investment strategies for each of the Funds is provided in the interviews with portfolio managers.

Fixed Income Investment Review

Interest rates trended higher in the second half of the year, with yields fluctuating based on expectations for the Fed's interest rate liftoff. Finally, the 25-basis point increase to the federal funds rate in December marked the first rate increase since 2006. Rising interest rates added to price declines for high-yield (or, "junk") bonds and bond funds, particularly those with investments in commodities and emerging markets. With crude oil prices continuing to fall, bonds of Energy-related companies sold off sharply with little regard to their financial health.

The Fed's decision to raise rates signals confidence in both the domestic and global economies as, historically, the Fed has typically raised rates during periods of economic strength. Interest rate fluctuations will likely continue as investors anticipate the Fed's upcoming rate increases. Importantly, though, Fed Chair Yellen emphasized a "gradual" pace of future rate increases, with rates likely to remain below historical levels.

Our investment strategy concentrates on fundamental characteristics, including liquidity ratios, financial strength, and expected capital spending. We have continued to focus on investment grade bonds with shorter-term maturities (e.g., 3-5 years), as well as corporate bonds temporarily out-of-favor that offer opportunities for higher yields. Further details on our fixed income strategy are provided in the Fund interviews.

Market Review • December 31, 2015

Index1 | Close | YTD Price Return | |||||||||

Dow Jones Industrial Avg | 17,425.03 | –2.23 | % | ||||||||

S&P 500® | 2,043.94 | –0.73 | % | ||||||||

NASDAQ | 5,007.41 | 5.73 | % | ||||||||

Russell Midcap® | 1,596.21 | –4.02 | % | ||||||||

Russell 2000® (small cap) | 1,135.89 | –5.71 | % | ||||||||

12/31/15 | 12/31/14 | ||||||||||

| 10-Year T-Note Yield | 2.27 | % | 2.17 | % | |||||||

Data: Bloomberg; Federal Reserve.

2

Looking Ahead

Some suggest that the lackluster market performance will lead to a recession; but, historically, the markets have been poor recession predictors. More importantly, the growing world economies support a more positive outlook; and, the usual indicators of a recession, such as higher inflation, rising interest rates, overheated economies and overvalued markets, are nowhere to be found.

Indeed, the world's major economies provided reason for optimism in 2015. Central bank policies designed to invigorate economies will continue; and, low gas prices will boost consumer spending. Most notably, Europe's recovery appears to have taken hold; the European Central Bank appears committed to accommodative monetary policies that, along with low oil prices, have helped the region achieve its fastest growth rate since 2011. Japan is once again on a path for recovery; after falling into a recession last year, the economy rebounded in the second and third quarters. And, the Chinese economy continues to expand at nearly 7% annually; the government's recent forecast of a 6.5% growth rate over the next five years would essentially double the country's 2010 output by 2020.

In 2015, headline events heavily influenced the markets; many stocks traded at distressed values which hardly reflected their financial strength or business outlooks. And yet, the current market turmoil is not unprecedented. As headline events recede and oil prices recover, we anticipate that economic fundamentals, which have recently been overwhelmed by negative investor sentiment, will once again reassert a more prominent role in determining prices. Our 20+ years of experience with disciplined, value-oriented investment strategies suggests that today's discounts for well-capitalized, proven businesses provide particularly enticing opportunities for future growth.

Sincerely,

George A. Henning

1 The Dow Jones Industrial Average is an unmanaged, price weighted measure of 30 U.S. stocks selected by the Averages Committee to represent the performance of all U.S. stocks outside the Transportation and Utilities sectors. The S&P 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. The NASDAQ Composite Index is an unmanaged, market capitalization weighted measure of all domestic and international common stocks (currently over 3,000 stocks) listed on The Nasdaq Stock Market. The Russell 2000® Index is an unmanaged, market-weighted measure of the 2,000 smallest publicly traded companies of the Russell 3000® Index. The Russell Midcap® Index is an unmanaged, weighted measure of the 800 smallest companies within the Russell 1000® Index based on a combination of their market cap and current index membership. These indices are not available for direct investment. Index returns assume the reinvestment of dividends.

Economic and performance information referenced is historical and past performance does not guarantee future results. The principal value and return of an investment will fluctuate so that an investor's shares may be worth less than the original cost when redeemed. For more information on the Pacific Advisors Funds, including information on charges, expenses and other classes offered, please obtain a copy of the prospectus by calling (800) 989-6693. Please read the prospectus and consider carefully the investment risks, objectives, charges and expenses before you invest or send money.

Shares of the Funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested. The views expressed represent the opinions and beliefs at the time of this commentary and are not meant as a market forecast. These views are subject to change at any time based on market or other conditions. This information may not be relied on as investment advice or as an indication of trading.

3

Pacific Advisors

Government Securities Fund

Fund Objective: High current income, preservation of capital, and rising future income consistent with prudent investment risk.

Investment Invests at least 80% of its assets in U.S. Government fixed income

Strategy: securities. These include securities issued or guaranteed by the U.S. Treasury; issued by a U.S. Government agency; or issued by a Government-Sponsored Enterprise (GSE). May also invest in high quality dividend-paying common stocks.

Investor Profile: Conservative. Income-focused; capital preservation aim.

TOTAL RETURNS | EXPENSE RATIOS1 | ||||||||||||||||||||||||||

For the year ended December 31, 2015 | Current | Prospectus | |||||||||||||||||||||||||

Net | Gross | Net | Gross | ||||||||||||||||||||||||

Class A | –1.97 | % | Class A | 3.88 | % | 7.05 | % | 3.50 | % | 6.37 | % | ||||||||||||||||

Class C | –2.63 | % | Class C | 4.61 | % | 7.78 | % | 4.23 | % | 7.09 | % | ||||||||||||||||

Barclays Capital U.S. Int T-Bond Index2 | 1.18 | % | |||||||||||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Rankings shown are for Class A shares; rankings for other share classes may be different. Returns and rankings do not take into account the maximum 4.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's board, but is expected to continue at current levels. Please see the Notes to Financial Statements in this report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Manager February 24, 2016

Jingjing Yan, CFA

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review as well as the Manager's general market outlook.

Fund Performance

The Fund's investment strategy is to manage interest rate risk for long-term and short-term investors seeking to protect principal. The Fund's fixed income investments were concentrated in short to intermediate-term bonds in response to the uncertainty surrounding the Federal Reserve's timeline for interest rate increases and concerns of a global economic slowdown.

For the year, Class A shares of the Fund returned –1.97% compared to 1.18% for its benchmark, the Barclays Capital U.S. Intermediate T-Bond Index; unlike the Fund, though, the benchmark is an unmanaged portfolio. Furthermore, the Index's longer average duration reflects a substantially greater exposure to principal loss as interest rates increase.

During the period, the Fund maintained an average duration of slightly less than 1.0 year; in contrast, the benchmark's average duration was 3.8 years. Duration measures a portfolio's sensitivity to interest

1 "Current" expense ratio as of 12/31/15. "Prospectus" expense ratio is for the fiscal year ended 12/31/14.

2 The Barclays Capital U.S. Intermediate Treasury Bond Index is an unmanaged index of U.S. government securities with one to ten years to maturity. It is not possible to invest directly in the Index.

4

rate movements; when rates increase by 1%, the value of a portfolio with a 4-year duration would decrease by approximately 4%. The Fund's short average duration reflected our commitment to minimize the negative effects of price volatility and rising interest rates on bond portfolios. In addition to price stability, the Fund's strategy also provides the flexibility to respond timely as investment opportunities arise.

The Fund's portfolio includes a small allocation to common stocks; these investments contribute to total return by providing dividend income and the potential for price appreciation. The Fund invests in high-quality, dividend-paying securities which help manage volatility by offsetting price changes in U.S. government securities holdings.

Market Overview

During the second half of the year, interest rates (as measured by the U.S. 10-year Treasury Note) fluctuated within a range of 50 basis points as investors anticipated the Federal Reserve's long-awaited interest rate increase (or "liftoff"). In September, the central bank cited global market turmoil and an apparent slowdown in China's economy in opting to delay the rate increase. Consequently, demand for U.S. Treasuries and other "safe-haven" investments rose; the yield on the 10-year Treasury Note, which was 2.35% by the end of the second quarter, fell to 1.99% in early October. In December, the Fed confirmed the market's expectations for an interest rate liftoff with a 25-basis point increase in the official federal funds rate, the first rate increase since 2006. The liftoff removed a cloud of uncertainty and signaled confidence in the U.S. economy. Importantly, Fed Chair Yellen emphasized a "gradual" pace of future rate increases, with rates likely to remain below historical levels. The yield on the 10-year Treasury Note ended the year at 2.27%.

The Fund continued to invest in shorter-term government securities in acknowledging the Fed's intention of continuing to raise rates during 2016; these bonds offer principal protection as rates increase. Specifically, the Fund invests in agency bonds with a "step-up" feature of scheduled coupon rate increases. Longer-term bonds would offer higher yields; but, we believe the long-term risk tradeoff of higher yields versus declining prices is unfavorable. For example, in 2013, portfolios that were invested in longer-term securities suffered significant losses when interest rates rose.

Fund Strategy

Fixed Income Strategy

Over 80% of the Fund's assets were invested in U.S. government agency bonds. These securities have higher coupon rates than U.S. Treasuries and enabled the Fund to generate additional income without materially increasing risk. The Fund invested in short-to-intermediate-term (e.g., three- to five-year maturities) callable government agency bonds; these bonds offer higher coupon rates than non-callable bonds because their issuing agencies are allowed to buy back, or "call," the bonds before maturity. To capture additional higher yields, the Fund invested in callable bonds that also included a "step-up" feature. Yields for step-up bonds increase at fixed intervals if they are not called back on the scheduled call dates; furthermore, as interest rates increase, they will preserve their value better than fixed-rate government securities with comparable maturities. And, if these bonds are called, they provide the flexibility to reinvest proceeds in other government agency securities according to prevailing market conditions.

The Fund does not utilize higher-risk strategies to enhance return. For example, the Fund does not invest in bonds with extended durations, use leverage strategies, or purchase mortgage-backed securities.

Equity Positioning

The Fund invests a small portion of its portfolio (less than 17% as of year-end) in high-quality, dividend-paying common stocks. Yet, the price appreciation potential offered by these holdings provided an important component of the Fund's total return and offset the limited price appreciation potential of short-to-intermediate-term U.S. government securities. Equity investments focus on blue-chip stocks that

5

Pacific Advisors

Government Securities Fund continued

offer attractive dividends and are less sensitive than the overall market to economic disruptions. Their relative price stability tends to counterbalance price movements in the fixed income markets without significantly increasing the Fund's risk exposure. We anticipate that, as interest rates rise, the Fund may reduce its equity allocation and shift the portfolio toward longer-term U.S. government securities.

Several Fund holdings3, including PPL, Southern Co. and Pepsi, had performed well as investors preferred the more conservative areas of the equity market. During the period, the Fund took profits and trimmed positions in companies such as Eli Lilly, Kimberly-Clark and Microsoft.

Looking Ahead

The Fed's actions will continue to strongly influence the fixed income market in 2016. Several factors, including economic growth rates abroad, the impact of higher interest rates, and the effects of oil prices, will affect the schedule and pace of the central bank's future rate increases. Additionally, market forces will likely influence longer-term rates separate and apart from any Fed actions. Regardless, the decision to raise short-term interest rates reflects the Fed's confidence in the U.S. and world economies. The move towards a more normal interest rate environment may prompt longer-term bond holders to reevaluate their willingness to hold these securities as interest rates rise.

The Fund will continue employing the conservative strategy of investing in short-to-intermediate-term U.S. government securities while monitoring opportunities to reinvest in suitable higher-yielding government bonds as interest rates increase. In a rising rate environment, we expect the Fund's portfolio to shift toward longer-term bonds. The Fund's flexibility to adjust holdings in response to economic and market conditions positions the Fund to successfully manage an upward trend in rates and provide improved performance.

3 For detailed information on Fund holdings, please see the Fund's Schedule of Investments in this Report.

6

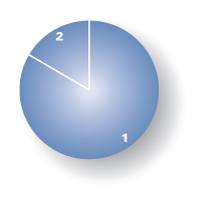

Portfolio Holdings as of 12/31/15 (Based on Total Investments)

1. | U.S. Government Agencies | 83.42 | % | ||||||||

2. | Equities | 16.58 | % | ||||||||

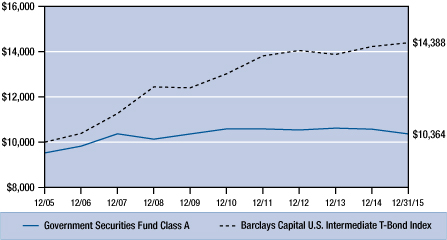

Change in Value of $10,000 Investment1

This chart compares the growth of a $10,000 investment in Class A shares of the Government Securities Fund for the period January 1, 2006 through December 31, 2015 with the same investment in the Barclays Capital U.S. Intermediate Treasury Bond Index2.

Average Annual Compounded Return as of December 31, 2015

Class A | Class C | Barclays Capital U.S. Int T-Bond Index | |||||||||||||

One Year | – 6.58 | % | – 3.60 | % | 1.18 | % | |||||||||

Five Year | – 1.39 | % | – 1.13 | % | 2.03 | % | |||||||||

Ten Year | 0.36 | % | 0.12 | % | 3.71 | % | |||||||||

Past performance does not guarantee future results. Performance quoted represents past performance. Current performance may be higher or lower than the performance data quoted. Returns include reinvested dividends and capital gains. Returns for Class A shares reflect a maximum front-end sales charge of 4.75%; and returns for Class C shares reflect the deduction of a contingent deferred sales charge of 1% on shares sold within the first year of purchase. Returns do not take into account individual taxes which may reduce actual returns when shares are sold. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Call (800) 989-6693 for the most recent month-end performance.

1 Fund results are shown for Class A shares and reflect deduction of the maximum front-end sales charge of 4.75% on the $10,000 investment for a net amount invested of $9,525. At the end of the same period, a $10,000 investment in Class C shares would have been valued at $10,120, and no contingent deferred sales charges would apply. Performance of the share classes will vary based on the difference in charges and expenses. The inception date is 02/08/93 for Class A shares and 04/01/98 for Class C shares. It is not possible to invest directly in the Index. Unlike the Fund's results, the results for the Index do not reflect sales charges, fees or expenses.

2 The Barclays Capital U.S. Intermediate Treasury Bond Index is an unmanaged index of U.S. government securities with one to ten years to maturity.

7

Pacific Advisors

Government Securities Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2015 through December 31, 2015.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 07/01/15 | Ending Account Value 12/31/15 | Expense Paid During Period 07/01/15 – 12/31/15 | |||||||||||||

Government Secs Fund Class A | |||||||||||||||

Actual | $ | 1,000.00 | $ | 997.80 | $ | 19.54 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,005.65 | $ | 19.61 | |||||||||

Government Secs Fund Class C | |||||||||||||||

Actual | $ | 1,000.00 | $ | 994.20 | $ | 23.17 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,001.97 | $ | 23.26 | |||||||||

3 Expenses are equal to the Fund's annualized expense ratio, net of expense waivers, of 3.88% for Class A shares and 4.61% for Class C shares, multiplied by the average account value over the period, multiplied by 184/365 days to reflect the one-half year period.

8

Pacific Advisors

Income and Equity Fund

Fund Objective: Current income and, secondarily, long-term capital appreciation.

Investment Invests primarily in investment grade U.S. corporate bonds and in dividend-paying

Strategy: stocks.

Investor Profile: Conservative. Some current income required; capital preservation aim.

TOTAL RETURNS | EXPENSE RATIOS1 | ||||||||||||||||||||||||||

For the year ended December 31, 2015 | Current | Prospectus | |||||||||||||||||||||||||

Net | Gross | Net | Gross | ||||||||||||||||||||||||

Class A | –2.57 | % | Class A | 2.06 | % | 2.81 | % | 1.91 | % | 2.66 | % | ||||||||||||||||

Class C | –3.21 | % | Class C | 2.81 | % | 3.56 | % | 2.66 | % | 3.41 | % | ||||||||||||||||

Barclays Capital U.S. Int Corp Bond Index2 | 1.08 | % | |||||||||||||||||||||||||

S&P 500® Index3 | 1.38 | % | |||||||||||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Rankings are shown for Class A shares; rankings for other share classes may be different. Returns and rankings do not take into account the maximum 4.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

The Fund's investment adviser is waiving a portion of its management fees pursuant to an Expense Limitation Agreement. The waiver may be discontinued at any time with ninety days written notice in consultation with the Fund's board, but is expected to continue at current levels. Please see the Notes to Financial Statements in this report for details. Performance shown reflects the waiver, without which the results would have been lower.

Discussion with Portfolio Managers February 24, 2016

Charles Suh, CFA

Jingjing Yan, CFA

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review as well as the Manager's general market outlook.

Fund Performance

For the year, Class A shares declined 2.57%. During the second half of the year, investors continued the trend from the first half of 2015 by fixating on Federal Reserve policy, the slow pace of global economic growth, and falling oil prices. Interest rate movements reflected the widely anticipated initiation of the Fed's rising interest rate policy (or "liftoff"). The yield on the benchmark U.S. 10-year Treasury Note, which ended the first half of the year at 2.35%, fell to 1.99% in early-October following the Fed's decision to delay raising the federal funds rate. In December, though, the long-awaited rate increase provided some reassurance in an otherwise uncertain market environment; interest rates drifted higher to end the year at 2.27%. Stocks, which had traded in a historically narrow range in the January-to-June period, fell

1 "Current" expense ratio as of 12/31/15. "Prospectus" expense ratio is for the fiscal year ended 12/31/14.

2 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity. It is not possible to invest directly in the Index.

3 The S&P 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses. It is not possible to invest directly in the Index.blicly issued investment grade U.S. corporate bonds with one to ten years to maturity. It is not possible to invest directly in the Index.

9

Pacific Advisors

Income and Equity Fund continued

sharply in the third quarter due to concerns about the possible impact from China's stock market selloff and currency devaluation. Broad market indices rebounded in the fourth quarter although the gains were mostly limited to a handful of relatively "safe" large cap stocks. Selling pressure for many stocks increased as investors stayed on the sidelines, awaiting a clearer view of the markets and the economy.

The Fund is well positioned as interest rates rise. The fixed income portfolio is focused on investment-grade bonds maturing in two to seven years. During the period, the Fund maintained an average duration of 2.4 years; in contrast, the average duration of the benchmark (the Barclays Capital U.S. Intermediate Corporate Bond Index, an unmanaged bond portfolio) was 4.3 years. Duration measures a portfolio's sensitivity to interest rate movements; when rates increase by 1%, the value of a portfolio with a 4-year duration would decrease by approximately 4%. The Fund's relatively short average duration reflected our commitment to minimize the negative effects of price volatility and rising interest rates on bond portfolios. The Fund's equity portfolio is concentrated in 30 to 40 high-quality, dividend-paying stocks with patterns of relatively low volatility and stable growth. In contrast, the Fund's equity benchmark, the S&P 500® Index, consists of companies across a broad range of quality, risk factors, and volatility. The market capitalization of the Fund's equity holdings are, on average, more than three times larger4 than the average for companies in the Index; this significant size variance highlights a fundamental difference between the Fund and the Index.

The composition of the Fund's fixed income holdings, and the Fund's equity holdings, differ from their respective benchmarks; nevertheless, overall Fund performance is best compared to a blended return based on the two benchmarks. For the year, the blended return5 for Fund's benchmarks was 1.23%. Importantly, the Fund maintained substantially lower volatility than the overall market as demonstrated by the Fund's one-year beta6 of 0.40, as of December 31st, versus the S&P 500® Index.

Fund Strategy

The Fund actively manages the allocation between fixed income and equity holdings to create risk-appropriate opportunities for both income and capital appreciation. The Fund seeks investment-quality bonds that provide current income and principal protection. The Fund also invests in a diverse selection of dividend-paying, blue-chip stocks. This equity approach has significantly contributed to Fund performance during the long period of low interest rates; that is, the dividend yields for portfolio stocks were often greater than the yields on corporate bonds issued by those same companies. We anticipate that the Fund's allocation to equities may decline as interest rates rise and we reinvest capital in bonds with prevailing higher yields.

Interest rates fluctuated in response to investor expectations of the Fed's liftoff. When the Fed postponed the commencement of its anticipated policy, demand for U.S. Treasuries and other "safe" investments rose and yields declined. Rates then rose following the first rate increase since 2006. In particular, short-term rates, which are most sensitive to the central bank's policy actions, increased sharply; the 2-year Treasury Bill, which closely tracks the official fed funds rate, moved from 0.57% in October to end the year at 1.06%. Rising interest rates pressured high-yield (or, "junk") bonds and bond funds, particularly those with investments in commodities and emerging markets. With crude oil prices continuing to fall, bonds of energy-related companies sold off sharply with little regard to their financial health.

We continue to monitor the fixed income markets to identify corporate bonds issued by good-quality companies that may be temporarily out-of-favor due to industry- or company-specific issues.

Fixed Income Strategy

The Fund's fixed income holdings focus on short-to-intermediate-term corporate bonds. Due to the extraordinary demand for these bonds during the period, we identified some high-quality bonds with

4 As of 12/31/15, the mean market cap was $120.6 billion for the Fund and $37.3 billion for the S&P 500® Index.

5 Blended return calculated from the benchmark index returns based on ratio of stocks to fixed-income securities in the Fund's portfolio as of the end of the period.

6 "Beta" measures volatility relative to the stock market or an alternative benchmark. A beta less than 1.0 indicates lower risk than the market or the benchmark; a beta greater than 1.0 indicates higher risk than the market or the benchmark.

10

attractive variable rate or call features. These securities offered better principal protection than longer-term bonds while also providing the flexibility to identify timely investment opportunities as fixed income markets evolved.

Several of the Fund's corporate bonds were called in as their issuers sought to refinance existing bonds or retire debt. The Fund reinvested capital from these transactions in similar investment-grade bonds7 of high-quality companies, including Pfizer and Block Financial. The Fund also purchased "fixed-to-floating" preferred stocks, such as Wells Fargo, in anticipation of rising interest rates. These securities' coupon rates and/or dividends periodically increase over time. In general, the Fund remains invested primarily in short-to-intermediate-term bonds which will help preserve principal when rates rise.

We continuously evaluate the fundamental characteristics of current investments. Corporate bonds issued by energy-related companies remained under pressure during the period; the Fund continued to hold investment-grade bonds of financially sound energy services companies; the Fund anticipates that these holdings, although undervalued due to lack of investor interest, will recover along with oil prices. The Fund sold its bond holding in the mining firm Freeport-McMoRan which we believed no longer provided a risk-appropriate opportunity for returns.

Equity Strategy

The Fund's equity portfolio is an important complement to corporate bond holdings especially during the historically low interest rate environment. The strategy seeks stocks that provide dividend income and price appreciation; we purchase high-quality, well-established companies from a wide range of industries.

The Fund continued to favor a select number of blue-chip stocks with attractive dividends and low volatility. The Fund's equity holdings had a weighted average dividend yield of 3.25% which compares favorably to the average yield for 5-year investment-grade corporate bonds of 2.98%. We believe the Fund's equity holdings offer attractive opportunities for total return compared to bonds, especially during periods of rising interest rates.

During the period, we purchased stocks of companies including Schlumberger, Mattel and Wal-Mart that typically provide stronger growth prospects during periods of global economic expansion; the Fund increased its allocation to industrial firms and businesses that offer consumer goods and services.

We anticipate adjusting the Fund's allocations between equity and fixed income holdings as the global economy strengthens and interest rates rise; we may reduce the Fund's equity allocation in favor of bonds with higher prevailing coupon yields.

Looking Ahead

The Fed's decision to raise interest rates signals confidence in the U.S. economy, and marks the beginning of a transitional phase in the markets. Importantly, though, Fed Chair Yellen emphasized a "gradual" pace of future rate increases while reiterating that rates will likely remain historically low for some time. The central bank's deliberate process should prevent market rates from rising quickly; yet, history has shown that the prices for fixed income securities, particularly longer-term bonds, often move independent of the Fed. During this market shift, the Fund's focus on shorter-term bonds to curtail price volatility may result in periods of underperformance. As interest rates move higher, the Fund should benefit from the flexibility of holding shorter-term bonds.

The Fund anticipates that, as its shorter-term bonds mature or are called, the proceeds will be invested at higher yields. Also, as rates trend higher, the Fund expects to gradually lengthen the average duration of its bond portfolio.

7 For detailed information on Fund holdings, please see the Fund's Schedule of Investments in this Report.

11

Pacific Advisors

Income and Equity Fund continued

The growing global economies support a more positive outlook for 2016. The European Central Bank appears committed to accommodative monetary policies that, along with low oil prices, enabled the region to achieve its fastest growth rate since 2011. China's transition to develop a consumer-driven economy will be critical to reducing the country's dependence on exports and more closely aligning its economy to those of developed nations; the International Monetary Fund acknowledged China's economic reforms in approving the inclusion of the yuan as a reserve currency. Amid this backdrop, the Fund will continue to identify stocks which are likely, over time, to increase dividends and provide price appreciation. Nevertheless, as future rate increases occur, the Fund may reduce its equity holdings to increase its fixed income allocation and take advantage of higher prevailing yields.

12

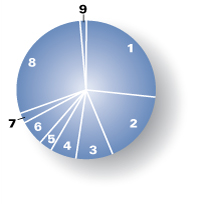

Portfolio Holdings as of 12/31/15 (Based on Total Investments)

1. | Corporate Bonds | 48.89 | % | ||||||||

| Equities | 46.73 | % | |||||||||

| 2. | Consumer Staples | 8.65 | % | ||||||||

| 3. | Industrials | 7.75 | % | ||||||||

| 4. | Consumer Discretionary | 5.26 | % | ||||||||

| 5. | Information Technology | 5.07 | % | ||||||||

| 6. | Utilities | 4.79 | % | ||||||||

| 7. | Health Care | 4.14 | % | ||||||||

| 8. | Telecommunication Services | 3.01 | % | ||||||||

| 9. | Others | 8.06 | % | ||||||||

10. | Preferred Stock | 2.51 | % | ||||||||

11. | Cash and Cash Equivalents | 1.87 | % | ||||||||

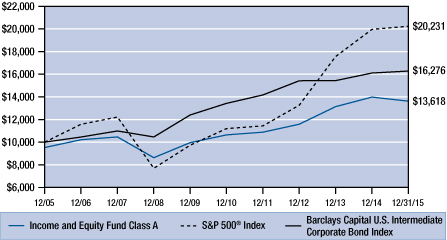

Change in Value of $10,000 Investment1

This chart compares the growth of a $10,000 investment in Class A shares of the Income and Equity Fund for the period January 1, 2006 through December 31, 2015 with the same investment in the S&P 500® Index2 and the Barclays Capital U.S. Intermediate Corporate Bond Index3.

Average Annual Compounded Returns as of December 31, 2015

Class A | Class C | Barclays Capital U.S. Int Corp Bond Index | S&P 500® Index | ||||||||||||||||

One Year | – 7.19 | % | – 4.18 | % | 1.08 | % | 1.38 | % | |||||||||||

Five Year | 4.04 | % | 4.30 | % | 3.93 | % | 12.57 | % | |||||||||||

Ten Year | 3.13 | % | 2.87 | % | 4.99 | % | 7.31 | % | |||||||||||

Past performance does not guarantee future results. Performance quoted represents past performance. Current performance may be higher or lower than the performance data quoted. Returns include reinvested dividends and capital gains. Returns for Class A shares reflect a maximum front-end sales charge of 4.75%; and returns for Class C shares reflect the deduction of a contingent deferred sales charge of 1% on shares sold within the first year of purchase. Returns do not take into account individual taxes which may reduce actual returns when shares are sold. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Call (800) 989-6693 for the most recent month-end performance.

1 Fund results are shown for Class A shares and reflect deduction of the maximum front-end sales charge of 4.75% on the $10,000 investment for a net amount invested of $9,525. At the end of the same period, a $10,000 investment in Class C shares would have been valued at $13,266, and no contingent deferred sales charges would apply. Performance of the share classes will vary based on the difference in charges and expenses. The inception date is 02/08/93 for Class A shares and 04/01/98 for Class C shares. It is not possible to invest directly in either Index. Index results assume reinvestment of dividends, but, unlike the Fund's results, do not reflect sales charges, fees or expenses.

2 The Standard & Poor's 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy.

3 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity.

13

Pacific Advisors

Income and Equity Fund continued

Expense Examples

As a shareholder of the Fund you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2015 through December 31, 2015.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during the period.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which in not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The following transaction costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a front-end sales charge (load) of 4.75% on Class A shares; (2) a 2% redemption fee if you sell or exchange shares within 30 days of purchase, with certain exceptions. The redemption fee does not apply to: (a) redemptions under an automatic withdrawal program or periodic asset reallocation plan, required minimum distributions (RMD), employer mandated distributions from a qualified plan, or redemptions under a qualified domestic relations order (QDRO); (b) redemptions to pay for expenses related to terminal illness, extended hospital or nursing home care, or other serious medical conditions, including death; (c) redemptions of shares acquired through dividend or capital gains reinvestments; (d) loans from a qualified plan account; and (e) redemptions initiated by the Fund; and (3) a $10 service fee on each exchange after the first five exchanges in each calendar year.

The following ongoing costs are not included in the expenses shown in the table and, if applicable, would increase the expenses that you paid over the period: (1) a $12 low balance fee on accounts with balances of less than $250 as of September 30th of each calendar year and no investment activity (excluding reinvestment of dividends and/or capital gains) during the prior calendar year or the first nine months of the current calendar year. This fee does not apply to IRAs, qualified plan accounts, or Coverdell Education Savings Accounts; (2) a $15 annual custodial fee on IRAs, SEPs, SIMPLE IRAs, and Coverdell Education Savings Accounts; and (3) a $20 annual custodial fee on 403(b) accounts.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 07/01/15 | Ending Account Value 12/31/15 | Expense Paid During Period 07/01/15 – 12/31/15 | |||||||||||||

Income & Equity Fund Class A | |||||||||||||||

Actual | $ | 1,000.00 | $ | 990.50 | $ | 10.34 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,014.82 | $ | 10.46 | |||||||||

Income & Equity Fund Class C | |||||||||||||||

Actual | $ | 1,000.00 | $ | 987.80 | $ | 14.08 | |||||||||

Hypothetical (5% return before expense) | $ | 1,000.00 | $ | 1,011.04 | $ | 14.24 | |||||||||

4 Expenses are equal to the Fund's annualized expense ratio, net of expense waivers, of 2.06% for Class A shares and 2.81% for Class C shares, multiplied by the average account value over the period, multiplied by 184/365 days to reflect the one-half year period.

14

Pacific Advisors

Balanced Fund

Fund Objective: Long-term capital appreciation and income consistent with reduced risk.

Investment Invests primarily in large cap common stocks and investment grade U.S. corporate

Strategy: bonds. Invests at least 25% of its assets in fixed income securities and preferred stocks and at least 25% in equities.

Investor Profile: Moderately conservative. Seeks combination of long-term growth, income, liquidity and reduced risk of price fluctuations.

TOTAL RETURNS | EXPENSE RATIOS1 | ||||||||||||||||||

For the year ended December 31, 2015 | Current | Prospectus | |||||||||||||||||

Class A | –16.73 | % | Class A | 3.27 | % | 2.84 | % | ||||||||||||

Class C | –17.31 | % | Class C | 4.05 | % | 3.58 | % | ||||||||||||

S&P 500® Index2 | 1.38 | % | |||||||||||||||||

Barclays Capital U.S. Int Corp Bond Index3 | 1.08 | % | |||||||||||||||||

Performance quoted is past performance which does not guarantee future results. Current performance may be higher or lower than the performance quoted. Call (800) 989-6693 for performance current to the most recent month-end. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Returns represent the change in value over the stated period assuming reinvestment of dividends and capital gains at net asset value. Rankings are shown for Class A shares; rankings for other share classes may be different. Returns and rankings do not take into account the maximum 5.75% sales charge on Class A shares or the 1% Contingent Deferred Sales Charge (CDSC) for Class C shares sold within one year of purchase. Returns would be lower if the applicable sales charge and CDSC were included. Returns do not take into account individual taxes which may reduce actual returns when shares are sold.

Discussion with Portfolio Managers February 24, 2016

Charles Suh, CFA

Jingjing Yan, CFA

Samuel C. Coquillard

Please see the Chairman's Letter at the beginning of this Report for a detailed market and economic review as well as the Manager's general market outlook.

Fund Performance

Fund performance, which reflected a diversified "all cap" equity strategy and "total return" approach to fixed income investing, lagged its benchmarks in 2015. Class A shares fell 16.73%; in comparison, the Fund's equity benchmark, the S&P 500® Index, gained 1.38% while the Fund's fixed income benchmark, the Barclays Capital U.S. Intermediate Corporate Bond Index, gained 1.08%. Market volatility rose in the third and fourth quarters as investors reacted to the Greek debt crisis, Chinese yuan devaluation, and the Federal Reserve's delays in initiating interest rate increases. These events prompted a shift to "safe haven" investments, such as U.S. Treasuries and relatively stable, dividend-paying mega-cap stocks. 35% of stocks in the S&P 500® Index fell 20% or more from than their 52-week highs. Notably, the S&P 500® Index benefitted from the performance of four holdings, Facebook, Amazon.com, Netflix, and Alphabet (formerly Google); for the year, these stocks rose between 34% and 178%. Small cap

1 "Current" expense ratio as of 12/31/15. "Prospectus" expense ratio is for the fiscal year ended 12/31/14.

2 The S&P 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy. Index returns assume the reinvestment of dividends, but, unlike the Fund's returns, do not reflect the effects of management fees or expenses. It is not possible to invest directly in the Index.

3 The Barclays Capital U.S. Intermediate Corporate Bond Index is an unmanaged index of publicly issued investment grade U.S. corporate bonds with one to ten years to maturity. It is not possible to invest directly in the Index.

15

Pacific Advisors

Balanced Fund continued

companies fared even worse: 56% of companies in the Russell 2000® Index fell 20% or more from their 52-week highs. A significant portion of Fund's equity holdings were allocated to small cap stocks. Also, Fund holdings were overweighted, compared to its equity benchmark, towards energy, manufacturing and global trade; these areas underperformed. As of December 31st, the Fund's volatility, as measured by its beta4, declined from 0.88 last year to 0.75 in comparison to the S&P 500® Index.

Fund Strategy

The Fund is designed for investors seeking to participate in the equity markets with reduced risk. The Fund's strategy combines high-quality stocks across all market capitalizations with investment-grade corporate bonds that provide additional income and appreciation potential. We identify leading, well-managed companies whose stocks trade at a discount to our internal price targets; in most cases, we anticipate that the stocks will appreciate over a medium-to-long-term time horizon as the companies' growth strategies unfold. The Fund may experience periods of underperformance when short-term market trends overshadow long-term outlooks; yet, over time, the Fund's performance should reflect the strength of these companies as they demonstrate the ability to grow during various economic and business cycles. We manage the Fund's asset allocation based on our assessment of risk-appropriate investments in the context of the overall economic, market, and interest rate outlook. This approach enables the Fund to take advantage of specific growth opportunities while reducing overall price volatility.

During the second half of 2015, the U.S. economy remained relatively healthy but fears of a global economic slowdown emerged following China's decision in August to devalue the yuan. Shortly thereafter, the Federal Reserve cited market turmoil and downward inflationary pressures in delaying its long-anticipated interest rate "liftoff". Investors began to favor less-risky areas of the market: the yield on the U.S. 10-year Treasury Note fell and corporate bond spreads (that is, the yield difference between higher and lower quality bonds) widened as demand for lower-grade debt diminished. Markets stabilized over the final two months of the year following the release of favorable economic data; however, shares of small and mid-sized companies, as well as stocks related to energy and industrial markets, continued to languish. The Fund's allocation to equities declined slightly primarily due to price depreciation for the portfolio's small and mid-cap holdings. Still, the emphasis on equity holdings reflects our confidence in the medium-to-longer-term prospects for the global economy as well as the appreciation potential of the Fund's individual stocks.

Equity Strategy

The Fund's "all cap" equity strategy diversifies investments among high-quality, well-managed companies with proven growth track records through various economic and business cycles. Large cap investments, which accounted for approximately 33% of the equity allocation, favor prominent global companies that offer stability with moderate growth potential. Mid-cap holdings, which represented approximately 36% (up from 33% as of June 30, 2015) of the equity allocation, feature industry leaders that are well-positioned to participate in sector or economic trends. The remainder of the Fund's equity allocation is invested in established small cap companies with attractive long-term growth prospects.

The Fund's positioning in the Energy and Industrials sectors anticipates ongoing growth in the domestic and global economy. However, China's slowdown in industrial production and subsequent currency devaluation fueled concerns of a global economic downturn and even the possibility of recession. As a result, investors moved out of sectors directly tied to general economic activity, such as manufacturing, transportation, and trade. Out-of-favor stocks included the Fund's holdings even though these investments are concentrated among market leading companies with experienced management teams with the wherewithal to survive a prolonged industry downturn. Many of these companies have

4 "Beta" measures volatility relative to the stock market or an alternative benchmark. A beta less than 1.0 indicates lower risk than the market or the benchmark; a beta greater than 1.0 indicates higher risk than the market or the benchmark.

16

used previous downturns to expand their market positioning. For example5, Genesee & Wyoming, the leading operator of "short-line" railroads, and Kirby, the leading provider of marine transportation along the river and coastal waterways, are ideally positioned to benefit from industry consolidation.

The deterioration in oil prices significantly impacted Energy-related holdings. Importantly, though, the Fund's Energy holdings are well-positioned with adequate financing, proprietary technologies, and high-quality assets. Core Labs, a new position, is the leading provider of global reservoir analysis; offshore driller Noble Corporation, a new position, and offshore service vessel operator Hornbeck Offshore Services should remain relatively insulated as their technically advanced fleets remain in demand even in the current depressed environment.

The Fund's large cap holdings, led by NIKE and Alphabet (formerly Google), performed well. NIKE is expanding its global footprint with recent quarterly sales increases of 34% in China and 36% in Japan; the company expects sales in Asian markets to surpass Western Europe, traditionally its second largest market, sometime in 2016. Alphabet delivered impressive results from mobile advertising and YouTube; the recent launch of subscription-based YouTube Red could provide further growth as the company pursues an original content strategy.

Our active management approach adjusts portfolio positions based on our evaluation of each company's potential for medium-to-long-term appreciation. During the period, we sold several positions including International Business Machines, Helix Energy Solutions Group, Navistar, and Omnicom Group in favor of more attractive opportunities; we also trimmed positions in CVS Health, Lithia Motors, NIKE, and O'Reilly Automotive as these companies approached our internal price targets. We used the proceeds to establish new positions in Core Labs, Noble, Spirit Airlines, and Gentherm. Ultra-low cost airline operator Spirit Airlines has established a profitable niche in the industry. Gentherm owns proprietary thermoelectric technologies that are used to provide energy-efficient heating and cooling for a range of products; the company maintains a dominant share of the automotive seating market and was recently awarded two contracts for a hybrid and electric vehicle batteries.

Fixed Income Strategy

The Fund's "total return" approach actively manages fixed income holdings in response to current interest rate trends. In selecting bonds, we examine each company's fundamentals including cash flow trends, liquidity ratios and debt maturity schedules, and then assess the income and capital appreciation potential. The Fund's investments have continued to focus on shorter-term bonds that are less sensitive to interest rate changes while avoiding higher risk investments. The extended period of low interest rates and our expectation for higher interest rates contributed to our decision to maintain the Fund's fixed income allocation near the lower end of its historical range.

Interest rates fluctuated in anticipation of the Fed's first interest rate increase since 2006; the yield on the U.S. 10-year Treasury Note fell from 2.35% at the end of the second quarter to a low of 1.99% in October before ending the year at 2.27%. Markets eventually settled down as the Fed ended its historic monetary policy with a rate hike in December.

The Fund's shorter-term investment grade corporate bonds, particularly, energy-related debt, underperformed. Our analysis of these holdings identified sufficient cash flows to cover operations and debt obligations. We anticipate improved energy market fundamentals in 2016; even so, any continued decline in oil prices could further depreciate bond prices and degrade underlying fundamentals.

The Fund has continued to invest in shorter-term investment grade corporate bonds which are designed to protect principal value in a rising interest rate environment. In contrast, the Fund's benchmark, the Barclays Capital U.S. Intermediate Corporate Bond Index, includes longer-term and lower quality bonds; these bonds are more susceptible to losses in value in response to rising interest rates.

5 For detailed information on Fund holdings, please see the Fund's Schedule of Investments in this Report.

17

Pacific Advisors

Balanced Fund continued

Looking Ahead

Despite the recent challenges, we remain confident in the long-term prospects of the Fund's holdings. Each of these companies is well managed with a track record of delivering attractive returns in difficult industry environments. In addition to the energy downturn, the recent economic slowdown can also be traced to the rise of the U.S. dollar; over the past two years, the dollar gained more than 20% against a basket of leading global currencies. Few analysts anticipate continued appreciation of the dollar; stabilization or a continuation of the recent weakening is perhaps more likely. Such a development could provide a meaningful lift to commodity-related companies and export-oriented manufacturers.

During the past two years, the Fund's large cap holdings have significantly outperformed its small and mid-cap holdings. We anticipate that this trend may reverse as the Fund's mid-cap and small cap holdings, including transportation companies such as Genesee & Wyoming, Kirby and Kansas City Southern, provide attractive opportunities along with a recovery in industrial and export activity. Two holdings, TAL International, a container leasing company, and Team, an industrial services provider, both industry leaders, recently announced transformative acquisitions; the transactions should lead to significant growth opportunities. And, Energy-related companies National Oilwell Varco, Hornbeck Offshore Services and Noble trade a fraction of book value, a conservative measure of a company's assets. Thus, any sign of stabilization in oil prices could lead to significant recoveries in their share prices.

Opportunities for conservative fixed income investors, meanwhile, may increase along with yields for investment grade debt. As Fund holdings mature or are called in, we anticipate reinvesting proceeds at more attractive yields, and, as the Fed continues to raise interest rates, we anticipate reinvesting in bonds with intermediate-to-longer-term maturities. The Fund's allocation strategy will continue to reflect not only our outlook for the economy and interest rates but also our assessment of the relative contributions of equity and fixed income holdings.

18

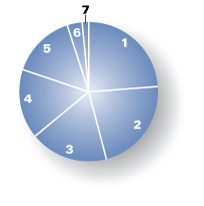

Portfolio Holdings as of 12/31/15 (Based on Total Investments)

| Equities | 69.51 | % | |||||||||

| 1. | Industrials | 26.64 | % | ||||||||

| 2. | Consumer Discretionary | 17.17 | % | ||||||||

| 3. | Energy | 8.57 | % | ||||||||

| 4. | Financials | 5.95 | % | ||||||||

| 5. | Consumer Staples | 3.07 | % | ||||||||

| 6. | Information Technology | 5.73 | % | ||||||||

| 7. | Health Care | 2.38 | % | ||||||||

8. | Corporate Bonds | 29.03 | % | ||||||||

9. | Preferred Stock | 1.46 | % | ||||||||

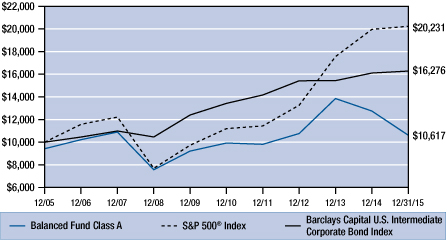

Change in Value of $10,000 Investment1

This chart compares the growth of a $10,000 investment in Class A shares of the Balanced Fund for the period January 1, 2006 through December 31, 2015 with the same investment in the S&P 500® Index2 and the Barclays Capital U.S. Intermediate Corporate Bond Index3.

Average Annual Compounded Returns as of December 31, 2015

Class A | Class C | S&P 500® Index | Barclays Capital U.S. Int Corp Bond Index | ||||||||||||||||

One Year | – 21.52 | % | – 18.13 | % | 1.38 | % | 1.08 | % | |||||||||||

Five Year | 0.16 | % | 0.60 | % | 12.57 | % | 3.93 | % | |||||||||||

Ten Year | 0.60 | % | 0.43 | % | 7.31 | % | 4.99 | % | |||||||||||

Past performance does not guarantee future results. Performance quoted represents past performance. Current performance may be higher or lower than the performance data quoted. Returns include reinvested dividends and capital gains. Returns for Class A shares reflect a maximum front-end sales charge of 5.75%; and returns for Class C shares reflect the deduction of a contingent deferred sales charge of 1% on shares sold within the first year of purchase. Returns do not take into account individual taxes which may reduce actual returns when shares are sold. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Call (800) 989-6693 for the most recent month-end performance.

1 Fund results are shown for Class A shares and reflect deduction of the maximum front-end sales charge of 5.75% on the $10,000 investment for a net amount invested of $9,425. At the end of the same period, a $10,000 investment in Class C shares would have been valued at $10,438, and no contingent deferred sales charges would apply. Performance of the share classes will vary based on the difference in charges and expenses. The inception date is 02/08/93 for Class A shares and 04/01/98 for Class C shares. It is not possible to invest directly in either Index. Index results assume reinvestment of dividends, but, unlike the Fund's results, do not reflect sales charges, fees or expenses.

2 The Standard & Poor's 500® Index is an unmanaged, market capitalization weighted index which measures the performance of the large cap segment of the U.S. equities market, covering approximately 75% of the U.S. equities market. The Index includes 500 leading companies in leading industries of the U.S. economy.