UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811- 7123 |

| |

| Advantage Funds, Inc. | |

| (Exact name of Registrant as specified in charter) | |

| | |

| c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 | |

| (Address of principal executive offices) (Zip code) | |

| | |

| Janette E. Farragher, Esq. 200 Park Avenue New York, New York 10166 | |

| (Name and address of agent for service) | |

|

Registrant's telephone number, including area code: | (212) 922-6000 |

| |

Date of fiscal year end: | 8/31 | |

Date of reporting period: | 8/31/2012 | |

| | | | | | | |

The following N-CSR relates only to the Registrant's series listed below and does not affect the other series of the Registrant, which has a different fiscal year end and, therefore, different N-CSR reporting requirements. A separate N-CSR Form will be filed for the remaining series as appropriate.

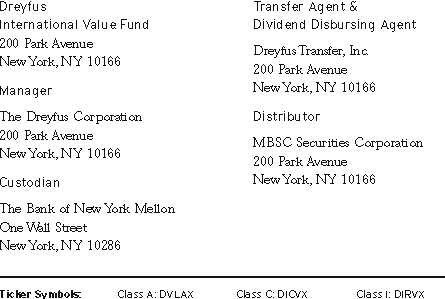

- DREYFUS INTERNATIONAL VALUE FUND

- DREYFUS OPPORTUNISTIC MIDCAP VALUE FUND

- DREYFUS OPPORTUNISTIC SMALL CAP FUND

- DREYFUS OPPORTUNISTIC U.S. STOCK FUND

- DREYFUS STRATEGIC VALUE FUND

- DREYFUS STRUCTURED MIDCAP FUND

- DREYFUS TECHNOLOGY GROWTH FUND

FORM N-CSR

Item 1. Reports to Stockholders.

Dreyfus

International

Value Fund

ANNUAL REPORT August 31, 2012

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.dreyfus.com and sign up for Dreyfus eCommunications. It’s simple and only takes a few minutes.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value

| |

| | Contents |

| |

| |

| | THE FUND |

| 2 | A Letter from the Chairman and CEO |

| 3 | Discussion of Fund Performance |

| 6 | Fund Performance |

| 8 | Understanding Your Fund’s Expenses |

| 8 | Comparing Your Fund’s Expenses |

| With Those of Other Funds |

| 9 | Statement of Investments |

| 14 | Statement of Assets and Liabilities |

| 15 | Statement of Operations |

| 16 | Statement of Changes in Net Assets |

| 18 | Financial Highlights |

| 21 | Notes to Financial Statements |

| 34 | Report of Independent Registered |

| | Public Accounting Firm |

| 35 | Important Tax Information |

| 36 | Proxy Results |

| 37 | Information About the Renewal of |

| | the Fund’s Management Agreement |

| 42 | Board Members Information |

| 44 | Officers of the Fund |

| |

| FOR MORE INFORMATION |

|

| | Back Cover |

Dreyfus

International Value Fund

The Fund

A LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholder:

We are pleased to present this annual report for Dreyfus International Value Fund, covering the 12-month period from September 1, 2011, throughAugust 31, 2012. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

While they produced flat returns, on average, for the past year overall, international equities proved unusually volatile as prices rose and fell according to investors’ changing expectations of global economic conditions. Europe has remained under severe economic pressure due to a persistent debt crisis and austerity-oriented fiscal policies adopted by many governments. In Japan, a strengthening currency dampened export activity and economic growth. The emerging markets have posted a slower rate of growth, reducing demand for industrial commodities and other goods and services. In contrast, the U.S. economy has grown relatively steadily, albeit at about half the average rate achieved in prior domestic recoveries.

Choppy economic conditions appear likely to persist over the foreseeable future. On one hand, the global economy has responded to a variety of stimulative measures, most notably aggressively accommodative monetary policies in most major markets. On the other hand, headwinds emanating from Europe and China may continue to weigh on economic growth and investor sentiment. Indeed, the ability of governments and economic policymakers to address these issues could go a long way toward shaping the 2013 market environment.As always, we urge you to speak regularly with your financial advisor to discuss how changing global economic conditions may affect your investments.

Thank you for your continued confidence and support.

Jonathan R. Baum

Chairman and Chief Executive Officer

The Dreyfus Corporation

September 17, 2012

2

DISCUSSION OF FUND PERFORMANCE

For the period of September 1, 2011, through August 31, 2012, as provided by D. Kirk Henry, Senior Portfolio Manager

Fund and Market Performance Overview

For the 12-month period ended August 31, 2012, Dreyfus International Value Fund’s Class A shares produced a total return of –5.89%, Class C shares returned –6.55% and Class I shares returned –5.41%.1 In comparison, the fund’s benchmark, the Morgan Stanley Capital International Europe, Australasia, Far East Index (“MSCI EAFE Index”), produced a total return of –0.04% for the same period.2 International stocks encountered heightened volatility throughout the reporting period due to changing economic conditions in Europe and the emerging markets. The fund produced lower returns than its benchmark, primarily due to investors’ preference for growth stocks over their value-oriented counterparts.

The Fund’s Investment Approach

The fund seeks long-term capital growth.The fund ordinarily invests most of its assets in securities of foreign companies which Dreyfus considers to be value companies.

The fund’s investment approach is value-oriented and research-driven. In selecting stocks, we attempt to identify potential investments through extensive quantitative and fundamental research. Emphasizing individual stock selection over economic or industry trends, the fund focuses on three key factors: value, or how a stock is valued relative to its intrinsic worth based on traditional value measures; business health, or overall efficiency and profitability as measured by return on assets and return on equity; and business momentum, or the presence of a catalyst (such as corporate restructuring, change in management or spin-off) that will trigger a price increase near term to midterm.

The fund typically sells a stock when it is no longer considered a value company, appears less likely to benefit from the current market and economic environment, shows deteriorating fundamentals or declining momentum, or falls short of our expectations.

The Fund 3

DISCUSSION OF FUND PERFORMANCE (continued)

Markets Reacted Sharply to Economic Developments

The reporting period began in the midst of major stock market declines throughout the world. The downgrade of one agency’s assessment of long-term U.S. government debt, an intensifying debt crisis in Europe and rising inflationary pressures in China triggered a flight away from stocks and toward traditional safe havens. Fortunately, better U.S. economic data and remedial measures from European and Chinese policymakers generally arrested the decline during the fall of 2011.

By the beginning of 2012, stocks were rallying amid U.S. employment gains, a quantitative easing program in Europe and a shift to less restrictive monetary and fiscal policies in China. Investors grew more tolerant of risks, focusing more intently on company fundamentals, including valuations. However, investors returned to a risk-averse posture during the spring, when measures designed to relieve fiscal pressures in Europe encountered resistance. The summer saw more encouraging global economic data, and the MSCI EAFE Index ended the reporting period close to where it began.

In this tumultuous environment, international investors tended to prefer large-cap companies with high dividend yields and positive earnings momentum. In contrast, investors did not favor the typical type of value companies invested in by the fund.

Mixed Investment Results in Volatile Markets

The fund’s relative performance over the reporting period was undermined by stocks in the United Kingdom, where metals producers Anglo American and Lonmin were hurt by the European debt crisis and reduced demand from the emerging markets. In addition, grocery chain Tesco weighed on results as the company lost market share, catalog retailer Home Retail Group encountered sluggish sales and the fund did not participate in gains posted by U.K. tobacco and spirits producers. In Hong Kong, apparel retailer Esprit Holdings was hurt by the downturn in Europe and overexpansion of its U.S. stores. Results from Finland were dampened by handset maker Nokia. In other areas, the fund suffered shortfalls stemming from Chinese clothing retailer China Dongxiang, Japanese technology company Ricoh, and European grocery chains Delhaize Group and Carrefour.

The fund achieved better results in the Netherlands, where successful positions included Koninklijke Philips Electronics, which posted strong quarterly results after a recent restructuring, and insurer Aegon, which

4

rallied late in the reporting period as the stock market outlook improved. Australia was home to several top performers, including agricultural chemicals producer Nufarm and medical center operator Primary Health Care. Overweighted exposure to Germany bolstered relative results, and successful stock selections there included utilities E.ON and RWE, which rallied from previous weakness, and health care company Bayer, which posted strong results in its pharmaceuticals division. In other parts of the world, the fund benefited from positions in Chinese electric utility Huaneng Power International, Japanese health care and household goods company Medipal Holdings and drug developer Astellas Pharma.

Finding Attractive Valuations Worldwide

The international equity markets’ gyrations have created some compelling valuations among companies we consider fundamentally sound as the market has priced in a worst-case macroeconomic scenario that we believe is unlikely to occur. In our judgment, the fund remains well positioned for a broad-based market rebound as global economic conditions gradually improve.

September 17, 2012

Please note, the position in any security highlighted with italicized typeface was sold during the reporting period.

Equity funds are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

The fund’s performance will be influenced by political, social and economic factors affecting investments in foreign companies. Special risks associated with investments in foreign companies include exposure to currency fluctuations, less liquidity, less developed or less efficient trading markets, lack of comprehensive company information, political instability and differing auditing and legal standards.These risks are enhanced in emerging market countries. Please read the prospectus for further discussion of these risks.

1 Total return includes reinvestment of dividends and any capital gains paid, and does not take into

consideration the maximum initial sales charge in the case of Class A shares, or the applicable

contingent deferred sales charge imposed on redemptions in the case of Class C shares. Had these

charges been reflected, returns would have been lower. Past performance is no guarantee of future

results. Share price, yield and investment return fluctuate such that upon redemption fund shares

may be worth more or less than their original cost.The fund’s returns reflect the absorption of

certain fund expenses by The Dreyfus Corporation pursuant to an agreement in effect through

March 31, 2013, at which time it may be extended, terminated or modified. Had these expenses

not been absorbed, the fund’s returns would have been lower.

2 SOURCE: LIPPER INC. — Reflects reinvestment of net dividends and, where applicable,

capital gain distributions.The Morgan Stanley Capital International Europe,Australasia, Far East

(MSCI EAFE) Index is an unmanaged index composed of a sample of companies representative

of the market structure of European and Pacific Basin countries.The Index does not take into

account fees and expenses to which the fund is subject. Investors cannot invest directly in any index.

The Fund 5

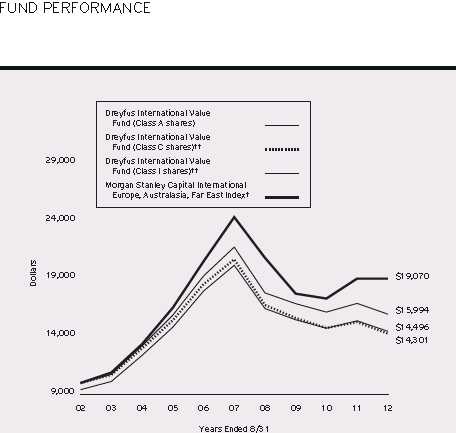

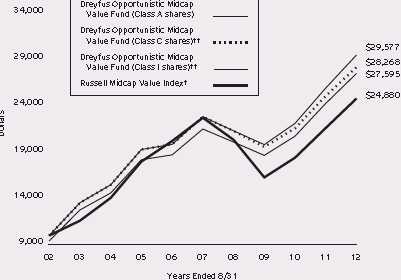

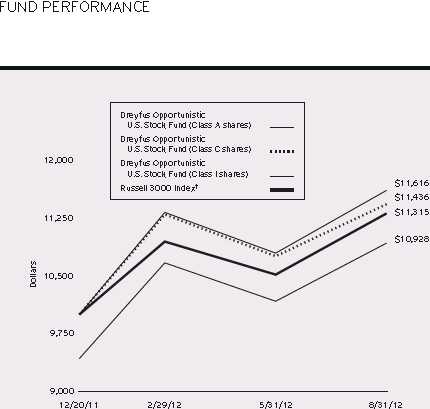

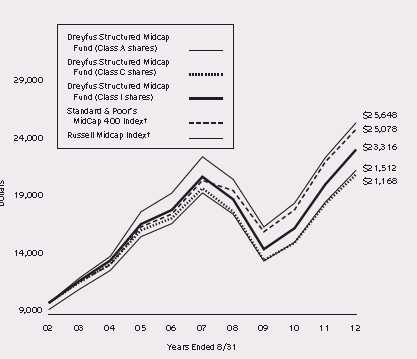

Comparison of change in value of $10,000 investment in Dreyfus International Value Fund Class A shares, Class C shares and Class I shares and the Morgan Stanley Capital International Europe, Australasia, Far East Index

† Source: Lipper Inc.

The total return figures presented for Class C shares of the fund reflect the performance of the fund’s Class A shares

for the period prior to 11/15/02 (the inception date for Class C shares), adjusted to reflect the applicable sales load

for this share class.

The total return figures presented for Class I shares of the fund reflect the performance of the fund’s Class A shares

for the period prior to 11/15/02 (the inception date for Class I shares).

Past performance is not predictive of future performance.

The above graph compares a $10,000 investment made in each of the Class A, Class C and Class I shares of Dreyfus International Value Fund on 8/31/02 to a $10,000 investment made in the Morgan Stanley Capital International Europe,Australasia, Far East Index (the “Index”) on that date.All dividends and capital gain distributions are reinvested. The fund’s performance shown in the line graph above takes into account the maximum initial sales charge on Class A shares and all other applicable fees and expenses on all classes.The Index is an unmanaged index composed of a sample of companies representative of the market structure of European and Pacific Basin countries. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors can not invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

| | | | | | | |

| Average Annual Total Returns as of 8/31/12 | | | | | | |

| |

| Inception |

| | Date | 1 | Year | 5 Years | | 10 Years | |

| Class A shares | | | | | | | |

| with maximum sales charge (5.75%) | 9/29/95 | –11.29 | % | –7.54 | % | 3.78 | % |

| without sales charge | 9/29/95 | –5.89 | % | –6.44 | % | 4.40 | % |

| Class C shares | | | | | | | |

| with applicable redemption charge † | 11/15/02 | –7.47 | % | –7.17 | % | 3.64 | %†† |

| without redemption | 11/15/02 | –6.55 | % | –7.17 | % | 3.64 | %†† |

| Class I shares | 11/15/02 | –5.41 | % | –6.00 | % | 4.81 | %†† |

| Morgan Stanley Capital | | | | | | | |

| International Europe, | | | | | | | |

| Australasia, Far East Index | | –0.04 | % | –4.81 | % | 6.67 | % |

Past performance is not predictive of future performance.The fund’s performance shown in the graph and table does not

reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

† The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the

date of purchase.

The total return performance figures presented for Class C shares of the fund reflect the performance of the fund’s

Class A shares for the period prior to 11/15/02 (the inception date for Class C shares), adjusted to reflect the

applicable sales load for this share class.

The total return performance figures presented for Class I shares of the fund reflect the performance of the fund’s Class

A shares for the period prior to 11/15/02 (the inception date for Class I shares).

The Fund 7

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus International Value Fund from March 1, 2012 to August 31, 2012. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment

assuming actual returns for the six months ended August 31, 2012

| | | | | | |

| | | Class A | | Class C | | Class I |

| Expenses paid per $1,000† | | $7.46 | | $11.08 | | $5.33 |

| Ending value (after expenses) | | $927.80 | | $924.20 | | $929.40 |

COMPARING YOUR FUND’S EXPENSES WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment

assuming a hypothetical 5% annualized return for the six months ended August 31, 2012

| | | | | | |

| | | Class A | | Class C | | Class I |

| Expenses paid per $1,000† | | $7.81 | | $11.59 | | $5.58 |

| Ending value (after expenses) | | $1,017.39 | | $1,013.62 | | $1,019.61 |

† Expenses are equal to the fund’s annualized expense ratio of 1.54% for Class A, 2.29% for Class C and 1.10%

for Class I, multiplied by the average account value over the period, multiplied by 184/366 (to reflect the one-half

year period).

8

STATEMENT OF INVESTMENTS

August 31, 2012

| | | |

| Common Stocks—96.2% | Shares | | Value ($) |

| Australia—3.2% | | | |

| Australia & New Zealand Banking Group | 63,730 | | 1,634,221 |

| Nufarm | 100,026 | | 604,552 |

| Primary Health Care | 349,673 | | 1,347,522 |

| QBE Insurance Group | 128,340 | | 1,727,712 |

| | | | 5,314,007 |

| Belgium—1.1% | | | |

| Delhaize Group | 45,580 | | 1,806,482 |

| Brazil—1.9% | | | |

| Banco Santander Brasil, ADS | 153,900 | | 1,166,562 |

| Oi, ADR | 135,510 | | 504,097 |

| Oi, ADR, Cl. C | 6,491 | | 28,755 |

| Petroleo Brasileiro, ADR | 66,140 | | 1,398,200 |

| | | | 3,097,614 |

| China—2.2% | | | |

| Beijing Capital International Airport, Cl. H | 410,000 | | 280,172 |

| China Railway Group, Cl. H | 987,000 | | 371,591 |

| Foxconn International Holdings | 1,615,000 | a | 508,074 |

| Guangzhou Automobile Group, Cl. H | 1,412,194 | | 985,046 |

| Huaneng Power International, Cl. H | 862,000 | | 594,602 |

| PetroChina, ADR | 7,451 | | 896,355 |

| | | | 3,635,840 |

| France—12.4% | | | |

| Alstom | 33,810 | | 1,203,916 |

| Carrefour | 134,672 | | 2,822,888 |

| Cie de St-Gobain | 40,530 | | 1,390,440 |

| Danone | 19,600 | | 1,221,549 |

| EDF | 49,680 | | 1,011,671 |

| France Telecom | 171,875 | | 2,376,944 |

| GDF Suez | 69,823 | | 1,719,140 |

| Sanofi | 38,411 | | 3,142,780 |

| Societe Generale | 45,374 | a | 1,201,352 |

| Total | 83,820 | | 4,186,045 |

| | | | 20,276,725 |

The Fund 9

STATEMENT OF INVESTMENTS (continued)

| | | |

| Common Stocks (continued) | Shares | | Value ($) |

| Germany—10.1% | | | |

| Aixtron | 65,690 | | 972,494 |

| Allianz | 11,810 | | 1,296,361 |

| Bayer | 13,340 | | 1,034,763 |

| Celesio | 66,340 | | 1,212,834 |

| Daimler | 37,606 | | 1,844,730 |

| Deutsche Bank | 59,920 | | 2,131,010 |

| Deutsche Telekom | 98,900 | | 1,179,899 |

| E.ON | 131,030 | | 3,013,538 |

| Muenchener Rueckversicherungs | 8,010 | | 1,185,823 |

| Siemens | 29,230 | | 2,772,850 |

| | | | 16,644,302 |

| Hong Kong—2.7% | | | |

| China Mobile, ADR | 6,410 | | 344,153 |

| Esprit Holdings | 1,107,070 | | 1,692,875 |

| Hang Seng Bank | 129,700 | | 1,846,180 |

| Pacific Basin Shipping | 1,315,000 | | 547,638 |

| | | | 4,430,846 |

| India—.6% | | | |

| Reliance Industries, GDR | 36,974 | b | 1,011,239 |

| Israel—1.5% | | | |

| Teva Pharmaceutical Industries, ADR | 63,230 | | 2,502,643 |

| Italy—2.0% | | | |

| Eni | 27,045 | | 599,382 |

| Finmeccanica | 161,006 | a | 714,466 |

| Saras | 1,816,710 | a | 1,966,290 |

| | | | 3,280,138 |

| Japan—22.7% | | | |

| Denso | 39,300 | | 1,310,084 |

| East Japan Railway | 15,600 | | 1,044,051 |

| Fujitsu | 374,000 | | 1,519,024 |

| INPEX | 314 | | 1,784,661 |

| Kao | 57,000 | | 1,721,029 |

| Kirin Holdings | 129,000 | | 1,606,424 |

| LIXIL Group | 52,300 | | 1,122,885 |

| Matsumotokiyoshi Holdings | 30,900 | | 740,779 |

| Mitsubishi UFJ Financial Group | 722,500 | | 3,285,140 |

10

| | | |

| Common Stocks (continued) | Shares | | Value ($) |

| Japan (continued) | | | |

| Nippon Electric Glass | 195,000 | | 926,496 |

| Nippon Express | 149,000 | | 584,239 |

| Nomura Holdings | 147,900 | | 487,364 |

| Nomura Research Institute | 46,400 | | 968,951 |

| Omron | 79,100 | | 1,543,710 |

| Panasonic | 60,400 | | 410,407 |

| Ricoh | 164,800 | | 1,296,594 |

| Shimachu | 71,700 | | 1,482,627 |

| Shin-Etsu Chemical | 52,220 | | 2,791,247 |

| Sumitomo Mitsui Financial Group | 65,500 | | 2,027,869 |

| Sumitomo Mitsui Trust Holdings | 369,560 | | 1,028,981 |

| Taiyo Nippon Sanso | 315,000 | | 1,569,066 |

| Tokyo Electron | 25,000 | | 1,173,447 |

| Tokyo Steel Manufacturing | 65,300 | | 212,676 |

| Toyota Motor | 107,800 | | 4,261,332 |

| Yamaha Motor | 155,300 | | 1,344,829 |

| Yamato Holdings | 63,400 | | 1,052,685 |

| | | | 37,296,597 |

| Netherlands—2.6% | | | |

| Aegon | 172,661 | | 886,716 |

| Koninklijke Philips Electronics | 111,861 | | 2,571,970 |

| Royal Dutch Shell, Cl. A | 23,712 | | 829,431 |

| | | | 4,288,117 |

| Norway—.6% | | | |

| Norsk Hydro | 216,268 | | 926,594 |

| Russia—.4% | | | |

| Gazprom, ADR | 60,140 | | 581,253 |

| Singapore—2.0% | | | |

| DBS Group Holdings | 114,539 | | 1,327,789 |

| Oversea-Chinese Banking | 260,000 | | 1,937,746 |

| | | | 3,265,535 |

| South Africa—.7% | | | |

| Murray & Roberts Holdings | 230,503 | a | 598,271 |

| Standard Bank Group | 37,590 | | 496,548 |

| | | | 1,094,819 |

The Fund 11

STATEMENT OF INVESTMENTS (continued)

| | | |

| Common Stocks (continued) | Shares | | Value ($) |

| South Korea—2.4% | | | |

| KB Financial Group | 6,100 | | 197,576 |

| KB Financial Group, ADR | 34,794 | | 1,125,934 |

| Korea Electric Power | 22,070 | a | 478,503 |

| Korea Electric Power, ADR | 65,394 | a | 700,370 |

| Korea Exchange Bank | 86,880 | a | 654,687 |

| KT, ADR | 14,300 | | 216,073 |

| SK Telecom, ADR | 35,330 | | 506,632 |

| | | | 3,879,775 |

| Sweden—3.5% | | | |

| Ericsson, Cl. B | 291,400 | | 2,728,217 |

| Husqvarna, Cl. B | 44,260 | | 212,204 |

| Investor, Cl. B | 26,950 | | 558,355 |

| Svenska Cellulosa, Cl. B | 120,940 | | 2,162,317 |

| | | | 5,661,093 |

| Switzerland—7.4% | | | |

| Adecco | 21,190 | a | 961,063 |

| Clariant | 113,410 | a | 1,272,254 |

| Novartis | 70,026 | | 4,125,864 |

| Roche Holding | 19,760 | | 3,597,243 |

| UBS | 189,628 | a | 2,121,323 |

| | | | 12,077,747 |

| Taiwan—.9% | | | |

| Hon Hai Precision Industry | 279,400 | | 791,063 |

| United Microelectronics | 1,868,720 | | 748,711 |

| | | | 1,539,774 |

| United Kingdom—15.3% | | | |

| Anglo American | 113,648 | | 3,157,992 |

| BP | 352,903 | | 2,473,145 |

| Home Retail Group | 536,056 | | 798,832 |

| HSBC Holdings | 651,257 | | 5,657,574 |

| Reed Elsevier | 111,551 | | 1,045,935 |

| Resolution | 553,287 | | 1,895,890 |

| Royal Dutch Shell, Cl. A | 100,718 | | 3,524,762 |

| Smith & Nephew | 172,857 | | 1,830,728 |

12

| | | | |

| Common Stocks (continued) | Shares | | Value ($) | |

| United Kingdom (continued) | | | | |

| Tesco | 165,435 | | 884,204 | |

| Unilever | 53,166 | | 1,911,268 | |

| Vodafone Group | 673,252 | | 1,940,285 | |

| | | | 25,120,615 | |

| Total Common Stocks | | | | |

| (cost $203,652,220) | | | 157,731,755 | |

| |

| Other Investment—6.9% | | | | |

| Registered Investment Company; | | | | |

| Dreyfus Institutional Preferred | | | | |

| Plus Money Market Fund | | | | |

| (cost $11,340,000) | 11,340,000 | c | 11,340,000 | |

| |

| Total Investments (cost $214,992,220) | 103.1 | % | 169,071,755 | |

| Liabilities, Less Cash and Receivables | (3.1 | %) | (5,030,705 | ) |

| Net Assets | 100.0 | % | 164,041,050 | |

ADR—American Depository Receipts

ADS—American Depository Shares

GDR—Global Depository Receipts

a Non-income producing security.

b Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933.This security may be

resold in transactions exempt from registration, normally to qualified institutional buyers.At August 31, 2012, this

security amounted to $1,011,239 or .6% of net assets.

c Investment in affiliated money market mutual fund.

| | | |

| Portfolio Summary (Unaudited)† | | |

| |

| | Value (%) | | Value (%) |

| Financial | 21.9 | Consumer Staples | 7.8 |

| Energy | 11.7 | Materials | 7.7 |

| Health Care | 11.5 | Money Market Investment | 6.9 |

| Consumer Discretionary | 9.4 | Utilities | 4.6 |

| Industrial | 9.3 | Telecommunication Services | 4.3 |

| Information Technology | 8.0 | | 103.1 |

| |

| † Based on net assets. | | | |

| See notes to financial statements. | | | |

The Fund 13

STATEMENT OF ASSETS AND LIABILITIES

August 31, 2012

| | | | |

| | | Cost | Value | |

| Assets ($): | | | | |

| Investments in securities—See Statement of Investments: | | | |

| Unaffiliated issuers | | 203,652,220 | 157,731,755 | |

| Affiliated issuers | | 11,340,000 | 11,340,000 | |

| Cash | | | 26,006 | |

| Cash denominated in foreign currencies | | 850,996 | 847,691 | |

| Receivable for investment securities sold | | | 683,064 | |

| Dividends receivable | | | 611,683 | |

| Receivable for shares of Common Stock subscribed | | | 59,816 | |

| Unrealized appreciation on forward foreign | | | | |

| currency exchange contracts—Note 4 | | | 2 | |

| Prepaid expenses | | | 22,082 | |

| | | | 171,322,099 | |

| Liabilities ($): | | | | |

| Due to The Dreyfus Corporation and affiliates—Note 3(c) | | 184,176 | |

| Payable for investment securities purchased | | | 6,603,804 | |

| Payable for shares of Common Stock redeemed | | | 395,815 | |

| Unrealized depreciation on forward foreign | | | | |

| currency exchange contracts—Note 4 | | | 1,965 | |

| Accrued expenses | | | 95,289 | |

| | | | 7,281,049 | |

| Net Assets ($) | | | 164,041,050 | |

| Composition of Net Assets ($): | | | | |

| Paid-in capital | | | 301,911,588 | |

| Accumulated undistributed investment income—net | | | 3,417,397 | |

| Accumulated net realized gain (loss) on investments | | | (95,332,171 | ) |

| Accumulated net unrealized appreciation (depreciation) | | | |

| on investments and foreign currency transactions | | | (45,955,764 | ) |

| Net Assets ($) | | | 164,041,050 | |

| |

| |

| Net Asset Value Per Share | | | | |

| | Class A | Class C | Class I | |

| Net Assets ($) | 93,078,260 | 7,998,128 | 62,964,662 | |

| Shares Outstanding | 9,535,075 | 829,618 | 6,463,591 | |

| Net Asset Value Per Share ($) | 9.76 | 9.64 | 9.74 | |

| |

| See notes to financial statements. | | | | |

14

| | |

| STATEMENT OF OPERATIONS | | |

| Year Ended August 31, 2012 | | |

| |

| |

| |

| |

| Investment Income ($): | | |

| Income: | | |

| Cash dividends (net of $573,796 foreign taxes withheld at source): | | |

| Unaffiliated issuers | 5,908,875 | |

| Affiliated issuers | 2,111 | |

| Total Income | 5,910,986 | |

| Expenses: | | |

| Management fee—Note 3(a) | 1,781,710 | |

| Shareholder servicing costs—Note 3(c) | 468,642 | |

| Custodian fees—Note 3(c) | 98,587 | |

| Distribution fees—Note 3(b) | 71,862 | |

| Professional fees | 70,900 | |

| Registration fees | 46,490 | |

| Prospectus and shareholders’ reports | 42,497 | |

| Directors’ fees and expenses—Note 3(d) | 10,524 | |

| Interest expense—Note 2 | 2,841 | |

| Loan commitment fees—Note 2 | 1,601 | |

| Miscellaneous | 33,263 | |

| Total Expenses | 2,628,917 | |

| Less—reduction in expenses due to undertaking—Note 3(a) | (178,171 | ) |

| Less—reduction in fees due to earnings credits—Note 3 (c) | (112 | ) |

| Net Expenses | 2,450,634 | |

| Investment Income—Net | 3,460,352 | |

| Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): | | |

| Net realized gain (loss) on investments and foreign currency transactions | (24,355,231 | ) |

| Net realized gain (loss) on forward foreign currency exchange contracts | (70,921 | ) |

| Net Realized Gain (Loss) | (24,426,152 | ) |

| Net unrealized appreciation (depreciation) on | | |

| investments and foreign currency transactions | 5,564,286 | |

| Net unrealized appreciation (depreciation) on | | |

| forward foreign currency exchange contracts | (1,342 | ) |

| Net Unrealized Appreciation (Depreciation) | 5,562,944 | |

| Net Realized and Unrealized Gain (Loss) on Investments | (18,863,208 | ) |

| Net (Decrease) in Net Assets Resulting from Operations | (15,402,856 | ) |

| |

| See notes to financial statements. | | |

The Fund 15

STATEMENT OF CHANGES IN NET ASSETS

| | | | |

| | Year Ended August 31, | |

| | 2012 | a | 2011 | |

| Operations ($): | | | | |

| Investment income—net | 3,460,352 | | 5,000,966 | |

| Net realized gain (loss) on investments | (24,426,152 | ) | 24,302,402 | |

| Net unrealized appreciation | | | | |

| (depreciation) on investments | 5,562,944 | | (17,601,048 | ) |

| Net Increase (Decrease) in Net Assets | | | | |

| Resulting from Operations | (15,402,856 | ) | 11,702,320 | |

| Dividends to Shareholders from ($): | | | | |

| Investment income—net: | | | | |

| Class A Shares | (2,772,443 | ) | (1,435,975 | ) |

| Class C Shares | (186,447 | ) | (49,595 | ) |

| Class I Shares | (2,975,318 | ) | (1,769,232 | ) |

| Total Dividends | (5,934,208 | ) | (3,254,802 | ) |

| Capital Stock Transactions ($): | | | | |

| Net proceeds from shares sold: | | | | |

| Class A Shares | 20,878,977 | | 16,430,509 | |

| Class B Shares | 13,986 | | 66,687 | |

| Class C Shares | 255,905 | | 421,682 | |

| Class I Shares | 16,118,621 | | 50,489,524 | |

| Dividends reinvested: | | | | |

| Class A Shares | 2,666,058 | | 1,362,852 | |

| Class C Shares | 98,544 | | 24,457 | |

| Class I Shares | 2,622,324 | | 1,536,803 | |

| Cost of shares redeemed: | | | | |

| Class A Shares | (23,471,434 | ) | (32,734,376 | ) |

| Class B Shares | (476,981 | ) | (2,141,296 | ) |

| Class C Shares | (2,885,040 | ) | (4,311,644 | ) |

| Class I Shares | (37,097,091 | ) | (59,952,698 | ) |

| Increase (Decrease) in Net Assets | | | | |

| from Capital Stock Transactions | (21,276,131 | ) | (28,807,500 | ) |

| Total Increase (Decrease) in Net Assets | (42,613,195 | ) | (20,359,982 | ) |

| Net Assets ($): | | | | |

| Beginning of Period | 206,654,245 | | 227,014,227 | |

| End of Period | 164,041,050 | | 206,654,245 | |

| Undistributed investment income—net | 3,417,397 | | 5,768,709 | |

16

| | | | |

| | Year Ended August 31, | |

| | 2012 | a | 2011 | |

| Capital Share Transactions: | | | | |

| Class Ab | | | | |

| Shares sold | 2,047,935 | | 1,392,368 | |

| Shares issued for dividends reinvested | 274,286 | | 119,339 | |

| Shares redeemed | (2,387,133 | ) | (2,777,334 | ) |

| Net Increase (Decrease) in Shares Outstanding | (64,912 | ) | (1,265,627 | ) |

| Class Bb | | | | |

| Shares sold | 1,369 | | 5,686 | |

| Shares redeemed | (46,819 | ) | (182,585 | ) |

| Net Increase (Decrease) in Shares Outstanding | (45,450 | ) | (176,899 | ) |

| Class C | | | | |

| Shares sold | 18,196 | | 35,827 | |

| Shares issued for dividends reinvested | 10,212 | | 2,166 | |

| Shares redeemed | (299,702 | ) | (369,728 | ) |

| Net Increase (Decrease) in Shares Outstanding | (271,294 | ) | (331,735 | ) |

| Class I | | | | |

| Shares sold | 1,535,195 | | 4,200,758 | |

| Shares issued for dividends reinvested | 271,462 | | 135,164 | |

| Shares redeemed | (3,962,000 | ) | (5,117,980 | ) |

| Net Increase (Decrease) in Shares Outstanding | (2,155,343 | ) | (782,058 | ) |

a Effective as of the close of business on March 13, 2012, the fund no longer offers Class B shares.

b During the period ended August 31, 2012, 27,053 Class B shares representing $272,804 were automatically

converted to 26,973 Class A shares and during the period ended August 31, 2011, 74,673 Class B shares

representing $882,387 were automatically converted to 73,675 Class A shares.

See notes to financial statements.

The Fund 17

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated.All information (except portfolio turnover rate) reflects financial results for a single fund share.Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| | | | | | | | | | |

| | | | Year Ended August 31, | | | |

| Class A Shares | 2012 | | 2011 | | 2010 | | 2009 | | 2008 | |

| Per Share Data ($): | | | | | | | | | | |

| Net asset value, beginning of period | 10.69 | | 10.37 | | 11.02 | | 12.30 | | 20.21 | |

| Investment Operations: | | | | | | | | | | |

| Investment income—neta | .17 | | .20 | | .15 | | .15 | | .27 | |

| Net realized and unrealized | | | | | | | | | | |

| gain (loss) on investments | (.80 | ) | .26 | | (.65 | ) | (1.01 | ) | (2.93 | ) |

| Total from Investment Operations | (.63 | ) | .46 | | (.50 | ) | (.86 | ) | (2.66 | ) |

| Distributions: | | | | | | | | | | |

| Dividends from investment income—net | (.30 | ) | (.14 | ) | (.15 | ) | (.42 | ) | (.32 | ) |

| Dividends from net realized | | | | | | | | | | |

| gain on investments | — | | — | | — | | — | | (4.93 | ) |

| Total Distributions | (.30 | ) | (.14 | ) | (.15 | ) | (.42 | ) | (5.25 | ) |

| Net asset value, end of period | 9.76 | | 10.69 | | 10.37 | | 11.02 | | 12.30 | |

| Total Return (%)b | (5.89 | ) | 4.32 | | (4.66 | ) | (5.97 | ) | (18.56 | ) |

| Ratios/Supplemental Data (%): | | | | | | | | | | |

| Ratio of total expenses | | | | | | | | | | |

| to average net assets | 1.63 | | 1.54 | | 1.54 | | 1.84 | | 1.57 | |

| Ratio of net expenses | | | | | | | | | | |

| to average net assets | 1.53 | | 1.49 | | 1.54 | | 1.84 | | 1.56 | |

| Ratio of net investment income | | | | | | | | | | |

| to average net assets | 1.74 | | 1.70 | | 1.29 | | 1.66 | | 1.71 | |

| Portfolio Turnover Rate | 40.93 | | 60.72 | | 55.35 | | 69.63 | | 46.96 | |

| Net Assets, end of period ($ x 1,000) | 93,078 | | 102,606 | | 112,716 | | 159,260 | | 228,308 | |

a Based on average shares outstanding at each month end.

b Exclusive of sales charge.

See notes to financial statements.

18

| | | | | | | | | | |

| | | | Year Ended August 31, | | | |

| Class C Shares | 2012 | | 2011 | | 2010 | | 2009 | | 2008 | |

| Per Share Data ($): | | | | | | | | | | |

| Net asset value, beginning of period | 10.51 | | 10.19 | | 10.84 | | 11.98 | | 19.79 | |

| Investment Operations: | | | | | | | | | | |

| Investment income—neta | .10 | | .11 | | .06 | | .08 | | .14 | |

| Net realized and unrealized | | | | | | | | | | |

| gain (loss) on investments | (.79 | ) | .25 | | (.65 | ) | (.96 | ) | (2.85 | ) |

| Total from Investment Operations | (.69 | ) | .36 | | (.59 | ) | (.88 | ) | (2.71 | ) |

| Distributions: | | | | | | | | | | |

| Dividends from investment income—net | (.18 | ) | (.04 | ) | (.06 | ) | (.26 | ) | (.17 | ) |

| Dividends from net realized | | | | | | | | | | |

| gain on investments | — | | — | | — | | — | | (4.93 | ) |

| Total Distributions | (.18 | ) | (.04 | ) | (.06 | ) | (.26 | ) | (5.10 | ) |

| Net asset value, end of period | 9.64 | | 10.51 | | 10.19 | | 10.84 | | 11.98 | |

| Total Return (%)b | (6.55 | ) | 3.48 | | (5.49 | ) | (6.71 | ) | (19.16 | ) |

| Ratios/Supplemental Data (%): | | | | | | | | | | |

| Ratio of total expenses | | | | | | | | | | |

| to average net assets | 2.38 | | 2.31 | | 2.33 | | 2.63 | | 2.32 | |

| Ratio of net expenses | | | | | | | | | | |

| to average net assets | 2.28 | | 2.26 | | 2.33 | | 2.63 | | 2.32 | |

| Ratio of net investment income | | | | | | | | | | |

| to average net assets | .99 | | .91 | | .56 | | .87 | | .91 | |

| Portfolio Turnover Rate | 40.93 | | 60.72 | | 55.35 | | 69.63 | | 46.96 | |

| Net Assets, end of period ($ x 1,000) | 7,998 | | 11,573 | | 14,604 | | 18,607 | | 30,965 | |

a Based on average shares outstanding at each month end.

b Exclusive of sales charge.

See notes to financial statements.

The Fund 19

FINANCIAL HIGHLIGHTS (continued)

| | | | | | | | | | |

| | | | Year Ended August 31, | | | |

| Class I Shares | 2012 | | 2011 | | 2010 | | 2009 | | 2008 | |

| Per Share Data ($): | | | | | | | | | | |

| Net asset value, beginning of period | 10.67 | | 10.36 | | 11.02 | | 12.31 | | 20.27 | |

| Investment Operations: | | | | | | | | | | |

| Investment income—neta | .23 | | .28 | | .22 | | .19 | | .34 | |

| Net realized and unrealized | | | | | | | | | | |

| gain (loss) on investments | (.81 | ) | .22 | | (.68 | ) | (.98 | ) | (2.93 | ) |

| Total from Investment Operations | (.58 | ) | .50 | | (.46 | ) | (.79 | ) | (2.59 | ) |

| Distributions: | | | | | | | | | | |

| Dividends from investment income—net | (.35 | ) | (.19 | ) | (.20 | ) | (.50 | ) | (.44 | ) |

| Dividends from net realized | | | | | | | | | | |

| gain on investments | — | | — | | — | | — | | (4.93 | ) |

| Total Distributions | (.35 | ) | (.19 | ) | (.20 | ) | (.50 | ) | (5.37 | ) |

| Net asset value, end of period | 9.74 | | 10.67 | | 10.36 | | 11.02 | | 12.31 | |

| Total Return (%) | (5.41 | ) | 4.67 | | (4.37 | ) | (5.21 | ) | (18.25 | ) |

| Ratios/Supplemental Data (%): | | | | | | | | | | |

| Ratio of total expenses | | | | | | | | | | |

| to average net assets | 1.19 | | 1.15 | | 1.22 | | 1.37 | | 1.21 | |

| Ratio of net expenses | | | | | | | | | | |

| to average net assets | 1.09 | | 1.09 | | 1.22 | | 1.36 | | 1.20 | |

| Ratio of net investment income | | | | | | | | | | |

| to average net assets | 2.29 | | 2.29 | | 1.93 | | 2.09 | | 2.16 | |

| Portfolio Turnover Rate | 40.93 | | 60.72 | | 55.35 | | 69.63 | | 46.96 | |

| Net Assets, end of period ($ x 1,000) | 62,965 | | 91,998 | | 97,429 | | 41,460 | | 42,444 | |

| |

| a Based on average shares outstanding at each month end. | | | | | | | | | |

| See notes to financial statements. | | | | | | | | | | |

20

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus International Value Fund (the “fund”) is a separate diversified series of Advantage Funds, Inc. (the “Company”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company and operates as a series company offering thirteen series, including the fund.The fund’s investment objective is to seek long-term capital growth.The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser.

MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares. The fund is authorized to issue 500 million shares of $.001 par value Common Stock.The fund currently offers three classes of shares: Class A (300 million shares authorized), Class C (100 million shares authorized) and Class I (100 million shares authorized). Class A shares are subject to a sales charge imposed at the time of purchase. Class C shares are subject to a contingent deferred sales charge (“CDSC”) imposed on Class C shares redeemed within one year of purchase. Class I shares are sold at net asset value per share only to institutional investors. The Company’s Board of Directors approved, effective as of the close of business on March 13, 2012, the transfer of shares authorized from Class B to Class A shares. Class B shares were subject to a CDSC imposed on Class B share redemptions made within six years of purchase and automatically converted to Class A shares after six years.The fund no longer offers Class B shares. Effective March 13, 2012, all outstanding Class B shares were automatically converted to Class A shares. Other differences between the classes include the services offered to and the expenses borne by each class, the allocation of certain transfer agency costs and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

The Fund 21

NOTES TO FINANCIAL STATEMENTS (continued)

The Company accounts separately for the assets, liabilities and operations of each series. Expenses directly attributable to each series are charged to that series’ operations; expenses which are applicable to all series are allocated among them on a pro rata basis.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions.Actual results could differ from those estimates.

The Company enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown.The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value.This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

22

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements.These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. Valuation techniques used to value the fund’s investments are as follows:

Investments in securities are valued at the last sales price on the securities exchange or national securities market on which such securities are primarily traded. Securities listed on the National Market System for which market quotations are available are valued at the official closing price or, if there is no official closing price that day, at the last sales price. Securities not listed on an exchange or the national securities market, or securities for which there were no transactions, are valued at the average of the most recent bid and asked prices, except for open short positions, where the asked price is used for valuation purposes. Bid price is used when no asked price is available. Registered investment companies that are not traded on an exchange are valued at their net asset value.All of the preceding securities are categorized within Level 1 of the fair value hierarchy.

The Fund 23

NOTES TO FINANCIAL STATEMENTS (continued)

Fair valuing of securities may be determined with the assistance of a pricing service using calculations based on indices of domestic securities and other appropriate indicators, such as prices of relevant ADRs and financial futures. Utilizing these techniques may result in transfers between Level 1 and Level 2 of the fair value hierarchy.

When market quotations or official closing prices are not readily available, or are determined not to reflect accurately fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded (for example, a foreign exchange or market), but before the fund calculates its net asset value, the fund may value these investments at fair value as determined in accordance with the procedures approved by the Company’s Board of Directors. Certain factors may be considered when fair valuing investments such as: fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold, and public trading in similar securities of the issuer or comparable issuers.These securities are either categorized as Level 2 or 3 depending on the relevant inputs used.

For restricted securities where observable inputs are limited, assumptions about market activity and risk are used and are categorized within Level 3 of the fair value hierarchy.

Investments denominated in foreign currencies are translated to U.S. dollars at the prevailing rates of exchange.

Forward foreign currency exchange contracts (“forward contracts”) are valued at the forward rate. These securities are generally categorized within Level 2 of the fair value hierarchy.

24

The following is a summary of the inputs used as of August 31, 2012 in valuing the fund’s investments:

| | | | | | |

| | | Level 2—Other | | Level 3— | | |

| | Level 1— | Significant | | Significant | | |

| | Unadjusted | Observable | | Unobservable | | |

| | Quoted Prices | Inputs | | Inputs | Total | |

| Assets ($) | | | | | | |

| Investments in Securities: | | | | | |

| Equity Securities— | | | | | | |

| Foreign† | 157,731,755 | — | | — | 157,731,755 | |

| Mutual Funds | 11,340,000 | — | | — | 11,340,000 | |

| Other Financial | | | | | | |

| Instruments: | | | | | | |

| Forward Foreign | | | | | | |

| Currency Exchange | | | | | | |

| Contracts†† | — | 2 | | — | 2 | |

| Liabilities ($) | | | | | | |

| Other Financial | | | | | | |

| Instruments: | | | | | | |

| Forward Foreign | | | | | | |

| Currency Exchange | | | | | | |

| Contracts†† | — | (1,965 | ) | — | (1,965 | ) |

† See Statement of Investments for additional detailed categorizations.

Amount shown represents unrealized appreciation (depreciation) at period end.

At August 31, 2012, there were no transfers between Level 1 and Level 2 of the fair value hierarchy.

(b) Foreign currency transactions: The fund does not isolate that portion of the results of operations resulting from changes in foreign exchange rates on investments from the fluctuations arising from changes in the market prices of securities held. Such fluctuations are included with the net realized and unrealized gain or loss on investments.

The Fund 25

NOTES TO FINANCIAL STATEMENTS (continued)

Net realized foreign exchange gains or losses arise from sales of foreign currencies, currency gains or losses realized on securities transactions between trade and settlement date, and the difference between the amounts of dividends, interest and foreign withholding taxes recorded on the fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in the value of assets and liabilities other than investments resulting from changes in exchange rates. Foreign currency gains and losses on investments are included with net realized and unrealized gain or loss on investments.

(c) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

(d) Risk: Investing in foreign markets may involve special risks and considerations not typically associated with investing in the U.S.These risks include revaluation of currencies, high rates of inflation, repatriation restrictions on income and capital, and adverse political and economic developments. Moreover, securities issued in these markets may be less liquid, subject to government ownership controls and delayed settlements, and their prices may be more volatile than those of comparable securities in the U.S.

(e) Affiliated issuers: Investments in other investment companies advised by Dreyfus are defined as “affiliated” in the Act. Investments in affiliated investment companies for the period ended August 31, 2012 were as follows:

| | | | | | |

| Affiliated | | | | | | |

| Investment | Value | | | | Value | Net |

| Company | 8/31/2011 | ($) | Purchases ($) | Sales($) | 8/31/2012 ($) | Assets (%) |

| Dreyfus | | | | | | |

| Institutional | | | | | | |

| Preferred | | | | | | |

| Plus Money | | | | | | |

| Market | | | | | | |

| Fund | 1,100,000 | | 55,125,000 | 44,885,000 | 11,340,000 | 6.9 |

26

(f) Dividends to shareholders: Dividends are recorded on the ex-dividend date. Dividends from investment income-net and dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”).To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

(g) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended August 31, 2012, the fund did not have any liabilities for any uncertain tax positions.The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period, the fund did not incur any interest or penalties.

Each of the tax years in the four-year period ended August 31, 2012 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At August 31, 2012, the components of accumulated earnings on a tax basis were as follows: undistributed ordinary income $3,473,906, accumulated capital losses $92,890,109 and unrealized depreciation $48,454,335.

Under the Regulated Investment Company Modernization Act of 2010 (the “2010 Act”), the fund is permitted to carry forward capital losses incurred in taxable years beginning after December 22, 2010 (“post-enactment losses”) for an unlimited period. Furthermore, post-enactment capital loss carryovers retain their character as either short-term or long-

The Fund 27

NOTES TO FINANCIAL STATEMENTS (continued)

term capital losses rather than short-term as they were under previous statute.The 2010 Act requires post-enactment losses to be utilized before the utilization of losses incurred in taxable years prior to the effective date of the 2010 Act (“pre-enactment losses”).As a result of this ordering rule, pre-enactment losses may be more likely to expire unused.

The accumulated capital loss carryover is available for federal income tax purposes to be applied against future net realized capital gains, if any, realized subsequent to August 31, 2012. If not applied, $24,770,979 of the carryover expires in fiscal year 2017 and $41,505,182 expires in fiscal year 2018.The fund has $3,162,451 of post-enactment short-term capital losses and $23,451,497 of post-enactment long-term capital losses that can be carried forward for an unlimited period.

The tax character of distributions paid to shareholders during the fiscal periods ended August 31, 2012 and August 31, 2011 were as follows: ordinary income $5,934,208 and $3,254,802, respectively.

During the period ended August 31, 2012, as a result of permanent book to tax differences, primarily due to the tax treatment for foreign exchange gains and losses and passive foreign investment companies, the fund increased accumulated undistributed investment income-net by $122,544 and decreased accumulated net realized gain (loss) on investments by the same amount. Net assets and net asset value per share were not affected by this reclassification.

(h) New Accounting Pronouncement: In December 2011, FASB issued Accounting Standards Update No. 2011-11 “Disclosures about Offsetting Assets and Liabilities” (“ASU 2011-11”). These disclosure requirements are intended to help investors and other financial statement users to better assess the effect or potential effect of offsetting arrangements on a company’s financial position.They also improve transparency in the reporting of how companies mitigate credit risk, including disclosure of related collateral pledged or received. In addition,ASU 2011-11 facilitates comparison between those entities that prepare their financial statements on the basis of GAAP and those entities that prepare their financial statements on the basis of International Financial Reporting

28

Standards (“IFRS”). ASU 2011-11 requires entities to: disclose both gross and net information about both instruments and transactions eligible for offset in the financial statements; and disclose instruments and transactions subject to an agreement similar to a master netting agreement. ASU 2011-11 is effective for fiscal years beginning on or after January 1, 2013, and interim periods within those annual periods. At this time, management is evaluating the implications of ASU 2011-11 and its impact on the funds’ financial statement disclosures.

NOTE 2—Bank Lines of Credit:

The fund participates with other Dreyfus-managed funds in a $225 million unsecured credit facility led by Citibank, N.A. and a $300 million unsecured credit facility provided by The Bank of NewYork Mellon, a subsidiary of BNY Mellon and an affiliate of Dreyfus (each, a“Facility”), each to be utilized primarily for temporary or emergency purposes, including the financing of redemptions. In connection therewith, the fund has agreed to pay its pro rata portion of commitment fees for each Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of borrowing.

The average amount of borrowings outstanding under the Facilities during the period ended August 31, 2012 was approximately $239,100, with a related weighted average annualized interest rate of 1.19%.

NOTE 3—Management Fee and Other Transactions with Affiliates:

(a) Pursuant to a management agreement with the Manager, the management fee is computed at the annual rate of 1% of the value of the fund’s average daily net assets and is payable monthly.

The Manager has agreed to waive receipt of a portion of the fund’s management fee, in the amount of .10% of the value of the fund’s average daily net assets, until March 31, 2013.The reduction in expenses, pursuant to the undertaking, amounted to $178,171 during the period ended August 31, 2012.

The Fund 29

NOTES TO FINANCIAL STATEMENTS (continued)

During the period ended August 31, 2012, the Distributor retained $1,829 from commissions earned on sales of the fund’s Class A shares, and $65 and $16 from CDSCs on redemptions of the fund’s Class B and Class C shares, respectively.

(b) Under the Distribution Plan adopted pursuant to Rule 12b-1 under the Act, Class B shares paid and Class C shares pay the Distributor for distributing their shares at an annual rate of .75% of the value of the average daily net assets of Class B and Class C shares. During the period ended August 31, 2012, Class B and Class C shares were charged $1,167 and $70,695, respectively, pursuant to the Distribution Plan.

(c) Under the Shareholder Services Plan, Class A and Class C shares pay and Class B shares paid the Distributor at an annual rate of .25% of the value of their average daily net assets for the provision of certain services. The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding the fund and providing reports and other information, and services related to the maintenance of shareholder accounts. The Distributor may make payments to Service Agents (securities dealers, financial institutions or other industry professionals) in respect of these services.The Distributor determines the amounts to be paid to Service Agents. During the period ended August 31, 2012, Class A, Class B and Class C shares were charged $221,513, $389 and $23,565, respectively, pursuant to the Shareholder Services Plan.

The fund has arrangements with the transfer agent and the custodian whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset transfer agency and custody fees. For financial reporting purposes, the fund includes net earnings credits as an expense offset in the Statement of Operations.

The fund compensates DreyfusTransfer, Inc. (“DTI”), a wholly-owned subsidiary of the Manager, under a transfer agency agreement for providing transfer agency services for the fund and, since May 29, 2012,

30

cash management services related to fund subscriptions and redemptions. During the period ended August 31, 2012, the fund was charged $29,956 for transfer agency services and $321 for cash management services. Cash management fees were partially offset by earnings credits of $38.These fees are included in Shareholder servicing costs in the Statement of Operations.

The fund compensatesThe Bank of NewYork Mellon under a custody agreement for providing custodial services for the fund. During the period ended August 31, 2012, the fund was charged $98,587 pursuant to the custody agreement.

Prior to May 29, 2012, the fund compensated The Bank of New York Mellon under a cash management agreement for performing cash management services related to fund subscriptions and redemptions. During the period ended August 31, 2012, the fund was charged $2,698 pursuant to the cash management agreement, which is included in Shareholder servicing costs in the Statement of Operations. These fees were partially offset by earnings credits of $74.

During the period ended August 31, 2012, the fund was charged $6,392 for services performed by the Chief Compliance Officer and his staff.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $132,304, Distribution Plan fees $5,172, Shareholder Services Plan fees $19,501, custodian fees $29,436, Chief Compliance Officer fees $4,243 and transfer agency per account fees $6,600, which are offset against an expense reimbursement currently in effect in the amount of $13,080.

(d) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

The Fund 31

NOTES TO FINANCIAL STATEMENTS (continued)

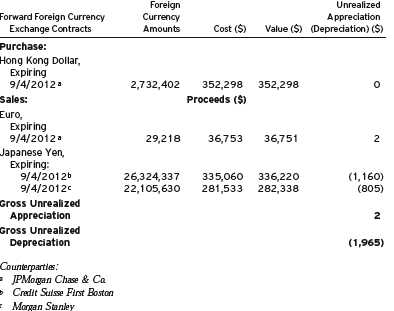

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales of investment securities, excluding short-term securities and forward contracts, during the period ended August 31, 2012 amounted to $72,354,691 and $98,884,959, respectively.

Derivatives: A derivative is a financial instrument whose performance is derived from the performance of another asset. Each type of derivative instrument that was held by the fund during the period ended August 31, 2012 is discussed below.

Forward Foreign Currency Exchange Contracts: The fund enters into forward contracts in order to hedge its exposure to changes in foreign currency exchange rates on its foreign portfolio holdings, to settle foreign currency transactions or as a part of its investment strategy.When executing forward contracts, the fund is obligated to buy or sell a foreign currency at a specified rate on a certain date in the future. With respect to sales of forward contracts, the fund incurs a loss if the value of the contract increases between the date the forward contract is opened and the date the forward contract is closed.The fund realizes a gain if the value of the contract decreases between those dates.With respect to purchases of forward contracts, the fund incurs a loss if the value of the contract decreases between the date the forward contract is opened and the date the forward contract is closed.The fund realizes a gain if the value of the contract increases between those dates. Any realized or unrealized gains or losses which occurred during the period are reflected in the Statement of Operations.The fund is exposed to foreign currency risk as a result of changes in value of underlying financial instruments. The fund is also exposed to credit risk associated with counterparty nonperformance on these forward contracts, which is typically limited

32

to the unrealized gain on each open contract.The following summarizes open forward contracts at August 31, 2012:

The following summarizes the average market value of derivatives outstanding during the period ended August 31, 2012:

| |

| | Average Market Value ($) |

| Forward contracts | 1,165,451 |

At August 31, 2012, the cost of investments for federal income tax purposes was $217,490,791; accordingly, accumulated net unrealized depreciation on investments was $48,419,036, consisting of $4,816,476 gross unrealized appreciation and $53,235,512 gross unrealized depreciation.

The Fund 33

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

Shareholders and Board of Directors

Dreyfus International Value Fund

We have audited the accompanying statement of assets and liabilities, including the statement of investments, of Dreyfus International Value Fund (one of the series comprising Advantage Funds, Inc.) as of August 31, 2012, and the related statement of operations for the year then ended, the statement of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement.We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of August 31, 2012 by correspondence with the custodian and others. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Dreyfus International Value Fund at August 31, 2012, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with U.S. generally accepted accounting principles.

New York, New York

October 29, 2012

34

IMPORTANT TAX INFORMATION (Unaudited)

In accordance with federal tax law, the fund elects to provide each shareholder with their portion of the fund’s foreign taxes paid and the income sourced from foreign countries. Accordingly, the fund hereby reports the following information regarding its fiscal year ended August 31, 2012:

—the total amount of taxes paid to foreign countries was $566,200

—the total amount of income sourced from foreign countries was $6,490,275.

Where required by federal tax law rules, shareholders will receive notification of their proportionate share of foreign taxes paid and foreign sourced income for the 2012 calendar year with Form 1099-DIV which will be mailed in early 2013.Also certain dividends paid by the fund may be subject to a maximum tax rate of 15%, as provided for by the Jobs and GrowthTax Relief Reconciliation Act of 2003. Of the distributions paid during the fiscal year, $5,934,208 represents the maximum amount that may be considered qualified dividend income.

The Fund 35

PROXY RESULTS (Unaudited)

The Company held a special meeting of shareholders on August 3, 2012.The proposal considered at the meeting, and the results, are as follows:

| | | |

| | | Shares | |

| | Votes For | | Authority Withheld |

| To elect additional Board Members: | | | |

| Lynn Martin† | 90,334,756 | | 3,252,629 |

| Robin A. Melvin† | 90,449,622 | | 3,137,763 |

| Philip L. Toia† | 90,229,928 | | 3,357,457 |

† Each new Board Member’s term commenced on September 1, 2012.

In addition Peggy C. Davis, Joseph S. DiMartino, David P. Feldman, Ehud Houminer and Dr. Martin Peretz continue

as Board Members of the Company.

36

INFORMATION ABOUT THE RENEWAL OF THE

FUND’S MANAGEMENT AGREEMENT (Unaudited)

At a meeting of the fund’s Board of Directors held on March 6, 2012, the Board considered the renewal of the fund’s Management Agreement pursuant to which Dreyfus provides the fund with investment advisory and administrative services (the “Agreement”). The Board members, none of whom are “interested persons” (as defined in the Investment Company Act of 1940, as amended) of the fund, were assisted in their review by independent legal counsel and met with counsel in executive session separate from Dreyfus representatives. In considering the renewal of the Agreement, the Board considered all factors that it believed to be relevant, including those discussed below.The Board did not identify any one factor as dispositive, and each Board member may have attributed different weights to the factors considered.

Analysis of Nature, Extent, and Quality of Services Provided to the Fund. The Board considered information previously provided to them in presentations from Dreyfus representatives regarding the nature, extent, and quality of the services provided to funds in the Dreyfus fund complex, and Dreyfus representatives confirmed that there had been no material changes in this information. Dreyfus provided the number of open accounts in the fund, the fund’s asset size and the allocation of fund assets among distribution channels. Dreyfus also had previously provided information regarding the diverse intermediary relationships and distribution channels of funds in the Dreyfus fund complex and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each distribution channel, including the distribution channel(s) for the fund.

The Board also considered research support available to, and portfolio management capabilities of, the fund’s portfolio management personnel and that Dreyfus also provides oversight of day-to-day fund operations, including fund accounting and administration and assistance in meeting legal and regulatory requirements.The Board also considered Dreyfus’

The Fund 37

INFORMATION ABOUT THE RENEWAL OF THE FUND’S

MANAGEMENT AGREEMENT (Unaudited) (continued)

extensive administrative, accounting, and compliance infrastructures.The Board also considered portfolio management’s brokerage policies and practices (including policies and practices regarding soft dollars) and the standards applied in seeking best execution.

Comparative Analysis of the Fund’s Performance and Management Fee and Expense Ratio. The Board reviewed reports prepared by Lipper, Inc. (“Lipper”), an independent provider of investment company data, which included information comparing (1) the fund’s performance with the performance of a group of comparable funds (the “Performance Group”) and with a broader group of funds (the “Performance Universe”), all for various periods ended December 31, 2011, and (2) the fund’s actual and contractual management fees and total expenses with those of a group of comparable funds (the “Expense Group”) and with a broader group of funds (the “Expense Universe”), the information for which was derived in part from fund financial statements available to Lipper as of the date of its analysis. Dreyfus previously had furnished the Board with a description of the methodology Lipper used to select the Performance Group and Performance Universe and the Expense Group and Expense Universe.

Dreyfus representatives stated that the usefulness of performance comparisons may be affected by a number of factors, including different investment limitations that may be applicable to the fund and comparison funds.They also noted that performance generally should be considered over longer periods of time, although it is possible that long-term performance can be adversely affected by even one period of significant underperformance so that a single investment decision or theme has the ability to affect disproportionately long-term performance. The Board discussed the results of the comparisons and noted that the fund’s total return performance was variously above and below the Performance Group and Performance Universe medians for the various

38

periods, and ranked in the fourth quartile of the Performance Group and Performance Universe for the three most recent periods ended December 31st. Dreyfus also provided a comparison of the fund’s calendar year total returns to the returns of the fund’s benchmark index. The Board indicated its expectation for improvements in the fund’s performance results in the future.

The Board also reviewed the range of actual and contractual management fees and total expenses of the Expense Group and Expense Universe funds and discussed the results of the comparisons.The Board noted that the fund’s contractual management fee was above the Expense Group median, and the fund’s actual management fee and total expenses were above the Expense Group and Expense Universe medians.

Dreyfus representatives noted that Dreyfus has agreed to waive receipt of a portion of the fund’s management fee in the amount of .10% of the value of the fund’s average daily net assets until September 30, 2012.

Dreyfus representatives reviewed with the Board the management or investment advisory fees (1) paid by funds advised or administered by Dreyfus that are in the same Lipper category as the fund and (2) paid to Dreyfus or the Dreyfus-affiliated primary employer of the fund’s primary portfolio manager(s) for advising any separate accounts and/or other types of client portfolios that are considered to have similar investment strategies and policies as the fund (the “Similar Clients”), and explained the nature of the Similar Clients.They discussed differences in fees paid and the relationship of the fees paid in light of any differences in the services provided and other relevant factors. The Board considered the relevance of the fee information provided for the Similar Clients to evaluate the appropriateness and reasonableness of the fund’s management fee.

The Fund 39

INFORMATION ABOUT THE RENEWAL OF THE FUND’S

MANAGEMENT AGREEMENT (Unaudited) (continued)

Analysis of Profitability and Economies of Scale. Dreyfus representatives reviewed the expenses allocated and profit received by Dreyfus and the resulting profitability percentage for managing the fund, and the method used to determine the expenses and profit. The Board concluded that the profitability results were not unreasonable, given the services rendered and service levels provided by Dreyfus. The Board previously had been provided with information prepared by an independent consulting firm regarding Dreyfus’ approach to allocating costs to, and determining the profitability of, individual funds and the entire Dreyfus fund complex. The consulting firm also had analyzed where any economies of scale might emerge in connection with the management of a fund.