As filed with the Securities and Exchange Commission on March 7, 2007

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-08200 |

BRIDGEWAY FUNDS, INC.

5615 Kirby Drive, Suite 518

Houston, Texas 77005-2448

Michael D. Mulcahy, President

Bridgeway Funds, Inc.

5615 Kirby Drive, Suite 518

Houston, Texas 77005-2448

Date of fiscal year end: June 30

Date of reporting period: July 1, 2006 - December 31, 2006

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

| ITEM 1. | REPORT TO STOCKHOLDERS |

A no-load mutual fund family of domestic funds

Semi-Annual Report

December 31, 2006 (Unaudited)

AGGRESSIVE INVESTORS 1

(Closed to New Investors)

AGGRESSIVE INVESTORS 2

ULTRA-SMALL COMPANY

(Closed)

ULTRA-SMALL COMPANY MARKET

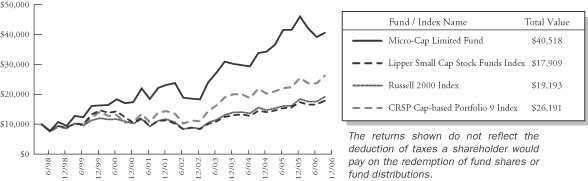

MICRO-CAP LIMITED

(Closed to New Investors)

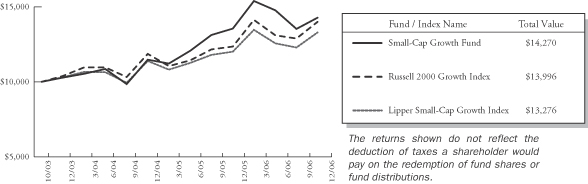

SMALL-CAP GROWTH

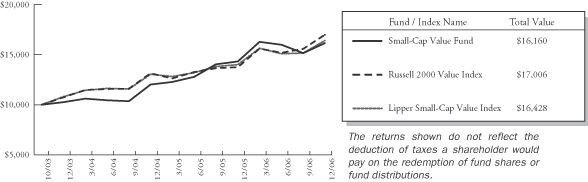

SMALL-CAP VALUE

LARGE-CAP GROWTH

LARGE-CAP VALUE

BLUE CHIP 35 INDEX

BALANCED

www.Bridgeway.com

| 1 | ||

AGGRESSIVE INVESTORS 1 | ||

| 8 | ||

| 14 | ||

AGGRESSIVE INVESTORS 2 | ||

| 16 | ||

| 22 | ||

ULTRA-SMALL COMPANY | ||

| 24 | ||

| 30 | ||

ULTRA-SMALL COMPANY MARKET | ||

| 32 | ||

| 36 | ||

MICRO-CAP LIMITED | ||

| 46 | ||

| 52 | ||

SMALL-CAP GROWTH | ||

| 54 | ||

| 60 | ||

SMALL-CAP VALUE | ||

| 62 | ||

| 68 | ||

LARGE-CAP GROWTH | ||

| 70 | ||

| 76 | ||

LARGE-CAP VALUE | ||

| 80 | ||

| 86 | ||

BLUE CHIP 35 INDEX | ||

| 88 | ||

| 92 | ||

BALANCED | ||

| 94 | ||

| 100 | ||

| 106 | ||

| 110 | ||

| 112 | ||

| 114 | ||

| 120 | ||

| 126 | ||

| 135 | ||

| 136 | ||

| 138 |

Bridgeway Funds Standardized Returns for One, Five and Ten Years and Inception to Date As of December 31, 2006*

| 1995 | 1996 | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | |||||||||||||

| Aggressive Investors 1 | 27.10% | 32.20% | 18.27% | 19.28% | 120.62% | 13.58% | -11.20% | -18.01% | 53.97% | 12.21% | 14.93% | 7.11% | ||||||||||||

| Aggressive Investors 2 | -19.02% | 44.01% | 16.23% | 18.59% | 5.43% | |||||||||||||||||||

| Ultra-Small Company | 39.84% | 29.74% | 37.99% | -13.11% | 40.41% | 4.75% | 34.00% | 3.98% | 88.57% | 23.33% | 2.99% | 21.55% | ||||||||||||

| Ultra-Small Company Market | -1.81% | 31.49% | 0.67% | 23.98% | 4.90% | 79.43% | 20.12% | 4.08% | 11.48% | |||||||||||||||

| Micro-Cap Limited | 49.55% | 6.02% | 30.20% | -16.61% | 66.97% | 9.46% | 22.55% | -2.34% | ||||||||||||||||

| Small-Cap Growth | 11.59% | 18.24% | 5.31% | |||||||||||||||||||||

| Small-Cap Value | 17.33% | 18.92% | 12.77% | |||||||||||||||||||||

| Large-Cap Growth | 6.77% | 9.33% | 4.99% | |||||||||||||||||||||

| Large-Cap Value | 15.15% | 11.62% | 18.52% | |||||||||||||||||||||

| Blue Chip 35 | 39.11% | 30.34% | -15.12% | -9.06% | -18.02% | 28.87% | 4.79% | 0.05% | 15.42% | |||||||||||||||

| Balanced | -3.51% | 17.82% | 7.61% | 6.96% | 6.65% |

| Fund | 1 Year | 5 Year | 10 Year | Inception to Date | Inception | |||||

| Aggressive Investors 1 | 7.11% | 11.76% | 18.53% | 20.40% | August 5, 1994 | |||||

| Aggressive Investors 2 | 5.43% | 11.13% | 11.61% | October 31, 2001 | ||||||

| Ultra-Small Company | 21.55% | 24.80% | 21.75% | 22.68% | August 5, 1994 | |||||

| Ultra-Small Company Market | 11.48% | 21.27% | 16.49% | July 31, 1997 | ||||||

| Micro-Cap Limited | -2.34% | 12.77% | 17.88% | June 30, 1998 | ||||||

| Small-Cap Growth | 5.31% | 11.88% | October 31, 2003 | |||||||

| Small-Cap Value | 12.77% | 16.36% | October 31, 2003 | |||||||

| Large-Cap Growth | 4.99% | 7.76% | October 31, 2003 | |||||||

| Large-Cap Value | 18.52% | 16.82% | October 31, 2003 | |||||||

| Blue Chip 35 Index | 15.42% | 5.03% | 6.37% | July 31, 1997 | ||||||

| Balanced | 6.65% | 6.89% | 5.80% | June 30, 2001 |

Performance figures quoted represent past performance and are no guarantee of future results. Current performance may be lower or higher than the performance figures quoted, and an investor’s shares, when redeemed, may be worth more or less than original cost. For the most recent month-end performance, please call 1-800-661-3550 or visit the Fund’s website at www.bridgeway.com.

*Numbers highlighted in green indicate periods when the Fund out performed its primary benchmark.

| i | www.Bridgeway.com |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM

January 31, 2007

Dear Fellow Shareholders,

The eleven Bridgeway Funds’ returns were mixed in the December quarter and calendar year 2006. Our best showing was from our “smallest fry” Ultra-Small Company Fund, which returned 12.19% in the quarter and 21.55% for the year. Very surprisingly, our worst performer was the Fund most similarly managed, Micro-Cap Limited Fund, demonstrating how different the returns of these two Funds can be in shorter time periods. Micro-Cap Limited Fund returned only 3.41% for the quarter and was our only Fund with a negative return for the calendar year, down 2.34%. (See the facing page for returns in the format required by the SEC.) Overall, this was a poor year for most of our quantitative models. As reflected in the returns to the left, we do not expect or even hope for market-beating returns every year, since our quantitative models are designed with longer-term performance in mind. Looking at the longer haul, eight of eleven Bridgeway Funds are beating their primary market benchmark since inception, and ten of eleven are beating their peer benchmarks since inception. While some may think we would be happy enough with this record, we never like lagging the market with any Fund since inception. Some “catch up” is in order with three of our younger Funds.

The recent market environment is most astonishing in what has not changed. In both the quarter and year, stocks of smaller size companies and more “value-oriented” ones (those which are priced cheaply based on some financial measures of worth) continue to lead the broader market. A turnaround toward larger and more growth-oriented stocks has been delayed another year, proving that even when things get “out of kilter” on a relative basis over a number of years, trends can always continue yet one more year. We present a brief discussion of the markets on page 2. Financial statements and notes begin on page 110.

In addition to performance, financial information, and market environment, we’d like to highlight several additional sections of this report. At Bridgeway, we like competition. In some prior years, in addition to market benchmarks, we’ve compared our performance to the recommended “picks” of a high profile rating agency. The analysis for 2006 is presented on page 3. Page 4 presents a discussion on “dollar weighted returns”, and what you can glean from this statistic.

As always, we appreciate your feedback. We take your comments seriously and discuss them regularly. Please keep your ideas coming—both favorable and critical. They are a vital tool in helping us serve you better.

Sincerely,

|  | |

| John Montgomery | Richard P. Cancelmo, Jr. | |

|  | |

Elena Khoziaeva | Michael A. Whipple | |

Your investment management team

| www.Bridgeway.com | 1 |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

Market Review

The Short Version: On the strength of the small company rally of the December quarter, 2006 was yet another year highly slanted toward small and value stocks. It might continue into 2007, but it’s gone on so long that the tide could shift quickly (in the direction of growth-oriented and large companies) when it does.

As you probably know, we don’t pay a lot of attention to market trends at Bridgeway. Our investment process looks the same in a bear or bull market, and we look at market trends primarily to explain what happened by way of looking in the rear view mirror.

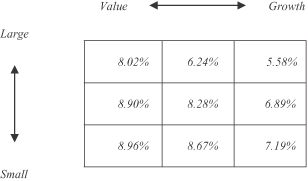

After last quarter’s both positive and negative results across the style box (various “niches” of the market), each corner of the stock market achieved a welcome positive return for the December quarter as follows from Morningstar data:

What is most remarkable about the last quarter and year is really what didn’t change. By many measures, 2006 was the eighth year in a row that the smallest companies, which we define as “ultra-small” or those in the smallest “decile” of the market, have outperformed the largest companies, those in the top “decile,” according to data from the Center for Research in Security Prices (“CRSP”). Through the middle part of the year, our large blue chip stocks (especially Blue Chip 35 Index Fund) made a great comeback, only to be somewhat left behind by year end. The longest “small cap run” in the 80-year history of the CRSP database thus continues. It won’t continue forever, but there’s never a guarantee it won’t last one more year.

Like small stocks, “value” stocks have also had a great run in recent years. In fact, if you compare larger growth-oriented stocks to small value-oriented ones, this is the seventh year that the latter have beaten the former. This factor has not been good for the more growth-oriented of our models, especially those of Aggressive Investors 1 and 2, and Large Cap Growth and Small Cap Growth. Similar to small stocks, we think growth stocks will again have their day in the sun.

What to Conclude? Before the last couple of years, the longest running period of small company dominance (outperformance relative to large stocks) was five years. This period has endured three years longer. Let’s consider three alternatives of what this might mean:

a. Large stocks just aren’t as good any more, and we can expect small company dominance to continue indefinitely.

| 2 | Semi-Annual Report | December 31, 2006 (Unaudited) |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

b. This trend has obviously gone on too long and large (especially growth) stocks are relatively undervalued, so 2007 will be a large company dominated year.

c. There is conflicting evidence. A firm trend has been established and confirmed (annual small company dominance), and this particular trend has tended to persist historically. On the other hand, the pendulum has swung out very far to one side (in favor of smaller companies), and statistically it is “overdue” to “correct” back the other direction. Thus, there is no assurance either large or smaller stocks will dominate in 2007. But of course, one of them will.

Historically, there have been continual periods of large and small company dominated periods, and I expect that to continue into the future. Therefore, I strongly disagree with alternative (a) above, but I hear the argument for such persistent trends to continue, surprisingly frequently. Although personally I’m a contrarian at heart and believe the pendulum will swing back in favor of large companies at some time in the future, it may not be next year. A major market trend, such as we have experienced, can always theoretically go on for another year. So I reject alternative (b). That leaves us with alternative (c), which is not very helpful if you want to time the market. However, at Bridgeway we don’t believe in timing the market anyway, and I’ll live with the ambiguity of (and vote for a wishy-washy) alternative (c).

Bridgeway 4, Morningstar 7

The Short Version: In 2006, the tide changed, and Morningstar’s “analyst picks” beat Bridgeway Funds in seven of eleven cases.

One of the arguments in favor of purchasing actively managed funds is the desire to have better than average returns. Usually, our Bridgeway Fund performance tables compare our returns to relevant market indexes. We think of indexes as “average,” but in fact we believe indexes have beaten roughly 80% of actively managed mutual funds over the long haul historically. So comparing our performance against indexes rather than the “average” mutual fund is actually a very high hurdle. Nevertheless, we’d still like to know that we don’t just beat the indexes or the average of our peers, but that we also beat the “predictably better” actively managed funds. After all, who wants an average doctor or teacher? We want superior ones. Likewise with mutual funds, we want to know how we stack up against other funds as chosen by an independent firm specializing in investment research.

Of course, the difficult part is identifying “best” funds up front, at the beginning of the performance period in question. For this purpose we turn to Morningstar, an independent Chicago-based firm, which publishes a list of fund “picks” selected by their analysts. We then look at how the performance of Bridgeway Funds compares with the average performance of these “best” funds. Thus, we pit the Bridgeway Funds in a given category against Morningstar’s candidates for best funds. Think of it as a friendly competition.

In 2006, the results of this competition shifted to Morningstar’s favor for the one-year period. The score was 4 to 7 in favor of Morningstar. The table below presents the results by category and Bridgeway Fund.

| Bridgeway Funds | Morningstar Analyst “Picks” | |||||

| Name | 2006 Return | Morningstar Category | 2006 Return | |||

| Large-Cap Value | 18.52% | Large-cap value | 17.85% | |||

| Blue Chip 35 Index | 15.42% | Large-cap blend | 14.59% | |||

| Large-Cap Growth | 4.99% | Large-cap growth | 6.48% | |||

| Aggressive Investors 1 | 7.11% | Mid-cap growth | 10.15% | |||

| Aggressive Investors 2 | 5.43% | Mid-cap growth | 10.15% | |||

| Small-Cap Value | 12.77% | Small-Value | 12.19% | |||

| Ultra-Small Co. Market | 11.48% | Small Blend | 13.36% | |||

| Ultra-Small Company | 21.55% | Small-Growth | 9.54% | |||

| Micro-Cap Limited | -2.34% | Small-Growth | 9.54% | |||

| Small-Cap Growth | 5.31% | Small-Growth | 9.54% | |||

| Balanced | 6.65% | Conservative Allocation | 9.98% | |||

| www.Bridgeway.com | 3 |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

Past performance is not an indicator of future results. The Bridgeway Funds’ adviser, Bridgeway Capital Management, Inc., does not have any influence on the selection of the funds chosen by Morningstar’s analysts. The number and specific funds used in the comparison are in the control and discretion of Morningstar and their analysts and are subject to change. Morningstar’s criteria for choosing Analyst Picks includes, but is not limited to, factors such as performance, expenses, and quality of fund management. In addition, the comparison of Bridgeway Funds to the Morningstar Analyst Picks is limited to performance only and does not take into consideration other factors that are considered by Morningstar when compiling their list of Analyst Picks.

Each Bridgeway Fund is compared to the average total return of the group of funds selected by Morningstar at the beginning of 2006 for the one year period ended December 31, 2006. Although these Analyst Picks changed from the beginning of the year to the final quarter, the same three out of four Bridgeway Funds beat the average of the end of year Morningstar picks as well. These averages in the table are comprised of between one and nine funds from within each category. In an effort to provide a complete and balanced assessment, all of the Bridgeway Funds are used in the comparison table shown above such that no attempt is made to cull out unfavorable results. The purpose of this comparison is to “raise the bar” on performance comparison as this analysis uses an arguably higher benchmark by comparing the Bridgeway Funds to other funds chosen by an independent source that specializes in investment research.

Preaching to the Choir about Statistics or Dollar-Weighted Returns

The Short Version: Most of us have a pretty clear idea of what we mean by a fund’s returns. If $10,000 grows to $11,000, that’s a 10% return. Some press and advisers have begun talking more frequently about “dollar-weighted returns,” an interesting, if highly problematic, alternative statistic to measure the return of a fund. An important lesson learned from this analysis? Overall, it’s probably best to stick with a well-managed fund with an objective and strategy that meets your needs, rather than “jump in and out” of funds based on trailing favorable or unfavorable performance.

A “quant firm” is an investment management firm that focuses on statistics and models to pick stocks rather than reading analyst research reports, talking to management, conducting industry and competitive analysis, etc. We’re always interested in new industry statistics or numerical ways of representing something about our funds or industry. Every statistic has certain advantages and disadvantages. I need to warn you though, if numbers aren’t what interest you or if they give you a headache, you may want to skip this section.

One of the statistics on performance I’ve been interested in for a long time is called dollar-weighted returns. Generally, when we speak of the “total return” of a fund, we mean time-weighted returns, or the return a hypothetical investor would receive between two dates, assuming they reinvested dividends and made no additional investments or withdrawals. For example, you invest $10,000 on 12/31/05, the investment appreciates and is worth $11,000 on 12/31/06, then you have a 10.0% (time weighted) total return. But what if you invested an additional $500 on 3/31/06 and withdrew $1,000 on 9/1/06. The fund’s total return doesn’t change, but your personal actual total return probably does. That’s where dollar-weighted (also known as asset-weighted) returns come in. The dollar-weighted return weights (or emphasizes) more heavily the returns during the period of time when there were more assets in the fund. The reason they are attractive in theory is that these can be considered as the returns that the aggregate of actual investors actually received. That has a lot of appeal to me. For this reason, Morningstar has added dollar-weighted returns to the statistics that they report.

Unfortunately, two disadvantages of this statistic are 1) while it may be the average return of all shareholders, it still doesn’t relate to what you’d probably really like to know (your own actual individual return), and 2) since the difference between the fund’s time-weighted return and a dollar-weighted return is driven by the timing of investors’ purchases and withdrawals, the fund company has little impact on this. Or do they? Morningstar recently added dollar-weighted returns to their lineup of statistics. Morningstar’s Don Phillips makes the following argument:

| 4 | Semi-Annual Report | December 31, 2006 (Unaudited) |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

Fund companies don’t have complete control over how investors use their funds, but that doesn’t mean they can’t exercise any control. Fund companies can influence investor behavior through fund design, the timing of launches and closings, marketing efforts, and shareholder communications.

I’m reasonably persuaded by this argument, but even these factors won’t necessarily eliminate (and may not significantly narrow) the gap between time-weighted and dollar-weighted returns. Let’s look at Bridgeway’s record in each of these areas:

a. Fund design. We have some very high octane funds (Aggressive Investors 1 and 2, Micro-Cap Limited, and Ultra-Small Company). If you think you might panic in a downturn or be tempted to invest more after an extended run, you should stay away from these funds. Our primary advice is don’t chase hot returns, including and especially ours. Know how volatile a given fund is likely to be, and invest in accordance with your risk tolerance and an asset allocation plan you have committed to writing. Even our “four corners funds” have higher short-term volatility (by some measures) than some of their peers. All our funds are intended for long-term investments. If you think you might be tempted to buy or sell on short-term whims or emotions, please look for lower volatility funds. Our lowest volatility fund is Bridgeway Balanced Fund, which seeks shorter term volatility equal to about 40% of the stock market. (You can find information on investment objective, risks and fees in our prospectus at www.bridgeway.com.)

b. Timing of fund launches. One industry problem is that a sales-driven organization will launch a new fund in a hot sector, e.g., Internet stocks in 1999. Investors are eager to invest, but do so near the “top of the market,” and are ultimately disappointed. Bridgeway has never launched a fund in a “hot” segment.

c. Timing of fund closings. Bridgeway has a stellar record in this department. We are known for closing small cap funds early. In 2003, we closed our Ultra-Small Company Market Fund at two-thirds the level we had anticipated, because the sector of ultra-small stocks was overheated and the money was coming in faster than we wanted. When things cooled down, we reopened it.

d. Marketing efforts. We have a web site, and we work very hard on investor communications and education. Beyond that we do little marketing, and thus don’t use abusive marketing practices, like advertising the returns of (only) our best performing funds.

e. Shareholder communications. This is one of the top three areas about which we get the most “kudos” from shareholders. We aim for honest, straight-forward, and educational communications.

Does this mean we have an excellent history with respect to dollar-weighted returns? The record is mixed. In our Aggressive Investors 2 Fund, for example, we outperformed the market in the first four years of our Fund’s history. During the same period, our dollar-weighted returns almost exactly matched our total fund returns. In the first year (2006) when we underperformed our benchmarks, however, our dollar-weighted returns significantly lagged our total fund return, indicating investors timed their purchases and sells poorly.

In conclusion, I think the statistic is interesting, but fund companies are only partially responsible for the timing of their shareholders’ purchases and redemptions. Even though we work very hard at the items on the list above, we still see some shareholders making buy and sell decisions at relatively poor times. Obviously, if you are still a shareholder after 2006, I’m preaching to the choir and you probably don’t have the problem of chasing hot returns (or at least if you got in after a “runup,” you stuck with us through our relatively poor short-term performance in mid-2006). Over the next decade, I hope to see many more investors just like you. We don’t want to be a vehicle through which people end up with returns poorer than the time-weighted returns we generate.

| www.Bridgeway.com | 5 |

LETTER FROM THE INVESTMENT MANAGEMENT TEAM (continued)

Interesting Reactions

The Short Version: As long as we keep “cranking the models,” we don’t get significantly distracted with respect to investment results.

We received a small number of interesting reactions to our underperformance in the September quarter among our actively managed accounts, which I will paraphrase into three groups. If you didn’t read our rather extensive explanations of third quarter results, they are available at www.bridgeway.com. I’ve put these comments into three categories:

a. “Eyes off the ball.” One interesting concern expressed is that Bridgeway’s interest in charitable service and mission, along with the death of one of our Foundation staff members caused us to “take our eyes off the ball” of our primary task of picking stocks. It is a most interesting and surprising comment to me, in that the only way to figuratively take your eyes off the ball with our investment management process would be to stop maintaining (“running”) our quantitative models. We didn’t at any point last year stop running models. One great thing about our quantitative process is that it takes all the emotion out of the process.

b. “Elena’s three-month leave.” Another question was, “Were you hamstrung by Elena’s absence?” If any of the investment management team is on vacation or out, we have backup plans and capabilities to continue to run the models. In this case, a team member was on maternity leave, which we obviously knew about (and made detailed plans for) months ahead of time. As leave time goes, this was an easy one. We missed Elena, but we didn’t stop running the models. Actually, I really appreciate this question because it emphasizes the very significant contribution of our other team members and that the success of our group is less and less dependent on me.

c. “It’s too bad that this was only a couple of quarters of underperformance.” It would be much healthier for Bridgeway and your shareholders if it were a couple of years of underperformance; then it would flush out the people that shouldn’t be in the funds to begin with.” By way of disclosure, this comment was from my brother, who is both a substantial Fund shareholder and a member of the advisory firm’s board of directors. Also, a bit amusing as a comment, but I honestly can’t argue with the logic of it.

In conclusion, it’s true that I don’t like underperforming the market in any reporting period, including a quarter or a year. But since our investment philosophy is to concentrate on long-term performance (at least three years and longer) and our models are calibrated over longer periods of time, my statistical view is that shorter time periods, while they may contribute helpful data points about the short-term riskiness of our funds, they do not contribute significant information about the effectiveness of our investment management process.

Another Instance of Timing the Market

At the opposite end of the spectrum from selling on a downturn is not buying while waiting for a better opportunity. Consider this text from a shareholder’s letter to Bridgeway:

Unfortunately, the national debt, the trade balance, the war, the oil problem, the yield curve and the further tightening of interest rates has been a cause for me to, at least temporarily, delay taking advantage of your offerings.

When I hear statements like this, I think, “so he wants to wait for all these things to be going simultaneously well, at which point the market will be undoubtedly higher?” That sounds like a formula for buying high, or worse (and I’ve actually seen this), missing the boat all together. Personally, I don’t have faith in any professional or individual investor calling this correctly, except by luck. If our Funds are too risky when times are difficult, they are probably all the more so when times are good.

| 6 | Semi-Annual Report | December 31, 2006 (Unaudited) |

THIS PAGE INTENTIONALLY LEFT BLANK

| www.Bridgeway.com | 7 |

Bridgeway Aggressive Investors 1 Fund

MANAGER’S COMMENTARY

(Unaudited)

January 31, 2007

Dear Fellow Aggressive Investors 1 Fund Shareholder,

Our Fund was up 7.88% in the December quarter compared to a gain of 6.70% for our primary benchmark, the S&P 500 Index and 5.46% for our peer benchmark, the Lipper Capital Appreciation Funds Index. Small stocks made a strong finish to extend an eighth year of dominance over large stocks. In this environment, the Russell 2000 Index was up a stronger 8.90% for the December quarter. Overall, it was a good quarter.

The Fund’s December quarter return was not nearly enough to make up for the lagging performance in the prior quarters, however, and our calendar year returns lagged our benchmarks as presented in the table below. The calendar year return was a dismal 7.11%, compared to a gain of 15.79% for our primary benchmark, the S&P 500 Index and 10.53% for our peer benchmark, the Lipper Capital Appreciation Funds Index.

Our poor showing was the result of poor performance across four of our five models and an unusual market environment that did not reward the favorable reports of some of our stocks, while pummeling our stocks with unfavorable reports. It was also the first calendar year since 1998 that we underperformed our primary market benchmark.

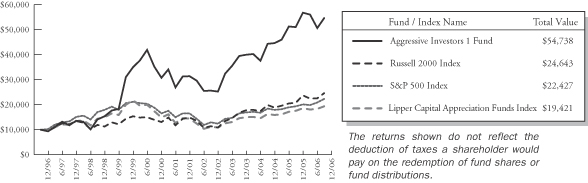

The table below presents our December quarter, one-year, five-year, ten-year and life-to-date financial results according to the formula required by the SEC. A graph of quarterly performance for the past ten years appears at the top of the following page.

Dec. Qtr. 10/1/06 to 12/31/06 | 1 Year 1/1/06 to 12/31/06 | 5 Year 1/1/02 to 12/31/06 | 10 Year 1/1/97 to 12/31/06 | Life-to-Date 8/5/94 to 12/31/06 | ||||||

Aggressive Investors 1 Fund | 7.88% | 7.11% | 11.76% | 18.53% | 20.40% | |||||

S&P 500 Index (large companies) | 6.70% | 15.79% | 6.19% | 8.41% | 11.49% | |||||

Russell 2000 Index (small companies) | 8.90% | 18.37% | 11.39% | 9.44% | 11.37% | |||||

Lipper Capital Appreciation Funds Index | 5.46% | 10.53% | 5.78% | 6.86% | 9.34% | |||||

Performance figures quoted represent past performance and are no guarantee of future results. Current performance may be lower or higher than the performance figures quoted, and an investor’s shares, when redeemed, may be worth more or less than original cost. For the most recent month-end performance, please call 1-800-661-3550 or visit the Fund’s website at www.bridgeway.com.

The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions based on the average of 500 widely held common stocks with dividends reinvested, while the Russell 2000 Index is an unmanaged, market value weighted index, that measures performance of the 2,000 companies that are between the 1,000th and 3,000th largest in the market with dividends reinvested. The Lipper Capital Appreciation Funds Index reflects the aggregate record of more aggressive domestic growth mutual funds, as reported by Lipper, Inc. It is not possible to invest directly in an index. Periods longer than one year are annualized.

According to data from Lipper, Inc. as of December 31, 2006, Aggressive Investors 1 Fund ranked 232nd of 354 capital appreciation funds for 2006, 23rd of 242 over the last five years, 2nd of 113 over the last ten years, and 1st of 68 since inception in August, 1994. Lipper, Inc. is an independent mutual fund rating service that ranks funds in various fund categories by making comparative calculations using total returns.

| 8 | Semi-Annual Report | December 31, 2006 (Unaudited) |

Bridgeway Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

Growth of $10,000 Invested in Aggressive Investors 1 Fund and Indexes from 1/1/97 to 12/31/06

Detailed Explanation of Quarterly Performance—What Worked Well

The Short Version: Of our Fund’s 71 holdings, 10 had better than 20% return for the December quarter, and only 3 were down more than 20%. Companies in the technology sector (semiconductor, software, and computers industries) added the most to performance, although only one, Amkor Technology, made the top ten.

These are the ten best performers for the December quarter:

| Rank | Description | Industry | % Gain | |||

| 1 | Amkor Technology, Inc. | Semiconductors | 59.2% | |||

| 2 | Tenaris SA | Iron/Steel | 41.0% | |||

| 3 | Ceradyne, Inc. | Misc. Manufacturing | 37.5% | |||

| 4 | CROCS, Inc. | Apparel | 27.3% | |||

| 5 | Cleveland-Cliffs, Inc. | Iron/Steel | 27.1% | |||

| 6 | Administaff, Inc. | Commercial Services | 26.9% | |||

| 7 | Dobson Communications Corp. | Telecommunications | 24.1% | |||

| 8 | McDermott International, Inc. | Engineering & Construction | 21.7% | |||

| 9 | ConocoPhillips | Oil & Gas | 20.9% | |||

| 10 | Marathon Oil Corp. | Oil & Gas | 20.3% | |||

Last quarter, I promised an update on our worst performer, Amkor Technology. At the time, I didn’t know just how interesting the story would get. Amkor is a leading provider of advanced semiconductor assembly and test services. As you may recall, through the summer and early fall, the company was fraught with problems that seemed to be one domino of bad news falling after another: the company warning of slowing growth rates, the SEC looking into option award practices, delays in filing its 10Q financial statements with the federal government pending the results of the stock option inquiry, threat of stock exchange delisting, announcement of likely restated financial results from the options probe, probable non-compliance with lending requirements (bondholder covenants) due to the delayed filings, and the specter of bankruptcy should the bondholders accelerate bond payment. On top of all this, the market environment was very unfriendly to this kind of stock, and for all these reasons, the stock price was pummeled. It would seem things just couldn’t get worse. (Things can always get worse.) In the midst of all this bad news, the company continued to report favorable underlying economic results. At the lower price, one of our models still liked the stock. This is where the advantage of quantitative investing comes into play—taking all the emotion out of the process. During the September quarter, we took a rather unusual action in the area of risk management (and cash management) in the Fund. We bought call options on the stock and shortly thereafter trimmed our position in the stock itself. This had the net effect of allowing us to participate in the stock’s recovery (should that happen), while providing some downside protection (as compared to owning the equivalent shares of the stock). And recover it did in the December quarter. Amkor had started out the September quarter at a price

| www.Bridgeway.com | 9 |

Bridgeway Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

of $9.46 and ended that quarter at $5.15. Thereafter, much of the “bad news” unwound as more facts came to light. The company reported another quarter of good financial results. The stock option inquiry exonerated all current members of management. Prior financials were restated, and the company was able to make their financial filings. The bondholders dropped their threat of accelerated payments, and the threat of bankruptcy filings vanished. With help from the market recovery in the fourth quarter, the stock price recovered to $9.34 at December quarter end. The net result to Aggressive Investors 1 shareholders? We decreased risk in Amkor by buying calls and selling a portion of our stock, and we participated in the stock price recovery. Combining our stock and call option positions, Amkor contributed a full 1.0% to our December quarter performance, significant for a single holding.

Although Amkor was our largest gainer for the quarter, McDermott International added almost as much (0.9%) to December quarter returns. Founded in 1923 in Bridgeway’s hometown of Houston, Texas, McDermott International, Inc., through its subsidiaries, operates as an energy services company worldwide. It operates in three segments: Marine Construction Services, Government Operations, and Power Generation Systems. Since our original purchase in the fall of 2005, it has been a steady performer for the Fund. Third quarter reports of higher earnings, revenues and operating income resulted in a 13% share price boost.

Detailed Explanation of Quarterly Performance—What Didn’t Work

The Short Version: For a number of our stocks, December quarter price movements were nearly a mirror image of the prior quarter. Three of the worst performers in the December quarter were among the best stocks in the September quarter: Motorola, Gymboree and Steven Madden. OM Group cost us the most in performance—a little more than a half percent. As losers go, it wasn’t a bad list.

These are the ten stocks that performed the worst in the December quarter:

| Rank | Description | Industry | % Loss | |||

| 1 | LifeCell Corp. | Biotechnology | -24.5% | |||

| 2 | Corning, Inc. | Telecommunications | -23.4% | |||

| 3 | OM Group, Inc. | Chemicals | -20.0% | |||

| 4 | Motorola, Inc. | Telecommunications | -16.4% | |||

| 5 | Archer-Daniels-Midland Co. | Agriculture | -15.9% | |||

| 6 | EGL, Inc. | Transportation | -15.3% | |||

| 7 | TXU Corp. | Electric | -13.3% | |||

| 8 | Encore Wire Corp. | Electrical Compo & Equip | -11.2% | |||

| 9 | Gymboree Corp. | Apparel | -9.5% | |||

| 10 | Steven Madden Ltd. | Apparel | -8.7% | |||

LifeCell Corporation engages in the development and marketing of human-derived tissue-based products for use in reconstructive, orthopedic, and urogynecologic surgical procedures to repair soft tissue defects. In late October, the company announced negative news on third quarter results. Even though earnings went from $2.5 million and 7 cents a share last year to $5.1 million and 15 cents a share this year, it had targeted 16 cents a share. You would think that investors would be happy with such an increase; however, LifeCell also lowered fourth quarter revenue and earnings projections, signaling a slow down in sales growth. Shares tumbled almost 25% on the news. We sold our position before quarter end.

Motorola, our third best performer in the September quarter, dropped to fourth worst this quarter. Cell phone competition has been fierce, not only with Nokia and Samsung, but also from its own Krzr, the new version of the popular slim phone, Razr, which has sold more than 50 million units world-wide (including the one I bought my wife last year). After announcing in mid-October that third quarter revenues fell short of expectations and that earnings fell 45% year-over-year, its share price fell 11% over the next few days. Nevertheless, the model that picked this stock still liked it enough to hold through quarter end.

| 10 | Semi-Annual Report | December 31, 2006 (Unaudited) |

Bridgeway Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

Detailed Explanation of Calendar Year Performance—What Worked Well

The Short Version: Although eight out of ten of the stocks below had better than 50% return, they were not enough to pull us ahead of our benchmarks for the calendar year.

These are the ten best performers for the calendar year:

| Rank | Description | Industry | % Gain | |||

| 1 | Tenaris SA | Iron/Steel | 117.9% | |||

| 2 | Nutri/System, Inc. | Internet | 76.0% | |||

| 3 | BellSouth Corp. | Telecommunications | 67.5% | |||

| 4 | CROCS, Inc. | Apparel | 65.3% | |||

| 5 | Hansen Natural Corp. | Beverages | 63.6% | |||

| 6 | McDermott International, Inc. | Engineering & Construction | 63.1% | |||

| 7 | BMC Software, Inc. | Software | 55.0% | |||

| 8 | NS Group, Inc. | Metal Fabricate/Hardware | 53.9% | |||

| 9 | WESCO International, Inc. | Distribution/Wholesale | 40.6% | |||

| 10 | AT&T, Inc. | Telecommunications | 40.3% | |||

Oil and gas companies world wide continue to increase their exploration and production spending in response to generally sustained high oil and gas prices. Our biggest gainer for the calendar year, Tenaris SA, has had a steady corresponding increase in demand for its products. Based in Luxembourg, the company manufactures seamless steel tubing in a number of countries, including Argentina, Brazil, Canada, Italy, Japan, Mexico and Venezuela. Its annual earnings growth rate over the past five years has been a huge 75.12%. Good third quarter results added fuel to rising share price, including a more than two-fold return for our Fund.

Detailed Explanation of Calendar Year Performance—What Didn’t Work

The Short Version: Five of the ten worst performers for the calendar year were in the industrial sector (electronics, building materials and transportation sectors).

These are the ten worst-performing stocks for the calendar year:

| Rank | Description | Industry | % Loss | |||

| 1 | Plexus Corp. | Electronics | -52.4% | |||

| 2 | American Science & Eng., Inc. | Electronics | -45.4% | |||

| 3 | Zoran Corp. | Semiconductors | -40.8% | |||

| 4 | Eagle Materials, Inc. | Building Materials | -39.3% | |||

| 5 | Brightpoint, Inc. | Distribution/Wholesale | -37.7% | |||

| 6 | USG Corp. | Building Materials | -36.1% | |||

| 7 | EGL, Inc. | Transportation | -34.2% | |||

| 8 | Advanced Micro Devices, Inc. | Semiconductors | -33.9% | |||

| 9 | Volt Information Sciences, Inc. | Commercial Services | -26.2% | |||

| 10 | Carpenter Technology Corp. | Iron/Steel | -25.9% | |||

There were no industry-related negative trends for these stocks. Nevertheless, although most of these companies have been good performers for the Fund at various times, they all “hit the skids” together, mostly in the early May through mid-September period. Is this just a fluke or was there a common statistical theme underlying their poor performance? From a statistical standpoint, it is too short a time period and too small a sample to draw any such conclusion (though part of our ongoing research seeks to determine the answer to such questions).

| www.Bridgeway.com | 11 |

Bridgeway Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

Top Ten Holdings as of December 31, 2006

Three of the largest holdings for the December quarter: BMC Software, McDermott International and Big Lots, were in the top quartile of performers, adding almost two and a half percentage points to our return. The top ten holdings represented 39.0% of net assets, higher than the average of domestic equity funds (35%), but slightly lower than the average aggressive growth fund (40%), according to data from Morningstar.

| Rank | Description | Industry | Percent of Net Assets | |||

| 1 | BMC Software, Inc. | Software | 5.6% | |||

| 2 | McDermott International, Inc. | Engineering & Construction | 5.1% | |||

| 3 | Big Lots, Inc. | Retail | 4.6% | |||

| 4 | Cephalon, Inc. | Pharmaceuticals | 4.0% | |||

| 5 | Dillard’s, Inc. | Retail | 3.8% | |||

| 6 | Digene Corp. | Biotechnology | 3.7% | |||

| 7 | Tesoro Corp. | Oil & Gas | 3.3% | |||

| 8 | Nutri/System, Inc. | Internet | 3.2% | |||

| 9 | AT&T, Inc. | Telecommunications | 3.1% | |||

| 10 | Cognizant Tech. Solutions Corp. | Computers | 2.6% | |||

| 39.0% |

Industry Sector Representation as of December 31, 2006

Consumer, cyclical was the largest sector representative at the end of the December quarter and also the sector in which we were most over weighted compared to the market—very slightly to our advantage. The Fund was most underweighted in the financial sector—very slightly to our disadvantage.

| % of Net Assets | % S&P 500 Index | Difference | ||||

Basic Materials | 6.9% | 2.9% | 4.0% | |||

Communications | 15.1% | 11.6% | 3.5% | |||

Consumer, Cyclical | 19.1% | 8.3% | 10.8% | |||

Consumer, Non-cyclical | 14.4% | 19.9% | -5.5% | |||

Energy | 11.4% | 9.9% | 1.5% | |||

Financial | 11.3% | 22.2% | -10.9% | |||

Industrial | 8.8% | 11.1% | -2.3% | |||

Technology | 12.5% | 10.6% | 1.9% | |||

Utilities | 0.9% | 3.5% | -2.6% | |||

Cash | -0.4% | 0.0% | -0.4% | |||

Total | 100.0% | 100.0% |

Disclaimer

The following is a reminder from the friendly folks at your Fund who worry about liability. The views expressed here are exclusively those of Fund management. These views, including those of market sectors or individual stocks, are not meant as investment advice and should not be considered predictive in nature. Any favorable (or unfavorable) description of a holding applies only as of the quarter end, December 31, 2006, unless otherwise stated. Security positions can and do change thereafter. Discussions of historical performance do not guarantee and are not indicative of future performance.

The Fund is subject to above average market risk (volatility) and is not an appropriate investment for short-term investors. Investments in the small companies within this multi-cap fund generally carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets (fewer investors), limited financial resources and greater trading difficulty.

| 12 | Semi-Annual Report | December 31, 2006 (Unaudited) |

Bridgeway Aggressive Investors 1 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

This report is submitted for the general information of the shareholders of the Fund. It is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus, which includes information regarding the Fund’s risks, objectives, fees and expenses, experience of its management, and other information. For questions or other Fund information, call 1-800-661-3550 or visit the Fund’s website www.bridgeway.com. Foreside Fund Services, LLC, distributor.

Conclusion

Thank you for your continued investment in Aggressive Investors 1 Fund. This Fund remains open only to current investors as we seek to keep the nimbleness that has fared very well over the long haul. As always, we appreciate your feedback.

Sincerely,

John Montgomery

| www.Bridgeway.com | 13 |

Bridgeway Aggressive Investors 1 Fund

SCHEDULE OF INVESTMENTS

Showing percentage of net assets as of December 31, 2006 (Unaudited)

| Industry | Company | Shares | Value | ||||

COMMON STOCKS - 100.53% | |||||||

Apparel - 6.32% | |||||||

CROCS, Inc.*+ | 145,400 | $ | 6,281,280 | ||||

Guess?, Inc.* | 129,000 | 8,182,470 | |||||

Gymboree Corp.* | 253,000 | 9,654,480 | |||||

| 24,118,230 | |||||||

Auto Manufacturers - 1.00% | |||||||

General Motors Corp.+ | 124,900 | 3,836,928 | |||||

Banks - 1.34% | |||||||

US Bancorp+ | 141,000 | 5,102,790 | |||||

Biotechnology - 5.41% | |||||||

Digene Corp.* | 292,300 | 14,007,016 | |||||

Illumina, Inc.*+ | 168,600 | 6,627,666 | |||||

| 20,634,682 | |||||||

Chemicals - 3.24% | |||||||

Albemarle Corp. | 117,000 | 8,400,600 | |||||

OM Group, Inc.* | 87,400 | 3,957,472 | |||||

| 12,358,072 | |||||||

Commercial Services - 1.09% | |||||||

Administaff, Inc. | 97,400 | 4,165,798 | |||||

Computers - 3.68% | |||||||

Cognizant Technology Solutions Corp.* | 129,900 | 10,023,084 | |||||

Research In Motion Ltd.* | 31,400 | 4,012,292 | |||||

| 14,035,376 | |||||||

Distribution/Wholesale - 1.95% | |||||||

WESCO International, Inc.* | 126,400 | 7,433,584 | |||||

Diversified Financial Services - 8.18% | |||||||

First Marblehead Corp.+ | 78,000 | 4,262,700 | |||||

Goldman Sachs Group, Inc.+ | 49,500 | 9,867,825 | |||||

Merrill Lynch & Co., Inc.+ | 92,400 | 8,602,440 | |||||

Morgan Stanley | 104,300 | 8,493,149 | |||||

| 31,226,114 | |||||||

Electric - 0.89% | |||||||

TXU Corp. | 62,700 | 3,398,967 | |||||

Engineering & Construction - 5.16% | |||||||

McDermott International, Inc.* | 387,000 | 19,682,820 | |||||

Insurance - 0.56% | |||||||

WR Berkley Corp.+ | 61,850 | 2,134,442 | |||||

| Industry | Company | Shares | Value | ||||

Internet - 3.24% | |||||||

Nutri/System, Inc.*+ | 195,000 | $ | 12,361,050 | ||||

Iron/Steel - 3.71% | |||||||

Cleveland-Cliffs, Inc.+ | 107,800 | 5,221,832 | |||||

Tenaris SA** | 179,000 | 8,930,310 | |||||

| 14,152,142 | |||||||

Machinery - Construction & Mining - 1.22% | |||||||

Joy Global, Inc.+ | 96,350 | 4,657,559 | |||||

Media - 1.19% | |||||||

Comcast Corp.*+ | 102,900 | 4,309,452 | |||||

Idearc, Inc.* | 7,850 | 224,903 | |||||

| 4,534,355 | |||||||

Miscellaneous Manufacturing - 2.39% | |||||||

Ceradyne, Inc.* | 90,300 | 5,101,950 | |||||

Freightcar America, Inc.+ | 72,800 | 4,036,760 | |||||

| 9,138,710 | |||||||

Oil & Gas - 7.52% | |||||||

Chesapeake Energy Corp.+ | 102,800 | 2,986,340 | |||||

ConocoPhillips | 121,300 | 8,727,535 | |||||

Marathon Oil Corp. | 46,000 | 4,255,000 | |||||

Tesoro Corp. | 193,400 | 12,719,918 | |||||

| 28,688,793 | |||||||

Oil & Gas Services - 3.94% | |||||||

Dril-Quip, Inc.* | 96,800 | 3,790,688 | |||||

Oceaneering International, Inc.* | 100,100 | 3,973,970 | |||||

Tetra Technologies, Inc.*+ | 283,600 | 7,254,488 | |||||

| 15,019,146 | |||||||

Pharmaceuticals - 7.92% | |||||||

Bristol-Myers Squibb Co.+ | 174,300 | 4,587,576 | |||||

Cephalon, Inc.* | 216,100 | 15,215,601 | |||||

Gilead Sciences, Inc.* | 58,800 | 3,817,884 | |||||

Merck & Co., Inc. | 151,200 | 6,592,320 | |||||

| 30,213,381 | |||||||

Retail - 9.84% | |||||||

Big Lots, Inc.* | 770,100 | 17,650,692 | |||||

Dillard’s, Inc.+ | 410,600 | 14,358,682 | |||||

Kohl’s Corp.*+ | 80,800 | 5,529,144 | |||||

| 37,538,518 | |||||||

| 14 | Semi-Annual Report | December 31, 2006 (Unaudited) |

Bridgeway Aggressive Investors 1 Fund

SCHEDULE OF INVESTMENTS (continued)

Showing percentage of net assets as of December 31, 2006 (Unaudited)

| Industry | Company | Shares | Value | |||||

Common Stocks (continued) |

| |||||||

Savings & Loans - 1.20% |

| |||||||

Washington Mutual, Inc.+ | 101,100 | $ | 4,599,039 | |||||

Semiconductors - 1.90% |

| |||||||

Amkor Technology, Inc.* | 774,700 | 7,235,698 | ||||||

Software - 6.98% |

| |||||||

BMC Software, Inc.* | 660,000 | 21,252,000 | ||||||

Oracle Corp.* | 315,200 | 5,402,528 | ||||||

| 26,654,528 | ||||||||

Telecommunications - 10.66% |

| |||||||

AT&T, Inc.+ | 327,300 | 11,700,975 | ||||||

BellSouth Corp. | 128,300 | 6,044,213 | ||||||

BT Group PLC** | 78,600 | 4,707,354 | ||||||

Corning, Inc.* | 209,000 | 3,910,390 | ||||||

Dobson Communications Corp.* | 594,500 | 5,178,095 | ||||||

Motorola, Inc.+ | 160,800 | 3,306,048 | ||||||

Verizon Communications, Inc. | 157,000 | 5,846,680 | ||||||

| 40,693,755 | ||||||||

Transportation - 0.00%# |

| |||||||

Kirby Corp.* | 20 | 683 | ||||||

TOTAL COMMON STOCKS | 383,615,160 | |||||||

(Cost $308,954,790) | ||||||||

TOTAL INVESTMENTS - 100.53% | $ | 383,615,160 | ||||||

(Cost $308,954,790) | ||||||||

Liabilities in Excess of Other Assets - (0.53)% | (2,038,336 | ) | ||||||

NET ASSETS - 100.00% | $ | 381,576,824 | ||||||

| * | Non Income Producing Security |

| ** | ADR - American Depositary Receipt |

| # | Less than 0.005% of Net Assets |

| + | This security or a portion of the security is out on loan at December 31, 2006. Total loaned securities had a market value of $109,170,543 at December 31, 2006. |

See Notes to Financial Statements.

| www.Bridgeway.com | 15 |

Bridgeway Aggressive Investors 2 Fund

MANAGER’S COMMENTARY

(Unaudited)

January 31, 2007

Dear Fellow Aggressive Investors 2 Fund Shareholder,

Our Fund had a positive return of 7.26% in the December quarter, compared with 6.70% for the S&P 500 Index and 5.46% for our peer benchmark, the Lipper Capital Appreciation Funds Index. Small stocks made a strong finish to extend an eighth year of dominance over large stocks. In this environment, the Russell 2000 Index was up a strong 8.90% for the December quarter. Overall, it was a good quarter.

The Fund’s December quarter return was not nearly enough to make up for the lagging performance in the prior quarters, however, and our calendar year returns lagged our benchmarks as presented in the table below. The calendar year return was a dismal 5.43%, compared to a gain of 15.79% for our primary benchmark, the S&P 500 Index and 10.53% for our peer benchmark, the Lipper Capital Appreciation Funds Index.

Our poor showing was the result of poor performance across four of our five models and an unusual market environment that did not reward the favorable reports of some of our stocks, while pummeling our stocks with unfavorable reports. It was the first time in the five calendar year history of our Fund that we underperformed the S&P 500 Index.

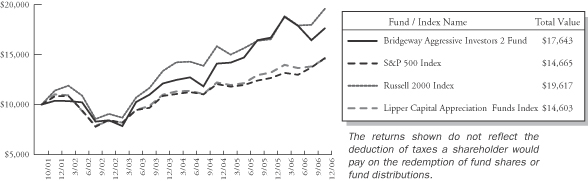

The table below presents our December quarter, one-year, five-year, and life-to-date financial results according to the formula required by the SEC. A graph of quarterly performance since inception appears on the following page.

Dec. Qtr. 10/1/06 to 12/31/06 | 1 Year 1/1/06 to 12/31/06 | 5 Year 1/1/02 to 12/31/06 | Life-to-Date 10/31/01 to 12/31/06 | |||||

Aggressive Investors 2 Fund | 7.26% | 5.43% | 11.13% | 11.61% | ||||

S&P 500 Index (large companies) | 6.70% | 15.79% | 6.19% | 7.69% | ||||

Russell 2000 Index (small companies) | 8.90% | 18.37% | 11.39% | 13.93% | ||||

Lipper Capital Appreciation Funds Index | 5.46% | 10.53% | 5.78% | 7.60% | ||||

Performance figures quoted represent past performance and are no guarantee of future results. Current performance may be lower or higher than the performance figures quoted, and an investor’s shares, when redeemed, may be worth more or less than original cost. For the most recent month-end performance, please call 1-800-661-3550 or visit the Fund’s website at www.bridgeway.com.

The S&P 500 Index is a broad-based, unmanaged measurement of changes in stock market conditions based on the average of 500 widely held common stocks with dividends reinvested, while the Russell 2000 Index is an unmanaged, market value weighted index that measures performance of the 2,000 companies that are between the 1,000th and 3,000th largest in the market with dividends reinvested. The Lipper Capital Appreciation Funds Index reflects the aggregate record of more aggressive domestic growth mutual funds, as reported by Lipper, Inc. It is not possible to invest directly in an index. Periods longer than one year are annualized.

According to data from Lipper, Inc. as of December 31, 2006, Aggressive Investors 2 Fund ranked 266th of 354 capital appreciation funds for 2006, 27th of 242 for the past five years and 53rd of 241 such funds since inception in October, 2001. Lipper, Inc. is an independent mutual fund rating service that ranks funds in various fund categories by making comparative calculations using total returns.

| 16 | Semi-Annual Report | December 31, 2006 (Unaudited) |

Bridgeway Aggressive Investors 2 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

Growth of $10,000 Invested in Aggressive Investors 2 Fund and Indexes from 10/31/01 (inception) to 12/31/06

Detailed Explanation of Quarterly Performance—What Worked Well

The Short Version: Of the 89 holdings at the end of the December quarter, 14 had returns greater than 20%, and only 4 had returns down 20% or more. Companies in communications and technology were bright spots, together adding about 3% to return.

These are the ten best performers for the December quarter:

| Rank | Description | Industry | % Gain | |||

| 1 | Amkor Technology, Inc. | Semiconductors | 64.0% | |||

| 2 | Tenaris SA | Iron/Steel | 41.0% | |||

| 3 | Ceradyne, Inc. | Miscellaneous Manufacturing | 37.5% | |||

| 4 | CDC Corp. Class A | Internet | 33.4% | |||

| 5 | CROCS, Inc. | Apparel | 27.3% | |||

| 6 | Cleveland-Cliffs, Inc. | Iron/Steel | 27.1% | |||

| 7 | Administaff, Inc. | Commercial Services | 26.9% | |||

| 8 | DIRECTV Group, Inc. | Media | 26.7% | |||

| 9 | Dobson Communications Corp. | Telecommunications | 24.1% | |||

| 10 | McDermott International, Inc. | Engineering & Construction | 21.7% | |||

Last quarter, I promised an update on our worst performer, Amkor Technology. At the time, I didn’t know just how interesting the story would get. Amkor is a leading provider of advanced semiconductor assembly and test services. As you may recall, through the summer and early fall, the company was fraught with problems that seemed to be one domino of bad news falling after another: the company warning of slowing growth rates, the SEC looking into option award practices, delays in filing its 10Q financial statements with the federal government pending the results of the stock option inquiry, threat of stock exchange delisting, announcement of likely restated financial results from the options probe, probable non-compliance with lending requirements (bondholder covenants) due to the delayed filings, and the specter of bankruptcy should the bondholders accelerate bond payment. On top of all this, the market environment was very unfriendly to this kind of stock, and for all these reasons the stock price was pummeled. It would seem things just couldn’t get worse. (Things can always get worse.) In the midst of all this bad news, the company continued to report favorable underlying economic results. At the lower price, one of our models still liked the stock. This is where the advantage of quantitative investing comes into play—taking all the emotion out of the process. During the September quarter, we took a rather unusual action in the area of risk management (and cash management) in the Fund. We bought call options on the stock and shortly thereafter trimmed our position in the stock itself. This had the net effect of allowing us to participate in the stock’s recovery (should that happen), while providing some downside protection (as compared to owning the equivalent shares of the stock). And recover it did in the December quarter. Amkor had started out the September quarter at a price

| www.Bridgeway.com | 17 |

Bridgeway Aggressive Investors 2 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

of $9.46 and ended that quarter at $5.15. Thereafter, much of the “bad news” unwound as more facts came to light. The company reported another quarter of good financial results. The stock option inquiry exonerated all current members of management. Prior financials were restated, and the company was able to make their financial filings. The bondholders dropped their threat of accelerated payments, and the threat of bankruptcy filings vanished. With help from the market recovery in the fourth quarter, the stock price recovered to $9.34 at December quarter end. The net result to Aggressive Investors 2 shareholders? We decreased risk in Amkor by buying calls and selling a portion of our stock, and we participated in the stock price recovery. Combining our stock and call option positions, Amkor contributed 0.8% to our December quarter performance, significant for a single holding.

Although Amkor was our largest gainer for the quarter, McDermott International added more to performance (0.9%). Founded in 1923 in Bridgeway’s hometown of Houston, Texas, McDermott International, Inc., through its subsidiaries, operates as an energy services company worldwide. It operates in three segments: Marine Construction Services, Government Operations, and Power Generation Systems. Since our original purchase in the fall of 2005, it has been a steady performer for the Fund. Third quarter reports of higher earnings, revenues and operating income resulted in a 21.7% share price boost.

Detailed Explanation of Quarterly Performance—What Didn’t Work

The Short Version: For a number of our stocks, December quarter price movements were nearly a mirror image of the prior quarter. Two of the worst performers in the December quarter were among the best stocks in the September quarter: NovAtel and Motorola. OM Group cost us the most in performance—more than a half percent. As losers go, it wasn’t a bad list.

These are the ten stocks that performed the worst in the December quarter:

| Rank | Description | Industry | % Loss | |||

| 1 | LifeCell Corp. | Biotechnology | -26.3% | |||

| 2 | Encore Wire Corp. | Electrical Compo & Equip | -25.0% | |||

| 3 | Corning, Inc. | Telecommunications | -23.4% | |||

| 4 | Aspreva Pharmaceuticals Corp. | Pharmaceuticals | -20.9% | |||

| 5 | OM Group, Inc. | Chemicals | -19.1% | |||

| 6 | Motorola, Inc. | Telecommunications | -17.8% | |||

| 7 | Archer-Daniels-Midland Co. | Agriculture | -16.3% | |||

| 8 | EGL, Inc. | Transportation | -14.6% | |||

| 9 | TXU Corp. | Electric | -13.3% | |||

| 10 | NovAtel, Inc. | Electronics | -13.1% | |||

What happened to NovAtel and Motorola? At the end of October, although NovAtel posted almost double third quarter profit from a year ago, it missed Wall Street expectations, and the price dropped 15%. It has recovered somewhat since then, and we continue to hold. Motorola, our fourth best performer in the September quarter, dropped to sixth worst this quarter. Cell phone competition has been fierce, not only with Nokia and Samsung, but also from its own Krzr, the new version of the popular slim phone, Razr, which has sold more than 50 million units world-wide (including the one I bought my wife last year). After announcing in mid-October that third quarter revenues fell short of expectations and that earnings fell 45% year-over-year, its share price fell 11% over the next few days. Nevertheless, the model that picked this stock liked it enough to hold through quarter end.

LifeCell Corporation engages in the development and marketing of human-derived tissue-based products for use in reconstructive, orthopedic, and urogynecologic surgical procedures to repair soft tissue defects. In late October, the company announced negative news on third quarter results. Even though earnings went from $2.5 million and 7 cents a share last year to $5.1 million and 15 cents a share this year, it had targeted 16 cents a share. You would think that investors would be happy with such an increase; however, LifeCell also lowered fourth quarter revenue and earnings projections, signaling a slow down in sales growth. Shares tumbled almost 25% on the news. We sold our position before quarter end.

| 18 | Semi-Annual Report | December 31, 2006 (Unaudited) |

Bridgeway Aggressive Investors 2 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

Detailed Explanation of Calendar Year Performance—What Worked Well

The Short Version: Although five out of ten of the stocks below had better than 50% return, they were not enough to pull us ahead of our benchmarks for the calendar year.

These are the ten best performers for the calendar year:

| Rank | Description | Industry | % Gain | |||

| 1 | Tenaris SA | Iron/Steel | 117.9% | |||

| 2 | BellSouth Corp. | Telecommunications | 73.8% | |||

| 3 | CROCS, Inc. | Apparel | 60.5% | |||

| 4 | NS Group, Inc. | Metal Fabricate/Hardware | 53.9% | |||

| 5 | BMC Software, Inc. | Software | 52.0% | |||

| 6 | DIRECTV Group, Inc. | Media | 49.7% | |||

| 7 | AT&T, Inc. | Telecommunications | 46.0% | |||

| 8 | McDermott International, Inc. | Engineering & Construction | 45.2% | |||

| 9 | NovAtel, Inc. | Electronics | 44.5% | |||

| 10 | Foundation Coal Holdings, Inc. | Coal | 40.1% | |||

Oil and gas companies world wide continue to increase their exploration and production spending in response to generally sustained high oil and gas prices. Our biggest gainer for the calendar year, Tenaris SA, has had a steady corresponding increase in demand for its products. Based in Luxembourg, the company manufactures seamless steel tubing in a number of countries, including Argentina, Brazil, Canada, Italy, Japan, Mexico and Venezuela. Its annual earnings growth rate over the past five years has been a huge 75.12%. Good third quarter results added fuel to rising share price, including a more than two-fold return for our Fund.

Detailed Explanation of Calendar Year Performance—What Didn’t Work

The Short Version: The four worst-performing companies in the industrial sector (electronics, building materials and transportation industries) practically cancelled the performance of their three counterparts in the best performers for the calendar year. In addition, the three tech companies below more than offset BMC Software. Not a winning combination for us for 2006.

The stocks that performed worst for the calendar year:

| Rank | Description | Industry | % Loss | |||

| 1 | Portalplayer, Inc. | Semiconductors | -60.3% | |||

| 2 | American Science & Eng., Inc. | Electronics | -49.7% | |||

| 3 | Advanced Micro Devices, Inc. | Semiconductors | -47.1% | |||

| 4 | Plexus Corp. | Electronics | -42.9% | |||

| 5 | Zoran Corp. | Semiconductors | -41.7% | |||

| 6 | Aspreva Pharmaceuticals Corp. | Pharmaceuticals | -38.0% | |||

| 7 | Brightpoint, Inc. | Distribution/Wholesale | -37.6% | |||

| 8 | Energy Partners Ltd. | Oil & Gas | -35.7% | |||

| 9 | Eagle Materials, Inc. | Building Materials | -34.9% | |||

| 10 | EGL, Inc. | Transportation | -31.1% | |||

Aspreva is the only stock of the ten that we continued to hold after year end. Aspreva Pharmaceuticals Corporation provides drugs for patients living with less common diseases. Its CellCept product was approved in 1995 for the prevention of rejection of kidney, heart and liver transplants and was being tested for its effectiveness in treating myasthenia gravis, a disease characterized by chronic fatigue and muscular weakness, especially in the face and neck. When CellCept failed to meet its primary and secondary endpoints in the Phase III clinical trial, Aspreva’s shares sank 14.1% to $19.03. Although we have trimmed our position, we continue to hold.

| www.Bridgeway.com | 19 |

Bridgeway Aggressive Investors 2 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

Top Ten Holdings as of December 31, 2006

Unfortunately, none of our largest holdings were ultra performers; however, only one was in negative performance territory. The top ten holdings represented 32.7% of net assets, below the average of both domestic equity funds (35%) and aggressive growth funds (40%), according to data from Morningstar.

| Rank | Description | Industry | Percent of Net Assets | |||

| 1 | McDermott International, Inc. | Engineering & Construction | 4.7% | |||

| 2 | Big Lots, Inc. | Retail | 4.4% | |||

| 3 | BMC Software, Inc. | Software | 4.0% | |||

| 4 | Cephalon, Inc. | Pharmaceuticals | 3.8% | |||

| 5 | Dillard’s, Inc. | Retail | 3.5% | |||

| 6 | Tetra Technologies, Inc. | Oil & Gas Services | 2.6% | |||

| 7 | Illumina, Inc. | Biotechnology | 2.5% | |||

| 8 | Goldman Sachs Group, Inc. | Diversified Finan Serv | 2.5% | |||

| 9 | America Movil SAB de CV | Telecommunications | 2.4% | |||

| 10 | Cognizant Tech. Solutions Corp. | Computers | 2.3% | |||

| 32.7% |

Industry Sector Representation as of December 31, 2006

Our significant underweighting in financial stocks compared to the market had a slightly negative effect in the quarter; strong stock selection nearly made up for fewer holdings. Fortunately, our overweighting and strong performance among technology stocks carried us into market-beating territory.

| % of Net Assets | % S&P 500 Index | Difference | ||||

Basic Materials | 6.1% | 2.9% | 3.2% | |||

Communications | 11.9% | 11.6% | 0.3% | |||

Consumer, Cyclical | 18.0% | 8.3% | 9.7% | |||

Consumer, Non-cyclical | 12.2% | 19.9% | -7.7% | |||

Energy | 15.6% | 9.9% | 5.7% | |||

Financial | 9.5% | 22.2% | -12.7% | |||

Industrial | 11.5% | 11.1% | 0.4% | |||

Technology | 13.2% | 10.6% | 2.6% | |||

Utilities | 1.8% | 3.5% | -1.7% | |||

Cash | 0.2% | 0.0% | 0.2% | |||

Total | 100.0% | 100.0% |

Disclaimer

The following is a reminder from the friendly folks at your Fund who worry about liability. The views expressed here are exclusively those of Fund management. These views, including those of market sectors or individual stocks, are not meant as investment advice and should not be considered predictive in nature. Any favorable (or unfavorable) description of a holding applies only as of the quarter end, December 31, 2006, unless otherwise stated. Security positions can and do change thereafter. Discussions of historical performance do not guarantee and are not indicative of future performance.

The Fund is subject to above average market risk (volatility) and is not an appropriate investment for short-term investors. Investments in the small companies within this multi-cap fund generally carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets (fewer investors), limited financial resources and greater trading difficulty.

| 20 | Semi-Annual Report | December 31, 2006 (Unaudited) |

Bridgeway Aggressive Investors 2 Fund

MANAGER’S COMMENTARY (continued)

(Unaudited)

This report is submitted for the general information of the shareholders of the Fund. It is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus, which includes information regarding the Fund’s risks, objectives, fees and expenses, experience of its management, and other information. For questions or other Fund information, call 1-800-661-3550 or visit the Fund’s website www.bridgeway.com. Foreside Fund Services, LLC, distributor.

Conclusion

Thank you for your continued investment in Aggressive Investors 2 Fund. This Fund remains open to both current and new investors. As always, we appreciate your feedback.

Sincerely,

John Montgomery

| www.Bridgeway.com | 21 |

Bridgeway Aggressive Investors 2 Fund

SCHEDULE OF INVESTMENTS

Showing percentage of net assets as of December 31, 2006 (Unaudited)

| Industry | Company | Shares | Value | ||||

COMMON STOCKS - 99.90% | |||||||

Apparel - 5.95% | |||||||

CROCS, Inc.*+ | 230,400 | $ | 9,953,280 | ||||

Guess?, Inc.* | 190,400 | 12,077,072 | |||||

Gymboree Corp.* | 337,400 | 12,875,184 | |||||

| 34,905,536 | |||||||

Auto Manufacturers - 0.97% | |||||||

General Motors Corp.+ | 184,300 | 5,661,696 | |||||

Banks - 0.49% | |||||||

US Bancorp+ | 79,000 | 2,859,010 | |||||

Biotechnology - 3.02% | |||||||

Amgen, Inc.* | 44,500 | 3,039,795 | |||||

Illumina, Inc.*+ | 373,400 | 14,678,354 | |||||

| 17,718,149 | |||||||

Chemicals - 3.50% | |||||||

Albemarle Corp. | 179,900 | 12,916,820 | |||||

OM Group, Inc.* | 167,771 | 7,596,671 | |||||

| 20,513,491 | |||||||

Commercial Services - 0.45% | |||||||

Administaff, Inc. | 62,100 | 2,656,017 | |||||

Computers - 3.27% | |||||||

Cognizant Technology Solutions Corp.* | 173,300 | 13,371,828 | |||||

Research In Motion Ltd.* | 45,600 | 5,826,768 | |||||

| 19,198,596 | |||||||

Distribution/Wholesale - 1.52% | |||||||

WESCO International, Inc.*+ | 151,800 | 8,927,358 | |||||

Diversified Financial Services - 7.73% | |||||||

First Marblehead Corp.+ | 113,850 | 6,221,903 | |||||

Goldman Sachs Group, Inc.+ | 73,300 | 14,612,355 | |||||

JPMorgan Chase & Co. | 138,400 | 6,684,720 | |||||

Merrill Lynch & Co., Inc.+ | 56,800 | 5,288,080 | |||||

Morgan Stanley | 153,600 | 12,507,648 | |||||

| 45,314,706 | |||||||

Electric - 0.85% | |||||||

TXU Corp. | 92,500 | 5,014,425 | |||||

Electronics - 2.99% | |||||||

Avnet, Inc.* | 466,700 | 11,914,851 | |||||

NovAtel, Inc.* | 141,300 | 5,637,870 | |||||

| 17,552,721 | |||||||

| Industry | Company | Shares | Value | ||||

Engineering & Construction - 4.73% | |||||||

McDermott International, Inc.* | 546,050 | $ | 27,772,103 | ||||

Gas - 0.92% | |||||||

Energen Corp. | 114,700 | 5,384,018 | |||||

Insurance - 0.90% | |||||||

Selective Insurance Group | 55,900 | 3,202,511 | |||||

WR Berkley Corp.+ | 59,950 | 2,068,874 | |||||

| 5,271,385 | |||||||

Internet - 2.32% | |||||||

CDC Corp.*+ | 864,200 | 8,209,900 | |||||

Nutri/System, Inc.*+ | 84,800 | 5,375,472 | |||||

| 13,585,372 | |||||||

Iron/Steel - 1.84% | |||||||

Cleveland-Cliffs, Inc.+ | 133,600 | 6,471,584 | |||||

Tenaris SA**+ | 86,500 | 4,315,485 | |||||

| 10,787,069 | |||||||

Machinery - Construction & Mining - 1.16% | |||||||

Joy Global, Inc.+ | 140,200 | 6,777,268 | |||||

Media - 1.47% | |||||||

DIRECTV Group, Inc.*+ | 339,900 | 8,477,106 | |||||

Idearc, Inc.* | 4,245 | 121,619 | |||||

| 8,598,725 | |||||||

Mining - 0.77% | |||||||

Alcoa, Inc. | 151,100 | 4,534,511 | |||||

Miscellaneous Manufacturers - 1.43% | |||||||

Ceradyne, Inc.* | 61,567 | 3,478,536 | |||||

Freightcar America, Inc.+ | 89,000 | 4,935,050 | |||||

| 8,413,586 | |||||||

Oil & Gas - 6.42% | |||||||

Chesapeake Energy Corp.+ | 85,060 | 2,470,993 | |||||

ConocoPhillips | 128,900 | 9,274,355 | |||||

EnCana Corp. | 107,000 | 4,916,650 | |||||

Frontier Oil Corp.+ | 192,600 | 5,535,324 | |||||

Marathon Oil Corp. | 66,500 | 6,151,250 | |||||

Tesoro Corp.+ | 69,300 | 4,557,861 | |||||

Unit Corp.* | 98,200 | 4,757,790 | |||||

| 37,664,223 | |||||||

| 22 | Semi-Annual Report | December 31, 2006 (Unaudited) |

Bridgeway Aggressive Investors 2 Fund

SCHEDULE OF INVESTMENTS (continued)

Showing percentage of net assets as of December 31, 2006 (Unaudited)

| Industry | Company | Shares | Value | ||||

Common Stocks (continued) | |||||||

Oil & Gas Services - 9.19% | |||||||

Dril-Quip, Inc.* | 278,600 | $ | 10,909,976 | ||||

Oceaneering International, Inc.* | 286,620 | 11,378,814 | |||||

Schlumberger Ltd.+ | 122,200 | 7,718,152 | |||||

Swift Energy Co.* | 186,500 | 8,357,065 | |||||

Tetra Technologies, Inc.*+ | 607,000 | 15,527,060 | |||||

| 53,891,067 | |||||||

Pharmaceuticals - 8.72% | |||||||

Aspreva Pharmaceuticals Corp.* | 190,000 | 3,898,800 | |||||

Bristol-Myers Squibb Co.+ | 465,500 | 12,251,960 | |||||

Cephalon, Inc.*+ | 314,300 | 22,129,863 | |||||

Gilead Sciences, Inc.* | 83,400 | 5,415,162 | |||||

Merck & Co., Inc.+ | 171,000 | 7,455,600 | |||||

| 51,151,385 | |||||||

Retail - 9.59% | |||||||

Big Lots, Inc.*+ | 1,128,200 | 25,858,344 | |||||

Dillard’s, Inc.+ | 591,600 | 20,688,252 | |||||

Kohl’s Corp.*+ | 141,500 | 9,682,845 | |||||

| 56,229,441 | |||||||

Savings & Loans - 0.45% | |||||||

Washington Mutual, Inc.+ | 58,000 | 2,638,420 | |||||

Semiconductors - 4.00% | |||||||

Amkor Technology, Inc.* | 1,114,300 | 10,407,562 | |||||

Varian Semiconductor Equipment Associates, Inc.*+ | 287,300 | 13,077,896 | |||||

| 23,485,458 | |||||||

Software - 5.93% | |||||||

BMC Software, Inc.* | 733,400 | 23,615,480 | |||||

Informatica Corp.* | 264,500 | 3,229,545 | |||||

Oracle Corp.* | 464,500 | 7,961,530 | |||||

| 34,806,555 | |||||||

| Industry | Company | Shares | Value | ||||

Telecommunications - 8.13% | |||||||

America Movil SAB de CV** | 311,000 | $ | 14,063,420 | ||||

AT&T, Inc.+ | 163,600 | 5,848,700 | |||||

BellSouth Corp. | 196,600 | 9,261,826 | |||||

BT Group PLC** | 116,000 | 6,947,240 | |||||

Corning, Inc.* | 180,200 | 3,371,542 | |||||

Dobson Communications Corp.* | 327,600 | 2,853,396 | |||||

Motorola, Inc.+ | 106,400 | 2,187,584 | |||||

Verizon Communications, Inc. | 84,900 | 3,161,676 | |||||

| 47,695,384 | |||||||

Transportation - 1.19% | |||||||

American Commercial Lines, Inc.* | 106,200 | 6,957,162 | |||||

TOTAL COMMON STOCKS | 585,964,837 | ||||||

(Cost $518,625,696) | |||||||

TOTAL INVESTMENTS - 99.90% | $ | 585,964,837 | |||||

(Cost $518,625,696) | |||||||

Other Assets in Excess of Liabilities - 0.10% | 605,644 | ||||||

NET ASSETS - 100.00% | $ | 586,570,481 | |||||

| * | Non Income Producing Security |

| ** | ADR - American Depositary Receipt |

| + | This security or a portion of the security is out on loan at December 31, 2006. Total loaned securities had a market value of $184,765,948 at December 31, 2006. |

See Notes to Financial Statements.

| www.Bridgeway.com | 23 |

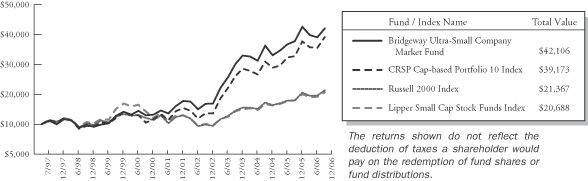

Bridgeway Ultra-Small Company Fund

MANAGER’S COMMENTARY

(Unaudited)

January 31, 2007

Dear Fellow Ultra-Small Company Fund Shareholder,

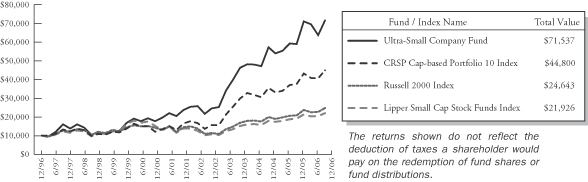

Our Fund was up 12.19% in the December quarter, compared to an 8.90% return for the Russell 2000 Index, 7.81% for our peer group, the Lipper Small-Cap Stock Funds Index, and 10.27% for our primary benchmark, the CRSP Cap-Based Portfolio 10 Index. It was a very good quarter.

For the calendar year 2006, we also had a “clean sweep.” Our Fund was up 21.55% for the full year, compared to 18.37% for the Russell 2000 Index, 14.66% for the Lipper Small-Cap Stock Funds Index, and 19.42% for the CRSP Cap-Based Portfolio 10 Index. Small stocks made a strong finish to extend a record-breaking eighth year of dominance over large stocks.